Interim report of the Atlantia Group for the nine months ended 30 September 2011

|

|

|

- Philomena Curtis

- 6 years ago

- Views:

Transcription

1 Interim report of the Atlantia Group for the nine months ended 30 September 2011

2 2 (This page intentionally left blank)

3 Contents 1. Introduction... 5 Corporate bodies... 7 Group structure... 8 Consolidated financial highlights... 9 Shareholder structure Atlantia share price performance Report on operations Consolidated financial review Operating review of the Group s operators Traffic Toll charges Network upgrade and modernisation Network operations Operating review of the other main subsidiaries Operating review of the Group s main investee companies Other information Workforce Significant regulatory aspects Events after 30 September Outlook Attestation

4 4

5 1. Introduction 5

6 6 (This page intentionally left blank)

7 Corporate bodies Board of Directors Chairman Fabio CERCHIAI in office for Chief Executive Officer Giovanni CASTELLUCCI Directors Gilberto BENETTON Alessandro BERTANI Alberto BOMBASSEI (independent) Stefano CAO Roberto CERA Alberto CLÔ (independent) Antonio FASSONE Carlo MALINCONICO (independent) Giuliano MARI (independent) Gianni MION Giuseppe PIAGGIO Antonino TURICCHI (independent) Paolo ZANNONI Secretary Andrea GRILLO Internal Control and Chairman Giuseppe PIAGGIO Corporate Governance Committee Members Giuliano MARI (independent) Antonino TURICCHI (independent) Committee of Independent Directors with responsibility for Related Party Transactions Chairman Giuliano MARI Alberto BOMBASSEI ( 1 ) Alberto CLÔ ( 2 ) Carlo MALINCONICO (independent) (independent) (independent) (independent) Human Resources Committee Chairman Carlo MALINCONICO ( 2 ) ( 3 ) (independent) Alberto BOMBASSEI ( 1 ) (independent) Members Stefano CAO Alberto CLÔ (independent) Giuseppe PIAGGIO Paolo ZANNONI Supervisory Board Chairman Renato GRANATA Members Simone BONTEMPO Pietro FRATTA Ethics Officer Coordinator Giuseppe LANGER Giulio BARREL Enzo SPOLETINI Board of Statutory Auditors Chairman Marco SPADACINI for three-year period Auditors Tommaso DI TANNO Raffaello LUPI Angelo MIGLIETTA Independent Auditors for the period Alternate Auditors KPMG SpA Alessandro TROTTER Giuseppe Maria CIPOLLA Giandomenico GENTA ( 1 ) Alberto Bombassei resigned from his position with effect from 9 June ( 2 ) Prof. Alberto Clô and Prof. Carlo Malinconico were elected by the Board of Directors meeting of 9 June ( 3 ) Prof. Carlo Malinconico was appointed Chairman of the Human Resources Committee at the meeting of 5 October

8 Group structure Tangenziale di Napoli SpA 100% Autostrada Torino-Savona SpA 99.98% Società Autostrada Tirrenica SpA 94% (1) Autostrade Meridionali SpA 58.98% Società Italiana pa Traforo del Monte Bianco 51% Raccordo Autostradale Valle d Aosta SpA 58% (2) Italian motorway operations 100% EsseDiEsse Società di Servizi SpA 100% Pavimental SpA 71.67% Pavimental Polska Spzoo 100% Spea Ingegneria Europea SpA 100% Ad Moving SpA 100% Port Mobility SpA 70% Newpass SpA 51% Giove Clear Srl 100% Tirreno Clear Srl 100% Autostrade Tech SpA 100% Telepass SpA 96.15% (3) Telepass France SAS 100% Infoblu SpA 75% IGLI SpA 33.3% (4) Impregilo SpA 29.96% (2)(4) Service companies TowerCo SpA 100% Pune Solapur Expressways Private Ltd. 50% (4) Alitalia Compagnia Aerea Italiana SpA 8.85% (4) Autostrade International US Holdings Inc. 75% (5) Autostrade International of Virginia O & M Inc. 100% Electronic Transaction Consultants Co. 45% Stalexport Autostrady SA 57.28% Biuro Centrum Spzoo 74.38% Stalexport Autostrada Dolnośląska SA 100% Stalexport Autostrada Malopolska SA 55.73%(6) Stalexport Autoroute SArl 100% Stalexport Transroute Autostrada SA 55% Autostrade dell Atlantico Srl 100% Autostrade Holding do Sur SA 100% Sociedad Concesionaria de Los Lagos SA100% Inversiones Holding do Sur Ltda. 100% Autostrade Portugal SA100% Autostrade Brasil Ltda. 100% Triangulo do Sol SA 70% Autostrade Sud America Srl 45.77% (4) Grupo Costanera SA 100% (4) Costanera Norte SA 100% (4) Acceso Vial AMB SA 100% (4) Inversiones Autostrade de Chile Ltda. 100% (4) Nororiente SA 100% (4) Gestion Vial SA 100% (4) Nueva Inversiones SA 50% (4)(7) Litoral SA 100% (4) Operalia SA 100% (4) Autostrade Urbane de Chile SA 100% (4) Vespucio Sur SA 100% (4) Autostrade Indian Infrastructure Development Private Ltd. 100% Ecomouv SAS 70% (8) Ecomouv D&B SAS 75% Tech Solutions Integrators SAS 100% (1) A 69.1% interest in this company is in the process of being sold. (2) The percentage refers to ordinary shares representing the issued capital. (3) The remaining 3.85% is held by Autostrade Tech SpA. (4) Unconsolidated company. (5) The remaining 25% is held by Autostrade Participations Srl. (6) The remaining 44.27% is held by Stalexport Autoroute SArl. (7) The remaining 50% is held by Inversiones Holding do Sur Ltda. (8) Following the issue of new shares to its French partners on 26 October 2011, Autostrade per l Italia has reduced its interest compared with the 100% interest held at 30 September

9 Consolidated financial highlights ( m) 9M 2011 (a) 9M 2010 (b) Total revenue Net toll revenue Other operating income Gross operating profit (EBITDA) EBITDA margin 62,1% 63,1% Operating profit (EBIT) EBIT margin 49,1% 49,2% Profit/(Loss) from continuing operations Profit margin from continuing operations 21,2% 20,5% Profit for the period (including non-controlling interests) Profit for the period attributable to owners of the parent Operating cash flow (c) Capital expenditure ( m) 30 September December 2010 Equity Net debt (a) The figures for the first nine months of 2011 benefit from the contribution of the Brazilian motorway operator, Triangulo do Sol Auto-Estradas, consolidated from 1 July 2011, following the acquisition of a further 20% stake during the third quarter of 2011, in addition to the 50% interest already held. (b) In view of the fact that consolidation of the contributions of Autostrada Tirrenica and Strada dei Parchi (until the date of deconsolidation) to the income statement for the first nine months of 2011 have been accounted for in accordance with IFRS 5, thus recognising the contributions to profit for the period in "Profit/(Loss) from discontinued operations", the two companies' contributions to the comparative consolidated income statement for the first nine months of 2010 have also been reclassified. Income statement amounts for the first nine months of 2010, other than profit for the period, are therefore different from those published in the interim report for the nine months ended 30 September 2010, due to the reclassifications carried out. (c) Operating cash flow is calculated as profit + amortisation/depreciation +/- provisions/releases of provisions + financial expenses from discounting of provisions +/- impairments/reversals of impairments of assets +/- share of profit/(loss) of investments accounted for using equity method +/- (losses)/gains on sale of assets +/- other non-cash items +/- portion of net deferred tax assets/liabilities recognised in the income statement. 9

10 Shareholder structure Edizione Srl Government of Singapore Investment Corporation Goldman Sachs Infrastructure Partners Mediobanca SpA 66.40% 17.68% 9.98% 5.94% 100% Geographical distribution of free float (2) 43.21% Rest of the world 14% Regno Unito 26% Fondazione CRT 6.76% 48.03% (1) Free float Rest of Europe 20% Italy (3) 7% (1) Excludes Atlantia SpA s treasury shares. (2) Source: CONSOB, Thomson Reuters (figures at 30 September 2011). (3) Includes retail investors. France 13% USA 20% 10

