Using Structured Events to Predict Stock Price Movement: An Empirical Investigation. Yue Zhang

|

|

|

- Bartholomew Franklin

- 5 years ago

- Views:

Transcription

1 Using Structured Events to Predict Stock Price Movement: An Empirical Investigation Yue Zhang

2 My research areas

3 This talk Reading news from the Internet and predicting the stock market

4 Outline Introduction Method Experiments Conclusion

5 Introduction Is it possible? Random walk theory Efficient market hypothesis Human/algorithm trading Examples Shares of Apple Inc. fell as trading began in New York on Tuesday morning, the day after former CEO Steve Jobs passed away Google s stock falls after grim earnings come out early

6 Why events? Previous work Bag-of-words Named Entities Noun Phrases Examples Oracle Corp would sue Google Inc., claiming Google s Android operating system Microsoft agrees to buy Nokia s mobile phone business for $ 7.2 billion.

7 Method Event Representation Event Extraction Event Generalization Prediction model

8 Method Event Representation E=(O 1, P, O 2, T) Actor Event Object Time

9 Method Event Extraction Syntactic parsing Open information extraction

10 Method Event Extraction Event Phrase Extraction Syntactic constraint every multi-word event phrase must begin with a verb, end with a preposition, and be a contiguous sequence of words in the sentence Lexical constraint an event phrase should appear with at least a minimal number of distinct argument pairs in a large corpus Argument Extraction For each event phrase Pv identified in the above step, we find the nearest noun phrase O 1 to the left of Pv in the sentence, and O 1 should contain the subject of the sentence (if it does not contain the subject of Pv, find the second nearest noun phrase)

11 Method Event Generalization First, we construct a morphological analysis tool based on the WordNet stemmer to extract lemma forms of inflected words Second, we generalize each verb to its class name in VerbNet For example Instant view: Private sector adds 114,000 jobs in July. (Private sector, adds, 114,000 jobs) (private sector, multiply_class, 114,000 job)

12 Method Prediction Model Linear model Most previous work uses linear models to predict the stock market. To make direct comparisons, this paper constructs a linear prediction model by using SVM with linear kernel Nonlinear model Intuitively, the relationship between events and the stock market may be more complex than linear, due to hidden and indirect relationships. We exploit a deep neural network model, the hidden layers of which is useful for learning such hidden relationships

13 Class +1 The polarity of the stock price movement is positive Class -1 The polarity of the stock price movement is negative Output Layer Hidden Layers Input Layer φ 1 φ 2 φ 3 φ M News documents

14 Method Feature Representation Bag-of-words TF*IDF Events O 1, P, O 2, O 1 + P, P + O 2, O 1 + P + O 2 For Example (Microsoft, buy, Nokia's mobile phone business) (#arg1=microsoft, #action=buy, #arg2= Nokia's mobile phone business, #arg1_action=microsoft buy, #action_arg2=buy Nokia's mobile phone business, #arg1_action_arg2= Microsoft buy Nokia's mobile phone business)

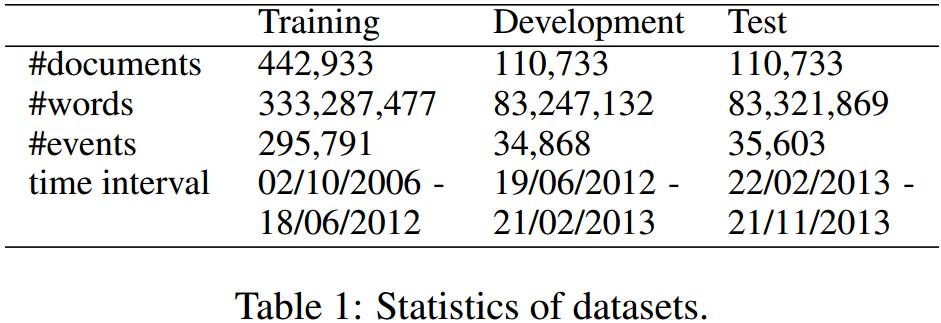

15 Experiments Data Description We use publicly available financial news from Reuters and Bloomberg over the period from October 2006 to November This time span witnesses a severe economic downturn in , followed by a modest recovery in There are 106,521 documents in total from Reuters News and 447,145 from Bloomberg News. We mainly focus on predicting the Standard &Poor's 500 stocks (S&P 500) index, obtaining indices and stock price from Yahoo Finance.

16 Evaluation Metrics Accuracy and MCC Experiments Overall Results

17 Experiments Experiments with Different Number of Hidden Layers of the Deep Neural Network Model

18 Experiments Experiments with Different Quantities of Data

19 Experiments Individual Stock Prediction

20 Experiments Individual Stock Prediction

21 Experiments Individual Stock Prediction

22 Section One Conclusion Events are useful. Events are more useful representations compared to bags-of-words for the task of stock market prediction. Hidden relations useful. A deep neural network model can be more accurate on predicting the stock market compared to the linear model. Robust results obtained. Our approach can achieve stable experiment results on S&P 500 index prediction and individual stock prediction over a large amount of data (eight years of stock prices and more than 550,000 pieces of news). Quality of information is more important than quantity. The most relevant information (i.e. news title vs news content, individual company news vs all news) is better than more, but less relevant information.

23 Section Two Overview Better event encodings Long term history

24 Event Embedding Previous work Learning entity embedding (Socher et al. 2013)

25 Neural Tensor Network Neural Network Neural Tensor Network

26 Neural Tensor Network for Event Embedding U R 1 R 2 T 3 O 1 T 1 P T 2 O 2

27 Neural Tensor Network for Event Embedding R 1 O 1 T 1 P

28 Training Minimize the margin loss 500 iterations Standard back-propagation Parameters Random replace with an object Regulation weight,set to

29 Deep Prediction Model We model long-, mid-, short-term events Long-term events (Last month) Mid-term events (Last week) Short-term events (Last day)

30 Architecture Deep Prediction Model

31 Deep Prediction Model Convolution and Max-pooling Convolution layer to obtain local feature Max-pooling to determine the global representative feature

32 Dataset Experiment

33 Experiment Baselines Input Method Luss and d Aspremont [2012] Bag of words NN Ding et al. [2014] (E-NN) Structured event NN WB-NN Word embedding NN WB-CNN Word embedding CNN E-CNN Structured event CNN EB-NN Event embedding NN EB-CNN Event embedding CNN

34 Experiment Index Prediction Events are better features than words Reducing sparsity if helpful in the task CNN-based is more powerfull

35 Experiment 15 companies from S&P 500 Consists of High-,mid- and low-ranking companies Evaluation metric: Accuarcy and MCC

36 Thanks!

STOCK MARKET PREDICTION AND ANALYSIS USING MACHINE LEARNING

STOCK MARKET PREDICTION AND ANALYSIS USING MACHINE LEARNING Sumedh Kapse 1, Rajan Kelaskar 2, Manojkumar Sahu 3, Rahul Kamble 4 1 Student, PVPPCOE, Computer engineering, PVPPCOE, Maharashtra, India 2 Student,

STOCK MARKET PREDICTION AND ANALYSIS USING MACHINE LEARNING Sumedh Kapse 1, Rajan Kelaskar 2, Manojkumar Sahu 3, Rahul Kamble 4 1 Student, PVPPCOE, Computer engineering, PVPPCOE, Maharashtra, India 2 Student,

$tock Forecasting using Machine Learning

$tock Forecasting using Machine Learning Greg Colvin, Garrett Hemann, and Simon Kalouche Abstract We present an implementation of 3 different machine learning algorithms gradient descent, support vector

