The Really Big Picture

|

|

|

- Ferdinand Evans

- 5 years ago

- Views:

Transcription

1 The Really Big Picture Debt The Economy Demographics Capital Markets Central Bank Policy Retirement Plans

2 Norwood Economics is a fee-only Registered Investment Advisor specializing in low-cost, small business 401(k) and Cash Balance Plans. Our mission is to provide low-cost, unbundled plans that are custom designed to meet the needs of your workforce based on your census. We can: Typically reduce plan costs by 40% to 50% Substantially improve plan design to better accomplish owner goals Provide plan administrators with the support and service they need to ensure the plan remains compliant and participants receive the administrative help they deserve Educate participants to help them better navigate the investment environment, making it more likely they ll achieve a successful retirement

3 Economics Is A Soft Science There is no law of gravity Humans are part of the equation, which means psychology matters An economy is a complex, dynamic system with many feedback loops Complex systems are systems whose behavior is intrinsically difficult to model due to the dependencies, relationships, or interactions between their parts or between a given system and its environment. Cause and effect can change as an economy evolves (As goes GM, so goes the Nation.Not!) Small variations can produce large changes in outcomes

4

5

6

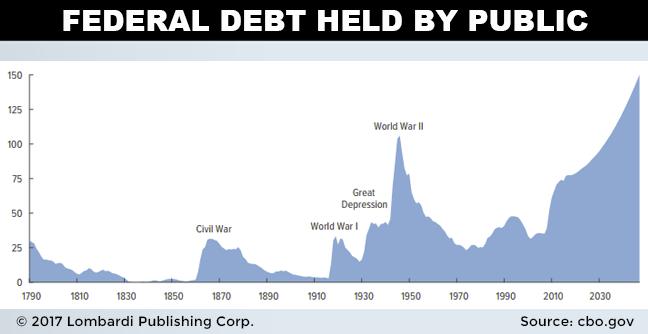

7

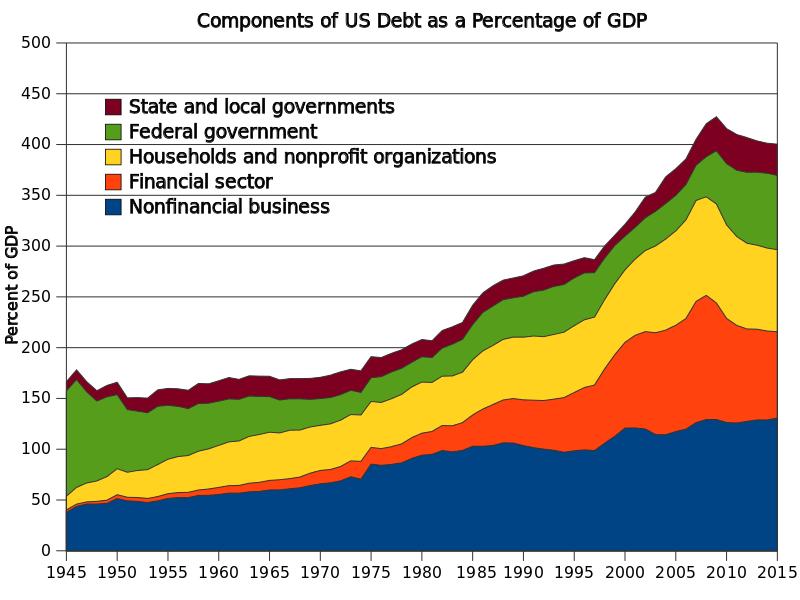

8 Household Debt Household Debt climbed to approximately $12.58 trillion by the end of 2016 (Federal Reserve Bank, NY) Total Household Debt stood at $12.68 trillion in 2008 (Federal Reserve Bank, NY) Savings rate fell to 2.9% in Nov from 3.7% the prior year (Dr. Lacy Hunt, Hoisington Asset Management, Q4 Newsletter)

