Welcome Personal Income Tax. Presented by Shohana Mohan

|

|

|

- Lee Quinn

- 6 years ago

- Views:

Transcription

1 Welcome 2016 Personal Income Tax Presented by Shohana Mohan

2 Upcoming CPD Events

3 Upcoming CPD Events Refer to our website for all upcoming events June 2016 Accounting & Bookkeeping Fundamentals for Tax Practitioners July 2016 VAT Fundamentals

4 2016 Personal Income Tax

5 Your objectives opening thoughts The Taxpayer The Legislation SARS The Tax Practitioner What to expect for the 2016 filing? How to file an accurate return? What s new in the 2016 PIT space? Managing risk? How to file a valid dispute?

6 What will we cover? Introduction Who should file a PIT return? Important dates for 2016 PIT return filing Consequences of not filing a PIT The PIT landscape Best practice methodology: collating of information to prepare PIT Tax treatment of certain Seventh Schedule benefits Our role as tax practitioners

7 What will we cover? cont d Gross income relevant paragraphs Resident vs Non-resident taxpayers The goal of Tax Treaties What happens when a taxpayer remains tax resident and renders services outside SA? What s new from SARS? How to prepare for a tax clearance in respect of foreign investments?

8 What will we cover? cont d When to approach the Office of the Tax Ombud? Pitfalls and challenges faced by tax practitioners Objection and Appeal Process important timelines Sources of taxpayer income Who is eligible for Voluntary Disclosure Relief? What is Special VDP?

9 A step back what is Income Tax Tax as a word appeared in the 14 th century Latin taxare to assess Income defined in section 1 of the Income Tax Act No. 58 of 1962 ( the Act ) income means the amount remaining of the gross income of any person for any year or period of assessment after deducting therefrom any amounts exempt from normal tax tax means tax or a penalty imposed in terms of the Act

10 Some interesting facts PIT 18.2 million registered taxpayers as at 1 March million are expected to submit returns PIT = bn (35.6% of revenue collected)

11 Who should file a personal income tax return? Public Notice of the persons required to submit personal income tax returns is given by the Commissioner. This notice is published on an annual basis (June each year) in the Government Gazette. Current Gazette published 3 June 2016 Number: Current persons are required to file returns: Every natural person: Who carried on any trade in South Africa (other than solely in his or her capacity as an employee); To whom a travel allowance was paid or granted (other than an amount reimbursed or advanced and whose gross income exceeded R for individuals under 65 years old); or R for individuals older than 65 years but under the age of 75; or R for individuals 75 years or older; who had capital gains or losses exceeding R ;

12 Who should file a personal income tax return? Cont d Who is resident and held any funds in foreign currency or owned any assets outside South Africa, if the total value of those funds and assets exceeded R at any stage during the year of assessment; Who is a resident and to whom any income or capital gains from funds in foreign currency or assets outside the Republic could be attributed Who is a resident and held any participation rights in a controlled foreign company; or To whom an income tax return is issued or who is requested by the Commissioner in writing to furnish a return, irrespective of the amount of income of that person.

13 Who should file a personal income tax return? Cont d Where a taxpayer has more than one source of remuneration, of which each income is less than R , the taxpayer is required to submit a tax return When is a return NOT required to be filed: Remuneration income that:» Is for the full year of assessment;» Is paid or payable from one single source (i.e. one employer);» Does not exceed R per annum;» Does not include any allowance or advance paid (example travel allowance, public office allowance); and» Employees tax has been deducted or withheld in terms of the deduction tables prescribed by the Commissioner.

14 Who should file a personal income tax return? Cont d Interest income from a South African source not exceeding: R in the case of an individual below the age of 65 years; or R in the case of an individual aged, or above the age, of 65 years. Dividends and the individual was a non-resident for the year of assessment.

15 Important dates for 2016 tax return filing Returns in respect of the 2016 year of assessment must be furnished within the following periods: In the case of all other persons (which include natural persons, trusts and other juristic persons, such as institutions, boards or bodies)- on or before 23 September 2016 is the return is submitted manually On or before 25 November 2016 is the return is submitted by using the SARS efiling platform or electronically through the assistance of a SARS official at an office of SARS; On or before 27 January 2017 if the return relates to a provisional taxpayer and is submitted using the SARS efiling platform.

16 Consequences for not filing an annual income tax return

17 Consequences for not filing an annual income tax return Government Gazette Administrative non-compliance penalty where a natural person fails to submit an annual income tax return as and when required under the Income Tax Act for the years of assessment commencing 1 March 2006 when that person has two or more outstanding returns for those years of assessments. Table: Amount of Administrative Non-Compliance Penalty is based on the taxable income or assessed loss for the preceding year. Ranges from R 250 per month to R per month Administrative non-compliance penalty is not subject to objection and appeal

18 The personal income tax cycle What does this entail Quality Control & Risk Management Information gathering Registration as a taxpayer (provided previously not registered)

19 What does the personal income tax return cycle look like? Past state Current state Dispute resolution process not documented in rules Manual income tax registration Dispute resolution rules contained in section 103 of the TAA Electronic registration process via SARS e- filing Tax assessment via post Tax return issued by SARS Tax assessment generated electronically Tax return requested via SARS e-filing unless Commissioner notifies otherwise Manual completion & submission of return Electronic completion & submission

20 Evolution of the South African personal income tax landscape Current state Is there a shift in focus? Increased regulatory compliance Liability on employer to ensure accurate information is processed Automatic Exchange of Information together with Country by Country reporting standards nowhere to hide Opportunities are limited to fly under the radar without being detected. Past state Electronic platform introduced Statistics PIT revenue collections increased; Tax Administration Act reduced propensity to engage in unethical behavior; and Administrative non-compliance penalties for non submission of returns.

21 Best practice methodology: How to collate information to prepare a tax return? SOME OF THE RISKS Inaccurate information Incomplete information Inflated claims/ Deductions Unsupported claims/deductions Nondisclosure of income What do you want to ensure? Accuracy of filing Reliability of information How do we ensure this? Information gathering phase key! Reviewing phase Controls we should have in place (mitigate risk) Preparer Control sheets Four eye review process

22 Risk Management Information request Review Best practice methodology: How to collate information to prepare a tax return? Cont d Take on process Tax Questionnaire Analyse quality of information 1 st Reviewer Preparer of tax return and PIT computation Information request and review 2 nd Reviewer and signoff

23 Best practice methodology: How to collate information to prepare a tax return? Cont d Source of information should be reliable documentation supporting claims should be original/original scanned documentation Questionnaire should be designed to ask relevant questions associated with the information that is being gathered (e.g. rental income: are there connected persons as tenants application of section 20A etc.) Non-disclosure response: I was not asked for the information!!!

24 SUPPORTING DOCUMENTATION Best practice methodology: How to collate information to prepare a tax return? Cont d IRP5/IT3(a) Employees tax certificates Documents and receipts for commission related income Bank account details Local interest income, foreign interest and dividend income certificates Documents relating to Medical expenditure Form ITR-DD Income tax certificates from financial institution to which Retirement Annuity contributions were made Logbook to claim against a travel allowance or use or motor vehicle Capital gains tax transaction Information relating to the letting of assets Financial statements for trading and farming activities Any other documentation relating to income that must be declared or deductions that may be claimed

25 Our role as Tax Practitioners Section 240 of the Tax Administration Act responsibility to ensure that tax practitioner is registered with the relevant Recognised Controlling Body (RCB) and with SARS. Tax practitioners who are not registered do not have the authority to prepare and submit tax returns on behalf of their clients. If not registered with the RCB and SARS, the tax practitioner can prepare and save the return but will not be in a position to submit the return. The submit return to SARS option is not available to unregistered tax practitioners = registered tax practitioners assisting three million taxpayers. Balance between SARS platform and advice from tax practitioners, so as to strike a balance to ensure optimal compliance.

26 Our role as Tax Practitioners Cont d SARS Discussion Paper dealing with regulation of tax practitioners provides for the following services: Assisting client to prepare and submit income tax returns Responding to queries from SARS of a non-routine nature Assisting clients in drafting objections to tax assessments Assisting clients in appealing tax decisions or assessments raised by SARS Providing advice by way of written technical tax opinions Increased tax compliance Non alignment and disconnect between what taxpayers want and what tax practitioners give Excerpt from Government Gazette No furnishing of tax returns for the 2016 tax year

27 Our role as Tax Practitioners Cont d RTP001 form used to report improper conduct of Tax Practitioners Nature of conduct to be reported: Not registered as a tax practitioner Unprofessional conduct Unlawful conduct Not acting in the taxpayer s interest

28 Our role as Tax Practitioners Cont d

29 Gross Income!! Definition of remuneration- does not require that an amount be received in respect of services rendered for it to constitute remuneration whether or not in respect of services rendered

30 Relevance? Is the amount received in respect of services rendered employer/employee relationship? Is the amount subject to PAYE withholding? Disclosure on the Employees Tax Certificate

31 Gross Income!! Severance benefits are taxed in accordance with the retirement lump sum tax table

32 Relevance? Cont d To qualify for the special severance tax rate, the employer must pay a lump sum as a result of the taxpayer s employment having been, amongst other things, terminated or lost, for example if: the employer stops (or intends to stop) trading; or the employer embarks on a general reduction in personnel (not applicable to restructuring of employees).

