JACKSON PARISH HOSPITAL SERVICE DISTRICT NO. 1

|

|

|

- Jane Jefferson

- 5 years ago

- Views:

Transcription

1 JACKSON PARISH HOSPITAL SERVICE DISTRICT NO. 1 INVESTIGATIVE AUDIT APRIL 8, 2015

2 LOUISIANA LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET POST OFFICE BOX BATON ROUGE, LOUISIANA LEGISLATIVE AUDITOR DARYL G. PURPERA, CPA, CFE DIRECTOR OF INVESTIGATIVE AUDIT ROGER W. HARRIS, J.D., CCEP Under the provisions of state law, this report is a public document. A copy of this report has been submitted to the Governor, to the Attorney General, and to other public officials as required by state law. A copy of this report is available for public inspection at the Baton Rouge office of the Louisiana Legislative Auditor and at the office of the parish clerk of court. This document is produced by the Louisiana Legislative Auditor, State of Louisiana, Post Office Box 94397, Baton Rouge, Louisiana in accordance with Louisiana Revised Statute 24:513. Eight copies of this public document were produced at an approximate cost of $8.40. This material was produced in accordance with the standards for state agencies established pursuant to R.S. 43:31. This report is available on the Legislative Auditor s website at When contacting the office, you may refer to Agency ID No or Report ID No for additional information. In compliance with the Americans With Disabilities Act, if you need special assistance relative to this document, or any documents of the Legislative Auditor, please contact Elizabeth Coxe, Chief Administrative Officer, at

3 LOUISIANA LEGISLATIVE AUDITOR DARYL G. PURPERA, CPA, CFE April 8, 2015 RICHARD LLOYD MONGER, ADMINISTRATOR, AND BOARD OF DIRECTORS JACKSON PARISH HOSPITAL SERVICE DISTRICT NO. 1 Jonesboro, Louisiana We have audited certain transactions of the Jackson Parish Hospital Service District No. 1. Our audit was conducted in accordance with Title 24 of the Louisiana Revised Statutes to determine the validity of allegations we received. Our audit consisted primarily of inquiries and the examination of selected financial records and other documentation. The scope of our audit was significantly less than that required by Government Auditing Standards. The accompanying report presents our findings and recommendations as well as management s response. This is a public report. Copies of this report have been delivered to the Attorney General for the State of Louisiana and others as required by law. Respectfully submitted, DGP/aa Daryl G. Purpera, CPA, CFE Legislative Auditor JPHSD NORTH THIRD STREET POST OFFICE BOX BATON ROUGE, LOUISIANA PHONE: FAX:

4

5 TABLE OF CONTENTS Page Executive Summary...2 Background and Methodology...3 Findings and Recommendations: Unearned and Unauthorized Payments of Accrued Time Off...4 Improper Payroll Deductions for Supplemental Insurance and Uniforms...7 Mismanagement of Payroll Deductions...8 Improper Insurance Stipend Payment...10 Former Employee Took Hospital Collections for Personal Use...10 Recommendations...12 Legal Provisions...13 Management s Response... Appendix A 1

6

7 EXECUTIVE SUMMARY Unearned and Unauthorized Payments of Accrued Time Off The Jackson Parish Hospital s (Hospital) former Human Resource employee, Elizabeth Cheatwood, and its former accounts payable clerk, Vickie Booker, received a combined $89,960 in excessive payments for accrued time off from January 2009 to November Based upon our review of Hospital documents, these payments were both unearned and unauthorized. Since Ms. Cheatwood and Ms. Booker were not entitled to these payments, they may have violated state and federal law. Improper Payroll Deductions for Supplemental Insurance and Uniforms Ms. Cheatwood and Ms. Booker improperly received a combined $25,723 of supplemental health insurance policies and $7,474 of uniforms offered through the Hospital from December 2008 to December Based on our review of Hospital records, Ms. Cheatwood and Ms. Booker did not pay for these benefits and, as such, may have violated state and federal law. Mismanagement of Payroll Deductions The Hospital did not reconcile its health and supplemental insurance invoices or other employee benefits to payroll deductions to ensure the Hospital received the proper amount from its employees. This resulted in undetected errors to employee payroll deductions and caused the Hospital to pay $200,997 for employee benefits that were not reimbursed by its employees from 2009 to Since the Hospital did not collect all amounts due from employees, the payments on behalf of employees without reimbursement may violate state law and the state constitution. Improper Insurance Stipend Payment Ms. Cheatwood received a stipend for health insurance in the amount of $26,072 from January 1, 2009 to December 31, Based on our review of Hospital records, Ms. Cheatwood was not entitled to receive these funds and, therefore, may have violated state and federal law. Former Employee Took Hospital Collections for Personal Use Hospital records indicate that from January 2012 to December 2014, the Hospital collected $121,968 in cash that was never deposited into its operating bank account. Ms. Booker stated that she took cash from Hospital collections and deposited it to her personal bank account or spent it. By taking cash from Hospital collections for her personal use, Ms. Booker may have violated state law. 2

8

9 BACKGROUND AND METHODOLOGY The Jackson Parish Hospital Service District No. 1 (District) is a component unit of the Jackson Parish Police Jury (Police Jury). The District was created by the Police Jury under the provisions of Louisiana Revised Statute (R.S.) 46:1051 and is governed by a seven-member board of commissioners (Board) appointed by the Police Jury. The District is responsible for the management and operations of the Jackson Parish Hospital (Hospital) and appoints a Hospital administrator to oversee the daily operations of the Hospital. The Hospital is located in Jonesboro, Louisiana, and is considered a critical access rural hospital. This audit was initiated after receiving information from the Louisiana State Police (LSP) regarding an ongoing investigation into improper payroll transactions. On March 13, 2015, LSP arrested four people as a result of its investigation: three former employees and the spouse of one of the former employees. During our audit, other matters and transactions came to our attention, and we expanded our scope to address them. The procedures performed during this audit included: (1) (2) (3) (4) (5) interviewing employees of the Hospital; interviewing other persons as appropriate; examining select Hospital documents and records; gathering documents from external parties; and reviewing applicable state and federal laws and regulations. 3

10

11 FINDINGS AND RECOMMENDATIONS Unearned and Unauthorized Payments of Accrued Time Off The Jackson Parish Hospital s (Hospital) former Human Resource employee, Elizabeth Cheatwood, and its former accounts payable clerk, Vickie Booker, received a combined $89,960 in excessive payments for accrued time off from January 2009 to November Based upon our review of Hospital documents, these payments were both unearned and unauthorized. Since Ms. Cheatwood and Ms. Booker were not entitled to these payments, they may have violated state and federal law. 1,2,3,4,5 The Hospital s policy manual encourages employees to use their accrued time off (vacation), but the policy also allows an exception for employees to receive cash for up to 10 days of accrued time off (ATO) when business requirements make the scheduling of a vacation impossible. This exception may be granted by the Hospital administrator when the administrator and the employee s department manager both agree the employee cannot use their accrued ATO. According to David Sanders, the Hospital s chief financial officer, to obtain an ATO payout, a Hospital employee had to complete a manual request form, obtain the employee s supervisor s approval, and obtain Mr. Sanders approval (after he verified that the employee had a sufficient ATO balance.) Once approved by Mr. Sanders, the form went to Ms. Booker for processing. Mr. Sanders stated that all Hospital checks are required to have two signatures to be valid and that Ms. Cheatwood had control over three signature stamps A used to process the payroll checks. In interviews with Mr. Sanders and Mr. Lloyd Monger, the chief executive officer, both said they trusted Ms. Cheatwood with their signature stamps. In December 2008, the Hospital changed its day-to-day business operations software system, which included the accounting and payroll systems. According to Ms. Booker, she and Ms. Cheatwood attended a software training session and learned that only the first payroll run made automatic deductions to employees ATO balances. Supplemental payroll runs are typically used for ATO payouts and to correct errors and do not automatically adjust employee ATO balances; therefore, a manual adjustment to an employee s ATO balance is required. Ms. Booker said that a couple of days after this training, Ms. Cheatwood said, Did you hear that? We can sell ATO time and not deduct it. Ms. Booker stated that shortly after the training, Ms. Cheatwood called her and wanted to sell ATO and not deduct the hours from her ATO balance. Ms. Booker stated that she told Ms. Cheatwood she was going to do the same thing and thought it was okay because they were friends. Ms. Booker added that both she and Ms. Cheatwood knew what they were doing and that the ATO payouts would not reduce their ATO balances. A Lloyd Monger - Chief Executive Officer, David Sanders - Chief Financial Officer, and one for the Board president. 4

12 Jackson Parish Hospital Service District No. 1 Findings and Recommendations The first three occasions of ATO payouts after the software training for Ms. Cheatwood and Ms. Booker were on the same days for the same number of hours as listed in the following table. First Three ATO Payouts to Ms. Cheatwood and Ms. Booker Date of ATO Payout Number of Hours for Elizabeth Cheatwood Number of Hours for Vickie Booker January 9, January 23, March 20, Hospital payroll records show Ms. Booker received ATO payouts 53 times totaling $52,763 and Ms. Cheatwood received ATO payouts 38 times totaling $52,584. The ATO payouts received by Ms. Cheatwood and Ms. Booker did not result in a reduction of either employee s ATO balances. During our audit, we applied all ATO payouts to the ATO balances of Ms. Cheatwood and Ms. Booker and discovered that their actual ATO balances were negative as of July 2009 (Ms. Cheatwood) and March 2010 (Ms. Booker) through their last date of employment with the Hospital in ATO Balances in Hours for Ms. Cheatwood and Ms. Booker Employee January 2009 December 2009 December 2010 December 2011 December 2012 December 2013 At termination E. Cheatwood (89.17) (432.09) (728.51) (1,098.43) (1,599.35) (1,848.35) V. Booker (381.19) (1,046.03) (1,574.87) (2,055.71) (2,484.21) Once they had negative ATO balances, neither Ms. Cheatwood nor Ms. Booker were entitled to receive the ATO payouts they initiated and authorized for themselves. As a result, Ms. Cheatwood received $46,947 in excess ATO payouts and Ms. Booker received $43,013 in excess ATO payouts. Ms. Booker stated that neither she nor Ms. Cheatwood would complete the proper forms or obtain proper approval to sell their ATO. Ms. Cheatwood s and Ms. Booker s personnel files contained approved ATO forms for payouts they received prior to 2009, but there were no forms for ATO payouts received in or after Since Ms. Cheatwood s job duties included the Human Resources function, Ms. Cheatwood was responsible for maintaining employee files. We telephoned Ms. Cheatwood s attorney multiple times to request an interview with Ms. Cheatwood, but he would not return our calls. Ms. Booker stated that when Ms. Cheatwood wanted an ATO payout, Ms. Cheatwood called Ms. Booker and told Ms. Booker how many hours to use. Ms. Booker had possession of the blank payroll account checks in her office and had the authority to print the checks at her desk; Ms. Cheatwood had possession of three Hospital officials signature stamps to authorize the ATO payout checks. Mr. Sanders stated that he reviewed and approved the payroll reports before the checks were distributed but was not aware that Ms. Cheatwood and Ms. Booker were receiving 5

