CHAPTER 2. GST Acts : CGST ACT, SGST ACT (KARNATAKA STATE) IGST ACT

|

|

|

- Gervase Gregory

- 5 years ago

- Views:

Transcription

1 CHAPTER 2 GST Acts : CGST ACT, SGST ACT (KARNATAKA STATE) IGST ACT

2

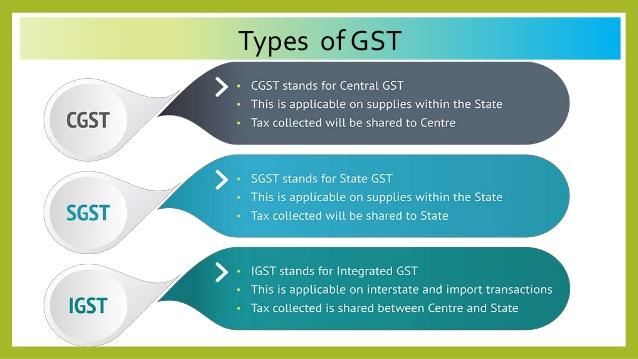

3 SALIENT FEATURES OF CGST ACT, A state-wise single registration for a taxpayer for filing returns, paying taxes, and to fulfil other compliance requirements. 2. Most of the compliance requirements would be fulfilled online. 3. A taxpayer has to file one single return state-wise to report all his supplies, whether made within or outside the state or exported out of the country and pay the applicable taxes on them. 4. A business entity with an annual turnover of upto Rs 20 lakh would not be required to take registration in the GST regime. 5. A business entity with turnover upto Rs 50 lakh can avail the benefit of a composition scheme under which it has to pay a much lower rate of tax 6. The Composition Scheme is available for all traders, select manufacturing sectors and for restaurants in the services sector.

4 SALIENT FEATURES OF SGST ACT, 2017 Levied by the States for all the transactions of goods and services made for a consideration. State GST would be paid to the accounts of the respective State. Exceptions would be exempted goods and services, goods kept out of GST and transactions below prescribed threshold limits. Basic features of law such as chargeability, taxable event, measure, valuation, classification would be uniform across the State.

5 SALIENT FEATURES OF IGST ACT, 2017 IGST equals to CGST+SGST. IGST model that the centre will levy tax at a rate approximately equal to CGST+SGST on Inter-State supply of goods & services. It is a destination based tax and will accrue to importing state. It will lower tax burden by taxing Inter-State transaction only once. B2B transactions tax will flow to the State where Purchaser claims Input Tax Credit. B2C transactions tax will flow to the State of Consumer, otherwise tax will remain in the State of Seller.

6 ADJUDICATING AUTHORITY Adjudication is the legal process by which an judge reviews evidence and argumentation, including legal reasoning set forth by opposing parties or litigants to come to a decision which determines rights and obligations between the parties involved.

7 APPOINTMENT OF ADJUDICATING AUTHORITY 1. Central Government will appoint as many officers as Adjudicating Authorities. 2. Against whom a complaint has been made under sub-section and imposing any penalty 3. Adjudicating Authority shall hold an enquiry and complaint in writing made by any officer authorized by a general or special order by the Central Government. 4. The said person may appear either in person or take the assistance of a legal practitioner or a chartered accountant of his choice for presenting his case before the Adjudicating Authority

8 5. On the date fixed, the Adjudicating Authority shall explain to the person against his legal practitioner or the chartered accountant, as the case committed by such person indicating the provisions of the Act or of rules, regulations, notifications, direction or orders or any condition. 6. The Adjudicating Authority shall, then, given an opportunity to such person to produce such documents or evidence as he may consider relevant to the inquiry. 7. Every Adjudicating Authority shall have the same powers of a civil court. 8. Every Adjudicating Authority shall deal with the compliant under sub-section (2) 9. Adjudicating Authority shall record periodically.

9 ADJUDICATING AUTHORITIES, COMPOSITION, POWERS 1. The Central Government shall appoint one or more Adjudicating Authorities to exercise jurisdiction, powers. 2. An Adjudicating Authority shall consist of a Chairperson and two other Members: Provided that one Member each shall be a person having experience in the field of law, administration, finance or accountancy. 3. A person shall in the field of law, is qualified for appointment as District Judge; 4. Has been a member of the Indian Legal Service and has held a post in Grade I of that service; 5. In the field of finance, accountancy or administration.

10 6. The Central Government shall appoint a Member to be the Chairperson of the Adjudicating Authority. 7. Subject to the provisions of this Act,- 8. The jurisdiction of the Adjudicating Authority may be exercised by Benches thereof; 9. a Bench may be constituted by the Chairperson of the Adjudicating Authority with one or two Members as the Chairperson. 10. The Benches of the Adjudicating Authority shall ordinarily sit at New Delhi. 11. Chairperson may transfer a Member from one Bench to another Bench.

11 12. The Chairperson and every Member shall hold office as for a term of five years from the date on which he enters upon his office: Provided that no Chairperson or other Member shall hold office as such after he has attained the age of sixty-two years. 13. The salary and allowances payable to and the other terms and conditions of service of the Member shall be such as may be prescribed. 14. For reasons other than temporary absence, any vacancy occurs in the office of the Chairperson or any other Member, then, the Central Government shall appoint another person to fill the vacancy.

12 15. The Chairperson or any other Member shall not be removed from his office except by an order made by the Central Government. 16. If Chairperson by reason of his death, resignation the senior-most Member shall act as the Chairperson of the Adjudicating Authority until the date on which a new Chairperson 17. The senior-most Member shall discharge the functions of the Chairperson of the Adjudicating Authority until the date on which the Chairperson of the Adjudicating Authority resumes his duties. 18. Adjudicating Authority shall have powers to regulate its own procedure.

13 AGENT As per Section 2(5) the term agent means a person, including a factor, broker, commission agent, an auctioneer or any other mercantile agent, by whatever name called, who carries on the business of supply or receipt of goods or services or both on behalf of another.

14 BUSINESS 1. any trade, commerce, manufacture, profession, vocation, adventure, wager or any other similar activity. 2. supply or acquisition of goods including capital goods and services in connection with commencement or closure of business; 3. provision by a club, association, society, or any such body of the facilities or benefits to its members;

15 CAPITAL GOODS As per Section 2(19), the term capital goods means goods, the value of which is capitalised in the books of account of the person claiming the input tax credit and which are used or intended to be used in the course business.

16 CASUAL TAXABLE PERSON As per Section 2(20) the term casual taxable person means a person who occasionally undertakes transactions involving supply of goods or services or both in the course or furtherance of business, whether as principal, agent or in any other capacity, in a State or a Union territory where he has no fixed place of business.

17 COMPOSITE SUPPLY As per Section 2(30) of the Central Goods and Services Tax (CGST) Act, 2017,the term composite supply means a supply made by a taxable person, consisting of two or more taxable supplies of goods and services, which are naturally bundled and supplied in conjunction with each other in the ordinary course of business. Illustration: Where goods are packed and transported with insurance, the supply of goods, packing materials, transport and insurance is a composite supply and supply of goods is a principal supply.

18 MIXED SUPPLY Section 2(66) defines this term as mixed supply means two or more individual supplies of goods or services, or any combination thereof, made in conjunction with each other by a taxable person for a single price where such supply does not constitute a composite supply. A supply of a package consisting of canned foods, sweets, chocolates, cakes, dry fruits and fruit juices when supplied for a single price is a mixed supply. Each of these items can be supplied separately and is not dependent on any other.

19 OUTWARD SUPPLY outward supply in relation to a taxable person, means supply of goods or services or both, whether by sale, transfer, exchange, licence, rental, lease or disposal or any other mode, made or agreed to be made by such person in the course or furtherance of business;

20 PRINCIPAL SUPPLY principal supply means the supply of goods or services which constitutes the predominant element of a composite supply and to which any other supply forming part of that composite supply is ancillary;

21 SUPPLIER supplier in relation to any goods or services or both, shall mean the person supplying the said goods or services or both and shall include an agent acting as such on behalf of such supplier in relation to the goods or services or both supplied;

22 TYPES OF SUPPLIERS Manufacturers and Vendors They produce the products and present them for purchase in bulk. The products are purchased by distributors, retailers, wholesalers, resellers, etc. at cheap prices and are sold at a profit. Wholesalers and Distributors They buy in bulk from different manufacturers and vendors; and keep the merchandise in warehouses for reselling these goods to local small distributors, wholesalers and retailers.