11 Atlantia share price performance Share information Number of shares (*) Price at 30 September ,82 Par value ( ) 1,00 Low (22 September 2011) 9,37 Type of shares Ordinary High (16 February 2011) 16,10 Final dividend per share for 2010, paid May 2011 ( ) 0,391 Capitalisation at 30 September 2011 ( m) Interim dividend per share for 2011, paid November 2011 ( ) 0,355 Average daily trading volume (m) 2,6 (*) After bonus issue of 6 June Volumes ('000) January February March April May June July August September 17,0 16,5 16,0 15,5 15,0 14,5 14,0 13,5 13,0 12,5 12,0 11,5 11,0 10,5 10,0 9,5 9,0 8,5 8,0 Price ( ) Volumes Atlantia Rebased FTSE/MIB 11

12 12

13 2. Report on operations 13

14 14 (This page intentionally left blank)

15 Consolidated financial review Introduction The Atlantia Group s interim report for the three months ended 31 March 2011 has been prepared on the basis of the provisions of art. 154-ter, Financial reporting, of the Consolidated Finance Act introduced by Legislative Decree 195/2007, in implementation of EU Directive 2004/109/EC (the socalled Transparency Directive) regarding periodic reporting, and in compliance with the international financial reporting standards (IFRS) issued by the International Accounting Standards Board (IASB), endorsed by the European Commission and in force at 30 September The financial review contained in this section includes and analyses the reclassified consolidated income statement, the statement of comprehensive income, the statement of changes in equity, the statement of changes in net debt and the statement of cash flows for the first nine months of 2011, in which amounts are compared with those for the same period of the previous year. The review also includes the reclassified statement of financial position as at 30 September 2011, compared with the corresponding amounts as at 31 December The reclassified consolidated income statement, the consolidated statement of changes in net debt and the consolidated statement of cash flows also include amounts for the third quarter of 2011, compared with those for the third quarter of The accounting standards applied during preparation of this document are consistent with those adopted for the consolidated financial statements as at and for the year ended 31 December It should be noted that the financial statements as at and for the nine months ended 30 September 2011 reflect the impact on taxation of the Ministerial Decree of 8 June 2011 (as provided for by the so- 15

16 called Milleproroghe, or Thousand postponements, legislation), of the response, received on 9 June 2011, to the request for a ruling submitted to the Italian tax authorities by Autostrade per l Italia in 2010 and, lastly, of Law Decree 98 of 6 July 2011, containing urgent measures to promote financial stability (converted into law, with amendments, by Law 111 of 15 July 2011). The Ministerial Decree of 8 June 2011 and the response to Autostrade per l Italia s request for a ruling have finally clarified the tax treatment of the new amounts accounted for in the financial statements as at and for the year ended 31 December 2009, substantially confirming the deductibility of the various components of the financial statements specifically recognised in application of IFRIC 12 (depreciation and amortisation, provisions and expenses from discounting to present value). The Decree and the response also permit deduction of the loss resulting from the realignment of carrying amounts with tax bases (Law Decree 185/2008) on a straight-line basis over concession terms (29 years in the case of Autostrade per l'italia), with immediate effect from the 2010 tax year. Law 111/2011, on the other hand, has, in the case of Italian operators, modified the deductible percentage of provisions for maintenance, repair and replacement obligations, which has been reduced from 5% to 1% of the historical cost of assets to be handed over, with immediate effect from the 2011 tax year. The basis of consolidation as at 30 September 2011 has changed with respect to the basis used in preparing the consolidated financial statements as at and for the year ended 31 December 2010, essentially due to the following: a) consolidation of the Brazilian motorway operator, Triangulo do Sol Auto-Estradas, from 1 July 2011, following the acquisition of a further 20% stake in the company during the third quarter of 2011 (the Group already held a 50% interest); b) deconsolidation of Strada dei Parchi, following completion of the sale of the related investment during the second quarter of Moreover, as required by IFRS 5 Non-current Assets Held for Sale and Discontinued Operations, Strada dei Parchi s contribution to the consolidated income statement for the first nine months of 2011 (up to the date of deconsolidation), and to the income 16

17 statement for the corresponding period of 2010, is accounted for in Profit/(Loss) from discontinued operations, rather than included in each component of the consolidated income statement for continuing operations. In addition, following the conclusion, during the second quarter of 2011, of an agreement to sell 69.1% of Autostrada Tirrenica, this company s contribution to the consolidated income statement for the first nine months of 2011 has also been accounted for in Profit/(Loss) from discontinued operations, in accordance with IFRS 5. As a result, in accordance with IFRS 5, Autostrada Tirrenica s contribution to the comparative consolidated income statement for the first nine months of 2010 has also been reclassified with respect to the statement published in the report for the nine months ended 30 September Again in accordance with IFRS 5, the consolidated assets and liabilities of Autostrada Tirrenica as at 30 September 2011 have been accounted for in the statement of financial position in financial and nonfinancial assets and liabilities related to discontinued operations, depending on their nature, whilst as at 31 December 2010 these items include the assets and liabilities of Strada dei Parchi, which, as noted above, has been deconsolidated as at 30 September The Group did not enter into material transactions, either with third or related parties, of a nonrecurring, atypical or unusual nature during the first nine months of This interim report has not been audited. 17

18 Consolidated results of operations Total revenue for the first nine months of 2011 amounts to 3,020.5 million, marking an increase of million (7.3%) on the same period of 2010 ( 2,814.9 million). In order to aid the reader s understanding of certain changes in the operating results, it should be noted that operating costs include the addition to the concession fee payable to ANAS by the Italian operators, whilst toll revenue includes the matching increase in tolls, without having any impact on the operators results (1). The total amount for the above toll increases for the first nine months of 2011 is million, compared with the million of the same period of After stripping out the contribution to revenue from Triangulo do Sol, following its consolidation from 1 July 2011, and the above toll increases matching the additional concession fee payable to ANAS, total revenue is up 40.7 million (1.5%). (1) The additional concession fees payable to ANAS, pursuant to laws 102/2009 and 122/2010, calculated on the basis of the number of kilometres travelled, amounted to 3 thousandths of a euro per kilometre for toll classes A and B and 9 thousandths of a euro per kilometre for classes 3, 4 and 5 for the first six months of 2010, whilst the additional amounts for the third quarter of 2010, following the increases introduced from 1 July 2010, were 4 thousandths of a euro per kilometre for toll classes A and B and 12 thousandths of a euro per kilometre for classes 3, 4 and 5. Following the further increases introduced from 1 January 2011, the additional amounts for the first nine months of 2011 amount to 6 thousandths of a euro per kilometre for toll classes A and B and 18 thousandths of a euro per kilometre for classes 3, 4 and 5. 18

19 19

20 Toll revenue of 2,550.1 million is up million (8.5%) on the first nine months of 2010 ( 2,350.2 million), primarily reflecting the combined effect of the following: a) the above toll increases (up million on the first nine months of 2010, representing 5.4% of total toll revenue) in connection with the matching increase in the concession fee; b) the application of annual toll increases by the Group s Italian operators from 1 January 2011 (a 1.92% increase for Autostrade per l Italia), boosting toll revenue by an estimated 41.6 million; c) the decline in traffic on the network operate by the Group s Italian operators (down 1.0%), resulting in an estimated overall reduction in toll revenue of 19.0 million; d) an increase in other toll revenue reported by Autostrade Meridionali (up 4.2 million) which, following the signature of the relevant Single Concession Arrangement, from 2009 no longer defers a portion of the X variable of tariffs, whilst continuing to partially release provisions made in previous years; e) consolidation, from 1 July 2011, of the Brazilian operator, Triangulo do Sol, which reports toll revenue of 36.0 million for the third quarter of 2011; f) increases in toll revenue reported by overseas operators (up 3.9 million), above all by Stalexport Autostrada Malopolska following the switch to direct tolling from the previous system of stickers for vehicles over 12 tonnes and an increase in traffic. Contract revenue of 45.2 million is down 3.1 million on the same period of 2010 ( 48.3 million), reflecting a reduction in work carried out for external customers by Pavimental and Spea, partly offset by revenue growth at the US company, Electronic Transaction Consultants, primarily as a result of contracts in Georgia, Texas and Illinois. Other operating income of million is up 8.8 million (2.1%) on the first nine months of 2010 ( million), due to the following: a) an increase in commercial revenue from service areas and payment systems (amounting to 6.5 million), reflecting annual contractual increases in service area royalties applied from 1 January 20

