Part 4. Comprehensive Example and Sample Forms Example One: Senior Minister

|

|

|

- Logan Cain

- 6 years ago

- Views:

Transcription

1 Part 4. Comprehensive Example and Sample Forms Example One: Senior Minister Note: This example is based on an illustrated example contained at the end of IRS Publication 517. Rev. John Michaels is the minister of the First Baptist Church. He is married and has one child. The child is considered a qualifying child for the child tax credit. Mrs. Michaels is not employed outside the home. Rev. Michaels is a commonlaw employee of the church, and he has not applied for an exemption from SE tax. The church paid Rev. Michaels a salary of $45,000. In addition, as a self-employed person, he earned $4,000 during the year for weddings, funerals, and honoraria. He made estimated tax payments during the year totaling $12,000. He taught a course at the local community college, for which he was paid $3,400. Rev. Michaels owns a home next to the church. He makes a $1,125 per month mortgage payment of principal and interest only. His utility bills and other housingrelated expenses for the year totaled $1,450, and the real estate taxes on his home amounted to $1,750 for the year. The church paid him $1,400 per month as his housing allowance. The home s fair rental value is $1,380 per month (including furnishings and utilities). The parts of Rev. and Mrs. Michaels income tax return are explained in the order they are completed. They are illustrated in the order that the Rev. Michaels will assemble the return to send it to the IRS. Form W 2 from Church The church completed Form W 2 for Rev. Michaels as follows: Box 1. The church entered Rev. Michaels $45,000 salary. Box 2. The church left this box blank because Rev. Michaels did not request federal income tax withholding. Boxes 3 through 6. Rev. Michaels is considered a self-employed person for purposes of Social Security and Medicare tax withholding, so the church left these boxes blank. Box 14. The church entered Rev. Michaels total housing allowance for the year and identified it. Turbo Tax tips: Listed below are tips for ministers who use Turbo Tax to complete their returns. We have listed our recommended responses to some of the questions asked by the software when entering your W 2 from your church. Please note that, at the time of publication, the 2010 Turbo Tax software had not been released, so the Turbo Tax tips listed throughout this example are based on the 2009 version of the software. These tips should not be construed as an endorsement or recommendation of the Turbo Tax software. 1. Do any of these apply to your W-2? Be sure to check the box that says, I earned this income for religious employment (clergy, nonclergy, religious sect). 2. What type of religious employment? Please note that ministers fall under the category of clergy employment. 3. Tell us about your clergy housing. Turbo Tax then asks for the Parsonage or Housing Allowance, as well as the amount of qualifying expenses. The amount you should enter for qualifying expenses is the lesser of your actual housing expenses, the annual fair rental value of your home (including furnishings and utilities) or the amount of your pay that was designated as ministerial housing allowance by your church. 4. How would you like us to calculate clergy selfemployment tax? Please note that self-employment tax should be paid on wages and housing allowance. See Schedule SE Turbo Tax Tip for additional information. Form W 2 from College The community college gave Rev. Michaels a Form W 2 that showed the following. Box 1. The college entered Rev. Michaels $3,400 salary. Box 2. The college withheld $272 in federal income tax on Rev. Michaels behalf. Boxes 3 and 5. As an employee of the college, Rev. Michaels is subject to Social Security and Medicare withholding on his full salary from the college. Box 4. The college withheld $ in Social Security taxes. Box 6. The college withheld $49.30 in Medicare taxes. Schedule C-EZ (Form 1040) Some of Rev. Michaels entries on Schedule C EZ are explained here. Line 1. Rev. Michaels reports the $4,000 from weddings, funerals and honoraria. Line 2. Michaels reports his expenses related to the line 1 amount. The total consisted of $87 for marriage and family Find IRS forms, instructions and publications at or call TAX-FORM. 41

2 booklets and $253 for 506 miles of business use of his car, mainly in connection with honoraria. Rev. Michaels used the standard mileage rate to figure his car expense. He multiplied the standard mileage rate of 50 cents by 506 miles for a total of $253. These expenses total $340 ($253 + $87). However, he cannot deduct the part of his expenses allocable to his tax-free housing allowance. He attaches the required statement, Attachment 1 (shown later), to his return showing that 25% (or $85) of his business expenses are not deductible because they are allocable to that tax-free allowance. He subtracts the $85 from the $340 and enters the $255 difference on line 2. Line 3. He enters his net profit of $3,745 both on line 3 and on Form 1040, line 12. Lines 4 through 8b. Rev. Michaels fills out these lines to report information about his car. Turbo Tax tips: Turbo Tax does not appear to calculate the nondeductible portion of the expenses which should be allocated to the tax-free portion of the housing allowance. The taxpayer will need to adjust the expenses (as shown in Attachment 1) and input the reduced figure into the software. Form 2106 EZ Rev. Michaels fills out Form 2106 EZ to report the unreimbursed business expenses he had as a common-law employee of First Baptist Church. Line 1. Before completing line 1, Rev. Michaels fills out Part II because he used his car for church business. His records show that he drove 2,860 business miles, which he reports in Part II. On line 1, he multiplies 2,860 miles driven by the mileage rate of 50 cents. The result of $1,430 is reported on line 1. Line 4. He enters $219 for his professional publications and booklets. Line 6. Before entering the total expenses on line 6, Rev. Michaels must reduce them by the amount allocable to his tax-free parsonage allowance. On the required Attachment 1 (shown later), he shows that 25% (or $412) of his employee business expenses are not deductible because they are allocable to the tax-free parsonage allowance. He subtracts $412 from $1,649 and enters the result, $1,237, on line 6. He also enters $1,237 on line 21 of Schedule A (Form 1040). Turbo Tax tips: Turbo Tax does not appear to calculate the nondeductible portion of the expenses which should be allocated to the tax-free portion of the housing allowance. The taxpayer will need to adjust the expenses (as shown in Attachment 1) and input the reduced figure into the software. Schedule A (Form 1040) Rev. Michaels fills out Schedule A as explained here. Line 5. In 2009, a taxpayer could elect to take an itemized deduction for state and local general sales taxes instead of the itemized deduction permitted for state and local income tax. This provision is not available for Since Rev. and Mrs. Michaels do not pay state income tax, no deduction is available to them on line 5. Line 6. Rev. Michaels deducts $1,750 in real estate taxes. Line 7. For 2010, a taxpayer can deduct certain state and local sales and excise taxes paid in 2010 for the purchase of a new motor vehicle after February 16, 2009 and before January 1, The deduction is limited to the taxes imposed on the first $49,500 of the purchase price of each new motor vehicle. Line 10. He deducts $6,810 of home mortgage interest. Line 16. Rev. and Mrs. Michaels contributed $4,800 in cash during the year to various qualifying charities. Each individual contribution was less than $250. For each contribution, Rev. and Mrs. Michaels maintain the required bank record (such as a canceled check) or written communication from the charity showing the charity s name, the amount of the contribution and the date of the contribution. (This substantiation is required in order for any contribution of money (cash, check or other monetary instrument) made in 2007 and thereafter to be deductible.) Line 21. Rev. Michaels enters his unreimbursed employee business expenses from Form 2106 EZ, line 6. Lines 25, 26 and 27. He can deduct only the part of his employee business expenses that exceeds 2% of his adjusted gross income. He fills out these lines to figure the amount he can deduct. Line 29. The total of all the Michaels itemized deductions is $13,639, which they enter on line 29 and on Form 1040, line 40a. Schedule M (Form 1040) For 2010, taxpayers should use Schedule M to figure the amount available for the Making Work Pay Credit. Rev. Michaels fills out Schedule M as explained here. Line 1a. Rev. and Mrs. Michaels have wages of more than $12,903 so they check Yes and enter $800 (for married filing jointly) on Line 4. Line 4. Rev. Michaels enters $800. Line 5. Rev. Michaels enters the amount from Form 1040, line 38. Line 6. Rev. Michaels enters $150,000 (for married filing jointly). 42

