Latest Tax Developments. November 2016

|

|

|

- Julian Willis

- 5 years ago

- Views:

Transcription

1 Latest Tax Developments November 2016

2 Introduction Monthly webinar Last webinar 2016 Recent developments This one November 2016; Cannot cover all developments in detail; Relevance of developments; Some will roll over - time; If we missed something that you would like us to cover, please let us know for inclusion in next webinar.

3 Introduction Overview General developments; Practical issues; Topics not covered.

; BMW v SARS; Cannon vs SARS; Public")

4 Overview Interpretation Note No. 91 ( IN91 ); BMW v SARS; Cannon vs SARS; Public Notice: Duty to Keep Records

5 General Developments SVDP can now be submitted at SARS branches in addition to efiling. VAT disputes can now be lodged via efiling. Special VDP at last in legislation. Taxation Laws Amendment Bill (Bill ) and Tax Administration Laws Amendment Bill (B ) have been finalised.

6 Practical Issues In the past SARS send out notifications on assessments indicating the number of the assessment for that year, so the original assessment would have been number one and additional assessments will be 2, 3 or 4. In the past on notifications, the specified what kind of correspondence was issued, objection allowance or disallowance, verification etc., nowadays the notification only states that a letter was issued. VDP01 application form problematic on e-filing.

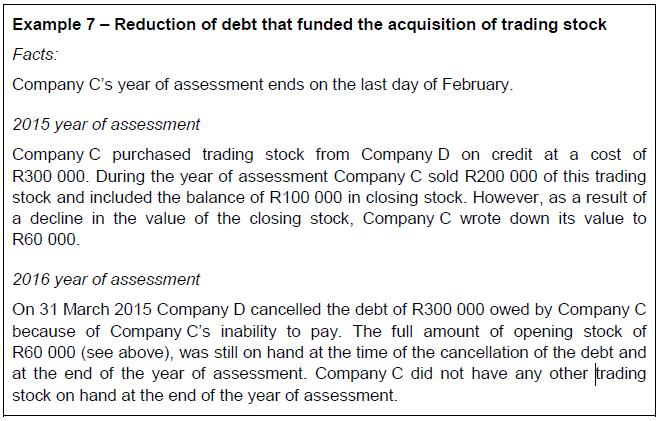

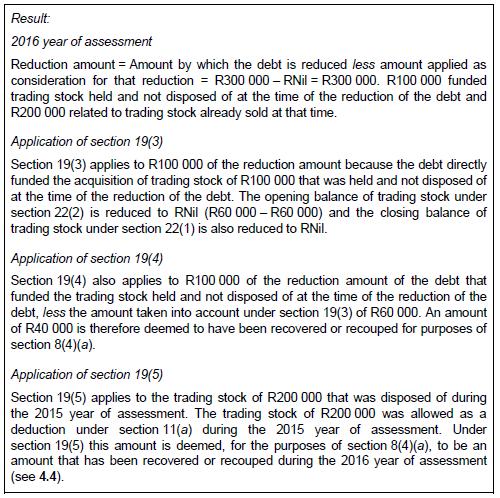

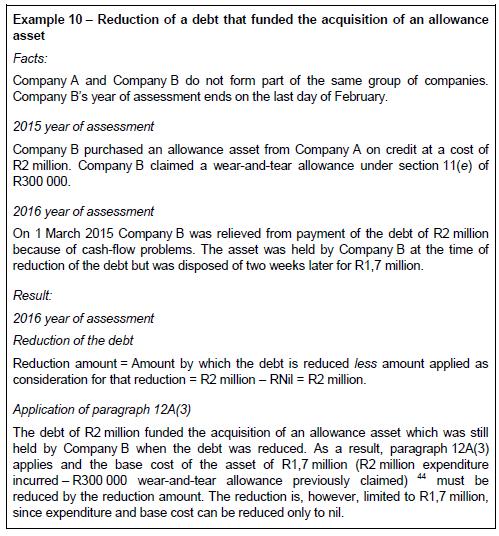

7 Issue date: 21 October Sections 19 and par. 2A of the 8 th Schedule. Purpose This note provides guidance on the interpretation and application of section 19 and par. 12A which deal with the reduction of debt. The Note does not address section 22 of the VAT Act dealing with irrecoverable debt. Background This new IN deals with scenarios where debt owed has been cancelled or reduced or waived. Different scenarios are dealt with depending on what the debt (cash received) was used to finance in the operations of the company. The general principle is that any previous deductions or allowances deducted from taxable income will be recouped or otherwise recovered to the extent the debt has been reduced.

8 Reduction amount A reduction amount in relation to a debt owed by a person means any amount by which that debt is reduced, less any amount that has been paid already by that debtor to the creditor as consideration for that reduction. The reference to that person in the definition of reduction amount is a reference to the debtor. Time of Reduction For purposes of section 19 and par 12A the time of reduction of the amount of a debt will depend on the facts of each case. A debt will be reduced when the event giving rise to the debt reduction takes place, for example, when a creditor decides not to enforce payment of a debt and informs the debtor accordingly.

9 Sequence of the application of the subsections of section 19 Any reduction amount in respect of trading stock must be applied in accordance with the sequence of the subsections of section 19. Thus, a debt that funded the acquisition of trading stock and which is partially reduced must first be allocated to trading stock that is held and not disposed of at the time of the debt reduction under section 19(3). Any remaining balance of the debt reduction must then be dealt with as a recoupment under section 19(4) or (5). Section 19(2) This subsection is the starting point and gives the scope of section 19. Section 19(3) This subsection tells us a debt that was used to finance trading stock that is still on hand at time of reduction we have to reduce the future cost of sale with the reduction amount.

10 Section 19(4) This subsection tells us a debt that funded expenditure that was incurred in respect of trading stock that is held and not disposed of at the time of the reduction of the debt. Section 19(4) provides that if the reduction amount of the debt exceeds the amount applied under section 19(3) to reduce the section 11(a), section 22(1) and section 22(2) amounts as appropriate, then the excess amount must, for the purposes of section 8(4)(a), be deemed to be an amount that has been recovered or recouped in the tax year.

11

12

13

14

15

16

17

18

19

20

21

22

23

24 Donations Tax Section 19(8)(b) and par. 12A(6)(b) do not require that the reduction amount of the debt be subject to donations tax. While a debt may be reduced by a donation as in section 55(1) and 58, the exclusions in section 19(8)(b) and paragraph 12A(6)(b) will apply even when the donation is exempt from donations tax under section 56. Not every reduction of a debt is motivated by pure liberality or disinterested benevolence. Only the reduction of a debt motivated by pure liberality or disinterested benevolence will be a debt reduced by way of a donation as defined in section 55(1).

25

26

27

28 Reduction in expenditure incurred under paragraph 20(1)(a) to (g) (paragraph 20(3)(b)) Double taxation could arise should both section 19 and par. 20(3)(b) apply to a reduction of debt. In this regard paragraph 20(3)(b) shall not apply to the extent that the amount was taken into account as a recoupment under section 8(4)(a) (it would have if section 19(4) or 19(6) applied); or the amount was applied to reduce an amount taken into account in respect of trading stock under section 19 (it would have if section 19(3) applied). This exclusion, therefore, ensures that the base cost of an asset must not be reduced under paragraph 20(3)(b) if section 19 has been applied to reduce an amount taken into account in respect of trading stock.

29 Summary Section 19 and par. 12A contain ordering rules for dealing with debt reduction and replace the previous rules that were contained in section 8(4)(m), the proviso to section 20(1)(a) and paragraph 12(5). The new ordering rules apply to trading stock, other deductible expenditure, allowance assets and capital assets financed by debt that is subsequently reduced. Briefly the rules provide as follows upon a reduction of such debt: Trading stock held and not disposed of Any section 11(a) deduction or the value of opening stock under section 22(2) as well as any closing stock under section 22(1) is reduced by the reduction amount of a debt under section 19(3). Any excess reduction amount is treated under section 19(4) as a recoupment for the purposes of section 8(4)(a). Trading stock not held and not disposed of at the time of the reduction of the debt and other deductible expenditure excluding allowance assets The reduction amount of a debt is deemed to be a recoupment under section 19(5) for the purposes of section 8(4)(a) to the extent that the expenditure that was funded by the debt was allowed as a deduction.

30 Summary (cont.) Allowance assets The reduction amount of a debt first reduces any base cost expenditure under paragraph 12A(3) after which any excess is deemed to be a recoupment under section 19(6) for the purposes of section 8(4)(a). Future capital allowances will be limited to the cost of the asset less the reduction amount and any previous allowances claimed on the asset, under section 19(7). Capital assets that are not allowance assets The base cost of the asset is reduced by the reduction amount of the debt under paragraph 12A(3). Any excess reduction amount reduces an assessed capital loss under paragraph 12A(4). The ordering rules do not apply to tax debt or debt that has been reduced by donation, bequest or by an employer (section 19(8) and paragraph 12A(6)(a), (b) and (c)).