33 Relevance? Since 1 March 2011 special tax rates apply to severance benefits, based on the retirement lump sum tax table. This means that the first R is not subject to tax, the next R is taxed at 18%, the subsequent R at 27%, and all amounts above R at 36%. Leave pay, notice pay and pro-rata bonuses that are paid at that time of termination do not form part of a severance benefit and are subject to normal income tax.

34 Gross Income

35 Relevance? Nature of the benefit will determine the cash equivalent of the value of the taxable benefit as well as the tax treatment thereof. Some of the common benefits provided in accordance with the Seventh Schedule to the Income Tax Act [contained in the slides below]

36 Resident vs Non Resident taxpayer Literature is derived from the following sources: Income Tax Act No. 58 of 1962 Case law Interpretation Notes (issued by SARS) Advanced Tax Rulings

37 Resident vs Non Resident taxpayer Generally, an individual must be subject to tax because he or she is resident or domiciled in at least one country. The domestic tax laws of a each country will determine whether an individual is a resident. Definition of gross income in section one of the Income Tax Act includes the word resident which is defined as being a natural person who is: Ordinarily resident in South Africa or Physically present in South Africa for a specified period of time (Physical Presence) In other words 2 tests apply to determine whether a person is a resident of South Africa, i.e. the ordinarily resident test and the physical presence residence test

38 Resident vs Non Resident taxpayer Cont d AEOI going forward, it will not be uncommon for SARS to query tax residence status by requesting a Certificate of Residence from another country Why is it important to determine tax residence status? Non-residents = liable to tax on their South African sourced income only Residents = liable to tax on worldwide income and capital gains (subject to certain exclusions)

39 Resident vs Non Resident taxpayer The term Ordinarily Resident is not defined in the Income Tax Act and therefore case law is used to ascribe a meaning. A person who regards South Africa as the place to which he would naturally and as a matter of course return to from his wanderings is regarded as ordinarily resident for tax purposes Although the test to determine OR is subjective, a host of objective factors are used to determine whether a person is to be regarded as OR. NB: Private Binding Ruling issued by SARS indicated the mere purchase of an investment property in SA is not sufficient to regard a person as OR to the extent he is on secondment to SA and will be repatriating upon termination of his/her secondment. Dual residence In certain instances, an individual may be regarded as a tax resident of both, the home country and the country in which he or she renders a service.

40 Resident vs Non Resident taxpayer In these circumstances, where an individual is resident of both contracting states, the tie-breaker rules (contained in most Double Taxation Agreements), need to be applied in order to tie break the individual to one particular state. In terms of the tie breaker rules: an individual is deemed to be a resident of the State where he has a permanent home available to him. [Note a rented property is also regarded as a permanent home] Where a taxpayer lets the property, such property may no longer be regarded as available. if the individual has property in both contracting states, he will be deemed to be a resident of the country in which his personal and economic relations are closer and significant (centre of vital interests). if state of vital interests cannot be determined and if he does not have a permanent home available in the home and host countries, he shall be a resident of the country in which he is considered to have a habitual abode.

41 Resident vs Non Resident taxpayer where an individual has a habitual abode in both countries, he shall be considered to be a resident of the country in which he is regarded as a national. if he is not considered a national of either state, the competent authorities will consider the position. NB: Depending on the facts and circumstances of a case, it may be advisable to refer the request to SARS to determine whether the taxpayer may be regarded as a tax resident of South Africa or the other country.

42 Example dual resident Dual resident

43 What is the goal of a Tax Treaty?

44 Resident vs Non Resident taxpayer Cont d Physical presence resident An individual who arrives to work in South Africa may trigger residence in his sixth year of being physically present in South Africa if he is present as follows: > 91 days in the current year of assessment; and > 91 days in the 5 preceding years of assessment; and > 915 days in aggregate in the preceding 5 years of assessment. A further requirement the individual must also not be regarded as exclusively a tax resident in another jurisdiction. The definition of Resident in the ITA excludes a person who remains exclusively resident in another country for purposes of the application of the DTA between South Africa and that other country.

45 An illustration physical presence residence test Current Year Preceding 5 fiscal years > 91 days > 91 days > 91 days > 91 days > 91 days > 91 days AND > 915 days in aggregate

46 Resident vs Non Resident taxpayer Cont d Physical presence residence test diagram

47 Resident vs Non Resident taxpayer Cont d

48 Physical presence residence test - Example Example 1 Calculation of days to determine physical presence Facts: X, who is not ordinarily resident in the Republic, was physically present in the Republic for the following number of days: Year of assessment Number of days Determine whether X is regarded as a resident under the physical presence test for the 2016 year of assessment.

49 Physical presence residence test - Example - Cont d Result: In order to meet the requirements of the physical presence test, X must satisfy all three elements of the test: (i) Was X present in the Republic for a period or periods exceeding 91 days in aggregate in the current (2016) year of assessment? This requirement is met, since X was physically present for 355 days. (ii) Was X present in the Republic for a period or periods exceeding 91 days in aggregate in each of the previous five years of assessment (2011 to 2015) This requirement is met, since X was physically present for more than 91 days in 2011 (95 days), 2012 (110 days), 2013 (115 days), 2014 (92 days) and 2015 (151 days). (iii) Was X present in the Republic for a period or periods exceeding 915 days in aggregate during the five previous years of assessment (2011 to 2016)

50 Physical presence residence test - Example - Cont d The aggregate of days during the five previous years of assessment amounts to 563 days ( ). As this does not exceed the required 915 days, the third requirement has not been met. The days present during the current year of assessment (2016) are not taken into account for purposes of this part of the calculation. All three requirements have not been met, therefore X is not resident in terms of the physical presence test for the 2016 year of assessment.

51 Resident vs Non Resident taxpayer Cont d What happens when a taxpayer remains tax resident and renders services abroad Section 10(1)(o)(ii) Remuneration exempt Domestic law prescribes to the extent any person renders services outside South Africa for and on behalf of an Employer for a period or periods exceeding 184 days of which 61 days are continuous during any 12 month period, the remuneration so earned is exempt from South African tax. The Employer may then elect not to withhold employees tax (PAYE) provided the days requirements will be met. The 12 month period relates to any period of 12 months and is not limited to a tax year, e.g. Mr X starts his assignment to ABC Limited on 01 May 2014, the 12 month period commences on 01 May 2014 and ends 30 April 2015.

52 Resident vs Non Resident taxpayer Cont d What happens when a taxpayer remains tax resident and renders services abroad

53 What s new from SARS? 18 April 2016 = launch of the Tax Compliance Status System (TCS) Tax compliance status is not static and changes according to the taxpayer s compliance status No real time information Use of a Tax Clearance Certificate (TCC) (hard copy) even if tax compliance status may have changed during the 12 month period for which the TCC is valid Activation of the Tax Compliance Verification system is a once-off process Tax Compliance Status PIN is issued for third parties to gain access to the electronic platform to verify the taxpayer s compliance status Tax Compliance Status is colour coded

54 What s new from SARS? Cont d What do the colours mean? Tax affairs are not in order and the taxpayer is not tax compliant Tax affairs are in order and the taxpayer is tax compliant To be tax compliant the taxpayer should ensure that: there are no outstanding returns He or she does not owe any money to SARS unless payment arrangement or suspension of debt has been agreed to Taxpayer is registered for all tax types she is liable to Registered particulars are updated All registered tax reference numbers are declared

55 What s new from SARS? Cont d Positive aspects Rectify areas of non-compliance. The Non-compliant status indicator should be selected to see what steps need to be taken to rectify the non-compliance. Empowers taxpayers with more reliable and accurate information. If the taxpayer s Tax Compliance Status reflects that he/she is non-compliant, the taxpayer will not receive a TCC until the non-compliance is rectified. The TCS can be challenged on SARS e-filing by clicking on the Challenge Status submission link.

56 What s new from SARS? Cont d Positive aspects Requests can be made online for: Good standing Tender FIA (individuals only) Emigration (individuals only) Nature of information required to facilitate the FIA001 application process

57 What s new from SARS? Cont d Nature of information required to facilitate the FIA001 (Application for tax clearance in respect of Foreign Investment Allowance) process: Is the taxpayer aware of any audit investigation against him/her? Expected annual income from the prospective investment What type of investment (i.e. details of the foreign investment to be made): call deposit, shares, other financial instruments etc. With which institution will the investment be made? When will this investment be made? What is the anticipated duration of the investment? In which country will this investment be made? What is the source of the capital to be invested, i.e. loan, donation, sale of property, inheritance, savings, cash bank account/other. In the case of Shares (Attach letter from institution stating the transfer of the funds containing the amount of shares and estimated current market value available).

