STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK June 2016

|

|

|

- Gwen Quinn

- 6 years ago

- Views:

Transcription

1 THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK GABRIEL F DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY Tel: (518) Fax: (518) June 2016 Luvelle Brown, Superintendent Members of the Board of Education Ithaca City School District 400 Lake Street Ithaca, NY Report Number: P Dear Dr. Brown and Members of the Board of Education: A top priority of the Office of the State Comptroller is to help school district officials manage their resources efficiently and effectively and, by so doing, provide accountability for money spent to support educational opportunities. The Comptroller oversees the fiscal affairs of districts statewide, as well as compliance with relevant statutes and observance of good business practices. This fiscal oversight is accomplished, in part, through our audits, which identify opportunities for improving operations and Board of Education (Board) governance. Audits also can identify strategies to reduce costs and to strengthen controls intended to safeguard district assets. In accordance with these goals, we conducted an audit of six school districts throughout New York State. The objective of our audit was to determine whether the Board ensured that district officials properly accounted for extra-classroom cash receipts and disbursements. We included the Ithaca City School District (District) in this audit. Within the scope of this audit, we examined the policies and procedures of the District and reviewed cash receipts and disbursements for the period July 1, 2013 through May 8, This audit was conducted pursuant to Article V, Section 1 of the State Constitution and the State Comptroller s authority as set forth in Article 3 of the New York State General Municipal Law. This report of examination letter contains our findings and recommendations specific to the District. We discussed our findings and recommendations with District officials and considered their comments, which appear in Appendix A, in preparing this report. District officials generally agreed with our recommendations and indicated they plan to initiate corrective action. At the completion of our audit of the six school districts, we prepared a global report that summarizes the significant issues we identified at all of the districts audited.

2 Summary of Findings We found that the Board and the District officials 1 need to strengthen the internal controls over cash receipts and disbursements. Additionally, while some clubs did maintain a complete second set of records as required, others were either missing some records or did not maintain any records. As a result, we could not determine if all cash collections were turned over to the Central Treasurers (Treasurers) 2 for deposit and were made in a timely fashion and intact. Generally, cash disbursements were properly approved and adequately supported by the Treasurers, although the clubs lacked support for the disbursements. Background and Methodology The District is located in the City of Ithaca and parts of the Towns of Caroline, Danby, Dryden, Enfield, Ithaca, Lansing, Newfield and Ulysses in Tompkins County; and parts of the Towns of Candor and Richfield in Tioga County. The District is governed by a nine-member Board. The Board has the responsibility for the general management and control of the District s financial and educational affairs, including the extra-classroom activity fund. The Superintendent of Schools (Superintendent) is responsible for recommending to the Board the staff necessary to fulfill duties related to extra-classroom activities, including the Treasurers. The Treasurers have custody of all extra-classroom funds, including checks and cash receipts. A faculty advisor guides and advises the students in planning extra-classroom activities and financial budgets, along with providing oversight of the deposit and disbursement of money, recordkeeping and, from time to time, checking the balancing of the student activity treasurers (student treasurer) accounts and the completeness of the supporting evidence. The faculty advisor is to work toward ensuring the largest educational return from the activities participated in by the students. The student treasurer is more directly involved in the receipt and disbursement of money and is responsible for maintaining a ledger showing all receipts and disbursements and indicating a daily running balance. The Superintendent, Board, District Treasurer and Business Official at the District have no involvement or oversight with extra-classroom activities. Each building has its own Treasurer. There are 181 active extra-classroom activities 3 within the District, each having its own student treasurer and faculty advisor, which report financial activities to the Treasurers. Students receive funds for extra-classroom activities from a number of sources, such as admissions, membership dues, sales, campaigns and donations. This money may be spent in any reasonable manner. The extra-classroom activity fund had approximately $527,000 in receipts and $485,000 in disbursements for the school year. 1 School principals, District Treasurer, Student Activities Director (High School only) and Treasurers 2 The District has four school buildings: Boynton Middle School (Boynton), DeWitt Middle School (DeWitt), Ithaca High School (High School) and Lehman Alternative Community School (LACS). Each building has its own Central Treasurer. 3 At LACS, clubs are set up as projects during the normal school day, not necessarily as extra-curricular activities. Not all clubs have faculty advisors as some clubs are simply set up in the system for recordkeeping purposes for allschool activities. 2

3 We examined the controls relating to extra-classroom activities cash receipts and disbursements of the District for the period July 1, 2013 through May 8, We conducted this performance audit in accordance with generally accepted government auditing standards (GAGAS). More information on the standards and the methodology used in performing this audit are included in Appendix B of this report. Unless otherwise indicated in this report, samples for testing were selected based on professional judgment, as it was not the intent to project the results onto the entire population. Where applicable, information is presented concerning the value and/or size of the relevant population and the sample selected for examination. Audit Results The Regulations of the Commissioner of Education (Regulations) of the New York State Education Department (SED) were formulated not only to safeguard the funds of extra-classroom activities, but also to provide school districts with the opportunity to teach students good business procedures through participation in handling such funds and operating a successful business. For many students, this may be the only business training they will receive in school. SED also published a pamphlet which presents a plan for the management and accounting of these funds. The Board is to follow this plan or make their own plan, which includes rules and regulations for the conduct, operation and maintenance of extra-classroom activities and for the safeguarding, accounting and auditing of all money received and derived therefrom. This plan shall include adopting policies and procedures that describe the records that District personnel and students must maintain and the duties and control procedures to be used. The Board-adopted policies require that a complete record of receipts and disbursements be kept, that the authority to expend money shall be distinct and separate from the custody of funds and records and that records, along with supporting documentation, are to be delivered to the District Treasurer for auditing. District policies, however, do not specify the procedures to establish an organization and what constitutes a complete set of records. The Board and District officials put some oversight controls in place whereby the District Treasurer audits the Treasurers quarterly reports. However, this did not happen for the duration of the audit period. 4 The District policies state that each Treasurer is to determine the policies and procedures for their respective building within the District. Three of the four Treasurers perform all functions of the cash receipt and disbursement process as well as bank reconciliations with no oversight. The High School Treasurer, however, does not have check-signing authority. Therefore, she does not perform all functions of the disbursement process. 5 Additionally, some clubs partially maintained or did not maintain a second set of receipt or disbursement records in accordance with the Regulations. Treasurers are providing the ledger balances to the clubs, making it easy for clubs to adjust their ledger balance to agree with the Treasurers. Alternatively, the clubs should be maintaining ledgers and verifying that their balance agrees with the Treasurers. 4 The District does have the extra-classroom activities fund audited annually by their external certified public accountant (CPA). 5 Additionally, the bank reconciliation is also sound because the Treasurer completes the bank reconciliations without check-writing authority. 3

