The Efficient Market Hypothesis. Presented by Luke Guerrero and Sarah Van der Elst

|

|

|

- Vanessa Laurel Hawkins

- 5 years ago

- Views:

Transcription

1 The Efficient Market Hypothesis Presented by Luke Guerrero and Sarah Van der Elst

2 Agenda Background and Definitions Tests of Efficiency Arguments against Efficiency Conclusions

3 Overview An ideal market is one in which prices provide accurate signals for resource allocation Extreme null hypothesis: a market is efficient if prices always fully reflect all available information Three forms of Efficiency: Weak form Semi-strong form Strong form

4 Defining Fully Reflect Most work based on assumption that market equilibrium can be stated in terms of expected returns E(p j,t+1 Փ t )=[1+E(r j,t+1 Փ t )p jt E = expected value operator, p jt = price of security j at time t, p j,t+1 = price at t+1, r j,t+1 = one-period percentage return, Փ t = information set assumed to be fully reflected Elevates concept of expected value One possible measure of distribution of returns Market efficiency does not per se instill it with any special importance

5 Expected return or fair game efficient market Market equilibrium can be stated in terms of expected returns Equilibrium returns are formed on basis of information set Փ t Rules out possibility of trading systems based only on information Փ t that have excess expected profits or returns Let x j,t+1 =p j,t+1 - E(p j,t+1 Փ t ) Then E(x j,t+1 Փ t )=0 So by definition the sequence {x jt } is fair game with respect to the information sequence {Փ t } Equivalently: z j,t+1 = rj,t+1 - E(r j,t+1 Փ t )

6 The Submartingale Model Suppose we assume that for all t and Փ t : E(p j,t+1 Փ t ) p jt equivalently, E(r j,t+1 Փ t ) 0 Expected value of next period s price is equal to or greater than the current price If submartingale, then trading rules based only on information Փ t in cannot have greater expected profits than policy of always buying-andholding the security during the future period

7 The Random Walk Model Successive price changes are independent and identically distributed Formally: f(r j,t+1 Փ t ) = f(r j,t+1 ) Entire distribution is independent of Փ t More detailed statement and extension of fair game efficient markets model Environment is such that return distributions repeat themselves

8 Market Conditions Consistent with Efficiency Sufficient but not necessary: No transactions costs in trading securities All available information is costlessly available to all market participants All agree on implications of current information for current price and distributions for future prices All potential sources of inefficiency All most likely exist somewhat in the real world

9 Weak Form Tests Most results for weak form tests come from Random Walk literature Filter Tests (Fama-Blume and Alexander): for very small filters it is possible to devise trading schemes based on very short-term price swings that will on average outperform buy-and-hold.5-1% filters Miniscule average profits Over long term outperform buy-and-hold With minimum trading costs small filters advantage disappears Statistically significant, economically insignificant

10 Serial Covariance of a fair game Serial covariance of a fair game and a random walk are zero E(x t+r +x t )= x t E(x t+r x t )f(x t )dx t and if x t is fair game: E(x t+r x t )=0 all serial covariances between lagged value are zero Observations are linearly independent Serial covariances of one-period returns aren t necessarily zero Deviation of return for t+1 from its conditional expectation is a fair game variable but conditional expectation itself can depend on the return observed for t A large approximation in estimating covariances but seems not to greatly affect the results of covariance tests for common stocks

11 Behavior of Stock Market Prices, Eugene F. Fama, Journal of Business

12 Weak Form Tests: Behavior of Stock Market Prices N= observations per stock Statistically significant deviations from zero covariance Small absolute levels of serial correlation observed EX: correlation as small as.06 almost double its standard error, but can also be used to explain about.36% of variation in the current price change Difficult to use as the basis of a substantially profitable trading system Also difficult to determine what degree of serial correlation would imply the existence of trading rules with substantial expected profits

13 Random Walk Literature Violations of independence assumption of random walk model expected Fair game expected return model as the basic model of market equilibrium Random walk arises when additional conditions are such that distributions of one-period returns repeat themselves through time Osborne, Fama: large daily price changes tend to be followed by large daily changes Signs of successor changes are random Violates random walk model but not market efficiency hypothesis Potential explanation: new information may not be evaluated precisely immediately

14 Niederhoffer and Osborne Reversals are 2-3x more likely than continuations Bunching on unexecuted buy and sell limit orders Continuations are more frequent after a proceeding continuation than after a reversal Tendency for limit orders to be concentrated at integers, halves, quarters, and odd eighths in descending order of preference Demonstrate statistically significant deviations from independence in price changes but Fama argues the types of dependence uncovered do not imply market inefficiency For specialist: unexecuted buy and sell limit orders Monopoly power of information and market inefficiency with respect to strong form tests

15 Distributional Evidence Statistical tools relevant for testing Interpretation of any results Fama and Blume: non-normal stable distributions are a better description of distributions of daily returns on common stocks than normal distributions Economists are hesitant to accept these results

16 Fair Game Models in Treasury Bill Market Roll: first weak form empirical work in fair game tradition Used 3 theories of term structure: Pure expectations hypothesis Two market segmentation hypotheses ( liquidity preference hypothesis) Three theories differ only in value assigned to liquidity premium r jt =E(r o,t+j-1 Փ t )+L jt L j,t : liquidity premium, r jt : rate observed from term structure at period t for one week loans to commence at t+j-1 ( futures rate ), r j+1,t-1: rate on one week loans to commence at t+j-1, but observed at t-1 Conditional expectation required in all three theories: E(r j,t Փ t-1 )=r j+1,t-1 +E (L jt Փ t-1 )-L j+1,t-1

17 Roll: Treasury Bill Market The two market segmentation hypotheses fit the data better than the pure expectations hypothesis (slight advantage to liquidity preference hypothesis) The market for Treasury Bills is efficient Z jt seems to be serially independent Non-normal distribution If he had assumed normal distribution, support would not be so strong

18 Multiple Security Expected Return Model Single Securities Test Are securities appropriately priced vis-a-vis one another? Sharpe and Lintner s Economic theory of equilibrium expected returns Expected one-period return on a security is the one-period riskless rate of interest plus a risk premium that is proportional to covariance Risk adjusted premium

19 Semi-Strong Form Tests Test whether current prices fully reflect all obviously available public information Each test is concerned with adjustment of prices to one kind of information generating event Fama, Fisher, Jensen, and Roll (FFJR): stock market able to respond efficiently to information implicit in a split

20 Splits and the Adjustment of Stock Prices (FFJR)

21 Public Announcements Annual Earnings Announcements (Ball and Brown): 261 firms from found no more than 10-15% of information in annual earnings announcement had not been anticipated by the month of the announcement Discount Rate changes by Federal Reserve Banks (Waud): Announcement effect for first trading day after announcement magnitude of adjustment <.5% If anything, the market anticipates the announcement Non-random patterns preceding announcement

22 Public Announcements Large Secondary Offerings of Common Stock and New issues of Stock On average secondary issues are associated with decline of 1-2% in cumulative average residual returns Magnitude of price adjustment unrelated to size of issue so not due to selling pressure Evidence that largest negative cumulative average residuals occur where vendor is the corporation itself or one of its officers Evidence that corporate insiders at least sometimes have important information about their firm not yet publicly known Supports semi-strong form but also provides evidence against strong-form model

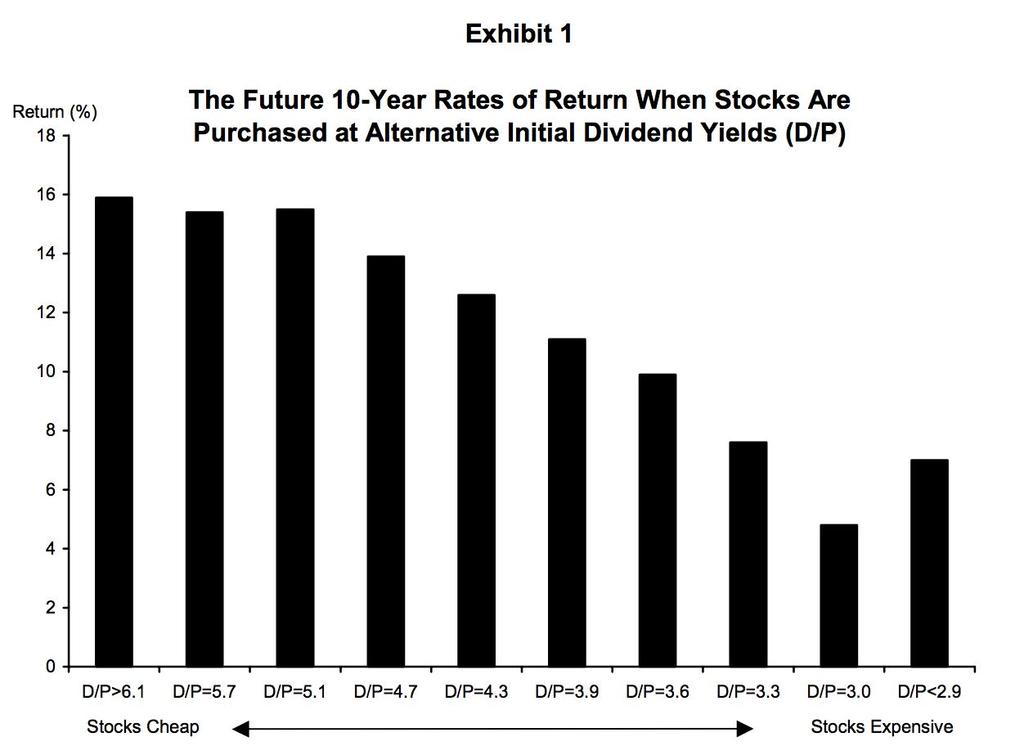

23 Strong Form Tests All available information is fully reflected in prices so that no individual has higher expected trading profits than others because he has monopolistic access to some information Previous contradictory example: NYSE specialists Officers of corporations Model not strictly valid but how far down through the investment community do deviations from the model permeate?

