Animal Spirits in the Foreign Exchange Market

|

|

|

- Brandon Byrd

- 5 years ago

- Views:

Transcription

1 Animal Spirits in the Foreign Exchange Market Paul De Grauwe (London School of Economics) 1

2 Introductory remarks Exchange rate modelling is still dominated by the rational-expectations-efficientmarket (REEM) paradigm: Agents continuously maximize utility in intertemporal framework Forecasts are rational, i.e. take all available information into account, including the one embedded in the model Markets are efficient: prices reflect all relevant information 2

3 Cracks in the REEM Construction One of the predictions is that exchange rates can only change because of news in the fundamentals. This prediction must surely be rejected 3

4 DEM-USD Euro-dollar rate ,3 Since 1980 dollar has been involved in bubble and crash scenarios more than half of the time News model can only explain this by first a very long series of positive news followed by long series of negative news There is just not enough news to do the trick 1,2 1,1 1 0,9 0,8 0,7 4 0,6 6/03/95 6/03/96 6/03/97 6/03/98 6/03/99 6/03/00 6/03/01 6/03/02 6/03/03 6/03/04

5 Dollar-DM/euro exchange rate, market and fundamental, Not only is there not enough positive and later negative news Quite often the news and the exchange rate move in opposite direction (cfr ) Source: Ehrmann, M., and Fratzscher, M., Exchange Rates and Fundamentals: New Evidence from Real-time Data, forthcoming in Journal of International Money and Finance, 2004 Other studies have confirmed that most of the time the exchange rate has changed in the absence of observable news 5

6 Previous graph also shows another empirical anomaly: Exchange rate is disconnected from underlying fundamentals most of the time This is the disconnect puzzle Spectacular example: failure of PPP 6

7 180 DM/Dollar : Market and PPP Rates 1973 = Market Rate PPP rate

8 Failure of uncovered interest parity 8

9 There are other anomalies that cannot be explained by the REEM-model Fat tails and excess kurtosis Volatility clustering 9

10 3/01/86 3/07/86 3/01/87 3/07/87 3/01/88 3/07/88 3/01/89 3/07/89 3/01/90 3/07/90 3/01/91 3/07/91 3/01/92 3/07/92 3/01/93 3/07/93 3/01/94 3/07/94 3/01/95 3/07/95 returns Returns DM-dollar ( ) daily observations 0,02 0,015 0,01 0,005 0 Sharp spikes and Clustering of volatility -0,005-0,01-0,015 There are five spikes that exceed 5 standard deviation -0,02 0,02 Normally distributed returns One such spike should be observed only once in 7000 years if exchange rate changes are normally distributed. 0,015 0,01 0, ,005-0,01-0,015-0,

11 These phenomena can only be explained in the news model by assuming that fat tails and volatility clustering is present in the news itself This is not an explanation. It shifts the need to explain to another level The REEM-model must be rejected on empirical grounds Only reason why economists continue to use this paradigm is its internal consistency and its elegance In science, esthetic criteria should not guide the selection of models 11

12 Implicit in the REEM model is the view that agents (at least some of them) understand the structure of the underlying model and that they use this information to make predictions This means that some agents can store and process in their individual brains the full complexity of the information lying out there in the world. An extraordinary assumption Such an extraordinary assumption should only be used if it leads to powerful empirical predictions The fact is that it does not. 12

13 Alternative APPROACH: behavioural finance tradition Agents have a limited capacity for understanding and processing the complex available information (bounded rationality). In order to cope with the uncertainty they use relatively simple behavioral rules (heuristics). This does not mean they are irrational. Because the world is so complex it is pointless to try to understand its full complexity Rationality in the model is introduced by assuming that agents are willing to learn. They follow a procedure that allows them to evaluate the simple rules 13

14 Two such procedures have been proposed Statistical learning Fitness learning We follow the second procedure: Agents compare the rule they currently use to alternative rules They decide to switch to the alternative if it turns out that this is more profitable (fitness criterion; evolutionary dynamics). This procedure is also a disciplining device: we have to avoid that all simple rules are possible; there must be a selection mechanism that only keeps the best rules 14

15 A behavioural model Consists of three blocks Optimal portfolio based on mean variance utility maximisation Expectations formation of heterogenous agents : simple behavioural rules Deciding about the forecasting rules: fitness criterion 15

16 16 1. Mean variance utility maximization 1, 1, 1, 2 1 t i i t i t t i W V E W W U Utility function of agent type i who has the choice between domestic and foreign asset t i t t i t i t t i d s W r d s r W,,, 1 * 1, 1 1 Wealth constraint 2, 1, *, 1 1 t i t t t i t i s r s E r d Optimal holdings of foreign assets Aggregation process to derive market clearing exchange rate

17 17 2, 1, *, 1 1 t i t t t i t i s r s E r d r r r R where s s RE d t i t i t i t t t i t i 1 ' 1 * 1 ' ) ( 2, 2, 2, 1,,

18 Aggregating individual demands: Equilibrium demand and supply: Market clearing exchange rate: 18

19 19 * 1 1 1, t t t t f s s s E Fundamentalists forecast: negative feedback T i t i t t c s s E 1 1 1, Chartists forecast: positive feedback 2. Expectations formation

20 3. Learning the forecasting rules: fitness criterion (discrete choice theory) Agents face discrete choice They are boundedly rational Utility has deterministic and random component This setup allows to derive fraction of agents choosing fundamentalist and chartist rules 20

21 Learning the forecasting rules: fitness criterion (discrete choice theory) switching is determined by relative risk-adjusted profitability Note: there is learning in the model; it is not statistical learning (Sargent(1993)) we use risk-adjusted profits; risk is time varying and is measured by the forecast errors of using the forecasting rule 21

22 Stochastic simulations Non-linear structure of the model does not allow for a simple analytical solution We use numerical methods We first show some examples of simulations of model in time domain Remember: fundamental exchange rate is random walk 22

23 Model predicts that exchange rate is disconnected from fundamental much of the time Periods during which exchange rate closely follows fundamental alternate with periods when exchange rate is disconnected from fundamentals The latter are periods during which technical traders completely dominate the market It appears that sometimes fundamentals matter at other times they do not. 23

24 Different degrees of risk aversion μ=0.1 μ=0.5 When risk aversion increases exchange rate departs from fundamental more persistently μ=0.75 μ=1 There is a failure of arbitrage when agents are too risk averse 24

γ =5")

25 Different gamma (sensitivity of switching with respect to profitability) γ =5 γ =2 γ =1 25

26 Model creates bubbles and crashes. The anatomy of bubbles and crashes First, self-fulfilling increase in relative profitability of technical trading and self-fulfilling decline in relative risk of technical trading Second, this dynamics reaches its limit when (almost) everybody has become a technical trader. Technical trading s profitability slows down. Third, an exogenous shock, e.g. in the fundamental can lead to a crash Technical traders share is brought back to normal level of tranquil market. Asymmetry in bubble and crash 26

27 In order to understand the nature of the results we analyse the deterministic part of the model 27

28 Deterministic solution Two types of attractors. Small disturbance: Fundamental attractor. Large disturbances: Non-fundamental ( bubble ) attractors. 28

29 Small disturbances: exchange rate converges to fundamental rate weight of technical traders and fundamentalists are equal to 50%. Their expectations are model-consistent For large initial disturbances Exchange rate converges to non-fundamental (bubble) attractor Technical traders' weight converges to 1. Absence of fundamentalists eliminates the mean reversion dynamics. Technical traders expectations are modelconsistent 29

there are fundamental and")

30 Risk aversion and the nature of equilibria When agents have low risk aversion (they perceive risk to be low and the world to be stable) only fundamental equilibria. This is an environment in which agents stick to their beliefs When agents have high risk aversion (they perceive risk to be high and the world to be highly uncertain) there are fundamental and nonfundamental equilibria. This is an environment in which agents easily switch to other beliefs (forecasting rules) 30

31 One possible interpretation of these results: When fundamentalists are very risk averse, they will not be willing to exploit the profit opportunities that arise when a bubble develops. There is a failure of arbitrage As a result, the mean reverting forces triggered by fundamentalists are weak and we have many bubbles (and crashes) Conversely when fundis have low risk aversion they are willing to exploit these profits during bubble Thus bubbles (non-fundamental equilibria) arise because of a failure of arbitrage. 31

")

32 Technical traders extrapolation and the nature of equilibria As beta increases zone of fundamental equilibria shrinks Beta measures strenght of extrapolative forecasting Smaller shocks lead to bubble equilibria Border between fundamental and bubble equilibria is complex (fractal) 32

33 The importance of memory We introduce memory by allowing agents to remember the past using weights with exponential decay When memory increases the space of fundamental equilibria increases 33

34 Why crashes occur It may not be clear yet why bubbles are always followed by crashes. Shocks in fundamental are key We performed following experiment We fix the initial condition such that it produces a bubble equilibrium We then compute the attractors for different shocks in fundamental 34

35 Suppose we are in a bubble equilibrium Then a sufficiently positive(negative) shock in fundamental brings us back to the fundamental equilibrium (a crash) Intuition: large displacement of fundamental strenghtens the hand of the fundamentalists Thus shocks in fundamentals are sources of bubbles and subsequent crash 35

36 Basins of attraction around the fundamental steady state: sensitivity with respect to initial condition y 0 = z 0 = 0 2 f,0 = 2 c,0 = 0.05 u 0 and s 0 varying parameters = 0.2 = 1 = 1 = 0.6 =0.83 =0.84 Basins of attraction fundamental bubble (a) (b) =0.85 =0.851 (c) (d) enlargement 37

parameters = 0.2 =1 = 1 = 0.6 (b) = 0.83 = 0.835 (c) (d) = 0.84 = 0.")

