UDC: NEW HIGHS AND PERCENTAGE RETURN. Marcus Davidsson. Independent Researcher, Sweden

|

|

|

- Randolph Taylor

- 6 years ago

- Views:

Transcription

1 UDC: NEW HIGHS AND PERCENTAGE RETURN Marcus Davidsson Independent Researcher, Sweden Abstract We will in this paper investigate the empirical relationship between the number of new highs (lows) and percentage return for 2500 stocks. The theoretical argument is that stocks that historically have produced large long (short) returns all have in common that they systematically made new highs (lows). We find that the number of highs (lows) is statistically significant and can together explain up to 35% of the variation of stock return. Keywords: trend following, new highs, investment Introduction Many different authors such as Markowitz (1959), Sharpe (1964), Covel (2004), Pedersen and Zwart (2004) and Gwilym et al (2010) have described the ben efit of using trend-following models when making investments in financial markets. A trend can be defined in many different ways. One way to define it is by using risk adjusted returns. The higher the risk adjusted return is the more the asset is trending. Another way is to look at price increase and price drawdown. The higher the percentage increase is and the lower the price drawdown is the more the asset is trending. A third way is to calculate the number of new highs (lows) a stock has made. The higher such a number is the more the asset is trending. The interesting thing to note is that all assets that historically have produced large long (short) returns all have in common that they systematically have made new highs (lows) over time. The price of a stock cannot increase without making new highs over time and a stock price cannot decrease without making new lows over time. Jegadeesh & Titman (1993) have shown that an investor that takes a long position in the stock that has outperformed and hold such positions for the next six months would on average made a twelve percentage annual return. Grinblatt, Titman, and Wermers (1995) 55

2 found that 77 percent of the mutual funds under investigation used a momentum investment strategy i.e. buying past winners. George and Hwang (2004) and Liu et al (2010) argue that the 52-week high price explains a large portion of the profits from momentum investing. Szakmarya, Shenb and Sharmac (2010) note that trend following strategies plays an important role in the commodity futures markets. They use monthly data for 28 markets for a 48 year time period to show that a trend following strategy has produced positive returns net of transaction costs in at least 22 markets out of 28. Jamesa (2003) argues that trend following strategies is an important tool when it comes to currency trading. The author shows by looking at FX data that a simple moving average can increase returns significantly. Such a strategy also results in an increase in the information ratio. The dynamic nature seems to be the key factor explaining such performance. Fung & Hsieh (2001) looked at empirical data for 407 trend -following funds. They found that trend following returns tends to be asymmetric which means that linear factor models might not be appropriate to analyze the performance of such funds. They also found that trend-following funds tend to do well when market crashes or rallies. Also benchmark indices as a proxy for risk might not be appropriate to use when it comes to trend-following funds due to the many different ways of implementations such basic strategy. The authors further explain that option models like look-back straddles can explain the trend following return much better than benchmark indices. This is also supported by authors such as Glosten and Jagannathan (1994) who came to the same conclusion by analyzing the performance of 130 mutual funds during the period Fung and Hsieh (2004) use eight dynamic risk factors which they show can explain up to 80% of diversified hedge funds monthly return variation. Capoccia and Hübner (2004) analyzed the performance of hedge funds by looking at a large database consisting of 2796 individual funds. They found that the general hedge fund showed little evidence of persistence in performance. However, they also found a small subsample, which was not representative for the group, that did have persistent performance. Kosowskia, Naikb and Teoc (2007) on the other hand argue that top hedge fund performance cannot be explained by luck since their performance persists on an annual basis. They also explain that Bayesian methods will produce increase performance predictability of hedge funds. Balia, Gokcanb and Liangc (2007) found that there exist a significant and positive relationship between hedge funds return and Value-at-Risk (VaR). They looked at a large dataset for the period 1995 to 56

3 2003 and discovered that funds with high VaR outperformed funds with low VaR with an annual return difference of 9%. I. We will in this section empirically investigate the relationship between the number of new highs (low) and percentage return. We will use two different datasets. One dataset consists of monthly data for SP500 (470 Stocks) for the period and one dataset consists of monthly data for NYSE (2038 Stocks) for the period In exhibit-1 you can find the summary of the regression models and its output. In exhibit-2 we can see how the number of new highs and lows are calculated. In exhibit-3 we can see the number of new highs (lows) and long (sh ort) percentage returns. In exhibit-4 to exhibit-7 we can see the regression models for the two datasets and the cumulative return for an investor that takes a long (short) position the stock that has had the largest number of new highs (lows) during the previous period. Finally in exhibit-8 we can see the regression result where the dependent variable is the absolute percentage return and the two independent variables are the number of new highs and the number of new lows. Exhibit-1 Data Sets and Regression Models SP500 (470 Stocks) NYSE (2038 Stocks) Monthly Data Monthly Data 74 Observations 71 Observations Long Return and New Highs Short Returns and New Lows y=a+b1*x1 y = long return, x1 = # of new highs a = -114 B1 = 7.5 TstatB1 = 8.77 (sign ificant) Rsquare = 0.14 y=a+b1*x2 y = short return, x2 = # of new lows a = -53 B1 = 11.4 TstatB1 = 8.3 (signifi cant) Rsquare = 0.12 y=a+b1*x1 y = long return, x1 = # of new highs a = B1 = 8.03 TstatB1 = (significant) Rsquare = 0.19 y=a+b1*x2 y = short return, x2 = # of new lows a = B1 = 8.19 TstatB1 = (significant) Rsquare =

4 Abs Returns y=a+b1*x1+b2*x2 y = abs return, x1 = # of new highs y=a+b1*x1+b2*x2 y = abs return, x1 = # of new and New x2 = # of new lows highs Lows and a = B1 = 4.96 B2 = 3.87 x2 = # of new lows New Highs TstatB1 = 5.06 (significant) a = B1 = 5.86 B2 = 2.25 TstatB2 = 2.4 (significant) TstatB1 = (significant) Rsquare = 0.05 TstatB2 = 4.54 (signifi cant) Rsquare = 0.09 Exhibit-2 Roadmap to Calculate New Highs and New Lows 58

5 p[t] = price time t New Highs P[0] p[1] p[2] p[3] p[4] p[5] p[6] p[7] NH=# of New Highs t=0 p[0]=max[0] and NH[0]=0 t=1 p[1]>max[t-1] -> max[t]=p[1] and NH[t] = NH[t-1] + 1 = 1 t=2 p[2]<max[t-1] -> max[t]=max[t-1] and NH[t] = NH[t-1] = 1 t=3 p[3]>max[t-1] -> max[t]=p[3] and NH[t] = NH[t-1] + 1 = 2 p[t] = price time t New Lows P[0] p[1] p[2] p[3] p[4] p[5] p[6] p[7] NL=# of New Lows t=0 p[0]=min[0] and NH[0]=0 t=1 p[1]<min[t-1] -> min[t]=p[1] and NL[t] = NL[t-1] + 1 = 1 t=2 p[2]>min[t-1] -> min[t]=min[t-1] and NL[t] = NL[t-1] = 1 t=3 p[3]<min[t-1] -> min[t]=p[3] and NL[t] = NL[t-1] + 1 = 2 59

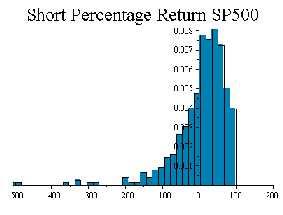

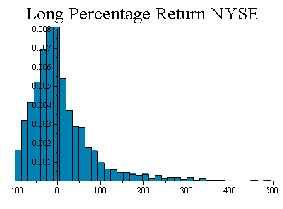

6 Exhibit-3 New Highs (Lows) and Long (Short) Returns for the two Datasets Exhibit-4 Percentage Long Returns and New Highs SP500 60

7 Exhibit-5 Percentage Short Returns and New Lows SP500 61

8 Exhibit-6 Percentage Long Returns and New Highs NYSE 62

9 Exhibit-7 Percentage Short Returns and New Lows NYSE 63

10 Exhibit-8 Absolute Returns and New Highs and New Lows 64

11 Conclusion We have in this paper analyzed the empirical relationship between the number of new highs (lows) and percentage return for a large sample of stocks. The theoretical argument is 65

