Michigan Public School Employees Retirement System Updates

|

|

|

- Jack Fisher

- 5 years ago

- Views:

Transcription

1 Michigan Public School Employees Retirement System Updates John Karagoulis Pension Administration Specialist, ORS Kayla Lintz Data Analyst, ORS Eric Formberg CPA, CGFM, Partner, Plante Moran MSBO CPA Workshop, June 6, 2018

2 Agenda Current Operating Expenditures (COE) Financial Highlights and System Funding GASB 75 Questions

3 UAAL Calculation in FY 2019

from one year to the next will be used to adjust the payroll on which the UAAL rate is charged.")

4 Employer Contributions - UAAL Effective FY 2019, percent change in Current Operating Expenditures (COE) from one year to the next will be used to adjust the payroll on which the UAAL rate is charged. 4

5 Employer Contributions - UAAL FY 2017 reported payroll will be adjusted by the percent change in COE from 2016 to 2017 to establish the FY19 adjusted payroll. Capped UAAL rate of 20.96% continues to be used in the calculation. UAAL contributions will no longer be calculated on member wages reported throughout the FY. 5

6 Year 1: COE Adjusted Payroll Calculation Calculate adjusted FY 2019 payroll Calculate the percent change in COE from FY 2016 to FY Apply the percentage difference to the actual FY 2017 payroll. 6

7 FY 2019 Required UAAL Determination Multiply 20.96% by your adjusted FY 2019 payroll from Step 1. 7

8 FY 2019 Required UAAL Payment Process The contributions due from Step 2 will be spread out over all Employer Statements in State FY 2019 (October 2018 through September 2019). 8

9 Adjusted Payroll Calculation Formulas: Yr. 1: Payroll 17 x (%ΔCOE ) = Adj Pyrl 19 Yr. 2: Adj Pyrl 19 x (%ΔCOE ) = Adj Pyrl 20 Yr. 3: Adj Pyrl 20 x (%ΔCOE ) = Adj Pyrl 21 9

10 Financial Highlights

11 2017 Investment Results 2017 was a great investment year. Actual returns exceeded the 7.5% assumption by nearly 6%. Excess was used to reduce future risk in the plan.

12 Investment Results and Dedicated Gains In August the DTMB-Director and MPSERS board adopted the Dedicated Gains policy where investment earnings above the assumed rate of return (AROR) are dedicated to reducing the AROR. Actual 2017 return exceeded the AROR by 5.89%. This was an excess investment gain of nearly $3B for pension resulting in a 45 basis point reduction in the AROR. $260M excess investment gain for OPEB resulting in a 35 basis point reduction in the AROR.

13 Investment Results and Dedicated Gains Reducing the AROR increases the actuarial accrued liability (AAL) in the plan, but the immediate recognition of the investment gains means there is a corresponding increase in the assets. Effect on contribution rates Normal cost rates will increase (contributions expected to earn less investment income in the future) UAAL rate will stay approximately level (can t go down due to PA 92 contribution rate floor).

14 Effect of Lowering AROR on 2019 Pension Contribution Rates 40.00% 35.00% 30.00% 25.00% 20.00% 15.00% 10.00% 5.00% 0.00% 36.92% 38.03% 12.21% 147c 12.21% 20.96% 147a(2) 20.96% 3.75% 4.86% 147a As-is Dedicated Gains Normal Cost District UAAL 147c.

15 Unfunded Actuarial Accrued Liabilities $50.0 $45.0 $40.0 $35.0 $39.3 $38.3 $37.7 $36.0 $34.5 $38.6 $35.9 $37.8 $30.0 Billions $ $25.0 $20.0 $15.0 $10.0 $5.0 $ * * 2017 Pension UAAL Retiree Healthcare UAAL

16 System Funding Pension Pension funding ratio for legacy Defined Benefit plans is 61.30% Pension Plus is 100% funded. Source: Annual Supplemental Report FY 2017

17 System Funding Retiree Healthcare Retiree Healthcare funding ratio is 38.11% The retirement system began pre-funding healthcare in FY Source: Annual Supplemental Report FY 2017

18 Pension Contribution Rates

19 FY 2018 State School Aid Retirement Appropriations K-12, ISD, PSA Above the Cap Funding Towards UAAL 147c. $960M Amount applied towards UAAL amortization payment. Beginning in FY2018, 100% applied to pension. 147c.(2) $200M Pre-payment of the final two years early retirement incentive from 2010.

20 FY 2018 State School Aid Retirement Appropriations K-12, ISD, and PSA Retirement Cost Off-set Appropriations 147a. $100M Offsets a portion of the retirement contributions owed by the district for the fiscal year in which it is received. 147a.(2) $48.9M Offsets increase in normal cost rates charged to districts as a result of reductions in the AROR. 147e. $23.1M Appropriation to offset the increase in employer normal cost due to PA 92 of 2017

21 System Funding ORS continues to take all steps to ensure responsible funding of all retirement systems. Annual actuarial valuations Experience study every five years Committed to paying off UAAL by 2038 Full payments ensured through detailed analyses and a robust reconciliation process Lowering the AROR from 8% to 7.05% for pension and 7.15% for OPEB.

22 GASB 67/68

23 GASB 68 Key take away ORS and OAG products are consistent with last year! Release of data tables and ORS Schedules Report (with audited data) targeted for mid-july Information provided on Employer Information website (mi.gov/psru) OAG audits of selected reporting units are underway

24 GASB: Employer Information Website The GASB 68 section of Employer Information website (mi.gov/psru) similar to last year will provide: Data Tables (universities and non-universities) Notes to Financial Statements sample language Required Supplemental Information (RSI) sample schedules and some data for these schedules Report: ORS Schedules of Employer Allocations and Schedule of Collective Pension Amounts (with OAG opinion letter) Additional resources (FAQ, Glossary)

25 GASB 68: Data Tables Table 1: Schedule of Pension Amounts by Employer Table 2: Schedule of Deferred Resources by Year by Employer Table 3: Schedule of Recognition of Outflow (Inflow) of Resources Due to Differences Between Actual and Expected Employer Contributions Table 4: Schedule of Recognition of Ouflow (Inflow) of Resources Due to Changes in Proportion Table 5: Schedule of Covered-Employee Payroll as of 9/30/17 and 6/30/18 (For use in RSI schedules; estimated availability: August 1.)

26 ORS Report with Audited Data Report consists of: OAG opinion letter ( Independent Auditor s Report ). Schedules of OAG-audited data Notes OAG will audit some but not all data Nothing after the measurement date, 9/30/17 Some data audited at the reporting unit level Some data audited at the plan level only Schedules: Schedules of Employer Allocations Proportionate share % for employers as of 9/30/17 Non-University and University on separate schedules Schedule of Collective Pension Amounts (plan-level) 9/30/17 balances for NPL Total deferred inflows/outflows Pension expense To Do focus on what the auditor s report covers, it does not cover everything on the ORS data tables!

27 GASB 68 Specific Elements Contribution After Measurement Date Determining/recording ending deferred outflows for defined benefit plan MPSERS contributions (made by Districts) after September 30, 2017 measurement date Reversing beginning of year deferred outflow 147c1 contribution treatment Considered part of statutorily required contribution May be a challenge to reconcile activity/amounts when including 147c1 contributions 147c1 revenue treatment on government-wide statements These amounts must be determined by each individual district and audited by district auditors. For measurement period portion is pension and portion is OPEB OPEB portion will be part of prior period adjustment for GASB 75

28 GASB 68 Recording and Reporting Recording and reporting issues consistent with prior years Other than the prior period adjustment pension and OPEB basic requirements are similar. Specifics are discussed in GASB 75 section

29 GASB 68 System-level numbers Expected Remaining Service Life of all Employees University (in years): Non- Expected Remaining Service Life of all Employees University (in years): Recognition Period For Assets (in years): Total Net Pension Liability Non-University: $25.9 billion Total Net Pension Liability University: $575 million Section 147(c) payments 72.88% of FY (c1) payments is for pension 100% of FY (c1) payments is for pension

30 GASB 74/75

31 What Does GASB 75 Require? GASB 75, like GASB 68 (Pension), adds: Liability called Net OPEB liability impacting government-wide and full accrual funds (generally enterprise funds) Deferred Inflows/Outflows OPEB expense under full accrual Segregations of contributions between defined benefit plans and defined contribution plans MORE disclosures 2 more RSI schedules Prior Period Adjustment as of July 1, 2017 for: Net OPEB Liability Deferred outflow for contributions subsequent to Sept. 30, 2016 Deferred inflow for 147c1 OPEB related revenues subsequent to Sept 30, 2016 Modified accrual funds continue to expense as contributions are paid/accrued

32 GASB 75 Overview of Impact MPSERS manages OPEB plan for Michigan school districts Net OPEB liability allocated to each participating government Allocation based on Statutory Required Contribution to the OPEB plan Structure similar to GASB 68 but not the same! ORS creating a separate section of web site for GASB 75, similar to 68 OAG expected to issue data tables and reports around the end of July 2018 Annual reporting at same time as GASB 68 information NOTE some districts provide district level plan impact will need to be assessed Examples paid insurance, supplemental benefits its more than health care!