$tock Forecasting using Machine Learning Greg Colvin, Garrett Hemann, and Simon Kalouche Abstract We present an implementation of 3 different machine learning algorithms gradient descent, support vector

Stock Market Trend Prediction Using Recurrent Convolutional Neural Networks

Stock Market Trend Prediction Using Recurrent Convolutional Neural Networks Bo Xu, Dongyu Zhang, Shaowu Zhang, Hengchao Li, and Hongfei Lin (&) School of Computer Science and Technology, Dalian University

Stock Market Trend Prediction Using Recurrent Convolutional Neural Networks Bo Xu, Dongyu Zhang, Shaowu Zhang, Hengchao Li, and Hongfei Lin (&) School of Computer Science and Technology, Dalian University

distribution of the best bid and ask prices upon the change in either of them. Architecture Each neural network has 4 layers. The standard neural netw

A Survey of Deep Learning Techniques Applied to Trading Published on July 31, 2016 by Greg Harris http://gregharris.info/a-survey-of-deep-learning-techniques-applied-t o-trading/ Deep learning has been

A Survey of Deep Learning Techniques Applied to Trading Published on July 31, 2016 by Greg Harris http://gregharris.info/a-survey-of-deep-learning-techniques-applied-t o-trading/ Deep learning has been

Real-Time Text Analytics for Event Detection in the Financial World

Real-Time Text Analytics for Event Detection in the Financial World Volker Stümpflen April 2015 Gaining value from Big Data Winner Information Delay - A Big Data Problem Markets are driven by news (and

Real-Time Text Analytics for Event Detection in the Financial World Volker Stümpflen April 2015 Gaining value from Big Data Winner Information Delay - A Big Data Problem Markets are driven by news (and

Novel Approaches to Sentiment Analysis for Stock Prediction

Novel Approaches to Sentiment Analysis for Stock Prediction Chris Wang, Yilun Xu, Qingyang Wang Stanford University chrwang, ylxu, iriswang @ stanford.edu Abstract Stock market predictions lend themselves

Novel Approaches to Sentiment Analysis for Stock Prediction Chris Wang, Yilun Xu, Qingyang Wang Stanford University chrwang, ylxu, iriswang @ stanford.edu Abstract Stock market predictions lend themselves

Leverage Financial News to Predict Stock Price Movements Using Word Embeddings and Deep Neural Networks

Leverage Financial News to Predict Stock Price Movements Using Word Embeddings and Deep Neural Networks Yangtuo Peng A THESIS SUBMITTED TO THE FACULTY OF GRADUATE STUDIES IN PARTIAL FULFILLMENT OF THE

Leverage Financial News to Predict Stock Price Movements Using Word Embeddings and Deep Neural Networks Yangtuo Peng A THESIS SUBMITTED TO THE FACULTY OF GRADUATE STUDIES IN PARTIAL FULFILLMENT OF THE

An enhanced artificial neural network for stock price predications

An enhanced artificial neural network for stock price predications Jiaxin MA Silin HUANG School of Engineering, The Hong Kong University of Science and Technology, Hong Kong SAR S. H. KWOK HKUST Business

An enhanced artificial neural network for stock price predications Jiaxin MA Silin HUANG School of Engineering, The Hong Kong University of Science and Technology, Hong Kong SAR S. H. KWOK HKUST Business

Stock Prediction Using Twitter Sentiment Analysis

Problem Statement Stock Prediction Using Twitter Sentiment Analysis Stock exchange is a subject that is highly affected by economic, social, and political factors. There are several factors e.g. external

Problem Statement Stock Prediction Using Twitter Sentiment Analysis Stock exchange is a subject that is highly affected by economic, social, and political factors. There are several factors e.g. external

Can Twitter predict the stock market?

1 Introduction Can Twitter predict the stock market? Volodymyr Kuleshov December 16, 2011 Last year, in a famous paper, Bollen et al. (2010) made the claim that Twitter mood is correlated with the Dow

1 Introduction Can Twitter predict the stock market? Volodymyr Kuleshov December 16, 2011 Last year, in a famous paper, Bollen et al. (2010) made the claim that Twitter mood is correlated with the Dow

Applications of Neural Networks

Applications of Neural Networks MPhil ACS Advanced Topics in NLP Laura Rimell 25 February 2016 1 NLP Neural Network Applications Language Models Word Embeddings Tagging Parsing Sentiment Machine Translation

Applications of Neural Networks MPhil ACS Advanced Topics in NLP Laura Rimell 25 February 2016 1 NLP Neural Network Applications Language Models Word Embeddings Tagging Parsing Sentiment Machine Translation

International Journal of Computer Engineering and Applications, Volume XII, Issue II, Feb. 18, ISSN

Volume XII, Issue II, Feb. 18, www.ijcea.com ISSN 31-3469 AN INVESTIGATION OF FINANCIAL TIME SERIES PREDICTION USING BACK PROPAGATION NEURAL NETWORKS K. Jayanthi, Dr. K. Suresh 1 Department of Computer

Volume XII, Issue II, Feb. 18, www.ijcea.com ISSN 31-3469 AN INVESTIGATION OF FINANCIAL TIME SERIES PREDICTION USING BACK PROPAGATION NEURAL NETWORKS K. Jayanthi, Dr. K. Suresh 1 Department of Computer

Artificially Intelligent Forecasting of Stock Market Indexes

Artificially Intelligent Forecasting of Stock Market Indexes Loyola Marymount University Math 560 Final Paper 05-01 - 2018 Daniel McGrath Advisor: Dr. Benjamin Fitzpatrick Contents I. Introduction II.

Artificially Intelligent Forecasting of Stock Market Indexes Loyola Marymount University Math 560 Final Paper 05-01 - 2018 Daniel McGrath Advisor: Dr. Benjamin Fitzpatrick Contents I. Introduction II.

Support Vector Machines: Training with Stochastic Gradient Descent

Support Vector Machines: Training with Stochastic Gradient Descent Machine Learning Spring 2018 The slides are mainly from Vivek Srikumar 1 Support vector machines Training by maximizing margin The SVM

Support Vector Machines: Training with Stochastic Gradient Descent Machine Learning Spring 2018 The slides are mainly from Vivek Srikumar 1 Support vector machines Training by maximizing margin The SVM

Analyzing Representational Schemes of Financial News Articles

Analyzing Representational Schemes of Financial News Articles Robert P. Schumaker Information Systems Dept. Iona College, New Rochelle, New York 10801, USA rschumaker@iona.edu Word Count: 2460 Abstract

Analyzing Representational Schemes of Financial News Articles Robert P. Schumaker Information Systems Dept. Iona College, New Rochelle, New York 10801, USA rschumaker@iona.edu Word Count: 2460 Abstract

The Influence of News Articles on The Stock Market.

The Influence of News Articles on The Stock Market. COMP4560 Presentation Supervisor: Dr Timothy Graham U6015364 Zhiheng Zhou Australian National University At Ian Ross Design Studio On 2018-5-18 Motivation

The Influence of News Articles on The Stock Market. COMP4560 Presentation Supervisor: Dr Timothy Graham U6015364 Zhiheng Zhou Australian National University At Ian Ross Design Studio On 2018-5-18 Motivation

Stock Price Prediction using Deep Learning

San Jose State University SJSU ScholarWorks Master's Projects Master's Theses and Graduate Research Spring 2018 Stock Price Prediction using Deep Learning Abhinav Tipirisetty San Jose State University

San Jose State University SJSU ScholarWorks Master's Projects Master's Theses and Graduate Research Spring 2018 Stock Price Prediction using Deep Learning Abhinav Tipirisetty San Jose State University

Stock Trading Following Stock Price Index Movement Classification Using Machine Learning Techniques

Stock Trading Following Stock Price Index Movement Classification Using Machine Learning Techniques 6.1 Introduction Trading in stock market is one of the most popular channels of financial investments.

