GASB 68 - Accounting and Financial Reporting for Pensions. Timothy J. Morgus, CPA, CGFM November 19 th, 2015

|

|

|

- Victor Morton

- 5 years ago

- Views:

Transcription

1 GASB 68 - Accounting and Financial Reporting for Pensions Timothy J. Morgus, CPA, CGFM November 19 th, 2015

2 Major Changes & Highlights Conceptually: - Each County is responsible for the net obligation for pension benefits, and it should be reported as a liability on the government wide financial statements (FS) - Similar information was reported in the notes to the FS previously 2

3 Major Changes & Highlights Conceptual shift from a funding approach to an earnings approach - Old way expense your pension when you make the required payment - New way fund your pension as the employees earn their pension - Pension expense no longer will equal pension contribution (ARC, or annually required contribution) 3

4 Major Changes & Highlights Requires consistent assumptions within actuarial valuations that are more strict than Act 293 of Requires use of entry age actuarial cost method vs. aggregate cost Immediate recognition of most expenses related to changes, as compared to amortization No phase in restate beginning balances 4

5 Major Changes & Highlights Expanded disclosure to 10 years Incorporate other financial reporting concepts brought about by other standards deferred inflows and outflows Changes relate to accounting and financial reporting NOT FUNDING 5

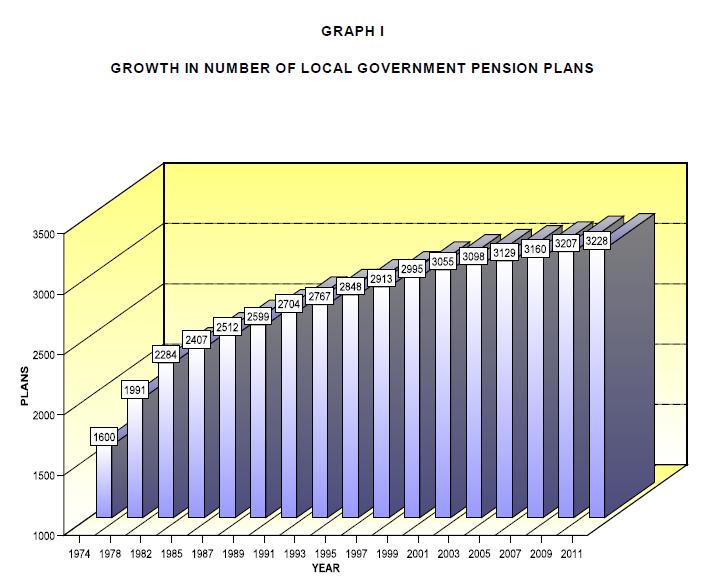

6 Some PA statistics Over 3,200 plans 6

7 Some PA statistics PA s local government pension plans comprise more than 25% of public employee pension plans in the U.S. 70% are defined benefit 98% have less than 100 members in the plan 7

8 Some PA statistics 8

9 9

10 Counties vs. Municipalities Entry age normal cost method is used by all municipal plans Most County plans (41) use the aggregate cost method - Will be required to perform actuarial valuation for GASB 67/68 using entry age normal impact unknown Most County plans have a hybrid plan consistent of defined benefit portion funded by the employer, and a defined contribution portion funded by the employee - Municipal Plans vary widely 10

11 Counties vs. Municipalities County pension plans have no specific actuarial funding standard, as compared to Municipalities (Act 205 of 1984) 11

12 Timing for implementation 12/31/15 will be GASB 68 adoption - Most Counties will be expanding upon the GASB 67 concept adopted in the prior year Will require reporting of the liability on the govtwide (full accrual) financial statements - Already have much of the information from GASB 67, this places the NPL on the statement of net position & adds some footnote information. 12

13 Example for a County Regular actuarial valuation completed for 1/1/15 sometime in early to mid 2015 Source information from that valuation is used, and the GASB requirements are applied to a completely new valuation following the GASB criteria - Although the report is based on 1/1/15 census data, it must be rolled forward to 12/31/15 for use in the 12/31/15 FS 13

14 Who/what is an actuary? A person who wanted to be an accountant, but couldn t handle all the excitement!

15 Components of the NPL 15

16 Total Pension Liability Total pension liability is: - The present value of projected benefit payments for current and former employees, based on members past service, allocated to past years 16

17 Projection of Benefit Payments Based on then-existing benefit terms and legal agreements Includes projected salary increases, service credits, and COLAs No significant change from prior practice 17

18 Pension Plan Assets Total pension plan assets: - In most cases, would be the fair market value of assets in the Pension Trust as of the financial reporting date - Would potentially include receivables to the plan as well (December employee contribution, for example) 18

19 Net Pension Liability (NPL) Net Pension Liability - Actuarially calculated liability as of the FS date - Less Pension Trust assets as of the FS date - Equals the NPL The NPL is the amount recorded on the government wide FS 19

20 Pension Expense Current standard pension cost expensed when paid (ARC) New standard pension cost expensed as service provided by employee 20

21 Pension Expense Current year pension expense on the govt-wide financial statements will be LESS under GASB 68 than under current practice for many governments how? In many cases a large part of the current year cost is for current and future retiree benefits that were already earned by the employee not paying for current year service by the employee 21

22 Example current practice Annual Required Contribution for 2015: $6.5 million - $4.0 million is normal cost (current year service cost) - $2.5 million is amortization of prior costs $2.5m is old costs being paid for now 22

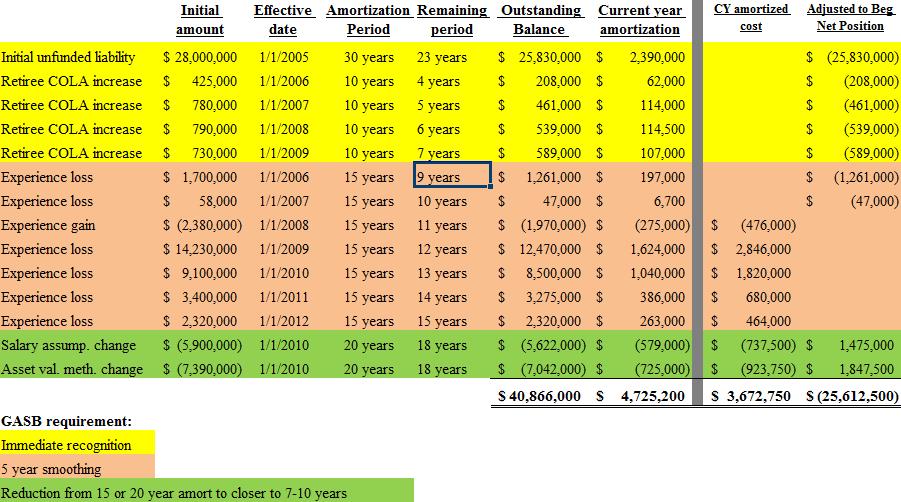

23 Amortization differences between current practice and GASB 67/68 Current practice (govt) Initial unfunded liability 30 year amortization Change in actuarial assumptions - 20 years or average future service life of participants Modification of benefits for retirees 20 years for active, 10 years for retired Actuarial experience adjustment 15 years GASB Initial unfunded liability immediate Change in actuarial assumptions average service life of participants (potentially zero for retirees) Modification of benefits for retirees immediate recognition Actuarial experience adjustment average service life of participants (potentially zero for retirees) 23

24 24

25 Example Government Wide FS 25

26 26

27 27

28 28

29 29

30 What about rating agencies? S&P will be incorporating it into their basis for analyzing pension liabilities Debt and Liability profile is one of the five major factors determining rating For SERS and PSERS type situations - S&P already historically allocated the plan s entire liability to the state sponsor - States liability will fall, local liabilities will increase 30

31 What about rating agencies? Does Standard & Poor's anticipate revising state government ratings based on changes to the new GASB statements? In our view, the changes to pension liabilities resulting from the new GASB standards, such as the use of the blended rate, are more likely to affect governments for which we have already factored their weak pension funding status into our ratings 31