33 GASB 75 Basic Formula Participating employers will now record the NET OPEB liability on the full accrual statements TOTAL OPEB liability OPEB Plan Net Position NET OPEB liability These amounts will be measured as of the measurement date Cost-sharing employers record their proportionate share of the net OPEB liability

34 GASB 75 Reporting Unit Liability Report proportionate share of collective net OPEB liability, OPEB expense, and deferred outflows/inflows of resources related to OPEB How is proportionate share determined? Consistent with the manner in which contributions to the OPEB plan are determined (essentially the statutory required contribution) ORS presumes it will result in reasonable allocation Multiply collective net OPEB liability and proportion % to determine employer s proportionate share Statewide liability approx. $8.9 billion as of ORS provides tables similar to GASB 68 For 6/30/18 District will record beginning of year and end of year liability (similar to GASB 68 adoption), prior period adjustment DB Employer s contributions subsequent to measurement date (since plan year different than the fiscal year end) deferred outflow (similar to GASB 68) DC contributions are not deferred and remain in expense

35 GASB 75 CAFR OPEB Summary Net OPEB Liability (in thousands) Total OPEB Liability $14,175,547 Plan Fiduciary Net Position 5,177,775 Net OPEB Liability $8,997,773 Plan Fiduciary Net Position as a Percentage of Total OPEB Liability 36.53% Net OPEB Liability as a percentage of Covered Employee Payroll % Total Covered Employee Payroll $8,452,983

36 GASB 75 Implementation details OPEB includes a DC plan and a DB plan Obligation is focused on DB plan Note, DC participants have a small DB benefit UAAL effective 11/1/17 the UAAL (147c1) amount is 100% pension Reporting Issues OAG report, likely 1 report with separate columns for pension and OPEB ORS data tables similar to GASB 68 2 sets of District disclosures for 68 and 75. Some elements may be combined Allocate pension expense to activities in Statement of Activities Unrestricted net position becomes a bigger negative amount Net Position deficit likely grows No change in fund level expense recognition

37 GASB 75 To Do List Obtain ORS data tables, plan information, and OAG report Capture district level contribution information and participant wage information Ensure census information on employee elections is available 9/30/17 obligation uses 9/30/16 participant data Discuss audit test requirements with auditor

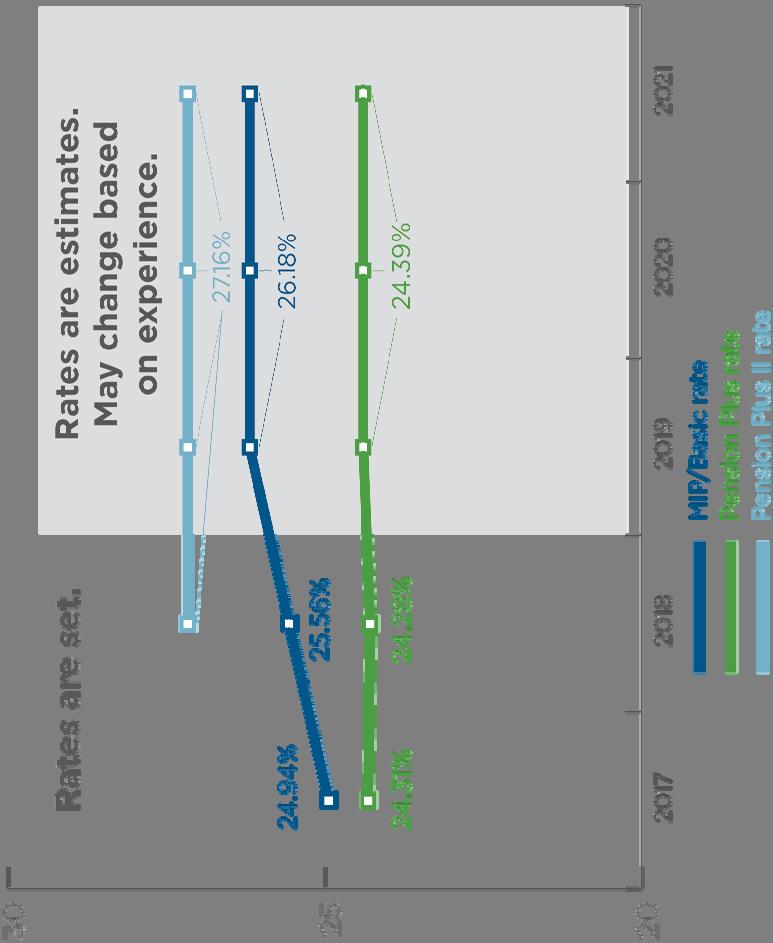

38 GASB 75 Compiling Information Compiling information for District footnotes information needs for 68 and 75 (See sample language on ORS website) 68 Deferred inflow/outflow table 68 5-year amortization table 75 Deferred inflow/outflow table 75 5-year amortization table Investment allocation tables for 68 and 75 1% change in discount rate tables for 68 and 75 Plan description and assumptions for 68 Plan description and assumptions for 75 Deferred inflow for 147c1 for 68 and 75 Contributions for 68 and 75 Covered payroll (reportable compensation) likely the same for 68 and 75 Payable to MPSERS under 68 and 75

39 GASB 75 Audit Requirements AICPA State and Local Audit Guide OPEB audit scope addressed in part 3 of new chapter: Cost- Sharing Employers Administered Through a Qualifying Trust Auditor tests Obtain/valdate OAG audit of the allocations to Data Tables, similar to GASB 68 Assess OAG assumptions, shared with the SD auditor Evaluate OAG assessment of actuary SD auditor Validate Statutory Required Contribution Validate Government-wide and full accrual expense recognized Validate allocation of OPEB obligation to elements of Net Position Validate proportionate share of Plan deferred inflows/outflows

40 GASB 75 Audit Requirements Auditor tests Validate post measurement period deferred inflows/outflows, including 147c1 Validate payroll data Assess completeness of disclosures Verify/agree RSI data Validate beginning Net OPEB liability Prior Period Adjustment, report letter modifications, change of accounting disclosure Communicate emphasis of matter, planning letter and end of audit letter Reconciliation between GASB 68 data and GASB 75 data Use of a specialist assessment Consideration of independence under Government Auditing Standards

41 GASB 75 Key Questions Key question: is key census data accurately reported to the actuary? When should District level census testing start? What should be tested? 9/30/15 census used for actuarial determined amount which is rolled forward to 9/30/16 (beginning balance) How can GASB 68 tests be leveraged?

42 GASB 75 Audit Issues Significant census elements may include (similar to GASB 68): a. Name b. Social Security number c. Date of birth d. Date of hire e. Marital status f. Gender g. Dependents h. Spouse s date of birth i. Class of employee j. Service credits (periods of time worked) k. Position or job code (or both) l. Date of termination or retirement m. Plan election of employee n. Contributions from inactive members receiving benefits o. Employment status (active, deferred, retired).

43 GASB 75 Questions What covered payroll number do we use? Since all participants in Pension have a contributed amount to OPEB, reportable compensation is the same as for GASB 68 Is Census testing required? YES, but it may be able to be combined with the GASB 68 tests. It would need to consider the correct OPEB participation 2018 AICPA State and Local Audit Guide includes outline of procedures to address What about 147a2, 147c2, 147e; how are those contributions handled? Amounts related to these sections do not directly impact the statutory required contributions 147a2 No deferral, similar to 147a1 147c2 Not tied to contribution rate, essentially a pay down of the ERIP liability 147e Will be small in 2018, related to DC/Pension Plus 2 plans, helps cover added cost of plans

44 GASB 75 Questions What contribution rate do we use to recalculate contribution? Unlike Pension the rate differential between employee elections is not significant. An average rate will likely be sufficient How do I record beginning balance? Recorded as a prior period adjustment for initial OPEB liability, no deferred inflows/outflows other than deferred outflow for contributions subsequent to the measurement date and 147c1 deferred inflow Government-wide statements and full accrual statements where payroll as an expenditure Emphasis of matter in audit opinion, accounting change footnote

45 GASB 75 Questions What reports will I need to complete GASB 75 information? ORS retirement rate sheets to , to and to OAG audit report on proportionate share ORS data tables (similar to GASB 68) Download Detail 2 reports ORS CAFR on GASB 68 and 75 (useful for disclosures) Internal reports for reportable compensation and contributions made 941s (or other documents) to verify compensation data

46 GASB 75 Post 1/31/2018 Contribution Requirements The updated FY MPSERS Contribution Rates due on members wages paid between February 1, 2018 and September 30, 2018, go into effect on February 1, These rates apply to K-12 school districts, intermediate school districts, community colleges, district libraries, charter schools, and public school academies. Updates include: Member rates are now included for DB (Defined Benefit) and DC (Defined Contribution) Active rates and retiree rates are all on one page Pension Plus 2 rates were added Employee DC matching changes for employees who are DC PHF UAAL Rate Stabilization table is now on a separate page

47 ASSETS Ending amounts Cash and cash equivalents $ 13,518,186 Investments 25,929,622 Receivables (net) 15,085,177 Capital assets (net of accumulated depreciation) Depreciable assets: 81,769,640 Non-depreciable assets: 88,253,120 TOTAL ASSETS 224,555,745 DEFERRED OUTFLOWS OF RESOURCES Deferred outflows related to pensions 1,050,000 Deferred outflows related to OPEB 980,000 TOTAL DEFERRED OUTFLOWS OF RESOURCES 2,030,000 LIABILITIES Accounts Payable 6,538,206 Non-current liabilities: Current portion of long-term debt 1,680,000 Long-term debt (net of current portion) 21,660,000 Net pension liability 24,589,000 Net OPEB liability 19,875,654 TOTAL LIABILITIES 74,342,860 DEFERRED INFLOWS OF RESOURCES Deferred inflows related to pensions 6,589,000 Deferred inflows related to OPEB 3,569,782 TOTAL DEFERRED INFLOWS OF RESOURCES 10,158,782 NET POSITION Net investment in capital assets 146,682,760 Restricted for: Capital projects 11,705,864 Debt service 11,046,053 Unrestricted (27,350,574) TOTAL NET POSITION $ 142,084,103

