2014 CliftonLarsonAllen LLP CliftonLarsonAllen LLP. GASB Update. Greg Bussink and Sean Walker October 22, CLAconnect.

|

|

|

- Samantha Fox

- 5 years ago

- Views:

Transcription

1 2014 CliftonLarsonAllen LLP GASB Update Greg Bussink and Sean Walker October 22, 2014 CLAconnect.com

2 Effective Dates Years beginning after December 15, 2012 (June 30, 2014) Statement 65 Items Previously Reported as Assets and Liabilities Statement 66 - Technical Corrections an amendment of GASB Statements No 10 and No 62 June 15, 2013 (June 30, 2014) Statement 67 Financial Reporting for Pension Plans - an amendment of GASB Statement No 25 Statement 70 - Accounting and Financial Reporting for Nonexchange Financial Guarantees December 15, 2013 (June 30, 2015) Statement 69 - Government Combinations and Disposals of Government Operations June 15, 2014 (June 30, 2015) Statement 68 Accounting and Financial Reporting for Pension Plans - an amendment of GASB Statement No 27 Statement 71 - Pension Transition for Contributions Made Subsequent to Measurement Date - an amendment of GASB Statement No. 68 2

3 GASB No. 65 Items Previously Reported as Assets and Liabilities

4 Background Certain items previously identified as assets and liabilities are not really considered to be assets or liabilities The use of the concept of deferred inflows and outflows was established to handle these items This statement establishes those items which are now to be recast as deferred inflows and outflows

5 Deferred Inflows/Outflows Previously restricted only to use in hedging and Service Concession arrangements Deferred Outflows A consumption of net position that is applicable to a future accounting period (e.g. dfd loss on refunding) Shown as a separate category below assets Deferred Inflows An acquisition of net position that is applicable to a future accounting period (e.g. Unavailable revenue in a governmentasl fund) Shown as a separate category below liabilities

6 Areas of Specific Guidance Refundings of Debt Nonexchange transactions Sales of Future Revenues Debt issuance costs Leases Acquisition costs related to insurance activities Lending activities Mortgage Banking activities Regulated Operations Revenue recognition in governmental funds Use of the term Deferred Major Fund criteria - effects

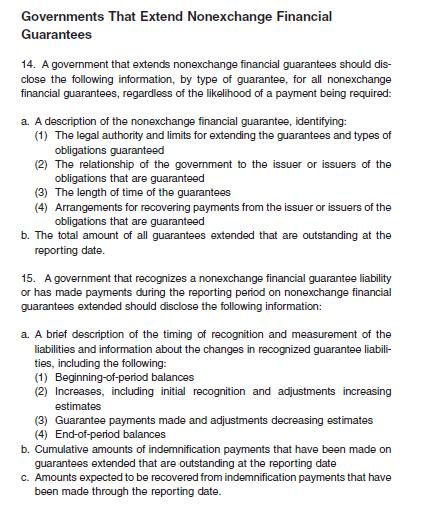

7 Specific Guidance Debt refundings Gain or Loss from a refunding resulting in a defeasance Deferred Inflow Gain Deferred Outflow - Loss Nonexchange transactions Deferred inflows when resources are received or reported as a receivable before: The period for which property taxes are levied The period when resources are required to be used or first permitted Deferred outflows are reported for resources received before time requirements are met, but eligibility requirements have been met

8 Specific Guidance (continued) Debt Issuance costs Report as a period expense when incurred, no longer amortized over the life of the debt Sale of Future Revenues Transferor reports a deferred inflow for resources in both the government-wide and fund financial statements Only exception is found in GASB 48, para 14 and has to do with revenue not previously recognized due to uncertainty of inability to measure Intra-entity sales - recognize as deferred inflow and outflow until all revenue recognition criteria met(gasb 48, para. 15)

9 Specific Guidance (continued) Leases Operating lease lessor Record initial direct costs (acquisition, legal, etc) as a period cost Sale/-Leaseback transaction Gain/loss on sale/leaseback should be recorded as either a deferred inflow or outflow, as applicable Revenue recognition in Governmental Funds Revenue not recognized because of availability criteria should be reported as deferred inflows (e.g. property taxes)

10 Specific Guidance (continued) Use of the term Deferred in GASB financial statements Limited only to use in connection with Deferred Inflows and Deferred Outflows Major Fund Criteria Utilize deferred Outflows as part of assets and deferred inflows as part of liabilities in the calculations in determining major funds

11 GASB No. 66 an amendment of GASB No. 10 and 62 Technical Corrections

12 Fixed GASB No. 54, removed the limitation on using general fund or internal service fund for risk financing activities. GASB No. 62, 13, and 48. Clarified language on issues related to: Operating leases Recognition of premium or discount on purchase of loans. Servicing fees for receivables that have been sold. 12

13 GASB No. 69 Government Combinations and Disposal of Government Operations 13

14 Background APB Opinion No. 16, Business Combinations Pooling of interests Purchase method Superseded by FASB No. 141 Business Combinations Did not apply to nonprofit organizations Eliminated pooling of interests FASB No. 164 NFP Entities: Mergers and Acquisitions Governments used superseded guidance in APB Opinion No. 16 Needed some GAAP for governments

15 Scope and Applicability Establishes standards for government combinations and disposals of government operations Government merger Government acquisition Transfer of operations Transactions Combinations of legally separate entities NFP, For profit, government (new or continuing government is formed) Mergers and acquisition of activities less than the entire legally separate entity

16 Scope and Applicability (cont.) Operations integrated set of activities conducted and managed for the purpose of providing identifiable services with associated assets and liabilities Examples: fire department, golf course, parking garage, etc. Disposal of operations Statement does not apply to: Assets and liabilities not considered an operation Line items Organizations that remain legally separate (GASB 14) Equity interests in an organization (GASB 14)

17 Definitions Government merger combination of legally separate entities without significant consideration exchanged. Transfer of operations combination of operations without significant consideration Government acquisition - combination of legally separate entities or operations with significant consideration exchanged. 17

18 Consideration Assets Assumption of liabilities Contingent assets NOT assumption of negative net position 18

19 Merger Government merger combination of legally separate entities without significant consideration exchanged. Two or more are now one Pooled, but don t use the word pooled. No revaluations Test for impairment Eliminate transactions between the parties 19

20 Transfer Transfer of operations combination of operations without significant consideration Pooling with an equity modification Net position transferred is a special item 20

21 Acquisition Government acquisition - combination of legally separate entities or operations with significant consideration exchanged. Purchase method (sort of) Intangible asset (i.e. goodwill-deferred outflow) Detailed measurement rules 21

22 Measurement Rules Acquisition date Control of assets Obligated for the liabilities Acquisition value market-based entry price Price that would be paid for acquiring similar assets, having similar service capacity or discharging the liabilities assumed Exceptions OPEB, pensions, compensated absences Landfill, pollution remediation Investments Deferred inflows and outflows

23 Disposals Gain or loss should be recorded as a special item 23

24 GASB No. 70 Accounting and Financial Reporting for Nonexchange Financial Guarantees

25 Background Investors are looking for more credit enhancements and assurances on obligations Minimize the possibility of nonpayment Government often provide guarantees and receive guarantees for free Belief nonpayment is not likely Currently, a liability is recorded when It is probable the government will be required to pay and amount can be reasonability estimated

26 Scope and Applicability Government provides a financial guarantee as a nonexchange transaction Government receives a financial guarantee as a nonexchange transaction Key considerations Three legally separate entities (component units qualify) Not deemed guarantees for this statement Withholding or garnishing revenues Pledges of future revenues Joint-and-several obligations

27 Three Legally Separate Entities Obligation Holder Guarantor Issuer

28 Government as the Grantor Assess the issuer s ability pay using qualitative factors If the government is more likely than not required to pay the issuer s debt, then book it More than 50% likelihood Book - The discounted present value of expected cash flows as the result of the guarantee, or If cash flows are within a range, the discounted present value of the minimum expected cash flows (low part of the range)

29 Qualitative Factors Bankruptcy or financial reorganizations Breach of debt contract Covenants Coverage ratios Default Other financial difficulty indicators Loss of major revenue source Debt holder concessions Using earmarked funding to pay debt

30 Book It Journal entry DR: Expense/Expenditures CR: Nonexchange Financial Guarantee Government-wide Financial Statements, and Fund Financial Statement to the extent the liability is normally expected to be liquidated with expendable available financial resources.

31 Government as a Guarantor to a Group You could analyze individually, or You could analyze as a group using qualitative factor of the group - Historical trends Economic factors Etc. May book a liability similar to an allowance on bad debt, historical trends

32 Practical Timing Issue The process should be ongoing and the books and records should be adjusted when the government becomes more likely than not to pay the debt of the issuer.

33 Disclosures 2014 CliftonLarsonAllen LLP

34 Government as Issuer Footnote disclosure explaining the guarantee If the government is required to repay the guarantor, then the liability should be reclassified as a liability to guarantor when the guarantor begins to pay the debt. If the government is legally released from the debt, a revenue is recognized for guarantor s assumption of the liability.

35 Disclosure 2014 CliftonLarsonAllen LLP

36 Intra-Entity Primary government guarantees a blended component unit s debt Blended component unit guarantees a primary government's debt Blended component unit guarantees another blended component unit A receivable should be booked in the amount of the liability booked by the guarantor.