31 BMW V CSARS Judgment date: 21 October Issue in dispute: Whether the Applicant was entitled to interest on the amount of penalties and interest paid by it under protest. Parties: Applicant: BMW South Africa The Respondent: Commissioner for the South Africa Revenue Services. Facts: Respondent had found that Applicant had not paid the value-added tax payable for the period October 2011 to February 2012 and therefore levied penalties and interest due. Applicant had made payment, which had not been properly allocated by the Respondent. Nevertheless, and despite proof of payment given to the Respondent by the Applicant, the Respondent continued to levy penalties and interest, and compelled payment thereof. Applicant did request suspension of payment, which request was not successful.

32 BMW V CSARS The Commissioner s finding of non-payment was corrected and the costs issue was dealt with, however repayment of the penalties and interest was still to be resolved. Applicant: Referred to Shuttleworth v South African Reserve Bank et al 2015 (1) SA 586 (SCA) and the Tax Administration Act of Said that they were entitled to interest on the amount of penalties and interest paid by it under protest. Respondent Referred to Commissioner for Inland Revenue v First National Industrial Bank Ltd. Said that no mora interest was payable on the amount relating to the penalties and interest.

33 BMW V CSARS Court found that the Shuttleworth judgment and the TAA were applicable. Applicant therefore entitled to interest on the amount paid in respect of penalties and interest levied by the Respondent. Respondent was ordered to pay back the provisional payment made to it by the Applicant, with interest a tempore morae.

34 Public Notice: Duty to Keep Records (Published in Government Gazette No , 28 October 2016) ( Public Notice ) Public Notice issued ito S29(1)(b) of the Tax Administration Act, 2011 ( TAA ). Public Notice applies to years of assessment commencing on/after 1 October Persons required to keep records, books of account or documents specified in this Public Notice: Persons who entered into potentially affected transaction (defined in S31 of Income Tax Act); and Aggregate of potentially affected transactions for YOA (without offsetting the transactions against each other) exceed R100 million.

35 Public Notice: Duty to Keep Records (Published in Government Gazette No , 28 October 2016) ( Public Notice ) Documents to be Kept iro Structure and Operations: Description of person s ownership structure; The name, address of the principal office, legal form and jurisdiction of tax residence of each of connected persons with which a potentially affected transaction has been entered into; Business operation summary, incl. Description of business and plans for principal trading operations; an organogram showing title and location of senior management team members; major economic and legal issues affecting profitability of person and industry;

36 Public Notice: Duty to Keep Records (Published in Government Gazette No , 28 October 2016) ( Public Notice ) Documents to be Kept iro Structure and Operations (contd.): Business operation summary, incl. (contd.) Description of any business restructurings or intangibles transfers that person has been affected by or involved in; Person s market share within industry, analysis of relevant market competition environment and key competitors; Key value drivers identified by available industry research findings or reports; Industry policy or industry incentives or restrictions affecting person s business; Role of person, as well as connected persons, in group s supply chain.

37 Public Notice: Duty to Keep Records (Published in Government Gazette No , 28 October 2016) ( Public Notice ) Documents to be Kept iro Transactions that exceed R5 million in value: Nature and terms (including pricing policy) of transactions; Contracts or agreements related to transactions; Any other governance and regulatory documents (e.g. complete board minutes and South African Reserve Bank applications and approvals); Indication and explanation of tested party, if applicable; Iro tested party (=selected for transfer pricing method) Detailed allocation of revenues, costs, expenses and profits between its connected person transactions and independent person transactions; or If the above cannot be directly allocated, an explanation and documents supporting the allocation rationale;

38 Public Notice: Duty to Keep Records (Published in Government Gazette No , 28 October 2016) ( Public Notice ) Documents to be Kept iro Transactions that exceed R5 million in value: (contd.) If tested party is tax resident outside RSA, documents evidencing the functional and risk classification of tested party, incl. Description of business; Contracts between tested party and its customers and suppliers; and Commercial invoices between tested party and its customers and suppliers. Description of functions, risks and assets; Description of intangible assets involved and their influence on classification of tested party;

39 Public Notice: Duty to Keep Records (Published in Government Gazette No , 28 October 2016) ( Public Notice ) Documents to be Kept iro Transactions that exceed R5 million in value: (contd.) Operational flows (incl. information flow, product flow, and cash flow); Data and methods used for determining arm s length return and transfer prices; Assumptions, policies and price negotiations, that influenced determination of the transfer prices or the allocations of profits or losses; Details of adjustments made to transfer prices to align them with the arm s length return; If potentially affected transactions = financial assistance transactions, the following records: Summary of financial forecasts; Analysis of financial strategy of business.

40 Public Notice: Duty to Keep Records (Published in Government Gazette No , 28 October 2016) ( Public Notice ) Documents to be Kept iro Transactions that exceed R5 million in value: (contd.) If potentially affected transactions = financial assistance transactions with a term exceeding 12 months, the following additional records: Description of funding structure in place; Group structure covering all relevant companies; Financial statements and management accounts. Existing unilateral, bilateral and multilateral advance pricing agreements and tax rulings. Documents to be kept where Transactions don t exceed R5 million: Documents that enable SRS to be satisfied that potentially affected transaction = arm s length.

41 Public Notice: Duty to Keep Records (Published in Government Gazette No , 28 October 2016) ( Public Notice ) Documents to be Kept by Connected Persons: Iro records to be kept iro structure and operations as well as transactions that exceed R5 million (discussed above) which are kept by connected person in ordinary course of business comply with requirements in S31 of TAA. Alternative Arrangements with SARS: If there are high volumes of potentially affected transactions which are also financial assistance transactions, SARS may agree to alternative records that may be kept re transaction being at arm s length.

42 CANNON SOUTH AFRICA v C:SARS (2671/2016P) [2016] ZAKZPHC 94 (7 October 2016) ( CANNON v SARS ) Cannon v SARS deals with review (ito HCR 48) of Taxing Master s disallowance of certain items on a bill of costs; Judgment Date: 7 October General Principals on Costs Depending on circumstances, taxpayer or SARS may be ordered by Tax Court to pay costs; Taxpayer may be awarded costs by Tax Court where SARS acts unreasonably;

43 General Principals on Costs Dispute Resolution Rules make no provision for payment of costs in the Tax Board; During ADR, parties can also agree to pay the other parties costs (this will form part of ADR agreement); Costs must be in accordance with fees prescribed by High Court Rules; If parties dispute amount of costs (as detailed in bill of costs document) Taxing Master (court official) may be called upon to tax the bill of costs;

44 General Principals on Costs For tax disputes, Registrar of Tax Court may perform functions of taxing master/ appoint someone to perform such functions; Taxing Master is granted a discretion as to which items in bill of costs to allow; Decisions by Taxing Master re bill of costs can be taken on review to High Court ito HCR 48.

45 Not covered Section 12l Tax Allowance Programme Changes made to rectify the implementation dates of decisions to approve or withdraw approval of applications received for the Tax Allowance programme in terms of section 12l (12)(a)(i) and (19)(d).

46 Thank you Thank you for listening Thanks to my technical team for assistance during the year: Matsika Vengesa; Rina Fourie; Craig Rocher; Marius Engelbrecht; Natasha Wilkinson; and Jessica Grobler. Tax Consulting South Africa Nico Theron

Latest Tax Developments. January 2017

Latest Tax Developments January 2017 Introduction Monthly webinar 1st of 11 webinars Recent developments: This one January 2017; Cannot cover all developments in detail; Relevance of developments; Some

Latest Tax Developments January 2017 Introduction Monthly webinar 1st of 11 webinars Recent developments: This one January 2017; Cannot cover all developments in detail; Relevance of developments; Some

Latest Tax Developments. June 2017

Latest Tax Developments June 2017 Introduction Monthly webinar 6th of 11 webinars Recent developments: This one June 2017; Cannot cover all developments in detail; Relevance of developments; Some will

Latest Tax Developments June 2017 Introduction Monthly webinar 6th of 11 webinars Recent developments: This one June 2017; Cannot cover all developments in detail; Relevance of developments; Some will

Estate Agency Affairs Board. Tax Notes

Estate Agency Affairs Board Tax Notes Contents Page Chapter 1: Tax Administration Act... 1 Part A - Objections... 2 A.1 What assessments and decisions may be objected against?... 2 A.2 SARS s decision

Estate Agency Affairs Board Tax Notes Contents Page Chapter 1: Tax Administration Act... 1 Part A - Objections... 2 A.1 What assessments and decisions may be objected against?... 2 A.2 SARS s decision