Stock Trading Following Stock Price Index Movement Classification Using Machine Learning Techniques 6.1 Introduction Trading in stock market is one of the most popular channels of financial investments.

International Journal of Computer Engineering and Applications, Volume XII, Issue II, Feb. 18, ISSN

International Journal of Computer Engineering and Applications, Volume XII, Issue II, Feb. 18, www.ijcea.com ISSN 31-3469 AN INVESTIGATION OF FINANCIAL TIME SERIES PREDICTION USING BACK PROPAGATION NEURAL

International Journal of Computer Engineering and Applications, Volume XII, Issue II, Feb. 18, www.ijcea.com ISSN 31-3469 AN INVESTIGATION OF FINANCIAL TIME SERIES PREDICTION USING BACK PROPAGATION NEURAL

Lazy Prices: Vector Representations of Financial Disclosures and Market Outperformance

Lazy Prices: Vector Representations of Financial Disclosures and Market Outperformance Kuspa Kai kuspakai@stanford.edu Victor Cheung hoche@stanford.edu Alex Lin alin719@stanford.edu Abstract The Efficient

Lazy Prices: Vector Representations of Financial Disclosures and Market Outperformance Kuspa Kai kuspakai@stanford.edu Victor Cheung hoche@stanford.edu Alex Lin alin719@stanford.edu Abstract The Efficient

Feedforward Neural Networks for Sentiment Detection in Financial News

World Journal of Social Sciences Vol. 2. No. 4. July 2012. Pp. 218 234 Feedforward Neural Networks for Sentiment Detection in Financial News Caslav Bozic* and Detlef Seese* With a rise of algorithmic trading

World Journal of Social Sciences Vol. 2. No. 4. July 2012. Pp. 218 234 Feedforward Neural Networks for Sentiment Detection in Financial News Caslav Bozic* and Detlef Seese* With a rise of algorithmic trading

Algorithmic Trading using Reinforcement Learning augmented with Hidden Markov Model

Algorithmic Trading using Reinforcement Learning augmented with Hidden Markov Model Simerjot Kaur (sk3391) Stanford University Abstract This work presents a novel algorithmic trading system based on reinforcement

Algorithmic Trading using Reinforcement Learning augmented with Hidden Markov Model Simerjot Kaur (sk3391) Stanford University Abstract This work presents a novel algorithmic trading system based on reinforcement

Y. Yang, Y. Zheng and T. Hospedales. Updated: 2016/09/21. Queen Mary, University of London

GATED NEURAL NETWORKS FOR OPTION PRICING ENFORCING SANITY IN A BLACK BOX MODEL Y. Yang, Y. Zheng and T. Hospedales Updated: 2016/09/21 Queen Mary, University of London Overview ML for Option Pricing. With

GATED NEURAL NETWORKS FOR OPTION PRICING ENFORCING SANITY IN A BLACK BOX MODEL Y. Yang, Y. Zheng and T. Hospedales Updated: 2016/09/21 Queen Mary, University of London Overview ML for Option Pricing. With

Two kinds of neural networks, a feed forward multi layer Perceptron (MLP)[1,3] and an Elman recurrent network[5], are used to predict a company's

![Two kinds of neural networks, a feed forward multi layer Perceptron (MLP)[1,3] and an Elman recurrent network[5], are used to predict a company's](/thumbs/87/97049831.jpg "Two kinds of neural networks, a feed forward multi layer Perceptron (MLP)[1,3] and an Elman recurrent network[5], are used to predict a company's") LITERATURE REVIEW 2. LITERATURE REVIEW Detecting trends of stock data is a decision support process. Although the Random Walk Theory claims that price changes are serially independent, traders and certain

LITERATURE REVIEW 2. LITERATURE REVIEW Detecting trends of stock data is a decision support process. Although the Random Walk Theory claims that price changes are serially independent, traders and certain

Is Greedy Coordinate Descent a Terrible Algorithm?

Is Greedy Coordinate Descent a Terrible Algorithm? Julie Nutini, Mark Schmidt, Issam Laradji, Michael Friedlander, Hoyt Koepke University of British Columbia Optimization and Big Data, 2015 Context: Random

Is Greedy Coordinate Descent a Terrible Algorithm? Julie Nutini, Mark Schmidt, Issam Laradji, Michael Friedlander, Hoyt Koepke University of British Columbia Optimization and Big Data, 2015 Context: Random

arxiv: v1 [cs.lg] 21 Oct 2018

![arxiv: v1 [cs.lg] 21 Oct 2018](/thumbs/92/111002177.jpg "arxiv: v1 [cs.lg] 21 Oct 2018") CNNPred: CNN-based stock market prediction using several data sources Ehsan Hoseinzade a, Saman Haratizadeh a arxiv:1810.08923v1 [cs.lg] 21 Oct 2018 a Faculty of New Sciences and Technologies, University

CNNPred: CNN-based stock market prediction using several data sources Ehsan Hoseinzade a, Saman Haratizadeh a arxiv:1810.08923v1 [cs.lg] 21 Oct 2018 a Faculty of New Sciences and Technologies, University

Application of Deep Learning to Algorithmic Trading

Application of Deep Learning to Algorithmic Trading Guanting Chen [guanting] 1, Yatong Chen [yatong] 2, and Takahiro Fushimi [tfushimi] 3 1 Institute of Computational and Mathematical Engineering, Stanford

Application of Deep Learning to Algorithmic Trading Guanting Chen [guanting] 1, Yatong Chen [yatong] 2, and Takahiro Fushimi [tfushimi] 3 1 Institute of Computational and Mathematical Engineering, Stanford

CS221 Project Final Report Deep Reinforcement Learning in Portfolio Management

CS221 Project Final Report Deep Reinforcement Learning in Portfolio Management Ruohan Zhan Tianchang He Yunpo Li rhzhan@stanford.edu th7@stanford.edu yunpoli@stanford.edu Abstract Portfolio management

CS221 Project Final Report Deep Reinforcement Learning in Portfolio Management Ruohan Zhan Tianchang He Yunpo Li rhzhan@stanford.edu th7@stanford.edu yunpoli@stanford.edu Abstract Portfolio management

Improving Long Term Stock Market Prediction with Text Analysis

Western University Scholarship@Western Electronic Thesis and Dissertation Repository May 2017 Improving Long Term Stock Market Prediction with Text Analysis Tanner A. Bohn The University of Western Ontario

Western University Scholarship@Western Electronic Thesis and Dissertation Repository May 2017 Improving Long Term Stock Market Prediction with Text Analysis Tanner A. Bohn The University of Western Ontario

Understanding Deep Learning Requires Rethinking Generalization

Understanding Deep Learning Requires Rethinking Generalization ChiyuanZhang 1 Samy Bengio 3 Moritz Hardt 3 Benjamin Recht 2 Oriol Vinyals 4 1 Massachusetts Institute of Technology 2 University of California,

Understanding Deep Learning Requires Rethinking Generalization ChiyuanZhang 1 Samy Bengio 3 Moritz Hardt 3 Benjamin Recht 2 Oriol Vinyals 4 1 Massachusetts Institute of Technology 2 University of California,