23 Affiliate Merchants Affiliate merchants sell their products online through banner ads and website links, which are posted on the web through a chain of affiliates. Franchisors Franchisors are business owners who through an agreement and at a price allow an individual for using their name, trademark, training, business know how, etc. the individual develops his own business with the benefit of already established franchisor s business system. Importers and Exporters Such suppliers either purchase products from manufacturers in a foreign country and import them to their own country; or export products from their country to some other country.

24 Independent Crafts People They are producers of self-designed or unique products which are manufactured on a small scale. These products are usually sold directly to retailers or individual customers through agents or trade show Drop Shippers Drop shippers are in contact with one or more supply companies and deliver their products directly to the buyer after the purchase has been made.

25 INPUT SERVICE DISTRIBUTOR Input Service Distributor means an office of the supplier of goods or services or both which receives tax invoices issued under section 31 towards the receipt of input services and issues a prescribed document for the purposes of distributing the credit of central tax, State tax, integrated tax or Union territory tax paid on the said services to a supplier of taxable goods or services or both having the same Permanent Account Number as that of the said office.

26 MANUFACTURER manufacture means processing of raw material or inputs in any manner that results in emergence of a new product having a distinct name, character and use and the term manufacturer shall be construed accordingly;

27 INPUT TAX input tax in relation to a registered person, means the central tax, State tax, integrated tax or Union territory tax charged on any supply of goods or services or both made to him and includes (a) the integrated goods and services tax charged on import of goods; (b) the tax payable under the provisions of subsections.

28 INPUT TAX CREDIT input tax credit is the credit manufacturer's received for paying input taxes towards inputs used in the manufacture of products. Similarly, a dealer is entitled to input tax credit if he has purchased goods for resale.

29 PERSON (a) an individual; (b) a Hindu Undivided Family; (c) a company; (d) a firm; (e) a Limited Liability Partnership; (f) an association of persons or a body of individuals, whether incorporated or not, in India or outside India; (g) Central Government or a State Government; (h) trust; and (i) every artificial juridical person, not falling within any of the above;

30 PLACE OF BUSINESS a) a place from where the business is ordinarily carried on, and includes a warehouse, a godown or any other place where a taxable person stores his goods, supplies or receives goods or services or both. (b) a place where a taxable person maintains his books of account; (c) a place where a taxable person is engaged in business through an agent, by whatever name called;

31 REVERSE CHARGE reverse charge means the liability to pay tax by the recipient of supply of goods or services or both instead of the supplier of such goods or services or both under sub-section (3).

32 WORKS CONTRACT works contract means a contract for building, construction, completion, installation, fitting out, improvement, modification, repair, maintenance, renovation, alteration or commissioning of any immovable property wherein transfer of property in goods.

33 NON - RESIDENT PERSON / NON- RESIDENT TAXABLE PERSON As per Section 2(77) of the Central Goods and Services Tax (CGST) Act, 2017, unless the context otherwise requires, the term non-resident taxable person means any person who occasionally undertakes transactions involving supply of goods or services or both, whether as principal or agent or in any other capacity, but who has no fixed place of business or residence in India.

34 EXPORT OF GOODS The term export means sending of goods or services produced in one country to another country. The seller of such goods and services is referred to as an exporter; the foreign buyer is referred to as an importer. Supplier of service is located in India Recipient of service is located outside India. The place of supply of service is outside India.

35 INWARD SUPPLY Inward supply in relation to a person, shall mean receipt of goods or services or both whether by purchase, acquisition or any other means with or without consideration;

36 PLACE OF SUPPLY TYPES location of the recipient of services location of the supplier of services

37 GST IMPACT ON MANUFACTURING SECTOR State incentives Area based incentives Increased working capital Free supplies Discounts Valuation of self supplies MRP valuation maximum retail price Reduction of cascading taxes Reduction of classification disputes Supply chain restructuring based on economic factors Exclusion of petroleum from GST

GST Concept and Road Map... Atul Gupta

GST Concept and Road Map... Atul Gupta Goods and Service Tax What will be incidence of tax (which Activity will attract GST Definition of Supply. Schedule 1 & 2 Classification Based on HSN, A/c Code for

GST Concept and Road Map... Atul Gupta Goods and Service Tax What will be incidence of tax (which Activity will attract GST Definition of Supply. Schedule 1 & 2 Classification Based on HSN, A/c Code for

THE CENTRAL GOODS AND SERVICES TAX ACT, 2017 CHAPTER I PRELIMINARY

THE CENTRAL GOODS AND SERVICES TAX ACT, 2017 NO. 12 OF 2017 [12th April, 2017.] An Act to make a provision for levy and collection of tax on intra-state supply of goods or services or both by the Central

THE CENTRAL GOODS AND SERVICES TAX ACT, 2017 NO. 12 OF 2017 [12th April, 2017.] An Act to make a provision for levy and collection of tax on intra-state supply of goods or services or both by the Central

Preliminary and Administration

Chapter I Preliminary and Administration FAQ s Definitions (Section 2) Section 2 of the Central Goods and Services Tax Act, 2017 ( the CGST Act, 2017 or the CGST Act ) Agriculturist [Section 2(7)] Q1.

Chapter I Preliminary and Administration FAQ s Definitions (Section 2) Section 2 of the Central Goods and Services Tax Act, 2017 ( the CGST Act, 2017 or the CGST Act ) Agriculturist [Section 2(7)] Q1.

Levy and Collection of Tax

FAQ Meaning and scope of supply (Section 7) Chapter I Levy and Collection of Tax Q1. What is the scope of the term supply as defined in CGST Act, 2017? Ans. As per Sub-section (1) of Section 7, Supply

FAQ Meaning and scope of supply (Section 7) Chapter I Levy and Collection of Tax Q1. What is the scope of the term supply as defined in CGST Act, 2017? Ans. As per Sub-section (1) of Section 7, Supply

DUAL TAX METHOD IN INTRA STATE SUPPLY

DUAL TAX METHOD IN INTRA STATE SUPPLY 1 INTRA STATE SUPPLY OF GOODS-Section 8(1) of IGST Act (1) Subject to the provisions of section 10, supply of goods where the location of the supplier and the place

DUAL TAX METHOD IN INTRA STATE SUPPLY 1 INTRA STATE SUPPLY OF GOODS-Section 8(1) of IGST Act (1) Subject to the provisions of section 10, supply of goods where the location of the supplier and the place

GST- VALUE OF SUPPLY

GST- VALUE OF SUPPLY TO DISCUSS Background Current regime Concept GST regime Examples Possible / open issues BACKGROUND CHARGING SECTION Service Tax Excise Customs There shall be levied a tax (hereinafter

GST- VALUE OF SUPPLY TO DISCUSS Background Current regime Concept GST regime Examples Possible / open issues BACKGROUND CHARGING SECTION Service Tax Excise Customs There shall be levied a tax (hereinafter

GOVERNMENT OF NAGALAND. The Nagaland Goods and Services Tax Act, 2017 (Act No. 4 of 2017)

") GOVERNMENT OF NAGALAND The Nagaland Goods and Services Tax Act, 2017 (Act No. 4 of 2017) The Nagaland Goods and Services Tax Act, 2017 (Act No. 4 of 2017) An ACT to make a provision for levy and collection

GOVERNMENT OF NAGALAND The Nagaland Goods and Services Tax Act, 2017 (Act No. 4 of 2017) The Nagaland Goods and Services Tax Act, 2017 (Act No. 4 of 2017) An ACT to make a provision for levy and collection

PUNJAB VIDHAN SABHA BILL NO. 10-PLA-2017 THE PUNJAB GOODS AND SERVICES TAX BILL, 2017 BILL

PUNJAB VIDHAN SABHA BILL NO. 10-PLA-2017 THE PUNJAB GOODS AND SERVICES TAX BILL, 2017 A BILL to make a provision for levy and collection of tax on intra-state supply of goods or services or both by the

PUNJAB VIDHAN SABHA BILL NO. 10-PLA-2017 THE PUNJAB GOODS AND SERVICES TAX BILL, 2017 A BILL to make a provision for levy and collection of tax on intra-state supply of goods or services or both by the

CENTRAL GOODS AND SERVICES TAX ACT, 2017

CENTRAL GOODS AND SERVICES TAX ACT, 2017 [12 OF 2017]* An Act to make a provision for levy and collection of tax on intra-state supply of goods or services or both by the Central Government and the matters

