Managing tax administration reforms

|

|

|

- Scott Jackson

- 6 years ago

- Views:

Transcription

1 Fiscal Affairs Department Effects of Good Government, by Ambrogio Lorenzetti, Siena, Italy, Managing tax administration reforms It all starts with a scoping mission Rene Ossa Fiscal Affairs Department - Revenue Administration 1

2 What I will talk about? 1. Undertaking a tax administration assessment The scoping mission 2. FAD tax administration assessment tools Introduction to RA-FIT, TADAT, RA-GAP 3. Strategy formulation Main challenges. 2

3 The scoping mission Pre-mission Questionnaire Questionnaire - timeline and objective Sent 4 weeks prior to the start of mission. Requests for numerical data and other information critical to the assessment process. Requests annual reports and other relevant documents. Questionnaire standard requests. Organization and management features: Taxpayers development services current initiatives Audit and investigation capacity and results. Arrears management strategy and results Legal, regulatory and dispute resolution framework Human resources and training management capacity Register of taxpayers adequacy and accuracy Effectiveness of tax returns and payment accounting systems Robustness of information and communication systems 3

4 The scoping mission During the Mission Opening meeting Acquaint senior officials with the objectives and outputs of the mission Seek their insights, specific guidance and expectations. Discuss mission work program. Meetings with key tax departments Go through the questionnaire and gather information and evidence in respect of each tax function. Discuss preliminary findings and recommendations to gauge counterparts feedback. Identify key challenges and priorities for reform Risk driven Resources available TA capacity availability and absorption 4

5 The scoping mission Post-Mission Finalize the Report Consider country s comments and feedback and make changes as appropriate. Consider Area department comments and make changes as appropriate. Send the report to the management First, the draft report is sent to the advisory committee for quality review. Second, the draft report incorporating country, Area department and advisory committee s comments and feedback is sent to the division chief for final review. and clearance Send the report to the country After clearance by the management, the team sends the final report to the country.. The team should seek permission of the country authorities to publish the report (disclosure policy) 5

6 What I will talk about 1. Undertaking a tax administration assessment The scoping mission 2. FAD tax administration assessment tools Introduction to RA-FIT, TADAT, RA-GAP 3. Strategy formulation Main challenges. 6

7 FAD s Fiscal Assessment Tools RA-FIT RA-GAP TADAT 7

8 RA-FIT PURPOSE AND BENEFITS RA-FIT VISION Elevate the importance of revenue administration performance reporting and measurement, globally; Establish RA-FIT as the single common online platform used by all institutions ; Gather data across a large number of tax and customs administrations to permit further analytical work, such as: Understanding historical performance; Establishing baselines by income group and other groupings; Identifying trends; Flagging policy and administrative inefficiencies; Refining performance measures to improve robustness; and Providing sufficient data to facilitate focused and in-depth research. Assist in developing international revenue administration performance, measurement, and reporting standards; 8

9 RA-FIT PURPOSE AND BENEFITS RA-FIT BENEFITS Provide a service to IMF members; Provide information for analysis for countries and for IMF (for improved cross-country/regional comparisons); Improve quality of revenue administration TA delivered (data in advance, better prep); Assist in developing an empirical basis for measuring revenue administration TA delivered ; Provide necessary data to better calibrate other FAD tools (TADAT); Elevate the importance of revenue administration performance reporting and measurement 9

10 TADAT Performance Outcome Areas (POAs) The tax administration is transparent in the conduct of its activities and accountable to the government and the community. All businesses, individuals, and other entities that are required to register are included in a taxpayer registration database. Information held in the database is complete and accurate. Tax administration operations are efficient and effective in performing key functions and achieving expected outcomes. The tax dispute resolution process is independent, accessible to taxpayers, and effective in resolving disputed matters in a timely manner. The tax administration s management of compliance risks results in higher levels of voluntary compliance and community confidence in the tax administration. Taxpayers have the necessary information and support to voluntarily comply at a reasonable cost to themselves. Taxpayers report complete and accurate information in their tax returns. Taxpayers file returns on time. Taxpayers pay their taxes in full on time. 10

11 TADAT PURPOSE AND BENEFITS Allows a better identification of the relative strengths and weaknesses in a tax administration. Understanding the strengths and weaknesses of a tax administration is critical to grasp what could be improved, and what is working well. Facilitates a shared view among all the stakeholders (Government authorities, international organizations, bilateral aid agencies and technical assistance providers ). A better understanding of what works and what does not, helps focus on setting the reform objectives, establishing priorities and sequencing implementation. 11

12 TADAT- HIERACHY OF PERFORMANCE MEASUREMENT Each dimension scored separately on a scale of A to D 9 POAs Each Performance Outcome Areas has 1-4 indicators 26 Indicators All indicators have 1 4 dimensions 51 Dimensions Basis of TADAT scoring POAs are not scored Indicator scores are based on scores for the dimensions some are averaged, others are based on weakest link 12

13 TADAT PURPOSE AND BENEFITS A Tax administration demonstrates strong performance and follows internationally accepted good practices in that dimension. B Tax administration shows sound performance fairly close to internationally accepted good practices in that dimension. C Tax administration just meets the minimum performance standards in that dimension. D Inadequate performance, where the minimum standards set in C are not met. OR Insufficient information to determine level of performance. 13

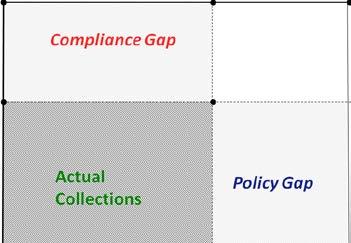

14 Revenue Administration Gap Analysis Program (RA-GAP): Visualizing the tax gap Potential Administrative Effectiveness 100 % Current Effectiven ess Compliance Gap Actual Collections Policy Gap Current Normative Structure Structure Potential Tax Structure Potential Collections 14

15 RA-GAP PURPOSE AND BENEFITS What is the RA-GAP? Revenue Administration s Gap Assessment Program is a systematic evaluation of a revenue administration s operations designed to assess their effectiveness in collecting taxes A long-run goal of the program is to build local capacity for execution of a similar domestic program. The ultimate goal of this assessment is to be able to estimate the tax gap. 15

16 RA-GAP PURPOSE AND BENEFITS What is the TAX-GAP? Loosely defined the tax gap is the difference between potential collections and actual collections. The gap would incorporate reduction in potential collections due to the policy structure (policy gap). Difference between potential collections and actual collections given the current policy framework. Revenue losses could directly tie to the effectiveness of the administration (compliance gap). 16

17 RA-GAP PURPOSE AND BENEFITS RA-GAP goes beyond an estimate of the tax gap One problem with a tax gap estimate is it doesn t tell you how to fix it. RA-GAP not only estimates the size of the tax gap, it narrows down which group of taxpayers are contributing the most to the gap, and identifies risk factors Estimating the tax gap requires the use of detailed tax record data. This allows for breaking the gap estimate down across various segments of taxpayers 17

18 What I will talk about 1. Undertaking a tax administration assessment The scoping mission 2. FAD tax administration assessment tools Introduction to RA-FIT, TADAT, RA-GAP 3. Strategy formulation Main challenges. 18