58 What s new from SARS? Cont d Nature of information required to facilitate the FIA001 process: In the case of Savings/Cash/Bank Account (attach 3 months statement of relevant bank account and proof of source proof of source being where and how the taxpayer obtained the money). Alternatively, an original letter from the Bank specifying the amount available for transfer and the source thereof. Statement of Assets & Liabilities if not provided in the previous tax return submissions.!! Request for R 10 million FIA can result in a lifestyle audit being triggered in respect of the taxpayer Ensure you have relevant supporting documentation from your client!

59 What s new from SARS? Cont d IRP5 certificates This year, employers are urged to accurately verify and update each employee s personal and financial details before submitting their Annual Reconciliation Declaration (EMP501) and Employees Income Tax Certificates [IRP5/IT3(a)s] to SARS. Should these details be incorrect on an IRP5 certificate, the employee will be unable to file his/her Income Tax Return for Individuals (ITR12) during Tax Season. Individuals will no longer be allowed to make any corrections to pre-populated IRP5 details on their returns. In cases where details are incorrect, employees will have to revert to their respective employers who will need to make changes on the IRP5 and resubmit these to SARS. This process can be time consuming and it may become problematic for employees to file on time.

60 What s new from SARS? Cont d Employers play a very important part in the income tax cycle which effectively starts on 18 April with the submission of the annual reconciliations. What does this mean for us? Upon commencement of the tax return filing process, the information reflected on the taxpayer s IRP5 certificate should be correct. For example, taxpayers that earn foreign sourced income will need to ensure that the correct source codes are used when generating the IRP5 certificate (e.g. meets requirements of section 10(1)(o)(ii)) foreign source codes should be applied (i.e. code 3651/3655) etc.

61 What s new from SARS? Cont d Non-resident taxpayers who derive income from a South African source together with income for services rendered outside South Africa, the income attributable to non-south African workdays should be disclosed appropriately on the IRP5/IT3(a) certificate. Should changes need to be made to the IRP5 certificate as opposed to a correction on an annual income tax return, SARS will request that the employer reissue the IRP5 certificate to reflect the correct position.

62 When to approach the Office of the Tax Ombud Section of the Tax Administration Act An Ombud is an independent and impartial officer who deals with complaints against an organization or an agency. The Tax Ombud deals with taxpayer s complaints against the South African Revenue Service.

63 When to approach the Office of the Tax Ombud (cont d) The Tax Ombud may only review a request if the requester has exhausted the available complaints resolution mechanisms in SARS (i.e. the SSMO/SARS Complaints Management Office) Section 18(4) of the TAA. The Tax Administration Act authorizes the Tax Ombud to: Review a complaint and if necessary, resolve it through mediation or conciliation; Act independently in resolving a complaint; Provide information to a taxpayer about the mandate of the Tax Ombud and the procedures to pursue a complaint; Facilitate access by taxpayers to complaint resolution mechanisms within SARS to address complaints; and

64 When to approach the Office of the Tax Ombud (cont d) identify and review systemic and emerging issues related to service matters or the application of the provisions of the TAA or procedural or administrative provisions of a tax Act that impact negatively on taxpayers. Section 18(5) of the TAA sets out the following factors that will be used to determine whether a circumstance may be regarded as compelling the request raises systemic issues; exhausting the complaints resolution mechanisms will cause undue hardship to the requester; exhausting the complaints resolution mechanisms is unlikely to produce a result within a period of time that the Tax Ombud considers reasonable.

65 When to approach the Office of the Tax Ombud (cont d) identify and review systemic and emerging issues related to service matters or the application of the provisions of the TAA or procedural or administrative provisions of a tax Act that impact negatively on taxpayers. NOTE OTO undertakes to respond to requests within 15 business days from date of submission of the complaint

66 When to approach the Office of the Tax Ombud (cont d) The OTO may not review legislation or tax policy; SARS policy or practice generally prevailing (other than to the extent that such policy or practice relates to a service matter or procedural or administrative matter arising from the application of the provisions of a tax Act by SARS;

67 When to approach the Office of the Tax Ombud (cont d) A matter subject to objection and appeal under a tax Act, except for an administrative matter relating to such objection and appeal; and A decision of, proceeding in, or matter before the tax court. NOTE Invalidation of NOO/DISP01

68 When to approach the Office of the Tax Ombud (cont d) The OTO has the authority to determine, independently of SARS, how a review should be conducted and whether a review should be terminated before it is completed. The decisions of the Tax Ombud are not binding on taxpayers or SARS. NOTE Valid POA in the case of taxpayer representation

69 Pitfalls and challenges faced by tax practitioners Registering a taxpayer Facilitating refund requests Require all relevant documentation, e.g. PAYE reference number for an electronic registration Manual registration process is onerous banking details etc. Verification process requires taxpayer to present him/herself at a branch Incorrect assessments Annualisation of income to clear tax refunds

70 Pitfalls and challenges faced by tax practitioners (cont d) Notice of Objection process System challenges appropriate source codes are not functional Pending verification of supporting documentation Request for suspension of payment until the outcome of the objection s164 of the TAA Objections cannot be filed which has the impact of delaying the process resulting in the objection being regarded as invalid due to lateness in filing No formal acknowledgement of receipt of the letter Collections department not aware of the position

71 Pitfalls and challenges faced by tax practitioners (cont d) Notice of Objection ( NOO ) process NOO partially allowed NOO late Full reason/grounds for the objection to be typed despite there being a limitation of characters (limited to 150 words) Source codes to be replicated e.g. if code 3601 is the first error, this is replicated for all further objections Deadlines are reflected as having been missed due to system glitches

72 Pitfalls and challenges faced by tax practitioners (cont d) Assessment challenges Part year employment require confirmation from employer to state start date of employment Notifications of additional information requests are not always received SARS Contact Centre should be called to request a list of complete information required Medical aid claims the receipt/proof of payment to be provided

73 Pitfalls and challenges faced by tax practitioners (cont d) Communication Inconsistent approach from branch to branch and SMS notifications requesting additional documentation is not always received Better option is to call into the SARS call centre and enquire regarding the request for additional supporting documentation

74 Pitfalls and challenges faced by tax practitioners (cont d) Take on of taxpayers on SARS e-filing Declined applications where banking details need to be verified SARS branch to be visited to manually update details Duplicate DOB and names

75 Timeline: Objection and Appeal per the Tax Administration Act (per the section 103 Rules) Submission of annual tax return on or before 21 November Upload supporting documentation within 5 10 days Review Notice of assessment within 30 business days from date of notice Assessment is incorrect lodge a Notice of Objection within 30 business days Lodge Notice of Objection following SARS notice of completion of general audit period may > 30 business days due to pending SARS general audit Resubmit Notice of Objection with detailed reason for late submission (i.e. SARS general audit) within 20 days of receipt of invalidity notice SARS request for supporting documentation Notice of assessment issued by SARS within 21 business days Notice of assessment correct provide an assessment review letter to taxpayer SARS issue notice of general audit. Notice of Objection to be lodged upon completion of general audit within 21 business days or longer period SARS issues notice of Invalid Objection on the grounds that the timeline for submission has been exceeded SARS responds to the Notice of Objection within 90 business days may request additional supporting documentation Section 103 of the TAA sets out Rules for dispute resolution

76 business day means a day which is not a Saturday, Sunday or public holiday, and for purposes of determining the days or a period allowed for complying with the provisions of Chapter 9, excludes the days between 16 December of each year and 15 January of the following year, both days inclusive.

77 Timeline: Objection and Appeal per the Tax Administration Act (Cont d) SARS issues notice to disallow the objection ADR proceedings must be finalised within 90 business days SARS will notify the taxpayer within 30 business days of receipt of the NOA whether or not the matter is appropriate for ADR Assessment notice provided to taxpayer Provide SARS with additional information within 5-10 days SARS requests for verification of banking details Notice of Appeal against the decision must be lodged within 30 business days from the date of receiving the notice of SARS decision Objection is not successful and the taxpayer indicates on the Notice of Appeal that he/she wishes to make use of the Alternative Dispute Resolution (ADR) Assessment is revised and correct in accordance with our calculations SARS refund verification process SARS may call for additional documentation example Contract of Employment SARS concludes verification Taxpayer is physically present in SA SARS requires personal verification of banking details in an attempt to mitigate fraud ADR PROCESS TAX REFUND PROCESS

78 Unpacking some of the key sources of taxpayer income Source Detail Remuneration Profits or losses Income or profits Director s fees Investment income Rental income or losses Income from employment, such as salaries, wages, bonuses, overtime pay, taxable (fringe) benefits, allowances and certain lump sum benefits Business or trade Beneficiary of a trust Board duties Interest income/foreign dividend income Letting of property

79 Unpacking some of the key sources of taxpayer income Cont d Source Detail Income from royalties Annuities pension Certain capital gains

80 Taxation of benefits Use of employer-provided motor vehicle Determined value is: Employer bought the vehicle Employer leases the vehicle other than under an operating lease and acquires the vehicle on termination of the lease Employer leases the vehicle under an operating lease With effect from 1 March 2015 Retail market value* Retail market value* Actual lease costs + fuel costs Calculation Determined Value X 3.5% or 3.25% where a maintenance plan is included Determined value X 3.5% or 3.25% where a maintenance plan is included Actual leasing costs + fuel costs *The retail market value as determined by the Minister by Regulation (28 April 2015)

81 Taxation of benefits Use of employer-provided motor vehicle Determined value is: 1 March February March February March February March February 2019 Motor vehicle manufacturers Dealer billing price (excluding VAT) reduced by 10 per cent Dealer billing price (excluding VAT) reduced by 5 per cent Dealer billing price (excluding VAT) Dealer billing price (including VAT) Motor vehicle dealers Dealer billing price (excluding VAT) Dealer billing price (excluding VAT) Dealer billing price (excluding VAT) Dealer billing price (including VAT)

82 Taxation of benefits Use of employer-provided motor vehicle Following NADA directive issued in April 2016 motor vehicle dealers may use the average cost of stock held in trade in the previous year of assessment to determine the fringe benefit for dealership employees that are required to use demonstration vehicles as a tool of trade.!! Employees must be required to regularly use multiple vehicles over short periods (i.e. 5 times or more during a year of assessment).

