Presentation by CA RITESH MEHTA, NAGPUR. B. Com., F.C.A., D.I.S.A (ICAI).

|

|

|

- Nigel Turner

- 6 years ago

- Views:

Transcription

1 Presentation by CA RITESH MEHTA, NAGPUR B. Com., F.C.A., D.I.S.A (ICAI). 1

2 Overview of GST Law Components of GST law Levy under GST Taxable event under GST Meaning & scope of the term Supply and its Implications Concept of CGST, SGST & IGST

3 Multiple Taxation Distinction between Goods and Services Double Taxation Overlapping of taxes Cross utilization of input Tax Credit Not Available Cascading Effect of Tax Dual Administration of Dealers Compliances of Various Laws

4 Article 246 to Article 256 Seventh Schedule of Constitution of India LIST II (Local Govt.) LIST I (UNION ) LIST II (STATE) Customs (Entry 83) VAT (Entry 54) Octroi State Excise (Entry 51) Property Tax Entertainment Tax (Entry 62) (Entry 5 read with Municipal Corporation Act) Central Excise (Entry 84) Service Tax (Entry 92C) CST (Entry 92A) Stamp Duty (Entry 63) Advertisement

5 122nd CAB Approved by Lok Sabha on Amended CAB Approved by Rajya Sabha on Amendments Approved in Lok Sabha on Endorsement by State Assemblies(50%) Presidents Assent for enactment of 122nd CAB 101st Constitution Amendment Act Formation of GST Council (GSTC) Recommendations of draft legislations by GSTC Drafting of Central and State GST Acts and Rules Passage of bills in State/Central Legislature Effective date to be decided by GSTC 5

6 State Legislature empowered to make law wrt Supply of Goods & Services within the state Parliament have exclusive power to make law wrt Supply of Goods & Services in interstate transactions IGST to be levied by Union govt. but revenue to be shared betn Union & States Subsuming of Various Central & State levies into GST Dispensing the concept of Declared Goods Formation of GST Council, its Role Compensation to State for the revenue loss upto five years.

7 Compensation for loss of revenue to states under new GST regime shall be provided for a period of 5 years from introduction of the levy of GST The 1% additional levy on interstate supply of goods has been scrapped. Establishing a mechanism for adjudicating any dispute between Centre and States or between the States, arising out of the recommendations of GST Council Note : In Nov.16 the GST ( Compensation to the States for Loss of Revenue) Bill has been proposed 7

8 Cap on GST Rates not included in the CAB as the rate will be first recommended by the GST Council. The Cap on GST Rates has been proposed in the Revised Model GST law. The recommendation for Adjudication of Assessees having turnover below Rs. 1.5 crore by the States is not considered in the CAB and will be decided by the GST Council 8

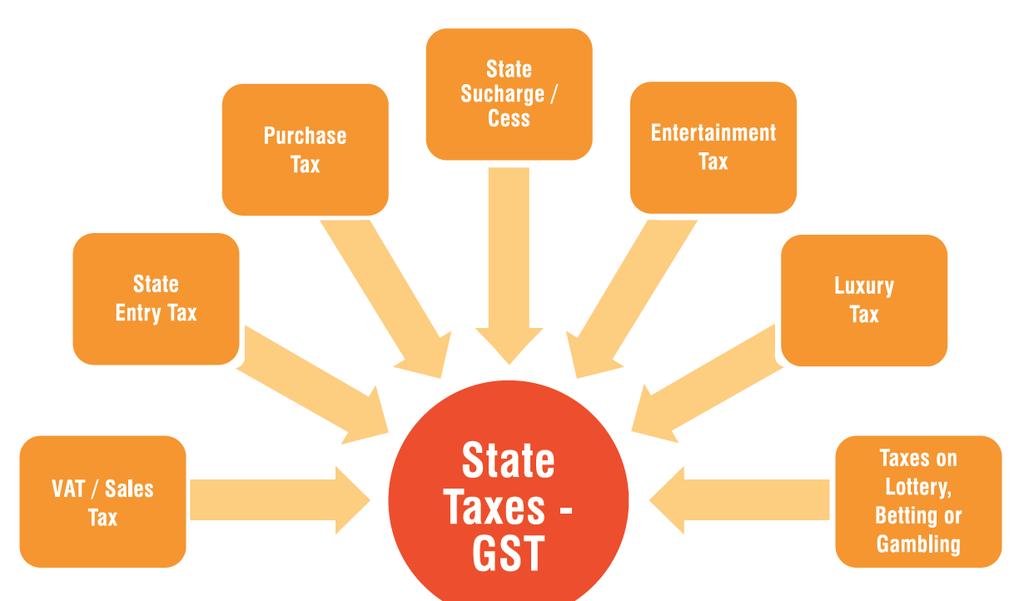

9 Tax Structure Indirect Tax Direct Tax Income Tax Wealth Tax (abolished in 15-16) Central Tax Excise Service Tax State Tax Customs VAT/CST Entry Tax, luxury tax, Lottery Tax, etc. 9

10

11

12 Exclusions from Subsuming under GST Basic Customs Duty (BCD) Stamp Duty Tax on Alcoholic Liquor for Human Consumption Petroleum Products levy to be made effective at a future date Tax on Entertainment and Amusement Levied & Collected by the Municipal Authorities

13 Ideally GST should be a singular tax on all supplies with a uniform rate and seamless credit for taxes paid at earlier stage. Considering Federal Structure of India EC has worked out the Dual Model of GST Central Govt.(CG) will levy Central GST ( CGST) State Govt.(SG) will levy State GST ( SGST) Supplies imported into the country - liable for GST Supplies exported from the country - Zero Rated 13

14 Interstate supplies ( Including Br. Trf.), Imports and exports will be governed by an Integrated GST ( IGST) which would consist of Two components - CGST & SGST The tax on Inter State supplies will accrue to the Destination State CGST will be held by Central Govt. and SGST will be trfd to the destination State Govt. IGST will enable smooth flow of credits between Origin and Destination States. 14

15 Export of Goods/Services to be Zero Rated All Goods/Services likely to be covered under GST except, o Alcohol for Human Consumption State Excise + VAT o Electricity Electricity Duty o Sale/Purchase of Real Estate Stamp Duty + Property Tax Five Specified Petroleum Products to be brought under GST from a later date on recommendation of GSTC Tobacco Products Under GST + Central Excise 15

16 To Trade: Reduction in Multiplicity of Taxes Mitigation of Cascading/Double Taxation Development of Common National Market Simpler Tax Regime -Fewer Rates & Exemptions -Distinction Betwn Goods & Services no longer required. To Consumers: Simpler Tax System Reduction in Price of Goods & Services Uniform Prices throughout the Nation Transparency in Taxation System Increase in employment Opportunities

17 Tax Structure Indirect Tax = GST (Except customs) Direct Tax Income Tax Intra- state CGST (Central) SGST (State) Inter State IGST (Central) 17

18 Basic Example on How would GST Work?

19 One Nation- One Tax Basic Threshold Limit for Registration Rs. 20 lacs All India Basis Withdrawal of Existing Exemption Limit of Rs.150 lacs to small manufacturers Concept of Supply of Goods and Services Inter-State Branch Transfers liable to GST ITC available. Supplies to SEZ Units - liable to GST ITC available. Sales in Transit - liable to GST ITC available. HighSeas Sales beyond the customs frontier ITC Matching Monthly Returns 19

20 GST Rates Finalized by GST Council Meeting on Zero Tax Rate 0% Essential Food Items & Mass Consumption Items 5% 12 % 18 % 28% Standard Rates Maximum Goods & all the Services Standard Rate May be Luxury Items, Pan Masala etc., Aerated Drinks Rate on Gold to be Decided Later Luxury Car, Aerated Water and Tobacco may be taxed more than 28% Additional Cess on Goods covered in 28%

21 GST Impact

22 CGST SGST IGST CGST SGST IGST IGST IGST CGST SGST *Cross utilization of credit of CGST and SGST shall not be allowed in Input Tax Credit 22

23 LEVY OF GST CHINA (Landed at Nava Mumbai) MAHARASHTRA GUJARAT M Imports from C of China T of Gujarat buys from G of Gujarat C Exports to M In INDIA M Pays Custom Duty + CVD (IGST)+ SAD (IGST) (M Is eligible for IGST Credit) Price + SGST + CGST (T is eligible for SGST & CGST Credit) A In Akola Purchases from M in Mumbai Price + SGST + CGST (A is eligible for SGST & CGST Credit) GUJARAT G in Gujarat buys from A of Akola Price + IGST (G is eligible for IGST Credit)

24 101st Constitution Amendment Act Registration Rules and Formats Refund Rules and Formats Payment Rules and Formats Returns Rules and Formats CGST, IGST, GST Compensation Loss to the States for Loss of Revenue bill. Revised Model SGST Law FAQ s by CBEC 24

25 GST Council Constituted wef 12/9/16 Ten Meetings held so far, Decision: Threshold limit for exemption to e Rs lakhs (Rs lakhs for North Eastern States) Compounding Threshold limit to be Rs lacs Not available to Manufacturers and Service Providers Govt. may convert are based exemption into refund based Formula for Compensation to States finalised Study of Draft law till Sec. 99 complete Four Rates of Tax Proposed

