Part 4. Comprehensive Examples and Forms Example One: Active minister

|

|

|

- Aleesha Greer

- 5 years ago

- Views:

Transcription

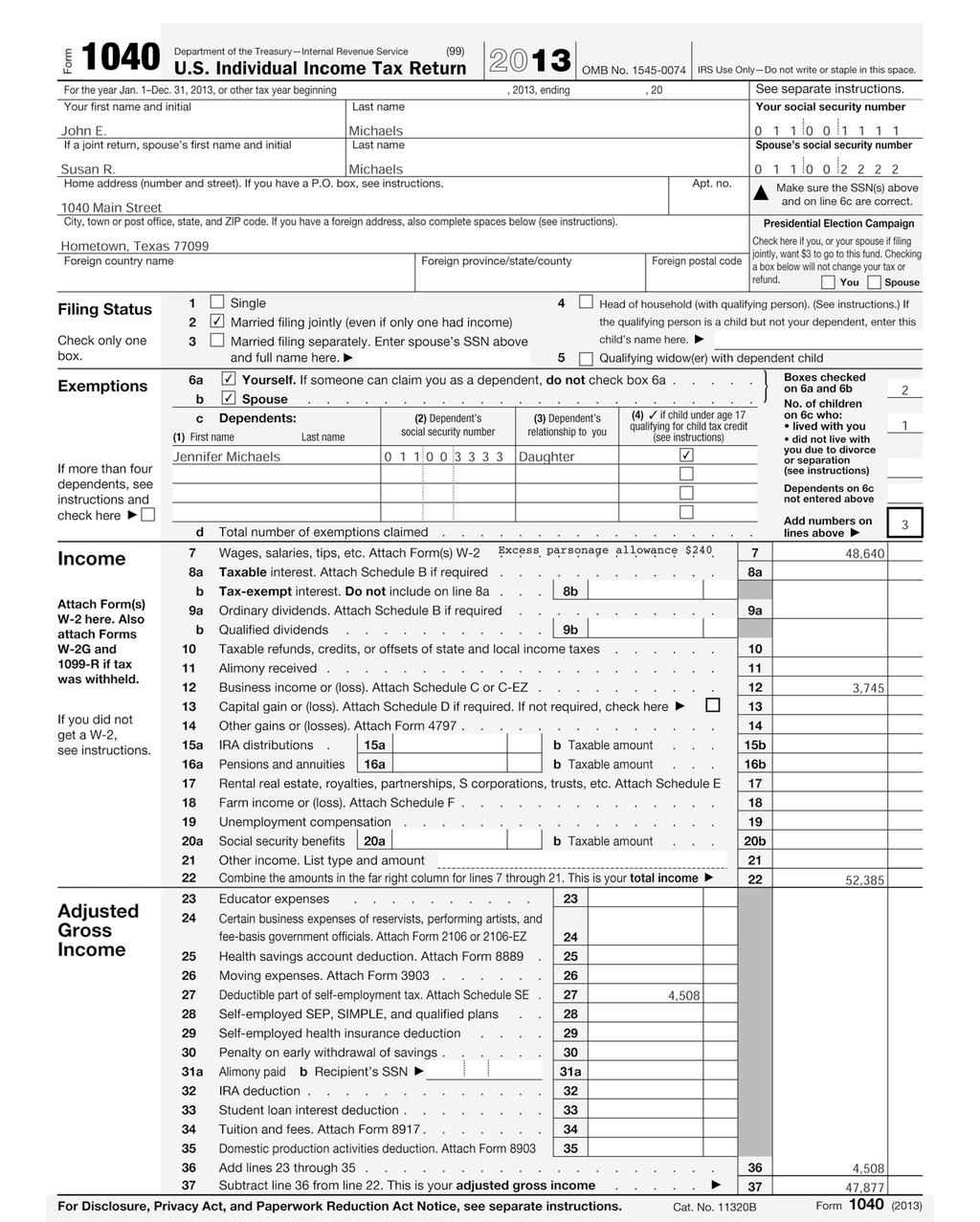

1 Part 4. Comprehensive Examples and Forms Example One: Active minister Note: This example is based on an illustrated example contained at the end of IRS Publication 517. Rev. John Michaels is the minister of the First United Church. He is married and has one child. The child is considered a qualifying child for the child tax credit. Mrs. Michaels is not employed outside the home. Rev. Michaels is a common-law employee of the church and he has not applied for an exemption from SE tax. The church paid Rev. Michaels a salary of $45,000. In addition, as a self-employed person, he earned $4,000 during the year for weddings, baptisms and honoraria. He made estimated tax payments during the year totaling $12,000. He taught a course at the local community college, for which he was paid $3,400. Rev. Michaels owns a home next to the church. He makes a $1,125 per month mortgage payment of principal and interest only. His utility bills and other housing-related expenses for the year totaled $1,450 and the real estate taxes on his home amounted to $1,750 for the year. The church paid him $1,400 per month as his parsonage allowance. The home s fair rental value is $1,380 per month (including furnishings and utilities). The parts of Rev. and Mrs. Michaels income tax return are explained in the order they are completed. They are illustrated in the order that Rev. Michaels will assemble the return to send it to the IRS. Form W 2 from church The church completed Form W 2 for Rev. Michaels as follows: Box 1. The church entered Rev. Michaels $45,000 salary. Box 2. The church left this box blank because Rev. Michaels did not request federal income tax withholding. Boxes 3 through 6. Rev. Michaels is considered a self-employed person for purposes of Social Security and Medicare tax withholding, so the church left these boxes blank. Box 14. The church entered Rev. Michaels total housing allowance for the year and identified it. TurboTax tips: Listed below are tips for ministers who use TurboTax to complete their returns. We have listed our recommended responses to some of the questions asked by the software when entering your W 2 from your church. Please note that, at the time of publication, the 2013 TurboTax software had not been released, so the TurboTax tips listed throughout this example are based on the 2012 version of the software. These tips should not be construed as an endorsement or recommendation of the TurboTax software. 1. Do any of these apply to this W 2? Be sure to check the box that says, I earned this income for religious employment (ministry, religious sect). 2. About your religious employment. Please note that ministers fall under the category of clergy employment. 3. Tell us about your minister housing. TurboTax then asks for the parsonage or housing allowance, as well as the amount of qualifying expenses. The amount you should enter for qualifying expenses is the lesser of your actual housing expenses, the annual fair rental value of your home (including furnishings and utilities) or the amount of your pay that was designated as ministerial housing allowance by your Church. 4. How would you like us to calculate ministry selfemployment tax? Please note that self-employment tax should be paid on wages and housing allowance. See Schedule SE TurboTax Tip for additional information. Form W 2 from college The community college gave Rev. Michaels a Form W 2 that showed the following: Box 1. The college entered Rev. Michaels $3,400 salary. Box 2. The college withheld $272 in federal income tax on Rev. Michaels behalf. Boxes 3 and 5. As an employee of the college, Rev. Rev. Michaels is subject to Social Security and Medicare withholding on his full salary from the college. Box 4. The college withheld $ in Social Security taxes. Box 6. The college withheld $49.30 in Medicare taxes. Schedule C-EZ (Form 1040) Some of Rev. Michaels entries on Schedule C EZ are explained here. Line 1. Rev. Michaels reports the $4,000 from weddings, baptisms and honoraria. Line 2. Rev. Michaels reports his expenses related to the line 1 amount. The total consisted of $87 for marriage and family booklets and $253 for 448 miles of business use of his car, mainly in connection with honoraria. Rev. Michaels used the standard mileage rate to figure his car expense. He multiplied 45