4 Cash Receipts District policies should describe the records that the faculty advisors and student treasurers must maintain and the duties and control procedures to be used. These should detail procedures and records, including such records as pre-numbered tickets or some other tracking of admissions, pre-numbered duplicate receipts, evidence that all money was turned over to the Treasurers (including types of money), individual club ledger requirements and profit and loss statements. 6 Profit and loss statements must contain sufficient detail such that the Treasurers can determine the total items sold and the prices charged for each item. The Board must also ensure the Treasurers do not perform all aspects of the cash receipts process, such as cash collection, recordkeeping, cash custody and bank reconciliations. If these duties cannot be separated, the Board should implement compensating controls, such as a comparison of club records to the Treasurers records. The policies relating to the Treasurers, faculty advisors and student treasurers financial responsibilities over cash receipts were adequate. However, the Treasurers did not ensure all procedures were performed and that all required records were maintained at the activity level. 7 The Treasurers are not directly involved in collecting cash for fundraising activities, as the cash receipts forms are turned over to the Treasurers by the faculty advisors or student treasurers. The student treasurers had very little involvement in the cash receipts process, 8 with the faculty advisors remitting cash receipts to the Treasurers. Additionally, District officials did not enforce the maintenance of a ledger by the student treasurers. Ledgers, if kept, were completed by the faculty advisors. 9 Each school appropriately had forms that were used to support cash receipts collected, although none of these forms were pre-numbered. The Treasurers did provide the faculty advisors or student treasurers with proof of remittance, such as duplicate receipts. In some cases, the Treasurers did provide numbered duplicate receipts to the faculty advisors once the receipts were entered into the financial software. Since we found that most clubs did not have support for receipts remitted, such as a profit and loss statement or other support, we could not ensure all money turned over to the Treasurers was deposited. Further, there was no standard process used to identify if all money collected by the faculty advisor was recorded on the deposit forms. None of the clubs we reviewed at any of the school buildings issued support, such as duplicate receipts, for money collected from payees. Therefore, there was no assurance that all money was turned over to the Treasurers. The Treasurers at each school building had varying processes to ensure the club records reconciled with theirs, while the High School had an adequate process. At Boynton, DeWitt and the High School, we tested 78 receipts totaling $54,900 and found the Treasurers deposited all of them timely and intact. At all four schools, we found clubs did not remit deposits timely to the Treasurers. We found 68 receipts totaling $47,200 that were either not submitted in a timely fashion to the Treasurers by the clubs or we could not determine timeliness due to lack of support. We also found student treasurers did not fill out profit and loss statements for fundraising activities at each school. Although the High School did use a standard profit and 6 A profit and loss statement summarizes the revenues, costs and expenses incurred during a specific period of time. 7 Activity level represents all financial records and processes in which the faculty advisor and student treasurer have control. 8 With the exception of student treasurers at the High School. These student treasurers collected cash for club activities, completed appropriate receipt forms, maintained ledgers and met with the Treasurer to ensure ledgers matched 9 With the exception of the High School, where student treasurers maintained ledgers. 4

5 loss form, which was completed the majority of the time, the other Treasurers do not require or provide these forms to clubs. We reviewed records for 13 fundraisers totaling $43,300 and found that 10 lacked profit and loss statements. Specific issues found are: 10 High School No significant issues relating to cash receipts were found. We discussed minor deficiencies with District officials. LACS We tested 61 receipts totaling $19,400. Of the 23 receipts from the clubs we tested totaling $8,000, we were unable to determine if two receipts, totaling $1,300, matched the Treasurer s copy as we were not provided with these. We could not determine if 43 receipts, totaling $8,400 were deposited in the bank because we were not provided with deposit slips or did not have sufficient support to trace to these receipts. The Treasurer aggregated receipts and did not have support for the deposit. Therefore, we cannot determine if these individual receipts were represented on the bank statement. Five receipts totaling $2,500 were not deposited in the bank in a timely manner by the Treasurer, or within five days of receiving the money. There were 534 unaccounted-for receipt numbers due to receipt books being used out of sequence and errors made by the Treasurer. Consequently, we cannot determine if all receipts remitted were deposited in the bank. Boynton No or minimal records existed for 13 cash receipts totaling $25,100. Therefore, we could not determine if the club deposited receipts in a timely manner or intact. DeWitt We could not determine if all receipts were accounted for due to record keeping practices. At the club level, seven receipts totaling $4,200 had no corresponding ledger entry at the activity level. For 37 cash receipts totaling $15,600, we could not determine if the receipts were deposited by the club either timely or intact. We could not determine if receipts were deposited either timely or intact at the activity level because no records existed to do so. We found one club that had an unreasonably low fundraiser profit. The vendor estimate for profit was $315, and the club reported revenue of $59. No explanation was provided from the Treasurer or faculty advisor. These weaknesses occurred due to the lack of record policies and their enforcement by the District. Treasurers told us they remind faculty advisors and student treasurers of the records that need to be kept. In addition, there was insufficient detail of the aggregated deposits because District officials did not have policies in place to ensure all deposits could be accounted for. Cash Disbursements The policies and procedures for disbursing extra-classroom activity money should ensure that the District only pays for goods or services that are supported by adequate documentation. The procedures and records to be used should include pre-numbered disbursing orders signed by the faculty advisor and student treasurer, support such as an invoice for these purchases, individual club ledger requirements and profit and loss statements. The requirement for multiple signatures on the disbursing order is essential to any plan, as it helps to ensure numerous levels of review prior to the disbursement being made. The Board must also ensure the Treasurers do not perform all aspects of the check writing process or implement compensating controls such 10 Total number of receipts that are not supported at the activity level is 38, totaling $26,900. 5