21 2011 and growth in the number of Telepass subscribers (approximately 400 thousand new devices in circulation and around 237 thousand new subscribers to the Premium option); b) a reduction in non-recurring income generated by the handover, free of charge, of buildings by sub-operators in the first nine months of 2010 (down 4.4 million); c) an increase in other income (up 5.5 million), essentially attributable to Autostrade per l Italia and relating above all to penalties receivable from suppliers and sales of solar energy; d) increased other income deriving from consolidation of Triangulo do Sol ( 1.2 million in the third quarter of 2011). Total net operating costs of 1,145.9 million are up million (10.2%) on the first nine months of 2010 ( 1,039.9 million). After stripping out Triangulo do Sol s contribution to operating costs and the impact the above increase in the concession fee, net operating costs are down 33.2 million (3.8%). The Cost of materials and external services amounts to million. This marks a reduction of 17.4 million on the same period of 2010 ( million), primarily due to the following: a) a reduction of 13.2 million in like-for-like maintenance costs (including a reduction of 10.1 million due to the lower costs incurred for winter operations, as a result of the reduced amount of snowfall in early 2011); b) the increased proportion of construction work carried out by the Group s own technical units, slightly offset by the increased cost of energy and fuel; c) the costs contributed by Triangulo do Sol, consolidated from 1 July 2011, totalling 8.6 million. Concession fees, totalling million, are up million compared with the first nine months of 2010 ( million), essentially due to the above increase in the concession fees payable by Italian operators. 21

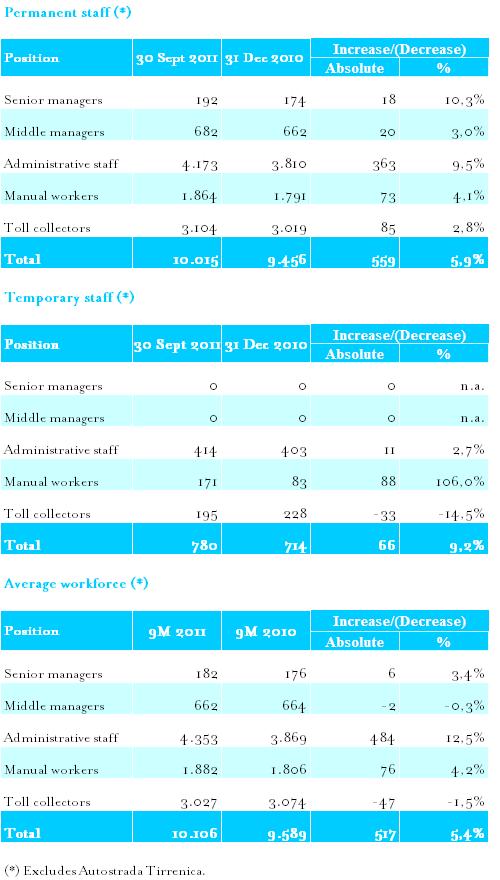

22 Staff costs, before deducting capitalised expenses, of million are up 8.1 million (1.7%) on the first nine months of 2010 ( million). This reflects: a) an increase of 517 in the average workforce (up 5.4%), primarily due to the increased volume of construction work carried out for the Group by Spea and Pavimental (up 239 on average), personnel hired by Electronic Transactions Consultants to work on the contracts acquired in Florida, Georgia and Texas (up 234 on average) and consolidation of Triangulo do Sol (up 117 on average); b) a decrease in the average unit cost (down 3.7%), primarily due to the different impact of long-term management incentive plans in the two comparative periods; after adjusting for the impact of these items, the average unit cost is down 0.4%, primarily due to the first-time consolidation of Triangulo do Sol and the above increase in the workforce at Electronic Transaction Consultants, both of which have average unit labour costs that are lower than the Group average, partly offset by contract renewals at motorway operators and construction companies. Capitalised staff costs are up from 47.4 million to 62.0 million (up 14.6 million), primarily due to the above increase in infrastructure construction work carried out for the Group by Spea and Pavimental. Gross operating profit (EBITDA) of 1,874.6 million is up 99.6 million (5.6%) on the same period of 2010 ( 1,775.0 million). On a like-for-like basis, after stripping out the contribution from Triangulo do Sol, gross operating profit is up 73.9 million (4.2%). Operating profit (EBIT) of 1,483.9 million is up 98.4 million (7.1%) on the same period of 2010 ( 1,385.5 million). The improvement in operating profit is in line with the increase in gross operating profit, as increased depreciation and amortisation (including 10.3 million attributable to Triangulo do Sol), above all of concession rights, and impairments of 25.2 million are almost totally offset by reduced provisions 22

23 and adjustments (down 24.0 million), primarily referring to provisions for the repair and replacement of assets to be handed over at the end of the various concession terms. Financial expenses, after deducting financial income, total million and are up 4.2 million (1.2%) on the same period of 2010 ( million). The increase primarily reflects the following: a) an impairment loss of 25 million in respect of the carrying amount of the investment in Alitalia Compagnia Aerea Italiana, already recognised in the Group s condensed interim financial statements for the six months ended 30 June 2011, and applied in view of the losses reported by the company and of the negative impact of the economic downturn on certain key aspects of its operating environment; b) a rise in net interest payable (up 7.7 million), essentially following an increase in the differential between the cost of borrowing incurred in order to provide the financial resources needed to redeem bonds of 2,000 million on 9 June 2011 and returns on the investment of liquidity; c) net financial expenses of 3.1 million contributed by Triangulo do Sol, following the company s consolidation from the third quarter of 2011; d) an increase in other net financial expenses (up 3.0 million), essentially reflecting non-recurring income of approximately 3.1 million recognised by Stalexport Autostrada Malopolska in the first nine months of 2010, following the restructuring of its debt to the Polish grantor; e) recognition of non-recurring financial income of 36.8 million deriving from the fair value measurement of the interest already held (amounting to 50%) in Triangulo do Sol, following the purchase of a further stake that has resulted in the acquisition of control of the company and its subsequent consolidation from 1 July Financial expenses from discounting of provisions for construction services required by contract and other provisions amount to million, marking an increase of 16.4 million on the first nine 23

24 months of 2010 (up 13.9%). This primarily reflects increases in the interest rates used at 31 December 2010 to discount the provisions. Capitalised financial expenses, amounting to 13.2 million, are up 3.5 million on the same period of 2010, reflecting the progressive increase in accumulated payments made for investment in assets for which the Group will receive additional economic benefits. The Share of the profit/(loss) of associates and joint ventures accounted for using the equity method has resulted in a loss of 0.5 million, compared with a loss of 10.5 million for the first nine months of The 10.0 million reduction in the loss primarily reflects the impairment loss of 18.2 million on the investment in IGLI for the first nine months of 2011, compared with the impairment loss of 30.8 million recognised in the first nine months of In both cases the losses were based on a comparison between the market value of Impregilo s shares and the relevant carrying amount. Income tax expense for the first nine months of 2011 amounts to million and is up 28.8 million (8.8%) on the first nine months of 2010 ( million). This is substantially in line with the improvement in Profit before tax from continuing operations. Profit from continuing operations amounts to million, marking an increase of 62.5 million (10.8%) on the same period of 2010 ( million). Profit from discontinued operations amounts to 87.4 million for the first nine months of 2011 (a loss of 0.1 million for the first nine months of 2010). The figure includes the after-tax gain of 96.7 million, already accounted for in the Group s condensed interim financial statements for the six months ended 30 June 2011, generated by the sale of the investment in Strada dei Parchi and including the fair value measurement of the remaining 2% interest covered by a call/put option agreed with Toto Costruzioni Generali. At the date of deconsolidation, Strada dei Parchi contributed negative equity to the consolidated statement of financial position, as calculated in compliance with the international accounting standards adopted by the Atlantia Group. This item also includes the effect of the impairment loss on the investment in the Portuguese company, Lusoponte, amounting to 20.0 million, after the related taxation, recognised in view of the macroeconomic and financial situation in 24

