OUR INSTRUCTOR FOR THE TWO DAY SEMINAR MICHAEL MIRANDA

|

|

|

- Herbert Wheeler

- 5 years ago

- Views:

Transcription

1 EXPLORING THE TAX AND PLANNING ASPECTS OF OUR PRIVATE AND PUBLIC RETIREMENT PLAN SYSTEMS WEBINAR PRESENTED BY KRISTY MAITRE AND MICHAEL MIRANDA OCTOBER 10 TH AND 11 TH OUR INSTRUCTOR FOR THE TWO DAY SEMINAR MICHAEL MIRANDA Michael Miranda, CPA, QKA, AEP, is the owner of Miranda CPA & Consulting LLC in Sioux Falls, South Dakota. Michael previously worked for Williams & Company CPA PC as a senior manager from 1989 to May of While at Williams & Company, Michael provided tax consulting, estate planning and employee benefit services. In 1976, he received a B.S. Degree in Accounting from Indiana University, South Bend, Indiana. Prior to joining Williams & Company, he was on staff as a Tax Specialist with Price Waterhouse in offices at South Bend and Minneapolis. Michael is currently the Treasurer and Liaison Board member for the Sioux Falls Estate Planning Councils. He holds CPA licenses in the states of Iowa, Minnesota and South Dakota. 2 1

and Roth IRAs Rollovers, distributions, and penalty issues Operational issues, including correction procedures Plan termination")

2 3 AGENDA Preparing for Retirement A Checklist Approach (October 10 th 2017 Webinar) Private Retirement Plans (October 10 th and 11 th 2017 Webinars) Qualified plan arrangements Choosing the right small business plan Regular IRAs (tax deferred) and Roth IRAs Rollovers, distributions, and penalty issues Operational issues, including correction procedures Plan termination considerations 4 2

3 AGENDA Social Security What s In It for Your Clients (October 11 th 2017 Webinar) Introduction Qualifying for benefit Retirement benefits Divorce Survivor benefits Disability Calculating the benefit brief overview Social security planning Questions & Answers 5 INDIVIDUAL RETIREMENT ACCOUNTS WEBINAR PRESENTED BY KRISTY MAITRE AND MICHAEL MIRANDA OCTOBER 10 TH AND 11 TH

4 CONTRIBUTIONS TO IRAS Executive Overview Introduction Traditional IRAs Roth IRAs Retirement savings contributions credit (saver s credit) What s new for CONTRIBUTIONS TO IRAS (CON T) Introduction What are some tax advantages of an IRA? Contributions and fully or partially deductible Tax treatment of earnings during the period that IRA funds are not distributed Setting up an IRA Contribution to an IRA Transferring money or property to / from an IRA Taking a credit for contributions to an IRA 8 4

5 CONTRIBUTIONS TO IRAS Introduction How Are a Traditional IRA and a Roth IRA Different? Question Answer Is there an age limit on when I can open and contribution to a. If I earned more than $5,500 in 2017 ($6,500 if I was 50 or older by end of 2017), is there a limit on how much I can contribution to a. Traditional IRA? Yes. You must not have reached age 70 ½ by the end of the year. Yes. For 2017, you can contribute $5,500 or $6,500 (catch-up) No upper limit on how much can earn and still contribute. Roth IRA? No. You can be any age. Yes. For 2017, you can contribute $5,500 or $6,500 (catch-up) But amount you contribute may be less depending on income, filing status, and if you contribute to another IRA. Can I deduct contributions to a. Yes. You may be able to deduct you contributions to a tradition IRA depending on income, filing, whether are covered by retirement plan and/or receive social security benefits No. You can never deduct contribution to a Roth IRA Do I have to file a form just because I contribute to a. Not unless you make nondeductible contributions to your traditional IRA. If so, you must file Form No. You do not have to file a form if you contribution to a Roth IRA. 9 CONTRIBUTIONS TO IRAS TRADITIONAL IRAS Introduction Who can open a traditional IRA? Both spouses have compensation What is compensation? When can a traditional IRA be opened? How can a traditional IRA be opened? Kinds of traditional IRAs COMPENSATION FOR PURPOSES OF AN IRA Includes Wages, Salaries, etc. Commissions Self-Employment Income Alimony and Separation Maintenance Nontaxable Combat Pay Does Not Include Earnings and Profits from Property Interest and Dividend Income Pension or Annuity Income Deferred Compensation Income from Certain Partnerships Any Amounts you Exclude from Income 10 5

6 CONTRIBUTIONS TO IRAS Traditional IRAs Types of Accounts Individual Retirement Account Individual Retirement Annuity Individual Retirement Bonds (suspended after 4/30/1982) SIMPLE IRAs Simplified Employee Pension (SEP) Employer and Employee Association Trust Accounts 11 CONTRIBUTIONS TO IRAS Traditional IRAs How Much Can Be Contributed? General Limit for 2017, lesser of (i) $5,500 ($6,500 if age 50 or older) or (ii) taxable compensation Kay Bailey Hutchinson spousal IRA limit Filing status may effect contribution amount if covered by retirement plan Less than maximum contribution More than maximum contribution 12 6

7 CONTRIBUTIONS TO IRAS Traditional IRAs When can contributions be made? How much can you deduct? Are you covered by an employer plan? Situations in which you are not covered? Limit if covered by employer plan Social security recipients Effect of modified AGI on deduction if you are covered by a retirement plan or not covered by a retirement plan See Table 1-2 and Table 1-3 Figuring your modified AGI See Worksheet 1-1 Figuring your reduced IRA deduction Worksheet

8

9 17 CONTRIBUTIONS TO IRAS EXAMPLES George, who is 34 years old and single, earns $24,000 in His IRA contributions for 2016 are limited to $5,500 Danny, an unmarried college student working part time, earns $3,500 in 2016 His IRA contributions for 2016 are limited to $3,500, the amount of his compensation 18 9

10 CONTRIBUTIONS TO IRAS Example Kay Bailey Hutchison Spousal IRA Limit Kristin, a full-time student with no taxable compensation, marries Carl during the year Neither of them was age 50 by the end of 2016 For the year, Carl has taxable compensation of $30,000 He plans to contribute (and deduct) $5,500 to a traditional IRA If he and Kristin file a joint return, each can contribute $5,500 to a traditional IRA This is because Kristin, who has no compensation, can add Carl's compensation, reduced by the amount of his IRA contribution ($30,000 $5,500 = $24,500), to her own compensation (-0-) to figure her maximum contribution to a traditional IRA In her case, $5,500 is her contribution limit, because $5,500 is less than $24,500 (her compensation for purposes of figuring her contribution limit) 19 CONTRIBUTIONS TO IRAS Example Filing Status Tom and Darcy are married and both are 53 They both work and each has a traditional IRA Tom earned $3,800 and Darcy earned $48,000 in 2016 Because of the Kay Bailey Hutchison Spousal IRA limit rule, even though Tom earned less than $6,500, they can con-tribute up to $6,500 to his IRA for 2016 if they file a joint return They can contribute up to $6,500 to Darcy's IRA If they file separate returns, the amount that can be contributed to Tom's IRA is limited by his earned income, $3,

11 CONTRIBUTIONS TO IRAS Example Less Than Maximum Contributions Rafael, who is 40, earns $30,000 in 2016 Although he can contribute up to $5,500 for 2016, he contributes only $3,000 After April 18, 2017, Rafael cannot make up the difference between his actual contributions for 2016 ($3,000) and his 2016 limit ($5,500) He cannot contribute $2,500 more than the limit for any later year 21 CONTRIBUTIONS TO IRAS Example Nondeductible Contributions Tony is 29 years old and single In 2016, he was covered by a retirement plan at work His salary is $67,000 His modified AGI is $80,000 Tony makes a $5,500 IRA contribution for 2016 Because he was covered by a retirement plan and his modified AGI is above $71,000, he cannot deduct his $5,500 IRA contribution He must designate this contribution as a nondeductible contribution by reporting it on Form

12 CONTRIBUTIONS TO IRAS Other Considerations for Traditional IRAs What if You Inherit an IRA? Can You Move Retirement Plan Assets? Trustee-to-Trustee Transfer Rollovers Time Limit for Making a Rollover Contribution Rollover From One IRA into Another Possible Waiver of the 60-day rollover requirement Rollover Chart Table

13 CONTRIBUTIONS TO IRAS Example Rollover From One IRA Into Another You have two traditional IRAs, IRA-1 and IRA-2 In 2016, you made a tax-free rollover of a distribution from IRA-1 into a new traditional IRA (IRA-3) You cannot, within 1 year of the distribution from IRA-1, make a tax-free rollover of any distribution from either IRA-1 or IRA-3 into another traditional IRA For 2016, the rollover from IRA-1 into IRA-3 prevents you from making a tax-free rollover from IRA-2 into any other traditional IRA This is because in 2016 you are only allowed to make one rollover within a 1-year period So when you make a rollover from IRA-1 to IRA-3, you cannot make a rollover from IRA-2 to any other traditional IRA. 25 CONTRIBUTIONS TO IRAS Example You received an eligible rollover distribution from your traditional IRA on June 30, 2016, that you intend to roll over to your 403(b) plan To postpone including the distribution in your income, you must complete the rollover by August 29, 2016, the 60th day following June 30 The IRS may waive the 60-day requirement where the failure to do so would be against equity or good conscience, such as in the event of a casualty, disaster, or other event beyond your reasonable control 26 13