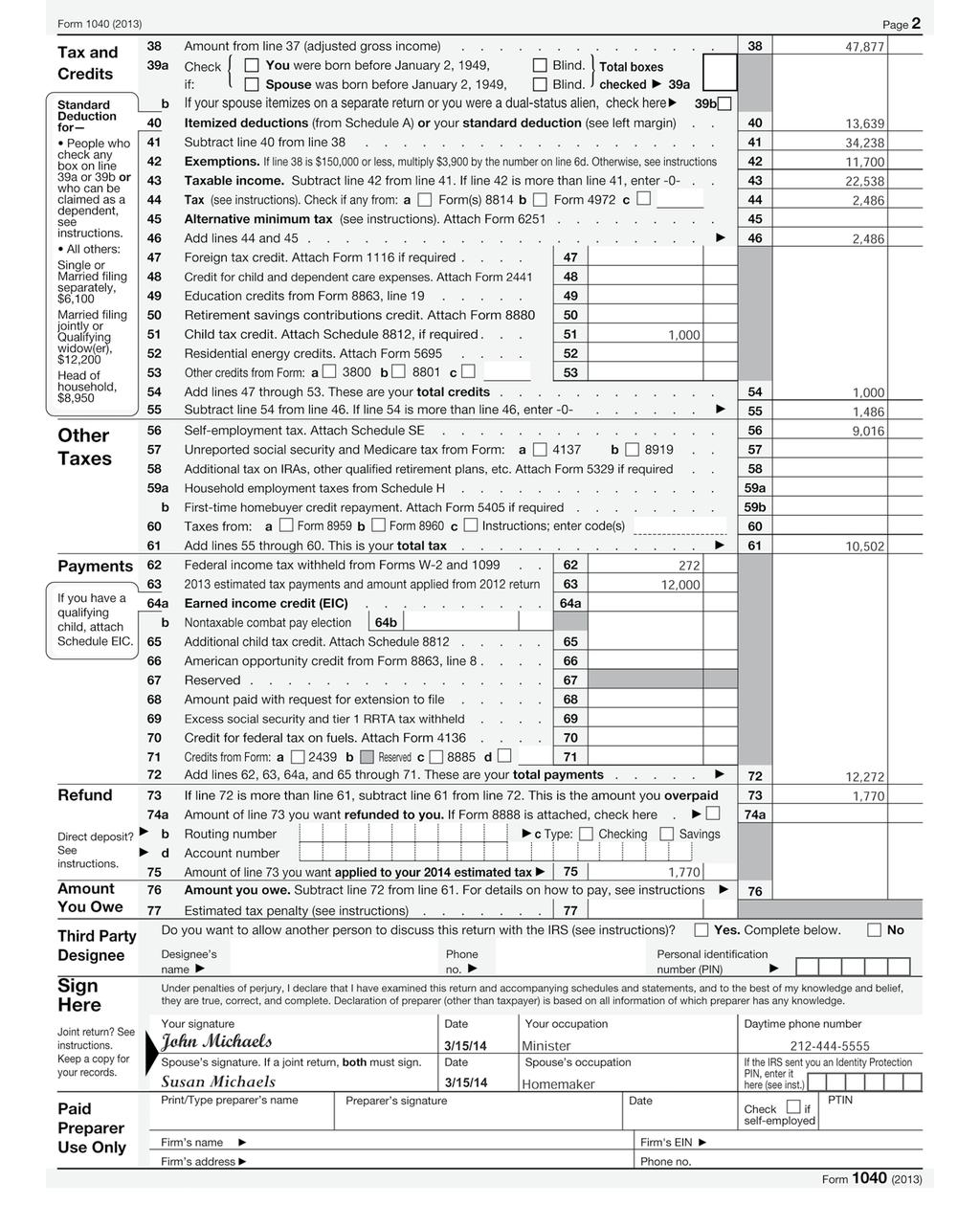

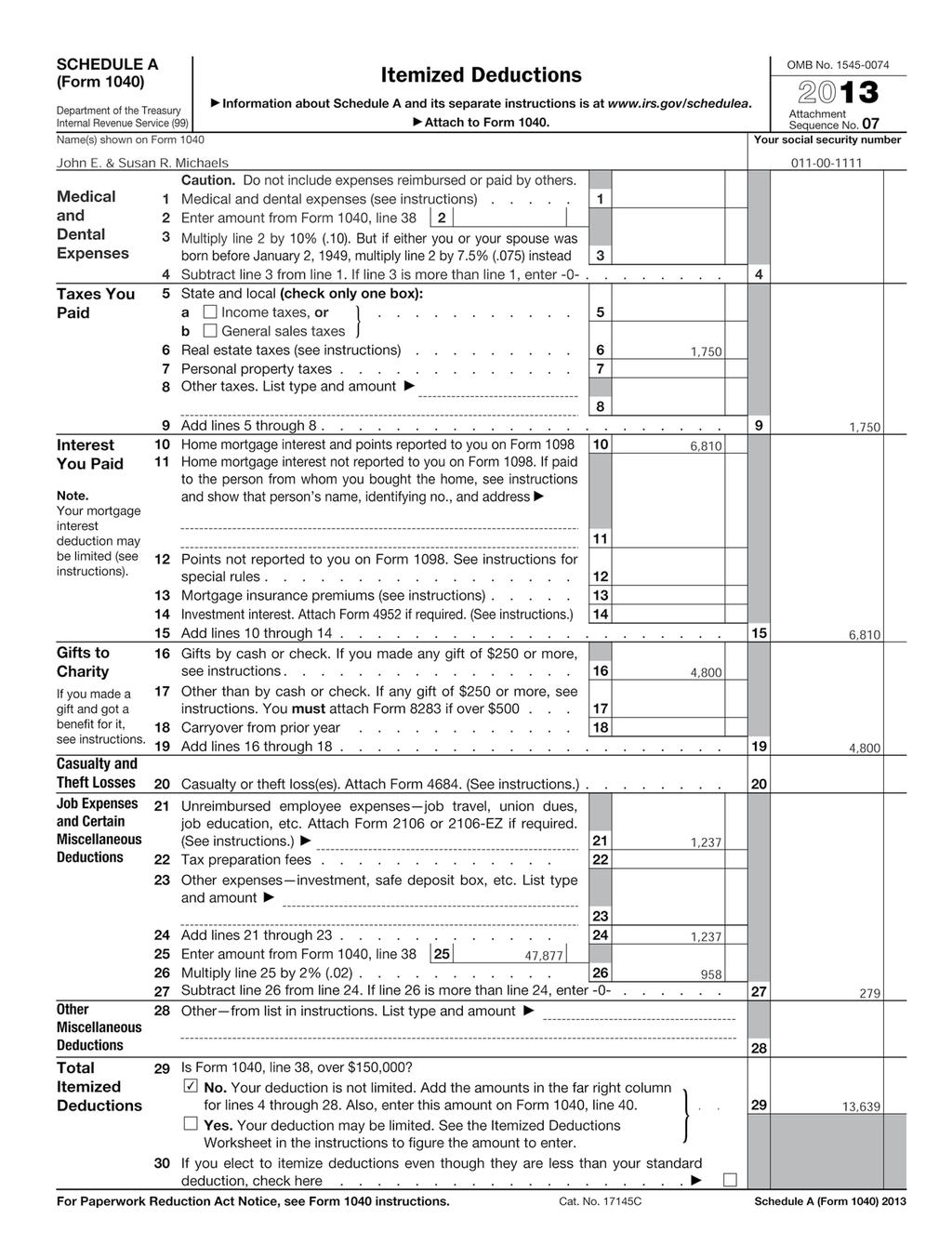

2 the standard mileage rate of 56.5 cents by 448 miles for a total of $253. These expenses total $340 ($253 + $87). However, he cannot deduct the part of his expenses allocable to his taxfree parsonage allowance. He attaches the required statement, Attachment 1 (shown later), to his return showing that 25% (or $85) of his business expenses are not deductible because they are allocable to that tax-free allowance. He subtracts the $85 from the $340 and enters the $255 difference on line 2. Line 3. He enters his net profit of $3,745 both on line 3 and on Form 1040, line 12. Lines 4 through 8b. Rev. Michaels fills out these lines to report information about his car. TurboTax tip: TurboTax does not appear to calculate the non-deductible portion of the expenses which should be allocated to the tax-free portion of the housing allowance. The taxpayer will need to adjust the expenses (as shown in Attachment 1) and input the reduced figure into the software. Form 2106 EZ Rev. Michaels fills out Form 2106-EZ to report the unreimbursed business expenses he had as a common-law employee of First United Church. Line 1. Before completing line 1, Rev. Michaels fills out Part II because he used his car for church business. His records show that he drove 2,531 business miles, which he reports in Part II. On line 1, he multiplies 2,531 miles driven by the mileage rate of 56.5 cents. The combined result of $1,430 is reported on line 1. Line 4. He enters $219 for his professional publications and booklets. Line 6. Before entering the total expenses on line 6, Rev. Michaels must reduce them by the amount allocable to his tax-free parsonage allowance. On the required Attachment 1 (shown later), he shows that 25% (or $412) of his employee business expenses are not deductible because they are allocable to the tax-free parsonage allowance. He subtracts $412 from $1,649 and enters the result, $1,237, on line 6. He also enters $1,237 on line 21 of Schedule A (Form 1040). TurboTax tip: TurboTax does not appear to calculate the non-deductible portion of the expenses which should be allocated to the tax-free portion of the housing allowance. The taxpayer will need to adjust the expenses (as shown in Attachment 1) and input the reduced figure into the software. Schedule A (Form 1040) Rev. Michaels fills out Schedule A as explained here. Line 5. Rev. and Mrs. Michaels do not pay state income tax; however, a deduction is available for state and local general sales taxes. For the purpose of this example, the author did not include an amount on Schedule A. Line 6. Rev. Michaels deducts $1,750 in real estate taxes. Line 10. He deducts $6,810 of home mortgage interest. Line 16. Rev. and Mrs. Michaels contributed $4,800 in cash during the year to various qualifying charities. Each individual contribution was less than $250. For each contribution, Rev. and Mrs. Michaels maintain the required bank record (such as a cancelled check) or written communication from the charity showing the charity s name, the amount of the contribution and the date of the contribution. (This substantiation is required in order for any contribution of money [cash, check or other monetary instrument] made in 2007 and thereafter to be deductible.) Line 21. Rev. Michaels enters his unreimbursed employee business expenses from Form 2106-EZ, line 6. Lines 25, 26 and 27. He can deduct only the part of his employee business expenses that exceeds 2% of his adjusted gross income. He fills out these lines to figure the amount he can deduct. Line 29. The total of all the Michaels itemized deductions is $13,639, which they enter on line 29 and on Form 1040, line 40. Schedule SE (Form 1040) After Rev. Michaels prepares Schedule C-EZ and Form 2106-EZ, he fills out Schedule SE (Form 1040). He reads the chart on page 1 of the schedule which tells him he can use Section A Short Schedule SE to figure his self-employment tax. Rev. Michaels is a minister, so his salary from the church is not considered church employee income. Thus, he does not have to use Section B Long Schedule SE. He fills out the following lines in Section A. Line 2. Rev. Michaels attaches a statement (see Attachment 2 later) that explains how he figures the amount ($63,811) he enters here. Line 4. He multiplies $63,811 by.9235 to get his net earnings from self-employment ($58,929). Line 5. The amount on line 4 is less than $113,700, so Rev. Michaels multiplies the amount on line 4 ($58,929) by.153 to get his self-employment tax of $9,016. He enters that amount here and on Form 1040, line 56. Line 6. Rev. Michaels multiplies the amount on line 5 by.50 to get his deduction for the employer-equivalent portion of self-employment tax of $4,508. He enters that amount here and on Form 1040, line

3 TurboTax tip: The software asks about self-employment tax on ministry wages. The taxpayer should check the box to pay self-employment tax on wages and housing allowance (assuming, as shown in this example, that the minister has not applied for exemption from the SE tax). Please note that the software does not appear to reduce self-employment wages by the business expenses allocated to tax-free income. The taxpayer will need to adjust net self-employment income (as shown in Attachment 2) and input the reduced figure into the software. Line 56. He enters the self-employment tax from Schedule SE, line 5. Line 62. He enters the federal income tax shown in box 2 of his Form W 2 from the college. Line 63. He enters the $12,000 estimated tax payments he made for the year. Form 1040 After Rev. Michaels prepares Form 2106-EZ and the other schedules, he fills out Form He files a joint return with his wife. First he fills out the address area and completes the appropriate lines for his filing status and exemptions. Then, he fills out the rest of the form as follows: Line 7. Rev. Michaels reports $48,640. This amount is the total of his $45,000 church salary, $3,400 college salary and $240, the excess of the amount designated and paid to him as a parsonage allowance over the lesser of his actual expenses and the fair rental value of his home (including furnishings and utilities). The two salaries were reported to him in box 1 of the Form W 2 he received. Line 12. He reports his net profit of $3,745 from Schedule C EZ, line 3. Line 27. He enters $4,508, the deductible part of his SE tax from Schedule SE, line 6. Line 37. Subtract line 36 from line 22. This is his adjusted gross income and he carries this amount forward to line 38. Line 40. He enters the total itemized deductions from Schedule A, line 29. Line 42. He multiplies the number of exemptions claimed (3 from Line 6d) by $3,900 and enters an exemption amount of $11,700 on line 42. Line 51. The Michaels s can take the child tax credit for their daughter, Jennifer. Rev. Michaels figures the credit by completing the Child Tax Credit Worksheet (not shown) contained in the Form 1040 general instructions. He enters the $1,000 credit. (Note: The Michaels are not required to attach Schedule 8812 to claim the child tax credit since their daughter does not have an individual taxpayer identification number (ITIN). The IRS issues ITINs to foreign nationals and others who have federal tax reporting or filing requirements and do not qualify for Social Security numbers (SSNs). Since Jennifer has a SSN, she is not required to obtain an ITIN and therefore Schedule 8812 is not applicable.) Find IRS forms, instructions and publications at or call TAX-FORM. 47