19 Strategy formulation From diagnosis to strategy Ensuring the needed complementary between tools and scoping missions FAD FAD Project managers are systematically informed of TADAT/RA-FIT missions in countries of their responsibility Project managers participate in to the TADAT/RA-GAP missions or at least are members of the TADAT/RA-GAP report advisory committee. Post-TADAT/RA-FIT TA missions are.requested to report on TADAT/RA- FIT findings and progress Field assessment missions are requested to use at the extent of possible RA-FIT data to help members countries improve the data collection and analysis. Countries Develop a proper understanding of the rationale behind every diagnostic tools to achieve expected results. Ensure that request for some diagnostic missions are consistent with current tax administration TA needs to avoid duplication or waste : Cautiously review tax administration reforms plans following diagnostic missions to ensure that new measures developed are sustainable and consistent with the ongoing reform strategy 19

20 Strategy formulation From diagnosis to strategy TA scoping missions pave the way to the following points: Usually begins with an environmental analysis - a means to understand where we are now. Can mean environmental scans and SWOT analyses. Reflects on our current processes, programs and their given strengths and weaknesses. What is the purpose of a each of the tools that can be used to help us analyze our business today? What do we want to continue to do and what do we need to change? What are key priorities for the government and the administration? Identify and articulate the main goals. Usually on a 3 to 5 year horizon. Published so administration is held to account 20

21 Strategic Management System STRATEGIC MANAGEMENT SYSTEM Environmental Analysis Foundation Statements Mission/Vision/Values Strategies (4-6 broad strategies) Strategic Objectives (2-4 for each strategy) Operational Plans Implementation of Operational Plans Monitoring and Performance Indicators Feedback STRATEGIC PLAN BUSINESS PLAN 21

An Update on TADAT. Tokyo Tax Conference April xx, Michael Keen

An Update on TADAT Tokyo Tax Conference April xx, 2015 Michael Keen A diagnostic tool to provide an objective and standardized performance assessment of a the strengths and weaknesses of a country s system

An Update on TADAT Tokyo Tax Conference April xx, 2015 Michael Keen A diagnostic tool to provide an objective and standardized performance assessment of a the strengths and weaknesses of a country s system

The TADAT Framework:

A Public Service to Support Domestic Revenue Mobilization The TADAT Framework: An Overview Prepared by the TADAT Secretariat September 2016 Email: secretariat@tadat.org Website: www.tadat.org 1 The TADAT

A Public Service to Support Domestic Revenue Mobilization The TADAT Framework: An Overview Prepared by the TADAT Secretariat September 2016 Email: secretariat@tadat.org Website: www.tadat.org 1 The TADAT

PEFA Training. Dakar, Senegal January & February 1, #PEFA. PEFA Secretariat

www.pefa.org #PEFA PEFA Training Dakar, Senegal January 30-31 & February 1, 2019 PEFA Secretariat Improving public financial management. Supporting sustainable development. INTRODUCTION Introductions Participant

www.pefa.org #PEFA PEFA Training Dakar, Senegal January 30-31 & February 1, 2019 PEFA Secretariat Improving public financial management. Supporting sustainable development. INTRODUCTION Introductions Participant

TADAT. The Tax Administration Diagnostic Assessment Tool (TADAT) Strategic Objectives and Observations To-date May 2017

Strategic Objectives and Observations To-date May 2017") The Tax Administration Diagnostic Assessment Tool (TADAT) Strategic Objectives and Observations To-date May 2017 TADAT TM TAX ADMINISTRATION DIAGNOSTIC ASSESSMENT TOOL Contributing to strengthened tax

The Tax Administration Diagnostic Assessment Tool (TADAT) Strategic Objectives and Observations To-date May 2017 TADAT TM TAX ADMINISTRATION DIAGNOSTIC ASSESSMENT TOOL Contributing to strengthened tax

Paper 3 Measuring Performance in Public Financial Management

Paper 3 Measuring Performance in Public Financial Management Key Issues 1. Effective financial management of public resources is essential to achieve the objectives of development programmes. It also promotes

Paper 3 Measuring Performance in Public Financial Management Key Issues 1. Effective financial management of public resources is essential to achieve the objectives of development programmes. It also promotes

I. Importance of Fiscal Transparency. II. The Fiscal Transparency Code. III. The Fiscal Transparency Evaluation

Fiscal Transparency Code & Evaluation: Outline of the Presentation I. Importance of Fiscal Transparency II. The Fiscal Transparency Code III. The Fiscal Transparency Evaluation IV. Fiscal Transparency

Fiscal Transparency Code & Evaluation: Outline of the Presentation I. Importance of Fiscal Transparency II. The Fiscal Transparency Code III. The Fiscal Transparency Evaluation IV. Fiscal Transparency

NYISO Capital Budgeting Process. Draft 01/13/03

NYISO Capital Budgeting Process Draft 01/13/03 1 1.0 INTRODUCTION An effective, capital budgeting process is essential to ensure sound capital investment decisions. This report details a recommended approach

NYISO Capital Budgeting Process Draft 01/13/03 1 1.0 INTRODUCTION An effective, capital budgeting process is essential to ensure sound capital investment decisions. This report details a recommended approach

Revenue Administration Gap Analysis Program (RA-GAP)

") The 5th IMF-Japan High-Level Tax Conference for Asian Countries April 21-23, 2014 Revenue Administration Gap Analysis Program (RA-GAP) David Kloeden What is the IMF RA-GAP program? 1. An evaluation of

The 5th IMF-Japan High-Level Tax Conference for Asian Countries April 21-23, 2014 Revenue Administration Gap Analysis Program (RA-GAP) David Kloeden What is the IMF RA-GAP program? 1. An evaluation of

Tax Administration Diagnostic Assessment Tool. Module 3: INTEGRITY OF THE REGISTERED TAXPAYER BASE

Tax Administration Diagnostic Assessment Tool Module 3: INTEGRITY OF THE REGISTERED TAXPAYER BASE Desired Outcome of POA 1 All businesses, individuals and other entities that are required to register are

Tax Administration Diagnostic Assessment Tool Module 3: INTEGRITY OF THE REGISTERED TAXPAYER BASE Desired Outcome of POA 1 All businesses, individuals and other entities that are required to register are

2. PEFA indicators and report

2. PEFA indicators and report Introduction to PEFA (2011 version) Skopje, Macedonia February 2015 PEFA Secretariat The PEFA Framework Launched in June 2005, updated 2011 (upgraded extensively 2015 - draft)

2. PEFA indicators and report Introduction to PEFA (2011 version) Skopje, Macedonia February 2015 PEFA Secretariat The PEFA Framework Launched in June 2005, updated 2011 (upgraded extensively 2015 - draft)

IMF EAST AFRITAC FY 2018 WORK PLAN REVENUE ADMINISTRATION

IMF EAST AFRITAC FY 2018 WORK PLAN REVENUE ADMINISTRATION Beneficiary Strategic Objective Topic Objective Activity Title Outcome Milestone AFE Complete AFE corporate activities Complete AFE corporate activities

IMF EAST AFRITAC FY 2018 WORK PLAN REVENUE ADMINISTRATION Beneficiary Strategic Objective Topic Objective Activity Title Outcome Milestone AFE Complete AFE corporate activities Complete AFE corporate activities

Third Monitoring Report of IFC s Response to: CAO Audit of a Sample of IFC Investments in Third-Party Financial Intermediaries

MONITORING REPORT CAO Audit of IFC CAO Compliance March 6, 2017 Third Monitoring Report of IFC s Response to: CAO Audit of a Sample of IFC Investments in Third-Party Financial Intermediaries Office of

MONITORING REPORT CAO Audit of IFC CAO Compliance March 6, 2017 Third Monitoring Report of IFC s Response to: CAO Audit of a Sample of IFC Investments in Third-Party Financial Intermediaries Office of

