GOODS AND SERVICE TAX (GST) IN INDIA Challenges Ahead. February 28, 2016

|

|

|

- Myles Nash

- 5 years ago

- Views:

Transcription

1 GOODS AND SERVICE TAX (GST) IN INDIA Challenges Ahead February 28, 2016

2 PRESENT SCENARIO: ISSUES & CONCERN Indian truck drivers clock an average of 280 km per day as against world average of 400 km per day and 700 km per day in US. Truck drivers in India spend 60% of their time off roads negotiating check posts & toll plazas. There are 650 odd check posts in the country and 11 categories of taxes. Introduction of GST will help in improving the Indian truck productivity

3 PRESENT SCENARIO: ISSUES & CONCERN A foreign company was advised by its tax planners to hold on its investment for a proposed manufacturing plant till the time country rolls out the GST regime. With an investment of around Rs. 100 crore, the company would have saved Rs. 10 to Rs. 15 crore through input tax credits under the GST regime. Similarly, many companies in corporate India are getting jittery on increasing working capital without complete visibility on tax rates and coverage of goods.

4 PRESENT SCENARIO: ISSUES & CONCERN At present the Restaurants are charging both Central Tax (Service Tax) and State Tax (VAT) After introduction of GST single tax will be applicable

on Rs.113/- 16 Add : CST @ 2% on Rs.")

on Rs.150/- 21 Add : VAT @ 12.")

5 PRESENT SCENARIO: ISSUES & CONCERN Within State Uttar Pradesh Amount Outside State: Maharastra Amount Manufacturer sells the product to Wholeseller 100 Manufacturer sells the product to Wholeseller 100 Add : Excise 12.5% 13 Add : Excise 12.5% Add : 14% (12.5%+1.5%)on Rs.113/- 16 Add : 2% on Rs. 113/- ( ) 2 Selling Price 128 Selling Price 115 Wholeseller sells the product to Retailer within the State 150 Wholeseller sells the product to Retailer within the State 125 Add : 14% (12.5%+1.5%) on Rs.150/- 21 Add : 12.5% 16 Selling Price 171 Selling Price 141 Impact Analysis: 200 Impact Analysis: Wholeseller paid Excise Duty at the time purchase 13 Wholeseller paid Excise Duty at the time purchase 13 Wholeseller paid VAT at the time purchase 16 Wholeseller paid CST at the time purchase 2 Input Tax Credit (ITC) Wholeseller takes Input Tax Credit on VAT 16 No Input Tax Credit (Rs.13+Rs.2) 15 No Input Tax Credit on Excise Duty paid 13 Output VAT liability 16 Output VAT liability 21 Net amount to be paid to Tax Department (Rs.16-0) 16 Net amount to be paid to Tax Department (21-16) 5 Impact of double on Rs. 13/- 2

6 PRESENT SCENARIO: GST Within State Uttar Pradesh Present GST Outside State: Maharastra Present GST Manufacturer sells the product to Wholeseller Manufacturer sells the product to Wholeseller Add : Excise 12.5% 13 Add : Excise 12.5% 13 Add : 14% (12.5%+1.5%)on Rs.113/- 16 Add : 2% on Rs. 112/- ( ) 2 10 IGST (CGST@10%+SGST@10%) % additional tax 1 Selling Price Selling Price Value Value Wholeseller sells the product to Retailer within the State Wholeseller sells the product to Retailer within the State Add : 14% (12.5%+1.5%) on Rs.150/- 20 Add : 12.5% Selling Price Selling Price Value Value Retailer sells the product to Customer within Retailer sells the product to Customer within the the State State Add : 14% (12.5%+1.5%) on Rs.150/- 26 Add : 12.5% Selling Price Selling Price Tax collected by Govt. Tax collected by Govt. Central Govt tax Central Govt tax State Govt State Govt Total tax collection Total tax collection 36 37

7 PRESENT INDIRECT TAX SCENARIO IN INDIA INDIRECT TAXATION CENTRAL Central Excise Custom Duty Service Tax Central sales Tax STATE Sales Tax / VAT Entertainment Tax Luxury Tax Taxes on lottery, betting and gambling Entry Tax Octroi etc.

8 Multiple Taxes CENTRAL STATE Customs Duty Basic Custom Duty Countervailing Duty Special Additional Duty Excise Duty: Basic Excise Duty, Add. Excise Duty Service Tax Product Specific Cess like Automobile Cess Research and Development Cess Swachh Bharat Cess Central Sales Tax Value Added Tax (VAT) Entry Tax Octroi charged by Municipality Local Body Tax Entertainment Tax Luxury Tax State cess & surcharge Stamp Duty & Registration Fees

9 SALIENT POINTS OF GST A Comprehensive Tax on Goods and Services Multi-point Tax on value added at each stage Tax is only cost to the end customer Consumption based tax not origin base No cascading due to input credit mechanism Self policing or voluntary compliances Reduction of Tax evasion /Widens the taxation base

10 SALIENT POINTS OF GST Enormous scope for augmenting revenue Lower taxes lead to better compliance and higher revenues Good opportunity to jointly work for better enforcement Uniform tax rate across the entire common market Reduces distribution cost as there is not tax barrier among the States GST will spur Growth and increase the GDP like Canada Making exports more competitive

11 GST JOURNEY SO FAR 2006 FM announces GST in India fm Joint Working Group set up by Empowered Committee of State Finance Ministers Joint Working Group submitted Report to Empowered Committee Report of Joint Working Group discussed by Empowered Committee and some changes made Views of Empowered Committee was sent to Government of India Comments received by Empowered Committee from Government of India Comments of Government of India considered by Empowered Committee and Committee was constituted to consider these comments 2009 Views accepted by Empowered Committee, a Working Group was formed by State/Central Govt office to submit recommendations of structure of GST. Interaction between Finance Minister and Empowered Committee for compensation for loss of Revenue to the State for phase out of the CST. First Discussion Paper released by Empowered Committee

12 GST JOURNEY SO FAR 2009 Report of the Task Force on GST constituted by the 13 th Finance Commission The Prime Minister s Economic Advisory Committee (PMEAC), Chairman C. Rangarajan has said The Centre could follow the pattern in which there is only one rate for goods and one rate for services, or one rate which is common to both goods and services The Constitution (One Hundred and Fifteenth Amendment) Bill, 2011 introduced in Parliament. The Constitution (One Hundred and Fifteenth Amendment) Bill, 2014 introduced in Parliament on December 19, Lok Sabha cleared the Constitution (122 nd Amendment )Bill on May 6, 2015

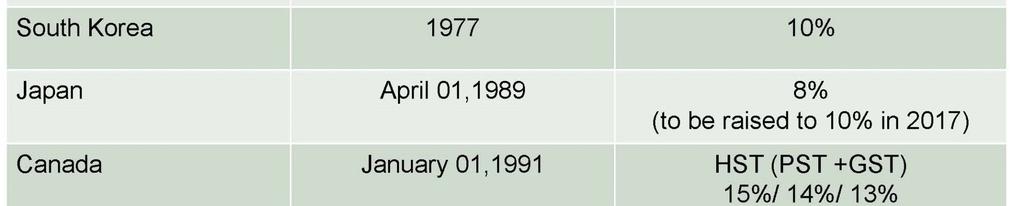

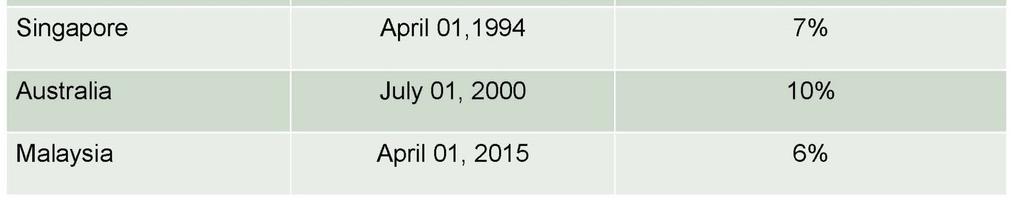

13 GST GLOBAL SCENARIO More than 160 countries have already introduced GST/ National Level VAT Typically GST is a unified Tax System in most of the Countries Canada and Brazil only have dual GST Standard rate of most of the Countries ranges between 16-20% As per KPMG international indirect tax survey 2014: 132 countries: Hungary- 27% and Aruba: 1.5% Out of

14 COMPARISON OF FEDERAL VAT SYSTEMS Nature of VAT Country Examples Disadvantages Independent VATs at Centre and Sates Brazil, Russia, Argentina Differences in base and rates weaken administration and compliance. Inter-state transactions difficult to manage VAT levied and administered at Centre Australia, Germany, Austria, Switzerland, etc. State government relieved of responsibility of raising taxes which also takes away fiscal discretion of States Dual VAT Canada and India today A combination of the above two and hence limits both their disadvantages "Clean" dual VAT India's GST Common base and common or similar rates facilitate administration and compliance, including for inter-state transactions, while continuing to provide some fiscal autonomy to States. Source : World Bank