24 Theoretical Framework: Mutual Fund Performance Tests for special information and whether some funds are better at uncovering special information

25 Empirical Results: Mutual Fund Performance Jensen: 115 mutual funds from out of 115 cases, fund s risk-return combination for 10 year period is below market line for the period Average deviation of ten year returns from market is -14.6% Ignoring loading charge, the average deviation of ten year returns from market line is -8.9% Adding back published expenses to their returns, risk return combinations for 58 funds were below market line, with average deviation of -2.5% (-2.5%-.9% estimating for commissions) Individual funds: returns above the norm in one subperiod do not seem to be associated with performance above the norm in other subperiods Number of funds with large positive deviations is less than by chance

26 Burton G. Malkiel (a non random walk)

27 Short-term Momentum Claim: Markets exhibit short term positive serial correlations Transactions Costs Odean (1990): Survey suggests momentum traders did worse in a period of time with positive momentum then buy-and-hold traders Positive in 90s, highly negative in 2000s Event Studies Fama (1998): Stock splits, surprise earnings, Dividends, IPOs Underreaction as common as overreaction Post event continuation as common as reversals January Effect

28 Long-run Return Reversals Claim: Negative serial correlation 25-40% of long period returns can be predicted Fama and French (1988) Behavioral Decision Theory Investors are overconfident in their ability to predict price and earnings Mean reversion weaker in some periods Empirical data based in periods like the depression If it exists, it signal efficiency Interest rates are volatility correcting and mean reverting Fluck, Malkiel, Quandt (1997) 13 year study

29 Valuation Parameters Trading strategies that involve analysis of initial valuation parameters Dividend Yield Price to Earnings Other factors

30 Dividend Yield Claim: up to 40% of the future returns from stocks can be predicted by initial dividend price ratios Higher rate of return when holding stocks with high initial Dividend Yields Lower rate of return when holding stocks with lower initial dividend yields Not inconsistent with efficiency High when interest rates are high, low when rates of low Prediction shows adjustments of economic conditions Strategy ineffective since 1980s 3% dividend yields with 15% returns Does not work with individual stocks Dogs of the Dow

31

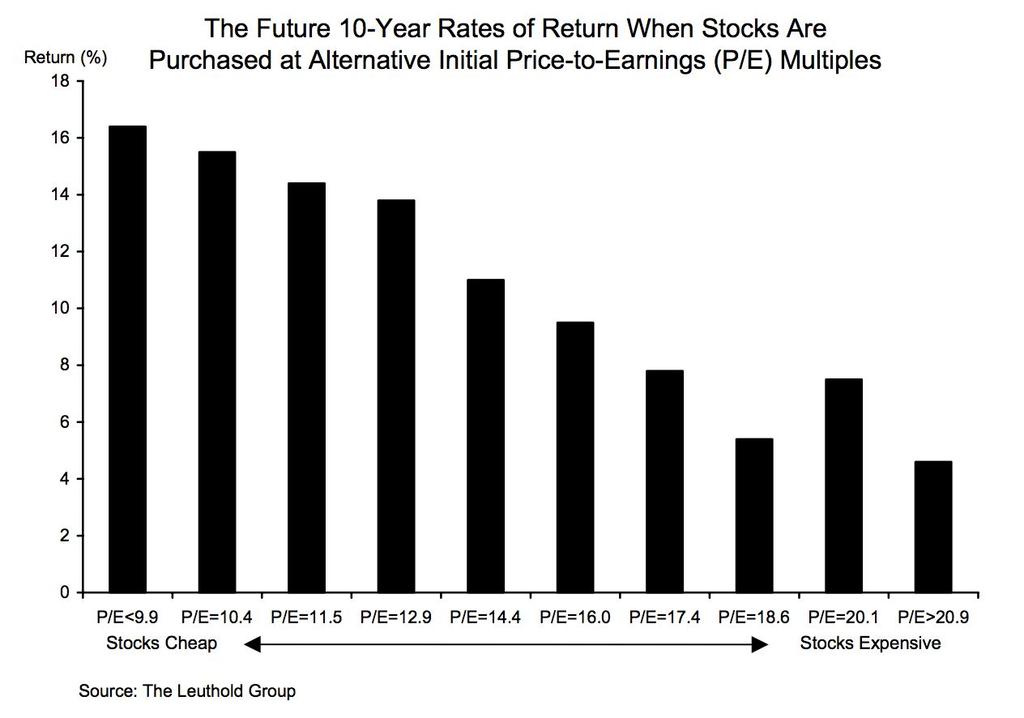

32 Price-Earnings Multiples Claim: Investors earn larger long-horizon returns when purchasing stocks at low P/E multiples Explanation of up to 40% of variance P/E of S&P 500 in low 20s in late 80s Rate of return 16.7% P/E of S&P 500 in mid 20s in early 2000s Rate of return around 11.2% Other assertions: term structure of i spreads, risk spreads, short term rates May exist, but may just point to required rates of return and different risk premiums

33

34 Long Term Firm Characteristics Size Value Stocks Equity Risk Premium Puzzle

35 The Size Effect Claim: Over long periods of time, smaller companies produce larger returns than larger companies: Exhibit 2 Predictable pattern to generate excess risk adjusted returns? Association with Beta Survivorship Bias Some companies fail

36

37 Value Stocks Claim: Value Stocks tend to outperform growth stocks Stock price to book value ratio Stock price / ((assets - liabilities)/shares outstanding) Low price to book shows value Fama and French suggest this idea is more prevalent in other world markets Seem to be at odds with efficiency or CAPM P/BV may imply a premium of risk not captured by model Rise of 3-factor model Bar the period of value strategy is negative with actively managed fund

38

39 Equity Risk Premium Puzzle Claim: Risk Premium inconsistant with risk of common stocks in general % on stocks but 5.5% on bonds Equity Risk higher during Great Depression Survivorship bias Data misconstrued by World War II US market was one of the few that stayed in continuous operation during whole period Ex ante vs Ex post risk premiums

40 Predictable Patterns For their to be true inefficiencies, patterns must be robust and proliferate through the period, not just be viable for short-term strategies January Effect More profitable a strategy is, the less likely it will survive Result of Data Mining Bias in academics towards disproving the consensus A statistician can massage any result out of data

41 Robert Shiller and Richard Role I have personally tried to invest money, my client s money and my own, in every single anomaly and predictive device that academics have dreamed up. I have attempted to exploit the so-called year-end anomalies and a whole variety of strategies supposedly documented by 23 academic research. And I have yet to make a nickel on any of these supposed market inefficiencies a true market inefficiency ought to be an exploitable opportunity. If there s nothing investors can exploit in a systematic way, time in and time out, then it s very hard to say that information is not being properly incorporated into stock prices.

