Imperfect Knowledge, Asset Price Swings and Structural Slumps: A Cointegrated VAR Analysis of their Interdependence

|

|

|

- Anastasia Lyons

- 5 years ago

- Views:

Transcription

1 Imperfect Knowledge, Asset Price Swings and Structural Slumps: A Cointegrated VAR Analysis of their Interdependence Katarina Juselius Department of Economics University of Copenhagen

2 Background There is more persistence and breaks in the data than standard (REH based) models can explain. Two important theories addressing this persistence: Edmund Phelps Structural Slumps 1994 book proposes a unified theory for booms and busts in a global economy. The theory of Imperfect Knowledge Economics (IKE) developed in 2007 by Roman Frydman and Michael Goldberg addresses speculation in the foreign currency market. Phelps theory is based on REH and does not fully incorporate financial market persistence, whereas the IKE theory does. To combine Structural Slumps with IKE seems a promising avenue.

3 Rational expectations based models

4 Imperfect Knowledge Based Models: Risk adjusted UIP is replaced by Uncertainty Adjusted UIP: where up is an uncertainty premium measuring individuals risk averseness.

5 The IKE equilibrium relation A cointegration relation between the real exchange rate, the nominal interest rate differential, and the inflation rate differential:

6 The assumption of uncertainty (imperfect knowledge) has important implications A tendency to generate more persistence than otherwise in nominal interests rates and nominal exchange rates, but not in goods prices. The latter are not in general affected by currency speculation. The result is real exchange rate persistence Empirically this is manifested in error-increasing financial behavior over the medium run while errorcorrecting behavior over the longer run.

7 Real exchange rate persistence Under IKE, the real exchange rate is a near I(2) process: and

8 The Cointegrated VAR: Using persistence as a structuring device The CVAR model is inherently consistent with a world where unanticipated shocks cumulate over time to generate stochastic trends which move the economic equilibria (the pushing forces) and where the deviations from these equilibria are corrected by means of the dynamics of the adjustment mechanism (the pulling forces). A theory consistent CVAR scenario translates all basic assumptions about the model's shock structure, equilibrium relations and steady-state behavior into testable hypotheses on common stochastic trends, cointegration, long-run impact and dynamic adjustment. Because the CVAR is able to structure the relevant data into economically meaningful directions without subjecting them to prior restrictions, it can provide broadly defined `confidence intervals' within which empirically relevant models should fall.

9 All basic assumptions of the REH and IKE based models were translated into hypotheses on the CVAR and tested The REH based model was rejected on all accounts, whereas the IKE based model obtained a remarkable support for every single hypothesis. For example, treating the real exchange rate as I(1) rather than near I(2) would leave two large characteristic roots in the model (0.96, 0.96).

10 Illustration

11

12 Illustration: short-long interest rate spreads

13 Why is IKE based speculation potentially so important for the macro economy? 1. IKE predicts persistent swings in the real exchange rate and similar persistent swings in the real interest rate differential. 2. IKE predicts that the Fisher parity (international as well as domestic) does not hold as a stationary condition. 3. A s a consequence the term structure of interest rates is no longer well described by the expectations hypothesis. 4. Persistent swings in real exchange rates, real interest rates and the term spreads are likely to generate persistent fluctuations in the macro economy.

14 Currency speculation, IKE and structural slumps: the role of the long-term interest rate The structural slumps theory explains how open economies connected by the world real interest rate and the real exchange rate can be hit by long episodes of unemployment It predicts that an exogenous shock to the world level of public debt and/or capital stock will change the world level of interest rates, whereas an exogenous shock to the public debt of an individual open economy tend to increase its interest rate relative to the world interest rate. Johansen et al. (2010), Frydman et al. (2010) and Juselius (2010) find that shocks to the long-term US bond rate (a proxy for the world interest rate) and to the US-German interest rate differential (measuring relative debt levels between the two countries) are the exogenous forces in a system comprising US-German prices, nominal exchange rates, and long-term interest rates.

15 The importance of a nonstationary Fisher Parity Under IKE, nominal interest rates and nominal exchange rates exhibit a pronounced persistence due to the uncertainty premium. Prices of tradable goods are essentially determined by supply and demand in a very competitive global world and, therefore, less susceptible to speculative currency movements When the nominal long-term interest rate increases but CPI inflation does not, the real interest rate will increase. Increasing real interest rates are likely to increase the speculative demand for the domestic currency, hence increasing its price. Thus, as predicted by IKE, there will be a tendency for the domestic real interest rate to increase and the real exchange rate to appreciate at the same time, aggravating domestic competitiveness. As the competitiveness of the economy worsens and the macroeconomic imbalances grow, this is likely to generate a reflexive process between changes in the real interest rates and the real exchange rate (Soros 1987).

16 Why can swings be so long-lasting? As long as the real interest rate differential moves in a compensating way, the deviations from long-run PPP benchmark values can be very persistent. The I(2) model is formulated precisely to describe an economy where persistent deviations from long-run static equilibrium values are compensated by similar deviations in other variables. Because a persistent movement away from long-run benchmarks is counteracted by another similar movement, an IKE economy is still characterized by equilibrating forces but in a dynamic rather than a static set-up

17 Fluctuations in the real economy When speculative behavior drives nominal exchange rates away from fundamental PPP values, enterprises cannot use constant mark-up pricing without loosing market shares. In the struggle for market shares, enterprises will be forced to adjust profits rather than prices: profits are likely to be squeezed in periods of persistent appreciation and increased during periods of depreciation. Thus, Phelps customer market pricing is likely to replace constant mark-up pricing in an IKE economy.

18 Implications for unemployment As enterprises struggle to survive in a period of real appreciation and increasing real long-term interest rates, they will tend to improve labor productivity by laying off the least productive part of the labor force. Thus, unemployment will tend to rise/decrease in periods of appreciation/depreciation while prices stay reasonably unchanged. The long-term real interest rate, unemployment rate and inflation rate would be co-moving in a relationship that Phelps (1994) calls an augmented Phillips Curve: Δp = -b₁(u-u ) where u = f(r) describes a nonstationary natural rate as a function of the (long-term) real interest rate level. However, this relationship would no longer hold in the present post crisis period due to large scale financial consolidation behavior (Koo, 2010).

19 Discussion Macroeconomic data have a reputation for not being sufficiently informative, thereby justifying the use of `mild force' to make them tell an economically relevant story. However, macroeconomic data are surprisingly informative, but only if you let them tell the story they want to tell.

20 Which stories do the data tell if they are allowed to speak freely? There is more persistence in the data than standard REH based theories can explain. In particular, basic parity conditions such as purchasing power parity, real interest rates, uncovered interest rate parity, and the term spread seem to exhibit a pronounced persistence untenable with I(0) type stationarity. This persistence seems to originate from complex interactions between speculative financial markets and the real economy. A synthesis between the theory of structural slumps by Phelps and the IKE theory by Frydman and Goldberg' (2007) is likely to improve our understanding of the long recurrent spells of high unemployment in our economies.