9

10

11

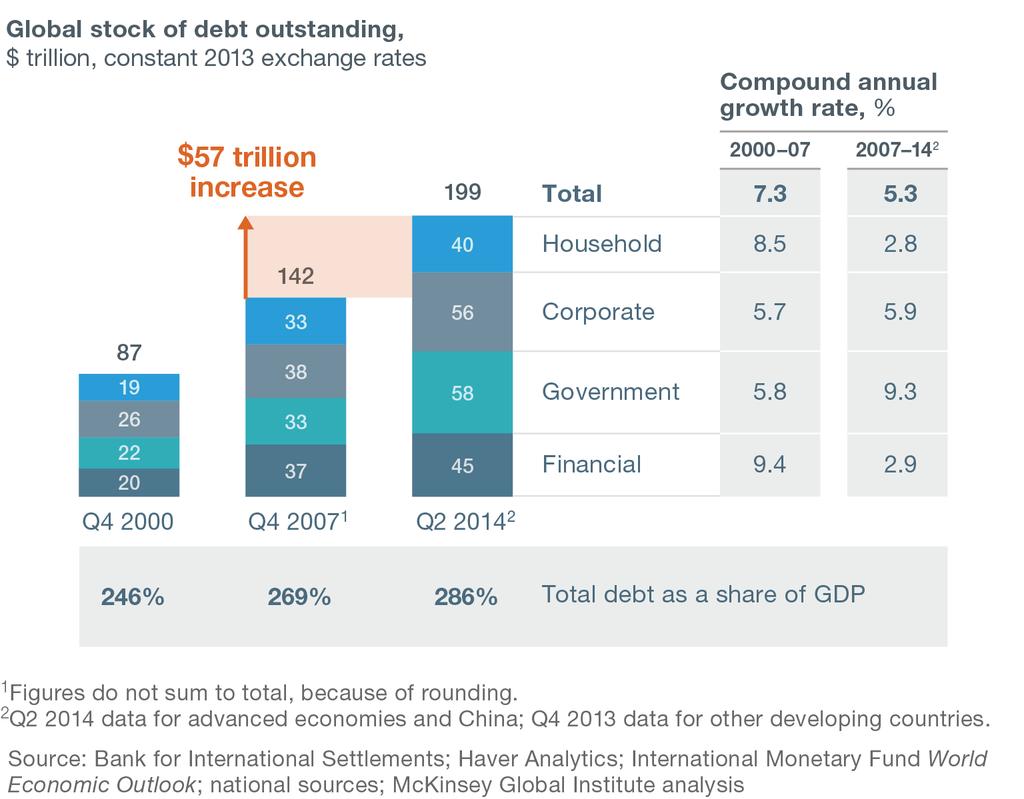

12 Institute For International Finance

13

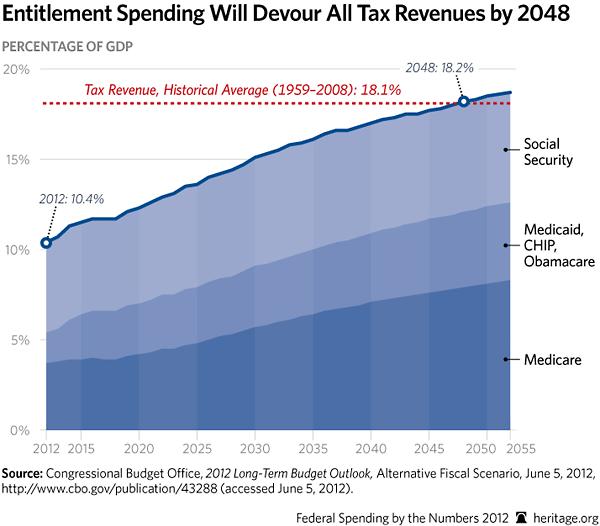

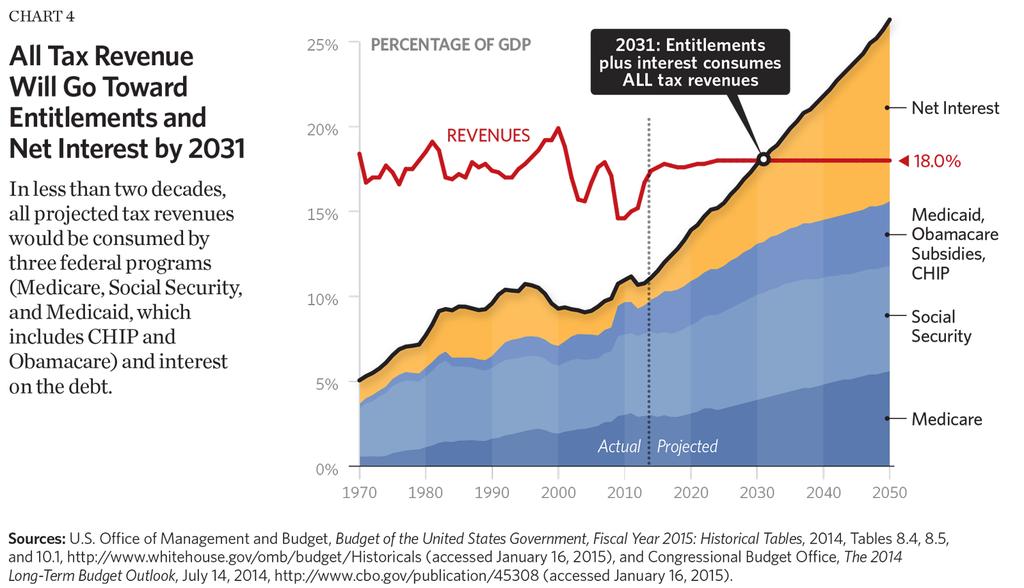

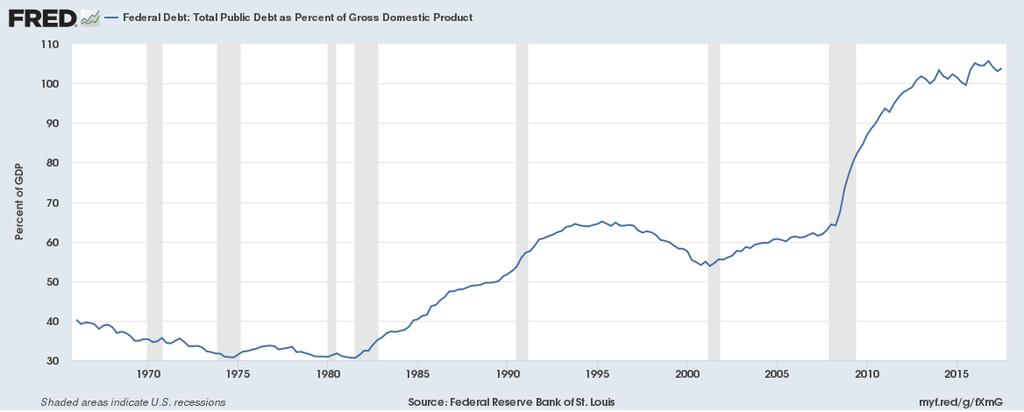

14 A Mountain of Debt U.S. Federal Debt at all time highs Total U.S. Debt at all time highs Worldwide Debt at all time highs Debt still rising sharply throughout the world and in the United States Debt must eventually be repaid, defaulted on, or inflated away

15 Demographics is Destiny The world working age population peaked in 2012 and is now falling. The world is aging rapidly, particularly in developed countries such as Japan, Germany, and the United States. There is a significant correlation between economic growth in the developed world over the last 30 years and immigration patterns. For example: Canada imports around one million new immigrants per year (3% of the population) the growth rate of the Canadian economy is usually around 3%. As countries in the developing world start to exploit the demographic advantage associated with young and growing populations, the developed world will continue to struggle with the economic challenges of an ageing population/workforce. This will cause significant disruption over the next years. (IFLA Trend Report, 2017)

16

17 Old-Age Dependency Ratio Over the coming decades, many countries in the developed and developing world alike will significantly age. Old-age dependency ratio - measures the number of those aged above 65 years (currently defined as old age) as a share of those between 15 to 64 years (currently defined as working age). The ratio tells us how many retired people a potential worker has to sustain.

18 Germany, Russia and America Countries like Germany, Russia, and the United States are all experiencing sharp increases Approximately five workers supported one old person in America in the 1990s an old-age dependency ratio of approximately 0.20 America will have an old-age dependency ratio of about 0.37 by workers per old person a big change

19 Source: United Nations World Population Prospects: the 2012 Revision (database)

20 Adult Dependency Ratio Adult dependency ratio: those inactive versus active in the entire adult population, aged 15 and older - gives us a much more positive and less divergent outlook across the three countries examined in this post

21 Source: Bussolo, Koettl, and Sinnott (Forthcoming). Golden Aging. Prospects for Healthy, Active, and Prosperous Aging in Europe and Central Asia. Washington, DC: World Bank.

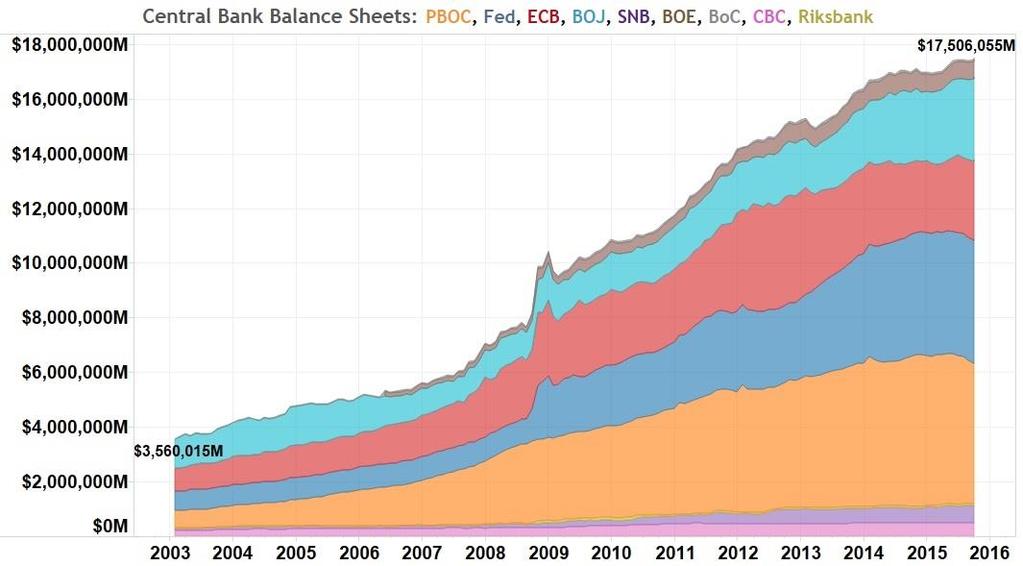

22 Central Bankers Response To The Great Recession Central banks have expanded their balance sheets, creating trillions in new base money Central banks have implemented Zero Interest Rate Policy (ZIRP) and Negative Interest Rate Policy (NIRP) at the short end of the yield curve Central banks have implemented unconventional monetary policy termed Quantitative Easing large scale asset purchases to lower interest rates and increase the money supply

23

24

25

26

27

28

29 Liquidity and Capital Markets Central Bankers have practiced unconventional monetary policy since the Great Recession Central Bank balance sheets have ballooned to unprecedented levels The Federal Reserve balance sheet grew from approximately $850 billion to $4.5 trillion Dollars are on the liability side of the Federal Reserve s balance sheet and someone has to hold those dollars

30

31

32

33

34

35

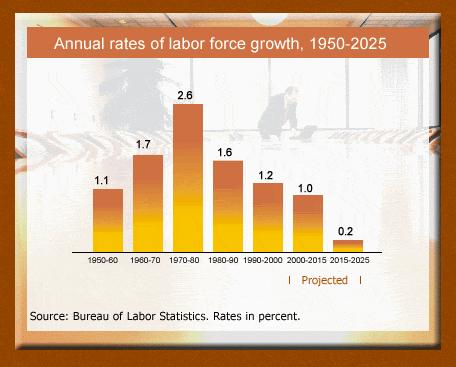

36

37

38

39 The Economy MV=PY

40 The Equation Of Exchange MV = PY M = money supply V = the velocity of money number of times per year the average dollar is spent P = the general price level Y = real output (quantity of goods and services)

41 Slow Economic Growth Velocity is currently low, standing at 1.43, its lowest level since 1949 Money growth has slowed to 5% as of Q The Federal Reserve continues to raise the Federal Funds Rate and also continues to shrink its balance sheet, putting additional downward pressure on money growth If money (M2) continues to decelerate, and V stabilizes (although it has declined at a 2.4% rate over the past eight years), then nominal GDP will record a lower growth rate in 2018 than the estimated 2017 pace of 4.0% Even nominal GDP growth of 4.0% equates to approximately a 2% real growth rate expect worse (Dr. Lacy Hunt and Van Hoisington, Hoisington Asset Management Q4 2017)

42 Debt And The Economy This Time Is Different: Eight Centuries of Financial Folly (Dr. Carmen Reinhart and Dr. Kenneth Rogoff) Countries with high debt levels rarely grow out of them Instead they: default, restructure, or allow inflation to reduce the real debt burden Countries with debt in excess of approximately 90% see reduced growth rates? A recent IMF study disputes that finding

43 Demographics and Growth Real GDP growth is the sum of labor force growth and productivity increases Currently the U.S. labor force is expected to grow at a 0.5% annual rate over the next 10 years (Bureau of Labor Statistics) During the current business cycle, which started in the fourth quarter of 2007, labor productivity has grown at an annualized rate of 1.1 percent (Bureau of Labor Statistics)

44

45 Debt Service Debt can t grow faster than the economy forever Low interest rates have allowed the Federal Government to sharply increase borrowing without raising the cost of servicing the debt Rising rates will sharply increase the cost of servicing the U.S. debt (Under current law, the Congressional Budget Office (CBO) projects interest payments to nearly triple in nominal dollars and double as a percent of GDP from $241 billion and 1.3 percent of GDP in Fiscal Year (FY) 2016 to $712 billion and 2.6 percent of GDP by FY 2026)

46

47 Retirement Plans Slower economic growth due to high debt levels, lower labor force growth rates, and lower productivity gains Lower capital market returns due to elevated asset levels and slower economic growth Continued low savings rates among baby boomers Rising inflation as the U.S. government struggles to meet rising debt servicing costs?

