dr Bartłomiej Rokicki Chair of Macroeconomics and International Trade Theory Faculty of Economic Sciences, University of Warsaw

|

|

|

- Victoria Berry

- 5 years ago

- Views:

Transcription

1 Chair of Macroeconomics and International Trade Theory Faculty of Economic Sciences, University of Warsaw

2 Determinants of the demand for foreign currencies To understand what factors determine the exchange rate, we should first consider what determines the demand for assets denominated in various currencies Demand for foreign currency assets is influenced by the same factors as the demand for other assets: mostly it is the expectation about future assets value The desire to have a deposit denominated in foreign currency depends on two factors: the interest rate it offers and expected changes in exchange rate

3 Rate of return from different assets The demand for various foreign currency deposits varies depending on the rate of return derived from them converted to a common currency how the investor makes the decision? Suppose that an investor has a million PLN that wants to invest for 6 months. Following are the options: o Investment in PLN bearing interest rate of 8% p a. o Investment in the euro with interest rate of 4% p a. o The current rate is EUR / PLN 3.93 o The investor expects that in six months, the rate will be equal to EUR / PLN 3.98 To make a rational decision the investor must compare the actual rate of return on both investments denominated in the same currency

4 Investor s decision 1 mln PLN PLN x 1, PLN , 93 EUR x 1, , 99 EUR

5 Is it an equilibrium? No, every investor can make such a comparison and conclude that investment in PLN brings a higher rate of return The result: rising demand for PLN (growing supply of EUR) and price of EUR falls If many investors will buy PLN, the investment rate falls and the PLN will become less profitable We can talk about an equilibrium when the rate of return on both investments is the same - investors will not have any incentive to change their investment behaviour

6 Question 1. Calculate the dollar rates of return on the following assets: A rare stamp whose price grows from $1500 to $2200 USD; A bottle of a rare Burgundy, Domaine de la Romanee-Conti 1978, whose price rises from 200 to 250 between 1999 and At the same time appreciates against $ by 5%; A painting whose price rises from GBP to GBP in a year while the exchange rate turns from $1.60/ to $1.50/ ; A deposit in a London bank in a year when the interest rate on pounds is 4.5% percent and the $ depreciates against the by 10%.

7 Foreign exchange market equilibrium interest rate parity In the equilibrium, the rate of return on domestic assets must equal the rate of return on foreign assets: the national interest rate equals the foreign interest rate plus the expected rate of appreciation of foreign currency (depreciation of home currency) Covered interest rate parity: 1 F 1+ i= (1+ i*) E i= i * + E Uncovered interest rate parity: E F E E where E F is forward exchange rate 1 e 1+ i= (1+ i*) E i= i * + E E e E E where E F is expected exchange rate

8 IRP as a model of current exchange rate Suppose that the expected dollar exchange rate in a year is equal to 3.10 PLN / USD The U.S. annual interest rate is equal to 3% and the domestic interest rate to 6% How will change the expected rate of return on dollar deposits depending on the current dollar exchange rate? E i i* (E e -E)/E i* + (E e -E)/E % 3% 8.40% 11.40% % 3% 6.54% 9.54% % 3% 4.74% 7.74% % 3% 3.00% 6.00% % 3% 1.32% 4.32% % 3% -0.31% 2.69% % 3% -1.89% 1.11% % 3% -3.42% -0.42% The current exchange rate reaches an equilibrium level when the rate of return on domestic assets (i) is equal to the rate of return on foreign assets (i* + (E e -E) / E). The latter, in turn, is negatively related to the current exchange rate.

9 IRP as a model of current exchange rate: growth of i

10 IRP as a model of current exchange rate: growth of i* and E e

11 Interest rate parity: a summary The current exchange rate reaches equilibrium when interest rate parity condition is satisfied: o an increase in domestic interest rate leads (ceteris paribus) to the appreciation of domestic currency o an increase in foreign interest rates (ceteris paribus) leads to a depreciation of domestic currency, o expectations of foreign currency appreciation, (ceteris paribus) result in its current appreciation

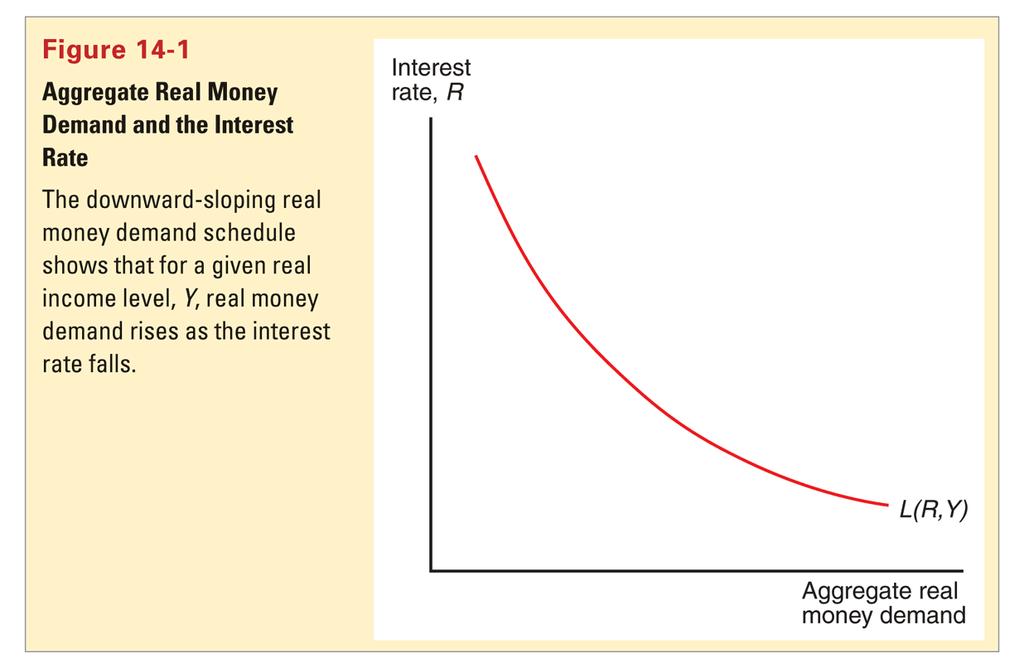

12 Adding money market equilibrium dr Bartłomiej Rokicki Exchange rate model based on the IRP can easily be extended by posing the question: what determines the interest rate? The interest rate is determined at the money market Having said that, we can better understand the factors determining the exchange rate in the short term Aggregated demand for money may be expressed as: M d = P x L(R,Y) where: o P is a price level o Y real GDP o R is an interest rate o L(R,Y) aggregated demand for money in real terms or: M d /P = L(R,Y) Real demand for money is a function of the interest rate and real GDP

