Introduction to Foreign Exchange Slides for International Finance (KOM Chapter 14)

|

|

|

- Antony Jackson

- 5 years ago

- Views:

Transcription

1 Slides for International Finance (KOM Chapter 14) American University

2 Preview Introduction to Exchange Rates Basics exchange rate concepts Exchange rates and the cost of foreign goods The foreign exchange markets The demand for currency deposits and other assets A model of foreign exchange markets effect of interest rates on currency deposits effect of expectations of exchange rates

3 What Is An Exchange Rate? Exchange Rate: The price of one currency in terms of another currency The number of units of the quote currency that it takes to buy one unit of the base currency USD-EUR 0.7 the quote currency is also called the terms currency or counter currency the base currency is also called the quoted currency or underlying currency USD is base currency; EUR is quote currency quote is in euros per dollar ( European terms ) EUR-USD 1.5 EUR is base currency; USD is quote currency quote is in dollars per euro terms ( dollar terms or American terms )

4 Direct Rate vs. Indirect Rate Direct rate: domestic currency per unit of foreign currency. in US, 1.5 USD per EUR in US, EUR-USD 1.5 Indirect rate: foreign currency per unit of domestic currency in US, 0.7 EUR per USD in US, USD-EUR 0.7 In class we will use the direct rate, but markets use both.

5 GBP-USD Introduction to Exchange Rates Source: series/exusuk?cid=95

6 USD-CAD Introduction to Exchange Rates Source: series/excaus?cid=95

7 Indirect and Direct Rates Currency 1 USD in USD ================== =========== ========= British Pound Canadian Dollar Chinese Yuan Euro Indian Rupee Japanese Yen Mexican Peso Russian Ruble Singapore Dollar South Korean Won Swiss Franc Taiwan Dollar Thai Baht ================== =========== =========

8 Cost of Foreign Goods Exchange rates allow us to express prices in a common currency make easier cost comparisons Example: In 2010, the Mercedes-Benz SLS AMG cost about EUR 150k. What was the dollar cost? Exchange rate (dollar terms): EUR-USD 1.3 Foreign price: EUR 150K Domestic price: (exchange rate) x (foreign price) (USD 1.3/EUR) x EUR 150k = USD 195k

9 EUR-USD Introduction to Exchange Rates Source: series/exuseu?cid=95

10 Depreciation and Appreciation Depreciation a fall in the exchange value of a currency. E rises (direct rate!) raises (cet. par.) the price of foreign goods relative to the price of our goods. Appreciation a rise in the exchange value of a currency. E falls (direct rate!) lowers (cet. par.) the price of foreign goods relative to the price of our goods.

11 Depreciation Example A depreciated currency buys a smaller amount of foreign currency. Example: EUR-USD 1.0 EUR-USD 1.50 the dollar has depreciated relative to the euro. The dollar is now less valuable. Equivalently, the euro has appreciated relative to the dollar: the euro is now more valuable. Given prices, a dollar buys fewer foreign goods after depreciating. Example: Suppose an AMG accord costs C150k C150k x $1/C1 = $150k C150k x $1.5/C1 = $225k Dollar depreciation imports into US become more expensive. Domestically produced goods, including our exports, are relatively less expensive.

12 Appreciation Example An appreciated currency buys a larger amount of foreign currency. Example: JPY-USD JPY-USD the dollar has appreciated relative to the yen. The dollar is more valuable. Equivalently, the yen has deppreciated relative to the dollar: the yen is now less valuable. Given prices, a dollar buys more foreign goods after appreciating. Example: suppose a Honda accord costs 1.5M 1,500,000 x $0.0100/ 1 = $15,000 1,500,000 x $0.0090/ 1 = $13,500 Dollar appreciation imports into US become less expensive. Domestically produced goods, including our exports, are relatively more expensive.

13 USD-JPY Introduction to Exchange Rates Source: series/exjpus?cid=95

14 Foreign Exchange Markets The set of markets where foreign currencies and other assets are exchanged for domestic ones Institutions buy and sell deposits of currencies or other assets for investment purposes. The daily volume of foreign exchange transactions was $4T in 2010 (vs. $3.2T in 2007) About 85% of transactions involved the USD USD-EUR transactions are just over 1/4 of the total Source:

15 Currency Composition

16 Foreign Exchange Market Participants 1 Commercial banks and other depository institutions: transactions involve buying/selling of deposits in different currencies for investment purposes. 2 Non-bank financial institutions (mutual funds, hedge funds, securities firms, insurance companies, pension funds) may buy/sell foreign assets for investment. 3 Non-financial businesses conduct foreign currency transactions to buy/sell goods, services and assets. 4 Central banks: conduct official international reserves transactions.

17 Global Foreign Exchange Turnover

18 Foreign Exchange Markets (cont.) Buying and selling in the foreign exchange market are dominated by commercial and investment banks. Inter-bank transactions of deposits in foreign currencies occur in amounts $1 million or more per transaction. Central banks sometimes intervene, but the direct effects of their transactions are small and transitory in many countries.

19 Arbitrage in Foreign Exchange Markets Arbitrage buying at a low price and selling at a high price for a profit. When other factors are the same, people will buy assets in New York and stop buying them in Hong Kong, so that their price in New York rises and their price in Hong Kong falls, until they are equal in the two markets. Computer and telecommunications technology transmit information rapidly and have integrated markets. The integration of markets implies that there are no significant arbitrage opportunities between markets.

20 Triangular Arbitrage Introduction to Exchange Rates Suppose geographical arbitrage equates bilateral exchange rates in all centers Q: Are any arbitrage opportunities left? A: Possibly a synthetic cross rate differs. An imaginary opportunity.

21 Spot Rates and Forward Rates Spot rate exchange rate for currency exchanges on the spot ; trading is executed in the present. Forward rate exchange rate for currency exchanges that will occur at a future ( forward ) date. Forward dates are typically 30, 90, 180, or 360 days in the future. Rates are negotiated between two parties in the present but the future present, exchange occurs in the future.

22 Fig. 13-1: Spot and Forward Exchange Rates GBP-USD day forward and spot exchange rates (end of month). Source: KO Figure 13-1 (Data Source: Datastream).

23 Covered R = R* + (F - E)/E where E is the spot (direct) exchange rate, F is the forward exchange rate, R is the domestic interest rate, and R* is the foreign interest rate. Covered interest parity relates interest rates across countries and the rate of change between forward exchange rates and the spot exchange rate: It says that rates of return on dollar deposits and covered foreign currency deposits are the same. How could you earn a risk-free return in the foreign exchange markets if covered interest parity did not hold? Covered positions using the forward rate involve little risk.

24 Other Methods of Currency Exchange Foreign exchange swaps: a combination of a spot sale with a forward repurchase. Swaps often result in lower fees or transactions costs because they combine two transactions, and they allow parties to meet each others needs for a temporary amount of time. Futures contracts: a contract designed by a third party for a standard amount of foreign currency delivered/received on a standard date. Contracts can be bought and sold on exchanges, and only the current owner is obliged to fulfill the contract.

25 Other Methods of Currency Exchange Options contracts: a contract designed by a third party for a standard amount of foreign currency delivered/received on or before a standard date. Contracts can be bought and sold in markets. A contract gives the owner the option, but not obligation, of buying or selling currency if the need arises.

26 Nondeliverable Forward Contracts Non-deliverable forward (NDF) contract: counterparties settle the difference cash settled : only difference flows contracted price vs. fixing price usually: fixing price = realized spot rate traded over-the-counter (OTC) direct trade between two parties (vs. trading on an exchange) offshore nondeliverable forward markets: NY (esp Latin America), London, Hong Kong, Singapore

27 Nondeliverable Forward Exchange NDF market became significant in early 1990s Initally mostly Latin American currencies NDFs are often a response to capital controls E.g., China restricts foreign ownership of renminbi deposits ISO: CNY; common: RMB; Latinized symbol:

28 SAFE Introduction to Exchange Rates China s State Administration for Foreign Exchange prohibits offshore conversion Thus offshort banks cannot deliver CNY to fulfill forward contracts One possibility: try to find a domestic (Chinese) bank that can offer forward delivery domestically. Not always possible. Another possibility: NDFs (all flows are in another currency (e.g., USD))

29 NDF Example Introduction to Exchange Rates Use NDF contracts to hedge future payments in Chinese yuan You need to pay CNY 10M in six months for equipment purchases. This exposes you to currency risk. Possible hedge: buy CNY six months forward at the NDF rate of CNY per U.S. dollar from an offshore bank. This bank cannot deliver CNY! Six months later, make a net settlement in dollars for the NDF contract. If fixing rate (Ef) is at par, there are no cash flows. If Ef > 6.72, the CNY is cheap. You fullfill your NDF contract by paying the bank USD(10M/ M/Ef) If Ef < 6.72, the CNY is expensive. The bank fullfills your NDF contract by paying you USD(10M/Ef - 10M/6.72) Because of your NDF hedge, your total cost is a certain USD 10M/6.72.