48 GASB 75 - RSI Table Example

49 GASB 75 - RSI Table Example

50 GASB 75 and 68 Key Take Aways ORS data tables key starting point, information expected near end of July OAG report covers statutory required contributions and some of the totals from the ORS data tables Auditors must audit the data, verify district recorded correctly Focus on PPA and communication requirements in report and with those charged with governance Document consideration of assumptions, including OAG assessments Create needed disclosures, addressing all the unique plan offerings and contribution requirements Audit elements of the disclosures Review/incorporate AICPA 2018 state & local audit guide requirements in audit programs

51 Questions?

MSBO Annual Conference Implementing GASB 75. Presented by Chris Geck and Eric Formberg

MSBO Annual Conference Implementing GASB 75 Presented by Chris Geck and Eric Formberg Accounting and Auditing Update Topics GASB 75 implementation year is here! GASB 68 - connecting the dots MPSERS contribution

MSBO Annual Conference Implementing GASB 75 Presented by Chris Geck and Eric Formberg Accounting and Auditing Update Topics GASB 75 implementation year is here! GASB 68 - connecting the dots MPSERS contribution

MSBO Finance Pre-Conference 2018 Accounting and Auditing Update. Presented by Donna Hanson and Eric Formberg

MSBO Finance Pre-Conference 2018 Accounting and Auditing Update Presented by Donna Hanson and Eric Formberg Accounting and Auditing Update Topics GASB 75 implementation year is here! GASBs on the horizon

MSBO Finance Pre-Conference 2018 Accounting and Auditing Update Presented by Donna Hanson and Eric Formberg Accounting and Auditing Update Topics GASB 75 implementation year is here! GASBs on the horizon

An Overview of the New GASB Pension Accounting and Reporting Standards. Presented By: Joel Knopp, CPA

An Overview of the New GASB Pension Accounting and Reporting Standards Presented By: Joel Knopp, CPA GASB Pension Accounting Standards GASB Resources: Statement 67 (plans) Statement 68 (employers) Statement

An Overview of the New GASB Pension Accounting and Reporting Standards Presented By: Joel Knopp, CPA GASB Pension Accounting Standards GASB Resources: Statement 67 (plans) Statement 68 (employers) Statement

GASB 74 & 75 The new GASB OPEB standards & an overview of upcoming pronouncements. Jeff Straus, CPA Principal

GASB 74 & 75 The new GASB OPEB standards & an overview of upcoming pronouncements Jeff Straus, CPA Principal jstraus@manercpa.com Session Overview 1. What are Other Post Employment Benefits (OPEB)? 2.

GASB 74 & 75 The new GASB OPEB standards & an overview of upcoming pronouncements Jeff Straus, CPA Principal jstraus@manercpa.com Session Overview 1. What are Other Post Employment Benefits (OPEB)? 2.

{Audit Update.} Presented by Katie Thornton to MCCBOA on March 6, 2014 PLANTE MORAN. plantemoran.com

{Audit Update.} Presented by Katie Thornton to MCCBOA on March 6, 2014 Agenda GASB Standards Update GASB Agenda Items Federal Update 1 GASB Standards Update 2 Summary of Recent GASB Statements Statement

{Audit Update.} Presented by Katie Thornton to MCCBOA on March 6, 2014 Agenda GASB Standards Update GASB Agenda Items Federal Update 1 GASB Standards Update 2 Summary of Recent GASB Statements Statement

GASB 68: Bet You Can t Wait! Presenters. Agenda. Date: October 7, 2014

GASB 68: Bet You Can t Wait! Taking a closer look at GASB s new pension standards Barrie Wilkes, Mary Hill Central Michigan University Katie Thornton Plante Moran, PLLC Date: October 7, 2014 Presenters

GASB 68: Bet You Can t Wait! Taking a closer look at GASB s new pension standards Barrie Wilkes, Mary Hill Central Michigan University Katie Thornton Plante Moran, PLLC Date: October 7, 2014 Presenters

GASB 74/75 Frequently Asked Questions

Page 1 of 15 GASB 74/75 Frequently Asked Questions General Information What is GASB? Governmental Accounting Standards Board is an independent, non-profit, nongovernmental regulatory body charged with

Page 1 of 15 GASB 74/75 Frequently Asked Questions General Information What is GASB? Governmental Accounting Standards Board is an independent, non-profit, nongovernmental regulatory body charged with

20/20 Vision: A Clear View of Pension Obligations:

20/20 Vision: A Clear View of Pension Obligations: Perspective on GASB 67/68 November 7, 2012 Presenters Eric Formberg, CPA, CGFM, Partner, Plante Moran Eric is the leader of the firm s K-12 education

20/20 Vision: A Clear View of Pension Obligations: Perspective on GASB 67/68 November 7, 2012 Presenters Eric Formberg, CPA, CGFM, Partner, Plante Moran Eric is the leader of the firm s K-12 education

5/6/2015. Completeness Assertion Risk approach How sample was selected:

1 Overall memo related to audit approach and summary of packet Schedules of Employer Allocations & Pension Amounts by Employer SOC 1 Type 2 report Note Disclosures and RSI info for a cost sharing employer

1 Overall memo related to audit approach and summary of packet Schedules of Employer Allocations & Pension Amounts by Employer SOC 1 Type 2 report Note Disclosures and RSI info for a cost sharing employer

INFORMATION SESSION Cd, 5/15/E

INFORMATION SESSION 1 50-923Cd, 5/15/E Background What is GASB 68? Governmental Accounting Standards Board (GASB) approved new rules that will affect employers Employers must include the following in their

INFORMATION SESSION 1 50-923Cd, 5/15/E Background What is GASB 68? Governmental Accounting Standards Board (GASB) approved new rules that will affect employers Employers must include the following in their

What you should know about the new Other Postemployment Benefits (OPEB) standard (GASB 75) WGFOA Spring Conference April 19, 2018

standard (GASB 75) WGFOA Spring Conference April 19, 2018") What you should know about the new Other Postemployment Benefits (OPEB) standard (GASB 75) WGFOA Spring Conference April 19, 2018 Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an independently

What you should know about the new Other Postemployment Benefits (OPEB) standard (GASB 75) WGFOA Spring Conference April 19, 2018 Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an independently

Implementing GASB 68

W a s h i n g t o n S t a t e A u d i t o r s O f f i c e Implementing GASB 68 GASB pension statements GASB number Title 78 Non-governmental plans 2016 73 Plans not within the scope of GASB 68 2017 71

W a s h i n g t o n S t a t e A u d i t o r s O f f i c e Implementing GASB 68 GASB pension statements GASB number Title 78 Non-governmental plans 2016 73 Plans not within the scope of GASB 68 2017 71

FPPA Affiliated Defined Benefit Plans

GASB 68 Implementation Guide For FPPA Affiliated Defined Benefit Plans Fire & Police Pension Association of Colorado GASB 68 Implementation Guide TABLE OF CONTENTS Overview & Timeline Overview Reports

GASB 68 Implementation Guide For FPPA Affiliated Defined Benefit Plans Fire & Police Pension Association of Colorado GASB 68 Implementation Guide TABLE OF CONTENTS Overview & Timeline Overview Reports

GASB 67/68 The New Pension Standards. The Reasoning Behind the Pronouncements

GASB 67/68 The New Pension Standards The Reasoning Behind the Pronouncements Presented by: Stephen W. Blann, CPA, CGFM, CGMA Director of Government Audit Quality Rehmann, Grand Rapids, MI Larry Langer,

GASB 67/68 The New Pension Standards The Reasoning Behind the Pronouncements Presented by: Stephen W. Blann, CPA, CGFM, CGMA Director of Government Audit Quality Rehmann, Grand Rapids, MI Larry Langer,

Kerrie Vanden Bosch, Executive Director

Kerrie Vanden Bosch, Executive Director Michigan School Business Officials August 17, 2017 Who We Are Our Purpose Statement ORS is an innovative retirement organization driven to empower our customers

Kerrie Vanden Bosch, Executive Director Michigan School Business Officials August 17, 2017 Who We Are Our Purpose Statement ORS is an innovative retirement organization driven to empower our customers

Healthcare Analytics Consulting. Actuarial Valuation of Postemployment Benefits as of Fiscal Year End June 30, Arthur J. Gallagher & Co.