26 MYTH REALITY WITH GST NO OTHER TAX TO BE LEVIED NO IMPACT ON DIRECT TAXES GST IS THE SINGLE LAW GST CONSISTS OF ICST, CGST & SGST LAWS GST IS A SINGLE TAX GST CONSISTS OF VARIOUS SLABS OF TAX RATE NO DISTINCTION NEEDED FOR GOODS & SERVICES TIME AND PLACE OF SUPPLY IS DIFFERENT FOR GOODS AS WELL AS SERVICES SEAMLESS CREDIT RESTRICTED ITC LESS COMPLIANCES 3 SETS OF MONTHLY RETURNS SINGLE ADMINISTRATOR DUAL CONTROL POSSIBLE LESS EXEMPTIONS SEPARATE LIST OF EXEMPTIONS

27 Incorporated on as section 25 Pvt. Ltd. Co. with authorized equity of Rs. 10 crore Strategic control to remain with Government Equity holders 1. Central Government 24.5% 2. EC and all states together 24.5% 3. Financial Institutions 51% To function as a common Pass-through portal for taxpayers- 1. Submit registration application 2. File Returns 3. Make tax payments Appointed Infosys as Managed Service Provider (MSP)

28 CGST/SGST Law (CGST Law Published in Gazette on 12/04/17) Released on 25/11/2016 Consists of 27 Chapters Consists of 197 Sections Five Schedules IGST Law Released on 25/11/16 Consists of 11 Chapters Consists of 24 Sections

29 Impact on Traders: 1) Tax on Value Addition 2) Reduce Cascading Effect 3) Dual GST On Local Transactions, IGST on Inter State Transactions 4) No Subsequent Sale or Sale in Transit 5) Export Supplies under Form H/SEZ Sale under Form I N.A 6) Stock Transfer/Consignment Transfers 7) Composition to Small Traders

30 Impact on Manufacturer: 1) Competitive in Market 2) Valuation of the supply of Goods 3) Cheaper Export 4) Ease of Doing Business 5) Transaction Cost 6) Manufacturers Under administration of State VAT Official

31 Impact on Service Provider 1) Present Origin based to Destination based levy 2) Service Tax SGST levied by State 3) Increased Set off with VAT

32 Section 9.Levy of CGST/SGST on all intra-state supplies of goods/services not exceeding 20% Except on Supply of alcoholic liquor for human Consumption On Value as determined under Sec. 15 Rates to be specified for each category of supply CGST/SGST to be paid by every taxable person [22] Levy of tax on following petroleum products from future date on recommendation of Council - Crude Oil -High Speed Diesel -Motor Spirit -Natural gas -Aviation turbine Fuel (ATF)

33 CG/SG may specify categories of supply of goods/services for payment of tax on reverse charge mechanism. [9(3)] Electronic Commerce operator (ECO).[9(4)] CG/SG may specify categories of service on which tax to be paid by ECO, if such service are supplied through it When ECO has no physical presence His Representative in taxable territory is liable Neither physical presence of ECO nor representative appointed ECO to appoint a person for paying tax

34 Section 5.Provides for Levy of IGST on all inter-state supplies of not exceeding 40% Except on Supply of Alcoholic Liquor for human consumption Rates to be specified in schedule for each category of supply Value to be determined as per Sec. 15 of CGST Act Levy on Petroleum Products to be levied form future date IGST on goods imported into India shall be levied & collected in accordance to section 3 of Custom tariff Act,1975. IGST to be paid by every taxable person [5(1)] CG/SG may specify categories of supply of goods/services for payment of tax on reverse charge mechanism [5(3)]

35 Present Tax Regime MANUFACTURE PAY EXCISE DUTY SERVICE SERVICES PAY SERVICE TAX Under GST SUPPLY OF GOODS &/OR Services Pay GST SALE SALE PAY VAT 35

36 Includes all forms of Supply of goods or services or both Sale, Transfer, barter, By Taxable person Exchange, License, rental, Lease or Disposal In course or Furtherance of business Consideration

37 Importation of Service, for a consideration whether or not in course or furtherance of business Deemed supply : Sec. 7(1)(b) Sec. 7(1)(c) Activities specified in Sch-I, made or agreed to be made without consideration. Sec.7(2) Activities to treated as supply of goods or services Sch. II Sec. 7(2)(a) Activity / Transactions which are neither supply goods nor services - Schedule III Sec. 7(2)(b) Activity / Transactions undertaken by CG/SG which are neither supply goods nor services (Schedule IV Removed)

38 Sec. 7(3) : CG/ SG may upon recommendation of the council, specify by notification transactions that are to be treated as: Supply of Goods and not as a supply of Services; or Supply of Services and not as a supply of Goods; or Neither Supply of Goods nor a supply of Services

39 composite supply means a supply made by a taxable person to a recipient comprising two or more supplies of goods or services, or any combination thereof, which are naturally bundled and supplied in conjunction with each other in the ordinary course of business, one of which is a principal supply; Illustration : Where goods are packed and transported with insurance, the supply of goods, packing materials, transport and insurance is a composite supply and supply of goods is the principal supply.

40 principal supply means the supply of goods or services which constitutes the predominant element of a composite supply and to which any other supply forming part of that composite supply is ancillary and does not constitute, for the recipient an aim in itself, but a means for better enjoyment of the principal supply

41 mixed supply means two or more individual supplies of goods or services, or any combination thereof, made in conjunction with each other by a taxable person for a single price where such supply does not constitute a composite supply; Illustration: A supply of a package consisting of canned foods, sweets, chocolates, cakes, dry fruits, aerated drink and fruit juices when supplied for a single price is a mixed supply. Each of these items can be supplied separately and is not dependent on any other. It shall not be a mixed supply if these items are supplied separately

42 8 The tax liability on a composite or a mixed supply shall be determined in the following manner (a) a composite supply comprising two or more supplies, one of which is a principal supply, shall be treated as a supply of such principal supply; (b) a mixed supply comprising two or more supplies shall be treated as supply of that particular supply which attracts the highest rate of tax.

43 Transactions Examples Permanent Transfer/disposal actions Examples of business asset where input credit availed on such asset Asset donated to trust Supply of goods or service between related person/distinct person, when made in course or furtherance of business Branch having a separate GSTIN Supply of Goods By principal to his agent where the agent undertakes to supply such goods on behalf of principal By agent to his principal where the agent undertakes to receive such goods on behalf of the principal Consignment Agent Importation of service by taxable person from a related person or from any of his other establishment outside India, in the course or furtherance of business Free Service from branch outside India Buying agent

44 NATURE OF TRANSACTION NATURE EXAMPLE TRANSFER OF TITLE IN GOODS GOODS Supply of goods TRANSFER OF GOODS/RIGHT IN GOODS OR UNDIVIDED SHARE IN GOODS WITHOUT TRANSFER OF TITLE SERVICE COMPUTER HIRING TRANSFER OF TITLE IN GOODS UNDER AGREEMENT ON A FUTURE DATE UPON PAYMENT OF CONSIDERATION GOODS HIRE PURCHASE LEASE /TENANCY/EASMENT/LICENSE TO OCCUPY LAND SERVICE TENANCY LEASE/LETTING OUT OF BUILDING FOR BUSINESS OR COMMERCE SERVICE LEAVE LICENSE JOB WORK ON ANOTHER PERSON S GOODS SERVICE PROCESSING TRANSFER OF BUSINESS ASSET GOODS SALE OF ASSET OTHER THAN STOCK IN TRADE MAKING AVAILABLE OF BUSINESS GOODS FOR PRIVATE USE SERVICE CAR GIVEN TO STAFF FOR MARRIAGE FUNCTION

45 NATURE OF TRANSACTION NATURE EXAMPLE GOODS/ASSET ON CLOSURE OF BUSINESS OTHER THAN GOODS TRANSFER AS GOING CONCERN OR TRANSFER TO REPRESENTATIVE WHO IS TAXABLE PERSON WITHDRAWAL BY PARTNER RENTING OF IMMOVABLE PROPERTY SERVICE RENTING SALE OF UNDER CONSTRUCTION UNITS SERVICE BUILDER TEMPORARY TRANSFER OF IPR SERVICE TRADE MARK, DESIGN DEVELOPMENT, DESIGN, CUSTOMISATION ETC. OF I.T. SERVICE SOFTWARE SOFTWARE DEVELOPMENT AGREEING TO OBLIGATION TO DO ACT OR REFRAIN AN ACT SERVICE NON COMPETE FEES WORKS CONTRACT SERVICE CIVIL CONTRACT TRANSFER OF RIGHT TO USE GOODS FOR ANY PURPOSE SERVICE RENT A CAB SUPPLY OF FOOD AS A PART OF SERVICE SERVICE RESTAURANT SUPPLY OF GOODS BY UNINCORPORATED ASSOCIATION TO GOODS ITS MEMBER

46 Service by Employee to Employer in course of or in relation to employment Service by court/tribunal under any law Function performed by MP/MLA/Corporator etc Duties performed by person who hold post in pursuance to constituion Duties by chairperson/director in body established by CG/SG Service of Funeral, burial, crematorium or mortuary including transportation of deceased Sale of Land/Building Actionable Claims