13 Jackson Parish Hospital Service District No. 1 Findings and Recommendations unearned and unauthorized ATO payouts. Mr. Sanders also said that both Ms. Cheatwood and Ms. Booker agreed to make restitution. The Hospital terminated Ms. Cheatwood on December 5, 2014, and Ms. Booker on December 8, Since Ms. Cheatwood and Ms. Booker did not obtain the proper authorization as required by Hospital policy and did not have available ATO hours to cash out, they may have violated state and federal law. 1,2,3,4,5 Ms. Booker also indicated in her interview that three additional employees were aware that they received an additional ATO payout without having their ATO balance reduced. Hospital records show that each of the three employees received numerous ATO payouts without a corresponding deduction to their ATO balances. After adjusting the ATO balance of these three employees for the ATO payouts they received, all three had negative balances between 359 and 653 hours as of December 5, One of the three employees stated she knew that on at least one occasion she received an ATO payout without having it deducted from her balance. She said she paid Ms. Booker $100 for receiving the ATO payout without a deduction to her ATO balance. This employee reviewed the endorsements on the back of all 19 checks payable to her for ATO payouts and claimed that she did not recognize her signature on eight checks. The second employee stated that she received an ATO payout and noticed that her ATO balance was not reduced. She asked Ms. Booker about why her ATO balance was not reduced and Ms. Booker told her that it was a favor and refused to correct it. This employee reviewed the endorsements on the back of all 13 checks payable to her for ATO payouts and identified one check where she did not recognize her signature. The third employee said that he did not know his ATO payouts were not being deducted from his ATO balance and that Ms. Booker had never approached him about an ATO payout without deducting it from his balance. He reviewed the endorsements on the back of all 41 checks payable to him for ATO payouts and identified five checks that he claimed were not endorsed by him. Ms. Booker did not recall printing checks with other employees names as the payee and cashing them for her use. She said she took checks to the bank for employees on a regular basis if a coworker asked. Ms. Booker also said on occasion she forgot to manually deduct employees ATO leave balances for ATO payouts. 6

14 Jackson Parish Hospital Service District No. 1 Findings and Recommendations Improper Payroll Deductions for Supplemental Insurance and Uniforms Ms. Cheatwood and Ms. Booker improperly received a combined $25,723 of supplemental health insurance policies and $7,474 of uniforms offered through the Hospital from December 2008 to December Based on our review of Hospital records, Ms. Cheatwood and Ms. Booker did not pay for these benefits and, as such, may have violated state and federal law. 1,2,3,4,5 The Hospital allowed its employees to purchase supplemental health insurance, uniforms, medication, and Sam s Club memberships from outside vendors. The Hospital paid the vendors on the employee s behalf and should have deducted the funds from the employee s payroll checks to recoup 100% of the amount the Hospital paid. Ms. Cheatwood was responsible for the Hospital s Human Resources function, which included entering payroll deductions for employee supplemental insurance. Ms. Booker stated that Ms. Cheatwood entered most payroll deductions to the payroll system. According to Hospital records, Ms. Cheatwood also entered her own payroll deductions. Ms. Cheatwood had numerous insurance policies that were offered through the Hospital. We compared the insurance invoices the Hospital paid for Ms. Cheatwood s insurance to her payroll deductions from 2009 to Those records show that Ms. Cheatwood received $19,414 of insurance that was not repaid through her payroll deductions. We telephoned Ms. Cheatwood s attorney multiple times to request an interview with Ms. Cheatwood, but he would not return our calls. Hospital records also show that Ms. Booker made numerous adjustments to her payroll deductions for supplemental insurance policies she obtained through the Hospital. We compared the insurance invoices the Hospital paid for Ms. Booker s insurance to her payroll deductions from 2009 to Those records show Ms. Booker received $6,309 of insurance that was not repaid through her payroll deductions. Ms. Booker claimed that she did not know her payroll deductions for supplemental insurance were less than the amount due to the Hospital. Since Ms. Cheatwood and Ms. Booker did not pay for the benefits they received, they may have violated state and federal law. 1,2,3,4,5 Uniforms The Hospital allowed its employees to purchase uniforms from a uniform company. The Hospital paid the uniform company in a lump sum and recovered those funds from employees through payroll deductions. Ms. Booker stated that she and Ms. Cheatwood purchased uniforms through the Hospital but never deducted the amounts they owed to the Hospital. According to Hospital records, Ms. Cheatwood received $2,779 of uniforms that she did not pay for, and Ms. Booker received $4,695 of uniforms for which she did not pay from December 2008 through December Since Ms. Cheatwood and Ms. Booker did not reimburse the Hospital for the uniforms they received, they may have violated state and federal law. 1,2,3,4,5 7

15 Jackson Parish Hospital Service District No. 1 Findings and Recommendations Mismanagement of Payroll Deductions The Hospital did not reconcile its health and supplemental insurance invoices or other employee benefits to payroll deductions to ensure the Hospital received the proper amount from its employees. This resulted in undetected errors to employee payroll deductions and caused the Hospital to pay $200,997 for employee benefits that were not reimbursed by its employees from 2009 to Since the Hospital did not collect all amounts due from employees, the payments on behalf of employees without reimbursement may violate state law and the state constitution. 4,6 We reconciled the Hospital s health and supplemental insurance payments to employee payroll deductions from January 2009 to December The reconciliation showed that the Hospital had paid $200,997 more than it had collected from employees through payroll deductions. The table below shows the results of the reconciliation and the amount the Hospital did not collect from its employees by year. Reconciliation of Payroll Deductions to Health Insurance and Supplemental Insurance Invoices Amount Paid to Employee Year Health Insurance Providers By Hospital Amount Deducted from Employees Pay Amount Under- Deducted 2009 $238,347 $210,136 ($28,212) , ,930 (28,843) , ,403 (26,221) , ,521 (41,359) , ,794 (45,487) , ,143 (30,875) Totals $2,437,923 $2,236,927 ($200,997) Mr. Sanders said that he reconciled the payroll deductions monthly in the payroll system with what the Hospital was invoiced and assumed the monthly shortfall was due to the doctor s portion of the Hospital s health insurance invoice and he plugged the difference. This means Mr. Sanders posted the shortfall, or under collection, to the accounting system and did not investigate the differences to determine why the payroll deductions were less than the insurance invoices. According to Mr. Sanders and Mr. Monger, the Hospital has employee contracts with its doctors that require the Hospital to pay 100% of the doctors health insurance premiums. The health insurance invoice typically included coverage for two doctors per month, but there were five different doctors on the invoice during the six-year period due to doctors leaving and the Hospital hiring new doctors. The Hospital could only provide three signed employment contracts with doctors named on the health insurance invoices. One of those contracts with a doctor called for the Hospital to pay 100% of family coverage, and the other two contracts with doctors required the doctors be treated as regular employees for health insurance (receive a stipend instead of health insurance). This means the Hospital misinterpreted two of the contracts and improperly paid 100% of the doctors health insurance. 8

16 Jackson Parish Hospital Service District No. 1 Findings and Recommendations Mr. Sanders stated that he trusted Ms. Cheatwood and assumed that she was doing her job and keeping the employees payroll deductions up to date in the system. Since Ms. Cheatwood was responsible for maintaining the employee payroll deductions and there were significant shortages to her deductions, we reconciled employee payroll deductions and health insurance and supplemental insurance invoices for one month for all employees. For the month of December 2014, the Hospital paid $4,724 more than required for employee benefits. The results of that reconciliation are in the following table. Reconciliation of Payroll Deductions for Health and Supplemental Insurance By Employee for December 2014 Number of Employees Amount Totals Employees Under-Deducted more than $5 61 ($5,103) B Employees Correctly-Deducted within $5 92 (5) Employees Over-Deducted more than $ Totals 162 ($4,724) Additional factors that contributed to the shortfall in employee payroll deductions included several employees who were listed on vendor invoices but no longer worked for the Hospital, one as far back as February Also, several employees did not have payroll checks for the time period reconciled due to extended leave of absence, but the Hospital continued to pay their insurance and did not collect funds from these employees to continue their insurance coverage. The Hospital s policy manual addresses employee insurance when the employee is on an extended leave of absence; however, the policy was not followed, and it appears the Hospital continued to pay employee premiums for the employees on extended leave. Additional Services and Products The Hospital allowed its employees to receive medication from the Hospital pharmacy and receive Sam s Club memberships. The Hospital s practice was to provide the employees with medication from the pharmacy and pay Sam s Club memberships and recover its funds through after-the-fact payroll deductions from the employee. However, the Hospital could not produce detailed records for prescription drugs received by employees, and the Sam s Club invoice paid by the Hospital did not contain enough detail to identify all employees who received a membership. Given that the Hospital did not have detailed records, it is unlikely the Hospital recovered all the public funds used for its employee pharmacy and Sam s Club membership costs. B This amount includes $828 for the doctor s portion of the Blue Cross Blue Shield medical insurance. 9

17 Jackson Parish Hospital Service District No. 1 Findings and Recommendations Improper Insurance Stipend Payment Ms. Cheatwood received a stipend for health insurance in the amount of $26,072 from January 1, 2009 to December 31, Based on our review of Hospital records, Ms. Cheatwood was not entitled to receive these funds and, therefore, may have violated state and federal law. 1,2,3,4,5 From January 2009 to December 2014, the Hospital did not provide a group health insurance policy for its employees due to the increasing cost of insurance. To replace this benefit, the Hospital allowed its employees to either use the Hospital services at no charge or receive a stipend to offset the cost to employees of personally purchased health insurance policies. The Hospital s policy required each employee to provide proof of insurance twice a year to receive the stipend. In 2009, the maximum stipend was $ per month. The stipend escalated to $500 per month in According to Hospital employees, Ms. Cheatwood was responsible for verifying employees proof of insurance and establishing the payment within the Hospital s accounts payable system. There was no evidence of proof of insurance in Ms. Cheatwood s human resources file for the period 2009 to Hospital records show Ms. Cheatwood received the maximum (or within $35 of the maximum) stipend for health insurance from 2009 to 2014, which totaled $26,072. In fact, according to records from her spouse s former employer, Ms. Cheatwood received no-cost health insurance from 2009 to 2014 through her husband s employer and, therefore, was not eligible to receive a stipend from the Hospital. Because Ms. Cheatwood received a health insurance stipend from the Hospital without incurring any personal cost for her health insurance, she may have violated state and federal law. 1,2,3,4,5 Former Employee Took Hospital Collections for Personal Use Hospital records indicate that from January 2012 to December 2014, the Hospital collected $121,968 in cash that was never deposited into its operating bank account. Former Hospital employee, Ms. Vickie Booker, stated that she took cash from Hospital collections and deposited it to her personal bank account or spent it. By taking cash from Hospital collections for her personal use, Ms. Booker may have violated state law. 1,2,3,4,5 Hospital records show that from January 2012 to December 2014, the Hospital collected $392,341 in cash; however, only $270,373 of these cash collections were deposited to the Hospital s operating bank account. Ms. Booker stated that she took cash from Hospital collections for her personal use or deposited the cash to her personal bank account. Ms. Booker acknowledged taking $200 to $300 per week, but denied taking the entire $121,968 of missing cash. Since Ms. Booker converted the Hospital s cash collections for her personal use, she may have violated state law. 1,2,3,4,5 10