13

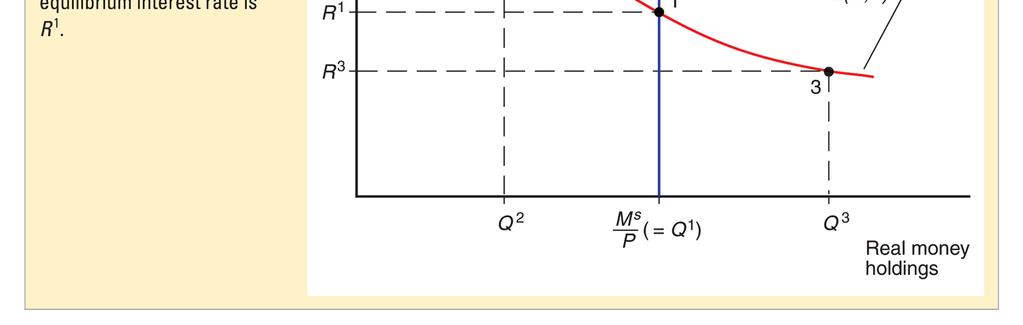

14 Money market equilibrium

15 Change in money supply

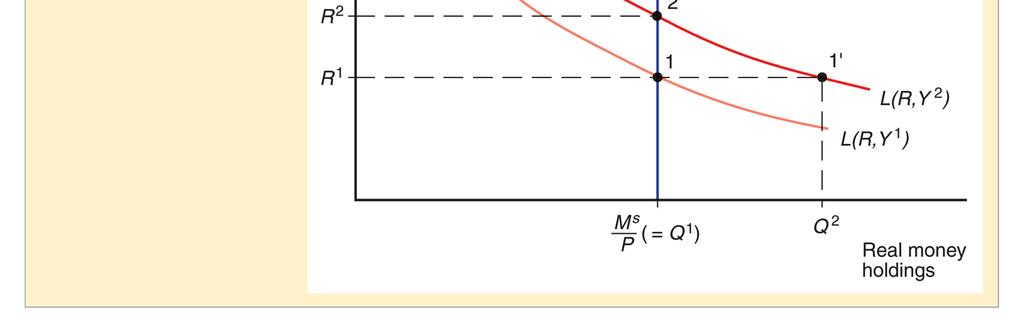

16 Change in GDP

17 Link between money market and foreign exchange market

18 Link between money market and foreign exchange market Since domestic interest rate can be considered as a rate of return on domestic assets than any change in money market equilibrium affects the domestic rate of return level. The intersection of domestic rate of return curve and foreign rate of return curve determines the spot exchange rate in equilibrium (assuming that interest rate parity holds).

19 Question 2. The one year T-bill rate in the U.S. is 5%, and the one year rate in the UK is 8%. The current spot rate (S) is $1.60/ and the one year forward rate (F) is $1.568/. a) Does interest rate parity hold? Show your work b) Individual A in the U.S. has $100,000 to invest for one year. Compare how much they would have at the end of one year by investing $100,000 in the U.S., compared to investing $100,000 in the U.K. for one year, using a one-year forward contract to cover currency risk. c) How would covered interest arbitrage restore interest rate parity? Address each of the four variables (S, F, i US and i UK ) indicate the direction of the change. d) Go back to the analysis in part b, and assume that investing in the U.K. at 8% involves a commission to buy the one-year security of 0.5% of the $100,000 investment (payable in dollars to a broker in the U.S.), and that there is a fixed fee of $350 to arrange the forward contract to sell the pounds in one year. Investing in the U.S. at the 5% interest rate includes all commissions and fees. Which country would you now invest in?

20 Question 3. The current ex-rate for the British pound is $1.67/. Interest rates for one year bank CDs are 4% in the U.S. and 8% in the U.K. Assuming interest rate parity holds, what are the expected forward rates for the British pound in 90 days, 180 days, and in one year? Question 4. In the table below you can find the 90-day spot and forward exchange rates of and CAD against $ and the 90-day interest rates in Germany and Canada. Germany Canada Spot Forward i per annum 3.48% 4% a) What should be the 90-day interest rate in the US in order that US investor receives the highest rate of return investing in domestic assets (as compared with foreign assets). b) If the spot rate change the way that interest rate parity holds, what spot rate of against CAD should be expected the next day?

21 Question 5. Use (uncovered) interest rate parity to explain why it might not be the deal of a lifetime to lend to the Reserve Bank of Zimbabwe, where deposits earn several thousand percent (nominal) interest. Question 6. Please, verify the following statement: if the uncovered interest rate parity holds, other things remaining constant, an increase in the U.K. nominal interest rate will increase the current value of the U.S. dollar against the British pound. Question 7. Lets assume that the interest rate parity holds. Using graphical presentation of the interest rates parity model, explain how would the following influence the spot exchange rate: a) a decrease in home interest rate (i HC ); b) an increase in foreign interest rate (i FC ); c) a decrease in expected exchange rate (E e HC/FC)

22 Question 8. Lets suppose again that the interest rate parity holds. Using graphical presentation of the interest rates parity model and the monetary market model, explain how would the following influence the spot exchange rate: a) an increase in foreign income; b) an increase in home income; c) an increase in nominal money supply in home country; d) an increase in price level in home country; e) an increase in home elasticity of money demand on change in interest rate.

Portfolio balanceapproachand the interest rateparity

Portfolio balanceapproachand the interest rateparity dr hab. Bartłomiej Rokicki Chair of Macroeconomics and International Trade Theory Faculty of conomic Sciences, University of Warsaw Rate of return from

Portfolio balanceapproachand the interest rateparity dr hab. Bartłomiej Rokicki Chair of Macroeconomics and International Trade Theory Faculty of conomic Sciences, University of Warsaw Rate of return from

dr Bartłomiej Rokicki Chair of Macroeconomics and International Trade Theory Faculty of Economic Sciences, University of Warsaw

Chair of Macroeconomics and International Trade Theory Faculty of Economic Sciences, University of Warsaw Purchasing Power Parity dr Bartłomiej Rokicki Purchasing power parity is derived from law of one

Chair of Macroeconomics and International Trade Theory Faculty of Economic Sciences, University of Warsaw Purchasing Power Parity dr Bartłomiej Rokicki Purchasing power parity is derived from law of one

Exchange ratein a shortrun

Exchange ratein a shortrun dr hab. Bartłomiej Rokicki Chair of Macroeconomics and International Trade Theory Faculty of Economic Sciences, University of Warsaw Main definitions Foreign exchange market

Exchange ratein a shortrun dr hab. Bartłomiej Rokicki Chair of Macroeconomics and International Trade Theory Faculty of Economic Sciences, University of Warsaw Main definitions Foreign exchange market

Exam 2 Sample Questions FINAN430 International Finance McBrayer Spring 2018

Sample Multiple Choice Questions 1. Suppose you observe a spot exchange rate of $1.0500/. If interest rates are 5% APR in the U.S. and 3% APR in the euro zone, what is the no-arbitrage 1-year forward rate?

Sample Multiple Choice Questions 1. Suppose you observe a spot exchange rate of $1.0500/. If interest rates are 5% APR in the U.S. and 3% APR in the euro zone, what is the no-arbitrage 1-year forward rate?

Exchange rate in a long run

Exchange rate in a long run dr hab. Bart Rokicki Chair of Macroeconomics and International Trade Theory Faculty of Economic Sciences, University of Warsaw urchasing ower arity Bart Rokicki urchasing power

Exchange rate in a long run dr hab. Bart Rokicki Chair of Macroeconomics and International Trade Theory Faculty of Economic Sciences, University of Warsaw urchasing ower arity Bart Rokicki urchasing power

3. If the price of a British pound increases from $1.50 per pound to $1.80 per pound, we say that:

HOMEWORK 7 (ON CHAPTERS 14 AND 15) ECO41 FALL 2015 UDAYAN ROY Each correct answer is worth 1 point. The maximum score is 20 points. This homework is due in class on Wednesday, December 2. Please show your

HOMEWORK 7 (ON CHAPTERS 14 AND 15) ECO41 FALL 2015 UDAYAN ROY Each correct answer is worth 1 point. The maximum score is 20 points. This homework is due in class on Wednesday, December 2. Please show your

Foreign exchange market based on chapter 14 (Exchange Rates and the Foreign Exchange Market: An Asset Approach) of the textbook

of the textbook") HOMEWORK 6 (ASSET MARKETS) ECO41 FALL 2011 UDAYAN ROY Each correct answer is worth 1 point. The maximum score is 20 points. This homework assignment is due on Wednesday, December 7. Please show your answers

HOMEWORK 6 (ASSET MARKETS) ECO41 FALL 2011 UDAYAN ROY Each correct answer is worth 1 point. The maximum score is 20 points. This homework assignment is due on Wednesday, December 7. Please show your answers