37 Basins of attraction around a bubble equilibrium : sensitivity with respect to initial condition y 0 = z 0 = 10 2 f,0 = 4 2 c,0 = 0 u 0 and s 0 varying (a) parameters = 0.2 =1 = 1 = 0.6 (b) = 0.83 = (c) (d) = 0.84 =

38 Informational issues Agents use simple forecasting rules because they cannot comprehend the full complexity of the underlying model. The results of the model suggest that this is the right strategy to follow. For despite its simplicity, the model creates an informational environment that is too complex for an individual to understand and to process. To show this we analyse the complex boundary between fundamental and bubble equilibria 39

39 Suppose we know initial condition to be exactly +5 We take a slice from 3D figure in slide 24 Assume the forecaster has estimated beta to be with standard error Is this enough information to predict whether we move to fundamental or bubble equilibria? Let s take a blow-up 40

40 Our forecaster has 23% probability of a fundamental equilibrium, and 77% probability of a bubble equilibrium Can he improve the precision of his forecast by better econometric techniques? Suppose that he reduces standard error by factor of 10 We take a new blow-up by a factor of 10 41

41 Despite much greater precision of his estimate of beta his precision in forecasting a bubble has not increased at all It does not pay to be a good econometrician This result has to do with the fractal nature of the border between the bubble and fundamental equilibria 42

42 Thus, even in a very simple model agents face enormous informational problems, that they cannot hope to solve. As a result, agents will not attempt to use all the information provided by the underlying structural model. 43

43 Sensitivity to initial conditions The fractal nature of the boundary between fundamental and non-fundamental equilibria produces a potential for sensitivity to initial conditions 44

44 We simulate the model twice with exactly the same realization of the fundamental variable Only initial conditions differ slightly, i.e

45 The exchange rate and the current account 46

46 In the previous chapters we used a model in which fundamental and bubble equilibria co-exist. As a result, the exchange rate is disconnected from the fundamentals much of the time. These results were obtained in a model where the real sector of the economy is exogenous. This implies that the exchange rate does not affect the real sector. 47

47 Thus there is no feedback of exchange rate changes into goods prices, output, export and import. In reality, however, it is likely that exchange rate movements affect real variables. In particular during a bubble the exchange rate becomes increasingly undervalued. This is likely to stimulate exports and discourage imports. 48

48 Will these feedback mechanisms affect our basic results? An increase in the exchange rate leads to more exports and less imports and thus to an improvement of the current account. The latter means that the supply of foreign assets to domestic wealth owners increases. But such an increase in the supply of the foreign asset must have some effect on its price. In general, as we will see, such an increase in the supply of foreign assets will tend to reduce its price 49

49 This mechanism implies that we have a potential mean reverting process in the exchange rate. i.e. when the exchange rate increases, say during a bubble, the ensuing increase in the supply of the foreign asset will tend to reduce the exchange rate again. Thus, even if there are no agents using fundamentalist forecasting rules anymore, there is still a mean reverting mechanism in the economy that can do its work of pushing back the exchange rate towards its fundamental value. 50

50 How can we model the interaction between exchange rate movements and the supply of foreign assets? We postulate that there is a stable relationship between the equilibrium supply of the foreign asset and the fundamental exchange rate, i.e. 51

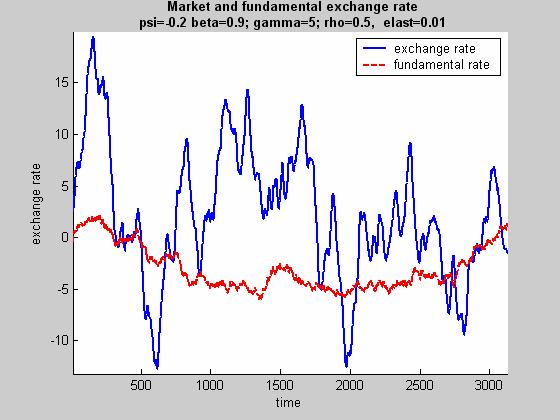

51 there is a one to one relationship between the fundamental exchange rate and the equilibrium supply of foreign assets. The parameter ε will be called the "elasticity". 52

52 the dynamics of the changes in the supply of foreign assets is described by the following equation: the adjustment of the supply to its long term value is gradual ρ z regulates the speed of adjustment of the supply of foreign assets 53

53 Stochastic simulation of the model (a) (b) (c) (d) 54

54 Thus the strength of the asset supply mechanism has the effect of tying down the exchange rate to its fundamental value. At the same time this mechanism creates additional short-term volatility around the fundamental. 55

has the effect of increasing the")

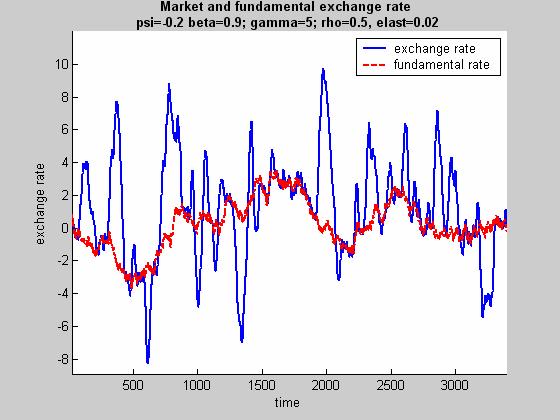

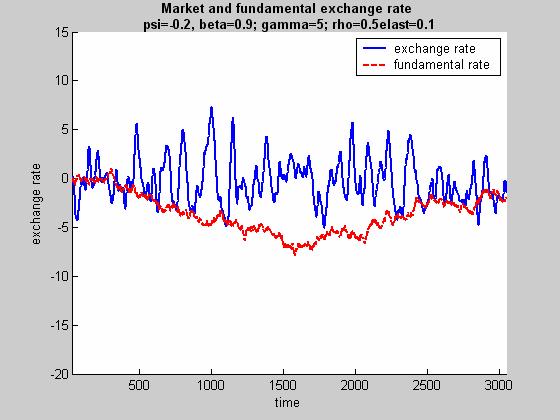

55 Deterministic analysis (a) (b) Importance of the elasticity As elasticity increases the zone of fundamental solutions increases. Note also the importance of the speed of adjustment. A high speed of adjustment (low ρ) has the effect of increasing the zone of fundamental equilibria. 56

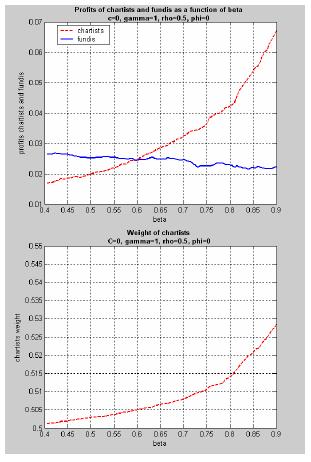

56 Interpretation The stronger and the speedier the supply of foreign assets reacts to the exchange rate the less likely it is that bubble equilibria occur. This is not really surprising. The asset supply mechanism that we modeled introduces a mean reversion process. If this mean reversion process is strong enough it strengthens the hands of the fundamentalists who use a mean-reverting forecasting rule. As a result, the probability that chartist rules will tend to dominate and generate bubbles is reduced. 57

57 Conclusion Exchange rate movements affect the current account. The latter in turn changes the net supply of foreign assets and feeds back on the exchange rate. The effect of making the supply of net foreign assets endogenous is that it can eliminate bubble equilibria. This will happen if the exchange rate changes have a sufficiently large and fast effect on the current account. In that case we also found that the profitability of fundamentalist rules is strongly increased, thereby also increasing the popularity of these rules in forecasting the exchange rate. 58

58 What is the empirical evidence of the sensitivity of the current account? The consensus today is that this sensitivity is rather weak. (see Krugman (1987), Frankel and Rose(1994), Obstfeld and Rogoff(2000)). In the short run, i.e. over periods extending to several quarters, there is very little evidence that the exchange rate affects the current account. This has a lot to do with the fact that firms tend to "price to market", As a result of this pricing to market, trade flows do not react much to (short-term) exchange rate movements. Trade flows appear to be disconnected from short-term exchange rate movements. 59