48 Public Pension Plan Funding As of June 30, 2017, the aggregate funded ratio is estimated to be 70.7% as assets experienced healthy growth One-third of the plans reduced the interest rate assumptions they use for determining contribution amounts The difference between the median sponsor reported discount rate (7.50%) and our independently determined assumption (6.71%) continues to widen, indicating that further reductions in interest rate assumptions are likely The Milliman Public Pension Funding Study 2017 the study annually explores the funded status of the 100 largest U.S. public pension plans.

49 Milliman 2017 Study

50 Range of Funding Among States Across the country, funded ratios for plans reviewed by The Pew Charitable Trusts ranged from 37% in New Jersey to 104% in South Dakota Indiana is 86% funded as of 2 Dec according to the State of Indiana

51 Baby Boomers One in four 65-year-olds today will live past age 90, while one in 10 will live past age 95 One out of every three Americans has no retirement savings whatsoever Over 40% of single seniors 65 and over get at least 90% of their income from Social Security

52 Baby Boomers A recent study by Fidelity Investments estimates that the average 65-year-old couple retiring this year will need $275,000 to pay for medical expenses during retirement. (Kiplinger, Sept. 2017) The number of bankruptcy filers age 65 and older more than tripled from 2.1% of seniors in 1991 to 7% in 2007, according to a recent study. (U.S. News & World, 2010)

53 Baby Boomers Only 54% of Boomers have retirement savings, the lowest recorded in the seven years of the Boomer report Only 23% of Boomers believe they will have enough money to last throughout retirement, and that they have done a good job preparing for retirement 82% of Boomers underestimate the percentage of their income that may be required to pay for health care At current savings levels, most Boomers with savings face a potential annual retirement income gap of between $3,864 and $12,072 Boomer Expectations For Retirement 2017, Insured Retirement Institute

54 Impact of Low Returns Public pension plans and individual households routinely use 7% to 8% return assumptions Likely expected returns of 0% over the coming 12 years, and perhaps 4% to 5% over the coming 20 years will exacerbate the savings deficit in the United States A retirement crisis is highly likely

55 Retirement Plan Specialists What can those of us in the retirement plans space do to help? Find ways to help plan participants increase savings: Auto-Enrollment, Auto-Escalation, HSA, Cash Balance Help people do a better job investing: Simplified investment choices such as pre-built, diversified portfolios lead to higher accumulation rates Reduce costs 1% saved is 1% earned Plan designs that encourage enrollment: Loan option, hardship distributions, shorter eligibility periods, more frequent start and change options)

CHARTS MAY 23, 2017 WASHINGTON, D.C.

CHARTS MAY 23, 2017 WASHINGTON, D.C. Peterson Foundation charts are available online and are free to use without modification for educational and editorial use, with credit to the Peter G. Peterson Foundation

CHARTS MAY 23, 2017 WASHINGTON, D.C. Peterson Foundation charts are available online and are free to use without modification for educational and editorial use, with credit to the Peter G. Peterson Foundation

The Province of Prince Edward Island Employment Trends and Data Poverty Reduction Action Plan Backgrounder

The Province of Prince Edward Island Employment Trends and Data Poverty Reduction Action Plan Backgrounder 5/17/2018 www.princeedwardisland.ca/poverty-reduction $000's Poverty Reduction Action Plan Backgrounder:

The Province of Prince Edward Island Employment Trends and Data Poverty Reduction Action Plan Backgrounder 5/17/2018 www.princeedwardisland.ca/poverty-reduction $000's Poverty Reduction Action Plan Backgrounder:

Data Brief. Dangerous Trends: The Growth of Debt in the U.S. Economy

cepr Center for Economic and Policy Research Data Brief Dangerous Trends: The Growth of Debt in the U.S. Economy Dean Baker 1 September 7, 2004 CENTER FOR ECONOMIC AND POLICY RESEARCH 1611 CONNECTICUT

cepr Center for Economic and Policy Research Data Brief Dangerous Trends: The Growth of Debt in the U.S. Economy Dean Baker 1 September 7, 2004 CENTER FOR ECONOMIC AND POLICY RESEARCH 1611 CONNECTICUT

Quarterly Review and Outlook, First Quarter 2018

Quarterly Review and Outlook, First Quarter 2018 April 19, 2018 by Lacy Hunt, Van Hoisington of Hoisington Investment Management Nearly nine years into the current economic expansion Federal Reserve policy

Quarterly Review and Outlook, First Quarter 2018 April 19, 2018 by Lacy Hunt, Van Hoisington of Hoisington Investment Management Nearly nine years into the current economic expansion Federal Reserve policy

Global Aging and Financial Markets

Global Aging and Financial Markets Overview Presentation by Richard Jackson CSIS Global Aging Initiative MA s 16th Annual Washington Policy Seminar Cosponsored by Macroeconomic Advisers, LLC Council on

Global Aging and Financial Markets Overview Presentation by Richard Jackson CSIS Global Aging Initiative MA s 16th Annual Washington Policy Seminar Cosponsored by Macroeconomic Advisers, LLC Council on

Chapter 6 ECONOMIC GROWTH. World Economic Growth. In this chapter-

Chapter 6 ECONOMIC GROWTH In this chapter- Define and calculate the growth rate and explain the implications of sustained growth in economic activity Briefly describe the economic growth trends in the

Chapter 6 ECONOMIC GROWTH In this chapter- Define and calculate the growth rate and explain the implications of sustained growth in economic activity Briefly describe the economic growth trends in the

In fiscal year 2016, for the first time since 2009, the

Summary In fiscal year 216, for the first time since 29, the federal budget deficit increased in relation to the nation s economic output. The Congressional Budget Office projects that over the next decade,

Summary In fiscal year 216, for the first time since 29, the federal budget deficit increased in relation to the nation s economic output. The Congressional Budget Office projects that over the next decade,

CHARTS MAY 10, 2018 WASHINGTON, D.C.

CHARTS MAY 10, 2018 WASHINGTON, D.C. Peterson Foundation charts are available online and are free to use without modification for educational and editorial use, with credit to the Peter G. Peterson Foundation

CHARTS MAY 10, 2018 WASHINGTON, D.C. Peterson Foundation charts are available online and are free to use without modification for educational and editorial use, with credit to the Peter G. Peterson Foundation

Report Documentation Page Form Approved OMB No Public reporting burden for the collection of information is estimated to average 1 hour per re

Testimony The Budget and Economic Outlook: 214 to 224 Douglas W. Elmendorf Director Before the Committee on the Budget U.S. House of Representatives February 5, 214 This document is embargoed until it

Testimony The Budget and Economic Outlook: 214 to 224 Douglas W. Elmendorf Director Before the Committee on the Budget U.S. House of Representatives February 5, 214 This document is embargoed until it

Federal Spending to Top a Record $4 Trillion in FY2017

Federal Spending to Top a Record $4 Trillion in FY2017 July 11, 2017 by Gary Halbert of Halbert Wealth Management 1. June Unemployment Report Was Better Than Expected 2. Federal Spending to Blow Through

Federal Spending to Top a Record $4 Trillion in FY2017 July 11, 2017 by Gary Halbert of Halbert Wealth Management 1. June Unemployment Report Was Better Than Expected 2. Federal Spending to Blow Through

Quarterly Review and Outlook Fourth Quarter 2013

6836 Bee Caves Rd. B2 S100, Austin, TX 78746 (512) 327-7200 www.hoisington.com Quarterly Review and Outlook Fourth Quarter 2013 In The Theory of Interest, Irving Fisher, who Nobel Laureate Milton Friedman

6836 Bee Caves Rd. B2 S100, Austin, TX 78746 (512) 327-7200 www.hoisington.com Quarterly Review and Outlook Fourth Quarter 2013 In The Theory of Interest, Irving Fisher, who Nobel Laureate Milton Friedman