6 as requiring independent reviews of canceled check images, to ensure disbursements are only for legitimate extra-classroom purposes. Generally, cash disbursement forms were appropriately signed, adequately supported and maintained on file by the Treasurers. With the exception of the High School, the other three school buildings have not adequately segregated duties over the disbursement process. The Treasurers perform all aspects of the cash disbursement process with limited oversight. No one reviews the monthly bank reconciliation, bank statements or the canceled check images. Further, at LACS, the Treasurer uses a credit union which is not a duly authorized banking institution for extra-classroom money. Specific issues noted at the school buildings are: High School We assessed and tested controls over cash disbursements and found the controls were appropriately designed and are operating effectively. LACS Overall, we found the clubs are not always maintaining copies of disbursement forms. For the 10 disbursements we tested, totaling $20,800, we found that clubs lacked eight forms, totaling $12,300, to support these disbursements. We found one instance where the Treasurer did not have a properly completed disbursement form on file. However, because the bank statements do not have check images, we are unable to confirm that payees matched what was recorded. We determined that the amount, check number and date associated with each disbursement matched the supporting documentation. In addition, seven of the disbursements tested, totaling $21,400, were for proper club purposes, but three disbursements, totaling $21,000, did not have adequate support. For the 15 electronic fund transfers/withdrawals we tested, totaling $18,500, we found 12, totaling $16,300, were not approved or we could not determine if they were approved. Boynton Generally, the clubs lacked support for disbursements. We tested 13 disbursements totaling $13,100 and found that 11, totaling $12,500, did not have any support at the activity level. DeWitt Generally, the clubs lacked support for disbursements. We tested 13 disbursements, totaling $6,700, and found that 12, totaling $5,800, did not have any support at the activity level. When cash receipts are not supported by appropriate documentation, it is difficult to determine if the actual amount collected was remitted to the Treasurers and in a timely fashion. This results in the District facing an increased risk of fraud or misuse of these funds. When student treasurers do not maintain ledgers, the students lose out on the business educational opportunity. Further, if club ledgers do not agree with the Treasurers ledger, the District faces an increased risk that errors or irregularities could occur and remain undetected. When District officials do not establish effective controls over cash disbursements, money disbursed may be for inappropriate purposes. Without retaining records from prior periods, faculty advisors and student treasurers may not have records available for audit or review. 6