Does Money Matter? An Artificial Intelligence Approach

An Artificial Intelligence Approach Peter Tiňo CERCIA, University of Birmingham, UK a collaboration with J. Binner Aston Business School, Aston University, UK B. Jones State University of New York, USA

An Artificial Intelligence Approach Peter Tiňo CERCIA, University of Birmingham, UK a collaboration with J. Binner Aston Business School, Aston University, UK B. Jones State University of New York, USA

Dr. P. O. Asagba Computer Science Department, Faculty of Science, University of Port Harcourt, Port Harcourt, PMB 5323, Choba, Nigeria

PREDICTING THE NIGERIAN STOCK MARKET USING ARTIFICIAL NEURAL NETWORK S. Neenwi Computer Science Department, Rivers State Polytechnic, Bori, PMB 20, Rivers State, Nigeria. Dr. P. O. Asagba Computer Science

PREDICTING THE NIGERIAN STOCK MARKET USING ARTIFICIAL NEURAL NETWORK S. Neenwi Computer Science Department, Rivers State Polytechnic, Bori, PMB 20, Rivers State, Nigeria. Dr. P. O. Asagba Computer Science

Foreign Exchange Forecasting via Machine Learning

Foreign Exchange Forecasting via Machine Learning Christian González Rojas cgrojas@stanford.edu Molly Herman mrherman@stanford.edu I. INTRODUCTION The finance industry has been revolutionized by the increased

Foreign Exchange Forecasting via Machine Learning Christian González Rojas cgrojas@stanford.edu Molly Herman mrherman@stanford.edu I. INTRODUCTION The finance industry has been revolutionized by the increased

Portfolio Recommendation System Stanford University CS 229 Project Report 2015

Portfolio Recommendation System Stanford University CS 229 Project Report 205 Berk Eserol Introduction Machine learning is one of the most important bricks that converges machine to human and beyond. Considering

Portfolio Recommendation System Stanford University CS 229 Project Report 205 Berk Eserol Introduction Machine learning is one of the most important bricks that converges machine to human and beyond. Considering

STOCK MARKET FORECASTING USING NEURAL NETWORKS

STOCK MARKET FORECASTING USING NEURAL NETWORKS Lakshmi Annabathuni University of Central Arkansas 400S Donaghey Ave, Apt#7 Conway, AR 72034 (845) 636-3443 lakshmiannabathuni@gmail.com Mark E. McMurtrey,

STOCK MARKET FORECASTING USING NEURAL NETWORKS Lakshmi Annabathuni University of Central Arkansas 400S Donaghey Ave, Apt#7 Conway, AR 72034 (845) 636-3443 lakshmiannabathuni@gmail.com Mark E. McMurtrey,

International Journal of Computer Engineering and Applications, Volume XII, Issue IV, April 18, ISSN

STOCK MARKET PREDICTION USING ARIMA MODEL Dr A.Haritha 1 Dr PVS Lakshmi 2 G.Lakshmi 3 E.Revathi 4 A.G S S Srinivas Deekshith 5 1,3 Assistant Professor, Department of IT, PVPSIT. 2 Professor, Department

STOCK MARKET PREDICTION USING ARIMA MODEL Dr A.Haritha 1 Dr PVS Lakshmi 2 G.Lakshmi 3 E.Revathi 4 A.G S S Srinivas Deekshith 5 1,3 Assistant Professor, Department of IT, PVPSIT. 2 Professor, Department

Stock Market Predictor and Analyser using Sentimental Analysis and Machine Learning Algorithms

Volume 119 No. 12 2018, 15395-15405 ISSN: 1314-3395 (on-line version) url: http://www.ijpam.eu ijpam.eu Stock Market Predictor and Analyser using Sentimental Analysis and Machine Learning Algorithms 1

Volume 119 No. 12 2018, 15395-15405 ISSN: 1314-3395 (on-line version) url: http://www.ijpam.eu ijpam.eu Stock Market Predictor and Analyser using Sentimental Analysis and Machine Learning Algorithms 1

Design and implementation of artificial neural network system for stock market prediction (A case study of first bank of Nigeria PLC Shares)

") International Journal of Advanced Engineering and Technology ISSN: 2456-7655 www.newengineeringjournal.com Volume 1; Issue 1; March 2017; Page No. 46-51 Design and implementation of artificial neural network

International Journal of Advanced Engineering and Technology ISSN: 2456-7655 www.newengineeringjournal.com Volume 1; Issue 1; March 2017; Page No. 46-51 Design and implementation of artificial neural network

Natural language based financial forecasting: a survey

Natural language based financial forecasting: a survey The MIT Faculty has made this article openly available. Please share how this access benefits you. Your story matters. Citation As Published Publisher

Natural language based financial forecasting: a survey The MIT Faculty has made this article openly available. Please share how this access benefits you. Your story matters. Citation As Published Publisher

Final Examination CS540: Introduction to Artificial Intelligence

Final Examination CS540: Introduction to Artificial Intelligence December 2008 LAST NAME: FIRST NAME: Problem Score Max Score 1 15 2 15 3 10 4 20 5 10 6 20 7 10 Total 100 Question 1. [15] Probabilistic

Final Examination CS540: Introduction to Artificial Intelligence December 2008 LAST NAME: FIRST NAME: Problem Score Max Score 1 15 2 15 3 10 4 20 5 10 6 20 7 10 Total 100 Question 1. [15] Probabilistic

Predicting stock prices for large-cap technology companies

Predicting stock prices for large-cap technology companies 15 th December 2017 Ang Li (al171@stanford.edu) Abstract The goal of the project is to predict price changes in the future for a given stock.

Predicting stock prices for large-cap technology companies 15 th December 2017 Ang Li (al171@stanford.edu) Abstract The goal of the project is to predict price changes in the future for a given stock.

Performance analysis of Neural Network Algorithms on Stock Market Forecasting

www.ijecs.in International Journal Of Engineering And Computer Science ISSN:2319-7242 Volume 3 Issue 9 September, 2014 Page No. 8347-8351 Performance analysis of Neural Network Algorithms on Stock Market

www.ijecs.in International Journal Of Engineering And Computer Science ISSN:2319-7242 Volume 3 Issue 9 September, 2014 Page No. 8347-8351 Performance analysis of Neural Network Algorithms on Stock Market

Relative and absolute equity performance prediction via supervised learning

Relative and absolute equity performance prediction via supervised learning Alex Alifimoff aalifimoff@stanford.edu Axel Sly axelsly@stanford.edu Introduction Investment managers and traders utilize two

Relative and absolute equity performance prediction via supervised learning Alex Alifimoff aalifimoff@stanford.edu Axel Sly axelsly@stanford.edu Introduction Investment managers and traders utilize two

Stock Market Index Prediction Using Multilayer Perceptron and Long Short Term Memory Networks: A Case Study on BSE Sensex

Stock Market Index Prediction Using Multilayer Perceptron and Long Short Term Memory Networks: A Case Study on BSE Sensex R. Arjun Raj # # Research Scholar, APJ Abdul Kalam Technological University, College

Stock Market Index Prediction Using Multilayer Perceptron and Long Short Term Memory Networks: A Case Study on BSE Sensex R. Arjun Raj # # Research Scholar, APJ Abdul Kalam Technological University, College