32 What about rating agencies? Moody s: - New pension disclosures under GASB 67/68 will have limited impact on US state and local government ratings - Will not change their methodology - Could impact the $$ amount they use for the liability based upon additional disclosures / discount rate sensitivity 32

33 Random items of note Proprietary Funds and Authorities - Since they use accrual accounting year round, this actually impacts numbers used for budgeting purposes - Will need to consider the impact, and potential allocation of the liability between the governmental funds vs. the business type funds 33

34 Random items of note Changes in the plan after the measurement date - Keep in mind your actuary needs to know if a significant change in benefit structure has occurred since 1/1/15 - An agreement or benefit change made during calendar 2015 would need to be considered in the NPL calculation for 12/31/15 34

35 35

36 Conclusion That s it! Except.OPEBs are coming soon Questions? 36

37 Contact Information Timothy J. Morgus, CPA, CGFM Partner

GASB 67/68 The New Pension Standards. The Reasoning Behind the Pronouncements

GASB 67/68 The New Pension Standards The Reasoning Behind the Pronouncements Presented by: Stephen W. Blann, CPA, CGFM, CGMA Director of Government Audit Quality Rehmann, Grand Rapids, MI Larry Langer,

GASB 67/68 The New Pension Standards The Reasoning Behind the Pronouncements Presented by: Stephen W. Blann, CPA, CGFM, CGMA Director of Government Audit Quality Rehmann, Grand Rapids, MI Larry Langer,

GASB 75 Accounting and Financial Reporting For Postemployment Benefits Other Than Pensions

GASB 75 Accounting and Financial Reporting For Postemployment Benefits Other Than Pensions Presented By: Marianne Van Duyne, CPA Managing Partner R.S. Abrams & Co., LLP 1 New York State Government Finance

GASB 75 Accounting and Financial Reporting For Postemployment Benefits Other Than Pensions Presented By: Marianne Van Duyne, CPA Managing Partner R.S. Abrams & Co., LLP 1 New York State Government Finance

GASB 74/75 The Accounting and Reporting of OPEBs Is Undergoing a Major Change

Pursuing the Profession While Promoting the Public Good GASB 74/75 The Accounting and Reporting of OPEBs Is Undergoing a Major Change 2016 Health Care Summit and Benefits Fair for Local Government What

Pursuing the Profession While Promoting the Public Good GASB 74/75 The Accounting and Reporting of OPEBs Is Undergoing a Major Change 2016 Health Care Summit and Benefits Fair for Local Government What

ICCCFO FALL 2012 CONFERENCE

ICCCFO FALL 2012 CONFERENCE GASB Statement No. 68, Accounting and Financial Reporting for Pensions Frederick G. Lantz, CPA Partner-in-Charge, Government Services Sikich LLP 1415 W. Diehl Road, Suite 400

ICCCFO FALL 2012 CONFERENCE GASB Statement No. 68, Accounting and Financial Reporting for Pensions Frederick G. Lantz, CPA Partner-in-Charge, Government Services Sikich LLP 1415 W. Diehl Road, Suite 400

Implementing GASB 68

W a s h i n g t o n S t a t e A u d i t o r s O f f i c e Implementing GASB 68 GASB pension statements GASB number Title 78 Non-governmental plans 2016 73 Plans not within the scope of GASB 68 2017 71

W a s h i n g t o n S t a t e A u d i t o r s O f f i c e Implementing GASB 68 GASB pension statements GASB number Title 78 Non-governmental plans 2016 73 Plans not within the scope of GASB 68 2017 71

What you should know about the new Other Postemployment Benefits (OPEB) standard (GASB 75) WGFOA Spring Conference April 19, 2018

standard (GASB 75) WGFOA Spring Conference April 19, 2018") What you should know about the new Other Postemployment Benefits (OPEB) standard (GASB 75) WGFOA Spring Conference April 19, 2018 Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an independently

What you should know about the new Other Postemployment Benefits (OPEB) standard (GASB 75) WGFOA Spring Conference April 19, 2018 Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an independently

Overview of GASB 74/75. The new OPEB accounting standard. Joshua Mayhue, F.S.A. Consulting Actuary

1 Overview of GASB 74/75 The new OPEB accounting standard Joshua Mayhue, F.S.A. Consulting Actuary GASB 74/75 Implementation 2 GASB 74 Plan Accounting (only applies if plan is funded) Replaces GASB 43

1 Overview of GASB 74/75 The new OPEB accounting standard Joshua Mayhue, F.S.A. Consulting Actuary GASB 74/75 Implementation 2 GASB 74 Plan Accounting (only applies if plan is funded) Replaces GASB 43

April 24, 2018 Webinar

Practical Implementation of GASB 75 (OPEB) April 24, 2018 Webinar Presented in association with Presented by: Stephen W. Blann, CPA, CGFM, CGMA Director of Governmental Audit Quality Rehmann 2 Session

Practical Implementation of GASB 75 (OPEB) April 24, 2018 Webinar Presented in association with Presented by: Stephen W. Blann, CPA, CGFM, CGMA Director of Governmental Audit Quality Rehmann 2 Session

GASB 67 and 68 The New World of Public Pension Plan Accounting

GASB 67 and 68 The New World of Public Pension Plan Accounting Presented by Mark Olleman, FSA, EA, MAAA Daniel Wade, FSA, EA, MAAA TERS Retirement Board Meeting October 10, 2013 Agenda Timing Notable Issues

GASB 67 and 68 The New World of Public Pension Plan Accounting Presented by Mark Olleman, FSA, EA, MAAA Daniel Wade, FSA, EA, MAAA TERS Retirement Board Meeting October 10, 2013 Agenda Timing Notable Issues

GOVERNMENTAL DEFINED BENEFIT PENSION PLANS

GOVERNMENTAL DEFINED BENEFIT PENSION PLANS UNDERSTANDING GASB 67 / 68 GGFOA 2014 ANNUAL CONFERENCE Presented By: Donald L. McGrath Jr., CPA, Partner Crace Galvis McGrath, LLC Sponsored By: Georgia Government

GOVERNMENTAL DEFINED BENEFIT PENSION PLANS UNDERSTANDING GASB 67 / 68 GGFOA 2014 ANNUAL CONFERENCE Presented By: Donald L. McGrath Jr., CPA, Partner Crace Galvis McGrath, LLC Sponsored By: Georgia Government

GASB 68 Implementation (The time is now upon us)

") GASB 68 Implementation (The time is now upon us) Maryland Association of Certified Public Accountants April 17, 2015 CLAconnect.com GASB No. 68 Accounting and Financial Reporting for Pension Plans Effective

GASB 68 Implementation (The time is now upon us) Maryland Association of Certified Public Accountants April 17, 2015 CLAconnect.com GASB No. 68 Accounting and Financial Reporting for Pension Plans Effective

Accounting Challenges & GASB Update. Presented by: Wendi Unger, Partner, CPA

Accounting Challenges & GASB Update April 23, 2015 Presented by: Wendi Unger, Partner, CPA 1 Agenda Challenging payroll related issues presented by Chad Koski GASB Update Accounting Challenges Clearing

Accounting Challenges & GASB Update April 23, 2015 Presented by: Wendi Unger, Partner, CPA 1 Agenda Challenging payroll related issues presented by Chad Koski GASB Update Accounting Challenges Clearing

An Overview of the New GASB Pension Accounting and Reporting Standards. Presented By: Joel Knopp, CPA

An Overview of the New GASB Pension Accounting and Reporting Standards Presented By: Joel Knopp, CPA GASB Pension Accounting Standards GASB Resources: Statement 67 (plans) Statement 68 (employers) Statement

An Overview of the New GASB Pension Accounting and Reporting Standards Presented By: Joel Knopp, CPA GASB Pension Accounting Standards GASB Resources: Statement 67 (plans) Statement 68 (employers) Statement

FPPA Affiliated Defined Benefit Plans

GASB 68 Implementation Guide For FPPA Affiliated Defined Benefit Plans Fire & Police Pension Association of Colorado GASB 68 Implementation Guide TABLE OF CONTENTS Overview & Timeline Overview Reports

GASB 68 Implementation Guide For FPPA Affiliated Defined Benefit Plans Fire & Police Pension Association of Colorado GASB 68 Implementation Guide TABLE OF CONTENTS Overview & Timeline Overview Reports

Implementing GASB 75 Accounting and financial reporting for other post-employment benefits

Implementing GASB 75 Accounting and financial reporting for other post-employment benefits Judy McNeal, Chief Financial Officer KPERS Michele Stromp, Partner KPMG LLP Julie Barrientos, Director KPMG LLP

Implementing GASB 75 Accounting and financial reporting for other post-employment benefits Judy McNeal, Chief Financial Officer KPERS Michele Stromp, Partner KPMG LLP Julie Barrientos, Director KPMG LLP

MEMORANDUM. CAFR Changes

MEMORANDUM DATE: February 2, 2015 TO: Members of the Board of Retirement FROM: Brenda Shott, Assistant CEO, Finance and Internal Operations SUBJECT: GASB 67/68 Update Recommendation: Receive and file.