83 Taxation of benefits Use of employer-provided motor vehicle 80% of the taxable benefit will be subject to PAYE on a monthly basis. The percentage may be reduced to 20% if the employer is satisfied that at least 80% of the use of the company car for the tax year will be for business purposes. The taxable income may be reduced on assessment of the employee s income tax return in accordance with the ratio of business kilometres travelled to total kilometres travelled. Further relief is available for the cost of licence, insurance, maintenance and fuel for private travel if the full cost was borne by the employee and the number of private kilometres travelled is substantiated by a logbook.

84 Taxation of benefits Employer-provided residential accommodation A taxable fringe benefit arises where an employer provides an employee with residential accommodation either free of charge, or for a consideration which is less than the rental value. The value of the benefit is, where the accommodation is owned by the employer or by an associated institution in relation to the employer, calculated with reference to a prescribed formula. From 1 March 2015, where the employer-provided accommodation is leased by the employer from an unconnected third party, the taxable value will be equal to the lower of the cost to the employer in providing the accommodation (i.e. rental) and the amount calculated with reference to the formula. Employer-owned accommodation and where it is customary for the employer to provide residential accommodation the formula value still applies!

85 Allowable deductions Travel allowance (3701) - An allowance or advance paid to an employee in respect of travelling expenses for business purposes including fixed travel allowances, petrol, garage- and maintenance cards. (provided if the employee is required to travel for business purposes as a term and condition of employment) A logbook confirming business kilometres travelled must be maintained in order to claim any deduction for business kilometres. PAYE must be withheld by the employer on 80% of the allowance granted to the employee. The percentage may be reduced to 20% PAYE withholding if the employer is satisfied that at least 80% of the use of the motor vehicle for the tax year is for business purposes.

86 Allowable deductions Reimbursive Travel allowance (3702) - Taxable A reimbursement for business kilometres exceeding kilometres per tax year or at a rate exceeding the prescribed rate per kilometre or the employee receives any other form of compensation for travel. Reimbursive Travel allowance (3703) Non-Taxable A reimbursement for business kilometres not exceeding kilometres per tax year and at a rate which does not exceed the prescribed rate per kilometre. Should only be used if the employee does not receive any other form of compensation for travel and may therefore not be used together with code 3701 and/or Also note the maximum value as prescribed in the relevant validation rules.

87 Allowable deductions Travel allowance Employees tax audits are often triggered where the following source codes (relating to travel) are reflected on IRP5 certificates: - Code 3701 = Travel Allowance - Code 3702 = Reimbursive Travel (taxable) - Code 3703 = Reimbursive Travel (non-taxable) Code = Correct Code = Not correct

88 Allowable deductions Pension Fund Contributions (prior to 1 March 2016) The deductible amount is the greater of: 7.5% of remuneration from retirement funding employment, or R Any excess may not be carried forward to the following year of assessment. Arrear Pension Fund Contributions (prior to 1 March 2016) Maximum of R per annum. Any excess over R may be carried forward to the following year of assessment.

89 Allowable deductions Current Retirement Annuity Fund contributions (prior to 1 March 2016) The deductible amount is the greater of: 15% of taxable income other than from retirement funding employment, or R less current contributions to a pension fund, or R Any excess may be carried forward to the following year of assessment. Arrear Retirement Annuity Fund Contributions (prior to 1 March 2016) Maximum of R per annum. Any excess over R may be carried forward to the following year of assessment.

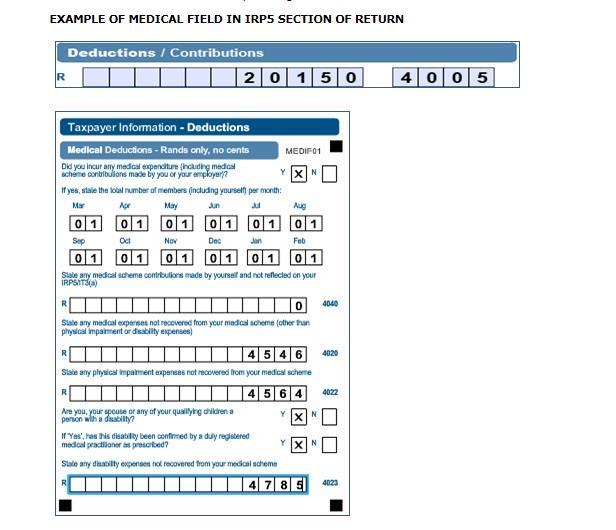

90 Allowable deductions Donations to Public Benefit Organisations The deductible is limited to 10% of taxable income before deducting medical expenses and donations. From 1 March 2014 and in respect of donations made on or after that date, any amount not allowed as a deduction solely by reason of the fact that the donation exceeded the maximum amount deductible may be carried forward to the following year of assessment.

91 Allowable deductions Donations to Public Benefit Organisations Example Mary donated R to an approved public benefit organization on 1 June She donated another R to the same PBO on 1 April She has taxable income of R for the 2015 year of assessment and R for the 2016 year of assessment. Calculate the s 18A deduction available to Mary for the 2015 and 2016 years of assessment. You can assume she was in possession of the relevant s 18 A certificates.

92 Allowable deductions Donations to Public Benefit Organisations Solution Year ended 28 February 2015 Donation of R , but maximum s 18A deduction is limited to 10% of R = R (excess deductible donation of R is rolled over to the 2016 year of assessment) Year ended 29 February 2016 Total deductible donations of R (2016) + R (excess deductible donation rolled over from 2015) = R Maximum deduction is limited to 10% of R = R 95,000 but limited to total deductible donation = R

93 Allowable deductions Medical and Disability expenses Medical Scheme Fees Tax Credit Taxpayers may deduct from their tax liability a tax credit of R270 for the first two beneficiaries and R 181 for each additional beneficiary, in respect of medical aid contributions. (section 6A) Additional medical expense deduction (section 6B) Taxpayers under the age of 65 years may deduct an additional tax credit equal to 25% of (a) medical aid contributions in excess of four times the total medical scheme fees tax credit (b) plus qualifying medical expenses (c) which exceeds 7.5% of the person s taxable income (excluding any retirement fund lump sum benefit, retirement fund lump sum withdrawal benefit and severance benefit).

94 Allowable deductions Medical and Disability expenses Example Mr Joe Soap is a 44 year old employee. He is married and has no children. His only source of income is his salary, which amounted to R for the current year of assessment. During the year he paid qualifying medical expenses of R and contributions to a medical scheme of R His employer contributed R the medical scheme on his behalf. Calculate Mr Soap s taxable income and normal tax liability for the year of assessment.

95 Allowable deductions Medical and disability expenses Solution 6A = MSFTC 6B = Additional Medical Expenses Tax Credit Note 1 Salary Add: Fringe benefit - para 12A Seventh Schedule Taxable income Normal tax payable per table Less: Primary rebate Section 6A credit R 540 x Section 6B credit (note 1) Normal tax liability Contributions Less: 4x s 6A credit (4 x 6480) Excess Plus: Medical expenses Less: 7.5% x R (taxable income) Section 6B credit (25% x 1187)

96 Allowable deductions Medical Scheme Fees Tax Credit Additional medical expense deduction (section 6B) Taxpayers 65 years and older and those with disabilities or with disabled dependants may deduct an additional medical expenses tax credit equal to (a) 33.3% of medical aid contributions in excess of 3 times the total allowable medical scheme fees tax credit (b) plus 33.3% of qualifying medical expenses NB! Even though the definition of qualifying medical expenses includes a physical impairment or disability in respect of any dependant (as defined), only a disability in respect of the person, his or her spouse and his or her child will cause the person to qualify for the increased 33.3%. In all other cases, the person will qualify for the 25% credit (Physical impairment will not qualify).

97 Allowable deductions What is regarded as a disability? As a result of changes to legislation, persons with a disability must have their disability re-confirmed in order to continue to claim the deduction. Section 18(3) of the Income Tax Act defines disability to mean a person with a moderate to severe limitation on a person s ability to perform daily activities as a result of a physical, sensory, communication, intellectual or mental impairment lasting more than a year and confirmed by a duly registered medical practitioner. An ITR-DD form - Confirmation of Diagnosis of Disability must be completed. Indicate whether you, your spouse or any of your qualifying children are considered to be a person with a disability by marking the yes or no block with an X. If yes indicate if this disability has been confirmed by a duly registered medical practitioner as prescribed, by marking the yes or no block with an X.