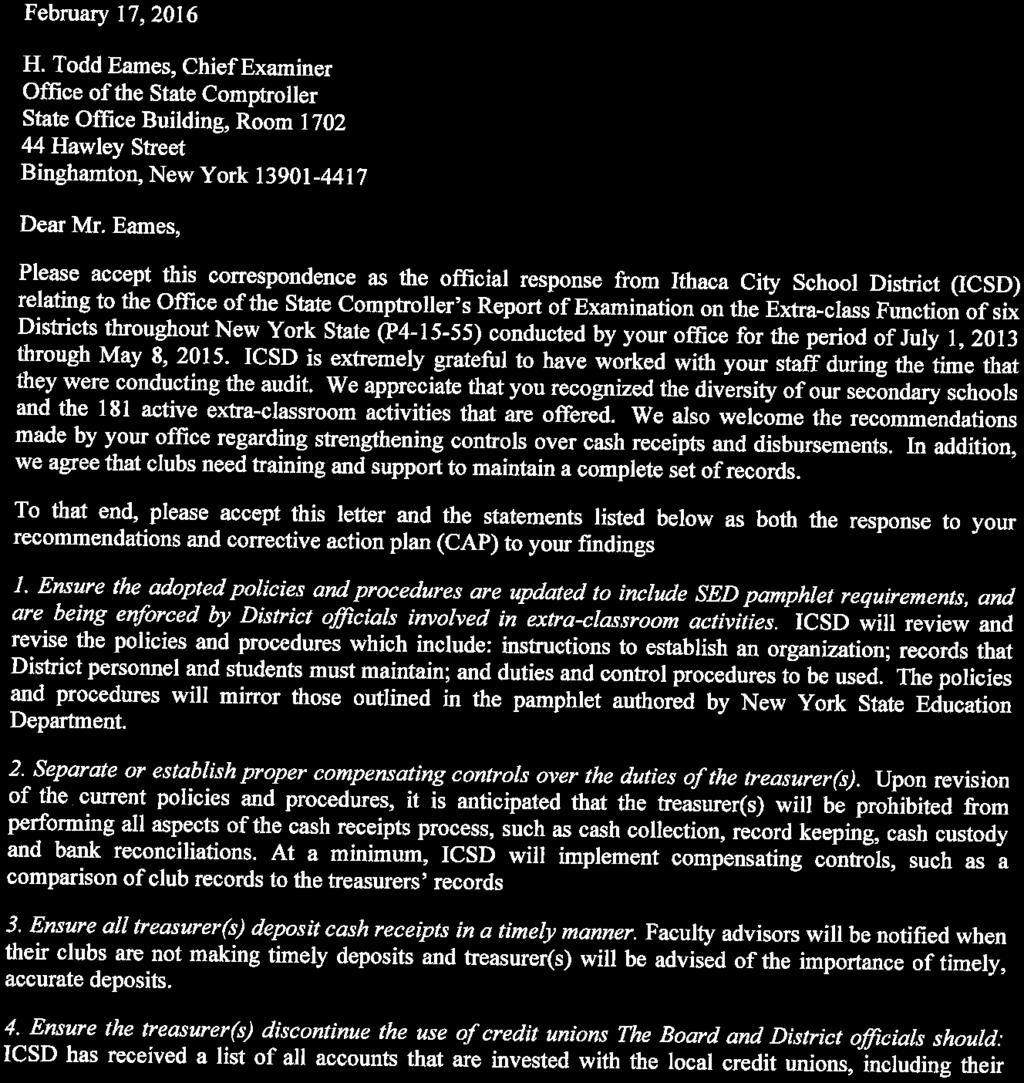

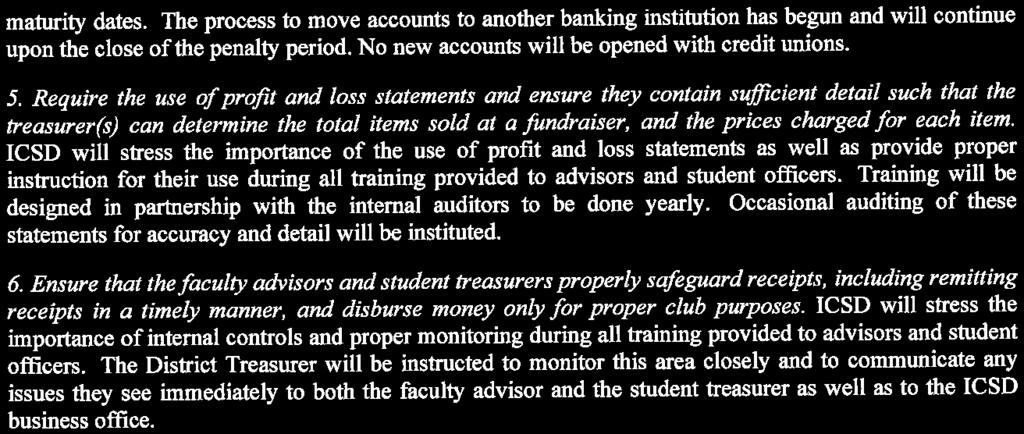

7 Recommendations The Board should: 1. Ensure the adopted policies and procedures are updated to include SED pamphlet requirements and are being enforced by District officials involved in extra-classroom activities. 2. Separate or establish proper compensating controls over the duties of the Treasurers. 3. Ensure all Treasurers deposit cash receipts in a timely manner. 4. Ensure the Treasurers discontinue the use of credit unions. The Board and District officials should: 5. Require the use of profit and loss statements and ensure they contain sufficient detail such so the Treasurers can determine the total items sold at a fundraiser and the prices charged for each item. 6. Ensure that the faculty advisors and student treasurers properly safeguard receipts, including remitting receipts in a timely manner, and disburse money only for proper club purposes. The Board has the responsibility to initiate corrective action. Pursuant to Section 35 of General Municipal Law, Section 2116-a (3)(c) of Education Law, and Section of the Regulations, a written corrective action plan (CAP) that addresses the findings and recommendations in this report must be prepared and forwarded to our office within 90 days. To the extent practicable, implementation of the CAP must begin by the end of the next fiscal year. For more information on preparing and filing your CAP, please refer to our brochure, Responding to an OSC Audit Report, which you received with the draft audit report. The Board should make the CAP available for public review in the District Clerk s office. We thank the officials and staff of the District for the courtesies and cooperation extended to our auditors during this audit. Sincerely, Gabriel F. Deyo Deputy Comptroller 7

8 APPENDIX A RESPONSE FROM DISTRICT OFFICIALS The District officials response to this audit can be found on the following pages. 8

9 9

10 10

11 APPENDIX B AUDIT METHODOLOGY AND STANDARDS To accomplish our objective, we reviewed the operations of the District extra-classroom activities for the period July 1, 2013 through May 8, Specific areas addressed in our audit included the cash receipts, cash disbursements and records and reports used. Our procedures included the following: We reviewed the Regulations as set forth by the Commissioner of Education for the treatment of extra-classroom activity funds from SED pamphlet number 2. We interviewed District officials and reviewed documentation relevant to the receipts and disbursements process (CPA audits for June 30, 2011 through 2014, the extra-classroom activities general ledger and club sub-ledgers) and applicable District policies relating to the extra-classroom activities. We judgmentally selected and reviewed the cash receipts for 10 clubs and the cash disbursements for seven clubs. We selected clubs with either greater than 5 percent of the total collected or paid in or the two clubs with the most activity at the High School, Boynton and DeWitt and three clubs with the most activity at LACS. We also randomly selected and reviewed the cash receipts and disbursements of two additional clubs. We examined 10 percent of the receipts collected for each club selected. We traced receipts from the cash receipts journal, to the Treasurer s duplicate deposit slip and to the bank statement to verify receipts were deposited in a timely fashion and intact. We judgmentally selected this non-biased sample by starting with the first receipt on the ledger and selecting every fourth for review. We examined 10 percent of the disbursements for each club selected. We selected our checks from the general ledger (LACS) and from the check images (at Boynton and DeWitt) by selecting the first disbursement for the clubs tested starting in July and skipping the next two checks to select the next disbursement for testing. For the disbursements from LACS, we did not have the canceled check images, but we still determined if they were being properly recorded in the club and Treasurer s ledgers and that they were properly supported and authorized. For the school buildings with bank statements that included check images, we verified the payee and amounts match and that the disbursement was supported by documentation and for proper club purposes. At the High School, we reviewed all disbursements in June 2014 and December 2014 (judgmentally selected based on June being the end of the school year and December being a holiday month) and ensured that all purchase orders were signed by the student treasurer, faculty advisor, student activities director and associate principal and were supported by an invoice or receipt. 11

12 We reviewed the general ledger for the audit period for all disbursements 11 made payable to the advisors and student treasurers for the clubs being tested, as well as the Treasurers, principals and associate principals (because they have check signing authority) to ensure it was supported by documentation and for proper club purposes. We judgmentally selected four fundraising activities at the High School, three at LACS, two at Boynton and four at DeWitt. We reviewed supporting documentation including profit and loss statements, where applicable, from the event and traced to records at the club, to the Treasurer s records and to the bank deposit. We verified from the bank deposit support that the receipts were deposited timely and intact. We scanned the list of receipts report from the software program at the High School and LACS and the receipt books at Boynton and DeWitt for any breaks in the numbering sequence and followed up with the respective Treasurer on any missing receipt numbers. We reviewed bank statements for the scope period at each school and verified any electronic transfers or withdrawals made had prior approval and went to District accounts or were for club purposes. We conducted this performance audit in accordance with GAGAS. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objective. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objective. 11 At the High School, we scanned check images for checks signed by the Treasurer or made payable to cash and found none that met this criteria. 12

Carmel Central School District

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-045 Carmel Central School District Extra-Classroom Activities JUNE 2018 Contents Report Highlights.............................