18 Jackson Parish Hospital Service District No. 1 Findings and Recommendations Mr. Sanders stated he has not been able to reconcile the Hospital s accounting records to the bank account for many years. In fact, Mr. Sanders stated that he plugged unreconciled cash differences to the contractual allowance for commercial insurance account. This means when the bank records show a different amount than the Hospital s records, Mr. Sanders adjusted the Hospital s records to match the bank s records. Hospital records also show that collections were rarely deposited within a day and were often misclassified. State law requires daily deposits when practicable. 7 In addition, the Hospital s records were incomplete. We found that some copies of payments made by Hospital employees were missing. Those records would indicate if the payment was made by cash or check. However, since some records were missing, we could not determine the exact amount of cash missing from the Hospital as a result of Ms. Booker s actions. 11

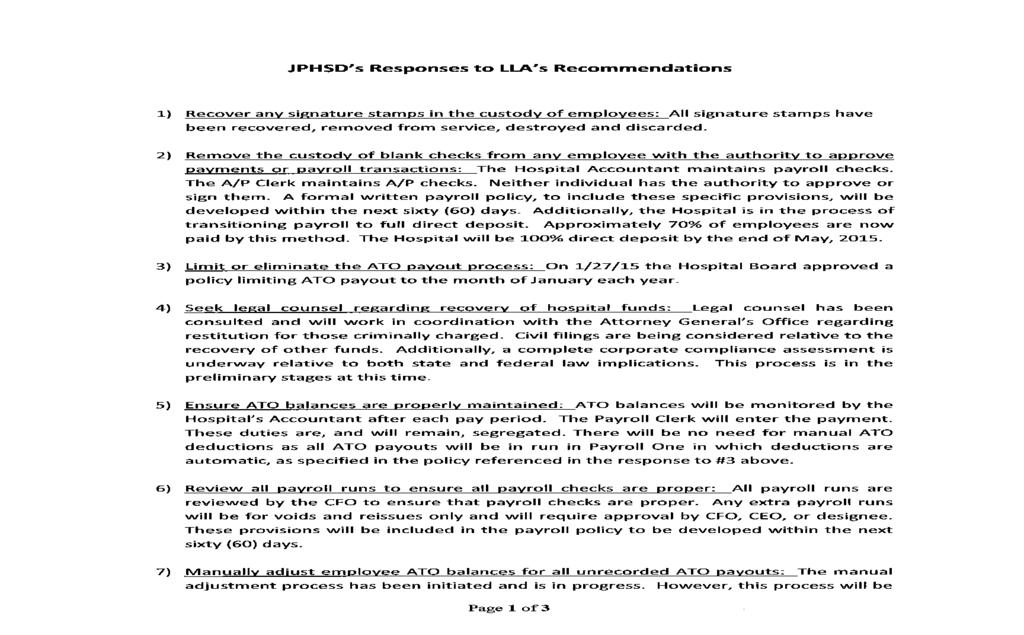

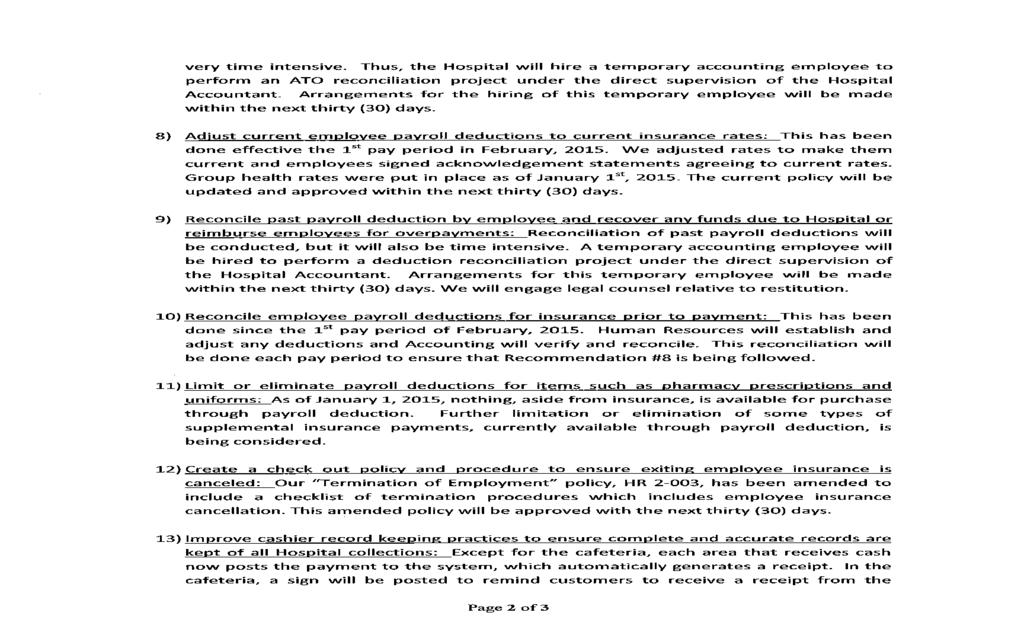

19 Jackson Parish Hospital Service District No. 1 Findings and Recommendations Recommendations We recommend the Hospital: (1) recover any signature stamps in the custody of employees; (2) remove the custody of blank checks from any employee with authority to approve payments or payroll transactions within the accounting system; (3) limit or eliminate the ATO payout practice; (4) seek legal counsel regarding recovery of Hospital funds; (5) ensure ATO balances are properly maintained; (6) review all payroll runs to ensure all payroll checks are proper; (7) manually adjust employee ATO balances for all unrecorded ATO payouts; (8) adjust current employee payroll deductions to current insurance rates; (9) reconcile past payroll deduction by employee and recover any funds due to Hospital or reimburse employees for overpayments; (10) reconcile employee payroll deductions for insurance prior to payment; (11) limit or eliminate payroll deductions for items such as pharmacy prescriptions and uniforms; (12) create a check-out policy and procedure to ensure exiting employee insurance is canceled; (13) improve cashier record keeping practices to ensure complete and accurate records are kept of all Hospital collections; (14) reconcile collections to deposits and investigate any discrepancies; (15) establish a chain of custody of collections; and (16) make daily deposits when practicable. 12

20

21 LEGAL PROVISIONS 1 Louisiana Revised Statute (La. R.S.) 14:67 (A) provides that, Theft is the misappropriation or taking of anything of value which belongs to another, either without the consent of the other to the misappropriation or taking, or by means of fraudulent conduct, practices, or representations. An intent to deprive the other permanently of whatever may be the subject of the misappropriation or taking is essential. 2 La. R.S. 14:134 (A) provides, in part, Malfeasance in office is committed when any public officer or public employee shall: (1) Intentionally refuse or fail to perform any duty lawfully required of him, as such officer or employee; or (2) Intentionally perform any such duty in an unlawful manner. 3 La. R.S. 14:230 (B) provides that, It is unlawful for any person knowingly to do any of the following: (1) Conduct, supervise, or facilitate a financial transaction involving proceeds known to be derived from criminal activity, when the transaction is designed in whole or in part to conceal or disguise the nature, location, source, ownership, or the control of proceeds known to be derived from such violation or to avoid a transaction reporting requirement under state or federal law. (2) Give, sell, transfer, trade, invest, conceal, transport, maintain an interest in, or otherwise make available anything of value known to be for the purpose of committing or furthering the commission of any criminal activity. (3) Direct, plan, organize, initiate, finance, manage, supervise, or facilitate the transportation or transfer of proceeds known to be derived from any violation of criminal activity. (4) Receive or acquire proceeds derived from any violation of criminal activity, or knowingly or intentionally engage in any transaction that the person knows involves proceeds from any such violations. (5) Acquire or maintain an interest in, receive, conceal, possess, transfer, or transport the proceeds of criminal activity. (6) Invest, expend, or receive, or offer to invest, expend, or receive, the proceeds of criminal activity. 4 La. R.S. 42:1461 (A) provides that, Officials, whether elected or appointed and whether compensated or not, and employees of any public entity, which, for purposes of this Section shall mean and include any department, division, office, board, agency, commission, or other organizational unit of any of the three branches of state government or of any parish, municipality, school board or district, court of limited jurisdiction, or other political subdivision or district, or the office of any sheriff, district attorney, coroner, or clerk of court, by the act of accepting such office or employment assume a personal obligation not to misappropriate, misapply, convert, misuse, or otherwise wrongfully take any funds, property, or other thing of value belonging to or under the custody or control of the public entity in which they hold office or are employed U.S.C.A states, in part, (a)(1) Whoever, knowing that the property involved in a financial transaction represents the proceeds of some form of unlawful activity, conducts or attempts to conduct such a financial transaction represents the proceeds of some form of unlawful activity, conducts or attempts to conduct such a financial transaction which in fact involves the proceeds of specified unlawful activity (A)(i) with the intent to promote the carrying on of specified unlawful activity; or (B) knowing that the transaction is designed in whole or in part (i) to conceal or disguise the nature, the location, the source, the ownership, or the control of the proceeds of specified unlawful activity. 6 Louisiana Constitution Article VII, Section 14(A) provides, in part, that, Prohibited Uses. Except as otherwise provided by this constitution, the funds, credit, property, or things of value of the state or of any political subdivision shall not be loaned, pledged, or donated to or for any person, association, or corporation, public or private. 7 La. R.S. 39:1211 states, The term, local depositing authorities, includes all parishes, municipalities, boards, commissions, sheriffs and tax collectors, judges, clerks of court, and any other public bodies or officers of any parish, municipality or township, but it does not include the state and its elected officials, and state commissions, boards, and other state agencies. La. R.S. 39:1212 states, After the expiration of existing contracts, all funds of local depositing authorities shall be deposited daily whenever practicable, in the fiscal agency provided for, upon the terms and conditions, and in the manner set forth in this Chapter. Deposits shall be made in the name of the depositing authority authorized by law to have custody and control over the disbursements. 13

22

23 APPENDIX A Management s Response

24

25 A.1

26 A.2

27 A.3

28 A.4

ST. BERNARD CULTURAL CENTER, INC.