The next 15 years Is there a New Normal ahead? Delaware Investments Presentation. Richard C Marston Wharton School, University of Pennsylvania

The next 15 years Is there a New Normal ahead? Delaware Investments Presentation Richard C Marston Wharton School, University of Pennsylvania Outline 1. Is there a New Normal ahead for stocks? 2. Is the

The next 15 years Is there a New Normal ahead? Delaware Investments Presentation Richard C Marston Wharton School, University of Pennsylvania Outline 1. Is there a New Normal ahead for stocks? 2. Is the

Notes Numbers in the text and tables may not add up to totals because of rounding. Unless otherwise indicated, years referred to in describing the bud

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE The Budget and Economic Outlook: 4 to 4 Percentage of GDP 4 Surpluses Actual Projected - -4-6 Average Deficit, 974 to Deficits -8-974 979 984 989

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE The Budget and Economic Outlook: 4 to 4 Percentage of GDP 4 Surpluses Actual Projected - -4-6 Average Deficit, 974 to Deficits -8-974 979 984 989

The Economics of the Federal Budget Deficit

Brian W. Cashell Specialist in Macroeconomic Policy February 2, 2010 Congressional Research Service CRS Report for Congress Prepared for Members and Committees of Congress 7-5700 www.crs.gov RL31235 Summary

Brian W. Cashell Specialist in Macroeconomic Policy February 2, 2010 Congressional Research Service CRS Report for Congress Prepared for Members and Committees of Congress 7-5700 www.crs.gov RL31235 Summary

Texas: Demographically Different

FEDERAL RESERVE BANK OF DALLAS ISSUE 3 99 : Demographically Different A s the st century nears, demographic changes are reshaping the U.S. economy. The largest impact is coming from the maturing of baby

FEDERAL RESERVE BANK OF DALLAS ISSUE 3 99 : Demographically Different A s the st century nears, demographic changes are reshaping the U.S. economy. The largest impact is coming from the maturing of baby

The yellow highlighted areas are bear markets with NO recession.

Part 3, Final Report: Major Market Reversal Model This is the third and final report on my major market reversal model. This portion of the model focuses on the domestic and international economy. I ve

Part 3, Final Report: Major Market Reversal Model This is the third and final report on my major market reversal model. This portion of the model focuses on the domestic and international economy. I ve

CRS Report for Congress

Order Code RL33519 CRS Report for Congress Received through the CRS Web Why Is Household Income Falling While GDP Is Rising? July 7, 2006 Marc Labonte Specialist in Macroeconomics Government and Finance

Order Code RL33519 CRS Report for Congress Received through the CRS Web Why Is Household Income Falling While GDP Is Rising? July 7, 2006 Marc Labonte Specialist in Macroeconomics Government and Finance

MACROECONOMICS. Economic Growth II: Technology, Empirics, and Policy MANKIW. In this chapter, you will learn. Introduction

C H A P T E R 8 Economic Growth II: Technology, Empirics, and Policy MACROECONOMICS N. GREGORY MANKIW 2007 Worth Publishers, all rights reserved SIXTH EDITION PowerPoint Slides by Ron Cronovich In this

C H A P T E R 8 Economic Growth II: Technology, Empirics, and Policy MACROECONOMICS N. GREGORY MANKIW 2007 Worth Publishers, all rights reserved SIXTH EDITION PowerPoint Slides by Ron Cronovich In this

The Congressional Budget Office s 2012 Long-Term Budget Outlook: An Analysis

The Congressional Budget Office s 2012 Long-Term Budget Outlook: An Analysis Jun 06, 2012 The Congressional Budget Office s (CBO) new update of its long-term fiscal outlook highlights the continued long-term

The Congressional Budget Office s 2012 Long-Term Budget Outlook: An Analysis Jun 06, 2012 The Congressional Budget Office s (CBO) new update of its long-term fiscal outlook highlights the continued long-term

FIRST LOOK AT MACROECONOMICS*

Chapter 4 A FIRST LOOK AT MACROECONOMICS* Key Concepts Origins and Issues of Macroeconomics Modern macroeconomics began during the Great Depression, 1929 1939. The Great Depression was a decade of high

Chapter 4 A FIRST LOOK AT MACROECONOMICS* Key Concepts Origins and Issues of Macroeconomics Modern macroeconomics began during the Great Depression, 1929 1939. The Great Depression was a decade of high

Briefing Paper. Business Week Restates the Nineties. By Dean Baker. April 22, 2002

cepr Center for Economic and Policy Research Briefing Paper Business Week Restates the Nineties By Dean Baker April 22, 2002 Center for Economic and Policy Research 1611 Connecticut Avenue NW, Suite 400

cepr Center for Economic and Policy Research Briefing Paper Business Week Restates the Nineties By Dean Baker April 22, 2002 Center for Economic and Policy Research 1611 Connecticut Avenue NW, Suite 400

U.S. Economic Outlook: recent developments

U.S. Economic Outlook Recent developments Washington, D.C., 6 February 2018 This document was prepared by Helvia Velloso, Economic Affairs Officer, under the supervision of Inés Bustillo, Director, ECLAC

U.S. Economic Outlook Recent developments Washington, D.C., 6 February 2018 This document was prepared by Helvia Velloso, Economic Affairs Officer, under the supervision of Inés Bustillo, Director, ECLAC

cepr Analysis of the Upcoming Release of 2003 Data on Income, Poverty, and Health Insurance Data Brief Paper Heather Boushey 1 August 2004

cepr Center for Economic and Policy Research Data Brief Paper Analysis of the Upcoming Release of 2003 Data on Income, Poverty, and Health Insurance Heather Boushey 1 August 2004 CENTER FOR ECONOMIC AND

cepr Center for Economic and Policy Research Data Brief Paper Analysis of the Upcoming Release of 2003 Data on Income, Poverty, and Health Insurance Heather Boushey 1 August 2004 CENTER FOR ECONOMIC AND

Savings Rate Lowest In A Decade, Credit Card Balances Soar

Savings Rate Lowest In A Decade, Credit Card Balances Soar January 24, 2018 by Gary Halbert of Halbert Wealth Management 1. US National Savings Rate Falls to 2.9%, Decade Low 2. Median Savings Rates by

Savings Rate Lowest In A Decade, Credit Card Balances Soar January 24, 2018 by Gary Halbert of Halbert Wealth Management 1. US National Savings Rate Falls to 2.9%, Decade Low 2. Median Savings Rates by

Massachusetts Outlook,

Massachusetts Outlook, 2016-2020 Highlights The state s economic growth will be pulled by two forces in opposite directions. Constraining growth will be a slower increase in the availability of workers

Massachusetts Outlook, 2016-2020 Highlights The state s economic growth will be pulled by two forces in opposite directions. Constraining growth will be a slower increase in the availability of workers

Monetary and financial trends in the fourth quarter of 2014

Monetary and financial trends in the fourth quarter of 2014 Oil prices have significantly contracted in the third and fourth quarters of 2014, in an international economic environment marked by fragile

Monetary and financial trends in the fourth quarter of 2014 Oil prices have significantly contracted in the third and fourth quarters of 2014, in an international economic environment marked by fragile

Growing Slowly, Getting Older:*

Growing Slowly, Getting Older:* Demographic Trends in the Third District States BY TIMOTHY SCHILLER N ational trends such as slower population growth, an aging population, and immigrants as a larger component

Growing Slowly, Getting Older:* Demographic Trends in the Third District States BY TIMOTHY SCHILLER N ational trends such as slower population growth, an aging population, and immigrants as a larger component

8.6% Unemployment Is a Myth

8.% Unemployment Is a Myth Sondra Albert Chief Economist, AFL-CIO Housing Investment Trust December 13, 2011 8.% unemployment is a myth! And, to the 13.3 million people who are currently counted as unemployed,

8.% Unemployment Is a Myth Sondra Albert Chief Economist, AFL-CIO Housing Investment Trust December 13, 2011 8.% unemployment is a myth! And, to the 13.3 million people who are currently counted as unemployed,

The Debt Monster. Daniel Stelter, Dirk Schilder, and Katrin van Dyken. May

The Debt Monster Daniel Stelter, Dirk Schilder, and Katrin van Dyken May AT A GLANCE Unprecedented levels of debt are creating the conditions for higher-than-expected inflation. W G I N A In many countries,

The Debt Monster Daniel Stelter, Dirk Schilder, and Katrin van Dyken May AT A GLANCE Unprecedented levels of debt are creating the conditions for higher-than-expected inflation. W G I N A In many countries,

Health Care Spending and the Aging of the Population

Order Code RS22619 March 13, 2007 Health Care Spending and the Aging of the Population Jennifer Jenson Specialist in Health Economics Domestic Social Policy Division Summary Health care spending has been