47 Cabinet Approval for SGST laws by all states Passage of CGST and IGST laws by Parliament and passage of SGST laws by all State Legislatures Notification of GST Rules Recommendation of GST Tax rates by GST Council Establishment and upgradation of IT Framework Notification of Implementation of GST

48 Meeting implementation challenges Effective coordination between Centre & State tax administrations Training of officials and Trade & Industry Spreading Accounting Literacy Developing IT Skills Reorganization of Audit procedures Harmonization of processes & procedures between CGST / IGST & SGST Law

49 riteshrmehta@yahoo.com Mob :

C. B. Thakar, Advocate

Refresher Course on GST by WIRC 26 th June,2017 Basic Concepts of GST Presentation by C. B. Thakar, Advocate B.Com., F.C.A., LLB C. B. THAKAR, Advocate 1 Journey towards GST 122 nd CAB Approved by Lok

Refresher Course on GST by WIRC 26 th June,2017 Basic Concepts of GST Presentation by C. B. Thakar, Advocate B.Com., F.C.A., LLB C. B. THAKAR, Advocate 1 Journey towards GST 122 nd CAB Approved by Lok

GOODS & SERVICES TAX (GST) (Status as on 01 st May, 2017)

(Status as on 01 st May, 2017)") GOODS & SERVICES TAX (GST) (Status as on 01 st May, 2017) 1 PRESENTATION PLAN WHY GST : BENEFITS EXISTING INDIRECT TAX STRUCTURE FEATURES OF CONSTITUTION AMENDMENT ACT GST COUNCIL MAIN FEATURES OF GST

GOODS & SERVICES TAX (GST) (Status as on 01 st May, 2017) 1 PRESENTATION PLAN WHY GST : BENEFITS EXISTING INDIRECT TAX STRUCTURE FEATURES OF CONSTITUTION AMENDMENT ACT GST COUNCIL MAIN FEATURES OF GST

BASIC CONCEPTS, SUPPLY, LEVY & COLLECTION OF GST

BASIC CONCEPTS, SUPPLY, LEVY & COLLECTION OF GST GST Basic Concepts Single Tax Payable on Taxable Supply of G&S Multi Stage & Destination based Consumption Tax GST Charged only on Value Addition No (Reduced)

BASIC CONCEPTS, SUPPLY, LEVY & COLLECTION OF GST GST Basic Concepts Single Tax Payable on Taxable Supply of G&S Multi Stage & Destination based Consumption Tax GST Charged only on Value Addition No (Reduced)

COMPONENTS OF GST GST. IGST (Interstate and Imports) CGST (Intrastate) SGST (Intrastate)

CGST (Intrastate) SGST (Intrastate)") WHAT IS GST Largest tax reform in the Indirect Taxation regime. PAN Based Registration Levied on supply of goods or services. Supply includes Stock Transfer. Supply being the Taxable Event, the concept

WHAT IS GST Largest tax reform in the Indirect Taxation regime. PAN Based Registration Levied on supply of goods or services. Supply includes Stock Transfer. Supply being the Taxable Event, the concept

Levy and Collection of Tax

FAQ Meaning and scope of supply (Section 7) Chapter I Levy and Collection of Tax Q1. What is the scope of the term supply as defined in CGST Act, 2017? Ans. As per Sub-section (1) of Section 7, Supply

FAQ Meaning and scope of supply (Section 7) Chapter I Levy and Collection of Tax Q1. What is the scope of the term supply as defined in CGST Act, 2017? Ans. As per Sub-section (1) of Section 7, Supply

THE CHAMBER OF TAX CONSULTANTS BASIC CONCEPTS O F G S T

THE CHAMBER OF TAX CONSULTANTS BASIC CONCEPTS O F G S T 1 Understanding GST Covering 2 Legislations, 174 Sections,3 Schedules TAXES IN INDIA There are mainly two types of taxes DIRECT TAXES INCOME TAX

THE CHAMBER OF TAX CONSULTANTS BASIC CONCEPTS O F G S T 1 Understanding GST Covering 2 Legislations, 174 Sections,3 Schedules TAXES IN INDIA There are mainly two types of taxes DIRECT TAXES INCOME TAX

GST Concept and Road Map... Atul Gupta

GST Concept and Road Map... Atul Gupta Goods and Service Tax What will be incidence of tax (which Activity will attract GST Definition of Supply. Schedule 1 & 2 Classification Based on HSN, A/c Code for

GST Concept and Road Map... Atul Gupta Goods and Service Tax What will be incidence of tax (which Activity will attract GST Definition of Supply. Schedule 1 & 2 Classification Based on HSN, A/c Code for

Downloaded from Update PPT on GST (As on 01 st January 2018)

") Update PPT on GST (As on 01 st January 2018) 1 This presentation is for education purposes only and holds no legal validity 2 The Journey to GST 2006 First Discussion Paper was released by the Empowered

Update PPT on GST (As on 01 st January 2018) 1 This presentation is for education purposes only and holds no legal validity 2 The Journey to GST 2006 First Discussion Paper was released by the Empowered

Activities to be treated as Neither Supply of Goods Nor a Supple of Service, Composite Supplies & Mixed Supplies, Intra-State and Inter-State Supply

1 Activities to be treated as Neither Supply of Goods Nor a Supple of Service, Composite Supplies & Mixed Supplies, Intra-State and Inter-State Supply 2 Activities to be treated as Neither Supply of Goods

1 Activities to be treated as Neither Supply of Goods Nor a Supple of Service, Composite Supplies & Mixed Supplies, Intra-State and Inter-State Supply 2 Activities to be treated as Neither Supply of Goods

GST Workshop 9th June 2017

GST Workshop 9 th June 2017 GST Model- Basic Features GST is tax on the supply of goods and services, right from the manufacturer/service provider to the consumer. Destination based consumption Tax (Tax

GST Workshop 9 th June 2017 GST Model- Basic Features GST is tax on the supply of goods and services, right from the manufacturer/service provider to the consumer. Destination based consumption Tax (Tax

Introduction to Goods and Services Tax (GST)

") Introduction to Goods and Services Tax (GST) CHAPTER 2 GST is the most ambitious and remarkable indirect tax reform in India s post-independence history. Its objective is to levy a single national uniform

Introduction to Goods and Services Tax (GST) CHAPTER 2 GST is the most ambitious and remarkable indirect tax reform in India s post-independence history. Its objective is to levy a single national uniform

GOODS AND SERVICES TAX

GOODS AND SERVICES TAX GOODS AND SERVICES TAX - AN INTRODUCTION Introduction to Goods and Services Tax GST and Centre-State Financial Relations Constitution (One Hundred and First) Amendment Act, 2016

GOODS AND SERVICES TAX GOODS AND SERVICES TAX - AN INTRODUCTION Introduction to Goods and Services Tax GST and Centre-State Financial Relations Constitution (One Hundred and First) Amendment Act, 2016

Goods and Service Tax (GST)

") Indirect Taxes Committee of ICAI Goods and Service Tax (GST) Globally Known As VAT Standardised PPT by Indirect Taxes Committee Institute of Chartered Accountants of India Major Initiative in 2014-15 Organized

Indirect Taxes Committee of ICAI Goods and Service Tax (GST) Globally Known As VAT Standardised PPT by Indirect Taxes Committee Institute of Chartered Accountants of India Major Initiative in 2014-15 Organized

GST Overview. ~CA Unmesh G. Patwardhan~ Mobile No Unmesh Patwardhan Mobile No

GST Overview ~CA Unmesh G. Patwardhan~ Mobile No.98224 24968 Unmesh Patwardhan Mobile No.98224 24968 1 Brief History & Concept of GST Unmesh Patwardhan Mobile No.98224 24968 2 1 st Jul 2017 The D Day Journey

GST Overview ~CA Unmesh G. Patwardhan~ Mobile No.98224 24968 Unmesh Patwardhan Mobile No.98224 24968 1 Brief History & Concept of GST Unmesh Patwardhan Mobile No.98224 24968 2 1 st Jul 2017 The D Day Journey

GST- VALUE OF SUPPLY

GST- VALUE OF SUPPLY TO DISCUSS Background Current regime Concept GST regime Examples Possible / open issues BACKGROUND CHARGING SECTION Service Tax Excise Customs There shall be levied a tax (hereinafter

GST- VALUE OF SUPPLY TO DISCUSS Background Current regime Concept GST regime Examples Possible / open issues BACKGROUND CHARGING SECTION Service Tax Excise Customs There shall be levied a tax (hereinafter

M/s PRANJAL JOSHI & CO

Introduction to GST Basic information GST stands for Goods and Service Tax. GST is a destination based tax on consumption of goods and services. It is proposed to be levied at all stages right from manufacture

Introduction to GST Basic information GST stands for Goods and Service Tax. GST is a destination based tax on consumption of goods and services. It is proposed to be levied at all stages right from manufacture

Goods and Service Tax (GST)

") Goods and Service Tax (GST) Globally Known As VAT Standardised PPT by Indirect Taxes Committee Institute of Chartered Accountants of India copyright@idtc_icai_2015 1 Indirect Taxes Committee of ICAI Major

Goods and Service Tax (GST) Globally Known As VAT Standardised PPT by Indirect Taxes Committee Institute of Chartered Accountants of India copyright@idtc_icai_2015 1 Indirect Taxes Committee of ICAI Major

GST GOODS & SERVICES TAX

ICAI Nagpur Branch Seminar on 5 th November 2016 GST GOODS & SERVICES TAX broad CONCEPTS By Ashok chandak sbcngp@gmail.com 1 CONTENTS Present Indirect Tax Structure in India. Enabling Constitutional Amendments.