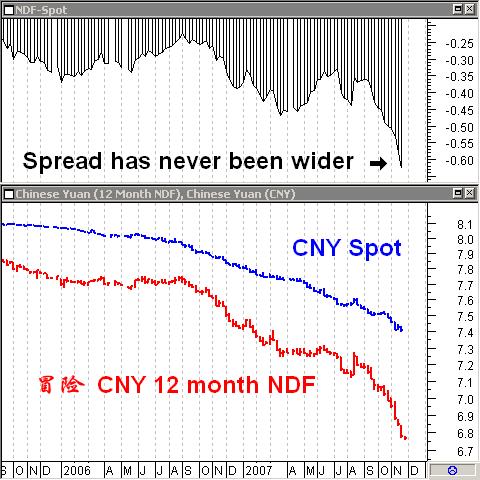

30 USD-CNY: Recent History

31 CNY Nondeliverable Forwards

32 Example: CNY NDF Introduction to Exchange Rates 8 Sep 2009 USD-CNY 6.83 (spot) Daily reference rate 20% appreciation since July 2005 (when fixed rate scrapped) USD-CNY (12 month NDF) implies ( )/6.83 = -1.3% expected change

33 Example: CNY NDF Introduction to Exchange Rates 10 Sep 2010 PBoC fixes mid-point at USD-CNY Sep 2010 USD-CNY (spot) vs predicted by the NDF market a year before USD-CNY (12 month NDF) 12-month implied yuan appreciation: 1.74% ( )/ = -1.74% CCN%2B12M:IND#chart

34 Rate of Return Introduction to Exchange Rates Currency Deposits Rate of return the percentage change in value that an asset produces during a time period. Real rate of return inflation-adjusted rate of return (approximately: interest rate - inflation rate) the addition to purchasing power (control over goods & services) Example: $1000 saving deposit, R=2%/yr, inflation = 1%/yr After 1 year the deposit is worth $1000 x 1.02 = $1020 So its rate of return is ($ $1000)/$1000 = 2%/yr The real rate of return is (approximately): 2% - 1.0% = 1.0%

35 Ignoring Inflation in SR Currency Deposits A rise in P reduces the goods and services controlled by a given nominal wealth. Suppose the inflation rate is 0%. Then prices are fixed, and nominal rates of return = real rates of return. Because trading of deposits in different currencies occurs on a daily basis, we often assume that prices do not change from day to day. A reasonable assumption to make for the short run.

36 Currency Deposits Other Influences on the Demand for Currency Deposits Risk: The volatility of real wealth Liquidity: the ease with which one can turn the asset into goods and services We will assume that the risk and liquidity of currency deposits does not depend on currency denomination. Assume: risk and liquidity are of secondary importance to individuals deciding to buy or sell currency deposits. Implication: investors in currency deposits are primarily concerned about the rates of return.

37 Currency Deposits Rate of Return on Currency Deposits The rate of return that an investor expects to earn on an interest bearing assets is determined by interest rate expectated exchange rate movements Domestic currency assets: expected return is just R Foreign currency assets: expected return is R* + (Ee-E)/E interest + expected depreciation of the domestic currency

38 Currency Deposits Summary: Demand for Currency Deposits Influences on the demand for deposits Deposits Risk Liquidity Expected rate of return we will emphasis this for now bear interest (at annual rate) denominated in domestic or foreign currency Foreign currency deposits additionally have capital gains or losses Exchange-rate risk

39 Currency Deposits Dollar and Yen Interest Rates (3 month rates, annualized) Source: KO Fig 13-2 (Original Data Source: Data Stream)

40 Currency Deposits The Demand for Currency Deposits (cont.) Suppose R = 1%/yr and R* = 2%/yr. Does a euro deposit yield a higher expected rate of return? To answer this, we must consider the expected change in the value of a euro. Suppose today the exchange rate is EUR-USD 1.5, and the expected rate one year in the future is EUR-USD 1.3. USD 150 can be exchanged today for EUR 100. These EUR 100 will yield EUR 102 after one year. These EUR 102 are expected to be worth (1.3 USD/EUR) EUR 102 = USD in one year. Clearly USD from investing at home is better than USD from investing abroad. The return is higher on domestic assets, despite the higher interest rate abroad.

41 Currency Deposits The Demand for Currency Deposits (cont.) Recap R = 1%. R* = 2% E = 1.50 Ee = 1.30 The rate of return from investing domestically is simply the interest rate, R=0.01=1%. The expected rate of return from investing abroad ( )/150 = = -11.6%. The euro deposit has higher interest rate but a lower expected rate of return. All investors should be willing to hold dollar deposits and none should be willing to hold euro deposits.

42 Currency Deposits The Demand for Currency Deposits (cont.) We simplify the analysis by saying that the dollar rate of return on euro deposits approximately equals: the interest rate on euro deposits plus the expected rate of appreciation of euro deposits 2% % = -11.3% (which is approximately our -11.6%) Return on foreign currency deposits: R* + (Ee - E)/E

43 Currency Deposits The Demand for Currency Deposits (cont.) The expected rate of return on euro deposits is R + E e E E interest rate on euro deposits, plus expected rate of depreciation of the dollar expected exchange rate current exchange rate

44 Currency Deposits Model of Foreign Exchange Markets (cont.) How do changes in the current exchange rate affect the expected rate of return of foreign currency deposits?

45 Currency Deposits Model of Foreign Exchange Markets (cont.) Depreciation of the domestic currency today lowers the expected rate of return on foreign currency deposits. Why? When the domestic currency depreciates, the initial cost of investing in foreign currency deposits increases, thereby lowering the expected rate of return of foreign currency deposits. Appreciation of the domestic currency today raises the expected return of deposits on foreign currency deposits. Why? When the domestic currency appreciates, the initial cost of investing in foreign currency deposits decreases, thereby raising the expected rate of return of foreign currency deposits.

46 Exchange Rate and Asset Return Currency Deposits Case E E e E E R + E e E E % -3.0% % -1.0% % 1.0% % 3.0% % 5.0% Constants: R = 1.0%, E e =1.33

47 Currency Deposits The Relation Between the Current Dollar/Euro Exchange Rate and the Expected Dollar Return on Euro Deposits Current Exchange Rate Expected USD Return on EUR Currency when E e = 1.33 Note: compare KO 8 Fig. 13-3

48 Equilibrium in the FX Market Currency Deposits Equilibrium in the market for foreign exchange requires equal desirability of competing assets. Interest parity comparable assets must bear comparable rates of return R = R* + (Ee-E)/E where expected return on dollar denominated deposits: R expected return on foreign currency denominated deposits: R* + (Ee-E)/E Interest parity implies that deposits in various currencies are equally desirable. Interest parity is the basic component of our first model of foreign exchange markets.

49 Currency Deposits Model of Foreign Exchange Markets (cont.) Interest parity says: R = R* + (Ee - E)/E Why should this condition hold? Suppose it didn t. Suppose R > R* + (Ee - E)/E Then no investor would want to hold euro deposits, driving down the demand and price of euros. Then all investors would want to hold dollar deposits, driving up the demand and price of dollars. The dollar would appreciate and the euro would depreciate, increasing the right side until equality was achieved:

50 Equilibrium in the FX Market Currency Deposits E E 1 R returns

51 Equilibrium in the FX Market Currency Deposits E E 1 R + Ee E E R returns

52 Equilibrium in the FX Market Currency Deposits E E 1 R + Ee E E R returns Note: compare KO 8 Fig 13-4

53 Currency Deposits Model of Foreign Exchange Markets Effect of changing R: an increase in the interest rate paid on deposits denominated in a particular currency will increase the rate of return on those deposits. This leads to an appreciation of the currency. Higher interest rates on dollar-denominated assets causes the dollar to appreciate. Higher interest rates on euro-denominated assets causes the dollar to depreciate

54 ^R _E Introduction to Exchange Rates Currency Deposits E E 1 E 2 R 1 R 2 R + Ee E E returns Note: compare KO 8 Fig 13-5

55 ^R* ^E Introduction to Exchange Rates Currency Deposits E E 2 R 2 + Ee E E E 1 R R 1 + Ee E E returns Note: compare KO 8 Fig 13-6

56 Appreciation of the Expected Euro Currency Deposits If people expect the euro to appreciate in the future, then euro-denominated assets will pay in valuable euros, so that these future euros will be able to buy many dollars and many dollar-denominated goods. The expected rate of return on euros therefore increases. An expected appreciation of a currency leads to an actual appreciation (a self-fulfilling prophecy). An expected depreciation of a currency leads to an actual depreciation (a self-fulfilling prophecy).