15 GST GLOBAL SCENARIO

16 INDIA: GST RATE SUGGESTED BY VARIOUS PANEL 13th Finance Commission task force: Centre 5% State - 7% Combined -12% Sub panel of Empowered committee: Centre % State % Combined-26.68% Select committee of RS: GST Rate-20%

17 DR. ARVIND SUBRAMANIAN COMMITTEE REPORT Source : Committee s calculations Note : All rates are the sum of rates at Centre and States

18 GST MODEL DUEL GST CENTRAL GST (CGST) STATE GST (SGST)

19 Key Features - Dual GST Dual GST Transactions within the State Interstate Transactions SGST CGST IGST Levied by State Levied by Centre Levied by Centre Implemented through Multiple Statues Paid to the account of State Govt. Implemented through Single Statue Paid to the account of Central Govt. Implemented through Single Statue Paid to the account of Central Govt. IGST = CGST+SGST Addl. 1% on goods for a period of 2 years

20 SUBSUMING OF CENTRAL GST Additional Excise Duty Additional Custom Duty (CVD) Central Excise Duty Central GST Service Tax Excise Duty levied under the MTP Act Central Surcharges and Cesses Special Additional Duty of Customs

21 SUBSUMING OF CENTRAL GST Purchase Tax State Cesses & Surcharges Entry Tax VAT / Sales Tax State GST Luxury Tax Entertainment Tax (other than levied by local body) Octroi and Entry Tax Taxes on lottery, betting & gambling

22 Petroleum products Tax on alcoholic liquor for human consumption Tax on entertainment and amusement levied and collected by Panchayat /Municipality/District Council (Local body of State) Stamp duty Customs duty NOT-SUBSUMING IN GST: Taxes on consumption or sale of electricity Petroleum products and natural gas are within the ambit of GST but will be kept in abeyance until GST council decides.

23 NOT-SUBSUMING IN GST Centre would impose the following taxes after the implementation of GST: Taxes on goods or passengers carried by railway, sea or air Stamp duty on bill of exchange etc. Taxes on sale or purchase of newspaper and advertising etc.

24 NOT-SUBSUMING IN GST State would impose the following taxes after the implementation of GST: Taxes on lands and buildings; Taxes on the consumption or sale of electricity; Taxes on goods and passengers carried by road or on inland waterways; Taxes on animals and boats Tolls Taxes on professions, trade etc. Stamp duty in respect of documents other than those specified of List 1;

25 CONSTITUTIONAL AMENDMENT BILL (122 nd ) 122nd Amendment Bill introduced in LS on 2014 Key Features o Concurrent jurisdiction for levy of GST by the Centre and the States proposed Article 246A o Authority for Centre to levy & collect of IGST on supplies in the course of inter-state trade or commerce including imports proposed Article 269A o Authority for Centre to levy non vatable Additional Tax to be retained by originating State o GST defined as any tax on supply of goods or services or both other than on alcohol for human consumption proposed Article 366 (12A)

26 FEATURES OF CONSTITUTIONAL AMENDMENT BILL contd. o Goods includes all materials, commodities & articles Article 366(12) o Services means anything other than goods- proposed Article 366 (26A) o Goods and Services Tax Council (GSTC) proposed Article 279A To be constituted by the President within 60 days from the coming into force of the Constitutional Amendments Consists of Union FM & Union MOS (Rev) Consists of all State Ministers of Finance Quoram is 50% of total members Decision by majority of 75% weighted votes of members present & voting 1/3rd weighted votes for Centre & 2/3rd for all States together

27 Council to make recommendations on Taxes, etc. to be submitted in GST Exemptions & thresholds GST rates Band of GST rates FEATURES OF CONSTITUTIONAL AMENDMENT BILL contd.. Model GST Law & procedures Special provisions for special category States Date from which GST would be levied on petroleum products To be constituted by the President within 60 days from the coming into force of the Constitutional Amendments o Compensation for loss of revenue to States for five years

28 Analysis of GST Bill Introduction of concurrent powers to levy the dual GST) Inter state sale of goods to attract additional Effect on make in India Campaign Additional 1% tax: confusion of origin vs. Destination tax Exclusion of Petroleum, alcohol, electricity and real estate negate the boost the GDP? Role of GST Council Reduced States fiscal and political autonomy States can t exempt some goods & services States would lost its right to fix own tax rate Centre can veto any measure under proposed GST Clause 20 of Amendment Bill: Transitional Provisions

29 Export would be zero rated EXPORT & EXEMPTION Similar benefits will be given to Special Economic Zones (SEZs). Industrial incentives & Special Industrial Area Scheme : The tax exemption, remission etc. related to industrial incentives would be converted into cash refund scheme after collection of tax. Area based exemptions will continue up to legitimate time. No new exemption, remission etc. would be allowed.

30 IGST MODEL: INTER-STATE TRANSACTIONS IGST (CGST+SGST) on all inter-state transactions of taxable goods and services Supplier will pay IGST after set-off available credit of IGST, CGST & SGST on his purchases. The exporting state will transfer to the central agency the credit of SGST used for payment of IGST The importing taxpayer will claim ITC of IGST against his IGST,CGST and SGST tax liability. The central agency will transfer to the importing state the credit of IGST used in payment of SGST.

31 ADVANTAGE OF IGST MODEL Uninterrupted ITC chain on inter-state transactions No upfront payment of tax or substantial blockage of funds for the inter-state seller or buyer No refund claim in exporting State Uniform E-registration /E-Return/common periodicity of return/ uniform cut-off date System based verifications /validations etc.

32 Draft Reports by the Joint Committee on GST Business Process Registration Existing registered business entities migrated to the GSTN portal Newly incorporated business entities would submit application within 30 days from turnover crossing taxable threshold State-wise registration May opt for multiple registrations for different business verticals within the same State Option for voluntary registration Taxable threshold for inter-state supplies and reverse charge would be Zero No ITC for default of application within the prescribed time. Regular defaulter s profile would be posted in public domain

33 Draft Reports by the Joint Committee on GST Business Processes - Payment Fill details of amount to be paid E-Payment OTC NEFT/RTGS Internet Banking Debit/Credit Cards Cheque DD Cash

34 Draft Reports by the Joint Committee on GST Business Process - Return Every registered person is required to file a return for the prescribed tax period even if there is no business activity (i.e. Return) Government entities / PSUs, etc. not dealing in GST supplies or persons exclusively dealing in exempted / Nil rated / non-gst goods or services would neither be required to obtain registration nor required to file returns under the GST law Self - assessment E-Return shall be common for CGST, SGST, IGST Following shall be the various returns for different categories: Normal / Regular & Casual Taxpayer (GSTR 1,2,3 & 8) Compounding Taxpayer (GSTR 4 & 8) Foreign Non-Resident Taxpayer (GSTR-5) Input Service Distributor (GSTR-5) Tax Deductor (GSTR 7)

35 Draft Reports by the Joint Committee on GST Business Process - Refund Verification shall take place online to the extent possible Communication through SMS and Dealer can check status of application on portal 90% of refund claimed by the taxpayer may be sanctioned automatically by the system. Balance 10% of refund claims, amount of refund may be granted after completion of verification of documents / accounts to be done at the end of the financial year and to be completed within a period of three months. Rate of interest in case of delayed refund may be around 6% and that in case of default in payment of taxes may be around 18%.

36 GST Impact across all business. Fiscal Business Processes Accounting Cash Flow GST IT Systems Product Pricing Supply Chain Marketing

37 IMPACT OF GST - ON INDIAN ECONOMY

38 Transitional Issues Status of Existing Input Credit lying under CENVAT and VAT Unutilized Cenvet credit in respect of inputs, capital goods and input services 50% Cenvat credit not availed on capital goods Rejection of materiel out of the material procured from the date of implementation and treatment of duty thereof

39 Transitional Issues Goods in Transit or sale of goods on approval basis; Ongoing contract / agreements, purchase orders, work orders Goods are supplied prior to GST but the invoice is not raised Services are provided / completed prior to GST but the invoice is not raised Services are provided partially and the invoice for the part of the services is not raised

40 Transitional Issues Where advances has been received but goods are not dispatched from the factory till implementation of GST and Excise duty is yet to be discharged Advances for services received and taxes thereon also has been paid prior to GST but the invoice and provision of services takes place under GST regime Advance for service received and the corresponding invoices also raised prior to GST but services is yet to be provided The invoices for goods/ services has been raised prior to GST but activities are yet to be completed

41 Transitional Issues Various forms like Form C, F not provided in relation to the transaction pertaining to pre GST regime In case of imported goods, Bill of Entry not filed / assessed till the time of implementation of GST Sales made prior to GST but sales return under GST regime Goods and services taxable at different rate(s) under pre and post GST regime Pending refund claims, litigations, assessments prior to GST

42 Transitional Issues Creating awareness / imparting training or education on GST Transitory Provisions Taxable Event in GST: The term supply has not been defined in the Constitution Amendment Bill. Advance Ruling