12 that stocks that historically have produced large long (short) returns all have in common that they systematically have made new highs (lows). See appendix-1 for further details. Hence, a stock that has a large number of new highs should also produce higher long returns than a stock with a small number of new highs. The same argument does also apply to short positions. The short return is simply -1*long return. We have seen in exhibit-1 that the variable the number of new highs is highly significant for the two dataset which means that the number of new highs can explain a lot of the variation in long percentage returns. The Rsquare was 0.14 and 0.19 for the two models. The variable the number of new lows was also highly significant for the two dataset which means that the number of new lows can explain a lot of the variation in short percentage returns. The Rsquare was 0.12 and 0.16 for the two models. The relationship between the number of new highs (low) and long (short) percentage returns is marginally stronger (weaker) due to differences in Rsquare. What was not expected was the low Rsquare (0.05 and 0.09) for multiple regression where the dependent variable was absolute percentage returns and the two independent variables where the number of new highs and the number of new lows. One would have expected a higher Rsquare than these models separately, however that was not the case. If we interpret the absolute return as volatility it makes more sense since volatility and new high (lows) usually don t go together. We can also see in appendix-2 how the number of new highs (lows) changes over time for different stocks included in the datasets. In appendix-3 a new dataset is introduced which consists of monthly data from for 23 global stock market indices. We can see the cumulative return for an investor that takes a long (short) position the market that has had the largest number of new highs (lows) during the previous period. References: Balia, T, Gokcanb, S and Liangc, B (2007) Value at risk and the cross-section of hedge fund returns, Journal of Banking & Finance, vol 31, issue 4, pp Capoccia, D and Hübner, G (2004) Analysis of hedge fund performance Journal of Empirical Finance, vol 11, issue 1, pp Covel, M (2004) Trend Following: How Great Traders Make Millions in Up or Down Markets, Pearson Education Inc Fung, W & Hsieh, D (2001) The Risk in Hedge Fund Strategies: Theory and Evidence from Trend Followers, the Review of Financial Studies, vol. 14, no. 2 66

13 Fung, W and Hsieh, D (2004) Hedge Fund Benchmarks: A Risk-Based Approach, Financial Analysts Journal, vol. 60, no. 5, pp George, T and Hwang, C (2004) The 52 -Week High and Momentum Investing, Journal of Finance, volume: 59, issue: 5, pp Gwilym, O, Clare, A, Seaton, J and Thomas, S (201 0) Price and Momentum as Robust Tactical Approaches to Global Equity Investing, The Journal of Investing, vol. 19, no. 3 Grinblatt, M, Titman, S, and Wermers, R (1995) Momentum Investment Strategies, Portfolio Performance, and Herding: A Study of Mutual Fund Behaviour. American Economic Review, vol 85, issue 5, pp Glosten, L and Jagannathan, R (1994) A Contingen t Claim Approach to Performance Evaluation, Journal of Empirical Finance, vol 1, issue 2, pp Jegadeesh, N & Titman, S (1993) Returns to buy ing winners and selling losers, Journal of Finance 48, Jamesa, J (2003) Simple trend-following strategies in currency trading Quantitative Finance, vol 3, issue 4, pp Kosowskia, R, Naikb, N and Teoc, M (2007) Do hedge funds deliver alpha? A Bayesian and bootstrap analysis, Journal of Financial Economics, vol 84, issue 1, pp Liu, M, Liu, Q and Ma, T (2010) The 52 -week high momentum strategy in international stock markets, Journal of International Money and Finance, volume 30, issue 1, pp Markowitz, H (1959) Portfolio Selection: Efficient Diversification of Investment. New York: John Wiley & Sons Pedersen, H and Zwart, G (2004) Uncoveri ng the Trend-Following Strategy The Journal of Portfolio Management, vol. 31, no. 1, pp Sharpe, W (1964) Capital Asset Prices - A Theory of Market Equilibrium Under Conditions of Risk, Journal of Finance, vol 19, issue 3, pp Szakmarya, A, Shenb, Q and Sharmac, S (2010) Trend -following trading strategies in commodity futures, Journal of Banking & Finance, volume 34, issue 2, pp

14 Appendix-1 Simulated Data and Number of New Highs 68

15 Appendix-2 Number of New Highs (Lows) over Time 69

16 70

17 Appendix-3 Global Stock Market Indices Dataset Monthly data from for 23 global stock market indices 71

Expected Return and Portfolio Rebalancing

Expected Return and Portfolio Rebalancing Marcus Davidsson Newcastle University Business School Citywall, Citygate, St James Boulevard, Newcastle upon Tyne, NE1 4JH E-mail: davidsson_marcus@hotmail.com

Expected Return and Portfolio Rebalancing Marcus Davidsson Newcastle University Business School Citywall, Citygate, St James Boulevard, Newcastle upon Tyne, NE1 4JH E-mail: davidsson_marcus@hotmail.com

Price and Momentum as Robust Tactical Approaches to Global Equity Investing

WORKING PAPER Price and Momentum as Robust Tactical Approaches to Global Equity Investing Owain ap Gwilym, Andrew Clare, James Seaton & Stephen Thomas May 2009 ISSN Centre for Asset Management Research

WORKING PAPER Price and Momentum as Robust Tactical Approaches to Global Equity Investing Owain ap Gwilym, Andrew Clare, James Seaton & Stephen Thomas May 2009 ISSN Centre for Asset Management Research

Enhancing equity portfolio diversification with fundamentally weighted strategies.

Enhancing equity portfolio diversification with fundamentally weighted strategies. This is the second update to a paper originally published in October, 2014. In this second revision, we have included

Enhancing equity portfolio diversification with fundamentally weighted strategies. This is the second update to a paper originally published in October, 2014. In this second revision, we have included

Short Term Alpha as a Predictor of Future Mutual Fund Performance

Short Term Alpha as a Predictor of Future Mutual Fund Performance Submitted for Review by the National Association of Active Investment Managers - Wagner Award 2012 - by Michael K. Hartmann, MSAcc, CPA

Short Term Alpha as a Predictor of Future Mutual Fund Performance Submitted for Review by the National Association of Active Investment Managers - Wagner Award 2012 - by Michael K. Hartmann, MSAcc, CPA

Just a One-Trick Pony? An Analysis of CTA Risk and Return

J.P. Morgan Center for Commodities at the University of Colorado Denver Business School Just a One-Trick Pony? An Analysis of CTA Risk and Return Jason Foran Mark Hutchinson David McCarthy John O Brien

J.P. Morgan Center for Commodities at the University of Colorado Denver Business School Just a One-Trick Pony? An Analysis of CTA Risk and Return Jason Foran Mark Hutchinson David McCarthy John O Brien

Portfolio Theory Forward Testing

Advances in Management & Applied Economics, vol. 3, no.3, 2013, 225-244 ISSN: 1792-7544 (print version), 1792-7552(online) Scienpress Ltd, 2013 Portfolio Theory Forward Testing Marcus Davidsson 1 Abstract

Advances in Management & Applied Economics, vol. 3, no.3, 2013, 225-244 ISSN: 1792-7544 (print version), 1792-7552(online) Scienpress Ltd, 2013 Portfolio Theory Forward Testing Marcus Davidsson 1 Abstract

The Trend is Your Friend: Time-series Momentum Strategies across Equity and Commodity Markets

The Trend is Your Friend: Time-series Momentum Strategies across Equity and Commodity Markets Athina Georgopoulou *, George Jiaguo Wang This version, June 2015 Abstract Using a dataset of 67 equity and

The Trend is Your Friend: Time-series Momentum Strategies across Equity and Commodity Markets Athina Georgopoulou *, George Jiaguo Wang This version, June 2015 Abstract Using a dataset of 67 equity and

Seminar HWS 2012: Hedge Funds and Liquidity

Universität Mannheim 68131 Mannheim 25.11.200925.11.2009 Besucheradresse: L9, 1-2 68161 Mannheim Telefon 0621/181-3755 Telefax 0621/181-1664 Nic Schaub schaub@bwl.uni-mannheim.de http://intfin.bwl.uni-mannheim.de