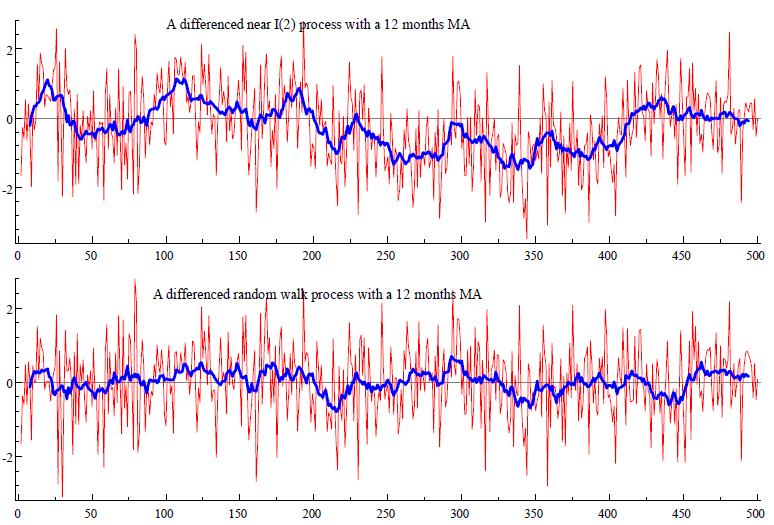

21 Difference between IKE and REH in simulated data REH: Real exchange rate at most I(1) IKE: real exchange rate near I(2)

22

23 Illustrations: real interest rates

24 Testable empirical regularities under REH and IKE Under IKE, the real exchange rate is near I(2). Under REH it is I(0) or most near I(1). Under IKE, the real exchange rate is co-moving with the real interest rate differential, so both are near I(2). Under REH the real interest rate differential is I(0) or at most near I(1). Under IKE, the real exchange rates and the real interest rate differential cointegrate to a stationary equilibrium relation. Under REH, they are individually stationary. Under IKE, the Fisher parity does not hold as a stationary condition. Under REH, the Fisher parity is stationary. Under IKE, interest rate spreads are nonstationary but cointegrated. Under REH, the expectations hypothesis holds and the spreads are stationary.

25 The purpose is to discuss: The role of speculative behavior in currency markets as a potentially important cause to persistent fluctuations in aggregate activity. The ability of REH based versus IKE based models to explain the observed nonstationary movements in basic parity conditions. How to combine the theory of IKE with the structural slumps theory in PheIps (1994) and its implication for the macro economy.

Models for Real-World Markets

Models for Real-World Markets Unanticipated Structural Change and Rationality in Macroeconomics and Finance Roman Frydman New York University and Institute for New Economic Thinking Prepared for the presentation

Models for Real-World Markets Unanticipated Structural Change and Rationality in Macroeconomics and Finance Roman Frydman New York University and Institute for New Economic Thinking Prepared for the presentation

Balance sheet recessions and time-varying coeffi cients in a Phillips curve relationship: An application to Finnish data

Balance sheet recessions and time-varying coeffi cients in a Phillips curve relationship: An application to Finnish data Katarina Juselius and Mikael Juselius University of Copenhagen and the Bank for

Balance sheet recessions and time-varying coeffi cients in a Phillips curve relationship: An application to Finnish data Katarina Juselius and Mikael Juselius University of Copenhagen and the Bank for

Balance sheet recessions and time-varying coe cients in a Phillips curve relationship: An application to Finnish data

Balance sheet recessions and time-varying coe cients in a Phillips curve relationship: An application to Finnish data Katarina Juselius and Mikael Juselius University of Copenhagen and the Bank for International

Balance sheet recessions and time-varying coe cients in a Phillips curve relationship: An application to Finnish data Katarina Juselius and Mikael Juselius University of Copenhagen and the Bank for International

INTRODUCTION TO ECONOMIC GROWTH. Dongpeng Liu Department of Economics Nanjing University

INTRODUCTION TO ECONOMIC GROWTH Dongpeng Liu Department of Economics Nanjing University ROADMAP INCOME EXPENDITURE LIQUIDITY PREFERENCE IS CURVE LM CURVE SHORT-RUN IS-LM MODEL AGGREGATE DEMAND AGGREGATE

INTRODUCTION TO ECONOMIC GROWTH Dongpeng Liu Department of Economics Nanjing University ROADMAP INCOME EXPENDITURE LIQUIDITY PREFERENCE IS CURVE LM CURVE SHORT-RUN IS-LM MODEL AGGREGATE DEMAND AGGREGATE

Are outcomes driving expectations or the other way around? An I(2) CVAR analysis of interest rate expectations in the dollar/pound market

CVAR analysis of interest rate expectations in the dollar/pound market") Are outcomes driving expectations or the other way around? An I(2) CVAR analysis of interest rate expectations in the dollar/pound market Abstract This paper uses consensus forecasts to address empirical

Are outcomes driving expectations or the other way around? An I(2) CVAR analysis of interest rate expectations in the dollar/pound market Abstract This paper uses consensus forecasts to address empirical

1 Figure 1 (A) shows what the IS LM model looks like for the case in which the Fed holds the

shows what the IS LM model looks like for the case in which the Fed holds the") 1 Figure 1 (A) shows what the IS LM model looks like for the case in which the Fed holds the money supply constant. Figure 1 (B) shows what the model looks like if the Fed adjusts the money supply to hold

1 Figure 1 (A) shows what the IS LM model looks like for the case in which the Fed holds the money supply constant. Figure 1 (B) shows what the model looks like if the Fed adjusts the money supply to hold

MONEY, PRICES AND THE EXCHANGE RATE: EVIDENCE FROM FOUR OECD COUNTRIES

money 15/10/98 MONEY, PRICES AND THE EXCHANGE RATE: EVIDENCE FROM FOUR OECD COUNTRIES Mehdi S. Monadjemi School of Economics University of New South Wales Sydney 2052 Australia m.monadjemi@unsw.edu.au

money 15/10/98 MONEY, PRICES AND THE EXCHANGE RATE: EVIDENCE FROM FOUR OECD COUNTRIES Mehdi S. Monadjemi School of Economics University of New South Wales Sydney 2052 Australia m.monadjemi@unsw.edu.au

In this chapter, we study a theory of how exchange rates are determined "in the long run." The theory we will develop has two parts:

1. INTRODUCTION 1 Introduction In the last chapter, uncovered interest parity (UIP) provided us with a theory of how the spot exchange rate is determined, given knowledge of three variables: the expected

1. INTRODUCTION 1 Introduction In the last chapter, uncovered interest parity (UIP) provided us with a theory of how the spot exchange rate is determined, given knowledge of three variables: the expected

Macroeconomics I International Group Course

Learning objectives Macroeconomics I International Group Course 2004-2005 Topic 4: INTRODUCTION TO MACROECONOMIC FLUCTUATIONS We have already studied how the economy adjusts in the long run: prices are

Learning objectives Macroeconomics I International Group Course 2004-2005 Topic 4: INTRODUCTION TO MACROECONOMIC FLUCTUATIONS We have already studied how the economy adjusts in the long run: prices are

Introduction The Story of Macroeconomics. September 2011

Introduction The Story of Macroeconomics September 2011 Keynes General Theory (1936) regards volatile expectations as the main source of economic fluctuations. animal spirits (shifts in expectations) econ

Introduction The Story of Macroeconomics September 2011 Keynes General Theory (1936) regards volatile expectations as the main source of economic fluctuations. animal spirits (shifts in expectations) econ

What Are Equilibrium Real Exchange Rates?