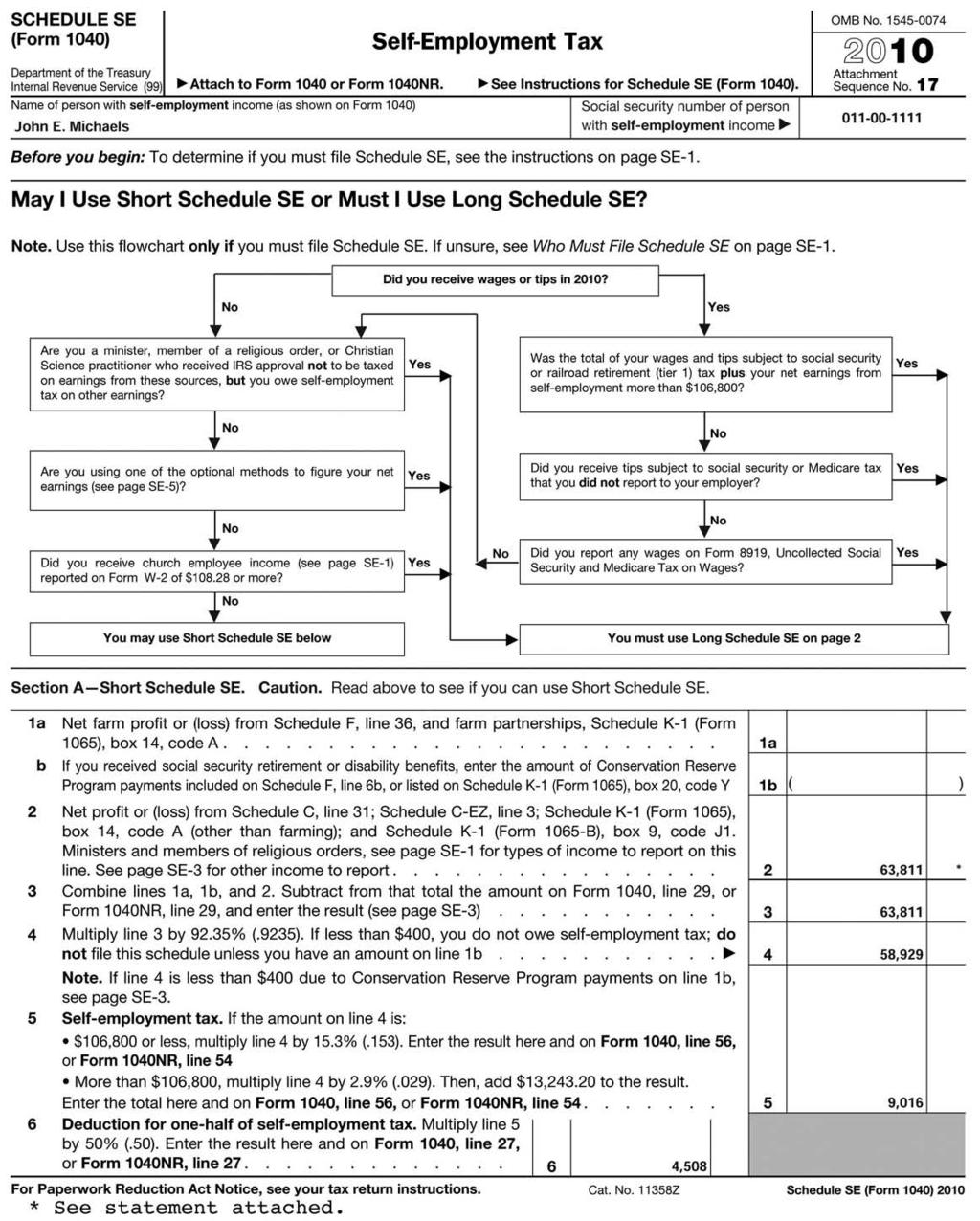

3 Line 7. Since the amount on line 5 is less than the amount on line 6, Rev. Michaels checks No and enters the amount from line 4 on line 9. Line 9. Rev. Michaels enters $800 from line 4. Line 10. Rev. Michaels did not receive an economic recovery payment in 2010, so he responds No and enters zero on line 10. Line 11. Rev. Michaels subtracts line 10 from line 9 and enters $800 here and on Form 1040, line 63. Schedule SE (Form 1040) After Rev. Michaels prepares Schedule C EZ and Form 2106 EZ, he fills out Schedule SE (Form 1040). He reads the chart on page 1 of the schedule which tells him he can use Section A Short Schedule SE to figure his self-employment tax. Rev. Michaels is a minister, so his salary from the church is not considered church employee income. Thus, he does not have to use Section B Long Schedule SE. He fills out the following lines in Section A. Line 2. Rev. Michaels attaches a statement (see Attachment 2, later) that explains how he figures the amount ($63,811) he enters here. Line 4. He multiplies $63,811 by to get his net earnings from self-employment ($58,929). Line 5. The amount on line 4 is less than $106,800, so Rev. Michaels multiplies the amount on line 4 ($58,929) by to get his selfemployment tax of $9,016. He enters that amount here and on Form 1040, line 56. Line 6. Rev. Michaels multiplies the amount on line 5 by 0.5 to get his deduction for one-half of self-employment tax of $4,508. He enters that amount here and on Form 1040, line 27. Turbo Tax tips: The software asks about self-employment tax on clergy wages. The taxpayer should check the box to pay selfemployment tax on wages and housing allowance (assuming, as shown in this example, that the minister has not applied for exemption from the SE tax). Please note that the software does not appear to reduce self-employment wages by the business expenses allocated to tax-free income. The taxpayer will need to adjust net self-employment income (as shown in Attachment 2) and input the reduced figure into the software. Line 7. Rev. Michaels reports $48,640. This amount is the total of his $45,000 church salary, $3,400 college salary, and $240, the excess of the amount designated and paid to him as a housing allowance over the lesser of his actual expenses and the fair rental value of his home (including furnishings and utilities). The two salaries were reported to him in Box 1 of the Forms W 2 he received. Line 12. He reports his net profit of $3,745 from Schedule C EZ, line 3. Line 27. He enters $4,508, one-half of his SE tax from Schedule SE, line 6. Line 37. Subtract line 36 from line 22. This is his adjusted gross income and he carries this amount forward to line 38. Line 40. He enters the total itemized deductions from Schedule A, line 29. Line 42. He multiplies the number of exemptions claimed (3 from Line 6d) by $3,650 and enters an exemption amount of $10,950 on line 42. Line 51. The Michaels can take the child tax credit for their daughter, Jennifer. Rev. Michaels figures the credit by completing the Child Tax Credit Worksheet (not shown) on page 43 of the Form 1040 general instructions. He enters the $1,000 credit. Line 56. He enters the self-employment tax from Schedule SE, line 5. Line 61. He enters the federal income tax shown in Box 2 of his Form W 2 from the college. Line 62. He enters the $12,000 estimated tax payments he made for the year. Line 63. He enters the $800 Making Work Pay Credit from Schedule M, line 11. Form 1040 After Rev. Michaels prepares Form 2106 EZ and the other schedules, he fills out Form He files a joint return with his wife. First he fills out the address area and completes the appropriate lines for his filing status and exemptions. Then he fills out the rest of the form as follows: 43

4 44

5 Find IRS forms, instructions and publications at or call TAX-FORM. 45

6 46

7 47

8 48

9 Find IRS forms, instructions and publications at or call TAX-FORM. 49

10 50

11 Find IRS forms, instructions and publications at or call TAX-FORM. 51

12 52

13 53

Part 4. Comprehensive Examples and Forms Example One: Active minister

Part 4. Comprehensive Examples and Forms Example One: Active minister Note: This example is based on an illustrated example contained at the end of IRS Publication 517. Rev. John Michaels is the minister

Part 4. Comprehensive Examples and Forms Example One: Active minister Note: This example is based on an illustrated example contained at the end of IRS Publication 517. Rev. John Michaels is the minister