INTERNATIONAL FINANCE

INTERNATIONAL FINANCE Ing. Zuzana STRÁPEKOVÁ, PhD. 1 10. 2017/2018 SUA-FEM Nitra The FOREX market is a two-tiered market: Interbank Market (Wholesale) FUNCTION AND STRUCTURE OF THE FOREX MARKET - about

INTERNATIONAL FINANCE Ing. Zuzana STRÁPEKOVÁ, PhD. 1 10. 2017/2018 SUA-FEM Nitra The FOREX market is a two-tiered market: Interbank Market (Wholesale) FUNCTION AND STRUCTURE OF THE FOREX MARKET - about

Exchange Rates. Exchange Rates. ECO 3704 International Macroeconomics. Chapter Exchange Rates

Exchange Rates CHAPTER 13 1 Exchange Rates What are they? How does one describe their movements? 2 Exchange Rates The nominal exchange rate is the price of one currency in terms of another. The spot rate

Exchange Rates CHAPTER 13 1 Exchange Rates What are they? How does one describe their movements? 2 Exchange Rates The nominal exchange rate is the price of one currency in terms of another. The spot rate

This is Interest Rate Parity, chapter 5 from the book Policy and Theory of International Finance (index.html) (v. 1.0).

(v. 1.0).") This is Interest Rate Parity, chapter 5 from the book Policy and Theory of International Finance (index.html) (v. 1.0). This book is licensed under a Creative Commons by-nc-sa 3.0 (http://creativecommons.org/licenses/by-nc-sa/

This is Interest Rate Parity, chapter 5 from the book Policy and Theory of International Finance (index.html) (v. 1.0). This book is licensed under a Creative Commons by-nc-sa 3.0 (http://creativecommons.org/licenses/by-nc-sa/

Exchange rateovershooting-the Dornbuschmodel

Exchange rateovershooting-the Dornbuschmodel dr hab. Bartłomiej Rokicki Chair of Macroeconomics and International Trade Theory Faculty of Economic Sciences, University of Warsaw Main assumptions of the

Exchange rateovershooting-the Dornbuschmodel dr hab. Bartłomiej Rokicki Chair of Macroeconomics and International Trade Theory Faculty of Economic Sciences, University of Warsaw Main assumptions of the

University of Colorado at Boulder. Department of Economics. ECON 4423: INTERNATIONAL FINANCE Term Test 2 Fall 2005

University of Colorado at Boulder Department of Economics ECON 4423: INTERNATIONAL FINANCE Term Test 2 Fall 2005 Name: Student ID: Instructions: This test is 1 hour in length. You may use a hand calculator

University of Colorado at Boulder Department of Economics ECON 4423: INTERNATIONAL FINANCE Term Test 2 Fall 2005 Name: Student ID: Instructions: This test is 1 hour in length. You may use a hand calculator

dr Bartłomiej Rokicki Chair of Macroeconomics and International Trade Theory Faculty of Economic Sciences, University of Warsaw

Chair of Macroeconomics and International Trade Theory Faculty of Economic Sciences, University of Warsaw Main assumptions of the model Small open economy Short term analysis constant prices and wages

Chair of Macroeconomics and International Trade Theory Faculty of Economic Sciences, University of Warsaw Main assumptions of the model Small open economy Short term analysis constant prices and wages

Arbitrage is a trading strategy that exploits any profit opportunities arising from price differences.

5. ARBITRAGE AND SPOT EXCHANGE RATES 5 Arbitrage and Spot Exchange Rates Arbitrage is a trading strategy that exploits any profit opportunities arising from price differences. Arbitrage is the most basic

5. ARBITRAGE AND SPOT EXCHANGE RATES 5 Arbitrage and Spot Exchange Rates Arbitrage is a trading strategy that exploits any profit opportunities arising from price differences. Arbitrage is the most basic

Homework Assignment #2, part 1 ECO 3203, Fall According to classical macroeconomic theory, money supply shocks are neutral.

Homework Assignment #2, part 1 ECO 3203, Fall 2017 Due: Friday, October 27 th at the beginning of class. 1. According to classical macroeconomic theory, money supply shocks are neutral. a. Explain what

Homework Assignment #2, part 1 ECO 3203, Fall 2017 Due: Friday, October 27 th at the beginning of class. 1. According to classical macroeconomic theory, money supply shocks are neutral. a. Explain what

Exchange rate: the price of one currency in terms of another. We will be using the notation E t = euro

Econ 330: Money and Banking Fall 2014, Handout 8 Chapter 17 : Foreign Exchange Market 1. Foreign Exchange Market Exchange rate: the price of one currency in terms of another. We will be using the notation

Econ 330: Money and Banking Fall 2014, Handout 8 Chapter 17 : Foreign Exchange Market 1. Foreign Exchange Market Exchange rate: the price of one currency in terms of another. We will be using the notation

Study Questions. Lecture 13. Exchange Rates

Study Questions Page 1 of 5 Study Questions Lecture 13 Part 1: Multiple Choice Select the best answer of those given. 1. The statement the yen rose today from 121 to 117 makes sense because a. The U.S.

Study Questions Page 1 of 5 Study Questions Lecture 13 Part 1: Multiple Choice Select the best answer of those given. 1. The statement the yen rose today from 121 to 117 makes sense because a. The U.S.

Openness in goods and financial markets II. Balance of payments. Uncovered interest rate parity. Goods market equilibrium in the open economy.

Openness in goods and financial markets II Balance of payments. Uncovered interest rate parity. Goods market equilibrium in the open economy. Openness in financial markets: The purchase and sale of foreign

Openness in goods and financial markets II Balance of payments. Uncovered interest rate parity. Goods market equilibrium in the open economy. Openness in financial markets: The purchase and sale of foreign

In frictionless markets, freely tradable goods should have the same price anywhere: S = P P $

Prices and Exchange Rates In frictionless markets, freely tradable goods should have the same price anywhere: P $ S = P P $ price in US$ S Exchange rate in yen per dollar P Price in Japanese yen Purchasing

Prices and Exchange Rates In frictionless markets, freely tradable goods should have the same price anywhere: P $ S = P P $ price in US$ S Exchange rate in yen per dollar P Price in Japanese yen Purchasing

Chapter 14 Exchange Rates and the Foreign Exchange Market: An Asset Approach

Chapter 14 Exchange Rates and the Foreign Exchange Market: An Asset Approach Copyright 2015 Pearson Education, Inc. All rights reserved. 1-1 Preview The basics of exchange rates Exchange rates and the

Chapter 14 Exchange Rates and the Foreign Exchange Market: An Asset Approach Copyright 2015 Pearson Education, Inc. All rights reserved. 1-1 Preview The basics of exchange rates Exchange rates and the

Study Questions (with Answers) Lecture 13. Exchange Rates

Lecture 13. Exchange Rates") Study Questions (with Answers) Page 1 of 5 Part 1: Multiple Choice Select the best answer of those given. Study Questions (with Answers) Lecture 13 1. The statement the yen rose today from 121 to 117 makes

Study Questions (with Answers) Page 1 of 5 Part 1: Multiple Choice Select the best answer of those given. Study Questions (with Answers) Lecture 13 1. The statement the yen rose today from 121 to 117 makes

Study Questions (with Answers) Lecture 13. Exchange Rates

Lecture 13. Exchange Rates") Study Questions (with Answers) Page 1 of 5 Part 1: Multiple Choice Select the best answer of those given. Study Questions (with Answers) Lecture 13 1. The statement the yen rose today from 121 to 117 makes

Study Questions (with Answers) Page 1 of 5 Part 1: Multiple Choice Select the best answer of those given. Study Questions (with Answers) Lecture 13 1. The statement the yen rose today from 121 to 117 makes

Study Questions. Lecture 13. Exchange Rates

Study Questions Page 1 of 5 Part 1: Multiple Choice Select the best answer of those given. Study Questions Lecture 13 1. The statement the yen rose today from 121 to 117 makes sense because a. The U.S.