CENTRAL GOODS AND SERVICES TAX ACT, 2017 [12 OF 2017]* An Act to make a provision for levy and collection of tax on intra-state supply of goods or services or both by the Central Government and the matters

DEPARTMENT OF LAW, JUSTICE AND LEGISLATIVE AFFARIS NOTIFICATION

PART IV] DELHI GAZETTE : EXTRAORDINARY 113 4 of 1882. DEPARTMENT OF LAW, JUSTICE AND LEGISLATIVE AFFARIS NOTIFICATION Delhi, the 14th June, 2017 No. F.14(3)/LA-2017/ cons2law / 49-58. The following Act

PART IV] DELHI GAZETTE : EXTRAORDINARY 113 4 of 1882. DEPARTMENT OF LAW, JUSTICE AND LEGISLATIVE AFFARIS NOTIFICATION Delhi, the 14th June, 2017 No. F.14(3)/LA-2017/ cons2law / 49-58. The following Act

THE Uttar Pradesh GOODS AND SERVICES TAX BILL, 2017 BILL

THE Uttar Pradesh GOODS AND SERVICES TAX BILL, 2017 A BILL to make a provision for levy and collection of tax on intra-state supply of goods or services or both by the State of Uttar Pradesh and the matters

THE Uttar Pradesh GOODS AND SERVICES TAX BILL, 2017 A BILL to make a provision for levy and collection of tax on intra-state supply of goods or services or both by the State of Uttar Pradesh and the matters

COMPONENTS OF GST GST. IGST (Interstate and Imports) CGST (Intrastate) SGST (Intrastate)

CGST (Intrastate) SGST (Intrastate)") WHAT IS GST Largest tax reform in the Indirect Taxation regime. PAN Based Registration Levied on supply of goods or services. Supply includes Stock Transfer. Supply being the Taxable Event, the concept

WHAT IS GST Largest tax reform in the Indirect Taxation regime. PAN Based Registration Levied on supply of goods or services. Supply includes Stock Transfer. Supply being the Taxable Event, the concept

Goods and Services Tax INPUT TAX CREDIT September 22, P V SRINIVASAN Corporate Advisor Mobile:

Goods and Services Tax INPUT TAX CREDIT September 22, 2016 P V SRINIVASAN Corporate Advisor Email: pvs@pvsadvisors.com Mobile: +919845057597 1 Input Tax Credit Key definitions 1. Input : S 2(54): means

Goods and Services Tax INPUT TAX CREDIT September 22, 2016 P V SRINIVASAN Corporate Advisor Email: pvs@pvsadvisors.com Mobile: +919845057597 1 Input Tax Credit Key definitions 1. Input : S 2(54): means

C. B. Thakar, Advocate

Refresher Course on GST by WIRC 26 th June,2017 Basic Concepts of GST Presentation by C. B. Thakar, Advocate B.Com., F.C.A., LLB C. B. THAKAR, Advocate 1 Journey towards GST 122 nd CAB Approved by Lok

Refresher Course on GST by WIRC 26 th June,2017 Basic Concepts of GST Presentation by C. B. Thakar, Advocate B.Com., F.C.A., LLB C. B. THAKAR, Advocate 1 Journey towards GST 122 nd CAB Approved by Lok

GST: Frequently Asked Questions(FAQs) for Traders

for Traders") GST: Frequently Asked Questions(FAQs) for Traders Q 1. How will GST benefit the Trading Community? Under GST, a trader would be entitled to avail input tax credit paid on their domestic procurements of

GST: Frequently Asked Questions(FAQs) for Traders Q 1. How will GST benefit the Trading Community? Under GST, a trader would be entitled to avail input tax credit paid on their domestic procurements of

Composition Levy Under GST- A Boon or Bane

Composition Levy Under GST- A Boon or Bane INTRODUCTION T he appointed date for Goods and Services Tax Law (GST Law or GST) role out is 1st of July, 2017. GST Law will affect, directly and indirectly,

Composition Levy Under GST- A Boon or Bane INTRODUCTION T he appointed date for Goods and Services Tax Law (GST Law or GST) role out is 1st of July, 2017. GST Law will affect, directly and indirectly,

GST IT/ITES SECTORAL SERIES CENTRAL BOARD OF EXCISE & CUSTOMS. Directorate General of Taxpayer Services. Follow

GST SECTORAL SERIES IT/ITES Directorate General of Taxpayer Services CENTRAL BOARD OF EXCISE & CUSTOMS www.cbec.gov.in FAQ: IT/ITES Question 1: Whether software is regarded as goods or services in GST?

GST SECTORAL SERIES IT/ITES Directorate General of Taxpayer Services CENTRAL BOARD OF EXCISE & CUSTOMS www.cbec.gov.in FAQ: IT/ITES Question 1: Whether software is regarded as goods or services in GST?

Activities to be treated as Neither Supply of Goods Nor a Supple of Service, Composite Supplies & Mixed Supplies, Intra-State and Inter-State Supply

1 Activities to be treated as Neither Supply of Goods Nor a Supple of Service, Composite Supplies & Mixed Supplies, Intra-State and Inter-State Supply 2 Activities to be treated as Neither Supply of Goods

1 Activities to be treated as Neither Supply of Goods Nor a Supple of Service, Composite Supplies & Mixed Supplies, Intra-State and Inter-State Supply 2 Activities to be treated as Neither Supply of Goods

Hkkx 4 ¼d½ jktlfkku jkt&i=] vizsy 28] ¼207½

![Hkkx 4 ¼d½ jktlfkku jkt&i=] vizsy 28] ¼207½](/thumbs/89/99936573.jpg "Hkkx 4 ¼d½ jktlfkku jkt&i=] vizsy 28] ¼207½") Hkkx 4 ¼d½ jktlfkku jkt&i=] vizsy 28] 2017 1¼207½ भन ज क भ य म स, प रभ ख श सन सध व LAW (LEGISLATIVE DRAFTING) DEPARTMENT (GROUP-II) NOTIFICATION Jaipur, April 28, 2017 No. F. 2 (34) Vidhi/2/2017.-In pursuance

Hkkx 4 ¼d½ jktlfkku jkt&i=] vizsy 28] 2017 1¼207½ भन ज क भ य म स, प रभ ख श सन सध व LAW (LEGISLATIVE DRAFTING) DEPARTMENT (GROUP-II) NOTIFICATION Jaipur, April 28, 2017 No. F. 2 (34) Vidhi/2/2017.-In pursuance

ISSUES IN COMPOSITION SCHEME UNDER GST PGS & ASSOCIATES

ISSUES IN COMPOSITION SCHEME UNDER GST PGS & ASSOCIATES DEFINITIONS:- Aggregate Turnover means the aggregate value of all taxable supplies, exempt supplies, exports of goods or services or both and Inter-State

ISSUES IN COMPOSITION SCHEME UNDER GST PGS & ASSOCIATES DEFINITIONS:- Aggregate Turnover means the aggregate value of all taxable supplies, exempt supplies, exports of goods or services or both and Inter-State

Goods and Service Tax in India. CA Ashutosh Thaker

Goods and Service Tax in India CA Ashutosh Thaker Ashutosh.thaker@verita.co.in Contents 01 Why &Salient features of Indian GST 02 Key Concept of GST 03 What should be of concern Central Govt. & State Govt.

Goods and Service Tax in India CA Ashutosh Thaker Ashutosh.thaker@verita.co.in Contents 01 Why &Salient features of Indian GST 02 Key Concept of GST 03 What should be of concern Central Govt. & State Govt.