1 What Are Equilibrium Real Exchange Rates? This chapter does not provide a definitive or comprehensive definition of FEERs. Many discussions of the concept already exist (e.g., Williamson 1983, 1985,

1 What Are Equilibrium Real Exchange Rates? This chapter does not provide a definitive or comprehensive definition of FEERs. Many discussions of the concept already exist (e.g., Williamson 1983, 1985,

Near-Rationality and Inflation in Two Monetary Regimes

Near-Rationality and Inflation in Two Monetary Regimes by Laurence Ball San Francisco Fed/Stanford Institute for Economic Policy Research Conference Structural Change and Monetary Policy March 3 4, 2000

Near-Rationality and Inflation in Two Monetary Regimes by Laurence Ball San Francisco Fed/Stanford Institute for Economic Policy Research Conference Structural Change and Monetary Policy March 3 4, 2000

Introduction. Learning Objectives. Chapter 17. Stabilization in an Integrated World Economy

Chapter 17 Stabilization in an Integrated World Economy Introduction For more than 50 years, many economists have used an inverse relationship involving the unemployment rate and real GDP as a guide to

Chapter 17 Stabilization in an Integrated World Economy Introduction For more than 50 years, many economists have used an inverse relationship involving the unemployment rate and real GDP as a guide to

Demographics and the behavior of interest rates

Demographics and the behavior of interest rates (C. Favero, A. Gozluklu and H. Yang) Discussion by Michele Lenza European Central Bank and ECARES-ULB Firenze 18-19 June 2015 Rubric Persistence in interest

Demographics and the behavior of interest rates (C. Favero, A. Gozluklu and H. Yang) Discussion by Michele Lenza European Central Bank and ECARES-ULB Firenze 18-19 June 2015 Rubric Persistence in interest

This PDF is a selection from a published volume from the National Bureau of Economic Research

This PDF is a selection from a published volume from the National Bureau of Economic Research Volume Title: Europe and the Euro Volume Author/Editor: Alberto Alesina and Francesco Giavazzi, editors Volume

This PDF is a selection from a published volume from the National Bureau of Economic Research Volume Title: Europe and the Euro Volume Author/Editor: Alberto Alesina and Francesco Giavazzi, editors Volume

QUEEN S UNIVERSITY FACULTY OF ARTS AND SCIENCE DEPARTMENT OF ECONOMICS. Economics 222 A&B Macroeconomic Theory I. Final Examination 20 April 2009

Page 1 of 9 QUEEN S UNIVERSITY FACULTY OF ARTS AND SCIENCE DEPARTMENT OF ECONOMICS Economics 222 A&B Macroeconomic Theory I Final Examination 20 April 2009 Instructors: Nicolas-Guillaume Martineau (Section

Page 1 of 9 QUEEN S UNIVERSITY FACULTY OF ARTS AND SCIENCE DEPARTMENT OF ECONOMICS Economics 222 A&B Macroeconomic Theory I Final Examination 20 April 2009 Instructors: Nicolas-Guillaume Martineau (Section

Classes and Lectures

Classes and Lectures There are no classes in week 24, apart from the cancelled ones You ve already had 9 classes, as promised, and no doubt you re keen to revise Answers for Question Sheet 5 are on the

Classes and Lectures There are no classes in week 24, apart from the cancelled ones You ve already had 9 classes, as promised, and no doubt you re keen to revise Answers for Question Sheet 5 are on the

CORRELATION BETWEEN MALTESE AND EURO AREA SOVEREIGN BOND YIELDS

CORRELATION BETWEEN MALTESE AND EURO AREA SOVEREIGN BOND YIELDS Article published in the Quarterly Review 2017:4, pp. 38-41 BOX 1: CORRELATION BETWEEN MALTESE AND EURO AREA SOVEREIGN BOND YIELDS 1 This

CORRELATION BETWEEN MALTESE AND EURO AREA SOVEREIGN BOND YIELDS Article published in the Quarterly Review 2017:4, pp. 38-41 BOX 1: CORRELATION BETWEEN MALTESE AND EURO AREA SOVEREIGN BOND YIELDS 1 This

Case Study: Predicting U.S. Saving Behavior after the 2008 Financial Crisis (proposed solution)

") 2 Case Study: Predicting U.S. Saving Behavior after the 2008 Financial Crisis (proposed solution) 1. Data on U.S. consumption, income, and saving for 1947:1 2014:3 can be found in MF_Data.wk1, pagefile

2 Case Study: Predicting U.S. Saving Behavior after the 2008 Financial Crisis (proposed solution) 1. Data on U.S. consumption, income, and saving for 1947:1 2014:3 can be found in MF_Data.wk1, pagefile

Midterm - Economics 160B, Fall 2011 Version A

Name Student ID Section (or TA) Midterm - Economics 160B, Fall 2011 Version A You will have 75 minutes to complete this exam. There are 5 pages and 108 points total. Good luck. Multiple choice: Mark best

Name Student ID Section (or TA) Midterm - Economics 160B, Fall 2011 Version A You will have 75 minutes to complete this exam. There are 5 pages and 108 points total. Good luck. Multiple choice: Mark best

Lectures 24 & 25: Determination of exchange rates

Lectures 24 & 25: Determination of exchange rates Building blocs - Interest rate parity - Money demand equation - Goods markets Flexible-price version: monetarist/lucas model - derivation - hyperinflation

Lectures 24 & 25: Determination of exchange rates Building blocs - Interest rate parity - Money demand equation - Goods markets Flexible-price version: monetarist/lucas model - derivation - hyperinflation

1 A Simple Model of the Term Structure

Comment on Dewachter and Lyrio s "Learning, Macroeconomic Dynamics, and the Term Structure of Interest Rates" 1 by Jordi Galí (CREI, MIT, and NBER) August 2006 The present paper by Dewachter and Lyrio

Comment on Dewachter and Lyrio s "Learning, Macroeconomic Dynamics, and the Term Structure of Interest Rates" 1 by Jordi Galí (CREI, MIT, and NBER) August 2006 The present paper by Dewachter and Lyrio

Chapter 9 Dynamic Models of Investment

George Alogoskoufis, Dynamic Macroeconomic Theory, 2015 Chapter 9 Dynamic Models of Investment In this chapter we present the main neoclassical model of investment, under convex adjustment costs. This

George Alogoskoufis, Dynamic Macroeconomic Theory, 2015 Chapter 9 Dynamic Models of Investment In this chapter we present the main neoclassical model of investment, under convex adjustment costs. This

Can P* Be a Basis for Core Inflation in the Philippines?

Philippine Institute for Development Studies Can P* Be a Basis for Core Inflation in the Philippines? Josef T. Yap DISCUSSION PAPER SERIES NO. 96-10 The PIDS Discussion Paper Series constitutes studies

Philippine Institute for Development Studies Can P* Be a Basis for Core Inflation in the Philippines? Josef T. Yap DISCUSSION PAPER SERIES NO. 96-10 The PIDS Discussion Paper Series constitutes studies

Lecture 9: Exchange rates

BURNABY SIMON FRASER UNIVERSITY BRITISH COLUMBIA Paul Klein Office: WMC 3635 Phone: (778) 782-9391 Email: paul klein 2@sfu.ca URL: http://paulklein.ca/newsite/teaching/305.php Economics 305 Intermediate

BURNABY SIMON FRASER UNIVERSITY BRITISH COLUMBIA Paul Klein Office: WMC 3635 Phone: (778) 782-9391 Email: paul klein 2@sfu.ca URL: http://paulklein.ca/newsite/teaching/305.php Economics 305 Intermediate

Inflation, Unemployment and the Federal Reserve Policy Chapter 16

Inflation, Unemployment and the Federal Reserve Policy Chapter 16 The Discover of the Short-Run Trade-off between Unemployment and Inflation Phillips curve: A curve showing the short-run relationship between

Inflation, Unemployment and the Federal Reserve Policy Chapter 16 The Discover of the Short-Run Trade-off between Unemployment and Inflation Phillips curve: A curve showing the short-run relationship between

Short Run vs Long Run Determinants of Exchange Rates

Fletcher School, Tufts University Short Run vs Long Run Determinants of Exchange Rates Prof. George Alogoskoufis Short Run Determinants of Exchange Rates We have seen that in the short run exchange rates

Fletcher School, Tufts University Short Run vs Long Run Determinants of Exchange Rates Prof. George Alogoskoufis Short Run Determinants of Exchange Rates We have seen that in the short run exchange rates

The Effects of Dollarization on Macroeconomic Stability

The Effects of Dollarization on Macroeconomic Stability Christopher J. Erceg and Andrew T. Levin Division of International Finance Board of Governors of the Federal Reserve System Washington, DC 2551 USA

The Effects of Dollarization on Macroeconomic Stability Christopher J. Erceg and Andrew T. Levin Division of International Finance Board of Governors of the Federal Reserve System Washington, DC 2551 USA

Please choose the most correct answer. You can choose only ONE answer for every question.