ICAI Nagpur Branch Seminar on 5 th November 2016 GST GOODS & SERVICES TAX broad CONCEPTS By Ashok chandak sbcngp@gmail.com 1 CONTENTS Present Indirect Tax Structure in India. Enabling Constitutional Amendments.

By: CA Sunnay Jariwala

By: CA Sunnay Jariwala Existing Indirect Tax Structure Source: cbec.gov.in What is Goods and Services Tax? Article 366 (12A) Tax on supply of goods or services or both. Except on supply of alcoholic liquor

By: CA Sunnay Jariwala Existing Indirect Tax Structure Source: cbec.gov.in What is Goods and Services Tax? Article 366 (12A) Tax on supply of goods or services or both. Except on supply of alcoholic liquor

CA ROHIT GAMBHIR. Page i

Page i INDEX Lesson Description Page No 1. Overview of GST -- 2. GST International Scenario 1 3. GST in India 3 4. Introduction to CGST Act, 2017 8 5. Supply 10 6. Composite and Mixed Supply 17 7. Composition

Page i INDEX Lesson Description Page No 1. Overview of GST -- 2. GST International Scenario 1 3. GST in India 3 4. Introduction to CGST Act, 2017 8 5. Supply 10 6. Composite and Mixed Supply 17 7. Composition

GST Tax of 21 st Century. V S Datey Website

GST Tax of 21 st Century V S Datey dateyvs@yahoo.com Website http://www.dateyvs.com Welcome Background of Indirect Taxes Present structure of indirect taxes is based on Constitutional Provisions giving

GST Tax of 21 st Century V S Datey dateyvs@yahoo.com Website http://www.dateyvs.com Welcome Background of Indirect Taxes Present structure of indirect taxes is based on Constitutional Provisions giving

BRIEF ON GST. GST is a destination based tax and levied at a single point at the time of consumption of goods or services by the ultimate consumer.

BRIEF ON GST GST is a destination based tax and levied at a single point at the time of consumption of goods or services by the ultimate consumer. GST will be levied on all goods and services except on

BRIEF ON GST GST is a destination based tax and levied at a single point at the time of consumption of goods or services by the ultimate consumer. GST will be levied on all goods and services except on

GOODS AND SERVICES TAX (COMPENSATION TO THE STATES FOR LOSS OF REVENUE) BILL, 2016

BILL, 2016") GOODS AND SERVICES TAX (COMPENSATION TO THE STATES FOR LOSS OF REVENUE) BILL, 2016 (No. of 2016) [ th, 2016] A Bill to provide for compensation to the States for loss of revenue arising on account of implementation

GOODS AND SERVICES TAX (COMPENSATION TO THE STATES FOR LOSS OF REVENUE) BILL, 2016 (No. of 2016) [ th, 2016] A Bill to provide for compensation to the States for loss of revenue arising on account of implementation

GST Law Guide. Introduction. 1.1 Background of GST. 1.2 What is Goods and Services Tax?

GST Law Guide Chapter 1 Introduction 1.1 Background of GST The structure of indirect taxes in India (as existing upto 30-6-2017) was based on three lists in Seventh Schedule to Constitution of India, which

GST Law Guide Chapter 1 Introduction 1.1 Background of GST The structure of indirect taxes in India (as existing upto 30-6-2017) was based on three lists in Seventh Schedule to Constitution of India, which

Most Expected Questions of GST CS EXECUTIVE (JUNE, 2018 STUDENTS) By

By") Most Expected Questions of GST CS EXECUTIVE (JUNE, 2018 STUDENTS) By CA Vivek Gaba 1. GST was first levied by? a) France in 1954 b) USA in 1985 c) India in 2017 d) U.K in 1970 2. Which of the following

Most Expected Questions of GST CS EXECUTIVE (JUNE, 2018 STUDENTS) By CA Vivek Gaba 1. GST was first levied by? a) France in 1954 b) USA in 1985 c) India in 2017 d) U.K in 1970 2. Which of the following

Basics of GST. Ganesh Pathuri

Basics of GST Ganesh Pathuri Background of Indian GST The Constitution (115th Amendment) Bill, 2011 The Constitution (122nd Amendment) Bill, 2014 Introduced in Lok Sabha on December 19, 2014. It was passed

Basics of GST Ganesh Pathuri Background of Indian GST The Constitution (115th Amendment) Bill, 2011 The Constitution (122nd Amendment) Bill, 2014 Introduced in Lok Sabha on December 19, 2014. It was passed

Virtual Certificate Course on GST Organised by: IDT Committee of ICAI

1 Virtual Certificate Course on GST Organised by: IDT Committee of ICAI Sector Specific Studies on Construction Information Technology Tourism Service Trader Manufacturer 23 of June 2017 2 HIGHLIGHTS OF

1 Virtual Certificate Course on GST Organised by: IDT Committee of ICAI Sector Specific Studies on Construction Information Technology Tourism Service Trader Manufacturer 23 of June 2017 2 HIGHLIGHTS OF

FDI. Investment by foreign investors directly in the productive assets of another nation.

FDI Investment by foreign investors directly in the productive assets of another nation. Financial investment in stocks or bonds denotes foreign portfolio investment. Factors for Rise in Fiscal Deficit

FDI Investment by foreign investors directly in the productive assets of another nation. Financial investment in stocks or bonds denotes foreign portfolio investment. Factors for Rise in Fiscal Deficit

SALIENT FEATURES OF PROPOSED GST

SALIENT FEATURES OF PROPOSED GST GST is a consumption based levy. Destination principle would be applicable in normal course of business to business [B2B] other than for few services and business to consumer.[

SALIENT FEATURES OF PROPOSED GST GST is a consumption based levy. Destination principle would be applicable in normal course of business to business [B2B] other than for few services and business to consumer.[

Goods and Service Tax in India. CA Ashutosh Thaker

Goods and Service Tax in India CA Ashutosh Thaker Ashutosh.thaker@verita.co.in Contents 01 Why &Salient features of Indian GST 02 Key Concept of GST 03 What should be of concern Central Govt. & State Govt.

Goods and Service Tax in India CA Ashutosh Thaker Ashutosh.thaker@verita.co.in Contents 01 Why &Salient features of Indian GST 02 Key Concept of GST 03 What should be of concern Central Govt. & State Govt.

Levy & Composition, Exemption from Tax

Levy & Composition, Exemption from Tax CA Ganesh Prabhu Balakumar B.Com, MFM, F.C.A, LL.B, DISA (ICAI) 1 All About GST Goods & Services Tax Single Tax Payable on Taxable Supply GST Single Tax on the Supply

Levy & Composition, Exemption from Tax CA Ganesh Prabhu Balakumar B.Com, MFM, F.C.A, LL.B, DISA (ICAI) 1 All About GST Goods & Services Tax Single Tax Payable on Taxable Supply GST Single Tax on the Supply

A Peek into GST... GST is commonly known as Destination based tax on consumption of goods and services.

Kharabanda Associates, Chartered Accountants A Peek into GST... Volume 1, Issue 1 Date : January 20, 2017 Inside this Issue : GST Demystified 2 Input tax credit, Supply & Liability GST Trend, VAT & Valuation

Kharabanda Associates, Chartered Accountants A Peek into GST... Volume 1, Issue 1 Date : January 20, 2017 Inside this Issue : GST Demystified 2 Input tax credit, Supply & Liability GST Trend, VAT & Valuation

GOODS & SERVICE TAX. Unleashing of the new era in the Indirect Taxation Arena. By CA. Chitresh Gupta

GOODS & SERVICE TAX Unleashing of the new era in the Indirect Taxation Arena Date : 22 nd May 2015 Venue: District Tax Bar Association, Faridabad By CA. Chitresh Gupta B.Com(H), FCA,IDT(Cert),IFRS(Cert)

GOODS & SERVICE TAX Unleashing of the new era in the Indirect Taxation Arena Date : 22 nd May 2015 Venue: District Tax Bar Association, Faridabad By CA. Chitresh Gupta B.Com(H), FCA,IDT(Cert),IFRS(Cert)

FAQ. Hindustan Shipyard Limited

FAQ Hindustan Shipyard Limited 1 Q 1. What is Goods and Service Tax (GST)? Ans. It is a destination based tax on consumption of goods and services. It is proposed to be levied at all stages right from

FAQ Hindustan Shipyard Limited 1 Q 1. What is Goods and Service Tax (GST)? Ans. It is a destination based tax on consumption of goods and services. It is proposed to be levied at all stages right from