ST. BERNARD CULTURAL CENTER, INC. INVESTIGATIVE AUDIT JANUARY 21, 2015 LOUISIANA LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET POST OFFICE BOX 94397 BATON ROUGE, LOUISIANA 70804-9397 LEGISLATIVE AUDITOR

ST. BERNARD CULTURAL CENTER, INC. INVESTIGATIVE AUDIT JANUARY 21, 2015 LOUISIANA LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET POST OFFICE BOX 94397 BATON ROUGE, LOUISIANA 70804-9397 LEGISLATIVE AUDITOR

TOWN OF BALDWIN INVESTIGATIVE AUDIT ISSUED JANUARY 6, 2016

TOWN OF BALDWIN INVESTIGATIVE AUDIT ISSUED JANUARY 6, 2016 LOUISIANA LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET POST OFFICE BOX 94397 BATON ROUGE, LOUISIANA 70804-9397 LEGISLATIVE AUDITOR DARYL G. PURPERA,

TOWN OF BALDWIN INVESTIGATIVE AUDIT ISSUED JANUARY 6, 2016 LOUISIANA LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET POST OFFICE BOX 94397 BATON ROUGE, LOUISIANA 70804-9397 LEGISLATIVE AUDITOR DARYL G. PURPERA,

TOWN OF EVERGREEN COMPLIANCE AUDIT ISSUED OCTOBER 18, 2006

TOWN OF EVERGREEN COMPLIANCE AUDIT ISSUED OCTOBER 18, 2006 LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET POST OFFICE BOX 94397 BATON ROUGE, LOUISIANA 70804-9397 LEGISLATIVE AUDIT ADVISORY COUNCIL SENATOR

TOWN OF EVERGREEN COMPLIANCE AUDIT ISSUED OCTOBER 18, 2006 LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET POST OFFICE BOX 94397 BATON ROUGE, LOUISIANA 70804-9397 LEGISLATIVE AUDIT ADVISORY COUNCIL SENATOR

March 30, School Board Improperly Paid Stipends to Employees

LOUISIANA LEGISLATIVE AUDITOR DARYL G. PURPERA, CPA, CFE March 30, 2017 Ronald Kevin Lemoine, Superintendent, and Members of the Pointe Coupee Parish School Board 337 Napoleon Street New Roads, Louisiana

LOUISIANA LEGISLATIVE AUDITOR DARYL G. PURPERA, CPA, CFE March 30, 2017 Ronald Kevin Lemoine, Superintendent, and Members of the Pointe Coupee Parish School Board 337 Napoleon Street New Roads, Louisiana

RENEW CHARTER MANAGEMENT ORGANIZATION

RENEW CHARTER MANAGEMENT ORGANIZATION INVESTIGATIVE AUDIT ISSUED MAY 28, 2014 LOUISIANA LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET POST OFFICE BOX 94397 BATON ROUGE, LOUISIANA 70804-9397 LEGISLATIVE AUDITOR

RENEW CHARTER MANAGEMENT ORGANIZATION INVESTIGATIVE AUDIT ISSUED MAY 28, 2014 LOUISIANA LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET POST OFFICE BOX 94397 BATON ROUGE, LOUISIANA 70804-9397 LEGISLATIVE AUDITOR

LOUISIANA INTERNATIONAL DEEP WATER GULF TRANSFER TERMINAL AUTHORITY STATE OF LOUISIANA

LOUISIANA INTERNATIONAL DEEP WATER GULF TRANSFER TERMINAL AUTHORITY STATE OF LOUISIANA FINANCIAL AUDIT SERVICES PROCEDURAL REPORT ISSUED DECEMBER 27, 2017 LOUISIANA LEGISLATIVE AUDITOR 1600 NORTH THIRD

LOUISIANA INTERNATIONAL DEEP WATER GULF TRANSFER TERMINAL AUTHORITY STATE OF LOUISIANA FINANCIAL AUDIT SERVICES PROCEDURAL REPORT ISSUED DECEMBER 27, 2017 LOUISIANA LEGISLATIVE AUDITOR 1600 NORTH THIRD

GRAMBLING STATE UNIVERSITY UNIVERSITY OF LOUISIANA SYSTEM STATE OF LOUISIANA

GRAMBLING STATE UNIVERSITY UNIVERSITY OF LOUISIANA SYSTEM STATE OF LOUISIANA MANAGEMENT LETTER ISSUED JANUARY 18, 2012 LOUISIANA LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET POST OFFICE BOX 94397 BATON

GRAMBLING STATE UNIVERSITY UNIVERSITY OF LOUISIANA SYSTEM STATE OF LOUISIANA MANAGEMENT LETTER ISSUED JANUARY 18, 2012 LOUISIANA LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET POST OFFICE BOX 94397 BATON

MADISON PARISH HOSPITAL SERVICE DISTRICT

MADISON PARISH HOSPITAL SERVICE DISTRICT INVESTIGATIVE AUDIT ISSUED JANUARY 2, 2013 LOUISIANA LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET POST OFFICE BOX 94397 BATON ROUGE, LOUISIANA 70804-9397 LEGISLATIVE

MADISON PARISH HOSPITAL SERVICE DISTRICT INVESTIGATIVE AUDIT ISSUED JANUARY 2, 2013 LOUISIANA LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET POST OFFICE BOX 94397 BATON ROUGE, LOUISIANA 70804-9397 LEGISLATIVE

DEPARTMENT OF PUBLIC SAFETY AND CORRECTIONS - CORRECTIONS SERVICES STATE OF LOUISIANA

DEPARTMENT OF PUBLIC SAFETY AND CORRECTIONS - CORRECTIONS SERVICES STATE OF LOUISIANA FINANCIAL AUDIT SERVICES PROCEDURAL REPORT ISSUED JUNE 17, 2015 LOUISIANA LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET

DEPARTMENT OF PUBLIC SAFETY AND CORRECTIONS - CORRECTIONS SERVICES STATE OF LOUISIANA FINANCIAL AUDIT SERVICES PROCEDURAL REPORT ISSUED JUNE 17, 2015 LOUISIANA LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET

THE MUNICIPAL EMPLOYEES RETIREMENT SYSTEM OF LOUISIANA

THE MUNICIPAL EMPLOYEES RETIREMENT SYSTEM OF LOUISIANA INVESTIGATIVE AUDIT DECEMBER 2, 2015 LOUISIANA LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET POST OFFICE BOX 94397 BATON ROUGE, LOUISIANA 70804-9397

THE MUNICIPAL EMPLOYEES RETIREMENT SYSTEM OF LOUISIANA INVESTIGATIVE AUDIT DECEMBER 2, 2015 LOUISIANA LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET POST OFFICE BOX 94397 BATON ROUGE, LOUISIANA 70804-9397

MEDICAL ASSISTANCE PROGRAMS FRAUD DETECTION FUND LOUISIANA DEPARTMENT OF HEALTH AND OFFICE OF THE LOUISIANA ATTORNEY GENERAL

MEDICAL ASSISTANCE PROGRAMS FRAUD DETECTION FUND LOUISIANA DEPARTMENT OF HEALTH AND OFFICE OF THE LOUISIANA ATTORNEY GENERAL PERFORMANCE AUDIT SERVICES JULY 25, 2018 LOUISIANA LEGISLATIVE AUDITOR 1600

MEDICAL ASSISTANCE PROGRAMS FRAUD DETECTION FUND LOUISIANA DEPARTMENT OF HEALTH AND OFFICE OF THE LOUISIANA ATTORNEY GENERAL PERFORMANCE AUDIT SERVICES JULY 25, 2018 LOUISIANA LEGISLATIVE AUDITOR 1600

ATHLETIC DEPARTMENT UNIVERSITY OF LOUISIANA AT LAFAYETTE UNIVERSITY OF LOUISIANA SYSTEM STATE OF LOUISIANA

ATHLETIC DEPARTMENT UNIVERSITY OF LOUISIANA AT LAFAYETTE UNIVERSITY OF LOUISIANA SYSTEM STATE OF LOUISIANA AGREED-UPON PROCEDURES REPORT ISSUED FEBRUARY 4, 2015 LOUISIANA LEGISLATIVE AUDITOR 1600 NORTH

ATHLETIC DEPARTMENT UNIVERSITY OF LOUISIANA AT LAFAYETTE UNIVERSITY OF LOUISIANA SYSTEM STATE OF LOUISIANA AGREED-UPON PROCEDURES REPORT ISSUED FEBRUARY 4, 2015 LOUISIANA LEGISLATIVE AUDITOR 1600 NORTH

CORRECTIONS SERVICES DEPARTMENT OF PUBLIC SAFETY AND CORRECTIONS STATE OF LOUISIANA

CORRECTIONS SERVICES DEPARTMENT OF PUBLIC SAFETY AND CORRECTIONS STATE OF LOUISIANA MANAGEMENT LETTER ISSUED APRIL 12, 2006 LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET POST OFFICE BOX 94397 BATON ROUGE,

CORRECTIONS SERVICES DEPARTMENT OF PUBLIC SAFETY AND CORRECTIONS STATE OF LOUISIANA MANAGEMENT LETTER ISSUED APRIL 12, 2006 LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET POST OFFICE BOX 94397 BATON ROUGE,

DEPARTMENT OF EDUCATION STATE OF LOUISIANA

DEPARTMENT OF EDUCATION STATE OF LOUISIANA FINANCIAL AUDIT SERVICES MANAGEMENT LETTER ISSUED NOVEMBER 26, 2014 LOUISIANA LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET POST OFFICE BOX 94397 BATON ROUGE, LOUISIANA

DEPARTMENT OF EDUCATION STATE OF LOUISIANA FINANCIAL AUDIT SERVICES MANAGEMENT LETTER ISSUED NOVEMBER 26, 2014 LOUISIANA LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET POST OFFICE BOX 94397 BATON ROUGE, LOUISIANA

LOUISIANA LEGISLATIVE AUDITOR DARYL G. PURPERA, CPA, CFE. March 11, 2015

LOUISIANA LEGISLATIVE AUDITOR DARYL G. PURPERA, CPA, CFE The Honorable Jeffrey Rouse, M.D. 2612 Martin Luther King Blvd. New Orleans, Louisiana 70113 Dear Dr. Rouse: At your request upon assuming office,

LOUISIANA LEGISLATIVE AUDITOR DARYL G. PURPERA, CPA, CFE The Honorable Jeffrey Rouse, M.D. 2612 Martin Luther King Blvd. New Orleans, Louisiana 70113 Dear Dr. Rouse: At your request upon assuming office,

UNIVERSITY OF LOUISIANA AT MONROE UNIVERSITY OF LOUISIANA SYSTEM STATE OF LOUISIANA

UNIVERSITY OF LOUISIANA AT MONROE UNIVERSITY OF LOUISIANA SYSTEM STATE OF LOUISIANA MANAGEMENT LETTER ISSUED FEBRUARY 23, 2011 LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET POST OFFICE BOX 94397 BATON ROUGE,

UNIVERSITY OF LOUISIANA AT MONROE UNIVERSITY OF LOUISIANA SYSTEM STATE OF LOUISIANA MANAGEMENT LETTER ISSUED FEBRUARY 23, 2011 LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET POST OFFICE BOX 94397 BATON ROUGE,

OFFICE OF THE VIRGIN ISLANDS INSPECTOR GENERAL

September 4, 2018 AR-01-39-18 THE UNITED STATES VIRGIN ISLANDS OFFICE OF THE VIRGIN ISLANDS INSPECTOR GENERAL AUDIT OF THE ADMINISTRATIVE FUNCTIONS OF THE VIRGIN ISLANDS CASINO CONTROL COMMISSION ILLEGAL

September 4, 2018 AR-01-39-18 THE UNITED STATES VIRGIN ISLANDS OFFICE OF THE VIRGIN ISLANDS INSPECTOR GENERAL AUDIT OF THE ADMINISTRATIVE FUNCTIONS OF THE VIRGIN ISLANDS CASINO CONTROL COMMISSION ILLEGAL

OVERSIGHT OF SURVEILLANCE AND UTILIZATION REVIEW SUBSYSTEM (SURS) MEDICAID PROGRAM INTEGRITY ACTIVITIES LOUISIANA DEPARTMENT OF HEALTH