Healthcare Analytics Consulting Village of Milford Actuarial Valuation of Postemployment Benefits as of Fiscal Year End June 30, 2017 July 31, 2017 Arthur J. Gallagher & Co. Healthcare Analytics Consulting

Healthcare Analytics Consulting Village of Milford Actuarial Valuation of Postemployment Benefits as of Fiscal Year End June 30, 2017 July 31, 2017 Arthur J. Gallagher & Co. Healthcare Analytics Consulting

GASB 67 & 68 in NC. State and Local Government Finance Division. July 22, 2014 Preeta Nayak

State and Local Government Finance Division July 22, 2014 Preeta Nayak Agenda: Overview of Standards, particularly 68 What are we doing in NC to prepare? How will all this new data be audited? Training

State and Local Government Finance Division July 22, 2014 Preeta Nayak Agenda: Overview of Standards, particularly 68 What are we doing in NC to prepare? How will all this new data be audited? Training

GASB 75 Accounting and Financial Reporting For Postemployment Benefits Other Than Pensions

GASB 75 Accounting and Financial Reporting For Postemployment Benefits Other Than Pensions Presented By: Marianne Van Duyne, CPA Managing Partner R.S. Abrams & Co., LLP 1 New York State Government Finance

GASB 75 Accounting and Financial Reporting For Postemployment Benefits Other Than Pensions Presented By: Marianne Van Duyne, CPA Managing Partner R.S. Abrams & Co., LLP 1 New York State Government Finance

5/1/15. Pension Accounting: Putting Theory into Practice. GASB 67 implementation. Pension Accounting Update: Putting Theory into Practice

Pension Accounting Update: Putting Theory into Practice Minnesota Association of School Business Officials (MASBO) Duluth Entertainment and Convention Center May 14, 2015 Presented by: John Wicklund, Assistant

Pension Accounting Update: Putting Theory into Practice Minnesota Association of School Business Officials (MASBO) Duluth Entertainment and Convention Center May 14, 2015 Presented by: John Wicklund, Assistant

Implementing GASB 75 Accounting and financial reporting for other post-employment benefits

Implementing GASB 75 Accounting and financial reporting for other post-employment benefits Judy McNeal, Chief Financial Officer KPERS Michele Stromp, Partner KPMG LLP Julie Barrientos, Director KPMG LLP

Implementing GASB 75 Accounting and financial reporting for other post-employment benefits Judy McNeal, Chief Financial Officer KPERS Michele Stromp, Partner KPMG LLP Julie Barrientos, Director KPMG LLP

Understanding GASB 74 and 75. Graham A. Schmidt, ASA, EA, FCA, MAAA Cheiron Anne Harper, FSA, EA, MAAA Cheiron

Understanding GASB 74 and 75 Graham A. Schmidt, ASA, EA, FCA, MAAA Cheiron Anne Harper, FSA, EA, MAAA Cheiron Background GASB Statements 67 and 68 issued in June 2012 Most retirement systems have reported

Understanding GASB 74 and 75 Graham A. Schmidt, ASA, EA, FCA, MAAA Cheiron Anne Harper, FSA, EA, MAAA Cheiron Background GASB Statements 67 and 68 issued in June 2012 Most retirement systems have reported

GASB Employer Reporting Guide

TEXAS MUNICIPAL RETIREMENT SYSTEM GASB Employer Reporting Guide July 2017 Table of Contents I. Introduction...3 II. III. IV. Timeline and Measurement Date...4 AICPA Audit Guidance...4 GRS GASB Employer

TEXAS MUNICIPAL RETIREMENT SYSTEM GASB Employer Reporting Guide July 2017 Table of Contents I. Introduction...3 II. III. IV. Timeline and Measurement Date...4 AICPA Audit Guidance...4 GRS GASB Employer

GASB 68 For the ALASBO POWER LUNCH

GASB 68 For the ALASBO POWER LUNCH BDO USA, LLP, a New York limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee, and forms part of the international

GASB 68 For the ALASBO POWER LUNCH BDO USA, LLP, a New York limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee, and forms part of the international

GASB 75 Overview. Presented by Josh Harner, WVDE School of Finance. GASB Statement No. 75

GASB 75 Overview Presented by Josh Harner, WVDE School of Finance GASB Statement No. 75 Accounting and Financial Reporting for Postemployment Benefits Other Than Pensions 2 1 General Information Objective

GASB 75 Overview Presented by Josh Harner, WVDE School of Finance GASB Statement No. 75 Accounting and Financial Reporting for Postemployment Benefits Other Than Pensions 2 1 General Information Objective

OPEB Reporting. Embracing GASB 74 and 75. May 16, PRESENTED TO Governmental Accounting & Auditing Conference

OPEB Reporting Embracing GASB 74 and 75 PRESENTED TO Governmental Accounting & Auditing Conference May 16, 2017 PRESENTED BY Jamie L. Rivette, CPA Ali N. Barnes, CPA 1 The Agenda What is OPEB? Implementation

OPEB Reporting Embracing GASB 74 and 75 PRESENTED TO Governmental Accounting & Auditing Conference May 16, 2017 PRESENTED BY Jamie L. Rivette, CPA Ali N. Barnes, CPA 1 The Agenda What is OPEB? Implementation

Upcoming Changes to Pension Reporting Under GASB 67 & 68 and the Impact to Municipalities Participating in PERA Retirement Plans

Upcoming Changes to Pension Reporting Under GASB 67 & 68 and the Impact to Municipalities Participating in PERA Retirement Plans Patricia (Patty) French, Board Chair, PERA Wayne Propst, Executive Director,

Upcoming Changes to Pension Reporting Under GASB 67 & 68 and the Impact to Municipalities Participating in PERA Retirement Plans Patricia (Patty) French, Board Chair, PERA Wayne Propst, Executive Director,

Accounting for the OPEB Obligation

Accounting for the OPEB Obligation Tom Swain, F.S.A. August 18, 2016 Agenda Overview and effective dates Significant changes Sample balance sheet pre/post changes Plan sponsor implications Planning steps

Accounting for the OPEB Obligation Tom Swain, F.S.A. August 18, 2016 Agenda Overview and effective dates Significant changes Sample balance sheet pre/post changes Plan sponsor implications Planning steps

Teacher Retirement System of Texas. GASB 68 Implementation Guide for TRS Employers

Teacher Retirement System of Texas GASB 68 Implementation Guide for TRS Employers Gloria Nichols, CPA June 18, 2015 Table of Contents GASB 68 Implementation of TRS Employers Chapter Topic Page 2 I. Overview

Teacher Retirement System of Texas GASB 68 Implementation Guide for TRS Employers Gloria Nichols, CPA June 18, 2015 Table of Contents GASB 68 Implementation of TRS Employers Chapter Topic Page 2 I. Overview

OPEB Reporting Overview: Implications of the Choice to Fund or Not Fund

OPEB Reporting Overview: Implications of the Choice to Fund or Not Fund Dean Michael Mead Research Manager, Governmental Accounting Standards Board March 12, 2008 Disclaimer: The opinions expressed in

OPEB Reporting Overview: Implications of the Choice to Fund or Not Fund Dean Michael Mead Research Manager, Governmental Accounting Standards Board March 12, 2008 Disclaimer: The opinions expressed in

Michigan Public School Employees Retirement System. Supreme Court Update GASB 68

Office of Retirement Services Serving more than 530,000 customers Michigan Public School Employees Retirement System June 2015 Agenda Supreme Court Update GASB 68 Overview Timelines for ORS and Reporting

Office of Retirement Services Serving more than 530,000 customers Michigan Public School Employees Retirement System June 2015 Agenda Supreme Court Update GASB 68 Overview Timelines for ORS and Reporting

GOVERNMENTAL DEFINED BENEFIT PENSION PLANS

GOVERNMENTAL DEFINED BENEFIT PENSION PLANS UNDERSTANDING GASB 67 / 68 GGFOA 2014 ANNUAL CONFERENCE Presented By: Donald L. McGrath Jr., CPA, Partner Crace Galvis McGrath, LLC Sponsored By: Georgia Government

GOVERNMENTAL DEFINED BENEFIT PENSION PLANS UNDERSTANDING GASB 67 / 68 GGFOA 2014 ANNUAL CONFERENCE Presented By: Donald L. McGrath Jr., CPA, Partner Crace Galvis McGrath, LLC Sponsored By: Georgia Government

GASB 68 ACCOUNTING VALUATION REPORT

GASB 68 ACCOUNTING VALUATION REPORT () Rate Plan Identifier: 595 Prepared for the SAN FRANCISCO COMMUNITY COLLEGE DISTRICT BOOKSTORE AUXILIARY MISCELLANEOUS PLAN, a Cost-Sharing Multiple-Employer Defined

GASB 68 ACCOUNTING VALUATION REPORT () Rate Plan Identifier: 595 Prepared for the SAN FRANCISCO COMMUNITY COLLEGE DISTRICT BOOKSTORE AUXILIARY MISCELLANEOUS PLAN, a Cost-Sharing Multiple-Employer Defined

April 24, 2018 Webinar

Practical Implementation of GASB 75 (OPEB) April 24, 2018 Webinar Presented in association with Presented by: Stephen W. Blann, CPA, CGFM, CGMA Director of Governmental Audit Quality Rehmann 2 Session

Practical Implementation of GASB 75 (OPEB) April 24, 2018 Webinar Presented in association with Presented by: Stephen W. Blann, CPA, CGFM, CGMA Director of Governmental Audit Quality Rehmann 2 Session

ACBO 2017 Spring Conference May 23, 2017

ACBO 2017 Spring Conference May 23, 2017 John Thompson, Director of Fiscal Services, Long Beach Community College District Geoffrey Kischuk, FSA, FCA, MAAA, President, Total Compensation Systems, Inc.

ACBO 2017 Spring Conference May 23, 2017 John Thompson, Director of Fiscal Services, Long Beach Community College District Geoffrey Kischuk, FSA, FCA, MAAA, President, Total Compensation Systems, Inc.