Goods and Service. By CMA Sachin Kathuria. CMA Sachin Kathuria

Goods and Service Tax (GST) in India By 1 Existing Tax structure in India 2 Tax Structure Direct Tax Indirect Tax Income Tax Wealth Tax (Now abolished) Central Tax State Tax Excise Service Tax Customs

Goods and Service Tax (GST) in India By 1 Existing Tax structure in India 2 Tax Structure Direct Tax Indirect Tax Income Tax Wealth Tax (Now abolished) Central Tax State Tax Excise Service Tax Customs

Air India. June Page 1

Air India June 2017 Page 1 Contents GST Overview Comparative tax scenarios: Current vs. GST Credit Mechanism Concept of Place & Time of Supply Valuation under GST Compliances under GST Page 2 Overview

Air India June 2017 Page 1 Contents GST Overview Comparative tax scenarios: Current vs. GST Credit Mechanism Concept of Place & Time of Supply Valuation under GST Compliances under GST Page 2 Overview

PARIMAL PATEL P. J. E-CONSULTANTS AHMEDABAD

SIMPLIFYING THE GST CODE PARIMAL PATEL P. J. E-CONSULTANTS AHMEDABAD CURRENT STRUCTURE CASCADING EFFECT TAX ON TAX Excise/VAT/CST/Entry Tax/BCD/CVD/AED, ETC. Excise/VAT/CST Branch Transfers VAT/CST WHY

SIMPLIFYING THE GST CODE PARIMAL PATEL P. J. E-CONSULTANTS AHMEDABAD CURRENT STRUCTURE CASCADING EFFECT TAX ON TAX Excise/VAT/CST/Entry Tax/BCD/CVD/AED, ETC. Excise/VAT/CST Branch Transfers VAT/CST WHY

Goods and Service Tax (GST)

") Goods and Service Tax (GST) 1. Basics of GST 2. Working Model of GST 3. GST Compliances- Monthly and Annual Filings 4. GST Impact on E-Commerce 5. GST Impact on Services ( IT/ITES) BASICS of GST GST is

Goods and Service Tax (GST) 1. Basics of GST 2. Working Model of GST 3. GST Compliances- Monthly and Annual Filings 4. GST Impact on E-Commerce 5. GST Impact on Services ( IT/ITES) BASICS of GST GST is

Press Information Bureau Government of India Ministry of Finance

Press Information Bureau Government of India Ministry of Finance Frequently Asked Questions (FAQs) on Goods and Services Tax (GST) 03 August 2016 15:32 IST Following are the answers to the various frequently

Press Information Bureau Government of India Ministry of Finance Frequently Asked Questions (FAQs) on Goods and Services Tax (GST) 03 August 2016 15:32 IST Following are the answers to the various frequently

INTRODUCTION TO GOODS AND SERVICE TAX

The Union Finance Minister Mr. P. Chidambaram in his budget speech in 2006 has said: It is my sense that there is a large consensus that the country should move towards a National Level Goods and Service

The Union Finance Minister Mr. P. Chidambaram in his budget speech in 2006 has said: It is my sense that there is a large consensus that the country should move towards a National Level Goods and Service

INTRODUCTION TO GST & CONSTITUTIONAL PROVISIONS

INTRODUCTION TO GST & CONSTITUTIONAL PROVISIONS Discussing the concept of GST and the basis of its levy - By Prakhar Jain HISTORY OF GST IN INDIA Idea of a national GST was first brought about by Kelkar

INTRODUCTION TO GST & CONSTITUTIONAL PROVISIONS Discussing the concept of GST and the basis of its levy - By Prakhar Jain HISTORY OF GST IN INDIA Idea of a national GST was first brought about by Kelkar

GST: An Integrated Tax

The Journey to GST 2006 First Discussion Paper was released by the Empowered Committee 2009 Constitution (115th Amendment) Bill introduced and subsequently lapsed 2011 The Constitution (122 n d Amendment)

The Journey to GST 2006 First Discussion Paper was released by the Empowered Committee 2009 Constitution (115th Amendment) Bill introduced and subsequently lapsed 2011 The Constitution (122 n d Amendment)

Dual GST Model CA Gadia Manish R 1. Marwadi Ghano Saro Tax

CA Gadia Manish R 3 Marwadi Ghano Saro Tax Doctor Glucose Stimulation Test Alia Bhatt Good night, Sweet dream, Take care FAQ : It is a destination based tax on consumption of goods and services. It is

CA Gadia Manish R 3 Marwadi Ghano Saro Tax Doctor Glucose Stimulation Test Alia Bhatt Good night, Sweet dream, Take care FAQ : It is a destination based tax on consumption of goods and services. It is

GST Implications. All India Distillers Association Hotel Crowne Plaza February 23, Discussion by: CA Gaurav Gupta

GST Implications All India Distillers Association Hotel Crowne Plaza February 23, 2017 Discussion by: CA Gaurav Gupta FCA, LLB, DISA Author GST Law & Practise - Service Tax Law & Practise Agenda GST exclusion

GST Implications All India Distillers Association Hotel Crowne Plaza February 23, 2017 Discussion by: CA Gaurav Gupta FCA, LLB, DISA Author GST Law & Practise - Service Tax Law & Practise Agenda GST exclusion

The Constitution (One Hundred and Twenty-Second Amendment) Bill, 2014, seeks to amend the Constitution of

Bill, 2014, seeks to amend the Constitution of") Concept Note on GST 1.Introduction The Constitution (One Hundred and Twenty-Second Amendment) Bill, 2014, seeks to amend the Constitution of India to facilitate the introduction of Goods and Services Tax

Concept Note on GST 1.Introduction The Constitution (One Hundred and Twenty-Second Amendment) Bill, 2014, seeks to amend the Constitution of India to facilitate the introduction of Goods and Services Tax

Goods & Service Tax. (GST) BBNL Vendor MEET

BBNL Vendor MEET") Goods & Service Tax (GST) BBNL Vendor MEET 28.6.2017 1 Overview GST In short How to Charge Tax Changes Now Tax on both goods and services when supplied Replacing - Central Excise, Service Tax, VAT, Entry

Goods & Service Tax (GST) BBNL Vendor MEET 28.6.2017 1 Overview GST In short How to Charge Tax Changes Now Tax on both goods and services when supplied Replacing - Central Excise, Service Tax, VAT, Entry

TITLE: GST LAW: AN EXECUTIVE SUMMARY

Pramod Kumar Rai, Advocate Managing Partner B.Tech (IITKanpur), LLB (Gold Medal), LLM (USA) Former Joint Commissioner of Customs, Excise & Service Tax (IRS). Email: pramodrai@ymail.com, pramod@athenalawassociates.com

Pramod Kumar Rai, Advocate Managing Partner B.Tech (IITKanpur), LLB (Gold Medal), LLM (USA) Former Joint Commissioner of Customs, Excise & Service Tax (IRS). Email: pramodrai@ymail.com, pramod@athenalawassociates.com

A PRESENTATION GOODS AND SERVICES TAX AN OVERVIEW

A PRESENTATION ON GOODS AND SERVICES TAX AN OVERVIEW BY ASHU DALMIA & ASSOCIATES CHARTERED ACCOUNTANTS A-36, 2 nd Floor, Guru Nanak Pura Laxmi Nagar, Delhi-110092, INDIA Tel: +91 11 22466591, 22422707,

A PRESENTATION ON GOODS AND SERVICES TAX AN OVERVIEW BY ASHU DALMIA & ASSOCIATES CHARTERED ACCOUNTANTS A-36, 2 nd Floor, Guru Nanak Pura Laxmi Nagar, Delhi-110092, INDIA Tel: +91 11 22466591, 22422707,

GST CONCEPT & STATUS As on 01 st May, Introduction

GST CONCEPT & STATUS As on 01 st May, 2017 Introduction The introduction of Goods and Services Tax (GST) would be a very significant step in the field of indirect tax reforms in India. By amalgamating

GST CONCEPT & STATUS As on 01 st May, 2017 Introduction The introduction of Goods and Services Tax (GST) would be a very significant step in the field of indirect tax reforms in India. By amalgamating

CHAPTER 2. GST Acts : CGST ACT, SGST ACT (KARNATAKA STATE) IGST ACT

IGST ACT") CHAPTER 2 GST Acts : CGST ACT, SGST ACT (KARNATAKA STATE) IGST ACT SALIENT FEATURES OF CGST ACT, 2017 1. A state-wise single registration for a taxpayer for filing returns, paying taxes, and to fulfil

CHAPTER 2 GST Acts : CGST ACT, SGST ACT (KARNATAKA STATE) IGST ACT SALIENT FEATURES OF CGST ACT, 2017 1. A state-wise single registration for a taxpayer for filing returns, paying taxes, and to fulfil

All About GST and Model GST Law

All About GST and Model GST Law 1 Contents GST Basics Supply Meaning & Scope Supply - Time & Place Valuation Rules Input Tax Credit Administration & Procedures Transitional Provisions 2 Basics of GST 3

All About GST and Model GST Law 1 Contents GST Basics Supply Meaning & Scope Supply - Time & Place Valuation Rules Input Tax Credit Administration & Procedures Transitional Provisions 2 Basics of GST 3

