LECTURES 11 and 12: Globalization of Financial Markets

|

|

|

- Dwight Ferdinand Jefferson

- 6 years ago

- Views:

Transcription

1 LECTURES 11 and 12: Globalization of Financial Markets Lecture 11: Measuring financial integration Foreign exchange markets (more in Appendix) Liberalization & interest rate arbitrage How to manage risk: The forward exchange market Lecture 12: Financial globalization, continued Should countries open up to international capital flows? Advantages of financial integration Disadvantages of financial integration

2 Measuring International Financial Integration I. Direct measures of barriers, e.g., IMF count of freedom from KA restrictions. II. Quantity tests III. Price tests All show general trend toward financial integration. Source: Kose, Prasad, Rogoff & Wei (2009)

3 I. Direct Measure of Financial Barriers: Chinn-Ito tally of capital controls, from IMF data Figure 1: Development of KAOPEN for Different Income Groups Rapid financial liberalization in 1990s year Industrial Countries Emerging Markets Less Developed Menzie Chinn & Hiro Ito, "A New Measure of Financial Openness" (Journal of Comparative Policy Analysis, 2008), updated July

4 Chinn-Ito Measure of Financial Openness The calculations are based on 4 categories in the IMF s Annual Report on Exchange Arrangements & Exchange Restrictions: multiple exchange rates, current account restrictions, capital account restrictions, and required surrender of export proceeds.

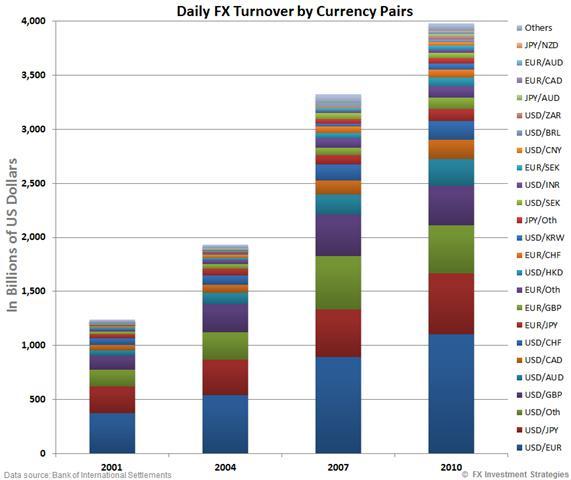

5 Graph 2 II. Quantity measures One comprehensive indicator of gross financial transactions: the volume of turnover in foreign exchange markets. FX trading has continued to grow rapidly. { Most trading is among banks; only 9% is with non-financial customers.

6 FX transactions now exceed $5 trillion per day Graph 3 } Spot transactions < ½. More are forwards & related derivatives.

7 IMF Quantity test shows rising integration

. } Higher prices onshore Robert McCauley, CFR conference on Internationalization of the RMB, Beijing, Nov.2011, Graph 5.")

8 III. Price Measure: Test arbitrage by price of the same asset across borders Chinese firms stock prices, onshore relative to offshore Premium of A shares (held domestically), over H shares (held in Hong Kong). } Higher prices onshore Robert McCauley, CFR conference on Internationalization of the RMB, Beijing, Nov.2011, Graph 5. Data Source: Bloomberg, BIS Note: company composition of the two indices differs. Investing in Chinese shares, Economist, Sept. 27, 2014

9 Price Measure: Covered interest arbitrage German interest rates in Frankfurt in 1973 >> rates available in marks offshore in London (whether measured in euromarks or covered eurodollars). { Why? Stringent capital controls penalized foreign investors who wanted to acquire German assets. Germany removed capital controls after the need to defend the fixed exchange rate had been overtaken by events, => The interest differential disappeared in {

, deposits in Tokyo until => 1979. interest differential. { Source: Frankel (1985), The Yen/Dollar Agreement Japan removed controls on outflows, 1979-83. Why?")

10 Liberalization in another country that had controls on capital inflows Similarly, Tokyo interest rates In 1978, were Japan higher still than prohibited those available foreigners in yen from offshore holding ( euroyen ), deposits in Tokyo until => interest differential. { Source: Frankel (1985), The Yen/Dollar Agreement Japan removed controls on outflows, Why? Foreign investors Again, were arbitrage banned eliminated from holding the interest Japanese differential. assets.

11 Liberalization in a country that had controls on outflows UK interest rates in were lower domestically than those available offshore. Controls against capital outflow kept domestic investors from taking money out. { Thatcher removed the controls in Interest differential fell to 0. {

12 COVERED INTEREST PARITY $ 1 + i US = (F $/ ) (1/S) (1+i UK ) where S is the spot rate in $/ and F is the forward rate. Forward discount: fd (F - S)/S => 1 + fd F/S => $ (1 + i US ) = $ (1 + fd)(1 + i UK ). Because (fd i UK ) is small, i US fd + i UK. = $ (1 + fd + i UK + fd i UK ). If the U.S. nominal interest rate exceeds the U.K. rate, the $ sells at a discount in the forward exchange market.

13 Daily exchange rates Spot rate Transaction cost Forward: Selling at a forward discount against the $: Turkish lire Argentine peso Brazilian real Selling at a forward premium against the $: Yen New Taiwan $ UAE dirham Source: Financial Times Accessed 11/2/2007

14 In late 2008 Covered Interest Parity surprisingly failed, in a Global-Financial-Crisis rush to the $ as safe haven. Covered interest differentials, using Overnight Index Swap interest rates, Significant determinants are apparently counterparty risk & liquidity, proxied by financial stock CDS, VIX, implied fx volatility, OIS bid-ask spreads & Fed swap lines. Inês Isabel Sequeira de Freitas Serra, Covered Interest Parity, NOVA School of Business & Economics, Lisbon, Jan

15 Appendix 1: Measuring International Financial Integration for Developing Countries For emerging markets, liberalization has been more rapid de facto than de jure: Capital controls are hard to enforce. I. Direct measures of barriers ( ), e.g., count of freedom from KA restrictions, IMF. II. Quantity tests Source: Kose, Prasad, Rogoff & Wei (2009)

16 III. Price test: Price of the same asset across borders Chinese firms stock prices, onshore relative to offshore: A shares, which domestic residents held, sold at a premium to B shares, which Chinese firms could issue to foreign investors. } Higher prices on-shore Source: Vicki Wei Tang (2011) In the 1990s, foreign residents held B shares, listed in Shenzhen or Shanghai. In 2001, Chinese citizens were allowed to buy B shares.

17 H shares (held in Hong Kong) became more important. Chinese firms stock prices, onshore relative to offshore:. Premium of A shares (held domestically), over H shares { Higher prices on-shore R. McCauley, CFR conference on Internationalization of the RMB, Beijing, Nov Data Source: Bloomberg, BIS Note: company composition of the two indices differs.

18 Liberalization in a country that had controls on outflows { From: M. Mussa and M. Goldstein, The Integration of World Capital Markets, Changing Capital Markets: Implications for Monetary Policy, Fed.Res.Bk. Kansas City, France kept its controls on capital outflows until the late 1980s. Again, they produced an offshore-onshore differential, which shot up whenever there was speculation of a franc devaluation. Again, the differential disappeared after controls were removed.

{ {")

19 Price test: Sovereign spread on Brazilian debt The forward premium + the country premium add up to the differential between Brazilian interest rates and $ interest rates in London (LIBOR) { { {

20 Appendix 2: Measures of activity in global foreign exchange markets. Trading volume in forex markets rose rapidly in the 1990s. Forward contracts (including swaps) became more than half of the total.