Order Code RS22619 March 13, 2007 Health Care Spending and the Aging of the Population Jennifer Jenson Specialist in Health Economics Domestic Social Policy Division Summary Health care spending has been

Regulatory Announcement RNS Number: RNS to insert number here Québec 27 November, 2017

ISSN 1718-836 Regulatory Announcement RNS Number: RNS to insert number here Québec 27 November, 2017 Re: Québec Excerpts from The Quebec Economic Plan November 2017 Update, Québec Public Accounts 2016-2017

ISSN 1718-836 Regulatory Announcement RNS Number: RNS to insert number here Québec 27 November, 2017 Re: Québec Excerpts from The Quebec Economic Plan November 2017 Update, Québec Public Accounts 2016-2017

BACKGROUNDER. U.S. Government Increases National Debt and Keeps 128 Million People on Government Programs

BACKGROUNDER U.S. Government Increases National Debt and Keeps 128 Million People on Government Programs Patrick D. Tyrrell and William W. Beach No. 2756 Abstract Between 1988 and 2011, the amount of the

BACKGROUNDER U.S. Government Increases National Debt and Keeps 128 Million People on Government Programs Patrick D. Tyrrell and William W. Beach No. 2756 Abstract Between 1988 and 2011, the amount of the

MACROECONOMICS. Economic Growth II: Technology, Empirics, and Policy. N. Gregory Mankiw. PowerPoint Slides by Ron Cronovich

9 : Technology, Empirics, and Policy MACROECONOMICS N. Gregory Mankiw Modified for EC 204 by Bob Murphy PowerPoint Slides by Ron Cronovich 2013 Worth Publishers, all rights reserved IN THIS CHAPTER, YOU

9 : Technology, Empirics, and Policy MACROECONOMICS N. Gregory Mankiw Modified for EC 204 by Bob Murphy PowerPoint Slides by Ron Cronovich 2013 Worth Publishers, all rights reserved IN THIS CHAPTER, YOU

OVERVIEW OF DEVELOPMENTS IN ICT INVESTMENT IN CANADA, 2011

September 212 151 Slater Street, Suite 71 Ottawa, Ontario K1P 5H3 613-233-8891, Fax 613-233-825 csls@csls.ca CENTRE FOR THE STUDY OF LIVING STANDARDS OVERVIEW OF DEVELOPMENTS IN ICT INVESTMENT IN CANADA,

September 212 151 Slater Street, Suite 71 Ottawa, Ontario K1P 5H3 613-233-8891, Fax 613-233-825 csls@csls.ca CENTRE FOR THE STUDY OF LIVING STANDARDS OVERVIEW OF DEVELOPMENTS IN ICT INVESTMENT IN CANADA,

Ready or Not... The Impact of Retirement-Plan Design

Ready or Not... The Impact of Retirement-Plan Design Some 10,000 baby boomers a day are heading into retirement. Will they have enough income to finance retirements that, for some, may last as long as

Ready or Not... The Impact of Retirement-Plan Design Some 10,000 baby boomers a day are heading into retirement. Will they have enough income to finance retirements that, for some, may last as long as

Do demographics explain structural inflation?

Do demographics explain structural inflation? May 2018 Executive summary In aggregate, the world s population is graying, caused by a combination of lower birthrates and longer lifespans. Another worldwide

Do demographics explain structural inflation? May 2018 Executive summary In aggregate, the world s population is graying, caused by a combination of lower birthrates and longer lifespans. Another worldwide

Who Wears the Diapers? A discussion about the economic implications of global demographic trends

Who Wears the Diapers? A discussion about the economic implications of global demographic trends Andrea Urban, CFA, CAIA AndreaUrban@kpmg.com kpmg.com Pro-Cyclical nature of fiscal balances wildly underestimated

Who Wears the Diapers? A discussion about the economic implications of global demographic trends Andrea Urban, CFA, CAIA AndreaUrban@kpmg.com kpmg.com Pro-Cyclical nature of fiscal balances wildly underestimated

NESGFOA Economic Assessment Impact on Rates

NESGFOA Economic Assessment Impact on Rates September 18, 2017 Not FDIC Insured May Lose Value No Bank Guarantee Not NCUA or NCUSIF insured. May lose value. No credit union guarantee. For institutional

NESGFOA Economic Assessment Impact on Rates September 18, 2017 Not FDIC Insured May Lose Value No Bank Guarantee Not NCUA or NCUSIF insured. May lose value. No credit union guarantee. For institutional

Socio-economic Series Changes in Household Net Worth in Canada:

research highlight October 2010 Socio-economic Series 10-018 Changes in Household Net Worth in Canada: 1990-2009 introduction For many households, buying a home is the largest single purchase they will

research highlight October 2010 Socio-economic Series 10-018 Changes in Household Net Worth in Canada: 1990-2009 introduction For many households, buying a home is the largest single purchase they will

Examining the Rural-Urban Income Gap. The Center for. Rural Pennsylvania. A Legislative Agency of the Pennsylvania General Assembly

Examining the Rural-Urban Income Gap The Center for Rural Pennsylvania A Legislative Agency of the Pennsylvania General Assembly Examining the Rural-Urban Income Gap A report by C.A. Christofides, Ph.D.,

Examining the Rural-Urban Income Gap The Center for Rural Pennsylvania A Legislative Agency of the Pennsylvania General Assembly Examining the Rural-Urban Income Gap A report by C.A. Christofides, Ph.D.,

Download the full paper»

Download the full paper» The U.S. Social Security system, which established old age benefits, is designed to be highly progressive by redistributing income from workers with high average lifetime earnings

Download the full paper» The U.S. Social Security system, which established old age benefits, is designed to be highly progressive by redistributing income from workers with high average lifetime earnings

AN ANALYSIS OF THE RECENT DETERIORATION IN THE FISCAL CONDITION OF THE U.S. GOVERNMENT

September 2004 AN ANALYSIS OF THE RECENT DETERIORATION IN THE FISCAL CONDITION OF THE U.S. GOVERNMENT Per Capita Net Federal Debt 1998 to 2004* (Actual Debt Compared to CBO January 2001 Forecast) $16,000

September 2004 AN ANALYSIS OF THE RECENT DETERIORATION IN THE FISCAL CONDITION OF THE U.S. GOVERNMENT Per Capita Net Federal Debt 1998 to 2004* (Actual Debt Compared to CBO January 2001 Forecast) $16,000

How Successful is China s Economic Rebalancing?*

How Successful is China s Economic Rebalancing?* C.P. Chandrasekhar and Jayati Ghosh Over the past decade, there has been much talk of global imbalances, and of the need to correct them in an orderly way.

How Successful is China s Economic Rebalancing?* C.P. Chandrasekhar and Jayati Ghosh Over the past decade, there has been much talk of global imbalances, and of the need to correct them in an orderly way.

Short- Term Employment Growth Forecast (as at February 19, 2015)

") Background According to Statistics Canada s Labour Force Survey records, employment conditions in Newfoundland and Labrador showed signs of weakening this past year. Having grown to a record level high

Background According to Statistics Canada s Labour Force Survey records, employment conditions in Newfoundland and Labrador showed signs of weakening this past year. Having grown to a record level high

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE CBO The Budget and Economic Outlook: 2016 to 2026 Percentage of GDP 100 Actual Projected 80

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE The Budget and Economic Outlook: 6 to 6 Percentage of GDP Actual Projected 8 In s projections, growing 6 deficits drive up debt over the next decade,

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE The Budget and Economic Outlook: 6 to 6 Percentage of GDP Actual Projected 8 In s projections, growing 6 deficits drive up debt over the next decade,

Vincent Reinhart on Debt and Growth in the U.S. and Japan By Robert Huebscher June 4, 2013

Vincent Reinhart on Debt and Growth in the U.S. and Japan By Robert Huebscher June 4, 2013 High debt levels translate to slower growth, according to Vincent Reinhart. That conclusion will be disheartening

Vincent Reinhart on Debt and Growth in the U.S. and Japan By Robert Huebscher June 4, 2013 High debt levels translate to slower growth, according to Vincent Reinhart. That conclusion will be disheartening

Minnesota s Economic Outlook for 2013 and Beyond. Tom Stinson October 2012

Minnesota s Economic Outlook for 2013 and Beyond Tom Stinson October 2012 FY 2014-15 Budget Planning ($ in millions) FY 2012-13 FY 2014-15 $ Difference % Change Forecast Revenues $33,867 $35,861 $1,994

Minnesota s Economic Outlook for 2013 and Beyond Tom Stinson October 2012 FY 2014-15 Budget Planning ($ in millions) FY 2012-13 FY 2014-15 $ Difference % Change Forecast Revenues $33,867 $35,861 $1,994