MEDICAID PROGRAM INTEGRITY ACTIVITIES LOUISIANA DEPARTMENT OF HEALTH") OVERSIGHT OF SURVEILLANCE AND UTILIZATION REVIEW SUBSYSTEM (SURS) MEDICAID PROGRAM INTEGRITY ACTIVITIES LOUISIANA DEPARTMENT OF HEALTH PERFORMANCE AUDIT SERVICES ISSUED DECEMBER 5, 2018 LOUISIANA LEGISLATIVE

OVERSIGHT OF SURVEILLANCE AND UTILIZATION REVIEW SUBSYSTEM (SURS) MEDICAID PROGRAM INTEGRITY ACTIVITIES LOUISIANA DEPARTMENT OF HEALTH PERFORMANCE AUDIT SERVICES ISSUED DECEMBER 5, 2018 LOUISIANA LEGISLATIVE

GLASA. Greater Los Angeles Softball Association. Accounting Policies & Procedures Manual

GLASA Greater Los Angeles Softball Association Accounting Policies & Procedures Manual 7/2015 TABLE OF CONTENTS I. General Practices... 1 II. Cash Receipts... 2 III. Cash Disbursements... 3 IV. Other Financial

GLASA Greater Los Angeles Softball Association Accounting Policies & Procedures Manual 7/2015 TABLE OF CONTENTS I. General Practices... 1 II. Cash Receipts... 2 III. Cash Disbursements... 3 IV. Other Financial

May 22, The Honorable Mayor and Members of City Commission City of Margate 1 South Washington Avenue Margate, N.J

May 22, 2012 The Honorable Mayor and Members of City Commission City of Margate 1 South Washington Avenue Margate, N.J. 08204 Dear Mayor and Commissioners: We have audited the financial statements of the

May 22, 2012 The Honorable Mayor and Members of City Commission City of Margate 1 South Washington Avenue Margate, N.J. 08204 Dear Mayor and Commissioners: We have audited the financial statements of the

MANAGEMENT CONTROLS, ACCURACY, AND RELIABILITY OF PROGRAM DATA REPORTED LOUISIANA ECONOMIC DEVELOPMENT

MANAGEMENT CONTROLS, ACCURACY, AND RELIABILITY OF PROGRAM DATA REPORTED IN THE UNIFIED ECONOMIC DEVELOPMENT BUDGET REPORT LOUISIANA ECONOMIC DEVELOPMENT PERFORMANCE AUDIT SERVICES ISSUED NOVEMBER 28, 2018

MANAGEMENT CONTROLS, ACCURACY, AND RELIABILITY OF PROGRAM DATA REPORTED IN THE UNIFIED ECONOMIC DEVELOPMENT BUDGET REPORT LOUISIANA ECONOMIC DEVELOPMENT PERFORMANCE AUDIT SERVICES ISSUED NOVEMBER 28, 2018

LOUISIANA SCHOOL EMPLOYEES RETIREMENT SYSTEM A COMPONENT UNIT OF THE STATE OF LOUISIANA

LOUISIANA SCHOOL EMPLOYEES RETIREMENT SYSTEM A COMPONENT UNIT OF THE STATE OF LOUISIANA FINANCIAL STATEMENT AUDIT FOR THE YEARS ENDED JUNE 30, 2018, AND 2017 ISSUED SEPTEMBER 28, 2018 LOUISIANA LEGISLATIVE

LOUISIANA SCHOOL EMPLOYEES RETIREMENT SYSTEM A COMPONENT UNIT OF THE STATE OF LOUISIANA FINANCIAL STATEMENT AUDIT FOR THE YEARS ENDED JUNE 30, 2018, AND 2017 ISSUED SEPTEMBER 28, 2018 LOUISIANA LEGISLATIVE

RS 39:1301 RS 39:1302

RS 39:1301 CHAPTER 9. LOUISIANA LOCAL GOVERNMENT BUDGET ACT 1301. Short title This Chapter may be cited as the "Louisiana Local Government Budget Act." Added by Acts 1980, No. 504, 1, eff. Sept. 1, 1980.

RS 39:1301 CHAPTER 9. LOUISIANA LOCAL GOVERNMENT BUDGET ACT 1301. Short title This Chapter may be cited as the "Louisiana Local Government Budget Act." Added by Acts 1980, No. 504, 1, eff. Sept. 1, 1980.

LOUISIANA COMPLIANCE QUESTIONNAIRE (For Audit Engagements)

") Dear Chief Executive Officer: LOUISIANA COMPLIANCE QUESTIONNAIRE (For Audit Engagements) Attached is the Louisiana Compliance Questionnaire that is to be completed by you or your staff. This questionnaire

Dear Chief Executive Officer: LOUISIANA COMPLIANCE QUESTIONNAIRE (For Audit Engagements) Attached is the Louisiana Compliance Questionnaire that is to be completed by you or your staff. This questionnaire

TOWN OF WHITE CASTLE COMPLIANCE AUDIT ISSUED MAY 2, 2007

TOWN OF WHITE CASTLE COMPLIANCE AUDIT ISSUED MAY 2, 2007 LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET POST OFFICE BOX 94397 BATON ROUGE, LOUISIANA 70804-9397 LEGISLATIVE AUDIT ADVISORY COUNCIL SENATOR J.

TOWN OF WHITE CASTLE COMPLIANCE AUDIT ISSUED MAY 2, 2007 LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET POST OFFICE BOX 94397 BATON ROUGE, LOUISIANA 70804-9397 LEGISLATIVE AUDIT ADVISORY COUNCIL SENATOR J.

STATE OF LOUISIANA LEGISLATIVE AUDITOR

STATE OF LOUISIANA Housing Authority of Abbeville December 10, 2003 LEGISLATIVE AUDIT ADVISORY COUNCIL MEMBERS Senator J. Tom Schedler, Chairman Representative Edwin R. Murray, Vice Chairman Senator Robert

STATE OF LOUISIANA Housing Authority of Abbeville December 10, 2003 LEGISLATIVE AUDIT ADVISORY COUNCIL MEMBERS Senator J. Tom Schedler, Chairman Representative Edwin R. Murray, Vice Chairman Senator Robert

LOUISIANA LOCAL GOVERNMENT ENVIRONMENTAL FACILITIES AND COMMUNITY DEVELOPMENT AUTHORITY FINANCIAL REPORT

LOUISIANA LOCAL GOVERNMENT ENVIRONMENTAL FACILITIES AND COMMUNITY DEVELOPMENT AUTHORITY FINANCIAL REPORT DECEMBER 31, 2013 LOUISIANA LOCAL GOVERNMENT ENVIRONMENTAL FACILITIES AND COMMUNITY DEVELOPMENT

LOUISIANA LOCAL GOVERNMENT ENVIRONMENTAL FACILITIES AND COMMUNITY DEVELOPMENT AUTHORITY FINANCIAL REPORT DECEMBER 31, 2013 LOUISIANA LOCAL GOVERNMENT ENVIRONMENTAL FACILITIES AND COMMUNITY DEVELOPMENT

LOUISIANA STATE UNIVERSITY HEALTH SCIENCES CENTER - HEALTH CARE SERVICES DIVISION STATE OF LOUISIANA

LOUISIANA STATE UNIVERSITY HEALTH SCIENCES CENTER - HEALTH CARE SERVICES DIVISION STATE OF LOUISIANA MANAGEMENT LETTER ISSUED APRIL 18, 2007 LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET POST OFFICE BOX

LOUISIANA STATE UNIVERSITY HEALTH SCIENCES CENTER - HEALTH CARE SERVICES DIVISION STATE OF LOUISIANA MANAGEMENT LETTER ISSUED APRIL 18, 2007 LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET POST OFFICE BOX

LOUISIANA TECH UNIVERSITY UNIVERSITY OF LOUISIANA SYSTEM STATE OF LOUISIANA

LOUISIANA TECH UNIVERSITY UNIVERSITY OF LOUISIANA SYSTEM STATE OF LOUISIANA INDEPENDENT ACCOUNTANT S REVIEW REPORT FOR THE YEAR ENDED JUNE 30, 2013 ISSUED DECEMBER 11, 2013 LOUISIANA LEGISLATIVE AUDITOR

LOUISIANA TECH UNIVERSITY UNIVERSITY OF LOUISIANA SYSTEM STATE OF LOUISIANA INDEPENDENT ACCOUNTANT S REVIEW REPORT FOR THE YEAR ENDED JUNE 30, 2013 ISSUED DECEMBER 11, 2013 LOUISIANA LEGISLATIVE AUDITOR

Employee Benefit Plan Fraud Examples

April 2013 Employee Benefit Plan Fraud Examples The following summary of actual fraud cases was compiled from submissions by auditor of employee benefit plans. The fraud cases are grouped in the following

April 2013 Employee Benefit Plan Fraud Examples The following summary of actual fraud cases was compiled from submissions by auditor of employee benefit plans. The fraud cases are grouped in the following

Jefferson County Soil and Water Conservation District

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Jefferson County Soil and Water Conservation District Internal Controls Over Selected Financial Operations

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Jefferson County Soil and Water Conservation District Internal Controls Over Selected Financial Operations

MMAAA Annual Meeting. Conducting an Investigative Audit June 13, Presented by: John J. Sullivan, CFE Melanson Heath

MMAAA Annual Meeting Conducting an Investigative Audit June 13, 2017 Presented by: John J. Sullivan, CFE Melanson Heath Association of Certified Fraud Examiners 2016 Global Fraud Study Figure 1. Statistics

MMAAA Annual Meeting Conducting an Investigative Audit June 13, 2017 Presented by: John J. Sullivan, CFE Melanson Heath Association of Certified Fraud Examiners 2016 Global Fraud Study Figure 1. Statistics

Town of Essex. Internal Controls Over Selected Financial Operations. Report of Examination. Period Covered: January 1, 2013 October 31, M-60

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of Local Government & School Accountability Town of Essex Internal Controls Over Selected Financial Operations Report of Examination

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of Local Government & School Accountability Town of Essex Internal Controls Over Selected Financial Operations Report of Examination

MEDICAID ELIGIBILITY: MODIFIED ADJUSTED GROSS INCOME DETERMINATION PROCESS LOUISIANA DEPARTMENT OF HEALTH

MEDICAID ELIGIBILITY: MODIFIED ADJUSTED GROSS INCOME DETERMINATION PROCESS LOUISIANA DEPARTMENT OF HEALTH MEDICAID AUDIT UNIT REPORT ISSUED DECEMBER 12, 2018 LOUISIANA LEGISLATIVE AUDITOR 1600 NORTH THIRD

MEDICAID ELIGIBILITY: MODIFIED ADJUSTED GROSS INCOME DETERMINATION PROCESS LOUISIANA DEPARTMENT OF HEALTH MEDICAID AUDIT UNIT REPORT ISSUED DECEMBER 12, 2018 LOUISIANA LEGISLATIVE AUDITOR 1600 NORTH THIRD

LOCAL GOVERNMENT BOND ISSUANCE COSTS STATE BOND COMMISSION

LOCAL GOVERNMENT BOND ISSUANCE COSTS STATE BOND COMMISSION PERFORMANCE AUDIT SERVICES ISSUED JULY 11, 2018 LOUISIANA LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET POST OFFICE BOX 94397 BATON ROUGE, LOUISIANA