Universität Mannheim 68131 Mannheim 25.11.200925.11.2009 Besucheradresse: L9, 1-2 68161 Mannheim Telefon 0621/181-3755 Telefax 0621/181-1664 Nic Schaub schaub@bwl.uni-mannheim.de http://intfin.bwl.uni-mannheim.de

A test of momentum strategies in funded pension systems - the case of Sweden. Tomas Sorensson*

A test of momentum strategies in funded pension systems - the case of Sweden Tomas Sorensson* This draft: January, 2013 Acknowledgement: I would like to thank Mikael Andersson and Jonas Murman for excellent

A test of momentum strategies in funded pension systems - the case of Sweden Tomas Sorensson* This draft: January, 2013 Acknowledgement: I would like to thank Mikael Andersson and Jonas Murman for excellent

Risk-Adjusted Momentum: A Superior Approach to Momentum Investing

Bridgeway Capital Management, Inc. Rasool Shaik, CFA Portfolio Manager Fall 2011 : A Superior Approach to Investing Synopsis This paper summarizes our methodology and findings on a risk-adjusted momentum

Bridgeway Capital Management, Inc. Rasool Shaik, CFA Portfolio Manager Fall 2011 : A Superior Approach to Investing Synopsis This paper summarizes our methodology and findings on a risk-adjusted momentum

Evaluating the Performance Persistence of Mutual Fund and Hedge Fund Managers

Evaluating the Performance Persistence of Mutual Fund and Hedge Fund Managers Iwan Meier Self-Declared Investment Objective Fund Basics Investment Objective Magellan Fund seeks capital appreciation. 1

Evaluating the Performance Persistence of Mutual Fund and Hedge Fund Managers Iwan Meier Self-Declared Investment Objective Fund Basics Investment Objective Magellan Fund seeks capital appreciation. 1

Man vs. Machine: Comparing Discretionary and Systematic Hedge Fund Performance

Man vs. Machine: Comparing Discretionary and Systematic Hedge Fund Performance Campbell R. Harvey, Sandy Rattray, Andrew Sinclair, Otto Van Hemert* This version: December 6 th, 2016 ABSTRACT We analyse

Man vs. Machine: Comparing Discretionary and Systematic Hedge Fund Performance Campbell R. Harvey, Sandy Rattray, Andrew Sinclair, Otto Van Hemert* This version: December 6 th, 2016 ABSTRACT We analyse

Mutual fund herding behavior and investment strategies in Chinese stock market

Mutual fund herding behavior and investment strategies in Chinese stock market AUTHORS ARTICLE INFO DOI John Wei-Shan Hu Yen-Hsien Lee Ying-Chuang Chen John Wei-Shan Hu, Yen-Hsien Lee and Ying-Chuang Chen

Mutual fund herding behavior and investment strategies in Chinese stock market AUTHORS ARTICLE INFO DOI John Wei-Shan Hu Yen-Hsien Lee Ying-Chuang Chen John Wei-Shan Hu, Yen-Hsien Lee and Ying-Chuang Chen

Economic Uncertainty and the Cross-Section of Hedge Fund Returns

Economic Uncertainty and the Cross-Section of Hedge Fund Returns Turan Bali, Georgetown University Stephen Brown, New York University Mustafa Caglayan, Ozyegin University Introduction Knight (1921) draws

Economic Uncertainty and the Cross-Section of Hedge Fund Returns Turan Bali, Georgetown University Stephen Brown, New York University Mustafa Caglayan, Ozyegin University Introduction Knight (1921) draws

NCER Working Paper Series

NCER Working Paper Series Momentum in Australian Stock Returns: An Update A. S. Hurn and V. Pavlov Working Paper #23 February 2008 Momentum in Australian Stock Returns: An Update A. S. Hurn and V. Pavlov

NCER Working Paper Series Momentum in Australian Stock Returns: An Update A. S. Hurn and V. Pavlov Working Paper #23 February 2008 Momentum in Australian Stock Returns: An Update A. S. Hurn and V. Pavlov

Strategy diversification: Combining momentum and carry strategies within a foreign exchange portfolio

Original Article Strategy diversification: Combining momentum and carry strategies within a foreign exchange portfolio Received (in revised form): 16th December 2013 Francis Olszweski is Managing Director

Original Article Strategy diversification: Combining momentum and carry strategies within a foreign exchange portfolio Received (in revised form): 16th December 2013 Francis Olszweski is Managing Director

Do Indian Mutual funds with high risk adjusted returns show more stability during an Economic downturn?

Do Indian Mutual funds with high risk adjusted returns show more stability during an Economic downturn? Kalpakam. G, Faculty Finance, KJ Somaiya Institute of management Studies & Research, Mumbai. India.

Do Indian Mutual funds with high risk adjusted returns show more stability during an Economic downturn? Kalpakam. G, Faculty Finance, KJ Somaiya Institute of management Studies & Research, Mumbai. India.

International Journal of Management Sciences and Business Research, 2013 ISSN ( ) Vol-2, Issue 12

Vol-2, Issue 12") Momentum and industry-dependence: the case of Shanghai stock exchange market. Author Detail: Dongbei University of Finance and Economics, Liaoning, Dalian, China Salvio.Elias. Macha Abstract A number of

Momentum and industry-dependence: the case of Shanghai stock exchange market. Author Detail: Dongbei University of Finance and Economics, Liaoning, Dalian, China Salvio.Elias. Macha Abstract A number of

Can Hedge Funds Time the Market?

International Review of Finance, 2017 Can Hedge Funds Time the Market? MICHAEL W. BRANDT,FEDERICO NUCERA AND GIORGIO VALENTE Duke University, The Fuqua School of Business, Durham, NC LUISS Guido Carli

International Review of Finance, 2017 Can Hedge Funds Time the Market? MICHAEL W. BRANDT,FEDERICO NUCERA AND GIORGIO VALENTE Duke University, The Fuqua School of Business, Durham, NC LUISS Guido Carli

AN INTRODUCTION TO FACTOR INVESTING

WHITE PAPER AN INTRODUCTION TO FACTOR INVESTING THIS DOCUMENT IS INTENDED FOR INSTITUTIONAL INVESTORS ONLY. IT SHOULD NOT BE DISTRIBUTED TO, OR USED BY, INDIVIDUAL INVESTORS. OUR RESEARCH COMMITMENT As

WHITE PAPER AN INTRODUCTION TO FACTOR INVESTING THIS DOCUMENT IS INTENDED FOR INSTITUTIONAL INVESTORS ONLY. IT SHOULD NOT BE DISTRIBUTED TO, OR USED BY, INDIVIDUAL INVESTORS. OUR RESEARCH COMMITMENT As

Chris Brightman, CFA, Feifei Li, Ph.D., FRM, and Xi Liu, CFA

Chasing Performance with ETFs Chris Brightman, CFA, Feifei Li, Ph.D., FRM, and Xi Liu, CFA Chris Brightman, CFA What s hot may change abruptly, but investors penchant for what s hot is steady. KEY POINTS

Chasing Performance with ETFs Chris Brightman, CFA, Feifei Li, Ph.D., FRM, and Xi Liu, CFA Chris Brightman, CFA What s hot may change abruptly, but investors penchant for what s hot is steady. KEY POINTS

ANALYZING MOMENTUM EFFECT IN HIGH AND LOW BOOK-TO-MARKET RATIO FIRMS WITH SPECIFIC REFERENCE TO INDIAN IT, BANKING AND PHARMACY FIRMS ABSTRACT

ANALYZING MOMENTUM EFFECT IN HIGH AND LOW BOOK-TO-MARKET RATIO FIRMS WITH SPECIFIC REFERENCE TO INDIAN IT, BANKING AND PHARMACY FIRMS 1 Dr.Madhu Tyagi, Professor, School of Management Studies, Ignou, New

ANALYZING MOMENTUM EFFECT IN HIGH AND LOW BOOK-TO-MARKET RATIO FIRMS WITH SPECIFIC REFERENCE TO INDIAN IT, BANKING AND PHARMACY FIRMS 1 Dr.Madhu Tyagi, Professor, School of Management Studies, Ignou, New