57 ^Ee ^E Introduction to Exchange Rates Currency Deposits E E 2 R 1 + Ee 2 E E E 1 R R 1 + Ee 1 E E returns

58 Summary Introduction to Exchange Rates Currency Deposits exchange rate (direct rate) the domestic-currency price of foreign exchange. foreign exchange interest-bearing deposits foreign currencies. (for the most part) spot exchange rate a contracted rate at which foreign exchange will be bought on sold on the spot. forward exchange rate a contracted rate at which foreign exchange will be bought on sold on a future date. By foreign exchange we primarily mean interest-bearing deposits foreign currencies.

59 Summary (cont) Introduction to Exchange Rates Currency Deposits Depreciation (of the domestic currency) E (direct rate) rises; the currency becomes less valuable. Goods priced in it (e.g., our exports) become relatively less expensive. Imports become relatively expensive. A depreciation hurts consumers (who buy imports) but helps exporters. Appreciation (of the domestic currency) E (direct rate) falls; the currency becomes more valuable. Goods priced in it (e.g., our exports) become relatively expensive. Imports become relatively cheap. An appreciation helps consumers (who buy imports) but hurts exporters.

60 Summary (cont) Introduction to Exchange Rates Currency Deposits The primary players in the market for foreign exchange are commercial and investment banks. Their arbitrage activities ensure interest parity holds: comparable assets should bear comparable rates of return. This implies covered interest parity. Ignoring risk factors, this implies uncovered interest parity.

61 Summary (cont) Introduction to Exchange Rates Currency Deposits Covered interest parity R = R* + (F - E)/E the rate of return on domestic currency deposits must equal the rate of return on covered foreign currency deposits. Foreign currency deposits can be covered with a forward exchange contract. Uncovered interest parity R = R* + (Ee - E)/E Expected rates of return on foreign and domestic currency deposits are equal Expected rates of return on currency deposits and determined by interest rates and expected exchange rates.

62 Summary (cont) Introduction to Exchange Rates Currency Deposits An increase in the domestic interest rate (an increase in its expected rate of return) leads to an appreciation of the domestic currency. An increase in the expected future exchange rate lead to a depreciation of the domestic currency.

Introduction to Foreign Exchange Slides for International Finance (KOM Chapter 14)

") Slides for International Finance (KOM Chapter 14) American University 2011-09-01 Preview Introduction to Exchange Rates Basics exchange rate concepts Exchange rates and the cost of foreign goods The foreign

Slides for International Finance (KOM Chapter 14) American University 2011-09-01 Preview Introduction to Exchange Rates Basics exchange rate concepts Exchange rates and the cost of foreign goods The foreign

Introduction to Foreign Exchange Slides for International Finance (KOMIF Chapter 3)

") Slides for International Finance (KOMIF Chapter 3) American University 2017-09-14 Preview Introduction to Exchange Rates Basic exchange rate concepts Exchange rates and the cost of foreign goods The foreign

Slides for International Finance (KOMIF Chapter 3) American University 2017-09-14 Preview Introduction to Exchange Rates Basic exchange rate concepts Exchange rates and the cost of foreign goods The foreign

Preview. Chapter 13. Depreciation and Appreciation. Definitions of Exchange Rates. Exchange Rates and the Foreign Exchange Market: An Asset Approach

Chapter 13 Exchange Rates and the Foreign Exchange Market: An Asset Approach Preview The basics of exchange rates Exchange rates and the prices of goods The foreign exchange markets The demand for currency

Chapter 13 Exchange Rates and the Foreign Exchange Market: An Asset Approach Preview The basics of exchange rates Exchange rates and the prices of goods The foreign exchange markets The demand for currency

Chapter 14 Exchange Rates and the Foreign Exchange Market: An Asset Approach

Chapter 14 Exchange Rates and the Foreign Exchange Market: An Asset Approach Copyright 2015 Pearson Education, Inc. All rights reserved. 1-1 Preview The basics of exchange rates Exchange rates and the

Chapter 14 Exchange Rates and the Foreign Exchange Market: An Asset Approach Copyright 2015 Pearson Education, Inc. All rights reserved. 1-1 Preview The basics of exchange rates Exchange rates and the

Financial markets in the open economy - the interest rate parity. Exchange rates in the short run.

Financial markets in the open economy - the interest rate parity. Exchange rates in the short run. Dr hab. Joanna Siwińska-Gorzelak Foreign Exchange Markets The set of markets where foreign currencies

Financial markets in the open economy - the interest rate parity. Exchange rates in the short run. Dr hab. Joanna Siwińska-Gorzelak Foreign Exchange Markets The set of markets where foreign currencies

Lecture 14 Internatinaa Ecinimics. Exchange Rates and the Fireign Exchange Market: An Asset Appriach

Lecture 14 Internatinaa Ecinimics Exchange Rates and the Fireign Exchange Market: An Asset Appriach Preview The basics of exchange rates: defnitons and computaton Exchange rates and the relatve prices

Lecture 14 Internatinaa Ecinimics Exchange Rates and the Fireign Exchange Market: An Asset Appriach Preview The basics of exchange rates: defnitons and computaton Exchange rates and the relatve prices

FOREIGN EXCHANGE MARKET. Luigi Vena 05/08/2015 Liuc Carlo Cattaneo

FOREIGN EXCHANGE MARKET Luigi Vena 05/08/2015 Liuc Carlo Cattaneo TABLE OF CONTENTS The FX market Exchange rates Exchange rates regimes Financial balances International Financial Markets 05/08/2015 Coopeland

FOREIGN EXCHANGE MARKET Luigi Vena 05/08/2015 Liuc Carlo Cattaneo TABLE OF CONTENTS The FX market Exchange rates Exchange rates regimes Financial balances International Financial Markets 05/08/2015 Coopeland

MPG End-2014 G-SIB template

Size Indicator Section 2 - Total Exposures GSIB Amount in thousand EUR a. Counterparty exposure of derivatives contracts 1012 2.324.745 2.a. b. Gross value of securities financing transactions (SFTs) 1013

Size Indicator Section 2 - Total Exposures GSIB Amount in thousand EUR a. Counterparty exposure of derivatives contracts 1012 2.324.745 2.a. b. Gross value of securities financing transactions (SFTs) 1013

End-2017 G-SIB Assessment Exercise

End-2017 G-SIB Assessment Exercise v4.4.2 General Bank Data Section 1 - General Information GSIB Response a. General information provided by the relevant supervisory authority: (1) Country code 1001 DE

End-2017 G-SIB Assessment Exercise v4.4.2 General Bank Data Section 1 - General Information GSIB Response a. General information provided by the relevant supervisory authority: (1) Country code 1001 DE

Currency Hedging and FX Trading Strategies using SGX-listed Futures by Tariq Dennison,

Presented by Exchange Partner Currency Hedging and FX Trading Strategies using SGX-listed Futures by Tariq Dennison, +852 9476 2868 Limited, www.gfmasset.com Disclaimer This presentation is for educational

Presented by Exchange Partner Currency Hedging and FX Trading Strategies using SGX-listed Futures by Tariq Dennison, +852 9476 2868 Limited, www.gfmasset.com Disclaimer This presentation is for educational

The renminbi as a global currency. By Zsanett Sütő

The renminbi as a global currency By Zsanett Sütő On 1 October 2016, the Chinese renminbi (yuan, CNY) was added to the SDR basket that comprises of the leading currencies of the world. This is also in

The renminbi as a global currency By Zsanett Sütő On 1 October 2016, the Chinese renminbi (yuan, CNY) was added to the SDR basket that comprises of the leading currencies of the world. This is also in

Results of the end 2015 G-SIB assessment exercise

DZ BANK AG Deutsche Zentral- Genossenschaftsbank 29 April 2016 Results of the end 2015 G-SIB assessment exercise Appendix 1 contains DZ BANK s results of the data collection to calculate the surcharge

DZ BANK AG Deutsche Zentral- Genossenschaftsbank 29 April 2016 Results of the end 2015 G-SIB assessment exercise Appendix 1 contains DZ BANK s results of the data collection to calculate the surcharge

Basics of Foreign Exchange Market in India

Basics of Foreign Exchange Market in India Foreign Exchange: Basics What is Foreign Exchange (Forex) How are currency prices determined What is foreign exchange rate policy in India Operation of Forex

Basics of Foreign Exchange Market in India Foreign Exchange: Basics What is Foreign Exchange (Forex) How are currency prices determined What is foreign exchange rate policy in India Operation of Forex

BLOOMBERG DOLLAR INDEX 2018 REBALANCE

BLOOMBERG DOLLAR INDEX 2018 REBALANCE 2018 REBALANCE HIGHLIGHTS Euro maintains largest weight 2018 BBDXY WEIGHTS Euro Canadian dollar largest percentage weight decrease Swiss franc has largest percentage

BLOOMBERG DOLLAR INDEX 2018 REBALANCE 2018 REBALANCE HIGHLIGHTS Euro maintains largest weight 2018 BBDXY WEIGHTS Euro Canadian dollar largest percentage weight decrease Swiss franc has largest percentage

An Extract from NIFD and CLS Joint Forum Publication: Foreign Exchange Market Infrastructure to Support Stability of RMB Internationally.