43 OPPORTUNITY FOR CS & OTHER PROFESSIONS Advisory /Support to Government Training to Corporate Staff Decision making functions such as market strategies, stock transfer etc. Registration of service tax in each State and cancellation of CST etc. Special Audit /Certification like non applicability, exemption etc. Helping the small business for composition scheme Impact on various sectors

44 Law cannot stand still, it must change with the changing social concepts and value. If the law fails to respond to the needs of the changing society, then either it will stifle the growth of society and choke its progress P N Bhawati THANKS

The Constitution (One Hundred and Twenty-Second Amendment) Bill, 2014, seeks to amend the Constitution of

Bill, 2014, seeks to amend the Constitution of") Concept Note on GST 1.Introduction The Constitution (One Hundred and Twenty-Second Amendment) Bill, 2014, seeks to amend the Constitution of India to facilitate the introduction of Goods and Services Tax

Concept Note on GST 1.Introduction The Constitution (One Hundred and Twenty-Second Amendment) Bill, 2014, seeks to amend the Constitution of India to facilitate the introduction of Goods and Services Tax

Goods and Service Tax (GST)

") Indirect Taxes Committee of ICAI Goods and Service Tax (GST) Globally Known As VAT Standardised PPT by Indirect Taxes Committee Institute of Chartered Accountants of India Major Initiative in 2014-15 Organized

Indirect Taxes Committee of ICAI Goods and Service Tax (GST) Globally Known As VAT Standardised PPT by Indirect Taxes Committee Institute of Chartered Accountants of India Major Initiative in 2014-15 Organized

Goods and Service Tax (GST)

") Goods and Service Tax (GST) Globally Known As VAT Standardised PPT by Indirect Taxes Committee Institute of Chartered Accountants of India copyright@idtc_icai_2015 1 Indirect Taxes Committee of ICAI Major

Goods and Service Tax (GST) Globally Known As VAT Standardised PPT by Indirect Taxes Committee Institute of Chartered Accountants of India copyright@idtc_icai_2015 1 Indirect Taxes Committee of ICAI Major

Press Information Bureau Government of India Ministry of Finance

Press Information Bureau Government of India Ministry of Finance Frequently Asked Questions (FAQs) on Goods and Services Tax (GST) 03 August 2016 15:32 IST Following are the answers to the various frequently

Press Information Bureau Government of India Ministry of Finance Frequently Asked Questions (FAQs) on Goods and Services Tax (GST) 03 August 2016 15:32 IST Following are the answers to the various frequently

M/s PRANJAL JOSHI & CO

Introduction to GST Basic information GST stands for Goods and Service Tax. GST is a destination based tax on consumption of goods and services. It is proposed to be levied at all stages right from manufacture

Introduction to GST Basic information GST stands for Goods and Service Tax. GST is a destination based tax on consumption of goods and services. It is proposed to be levied at all stages right from manufacture

CHARTERED ACCOUNTANTS THE ROADMAP TO GST

CHARTERED ACCOUNTANTS THE ROADMAP TO GST Target date of GST Roll Out: 1st April 2017 R.Tulsian and Co LLP 2016 1 Shashwat Tulsian,Partner GST is one indirect tax for the whole nation, which will make India

CHARTERED ACCOUNTANTS THE ROADMAP TO GST Target date of GST Roll Out: 1st April 2017 R.Tulsian and Co LLP 2016 1 Shashwat Tulsian,Partner GST is one indirect tax for the whole nation, which will make India

Downloaded from Update PPT on GST (As on 01 st January 2018)

") Update PPT on GST (As on 01 st January 2018) 1 This presentation is for education purposes only and holds no legal validity 2 The Journey to GST 2006 First Discussion Paper was released by the Empowered

Update PPT on GST (As on 01 st January 2018) 1 This presentation is for education purposes only and holds no legal validity 2 The Journey to GST 2006 First Discussion Paper was released by the Empowered

GOODS & SERVICES TAX (GST) (Status as on 01 st May, 2017)

(Status as on 01 st May, 2017)") GOODS & SERVICES TAX (GST) (Status as on 01 st May, 2017) 1 PRESENTATION PLAN WHY GST : BENEFITS EXISTING INDIRECT TAX STRUCTURE FEATURES OF CONSTITUTION AMENDMENT ACT GST COUNCIL MAIN FEATURES OF GST

GOODS & SERVICES TAX (GST) (Status as on 01 st May, 2017) 1 PRESENTATION PLAN WHY GST : BENEFITS EXISTING INDIRECT TAX STRUCTURE FEATURES OF CONSTITUTION AMENDMENT ACT GST COUNCIL MAIN FEATURES OF GST

GST: An Integrated Tax

The Journey to GST 2006 First Discussion Paper was released by the Empowered Committee 2009 Constitution (115th Amendment) Bill introduced and subsequently lapsed 2011 The Constitution (122 n d Amendment)

The Journey to GST 2006 First Discussion Paper was released by the Empowered Committee 2009 Constitution (115th Amendment) Bill introduced and subsequently lapsed 2011 The Constitution (122 n d Amendment)

GST GOODS & SERVICES TAX

ICAI Nagpur Branch Seminar on 5 th November 2016 GST GOODS & SERVICES TAX broad CONCEPTS By Ashok chandak sbcngp@gmail.com 1 CONTENTS Present Indirect Tax Structure in India. Enabling Constitutional Amendments.

ICAI Nagpur Branch Seminar on 5 th November 2016 GST GOODS & SERVICES TAX broad CONCEPTS By Ashok chandak sbcngp@gmail.com 1 CONTENTS Present Indirect Tax Structure in India. Enabling Constitutional Amendments.

Implementation of Goods and Service Tax (GST) in India. Opportunities and Challenges for CMA

in India. Opportunities and Challenges for CMA") Implementation of Goods and Service Tax (GST) in India Opportunities and Challenges for CMA CMA Rajesh Shukla At ICWA Chapter meet 14 th August 2015 Aurangabad Present Indirect Taxation Structure 2 Background

Implementation of Goods and Service Tax (GST) in India Opportunities and Challenges for CMA CMA Rajesh Shukla At ICWA Chapter meet 14 th August 2015 Aurangabad Present Indirect Taxation Structure 2 Background

GOODS & SERVICE TAX. Unleashing of the new era in the Indirect Taxation Arena. By CA. Chitresh Gupta

GOODS & SERVICE TAX Unleashing of the new era in the Indirect Taxation Arena Date : 22 nd May 2015 Venue: District Tax Bar Association, Faridabad By CA. Chitresh Gupta B.Com(H), FCA,IDT(Cert),IFRS(Cert)

GOODS & SERVICE TAX Unleashing of the new era in the Indirect Taxation Arena Date : 22 nd May 2015 Venue: District Tax Bar Association, Faridabad By CA. Chitresh Gupta B.Com(H), FCA,IDT(Cert),IFRS(Cert)

C A. S H A S H A N K S H E K H A R G U P T A P A R T N E R - I N D I R E C T T A X

OM HARE GURVEY NAMAH GOODS AND SERVICES TAX A DISCUSSION C A. S H A S H A N K S H E K H A R G U P T A P A R T N E R - I N D I R E C T T A X J U N E 2 0 1 6 BACKGROUND WHAT IS GST? WHY GST? (a) & (b) BRIEF

OM HARE GURVEY NAMAH GOODS AND SERVICES TAX A DISCUSSION C A. S H A S H A N K S H E K H A R G U P T A P A R T N E R - I N D I R E C T T A X J U N E 2 0 1 6 BACKGROUND WHAT IS GST? WHY GST? (a) & (b) BRIEF

PARIMAL PATEL P. J. E-CONSULTANTS AHMEDABAD

SIMPLIFYING THE GST CODE PARIMAL PATEL P. J. E-CONSULTANTS AHMEDABAD CURRENT STRUCTURE CASCADING EFFECT TAX ON TAX Excise/VAT/CST/Entry Tax/BCD/CVD/AED, ETC. Excise/VAT/CST Branch Transfers VAT/CST WHY

SIMPLIFYING THE GST CODE PARIMAL PATEL P. J. E-CONSULTANTS AHMEDABAD CURRENT STRUCTURE CASCADING EFFECT TAX ON TAX Excise/VAT/CST/Entry Tax/BCD/CVD/AED, ETC. Excise/VAT/CST Branch Transfers VAT/CST WHY

GST. Concept & Roadmap By CA. Ashwarya Agarwal

GST Concept & Roadmap By CA. Ashwarya Agarwal 1 What is GST?? GST Goods and Services Tax Clause 12A of Article 366 of The Constitution of India goods and services tax means any tax on supply of goods,

GST Concept & Roadmap By CA. Ashwarya Agarwal 1 What is GST?? GST Goods and Services Tax Clause 12A of Article 366 of The Constitution of India goods and services tax means any tax on supply of goods,

FDI. Investment by foreign investors directly in the productive assets of another nation.