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-045 Carmel Central School District Extra-Classroom Activities JUNE 2018 Contents Report Highlights.............................

Queensbury Union Free School District

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2017M-164 Queensbury Union Free School District Extra-Classroom Activities JANUARY 2018 Contents Report Highlights.............................

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2017M-164 Queensbury Union Free School District Extra-Classroom Activities JANUARY 2018 Contents Report Highlights.............................

Peru Central School District

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2017M-69 Peru Central School District Extra-Classroom Activity Funds JUNE 2017 Contents Report Highlights.............................

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2017M-69 Peru Central School District Extra-Classroom Activity Funds JUNE 2017 Contents Report Highlights.............................

Ticonderoga Central School District

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2017M-182 Ticonderoga Central School District Transportation State Aid and Extra-Classroom Activity Funds DECEMBER 2017 Contents

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2017M-182 Ticonderoga Central School District Transportation State Aid and Extra-Classroom Activity Funds DECEMBER 2017 Contents

OFFICE OF THE STATE COMPTROLLER

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

Voorheesville Central School District

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2017M-181 Voorheesville Central School District Extra-Classroom Activities DECEMBER 2017 Contents Report Highlights.............................

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2017M-181 Voorheesville Central School District Extra-Classroom Activities DECEMBER 2017 Contents Report Highlights.............................

Are controls adequate to ensure that the Program s financial activity is properly recorded and reported and that Program moneys are safeguarded?

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 October 2016 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 October 2016 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND

Saugerties Central School District

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Saugerties Central School District Extra-Classroom Activities Report of Examination Period Covered: July 1,

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Saugerties Central School District Extra-Classroom Activities Report of Examination Period Covered: July 1,

Dear Ms. Lawrence and Members of the Board of Commissioners:

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

Otsego Northern Catskills Board of Cooperative Educational Services

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Otsego Northern Catskills Board of Cooperative Educational Services Extra-Classroom Activity Funds Report

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Otsego Northern Catskills Board of Cooperative Educational Services Extra-Classroom Activity Funds Report

STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK September 5, 2014

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

August Report Number: P Dear Dr. Murphy and Members of the Board of Education:

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 August 2015 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 August 2015 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND

STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

East Aurora Union Free School District

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY East Aurora Union Free School District High School Extra-Classroom Activity Funds Report of Examination Period

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY East Aurora Union Free School District High School Extra-Classroom Activity Funds Report of Examination Period

STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK April 2018

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

Syracuse City School District

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Syracuse City School District Internal Controls Over Selected Financial Operations Report of Examination Period

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Syracuse City School District Internal Controls Over Selected Financial Operations Report of Examination Period

McLean Fire Department

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-40 McLean Fire Department Financial Operations MAY 2018 Contents Report Highlights............................. 1 Financial

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-40 McLean Fire Department Financial Operations MAY 2018 Contents Report Highlights............................. 1 Financial

Scotia-Glenville Central School District

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2017M-288 Scotia-Glenville Central School District Financial Condition Management and Extra-Classroom Activities JUNE 2018 Contents

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2017M-288 Scotia-Glenville Central School District Financial Condition Management and Extra-Classroom Activities JUNE 2018 Contents

STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

Dear Chairman Eck and Members of the Board of Fire Commissioners:

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

OFFICE OF THE STATE COMPTROLLER

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK April 2018

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

Dear Superintendent Cardillo and Members of the Board of Education:

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 August 2015 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 August 2015 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND

Levittown Union Free School District

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of Local Government & School Accountability Levittown Union Free School District Reserve Funds and Extra-Classroom Activity

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of Local Government & School Accountability Levittown Union Free School District Reserve Funds and Extra-Classroom Activity

Town of Essex. Internal Controls Over Selected Financial Operations. Report of Examination. Period Covered: January 1, 2013 October 31, M-60

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of Local Government & School Accountability Town of Essex Internal Controls Over Selected Financial Operations Report of Examination

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of Local Government & School Accountability Town of Essex Internal Controls Over Selected Financial Operations Report of Examination

Town of Callicoon. Cash Receipts and Disbursements. Report of Examination. Period Covered: January 1, 2011 October 19, M-16

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Town of Callicoon Cash Receipts and Disbursements Report of Examination Period Covered: January 1, 2011 October

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Town of Callicoon Cash Receipts and Disbursements Report of Examination Period Covered: January 1, 2011 October

STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

EXTRACLASSROOM ACTIVITY FUNDS MANAGEMENT COMMENT LETTER

EXTRACLASSROOM ACTIVITY FUNDS MANAGEMENT COMMENT LETTER Board of Education Elmira City School District Elmira, New York In planning and performing our audit of the financial statements of the Extraclassroom

EXTRACLASSROOM ACTIVITY FUNDS MANAGEMENT COMMENT LETTER Board of Education Elmira City School District Elmira, New York In planning and performing our audit of the financial statements of the Extraclassroom

Chautauqua Utility District

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Chautauqua Utility District Banking Report of Examination Period Covered: January 1, 2014 March 27, 2017 2017M-121

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Chautauqua Utility District Banking Report of Examination Period Covered: January 1, 2014 March 27, 2017 2017M-121

January 13, Dear Mr. Sweeney and Members of the Board of Fire Commissioners:

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 STEVEN J. HANCOX DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 STEVEN J. HANCOX DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

Willsboro Fire Department

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Willsboro Fire Department Financial Operations Report of Examination Period Covered: January 1, 2013 April

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Willsboro Fire Department Financial Operations Report of Examination Period Covered: January 1, 2013 April

STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

Altona Volunteer Fire Company, Inc.

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of Local Government & School Accountability Altona Volunteer Fire Company, Inc. Financial Operations Report of Examination Period

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of Local Government & School Accountability Altona Volunteer Fire Company, Inc. Financial Operations Report of Examination Period

Broadalbin Youth Commission

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-19 Broadalbin Youth Commission Financial Operations OCTOBER 2018 Contents Report Highlights.............................