Recent VRS Changes and the New Pension GASB Standard. VGFOA Fall Conference October 17 th, 2012

Recent VRS Changes and the New Pension GASB Standard VGFOA Fall Conference October 17 th, 2012 Panel: William H Leighty, DecideSmart, LLC Robert H Churchman, CPA William M Dowd, Sageview Consulting Barry

Recent VRS Changes and the New Pension GASB Standard VGFOA Fall Conference October 17 th, 2012 Panel: William H Leighty, DecideSmart, LLC Robert H Churchman, CPA William M Dowd, Sageview Consulting Barry

A.G.B.U. ALEX AND MARIE MANOOGIAN SCHOOL. MICHIGAN PUBLIC SCHOOL ACADEMY (A Michigan Nonprofit Corporation)

") A.G.B.U. ALEX AND MARIE MANOOGIAN SCHOOL MICHIGAN PUBLIC SCHOOL ACADEMY (A Michigan Nonprofit Corporation) FINANCIAL STATEMENT WITH SUPPLEMENTAL INFORMATION JUNE 30, 2018 REPORT TO MANAGEMENT ON COMPLIANCE

A.G.B.U. ALEX AND MARIE MANOOGIAN SCHOOL MICHIGAN PUBLIC SCHOOL ACADEMY (A Michigan Nonprofit Corporation) FINANCIAL STATEMENT WITH SUPPLEMENTAL INFORMATION JUNE 30, 2018 REPORT TO MANAGEMENT ON COMPLIANCE

Agenda. Pension and OPEB News GASB 67, 68, 71, 73, 74, and 75. July 23, 2015

Pension and OPEB News GASB 67, 68, 71, 73, 74, and 75 July 23, 2015 Mary Beth Redding mbredding@bartel-associates.com www.bartel-associates.com Agenda GASB 68 Overview 1 GASB68C CalPERS lpersreports 12

Pension and OPEB News GASB 67, 68, 71, 73, 74, and 75 July 23, 2015 Mary Beth Redding mbredding@bartel-associates.com www.bartel-associates.com Agenda GASB 68 Overview 1 GASB68C CalPERS lpersreports 12

GASB UPDATE. Kathryn Barrett, CPA Freed Maxick CPAs, PC Alexandria Battaglia, CPA R.S. Abrams & Co., LLP

GASB UPDATE Kathryn Barrett, CPA Freed Maxick CPAs, PC Alexandria Battaglia, CPA R.S. Abrams & Co., LLP 1 Effective for June 30, 2018 Statement No. 75 OPEB (employers) Statement No. 81 Irrevocable Split

GASB UPDATE Kathryn Barrett, CPA Freed Maxick CPAs, PC Alexandria Battaglia, CPA R.S. Abrams & Co., LLP 1 Effective for June 30, 2018 Statement No. 75 OPEB (employers) Statement No. 81 Irrevocable Split

Prepared by: Questar III - BOCES

Huntington Union Free School District Actuarial Valuation Postretirement Benefits (GASB 45) as of July 1, 2012 With Disclosures for the Year Ended June 30, 2013 Prepared by: Questar III - BOCES TABLE OF

Huntington Union Free School District Actuarial Valuation Postretirement Benefits (GASB 45) as of July 1, 2012 With Disclosures for the Year Ended June 30, 2013 Prepared by: Questar III - BOCES TABLE OF

The Future is Now: Implementing GASB Guidance on Pension and OPEB Tuesday, May 24, 2016 I 10:20 a.m. to 12:00 p.m. I 1.5 CPE

The Future is Now: Implementing GASB Guidance on Pension and OPEB Tuesday, May 24, 2016 I 10:20 a.m. to 12:00 p.m. I 1.5 CPE Moderator: Debra Roberts, MBA, CPA, CRC, Director of Finance, Maryland Supplemental

The Future is Now: Implementing GASB Guidance on Pension and OPEB Tuesday, May 24, 2016 I 10:20 a.m. to 12:00 p.m. I 1.5 CPE Moderator: Debra Roberts, MBA, CPA, CRC, Director of Finance, Maryland Supplemental

October 3, 2014 Hilton Garden Inn DTC Denver, Colorado

October 3, 2014 Hilton Garden Inn DTC Denver, Colorado Governmental Accounting Standards Board Statements 67 and 68 (GASB 67/68)Update Two Accounting Standards GASB 67 Accounting and Financial Reporting

October 3, 2014 Hilton Garden Inn DTC Denver, Colorado Governmental Accounting Standards Board Statements 67 and 68 (GASB 67/68)Update Two Accounting Standards GASB 67 Accounting and Financial Reporting

Sample Notes to the Financial Statements Cost-Sharing Employer Plans VRS State Employee Health Insurance Credit Program For the Fiscal Year Ended June 30, 2018 Instructions The Sample Notes to the Financial

Sample Notes to the Financial Statements Cost-Sharing Employer Plans VRS State Employee Health Insurance Credit Program For the Fiscal Year Ended June 30, 2018 Instructions The Sample Notes to the Financial

Overview of GASB 67 and 68

Overview of GASB 67 and 68 Community College Internal Auditors May 7, 2015 Crowe Horwath LLP Jeff Jensen, Partner Audit Tax Advisory Risk Performance 2014 Crowe Horwath LLP Implementation Dates When will

Overview of GASB 67 and 68 Community College Internal Auditors May 7, 2015 Crowe Horwath LLP Jeff Jensen, Partner Audit Tax Advisory Risk Performance 2014 Crowe Horwath LLP Implementation Dates When will

GASB 67 and 68 The New World of Public Pension Plan Accounting

GASB 67 and 68 The New World of Public Pension Plan Accounting Presented by Mark Olleman, FSA, EA, MAAA Daniel Wade, FSA, EA, MAAA TERS Retirement Board Meeting October 10, 2013 Agenda Timing Notable Issues

GASB 67 and 68 The New World of Public Pension Plan Accounting Presented by Mark Olleman, FSA, EA, MAAA Daniel Wade, FSA, EA, MAAA TERS Retirement Board Meeting October 10, 2013 Agenda Timing Notable Issues

Local Government Finance Officials and Their Independent Auditors

NORTH CAROLINA DEPARTMENT OF STATE TREASURER STATE AND LOCAL GOVERNMENT FINANCE DIVISION AND THE LOCAL GOVERNMENT COMMISSION JANET COWELL TREASURER T. VANCE HOLLOMAN DEPUTY TREASURER Memorandum #2015-06

NORTH CAROLINA DEPARTMENT OF STATE TREASURER STATE AND LOCAL GOVERNMENT FINANCE DIVISION AND THE LOCAL GOVERNMENT COMMISSION JANET COWELL TREASURER T. VANCE HOLLOMAN DEPUTY TREASURER Memorandum #2015-06

GASB 67 & 68 Frequently Asked Questions (FAQs)

") GASB 67 & 68 Frequently Asked Questions (FAQs) 1. When do these new standards go into effect? Statement No. 67 replaces the requirements of the existing Statement No. 25, Financial Reporting for Defined

GASB 67 & 68 Frequently Asked Questions (FAQs) 1. When do these new standards go into effect? Statement No. 67 replaces the requirements of the existing Statement No. 25, Financial Reporting for Defined

GASB Pension Reporting Update

GASB Pension Reporting Update Minnesota Society of CPAs: School District Audit Conference June 2, 2014 Presented by: Dave DeJonge, Assistant Executive Director, PERA John Wicklund, Assistant Executive

GASB Pension Reporting Update Minnesota Society of CPAs: School District Audit Conference June 2, 2014 Presented by: Dave DeJonge, Assistant Executive Director, PERA John Wicklund, Assistant Executive

MEMORANDUM. CAFR Changes

MEMORANDUM DATE: February 2, 2015 TO: Members of the Board of Retirement FROM: Brenda Shott, Assistant CEO, Finance and Internal Operations SUBJECT: GASB 67/68 Update Recommendation: Receive and file.

MEMORANDUM DATE: February 2, 2015 TO: Members of the Board of Retirement FROM: Brenda Shott, Assistant CEO, Finance and Internal Operations SUBJECT: GASB 67/68 Update Recommendation: Receive and file.

GASB Fast Facts. GASB 67/68 requires the unfunded net pension liability be reported for the first time for many governmental entities.

Teacher Retirement System of Texas GASB 68 Implementation Update Gloria Nichols, CPA February 9, 2015 GASB Fast Facts GASB 67/68 requires the unfunded net pension liability be reported for the first time

Teacher Retirement System of Texas GASB 68 Implementation Update Gloria Nichols, CPA February 9, 2015 GASB Fast Facts GASB 67/68 requires the unfunded net pension liability be reported for the first time

GASB Revised Pension Standards:

GASB Revised Pension Standards: What Arizona governments need to know DONNA MILLER, PROFESSIONAL PRACTICE DIRECTOR ARIZONA OFFICE OF THE AUDITOR GENERAL NANCY BENNETT, CFO, ARIZONA STATE RETIREMENT SYSTEM

GASB Revised Pension Standards: What Arizona governments need to know DONNA MILLER, PROFESSIONAL PRACTICE DIRECTOR ARIZONA OFFICE OF THE AUDITOR GENERAL NANCY BENNETT, CFO, ARIZONA STATE RETIREMENT SYSTEM

Overview of OPEB Accounting Changes

Overview of OPEB Accounting Changes More matter with less art Hamlet Act 2, Scene 2 Get your facts first, then you can distort them as you please. - Mark Twain 2 Bolton Partners. Inc. Bolton Partners Inc.

Overview of OPEB Accounting Changes More matter with less art Hamlet Act 2, Scene 2 Get your facts first, then you can distort them as you please. - Mark Twain 2 Bolton Partners. Inc. Bolton Partners Inc.