By: CA Sanjay Dhariwal

By: CA Sanjay Dhariwal sanjay@dnsconsulting.net 9972070601 Specific issues under Stock transfer: Consignment Sales, Inter unit transaction (Separate and Centralized Registration within State), E-commerce,

By: CA Sanjay Dhariwal sanjay@dnsconsulting.net 9972070601 Specific issues under Stock transfer: Consignment Sales, Inter unit transaction (Separate and Centralized Registration within State), E-commerce,

GOODS AND SERVICE TAX FILING OF RETURN. Prepared by Dharmendra Academy of GST Awareness

GOODS AND SERVICE TAX FILING OF RETURN 1 Returns Chapter IX of the CGST/SGST Act, 2017 GST Return Rules, 2017 2 RETURNS: SALIENT FEATURES A return is a statement of specified particulars relating to business

GOODS AND SERVICE TAX FILING OF RETURN 1 Returns Chapter IX of the CGST/SGST Act, 2017 GST Return Rules, 2017 2 RETURNS: SALIENT FEATURES A return is a statement of specified particulars relating to business

DEFINITION AND CONCEPT UNDER GST: SGST,CGST & IGST C.A.PURUSHOTHAMA N.J DATE:

1 DEFINITION AND CONCEPT UNDER GST: SGST,CGST & IGST C.A.PURUSHOTHAMA N.J DATE:19.01.2017 GST is biggest indirect tax reform 2 CA PURUSHOTHAMAN J 1/20/17 INTRODUCTION Present system of taxation What is

1 DEFINITION AND CONCEPT UNDER GST: SGST,CGST & IGST C.A.PURUSHOTHAMA N.J DATE:19.01.2017 GST is biggest indirect tax reform 2 CA PURUSHOTHAMAN J 1/20/17 INTRODUCTION Present system of taxation What is

SUPPLY, LEVY AND COLLECTION

3 CHAPTER SUPPLY, LEVY AND COLLECTION 3.1 relevant definition 3.1.1 meaning of GSt It is a destination based tax on consumption of goods and services. It is proposed to be levied at all stages right from

3 CHAPTER SUPPLY, LEVY AND COLLECTION 3.1 relevant definition 3.1.1 meaning of GSt It is a destination based tax on consumption of goods and services. It is proposed to be levied at all stages right from

Definitions, Scope of Supply, Levy & Collection Under GST

Definitions, Scope of Supply, Levy & Collection Under GST CA Ganesh Prabhu Balakumar B.Com, MFM, F.C.A, LL.B, DISA (ICAI) 1 Introduction of GST Goods & Services Tax Dual GST : CGST/SGST Or IGST Single

Definitions, Scope of Supply, Levy & Collection Under GST CA Ganesh Prabhu Balakumar B.Com, MFM, F.C.A, LL.B, DISA (ICAI) 1 Introduction of GST Goods & Services Tax Dual GST : CGST/SGST Or IGST Single

GST & YOU. Tally Solutions Pvt. Ltd. All Rights Reserved 2. Tally Solutions Pvt. Ltd. All Rights Reserved Business Presentation

WELCOME 1 GST & YOU Tally Solutions Pvt. Ltd. All Rights Reserved 2 Tally Solutions Pvt. Ltd. All Rights Reserved Business Presentation Presentation Agenda GST Basics What is GST Why GST GST concepts How

WELCOME 1 GST & YOU Tally Solutions Pvt. Ltd. All Rights Reserved 2 Tally Solutions Pvt. Ltd. All Rights Reserved Business Presentation Presentation Agenda GST Basics What is GST Why GST GST concepts How

A BRIEF INTRODUCTION TO CGST, SGST/UTGST, IGST & COMPENSATION CESS ACT(S)

") A BRIEF INTRODUCTION TO CGST, SGST/UTGST, IGST & COMPENSATION CESS ACT(S) 1 PRESENTATION PLAN: LEGAL PROVISIONS COMMON TO THE GST LAW(S) LEGAL PROVISIONS SPECIFIC TO IGST ACT & COMPENSATION CESS ACT NEERAJ

A BRIEF INTRODUCTION TO CGST, SGST/UTGST, IGST & COMPENSATION CESS ACT(S) 1 PRESENTATION PLAN: LEGAL PROVISIONS COMMON TO THE GST LAW(S) LEGAL PROVISIONS SPECIFIC TO IGST ACT & COMPENSATION CESS ACT NEERAJ

The Goa Goods and Services Tax Act, 2017; Published in the Official Gazette Series I No. 8 dated Arrangement of Sections Sr.

The Goa Goods and Services Tax Act, 2017; Published in the Official Gazette Series I No. 8 dated 26-5-2017 Arrangement of Sections Sr. Short Title No 1 Short title, extent and commencement 2 Definitions

The Goa Goods and Services Tax Act, 2017; Published in the Official Gazette Series I No. 8 dated 26-5-2017 Arrangement of Sections Sr. Short Title No 1 Short title, extent and commencement 2 Definitions

Goods and Service Tax (GST)

") Goods and Service Tax (GST) 1. Basics of GST 2. Working Model of GST 3. GST Compliances- Monthly and Annual Filings 4. GST Impact on E-Commerce 5. GST Impact on Services ( IT/ITES) BASICS of GST GST is

Goods and Service Tax (GST) 1. Basics of GST 2. Working Model of GST 3. GST Compliances- Monthly and Annual Filings 4. GST Impact on E-Commerce 5. GST Impact on Services ( IT/ITES) BASICS of GST GST is

Goods and Service. By CMA Sachin Kathuria. CMA Sachin Kathuria

Goods and Service Tax (GST) in India By 1 Existing Tax structure in India 2 Tax Structure Direct Tax Indirect Tax Income Tax Wealth Tax (Now abolished) Central Tax State Tax Excise Service Tax Customs

Goods and Service Tax (GST) in India By 1 Existing Tax structure in India 2 Tax Structure Direct Tax Indirect Tax Income Tax Wealth Tax (Now abolished) Central Tax State Tax Excise Service Tax Customs

Virtual Certificate Course on GST Organised by: IDT Committee of ICAI

1 Virtual Certificate Course on GST Organised by: IDT Committee of ICAI Sector Specific Studies on Construction Information Technology Tourism Service Trader Manufacturer 23 of June 2017 2 HIGHLIGHTS OF

1 Virtual Certificate Course on GST Organised by: IDT Committee of ICAI Sector Specific Studies on Construction Information Technology Tourism Service Trader Manufacturer 23 of June 2017 2 HIGHLIGHTS OF

The Goa Goods and Services Tax Act, 2017; The Goa Goods and Services Tax (Amendment) Ordinance, 2018;

Ordinance, 2018;") 1. The Goa Goods and Services Tax Act, 2017; published in the Official Gazette Series I No. 8 dated 26-5-2017; 2. The Goa Goods and Services Tax (Amendment) Ordinance, 2018; published in the Official Gazette

1. The Goa Goods and Services Tax Act, 2017; published in the Official Gazette Series I No. 8 dated 26-5-2017; 2. The Goa Goods and Services Tax (Amendment) Ordinance, 2018; published in the Official Gazette

CHAPTER 1: INTRODUCTION TO GST 1.1 BASICS OF GST What is GST?

CHAPTER 1: INTRODUCTION TO GST 1.1 BASICS OF GST 1.1.1 What is GST? Goods and Services Tax (GST) is a value-added indirect tax at each stage of the supply of goods and services precisely on the amount

CHAPTER 1: INTRODUCTION TO GST 1.1 BASICS OF GST 1.1.1 What is GST? Goods and Services Tax (GST) is a value-added indirect tax at each stage of the supply of goods and services precisely on the amount

By: CA Sunnay Jariwala

By: CA Sunnay Jariwala Existing Indirect Tax Structure Source: cbec.gov.in What is Goods and Services Tax? Article 366 (12A) Tax on supply of goods or services or both. Except on supply of alcoholic liquor

By: CA Sunnay Jariwala Existing Indirect Tax Structure Source: cbec.gov.in What is Goods and Services Tax? Article 366 (12A) Tax on supply of goods or services or both. Except on supply of alcoholic liquor

THE TELANGANA STATE GOODS AND SERVICES TAX BILL, 2017

THE TELANGANA STATE GOODS AND SERVICES TAX BILL, 2017 CLAUSES THE TELANGANA GOODS AND SERVICES TAX BILL, 2017 ARRANGEMENT OF CLAUSES CHAPTER I PRELIMINARY PAGE 1. Short title, extent and commencement.

THE TELANGANA STATE GOODS AND SERVICES TAX BILL, 2017 CLAUSES THE TELANGANA GOODS AND SERVICES TAX BILL, 2017 ARRANGEMENT OF CLAUSES CHAPTER I PRELIMINARY PAGE 1. Short title, extent and commencement.