FDI Investment by foreign investors directly in the productive assets of another nation. Financial investment in stocks or bonds denotes foreign portfolio investment. Factors for Rise in Fiscal Deficit

FDI Investment by foreign investors directly in the productive assets of another nation. Financial investment in stocks or bonds denotes foreign portfolio investment. Factors for Rise in Fiscal Deficit

All About GST and Model GST Law

All About GST and Model GST Law 1 Contents GST Basics Supply Meaning & Scope Supply - Time & Place Valuation Rules Input Tax Credit Administration & Procedures Transitional Provisions 2 Basics of GST 3

All About GST and Model GST Law 1 Contents GST Basics Supply Meaning & Scope Supply - Time & Place Valuation Rules Input Tax Credit Administration & Procedures Transitional Provisions 2 Basics of GST 3

Goods and Service Tax (GST)

") Goods and Service Tax (GST) 1. Basics of GST 2. Working Model of GST 3. GST Compliances- Monthly and Annual Filings 4. GST Impact on E-Commerce 5. GST Impact on Services ( IT/ITES) BASICS of GST GST is

Goods and Service Tax (GST) 1. Basics of GST 2. Working Model of GST 3. GST Compliances- Monthly and Annual Filings 4. GST Impact on E-Commerce 5. GST Impact on Services ( IT/ITES) BASICS of GST GST is

INTRODUCTION TO GOODS AND SERVICE TAX

The Union Finance Minister Mr. P. Chidambaram in his budget speech in 2006 has said: It is my sense that there is a large consensus that the country should move towards a National Level Goods and Service

The Union Finance Minister Mr. P. Chidambaram in his budget speech in 2006 has said: It is my sense that there is a large consensus that the country should move towards a National Level Goods and Service

THE CHAMBER OF TAX CONSULTANTS BASIC CONCEPTS O F G S T

THE CHAMBER OF TAX CONSULTANTS BASIC CONCEPTS O F G S T 1 Understanding GST Covering 2 Legislations, 174 Sections,3 Schedules TAXES IN INDIA There are mainly two types of taxes DIRECT TAXES INCOME TAX

THE CHAMBER OF TAX CONSULTANTS BASIC CONCEPTS O F G S T 1 Understanding GST Covering 2 Legislations, 174 Sections,3 Schedules TAXES IN INDIA There are mainly two types of taxes DIRECT TAXES INCOME TAX

Goods and Service. By CMA Sachin Kathuria. CMA Sachin Kathuria

Goods and Service Tax (GST) in India By 1 Existing Tax structure in India 2 Tax Structure Direct Tax Indirect Tax Income Tax Wealth Tax (Now abolished) Central Tax State Tax Excise Service Tax Customs

Goods and Service Tax (GST) in India By 1 Existing Tax structure in India 2 Tax Structure Direct Tax Indirect Tax Income Tax Wealth Tax (Now abolished) Central Tax State Tax Excise Service Tax Customs

GST Workshop 9th June 2017

GST Workshop 9 th June 2017 GST Model- Basic Features GST is tax on the supply of goods and services, right from the manufacturer/service provider to the consumer. Destination based consumption Tax (Tax

GST Workshop 9 th June 2017 GST Model- Basic Features GST is tax on the supply of goods and services, right from the manufacturer/service provider to the consumer. Destination based consumption Tax (Tax

FAQ. Hindustan Shipyard Limited

FAQ Hindustan Shipyard Limited 1 Q 1. What is Goods and Service Tax (GST)? Ans. It is a destination based tax on consumption of goods and services. It is proposed to be levied at all stages right from

FAQ Hindustan Shipyard Limited 1 Q 1. What is Goods and Service Tax (GST)? Ans. It is a destination based tax on consumption of goods and services. It is proposed to be levied at all stages right from

GST Concept and Design

GST Concept and Design GST Understanding from the First discussion paper released by the Empowered Committee of State Finance Ministers on November 10, 2009 1 Understanding GST Brief History Need for GST

GST Concept and Design GST Understanding from the First discussion paper released by the Empowered Committee of State Finance Ministers on November 10, 2009 1 Understanding GST Brief History Need for GST

Asian Research Consortium

Asian Research Consortium Asian Journal of Research in Business Economics and Management Vol. 5, No. 8, August 2015, pp. 58-68. ISSN 2249-7307 Asian Journal of Research in Business Economics and Management

Asian Research Consortium Asian Journal of Research in Business Economics and Management Vol. 5, No. 8, August 2015, pp. 58-68. ISSN 2249-7307 Asian Journal of Research in Business Economics and Management

GOODS AND SERVICES TAX AN OVERVIEW

GOODS AND SERVICES TAX AN OVERVIEW CENTRAL BOARD OF EXCISE & CUSTOMS GOODS AND SERVICES TAX (GST) 1. Benefits: 1. GST is a win-win situation for the entire country. It brings benefits to all the stakeholders

GOODS AND SERVICES TAX AN OVERVIEW CENTRAL BOARD OF EXCISE & CUSTOMS GOODS AND SERVICES TAX (GST) 1. Benefits: 1. GST is a win-win situation for the entire country. It brings benefits to all the stakeholders

Goods and Service Tax in India. CA Ashutosh Thaker

Goods and Service Tax in India CA Ashutosh Thaker Ashutosh.thaker@verita.co.in Contents 01 Why &Salient features of Indian GST 02 Key Concept of GST 03 What should be of concern Central Govt. & State Govt.

Goods and Service Tax in India CA Ashutosh Thaker Ashutosh.thaker@verita.co.in Contents 01 Why &Salient features of Indian GST 02 Key Concept of GST 03 What should be of concern Central Govt. & State Govt.

A PRESENTATION GOODS AND SERVICES TAX AN OVERVIEW

A PRESENTATION ON GOODS AND SERVICES TAX AN OVERVIEW BY ASHU DALMIA & ASSOCIATES CHARTERED ACCOUNTANTS A-36, 2 nd Floor, Guru Nanak Pura Laxmi Nagar, Delhi-110092, INDIA Tel: +91 11 22466591, 22422707,

A PRESENTATION ON GOODS AND SERVICES TAX AN OVERVIEW BY ASHU DALMIA & ASSOCIATES CHARTERED ACCOUNTANTS A-36, 2 nd Floor, Guru Nanak Pura Laxmi Nagar, Delhi-110092, INDIA Tel: +91 11 22466591, 22422707,

Goods and Services Tax in India

Goods and Services Tax in India Satya Poddar December 1, 2011 Current Patchwork State VAT CENVAT/Service Tax Primary Producers Service Providers Primary Producers Service Providers Manufacturers Service

Goods and Services Tax in India Satya Poddar December 1, 2011 Current Patchwork State VAT CENVAT/Service Tax Primary Producers Service Providers Primary Producers Service Providers Manufacturers Service

GOODS AND SERVICE TAX (G.S.T.) OPPORTUNITIES AND CHALLENGES

OPPORTUNITIES AND CHALLENGES") 62 News & Views 2010 NTN I II GOODS AND SERVICE TAX (G.S.T.) OPPORTUNITIES AND CHALLENGES Sudhir Kumar Arora Advocate 140, Ist Floor, Navyug Market, Implementation of G.S.T. Principal Costing Impact. Possibility

62 News & Views 2010 NTN I II GOODS AND SERVICE TAX (G.S.T.) OPPORTUNITIES AND CHALLENGES Sudhir Kumar Arora Advocate 140, Ist Floor, Navyug Market, Implementation of G.S.T. Principal Costing Impact. Possibility

Current Tax Structure in India

History of GST More than 150 countries have already introduced GST. France was the first country to introduce GST system in 1954. Typically it is a single rate system but two/three rate systems are also

History of GST More than 150 countries have already introduced GST. France was the first country to introduce GST system in 1954. Typically it is a single rate system but two/three rate systems are also

26 th Year of Publication. A monthly publication from South Indian Bank. To kindle interest in economic affairs... To empower the student community...