42 Seemingly Irrefutable Cases Recent Evidence could not possibly have been set by rational investors Market Crash of 1987 Can prices be efficient at the beginning and end of a crash? Internet Bubble of 1990s Pricing of internet stocks could not possibly have been rational

43 Market Crash of 1987 Claim: Rapid market changes prove that pricing is based on psychology and not logic ⅓ market drop in October of 1987 Can be broken down into a logic based argument Yields on Long term treasuries increased from 9% to 10 ½% prior to crash Threats of a merger tax James Baker says he will encourage further fall in exchange value of USD Scared foreign and domestic investors Impossible to say that psychology had nothing to to with price changes, but many innocuous problems can coalesce to create a perfect storm

44 Market Crash of 1987 R=D/P + G R is Rate of Return of a stock D is dividend paid by company P is price of Stock G is growth rate Look at R as the required rate of return Government Yield increase scares investors Investors now require a higher rate of return Price falls as a result

45 1990s Internet Bubble Claim: Over pricing of internet companies can not be based in rational expectations Easy to see ex post No arbitrage opportunities existed before the bubble popped Hindsight is 20/20 Internet use double every several months Alan Greenspan fell in line Arbitrage and the Greater Fool Stock may be at 2x value, but someone may be willing to pay 3x value Markets may have temporarily failed Bubbles are exception, not the rule

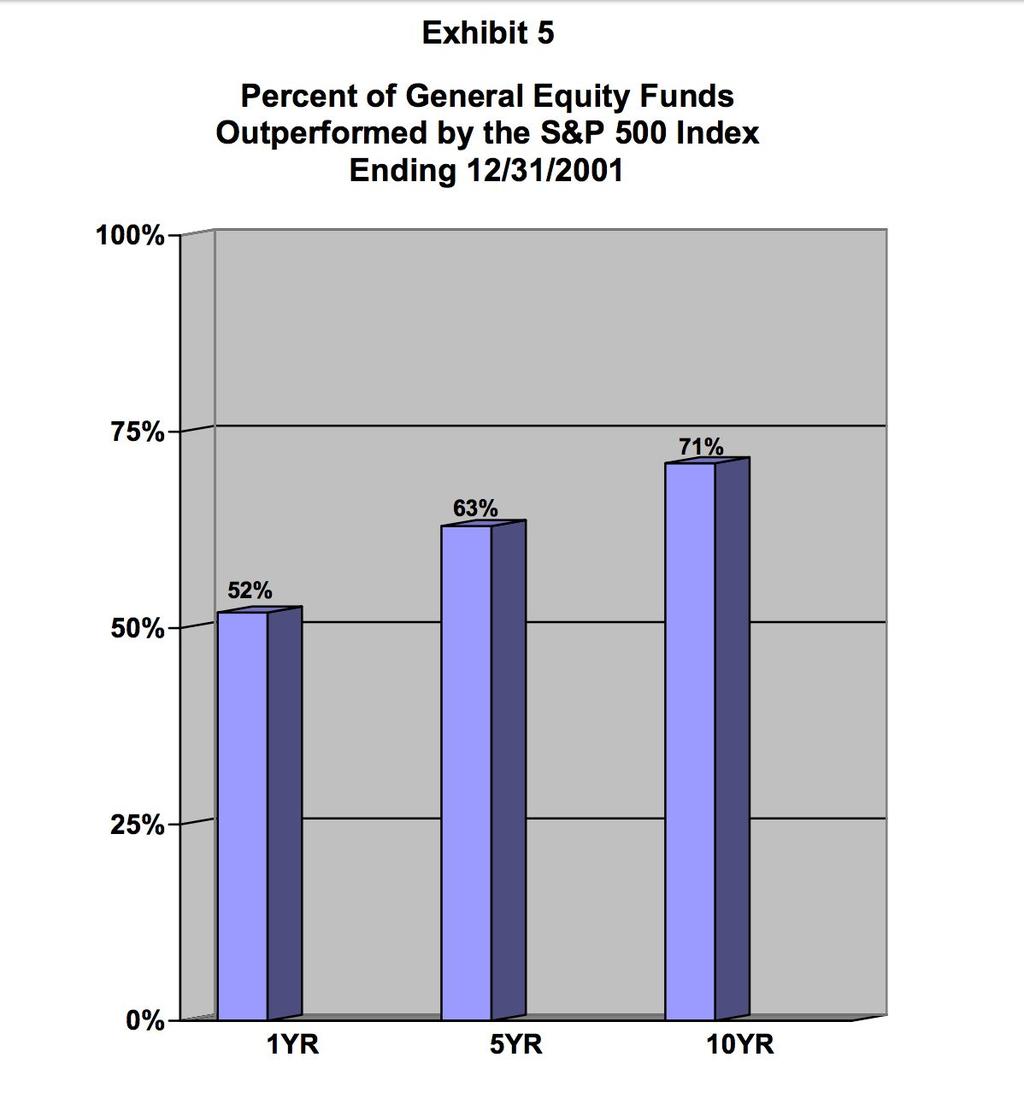

46 Professional Investor Performance Professional investors should be able to beat a market that is inefficient Jensen (1969) and Malkiel (1995) show managers underperform broad market ETFs More Survivorship Bias Top 20 mutual funds in the 70s doubled the performance of ETFs The next decade, those Funds underperformed Top 20 funds in 1998 and 1999 tripled ETF In 2000 and 2001, they did 3x worse

47

48 Conclusions Most of the debate about efficient markets is based upon definitions Prices fully reflect information Professional consensus Long-term efficiency Highly exploitable trends live short lives Prices are not always correct in the short-term Markets more efficient than ever Internet 24 hour news cycle

49 Questions?

50 Bibliography Efficient Capital Markets: A Review of Theory and Empirical Work, Eugene F. Fama, The Journal of Finance, 1970 The Efficient Market Hypothesis and Its Critics, Burton G. Malkiel, Journal of Economic Perspectives, 2003

Chapter 13. Efficient Capital Markets and Behavioral Challenges

Chapter 13 Efficient Capital Markets and Behavioral Challenges Articulate the importance of capital market efficiency Define the three forms of efficiency Know the empirical tests of market efficiency

Chapter 13 Efficient Capital Markets and Behavioral Challenges Articulate the importance of capital market efficiency Define the three forms of efficiency Know the empirical tests of market efficiency

The Efficient Market Hypothesis

Efficient Market Hypothesis (EMH) 11-2 The Efficient Market Hypothesis Maurice Kendall (1953) found no predictable pattern in stock prices. Prices are as likely to go up as to go down on any particular

Efficient Market Hypothesis (EMH) 11-2 The Efficient Market Hypothesis Maurice Kendall (1953) found no predictable pattern in stock prices. Prices are as likely to go up as to go down on any particular

AFM 371 Winter 2008 Chapter 14 - Efficient Capital Markets

AFM 371 Winter 2008 Chapter 14 - Efficient Capital Markets 1 / 24 Outline Background What Is Market Efficiency? Different Levels Of Efficiency Empirical Evidence Implications Of Market Efficiency For Corporate

AFM 371 Winter 2008 Chapter 14 - Efficient Capital Markets 1 / 24 Outline Background What Is Market Efficiency? Different Levels Of Efficiency Empirical Evidence Implications Of Market Efficiency For Corporate

CHAPTER 12: MARKET EFFICIENCY AND BEHAVIORAL FINANCE

CHAPTER 12: MARKET EFFICIENCY AND BEHAVIORAL FINANCE 1. The correlation coefficient between stock returns for two non-overlapping periods should be zero. If not, one could use returns from one period to

CHAPTER 12: MARKET EFFICIENCY AND BEHAVIORAL FINANCE 1. The correlation coefficient between stock returns for two non-overlapping periods should be zero. If not, one could use returns from one period to

A Random Walk Down Wall Street

FIN 614 Capital Market Efficiency Professor Robert B.H. Hauswald Kogod School of Business, AU A Random Walk Down Wall Street From theory of return behavior to its practice Capital market efficiency: the

FIN 614 Capital Market Efficiency Professor Robert B.H. Hauswald Kogod School of Business, AU A Random Walk Down Wall Street From theory of return behavior to its practice Capital market efficiency: the

Economics 430 Handout on Rational Expectations: Part I. Review of Statistics: Notation and Definitions

Economics 430 Chris Georges Handout on Rational Expectations: Part I Review of Statistics: Notation and Definitions Consider two random variables X and Y defined over m distinct possible events. Event

Economics 430 Chris Georges Handout on Rational Expectations: Part I Review of Statistics: Notation and Definitions Consider two random variables X and Y defined over m distinct possible events. Event

Efficient Market Hypothesis & Behavioral Finance

Efficient Market Hypothesis & Behavioral Finance Supervision: Ing. Luděk Benada Prepared by: Danial Hasan 1 P a g e Contents: 1. Introduction 2. Efficient Market Hypothesis (EMH) 3. Versions of the EMH

Efficient Market Hypothesis & Behavioral Finance Supervision: Ing. Luděk Benada Prepared by: Danial Hasan 1 P a g e Contents: 1. Introduction 2. Efficient Market Hypothesis (EMH) 3. Versions of the EMH

Research Methods in Accounting

01130591 Research Methods in Accounting Capital Markets Research in Accounting Dr Polwat Lerskullawat: fbuspwl@ku.ac.th Dr Suthawan Prukumpai: fbusswp@ku.ac.th Assoc Prof Tipparat Laohavichien: fbustrl@ku.ac.th

01130591 Research Methods in Accounting Capital Markets Research in Accounting Dr Polwat Lerskullawat: fbuspwl@ku.ac.th Dr Suthawan Prukumpai: fbusswp@ku.ac.th Assoc Prof Tipparat Laohavichien: fbustrl@ku.ac.th

CHAPTER 13 EFFICIENT CAPITAL MARKETS AND BEHAVIORAL CHALLENGES

CHAPTER 13 EFFICIENT CAPITAL MARKETS AND BEHAVIORAL CHALLENGES Answers to Concept Questions 1. To create value, firms should accept financing proposals with positive net present values. Firms can create

CHAPTER 13 EFFICIENT CAPITAL MARKETS AND BEHAVIORAL CHALLENGES Answers to Concept Questions 1. To create value, firms should accept financing proposals with positive net present values. Firms can create