98 Allowable deductions Top Tip: The ITR-DD must be completed by you and the duly registered medical practitioner, for yes to be selected. The ITR-DD must not be submitted to SARS with the return, but must be kept with all the relevant material for a period of five (5) years should SARS ask for it in the future. If you are a person with a disability, or your spouse or your child is a person with a disability and expenditure was incurred as a result of the disability and was not included in the amount reflected on the medical statement received from the medical aid scheme (if applicable), this amounts must be shown next to code 4023.

99 Allowable deductions

100 How to complete a PIT return CREATE THE TAXPAYER S PERSONAL INCOME TAX RETURN EMPLOYMENT STATUS REMUNERATION FOR FOREIGN SERVICES Customise on efiling How many IRP5 certificates Residency Manual answer mandatory questions Medical expenses incurred Retirement annuity fund (code 4006) Expenditure against a travel allowance Expenditure against an employer provided motor vehicle

101 How to complete a PIT return INVESTMENT INCOME Interest local/foreign MEMBER OF A CLOSE CORPORATION Statement of Assets & Liabilities required DONATIONS Indicate how many contributions made OTHER INCOME AND ALLOWABLE EXPENDITURE Any other income and/or allowable expenses Exempt local dividends gross dividend to be declared Foreign dividend income

102 How to complete a PIT return CAPITAL GAIN/LOSS FOREIGN TAX CREDITS NON- TAXABLE AMOUNTS MEDICAL/ RETIREMENT OTHER EXPENDITURE Disposal of local assets Disposal of foreign assets Section 6quin Foreign tax credits from prior years (6quat) Income considered non-taxable Contributions toward Retirement Any other expenditure not addressed before

103 Eligibility to qualify for relief in terms of the Voluntary Disclosure Programme Part B of the Tax Administration Act permanent VDP Impetus for taxpayers to come forth to regularise their tax affairs ********************************************* What is a default default means the submission of inaccurate or incomplete information to SARS, or the failure to submit information or the adoption of a tax position, where such submission, nonsubmission, or adoption resulted in an understatement.

104 Eligibility to qualify for relief in terms of the Voluntary Disclosure Programme (cont d) Examples of defaults Tax return erroneously excluded taxable income NB: one needs to consider that there may not be an understatement penalty, in which case, the additional income should be disclosed to SARS by reopening an assessment. Where income (subject to provisional tax), is erroneously omitted from the return, given that there is a likely understatement penalty to be imposed, application for relief may be sought in terms of the VDP process. Non-submission of annual tax returns subject to administrative non-compliance penalty if 2 or more returns are outstanding

105 Eligibility to qualify for relief in terms of the Voluntary Disclosure Programme (cont d) Will the application result in a refund to the taxpayer? Is the taxpayer aware of any pending audit or investigation? Is the taxpayer aware of any verification or inspection procedure?

106 Special Voluntary Disclosure Programme (SVDP) Not an amnesty Primary intention of the SVDP is to provide taxpayers with a window of opportunity to regularize their affairs prior to the introduction of the Automatic Exchange of Information dispensation The primary focus is therefore NOT the revenue which may be collected Business as usual at SARS and SARB. Audits and investigations are therefore not being halted pending the commencement date of the SVDP Taxpayers wishing to make use of the SVDP are currently still open to audit and investigation

107 Special Voluntary Disclosure Programme (SVDP) Effective date of SVDP is likely to be 1 October 2016 and will last for a 6 month period The Tax and Exchange Control SVDP can be accessed independently Taxpayers can still make use of the normal VDP process to regularise their affairs Legislation may be introduced which states that SARS may notify taxpayers where information is obtained under an International Tax Agreement (AEOI) that the taxpayer is disqualified from accessing the SVDP. SARB will issue a circular later this month (June 2016) dealing with the exchange control regime

108 Seventh Schedule Exposition of Fringe benefits

109 Relevance? Fringe benefits (Seventh Schedule to the Act) Acquisition of an asset at less than actual value: Asset acquired by an employee market value thereof Asset acquired to give to the employee cost thereof to the employer Asset held as trading stock cost thereof to the employer or market value if the market value is less than such cost No value placed on long service awards R5 000 Long service initial unbroken period of service of not less than 15 years or any subsequent unbroken period of service of not less than 10 years.

110 Relevance? Right of use of any asset (other than residential accommodation or any motor vehicle) (para 6). Asset leased by employer rental payable by the employer over period during which the asset was used Asset owned by employer 15 % per annum of the lesser of the cost or the market value thereof Employee has sole right of use over the useful lifetime cost to the employer No taxable value where: o Private or domestic use is incidental o Asset consists of any equipment or machine which all employees are allowed to use for short periods of time o Asset consists of telephone or computer equipment which the employee uses mainly for business purposes.

GUIDE ON INCOME TAX AND THE INDIVIDUAL (2010/11)

") SOUTH AFRICAN REVENUE SERVICE GUIDE ON INCOME TAX AND THE INDIVIDUAL (2010/11) Another helpful guide brought to you by the South African Revenue Service Foreword Guide on Income Tax and the Individual

SOUTH AFRICAN REVENUE SERVICE GUIDE ON INCOME TAX AND THE INDIVIDUAL (2010/11) Another helpful guide brought to you by the South African Revenue Service Foreword Guide on Income Tax and the Individual

SARS Tax Guide 2014 / 2015

This SARS pocket tax guide has been developed to provide a synopsis of the most important tax, duty and levy related information for 2014/15. SARS Tax Guide 2014 / 2015 INCOME TAX: INDIVIDUALS AND TRUSTS

This SARS pocket tax guide has been developed to provide a synopsis of the most important tax, duty and levy related information for 2014/15. SARS Tax Guide 2014 / 2015 INCOME TAX: INDIVIDUALS AND TRUSTS

BUDGET 2019 TAX GUIDE

BUDGET 2019 TAX GUIDE 1 This SARS pocket tax guide has been developed to provide a synopsis of the most important tax, duty and levy related information for 2019/20. INCOME TAX: INDIVIDUALS AND TRUSTS

BUDGET 2019 TAX GUIDE 1 This SARS pocket tax guide has been developed to provide a synopsis of the most important tax, duty and levy related information for 2019/20. INCOME TAX: INDIVIDUALS AND TRUSTS

INCOME TAX: INDIVIDUALS AND TRUSTS

The SARS Tax Guide: A synopsis of the most important tax, duty and levy related information for 2015/16. INCOME TAX: INDIVIDUALS AND TRUSTS Tax rates (year of assessment ending 29 February 2016) Individuals

The SARS Tax Guide: A synopsis of the most important tax, duty and levy related information for 2015/16. INCOME TAX: INDIVIDUALS AND TRUSTS Tax rates (year of assessment ending 29 February 2016) Individuals

This SARS pocket tax guide has been developed to provide a synopsis of the most important tax, duty and levy related information for 2015/16.

BUDGET2015 TAX GUIDE This SARS pocket tax guide has been developed to provide a synopsis of the most important tax, duty and levy related information for 2015/16. INCOME TAX: INDIVIDUALS AND TRUSTS Tax

BUDGET2015 TAX GUIDE This SARS pocket tax guide has been developed to provide a synopsis of the most important tax, duty and levy related information for 2015/16. INCOME TAX: INDIVIDUALS AND TRUSTS Tax

NEWS FLASH - February 2016

NEWS FLASH - February 2016 Africa: South Africa CRS TAX POCKET GUIDE 2016/2017 it is important that Employers note the following TAX RATES (TAX YEAR ENDING 28 FEBRUARY 2017) Individuals and special trusts

NEWS FLASH - February 2016 Africa: South Africa CRS TAX POCKET GUIDE 2016/2017 it is important that Employers note the following TAX RATES (TAX YEAR ENDING 28 FEBRUARY 2017) Individuals and special trusts

South African Income Tax Guide for 2013/2014

South African Income Tax Guide for 2013/2014 Individuals and trusts Income tax rates for natural persons and special trusts Year of assessment ending 28 February 2014 Taxable income Taxable rates 0 165

South African Income Tax Guide for 2013/2014 Individuals and trusts Income tax rates for natural persons and special trusts Year of assessment ending 28 February 2014 Taxable income Taxable rates 0 165

Budget Highlights 2018

Budget Highlights 2018 14 March 2018 Budget Highlights Value-Added Tax rate increases from 14% to 15% on 1 April 2018 Limited relief for the effect of inflation in adjusting Personal Income Tax rates resulting

Budget Highlights 2018 14 March 2018 Budget Highlights Value-Added Tax rate increases from 14% to 15% on 1 April 2018 Limited relief for the effect of inflation in adjusting Personal Income Tax rates resulting