The Centre of Excellence for GST. GST: Returns. JULY 09, 2017 ICAI Tower, BKC MUMBAI. CA. Hemant P. Vastani. The Centre of Excellence for GST

GST: Returns JULY 09, 2017 ICAI Tower, BKC MUMBAI CA. Hemant P. Vastani 1 Sections Covering Returns 37. Furnishing details of outward supplies. 38. Furnishing details of inward supplies. 39. Furnishing

GST: Returns JULY 09, 2017 ICAI Tower, BKC MUMBAI CA. Hemant P. Vastani 1 Sections Covering Returns 37. Furnishing details of outward supplies. 38. Furnishing details of inward supplies. 39. Furnishing

Bengaluru, Tuesday, June 27, 2017 (Ashada 06, Shaka Varsha 1939)

") 0 RNI No. KARBIL/2001/47147 apple Òûª ª apple «Ò  apple appleê sáuà IVA Part IVA C üpàèvàªáv ÀæPÀn À ÁzÀÄzÀÄ «±ÉõÀ gádå ÀwæPÉ ÉAUÀ¼ÀÆgÀÄ, ªÀÄAUÀ¼ÀªÁgÀ, dæ ï 27, 2017 (DµÁqsÀ 06, ±ÀPÀ ªÀµÀð 1939) Bengaluru,

0 RNI No. KARBIL/2001/47147 apple Òûª ª apple «Ò  apple appleê sáuà IVA Part IVA C üpàèvàªáv ÀæPÀn À ÁzÀÄzÀÄ «±ÉõÀ gádå ÀwæPÉ ÉAUÀ¼ÀÆgÀÄ, ªÀÄAUÀ¼ÀªÁgÀ, dæ ï 27, 2017 (DµÁqsÀ 06, ±ÀPÀ ªÀµÀð 1939) Bengaluru,

FAQ. Hindustan Shipyard Limited

FAQ Hindustan Shipyard Limited 1 Q 1. What is Goods and Service Tax (GST)? Ans. It is a destination based tax on consumption of goods and services. It is proposed to be levied at all stages right from

FAQ Hindustan Shipyard Limited 1 Q 1. What is Goods and Service Tax (GST)? Ans. It is a destination based tax on consumption of goods and services. It is proposed to be levied at all stages right from

THE CENTRAL GOODS AND SERVICES TAX ACT, 2017 ARRANGEMENT OF SECTIONS

THE CENTRAL GOODS AND SERVICES TAX ACT, 2017 ARRANGEMENT OF SECTIONS CHAPTER I SECTIONS 1. Short title, extent and commencement. 2. Definitions. PRELIMINARY CHAPTER II ADMINISTRATION 3. Officers under

THE CENTRAL GOODS AND SERVICES TAX ACT, 2017 ARRANGEMENT OF SECTIONS CHAPTER I SECTIONS 1. Short title, extent and commencement. 2. Definitions. PRELIMINARY CHAPTER II ADMINISTRATION 3. Officers under

GST Workshop 9th June 2017

GST Workshop 9 th June 2017 GST Model- Basic Features GST is tax on the supply of goods and services, right from the manufacturer/service provider to the consumer. Destination based consumption Tax (Tax

GST Workshop 9 th June 2017 GST Model- Basic Features GST is tax on the supply of goods and services, right from the manufacturer/service provider to the consumer. Destination based consumption Tax (Tax

Composition. Exports

Email FAQs The emails were received by the GST Policy Wing from various sources and were scrutinized and developed into a short FAQ of 100 emails. It should be noted that the emails received or the replies

Email FAQs The emails were received by the GST Policy Wing from various sources and were scrutinized and developed into a short FAQ of 100 emails. It should be noted that the emails received or the replies

Input Tax Credit Under GST Law, Rules & Forms. 2 December 2017 Copyrights Reserved of 33

Input Tax Credit Under GST Law, Rules & Forms www.alankitgst.com 2 December 2017 Copyrights Reserved 2017 1 of 33 What is GST? Goods & Services Tax Law in India is a comprehensive, multi-stage, destinationbased

Input Tax Credit Under GST Law, Rules & Forms www.alankitgst.com 2 December 2017 Copyrights Reserved 2017 1 of 33 What is GST? Goods & Services Tax Law in India is a comprehensive, multi-stage, destinationbased

Current Tax Structure in India

History of GST More than 150 countries have already introduced GST. France was the first country to introduce GST system in 1954. Typically it is a single rate system but two/three rate systems are also

History of GST More than 150 countries have already introduced GST. France was the first country to introduce GST system in 1954. Typically it is a single rate system but two/three rate systems are also

GST Customised FAQs for Gems and Jewelry industry. ANSWER The rate of GST applicable on gold bullion and gold jewellery is the same 3%.

GST Customised FAQs for Gems and Jewelry industry Updated on: June 17, 2017 SUPPLY Is there separate GST on gold bullion and gold jewellery? The rate of GST applicable on gold bullion and gold jewellery

GST Customised FAQs for Gems and Jewelry industry Updated on: June 17, 2017 SUPPLY Is there separate GST on gold bullion and gold jewellery? The rate of GST applicable on gold bullion and gold jewellery

The. Extraordinary Published by Authority JYAISTHA 25] THURSDAY, JUNE 15, 2017 [SAKA 1939 GOVERNMENT OF WEST BENGAL. LAW DEPARTMENT Legislative

![The. Extraordinary Published by Authority JYAISTHA 25] THURSDAY, JUNE 15, 2017 [SAKA 1939 GOVERNMENT OF WEST BENGAL. LAW DEPARTMENT Legislative](/thumbs/75/72847969.jpg "The. Extraordinary Published by Authority JYAISTHA 25] THURSDAY, JUNE 15, 2017 [SAKA 1939 GOVERNMENT OF WEST BENGAL. LAW DEPARTMENT Legislative") Registered No. WB/SC-247 No. WB(Part-IIIA)/2017/SAR-2 The Kolkata Gazette Extraordinary Published by Authority JYAISTHA 25] THURSDAY, JUNE 15, 2017 [SAKA 1939 PART IIIA Ordinances promulgated by the Governor

Registered No. WB/SC-247 No. WB(Part-IIIA)/2017/SAR-2 The Kolkata Gazette Extraordinary Published by Authority JYAISTHA 25] THURSDAY, JUNE 15, 2017 [SAKA 1939 PART IIIA Ordinances promulgated by the Governor

C A. S H A S H A N K S H E K H A R G U P T A P A R T N E R - I N D I R E C T T A X

OM HARE GURVEY NAMAH GOODS AND SERVICES TAX A DISCUSSION C A. S H A S H A N K S H E K H A R G U P T A P A R T N E R - I N D I R E C T T A X J U N E 2 0 1 6 BACKGROUND WHAT IS GST? WHY GST? (a) & (b) BRIEF

OM HARE GURVEY NAMAH GOODS AND SERVICES TAX A DISCUSSION C A. S H A S H A N K S H E K H A R G U P T A P A R T N E R - I N D I R E C T T A X J U N E 2 0 1 6 BACKGROUND WHAT IS GST? WHY GST? (a) & (b) BRIEF

COMPOSITION LEVY DISCLAIMER: Threshold limit for Composition scheme: Act

COMPOSITION LEVY DISCLAIMER: The views expressed in this article are of the author(s). The Institute of Chartered Accountants of India may not necessarily subscribe to the views expressed by the author(s).

COMPOSITION LEVY DISCLAIMER: The views expressed in this article are of the author(s). The Institute of Chartered Accountants of India may not necessarily subscribe to the views expressed by the author(s).

GST Overview. ~CA Unmesh G. Patwardhan~ Mobile No Unmesh Patwardhan Mobile No

GST Overview ~CA Unmesh G. Patwardhan~ Mobile No.98224 24968 Unmesh Patwardhan Mobile No.98224 24968 1 Brief History & Concept of GST Unmesh Patwardhan Mobile No.98224 24968 2 1 st Jul 2017 The D Day Journey

GST Overview ~CA Unmesh G. Patwardhan~ Mobile No.98224 24968 Unmesh Patwardhan Mobile No.98224 24968 1 Brief History & Concept of GST Unmesh Patwardhan Mobile No.98224 24968 2 1 st Jul 2017 The D Day Journey

Chapter IX Returns Statutory Provision 37. Furnishing details of outward supplies

Chapter IX Returns Statutory Provision 37. Furnishing details of outward supplies (1) Every registered taxable person, other than an input service distributor, a non-resident taxable person and a person

Chapter IX Returns Statutory Provision 37. Furnishing details of outward supplies (1) Every registered taxable person, other than an input service distributor, a non-resident taxable person and a person

GST on Traders. 1. Introduction Levy Time of Supply of Goods Place of Supply of Goods Value of Supply 23

GST on Traders DISCLAIMER The views expressed in this article are of the author(s). The Institute of Chartered Accountants of India may not necessarily subscribe to the views expressed by the author(s).