21 The world s largest financial center, as measured by FX, is London, not New York. In 2010, UK banks accounted for 36.7% of forex turnover, followed by the US (18%), Japan (6%), Singapore (5%), Switzerland (5%), Hong Kong SAR (5%) & Australia (4%).

22

23 Global fx market turnover was 20% higher in 2010 than in 2007, with average daily turnover of $4.0 trillion compared to $3.3 trillion. The rise was driven by the 48% growth in turnover of spot transactions, (=37% of fx turnover; spot turnover rose to $1.5 tr. in 2010 from $1.0 tr. in 2007.) Daily turnover in OTC interest rate derivatives grew by 24%, to $2.1 trillion in The dollar remains the leading vehicle currency, used in 85% of transactions. Source: BIS, Triennial Central Bank Survey: Report on global foreign exchange market activity in 2010 (Basel, Dec.2010).

24 2004

25 Securitization, internationally 1982 International debt crisis: Banks lose enthusiasm for lending to developing countries Basel I Agreement sets standards for international banks (e.g., minimum capital requirements) Brady bonds securitize bad bank loans to developing countries Mexican peso crisis hits when foreign investors lose willingness to hold CETES & tesobonos Thai baht crisis also features a larger role for securities International securitization of US mortgages ( MBS ) ends in tears, with the sub-prime mortgage market crisis Basel III: AAA ratings for MBSs, ABSs or CDOs > 0 risk.

LECTURES 11 and 12: Globalization of Financial Markets

LECTURES 11 and 12: Globalization of Financial Markets Lecture 11: Measuring financial integration I) Direct measures of barriers II) Quantity measures III) Price tests, esp. interest rate arbitrage Managing

LECTURES 11 and 12: Globalization of Financial Markets Lecture 11: Measuring financial integration I) Direct measures of barriers II) Quantity measures III) Price tests, esp. interest rate arbitrage Managing

(VII) INTERNATIONAL INTEGRATION OF FINANCIAL MARKETS

INTERNATIONAL INTEGRATION OF FINANCIAL MARKETS") (VII) INTERNATIONAL INTEGRATION OF FINANCIAL MARKETS LECTURES 20-22 Question 1: What are the arguments in favor of open financial markets? Question 2: Does it really work this way? Question 3: How integrated

(VII) INTERNATIONAL INTEGRATION OF FINANCIAL MARKETS LECTURES 20-22 Question 1: What are the arguments in favor of open financial markets? Question 2: Does it really work this way? Question 3: How integrated

Bank of Canada Triennial Central Bank Survey of Foreign Exchange and Over-the-Counter (OTC) Derivatives Markets Turnover for April, 2010 and Amounts

Derivatives Markets Turnover for April, 2010 and Amounts") Bank of Canada Triennial Central Bank Survey of Foreign Exchange and Over-the-Counter (OTC) Derivatives Markets Turnover for April, 2010 and Amounts Outstanding as at June 30, 2010 December 20, 2010 Table

Bank of Canada Triennial Central Bank Survey of Foreign Exchange and Over-the-Counter (OTC) Derivatives Markets Turnover for April, 2010 and Amounts Outstanding as at June 30, 2010 December 20, 2010 Table

Global liquidity: selected indicators 1

8 October 14 Global liquidity: selected indicators 1 Highlights Indicators of global liquidity point to a continued strengthening of risk appetite and loosening of credit conditions in the spring and summer

8 October 14 Global liquidity: selected indicators 1 Highlights Indicators of global liquidity point to a continued strengthening of risk appetite and loosening of credit conditions in the spring and summer

Bank of Canada Triennial Central Bank Surveys of Foreign Exchange and Over-the-Counter (OTC) Derivatives Markets Turnover for April, 2007 and Amounts

Derivatives Markets Turnover for April, 2007 and Amounts") Bank of Canada Triennial Central Bank Surveys of Foreign Exchange and Over-the-Counter (OTC) Derivatives Markets Turnover for April, 2007 and Amounts Outstanding as at June 30, 2007 January 4, 2008 Table

Bank of Canada Triennial Central Bank Surveys of Foreign Exchange and Over-the-Counter (OTC) Derivatives Markets Turnover for April, 2007 and Amounts Outstanding as at June 30, 2007 January 4, 2008 Table

THE CANADIAN FOREIGN EXCHANGE COMMITTEE LE COMITÉ CANADIEN DU MARCHÉ DES CHANGES

THE CANADIAN FOREIGN EXCHANGE COMMITTEE LE COMITÉ CANADIEN DU MARCHÉ DES CHANGES 150 King Street West Contact: Rob Ogrodnick Suite 2000 Telephone: (416) 542-1339 Toronto, Ontario Email: rogrodnick@bankofcanada.ca

THE CANADIAN FOREIGN EXCHANGE COMMITTEE LE COMITÉ CANADIEN DU MARCHÉ DES CHANGES 150 King Street West Contact: Rob Ogrodnick Suite 2000 Telephone: (416) 542-1339 Toronto, Ontario Email: rogrodnick@bankofcanada.ca

Table 1: Foreign exchange turnover: Summary of surveys Billions of U.S. dollars. Number of business days

Table 1: Foreign exchange turnover: Summary of surveys Billions of U.S. dollars Total turnover Number of business days Average daily turnover change 1983 103.2 20 5.2 1986 191.2 20 9.6 84.6 1989 299.9

Table 1: Foreign exchange turnover: Summary of surveys Billions of U.S. dollars Total turnover Number of business days Average daily turnover change 1983 103.2 20 5.2 1986 191.2 20 9.6 84.6 1989 299.9

Bank of Canada Triennial Central Bank Survey of Foreign Exchange and Over-the-Counter (OTC) Derivatives Markets

Derivatives Markets") Bank of Canada Triennial Central Bank Survey of Foreign Exchange and Over-the-Counter (OTC) Derivatives Markets Turnover for, and Amounts Outstanding as at June 30, March, 2005 Turnover data for, Table

Bank of Canada Triennial Central Bank Survey of Foreign Exchange and Over-the-Counter (OTC) Derivatives Markets Turnover for, and Amounts Outstanding as at June 30, March, 2005 Turnover data for, Table

RMB internationalization:

RMB internationalization: Recent Development and headwinds Alicia Garcia-Herrero Chief Economist for Emerging Markets, BBVA Key points 1 Why is China pushing to internationalize the RMB? 2 Recent development

RMB internationalization: Recent Development and headwinds Alicia Garcia-Herrero Chief Economist for Emerging Markets, BBVA Key points 1 Why is China pushing to internationalize the RMB? 2 Recent development

1 THE EURODOLLAR MARKET

Roberto Perotti September 15 2016 Version 1.0 1 THE EURODOLLAR MARKET WHAT ARE EURODOLLARS? Eurodollars are bank deposits denominated in dollars but held in banks located outside the US, including foreign

Roberto Perotti September 15 2016 Version 1.0 1 THE EURODOLLAR MARKET WHAT ARE EURODOLLARS? Eurodollars are bank deposits denominated in dollars but held in banks located outside the US, including foreign

Internationalization of the RMB: Developments, Problems and Policies

Internationalization of the RMB: Developments, Problems and Policies 23 October 2015 Zheng Liansheng Outline Introduction The development of RMB internationalization RMB Offshore markets The problems behind