Study Questions Page 1 of 5 Part 1: Multiple Choice Select the best answer of those given. Study Questions Lecture 13 1. The statement the yen rose today from 121 to 117 makes sense because a. The U.S.

Introduction to Foreign Exchange Slides for International Finance (KOM Chapter 14)

") Slides for International Finance (KOM Chapter 14) American University 2011-09-01 Preview Introduction to Exchange Rates Basics exchange rate concepts Exchange rates and the cost of foreign goods The foreign

Slides for International Finance (KOM Chapter 14) American University 2011-09-01 Preview Introduction to Exchange Rates Basics exchange rate concepts Exchange rates and the cost of foreign goods The foreign

International Parity Conditions

International Parity Conditions Eiteman et al., Chapter 6 Winter 2004 Outline of the Chapter How are exchange rates determined? Can we predict them? Prices and Exchange Rates Prices Indices Inflation Rates

International Parity Conditions Eiteman et al., Chapter 6 Winter 2004 Outline of the Chapter How are exchange rates determined? Can we predict them? Prices and Exchange Rates Prices Indices Inflation Rates

Introduction to Foreign Exchange Slides for International Finance (KOM Chapter 14)

") Slides for International Finance (KOM Chapter 14) American University 2011-09-01 Preview Introduction to Exchange Rates Basics exchange rate concepts Exchange rates and the cost of foreign goods The foreign

Slides for International Finance (KOM Chapter 14) American University 2011-09-01 Preview Introduction to Exchange Rates Basics exchange rate concepts Exchange rates and the cost of foreign goods The foreign

Midterm - Economics 160B, Spring 2012 Version A

Name Student ID Section (or TA) Midterm - Economics 160B, Spring 2012 Version A You will have 75 minutes to complete this exam. There are 6 pages and 111 points total. Good luck. Multiple choice: Mark

Name Student ID Section (or TA) Midterm - Economics 160B, Spring 2012 Version A You will have 75 minutes to complete this exam. There are 6 pages and 111 points total. Good luck. Multiple choice: Mark

The Mundell-Fleming model

The Mundell-Fleming model dr hab. Bartłomiej Rokicki Chair of Macroeconomics and International Trade Theory Faculty of Economic Sciences, University of Warsaw Main assumptions of the model Small open economy

The Mundell-Fleming model dr hab. Bartłomiej Rokicki Chair of Macroeconomics and International Trade Theory Faculty of Economic Sciences, University of Warsaw Main assumptions of the model Small open economy

Lessons V and VI: FX Parity Conditions

Lessons V and VI: FX March 27, 2017 Table of Contents Does the PPP Hold Parity s should be thought of as break-even values, where the decision-maker is indifferent between two available strategies. Parity

Lessons V and VI: FX March 27, 2017 Table of Contents Does the PPP Hold Parity s should be thought of as break-even values, where the decision-maker is indifferent between two available strategies. Parity

Midterm - Economics 160B, Fall 2011 Version A

Name Student ID Section (or TA) Midterm - Economics 160B, Fall 2011 Version A You will have 75 minutes to complete this exam. There are 5 pages and 108 points total. Good luck. Multiple choice: Mark best

Name Student ID Section (or TA) Midterm - Economics 160B, Fall 2011 Version A You will have 75 minutes to complete this exam. There are 5 pages and 108 points total. Good luck. Multiple choice: Mark best

Financial markets in the open economy - the interest rate parity. Exchange rates in the short run.

Financial markets in the open economy - the interest rate parity. Exchange rates in the short run. Dr hab. Joanna Siwińska-Gorzelak Foreign Exchange Markets The set of markets where foreign currencies

Financial markets in the open economy - the interest rate parity. Exchange rates in the short run. Dr hab. Joanna Siwińska-Gorzelak Foreign Exchange Markets The set of markets where foreign currencies

Week-7. Dr. Ahmed. Domestic Firms International Firms Multinational Firms Global Firms

FINC 5880 Dr. Ahmed Week-7 Name Domestic Firms International Firms Multinational Firms Global Firms Factors that make multinational financial management different Exchange rates and trading International

FINC 5880 Dr. Ahmed Week-7 Name Domestic Firms International Firms Multinational Firms Global Firms Factors that make multinational financial management different Exchange rates and trading International

International Financial and Foreign Exchange Markets. Parity Relationships. Currency Options. Currency Arbitrages. Exercise Handbook.

Exercise Handbook March 30, 2018 Table of Contents Exercise XXXII In the 1990s, Russia was attempting to import more goods, but had little to offer to other countries in terms of potential exports. In

Exercise Handbook March 30, 2018 Table of Contents Exercise XXXII In the 1990s, Russia was attempting to import more goods, but had little to offer to other countries in terms of potential exports. In

Preview. Chapter 13. Depreciation and Appreciation. Definitions of Exchange Rates. Exchange Rates and the Foreign Exchange Market: An Asset Approach

Chapter 13 Exchange Rates and the Foreign Exchange Market: An Asset Approach Preview The basics of exchange rates Exchange rates and the prices of goods The foreign exchange markets The demand for currency

Chapter 13 Exchange Rates and the Foreign Exchange Market: An Asset Approach Preview The basics of exchange rates Exchange rates and the prices of goods The foreign exchange markets The demand for currency

Lessons V and VI: Overview

Lessons V and VI: Overview 1. FX parity conditions 2. Do the PPP and the IRPs (CIRP and UIRP) hold in practice? 1 FX parity conditions 2 FX parity conditions 1. The Law of One Price and the Purchasing

Lessons V and VI: Overview 1. FX parity conditions 2. Do the PPP and the IRPs (CIRP and UIRP) hold in practice? 1 FX parity conditions 2 FX parity conditions 1. The Law of One Price and the Purchasing

The Global Economy II I (4.5)

") The Global Economy II Nova SBE Fall 2017 Miguel Lebre de Freitas, Sharmin Sazedj Exam 5/1/2018 Duration: 2h00 I (4.5) Define three of the following concepts (3-5 lines each): i. Foreign exchange put option

The Global Economy II Nova SBE Fall 2017 Miguel Lebre de Freitas, Sharmin Sazedj Exam 5/1/2018 Duration: 2h00 I (4.5) Define three of the following concepts (3-5 lines each): i. Foreign exchange put option

Future Market Rates for Scenario Analysis

Future Market Rates for Scenario Analysis MTDS: Step 4 1 Step 4 (Market variables) Objective Identify baseline projections for market variables and the main risks to these Outcome A clearly defined baseline

Future Market Rates for Scenario Analysis MTDS: Step 4 1 Step 4 (Market variables) Objective Identify baseline projections for market variables and the main risks to these Outcome A clearly defined baseline

International Parity Conditions. 1. The Law of One Price. 2. Absolute Purchasing Power Parity

International Parity Conditions Some fundamental questions of international financial managers are: - What are the determinants of exchange rates? - Are changes in exchange rates predictable? The economic

International Parity Conditions Some fundamental questions of international financial managers are: - What are the determinants of exchange rates? - Are changes in exchange rates predictable? The economic

Lecture 2. Agenda: Basic descriptions for derivatives. 1. Standard derivatives Forward Futures Options

Lecture 2 Basic descriptions for derivatives Agenda: 1. Standard derivatives Forward Futures Options 2. Nonstandard derivatives ICON Range forward contract 1. Standard derivatives ~ Forward contracts:

Lecture 2 Basic descriptions for derivatives Agenda: 1. Standard derivatives Forward Futures Options 2. Nonstandard derivatives ICON Range forward contract 1. Standard derivatives ~ Forward contracts:

Relationships among Exchange Rates, Inflation, and Interest Rates

Relationships among Exchange Rates, Inflation, and Interest Rates Chapter Objectives To explain the purchasing power parity (PPP) and international Fisher effect (IFE) theories, and their implications

Relationships among Exchange Rates, Inflation, and Interest Rates Chapter Objectives To explain the purchasing power parity (PPP) and international Fisher effect (IFE) theories, and their implications

Rutgers University Spring Econ 336 International Balance of Payments Professor Roberto Chang. Problem Set 2. Deadline: March 1st.