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-19 Broadalbin Youth Commission Financial Operations OCTOBER 2018 Contents Report Highlights.............................

Jefferson County Soil and Water Conservation District

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Jefferson County Soil and Water Conservation District Internal Controls Over Selected Financial Operations

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Jefferson County Soil and Water Conservation District Internal Controls Over Selected Financial Operations

New York City Department of Education

New York State Office of the State Comptroller Thomas P. DiNapoli Division of State Government Accountability Michelangelo Middle School: Management of General School Funds New York City Department of

New York State Office of the State Comptroller Thomas P. DiNapoli Division of State Government Accountability Michelangelo Middle School: Management of General School Funds New York City Department of

Pocatello Fire District

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Pocatello Fire District Board Oversight and Treasurer s Records and Reports Report of Examination Period Covered:

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Pocatello Fire District Board Oversight and Treasurer s Records and Reports Report of Examination Period Covered:

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-101. Village of Owego. Board Oversight and Financial Operations

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-101 Village of Owego Board Oversight and Financial Operations SEPTEMBER 2018 Contents Report Highlights.............................

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-101 Village of Owego Board Oversight and Financial Operations SEPTEMBER 2018 Contents Report Highlights.............................

Burnt Hills Ballston Lake Youth Recreation Commission

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2017M-68 Burnt Hills Ballston Lake Youth Recreation Commission Financial Activities OCTOBER 2017 Contents Report Highlights............................

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2017M-68 Burnt Hills Ballston Lake Youth Recreation Commission Financial Activities OCTOBER 2017 Contents Report Highlights............................

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-196. Town of Westford. Financial Operations Oversight JANUARY 2019

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-196 Town of Westford Financial Operations Oversight JANUARY 2019 Contents Report Highlights.............................

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-196 Town of Westford Financial Operations Oversight JANUARY 2019 Contents Report Highlights.............................

Village of Clinton. Financial Management. Report of Examination. Thomas P. DiNapoli. Period Covered: June 1, 2012 January 31, M-316

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Village of Clinton Financial Management Report of Examination Period Covered: June 1, 2012 January 31, 2014

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Village of Clinton Financial Management Report of Examination Period Covered: June 1, 2012 January 31, 2014

Richland Fire District

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of Local Government & School Accountability Richland Fire District Board Oversight Report of Examination Period Covered: January

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of Local Government & School Accountability Richland Fire District Board Oversight Report of Examination Period Covered: January

STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

Beaver Dams Volunteer Fire Company, Inc.

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-17 Beaver Dams Volunteer Fire Company, Inc. Financial Activities JUNE 2018 Contents Report Highlights.............................

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-17 Beaver Dams Volunteer Fire Company, Inc. Financial Activities JUNE 2018 Contents Report Highlights.............................

Town of Sand Lake. Justice Court. Report of Examination. Period Covered: January 1, 2013 February 28, M-121

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of Local Government & School Accountability Town of Sand Lake Justice Court Report of Examination Period Covered: January 1,

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of Local Government & School Accountability Town of Sand Lake Justice Court Report of Examination Period Covered: January 1,

Village of New Paltz. Internal Controls Over Building Department Operations REPORT OF EXAMINATION 2017M-201

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2017M-201 Village of New Paltz Internal Controls Over Building Department Operations DECEMBER 2017 Contents Report Highlights.............................

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2017M-201 Village of New Paltz Internal Controls Over Building Department Operations DECEMBER 2017 Contents Report Highlights.............................

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-154. Town of Yates. Town Supervisor s Records and Reports

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-154 Town of Yates Town Supervisor s Records and Reports OCTOBER 2018 Contents Report Highlights.............................

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-154 Town of Yates Town Supervisor s Records and Reports OCTOBER 2018 Contents Report Highlights.............................

New York City Department of Education

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of State Government Accountability New York City Department of Education James Monroe Educational Campus Management of General

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of State Government Accountability New York City Department of Education James Monroe Educational Campus Management of General

Walden Fire District

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Walden Fire District Disbursements Report of Examination Period Covered: January 1, 2013 February 18, 2014

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Walden Fire District Disbursements Report of Examination Period Covered: January 1, 2013 February 18, 2014

STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

Village of East Rockaway

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2017M-206 Village of East Rockaway Justice Court Operations DECEMBER 2017 Contents Report Highlights.............................

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2017M-206 Village of East Rockaway Justice Court Operations DECEMBER 2017 Contents Report Highlights.............................

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2017M-56. Village of Ravena. Departmental Collections and Leave Accruals

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2017M-56 Village of Ravena Departmental Collections and Leave Accruals SEPTEMBER 2017 Contents Report Highlights.............................

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2017M-56 Village of Ravena Departmental Collections and Leave Accruals SEPTEMBER 2017 Contents Report Highlights.............................

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-85. Town of Davenport. Transparency AUGUST 2018

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-85 Town of Davenport Transparency AUGUST 2018 Contents Report Highlights............................. 1. Transparency...............................

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-85 Town of Davenport Transparency AUGUST 2018 Contents Report Highlights............................. 1. Transparency...............................