PN: The basic rule, as found in section 9(1) of the Value-added Tax Act, applies. It reads as follows:

of the Value-added Tax Act, applies. It reads as follows:") Webinar = 22 June 1. What is the meaning of In Duplum? PN: The in duplum states that unpaid interest on a money debt owing ceases to accumulate once it reaches the amount of the capital sum. In other words,

Webinar = 22 June 1. What is the meaning of In Duplum? PN: The in duplum states that unpaid interest on a money debt owing ceases to accumulate once it reaches the amount of the capital sum. In other words,

A closer look at the new Debt Reduction Regime

A closer look at the new Debt Reduction Regime Herman Viviers 20 November 2014 Disclaimer Nothing in this presentation should be construed as constituting tax advice or a tax opinion. An expert should

A closer look at the new Debt Reduction Regime Herman Viviers 20 November 2014 Disclaimer Nothing in this presentation should be construed as constituting tax advice or a tax opinion. An expert should

EXTERNAL FREQUENTLY ASKED QUESTIONS DISPUTE ADMINISTRATION

EXTERNAL FREQUENTLY ASKED QUESTIONS Revision: 5 Page 1 of 9 1 PURPOSE These frequently asked questions (FAQ) deal with the basic principles of objections and appeals applicable to individual and corporate

EXTERNAL FREQUENTLY ASKED QUESTIONS Revision: 5 Page 1 of 9 1 PURPOSE These frequently asked questions (FAQ) deal with the basic principles of objections and appeals applicable to individual and corporate

THE TAX PROFESSIONAL KNOWLEDGE COMPETENCY ASSESSMENT NOVEMBER 2013 SAMPLE PAPER 1 SUGGESTED SOLUTION

THE TAX PROFESSIONAL KNOWLEDGE COMPETENCY ASSESSMENT NOVEMBER 2013 SAMPLE PAPER 1 SUGGESTED SOLUTION Question Topic Marks 1 Various Advisory 50 2 VAT, CGT and Capital Allowances 30 3 Normal Tax Calculation

THE TAX PROFESSIONAL KNOWLEDGE COMPETENCY ASSESSMENT NOVEMBER 2013 SAMPLE PAPER 1 SUGGESTED SOLUTION Question Topic Marks 1 Various Advisory 50 2 VAT, CGT and Capital Allowances 30 3 Normal Tax Calculation

Occupational Certificate: Tax Professional

Occupational Certificate: Tax Professional External Integrated Summative Assessment (EISA) Personal Taxation Question EXEMPLAR Part A Aspect of the answer Details of aspects to be included in answer Comp

Occupational Certificate: Tax Professional External Integrated Summative Assessment (EISA) Personal Taxation Question EXEMPLAR Part A Aspect of the answer Details of aspects to be included in answer Comp

VDP applications. August 2015

VDP applications August 2015 Overview for this webinar VDP Relief offered under the VDP; Overview of the VDP process; When VDP is not available: Pending or current audit/investigation Requirements for

VDP applications August 2015 Overview for this webinar VDP Relief offered under the VDP; Overview of the VDP process; When VDP is not available: Pending or current audit/investigation Requirements for

Tax Professional 2013 Knowledge Competency Assessment Paper 2: Solution

Tax Professional 2013 Knowledge Competency Assessment Paper 2: Solution P a g e 0 Suggested Solutions Question Topic Marks 1 Individual Tax 40 2 Trust Estate Duty and Donations Tax 50 3 Partnership 30

Tax Professional 2013 Knowledge Competency Assessment Paper 2: Solution P a g e 0 Suggested Solutions Question Topic Marks 1 Individual Tax 40 2 Trust Estate Duty and Donations Tax 50 3 Partnership 30

Mini-Panel: International Reporting Heavy Compliance Burden Ahead. Amit Chadha KPMG JP Borman PwC Wally Horak Bowman Gilfillan Franz Tomasek SARS

Mini-Panel: International Reporting Heavy Compliance Burden Ahead Amit Chadha KPMG JP Borman PwC Wally Horak Bowman Gilfillan Franz Tomasek SARS Country-by-Country Reporting (CbyCR) Background On October

Mini-Panel: International Reporting Heavy Compliance Burden Ahead Amit Chadha KPMG JP Borman PwC Wally Horak Bowman Gilfillan Franz Tomasek SARS Country-by-Country Reporting (CbyCR) Background On October

Value Added Tax. The debt collection industry

Value Added Tax The debt collection industry Presenter: Christo Theron Founder: TradeTaxPlus Centre of Excellence Email address: christo.theron@tradetaxplus.com Mobile number: 083 283 7242 Website: www.tradetaxplus.com

Value Added Tax The debt collection industry Presenter: Christo Theron Founder: TradeTaxPlus Centre of Excellence Email address: christo.theron@tradetaxplus.com Mobile number: 083 283 7242 Website: www.tradetaxplus.com

OFFICE OF THE TAX OMBUD Limitations to the OTO Mandate and SARS Objections Procedure

OFFICE OF THE TAX OMBUD Limitations to the OTO Mandate and SARS Objections Procedure MANDATE OF TAX OMBUD s16. Review and address any complaint by a taxpayer regarding a service matter or a procedural

OFFICE OF THE TAX OMBUD Limitations to the OTO Mandate and SARS Objections Procedure MANDATE OF TAX OMBUD s16. Review and address any complaint by a taxpayer regarding a service matter or a procedural

IMPORTER GUIDE PROVISIONAL VALUES SCHEME

IMPORTER GUIDE PROVISIONAL VALUES SCHEME Date: October 2018 Contents Provisional values scheme... 1 Overview of the provisional values scheme... 3 When you can automatically qualify... 15 What to do if

IMPORTER GUIDE PROVISIONAL VALUES SCHEME Date: October 2018 Contents Provisional values scheme... 1 Overview of the provisional values scheme... 3 When you can automatically qualify... 15 What to do if

1. Purpose This Note provides guidance on the application and interpretation of paragraph (ja) and its interaction with other provisions of the Act.

and its interaction with other provisions of the Act.") INTERPRETATION NOTE 11 (Issue 4) DATE: 6 February 2017 ACT : INCOME TAX ACT 58 OF 1962 SECTION : PARAGRAPH (ja) OF THE DEFINITION OF GROSS INCOME IN SECTION 1(1) SUBJECT : TRADING STOCK: ASSETS NOT USED

INTERPRETATION NOTE 11 (Issue 4) DATE: 6 February 2017 ACT : INCOME TAX ACT 58 OF 1962 SECTION : PARAGRAPH (ja) OF THE DEFINITION OF GROSS INCOME IN SECTION 1(1) SUBJECT : TRADING STOCK: ASSETS NOT USED

SAIT Webinar. 26 July Gert van Heerden Senior Legal Manager: Office of the Tax Ombud

SAIT Webinar 26 July 2017 Gert van Heerden Senior Legal Manager: Office of the Tax Ombud GENERAL INFORMATION 1. Any complaints about the OTO services or cases can be escalated to: Reason Dube: Manager

SAIT Webinar 26 July 2017 Gert van Heerden Senior Legal Manager: Office of the Tax Ombud GENERAL INFORMATION 1. Any complaints about the OTO services or cases can be escalated to: Reason Dube: Manager

12I. Additional investment and training allowances in respect of industrial policy projects. (1) For the purposes of this section

For the purposes of this section") Section 12 I of the Income Tax Act No. 58 of 1962 SOURCE: Lexis Nexis Butterworths (24 May 2010) 12I. Additional investment and training allowances in respect of industrial policy projects. (1) For the

Section 12 I of the Income Tax Act No. 58 of 1962 SOURCE: Lexis Nexis Butterworths (24 May 2010) 12I. Additional investment and training allowances in respect of industrial policy projects. (1) For the

2017 Budget and Tax Update

2017 Budget and Tax Update Presented by Nico Theron MTP(SA), BCom Law (cum laude), BCom Honours Taxation, MCom Taxation (SA and International Tax) Nico, a partner at Tax Consulting South Africa, has been

2017 Budget and Tax Update Presented by Nico Theron MTP(SA), BCom Law (cum laude), BCom Honours Taxation, MCom Taxation (SA and International Tax) Nico, a partner at Tax Consulting South Africa, has been

Tax Technician Knowledge Competency Assessment June 2015 Paper 2: Solutions

Tax Technician Knowledge Competency Assessment June 205 Paper 2: Solutions Instructions to Candidates. This competency assessment paper consists of two questions. 2. Answer each question in a separate

Tax Technician Knowledge Competency Assessment June 205 Paper 2: Solutions Instructions to Candidates. This competency assessment paper consists of two questions. 2. Answer each question in a separate

Republic of Korea Dispute Resolution Profile. (Last updated: 30 August 2017) General Information

General Information") 1 Republic of Korea Dispute Resolution Profile (Last updated: 30 August 2017) General Information Korea tax treaties are available at: www.nts.go.kr/eng/ [Please see Resources-Tax Law/Treaty] MAP request