25 Portugal and deterioration in a number of the operator s performance indicators. Finally, as noted previously and as required by IFRS 5, this item also includes the operating results of Strada dei Parchi, until the date of this company s deconsolidation, and of Autostrada Tirrenica. As a result, Autostrada Tirrenica s contribution to the comparative consolidated income statement for the first nine months of 2010 has also been reclassified with respect to the amount published in the interim report for the nine months ended 30 September 2010, which already included Strada dei Parchi s operating result for the period in the component relating to discontinued operations. Profit for the period, amounting to million, is up million (26.0%) on the first nine months of 2010 ( million). Profit for the period attributable to owners of the parent ( million) is up million (24.6%) on the figure for the first nine months of 2010 ( million), whilst the profit attributable to non-controlling interests amounts to 13.7 million (in the first nine months of 2010 a profit of 4.3 million). On a like-for-like basis, after stripping out the contribution from Triangulo do Sol and the impact of impairments and non-recurring gains and income, profit attributable to owners of the parent is up 33.4 million (5.5%). Operating cash flow, as defined in the section Consolidated financial highlights, to which reference should be made, amounts to 1,365.5 million, up million (19.7%) on the figure for the first nine months of This essentially reflects the impact of recognition of the deductibility of the carrying amounts recorded by Autostrade per l Italia in application of IFRIC 12, reflecting the response of the tax authorities to the company s request for a ruling on the matter and the provisions of the Ministerial Decree of 8 June Operating cash flow was primarily used to fund the Group s capital expenditure (motorway infrastructure, property, plant and equipment and intangible assets) during the first nine months of

26 CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME ( m) 9M M 2010 Profit for the period (A) 726,3 576,3 Fair value gains/(losses) on cash flow hedges -5,3-14,4 Gains/(losses) from translation of financial statements denominated in functional currencies other than the euro -62,7 13,9 Gains/(losses) from measurement of associates and joint ventures using the equity method -20,5 31,3 Other fair value gains/(losses) -0,6 - Other comprehensive income for the period, after related taxation -89,1 30,8 Reclassifications of components of comprehensive income in profit/(loss) for the period Fair value gains on cash flow hedges reclassified to profit/(loss) for the period 0,6 - Total other comprehensive income for the period, after related taxation and reclassifications to profit/(loss) for the period (B) -88,5 30,8 Comprehensive income for the period (A+B) 637,8 607,1 Of which attributable to owners of the parent 641,4 601,7 Of which attributable to non-controlling interests -3,6 5,4 The consolidated statement of comprehensive income reports comprehensive income for the period of million ( million in the first nine months of 2010). The loss, after the related taxation, of 88.5 million resulting from other components of comprehensive income (net income of 30.8 million in the first nine months of 2010), essentially reflecting the following components: a) a fair value loss on the measurement of cash flow hedges of 5.3 million (a loss of 14.4 million for the first nine months of 2010), reflecting interest rate trends in the two comparative periods; b) a loss on the translation of the financial statements of subsidiaries, totalling 62.7 million (a gain of 13.9 million for the first nine months of 2010), primarily reflecting the decline in 26

27 value of the Chilean peso and the Brazilian real versus the euro at the end of the period (inverse exchange rate trends in the first nine months of 2010); c) a loss of 20.5 million resulting from the measurement of associates and joint ventures using the equity method (a gain of 31.3 million for the first nine months of 2010 due to a strengthening of the Chilean peso at that time), essentially due to the above decline in value of the Chilean peso versus the euro, which has had a negative impact on the carrying amount of the investment in Autostrade Sud America). 27

28 28

29 The reclassified consolidated income statement for the third quarter of 2011 reports revenue of 1,140.6 million, marking an improvement of 91.4 million (8.7%) on the same period of 2010, essentially attributable to toll revenue. After stripping out Triangulo do Sol s contribution to revenue, following its consolidation from the second half of 2011, and the toll increases designed to match the rise in the concession fee, like-forlike total revenue is up 17.7 million (1.8%). The 89.3 million improvement in toll revenue primarily reflects: a) consolidation, from 1 July 2011, of the Brazilian operator, Triangulo do Sol, which reports toll revenue of 36.0 million; b) the impact of the above legislative changes to tolls ( 36.5 million); c) the application of annual toll increases by the Group s Italian operators from 1 January 2011 (a 1.92% increase for Autostrade per l Italia), boosting toll revenue by an estimated 17.9 million; d) the decline in traffic on the network operate by the Group s Italian operators, above all with regard to vehicles with 3 or more axles, which are down 1.7% with respect to the same quarter of 2010, whilst the reduction in the 2 axle is less accentuated (down 0.7%), resulting in an overall reduction in toll revenue of 8.3 million. Other operating income is up 2.1 million on the third quarter of 2010, essentially reflecting the contribution from Triangulo do Sol ( 1.2 million), increased revenue from service areas, a rise in payouts and greater income from solar energy, offset by a decline in revenue from work carried out for external customers by Pavimental. Net operating costs of million are up 58.4 million (16.9%) on the third quarter of 2010, primarily reflecting the contribution from Triangulo do Sol, the increase in the concession fee and an increase in maintenance activity. After stripping out Triangulo do Sol s contribution to operating costs 29

30 and the impact the above increase in the concession fee, net operating costs are up 10.4 million (3.8%), essentially due to the above increase in maintenance activity. Gross operating profit (EBITDA) for the third quarter of 2011 amounts to million, marking an increase of 33.0 million (4.7%) on the same period of 2010 ( million). On a like-for-like basis, gross operating profit is up 7.3 million (1.0%). Profit from continuing operations of million is up 38.9 million (14.8%) on the third quarter of 2010 ( million). The improvement substantially reflects recognition of nonrecurring financial income of 36.8 million deriving from the fair value measurement of the interest already held (amounting to 50%) in Triangulo do Sol, following the purchase of a further stake that has resulted in the acquisition of control of the company and its subsequent consolidation from 1 July The Loss from discontinued operations, which includes Autostrada Tirrenica s contribution to the Group s results for both comparative quarters, amounts to 14.7 million for the third quarter of This reflects the impairment loss on the investment in the Portuguese company, Lusoponte, amounting to 20.0 million, after the related taxation. Profit for the third quarter of 2011 is million ( million for the third quarter of 2010), of which million is attributable to owners of the parent ( million attributable to owners of the parent for the third quarter of 2010). 30

31 Consolidated financial position As at 30 September 2011 Non-current non-financial assets of 19,515.5 million are up million on the figure for 31 December 2010 ( 18,942.8 million). Property, plant and equipment, amounting to million, has not undergone significant changes during the period. Intangible assets total 17,114.7 million ( 16,187.6 million as at 31 December 2010). In addition to the goodwill ( 4,382.9 million) recognised as at 31 December 2003, following acquisition of the majority shareholding in the former Autostrade Concessioni e Costruzioni Autostrade SpA, these assets include the Group s concession rights, amounting to 12,673.4 million ( 11,752.0 million as at 31 December 2010). These rights refer to concession rights accruing from construction services for which no additional economic benefits are received, totalling 9,354.2 million ( 9,257.3 million as at 31 December 2010) and construction services for which additional economic benefits are received, totalling 2,714.4 million ( 2,216.9 million as at 31 December 2010). The increase in intangible assets, amounting to million, is essentially due to the following: a) investment in construction services for which additional economic benefits are received (up million); b) adjustment of the present value on completion of investment in construction services for which no additional benefits are received (up million); c) recognition of the concession rights of the newly consolidated company, Triangulo do Sol (up million), primarily reflecting the fair value of the assets acquired, identified using the purchase method; d) amortisation for the period, totalling million; e) reclassification of Autostrada Tirrenica s intangible assets ( million) to Non-financial assets held for sale or related to discontinued operations, following the above agreement to sell the Group s majority stake in the company. 31

32 32

33 33

34 As at 30 September 2011 Investments, totalling million ( million as at 31 December 2010), are down million, resulting from the following: a) consolidation on a line-by-line basis, from 1 July 2011, of Triangulo do Sol, following the above-mentioned acquisition of control (as at 31 December 2010 the investment was accounted for at a carrying amount of million); b) the impairment loss of 25 million on the investment in Alitalia Compagnia Aerea Italiana, already recognised in the condensed interim financial statements for the six months ended 30 June 2011; c) the full write-down of the residual carrying amount of the investment in IGLI, amounting to 13.1 million for the first nine months of 2011 (with provisions made for impairments exceeding the carrying amount of investments, totalling 3.9 million); d) the injection of 17.4 million of further equity into Tangenziali Esterne di Milano ( 9.6 million) and into the Indian operator, Pune Solapur ( 7.8 million). Deferred tax assets, after offsetting against deferred tax liabilities, amount to 1,881.4 million ( 2,101.8 million as at 31 December 2010), marking a reduction of million. This primarily reflects the release of deferred tax assets linked primarily to the positive impact of recognition of the tax deductibility of the carrying amounts recorded by Autostrade per l Italia in application of IFRIC 12, in addition to the release of deferred tax assets recognised on the intercompany gain arising in 2003 as a result of the transfer of motorway assets to Autostrade per l Italia, totalling 79.3 million. Consolidated working capital reports a negative balance of 1,209.2 million as at 30 September 2011, marking a change of million compared with the negative balance of million as at 31 December The change basically reflects the deconsolidation of Strada dei Parchi, after closure of the sale of the related investment, partially offset by an increase in non-financial assets held for sale or related to discontinued operations as a result of reclassification of the assets of Autostrade Tirrenica, the 34