Please choose the most correct answer. You can choose only ONE answer for every question. 1. Only when inflation increases unexpectedly a. the real interest rate will be lower than the nominal inflation

Please choose the most correct answer. You can choose only ONE answer for every question. 1. Only when inflation increases unexpectedly a. the real interest rate will be lower than the nominal inflation

Tradeoff Between Inflation and Unemployment

CHAPTER 13 Aggregate Supply and the Short-Run Tradeoff Between Inflation and Unemployment Questions for Review 1. In this chapter we looked at two models of the short-run aggregate supply curve. Both models

CHAPTER 13 Aggregate Supply and the Short-Run Tradeoff Between Inflation and Unemployment Questions for Review 1. In this chapter we looked at two models of the short-run aggregate supply curve. Both models

Interest Rate Linkages and Capital Market Integration: Evidence from the Americas

Interest Rate Linkages and Capital Market Integration: Evidence from the Americas Bharat Bhalla, Ph. D. Fairfield University Bbhalla@mail.fairfield.edu 203 254 4000 Anand Shetty, Ph. D., Iona College Ashetty@iona.edu

Interest Rate Linkages and Capital Market Integration: Evidence from the Americas Bharat Bhalla, Ph. D. Fairfield University Bbhalla@mail.fairfield.edu 203 254 4000 Anand Shetty, Ph. D., Iona College Ashetty@iona.edu

Balance sheet recessions and time-varying coe cients in a Phillips curve relationship: An application to Finnish data

Balance sheet recessions and time-varying coe cients in a Phillips curve relationship: An application to Finnish data Katarina Juselius and Mikael Juselius University of Copenhagen and the Bank for International

Balance sheet recessions and time-varying coe cients in a Phillips curve relationship: An application to Finnish data Katarina Juselius and Mikael Juselius University of Copenhagen and the Bank for International

EC202 Macroeconomics

EC202 Macroeconomics Koç University, Summer 2014 by Arhan Ertan Study Questions - 3 1. Suppose a government is able to permanently reduce its budget deficit. Use the Solow growth model of Chapter 9 to

EC202 Macroeconomics Koç University, Summer 2014 by Arhan Ertan Study Questions - 3 1. Suppose a government is able to permanently reduce its budget deficit. Use the Solow growth model of Chapter 9 to

Lessons V and VI: FX Parity Conditions

Lessons V and VI: FX March 27, 2017 Table of Contents Does the PPP Hold Parity s should be thought of as break-even values, where the decision-maker is indifferent between two available strategies. Parity

Lessons V and VI: FX March 27, 2017 Table of Contents Does the PPP Hold Parity s should be thought of as break-even values, where the decision-maker is indifferent between two available strategies. Parity

11. Short Run versus Medium Run Determinants of Exchange Rates

Fletcher School of Law and Diplomacy, Tufts University 11. Short Run versus Medium Run Determinants of Exchange Rates E212 Macroeconomics Prof. George Alogoskoufis Short Run versus Medium Run Determinants

Fletcher School of Law and Diplomacy, Tufts University 11. Short Run versus Medium Run Determinants of Exchange Rates E212 Macroeconomics Prof. George Alogoskoufis Short Run versus Medium Run Determinants

Lecture 1: Traditional Open Macro Models and Monetary Policy

Lecture 1: Traditional Open Macro Models and Monetary Policy Isabelle Méjean isabelle.mejean@polytechnique.edu http://mejean.isabelle.googlepages.com/ Master Economics and Public Policy, International

Lecture 1: Traditional Open Macro Models and Monetary Policy Isabelle Méjean isabelle.mejean@polytechnique.edu http://mejean.isabelle.googlepages.com/ Master Economics and Public Policy, International

Dynamic Macroeconomics

Chapter 1 Introduction Dynamic Macroeconomics Prof. George Alogoskoufis Fletcher School, Tufts University and Athens University of Economics and Business 1.1 The Nature and Evolution of Macroeconomics

Chapter 1 Introduction Dynamic Macroeconomics Prof. George Alogoskoufis Fletcher School, Tufts University and Athens University of Economics and Business 1.1 The Nature and Evolution of Macroeconomics

A Study on Impact of WPI, IIP and M3 on the Performance of Selected Sectoral Indices of BSE

A Study on Impact of WPI, IIP and M3 on the Performance of Selected Sectoral Indices of BSE J. Gayathiri 1 and Dr. L. Ganesamoorthy 2 1 (Research Scholar, Department of Commerce, Annamalai University,

A Study on Impact of WPI, IIP and M3 on the Performance of Selected Sectoral Indices of BSE J. Gayathiri 1 and Dr. L. Ganesamoorthy 2 1 (Research Scholar, Department of Commerce, Annamalai University,

Volume 35, Issue 1. Thai-Ha Le RMIT University (Vietnam Campus)

") Volume 35, Issue 1 Exchange rate determination in Vietnam Thai-Ha Le RMIT University (Vietnam Campus) Abstract This study investigates the determinants of the exchange rate in Vietnam and suggests policy

Volume 35, Issue 1 Exchange rate determination in Vietnam Thai-Ha Le RMIT University (Vietnam Campus) Abstract This study investigates the determinants of the exchange rate in Vietnam and suggests policy

Lecture 2, November 16: A Classical Model (Galí, Chapter 2)

") MakØk3, Fall 2010 (blok 2) Business cycles and monetary stabilization policies Henrik Jensen Department of Economics University of Copenhagen Lecture 2, November 16: A Classical Model (Galí, Chapter 2)

MakØk3, Fall 2010 (blok 2) Business cycles and monetary stabilization policies Henrik Jensen Department of Economics University of Copenhagen Lecture 2, November 16: A Classical Model (Galí, Chapter 2)

Chapter 8 A Short Run Keynesian Model of Interdependent Economies

George Alogoskoufis, International Macroeconomics, 2016 Chapter 8 A Short Run Keynesian Model of Interdependent Economies Our analysis up to now was related to small open economies, which took developments

George Alogoskoufis, International Macroeconomics, 2016 Chapter 8 A Short Run Keynesian Model of Interdependent Economies Our analysis up to now was related to small open economies, which took developments

International Parity Relationships Between Germany and the United States: A Joint Modelling Approach

International Parity Relationships Between Germany and the United States: A Joint Modelling Approach Katarina Juselius Institute of Economics, University of Copenhagen Ronald MacDonald Department of Economics,

International Parity Relationships Between Germany and the United States: A Joint Modelling Approach Katarina Juselius Institute of Economics, University of Copenhagen Ronald MacDonald Department of Economics,

Monetary Transmission Mechanisms in Spain: The Effect of Monetization, Financial Deregulation, and the EMS

Monetary Transmission Mechanisms in Spain: The Effect of Monetization, Financial Deregulation, and the EMS Katarina Juselius University of Copenhagen and Juan Toro University of Oxford Abstract The paper