The Federal Reserve Bank of Kansas City and Community Development

The Federal Reserve Bank of Kansas City and Community Development ECON 336: The Kansas City Economy University of Missouri Kansas City April 11, 2012 Kelly D. Edmiston Outline The Federal Reserve System

The Federal Reserve Bank of Kansas City and Community Development ECON 336: The Kansas City Economy University of Missouri Kansas City April 11, 2012 Kelly D. Edmiston Outline The Federal Reserve System

Quarterly Review and Outlook

6836 Bee Caves Rd. B2 S100, Austin, TX 78746 (512) 327-7200 www.hoisington.com Quarterly Review and Outlook Fourth Quarter 2017 Optimism is pervasive regarding U.S. economic growth in 2018. Based on the

6836 Bee Caves Rd. B2 S100, Austin, TX 78746 (512) 327-7200 www.hoisington.com Quarterly Review and Outlook Fourth Quarter 2017 Optimism is pervasive regarding U.S. economic growth in 2018. Based on the

The Economics of the Federal Budget Deficit

Order Code RL31235 The Economics of the Federal Budget Deficit Updated January 24, 2007 Brian W. Cashell Specialist in Quantitative Economics Government and Finance Division The Economics of the Federal

Order Code RL31235 The Economics of the Federal Budget Deficit Updated January 24, 2007 Brian W. Cashell Specialist in Quantitative Economics Government and Finance Division The Economics of the Federal

The US Economy Disappointed In The Fourth Quarter

The US Economy Disappointed In The Fourth Quarter January 31, 2018 by Gary Halbert of Halbert Wealth Management 1. Advance GDP Report Missed Expectations at Only 2.6% 2. US Economic Strength Lifts Other

The US Economy Disappointed In The Fourth Quarter January 31, 2018 by Gary Halbert of Halbert Wealth Management 1. Advance GDP Report Missed Expectations at Only 2.6% 2. US Economic Strength Lifts Other

COMMENTS ON SESSION 1 PENSION REFORM AND THE LABOUR MARKET. Walpurga Köhler-Töglhofer *

COMMENTS ON SESSION 1 PENSION REFORM AND THE LABOUR MARKET Walpurga Köhler-Töglhofer * 1 Introduction OECD countries, in particular the European countries within the OECD, will face major demographic challenges

COMMENTS ON SESSION 1 PENSION REFORM AND THE LABOUR MARKET Walpurga Köhler-Töglhofer * 1 Introduction OECD countries, in particular the European countries within the OECD, will face major demographic challenges

Lacy Hunt: Keynes was Wrong (and Ricardo was Right)

") Lacy Hunt: Keynes was Wrong (and Ricardo was Right) May 4, 2010 by Robert Huebscher Underpinning the Obama administration s economic policies is the work of John Maynard Keynes, the legendary British economist

Lacy Hunt: Keynes was Wrong (and Ricardo was Right) May 4, 2010 by Robert Huebscher Underpinning the Obama administration s economic policies is the work of John Maynard Keynes, the legendary British economist

The state of the nation s Housing 2013

The state of the nation s Housing 2013 Fact Sheet PURPOSE The State of the Nation s Housing report has been released annually by Harvard University s Joint Center for Housing Studies since 1988. Now in

The state of the nation s Housing 2013 Fact Sheet PURPOSE The State of the Nation s Housing report has been released annually by Harvard University s Joint Center for Housing Studies since 1988. Now in

Economic Outlook, January 2016 Jeffrey M. Lacker President, Federal Reserve Bank of Richmond

Economic Outlook, January 2016 Jeffrey M. Lacker President, Federal Reserve Bank of Richmond Annual Meeting of the South Carolina Business & Industry Political Education Committee Columbia, South Carolina

Economic Outlook, January 2016 Jeffrey M. Lacker President, Federal Reserve Bank of Richmond Annual Meeting of the South Carolina Business & Industry Political Education Committee Columbia, South Carolina

The Challenge of Global Aging

The Challenge of Global Aging Richard Jackson President Global Aging Institute Department of Work and Pensions February 11, 2015 Washington, DC The Demographic Transformation The developed world is being

The Challenge of Global Aging Richard Jackson President Global Aging Institute Department of Work and Pensions February 11, 2015 Washington, DC The Demographic Transformation The developed world is being

Don t Raise the Federal Debt Ceiling, Torpedo the U.S. Housing Market

Don t Raise the Federal Debt Ceiling, Torpedo the U.S. Housing Market Failure to Act Would Have Serious Consequences for Housing Just as the Market Is Showing Signs of Recovery Christian E. Weller May

Don t Raise the Federal Debt Ceiling, Torpedo the U.S. Housing Market Failure to Act Would Have Serious Consequences for Housing Just as the Market Is Showing Signs of Recovery Christian E. Weller May

Chapter 5. Measuring a Nation s Production and Income. Macroeconomics: Principles, Applications, and Tools NINTH EDITION

Macroeconomics: Principles, Applications, and Tools NINTH EDITION Chapter 5 Measuring a Nation s Production and Income During the recent deep economic downturn, economists, business writers, and politicians

Macroeconomics: Principles, Applications, and Tools NINTH EDITION Chapter 5 Measuring a Nation s Production and Income During the recent deep economic downturn, economists, business writers, and politicians

Multifamily Market Commentary May 2017

Millions Multifamily Market Commentary May 2017 : Fundamentals Soften but Remain Healthy in First Quarter 2017 Seniors housing fundamentals softened modestly in the first quarter of 2017, with elevated

Millions Multifamily Market Commentary May 2017 : Fundamentals Soften but Remain Healthy in First Quarter 2017 Seniors housing fundamentals softened modestly in the first quarter of 2017, with elevated

The U.S. Economy After the Great Recession: America s Deleveraging and Recovery Experience

The U.S. Economy After the Great Recession: America s Deleveraging and Recovery Experience Sherle R. Schwenninger and Samuel Sherraden Economic Growth Program March 2014 Introduction The bursting of the

The U.S. Economy After the Great Recession: America s Deleveraging and Recovery Experience Sherle R. Schwenninger and Samuel Sherraden Economic Growth Program March 2014 Introduction The bursting of the

Florida: An Economic Overview

Florida: An Economic Overview December 26, 2018 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Shifting in Key Economic Variables

Florida: An Economic Overview December 26, 2018 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Shifting in Key Economic Variables

Not All Deleveragings Are Created Equal

INSIGHT Ruben Hovhannisyan, CFA Senior Vice President Fixed Income Mr. Hovhannisyan is a Generalist Analyst in the Fixed Income group. Mr. Hovhannisyan joined TCW in 2009 during the acquisition of Metropolitan

INSIGHT Ruben Hovhannisyan, CFA Senior Vice President Fixed Income Mr. Hovhannisyan is a Generalist Analyst in the Fixed Income group. Mr. Hovhannisyan joined TCW in 2009 during the acquisition of Metropolitan

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE The Budget and Economic Outlook: 2017 to 2027 Percentage of GDP 4 2 Surpluses Actual Current-Law Projection 0 Growth in revenues is projected -2-4

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE The Budget and Economic Outlook: 2017 to 2027 Percentage of GDP 4 2 Surpluses Actual Current-Law Projection 0 Growth in revenues is projected -2-4

Quarterly Review and Outlook

6836 Bee Caves Rd. B2 S100, Austin, TX 78746 (512) 327-7200 www.hoisington.com Quarterly Review and Outlook First Quarter 2018 Nearly nine years into the current economic expansion Federal Reserve policy

6836 Bee Caves Rd. B2 S100, Austin, TX 78746 (512) 327-7200 www.hoisington.com Quarterly Review and Outlook First Quarter 2018 Nearly nine years into the current economic expansion Federal Reserve policy

Policy Note 2000/6 Drowning In Debt

Policy Note 2000/6 Drowning In Debt Wynne Godley The U.S. expansion has been driven to an unusual extent by falling personal saving and rising borrowing by the private sector. If this process goes into

Policy Note 2000/6 Drowning In Debt Wynne Godley The U.S. expansion has been driven to an unusual extent by falling personal saving and rising borrowing by the private sector. If this process goes into

The Labor Force Participation Puzzle

The Labor Force Participation Puzzle May 23, 2013 by David Kelly of J.P. Morgan Funds Slow growth and mediocre job creation have been common themes used to describe the U.S. economy in recent years, as

The Labor Force Participation Puzzle May 23, 2013 by David Kelly of J.P. Morgan Funds Slow growth and mediocre job creation have been common themes used to describe the U.S. economy in recent years, as

A Demographic Dividend for the Developing Countries? Consequences of the Global Aging Process

Briefing Paper 6/2007 A Demographic Dividend for the Developing Countries? Consequences of the Global Aging Process Even in the countries of the South life expectancy is rising and birth rates are falling.