Example Two: Retired Minister

Example Two: Retired Minister Form 1040 Rev. William K. Green is a retired minister. He is 69 years old. He is married to Sarah J. Green. She is 65 years old and is also retired. For 2010, Rev. Green received

Example Two: Retired Minister Form 1040 Rev. William K. Green is a retired minister. He is 69 years old. He is married to Sarah J. Green. She is 65 years old and is also retired. For 2010, Rev. Green received

CLERGY TAX & BENEFITS SEMINAR. Insight Into the World of Clergy Taxes and Benefits

CLERGY TAX & BENEFITS SEMINAR Insight Into the World of Clergy Taxes and Benefits AGENDA Welcome and Prayer Introductions & Overview Clergy Compensation Clergy Benefits Other Tax Matters Q&A 2 Clergy Tax

CLERGY TAX & BENEFITS SEMINAR Insight Into the World of Clergy Taxes and Benefits AGENDA Welcome and Prayer Introductions & Overview Clergy Compensation Clergy Benefits Other Tax Matters Q&A 2 Clergy Tax

2011 Tax Return Preparation

2011 Tax Return Preparation and Federal Reporting Guide Tax Guide for 2010 Returns for Ministers Prepared by Richard R. Hammar, J.D., LL.M., CPA Edited by GuideStone Financial Resources of the Southern

2011 Tax Return Preparation and Federal Reporting Guide Tax Guide for 2010 Returns for Ministers Prepared by Richard R. Hammar, J.D., LL.M., CPA Edited by GuideStone Financial Resources of the Southern

See separate instructions. Your social security number GREEN BEAN If a joint return, spouse's first name and initial

Form Department of the Treasury - Internal Revenue Service (99) 1040 U.S. Individual Income Tax Return OMB. 1545-0074 For the year Jan. 1-Dec. 31,, or other tax year beginning,, ending, 0 Your first name

Form Department of the Treasury - Internal Revenue Service (99) 1040 U.S. Individual Income Tax Return OMB. 1545-0074 For the year Jan. 1-Dec. 31,, or other tax year beginning,, ending, 0 Your first name

8/3/2016. Presented by: John L Crandell EA MBA CTRS

Presented by: John L Crandell EA MBA CTRS 1 2 1 At the end of this webinar, you should be able to: Understand what Clergy means Understand what a Housing Allowance is Be able to calculate Self Employment

Presented by: John L Crandell EA MBA CTRS 1 2 1 At the end of this webinar, you should be able to: Understand what Clergy means Understand what a Housing Allowance is Be able to calculate Self Employment

Minister Tax Law. Topics Unique to Ministers. Important Tax Cases and IRS Rulings 8/5/2015

Minister Tax Law Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation August 5, 2015 Topics Unique to Ministers Income Issue: Parsonage/Housing Allowance Gift or Compensation SE Issue:

Minister Tax Law Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation August 5, 2015 Topics Unique to Ministers Income Issue: Parsonage/Housing Allowance Gift or Compensation SE Issue:

Clergy ************************************************************************

Clergy Contents In this webinar, the student will learn the tax treatment of income received by a minister. Objectives After completing this webinar, the student will be able to: Determine if clergy are

Clergy Contents In this webinar, the student will learn the tax treatment of income received by a minister. Objectives After completing this webinar, the student will be able to: Determine if clergy are

Bus. Admin: Ministers Tax Issues Course #E913

Bus. Admin: Ministers Tax Issues Course #E913 Presented by: Stephanie Buduhan, CPA PSK LLP 2018 Shelby Systems, Inc. Other brand and product names are trademarks or registered trademarks of the respective

Bus. Admin: Ministers Tax Issues Course #E913 Presented by: Stephanie Buduhan, CPA PSK LLP 2018 Shelby Systems, Inc. Other brand and product names are trademarks or registered trademarks of the respective

Minister Taxes San Jacinto Baptist Association October 2014

Minister Taxes San Jacinto Baptist Association October 2014 Minister Criteria Credential - Licensed - Commissioned or - Ordained Performance - Conduct of religious worship - Administration & maintenance

Minister Taxes San Jacinto Baptist Association October 2014 Minister Criteria Credential - Licensed - Commissioned or - Ordained Performance - Conduct of religious worship - Administration & maintenance

Tax Guide. for Ministers. Filing Year. The Pension Boards United Church of Christ, Inc.

The Pension Boards United Church of Christ, Inc. 2017 Filing Year Tax Guide for Ministers Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Tax Guide for

The Pension Boards United Church of Christ, Inc. 2017 Filing Year Tax Guide for Ministers Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Tax Guide for

Ministerial Taxation

Ministerial Taxation Minister s Taxation & Reporting Ministers qualify for four special tax rules: Housing allowance exclusion Self-employed status for social security taxation Exemption from withholding

Ministerial Taxation Minister s Taxation & Reporting Ministers qualify for four special tax rules: Housing allowance exclusion Self-employed status for social security taxation Exemption from withholding

Chapter 6. Paying Taxes Pearson Education, Inc. All rights reserved

Chapter 6 Paying Taxes 2010 Pearson Education, Inc. All rights reserved Learning Objectives Describe the basic principles of taxation and the major categories of taxes. Explain payroll taxes Describe the

Chapter 6 Paying Taxes 2010 Pearson Education, Inc. All rights reserved Learning Objectives Describe the basic principles of taxation and the major categories of taxes. Explain payroll taxes Describe the

Part 3. Step-by-Step Tax Return Preparation

Part 3. Step-by-Step Tax Return Preparation TAX FORMS AND SCHEDULES This step-by-step analysis covers these forms and schedules: Form 1040 is the basic document you will use. It summarizes all of your

Part 3. Step-by-Step Tax Return Preparation TAX FORMS AND SCHEDULES This step-by-step analysis covers these forms and schedules: Form 1040 is the basic document you will use. It summarizes all of your

Taxable income (Federal and Social Security) The following are various types of income commonly found on a priest s tax filing:

The following are various types of income commonly found on a priest s tax filing:") Diocese of Madison Policy for Priest Compensation Taxable income (Federal and Social Security) The following are various types of income commonly found on a priest s tax filing: A. Salary and Supplements

Diocese of Madison Policy for Priest Compensation Taxable income (Federal and Social Security) The following are various types of income commonly found on a priest s tax filing: A. Salary and Supplements

TAX RETURN PREPARATION & FEDERAL REPORTING. Ministers Tax Guide for 2015 Returns

Ministers Tax Guide for 2015 Returns 2016 TAX RETURN PREPARATION & FEDERAL REPORTING G U I D E Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Copyright 2016 Christianity Today

Ministers Tax Guide for 2015 Returns 2016 TAX RETURN PREPARATION & FEDERAL REPORTING G U I D E Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Copyright 2016 Christianity Today

WHAT'S NEW ON FORM 1040 FOR TAX YEAR 2014

Page 1 of 5 WHAT'S NEW ON FORM 1040 FOR TAX YEAR 2014 The IRS has electronically released final tax forms and instructions for the 2014 tax year, including Forms 1040, 1040-A, and 1040-EZ, along with some

Page 1 of 5 WHAT'S NEW ON FORM 1040 FOR TAX YEAR 2014 The IRS has electronically released final tax forms and instructions for the 2014 tax year, including Forms 1040, 1040-A, and 1040-EZ, along with some

1 of 14 8/10/ :45 PM

1 of 14 8/10/2016 11:45 PM Publication 503 - Main Content Table of Contents Tests To Claim the Credit Qualifying Person Test Earned Income Test Work-Related Expense Test Joint Return Test Provider Identification

1 of 14 8/10/2016 11:45 PM Publication 503 - Main Content Table of Contents Tests To Claim the Credit Qualifying Person Test Earned Income Test Work-Related Expense Test Joint Return Test Provider Identification

Income Tax Guide and Organizer for 2017

Income Tax Guide and Organizer for 2017 Email: rwa@blueriver.net Web site: www.rwataxservice.com phone: 812.586.0420 Before doing the booklet, please print out or read the informational sheet as it has

Income Tax Guide and Organizer for 2017 Email: rwa@blueriver.net Web site: www.rwataxservice.com phone: 812.586.0420 Before doing the booklet, please print out or read the informational sheet as it has

TABLE OF CONTENTS. Overview Who Qualifies for Special Tax Treatment as a Minister Income to Be Reported The Parsonage Allowance...