59 Thus, the disconnect puzzle has two dimensions. It relates to the fact that trade flows are not very responsive to exchange rate changes, and it also means that the exchange rate is disconnected from its underlying fundamental. The existence of a disconnect phenomenon whereby the current account is only weakly sensitive to the exchange rate implies that the feedback mechanism is a weak force so that it will most often not prevent bubbles and crashes in the exchange rate from emerging. 60

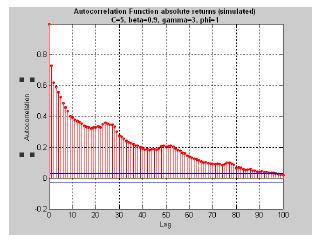

60 Empirical relevance of model We calibrate the model in such a way as to mimick main empirical regularities Disconnect puzzle Excess volatility Fat tails and excess kurtosis Volatility clustering (GARCH) 61

61 Disconnect puzzle The major puzzle in exchange rate economics Our model mimicks this puzzle 62

62 Dollar-DM/euro exchange rate, market and fundamental, Source: Ehrmann, M., and Fratzscher, M., Exchange Rates and Fundamentals: New Evidence from Real-time Data, forthcoming in Journal of International Money and Finance,

63 Error correction model of simulated exchange rate and fundamental We specify an error correction model on the simulated exchange rate and fundamental. We replicate an empirical finding that: There is a long run cointegration relationship between the exchange rate and the fundamental the speed of adjustment of both the exchange rate towards this long run equilibrium relationship is very weak Thus, there is a disconnect puzzle 64

64 Returns have fat tails and excess kurtosis Normal distribution Real life distribution of returns Simulated distribution of returns 65

65 Our model also mimicks other empirical puzzles of the foreign exchange markets Volatility clustering 66

66 67

67 Is chartism evolutionary stable? Traditional analysis is scornful about chartism and technical analysis In the REEM model there is no place for these rules. Reality is that technical analysis is widely used, in fact more so than fundamental analysis Can our model replicate this empirical observation? 68

68 We compute the profitability of chartist and fundamentalist rules Profitability of chartist rules increases with gamma Weight of chartists increases with gamma 69

69 70

70 Some results are noteworthy. Chartist forecasting rules turn out to be more profitable than fundamentalist rules for most parameter values, leading to systematically larger share of chartism compared to fundamentalism. Second when γ and β increase the profitability of chartist rules increases relative to the profitability of fundamentalist rules. 71

71 This result is related to the fact that as these parameters increase, the probability of the occurrence of bubbles increases. Chartist forecasting rules become more profitable in an environment of turbulence during which the exchange rate deviates from its fundamental. 72

")

72 During bubbles chartists make dramatically more profits (a) Fundamentalists make major losses; that s why they drop out of the market during bubbles 73

73 Fundamentalist rules appear to be loss making on average. Does this mean that instead of chartists, the fundamentalists are in danger of extinction? We measure the profitability of forecasting rules. During the bubble phases the use of chartist rules is very profitable while the use of fundamentalist rules is loss making. As a result, most agents switch to the use of chartist rules and few if any agents continue to use fundamentalist rules during these bubble phases. 74

74 Conclusion The world we have modelled is one in which agents do not understand its complexity Therefore they use simple rules of behaviour which they check ex post (fitness criterion) This is the way to introduce discipline into the model In such a world we get a very different dynamics compared to rational expectations world 75

75 Conclusion Nature of the dynamics There are bubble equilibria that attract the asset prices They will be reached as a result of shocks which makes extrapolating forecasting profitable Sensitivity to initial conditions, or the importance of trivial events 76

76 Once in a bubble equilibrium one can stay there for a long time or for a very short time As a result, asset price is disconnected from fundamentals very often. The switch from one regime to the other creates turbulence 77

77 Policy implications In the world we have modeled, policies can have powerful effects Interventions in the market can move the asset price, and push it towards a new equilibrium Thus, potentially effect of policy is strong 78

Dynamic Forecasting Rules and the Complexity of Exchange Rate Dynamics

Inspirar para Transformar Dynamic Forecasting Rules and the Complexity of Exchange Rate Dynamics Hans Dewachter Romain Houssa Marco Lyrio Pablo Rovira Kaltwasser Insper Working Paper WPE: 26/2 Dynamic

Inspirar para Transformar Dynamic Forecasting Rules and the Complexity of Exchange Rate Dynamics Hans Dewachter Romain Houssa Marco Lyrio Pablo Rovira Kaltwasser Insper Working Paper WPE: 26/2 Dynamic

Finance when no one believes the textbooks. Roy Batchelor Director, Cass EMBA Dubai Cass Business School, London

Finance when no one believes the textbooks Roy Batchelor Director, Cass EMBA Dubai Cass Business School, London What to expect Your fat finance textbook A class test Inside investors heads Something about

Finance when no one believes the textbooks Roy Batchelor Director, Cass EMBA Dubai Cass Business School, London What to expect Your fat finance textbook A class test Inside investors heads Something about

Lecture One. Dynamics of Moving Averages. Tony He University of Technology, Sydney, Australia

Lecture One Dynamics of Moving Averages Tony He University of Technology, Sydney, Australia AI-ECON (NCCU) Lectures on Financial Market Behaviour with Heterogeneous Investors August 2007 Outline Related

Lecture One Dynamics of Moving Averages Tony He University of Technology, Sydney, Australia AI-ECON (NCCU) Lectures on Financial Market Behaviour with Heterogeneous Investors August 2007 Outline Related

Capital markets liberalization and global imbalances

Capital markets liberalization and global imbalances Vincenzo Quadrini University of Southern California, CEPR and NBER February 11, 2006 VERY PRELIMINARY AND INCOMPLETE Abstract This paper studies the

Capital markets liberalization and global imbalances Vincenzo Quadrini University of Southern California, CEPR and NBER February 11, 2006 VERY PRELIMINARY AND INCOMPLETE Abstract This paper studies the

effect on foreign exchange dynamics as transaction taxes. Transaction taxes seek to curb

On central bank interventions and transaction taxes Frank H. Westerhoff University of Osnabrueck Department of Economics Rolandstrasse 8 D-49069 Osnabrueck Germany Email: frank.westerhoff@uos.de Abstract

On central bank interventions and transaction taxes Frank H. Westerhoff University of Osnabrueck Department of Economics Rolandstrasse 8 D-49069 Osnabrueck Germany Email: frank.westerhoff@uos.de Abstract

General Examination in Macroeconomic Theory SPRING 2016

HARVARD UNIVERSITY DEPARTMENT OF ECONOMICS General Examination in Macroeconomic Theory SPRING 2016 You have FOUR hours. Answer all questions Part A (Prof. Laibson): 60 minutes Part B (Prof. Barro): 60

HARVARD UNIVERSITY DEPARTMENT OF ECONOMICS General Examination in Macroeconomic Theory SPRING 2016 You have FOUR hours. Answer all questions Part A (Prof. Laibson): 60 minutes Part B (Prof. Barro): 60

Modeling optimism and pessimism in the foreign exchange market

Modeling optimism and pessimism in the foreign exchange market Paul De Grauwe Pablo Rovira Kaltwasser University of Leuven, Department of Economics, Naamsestraat 69, 3000 Leuven, Belgium This Draft: January

Modeling optimism and pessimism in the foreign exchange market Paul De Grauwe Pablo Rovira Kaltwasser University of Leuven, Department of Economics, Naamsestraat 69, 3000 Leuven, Belgium This Draft: January

CHAPTER 7 FOREIGN EXCHANGE MARKET EFFICIENCY

CHAPTER 7 FOREIGN EXCHANGE MARKET EFFICIENCY Chapter Overview This chapter has two major parts: the introduction to the principles of market efficiency and a review of the empirical evidence on efficiency

CHAPTER 7 FOREIGN EXCHANGE MARKET EFFICIENCY Chapter Overview This chapter has two major parts: the introduction to the principles of market efficiency and a review of the empirical evidence on efficiency

What Are Equilibrium Real Exchange Rates?

1 What Are Equilibrium Real Exchange Rates? This chapter does not provide a definitive or comprehensive definition of FEERs. Many discussions of the concept already exist (e.g., Williamson 1983, 1985,

1 What Are Equilibrium Real Exchange Rates? This chapter does not provide a definitive or comprehensive definition of FEERs. Many discussions of the concept already exist (e.g., Williamson 1983, 1985,

Has the Inflation Process Changed?

Has the Inflation Process Changed? by S. Cecchetti and G. Debelle Discussion by I. Angeloni (ECB) * Cecchetti and Debelle (CD) could hardly have chosen a more relevant and timely topic for their paper.

Has the Inflation Process Changed? by S. Cecchetti and G. Debelle Discussion by I. Angeloni (ECB) * Cecchetti and Debelle (CD) could hardly have chosen a more relevant and timely topic for their paper.