Monetary Transmission Mechanisms in Spain: The Effect of Monetization, Financial Deregulation, and the EMS Katarina Juselius University of Copenhagen and Juan Toro University of Oxford Abstract The paper

Monetary Theory and Policy. Fourth Edition. Carl E. Walsh. The MIT Press Cambridge, Massachusetts London, England

Monetary Theory and Policy Fourth Edition Carl E. Walsh The MIT Press Cambridge, Massachusetts London, England Contents Preface Introduction xiii xvii 1 Evidence on Money, Prices, and Output 1 1.1 Introduction

Monetary Theory and Policy Fourth Edition Carl E. Walsh The MIT Press Cambridge, Massachusetts London, England Contents Preface Introduction xiii xvii 1 Evidence on Money, Prices, and Output 1 1.1 Introduction

CFA Level II - LOS Changes

CFA Level II - LOS Changes 2018-2019 Topic LOS Level II - 2018 (465 LOS) LOS Level II - 2019 (471 LOS) Compared Ethics 1.1.a describe the six components of the Code of Ethics and the seven Standards of

CFA Level II - LOS Changes 2018-2019 Topic LOS Level II - 2018 (465 LOS) LOS Level II - 2019 (471 LOS) Compared Ethics 1.1.a describe the six components of the Code of Ethics and the seven Standards of

CFA Level II - LOS Changes

CFA Level II - LOS Changes 2017-2018 Ethics Ethics Ethics Ethics Ethics Ethics Ethics Ethics Ethics Topic LOS Level II - 2017 (464 LOS) LOS Level II - 2018 (465 LOS) Compared 1.1.a 1.1.b 1.2.a 1.2.b 1.3.a

CFA Level II - LOS Changes 2017-2018 Ethics Ethics Ethics Ethics Ethics Ethics Ethics Ethics Ethics Topic LOS Level II - 2017 (464 LOS) LOS Level II - 2018 (465 LOS) Compared 1.1.a 1.1.b 1.2.a 1.2.b 1.3.a

The Importance of Being Predictable. John B. Taylor Stanford University. Remarks Prepared for the Policy Panel on Monetary Policy Under Uncertainty

The Importance of Being Predictable John B. Taylor Stanford University Remarks Prepared for the Policy Panel on Monetary Policy Under Uncertainty 23 rd Annual Policy Conference Federal Reserve Bank of

The Importance of Being Predictable John B. Taylor Stanford University Remarks Prepared for the Policy Panel on Monetary Policy Under Uncertainty 23 rd Annual Policy Conference Federal Reserve Bank of

ECON 3312 Macroeconomics Exam 4 Crowder Fall 2016

ECON 3312 Macroeconomics Exam 4 Crowder Fall 2016 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) When the economy is hit by a temporary positive

ECON 3312 Macroeconomics Exam 4 Crowder Fall 2016 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) When the economy is hit by a temporary positive

Part III. Cycles and Growth:

Part III. Cycles and Growth: UMSL Max Gillman Max Gillman () AS-AD 1 / 56 AS-AD, Relative Prices & Business Cycles Facts: Nominal Prices are Not Real Prices Price of goods in nominal terms: eg. Consumer

Part III. Cycles and Growth: UMSL Max Gillman Max Gillman () AS-AD 1 / 56 AS-AD, Relative Prices & Business Cycles Facts: Nominal Prices are Not Real Prices Price of goods in nominal terms: eg. Consumer

1 Business-Cycle Facts Around the World 1

Contents Preface xvii 1 Business-Cycle Facts Around the World 1 1.1 Measuring Business Cycles 1 1.2 Business-Cycle Facts Around the World 4 1.3 Business Cycles in Poor, Emerging, and Rich Countries 7 1.4

Contents Preface xvii 1 Business-Cycle Facts Around the World 1 1.1 Measuring Business Cycles 1 1.2 Business-Cycle Facts Around the World 4 1.3 Business Cycles in Poor, Emerging, and Rich Countries 7 1.4

3. If the price of a British pound increases from $1.50 per pound to $1.80 per pound, we say that:

STUDY GUIDE FINAL ECO41 FALL 2013 UDAYAN ROY Ch 13 National Income Accounting See the questions in Homework 7 and Homework 8. CHAPTER 14 Exchange Rates and Interest Parity 1. How many dollars would it

STUDY GUIDE FINAL ECO41 FALL 2013 UDAYAN ROY Ch 13 National Income Accounting See the questions in Homework 7 and Homework 8. CHAPTER 14 Exchange Rates and Interest Parity 1. How many dollars would it

Satya P. Das NIPFP) Open Economy Keynesian Macro: CGG (2001, 2002), Obstfeld-Rogoff Redux Model 1 / 18

Open Economy Keynesian Macro: CGG (2001, 2002), Obstfeld-Rogoff Redux Model 1 / 18") Open Economy Keynesian Macro: CGG (2001, 2002), Obstfeld-Rogoff Redux Model Satya P. Das @ NIPFP Open Economy Keynesian Macro: CGG (2001, 2002), Obstfeld-Rogoff Redux Model 1 / 18 1 CGG (2001) 2 CGG (2002)

Open Economy Keynesian Macro: CGG (2001, 2002), Obstfeld-Rogoff Redux Model Satya P. Das @ NIPFP Open Economy Keynesian Macro: CGG (2001, 2002), Obstfeld-Rogoff Redux Model 1 / 18 1 CGG (2001) 2 CGG (2002)

Portfolio Balance Models of Exchange

Lecture Notes 10 Portfolio Balance Models of Exchange Rate Determination When economists speak of the portfolio balance approach, they are referring to a diverse set of models. There are a few common features,

Lecture Notes 10 Portfolio Balance Models of Exchange Rate Determination When economists speak of the portfolio balance approach, they are referring to a diverse set of models. There are a few common features,

Currency Intervention vs. Speculative Sentiment:

Currency Intervention vs. Speculative Sentiment: Analysis of Japanese and US FOREX Markets Xuxin Mao Feb 2012 University of Glasgow Motivation and Plan Yen s Appreciation against USD is a puzzle in international

Currency Intervention vs. Speculative Sentiment: Analysis of Japanese and US FOREX Markets Xuxin Mao Feb 2012 University of Glasgow Motivation and Plan Yen s Appreciation against USD is a puzzle in international

CHAPTER 17 (7e) 1. Using the information in this chapter, label each of the following statements true, false, or uncertain. Explain briefly.

1. Using the information in this chapter, label each of the following statements true, false, or uncertain. Explain briefly.") Self-practice (Open Economy) Ch 17(7e): Q1, Q2, Q5 Ch 18(7e): Q1, Q2, Q5, Q7, Ch 20(6e): Q1-Q5 CHAPTER 17 (7e) 1. Using the information in this chapter, label each of the following statements true, false,

Self-practice (Open Economy) Ch 17(7e): Q1, Q2, Q5 Ch 18(7e): Q1, Q2, Q5, Q7, Ch 20(6e): Q1-Q5 CHAPTER 17 (7e) 1. Using the information in this chapter, label each of the following statements true, false,

Chapter 13. Introduction. Goods Market Equilibrium. Modeling Strategy. Nominal Exchange Rate: A Convention. The Nominal Exchange Rate

Introduction Chapter 13 Open Economy Macroeconomics Our previous model has assumed a single country exists in isolation, with no trade or financial flows with any other country. This chapter relaxes the

Introduction Chapter 13 Open Economy Macroeconomics Our previous model has assumed a single country exists in isolation, with no trade or financial flows with any other country. This chapter relaxes the

Monetary Policy, Financial Stability and Interest Rate Rules Giorgio Di Giorgio and Zeno Rotondi