35 controlling interest in which is in the process of being sold, and of the investment in Nueva Inversiones (accounted for as at 30 September 2011 at a carrying amount of million). A full description of the transaction involved in this latest investment in Chile is provided in the section, Operating review of the Group s main investee companies. The remaining million reduction in working capital primarily reflects the following: a) an increase of million in trading liabilities, primarily due to a million increase in amounts payable to the operators of interconnecting motorways, reflecting the contractually agreed timing of the settlement of amounts due to and from other motorway operators, as well as increased turnover for the period, reflected in a 62.5 million rise in tolls awaiting payment; amounts payable to suppliers are also up 28.9 million, reflecting increased capital expenditure; b) a rise in the current portion of provisions for construction services required by contract (up million), reflecting the forecast volume of construction services for which no additional economic benefits are received; c) an increase of 88.9 million in net current tax liabilities, reflecting income tax expense for the period, after the impact of recognition of the tax deductibility of the carrying amounts recorded by Autostrade per l Italia in application of IFRIC 12; d) an increase in trade receivables of million, primarily reflecting an increase in tolls receivable, partly due to amounts billed in September, and the toll increases applied by the Italian operators in order to match the rise in the concession fee, in addition to an increase in VAT billed to customers. The carrying amount of Non-current non-financial liabilities, totalling 5,373.4 million, is substantially in line with the figure for 31 December 2010 ( 5,334.8 million), primarily reflecting a reduction in provisions for construction services required by contract (down million), partially offset by an increase in deferred tax liabilities (up million). Provisions for construction services required by contract have fallen as a result of the reclassification of the current portion (down 35

36 552.5 million), partially offset by an increase resulting from an adjustment, following increases in current and prospective interest rates, of the present value on completion of investment in construction services for which no additional benefits are received (up million) and recognition in the income statement of the impact of discounting to present value (up 98.4 million). Deferred tax liabilities have increased as a result of the first-time consolidation of Triangulo do Sol (up million). As a result, Net invested capital, totalling 12,932.9 million as at 30 September 2011, is down million on the figure for 31 December 2010 ( 13,244.2 million). Equity attributable to owners of the parent and non-controlling interests totals 4,089.4 million ( 3,586.9 million as at 31 December 2010). Equity attributable to owners of the parent, totalling 3,601.8 million, is up million, primarily reflecting comprehensive income for the period ( million), after payment of the final dividend for 2010, approved in the first nine months of 2011 ( million). Equity attributable to non-controlling interests, totalling million, is up 84.1 million on the figure for 31 December 2010 ( million), essentially due to consolidation of Triangulo do Sol. The Group s net debt as at 30 September 2011 amounts to 8,843.5 million, marking a reduction of million compared with 31 December 2010 ( 9,657.3 million), primarily due to the deconsolidation of Strada dei Parchi following the sale of the investment in this company. Non-current net debt, amounting to 9,464.2 million ( 9,131.5 million at 31 December 2010) is up million, primarily due to the following: a) an increase of million in non-current financial liabilities, essentially reflecting: 1) new medium/long-term borrowings, following the drawdown of a new tranche with a face value of million of the floating rate loan granted to Autostrade per l Italia by Cassa Depositi e Prestiti (with final repayment maturing in 2034), the signature by the Chilean operator, Los 36

37 Lagos, of a new medium/long-term loan agreement (a face value of 92.3 million), and the assumption of debt of 55.3 million following the consolidation of Triangulo do Sol, partially offset by the reclassification to current liabilities of the portion of borrowings maturing within the next 12 months ( 90.6 million), reclassification to liabilities related to discontinued operations of the interest-free loan from the Central Guarantee Fund to Autostrade Tirrenica ( 36.5 million) and a reduction of 37.1 million in foreign currency financial liabilities as a result of exchange rate movements; 2) reclassification to liabilities related to discontinued operations of deferred financial income of 21.9 million, essentially consisting of interest rate subsidies relating to the interest-free loan from the Central Guarantee Fund to Autostrade Tirrenica; b) an increase of 1.4 million in non-current financial assets, substantially due to the following, which almost entirely cancel each other out: 1) an increase of 25.5 million in the term deposits provided for by laws 662/96, 135/97 and 345/97, following a review of the timing of their release; 2) an increase of 21.6 million in other financial assets, which include the remaining portion of the amount due from Toto Costruzioni Generali in connection with the sale of the investment in Strada dei Parchi; 3) an increase of 18.7 million in non-current financial assets deriving from concessions, essentially reflecting investments in motorway infrastructure by Autostrade Meridionali during the first nine months of 2011; 4) a reduction of 50.5 million in financial assets deriving from accrued government grants, resulting from the reclassification to current assets of grants accruing from construction services rendered during the period by the Group s motorway operators, which are expected to be collected within the next 12 months; 5) a reduction in fair value gains (down 13.8 million) on the derivatives hedging the yen denominated bond issue, primarily due to a decline in the interest rates used for their measurement as at 30 September 2011, partially offset by a strengthening of the currency in 37

38 which the bonds were issued with respect to the euro, accounted for as a change in the hedged liability. As at 30 September 2011 current net funds amount to million (net debt of million as at 31 December 2010). The change of 1,146.5 million reflects: a) a reduction of 2,872.0 million in current financial liabilities, essentially due to the following: 1) the redemption of bonds totalling 2,000 million and unwinding of the related cash flow hedges (down 26.0 million; 2) a reduction of million in financial liabilities related to discontinued operations, primarily following the sale of the investment in Strada dei Parchi, partially offset by reclassification of Autostrade Tirrenica s financial liabilities; 3) a decrease of 99.0 million in accrued borrowing costs following the payment of interest on bond issues and of differentials on derivatives; 4) a reduction of 63.7 million in the current portion of medium/long-term borrowings, following repayments during the period, totalling million, and a reduction of 32.6 million in the amount payable to ANAS deriving from the progressive collection of government grants, partially offset by the reclassification to current financial liabilities (up 90.6 million) of portions of borrowings maturing within the next 12 months, and the assumption of Triangulo do Sol s current borrowings ( 25.0 million); 5) a short-term loan obtained by Holding do Sur (with a face value of million) to fund the acquisition, via the issue of new shares, of a 50% interest in Nueva Inversiones, the Chilean company set up by the Atlantia Group to acquire the investments covered by the agreement reached with the Acciona group on 18 April 2011; 6) increased use of short-term facilities, amounting to 52.5 million; b) a reduction of 1,635.1 million in cash and cash equivalents, primarily due to the above redemption of bonds totalling 2,000 million and payment of the final dividend for 2010 ( million), partially offset by cash generated during the period in the form of new 38

39 borrowings and operating cash flow, and from the collection of 60.6 million from Toto Costruzioni Generali as the initial instalment of the amount due in relation to the sale of Strada dei Parchi; c) a reduction of 90.4 million in other current financial assets, due to the following: 1) a reduction of million in the short-term portion of term deposits, primarily due to release of the related certificates during the first nine months of 2011; 2) a reduction in current financial assets deriving from government grants for construction services rendered, totalling 39.9 million, after the collection of grants with a value of million, partially offset by the increase resulting from the reclassification from non-current assets of amounts expected to be collected within the next 12 months, totalling 41.7 million, and by grants accruing on the completion of construction services, totalling 52.1 million; 3) an increase of 63.6 million in other current financial assets, essentially reflecting an increase of 59.0 million in the amount receivable from ANAS linked to the progressive release of certificates. The Group s ordinary operating and financing activities expose it to market risks, primarily regarding interest rate and currency risks linked to the financial assets acquired and the financial liabilities assumed, in addition to liquidity and credit risks. The Group s financial risk management strategy is consistent with the objectives set by Atlantia s Board of Directors. The strategy aims to both manage and control such risks, wherever possible mitigating interest rate and currency risks and minimising borrowing costs, as defined in the approved Financial Policy. The components of the Group s derivatives portfolio as at 30 September 2011 are classified, in application of IAS 39, as cash flow hedges. Based on the positive outcome of tests of effectiveness of cash flow hedges as at 30 September 2011, changes in fair value have been recognised in full in comprehensive income, with no recognition of any ineffective portion in profit or loss. 39