LOCAL GOVERNMENT BOND ISSUANCE COSTS STATE BOND COMMISSION PERFORMANCE AUDIT SERVICES ISSUED JULY 11, 2018 LOUISIANA LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET POST OFFICE BOX 94397 BATON ROUGE, LOUISIANA

Louisiana Asset Management Pool (LAMP)

") Report Highlights Louisiana Asset Management Pool (LAMP) DARYL G. PURPERA, CPA, CFE Audit Control # 80130167 Financial Audit Services June 2014 Why We Conducted This Audit We conducted our audit of LAMP

Report Highlights Louisiana Asset Management Pool (LAMP) DARYL G. PURPERA, CPA, CFE Audit Control # 80130167 Financial Audit Services June 2014 Why We Conducted This Audit We conducted our audit of LAMP

SEWERAGE DISTRICT NO. 2 OF RAPIDES PARISH RAPIDES PARISH POLICE JURY Alexandria, Louisiana

3 05^ RECEIVED, c,-.,-? iv\\;~ AM wm IPI -3 t-uu 1 - *-"wl_ *-* SEWERAGE DISTRICT NO. 2 OF RAPIDES PARISH FINANCIAL STATEMENTS WITH INDEPENDENT AUDITOR'S REPORTS AS OF AND FOR THE YEAR ENDED DECEMBER 31,2007

3 05^ RECEIVED, c,-.,-? iv\\;~ AM wm IPI -3 t-uu 1 - *-"wl_ *-* SEWERAGE DISTRICT NO. 2 OF RAPIDES PARISH FINANCIAL STATEMENTS WITH INDEPENDENT AUDITOR'S REPORTS AS OF AND FOR THE YEAR ENDED DECEMBER 31,2007

UNIVERSITY OF LOUISIANA SYSTEM A COMPONENT OF THE STATE OF LOUISIANA

UNIVERSITY OF LOUISIANA SYSTEM A COMPONENT OF THE STATE OF LOUISIANA FINANCIAL STATEMENT REPORT FOR THE YEAR ENDED JUNE 30, 2012 ISSUED MARCH 6, 2013 LOUISIANA LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET

UNIVERSITY OF LOUISIANA SYSTEM A COMPONENT OF THE STATE OF LOUISIANA FINANCIAL STATEMENT REPORT FOR THE YEAR ENDED JUNE 30, 2012 ISSUED MARCH 6, 2013 LOUISIANA LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET

STATE OF MINNESOTA Office of the State Auditor

STATE OF MINNESOTA Office of the State Auditor Patricia Anderson State Auditor MANAGEMENT AND COMPLIANCE REPORT PREPARED AS A RESULT OF THE AUDIT OF THE FINANCIAL AFFAIRS OF THE CITY OF GREENFIELD GREENFIELD,

STATE OF MINNESOTA Office of the State Auditor Patricia Anderson State Auditor MANAGEMENT AND COMPLIANCE REPORT PREPARED AS A RESULT OF THE AUDIT OF THE FINANCIAL AFFAIRS OF THE CITY OF GREENFIELD GREENFIELD,

JACKSON PARISH AMBULANCE SERVICE DISTRICT JONESBORO, LOUISIANA ANNUAL FINANCIAL REPORT DECEMBER 31,2005

JACKSON PARISH AMBULANCE SERVICE DISTRICT JONESBORO, LOUISIANA ANNUAL FINANCIAL REPORT DECEMBER 31,2005 Under provisions of state law, this report is a public document. Acopy of the report has been submitted

JACKSON PARISH AMBULANCE SERVICE DISTRICT JONESBORO, LOUISIANA ANNUAL FINANCIAL REPORT DECEMBER 31,2005 Under provisions of state law, this report is a public document. Acopy of the report has been submitted

RIGHTS OF MASSACHUSETTS INDIVIDUALS WITH A REPRESENTATIVE PAYEE. Prepared by the Mental Health Legal Advisors Committee August 2017

RIGHTS OF MASSACHUSETTS INDIVIDUALS WITH A REPRESENTATIVE PAYEE Prepared by the Mental Health Legal Advisors Committee August 2017 What is a representative payee? 2 When does the Social Security Administration

RIGHTS OF MASSACHUSETTS INDIVIDUALS WITH A REPRESENTATIVE PAYEE Prepared by the Mental Health Legal Advisors Committee August 2017 What is a representative payee? 2 When does the Social Security Administration

MONITORING OF MEDICAID CLAIMS USING ALL-INCLUSIVE CODE (T1015) LOUISIANA DEPARTMENT OF HEALTH STATE OF LOUISIANA

LOUISIANA DEPARTMENT OF HEALTH STATE OF LOUISIANA") MONITORING OF MEDICAID CLAIMS USING ALL-INCLUSIVE CODE (T1015) LOUISIANA DEPARTMENT OF HEALTH STATE OF LOUISIANA MEDICAID AUDIT UNIT ISSUED OCTOBER 4, 2017 LOUISIANA LEGISLATIVE AUDITOR 1600 NORTH THIRD

MONITORING OF MEDICAID CLAIMS USING ALL-INCLUSIVE CODE (T1015) LOUISIANA DEPARTMENT OF HEALTH STATE OF LOUISIANA MEDICAID AUDIT UNIT ISSUED OCTOBER 4, 2017 LOUISIANA LEGISLATIVE AUDITOR 1600 NORTH THIRD

DEPARTMENT OF CULTURE, RECREATION AND TOURISM STATE OF LOUISIANA

DEPARTMENT OF CULTURE, RECREATION AND TOURISM STATE OF LOUISIANA PROCEDURAL REPORT ISSUED DECEMBER 22, 2010 LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET POST OFFICE BOX 94397 BATON ROUGE, LOUISIANA 70804-9397

DEPARTMENT OF CULTURE, RECREATION AND TOURISM STATE OF LOUISIANA PROCEDURAL REPORT ISSUED DECEMBER 22, 2010 LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET POST OFFICE BOX 94397 BATON ROUGE, LOUISIANA 70804-9397

LIVE OAK MANOR VOLUNTEER FIRE COMPANY, INC. FINANCIAL REPORT YEAR ENDED DECEMBER 31, 2007

LIVE OAK MANOR VOLUNTEER FIRE COMPANY, INC. FINANCIAL REPORT YEAR ENDED DECEMBER 31, 2007 Under provisions of state law, this report is a public document. A copy of the report has been submitted to the

LIVE OAK MANOR VOLUNTEER FIRE COMPANY, INC. FINANCIAL REPORT YEAR ENDED DECEMBER 31, 2007 Under provisions of state law, this report is a public document. A copy of the report has been submitted to the

Cash Operations Training Mary H. Loomis, CPA, Comptroller

Cash Operations Training - 2012 Mary H. Loomis, CPA, Comptroller Purpose of the Cash Operations Manual The purpose of the cash operations manual is to consolidate the cash handling/cash operations policies

Cash Operations Training - 2012 Mary H. Loomis, CPA, Comptroller Purpose of the Cash Operations Manual The purpose of the cash operations manual is to consolidate the cash handling/cash operations policies

Sheriff Kemuel A. Kem Kimbrough Sr.

Clayton County Sheriff s Office Sheriff Kemuel A. Kem Kimbrough Sr. 9157 Tara Boulevard, Jonesboro, Georgia 30236 Telephone No. (770) 471-1122 Internet: www.claytonsheriff.com In February 2011, Sheriff

Clayton County Sheriff s Office Sheriff Kemuel A. Kem Kimbrough Sr. 9157 Tara Boulevard, Jonesboro, Georgia 30236 Telephone No. (770) 471-1122 Internet: www.claytonsheriff.com In February 2011, Sheriff

STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK June 2016

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

CASH HANDLING POLICIES

CASH HANDLING POLICIES Administered by the Skagit County Treasurer Revised May 8, 2017 Policy TABLE OF CONTENTS I. Mandatory training for Cash Handlers 3 II. Temporary Employees as Cash Handlers 4 III.

CASH HANDLING POLICIES Administered by the Skagit County Treasurer Revised May 8, 2017 Policy TABLE OF CONTENTS I. Mandatory training for Cash Handlers 3 II. Temporary Employees as Cash Handlers 4 III.

LOUISIANA DISTRICT PUBLIC DEFENDERS COMPLIANCE WITH REPORT REQUIREMENTS

LOUISIANA DISTRICT PUBLIC DEFENDERS COMPLIANCE WITH REPORT REQUIREMENTS ADVISORY SERVICES REPORT ISSUED MAY 2, 2012 LOUISIANA LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET POST OFFICE BOX 94397 BATON ROUGE,

LOUISIANA DISTRICT PUBLIC DEFENDERS COMPLIANCE WITH REPORT REQUIREMENTS ADVISORY SERVICES REPORT ISSUED MAY 2, 2012 LOUISIANA LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET POST OFFICE BOX 94397 BATON ROUGE,

State Capitol Building Des Moines, Iowa

OFFICE OF AUDITOR OF STATE STATE OF IOWA State Capitol Building Des Moines, Iowa 50319-0006 Mary Mosiman, CPA Auditor of State Telephone (515) 281-5834 Facsimile (515) 242-6134 NEWS RELEASE Contact: Mary

OFFICE OF AUDITOR OF STATE STATE OF IOWA State Capitol Building Des Moines, Iowa 50319-0006 Mary Mosiman, CPA Auditor of State Telephone (515) 281-5834 Facsimile (515) 242-6134 NEWS RELEASE Contact: Mary

IN THE SUPREME COURT OF FLORIDA (Before a Referee) REPORT OF REFEREE

REPORT OF REFEREE") IN THE SUPREME COURT OF FLORIDA (Before a Referee) THE FLORIDA BAR, Complainant, v. CASE NO.: SC10-1824 TFB NOS.: 2009-10,429(12C) 2009-11,531(12C) GERI LYNN HALLERMAN WAKSLER, Respondent. / REPORT OF

IN THE SUPREME COURT OF FLORIDA (Before a Referee) THE FLORIDA BAR, Complainant, v. CASE NO.: SC10-1824 TFB NOS.: 2009-10,429(12C) 2009-11,531(12C) GERI LYNN HALLERMAN WAKSLER, Respondent. / REPORT OF

INTERNAL CONTROL AND LOSS PREVENTION SUPPLEMENTAL APPLICATION FOR INVESTMENT FIRMS

Name of Insurance Company to which application is made INTERNAL CONTROL AND LOSS PREVENTION SUPPLEMENTAL APPLICATION FOR INVESTMENT FIRMS A. AUDITS NAME OF INSTITUTION: PRINCIPAL ADDRESS: DATE: 1. Are

Name of Insurance Company to which application is made INTERNAL CONTROL AND LOSS PREVENTION SUPPLEMENTAL APPLICATION FOR INVESTMENT FIRMS A. AUDITS NAME OF INSTITUTION: PRINCIPAL ADDRESS: DATE: 1. Are