Behavioral Finance 1-1. Chapter 4 Challenges to Market Efficiency

Behavioral Finance 1-1 Chapter 4 Challenges to Market Efficiency 1 Introduction 1-2 Early tests of market efficiency were largely positive However, more recent empirical evidence has uncovered a series

Behavioral Finance 1-1 Chapter 4 Challenges to Market Efficiency 1 Introduction 1-2 Early tests of market efficiency were largely positive However, more recent empirical evidence has uncovered a series

Testing Semi-Strong Form Efficiency and the PEAD Anomaly in ATHEX

Testing Semi-Strong Form Efficiency and the PEAD Anomaly in ATHEX An Event Study based on Annual Earnings Announcements Stavros I. Derdas DISSERTATION.COM Boca Raton Testing Semi-Strong Form Efficiency

Testing Semi-Strong Form Efficiency and the PEAD Anomaly in ATHEX An Event Study based on Annual Earnings Announcements Stavros I. Derdas DISSERTATION.COM Boca Raton Testing Semi-Strong Form Efficiency

CORPORATE FINANCING and MARKET EFFICIENCY FINANCING STRATEGY

CHAPTER 13 CORPORATE FINANCING and MARKET EFFICIENCY FINANCING STRATEGY WE NOW MOVE FROM LEFT-HAND SIDE TO RIGHT HAND SIDE OF THE BALANCE SHEET GIVEN THE FIRM S CURRENT PORTFOLIO OF REAL ASSETS AND ITS

CHAPTER 13 CORPORATE FINANCING and MARKET EFFICIENCY FINANCING STRATEGY WE NOW MOVE FROM LEFT-HAND SIDE TO RIGHT HAND SIDE OF THE BALANCE SHEET GIVEN THE FIRM S CURRENT PORTFOLIO OF REAL ASSETS AND ITS

Economics of Money, Banking, and Fin. Markets, 10e

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 7 The Stock Market, the Theory of Rational Expectations, and the Efficient Market Hypothesis 7.1 Computing the Price of Common Stock

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 7 The Stock Market, the Theory of Rational Expectations, and the Efficient Market Hypothesis 7.1 Computing the Price of Common Stock

Economics of Behavioral Finance. Lecture 3

Economics of Behavioral Finance Lecture 3 Security Market Line CAPM predicts a linear relationship between a stock s Beta and its excess return. E[r i ] r f = β i E r m r f Practically, testing CAPM empirically

Economics of Behavioral Finance Lecture 3 Security Market Line CAPM predicts a linear relationship between a stock s Beta and its excess return. E[r i ] r f = β i E r m r f Practically, testing CAPM empirically

Early evidence on the efficient market hypothesis was quite favorable to it. In recent

Appendix to chapter 7 Evidence on the Efficient Market Hypothesis Early evidence on the efficient market hypothesis was quite favorable to it. In recent years, however, deeper analysis of the evidence

Appendix to chapter 7 Evidence on the Efficient Market Hypothesis Early evidence on the efficient market hypothesis was quite favorable to it. In recent years, however, deeper analysis of the evidence

Efficient Capital Markets

Efficient Capital Markets Why Should Capital Markets Be Efficient? Alternative Efficient Market Hypotheses Tests and Results of the Hypotheses Behavioural Finance Implications of Efficient Capital Markets

Efficient Capital Markets Why Should Capital Markets Be Efficient? Alternative Efficient Market Hypotheses Tests and Results of the Hypotheses Behavioural Finance Implications of Efficient Capital Markets

Note on Cost of Capital

DUKE UNIVERSITY, FUQUA SCHOOL OF BUSINESS ACCOUNTG 512F: FUNDAMENTALS OF FINANCIAL ANALYSIS Note on Cost of Capital For the course, you should concentrate on the CAPM and the weighted average cost of capital.

DUKE UNIVERSITY, FUQUA SCHOOL OF BUSINESS ACCOUNTG 512F: FUNDAMENTALS OF FINANCIAL ANALYSIS Note on Cost of Capital For the course, you should concentrate on the CAPM and the weighted average cost of capital.

Testing for efficient markets

IGIDR, Bombay May 17, 2011 What is market efficiency? A market is efficient if prices contain all information about the value of a stock. An attempt at a more precise definition: an efficient market is

IGIDR, Bombay May 17, 2011 What is market efficiency? A market is efficient if prices contain all information about the value of a stock. An attempt at a more precise definition: an efficient market is

Testing Capital Asset Pricing Model on KSE Stocks Salman Ahmed Shaikh

Abstract Capital Asset Pricing Model (CAPM) is one of the first asset pricing models to be applied in security valuation. It has had its share of criticism, both empirical and theoretical; however, with

Abstract Capital Asset Pricing Model (CAPM) is one of the first asset pricing models to be applied in security valuation. It has had its share of criticism, both empirical and theoretical; however, with

Monetary Economics Efficient Markets and Alternatives. Gerald P. Dwyer Fall 2015

Monetary Economics Efficient Markets and Alternatives Gerald P. Dwyer Fall 2015 Readings This lecture, Malkiel Part 3 Next lecture, Cuthbertson, Chapter 6 Behavioral Finance Behavioral finance is not a

Monetary Economics Efficient Markets and Alternatives Gerald P. Dwyer Fall 2015 Readings This lecture, Malkiel Part 3 Next lecture, Cuthbertson, Chapter 6 Behavioral Finance Behavioral finance is not a

Empirical Evidence. r Mt r ft e i. now do second-pass regression (cross-sectional with N 100): r i r f γ 0 γ 1 b i u i

: r i r f γ 0 γ 1 b i u i") Empirical Evidence (Text reference: Chapter 10) Tests of single factor CAPM/APT Roll s critique Tests of multifactor CAPM/APT The debate over anomalies Time varying volatility The equity premium puzzle

Empirical Evidence (Text reference: Chapter 10) Tests of single factor CAPM/APT Roll s critique Tests of multifactor CAPM/APT The debate over anomalies Time varying volatility The equity premium puzzle

Derivation of zero-beta CAPM: Efficient portfolios

Derivation of zero-beta CAPM: Efficient portfolios AssumptionsasCAPM,exceptR f does not exist. Argument which leads to Capital Market Line is invalid. (No straight line through R f, tilted up as far as

Derivation of zero-beta CAPM: Efficient portfolios AssumptionsasCAPM,exceptR f does not exist. Argument which leads to Capital Market Line is invalid. (No straight line through R f, tilted up as far as

Chapter 6 Investment Analysis and Portfolio Management

Chapter 6 Investment Analysis and Portfolio Management Frank K. Reilly & Keith C. Brown Part 2: INVESTMENT THEORY 6 Pasar Efisien 7 Mnj Portofolio Konsep RETURN, RISIKO, Investasi 9 Model Ret, Risiko 8

Chapter 6 Investment Analysis and Portfolio Management Frank K. Reilly & Keith C. Brown Part 2: INVESTMENT THEORY 6 Pasar Efisien 7 Mnj Portofolio Konsep RETURN, RISIKO, Investasi 9 Model Ret, Risiko 8

Absolute Alpha with Moving Averages

a Consistent Trading Strategy University of Rochester April 23, 2016 Carhart (1995, 1997) discussed a 4-factor model using Fama and French s (1993) 3-factor model plus an additional factor capturing Jegadeesh

a Consistent Trading Strategy University of Rochester April 23, 2016 Carhart (1995, 1997) discussed a 4-factor model using Fama and French s (1993) 3-factor model plus an additional factor capturing Jegadeesh

MBF2253 Modern Security Analysis

MBF2253 Modern Security Analysis Prepared by Dr Khairul Anuar L8: Efficient Capital Market www.notes638.wordpress.com Capital Market Efficiency Capital market history suggests that the market values of

MBF2253 Modern Security Analysis Prepared by Dr Khairul Anuar L8: Efficient Capital Market www.notes638.wordpress.com Capital Market Efficiency Capital market history suggests that the market values of

Applied Macro Finance

Master in Money and Finance Goethe University Frankfurt Week 2: Factor models and the cross-section of stock returns Fall 2012/2013 Please note the disclaimer on the last page Announcements Next week (30

Master in Money and Finance Goethe University Frankfurt Week 2: Factor models and the cross-section of stock returns Fall 2012/2013 Please note the disclaimer on the last page Announcements Next week (30

CHAPTER 6. Are Financial Markets Efficient? Copyright 2012 Pearson Prentice Hall. All rights reserved.

CHAPTER 6 Are Financial Markets Efficient? Copyright 2012 Pearson Prentice Hall. All rights reserved. Chapter Preview Expectations are very important in our financial system. Expectations of returns, risk,

CHAPTER 6 Are Financial Markets Efficient? Copyright 2012 Pearson Prentice Hall. All rights reserved. Chapter Preview Expectations are very important in our financial system. Expectations of returns, risk,

CHAPTER 11. The Efficient Market Hypothesis INVESTMENTS BODIE, KANE, MARCUS. Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved.