4 : From church 48

5 : From college Find IRS forms, instructions and publications at or call TAX-FORM. 49

6 50

7 51

8 52

9 53

10 54

11 Find IRS forms, instructions and publications at or call TAX-FORM. 55

12 56

13 57

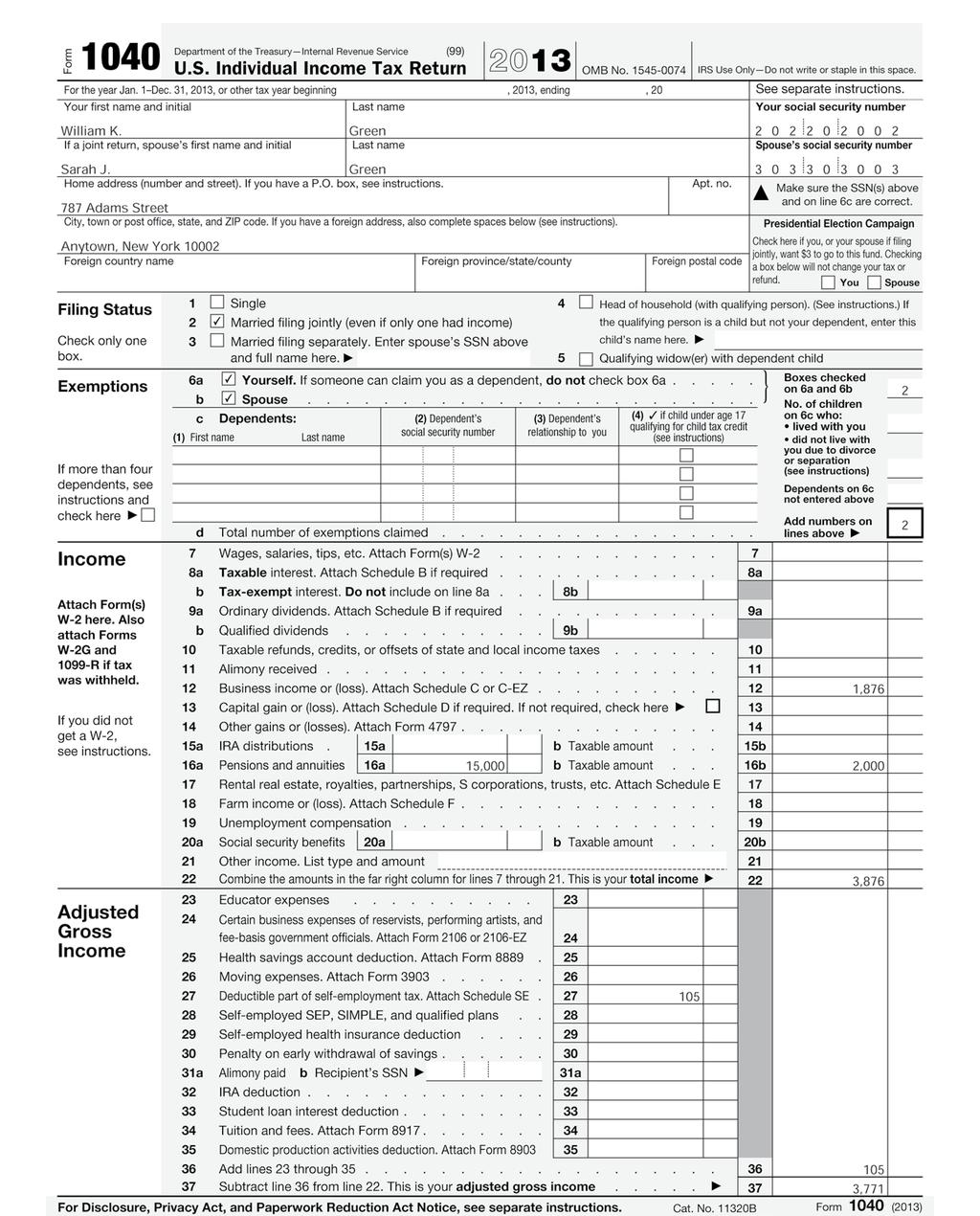

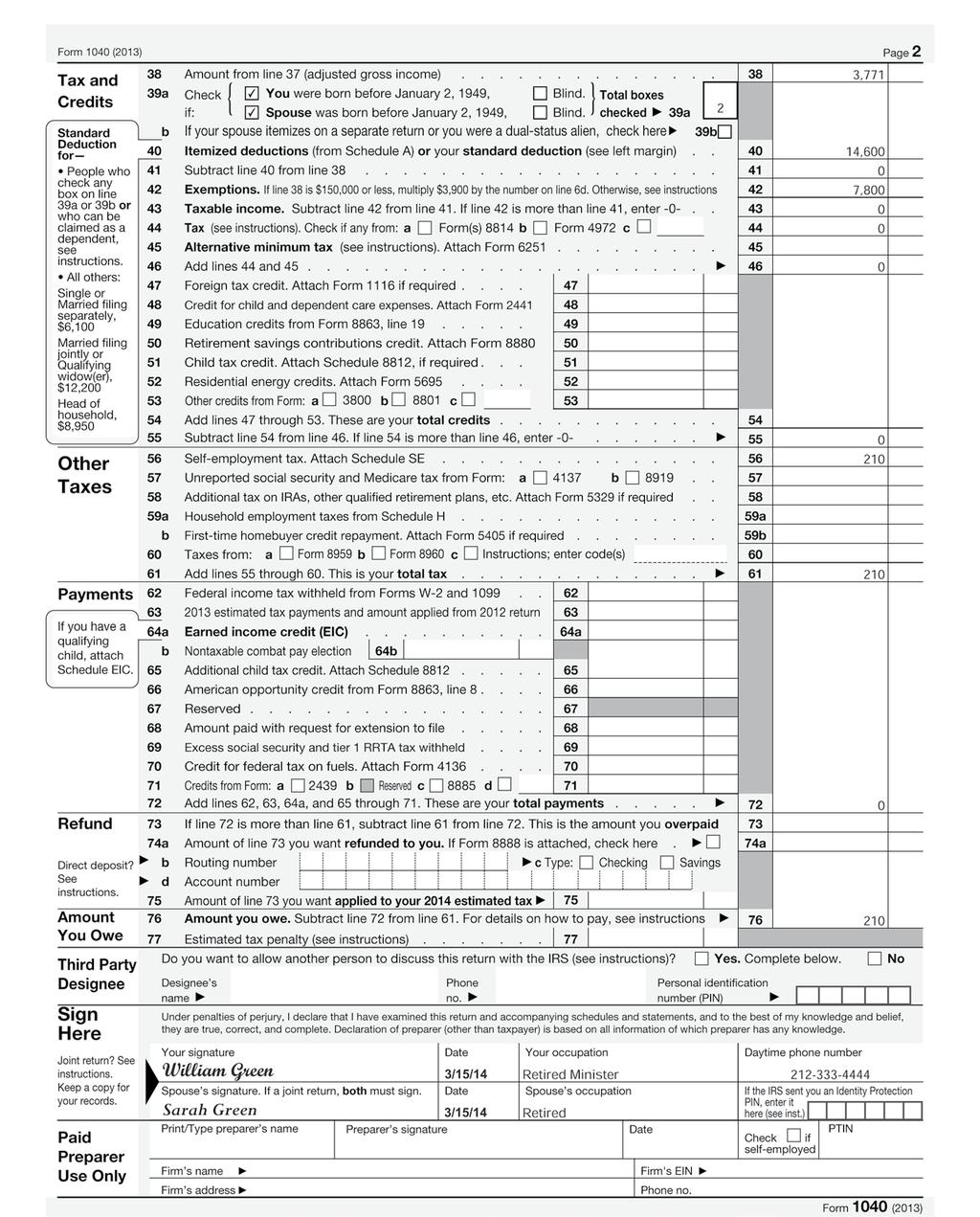

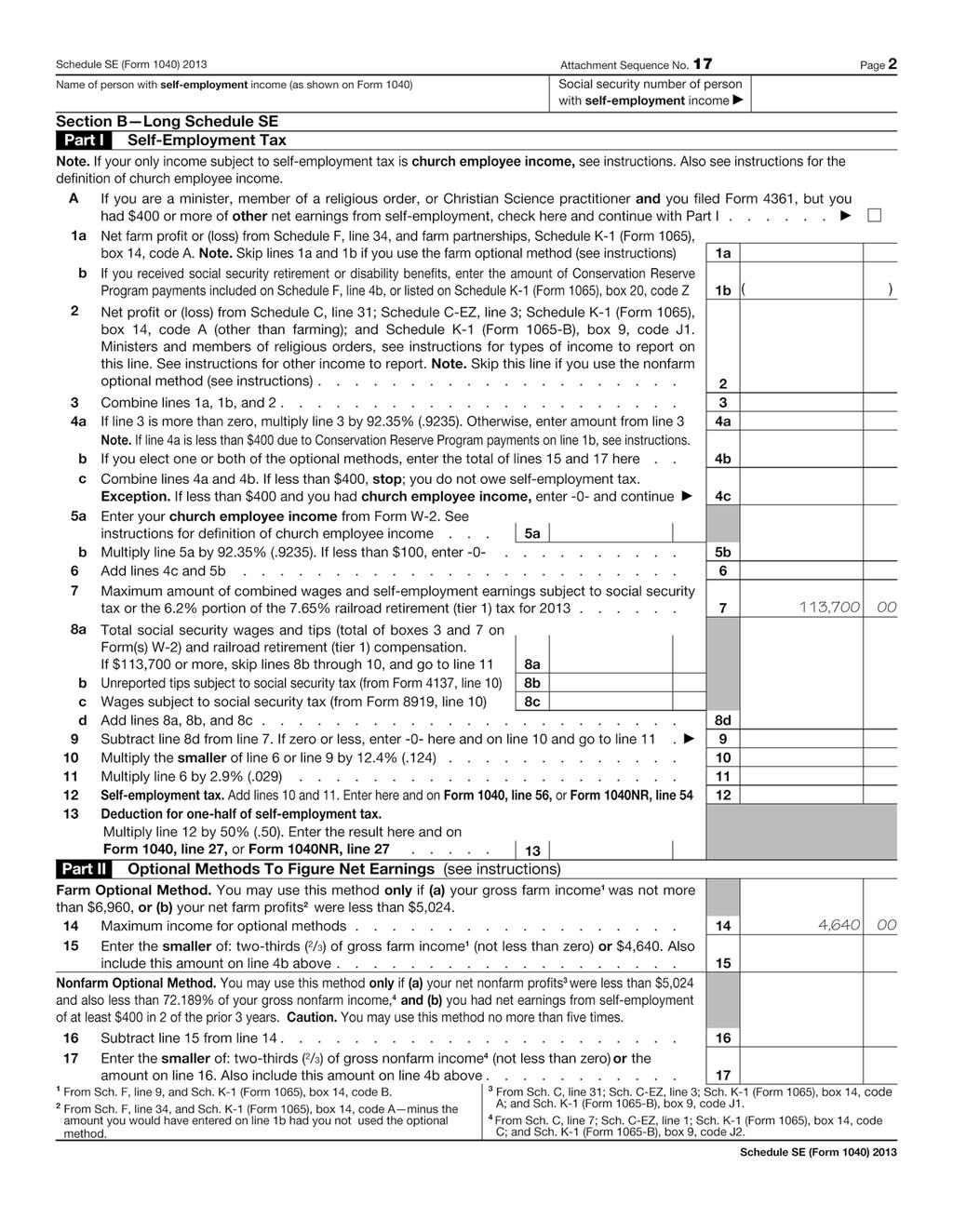

14 Example Two: Retired minister Rev. William K. Green is a retired minister. He is 69 years old. He is married to Sarah J. Green. She is 65 years old and is also retired. For 2013, Rev. Green received $15,000 in annuity income, all of which was designated in advance by GuideStone as a housing allowance. Rev. Green had housing expenses of $13,000. The home s fair rental value is $1,200 per month (including furnishings and utilities). Housing allowances for retired ministers are not taxable in computing federal income tax to the extent that they do not exceed the lesser of actual housing expenses or the annual fair rental value of the home (including furnishings and utilities). Retirement benefits, whether or not designated in advance as a housing allowance, are not subject to self-employment taxes. Rev. Green received $12,000 of Social Security benefits in 2013 and his wife received $6,000. None of this income is taxable, however, because the Green s income is not enough to expose their Social Security benefits to tax. In 2013, Rev. Green received $2,000 from occasional guest preaching engagements. He incurred $590 in expenses as a result of these activities ($440 of travel expenses and $150 of meal expenses). Note that Rev. Green will pay self-employment tax on this income (see Schedule SE), since it represents compensation from active ministry. The parts of Rev. and Mrs. Green s income tax return are explained in the order they are completed. They are illustrated in the order that the Rev. Green will assemble the return to send it to the IRS. Form 1099-R from GuideStone GuideStone completed Form 1099-R for Rev. Green as follows: Box 1. The $15,000 pension income Rev. Green receives from GuideStone. Box 2b. Taxable amount not determined. GuideStone designated in advance 100% of pension income as a housing allowance. It is not taxable to the extent that it does not exceed the lesser of actual housing expenses or the annual fair rental value of the home (including furnishings and utilities). Box 7. Rev. Green s pension income is a normal distribution. Schedule C-EZ (Form 1040) Some of Rev. Green s entries on Schedule C-EZ are explained here. Line 1b. Rev. Green reports the $2,000 from occasional guest preaching engagements. Line 2. Green reports his expenses related to the line 1 amount. He drove 779 miles of business use of his car, in connection with guest preaching. Rev. Green used the standard business mileage rate to figure his car expense. He multiplied the standard mileage rate of 56.5 cents by 779 miles for a total of $440. He also incurred $75 ($150 x 50% non-deductible) in meal expenses in connection with the guest preaching for total expenses of $515. However, he cannot deduct the part of his expenses allocable to his tax-free parsonage allowance. He attaches the required statement, Attachment 1 (shown later), to his return showing that 76% (or $391) of his business expenses are not deductible because they are allocable to that tax-free allowance. He subtracts the $391 from the $515 and enters the $124 difference on line 2. Line 3. He enters his net profit of $1,876 both on line 3 and on Form 1040, line 12. Lines 4 through 8b. Rev. Green fills out these lines to report information about his car. TurboTax tips: Listed below are tips for ministers who use TurboTax to complete their returns. Please note that, at the time of publication, the 2013 TurboTax software had not been released, so the TurboTax tips listed throughout this example are based on the 2012 version of the software. These tips should not be construed as an endorsement or recommendation of the TurboTax software. TurboTax does not appear to calculate the non-deductible portion of the expenses which should be allocated to the taxfree portion of the housing allowance. The taxpayer will need to adjust the expenses (as shown in Attachment 1) and input the reduced figure into the software. Schedule SE (Form 1040) After Rev. Green prepares Schedule C-EZ he fills out Schedule SE (Form 1040). He reads the chart on page 1 of the schedule, which tells him he can use Section A Short Schedule SE to figure his self-employment tax. Ministers are not church employees under this definition. He fills out the following lines in Section A. Line 2. Rev. Green attaches a statement (see Attachment 2 later) that calculates his net profit of $1,485 and he enters that amount here. Line 4. He multiplies the $1,485 by.9235 to get his net earnings from self-employment ($1,371). Line 5. The amount on line 4 is less than $113,700, so Rev. Green multiplies the amount on line 4 ($1,371) by.153 to get his self-employment tax of $210. He enters that amount here and on Form 1040, line 56. Line 6. Rev. Green multiplies the amount on line 5 by.50 to get his deduction for the employer-equivalent portion of selfemployment tax of $105. He enters that amount here and on Form 1040, line

