Developing Financial Capability Over the Life Course

|

|

|

- Debra Sharyl Briggs

- 6 years ago

- Views:

Transcription

1 1 / 51 Developing Financial Capability Over the Life Course J. Michael Collins University of Wisconsin-Madison June 3,

2 2 / 51 Table of Contents

3 3 / 51 Financial Capability Over the Life Course 1 Defining Capability 2 Stages of the Life Course 3 Recommendations

4 4 / 51 Financial Capability Shifting financial decision making to individuals ->Knowledge, Skills, Behaviors, Attitudes ->Life Course ->Financial Access ->Adaptability & Confidence ->Goal: Economic Well-being

5 5 / 51 Financial Capability Model Program Experience Personality Knowledge Skills Attitude Behavior

6 6 / 51 FINRA Financial Capability Survey - clickable map 55 percent living paycheck-to-paycheck 60 percent do not have a rainy day fund to cover three months of unanticipated financial emergencies. On average 3/5 financial literacy questions correctly Data Just Released...

7 7 / 51 Re-Frame: Understanding Decisions in Context Goal = financial security Choices = tradeoffs Savings may not be goal; paying bills, debts, paying for needs e.g. Emergency savings = cash in pinch or spending on social mobility

8

9 9 / 51 Compared to What?

10 10 / 51 Life Course Stages

11 11 / 51 Table of Contents

12 12 / 51 School Age Children Kids Themselves Parents Allowance (be consistent) Savings in school and/or in home Basic Concepts: opportunity cost/tradeoffs Education Savings (529 plans as example) Family Budget Include in Decisions observe you doing your homework

13 13 / 51 Rules of Thumb I for (Parents/Teachers) 1 School-partnerships: financial institutions, community organizations 2 Family & financial discussions need not be taboo, but not easy 3 Focus on tradeoffs not hard and fast rules 4 Investing in human capital as primary goal

14 14 / 51 Table of Contents

15 15 / 51 Post Secondary Schooling to Early 30s School-work blend: Building earning power Financial Services: Transitions to independence Spending: Managing Short and longer term Health Insurance: Being uninsured is risky financial choice Debt: Access to debt is good and important but must be well-managed

16 16 / to 30 Year Olds: School to Work Education & Student Loans Returns to college are strong Federal/subsidized students loans are still a good deal in school can slow you down Getting Going Credit Management Matters...even for dating The Employee Benefits Maze Health care: covered, but increasingly complex Savings: start early even if small * Automate!

17

18 18 / 51 Student Loans: New Options Know your options: Standard Repayment Graduated Repayment Extended Repayment Income-Based Repayment (IBR) Income-Contingent (ICR) (Direct) Income-Sensitive Repayment (FFEL) Alternative Repayment Plans (Direct ) http: //

- February 2 nd (2/2): (Experian) - June 6 th (6/6): (Equifax) - October 10 th")

19 Check Your Credit Report Campaign 5 minutes 3 times per year 2/2, 6/6, 10/ out of 200+ million consumers use AnnualCreditReport.com annually (CFPB, 2012) 5% of records have errors that could have negative consequence (FTC, ) - February 2 nd (2/2): (Experian) - June 6 th (6/6): (Equifax) - October 10 th (10/10): (TransUnion)

20 20 / 51 Rules of Thumb II for 1 Invest in Yourself: consider costs of delay 2 Manage student loans: consolidation, IBR, deferment 3 Check Your Credit 3xs per year: 4 Funds maximize employer matches Make it automatic Watch for fees (on financial products of all types) 5 #1 risk? You cannot work. Need (term) life insurance & Disability

21 21 / 51 Table of Contents

22 22 / Year Old Housing Rent vs. Own Buying a home for lifestyle not investment Saving for Keep it Simple Beware: Sold not sought There is no free lunch

23 23 / 51 A House is a Home Historically ownership is a means for building wealth : expansion Home equity used for consumption 2008 unemployment & home values fall 4 million foreclosures later...

24 Focus on Fees

25 retirement-fees/

26 Passive Investing: Hands Off is Better Very unlikely to beat market consistently A few funds or investments will beat the average, but rarely will that happen every year Number of Funds 5 years 10 years 20 years 3 funds 17% 9% 3% 5 funds 1 14% 8% 2% 10 funds 9% 6% 1% Source: The Power of Passive Investing: More Wealth with Less Work by Richard A. Ferri, / 51 1 average number of funds held by typical investor

27 Why Play the Lottery?

28 28 / 51 Rules of Thumb III for 1 Buy a home (not a real estate investment you happen to live in) 2 Mortgages shop around and refinance strategically 3 401k funds (a) focus on expense ratios and fees (not returns) 4 401k funds (b) use simple, broad market index funds 5 Save for kid s college it sends a signal 6 Just say no to financial sales people.