MEMORANDUM DATE: February 2, 2015 TO: Members of the Board of Retirement FROM: Brenda Shott, Assistant CEO, Finance and Internal Operations SUBJECT: GASB 67/68 Update Recommendation: Receive and file.

Implementing GASB 67 & 68 for Pensions

Implementing GASB 67 & 68 for Pensions Government Officers Association of Pennsylvania Webinar Wednesday April 16, 2014 Charles B. Friedlander, F.S.A. Director, Actuarial Services Course Objectives To

Implementing GASB 67 & 68 for Pensions Government Officers Association of Pennsylvania Webinar Wednesday April 16, 2014 Charles B. Friedlander, F.S.A. Director, Actuarial Services Course Objectives To

GASB Statement No. 75: Accounting and Financial Reporting for Postemployment Benefits Other Than Pensions

GASB Statement No. 75: Accounting and Financial Reporting for Postemployment Benefits Other Than Pensions April 4, 2017 The webinar will begin at 12:30 pm CT. Tara Laughlin, CPA, CGFM Senior Manager, Assurance

GASB Statement No. 75: Accounting and Financial Reporting for Postemployment Benefits Other Than Pensions April 4, 2017 The webinar will begin at 12:30 pm CT. Tara Laughlin, CPA, CGFM Senior Manager, Assurance

GASB 67 & 68 Frequently Asked Questions (FAQs)

") GASB 67 & 68 Frequently Asked Questions (FAQs) 1. When do these new standards go into effect? Statement No. 67 replaces the requirements of the existing Statement No. 25, Financial Reporting for Defined

GASB 67 & 68 Frequently Asked Questions (FAQs) 1. When do these new standards go into effect? Statement No. 67 replaces the requirements of the existing Statement No. 25, Financial Reporting for Defined

GASB Revised Pension Standards:

GASB Revised Pension Standards: What Arizona governments need to know DONNA MILLER, PROFESSIONAL PRACTICE DIRECTOR ARIZONA OFFICE OF THE AUDITOR GENERAL NANCY BENNETT, CFO, ARIZONA STATE RETIREMENT SYSTEM

GASB Revised Pension Standards: What Arizona governments need to know DONNA MILLER, PROFESSIONAL PRACTICE DIRECTOR ARIZONA OFFICE OF THE AUDITOR GENERAL NANCY BENNETT, CFO, ARIZONA STATE RETIREMENT SYSTEM

2014 CliftonLarsonAllen LLP CliftonLarsonAllen LLP. GASB Update. Greg Bussink and Sean Walker October 22, CLAconnect.

2014 CliftonLarsonAllen LLP GASB Update Greg Bussink and Sean Walker October 22, 2014 CLAconnect.com Effective Dates Years beginning after December 15, 2012 (June 30, 2014) Statement 65 Items Previously

2014 CliftonLarsonAllen LLP GASB Update Greg Bussink and Sean Walker October 22, 2014 CLAconnect.com Effective Dates Years beginning after December 15, 2012 (June 30, 2014) Statement 65 Items Previously

Texas Municipal Retirement System. September 19, GASB Update. Joseph Newton, Leslee Hardy and Rhonda Covarrubias

Texas Municipal Retirement System GASB Update September 19, 2014 Joseph Newton, Leslee Hardy and Rhonda Covarrubias Copyright 2013 GRS All rights reserved. Today s Agenda GASB Recap New Pension Expense

Texas Municipal Retirement System GASB Update September 19, 2014 Joseph Newton, Leslee Hardy and Rhonda Covarrubias Copyright 2013 GRS All rights reserved. Today s Agenda GASB Recap New Pension Expense

GASB Statement 68 Government Financial Reporting of Pension Finances Summary Explanation of Predictor Model 10/16/12

GASB Statement 68 Government Financial Reporting of Pension Finances Summary Explanation of Predictor Model 10/16/12 The Governmental Accounting Standards Board (GASB) voted to approve new standards that

GASB Statement 68 Government Financial Reporting of Pension Finances Summary Explanation of Predictor Model 10/16/12 The Governmental Accounting Standards Board (GASB) voted to approve new standards that

GASB UPDATE. Kathryn Barrett, CPA Freed Maxick CPAs, PC Alexandria Battaglia, CPA R.S. Abrams & Co., LLP

GASB UPDATE Kathryn Barrett, CPA Freed Maxick CPAs, PC Alexandria Battaglia, CPA R.S. Abrams & Co., LLP 1 Effective for June 30, 2018 Statement No. 75 OPEB (employers) Statement No. 81 Irrevocable Split

GASB UPDATE Kathryn Barrett, CPA Freed Maxick CPAs, PC Alexandria Battaglia, CPA R.S. Abrams & Co., LLP 1 Effective for June 30, 2018 Statement No. 75 OPEB (employers) Statement No. 81 Irrevocable Split

Impacts of GASB 74/75 on CalSTRS and Employers. Presented on July 13, 2017

Impacts of GASB 74/75 on CalSTRS and Employers Presented on July 13, 2017 GASB Implementation Effective for CalSTRS FY 2016-17 Statement 74, Financial Reporting for Postemployment Benefit Plans Other Than

Impacts of GASB 74/75 on CalSTRS and Employers Presented on July 13, 2017 GASB Implementation Effective for CalSTRS FY 2016-17 Statement 74, Financial Reporting for Postemployment Benefit Plans Other Than

GASB Update OPEB, Fair Value and Abatements

GASB Update OPEB, Fair Value and Abatements Rob Churchman, Partner October 23, 2015 Type of Plan Defined benefit OPEB plan Benefit after separation is defined by benefit terms May be stated as a dollar

GASB Update OPEB, Fair Value and Abatements Rob Churchman, Partner October 23, 2015 Type of Plan Defined benefit OPEB plan Benefit after separation is defined by benefit terms May be stated as a dollar

20/20 Vision: A Clear View of Pension Obligations:

20/20 Vision: A Clear View of Pension Obligations: Perspective on GASB 67/68 November 7, 2012 Presenters Eric Formberg, CPA, CGFM, Partner, Plante Moran Eric is the leader of the firm s K-12 education

20/20 Vision: A Clear View of Pension Obligations: Perspective on GASB 67/68 November 7, 2012 Presenters Eric Formberg, CPA, CGFM, Partner, Plante Moran Eric is the leader of the firm s K-12 education

Joel Black & Miller Edwards. GASB 68 Allocation of the Net Pension Liability and Required Note Disclosures

Joel Black & Miller Edwards GASB 68 Allocation of the Net Pension Liability and Required Note Disclosures Today s Presenters Joel Black, CPA, is a partner with Mauldin & Jenkins LLC specializing in serving

Joel Black & Miller Edwards GASB 68 Allocation of the Net Pension Liability and Required Note Disclosures Today s Presenters Joel Black, CPA, is a partner with Mauldin & Jenkins LLC specializing in serving

INFORMATION SESSION Cd, 5/15/E

INFORMATION SESSION 1 50-923Cd, 5/15/E Background What is GASB 68? Governmental Accounting Standards Board (GASB) approved new rules that will affect employers Employers must include the following in their

INFORMATION SESSION 1 50-923Cd, 5/15/E Background What is GASB 68? Governmental Accounting Standards Board (GASB) approved new rules that will affect employers Employers must include the following in their

GASB Fast Facts. GASB 67/68 requires the unfunded net pension liability be reported for the first time for many governmental entities.