37 GASB No. 67 Financial Reporting for Pension Plans

38 Scope and Applicability Replaces previous guidance under GASB No. 25, Financial Reporting for Defined Pension Plans and Note Disclosures Establishes financial reporting standards for pension plans administered through trusts in which: Contributions to the plans and related earnings are irrevocable Plan assets are dedicated to providing pensions to plan members in accordance with benefit terms Plan assets are legally protected from creditors of employers, nonemployer contributing entities and plan administrators Applicable for defined benefit plans and defined contribution plans Does not include OPEB plans

39 Defined Benefit Pension Plans Recognition, measurement and presentation of the financial statement amounts generally similar to current guidance Incorporates deferred outflows of resources and deferred inflows of resources, where applicable

40 Defined Benefit Pension Plans (continued) Required Financial Statements Statement of Fiduciary Net Position Assets + Dfd Outflows Liabilities Dfd Inflows = Fiduciary Net Position Statement of Changes in Fiduciary Net Position

41 Defined Benefit Pension Plans (continued) Notes to the Financial Statements: Plan description Allocated insurance contracts excluded from plan assets Plan investments, including investment policy, determination of fair value, annual money-weighted rate of return and identification of investments that represent 5% or more of plan net position Receivables - terms of any long term contracts for contributions to the plan Deferred retirement option program (DROP) balances Policy for reserves of plan net position

42 Defined Benefit Pension Plans (continued) Notes to the Financial Statements: Components of the net pension liability, including Total pension liability Pension plan s fiduciary net position Net pension liability Pension plan s fiduciary net position as a percentage of total pension liability Significant assumptions used to measure the total pension liability Date of actuarial valuation and if applicable, disclosure that roll forward procedures were used to roll forward the total pension liability from the actuarial valuation date to the plan s fiscal year end

43 Defined Benefit Pension Plans (continued) Required Supplementary Information: 10 year schedule of Changes in net pension liability Net pension liability Contributions Annual money weighted rate of return Encouraged to present all years retroactively in implementation year If retroactive information is not available for all 10 years, only include those years where information is available in transition year and until 10 yrs of such information is available Notes to the Required Schedules: Significant methods and assumptions used in calculating the actuarially determined contributions

44 Schedule of Changes in Net Pension Liability Last 10 Fiscal Years Schedules of Required Supplementary Information SCHEDULE OF CHANGES IN THE SCHOOL DISTRICTS NET PENSION LIABILITY Last 10 Fiscal Years 2014 CliftonLarsonAllen LLP

45 Schedule of Net Pension Liability Last 10 Fiscal Years SCHEDULE OF THE SCHOOL DISTRICTS NET PENSION LIABILITY Last 10 Fiscal Years (Dollar amounts in thousands) 2014 CliftonLarsonAllen LLP

46 Schedule of Contributions Last 10 Fiscal Years SCHEDULE OF SCHOOL DISTRICTS CONTRIBUTIONS Last 10 Fiscal Years (Dollar amounts in thousands)

47 Schedule of Investment Returns Last 10 Fiscal Years SCHEDULE OF INVESTMENT RETURNS Last 10 Fiscal Years

48 Defined Benefit Pension Plans (continued) Net Pension Liability Total pension liability, net of plan s fiduciary net position Measurement of Total Pension Liability Timing and frequency of actuarial valuations As of plan s most recent fiscal year end or The use of update procedures to roll forward to plan s most recent fiscal year end from actuarial valuation Actuarial valuation date can be no more than 24 months prior to plan s fiscal year end

49 Defined Benefit Pension Plans (continued) Measurement of Total Pension Liability Discount rate Long term expected rate of return on investments that are expected to be used to finance payment of benefits, to the extent that net position is sufficient to make projected benefits and assets are invested using a strategy to achieve that return, Yield or index rate for 20 yr, tax exempt general obligation municipal bonds with an average rating of AA/Aa or higher to the extent the conditions used for the long term expected rate of return are not met. Actuarial cost method Entry age actuarial cost method should be used to attribute the actuarial present value of projected benefit payments to periods

50 Defined Contribution Plans Footnote disclosures should include: Identification of the pension plan as a defined contribution pension plan Classes of members covered Number of plan members Participating employers for multiple-employer plans Nonemployer contributing entities, if applicable The authority under which the plan is established or may be amended.

51 Additional Resources GASB Toolkit (available at the GASB website) Guide to Implementation of GASB Statement 67 on Financial Reporting for Pension Plans Podcast discussing the types of pension plans affected by Statement 67 and most significant changes Article on the key implementation issues Summary and Full Text of Statement 67

52 GASB No. 68 Accounting and Financial Reporting for Pension Plans 52

53 Background Part of the effort which goes back to GASB 34 to make government statements more usable, comparable and on par with the corporate world Investors understand full accrual accounting and get confused with multiple levels of government reporting Gives a better perspective as to both financial position and financial condition

54 Scope and Applicability Applies to: Employers in single-employer and agent multipleemployer defined benefit plans Employers in cost-sharing plans Special funding situations One government makes payments on behalf of another Employers in defined contribution plans

55 Defined Benefit Pensions Employer liability Current: Difference between the annual required contribution (ARC) and actual contributions = Net pension obligation Only record a liability if required funding not made New: Difference between the total pension liability and the fiduciary net position = Net pension liability Record net liability of the governmental entity Measured as of a date no earlier than the end of the employer s prior fiscal year (measurement date)

56 Defined Benefit Plans (continued) Changes in the pension liability Service cost, interest on the pension liability and changes in benefit terms Recorded as pension expense immediately Changes in economic and demographic assumptions and differences between economic and demographic assumptions and actual experience Amortized over a closed period equal to the average remaining service period for plan members Current portion recorded as pension expense Remaining portion recorded as deferred outflows or deferred inflows of resources

57 Defined Benefit Plans (continued) Changes in the pension liability (continued) Differences between expected and actual rates of investment returns Amortized over a closed 5 year period (including current period) Current portion recorded as pension expense Remaining portion recorded as deferred outflows or deferred inflows of resources Employer contributions made subsequent to the measurement date of the net pension liability are recorded as deferred outflows of resources

58 Defined Benefit Plans (continued) Actuarial valuations Required at least every two years Total pension liability should be determined by An actuarial valuation as of the measurement date which must be within 1 year and 1 day of the report date or The use of update procedures to roll forward from the actuarial valuation to the measurement date no more than 30 months and 1 day before employers year end Entry age method only Consistency multiple methods no longer accepted No tie to actuarial method used for funding Service cost determined as a percentage of pay

59 Timing of Measurement of Total Pension Liability Pension Expense (measurement period) Deferred Outflows of Resources Plan Prior Year-End Employer Prior Year-End Plan Current Year-End Employer Current Year-End Measurement Date June 2014 December 2014 June 2015 December 2015 Measurement date will most likely correspond to year-end of plan. Employer contributions made directly by the employer subsequent to the measurement date of the net pension liability and before the end of the employer s fiscal year should be recognized as a deferred outflow of resources. 59

60 Example Impact of Using Prior Year Measurement Date Pension Expense (measurement period) Deferred Outflows of Resources Employer Prior Year-End Employer Current Year-End Plan Year-End Plan Year-End Measurement Date June 2013 June 2014 June

61 Example Impact of Using Current Year Measurement Date Pension Expense (measurement period) Employer Prior Year-End Employer Current Year-End Plan Year-End Plan Year-End Plan Year-End June 2013 June 2014 Measurement Date June

62 Projection of Benefit Payments Projections Include: Automatic cost of living adjustments (COLAs) and other automatic retroactive benefit changes Ad hoc COLAs and ad hoc retroactive benefit changes substantively automatic Projected future salary increases if benefit formula is based on future levels Projected future service credits (when determining probability of eligibility for benefits and when formula is based on years of service)

63 New Blended Discount Rate Single rate reflective of: Long-term expected rate of return to extent plan net position for specified source is: Projected sufficient to make benefit payments Expected to be invested using long-term investment strategy Otherwise, index rate for a tax-exempt 20-year GO rated AA/Aa (or equivalent) or higher

64 Example Scenario- Discount Rate Current Situation 8% discount rate, same as historical rate of return 75% funded plan 20 year GO rate is 4%

65 Example Scenario- Discount Rate (cont d) New Calculation: Blended rate Calculation Step Funded % X Historical Rate of Return Unfunded % X Tax Exempt 20yr Rate Example 75% X 8% 6% 25% X 4% 1% Blended Discount Rate 6% + 1% = 7%

66 Discount rate calculation Projected Benefit Payments Actuarial Present Values of Projected Benefit Payments Year (a) Projected Beginning Fiduciary Net Position (b) Projected Benefit Payments (c) "Funded" Portion of Benefit Payments (d) "Unfunded" Portion of Benefit Payments (e) Present Value of "Funded" Benefit Payments (f) = (d) ( %) (a) Present Value of "Unfunded" Benefit Payments (g) = (e) (1 + 4%) (a) Present Value of Benefit Payments Using the Single Discount Rate (h) = (c) ( %) (a) $ 1,431,956 $ 109,951 $ 109,951 $ - $ 102,280 $ - $ 104,427 1,500, , , , ,088 1,565, , ,749-99, ,019 1,628, , ,690-98, ,154 1,687, , ,229-97, ,370 1,742, , ,168-96, ,487 1,792, , ,466-95, ,468 1,835, , ,332-94, ,450 1,871, , ,591-93, ,302 1,898, , ,069-91, ,918 The sum of the present values of the two benefit payment streams is calculated. 547, , ,779-49,236-84, , , , ,175 81,140 64, , , ,713 77, , , ,032 74, , , ,135 70, Total $ 2,109,333 + $ 1,724,534 = $ 3,833,867 66