REPORT OF THE AUDIT OF THE BREATHITT COUNTY SHERIFF

REPORT OF THE AUDIT OF THE BREATHITT COUNTY SHERIFF For The Year Ended December 31, 2007 CRIT LUALLEN AUDITOR OF PUBLIC ACCOUNTS www.auditor.ky.gov 105 SEA HERO ROAD, SUITE 2 FRANKFORT, KY 40601-5404 TELEPHONE

REPORT OF THE AUDIT OF THE BREATHITT COUNTY SHERIFF For The Year Ended December 31, 2007 CRIT LUALLEN AUDITOR OF PUBLIC ACCOUNTS www.auditor.ky.gov 105 SEA HERO ROAD, SUITE 2 FRANKFORT, KY 40601-5404 TELEPHONE

Village of Riverside

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Village of Riverside Treasurer s Misappropriation of Funds Report of Examination Period Covered: August 1,

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Village of Riverside Treasurer s Misappropriation of Funds Report of Examination Period Covered: August 1,

OFFICE OF THE VIRGIN ISLANDS INSPECTOR GENERAL

October 1, 2018 IR-01-36-19 THE UNITED STATES VIRGIN ISLANDS OFFICE OF THE VIRGIN ISLANDS INSPECTOR GENERAL INVESTIGATION INTO ALLEGATION OF THE UNAUTHORIZED REGISTRATION OF MOTOR VEHICLES ILLEGAL OR WASTEFUL

October 1, 2018 IR-01-36-19 THE UNITED STATES VIRGIN ISLANDS OFFICE OF THE VIRGIN ISLANDS INSPECTOR GENERAL INVESTIGATION INTO ALLEGATION OF THE UNAUTHORIZED REGISTRATION OF MOTOR VEHICLES ILLEGAL OR WASTEFUL

MICHIGAN ASSOCIATION OF COUNTY TREASURERS Summer Conference Amway Grand Hotel Grand Rapids, Michigan. August 10, 1998

MICHIGAN ASSOCIATION OF COUNTY TREASURERS Summer Conference Amway Grand Hotel Grand Rapids, Michigan August 10, 1998 County Treasurer's Responsibility for Trust Accounts Prepared by Richard L. Baldermann,

MICHIGAN ASSOCIATION OF COUNTY TREASURERS Summer Conference Amway Grand Hotel Grand Rapids, Michigan August 10, 1998 County Treasurer's Responsibility for Trust Accounts Prepared by Richard L. Baldermann,

DEPARTMENT OF CHILDREN AND FAMILY SERVICES - PROCESSES TO PREVENT, IDENTIFY, AND RECOVER IMPROPER PAYMENTS IN THE CHILD CARE ASSISTANCE PROGRAM

DEPARTMENT OF CHILDREN AND FAMILY SERVICES - PROCESSES TO PREVENT, IDENTIFY, AND RECOVER IMPROPER PAYMENTS IN THE CHILD CARE ASSISTANCE PROGRAM PERFORMANCE AUDIT ISSUED APRIL 18, 2012 LOUISIANA LEGISLATIVE

DEPARTMENT OF CHILDREN AND FAMILY SERVICES - PROCESSES TO PREVENT, IDENTIFY, AND RECOVER IMPROPER PAYMENTS IN THE CHILD CARE ASSISTANCE PROGRAM PERFORMANCE AUDIT ISSUED APRIL 18, 2012 LOUISIANA LEGISLATIVE

Syracuse City School District

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Syracuse City School District Internal Controls Over Selected Financial Operations Report of Examination Period

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Syracuse City School District Internal Controls Over Selected Financial Operations Report of Examination Period

LOUISIANA TRANSPORTATION AUTHORITY DEPARTMENT OF TRANSPORTATION AND DEVELOPMENT A COMPONENT UNIT OF THE STATE OF LOUISIANA

LOUISIANA TRANSPORTATION AUTHORITY DEPARTMENT OF TRANSPORTATION AND DEVELOPMENT A COMPONENT UNIT OF THE STATE OF LOUISIANA FINANCIAL STATEMENT AUDIT FOR THE YEAR ENDED JUNE 30, 2011 ISSUED JULY 25, 2012

LOUISIANA TRANSPORTATION AUTHORITY DEPARTMENT OF TRANSPORTATION AND DEVELOPMENT A COMPONENT UNIT OF THE STATE OF LOUISIANA FINANCIAL STATEMENT AUDIT FOR THE YEAR ENDED JUNE 30, 2011 ISSUED JULY 25, 2012

CREIA ACCOUNTING POLICIES AND PROCEDURES

CREIA ACCOUNTING POLICIES AND PROCEDURES Updated June 2015 1 Table of Contents I. Introduction... 3 II. Division of Responsibilities... 4 Board of Directors... 4 Executive Director/Chief Executive Officer...

CREIA ACCOUNTING POLICIES AND PROCEDURES Updated June 2015 1 Table of Contents I. Introduction... 3 II. Division of Responsibilities... 4 Board of Directors... 4 Executive Director/Chief Executive Officer...

ASSUMPTION PARISH CLERK OF COURT NAPOLEONVILLE, LOUISIANA

/ I ASSUMPTION PARISH CLERK OF COURT NAPOLEONVILLE, LOUISIANA BASIC FINANCIAL STATEMENTS, REQUIRED SUPPLEMENTARY INFORMATION, INDEPENDENT AUDITORS' REPORT AND OTHER REPORTS REQUIRED BY GOVERNMENTAL AUDITING

/ I ASSUMPTION PARISH CLERK OF COURT NAPOLEONVILLE, LOUISIANA BASIC FINANCIAL STATEMENTS, REQUIRED SUPPLEMENTARY INFORMATION, INDEPENDENT AUDITORS' REPORT AND OTHER REPORTS REQUIRED BY GOVERNMENTAL AUDITING

STATE OF MINNESOTA OFFICE OF THE STATE AUDITOR

JUDITH H. DUTCHER STATE AUDITOR STATE OF MINNESOTA OFFICE OF THE STATE AUDITOR SUITE 400 525 PARK STREET SAINT PAUL, MN 55103-2139 (651) 296-2551 (Voice) (651) 296-4755 (Fax) stateauditor@osa.state.mn.us

JUDITH H. DUTCHER STATE AUDITOR STATE OF MINNESOTA OFFICE OF THE STATE AUDITOR SUITE 400 525 PARK STREET SAINT PAUL, MN 55103-2139 (651) 296-2551 (Voice) (651) 296-4755 (Fax) stateauditor@osa.state.mn.us

New York City Department of Education

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of State Government Accountability New York City Department of Education James Monroe Educational Campus Management of General

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of State Government Accountability New York City Department of Education James Monroe Educational Campus Management of General

DESCHUTES COUNTY ADULT JAIL L. Shane Nelson, Sheriff Jail Operations Approved by: February 8, 2016 INMATE ACCOUNT

DESCHUTES COUNTY ADULT JAIL CD-1-3 L. Shane Nelson, Sheriff Jail Operations Approved by: February 8, 2016 INMATE ACCOUNT POLICY. Cash in an inmate s possession at the time of dress-in will be deposited

DESCHUTES COUNTY ADULT JAIL CD-1-3 L. Shane Nelson, Sheriff Jail Operations Approved by: February 8, 2016 INMATE ACCOUNT POLICY. Cash in an inmate s possession at the time of dress-in will be deposited

Town of Moira. Fiscal Oversight and Selected Financial Operations. Report of Examination. Thomas P. DiNapoli

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Town of Moira Fiscal Oversight and Selected Financial Operations Report of Examination Period Covered: January

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Town of Moira Fiscal Oversight and Selected Financial Operations Report of Examination Period Covered: January

Department of Health and Hospitals Baton Rouge Main Office Operations

Report Highlights Department of Health and Hospitals Baton Rouge Main Office Operations DARYL G. PURPERA, CPA, CFE Audit Control # 80120027 Financial Audit Services January 2013 Why We Conducted This Audit

Report Highlights Department of Health and Hospitals Baton Rouge Main Office Operations DARYL G. PURPERA, CPA, CFE Audit Control # 80120027 Financial Audit Services January 2013 Why We Conducted This Audit

INTERNAL CONTROL MANUAL

INTERNAL CONTROL MANUAL Revised May 2018 Table of Contents 1 Introduction 1 2 Considerations in Development of Internal Controls 2 3 Five Components of Internal Control 3 Control Environment 3 3 Policies

INTERNAL CONTROL MANUAL Revised May 2018 Table of Contents 1 Introduction 1 2 Considerations in Development of Internal Controls 2 3 Five Components of Internal Control 3 Control Environment 3 3 Policies

Stop Fraud in Your Office. Presented by: Margaret A. (Peggy) McGarrity, Esq., CPA

McGarrity, Esq., CPA") Stop Fraud in Your Office Presented by: Margaret A. (Peggy) McGarrity, Esq., CPA 1 White-Collar Crime EDWIN H. SUTHERLAND 1939 First defined white-collar crime Criminal acts of corporations Individuals

Stop Fraud in Your Office Presented by: Margaret A. (Peggy) McGarrity, Esq., CPA 1 White-Collar Crime EDWIN H. SUTHERLAND 1939 First defined white-collar crime Criminal acts of corporations Individuals

OFFICE OF AUDITOR OF STATE STATE OF IOWA

OFFICE OF AUDITOR OF STATE STATE OF IOWA State Capitol Building Des Moines, Iowa 50319-0004 Mary Mosiman, CPA Auditor of State Telephone (515) 281-5834 Facsimile (515) 242-6134 NEWS RELEASE Contact: Mary

OFFICE OF AUDITOR OF STATE STATE OF IOWA State Capitol Building Des Moines, Iowa 50319-0004 Mary Mosiman, CPA Auditor of State Telephone (515) 281-5834 Facsimile (515) 242-6134 NEWS RELEASE Contact: Mary

ATHLETIC DEPARTMENT LOUISIANA STATE UNIVERSITY LOUISIANA STATE UNIVERSITY SYSTEM STATE OF LOUISIANA

ATHLETIC DEPARTMENT LOUISIANA STATE UNIVERSITY LOUISIANA STATE UNIVERSITY SYSTEM STATE OF LOUISIANA AGREED-UPON PROCEDURES REPORT ISSUED FEBRUARY 15, 2017 LOUISIANA LEGISLATIVE AUDITOR 1600 NORTH THIRD

ATHLETIC DEPARTMENT LOUISIANA STATE UNIVERSITY LOUISIANA STATE UNIVERSITY SYSTEM STATE OF LOUISIANA AGREED-UPON PROCEDURES REPORT ISSUED FEBRUARY 15, 2017 LOUISIANA LEGISLATIVE AUDITOR 1600 NORTH THIRD

As defined by state law, some of the treasurer s duties include the following activities:

Investigative Report ity of Ronneby May 31, 2000 Page 2 The OSA s investigation revealed that lerk-treasurer Linn disbursed ity checks to herself which 3 were not authorized by the ity ouncil as required

Investigative Report ity of Ronneby May 31, 2000 Page 2 The OSA s investigation revealed that lerk-treasurer Linn disbursed ity checks to herself which 3 were not authorized by the ity ouncil as required

Fraud Prevention for Nonprofits

Fraud Prevention for Nonprofits January 11, 2017 Fraud Myths It hardly ever happens to nonprofits. It won t happen in our organization. Jane is the most dedicated and honest person I ve ever met. Mary