Phase 1: Written Qualifications. Phase 2: Client Reference Checks. Phase 3: Evaluation: Oral Interviews

APPENDIX C-1: SAMPLE EVALUATION FORMS Phase 1: Written Qualifications Phase 2: Client Reference Checks Phase 3: Evaluation: Oral Interviews Appendix C-1: Page 1 Insert Name of Institution Energy Performance

APPENDIX C-1: SAMPLE EVALUATION FORMS Phase 1: Written Qualifications Phase 2: Client Reference Checks Phase 3: Evaluation: Oral Interviews Appendix C-1: Page 1 Insert Name of Institution Energy Performance

Debt Statistics and Management: Issues at the National Level

Debt Statistics and Management: Issues at the National Level Punam Chuhan-Pole Development Economics Fiscal Transparency and Data Management Workshop For Delegation from the Ministry of Finance, China

Debt Statistics and Management: Issues at the National Level Punam Chuhan-Pole Development Economics Fiscal Transparency and Data Management Workshop For Delegation from the Ministry of Finance, China

IFC Response to Third Monitoring Report of IFC s Response to: CAO Audit of a Sample of IFC Investments in Third-Party Financial Intermediaries

March 9, 2017 IFC Response to Third Monitoring Report of IFC s Response to: CAO Audit of a Sample of IFC Investments in Third-Party Financial Intermediaries IFC would like to thank CAO for the monitoring

March 9, 2017 IFC Response to Third Monitoring Report of IFC s Response to: CAO Audit of a Sample of IFC Investments in Third-Party Financial Intermediaries IFC would like to thank CAO for the monitoring

Fiscal Year 2018 Workplan. May April 2018

Fiscal Year 2018 Workplan May 2017 - April 2018 Banking Supervision Objective Description /Activity Medium-Term Outcome Milestones Output Quarter Regional Workshops Implement Basel II and III Standards.

Fiscal Year 2018 Workplan May 2017 - April 2018 Banking Supervision Objective Description /Activity Medium-Term Outcome Milestones Output Quarter Regional Workshops Implement Basel II and III Standards.

OUTPUT CLASS 1 POLICY ADVICE OUTPUT DELIVERY TARGETS

OUTPUT CLASS 1 POLICY ADVICE OUTPUT DELIVERY TARGETS Performance Delivery and Measurement Document 2011/12 Page 1 of 16 Output 1.1 Policy Advice in Relation to Tax and Social Policy Performance Measures

OUTPUT CLASS 1 POLICY ADVICE OUTPUT DELIVERY TARGETS Performance Delivery and Measurement Document 2011/12 Page 1 of 16 Output 1.1 Policy Advice in Relation to Tax and Social Policy Performance Measures

Public Financial Management (PFMx) Module 7

Module 7") Public Financial Management (PFMx) Module 7 Budget Execution and Control Processes This training material is the property of the International Monetary Fund (IMF) and is intended for use in IMF Fiscal

Public Financial Management (PFMx) Module 7 Budget Execution and Control Processes This training material is the property of the International Monetary Fund (IMF) and is intended for use in IMF Fiscal

STRATEGY NORGES BANK INVESTMENT MANAGEMENT

STRATEGY 2017 2019 NORGES BANK INVESTMENT MANAGEMENT Our mission is to safeguard and build financial wealth for future generations. Contents Strategy 2017 2019 We are a large global investor and a long-term

STRATEGY 2017 2019 NORGES BANK INVESTMENT MANAGEMENT Our mission is to safeguard and build financial wealth for future generations. Contents Strategy 2017 2019 We are a large global investor and a long-term

TADAT REFLECTIONS: Impacts, Lessons and Beyond

TAAT REFLECTIONS: Impacts, Lessons and Beyond International Monetary Fund Seminar Panel iscussion 1: The TAAT Assessment Experience Key Takeaways Mr. George Santoro Secretary of State for Finance Alagoas/Brazil

TAAT REFLECTIONS: Impacts, Lessons and Beyond International Monetary Fund Seminar Panel iscussion 1: The TAAT Assessment Experience Key Takeaways Mr. George Santoro Secretary of State for Finance Alagoas/Brazil

VANUATU NATIONAL INFRASTRUCTURE MASTERPLAN. Terms of Reference for Consultants

VANUATU NATIONAL INFRASTRUCTURE MASTERPLAN Terms of Reference for Consultants 1. BACKGROUND INFORMATION Government of Vanuatu has requested TA support in the formulation and preparation of a national infrastructure

VANUATU NATIONAL INFRASTRUCTURE MASTERPLAN Terms of Reference for Consultants 1. BACKGROUND INFORMATION Government of Vanuatu has requested TA support in the formulation and preparation of a national infrastructure

Technical Assistance (TA) on Public Debt Management

on Public Debt Management") The World Bank Technical Assistance (TA) on Public Debt Management OIC-COMCEC Financial Cooperation Working Group Meeting Ankara / Turkey Emre Balibek Senior Debt Specialist Macroeconomics and Fiscal Management

The World Bank Technical Assistance (TA) on Public Debt Management OIC-COMCEC Financial Cooperation Working Group Meeting Ankara / Turkey Emre Balibek Senior Debt Specialist Macroeconomics and Fiscal Management

TERMS OF REFERENCE FOR INTERNATIONAL CONSULTANT

TERMS OF REFERENCE FOR INTERNATIONAL CONSULTANT Title: Countries: Duration: Analysis and Advocacy for Child-Centred Budgeting Botswana, Lesotho, Namibia, South Africa and Swaziland 40 working days, spread

TERMS OF REFERENCE FOR INTERNATIONAL CONSULTANT Title: Countries: Duration: Analysis and Advocacy for Child-Centred Budgeting Botswana, Lesotho, Namibia, South Africa and Swaziland 40 working days, spread

Cabinet (Performance Management) Panel 12 June 2017

Panel 12 June 2017") Cabinet (Performance Management) Panel 12 June 2017 Report title Decision designation Cabinet member with lead responsibility Key decision In forward plan Wards affected Accountable director Originating

Cabinet (Performance Management) Panel 12 June 2017 Report title Decision designation Cabinet member with lead responsibility Key decision In forward plan Wards affected Accountable director Originating

POLICY DEVELOPMENT POLICY CODE: B 3.15

POLICY CODE: B 3.15 Policy Statement: The London District Catholic School Board of Trustees in recognition of its public responsibility and the confidence placed in the educational system establishes a

POLICY CODE: B 3.15 Policy Statement: The London District Catholic School Board of Trustees in recognition of its public responsibility and the confidence placed in the educational system establishes a

Challenge: The Gambia lacked a medium-term fiscal framework (MTFF) and a medium-term expenditure framework (MTEF) to direct public expenditures

and a medium-term expenditure framework (MTEF) to direct public expenditures") 00 The Gambia INTRODUCTION The Gambia is a low-income country with a gross national income (GNI) of USD 440 per capita (2009) which has grown at an average rate of 3% annually since 2005 (WDI, 2011). It

00 The Gambia INTRODUCTION The Gambia is a low-income country with a gross national income (GNI) of USD 440 per capita (2009) which has grown at an average rate of 3% annually since 2005 (WDI, 2011). It

North Orange County Community College District Integrated. Planning Manual March 2014 Update

2013 Integrated Planning Manual March 2014 Update 2013 Integrated Planning Manual NOCCCD Mission Statement The mission of the is to serve and enrich our diverse communities by providing a comprehensive