Evolution of Market Heuristics

Evolution of Market Heuristics Mikhail Anufriev Cars Hommes CeNDEF, Department of Economics, University of Amsterdam, Roetersstraat 11, NL-1018 WB Amsterdam, Netherlands July 2007 This paper is forthcoming

Evolution of Market Heuristics Mikhail Anufriev Cars Hommes CeNDEF, Department of Economics, University of Amsterdam, Roetersstraat 11, NL-1018 WB Amsterdam, Netherlands July 2007 This paper is forthcoming

Characterization of the Optimum

ECO 317 Economics of Uncertainty Fall Term 2009 Notes for lectures 5. Portfolio Allocation with One Riskless, One Risky Asset Characterization of the Optimum Consider a risk-averse, expected-utility-maximizing

ECO 317 Economics of Uncertainty Fall Term 2009 Notes for lectures 5. Portfolio Allocation with One Riskless, One Risky Asset Characterization of the Optimum Consider a risk-averse, expected-utility-maximizing

Universidade de Aveiro Departamento de Economia, Gestão e Engenharia Industrial. Documentos de Trabalho em Economia Working Papers in Economics

Universidade de Aveiro Departamento de Economia, Gestão e Engenharia Industrial Documentos de Trabalho em Economia Working Papers in Economics Área Científica de Economia E/nº 25/2004 Bubbles and crashes

Universidade de Aveiro Departamento de Economia, Gestão e Engenharia Industrial Documentos de Trabalho em Economia Working Papers in Economics Área Científica de Economia E/nº 25/2004 Bubbles and crashes

Understanding Krugman s Third-Generation Model of Currency and Financial Crises

Hisayuki Mitsuo ed., Financial Fragilities in Developing Countries, Chosakenkyu-Hokokusho, IDE-JETRO, 2007. Chapter 2 Understanding Krugman s Third-Generation Model of Currency and Financial Crises Hidehiko

Hisayuki Mitsuo ed., Financial Fragilities in Developing Countries, Chosakenkyu-Hokokusho, IDE-JETRO, 2007. Chapter 2 Understanding Krugman s Third-Generation Model of Currency and Financial Crises Hidehiko

Heterogeneous Agent Models Lecture 1. Introduction Rational vs. Agent Based Modelling Heterogeneous Agent Modelling

Heterogeneous Agent Models Lecture 1 Introduction Rational vs. Agent Based Modelling Heterogeneous Agent Modelling Mikhail Anufriev EDG, Faculty of Business, University of Technology Sydney (UTS) July,

Heterogeneous Agent Models Lecture 1 Introduction Rational vs. Agent Based Modelling Heterogeneous Agent Modelling Mikhail Anufriev EDG, Faculty of Business, University of Technology Sydney (UTS) July,

Problem set 1 Answers: 0 ( )= [ 0 ( +1 )] = [ ( +1 )]

![Problem set 1 Answers: 0 ( )= [ 0 ( +1 )] = [ ( +1 )]](/thumbs/90/101609040.jpg "Problem set 1 Answers: 0 ( )= [ 0 ( +1 )] = [ ( +1 )]") Problem set 1 Answers: 1. (a) The first order conditions are with 1+ 1so 0 ( ) [ 0 ( +1 )] [( +1 )] ( +1 ) Consumption follows a random walk. This is approximately true in many nonlinear models. Now we

Problem set 1 Answers: 1. (a) The first order conditions are with 1+ 1so 0 ( ) [ 0 ( +1 )] [( +1 )] ( +1 ) Consumption follows a random walk. This is approximately true in many nonlinear models. Now we

Nominal Exchange Rates Obstfeld and Rogoff, Chapter 8

Nominal Exchange Rates Obstfeld and Rogoff, Chapter 8 1 Cagan Model of Money Demand 1.1 Money Demand Demand for real money balances ( M P ) depends negatively on expected inflation In logs m d t p t =

Nominal Exchange Rates Obstfeld and Rogoff, Chapter 8 1 Cagan Model of Money Demand 1.1 Money Demand Demand for real money balances ( M P ) depends negatively on expected inflation In logs m d t p t =

Discussion. Benoît Carmichael

Discussion Benoît Carmichael The two studies presented in the first session of the conference take quite different approaches to the question of price indexes. On the one hand, Coulombe s study develops

Discussion Benoît Carmichael The two studies presented in the first session of the conference take quite different approaches to the question of price indexes. On the one hand, Coulombe s study develops

Expectations and market microstructure when liquidity is lost

Expectations and market microstructure when liquidity is lost Jun Muranaga and Tokiko Shimizu* Bank of Japan Abstract In this paper, we focus on the halt of discovery function in the financial markets

Expectations and market microstructure when liquidity is lost Jun Muranaga and Tokiko Shimizu* Bank of Japan Abstract In this paper, we focus on the halt of discovery function in the financial markets

MARKET DEPTH AND PRICE DYNAMICS: A NOTE

International Journal of Modern hysics C Vol. 5, No. 7 (24) 5 2 c World Scientific ublishing Company MARKET DETH AND RICE DYNAMICS: A NOTE FRANK H. WESTERHOFF Department of Economics, University of Osnabrueck

International Journal of Modern hysics C Vol. 5, No. 7 (24) 5 2 c World Scientific ublishing Company MARKET DETH AND RICE DYNAMICS: A NOTE FRANK H. WESTERHOFF Department of Economics, University of Osnabrueck

Labor Economics Field Exam Spring 2011

Labor Economics Field Exam Spring 2011 Instructions You have 4 hours to complete this exam. This is a closed book examination. No written materials are allowed. You can use a calculator. THE EXAM IS COMPOSED

Labor Economics Field Exam Spring 2011 Instructions You have 4 hours to complete this exam. This is a closed book examination. No written materials are allowed. You can use a calculator. THE EXAM IS COMPOSED

1 Consumption and saving under uncertainty

1 Consumption and saving under uncertainty 1.1 Modelling uncertainty As in the deterministic case, we keep assuming that agents live for two periods. The novelty here is that their earnings in the second

1 Consumption and saving under uncertainty 1.1 Modelling uncertainty As in the deterministic case, we keep assuming that agents live for two periods. The novelty here is that their earnings in the second

Chapter 1. Chaos in the Dornbusch Model of the Exchange Rate

Chapter 1 Chaos in the Dornbusch Model of the Exchange Rate Paul De Grauwe and Hans Dewachter 1. Introduction Ever since the empirical breakdown of (linear) structural exchange rate models, the predominant

Chapter 1 Chaos in the Dornbusch Model of the Exchange Rate Paul De Grauwe and Hans Dewachter 1. Introduction Ever since the empirical breakdown of (linear) structural exchange rate models, the predominant

Consumption and Asset Pricing

Consumption and Asset Pricing Yin-Chi Wang The Chinese University of Hong Kong November, 2012 References: Williamson s lecture notes (2006) ch5 and ch 6 Further references: Stochastic dynamic programming:

Consumption and Asset Pricing Yin-Chi Wang The Chinese University of Hong Kong November, 2012 References: Williamson s lecture notes (2006) ch5 and ch 6 Further references: Stochastic dynamic programming:

Lower prices. Lower costs, esp. wages. Higher productivity. Higher quality/more desirable exports. Greater natural resources. Higher interest rates

1 Goods market Reason to Hold Currency To acquire goods and services from that country Important in... Long run (years to decades) Currency Will Appreciate If... Lower prices Lower costs, esp. wages Higher

1 Goods market Reason to Hold Currency To acquire goods and services from that country Important in... Long run (years to decades) Currency Will Appreciate If... Lower prices Lower costs, esp. wages Higher

PART II IT Methods in Finance

PART II IT Methods in Finance Introduction to Part II This part contains 12 chapters and is devoted to IT methods in finance. There are essentially two ways where IT enters and influences methods used

PART II IT Methods in Finance Introduction to Part II This part contains 12 chapters and is devoted to IT methods in finance. There are essentially two ways where IT enters and influences methods used

Is regulatory capital pro-cyclical? A macroeconomic assessment of Basel II

Is regulatory capital pro-cyclical? A macroeconomic assessment of Basel II (preliminary version) Frank Heid Deutsche Bundesbank 2003 1 Introduction Capital requirements play a prominent role in international

Is regulatory capital pro-cyclical? A macroeconomic assessment of Basel II (preliminary version) Frank Heid Deutsche Bundesbank 2003 1 Introduction Capital requirements play a prominent role in international

Lecture 1: Traditional Open Macro Models and Monetary Policy

Lecture 1: Traditional Open Macro Models and Monetary Policy Isabelle Méjean isabelle.mejean@polytechnique.edu http://mejean.isabelle.googlepages.com/ Master Economics and Public Policy, International

Lecture 1: Traditional Open Macro Models and Monetary Policy Isabelle Méjean isabelle.mejean@polytechnique.edu http://mejean.isabelle.googlepages.com/ Master Economics and Public Policy, International

ACTIVE FISCAL, PASSIVE MONEY EQUILIBRIUM IN A PURELY BACKWARD-LOOKING MODEL

ACTIVE FISCAL, PASSIVE MONEY EQUILIBRIUM IN A PURELY BACKWARD-LOOKING MODEL CHRISTOPHER A. SIMS ABSTRACT. The active money, passive fiscal policy equilibrium that the fiscal theory of the price level shows