Fraud Prevention for Nonprofits January 11, 2017 Fraud Myths It hardly ever happens to nonprofits. It won t happen in our organization. Jane is the most dedicated and honest person I ve ever met. Mary

SEWERAGE DISTRICT NO. 1 OF RAPIDES PARISH RAPIDES PARISH POLICE JURY Alexandria, Louisiana

06JUL-5 PMI2.-33 SEWERAGE DISTRICT NO. 1 OF RAPIDES PARISH FINANCIAL STATEMENTS WITH INDEPENDENT AUDITOR'S REPORTS AS OF AND FOR THE YEARS ENDED DECEMBER 31, 2004 AND DECEMBER 31,2005 WITH SUPPLEMENTAL

06JUL-5 PMI2.-33 SEWERAGE DISTRICT NO. 1 OF RAPIDES PARISH FINANCIAL STATEMENTS WITH INDEPENDENT AUDITOR'S REPORTS AS OF AND FOR THE YEARS ENDED DECEMBER 31, 2004 AND DECEMBER 31,2005 WITH SUPPLEMENTAL

Salt Lake County Library Imprest Fund

A Review of the A Report to the Citizens of Salt Lake County, the Mayor, and the County Council Salt Lake County Library Imprest Fund December 2010 Jeff Hatch Salt Lake County Auditor A Review of the

A Review of the A Report to the Citizens of Salt Lake County, the Mayor, and the County Council Salt Lake County Library Imprest Fund December 2010 Jeff Hatch Salt Lake County Auditor A Review of the

Financial Statements. St. Tammany Parish Recreation District No. 4. Lacombe, Louisiana. December 31, 2004

r RECEIVED 05MAR1L* AWll'SU Financial Statements St. Tammany Parish Recreation District No. 4 Lacombe, Louisiana December 31, 2004 Under provisions) u'&idtelaw. this report is a r"blic document. Acopy

r RECEIVED 05MAR1L* AWll'SU Financial Statements St. Tammany Parish Recreation District No. 4 Lacombe, Louisiana December 31, 2004 Under provisions) u'&idtelaw. this report is a r"blic document. Acopy

ANNUAL FINANCIAL STATEMENTS

PONCHATOULA VOLUNTEER FIRE DEPARTMENT, INC. ANNUAL FINANCIAL STATEMENTS As of December 31, 2006 and for the Year Then Ended With Supplemental Information Schedules Under provisions of state law, this report

PONCHATOULA VOLUNTEER FIRE DEPARTMENT, INC. ANNUAL FINANCIAL STATEMENTS As of December 31, 2006 and for the Year Then Ended With Supplemental Information Schedules Under provisions of state law, this report

REPORT OF THE AUDIT OF THE FORMER PERRY COUNTY SHERIFF S SETTLEMENT TAXES

REPORT OF THE AUDIT OF THE FORMER PERRY COUNTY SHERIFF S SETTLEMENT - 2005 TAXES July 28, 2006 CRIT LUALLEN AUDITOR OF PUBLIC ACCOUNTS www.auditor.ky.gov 105 SEA HERO ROAD, SUITE 2 FRANKFORT, KY 40601-5404

REPORT OF THE AUDIT OF THE FORMER PERRY COUNTY SHERIFF S SETTLEMENT - 2005 TAXES July 28, 2006 CRIT LUALLEN AUDITOR OF PUBLIC ACCOUNTS www.auditor.ky.gov 105 SEA HERO ROAD, SUITE 2 FRANKFORT, KY 40601-5404

INVESTIGATIVE AUDIT REPORT

INVESTIGATIVE AUDIT REPORT ARLINGTON HIGH SCHOOL SHELBY COUNTY SCHOOL SYSTEM JULY 1, 2008, THROUGH JUNE 30, 2010 State of Tennessee Comptroller of the Treasury Department of Audit Division of Investigations

INVESTIGATIVE AUDIT REPORT ARLINGTON HIGH SCHOOL SHELBY COUNTY SCHOOL SYSTEM JULY 1, 2008, THROUGH JUNE 30, 2010 State of Tennessee Comptroller of the Treasury Department of Audit Division of Investigations

O L A. Minnesota State Arts Board Employee Payroll Misappropriation OFFICE OF THE LEGISLATIVE AUDITOR STATE OF MINNESOTA.

O L A OFFICE OF THE LEGISLATIVE AUDITOR STATE OF MINNESOTA Special Review Minnesota State Arts Board SEPTEMBER 12, 2003 03-50 Financial Audit Division The Office of the Legislative Auditor (OLA) is a professional,

O L A OFFICE OF THE LEGISLATIVE AUDITOR STATE OF MINNESOTA Special Review Minnesota State Arts Board SEPTEMBER 12, 2003 03-50 Financial Audit Division The Office of the Legislative Auditor (OLA) is a professional,

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2017M-56. Village of Ravena. Departmental Collections and Leave Accruals

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2017M-56 Village of Ravena Departmental Collections and Leave Accruals SEPTEMBER 2017 Contents Report Highlights.............................

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2017M-56 Village of Ravena Departmental Collections and Leave Accruals SEPTEMBER 2017 Contents Report Highlights.............................

Audit Report. Judiciary. August 2010 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY

Audit Report Judiciary August 2010 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related follow-up correspondence are available to the public

Audit Report Judiciary August 2010 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related follow-up correspondence are available to the public

TOWN OF EMERALD ISLE INTERNAL CONTROL POLICY

TOWN OF EMERALD ISLE INTERNAL CONTROL POLICY Goals The Town of Emerald Isle has set forth the following internal control procedures to ensure compliance with all applicable laws and regulations. Internal

TOWN OF EMERALD ISLE INTERNAL CONTROL POLICY Goals The Town of Emerald Isle has set forth the following internal control procedures to ensure compliance with all applicable laws and regulations. Internal

FOURTH JUDICIAL DISTRICT INDIGENT DEFENDER BOARD Parishes of Morehouse and Ouachita, Louisiana

Annual Financial Statements With Independent Auditor's Report As of and for the Year Ended December 31,2006 With Supplemental Information Schedules Under provisions of state law, this report is a public

Annual Financial Statements With Independent Auditor's Report As of and for the Year Ended December 31,2006 With Supplemental Information Schedules Under provisions of state law, this report is a public

GOVERNMENT OF GUAM RETIREMENT FUND (A Public Corporation) Schedule of Findings. September 30, 2001 and 2000

Schedule of Findings. September 30, 2001 and 2000") GOVERNMENT OF GUAM RETIREMENT FUND (A Public Corporation) Schedule of Findings CURRENT YEAR (2001) FINDINGS Finding No. 2001-1 Verification of Disability Annuitants 4GCA, Chapter 8, Article 1, 8127(a)

GOVERNMENT OF GUAM RETIREMENT FUND (A Public Corporation) Schedule of Findings CURRENT YEAR (2001) FINDINGS Finding No. 2001-1 Verification of Disability Annuitants 4GCA, Chapter 8, Article 1, 8127(a)

DEPARTMENT OF REVENUE STATE OF LOUISIANA

DEPARTMENT OF REVENUE STATE OF LOUISIANA FINANCIAL AUDIT SERVICES MANAGEMENT LETTER ISSUED DECEMBER 19, 2018 LOUISIANA LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET POST OFFICE BOX 94397 BATON ROUGE, LOUISIANA

DEPARTMENT OF REVENUE STATE OF LOUISIANA FINANCIAL AUDIT SERVICES MANAGEMENT LETTER ISSUED DECEMBER 19, 2018 LOUISIANA LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET POST OFFICE BOX 94397 BATON ROUGE, LOUISIANA

LOUISIANA COMPLIANCE QUESTIONNAIRE

Dear Chief Executive Officer: Attached is the Louisiana Compliance Questionnaire that is to be completed by you or your staff. This questionnaire is a required part of a financial audit of Louisiana state

Dear Chief Executive Officer: Attached is the Louisiana Compliance Questionnaire that is to be completed by you or your staff. This questionnaire is a required part of a financial audit of Louisiana state

Code of Conduct. This Code of Conduct covers all associates. When appropriate, it also covers all members of the Company's Board of Directors.

Code of Conduct This Code of Conduct has been adopted for the purpose of ensuring that the Company's "Associates" (Officers and Employees) conduct themselves and operate the Company's business in accordance

Code of Conduct This Code of Conduct has been adopted for the purpose of ensuring that the Company's "Associates" (Officers and Employees) conduct themselves and operate the Company's business in accordance

ATHLETIC DEPARTMENT NORTHWESTERN STATE UNIVERSITY UNIVERSITY OF LOUISIANA SYSTEM STATE OF LOUISIANA

ATHLETIC DEPARTMENT NORTHWESTERN STATE UNIVERSITY UNIVERSITY OF LOUISIANA SYSTEM STATE OF LOUISIANA AGREED-UPON PROCEDURES REPORT ISSUED DECEMBER 13, 2006 LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET POST

ATHLETIC DEPARTMENT NORTHWESTERN STATE UNIVERSITY UNIVERSITY OF LOUISIANA SYSTEM STATE OF LOUISIANA AGREED-UPON PROCEDURES REPORT ISSUED DECEMBER 13, 2006 LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET POST

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-196. Town of Westford. Financial Operations Oversight JANUARY 2019

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-196 Town of Westford Financial Operations Oversight JANUARY 2019 Contents Report Highlights.............................

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-196 Town of Westford Financial Operations Oversight JANUARY 2019 Contents Report Highlights.............................

STATE OF NORTH CAROLINA

STATE OF NORTH CAROLINA SPECIAL REVIEW NORTH CAROLINA DEPARTMENT OF TRANSPORTATION RALEIGH, NORTH CAROLINA FEBRUARY 2006 OFFICE OF THE STATE AUDITOR LESLIE W. MERRITT, JR., CPA, CFP STATE AUDITOR SPECIAL

STATE OF NORTH CAROLINA SPECIAL REVIEW NORTH CAROLINA DEPARTMENT OF TRANSPORTATION RALEIGH, NORTH CAROLINA FEBRUARY 2006 OFFICE OF THE STATE AUDITOR LESLIE W. MERRITT, JR., CPA, CFP STATE AUDITOR SPECIAL

LOUISIANA DELTA COMMUNITY COLLEGE LOUISIANA COMMUNITY AND TECHNICAL COLLEGE SYSTEM STATE OF LOUISIANA Monroe, Louisiana

Monroe, Louisiana Basic Financial Statements and Independent Auditor's Reports As of and for the Years Ended June 30, 2003 and 2002 January 28, 2004 DIRECTOR OF FINANCIAL AND COMPLIANCE AUDIT Albert J.

Monroe, Louisiana Basic Financial Statements and Independent Auditor's Reports As of and for the Years Ended June 30, 2003 and 2002 January 28, 2004 DIRECTOR OF FINANCIAL AND COMPLIANCE AUDIT Albert J.

STATE OF NORTH CAROLINA

STATE OF NORTH CAROLINA PITT COUNTY- CITY OF GREENVILLE AIRPORT AUTHORITY FISCAL CONTROL AUDIT OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA STATE AUDITOR PITT COUNTY - CITY OF GREENVILLE AIRPORT AUTHORITY