Briefing Paper 6/2007 A Demographic Dividend for the Developing Countries? Consequences of the Global Aging Process Even in the countries of the South life expectancy is rising and birth rates are falling.

Student Loan Debt Worries May Be Overstated

WEEKLY GUIDANCE ON ECONOMIC AND GEOPOLITICAL EVENTS June 12, 2018 Michael Taylor, CFA Investment Strategy Analyst Student Loan Debt Worries May Be Overstated Key takeaways» Today, U.S. student loan debt

WEEKLY GUIDANCE ON ECONOMIC AND GEOPOLITICAL EVENTS June 12, 2018 Michael Taylor, CFA Investment Strategy Analyst Student Loan Debt Worries May Be Overstated Key takeaways» Today, U.S. student loan debt

From the Great Moderation to the Great Recession and Beyond

From the Great Moderation to the Great Recession and Beyond Kenneth Rogoff, Harvard University Washington DC October 24 2018 THE WORLD BANK SOVEREIGN DEBT FORUM Low real rates --- if they stay low -- imply

From the Great Moderation to the Great Recession and Beyond Kenneth Rogoff, Harvard University Washington DC October 24 2018 THE WORLD BANK SOVEREIGN DEBT FORUM Low real rates --- if they stay low -- imply

Supply and Demand over the Business Cycle

Session 9. The Model at Work. v Business Cycles v The Economy in the Long Run: Recession and recovery Monetary expansion The everyday business of the central bank v Summing up: The IS/LM Model in Closed

Session 9. The Model at Work. v Business Cycles v The Economy in the Long Run: Recession and recovery Monetary expansion The everyday business of the central bank v Summing up: The IS/LM Model in Closed

EXECUTIVE OFFICE OF THE PRESIDENT COUNCIL OF ECONOMIC ADVISERS WASHINGTON, DC 20502

EXECUTIVE OFFICE OF THE PRESIDENT COUNCIL OF ECONOMIC ADVISERS WASHINGTON, DC 20502 Prepared Remarks of Edward P. Lazear, Chairman Productivity and Wages At the National Association of Business Economics

EXECUTIVE OFFICE OF THE PRESIDENT COUNCIL OF ECONOMIC ADVISERS WASHINGTON, DC 20502 Prepared Remarks of Edward P. Lazear, Chairman Productivity and Wages At the National Association of Business Economics

Q WestEnd Advisors. Macroeconomic Highlights. (888)

") Q1 2017 WestEnd Advisors Macroeconomic Highlights www.westendadvisors.com info@westendadvisors.com (888) 500-9025 1 U.S. Economic Picture Prior to the November Election 3-Month Moving Average 1.0 0.5 0.0-0.5-1.0-1.5-2.0

Q1 2017 WestEnd Advisors Macroeconomic Highlights www.westendadvisors.com info@westendadvisors.com (888) 500-9025 1 U.S. Economic Picture Prior to the November Election 3-Month Moving Average 1.0 0.5 0.0-0.5-1.0-1.5-2.0

The Basics of Economic Growth. Real GDP per person in Canada tripled in the 50 years between 1958 and 2008.

Real GDP per person in Canada tripled in the 50 years between 1958 and 2008. What has brought about this growth in production, incomes, and living standards? We see even greater economic growth in modern

Real GDP per person in Canada tripled in the 50 years between 1958 and 2008. What has brought about this growth in production, incomes, and living standards? We see even greater economic growth in modern

THE STATE OF THE ECONOMY

THE STATE OF THE ECONOMY ANGELA GUO Portland State University The United States economy in the fourth quarter of 2013 appears to have a more robust foothold pointing to a healthier outlook for 2014. Much

THE STATE OF THE ECONOMY ANGELA GUO Portland State University The United States economy in the fourth quarter of 2013 appears to have a more robust foothold pointing to a healthier outlook for 2014. Much

AUGUST 2012 An Update to the Budget and Economic Outlook: Fiscal Years 2012 to 2022 Provided as a convenience, this screen-friendly version is identic

AUGUST 2012 An Update to the Budget and Economic Outlook: Fiscal Years 2012 to 2022 Provided as a convenience, this screen-friendly version is identical in content to the principal, printer-friendly version

AUGUST 2012 An Update to the Budget and Economic Outlook: Fiscal Years 2012 to 2022 Provided as a convenience, this screen-friendly version is identical in content to the principal, printer-friendly version

Estimating Key Economic Variables: The Policy Implications

EMBARGOED UNTIL 11:45 A.M. Eastern Time on Saturday, October 7, 2017 OR UPON DELIVERY Estimating Key Economic Variables: The Policy Implications Eric S. Rosengren President & Chief Executive Officer Federal

EMBARGOED UNTIL 11:45 A.M. Eastern Time on Saturday, October 7, 2017 OR UPON DELIVERY Estimating Key Economic Variables: The Policy Implications Eric S. Rosengren President & Chief Executive Officer Federal

2014 Annual Review & Outlook

2014 Annual Review & Outlook As we enter 2014, the current economic expansion is 4.5 years in duration, roughly the average life of U.S. economic expansions. There is every reason to believe it will continue,

2014 Annual Review & Outlook As we enter 2014, the current economic expansion is 4.5 years in duration, roughly the average life of U.S. economic expansions. There is every reason to believe it will continue,

FRBSF ECONOMIC LETTER

FRBSF ECONOMIC LETTER 2013-38 December 23, 2013 Labor Markets in the Global Financial Crisis BY MARY C. DALY, JOHN FERNALD, ÒSCAR JORDÀ, AND FERNANDA NECHIO The impact of the global financial crisis on

FRBSF ECONOMIC LETTER 2013-38 December 23, 2013 Labor Markets in the Global Financial Crisis BY MARY C. DALY, JOHN FERNALD, ÒSCAR JORDÀ, AND FERNANDA NECHIO The impact of the global financial crisis on

Canada s Economic Future: What Have We Learned from the 1990s?

Remarks by Gordon Thiessen Governor of the Bank of Canada to the Canadian Club of Toronto Toronto, Ontario 22 January 2001 Canada s Economic Future: What Have We Learned from the 1990s? It was to the Canadian

Remarks by Gordon Thiessen Governor of the Bank of Canada to the Canadian Club of Toronto Toronto, Ontario 22 January 2001 Canada s Economic Future: What Have We Learned from the 1990s? It was to the Canadian

Retirement Solutions. Engaging the Next Generations in Retirement Savings

www.calamos.com Retirement Solutions Engaging the Next Generations in Retirement Savings Improving Retirement Readiness for the Next Generations by Applying Behavioral Finance & Thoughtful Plan Design

www.calamos.com Retirement Solutions Engaging the Next Generations in Retirement Savings Improving Retirement Readiness for the Next Generations by Applying Behavioral Finance & Thoughtful Plan Design

Game-Changers in the Era of Dissonance

Game-Changers in the Era of Dissonance The research views expressed herein are those of the author and do not necessarily represent the views of the CME Group or its affiliates. All examples in this presentation

Game-Changers in the Era of Dissonance The research views expressed herein are those of the author and do not necessarily represent the views of the CME Group or its affiliates. All examples in this presentation

A Discussion of Key Secular Trends, Economic Conditions and Monetary Policy

A Discussion of Key Secular Trends, Economic Conditions and Monetary Policy Remarks before the Official Monetary and Financial Institutions Forum Robert S. Kaplan President and CEO Federal Reserve Bank

A Discussion of Key Secular Trends, Economic Conditions and Monetary Policy Remarks before the Official Monetary and Financial Institutions Forum Robert S. Kaplan President and CEO Federal Reserve Bank

Income Progress across the American Income Distribution,

Income Progress across the American Income Distribution, 2000-2005 Testimony for the Committee on Finance U.S. Senate Room 215 Dirksen Senate Office Building 10:00 a.m. May 10, 2007 by GARY BURTLESS* *

Income Progress across the American Income Distribution, 2000-2005 Testimony for the Committee on Finance U.S. Senate Room 215 Dirksen Senate Office Building 10:00 a.m. May 10, 2007 by GARY BURTLESS* *

Growth in the US: A Macro and Global Perspective. Professor Pierre Yared. Columbia Business School Executive Education Program July 29-30, 2013

Growth in the US: A Macro and Global Perspective Professor Pierre Yared Columbia Business School Executive Education Program July 29-30, 2013 US Economic Recovery 2 US Economic Recovery 3 Exacerbated by

Growth in the US: A Macro and Global Perspective Professor Pierre Yared Columbia Business School Executive Education Program July 29-30, 2013 US Economic Recovery 2 US Economic Recovery 3 Exacerbated by