67 Cost Sharing Plans Cost Sharing Employers Current: New: Liability recorded only if the actual employer contribution is less than annual required contribution Expense is equal to annual required contribution Liability is equal to the employers proportionate share of the total net pension liability of all participating employers Will now allow readers to determine overall liabilities currently not easily determinable More pressure to adequately fund Expense is equal to the employer s proportionate share of the pension expense of all participating employers Both liability and expense are reported as of the date reported by the plan No need to adjust/rollforward to actual report date of the government

68 Cost Sharing Plans (continued) Employer s recognize their proportionate share of collective: Net pension liability Pension expense Deferred outflows of resources Deferred inflows of resources This will provide audit challenges

69 Special Funding Situations Nonemployer entity legally responsible for making contributions directly to a pension plan for the employees of another entity and either: The amount of contributions for which the nonemployer entity legally is responsible is not dependent upon one or more events unrelated to pensions or The nonemployer is the only entity with a legal obligation to make contributions directly to the pension plan Nonemployer contributor accounting patterned on accounting for employers in cost-sharing plans

70 Defined Contribution Plans No significant changes Expense Amount of contributions (employee and employer) to the employee accounts, net of forfeited amounts Liability Difference between the amount of the expense recorded and amount paid to the plan

71 Note Disclosures Description of the Plan Assumptions Used to Measure Total Pension Liability Brief Description of Changes in Benefit Terms and Assumptions that Affect Measurement of Total Pension Liability

72 Required Supplementary Information Single Employer Plan SCHEDULE OF CHANGES IN THE COUNTY S NET PENSION LIABILITY AND RELATED RATIOS Last 10 Fiscal Years

73 Required Supplementary Information Single Employer Plan (continued) SCHEDULE OF COUNTY CONTRIBUTIONS Last 10 Fiscal Years

74 Required Supplementary Information Cost-Sharing Employer Plan SCHEDULE OF THE DISTRICT S PROPORTIONATE SHARE OF THE NET PENSION LIABILITY Teachers Pension Plan Last 10 Fiscal Years*

75 Required Supplementary Information Cost-Sharing Employer Plan (continued) SCHEDULE OF DISTRICT CONTRIBUTIONS Teachers Pension Plan Last 10 Fiscal Years

76 Required Supplementary Information Special Funding Situation SCHEDULE OF THE DISTRICT S PROPORTIONATE SHARE OF THE NET PENSION LIABILITY Teachers Pension Plan Last 10 Fiscal Years*

77 Required Supplementary Information Special Funding Situation (Continued) SCHEDULE OF THE DISTRICT CONTRIBUTIONS Teachers Pension Plan Last 10 Fiscal Years*

78 Required Supplementary Information Special Funding Situation: Nonemployer Contributing Entity SCHEDULE OF THE STATE S PROPORTIONATE SHARE OF THE NET PENSION LIABILITY Teachers Pension Plan Last 10 Fiscal Years*

79 Required Supplementary Information Special Funding Situation: Nonemployer Contributing Entity (continued) SCHEDULE OF THE STATE CONTRIBUTIONS Teachers Pension Plan Last 10 Fiscal Years*

80 Additional Guidance AICPA White Paper: Governmental Employer Participation in Cost-Sharing Multiple-Employer Plans: Issues Related to Information for Employer Reporting Provides guidance on employer challenges related to recognizing proportionate share of collective pension amounts and related auditor issues Recommends cost-sharing plans calculate each employer s allocation percentage and collective pension amounts Prepare a Schedule of Employer Contributions and related Notes to the Schedule Plan engage its auditor to form an opinion on the schedule in accordance with AU-C section 805, Special Considerations Audits of Single Financial Statements and Specific Elements, Accounts, or Items of a Financial Statement

81 Additional Guidance (continued) GASB Toolkit (available at the GASB website) Guide to Implementation of GASB Statement 68 on Accounting and Financial Reporting for Pensions Videos outlining key issues, discussing stakeholder outreach, and top implementation issues Podcasts discussing the most significant changes to accounting and financial reporting for pensions Background documents and fact sheets A Setting the Record Straight document addressing common misperceptions about the new pension standards

82 GASB No. 71 Pension Transition for Contributions Made Subsequent to the Measurement Date

83 Background GASB 68 requires: Recognition of a net pension liability measured as of a date no earlier than the end of its prior fiscal year If a contribution is made between the measurement date and the end of the reporting period, its recognized as a deferred outflow of resources Recognition of deferred outflows and inflows of resources for other pension-related events Differences arising between expected and actual experience in relation to economic and/or demographic factors Effects of changes of assumptions about future economic or demographic factors Differences between projected and actual investment earnings

84 Background (continued) At transition, if it s not practical to determine the amounts of all deferred inflows and outflows of resources related to pensions, no beginning balances for deferred inflows and outflows be reported Potential for significant misstatement of beginning net position and subsequent expense in accrual based statements if the employer does not recognize its contributions made after the measurement date of the beginning net pension liability as deferred outflows of resources at transition

85 Summary When it s not practical to determine all amounts of deferred inflows and outflows of resources related to pensions, GASB 71 states: Employers should recognize a beginning deferred outflow of resources for pension contributions, if any made subsequent to the measurement date of the beginning net pension liability No beginning balances for other deferred inflows and outflows of resources related to pensions should be recognized

86 2014 CliftonLarsonAllen LLP Greg Bussink, CPA, CGFM Principal, State and Local Government Sean Walker, CPA, CGFM, CGMS Principal, State and Local Government CLAconnect.com twitter.com/ CLAconnect facebook.com/ cliftonlarsonallen linkedin.com/company/ cliftonlarsonallen 86

2014 CliftonLarsonAllen LLP. GASB Update. May 20, CLAconnect.com

GASB Update May 20, 2014 CLAconnect.com Effective Dates Years beginning after December 15, 2012 (June 30, 2014) Statement 65 Items Previously Reported as Assets and Liabilities Statement 66 - Technical

GASB Update May 20, 2014 CLAconnect.com Effective Dates Years beginning after December 15, 2012 (June 30, 2014) Statement 65 Items Previously Reported as Assets and Liabilities Statement 66 - Technical

GASB 68 Implementation (The time is now upon us)

") GASB 68 Implementation (The time is now upon us) Maryland Association of Certified Public Accountants April 17, 2015 CLAconnect.com GASB No. 68 Accounting and Financial Reporting for Pension Plans Effective

GASB 68 Implementation (The time is now upon us) Maryland Association of Certified Public Accountants April 17, 2015 CLAconnect.com GASB No. 68 Accounting and Financial Reporting for Pension Plans Effective

GASB Update. Rob Churchman, Partner. April 9, 2013

GASB Update Rob Churchman, Partner April 9, 2013 Agenda GASB 60: Service Concession Arrangements GASB 61: The Financial Reporting Entity GASB 62 & 66: Pre-1989 FASB/AICPA Pronouncements & Technical Corrections

GASB Update Rob Churchman, Partner April 9, 2013 Agenda GASB 60: Service Concession Arrangements GASB 61: The Financial Reporting Entity GASB 62 & 66: Pre-1989 FASB/AICPA Pronouncements & Technical Corrections

Governmental Accounting Standards Board (GASB) Updates. Summary of GASB Updates

Updates. Summary of GASB Updates") Governmental Accounting Standards Board (GASB) Updates Effective Dates Recently Issued GASB Standards June 30, 2013 GASB Statement No. 60, Accounting and Financial Reporting for Service Concession Arrangements*

Governmental Accounting Standards Board (GASB) Updates Effective Dates Recently Issued GASB Standards June 30, 2013 GASB Statement No. 60, Accounting and Financial Reporting for Service Concession Arrangements*

GASB Review Session Handout

GASB Review Session Handout 56th County Auditors Institute Austin, Texas May 15, 2014 PATTILLO, BROWN & HILL, L.L.P. Paula Lowe, CPA Johnasan Gregory, CPA GASB Concepts Statement No. 4, Elements of Financial

GASB Review Session Handout 56th County Auditors Institute Austin, Texas May 15, 2014 PATTILLO, BROWN & HILL, L.L.P. Paula Lowe, CPA Johnasan Gregory, CPA GASB Concepts Statement No. 4, Elements of Financial

Government Accounting Standards Board Update. GASB 65 Through GASB 70: How Do These Statements Affect Public Ports in Washington?

Government Accounting Standards Board Update GASB 65 Through GASB 70: How Do These Statements Affect Public Ports in Washington? Introduction FOX & COMPANY CPAs, LLC George@cpafox.net (360) 597-0400 GASB:

Government Accounting Standards Board Update GASB 65 Through GASB 70: How Do These Statements Affect Public Ports in Washington? Introduction FOX & COMPANY CPAs, LLC George@cpafox.net (360) 597-0400 GASB:

GASB Update. Presented by: Miller Edwards, CPA of Mauldin & Jenkins, LLC

Presented by: Miller Edwards, CPA of Mauldin & Jenkins, LLC medwards@mjcpa.com 2013 GGFOA Annual Conference Legacy Lodge & Conference Center Lake Lanier Islands Resort September 30, 2013 The materials

Presented by: Miller Edwards, CPA of Mauldin & Jenkins, LLC medwards@mjcpa.com 2013 GGFOA Annual Conference Legacy Lodge & Conference Center Lake Lanier Islands Resort September 30, 2013 The materials

GASB Update. Presented by: Craig Moye, CPA of Mauldin & Jenkins, LLC

Presented by: Craig Moye, CPA of Mauldin & Jenkins, LLC cmoye@mjcpa.com 2013 GGFOA Annual Conference Legacy Lodge & Conference Center Lake Lanier Islands Resort September 30, 2013 The materials & oral

Presented by: Craig Moye, CPA of Mauldin & Jenkins, LLC cmoye@mjcpa.com 2013 GGFOA Annual Conference Legacy Lodge & Conference Center Lake Lanier Islands Resort September 30, 2013 The materials & oral