CHAPTER 11 The Efficient Market Hypothesis McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 11-2 Efficient Market Hypothesis (EMH) Maurice Kendall (1953) found no

CHAPTER 11 The Efficient Market Hypothesis McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 11-2 Efficient Market Hypothesis (EMH) Maurice Kendall (1953) found no

EQUITY RESEARCH AND PORTFOLIO MANAGEMENT

EQUITY RESEARCH AND PORTFOLIO MANAGEMENT By P K AGARWAL IIFT, NEW DELHI 1 MARKOWITZ APPROACH Requires huge number of estimates to fill the covariance matrix (N(N+3))/2 Eg: For a 2 security case: Require

EQUITY RESEARCH AND PORTFOLIO MANAGEMENT By P K AGARWAL IIFT, NEW DELHI 1 MARKOWITZ APPROACH Requires huge number of estimates to fill the covariance matrix (N(N+3))/2 Eg: For a 2 security case: Require

The Value Premium and the January Effect

The Value Premium and the January Effect Julia Chou, Praveen Kumar Das * Current Version: January 2010 * Chou is from College of Business Administration, Florida International University, Miami, FL 33199;

The Value Premium and the January Effect Julia Chou, Praveen Kumar Das * Current Version: January 2010 * Chou is from College of Business Administration, Florida International University, Miami, FL 33199;

Discussion of Value Investing: The Use of Historical Financial Statement Information to Separate Winners from Losers

Discussion of Value Investing: The Use of Historical Financial Statement Information to Separate Winners from Losers Wayne Guay The Wharton School University of Pennsylvania 2400 Steinberg-Dietrich Hall

Discussion of Value Investing: The Use of Historical Financial Statement Information to Separate Winners from Losers Wayne Guay The Wharton School University of Pennsylvania 2400 Steinberg-Dietrich Hall

EFFICIENT MARKETS HYPOTHESIS

EFFICIENT MARKETS HYPOTHESIS when economists speak of capital markets as being efficient, they usually consider asset prices and returns as being determined as the outcome of supply and demand in a competitive

EFFICIENT MARKETS HYPOTHESIS when economists speak of capital markets as being efficient, they usually consider asset prices and returns as being determined as the outcome of supply and demand in a competitive

The Conditional Relation between Beta and Returns

Articles I INTRODUCTION The Conditional Relation between Beta and Returns Evidence from Japan and Sri Lanka * Department of Finance, University of Sri Jayewardenepura / Senior Lecturer ** Department of

Articles I INTRODUCTION The Conditional Relation between Beta and Returns Evidence from Japan and Sri Lanka * Department of Finance, University of Sri Jayewardenepura / Senior Lecturer ** Department of

Quantitative Trading System For The E-mini S&P

AURORA PRO Aurora Pro Automated Trading System Aurora Pro v1.11 For TradeStation 9.1 August 2015 Quantitative Trading System For The E-mini S&P By Capital Evolution LLC Aurora Pro is a quantitative trading

AURORA PRO Aurora Pro Automated Trading System Aurora Pro v1.11 For TradeStation 9.1 August 2015 Quantitative Trading System For The E-mini S&P By Capital Evolution LLC Aurora Pro is a quantitative trading

15 Week 5b Mutual Funds

15 Week 5b Mutual Funds 15.1 Background 1. It would be natural, and completely sensible, (and good marketing for MBA programs) if funds outperform darts! Pros outperform in any other field. 2. Except for...

15 Week 5b Mutual Funds 15.1 Background 1. It would be natural, and completely sensible, (and good marketing for MBA programs) if funds outperform darts! Pros outperform in any other field. 2. Except for...

Premium Timing with Valuation Ratios

RESEARCH Premium Timing with Valuation Ratios March 2016 Wei Dai, PhD Research The predictability of expected stock returns is an old topic and an important one. While investors may increase expected returns

RESEARCH Premium Timing with Valuation Ratios March 2016 Wei Dai, PhD Research The predictability of expected stock returns is an old topic and an important one. While investors may increase expected returns

COMM 324 INVESTMENTS AND PORTFOLIO MANAGEMENT ASSIGNMENT 2 Due: October 20

COMM 34 INVESTMENTS ND PORTFOLIO MNGEMENT SSIGNMENT Due: October 0 1. In 1998 the rate of return on short term government securities (perceived to be risk-free) was about 4.5%. Suppose the expected rate

COMM 34 INVESTMENTS ND PORTFOLIO MNGEMENT SSIGNMENT Due: October 0 1. In 1998 the rate of return on short term government securities (perceived to be risk-free) was about 4.5%. Suppose the expected rate

Institutional Finance Financial Crises, Risk Management and Liquidity

Institutional Finance Financial Crises, Risk Management and Liquidity Markus K. Brunnermeier Preceptor: Dong Beom Choi Princeton University 1 Overview Efficiency concepts EMH implies Martingale Property

Institutional Finance Financial Crises, Risk Management and Liquidity Markus K. Brunnermeier Preceptor: Dong Beom Choi Princeton University 1 Overview Efficiency concepts EMH implies Martingale Property

An Introduction to Behavioral Finance

Topics An Introduction to Behavioral Finance Efficient Market Hypothesis Empirical Support of Efficient Market Hypothesis Empirical Challenges to the Efficient Market Hypothesis Theoretical Challenges

Topics An Introduction to Behavioral Finance Efficient Market Hypothesis Empirical Support of Efficient Market Hypothesis Empirical Challenges to the Efficient Market Hypothesis Theoretical Challenges

in-depth Invesco Actively Managed Low Volatility Strategies The Case for

Invesco in-depth The Case for Actively Managed Low Volatility Strategies We believe that active LVPs offer the best opportunity to achieve a higher risk-adjusted return over the long term. Donna C. Wilson

Invesco in-depth The Case for Actively Managed Low Volatility Strategies We believe that active LVPs offer the best opportunity to achieve a higher risk-adjusted return over the long term. Donna C. Wilson

Chapter 7 The Stock Market, the Theory of Rational Expectations, and the Efficient Markets Hypothesis

Chapter 7 The Stock Market, the Theory of Rational Expectations, and the Efficient Markets Hypothesis Multiple Choice 1) Stockholders rights include (a) the right to vote. (b) the right to manage. (c)

Chapter 7 The Stock Market, the Theory of Rational Expectations, and the Efficient Markets Hypothesis Multiple Choice 1) Stockholders rights include (a) the right to vote. (b) the right to manage. (c)

The Great Divide. Cliff Asness, Ph.D. Managing and Founding Principal. October For Investment Professional Use Only. AQR Capital Management, LLC

The Great Divide Cliff Asness, Ph.D. Managing and Founding Principal October 2014 AQR Capital Management, LLC Two Greenwich Plaza Greenwich, CT 06830 p: +1.203.742.3600 w: aqr.com Disclosures, in English

The Great Divide Cliff Asness, Ph.D. Managing and Founding Principal October 2014 AQR Capital Management, LLC Two Greenwich Plaza Greenwich, CT 06830 p: +1.203.742.3600 w: aqr.com Disclosures, in English

Chapter 13: Investor Behavior and Capital Market Efficiency

Chapter 13: Investor Behavior and Capital Market Efficiency -1 Chapter 13: Investor Behavior and Capital Market Efficiency Note: Only responsible for sections 13.1 through 13.6 Fundamental question: Is

Chapter 13: Investor Behavior and Capital Market Efficiency -1 Chapter 13: Investor Behavior and Capital Market Efficiency Note: Only responsible for sections 13.1 through 13.6 Fundamental question: Is

Analysis of Stock Price Behaviour around Bonus Issue:

BHAVAN S INTERNATIONAL JOURNAL of BUSINESS Vol:3, 1 (2009) 18-31 ISSN 0974-0082 Analysis of Stock Price Behaviour around Bonus Issue: A Test of Semi-Strong Efficiency of Indian Capital Market Charles Lasrado

BHAVAN S INTERNATIONAL JOURNAL of BUSINESS Vol:3, 1 (2009) 18-31 ISSN 0974-0082 Analysis of Stock Price Behaviour around Bonus Issue: A Test of Semi-Strong Efficiency of Indian Capital Market Charles Lasrado

Institutional Finance Financial Crises, Risk Management and Liquidity

Institutional Finance Financial Crises, Risk Management and Liquidity Markus K. Brunnermeier Preceptor: Delwin Olivan Princeton University 1 Overview Efficiency concepts EMH implies Martingale Property

Institutional Finance Financial Crises, Risk Management and Liquidity Markus K. Brunnermeier Preceptor: Delwin Olivan Princeton University 1 Overview Efficiency concepts EMH implies Martingale Property

Another Look at Market Responses to Tangible and Intangible Information

Critical Finance Review, 2016, 5: 165 175 Another Look at Market Responses to Tangible and Intangible Information Kent Daniel Sheridan Titman 1 Columbia Business School, Columbia University, New York,

Critical Finance Review, 2016, 5: 165 175 Another Look at Market Responses to Tangible and Intangible Information Kent Daniel Sheridan Titman 1 Columbia Business School, Columbia University, New York,