1 Republic of Korea Dispute Resolution Profile (Last updated: 30 August 2017) General Information Korea tax treaties are available at: www.nts.go.kr/eng/ [Please see Resources-Tax Law/Treaty] MAP request

Latest Tax Developments. February 2017

Latest Tax Developments February 2017 Introduction Monthly webinar 2nd of 11 webinars Recent developments: This one February 2017; Cannot cover all developments in detail; Relevance of developments; Some

Latest Tax Developments February 2017 Introduction Monthly webinar 2nd of 11 webinars Recent developments: This one February 2017; Cannot cover all developments in detail; Relevance of developments; Some

TAX UPDATE SEMINAR APRIL / MAY 2017

TAX UPDATE SEMINAR APRIL / MAY 2017 OVERVIEW Budget Speech Chapter 4 and Annexure C. Recent Rulings. Taxation Laws Amendment Act, 2016 ( 2016 TLA ). Recent Case Law. Amendments set out in Tax Administration

TAX UPDATE SEMINAR APRIL / MAY 2017 OVERVIEW Budget Speech Chapter 4 and Annexure C. Recent Rulings. Taxation Laws Amendment Act, 2016 ( 2016 TLA ). Recent Case Law. Amendments set out in Tax Administration

CANDIDATE NUMBER No Aspect of the Answer Marks Candidate Mark Obtained 1 To Mr. Anil Naidoo

CANDIDATE NUMBER No Aspect of the Answer Marks Candidate Mark Obtained To Mr. Anil Naidoo From Tax Manager Subject Tax implications of issues discussed Date 4 December 207 Sub Total Scope We refer to our

CANDIDATE NUMBER No Aspect of the Answer Marks Candidate Mark Obtained To Mr. Anil Naidoo From Tax Manager Subject Tax implications of issues discussed Date 4 December 207 Sub Total Scope We refer to our

Income Tax. ABC of Capital Gains Tax for Companies (Issue 7) ABC of Capital Gains Tax for Companies (Issue 7) 1

ABC of Capital Gains Tax for Companies (Issue 7) 1") Income Tax ABC of Capital Gains Tax for Companies (Issue 7) ABC of Capital Gains Tax for Companies (Issue 7) 1 Preface ABC of Capital Gains Tax for Companies This guide provides a basic introduction to

Income Tax ABC of Capital Gains Tax for Companies (Issue 7) ABC of Capital Gains Tax for Companies (Issue 7) 1 Preface ABC of Capital Gains Tax for Companies This guide provides a basic introduction to

SAIT TAX INDABA 2016

SAIT TAX INDABA 2016 TOPIC: PRESCRIPTION: S99 OF TAA Betsie Strydom 011 669 9396 / 082 900 1442 betsie.strydom@bowmanslaw.com Mogola Makola 011 669 9398 / 073 123 1373 mogola.makola@bowmanslaw.com SECTION

SAIT TAX INDABA 2016 TOPIC: PRESCRIPTION: S99 OF TAA Betsie Strydom 011 669 9396 / 082 900 1442 betsie.strydom@bowmanslaw.com Mogola Makola 011 669 9398 / 073 123 1373 mogola.makola@bowmanslaw.com SECTION

Service Charter. South African Revenue Service Service Charter

Service Charter South African Revenue Service Service Charter 1 South African Revenue Service Your Rights Obligations and Service timelines 2 Service Charter WHAT WE DO IN SOUTH AFRICA We, the South African

Service Charter South African Revenue Service Service Charter 1 South African Revenue Service Your Rights Obligations and Service timelines 2 Service Charter WHAT WE DO IN SOUTH AFRICA We, the South African

FAQs: Increase in the VAT rate from 1 April 2018 Value-Added Tax

Value-Added Tax Frequently Asked Questions: Increase in the VAT rate 1 In the Minister s Budget speech on 21 February 2018, an increase in the standard rate of VAT was announced. The rate increase applies

Value-Added Tax Frequently Asked Questions: Increase in the VAT rate 1 In the Minister s Budget speech on 21 February 2018, an increase in the standard rate of VAT was announced. The rate increase applies

Paper F6 (ZAF) Taxation (South Africa) Tuesday 4 June Fundamentals Level Skills Module. The Association of Chartered Certified Accountants

Taxation (South Africa) Tuesday 4 June Fundamentals Level Skills Module. The Association of Chartered Certified Accountants") Fundamentals Level Skills Module Taxation (South Africa) Tuesday 4 June 2013 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. Tax

Fundamentals Level Skills Module Taxation (South Africa) Tuesday 4 June 2013 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. Tax

Special Voluntary Disclosure Programme. GUIDE: SPECIAL VOLUNTARY DISCLOSURE PROGRAMME (v1.2)

") GUIDE: SPECIAL VOLUNTARY DISCLOSURE PROGRAMME (v1.2) This is a preliminary guide, which is subject to Parliamentary legislative processes. This version is based on the proposals to Parliament following

GUIDE: SPECIAL VOLUNTARY DISCLOSURE PROGRAMME (v1.2) This is a preliminary guide, which is subject to Parliamentary legislative processes. This version is based on the proposals to Parliament following

Value-Added Tax. Guide for Vendors

VAT 404 Guide for Vendors 10 Important principles Value-Added Tax VAT 404 Guide for Vendors VAT 404 Guide for Vendors 10 Important principles 10 Important principles All prices charged, advertised or quoted

VAT 404 Guide for Vendors 10 Important principles Value-Added Tax VAT 404 Guide for Vendors VAT 404 Guide for Vendors 10 Important principles 10 Important principles All prices charged, advertised or quoted

Latest tax developments. May 2016

Latest tax developments May 2016 Introduction Monthly webinar 5 th of 11 webinars Recent developments This one May 2016; Cannot cover all developments in detail; Relevance of developments; Some will roll

Latest tax developments May 2016 Introduction Monthly webinar 5 th of 11 webinars Recent developments This one May 2016; Cannot cover all developments in detail; Relevance of developments; Some will roll

VAT: Supply of a business as a going concern - New Draft Interpretation Note 57. Severus Smuts

VAT: Supply of a business as a going concern - New Draft Interpretation Note 57 Severus Smuts Background South African legislation based on the New Zealand practise IN 57 deals with taxable going concern

VAT: Supply of a business as a going concern - New Draft Interpretation Note 57 Severus Smuts Background South African legislation based on the New Zealand practise IN 57 deals with taxable going concern

Tax Professional Knowledge Competency Assessment. June 2014 Paper 1: Solution

Tax Professional Knowledge Competency Assessment June 2014 Paper 1: Solution Suggested Solution Question Topic Marks 1 Company Tax Calculation and Advisory 40 2 Analysis of Financial Statements 45 3 Value-Added

Tax Professional Knowledge Competency Assessment June 2014 Paper 1: Solution Suggested Solution Question Topic Marks 1 Company Tax Calculation and Advisory 40 2 Analysis of Financial Statements 45 3 Value-Added

2016 Dispute Resolution

2016 Dispute Resolution Presented by Nico Theron MTP(SA), BCom Law (cum laude), BCom Honours Taxation, MCom Taxation Nico, previously from PKF/Grant Thornton, holds the degrees, BCom Law (cum laude), BCom

2016 Dispute Resolution Presented by Nico Theron MTP(SA), BCom Law (cum laude), BCom Honours Taxation, MCom Taxation Nico, previously from PKF/Grant Thornton, holds the degrees, BCom Law (cum laude), BCom

SOUTH AFRICA GLOBAL GUIDE TO M&A TAX: 2017 EDITION

SOUTH AFRICA 1 SOUTH AFRICA INTERNATIONAL DEVELOPMENTS 1. WHAT ARE RECENT TAX DEVELOPMENTS IN YOUR COUNTRY WHICH ARE RELEVANT FOR M&A DEALS AND PRIVATE EQUITY? In the 2016 Budget Review, tax avoidance

SOUTH AFRICA 1 SOUTH AFRICA INTERNATIONAL DEVELOPMENTS 1. WHAT ARE RECENT TAX DEVELOPMENTS IN YOUR COUNTRY WHICH ARE RELEVANT FOR M&A DEALS AND PRIVATE EQUITY? In the 2016 Budget Review, tax avoidance

DEPARTMENTAL INTERPRETATION AND PRACTICE NOTES NO. 45 RELIEF FROM DOUBLE TAXATION DUE TO TRANSFER PRICING OR PROFIT REALLOCATION ADJUSTMENTS

Inland Revenue Department Hong Kong DEPARTMENTAL INTERPRETATION AND PRACTICE NOTES NO. 45 RELIEF FROM DOUBLE TAXATION DUE TO TRANSFER PRICING OR PROFIT REALLOCATION ADJUSTMENTS These notes are issued for