15 TurboTax tips: The software does not appear to reduce selfemployment wages by the business expenses allocated to taxfree income. The taxpayer will need to adjust net self-employment income (as shown in Attachment 2) and input the reduced figure into the software. Form 1040 After Rev. Green prepares Schedule C-EZ and Schedule SE, he fills out Form Rev. Green files a joint return with his wife. First, he fills out the address area and completes the appropriate lines for his filing status and exemptions. Then, he fills out the rest of the form as follows: Line 12. He reports his net profit of $1,876 from Schedule C-EZ, line 3. Line 16a and 16b. Rev. Green reports his total annuity income of $15,000 on line 16a. He reports the taxable amount ($2,000) as computed on Attachment 1 (shown later) on line 16b. Line 20a and 20b. Since none of Rev. Green s Social Security benefits are taxable, he does not report any amounts on line 20a or 20b. Line 27. He enters $105, the deductible part of his SE tax from Schedule SE, line 6. Line 37. Subtract line 36 from line 22. This is his adjusted gross income, and he carries this amount forward to line 38. Line 39a. He checks the boxes indicating that he and his wife were born before January 2, 1949 and enters 2 in the total box. Line 40. Rev. Green enters his standard deduction of $14,600 which takes into consideration the fact he and his wife were born before January 2, Line 42. He multiplies the number of exemptions claimed (2 from Line 6d) by $3,900 and enters an exemption amount of $7,800 on line 42. Line 43. Rev. Green has no taxable income. Line 56. He enters the self-employment tax from Schedule SE, line 5. Line 62. Rev. Green did not have any income tax withheld from his pension. Line 76. Amount Rev. Green owes to the IRS. Find IRS forms, instructions and publications at or call TAX-FORM. 59

16 GuideStone Financial Resources of the Southern Baptist Convention 2401 Cedar Springs Rd Dallas, TX

17 61

18 62

19 63

20 64

21 65

22 66

23 This page intentionally left blank. 67

24 68 This page intentionally left blank.

Part 4. Comprehensive Example and Sample Forms Example One: Senior Minister

Part 4. Comprehensive Example and Sample Forms Example One: Senior Minister Note: This example is based on an illustrated example contained at the end of IRS Publication 517. Rev. John Michaels is the

Part 4. Comprehensive Example and Sample Forms Example One: Senior Minister Note: This example is based on an illustrated example contained at the end of IRS Publication 517. Rev. John Michaels is the

Example Two: Retired Minister

Example Two: Retired Minister Form 1040 Rev. William K. Green is a retired minister. He is 69 years old. He is married to Sarah J. Green. She is 65 years old and is also retired. For 2010, Rev. Green received

Example Two: Retired Minister Form 1040 Rev. William K. Green is a retired minister. He is 69 years old. He is married to Sarah J. Green. She is 65 years old and is also retired. For 2010, Rev. Green received

CLERGY TAX & BENEFITS SEMINAR. Insight Into the World of Clergy Taxes and Benefits

CLERGY TAX & BENEFITS SEMINAR Insight Into the World of Clergy Taxes and Benefits AGENDA Welcome and Prayer Introductions & Overview Clergy Compensation Clergy Benefits Other Tax Matters Q&A 2 Clergy Tax

CLERGY TAX & BENEFITS SEMINAR Insight Into the World of Clergy Taxes and Benefits AGENDA Welcome and Prayer Introductions & Overview Clergy Compensation Clergy Benefits Other Tax Matters Q&A 2 Clergy Tax

See separate instructions. Your social security number GREEN BEAN If a joint return, spouse's first name and initial

Form Department of the Treasury - Internal Revenue Service (99) 1040 U.S. Individual Income Tax Return OMB. 1545-0074 For the year Jan. 1-Dec. 31,, or other tax year beginning,, ending, 0 Your first name

Form Department of the Treasury - Internal Revenue Service (99) 1040 U.S. Individual Income Tax Return OMB. 1545-0074 For the year Jan. 1-Dec. 31,, or other tax year beginning,, ending, 0 Your first name

2011 Tax Return Preparation

2011 Tax Return Preparation and Federal Reporting Guide Tax Guide for 2010 Returns for Ministers Prepared by Richard R. Hammar, J.D., LL.M., CPA Edited by GuideStone Financial Resources of the Southern

2011 Tax Return Preparation and Federal Reporting Guide Tax Guide for 2010 Returns for Ministers Prepared by Richard R. Hammar, J.D., LL.M., CPA Edited by GuideStone Financial Resources of the Southern

8/3/2016. Presented by: John L Crandell EA MBA CTRS

Presented by: John L Crandell EA MBA CTRS 1 2 1 At the end of this webinar, you should be able to: Understand what Clergy means Understand what a Housing Allowance is Be able to calculate Self Employment

Presented by: John L Crandell EA MBA CTRS 1 2 1 At the end of this webinar, you should be able to: Understand what Clergy means Understand what a Housing Allowance is Be able to calculate Self Employment

Minister Taxes San Jacinto Baptist Association October 2014

Minister Taxes San Jacinto Baptist Association October 2014 Minister Criteria Credential - Licensed - Commissioned or - Ordained Performance - Conduct of religious worship - Administration & maintenance

Minister Taxes San Jacinto Baptist Association October 2014 Minister Criteria Credential - Licensed - Commissioned or - Ordained Performance - Conduct of religious worship - Administration & maintenance

Filing status: Single Married filing jointly Married filing separately Head of household Qualifying widow(er)

") -Internal Revenue Service (99) 1040 U.S. Individual Income Tax Return 018 IRS Use Only-Do not write or staple in this space. Filing status: Single Married filing jointly Married filing separately Head