Rutgers University Spring 2012 Econ 336 International Balance of Payments Professor Roberto Chang Problem Set 2. Deadline: March 1st Name: 1. The law of one price works under some assumptions. Which of

Rutgers University Spring 2012 Econ 336 International Balance of Payments Professor Roberto Chang Problem Set 2. Deadline: March 1st Name: 1. The law of one price works under some assumptions. Which of

INTERNATIONAL FINANCE TOPIC

INTERNATIONAL FINANCE 11 TOPIC The Foreign Exchange Market The dollar ($), the euro ( ), and the yen ( ) are three of the world s monies and most international payments are made using one of them. But

INTERNATIONAL FINANCE 11 TOPIC The Foreign Exchange Market The dollar ($), the euro ( ), and the yen ( ) are three of the world s monies and most international payments are made using one of them. But

Chapter 17 Appendix A

Chapter 17 Appendix A The Interest Parity Condition We can derive all the results in the text with a concept that is widely used in international finance. The interest parity condition shows the relationship

Chapter 17 Appendix A The Interest Parity Condition We can derive all the results in the text with a concept that is widely used in international finance. The interest parity condition shows the relationship

Prepared by Iordanis Petsas To Accompany. by Paul R. Krugman and Maurice Obstfeld

Chapter 13 Exchange Rates and the Foreign Exchange Market: An Asset Approach Prepared by Iordanis Petsas To Accompany International Economics: Theory and Policy, Sixth Edition by Paul R. Krugman and Maurice

Chapter 13 Exchange Rates and the Foreign Exchange Market: An Asset Approach Prepared by Iordanis Petsas To Accompany International Economics: Theory and Policy, Sixth Edition by Paul R. Krugman and Maurice

14.05 Intermediate Applied Macroeconomics Problem Set 5

14.05 Intermediate Applied Macroeconomics Problem Set 5 Distributed: November 15, 2005 Due: November 22, 2005 TA: Jose Tessada Frantisek Ricka 1. Rational exchange rate expectations and overshooting The

14.05 Intermediate Applied Macroeconomics Problem Set 5 Distributed: November 15, 2005 Due: November 22, 2005 TA: Jose Tessada Frantisek Ricka 1. Rational exchange rate expectations and overshooting The

05/07/55. International Parity Conditions. 1. The Law of One Price

International Parity Conditions Some fundamental questions of international financial managers are: - What are the determinants of exchange rates? - Are changes in exchange rates predictable? The economic

International Parity Conditions Some fundamental questions of international financial managers are: - What are the determinants of exchange rates? - Are changes in exchange rates predictable? The economic

International Parity Conditions

International Parity Conditions Some fundamental questions of international financial managers are: - What are the determinants of exchange rates? - Are changes in exchange rates predictable? The economic

International Parity Conditions Some fundamental questions of international financial managers are: - What are the determinants of exchange rates? - Are changes in exchange rates predictable? The economic

CHAPTER 8 MANAGEMENT OF TRANSACTION EXPOSURE ANSWERS & SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS

CHAPTER 8 MANAGEMENT OF TRANSACTION EXPOSURE ANSWERS & SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. How would you define transaction exposure? How is it different from economic exposure?

CHAPTER 8 MANAGEMENT OF TRANSACTION EXPOSURE ANSWERS & SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. How would you define transaction exposure? How is it different from economic exposure?

FETP/MPP8/Macroeconomics/Riedel. General Equilibrium in the Short Run

FETP/MPP8/Macroeconomics/Riedel General Equilibrium in the Short Run Determinants of aggregate demand in the short run A short-run model of output markets A short-run model of asset markets A short-run

FETP/MPP8/Macroeconomics/Riedel General Equilibrium in the Short Run Determinants of aggregate demand in the short run A short-run model of output markets A short-run model of asset markets A short-run

ECO 209Y MACROECONOMIC THEORY AND POLICY LECTURE 7: INTRODUCTION TO THE OPEN ECONOMY

ECO 209Y MACROECONOMIC THEORY AND POLICY LECTURE 7: INTRODUCTION TO THE OPEN ECONOMY Gustavo Indart Slide 1 THE BALANCE OF PAYMENTS On the one hand, the home country will export goods and services to other

ECO 209Y MACROECONOMIC THEORY AND POLICY LECTURE 7: INTRODUCTION TO THE OPEN ECONOMY Gustavo Indart Slide 1 THE BALANCE OF PAYMENTS On the one hand, the home country will export goods and services to other

ECO 209Y MACROECONOMIC THEORY AND POLICY LECTURE 3: AGGREGATE EXPENDITURE AND EQUILIBRIUM INCOME

ECO 209Y MACROECONOMIC THEORY AND POLICY LECTURE 3: AGGREGATE EXPENDITURE AND EQUILIBRIUM INCOME Gustavo Indart Slide 1 ASSUMPTIONS We will assume that: There is no depreciation There are no indirect taxes

ECO 209Y MACROECONOMIC THEORY AND POLICY LECTURE 3: AGGREGATE EXPENDITURE AND EQUILIBRIUM INCOME Gustavo Indart Slide 1 ASSUMPTIONS We will assume that: There is no depreciation There are no indirect taxes

Less Reliable International Parity Conditions

The International Parity Conditions The Law of One Price Interest Rate Parity Less Reliable International Parity Conditions The Real Exchange Rate 1 The International Parity Conditions Though this be madness,

The International Parity Conditions The Law of One Price Interest Rate Parity Less Reliable International Parity Conditions The Real Exchange Rate 1 The International Parity Conditions Though this be madness,

ECO 328 SUMMER Sample Questions Topics I.1-3. I.1 National Income Accounting and the Balance of Payments

ECO 328 SUMMER 2004--Sample Questions Topics I.1-3 I.1 National Income Accounting and the Balance of Payments 1. National income equals GNP A. less depreciation, less net unilateral transfers, less indirect

ECO 328 SUMMER 2004--Sample Questions Topics I.1-3 I.1 National Income Accounting and the Balance of Payments 1. National income equals GNP A. less depreciation, less net unilateral transfers, less indirect

NAME: ID Number: 3. Lump sum taxes cause effects. a) Do not; wealth b) do; wealth c) do; substitution d) both (b) and (c).

Do not; wealth b) do; wealth c) do; substitution d) both (b) and (c).") NAME: ID Number: Econ 302 Final May 11, 5:05 PM 7:05 PM Instructions: This exam consists of two parts. There are twenty-five multiple choice questions, each worth 2 points (totaling 50 points). The second

NAME: ID Number: Econ 302 Final May 11, 5:05 PM 7:05 PM Instructions: This exam consists of two parts. There are twenty-five multiple choice questions, each worth 2 points (totaling 50 points). The second

::Solutions:: Exam 1. You may use a calculator; you may not use any other device (cell phone, etc.)