The evaluation of the performance of UK American unit trusts

International Review of Economics and Finance 8 (1999) 455 466 The evaluation of the performance of UK American unit trusts Jonathan Fletcher* Department of Finance and Accounting, Glasgow Caledonian University,

International Review of Economics and Finance 8 (1999) 455 466 The evaluation of the performance of UK American unit trusts Jonathan Fletcher* Department of Finance and Accounting, Glasgow Caledonian University,

Long-run Consumption Risks in Assets Returns: Evidence from Economic Divisions

Long-run Consumption Risks in Assets Returns: Evidence from Economic Divisions Abdulrahman Alharbi 1 Abdullah Noman 2 Abstract: Bansal et al (2009) paper focus on measuring risk in consumption especially

Long-run Consumption Risks in Assets Returns: Evidence from Economic Divisions Abdulrahman Alharbi 1 Abdullah Noman 2 Abstract: Bansal et al (2009) paper focus on measuring risk in consumption especially

Advanced Corporate Finance. 7. Investor behavior and capital market efficiency

Advanced Corporate Finance 7. Investor behavior and capital market efficiency Objectives of the session 1. So far => analysis of company value, of projects and of derivatives. Intuitively => Important

Advanced Corporate Finance 7. Investor behavior and capital market efficiency Objectives of the session 1. So far => analysis of company value, of projects and of derivatives. Intuitively => Important

Dynamic Smart Beta Investing Relative Risk Control and Tactical Bets, Making the Most of Smart Betas

Dynamic Smart Beta Investing Relative Risk Control and Tactical Bets, Making the Most of Smart Betas Koris International June 2014 Emilien Audeguil Research & Development ORIAS n 13000579 (www.orias.fr).

Dynamic Smart Beta Investing Relative Risk Control and Tactical Bets, Making the Most of Smart Betas Koris International June 2014 Emilien Audeguil Research & Development ORIAS n 13000579 (www.orias.fr).

Financial Mathematics III Theory summary

Financial Mathematics III Theory summary Table of Contents Lecture 1... 7 1. State the objective of modern portfolio theory... 7 2. Define the return of an asset... 7 3. How is expected return defined?...

Financial Mathematics III Theory summary Table of Contents Lecture 1... 7 1. State the objective of modern portfolio theory... 7 2. Define the return of an asset... 7 3. How is expected return defined?...

Efficient capital markets. Skema Business School. Portfolio Management 1. Course Outline

Efficient capital markets bertrand.groslambert@skema.edu Skema Business School Portfolio Management 1 Course Outline Introduction (lecture 1) Presentation of portfolio management Chap.2,3,5 Introduction

Efficient capital markets bertrand.groslambert@skema.edu Skema Business School Portfolio Management 1 Course Outline Introduction (lecture 1) Presentation of portfolio management Chap.2,3,5 Introduction

Optimal Financial Education. Avanidhar Subrahmanyam

Optimal Financial Education Avanidhar Subrahmanyam Motivation The notion that irrational investors may be prevalent in financial markets has taken on increased impetus in recent years. For example, Daniel

Optimal Financial Education Avanidhar Subrahmanyam Motivation The notion that irrational investors may be prevalent in financial markets has taken on increased impetus in recent years. For example, Daniel

RISK FACTORS RELATING TO THE CITI FLEXIBLE ALLOCATION 6 EXCESS RETURN INDEX

RISK FACTORS RELATING TO THE CITI FLEXIBLE ALLOCATION 6 EXCESS RETURN INDEX The following discussion of risks relating to the Citi Flexible Allocation 6 Excess Return Index (the Index ) should be read

RISK FACTORS RELATING TO THE CITI FLEXIBLE ALLOCATION 6 EXCESS RETURN INDEX The following discussion of risks relating to the Citi Flexible Allocation 6 Excess Return Index (the Index ) should be read

Expectations are very important in our financial system.

Chapter 6 Are Financial Markets Efficient? Chapter Preview Expectations are very important in our financial system. Expectations of returns, risk, and liquidity impact asset demand Inflationary expectations

Chapter 6 Are Financial Markets Efficient? Chapter Preview Expectations are very important in our financial system. Expectations of returns, risk, and liquidity impact asset demand Inflationary expectations

Lesson XI: Overview. 1. FX market efficiency 2. The art of foreign exchange rate

Lesson XI: Overview 1. FX market efficiency 2. The art of foreign exchange rate forecasting 1 FX market efficiency 2 Terminology I K markets are said to be efficient whenever their prices fully reflect

Lesson XI: Overview 1. FX market efficiency 2. The art of foreign exchange rate forecasting 1 FX market efficiency 2 Terminology I K markets are said to be efficient whenever their prices fully reflect

ANOMALIES AND NEWS JOEY ENGELBERG (UCSD) R. DAVID MCLEAN (GEORGETOWN) JEFFREY PONTIFF (BOSTON COLLEGE)

R. DAVID MCLEAN (GEORGETOWN) JEFFREY PONTIFF (BOSTON COLLEGE)") ANOMALIES AND NEWS JOEY ENGELBERG (UCSD) R. DAVID MCLEAN (GEORGETOWN) JEFFREY PONTIFF (BOSTON COLLEGE) 3 RD ANNUAL NEWS & FINANCE CONFERENCE COLUMBIA UNIVERSITY MARCH 8, 2018 Background and Motivation

ANOMALIES AND NEWS JOEY ENGELBERG (UCSD) R. DAVID MCLEAN (GEORGETOWN) JEFFREY PONTIFF (BOSTON COLLEGE) 3 RD ANNUAL NEWS & FINANCE CONFERENCE COLUMBIA UNIVERSITY MARCH 8, 2018 Background and Motivation

Discussion of Information Uncertainty and Post-Earnings-Announcement-Drift

Journal of Business Finance & Accounting, 34(3) & (4), 434 438, April/May 2007, 0306-686X doi: 10.1111/j.1468-5957.2007.02031.x Discussion of Information Uncertainty and Post-Earnings-Announcement-Drift

Journal of Business Finance & Accounting, 34(3) & (4), 434 438, April/May 2007, 0306-686X doi: 10.1111/j.1468-5957.2007.02031.x Discussion of Information Uncertainty and Post-Earnings-Announcement-Drift

Capital Asset Pricing Model - CAPM

Capital Asset Pricing Model - CAPM The capital asset pricing model (CAPM) is a model that describes the relationship between systematic risk and expected return for assets, particularly stocks. CAPM is

Capital Asset Pricing Model - CAPM The capital asset pricing model (CAPM) is a model that describes the relationship between systematic risk and expected return for assets, particularly stocks. CAPM is

Would You Follow MM or a Profitable Trading Strategy? Brian Baturevich. Gulnur Muradoglu*

Would You Follow MM or a Profitable Trading Strategy? Brian Baturevich Gulnur Muradoglu* Abstract We investigate the ability of company capital structures to be used as a predictor for abnormal returns.

Would You Follow MM or a Profitable Trading Strategy? Brian Baturevich Gulnur Muradoglu* Abstract We investigate the ability of company capital structures to be used as a predictor for abnormal returns.

Portfolio Construction through Price Earnings Ratio: Indian Evidence

Portfolio Construction through Price Earnings Ratio: Indian Evidence Abhay Raja* Abstract: Fundamental and Technical analyses are bases for market participants to trade in. The objective of all tools is

Portfolio Construction through Price Earnings Ratio: Indian Evidence Abhay Raja* Abstract: Fundamental and Technical analyses are bases for market participants to trade in. The objective of all tools is

Seasonal Analysis of Abnormal Returns after Quarterly Earnings Announcements

Seasonal Analysis of Abnormal Returns after Quarterly Earnings Announcements Dr. Iqbal Associate Professor and Dean, College of Business Administration The Kingdom University P.O. Box 40434, Manama, Bahrain

Seasonal Analysis of Abnormal Returns after Quarterly Earnings Announcements Dr. Iqbal Associate Professor and Dean, College of Business Administration The Kingdom University P.O. Box 40434, Manama, Bahrain

University of Pennsylvania The Wharton School

University of Pennsylvania The Wharton School FNCE 100 PROBLEM SET #5 Fall Term 2005 A. Craig MacKinlay Market Efficiency 1. Money manager Robert J. Betaman of Betaman-Rubin Associates has shown an uncanny

University of Pennsylvania The Wharton School FNCE 100 PROBLEM SET #5 Fall Term 2005 A. Craig MacKinlay Market Efficiency 1. Money manager Robert J. Betaman of Betaman-Rubin Associates has shown an uncanny

Module 6 Portfolio risk and return

Module 6 Portfolio risk and return Prepared by Pamela Peterson Drake, Ph.D., CFA 1. Overview Security analysts and portfolio managers are concerned about an investment s return, its risk, and whether it

Module 6 Portfolio risk and return Prepared by Pamela Peterson Drake, Ph.D., CFA 1. Overview Security analysts and portfolio managers are concerned about an investment s return, its risk, and whether it