Internationalization of the RMB: Developments, Problems and Policies 23 October 2015 Zheng Liansheng Outline Introduction The development of RMB internationalization RMB Offshore markets The problems behind

The Development of the Offshore. Bonds. Peter J. Morgan, PhD Senior Consultant for Research Asian Development Bank Institute

The Development of the Offshore Market of the Yuan-Denominated Bonds Peter J. Morgan, PhD Senior Consultant for Research Asian Development Bank Institute ADBI-OECD Roundtable on Capital Market Reform in

The Development of the Offshore Market of the Yuan-Denominated Bonds Peter J. Morgan, PhD Senior Consultant for Research Asian Development Bank Institute ADBI-OECD Roundtable on Capital Market Reform in

Monetary Policy Divergence and Global Financial Stability: From the Perspective of Demand and Supply of Safe Assets

Monetary Policy Divergence and Global Financial Stability: From the Perspective of Demand and Supply of Safe Assets January, 7 Speech at a Meeting Hosted by the International Bankers Association of Japan

Monetary Policy Divergence and Global Financial Stability: From the Perspective of Demand and Supply of Safe Assets January, 7 Speech at a Meeting Hosted by the International Bankers Association of Japan

1)International Monetary System

International Monetary System") 1) (International Monetary System) 2) 3) (Balance of Payments) 4) (Foreign Exchange Market) 5) Interest Rate Parity (IRP) 6) Covered Interest Arbitrage 1 1)International Monetary System 1.1 The Gold Standard

1) (International Monetary System) 2) 3) (Balance of Payments) 4) (Foreign Exchange Market) 5) Interest Rate Parity (IRP) 6) Covered Interest Arbitrage 1 1)International Monetary System 1.1 The Gold Standard

THE CANADIAN FOREIGN EXCHANGE COMMITTEE LE COMITÉ CANADIEN DU MARCHÉ DES CHANGES

THE CANADIAN FOREIGN EXCHANGE COMMITTEE LE COMITÉ CANADIEN DU MARCHÉ DES CHANGES 150 King Street West Contact: Rob Ogrodnick Suite 2000 Telephone: (416) 542-1339 Toronto, Ontario Email: rogrodnick@bankofcanada.ca

THE CANADIAN FOREIGN EXCHANGE COMMITTEE LE COMITÉ CANADIEN DU MARCHÉ DES CHANGES 150 King Street West Contact: Rob Ogrodnick Suite 2000 Telephone: (416) 542-1339 Toronto, Ontario Email: rogrodnick@bankofcanada.ca

Monetary and Economic Department. OTC derivatives market activity in the second half of 2005

Monetary and Economic Department OTC derivatives market activity in the second half of 2005 May 2006 Queries concerning this release should be addressed to the authors listed below: Section I: Christian

Monetary and Economic Department OTC derivatives market activity in the second half of 2005 May 2006 Queries concerning this release should be addressed to the authors listed below: Section I: Christian

RMB Internationalization Status and Its Implications

International Finance RMB Internationalization Status and Its Implications Hansoo Kim, Research Fellow* 1) China announced the RMB internationalization policy in 2009 and has carried forward many initiatives

International Finance RMB Internationalization Status and Its Implications Hansoo Kim, Research Fellow* 1) China announced the RMB internationalization policy in 2009 and has carried forward many initiatives

Study Questions (with Answers) Lecture 13. Exchange Rates

Lecture 13. Exchange Rates") Study Questions (with Answers) Page 1 of 5 Part 1: Multiple Choice Select the best answer of those given. Study Questions (with Answers) Lecture 13 1. The statement the yen rose today from 121 to 117 makes

Study Questions (with Answers) Page 1 of 5 Part 1: Multiple Choice Select the best answer of those given. Study Questions (with Answers) Lecture 13 1. The statement the yen rose today from 121 to 117 makes

Introduction to Foreign Exchange Slides for International Finance (KOM Chapter 14)

") Slides for International Finance (KOM Chapter 14) American University 2011-09-01 Preview Introduction to Exchange Rates Basics exchange rate concepts Exchange rates and the cost of foreign goods The foreign

Slides for International Finance (KOM Chapter 14) American University 2011-09-01 Preview Introduction to Exchange Rates Basics exchange rate concepts Exchange rates and the cost of foreign goods The foreign

Arbitrage Activities between Offshore and Domestic Yen Money Markets since the End of the Quantitative Easing Policy

Bank of Japan Review 27-E-2 Arbitrage Activities between Offshore and Domestic Yen Money Markets since the End of the Quantitative Easing Policy Teppei Nagano, Eiko Ooka, and Naohiko Baba Money Markets

Bank of Japan Review 27-E-2 Arbitrage Activities between Offshore and Domestic Yen Money Markets since the End of the Quantitative Easing Policy Teppei Nagano, Eiko Ooka, and Naohiko Baba Money Markets

THE CANADIAN FOREIGN EXCHANGE COMMITTEE LE COMITÉ CANADIEN DU MARCHÉ DES CHANGES

THE CANADIAN FOREIGN EXCHANGE COMMITTEE LE COMITÉ CANADIEN DU MARCHÉ DES CHANGES 150 King Street West Contact: Rob Ogrodnick Suite 2000 Telephone: (416) 542-1339 Toronto, Ontario Email: rogrodnick@bankofcanada.ca

THE CANADIAN FOREIGN EXCHANGE COMMITTEE LE COMITÉ CANADIEN DU MARCHÉ DES CHANGES 150 King Street West Contact: Rob Ogrodnick Suite 2000 Telephone: (416) 542-1339 Toronto, Ontario Email: rogrodnick@bankofcanada.ca

TREASURY AND FEDERAL RESERVE FOREIGN EXCHANGE OPERATIONS

EMBARGOED: FOR RELEASE AT 4:00 PM, EST, THURSDAY, JANUARY 29, 1998 TREASURY AND FEDERAL RESERVE FOREIGN EXCHANGE OPERATIONS October December In a period marked by dramatic developments in Asia, the dollar

EMBARGOED: FOR RELEASE AT 4:00 PM, EST, THURSDAY, JANUARY 29, 1998 TREASURY AND FEDERAL RESERVE FOREIGN EXCHANGE OPERATIONS October December In a period marked by dramatic developments in Asia, the dollar

Study Questions. Lecture 13. Exchange Rates

Study Questions Page 1 of 5 Study Questions Lecture 13 Part 1: Multiple Choice Select the best answer of those given. 1. The statement the yen rose today from 121 to 117 makes sense because a. The U.S.

Study Questions Page 1 of 5 Study Questions Lecture 13 Part 1: Multiple Choice Select the best answer of those given. 1. The statement the yen rose today from 121 to 117 makes sense because a. The U.S.