2013 Integrated Planning Manual March 2014 Update 2013 Integrated Planning Manual NOCCCD Mission Statement The mission of the is to serve and enrich our diverse communities by providing a comprehensive

HIGHLIGHTS AND WORK AGENDA

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized HIGHLIGHTS AND WORK AGENDA 1. Public debt transparency plays a critical role in ensuring

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized HIGHLIGHTS AND WORK AGENDA 1. Public debt transparency plays a critical role in ensuring

September Preparing a Government Debt Management Reform Plan

September 2012 Preparing a Government Debt Management Reform Plan Introduction Preparing a Government Debt Management Reform Plan The World Bank supports the strengthening of government debt management

September 2012 Preparing a Government Debt Management Reform Plan Introduction Preparing a Government Debt Management Reform Plan The World Bank supports the strengthening of government debt management

Georgia: Strengthening Domestic Resource Mobilization

Technical Assistance Report Project Number: 48044-003 Policy and Advisory Technical Assistance (PATA) September 2014 Georgia: Strengthening Domestic Resource Mobilization This document is being disclosed

Technical Assistance Report Project Number: 48044-003 Policy and Advisory Technical Assistance (PATA) September 2014 Georgia: Strengthening Domestic Resource Mobilization This document is being disclosed

Public financial management is an essential part of the development process.

IDA at Work Public Financial Management: Tracking Resources for Better Results Public financial management is an essential part of the development process. It supports the efficient and accountable use

IDA at Work Public Financial Management: Tracking Resources for Better Results Public financial management is an essential part of the development process. It supports the efficient and accountable use

2016 Strategic Planning Process

Page 1 of 8 2016 Strategic Planning Process Item 9 January 18, 2016 Board of Directors Report: To: From: TCHC:2015-03 Board of Directors President and Chief Executive Officer (Interim) Date: January 5,

Page 1 of 8 2016 Strategic Planning Process Item 9 January 18, 2016 Board of Directors Report: To: From: TCHC:2015-03 Board of Directors President and Chief Executive Officer (Interim) Date: January 5,

Base Erosion and Profit Sharing Action Plan 11, 12, 14 & 15. Mr. S.P. Singh, Ex-IRS 7th November, 2015

Base Erosion and Profit Sharing Action Plan 11, 12, 14 & 15 Mr. S.P. Singh, Ex-IRS 7th November, 2015 Contents Action 11 - Establishing Methodologies to Collect and Analyze Data on BEPS Action 12 Requiring

Base Erosion and Profit Sharing Action Plan 11, 12, 14 & 15 Mr. S.P. Singh, Ex-IRS 7th November, 2015 Contents Action 11 - Establishing Methodologies to Collect and Analyze Data on BEPS Action 12 Requiring

The PEFA Performance Measurement Framework and the Strengthened Approach to Supporting PFM Reform

The PEFA Performance Measurement Framework and the Strengthened Approach to Supporting PFM Reform Budgeting and Public Financial Management September 2007 Ivor Beazley World Bank Page 1 CONTENT What is

The PEFA Performance Measurement Framework and the Strengthened Approach to Supporting PFM Reform Budgeting and Public Financial Management September 2007 Ivor Beazley World Bank Page 1 CONTENT What is

AN INTEGRATED ASSESSMENT MODEL FOR TAX ADMINISTRATION

Poverty Reduction and Economic Management Public Sector and Governance Group AN INTEGRATED ASSESSMENT MODEL FOR TAX ADMINISTRATION Final Version, 2011 INTEGRATED ASSESSMENT MODEL FOR TAX ADMINISTRATION

Poverty Reduction and Economic Management Public Sector and Governance Group AN INTEGRATED ASSESSMENT MODEL FOR TAX ADMINISTRATION Final Version, 2011 INTEGRATED ASSESSMENT MODEL FOR TAX ADMINISTRATION

CLIMATE INVESTMENT READINESS INDEX (CIRI) - A Tool to Assess Investment Climate for Climate Investments

- A Tool to Assess Investment Climate for Climate Investments") CLIMATE INVESTMENT READINESS INDEX (CIRI) - A Tool to Assess Investment Climate for Climate Investments Background Mitigating climate-change while addressing development needs will involve massive scale-up

CLIMATE INVESTMENT READINESS INDEX (CIRI) - A Tool to Assess Investment Climate for Climate Investments Background Mitigating climate-change while addressing development needs will involve massive scale-up

People s Republic of China: Promotion of a Legal Framework for Financial Consumer Protection

Technical Assistance Report Project Number: 47042-001 Policy and Advisory Technical Assistance (PATA) October 2013 People s Republic of China: Promotion of a Legal Framework for Financial Consumer Protection

Technical Assistance Report Project Number: 47042-001 Policy and Advisory Technical Assistance (PATA) October 2013 People s Republic of China: Promotion of a Legal Framework for Financial Consumer Protection

Tax Administration Diagnostic Assessment Tool. Module 7: TIMELY PAYMENT OF TAXES

Tax Administration Diagnostic Assessment Tool Module 7: TIMELY PAYMENT OF TAXES Desired Outcome of POA 5 Taxpayers pay their taxes in full on time. Taxpayers are expected to pay taxes on time according

Tax Administration Diagnostic Assessment Tool Module 7: TIMELY PAYMENT OF TAXES Desired Outcome of POA 5 Taxpayers pay their taxes in full on time. Taxpayers are expected to pay taxes on time according

TAX REFORM TO IMPROVE TAX COMPLIANCE

TAX REFORM TO IMPROVE TAX COMPLIANCE Juan Toro IMF s Fiscal Affairs Department -- Assistant Director 7th IMF-Japan High-Level Tax Conference For Asian Countries Tokyo, April 5-7, 2016 Outline Challenges

TAX REFORM TO IMPROVE TAX COMPLIANCE Juan Toro IMF s Fiscal Affairs Department -- Assistant Director 7th IMF-Japan High-Level Tax Conference For Asian Countries Tokyo, April 5-7, 2016 Outline Challenges

PEFA Handbook. Volume I: The PEFA Assessment Process Planning, Managing and Using PEFA

PEFA Handbook Volume I: The PEFA Assessment Process Planning, Managing and Using PEFA October 18, 2016 PEFA Secretariat Washington DC USA 1 Table of Contents PEFA ASSESSMENT HANDBOOK... 5 Preface... 5

PEFA Handbook Volume I: The PEFA Assessment Process Planning, Managing and Using PEFA October 18, 2016 PEFA Secretariat Washington DC USA 1 Table of Contents PEFA ASSESSMENT HANDBOOK... 5 Preface... 5

Strengthening National Comprehensive Agricultural Public Expenditure. in Sub-Saharan Africa. Public Expenditure Tracking Survey

Strengthening National Comprehensive Agricultural Public Expenditure in Sub-Saharan Africa Public Expenditure Tracking Survey Template Terms of Reference web page: www.worldbank.org/afr/agperprogram email

Strengthening National Comprehensive Agricultural Public Expenditure in Sub-Saharan Africa Public Expenditure Tracking Survey Template Terms of Reference web page: www.worldbank.org/afr/agperprogram email

Introduction Chapter 1, Page 1 of 9 1. INTRODUCTION

Introduction Chapter 1, Page 1 of 9 1. INTRODUCTION 1.1 OVERVIEW Preamble 1.1.1 The African Development Bank is the premier financial development institution in Africa dedicated to combating poverty and

Introduction Chapter 1, Page 1 of 9 1. INTRODUCTION 1.1 OVERVIEW Preamble 1.1.1 The African Development Bank is the premier financial development institution in Africa dedicated to combating poverty and