REVIEW OF OVERREACTION AND UNDERREACTION IN STOCK MARKETS

International Journal of Economics, Commerce and Management United Kingdom Vol. IV, Issue 12, December 2016 http://ijecm.co.uk/ ISSN 2348 0386 REVIEW OF OVERREACTION AND UNDERREACTION IN STOCK MARKETS

International Journal of Economics, Commerce and Management United Kingdom Vol. IV, Issue 12, December 2016 http://ijecm.co.uk/ ISSN 2348 0386 REVIEW OF OVERREACTION AND UNDERREACTION IN STOCK MARKETS

PAPER No.14 : Security Analysis and Portfolio Management MODULE No.24 : Efficient market hypothesis: Weak, semi strong and strong market)

") Subject Paper No and Title Module No and Title Module Tag 14. Security Analysis and Portfolio M24 Efficient market hypothesis: Weak, semi strong and strong market COM_P14_M24 TABLE OF CONTENTS After going

Subject Paper No and Title Module No and Title Module Tag 14. Security Analysis and Portfolio M24 Efficient market hypothesis: Weak, semi strong and strong market COM_P14_M24 TABLE OF CONTENTS After going

Exchange Rate Forecasting

Exchange Rate Forecasting Controversies in Exchange Rate Forecasting The Cases For & Against FX Forecasting Performance Evaluation: Accurate vs. Useful A Framework for Currency Forecasting Empirical Evidence

Exchange Rate Forecasting Controversies in Exchange Rate Forecasting The Cases For & Against FX Forecasting Performance Evaluation: Accurate vs. Useful A Framework for Currency Forecasting Empirical Evidence

+ = Smart Beta 2.0 Bringing clarity to equity smart beta. Drawbacks of Market Cap Indices. A Lesson from History

Benoit Autier Head of Product Management benoit.autier@etfsecurities.com Mike McGlone Head of Research (US) mike.mcglone@etfsecurities.com Alexander Channing Director of Quantitative Investment Strategies

Benoit Autier Head of Product Management benoit.autier@etfsecurities.com Mike McGlone Head of Research (US) mike.mcglone@etfsecurities.com Alexander Channing Director of Quantitative Investment Strategies

Stock Price Behavior. Stock Price Behavior

Major Topics Statistical Properties Volatility Cross-Country Relationships Business Cycle Behavior Page 1 Statistical Behavior Previously examined from theoretical point the issue: To what extent can the

Major Topics Statistical Properties Volatility Cross-Country Relationships Business Cycle Behavior Page 1 Statistical Behavior Previously examined from theoretical point the issue: To what extent can the

Optimal Portfolio Inputs: Various Methods

Optimal Portfolio Inputs: Various Methods Prepared by Kevin Pei for The Fund @ Sprott Abstract: In this document, I will model and back test our portfolio with various proposed models. It goes without

Optimal Portfolio Inputs: Various Methods Prepared by Kevin Pei for The Fund @ Sprott Abstract: In this document, I will model and back test our portfolio with various proposed models. It goes without

Financial Economics. Runs Test

Test A simple statistical test of the random-walk theory is a runs test. For daily data, a run is defined as a sequence of days in which the stock price changes in the same direction. For example, consider

Test A simple statistical test of the random-walk theory is a runs test. For daily data, a run is defined as a sequence of days in which the stock price changes in the same direction. For example, consider

Irrational markets, rational fiduciaries

fi360 Conference, April 26, 2012 Justin Fox Irrational markets, rational fiduciaries A prelude, courtesy of Irving Fisher If we take the history of the prices of stocks and bonds, we shall find it chiefly

fi360 Conference, April 26, 2012 Justin Fox Irrational markets, rational fiduciaries A prelude, courtesy of Irving Fisher If we take the history of the prices of stocks and bonds, we shall find it chiefly

Unit01. Introduction, Creation of Financial Assets, and Security Markets

FCS 5510 Concept Review Notes: Unit01. Introduction, Creation of Financial Assets, and Security Markets Chapter 01. Definition of investment Portfolio Primary and secondary markets Value and valuation

FCS 5510 Concept Review Notes: Unit01. Introduction, Creation of Financial Assets, and Security Markets Chapter 01. Definition of investment Portfolio Primary and secondary markets Value and valuation

Post-Earnings-Announcement Drift: The Role of Revenue Surprises and Earnings Persistence

Post-Earnings-Announcement Drift: The Role of Revenue Surprises and Earnings Persistence Joshua Livnat Department of Accounting Stern School of Business Administration New York University 311 Tisch Hall

Post-Earnings-Announcement Drift: The Role of Revenue Surprises and Earnings Persistence Joshua Livnat Department of Accounting Stern School of Business Administration New York University 311 Tisch Hall

Market efficiency, questions 1 to 10

Market efficiency, questions 1 to 10 1. Is it possible to forecast future prices on an efficient market? 2. Many financial analysts try to predict future prices. Does it imply that markets are inefficient?

Market efficiency, questions 1 to 10 1. Is it possible to forecast future prices on an efficient market? 2. Many financial analysts try to predict future prices. Does it imply that markets are inefficient?

Lesson XI: Market Efficiency and FX. Forecasting

Lesson XI: May 15, 2017 Table of Contents Getting Started Market efficiency is an equilibrium condition, such that prices reflect all the available information and no abnormal returns can thus be earned

Lesson XI: May 15, 2017 Table of Contents Getting Started Market efficiency is an equilibrium condition, such that prices reflect all the available information and no abnormal returns can thus be earned

Chapter Ten. The Efficient Market Hypothesis

Chapter Ten The Efficient Market Hypothesis Slide 10 3 Topics Covered We Always Come Back to NPV What is an Efficient Market? Random Walk Efficient Market Theory The Evidence on Market Efficiency Puzzles

Chapter Ten The Efficient Market Hypothesis Slide 10 3 Topics Covered We Always Come Back to NPV What is an Efficient Market? Random Walk Efficient Market Theory The Evidence on Market Efficiency Puzzles

The Importance (or Non-Importance) of Distributional Assumptions in Monte Carlo Models of Saving. James P. Dow, Jr.

of Distributional Assumptions in Monte Carlo Models of Saving. James P. Dow, Jr.") The Importance (or Non-Importance) of Distributional Assumptions in Monte Carlo Models of Saving James P. Dow, Jr. Department of Finance, Real Estate and Insurance California State University, Northridge

The Importance (or Non-Importance) of Distributional Assumptions in Monte Carlo Models of Saving James P. Dow, Jr. Department of Finance, Real Estate and Insurance California State University, Northridge

Discussion Paper No. DP 07/02

SCHOOL OF ACCOUNTING, FINANCE AND MANAGEMENT Essex Finance Centre Can the Cross-Section Variation in Expected Stock Returns Explain Momentum George Bulkley University of Exeter Vivekanand Nawosah University

SCHOOL OF ACCOUNTING, FINANCE AND MANAGEMENT Essex Finance Centre Can the Cross-Section Variation in Expected Stock Returns Explain Momentum George Bulkley University of Exeter Vivekanand Nawosah University

Answer FOUR questions out of the following FIVE. Each question carries 25 Marks.

UNIVERSITY OF EAST ANGLIA School of Economics Main Series PGT Examination 2017-18 FINANCIAL MARKETS ECO-7012A Time allowed: 2 hours Answer FOUR questions out of the following FIVE. Each question carries

UNIVERSITY OF EAST ANGLIA School of Economics Main Series PGT Examination 2017-18 FINANCIAL MARKETS ECO-7012A Time allowed: 2 hours Answer FOUR questions out of the following FIVE. Each question carries

Expected Return and Portfolio Rebalancing

Expected Return and Portfolio Rebalancing Marcus Davidsson Newcastle University Business School Citywall, Citygate, St James Boulevard, Newcastle upon Tyne, NE1 4JH E-mail: davidsson_marcus@hotmail.com

Expected Return and Portfolio Rebalancing Marcus Davidsson Newcastle University Business School Citywall, Citygate, St James Boulevard, Newcastle upon Tyne, NE1 4JH E-mail: davidsson_marcus@hotmail.com

Principles of Finance

Principles of Finance Grzegorz Trojanowski Lecture 7: Arbitrage Pricing Theory Principles of Finance - Lecture 7 1 Lecture 7 material Required reading: Elton et al., Chapter 16 Supplementary reading: Luenberger,

Principles of Finance Grzegorz Trojanowski Lecture 7: Arbitrage Pricing Theory Principles of Finance - Lecture 7 1 Lecture 7 material Required reading: Elton et al., Chapter 16 Supplementary reading: Luenberger,

Steve Monahan. Discussion of Using earnings forecasts to simultaneously estimate firm-specific cost of equity and long-term growth

Steve Monahan Discussion of Using earnings forecasts to simultaneously estimate firm-specific cost of equity and long-term growth E 0 [r] and E 0 [g] are Important Businesses are institutional arrangements

Steve Monahan Discussion of Using earnings forecasts to simultaneously estimate firm-specific cost of equity and long-term growth E 0 [r] and E 0 [g] are Important Businesses are institutional arrangements