") Issues in International Finance ::Solutions:: Exam 1 You have 75 minutes to complete this exam. You may use a calculator; you may not use any other device (cell phone, etc.) You may consult one page of

Issues in International Finance ::Solutions:: Exam 1 You have 75 minutes to complete this exam. You may use a calculator; you may not use any other device (cell phone, etc.) You may consult one page of

Chapter 2 Foreign Exchange Parity Relations

Chapter 2 Foreign Exchange Parity Relations Note: In the sixth edition of Global Investments, the exchange rate quotation symbols differ from previous editions. We adopted the convention that the first

Chapter 2 Foreign Exchange Parity Relations Note: In the sixth edition of Global Investments, the exchange rate quotation symbols differ from previous editions. We adopted the convention that the first

LINES AND SLOPES. Required concepts for the courses : Micro economic analysis, Managerial economy.

LINES AND SLOPES Summary 1. Elements of a line equation... 1 2. How to obtain a straight line equation... 2 3. Microeconomic applications... 3 3.1. Demand curve... 3 3.2. Elasticity problems... 7 4. Exercises...

LINES AND SLOPES Summary 1. Elements of a line equation... 1 2. How to obtain a straight line equation... 2 3. Microeconomic applications... 3 3.1. Demand curve... 3 3.2. Elasticity problems... 7 4. Exercises...

A CLOSED ECONOMY. 2-) In a closed economy, Y-C-G equals: a-) national saving. b-) private saving. c-) public saving. d-) nancial saving.

In a closed economy, Y-C-G equals: a-) national saving. b-) private saving. c-) public saving. d-) nancial saving.") TOBB-ETU, Economics Department Macroeconomics II (IKT 234) Closed and Open Economies in the Medium Run Intro 1 - Practice Questions (Ozan Eksi) A CLOSED ECONOMY 1-) In the classical model with xed output,

TOBB-ETU, Economics Department Macroeconomics II (IKT 234) Closed and Open Economies in the Medium Run Intro 1 - Practice Questions (Ozan Eksi) A CLOSED ECONOMY 1-) In the classical model with xed output,

Ch. 7 International Arbitrage and IRP. International Arbitrage. International Arbitrage

Ch. 7 and IRP Topics Locational Arbitrage Triangular Arbitrage Covered Interest Arbitrage Impact of Arbitrage on an MNC s Value Arbitrage: The simultaneous purchase and sale of securities or foreign exchange

Ch. 7 and IRP Topics Locational Arbitrage Triangular Arbitrage Covered Interest Arbitrage Impact of Arbitrage on an MNC s Value Arbitrage: The simultaneous purchase and sale of securities or foreign exchange

2. Discuss the implications of the interest rate parity for the exchange rate determination.

CHAPTER 5 INTERNATIONAL PARITY RELATIONSHIPS AND FORECASTING FOREIGN EXCHANGE RELATIONSHIPS SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. Give a full definition

CHAPTER 5 INTERNATIONAL PARITY RELATIONSHIPS AND FORECASTING FOREIGN EXCHANGE RELATIONSHIPS SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. Give a full definition

Problems involving Foreign Exchange Solutions

Problems involving Foreign Exchange Solutions 1. A bank quotes the following rates: CHF/USD 1.0898-1.0910 and JPY/USD 119 121. What is the minimum JPY/CHF bid and the maximum ask rate that the bank would

Problems involving Foreign Exchange Solutions 1. A bank quotes the following rates: CHF/USD 1.0898-1.0910 and JPY/USD 119 121. What is the minimum JPY/CHF bid and the maximum ask rate that the bank would

1)International Monetary System

International Monetary System") 1) (International Monetary System) 2) 3) (Balance of Payments) 4) (Foreign Exchange Market) 5) Interest Rate Parity (IRP) 6) Covered Interest Arbitrage 1 1)International Monetary System 1.1 The Gold Standard

1) (International Monetary System) 2) 3) (Balance of Payments) 4) (Foreign Exchange Market) 5) Interest Rate Parity (IRP) 6) Covered Interest Arbitrage 1 1)International Monetary System 1.1 The Gold Standard

Lecture 9: Exchange rates

BURNABY SIMON FRASER UNIVERSITY BRITISH COLUMBIA Paul Klein Office: WMC 3635 Phone: (778) 782-9391 Email: paul klein 2@sfu.ca URL: http://paulklein.ca/newsite/teaching/305.php Economics 305 Intermediate

BURNABY SIMON FRASER UNIVERSITY BRITISH COLUMBIA Paul Klein Office: WMC 3635 Phone: (778) 782-9391 Email: paul klein 2@sfu.ca URL: http://paulklein.ca/newsite/teaching/305.php Economics 305 Intermediate

A) decrease; decrease B) decrease; not change C) decrease; increase D) increase; decrease E) not change; increase

decrease; decrease B) decrease; not change C) decrease; increase D) increase; decrease E) not change; increase") Multiple Choice: On your answer sheet darken in the letter of your choice for each question. You should choose the suggested answer that BEST complete the statement or answers the question. 1) Suppose

Multiple Choice: On your answer sheet darken in the letter of your choice for each question. You should choose the suggested answer that BEST complete the statement or answers the question. 1) Suppose

MIDSUMMER EXAMINATIONS 2008

No. of Pages: (A) 8 No. of Questions: 38 EC1001A vv MIDSUMMER EXAMINATIONS 2008 Subject Title of Paper ECONOMICS EC1001 MACROECONOMICS Time Allowed Two Hours (2 Hours) Instructions to candidates This paper

No. of Pages: (A) 8 No. of Questions: 38 EC1001A vv MIDSUMMER EXAMINATIONS 2008 Subject Title of Paper ECONOMICS EC1001 MACROECONOMICS Time Allowed Two Hours (2 Hours) Instructions to candidates This paper

3. If the price of a British pound increases from $1.50 per pound to $1.80 per pound, we say that:

STUDY GUIDE FINAL ECO41 FALL 2013 UDAYAN ROY Ch 13 National Income Accounting See the questions in Homework 7 and Homework 8. CHAPTER 14 Exchange Rates and Interest Parity 1. How many dollars would it

STUDY GUIDE FINAL ECO41 FALL 2013 UDAYAN ROY Ch 13 National Income Accounting See the questions in Homework 7 and Homework 8. CHAPTER 14 Exchange Rates and Interest Parity 1. How many dollars would it

::Solutions:: Problem Set #2: Due end of class October 2, 2018

Issues in International Finance ::Solutions:: Problem Set #2: Due end of class October 2, 2018 You may discuss this problem set with your classmates, but everything you turn in must be your own work. Questions

Issues in International Finance ::Solutions:: Problem Set #2: Due end of class October 2, 2018 You may discuss this problem set with your classmates, but everything you turn in must be your own work. Questions

The Economics of International Financial Crises 4. Foreign Exchange Markets, Interest Rates and Exchange Rate Determination

Fletcher School of Law and Diplomacy, Tufts University The Economics of International Financial Crises 4. Foreign Exchange Markets, Interest Rates and Exchange Rate Determination Prof. George Alogoskoufis

Fletcher School of Law and Diplomacy, Tufts University The Economics of International Financial Crises 4. Foreign Exchange Markets, Interest Rates and Exchange Rate Determination Prof. George Alogoskoufis

LECTURE XIII. 30 July Monday, July 30, 12

LECTURE XIII 30 July 2012 TOPIC 15 Exchange Rates BIG PICTURE How do we evaluate currency across countries? How is the exchange rate determined? What is the relationship of the foreign exchange market

LECTURE XIII 30 July 2012 TOPIC 15 Exchange Rates BIG PICTURE How do we evaluate currency across countries? How is the exchange rate determined? What is the relationship of the foreign exchange market

Aggregate Supply and Demand

Aggregate demand is the relationship between GDP and the price level. When only the price level changes, GDP changes and we move along the Aggregate Demand curve. The total amount of goods and services,