Research Note. Asia-Pacific Derivatives Survey. April 2019

April 19 Research Note In anticipation of ISDA s 34th Annual General Meeting in Hong Kong, ISDA conducted a survey of derivatives markets in the Asia-Pacific region. The survey reveals that market participants

April 19 Research Note In anticipation of ISDA s 34th Annual General Meeting in Hong Kong, ISDA conducted a survey of derivatives markets in the Asia-Pacific region. The survey reveals that market participants

Efficacy of China s capital controls

Efficacy of China s capital controls RIETI/BIS/BOC conference Globalisation of financial servceis in China: implications for capital flows, supervision and monetary policy Beijing, 19 March 2005 Guonan

Efficacy of China s capital controls RIETI/BIS/BOC conference Globalisation of financial servceis in China: implications for capital flows, supervision and monetary policy Beijing, 19 March 2005 Guonan

483 Subject Index. Global Depositiory Receipts, 250 Grassman s law, 148, 160

Subject Index Adjustabonos, 401-3 Agency for International Development, 100 American depository receipts (ADRs): considered as foreign securities, 250; traded on over-the-counter market, 245 Arbitrage:

Subject Index Adjustabonos, 401-3 Agency for International Development, 100 American depository receipts (ADRs): considered as foreign securities, 250; traded on over-the-counter market, 245 Arbitrage:

Hong Kong s Experience

Cross Border Issues IMF Conference on Operationalizing Systemic Risk Monitoring Washington, D. C. 26 May 21 Hong Kong s Experience Dong He Executive Director (Research) Hong Kong Monetary Authority 1 Outline

Cross Border Issues IMF Conference on Operationalizing Systemic Risk Monitoring Washington, D. C. 26 May 21 Hong Kong s Experience Dong He Executive Director (Research) Hong Kong Monetary Authority 1 Outline

Introduction to Foreign Exchange Slides for International Finance (KOM Chapter 14)

") Slides for International Finance (KOM Chapter 14) American University 2011-09-01 Preview Introduction to Exchange Rates Basics exchange rate concepts Exchange rates and the cost of foreign goods The foreign

Slides for International Finance (KOM Chapter 14) American University 2011-09-01 Preview Introduction to Exchange Rates Basics exchange rate concepts Exchange rates and the cost of foreign goods The foreign

Triennial Central Bank Survey of Foreign Exchange and Derivatives Market Activity in Canada during April 2013

For Immediate Release Contact: Bank of Canada 5 September 2013, 09:00 ET Media Relations (613) 782-8782 Triennial Central Bank Survey of Foreign Exchange and Derivatives Market Activity in Canada during

For Immediate Release Contact: Bank of Canada 5 September 2013, 09:00 ET Media Relations (613) 782-8782 Triennial Central Bank Survey of Foreign Exchange and Derivatives Market Activity in Canada during

Advanced and Emerging Economies Two speed Recovery

Advanced and Emerging Economies Two speed Recovery 23 November 2 Bauhinia Foundation Research Centre Masaaki Shirakawa Governor of the Bank of Japan Slide 1 Japan s Silver Yen and Hong Kong s Silver Yuan

Advanced and Emerging Economies Two speed Recovery 23 November 2 Bauhinia Foundation Research Centre Masaaki Shirakawa Governor of the Bank of Japan Slide 1 Japan s Silver Yen and Hong Kong s Silver Yuan

Foreign Exchange Markets

Foreign Exchange Markets Foreign exchange: Money of another country. Foreign exchange transaction: and the seller of a currency. Agreement between the buyer Foreign exchange market (FOREX market): Physical

Foreign Exchange Markets Foreign exchange: Money of another country. Foreign exchange transaction: and the seller of a currency. Agreement between the buyer Foreign exchange market (FOREX market): Physical

EconS 327 Test 2 Spring 2010

1. Credit (+) items in the balance of payments correspond to anything that: a. Involves payments to foreigners b. Decreases the domestic money supply c. Involves receipts from foreigners d. Reduces international

1. Credit (+) items in the balance of payments correspond to anything that: a. Involves payments to foreigners b. Decreases the domestic money supply c. Involves receipts from foreigners d. Reduces international

Definitions and BoP Accounting

Lecture 2: Definitions and BoP Accounting Spring 2008 Concepts/Definitions GDP Real versus nominal Price level, inflation Money Interest rates GDP Sum of value of all goods and services produced within

Lecture 2: Definitions and BoP Accounting Spring 2008 Concepts/Definitions GDP Real versus nominal Price level, inflation Money Interest rates GDP Sum of value of all goods and services produced within

The Renminbi s Ascendance in International Finance

257 COMMENTARY The Renminbi s Ascendance in International Finance Menzie Chinn In this wide-ranging review of recent developments involving the progress in renminbi internationalization, Eswar Prasad concludes,

257 COMMENTARY The Renminbi s Ascendance in International Finance Menzie Chinn In this wide-ranging review of recent developments involving the progress in renminbi internationalization, Eswar Prasad concludes,

Chapter 5. The Foreign Exchange Market. Foreign Exchange Markets: Learning Objectives. Foreign Exchange Markets. Foreign Exchange Markets

Chapter 5 The Foreign Exchange Market Foreign Exchange Markets: Learning Objectives Examine the functions performed by the foreign exchange (FOREX) market, its participants, size, geographic and currency

Chapter 5 The Foreign Exchange Market Foreign Exchange Markets: Learning Objectives Examine the functions performed by the foreign exchange (FOREX) market, its participants, size, geographic and currency

Japanese Capital Market

Japanese Capital Market The objectives of the chapter are to provide an understanding of: o o o o o o Financial system reforms. The banking sector. Japanese government bonds. Corporate debt markets. Stock

Japanese Capital Market The objectives of the chapter are to provide an understanding of: o o o o o o Financial system reforms. The banking sector. Japanese government bonds. Corporate debt markets. Stock

Definitions and BoP Accounting

Lecture 2: Definitions and BoP Accounting Prof. Menzie Chinn PA 854 Spring 2010 Concepts/Definitions GDP Real versus nominal Price level, inflation Money Interest rates GDP Sum of value of all goods and

Lecture 2: Definitions and BoP Accounting Prof. Menzie Chinn PA 854 Spring 2010 Concepts/Definitions GDP Real versus nominal Price level, inflation Money Interest rates GDP Sum of value of all goods and

THE CANADIAN FOREIGN EXCHANGE COMMITTEE LE COMITÉ CANADIEN DU MARCHÉ DES CHANGES

THE CANADIAN FOREIGN EXCHANGE COMMITTEE LE COMITÉ CANADIEN DU MARCHÉ DES CHANGES 150 King Street West Contact: Rob Ogrodnick Suite 2000 Telephone: (416) 542-1339 Toronto, Ontario Email: rogrodnick@bankofcanada.ca

THE CANADIAN FOREIGN EXCHANGE COMMITTEE LE COMITÉ CANADIEN DU MARCHÉ DES CHANGES 150 King Street West Contact: Rob Ogrodnick Suite 2000 Telephone: (416) 542-1339 Toronto, Ontario Email: rogrodnick@bankofcanada.ca

Preview PP542. International Capital Markets. Gains from Trade. International Capital Markets. The Three Types of International Transaction Trade

Preview PP542 International Capital Markets Gains from trade Portfolio diversification Players in the international capital markets Attainable policies with international capital markets Offshore banking

Preview PP542 International Capital Markets Gains from trade Portfolio diversification Players in the international capital markets Attainable policies with international capital markets Offshore banking

The Economics of International Financial Crises 4. Foreign Exchange Markets, Interest Rates and Exchange Rate Determination

Fletcher School of Law and Diplomacy, Tufts University The Economics of International Financial Crises 4. Foreign Exchange Markets, Interest Rates and Exchange Rate Determination Prof. George Alogoskoufis

Fletcher School of Law and Diplomacy, Tufts University The Economics of International Financial Crises 4. Foreign Exchange Markets, Interest Rates and Exchange Rate Determination Prof. George Alogoskoufis

Study Questions (with Answers) Lecture 13. Exchange Rates

Lecture 13. Exchange Rates") Study Questions (with Answers) Page 1 of 5 Part 1: Multiple Choice Select the best answer of those given. Study Questions (with Answers) Lecture 13 1. The statement the yen rose today from 121 to 117 makes

Study Questions (with Answers) Page 1 of 5 Part 1: Multiple Choice Select the best answer of those given. Study Questions (with Answers) Lecture 13 1. The statement the yen rose today from 121 to 117 makes

Study Questions. Lecture 13. Exchange Rates

Study Questions Page 1 of 5 Part 1: Multiple Choice Select the best answer of those given. Study Questions Lecture 13 1. The statement the yen rose today from 121 to 117 makes sense because a. The U.S.