Implementing GASB 75 Accounting and financial reporting for other post-employment benefits

Implementing GASB 75 Accounting and financial reporting for other post-employment benefits Judy McNeal, Chief Financial Officer KPERS Michele Stromp, Partner KPMG LLP Julie Barrientos, Director KPMG LLP

Implementing GASB 75 Accounting and financial reporting for other post-employment benefits Judy McNeal, Chief Financial Officer KPERS Michele Stromp, Partner KPMG LLP Julie Barrientos, Director KPMG LLP

GASB STATEMENTS AND EFFECTIVE DATES

1 Authoritative Status of NCGA On issuance July 1984 Pronouncements and AICPA Industry Audit Guide 2 Financial Reporting of Deferred Financial statements for periods ending after 12/15/86 Compensation

1 Authoritative Status of NCGA On issuance July 1984 Pronouncements and AICPA Industry Audit Guide 2 Financial Reporting of Deferred Financial statements for periods ending after 12/15/86 Compensation

State Association of County Auditors GASB Update

State Association of County Auditors GASB Update The views expressed in this presentation are those of Mr. Sundstrom. Official positions of the GASB are determined only after extensive due process and

State Association of County Auditors GASB Update The views expressed in this presentation are those of Mr. Sundstrom. Official positions of the GASB are determined only after extensive due process and

ANNUAL STATE AND LOCAL GOVERNMENT ACCOUNTING UPDATE WHAT S NEW AND WHAT S NEXT? 4/17/18

ANNUAL STATE AND LOCAL GOVERNMENT ACCOUNTING UPDATE WHAT S NEW AND WHAT S NEXT? 4/17/18 Today s presenter Michelle Horaney Partner, National Professional Standards Group/National Leader for Education RSM

ANNUAL STATE AND LOCAL GOVERNMENT ACCOUNTING UPDATE WHAT S NEW AND WHAT S NEXT? 4/17/18 Today s presenter Michelle Horaney Partner, National Professional Standards Group/National Leader for Education RSM

Government Combinations and Disposals of Government Operations

What s Next?! Government Combinations and Disposals of Government Operations Why issue GASB 69? Effective for periods beginning after December 15, 2015, applied on a prospective basis. Early adoption

What s Next?! Government Combinations and Disposals of Government Operations Why issue GASB 69? Effective for periods beginning after December 15, 2015, applied on a prospective basis. Early adoption

The opinions expressed in this presentation are those of Mrs. Parker. Official positions of the GASB are established only after extensive public due

GASB Update Lisa R. Parker, CPA Project Manager, Governmental Accounting Standards Board Florida Institute of CPA s September 21, 2012 Ft. Lauderdale, Florida The opinions expressed in this presentation

GASB Update Lisa R. Parker, CPA Project Manager, Governmental Accounting Standards Board Florida Institute of CPA s September 21, 2012 Ft. Lauderdale, Florida The opinions expressed in this presentation

GASB Issues Final Rules Governing Reporting for Postemployment Benefits Other Than Pensions

GASB Issues Final Rules Governing Reporting for Postemployment Benefits Other Than Pensions Table of Contents EXECUTIVE SUMMARY... 3 GASB 75 EMPLOYER STANDARD... 5 BACKGROUND & IMPACT OF CHANGE... 5 SCOPE...

GASB Issues Final Rules Governing Reporting for Postemployment Benefits Other Than Pensions Table of Contents EXECUTIVE SUMMARY... 3 GASB 75 EMPLOYER STANDARD... 5 BACKGROUND & IMPACT OF CHANGE... 5 SCOPE...

GASB Update. Louisiana Association of School Business Officials March 19, 2015

GASB Update Louisiana Association of School Business Officials March 19, 2015 GAO Green Book Out-of-date (last issued in November 1999) Desire to harmonize Green Book with the updated COSO framework Retains

GASB Update Louisiana Association of School Business Officials March 19, 2015 GAO Green Book Out-of-date (last issued in November 1999) Desire to harmonize Green Book with the updated COSO framework Retains

GASB UPDATE. Kathryn Barrett, CPA Freed Maxick CPAs, PC Alexandria Battaglia, CPA R.S. Abrams & Co., LLP

GASB UPDATE Kathryn Barrett, CPA Freed Maxick CPAs, PC Alexandria Battaglia, CPA R.S. Abrams & Co., LLP 1 Effective for June 30, 2018 Statement No. 75 OPEB (employers) Statement No. 81 Irrevocable Split

GASB UPDATE Kathryn Barrett, CPA Freed Maxick CPAs, PC Alexandria Battaglia, CPA R.S. Abrams & Co., LLP 1 Effective for June 30, 2018 Statement No. 75 OPEB (employers) Statement No. 81 Irrevocable Split

GASB Update. Walker Wilkerson, CPA, MBA, Partner. Statements No cliftonlarsonallen.com CliftonLarsonAllen LLP

GASB Update Statements No. 63-70 Walker Wilkerson, CPA, MBA, Partner cliftonlarsonallen.com Learning Objectives Discuss the details of GASB No. 63 and 65, Deferred inflows, outflows, and net position.

GASB Update Statements No. 63-70 Walker Wilkerson, CPA, MBA, Partner cliftonlarsonallen.com Learning Objectives Discuss the details of GASB No. 63 and 65, Deferred inflows, outflows, and net position.

GASB Standards Update

GASB Standards Update Nathan Baldermann, CPA, CGFM Governmental Training Series June 17, 2015 - Gem Theatre, Detroit Session Outline Newly issued standards Newly effective standards Upcoming standards

GASB Standards Update Nathan Baldermann, CPA, CGFM Governmental Training Series June 17, 2015 - Gem Theatre, Detroit Session Outline Newly issued standards Newly effective standards Upcoming standards

Governmental GAAP Edition. Warren Ruppel

Governmental GAAP 2016 Edition Warren Ruppel Chapter 1 New Developments... 1 Introduction... 1 Recently Issued GASB Statements and Their Effective Dates... 1 Exposure Drafts... 1 Exposure Draft Implementation

Governmental GAAP 2016 Edition Warren Ruppel Chapter 1 New Developments... 1 Introduction... 1 Recently Issued GASB Statements and Their Effective Dates... 1 Exposure Drafts... 1 Exposure Draft Implementation

May 28, 2014 Comments Due: August 29, Proposed Statement of the Governmental Accounting Standards Board

May 28, 2014 Comments Due: August 29, 2014 Proposed Statement of the Governmental Accounting Standards Board Accounting and Financial Reporting for Pensions and Financial Reporting for Pension Plans That

May 28, 2014 Comments Due: August 29, 2014 Proposed Statement of the Governmental Accounting Standards Board Accounting and Financial Reporting for Pensions and Financial Reporting for Pension Plans That

AUDITOR S RESPONSIBILITY UNDER AUDITING STANDARDS GENERALLY ACCEPTED IN THE UNITED STATES OF AMERICA

Crowe Horwath LLP Independent Member Crowe Horwath International Board of Trustees Gavilan Joint Community College District Gilroy, California Professional standards require that we communicate certain

Crowe Horwath LLP Independent Member Crowe Horwath International Board of Trustees Gavilan Joint Community College District Gilroy, California Professional standards require that we communicate certain

Summary of GASB Updates Effective Dates Recently Issued GASB Standards June 30, 2012

Effective Dates Recently Issued GASB Standards June 30, 2012 GASB Statement No. 64, Derivative Instruments: Application of Hedge Accounting Termination Provisions Effective Dates Recently Issued GASB Standards

Effective Dates Recently Issued GASB Standards June 30, 2012 GASB Statement No. 64, Derivative Instruments: Application of Hedge Accounting Termination Provisions Effective Dates Recently Issued GASB Standards

GASB & AUDIT UPDATE NOVEMBER 2018

GASB & AUDIT UPDATE NOVEMBER 2018 Alaska Government Finance Officers Association BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited

GASB & AUDIT UPDATE NOVEMBER 2018 Alaska Government Finance Officers Association BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited

Governmental Audit & Accounting Update

Presented by: Miller Edwards, CPA of Mauldin & Jenkins, LLC medwards@mjcpa.com October 14, 2014-10:50 am 11:402013 am GGFOA Annual Conference Legacy Lodge & Conference Center Lake Lanier Islands Resort

Presented by: Miller Edwards, CPA of Mauldin & Jenkins, LLC medwards@mjcpa.com October 14, 2014-10:50 am 11:402013 am GGFOA Annual Conference Legacy Lodge & Conference Center Lake Lanier Islands Resort

October 13, Dear Mr. Bean:

October 13, 2011 Deloitte & Touche LLP 10 Westport Road P.O. Box 820 Wilton, CT 06897-0820 USA Tel: +1 203 761 3000 Fax: +1 203 834 2200 www.deloitte.com Mr. David R. Bean Director of Research and Technical

October 13, 2011 Deloitte & Touche LLP 10 Westport Road P.O. Box 820 Wilton, CT 06897-0820 USA Tel: +1 203 761 3000 Fax: +1 203 834 2200 www.deloitte.com Mr. David R. Bean Director of Research and Technical

Governmental GAAP Edition. Warren Ruppel

Governmental GAAP 2017 Edition Warren Ruppel Chapter 1 New Developments... 1 Introduction... 1 Recently Issued GASB Statements and Their Effective Dates... 1 Exposure Drafts... 2 Exposure Drafts Implementation

Governmental GAAP 2017 Edition Warren Ruppel Chapter 1 New Developments... 1 Introduction... 1 Recently Issued GASB Statements and Their Effective Dates... 1 Exposure Drafts... 2 Exposure Drafts Implementation