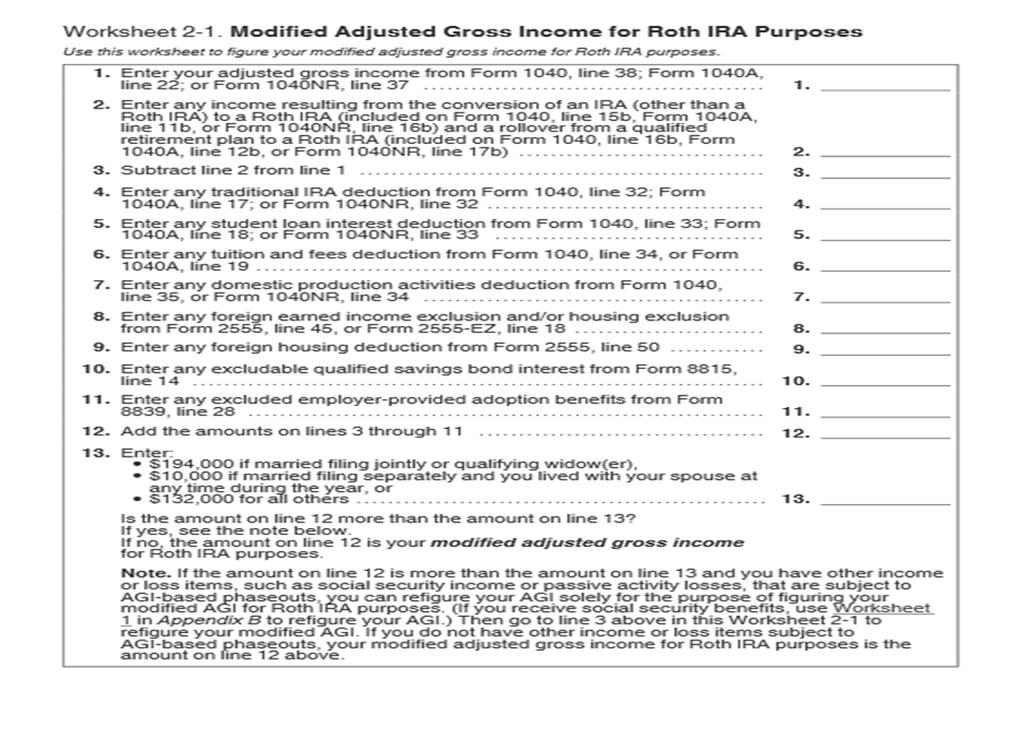

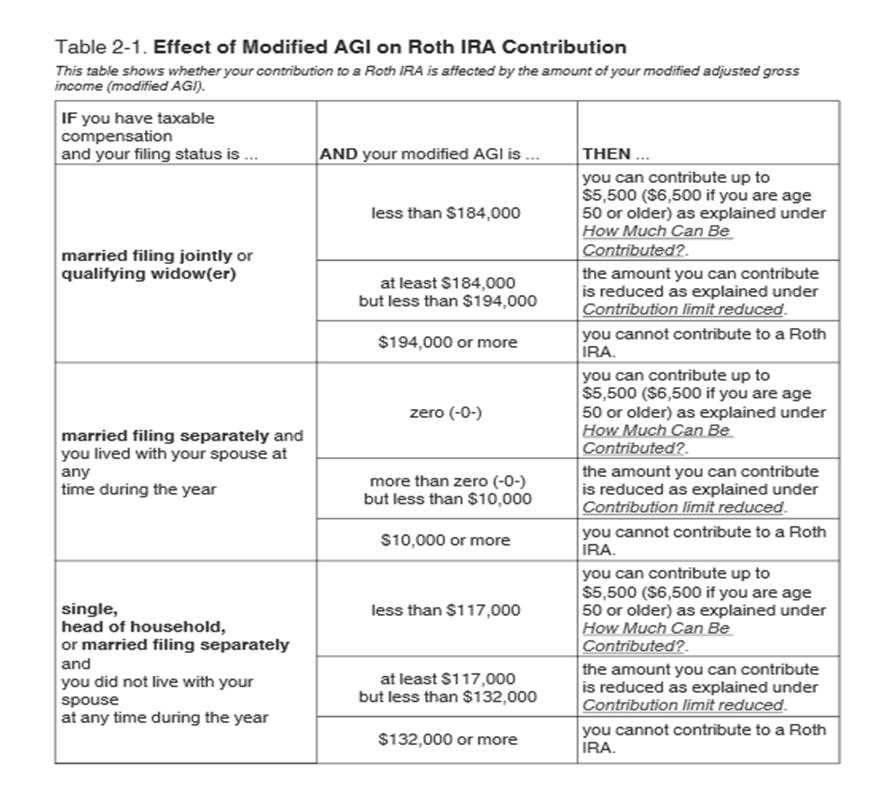

14 CONTRIBUTIONS TO IRAS Ways to get a waiver of the 60day rollover requirement. There are three ways to obtain a waiver of the 60- day rollover requirement: You qualify for an automatic waiver You self-certify that you met the requirements of a waiver or You request and receive a private letter ruling granting a waiver How do you qualify for an automatic waiver? You qualify for an automatic waiver if all of the following apply: The financial institution receives the funds on your be-half before the end of the 60-day rollover period You followed all of the procedures set by the financial institution for depositing the funds into an IRA or other eligible retirement plan within the 60-day rollover period (including giving instructions to deposit the funds into a plan or IRA) The funds are not deposited into a plan or IRA within the 60-day rollover period solely because of an error on the part of the financial institution The funds are deposited into a plan or IRA within 1 year from the beginning of the 60-day rollover period It would have been a valid rollover if the financial institution had deposited the funds as instructed If you do not qualify for an automatic waiver, you can use the self-certification procedure to make a late rollover contribution or you can apply to the IRS for a waiver of the 60- day rollover requirement 27 CONTRIBUTIONS TO IRAS Roth IRAs Introduction What is a Roth IRA? When can a Roth IRA be opened Can you contribute to a Roth IRA? How much can be contributed? Roth IRAs only Roth IRAs and traditional IRAs Modified AGI for Roth IRA purposes Worksheet 2-1 Effect of Modified AGI on Roth IRA contribution Table 2-1 Determining your reduced Roth IRA contribution limit Worksheet 2-2 Illustrated 28 14

15

16 CONTRIBUTIONS TO IRAS EXAMPLE Reduced Roth IRA Contribution You are a 45-year-old, single individual with taxable compensation of $118,000 You want to make the maximum allowable contribution to your Roth IRA for 2016 Your modified AGI for 2016 is $118,000 You have not contributed to any traditional IRA, so the maximum contribution limit before the modified AGI reduction is $5,500 You figure your reduced Roth IRA contribution of $5,140 as shown on Worksheet Illustrated

17 CONTRIBUTIONS TO IRAS Roth IRAs Can you move amounts into a Roth IRA? Conversions Rollover Trustee-to-trustee transfer Same trustee transfer Same trustee Income includes Rollover from employer s plan into a Roth IRA Rollover from a Roth IRA 33 CONTRIBUTIONS TO IRAS Retirement Savings Contributions Credit (Saver s Credit) Introduction Can you claim the credit? Full-time student Adjusted gross income Eligible contributions Reducing eligible contribution (for distributions received while making contributions) Maximum eligible contributions Maximum credit Nonrefundable credit How to figure and report the credit Form

18 CONTRIBUTIONS TO IRAS (CON T) What s New for 2017 Modified AGI limit for Traditional IRA contributions Joint Return - $99K - $119K Single or HOH - $62K - $72K MFS Less than $10K Joint return and one spouse not covered - $186K - $196K Modified AGI limit for Roth IRA contributions Joint return - $186K 196K Single or HOH or MFS MAGI - $118K ($0 if MAGI is $133K) MFS and lived with spouse Less than $10K 35 MYRA 18

19 PHASING OUT THE MYRA PROGRAM The U.S. Department of the Treasury has decided to phase out the myra retirement savings program, and the program is no longer accepting new enrollments Existing accounts can remain open until further notice What is happening to accounts? The account remains open and taxpayers can continue to manage the account until further notice The funds in the account remain safe and in an investment issued by the U.S. Department of the Treasury PHASING OUT THE MYRA PROGRAM Any myra with a zero ($0) balance as of September 15, 2017 or later, will be subject to possible automatic closure beginning on September 18, 2017 Treasury will be reaching out to all of the account holders with more information regarding the transfer or closure of the account over the next few weeks outlining when they will stop accepting and processing deposits 19

20 PHASING OUT THE MYRA PROGRAM It is recommended taxpayers log in to their account to make sure their contact information is complete and up to date They can also update their information by contacting customer service They can initiate a direct transfer of their full account balance to another Roth IRA at any time First identify or open an account at the new Roth IRA provider where they will continue to save and invest PHASING OUT THE MYRA PROGRAM Then, work with a new Roth IRA provider selected to transfer the myra balance to the new Roth IRA By opening another Roth IRA and working with the new Roth IRA provider to initiate a transfer of the funds in the myra to the new Roth IRA, taxpayers avoid withholding and potential tax liabilities (including potential tax penalties) that may apply to earnings if funds are paid directly to them To request closure of the account, call myra customer support at or TTY/TDD or International

21 PHASING OUT THE MYRA PROGRAM Remember that a myra follows Roth IRA rules To avoid tax liabilities that may apply to earnings if funds are paid directly to the taxpayer they will need to deposit the amount of the distribution (including any tax withholding) into a private-sector Roth IRA within 60 days of the distribution Taxpayers may receive an additional payment due to a timing difference between when interest earned was reflected in the account balance, and when the requested a withdrawal or distribution is issued PHASING OUT THE MYRA PROGRAM Transferring the account - myra has no fees to move funds to another Roth IRA provider (or to withdraw funds and close the account) Have the taxpayer check with the new Roth IRA provider to learn whether they have applicable fees Can the taxpayer transfer or roll over the account into my employer-sponsored retirement plan, such as a 401(k), or into a traditional IRA? No. As is the case with all Roth IRAs, the myra can t be transferred or rolled over into an employer-sponsored retirement plan or a traditional IRA Roth IRAs must be transferred or rolled over into other Roth IRAs 21

22 DISTRIBUTIONS FROM IRAS WEBINAR PRESENTED BY KRISTY MAITRE AND MICHAEL MIRANDA OCTOBER 10 TH AND 11 TH Executive Overview Introduction Traditional IRAs Roth IRAs Reminders 44 22

23 Introduction Receiving distributions from an IRA Making withholdings from an IRA Potential penalties associated with IRA distributions and/or withdrawals Required Minimum Distributions (RMDs) Distributions or withdrawals associated with the death or owners 45 How Are Traditional IRA and a Roth Different? Question Do I have to start taking distribution when I reach a certain age from a. How are distributions taxed from a. Do I have to file a form just because I received distributions from a. Answer Traditional IRA? Yes. You must begin receiving RMDs by 4/1 of year following year you reach age 70 ½ Distributions from a Traditional IRA are taxed as ordinary income, but if you made nondeductible contributions, not all of the distributions is taxable Not unless you have ever made a nondeductible contribution to a traditional IRA (Form 8606) Roth IRA? No. If you are the original owners of Roth IRA, you do not have to take distributions regardless of age Distributions from a Roth IRA are not taxed as long as you meet certain criteria Yes. File Form 8606 if you received distributions from a Roth IRA (other than a rollover, QCD, HSA rollover, recharacterization distributions, or return of certain contributions 46 23