-Internal Revenue Service (99) 1040 U.S. Individual Income Tax Return 018 IRS Use Only-Do not write or staple in this space. Filing status: Single Married filing jointly Married filing separately Head

1 of 14 8/10/ :45 PM

1 of 14 8/10/2016 11:45 PM Publication 503 - Main Content Table of Contents Tests To Claim the Credit Qualifying Person Test Earned Income Test Work-Related Expense Test Joint Return Test Provider Identification

1 of 14 8/10/2016 11:45 PM Publication 503 - Main Content Table of Contents Tests To Claim the Credit Qualifying Person Test Earned Income Test Work-Related Expense Test Joint Return Test Provider Identification

Form 1040-V. Department of the Treasury. Internal Revenue Service $ 3, Dave Dave Sarah Sarah Terrace Glenview, IL 60001

2006 Form 040-V Department of the Treasury Internal Revenue Service For Privacy Act and Paperwork Reduction Act tice, see separate instructions. DETACH HERE Form 040 (2006) Department of the Treasury Internal

2006 Form 040-V Department of the Treasury Internal Revenue Service For Privacy Act and Paperwork Reduction Act tice, see separate instructions. DETACH HERE Form 040 (2006) Department of the Treasury Internal

Taxable income (Federal and Social Security) The following are various types of income commonly found on a priest s tax filing:

The following are various types of income commonly found on a priest s tax filing:") Diocese of Madison Policy for Priest Compensation Taxable income (Federal and Social Security) The following are various types of income commonly found on a priest s tax filing: A. Salary and Supplements

Diocese of Madison Policy for Priest Compensation Taxable income (Federal and Social Security) The following are various types of income commonly found on a priest s tax filing: A. Salary and Supplements

Ministerial Taxation

Ministerial Taxation Minister s Taxation & Reporting Ministers qualify for four special tax rules: Housing allowance exclusion Self-employed status for social security taxation Exemption from withholding

Ministerial Taxation Minister s Taxation & Reporting Ministers qualify for four special tax rules: Housing allowance exclusion Self-employed status for social security taxation Exemption from withholding

COVER PAGE. Filing Checklist for 2014 Tax Return Filed On Standard Forms. Prepared on: 11/05/ :49:43 am

COVER PAGE Filing Checklist for 214 Tax Return Filed On Standard Forms Prepared on: 11/5/215 5:49:43 am Return: :\IAG\Presentations\Self-Employment Child Support 11515\Jim Fardashian 214 Tax Return.T14

COVER PAGE Filing Checklist for 214 Tax Return Filed On Standard Forms Prepared on: 11/5/215 5:49:43 am Return: :\IAG\Presentations\Self-Employment Child Support 11515\Jim Fardashian 214 Tax Return.T14

A & B Office. Education Benefits. A Self-Improvement Mini-Course. Student Loan Interest & Education Expenses. Income Tax Training School

A & B Office Income Tax Training School Education Benefits Student Loan Interest & Education Expenses Key Features: Learn how to properly calculate education expenses. Step-by-step description of the education

A & B Office Income Tax Training School Education Benefits Student Loan Interest & Education Expenses Key Features: Learn how to properly calculate education expenses. Step-by-step description of the education

TABLE OF CONTENTS. Overview Who Qualifies for Special Tax Treatment as a Minister Income to Be Reported The Parsonage Allowance...

TABLE OF CONTENTS Overview... 1 Who Qualifies for Special Tax Treatment as a Minister... 2 Income to Be Reported... 5 The Parsonage Allowance... 6 Business Expenses... 11 Self-Employment Tax: Exemption...

TABLE OF CONTENTS Overview... 1 Who Qualifies for Special Tax Treatment as a Minister... 2 Income to Be Reported... 5 The Parsonage Allowance... 6 Business Expenses... 11 Self-Employment Tax: Exemption...

Bus. Admin: Ministers Tax Issues Course #E913

Bus. Admin: Ministers Tax Issues Course #E913 Presented by: Stephanie Buduhan, CPA PSK LLP 2018 Shelby Systems, Inc. Other brand and product names are trademarks or registered trademarks of the respective

Bus. Admin: Ministers Tax Issues Course #E913 Presented by: Stephanie Buduhan, CPA PSK LLP 2018 Shelby Systems, Inc. Other brand and product names are trademarks or registered trademarks of the respective

Minister Tax Law. Topics Unique to Ministers. Important Tax Cases and IRS Rulings 8/5/2015

Minister Tax Law Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation August 5, 2015 Topics Unique to Ministers Income Issue: Parsonage/Housing Allowance Gift or Compensation SE Issue:

Minister Tax Law Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation August 5, 2015 Topics Unique to Ministers Income Issue: Parsonage/Housing Allowance Gift or Compensation SE Issue:

Part 3. Step-by-Step Tax Return Preparation

Part 3. Step-by-Step Tax Return Preparation TAX FORMS AND SCHEDULES This step-by-step analysis covers these forms and schedules: Form 1040 is the basic document you will use. It summarizes all of your

Part 3. Step-by-Step Tax Return Preparation TAX FORMS AND SCHEDULES This step-by-step analysis covers these forms and schedules: Form 1040 is the basic document you will use. It summarizes all of your

PART 3 Step-by-Step Tax Return Preparation

PART 3 Step-by-Step Tax Return Preparation TAX FORMS AND SCHEDULES This step-by-step analysis covers these forms and schedules: Form 1040 is the basic document you will use. It summarizes all of your tax

PART 3 Step-by-Step Tax Return Preparation TAX FORMS AND SCHEDULES This step-by-step analysis covers these forms and schedules: Form 1040 is the basic document you will use. It summarizes all of your tax

Disability Income Benefit. Retirement

Disability Income Benefit Retirement General information This brochure accompanies the Disability Income Benefit Estimate of Benefits. Information in this brochure will help you understand the general

Disability Income Benefit Retirement General information This brochure accompanies the Disability Income Benefit Estimate of Benefits. Information in this brochure will help you understand the general

Church and Taxes. San Jacinto Baptist Association October 2014

Church and Taxes San Jacinto Baptist Association October 2014 The Affordable Care Act 1. Health FSA (flexible spending accounts) capped $2,500 2. Modified the itemized deduction for medical expenses increased

Church and Taxes San Jacinto Baptist Association October 2014 The Affordable Care Act 1. Health FSA (flexible spending accounts) capped $2,500 2. Modified the itemized deduction for medical expenses increased

TAXATION OF CLERGY & OTHER CALLED WORKERS

TAXATION OF CLERGY & OTHER CALLED WORKERS January 2017 Presented by David Mellem, EA This text is written to provide accurate and authoritative information regarding the subject matter. The information

TAXATION OF CLERGY & OTHER CALLED WORKERS January 2017 Presented by David Mellem, EA This text is written to provide accurate and authoritative information regarding the subject matter. The information

5 Qualifying widow(er) (see instructions) 6a Yourself. If someone can claim you as a dependent, do not check box 6a...

(see instructions) 6a Yourself. If someone can claim you as a dependent, do not check box 6a...") Form 1040 Department of the Treasury Internal Revenue Service (99) U.S. Individual Income Tax Return 2017 OMB No. 1545-0074 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31,

Form 1040 Department of the Treasury Internal Revenue Service (99) U.S. Individual Income Tax Return 2017 OMB No. 1545-0074 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31,

Clergy ************************************************************************

Clergy Contents In this webinar, the student will learn the tax treatment of income received by a minister. Objectives After completing this webinar, the student will be able to: Determine if clergy are

Clergy Contents In this webinar, the student will learn the tax treatment of income received by a minister. Objectives After completing this webinar, the student will be able to: Determine if clergy are

TAX RETURN PREPARATION & FEDERAL REPORTING. Ministers Tax Guide for 2015 Returns

Ministers Tax Guide for 2015 Returns 2016 TAX RETURN PREPARATION & FEDERAL REPORTING G U I D E Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Copyright 2016 Christianity Today

Ministers Tax Guide for 2015 Returns 2016 TAX RETURN PREPARATION & FEDERAL REPORTING G U I D E Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Copyright 2016 Christianity Today

SCHEDULE C AUDIT RISKS

7/15/2017 SCHEDULE C AUDIT RISKS C. FORREST DAVIS, E.A. A LOOK AT TAX RETURNS (2014) 148.6M individual returns 63.7M Form 1040A and EZ 84.9M Form 1040 27.6M Schedule C or C-EZ 22.6M Schedule C 5.0M Sch

7/15/2017 SCHEDULE C AUDIT RISKS C. FORREST DAVIS, E.A. A LOOK AT TAX RETURNS (2014) 148.6M individual returns 63.7M Form 1040A and EZ 84.9M Form 1040 27.6M Schedule C or C-EZ 22.6M Schedule C 5.0M Sch

Your first name and initial Last name Your social security number

Form 1040 Internal Revenue Service (99) U.S. Individual Income Tax Return OMB. 1545-0074 IRS Use Only Do not write or staple in this space. Filing status: Single Married filing jointly Married filing separately

Form 1040 Internal Revenue Service (99) U.S. Individual Income Tax Return OMB. 1545-0074 IRS Use Only Do not write or staple in this space. Filing status: Single Married filing jointly Married filing separately

JOSEPH COHEN If a joint return, spouse's first name and initial Last name Spouse's social security number

Department of the Treasury ' Internal Revenue Service (99) Form 1040 U.S. Individual Income Tax Return 2012 OMB No. 1545-0074 IRS Use Only ' Do not write or staple in this space. For the year Jan 1 - Dec

Department of the Treasury ' Internal Revenue Service (99) Form 1040 U.S. Individual Income Tax Return 2012 OMB No. 1545-0074 IRS Use Only ' Do not write or staple in this space. For the year Jan 1 - Dec

Tax Guide. for Ministers. Filing Year. The Pension Boards United Church of Christ, Inc.