Monetary Policy, Financial Stability and Interest Rate Rules Giorgio Di Giorgio and Zeno Rotondi Alessandra Vincenzi VR 097844 Marco Novello VR 362520 The paper is focus on This paper deals with the empirical

Monetary Policy, Financial Stability and Interest Rate Rules Giorgio Di Giorgio and Zeno Rotondi Alessandra Vincenzi VR 097844 Marco Novello VR 362520 The paper is focus on This paper deals with the empirical

24/01/2016. Uniwersytet Ekonomiczny. George Matysiak. Agenda. Modelling & Forecasting Process

Uniwersytet Ekonomiczny George Matysiak Building and estimating models 11 th January, 2016 Agenda Modelling and forecasting commercial real estate markets Modelling process Model specification Drivers

Uniwersytet Ekonomiczny George Matysiak Building and estimating models 11 th January, 2016 Agenda Modelling and forecasting commercial real estate markets Modelling process Model specification Drivers

Monetary Policy and Medium-Term Fiscal Planning

Doug Hostland Department of Finance Working Paper * 2001-20 * The views expressed in this paper are those of the author and do not reflect those of the Department of Finance. A previous version of this

Doug Hostland Department of Finance Working Paper * 2001-20 * The views expressed in this paper are those of the author and do not reflect those of the Department of Finance. A previous version of this

Zhenyu Wu 1 & Maoguo Wu 1

International Journal of Economics and Finance; Vol. 10, No. 5; 2018 ISSN 1916-971X E-ISSN 1916-9728 Published by Canadian Center of Science and Education The Impact of Financial Liquidity on the Exchange

International Journal of Economics and Finance; Vol. 10, No. 5; 2018 ISSN 1916-971X E-ISSN 1916-9728 Published by Canadian Center of Science and Education The Impact of Financial Liquidity on the Exchange

Topic 4: Introduction to Exchange Rates Part 1: Definitions and empirical regularities

Topic 4: Introduction to Exchange Rates Part 1: Definitions and empirical regularities - The models we studied earlier include only real variables and relative prices. We now extend these models to have

Topic 4: Introduction to Exchange Rates Part 1: Definitions and empirical regularities - The models we studied earlier include only real variables and relative prices. We now extend these models to have

7.1 Assumptions: prices sticky in SR, but flex in MR, endogenous expectations

7 Lecture 7(I): Exchange rate overshooting - Dornbusch model Reference: Krugman-Obstfeld, p. 356-365 7.1 Assumptions: prices sticky in SR, but flex in MR, endogenous expectations Clearly it applies only

7 Lecture 7(I): Exchange rate overshooting - Dornbusch model Reference: Krugman-Obstfeld, p. 356-365 7.1 Assumptions: prices sticky in SR, but flex in MR, endogenous expectations Clearly it applies only

Lecture 3, Part 1 (Bubbles, Portfolio Balance Models)

") Lecture 3, Part 1 (Bubbles, Portfolio Balance Models) 1. Rational Bubbles in Theory 2. An Early Test for Price Bubbles 3. Meese's Tests Foreign Exchange Bubbles 4. Limitations of Bubble Tests 5. A Simple

Lecture 3, Part 1 (Bubbles, Portfolio Balance Models) 1. Rational Bubbles in Theory 2. An Early Test for Price Bubbles 3. Meese's Tests Foreign Exchange Bubbles 4. Limitations of Bubble Tests 5. A Simple

Canada s Pioneering Experience with a Flexible Exchange Rate in the 1950s: (Hard) Lessons Learned for Monetary Policy in a Small Open Economy.

Lessons Learned for Monetary Policy in a Small Open Economy.") Canada s Pioneering Experience with a Flexible Exchange Rate in the 1950s: (Hard) Lessons Learned for Monetary Policy in a Small Open Economy. Lawrence Schembri International Department Bank of Canada

Canada s Pioneering Experience with a Flexible Exchange Rate in the 1950s: (Hard) Lessons Learned for Monetary Policy in a Small Open Economy. Lawrence Schembri International Department Bank of Canada

Chapter 9, section 3 from the 3rd edition: Policy Coordination

Chapter 9, section 3 from the 3rd edition: Policy Coordination Carl E. Walsh March 8, 017 Contents 1 Policy Coordination 1 1.1 The Basic Model..................................... 1. Equilibrium with Coordination.............................

Chapter 9, section 3 from the 3rd edition: Policy Coordination Carl E. Walsh March 8, 017 Contents 1 Policy Coordination 1 1.1 The Basic Model..................................... 1. Equilibrium with Coordination.............................

Overview Panel: Re-Anchoring Inflation Expectations via Quantitative and Qualitative Monetary Easing with a Negative Interest Rate

Overview Panel: Re-Anchoring Inflation Expectations via Quantitative and Qualitative Monetary Easing with a Negative Interest Rate Haruhiko Kuroda I. Introduction Over the past two decades, Japan has found

Overview Panel: Re-Anchoring Inflation Expectations via Quantitative and Qualitative Monetary Easing with a Negative Interest Rate Haruhiko Kuroda I. Introduction Over the past two decades, Japan has found

Is regulatory capital pro-cyclical? A macroeconomic assessment of Basel II

Is regulatory capital pro-cyclical? A macroeconomic assessment of Basel II (preliminary version) Frank Heid Deutsche Bundesbank 2003 1 Introduction Capital requirements play a prominent role in international

Is regulatory capital pro-cyclical? A macroeconomic assessment of Basel II (preliminary version) Frank Heid Deutsche Bundesbank 2003 1 Introduction Capital requirements play a prominent role in international

Innovations in Macroeconomics

Paul JJ. Welfens Innovations in Macroeconomics Third Edition 4y Springer Contents A. Globalization, Specialization and Innovation Dynamics 1 A. 1 Introduction 1 A.2 Approaches in Modern Macroeconomics

Paul JJ. Welfens Innovations in Macroeconomics Third Edition 4y Springer Contents A. Globalization, Specialization and Innovation Dynamics 1 A. 1 Introduction 1 A.2 Approaches in Modern Macroeconomics

Answers To Chapter 14

nswers To Chapter 14 eview Questions 1. nswer a. U 15 u = 0.10. U + E = 15 + 135 = 2. nswer a. The degree of economic hardship is clearly influenced by the percentage of the population that is employed,

nswers To Chapter 14 eview Questions 1. nswer a. U 15 u = 0.10. U + E = 15 + 135 = 2. nswer a. The degree of economic hardship is clearly influenced by the percentage of the population that is employed,

FETP/MPP8/Macroeconomics/Riedel. Money, Interest Rates and the Exchange Rate

FETP/MPP8/Macroeconomics/Riedel Money, Interest Rates and the Exchange Rate Money, Interest Rates and the Exchange Rate In the previous lecture we learned that the exchange rate between two currencies

FETP/MPP8/Macroeconomics/Riedel Money, Interest Rates and the Exchange Rate Money, Interest Rates and the Exchange Rate In the previous lecture we learned that the exchange rate between two currencies

Theory. 2.1 One Country Background

2 Theory 2.1 One Country 2.1.1 Background The theory that has guided the specification of the US model was first presented in Fair (1974) and then in Chapter 3 in Fair (1984). This work stresses three

2 Theory 2.1 One Country 2.1.1 Background The theory that has guided the specification of the US model was first presented in Fair (1974) and then in Chapter 3 in Fair (1984). This work stresses three

1. Money in the utility function (continued)

") Monetary Economics: Macro Aspects, 19/2 2013 Henrik Jensen Department of Economics University of Copenhagen 1. Money in the utility function (continued) a. Welfare costs of in ation b. Potential non-superneutrality