GST on Traders DISCLAIMER The views expressed in this article are of the author(s). The Institute of Chartered Accountants of India may not necessarily subscribe to the views expressed by the author(s).

Proposed Amendments in GST Law

Proposed Amendments in GST Law On 09.07.2018, the Goods and Service Tax Council has issued draft proposal for the amendment in the "Goods and Services Tax" Law. The entire proposal gives brief view on

Proposed Amendments in GST Law On 09.07.2018, the Goods and Service Tax Council has issued draft proposal for the amendment in the "Goods and Services Tax" Law. The entire proposal gives brief view on

i. On or before the due date of furnishing the return for the month of September 2018 i.e (unless extended). OR

. OR") Points to consider before filing GSTR-3B/GSTR-1 for September 1. Pending Input Tax Credit to be availed before filing GSTR- 3B of Sept 18: Section 16 (4) of Central Goods and Services Tax Act, 2017 provides

Points to consider before filing GSTR-3B/GSTR-1 for September 1. Pending Input Tax Credit to be availed before filing GSTR- 3B of Sept 18: Section 16 (4) of Central Goods and Services Tax Act, 2017 provides

Payment of tax, interest, penalty and other amounts (Section 49)

") FAQ s Chapter VIII Payment of Tax Payment of tax, interest, penalty and other amounts (Section 49) Section 49 of the CGST Act, 2017 made applicable to IGST vide Section 20 of the IGST Act, 2017 and UTGST

FAQ s Chapter VIII Payment of Tax Payment of tax, interest, penalty and other amounts (Section 49) Section 49 of the CGST Act, 2017 made applicable to IGST vide Section 20 of the IGST Act, 2017 and UTGST

FAQs. Yes. He is liable for registration as he is engaged in Inter State supplies.

FAQs 1. A registered person s business is in many states. All supplies are below 10 lakhs. He makes an Inter State supply from one state. Is he liable for registration? Yes. He is liable for registration

FAQs 1. A registered person s business is in many states. All supplies are below 10 lakhs. He makes an Inter State supply from one state. Is he liable for registration? Yes. He is liable for registration

THE CHAMBER OF TAX CONSULTANTS BASIC CONCEPTS O F G S T

THE CHAMBER OF TAX CONSULTANTS BASIC CONCEPTS O F G S T 1 Understanding GST Covering 2 Legislations, 174 Sections,3 Schedules TAXES IN INDIA There are mainly two types of taxes DIRECT TAXES INCOME TAX

THE CHAMBER OF TAX CONSULTANTS BASIC CONCEPTS O F G S T 1 Understanding GST Covering 2 Legislations, 174 Sections,3 Schedules TAXES IN INDIA There are mainly two types of taxes DIRECT TAXES INCOME TAX

Answer to MTP_Intermediate_Syllabus 2016_Jun2018_Set 2 Paper 11- Indirect Taxation

Paper 11- Indirect Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 11- Indirect Taxation Full Marks: 100 Time allowed:

Paper 11- Indirect Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 11- Indirect Taxation Full Marks: 100 Time allowed:

UPDATE ON AMENDMENTS TO CGST ACT, 2017

UPDATE ON AMENDMENTS TO CGST ACT, 2017 Dear Person, August 31, 2018 TEAM TRD An amendment to CGST Act, 2017 has been introduced on 29 th August, 2018 with the following objective by The Central Government:-

UPDATE ON AMENDMENTS TO CGST ACT, 2017 Dear Person, August 31, 2018 TEAM TRD An amendment to CGST Act, 2017 has been introduced on 29 th August, 2018 with the following objective by The Central Government:-

REGISTRATION & RETURN PROCESS UNDER GOODS AND SERVICES TAX (GST) By CA Sandip Agrawal Sandip Satyanarayan & Co Chartered Accountants

By CA Sandip Agrawal Sandip Satyanarayan & Co Chartered Accountants") REGISTRATION & RETURN PROCESS UNDER GOODS AND SERVICES TAX (GST) By BRIEF INTRODUCTION TO GST GST is a Tax on Goods and services and it is proposed to be a comprehensive indirect tax levy on manufacture,

REGISTRATION & RETURN PROCESS UNDER GOODS AND SERVICES TAX (GST) By BRIEF INTRODUCTION TO GST GST is a Tax on Goods and services and it is proposed to be a comprehensive indirect tax levy on manufacture,

VAT CONCEPT AND ITS APPLICATION IN GST

CONTENTS DIVISION 1 INPUT TAX CREDIT 1 VAT CONCEPT AND ITS APPLICATION IN GST 1.1 Background of VAT 3 1.2 Basic Concept of VAT 4 1.2-1 VAT to avoid the cascading effect 5 1.2-2 Input Tax credit system

CONTENTS DIVISION 1 INPUT TAX CREDIT 1 VAT CONCEPT AND ITS APPLICATION IN GST 1.1 Background of VAT 3 1.2 Basic Concept of VAT 4 1.2-1 VAT to avoid the cascading effect 5 1.2-2 Input Tax credit system

Goods and Services Tax (GST)

") JUNE 2017 Goods and Services Tax (GST) Frequently Asked Questions GST is one of the most significant tax reforms of the country towards a seamless indirect tax regime. The new tax regime is transformational

JUNE 2017 Goods and Services Tax (GST) Frequently Asked Questions GST is one of the most significant tax reforms of the country towards a seamless indirect tax regime. The new tax regime is transformational

GST -Some Basic Concepts. Presented By: CA Madhukar Hiregange

GST -Some Basic Concepts Presented By: CA Madhukar Hiregange Necessity for GST Present system of indirect tax has multiplicity of taxes levied by Centre & State Tax on tax, increases cost - Cascading No

GST -Some Basic Concepts Presented By: CA Madhukar Hiregange Necessity for GST Present system of indirect tax has multiplicity of taxes levied by Centre & State Tax on tax, increases cost - Cascading No

BRIEF ON GST. GST is a destination based tax and levied at a single point at the time of consumption of goods or services by the ultimate consumer.

BRIEF ON GST GST is a destination based tax and levied at a single point at the time of consumption of goods or services by the ultimate consumer. GST will be levied on all goods and services except on

BRIEF ON GST GST is a destination based tax and levied at a single point at the time of consumption of goods or services by the ultimate consumer. GST will be levied on all goods and services except on

Sampat & Mehta GST - FAQ

Sr. No. Particulars Suggestions 1. What documents are required to accompany movement of Goods outside own premises E Way Bill to be generated from GSTN Portal before or at the time of movement of Goods

Sr. No. Particulars Suggestions 1. What documents are required to accompany movement of Goods outside own premises E Way Bill to be generated from GSTN Portal before or at the time of movement of Goods

Transitional Provisions

FAQ s Migration of Existing Tax Payers (Section 139) Similar provisions have been specified in the UTGST Act, 2017 Chapter XVIII Transitional Provisions Q1. What is the primary condition for provisional

FAQ s Migration of Existing Tax Payers (Section 139) Similar provisions have been specified in the UTGST Act, 2017 Chapter XVIII Transitional Provisions Q1. What is the primary condition for provisional

Response to questions raised by members in relation to Goods and Services Tax ( GST )

") Response to questions raised by members in relation to Goods and Services Tax ( GST ) 1. What will be the treatment for hallmarking charges recovered from Customer? As per Section 15 of the CGST Act, 2017,

Response to questions raised by members in relation to Goods and Services Tax ( GST ) 1. What will be the treatment for hallmarking charges recovered from Customer? As per Section 15 of the CGST Act, 2017,

GST: FREQUENTLY ASKED QUESTIONS [FAQS] FOR COMPOSITION SCHEME

![GST: FREQUENTLY ASKED QUESTIONS [FAQS] FOR COMPOSITION SCHEME](/thumbs/79/79563057.jpg "GST: FREQUENTLY ASKED QUESTIONS [FAQS] FOR COMPOSITION SCHEME") Q 1. What is composition levy under GST? Ans. The composition levy is an alternative method of levy of tax designed for small taxpayers whose turnover is up to Rs. 75 lakhs (Rs. 50 lakhs in case of few