The Pension Boards United Church of Christ, Inc. 2017 Filing Year Tax Guide for Ministers Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Tax Guide for

The Pension Boards United Church of Christ, Inc. 2017 Filing Year Tax Guide for Ministers Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Tax Guide for

ADVANCED CERTIFICATION STUDY GUIDE Tax Year 2018

ADVANCED CERTIFICATION STUDY GUIDE Tax Year 2018 Table of Contents ADVANCED SCENARIO 1: Aiden Smith... 1 ADVANCED SCENARIO 2: Sean Yale... 2 ADVANCED SCENARIO 3: Tom and Carol Baker... 3 ADVANCED SCENARIO

ADVANCED CERTIFICATION STUDY GUIDE Tax Year 2018 Table of Contents ADVANCED SCENARIO 1: Aiden Smith... 1 ADVANCED SCENARIO 2: Sean Yale... 2 ADVANCED SCENARIO 3: Tom and Carol Baker... 3 ADVANCED SCENARIO

Advanced Course Scenarios and Test Questions

Advanced Course Scenarios and Test Questions Directions The first four scenarios do not require you to prepare a tax return. Read the interview notes for each scenario carefully and use your training and

Advanced Course Scenarios and Test Questions Directions The first four scenarios do not require you to prepare a tax return. Read the interview notes for each scenario carefully and use your training and

See separate instructions. Your social security number RIGHT ANGLE XXX-XX-XXXX If a joint return, spouse's first name and initial

Form Department of the Treasury - Internal Revenue Service (99) 14 U.S. Individual Income Tax Return 216 OMB No. 1545-74 For the year Jan. 1-Dec. 31, 216, or other tax year beginning, 216, ending, 2 Your

Form Department of the Treasury - Internal Revenue Service (99) 14 U.S. Individual Income Tax Return 216 OMB No. 1545-74 For the year Jan. 1-Dec. 31, 216, or other tax year beginning, 216, ending, 2 Your

2018 Compensation Policy

Summary 2018 Compensation Policy It is the policy of Newark Presbytery that its member churches shall provide equitable compensation of pastors and shall meet or exceed the minimum amounts specified for

Summary 2018 Compensation Policy It is the policy of Newark Presbytery that its member churches shall provide equitable compensation of pastors and shall meet or exceed the minimum amounts specified for

social security number relationship to you

Form 1040 Department of the Treasury Internal Revenue Service (99) OMB. 1545-0074 U.S. Individual Income Tax Return IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31,, or other

Form 1040 Department of the Treasury Internal Revenue Service (99) OMB. 1545-0074 U.S. Individual Income Tax Return IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31,, or other

Appendix B Pali Rao, istockphoto

Appendix B Pali Rao, istockphoto Tax Forms (Tax forms can be obtained from the IRS website: www.irs.gov) Form 1040 U.S. Individual Income Tax Return B-2 Schedule C Profit or Loss from Business B-4 Schedule

Appendix B Pali Rao, istockphoto Tax Forms (Tax forms can be obtained from the IRS website: www.irs.gov) Form 1040 U.S. Individual Income Tax Return B-2 Schedule C Profit or Loss from Business B-4 Schedule

2017 Minister s Tax Organizer Supplement

Please make a copy of this tax organizer for your records before you send to us. 2017 Minister s Tax Organizer Supplement Peachtree Tax Advisors, LLC 500 East Second Street Rome, GA 30161-3112 706-234-7468

Please make a copy of this tax organizer for your records before you send to us. 2017 Minister s Tax Organizer Supplement Peachtree Tax Advisors, LLC 500 East Second Street Rome, GA 30161-3112 706-234-7468

File by Mail Instructions for your 2017 Federal Tax Return Important: Your taxes are not finished until all required steps are completed.

File by Mail Instructions for your 2017 Federal Tax Return Important: Your taxes are not finished until all required steps are completed. calvin & kerty L Satur 1651 Deer Run Dr. Burlington, KY 41005 Balance

File by Mail Instructions for your 2017 Federal Tax Return Important: Your taxes are not finished until all required steps are completed. calvin & kerty L Satur 1651 Deer Run Dr. Burlington, KY 41005 Balance

2018 Process for Establishing Compensation for Authorized Ordained Ministers within the Penn Central Conference, United Church of Christ

2018 Process for Establishing Compensation for Authorized Ordained Ministers within the Penn Central Conference, United Church of Christ A. CASH SALARY These guidelines of the Penn Central Conference are

2018 Process for Establishing Compensation for Authorized Ordained Ministers within the Penn Central Conference, United Church of Christ A. CASH SALARY These guidelines of the Penn Central Conference are

Do your taxes online with H&R Block. Do your taxes online with H&R Block. Do your taxes online with H&R Block.

Send Friend (2004) FDFRNDOL-1WV 1.0 Send a friend to us. We'll thank you both with cash! 5 for you. 10 for your friend! Easy-to-follow instructions: 1. 2. 3. Give one of the forms below to a friend and

Send Friend (2004) FDFRNDOL-1WV 1.0 Send a friend to us. We'll thank you both with cash! 5 for you. 10 for your friend! Easy-to-follow instructions: 1. 2. 3. Give one of the forms below to a friend and

2017 Instructions for Schedule 8812

Department of the Treasury Internal Revenue Service 2017 Instructions for Schedule 8812 Child Tax Credit Part I of Schedule 8812 documents that any qualifying child whom you identify with an ITIN is a

Department of the Treasury Internal Revenue Service 2017 Instructions for Schedule 8812 Child Tax Credit Part I of Schedule 8812 documents that any qualifying child whom you identify with an ITIN is a

Your first name and initial Last name Your social security number

1040 Department of the Treasury Internal Revenue Service (99) U.S. Individual Income Tax Return OMB No. 1545-0074 IRS Use Only Do not write or staple in this space. Filing status: Single X Married filing

1040 Department of the Treasury Internal Revenue Service (99) U.S. Individual Income Tax Return OMB No. 1545-0074 IRS Use Only Do not write or staple in this space. Filing status: Single X Married filing

Church and Taxes. San Jacinto Baptist Association October 2015

Church and Taxes San Jacinto Baptist Association October 2015 Updates for 2015 1. Standard mileage rate 56 cents per mile, 14 cents charity 2. $18,000 maximum contribution deferral to 403(b) or 401(k)

Church and Taxes San Jacinto Baptist Association October 2015 Updates for 2015 1. Standard mileage rate 56 cents per mile, 14 cents charity 2. $18,000 maximum contribution deferral to 403(b) or 401(k)

JANUARY 2017 EMPLOYEE OR INDEPENDENT CONTRACTOR

JANUARY 2017 GUIDELINES TO OBLIGATIONS OF BRANCH CHURCHES AND SOCIETIES TO WITHHOLD FEDERAL INCOME AND SOCIAL SECURITY TAXES AND TO REPORT COMPENSATION; AND OTHER INFORMATION EMPLOYEE OR INDEPENDENT CONTRACTOR

JANUARY 2017 GUIDELINES TO OBLIGATIONS OF BRANCH CHURCHES AND SOCIETIES TO WITHHOLD FEDERAL INCOME AND SOCIAL SECURITY TAXES AND TO REPORT COMPENSATION; AND OTHER INFORMATION EMPLOYEE OR INDEPENDENT CONTRACTOR

CHAPTER 12 TAX RETURN ASSIGNMENT

A-PDF Merger DEMO : Purchase from www.a-pdf.com to remove the watermark Name: Nargiz CHAPTER 12 TAX RETURN ASSIGNMENT Using the data for NOAH AND JOAN ARC (Comprehensive Problem One from Appendix D, on

A-PDF Merger DEMO : Purchase from www.a-pdf.com to remove the watermark Name: Nargiz CHAPTER 12 TAX RETURN ASSIGNMENT Using the data for NOAH AND JOAN ARC (Comprehensive Problem One from Appendix D, on

Non-Resident Alien Frequently Asked Questions

Materials Management: Payroll Time and Attendance Unit Non-Resident Alien Frequently Asked Questions TAX FILING: DO I NEED TO FILE / WHEN DO I FILE? What happens if I fail to file my taxes? If you owe

Materials Management: Payroll Time and Attendance Unit Non-Resident Alien Frequently Asked Questions TAX FILING: DO I NEED TO FILE / WHEN DO I FILE? What happens if I fail to file my taxes? If you owe

1040 U.S. Individual Income Tax Return 2017

F or Department of the Treasury Internal Revenue Service (99) 14 U.S. Individual Income Tax Return 17 m OMB No. 1545-74 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31, 17,

F or Department of the Treasury Internal Revenue Service (99) 14 U.S. Individual Income Tax Return 17 m OMB No. 1545-74 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31, 17,

CONGREGATIONAL/MINISTERIAL INCOME TAX GUIDELINES

CONGREGATIONAL/MINISTERIAL INCOME TAX GUIDELINES Updated For 2016 Tax Returns By Carl A. Hess The new year brings a reminder that tax season is also here and deserves our attention. This document is to

CONGREGATIONAL/MINISTERIAL INCOME TAX GUIDELINES Updated For 2016 Tax Returns By Carl A. Hess The new year brings a reminder that tax season is also here and deserves our attention. This document is to

Chapter 6. Paying Taxes Pearson Education, Inc. All rights reserved

Chapter 6 Paying Taxes 2010 Pearson Education, Inc. All rights reserved Learning Objectives Describe the basic principles of taxation and the major categories of taxes. Explain payroll taxes Describe the

Chapter 6 Paying Taxes 2010 Pearson Education, Inc. All rights reserved Learning Objectives Describe the basic principles of taxation and the major categories of taxes. Explain payroll taxes Describe the

5 Qualifying widow(er) with dependent child 6a Yourself. If someone can claim you as a dependent, do not check box 6a...

with dependent child 6a Yourself. If someone can claim you as a dependent, do not check box 6a...") Form 1040 Department of the Treasury Internal Revenue Service (99) U.S. Individual Income Tax Return 2016 OMB No. 1545-0074 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31,

Form 1040 Department of the Treasury Internal Revenue Service (99) U.S. Individual Income Tax Return 2016 OMB No. 1545-0074 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31,

1040 U.S. Individual Income Tax Return 2017

F or Department of the Treasury Internal Revenue Service (99) 14 U.S. Individual Income Tax Return 217 m OMB No. 1545-74 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31,

F or Department of the Treasury Internal Revenue Service (99) 14 U.S. Individual Income Tax Return 217 m OMB No. 1545-74 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31,

ELIGIBLE. Earned Income Credit (EIC)

") Department of the Treasury Internal Revenue Service Publication 596 Cat. No. 15173A Earned Income Credit (EIC) For use in preparing 2003 Returns?ARE YOU ELIGIBLE Look inside for... Detailed Examples Eligibility

Department of the Treasury Internal Revenue Service Publication 596 Cat. No. 15173A Earned Income Credit (EIC) For use in preparing 2003 Returns?ARE YOU ELIGIBLE Look inside for... Detailed Examples Eligibility

Planning Guide. Compensation. V isit. For ministers and church employees. BudgetResources

Compensation Planning Guide V isit www.guidestone.org/ BudgetResources to view this material online along with our other helpful resources. For ministers and church employees Three things you need to know

Compensation Planning Guide V isit www.guidestone.org/ BudgetResources to view this material online along with our other helpful resources. For ministers and church employees Three things you need to know

5 Qualifying widow(er) with dependent child 6a Yourself. If someone can claim you as a dependent, do not check box 6a...

with dependent child 6a Yourself. If someone can claim you as a dependent, do not check box 6a...") Form 1040 Department of the Treasury Internal Revenue Service (99) U.S. Individual Income Tax Return OMB No. 1545-0074 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31,, or

Form 1040 Department of the Treasury Internal Revenue Service (99) U.S. Individual Income Tax Return OMB No. 1545-0074 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31,, or

The IRS Will Figure Your Tax

Department of the Treasury Internal Revenue Service Publication 967 Cat. No. 22402M The IRS Will Figure Your Tax Introduction You can have the IRS figure your tax on Form 1040EZ, Form 1040A, or Form 1040

Department of the Treasury Internal Revenue Service Publication 967 Cat. No. 22402M The IRS Will Figure Your Tax Introduction You can have the IRS figure your tax on Form 1040EZ, Form 1040A, or Form 1040

You Spouse 1 Single. name here.. G 5 Qualifying widow(er) with dependent child

with dependent child") ' Form 1040 U.S. Individual Income Tax Return 2014 IRS Use Only ' Do not write or staple in this space. For the year Jan 1 - Dec 31, 2014, or other tax year beginning, 2014, ending, 20 See separate instructions.