GST MSME SECTORAL SERIES CENTRAL BOARD OF EXCISE & CUSTOMS. Directorate General of Taxpayer Services. Follow

GST SECTORAL SERIES MSME Directorate General of Taxpayer Services CENTRAL BOARD OF EXCISE & CUSTOMS www.cbec.gov.in Question 55: Whether a registered person under the composition scheme needs to learn

GST SECTORAL SERIES MSME Directorate General of Taxpayer Services CENTRAL BOARD OF EXCISE & CUSTOMS www.cbec.gov.in Question 55: Whether a registered person under the composition scheme needs to learn

Implementation of Goods and Service Tax (GST) in India. Opportunities and Challenges for CMA

in India. Opportunities and Challenges for CMA") Implementation of Goods and Service Tax (GST) in India Opportunities and Challenges for CMA CMA Rajesh Shukla At ICWA Chapter meet 14 th August 2015 Aurangabad Present Indirect Taxation Structure 2 Background

Implementation of Goods and Service Tax (GST) in India Opportunities and Challenges for CMA CMA Rajesh Shukla At ICWA Chapter meet 14 th August 2015 Aurangabad Present Indirect Taxation Structure 2 Background

OVERVIEW OF GOODS & SERVICES TAX (GST) CA. JINIT R SHAH GMJ & Co. J.B. Nagar CPE Study Circle of WIRC 18 th October, 2015

CA. JINIT R SHAH GMJ & Co. J.B. Nagar CPE Study Circle of WIRC 18 th October, 2015") OVERVIEW OF GOODS & SERVICES TAX (GST) CA. JINIT R SHAH GMJ & Co J.B. Nagar CPE Study Circle of WIRC 18 th October, 2015 GST Biggest Tax Reform JOURNEY OF GST IN INDIA UPTO 2014 S. N. Event Year 1 Announcement

OVERVIEW OF GOODS & SERVICES TAX (GST) CA. JINIT R SHAH GMJ & Co J.B. Nagar CPE Study Circle of WIRC 18 th October, 2015 GST Biggest Tax Reform JOURNEY OF GST IN INDIA UPTO 2014 S. N. Event Year 1 Announcement

GST Overview (Concept of GST, Supply, Intra-State and Inter-State Supply) -Karan Talwar, Advocate

-Karan Talwar, Advocate") GST Overview (Concept of GST, Supply, Intra-State and Inter-State Supply) -Karan Talwar, Advocate GST Overview - Objective Destination based consumption tax Multi Stage Value Added Tax One nation one tax

GST Overview (Concept of GST, Supply, Intra-State and Inter-State Supply) -Karan Talwar, Advocate GST Overview - Objective Destination based consumption tax Multi Stage Value Added Tax One nation one tax

EXECUTIVE PROGRAMME SUPPLEMENT FOR TAX LAWS & PRACTICE

EXECUTIVE PROGRAMME SUPPLEMENT FOR TAX LAWS & PRACTICE (INDIRECT TAX PART-B) (Relevant for Students appearing in December 2017 Examination) Module I-Paper 4 Disclaimer- This document has been prepared

EXECUTIVE PROGRAMME SUPPLEMENT FOR TAX LAWS & PRACTICE (INDIRECT TAX PART-B) (Relevant for Students appearing in December 2017 Examination) Module I-Paper 4 Disclaimer- This document has been prepared

Marking Scheme. Session TAXATION (782) CLASS XII. Total marks: 100 Theory: 60 Marks Practical: 40 Marks. 1 Deduction From Gross Total Income

CLASS XII. Total marks: 100 Theory: 60 Marks Practical: 40 Marks. 1 Deduction From Gross Total Income") Marking Scheme Session 2018-19 TAXATION (782) CLASS XII Total marks: 100 Theory: 60 Marks Practical: 40 Marks UNITS UNIT NAME TOTAL 1 Deduction From Gross Total Income 2 Computation Of Ta x Liability Of

Marking Scheme Session 2018-19 TAXATION (782) CLASS XII Total marks: 100 Theory: 60 Marks Practical: 40 Marks UNITS UNIT NAME TOTAL 1 Deduction From Gross Total Income 2 Computation Of Ta x Liability Of

GOODS AND SERVICES TAX AN OVERVIEW

GOODS AND SERVICES TAX AN OVERVIEW CENTRAL BOARD OF EXCISE & CUSTOMS GOODS AND SERVICES TAX (GST) 1. Benefits: 1. GST is a win-win situation for the entire country. It brings benefits to all the stakeholders

GOODS AND SERVICES TAX AN OVERVIEW CENTRAL BOARD OF EXCISE & CUSTOMS GOODS AND SERVICES TAX (GST) 1. Benefits: 1. GST is a win-win situation for the entire country. It brings benefits to all the stakeholders

Goods and Services Tax in India

Goods and Services Tax in India Satya Poddar December 1, 2011 Current Patchwork State VAT CENVAT/Service Tax Primary Producers Service Providers Primary Producers Service Providers Manufacturers Service

Goods and Services Tax in India Satya Poddar December 1, 2011 Current Patchwork State VAT CENVAT/Service Tax Primary Producers Service Providers Primary Producers Service Providers Manufacturers Service

GST on Traders. 1. Introduction Levy Time of Supply of Goods Place of Supply of Goods Value of Supply 23

GST on Traders DISCLAIMER The views expressed in this article are of the author(s). The Institute of Chartered Accountants of India may not necessarily subscribe to the views expressed by the author(s).

GST on Traders DISCLAIMER The views expressed in this article are of the author(s). The Institute of Chartered Accountants of India may not necessarily subscribe to the views expressed by the author(s).

VALUATION OF TAXABLE SUPPLY UNDER REVISED GST LAW & VALUATION RULES UNDER DRAFT MODEL GST LAW FEW THOUGHTS. Indirect Taxes Committee, ICAI

VALUATION OF TAXABLE SUPPLY UNDER REVISED GST LAW & VALUATION RULES UNDER DRAFT MODEL GST LAW FEW THOUGHTS Indirect Taxes Committee, ICAI 1 VALUE OF TAXABLE SUPPLY Sec 15 For any levy / tax, apart from

VALUATION OF TAXABLE SUPPLY UNDER REVISED GST LAW & VALUATION RULES UNDER DRAFT MODEL GST LAW FEW THOUGHTS Indirect Taxes Committee, ICAI 1 VALUE OF TAXABLE SUPPLY Sec 15 For any levy / tax, apart from

Indirect Taxes Committee, ICAI

1 GST Constitutional Provisions and Features of Constitution (101 st Amendment) Act, 2016 101st Constitution Amendment Act 2 Under current regime - Centre levies Excise duty on manufacture, Service tax

1 GST Constitutional Provisions and Features of Constitution (101 st Amendment) Act, 2016 101st Constitution Amendment Act 2 Under current regime - Centre levies Excise duty on manufacture, Service tax

GOODS AND SERVICES TAX

GOODS AND SERVICES TAX The Ultimate Indirect Tax reform The information provided in this document is for general information only. It is based on the information available publicly and the advice received

GOODS AND SERVICES TAX The Ultimate Indirect Tax reform The information provided in this document is for general information only. It is based on the information available publicly and the advice received

FAQs. Yes. He is liable for registration as he is engaged in Inter State supplies.

FAQs 1. A registered person s business is in many states. All supplies are below 10 lakhs. He makes an Inter State supply from one state. Is he liable for registration? Yes. He is liable for registration

FAQs 1. A registered person s business is in many states. All supplies are below 10 lakhs. He makes an Inter State supply from one state. Is he liable for registration? Yes. He is liable for registration

Important MCQ of GST

Important MCQ of GST By CA Vivek Gaba (Expected in Exam) 1. Compensation to states under GST (Compensation to States) Act, 2017 is paid by a) Central Government from consolidated fund of India b) Central

Important MCQ of GST By CA Vivek Gaba (Expected in Exam) 1. Compensation to states under GST (Compensation to States) Act, 2017 is paid by a) Central Government from consolidated fund of India b) Central

THE GOODS AND SERVICES TAX (GST) IN INDIA: CONCEPTUAL FRAMEWORK AND CHALLENGES

IN INDIA: CONCEPTUAL FRAMEWORK AND CHALLENGES") Inspira-Journal of Commerce, Economics & Computer Science (JCECS) 273 ISSN : 2395-7069 General Impact Factor : 2.4668, Volume 04, No. 01, January-March, 2018, pp. 273-280 THE GOODS AND SERVICES TAX (GST)

Inspira-Journal of Commerce, Economics & Computer Science (JCECS) 273 ISSN : 2395-7069 General Impact Factor : 2.4668, Volume 04, No. 01, January-March, 2018, pp. 273-280 THE GOODS AND SERVICES TAX (GST)

THE CONSTITUTION (ONE HUNDRED AND FIFTEENTH AMENDMENT) BILL, 2011

BILL, 2011") Bill No. 22 of 2011 5 THE CONSTITUTION (ONE HUNDRED AND FIFTEENTH AMENDMENT) BILL, 2011 A BILL further to amend the Constitution of India. BE it enacted by Parliament in the Sixty-second Year of the Republic

Bill No. 22 of 2011 5 THE CONSTITUTION (ONE HUNDRED AND FIFTEENTH AMENDMENT) BILL, 2011 A BILL further to amend the Constitution of India. BE it enacted by Parliament in the Sixty-second Year of the Republic

Current Tax Structure in India

History of GST More than 150 countries have already introduced GST. France was the first country to introduce GST system in 1954. Typically it is a single rate system but two/three rate systems are also

History of GST More than 150 countries have already introduced GST. France was the first country to introduce GST system in 1954. Typically it is a single rate system but two/three rate systems are also

Simple Handbook on GST

Simple Handbook on GST Team Hiregange 01.12.2017 Published by Team Hiregange #1010, 26th Main (Above Corporation Bank), 4 th T Block, Jayanagar, Bangalore 560041 www.hiregange.com 1 P a g e Contents 1.