An Overview of the New GASB Pension Accounting and Reporting Standards. Presented By: Joel Knopp, CPA

An Overview of the New GASB Pension Accounting and Reporting Standards Presented By: Joel Knopp, CPA GASB Pension Accounting Standards GASB Resources: Statement 67 (plans) Statement 68 (employers) Statement

An Overview of the New GASB Pension Accounting and Reporting Standards Presented By: Joel Knopp, CPA GASB Pension Accounting Standards GASB Resources: Statement 67 (plans) Statement 68 (employers) Statement

GASB Update Florida School Finance Officers Association June 12, 2018

GASB Update Florida School Finance Officers Association June 12, 2018 2017 Becker Professional Education Corporation. All rights reserved. The copyright in this material is owned by Becker Professional

GASB Update Florida School Finance Officers Association June 12, 2018 2017 Becker Professional Education Corporation. All rights reserved. The copyright in this material is owned by Becker Professional

GASB Statement No. 75: Accounting and Financial Reporting for Postemployment Benefits Other Than Pensions

GASB Statement No. 75: Accounting and Financial Reporting for Postemployment Benefits Other Than Pensions April 4, 2017 The webinar will begin at 12:30 pm CT. Tara Laughlin, CPA, CGFM Senior Manager, Assurance

GASB Statement No. 75: Accounting and Financial Reporting for Postemployment Benefits Other Than Pensions April 4, 2017 The webinar will begin at 12:30 pm CT. Tara Laughlin, CPA, CGFM Senior Manager, Assurance

Implementing the New Pension Accounting Rules for Public Pension Plans

Implementing the New Pension Accounting Rules for Public Pension Plans William G. Karbon, MSPA, CPC Sr. Vice President, Dir. of Compliance CBIZ Benefits & Insurance Services, Inc. Lawrenceville, NJ What

Implementing the New Pension Accounting Rules for Public Pension Plans William G. Karbon, MSPA, CPC Sr. Vice President, Dir. of Compliance CBIZ Benefits & Insurance Services, Inc. Lawrenceville, NJ What

The City of Alpharetta, Georgia

The City of Alpharetta, Georgia Presented by: Engagement Team. Overview of: PURPOSE OF AUDITORS DISCUSSION & ANALYSIS o Independent Auditor s Report o Financial Statements and Footnotes and Supplementary

The City of Alpharetta, Georgia Presented by: Engagement Team. Overview of: PURPOSE OF AUDITORS DISCUSSION & ANALYSIS o Independent Auditor s Report o Financial Statements and Footnotes and Supplementary

What you should know about the new Other Postemployment Benefits (OPEB) standard (GASB 75) WGFOA Spring Conference April 19, 2018

standard (GASB 75) WGFOA Spring Conference April 19, 2018") What you should know about the new Other Postemployment Benefits (OPEB) standard (GASB 75) WGFOA Spring Conference April 19, 2018 Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an independently

What you should know about the new Other Postemployment Benefits (OPEB) standard (GASB 75) WGFOA Spring Conference April 19, 2018 Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an independently

Accounting Update: GASB/FASB/AICPA/COSO

1 Accounting Update: GASB/FASB/AICPA/COSO American Association of Port Authorities April 17, 2012 2 Section 1 GASB/ Nonprofit Update 3 GASB Standards-Old standards GASB Statement 54 Fund Balance Reporting

1 Accounting Update: GASB/FASB/AICPA/COSO American Association of Port Authorities April 17, 2012 2 Section 1 GASB/ Nonprofit Update 3 GASB Standards-Old standards GASB Statement 54 Fund Balance Reporting

GASB Update OPEB, Fair Value and Abatements

GASB Update OPEB, Fair Value and Abatements Rob Churchman, Partner October 23, 2015 Type of Plan Defined benefit OPEB plan Benefit after separation is defined by benefit terms May be stated as a dollar

GASB Update OPEB, Fair Value and Abatements Rob Churchman, Partner October 23, 2015 Type of Plan Defined benefit OPEB plan Benefit after separation is defined by benefit terms May be stated as a dollar

FSFOA GASB Update. November 14, 2017

FSFOA GASB Update November 14, 2017 Course Topics Investments Fair Value OPEB Tax Abatements Pension Amendments Blending Criteria Irrevocable Split Interest Agreements Asset Retirement Obligations Fiduciary

FSFOA GASB Update November 14, 2017 Course Topics Investments Fair Value OPEB Tax Abatements Pension Amendments Blending Criteria Irrevocable Split Interest Agreements Asset Retirement Obligations Fiduciary

2013 GASB Update. WVDE Office of School Finance Summer Conference. Agenda. GASB Statement No. 65. Items Previously Reported as Assets and Liabilities

2013 GASB Update WVDE Office of School Finance Summer Conference Presented by Gregory S. Allison, CPA UNC School of Government Agenda GASB Update Items Previously Reported as Assets and Liabilities (GASB

2013 GASB Update WVDE Office of School Finance Summer Conference Presented by Gregory S. Allison, CPA UNC School of Government Agenda GASB Update Items Previously Reported as Assets and Liabilities (GASB

ICCCFO FALL 2012 CONFERENCE

ICCCFO FALL 2012 CONFERENCE GASB Statement No. 68, Accounting and Financial Reporting for Pensions Frederick G. Lantz, CPA Partner-in-Charge, Government Services Sikich LLP 1415 W. Diehl Road, Suite 400

ICCCFO FALL 2012 CONFERENCE GASB Statement No. 68, Accounting and Financial Reporting for Pensions Frederick G. Lantz, CPA Partner-in-Charge, Government Services Sikich LLP 1415 W. Diehl Road, Suite 400

11/7/2018. Emily Sobczak Greene Finney, LLP November, 2018

GAAP UPDATE 2018 Emily Sobczak Greene Finney, LLP November, 2018 GAAP Update Current Topics GASB 75 OPEB Reporting for Employers GASB 81 Irrevocable Split-Interest Agreements GASB 85 Omnibus 2017 GASB

GAAP UPDATE 2018 Emily Sobczak Greene Finney, LLP November, 2018 GAAP Update Current Topics GASB 75 OPEB Reporting for Employers GASB 81 Irrevocable Split-Interest Agreements GASB 85 Omnibus 2017 GASB

WEST BAY SANITARY DISTRICT FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORT JUNE 30, 2015 * * *

WEST BAY SANITARY DISTRICT FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORT JUNE 30, 2015 * * * CHAVAN & ASSOCIATES LLP CERTIFIED PUBLIC ACCOUNTANTS 1475 SARATOGA AVE, SUITE 180 SAN JOSE, CA 95129

WEST BAY SANITARY DISTRICT FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORT JUNE 30, 2015 * * * CHAVAN & ASSOCIATES LLP CERTIFIED PUBLIC ACCOUNTANTS 1475 SARATOGA AVE, SUITE 180 SAN JOSE, CA 95129

1 NEW DEVELOPMENTS COPYRIGHTED MATERIAL

1 NEW DEVELOPMENTS Introduction 2 GASB Statement 43, Financial Reporting for Postemployment Benefit Plans other than Pension Plans and GASB Statement 45, Accounting and Financial Reporting by Employers

1 NEW DEVELOPMENTS Introduction 2 GASB Statement 43, Financial Reporting for Postemployment Benefit Plans other than Pension Plans and GASB Statement 45, Accounting and Financial Reporting by Employers

GAAP Update. Dean Michael Mead. Research Manager Governmental Accounting Standards Board. Maryland Association of CPAs April 30, 2010

GAAP Update Dean Michael Mead Research Manager Governmental Accounting Standards Board Maryland Association of CPAs April 30, 2010 The opinions expressed in this presentation are those of the presenter.

GAAP Update Dean Michael Mead Research Manager Governmental Accounting Standards Board Maryland Association of CPAs April 30, 2010 The opinions expressed in this presentation are those of the presenter.

GASB Update 2015 GFOAA Annual Conference Wesley A. Galloway, Project Manager Governmental Accounting Standards Board

GASB Update 2015 GFOAA Annual Conference Wesley A. Galloway, Project Manager Governmental Accounting Standards Board The views expressed in this presentation are those of [Mr./Ms. last name]. Official

GASB Update 2015 GFOAA Annual Conference Wesley A. Galloway, Project Manager Governmental Accounting Standards Board The views expressed in this presentation are those of [Mr./Ms. last name]. Official

Accounting and Financial Reporting for Pensions A summary of changes and recommended steps

Accounting and Financial Reporting for Pensions A summary of changes and recommended steps January 29, 2013 2012 McGladrey LLP. All Rights Reserved. Today s presenters Patrick Hagan National Managing Partner

Accounting and Financial Reporting for Pensions A summary of changes and recommended steps January 29, 2013 2012 McGladrey LLP. All Rights Reserved. Today s presenters Patrick Hagan National Managing Partner

GASB 70, Accounting and Financial Reporting for Nonexchange Financial Guarantees

GASB 70, Accounting and Financial Reporting for Nonexchange Financial Guarantees Presented by J. Chris Hollifield, CPA CFF GASB 70 The GASB has issued Statement No. 70, Accounting and Financial Reporting

GASB 70, Accounting and Financial Reporting for Nonexchange Financial Guarantees Presented by J. Chris Hollifield, CPA CFF GASB 70 The GASB has issued Statement No. 70, Accounting and Financial Reporting

GASB 74/75 The Accounting and Reporting of OPEBs Is Undergoing a Major Change

Pursuing the Profession While Promoting the Public Good GASB 74/75 The Accounting and Reporting of OPEBs Is Undergoing a Major Change December 17, 2018 1 What is an OPEB? Other Postemployment Benefits