Bond Market Prediction using an Ensemble of Neural Networks

Bond Market Prediction using an Ensemble of Neural Networks Bhagya Parekh Naineel Shah Rushabh Mehta Harshil Shah ABSTRACT The characteristics of a successful financial forecasting system are the exploitation

Bond Market Prediction using an Ensemble of Neural Networks Bhagya Parekh Naineel Shah Rushabh Mehta Harshil Shah ABSTRACT The characteristics of a successful financial forecasting system are the exploitation

Development and Performance Evaluation of Three Novel Prediction Models for Mutual Fund NAV Prediction

Development and Performance Evaluation of Three Novel Prediction Models for Mutual Fund NAV Prediction Ananya Narula *, Chandra Bhanu Jha * and Ganapati Panda ** E-mail: an14@iitbbs.ac.in; cbj10@iitbbs.ac.in;

Development and Performance Evaluation of Three Novel Prediction Models for Mutual Fund NAV Prediction Ananya Narula *, Chandra Bhanu Jha * and Ganapati Panda ** E-mail: an14@iitbbs.ac.in; cbj10@iitbbs.ac.in;

LITERATURE REVIEW. can mimic the brain. A neural network consists of an interconnected nnected group of

10 CHAPTER 2 LITERATURE REVIEW 2.1 Artificial Neural Network Artificial neural network (ANN), usually ly called led Neural Network (NN), is an algorithm that was originally motivated ted by the goal of

10 CHAPTER 2 LITERATURE REVIEW 2.1 Artificial Neural Network Artificial neural network (ANN), usually ly called led Neural Network (NN), is an algorithm that was originally motivated ted by the goal of

Measuring the Impact of Financial News and Social Media on Stock Market Modeling Using Time Series Mining Techniques

algorithms Article Measuring the Impact of Financial News and Social Media on Stock Market Modeling Using Time Series Mining Techniques Foteini Kollintza-Kyriakoulia 1, Manolis Maragoudakis 1, * and Anastasia

algorithms Article Measuring the Impact of Financial News and Social Media on Stock Market Modeling Using Time Series Mining Techniques Foteini Kollintza-Kyriakoulia 1, Manolis Maragoudakis 1, * and Anastasia

Session 5. Predictive Modeling in Life Insurance

SOA Predictive Analytics Seminar Hong Kong 29 Aug. 2018 Hong Kong Session 5 Predictive Modeling in Life Insurance Jingyi Zhang, Ph.D Predictive Modeling in Life Insurance JINGYI ZHANG PhD Scientist Global

SOA Predictive Analytics Seminar Hong Kong 29 Aug. 2018 Hong Kong Session 5 Predictive Modeling in Life Insurance Jingyi Zhang, Ph.D Predictive Modeling in Life Insurance JINGYI ZHANG PhD Scientist Global

COGNITIVE LEARNING OF INTELLIGENCE SYSTEMS USING NEURAL NETWORKS: EVIDENCE FROM THE AUSTRALIAN CAPITAL MARKETS

Asian Academy of Management Journal, Vol. 7, No. 2, 17 25, July 2002 COGNITIVE LEARNING OF INTELLIGENCE SYSTEMS USING NEURAL NETWORKS: EVIDENCE FROM THE AUSTRALIAN CAPITAL MARKETS Joachim Tan Edward Sek

Asian Academy of Management Journal, Vol. 7, No. 2, 17 25, July 2002 COGNITIVE LEARNING OF INTELLIGENCE SYSTEMS USING NEURAL NETWORKS: EVIDENCE FROM THE AUSTRALIAN CAPITAL MARKETS Joachim Tan Edward Sek

Backpropagation and Recurrent Neural Networks in Financial Analysis of Multiple Stock Market Returns

Backpropagation and Recurrent Neural Networks in Financial Analysis of Multiple Stock Market Returns Jovina Roman and Akhtar Jameel Department of Computer Science Xavier University of Louisiana 7325 Palmetto

Backpropagation and Recurrent Neural Networks in Financial Analysis of Multiple Stock Market Returns Jovina Roman and Akhtar Jameel Department of Computer Science Xavier University of Louisiana 7325 Palmetto

A Dynamic Hedging Strategy for Option Transaction Using Artificial Neural Networks

A Dynamic Hedging Strategy for Option Transaction Using Artificial Neural Networks Hyun Joon Shin and Jaepil Ryu Dept. of Management Eng. Sangmyung University {hjshin, jpru}@smu.ac.kr Abstract In order

A Dynamic Hedging Strategy for Option Transaction Using Artificial Neural Networks Hyun Joon Shin and Jaepil Ryu Dept. of Management Eng. Sangmyung University {hjshin, jpru}@smu.ac.kr Abstract In order

Prediction Algorithm using Lexicons and Heuristics based Sentiment Analysis

IOSR Journal of Computer Engineering (IOSR-JCE) e-issn: 2278-0661,p-ISSN: 2278-8727 PP 16-20 www.iosrjournals.org Prediction Algorithm using Lexicons and Heuristics based Sentiment Analysis Aakash Kamble

IOSR Journal of Computer Engineering (IOSR-JCE) e-issn: 2278-0661,p-ISSN: 2278-8727 PP 16-20 www.iosrjournals.org Prediction Algorithm using Lexicons and Heuristics based Sentiment Analysis Aakash Kamble

Notes on the EM Algorithm Michael Collins, September 24th 2005

Notes on the EM Algorithm Michael Collins, September 24th 2005 1 Hidden Markov Models A hidden Markov model (N, Σ, Θ) consists of the following elements: N is a positive integer specifying the number of

Notes on the EM Algorithm Michael Collins, September 24th 2005 1 Hidden Markov Models A hidden Markov model (N, Σ, Θ) consists of the following elements: N is a positive integer specifying the number of

Market Microstructure Invariants

Market Microstructure Invariants Albert S. Kyle and Anna A. Obizhaeva University of Maryland TI-SoFiE Conference 212 Amsterdam, Netherlands March 27, 212 Kyle and Obizhaeva Market Microstructure Invariants

Market Microstructure Invariants Albert S. Kyle and Anna A. Obizhaeva University of Maryland TI-SoFiE Conference 212 Amsterdam, Netherlands March 27, 212 Kyle and Obizhaeva Market Microstructure Invariants

Chapter 5: Estimating Project Times and Costs 4KF3

Lecture Notes Importance of Estimates Support good decisions Schedule work o Make sure your team members can take on added work of project Determine length of project and costs o Projects can be cancelled

Lecture Notes Importance of Estimates Support good decisions Schedule work o Make sure your team members can take on added work of project Determine length of project and costs o Projects can be cancelled

Dependency Parsing. CS5740: Natural Language Processing Spring Instructor: Yoav Artzi

CS5740: Natural Language Processing Spring 2018 Dependency Parsing Instructor: Yoav Artzi Slides adapted from Dan Klein, Luke Zettlemoyer, Chris Manning, and Dan Jurafsky, and David Weiss Overview The

CS5740: Natural Language Processing Spring 2018 Dependency Parsing Instructor: Yoav Artzi Slides adapted from Dan Klein, Luke Zettlemoyer, Chris Manning, and Dan Jurafsky, and David Weiss Overview The

Textual Analysis of Stock Market Prediction Using Financial News Articles

Association for Information Systems AIS Electronic Library (AISeL) AMCIS 2006 Proceedings Americas Conference on Information Systems (AMCIS) December 2006 Textual Analysis of Stock Market Prediction Using

Association for Information Systems AIS Electronic Library (AISeL) AMCIS 2006 Proceedings Americas Conference on Information Systems (AMCIS) December 2006 Textual Analysis of Stock Market Prediction Using

Prepayments in depth - part 2: Deeper into the forest

: Deeper into the forest Anders S. Aalund & Peder C. F. Møller October 12, 2018 Contents 1 Summary 1 2 Pool factor and prepayments - a subtle relation 2 2.1 In-sample analysis.................................