Simple Handbook on GST Team Hiregange 01.12.2017 Published by Team Hiregange #1010, 26th Main (Above Corporation Bank), 4 th T Block, Jayanagar, Bangalore 560041 www.hiregange.com 1 P a g e Contents 1.

THE CONSTITUTION (ONE HUNDRED AND FIFTEENTH AMENDMENT) BILL, 2011

BILL, 2011") 1 AS INTRODUCED IN LOK SABHA Bill No. 22 of 2011 5 10 THE CONSTITUTION (ONE HUNDRED AND FIFTEENTH AMENDMENT) BILL, 2011 A BILL further to amend the Constitution of India. BE it enacted by Parliament in

1 AS INTRODUCED IN LOK SABHA Bill No. 22 of 2011 5 10 THE CONSTITUTION (ONE HUNDRED AND FIFTEENTH AMENDMENT) BILL, 2011 A BILL further to amend the Constitution of India. BE it enacted by Parliament in

26 th Year of Publication. A monthly publication from South Indian Bank. To kindle interest in economic affairs... To empower the student community...

Experience Next Generation Banking A monthly publication from South Indian Bank To kindle interest in economic affairs... To empower the student community... www.southindianbank.com Student s corner ho2099@sib.co.in

Experience Next Generation Banking A monthly publication from South Indian Bank To kindle interest in economic affairs... To empower the student community... www.southindianbank.com Student s corner ho2099@sib.co.in

for 3-DAYS REFRESHER COURSE GOODS AND SERVICE TAX (GST)

") BACKGROUND MATERIAL for 3-DAYS REFRESHER COURSE on GOODS AND SERVICE TAX (GST) I. INTRODUCTION The present system of indirect taxation has multiplicity of taxes levied by the Centre and State. This has

BACKGROUND MATERIAL for 3-DAYS REFRESHER COURSE on GOODS AND SERVICE TAX (GST) I. INTRODUCTION The present system of indirect taxation has multiplicity of taxes levied by the Centre and State. This has

BACKGROUND OF GST. As per Statement of Objects and Reasons appended to the Constitutional Amendment bill the object of GST is :

BACKGROUND OF GST INTRODUCTION The introduction of Goods and Services Tax (GST) is a very significant step in the field of indirect tax reforms in India. In the pre GST regime, there was multiplicity of

BACKGROUND OF GST INTRODUCTION The introduction of Goods and Services Tax (GST) is a very significant step in the field of indirect tax reforms in India. In the pre GST regime, there was multiplicity of

Goods and Services Tax

Goods and Services Tax Overview and Impact Analysis CA Neeraj Menon THE PROPOSED GST FRAMEWORK IN INDIA Dual-GST Centre and States to levy GST on common base (CGST & SGST) Salient features IGST on interstate

Goods and Services Tax Overview and Impact Analysis CA Neeraj Menon THE PROPOSED GST FRAMEWORK IN INDIA Dual-GST Centre and States to levy GST on common base (CGST & SGST) Salient features IGST on interstate

Levy and Collection of Tax

FAQ Levy and collection of Tax (Section 5) Q 1. What type of tax is levied on inter-state supply? Chapter I Levy and Collection of Tax Ans. In terms of Section 5 of the IGST Act, 2017, inter-state supplies

FAQ Levy and collection of Tax (Section 5) Q 1. What type of tax is levied on inter-state supply? Chapter I Levy and Collection of Tax Ans. In terms of Section 5 of the IGST Act, 2017, inter-state supplies

Goods & Services Tax (GST) One Nation One Tax

One Nation One Tax") Goods & Services Tax (GST) One Nation One Tax Why In News: After being subject to years of haggling and histrionics, the Goods & Services Tax (GST) finally had its historic day in the Parliament with the

Goods & Services Tax (GST) One Nation One Tax Why In News: After being subject to years of haggling and histrionics, the Goods & Services Tax (GST) finally had its historic day in the Parliament with the

A BRIEF INTRODUCTION TO CGST, SGST/UTGST, IGST & COMPENSATION CESS ACT(S)

") A BRIEF INTRODUCTION TO CGST, SGST/UTGST, IGST & COMPENSATION CESS ACT(S) 1 PRESENTATION PLAN: LEGAL PROVISIONS COMMON TO THE GST LAW(S) LEGAL PROVISIONS SPECIFIC TO IGST ACT & COMPENSATION CESS ACT NEERAJ

A BRIEF INTRODUCTION TO CGST, SGST/UTGST, IGST & COMPENSATION CESS ACT(S) 1 PRESENTATION PLAN: LEGAL PROVISIONS COMMON TO THE GST LAW(S) LEGAL PROVISIONS SPECIFIC TO IGST ACT & COMPENSATION CESS ACT NEERAJ

CHARTERED ACCOUNTANTS THE ROADMAP TO GST

CHARTERED ACCOUNTANTS THE ROADMAP TO GST Target date of GST Roll Out: 1st April 2017 R.Tulsian and Co LLP 2016 1 Shashwat Tulsian,Partner GST is one indirect tax for the whole nation, which will make India

CHARTERED ACCOUNTANTS THE ROADMAP TO GST Target date of GST Roll Out: 1st April 2017 R.Tulsian and Co LLP 2016 1 Shashwat Tulsian,Partner GST is one indirect tax for the whole nation, which will make India

GST CGST SUPPLY, TIME AND PLACE OF SUPPLY THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA. Scope of Supply

GST SUPPLY, TIME AND PLACE OF SUPPLY THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA BY :-CA SUNIL P JAIN (FCA, DISA) (STUDY GROUP MEMBER & FACULTY-IDT) CGST Section 7 Scope of Supply 2 1) For the purposes

GST SUPPLY, TIME AND PLACE OF SUPPLY THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA BY :-CA SUNIL P JAIN (FCA, DISA) (STUDY GROUP MEMBER & FACULTY-IDT) CGST Section 7 Scope of Supply 2 1) For the purposes

GST & YOU. Tally Solutions Pvt. Ltd. All Rights Reserved 2. Tally Solutions Pvt. Ltd. All Rights Reserved Business Presentation

WELCOME 1 GST & YOU Tally Solutions Pvt. Ltd. All Rights Reserved 2 Tally Solutions Pvt. Ltd. All Rights Reserved Business Presentation Presentation Agenda GST Basics What is GST Why GST GST concepts How

WELCOME 1 GST & YOU Tally Solutions Pvt. Ltd. All Rights Reserved 2 Tally Solutions Pvt. Ltd. All Rights Reserved Business Presentation Presentation Agenda GST Basics What is GST Why GST GST concepts How

GST CONCEPT & STATUS

GST CONCEPT & STATUS Updated as on 01 st January 2018 INTRODUCTION: The introduction of Goods and Services Tax on 1 st of July 2017 was a very significant step in the field of indirect tax reforms in India.

GST CONCEPT & STATUS Updated as on 01 st January 2018 INTRODUCTION: The introduction of Goods and Services Tax on 1 st of July 2017 was a very significant step in the field of indirect tax reforms in India.

CHAPTER 1: INTRODUCTION TO GST 1.1 BASICS OF GST What is GST?