' Form 1040 U.S. Individual Income Tax Return 2014 IRS Use Only ' Do not write or staple in this space. For the year Jan 1 - Dec 31, 2014, or other tax year beginning, 2014, ending, 20 See separate instructions.

Northwestern Pennsylvania Synod, ELCA Compensation Guidelines Compensation Standards for Rostered Leaders

Northwestern Pennsylvania Synod, ELCA Compensation Guidelines Compensation Standards for Rostered Leaders -- 2018 Rostered Leader compensation is to be revisited and renegotiated annually. Compensation

Northwestern Pennsylvania Synod, ELCA Compensation Guidelines Compensation Standards for Rostered Leaders -- 2018 Rostered Leader compensation is to be revisited and renegotiated annually. Compensation

Planning Financial Support. Planning Financial Support. For ministers and church employees. Visit

Planning Financial Support Visit www.guidestone.org for an online version of this workbook or view the Planning Financial Support presentation. For ministers and church employees Well done... M A T T H

Planning Financial Support Visit www.guidestone.org for an online version of this workbook or view the Planning Financial Support presentation. For ministers and church employees Well done... M A T T H

US Tax Information for Diplomatic Families at the Australian Embassy

US Tax Information for Diplomatic Families at the Australian Rick Ward LLC January 25, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of

US Tax Information for Diplomatic Families at the Australian Rick Ward LLC January 25, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of

Tax Guide. for Ministers. Filing Year. The Pension Boards United Church of Christ, Inc.

The Pension Boards United Church of Christ, Inc. 2012 Filing Year Tax Guide for Ministers Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Tax Guide for

The Pension Boards United Church of Christ, Inc. 2012 Filing Year Tax Guide for Ministers Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Tax Guide for

SAMPLE FEDERAL REPORTING REQUIREMENTS. for Churches. Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report

Attachment 1. Computation of expenses, allocable to tax-free ministerial income, that are nondeductible. % of Nondeductible Expenses Parsonage allowance: Taxable Tax-Free Total M inisterial retirement

Attachment 1. Computation of expenses, allocable to tax-free ministerial income, that are nondeductible. % of Nondeductible Expenses Parsonage allowance: Taxable Tax-Free Total M inisterial retirement

Ministers Tax Guide for 2017 Returns TAX RETURN PREPARATION. Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report

Ministers Tax Guide for 2017 Returns 2018 TAX RETURN PREPARATION G U I D E Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Copyright 2018 Christianity Today International. Clergy

Ministers Tax Guide for 2017 Returns 2018 TAX RETURN PREPARATION G U I D E Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Copyright 2018 Christianity Today International. Clergy

Accounting for Churches. Jerry L Walker, CPA

Accounting for Churches By Jerry L Walker, CPA TABLE OF CONTENTS Worker Classifications... 1 Do ministers receive special tax treatment?... 1 Who is considered a minister for tax purposes?... 1 Is a part-time

Accounting for Churches By Jerry L Walker, CPA TABLE OF CONTENTS Worker Classifications... 1 Do ministers receive special tax treatment?... 1 Who is considered a minister for tax purposes?... 1 Is a part-time

SOLUTIONS FOR QUESTIONS AND PROBLEMS

Solutions for Questions and Problems Chapter 1 25 SOLUTIONS FOR QUESTIONS AND PROBLEMS 26 Chapter 1 The Individual Income Tax Return Solutions for Questions and Problems Chapter 1 27 CHAPTER 1 THE INDIVIDUAL

Solutions for Questions and Problems Chapter 1 25 SOLUTIONS FOR QUESTIONS AND PROBLEMS 26 Chapter 1 The Individual Income Tax Return Solutions for Questions and Problems Chapter 1 27 CHAPTER 1 THE INDIVIDUAL

5 Qualifying widow(er) (see instructions) 6a Yourself. If someone can claim you as a dependent, do not check box 6a...

(see instructions) 6a Yourself. If someone can claim you as a dependent, do not check box 6a...") Form 1040 Department of the Treasury Internal Revenue Service (99) US Individual Income Tax Return OMB No 1545-0074 IRS Use Only Do not write or staple in this space For the year Jan 1 Dec 31,, or other

Form 1040 Department of the Treasury Internal Revenue Service (99) US Individual Income Tax Return OMB No 1545-0074 IRS Use Only Do not write or staple in this space For the year Jan 1 Dec 31,, or other

Legal and Business Issues Pertaining to Church Life

Legal and Business Issues Pertaining to Church Life There are various government entities and businesses with whom an established church will transact business on a regular basis and with whom a new church

Legal and Business Issues Pertaining to Church Life There are various government entities and businesses with whom an established church will transact business on a regular basis and with whom a new church

Oregon-Idaho Annual Conference

Oregon-Idaho Annual Conference The United Methodist Church 1505 SW 18 th Avenue Portland OR 97201 503.226.7931 1.800.593.7539 www.umoi.org W-2 Instructions and other General Tax Information Remember that

Oregon-Idaho Annual Conference The United Methodist Church 1505 SW 18 th Avenue Portland OR 97201 503.226.7931 1.800.593.7539 www.umoi.org W-2 Instructions and other General Tax Information Remember that

Form1040-ES/V (OCR) Department of the Treasury Internal Revenue Service

Department of the Treasury Internal Revenue Service") Form1040-ES/V (OCR) Department Treasury Internal Revenue Service Purpose of This Package Use this package to figure and pay your estimated tax. If you are not required to make estimated tax payments for

Form1040-ES/V (OCR) Department Treasury Internal Revenue Service Purpose of This Package Use this package to figure and pay your estimated tax. If you are not required to make estimated tax payments for

1040 U.S. Individual Income Tax Return 2011

F or Department of the Treasury Internal Revenue Service (99) 14 U.S. Individual Income Tax Return 211 m OMB. 1545-74 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31, 211,

F or Department of the Treasury Internal Revenue Service (99) 14 U.S. Individual Income Tax Return 211 m OMB. 1545-74 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31, 211,

WHAT'S NEW ON FORM 1040 FOR TAX YEAR 2014

Page 1 of 5 WHAT'S NEW ON FORM 1040 FOR TAX YEAR 2014 The IRS has electronically released final tax forms and instructions for the 2014 tax year, including Forms 1040, 1040-A, and 1040-EZ, along with some

Page 1 of 5 WHAT'S NEW ON FORM 1040 FOR TAX YEAR 2014 The IRS has electronically released final tax forms and instructions for the 2014 tax year, including Forms 1040, 1040-A, and 1040-EZ, along with some

SECTION 1: FILLING OUT THE COMPENSATION PACKAGE

STATED SUPPLY AGREEMENT for Minister Members of New Hope Presbytery Section 1. Filling out the Compensation Pkg. Page 1-2 Section 3. Min. Standards of Compensation Page 4 Section 2. Effective Salary Information

STATED SUPPLY AGREEMENT for Minister Members of New Hope Presbytery Section 1. Filling out the Compensation Pkg. Page 1-2 Section 3. Min. Standards of Compensation Page 4 Section 2. Effective Salary Information

C Consumer Information on the Earned Income Tax Credit

APPENDIX C Consumer Information on the Earned Income Tax Credit The Earned Income Credit: A Powerful Benefit for People Who Work What is the Earned Income Credit (EIC)? The EIC is a tax benefit for working

APPENDIX C Consumer Information on the Earned Income Tax Credit The Earned Income Credit: A Powerful Benefit for People Who Work What is the Earned Income Credit (EIC)? The EIC is a tax benefit for working

Income Tax Guide and Organizer for 2017

Income Tax Guide and Organizer for 2017 Email: rwa@blueriver.net Web site: www.rwataxservice.com phone: 812.586.0420 Before doing the booklet, please print out or read the informational sheet as it has

Income Tax Guide and Organizer for 2017 Email: rwa@blueriver.net Web site: www.rwataxservice.com phone: 812.586.0420 Before doing the booklet, please print out or read the informational sheet as it has

See separate instructions. Your social security number RIGHT ANGLE If a joint return, spouse's first name and initial

Form Department of the Treasury - Internal Revenue Service (99) 14 U.S. Individual Income Tax Return OMB No. 1545-74 For the year Jan. 1-Dec. 31,, or other tax year beginning,, ending, 2 Your first name

Form Department of the Treasury - Internal Revenue Service (99) 14 U.S. Individual Income Tax Return OMB No. 1545-74 For the year Jan. 1-Dec. 31,, or other tax year beginning,, ending, 2 Your first name

US Tax Information for Diplomatic Families at the German Embassy

US Tax Information for Diplomatic Families at the German Rick Ward LLC February 26, 2018 Disclosure This presentation has been prepared for employees of the World Bank by LLC. The information in this presentation

US Tax Information for Diplomatic Families at the German Rick Ward LLC February 26, 2018 Disclosure This presentation has been prepared for employees of the World Bank by LLC. The information in this presentation

Military Scenario Tax Year 2016 Interview Notes

Military Training Tax Year 2016 Military Scenario Tax Year 2016 Interview Notes Michael and Jessica Williams are married and want to file a joint return. They do not have any dependents. Michael is active

Military Training Tax Year 2016 Military Scenario Tax Year 2016 Interview Notes Michael and Jessica Williams are married and want to file a joint return. They do not have any dependents. Michael is active

US Tax Information for Diplomatic Families at the Canadian Embassy

US Tax Information for Diplomatic Families at the Canadian Rick Ward LLC January 16, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of January

US Tax Information for Diplomatic Families at the Canadian Rick Ward LLC January 16, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of January

City, town or post office, state, and ZIP code. If you have a foreign address, see page 14.

Form 1040 Label (See instructions on page 14.) Use the IRS label. Otherwise, please print or type. L E L H E R E Department of the Treasury Internal Revenue Service U.S. Individual Income Tax Return 2009

Form 1040 Label (See instructions on page 14.) Use the IRS label. Otherwise, please print or type. L E L H E R E Department of the Treasury Internal Revenue Service U.S. Individual Income Tax Return 2009

Payment Options. Disability

Payment Options Disability Choosing your payment option Information in this brochure is provided to assist you in understanding your pay ment options and the Disability Retirement Income Estimate(s).