29 29 / 51 Table of Contents

30 30 / 51 Transitions and Planning How long will you work? What does work mean? How healthy are you? What will your life be like in retirement?

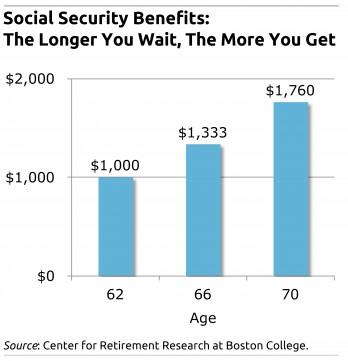

31 31 / 51 Claiming Social Security Social Security Payments are a Form of Annuity Inflation adjusted payments for life Core of retirement for many people Most people claim as soon as possible... Don t unless you have no other options Social Security Survivor benefits also valuable for spouse Use tools at:

32 32 / 51 Understanding Claiming Options

33

34 34 / 51 Rules of Thumb IV for ing 1 Boost savings rate as other expenses decline 2 Manage health care costs & coverage 3 Stay healthy, but prepare for not being healthy 4 Give a lot of thought to Social Security claiming choices (with spouse) 5 Remember: work may continue. becoming less of an event.

35 35 / 51 Table of Contents

36 36 / 51 Thinking Ahead is not about money Replacement rate fallacy You may not need as much as you think Health care is the wild card Expectations, health & well-being are complex! Living too long is a real risk Costs of maintaining complicated investments Simplify, especially as we age Keeping trusts, wills, estates fresh Preventing Financial Fraud & Elder Abuse

37 37 / 51 Plan for Loss in Cognitive Functioning Ability to make financial decisions? 30% of people in their 80s show cognitive impairment 20% of people in 80s show evidence of dementia That s 50% chance you will lose cognitive acumen. Agarwal, Driscoll, Gabaix, and Laibson Brookings Papers on Economic Activity 2:

38 38 / 51 Rules of Thumb V for Seniors 1 Organize documents Will DPA: Durable Power of Attorney Living will Health care proxy 2 Simplify & Consolidate 3 Manage Longevity Risk Annuity contracts: Yes, but read fine print 4 Talk to your spouse and family about managing finances regularly

39 39 / 51 Table of Contents

40 40 / 51 Keeping Up in Modern Consumer Financial Market Accelerated use of technology Prepaid debit cards Electronic payments SmartPhone Wallet Instant liquidity

41 Financial Capability Strategies Financial Capacity Building Information Models Disclosures Print/Web Interactive Web Workshops One:One Advice Models Technical expert (credentialed) Transactional guide (may have sales focus) Counseling (acute problem solving) Coaching Mechanism Models Defaults Automatic Deposit Product constraints Reminders: Salience Monitoring Executive Attention 41 / 51

42 Role of Education Workshops, Seminars, Brochures, Websites etc. Reduce the cost of acquiring information If people make better choices with more information Evidence of effects of financial literacy education are weak at best 2 But, be careful about right outcomes 42 /

43 43 / 51 More Information = More Debt Use //ssc.wisc.edu/~jmcollin/jebo_12.pdf http:

44 44 / 51 Multilevel Approaches Communitybased orgs Helping professionals Partnerships with the financial sector Social Ecological Model Social Ecological Model PUBLIC POLICY COMMUNITY ORGANIZATIONAL INTERPERSONAL INDIVIDUAL

45 45 / 51 Be Realistic: Financial Interventions Have Limits Limits of technical sciences... Exercise, Monitoring, Nutrition, Food Access, Counseling

46 46 / 51 Building Capability: When? Teachable Moments Life events Transitions Not just a class; not just in school Just in Time Decision making tools Linking to financial product access

47 47 / 51 What About Behavioral Nudges? Defaults Procrastination /Impatience Inattention Reminders Following the Crowd Social comparisons - Pro: Can be very powerful - Con: Indiscriminate Still need to have the ability to make decisions

48 48 / 51 Emerging Strategies Peers, Couples, Generational Focus on Goals Translating into impacts on future self Leverage Peers (and peer networks) Examples: Financial Coaching Emergency Savings

49 49 / 51 Focus on Well-Being More than Finances Being a steward of all resources Stability especially in housing Being able to response to shocks Mental and physical health Adaptability as contexts change Stress Confidence Trust

50 50 / 51 Moving Forward Rules of thumb help......but one size fits all solutions may not fit everyone Context matters A lot still to learn!