CHAPTER 1: INTRODUCTION TO GST 1.1 BASICS OF GST 1.1.1 What is GST? Goods and Services Tax (GST) is a value-added indirect tax at each stage of the supply of goods and services precisely on the amount

CHAPTER 1: INTRODUCTION TO GST 1.1 BASICS OF GST 1.1.1 What is GST? Goods and Services Tax (GST) is a value-added indirect tax at each stage of the supply of goods and services precisely on the amount

GST. Concept & Roadmap By CA. Ashwarya Agarwal

GST Concept & Roadmap By CA. Ashwarya Agarwal 1 What is GST?? GST Goods and Services Tax Clause 12A of Article 366 of The Constitution of India goods and services tax means any tax on supply of goods,

GST Concept & Roadmap By CA. Ashwarya Agarwal 1 What is GST?? GST Goods and Services Tax Clause 12A of Article 366 of The Constitution of India goods and services tax means any tax on supply of goods,

GOODS AND SERVICE TAX (GST) IN INDIA Challenges Ahead. February 28, 2016

IN INDIA Challenges Ahead. February 28, 2016") GOODS AND SERVICE TAX (GST) IN INDIA Challenges Ahead February 28, 2016 PRESENT SCENARIO: ISSUES & CONCERN Indian truck drivers clock an average of 280 km per day as against world average of 400 km per

GOODS AND SERVICE TAX (GST) IN INDIA Challenges Ahead February 28, 2016 PRESENT SCENARIO: ISSUES & CONCERN Indian truck drivers clock an average of 280 km per day as against world average of 400 km per

WIRC Refresher Course on GST

WIRC Refresher Course on GST Date & Day : 25 th May, 2017 (Thursday) Subject : 1) Basic Concepts and Applicability of GST 2) Levy, meaning and scope of Supply 3) Relevant transitional provision Venue :

WIRC Refresher Course on GST Date & Day : 25 th May, 2017 (Thursday) Subject : 1) Basic Concepts and Applicability of GST 2) Levy, meaning and scope of Supply 3) Relevant transitional provision Venue :

BIRD S EYE VIEW OF GST LAW

BIRD S EYE VIEW OF GST LAW This Chapter covers major aspects of CGST Bill, IGST Bill for understanding what GST is all about. It does not cover the dispute resolution mechanism as that stage shall come

BIRD S EYE VIEW OF GST LAW This Chapter covers major aspects of CGST Bill, IGST Bill for understanding what GST is all about. It does not cover the dispute resolution mechanism as that stage shall come

HANDBOOK TO G S T AUDIT. (with GSTR-9 and 9C) BY :- CA ATUL KUMAR GUPTA ASSISTED BY :- CA SMELLY KINRA CA MOHIT GUPTA

BY :- CA ATUL KUMAR GUPTA ASSISTED BY :- CA SMELLY KINRA CA MOHIT GUPTA") HANDBOOK TO G S T AUDIT (with GSTR-9 and 9C) BY :- CA ATUL KUMAR GUPTA ASSISTED BY :- CA SMELLY KINRA CA MOHIT GUPTA HANDBOOK TO GST AUDIT (With GSTR 9 & GSTR 9C) By- CA Atul Kumar Gupta Assisted by-

HANDBOOK TO G S T AUDIT (with GSTR-9 and 9C) BY :- CA ATUL KUMAR GUPTA ASSISTED BY :- CA SMELLY KINRA CA MOHIT GUPTA HANDBOOK TO GST AUDIT (With GSTR 9 & GSTR 9C) By- CA Atul Kumar Gupta Assisted by-

C A. S H A S H A N K S H E K H A R G U P T A P A R T N E R - I N D I R E C T T A X

OM HARE GURVEY NAMAH GOODS AND SERVICES TAX A DISCUSSION C A. S H A S H A N K S H E K H A R G U P T A P A R T N E R - I N D I R E C T T A X J U N E 2 0 1 6 BACKGROUND WHAT IS GST? WHY GST? (a) & (b) BRIEF

OM HARE GURVEY NAMAH GOODS AND SERVICES TAX A DISCUSSION C A. S H A S H A N K S H E K H A R G U P T A P A R T N E R - I N D I R E C T T A X J U N E 2 0 1 6 BACKGROUND WHAT IS GST? WHY GST? (a) & (b) BRIEF

Taxation principles of GST and experience of present law as relevant to GST

Taxation principles of GST and experience of present law as relevant to GST Outline of discussion General Taxation principles Indian indirect Tax system Road to GST Introduction of GST Benefits of GST

Taxation principles of GST and experience of present law as relevant to GST Outline of discussion General Taxation principles Indian indirect Tax system Road to GST Introduction of GST Benefits of GST

VAT CONCEPT AND ITS APPLICATION IN GST

CONTENTS DIVISION 1 INPUT TAX CREDIT 1 VAT CONCEPT AND ITS APPLICATION IN GST 1.1 Background of VAT 3 1.2 Basic Concept of VAT 4 1.2-1 VAT to avoid the cascading effect 5 1.2-2 Input Tax credit system

CONTENTS DIVISION 1 INPUT TAX CREDIT 1 VAT CONCEPT AND ITS APPLICATION IN GST 1.1 Background of VAT 3 1.2 Basic Concept of VAT 4 1.2-1 VAT to avoid the cascading effect 5 1.2-2 Input Tax credit system

A. Introduction on GST:

GST FAQ S Contents A. Introduction on GST: 02 B. Meaning and Scope of Supply: 04 C. Tax liability on composite and mixed supplies 06 D. Registration under GST 07 E. Levy of GST 11 F. Time of supply of

GST FAQ S Contents A. Introduction on GST: 02 B. Meaning and Scope of Supply: 04 C. Tax liability on composite and mixed supplies 06 D. Registration under GST 07 E. Levy of GST 11 F. Time of supply of

Integrated Goods and Services Tax (IGST)

") 1. The introduction of Goods and Services Tax (GST) is a significant reform in the field of indirect taxes in our country. Multiple taxes levied and collected by the Centre and the States will be replaced

1. The introduction of Goods and Services Tax (GST) is a significant reform in the field of indirect taxes in our country. Multiple taxes levied and collected by the Centre and the States will be replaced

GST- A NEW BEGINNING IN INDIAN FINANCIAL SYSTEM

GST- A NEW BEGINNING IN INDIAN FINANCIAL SYSTEM Dr. Anita Sharma, Reader, Maharaja Surajmal Institute (GGSIPU), New Delhi Abstract: GST means Goods and Services Tax. The main aim of GST is to abolish all

GST- A NEW BEGINNING IN INDIAN FINANCIAL SYSTEM Dr. Anita Sharma, Reader, Maharaja Surajmal Institute (GGSIPU), New Delhi Abstract: GST means Goods and Services Tax. The main aim of GST is to abolish all

An Overview of Indirect Taxes. By PROF V.N. PARTHIBAN, FICWA, ACS, FIII, ASM, ADIM, MBA, LLM

An Overview of Indirect Taxes By PROF V.N. PARTHIBAN, FICWA, ACS, FIII, ASM, ADIM, MBA, LLM Customs Duty Basic Customs Duty :Levied under Customs Act, 1962 on : Imported goods: (means any goods brought

An Overview of Indirect Taxes By PROF V.N. PARTHIBAN, FICWA, ACS, FIII, ASM, ADIM, MBA, LLM Customs Duty Basic Customs Duty :Levied under Customs Act, 1962 on : Imported goods: (means any goods brought

BIRD S EYE VIEW OF GST LAW

BIRD S EYE VIEW OF GST LAW This part covers major aspects of CGST, IGST Act for understanding what GST is all about. The UTGST and State GST laws are expected to follow the same principles. Comparison

BIRD S EYE VIEW OF GST LAW This part covers major aspects of CGST, IGST Act for understanding what GST is all about. The UTGST and State GST laws are expected to follow the same principles. Comparison

Asian Research Consortium

Asian Research Consortium Asian Journal of Research in Business Economics and Management Vol. 5, No. 8, August 2015, pp. 58-68. ISSN 2249-7307 Asian Journal of Research in Business Economics and Management

Asian Research Consortium Asian Journal of Research in Business Economics and Management Vol. 5, No. 8, August 2015, pp. 58-68. ISSN 2249-7307 Asian Journal of Research in Business Economics and Management

IMPACTS OF GST ON INDIAN ECONOMY. Mrs.D.Sivasakthi Assistant Professor: B.Com (PA) Dr. N.G.P. Arts and science college (Autonomous) Coimbatore

Dr. N.G.P. Arts and science college (Autonomous) Coimbatore") 141 Journal of Management and Science ISSN: 2249-1260 e-issn: 2250-1819 Special Issue. No.1 Sep 17 IMPACTS OF GST ON INDIAN ECONOMY Mrs.D.Sivasakthi Assistant Professor: B.Com (PA) Dr. N.G.P. Arts and

141 Journal of Management and Science ISSN: 2249-1260 e-issn: 2250-1819 Special Issue. No.1 Sep 17 IMPACTS OF GST ON INDIAN ECONOMY Mrs.D.Sivasakthi Assistant Professor: B.Com (PA) Dr. N.G.P. Arts and

Goods and Services Tax (GST): An Overview

: An Overview") Goods and Services Tax (GST): An Overview I. Introduction Introduction of GST would be a significant step in the field of indirect tax reforms in India. By amalgamating a large number of Central and State

Goods and Services Tax (GST): An Overview I. Introduction Introduction of GST would be a significant step in the field of indirect tax reforms in India. By amalgamating a large number of Central and State

Response to questions raised by members in relation to Goods and Services Tax ( GST )

") Response to questions raised by members in relation to Goods and Services Tax ( GST ) 1. What will be the treatment for hallmarking charges recovered from Customer? As per Section 15 of the CGST Act, 2017,

Response to questions raised by members in relation to Goods and Services Tax ( GST ) 1. What will be the treatment for hallmarking charges recovered from Customer? As per Section 15 of the CGST Act, 2017,

Proposed Amendments in GST Law

Proposed Amendments in GST Law On 09.07.2018, the Goods and Service Tax Council has issued draft proposal for the amendment in the "Goods and Services Tax" Law. The entire proposal gives brief view on

Proposed Amendments in GST Law On 09.07.2018, the Goods and Service Tax Council has issued draft proposal for the amendment in the "Goods and Services Tax" Law. The entire proposal gives brief view on