Payment Options Disability Choosing your payment option Information in this brochure is provided to assist you in understanding your pay ment options and the Disability Retirement Income Estimate(s).

Frequently asked Questions: Donations. General Council of the Assemblies of God Division of the Treasury

Frequently asked Questions: Donations General Council of the Assemblies of God Division of the Treasury 1 FREQUENTLY ASKED QUESTIONS CONCERNING DONATIONS QUESTIONS ADDRESSED IN THIS PAMPHLET What are appropriate

Frequently asked Questions: Donations General Council of the Assemblies of God Division of the Treasury 1 FREQUENTLY ASKED QUESTIONS CONCERNING DONATIONS QUESTIONS ADDRESSED IN THIS PAMPHLET What are appropriate

US Tax Information for Diplomatic Families at the Swiss Embassy

US Tax Information for Diplomatic Families at the Swiss Rick Ward LLC October 18, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of October

US Tax Information for Diplomatic Families at the Swiss Rick Ward LLC October 18, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of October

2014 Tax Guide. For Episcopal Ministers For 2013 Tax Returns. Prepared by Richard R. Hammar, J.D., LL.M., CPA. Publish date: February 6, 2014

2014 Tax Guide For Episcopal Ministers For 2013 Tax Returns Prepared by Richard R. Hammar, J.D., LL.M., CPA Publish date: February 6, 2014 Editors: Matthew K. Chew, CPA The Reverend Canon William F. Geisler,

2014 Tax Guide For Episcopal Ministers For 2013 Tax Returns Prepared by Richard R. Hammar, J.D., LL.M., CPA Publish date: February 6, 2014 Editors: Matthew K. Chew, CPA The Reverend Canon William F. Geisler,

Earned Income Credit i

Earned Income Credit i ALL RIGHTS RESERVED. NO PART OF THIS COURSE MAY BE REPRODUCED IN ANY FORM OR BY ANY MEANS WITHOUT THE WRITTEN PERMISSION OF THE COPYRIGHT HOLDER. All materials relating to this course

Earned Income Credit i ALL RIGHTS RESERVED. NO PART OF THIS COURSE MAY BE REPRODUCED IN ANY FORM OR BY ANY MEANS WITHOUT THE WRITTEN PERMISSION OF THE COPYRIGHT HOLDER. All materials relating to this course

Homer J. Sampson If a joint return, spouse's first name and initial Last name Spouse's social security number

Department of the Treasury ' Internal Revenue Service (99) Form 1040 U.S. Individual Income Tax Return 2017 OMB. 1545-0074 IRS Use Only ' Do not write or staple in this space. For the year Jan. 1 - Dec.

Department of the Treasury ' Internal Revenue Service (99) Form 1040 U.S. Individual Income Tax Return 2017 OMB. 1545-0074 IRS Use Only ' Do not write or staple in this space. For the year Jan. 1 - Dec.

US Tax Information for Diplomatic Families at the British Embassy

US Tax Information for Diplomatic Families at the British Rick Ward LLC February 22, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of February

US Tax Information for Diplomatic Families at the British Rick Ward LLC February 22, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of February

COVER PAGE. Filing Checklist For 2008 Tax Return Filed On Standard Forms. Prepared on: 01/13/ :55:49 am

COVER PAGE Filing Checklist For 28 Tax Return Filed On Standard Forms Prepared on: 1/13/29 12:55:49 am Return: C:\Documents and Settings\Owner.gateway\My Documents\TaxCut\Donna Harp 28 Tax Return.T8 To

COVER PAGE Filing Checklist For 28 Tax Return Filed On Standard Forms Prepared on: 1/13/29 12:55:49 am Return: C:\Documents and Settings\Owner.gateway\My Documents\TaxCut\Donna Harp 28 Tax Return.T8 To

Federal Reporting Requirements for Churches

Federal Reporting Requirements for Churches Prepared by Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Copyright 2014 Christianity Today International. Federal Reporting Requirements

Federal Reporting Requirements for Churches Prepared by Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Copyright 2014 Christianity Today International. Federal Reporting Requirements

2018 Tax Return Organizer

2018 Tax Return Organizer Name(s): Primary Contact: Phone: Primary Contact Email: Spouse s Email: Spouse Phone: My forms W 2, 1099, K 1, 1095, 1098, 1098 T, etc. have been provided via (Check one): Original

2018 Tax Return Organizer Name(s): Primary Contact: Phone: Primary Contact Email: Spouse s Email: Spouse Phone: My forms W 2, 1099, K 1, 1095, 1098, 1098 T, etc. have been provided via (Check one): Original

Your first name and initial Last name Your social security number

Form 1040 Department of the Treasury Internal Revenue Service (99) U.S. Individual Income Tax Return 2018 OMB. 1545-0074 IRS Use Only Do not write or staple in this space. Filing status: Single Married

Form 1040 Department of the Treasury Internal Revenue Service (99) U.S. Individual Income Tax Return 2018 OMB. 1545-0074 IRS Use Only Do not write or staple in this space. Filing status: Single Married

Name Social Security No. Birth Date. Name SSN Relation- Birth 2013 Gross *Full-Time (required) ship date Income Student

ship date Income Student") Tax Data Questionnaire 2013 The Stewardship Services Foundation (661) 362-2TAX (362-2829) Check here if this is the first year we have prepared your return. Name Social Security No. Birth Date Name of

Tax Data Questionnaire 2013 The Stewardship Services Foundation (661) 362-2TAX (362-2829) Check here if this is the first year we have prepared your return. Name Social Security No. Birth Date Name of

Name Social Security No. Birth Date

Tax Data Questionnaire 2017 The Stewardship Services Foundation (661) 362-2TAX (362-2829) stewardship@ssfoundation.net Check here if this is the first year we have prepared your return. Name Social Security

Tax Data Questionnaire 2017 The Stewardship Services Foundation (661) 362-2TAX (362-2829) stewardship@ssfoundation.net Check here if this is the first year we have prepared your return. Name Social Security

Contents. What s New... 1 Reminders... 1 Publication 503

Department of the Treasury Internal Revenue Service Contents What s New... 1 Reminders... 1 Publication 503 Introduction... 2 Cat.. 15004M Tests To Claim the Credit... 2 Qualifying Person Test... 4 Keeping

Department of the Treasury Internal Revenue Service Contents What s New... 1 Reminders... 1 Publication 503 Introduction... 2 Cat.. 15004M Tests To Claim the Credit... 2 Qualifying Person Test... 4 Keeping

Filing Instructions. Amount to be refunded to you...$ 5,056

Prepared for: Filing Instructions Prepared by: Stephen M. & Jaime M. Weinress Accounting Specialists, Inc. Po Box 773150 P.O. Box 1040 Steamboat Springs, CO 80477 Nederland, CO 80466 2016 U.S. INDIVIDUAL

Prepared for: Filing Instructions Prepared by: Stephen M. & Jaime M. Weinress Accounting Specialists, Inc. Po Box 773150 P.O. Box 1040 Steamboat Springs, CO 80477 Nederland, CO 80466 2016 U.S. INDIVIDUAL

Pension and Annuity Income

Department of the Treasury Internal Revenue Service Publication 575 Cat. No. 15142B Pension and Annuity Income For use in preparing 1998 Returns Contents Important Changes for 1998... 1 Introduction...

Department of the Treasury Internal Revenue Service Publication 575 Cat. No. 15142B Pension and Annuity Income For use in preparing 1998 Returns Contents Important Changes for 1998... 1 Introduction...

Federal Reporting Requirements for Churches

Federal Reporting Requirements for Churches Prepared by Richard R. Hammar, J.D., LL.M., CPA Senior Editor, CHURCH LAW & TAX REPORT Copyright 2013 Christianity Today International. Federal Reporting Requirements

Federal Reporting Requirements for Churches Prepared by Richard R. Hammar, J.D., LL.M., CPA Senior Editor, CHURCH LAW & TAX REPORT Copyright 2013 Christianity Today International. Federal Reporting Requirements

Determining your 2016 stock plan tax requirements a step-by-step guide

Determining your 2016 stock plan tax requirements a step-by-step guide INSIDE How to use the Supplemental Form to avoid overpaying taxes Upon selling shares acquired from a nonqualified employee stock

Determining your 2016 stock plan tax requirements a step-by-step guide INSIDE How to use the Supplemental Form to avoid overpaying taxes Upon selling shares acquired from a nonqualified employee stock

Advanced Course Scenarios and Test Questions

Advanced Course Scenarios and Test Questions Directions The first four scenarios do not require you to prepare a tax return. Read the interview notes for each scenario carefully and use your training and

Advanced Course Scenarios and Test Questions Directions The first four scenarios do not require you to prepare a tax return. Read the interview notes for each scenario carefully and use your training and

Above lists are not all-inclusive. For more information, contact (937)

") In this packet you, will find general tax information about the City of Springboro Income Tax Return. We encourage you to bring your income tax information to our office and we will gladly prepare your

In this packet you, will find general tax information about the City of Springboro Income Tax Return. We encourage you to bring your income tax information to our office and we will gladly prepare your

Taxes and Ministers TOPICS: 2011 edition (rev. 10/11) The IRS s definition of minister. Employment status: W-2 or Housing/Parsonage allowance

The IRS s definition of minister. Employment status: W-2 or Housing/Parsonage allowance") Taxes and Ministers 2011 edition (rev. ) TOPICS: The IRS s definition of minister Employment status: W-2 or 1099 Housing/Parsonage allowance Reporting income and expenses Paying federal and state taxes

Taxes and Ministers 2011 edition (rev. ) TOPICS: The IRS s definition of minister Employment status: W-2 or 1099 Housing/Parsonage allowance Reporting income and expenses Paying federal and state taxes

Advanced Course Scenarios and Test Questions

Advanced Course Scenarios and Test Questions Directions The first four scenarios do not require you to prepare a tax return. Read the interview notes for each scenario carefully and use your training and

Advanced Course Scenarios and Test Questions Directions The first four scenarios do not require you to prepare a tax return. Read the interview notes for each scenario carefully and use your training and

City of Detroit City of Detroit. Forms and Instructions. Filing Due Date: April 18, 2016

City of Detroit 2015 City of Detroit aa aa Income Tax Returns Forms and Instructions Starting with tax year 2015, the Michigan Department of Treasury will begin processing City of Detroit Individual Income

City of Detroit 2015 City of Detroit aa aa Income Tax Returns Forms and Instructions Starting with tax year 2015, the Michigan Department of Treasury will begin processing City of Detroit Individual Income