Performance audit report. Inland Revenue Department: Performance of taxpayer audit follow-up audit

Performance audit report Inland Revenue Department: Performance of taxpayer audit follow-up audit Office of the Auditor-General Private Box 3928, Wellington Telephone: (04) 917 1500 Facsimile: (04) 917

Performance audit report Inland Revenue Department: Performance of taxpayer audit follow-up audit Office of the Auditor-General Private Box 3928, Wellington Telephone: (04) 917 1500 Facsimile: (04) 917

Project Administration Instructions

Project Administration Instructions PAI 6.02 Page 1 of 2 PROJECT ADMINISTRATION MISSIONS A. Introduction 1. ADB missions dispatched for loan and technical assistance (TA) project administration are classified

Project Administration Instructions PAI 6.02 Page 1 of 2 PROJECT ADMINISTRATION MISSIONS A. Introduction 1. ADB missions dispatched for loan and technical assistance (TA) project administration are classified

GFOA AWARD FOR BEST PRACTICES IN SCHOOL BUDGETING. Applicant and Judge's Guide

GFOA AWARD FOR BEST PRACTICES IN SCHOOL BUDGETING Applicant and Judge's Guide GFOA Award for Best Practices in School Budgeting Applicant and Judges Guide Introduction... 2 Definitions... 2 About the Award...

GFOA AWARD FOR BEST PRACTICES IN SCHOOL BUDGETING Applicant and Judge's Guide GFOA Award for Best Practices in School Budgeting Applicant and Judges Guide Introduction... 2 Definitions... 2 About the Award...

SURVEY GUIDANCE CONTENTS Survey on Monitoring the Paris Declaration Fourth High Level Forum on Aid Effectiveness

SURVEY GUIDANCE 2011 Survey on Monitoring the Paris Declaration Fourth High Level Forum on Aid Effectiveness This document explains the objectives, process and methodology agreed for the 2011 Survey on

SURVEY GUIDANCE 2011 Survey on Monitoring the Paris Declaration Fourth High Level Forum on Aid Effectiveness This document explains the objectives, process and methodology agreed for the 2011 Survey on

California State University, Los Angeles University Resource Allocation Process for Change CURRENT ALLOCATION MODEL OVERVIEW

Overview California State University, Los Angeles University Resource Allocation Process for Change CURRENT ALLOCATION MODEL OVERVIEW The University Resource Allocation, as defined by Administrative Procedure

Overview California State University, Los Angeles University Resource Allocation Process for Change CURRENT ALLOCATION MODEL OVERVIEW The University Resource Allocation, as defined by Administrative Procedure

PEFA Handbook. Volume I: The PEFA Assessment Process Planning, Managing and Using PEFA

PEFA Handbook Volume I: The PEFA Assessment Process Planning, Managing and Using PEFA Second edition November 20, 2018 PEFA Secretariat Washington DC, USA Table of Contents PEFA ASSESSMENT HANDBOOK...

PEFA Handbook Volume I: The PEFA Assessment Process Planning, Managing and Using PEFA Second edition November 20, 2018 PEFA Secretariat Washington DC, USA Table of Contents PEFA ASSESSMENT HANDBOOK...

REPORT 2015/174 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2015/174 Audit of management of selected subprogrammes and related capacity development projects in the United Nations Economic and Social Commission for Asia and the Pacific

INTERNAL AUDIT DIVISION REPORT 2015/174 Audit of management of selected subprogrammes and related capacity development projects in the United Nations Economic and Social Commission for Asia and the Pacific

Report of the Auditor General of Alberta

Report of the Auditor General of Alberta JULY 2014 Mr. Matt Jeneroux, MLA Chair Standing Committee on Legislative Offices I am honoured to send my Report of the Auditor General of Alberta July 2014 to

Report of the Auditor General of Alberta JULY 2014 Mr. Matt Jeneroux, MLA Chair Standing Committee on Legislative Offices I am honoured to send my Report of the Auditor General of Alberta July 2014 to

Treasury and Policy Board Office Accountability Report

Treasury and Policy Board Office 2003-2004 Accountability Report TABLE OF CONTENTS Accountability Statement... 1 Message from the Minister... 2 Introduction... 3 Progress and... 5 Financial Results...

Treasury and Policy Board Office 2003-2004 Accountability Report TABLE OF CONTENTS Accountability Statement... 1 Message from the Minister... 2 Introduction... 3 Progress and... 5 Financial Results...

Public Financial Management

UNITAR Mustofi Fellowship Hiroshima, Japan 18 22 February 2012! Index! Overview and Objectives! Limitations and Problems! Public Financial Systems! Financial Management System Boundaries! Framework! Government

UNITAR Mustofi Fellowship Hiroshima, Japan 18 22 February 2012! Index! Overview and Objectives! Limitations and Problems! Public Financial Systems! Financial Management System Boundaries! Framework! Government

Tax Administration Diagnostic Assessment Tool

Tax Administration Diagnostic Assessment Tool Pre-Assessment Module 6: TIMELY FILING OF TAX DECLARATIONS Desired Outcome of POA 4 The desired outcome is: Taxpayers file their tax on time. Tax are the principal

Tax Administration Diagnostic Assessment Tool Pre-Assessment Module 6: TIMELY FILING OF TAX DECLARATIONS Desired Outcome of POA 4 The desired outcome is: Taxpayers file their tax on time. Tax are the principal

Pensions and Long-Run Investment

Organisation de Coopération et de Développement Economiques Organisation for Economic Co-operation and Development DIRECTION DES AFFAIRES FINANCIERES, FISCALES ET DES ENTREPRISES DIRECTORATE FOR FINANCIAL,

Organisation de Coopération et de Développement Economiques Organisation for Economic Co-operation and Development DIRECTION DES AFFAIRES FINANCIERES, FISCALES ET DES ENTREPRISES DIRECTORATE FOR FINANCIAL,

Audit of Regional Operations Manitoba Region

Audit of Regional Operations Manitoba Region WESTERN ECONOMIC DIVERSIFICATION CANADA Audit & Evaluation Branch December 2010 Table of Contents 1.0 Executive Summary 2 Findings 2 Statement of Assurance

Audit of Regional Operations Manitoba Region WESTERN ECONOMIC DIVERSIFICATION CANADA Audit & Evaluation Branch December 2010 Table of Contents 1.0 Executive Summary 2 Findings 2 Statement of Assurance

ABBREVIATIONS AND ACRONYMS...4 PREFACE...5 EXECUTIVE SUMMARY...6

1 Jordan 2 Contents Page ABBREVIATIONS AND ACRONYMS...4 PREFACE...5 EXECUTIVE SUMMARY...6 II. COUNTRY BACKGROUND INFORMATION...13 A. Country Profile...13 B. Data Tables...13 C. Economic Situation...14

1 Jordan 2 Contents Page ABBREVIATIONS AND ACRONYMS...4 PREFACE...5 EXECUTIVE SUMMARY...6 II. COUNTRY BACKGROUND INFORMATION...13 A. Country Profile...13 B. Data Tables...13 C. Economic Situation...14

75 working days spread over 4 months with possibility of extension 1. BACKGROUND

TERMS OF REFERENCE 1. Environmental Finance Expert Contracting Agency: Coordinating Agency: Place: Expected duration: United Nations Development Programme (UNDP) Bhutan UNDP Country Office Thimphu, Bhutan.