51 51 / 51 Learning More J. Michael Collins Center for Financial Security wisc.edu cfs.wisc.edu ssc.wisc.edu/~jmcollin/

Financial Capability Over the Life Course

1 / 38 Over the Life Course J. Michael Collins University of Wisconsin-Madison 2013 2 / 38 Survey for Wisconsin www.usfinancialcapability.org - clickable map 55 percent of Wisconsinites are living paycheck-to-paycheck

1 / 38 Over the Life Course J. Michael Collins University of Wisconsin-Madison 2013 2 / 38 Survey for Wisconsin www.usfinancialcapability.org - clickable map 55 percent of Wisconsinites are living paycheck-to-paycheck

TABLE OF CONTENTS Spring Schedule of Spring 2016 Events January

TABLE OF CONTENTS Spring 2016...93 Schedule of Spring 2016 Events... 94 January 2016......95 Financial Management Counseling: Lunch and Learn...96 Financial Literacy Presentation...97 Student Loans 101

TABLE OF CONTENTS Spring 2016...93 Schedule of Spring 2016 Events... 94 January 2016......95 Financial Management Counseling: Lunch and Learn...96 Financial Literacy Presentation...97 Student Loans 101

Financial Literacy and Your Financial Security. Academic Staff Institute April 1, 2014

Financial Literacy and Your Financial Security Academic Staff Institute April 1, 2014 What Does Financial Security Mean For You? What makes for Financial Security? Common Survey Question Let s say you

Financial Literacy and Your Financial Security Academic Staff Institute April 1, 2014 What Does Financial Security Mean For You? What makes for Financial Security? Common Survey Question Let s say you

Snapshots of Financial Coaching. Bank of America & Annie E. Casey Foundation Meeting April 26, 2010

Snapshots of Financial Coaching Bank of America & Annie E. Casey Foundation Meeting April 26, 2010 Context for Coaching Financial Capacity Building Information Models Advice Models Mechanism Models Disclosures

Snapshots of Financial Coaching Bank of America & Annie E. Casey Foundation Meeting April 26, 2010 Context for Coaching Financial Capacity Building Information Models Advice Models Mechanism Models Disclosures

STUDENT LOAN REPAYMENT. Leslie Tobakos Registrar, Financial Aid & Admissions Manager Cranbrook Academy of Art

STUDENT LOAN REPAYMENT Leslie Tobakos Registrar, Financial Aid & Admissions Manager Cranbrook Academy of Art In this world nothing can be said to be certain, except death and taxes. Benjamin Franklin,

STUDENT LOAN REPAYMENT Leslie Tobakos Registrar, Financial Aid & Admissions Manager Cranbrook Academy of Art In this world nothing can be said to be certain, except death and taxes. Benjamin Franklin,

Money 101 Presenter s Guide

For College Students Money 101 Presenter s Guide A Crash Course in Better Money Management For College Students Getting Started The What s My Score Money 101 presentation features six topics that should

For College Students Money 101 Presenter s Guide A Crash Course in Better Money Management For College Students Getting Started The What s My Score Money 101 presentation features six topics that should

How to Strategically Manage Your Debt

Debt. Funny how four little letters can feel so dirty. Most of us have it in one shape or another, but none of us like to talk about it. Debt can get us into trouble, especially if it is unplanned and

Debt. Funny how four little letters can feel so dirty. Most of us have it in one shape or another, but none of us like to talk about it. Debt can get us into trouble, especially if it is unplanned and

50 Personal Finance Habits Everyone Should Follow

50 Personal Finance Habits Everyone Should Follow Len Penzo Start by spending less than you earn every month. From time to time we bring you posts from our partners that may not be new but contain advice

50 Personal Finance Habits Everyone Should Follow Len Penzo Start by spending less than you earn every month. From time to time we bring you posts from our partners that may not be new but contain advice

YOU ARE NOT ALONE Hello, my name is <name> and I m <title>.

So I know why you re here: I bet you ve got some questions about your money: what to do with it, how to make the most of it and how to hopefully get more of it. You ve got questions and the good news is

So I know why you re here: I bet you ve got some questions about your money: what to do with it, how to make the most of it and how to hopefully get more of it. You ve got questions and the good news is

Project Pro$per. Credit Reports and Credit Scores

Project Pro$per Presents Credit Reports and Credit Scores Participant Guide www.projectprosper.org www.facebook.com/projectprosper Based on Wells Fargo s Hands on Banking The Hands on Banking program is

Project Pro$per Presents Credit Reports and Credit Scores Participant Guide www.projectprosper.org www.facebook.com/projectprosper Based on Wells Fargo s Hands on Banking The Hands on Banking program is

THE ROAD TO ZERO. A Strategic Approach to Student Loan Repayment. Financial education resources from a nonprofit you can trust. AccessLex.