Study Questions Page 1 of 5 Part 1: Multiple Choice Select the best answer of those given. Study Questions Lecture 13 1. The statement the yen rose today from 121 to 117 makes sense because a. The U.S.

CHINA FOCUS II AIMING FOR THE SDR BASKET

AIMING FOR THE SDR BASKET With its rising economic size and position as a top trading nation, China is aiming for the RMB to be included into the SDR basket of currencies at the 2015 IMF review, which

AIMING FOR THE SDR BASKET With its rising economic size and position as a top trading nation, China is aiming for the RMB to be included into the SDR basket of currencies at the 2015 IMF review, which

The Rise of China and the International Monetary System

The Rise of China and the International Monetary System Masahiro Kawai Asian Development Bank Institute Macro Economy Research Conference China and the Global Economy Hosted by the Nomura Foundation Tokyo,

The Rise of China and the International Monetary System Masahiro Kawai Asian Development Bank Institute Macro Economy Research Conference China and the Global Economy Hosted by the Nomura Foundation Tokyo,

VI. International Monetary Study II for KUINEP The Internationalization of the Yen. its importance and issues to overcome.

VI. International Monetary Study II for KUINEP The Internationalization of the Yen its importance and issues to overcome April-July 2004 1 1.What is the internationalization of the yen? What is the internationalization

VI. International Monetary Study II for KUINEP The Internationalization of the Yen its importance and issues to overcome April-July 2004 1 1.What is the internationalization of the yen? What is the internationalization

The Renminbi s Ascendance in International Finance

207 The Renminbi s Ascendance in International Finance Eswar S. Prasad The renminbi is gaining prominence as an international currency that is being used more widely to denominate and settle cross-border

207 The Renminbi s Ascendance in International Finance Eswar S. Prasad The renminbi is gaining prominence as an international currency that is being used more widely to denominate and settle cross-border

3) In 2010, what was the top remittance-receiving country in the world? A) Brazil B) Mexico C) India D) China

In 2010, what was the top remittance-receiving country in the world? A) Brazil B) Mexico C) India D) China") HSE-IB Test Syllabus: International Business: Environments and Operations, 15e, Global Edition (Daniels et al.). For use of the student for an educational purpose only, do not reproduce or redistribute.

HSE-IB Test Syllabus: International Business: Environments and Operations, 15e, Global Edition (Daniels et al.). For use of the student for an educational purpose only, do not reproduce or redistribute.

Statistical release: OTC derivatives statistics at end-december Monetary and Economic Department

Statistical release: OTC derivatives statistics at end-december 2011 Monetary and Economic Department May 2012 Queries concerning this release should be addressed to the authors listed below: Section I:

Statistical release: OTC derivatives statistics at end-december 2011 Monetary and Economic Department May 2012 Queries concerning this release should be addressed to the authors listed below: Section I:

Study Questions. Lecture 1 Overview of the World Economy

Study Questions (with Answers) Page 1 of 5 (7) Study Questions Lecture 1 of the World Economy Part 1: Multiple Choice Select the best answer of those given. 1. How many countries are there in the world?

Study Questions (with Answers) Page 1 of 5 (7) Study Questions Lecture 1 of the World Economy Part 1: Multiple Choice Select the best answer of those given. 1. How many countries are there in the world?

SELECTED INTEREST & EXCHANGE RATES FOR MAJOR COUNTRIES & THE U.S.

\«April 1, 1970 No. 448 f / A t *^ f,, H«13 Division of IntomotiMoiJxnyce Europe and British Common wealth Section f j y SELECTED INTEREST & EXCHANGE RATES FOR MAJOR COUNTRIES & THE U.S. WEEKLY SERIES

\«April 1, 1970 No. 448 f / A t *^ f,, H«13 Division of IntomotiMoiJxnyce Europe and British Common wealth Section f j y SELECTED INTEREST & EXCHANGE RATES FOR MAJOR COUNTRIES & THE U.S. WEEKLY SERIES

FOREIGN EXCHANGE MARKET. Luigi Vena 05/08/2015 Liuc Carlo Cattaneo

FOREIGN EXCHANGE MARKET Luigi Vena 05/08/2015 Liuc Carlo Cattaneo TABLE OF CONTENTS The FX market Exchange rates Exchange rates regimes Financial balances International Financial Markets 05/08/2015 Coopeland

FOREIGN EXCHANGE MARKET Luigi Vena 05/08/2015 Liuc Carlo Cattaneo TABLE OF CONTENTS The FX market Exchange rates Exchange rates regimes Financial balances International Financial Markets 05/08/2015 Coopeland

Introduction to Foreign Exchange Slides for International Finance (KOMIF Chapter 3)

") Slides for International Finance (KOMIF Chapter 3) American University 2017-09-14 Preview Introduction to Exchange Rates Basic exchange rate concepts Exchange rates and the cost of foreign goods The foreign

Slides for International Finance (KOMIF Chapter 3) American University 2017-09-14 Preview Introduction to Exchange Rates Basic exchange rate concepts Exchange rates and the cost of foreign goods The foreign

Government Intervention during the Asian Crisis

Government Intervention during the Asian Crisis From 990 to 997, Asian countries achieved higher economic growth than any other countries. They were viewed as models for advances in technology and economic

Government Intervention during the Asian Crisis From 990 to 997, Asian countries achieved higher economic growth than any other countries. They were viewed as models for advances in technology and economic

Selected Interest & Exchange Rates

(51/51) Selected Interest & Exchange Rates Weekly Series of Charts December 19,199 HNANCE Prepared by the BOARD OF GOVERNORS FINANCIAL MARKETS FEDERAL RESERVE SYSTEM SECTION Washington, DC. 0551 Table

(51/51) Selected Interest & Exchange Rates Weekly Series of Charts December 19,199 HNANCE Prepared by the BOARD OF GOVERNORS FINANCIAL MARKETS FEDERAL RESERVE SYSTEM SECTION Washington, DC. 0551 Table

Selected Interest & Exchange Rates

(51/51) Selected Interest & Exchange Rates Weekly Series of Charts February,1995 j Prepared by the FINANCIAL MARKETS SECTION DIVISION OF INTERNATIONAL FINANCE BOARD OF GOVERNORS FEDERAL RESERVE SYSTEM

(51/51) Selected Interest & Exchange Rates Weekly Series of Charts February,1995 j Prepared by the FINANCIAL MARKETS SECTION DIVISION OF INTERNATIONAL FINANCE BOARD OF GOVERNORS FEDERAL RESERVE SYSTEM

UNESCAP WORKING PAPER

WP/09/04 UNESCAP WORKING PAPER Cross-Border Investment and the Global Financial Crisis in the Asia-Pacific Region Sayuri Shirai Cross-Border Investment and the Global Financial Crisis in the Asia-Pacific

WP/09/04 UNESCAP WORKING PAPER Cross-Border Investment and the Global Financial Crisis in the Asia-Pacific Region Sayuri Shirai Cross-Border Investment and the Global Financial Crisis in the Asia-Pacific