TABLE OF CONTENTS Overview... 1 Who Qualifies for Special Tax Treatment as a Minister... 2 Income to Be Reported... 5 The Parsonage Allowance... 6 Business Expenses... 11 Self-Employment Tax: Exemption...

TABLE OF CONTENTS Overview... 1 Who Qualifies for Special Tax Treatment as a Minister... 2 Income to Be Reported... 5 The Parsonage Allowance... 6 Business Expenses... 11 Self-Employment Tax: Exemption...

Form 1040-V. Department of the Treasury. Internal Revenue Service $ 3, Dave Dave Sarah Sarah Terrace Glenview, IL 60001

2006 Form 040-V Department of the Treasury Internal Revenue Service For Privacy Act and Paperwork Reduction Act tice, see separate instructions. DETACH HERE Form 040 (2006) Department of the Treasury Internal

2006 Form 040-V Department of the Treasury Internal Revenue Service For Privacy Act and Paperwork Reduction Act tice, see separate instructions. DETACH HERE Form 040 (2006) Department of the Treasury Internal

PART 3 Step-by-Step Tax Return Preparation

PART 3 Step-by-Step Tax Return Preparation TAX FORMS AND SCHEDULES This step-by-step analysis covers these forms and schedules: Form 1040 is the basic document you will use. It summarizes all of your tax

PART 3 Step-by-Step Tax Return Preparation TAX FORMS AND SCHEDULES This step-by-step analysis covers these forms and schedules: Form 1040 is the basic document you will use. It summarizes all of your tax

2014 Tax Guide. For Episcopal Ministers For 2013 Tax Returns. Prepared by Richard R. Hammar, J.D., LL.M., CPA. Publish date: February 6, 2014

2014 Tax Guide For Episcopal Ministers For 2013 Tax Returns Prepared by Richard R. Hammar, J.D., LL.M., CPA Publish date: February 6, 2014 Editors: Matthew K. Chew, CPA The Reverend Canon William F. Geisler,

2014 Tax Guide For Episcopal Ministers For 2013 Tax Returns Prepared by Richard R. Hammar, J.D., LL.M., CPA Publish date: February 6, 2014 Editors: Matthew K. Chew, CPA The Reverend Canon William F. Geisler,

Company Car Guidelines

December 2017 Company Car Guidelines As year end approaches, it is time to start thinking about preparing W-2 s. One commonly asked question is How should employees personal use of company automobiles

December 2017 Company Car Guidelines As year end approaches, it is time to start thinking about preparing W-2 s. One commonly asked question is How should employees personal use of company automobiles

CONGREGATIONAL/MINISTERIAL INCOME TAX GUIDELINES

CONGREGATIONAL/MINISTERIAL INCOME TAX GUIDELINES Updated For 2016 Tax Returns By Carl A. Hess The new year brings a reminder that tax season is also here and deserves our attention. This document is to

CONGREGATIONAL/MINISTERIAL INCOME TAX GUIDELINES Updated For 2016 Tax Returns By Carl A. Hess The new year brings a reminder that tax season is also here and deserves our attention. This document is to

Tax Guide. for Ministers. Filing Year. The Pension Boards United Church of Christ, Inc.

The Pension Boards United Church of Christ, Inc. 2012 Filing Year Tax Guide for Ministers Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Tax Guide for

The Pension Boards United Church of Christ, Inc. 2012 Filing Year Tax Guide for Ministers Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Tax Guide for

Filing status: Single Married filing jointly Married filing separately Head of household Qualifying widow(er)

") -Internal Revenue Service (99) 1040 U.S. Individual Income Tax Return 018 IRS Use Only-Do not write or staple in this space. Filing status: Single Married filing jointly Married filing separately Head

-Internal Revenue Service (99) 1040 U.S. Individual Income Tax Return 018 IRS Use Only-Do not write or staple in this space. Filing status: Single Married filing jointly Married filing separately Head

Appendix B Pali Rao, istockphoto

Appendix B Pali Rao, istockphoto Tax Forms (Tax forms can be obtained from the IRS website: www.irs.gov) Form 1040 U.S. Individual Income Tax Return B-2 Schedule C Profit or Loss from Business B-4 Schedule

Appendix B Pali Rao, istockphoto Tax Forms (Tax forms can be obtained from the IRS website: www.irs.gov) Form 1040 U.S. Individual Income Tax Return B-2 Schedule C Profit or Loss from Business B-4 Schedule

2017 Minister s Tax Organizer Supplement

Please make a copy of this tax organizer for your records before you send to us. 2017 Minister s Tax Organizer Supplement Peachtree Tax Advisors, LLC 500 East Second Street Rome, GA 30161-3112 706-234-7468

Please make a copy of this tax organizer for your records before you send to us. 2017 Minister s Tax Organizer Supplement Peachtree Tax Advisors, LLC 500 East Second Street Rome, GA 30161-3112 706-234-7468

Ministers Tax Guide for 2017 Returns TAX RETURN PREPARATION. Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report

Ministers Tax Guide for 2017 Returns 2018 TAX RETURN PREPARATION G U I D E Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Copyright 2018 Christianity Today International. Clergy

Ministers Tax Guide for 2017 Returns 2018 TAX RETURN PREPARATION G U I D E Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Copyright 2018 Christianity Today International. Clergy

JOSEPH COHEN If a joint return, spouse's first name and initial Last name Spouse's social security number

Department of the Treasury ' Internal Revenue Service (99) Form 1040 U.S. Individual Income Tax Return 2012 OMB No. 1545-0074 IRS Use Only ' Do not write or staple in this space. For the year Jan 1 - Dec

Department of the Treasury ' Internal Revenue Service (99) Form 1040 U.S. Individual Income Tax Return 2012 OMB No. 1545-0074 IRS Use Only ' Do not write or staple in this space. For the year Jan 1 - Dec

TAXATION OF CLERGY & OTHER CALLED WORKERS

TAXATION OF CLERGY & OTHER CALLED WORKERS January 2017 Presented by David Mellem, EA This text is written to provide accurate and authoritative information regarding the subject matter. The information

TAXATION OF CLERGY & OTHER CALLED WORKERS January 2017 Presented by David Mellem, EA This text is written to provide accurate and authoritative information regarding the subject matter. The information

Vehicle Non-Cash Fringe Benefits Reporting Requirements

PERCY S. YANG, CPA, ABV KATHLEEN M. ALAMEDA, CPA DEBRA K. DOBLE, CPA JENNIFER D. CASTELLUCCIO, CPA YUAN CAI, CPA ALAN HA, CPA VENUS JANDU, CPA JAN L. JONES, CPA MICHAEL R. RAMIL, CPA JOHN ROSENTHAL, CPA

PERCY S. YANG, CPA, ABV KATHLEEN M. ALAMEDA, CPA DEBRA K. DOBLE, CPA JENNIFER D. CASTELLUCCIO, CPA YUAN CAI, CPA ALAN HA, CPA VENUS JANDU, CPA JAN L. JONES, CPA MICHAEL R. RAMIL, CPA JOHN ROSENTHAL, CPA

5 Qualifying widow(er) (see instructions) 6a Yourself. If someone can claim you as a dependent, do not check box 6a...

(see instructions) 6a Yourself. If someone can claim you as a dependent, do not check box 6a...") Form 1040 Department of the Treasury Internal Revenue Service (99) U.S. Individual Income Tax Return 2017 OMB No. 1545-0074 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31,

Form 1040 Department of the Treasury Internal Revenue Service (99) U.S. Individual Income Tax Return 2017 OMB No. 1545-0074 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31,

JANUARY 2017 EMPLOYEE OR INDEPENDENT CONTRACTOR

JANUARY 2017 GUIDELINES TO OBLIGATIONS OF BRANCH CHURCHES AND SOCIETIES TO WITHHOLD FEDERAL INCOME AND SOCIAL SECURITY TAXES AND TO REPORT COMPENSATION; AND OTHER INFORMATION EMPLOYEE OR INDEPENDENT CONTRACTOR

JANUARY 2017 GUIDELINES TO OBLIGATIONS OF BRANCH CHURCHES AND SOCIETIES TO WITHHOLD FEDERAL INCOME AND SOCIAL SECURITY TAXES AND TO REPORT COMPENSATION; AND OTHER INFORMATION EMPLOYEE OR INDEPENDENT CONTRACTOR

Q1. Why is it necessary for me to complete a new Employee s Withholding Allowance Certificate for tax year 2014?