THE ROAD TO ZERO A Strategic Approach to Student Loan Repayment Financial education resources from a nonprofit you can trust. AccessLex.org 1 GET STARTED. 3 KNOW WHAT YOU OWE. 4 KNOW YOUR OPTIONS. 6 Debt-Driven

THE ROAD TO ZERO A Strategic Approach to Student Loan Repayment Financial education resources from a nonprofit you can trust. AccessLex.org 1 GET STARTED. 3 KNOW WHAT YOU OWE. 4 KNOW YOUR OPTIONS. 6 Debt-Driven

September 13, Financial Planning for First Time Homebuyers

Welcome to the Center for Financial Security Family Financial Security Webinar Series September 13, 2011 Financial Planning for First Time Homebuyers Sponsored by a grant from the UW-Madison School of

Welcome to the Center for Financial Security Family Financial Security Webinar Series September 13, 2011 Financial Planning for First Time Homebuyers Sponsored by a grant from the UW-Madison School of

About Salt Money Management Student Loan Repayment

About Salt Money Management Student Loan Repayment Michele Almeida Senior Associate Director of SFS Jane Aube Loan Programs & Compliance Specialist Kim Downs-Burns AVP Student Financial Services American

About Salt Money Management Student Loan Repayment Michele Almeida Senior Associate Director of SFS Jane Aube Loan Programs & Compliance Specialist Kim Downs-Burns AVP Student Financial Services American

Appendix 1V Baby Boomer Contemplating Retirement

Checkpoint Contents Federal Library Federal Editorial Materials PPC's Tax and Financial Planning Library Retirement Planning Chapter 1 A Step-by-step Planning Approach Appendix 1V Baby Boomer Contemplating

Checkpoint Contents Federal Library Federal Editorial Materials PPC's Tax and Financial Planning Library Retirement Planning Chapter 1 A Step-by-step Planning Approach Appendix 1V Baby Boomer Contemplating

You Know You ve Reached Middle Age IF? There s no need to run out and buy a home pregnancy kit Happy Hour with free Hors d oeuvres no long constitutes

Financial Secrets one CRNA to Another Major Peter Strube CRNA MSNA APNP You Know You ve Reached Middle Age IF? There s no need to run out and buy a home pregnancy kit Happy Hour with free Hors d oeuvres

Financial Secrets one CRNA to Another Major Peter Strube CRNA MSNA APNP You Know You ve Reached Middle Age IF? There s no need to run out and buy a home pregnancy kit Happy Hour with free Hors d oeuvres

Curriculum Guide

EverFi @Work Curriculum Guide Table of Contents Overview... 3 Detailed Module Summaries... 4 Auto Loans... 4 Benefits of a Credit Union... 4 Budgeting Tool... 4 Building Emergency Savings... 4 Checking

EverFi @Work Curriculum Guide Table of Contents Overview... 3 Detailed Module Summaries... 4 Auto Loans... 4 Benefits of a Credit Union... 4 Budgeting Tool... 4 Building Emergency Savings... 4 Checking

FarmHouse International Fraternity New Member Education Program Topic Summary: Personal Finance

FarmHouse International Fraternity New Member Education Program Topic Summary: Personal Finance 11 College is a challenging time both in and out of class. As a student you are coping with a new environment

FarmHouse International Fraternity New Member Education Program Topic Summary: Personal Finance 11 College is a challenging time both in and out of class. As a student you are coping with a new environment

Your guide to the fundamentals of investing

Your guide to the fundamentals of investing Your money. Our expertise. This guide is for information purposes only. It should not be seen as advice. Investments in the stock market may fall as well as

Your guide to the fundamentals of investing Your money. Our expertise. This guide is for information purposes only. It should not be seen as advice. Investments in the stock market may fall as well as

GREENPATH FINANCIAL WELLNESS SERIES

GREENPATH FINANCIAL WELLNESS SERIES UNDERSTANDING YOUR CREDIT REPORT & SCORE Empowering people to lead financially healthy lives. TABLE OF CONTENTS Understanding credit reports...2 What s in a credit