Experience Next Generation Banking A monthly publication from South Indian Bank To kindle interest in economic affairs... To empower the student community... www.southindianbank.com Student s corner ho2099@sib.co.in

Experience Next Generation Banking A monthly publication from South Indian Bank To kindle interest in economic affairs... To empower the student community... www.southindianbank.com Student s corner ho2099@sib.co.in

IMPACT OF GOODS AND SERVICE TAX (GST)

") 244 Journal of Management and Science ISSN: 2249-1260 e-issn: 2250-1819 Special Issue. No.1 Sep 17 IMPACT OF GOODS AND SERVICE TAX (GST) Mrs. M.Shanthini Devi Assistant professor Department of Commerce

244 Journal of Management and Science ISSN: 2249-1260 e-issn: 2250-1819 Special Issue. No.1 Sep 17 IMPACT OF GOODS AND SERVICE TAX (GST) Mrs. M.Shanthini Devi Assistant professor Department of Commerce

TITLE: GST LAW: AN EXECUTIVE SUMMARY

Pramod Kumar Rai, Advocate Managing Partner B.Tech (IITKanpur), LLB (Gold Medal), LLM (USA) Former Joint Commissioner of Customs, Excise & Service Tax (IRS). Email: pramodrai@ymail.com, pramod@athenalawassociates.com

Pramod Kumar Rai, Advocate Managing Partner B.Tech (IITKanpur), LLB (Gold Medal), LLM (USA) Former Joint Commissioner of Customs, Excise & Service Tax (IRS). Email: pramodrai@ymail.com, pramod@athenalawassociates.com

COMPONENTS OF GST GST. IGST (Interstate and Imports) CGST (Intrastate) SGST (Intrastate)

CGST (Intrastate) SGST (Intrastate)") WHAT IS GST Largest tax reform in the Indirect Taxation regime. PAN Based Registration Levied on supply of goods or services. Supply includes Stock Transfer. Supply being the Taxable Event, the concept

WHAT IS GST Largest tax reform in the Indirect Taxation regime. PAN Based Registration Levied on supply of goods or services. Supply includes Stock Transfer. Supply being the Taxable Event, the concept

C. B. Thakar, Advocate

Refresher Course on GST by WIRC 26 th June,2017 Basic Concepts of GST Presentation by C. B. Thakar, Advocate B.Com., F.C.A., LLB C. B. THAKAR, Advocate 1 Journey towards GST 122 nd CAB Approved by Lok

Refresher Course on GST by WIRC 26 th June,2017 Basic Concepts of GST Presentation by C. B. Thakar, Advocate B.Com., F.C.A., LLB C. B. THAKAR, Advocate 1 Journey towards GST 122 nd CAB Approved by Lok

Goods and Services Tax

Goods and Services Tax Overview and Impact Analysis CA Neeraj Menon THE PROPOSED GST FRAMEWORK IN INDIA Dual-GST Centre and States to levy GST on common base (CGST & SGST) Salient features IGST on interstate

Goods and Services Tax Overview and Impact Analysis CA Neeraj Menon THE PROPOSED GST FRAMEWORK IN INDIA Dual-GST Centre and States to levy GST on common base (CGST & SGST) Salient features IGST on interstate

GST- A NEW BEGINNING IN INDIAN FINANCIAL SYSTEM

GST- A NEW BEGINNING IN INDIAN FINANCIAL SYSTEM Dr. Anita Sharma, Reader, Maharaja Surajmal Institute (GGSIPU), New Delhi Abstract: GST means Goods and Services Tax. The main aim of GST is to abolish all

GST- A NEW BEGINNING IN INDIAN FINANCIAL SYSTEM Dr. Anita Sharma, Reader, Maharaja Surajmal Institute (GGSIPU), New Delhi Abstract: GST means Goods and Services Tax. The main aim of GST is to abolish all

BRIEF ON GST. GST is a destination based tax and levied at a single point at the time of consumption of goods or services by the ultimate consumer.

BRIEF ON GST GST is a destination based tax and levied at a single point at the time of consumption of goods or services by the ultimate consumer. GST will be levied on all goods and services except on

BRIEF ON GST GST is a destination based tax and levied at a single point at the time of consumption of goods or services by the ultimate consumer. GST will be levied on all goods and services except on

Goods & Service Tax. (GST) BBNL Vendor MEET

BBNL Vendor MEET") Goods & Service Tax (GST) BBNL Vendor MEET 28.6.2017 1 Overview GST In short How to Charge Tax Changes Now Tax on both goods and services when supplied Replacing - Central Excise, Service Tax, VAT, Entry

Goods & Service Tax (GST) BBNL Vendor MEET 28.6.2017 1 Overview GST In short How to Charge Tax Changes Now Tax on both goods and services when supplied Replacing - Central Excise, Service Tax, VAT, Entry

Introduction to Goods and Services Tax (GST)

") Introduction to Goods and Services Tax (GST) CHAPTER 2 GST is the most ambitious and remarkable indirect tax reform in India s post-independence history. Its objective is to levy a single national uniform

Introduction to Goods and Services Tax (GST) CHAPTER 2 GST is the most ambitious and remarkable indirect tax reform in India s post-independence history. Its objective is to levy a single national uniform

Goods & Services Tax (GST) One Nation One Tax

One Nation One Tax") Goods & Services Tax (GST) One Nation One Tax Why In News: After being subject to years of haggling and histrionics, the Goods & Services Tax (GST) finally had its historic day in the Parliament with the

Goods & Services Tax (GST) One Nation One Tax Why In News: After being subject to years of haggling and histrionics, the Goods & Services Tax (GST) finally had its historic day in the Parliament with the

REGISTRATION & RETURN PROCESS UNDER GOODS AND SERVICES TAX (GST) By CA Sandip Agrawal Sandip Satyanarayan & Co Chartered Accountants

By CA Sandip Agrawal Sandip Satyanarayan & Co Chartered Accountants") REGISTRATION & RETURN PROCESS UNDER GOODS AND SERVICES TAX (GST) By BRIEF INTRODUCTION TO GST GST is a Tax on Goods and services and it is proposed to be a comprehensive indirect tax levy on manufacture,

REGISTRATION & RETURN PROCESS UNDER GOODS AND SERVICES TAX (GST) By BRIEF INTRODUCTION TO GST GST is a Tax on Goods and services and it is proposed to be a comprehensive indirect tax levy on manufacture,

GST Implications. All India Distillers Association Hotel Crowne Plaza February 23, Discussion by: CA Gaurav Gupta

GST Implications All India Distillers Association Hotel Crowne Plaza February 23, 2017 Discussion by: CA Gaurav Gupta FCA, LLB, DISA Author GST Law & Practise - Service Tax Law & Practise Agenda GST exclusion

GST Implications All India Distillers Association Hotel Crowne Plaza February 23, 2017 Discussion by: CA Gaurav Gupta FCA, LLB, DISA Author GST Law & Practise - Service Tax Law & Practise Agenda GST exclusion

VAT CONCEPT AND ITS APPLICATION IN GST

CONTENTS DIVISION 1 INPUT TAX CREDIT 1 VAT CONCEPT AND ITS APPLICATION IN GST 1.1 Background of VAT 3 1.2 Basic Concept of VAT 4 1.2-1 VAT to avoid the cascading effect 5 1.2-2 Input Tax credit system

CONTENTS DIVISION 1 INPUT TAX CREDIT 1 VAT CONCEPT AND ITS APPLICATION IN GST 1.1 Background of VAT 3 1.2 Basic Concept of VAT 4 1.2-1 VAT to avoid the cascading effect 5 1.2-2 Input Tax credit system

INTRODUCTION TO GST. 1.1 constitutional framework of taxes before gst

1 C H A P T E R INTRODUCTION TO GST LEARNING OBJECTIVES 1.1 Constitutional Framework of Taxes Before GST 1.2 Defects in structure of indirect taxes before GST 1.3 Rationale for GST 1.4 Features and Structure

1 C H A P T E R INTRODUCTION TO GST LEARNING OBJECTIVES 1.1 Constitutional Framework of Taxes Before GST 1.2 Defects in structure of indirect taxes before GST 1.3 Rationale for GST 1.4 Features and Structure

GST Tax of 21 st Century. V S Datey Website

GST Tax of 21 st Century V S Datey dateyvs@yahoo.com Website http://www.dateyvs.com Welcome Background of Indirect Taxes Present structure of indirect taxes is based on Constitutional Provisions giving

GST Tax of 21 st Century V S Datey dateyvs@yahoo.com Website http://www.dateyvs.com Welcome Background of Indirect Taxes Present structure of indirect taxes is based on Constitutional Provisions giving

An Overview of Indirect Taxes. By PROF V.N. PARTHIBAN, FICWA, ACS, FIII, ASM, ADIM, MBA, LLM

An Overview of Indirect Taxes By PROF V.N. PARTHIBAN, FICWA, ACS, FIII, ASM, ADIM, MBA, LLM Customs Duty Basic Customs Duty :Levied under Customs Act, 1962 on : Imported goods: (means any goods brought

An Overview of Indirect Taxes By PROF V.N. PARTHIBAN, FICWA, ACS, FIII, ASM, ADIM, MBA, LLM Customs Duty Basic Customs Duty :Levied under Customs Act, 1962 on : Imported goods: (means any goods brought

Taxation principles of GST and experience of present law as relevant to GST

Taxation principles of GST and experience of present law as relevant to GST Outline of discussion General Taxation principles Indian indirect Tax system Road to GST Introduction of GST Benefits of GST

Taxation principles of GST and experience of present law as relevant to GST Outline of discussion General Taxation principles Indian indirect Tax system Road to GST Introduction of GST Benefits of GST

A Note on GST. 1. GST (Goods & Services Tax) is a single tax on the supply of goods and services, right

is a single tax on the supply of goods and services, right") A Note on GST 1. GST (Goods & Services Tax) is a single tax on the supply of goods and services, right from the manufacturer to the consumer. The final consumer will thus bear only the GST charged by the

A Note on GST 1. GST (Goods & Services Tax) is a single tax on the supply of goods and services, right from the manufacturer to the consumer. The final consumer will thus bear only the GST charged by the