24 Traditional IRAs What if you inherit an IRA? Inherited from spouse Treating it as you own Inherited from someone other than spouse IRA with basis Federal (and possibly state) estate tax deduction 47 (CON T) Traditional IRAs When can you withdraw or use assets? When must you withdrawal assets? (RMDs) IRA owners and RMD rules Required beginning date (RBD) Distribution calendar year and calendar year of age 70 ½ Distributions after the RBD Change in marital status and change in beneficiary Example 48 24

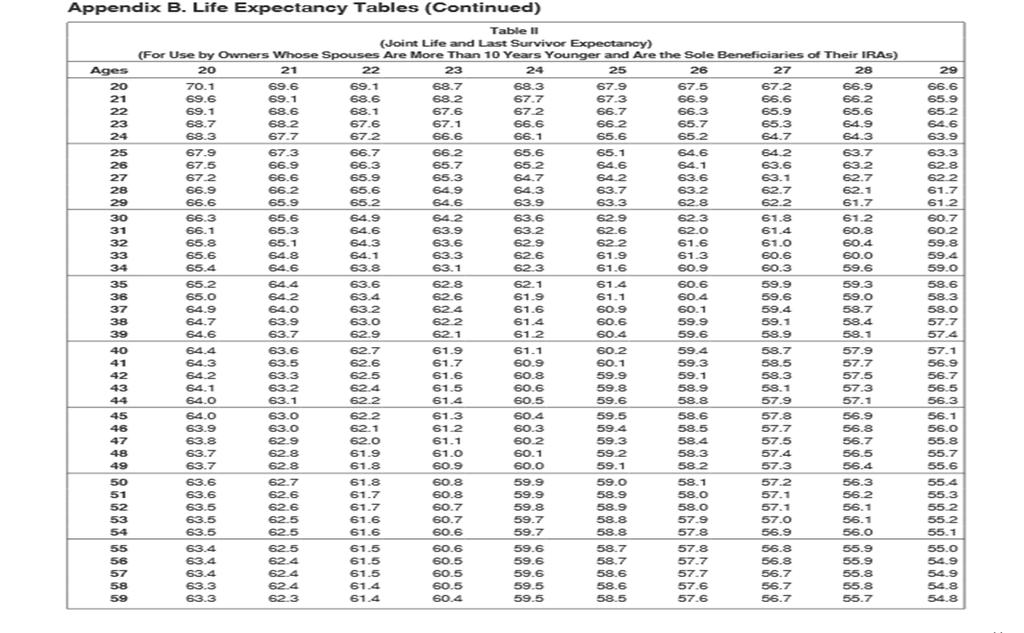

25 EXAMPLE You reach age 70 ½ on August 20, 2016 For 2016, you must receive the required minimum distribution from your IRA by April 1, 2017 You must receive the required minimum distribution for 2017 by December 31, 2017 Creates a bunching of gross income in one calendar year Consider accelerating the 2016 RMD into the 2016 calendar year 49 (CON T) Traditional IRAs Figuring the owner s RMD Review distribution Table I, Table II, and Table III Table I Single Life Expectancy For Use by Beneficiaries Table II Joint Life and Last Survivor Expectancy Owners whose spouses are more than 10 years younger and spouse is sole beneficiary of owner s IRA Table III Uniform Lifetime Unmarried owners Married owners whose spouses are not more than 10 years younger and Married owners whose spouses are not the sole beneficiaries of their IRAs 50 25

26

27 53 Traditional IRAs More on figuring the owner s RMD IRA account balance (end of preceding year) Contributions Outstanding rollovers and recharacterizations Distributions Examples 54 27

28 Example Laura was born on October 1, 1945 She reaches age 70 ½ in 2016 Her required beginning date is April 1, 2017 As of December 31, 2015, her IRA account balance was $26,500 No rollover or recharacterization amounts were outstanding Using Table III, the applicable distribution period for someone her age (71) is 26.5 years Her required minimum distribution for 2016 is $1,000 ($26, ) That amount is distributed to her on April 1, Example Joe, born October 1, 1945, reached 70 ½ in 2016 His wife (his beneficiary) turned 56 in September 2016 He must begin receiving distributions by April 1, 2017 Joe's IRA account balance as of December 31, 2015, is $30,100 Because Joe's wife is more than 10 years younger than Joe and is the sole beneficiary of his IRA, Joe uses Table II Based on their ages at year end (December 31, 2016), the joint life expectancy for Joe (age 71) and his wife (age 56) is 30.1 years The required minimum distribution for 2016, Joe's first distribution year, is $1,000 ($30, ) This amount is distributed to Joe on April 1,

29 Example Distributions during your lifetime (spouse not 10 years older) You own a traditional IRA Your account balance at the end of 2016 was $100,000 You are married and your spouse, who is the sole beneficiary of your IRA, is 6 years younger than you You turn 75 years old in 2017 You use Table III. Your distribution period is 22.9 Your required minimum distribution for 2017 would be $4,367 ($100, ) 57 Example Distributions during your lifetime (spouse is 10 years older) You own a traditional IRA Your account balance at the end of 2016 was $100,000 You are married and your spouse, who is the sole beneficiary of your IRA, is 11 years younger than you You turn 75 in 2017 and your spouse turns 64 You use Table II Your joint life and last survivor expectancy is 23.6 Your required minimum distribution for 2017 would be $4,237 ($100, ) 58 29

30 Traditional IRAs Distributions in year of owner s death Key Death before or after RBD If death before RBD then no RMD in year of death of owner If owner died on or after RBD, IRS beneficiaries are responsible for figuring and distributing RMD in year of death Note Figure RMD for year in which IRA owners dies as if owner lived for the entire year 59 Traditional IRAs IRA Beneficiaries Beneficiary is surviving spouse Beneficiary is an individual (other than the surviving spouse) Beneficiary is not an individual IRA owner died before RBD or after RBD 60 30

31 Traditional IRAs Surviving spouse If you are the surviving spouse who is the sole beneficiary of your deceased spouse's IRA, you may elect to be treated as the owner and not as the beneficiary If you elect to be treated as the owner, you determine the required minimum distribution (if any) as if you were the owner beginning with the year you elect or are deemed to be the owner NOTE: If you become the owner in the year your deceased spouse died, do not determine the required mini-mum distribution for that year using your life; rather, you must take the deceased owner's required minimum distribution for that year (to the extent it was not already distributed to the owner before his or her death) 61 Traditional IRAs Date the designated beneficiary is determined Generally, the designated beneficiary is determined on September 30 of the calendar year following the calendar year of the IRA owner's death In order to be a designated beneficiary, an individual must be a beneficiary as of the date of death Any person who was a beneficiary on the date of the owner's death, but is not a beneficiary on September 30 of the calendar year following the calendar year of the owner's death (because, for example, he or she disclaimed entitlement or received his or her entire benefit), will not be taken into account in determining the designated beneficiary An individual may be designated as a beneficiary either by the terms of the plan or, if the plan permits, by affirmative election by the employee specifying the beneficiary 62 31

32 Traditional IRAs Death of a beneficiary More than one beneficiary Owner died on or after RBD Designated beneficiary base RMDs on the longer of: Single life expectancy (Table I), or Owner s life expectancy Surviving spouse is sole designated beneficiary 63 Traditional IRAs Owner died before RBD Designated beneficiary generally must base RMDs for years after owner s death using your single life expectancy (Table I) Special rules for surviving spouse Year of first required distribution Death of surviving spouse prior to date distributions being This rule does not apply to the surviving spouse of a surviving spouse Examples 64 32

33 Example #1 Your spouse died in 2014, at age 65 ½ You are the sole designated beneficiary of your spouse s traditional IRA You do not need to take any required minimum distribution until December 31 of 2019, the year your spouse would have reached age 70 ½ If you die prior to that date, you will be treated as the owner of the IRA for purposes of determining the required distributions to your beneficiaries For example, if you die in 2016, your beneficiaries will not have any required minimum distribution for 2016 (because you are treated as the owner, died prior to your required beginning date) They must start taking distributions under the general rules for an owner who died prior to the required beginning date 65 Example #2 Same facts as Example 1, except your sole beneficiary upon your death in 2016 is your surviving spouse (the original spouse beneficiary remarried) Your surviving spouse cannot wait until the year you would have turned 701/2 to take distributions using his or her life expectancy Also, if your surviving spouse dies prior to the date he or she is required to take a distribution, he or she is not treated as the owner of the account Just like any other individual beneficiary of an owner who dies before the required beginning date, your surviving spouse must start taking distributions in 2017 based on his or her life expectancy (or elect to fully distribute the account under the 5-year rule by the end of 2021) 66 33

34 TIP from Example #2 The second surviving spouse from Example 2 above can still elect to treat the IRA as his or her own IRA or rollover any distributions that are not required minimum distributions into his or her own IRA 67 Traditional IRAs 5-year rule The 5-year rule requires the IRA beneficiaries to withdraw 100% of the IRA by December 31 of the year containing the fifth anniversary of the owner s death For example, if the owner died in 2016, the beneficiary would have to fully distribute the plan by December 31, 2021 The beneficiary is allowed, but not required, to take distributions prior to that date The 5-year rule never applies if the owner died on or after his or her required beginning date 68 34

35 Traditional IRAs Individual designated beneficiaries The terms of most IRA plans require individual designated beneficiaries to take required minimum distributions using the life expectancy rules (explained earlier) unless such beneficiaries elect to take distributions using the 5-year rule The deadline for making this election is December 31 of the year the beneficiary must take the first required distribution using his or her life expectancy (or December 31 of the year containing the fifth anniversary of the owner's death, if earlier) 69 Traditional IRAs Beneficiary not an individual The 5-year rule applies in all cases where there is no individual designated beneficiary by September 30 of the year following the year of the owner s death or where any beneficiary is not an individual (for example, the owner named his or her estate as the beneficiary) TIP Review IRA plan documents on 5-year rule provisions of any particular Plan Caution If any residue remains after the 5-year period on 12/31 is may be subject to the 50% excise tax 70 35

36 Traditional IRAs Figuring the beneficiary s required minimum distribution Beneficiary an individual Spouse as sole designated beneficiary Other designated beneficiary Beneficiary not an individual Death on or after RBD Death before RBD Examples 71 Example Beneficiary an Individual Your father died in 2016 You are the designated beneficiary of your father's traditional IRA You are 53 years old in 2017, which is the year following your father's death You use Table I and see that your life expectancy in 2017 is 31.4 If the IRA was worth $100,000 at the end of 2016, your required minimum distribution for 2017 would be $3,185 ($100, ) If the value of the IRA at the end of 2017 was again $100,000, your required minimum distribution for 2018 would be $3,289 ($100, (31.4 reduced by 1, which is the number of years following the year after your father's death in 2016)) 72 36