Teacher Retirement System of Texas GASB 68 Implementation Update Gloria Nichols, CPA February 9, 2015 GASB Fast Facts GASB 67/68 requires the unfunded net pension liability be reported for the first time

Teacher Retirement System of Texas GASB 68 Implementation Update Gloria Nichols, CPA February 9, 2015 GASB Fast Facts GASB 67/68 requires the unfunded net pension liability be reported for the first time

The Future is Now: Implementing GASB Guidance on Pension and OPEB Tuesday, May 24, 2016 I 10:20 a.m. to 12:00 p.m. I 1.5 CPE

The Future is Now: Implementing GASB Guidance on Pension and OPEB Tuesday, May 24, 2016 I 10:20 a.m. to 12:00 p.m. I 1.5 CPE Moderator: Debra Roberts, MBA, CPA, CRC, Director of Finance, Maryland Supplemental

The Future is Now: Implementing GASB Guidance on Pension and OPEB Tuesday, May 24, 2016 I 10:20 a.m. to 12:00 p.m. I 1.5 CPE Moderator: Debra Roberts, MBA, CPA, CRC, Director of Finance, Maryland Supplemental

G O G E B I C C OUNTY EMPLO Y E E S R E T I R E M E N T S YS T EM

G O G E B I C C OUNTY EMPLO Y E E S R E T I R E M E N T S YS T EM G A S B S T A T E M E N T NOS. 6 7 A N D 6 8 A C C O U N T I N G A N D F I N A N C I A L R E P O R T I N G F O R P E N S I O N S D E C

G O G E B I C C OUNTY EMPLO Y E E S R E T I R E M E N T S YS T EM G A S B S T A T E M E N T NOS. 6 7 A N D 6 8 A C C O U N T I N G A N D F I N A N C I A L R E P O R T I N G F O R P E N S I O N S D E C

GASB 68 ACCOUNTING VALUATION REPORT

GASB 68 ACCOUNTING VALUATION REPORT () Rate Plan Identifier: 47 Prepared for COUNTY OF BUTTE MISCELLANEOUS PLAN, an Agent Multiple-Employer Defined Benefit Pension Plan Measurement Date of June 30, 2016

GASB 68 ACCOUNTING VALUATION REPORT () Rate Plan Identifier: 47 Prepared for COUNTY OF BUTTE MISCELLANEOUS PLAN, an Agent Multiple-Employer Defined Benefit Pension Plan Measurement Date of June 30, 2016

ILLINOIS COMMUNITY COLLEGE CHIEF FINANCIAL OFFICERS SPRING 2015 CONFERENCE IMPLEMENTING GASB S68 Presented by: Frederick G.

ILLINOIS COMMUNITY COLLEGE CHIEF FINANCIAL OFFICERS SPRING 2015 CONFERENCE IMPLEMENTING GASB S68 Presented by: Frederick G. Lantz, CPA Partner-in-Charge, Government Services Sikich LLP 1415 W. Diehl Road,

ILLINOIS COMMUNITY COLLEGE CHIEF FINANCIAL OFFICERS SPRING 2015 CONFERENCE IMPLEMENTING GASB S68 Presented by: Frederick G. Lantz, CPA Partner-in-Charge, Government Services Sikich LLP 1415 W. Diehl Road,

GASB 68 ACCOUNTING VALUATION REPORT

GASB 68 ACCOUNTING VALUATION REPORT () Rate Plan Identifier: 48 Prepared for COUNTY OF BUTTE SAFETY PLAN, an Agent Multiple-Employer Defined Benefit Pension Plan Measurement Date of June 30, 2017 TABLE

GASB 68 ACCOUNTING VALUATION REPORT () Rate Plan Identifier: 48 Prepared for COUNTY OF BUTTE SAFETY PLAN, an Agent Multiple-Employer Defined Benefit Pension Plan Measurement Date of June 30, 2017 TABLE

Minnesota School Boards Association Roundtable

GASB Click 67/68 here School to add District title Implementation one or two Impacts lines Minnesota School Boards Association Roundtable January 16, 2015 Presented by: Jay Stoffel, Deputy Executive Director

GASB Click 67/68 here School to add District title Implementation one or two Impacts lines Minnesota School Boards Association Roundtable January 16, 2015 Presented by: Jay Stoffel, Deputy Executive Director

GASB 68 Nuts and Bolts

GASB 68 Nuts and Bolts Paul Niedermuller, CPA, Principal cliftonlarsonallen.com Learning Objectives/Agenda Information from plan now WHAT? Impact of Measurement Date & Coordination with Auditors Accounting

GASB 68 Nuts and Bolts Paul Niedermuller, CPA, Principal cliftonlarsonallen.com Learning Objectives/Agenda Information from plan now WHAT? Impact of Measurement Date & Coordination with Auditors Accounting

Jerry E. Durham, CPA, CGFM, CFE

Jerry E. Durham, CPA, CGFM, CFE 1 2015 Effective Dates June 30 Statement 68 Pensions Employers Statement 69 Government Combinations and Disposals of Government Operations Statement 71 Pension Transition

Jerry E. Durham, CPA, CGFM, CFE 1 2015 Effective Dates June 30 Statement 68 Pensions Employers Statement 69 Government Combinations and Disposals of Government Operations Statement 71 Pension Transition

2014 CliftonLarsonAllen LLP. GASB Update. May 20, CLAconnect.com

GASB Update May 20, 2014 CLAconnect.com Effective Dates Years beginning after December 15, 2012 (June 30, 2014) Statement 65 Items Previously Reported as Assets and Liabilities Statement 66 - Technical

GASB Update May 20, 2014 CLAconnect.com Effective Dates Years beginning after December 15, 2012 (June 30, 2014) Statement 65 Items Previously Reported as Assets and Liabilities Statement 66 - Technical

Town of Scituate Retirement Plan for the Police Department Employees

Town of Scituate Retirement Plan for the Police Department Employees Financial Disclosure Information in accordance with Statements of Governmental Accounting Standards Board Statement No. 67 ( GASB 67

Town of Scituate Retirement Plan for the Police Department Employees Financial Disclosure Information in accordance with Statements of Governmental Accounting Standards Board Statement No. 67 ( GASB 67

Ohio Police & Fire Pension Fund

Ohio Police & Fire Pension Fund Retiree Health Care Benefits for Fiscal Year Ending Dec. 31, 2017 Information Required Under Governmental Accounting Standards Board Statement No. 75 August 24, 2018 200

Ohio Police & Fire Pension Fund Retiree Health Care Benefits for Fiscal Year Ending Dec. 31, 2017 Information Required Under Governmental Accounting Standards Board Statement No. 75 August 24, 2018 200

OPEB Preparing for Your Audit

OPEB Preparing for Your Audit Civic Federation and the Federal Reserve Bank of Chicago March 12, 2008 Bert Nuehring, CPA Executive Crowe Chizek and Company LLC BNuehring@crowechizek.com 1 OPEB Preparing

OPEB Preparing for Your Audit Civic Federation and the Federal Reserve Bank of Chicago March 12, 2008 Bert Nuehring, CPA Executive Crowe Chizek and Company LLC BNuehring@crowechizek.com 1 OPEB Preparing

Georgia Municipal Association Pre-Convention Workshop: Big Changes Coming to Retirement Plans

Georgia Municipal Association Pre-Convention Workshop: Big Changes Coming to Retirement Plans June 21, 2013 Leon F. (Rocky) Joyner, Jr. GMEBS Actuary Copyright 2013 by The Segal Group, Inc., parent of

Georgia Municipal Association Pre-Convention Workshop: Big Changes Coming to Retirement Plans June 21, 2013 Leon F. (Rocky) Joyner, Jr. GMEBS Actuary Copyright 2013 by The Segal Group, Inc., parent of