General Frequently Asked Questions Q1. Why is it necessary for me to complete a new Employee s Withholding Allowance Certificate for tax year 2014? A1. The North Carolina General Assembly recently enacted

General Frequently Asked Questions Q1. Why is it necessary for me to complete a new Employee s Withholding Allowance Certificate for tax year 2014? A1. The North Carolina General Assembly recently enacted

Don t fill in cents. Round off cents to the nearest dollar. For example, $99.49 becomes $99.00, and $99.50 becomes $

Page 1 of 3, 150-206-643 (Rev. 08-18) Oregon Department of Revenue 04131801010000 Instructions: Read Oregon Income Tax Withholding Information prior to completing this worksheet. Complete Part A to determine

Page 1 of 3, 150-206-643 (Rev. 08-18) Oregon Department of Revenue 04131801010000 Instructions: Read Oregon Income Tax Withholding Information prior to completing this worksheet. Complete Part A to determine

Tax Preparation Guide. for 2012 returns RETIREMENT. Including the Federal Reporting Requirements for Churches PCA & BENEFITS, INC.

PCA RETIREMENT & BENEFITS, INC. 2013 Tax Preparation Guide for 2012 returns Including the Federal Reporting Requirements for Churches Prepared by Richard R. Hammar, J.D., LL.M., CPA Senior Editor, CHURCH

PCA RETIREMENT & BENEFITS, INC. 2013 Tax Preparation Guide for 2012 returns Including the Federal Reporting Requirements for Churches Prepared by Richard R. Hammar, J.D., LL.M., CPA Senior Editor, CHURCH

Clergy Tax Return Preparation Guide for 2017 Returns*

2018 Clergy Tax Return Preparation Guide for 2017 Returns* Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Copyright 2018 Christianity Today International. Clergy Tax Return

2018 Clergy Tax Return Preparation Guide for 2017 Returns* Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Copyright 2018 Christianity Today International. Clergy Tax Return

See separate instructions. Your social security number RIGHT ANGLE If a joint return, spouse's first name and initial

Form Department of the Treasury - Internal Revenue Service (99) 14 U.S. Individual Income Tax Return OMB No. 1545-74 For the year Jan. 1-Dec. 31,, or other tax year beginning,, ending, 2 Your first name

Form Department of the Treasury - Internal Revenue Service (99) 14 U.S. Individual Income Tax Return OMB No. 1545-74 For the year Jan. 1-Dec. 31,, or other tax year beginning,, ending, 2 Your first name

CLERGY TAXES Q & A **Updated Feb. 22, 2018**

CLERGY TAXES Q & A **Updated Feb. 22, 2018** On Monday, Feb. 12, 2018 Discipleship Ministries presented a webinar on clergy taxes, and at the end we asked attendees to send us their questions. While this

CLERGY TAXES Q & A **Updated Feb. 22, 2018** On Monday, Feb. 12, 2018 Discipleship Ministries presented a webinar on clergy taxes, and at the end we asked attendees to send us their questions. While this

See separate instructions. Your social security number RIGHT ANGLE XXX-XX-XXXX If a joint return, spouse's first name and initial

Form Department of the Treasury - Internal Revenue Service (99) 14 U.S. Individual Income Tax Return 216 OMB No. 1545-74 For the year Jan. 1-Dec. 31, 216, or other tax year beginning, 216, ending, 2 Your

Form Department of the Treasury - Internal Revenue Service (99) 14 U.S. Individual Income Tax Return 216 OMB No. 1545-74 For the year Jan. 1-Dec. 31, 216, or other tax year beginning, 216, ending, 2 Your

How Do I Adjust My Tax Withholding?

Contents Department of the Treasury Internal Revenue Service What s New for 2011... 2 Reminder.... Publication 919 Introduction... 3 Cat. No. 63900P How Do I Adjust My Tax Withholding? Checking Your Withholding...

Contents Department of the Treasury Internal Revenue Service What s New for 2011... 2 Reminder.... Publication 919 Introduction... 3 Cat. No. 63900P How Do I Adjust My Tax Withholding? Checking Your Withholding...

Tax Guide Appendix

ThePe ns i onboa r ds Uni t e dchur c hofchr i s t,i nc. 2 0 1 8 F i l i ngye a r T a xg u i d e f ormi ni s t e r s Pr e pa r e dbychur c hl a w &T a xre por t Publ i s he dbythepe ns i onboa r ds Uni

ThePe ns i onboa r ds Uni t e dchur c hofchr i s t,i nc. 2 0 1 8 F i l i ngye a r T a xg u i d e f ormi ni s t e r s Pr e pa r e dbychur c hl a w &T a xre por t Publ i s he dbythepe ns i onboa r ds Uni

COVER PAGE. Filing Checklist for 2014 Tax Return Filed On Standard Forms. Prepared on: 11/05/ :49:43 am

COVER PAGE Filing Checklist for 214 Tax Return Filed On Standard Forms Prepared on: 11/5/215 5:49:43 am Return: :\IAG\Presentations\Self-Employment Child Support 11515\Jim Fardashian 214 Tax Return.T14

COVER PAGE Filing Checklist for 214 Tax Return Filed On Standard Forms Prepared on: 11/5/215 5:49:43 am Return: :\IAG\Presentations\Self-Employment Child Support 11515\Jim Fardashian 214 Tax Return.T14

MINISTERS FOR 2016 RETURNS

TAX GUIDE for MINISTERS FOR 2016 RETURNS Prepared by Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Presented by Board University of The Board of Pensions of the Presbyterian

TAX GUIDE for MINISTERS FOR 2016 RETURNS Prepared by Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Presented by Board University of The Board of Pensions of the Presbyterian

2018 Compensation Policy

Summary 2018 Compensation Policy It is the policy of Newark Presbytery that its member churches shall provide equitable compensation of pastors and shall meet or exceed the minimum amounts specified for

Summary 2018 Compensation Policy It is the policy of Newark Presbytery that its member churches shall provide equitable compensation of pastors and shall meet or exceed the minimum amounts specified for

Do your taxes online with H&R Block. Do your taxes online with H&R Block. Do your taxes online with H&R Block.