: Deeper into the forest Anders S. Aalund & Peder C. F. Møller October 12, 2018 Contents 1 Summary 1 2 Pool factor and prepayments - a subtle relation 2 2.1 In-sample analysis.................................

Exploring the Potential of Image-based Deep Learning in Insurance. Luisa F. Polanía Cabrera

Exploring the Potential of Image-based Deep Learning in Insurance Luisa F. Polanía Cabrera 1 Madison, Wisconsin based American Family Insurance is the nation's third-largest mutual property/casualty insurance

Exploring the Potential of Image-based Deep Learning in Insurance Luisa F. Polanía Cabrera 1 Madison, Wisconsin based American Family Insurance is the nation's third-largest mutual property/casualty insurance

Statistical and Machine Learning Approach in Forex Prediction Based on Empirical Data

Statistical and Machine Learning Approach in Forex Prediction Based on Empirical Data Sitti Wetenriajeng Sidehabi Department of Electrical Engineering Politeknik ATI Makassar Makassar, Indonesia tenri616@gmail.com

Statistical and Machine Learning Approach in Forex Prediction Based on Empirical Data Sitti Wetenriajeng Sidehabi Department of Electrical Engineering Politeknik ATI Makassar Makassar, Indonesia tenri616@gmail.com

Deep Learning in Asset Pricing

Deep Learning in Asset Pricing Luyang Chen 1 Markus Pelger 1 Jason Zhu 1 1 Stanford University November 17th 2018 Western Mathematical Finance Conference 2018 Motivation Hype: Machine Learning in Investment

Deep Learning in Asset Pricing Luyang Chen 1 Markus Pelger 1 Jason Zhu 1 1 Stanford University November 17th 2018 Western Mathematical Finance Conference 2018 Motivation Hype: Machine Learning in Investment

Pattern Recognition by Neural Network Ensemble

IT691 2009 1 Pattern Recognition by Neural Network Ensemble Joseph Cestra, Babu Johnson, Nikolaos Kartalis, Rasul Mehrab, Robb Zucker Pace University Abstract This is an investigation of artificial neural

IT691 2009 1 Pattern Recognition by Neural Network Ensemble Joseph Cestra, Babu Johnson, Nikolaos Kartalis, Rasul Mehrab, Robb Zucker Pace University Abstract This is an investigation of artificial neural

Wide and Deep Learning for Peer-to-Peer Lending

Wide and Deep Learning for Peer-to-Peer Lending Kaveh Bastani 1 *, Elham Asgari 2, Hamed Namavari 3 1 Unifund CCR, LLC, Cincinnati, OH 2 Pamplin College of Business, Virginia Polytechnic Institute, Blacksburg,

Wide and Deep Learning for Peer-to-Peer Lending Kaveh Bastani 1 *, Elham Asgari 2, Hamed Namavari 3 1 Unifund CCR, LLC, Cincinnati, OH 2 Pamplin College of Business, Virginia Polytechnic Institute, Blacksburg,

IN traditional finance, the efficient market hypothesis states

IEEE TRANSACTIONS ON KNOWLEDGE AND DATA ENGINEERING, VOL. 30, NO. 2, FEBRUARY 2018 381 Web Media and Stock Markets : A Survey and Future Directions from a Big Data Perspective Qing Li, Member, IEEE, Yan

IEEE TRANSACTIONS ON KNOWLEDGE AND DATA ENGINEERING, VOL. 30, NO. 2, FEBRUARY 2018 381 Web Media and Stock Markets : A Survey and Future Directions from a Big Data Perspective Qing Li, Member, IEEE, Yan

Applications of Neural Networks in Stock Market Prediction

Applications of Neural Networks in Stock Market Prediction -An Approach Based Analysis Shiv Kumar Goel 1, Bindu Poovathingal 2, Neha Kumari 3 1Asst. Professor, Vivekanand Education Society Institute of

Applications of Neural Networks in Stock Market Prediction -An Approach Based Analysis Shiv Kumar Goel 1, Bindu Poovathingal 2, Neha Kumari 3 1Asst. Professor, Vivekanand Education Society Institute of

Multi-armed bandits in dynamic pricing

Multi-armed bandits in dynamic pricing Arnoud den Boer University of Twente, Centrum Wiskunde & Informatica Amsterdam Lancaster, January 11, 2016 Dynamic pricing A firm sells a product, with abundant inventory,

Multi-armed bandits in dynamic pricing Arnoud den Boer University of Twente, Centrum Wiskunde & Informatica Amsterdam Lancaster, January 11, 2016 Dynamic pricing A firm sells a product, with abundant inventory,

Shynkevich, Y, McGinnity, M, Coleman, S, Belatreche, A and Li, Y

Forecasting price movements using technical indicators : investigating the impact of varying input window length Shynkevich, Y, McGinnity, M, Coleman, S, Belatreche, A and Li, Y http://dx.doi.org/10.1016/j.neucom.2016.11.095

Forecasting price movements using technical indicators : investigating the impact of varying input window length Shynkevich, Y, McGinnity, M, Coleman, S, Belatreche, A and Li, Y http://dx.doi.org/10.1016/j.neucom.2016.11.095

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2010, Mr. Ruey S. Tsay Solutions to Final Exam

The University of Chicago, Booth School of Business Business 410, Spring Quarter 010, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (4 pts) Answer briefly the following questions. 1. Questions 1

The University of Chicago, Booth School of Business Business 410, Spring Quarter 010, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (4 pts) Answer briefly the following questions. 1. Questions 1

Predicting Risk from Financial Reports with Regression

Predicting Risk from Financial Reports with Regression Shimon Kogan, University of Texas at Austin Dimitry Levin, Carnegie Mellon University Bryan R. Routledge, Carnegie Mellon University Jacob S. Sagi,

Predicting Risk from Financial Reports with Regression Shimon Kogan, University of Texas at Austin Dimitry Levin, Carnegie Mellon University Bryan R. Routledge, Carnegie Mellon University Jacob S. Sagi,

Estimating Term Structure of U.S. Treasury Securities: An Interpolation Approach

Estimating Term Structure of U.S. Treasury Securities: An Interpolation Approach Feng Guo J. Huston McCulloch Our Task Empirical TS are unobservable. Without a continuous spectrum of zero-coupon securities;

Estimating Term Structure of U.S. Treasury Securities: An Interpolation Approach Feng Guo J. Huston McCulloch Our Task Empirical TS are unobservable. Without a continuous spectrum of zero-coupon securities;

Data based stock portfolio construction using Computational Intelligence

Data based stock portfolio construction using Computational Intelligence Asimina Dimara and Christos-Nikolaos Anagnostopoulos Data Economy workshop: How online data change economy and business Introduction

Data based stock portfolio construction using Computational Intelligence Asimina Dimara and Christos-Nikolaos Anagnostopoulos Data Economy workshop: How online data change economy and business Introduction

Multi-factor Stock Selection Model Based on Kernel Support Vector Machine

Journal of Mathematics Research; Vol. 10, No. 5; October 2018 ISSN 1916-9795 E-ISSN 1916-9809 Published by Canadian Center of Science and Education Multi-factor Stock Selection Model Based on Kernel Support