Monetary Economics: Macro Aspects, 19/2 2013 Henrik Jensen Department of Economics University of Copenhagen 1. Money in the utility function (continued) a. Welfare costs of in ation b. Potential non-superneutrality

TOPICS IN MACROECONOMICS: MODELLING INFORMATION, LEARNING AND EXPECTATIONS LECTURE NOTES. Lucas Island Model

TOPICS IN MACROECONOMICS: MODELLING INFORMATION, LEARNING AND EXPECTATIONS LECTURE NOTES KRISTOFFER P. NIMARK Lucas Island Model The Lucas Island model appeared in a series of papers in the early 970s

TOPICS IN MACROECONOMICS: MODELLING INFORMATION, LEARNING AND EXPECTATIONS LECTURE NOTES KRISTOFFER P. NIMARK Lucas Island Model The Lucas Island model appeared in a series of papers in the early 970s

CHAPTER 5 RESULT AND ANALYSIS

CHAPTER 5 RESULT AND ANALYSIS This chapter presents the results of the study and its analysis in order to meet the objectives. These results confirm the presence and impact of the biases taken into consideration,

CHAPTER 5 RESULT AND ANALYSIS This chapter presents the results of the study and its analysis in order to meet the objectives. These results confirm the presence and impact of the biases taken into consideration,

ECONOMICS. of Macroeconomic. Paper 4: Basic Macroeconomics Module 1: Introduction: Issues studied in Macroeconomics, Schools of Macroeconomic

Subject Paper No and Title Module No and Title Module Tag 4: Basic s 1: Introduction: Issues studied in s, Schools of ECO_P4_M1 Paper 4: Basic s Module 1: Introduction: Issues studied in s, Schools of

Subject Paper No and Title Module No and Title Module Tag 4: Basic s 1: Introduction: Issues studied in s, Schools of ECO_P4_M1 Paper 4: Basic s Module 1: Introduction: Issues studied in s, Schools of

The Dornbusch overshooting model. The short run and long run together

The Dornbusch overshooting model. The short run and long run together Overview of the Dornbusch model Weaknesses of preceding models: Long run Monetary Model: exchange rate far more volatile than monetary

The Dornbusch overshooting model. The short run and long run together Overview of the Dornbusch model Weaknesses of preceding models: Long run Monetary Model: exchange rate far more volatile than monetary

Introduction to Macroeconomics M

Introduction to Macroeconomics M5 2015-16 Problem Set 4 Multiple choice questions 1. Arbitrage and speculation differ from each other (a) in that arbitrage only takes place in the currency market, whereas

Introduction to Macroeconomics M5 2015-16 Problem Set 4 Multiple choice questions 1. Arbitrage and speculation differ from each other (a) in that arbitrage only takes place in the currency market, whereas

III Econometric Policy Evaluation

III Econometric Policy Evaluation 6 Design of Policy Systems This chapter considers the design of macroeconomic policy systems. Three questions are addressed. First, is a worldwide system of fixed exchange

III Econometric Policy Evaluation 6 Design of Policy Systems This chapter considers the design of macroeconomic policy systems. Three questions are addressed. First, is a worldwide system of fixed exchange

List of tables List of boxes List of screenshots Preface to the third edition Acknowledgements

Table of List of figures List of tables List of boxes List of screenshots Preface to the third edition Acknowledgements page xii xv xvii xix xxi xxv 1 Introduction 1 1.1 What is econometrics? 2 1.2 Is

Table of List of figures List of tables List of boxes List of screenshots Preface to the third edition Acknowledgements page xii xv xvii xix xxi xxv 1 Introduction 1 1.1 What is econometrics? 2 1.2 Is

Unemployment Persistence, Inflation and Monetary Policy, in a Dynamic Stochastic Model of the Natural Rate.

Unemployment Persistence, Inflation and Monetary Policy, in a Dynamic Stochastic Model of the Natural Rate. George Alogoskoufis * October 11, 2017 Abstract This paper analyzes monetary policy in the context

Unemployment Persistence, Inflation and Monetary Policy, in a Dynamic Stochastic Model of the Natural Rate. George Alogoskoufis * October 11, 2017 Abstract This paper analyzes monetary policy in the context

Money Market Uncertainty and Retail Interest Rate Fluctuations: A Cross-Country Comparison

DEPARTMENT OF ECONOMICS JOHANNES KEPLER UNIVERSITY LINZ Money Market Uncertainty and Retail Interest Rate Fluctuations: A Cross-Country Comparison by Burkhard Raunig and Johann Scharler* Working Paper

DEPARTMENT OF ECONOMICS JOHANNES KEPLER UNIVERSITY LINZ Money Market Uncertainty and Retail Interest Rate Fluctuations: A Cross-Country Comparison by Burkhard Raunig and Johann Scharler* Working Paper

Final Exam - Economics 101 (Fall 2009) You will have 120 minutes to complete this exam. There are 105 points and 7 pages

You will have 120 minutes to complete this exam. There are 105 points and 7 pages") Name Student ID Section day and time Final Exam - Economics 101 (Fall 2009) You will have 120 minutes to complete this exam. There are 105 points and 7 pages Multiple Choice: (20 points total, 2 points

Name Student ID Section day and time Final Exam - Economics 101 (Fall 2009) You will have 120 minutes to complete this exam. There are 105 points and 7 pages Multiple Choice: (20 points total, 2 points

Structural Cointegration Analysis of Private and Public Investment

International Journal of Business and Economics, 2002, Vol. 1, No. 1, 59-67 Structural Cointegration Analysis of Private and Public Investment Rosemary Rossiter * Department of Economics, Ohio University,

International Journal of Business and Economics, 2002, Vol. 1, No. 1, 59-67 Structural Cointegration Analysis of Private and Public Investment Rosemary Rossiter * Department of Economics, Ohio University,

A Resolution of the Purchasing Power Parity Puzzle: Imperfect Knowledge and Long Swings

A Resolution of the Purchasing Power Parity Puzzle: Imperfect Knowledge and Long Swings Roman Frydman 1, Michael D. Goldberg 2, Søren Johansen 3, and Katarina Juselius 4 December 8, 2008 Abstract Asset

A Resolution of the Purchasing Power Parity Puzzle: Imperfect Knowledge and Long Swings Roman Frydman 1, Michael D. Goldberg 2, Søren Johansen 3, and Katarina Juselius 4 December 8, 2008 Abstract Asset

How To Calculate FEERs

3 How To Calculate FEERs This chapter specifies the partial-equilibrium model we use to calculate FEERs. Chapter 4 estimates key relationships from this model and chapter 5 uses the model to calculate

3 How To Calculate FEERs This chapter specifies the partial-equilibrium model we use to calculate FEERs. Chapter 4 estimates key relationships from this model and chapter 5 uses the model to calculate

Assignment 5 The New Keynesian Phillips Curve

Econometrics II Fall 2017 Department of Economics, University of Copenhagen Assignment 5 The New Keynesian Phillips Curve The Case: Inflation tends to be pro-cycical with high inflation during times of

Econometrics II Fall 2017 Department of Economics, University of Copenhagen Assignment 5 The New Keynesian Phillips Curve The Case: Inflation tends to be pro-cycical with high inflation during times of

2/10/2011 PREDICTING EXCHANGE RATES: THE LONG-RUN MONETARY APPROACH and the The SHORT-RUN ASSET APPROACH

PREDICTING EXCHANGE RATES: THE LONG-RUN MONETARY APPROACH and the The SHORT-RUN ASSET APPROACH Introduction to Exchange Rates and Prices Consider some hypothetical data on prices and exchange rates in