Pursuing the Profession While Promoting the Public Good GASB 74/75 The Accounting and Reporting of OPEBs Is Undergoing a Major Change December 17, 2018 1 What is an OPEB? Other Postemployment Benefits

Pursuing the Profession While Promoting the Public Good. GASB 74/75 The Accounting and Reporting of OPEBs Is Undergoing a Major Change

Pursuing the Profession While Promoting the Public Good GASB 74/75 The Accounting and Reporting of OPEBs Is Undergoing a Major Change December 17, 2018 What is an OPEB? Other Postemployment Benefits (or

Pursuing the Profession While Promoting the Public Good GASB 74/75 The Accounting and Reporting of OPEBs Is Undergoing a Major Change December 17, 2018 What is an OPEB? Other Postemployment Benefits (or

Omnibus 201X. September 13, 2016 Comments Due: November 23, Proposed Statement of the Governmental Accounting Standards Board

September 13, 2016 Comments Due: November 23, 2016 Proposed Statement of the Governmental Accounting Standards Board Omnibus 201X This Exposure Draft of a proposed Statement of Governmental Accounting

September 13, 2016 Comments Due: November 23, 2016 Proposed Statement of the Governmental Accounting Standards Board Omnibus 201X This Exposure Draft of a proposed Statement of Governmental Accounting

Overview: GASB Statement 68 on Pensions

Overview: GASB Statement 68 on Pensions Michelle Czerkawski, GASB Project Manager The views expressed in this presentation are those of Ms. Czerkawski. Official positions of the Governmental Accounting

Overview: GASB Statement 68 on Pensions Michelle Czerkawski, GASB Project Manager The views expressed in this presentation are those of Ms. Czerkawski. Official positions of the Governmental Accounting

GASB 74/75 The Accounting and Reporting of OPEBs Is Undergoing a Major Change

Pursuing the Profession While Promoting the Public Good GASB 74/75 The Accounting and Reporting of OPEBs Is Undergoing a Major Change 2016 Health Care Summit and Benefits Fair for Local Government What

Pursuing the Profession While Promoting the Public Good GASB 74/75 The Accounting and Reporting of OPEBs Is Undergoing a Major Change 2016 Health Care Summit and Benefits Fair for Local Government What

Current Board Members [continued]

![Current Board Members [continued]](/thumbs/94/121320560.jpg "Current Board Members [continued]") ASSOCIATION OF GOVERNMENT ACCOUNTANTS 2013 Southeast Region PDC GASB Update April 5, 2013 The views expressed in this presentation are those of Dr. Smith. Official positions of the GASB are determined

ASSOCIATION OF GOVERNMENT ACCOUNTANTS 2013 Southeast Region PDC GASB Update April 5, 2013 The views expressed in this presentation are those of Dr. Smith. Official positions of the GASB are determined

GAAP Update. Introduction / Summary 6/1/17. GASB Statement No. 73

GAAP Update Greg Allison, Teaching Professor UNC-CH SOG Lee Carter, Vice President Capital Management of the Carolinas GASB Statement No. 73 Accounting and Financial Reporting for Pensions and Financial

GAAP Update Greg Allison, Teaching Professor UNC-CH SOG Lee Carter, Vice President Capital Management of the Carolinas GASB Statement No. 73 Accounting and Financial Reporting for Pensions and Financial

August 28, Dear Mr. Bean:

Deloitte & Touche LLP Ten Westport Road P.O. Box 820 Wilton, CT 06897-0820 Tel: +1 203 761 3000 Fax: +1 203 834 2200 www.deloitte.com Mr. David R. Bean Director of Research and Technical Activities Governmental

Deloitte & Touche LLP Ten Westport Road P.O. Box 820 Wilton, CT 06897-0820 Tel: +1 203 761 3000 Fax: +1 203 834 2200 www.deloitte.com Mr. David R. Bean Director of Research and Technical Activities Governmental

NANTUCKET REGIONAL TRANSIT AUTHORITY (a component Unit of the Massachusetts Department of Transportation)

") (a component Unit of the Massachusetts Department of Transportation) Basic Financial Statements, Supplementary Data For the Year Ended June 30, 2015 Table of Contents Management s Discussion and Analysis

(a component Unit of the Massachusetts Department of Transportation) Basic Financial Statements, Supplementary Data For the Year Ended June 30, 2015 Table of Contents Management s Discussion and Analysis

BARSTOW COMMUNITY COLLEGE DISTRICT

BARSTOW COMMUNITY COLLEGE DISTRICT San Bernardino County Barstow, California Report on Audit Barstow Community College District TABLE OF CONTENTS FINANCIAL SECTION STATEMENT OF NET POSITION...9 STATEMENT

BARSTOW COMMUNITY COLLEGE DISTRICT San Bernardino County Barstow, California Report on Audit Barstow Community College District TABLE OF CONTENTS FINANCIAL SECTION STATEMENT OF NET POSITION...9 STATEMENT

The opinions expressed in this presentation are those of Mrs. Parker. Official positions of the GASB are established only after extensive public due

GASB Update Lisa R. Parker, CPA Project Manager, Governmental Accounting Standards Board 22nd Governmental Accounting and Auditing Conference Alabama Society of CPA s December 2, 2010 Birmingham, Alabama

GASB Update Lisa R. Parker, CPA Project Manager, Governmental Accounting Standards Board 22nd Governmental Accounting and Auditing Conference Alabama Society of CPA s December 2, 2010 Birmingham, Alabama

2014 FINANCIAL ACCOUNTING AND REPORTING ISSUES SEMINAR (AND GAAP UPDATE) Presented by Paul E. Glick, Glick Consulting Group

Presented by Paul E. Glick, Glick Consulting Group") 2014 FINANCIAL ACCOUNTING AND REPORTING ISSUES SEMINAR (AND GAAP UPDATE) Presented by Paul E. Glick, Primary Seminar Objectives Review the GASB Pronouncements Becoming Effective in The Near Future Emphasis

2014 FINANCIAL ACCOUNTING AND REPORTING ISSUES SEMINAR (AND GAAP UPDATE) Presented by Paul E. Glick, Primary Seminar Objectives Review the GASB Pronouncements Becoming Effective in The Near Future Emphasis

Governmental Update. GASB Statements 5/15/2018 RACHEL WALLEN, CPA.CFE RACHEL SQUIBB, CPA GASB 75. June 15,

Governmental Update RACHEL WALLEN, CPA.CFE RACHEL SQUIBB, CPA GASB Statements GASB Statement Number Description Effective for Fiscal Years / Reporting Periods Beginning After Effective Fiscal Year for

Governmental Update RACHEL WALLEN, CPA.CFE RACHEL SQUIBB, CPA GASB Statements GASB Statement Number Description Effective for Fiscal Years / Reporting Periods Beginning After Effective Fiscal Year for

Atlanta Independent Schools System

Atlanta Independent Schools System Auditor s Discussion & Analysis Financial & Compliance Audit Summary Presented by: Douglas A. Moses, CPA Miller G. Edwards, CPA Timothy M. Lyons, CPA, CGMA (770) 955

Atlanta Independent Schools System Auditor s Discussion & Analysis Financial & Compliance Audit Summary Presented by: Douglas A. Moses, CPA Miller G. Edwards, CPA Timothy M. Lyons, CPA, CGMA (770) 955

GASB 75 Accounting and Financial Reporting For Postemployment Benefits Other Than Pensions

GASB 75 Accounting and Financial Reporting For Postemployment Benefits Other Than Pensions Presented By: Marianne Van Duyne, CPA Managing Partner R.S. Abrams & Co., LLP 1 New York State Government Finance

GASB 75 Accounting and Financial Reporting For Postemployment Benefits Other Than Pensions Presented By: Marianne Van Duyne, CPA Managing Partner R.S. Abrams & Co., LLP 1 New York State Government Finance

NEW JERSEY ENVIRONMENTAL INFRASTRUCTURE TRUST (A Component Unit of the State of New Jersey)

") NEW JERSEY ENVIRONMENTAL INFRASTRUCTURE TRUST (A Component Unit of the State of New Jersey) Report of Audit For the Years Ended June 30, 2013 and 2012 NEW JERSEY ENVIRONMENTAL INFRASTRUCTURE TRUST (A Component

NEW JERSEY ENVIRONMENTAL INFRASTRUCTURE TRUST (A Component Unit of the State of New Jersey) Report of Audit For the Years Ended June 30, 2013 and 2012 NEW JERSEY ENVIRONMENTAL INFRASTRUCTURE TRUST (A Component

The Future is Now: Implementing GASB Guidance on Pension and OPEB Tuesday, May 24, 2016 I 10:20 a.m. to 12:00 p.m. I 1.5 CPE

The Future is Now: Implementing GASB Guidance on Pension and OPEB Tuesday, May 24, 2016 I 10:20 a.m. to 12:00 p.m. I 1.5 CPE Moderator: Debra Roberts, MBA, CPA, CRC, Director of Finance, Maryland Supplemental

The Future is Now: Implementing GASB Guidance on Pension and OPEB Tuesday, May 24, 2016 I 10:20 a.m. to 12:00 p.m. I 1.5 CPE Moderator: Debra Roberts, MBA, CPA, CRC, Director of Finance, Maryland Supplemental

GASB Update. August 2018

GASB Update August 2018 Agenda GASB 75 OPEB GASB 84 Fiduciary Activities GASB 85 Omnibus 2017 GASB 87 Leases GASB 88 Certain Disclosures Related to Debt GASB 89 Accounting for Interest Cost Incurred Before