GREENPATH FINANCIAL WELLNESS SERIES UNDERSTANDING YOUR CREDIT REPORT & SCORE Empowering people to lead financially healthy lives. TABLE OF CONTENTS Understanding credit reports...2 What s in a credit

LOAN REPAYMENT STRATEGIES

LOAN REPAYMENT STRATEGIES Be Ready! Develop a Plan! Fall 2017 Jeffrey Hanson Education Services Boston University School of Law You have CHOICES Decisions to be made 2 Should you pay the interest on your

LOAN REPAYMENT STRATEGIES Be Ready! Develop a Plan! Fall 2017 Jeffrey Hanson Education Services Boston University School of Law You have CHOICES Decisions to be made 2 Should you pay the interest on your

Curriculum Guide

EverFi @Work Curriculum Guide Table of Contents Overview... 3 Detailed Module Summaries... 4 Auto Loans... 4 Building Emergency Savings... 4 Checking Accounts... 4 Considering Home Ownership... 5 Credit

EverFi @Work Curriculum Guide Table of Contents Overview... 3 Detailed Module Summaries... 4 Auto Loans... 4 Building Emergency Savings... 4 Checking Accounts... 4 Considering Home Ownership... 5 Credit

Financial Capability in the U.S. Data from the State-by-State Survey Component of the National Financial Capability Study April 13, 2011

Financial Capability in the U.S. Data from the State-by-State Survey Component of the National Financial Capability Study April 13, 2011 INFORMING TODAY S INVESTORS Financial Industry Regulatory Authority

Financial Capability in the U.S. Data from the State-by-State Survey Component of the National Financial Capability Study April 13, 2011 INFORMING TODAY S INVESTORS Financial Industry Regulatory Authority

Understanding Credit

Understanding Credit LAURA STEINBECK DIRECTOR OF BUSINESS DEVELOPMENT, SALLIE MAE 2018 MASFAP CONFERENCE Agenda 2 Credit Management Protect Yourself Understanding Credit Reports Summary: Financial Health

Understanding Credit LAURA STEINBECK DIRECTOR OF BUSINESS DEVELOPMENT, SALLIE MAE 2018 MASFAP CONFERENCE Agenda 2 Credit Management Protect Yourself Understanding Credit Reports Summary: Financial Health

Lending with a Purpose

Lending with a Purpose 7 Steps to Loaning Money to Family and Friends 2 Table of Contents Family and Friend Loans Risks and Rewards... 3 When it goes well... 3 When it goes bad... 3 A matter of trust...

Lending with a Purpose 7 Steps to Loaning Money to Family and Friends 2 Table of Contents Family and Friend Loans Risks and Rewards... 3 When it goes well... 3 When it goes bad... 3 A matter of trust...

Checking, Saving, Investing, and Protecting your money Unit 3

Checking, Saving, Investing, and Protecting your money Unit 3 Banks Financial Institutions licensed to receive and utilize deposits There are 2 main types of Banks Retail/Commercial Banks- Financial Institutions

Checking, Saving, Investing, and Protecting your money Unit 3 Banks Financial Institutions licensed to receive and utilize deposits There are 2 main types of Banks Retail/Commercial Banks- Financial Institutions

Financial Well-being SAVINGS

Financial Well-being SAVINGS SAVINGS Savings is a key part of a successful financial wellness plan. Specifically, having not only a basic savings level (emergency fund), but also building up enough savings

Financial Well-being SAVINGS SAVINGS Savings is a key part of a successful financial wellness plan. Specifically, having not only a basic savings level (emergency fund), but also building up enough savings

Building Credit. Inside this issue:

CCCS of Rochester/RethinkingDebt Headquarters: 1000 University Ave, Rochester, NY 14607 **Fall 2018** Inside this issue: Building Credit Building Credit 1 Retail Credit Cards 2 By: CCCS of Rochester Student

CCCS of Rochester/RethinkingDebt Headquarters: 1000 University Ave, Rochester, NY 14607 **Fall 2018** Inside this issue: Building Credit Building Credit 1 Retail Credit Cards 2 By: CCCS of Rochester Student

What is a Robo Advisor? A publication of Paladin Research.

What is a Robo Advisor? A publication of Paladin Research www.paladinregistry.com The word Robo is catchy and easy to remember. Your assets are managed by computer programs and not by investment professionals.

What is a Robo Advisor? A publication of Paladin Research www.paladinregistry.com The word Robo is catchy and easy to remember. Your assets are managed by computer programs and not by investment professionals.