37 (CON T) Example Beneficiary in not an Individual The owner died in 2016 at the age of 80 The owner's traditional IRA went to his estate The account balance at the end of 2016 was $100,000. In 2017, the required minimum distribution would be $10,870 ($100, ) (The owner's life expectancy in the year of death, 10.2, reduced by one) If the owner had died in 2016 at the age of 70, the entire account would have to be distributed by the end of Traditional IRAs Installments allowed More than one IRA (see example) More than minimum received (see example) Multiple individual beneficiaries separate accounts Trust as beneficiary 74 37

38 Example More than one IRA Sara, born August 1, 1945, became 70 1/2 on February 1, 2016 She has two traditional IRAs She must begin receiving her IRA distributions by April 1, 2017 On December 31, 2015, Sara's account balance from IRA A was $10,000; her account balance from IRA B was $20,000 Sara's brother, age 64 as of his birthday in 2016, is the beneficiary of IRA A Her husband, age 78 as of his birthday in 2016, is the beneficiary of IRA B Sara's required minimum distribution from IRA A is $377 ($10, (the distribution period for age 71 per Table III)) The amount of the required minimum distribution from IRA B is $755 ($20, ) The amount that must be withdrawn by Sara from her IRA accounts by April 1, 2017, is $1,132 ($377 + $755) 75 Example More than minimum received Justin became 70 ½ on December 15, 2016 Justin's IRA account balance on December 31, 2015, was $38,400 He figured his required minimum distribution for 2016 was $1,401 ($38, (the distribution period for age 70 per Table III)) By December 31, 2016, he had actually received distributions totaling $3,600, $2,199 more than was required. Justin cannot use that $2,199 to reduce the amount he is required to withdraw for 2017, but his IRA account balance is reduced by the full $3,600 to figure his required minimum distribution for 2017 Justin's reduced IRA account balance on December 31, 2016, was $34,800 Justin figured his required minimum distribution for 2017 is $1,313 ($34, (the distribution period for age 71 per Table III)) During 2017, he must receive distributions of at least that amount 76 38

39 Traditional IRAs Trust as beneficiary (cannot be a designated beneficiary) However, the beneficiaries of a Trust will be treated as designated beneficiaries is the following are true: Trust is valid under state law Trust is irrevocable or becomes such by its terms upon owner s death Beneficiaries are identifiable from the trust instrument Trustee provides IRA custodian or trustee with the documentation 77 Traditional IRAs Are Distributions Taxable? In general Exceptions Rollovers Qualified charitable distributions (QCDs) Tax-free withdrawals of contributions Return of nondeductible contributions One-time qualified HSA funding distribution Ordinary income No special treatment (i.e., 10-year tax option or capital gain treatment 78 39

40 Example Qualified charitable distributions Part 1 On December 23, 2016, Jeff, age 75, directed the trustee of his IRA to make a distribution of $25,000 directly to a qualified 501(c)(3) organization (a charitable organization eligible to receive tax-deductible contributions) The total value of Jeff's IRA is $30,000 and consists of $20,000 of deductible contributions and earnings and $10,000 of nondeductible contributions (basis) Since Jeff is at least age 70 ½ and the distribution is made directly by the trustee to a qualified organization, the part of the distribution that would otherwise be includible in Jeff's income ($20,000) is a QCD 79 Example Qualified charitable distributions Part 2 In this case, Jeff has made a QCD of $20,000 (his deductible contributions and earnings) Because Jeff made a distribution of nondeductible contributions from his IRA, he must file Form 8606 with his return Jeff includes the total distribution ($25,000) on line 15a of Form 1040 He completes Form 8606 to determine the amount to enter on line 15b of Form 1040 and the remaining basis in his IRA Jeff enters -0- on line 15b This is Jeff's only IRA and he took no other distributions in 2016 He also enters QCD next to line 15b to indicate a qualified charitable distribution 80 40

41 Example Qualified charitable distributions Part 3 After the distribution, his basis in his IRA is $5,000 If Jeff itemizes deductions and files Schedule A with Form 1040, the $5,000 portion of the distribution attributable to the nondeductible contributions can be deducted as a charitable contribution, subject to AGI limits He cannot take the charitable contribution deduction for the $20,000 portion of the distribution that was not included in his income 81 Traditional IRAs Distributions fully or partly taxable Fully taxable Partly taxable Form 8606 IRS Worksheets Figuring the taxable part of your IRA distribution 82 41

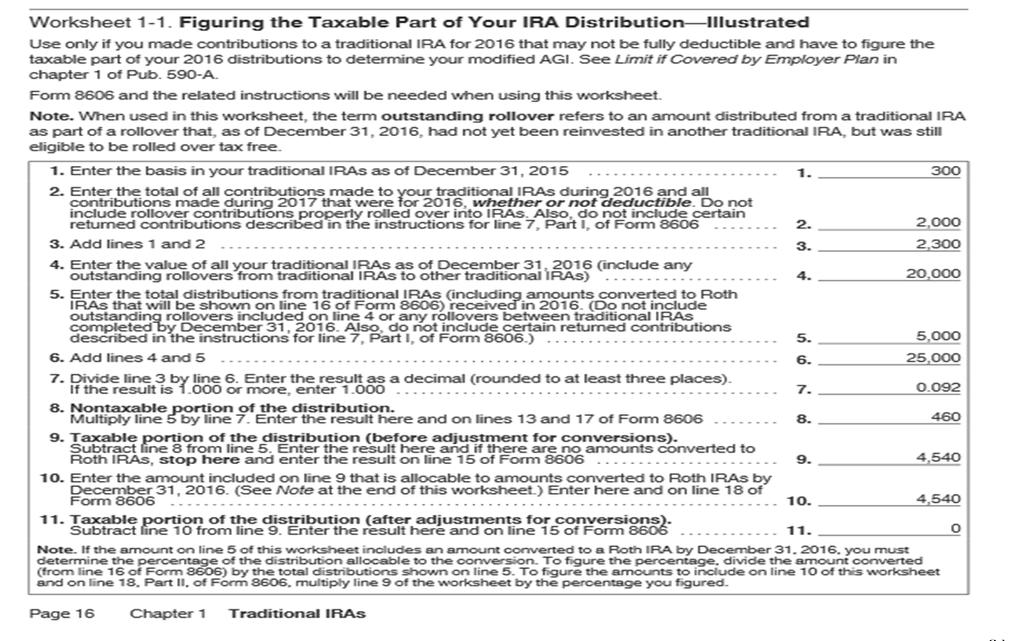

42 EXAMPLE Rose Green has made the following contributions to her traditional IRAs. Year Deductible Nondeductible , , , , , , Totals $9,700 $ Rose s example continues - Rose needs to complete Worksheet 1-1 Figuring the Taxable Part of Your IRA Distribution to determine if her IRA deduction for 2016 will be reduced or eliminated In 2016, she makes a $2,000 contribution that may be partly non-deductible She also receives a distribution of $5,000 for conversion to a Roth IRA She completed the conversion before December 31, 2016, and did not recharacterize any contributions At the end of 2016, the fair market values of her accounts, including earnings, total $20,000 She did not receive any tax-free distributions in earlier years 84 42

43

44 87 Traditional IRAs What acts result in penalties or additional taxes? Investment in collectibles Making excess contributions Taking early distribution Allowing excess amounts to accumulate (failure to take RMDs) 88 44

45 Traditional IRAs Prohibited Transactions Disqualified persons Prohibited transactions borrowing, selling, using assets as security, buying property for personal use Effect on IRA account Exempt Transactions 89 Traditional IRAs Early Distributions Age 59 ½ rule Exceptions Medical expenses Medical insurance Disability Beneficiary Higher education expenses First home Qualified reservist distributions 90 45

46 EXAMPLE Tom Jones, who is 35 years old, receives a $3,000 distribution from his traditional IRA account Tom does not meet any of the exceptions to the 10% additional tax, so the $3,000 is an early distribution Tom never made any nondeductible contributions to his IRA He must include the $3,000 in his gross income for the year of the distribution and pay income tax on it Tom must also pay an additional tax of $300 (10% $3,000) He files Form

47 Traditional IRAs Excess Accumulations Tax on excess 50% excise tax of RMD amount Reporting the tax Form 5329 Request to waive the tax (do not ignore this opportunity my experience with this matter has been good) 93 Roth IRAs What is a Roth IRA? Are distributions taxable? What are qualified distribution? Made after the 5-year period beginning with first taxable year for which a contribution was made to a Roth IRA Payment or distribution is Made after 59 ½ Made because of disability Made to beneficiary or estate, Meet First Home requirements discussed above 94 47

48 Roth IRAs Additional Tax on Early Distribution Distributions of conversion and certain rollover contributions with 5-year period Other early distributions Exception to 10% additional tax similar to previous exceptions for early withdrawal under age 59 ½ Flow chart Is the distribution from your Roth IRA a Qualified Distribution?

49 Roth IRAs Ordering Rules for Distributions Regular contributions Conversion and rollover contributions (FIFO basis) Earnings on contributions Disregard rollovers from other Roth IRAs Aggregation (grouping and adding) rules Example 97 EXAMPLE On October 15, 2012, Justin converted all $80,000 in his traditional IRA to his Roth IRA. His Forms 8606 from prior years show that $20,000 of the amount converted is his basis. Justin included $60,000 ($80,000 $20,000) in his gross income On February 23, 2016, Justin made a regular contribution of $5,000 to a Roth IRA. On November 8, 2016, at age 60, Justin took a $7,000 distribution from his Roth IRA The first $5,000 of the distribution is a return of Justin's regular contribution and is not includible in his income. The next $2,000 of the distribution is not includible in income because it was included previously 98 49

50 Roth IRAs Must you withdraw or use assets? Recognizing losses on investments Distributions after owner s death Distributions to beneficiaries (5-year rule) Special rules for surviving spouse Distributions that are not qualified distributions Example 99 (CON T) EXAMPLE When Ms. Hibbard died in 2016, her Roth IRA contained regular contributions of $4,000, a conversion contribution of $10,000 that was made in 2012, and earnings of $2,000. No distributions had been made from her IRA. She had no basis in the conversion contribution in 2012 When she established this Roth IRA (her first) in 2012, she named each of her four children as equal beneficiaries. Each child will receive one-fourth of each type of contribution and one-fourth of the earnings. An immediate distribution of $4,000 to each child will be treated as $1,000 from regular contributions, $2,500 from conversion contributions, and $500 from earnings In this case, because the distributions are made before the end of the applicable 5-year period for a qualified distribution, each beneficiary includes $500 in income for The 10% additional tax on early distributions does not apply because the distribution was made to the beneficiaries as a result of the death of the IRA owner