SALIENT FEATURES OF PROPOSED GST

SALIENT FEATURES OF PROPOSED GST GST is a consumption based levy. Destination principle would be applicable in normal course of business to business [B2B] other than for few services and business to consumer.[

SALIENT FEATURES OF PROPOSED GST GST is a consumption based levy. Destination principle would be applicable in normal course of business to business [B2B] other than for few services and business to consumer.[

Goods and Services Tax A benchmark transformation from present tax regime to the unified tax framework

Goods and Services Tax A benchmark transformation from present tax regime to the unified tax framework Edition 2 September 15, 2016 Introduction GST Regime The much-awaited GST now becomes a law with President

Goods and Services Tax A benchmark transformation from present tax regime to the unified tax framework Edition 2 September 15, 2016 Introduction GST Regime The much-awaited GST now becomes a law with President

GOODS AND SERVICE TAX (GST) AND ITS IMPACT

AND ITS IMPACT") 104 Journal of Management and Science ISSN: 2249-1260 e-issn: 2250-1819 Special Issue. No.1 Sep 17 GOODS AND SERVICE TAX (GST) AND ITS IMPACT P.KANAGARAJ Assistant Professor in Commerce Department of Commerce

104 Journal of Management and Science ISSN: 2249-1260 e-issn: 2250-1819 Special Issue. No.1 Sep 17 GOODS AND SERVICE TAX (GST) AND ITS IMPACT P.KANAGARAJ Assistant Professor in Commerce Department of Commerce

GST Overview. ~CA Unmesh G. Patwardhan~ Mobile No Unmesh Patwardhan Mobile No

GST Overview ~CA Unmesh G. Patwardhan~ Mobile No.98224 24968 Unmesh Patwardhan Mobile No.98224 24968 1 Brief History & Concept of GST Unmesh Patwardhan Mobile No.98224 24968 2 1 st Jul 2017 The D Day Journey

GST Overview ~CA Unmesh G. Patwardhan~ Mobile No.98224 24968 Unmesh Patwardhan Mobile No.98224 24968 1 Brief History & Concept of GST Unmesh Patwardhan Mobile No.98224 24968 2 1 st Jul 2017 The D Day Journey

CENTRAL BOARD OF EXCISE & CUSTOMS

CENTRAL BOARD OF EXCISE & CUSTOMS GST (Goods and Services Tax) www.cbec.gov.in www.aces.gov.in CENTRAL BOARD OF EXCISE & CUSTOMS Concept of GST Registration g ITC Return PRESENTATION PLAN www.cbec.gov.in

CENTRAL BOARD OF EXCISE & CUSTOMS GST (Goods and Services Tax) www.cbec.gov.in www.aces.gov.in CENTRAL BOARD OF EXCISE & CUSTOMS Concept of GST Registration g ITC Return PRESENTATION PLAN www.cbec.gov.in

Indirect Taxes Committee, ICAI

1 GST Constitutional Provisions and Features of Constitution (101 st Amendment) Act, 2016 101st Constitution Amendment Act 2 Under current regime - Centre levies Excise duty on manufacture, Service tax

1 GST Constitutional Provisions and Features of Constitution (101 st Amendment) Act, 2016 101st Constitution Amendment Act 2 Under current regime - Centre levies Excise duty on manufacture, Service tax

IMPACTS OF GST ON INDIAN ECONOMY. Mrs.D.Sivasakthi Assistant Professor: B.Com (PA) Dr. N.G.P. Arts and science college (Autonomous) Coimbatore

Dr. N.G.P. Arts and science college (Autonomous) Coimbatore") 141 Journal of Management and Science ISSN: 2249-1260 e-issn: 2250-1819 Special Issue. No.1 Sep 17 IMPACTS OF GST ON INDIAN ECONOMY Mrs.D.Sivasakthi Assistant Professor: B.Com (PA) Dr. N.G.P. Arts and

141 Journal of Management and Science ISSN: 2249-1260 e-issn: 2250-1819 Special Issue. No.1 Sep 17 IMPACTS OF GST ON INDIAN ECONOMY Mrs.D.Sivasakthi Assistant Professor: B.Com (PA) Dr. N.G.P. Arts and

OVERVIEW OF GST. Knowledge update. 29 th August Introduction

29 th August 2016 Knowledge update OVERVIEW OF GST Introduction The existing indirect tax regime in India carries some inherent shortcomings which not only results in instances of double taxation, but

29 th August 2016 Knowledge update OVERVIEW OF GST Introduction The existing indirect tax regime in India carries some inherent shortcomings which not only results in instances of double taxation, but

GOODS AND SERVICE TAX IN INDIA PROBLEMS AND PROSPECTS

82 Journal of Management and Science ISSN: 2249-1260 e-issn: 2250-1819 Special Issue. No.1 Sep 17 GOODS AND SERVICE TAX IN INDIA PROBLEMS AND PROSPECTS DR.T.DURAIPANDI Assistant Professor Department of

82 Journal of Management and Science ISSN: 2249-1260 e-issn: 2250-1819 Special Issue. No.1 Sep 17 GOODS AND SERVICE TAX IN INDIA PROBLEMS AND PROSPECTS DR.T.DURAIPANDI Assistant Professor Department of

Transitional Provisions

FAQ s Migration of Existing Tax Payers (Section 139) Similar provisions have been specified in the UTGST Act, 2017 Chapter XVIII Transitional Provisions Q1. What is the primary condition for provisional

FAQ s Migration of Existing Tax Payers (Section 139) Similar provisions have been specified in the UTGST Act, 2017 Chapter XVIII Transitional Provisions Q1. What is the primary condition for provisional

Basics of GST. Ganesh Pathuri

Basics of GST Ganesh Pathuri Background of Indian GST The Constitution (115th Amendment) Bill, 2011 The Constitution (122nd Amendment) Bill, 2014 Introduced in Lok Sabha on December 19, 2014. It was passed

Basics of GST Ganesh Pathuri Background of Indian GST The Constitution (115th Amendment) Bill, 2011 The Constitution (122nd Amendment) Bill, 2014 Introduced in Lok Sabha on December 19, 2014. It was passed

GST & YOU. Tally Solutions Pvt. Ltd. All Rights Reserved 2. Tally Solutions Pvt. Ltd. All Rights Reserved Business Presentation

WELCOME 1 GST & YOU Tally Solutions Pvt. Ltd. All Rights Reserved 2 Tally Solutions Pvt. Ltd. All Rights Reserved Business Presentation Presentation Agenda GST Basics What is GST Why GST GST concepts How

WELCOME 1 GST & YOU Tally Solutions Pvt. Ltd. All Rights Reserved 2 Tally Solutions Pvt. Ltd. All Rights Reserved Business Presentation Presentation Agenda GST Basics What is GST Why GST GST concepts How

The study of conversion of Indirect Taxes into GST in India

International Journal of Management, IT & Engineering Vol. 7 Issue 5, May 2017, ISSN: 2249-0558 Impact Factor: 7.119 Journal Homepage: Double-Blind Peer Reviewed Refereed Open Access International Journal

International Journal of Management, IT & Engineering Vol. 7 Issue 5, May 2017, ISSN: 2249-0558 Impact Factor: 7.119 Journal Homepage: Double-Blind Peer Reviewed Refereed Open Access International Journal

By: CA Sunnay Jariwala

By: CA Sunnay Jariwala Existing Indirect Tax Structure Source: cbec.gov.in What is Goods and Services Tax? Article 366 (12A) Tax on supply of goods or services or both. Except on supply of alcoholic liquor

By: CA Sunnay Jariwala Existing Indirect Tax Structure Source: cbec.gov.in What is Goods and Services Tax? Article 366 (12A) Tax on supply of goods or services or both. Except on supply of alcoholic liquor

GST - AN OVERVIEW I-5

Contents 1 GST - AN OVERVIEW 1.1 What is Goods and Services Tax? 1 1.1-1 Broad definition of service 3 1.1-2 Dual GST for supply of goods and services within State 3 1.1-3 IGST for inter-state transactions

Contents 1 GST - AN OVERVIEW 1.1 What is Goods and Services Tax? 1 1.1-1 Broad definition of service 3 1.1-2 Dual GST for supply of goods and services within State 3 1.1-3 IGST for inter-state transactions

GST - AN OVERVIEW I-5

Contents 1 GST - AN OVERVIEW 1.1 What is Goods and Services Tax? 1 1.1-1 Amendments made to GST Acts vide Amendment Act, 2018 3 1.1-2 Broad definition of service 6 1.1-3 Dual GST for supply of goods and

Contents 1 GST - AN OVERVIEW 1.1 What is Goods and Services Tax? 1 1.1-1 Amendments made to GST Acts vide Amendment Act, 2018 3 1.1-2 Broad definition of service 6 1.1-3 Dual GST for supply of goods and

GST with multiple tax rates boon or bane?