GASB 67 and 68: Pension Fund Reporting. Presented By: Jamie Wilkey, Partner Todd Schroeder, Principle, Actuary

GASB 67 and 68: Pension Fund Reporting Presented By: Jamie Wilkey, Partner Todd Schroeder, Principle, Actuary GASB 67/68 - Accounting and Financial Reporting for Pensions Topics for discussion Employer

GASB 67 and 68: Pension Fund Reporting Presented By: Jamie Wilkey, Partner Todd Schroeder, Principle, Actuary GASB 67/68 - Accounting and Financial Reporting for Pensions Topics for discussion Employer

S A M P L E OLD HIRE FIRE P E N S I ON FUND

S A M P L E OLD HIRE FIRE P E N S I ON FUND G A S B S T A T E M E N T N O. 6 8 E M P L O Y E R R E P O R T I N G A C C O U N T I N G S C H E D U L E S F O R T H E M E A S U R E M E N T P E R I O D E N

S A M P L E OLD HIRE FIRE P E N S I ON FUND G A S B S T A T E M E N T N O. 6 8 E M P L O Y E R R E P O R T I N G A C C O U N T I N G S C H E D U L E S F O R T H E M E A S U R E M E N T P E R I O D E N

Accounting for the OPEB Obligation

Accounting for the OPEB Obligation Tom Swain, F.S.A. August 18, 2016 Agenda Overview and effective dates Significant changes Sample balance sheet pre/post changes Plan sponsor implications Planning steps

Accounting for the OPEB Obligation Tom Swain, F.S.A. August 18, 2016 Agenda Overview and effective dates Significant changes Sample balance sheet pre/post changes Plan sponsor implications Planning steps

Overview of OPEB Accounting Changes

Overview of OPEB Accounting Changes More matter with less art Hamlet Act 2, Scene 2 Get your facts first, then you can distort them as you please. - Mark Twain 2 Bolton Partners. Inc. Bolton Partners Inc.

Overview of OPEB Accounting Changes More matter with less art Hamlet Act 2, Scene 2 Get your facts first, then you can distort them as you please. - Mark Twain 2 Bolton Partners. Inc. Bolton Partners Inc.

Understanding Your Financial Statements

Understanding Your Financial Statements NHSAA & NHASBO BEST PRACTICES CONFERENCE 10.30.2017 & 10.31.2017 PLODZIK & SANDERSON, PA SCOTT EAGEN, CFE SENIOR MANAGER What s In Your Annual Financial Report *

Understanding Your Financial Statements NHSAA & NHASBO BEST PRACTICES CONFERENCE 10.30.2017 & 10.31.2017 PLODZIK & SANDERSON, PA SCOTT EAGEN, CFE SENIOR MANAGER What s In Your Annual Financial Report *

OPEB - GASB 75: GAQC Web Event: OPEB GASB 75: Special Emphasis and Considerations for Nontrusted Plans. Administrative Notes.

OPEB - GASB 75: Special Emphasis and Considerations for Nontrusted Plans A Governmental Audit Quality Center Web Event Administrative Notes Please ensure your pop-up blocker is disabled. Note the interactive

OPEB - GASB 75: Special Emphasis and Considerations for Nontrusted Plans A Governmental Audit Quality Center Web Event Administrative Notes Please ensure your pop-up blocker is disabled. Note the interactive

1.02 TRINITY COUNTY. County Contract No. Board Item Request Form Department Personnel. Contact Carol Martin

County Contract No. Department Personnel TRINITY COUNTY 1.02 Board Item Request Form 2016-09-20 Contact Carol Martin Phone 530-623-1325 Requested Agenda Location Presentations Requested Board Action: Receive

County Contract No. Department Personnel TRINITY COUNTY 1.02 Board Item Request Form 2016-09-20 Contact Carol Martin Phone 530-623-1325 Requested Agenda Location Presentations Requested Board Action: Receive

OPEB: A Closer Look at the Present and Future

Menard Consulting, Inc. Actuaries & Consultants OPEB: A Closer Look at the Present and Future GASB Statements No. 43 & No. 45 Agenda Overview The Actuarial Calculation Accounting GASB OPEB Accounting Exposure

Menard Consulting, Inc. Actuaries & Consultants OPEB: A Closer Look at the Present and Future GASB Statements No. 43 & No. 45 Agenda Overview The Actuarial Calculation Accounting GASB OPEB Accounting Exposure

Michigan Public School Employees Retirement System Updates

Michigan Public School Employees Retirement System Updates John Karagoulis Pension Administration Specialist, ORS Kayla Lintz Data Analyst, ORS Eric Formberg CPA, CGFM, Partner, Plante Moran MSBO CPA Workshop,

Michigan Public School Employees Retirement System Updates John Karagoulis Pension Administration Specialist, ORS Kayla Lintz Data Analyst, ORS Eric Formberg CPA, CGFM, Partner, Plante Moran MSBO CPA Workshop,

Overview of GASB 67 and 68

Overview of GASB 67 and 68 Community College Internal Auditors May 7, 2015 Crowe Horwath LLP Jeff Jensen, Partner Audit Tax Advisory Risk Performance 2014 Crowe Horwath LLP Implementation Dates When will

Overview of GASB 67 and 68 Community College Internal Auditors May 7, 2015 Crowe Horwath LLP Jeff Jensen, Partner Audit Tax Advisory Risk Performance 2014 Crowe Horwath LLP Implementation Dates When will

Oh No It s OPEB! Other Postemployment Benefits Implementation of GASB Statement No. 75. GFOAT Spring Institute Deborah Beams, CPA.

Government Oh No It s OPEB! Other Postemployment Benefits Implementation of GASB Statement No. 75 GFOAT Spring Institute 2018 Deborah Beams, CPA Director, BKD Does OPEB Make You Want to Scream? *Disclaimer:

Government Oh No It s OPEB! Other Postemployment Benefits Implementation of GASB Statement No. 75 GFOAT Spring Institute 2018 Deborah Beams, CPA Director, BKD Does OPEB Make You Want to Scream? *Disclaimer:

GASB 74 & 75 The new GASB OPEB standards & an overview of upcoming pronouncements. Jeff Straus, CPA Principal

GASB 74 & 75 The new GASB OPEB standards & an overview of upcoming pronouncements Jeff Straus, CPA Principal jstraus@manercpa.com Session Overview 1. What are Other Post Employment Benefits (OPEB)? 2.

GASB 74 & 75 The new GASB OPEB standards & an overview of upcoming pronouncements Jeff Straus, CPA Principal jstraus@manercpa.com Session Overview 1. What are Other Post Employment Benefits (OPEB)? 2.

GASB 68 ACCOUNTING VALUATION REPORT

GASB 68 ACCOUNTING VALUATION REPORT () Rate Plan Identifier: 595 Prepared for the SAN FRANCISCO COMMUNITY COLLEGE DISTRICT BOOKSTORE AUXILIARY MISCELLANEOUS PLAN, a Cost-Sharing Multiple-Employer Defined

GASB 68 ACCOUNTING VALUATION REPORT () Rate Plan Identifier: 595 Prepared for the SAN FRANCISCO COMMUNITY COLLEGE DISTRICT BOOKSTORE AUXILIARY MISCELLANEOUS PLAN, a Cost-Sharing Multiple-Employer Defined

Local Municipal Workshop

Local Municipal Workshop Assessing your Pension Plan Joe Newton January 24, 2012 Copyright 2011 GRS All rights reserved. Look At Critical Issues Facing Both Member And dthe Employer Income Replacement

Local Municipal Workshop Assessing your Pension Plan Joe Newton January 24, 2012 Copyright 2011 GRS All rights reserved. Look At Critical Issues Facing Both Member And dthe Employer Income Replacement

MSBO Annual Conference Implementing GASB 75. Presented by Chris Geck and Eric Formberg

MSBO Annual Conference Implementing GASB 75 Presented by Chris Geck and Eric Formberg Accounting and Auditing Update Topics GASB 75 implementation year is here! GASB 68 - connecting the dots MPSERS contribution