51 Reminders Application of one-rollover-per-year limitation Deemed IRAs Statement of required minimum distribution (RMD) IRA interest Net investment income tax (NIIT) Designated Roth accounts (not Roth IRAs) 101 SOCIAL SECURITY (SS) - INTRODUCTION Please note that today s presentation used as reference material, copyrighted information by Bob Jennings CPA, EA and Ron Roberson CPA co-authors of the 2016 Social Security Understanding Your Clients Future a 2016 live CPE presentation Background & Short History The 2016 changes in social security Resources don t believe what s on the internet Terminology How is SS Funded The Main Categories of SS and Medicare Benefits Miscellaneous Issues Windfall elimination provision / government pension offset How to sign up Myth I have paid in more than I will ever receive as a benefit

52 SOCIAL SECURITY (SS) QUALIFYING FOR BENEFITS Insured Status Fully Currently Disability Special Persons Disable Before Age Thirty-One Lump Sum Death Payment Foreign Earnings Income Qualifying for SS Earned as Employee (including Agriculture and Domestic Labor) Earned as Self-Employed Income That Does Not Qualify for SS Credits Special Planning Tip Optional SE Tax Method for Small Business Owners 103 SOCIAL SECURITY (SS) RETIREMENT BENEFITS Full Retirement Age Situations When Retirement Benefits NOT Payable (or Partially Payable) The Impact of Delayed Retirement Retirement Benefit Estimates Retirement Benefits for Widows and Widowers Spouse s Benefits Deemed Filing Rule File and Suspend Restricted Application Rule Who Is a Spouse?

53 SOCIAL SECURITY (SS) RETIREMENT BENEFITS Child in Care Spousal Benefits Discontinued Maximum Family Benefits Benefits for a Divorced Spouse Child Benefits Examples Special Monthly Rule Do-Over Options 105 SOCIAL SECURITY (SS) - DIVORCE Keys to Obtaining Retirement Benefits 10 years of marriage prior to the divorce being final Age 62 or older Not currently married Ex-spouse must have claimed their benefit OR Eligible to Claim their Benefit and divorce was finalized more than two years prior EXAMPLES

54 SOCIAL SECURITY (SS) SURVIVOR S BENEFITS Survivor s Benefits In General Remarriage Rules The Amount of Retirement Benefit Requirements for a Widow/Widower or Ex-Spouse to Draw Survivor s Benefit EXAMPLES 107 SOCIAL SECURITY (SS) - DISABILITY The Eight Types of Disability Protection Amount of Disability Benefit When Do Benefits End Definition of Disability Widow / Widower Disability Benefit Child Disability Working While Disabled SSA Notification Requirements Applying for Benefits Appeals SSA s Listing of Impairments

55 SOCIAL SECURITY (SS) CALCULATING THE BENEFIT Primary Insurance Amount (PIA) for Eligibility or Death for Years after 1978 Computation Years Elapsed Years Base Years Determining PIA Special Minimum PIA Cost of Living Adjustments Delayed Retirement Credits Reduction of Benefits Basic Reduction Formulas for Early Retirement Child in Care Exceeds Age Sixteen Maximum Family Benefits Earnings Reports 109 SOCIAL SECURITY (SS) - PLANNING Myths vs Facts SS s Biggest Financial Worry SS Planning and Case Studies Introduction Balancing Wages, SE Earnings & SE Taxation SS Benefits Early, at Full Retirement Age, or Delayed Spousal and Family Benefit Options Spouse and Former Spouse Benefit Summary Maximizing SS for Married Couples SS Disability Benefit Planning Survivor Benefit Planning

56 SOCIAL SECURITY (SS) - CONSULTING Marketing to Existing Clients Marketing to the General Public Consider Adding a SS Consulting Division to your Firm Case Studies Question and Answers 111 EXPLORING THE TAX AND PLANNING ASPECTS OF OUR PRIVATE AND PUBLIC RETIREMENT PLAN SYSTEMS QUESTIONS AND ANSWERS Thank you for Participating in Today s Webinar

57 THE SCOOP UPCOMING DATES October 18, 2017 November 1 December 13, 2017 Held at 8:00 am and 12:00 pm Central time 113 UP COMING ETHICS CLASSES Ethics Part 1 and Part 2 (November 13) Ethics Part 1 and Part 2 (November 14) Ethics Part 1 and Part 2 (December 15) Ethics Part 1 and Part 2 (December 18) Ethics Part 1 and Part 2 (December 19)

October 12 Iowa Rural Property (Legal Issues) October 13 New Law Update October 17")

58 UP COMING WEBINARS SEMINAR-DATE/MONTH Iowa Farm Leases (Legal Issues) October 12 Iowa Rural Property (Legal Issues) October 13 New Law Update October 17 New Partnership Audit Rules October 19 Farm Expenses October 24, 2017 Farm Income October 26, THE CALT STAFF WILLIAM EDWARDS INTERIM DIRECTOR FOR THE BEGINNING FARMER CENTER INTERIM DIRECTOR FOR THE CENTER FOR AGRICULTURAL LAW AND TAXATION HEADY 518 FARM HOUSE LN AMES. IOWA KRISTINE A. TIDGREN ASSISTANT DIRECTOR PHONE: (515) FAX: (515)

59 THE CALT STAFF KRISTY S. MAITRE TAX SPECIALIST PHONE: (515) FAX: (515) TIFFANY L. KAYSER PROGRAM ADMINISTRATOR PHONE: (515) FAX: (515)

chart RETIREMENT PLANS 8 RETIREMENT PLAN BENEFITS AVAILABLE RETIREMENT PLANS Retirement plans available to self-employed individuals include:

retirement plans Contributing to retirement plans can provide you with financial security as well as reducing and/or deferring your taxes. However, there are complex rules that govern the type of plans

retirement plans Contributing to retirement plans can provide you with financial security as well as reducing and/or deferring your taxes. However, there are complex rules that govern the type of plans

UMB Bank, n.a. Universal IRA Information Kit

UMB Bank, n.a. Universal IRA Information Kit INTRODUCTION: What is the Difference between a Traditional IRA and a Roth IRA? With a traditional IRA, an individual may be able to deduct the contribution

UMB Bank, n.a. Universal IRA Information Kit INTRODUCTION: What is the Difference between a Traditional IRA and a Roth IRA? With a traditional IRA, an individual may be able to deduct the contribution

Publication 590-A and. Publication 590-B

Publication 590-A and Publication 590-B This material is not intended to replace the advice of a qualified attorney, tax advisor, financial advisor, or insurance agent Before making any financial commitment

Publication 590-A and Publication 590-B This material is not intended to replace the advice of a qualified attorney, tax advisor, financial advisor, or insurance agent Before making any financial commitment

Individual Retirement Account (IRA) Information Kit

Information Kit") Individual Retirement Account (IRA) Information Kit (Effective January 1, 2018) Pear Tree Funds 55 Old Bedford Road Suite 202 Lincoln, MA 01773 1-800-326-2151 PEAR TREE FUNDS Individual Retirement Account

Individual Retirement Account (IRA) Information Kit (Effective January 1, 2018) Pear Tree Funds 55 Old Bedford Road Suite 202 Lincoln, MA 01773 1-800-326-2151 PEAR TREE FUNDS Individual Retirement Account

Individual Retirement Account (IRA) Information Kit

Information Kit") Individual Retirement Account (IRA) Information Kit (Effective January 1, 2013) Pear Tree Funds 55 Old Bedford Road Suite 202 Lincoln, MA 01773 1-800-326-2151 1117-03-0713 PEAR TREE FUNDS Individual Retirement

Individual Retirement Account (IRA) Information Kit (Effective January 1, 2013) Pear Tree Funds 55 Old Bedford Road Suite 202 Lincoln, MA 01773 1-800-326-2151 1117-03-0713 PEAR TREE FUNDS Individual Retirement

Traditional and Roth IRAs. Information Kit, Disclosure Statement and Custodial Agreement

Traditional and Roth IRAs Information Kit, Disclosure Statement and Custodial Agreement UMB Bank, n.a. Universal Individual Retirement Account Disclosure Statement (EFFECTIVE DECEMBER 1, 2016) Part One:

Traditional and Roth IRAs Information Kit, Disclosure Statement and Custodial Agreement UMB Bank, n.a. Universal Individual Retirement Account Disclosure Statement (EFFECTIVE DECEMBER 1, 2016) Part One:

Janus Universal IRA. Disclosure Statement & Custodial Agreement

Janus Universal IRA Disclosure Statement & Custodial Agreement Janus Universal Individual Retirement Account Disclosure Statement Part One: Description of Traditional IRAs SPECIAL NOTE State Street Bank

Janus Universal IRA Disclosure Statement & Custodial Agreement Janus Universal Individual Retirement Account Disclosure Statement Part One: Description of Traditional IRAs SPECIAL NOTE State Street Bank

Contributions to Individual Retirement Arrangements (IRAs)

") Department of the Treasury Internal Revenue Service Contents What's New for 2016 1 Publication 590-A What's New for 2017 2 Cat No 66302J Reminders 2 Contributions to Individual Retirement Arrangements

Department of the Treasury Internal Revenue Service Contents What's New for 2016 1 Publication 590-A What's New for 2017 2 Cat No 66302J Reminders 2 Contributions to Individual Retirement Arrangements

Traditional Individual Retirement Account Disclosure Statement and Custodial Agreement

Traditional Individual Retirement Account Disclosure Statement and Custodial Agreement Effective November 11, 2016 Page 1 of 26 Table of Contents Section I: Disclosure Statement A. Introduction... B. Contributions

Traditional Individual Retirement Account Disclosure Statement and Custodial Agreement Effective November 11, 2016 Page 1 of 26 Table of Contents Section I: Disclosure Statement A. Introduction... B. Contributions

UMB Bank, n.a. Universal Individual Retirement Account Disclosure Statement

UMB Bank, n.a. Universal Individual Retirement Account Disclosure Statement PART ONE:DESCRIPTION OF TRADITIONAL IRAs Part One of the Disclosure Statement describes the rules applicable to traditional IRAs.

UMB Bank, n.a. Universal Individual Retirement Account Disclosure Statement PART ONE:DESCRIPTION OF TRADITIONAL IRAs Part One of the Disclosure Statement describes the rules applicable to traditional IRAs.