GASB Update August 2018 Agenda GASB 75 OPEB GASB 84 Fiduciary Activities GASB 85 Omnibus 2017 GASB 87 Leases GASB 88 Certain Disclosures Related to Debt GASB 89 Accounting for Interest Cost Incurred Before

CERTIFICATE OF EXCELLENCE IN FINANCIAL REPORTING (COE)

") CHECKLIST ESSENTIALS COE CHECKLIST UPDATES For Comprehensive Annual Financial Reports (CAFR) for the fiscal year ending June 30 or August 31, 2017. The following GASB Standards are addressed in this update:

CHECKLIST ESSENTIALS COE CHECKLIST UPDATES For Comprehensive Annual Financial Reports (CAFR) for the fiscal year ending June 30 or August 31, 2017. The following GASB Standards are addressed in this update:

Miscellaneous Reporting Issues and Best Practices

2014 CliftonLarsonAllen LLP 2013 CliftonLarsonAllen LLP Miscellaneous Reporting Issues and Best Practices Government Finance Officers Association of South Carolina October 14, 2014 cliftonlarsonallen.com

2014 CliftonLarsonAllen LLP 2013 CliftonLarsonAllen LLP Miscellaneous Reporting Issues and Best Practices Government Finance Officers Association of South Carolina October 14, 2014 cliftonlarsonallen.com

1 NEW DEVELOPMENTS COPYRIGHTED MATERIAL

1 NEW DEVELOPMENTS Introduction 3 GASB Statement 43, Financial Reporting for Postemployment Benefit Plans other than Pension Plans and GASB Statement 45, Accounting and Financial Reporting by Employers

1 NEW DEVELOPMENTS Introduction 3 GASB Statement 43, Financial Reporting for Postemployment Benefit Plans other than Pension Plans and GASB Statement 45, Accounting and Financial Reporting by Employers

Special Funding Situations

Special Funding Situations Special Funding Situation Overview Special funding situations are circumstances in which a nonemployer entity is legally responsible for making contributions directly to a pension

Special Funding Situations Special Funding Situation Overview Special funding situations are circumstances in which a nonemployer entity is legally responsible for making contributions directly to a pension

2012 Governmental GAAP Update

2012 Governmental GAAP Update Interactive Webinar February 2, 2012 Presented by Presented by: Stephen W. Blann, CPA, CGFM Director of Governmental Audit Quality Principal Government/Nonprofit Services

2012 Governmental GAAP Update Interactive Webinar February 2, 2012 Presented by Presented by: Stephen W. Blann, CPA, CGFM Director of Governmental Audit Quality Principal Government/Nonprofit Services

INDEPENDENT AUDITOR'S REPORT

Board of Trustees Lake Tahoe Community College District South Lake Tahoe, California Report on the Financial Statements INDEPENDENT AUDITOR'S REPORT We have audited the accompanying financial statements

Board of Trustees Lake Tahoe Community College District South Lake Tahoe, California Report on the Financial Statements INDEPENDENT AUDITOR'S REPORT We have audited the accompanying financial statements

ILLINOIS CPA SOCIETY. Governmental Report Review Program 2015 Review Session Check List for Pension Disclosures - In compliance with GASB Statement 68

ILLINOIS CPA SOCIETY Governmental Report Review Program 2015 Review Session Check List for Pension Disclosures - In compliance with GASB Statement 68 Your Name Report # This check list has been developed

ILLINOIS CPA SOCIETY Governmental Report Review Program 2015 Review Session Check List for Pension Disclosures - In compliance with GASB Statement 68 Your Name Report # This check list has been developed

GASB Update. Florida Court Clerks & Comptrollers 2018 Winter Conference. February 28, Christopher M. Davis, CPA, MBA, CFST

GASB Update Florida Court Clerks & Comptrollers 2018 Winter Conference February 28, 2018 Christopher M. Davis, CPA, MBA, CFST 2018 Crowe Horwath LLP 2018 Crowe Horwath LLP Course Objectives At the end

GASB Update Florida Court Clerks & Comptrollers 2018 Winter Conference February 28, 2018 Christopher M. Davis, CPA, MBA, CFST 2018 Crowe Horwath LLP 2018 Crowe Horwath LLP Course Objectives At the end

i Reporting Standards

The KPMG Government Institute Webcast Series: GASB Pension Accounting and Financial Reporting Standards Jeff Markert, KPMG Greg Driscoll, KPMG July 19, 2012 KPMG Government Institute Webcast Series: GASB

The KPMG Government Institute Webcast Series: GASB Pension Accounting and Financial Reporting Standards Jeff Markert, KPMG Greg Driscoll, KPMG July 19, 2012 KPMG Government Institute Webcast Series: GASB

GASB STATEMENTS AND EFFECTIVE DATES

1 Authoritative Status of NCGA On issuance July 1984 Pronouncements and AICPA Industry Audit Guide 2 Financial Reporting of Deferred Financial statements for periods ending after 12/15/86 Compensation

1 Authoritative Status of NCGA On issuance July 1984 Pronouncements and AICPA Industry Audit Guide 2 Financial Reporting of Deferred Financial statements for periods ending after 12/15/86 Compensation

Government Finance Officers Association November 7, 2013

Government Finance Officers Association November 7, 2013 1 Final GASB pronouncements Government Combinations and Disposals of Government Operations GASB Statement No. 69 Accounting and Financial Reporting

Government Finance Officers Association November 7, 2013 1 Final GASB pronouncements Government Combinations and Disposals of Government Operations GASB Statement No. 69 Accounting and Financial Reporting

Proposed Statement of the Governmental Accounting Standards Board

Issue Paper Attachment B June 0 Meeting NO. - JUNE XX, 0 Governmental Accounting Standards Series EXPOSURE DRAFT Proposed Statement of the Governmental Accounting Standards Board Financial Reporting for

Issue Paper Attachment B June 0 Meeting NO. - JUNE XX, 0 Governmental Accounting Standards Series EXPOSURE DRAFT Proposed Statement of the Governmental Accounting Standards Board Financial Reporting for

CLARION UNIVERSITY OF PENNSYLVANIA OF THE STATE SYSTEM OF HIGHER EDUCATION FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION

FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION YEARS ENDED TABLE OF CONTENTS YEARS ENDED INDEPENDENT AUDITORS' REPORT 1 FINANCIAL STATEMENTS BALANCE SHEETS PRIMARY INSTITUTION 3 STATEMENTS OF REVENUES,

FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION YEARS ENDED TABLE OF CONTENTS YEARS ENDED INDEPENDENT AUDITORS' REPORT 1 FINANCIAL STATEMENTS BALANCE SHEETS PRIMARY INSTITUTION 3 STATEMENTS OF REVENUES,

MARTHA S VINEYARD REGIONAL TRANSIT AUTHORITY (a component Unit of the Massachusetts Department of Transportation)

") (a component Unit of the Massachusetts Department of Transportation) Basic Financial Statements, Supplementary Data For the Year Ended Table of Contents Management s Discussion and Analysis i vii Independent

(a component Unit of the Massachusetts Department of Transportation) Basic Financial Statements, Supplementary Data For the Year Ended Table of Contents Management s Discussion and Analysis i vii Independent

GASB 68 For the ALASBO POWER LUNCH

GASB 68 For the ALASBO POWER LUNCH BDO USA, LLP, a New York limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee, and forms part of the international

GASB 68 For the ALASBO POWER LUNCH BDO USA, LLP, a New York limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee, and forms part of the international

Upcoming Changes to Pension Reporting Under GASB 67 & 68 and the Impact to Municipalities Participating in PERA Retirement Plans

Upcoming Changes to Pension Reporting Under GASB 67 & 68 and the Impact to Municipalities Participating in PERA Retirement Plans Patricia (Patty) French, Board Chair, PERA Wayne Propst, Executive Director,

Upcoming Changes to Pension Reporting Under GASB 67 & 68 and the Impact to Municipalities Participating in PERA Retirement Plans Patricia (Patty) French, Board Chair, PERA Wayne Propst, Executive Director,

CHEROKEE COUNTY WATER AND SEWERAGE AUTHORITY CHEROKEE COUNTY, GEORGIA FINANCIAL STATEMENTS FOR THE FISCAL YEAR ENDED AUGUST 31, 2017

CHEROKEE COUNTY WATER AND SEWERAGE AUTHORITY CHEROKEE COUNTY, GEORGIA FINANCIAL STATEMENTS FOR THE FISCAL YEAR ENDED AUGUST 31, 2017 TOGETHER WITH INDEPENDENT AUDITORS REPORTS FINANCIAL STATEMENTS AUGUST

CHEROKEE COUNTY WATER AND SEWERAGE AUTHORITY CHEROKEE COUNTY, GEORGIA FINANCIAL STATEMENTS FOR THE FISCAL YEAR ENDED AUGUST 31, 2017 TOGETHER WITH INDEPENDENT AUDITORS REPORTS FINANCIAL STATEMENTS AUGUST

City of Del Rey Oaks. Annual Financial Report June 30, Chavan & Associates, LLP Certified Public Accountants

City of Del Rey Oaks Annual Financial Report Chavan & Associates, LLP Certified Public Accountants www.cnallp.com Page Intentionally Left Blank Annual Financial Report For the year ended TABLE OF CONTENTS

City of Del Rey Oaks Annual Financial Report Chavan & Associates, LLP Certified Public Accountants www.cnallp.com Page Intentionally Left Blank Annual Financial Report For the year ended TABLE OF CONTENTS

Annual Audit Agenda June 30, Presented by: Adam Fraley of

Presented by: Adam Fraley of PURPOSE OF ANNUAL AUDIT AGENDA Engagement Team Overview of: o Audit Opinion o Financial Statements, Footnotes and Supplementary Information o Compliance Reports o Audit Scopes

Presented by: Adam Fraley of PURPOSE OF ANNUAL AUDIT AGENDA Engagement Team Overview of: o Audit Opinion o Financial Statements, Footnotes and Supplementary Information o Compliance Reports o Audit Scopes

GASB Update Lisa R. Parker, CPA, CGMA Project Manager Governmental Accounting Standards Board

GASB Update Lisa R. Parker, CPA, CGMA Project Manager Governmental Accounting Standards Board The views expressed in this presentation are those of Ms. Parker. Official positions of the GASB on accounting

GASB Update Lisa R. Parker, CPA, CGMA Project Manager Governmental Accounting Standards Board The views expressed in this presentation are those of Ms. Parker. Official positions of the GASB on accounting

Standards and statements Where do we go from here?