MSBO Annual Conference Implementing GASB 75 Presented by Chris Geck and Eric Formberg Accounting and Auditing Update Topics GASB 75 implementation year is here! GASB 68 - connecting the dots MPSERS contribution

THE EATONTOWN SEWERAGE AUTHORITY A COMPONENT UNIT OF THE BOROUGH OF EATONTOWN FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION AND

THE EATONTOWN SEWERAGE AUTHORITY A COMPONENT UNIT OF THE BOROUGH OF EATONTOWN FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION AND INDEPENDENT AUDITOR'S REPORTS YEARS ENDED DECEMBER 31, 2015 AND 2014

THE EATONTOWN SEWERAGE AUTHORITY A COMPONENT UNIT OF THE BOROUGH OF EATONTOWN FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION AND INDEPENDENT AUDITOR'S REPORTS YEARS ENDED DECEMBER 31, 2015 AND 2014

GASB Issues Final Rules Governing Reporting for Postemployment Benefits Other Than Pensions

GASB Issues Final Rules Governing Reporting for Postemployment Benefits Other Than Pensions Table of Contents EXECUTIVE SUMMARY... 3 GASB 75 EMPLOYER STANDARD... 5 BACKGROUND & IMPACT OF CHANGE... 5 SCOPE...

GASB Issues Final Rules Governing Reporting for Postemployment Benefits Other Than Pensions Table of Contents EXECUTIVE SUMMARY... 3 GASB 75 EMPLOYER STANDARD... 5 BACKGROUND & IMPACT OF CHANGE... 5 SCOPE...

ARKANSAS STATE HIGHWAY EMPLOYEES RETIREMENT SYSTEM (ASHERS)

") ARKANSAS STATE HIGHWAY EMPLOYEES RETIREMENT SYSTEM (ASHERS) GASB 67/68 DISCLOSURES AS OF JUNE 30, 2018 Osborn, Carreiro & Associates, Inc. ACTUARIES CONSULTANTS ANALYSTS 124 West Capitol Avenue, Suite

ARKANSAS STATE HIGHWAY EMPLOYEES RETIREMENT SYSTEM (ASHERS) GASB 67/68 DISCLOSURES AS OF JUNE 30, 2018 Osborn, Carreiro & Associates, Inc. ACTUARIES CONSULTANTS ANALYSTS 124 West Capitol Avenue, Suite

GASB Pension Accounting Standards

GASB Pension Accounting Standards Michelle Czerkawski, Senior Project Manager Governmental Accounting Standards Board The views expressed in this presentation are those of Ms. Czerkawski. Official positions

GASB Pension Accounting Standards Michelle Czerkawski, Senior Project Manager Governmental Accounting Standards Board The views expressed in this presentation are those of Ms. Czerkawski. Official positions

11/15/2017 IMPLEMENTING GASB 75: WHAT YOU NEED TO KNOW. Lindsey Oakley, CPA Director November 15, 2017

IMPLEMENTING GASB 75: WHAT YOU NEED TO KNOW November 15, 2017 Lindsey Oakley, CPA Director loakley@bkd.com 1 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you

IMPLEMENTING GASB 75: WHAT YOU NEED TO KNOW November 15, 2017 Lindsey Oakley, CPA Director loakley@bkd.com 1 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you

Recent VRS Changes and the New Pension GASB Standard. VGFOA Fall Conference October 17 th, 2012

Recent VRS Changes and the New Pension GASB Standard VGFOA Fall Conference October 17 th, 2012 Panel: William H Leighty, DecideSmart, LLC Robert H Churchman, CPA William M Dowd, Sageview Consulting Barry

Recent VRS Changes and the New Pension GASB Standard VGFOA Fall Conference October 17 th, 2012 Panel: William H Leighty, DecideSmart, LLC Robert H Churchman, CPA William M Dowd, Sageview Consulting Barry

OPEB Reporting Overview: Implications of the Choice to Fund or Not Fund

OPEB Reporting Overview: Implications of the Choice to Fund or Not Fund Dean Michael Mead Research Manager, Governmental Accounting Standards Board March 12, 2008 Disclaimer: The opinions expressed in

OPEB Reporting Overview: Implications of the Choice to Fund or Not Fund Dean Michael Mead Research Manager, Governmental Accounting Standards Board March 12, 2008 Disclaimer: The opinions expressed in

The General Retirement System of the City of Detroit GASB Statement Nos. 67 and 68 Accounting and Financial Reporting for Pension Plans of Component

The General Retirement System of the City of Detroit GASB Statement Nos. 67 and 68 Accounting and Financial Reporting for Pension Plans of Component I June 30, 2018 October 31, 2018 Board of Trustees The

The General Retirement System of the City of Detroit GASB Statement Nos. 67 and 68 Accounting and Financial Reporting for Pension Plans of Component I June 30, 2018 October 31, 2018 Board of Trustees The

Pension Reporting What you need to know about GASB 67 and 68. Sherry Chan, Chief Actuary Paul Snyder, Chief Financial Officer

Pension Reporting What you need to know about GASB 67 and 68 Sherry Chan, Chief Actuary Paul Snyder, Chief Financial Officer 1 Generally Accepted Accounting Principles FAF Financial Accounting Foundation

Pension Reporting What you need to know about GASB 67 and 68 Sherry Chan, Chief Actuary Paul Snyder, Chief Financial Officer 1 Generally Accepted Accounting Principles FAF Financial Accounting Foundation

GASB 68 For the ALASBO POWER LUNCH

GASB 68 For the ALASBO POWER LUNCH BDO USA, LLP, a New York limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee, and forms part of the international

GASB 68 For the ALASBO POWER LUNCH BDO USA, LLP, a New York limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee, and forms part of the international

GASB Review Session Handout

GASB Review Session Handout 56th County Auditors Institute Austin, Texas May 15, 2014 PATTILLO, BROWN & HILL, L.L.P. Paula Lowe, CPA Johnasan Gregory, CPA GASB Concepts Statement No. 4, Elements of Financial

GASB Review Session Handout 56th County Auditors Institute Austin, Texas May 15, 2014 PATTILLO, BROWN & HILL, L.L.P. Paula Lowe, CPA Johnasan Gregory, CPA GASB Concepts Statement No. 4, Elements of Financial

Session 604. GASB Statements 67 and 68 Update. Michelle Czerkawski GASB. Bill Hallmark Cheiron, Inc. March 25, 2014

Session 604 GASB Statements 67 and 68 Update Jointly sponsored by the American Academy of Actuaries And the Conference of Consulting Actuaries In cooperation with the Society of Actuaries Michelle Czerkawski

Session 604 GASB Statements 67 and 68 Update Jointly sponsored by the American Academy of Actuaries And the Conference of Consulting Actuaries In cooperation with the Society of Actuaries Michelle Czerkawski

A Walkthrough of the New GASB Pension Standards

A Walkthrough of the New GASB Pension Standards Implementing and Explaining the Accounting, Notes, RSI and Journal Entries Presented by: Scott Anderson, CPA November 3, 2015 Session Objectives Assuming

A Walkthrough of the New GASB Pension Standards Implementing and Explaining the Accounting, Notes, RSI and Journal Entries Presented by: Scott Anderson, CPA November 3, 2015 Session Objectives Assuming

Overview of OPEB Accounting Changes. More matter with less art Hamlet Act 2, Scene 2

Overview of OPEB Accounting Changes More matter with less art Hamlet Act 2, Scene 2 2 Presenters Kevin Binder, FSA, EA, MAAA, FCA As the leader of Bolton s OPEB practice, Kevin is responsible for the actuarial

Overview of OPEB Accounting Changes More matter with less art Hamlet Act 2, Scene 2 2 Presenters Kevin Binder, FSA, EA, MAAA, FCA As the leader of Bolton s OPEB practice, Kevin is responsible for the actuarial

A R K A N S A S P U B L I C E M P L O Y E E S R E T I R E M E N T S Y S T E M ( I N C L U D I N G D I S T R I C T J U D G E S ) G A S B S T A T E M E