Aggregate demand is the relationship between GDP and the price level. When only the price level changes, GDP changes and we move along the Aggregate Demand curve. The total amount of goods and services,

Foreign Exchange Markets: Key Institutional Features (cont)

") Foreign Exchange Markets FOREIGN EXCHANGE MARKETS Professor Anant Sundaram AGENDA Basic characteristics of FX markets: Institutional features Spot markets Forward markets Appreciation, depreciation, premium,

Foreign Exchange Markets FOREIGN EXCHANGE MARKETS Professor Anant Sundaram AGENDA Basic characteristics of FX markets: Institutional features Spot markets Forward markets Appreciation, depreciation, premium,

1. The short-run asset market approach model assumes A) fixed money supply B) fixed nominal exchange rate C) sticky price D) growing national income

fixed money supply B) fixed nominal exchange rate C) sticky price D) growing national income") 1. The short-run asset market approach model assumes A) fixed money supply B) fixed nominal exchange rate C) sticky price D) growing national income 2. Which of the following is true regarding the money

1. The short-run asset market approach model assumes A) fixed money supply B) fixed nominal exchange rate C) sticky price D) growing national income 2. Which of the following is true regarding the money

Name Student ID Summer Session II Midterm ECON160B There are 7 pages and 100 points. You have 100 minutes to complete the exam.

Name Student ID Summer Session II 2013 Midterm ECON160B There are 7 pages and 100 points. You have 100 minutes to complete the exam. Multiple Choice Choose the best answer. (2.5 points each, 30 points

Name Student ID Summer Session II 2013 Midterm ECON160B There are 7 pages and 100 points. You have 100 minutes to complete the exam. Multiple Choice Choose the best answer. (2.5 points each, 30 points

Policy Discussion Assignment 1

Management 495 Spring 2016 Topics in Finance: International Macroeconomics Policy Discussion Assignment 1 April 6, 2016 Due: Instructor: E-mail: Wed, April 27, before 9:30am Marc-Andreas Muendler muendler@ucsd.edu

Management 495 Spring 2016 Topics in Finance: International Macroeconomics Policy Discussion Assignment 1 April 6, 2016 Due: Instructor: E-mail: Wed, April 27, before 9:30am Marc-Andreas Muendler muendler@ucsd.edu

Chapter 17: Output and the Exchange Rate in the Short Run

Chapter 17: Output and the Exchange Rate in the Short Run Krugman, P.R., Obstfeld, M.: International Economics: Theory and Policy, 8th Edition, Pearson Addison-Wesley, 420-459 1 Preview Determinants of

Chapter 17: Output and the Exchange Rate in the Short Run Krugman, P.R., Obstfeld, M.: International Economics: Theory and Policy, 8th Edition, Pearson Addison-Wesley, 420-459 1 Preview Determinants of

Global Finance : PPP, IFE, IRP Project

Global Finance : PPP, IFE, IRP Project JRL 咨询公司 (JRL Consulting) 科技管理职场发展咨询电邮 : tech@jrleeconsulting.com 网站 : www.jrleeconsulting.com Two countries (Canada and Japan) were selected for this exercise to

Global Finance : PPP, IFE, IRP Project JRL 咨询公司 (JRL Consulting) 科技管理职场发展咨询电邮 : tech@jrleeconsulting.com 网站 : www.jrleeconsulting.com Two countries (Canada and Japan) were selected for this exercise to

ECON Intermediate Macroeconomics (Professor Gordon) Second Midterm Examination: Fall 2014 Answer sheet

Second Midterm Examination: Fall 2014 Answer sheet") ECON 311 - Intermediate Macroeconomics (Professor Gordon) Second Midterm Examination: Fall 2014 Answer sheet YOUR NAME: Student ID: Circle the TA session you attend: Chris - 3PM Andreas - 3PM Hugh - 3PM

ECON 311 - Intermediate Macroeconomics (Professor Gordon) Second Midterm Examination: Fall 2014 Answer sheet YOUR NAME: Student ID: Circle the TA session you attend: Chris - 3PM Andreas - 3PM Hugh - 3PM

Forward Foreign Exchange

Forward Foreign Exchange Concept of exchange rate risk or exposure» Hedging: Reducing exposure to exchange rate risk» Speculation: Increasing exposure to exchange rate risk Using the forward market to

Forward Foreign Exchange Concept of exchange rate risk or exposure» Hedging: Reducing exposure to exchange rate risk» Speculation: Increasing exposure to exchange rate risk Using the forward market to

International Parity Conditions

International Parity Conditions Fall 2013 Stephen Sapp Introduction The costs should be the same for buying and selling goods, services and financial assets in different countries when converted to a common

International Parity Conditions Fall 2013 Stephen Sapp Introduction The costs should be the same for buying and selling goods, services and financial assets in different countries when converted to a common

Financial Management in IB. Exercises

Financial Management in IB Exercises I. Foreign Exchange Market Locational Arbitrage Paris Interbank market: EUR/USD 1.2548/1.2552 London Interbank market: EUR/USD 1.2543/1.2546 =(1.2548-1.2546)*10000000=

Financial Management in IB Exercises I. Foreign Exchange Market Locational Arbitrage Paris Interbank market: EUR/USD 1.2548/1.2552 London Interbank market: EUR/USD 1.2543/1.2546 =(1.2548-1.2546)*10000000=

Print last name: Solution Given name: Student number: Section number

Department of Economics University of Toronto at Mississauga ECO202Y5Y Macroeconomic Theory and Policy July 2003 Test Two Dr. Gu Date: Tuesday, July 8, 2003 Time allowed: Two hours Aids allowed: Calculator

Department of Economics University of Toronto at Mississauga ECO202Y5Y Macroeconomic Theory and Policy July 2003 Test Two Dr. Gu Date: Tuesday, July 8, 2003 Time allowed: Two hours Aids allowed: Calculator

Chapter 17 (6) Output and the Exchange Rate in the Short Run

Output and the Exchange Rate in the Short Run") Chapter 17 (6) Output and the Exchange Rate in the Short Run Preview Determinants of aggregate demand in the short run A short-run model of output markets A short-run model of asset markets A short-run

Chapter 17 (6) Output and the Exchange Rate in the Short Run Preview Determinants of aggregate demand in the short run A short-run model of output markets A short-run model of asset markets A short-run

International Economics: Theory and Policy

International Economics: Theory and Policy Eleventh Edition Chapter 15 Money, Interest Rates, and Exchange Rates Learning Objectives 15.1 Describe and discuss the national money markets in which interest

International Economics: Theory and Policy Eleventh Edition Chapter 15 Money, Interest Rates, and Exchange Rates Learning Objectives 15.1 Describe and discuss the national money markets in which interest

ECON Intermediate Macroeconomics (Professor Gordon) Second Midterm Examination: Fall 2013 Answer sheet

Second Midterm Examination: Fall 2013 Answer sheet") ECON 311 - Intermediate Macroeconomics (Professor Gordon) Second Midterm Examination: Fall 2013 Answer sheet YOUR NAME: Student ID: Circle the TA session you attend: Chris - 10AM Chris - 1PM Andreas -

ECON 311 - Intermediate Macroeconomics (Professor Gordon) Second Midterm Examination: Fall 2013 Answer sheet YOUR NAME: Student ID: Circle the TA session you attend: Chris - 10AM Chris - 1PM Andreas -

11. Short Run versus Medium Run Determinants of Exchange Rates

Fletcher School of Law and Diplomacy, Tufts University 11. Short Run versus Medium Run Determinants of Exchange Rates E212 Macroeconomics Prof. George Alogoskoufis Short Run versus Medium Run Determinants

Fletcher School of Law and Diplomacy, Tufts University 11. Short Run versus Medium Run Determinants of Exchange Rates E212 Macroeconomics Prof. George Alogoskoufis Short Run versus Medium Run Determinants

1. Exchange Rates Definition: An exchange rate is a price: The relative price of two currencies.

Rauli Susmel Dept. of Finance Univ. of Houston FINA 4360 International Financial Management International Finance Many of the concepts and techniques are the same as the one used in other Finance classes.