An Extract from NIFD and CLS Joint Forum Publication: Foreign Exchange Market Infrastructure to Support Stability of RMB Internationally. 1. Introduction As China moves toward a more market driven financial

An Extract from NIFD and CLS Joint Forum Publication: Foreign Exchange Market Infrastructure to Support Stability of RMB Internationally. 1. Introduction As China moves toward a more market driven financial

Prepared by Iordanis Petsas To Accompany. by Paul R. Krugman and Maurice Obstfeld

Chapter 13 Exchange Rates and the Foreign Exchange Market: An Asset Approach Prepared by Iordanis Petsas To Accompany International Economics: Theory and Policy, Sixth Edition by Paul R. Krugman and Maurice

Chapter 13 Exchange Rates and the Foreign Exchange Market: An Asset Approach Prepared by Iordanis Petsas To Accompany International Economics: Theory and Policy, Sixth Edition by Paul R. Krugman and Maurice

Chapter 5. The Foreign Exchange Market. Foreign Exchange Markets: Learning Objectives. Foreign Exchange Markets. Foreign Exchange Markets

Chapter 5 The Foreign Exchange Market Foreign Exchange Markets: Learning Objectives Examine the functions performed by the foreign exchange (FOREX) market, its participants, size, geographic and currency

Chapter 5 The Foreign Exchange Market Foreign Exchange Markets: Learning Objectives Examine the functions performed by the foreign exchange (FOREX) market, its participants, size, geographic and currency

TREASURY AND FEDERAL RESERVE FOREIGN EXCHANGE OPERATIONS

October December 2015 This report, presented by Simon Potter, Executive Vice President, Federal Reserve Bank of New York, and Manager of the System Open Market Account, describes the foreign exchange operations

October December 2015 This report, presented by Simon Potter, Executive Vice President, Federal Reserve Bank of New York, and Manager of the System Open Market Account, describes the foreign exchange operations

THE CANADIAN FOREIGN EXCHANGE COMMITTEE LE COMITÉ CANADIEN DU MARCHÉ DES CHANGES

THE CANADIAN FOREIGN EXCHANGE COMMITTEE LE COMITÉ CANADIEN DU MARCHÉ DES CHANGES 150 King Street West Contact: Rob Ogrodnick Suite 2000 Telephone: (416) 542-1339 Toronto, Ontario Email: rogrodnick@bankofcanada.ca

THE CANADIAN FOREIGN EXCHANGE COMMITTEE LE COMITÉ CANADIEN DU MARCHÉ DES CHANGES 150 King Street West Contact: Rob Ogrodnick Suite 2000 Telephone: (416) 542-1339 Toronto, Ontario Email: rogrodnick@bankofcanada.ca

Exchange rates and aviation: examining the links

-50%+ -48% to -50% -44% to -46% -40% to -42% -36% to -38% -32% to -34% -28% to -30% -24% to -26% -20% to -22% -16% to -18% -12% to -14% -8% to -10% -4% to -6% 0% to -2% 0% to 2% 4% to 6% 8% to 10% 12%

-50%+ -48% to -50% -44% to -46% -40% to -42% -36% to -38% -32% to -34% -28% to -30% -24% to -26% -20% to -22% -16% to -18% -12% to -14% -8% to -10% -4% to -6% 0% to -2% 0% to 2% 4% to 6% 8% to 10% 12%

Finding Quality Income

KCNY 9/30/2018 Finding Quality Income An Overview of Opportunities Within China s Interbank Bond Market info@kraneshares.com 1 Introduction to KraneShares About KraneShares Krane Funds Advisors, LLC is

KCNY 9/30/2018 Finding Quality Income An Overview of Opportunities Within China s Interbank Bond Market info@kraneshares.com 1 Introduction to KraneShares About KraneShares Krane Funds Advisors, LLC is

Q3 and 9M 2018 Trading Update

Q3 and 9M 2018 Trading Update DISCLAIMER This presentation may contain forward looking statements based on current expectations and projects of the Group in relation to future events. Due to their specific

Q3 and 9M 2018 Trading Update DISCLAIMER This presentation may contain forward looking statements based on current expectations and projects of the Group in relation to future events. Due to their specific

INTRODUCTION TO EXCHANGE RATES AND THE FOREIGN EXCHANGE MARKET

INTRODUCTION TO EXCHANGE RATES AND THE FOREIGN EXCHANGE MARKET 13 1 Exchange Rate Essentials 2 Exchange Rates in Practice 3 The Market for Foreign Exchange 4 Arbitrage and Spot Exchange Rates 5 Arbitrage

INTRODUCTION TO EXCHANGE RATES AND THE FOREIGN EXCHANGE MARKET 13 1 Exchange Rate Essentials 2 Exchange Rates in Practice 3 The Market for Foreign Exchange 4 Arbitrage and Spot Exchange Rates 5 Arbitrage

THE CANADIAN FOREIGN EXCHANGE COMMITTEE LE COMITÉ CANADIEN DU MARCHÉ DES CHANGES

THE CANADIAN FOREIGN EXCHANGE COMMITTEE LE COMITÉ CANADIEN DU MARCHÉ DES CHANGES 150 King Street West Contact: Rob Ogrodnick Suite 2000 Telephone: (416) 542-1339 Toronto, Ontario Email: rogrodnick@bankofcanada.ca

THE CANADIAN FOREIGN EXCHANGE COMMITTEE LE COMITÉ CANADIEN DU MARCHÉ DES CHANGES 150 King Street West Contact: Rob Ogrodnick Suite 2000 Telephone: (416) 542-1339 Toronto, Ontario Email: rogrodnick@bankofcanada.ca

G-SIBs Quantitative indicators as at December 31 st, 2016

G-SIBs Quantitative indicators as at December 31 st, 2016 Dec 2 >> G-SIBs Quantitative indicators Disclosure of all the values used for the 12 quantitative Indicators of G-SIB at December 31 st, 2016 (Article

G-SIBs Quantitative indicators as at December 31 st, 2016 Dec 2 >> G-SIBs Quantitative indicators Disclosure of all the values used for the 12 quantitative Indicators of G-SIB at December 31 st, 2016 (Article

Rutgers University Spring Econ 336 International Balance of Payments Professor Roberto Chang. Problem Set 1. Name:

Rutgers University Spring 2013 Econ 336 International Balance of Payments Professor Roberto Chang Problem Set 1 Name: 1. When the exchange value of the euro rises in terms of the U.S. dollar, U.S. residents

Rutgers University Spring 2013 Econ 336 International Balance of Payments Professor Roberto Chang Problem Set 1 Name: 1. When the exchange value of the euro rises in terms of the U.S. dollar, U.S. residents

Management of Transaction Exposure

INTERNATIONAL FINANCIAL MANAGEMENT Seventh Edition EUN / RESNICK 8-0 Copyright 2015 by The McGraw-Hill Companies, Inc. All rights reserved. Management of Transaction Exposure 8 Chapter Eight INTERNATIONAL

INTERNATIONAL FINANCIAL MANAGEMENT Seventh Edition EUN / RESNICK 8-0 Copyright 2015 by The McGraw-Hill Companies, Inc. All rights reserved. Management of Transaction Exposure 8 Chapter Eight INTERNATIONAL

Guidance regarding the completion of the Market Risk prudential reporting module for deposit-taking branches Issued May 2008

Guidance regarding the completion of the Market Risk prudential reporting module for deposit-taking branches Issued May 2008 Branch Market Risk Reporting Guide May 2008 1 Glossary The following abbreviations

Guidance regarding the completion of the Market Risk prudential reporting module for deposit-taking branches Issued May 2008 Branch Market Risk Reporting Guide May 2008 1 Glossary The following abbreviations

Chapter 6. Government Influence on Exchange Rates. Lecture Outline

Chapter 6 Government Influence on Exchange Rates Lecture Outline Exchange Rate Systems Fixed Exchange Rate System Freely Floating Exchange Rate System Managed Float Exchange Rate System Pegged Exchange

Chapter 6 Government Influence on Exchange Rates Lecture Outline Exchange Rate Systems Fixed Exchange Rate System Freely Floating Exchange Rate System Managed Float Exchange Rate System Pegged Exchange

INFORMATION FROM EUROPEAN UNION INSTITUTIONS, BODIES, OFFICES AND AGENCIES

Official Journal C 1 of the European Union Volume 62 English edition Information and Notices 3 January 2019 Contents II Information INFORMATION FROM EUROPEAN UNION INSTITUTIONS, BODIES, OFFICES AND AGENCIES

Official Journal C 1 of the European Union Volume 62 English edition Information and Notices 3 January 2019 Contents II Information INFORMATION FROM EUROPEAN UNION INSTITUTIONS, BODIES, OFFICES AND AGENCIES

Management of Transaction Exposure

INTERNATIONAL FINANCIAL MANAGEMENT Seventh Edition EUN / RESNICK 8-0 Copyright 2015 by The McGraw-Hill Companies, Inc. All rights reserved. Management of Transaction Exposure 8 Chapter Eight INTERNATIONAL

INTERNATIONAL FINANCIAL MANAGEMENT Seventh Edition EUN / RESNICK 8-0 Copyright 2015 by The McGraw-Hill Companies, Inc. All rights reserved. Management of Transaction Exposure 8 Chapter Eight INTERNATIONAL

Exam 2 Sample Questions FINAN430 International Finance McBrayer Spring 2018

Sample Multiple Choice Questions 1. Suppose you observe a spot exchange rate of $1.0500/. If interest rates are 5% APR in the U.S. and 3% APR in the euro zone, what is the no-arbitrage 1-year forward rate?