The Asian Financial Crisis

The Asian Financial Crisis The Asian crisis 1996 Miraculous growth in EA But some signs of worsening current accounts in Korea and Thailand Signs of worsening financial institutions in Thailand 1997 January

The Asian Financial Crisis The Asian crisis 1996 Miraculous growth in EA But some signs of worsening current accounts in Korea and Thailand Signs of worsening financial institutions in Thailand 1997 January

What we will cover today. IFLR Asia Capital Markets Forum. Internationalization of the RMB Market: how you can benefit from China s financial opening

IFLR Asia Capital Markets Forum Internationalization of the RMB Market: how you can benefit from s financial opening Jay Lee Partner, Hong Kong What we will cover today 1. RMB internationalization 2. Structural

IFLR Asia Capital Markets Forum Internationalization of the RMB Market: how you can benefit from s financial opening Jay Lee Partner, Hong Kong What we will cover today 1. RMB internationalization 2. Structural

Turnover in the Foreign-Exchange and Derivatives Markets in April 2004

85 Turnover in the Foreign-Exchange and Derivatives Markets in April 2004 Peter Askjær Drejer and Vibeke Buur Hove, Statistics INTRODUCTION In April 2004, Danmarks Nationalbank conducted a survey of turnover

85 Turnover in the Foreign-Exchange and Derivatives Markets in April 2004 Peter Askjær Drejer and Vibeke Buur Hove, Statistics INTRODUCTION In April 2004, Danmarks Nationalbank conducted a survey of turnover

Monetary and Economic Department OTC derivatives market activity in the first half of 2006

Monetary and Economic Department OTC derivatives market activity in the first half of 2006 November 2006 Queries concerning this release should be addressed to the authors listed below: Section I: Christian

Monetary and Economic Department OTC derivatives market activity in the first half of 2006 November 2006 Queries concerning this release should be addressed to the authors listed below: Section I: Christian

International Monetary System Reform and Asian Monetary and Financial Cooperation

International Monetary System Reform and Asian Monetary and Financial Cooperation Dr. Zong Liang Deputy General Manager Strategic Development Department Bank of China New Delhi, March 20, 2012 0 Contents

International Monetary System Reform and Asian Monetary and Financial Cooperation Dr. Zong Liang Deputy General Manager Strategic Development Department Bank of China New Delhi, March 20, 2012 0 Contents

Statistical release: OTC derivatives statistics at end-june Monetary and Economic Department

Statistical release: OTC derivatives statistics at end-june 202 Monetary and Economic Department November 202 Queries concerning this release should be addressed to ibfs.derivatives@bis.org. Bank for International

Statistical release: OTC derivatives statistics at end-june 202 Monetary and Economic Department November 202 Queries concerning this release should be addressed to ibfs.derivatives@bis.org. Bank for International

Chapter 3 Foreign Exchange Determination and Forecasting

Chapter 3 Foreign Exchange Determination and Forecasting Note: In the sixth edition of Global Investments, the exchange rate quotation symbols differ from previous editions. We adopted the convention that

Chapter 3 Foreign Exchange Determination and Forecasting Note: In the sixth edition of Global Investments, the exchange rate quotation symbols differ from previous editions. We adopted the convention that

Chapter 10. The Foreign Exchange Market

Chapter 10 The Foreign Exchange Market Why Is The Foreign Exchange Market Important? The foreign exchange market 1. is used to convert the currency of one country into the currency of another 2. provides

Chapter 10 The Foreign Exchange Market Why Is The Foreign Exchange Market Important? The foreign exchange market 1. is used to convert the currency of one country into the currency of another 2. provides

Interest Rate Policies for the People s Republic of China: Some Considerations

Interest Rate Policies for the People s Republic of China: Some Considerations 1.The Objectives of Interest Rate Policies The rate of interest (and its term structure) is an extremely important instrument

Interest Rate Policies for the People s Republic of China: Some Considerations 1.The Objectives of Interest Rate Policies The rate of interest (and its term structure) is an extremely important instrument

Selected Interest & Exchange Rates

(51/517) Selected Interest & Exchange Rates Weekly Series of Charts May 1,199 Prepared by the FINANCIAL MARKETS SECTION DIVISION OF INTERNATIONAL FINANCE BOARD OF GOVERNORS FEDERAL RESERVE SYSTEM Washington,

(51/517) Selected Interest & Exchange Rates Weekly Series of Charts May 1,199 Prepared by the FINANCIAL MARKETS SECTION DIVISION OF INTERNATIONAL FINANCE BOARD OF GOVERNORS FEDERAL RESERVE SYSTEM Washington,

H. 13 No. 374 CAPITAL MARKET DEVELOPMENTS ABROAD

H. 13 No. 374 CAPITAL MARKET DEVELOPMENTS ABROAD October 30, 1968. Lisr j l. Ten Charts on Financial Markets Abroad \u\ zl oo' Ijl. Latest Figures Plotted in H. 13 Chart Series, 1968 dci^t'tcll I. Ten

H. 13 No. 374 CAPITAL MARKET DEVELOPMENTS ABROAD October 30, 1968. Lisr j l. Ten Charts on Financial Markets Abroad \u\ zl oo' Ijl. Latest Figures Plotted in H. 13 Chart Series, 1968 dci^t'tcll I. Ten

Derivative Instruments

Derivative Instruments Paris Dauphine University - Master I.E.F. (272) Autumn 2016 Jérôme MATHIS jerome.mathis@dauphine.fr (object: IEF272) http://jerome.mathis.free.fr/ief272 Slides on book: John C. Hull,

Derivative Instruments Paris Dauphine University - Master I.E.F. (272) Autumn 2016 Jérôme MATHIS jerome.mathis@dauphine.fr (object: IEF272) http://jerome.mathis.free.fr/ief272 Slides on book: John C. Hull,

1. Which of the following is not a money market instrument? A. Treasury bill B. commercial paper C. preferred stock D. bankers' acceptance

Student: 1. Which of the following is not a money market instrument? A. Treasury bill B. commercial paper C. preferred stock D. bankers' acceptance 2. T-bills are issued with initial maturities of: I.

Student: 1. Which of the following is not a money market instrument? A. Treasury bill B. commercial paper C. preferred stock D. bankers' acceptance 2. T-bills are issued with initial maturities of: I.

Asset Securitisation in East Asia

East Asian Finance-Road to Robust Markets Asset Securitisation in East Asia Ismail Dalla Hong Kong June 22-23, 06 Views expressed in this presentation do not represent official views of the World Bank

East Asian Finance-Road to Robust Markets Asset Securitisation in East Asia Ismail Dalla Hong Kong June 22-23, 06 Views expressed in this presentation do not represent official views of the World Bank

The LBMA Bullion Market Forum June The World Needs New Reserve Currency: from the perspective of global liquidity

The World Needs New Reserve Currency: from the perspective of global liquidity Yao Yudong People s Bank of China 215-6-25 Outline 1 Global liquidity provision: History and Status quo 2 Global liquidity

The World Needs New Reserve Currency: from the perspective of global liquidity Yao Yudong People s Bank of China 215-6-25 Outline 1 Global liquidity provision: History and Status quo 2 Global liquidity

Foreign Bank Agency Business regime: time to review and repeal

Foreign Bank Agency Business regime: time to review and repeal Background 1. Foreign banks have for many years been serving Japanese customers including leveraging off their global network which is often

Foreign Bank Agency Business regime: time to review and repeal Background 1. Foreign banks have for many years been serving Japanese customers including leveraging off their global network which is often