Exploiting Factor Autocorrelation to Improve Risk Adjusted Returns

Exploiting Factor Autocorrelation to Improve Risk Adjusted Returns Kevin Oversby 22 February 2014 ABSTRACT The Fama-French three factor model is ubiquitous in modern finance. Returns are modeled as a linear

Exploiting Factor Autocorrelation to Improve Risk Adjusted Returns Kevin Oversby 22 February 2014 ABSTRACT The Fama-French three factor model is ubiquitous in modern finance. Returns are modeled as a linear

Risk-managed 52-week high industry momentum, momentum crashes, and hedging macroeconomic risk

Risk-managed 52-week high industry momentum, momentum crashes, and hedging macroeconomic risk Klaus Grobys¹ This draft: January 23, 2017 Abstract This is the first study that investigates the profitability

Risk-managed 52-week high industry momentum, momentum crashes, and hedging macroeconomic risk Klaus Grobys¹ This draft: January 23, 2017 Abstract This is the first study that investigates the profitability

Quantitative Analysis in Finance

*** This syllabus is tentative and subject to change as needed. Quantitative Analysis in Finance Professor: E-mail: sean.shin@aalto.fi Phone: +358-50-304-3004 Office: G2.10 (Office hours: by appointment)

*** This syllabus is tentative and subject to change as needed. Quantitative Analysis in Finance Professor: E-mail: sean.shin@aalto.fi Phone: +358-50-304-3004 Office: G2.10 (Office hours: by appointment)

APPLIED FINANCE LETTERS

APPLIED FINANCE LETTERS VOLUME 5, ISSUE 1, 2016 THE MEASUREMENT OF TRACKING ERRORS OF GOLD ETFS: EVIDENCE FROM CHINA Wei-Fong Pan 1*, Ting Li 2 1. Investment Analyst, Sales and Trading Department, Ping

APPLIED FINANCE LETTERS VOLUME 5, ISSUE 1, 2016 THE MEASUREMENT OF TRACKING ERRORS OF GOLD ETFS: EVIDENCE FROM CHINA Wei-Fong Pan 1*, Ting Li 2 1. Investment Analyst, Sales and Trading Department, Ping

International Finance. Investment Styles. Campbell R. Harvey. Duke University, NBER and Investment Strategy Advisor, Man Group, plc.

International Finance Investment Styles Campbell R. Harvey Duke University, NBER and Investment Strategy Advisor, Man Group, plc February 12, 2017 2 1. Passive Follow the advice of the CAPM Most influential

International Finance Investment Styles Campbell R. Harvey Duke University, NBER and Investment Strategy Advisor, Man Group, plc February 12, 2017 2 1. Passive Follow the advice of the CAPM Most influential

A Short Note on the Potential for a Momentum Based Investment Strategy in Sector ETFs

Journal of Finance and Economics Volume 8, No. 1 (2018), 35-41 ISSN 2291-4951 E-ISSN 2291-496X Published by Science and Education Centre of North America A Short Note on the Potential for a Momentum Based

Journal of Finance and Economics Volume 8, No. 1 (2018), 35-41 ISSN 2291-4951 E-ISSN 2291-496X Published by Science and Education Centre of North America A Short Note on the Potential for a Momentum Based

Dynamic Smart Beta Investing Relative Risk Control and Tactical Bets, Making the Most of Smart Betas

Dynamic Smart Beta Investing Relative Risk Control and Tactical Bets, Making the Most of Smart Betas Koris International June 2014 Emilien Audeguil Research & Development ORIAS n 13000579 (www.orias.fr).

Dynamic Smart Beta Investing Relative Risk Control and Tactical Bets, Making the Most of Smart Betas Koris International June 2014 Emilien Audeguil Research & Development ORIAS n 13000579 (www.orias.fr).

TREND FOLLOWING AND MOMENTUM STRATEGIES FOR GLOBAL REITS

J R E P M TREND FOLLOWING AND MOMENTUM STRATEGIES FOR GLOBAL REITS Executive Summary. In this study, we investigate whether the risk-adjusted returns of a global REIT portfolio would be enhanced by adopting

J R E P M TREND FOLLOWING AND MOMENTUM STRATEGIES FOR GLOBAL REITS Executive Summary. In this study, we investigate whether the risk-adjusted returns of a global REIT portfolio would be enhanced by adopting

15 Week 5b Mutual Funds

15 Week 5b Mutual Funds 15.1 Background 1. It would be natural, and completely sensible, (and good marketing for MBA programs) if funds outperform darts! Pros outperform in any other field. 2. Except for...

15 Week 5b Mutual Funds 15.1 Background 1. It would be natural, and completely sensible, (and good marketing for MBA programs) if funds outperform darts! Pros outperform in any other field. 2. Except for...

Behind the Scenes of Mutual Fund Alpha

Behind the Scenes of Mutual Fund Alpha Qiang Bu Penn State University-Harrisburg This study examines whether fund alpha exists and whether it comes from manager skill. We found that the probability and

Behind the Scenes of Mutual Fund Alpha Qiang Bu Penn State University-Harrisburg This study examines whether fund alpha exists and whether it comes from manager skill. We found that the probability and

Keep Up The Momentum

Thierry Roncalli Quantitative Research Amundi Asset Management, Paris thierry.roncalli@amundi.com December 2017 Abstract The momentum risk premium is one of the most important alternative risk premia alongside

Thierry Roncalli Quantitative Research Amundi Asset Management, Paris thierry.roncalli@amundi.com December 2017 Abstract The momentum risk premium is one of the most important alternative risk premia alongside

Further Evidence on the Performance of Funds of Funds: The Case of Real Estate Mutual Funds. Kevin C.H. Chiang*

Further Evidence on the Performance of Funds of Funds: The Case of Real Estate Mutual Funds Kevin C.H. Chiang* School of Management University of Alaska Fairbanks Fairbanks, AK 99775 Kirill Kozhevnikov

Further Evidence on the Performance of Funds of Funds: The Case of Real Estate Mutual Funds Kevin C.H. Chiang* School of Management University of Alaska Fairbanks Fairbanks, AK 99775 Kirill Kozhevnikov

CTAs and Commodity Indices: A Fresh Perspective. Joint PRMIA and CAIA Meeting at the Monadnock Building, Chicago. May 19, 2016

CTAs and Commodity Indices: A Fresh Perspective Joint PRMIA and CAIA Meeting at the Monadnock Building, Chicago May 19, 2016 Ms. Hilary Till Principal, Premia Capital Management, LLC; Research Associate,

CTAs and Commodity Indices: A Fresh Perspective Joint PRMIA and CAIA Meeting at the Monadnock Building, Chicago May 19, 2016 Ms. Hilary Till Principal, Premia Capital Management, LLC; Research Associate,

Economics of Behavioral Finance. Lecture 3

Economics of Behavioral Finance Lecture 3 Security Market Line CAPM predicts a linear relationship between a stock s Beta and its excess return. E[r i ] r f = β i E r m r f Practically, testing CAPM empirically

Economics of Behavioral Finance Lecture 3 Security Market Line CAPM predicts a linear relationship between a stock s Beta and its excess return. E[r i ] r f = β i E r m r f Practically, testing CAPM empirically

Aiming to deliver attractive absolute returns with style

For professional investors only Aiming to deliver attractive absolute returns with style BMO Global Equity Market Neutral (SICAV) 2 BMO Global Equity Market Neutral (SICAV) Leveraging our proven capabilities

For professional investors only Aiming to deliver attractive absolute returns with style BMO Global Equity Market Neutral (SICAV) 2 BMO Global Equity Market Neutral (SICAV) Leveraging our proven capabilities

Factor Investing: Smart Beta Pursuing Alpha TM

In the spectrum of investing from passive (index based) to active management there are no shortage of considerations. Passive tends to be cheaper and should deliver returns very close to the index it tracks,

In the spectrum of investing from passive (index based) to active management there are no shortage of considerations. Passive tends to be cheaper and should deliver returns very close to the index it tracks,