Sample Multiple Choice Questions 1. Suppose you observe a spot exchange rate of $1.0500/. If interest rates are 5% APR in the U.S. and 3% APR in the euro zone, what is the no-arbitrage 1-year forward rate?

Disclosure for global systemically important banks (G-SIBs) indicators as of 31 December 2017

indicators as of 31 December 2017") Disclosure for global systemically important banks (G-SIBs) indicators as of 31 December 2017 In order to comply with disclosure requirements and methodology described in the July 2013 document entitled

Disclosure for global systemically important banks (G-SIBs) indicators as of 31 December 2017 In order to comply with disclosure requirements and methodology described in the July 2013 document entitled

Alpha-Beta Series: Currency ETFs. November 10, 2011, 2pm EDT

Alpha-Beta Series: Currency ETFs November 10, 2011, 2pm EDT Speakers: Ugo Egbunike ETF Analyst IndexUniverse Dave Nadig Director of Research IndexUniverse Tony Davidow Managing Director Guggenheim Investments

Alpha-Beta Series: Currency ETFs November 10, 2011, 2pm EDT Speakers: Ugo Egbunike ETF Analyst IndexUniverse Dave Nadig Director of Research IndexUniverse Tony Davidow Managing Director Guggenheim Investments

Quarterly Market Review

Quarterly Market Review THEMES FOR THE QUARTER Emerging Markets the Standout in Mixed Q1 Global Equity Returns Developed Markets Positive; Australia and NZ Negative Value Premium Positive in Emerging Markets;

Quarterly Market Review THEMES FOR THE QUARTER Emerging Markets the Standout in Mixed Q1 Global Equity Returns Developed Markets Positive; Australia and NZ Negative Value Premium Positive in Emerging Markets;

The U.S. dollar continues to be a primary beneficiary during times of market stress. In our view:

WisdomTree Bloomberg U.S. Dollar Bullish Fund USDU Over the past few years, investors have become increasingly sophisticated. Not only do they understand the benefits of expanding their holdings beyond

WisdomTree Bloomberg U.S. Dollar Bullish Fund USDU Over the past few years, investors have become increasingly sophisticated. Not only do they understand the benefits of expanding their holdings beyond

foreign, and hence it is where the prices of many currencies are set. The price of foreign money is

Chapter 2: The BOP and the Foreign Exchange Market The foreign exchange market is the market where domestic money can be exchanged for foreign, and hence it is where the prices of many currencies are set.

Chapter 2: The BOP and the Foreign Exchange Market The foreign exchange market is the market where domestic money can be exchanged for foreign, and hence it is where the prices of many currencies are set.

Management of Transaction Exposure

INTERNATIONAL FINANCIAL MANAGEMENT Seventh Edition EUN / RESNICK Management of Transaction Exposure 8 Chapter Eight INTERNATIONAL Chapter Objective: FINANCIAL MANAGEMENT This chapter discusses various

INTERNATIONAL FINANCIAL MANAGEMENT Seventh Edition EUN / RESNICK Management of Transaction Exposure 8 Chapter Eight INTERNATIONAL Chapter Objective: FINANCIAL MANAGEMENT This chapter discusses various

Official Journal C 313

Official Journal C 313 of the European Union Volume 61 English edition Information and Notices 5 September 2018 Contents IV Notices NOTICES FROM EUROPEAN UNION INSTITUTIONS, BODIES, OFFICES AND AGENCIES

Official Journal C 313 of the European Union Volume 61 English edition Information and Notices 5 September 2018 Contents IV Notices NOTICES FROM EUROPEAN UNION INSTITUTIONS, BODIES, OFFICES AND AGENCIES

Triennial Central Bank Survey of Foreign Exchange and Derivatives Market Activity in Canada during April 2013

For Immediate Release Contact: Bank of Canada 5 September 2013, 09:00 ET Media Relations (613) 782-8782 Triennial Central Bank Survey of Foreign Exchange and Derivatives Market Activity in Canada during

For Immediate Release Contact: Bank of Canada 5 September 2013, 09:00 ET Media Relations (613) 782-8782 Triennial Central Bank Survey of Foreign Exchange and Derivatives Market Activity in Canada during

Chapter 8 Outline. Transaction exposure Should the Firm Hedge? Contractual hedge Risk Management in practice

Chapter 8 Outline Transaction exposure Should the Firm Hedge? Contractual hedge Risk Management in practice 1 / 51 Transaction exposure Transaction exposure measures gains or losses that arise from the

Chapter 8 Outline Transaction exposure Should the Firm Hedge? Contractual hedge Risk Management in practice 1 / 51 Transaction exposure Transaction exposure measures gains or losses that arise from the

Types of Exposure. Forward Market Hedge. Transaction Exposure. Forward Market Hedge. Forward Market Hedge: an Example INTERNATIONAL FINANCE.

Types of Exposure INTERNATIONAL FINANCE Chapter 8 Transaction exposure sensitivity of realized domestic currency values of the firm s contractual cash flows denominated in foreign currencies to unexpected

Types of Exposure INTERNATIONAL FINANCE Chapter 8 Transaction exposure sensitivity of realized domestic currency values of the firm s contractual cash flows denominated in foreign currencies to unexpected

Exchange rate and interest rates. Rodolfo Helg, February 2018 (adapted from Feenstra Taylor)

") Exchange rate and interest rates Rodolfo Helg, February 2018 (adapted from Feenstra Taylor) Defining the Exchange Rate Exchange rate (E domestic/foreign ) The price of a unit of foreign currency in terms

Exchange rate and interest rates Rodolfo Helg, February 2018 (adapted from Feenstra Taylor) Defining the Exchange Rate Exchange rate (E domestic/foreign ) The price of a unit of foreign currency in terms

5: Currency Derivatives

5: Currency Derivatives Given the potential shifts in the supply of or demand for currency (as explained in the previous chapter), fi rms and individuals who have assets denominated in foreign currencies

5: Currency Derivatives Given the potential shifts in the supply of or demand for currency (as explained in the previous chapter), fi rms and individuals who have assets denominated in foreign currencies

Chapter 2. The Foreign Exchange Market Cambridge University Press 2-1

Chapter 2 The Foreign Exchange Market 2018 Cambridge University Press 2-1 Exhibit 2.1 The Structure of the Foreign Exchange Market Most important cities: London, New York, Tokyo ForEx (or FX) operates

Chapter 2 The Foreign Exchange Market 2018 Cambridge University Press 2-1 Exhibit 2.1 The Structure of the Foreign Exchange Market Most important cities: London, New York, Tokyo ForEx (or FX) operates

THE CANADIAN FOREIGN EXCHANGE COMMITTEE LE COMITÉ CANADIEN DU MARCHÉ DES CHANGES

THE CANADIAN FOREIGN EXCHANGE COMMITTEE LE COMITÉ CANADIEN DU MARCHÉ DES CHANGES 150 King Street West Contact: Rob Ogrodnick Suite 2000 Telephone: (416) 542-1339 Toronto, Ontario Email: rogrodnick@bankofcanada.ca

THE CANADIAN FOREIGN EXCHANGE COMMITTEE LE COMITÉ CANADIEN DU MARCHÉ DES CHANGES 150 King Street West Contact: Rob Ogrodnick Suite 2000 Telephone: (416) 542-1339 Toronto, Ontario Email: rogrodnick@bankofcanada.ca

THE CANADIAN FOREIGN EXCHANGE COMMITTEE LE COMITÉ CANADIEN DU MARCHÉ DES CHANGES

THE CANADIAN FOREIGN EXCHANGE COMMITTEE LE COMITÉ CANADIEN DU MARCHÉ DES CHANGES 150 King Street West Contact: Rob Ogrodnick Suite 2000 Telephone: (416) 542-1339 Toronto, Ontario Email: rogrodnick@bankofcanada.ca

THE CANADIAN FOREIGN EXCHANGE COMMITTEE LE COMITÉ CANADIEN DU MARCHÉ DES CHANGES 150 King Street West Contact: Rob Ogrodnick Suite 2000 Telephone: (416) 542-1339 Toronto, Ontario Email: rogrodnick@bankofcanada.ca

UNIVERSITY OF TORONTO (OISE) PENSION PLAN FINANCIAL STATEMENTS JUNE 30, 2015

PENSION PLAN FINANCIAL STATEMENTS JUNE 30, 2015") UNIVERSITY OF TORONTO (OISE) PENSION PLAN FINANCIAL STATEMENTS JUNE 30, 2015 INDEPENDENT AUDITORS' REPORT To the Administrator of the University of Toronto (OISE) Pension Plan We have audited the accompanying

UNIVERSITY OF TORONTO (OISE) PENSION PLAN FINANCIAL STATEMENTS JUNE 30, 2015 INDEPENDENT AUDITORS' REPORT To the Administrator of the University of Toronto (OISE) Pension Plan We have audited the accompanying

After You Read. Find the missing expressions from the reading. Paragraph numbers are given. Write your answer on line.