40 In September 2011 the Group entered into new Interest Rate Swaps, classified as cash flow hedges in application of IAS 39, to hedge interest rate risk on the million medium/long-term floating rate loan from Cassa Depositi e Prestiti, using EIB funding, which has a residual weighted average term to maturity of approximately 13 years. This transaction has converted the overall exposure to a fixed rate of approximately 3.99%. The residual weighted average term to maturity of the Group s interest bearing debt is approximately 7 years and 3 months, with 95% fixed rate. 12% of the Group s medium/long-term debt is denominated in currencies other than the euro. Taking account of foreign exchange hedges and the proportion of debt denominated in the local currency of the country in which the relevant Group company operates (around 4%), the Group is not exposed to currency risk on translation into euros. The average cost of the Group s medium/long-term borrowings in the first nine months of 2011, after adjusting for Strada dei Parchi s debt, was approximately 4.9%. As at 30 September 2011 the Group has cash reserves (cash, term deposits and undrawn committed lines of credit) of 4,094 million, consisting of: a) 913 million in cash and/or investments maturing within 120 days; b) 381 million in term deposits allocated primarily to finance the execution of specific construction services; c) 2,800 million in undrawn committed lines of credit. The Group s net debt, as defined according to the CESR recommendation of 10 February 2005 (which does not permit the deduction of non-current financial assets from debt), amounts to 9,780.3 million as at 30 September 2011, compared with net debt of 10,592.7 million as at 31 December

41 41

42 Consolidated cash flow Net debt decreased by million during the first nine months of 2011, compared with a reduction of million in the first nine months of Operating activities generated cash flows of 1,572.4 million in the first nine months of 2011 ( 1,530.4 million in the first nine months of 2010). Cash generated by operating activities is up 42.0 million on the first nine months of 2010, bearing in mind that, alongside an improvement in profit from continuing operations for the first nine months of 2011 and the positive impact of recognition of the deductibility of the carrying amounts recorded by Autostrade per l Italia in application of IFRIC 12 (operating cash flow up million), the contribution from operating capital and other components of working capital, whilst positive, is much lower than the corresponding contribution for the first nine months of 2010, which essentially resulted from significant increases in trade payables and in the amount payable to ANAS as a result of the above-mentioned increase in concession fees. Cash used for investments in non-financial assets amounts to million, compared with an outflow of million in the first nine months of Cash used in the first nine months of 2011 essentially reflects investment in motorway infrastructure, after the related government grants (an outflow of 1,017.1 million), the cost of acquiring interests in consolidated investments ( million), regarding the acquisition of a further stake in Triangulo do Sol and including debt resulting from consolidation of the company, and the cost of acquiring interests in unconsolidated investments ( million), primarily referring to the purchase of 50% of Nueva Inversiones by Inversiones Autostrade Holding do Sur. These outflows are, however, partially offset by the gain realised on the sale of Strada dei Parchi, and by the resulting deconsolidation of this company s net debt (with an overall impact on consolidated debt of 1,021.2 million). 42

43 The outflow in the first nine months of 2010 was primarily due to investment in motorway infrastructure, after the related government grants, and an increase in takeover rights resulting from capital expenditure. The cash outflow resulting from changes in equity amounts to million in the first nine months of 2011 ( million in the same period of 2010), essentially due to the dividends approved by Group companies during the period. The overall impact of the above cash flows was to reduce net debt by million in the first nine months of 2011 ( million in the same period of 2010). In addition, in the first nine months of 2011 net debt was increased by changes in the fair value of cash flow hedges recognised in comprehensive income (amounting to 5.7 million), with the corresponding effect in the same period of 2010 resulting in an increase in net debt of 16.5 million. This reflects falling interest rates from one comparative period to the other. 43

44 44

45 45

46 46

47 Operating review of the Group s operators Traffic The number of kilometres travelled on the network managed by Autostrade per l Italia and its Italian motorway subsidiaries (excluding Autostrada Tirrenica, 69.1% of which is in the process of being sold) during the first nine months of 2011 amounts to 39,804.8 million: 34,934.8 million by vehicles with 2 axles (cars and vans, representing 87.8% of the total) and 4,870.0 million by vehicles with 3 or more axles (12.2% of the total). In terms of total kilometres travelled, traffic using the Group s Italian network is 1.0% down on the same period of 2010, with vehicles with 2 axles down 1.1% and those with 3 or more axles down 0.6%. Traffic using Autostrade per l Italia s network during the first nine months of 2011 is down 0.9%, with vehicles with 2 axles down 0.9% and those with 3 or more axles down 0.7%. The two motorways serving the Naples metropolitan area saw a significant decline in traffic, with the number of vehicles down 3.3% on the Naples Ring Road and 3.8% on the A3 Naples Salerno. In contrast, the motorways in the Valle d Aosta recorded a positive performance (traffic using the Mont Blanc Tunnel up 3.2% and vehicles using the Valle d Aosta Motorway Link Road up 0.3%), whilst Autostrada Torino-Savona reports a slight decline (down 0.2%). The third quarter of 2011, on the other hand, saw a reduction in traffic for all the Group s companies. 47

48 The biggest drop was recorded by vehicles with 3 or more axles, which are down 1.7% on the same quarter of 2010, whilst the decline in the 2-axle component was less significant (down 0.7%) and related primarily to working days. Traffic on the network operated under concession in Italy during the first nine months of 2011 Overseas, the Polish operator, Stalexport Autostrada Malopolska, recorded a 3.6% increase in traffic during the first nine months of 2011, compared with the same period of The average daily volume of light vehicles is up 5.6%, whilst heavy vehicles are down 3.2%, reflecting the adoption of direct tolling (in place of the previous government-funded system of shadow tolling ) from 1 July The Chilean operator, Los Lagos, saw an increase in traffic using its network, which was up 9.5% on the first nine months of Vehicles with 2 axles are up 8.8% and those with 3 or more axles up 16.8%. It should be noted that the figures for 2010 were affected by damage to the network to the north of the section operated by Los Lagos (which instead escaped damage), as a result of the earthquake that hit Chile on 27 February

49 In the first nine months of 2011 the Brazilian operator, Triangulo do Sol, registered growth of 5.9% in terms of kilometres travelled, compared with the same period of Light vehicles are up 6.2%, whilst heavy traffic is up 5.6%. Traffic growth remained strong on the networks operated by the Group s other main investee companies: Costanera Norte, Litoral Central, Nororiente and Vespucio Sur in Chile recorded traffic growth of 6.6%, 7.8%, 14.0% and 10.8%, respectively, in terms of kilometres travelled, compared with the same period of Traffic on the network operated under concession overseas during the first nine months of 2011 Traffic (millions of km travelled) (a) Traffic (thousands of transits) (a) % inc./(dec.) % inc./(dec.) 9M M 2010 on M M 2010 on 2010 Consolidated foreign operations Stalexport Autostrada Malopolska 522,3 504,0 3,6% , ,0 3,6% Los Lagos 344,4 314,1 9,6% 8.982, ,0 9,5% Triangulo do Sol 963,4 909,5 5,9% , ,0 6,0% Foreign investee companies Autostrade Sud America -Nororiente (b) 34,8 30,5 14,0% 2.944, ,5 14,0% -Litoral Central 56,9 52,8 7,8% 2.264, ,0 8,4% -Vespucio Sur 485,0 437,6 10,8% , ,0 10,6% -Costanera Norte 646,5 606,7 6,6% , ,0 5,9% Total 3.053, ,2 6,9% , ,5 8,1% (a) Provisional data (b) Traffic figure in millions of km travelled is based on the new method of calculation applied from August Toll charges The following annual tariff increases were introduced by Autostrade per l Italia and the Group s Italian motorway operators, in accordance with their respective concession arrangements, from 1 January 2011: 49