Chapter 5 CHAPTER 5. Pensions Employer and Plan and Employer Accounting and Reporting

Chapter 5 CHAPTER 5 Pensions Employer and Plan and Employer Accounting and Reporting Primary Pronouncements: GASB Statement 25, GASB Statement 27, GASB Statement 50, GASB Statement 67, GASB Statement 68

Chapter 5 CHAPTER 5 Pensions Employer and Plan and Employer Accounting and Reporting Primary Pronouncements: GASB Statement 25, GASB Statement 27, GASB Statement 50, GASB Statement 67, GASB Statement 68

Overview: GASB Statement 68 on Pensions

Overview: GASB Statement 68 on Pensions Michelle Czerkawski, GASB Project Manager The views expressed in this presentation are those of Ms. Czerkawski. Official positions of the Governmental Accounting

Overview: GASB Statement 68 on Pensions Michelle Czerkawski, GASB Project Manager The views expressed in this presentation are those of Ms. Czerkawski. Official positions of the Governmental Accounting

GASB Update. August 2018

GASB Update August 2018 Agenda GASB 75 OPEB GASB 84 Fiduciary Activities GASB 85 Omnibus 2017 GASB 87 Leases GASB 88 Certain Disclosures Related to Debt GASB 89 Accounting for Interest Cost Incurred Before

GASB Update August 2018 Agenda GASB 75 OPEB GASB 84 Fiduciary Activities GASB 85 Omnibus 2017 GASB 87 Leases GASB 88 Certain Disclosures Related to Debt GASB 89 Accounting for Interest Cost Incurred Before

Overview of GASB 74/75. The new OPEB accounting standard. Joshua Mayhue, F.S.A. Consulting Actuary

1 Overview of GASB 74/75 The new OPEB accounting standard Joshua Mayhue, F.S.A. Consulting Actuary GASB 74/75 Implementation 2 GASB 74 Plan Accounting (only applies if plan is funded) Replaces GASB 43

1 Overview of GASB 74/75 The new OPEB accounting standard Joshua Mayhue, F.S.A. Consulting Actuary GASB 74/75 Implementation 2 GASB 74 Plan Accounting (only applies if plan is funded) Replaces GASB 43

IMPLEMENTING GASB STATEMENT NO. 75 ACCOUNTING AND FINANCIAL REPORTING FOR POSTEMPLOYMENT BENEFITS OTHER THAN PENSIONS

IMPLEMENTING GASB STATEMENT NO. 75 ACCOUNTING AND FINANCIAL REPORTING FOR POSTEMPLOYMENT BENEFITS OTHER THAN PENSIONS A CCMA WHITE PAPER FOR CALIFORNIA LOCAL GOVERNMENTS Issued February 2018 PUBLISHED

IMPLEMENTING GASB STATEMENT NO. 75 ACCOUNTING AND FINANCIAL REPORTING FOR POSTEMPLOYMENT BENEFITS OTHER THAN PENSIONS A CCMA WHITE PAPER FOR CALIFORNIA LOCAL GOVERNMENTS Issued February 2018 PUBLISHED

KALKASKA COUNTY ROAD COMMISSION OPEB BENEFITS Kalkaska County Road Commission

Kalkaska County Road Commission ACCOUNTING REPORT AND VALUATION AS PROVIDED FOR UNDER THE ALTERNATE CALCULATION PROVISIONS OF GASB STATEMENTS NO. 43 & 45 For the Period January 1, 2016 to December 31,

Kalkaska County Road Commission ACCOUNTING REPORT AND VALUATION AS PROVIDED FOR UNDER THE ALTERNATE CALCULATION PROVISIONS OF GASB STATEMENTS NO. 43 & 45 For the Period January 1, 2016 to December 31,

City of Richmond Heights Policemen s and Firemen s Retirement Fund GASB Statement No. 68 Employer Reporting Accounting Schedules July 1, 2017

City of Richmond Heights Policemen s and Firemen s Retirement Fund GASB Statement No. 68 Employer Reporting Accounting Schedules July 1, 2017 December 20, 2017 Board of Trustees City of Richmond Heights

City of Richmond Heights Policemen s and Firemen s Retirement Fund GASB Statement No. 68 Employer Reporting Accounting Schedules July 1, 2017 December 20, 2017 Board of Trustees City of Richmond Heights

NEW AMERICA SCHOOL - LAKEWOOD BASIC FINANCIAL STATEMENTS

BASIC FINANCIAL STATEMENTS TABLE OF CONTENTS INTRODUCTORY SECTION PAGE Title Page Table of Contents FINANCIAL SECTION Independent Auditors Report Management s Discussion and Analysis i - v Basic Financial

BASIC FINANCIAL STATEMENTS TABLE OF CONTENTS INTRODUCTORY SECTION PAGE Title Page Table of Contents FINANCIAL SECTION Independent Auditors Report Management s Discussion and Analysis i - v Basic Financial

CITY OF PARK RIDGE SLEP GASB STATEMENT NO. 68 EMPLOYER REPORTING ACCOUNTING SCHEDULES DECEMBER 31, 2014

CITY OF PARK RIDGE SLEP GASB STATEMENT NO. 68 EMPLOYER REPORTING ACCOUNTING SCHEDULES DECEMBER 31, 2014 PRELIMINARY - WILL NOT IMPLEMENT GASB 68 UNTIL NEXT YEAR TABLE OF CONTENTS Page Certification Letter

CITY OF PARK RIDGE SLEP GASB STATEMENT NO. 68 EMPLOYER REPORTING ACCOUNTING SCHEDULES DECEMBER 31, 2014 PRELIMINARY - WILL NOT IMPLEMENT GASB 68 UNTIL NEXT YEAR TABLE OF CONTENTS Page Certification Letter

GASB Statements No. 67 and 68 Net Pension Liability Changes to the Net Pension Liability [GASB 68, Paragraph 80]... 3

![GASB Statements No. 67 and 68 Net Pension Liability Changes to the Net Pension Liability [GASB 68, Paragraph 80]... 3](/thumbs/94/121299525.jpg "GASB Statements No. 67 and 68 Net Pension Liability Changes to the Net Pension Liability [GASB 68, Paragraph 80]... 3") Weymouth Retirement System GASB Statements No. 67 and 68 TABLE OF CONTENTS PAGE Actuarial Certification GASB Statements No. 67 and 68 Net Pension Liability... 3 Changes to the Net Pension Liability [GASB

Weymouth Retirement System GASB Statements No. 67 and 68 TABLE OF CONTENTS PAGE Actuarial Certification GASB Statements No. 67 and 68 Net Pension Liability... 3 Changes to the Net Pension Liability [GASB

GASB Pension Standards: An Educational Overview

GASB Pension Standards: An Educational Overview PEBA Retirement Division GFOA Fall Conference October 12, 2014 1 Governmental Accounting Standards Board New GASB Pension Accounting Standards GASB 67, Financial

GASB Pension Standards: An Educational Overview PEBA Retirement Division GFOA Fall Conference October 12, 2014 1 Governmental Accounting Standards Board New GASB Pension Accounting Standards GASB 67, Financial

EL-HAJJ MALIK EL-SHABAZZ ACADEMY. Financial Report with Supplemental Information June 30, 2018

EL-HAJJ MALIK EL-SHABAZZ ACADEMY Financial Report with Supplemental Information June 30, 2018 EL-HAJJ MALIK EL-SHABAZZ ACADEMY CONTENTS FINANCIAL STATEMENTS Independent auditor's report 1-2 Report on internal

EL-HAJJ MALIK EL-SHABAZZ ACADEMY Financial Report with Supplemental Information June 30, 2018 EL-HAJJ MALIK EL-SHABAZZ ACADEMY CONTENTS FINANCIAL STATEMENTS Independent auditor's report 1-2 Report on internal

YEO & YEO CPAs & BUSINESS CONSULTANTS

Financial Statements June 30, 2018 YEO & YEO CPAs & BUSINESS CONSULTANTS Table of Contents Section Page 1 Members of the Board of Education and Administration 1-1 2 Independent Auditors Report 2-1 3 Management

Financial Statements June 30, 2018 YEO & YEO CPAs & BUSINESS CONSULTANTS Table of Contents Section Page 1 Members of the Board of Education and Administration 1-1 2 Independent Auditors Report 2-1 3 Management

GASB 74/75 The Accounting and Reporting of OPEBs Is Undergoing a Major Change

Pursuing the Profession While Promoting the Public Good GASB 74/75 The Accounting and Reporting of OPEBs Is Undergoing a Major Change 2016 Health Care Summit and Benefits Fair for Local Government What

Pursuing the Profession While Promoting the Public Good GASB 74/75 The Accounting and Reporting of OPEBs Is Undergoing a Major Change 2016 Health Care Summit and Benefits Fair for Local Government What

BOARD OF EDUCATION OF THE CITY OF CHICAGO ANNUAL PENSIONS AND OTHER POST-EMPLOYMENT OBLIGATIONS DISCLOSURE. As of June 21, 2017

BOARD OF EDUCATION OF THE CITY OF CHICAGO ANNUAL PENSIONS AND OTHER POST-EMPLOYMENT OBLIGATIONS DISCLOSURE As of June 21, 2017 The information contained herein regarding annual pensions and other post-employment

BOARD OF EDUCATION OF THE CITY OF CHICAGO ANNUAL PENSIONS AND OTHER POST-EMPLOYMENT OBLIGATIONS DISCLOSURE As of June 21, 2017 The information contained herein regarding annual pensions and other post-employment

August 13, Segal Consulting, a Member of The Segal Group, Inc. By: JB/hy

Alameda County Employees Retirement Association Governmental Accounting Standards Board (GASB) Statement 68 Actuarial Valuation Based on December 31, 2014 Measurement Date for Employer Reporting as of

Alameda County Employees Retirement Association Governmental Accounting Standards Board (GASB) Statement 68 Actuarial Valuation Based on December 31, 2014 Measurement Date for Employer Reporting as of

BANGOR TOWNSHIP SCHOOL DISTRICT NO. 8. REPORT ON FINANCIAL STATEMENTS (with required supplementary information) YEAR ENDED JUNE 30, 2017