GUIDE FOR EMPLOYERS IN RESPECT OF THE UNEMPLOYEMENT INSURANCE FUND

GUIDE FOR EMPLOYERS IN RESPECT OF THE UNEMPLOYEMENT INSURANCE FUND Revision: 8 Page 1 of 15 TABLE OF CONTENTS 1 PURPOSE 3 2 SCOPE 3 3 REFERENCES 3 3.1 LEGISLATION 3 3.2 CROSS REFERENCES 3 4 DEFINITIONS

GUIDE FOR EMPLOYERS IN RESPECT OF THE UNEMPLOYEMENT INSURANCE FUND Revision: 8 Page 1 of 15 TABLE OF CONTENTS 1 PURPOSE 3 2 SCOPE 3 3 REFERENCES 3 3.1 LEGISLATION 3 3.2 CROSS REFERENCES 3 4 DEFINITIONS

Change, the new certainty

Change, the new certainty Tax Facts February 2018/2019 Income Tax Residence basis of taxation South Africa has a residence basis of taxation. Residents are taxable on worldwide income and capital gains,

Change, the new certainty Tax Facts February 2018/2019 Income Tax Residence basis of taxation South Africa has a residence basis of taxation. Residents are taxable on worldwide income and capital gains,

WHAT TO DO WITH YOUR IRP YEAR OF ASSESSMENT

WHAT TO DO WITH YOUR IRP5 2014 YEAR OF ASSESSMENT Office staff must take into account the undermentioned on receipt of their IRP5 tax certificates for the 2014 tax year ended 28 February 2014. Contact

WHAT TO DO WITH YOUR IRP5 2014 YEAR OF ASSESSMENT Office staff must take into account the undermentioned on receipt of their IRP5 tax certificates for the 2014 tax year ended 28 February 2014. Contact

Welcome to the SARS Tax Workshop

Tax Directives Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the legislation

Tax Directives Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the legislation

REPUBLIC OF SOUTH AFRICA

Please note that most Acts are published in English and another South African official language. Currently we only have capacity to publish the English versions. This means that this document will only

Please note that most Acts are published in English and another South African official language. Currently we only have capacity to publish the English versions. This means that this document will only

TODAY S THE DAY GET GREAT FINANCIAL ADVICE DO GREAT THINGS

TODAY S THE DAY GET GREAT FINANCIAL ADVICE DO GREAT THINGS BUDGET SPEECH 2017 RATES OF TAXES Individual, special trusts, insolvent and deceased estates Year of assessment ending 28 February 2017 Taxable

TODAY S THE DAY GET GREAT FINANCIAL ADVICE DO GREAT THINGS BUDGET SPEECH 2017 RATES OF TAXES Individual, special trusts, insolvent and deceased estates Year of assessment ending 28 February 2017 Taxable

Global Mobility Services: Taxation of International Assignees - Namibia

www.pwc.com/na/en Global Mobility Services: Taxation of International Assignees - Namibia Taxation issues & related matters for employers & employees 2018 Last Updated: May 2018 This document was not intended

www.pwc.com/na/en Global Mobility Services: Taxation of International Assignees - Namibia Taxation issues & related matters for employers & employees 2018 Last Updated: May 2018 This document was not intended

IN RESPECT OF FRINGE BENEFITS

GUIDE FOR EMPLOYERS IN RESPECT OF (2016 TAX YEAR) 1 PURPOSE 3 2 SCOPE 3 3 OBLIGATIONS OF THE EMPLOYER 3 4 BENEFITS GRANTED TO RELATIVES OF EMPLOYEES AND OTHERS 4 5 TAXABLE BENEFITS 4 5.1 ACQUISITION OF

GUIDE FOR EMPLOYERS IN RESPECT OF (2016 TAX YEAR) 1 PURPOSE 3 2 SCOPE 3 3 OBLIGATIONS OF THE EMPLOYER 3 4 BENEFITS GRANTED TO RELATIVES OF EMPLOYEES AND OTHERS 4 5 TAXABLE BENEFITS 4 5.1 ACQUISITION OF

Global Mobility Services: Taxation of International Assignees - Swaziland

www.pwc.com/sz/en Global Mobility Services: Taxation of International Assignees - Swaziland People and Organisation Global Mobility Country Guide (Folio) Last Updated: June 2018 This document was not intended

www.pwc.com/sz/en Global Mobility Services: Taxation of International Assignees - Swaziland People and Organisation Global Mobility Country Guide (Folio) Last Updated: June 2018 This document was not intended

Welcome to the SARS Tax Workshop

Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the legislation more accessible

Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the legislation more accessible

Budget Highlight 2017

Budget Highlight 2017 Budget Highlights A new top marginal tax rate of 45% on taxable income of above R 1 500 000.00 was introduced The tax threshold increased from R75 000 to R75 750 p.a Dividends tax

Budget Highlight 2017 Budget Highlights A new top marginal tax rate of 45% on taxable income of above R 1 500 000.00 was introduced The tax threshold increased from R75 000 to R75 750 p.a Dividends tax

Individual Income Tax

Individual Income Tax Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the

Individual Income Tax Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the provisions of the

Global Mobility Services: Taxation of International Assignees - Malawi

www.pwc.com/mw/en Global Mobility Services: Taxation of International Assignees - Malawi Taxation issues & related matters for employers & employees 2017/18 Last Updated: June 2018 This document was not

www.pwc.com/mw/en Global Mobility Services: Taxation of International Assignees - Malawi Taxation issues & related matters for employers & employees 2017/18 Last Updated: June 2018 This document was not

OFFICE OF THE TAX OMBUD Limitations to the OTO Mandate and SARS Objections Procedure

OFFICE OF THE TAX OMBUD Limitations to the OTO Mandate and SARS Objections Procedure MANDATE OF TAX OMBUD s16. Review and address any complaint by a taxpayer regarding a service matter or a procedural

OFFICE OF THE TAX OMBUD Limitations to the OTO Mandate and SARS Objections Procedure MANDATE OF TAX OMBUD s16. Review and address any complaint by a taxpayer regarding a service matter or a procedural

A guide to understanding the medical scheme fees tax credit

A guide to understanding the medical scheme fees tax credit A guide to understanding the medical scheme fees tax credit 1 TABLE OF CONTENTS 1. INTRODUCTION... 3 2. WHAT ARE THE CHANGES?... 3 3. THE CHANGES

A guide to understanding the medical scheme fees tax credit A guide to understanding the medical scheme fees tax credit 1 TABLE OF CONTENTS 1. INTRODUCTION... 3 2. WHAT ARE THE CHANGES?... 3 3. THE CHANGES

Tax data card 2018/2019

Tax data card 2018/2019 1 Contents 1 Individuals and trusts 4 Companies 5 Capital allowances 6 Capital gains tax 7 Tax Administration Act penalties 8 Value-added tax 8 Other taxes, duties & levies 10 Exchange

Tax data card 2018/2019 1 Contents 1 Individuals and trusts 4 Companies 5 Capital allowances 6 Capital gains tax 7 Tax Administration Act penalties 8 Value-added tax 8 Other taxes, duties & levies 10 Exchange

GUIDE TO DETERMINE FRINGE BENEFIT VALUE ON ACCOMMODATION

GUIDE TO DETERMINE FRINGE BENEFIT VALUE ON Revision: 3 Page 1 of 14 TABLE OF CONTENTS 1 PURPOSE 3 2 SCOPE 3 3 REFERENCES 3 3.1 LEGISLATION 3 3.2 CROSS REFERENCES 3 4 DEFINITIONS AND ACRONYMS 3 5 BACKGROUND

GUIDE TO DETERMINE FRINGE BENEFIT VALUE ON Revision: 3 Page 1 of 14 TABLE OF CONTENTS 1 PURPOSE 3 2 SCOPE 3 3 REFERENCES 3 3.1 LEGISLATION 3 3.2 CROSS REFERENCES 3 4 DEFINITIONS AND ACRONYMS 3 5 BACKGROUND

Occupational Certificate: Tax Professional

Occupational Certificate: Tax Professional External Integrated Summative Assessment (EISA) Personal Taxation Question EXEMPLAR Part A Aspect of the answer Details of aspects to be included in answer Comp

Occupational Certificate: Tax Professional External Integrated Summative Assessment (EISA) Personal Taxation Question EXEMPLAR Part A Aspect of the answer Details of aspects to be included in answer Comp

Tax guide 2018/2019 TAX FACTS

Tax guide 2018/2019 TAX FACTS CONTENTS 1 1 RATES OF TAXES, 3 USEFUL INFORMATION AT A GLANCE, 4 TRAVEL ALLOWANCE, 6 COMPANY CAR, 6 OFFICIAL RATE OF INTEREST, 7 DEDUCTIONS FROM INCOME, 7 TRANSFER DUTY, 8

Tax guide 2018/2019 TAX FACTS CONTENTS 1 1 RATES OF TAXES, 3 USEFUL INFORMATION AT A GLANCE, 4 TRAVEL ALLOWANCE, 6 COMPANY CAR, 6 OFFICIAL RATE OF INTEREST, 7 DEDUCTIONS FROM INCOME, 7 TRANSFER DUTY, 8