ACTIVE FISCAL, PASSIVE MONEY EQUILIBRIUM IN A PURELY BACKWARD-LOOKING MODEL CHRISTOPHER A. SIMS ABSTRACT. The active money, passive fiscal policy equilibrium that the fiscal theory of the price level shows

Capital Constraints, Lending over the Cycle and the Precautionary Motive: A Quantitative Exploration

Capital Constraints, Lending over the Cycle and the Precautionary Motive: A Quantitative Exploration Angus Armstrong and Monique Ebell National Institute of Economic and Social Research 1. Introduction

Capital Constraints, Lending over the Cycle and the Precautionary Motive: A Quantitative Exploration Angus Armstrong and Monique Ebell National Institute of Economic and Social Research 1. Introduction

1 Volatility Definition and Estimation

1 Volatility Definition and Estimation 1.1 WHAT IS VOLATILITY? It is useful to start with an explanation of what volatility is, at least for the purpose of clarifying the scope of this book. Volatility

1 Volatility Definition and Estimation 1.1 WHAT IS VOLATILITY? It is useful to start with an explanation of what volatility is, at least for the purpose of clarifying the scope of this book. Volatility

Quantitative Modelling of Market Booms and Crashes

Quantitative Modelling of Market Booms and Crashes Ilya Sheynzon (LSE) Workhop on Mathematics of Financial Risk Management Isaac Newton Institute for Mathematical Sciences March 28, 2013 October. This

Quantitative Modelling of Market Booms and Crashes Ilya Sheynzon (LSE) Workhop on Mathematics of Financial Risk Management Isaac Newton Institute for Mathematical Sciences March 28, 2013 October. This

An Agent-Based Simulation of Stock Market to Analyze the Influence of Trader Characteristics on Financial Market Phenomena

An Agent-Based Simulation of Stock Market to Analyze the Influence of Trader Characteristics on Financial Market Phenomena Y. KAMYAB HESSARY 1 and M. HADZIKADIC 2 Complex System Institute, College of Computing

An Agent-Based Simulation of Stock Market to Analyze the Influence of Trader Characteristics on Financial Market Phenomena Y. KAMYAB HESSARY 1 and M. HADZIKADIC 2 Complex System Institute, College of Computing

DEPARTMENT OF ECONOMICS Fall 2013 D. Romer

UNIVERSITY OF CALIFORNIA Economics 202A DEPARTMENT OF ECONOMICS Fall 203 D. Romer FORCES LIMITING THE EXTENT TO WHICH SOPHISTICATED INVESTORS ARE WILLING TO MAKE TRADES THAT MOVE ASSET PRICES BACK TOWARD

UNIVERSITY OF CALIFORNIA Economics 202A DEPARTMENT OF ECONOMICS Fall 203 D. Romer FORCES LIMITING THE EXTENT TO WHICH SOPHISTICATED INVESTORS ARE WILLING TO MAKE TRADES THAT MOVE ASSET PRICES BACK TOWARD

Technical Report: CES-497 A summary for the Brock and Hommes Heterogeneous beliefs and routes to chaos in a simple asset pricing model 1998 JEDC paper

Technical Report: CES-497 A summary for the Brock and Hommes Heterogeneous beliefs and routes to chaos in a simple asset pricing model 1998 JEDC paper Michael Kampouridis, Shu-Heng Chen, Edward P.K. Tsang

Technical Report: CES-497 A summary for the Brock and Hommes Heterogeneous beliefs and routes to chaos in a simple asset pricing model 1998 JEDC paper Michael Kampouridis, Shu-Heng Chen, Edward P.K. Tsang

ALM Analysis for a Pensionskasse

ALM Analysis for a Pensionskasse Asset Liability Management Study Francesco Sandrini MSc, PhD New Thinking in Finance London, February 14 th 2014 For Internal Use Only. Not to be Distributed to the Public.

ALM Analysis for a Pensionskasse Asset Liability Management Study Francesco Sandrini MSc, PhD New Thinking in Finance London, February 14 th 2014 For Internal Use Only. Not to be Distributed to the Public.

Optimal Negative Interest Rates in the Liquidity Trap

Optimal Negative Interest Rates in the Liquidity Trap Davide Porcellacchia 8 February 2017 Abstract The canonical New Keynesian model features a zero lower bound on the interest rate. In the simple setting

Optimal Negative Interest Rates in the Liquidity Trap Davide Porcellacchia 8 February 2017 Abstract The canonical New Keynesian model features a zero lower bound on the interest rate. In the simple setting

Topic 4: Introduction to Exchange Rates Part 1: Definitions and empirical regularities

Topic 4: Introduction to Exchange Rates Part 1: Definitions and empirical regularities - The models we studied earlier include only real variables and relative prices. We now extend these models to have

Topic 4: Introduction to Exchange Rates Part 1: Definitions and empirical regularities - The models we studied earlier include only real variables and relative prices. We now extend these models to have

G R E D E G Documents de travail

G R E D E G Documents de travail WP n 2008-08 ASSET MISPRICING AND HETEROGENEOUS BELIEFS AMONG ARBITRAGEURS *** Sandrine Jacob Leal GREDEG Groupe de Recherche en Droit, Economie et Gestion 250 rue Albert

G R E D E G Documents de travail WP n 2008-08 ASSET MISPRICING AND HETEROGENEOUS BELIEFS AMONG ARBITRAGEURS *** Sandrine Jacob Leal GREDEG Groupe de Recherche en Droit, Economie et Gestion 250 rue Albert

Exchange Rates and Fundamentals: A General Equilibrium Exploration

Exchange Rates and Fundamentals: A General Equilibrium Exploration Takashi Kano Hitotsubashi University @HIAS, IER, AJRC Joint Workshop Frontiers in Macroeconomics and Macroeconometrics November 3-4, 2017

Exchange Rates and Fundamentals: A General Equilibrium Exploration Takashi Kano Hitotsubashi University @HIAS, IER, AJRC Joint Workshop Frontiers in Macroeconomics and Macroeconometrics November 3-4, 2017

Oesterreichische Nationalbank. Eurosystem. Workshops. Proceedings of OeNB Workshops. Macroeconomic Models and Forecasts for Austria

Oesterreichische Nationalbank Eurosystem Workshops Proceedings of OeNB Workshops Macroeconomic Models and Forecasts for Austria November 11 to 12, 2004 No. 5 Comment on Evaluating Euro Exchange Rate Predictions

Oesterreichische Nationalbank Eurosystem Workshops Proceedings of OeNB Workshops Macroeconomic Models and Forecasts for Austria November 11 to 12, 2004 No. 5 Comment on Evaluating Euro Exchange Rate Predictions

EFFICIENT MARKETS HYPOTHESIS

EFFICIENT MARKETS HYPOTHESIS when economists speak of capital markets as being efficient, they usually consider asset prices and returns as being determined as the outcome of supply and demand in a competitive

EFFICIENT MARKETS HYPOTHESIS when economists speak of capital markets as being efficient, they usually consider asset prices and returns as being determined as the outcome of supply and demand in a competitive

CONSUMPTION-BASED MACROECONOMIC MODELS OF ASSET PRICING THEORY

ECONOMIC ANNALS, Volume LXI, No. 211 / October December 2016 UDC: 3.33 ISSN: 0013-3264 DOI:10.2298/EKA1611007D Marija Đorđević* CONSUMPTION-BASED MACROECONOMIC MODELS OF ASSET PRICING THEORY ABSTRACT:

ECONOMIC ANNALS, Volume LXI, No. 211 / October December 2016 UDC: 3.33 ISSN: 0013-3264 DOI:10.2298/EKA1611007D Marija Đorđević* CONSUMPTION-BASED MACROECONOMIC MODELS OF ASSET PRICING THEORY ABSTRACT:

0. Finish the Auberbach/Obsfeld model (last lecture s slides, 13 March, pp. 13 )

") Monetary Policy, 16/3 2017 Henrik Jensen Department of Economics University of Copenhagen 0. Finish the Auberbach/Obsfeld model (last lecture s slides, 13 March, pp. 13 ) 1. Money in the short run: Incomplete

Monetary Policy, 16/3 2017 Henrik Jensen Department of Economics University of Copenhagen 0. Finish the Auberbach/Obsfeld model (last lecture s slides, 13 March, pp. 13 ) 1. Money in the short run: Incomplete

Stock Market Forecast: Chaos Theory Revealing How the Market Works March 25, 2018 I Know First Research

Stock Market Forecast: Chaos Theory Revealing How the Market Works March 25, 2018 I Know First Research Stock Market Forecast : How Can We Predict the Financial Markets by Using Algorithms? Common fallacies

Stock Market Forecast: Chaos Theory Revealing How the Market Works March 25, 2018 I Know First Research Stock Market Forecast : How Can We Predict the Financial Markets by Using Algorithms? Common fallacies

Market Risk Analysis Volume II. Practical Financial Econometrics

Market Risk Analysis Volume II Practical Financial Econometrics Carol Alexander John Wiley & Sons, Ltd List of Figures List of Tables List of Examples Foreword Preface to Volume II xiii xvii xx xxii xxvi