Addendum to the Traditional IRA Custodial Agreement and Disclosures

Effective January 1, 2018 Addendum to the Traditional IRA Custodial Agreement and Disclosures This Addendum changes the Traditional IRA Custodial Agreement and Disclosures ( Agreement ) document and uses

Effective January 1, 2018 Addendum to the Traditional IRA Custodial Agreement and Disclosures This Addendum changes the Traditional IRA Custodial Agreement and Disclosures ( Agreement ) document and uses

Contributions to Individual Retirement Arrangements (IRAs)

") Department of the Treasury Internal Revenue Service Publication 590-A Contents What's New for 2018 1 What s New for 2019 2 Cat No 66302J Reminders 2 Contributions to Individual Retirement Arrangements

Department of the Treasury Internal Revenue Service Publication 590-A Contents What's New for 2018 1 What s New for 2019 2 Cat No 66302J Reminders 2 Contributions to Individual Retirement Arrangements

Traditional Individual Retirement Account (Trust) Disclosure Statement

Disclosure Statement") Traditional Individual Retirement Account (Trust) Disclosure Statement This Disclosure Statement contains important information about traditional Individual Retirement Accounts ( traditional IRA ) described

Traditional Individual Retirement Account (Trust) Disclosure Statement This Disclosure Statement contains important information about traditional Individual Retirement Accounts ( traditional IRA ) described

UMB BANK, N.A INFORMATION KIT

UMB BANK, N.A UNIVERSAL INDIVIDUAL RETIREMENT ACCOUNT INFORMATION KIT (EFFECTIVE DECEMBER 1, 2016) 600 University Street, Suite 2412 Seattle, WA 98101 Main: 206.838.9850 Toll Free: 877.701.2883 Fax: 206.838.9851

UMB BANK, N.A UNIVERSAL INDIVIDUAL RETIREMENT ACCOUNT INFORMATION KIT (EFFECTIVE DECEMBER 1, 2016) 600 University Street, Suite 2412 Seattle, WA 98101 Main: 206.838.9850 Toll Free: 877.701.2883 Fax: 206.838.9851

Roth Individual Retirement Account (Trust) Disclosure Statement

Disclosure Statement") Roth Individual Retirement Account (Trust) Disclosure Statement This Disclosure Statement contains important information about traditional Individual Retirement Accounts ( traditional IRA ) described in

Roth Individual Retirement Account (Trust) Disclosure Statement This Disclosure Statement contains important information about traditional Individual Retirement Accounts ( traditional IRA ) described in

P A R N A S S U S F U N D S

PARNASSUS FUNDS P A R N A S S U S F U N D S Useful information about IRAs What is a Traditional IRA? A traditional IRA is an Individual Retirement Account that allows you to put away money for your retirement

PARNASSUS FUNDS P A R N A S S U S F U N D S Useful information about IRAs What is a Traditional IRA? A traditional IRA is an Individual Retirement Account that allows you to put away money for your retirement

Required Minimum Distributions

Required Minimum Distributions What You Need To Know When It Is Time To Start Distributions From Your Retirement Accounts What Are Required Minimum Distributions? Required minimum distributions (RMDs)

Required Minimum Distributions What You Need To Know When It Is Time To Start Distributions From Your Retirement Accounts What Are Required Minimum Distributions? Required minimum distributions (RMDs)

TRADITIONAL IRA DISCLOSURE STATEMENT

TRADITIONAL IRA DISCLOSURE STATEMENT RIGHT TO REVOKE YOUR IRA ACCOUNT The W-2 form will have a check in the "retirement plan" box if you are covered by a retirement plan. You can also obtain IRS Notice

TRADITIONAL IRA DISCLOSURE STATEMENT RIGHT TO REVOKE YOUR IRA ACCOUNT The W-2 form will have a check in the "retirement plan" box if you are covered by a retirement plan. You can also obtain IRS Notice

DISCLOSURE STATEMENTS AND CUSTODIAL ACCOUNT AGREEMENT

Traditional and Roth Individual Retirement Account Informational Booklet DISCLOSURE STATEMENTS AND CUSTODIAL ACCOUNT AGREEMENT 15810M REV 01-18 TABLE OF CONTENTS THE LIVEWELL MUTUAL FUND TRADITIONAL INDIVIDUAL

Traditional and Roth Individual Retirement Account Informational Booklet DISCLOSURE STATEMENTS AND CUSTODIAL ACCOUNT AGREEMENT 15810M REV 01-18 TABLE OF CONTENTS THE LIVEWELL MUTUAL FUND TRADITIONAL INDIVIDUAL

Roth Individual Retirement Account Disclosure Statement and Custodial Agreement

Wells Fargo Clearing Services, LLC Roth Individual Retirement Account Disclosure Statement and Custodial Agreement Effective November 11, 2016 Table of Contents Section I: Disclosure Statement A. Introduction...3

Wells Fargo Clearing Services, LLC Roth Individual Retirement Account Disclosure Statement and Custodial Agreement Effective November 11, 2016 Table of Contents Section I: Disclosure Statement A. Introduction...3

Street Address. City, State, ZIP

ROTH IRA CUSTODIAL APPLICATION PACKET (FORM ) Please Print or Type CUID (Credit union will complete.) - - IRA Owner s Social Security Number IRA Owner s Name (First, Initial, Last) Street Address IRA Owner

ROTH IRA CUSTODIAL APPLICATION PACKET (FORM ) Please Print or Type CUID (Credit union will complete.) - - IRA Owner s Social Security Number IRA Owner s Name (First, Initial, Last) Street Address IRA Owner

What You Need To Know When It Is Time To Start Distributions From Your Retirement Accounts

Retirement Planning Required Minimum Distributions What You Need To Know When It Is Time To Start Distributions From Your Retirement Accounts WHAT ARE REQUIRED MINIMUM DISTRIBUTIONS? Required minimum distributions

Retirement Planning Required Minimum Distributions What You Need To Know When It Is Time To Start Distributions From Your Retirement Accounts WHAT ARE REQUIRED MINIMUM DISTRIBUTIONS? Required minimum distributions

Universal Individual Retirement Account Information Kit

Universal Individual Retirement Account Information Kit Universal Individual Retirement Custodial Account Instructions for Opening Your Traditional IRA or Roth IRA 1. Please review the applicable sections

Universal Individual Retirement Account Information Kit Universal Individual Retirement Custodial Account Instructions for Opening Your Traditional IRA or Roth IRA 1. Please review the applicable sections

Roth Individual Retirement Account Disclosure Statement and Custodial Agreement Effective November 11, 2016

Roth Individual Retirement Account Disclosure Statement and Custodial Agreement Effective November 11, 2016 544260 (Rev 17-06/17) Page 1 of 25 Table of Contents Section I: Disclosure Statement A. Introduction...

Roth Individual Retirement Account Disclosure Statement and Custodial Agreement Effective November 11, 2016 544260 (Rev 17-06/17) Page 1 of 25 Table of Contents Section I: Disclosure Statement A. Introduction...

TRADITIONAL IRA DISCLOSURE STATMENT

TRADITIONAL IRA DISCLOSURE STATMENT The Traditional Individual Retirement Account ( Traditional IRA ) presented with this Disclosure Statement is a retirement plan made available to individuals. An individual

TRADITIONAL IRA DISCLOSURE STATMENT The Traditional Individual Retirement Account ( Traditional IRA ) presented with this Disclosure Statement is a retirement plan made available to individuals. An individual

TRANSAMERICA PREMIER FUNDS. Disclosure Statement and Custodial Agreement for IRAs. Table of Contents

TRANSAMERICA PREMIER FUNDS Disclosure Statement and Custodial Agreement for IRAs Table of Contents IRA DISCLOSURE STATEMENT Part One: Description of Traditional IRAs 1 Special Note 1 Your Traditional IRA

TRANSAMERICA PREMIER FUNDS Disclosure Statement and Custodial Agreement for IRAs Table of Contents IRA DISCLOSURE STATEMENT Part One: Description of Traditional IRAs 1 Special Note 1 Your Traditional IRA

Exploring Your IRA Options

Exploring Your IRA Options Traditional IRA Q & A.................. Page 2 Roth IRA Q & A...................... Page 5 Traditional vs. Roth IRAs............... Page 8 How does a Traditional IRA differ from

Exploring Your IRA Options Traditional IRA Q & A.................. Page 2 Roth IRA Q & A...................... Page 5 Traditional vs. Roth IRAs............... Page 8 How does a Traditional IRA differ from

Universal Individual Retirement Account

December 30, 2017 Universal Individual Retirement Account Baron Asset Fund Baron Discovery Fund Baron Durable Advantage Fund Baron Emerging Markets Fund Baron Energy and Resources Fund Baron Fifth Avenue

December 30, 2017 Universal Individual Retirement Account Baron Asset Fund Baron Discovery Fund Baron Durable Advantage Fund Baron Emerging Markets Fund Baron Energy and Resources Fund Baron Fifth Avenue

A Guide to Roth IRAs. Contribution Limits and Deadlines. Who Can Contribute to a Roth IRA? Retirement Planning

A Guide to Roth IRAs A Roth IRA is an individual retirement account named for the late Senate Finance Committee Chairman, William Roth, Jr. who championed its creation. Traditional and Roth IRAs are both

A Guide to Roth IRAs A Roth IRA is an individual retirement account named for the late Senate Finance Committee Chairman, William Roth, Jr. who championed its creation. Traditional and Roth IRAs are both

SIMPLE Individual Retirement Account Disclosure Statement and Custodial Agreement Effective November 11, 2016

SIMPLE Individual Retirement Account Disclosure Statement and Custodial Agreement Effective November 11, 2016 550308 (Rev 15-06/17) Page 1 of 26 Table of Contents Section I: Disclosure Statement A. Introduction...

SIMPLE Individual Retirement Account Disclosure Statement and Custodial Agreement Effective November 11, 2016 550308 (Rev 15-06/17) Page 1 of 26 Table of Contents Section I: Disclosure Statement A. Introduction...