Empirical Option Pricing

Empirical Option Pricing Holes in Black& Scholes Overpricing Price pressures in derivatives and underlying Estimating volatility and VAR Put-Call Parity Arguments Put-call parity p +S 0 e -dt = c +EX e

Empirical Option Pricing Holes in Black& Scholes Overpricing Price pressures in derivatives and underlying Estimating volatility and VAR Put-Call Parity Arguments Put-call parity p +S 0 e -dt = c +EX e

Optimal Portfolio Inputs: Various Methods

Optimal Portfolio Inputs: Various Methods Prepared by Kevin Pei for The Fund @ Sprott Abstract: In this document, I will model and back test our portfolio with various proposed models. It goes without

Optimal Portfolio Inputs: Various Methods Prepared by Kevin Pei for The Fund @ Sprott Abstract: In this document, I will model and back test our portfolio with various proposed models. It goes without

Global Tactical Asset Allocation (GTAA)

") JPMorgan Global Access Portfolios Presented at 2014 Matlab Computational Finance Conference April 2010 JPMorgan Global Access Investment Team Global Tactical Asset Allocation (GTAA) Jeff Song, Ph.D. CFA

JPMorgan Global Access Portfolios Presented at 2014 Matlab Computational Finance Conference April 2010 JPMorgan Global Access Investment Team Global Tactical Asset Allocation (GTAA) Jeff Song, Ph.D. CFA

Discussion Paper No. DP 07/02

SCHOOL OF ACCOUNTING, FINANCE AND MANAGEMENT Essex Finance Centre Can the Cross-Section Variation in Expected Stock Returns Explain Momentum George Bulkley University of Exeter Vivekanand Nawosah University

SCHOOL OF ACCOUNTING, FINANCE AND MANAGEMENT Essex Finance Centre Can the Cross-Section Variation in Expected Stock Returns Explain Momentum George Bulkley University of Exeter Vivekanand Nawosah University

ALTERNATIVE MOMENTUM STRATEGIES. Faculdade de Economia da Universidade do Porto Rua Dr. Roberto Frias Porto Portugal

FINANCIAL MARKETS ALTERNATIVE MOMENTUM STRATEGIES António de Melo da Costa Cerqueira, amelo@fep.up.pt, Faculdade de Economia da UP Elísio Fernando Moreira Brandão, ebrandao@fep.up.pt, Faculdade de Economia

FINANCIAL MARKETS ALTERNATIVE MOMENTUM STRATEGIES António de Melo da Costa Cerqueira, amelo@fep.up.pt, Faculdade de Economia da UP Elísio Fernando Moreira Brandão, ebrandao@fep.up.pt, Faculdade de Economia

PROFITABILITY OF CAPM MOMENTUM STRATEGIES IN THE US STOCK MARKET

International Journal of Business and Society, Vol. 18 No. 2, 2017, 347-362 PROFITABILITY OF CAPM MOMENTUM STRATEGIES IN THE US STOCK MARKET Terence Tai-Leung Chong The Chinese University of Hong Kong

International Journal of Business and Society, Vol. 18 No. 2, 2017, 347-362 PROFITABILITY OF CAPM MOMENTUM STRATEGIES IN THE US STOCK MARKET Terence Tai-Leung Chong The Chinese University of Hong Kong

An analysis of momentum and contrarian strategies using an optimal orthogonal portfolio approach

An analysis of momentum and contrarian strategies using an optimal orthogonal portfolio approach Hossein Asgharian and Björn Hansson Department of Economics, Lund University Box 7082 S-22007 Lund, Sweden

An analysis of momentum and contrarian strategies using an optimal orthogonal portfolio approach Hossein Asgharian and Björn Hansson Department of Economics, Lund University Box 7082 S-22007 Lund, Sweden

Procedia - Social and Behavioral Sciences 109 ( 2014 ) Yigit Bora Senyigit *, Yusuf Ag

Yigit Bora Senyigit *, Yusuf Ag") Available online at www.sciencedirect.com ScienceDirect Procedia - Social and Behavioral Sciences 109 ( 2014 ) 327 332 2 nd World Conference on Business, Economics and Management WCBEM 2013 Explaining

Available online at www.sciencedirect.com ScienceDirect Procedia - Social and Behavioral Sciences 109 ( 2014 ) 327 332 2 nd World Conference on Business, Economics and Management WCBEM 2013 Explaining

Performance Attribution: Are Sector Fund Managers Superior Stock Selectors?

Performance Attribution: Are Sector Fund Managers Superior Stock Selectors? Nicholas Scala December 2010 Abstract: Do equity sector fund managers outperform diversified equity fund managers? This paper

Performance Attribution: Are Sector Fund Managers Superior Stock Selectors? Nicholas Scala December 2010 Abstract: Do equity sector fund managers outperform diversified equity fund managers? This paper

A Performance Analysis of Risk Parity

Investment Research A Performance Analysis of Do Asset Allocations Outperform and What Are the Return Sources of Portfolios? Stephen Marra, CFA, Director, Portfolio Manager/Analyst¹ A risk parity model

Investment Research A Performance Analysis of Do Asset Allocations Outperform and What Are the Return Sources of Portfolios? Stephen Marra, CFA, Director, Portfolio Manager/Analyst¹ A risk parity model

Portfolio Construction Using Alternative Strategy Allocations in Farmland and Venture Capital. Stephen Johnston, Barclay Laughland & Karim Kadry

Portfolio Construction Using Alternative Strategy Allocations in Farmland and Venture Capital Stephen Johnston, Barclay Laughland & Karim Kadry Copyright 2017 All rights reserved. Readers may make verbatim

Portfolio Construction Using Alternative Strategy Allocations in Farmland and Venture Capital Stephen Johnston, Barclay Laughland & Karim Kadry Copyright 2017 All rights reserved. Readers may make verbatim

MULTI FACTOR PRICING MODEL: AN ALTERNATIVE APPROACH TO CAPM

MULTI FACTOR PRICING MODEL: AN ALTERNATIVE APPROACH TO CAPM Samit Majumdar Virginia Commonwealth University majumdars@vcu.edu Frank W. Bacon Longwood University baconfw@longwood.edu ABSTRACT: This study

MULTI FACTOR PRICING MODEL: AN ALTERNATIVE APPROACH TO CAPM Samit Majumdar Virginia Commonwealth University majumdars@vcu.edu Frank W. Bacon Longwood University baconfw@longwood.edu ABSTRACT: This study

Eclipse Capital. Strategy Diversification: Combining Momentum and Carry Strategies Within a Foreign Exchange Portfolio. Collaborative Research Q3.

Eclipse Capital Francis Olszweski Managing Director, Chief Portfolio Manager Eclipse Capital Management, Inc. Guofu Zhou, Ph.D. Frederick Bierman and James E. Spears Professor of Finance Olin Business

Eclipse Capital Francis Olszweski Managing Director, Chief Portfolio Manager Eclipse Capital Management, Inc. Guofu Zhou, Ph.D. Frederick Bierman and James E. Spears Professor of Finance Olin Business

Implementing Momentum Strategy with Options: Dynamic Scaling and Optimization

Implementing Momentum Strategy with Options: Dynamic Scaling and Optimization Abstract: Momentum strategy and its option implementation are studied in this paper. Four basic strategies are constructed

Implementing Momentum Strategy with Options: Dynamic Scaling and Optimization Abstract: Momentum strategy and its option implementation are studied in this paper. Four basic strategies are constructed

REVISITING THE ASSET PRICING MODELS

REVISITING THE ASSET PRICING MODELS Mehak Jain 1, Dr. Ravi Singla 2 1 Dept. of Commerce, Punjabi University, Patiala, (India) 2 University School of Applied Management, Punjabi University, Patiala, (India)

REVISITING THE ASSET PRICING MODELS Mehak Jain 1, Dr. Ravi Singla 2 1 Dept. of Commerce, Punjabi University, Patiala, (India) 2 University School of Applied Management, Punjabi University, Patiala, (India)

Active portfolios: diversification across trading strategies

Computational Finance and its Applications III 119 Active portfolios: diversification across trading strategies C. Murray Goldman Sachs and Co., New York, USA Abstract Several characteristics of a firm