The Importance of Comprehensive Estate Planning as Cognitive Challenges Become More Significant

The Importance of Comprehensive Estate Planning as Cognitive Challenges Become More Significant Creating a hierarchical organization chart of family members who need to be involved in the decision-making

The Importance of Comprehensive Estate Planning as Cognitive Challenges Become More Significant Creating a hierarchical organization chart of family members who need to be involved in the decision-making

12 Steps to Improved Credit Steven K. Shapiro

12 Steps to Improved Credit Steven K. Shapiro 2009 2018 sks@skscci.com In my previous article, I wrote about becoming debt-free and buying everything with cash. Even while I was writing the article, I

12 Steps to Improved Credit Steven K. Shapiro 2009 2018 sks@skscci.com In my previous article, I wrote about becoming debt-free and buying everything with cash. Even while I was writing the article, I

UNDERSTANDING CREDIT. KASFAA Conference Manhattan, KS April 21, Robb Cummings Director of Business Development

UNDERSTANDING CREDIT KASFAA Conference Manhattan, KS April 21, 2016 Robb Cummings Director of Business Development FICO Score 2 A FICO Score is a three-digit number calculated from the credit information

UNDERSTANDING CREDIT KASFAA Conference Manhattan, KS April 21, 2016 Robb Cummings Director of Business Development FICO Score 2 A FICO Score is a three-digit number calculated from the credit information

Comprehensive wealth management for Accenture consultants SENIOR MANAGERS, MANAGING DIRECTORS AND PARTNERS

Comprehensive wealth management for Accenture consultants SENIOR MANAGERS, MANAGING DIRECTORS AND PARTNERS Executive Summary Because the majority of you will only read one slide Our team Our advisors share

Comprehensive wealth management for Accenture consultants SENIOR MANAGERS, MANAGING DIRECTORS AND PARTNERS Executive Summary Because the majority of you will only read one slide Our team Our advisors share

Post-Loan (Exit) Counseling Supplement:

Counseling Supplement:") Post-Loan (Exit) Counseling Supplement: Prepared by: Dr. Deb Figart Director, Stockton Center for Economic & Financial Literacy Deb.Figart@stockton.edu Why this Presentation? The federal online, required

Post-Loan (Exit) Counseling Supplement: Prepared by: Dr. Deb Figart Director, Stockton Center for Economic & Financial Literacy Deb.Figart@stockton.edu Why this Presentation? The federal online, required

General Financial Literacy

General Financial Literacy Levels: Grades 11-12 Units of Credit: 0.50 Core Code: 01-00- 00-00- 100 Prerequisite: None COURSE DESRIPTION The General Financial Literacy course for juniors and seniors encompasses

General Financial Literacy Levels: Grades 11-12 Units of Credit: 0.50 Core Code: 01-00- 00-00- 100 Prerequisite: None COURSE DESRIPTION The General Financial Literacy course for juniors and seniors encompasses

YOUR MONEY, YOUR GOALS. A financial empowerment toolkit

YOUR MONEY, YOUR GOALS A financial empowerment toolkit Consumer Financial Protection Bureau December 2016 About the Consumer Financial Protection Bureau The Consumer Financial Protection Bureau (CFPB)

YOUR MONEY, YOUR GOALS A financial empowerment toolkit Consumer Financial Protection Bureau December 2016 About the Consumer Financial Protection Bureau The Consumer Financial Protection Bureau (CFPB)

Meet The Speakers. Sasha Grabenstetter, AFC Consumer Economics Educator University of Illinois Extension

Welcome to 1 Meet The Speakers Sasha Grabenstetter, AFC Consumer Economics Educator University of Illinois Extension Andrea Pellegrini Assistant Director Student Money Management Center 2 Where are you

Welcome to 1 Meet The Speakers Sasha Grabenstetter, AFC Consumer Economics Educator University of Illinois Extension Andrea Pellegrini Assistant Director Student Money Management Center 2 Where are you

FAQ s. Why should I hire Social Security Advocates for the Disabled? How can you help me if I don t live near your office?