YEAR ENDED JUNE 30, 2017") REPORT ON FINANCIAL STATEMENTS (with required supplementary information) YEAR ENDED JUNE 30, 2017 1 C O N T E N T S Independent auditor s report... 3-4 Page Management s Discussion and Analysis... 5-9

REPORT ON FINANCIAL STATEMENTS (with required supplementary information) YEAR ENDED JUNE 30, 2017 1 C O N T E N T S Independent auditor s report... 3-4 Page Management s Discussion and Analysis... 5-9

11/7/2018. Emily Sobczak Greene Finney, LLP November, 2018

GAAP UPDATE 2018 Emily Sobczak Greene Finney, LLP November, 2018 GAAP Update Current Topics GASB 75 OPEB Reporting for Employers GASB 81 Irrevocable Split-Interest Agreements GASB 85 Omnibus 2017 GASB

GAAP UPDATE 2018 Emily Sobczak Greene Finney, LLP November, 2018 GAAP Update Current Topics GASB 75 OPEB Reporting for Employers GASB 81 Irrevocable Split-Interest Agreements GASB 85 Omnibus 2017 GASB

YourPublicMoney.Com Memo 6/21/2010 v.1c. One Page Summary - Key Proposed Changes

Possible Changes in Pension Accounting and Financial Reporting Plain-Language Supplement to Preliminary Views Governmental Accounting Standards Board June 16, 2010 YourPublicMoney.Com Memo 6/21/2010 v.1c

Possible Changes in Pension Accounting and Financial Reporting Plain-Language Supplement to Preliminary Views Governmental Accounting Standards Board June 16, 2010 YourPublicMoney.Com Memo 6/21/2010 v.1c

Berrien County Road Commission. Financial Report with Supplemental Information September 28, 2017

Financial Report with Supplemental Information Contents Report Letter 1-3 Management's Discussion and Analysis 4-7 Basic Financial Statements Statement of Net Position/Governmental Fund Balance Sheet 8

Financial Report with Supplemental Information Contents Report Letter 1-3 Management's Discussion and Analysis 4-7 Basic Financial Statements Statement of Net Position/Governmental Fund Balance Sheet 8

GASB 68 - Accounting and Financial Reporting for Pensions. Timothy J. Morgus, CPA, CGFM November 19 th, 2015

GASB 68 - Accounting and Financial Reporting for Pensions Timothy J. Morgus, CPA, CGFM November 19 th, 2015 Major Changes & Highlights Conceptually: - Each County is responsible for the net obligation

GASB 68 - Accounting and Financial Reporting for Pensions Timothy J. Morgus, CPA, CGFM November 19 th, 2015 Major Changes & Highlights Conceptually: - Each County is responsible for the net obligation

i Reporting Standards

The KPMG Government Institute Webcast Series: GASB Pension Accounting and Financial Reporting Standards Jeff Markert, KPMG Greg Driscoll, KPMG July 19, 2012 KPMG Government Institute Webcast Series: GASB

The KPMG Government Institute Webcast Series: GASB Pension Accounting and Financial Reporting Standards Jeff Markert, KPMG Greg Driscoll, KPMG July 19, 2012 KPMG Government Institute Webcast Series: GASB

Today s agenda. Overview of GASB 74/75. VGFOA Conference Spring, Presented by: William Dowd, MAAA, EA, FCA Daniel Homan, MAAA, EA

Today s agenda Overview of GASB 74/75 VGFOA Conference Spring, 2018 Presented by: William Dowd, MAAA, EA, FCA Daniel Homan, MAAA, EA Agenda» Why this? Why now?» Understanding the new reporting standards»

Today s agenda Overview of GASB 74/75 VGFOA Conference Spring, 2018 Presented by: William Dowd, MAAA, EA, FCA Daniel Homan, MAAA, EA Agenda» Why this? Why now?» Understanding the new reporting standards»

Public Schools of the City of Ann Arbor, Michigan. Report to the Board of Education June 30, 2012

Public Schools of the City of Ann Arbor, Michigan Report to the Board of Education June 30, 2012 To the Board of Education Public Schools of the City of Ann Arbor, Michigan We have recently completed our

Public Schools of the City of Ann Arbor, Michigan Report to the Board of Education June 30, 2012 To the Board of Education Public Schools of the City of Ann Arbor, Michigan We have recently completed our

Other Postemployment Benefits (OPEB)

") Other Postemployment Benefits (OPEB) A Webinar for Users of State & Local Government Financial Information Scott Reeser, Project Manager Emily Clark, Project Research Associate Dean Mead, Research Manager

Other Postemployment Benefits (OPEB) A Webinar for Users of State & Local Government Financial Information Scott Reeser, Project Manager Emily Clark, Project Research Associate Dean Mead, Research Manager

Section I - Required Communications with Those Charged with Governance

November 8, 2017 To the Board of Trustees and Management Kellogg Community College We have audited the financial statements of Kellogg Community College (the College ) as of and for the year ended June

November 8, 2017 To the Board of Trustees and Management Kellogg Community College We have audited the financial statements of Kellogg Community College (the College ) as of and for the year ended June

GASB Statement No. 75: Accounting and Financial Reporting for Postemployment Benefits Other Than Pensions

GASB Statement No. 75: Accounting and Financial Reporting for Postemployment Benefits Other Than Pensions April 4, 2017 The webinar will begin at 12:30 pm CT. Tara Laughlin, CPA, CGFM Senior Manager, Assurance

GASB Statement No. 75: Accounting and Financial Reporting for Postemployment Benefits Other Than Pensions April 4, 2017 The webinar will begin at 12:30 pm CT. Tara Laughlin, CPA, CGFM Senior Manager, Assurance

Total Compensation Systems, Inc.

College of Marin Actuarial Study of Retiree Health Liabilities Under GASB 74/75 Roll-forward Valuation Valuation Date: June 30, 2017 Measurement Date: June 30, 2017 Prepared by: Date: November 30, 2017

College of Marin Actuarial Study of Retiree Health Liabilities Under GASB 74/75 Roll-forward Valuation Valuation Date: June 30, 2017 Measurement Date: June 30, 2017 Prepared by: Date: November 30, 2017

Overview of OPEB Accounting Changes. More matter with less art Hamlet Act 2, Scene 2

Overview of OPEB Accounting Changes More matter with less art Hamlet Act 2, Scene 2 2 Presenters Kevin Binder, FSA, EA, MAAA, FCA As the leader of Bolton s OPEB practice, Kevin is responsible for the actuarial

Overview of OPEB Accounting Changes More matter with less art Hamlet Act 2, Scene 2 2 Presenters Kevin Binder, FSA, EA, MAAA, FCA As the leader of Bolton s OPEB practice, Kevin is responsible for the actuarial

LOWELL LIGHT & POWER LOWELL, MICHIGAN

LOWELL, MICHIGAN FINANCIAL STATEMENTS Vredeveld Haefner LLC TABLE OF CONTENTS PAGE Independent Auditors Report 1-2 Management s Discussion and Analysis 3-6 Basic Financial Statements Statement of Net Assets

LOWELL, MICHIGAN FINANCIAL STATEMENTS Vredeveld Haefner LLC TABLE OF CONTENTS PAGE Independent Auditors Report 1-2 Management s Discussion and Analysis 3-6 Basic Financial Statements Statement of Net Assets

NORTHWEST FLORIDA STATE COLLEGE COLLEGIATE HIGH SCHOOL A CHARTER SCHOOL AND RESTRICTED FUND OF NORTHWEST FLORIDA STATE COLLEGE

COLLEGIATE HIGH SCHOOL FINANCIAL STATEMENTS June 30, 2015 and 2014 TABLE OF CONTENTS INDEPENDENT AUDITOR'S REPORT... 1 MANAGEMENT'S DISCUSSION AND ANALYSIS... 4 FINANCIAL STATEMENTS Statements of Net Position...

COLLEGIATE HIGH SCHOOL FINANCIAL STATEMENTS June 30, 2015 and 2014 TABLE OF CONTENTS INDEPENDENT AUDITOR'S REPORT... 1 MANAGEMENT'S DISCUSSION AND ANALYSIS... 4 FINANCIAL STATEMENTS Statements of Net Position...