Market Risk Analysis Volume II Practical Financial Econometrics Carol Alexander John Wiley & Sons, Ltd List of Figures List of Tables List of Examples Foreword Preface to Volume II xiii xvii xx xxii xxvi

Financial Economics Field Exam January 2008

Financial Economics Field Exam January 2008 There are two questions on the exam, representing Asset Pricing (236D = 234A) and Corporate Finance (234C). Please answer both questions to the best of your

Financial Economics Field Exam January 2008 There are two questions on the exam, representing Asset Pricing (236D = 234A) and Corporate Finance (234C). Please answer both questions to the best of your

Chapter 9 Dynamic Models of Investment

George Alogoskoufis, Dynamic Macroeconomic Theory, 2015 Chapter 9 Dynamic Models of Investment In this chapter we present the main neoclassical model of investment, under convex adjustment costs. This

George Alogoskoufis, Dynamic Macroeconomic Theory, 2015 Chapter 9 Dynamic Models of Investment In this chapter we present the main neoclassical model of investment, under convex adjustment costs. This

Eco504 Spring 2010 C. Sims FINAL EXAM. β t 1 2 φτ2 t subject to (1)

") Eco54 Spring 21 C. Sims FINAL EXAM There are three questions that will be equally weighted in grading. Since you may find some questions take longer to answer than others, and partial credit will be given

Eco54 Spring 21 C. Sims FINAL EXAM There are three questions that will be equally weighted in grading. Since you may find some questions take longer to answer than others, and partial credit will be given

Project Proposals for MS&E 444. Lisa Borland and Jeremy Evnine. Evnine and Associates, Inc. April 2008

Project Proposals for MS&E 444 Lisa Borland and Jeremy Evnine Evnine and Associates, Inc. April 2008 1 Portfolio Construction using Prospect Theory Single asset: -Maximize expected long run profit based

Project Proposals for MS&E 444 Lisa Borland and Jeremy Evnine Evnine and Associates, Inc. April 2008 1 Portfolio Construction using Prospect Theory Single asset: -Maximize expected long run profit based

Modeling Interest Rate Parity: A System Dynamics Approach

Modeling Interest Rate Parity: A System Dynamics Approach John T. Harvey Professor of Economics Department of Economics Box 98510 Texas Christian University Fort Worth, Texas 7619 (817)57-730 j.harvey@tcu.edu

Modeling Interest Rate Parity: A System Dynamics Approach John T. Harvey Professor of Economics Department of Economics Box 98510 Texas Christian University Fort Worth, Texas 7619 (817)57-730 j.harvey@tcu.edu

Volatility and Dynamics in Agricultural and Trade Policy Impact Assessment Modelling Advances Needed. Thomas Heckelei

Volatility and Dynamics in Agricultural and Trade Policy Impact Assessment Modelling Advances Needed Thomas Heckelei Selected Paper prepared for presentation at the International Agricultural Trade Research

Volatility and Dynamics in Agricultural and Trade Policy Impact Assessment Modelling Advances Needed Thomas Heckelei Selected Paper prepared for presentation at the International Agricultural Trade Research

ARCH Models and Financial Applications

Christian Gourieroux ARCH Models and Financial Applications With 26 Figures Springer Contents 1 Introduction 1 1.1 The Development of ARCH Models 1 1.2 Book Content 4 2 Linear and Nonlinear Processes 5

Christian Gourieroux ARCH Models and Financial Applications With 26 Figures Springer Contents 1 Introduction 1 1.1 The Development of ARCH Models 1 1.2 Book Content 4 2 Linear and Nonlinear Processes 5

Financial Mathematics III Theory summary

Financial Mathematics III Theory summary Table of Contents Lecture 1... 7 1. State the objective of modern portfolio theory... 7 2. Define the return of an asset... 7 3. How is expected return defined?...

Financial Mathematics III Theory summary Table of Contents Lecture 1... 7 1. State the objective of modern portfolio theory... 7 2. Define the return of an asset... 7 3. How is expected return defined?...

Is there a significant connection between commodity prices and exchange rates?

Is there a significant connection between commodity prices and exchange rates? Preliminary Thesis Report Study programme: MSc in Business w/ Major in Finance Supervisor: Håkon Tretvoll Table of content

Is there a significant connection between commodity prices and exchange rates? Preliminary Thesis Report Study programme: MSc in Business w/ Major in Finance Supervisor: Håkon Tretvoll Table of content

Volatility Clustering in High-Frequency Data: A self-fulfilling prophecy? Abstract

Volatility Clustering in High-Frequency Data: A self-fulfilling prophecy? Matei Demetrescu Goethe University Frankfurt Abstract Clustering volatility is shown to appear in a simple market model with noise

Volatility Clustering in High-Frequency Data: A self-fulfilling prophecy? Matei Demetrescu Goethe University Frankfurt Abstract Clustering volatility is shown to appear in a simple market model with noise

Macroeconomics Sequence, Block I. Introduction to Consumption Asset Pricing

Macroeconomics Sequence, Block I Introduction to Consumption Asset Pricing Nicola Pavoni October 21, 2016 The Lucas Tree Model This is a general equilibrium model where instead of deriving properties of

Macroeconomics Sequence, Block I Introduction to Consumption Asset Pricing Nicola Pavoni October 21, 2016 The Lucas Tree Model This is a general equilibrium model where instead of deriving properties of

Discussion of Charles Engel and Feng Zhu s paper

Discussion of Charles Engel and Feng Zhu s paper Michael B Devereux 1 1. Introduction This is a creative and thought-provoking paper. In many ways, it covers familiar ground for students of open economy

Discussion of Charles Engel and Feng Zhu s paper Michael B Devereux 1 1. Introduction This is a creative and thought-provoking paper. In many ways, it covers familiar ground for students of open economy

AGGREGATION OF HETEROGENEOUS BELIEFS AND ASSET PRICING: A MEAN-VARIANCE ANALYSIS

AGGREGATION OF HETEROGENEOUS BELIEFS AND ASSET PRICING: A MEAN-VARIANCE ANALYSIS CARL CHIARELLA*, ROBERTO DIECI** AND XUE-ZHONG HE* *School of Finance and Economics University of Technology, Sydney PO

AGGREGATION OF HETEROGENEOUS BELIEFS AND ASSET PRICING: A MEAN-VARIANCE ANALYSIS CARL CHIARELLA*, ROBERTO DIECI** AND XUE-ZHONG HE* *School of Finance and Economics University of Technology, Sydney PO

Endogenous risk in a DSGE model with capital-constrained financial intermediaries

Endogenous risk in a DSGE model with capital-constrained financial intermediaries Hans Dewachter (NBB-KUL) and Raf Wouters (NBB) NBB-Conference, Brussels, 11-12 October 2012 PP 1 motivation/objective introduce

Endogenous risk in a DSGE model with capital-constrained financial intermediaries Hans Dewachter (NBB-KUL) and Raf Wouters (NBB) NBB-Conference, Brussels, 11-12 October 2012 PP 1 motivation/objective introduce

Fundamental and Non-Fundamental Explanations for House Price Fluctuations

Fundamental and Non-Fundamental Explanations for House Price Fluctuations Christian Hott Economic Advice 1 Unexplained Real Estate Crises Several countries were affected by a real estate crisis in recent

Fundamental and Non-Fundamental Explanations for House Price Fluctuations Christian Hott Economic Advice 1 Unexplained Real Estate Crises Several countries were affected by a real estate crisis in recent

Economics, Complexity and Agent Based Models

Economics, Complexity and Agent Based Models Francesco LAMPERTI 1,2, 1 Institute 2 Universite of Economics and LEM, Scuola Superiore Sant Anna (Pisa) Paris 1 Pathe on-sorbonne, Centre d Economie de la

Economics, Complexity and Agent Based Models Francesco LAMPERTI 1,2, 1 Institute 2 Universite of Economics and LEM, Scuola Superiore Sant Anna (Pisa) Paris 1 Pathe on-sorbonne, Centre d Economie de la

LONG MEMORY IN VOLATILITY

LONG MEMORY IN VOLATILITY How persistent is volatility? In other words, how quickly do financial markets forget large volatility shocks? Figure 1.1, Shephard (attached) shows that daily squared returns

LONG MEMORY IN VOLATILITY How persistent is volatility? In other words, how quickly do financial markets forget large volatility shocks? Figure 1.1, Shephard (attached) shows that daily squared returns

Financial Market Feedback and Disclosure

Financial Market Feedback and Disclosure Itay Goldstein Wharton School, University of Pennsylvania Information in prices A basic premise in financial economics: market prices are very informative about

Financial Market Feedback and Disclosure Itay Goldstein Wharton School, University of Pennsylvania Information in prices A basic premise in financial economics: market prices are very informative about

Identification and Price Determination with Taylor Rules: A Critical Review by John H. Cochrane. Discussion. Eric M. Leeper