Journal of Mathematics Research; Vol. 10, No. 5; October 2018 ISSN 1916-9795 E-ISSN 1916-9809 Published by Canadian Center of Science and Education Multi-factor Stock Selection Model Based on Kernel Support

COMMIT at SemEval-2017 Task 5: Ontology-based Method for Sentiment Analysis of Financial Headlines

COMMIT at SemEval-2017 Task 5: Ontology-based Method for Sentiment Analysis of Financial Headlines Kim Schouten Flavius Frasincar Erasmus University Rotterdam P.O. Box 1738, NL-3000 DR Rotterdam, The Netherlands

COMMIT at SemEval-2017 Task 5: Ontology-based Method for Sentiment Analysis of Financial Headlines Kim Schouten Flavius Frasincar Erasmus University Rotterdam P.O. Box 1738, NL-3000 DR Rotterdam, The Netherlands

2D5362 Machine Learning

2D5362 Machine Learning Reinforcement Learning MIT GALib Available at http://lancet.mit.edu/ga/ download galib245.tar.gz gunzip galib245.tar.gz tar xvf galib245.tar cd galib245 make or access my files

2D5362 Machine Learning Reinforcement Learning MIT GALib Available at http://lancet.mit.edu/ga/ download galib245.tar.gz gunzip galib245.tar.gz tar xvf galib245.tar cd galib245 make or access my files

Gradient Descent and the Structure of Neural Network Cost Functions. presentation by Ian Goodfellow

Gradient Descent and the Structure of Neural Network Cost Functions presentation by Ian Goodfellow adapted for www.deeplearningbook.org from a presentation to the CIFAR Deep Learning summer school on August

Gradient Descent and the Structure of Neural Network Cost Functions presentation by Ian Goodfellow adapted for www.deeplearningbook.org from a presentation to the CIFAR Deep Learning summer school on August

Cooperative Game Theory

Cooperative Game Theory Non-cooperative game theory specifies the strategic structure of an interaction: The participants (players) in a strategic interaction Who can do what and when, and what they know

Cooperative Game Theory Non-cooperative game theory specifies the strategic structure of an interaction: The participants (players) in a strategic interaction Who can do what and when, and what they know

Fast R-CNN. Ross Girshick Facebook AI Research (FAIR) Work done at Microsoft Research. Presented by: Nick Joodi Doug Sherman

Work done at Microsoft Research. Presented by: Nick Joodi Doug Sherman") Fast R-CNN Ross Girshick Facebook AI Research (FAIR) Work done at Microsoft Research Presented by: Nick Joodi Doug Sherman Fast Region-based ConvNets (R-CNNs) Fast Sorry about the black BG, Girshick s

Fast R-CNN Ross Girshick Facebook AI Research (FAIR) Work done at Microsoft Research Presented by: Nick Joodi Doug Sherman Fast Region-based ConvNets (R-CNNs) Fast Sorry about the black BG, Girshick s

Forecasting Movements of Health-Care Stock Prices Based on Different Categories of News Articles. using Multiple Kernel Learning

Forecasting Movements of Health-Care Stock Prices Based on Different Categories of News Articles using Multiple Kernel Learning Yauheniya Shynkevich 1,*, T.M. McGinnity 1,, Sonya Coleman 1, Ammar Belatreche

Forecasting Movements of Health-Care Stock Prices Based on Different Categories of News Articles using Multiple Kernel Learning Yauheniya Shynkevich 1,*, T.M. McGinnity 1,, Sonya Coleman 1, Ammar Belatreche

Prediction Using Back Propagation and k- Nearest Neighbor (k-nn) Algorithm

Algorithm") Prediction Using Back Propagation and k- Nearest Neighbor (k-nn) Algorithm Tejaswini patil 1, Karishma patil 2, Devyani Sonawane 3, Chandraprakash 4 Student, Dept. of computer, SSBT COET, North Maharashtra

Prediction Using Back Propagation and k- Nearest Neighbor (k-nn) Algorithm Tejaswini patil 1, Karishma patil 2, Devyani Sonawane 3, Chandraprakash 4 Student, Dept. of computer, SSBT COET, North Maharashtra

Visualization on Financial Terms via Risk Ranking from Financial Reports

Visualization on Financial Terms via Risk Ranking from Financial Reports Ming-Feng Tsai 1,2 Chuan-Ju Wang 3 (1) Department of Computer Science, National Chengchi University, Taipei 116, Taiwan (2) Program

Visualization on Financial Terms via Risk Ranking from Financial Reports Ming-Feng Tsai 1,2 Chuan-Ju Wang 3 (1) Department of Computer Science, National Chengchi University, Taipei 116, Taiwan (2) Program

Future Market Rates for Scenario Analysis

Future Market Rates for Scenario Analysis MTDS: Step 4 1 Step 4 (Market variables) Objective Identify baseline projections for market variables and the main risks to these Outcome A clearly defined baseline

Future Market Rates for Scenario Analysis MTDS: Step 4 1 Step 4 (Market variables) Objective Identify baseline projections for market variables and the main risks to these Outcome A clearly defined baseline

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2009, Mr. Ruey S. Tsay. Solutions to Final Exam

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2009, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (42 pts) Answer briefly the following questions. 1. Questions

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2009, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (42 pts) Answer briefly the following questions. 1. Questions

Topic-based vector space modeling of Twitter data with application in predictive analytics

Topic-based vector space modeling of Twitter data with application in predictive analytics Guangnan Zhu (U6023358) Australian National University COMP4560 Individual Project Presentation Supervisor: Dr.

Topic-based vector space modeling of Twitter data with application in predictive analytics Guangnan Zhu (U6023358) Australian National University COMP4560 Individual Project Presentation Supervisor: Dr.

A Lattice-based Framework for Joint Chinese Word Segmentation, POS Tagging and Parsing

A Lattice-based Framework for Joint Chinese Word Segmentation, OS Tagging and arsing Zhiguo Wang 1, Chengqing Zong 1 and Nianwen Xue 2 1 National Laboratory of attern Recognition, Institute of Automation,

A Lattice-based Framework for Joint Chinese Word Segmentation, OS Tagging and arsing Zhiguo Wang 1, Chengqing Zong 1 and Nianwen Xue 2 1 National Laboratory of attern Recognition, Institute of Automation,

A Machine Learning Investigation of One-Month Momentum. Ben Gum

A Machine Learning Investigation of One-Month Momentum Ben Gum Contents Problem Data Recent Literature Simple Improvements Neural Network Approach Conclusion Appendix : Some Background on Neural Networks

A Machine Learning Investigation of One-Month Momentum Ben Gum Contents Problem Data Recent Literature Simple Improvements Neural Network Approach Conclusion Appendix : Some Background on Neural Networks

arxiv: v1 [cs.ai] 7 Jan 2018

![arxiv: v1 [cs.ai] 7 Jan 2018](/thumbs/90/101210477.jpg "arxiv: v1 [cs.ai] 7 Jan 2018") Trading the Twitter Sentiment with Reinforcement Learning Catherine Xiao catherine.xiao1@gmail.com Wanfeng Chen wanfengc@gmail.com arxiv:1801.02243v1 [cs.ai] 7 Jan 2018 Abstract This paper is to explore