TERMS OF REFERENCE 1. Environmental Finance Expert Contracting Agency: Coordinating Agency: Place: Expected duration: United Nations Development Programme (UNDP) Bhutan UNDP Country Office Thimphu, Bhutan.

OXFORD ECONOMICS. Stress testing and risk management services

OXFORD ECONOMICS Stress testing and risk management services September 2014 The rising need for rigorous stress testing Stress testing has become a critical component of the risk identification and risk

OXFORD ECONOMICS Stress testing and risk management services September 2014 The rising need for rigorous stress testing Stress testing has become a critical component of the risk identification and risk

Managing Uncertainty In The SEC Fair Fund Process: Part 2

Portfolio Media. Inc. 111 West 19 th Street, 5th Floor New York, NY 10011 www.law360.com Phone: +1 646 783 7100 Fax: +1 646 783 7161 customerservice@law360.com Managing Uncertainty In The SEC Fair Fund

Portfolio Media. Inc. 111 West 19 th Street, 5th Floor New York, NY 10011 www.law360.com Phone: +1 646 783 7100 Fax: +1 646 783 7161 customerservice@law360.com Managing Uncertainty In The SEC Fair Fund

Executive Summary of the National Report on the Implementation of the 2030 Agenda for Sustainable Development. Czech Republic

Office of the Government of the Czech Republic Sustainable Development Department Executive Summary of the National Report on the Implementation of the 2030 Agenda for Sustainable Development Czech Republic

Office of the Government of the Czech Republic Sustainable Development Department Executive Summary of the National Report on the Implementation of the 2030 Agenda for Sustainable Development Czech Republic

OECD, UN, IMF and World Bank issue toolkit for addressing difficulties in accessing comparable data for transfer pricing analysis

6 July 2017 Global Tax Alert OECD, UN, IMF and World Bank issue toolkit for addressing difficulties in accessing comparable data for transfer pricing analysis EY Global Tax Alert Library Access both online

6 July 2017 Global Tax Alert OECD, UN, IMF and World Bank issue toolkit for addressing difficulties in accessing comparable data for transfer pricing analysis EY Global Tax Alert Library Access both online

ECB guide to internal models. Risk-type-specific chapters

ECB guide to internal models Risk-type-specific chapters September 2018 Contents Foreword 3 Credit risk 5 1 Scope of the credit risk chapter 5 2 Data maintenance for the IRB approach 5 3 Data requirements

ECB guide to internal models Risk-type-specific chapters September 2018 Contents Foreword 3 Credit risk 5 1 Scope of the credit risk chapter 5 2 Data maintenance for the IRB approach 5 3 Data requirements

Handbook for the Corruption Impact Assessment

Handbook for the Corruption Impact Assessment Handbook for the Corruption Impact Assessment Handbook for the Corruption Impact Assessment Government Complex Sejong 20, Doum 5-ro, Sejong-si, 30102, Republic

Handbook for the Corruption Impact Assessment Handbook for the Corruption Impact Assessment Handbook for the Corruption Impact Assessment Government Complex Sejong 20, Doum 5-ro, Sejong-si, 30102, Republic

Mn/DOT Scoping Process Narrative

Table of Contents 1 Project Planning Phase...3 1.1 Identify Needs...4 1.2 Compile List of Needs = Needs List...4 1.3 Define Project Concept...5 1.4 Apply Fiscal/Other Constraints...5 1.5 Compile List of

Table of Contents 1 Project Planning Phase...3 1.1 Identify Needs...4 1.2 Compile List of Needs = Needs List...4 1.3 Define Project Concept...5 1.4 Apply Fiscal/Other Constraints...5 1.5 Compile List of

National Accounts. The System of National Accounts

National Accounts The United Nations Statistics Division (UNSD) contributes to the international coordination, development and implementation of the System of National Accounts (SNA). It undertakes methodological

National Accounts The United Nations Statistics Division (UNSD) contributes to the international coordination, development and implementation of the System of National Accounts (SNA). It undertakes methodological

ATI Work Plan 2017 / 2018 facilitated by funded by

ATI Work Plan 2017 / 2018 facilitated by funded by Imprint The International Tax Compact (ITC) is an informal platform that aims to enhance domestic revenue mobilisation in partner countries, and to promote

ATI Work Plan 2017 / 2018 facilitated by funded by Imprint The International Tax Compact (ITC) is an informal platform that aims to enhance domestic revenue mobilisation in partner countries, and to promote

Project Administration Instructions

Project Administration Instructions PAI 6.07A Page 1 of 4 PROJECT COMPLETION REPORT FOR SOVEREIGN OPERATIONS 1 A. Objective and Scope 1. The main objective of a project completion report (PCR) 1 is to

Project Administration Instructions PAI 6.07A Page 1 of 4 PROJECT COMPLETION REPORT FOR SOVEREIGN OPERATIONS 1 A. Objective and Scope 1. The main objective of a project completion report (PCR) 1 is to

INSTITUTIONAL EFFECTIVENESS Procedures Manual. Developed by the Office of Institutional Effectiveness

INSTITUTIONAL EFFECTIVENESS Procedures Manual Developed by the Office of Institutional Effectiveness 2014-2018 INSTITUTIONAL EFFECTIVENESS PROCEDURES MANUAL Purpose < To support a comprehensive institutional

INSTITUTIONAL EFFECTIVENESS Procedures Manual Developed by the Office of Institutional Effectiveness 2014-2018 INSTITUTIONAL EFFECTIVENESS PROCEDURES MANUAL Purpose < To support a comprehensive institutional

Vanuatu. Vanuatu is a lower-middle-income country with a gross national income (GNI) of

of") 00 Vanuatu INTRODUCTION Vanuatu is a lower-middle-income country with a gross national income (GNI) of USD 2 620 per capita (2009) and a population of 240 000 (WDI, 2011). Net official development assistance

00 Vanuatu INTRODUCTION Vanuatu is a lower-middle-income country with a gross national income (GNI) of USD 2 620 per capita (2009) and a population of 240 000 (WDI, 2011). Net official development assistance

Perspectives on possible deliverables in the investment area

Perspectives on possible deliverables in the investment area Presentation by International Organizations to the G20 Trade and Investment Working Group Beijing, January 2016 Contents UNCTAD (Overview) James

Perspectives on possible deliverables in the investment area Presentation by International Organizations to the G20 Trade and Investment Working Group Beijing, January 2016 Contents UNCTAD (Overview) James

COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL. Towards robust quality management for European Statistics

EN EN EN EUROPEAN COMMISSION Brussels, 15.4.2011 COM(2011) 211 final COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL Towards robust quality management for European Statistics

EN EN EN EUROPEAN COMMISSION Brussels, 15.4.2011 COM(2011) 211 final COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL Towards robust quality management for European Statistics

Aboriginal Affairs and Northern Development Canada. Internal Audit Report. Audit of the Income Assistance Program. Prepared by:

Aboriginal Affairs and Northern Development Canada Internal Audit Report Audit of the Income Assistance Program Prepared by: Audit and Assurance Services Branch Project # 12-07 February 2013 TABLE OF CONTENTS

Aboriginal Affairs and Northern Development Canada Internal Audit Report Audit of the Income Assistance Program Prepared by: Audit and Assurance Services Branch Project # 12-07 February 2013 TABLE OF CONTENTS

Expected results of the Trust Fund and corresponding indicators (including baselines, result goals and sources of data) are set out in Annex 4.

are set out in Annex 4.") Administration Agreement between the European Commission and the International Bank for Reconstruction and Development concerning the Part H Europe 2020 Programmatic Single-Donor Trust Fund Trust Fund