Inland Revenue Department Hong Kong DEPARTMENTAL INTERPRETATION AND PRACTICE NOTES NO. 45 RELIEF FROM DOUBLE TAXATION DUE TO TRANSFER PRICING OR PROFIT REALLOCATION ADJUSTMENTS These notes are issued for

Disputing an assessment

IR776 June 2018 Disputing an assessment What to do if you dispute an assessment 2 DISPUTING AN ASSESSMENT Introduction While we make every effort to apply the tax laws fairly and correctly, there may be

IR776 June 2018 Disputing an assessment What to do if you dispute an assessment 2 DISPUTING AN ASSESSMENT Introduction While we make every effort to apply the tax laws fairly and correctly, there may be

EIGHTH SCHEDULE DETERMINATION OF TAXABLE CAPITAL GAINS AND ASSESSED CAPITAL LOSSES (SECTION 26A OF THIS ACT)

") 1 This document is an unofficial consolidation of the Eighth Schedule to the Income Tax Act, 58 of 1962, introduced by the Taxation Laws Amendment Act, 5 of 2001, the amendments effected by the Revenue

1 This document is an unofficial consolidation of the Eighth Schedule to the Income Tax Act, 58 of 1962, introduced by the Taxation Laws Amendment Act, 5 of 2001, the amendments effected by the Revenue

International Tax South Africa Highlights 2018

International Tax South Africa Highlights 2018 Investment basics: Currency South African Rand (ZAR) Foreign exchange control Exchange control is administered by the South African Reserve Bank, which has

International Tax South Africa Highlights 2018 Investment basics: Currency South African Rand (ZAR) Foreign exchange control Exchange control is administered by the South African Reserve Bank, which has

INTERPRETATION NOTE: NO.15 (Issue 3) DATE: 10 July 2013

DATE: 10 July 2013") INTERPRETATION NOTE: NO.15 (Issue 3) DATE: 10 July 2013 ACT : TAX ADMINISTRATION ACT NO. 28 OF 2011 (TA Act) SECTION : SECTIONS 104, 106 and 107 SUBJECT : EXERCISE OF DISCRETION IN CASE OF LATE OBJECTION

INTERPRETATION NOTE: NO.15 (Issue 3) DATE: 10 July 2013 ACT : TAX ADMINISTRATION ACT NO. 28 OF 2011 (TA Act) SECTION : SECTIONS 104, 106 and 107 SUBJECT : EXERCISE OF DISCRETION IN CASE OF LATE OBJECTION

Value-Added Tax VAT 413

Value-Added Tax VAT 413 Guide for Estates ii VAT 413 Guide for Estates Preface PREFACE This guide concerns the application of the value-added tax (VAT) law in respect of deceased and insolvent estates

Value-Added Tax VAT 413 Guide for Estates ii VAT 413 Guide for Estates Preface PREFACE This guide concerns the application of the value-added tax (VAT) law in respect of deceased and insolvent estates

Australia. Transfer Pricing Country Profile. Updated February The Arm s Length Principle

Australia Transfer Pricing Country Profile Updated February 2018 SUMMARY REFERENCE 1 Does your domestic legislation or regulation make reference to the Arm s Length Principle? 2 What is the role of the

Australia Transfer Pricing Country Profile Updated February 2018 SUMMARY REFERENCE 1 Does your domestic legislation or regulation make reference to the Arm s Length Principle? 2 What is the role of the

Case No.: IT In the matter between: Appellant. and. Respondent. ") for just over sixteen years, IN THE TAX COURT OF SOUTH AFRICA

for just over sixteen years, IN THE TAX COURT OF SOUTH AFRICA") IN THE TAX COURT OF SOUTH AFRICA AT PORT ELIZABEH Case No.: IT13726 In the matter between: Appellant and THE COMMISSIONER FOR THE SOUTH AFRICAN REVENUE SERVICE Respondent JUDGMENT REVELAS J: [1] The appellant

IN THE TAX COURT OF SOUTH AFRICA AT PORT ELIZABEH Case No.: IT13726 In the matter between: Appellant and THE COMMISSIONER FOR THE SOUTH AFRICAN REVENUE SERVICE Respondent JUDGMENT REVELAS J: [1] The appellant

24 November 2016 The National Treasury 240 Vermeulen Street PRETORIA 0001

24 November 2016 The National Treasury 240 Vermeulen Street PRETORIA 0001 The South African Revenue Service Lehae La SARS, 299 Bronkhorst Street PRETORIA 0181 BY EMAIL: Mmule Majola (mmule.majola@treasury.gov.za)

24 November 2016 The National Treasury 240 Vermeulen Street PRETORIA 0001 The South African Revenue Service Lehae La SARS, 299 Bronkhorst Street PRETORIA 0181 BY EMAIL: Mmule Majola (mmule.majola@treasury.gov.za)

HONG KONG. 1. Introduction. Contact Information Henry Fung Candice Ng

HONG KONG Contact Information Henry Fung +852 2969 4054 hernyfung@pkf-hk.com Candice Ng +852 2969 4016 candiceng@pkf-hk.com 1. Introduction 1.1. Legal context Currently, the Hong Kong Inland Revenue Ordinance

HONG KONG Contact Information Henry Fung +852 2969 4054 hernyfung@pkf-hk.com Candice Ng +852 2969 4016 candiceng@pkf-hk.com 1. Introduction 1.1. Legal context Currently, the Hong Kong Inland Revenue Ordinance

Government Gazette REPUBLIC OF SOUTH AFRICA. Vol. 475 Cape Town 24 January 2005 No

Government Gazette REPUBLIC OF SOUTH AFRICA Vol. 475 Cape Town 24 January 2005 No. 27188 THE PRESIDENCY No. 46 24 January 2005 It is hereby notified that the President has assented to the following Act,

Government Gazette REPUBLIC OF SOUTH AFRICA Vol. 475 Cape Town 24 January 2005 No. 27188 THE PRESIDENCY No. 46 24 January 2005 It is hereby notified that the President has assented to the following Act,

Welcome Personal Income Tax. Presented by Shohana Mohan

Welcome 2016 Personal Income Tax Presented by Shohana Mohan Upcoming CPD Events Upcoming CPD Events Refer to our website for all upcoming events June 2016 Accounting & Bookkeeping Fundamentals for Tax

Welcome 2016 Personal Income Tax Presented by Shohana Mohan Upcoming CPD Events Upcoming CPD Events Refer to our website for all upcoming events June 2016 Accounting & Bookkeeping Fundamentals for Tax

A QUICK GUIDE TO DIVIDENDS TAX

A QUICK GUIDE TO DIVIDENDS TAX i A QUICK GUIDE TO DIVIDENDS TAX 1. INTRODUCTION TO DIVIDENDS TAX In 2007, the Minister of Finance announced that Secondary Tax on Companies (STC) would be replaced by Dividends

A QUICK GUIDE TO DIVIDENDS TAX i A QUICK GUIDE TO DIVIDENDS TAX 1. INTRODUCTION TO DIVIDENDS TAX In 2007, the Minister of Finance announced that Secondary Tax on Companies (STC) would be replaced by Dividends

Photo credits: Cover Rawpixel.com - Shutterstock.com

Photo credits: Cover Rawpixel.com - Shutterstock.com TABLE OF CONTENTS 5 Table of contents Abbreviations and acronyms... 7 Introduction... 9 Part A Preventing Disputes... 11 [BP.1] Implement bilateral

Photo credits: Cover Rawpixel.com - Shutterstock.com TABLE OF CONTENTS 5 Table of contents Abbreviations and acronyms... 7 Introduction... 9 Part A Preventing Disputes... 11 [BP.1] Implement bilateral

Donating to Public Benefit Organisations

Donating to Public Benefit Organisations Public benefit organisations ( PBOs ) provide invaluable healthcare, education, poverty alleviation, housing, conservation, environmental, cultural and religious

Donating to Public Benefit Organisations Public benefit organisations ( PBOs ) provide invaluable healthcare, education, poverty alleviation, housing, conservation, environmental, cultural and religious

University of the Witwatersrand, Johannesburg DEBT REDUCTION: NEW LEGISLATION, NEW CHALLENGES

University of the Witwatersrand, Johannesburg 캒A research report submitted to the Faculty of Commerce, Law and Management in A research report submitted to the Faculty of Commerce, Law and Management in

University of the Witwatersrand, Johannesburg 캒A research report submitted to the Faculty of Commerce, Law and Management in A research report submitted to the Faculty of Commerce, Law and Management in

Professional Level Options Module, Paper P6 (ZAF) 1 David Sole

1 David Sole") Answers Professional Level Options Module, Paper P6 (ZAF) Advanced Taxation (South Africa) June 008 Answers 1 David Sole (a) Taxable income for the year of assessment ended 9 February 008 R Orgshops taxable