2015 Continuing Education Course. THE TAX INSTITUTE th St Bakersfield CA THE TAX INSTITUTE S ANNUAL CPE COURSE 15HR COURSE

THE TAX INSTITUTE 424 18 th St Bakersfield CA 93301. 2015 Continuing Education Course THE TAX INSTITUTE S ANNUAL CPE COURSE 15HR COURSE IRS # N56QT-T-00018-15-S, N56QT-U-00017-15-S, & N56QT-E-00019-15-S

THE TAX INSTITUTE 424 18 th St Bakersfield CA 93301. 2015 Continuing Education Course THE TAX INSTITUTE S ANNUAL CPE COURSE 15HR COURSE IRS # N56QT-T-00018-15-S, N56QT-U-00017-15-S, & N56QT-E-00019-15-S

1. New IRA Contribution Limits for IRA Transfers 3. IRA Rollovers (k) Direct Rollovers 5. Fraudulent contributions

Direct Rollovers 5. Fraudulent contributions") 1. New IRA Contribution Limits for 2013 2. IRA Transfers 3. IRA Rollovers 4. 401(k) Direct Rollovers 5. Fraudulent contributions Rev 12-5-2012 Just a Reminder: This is copyrighted material. No Video or

1. New IRA Contribution Limits for 2013 2. IRA Transfers 3. IRA Rollovers 4. 401(k) Direct Rollovers 5. Fraudulent contributions Rev 12-5-2012 Just a Reminder: This is copyrighted material. No Video or

What You Should Know: Required Minimum Distributions (RMDs)

") Brian D. Goguen, P.C. Brian D. Goguen, CPA CFP 164 Concord Road Billerica, MA 01821 978-667-4595 bdgoguen@comcast.net www.bgoguen.com What You Should Know: Required Minimum Distributions (RMDs) Page 1

Brian D. Goguen, P.C. Brian D. Goguen, CPA CFP 164 Concord Road Billerica, MA 01821 978-667-4595 bdgoguen@comcast.net www.bgoguen.com What You Should Know: Required Minimum Distributions (RMDs) Page 1

Required Minimum Distributions (RMDs)

") Jennifer J. Cole, CFA, MBA P.O. Box 1109 Sandia Park, NM 505-286-7915 JCole@ColeFinancialConsulting.com ColeFinancialConsulting.com Required Minimum Distributions (RMDs) Page 2 of 7 Required Minimum Distributions

Jennifer J. Cole, CFA, MBA P.O. Box 1109 Sandia Park, NM 505-286-7915 JCole@ColeFinancialConsulting.com ColeFinancialConsulting.com Required Minimum Distributions (RMDs) Page 2 of 7 Required Minimum Distributions

Roth IRA Owner Resource Book

Roth IRA Owner Resource Book A benefit under the Issued February 2018 Defined Contribution Retirement Accounts of the Pension Fund of the Christian Church (Disciples of Christ) ("DCRA") TABLE OF CONTENTS

Roth IRA Owner Resource Book A benefit under the Issued February 2018 Defined Contribution Retirement Accounts of the Pension Fund of the Christian Church (Disciples of Christ) ("DCRA") TABLE OF CONTENTS

The statutory requirements for a traditional IRA, which are described in section 408(a) of the Internal Revenue Code (Code), are as follows:

of the Internal Revenue Code (Code), are as follows:") Page 1 of 9 This Disclosure Statement is provided in accordance with the tax laws applicable to your individual retirement account (IRA). It provides only a summary of the rules that apply to your IRA.

Page 1 of 9 This Disclosure Statement is provided in accordance with the tax laws applicable to your individual retirement account (IRA). It provides only a summary of the rules that apply to your IRA.

Traditional SEP, and SIMPLE IRAs

Traditional SEP, and SIMPLE IRAs Understanding Required Distributions at 70 1 / 2 Questions & Answers Why must I and others age 70 1/2 or older have to take a required distribution? The purpose of an IRA

Traditional SEP, and SIMPLE IRAs Understanding Required Distributions at 70 1 / 2 Questions & Answers Why must I and others age 70 1/2 or older have to take a required distribution? The purpose of an IRA

Recent Changes to IRAs

Recent Changes to IRAs Federal legislation and new IRS regulations have created several changes to IRAs in the past year. Prohibition on recharacterization of IRA conversions: Effective for taxable years

Recent Changes to IRAs Federal legislation and new IRS regulations have created several changes to IRAs in the past year. Prohibition on recharacterization of IRA conversions: Effective for taxable years

Street Address. PRIMARY Beneficiary(ies) % Column MUST total 100% % Name Mailing Address Relationship Birth Date SS #

% Column MUST total 100% % Name Mailing Address Relationship Birth Date SS #") TRADITIONAL IRA CUSTODIAL APPLICATION PACKET (FORM ) Please Print or Type CUID (Credit union will complete.) - - IRA Owner s Social Security Number IRA Owner s Name (First, Initial, Last) Street Address

TRADITIONAL IRA CUSTODIAL APPLICATION PACKET (FORM ) Please Print or Type CUID (Credit union will complete.) - - IRA Owner s Social Security Number IRA Owner s Name (First, Initial, Last) Street Address

A Guide to Understanding Social Security Retirement Benefits

Private Wealth Management Products & Services A Guide to Understanding Social Security Retirement Benefits Social Security Eligibility Requirements Workers who pay Social Security taxes on their wages

Private Wealth Management Products & Services A Guide to Understanding Social Security Retirement Benefits Social Security Eligibility Requirements Workers who pay Social Security taxes on their wages

Required Minimum Distributions (RMDs)

") Required Minimum Distributions (RMDs) March 21, 2012 Page 1 of 7, see disclaimer on final page What Are Required Minimum Distributions (RMDs)? Required minimum distributions, often referred to as RMDs

Required Minimum Distributions (RMDs) March 21, 2012 Page 1 of 7, see disclaimer on final page What Are Required Minimum Distributions (RMDs)? Required minimum distributions, often referred to as RMDs

Roth IRA Owner Resource Book

Roth IRA Owner Resource Book A benefit under the Issued May 2017 Defined Contribution Retirement Accounts of the Pension Fund of the Christian Church (Disciples of Christ) ("DCRA") TABLE OF CONTENTS INTRODUCTION...

Roth IRA Owner Resource Book A benefit under the Issued May 2017 Defined Contribution Retirement Accounts of the Pension Fund of the Christian Church (Disciples of Christ) ("DCRA") TABLE OF CONTENTS INTRODUCTION...

Required Minimum Distributions (RMDs)

") Weller Group LLC Timothy Weller, CFP CERTIFIED FINANCIAL PLANNER 6206 Slocum Road Ontario, NY 14519 315-524-8000 tim@wellergroupllc.com www.wellergroupllc.com Required Minimum Distributions (RMDs) March

Weller Group LLC Timothy Weller, CFP CERTIFIED FINANCIAL PLANNER 6206 Slocum Road Ontario, NY 14519 315-524-8000 tim@wellergroupllc.com www.wellergroupllc.com Required Minimum Distributions (RMDs) March

Traditional Individual Retirement Custodial Account (Under section 408(a) of the Internal Revenue Code) determined as follows:

of the Internal Revenue Code) determined as follows:") 0-A Form (Rev. April 07) Department of the Treasury Internal Revenue Service Traditional Individual Retirement Custodial Account (Under section 08(a) of the Internal Revenue Code) Introduction The Depositor

0-A Form (Rev. April 07) Department of the Treasury Internal Revenue Service Traditional Individual Retirement Custodial Account (Under section 08(a) of the Internal Revenue Code) Introduction The Depositor

Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure Statement

Disclosure Statement") BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure Statement Deadline Extension for 2016 Contributions to a Traditional

BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure Statement Deadline Extension for 2016 Contributions to a Traditional

DISTRIBUTION PLANNING

DISTRIBUTION PLANNING In 5 Easy Steps 2.5 Million Baby Boomers Will Turn Age 70 in 2016 Get the Definitive Guide to RMD Planning at: www.irahelp.com/rmd-guide Calculating the Pro-Rata Rule in 5 Easy Steps

DISTRIBUTION PLANNING In 5 Easy Steps 2.5 Million Baby Boomers Will Turn Age 70 in 2016 Get the Definitive Guide to RMD Planning at: www.irahelp.com/rmd-guide Calculating the Pro-Rata Rule in 5 Easy Steps

AMERUS LIFE INSURANCE COMPANY

AMERUS LIFE INSURANCE COMPANY IRA DISCLOSURE STATEMENT INTRODUCTION This Individual Retirement Annuity ("IRA") is an annuity contract issued by AmerUs Life Insurance Company ("AMERUS") to fund an individual's

AMERUS LIFE INSURANCE COMPANY IRA DISCLOSURE STATEMENT INTRODUCTION This Individual Retirement Annuity ("IRA") is an annuity contract issued by AmerUs Life Insurance Company ("AMERUS") to fund an individual's

Traditional IRA Owner Resource Book

Traditional IRA Owner Resource Book A benefit under the Issued May 2017 Defined Contribution Retirement Accounts of the Pension Fund of the Christian Church (Disciples of Christ) ("DCRA") TABLE OF CONTENTS

Traditional IRA Owner Resource Book A benefit under the Issued May 2017 Defined Contribution Retirement Accounts of the Pension Fund of the Christian Church (Disciples of Christ) ("DCRA") TABLE OF CONTENTS

A Guide to Understanding Social Security Retirement Benefits

Private Wealth Management Products & Services A Guide to Understanding Social Security Retirement Benefits Social Security Eligibility Requirements Workers who pay Social Security taxes on their wages

Private Wealth Management Products & Services A Guide to Understanding Social Security Retirement Benefits Social Security Eligibility Requirements Workers who pay Social Security taxes on their wages

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy March 2018 TABLE OF CONTENTS DISCLOSURE STATEMENT Introduction 3 Section I Revocation 3

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy March 2018 TABLE OF CONTENTS DISCLOSURE STATEMENT Introduction 3 Section I Revocation 3

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy Effective November 2016 TABLE OF CONTENTS DISCLOSURE STATEMENT Introduction 3 Section I

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy Effective November 2016 TABLE OF CONTENTS DISCLOSURE STATEMENT Introduction 3 Section I

Session # 1 Establishing and Contributing

11/15/2018 Session # 1 Establishing and Contributing We request you sign in by 8:20 and 12:20 as this allows an efficient start of the webinar The Webinar will be starting shortly 8:30 am CST or 12:30

11/15/2018 Session # 1 Establishing and Contributing We request you sign in by 8:20 and 12:20 as this allows an efficient start of the webinar The Webinar will be starting shortly 8:30 am CST or 12:30

Understanding Required Minimum Distributions for Individual Retirement Accounts

Understanding Required Minimum Distributions for Individual Retirement Accounts What are required minimum distributions (RMDs)? Required minimum distributions, often referred to as RMDs or minimum required

Understanding Required Minimum Distributions for Individual Retirement Accounts What are required minimum distributions (RMDs)? Required minimum distributions, often referred to as RMDs or minimum required

INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA

TRADITIONAL IRA SEP IRA ROTH IRA") INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure

INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure

How to Maximize Social Security Benefits Now

MERS of Michigan 2018 Retirement Conference October 5, 2018 How to Maximize Social Security Benefits Now Mary Beth Franklin, CFP Contributing Editor Investment News MBF01 For most retirees, Social Security