Administration Agreement between the European Commission and the International Bank for Reconstruction and Development concerning the Part H Europe 2020 Programmatic Single-Donor Trust Fund Trust Fund

Strategic Science Investment Fund Programmes. Performance Framework

Strategic Science Investment Fund Programmes Performance Framework 2018 Contents THE PURPOSE OF THIS DOCUMENT 1 Who It Is Intended For 1 Strategic Science Investment Fund 1 SSIF Programmes 2 Key Elements

Strategic Science Investment Fund Programmes Performance Framework 2018 Contents THE PURPOSE OF THIS DOCUMENT 1 Who It Is Intended For 1 Strategic Science Investment Fund 1 SSIF Programmes 2 Key Elements

Corporate Governance in Transition Economies Armenia Country Report

Comments are welcome: please provide comments to cignag@ebrd.com Corporate Governance in Transition Economies Armenia Country Report May 2017 Prepared by: Gian Piero Cigna Pavle Djuric Yaryna Kobel Alina

Comments are welcome: please provide comments to cignag@ebrd.com Corporate Governance in Transition Economies Armenia Country Report May 2017 Prepared by: Gian Piero Cigna Pavle Djuric Yaryna Kobel Alina

International Monetary Fund Washington, D.C.

2010 International Monetary Fund May 2010 IMF Country Report No. 10/138 November 2009 January 29, 2001 January 29, 2001 January 29, 2001 January 29, 2001 Maldives: Action Plan for PFM Reforms Based on

2010 International Monetary Fund May 2010 IMF Country Report No. 10/138 November 2009 January 29, 2001 January 29, 2001 January 29, 2001 January 29, 2001 Maldives: Action Plan for PFM Reforms Based on

African, Caribbean and Pacific Group of States TRADE REGULATORY IMPACT ASSESSMENT - MAURITIUS ACP-EU TBT PROGRAMME (REG/FED/ )

") African, Caribbean and Pacific Group of States TRADE REGULATORY IMPACT ASSESSMENT - MAURITIUS ACP-EU TBT PROGRAMME (REG/FED/022-667) Project code: 020/15 FINAL REPORT 4 October 2015 Table of Contents GLOSSARY...

African, Caribbean and Pacific Group of States TRADE REGULATORY IMPACT ASSESSMENT - MAURITIUS ACP-EU TBT PROGRAMME (REG/FED/022-667) Project code: 020/15 FINAL REPORT 4 October 2015 Table of Contents GLOSSARY...

The Big Business of Small Enterprises

The Big Business of Small Enterprises An IEG Evaluation of WBG Experience with Targeted Support for SMEs 2006-12 Andrew H. W. Stone IEG, Private Sector JOINT MNSFP-MENA Chief Economist Seminar January

The Big Business of Small Enterprises An IEG Evaluation of WBG Experience with Targeted Support for SMEs 2006-12 Andrew H. W. Stone IEG, Private Sector JOINT MNSFP-MENA Chief Economist Seminar January

Loss Prevention Strategy & Framework for Manitoba Public Insurance

Loss Prevention Strategy & Framework for Manitoba Public Insurance May Version:. Date Revised: May, Document Name: MAIN_MPI Loss Prevention Strategy and Framework.docx Page 0 Executive Summary Manitoba

Loss Prevention Strategy & Framework for Manitoba Public Insurance May Version:. Date Revised: May, Document Name: MAIN_MPI Loss Prevention Strategy and Framework.docx Page 0 Executive Summary Manitoba

Project Information Document/ Identification/Concept Stage (PID)

") Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Project Information Document/ Identification/Concept Stage (PID) Concept Stage Date Prepared/Updated: 25-Apr-2018

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Project Information Document/ Identification/Concept Stage (PID) Concept Stage Date Prepared/Updated: 25-Apr-2018

ASIAN DEVELOPMENT BANK SST:REG 99025

ASIAN DEVELOPMENT BANK SST:REG 99025 SPECIAL EVALUATION STUDY OF EFFECTIVENESS AND IMPACT OF ASIAN DEVELOPMENT BANK ASSISTANCE TO THE REFORM OF PUBLIC EXPENDITURE MANAGEMENT I N BHUTAN, INDIA, KIRIBATI,

ASIAN DEVELOPMENT BANK SST:REG 99025 SPECIAL EVALUATION STUDY OF EFFECTIVENESS AND IMPACT OF ASIAN DEVELOPMENT BANK ASSISTANCE TO THE REFORM OF PUBLIC EXPENDITURE MANAGEMENT I N BHUTAN, INDIA, KIRIBATI,

PCT WBG IMF OECD. The Platform for Collaboration on Tax (PCT) The Platform for Collaboration on Tax (PCT) Workplan: PCT 14 Actions

The Platform for Collaboration on Tax (PCT) Workplan: PCT 14 Actions") The Platform for Collaboration on Tax (PCT) The (PCT) Strengthening Tax Capacity in Developing Countries: Inter-agency ECOSOC Special Meeting on International Cooperation in Tax Matters New York, 18 May

The Platform for Collaboration on Tax (PCT) The (PCT) Strengthening Tax Capacity in Developing Countries: Inter-agency ECOSOC Special Meeting on International Cooperation in Tax Matters New York, 18 May

TAXPAYER S SERVICE CHARTER

ISO 9001:2008 Certified TAXPAYER S SERVICE CHARTER April 2012 5 th Edition VISION To be a Modern Tax Administration MISSION STATEMENT To be an effective and efficient Tax Administration which promotes

ISO 9001:2008 Certified TAXPAYER S SERVICE CHARTER April 2012 5 th Edition VISION To be a Modern Tax Administration MISSION STATEMENT To be an effective and efficient Tax Administration which promotes

Ninth UNCTAD Debt Management Conference

Ninth UNCTAD Debt Management Conference Geneva, 11-13 November 2013 The Debt manager and Transparency: Responses from International Organisations by Mr. Gerry Teeling Chief, Debt Management and Financial

Ninth UNCTAD Debt Management Conference Geneva, 11-13 November 2013 The Debt manager and Transparency: Responses from International Organisations by Mr. Gerry Teeling Chief, Debt Management and Financial

Financial Crisis and the Information Gaps: Implementing the G20 Recommendations Recommendation 6: Structured Products

Financial Crisis and the Information Gaps: Implementing the G20 Recommendations Recommendation 6: Structured Products By Werner Bijkerk Senior Officials Conference Basel 8 April 2010 Agenda IOSCO Policy

Financial Crisis and the Information Gaps: Implementing the G20 Recommendations Recommendation 6: Structured Products By Werner Bijkerk Senior Officials Conference Basel 8 April 2010 Agenda IOSCO Policy

Services Trade Restrictiveness Index. Raed Safadi

Services Trade Restrictiveness Index Raed Safadi Background: importance of services Services share of GDP Services share of total trade OECD Trade & Agriculture 2 Cross-border trade in services by sector,

Services Trade Restrictiveness Index Raed Safadi Background: importance of services Services share of GDP Services share of total trade OECD Trade & Agriculture 2 Cross-border trade in services by sector,

TRENDS, CHALLENGES AND OPPORTUNITIES ADMINISTRATIVE FOCUS

TRENDS, CHALLENGES AND OPPORTUNITIES ADMINISTRATIVE FOCUS Juan Toro IMF Conference on Revenue Mobilization and Development April 17, 2011 As pointed out Reform of revenue and customs administrations is