800.825.7735 136 Long water Drive, Suite 100, Norwell, MA 02150 FAQ s Why should I hire Social Security Advocates for the Disabled? Hire us because we win, and we ve been winning since 1994. People that

800.825.7735 136 Long water Drive, Suite 100, Norwell, MA 02150 FAQ s Why should I hire Social Security Advocates for the Disabled? Hire us because we win, and we ve been winning since 1994. People that

Money Math for Teens. The Emergency Fund

Money Math for Teens The Emergency Fund This Money Math for Teens lesson is part of a series created by Generation Money, a multimedia financial literacy initiative of the FINRA Investor Education Foundation,

Money Math for Teens The Emergency Fund This Money Math for Teens lesson is part of a series created by Generation Money, a multimedia financial literacy initiative of the FINRA Investor Education Foundation,

Consumer Literacy & Credit Worthiness

Consumer Literacy & Credit Worthiness June 1, 2005 Marsha J. Courchane, Principal, ERS Group Peter M. Zorn, VP, Housing Analysis, Research & Policy, FMAC Prepared for: Wisconsin Department of Financial

Consumer Literacy & Credit Worthiness June 1, 2005 Marsha J. Courchane, Principal, ERS Group Peter M. Zorn, VP, Housing Analysis, Research & Policy, FMAC Prepared for: Wisconsin Department of Financial

Welcome to Student Loan Repayment Strategies

Welcome to Student Loan Repayment Strategies Kathy Sweedler Consumer Economics Educator University of Illinois Extension sweedler@illinois.edu 1 Make Plan: Take Action Where are you now? Evaluate repayment

Welcome to Student Loan Repayment Strategies Kathy Sweedler Consumer Economics Educator University of Illinois Extension sweedler@illinois.edu 1 Make Plan: Take Action Where are you now? Evaluate repayment

Employee Education Catalog

2017 CUNA Mutual Retirement Solutions Education Curriculum Employee Education Catalog CUNA MUTUAL RETIREMENT SOLUTIONS People driven. Outcome focused. Improving employees financial wellness is the theme

2017 CUNA Mutual Retirement Solutions Education Curriculum Employee Education Catalog CUNA MUTUAL RETIREMENT SOLUTIONS People driven. Outcome focused. Improving employees financial wellness is the theme

Financial Wellness Programs

GET OFF THE CAR LOAN CAROUSEL Many people just assume that they will be burdened with a car loan for life. However, with well-planned, prudent choices an individual can rid themselves of car loans and

GET OFF THE CAR LOAN CAROUSEL Many people just assume that they will be burdened with a car loan for life. However, with well-planned, prudent choices an individual can rid themselves of car loans and

Preparing for Cognitive Impairment: Three Items You Can t Do Without By Renée Kwok CFP, President, TFC Financial Management

Reprinted from Forbes.com Preparing for Cognitive Impairment: Three Items You Can t Do Without By Renée Kwok CFP, President, TFC Financial Management The way in which families interact changes as life

Reprinted from Forbes.com Preparing for Cognitive Impairment: Three Items You Can t Do Without By Renée Kwok CFP, President, TFC Financial Management The way in which families interact changes as life

Student Loan Repayment Workshop. Amanda Seitz Direct Loan Coordinator - Student Financial Services

Student Loan Repayment Workshop Amanda Seitz Direct Loan Coordinator - Student Financial Services Amanda.seitz@purchase.edu (914) 251-6080 Types of Student Loans Subsidized Direct Loan fixed interest loan

Student Loan Repayment Workshop Amanda Seitz Direct Loan Coordinator - Student Financial Services Amanda.seitz@purchase.edu (914) 251-6080 Types of Student Loans Subsidized Direct Loan fixed interest loan

A Financial Primer: 12 Tips to Help Secure Your Financial Future

A Financial Primer: 12 Tips to Help Secure Your Financial Future What will you do with your earning power and what will you have to show for it in the future? Table of Contents Page Your Earning Power

A Financial Primer: 12 Tips to Help Secure Your Financial Future What will you do with your earning power and what will you have to show for it in the future? Table of Contents Page Your Earning Power

Highlights of The Tax-Sheltered Annuity Program. The California State University

Highlights of The Tax-Sheltered Annuity Program The California State University Tax-Sheltered Annuity Program TABLE OF CONTENTS TSA Program Overview... 1 Saving Through the TSA Program... 2 Making Investment

Highlights of The Tax-Sheltered Annuity Program The California State University Tax-Sheltered Annuity Program TABLE OF CONTENTS TSA Program Overview... 1 Saving Through the TSA Program... 2 Making Investment

Welcome! Credit Scoring and Sub-Prime Lending

Welcome! Credit Scoring and Sub-Prime Lending What is Credit Scoring? It s the use of a statistical model to objectively evaluate all the credit information available in a single repository What is a repository?

Welcome! Credit Scoring and Sub-Prime Lending What is Credit Scoring? It s the use of a statistical model to objectively evaluate all the credit information available in a single repository What is a repository?