Answers Professional Level Options Module, Paper P6 (ZAF) Advanced Taxation (South Africa) June 008 Answers 1 David Sole (a) Taxable income for the year of assessment ended 9 February 008 R Orgshops taxable

SUBJECT : THE MASTER CURRENCY CASE AND THE ZERO-RATING OF SUPPLIES MADE TO NON-RESIDENTS

DRAFT DRAFT INTERPRETATION NOTE DATE : ACT : VALUE-ADDED TAX ACT, NO. 89 OF 1991 SECTIONS : SECTION 11(2)(l) SUBJECT : THE MASTER CURRENCY CASE AND THE ZERO-RATING OF SUPPLIES MADE TO NON-RESIDENTS Preamble

DRAFT DRAFT INTERPRETATION NOTE DATE : ACT : VALUE-ADDED TAX ACT, NO. 89 OF 1991 SECTIONS : SECTION 11(2)(l) SUBJECT : THE MASTER CURRENCY CASE AND THE ZERO-RATING OF SUPPLIES MADE TO NON-RESIDENTS Preamble

Future of TP. Documentation & Certification. 7th October Presented by- CA Dilip Gupta

Future of TP Documentation & Certification 7th October 2017 Presented by- CA Dilip Gupta Journey of TP regulations in India Major Milestones Final Rules on Range and multiple year data concept Introduction

Future of TP Documentation & Certification 7th October 2017 Presented by- CA Dilip Gupta Journey of TP regulations in India Major Milestones Final Rules on Range and multiple year data concept Introduction

Occupational Certificate Tax Professional

Occupational Certificate Tax Professional External Integrated Summative Assessment (EISA) SAQA ID: 93624 November 2017 Paper 1: Tax Awareness MULTIPLE CHOICE QUESTIONS TRUE/FALSE QUESTIONS CANDIDATE NUMBER

Occupational Certificate Tax Professional External Integrated Summative Assessment (EISA) SAQA ID: 93624 November 2017 Paper 1: Tax Awareness MULTIPLE CHOICE QUESTIONS TRUE/FALSE QUESTIONS CANDIDATE NUMBER

TAXATION LAWS AMENDMENT BILL

REPUBLIC OF SOUTH AFRICA TAXATION LAWS AMENDMENT BILL (As introduced in the National Assembly (proposed section 77)) (The English text is the offıcial text of the Bill) (MINISTER OF FINANCE) [B 13 14]

REPUBLIC OF SOUTH AFRICA TAXATION LAWS AMENDMENT BILL (As introduced in the National Assembly (proposed section 77)) (The English text is the offıcial text of the Bill) (MINISTER OF FINANCE) [B 13 14]

ADJUSTMENT OF INTERNATIONAL TAXES ACT

ADJUSTMENT OF INTERNATIONAL TAXES ACT Act No. 4981, Dec. 6, 1995 Amended by Act No. 5193, Dec. 30, 1996 Act No. 5581, Dec. 28, 1998 Act No. 5584, Dec. 28, 1998 Act No. 6299, Dec. 29, 2000 Act No. 6304,

ADJUSTMENT OF INTERNATIONAL TAXES ACT Act No. 4981, Dec. 6, 1995 Amended by Act No. 5193, Dec. 30, 1996 Act No. 5581, Dec. 28, 1998 Act No. 5584, Dec. 28, 1998 Act No. 6299, Dec. 29, 2000 Act No. 6304,

ANNEXURE C FOR 2018 BUDGET: INTERNATIONAL TAX

24 November 2017 The National Treasury 240 Madiba Street PRETORIA 0001 The South African Revenue Service Lehae La SARS, 299 Bronkhorst Street PRETORIA 0181 BY EMAIL: Nombasa Langeni (Nombasa.Langeni@treasury.gov.za)

24 November 2017 The National Treasury 240 Madiba Street PRETORIA 0001 The South African Revenue Service Lehae La SARS, 299 Bronkhorst Street PRETORIA 0181 BY EMAIL: Nombasa Langeni (Nombasa.Langeni@treasury.gov.za)

THE CORPORATE INCOME TAX EFFECT OF GROUP RESTRUCTURINGS IN SOUTH AFRICA

University of the Witwatersrand, Johannesburg THE CORPORATE INCOME TAX EFFECT OF GROUP RESTRUCTURINGS IN SOUTH AFRICA Candyce Blew A research report submitted to the Faculty of Commerce, Law and Management,

University of the Witwatersrand, Johannesburg THE CORPORATE INCOME TAX EFFECT OF GROUP RESTRUCTURINGS IN SOUTH AFRICA Candyce Blew A research report submitted to the Faculty of Commerce, Law and Management,

New Zealand. Transfer Pricing Country Profile. Updated October The Arm s Length Principle

New Zealand Transfer Pricing Country Profile Updated October 2017 SUMMARY REFERENCE The Arm s Length Principle 1 Does your domestic legislation or regulation make reference to the Arm s Length Principle?

New Zealand Transfer Pricing Country Profile Updated October 2017 SUMMARY REFERENCE The Arm s Length Principle 1 Does your domestic legislation or regulation make reference to the Arm s Length Principle?

REPUBLIC OF SOUTH AFRICA

Please note that most Acts are published in English and another South African official language. Currently we only have capacity to publish the English versions. This means that this document will only

Please note that most Acts are published in English and another South African official language. Currently we only have capacity to publish the English versions. This means that this document will only

Taxation (F6) Lesotho (LSO) June & December 2017

Lesotho (LSO) June & December 2017") Taxation (F6) Lesotho (LSO) June & December 2017 This syllabus and study guide is designed to help with planning study and to provide detailed information on what could be assessed in any examination session.

Taxation (F6) Lesotho (LSO) June & December 2017 This syllabus and study guide is designed to help with planning study and to provide detailed information on what could be assessed in any examination session.

Cape Town Johannesburg Durban

APPOINTMENT AS ACCOUNTANTS TO: SIR / MADAM We hereby wish to confirm our appointment as accountants and financial advisors to the above business and its owners / members / directors. The terms and conditions

APPOINTMENT AS ACCOUNTANTS TO: SIR / MADAM We hereby wish to confirm our appointment as accountants and financial advisors to the above business and its owners / members / directors. The terms and conditions

ROMANIA TRANSFER PRICING COUNTRY PROFILE

ROMANIA TRANSFER PRICING COUNTRY PROFILE 1. Reference to the Arm s Length Principle Latest update April 2018 The arm's length principle was introduced in the domestic tax law in 1994 and is applicable

ROMANIA TRANSFER PRICING COUNTRY PROFILE 1. Reference to the Arm s Length Principle Latest update April 2018 The arm's length principle was introduced in the domestic tax law in 1994 and is applicable

Professional Level Options Module, Paper P6 (ZAF)

") Answers Professional Level Options Module, Paper P6 (ZAF) Advanced Taxation (South Africa) December 2016 Answers Note: ACCA does not require candidates to quote section numbers or other statutory or case

Answers Professional Level Options Module, Paper P6 (ZAF) Advanced Taxation (South Africa) December 2016 Answers Note: ACCA does not require candidates to quote section numbers or other statutory or case

Retirement Annuity Fund

Retirement Annuity Fund Background information... 3 Purpose... 3 Benefits of investing in a RA... 5 Definitions... 5 Member... 5 Nominee... 5 Dependant... 6 Beneficiary... 6 General information... 6 Registration...

Retirement Annuity Fund Background information... 3 Purpose... 3 Benefits of investing in a RA... 5 Definitions... 5 Member... 5 Nominee... 5 Dependant... 6 Beneficiary... 6 General information... 6 Registration...