MERS of Michigan 2018 Retirement Conference October 5, 2018 How to Maximize Social Security Benefits Now Mary Beth Franklin, CFP Contributing Editor Investment News MBF01 For most retirees, Social Security

BNY MELLON INVESTMENT SERVICING TRUST COMPANY. Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure Statement

Disclosure Statement") BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure Statement IMPORTANT CHANGES TO THE RULES GOVERNING INDIRECT (60-DAY)

BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure Statement IMPORTANT CHANGES TO THE RULES GOVERNING INDIRECT (60-DAY)

BNY MELLON INVESTMENT SERVICING TRUST COMPANY. Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure Statement

Disclosure Statement") BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure Statement DEADLINE EXTENSION FOR 2016 CONTRIBUTIONS TO A TRADITIONAL

BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure Statement DEADLINE EXTENSION FOR 2016 CONTRIBUTIONS TO A TRADITIONAL

Gabelli Funds IRA Information Guide

The Gabelli Funds IRA Information Guide Contains: IRA Q & A Disclosure Statement Custodial Agreement Distributed by Gabelli & Company, Inc. One Corporate Center Rye, New York 10580 This material must be

The Gabelli Funds IRA Information Guide Contains: IRA Q & A Disclosure Statement Custodial Agreement Distributed by Gabelli & Company, Inc. One Corporate Center Rye, New York 10580 This material must be

Traditional IRAs. Understanding Required Distributions at 70 1 / 2. Questions & Answers

Traditional IRAs Understanding Required Distributions at 70 1 / 2 Questions & Answers Why are there federal tax rules mandating required minimum distributions from a traditional IRA? The primary purpose

Traditional IRAs Understanding Required Distributions at 70 1 / 2 Questions & Answers Why are there federal tax rules mandating required minimum distributions from a traditional IRA? The primary purpose

Law Office Of Keith R. Miles, LLC July 28, 2015

Law Office Of Keith R. Miles, LLC Keith Miles Attorney-at-Law 2250 Oak Road PO Box 430 Snellville, GA 30078 678-666-0618 keithmiles@timetoestateplan.com www.timetoestateplan.com Traditional IRAs Page 1

Law Office Of Keith R. Miles, LLC Keith Miles Attorney-at-Law 2250 Oak Road PO Box 430 Snellville, GA 30078 678-666-0618 keithmiles@timetoestateplan.com www.timetoestateplan.com Traditional IRAs Page 1

USAA TRADITIONAL / ROTH IRA

USAA TRADITIONAL / ROTH Disclosure Statements and Custodial Agreements 49630-1215 Table of Contents USAA Traditional Disclosure Statement 2 USAA Roth Disclosure Statement 11 USAA Traditional Custodial

USAA TRADITIONAL / ROTH Disclosure Statements and Custodial Agreements 49630-1215 Table of Contents USAA Traditional Disclosure Statement 2 USAA Roth Disclosure Statement 11 USAA Traditional Custodial

PRIVACY POLICIES, DISCLOSURES, INSTRUCTIONS & AGREEMENTS FOR: Individual Retirement Account (IRA) Traditional IRA SEP IRA.

Traditional IRA SEP IRA.") PRIVACY POLICIES, DISCLOSURES, INSTRUCTIONS & AGREEMENTS FOR: Individual Retirement Account (IRA) Traditional IRA SEP IRA Roth IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional

PRIVACY POLICIES, DISCLOSURES, INSTRUCTIONS & AGREEMENTS FOR: Individual Retirement Account (IRA) Traditional IRA SEP IRA Roth IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional

IRA: Traditional SEP APPLICATION TO PARTICIPATE Name of Financial Organization

IRA: Traditional SEP APPLICATION TO PARTICIPATE Name of Financial Organization IRA Owner Information Check here if Amendment - - Name Social Security Number Date of Birth - - E-mail Home Phone Number -

IRA: Traditional SEP APPLICATION TO PARTICIPATE Name of Financial Organization IRA Owner Information Check here if Amendment - - Name Social Security Number Date of Birth - - E-mail Home Phone Number -

Required Minimum Distributions

Required Minimum Distributions Page 1 of 6, see disclaimer on final page Required Minimum Distributions What are required minimum distributions (RMDs)? Required minimum distributions, often referred to

Required Minimum Distributions Page 1 of 6, see disclaimer on final page Required Minimum Distributions What are required minimum distributions (RMDs)? Required minimum distributions, often referred to

INFORMATION KIT GABELLI FUNDS

STATE STREET BANK AND TRUST COMPANY UNIVERSAL INDIVIDUAL RETIREMENT ACCOUNT INFORMATION KIT -------------- GABELLI FUNDS State Street Bank and Trust Company Universal IRA Information Kit Supplement to

STATE STREET BANK AND TRUST COMPANY UNIVERSAL INDIVIDUAL RETIREMENT ACCOUNT INFORMATION KIT -------------- GABELLI FUNDS State Street Bank and Trust Company Universal IRA Information Kit Supplement to

BNY MELLON INVESTMENT SERVICING TRUST COMPANY. Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure Statement

Disclosure Statement") BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure Statement DEADLINE EXTENSION FOR 2016 CONTRIBUTIONS TO A TRADITIONAL

BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure Statement DEADLINE EXTENSION FOR 2016 CONTRIBUTIONS TO A TRADITIONAL

Traditional IRA SEP IRA Roth IRA. Disclosure Statement & Custodial Account Agreement

Traditional IRA SEP IRA Roth IRA Disclosure Statement & Custodial Account Agreement Table of Contents Page in Document PART I COMBINED DISCLOSURE STATEMENT AND CUSTODIAL ACCOUNT AGREEMENT... 1 TRADITIONAL

Traditional IRA SEP IRA Roth IRA Disclosure Statement & Custodial Account Agreement Table of Contents Page in Document PART I COMBINED DISCLOSURE STATEMENT AND CUSTODIAL ACCOUNT AGREEMENT... 1 TRADITIONAL

Traditional Individual Retirement Account Disclosure Statement

Traditional Individual Retirement Account Disclosure Statement This Disclosure Statement contains important information about traditional Individual Retirement Accounts ( traditional IRA ) described in

Traditional Individual Retirement Account Disclosure Statement This Disclosure Statement contains important information about traditional Individual Retirement Accounts ( traditional IRA ) described in

Individual Retirement Account (IRA)

") Longleaf Partners Funds Individual Retirement Account (IRA) Traditional IRA SEP IRA Roth IRA Contents BNY Mellon Investment Servicing Trust Company 2 Traditional and Roth IRA Combined Disclosure Statement

Longleaf Partners Funds Individual Retirement Account (IRA) Traditional IRA SEP IRA Roth IRA Contents BNY Mellon Investment Servicing Trust Company 2 Traditional and Roth IRA Combined Disclosure Statement

REQUIRED MINIMUM DISTRIBUTIONS (RMDs)

") REQUIRED MINIMUM DISTRIBUTIONS (RMDs) Everything you need to know about Required Minimum Distributions. What are required minimum distributions (RMDs)? A required minimum distribution, also referred to

REQUIRED MINIMUM DISTRIBUTIONS (RMDs) Everything you need to know about Required Minimum Distributions. What are required minimum distributions (RMDs)? A required minimum distribution, also referred to

Individual Retirement Arrangements (IRAs)

") PAGER/SGML Userid: SD_FMZHB DTD tipx Leadpct: 0% Pt. size: 10 Fileid: D:\Users\fmzhb\documents\Epicfiles\08P590.xml Page 1 of 114 of Publication 590 Draft (Init. & date) Ok to Print 16:51-30-JAN-2009 The

PAGER/SGML Userid: SD_FMZHB DTD tipx Leadpct: 0% Pt. size: 10 Fileid: D:\Users\fmzhb\documents\Epicfiles\08P590.xml Page 1 of 114 of Publication 590 Draft (Init. & date) Ok to Print 16:51-30-JAN-2009 The

Traditional Individual Retirement Account and Roth Individual Retirement Account

ING EXPRESS MUTUAL FUND IRA Traditional Individual Retirement Account and Roth Individual Retirement Account Disclosure Statement and Custodial Account Agreement Table of Contents I. ING express Mutual

ING EXPRESS MUTUAL FUND IRA Traditional Individual Retirement Account and Roth Individual Retirement Account Disclosure Statement and Custodial Account Agreement Table of Contents I. ING express Mutual

A Surviving Spouse s Options with Respect to Their Deceased Spouse s IRA

Rev 7/11/2018 A Surviving Spouse s Options with Respect to Their Deceased Spouse s IRA We request you sign in by 8:20 and 12:20 as this allows an efficient start of the webinar The Webinar will be starting

Rev 7/11/2018 A Surviving Spouse s Options with Respect to Their Deceased Spouse s IRA We request you sign in by 8:20 and 12:20 as this allows an efficient start of the webinar The Webinar will be starting

Table of Contents. Disclaimer Notice... 1 Roth IRAs... 2 Roth IRA Conversion - Factors to Consider...7

Table of Contents Disclaimer Notice... 1 Roth IRAs... 2 Roth IRA Conversion - Factors to Consider...7 ImportantNotice Thisreportisintendedtoserveasabasisforfurtherdiscussionwithyourotherprofessionaladvisors.

Table of Contents Disclaimer Notice... 1 Roth IRAs... 2 Roth IRA Conversion - Factors to Consider...7 ImportantNotice Thisreportisintendedtoserveasabasisforfurtherdiscussionwithyourotherprofessionaladvisors.

Manning & Napier Fund, Inc. Individual Retirement Account (IRA) TRADITIONAL IRA ROLLOVER IRA ROTH IRA SEP IRA BENEFICIARY IRA

TRADITIONAL IRA ROLLOVER IRA ROTH IRA SEP IRA BENEFICIARY IRA") Manning & Napier Fund, Inc. Individual Retirement Account (IRA) TRADITIONAL IRA ROLLOVER IRA ROTH IRA SEP IRA BENEFICIARY IRA TABLE OF CONTENTS SUPPLEMENT TO THE COMBINED IRA DISCLOSURE STATEMENT 3 COMBINED

Manning & Napier Fund, Inc. Individual Retirement Account (IRA) TRADITIONAL IRA ROLLOVER IRA ROTH IRA SEP IRA BENEFICIARY IRA TABLE OF CONTENTS SUPPLEMENT TO THE COMBINED IRA DISCLOSURE STATEMENT 3 COMBINED