Identification and Price Determination with Taylor Rules: A Critical Review by John H. Cochrane Discussion Eric M. Leeper September 29, 2006 NBER Economic Fluctuations & Growth Federal Reserve Bank of

Identification and Price Determination with Taylor Rules: A Critical Review by John H. Cochrane Discussion Eric M. Leeper September 29, 2006 NBER Economic Fluctuations & Growth Federal Reserve Bank of

Smooth pasting as rate of return equalisation: A note

mooth pasting as rate of return equalisation: A note Mark hackleton & igbjørn ødal May 2004 Abstract In this short paper we further elucidate the smooth pasting condition that is behind the optimal early

mooth pasting as rate of return equalisation: A note Mark hackleton & igbjørn ødal May 2004 Abstract In this short paper we further elucidate the smooth pasting condition that is behind the optimal early

TOPICS IN MACROECONOMICS: MODELLING INFORMATION, LEARNING AND EXPECTATIONS LECTURE NOTES. Lucas Island Model

TOPICS IN MACROECONOMICS: MODELLING INFORMATION, LEARNING AND EXPECTATIONS LECTURE NOTES KRISTOFFER P. NIMARK Lucas Island Model The Lucas Island model appeared in a series of papers in the early 970s

TOPICS IN MACROECONOMICS: MODELLING INFORMATION, LEARNING AND EXPECTATIONS LECTURE NOTES KRISTOFFER P. NIMARK Lucas Island Model The Lucas Island model appeared in a series of papers in the early 970s

Lesson XI: Overview. 1. FX market efficiency 2. The art of foreign exchange rate

Lesson XI: Overview 1. FX market efficiency 2. The art of foreign exchange rate forecasting 1 FX market efficiency 2 Terminology I K markets are said to be efficient whenever their prices fully reflect

Lesson XI: Overview 1. FX market efficiency 2. The art of foreign exchange rate forecasting 1 FX market efficiency 2 Terminology I K markets are said to be efficient whenever their prices fully reflect

u (x) < 0. and if you believe in diminishing return of the wealth, then you would require

< 0. and if you believe in diminishing return of the wealth, then you would require") Chapter 8 Markowitz Portfolio Theory 8.7 Investor Utility Functions People are always asked the question: would more money make you happier? The answer is usually yes. The next question is how much more

Chapter 8 Markowitz Portfolio Theory 8.7 Investor Utility Functions People are always asked the question: would more money make you happier? The answer is usually yes. The next question is how much more

1 Dynamic programming

1 Dynamic programming A country has just discovered a natural resource which yields an income per period R measured in terms of traded goods. The cost of exploitation is negligible. The government wants

1 Dynamic programming A country has just discovered a natural resource which yields an income per period R measured in terms of traded goods. The cost of exploitation is negligible. The government wants

Exercises on the New-Keynesian Model

Advanced Macroeconomics II Professor Lorenza Rossi/Jordi Gali T.A. Daniël van Schoot, daniel.vanschoot@upf.edu Exercises on the New-Keynesian Model Schedule: 28th of May (seminar 4): Exercises 1, 2 and

Advanced Macroeconomics II Professor Lorenza Rossi/Jordi Gali T.A. Daniël van Schoot, daniel.vanschoot@upf.edu Exercises on the New-Keynesian Model Schedule: 28th of May (seminar 4): Exercises 1, 2 and

Discussion of Risks to Price Stability, The Zero Lower Bound, and Forward Guidance: A Real-Time Assessment

Discussion of Risks to Price Stability, The Zero Lower Bound, and Forward Guidance: A Real-Time Assessment Ragna Alstadheim Norges Bank 1. Introduction The topic of Coenen and Warne (this issue) is of

Discussion of Risks to Price Stability, The Zero Lower Bound, and Forward Guidance: A Real-Time Assessment Ragna Alstadheim Norges Bank 1. Introduction The topic of Coenen and Warne (this issue) is of

Monetary Theory and Policy. Fourth Edition. Carl E. Walsh. The MIT Press Cambridge, Massachusetts London, England

Monetary Theory and Policy Fourth Edition Carl E. Walsh The MIT Press Cambridge, Massachusetts London, England Contents Preface Introduction xiii xvii 1 Evidence on Money, Prices, and Output 1 1.1 Introduction

Monetary Theory and Policy Fourth Edition Carl E. Walsh The MIT Press Cambridge, Massachusetts London, England Contents Preface Introduction xiii xvii 1 Evidence on Money, Prices, and Output 1 1.1 Introduction

Universal Properties of Financial Markets as a Consequence of Traders Behavior: an Analytical Solution

Universal Properties of Financial Markets as a Consequence of Traders Behavior: an Analytical Solution Simone Alfarano, Friedrich Wagner, and Thomas Lux Institut für Volkswirtschaftslehre der Christian

Universal Properties of Financial Markets as a Consequence of Traders Behavior: an Analytical Solution Simone Alfarano, Friedrich Wagner, and Thomas Lux Institut für Volkswirtschaftslehre der Christian

Menu Costs and Phillips Curve by Mikhail Golosov and Robert Lucas. JPE (2007)

") Menu Costs and Phillips Curve by Mikhail Golosov and Robert Lucas. JPE (2007) Virginia Olivella and Jose Ignacio Lopez October 2008 Motivation Menu costs and repricing decisions Micro foundation of sticky

Menu Costs and Phillips Curve by Mikhail Golosov and Robert Lucas. JPE (2007) Virginia Olivella and Jose Ignacio Lopez October 2008 Motivation Menu costs and repricing decisions Micro foundation of sticky

Barro-Gordon Revisited: Reputational Equilibria with Inferential Expectations

Barro-Gordon Revisited: Reputational Equilibria with Inferential Expectations Timo Henckel Australian National University Gordon D. Menzies University of Technology Sydney Nicholas Prokhovnik University

Barro-Gordon Revisited: Reputational Equilibria with Inferential Expectations Timo Henckel Australian National University Gordon D. Menzies University of Technology Sydney Nicholas Prokhovnik University

NBER WORKING PAPER SERIES A BRAZILIAN DEBT-CRISIS MODEL. Assaf Razin Efraim Sadka. Working Paper

NBER WORKING PAPER SERIES A BRAZILIAN DEBT-CRISIS MODEL Assaf Razin Efraim Sadka Working Paper 9211 http://www.nber.org/papers/w9211 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge,

NBER WORKING PAPER SERIES A BRAZILIAN DEBT-CRISIS MODEL Assaf Razin Efraim Sadka Working Paper 9211 http://www.nber.org/papers/w9211 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge,

Is the Extension of Trading Hours Always Beneficial? An Artificial Agent-Based Analysis

Is the Extension of Trading Hours Always Beneficial? An Artificial Agent-Based Analysis KOTARO MIWA Tokio Marine Asset Management Co., Ltd KAZUHIRO UEDA Interfaculty Initiative in Information Studies,

Is the Extension of Trading Hours Always Beneficial? An Artificial Agent-Based Analysis KOTARO MIWA Tokio Marine Asset Management Co., Ltd KAZUHIRO UEDA Interfaculty Initiative in Information Studies,

Booms and Busts in Asset Prices. May 2010

Booms and Busts in Asset Prices Klaus Adam Mannheim University & CEPR Albert Marcet London School of Economics & CEPR May 2010 Adam & Marcet ( Mannheim Booms University and Busts & CEPR London School of

Booms and Busts in Asset Prices Klaus Adam Mannheim University & CEPR Albert Marcet London School of Economics & CEPR May 2010 Adam & Marcet ( Mannheim Booms University and Busts & CEPR London School of

ASSET PRICING AND WEALTH DYNAMICS AN ADAPTIVE MODEL WITH HETEROGENEOUS AGENTS

ASSET PRICING AND WEALTH DYNAMICS AN ADAPTIVE MODEL WITH HETEROGENEOUS AGENTS CARL CHIARELLA AND XUE-ZHONG HE School of Finance and Economics University of Technology, Sydney PO Box 123 Broadway NSW 2007,

ASSET PRICING AND WEALTH DYNAMICS AN ADAPTIVE MODEL WITH HETEROGENEOUS AGENTS CARL CHIARELLA AND XUE-ZHONG HE School of Finance and Economics University of Technology, Sydney PO Box 123 Broadway NSW 2007,

Exchange Rate Uncertainty and Optimal Participation in International Trade

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Policy Research Working Paper 5593 Exchange Rate Uncertainty and Optimal Participation

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Policy Research Working Paper 5593 Exchange Rate Uncertainty and Optimal Participation

A Unified Theory of Bond and Currency Markets

A Unified Theory of Bond and Currency Markets Andrey Ermolov Columbia Business School April 24, 2014 1 / 41 Stylized Facts about Bond Markets US Fact 1: Upward Sloping Real Yield Curve In US, real long

A Unified Theory of Bond and Currency Markets Andrey Ermolov Columbia Business School April 24, 2014 1 / 41 Stylized Facts about Bond Markets US Fact 1: Upward Sloping Real Yield Curve In US, real long

Imperfect Knowledge, Asset Price Swings and Structural Slumps: A Cointegrated VAR Analysis of their Interdependence

Imperfect Knowledge, Asset Price Swings and Structural Slumps: A Cointegrated VAR Analysis of their Interdependence Katarina Juselius Department of Economics University of Copenhagen Background There is

Imperfect Knowledge, Asset Price Swings and Structural Slumps: A Cointegrated VAR Analysis of their Interdependence Katarina Juselius Department of Economics University of Copenhagen Background There is

Chapter 9, section 3 from the 3rd edition: Policy Coordination

Chapter 9, section 3 from the 3rd edition: Policy Coordination Carl E. Walsh March 8, 017 Contents 1 Policy Coordination 1 1.1 The Basic Model..................................... 1. Equilibrium with Coordination.............................