Qualification Programme Examination Panelists Report. Module D Taxation (December 2015 Session)

") Qualification Programme Examination Panelists Report Module D Taxation (December 2015 Session) (The main purpose of the following report is to summarise candidates common weaknesses and make recommendations

Qualification Programme Examination Panelists Report Module D Taxation (December 2015 Session) (The main purpose of the following report is to summarise candidates common weaknesses and make recommendations

1. Purpose This Note provides guidance on the income tax implications of the letting of tank containers.

INTERPRETATION NOTE: NO. 73 DATE: 24 April 2013 ACT : INCOME TAX ACT NO. 58 OF 1962 (the Act) SECTION : SECTIONS 11(a), 11(e), 20(1), 23A AND 25D SUBJECT : TAX IMPLICATIONS OF RENTAL INCOME FROM TANK CONTAINERS

INTERPRETATION NOTE: NO. 73 DATE: 24 April 2013 ACT : INCOME TAX ACT NO. 58 OF 1962 (the Act) SECTION : SECTIONS 11(a), 11(e), 20(1), 23A AND 25D SUBJECT : TAX IMPLICATIONS OF RENTAL INCOME FROM TANK CONTAINERS

STANDARD CONDITIONS FOR INDIVIDUAL VOLUNTARY ARRANGEMENTS. Produced by the IVA FORUM

Protocol Annex 4 STANDARD CONDITIONS FOR INDIVIDUAL VOLUNTARY ARRANGEMENTS Produced by the IVA FORUM Revised November 2013 For use in proposals issued on or after 1 January 2014 TABLE OF CONTENTS FOR STANDARD

Protocol Annex 4 STANDARD CONDITIONS FOR INDIVIDUAL VOLUNTARY ARRANGEMENTS Produced by the IVA FORUM Revised November 2013 For use in proposals issued on or after 1 January 2014 TABLE OF CONTENTS FOR STANDARD

Global Transfer Pricing Review kpmg.com/gtps

Global Transfer Pricing Review Czech Australia Republic kpmg.com/gtps TAX 2 Global Transfer Pricing Review Australia KPMG observation The transfer pricing landscape in Australia continues to be one of

Global Transfer Pricing Review Czech Australia Republic kpmg.com/gtps TAX 2 Global Transfer Pricing Review Australia KPMG observation The transfer pricing landscape in Australia continues to be one of

Administrative measures

August 2018 A special report from Policy and Strategy, Inland Revenue Administrative measures DEFINITION OF LARGE MULTINATIONAL GROUP Section YA 1 The new legislation introduces the term large multinational

August 2018 A special report from Policy and Strategy, Inland Revenue Administrative measures DEFINITION OF LARGE MULTINATIONAL GROUP Section YA 1 The new legislation introduces the term large multinational

IN THE TAX COURT. [1] This is an appeal referred to this court in terms of section 83A(13)(a) of

![IN THE TAX COURT. [1] This is an appeal referred to this court in terms of section 83A(13)(a) of](/thumbs/89/100525653.jpg "IN THE TAX COURT. [1] This is an appeal referred to this court in terms of section 83A(13)(a) of") JUDGMENT IN THE TAX COURT CASE NO: 11398 BEFORE THE HONOURABLE MR JUSTICE B H MBHA PRESIDENT Y WAJA E TAYOB In the matter between: ACCOUNTANT MEMBER COMMERCIAL MEMBER Appellant and THE COMMISSIONER FOR

JUDGMENT IN THE TAX COURT CASE NO: 11398 BEFORE THE HONOURABLE MR JUSTICE B H MBHA PRESIDENT Y WAJA E TAYOB In the matter between: ACCOUNTANT MEMBER COMMERCIAL MEMBER Appellant and THE COMMISSIONER FOR

VAT 404. Value-Added Tax. Guide for Vendors /02/25 SPC V2.000

VAT 404 Value-Added Tax Guide for Vendors 2009/02/25 SPC V2.000 www.sars.gov.za 10 IMPORTANT PRINCIPLES 1. All prices charged, advertised or quoted by a vendor must include VAT at the applicable rate.

VAT 404 Value-Added Tax Guide for Vendors 2009/02/25 SPC V2.000 www.sars.gov.za 10 IMPORTANT PRINCIPLES 1. All prices charged, advertised or quoted by a vendor must include VAT at the applicable rate.

CR 2017/38. Summary what this ruling is about

Page status: legally binding Page 1 of 12 Class Ruling Fringe benefits tax: employer clients of Community Sector Banking Pty Limited who are subject to the provisions of either section 57A or 65J of the

Page status: legally binding Page 1 of 12 Class Ruling Fringe benefits tax: employer clients of Community Sector Banking Pty Limited who are subject to the provisions of either section 57A or 65J of the

Comments on the United Nations Practical Manual on Transfer Pricing Countries for Developing Countries

To: United Nations From: Repsol, S.A. Date: 02/28/2014 Comments on the United Nations Practical Manual on Transfer Pricing Countries for Developing Countries REPSOL appreciates the opportunity to contribute

To: United Nations From: Repsol, S.A. Date: 02/28/2014 Comments on the United Nations Practical Manual on Transfer Pricing Countries for Developing Countries REPSOL appreciates the opportunity to contribute

South African Revenue Service releases public notice on recordkeeping for transfer pricing transactions

9 November 2016 Global Tax Alert News from Transfer Pricing South African Revenue Service releases public notice on recordkeeping for transfer pricing transactions EY Global Tax Alert Library Access both

9 November 2016 Global Tax Alert News from Transfer Pricing South African Revenue Service releases public notice on recordkeeping for transfer pricing transactions EY Global Tax Alert Library Access both

Deloitte School of Tax & Legal Corporate Tax Bootcamp

South Africa Deloitte School of Tax & Legal October - December 2018 Deloitte School of Tax & Legal Corporate Tax Bootcamp We have the pleasure of inviting you to our two-day Corporate tax Bootcamp Workshop.

South Africa Deloitte School of Tax & Legal October - December 2018 Deloitte School of Tax & Legal Corporate Tax Bootcamp We have the pleasure of inviting you to our two-day Corporate tax Bootcamp Workshop.

Points of Discussion

Provisional Tax Points of Discussion Overview of Provisional Tax Who is liable for Provisional Tax Exclusions for Provisional Tax IRP6 Submission on efiling Payments on efiling Payment dates for 2019 YOA

Provisional Tax Points of Discussion Overview of Provisional Tax Who is liable for Provisional Tax Exclusions for Provisional Tax IRP6 Submission on efiling Payments on efiling Payment dates for 2019 YOA

INTERPRETATION NOTE: NO. 70. DATE: 14 March 2013

INTERPRETATION NOTE: NO. 70 DATE: 14 March 2013 ACT : VALUE-ADDED TAX ACT NO. 89 OF 1991 (the VAT Act) SECTION : SECTION 1(1) DEFINITION OF THE TERMS ENTERPRISE, TAXABLE SUPPLY, INPUT TAX, DONATION AND

INTERPRETATION NOTE: NO. 70 DATE: 14 March 2013 ACT : VALUE-ADDED TAX ACT NO. 89 OF 1991 (the VAT Act) SECTION : SECTION 1(1) DEFINITION OF THE TERMS ENTERPRISE, TAXABLE SUPPLY, INPUT TAX, DONATION AND

ACT : INCOME TAX ACT 58 OF 1962 SECTION : SECTIONS 11(a), 11(e), 20(1), 23A AND 25D SUBJECT : TAX IMPLICATIONS OF RENTAL INCOME FROM TANK CONTAINERS

, 11(e), 20(1), 23A AND 25D SUBJECT : TAX IMPLICATIONS OF RENTAL INCOME FROM TANK CONTAINERS") INTERPRETATION NOTE 73 (Issue 3) DATE: 20 December 2017 ACT : INCOME TAX ACT 58 OF 1962 SECTION : SECTIONS 11(a), 11(e), 20(1), 23A AND 25D SUBJECT : TAX IMPLICATIONS OF RENTAL INCOME FROM TANK CONTAINERS

INTERPRETATION NOTE 73 (Issue 3) DATE: 20 December 2017 ACT : INCOME TAX ACT 58 OF 1962 SECTION : SECTIONS 11(a), 11(e), 20(1), 23A AND 25D SUBJECT : TAX IMPLICATIONS OF RENTAL INCOME FROM TANK CONTAINERS

RE: CALL FOR COMMENT: DRAFT TAXATION LAWS AMENDMENT BILL ( TLAB )

") 5 August 2013 Ms N. Mpotulo The National Treasury 240 Vermuelen Street PRETORIA 0001 Ms A. Collins Legal & Policy The South African Revenue Service Lehae La SARS PRETORIA 8000 BY E-MAIL: nomfanelo.mpotulo@treasury.gov.za

5 August 2013 Ms N. Mpotulo The National Treasury 240 Vermuelen Street PRETORIA 0001 Ms A. Collins Legal & Policy The South African Revenue Service Lehae La SARS PRETORIA 8000 BY E-MAIL: nomfanelo.mpotulo@treasury.gov.za

SOUTH AFRICAN REVENUE SERVICE

SOUTH AFRICAN REVENUE SERVICE INTERPRETATION NOTE NO. 41 (ISSUE 2) DATE: 31 March 2008 ACT: SECTION: SUBJECT: VALUE-ADDED TAX ACT, NO. 89 OF 1991 (the VAT Act) SECTIONS 1, 8(13), 8(13A), 9(3)(e), 16(3)(a),

SOUTH AFRICAN REVENUE SERVICE INTERPRETATION NOTE NO. 41 (ISSUE 2) DATE: 31 March 2008 ACT: SECTION: SUBJECT: VALUE-ADDED TAX ACT, NO. 89 OF 1991 (the VAT Act) SECTIONS 1, 8(13), 8(13A), 9(3)(e), 16(3)(a),

An Act to make provision for the law relating to Value Added Tax. CHAPTER I PRELIMINARY