Send Friend (2004) FDFRNDOL-1WV 1.0 Send a friend to us. We'll thank you both with cash! 5 for you. 10 for your friend! Easy-to-follow instructions: 1. 2. 3. Give one of the forms below to a friend and

Send Friend (2004) FDFRNDOL-1WV 1.0 Send a friend to us. We'll thank you both with cash! 5 for you. 10 for your friend! Easy-to-follow instructions: 1. 2. 3. Give one of the forms below to a friend and

Northwestern Pennsylvania Synod, ELCA Compensation Guidelines Compensation Standards for Rostered Leaders

Northwestern Pennsylvania Synod, ELCA Compensation Guidelines Compensation Standards for Rostered Leaders -- 2018 Rostered Leader compensation is to be revisited and renegotiated annually. Compensation

Northwestern Pennsylvania Synod, ELCA Compensation Guidelines Compensation Standards for Rostered Leaders -- 2018 Rostered Leader compensation is to be revisited and renegotiated annually. Compensation

Persons Not Eligible for the Standard Deduction

Exhibit 1 Standard Deduction for Most People* This table provides the standard deduction amounts for tax year 2016. If the taxpayer s filing status is... Your standard deduction is... Single or married

Exhibit 1 Standard Deduction for Most People* This table provides the standard deduction amounts for tax year 2016. If the taxpayer s filing status is... Your standard deduction is... Single or married

SCHEDULE C AUDIT RISKS

7/15/2017 SCHEDULE C AUDIT RISKS C. FORREST DAVIS, E.A. A LOOK AT TAX RETURNS (2014) 148.6M individual returns 63.7M Form 1040A and EZ 84.9M Form 1040 27.6M Schedule C or C-EZ 22.6M Schedule C 5.0M Sch

7/15/2017 SCHEDULE C AUDIT RISKS C. FORREST DAVIS, E.A. A LOOK AT TAX RETURNS (2014) 148.6M individual returns 63.7M Form 1040A and EZ 84.9M Form 1040 27.6M Schedule C or C-EZ 22.6M Schedule C 5.0M Sch

Individual Tax Deductions

Individual Tax Deductions What you need to know for 2017 filings. A review of the most often used deductions for individuals, including which ones ARE (temporarily) going away. Disclaimer Presentations,

Individual Tax Deductions What you need to know for 2017 filings. A review of the most often used deductions for individuals, including which ones ARE (temporarily) going away. Disclaimer Presentations,

The IRS Will Figure Your Tax

Department of the Treasury Internal Revenue Service Publication 967 Cat. No. 22402M The IRS Will Figure Your Tax Introduction You can have the IRS figure your tax on Form 1040EZ, Form 1040A, or Form 1040

Department of the Treasury Internal Revenue Service Publication 967 Cat. No. 22402M The IRS Will Figure Your Tax Introduction You can have the IRS figure your tax on Form 1040EZ, Form 1040A, or Form 1040

Tax Withholding and Estimated Tax

This publication was cited in a footnote at the Bradford Tax Institute. ClLICK HERE to go to the home page. Department of the Treasury Internal Revenue Service Publication 505 Cat. No. 15008E Tax Withholding

This publication was cited in a footnote at the Bradford Tax Institute. ClLICK HERE to go to the home page. Department of the Treasury Internal Revenue Service Publication 505 Cat. No. 15008E Tax Withholding

Church and Taxes. San Jacinto Baptist Association October 2014

Church and Taxes San Jacinto Baptist Association October 2014 The Affordable Care Act 1. Health FSA (flexible spending accounts) capped $2,500 2. Modified the itemized deduction for medical expenses increased

Church and Taxes San Jacinto Baptist Association October 2014 The Affordable Care Act 1. Health FSA (flexible spending accounts) capped $2,500 2. Modified the itemized deduction for medical expenses increased

CHAPTER 12 TAX RETURN ASSIGNMENT

A-PDF Merger DEMO : Purchase from www.a-pdf.com to remove the watermark Name: Nargiz CHAPTER 12 TAX RETURN ASSIGNMENT Using the data for NOAH AND JOAN ARC (Comprehensive Problem One from Appendix D, on

A-PDF Merger DEMO : Purchase from www.a-pdf.com to remove the watermark Name: Nargiz CHAPTER 12 TAX RETURN ASSIGNMENT Using the data for NOAH AND JOAN ARC (Comprehensive Problem One from Appendix D, on

1040 U.S. Individual Income Tax Return 2017

F or Department of the Treasury Internal Revenue Service (99) 14 U.S. Individual Income Tax Return 17 m OMB No. 1545-74 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31, 17,

F or Department of the Treasury Internal Revenue Service (99) 14 U.S. Individual Income Tax Return 17 m OMB No. 1545-74 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31, 17,

Frequently asked Questions: Donations. General Council of the Assemblies of God Division of the Treasury

Frequently asked Questions: Donations General Council of the Assemblies of God Division of the Treasury 1 FREQUENTLY ASKED QUESTIONS CONCERNING DONATIONS QUESTIONS ADDRESSED IN THIS PAMPHLET What are appropriate

Frequently asked Questions: Donations General Council of the Assemblies of God Division of the Treasury 1 FREQUENTLY ASKED QUESTIONS CONCERNING DONATIONS QUESTIONS ADDRESSED IN THIS PAMPHLET What are appropriate

Understanding Taxes. and understanding your paycheck!

Understanding Taxes and understanding your paycheck! Summarize the purpose of paying taxes. Recognize the parts of a paystub. Differentiate between net and gross income. Explain what W-2 and W-4 forms

Understanding Taxes and understanding your paycheck! Summarize the purpose of paying taxes. Recognize the parts of a paystub. Differentiate between net and gross income. Explain what W-2 and W-4 forms

Oregon-Idaho Annual Conference

Oregon-Idaho Annual Conference The United Methodist Church 1505 SW 18 th Avenue Portland OR 97201 503.226.7931 1.800.593.7539 www.umoi.org W-2 Instructions and other General Tax Information Remember that

Oregon-Idaho Annual Conference The United Methodist Church 1505 SW 18 th Avenue Portland OR 97201 503.226.7931 1.800.593.7539 www.umoi.org W-2 Instructions and other General Tax Information Remember that

INSTRUCTIONS FOR 2009 PIT-RC SCHEDULE NEW MEXICO REBATE AND CREDIT SCHEDULE

INSTRUCTIONS FOR 2009 PIT-RC SCHEDULE NEW MEXICO REBATE AND CREDIT SCHEDULE GENERAL INFORMATION SECTION I The questions in SECTION I must be answered to claim any of the rebates or credits reported in

INSTRUCTIONS FOR 2009 PIT-RC SCHEDULE NEW MEXICO REBATE AND CREDIT SCHEDULE GENERAL INFORMATION SECTION I The questions in SECTION I must be answered to claim any of the rebates or credits reported in

SECTION 1: FILLING OUT THE COMPENSATION PACKAGE

STATED SUPPLY AGREEMENT for Minister Members of New Hope Presbytery Section 1. Filling out the Compensation Pkg. Page 1-2 Section 3. Min. Standards of Compensation Page 4 Section 2. Effective Salary Information

STATED SUPPLY AGREEMENT for Minister Members of New Hope Presbytery Section 1. Filling out the Compensation Pkg. Page 1-2 Section 3. Min. Standards of Compensation Page 4 Section 2. Effective Salary Information

Standard Deductions. MACRS Recovery Periods. Tax Preparers Due Diligence Requirements for EITC Medical Savings Accounts (MSA)

") Tax Preparers Due Diligence Requirements for EITC Paid preparers who file EITC returns or claims for refunds for clients must meet four due diligence requirements. Those who fail to do so can be assessed

Tax Preparers Due Diligence Requirements for EITC Paid preparers who file EITC returns or claims for refunds for clients must meet four due diligence requirements. Those who fail to do so can be assessed

WORKSHEET #2 - Employee Statement to Employer Employee using vehicle completes ALL OF Worksheet #2 and gives to employer.

October 2015 Dear Employer: As you know, the Internal Revenue Service (IRS) treats an employee s personal use of a company vehicle as an employee benefit, to be either reimbursed to the company by the

October 2015 Dear Employer: As you know, the Internal Revenue Service (IRS) treats an employee s personal use of a company vehicle as an employee benefit, to be either reimbursed to the company by the

2013 Instructions for Schedule E (Form 1040)

") Department of the Treasury Internal Revenue Service 2013 Instructions for Schedule E (Form 1040) Supplemental Income and Loss Use Schedule E (Form 1040) to report income or loss from rental real estate,

Department of the Treasury Internal Revenue Service 2013 Instructions for Schedule E (Form 1040) Supplemental Income and Loss Use Schedule E (Form 1040) to report income or loss from rental real estate,

Top 10 Questions that Ministers, Missionaries, and Church Treasurers Ask Tax Preparers (Updated: December 11, 2014)

") Based on our experience, the following are frequent questions asked by ministers, missionaries, church treasurers, and others serving in ministry positions as licensed or ordained ministers. Our answers

Based on our experience, the following are frequent questions asked by ministers, missionaries, church treasurers, and others serving in ministry positions as licensed or ordained ministers. Our answers

Form CT-1040ES Estimated Connecticut Income Tax Payment Coupon for Individuals

Department of Revenue Services State of Connecticut Form CT-1040ES 2017 Estimated Connecticut Income Tax Payment Coupon for Individuals 2017 (Rev. 01/17) Complete this form in blue or black ink only. Who

Department of Revenue Services State of Connecticut Form CT-1040ES 2017 Estimated Connecticut Income Tax Payment Coupon for Individuals 2017 (Rev. 01/17) Complete this form in blue or black ink only. Who

1040 U.S. Individual Income Tax Return 2017

F or Department of the Treasury Internal Revenue Service (99) 14 U.S. Individual Income Tax Return 217 m OMB No. 1545-74 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31,

F or Department of the Treasury Internal Revenue Service (99) 14 U.S. Individual Income Tax Return 217 m OMB No. 1545-74 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31,

Federal Reporting. The Pension Boards United Church of Christ, Inc.