Standards and statements Where do we go from here? 2018 MACATFO Summer Conference June 21, 2018 Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an independently owned and managed member of Baker

Standards and statements Where do we go from here? 2018 MACATFO Summer Conference June 21, 2018 Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an independently owned and managed member of Baker

Other Postemployment Benefits (OPEB)

") Other Postemployment Benefits (OPEB) A Webinar for Users of State & Local Government Financial Information Scott Reeser, Project Manager Emily Clark, Project Research Associate Dean Mead, Research Manager

Other Postemployment Benefits (OPEB) A Webinar for Users of State & Local Government Financial Information Scott Reeser, Project Manager Emily Clark, Project Research Associate Dean Mead, Research Manager

BARSTOW COMMUNITY COLLEGE DISTRICT

BARSTOW COMMUNITY COLLEGE DISTRICT San Bernardino County Barstow, California Report on Audit TABLE OF CONTENTS FINANCIAL SECTION STATEMENT OF NET POSITION...9 STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES

BARSTOW COMMUNITY COLLEGE DISTRICT San Bernardino County Barstow, California Report on Audit TABLE OF CONTENTS FINANCIAL SECTION STATEMENT OF NET POSITION...9 STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES

Financial Reporting for Postemployment Benefit Plans Other Than Pension Plans

May 28, 2014 Comments Due: August 29, 2014 Proposed Statement of the Governmental Accounting Standards Board Financial Reporting for Postemployment Benefit Plans Other Than Pension Plans This Exposure

May 28, 2014 Comments Due: August 29, 2014 Proposed Statement of the Governmental Accounting Standards Board Financial Reporting for Postemployment Benefit Plans Other Than Pension Plans This Exposure

Chapter 5 CHAPTER 5. Pensions Employer and Plan and Employer Accounting and Reporting

Chapter 5 CHAPTER 5 Pensions Employer and Plan and Employer Accounting and Reporting Primary Pronouncements: GASB Statement 25, GASB Statement 27, GASB Statement 50, GASB Statement 67, GASB Statement 68

Chapter 5 CHAPTER 5 Pensions Employer and Plan and Employer Accounting and Reporting Primary Pronouncements: GASB Statement 25, GASB Statement 27, GASB Statement 50, GASB Statement 67, GASB Statement 68

EAST AURORA SCHOOL DISTRICT 131. FINANCIAL STATEMENTS June 30, (With Independent Auditor s Report Therein)

") FINANCIAL STATEMENTS (With Independent Auditor s Report Therein) FINANCIAL STATEMENTS CONTENTS INDEPENDENT AUDITOR S REPORT... 1 BASIC FINANCIAL STATEMENTS Government-Wide Financial Statements: Statement

FINANCIAL STATEMENTS (With Independent Auditor s Report Therein) FINANCIAL STATEMENTS CONTENTS INDEPENDENT AUDITOR S REPORT... 1 BASIC FINANCIAL STATEMENTS Government-Wide Financial Statements: Statement

GASB 45 Exposure Draft. Two New Exposure Drafts for OPEB

GASB 45 Exposure Draft Presented by Kathleen Cost Solving Tomorrow s Benefit Plan Challenges...Today Two New Exposure Drafts for OPEB 1. Financial Reporting for Postemployment Benefit Plans Other Than

GASB 45 Exposure Draft Presented by Kathleen Cost Solving Tomorrow s Benefit Plan Challenges...Today Two New Exposure Drafts for OPEB 1. Financial Reporting for Postemployment Benefit Plans Other Than

American Association of Port Authorities 2008 Port Finance Seminar GASB Update. Jim Lanzarotta Moss Adams LLP June 12, 2008

American Association of Port Authorities 2008 Port Finance Seminar GASB Update Jim Lanzarotta Moss Adams LLP June 12, 2008 What we will cover Recent activities of the AICPA SLG Expert Panel Review of implementation

American Association of Port Authorities 2008 Port Finance Seminar GASB Update Jim Lanzarotta Moss Adams LLP June 12, 2008 What we will cover Recent activities of the AICPA SLG Expert Panel Review of implementation

Pension Reporting What you need to know about GASB 67 and 68. Sherry Chan, Chief Actuary Paul Snyder, Chief Financial Officer

Pension Reporting What you need to know about GASB 67 and 68 Sherry Chan, Chief Actuary Paul Snyder, Chief Financial Officer 1 Generally Accepted Accounting Principles FAF Financial Accounting Foundation

Pension Reporting What you need to know about GASB 67 and 68 Sherry Chan, Chief Actuary Paul Snyder, Chief Financial Officer 1 Generally Accepted Accounting Principles FAF Financial Accounting Foundation

June 28, 2017 Comments Due: September 25, Proposed Implementation Guide of the Governmental Accounting Standards Board

June 28, 2017 Comments Due: September 25, 2017 Proposed Implementation Guide of the Governmental Accounting Standards Board Implementation Guide No. 201X-Z, Accounting and Financial Reporting for Postemployment

June 28, 2017 Comments Due: September 25, 2017 Proposed Implementation Guide of the Governmental Accounting Standards Board Implementation Guide No. 201X-Z, Accounting and Financial Reporting for Postemployment

The KPMG Government Institute Webcast Series: GASB Pension Accounting and Financial Reporting Standards

The KPMG Government Institute Webcast Series: GASB Pension Accounting and Financial Reporting Standards Jeff Markert, KPMG Greg Driscoll, KPMG July 19, 2012 KPMG Government Institute Webcast Series: GASB

The KPMG Government Institute Webcast Series: GASB Pension Accounting and Financial Reporting Standards Jeff Markert, KPMG Greg Driscoll, KPMG July 19, 2012 KPMG Government Institute Webcast Series: GASB

CAPE COD REGIONAL TRANSIT AUTHORITY (a component Unit of the Massachusetts Department of Transportation)

") (a component Unit of the Massachusetts Department of Transportation) Basic Financial Statements, Supplementary Data For the Year Ended June 30, 2015 Table of Contents Management s Discussion and Analysis

(a component Unit of the Massachusetts Department of Transportation) Basic Financial Statements, Supplementary Data For the Year Ended June 30, 2015 Table of Contents Management s Discussion and Analysis

City of Chicago Department of Water Management Water Fund Comprehensive Annual Financial Report For the Years Ended December 31, 2016 and 2015

City of Chicago Department of Water Management Water Fund Comprehensive Annual Financial Report For the Years Ended December 31, 2016 and 2015 Rahm Emanuel, Mayor Carole L. Brown, Chief Financial Officer

City of Chicago Department of Water Management Water Fund Comprehensive Annual Financial Report For the Years Ended December 31, 2016 and 2015 Rahm Emanuel, Mayor Carole L. Brown, Chief Financial Officer

Overview of GASB 67 and 68

Overview of GASB 67 and 68 Community College Internal Auditors May 7, 2015 Crowe Horwath LLP Jeff Jensen, Partner Audit Tax Advisory Risk Performance 2014 Crowe Horwath LLP Implementation Dates When will

Overview of GASB 67 and 68 Community College Internal Auditors May 7, 2015 Crowe Horwath LLP Jeff Jensen, Partner Audit Tax Advisory Risk Performance 2014 Crowe Horwath LLP Implementation Dates When will

Agenda / Learning Objectives

Audit and Accounting Update: Navigating Uncharted Waters Tyler Bernier, CPA, CHFP August 18, 2016 Agenda / Learning Objectives Understand significant FASB and GASB Standards changes Consider the effects

Audit and Accounting Update: Navigating Uncharted Waters Tyler Bernier, CPA, CHFP August 18, 2016 Agenda / Learning Objectives Understand significant FASB and GASB Standards changes Consider the effects

MAKING SENSE OF DEFERRED INFLOWS AND OUTFLOWS OF RESOURCES

MAKING SENSE OF DEFERRED INFLOWS AND OUTFLOWS OF RESOURCES Presented by: Beila Sherman, CPA Director November 4, 2015 marcumllp.com Objectives of This Session This session will address why the Board established:

MAKING SENSE OF DEFERRED INFLOWS AND OUTFLOWS OF RESOURCES Presented by: Beila Sherman, CPA Director November 4, 2015 marcumllp.com Objectives of This Session This session will address why the Board established:

Proposed Statement of the Governmental Accounting Standards Board

NO. 34-P JUNE 27, 2011 Governmental Accounting Standards Series EXPOSURE DRAFT Proposed Statement of the Governmental Accounting Standards Board Financial Reporting for Pension Plans an amendment of GASB

NO. 34-P JUNE 27, 2011 Governmental Accounting Standards Series EXPOSURE DRAFT Proposed Statement of the Governmental Accounting Standards Board Financial Reporting for Pension Plans an amendment of GASB