Computational Finance and its Applications III 119 Active portfolios: diversification across trading strategies C. Murray Goldman Sachs and Co., New York, USA Abstract Several characteristics of a firm

Quantitative investing, which deploys

CAMPBELL R. HARVEY is a professor of finance at Duke University in Durham, NC, and an investment strategy advisor at Man Group in London, UK. cam.harvey@duke.edu SANDY RATTRAY is the CIO of Man Group and

CAMPBELL R. HARVEY is a professor of finance at Duke University in Durham, NC, and an investment strategy advisor at Man Group in London, UK. cam.harvey@duke.edu SANDY RATTRAY is the CIO of Man Group and

The Trend is Our Friend: Risk Parity, Momentum and Trend Following in Global Asset Allocation

The Trend is Our Friend: Risk Parity, Momentum and Trend Following in Global Asset Allocation Andrew Clare*, James Seaton*, Peter N. Smith and Stephen Thomas* *Cass Business School, London University of

The Trend is Our Friend: Risk Parity, Momentum and Trend Following in Global Asset Allocation Andrew Clare*, James Seaton*, Peter N. Smith and Stephen Thomas* *Cass Business School, London University of

ARE MOMENTUM PROFITS DRIVEN BY DIVIDEND STRATEGY?

ARE MOMENTUM PROFITS DRIVEN BY DIVIDEND STRATEGY? Huei-Hwa Lai Department of Finance National Yunlin University of Science and Technology, Taiwan R.O.C. Szu-Hsien Lin* Department of Finance TransWorld

ARE MOMENTUM PROFITS DRIVEN BY DIVIDEND STRATEGY? Huei-Hwa Lai Department of Finance National Yunlin University of Science and Technology, Taiwan R.O.C. Szu-Hsien Lin* Department of Finance TransWorld

Momentum Crashes. Kent Daniel. Columbia University Graduate School of Business. Columbia University Quantitative Trading & Asset Management Conference

Crashes Kent Daniel Columbia University Graduate School of Business Columbia University Quantitative Trading & Asset Management Conference 9 November 2010 Kent Daniel, Crashes Columbia - Quant. Trading

Crashes Kent Daniel Columbia University Graduate School of Business Columbia University Quantitative Trading & Asset Management Conference 9 November 2010 Kent Daniel, Crashes Columbia - Quant. Trading

The bottom-up beta of momentum

The bottom-up beta of momentum Pedro Barroso First version: September 2012 This version: November 2014 Abstract A direct measure of the cyclicality of momentum at a given point in time, its bottom-up beta

The bottom-up beta of momentum Pedro Barroso First version: September 2012 This version: November 2014 Abstract A direct measure of the cyclicality of momentum at a given point in time, its bottom-up beta

The evaluation of the performance of UK American unit trusts

International Review of Economics and Finance 8 (1999) 455 466 The evaluation of the performance of UK American unit trusts Jonathan Fletcher* Department of Finance and Accounting, Glasgow Caledonian University,

International Review of Economics and Finance 8 (1999) 455 466 The evaluation of the performance of UK American unit trusts Jonathan Fletcher* Department of Finance and Accounting, Glasgow Caledonian University,

Diversification and Yield Enhancement with Hedge Funds

ALTERNATIVE INVESTMENT RESEARCH CENTRE WORKING PAPER SERIES Working Paper # 0008 Diversification and Yield Enhancement with Hedge Funds Gaurav S. Amin Manager Schroder Hedge Funds, London Harry M. Kat

ALTERNATIVE INVESTMENT RESEARCH CENTRE WORKING PAPER SERIES Working Paper # 0008 Diversification and Yield Enhancement with Hedge Funds Gaurav S. Amin Manager Schroder Hedge Funds, London Harry M. Kat

Electronic copy available at:

Does active management add value? The Brazilian mutual fund market Track: Financial s, Investments and Risk Management William Eid Junior Full Professor FGV/EAESP Escola de Administração de Empresas de

Does active management add value? The Brazilian mutual fund market Track: Financial s, Investments and Risk Management William Eid Junior Full Professor FGV/EAESP Escola de Administração de Empresas de

Abstract. Introduction

2009 Update to An Examination of Fund Age and Size and Its Impact on Hedge Fund Performance Meredith Jones, Managing Director, PerTrac Financial Solutions Abstract This short paper updates research originally

2009 Update to An Examination of Fund Age and Size and Its Impact on Hedge Fund Performance Meredith Jones, Managing Director, PerTrac Financial Solutions Abstract This short paper updates research originally

Market Timing With a Robust Moving Average

Market Timing With a Robust Moving Average Valeriy Zakamulin This revision: May 29, 2015 Abstract In this paper we entertain a method of finding the most robust moving average weighting scheme to use for

Market Timing With a Robust Moving Average Valeriy Zakamulin This revision: May 29, 2015 Abstract In this paper we entertain a method of finding the most robust moving average weighting scheme to use for

Dual Momentum Investing. Gary Antonacci Portfolio Management Consultants

Dual Momentum Investing Gary Antonacci Portfolio Management Consultants Gary Antonacci Over 4 years experience with underexploited investments first place winner of the NAAIM Wagner Award Author of Dual

Dual Momentum Investing Gary Antonacci Portfolio Management Consultants Gary Antonacci Over 4 years experience with underexploited investments first place winner of the NAAIM Wagner Award Author of Dual

Empirical Study on Market Value Balance Sheet (MVBS)

") Empirical Study on Market Value Balance Sheet (MVBS) Yiqiao Yin Simon Business School November 2015 Abstract This paper presents the results of an empirical study on Market Value Balance Sheet (MVBS).

Empirical Study on Market Value Balance Sheet (MVBS) Yiqiao Yin Simon Business School November 2015 Abstract This paper presents the results of an empirical study on Market Value Balance Sheet (MVBS).

Empirical Option Pricing. Matti Suominen

Empirical Option Pricing Matti Suominen Put-Call Parity Arguments Put-call parity p +S 0 e -dt = c +EX e r T holds regardless of the assumptions made about the stock price distribution It follows that

Empirical Option Pricing Matti Suominen Put-Call Parity Arguments Put-call parity p +S 0 e -dt = c +EX e r T holds regardless of the assumptions made about the stock price distribution It follows that

STRATEGY OVERVIEW. Long/Short Equity. Related Funds: 361 Domestic Long/Short Equity Fund (ADMZX) 361 Global Long/Short Equity Fund (AGAZX)

361 Global Long/Short Equity Fund (AGAZX)") STRATEGY OVERVIEW Long/Short Equity Related Funds: 361 Domestic Long/Short Equity Fund (ADMZX) 361 Global Long/Short Equity Fund (AGAZX) Strategy Thesis The thesis driving 361 s Long/Short Equity strategies

STRATEGY OVERVIEW Long/Short Equity Related Funds: 361 Domestic Long/Short Equity Fund (ADMZX) 361 Global Long/Short Equity Fund (AGAZX) Strategy Thesis The thesis driving 361 s Long/Short Equity strategies

THE ROLE OF EXCHANGE RATES IN MONETARY POLICY RULE: THE CASE OF INFLATION TARGETING COUNTRIES

THE ROLE OF EXCHANGE RATES IN MONETARY POLICY RULE: THE CASE OF INFLATION TARGETING COUNTRIES Mahir Binici Central Bank of Turkey Istiklal Cad. No:10 Ulus, Ankara/Turkey E-mail: mahir.binici@tcmb.gov.tr

THE ROLE OF EXCHANGE RATES IN MONETARY POLICY RULE: THE CASE OF INFLATION TARGETING COUNTRIES Mahir Binici Central Bank of Turkey Istiklal Cad. No:10 Ulus, Ankara/Turkey E-mail: mahir.binici@tcmb.gov.tr

Application of Conditional Autoregressive Value at Risk Model to Kenyan Stocks: A Comparative Study

American Journal of Theoretical and Applied Statistics 2017; 6(3): 150-155 http://www.sciencepublishinggroup.com/j/ajtas doi: 10.11648/j.ajtas.20170603.13 ISSN: 2326-8999 (Print); ISSN: 2326-9006 (Online)