Houghton County Medical Care Facility. Financial Report with Supplemental Information September 30, 2016

Financial Report with Supplemental Information September 30, 2016 Contents Independent Auditor's Report 1-2 Management's Discussion and Analysis 3-5 Basic Financial Statements Proprietary Funds: Statement

Financial Report with Supplemental Information September 30, 2016 Contents Independent Auditor's Report 1-2 Management's Discussion and Analysis 3-5 Basic Financial Statements Proprietary Funds: Statement

MILTON CONTRIBUTORY RETIREMENT SYSTEM AUDIT OF SPECIFIC ELEMENTS, ACCOUNTS AND ITEMS OF FINANCIAL STATEMENTS

MILTON CONTRIBUTORY RETIREMENT SYSTEM AUDIT OF SPECIFIC ELEMENTS, ACCOUNTS AND ITEMS OF FINANCIAL STATEMENTS YEAR ENDED DECEMBER 31, 2016 MILTON CONTRIBUTORY RETIREMENT SYSTEM AUDIT OF SPECIFIC ELEMENTS,

MILTON CONTRIBUTORY RETIREMENT SYSTEM AUDIT OF SPECIFIC ELEMENTS, ACCOUNTS AND ITEMS OF FINANCIAL STATEMENTS YEAR ENDED DECEMBER 31, 2016 MILTON CONTRIBUTORY RETIREMENT SYSTEM AUDIT OF SPECIFIC ELEMENTS,

The KPMG Government Institute Webcast Series: GASB Pension Accounting and Financial Reporting Standards

The KPMG Government Institute Webcast Series: GASB Pension Accounting and Financial Reporting Standards Jeff Markert, KPMG Greg Driscoll, KPMG July 19, 2012 KPMG Government Institute Webcast Series: GASB

The KPMG Government Institute Webcast Series: GASB Pension Accounting and Financial Reporting Standards Jeff Markert, KPMG Greg Driscoll, KPMG July 19, 2012 KPMG Government Institute Webcast Series: GASB

PETROLEUM STORAGE TANK INSURANCE FUND (A Major Fund of the State of Missouri)

") PETROLEUM STORAGE TANK INSURANCE FUND (A Major Fund of the State of Missouri) INDEPENDENT AUDITOR S REPORT For the Year Ended June 30, 2018 TABLE OF CONTENTS PAGE INDEPENDENT AUDITOR'S REPORT 1-2 FINANCIAL

PETROLEUM STORAGE TANK INSURANCE FUND (A Major Fund of the State of Missouri) INDEPENDENT AUDITOR S REPORT For the Year Ended June 30, 2018 TABLE OF CONTENTS PAGE INDEPENDENT AUDITOR'S REPORT 1-2 FINANCIAL

NORTH CAROLINA STATE BOARD OF BARBER EXAMINERS

NORTH CAROLINA STATE BOARD OF BARBER EXAMINERS FINANCIAL STATEMENTS YEARS ENDED JUNE 30, 2018 AND 2017 Table of Contents Page No. Management's Discussion and Analysis 1-3 Independent Auditor's Report 4-5

NORTH CAROLINA STATE BOARD OF BARBER EXAMINERS FINANCIAL STATEMENTS YEARS ENDED JUNE 30, 2018 AND 2017 Table of Contents Page No. Management's Discussion and Analysis 1-3 Independent Auditor's Report 4-5

ICCCFO FALL 2012 CONFERENCE

ICCCFO FALL 2012 CONFERENCE GASB Statement No. 68, Accounting and Financial Reporting for Pensions Frederick G. Lantz, CPA Partner-in-Charge, Government Services Sikich LLP 1415 W. Diehl Road, Suite 400

ICCCFO FALL 2012 CONFERENCE GASB Statement No. 68, Accounting and Financial Reporting for Pensions Frederick G. Lantz, CPA Partner-in-Charge, Government Services Sikich LLP 1415 W. Diehl Road, Suite 400

OPEB: A Closer Look at the Present and Future

Menard Consulting, Inc. Actuaries & Consultants OPEB: A Closer Look at the Present and Future GASB Statements No. 43 & No. 45 Agenda Overview The Actuarial Calculation Accounting GASB OPEB Accounting Exposure

Menard Consulting, Inc. Actuaries & Consultants OPEB: A Closer Look at the Present and Future GASB Statements No. 43 & No. 45 Agenda Overview The Actuarial Calculation Accounting GASB OPEB Accounting Exposure

System Keynotes. Investment Strategy Actuarial Results, Funded Levels, Contributions, Demographics

City Council Working Session February 13, 2012 Agenda System Keynotes Trust Performance, Market Returns, Investment Strategy Actuarial Results, Funded Levels, Contributions, Demographics 1 City Ordinance

City Council Working Session February 13, 2012 Agenda System Keynotes Trust Performance, Market Returns, Investment Strategy Actuarial Results, Funded Levels, Contributions, Demographics 1 City Ordinance

METROPOLITAN WATER RECLAMATION DISTRICT OF CHICAGO OTHER POSTEMPLOYMENT BENEFITS PROGRAM ACTUARIAL VALUATION AS OF DECEMBER 31, 2017 INCLUDING:

METROPOLITAN WATER RECLAMATION DISTRICT OF CHICAGO OTHER POSTEMPLOYMENT BENEFITS PROGRAM ACTUARIAL VALUATION AS OF DECEMBER 31, 2017 INCLUDING: GASB 45 DISCLOSURES FOR THE PLAN/FISCAL YEAR ENDING DECEMBER

METROPOLITAN WATER RECLAMATION DISTRICT OF CHICAGO OTHER POSTEMPLOYMENT BENEFITS PROGRAM ACTUARIAL VALUATION AS OF DECEMBER 31, 2017 INCLUDING: GASB 45 DISCLOSURES FOR THE PLAN/FISCAL YEAR ENDING DECEMBER

WASHTENAW TECHNICAL MIDDLE COLLEGE

WASHTENAW TECHNICAL MIDDLE COLLEGE AUDITED FINANCIAL STATEMENTS AND SUPPLEMENTAL INFORMATION Year ended TABLE OF CONTENTS Page Independent Auditor s Report 1 Management s Discussion and Analysis 4 Financial

WASHTENAW TECHNICAL MIDDLE COLLEGE AUDITED FINANCIAL STATEMENTS AND SUPPLEMENTAL INFORMATION Year ended TABLE OF CONTENTS Page Independent Auditor s Report 1 Management s Discussion and Analysis 4 Financial

Total Compensation Systems, Inc.

Merced Union High School District Actuarial Study of Retiree Health Liabilities Under GASB 74/75 Valuation Date: June 30, 2017 Measurement Date: June 30, 2017 Prepared by: Date: May 24, 2018 Table of Contents

Merced Union High School District Actuarial Study of Retiree Health Liabilities Under GASB 74/75 Valuation Date: June 30, 2017 Measurement Date: June 30, 2017 Prepared by: Date: May 24, 2018 Table of Contents

Central Michigan University. State of Michigan CAFR Financial Schedules June 30, 2018

State of Michigan CAFR Financial Schedules June 30, 2018 Contents Independent Auditor s Report 1 Basic Financial Statements Exhibit I Reclassified Statement of Net Position and Reclassifying Entries 2-4

State of Michigan CAFR Financial Schedules June 30, 2018 Contents Independent Auditor s Report 1 Basic Financial Statements Exhibit I Reclassified Statement of Net Position and Reclassifying Entries 2-4

Implementing the New Pension Accounting Rules for Public Pension Plans

Implementing the New Pension Accounting Rules for Public Pension Plans William G. Karbon, MSPA, CPC Sr. Vice President, Dir. of Compliance CBIZ Benefits & Insurance Services, Inc. Lawrenceville, NJ What

Implementing the New Pension Accounting Rules for Public Pension Plans William G. Karbon, MSPA, CPC Sr. Vice President, Dir. of Compliance CBIZ Benefits & Insurance Services, Inc. Lawrenceville, NJ What

OPEB Preparing for Your Audit

OPEB Preparing for Your Audit Civic Federation and the Federal Reserve Bank of Chicago March 12, 2008 Bert Nuehring, CPA Executive Crowe Chizek and Company LLC BNuehring@crowechizek.com 1 OPEB Preparing

OPEB Preparing for Your Audit Civic Federation and the Federal Reserve Bank of Chicago March 12, 2008 Bert Nuehring, CPA Executive Crowe Chizek and Company LLC BNuehring@crowechizek.com 1 OPEB Preparing

Georgia Municipal Association Pre-Convention Workshop: Big Changes Coming to Retirement Plans

Georgia Municipal Association Pre-Convention Workshop: Big Changes Coming to Retirement Plans June 21, 2013 Leon F. (Rocky) Joyner, Jr. GMEBS Actuary Copyright 2013 by The Segal Group, Inc., parent of

Georgia Municipal Association Pre-Convention Workshop: Big Changes Coming to Retirement Plans June 21, 2013 Leon F. (Rocky) Joyner, Jr. GMEBS Actuary Copyright 2013 by The Segal Group, Inc., parent of

Governmental Audit & Accounting Update

Presented by: Miller Edwards, CPA of Mauldin & Jenkins, LLC medwards@mjcpa.com October 14, 2014-10:50 am 11:402013 am GGFOA Annual Conference Legacy Lodge & Conference Center Lake Lanier Islands Resort

Presented by: Miller Edwards, CPA of Mauldin & Jenkins, LLC medwards@mjcpa.com October 14, 2014-10:50 am 11:402013 am GGFOA Annual Conference Legacy Lodge & Conference Center Lake Lanier Islands Resort

OPEB - GASB 75: GAQC Web Event: OPEB GASB 75: Special Emphasis and Considerations for Nontrusted Plans. Administrative Notes.

OPEB - GASB 75: Special Emphasis and Considerations for Nontrusted Plans A Governmental Audit Quality Center Web Event Administrative Notes Please ensure your pop-up blocker is disabled. Note the interactive

OPEB - GASB 75: Special Emphasis and Considerations for Nontrusted Plans A Governmental Audit Quality Center Web Event Administrative Notes Please ensure your pop-up blocker is disabled. Note the interactive

THE AUDITORS AUDITORS OF MICHIGAN SCHOOLS

THE AUDITORS AUDITORS OF MICHIGAN SCHOOLS Kim Lindsay, CPA Jamie Essenmacher, CPA Jennifer Watkins, CPA Bruce Dunn, CPA 1 GASB 75 OPEB Reporting Kim Lindsay, CPA klindsay@lewis knopf.com Accounting and

THE AUDITORS AUDITORS OF MICHIGAN SCHOOLS Kim Lindsay, CPA Jamie Essenmacher, CPA Jennifer Watkins, CPA Bruce Dunn, CPA 1 GASB 75 OPEB Reporting Kim Lindsay, CPA klindsay@lewis knopf.com Accounting and