GST with multiple tax rates boon or bane? By Kishan Pandey From City Academy of Law College Introduction:- GST is a very important tool for the purpose of tax collection because it is a very dynamic concept

GST with multiple tax rates boon or bane? By Kishan Pandey From City Academy of Law College Introduction:- GST is a very important tool for the purpose of tax collection because it is a very dynamic concept

INTRODUCTION TO GST & CONSTITUTIONAL PROVISIONS

INTRODUCTION TO GST & CONSTITUTIONAL PROVISIONS Discussing the concept of GST and the basis of its levy - By Prakhar Jain HISTORY OF GST IN INDIA Idea of a national GST was first brought about by Kelkar

INTRODUCTION TO GST & CONSTITUTIONAL PROVISIONS Discussing the concept of GST and the basis of its levy - By Prakhar Jain HISTORY OF GST IN INDIA Idea of a national GST was first brought about by Kelkar

GST AND ITS IMPACT ON VARIOUS SECTOR

65 Journal of Management and Science ISSN: 2249-1260 e-issn: 2250-1819 Special Issue. No.1 Sep 17 GST AND ITS IMPACT ON VARIOUS SECTOR Ms.N.Ramya Assistant Professor, Department of Commerce with Professional

65 Journal of Management and Science ISSN: 2249-1260 e-issn: 2250-1819 Special Issue. No.1 Sep 17 GST AND ITS IMPACT ON VARIOUS SECTOR Ms.N.Ramya Assistant Professor, Department of Commerce with Professional

Air India. June Page 1

Air India June 2017 Page 1 Contents GST Overview Comparative tax scenarios: Current vs. GST Credit Mechanism Concept of Place & Time of Supply Valuation under GST Compliances under GST Page 2 Overview

Air India June 2017 Page 1 Contents GST Overview Comparative tax scenarios: Current vs. GST Credit Mechanism Concept of Place & Time of Supply Valuation under GST Compliances under GST Page 2 Overview

GST. The New Fiscal Baby

GST The New Fiscal Baby GST A Major Reform in Indirect Taxation post Indian Independence INDIRECT TAXATION PARENT ACTS Central Excise & Salt Act, 1944 Central Excise Tariff Act, 1975 Customs Act, 1962

GST The New Fiscal Baby GST A Major Reform in Indirect Taxation post Indian Independence INDIRECT TAXATION PARENT ACTS Central Excise & Salt Act, 1944 Central Excise Tariff Act, 1975 Customs Act, 1962

THE GOODS AND SERVICES TAX (GST) IN INDIA: CONCEPTUAL FRAMEWORK AND CHALLENGES

IN INDIA: CONCEPTUAL FRAMEWORK AND CHALLENGES") Inspira-Journal of Commerce, Economics & Computer Science (JCECS) 273 ISSN : 2395-7069 General Impact Factor : 2.4668, Volume 04, No. 01, January-March, 2018, pp. 273-280 THE GOODS AND SERVICES TAX (GST)

Inspira-Journal of Commerce, Economics & Computer Science (JCECS) 273 ISSN : 2395-7069 General Impact Factor : 2.4668, Volume 04, No. 01, January-March, 2018, pp. 273-280 THE GOODS AND SERVICES TAX (GST)

OVERVIEW OF GOODS & SERVICES TAX (GST) CA. JINIT R SHAH GMJ & Co. J.B. Nagar CPE Study Circle of WIRC 18 th October, 2015

CA. JINIT R SHAH GMJ & Co. J.B. Nagar CPE Study Circle of WIRC 18 th October, 2015") OVERVIEW OF GOODS & SERVICES TAX (GST) CA. JINIT R SHAH GMJ & Co J.B. Nagar CPE Study Circle of WIRC 18 th October, 2015 GST Biggest Tax Reform JOURNEY OF GST IN INDIA UPTO 2014 S. N. Event Year 1 Announcement

OVERVIEW OF GOODS & SERVICES TAX (GST) CA. JINIT R SHAH GMJ & Co J.B. Nagar CPE Study Circle of WIRC 18 th October, 2015 GST Biggest Tax Reform JOURNEY OF GST IN INDIA UPTO 2014 S. N. Event Year 1 Announcement

GOODS AND SERVICES TAX

GOODS AND SERVICES TAX GOODS AND SERVICES TAX - AN INTRODUCTION Introduction to Goods and Services Tax GST and Centre-State Financial Relations Constitution (One Hundred and First) Amendment Act, 2016

GOODS AND SERVICES TAX GOODS AND SERVICES TAX - AN INTRODUCTION Introduction to Goods and Services Tax GST and Centre-State Financial Relations Constitution (One Hundred and First) Amendment Act, 2016

A Peek into GST... GST is commonly known as Destination based tax on consumption of goods and services.

Kharabanda Associates, Chartered Accountants A Peek into GST... Volume 1, Issue 1 Date : January 20, 2017 Inside this Issue : GST Demystified 2 Input tax credit, Supply & Liability GST Trend, VAT & Valuation

Kharabanda Associates, Chartered Accountants A Peek into GST... Volume 1, Issue 1 Date : January 20, 2017 Inside this Issue : GST Demystified 2 Input tax credit, Supply & Liability GST Trend, VAT & Valuation

VALUATION OF TAXABLE SUPPLY UNDER REVISED GST LAW & VALUATION RULES UNDER DRAFT MODEL GST LAW FEW THOUGHTS. Indirect Taxes Committee, ICAI

VALUATION OF TAXABLE SUPPLY UNDER REVISED GST LAW & VALUATION RULES UNDER DRAFT MODEL GST LAW FEW THOUGHTS Indirect Taxes Committee, ICAI 1 VALUE OF TAXABLE SUPPLY Sec 15 For any levy / tax, apart from

VALUATION OF TAXABLE SUPPLY UNDER REVISED GST LAW & VALUATION RULES UNDER DRAFT MODEL GST LAW FEW THOUGHTS Indirect Taxes Committee, ICAI 1 VALUE OF TAXABLE SUPPLY Sec 15 For any levy / tax, apart from

S. No. Questions / Tweets Received Replies Registration 1. Does aggregate turnover include value of inward supplies Refer Section 2(6) of CGST Act.

of CGST Act.") S. No. Questions / Tweets Received Replies Registration 1. Does aggregate turnover include value of inward supplies Refer Section 2(6) of CGST Act. received on which RCM is payable? Aggregate turnover

S. No. Questions / Tweets Received Replies Registration 1. Does aggregate turnover include value of inward supplies Refer Section 2(6) of CGST Act. received on which RCM is payable? Aggregate turnover

Most Expected Questions of GST CS EXECUTIVE (JUNE, 2018 STUDENTS) By

By") Most Expected Questions of GST CS EXECUTIVE (JUNE, 2018 STUDENTS) By CA Vivek Gaba 1. GST was first levied by? a) France in 1954 b) USA in 1985 c) India in 2017 d) U.K in 1970 2. Which of the following

Most Expected Questions of GST CS EXECUTIVE (JUNE, 2018 STUDENTS) By CA Vivek Gaba 1. GST was first levied by? a) France in 1954 b) USA in 1985 c) India in 2017 d) U.K in 1970 2. Which of the following

Impact of GST on various sectors

of GST on various sectors S. Thirumalai November 2016 Overview of GST implications Service Provider Output Service Procurements Service tax Present regime rate is 15% GST regime - rate in the range of

of GST on various sectors S. Thirumalai November 2016 Overview of GST implications Service Provider Output Service Procurements Service tax Present regime rate is 15% GST regime - rate in the range of

Presentation by CA RITESH MEHTA, NAGPUR. B. Com., F.C.A., D.I.S.A (ICAI).

.") Presentation by CA RITESH MEHTA, NAGPUR B. Com., F.C.A., D.I.S.A (ICAI). 1 Overview of GST Law Components of GST law Levy under GST Taxable event under GST Meaning & scope of the term Supply and its Implications

Presentation by CA RITESH MEHTA, NAGPUR B. Com., F.C.A., D.I.S.A (ICAI). 1 Overview of GST Law Components of GST law Levy under GST Taxable event under GST Meaning & scope of the term Supply and its Implications

MODEL GST LAW Decoding The Regulation. Khandhar Mehta & Shah

MODEL GST LAW Decoding The Regulation Khandhar Mehta & Shah 1 CONTENTS BASICS OF GST LEVY IN GST REGIME TIME AND PLACE OF SUPPLY GST VALUATION RULES INPUT TAX CREDIT (ITC) TAX ADMINISTRATION SECTOR-SPECIFIC

MODEL GST LAW Decoding The Regulation Khandhar Mehta & Shah 1 CONTENTS BASICS OF GST LEVY IN GST REGIME TIME AND PLACE OF SUPPLY GST VALUATION RULES INPUT TAX CREDIT (ITC) TAX ADMINISTRATION SECTOR-SPECIFIC

The Empowered Committee of State Finance Ministers have worked out a dual GST model for India. In

GST is proposed to be a comprehensive indirect tax levy on manufacture, sale and consumption of goods as well as on the services at a national level. In an utopian situation, the tax has to be a singular

GST is proposed to be a comprehensive indirect tax levy on manufacture, sale and consumption of goods as well as on the services at a national level. In an utopian situation, the tax has to be a singular