Trading the Twitter Sentiment with Reinforcement Learning Catherine Xiao catherine.xiao1@gmail.com Wanfeng Chen wanfengc@gmail.com arxiv:1801.02243v1 [cs.ai] 7 Jan 2018 Abstract This paper is to explore

arxiv: v1 [cs.ce] 11 Sep 2018

![arxiv: v1 [cs.ce] 11 Sep 2018](/thumbs/90/103888497.jpg "arxiv: v1 [cs.ce] 11 Sep 2018") Visual Attention Model for Cross-sectional Stock Return Prediction and End-to-End Multimodal Market Representation Learning Ran Zhao Carnegie Mellon University rzhao1@cs.cmu.edu Arun Verma Bloomberg averma3@bloomberg.net

Visual Attention Model for Cross-sectional Stock Return Prediction and End-to-End Multimodal Market Representation Learning Ran Zhao Carnegie Mellon University rzhao1@cs.cmu.edu Arun Verma Bloomberg averma3@bloomberg.net

HEDGING WITH GENERALIZED BASIS RISK: Empirical Results

HEDGING WITH GENERALIZED BASIS RISK: Empirical Results 1 OUTLINE OF PRESENTATION INTRODUCTION MOTIVATION FOR THE TOPIC GOALS LITERATURE REVIEW THE MODEL THE DATA FUTURE WORK 2 INTRODUCTION Hedging is used

HEDGING WITH GENERALIZED BASIS RISK: Empirical Results 1 OUTLINE OF PRESENTATION INTRODUCTION MOTIVATION FOR THE TOPIC GOALS LITERATURE REVIEW THE MODEL THE DATA FUTURE WORK 2 INTRODUCTION Hedging is used

Cognitive Pattern Analysis Employing Neural Networks: Evidence from the Australian Capital Markets

76 Cognitive Pattern Analysis Employing Neural Networks: Evidence from the Australian Capital Markets Edward Sek Khin Wong Faculty of Business & Accountancy University of Malaya 50603, Kuala Lumpur, Malaysia

76 Cognitive Pattern Analysis Employing Neural Networks: Evidence from the Australian Capital Markets Edward Sek Khin Wong Faculty of Business & Accountancy University of Malaya 50603, Kuala Lumpur, Malaysia

Predicting the Success of a Retirement Plan Based on Early Performance of Investments

Predicting the Success of a Retirement Plan Based on Early Performance of Investments CS229 Autumn 2010 Final Project Darrell Cain, AJ Minich Abstract Using historical data on the stock market, it is possible

Predicting the Success of a Retirement Plan Based on Early Performance of Investments CS229 Autumn 2010 Final Project Darrell Cain, AJ Minich Abstract Using historical data on the stock market, it is possible

D I S C O N T I N U O U S DEMAND FUNCTIONS: ESTIMATION AND PRICING. Rotterdam May 24, 2018

D I S C O N T I N U O U S DEMAND FUNCTIONS: ESTIMATION AND PRICING Arnoud V. den Boer University of Amsterdam N. Bora Keskin Duke University Rotterdam May 24, 2018 Dynamic pricing and learning: Learning

D I S C O N T I N U O U S DEMAND FUNCTIONS: ESTIMATION AND PRICING Arnoud V. den Boer University of Amsterdam N. Bora Keskin Duke University Rotterdam May 24, 2018 Dynamic pricing and learning: Learning

Neural Network Prediction of Stock Price Trend Based on RS with Entropy Discretization

2017 International Conference on Materials, Energy, Civil Engineering and Computer (MATECC 2017) Neural Network Prediction of Stock Price Trend Based on RS with Entropy Discretization Huang Haiqing1,a,

2017 International Conference on Materials, Energy, Civil Engineering and Computer (MATECC 2017) Neural Network Prediction of Stock Price Trend Based on RS with Entropy Discretization Huang Haiqing1,a,

Stock Market Analysis Using Artificial Neural Network on Big Data

Available online www.ejaet.com European Journal of Advances in Engineering and Technology, 2016, 3(1): 26-33 Research Article ISSN: 2394-658X Stock Market Analysis Using Artificial Neural Network on Big

Available online www.ejaet.com European Journal of Advances in Engineering and Technology, 2016, 3(1): 26-33 Research Article ISSN: 2394-658X Stock Market Analysis Using Artificial Neural Network on Big

An Online Algorithm for Multi-Strategy Trading Utilizing Market Regimes

An Online Algorithm for Multi-Strategy Trading Utilizing Market Regimes Hynek Mlnařík 1 Subramanian Ramamoorthy 2 Rahul Savani 1 1 Warwick Institute for Financial Computing Department of Computer Science

An Online Algorithm for Multi-Strategy Trading Utilizing Market Regimes Hynek Mlnařík 1 Subramanian Ramamoorthy 2 Rahul Savani 1 1 Warwick Institute for Financial Computing Department of Computer Science

Algorithmic Trading using Sentiment Analysis and Reinforcement Learning Simerjot Kaur (SUNetID: sk3391 and TeamID: 035)

") Algorithmic Trading using Sentiment Analysis and Reinforcement Learning Simerjot Kaur (SUNetID: sk3391 and TeamID: 035) Abstract This work presents a novel algorithmic trading system based on reinforcement

Algorithmic Trading using Sentiment Analysis and Reinforcement Learning Simerjot Kaur (SUNetID: sk3391 and TeamID: 035) Abstract This work presents a novel algorithmic trading system based on reinforcement

PREDICTION OF STOCK MARKET TRENDS BY SENTIMENT FARMING USING OPINION MINING

TITLE OF THE THESIS PREDICTION OF STOCK MARKET TRENDS BY SENTIMENT FARMING USING OPINION MINING A RESEARCH PROPOSAL SUBMITTED TO THE SHRI RAMDEOBABA COLLEGE OF ENGINEERING AND MANAGEMENT, FOR THE DEGREE

TITLE OF THE THESIS PREDICTION OF STOCK MARKET TRENDS BY SENTIMENT FARMING USING OPINION MINING A RESEARCH PROPOSAL SUBMITTED TO THE SHRI RAMDEOBABA COLLEGE OF ENGINEERING AND MANAGEMENT, FOR THE DEGREE

TTIC An Introduction to the Theory of Machine Learning. The Adversarial Multi-armed Bandit Problem Avrim Blum.

TTIC 31250 An Introduction to the Theory of Machine Learning The Adversarial Multi-armed Bandit Problem Avrim Blum Start with recap 1 Algorithm Consider the following setting Each morning, you need to

TTIC 31250 An Introduction to the Theory of Machine Learning The Adversarial Multi-armed Bandit Problem Avrim Blum Start with recap 1 Algorithm Consider the following setting Each morning, you need to

Machine Learning in Risk Forecasting and its Application in Low Volatility Strategies

NEW THINKING Machine Learning in Risk Forecasting and its Application in Strategies By Yuriy Bodjov Artificial intelligence and machine learning are two terms that have gained increased popularity within

NEW THINKING Machine Learning in Risk Forecasting and its Application in Strategies By Yuriy Bodjov Artificial intelligence and machine learning are two terms that have gained increased popularity within

Stock Price Prediction Using Neural Network Models Based on Tweets Sentiment Scores

Journal of Computer Sciences and Applications, 2017, Vol. 5, No. 2, 64-75 Available online at http://pubs.sciepub.com/jcsa/5/2/3 Science and Education Publishing DOI:10.12691/jcsa-5-2-3 Stock Price Prediction

Journal of Computer Sciences and Applications, 2017, Vol. 5, No. 2, 64-75 Available online at http://pubs.sciepub.com/jcsa/5/2/3 Science and Education Publishing DOI:10.12691/jcsa-5-2-3 Stock Price Prediction