American Journal of Theoretical and Applied Statistics 2017; 6(3): 150-155 http://www.sciencepublishinggroup.com/j/ajtas doi: 10.11648/j.ajtas.20170603.13 ISSN: 2326-8999 (Print); ISSN: 2326-9006 (Online)

Portfolios with Hedge Funds and Other Alternative Investments Introduction to a Work in Progress

Portfolios with Hedge Funds and Other Alternative Investments Introduction to a Work in Progress July 16, 2002 Peng Chen Barry Feldman Chandra Goda Ibbotson Associates 225 N. Michigan Ave. Chicago, IL

Portfolios with Hedge Funds and Other Alternative Investments Introduction to a Work in Progress July 16, 2002 Peng Chen Barry Feldman Chandra Goda Ibbotson Associates 225 N. Michigan Ave. Chicago, IL

NAMHOON AUGUST LEE Southern Wesleyan University 907 Wesleyan Dr. Central, SC O

NAMHOON AUGUST LEE Southern Wesleyan University 907 Wesleyan Dr. Central, SC 29630 Email: nlee@swu.edu, O. 864.644.5487 Education Illinois Institute of Technology, IL Ph.D. in Management Science with Finance

NAMHOON AUGUST LEE Southern Wesleyan University 907 Wesleyan Dr. Central, SC 29630 Email: nlee@swu.edu, O. 864.644.5487 Education Illinois Institute of Technology, IL Ph.D. in Management Science with Finance

Tests of the Overreaction Hypothesis and the Timing of Mean Reversals on the JSE Securities Exchange (JSE): the Case of South Africa

: the Case of South Africa") Journal of Applied Finance & Banking, vol.1, no.1, 2011, 107-130 ISSN: 1792-6580 (print version), 1792-6599 (online) International Scientific Press, 2011 Tests of the Overreaction Hypothesis and the Timing

Journal of Applied Finance & Banking, vol.1, no.1, 2011, 107-130 ISSN: 1792-6580 (print version), 1792-6599 (online) International Scientific Press, 2011 Tests of the Overreaction Hypothesis and the Timing

The Effect of Kurtosis on the Cross-Section of Stock Returns

Utah State University DigitalCommons@USU All Graduate Plan B and other Reports Graduate Studies 5-2012 The Effect of Kurtosis on the Cross-Section of Stock Returns Abdullah Al Masud Utah State University

Utah State University DigitalCommons@USU All Graduate Plan B and other Reports Graduate Studies 5-2012 The Effect of Kurtosis on the Cross-Section of Stock Returns Abdullah Al Masud Utah State University

The Impact of Institutional Investors on the Monday Seasonal*

Su Han Chan Department of Finance, California State University-Fullerton Wai-Kin Leung Faculty of Business Administration, Chinese University of Hong Kong Ko Wang Department of Finance, California State

Su Han Chan Department of Finance, California State University-Fullerton Wai-Kin Leung Faculty of Business Administration, Chinese University of Hong Kong Ko Wang Department of Finance, California State

The Role of Industry Effect and Market States in Taiwanese Momentum

The Role of Industry Effect and Market States in Taiwanese Momentum Hsiao-Peng Fu 1 1 Department of Finance, Providence University, Taiwan, R.O.C. Correspondence: Hsiao-Peng Fu, Department of Finance,

The Role of Industry Effect and Market States in Taiwanese Momentum Hsiao-Peng Fu 1 1 Department of Finance, Providence University, Taiwan, R.O.C. Correspondence: Hsiao-Peng Fu, Department of Finance,

Tuomo Lampinen Silicon Cloud Technologies LLC

Tuomo Lampinen Silicon Cloud Technologies LLC www.portfoliovisualizer.com Background and Motivation Portfolio Visualizer Tools for Investors Overview of tools and related theoretical background Investment

Tuomo Lampinen Silicon Cloud Technologies LLC www.portfoliovisualizer.com Background and Motivation Portfolio Visualizer Tools for Investors Overview of tools and related theoretical background Investment

Occasional Paper. Risk Measurement Illiquidity Distortions. Jiaqi Chen and Michael L. Tindall

DALLASFED Occasional Paper Risk Measurement Illiquidity Distortions Jiaqi Chen and Michael L. Tindall Federal Reserve Bank of Dallas Financial Industry Studies Department Occasional Paper 12-2 December

DALLASFED Occasional Paper Risk Measurement Illiquidity Distortions Jiaqi Chen and Michael L. Tindall Federal Reserve Bank of Dallas Financial Industry Studies Department Occasional Paper 12-2 December

Persistence in Mutual Fund Performance: Analysis of Holdings Returns

Persistence in Mutual Fund Performance: Analysis of Holdings Returns Samuel Kruger * June 2007 Abstract: Do mutual funds that performed well in the past select stocks that perform well in the future? I

Persistence in Mutual Fund Performance: Analysis of Holdings Returns Samuel Kruger * June 2007 Abstract: Do mutual funds that performed well in the past select stocks that perform well in the future? I

Does my beta look big in this?

Does my beta look big in this? Patrick Burns 15th July 2003 Abstract Simulations are performed which show the difficulty of actually achieving realized market neutrality. Results suggest that restrictions

Does my beta look big in this? Patrick Burns 15th July 2003 Abstract Simulations are performed which show the difficulty of actually achieving realized market neutrality. Results suggest that restrictions

Long-run Consumption Risks in Assets Returns: Evidence from Economic Divisions

Long-run Consumption Risks in Assets Returns: Evidence from Economic Divisions Abdulrahman Alharbi 1 Abdullah Noman 2 Abstract: Bansal et al (2009) paper focus on measuring risk in consumption especially

Long-run Consumption Risks in Assets Returns: Evidence from Economic Divisions Abdulrahman Alharbi 1 Abdullah Noman 2 Abstract: Bansal et al (2009) paper focus on measuring risk in consumption especially

How Markets React to Different Types of Mergers

How Markets React to Different Types of Mergers By Pranit Chowhan Bachelor of Business Administration, University of Mumbai, 2014 And Vishal Bane Bachelor of Commerce, University of Mumbai, 2006 PROJECT

How Markets React to Different Types of Mergers By Pranit Chowhan Bachelor of Business Administration, University of Mumbai, 2014 And Vishal Bane Bachelor of Commerce, University of Mumbai, 2006 PROJECT

UNIVERSITY Of ILLINOIS LIBRARY AT URBANA-CHAMPA1GN STACKS

UNIVERSITY Of ILLINOIS LIBRARY AT URBANA-CHAMPA1GN STACKS Digitized by the Internet Archive in University of Illinois 2011 with funding from Urbana-Champaign http://www.archive.org/details/analysisofnonsym436kimm

UNIVERSITY Of ILLINOIS LIBRARY AT URBANA-CHAMPA1GN STACKS Digitized by the Internet Archive in University of Illinois 2011 with funding from Urbana-Champaign http://www.archive.org/details/analysisofnonsym436kimm

Key reasons why you must attend this groundbreaking training course: Introducing the Investment Markets and Investment Fundamentals

Investment Management Effective Methods Course Highlights and Agenda Key reasons why you must attend this groundbreaking training course: You will get to grips with the practicalities of cutting-edge investment

Investment Management Effective Methods Course Highlights and Agenda Key reasons why you must attend this groundbreaking training course: You will get to grips with the practicalities of cutting-edge investment

COMPARISON OF NATURAL HEDGES FROM DIVERSIFICATION AND DERIVATE INSTRUMENTS AGAINST COMMODITY PRICE RISK : A CASE STUDY OF PT ANEKA TAMBANG TBK

THE INDONESIAN JOURNAL OF BUSINESS ADMINISTRATION Vol. 2, No. 13, 2013:1651-1664 COMPARISON OF NATURAL HEDGES FROM DIVERSIFICATION AND DERIVATE INSTRUMENTS AGAINST COMMODITY PRICE RISK : A CASE STUDY OF

THE INDONESIAN JOURNAL OF BUSINESS ADMINISTRATION Vol. 2, No. 13, 2013:1651-1664 COMPARISON OF NATURAL HEDGES FROM DIVERSIFICATION AND DERIVATE INSTRUMENTS AGAINST COMMODITY PRICE RISK : A CASE STUDY OF

Does an Optimal Static Policy Foreign Currency Hedge Ratio Exist?