COVER STORY A to Z of Goods and Services Tax

COVER STORY A to Z of Goods and Services Tax The Goods and Services Tax (GST), the biggest reform in India s indirect tax structure since the economy began to be opened up 25 years ago, at last became

COVER STORY A to Z of Goods and Services Tax The Goods and Services Tax (GST), the biggest reform in India s indirect tax structure since the economy began to be opened up 25 years ago, at last became

Offences & Penalties, Search, Seizure, Arrest, Demand and Recovery under GST Laws

E-Book on Offences & Penalties, Search, Seizure, Arrest, Demand and Recovery under GST Laws Written By Anand Singh IRS Retd. Additional Commissioner (Customs) New Delhi, India Buyer of This E-Book Will

E-Book on Offences & Penalties, Search, Seizure, Arrest, Demand and Recovery under GST Laws Written By Anand Singh IRS Retd. Additional Commissioner (Customs) New Delhi, India Buyer of This E-Book Will

BACKGROUND OF GST. As per Statement of Objects and Reasons appended to the Constitutional Amendment bill the object of GST is :

BACKGROUND OF GST INTRODUCTION The introduction of Goods and Services Tax (GST) is a very significant step in the field of indirect tax reforms in India. In the pre GST regime, there was multiplicity of

BACKGROUND OF GST INTRODUCTION The introduction of Goods and Services Tax (GST) is a very significant step in the field of indirect tax reforms in India. In the pre GST regime, there was multiplicity of

Tweet FAQs. The tweets received by askgst_goi handle were scrutinized and developed into a short FAQ of 100 tweets.

Tweet FAQs The tweets received by askgst_goi handle were scrutinized and developed into a short FAQ of 100 tweets. S. No. Questions / Tweets Received Replies Registration 1. Does aggregate turnover include

Tweet FAQs The tweets received by askgst_goi handle were scrutinized and developed into a short FAQ of 100 tweets. S. No. Questions / Tweets Received Replies Registration 1. Does aggregate turnover include

Updates on GST GST Hope For Betterment Released.. For ICMAI Members Here Today

Updates on GST GST Hope For Betterment Released.. For ICMAI Members Here Today WELCOME DELEGATES Humble Request : Silence Please and Urgent Calls Only CMA Dr. Pawan Jaiswal Special Invited Member on GST

Updates on GST GST Hope For Betterment Released.. For ICMAI Members Here Today WELCOME DELEGATES Humble Request : Silence Please and Urgent Calls Only CMA Dr. Pawan Jaiswal Special Invited Member on GST

GOODS AND SERVICES TAX (COMPENSATION TO THE STATES FOR LOSS OF REVENUE) BILL, 2016

BILL, 2016") GOODS AND SERVICES TAX (COMPENSATION TO THE STATES FOR LOSS OF REVENUE) BILL, 2016 (No. of 2016) [ th, 2016] A Bill to provide for compensation to the States for loss of revenue arising on account of implementation

GOODS AND SERVICES TAX (COMPENSATION TO THE STATES FOR LOSS OF REVENUE) BILL, 2016 (No. of 2016) [ th, 2016] A Bill to provide for compensation to the States for loss of revenue arising on account of implementation

Goods and Services Tax Users Manual

E-Book on Goods and Services Tax Users Manual Written By Anand Singh IRS Retd. Additional Commissioner (Customs) New Delhi, India Email: easylawmatebooks@gmail.com All Rights Reserved. Copyright 2017 by

E-Book on Goods and Services Tax Users Manual Written By Anand Singh IRS Retd. Additional Commissioner (Customs) New Delhi, India Email: easylawmatebooks@gmail.com All Rights Reserved. Copyright 2017 by

Goods and Services Tax (GST): An Overview

: An Overview") Goods and Services Tax (GST): An Overview I. Introduction Introduction of GST would be a significant step in the field of indirect tax reforms in India. By amalgamating a large number of Central and State

Goods and Services Tax (GST): An Overview I. Introduction Introduction of GST would be a significant step in the field of indirect tax reforms in India. By amalgamating a large number of Central and State

FAQs. Yes. He is liable for registration as he is engaged in Inter State supplies.

FAQs 1. A registered person s business is in many states. All supplies are below 10 lakhs. He makes an Inter State supply from one state. Is he liable for registration? Yes. He is liable for registration

FAQs 1. A registered person s business is in many states. All supplies are below 10 lakhs. He makes an Inter State supply from one state. Is he liable for registration? Yes. He is liable for registration

GST & Constitutional Amendment

GST & Constitutional Amendment S M Sinha Addl.Commissioner, Commercial Tax (Retd.) Lucknow, UP The proposed 122 nd Constitutional Amendment to the Constitution has paved the way for introduction of GST

GST & Constitutional Amendment S M Sinha Addl.Commissioner, Commercial Tax (Retd.) Lucknow, UP The proposed 122 nd Constitutional Amendment to the Constitution has paved the way for introduction of GST

GST: Frequently Asked Questions(FAQs) for Traders

for Traders") GST: Frequently Asked Questions(FAQs) for Traders Q 1. How will GST benefit the Trading Community? Under GST, a trader would be entitled to avail input tax credit paid on their domestic procurements of

GST: Frequently Asked Questions(FAQs) for Traders Q 1. How will GST benefit the Trading Community? Under GST, a trader would be entitled to avail input tax credit paid on their domestic procurements of

Overview of Goods and Services Tax. Prashant Deshpande 31st July 2015 WIRC

Overview of Goods and Services Tax Prashant Deshpande 31st July 2015 WIRC 1 Contents Setting the Context Potential Implications Key Considerations Proactive Approach to GST Questions 2015 Deloitte Touché

Overview of Goods and Services Tax Prashant Deshpande 31st July 2015 WIRC 1 Contents Setting the Context Potential Implications Key Considerations Proactive Approach to GST Questions 2015 Deloitte Touché

Goods and Services Tax in India

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668 PP 32-36 www.iosrjournals.org Dr. Savitha. P Dept of Management, KSOU, Mukthagangothri, Mysuru 06. Abstract: GST

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668 PP 32-36 www.iosrjournals.org Dr. Savitha. P Dept of Management, KSOU, Mukthagangothri, Mysuru 06. Abstract: GST

THE CONSTITUTION (ONE HUNDRED AND FIFTEENTH AMENDMENT) BILL, 2011

BILL, 2011") Bill No. 22 of 2011 5 THE CONSTITUTION (ONE HUNDRED AND FIFTEENTH AMENDMENT) BILL, 2011 A BILL further to amend the Constitution of India. BE it enacted by Parliament in the Sixty-second Year of the Republic

Bill No. 22 of 2011 5 THE CONSTITUTION (ONE HUNDRED AND FIFTEENTH AMENDMENT) BILL, 2011 A BILL further to amend the Constitution of India. BE it enacted by Parliament in the Sixty-second Year of the Republic

The Proposed GST (Goods and Services Tax) and Indian Economy

and Indian Economy") The Proposed GST (Goods and Services Tax) and Indian Economy Bikram Pegu Research scholar,department of Economics, Gauhati University Assam, India ABSTRACT : The GST (GOODS AND SERVICES TAX) is defined

The Proposed GST (Goods and Services Tax) and Indian Economy Bikram Pegu Research scholar,department of Economics, Gauhati University Assam, India ABSTRACT : The GST (GOODS AND SERVICES TAX) is defined

GOODS AND SERVICE TAX (GST) CONCEPT. Introduction:

CONCEPT. Introduction:") GOODS AND SERVICE TAX (GST) CONCEPT Introduction: The introduction of Goods and Services Tax (GST) would be a very significant step in the field of indirect tax reforms in India. By amalgamating a large

GOODS AND SERVICE TAX (GST) CONCEPT Introduction: The introduction of Goods and Services Tax (GST) would be a very significant step in the field of indirect tax reforms in India. By amalgamating a large

Goods and Services Tax (GST) M.R.Narain & Co., Chartered Accountants 1

M.R.Narain & Co., Chartered Accountants 1") Goods and Services Tax (GST) 1 How GST Works Following are the Important Features of GST 1. Tax on Supply of Goods and Service (Except Alcoholic Liquor) 2. Multistage Tax 3. Tax on Value Added 4. Destination/Consumption

Goods and Services Tax (GST) 1 How GST Works Following are the Important Features of GST 1. Tax on Supply of Goods and Service (Except Alcoholic Liquor) 2. Multistage Tax 3. Tax on Value Added 4. Destination/Consumption

Will the impact of GST benefit to our economy?

Will the impact of GST benefit to our economy? Jaseena K B M. Phil.Scholar Sree Narayana GuruCollege Chavadi, Coimbatore, Tamilnadu S Reena Assistant Professor of Commerce Sree Narayana Guru College Chavadi,

Will the impact of GST benefit to our economy? Jaseena K B M. Phil.Scholar Sree Narayana GuruCollege Chavadi, Coimbatore, Tamilnadu S Reena Assistant Professor of Commerce Sree Narayana Guru College Chavadi,