Central Valley School District

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Central Valley School District Claims Audit Report of Examination Period Covered: July 1, 2013 November 30,

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Central Valley School District Claims Audit Report of Examination Period Covered: July 1, 2013 November 30,

Town of New Lisbon. Financial Oversight. Report of Examination. Thomas P. DiNapoli. Period Covered: January 1, 2011 September 27, M-12

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Town of New Lisbon Financial Oversight Report of Examination Period Covered: January 1, 2011 September 27,

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Town of New Lisbon Financial Oversight Report of Examination Period Covered: January 1, 2011 September 27,

STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 ANDREW A SANFILIPPO EXECUTIVE DEPUTY COMPTROLLER OFFICE OF STATE AND LOCAL GOVERNMENT

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 ANDREW A SANFILIPPO EXECUTIVE DEPUTY COMPTROLLER OFFICE OF STATE AND LOCAL GOVERNMENT

Bainbridge Fire District

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-252 Bainbridge Fire District Board Oversight FEBRUARY 2019 Contents Report Highlights............................. 1 Board

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-252 Bainbridge Fire District Board Oversight FEBRUARY 2019 Contents Report Highlights............................. 1 Board

Canaseraga Central School District

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Canaseraga Central School District Cafeteria Cash Receipts Report of Examination Period Covered: July 1, 2012

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Canaseraga Central School District Cafeteria Cash Receipts Report of Examination Period Covered: July 1, 2012

TOWN OF MILLIS, MASSACHUSETTS. Independent Accountant s Report On Applying Agreed-Upon Procedures Over Student Activity Funds. As of June 30, 2010

TOWN OF MILLIS, MASSACHUSETTS Independent Accountant s Report On Applying Agreed-Upon Procedures Over Student Activity Funds As of June 30, 2010 TABLE OF CONTENTS INDEPENDENT ACCOUNTANT S REPORT ON APPLYING

TOWN OF MILLIS, MASSACHUSETTS Independent Accountant s Report On Applying Agreed-Upon Procedures Over Student Activity Funds As of June 30, 2010 TABLE OF CONTENTS INDEPENDENT ACCOUNTANT S REPORT ON APPLYING

Forestburgh Fire District

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of Local Government & School Accountability Forestburgh Fire District Financial Activities Report of Examination Period Covered:

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of Local Government & School Accountability Forestburgh Fire District Financial Activities Report of Examination Period Covered:

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-94. Town of Binghamton. Credit Cards and Non-Payroll Disbursements

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-94 Town of Binghamton Credit Cards and Non-Payroll Disbursements DECEMBER 2018 Contents Report Highlights.............................

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-94 Town of Binghamton Credit Cards and Non-Payroll Disbursements DECEMBER 2018 Contents Report Highlights.............................

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2017M-42. Town of Chazy. Water and Sewer District Financial Operations

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2017M-42 Town of Chazy Water and Sewer District Financial Operations MAY 2017 Contents Report Highlights.............................

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2017M-42 Town of Chazy Water and Sewer District Financial Operations MAY 2017 Contents Report Highlights.............................

Town of Tuxedo. Financial Operations. Report of Examination. Period Covered: January 1, 2013 January 29, M-284

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of Local Government & School Accountability Town of Tuxedo Financial Operations Report of Examination Period Covered: January

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of Local Government & School Accountability Town of Tuxedo Financial Operations Report of Examination Period Covered: January

Coxsackie-Athens Central School District

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-180 Coxsackie-Athens Central School District Procurement and Claims Audit DECEMBER 2018 Contents Report Highlights.............................

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-180 Coxsackie-Athens Central School District Procurement and Claims Audit DECEMBER 2018 Contents Report Highlights.............................

Directors of the Rochester Firefighters Two Percent Committee Inc Mt. Read Boulevard, Suite 245 Rochester, New York 14606

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

Town of Moira. Fiscal Oversight and Selected Financial Operations. Report of Examination. Thomas P. DiNapoli

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Town of Moira Fiscal Oversight and Selected Financial Operations Report of Examination Period Covered: January

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Town of Moira Fiscal Oversight and Selected Financial Operations Report of Examination Period Covered: January

Smithtown Central School District

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of Local Government & School Accountability Smithtown Central School District Capital Projects Report of Examination Period

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of Local Government & School Accountability Smithtown Central School District Capital Projects Report of Examination Period

Village of Rushville. Board Oversight and Information Technology REPORT OF EXAMINATION 2018M-118

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-118 Village of Rushville Board Oversight and Information Technology AUGUST 2018 Contents Report Highlights.............................

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-118 Village of Rushville Board Oversight and Information Technology AUGUST 2018 Contents Report Highlights.............................

Dear Chairman Dunn and Members of the Board of Fire Commissioners:

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 March 2017 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 March 2017 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL

Beacon City School District

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of Local Government & School Accountability Beacon City School District Claims Auditing Report of Examination Period Covered:

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of Local Government & School Accountability Beacon City School District Claims Auditing Report of Examination Period Covered:

Mattituck Park District

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Mattituck Park District Credit Cards and Segregation of Duties Report of Examination Period Covered: January

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Mattituck Park District Credit Cards and Segregation of Duties Report of Examination Period Covered: January

Town of Galen. Financial Management. Report of Examination. Thomas P. DiNapoli. Period Covered: January 1, 2013 June 12, M-341

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Town of Galen Financial Management Report of Examination Period Covered: January 1, 2013 June 12, 2014 2014M-341

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Town of Galen Financial Management Report of Examination Period Covered: January 1, 2013 June 12, 2014 2014M-341

Village of Homer. Purchasing and Credit Cards. Report of Examination. Thomas P. DiNapoli. Period Covered: March 1, 2015 April 13, M-112

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Village of Homer Purchasing and Credit Cards Report of Examination Period Covered: March 1, 2015 April 13,

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Village of Homer Purchasing and Credit Cards Report of Examination Period Covered: March 1, 2015 April 13,

Poland Central School District

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-214 Poland Central School District Claims Audit Process JANUARY 2019 Contents Report Highlights.............................

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-214 Poland Central School District Claims Audit Process JANUARY 2019 Contents Report Highlights.............................