50 Toll increases from 1 January 2011 (excluding increases pursuant to Law 122/2010) Italian motorway operator Toll charge increase Autostrade per l'italia 1.92% Raccordo Autostradale Valle D'Aosta 14.15% Autostrada Torino-Savona 0.63% Tangenziale di Napoli 3.80% Autostrade Meridionali -6.56%(*) Società Italiana Traforo del Monte Bianco 4.96% Autostrada Tirrenica (**) 4.08% (*)As a result of rounding, the impact on the final tolls paid by road users is limited to classes B and 5. (**)A 69.1% interest in this company is in the process of being sold. In accordance with the existing Single Concession Arrangement, the toll increase applied by Autostrade per l'italia for 2011 was 1.92%. This was calculated on the basis of two components: 0.63%, equivalent to 70% of the inflation rate in the period from 1 July 2009 to 30 June 2010; 1.29%, relating to the X investments component of the tariff formula, designed to cover the additional capital expenditure inserted into the IV Addendum of The inflation-linked component (0.63%) was calculated on the basis of consumer price inflation for the Italian population as a whole, as calculated by ISTAT (the NIC index), for the period between 1 July 2009 and 30 June 2010, equal to 0.90%, compared with the period from 1 July 2008 to 30 June The toll component relating to capital expenditure inserted into the IV Addendum (1.29%) is based on the state of progress of work on the individual projects, as reported in the statement of financial position as at 30 September The subsidiaries, Raccordo Autostradale Valle d'aosta, Autostrada Tirrenica, Tangenziale di Napoli and Autostrade Meridionali, whose single concession arrangements, involving the rebalancing of their 50

51 respective financial plans, became effective 2010, have for the first time applied the new formula for calculating their toll increases. The various factors taken into account include the target inflation rate, the rebalancing component and the return on investment, in addition to quality. The increases granted from 1 January 2011 represented the sum of the increases granted in compliance with the new arrangements for the years 2010 and 2011, after deducting the increase already applied from 1 January 2010 on the basis of the arrangements in force at that time. The toll increase for Autostrada Torino-Savona is 0.63%, which was granted on the basis of the single concession arrangement that came into effect in This increase is equal to 70% of the inflation rate in the period from 1 July 2009 to 30 June Società Traforo del Monte Bianco, which operates under a different concession regime based on bilateral agreements between Italy and France, applied a total increase of 4.96% from 1 January 2011, in accordance with the resolution approved by the Intergovernmental Committee for the Mont Blanc Tunnel on 22 October This increase is based on the combination of two elements: 1.46% representing the average inflation rate in France and Italy for the period from 1 September 2009 to 31 August 2010; 3.50% in accordance with the agreement between the Italian and French governments dated 24 February 2009, with use of the proceeds still be decided on by the two governments. The shadow toll paid by the Grantor to the Polish operator, Stalexport Autostrada Malopolska, for heavy vehicles weighing more than 12 tonnes was abolished from 1 July 2011, to be replaced by a direct polling system, with charges paid by users of the motorway network. The switch to a direct polling system has raised tolls by 114% compared with those previously paid by the Grantor. The toll paid by heavy vehicles weighing less than 12 tonnes has, on the other hand, risen 11.1% from 1 July Under the terms of its concession arrangement, the tolls applied by Chilean operator, Los Lagos, did not change from 1 January 2011, reflecting the combined effect of: the inflation-linked increase of 2.5% (calculated between 1 December 2009 and 30 November 2010); 51

52 the negative impact of the safety factor between 2010 (equal to 3.5%) and 2011 (equal to 0.0%); the rounding off of tariffs to the nearest 100 pesos (up 1.0%). From 1 July 2011 the tolls charged by the Brazilian operator, Triangulo do Sol, were raised by 9.7%, in accordance with the terms of the company s concession arrangement, which link toll increases to the General Market Price Index. Network upgrade and modernisation During the first nine months of 2011 the Group invested a total of 1,128.2 million, marking an increase of million (14%) on the first nine months of Capital expenditure by the Atlantia Group ( m) 9M M 2010 % inc./(dec.) Autostrade per l'italia -projects in Agreement of ,9 384,6-27% Autostrade per l'italia - projects in IV Addendum of ,4 263,7 98% Investments in major works by other subsidiaries 69,6 80,0-13% Other investments in the network and capitalised costs (staff, maintenance, other) 199,3 212,5-6% Total investments in motorway assets 1.069,2 940,8 14% Investments in other intangible assets 21,5 15,7 37% Investments in property, plant and equipment 37,5 37,4 - Total capital expenditure by the Group 1.128,2 994,0 14% Investment relating to Autostrade per l Italia s Agreement of 1997 is down million on the first nine months of 2010, primarily following completion of excavation of the Base Tunnel and of the tunnels for Lot 12 of the Variante di Valico and Lots and 7-8 on the Florence North-Florence South section of motorway. These reductions have not yet been offset by work being carried out on the Barberino-Florence North 52

53 section, which began in January 2011, and investment in the Florence South-Incisa section, the design for which was only partially approved by the Services Conference of 31 May 2011 and submitted to ANAS for approval. Investment envisaged under the IV Addendum of 2002 is up million on the first nine months of 2010, primarily due to increased work on the A14 between Rimini North and Porto Sant Elpidio, on the A1 between Fiano and Settebagni and on the A9 Lainate-Como section, partly as a result of contractual agreements with certain contractors designed to speed up construction. Investment in major works by the Group s other motorway operators is down 10.4 million compared with the same period of This primarily reflects a reduction in work carried out by Autostrade Meridionali on the widening of the A3, which is approximately 90% complete. This reduction was partially offset by a rise in investment by Autostrada Tirrenica, reflecting increased work on the Rosignano-San Pietro in Palazzi section and on the final designs for the remaining lots. Investment in major works by Autostrade per l Italia 1997 Agreement Of the works included in Autostrade per l Italia SpA s Agreement of 1997, as at 30 September 2011 approximately 95% of the works have been authorised, around 78% have been contracted out, and more than 62% of the works have been completed. Variante di Valico This section of motorway is scheduled to open to traffic in 2013, partly thanks to the use of a mechanised EPB (Earth Pressure Balance) tunnelling machine for the Sparvo tunnel (2.5 km), enabling full mechanisation of both the excavation and tunnel cladding process and thereby speeding up excavation time. 53

54 Florence North Florence South Despite the financial difficulties experienced by the contractor early in the year, the 13.5-km stretch of the new 3-lane southbound carriageway of the A1 between Florence Scandicci and Florence South was opened to traffic on 3 August The opening means that the full 22-km stretch of the 3-lane southbound carriageway of the A1 from Florence North to Florence South is now open to traffic. In addition, the 3-lane northbound carriageway was opened on 19 August, in time for the start of the peak period corresponding with the end of the summer holidays. Barberino - Florence North The works for Lot 0, including site preparation, service roads and certain pre-construction works, were handed over to Pavimental on 26 January In terms of completion work, Autostrade per l Italia has opted to use an EPB (Earth Pressure Balance) tunnelling machine to build a single tunnel in place of nine tunnels originally to be excavated using the traditional method. This will significantly cut construction time, provide enhanced safety guarantees for workers, reduce the environmental impact and result in cost savings. The design using mechanised excavation received final approval for the purposes of environmental compatibility on 27 June 2011 and is now awaiting approval by a national Services Conference. In the meantime, in order to ensure continuity of the work already started at Lot 0, on 31 May 2011 Autostrade per l Italia sent ANAS the final design for Lot 1, including the motorway widening work not affected by the variation. Florence South - Incisa The Services Conference was concluded positively on 31 May 2011 solely in respect of the sections external to the San Donato tunnel (Lot 1), and on 8 August 2011 the Ministry of Infrastructure 54

55 announced confirmation of the final agreement between central government and the regional authority. On 4 October 2011 Autostrade per l Italia submitted the final design for Lot 1 to ANAS for approval. The Environmental Impact Assessment (EIA) for the sections relating to the San Donato tunnel began on 23 June 2011 with publication of the Final Design and Environmental Impact Study. Investment in major works by Autostrade per l Italia IV Addendum 2002 As at 30 September 2011 over 66% of the works have been authorised, over 65% have been contracted out and more than 33% have been completed. Lainate - Como Work on the third lane of the A9 between Lainate and Como Grandate is proceeding apace. Thanks to award of the contract to the subsidiary, Pavimental, the new Lainate interchange was opened to traffic 14 months ahead of schedule on 26 July 2011, smoothing traffic flow and improving safety for vehicles switching between the A8 and A9 motorways. The Group expects to have the entire section open to traffic by 31 July 2012, seven months ahead of the original completion date. Rimini North Porto Sant Elpidio Work on the section between Ancona South and Porto Sant Elpidio (Lot 6A) is substantially complete and the road open to traffic. Widening work is currently underway on the remaining section, with the exception of the 17.2 km between Ancona North and Ancona South (Lot 5), for which Autostrade per l Italia sent ANAS the executive design prepared by the contractor on 28 July Autostrade per l Italia aims to be able to give the go-ahead for work to start by the end of 2011, after ANAS has approved the design submitted. Contractual agreements have been entered into speeding up work on Lots 1A, 2, 3 and 55