An Act to make provision for the law relating to Value Added Tax. Enacted by the Parliament of Lesotho Short Title CHAPTER I PRELIMINARY 1. This Act may be cited as the Value Added Tax Act, 2001. Commencement

An Act to make provision for the law relating to Value Added Tax. Enacted by the Parliament of Lesotho Short Title CHAPTER I PRELIMINARY 1. This Act may be cited as the Value Added Tax Act, 2001. Commencement

Adjustment of International Taxes Act

Adjustment of International Taxes Act INTRODUCTION Details of Enactment and Amendment Enactment: This Act was enacted in 1995 opportunely at this time when the World Trade Organization (WTO) is about to

Adjustment of International Taxes Act INTRODUCTION Details of Enactment and Amendment Enactment: This Act was enacted in 1995 opportunely at this time when the World Trade Organization (WTO) is about to

Guide on Valuation of Assets for Capital Gains Tax Purposes

Guide on Valuation of Assets for Capital Gains Tax Purposes Guide on Valuation of Assets for Capital Gains Tax Purposes FOREWORD This guide provides general guidelines regarding valuation of assets as

Guide on Valuation of Assets for Capital Gains Tax Purposes Guide on Valuation of Assets for Capital Gains Tax Purposes FOREWORD This guide provides general guidelines regarding valuation of assets as

Spain. Transfer Pricing Country Profile. Updated October The Arm s Length Principle

Spain Transfer Pricing Country Profile Updated October 2017 SUMMARY REFERENCE The Arm s Length Principle 1 Does your domestic legislation or regulation make reference to the Arm s Length Principle? 2 What

Spain Transfer Pricing Country Profile Updated October 2017 SUMMARY REFERENCE The Arm s Length Principle 1 Does your domestic legislation or regulation make reference to the Arm s Length Principle? 2 What

Tax Professional Knowledge Competency Assessment. June 2014 Paper 2: Solution

Tax Professional Knowledge Competency Assessment June 2014 Paper 2: Solution Suggested Solutions Question Topic Marks 1 Taxable Income 40 2 Calculate Estate Duty 40 3 Explain Tax Implications & Liabilities

Tax Professional Knowledge Competency Assessment June 2014 Paper 2: Solution Suggested Solutions Question Topic Marks 1 Taxable Income 40 2 Calculate Estate Duty 40 3 Explain Tax Implications & Liabilities

Occupational Certificate Tax Professional

Occupational Certificate Tax Professional External Integrated Summative Assessment (EISA) SAQA ID: 93624 July 2017 SUPPLEMENTARY Paper 2: Corporate Taxation Question CASE STUDY AND REQUIRED CANDIDATE NUMBER

Occupational Certificate Tax Professional External Integrated Summative Assessment (EISA) SAQA ID: 93624 July 2017 SUPPLEMENTARY Paper 2: Corporate Taxation Question CASE STUDY AND REQUIRED CANDIDATE NUMBER

Content of the session. Basics Small business asset exclusion Primary residence Discharge of debt Roll-over provisions

Capital Gains Tax Content of the session Basics Small business asset exclusion Primary residence Discharge of debt Roll-over provisions Basics Updates and amendments Inclusion rate Individuals Companies

Capital Gains Tax Content of the session Basics Small business asset exclusion Primary residence Discharge of debt Roll-over provisions Basics Updates and amendments Inclusion rate Individuals Companies

JUTA'S TAX LAW REVIEW

JUTA'S TAX LAW REVIEW November 2016 Dear Subscriber to Juta's Tax Law Review publications Welcome to the November edition of Juta's Tax Law Review. We thank you for your constructive suggestions and comments

JUTA'S TAX LAW REVIEW November 2016 Dear Subscriber to Juta's Tax Law Review publications Welcome to the November edition of Juta's Tax Law Review. We thank you for your constructive suggestions and comments

Company distributions in perspective

Company distributions in perspective Herman Viviers 22 September 2015 Disclaimer Nothing in this presentation should be construed as constituting tax advice or a tax opinion. An expert should be consulted

Company distributions in perspective Herman Viviers 22 September 2015 Disclaimer Nothing in this presentation should be construed as constituting tax advice or a tax opinion. An expert should be consulted

THE SUPREME COURT OF APPEAL OF SOUTH AFRICA JUDGMENT

THE SUPREME COURT OF APPEAL OF SOUTH AFRICA JUDGMENT Reportable Case no: 830/2011 In the matter between H R COMPUTEK (PTY) LTD Appellant and THE COMMISSIONER FOR THE SOUTH AFRICAN REVENUE SERVICE Respondent

THE SUPREME COURT OF APPEAL OF SOUTH AFRICA JUDGMENT Reportable Case no: 830/2011 In the matter between H R COMPUTEK (PTY) LTD Appellant and THE COMMISSIONER FOR THE SOUTH AFRICAN REVENUE SERVICE Respondent

South African Income Tax Guide for 2013/2014

South African Income Tax Guide for 2013/2014 Individuals and trusts Income tax rates for natural persons and special trusts Year of assessment ending 28 February 2014 Taxable income Taxable rates 0 165

South African Income Tax Guide for 2013/2014 Individuals and trusts Income tax rates for natural persons and special trusts Year of assessment ending 28 February 2014 Taxable income Taxable rates 0 165

Germany. Transfer Pricing Country Profile. Updated October The Arm s Length Principle

Germany Transfer Pricing Country Profile Updated October 2017 SUMMARY REFERENCE The Arm s Length Principle 1 Does your domestic legislation or regulation make reference to the Arm s Length Principle? Foreign

Germany Transfer Pricing Country Profile Updated October 2017 SUMMARY REFERENCE The Arm s Length Principle 1 Does your domestic legislation or regulation make reference to the Arm s Length Principle? Foreign

VALUE ADDED TAX PUBLIC RULING

4/30/2010 W Invoice Fuel & Maintenance -390.00 4/29/2010 W INV9972 Telephone -652.00 5/1/2010 4/29/2010 W Debit Order Internet Service Provider -210.00 4/29/2010 4/28/2010 W Bank Statement Monthly Service

4/30/2010 W Invoice Fuel & Maintenance -390.00 4/29/2010 W INV9972 Telephone -652.00 5/1/2010 4/29/2010 W Debit Order Internet Service Provider -210.00 4/29/2010 4/28/2010 W Bank Statement Monthly Service

Transfer Pricing Country Summary Belgium

Page 1 of 8 Transfer Pricing Country Summary Belgium July 2018 Page 2 of 8 Legislation Existence of Transfer Pricing Laws/Guidelines The arm s length principle is codified in Article 185, Par 2, of the

Page 1 of 8 Transfer Pricing Country Summary Belgium July 2018 Page 2 of 8 Legislation Existence of Transfer Pricing Laws/Guidelines The arm s length principle is codified in Article 185, Par 2, of the

Bilateral Advance Pricing Agreement Guidelines

September 2016 Bilateral Advance Pricing Agreement Guidelines Page 1 Contents PART 1 INTRODUCTION...5 PART 2 BILATERAL APA PROGRAMME OVERVIEW...5 PART 3 PURPOSE AND SCOPE OF APA...7 What is an APA?...7

September 2016 Bilateral Advance Pricing Agreement Guidelines Page 1 Contents PART 1 INTRODUCTION...5 PART 2 BILATERAL APA PROGRAMME OVERVIEW...5 PART 3 PURPOSE AND SCOPE OF APA...7 What is an APA?...7

DECEASED ESTATES REGISTRATION & ASSESSMENT

DECEASED ESTATES REGISTRATION & ASSESSMENT Agenda Introduction Position - deaths prior to 1 March 2016 Position - deaths post 1 March 2016 Registration process for Deceased Person Registration process

DECEASED ESTATES REGISTRATION & ASSESSMENT Agenda Introduction Position - deaths prior to 1 March 2016 Position - deaths post 1 March 2016 Registration process for Deceased Person Registration process

Annexure C Section 18A of the Income Tax Act, 1962

Annexure C Section 18A of the Income Tax Act, 1962 18A. Deduction of donations to certain organisations. (1) Notwithstanding the provisions of section 23, there shall be allowed to be deducted from the

Annexure C Section 18A of the Income Tax Act, 1962 18A. Deduction of donations to certain organisations. (1) Notwithstanding the provisions of section 23, there shall be allowed to be deducted from the

Tax Professional EISA Supplementary Examination July 2017 Paper 2: Solution

Tax Professional EISA Supplementary Examination July 07 Paper : Solution PROFESSIONAL WRITING: PART A Aspect of the answer Details of aspects to be included in answer s s by candidate Format of opinions

Tax Professional EISA Supplementary Examination July 07 Paper : Solution PROFESSIONAL WRITING: PART A Aspect of the answer Details of aspects to be included in answer s s by candidate Format of opinions