Q 1. What is composition levy under GST? Ans. The composition levy is an alternative method of levy of tax designed for small taxpayers whose turnover is up to Rs. 75 lakhs (Rs. 50 lakhs in case of few

Reverse Charge Mechanism - Reverse gear of tax burden

Reverse Charge Mechanism - Reverse gear of tax burden A. Introductory provisions of reverse charge under GST Law. In terms of section 9(1) of Central Goods and Services Tax Act, 2017, Central Goods and

Reverse Charge Mechanism - Reverse gear of tax burden A. Introductory provisions of reverse charge under GST Law. In terms of section 9(1) of Central Goods and Services Tax Act, 2017, Central Goods and

GST- COMPOSITION SCHEME - BOON FOR SMALL TAXABLE PERSONS

GST- COMPOSITION SCHEME - BOON FOR SMALL TAXABLE PERSONS BY: PRADEEP K. MITTAL, ADVOCATE 1 INTRODUCTION: 1: The new composition scheme provides for a simple and easy method of charge and payment of tax

GST- COMPOSITION SCHEME - BOON FOR SMALL TAXABLE PERSONS BY: PRADEEP K. MITTAL, ADVOCATE 1 INTRODUCTION: 1: The new composition scheme provides for a simple and easy method of charge and payment of tax

Returns in goods and services tax

Returns in goods and services tax A brief overview by Shri Sunil Lahane, Dy Commissioner, Sales Tax Outline What s special about GST return? Overview of Returns to be submitted by regular tax payers Process

Returns in goods and services tax A brief overview by Shri Sunil Lahane, Dy Commissioner, Sales Tax Outline What s special about GST return? Overview of Returns to be submitted by regular tax payers Process

Vasai Branch of WIRC of ICAI

Vasai Branch of WIRC of ICAI Event : Two Days Mega Members Conference on GST Date & Day : 16 th October,2016 (Sunday) Subject : Job-work and E-commerce under GST Venue : Green Court Club (GCC), GCC International

Vasai Branch of WIRC of ICAI Event : Two Days Mega Members Conference on GST Date & Day : 16 th October,2016 (Sunday) Subject : Job-work and E-commerce under GST Venue : Green Court Club (GCC), GCC International

Air India. June Page 1

Air India June 2017 Page 1 Contents GST Overview Comparative tax scenarios: Current vs. GST Credit Mechanism Concept of Place & Time of Supply Valuation under GST Compliances under GST Page 2 Overview

Air India June 2017 Page 1 Contents GST Overview Comparative tax scenarios: Current vs. GST Credit Mechanism Concept of Place & Time of Supply Valuation under GST Compliances under GST Page 2 Overview

All About GST and Model GST Law

All About GST and Model GST Law 1 Contents GST Basics Supply Meaning & Scope Supply - Time & Place Valuation Rules Input Tax Credit Administration & Procedures Transitional Provisions 2 Basics of GST 3

All About GST and Model GST Law 1 Contents GST Basics Supply Meaning & Scope Supply - Time & Place Valuation Rules Input Tax Credit Administration & Procedures Transitional Provisions 2 Basics of GST 3

ISSUES ON GST FOR PANEL DISCUSSION TO BE HELD ON 13 th AUGUST, 2017

ISSUES ON GST FOR PANEL DISCUSSION TO BE HELD ON 13 th AUGUST, 2017 1. Developer has given work contract to construct the building to a work contractor in 2016. Developer had made the payment after deducting

ISSUES ON GST FOR PANEL DISCUSSION TO BE HELD ON 13 th AUGUST, 2017 1. Developer has given work contract to construct the building to a work contractor in 2016. Developer had made the payment after deducting

WHITE PAPER - ISD AND CROSS CHARGE MECHANISM UNDER GST REGIME.

WHITE PAPER - ISD AND CROSS CHARGE MECHANISM UNDER GST REGIME www.rsmindia.in 1.0 Introduction GST was introduced on 01 July 2017 replacing multiple Indirect Taxes with a single tax. However, a lot of

WHITE PAPER - ISD AND CROSS CHARGE MECHANISM UNDER GST REGIME www.rsmindia.in 1.0 Introduction GST was introduced on 01 July 2017 replacing multiple Indirect Taxes with a single tax. However, a lot of

Master class on GST. Institute of Company Secretaries of India - WIRC. CA Ashit Shah. Shah & Savla LLP. Chartered Accountants

Master class on GST Institute of Company Secretaries of India - WIRC CA Ashit Shah Chartered Accountants Matters to be covered Job work E-Commerce Valuation of Goods and Services Accounts & Records Tax

Master class on GST Institute of Company Secretaries of India - WIRC CA Ashit Shah Chartered Accountants Matters to be covered Job work E-Commerce Valuation of Goods and Services Accounts & Records Tax

GOODS AND SERVICE TAX (GST) TRANSITIONAL PROVISIONS COMPILED AND PREPARED BY : CA SAGAR THAKKAR

TRANSITIONAL PROVISIONS COMPILED AND PREPARED BY : CA SAGAR THAKKAR") GOODS AND SERVICE TAX (GST) TRANSITIONAL PROVISIONS COMPILED AND PREPARED BY : CA SAGAR THAKKAR PRESENTATION COVERAGE TRANSITIONAL PROVISIONS UNDER CGST/SGST ACT SEC. 139 TO 142 OF CGST ACT TRANSITIONAL

GOODS AND SERVICE TAX (GST) TRANSITIONAL PROVISIONS COMPILED AND PREPARED BY : CA SAGAR THAKKAR PRESENTATION COVERAGE TRANSITIONAL PROVISIONS UNDER CGST/SGST ACT SEC. 139 TO 142 OF CGST ACT TRANSITIONAL

Frequently Asked Questions on Composition Levy

Frequently Asked Questions on Composition Levy Q 1. What is composition levy under GST? Ans. The composition levy is an alternative method of levy of tax designed for small taxpayers whose turnover is

Frequently Asked Questions on Composition Levy Q 1. What is composition levy under GST? Ans. The composition levy is an alternative method of levy of tax designed for small taxpayers whose turnover is

Dual GST Model CA Gadia Manish R 1. Marwadi Ghano Saro Tax

CA Gadia Manish R 3 Marwadi Ghano Saro Tax Doctor Glucose Stimulation Test Alia Bhatt Good night, Sweet dream, Take care FAQ : It is a destination based tax on consumption of goods and services. It is

CA Gadia Manish R 3 Marwadi Ghano Saro Tax Doctor Glucose Stimulation Test Alia Bhatt Good night, Sweet dream, Take care FAQ : It is a destination based tax on consumption of goods and services. It is

The Empowered Committee of State Finance Ministers have worked out a dual GST model for India. In

GST is proposed to be a comprehensive indirect tax levy on manufacture, sale and consumption of goods as well as on the services at a national level. In an utopian situation, the tax has to be a singular

GST is proposed to be a comprehensive indirect tax levy on manufacture, sale and consumption of goods as well as on the services at a national level. In an utopian situation, the tax has to be a singular

Integrated Goods and Services Tax (IGST)

") 1. The introduction of Goods and Services Tax (GST) is a significant reform in the field of indirect taxes in our country. Multiple taxes levied and collected by the Centre and the States will be replaced

1. The introduction of Goods and Services Tax (GST) is a significant reform in the field of indirect taxes in our country. Multiple taxes levied and collected by the Centre and the States will be replaced

Presentation by CA RITESH MEHTA, NAGPUR. B. Com., F.C.A., D.I.S.A (ICAI).