FROM POWERFUL PARTNERSHIPS COME POWERFUL SOLUTIONS. Budget Pocket Guide 2018/2019 TAX & EXCHANGE CONTROL

FROM POWERFUL PARTNERSHIPS COME POWERFUL SOLUTIONS Budget Pocket Guide 2018/2019 TAX & EXCHANGE CONTROL CONTENTS 1 1 RATES OF TAXES, 3 USEFUL INFORMATION AT A GLANCE, 4 TRAVEL ALLOWANCE, 6 COMPANY CAR,

FROM POWERFUL PARTNERSHIPS COME POWERFUL SOLUTIONS Budget Pocket Guide 2018/2019 TAX & EXCHANGE CONTROL CONTENTS 1 1 RATES OF TAXES, 3 USEFUL INFORMATION AT A GLANCE, 4 TRAVEL ALLOWANCE, 6 COMPANY CAR,

VDP applications. August 2015

VDP applications August 2015 Overview for this webinar VDP Relief offered under the VDP; Overview of the VDP process; When VDP is not available: Pending or current audit/investigation Requirements for

VDP applications August 2015 Overview for this webinar VDP Relief offered under the VDP; Overview of the VDP process; When VDP is not available: Pending or current audit/investigation Requirements for

Tax Professional 2013 Knowledge Competency Assessment Paper 2: Solution

Tax Professional 2013 Knowledge Competency Assessment Paper 2: Solution P a g e 0 Suggested Solutions Question Topic Marks 1 Individual Tax 40 2 Trust Estate Duty and Donations Tax 50 3 Partnership 30

Tax Professional 2013 Knowledge Competency Assessment Paper 2: Solution P a g e 0 Suggested Solutions Question Topic Marks 1 Individual Tax 40 2 Trust Estate Duty and Donations Tax 50 3 Partnership 30

Payroll Tax Pocket Guide 2017/18

Payroll Tax Pocket Guide 2017/18 A complete reference guide covering legislative matters that affect the HR & payroll practitioner in South Africa. Quick Reference Subsistence Allowance Travel inside RSA

Payroll Tax Pocket Guide 2017/18 A complete reference guide covering legislative matters that affect the HR & payroll practitioner in South Africa. Quick Reference Subsistence Allowance Travel inside RSA

Paper P6 (ZAF) Advanced Taxation (South Africa) Friday 5 June Professional Level Options Module

Advanced Taxation (South Africa) Friday 5 June Professional Level Options Module") Professional Level Options Module Advanced Taxation (South Africa) Friday 5 June 2015 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section A BOTH

Professional Level Options Module Advanced Taxation (South Africa) Friday 5 June 2015 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section A BOTH

Service Charter. South African Revenue Service Service Charter

Service Charter South African Revenue Service Service Charter 1 South African Revenue Service Your Rights Obligations and Service timelines 2 Service Charter WHAT WE DO IN SOUTH AFRICA We, the South African

Service Charter South African Revenue Service Service Charter 1 South African Revenue Service Your Rights Obligations and Service timelines 2 Service Charter WHAT WE DO IN SOUTH AFRICA We, the South African

INCOME TAX / TAXATION

INCBUS JUNE 2012 EXAMINATION DATE: 6 JUNE 2012 TIME: 09H00 12H00 TOTAL: 100 MARKS DURATION: 3 HOURS PASS MARK: 40% (KJ-59 / BUS-LT) INCOME TAX / TAXATION THIS EXAMINATION PAPER CONSISTS OF 2 SECTIONS:

INCBUS JUNE 2012 EXAMINATION DATE: 6 JUNE 2012 TIME: 09H00 12H00 TOTAL: 100 MARKS DURATION: 3 HOURS PASS MARK: 40% (KJ-59 / BUS-LT) INCOME TAX / TAXATION THIS EXAMINATION PAPER CONSISTS OF 2 SECTIONS:

HOW TO EFFECTIVELY MANAGE EXPATRIATE PAYROLLS? 6 September 2017 [Shohana Mohan, Johannesburg South Africa]

![HOW TO EFFECTIVELY MANAGE EXPATRIATE PAYROLLS? 6 September 2017 [Shohana Mohan, Johannesburg South Africa]](/thumbs/87/96816836.jpg "HOW TO EFFECTIVELY MANAGE EXPATRIATE PAYROLLS? 6 September 2017 [Shohana Mohan, Johannesburg South Africa]") HOW TO EFFECTIVELY MANAGE EXPATRIATE PAYROLLS? 6 September 2017 [Shohana Mohan, Johannesburg South Africa] 1 LET S TEST YOUR KNOWLEDGE ON EXPATRIATE TAX What does an expatriate mean? A a person who lives

HOW TO EFFECTIVELY MANAGE EXPATRIATE PAYROLLS? 6 September 2017 [Shohana Mohan, Johannesburg South Africa] 1 LET S TEST YOUR KNOWLEDGE ON EXPATRIATE TAX What does an expatriate mean? A a person who lives

Payroll Pocket Guide. as at March A complete reference guide covering legislative matters that affect the payroll practitioner in South Africa

Payroll Pocket Guide as at March 2013 A complete reference guide covering legislative matters that affect the payroll practitioner in South Africa Quick Reference Subsistence Allowance Travel inside RSA

Payroll Pocket Guide as at March 2013 A complete reference guide covering legislative matters that affect the payroll practitioner in South Africa Quick Reference Subsistence Allowance Travel inside RSA

Points Of Discussion

Provisional Tax Provisional Tax Points Of Discussion Overview Who is liable for Provisional Tax Who is not liable Exemption: Interest Income Estimates of Taxable Income When is Provisional Tax Paid Provisional

Provisional Tax Provisional Tax Points Of Discussion Overview Who is liable for Provisional Tax Who is not liable Exemption: Interest Income Estimates of Taxable Income When is Provisional Tax Paid Provisional

EXTERNAL FREQUENTLY ASKED QUESTIONS DISPUTE ADMINISTRATION

EXTERNAL FREQUENTLY ASKED QUESTIONS Revision: 5 Page 1 of 9 1 PURPOSE These frequently asked questions (FAQ) deal with the basic principles of objections and appeals applicable to individual and corporate

EXTERNAL FREQUENTLY ASKED QUESTIONS Revision: 5 Page 1 of 9 1 PURPOSE These frequently asked questions (FAQ) deal with the basic principles of objections and appeals applicable to individual and corporate

FINANCIAL & TAXATION. Directory 2017 / 2018

FINANCIAL & TAXATION Directory 2017 / 2018 BDO IN SOUTH AFRICA We are the South African member firm of BDO International. The global BDO network provides audit, tax and advisory services in 157 countries,

FINANCIAL & TAXATION Directory 2017 / 2018 BDO IN SOUTH AFRICA We are the South African member firm of BDO International. The global BDO network provides audit, tax and advisory services in 157 countries,

Tax and ETI Amendments 2017/2018

Tax and ETI Amendments 2017/2018 Contents 1 Employment Tax Incentive (ETI) Changes... 2 1.1 Wage Qualifying Test... 2 1.1.1 Before March 2017... 2 1.1.2 From March 2017... 3 1.1.3 Employed and Remunerated

Tax and ETI Amendments 2017/2018 Contents 1 Employment Tax Incentive (ETI) Changes... 2 1.1 Wage Qualifying Test... 2 1.1.1 Before March 2017... 2 1.1.2 From March 2017... 3 1.1.3 Employed and Remunerated

GREATSOFT CRM CLIENT RELEASE NOTES

GREATSOFT CRM 2016.1.0 CLIENT RELEASE NOTES CONTENTS INTRODUCTION...1 Prerequisites...1 CRM...2 Tasks...2 Billings...2 Disbursements...2 TAX...2 ITR12 Changes for 2016...2 Other ITR12 Changes... 15 ITR14

GREATSOFT CRM 2016.1.0 CLIENT RELEASE NOTES CONTENTS INTRODUCTION...1 Prerequisites...1 CRM...2 Tasks...2 Billings...2 Disbursements...2 TAX...2 ITR12 Changes for 2016...2 Other ITR12 Changes... 15 ITR14

PAYROLL TAX POCKET GUIDE. A complete reference guide covering legislative matters that affect the HR and payroll practitioner in South Africa.