PREDICTING EXCHANGE RATES: THE LONG-RUN MONETARY APPROACH and the The SHORT-RUN ASSET APPROACH Introduction to Exchange Rates and Prices Consider some hypothetical data on prices and exchange rates in

EMPIRICAL STUDY ON RELATIONS BETWEEN MACROECONOMIC VARIABLES AND THE KOREAN STOCK PRICES: AN APPLICATION OF A VECTOR ERROR CORRECTION MODEL

FULL PAPER PROCEEDING Multidisciplinary Studies Available online at www.academicfora.com Full Paper Proceeding BESSH-2016, Vol. 76- Issue.3, 56-61 ISBN 978-969-670-180-4 BESSH-16 EMPIRICAL STUDY ON RELATIONS

FULL PAPER PROCEEDING Multidisciplinary Studies Available online at www.academicfora.com Full Paper Proceeding BESSH-2016, Vol. 76- Issue.3, 56-61 ISBN 978-969-670-180-4 BESSH-16 EMPIRICAL STUDY ON RELATIONS

Equilibrium exchange rate in Ukraine:

Policy Briefing Series [PB/18/2011] Equilibrium exchange rate in Ukraine: Quantitative assessment and policy implications for 2011/2012 Prof. Dr. Enzo Weber, Robert Kirchner, Dr. Ricardo Giucci German

Policy Briefing Series [PB/18/2011] Equilibrium exchange rate in Ukraine: Quantitative assessment and policy implications for 2011/2012 Prof. Dr. Enzo Weber, Robert Kirchner, Dr. Ricardo Giucci German

CHAPTER 5: LEARNING ABOUT RETURN AND RISK FROM THE HISTORICAL RECORD

CHAPTER 5: LEARNING ABOUT RETURN AND RISK FROM THE HISTORICAL RECORD PROBLEM SETS 1. The Fisher equation predicts that the nominal rate will equal the equilibrium real rate plus the expected inflation

CHAPTER 5: LEARNING ABOUT RETURN AND RISK FROM THE HISTORICAL RECORD PROBLEM SETS 1. The Fisher equation predicts that the nominal rate will equal the equilibrium real rate plus the expected inflation

HOMEWORK 8 (CHAPTER 16 PRICE LEVELS AND THE EXCHANGE RATE IN THE LONG RUN) ECO41 FALL 2015 UDAYAN ROY

ECO41 FALL 2015 UDAYAN ROY") HOMEWORK 8 (CHAPTER 16 PRICE LEVELS AND THE EXCHANGE RATE IN THE LONG RUN) ECO41 FALL 2015 UDAYAN ROY Each correct answer is worth 1 point. The maximum score is 20 points. This homework is due in class

HOMEWORK 8 (CHAPTER 16 PRICE LEVELS AND THE EXCHANGE RATE IN THE LONG RUN) ECO41 FALL 2015 UDAYAN ROY Each correct answer is worth 1 point. The maximum score is 20 points. This homework is due in class

CFA Level 2 - LOS Changes

CFA Level 2 - LOS s 2014-2015 Ethics Ethics Ethics Ethics Ethics Ethics Topic LOS Level II - 2014 (477 LOS) LOS Level II - 2015 (468 LOS) Compared 1.1.a 1.1.b 1.2.a 1.2.b 1.3.a 1.3.b describe the six components

CFA Level 2 - LOS s 2014-2015 Ethics Ethics Ethics Ethics Ethics Ethics Topic LOS Level II - 2014 (477 LOS) LOS Level II - 2015 (468 LOS) Compared 1.1.a 1.1.b 1.2.a 1.2.b 1.3.a 1.3.b describe the six components

1) Real and Nominal exchange rates are highly positively correlated. 2) Real and nominal exchange rates are well approximated by a random walk.

Real and Nominal exchange rates are highly positively correlated. 2) Real and nominal exchange rates are well approximated by a random walk.") Stylized Facts Most of the large industrialized countries floated their exchange rates in early 1973, after the demise of the post-war Bretton Woods system of fixed exchange rates. While there have been

Stylized Facts Most of the large industrialized countries floated their exchange rates in early 1973, after the demise of the post-war Bretton Woods system of fixed exchange rates. While there have been

Re-anchoring Inflation Expectations via "Quantitative and Qualitative Monetary Easing with a Negative Interest Rate"

August 27, 2016 Bank of Japan Re-anchoring Inflation Expectations via "Quantitative and Qualitative Monetary Easing with a Negative Interest Rate" Remarks at the Economic Policy Symposium Held by the Federal

August 27, 2016 Bank of Japan Re-anchoring Inflation Expectations via "Quantitative and Qualitative Monetary Easing with a Negative Interest Rate" Remarks at the Economic Policy Symposium Held by the Federal

The papers and comments presented at the Federal Reserve Bank of

Preface The papers and comments presented at the Federal Reserve Bank of St. Louis s Tenth Annual Economic Conference are contained in this book. The topic of this conference, held on October 12 13, 1985,

Preface The papers and comments presented at the Federal Reserve Bank of St. Louis s Tenth Annual Economic Conference are contained in this book. The topic of this conference, held on October 12 13, 1985,

Does the Unemployment Invariance Hypothesis Hold for Canada?

DISCUSSION PAPER SERIES IZA DP No. 10178 Does the Unemployment Invariance Hypothesis Hold for Canada? Aysit Tansel Zeynel Abidin Ozdemir Emre Aksoy August 2016 Forschungsinstitut zur Zukunft der Arbeit

DISCUSSION PAPER SERIES IZA DP No. 10178 Does the Unemployment Invariance Hypothesis Hold for Canada? Aysit Tansel Zeynel Abidin Ozdemir Emre Aksoy August 2016 Forschungsinstitut zur Zukunft der Arbeit

Volume 29, Issue 3. Application of the monetary policy function to output fluctuations in Bangladesh

Volume 29, Issue 3 Application of the monetary policy function to output fluctuations in Bangladesh Yu Hsing Southeastern Louisiana University A. M. M. Jamal Southeastern Louisiana University Wen-jen Hsieh

Volume 29, Issue 3 Application of the monetary policy function to output fluctuations in Bangladesh Yu Hsing Southeastern Louisiana University A. M. M. Jamal Southeastern Louisiana University Wen-jen Hsieh

Chapter 12 Keynesian Models and the Phillips Curve

George Alogoskoufis, Dynamic Macroeconomics, 2016 Chapter 12 Keynesian Models and the Phillips Curve As we have already mentioned, following the Great Depression of the 1930s, the analysis of aggregate

George Alogoskoufis, Dynamic Macroeconomics, 2016 Chapter 12 Keynesian Models and the Phillips Curve As we have already mentioned, following the Great Depression of the 1930s, the analysis of aggregate

Inflation Targeting and Inflation Prospects in Canada

Inflation Targeting and Inflation Prospects in Canada CPP Interdisciplinary Seminar March 2006 Don Coletti Research Director International Department Bank of Canada Overview Objective: answer questions

Inflation Targeting and Inflation Prospects in Canada CPP Interdisciplinary Seminar March 2006 Don Coletti Research Director International Department Bank of Canada Overview Objective: answer questions

Comments on Credit Frictions and Optimal Monetary Policy, by Cúrdia and Woodford

Comments on Credit Frictions and Optimal Monetary Policy, by Cúrdia and Woodford Olivier Blanchard August 2008 Cúrdia and Woodford (CW) have written a topical and important paper. There is no doubt in

Comments on Credit Frictions and Optimal Monetary Policy, by Cúrdia and Woodford Olivier Blanchard August 2008 Cúrdia and Woodford (CW) have written a topical and important paper. There is no doubt in