G A S B S T A T E M E") A R K A N S A S P U B L I C E M P L O Y E E S R E T I R E M E N T S Y S T E M ( I N C L U D I N G D I S T R I C T J U D G E S ) G A S B S T A T E M E N T N O S. 6 7 A N D 6 8 A C C O U N T I N G A N D

A R K A N S A S P U B L I C E M P L O Y E E S R E T I R E M E N T S Y S T E M ( I N C L U D I N G D I S T R I C T J U D G E S ) G A S B S T A T E M E N T N O S. 6 7 A N D 6 8 A C C O U N T I N G A N D

In June, 2004 the Governmental Accounting Standards Board issued

National Conference on Public Employee Retirement Systems NCPERS Research Series January 2008 GASB 45 Survey of NCPERS Members In June, 2004 the Governmental Accounting Standards Board issued Statement

National Conference on Public Employee Retirement Systems NCPERS Research Series January 2008 GASB 45 Survey of NCPERS Members In June, 2004 the Governmental Accounting Standards Board issued Statement

GASB 45 Exposure Draft. Two New Exposure Drafts for OPEB

GASB 45 Exposure Draft Presented by Kathleen Cost Solving Tomorrow s Benefit Plan Challenges...Today Two New Exposure Drafts for OPEB 1. Financial Reporting for Postemployment Benefit Plans Other Than

GASB 45 Exposure Draft Presented by Kathleen Cost Solving Tomorrow s Benefit Plan Challenges...Today Two New Exposure Drafts for OPEB 1. Financial Reporting for Postemployment Benefit Plans Other Than

The following document was not prepared by the Office of the State Auditor, but was prepared by and submitted to the Office of the State Auditor by a

The following document was not prepared by the Office of the State Auditor, but was prepared by and submitted to the Office of the State Auditor by a private CPA firm. The document was placed on this web

The following document was not prepared by the Office of the State Auditor, but was prepared by and submitted to the Office of the State Auditor by a private CPA firm. The document was placed on this web

West Virginia Emergency Medical Services Retirement System

Audited Schedules of Allocations and Pension Amounts By West Virginia Emergency Medical Services Retirement System Administered by The West Virginia Consolidated Public Retirement Board As of and for the

Audited Schedules of Allocations and Pension Amounts By West Virginia Emergency Medical Services Retirement System Administered by The West Virginia Consolidated Public Retirement Board As of and for the

FISCAL YEAR 2017 GaDOE FINANCIAL REVIEW SECTION Instructions for Posting the Net Pension Liability

FISCAL YEAR 2017 GaDOE FINANCIAL REVIEW SECTION Instructions for Posting the Net Pension Liability 2017 INSTRUCTIONS FOR POSTING THE NET PENSION LIABILITY Step A Accumulating the Resources Begin by obtaining/downloading

FISCAL YEAR 2017 GaDOE FINANCIAL REVIEW SECTION Instructions for Posting the Net Pension Liability 2017 INSTRUCTIONS FOR POSTING THE NET PENSION LIABILITY Step A Accumulating the Resources Begin by obtaining/downloading

Government Accounting Standards Board Update. GASB 65 Through GASB 70: How Do These Statements Affect Public Ports in Washington?

Government Accounting Standards Board Update GASB 65 Through GASB 70: How Do These Statements Affect Public Ports in Washington? Introduction FOX & COMPANY CPAs, LLC George@cpafox.net (360) 597-0400 GASB:

Government Accounting Standards Board Update GASB 65 Through GASB 70: How Do These Statements Affect Public Ports in Washington? Introduction FOX & COMPANY CPAs, LLC George@cpafox.net (360) 597-0400 GASB:

CITY OF PARK RIDGE SLEP GASB STATEMENT NO. 68 EMPLOYER REPORTING ACCOUNTING SCHEDULES DECEMBER 31, 2014

CITY OF PARK RIDGE SLEP GASB STATEMENT NO. 68 EMPLOYER REPORTING ACCOUNTING SCHEDULES DECEMBER 31, 2014 PRELIMINARY - WILL NOT IMPLEMENT GASB 68 UNTIL NEXT YEAR TABLE OF CONTENTS Page Certification Letter

CITY OF PARK RIDGE SLEP GASB STATEMENT NO. 68 EMPLOYER REPORTING ACCOUNTING SCHEDULES DECEMBER 31, 2014 PRELIMINARY - WILL NOT IMPLEMENT GASB 68 UNTIL NEXT YEAR TABLE OF CONTENTS Page Certification Letter

Interim Charge #4: State Pension Review Board (PRB) Report on GASB Rule Changes and House Bill 13

Report on GASB Rule Changes and House Bill 13") Interim Charge #4: State Pension Review Board (PRB) Report on GASB Rule Changes and House Bill 13 State Pension Review Board House Pensions Committee July 9, 2014 Interim Hearing Interim Charge #4 (GASB

Interim Charge #4: State Pension Review Board (PRB) Report on GASB Rule Changes and House Bill 13 State Pension Review Board House Pensions Committee July 9, 2014 Interim Hearing Interim Charge #4 (GASB

Governmental Accounting and Audit Update

Governmental Accounting and Audit Update Joey Richard and Freddy Smith jrichard@pncpa.com; fsmith@pncpa.com Financial Pressures on Government o Employees\Unions o Revenue declines o Legislation o Media

Governmental Accounting and Audit Update Joey Richard and Freddy Smith jrichard@pncpa.com; fsmith@pncpa.com Financial Pressures on Government o Employees\Unions o Revenue declines o Legislation o Media

Teacher Retirement System of Texas. GASB 68 Implementation Guide for TRS Employers

Teacher Retirement System of Texas GASB 68 Implementation Guide for TRS Employers Gloria Nichols, CPA June 18, 2015 Table of Contents GASB 68 Implementation of TRS Employers Chapter Topic Page 2 I. Overview

Teacher Retirement System of Texas GASB 68 Implementation Guide for TRS Employers Gloria Nichols, CPA June 18, 2015 Table of Contents GASB 68 Implementation of TRS Employers Chapter Topic Page 2 I. Overview

Upcoming Changes to Pension Reporting Under GASB 67 & 68 and the Impact to Municipalities Participating in PERA Retirement Plans

Upcoming Changes to Pension Reporting Under GASB 67 & 68 and the Impact to Municipalities Participating in PERA Retirement Plans Patricia (Patty) French, Board Chair, PERA Wayne Propst, Executive Director,

Upcoming Changes to Pension Reporting Under GASB 67 & 68 and the Impact to Municipalities Participating in PERA Retirement Plans Patricia (Patty) French, Board Chair, PERA Wayne Propst, Executive Director,

Minnesota Association of School Business Officials (MASBO) Employer Pension Reporting Under GASB 68

Employer Pension Reporting Under GASB 68") Minnesota Association of School Business Officials (MASBO) Employer Pension Reporting Under GASB 68 November 15, 2013 Presented by: Dave DeJonge, Assistant Executive Director, PERA John Wicklund, Assistant

Minnesota Association of School Business Officials (MASBO) Employer Pension Reporting Under GASB 68 November 15, 2013 Presented by: Dave DeJonge, Assistant Executive Director, PERA John Wicklund, Assistant

FISCAL YEAR GADOE FINANCIAL REVIEW SECTION Implementation of GASB 68 for School Districts

FISCAL YEAR 2015 GADOE FINANCIAL REVIEW SECTION Implementation of GASB 68 for School Districts HOW THE IMPLEMENTATION OF GASB 68 AFFECTS THE SCHOOL DISTRICTS Background Information In June 2012, the Governmental

FISCAL YEAR 2015 GADOE FINANCIAL REVIEW SECTION Implementation of GASB 68 for School Districts HOW THE IMPLEMENTATION OF GASB 68 AFFECTS THE SCHOOL DISTRICTS Background Information In June 2012, the Governmental