BAM Intelligence. 1 of 7 11/6/2017, 12:02 PM

1 of 7 11/6/2017, 12:02 PM BAM Intelligence Larry Swedroe, Director of Research, 6/22/2016 For about ree decades, e working asset pricing model was e capital asset pricing model (CAPM), wi beta specifically

1 of 7 11/6/2017, 12:02 PM BAM Intelligence Larry Swedroe, Director of Research, 6/22/2016 For about ree decades, e working asset pricing model was e capital asset pricing model (CAPM), wi beta specifically

What is an efficient market? What does it imply for investment and valuation

ch06_p111_153.qxp 12/2/11 2:07 PM Page 111 CHAPTER 6 Market Efficiency Definition, Tests, and Evidence What is an efficient market? What does it imply for investment and valuation models? Clearly, market

ch06_p111_153.qxp 12/2/11 2:07 PM Page 111 CHAPTER 6 Market Efficiency Definition, Tests, and Evidence What is an efficient market? What does it imply for investment and valuation models? Clearly, market

CORPORATE ANNOUNCEMENTS OF EARNINGS AND STOCK PRICE BEHAVIOR: EMPIRICAL EVIDENCE

CORPORATE ANNOUNCEMENTS OF EARNINGS AND STOCK PRICE BEHAVIOR: EMPIRICAL EVIDENCE By Ms Swati Goyal & Dr. Harpreet kaur ABSTRACT: This paper empirically examines whether earnings reports possess informational

CORPORATE ANNOUNCEMENTS OF EARNINGS AND STOCK PRICE BEHAVIOR: EMPIRICAL EVIDENCE By Ms Swati Goyal & Dr. Harpreet kaur ABSTRACT: This paper empirically examines whether earnings reports possess informational

Cascades in Experimental Asset Marktes

Cascades in Experimental Asset Marktes Christoph Brunner September 6, 2010 Abstract It has been suggested that information cascades might affect prices in financial markets. To test this conjecture, we

Cascades in Experimental Asset Marktes Christoph Brunner September 6, 2010 Abstract It has been suggested that information cascades might affect prices in financial markets. To test this conjecture, we

BARUCH COLLEGE DEPARTMENT OF ECONOMICS & FINANCE Professor Chris Droussiotis LECTURE 6. Modern Portfolio Theory (MPT): The Keynesian Animal Spirits

: The Keynesian Animal Spirits") LECTURE 6 Modern Portfolio Theory (MPT): CHALLENGED BY BEHAVIORAL ECONOMICS Efficient Frontier is the intersection of the Set of Portfolios with Minimum Variance (MVS) and set of portfolios with Maximum

LECTURE 6 Modern Portfolio Theory (MPT): CHALLENGED BY BEHAVIORAL ECONOMICS Efficient Frontier is the intersection of the Set of Portfolios with Minimum Variance (MVS) and set of portfolios with Maximum

MARKET EFFICIENCY & MUTUAL FUNDS

MARKET EFFICIENCY & MUTUAL FUNDS Topics: Market Efficiency Random Walks Different Forms of Market Efficiency Investing in Mutual Funds Introduction to mutual funds Evaluating mutual fund performance Evaluating

MARKET EFFICIENCY & MUTUAL FUNDS Topics: Market Efficiency Random Walks Different Forms of Market Efficiency Investing in Mutual Funds Introduction to mutual funds Evaluating mutual fund performance Evaluating

HOW TO GENERATE ABNORMAL RETURNS.

STOCKHOLM SCHOOL OF ECONOMICS Bachelor Thesis in Finance, Spring 2010 HOW TO GENERATE ABNORMAL RETURNS. An evaluation of how two famous trading strategies worked during the last two decades. HENRIK MELANDER

STOCKHOLM SCHOOL OF ECONOMICS Bachelor Thesis in Finance, Spring 2010 HOW TO GENERATE ABNORMAL RETURNS. An evaluation of how two famous trading strategies worked during the last two decades. HENRIK MELANDER

Technical Anomalies: A Theoretical Review

Malaysian Journal of Business and Economics Vol. 1, No. 1, June 2014, 103 110 ISSN 2289-6856 Kok Sook Ching a*, Qaiser Munir a and Arsiah Bahron a a Faculty of Business, Economics and Accountancy, Universiti

Malaysian Journal of Business and Economics Vol. 1, No. 1, June 2014, 103 110 ISSN 2289-6856 Kok Sook Ching a*, Qaiser Munir a and Arsiah Bahron a a Faculty of Business, Economics and Accountancy, Universiti

Portfolio strategies based on stock

ERIK HJALMARSSON is a professor at Queen Mary, University of London, School of Economics and Finance in London, UK. e.hjalmarsson@qmul.ac.uk Portfolio Diversification Across Characteristics ERIK HJALMARSSON

ERIK HJALMARSSON is a professor at Queen Mary, University of London, School of Economics and Finance in London, UK. e.hjalmarsson@qmul.ac.uk Portfolio Diversification Across Characteristics ERIK HJALMARSSON

Introduction to Equity Valuation

Introduction to Equity Valuation FINANCE 352 INVESTMENTS Professor Alon Brav Fuqua School of Business Duke University Alon Brav 2004 Finance 352, Equity Valuation 1 1 Overview Stocks and stock markets

Introduction to Equity Valuation FINANCE 352 INVESTMENTS Professor Alon Brav Fuqua School of Business Duke University Alon Brav 2004 Finance 352, Equity Valuation 1 1 Overview Stocks and stock markets

M A R K E T E F F I C I E N C Y & R O B E R T SHILLER S I R R A T I O N A L E X U B E R A N C E

M A R K E T E F F I C I E N C Y & R O B E R T SHILLER S I R R A T I O N A L E X U B E R A N C E K E L L Y J I A N G E C O N 4 9 0 5 : F I N A N C I A L F R A G I L I T Y O F T H E M A C R O E C O N O M

M A R K E T E F F I C I E N C Y & R O B E R T SHILLER S I R R A T I O N A L E X U B E R A N C E K E L L Y J I A N G E C O N 4 9 0 5 : F I N A N C I A L F R A G I L I T Y O F T H E M A C R O E C O N O M

FTSE ActiveBeta Index Series: A New Approach to Equity Investing

FTSE ActiveBeta Index Series: A New Approach to Equity Investing 2010: No 1 March 2010 Khalid Ghayur, CEO, Westpeak Global Advisors Patent Pending Abstract The ActiveBeta Framework asserts that a significant

FTSE ActiveBeta Index Series: A New Approach to Equity Investing 2010: No 1 March 2010 Khalid Ghayur, CEO, Westpeak Global Advisors Patent Pending Abstract The ActiveBeta Framework asserts that a significant

An Empirical Study of Serial Correlation in Stock Returns

NORGES HANDELSHØYSKOLE An Empirical Study of Serial Correlation in Stock Returns Cause effect relationship for excess returns from momentum trading in the Norwegian market Maximilian Brodin and Øyvind

NORGES HANDELSHØYSKOLE An Empirical Study of Serial Correlation in Stock Returns Cause effect relationship for excess returns from momentum trading in the Norwegian market Maximilian Brodin and Øyvind

The mood beta concept of Hirshleifer, Jiang & Meng (2017) examined by incorporating soccer results.

examined by incorporating soccer results.") The mood beta concept of Hirshleifer, Jiang & Meng (2017) examined by incorporating soccer results. Master Thesis in Financial Economics Nijmegen School of Management Written by Kees Revenberg Student

The mood beta concept of Hirshleifer, Jiang & Meng (2017) examined by incorporating soccer results. Master Thesis in Financial Economics Nijmegen School of Management Written by Kees Revenberg Student

Exploiting Factor Autocorrelation to Improve Risk Adjusted Returns

Exploiting Factor Autocorrelation to Improve Risk Adjusted Returns Kevin Oversby 22 February 2014 ABSTRACT The Fama-French three factor model is ubiquitous in modern finance. Returns are modeled as a linear

Exploiting Factor Autocorrelation to Improve Risk Adjusted Returns Kevin Oversby 22 February 2014 ABSTRACT The Fama-French three factor model is ubiquitous in modern finance. Returns are modeled as a linear

Evolving Equity Investing: Delivering Long-Term Returns in Short-Tempered Markets

March 2012 Evolving Equity Investing: Delivering Long-Term Returns in Short-Tempered Markets Kent Hargis Portfolio Manager Low Volatility Equities Director of Quantitative Research Equities This information

March 2012 Evolving Equity Investing: Delivering Long-Term Returns in Short-Tempered Markets Kent Hargis Portfolio Manager Low Volatility Equities Director of Quantitative Research Equities This information

Stock Market Basics. Capital Market A market for intermediate or long-term debt or corporate stocks.

Stock Market Basics Capital Market A market for intermediate or long-term debt or corporate stocks. Stock Market and Stock Exchange A stock exchange is the most important component of a stock market. It

Stock Market Basics Capital Market A market for intermediate or long-term debt or corporate stocks. Stock Market and Stock Exchange A stock exchange is the most important component of a stock market. It