3 After You Read. Find the missing expressions from the reading. Paragraph numbers are given. Write your answer on line. 1. Par. 1: Countries do not exchange goods and services directly, but use money

3 After You Read. Find the missing expressions from the reading. Paragraph numbers are given. Write your answer on line. 1. Par. 1: Countries do not exchange goods and services directly, but use money

Currency Futures or FX Futures Introduction and Pricing Guide

s or FX Futures Introduction and Pricing Guide Michael Taylor FinPricing A currency future or an FX future is a future contract between two parties to exchange one currency for another at a fixed exchange

s or FX Futures Introduction and Pricing Guide Michael Taylor FinPricing A currency future or an FX future is a future contract between two parties to exchange one currency for another at a fixed exchange

RMB internationalization:

RMB internationalization: Recent Development and headwinds Alicia Garcia-Herrero Chief Economist for Emerging Markets, BBVA Key points 1 Why is China pushing to internationalize the RMB? 2 Recent development

RMB internationalization: Recent Development and headwinds Alicia Garcia-Herrero Chief Economist for Emerging Markets, BBVA Key points 1 Why is China pushing to internationalize the RMB? 2 Recent development

Bank of Canada Triennial Central Bank Survey of Foreign Exchange and Over-the-Counter (OTC) Derivatives Markets

Derivatives Markets") Bank of Canada Triennial Central Bank Survey of Foreign Exchange and Over-the-Counter (OTC) Derivatives Markets Turnover for, and Amounts Outstanding as at June 30, March, 2005 Turnover data for, Table

Bank of Canada Triennial Central Bank Survey of Foreign Exchange and Over-the-Counter (OTC) Derivatives Markets Turnover for, and Amounts Outstanding as at June 30, March, 2005 Turnover data for, Table

Lyxor Asia 10US$(P60) SGX-ST Listing Date 19 October 2006

SGX-ST Listing Date 19 October 2006") 1 Prepared on: 20/03/2012 This Product Highlights Sheet ( PHS ) is an important document. It highlights the key terms and risks of this investment product and complements the prospectus of the Fund dated

1 Prepared on: 20/03/2012 This Product Highlights Sheet ( PHS ) is an important document. It highlights the key terms and risks of this investment product and complements the prospectus of the Fund dated

Learning Goal: How do we convert money into different currencies?

Name IB Math Studies Year 1 Date 7-2 Buy, Sell, and Commission Rates Learning Goal: How do we convert money into different currencies? Warm-Up: In this question give all answers correct to two decimal

Name IB Math Studies Year 1 Date 7-2 Buy, Sell, and Commission Rates Learning Goal: How do we convert money into different currencies? Warm-Up: In this question give all answers correct to two decimal

An Overview of Opportunities Within China s Interbank Bond Market

KCNY 2/3/207 Finding Quality Income An Overview of Opportunities Within China s Interbank Bond Market info@kraneshares.com Introduction to KraneShares About KraneShares Krane Funds Advisors, LLC is the

KCNY 2/3/207 Finding Quality Income An Overview of Opportunities Within China s Interbank Bond Market info@kraneshares.com Introduction to KraneShares About KraneShares Krane Funds Advisors, LLC is the

Replies to one minute memos, 9/21/03

Replies to one minute memos, 9/21/03 Dear Students, Thank you for asking these great questions. The answer to my question (what is the difference b/n the covered & uncovered interest rate arbitrage? If

Replies to one minute memos, 9/21/03 Dear Students, Thank you for asking these great questions. The answer to my question (what is the difference b/n the covered & uncovered interest rate arbitrage? If

UNIVERSITY OF TORONTO PENSION PLAN FINANCIAL STATEMENTS JUNE 30, 2016

UNIVERSITY OF TORONTO PENSION PLAN FINANCIAL STATEMENTS JUNE 30, 2016 INDEPENDENT AUDITORS' REPORT To the Administrator of the University of Toronto Pension Plan We have audited the accompanying financial

UNIVERSITY OF TORONTO PENSION PLAN FINANCIAL STATEMENTS JUNE 30, 2016 INDEPENDENT AUDITORS' REPORT To the Administrator of the University of Toronto Pension Plan We have audited the accompanying financial

Agenda. Learning Objectives. Chapter 19. International Business Finance. Learning Objectives Principles Used in This Chapter

Chapter 19 International Business Finance Agenda Learning Objectives Principles Used in This Chapter 1. Foreign Exchange Markets and Currency Exchange Rates 2. Interest Rate and Purchasing-Power Parity

Chapter 19 International Business Finance Agenda Learning Objectives Principles Used in This Chapter 1. Foreign Exchange Markets and Currency Exchange Rates 2. Interest Rate and Purchasing-Power Parity

Bank of Canada Triennial Central Bank Survey of Foreign Exchange and Over-the-Counter (OTC) Derivatives Markets Turnover for April, 2010 and Amounts

Derivatives Markets Turnover for April, 2010 and Amounts") Bank of Canada Triennial Central Bank Survey of Foreign Exchange and Over-the-Counter (OTC) Derivatives Markets Turnover for April, 2010 and Amounts Outstanding as at June 30, 2010 December 20, 2010 Table

Bank of Canada Triennial Central Bank Survey of Foreign Exchange and Over-the-Counter (OTC) Derivatives Markets Turnover for April, 2010 and Amounts Outstanding as at June 30, 2010 December 20, 2010 Table

Copyright Alpha Markets Ltd. Page 1

Copyright Alpha Markets Ltd. Page 1 Financial Industry - Module 1 Welcome to this unit on the Financial Industry. In this module we will be explaining the various aspects of the Financial Industry as well

Copyright Alpha Markets Ltd. Page 1 Financial Industry - Module 1 Welcome to this unit on the Financial Industry. In this module we will be explaining the various aspects of the Financial Industry as well

APPENDIX ECONOMIC INDICATORS DEVELOPED ECONOMIES

QUARTERLY INVESTMENT STRATEGY Third Quarter 15 19 APPENDIX ECONOMIC INDICATORS DEVELOPED ECONOMIES Purchasing Managers EMERGING ECONOMIES Purchasing Managers US Eurozone Japan Brazil Russia India China

QUARTERLY INVESTMENT STRATEGY Third Quarter 15 19 APPENDIX ECONOMIC INDICATORS DEVELOPED ECONOMIES Purchasing Managers EMERGING ECONOMIES Purchasing Managers US Eurozone Japan Brazil Russia India China

INTERNATIONAL FINANCE

INTERNATIONAL FINANCE 5. 2017/2018 Ing. Zuzana STRÁPEKOVÁ, PhD. SUA-FEM Nitra CONTENTS: Eexchange rate quotation Cross exchange rates Bilateral arbitration Trilateral arbitration Quotation of forward ER

INTERNATIONAL FINANCE 5. 2017/2018 Ing. Zuzana STRÁPEKOVÁ, PhD. SUA-FEM Nitra CONTENTS: Eexchange rate quotation Cross exchange rates Bilateral arbitration Trilateral arbitration Quotation of forward ER

Chapter 25 The Exchange Rate and the Balance of Payments The Foreign Exchange Market

Chapter 25 The Exchange Rate and the Balance of Payments 25.1 The Foreign Exchange Market 1) Foreign currency is A) the market for foreign exchange. B) the price at which one currency exchanges for another

Chapter 25 The Exchange Rate and the Balance of Payments 25.1 The Foreign Exchange Market 1) Foreign currency is A) the market for foreign exchange. B) the price at which one currency exchanges for another

Disclosures for Global Systemically Important Institutions (G-SIIs) 2016

2016") Disclosures for Global Systemically Important Institutions (G-SIIs) 2016 Deutsche Bank s disclosure with regard to Global Systemically Important Institutions (G-SII s) indicators as of December 31, 2016

Disclosures for Global Systemically Important Institutions (G-SIIs) 2016 Deutsche Bank s disclosure with regard to Global Systemically Important Institutions (G-SII s) indicators as of December 31, 2016

3) In 2010, what was the top remittance-receiving country in the world? A) Brazil B) Mexico C) India D) China

In 2010, what was the top remittance-receiving country in the world? A) Brazil B) Mexico C) India D) China") HSE-IB Test Syllabus: International Business: Environments and Operations, 15e, Global Edition (Daniels et al.). For use of the student for an educational purpose only, do not reproduce or redistribute.