The Pension Boards United Church of Christ, Inc. 2019 Federal Reporting Requirements for Churches Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Click

The Pension Boards United Church of Christ, Inc. 2019 Federal Reporting Requirements for Churches Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Click

Social Security Card(s) or Numbers for all family members listed on return.

or Numbers for all family members listed on return.") Social Security Card(s) or Numbers for all family members listed on return. If you have your Social Security card, bring it with you to the appointment. If you have changed your name (due to marriage,

Social Security Card(s) or Numbers for all family members listed on return. If you have your Social Security card, bring it with you to the appointment. If you have changed your name (due to marriage,

Accounting for Churches. Jerry L Walker, CPA

Accounting for Churches By Jerry L Walker, CPA TABLE OF CONTENTS Worker Classifications... 1 Do ministers receive special tax treatment?... 1 Who is considered a minister for tax purposes?... 1 Is a part-time

Accounting for Churches By Jerry L Walker, CPA TABLE OF CONTENTS Worker Classifications... 1 Do ministers receive special tax treatment?... 1 Who is considered a minister for tax purposes?... 1 Is a part-time

Student's Guide to Federal Income Tax

Publication 4 Cat. No. 46073X Department of the Treasury Internal Revenue Service Student's Guide to Federal Income Tax For use in preparing 1998 Returns Contents Introduction... 2 Where Do My Tax Dollars

Publication 4 Cat. No. 46073X Department of the Treasury Internal Revenue Service Student's Guide to Federal Income Tax For use in preparing 1998 Returns Contents Introduction... 2 Where Do My Tax Dollars

Federal Reporting Requirements for Churches

Federal Reporting Requirements for Churches Prepared by Richard R. Hammar, J.D., LL.M., CPA Senior Editor, CHURCH LAW & TAX REPORT Copyright 2013 Christianity Today International. Federal Reporting Requirements

Federal Reporting Requirements for Churches Prepared by Richard R. Hammar, J.D., LL.M., CPA Senior Editor, CHURCH LAW & TAX REPORT Copyright 2013 Christianity Today International. Federal Reporting Requirements

social security number relationship to you ASHLEY SPOCK DAUGHTER X MORGAN SPOCK DAUGHTER X Dependents on 6c not entered above

Form 1040 Department of the Treasury Internal Revenue Service (99) U.S. Individual Income Tax Return 2017 OMB No. 1545-0074 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31,

Form 1040 Department of the Treasury Internal Revenue Service (99) U.S. Individual Income Tax Return 2017 OMB No. 1545-0074 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31,

Prepare, print, and e-file your federal tax return for free!

Prepare, print, and e-file your federal tax return for free! www.freetaxusa.com SCHEDULE 8812 (Form A or ) Department of the Treasury Internal Revenue Service (99) Name(s) shown on return Child Tax Credit

Prepare, print, and e-file your federal tax return for free! www.freetaxusa.com SCHEDULE 8812 (Form A or ) Department of the Treasury Internal Revenue Service (99) Name(s) shown on return Child Tax Credit

Paying Your Income Taxes. Advanced Level

Paying Your Income Taxes Advanced Level What are taxes? A sum of money demanded by a government for support of itself and specific programs and services; paid by taxpayers Take Charge Today February 2017

Paying Your Income Taxes Advanced Level What are taxes? A sum of money demanded by a government for support of itself and specific programs and services; paid by taxpayers Take Charge Today February 2017

Federal Reporting. The Pension Boards United Church of Christ, Inc.

The Pension Boards United Church of Christ, Inc. 2015 Federal Reporting Requirements for Churches Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Federal

The Pension Boards United Church of Christ, Inc. 2015 Federal Reporting Requirements for Churches Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Federal

5 Qualifying widow(er) with dependent child 6a Yourself. If someone can claim you as a dependent, do not check box 6a...

with dependent child 6a Yourself. If someone can claim you as a dependent, do not check box 6a...") Form 1040 Department of the Treasury Internal Revenue Service (99) U.S. Individual Income Tax Return OMB No. 1545-0074 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31,, or

Form 1040 Department of the Treasury Internal Revenue Service (99) U.S. Individual Income Tax Return OMB No. 1545-0074 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31,, or

Advanced Course Scenarios and Test Questions

Advanced Course Scenarios and Test Questions Directions The first four scenarios do not require you to prepare a tax return. Read the interview notes for each scenario carefully and use your training and

Advanced Course Scenarios and Test Questions Directions The first four scenarios do not require you to prepare a tax return. Read the interview notes for each scenario carefully and use your training and

2018 Tax Guide For Episcopal Ministers For 2017 Tax Returns

2018 Tax Guide For Episcopal Ministers For 2017 Tax Returns Prepared by Richard R. Hammar, J.D., LL.M., CPA Publish date: February 23, 2018 Editors: The Reverend Canon William F. Geisler, CPA-Retired Nancy

2018 Tax Guide For Episcopal Ministers For 2017 Tax Returns Prepared by Richard R. Hammar, J.D., LL.M., CPA Publish date: February 23, 2018 Editors: The Reverend Canon William F. Geisler, CPA-Retired Nancy

Determining your 2016 stock plan tax requirements a step-by-step guide

Determining your 2016 stock plan tax requirements a step-by-step guide INSIDE How to use the Supplemental Form to avoid overpaying taxes Upon selling shares acquired from a nonqualified employee stock

Determining your 2016 stock plan tax requirements a step-by-step guide INSIDE How to use the Supplemental Form to avoid overpaying taxes Upon selling shares acquired from a nonqualified employee stock

Form1040-ES/V (OCR) Department of the Treasury Internal Revenue Service

Department of the Treasury Internal Revenue Service") Form1040-ES/V (OCR) Department Treasury Internal Revenue Service Purpose of This Package Use this package to figure and pay your estimated tax. If you are not required to make estimated tax payments for

Form1040-ES/V (OCR) Department Treasury Internal Revenue Service Purpose of This Package Use this package to figure and pay your estimated tax. If you are not required to make estimated tax payments for

2001 Instructions for Schedule E, Supplemental Income and Loss

2001 Instructions for Schedule E, Supplemental Income and Loss Use Schedule E (Form 1040) to report income or loss from rental real estate, royalties, partnerships, S corporations, estates, trusts, and

2001 Instructions for Schedule E, Supplemental Income and Loss Use Schedule E (Form 1040) to report income or loss from rental real estate, royalties, partnerships, S corporations, estates, trusts, and

A & B Office. Education Benefits. A Self-Improvement Mini-Course. Student Loan Interest & Education Expenses. Income Tax Training School

A & B Office Income Tax Training School Education Benefits Student Loan Interest & Education Expenses Key Features: Learn how to properly calculate education expenses. Step-by-step description of the education

A & B Office Income Tax Training School Education Benefits Student Loan Interest & Education Expenses Key Features: Learn how to properly calculate education expenses. Step-by-step description of the education

Orthodox Church in America Tax Help for Parish Treasurers

Orthodox Church in America Tax Help for Parish Treasurers INTRODUCTION Taxes in the United States are complex and consequences for noncompliance can be significant. Furthermore, there are nuances in the