TRENDS, CHALLENGES AND OPPORTUNITIES ADMINISTRATIVE FOCUS Juan Toro IMF Conference on Revenue Mobilization and Development April 17, 2011 As pointed out Reform of revenue and customs administrations is

MUTUAL ACCOUNTABILITY FOR LDCs: A FRAMEWORK FOR AID QUALITY AND BEYOND

Special Event Fourth United Nations Conference on Least Developed Countries (LDC-IV) Thursday 12 May 2011 6:15 pm-8 pm Istanbul Congress Centre Çamlica Hall Background Note MUTUAL ACCOUNTABILITY FOR LDCs:

Special Event Fourth United Nations Conference on Least Developed Countries (LDC-IV) Thursday 12 May 2011 6:15 pm-8 pm Istanbul Congress Centre Çamlica Hall Background Note MUTUAL ACCOUNTABILITY FOR LDCs:

Public Disclosure Copy. Implementation Status & Results Report Revenue Mobilization Program for Results: VAT Improvement Program (VIP) (P129770)

(P129770)") Public Disclosure Authorized SOUTH ASIA Bangladesh Governance Global Practice IBRD/IDA Program-for-Results FY 2014 Seq No: 7 ARCHIVED on 05-Jun-2017 ISR28344 Implementing Agencies: National Board of Revenue,

Public Disclosure Authorized SOUTH ASIA Bangladesh Governance Global Practice IBRD/IDA Program-for-Results FY 2014 Seq No: 7 ARCHIVED on 05-Jun-2017 ISR28344 Implementing Agencies: National Board of Revenue,

Joint Technical Advice

JC 2017 43 28 July 2017 Joint Technical Advice on the procedures used to establish whether a PRIIP targets specific environmental or social objectives pursuant to Article 8 (4) of Regulation (EU) No 1286/2014

JC 2017 43 28 July 2017 Joint Technical Advice on the procedures used to establish whether a PRIIP targets specific environmental or social objectives pursuant to Article 8 (4) of Regulation (EU) No 1286/2014

Review Criteria. Robotics Program. Reviewer SCORE SUMMARY. Extent of Need 25 Goals Objectives and Milestones

Proposal Lead Agency: Proposal Title: Review Criteria [Additional Information]: Robotics Program Reviewer Reviewer: Signature: Date: SCORE SUMMARY Section Maximum Score Extent of Need 25 Goals Objectives

Proposal Lead Agency: Proposal Title: Review Criteria [Additional Information]: Robotics Program Reviewer Reviewer: Signature: Date: SCORE SUMMARY Section Maximum Score Extent of Need 25 Goals Objectives

KANPUR City Development Plan (CDP)

") Annexure-IV JNNURM AND METHODOLOGY FOR DEVELOPING CITY DEVELOPMENT PLAN BACKGROUND Urban population of India has increased from 23.34 percent in 1981 to 27.8 percent in 2001 (Census of India 1991, 2001).

Annexure-IV JNNURM AND METHODOLOGY FOR DEVELOPING CITY DEVELOPMENT PLAN BACKGROUND Urban population of India has increased from 23.34 percent in 1981 to 27.8 percent in 2001 (Census of India 1991, 2001).

INTERNATIONAL RESERVES: IMF ADVICE AND COUNTRY PERSPECTIVES ISSUES PAPER FOR AN EVALUATION BY THE INDEPENDENT EVALUATION OFFICE (IEO)

") INTERNATIONAL RESERVES: IMF ADVICE AND COUNTRY PERSPECTIVES ISSUES PAPER FOR AN EVALUATION BY THE INDEPENDENT EVALUATION OFFICE (IEO) September 20, 2011 I. BACKGROUND AND MOTIVATION 1. The IEO will undertake

INTERNATIONAL RESERVES: IMF ADVICE AND COUNTRY PERSPECTIVES ISSUES PAPER FOR AN EVALUATION BY THE INDEPENDENT EVALUATION OFFICE (IEO) September 20, 2011 I. BACKGROUND AND MOTIVATION 1. The IEO will undertake

ASIAN DEVELOPMENT BANK

ASIAN DEVELOPMENT BANK R191-00 12 September 2000 TECHNICAL ASSISTANCE TO INDONESIA FOR CORPORATE GOVERNANCE REFORM The attached Report is circulated for the information of the Board. The President approved

ASIAN DEVELOPMENT BANK R191-00 12 September 2000 TECHNICAL ASSISTANCE TO INDONESIA FOR CORPORATE GOVERNANCE REFORM The attached Report is circulated for the information of the Board. The President approved

Partner Reporting System on Statistical Development (PRESS) Task Team Developments during July 07-January 08

Task Team Developments during July 07-January 08") Partner Reporting System on Statistical Development (PRESS) Task Team Developments during July 07-January 08 1. This note attempts to present the activities completed by the Task Team on PRESS since its

Partner Reporting System on Statistical Development (PRESS) Task Team Developments during July 07-January 08 1. This note attempts to present the activities completed by the Task Team on PRESS since its

CAMBODIA. Cambodia is a low-income country with a gross national income (GNI) of USD 610 per

of USD 610 per") 00 CAMBODIA INTRODUCTION Cambodia is a low-income country with a gross national income (GNI) of USD 610 per capita in 2009 (WDI, 2011). It has a population of approximately 15 million and more than a quarter

00 CAMBODIA INTRODUCTION Cambodia is a low-income country with a gross national income (GNI) of USD 610 per capita in 2009 (WDI, 2011). It has a population of approximately 15 million and more than a quarter

M2i s Experience in Microfinance

M2i s Experience in Microfinance Title Duration Client Page Implementation of Risk Management International Finance June 2012-May 2015 Framework in 5 MFIs Corporation 3 Adaptation of Global Risk International

M2i s Experience in Microfinance Title Duration Client Page Implementation of Risk Management International Finance June 2012-May 2015 Framework in 5 MFIs Corporation 3 Adaptation of Global Risk International

Event Performance Indices (EPI) Report

Report") Event Performance Indices (EPI) Report MeetingMetrics SM A comprehensive snapshot report to help you and your organization understand the value and performance of your meetings. Use this report to evaluate,

Event Performance Indices (EPI) Report MeetingMetrics SM A comprehensive snapshot report to help you and your organization understand the value and performance of your meetings. Use this report to evaluate,

FRAMEWORK AND WORK PROGRAM FOR GEF S MONITORING, EVALUATION AND DISSEMINATION ACTIVITIES

GEF/C.8/4 GEF Council October 8-10, 1996 Agenda Item 6 FRAMEWORK AND WORK PROGRAM FOR GEF S MONITORING, EVALUATION AND DISSEMINATION ACTIVITIES RECOMMENDED DRAFT COUNCIL DECISION The Council reviewed document

GEF/C.8/4 GEF Council October 8-10, 1996 Agenda Item 6 FRAMEWORK AND WORK PROGRAM FOR GEF S MONITORING, EVALUATION AND DISSEMINATION ACTIVITIES RECOMMENDED DRAFT COUNCIL DECISION The Council reviewed document

The Canadian Government, the World Bank and the International Monetary Fund:

The Canadian Government, the World Bank and the International Monetary Fund: A REPORT CARD on FINANCE CANADA S 2006 ANNUAL REPORT to PARLIAMENT Every year at the end of March, i the Minister of Finance

The Canadian Government, the World Bank and the International Monetary Fund: A REPORT CARD on FINANCE CANADA S 2006 ANNUAL REPORT to PARLIAMENT Every year at the end of March, i the Minister of Finance