HSE-IB Test Syllabus: International Business: Environments and Operations, 15e, Global Edition (Daniels et al.). For use of the student for an educational purpose only, do not reproduce or redistribute.

Chapter 18 (7) Fixed Exchange Rates and Foreign Exchange Intervention

Fixed Exchange Rates and Foreign Exchange Intervention") Chapter 18 (7) Fixed Exchange Rates and Foreign Exchange Intervention Preview Balance sheets of central banks Intervention in the foreign exchange markets and the money supply How the central bank fixes

Chapter 18 (7) Fixed Exchange Rates and Foreign Exchange Intervention Preview Balance sheets of central banks Intervention in the foreign exchange markets and the money supply How the central bank fixes

G-SIB Disclosure for global systemically important banks (G-SIBs) indicators as of 31 December April 2017

indicators as of 31 December April 2017") Disclosure for global systemically important banks (G-SIBs) indicators as of 31 December 2016 28 April 2017 Introduction In November 2011 the FSB published an integrated set of policy measures to address

Disclosure for global systemically important banks (G-SIBs) indicators as of 31 December 2016 28 April 2017 Introduction In November 2011 the FSB published an integrated set of policy measures to address

Advanced and Emerging Economies Two speed Recovery

Advanced and Emerging Economies Two speed Recovery 23 November 2 Bauhinia Foundation Research Centre Masaaki Shirakawa Governor of the Bank of Japan Slide 1 Japan s Silver Yen and Hong Kong s Silver Yuan

Advanced and Emerging Economies Two speed Recovery 23 November 2 Bauhinia Foundation Research Centre Masaaki Shirakawa Governor of the Bank of Japan Slide 1 Japan s Silver Yen and Hong Kong s Silver Yuan

Disclaimer. Notes in the presentation

Q1 2015 Results Disclaimer This presentation may contain forward looking statements based on current expectations and projects of the Group in relation to future events. Due to their specific nature, these

Q1 2015 Results Disclaimer This presentation may contain forward looking statements based on current expectations and projects of the Group in relation to future events. Due to their specific nature, these

The Internationalization of the RMB: A Treasury Perspective

ctc guide to The Internationalization of the RMB: A Treasury Perspective Executive Summary Underwritten by: CTC GUIDE: The Internationalization of the RMB: A Treasury Perspective Executive Summary The

ctc guide to The Internationalization of the RMB: A Treasury Perspective Executive Summary Underwritten by: CTC GUIDE: The Internationalization of the RMB: A Treasury Perspective Executive Summary The

Risk-free interest rate term structures. Report on the. Calculation of the UFR for 2019

EIOPA-BoS-18/141 21 March 2018 Risk-free interest rate term structures Report on the Calculation of the UFR for 2019 Executive summary EIOPA has calculated the ultimate forward rate (UFR) for 2019 in accordance

EIOPA-BoS-18/141 21 March 2018 Risk-free interest rate term structures Report on the Calculation of the UFR for 2019 Executive summary EIOPA has calculated the ultimate forward rate (UFR) for 2019 in accordance

UNIVERSITY OF TORONTO PENSION PLAN FINANCIAL STATEMENTS JUNE 30, 2017

UNIVERSITY OF TORONTO PENSION PLAN FINANCIAL STATEMENTS JUNE 30, 2017 INDEPENDENT AUDITORS' REPORT To the Administrator of the University of Toronto Pension Plan We have audited the accompanying financial

UNIVERSITY OF TORONTO PENSION PLAN FINANCIAL STATEMENTS JUNE 30, 2017 INDEPENDENT AUDITORS' REPORT To the Administrator of the University of Toronto Pension Plan We have audited the accompanying financial

UNIVERSITY OF TORONTO PENSION PLAN FINANCIAL STATEMENTS JUNE 30, 2018

UNIVERSITY OF TORONTO PENSION PLAN FINANCIAL STATEMENTS JUNE 30, 2018 INDEPENDENT AUDITORS' REPORT To the Administrator of the University of Toronto Pension Plan We have audited the accompanying financial

UNIVERSITY OF TORONTO PENSION PLAN FINANCIAL STATEMENTS JUNE 30, 2018 INDEPENDENT AUDITORS' REPORT To the Administrator of the University of Toronto Pension Plan We have audited the accompanying financial

March 26, Why Hedge? How to Hedge? Trends and Strategies in Interest Rate and FX Risk Management

Establishing and Maintaining an FX and Interest Rate Hedging Program: The Lifecycle of a Hedge presented by Thomas Armes, Managing Director Foreign Exchange, PNC Capital Markets Steve Goel, Assistant Treasurer,

Establishing and Maintaining an FX and Interest Rate Hedging Program: The Lifecycle of a Hedge presented by Thomas Armes, Managing Director Foreign Exchange, PNC Capital Markets Steve Goel, Assistant Treasurer,

Fx Derivatives- Simplified CA NAVEEN JAIN AUGUST 1, 2015

1 Fx Derivatives- Simplified CA NAVEEN JAIN AUGUST 1, 2015 Agenda 2 History of Fx Overview of Forex Markets Understanding Forex Concepts Hedging Instruments RBI Guidelines Current Forex Markets History

1 Fx Derivatives- Simplified CA NAVEEN JAIN AUGUST 1, 2015 Agenda 2 History of Fx Overview of Forex Markets Understanding Forex Concepts Hedging Instruments RBI Guidelines Current Forex Markets History

Foreign Exchange Markets

Foreign Exchange Markets Foreign exchange: Money of another country. Foreign exchange transaction: and the seller of a currency. Agreement between the buyer Foreign exchange market (FOREX market): Physical

Foreign Exchange Markets Foreign exchange: Money of another country. Foreign exchange transaction: and the seller of a currency. Agreement between the buyer Foreign exchange market (FOREX market): Physical

Bank of Canada Triennial Central Bank Surveys of Foreign Exchange and Over-the-Counter (OTC) Derivatives Markets Turnover for April, 2007 and Amounts

Derivatives Markets Turnover for April, 2007 and Amounts") Bank of Canada Triennial Central Bank Surveys of Foreign Exchange and Over-the-Counter (OTC) Derivatives Markets Turnover for April, 2007 and Amounts Outstanding as at June 30, 2007 January 4, 2008 Table

Bank of Canada Triennial Central Bank Surveys of Foreign Exchange and Over-the-Counter (OTC) Derivatives Markets Turnover for April, 2007 and Amounts Outstanding as at June 30, 2007 January 4, 2008 Table

Chapter 17 Appendix A

Chapter 17 Appendix A The Interest Parity Condition We can derive all the results in the text with a concept that is widely used in international finance. The interest parity condition shows the relationship

Chapter 17 Appendix A The Interest Parity Condition We can derive all the results in the text with a concept that is widely used in international finance. The interest parity condition shows the relationship

Listing of bonds. at the Stuttgart Stock Exchange

Listing of bonds at the Stuttgart Stock Exchange Agenda 1. Two Market segments for different demands 2. Listing criteria in general 3. Listing Criteria specifically for bonds 4. Trading and settlement

Listing of bonds at the Stuttgart Stock Exchange Agenda 1. Two Market segments for different demands 2. Listing criteria in general 3. Listing Criteria specifically for bonds 4. Trading and settlement

THE EVOLUTION OF OTC CURRENCY DERIVATIVES MARKET. Associate professor Codruța Făt, Associate professor Fănuța Pop

THE EVOLUTION OF OTC CURRENCY DERIVATIVES MARKET Associate professor Codruța Făt, Associate professor Fănuța Pop Abstract The exchange rate risk is the risk that affect the companies, the individuals,

THE EVOLUTION OF OTC CURRENCY DERIVATIVES MARKET Associate professor Codruța Făt, Associate professor Fănuța Pop Abstract The exchange rate risk is the risk that affect the companies, the individuals,

Currency Hedged Indexes

ISSUE BRIEF Currency Hedged Indexes Why Currency Returns and Currency Hedging Matter JULY 2015 The growth of international investing makes it important to understand the impact of currency movements. Institutional

ISSUE BRIEF Currency Hedged Indexes Why Currency Returns and Currency Hedging Matter JULY 2015 The growth of international investing makes it important to understand the impact of currency movements. Institutional

Chapter 18 (7) Fixed Exchange Rates and Foreign Exchange Intervention

Fixed Exchange Rates and Foreign Exchange Intervention") Chapter 18 (7) Fixed Exchange Rates and Foreign Exchange Intervention Preview Balance sheets of central banks Intervention in the foreign exchange markets and the money supply How the central bank fixes

Chapter 18 (7) Fixed Exchange Rates and Foreign Exchange Intervention Preview Balance sheets of central banks Intervention in the foreign exchange markets and the money supply How the central bank fixes

The Renminbi: Now in the Basket of Special Drawing Rights (SDR)

") The Renminbi: Now in the Basket of Special Drawing Rights (SDR) Lawrence J. Lau 刘遵义 Ralph and Claire Landau Professor of Economics, The Chinese University of Hong Kong and Kwoh-Ting Li Professor in Economic

The Renminbi: Now in the Basket of Special Drawing Rights (SDR) Lawrence J. Lau 刘遵义 Ralph and Claire Landau Professor of Economics, The Chinese University of Hong Kong and Kwoh-Ting Li Professor in Economic

Arbitrage is a trading strategy that exploits any profit opportunities arising from price differences.