PAYROLL TAX POCKET GUIDE 2019 2020 A complete reference guide covering legislative matters that affect the HR and payroll practitioner in South Africa. Quick Reference Subsistence Allowance Travel inside

PAYROLL TAX POCKET GUIDE 2019 2020 A complete reference guide covering legislative matters that affect the HR and payroll practitioner in South Africa. Quick Reference Subsistence Allowance Travel inside

Quick Tax Guide 2013/14 Simplicity from complexity

Quick Tax Guide 2013/14 Simplicity from complexity Income Tax for Individuals Tax rates and rebates Individuals, Estates & Special Trusts 1 (Year ending 28 February 2014) Taxable income as exceeds But

Quick Tax Guide 2013/14 Simplicity from complexity Income Tax for Individuals Tax rates and rebates Individuals, Estates & Special Trusts 1 (Year ending 28 February 2014) Taxable income as exceeds But

BBR VAN DER GRIJP & ASSOCIATES

BB VAN DE GIJP & ASSOCIATES CHATEED ACCOUNTANTS (S.A.) P. O. BOX 1448 1106 COUTYAD egistration: 920 932 E SOMESET WEST 7129 GANTS CENTE, STAND 7140 Tel: (021) 854 9060 Knysna Office: P.O. Box 2602 3 Hill

BB VAN DE GIJP & ASSOCIATES CHATEED ACCOUNTANTS (S.A.) P. O. BOX 1448 1106 COUTYAD egistration: 920 932 E SOMESET WEST 7129 GANTS CENTE, STAND 7140 Tel: (021) 854 9060 Knysna Office: P.O. Box 2602 3 Hill

TCS (Tax Clearance Status) November 2018

November 2018") TCS (Tax Clearance Status) November 2018 Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the

TCS (Tax Clearance Status) November 2018 Welcome to the SARS Tax Workshop The purpose of this presentation is merely to provide information in an easily understandable format and is intended to make the

Tax, ETI and UIF Amendments 2018/2019

Tax, ETI and UIF Amendments 2018/2019 Contents 1 General Explanatory Note 3 2 Explanation of Changes Affecting the System 3 2.1 Reimbursive Travel Allowance Included in Remuneration 3 2.2 Certain Dividends

Tax, ETI and UIF Amendments 2018/2019 Contents 1 General Explanatory Note 3 2 Explanation of Changes Affecting the System 3 2.1 Reimbursive Travel Allowance Included in Remuneration 3 2.2 Certain Dividends

EXTERNAL GUIDE COMPREHENSIVE GUIDE TO THE ITR12T RETURN FOR TRUSTS

THE ITR12T RETURN FOR TABLE OF CONTENTS 1 INTRODUCTION... 6 2 GENERAL INFORMATION... 6 2.1 WHO MUST COMPLETE AND SUBMIT THE IT12T... 6 2.2 HOW TO OBTAIN A RETURN... 7 2.3 HOW TO SUBMIT A RETURN... 8 2.4

THE ITR12T RETURN FOR TABLE OF CONTENTS 1 INTRODUCTION... 6 2 GENERAL INFORMATION... 6 2.1 WHO MUST COMPLETE AND SUBMIT THE IT12T... 6 2.2 HOW TO OBTAIN A RETURN... 7 2.3 HOW TO SUBMIT A RETURN... 8 2.4

Special Voluntary Disclosure Programme. GUIDE: SPECIAL VOLUNTARY DISCLOSURE PROGRAMME (v1.2)

") GUIDE: SPECIAL VOLUNTARY DISCLOSURE PROGRAMME (v1.2) This is a preliminary guide, which is subject to Parliamentary legislative processes. This version is based on the proposals to Parliament following

GUIDE: SPECIAL VOLUNTARY DISCLOSURE PROGRAMME (v1.2) This is a preliminary guide, which is subject to Parliamentary legislative processes. This version is based on the proposals to Parliament following

THE PRESIDENCY. No June 2001

THE PRESIDENCY No. 550 20 June 2001 It is hereby notified that the Acting President has assented to the following Act which is hereby published for general information: - NO. 5 OF 2001: TAXATION LAWS AMENDMENT

THE PRESIDENCY No. 550 20 June 2001 It is hereby notified that the Acting President has assented to the following Act which is hereby published for general information: - NO. 5 OF 2001: TAXATION LAWS AMENDMENT

Luxembourg income tax 2018 Guide for individuals

Luxembourg income tax 2018 Guide for individuals www.pwc.lu 2 Table of Contents Basic principles Employment income Directors fees Dividend and interest income 1 2 3 4 5 Capital gains p4 p8 p9 p9 p10 Real

Luxembourg income tax 2018 Guide for individuals www.pwc.lu 2 Table of Contents Basic principles Employment income Directors fees Dividend and interest income 1 2 3 4 5 Capital gains p4 p8 p9 p9 p10 Real

Tax Guide

2017-2018 Tax Guide - 1 - CONTENTS INCOME TAX RATES 2 DIFFERENT TYPES OF ENTITIES TAX REBATES 2 Small business corporations 24 TAX THRESHOLDS 2 Personal service providers 26 MEDICAL SCHEME TAX CREDITS

2017-2018 Tax Guide - 1 - CONTENTS INCOME TAX RATES 2 DIFFERENT TYPES OF ENTITIES TAX REBATES 2 Small business corporations 24 TAX THRESHOLDS 2 Personal service providers 26 MEDICAL SCHEME TAX CREDITS

Latest Tax Developments. November 2016

Latest Tax Developments November 2016 Introduction Monthly webinar Last webinar 2016 Recent developments This one November 2016; Cannot cover all developments in detail; Relevance of developments; Some

Latest Tax Developments November 2016 Introduction Monthly webinar Last webinar 2016 Recent developments This one November 2016; Cannot cover all developments in detail; Relevance of developments; Some

Financial and Taxation Directory 2006/2007

Financial and Taxation Directory 2006/2007 Cliffe Dekker is part of DLA Piper Group, an alliance of legal practices CONTENTS South African Taxation Highlights of the 2006/2007 Budget 2-5 Calculation of

Financial and Taxation Directory 2006/2007 Cliffe Dekker is part of DLA Piper Group, an alliance of legal practices CONTENTS South African Taxation Highlights of the 2006/2007 Budget 2-5 Calculation of

- 2 - INCOME TAX RATES Rate of normal income tax on taxable income of any natural person or special trust: 2014/2015

TAX GUIDE 2014-2015 - 1 - CONTENTS INCOME TAX RATES, REBATES AND THRESHOLDS 2 WEAR AND TEAR ALLOWANCES General 3 Capital allowances 3 RESIDENCE BASIS OF TAXATION Resident 4 Non-resident 4 INTEREST AND

TAX GUIDE 2014-2015 - 1 - CONTENTS INCOME TAX RATES, REBATES AND THRESHOLDS 2 WEAR AND TEAR ALLOWANCES General 3 Capital allowances 3 RESIDENCE BASIS OF TAXATION Resident 4 Non-resident 4 INTEREST AND

CANDIDATE NUMBER No Aspect of the Answer Marks Candidate Mark Obtained 1 To Mr. Anil Naidoo

CANDIDATE NUMBER No Aspect of the Answer Marks Candidate Mark Obtained To Mr. Anil Naidoo From Tax Manager Subject Tax implications of issues discussed Date 4 December 207 Sub Total Scope We refer to our

CANDIDATE NUMBER No Aspect of the Answer Marks Candidate Mark Obtained To Mr. Anil Naidoo From Tax Manager Subject Tax implications of issues discussed Date 4 December 207 Sub Total Scope We refer to our

PUBLIC RELEASE. Document Classification: Official Publication. South African Revenue Service 2009

PUBLIC RELEASE Document Classification: Official Publication South African Revenue Service 2009 Page 1 of 49 Revision History Date Version Description Author/s 2008/11/14 V1.0.0 Draft release for public

PUBLIC RELEASE Document Classification: Official Publication South African Revenue Service 2009 Page 1 of 49 Revision History Date Version Description Author/s 2008/11/14 V1.0.0 Draft release for public

ATX ZAF. Advanced Taxation South Africa (ATX ZAF) Strategic Professional Options. Tuesday 4 December 2018

Strategic Professional Options. Tuesday 4 December 2018") Strategic Professional Options Advanced Taxation South Africa (ATX ZAF) Tuesday 4 December 2018 ATX ZAF ACCA Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A

Strategic Professional Options Advanced Taxation South Africa (ATX ZAF) Tuesday 4 December 2018 ATX ZAF ACCA Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A

Disclaimer. Copyright notice

Disclaimer The DVD lectures and related study material (consisting of Powerpoint slides, summary modules, integrated question banks and other academic material) are based on the views and/or opinions of

Disclaimer The DVD lectures and related study material (consisting of Powerpoint slides, summary modules, integrated question banks and other academic material) are based on the views and/or opinions of

Tax Professional Knowledge Competency Assessment

Tax Professional Knowledge Competency Assessment JUNE 2016 Paper 2 Instructions to Candidates 1. This competency assessment paper consists of four questions. 2. Answer each question in a separate answer

Tax Professional Knowledge Competency Assessment JUNE 2016 Paper 2 Instructions to Candidates 1. This competency assessment paper consists of four questions. 2. Answer each question in a separate answer

% 28% funds Trusts 45% 45% Small Business Funding Entities 28% 28%

- 1 - CONTENTS INCOME TAX RATES 2 DIFFERENT TYPES OF ENTITIES TAX REBATES 2 Small business corporations 25 TAX THRESHOLDS 2 Personal service providers 26 MEDICAL SCHEME TAX CREDITS 2 Micro businesses 27

- 1 - CONTENTS INCOME TAX RATES 2 DIFFERENT TYPES OF ENTITIES TAX REBATES 2 Small business corporations 25 TAX THRESHOLDS 2 Personal service providers 26 MEDICAL SCHEME TAX CREDITS 2 Micro businesses 27

training (pty) ltd Tax Guide