May 2015 Does an Optimal Static Policy Foreign Currency Hedge Ratio Exist? FQ Perspective DORI LEVANONI Partner, Investments Investing in foreign assets comes with the additional question of what to do

May 2015 Does an Optimal Static Policy Foreign Currency Hedge Ratio Exist? FQ Perspective DORI LEVANONI Partner, Investments Investing in foreign assets comes with the additional question of what to do

Mutual Fund Performance and Performance Persistence

Peter Luckoff Mutual Fund Performance and Performance Persistence The Impact of Fund Flows and Manager Changes With a foreword by Prof. Dr. Wolfgang Bessler GABLER RESEARCH List of Tables List of Figures

Peter Luckoff Mutual Fund Performance and Performance Persistence The Impact of Fund Flows and Manager Changes With a foreword by Prof. Dr. Wolfgang Bessler GABLER RESEARCH List of Tables List of Figures

MEMBER CONTRIBUTION. 20 years of VIX: Implications for Alternative Investment Strategies

MEMBER CONTRIBUTION 20 years of VIX: Implications for Alternative Investment Strategies Mikhail Munenzon, CFA, CAIA, PRM Director of Asset Allocation and Risk, The Observatory mikhail@247lookout.com Copyright

MEMBER CONTRIBUTION 20 years of VIX: Implications for Alternative Investment Strategies Mikhail Munenzon, CFA, CAIA, PRM Director of Asset Allocation and Risk, The Observatory mikhail@247lookout.com Copyright

The Case for TD Low Volatility Equities

The Case for TD Low Volatility Equities By: Jean Masson, Ph.D., Managing Director April 05 Most investors like generating returns but dislike taking risks, which leads to a natural assumption that competition

The Case for TD Low Volatility Equities By: Jean Masson, Ph.D., Managing Director April 05 Most investors like generating returns but dislike taking risks, which leads to a natural assumption that competition

A White Paper from Landry Investment Management Turning Behavioral Science into Performance Landry Investment Management Inc.

PRICE MOMENTUM & GLOBAL ASSET ALLOCATION A White Paper from Landry Investment Management Turning Behavioral Science into Performance MULTI-ASSET ETF STRATEGY February 2015 Page 2 TABLE OF CONTENTS MULTI-ASSET

PRICE MOMENTUM & GLOBAL ASSET ALLOCATION A White Paper from Landry Investment Management Turning Behavioral Science into Performance MULTI-ASSET ETF STRATEGY February 2015 Page 2 TABLE OF CONTENTS MULTI-ASSET

Discussion Papers in Economics

Discussion Papers in Economics No. 14/02 European Equity Investing through the Financial Crisis: Can Risk Parity, Momentum or Trend Following Help to Reduce Tail Risk? Andrew Clare, James Seaton, Peter

Discussion Papers in Economics No. 14/02 European Equity Investing through the Financial Crisis: Can Risk Parity, Momentum or Trend Following Help to Reduce Tail Risk? Andrew Clare, James Seaton, Peter

Changes in Analysts' Recommendations and Abnormal Returns. Qiming Sun. Bachelor of Commerce, University of Calgary, 2011.

Changes in Analysts' Recommendations and Abnormal Returns By Qiming Sun Bachelor of Commerce, University of Calgary, 2011 Yuhang Zhang Bachelor of Economics, Capital Unv of Econ and Bus, 2011 RESEARCH

Changes in Analysts' Recommendations and Abnormal Returns By Qiming Sun Bachelor of Commerce, University of Calgary, 2011 Yuhang Zhang Bachelor of Economics, Capital Unv of Econ and Bus, 2011 RESEARCH

Black Box Trend Following Lifting the Veil

AlphaQuest CTA Research Series #1 The goal of this research series is to demystify specific black box CTA trend following strategies and to analyze their characteristics both as a stand-alone product as

AlphaQuest CTA Research Series #1 The goal of this research series is to demystify specific black box CTA trend following strategies and to analyze their characteristics both as a stand-alone product as

The Use of Financial Futures as Hedging Vehicles

Journal of Business and Economics, ISSN 2155-7950, USA May 2013, Volume 4, No. 5, pp. 413-418 Academic Star Publishing Company, 2013 http://www.academicstar.us The Use of Financial Futures as Hedging Vehicles

Journal of Business and Economics, ISSN 2155-7950, USA May 2013, Volume 4, No. 5, pp. 413-418 Academic Star Publishing Company, 2013 http://www.academicstar.us The Use of Financial Futures as Hedging Vehicles

Great Company, Great Investment Revisited. Gary Smith. Fletcher Jones Professor. Department of Economics. Pomona College. 425 N.

!1 Great Company, Great Investment Revisited Gary Smith Fletcher Jones Professor Department of Economics Pomona College 425 N. College Avenue Claremont CA 91711 gsmith@pomona.edu !2 Great Company, Great

!1 Great Company, Great Investment Revisited Gary Smith Fletcher Jones Professor Department of Economics Pomona College 425 N. College Avenue Claremont CA 91711 gsmith@pomona.edu !2 Great Company, Great

INTRODUCTION TO HEDGE-FUNDS. 11 May 2016 Matti Suominen (Aalto) 1

1") INTRODUCTION TO HEDGE-FUNDS 11 May 2016 Matti Suominen (Aalto) 1 Traditional investments: Static invevestments Risk measured with β Expected return according to CAPM: E(R) = R f + β (R m R f ) 11 May 2016

INTRODUCTION TO HEDGE-FUNDS 11 May 2016 Matti Suominen (Aalto) 1 Traditional investments: Static invevestments Risk measured with β Expected return according to CAPM: E(R) = R f + β (R m R f ) 11 May 2016

Incorporating Risk Premia Mandates in a Strategic Allocation

Incorporating Risk Premia Mandates in a Strategic Allocation A Client Case Study: Wyoming Retirement System Raman Aylur Subramanian The Challenge Wyoming Retirement System (WRS), a public pension plan

Incorporating Risk Premia Mandates in a Strategic Allocation A Client Case Study: Wyoming Retirement System Raman Aylur Subramanian The Challenge Wyoming Retirement System (WRS), a public pension plan

TIME SERIES RISK FACTORS OF HEDGE FUND

OULU BUSINESS SCHOOL Nguyen Kim Lien TIME SERIES RISK FACTORS OF HEDGE FUND INVESTMENT OBJECTIVES Master thesis Department of Finance October 2013 UNIVERSITY OF OULU Oulu Business School Unit Department

OULU BUSINESS SCHOOL Nguyen Kim Lien TIME SERIES RISK FACTORS OF HEDGE FUND INVESTMENT OBJECTIVES Master thesis Department of Finance October 2013 UNIVERSITY OF OULU Oulu Business School Unit Department

APPLICATION OF CAPITAL ASSET PRICING MODEL BASED ON THE SECURITY MARKET LINE

APPLICATION OF CAPITAL ASSET PRICING MODEL BASED ON THE SECURITY MARKET LINE Dr. Ritika Sinha ABSTRACT The CAPM is a model for pricing an individual security (asset) or a portfolio. For individual security

APPLICATION OF CAPITAL ASSET PRICING MODEL BASED ON THE SECURITY MARKET LINE Dr. Ritika Sinha ABSTRACT The CAPM is a model for pricing an individual security (asset) or a portfolio. For individual security

Optimal Debt-to-Equity Ratios and Stock Returns

Utah State University DigitalCommons@USU All Graduate Plan B and other Reports Graduate Studies 5-2014 Optimal Debt-to-Equity Ratios and Stock Returns Courtney D. Winn Utah State University Follow this

Utah State University DigitalCommons@USU All Graduate Plan B and other Reports Graduate Studies 5-2014 Optimal Debt-to-Equity Ratios and Stock Returns Courtney D. Winn Utah State University Follow this