Rauli Susmel Dept. of Finance Univ. of Houston FINA 4360 International Financial Management International Finance Many of the concepts and techniques are the same as the one used in other Finance classes.

Part B (Long Questions)

") Part B (Long Questions) Question B.1: Mundell-Fleming Model with Flexible Exchange Rates Suppose that a small open economy can be represented by the following model with a flexible exchange rate: C d =

Part B (Long Questions) Question B.1: Mundell-Fleming Model with Flexible Exchange Rates Suppose that a small open economy can be represented by the following model with a flexible exchange rate: C d =

Part I: Multiple Choice (36%) circle the correct answer

circle the correct answer") Econ 434 Professor Ickes Fall 2009 Midterm Exam II: Answer Sheet Instructions: Read the entire exam over carefully before beginning. The value of each question is given. Allocate your time efficiently

Econ 434 Professor Ickes Fall 2009 Midterm Exam II: Answer Sheet Instructions: Read the entire exam over carefully before beginning. The value of each question is given. Allocate your time efficiently

FETP/MPP8/Macroeconomics/Riedel. General Equilibrium in the Short Run II The IS-LM model

FETP/MPP8/Macroeconomics/iedel General Equilibrium in the Short un II The -LM model The -LM Model Like the AA-DD model, the -LM model is a general equilibrium model, which derives the conditions for simultaneous

FETP/MPP8/Macroeconomics/iedel General Equilibrium in the Short un II The -LM model The -LM Model Like the AA-DD model, the -LM model is a general equilibrium model, which derives the conditions for simultaneous

Chapter 10 3/19/2018. AGGREGATE SUPPLY AND AGGREGATE DEMAND (Part 1) Objectives. Aggregate Supply

Objectives. Aggregate Supply") Chapter 10 AGGREGATE SUPPLY AND AGGREGATE DEMAND (Part 1) Objectives Explain what determines aggregate supply in the long run and in the short run Explain what determines aggregate demand Explain how real

Chapter 10 AGGREGATE SUPPLY AND AGGREGATE DEMAND (Part 1) Objectives Explain what determines aggregate supply in the long run and in the short run Explain what determines aggregate demand Explain how real

Parity Conditions in International Finance and Currency Forecasting. Chapter 4

Parity Conditions in International Finance and Currency Forecasting Chapter 4 ١ ARBITRAGE AND THE LAW OF ONE PRICE Five Parity Conditions Result From Arbitrage Activities 1. Purchasing Power Parity (PPP)

Parity Conditions in International Finance and Currency Forecasting Chapter 4 ١ ARBITRAGE AND THE LAW OF ONE PRICE Five Parity Conditions Result From Arbitrage Activities 1. Purchasing Power Parity (PPP)

Capital & Money Markets

Πανεπιστήμιο Πειραιώς, Τμήμα Τραπεζικής και Χρηματοοικονομικής Διοικητικής Μεταπτυχιακό Πρόγραμμα «Χρηματοοικονομική και Τραπεζική Διοικητική» Capital & Money Markets Section 1 Foreign Exchange Markets

Πανεπιστήμιο Πειραιώς, Τμήμα Τραπεζικής και Χρηματοοικονομικής Διοικητικής Μεταπτυχιακό Πρόγραμμα «Χρηματοοικονομική και Τραπεζική Διοικητική» Capital & Money Markets Section 1 Foreign Exchange Markets

The Mundell Fleming Model. The Mundell Fleming Model is a simple open economy version of the IS LM model.

International Finance Lecture 4 Autumn 2011 The Mundell Fleming Model The Mundell Fleming Model is a simple open economy version of the IS LM model. I. The Model A. The goods market Goods market equilibrium

International Finance Lecture 4 Autumn 2011 The Mundell Fleming Model The Mundell Fleming Model is a simple open economy version of the IS LM model. I. The Model A. The goods market Goods market equilibrium

Economics 3422 Sample Midterm examination. Part A: Multiple-choice questions. Choose the best alternative. The total for Part A is 25 points.

Economics 3422 Sample Midterm examination Instruction: Put your name and PeopleSoft ID on the question sheets and the blue book. Put your answers in the blue book only. Turn in both at the end of the examination.

Economics 3422 Sample Midterm examination Instruction: Put your name and PeopleSoft ID on the question sheets and the blue book. Put your answers in the blue book only. Turn in both at the end of the examination.

Madura: International Financial Management Chapter 8

Madura: International Financial Management Chapter Chapter Relationships Between Inflation, Interest Rates, and Exchange Rates Chapter Objectives To explain the theories of purchasing power parity (PPP)

Madura: International Financial Management Chapter Chapter Relationships Between Inflation, Interest Rates, and Exchange Rates Chapter Objectives To explain the theories of purchasing power parity (PPP)

RPH GLOBAL SOVEREIGN BOND FUND L.P. NOTES TO FINANCIAL STATEMENTS

1. ESTABLISHMENT OF FUND RPH Global Sovereign Bond Fund L.P. [the "Fund"] is a limited partnership established under the laws of the Province of Ontario. Investors in the Fund will become limited partners

1. ESTABLISHMENT OF FUND RPH Global Sovereign Bond Fund L.P. [the "Fund"] is a limited partnership established under the laws of the Province of Ontario. Investors in the Fund will become limited partners

Introduction to Foreign Exchange Slides for International Finance (KOMIF Chapter 3)

") Slides for International Finance (KOMIF Chapter 3) American University 2017-09-14 Preview Introduction to Exchange Rates Basic exchange rate concepts Exchange rates and the cost of foreign goods The foreign

Slides for International Finance (KOMIF Chapter 3) American University 2017-09-14 Preview Introduction to Exchange Rates Basic exchange rate concepts Exchange rates and the cost of foreign goods The foreign

LESSON - 26 FOREIGN EXCHANGE - 1. Learning outcomes

LESSON - 26 FOREIGN EXCHANGE - 1 Learning outcomes After studying this unit, you should be able to: Define foreign exchange Know foreign exchange markets functions of foreign exchange market methods affecting

LESSON - 26 FOREIGN EXCHANGE - 1 Learning outcomes After studying this unit, you should be able to: Define foreign exchange Know foreign exchange markets functions of foreign exchange market methods affecting

QUEEN S UNIVERSITY FACULTY OF ARTS AND SCIENCE DEPARTMENT OF ECONOMICS. Economics 222 A&B Macroeconomic Theory I. Final Examination 20 April 2009

Page 1 of 9 QUEEN S UNIVERSITY FACULTY OF ARTS AND SCIENCE DEPARTMENT OF ECONOMICS Economics 222 A&B Macroeconomic Theory I Final Examination 20 April 2009 Instructors: Nicolas-Guillaume Martineau (Section

Page 1 of 9 QUEEN S UNIVERSITY FACULTY OF ARTS AND SCIENCE DEPARTMENT OF ECONOMICS Economics 222 A&B Macroeconomic Theory I Final Examination 20 April 2009 Instructors: Nicolas-Guillaume Martineau (Section

Ex-ante cost and charges disclosure 1

Ex-ante cost and charges disclosure 1 Introduction An important element which needs to be taken into consideration when trading with Rabobank, is the cost of our services and the cost related to the financial

Ex-ante cost and charges disclosure 1 Introduction An important element which needs to be taken into consideration when trading with Rabobank, is the cost of our services and the cost related to the financial