5. ARBITRAGE AND SPOT EXCHANGE RATES 5 Arbitrage and Spot Exchange Rates Arbitrage is a trading strategy that exploits any profit opportunities arising from price differences. Arbitrage is the most basic

5. ARBITRAGE AND SPOT EXCHANGE RATES 5 Arbitrage and Spot Exchange Rates Arbitrage is a trading strategy that exploits any profit opportunities arising from price differences. Arbitrage is the most basic

CME Chapter 13 Spot FX Transactions

CME Chapter 13 Spot FX Transactions 1300. SCOPE OF CHAPTER 1301. SPOT FX TRANSACTION SPECIFICATIONS 1302. DEFINITIONS 1303. GENERAL PROVISIONS 1304. [RESERVED] 1305. PERMITTED USER 1306. END-USERS AND

CME Chapter 13 Spot FX Transactions 1300. SCOPE OF CHAPTER 1301. SPOT FX TRANSACTION SPECIFICATIONS 1302. DEFINITIONS 1303. GENERAL PROVISIONS 1304. [RESERVED] 1305. PERMITTED USER 1306. END-USERS AND

Condensed Interim Consolidated Financial Statements of. Canada Pension Plan Investment Board

Condensed Interim Consolidated Financial Statements of Canada Pension Plan Investment Board December 31, 2016 Condensed Interim Consolidated Balance Sheet December 31, 2016 December 31, 2016 March 31,

Condensed Interim Consolidated Financial Statements of Canada Pension Plan Investment Board December 31, 2016 Condensed Interim Consolidated Balance Sheet December 31, 2016 December 31, 2016 March 31,

Answers to Questions: Chapter 7

Answers to Questions in Textbook 1 Answers to Questions: Chapter 7 1. Any international transaction that creates a payment of money to a U.S. resident generates a credit. Any international transaction

Answers to Questions in Textbook 1 Answers to Questions: Chapter 7 1. Any international transaction that creates a payment of money to a U.S. resident generates a credit. Any international transaction

INTERNATIONAL FINANCE

INTERNATIONAL FINANCE Ing. Zuzana STRÁPEKOVÁ, PhD. 1 10. 2017/2018 SUA-FEM Nitra The FOREX market is a two-tiered market: Interbank Market (Wholesale) FUNCTION AND STRUCTURE OF THE FOREX MARKET - about

INTERNATIONAL FINANCE Ing. Zuzana STRÁPEKOVÁ, PhD. 1 10. 2017/2018 SUA-FEM Nitra The FOREX market is a two-tiered market: Interbank Market (Wholesale) FUNCTION AND STRUCTURE OF THE FOREX MARKET - about

UNIT FIVE (5) The International Monetary Environment and Financial Management in the Global Firm

The International Monetary Environment and Financial Management in the Global Firm") UNIT FIVE (5) The International Monetary Environment and Financial Management in the Global Firm Objectives Exchange rates and currencies How exchange rates are determined The monetary and financial systems

UNIT FIVE (5) The International Monetary Environment and Financial Management in the Global Firm Objectives Exchange rates and currencies How exchange rates are determined The monetary and financial systems

Study Questions. Lecture 13. Exchange Rates

Study Questions Page 1 of 5 Study Questions Lecture 13 Part 1: Multiple Choice Select the best answer of those given. 1. The statement the yen rose today from 121 to 117 makes sense because a. The U.S.

Study Questions Page 1 of 5 Study Questions Lecture 13 Part 1: Multiple Choice Select the best answer of those given. 1. The statement the yen rose today from 121 to 117 makes sense because a. The U.S.

Schweser Printable Answers - Session Financial Statement Analysis: Business Combinations and International Operations

1 of 18 18/12/2006 6:50 Schweser Printable Answers - Session Financial Statement Analysis: Business Combinations and International Operations Test ID#: 1362407 2 of 18 18/12/2006 6:50 Back to Test Review

1 of 18 18/12/2006 6:50 Schweser Printable Answers - Session Financial Statement Analysis: Business Combinations and International Operations Test ID#: 1362407 2 of 18 18/12/2006 6:50 Back to Test Review

Lesson II: Overview. 1. Foreign exchange markets: everyday market practice

Lesson II: Overview 1. Foreign exchange markets: everyday market practice 2. Forward foreign exchange market 1 Foreign exchange markets: everyday market practice 2 Getting started I The exchange rates

Lesson II: Overview 1. Foreign exchange markets: everyday market practice 2. Forward foreign exchange market 1 Foreign exchange markets: everyday market practice 2 Getting started I The exchange rates

Official Journal C 373

Official Journal C 373 of the European Union Volume 60 English edition Information and Notices 4 November 2017 Contents IV Notices NOTICES FROM EUROPEAN UNION INSTITUTIONS, BODIES, OFFICES AND AGENCIES

Official Journal C 373 of the European Union Volume 60 English edition Information and Notices 4 November 2017 Contents IV Notices NOTICES FROM EUROPEAN UNION INSTITUTIONS, BODIES, OFFICES AND AGENCIES

ECO 328 SUMMER Sample Questions Topics I.1-3. I.1 National Income Accounting and the Balance of Payments

ECO 328 SUMMER 2004--Sample Questions Topics I.1-3 I.1 National Income Accounting and the Balance of Payments 1. National income equals GNP A. less depreciation, less net unilateral transfers, less indirect

ECO 328 SUMMER 2004--Sample Questions Topics I.1-3 I.1 National Income Accounting and the Balance of Payments 1. National income equals GNP A. less depreciation, less net unilateral transfers, less indirect

(Important Basic Matters for Preparation of Consolidated Financial Statements)

") [Notes] (Important Basic Matters for Preparation of Consolidated Financial Statements) 1. Matters related to the scope of consolidation All of our 303 subsidiaries are included in the scope of consolidation.

[Notes] (Important Basic Matters for Preparation of Consolidated Financial Statements) 1. Matters related to the scope of consolidation All of our 303 subsidiaries are included in the scope of consolidation.

Official Journal C 398

Official Journal C 398 of the European Union Volume 60 English edition Information and Notices 24 November 2017 Contents II Information INFORMATION FROM EUROPEAN UNION INSTITUTIONS, BODIES, OFFICES AND

Official Journal C 398 of the European Union Volume 60 English edition Information and Notices 24 November 2017 Contents II Information INFORMATION FROM EUROPEAN UNION INSTITUTIONS, BODIES, OFFICES AND

An Overview of Opportunities Within China s Interbank Bond Market

KCNY 2/3/208 Finding Quality Income An Overview of Opportunities Within China s Interbank Bond Market info@kraneshares.com Introduction to KraneShares About KraneShares Krane Funds Advisors, LLC is the

KCNY 2/3/208 Finding Quality Income An Overview of Opportunities Within China s Interbank Bond Market info@kraneshares.com Introduction to KraneShares About KraneShares Krane Funds Advisors, LLC is the

Investment Management FX markets and International Portfolio Management

Investment Management FX markets and International Portfolio Management Road Map International portfolio diversification Home bias FX risk FX markets Spot and forward/futures FX rates FX parities Hedging

Investment Management FX markets and International Portfolio Management Road Map International portfolio diversification Home bias FX risk FX markets Spot and forward/futures FX rates FX parities Hedging

dr Bartłomiej Rokicki Chair of Macroeconomics and International Trade Theory Faculty of Economic Sciences, University of Warsaw

Chair of Macroeconomics and International Trade Theory Faculty of Economic Sciences, University of Warsaw Determinants of the demand for foreign currencies To understand what factors determine the exchange

Chair of Macroeconomics and International Trade Theory Faculty of Economic Sciences, University of Warsaw Determinants of the demand for foreign currencies To understand what factors determine the exchange

FX BRIEFLY. 8 June Helaba Research. Performance on a month-over-month basis

Helaba Research FX BRIEFLY 8 June 2018 AUTHOR Christian Apelt, CFA phone: +49 69/91 32-47 26 research@helaba.de EDITOR Claudia Windt PUBLISHER: Dr. Gertrud R. Traud Chief Economist/ Head of Research The

Helaba Research FX BRIEFLY 8 June 2018 AUTHOR Christian Apelt, CFA phone: +49 69/91 32-47 26 research@helaba.de EDITOR Claudia Windt PUBLISHER: Dr. Gertrud R. Traud Chief Economist/ Head of Research The