Town of Beekman. Dover Ridge Sewer and Water Districts Financial Operations. Report of Examination

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of Local Government & School Accountability Town of Beekman Dover Ridge Sewer and Water Districts Financial Operations Report

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of Local Government & School Accountability Town of Beekman Dover Ridge Sewer and Water Districts Financial Operations Report

Rutland Fire District

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2017M-262 Rutland Fire District Board Oversight FEBRUARY 2018 Contents Report Highlights............................. 1 Board

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2017M-262 Rutland Fire District Board Oversight FEBRUARY 2018 Contents Report Highlights............................. 1 Board

Village of Bainbridge

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Village of Bainbridge Financial Operations Report of Examination Period Covered: June 1, 2012 May 31, 2014

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Village of Bainbridge Financial Operations Report of Examination Period Covered: June 1, 2012 May 31, 2014

Town of Hampton. Justice Court Operations. Report of Examination. Thomas P. DiNapoli. Period Covered: January 1, 2012 June 30, M-305

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Town of Hampton Justice Court Operations Report of Examination Period Covered: January 1, 2012 June 30, 2013

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Town of Hampton Justice Court Operations Report of Examination Period Covered: January 1, 2012 June 30, 2013

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-63. Town of Broadalbin. Records and Reports

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-63 Town of Broadalbin Records and Reports JUNE 2018 Contents Report Highlights............................ 1 Records and

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-63 Town of Broadalbin Records and Reports JUNE 2018 Contents Report Highlights............................ 1 Records and

Prattsburgh Central School District

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of Local Government & School Accountability Prattsburgh Central School District Tax Collection Report of Examination Period

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of Local Government & School Accountability Prattsburgh Central School District Tax Collection Report of Examination Period

Town of Canaan. Board Oversight. Report of Examination. Period Covered: January 1, 2016 December 31, M-183

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of Local Government & School Accountability Town of Canaan Board Oversight Report of Examination Period Covered: January 1,

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of Local Government & School Accountability Town of Canaan Board Oversight Report of Examination Period Covered: January 1,

STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK July 19, 2013

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 July 19, 2013 ANDREW S. SANFILIPPO EXECUTIVE DEPUTY COMPTROLLER OFFICE OF STATE

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 July 19, 2013 ANDREW S. SANFILIPPO EXECUTIVE DEPUTY COMPTROLLER OFFICE OF STATE

Bethpage Union Free School District

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of Local Government & School Accountability Bethpage Union Free School District Leave Accruals Report of Examination Period

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of Local Government & School Accountability Bethpage Union Free School District Leave Accruals Report of Examination Period

Oneida-Herkimer- Madison Board of Cooperative Educational Services

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Oneida-Herkimer- Madison Board of Cooperative Educational Services Claim Payments Report of Examination Period

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Oneida-Herkimer- Madison Board of Cooperative Educational Services Claim Payments Report of Examination Period

Hartford Central School District

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-10 Hartford Central School District Cafeteria Collections MARCH 2018 Contents Report Highlights............................

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-10 Hartford Central School District Cafeteria Collections MARCH 2018 Contents Report Highlights............................

Student Activity Account Guidelines For Burlington Public Schools

Student Activity Account Guidelines For Burlington Public Schools * Information and text in this document was adapted for the Burlington Public Schools by the Finance Manager from the Student Activity

Student Activity Account Guidelines For Burlington Public Schools * Information and text in this document was adapted for the Burlington Public Schools by the Finance Manager from the Student Activity

Town of Potsdam. Justice Court. Report of Examination. Thomas P. DiNapoli. Period Covered: January 1, 2009 August 5, M-14

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Town of Potsdam Justice Court Report of Examination Period Covered: January 1, 2009 August 5, 2013 2014M-14

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Town of Potsdam Justice Court Report of Examination Period Covered: January 1, 2009 August 5, 2013 2014M-14

Magee Volunteer Fire Department, Inc.

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2017M-294 Magee Volunteer Fire Department, Inc. Financial Activities MARCH 2018 Contents Report Highlights.............................

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2017M-294 Magee Volunteer Fire Department, Inc. Financial Activities MARCH 2018 Contents Report Highlights.............................

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-213. Town of Freetown. Records and Reports JANUARY 2019

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-213 Town of Freetown Records and Reports JANUARY 2019 Contents Report Highlights............................. 1. Records

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-213 Town of Freetown Records and Reports JANUARY 2019 Contents Report Highlights............................. 1. Records

Norwood-Norfolk Central School District

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Norwood-Norfolk Central School District Claims Auditing Report of Examination Period Covered: July 1, 2014

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Norwood-Norfolk Central School District Claims Auditing Report of Examination Period Covered: July 1, 2014

Geneva Housing Authority

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of Local Government & School Accountability Geneva Housing Authority Cash Receipts Report of Examination Period Covered: October

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of Local Government & School Accountability Geneva Housing Authority Cash Receipts Report of Examination Period Covered: October

February 17, Dear Mr. Wallace, Sheriff Farber and Members of the County Legislature:

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 February 17, 2015 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 February 17, 2015 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT

Town of Plymouth. Board Oversight. Report of Examination. Thomas P. DiNapoli. Period Covered: January 1, 2015 March 31, M-190

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Town of Plymouth Board Oversight Report of Examination Period Covered: January 1, 2015 March 31, 2016 2016M-190

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Town of Plymouth Board Oversight Report of Examination Period Covered: January 1, 2015 March 31, 2016 2016M-190

North Colonie Central School District

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY North Colonie Central School District Claims Processing Report of Examination Period Covered: July 1, 2011

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY North Colonie Central School District Claims Processing Report of Examination Period Covered: July 1, 2011

Village of Old Brookville

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Village of Old Brookville Cash Receipts Report of Examination Period Covered: January 1, 2014 July 31, 2015

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Village of Old Brookville Cash Receipts Report of Examination Period Covered: January 1, 2014 July 31, 2015

Hawthorne Cedar Knolls Union Free School District

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of Local Government & School Accountability Hawthorne Cedar Knolls Union Free School District Internal Controls Over Wire Transfers

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of Local Government & School Accountability Hawthorne Cedar Knolls Union Free School District Internal Controls Over Wire Transfers

Dear Mayor Brown, Comptroller Schroeder, Members of the Common Council and Trustees of the Buffalo Firefighters Two Percent Fund:

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-183. Town of Amity. Town Clerk JANUARY 2019

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-183 Town of Amity Town Clerk JANUARY 2019 Contents Report Highlights............................. 1 Town Clerk................................

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-183 Town of Amity Town Clerk JANUARY 2019 Contents Report Highlights............................. 1 Town Clerk................................

Champlain Joint Youth Program

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of Local Government & School Accountability Champlain Joint Youth Program Oversight of Financial Activities Report of Examination

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of Local Government & School Accountability Champlain Joint Youth Program Oversight of Financial Activities Report of Examination