Orthodox Church in America Tax Help for Parish Treasurers INTRODUCTION Taxes in the United States are complex and consequences for noncompliance can be significant. Furthermore, there are nuances in the

Your first name and initial Last name Your social security number

Form 1040 Internal Revenue Service (99) U.S. Individual Income Tax Return OMB. 1545-0074 IRS Use Only Do not write or staple in this space. Filing status: Single Married filing jointly Married filing separately

Form 1040 Internal Revenue Service (99) U.S. Individual Income Tax Return OMB. 1545-0074 IRS Use Only Do not write or staple in this space. Filing status: Single Married filing jointly Married filing separately

ELIGIBLE. Earned Income Credit (EIC)

") Department of the Treasury Internal Revenue Service Publication 596 Cat. No. 15173A Earned Income Credit (EIC) For use in preparing 2003 Returns?ARE YOU ELIGIBLE Look inside for... Detailed Examples Eligibility

Department of the Treasury Internal Revenue Service Publication 596 Cat. No. 15173A Earned Income Credit (EIC) For use in preparing 2003 Returns?ARE YOU ELIGIBLE Look inside for... Detailed Examples Eligibility

New IRS Audit Guidelines for Ministers

New IRS Audit Guidelines for Ministers In April 2009 the IRS released the new audit guidelines for ministers. Now this doesn t necessarily mean that ministers will be targets of audits in 2010 but it could

New IRS Audit Guidelines for Ministers In April 2009 the IRS released the new audit guidelines for ministers. Now this doesn t necessarily mean that ministers will be targets of audits in 2010 but it could

Compensation and Benefits Guidelines for Lay and Clergy Employees. Revised October 2014

2015 Compensation and Benefits Guidelines for Lay and Clergy Employees Revised October 2014 Page 2 Page 3 Table of Contents INTRODUCTION... 5 COMPENSATION... 6 COMPENSATION FOR PRIESTS AND TRANSITIONAL

2015 Compensation and Benefits Guidelines for Lay and Clergy Employees Revised October 2014 Page 2 Page 3 Table of Contents INTRODUCTION... 5 COMPENSATION... 6 COMPENSATION FOR PRIESTS AND TRANSITIONAL

Your first name and initial Last name Your social security number

1040 Department of the Treasury Internal Revenue Service (99) U.S. Individual Income Tax Return OMB No. 1545-0074 IRS Use Only Do not write or staple in this space. Filing status: Single X Married filing

1040 Department of the Treasury Internal Revenue Service (99) U.S. Individual Income Tax Return OMB No. 1545-0074 IRS Use Only Do not write or staple in this space. Filing status: Single X Married filing

Earned Income Credit i

Earned Income Credit i ALL RIGHTS RESERVED. NO PART OF THIS COURSE MAY BE REPRODUCED IN ANY FORM OR BY ANY MEANS WITHOUT THE WRITTEN PERMISSION OF THE COPYRIGHT HOLDER. All materials relating to this course

Earned Income Credit i ALL RIGHTS RESERVED. NO PART OF THIS COURSE MAY BE REPRODUCED IN ANY FORM OR BY ANY MEANS WITHOUT THE WRITTEN PERMISSION OF THE COPYRIGHT HOLDER. All materials relating to this course

MINISTER S GUIDE for 2017 Income Tax

Sixty-Second Annual Edition MINISTER S GUIDE for 2017 Income Tax by Conrad Teitell, LL.B., LL.M. . TABLE OF CONTENTS I. Are You a Church Employee or a Self-Employed Minister?......... 5 A. Form W-2.........................................

Sixty-Second Annual Edition MINISTER S GUIDE for 2017 Income Tax by Conrad Teitell, LL.B., LL.M. . TABLE OF CONTENTS I. Are You a Church Employee or a Self-Employed Minister?......... 5 A. Form W-2.........................................

COVER PAGE. Filing Checklist For 2009 Tax Return Filed On Standard Forms. Prepared on: 12/01/ :27:26 pm

COVER PAGE Filing Checklist For 29 Tax Return Filed On Standard Forms Prepared on: 12/1/21 11:27:26 pm Return: C:\Users\Aarons\Documents\HRBlock\MARVIN HALL 1 29 Tax Return.T9 To file your 29 tax return,

COVER PAGE Filing Checklist For 29 Tax Return Filed On Standard Forms Prepared on: 12/1/21 11:27:26 pm Return: C:\Users\Aarons\Documents\HRBlock\MARVIN HALL 1 29 Tax Return.T9 To file your 29 tax return,

social security number relationship to you

Form 1040 Department of the Treasury Internal Revenue Service (99) OMB. 1545-0074 U.S. Individual Income Tax Return IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31,, or other

Form 1040 Department of the Treasury Internal Revenue Service (99) OMB. 1545-0074 U.S. Individual Income Tax Return IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31,, or other

Why Keep Records? Kinds of Records To Keep

Why Keep Records? There are many reasons to keep records. In addition to tax purposes, you may need to keep records for insurance purposes or for getting a loan. Good records will help you: Identify sources

Why Keep Records? There are many reasons to keep records. In addition to tax purposes, you may need to keep records for insurance purposes or for getting a loan. Good records will help you: Identify sources

Tax. and Estimated Tax. Contents. For use in. Introduction. Publication

Publication 505 Contents Tax Withholding and Estimated Tax Introduction 1 Cat No 15008E Department of the Treasury Internal Revenue Service For use in 2016 What's New for 2016 2 Reminders 2 Chapter 1 Tax

Publication 505 Contents Tax Withholding and Estimated Tax Introduction 1 Cat No 15008E Department of the Treasury Internal Revenue Service For use in 2016 What's New for 2016 2 Reminders 2 Chapter 1 Tax

5 Qualifying widow(er) with dependent child 6a Yourself. If someone can claim you as a dependent, do not check box 6a...

with dependent child 6a Yourself. If someone can claim you as a dependent, do not check box 6a...") Form 1040 Department of the Treasury Internal Revenue Service (99) U.S. Individual Income Tax Return 2016 OMB No. 1545-0074 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31,

Form 1040 Department of the Treasury Internal Revenue Service (99) U.S. Individual Income Tax Return 2016 OMB No. 1545-0074 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31,

STANDARD DEDUCTIONS MACRS RECOVERY PERIODS

217 Medical Savings Accounts (MSA) 217 Annual Deductible Range Self-Only Coverage 2,25-3,35 Family Coverage 4,5-6,75 Maximum Out of Pocket Self-Only Coverage 4,5 Family Coverage 8,25 STANDARD DEDUCTIONS

217 Medical Savings Accounts (MSA) 217 Annual Deductible Range Self-Only Coverage 2,25-3,35 Family Coverage 4,5-6,75 Maximum Out of Pocket Self-Only Coverage 4,5 Family Coverage 8,25 STANDARD DEDUCTIONS

5 Qualifying widow(er) (see instructions) 6a Yourself. If someone can claim you as a dependent, do not check box 6a...

(see instructions) 6a Yourself. If someone can claim you as a dependent, do not check box 6a...") Form 1040 Department of the Treasury Internal Revenue Service (99) US Individual Income Tax Return OMB No 1545-0074 IRS Use Only Do not write or staple in this space For the year Jan 1 Dec 31,, or other

Form 1040 Department of the Treasury Internal Revenue Service (99) US Individual Income Tax Return OMB No 1545-0074 IRS Use Only Do not write or staple in this space For the year Jan 1 Dec 31,, or other

Church and Taxes. San Jacinto Baptist Association October 2015

Church and Taxes San Jacinto Baptist Association October 2015 Updates for 2015 1. Standard mileage rate 56 cents per mile, 14 cents charity 2. $18,000 maximum contribution deferral to 403(b) or 401(k)

Church and Taxes San Jacinto Baptist Association October 2015 Updates for 2015 1. Standard mileage rate 56 cents per mile, 14 cents charity 2. $18,000 maximum contribution deferral to 403(b) or 401(k)