LETTER. economic THE CANADA / U.S. PRODUCTIVITY GAP: THE EFFECT OF FIRM SIZE FEBRUARY Canada. United States. Interest rates.

economic LETTER FEBRUARY 2014 THE CANADA / U.S. PRODUCTIVITY GAP: THE EFFECT OF FIRM SIZE For many years now, Canada s labour productivity has been weaker than that of the United States. One of the theories

economic LETTER FEBRUARY 2014 THE CANADA / U.S. PRODUCTIVITY GAP: THE EFFECT OF FIRM SIZE For many years now, Canada s labour productivity has been weaker than that of the United States. One of the theories

Ontario Economic Overview: International and National Context and Fiscal Implications

Ontario Economic Overview: International and National Context and Fiscal Implications Livio Di Matteo, Economics, Lakehead University Presentation for OCSBOA/OCSTA Seminar, Valhalla Inn, Thunder Bay, April

Ontario Economic Overview: International and National Context and Fiscal Implications Livio Di Matteo, Economics, Lakehead University Presentation for OCSBOA/OCSTA Seminar, Valhalla Inn, Thunder Bay, April

Achieving Long-Run Fiscal Sustainability

Achieving Long-Run Fiscal Sustainability William R. Emmons, Assistant Vice President and Economist April 8, 213 The views expressed here are those of the speakers, and do not necessarily represent the

Achieving Long-Run Fiscal Sustainability William R. Emmons, Assistant Vice President and Economist April 8, 213 The views expressed here are those of the speakers, and do not necessarily represent the

Notes The Congressional udget Office s extended baseline shows the budget s long-term path under most of the same assumptions that the agency uses, in

CONGRESS OF THE UNITED STATES CONGRESSIONAL UDGET OFFICE The 2016 Long-Term udget Outlook Percentage of GDP 2046 30 Net Interest 2016 20 Deficit Other Revenues Corporate Income Taxes Payroll Taxes Major

CONGRESS OF THE UNITED STATES CONGRESSIONAL UDGET OFFICE The 2016 Long-Term udget Outlook Percentage of GDP 2046 30 Net Interest 2016 20 Deficit Other Revenues Corporate Income Taxes Payroll Taxes Major

NEBRASKA SNAPS BACK By the Bureau of Business Research and the Nebraska Business Forecast Council

VOLUME 72, NO. 721 PRESENTED BY THE UNL BUREAU OF BUSINESS RESEARCH (BBR) DECEMBER 2017 NEBRASKA SNAPS BACK By the Bureau of Business Research and the Nebraska Business Forecast Council U.S. Macroeconomic

VOLUME 72, NO. 721 PRESENTED BY THE UNL BUREAU OF BUSINESS RESEARCH (BBR) DECEMBER 2017 NEBRASKA SNAPS BACK By the Bureau of Business Research and the Nebraska Business Forecast Council U.S. Macroeconomic

The Urgent Need for Job Creation

The Urgent Need for Job Creation John Schmitt and Tessa Conroy July 21 Center for Economic and Policy Research 1611 Connecticut Avenue, NW, Suite 4 Washington, D.C. 29 22-29338 www.cepr.net CEPR The Urgent

The Urgent Need for Job Creation John Schmitt and Tessa Conroy July 21 Center for Economic and Policy Research 1611 Connecticut Avenue, NW, Suite 4 Washington, D.C. 29 22-29338 www.cepr.net CEPR The Urgent

Post-Election Special Analysis November 27, 2016 by The GaveKal USA Team of GaveKal Capital

Post-Election Special Analysis November 27, 2016 by The GaveKal USA Team of GaveKal Capital Page 1, 2018 Advisor Perspectives, Inc. All rights reserved. Source: Center for Responsible Federal Budget Page

Post-Election Special Analysis November 27, 2016 by The GaveKal USA Team of GaveKal Capital Page 1, 2018 Advisor Perspectives, Inc. All rights reserved. Source: Center for Responsible Federal Budget Page

The Economy: Growth Has Been Weak But Long-Lasting

The Economy: Growth Has Been Weak But Long-Lasting October 19, 2016 by Gary Halbert of Halbert Wealth Management 1. Why This Economic Recovery Has Been So Disappointing 2. The Fourth Longest Economic Expansion

The Economy: Growth Has Been Weak But Long-Lasting October 19, 2016 by Gary Halbert of Halbert Wealth Management 1. Why This Economic Recovery Has Been So Disappointing 2. The Fourth Longest Economic Expansion

China & Commodities - the First Major Trend Reversal of the 21st Century

China & Commodities - the First Major Trend Reversal of the 21 st Century There are major economic and investment trends that happen about every 10 years. In 2013, I wrote the reversal of a major trend,

China & Commodities - the First Major Trend Reversal of the 21 st Century There are major economic and investment trends that happen about every 10 years. In 2013, I wrote the reversal of a major trend,

Statement of. Ben S. Bernanke. Chairman. Board of Governors of the Federal Reserve System. before the. Committee on the Budget

For release on delivery 10:00 a.m. EST February 28, 2007 Statement of Ben S. Bernanke Chairman Board of Governors of the Federal Reserve System before the Committee on the Budget U.S. House of Representatives

For release on delivery 10:00 a.m. EST February 28, 2007 Statement of Ben S. Bernanke Chairman Board of Governors of the Federal Reserve System before the Committee on the Budget U.S. House of Representatives

2017 MORTGAGE MARKET OUTLOOK: EXECUTIVE ECONOMIC REPORT JANUARY 2017

2017 MORTGAGE MARKET OUTLOOK: EXECUTIVE ECONOMIC REPORT JANUARY 2017 1 2017 FORECAST OVERVIEW For the 2017 housing market, the outlook is generally positive. The long recovery from the elevated delinquency

2017 MORTGAGE MARKET OUTLOOK: EXECUTIVE ECONOMIC REPORT JANUARY 2017 1 2017 FORECAST OVERVIEW For the 2017 housing market, the outlook is generally positive. The long recovery from the elevated delinquency

Greece. Eurozone rebalancing. EY Eurozone Forecast June Portugal Slovakia Slovenia Spain. Latvia Lithuania Luxembourg Malta Netherlands

EY Forecast June 215 rebalancing recovery Outlook for Delay in agreeing reform agenda has undermined the recovery Published in collaboration with Highlights The immediate economic outlook for continues

EY Forecast June 215 rebalancing recovery Outlook for Delay in agreeing reform agenda has undermined the recovery Published in collaboration with Highlights The immediate economic outlook for continues

KING COUNTY AND SEATTLE MOTOR VEHICLE EXCISE TAX BASE PROJECTIONS

KING COUNTY AND SEATTLE MOTOR VEHICLE EXCISE TAX BASE PROJECTIONS 1. SUMMARY Based on my current work for Sound Transit ( Sound Transit Tax Base Forecast, Dick Conway & Associates, August 2005), I expect

KING COUNTY AND SEATTLE MOTOR VEHICLE EXCISE TAX BASE PROJECTIONS 1. SUMMARY Based on my current work for Sound Transit ( Sound Transit Tax Base Forecast, Dick Conway & Associates, August 2005), I expect

HOW PUBLIC PENSION PLAN DEMOGRAPHIC CHARACTERISTICS AFFECT FUNDING

PENSION SIMULATION PROJECT HOW PUBLIC PENSION PLAN DEMOGRAPHIC CHARACTERISTICS AFFECT FUNDING ANDCONTRIBUTION RISK The Nelson A. Rockefeller Institute of Government, the public policy research arm of the

PENSION SIMULATION PROJECT HOW PUBLIC PENSION PLAN DEMOGRAPHIC CHARACTERISTICS AFFECT FUNDING ANDCONTRIBUTION RISK The Nelson A. Rockefeller Institute of Government, the public policy research arm of the

THE GROWTH RATE OF GNP AND ITS IMPLICATIONS FOR MONETARY POLICY. Remarks by. Emmett J. Rice. Member. Board of Governors of the Federal Reserve System

THE GROWTH RATE OF GNP AND ITS IMPLICATIONS FOR MONETARY POLICY Remarks by Emmett J. Rice Member Board of Governors of the Federal Reserve System before The Financial Executive Institute Chicago, Illinois

THE GROWTH RATE OF GNP AND ITS IMPLICATIONS FOR MONETARY POLICY Remarks by Emmett J. Rice Member Board of Governors of the Federal Reserve System before The Financial Executive Institute Chicago, Illinois

Investment Company Institute and the Securities Industry Association. Equity Ownership

Investment Company Institute and the Securities Industry Association Equity Ownership in America, 2005 Investment Company Institute and the Securities Industry Association Equity Ownership in America,

Investment Company Institute and the Securities Industry Association Equity Ownership in America, 2005 Investment Company Institute and the Securities Industry Association Equity Ownership in America,