Study Questions. Lecture 14 Pegging the Exchange Rate

Study Questions Page 1 of 7 Study Questions Lecture 14 the Exchange Rate Part 1: Multiple Choice Select the best answer of those given. 1. Suppose the central bank of Mexico is pegging its currency, the

Study Questions Page 1 of 7 Study Questions Lecture 14 the Exchange Rate Part 1: Multiple Choice Select the best answer of those given. 1. Suppose the central bank of Mexico is pegging its currency, the

OECD-ADBI Roundtable on Capital Market Reform in Asia, Tokyo. Session Measures taken by supervisors or regulators short selling restrictions

OECD-ADBI Roundtable on Capital Market Reform in Asia, Tokyo Session 3.1.2 Measures taken by supervisors or regulators short selling restrictions 2 March 2009 Keith Lui, Executive Director, Securities

OECD-ADBI Roundtable on Capital Market Reform in Asia, Tokyo Session 3.1.2 Measures taken by supervisors or regulators short selling restrictions 2 March 2009 Keith Lui, Executive Director, Securities

RMB Internationalization and Offshore Markets Developments. Zhihuan E. I. A brief history of dollar internationalization and its main factors

RMB Internationalization and Offshore Markets Developments Zhihuan E As the RMB is increasingly used in cross-border trade and investment, a number of offshore RMB centers have rapidly emerged. With consistently

RMB Internationalization and Offshore Markets Developments Zhihuan E As the RMB is increasingly used in cross-border trade and investment, a number of offshore RMB centers have rapidly emerged. With consistently

Finding Quality Income

KCNY 9/30/2018 Finding Quality Income An Overview of Opportunities Within China s Interbank Bond Market info@kraneshares.com 1 Introduction to KraneShares About KraneShares Krane Funds Advisors, LLC is

KCNY 9/30/2018 Finding Quality Income An Overview of Opportunities Within China s Interbank Bond Market info@kraneshares.com 1 Introduction to KraneShares About KraneShares Krane Funds Advisors, LLC is

Agenda. Learning Objectives. Chapter 19. International Business Finance. Learning Objectives Principles Used in This Chapter

Chapter 19 International Business Finance Agenda Learning Objectives Principles Used in This Chapter 1. Foreign Exchange Markets and Currency Exchange Rates 2. Interest Rate and Purchasing-Power Parity

Chapter 19 International Business Finance Agenda Learning Objectives Principles Used in This Chapter 1. Foreign Exchange Markets and Currency Exchange Rates 2. Interest Rate and Purchasing-Power Parity

SELECTED INTEREST & EXCHANGE RATES FOR MAJOR COUNTRIES & THE US.

September 1, 1971 No. 521 Britii SELECTED INTEREST & EXCHANGE RATES FOR MAJOR COUNTRIES & THE US. WEEKLY SERIES OF CHARTS BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM TABLE OF CONTENTS PART I. EXCHANGE

September 1, 1971 No. 521 Britii SELECTED INTEREST & EXCHANGE RATES FOR MAJOR COUNTRIES & THE US. WEEKLY SERIES OF CHARTS BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM TABLE OF CONTENTS PART I. EXCHANGE

Are China s capital controls still binding?

15 March 25 Are China s capital controls still binding? Joint RIETI/BIS/BOC conference Globalisation of financial services in China: implications for capital flows, supervision and monetary policy Beijing,

15 March 25 Are China s capital controls still binding? Joint RIETI/BIS/BOC conference Globalisation of financial services in China: implications for capital flows, supervision and monetary policy Beijing,

The Evolution of The Canadian. Derivatives Market. Canadian Annual Derivatives Conference. Head of Derivatives Research. November 17-19, 2014

The Evolution of The Canadian Derivatives Market Andy Nybo Head of Derivatives Research Canadian Annual Derivatives Conference November 17-19, 2014 Focus Introduction Trends in global derivatives markets

The Evolution of The Canadian Derivatives Market Andy Nybo Head of Derivatives Research Canadian Annual Derivatives Conference November 17-19, 2014 Focus Introduction Trends in global derivatives markets

Monetary and Economic Department Triennial and semiannual surveys on positions in global over-the-counter (OTC) derivatives markets at end-june 2007

derivatives markets at end-june 2007") Monetary and Economic Department Triennial and semiannual surveys on positions in global over-the-counter (OTC) derivatives markets at end-e 27 November 27 Queries concerning this release should be addressed

Monetary and Economic Department Triennial and semiannual surveys on positions in global over-the-counter (OTC) derivatives markets at end-e 27 November 27 Queries concerning this release should be addressed

Comments on Capital Controls in India and Interest Rate Arbitrage by Hutchison, Kendall, Pasrischa, Singh

Comments on Capital Controls in India and Interest Rate Arbitrage by Hutchison, Kendall, Pasrischa, Singh Sergio Schmukler 2nd Research Meeting of the NIPFP-DEA Program New Delhi March 2008 Comments Caveat:

Comments on Capital Controls in India and Interest Rate Arbitrage by Hutchison, Kendall, Pasrischa, Singh Sergio Schmukler 2nd Research Meeting of the NIPFP-DEA Program New Delhi March 2008 Comments Caveat:

East Asia s Foreign Exchange Rate Policies

Order Code RS22860 April 10, 2008 East Asia s Foreign Exchange Rate Policies Summary Michael F. Martin Analyst in Asian Trade and Finance Foreign Affairs, Defense, and Trade Division The economies of East

Order Code RS22860 April 10, 2008 East Asia s Foreign Exchange Rate Policies Summary Michael F. Martin Analyst in Asian Trade and Finance Foreign Affairs, Defense, and Trade Division The economies of East

16. Foreign Exchange

16. Foreign Exchange Last time we introduced two new Dealer diagrams in order to help us understand our third price of money, the exchange rate, but under the special conditions of the gold standard. In

16. Foreign Exchange Last time we introduced two new Dealer diagrams in order to help us understand our third price of money, the exchange rate, but under the special conditions of the gold standard. In

Is There Really a RMB Bloc in Asia?

Is There Really a RMB Bloc in Asia? Masahiro Kawai Graduate School of Public Policy University of Tokyo Victor Pontines Asian Development Bank Institute 13th Research Meeting of NIPFP-DEA Research Program

Is There Really a RMB Bloc in Asia? Masahiro Kawai Graduate School of Public Policy University of Tokyo Victor Pontines Asian Development Bank Institute 13th Research Meeting of NIPFP-DEA Research Program

Selected Interest & Exchange Rates

(5/5) Selected Interest & Exchange Rates Weekly Series of Charts October 2, 995 DIVISION OF INTERNATIONAL FINANCE Prepared by the FINANCIAL MARKETS SECTION BOARD OF GOVERNORS FEDERAL RESERVE SYSTEM Washington,

(5/5) Selected Interest & Exchange Rates Weekly Series of Charts October 2, 995 DIVISION OF INTERNATIONAL FINANCE Prepared by the FINANCIAL MARKETS SECTION BOARD OF GOVERNORS FEDERAL RESERVE SYSTEM Washington,

INTRODUCTION TO EXCHANGE RATES AND THE FOREIGN EXCHANGE MARKET

INTRODUCTION TO EXCHANGE RATES AND THE FOREIGN EXCHANGE MARKET 13 1 Exchange Rate Essentials 2 Exchange Rates in Practice 3 The Market for Foreign Exchange 4 Arbitrage and Spot Exchange Rates 5 Arbitrage