56 6B (53.8 km), so as to be able to open the relevant motorway to traffic 4 to 8 months ahead of the original completion date. The new Senigallia toll station (Lot 3) was opened to traffic around 5 months ahead of schedule on 21 April km of the new third lane on the northbound stretch between Fano and Senigallia (Lot 3) was opened to traffic 3 months ahead of schedule on 21 July The new Porto Sant Elpidio junction (Lot 6B) was opened to traffic 4 months ahead of schedule on 29 July Fiano - Settebagni di Roma Award of the contract directly to the subsidiary, Pavimental, made it possible to open the Castelnuovo di Porto junction to traffic 7 months ahead of schedule on 27 July The entire section of motorway was opened to traffic on 1 August 2011, 9 months ahead of schedule. Genoa Bypass Following conclusion of the public consultation process on 8 February 2010, and after receiving approval from the various entities involved, the Ministry of Infrastructure and Transport, Genoa Provincial Authority, the Municipality of Genoa, the Genoa Port Authority, ANAS and Autostrade per l Italia signed the new memorandum of understanding, which sets out the new agreed upon solution and identifies the next steps to be taken in order to proceed with work on the project. The Memorandum of Understanding was also signed by Liguria Regional Authority on 13 April An initial estimate contained in the preliminary design indicates that the total cost of constructing the Genoa Interchange will be 3.1 billion. This figure will be confirmed in the final and executive designs. Autostrade per l Italia has prepared the final design and the environmental impact study for the Genoa Interchange (or Gronda di Ponente). On 15 June 2011 the company submitted a request, pursuant to art. 23 of Legislative Decree 152/06, to start the EIA procedure and for permission to 56

57 file and publish the final design and the environmental impact study. The Services Conference for the San Benigno Interchange began on 14 April 2011 and ended on 4 August Revision of the Final Design has begun in accordance with the requirements expressed by the various bodies involved in the Services Conference. Tunnel Safety Plan As at 30 September 2011 the upgrade of 317 tunnels has been completed out of a total of 548 designs, whilst work on the remaining 231 is underway. 297 tunnels out of a total of 405 have been completed, whilst work is underway on the remaining 108. Planned investment in major works by the Group s other motorway operators With regard to investment in new works by Autostrade per l Italia s subsidiaries (Raccordo Autostradale Valle d Aosta, Autostrade Meridionali and Autostrada Tirrenica), as at 30 September 2011 approximately 38% of the works have been authorised, around 32% of the works are being carried out or completed, and 32% have been completed. Contract reserves quantified by contractors As at 30 September 2011 operators have recognised contract reserves quantified by contractors amounting to 830 million, including 400 million regarding works envisaged in Autostrade per l Italia s Agreement of 1997, the additional cost of which cannot be recovered via toll charges. 57

58 Network operations Safety, maintenance and traffic management The death rate on the network operated by Autostrade per l Italia in the first nine months of 2011 was 0.30 (down on the same period of 2010, when the figure was 0.33), whilst the accident rate was 28.2 (30.4 in the first nine months of 2010). Rollout of the system for measuring the average speeds of vehicles using a particular stretch of motorway ( Tutor ) continues. One year on from its installation on a number of sections of motorway, the new system has in general resulted in a 19% reduction in accidents, with the number of deaths falling 51%. As at 30 September 2011 Tutor has been installed along approximately 2,500 km of carriageway, representing approximately 39% of the network operated by Autostrade per l Italia and the Group s other Italian motorway operators. The system will soon be installed on the network operated by Autostrade per l Italia and its subsidiaries on the A16 between Naples and Canosa and on the A12 between Genoa and Sestri Levante. Routine and unscheduled maintenance continued as part the operators commitment to guaranteeing ever better operating standards. Draining pavement now covers 81.7% of Autostrade per l'italia s network, with the percentage rising to nearly 100% of the network where it is possible to lay draining pavement, thus excluding mountain stretches, tunnels and sections where new road construction work is taking place. During the first nine months of 2011 traffic conditions on Autostrade per l Italia s network also benefitted from a 60% reduction in the hours of snowfall per kilometre compared with the same period of Toll collection and payment systems Transactions handled by automated tolling systems on the network operated by Autostrade per l Italia 58

59 and its Italian subsidiaries, excluding Autostrada Tirrenica, accounted for 77.21% of total transactions in the first nine months of 2011 (75.54% in the same period of 2010). Payments using Telepass accounted for 56.95% of total transactions, compared with 55.54% in the same period of As at 30 September 2011 approximately 7.7 million Telepass devices are in use on the Italian motorway network. Service areas and advertising Royalties on the revenues generated by the retail activities of sub-operators at service areas on the network managed by Autostrade per l'italia and its subsidiaries (including Stalexport Autostrada Malopolska and excluding Autostrada Tirrenica) amount to million for the first nine months of 2011, marking an increase of 1.6% in recurring royalties compared with the same period of This primarily reflects the annual increases applied from 1 January As at 30 September 2011 approximately 95.3% of the works included in the 800 million service area upgrade programme for Autostrade per l Italia s network, covering works to be carried out by both Autostrade per l Italia and sub-operators, had either been started or completed. Work on 192 service areas has already been completed by Autostrade per l Italia and sub-operators, whilst expansion and renovation work is being carried out by Autostrade per l Italia at a further 9 service areas. In the first nine months of 2011 the subsidiary, AD Moving SpA, earned revenue of approximately 10.7 million (down 1.4 million on the same period of 2010) from the management and marketing of advertising space along the motorway network and at other locations. This reflects a downturn in the billboard market. 59

60 Operating review of the other main subsidiaries Pavimental The company operates as a motorway maintenance provider and is carrying out a number of major infrastructure works for the Group. Compared with the first nine months of 2010, revenue of million is up million (49.4%). This is primarily due to the increased volume of infrastructure construction work carried out for Autostrade per l Italia (up million) and increased work on other contracts awarded by the same company (maintenance, roadside barriers, the elimination of noise pollution and junctions) and other Group companies (Autostrada Tirrenica, up 10.8 million). EBITDA is 16.7 million for the first nine months of 2011, compared with EBITDA of 7.4 million for the same period of Spea Ingegneria Europea The company supplies engineering services, primarily to the Group. It offers design, project management and monitoring services for upgrade and extraordinary maintenance of the network. Revenue of 113 million for the first nine months of 2011 is up 5.35% ( 5.7 million) on the same period of the previous year. This is primarily due to an increase in project management activities, above all on the A14 Rimini-Pedaso and Variante di Valico sections, partially offset by a reduction in design work for infrastructure projects, including the final design for the Genoa Interchange on behalf of Autostrade per l Italia, completion of the A12 Livorno-Civitavecchia for Autostrada Tirrenica and new projects provided for in Autostrade per l Italia s Single Concession Arrangement. 97.1% of the company s revenue in the first nine months of 2011 was earned on services provided to 60

61 the Group. EBITDA is 43.4 million for the first nine months of 2011, up 5.4 million on the same period of the previous year. Telepass The company is responsible for operating motorway toll collection systems providing an alternative to cash payments: the Viacard direct debit card and Telepass devices. As at 30 September 2011 the number of Telepass devices in circulation exceeds 7.7 million (up 400,000 on 30 September 2010), with the number of subscribers of the Premium option totalling 1.4 million (up 237,000 on 30 September 2010). Revenue of 95.9 million in the first nine months of 2011 was primarily generated by Viacard subscription fees of 16.1 million (in line with the same period of the previous year), Telepass fees of 64.5 million (up 2.3 million on the first nine months of 2010) and payments for Telepass Premium services of 7.8 million (up 1.5 million on the same period of 2010). Telepass fees were impacted by discounts, totalling 0.9 million, applied to Telepass Family customers to take account of the increased amount of VAT payable for motorway use prior to the date on which the increase in rate from 20% to 21% came into force on 17 September 2011, in compliance with Law 148 of 14 September Telepass decided to absorb the retroactive increase in VAT on tolls, giving Telepass Family customers, who cannot deduct VAT, a discount of an equal amount when billing Telepass fees accruing prior to 17 September The company s EBITDA for the first nine months of 2011, amounting to 53.5 million, compares with EBITDA of 49.5 million for the same period of Autostrade Tech Formed as a result of the spin-off of the Group s technology unit in January 2010, Autostrade Tech 61