.") Presentation by CA RITESH MEHTA, NAGPUR B. Com., F.C.A., D.I.S.A (ICAI). 1 Overview of GST Law Components of GST law Levy under GST Taxable event under GST Meaning & scope of the term Supply and its Implications

Presentation by CA RITESH MEHTA, NAGPUR B. Com., F.C.A., D.I.S.A (ICAI). 1 Overview of GST Law Components of GST law Levy under GST Taxable event under GST Meaning & scope of the term Supply and its Implications

M/s PRANJAL JOSHI & CO

Introduction to GST Basic information GST stands for Goods and Service Tax. GST is a destination based tax on consumption of goods and services. It is proposed to be levied at all stages right from manufacture

Introduction to GST Basic information GST stands for Goods and Service Tax. GST is a destination based tax on consumption of goods and services. It is proposed to be levied at all stages right from manufacture

Goods & Service Tax. (GST) BBNL Vendor MEET

BBNL Vendor MEET") Goods & Service Tax (GST) BBNL Vendor MEET 28.6.2017 1 Overview GST In short How to Charge Tax Changes Now Tax on both goods and services when supplied Replacing - Central Excise, Service Tax, VAT, Entry

Goods & Service Tax (GST) BBNL Vendor MEET 28.6.2017 1 Overview GST In short How to Charge Tax Changes Now Tax on both goods and services when supplied Replacing - Central Excise, Service Tax, VAT, Entry

FAQ s on Form GSTR-9 Annual Return

FAQ s on Form GSTR-9 Annual Return DISCLAIMER The views expressed in this write up are of the author(s). The Institute of Chartered Accountants of India may not necessarily subscribe to the views expressed

FAQ s on Form GSTR-9 Annual Return DISCLAIMER The views expressed in this write up are of the author(s). The Institute of Chartered Accountants of India may not necessarily subscribe to the views expressed

Q. 1. If I have multiple manufacturing units in a State/UT, do I have to register all my companies separately or as a group?

Q. 1. If I have multiple manufacturing units in a State/UT, do I have to register all my companies separately or as a group? Ans: You shall be granted a single registration in the State/UT. However, you

Q. 1. If I have multiple manufacturing units in a State/UT, do I have to register all my companies separately or as a group? Ans: You shall be granted a single registration in the State/UT. However, you

GUIDANCE NOTE ON GST FOR EVENT MANAGEMENT COMPANIES

GUIDANCE NOTE ON GST FOR EVENT MANAGEMENT COMPANIES Being a CA in practice for last 26 years and consultant to several Event Management, Advertising and Marketing Companies, I thought it would be good

GUIDANCE NOTE ON GST FOR EVENT MANAGEMENT COMPANIES Being a CA in practice for last 26 years and consultant to several Event Management, Advertising and Marketing Companies, I thought it would be good

SALIENT FEATURES OF PROPOSED GST

SALIENT FEATURES OF PROPOSED GST GST is a consumption based levy. Destination principle would be applicable in normal course of business to business [B2B] other than for few services and business to consumer.[

SALIENT FEATURES OF PROPOSED GST GST is a consumption based levy. Destination principle would be applicable in normal course of business to business [B2B] other than for few services and business to consumer.[

GOODS AND SERVICES TAX

GOODS AND SERVICES TAX GOODS AND SERVICES TAX - AN INTRODUCTION Introduction to Goods and Services Tax GST and Centre-State Financial Relations Constitution (One Hundred and First) Amendment Act, 2016

GOODS AND SERVICES TAX GOODS AND SERVICES TAX - AN INTRODUCTION Introduction to Goods and Services Tax GST and Centre-State Financial Relations Constitution (One Hundred and First) Amendment Act, 2016

GST MSME SECTORAL SERIES CENTRAL BOARD OF EXCISE & CUSTOMS. Directorate General of Taxpayer Services. Follow

GST SECTORAL SERIES MSME Directorate General of Taxpayer Services CENTRAL BOARD OF EXCISE & CUSTOMS www.cbec.gov.in Question 55: Whether a registered person under the composition scheme needs to learn

GST SECTORAL SERIES MSME Directorate General of Taxpayer Services CENTRAL BOARD OF EXCISE & CUSTOMS www.cbec.gov.in Question 55: Whether a registered person under the composition scheme needs to learn

Answer to MTP_Intermediate_Syllabus 2016_Dec 2018_Set 1 Paper 11- Indirect Taxation

Paper 11- Indirect Taxation DoS, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 11- Indirect Taxation Full Marks: 100 Time allowed: 3 hours The figures

Paper 11- Indirect Taxation DoS, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 11- Indirect Taxation Full Marks: 100 Time allowed: 3 hours The figures

FAQs and MCQs on Revised Model GST Law

FAQs and MCQs on Revised Model GST Law The Institute of Chartered Accountants of India (Set up by an Act of Parliament) New Delhi The Institute of Chartered Accountants of India All rights reserved. No

FAQs and MCQs on Revised Model GST Law The Institute of Chartered Accountants of India (Set up by an Act of Parliament) New Delhi The Institute of Chartered Accountants of India All rights reserved. No

CA. Hrishikesh Wandrekar Wandrekar & Co.

Wandrekar & Co. Basic Concept of GST Destination Based Consumption Tax Tax leviable on value added in the transaction chain Tax on goods & services borne by the ultimate consumer Input tax credit available

Wandrekar & Co. Basic Concept of GST Destination Based Consumption Tax Tax leviable on value added in the transaction chain Tax on goods & services borne by the ultimate consumer Input tax credit available

Marking Scheme. Session TAXATION (782) CLASS XII. Total marks: 100 Theory: 60 Marks Practical: 40 Marks. 1 Deduction From Gross Total Income

CLASS XII. Total marks: 100 Theory: 60 Marks Practical: 40 Marks. 1 Deduction From Gross Total Income") Marking Scheme Session 2018-19 TAXATION (782) CLASS XII Total marks: 100 Theory: 60 Marks Practical: 40 Marks UNITS UNIT NAME TOTAL 1 Deduction From Gross Total Income 2 Computation Of Ta x Liability Of

Marking Scheme Session 2018-19 TAXATION (782) CLASS XII Total marks: 100 Theory: 60 Marks Practical: 40 Marks UNITS UNIT NAME TOTAL 1 Deduction From Gross Total Income 2 Computation Of Ta x Liability Of

Chapter - RETURNS. 1. Form and manner of furnishing details of outward supplies

Chapter - RETURNS 1. Form and manner of furnishing details of outward supplies (1) Every registered person (other than a person referred to in section 14 of the Integrated Goods and Services Tax Act, 2017)

Chapter - RETURNS 1. Form and manner of furnishing details of outward supplies (1) Every registered person (other than a person referred to in section 14 of the Integrated Goods and Services Tax Act, 2017)

Presentation on GST Annual Return & GST Audit

Optitax s R Presentation on GST Annual Return & GST Audit 25th Nov 2018 1 1 Legal provisions 2 Legal provision Applicability Section 44 (1) - Every registered person, other than an Input Service Distributor,

Optitax s R Presentation on GST Annual Return & GST Audit 25th Nov 2018 1 1 Legal provisions 2 Legal provision Applicability Section 44 (1) - Every registered person, other than an Input Service Distributor,

A. Introduction on GST:

GST FAQ S Contents A. Introduction on GST: 02 B. Meaning and Scope of Supply: 04 C. Tax liability on composite and mixed supplies 06 D. Registration under GST 07 E. Levy of GST 11 F. Time of supply of

GST FAQ S Contents A. Introduction on GST: 02 B. Meaning and Scope of Supply: 04 C. Tax liability on composite and mixed supplies 06 D. Registration under GST 07 E. Levy of GST 11 F. Time of supply of

GST for Hospitality Industry Practical Aspects in Implementation

GST for Hospitality Industry Practical Aspects in Implementation CA KURESH S KAGALWALA kuresh@alifsystems.com +91 98201 69660 +91 22 43441717 Topics covered Introduction and Concepts Hospitality Industry

GST for Hospitality Industry Practical Aspects in Implementation CA KURESH S KAGALWALA kuresh@alifsystems.com +91 98201 69660 +91 22 43441717 Topics covered Introduction and Concepts Hospitality Industry

CA ROHIT GAMBHIR. Page i

Page i INDEX Lesson Description Page No 1. Overview of GST -- 2. GST International Scenario 1 3. GST in India 3 4. Introduction to CGST Act, 2017 8 5. Supply 10 6. Composite and Mixed Supply 17 7. Composition

Page i INDEX Lesson Description Page No 1. Overview of GST -- 2. GST International Scenario 1 3. GST in India 3 4. Introduction to CGST Act, 2017 8 5. Supply 10 6. Composite and Mixed Supply 17 7. Composition

GST. Concept & Roadmap By CA. Ashwarya Agarwal

GST Concept & Roadmap By CA. Ashwarya Agarwal 1 What is GST?? GST Goods and Services Tax Clause 12A of Article 366 of The Constitution of India goods and services tax means any tax on supply of goods,

GST Concept & Roadmap By CA. Ashwarya Agarwal 1 What is GST?? GST Goods and Services Tax Clause 12A of Article 366 of The Constitution of India goods and services tax means any tax on supply of goods,