INTRODUCTION TO EXCHANGE RATES AND THE FOREIGN EXCHANGE MARKET 13 1 Exchange Rate Essentials 2 Exchange Rates in Practice 3 The Market for Foreign Exchange 4 Arbitrage and Spot Exchange Rates 5 Arbitrage

Financial Highlights

June 2, 2010 Financial Highlights Federal Reserve Balance Sheet 1 European Debt Bond Spreads 2 CDS Spreads 2 Consumer Credit ABS Issuance 3 ABS Spreads 3 Outstanding Amounts 4 Charge-Off Rates 4 Credit

June 2, 2010 Financial Highlights Federal Reserve Balance Sheet 1 European Debt Bond Spreads 2 CDS Spreads 2 Consumer Credit ABS Issuance 3 ABS Spreads 3 Outstanding Amounts 4 Charge-Off Rates 4 Credit

BSM939 Risk and Uncertainty in Business

BSM939 Risk and Uncertainty in Business Lectures 3 & 4 Interest rate and exchange rate risk Sumon Bhaumik http://www.sumonbhaumik.net How volatile are interest and exchange rates? Interest rate volatility

BSM939 Risk and Uncertainty in Business Lectures 3 & 4 Interest rate and exchange rate risk Sumon Bhaumik http://www.sumonbhaumik.net How volatile are interest and exchange rates? Interest rate volatility

2015 Outlook: China s Economy and Bond Markets

Special Comment 215 Outlook: China s Economy and Bond Markets January 215 Elle Hu +852-2868 317 elle_hu@ccxap.com Carter Liu +852-2868 377 carter_liu@ccxap.com Jolie Li +852-2868 319 jolie_li@ccxap.com

Special Comment 215 Outlook: China s Economy and Bond Markets January 215 Elle Hu +852-2868 317 elle_hu@ccxap.com Carter Liu +852-2868 377 carter_liu@ccxap.com Jolie Li +852-2868 319 jolie_li@ccxap.com

The Slow, Uneven Rise of the Renminbi

The Slow, Uneven Rise of the Renminbi Eswar S. Prasad The Chinese renminbi (RMB) has come a long way in a short period. It was only in the early 2000s that the Chinese government began the process of gradually

The Slow, Uneven Rise of the Renminbi Eswar S. Prasad The Chinese renminbi (RMB) has come a long way in a short period. It was only in the early 2000s that the Chinese government began the process of gradually

Reform of Global Reserve System and China s Choice 1

Reform of Global Reserve System and China s Choice 1 Liqing Zhang Professor and Dean, School of Finance, Central University of Finance and Economics, Beijing Email: zhlq@cufe.edu.cn 1. Why the Regime should

Reform of Global Reserve System and China s Choice 1 Liqing Zhang Professor and Dean, School of Finance, Central University of Finance and Economics, Beijing Email: zhlq@cufe.edu.cn 1. Why the Regime should

SELECTED INTEREST & EXCHANGE RATES FOR MAJOR COUNTRIES & THE U.S.

August 18, 1971 No. 519 V H«13 Division of lnttn^tionol Finonc# Europe and British Common weolth Section r ' ;;,3 SELECTED INTEREST & EXCHANGE RATES FOR MAJOR COUNTRIES & THE U.S. WEEKLY SERIES OF CHARTS

August 18, 1971 No. 519 V H«13 Division of lnttn^tionol Finonc# Europe and British Common weolth Section r ' ;;,3 SELECTED INTEREST & EXCHANGE RATES FOR MAJOR COUNTRIES & THE U.S. WEEKLY SERIES OF CHARTS

TREASURY AND FEDERAL RESERVE FOREIGN EXCHANGE OPERATIONS

EMBARGOED: FOR RELEASE AT 4:00 P.M., EDT, THURSDAY, AUGUST 2, TREASURY AND FEDERAL RESERVE FOREIGN EXCHANGE OPERATIONS During the second quarter of, the dollar appreciated 3.3 percent against the euro

EMBARGOED: FOR RELEASE AT 4:00 P.M., EDT, THURSDAY, AUGUST 2, TREASURY AND FEDERAL RESERVE FOREIGN EXCHANGE OPERATIONS During the second quarter of, the dollar appreciated 3.3 percent against the euro

Press release Press enquiries: /

BANK FOR INTERNATIONAL SETTLEMENTS CH-4002 BASEL, SWITZERLAND Press release Press enquiries: +41 61 / 280 81 88 Ref. No.: 36/E 13 November The global OTC derivatives market continues to grow Data released

BANK FOR INTERNATIONAL SETTLEMENTS CH-4002 BASEL, SWITZERLAND Press release Press enquiries: +41 61 / 280 81 88 Ref. No.: 36/E 13 November The global OTC derivatives market continues to grow Data released

Renminbi Internationalisation The Journey Begins

Treasury Division Renminbi Monitor January 2013 Joanne Yim Chief Economist joanneyim@hangseng.com Renminbi Internationalisation The Journey Begins After decades of rapid growth, mainland China has become

Treasury Division Renminbi Monitor January 2013 Joanne Yim Chief Economist joanneyim@hangseng.com Renminbi Internationalisation The Journey Begins After decades of rapid growth, mainland China has become

SEcicTED INTEREST & EXCHANGE RATES FOR MAJOR COUNTRIES & THE U.S.

June 2, 1971 No. 508 t H-13 Division of international Finance Europe and British Commonwealth Section ' / (bei % 6"" i JU, \ f O & p i - b - t. n - w j J u i /V/3 SEcicTED INTEREST & EXCHANGE RATES FOR

June 2, 1971 No. 508 t H-13 Division of international Finance Europe and British Commonwealth Section ' / (bei % 6"" i JU, \ f O & p i - b - t. n - w j J u i /V/3 SEcicTED INTEREST & EXCHANGE RATES FOR

Increasing Competition among Markets for Offshore Renminbi Business

Increasing Competition among Markets for Offshore Renminbi Business Eiichi Sekine Chief Representative, Beijing Representative Office Nomura Institute of Capital Markets Research Masanobu Iwatani Financial

Increasing Competition among Markets for Offshore Renminbi Business Eiichi Sekine Chief Representative, Beijing Representative Office Nomura Institute of Capital Markets Research Masanobu Iwatani Financial

Selected Interest & Exchange Rates Weekly Series of Charts

t i Selected Interest & Exchange Rates Weekly Series of Charts V:,: v:,:ir. : x Bqnl of * n n ft'c irism i.://!,r " ^ JANUARY 1,1977 DIVISION OF INTERNATIONAL FINANCE Prepared by the BOARD OF GOVERNORS

t i Selected Interest & Exchange Rates Weekly Series of Charts V:,: v:,:ir. : x Bqnl of * n n ft'c irism i.://!,r " ^ JANUARY 1,1977 DIVISION OF INTERNATIONAL FINANCE Prepared by the BOARD OF GOVERNORS

CHNB. Chinese Onshore Bonds: CHNB provides direct access to Chinese onshore bonds that are among the highest quality in the credit spectrum.

Chinese Onshore Bonds: CHNB provides direct access to Chinese onshore bonds that are among the highest quality in the credit spectrum. KEY FEATURES Attractive Yield Onshore bonds typically have offered

Chinese Onshore Bonds: CHNB provides direct access to Chinese onshore bonds that are among the highest quality in the credit spectrum. KEY FEATURES Attractive Yield Onshore bonds typically have offered