IMPLEMENTING GASB STATEMENT NO. 75 ACCOUNTING AND FINANCIAL REPORTING FOR POSTEMPLOYMENT BENEFITS OTHER THAN PENSIONS

IMPLEMENTING GASB STATEMENT NO. 75 ACCOUNTING AND FINANCIAL REPORTING FOR POSTEMPLOYMENT BENEFITS OTHER THAN PENSIONS A CCMA WHITE PAPER FOR CALIFORNIA LOCAL GOVERNMENTS Issued February 2018 PUBLISHED

IMPLEMENTING GASB STATEMENT NO. 75 ACCOUNTING AND FINANCIAL REPORTING FOR POSTEMPLOYMENT BENEFITS OTHER THAN PENSIONS A CCMA WHITE PAPER FOR CALIFORNIA LOCAL GOVERNMENTS Issued February 2018 PUBLISHED

P O L I C E M E N S A N N U I T Y A N D B E N E F I T F U N D O F C H I C A G O G A S B S T A T E M E N T S N O S. 6 7 A N D 6 8 A C C O U N T I N G

P O L I C E M E N S A N N U I T Y A N D B E N E F I T F U N D O F C H I C A G O G A S B S T A T E M E N T S N O S. 6 7 A N D 6 8 A C C O U N T I N G A N D F I N A N C I A L R E P O R T I N G F O R P E

P O L I C E M E N S A N N U I T Y A N D B E N E F I T F U N D O F C H I C A G O G A S B S T A T E M E N T S N O S. 6 7 A N D 6 8 A C C O U N T I N G A N D F I N A N C I A L R E P O R T I N G F O R P E

GASB: What Legislative Staff Need to Know

GASB: What Legislative Staff Need to Know Fiscal Analysts Seminar Dean Michael Mead October 22, 2014 The views expressed in this presentation are those of Mr. Mead. Official positions of the GASB on accounting

GASB: What Legislative Staff Need to Know Fiscal Analysts Seminar Dean Michael Mead October 22, 2014 The views expressed in this presentation are those of Mr. Mead. Official positions of the GASB on accounting

If you have questions or require additional assistance, please contact TMRS at or to

July 11, 2018 Finance Director City of McKinney P.O. Box 517 McKinney, TX 75070-0517 City # 00830 Subject: 2018 Governmental Accounting Standards Board (GASB) Employer Reporting Package For Pensions (GASB

July 11, 2018 Finance Director City of McKinney P.O. Box 517 McKinney, TX 75070-0517 City # 00830 Subject: 2018 Governmental Accounting Standards Board (GASB) Employer Reporting Package For Pensions (GASB

City of Richmond Heights Policemen s and Firemen s Retirement Fund GASB Statement No. 68 Employer Reporting Accounting Schedules July 1, 2017

City of Richmond Heights Policemen s and Firemen s Retirement Fund GASB Statement No. 68 Employer Reporting Accounting Schedules July 1, 2017 December 20, 2017 Board of Trustees City of Richmond Heights

City of Richmond Heights Policemen s and Firemen s Retirement Fund GASB Statement No. 68 Employer Reporting Accounting Schedules July 1, 2017 December 20, 2017 Board of Trustees City of Richmond Heights

Re: Exposure Draft on Pension Accounting and Financial Reporting by Employers

October 4, 2011 Director of Research and Technical Activities Project No. E-34 Governmental Accounting Standards Board 401 Merritt 7, PO Box 5116 Norwalk, CT 06856-5116 director@gasb.org Re: Exposure Draft

October 4, 2011 Director of Research and Technical Activities Project No. E-34 Governmental Accounting Standards Board 401 Merritt 7, PO Box 5116 Norwalk, CT 06856-5116 director@gasb.org Re: Exposure Draft

Subject: 2016 Governmental Accounting Standards Board (GASB) Employer Reporting Package. Based on the Actuarial Valuation dated December 31, 2015

Employer Reporting Package. Based on the Actuarial Valuation dated December 31, 2015") July 15, 2016 Finance Director City of Plano P.O. Box 860358 Plano, TX 75086-0358 City No. 01010 Subject: 2016 Governmental Accounting Standards Board (GASB) Employer Reporting Package Dear Finance Director:

July 15, 2016 Finance Director City of Plano P.O. Box 860358 Plano, TX 75086-0358 City No. 01010 Subject: 2016 Governmental Accounting Standards Board (GASB) Employer Reporting Package Dear Finance Director:

SPRINGFIELD FIREFIGHTERS PENSION FUND

Lauterbach & Amen, LLP 27W457 Warrenville Road Warrenville, IL 60555-3902 Actuarial Valuation as of March 1, 2017 SPRINGFIELD FIREFIGHTERS PENSION FUND GASB 67/68 Reporting LAUTERBACH & AMEN, LLP Actuarial

Lauterbach & Amen, LLP 27W457 Warrenville Road Warrenville, IL 60555-3902 Actuarial Valuation as of March 1, 2017 SPRINGFIELD FIREFIGHTERS PENSION FUND GASB 67/68 Reporting LAUTERBACH & AMEN, LLP Actuarial

TOWN OF TEMPLETON, MASSACHUSETTS MUNICIPAL WATER DEPARTMENT Financial Statements June 30, 2016 and 2015

Financial Statements June 30, 2016 and 2015 TABLE OF CONTENTS Page Independent Auditors' Report 1,2 Management s Discussion and Analysis 3-5 Financial Statements: Statements of Net Position 6,7 Statements

Financial Statements June 30, 2016 and 2015 TABLE OF CONTENTS Page Independent Auditors' Report 1,2 Management s Discussion and Analysis 3-5 Financial Statements: Statements of Net Position 6,7 Statements

The opinions expressed in this presentation are those of Mrs. Parker. Official positions of the GASB are established only after extensive public due

GASB Update Lisa R. Parker, CPA Project Manager, Governmental Accounting Standards Board Florida Institute of CPA s September 21, 2012 Ft. Lauderdale, Florida The opinions expressed in this presentation

GASB Update Lisa R. Parker, CPA Project Manager, Governmental Accounting Standards Board Florida Institute of CPA s September 21, 2012 Ft. Lauderdale, Florida The opinions expressed in this presentation

KALKASKA COUNTY ROAD COMMISSION OPEB BENEFITS Kalkaska County Road Commission

Kalkaska County Road Commission ACCOUNTING REPORT AND VALUATION AS PROVIDED FOR UNDER THE ALTERNATE CALCULATION PROVISIONS OF GASB STATEMENTS NO. 43 & 45 For the Period January 1, 2016 to December 31,

Kalkaska County Road Commission ACCOUNTING REPORT AND VALUATION AS PROVIDED FOR UNDER THE ALTERNATE CALCULATION PROVISIONS OF GASB STATEMENTS NO. 43 & 45 For the Period January 1, 2016 to December 31,

Conduent Human Resource Services Retirement Consulting. Public Employees Retirement System of New Jersey

Conduent Human Resource Services Retirement Consulting Public Employees Retirement System of New Jersey Information Required Under Governmental Accounting Standards Board Statement No. 68 as of June 30,

Conduent Human Resource Services Retirement Consulting Public Employees Retirement System of New Jersey Information Required Under Governmental Accounting Standards Board Statement No. 68 as of June 30,

Presented by Steve Toole & Sam Watts, N.C. Department of State Treasurer

State Retirement Valuations/Annual Required Contribution Information Presented by Steve Toole & Sam Watts, N.C. Department of State Treasurer Larry Langer, Buck Consultants November 13, 2012 Agenda Overview

State Retirement Valuations/Annual Required Contribution Information Presented by Steve Toole & Sam Watts, N.C. Department of State Treasurer Larry Langer, Buck Consultants November 13, 2012 Agenda Overview

GASB 68: Bet You Can t Wait! Presenters. Agenda. Date: October 7, 2014

GASB 68: Bet You Can t Wait! Taking a closer look at GASB s new pension standards Barrie Wilkes, Mary Hill Central Michigan University Katie Thornton Plante Moran, PLLC Date: October 7, 2014 Presenters

GASB 68: Bet You Can t Wait! Taking a closer look at GASB s new pension standards Barrie Wilkes, Mary Hill Central Michigan University Katie Thornton Plante Moran, PLLC Date: October 7, 2014 Presenters