Chapter 9, section 3 from the 3rd edition: Policy Coordination Carl E. Walsh March 8, 017 Contents 1 Policy Coordination 1 1.1 The Basic Model..................................... 1. Equilibrium with Coordination.............................

Assessing the Spillover Effects of Changes in Bank Capital Regulation Using BoC-GEM-Fin: A Non-Technical Description

Assessing the Spillover Effects of Changes in Bank Capital Regulation Using BoC-GEM-Fin: A Non-Technical Description Carlos de Resende, Ali Dib, and Nikita Perevalov International Economic Analysis Department

Assessing the Spillover Effects of Changes in Bank Capital Regulation Using BoC-GEM-Fin: A Non-Technical Description Carlos de Resende, Ali Dib, and Nikita Perevalov International Economic Analysis Department

Markets Do Not Select For a Liquidity Preference as Behavior Towards Risk

Markets Do Not Select For a Liquidity Preference as Behavior Towards Risk Thorsten Hens a Klaus Reiner Schenk-Hoppé b October 4, 003 Abstract Tobin 958 has argued that in the face of potential capital

Markets Do Not Select For a Liquidity Preference as Behavior Towards Risk Thorsten Hens a Klaus Reiner Schenk-Hoppé b October 4, 003 Abstract Tobin 958 has argued that in the face of potential capital

Assicurazioni Generali: An Option Pricing Case with NAGARCH

Assicurazioni Generali: An Option Pricing Case with NAGARCH Assicurazioni Generali: Business Snapshot Find our latest analyses and trade ideas on bsic.it Assicurazioni Generali SpA is an Italy-based insurance

Assicurazioni Generali: An Option Pricing Case with NAGARCH Assicurazioni Generali: Business Snapshot Find our latest analyses and trade ideas on bsic.it Assicurazioni Generali SpA is an Italy-based insurance

WHAT IT TAKES TO SOLVE THE U.S. GOVERNMENT DEFICIT PROBLEM

WHAT IT TAKES TO SOLVE THE U.S. GOVERNMENT DEFICIT PROBLEM RAY C. FAIR This paper uses a structural multi-country macroeconometric model to estimate the size of the decrease in transfer payments (or tax

WHAT IT TAKES TO SOLVE THE U.S. GOVERNMENT DEFICIT PROBLEM RAY C. FAIR This paper uses a structural multi-country macroeconometric model to estimate the size of the decrease in transfer payments (or tax

1 Introduction. Term Paper: The Hall and Taylor Model in Duali 1. Yumin Li 5/8/2012

Term Paper: The Hall and Taylor Model in Duali 1 Yumin Li 5/8/2012 1 Introduction In macroeconomics and policy making arena, it is extremely important to have the ability to manipulate a set of control

Term Paper: The Hall and Taylor Model in Duali 1 Yumin Li 5/8/2012 1 Introduction In macroeconomics and policy making arena, it is extremely important to have the ability to manipulate a set of control

Appendix to: AMoreElaborateModel

Appendix to: Why Do Demand Curves for Stocks Slope Down? AMoreElaborateModel Antti Petajisto Yale School of Management February 2004 1 A More Elaborate Model 1.1 Motivation Our earlier model provides a

Appendix to: Why Do Demand Curves for Stocks Slope Down? AMoreElaborateModel Antti Petajisto Yale School of Management February 2004 1 A More Elaborate Model 1.1 Motivation Our earlier model provides a

Exploring Financial Instability Through Agent-based Modeling Part 2: Time Series, Adaptation, and Survival

Mini course CIGI-INET: False Dichotomies Exploring Financial Instability Through Agent-based Modeling Part 2: Time Series, Adaptation, and Survival Blake LeBaron International Business School Brandeis

Mini course CIGI-INET: False Dichotomies Exploring Financial Instability Through Agent-based Modeling Part 2: Time Series, Adaptation, and Survival Blake LeBaron International Business School Brandeis

On Effects of Asymmetric Information on Non-Life Insurance Prices under Competition

On Effects of Asymmetric Information on Non-Life Insurance Prices under Competition Albrecher Hansjörg Department of Actuarial Science, Faculty of Business and Economics, University of Lausanne, UNIL-Dorigny,

On Effects of Asymmetric Information on Non-Life Insurance Prices under Competition Albrecher Hansjörg Department of Actuarial Science, Faculty of Business and Economics, University of Lausanne, UNIL-Dorigny,

II. Determinants of Asset Demand. Figure 1

University of California, Merced EC 121-Money and Banking Chapter 5 Lecture otes Professor Jason Lee I. Introduction Figure 1 shows the interest rates for 3 month treasury bills. As evidenced by the figure,

University of California, Merced EC 121-Money and Banking Chapter 5 Lecture otes Professor Jason Lee I. Introduction Figure 1 shows the interest rates for 3 month treasury bills. As evidenced by the figure,

Limitations of demand constraints in stabilising financial markets with heterogeneous beliefs.

Limitations of demand constraints in stabilising financial markets with heterogeneous beliefs. Daan in t Veld a a CeNDEF, Department of Quantitative Economics, University of Amsterdam, Valckeniersstraat

Limitations of demand constraints in stabilising financial markets with heterogeneous beliefs. Daan in t Veld a a CeNDEF, Department of Quantitative Economics, University of Amsterdam, Valckeniersstraat

Macroeconomics I Chapter 3. Consumption

Toulouse School of Economics Notes written by Ernesto Pasten (epasten@cict.fr) Slightly re-edited by Frank Portier (fportier@cict.fr) M-TSE. Macro I. 200-20. Chapter 3: Consumption Macroeconomics I Chapter

Toulouse School of Economics Notes written by Ernesto Pasten (epasten@cict.fr) Slightly re-edited by Frank Portier (fportier@cict.fr) M-TSE. Macro I. 200-20. Chapter 3: Consumption Macroeconomics I Chapter

Heterogeneous Firm, Financial Market Integration and International Risk Sharing

Heterogeneous Firm, Financial Market Integration and International Risk Sharing Ming-Jen Chang, Shikuan Chen and Yen-Chen Wu National DongHwa University Thursday 22 nd November 2018 Department of Economics,

Heterogeneous Firm, Financial Market Integration and International Risk Sharing Ming-Jen Chang, Shikuan Chen and Yen-Chen Wu National DongHwa University Thursday 22 nd November 2018 Department of Economics,

9. Real business cycles in a two period economy

9. Real business cycles in a two period economy Index: 9. Real business cycles in a two period economy... 9. Introduction... 9. The Representative Agent Two Period Production Economy... 9.. The representative

9. Real business cycles in a two period economy Index: 9. Real business cycles in a two period economy... 9. Introduction... 9. The Representative Agent Two Period Production Economy... 9.. The representative

G97/4. Current account and exchange rate behaviour under inflation targeting in a small open economy. Francisco Nadal De Simone.

G97/4 Current account and exchange rate behaviour under inflation targeting in a small open economy Francisco Nadal De Simone July 1997 JEL: E13, E5, F41 G97/4 Current account and exchange rate behaviour

G97/4 Current account and exchange rate behaviour under inflation targeting in a small open economy Francisco Nadal De Simone July 1997 JEL: E13, E5, F41 G97/4 Current account and exchange rate behaviour

S9/ex Minor Option K HANDOUT 1 OF 7 Financial Physics

S9/ex Minor Option K HANDOUT 1 OF 7 Financial Physics Professor Neil F. Johnson, Physics Department n.johnson@physics.ox.ac.uk The course has 7 handouts which are Chapters from the textbook shown above:

S9/ex Minor Option K HANDOUT 1 OF 7 Financial Physics Professor Neil F. Johnson, Physics Department n.johnson@physics.ox.ac.uk The course has 7 handouts which are Chapters from the textbook shown above:

Should Norway Change the 60% Equity portion of the GPFG fund?

Should Norway Change the 60% Equity portion of the GPFG fund? Pierre Collin-Dufresne EPFL & SFI, and CEPR April 2016 Outline Endowment Consumption Commitments Return Predictability and Trading Costs General

Should Norway Change the 60% Equity portion of the GPFG fund? Pierre Collin-Dufresne EPFL & SFI, and CEPR April 2016 Outline Endowment Consumption Commitments Return Predictability and Trading Costs General