Valuation of Equity and Investment Decisions. Shyam Sunder, Yale University Amrut Modi School of Management Ahmedabad University January 1, 2015

Valuation of Equity and Investment Decisions Shyam Sunder, Yale University Amrut Modi School of Management Ahmedabad University January 1, 2015 An Overview What is your purpose? What is in your opportunity

Valuation of Equity and Investment Decisions Shyam Sunder, Yale University Amrut Modi School of Management Ahmedabad University January 1, 2015 An Overview What is your purpose? What is in your opportunity

WHAT MATTERS MOST. A woman s guide to an inspired retirement strategy

WHAT MATTERS MOST A woman s guide to an inspired retirement strategy Issued by Pruco Life Insurance Company (in New York, issued by Pruco Life Insurance Company of New Jersey). 0250519-00002-00 Ed. 01/2014

WHAT MATTERS MOST A woman s guide to an inspired retirement strategy Issued by Pruco Life Insurance Company (in New York, issued by Pruco Life Insurance Company of New Jersey). 0250519-00002-00 Ed. 01/2014

THE EMPLOYEE EDUCATION SOLUTION

THE EMPLOYEE EDUCATION SOLUTION A Comprehensive Overview of Tools and Resources WORKSITE FINANCIAL SOLUTIONS THE EMPLOYEE EDUCATION SOLUTION A Customized Financial Wellness Program for Your Employees CONTENTS

THE EMPLOYEE EDUCATION SOLUTION A Comprehensive Overview of Tools and Resources WORKSITE FINANCIAL SOLUTIONS THE EMPLOYEE EDUCATION SOLUTION A Customized Financial Wellness Program for Your Employees CONTENTS

PIONEERING WORKPLACE FINANCIAL WELLNESS

PIONEERING WORKPLACE FINANCIAL WELLNESS It s no secret that workers are shouldering more responsibility and risk for their healthcare and retirement expenses. Coupled with higher costs for buying a home

PIONEERING WORKPLACE FINANCIAL WELLNESS It s no secret that workers are shouldering more responsibility and risk for their healthcare and retirement expenses. Coupled with higher costs for buying a home

10 Things to Consider in

RETIREMENT INCOME PLANNING for Ages 35 to 50 Compliments of Jennifer & Eric Lahaie Jennifer & Eric Lahaie Eric and Jennifer Lahaie are the owners and founders of JEHM Wealth & Retirement. With years of

RETIREMENT INCOME PLANNING for Ages 35 to 50 Compliments of Jennifer & Eric Lahaie Jennifer & Eric Lahaie Eric and Jennifer Lahaie are the owners and founders of JEHM Wealth & Retirement. With years of

Miami-Dade County Public Schools Department of Social Sciences. Financial Literacy Tip of the Week: Secondary

Miami-Dade County Public Schools Department of Social Sciences Financial Literacy Tip of the Week: Secondary Financial Literacy Tip of the Week Secondary: Below are statements that can be shared via school

Miami-Dade County Public Schools Department of Social Sciences Financial Literacy Tip of the Week: Secondary Financial Literacy Tip of the Week Secondary: Below are statements that can be shared via school

FINANCIAL LITERACY WHAT YOU NEED TO KNOW TO SURVIVE IN TODAY S ECONOMY

FINANCIAL LITERACY WHAT YOU NEED TO KNOW TO SURVIVE IN TODAY S ECONOMY Presented by: Terry Lawson Lawson Law Center 700 E. 8 th St. Kansas City, MO 64106 www.llckc.com LAWSON LAW CENTER LLC WWW. LLCKC.COM

FINANCIAL LITERACY WHAT YOU NEED TO KNOW TO SURVIVE IN TODAY S ECONOMY Presented by: Terry Lawson Lawson Law Center 700 E. 8 th St. Kansas City, MO 64106 www.llckc.com LAWSON LAW CENTER LLC WWW. LLCKC.COM

steps to financial fitne $$

#1 Fit or fat? Take our financial quiz Do you have a written household budget? Do you pay more than the minimum amount on your credit card or have no credit card debt? Do you have an emergency savings

#1 Fit or fat? Take our financial quiz Do you have a written household budget? Do you pay more than the minimum amount on your credit card or have no credit card debt? Do you have an emergency savings

General Financial Literacy

PRECISION EXAMS General Financial Literacy EXAM INFORMATION Items 75 Points 85 Prerequisites NONE Grade Level 10-12 Course Length ONE SEMESTER Career Cluster 21 ST CENTURY SKILLS FINANCE Performance Standards

PRECISION EXAMS General Financial Literacy EXAM INFORMATION Items 75 Points 85 Prerequisites NONE Grade Level 10-12 Course Length ONE SEMESTER Career Cluster 21 ST CENTURY SKILLS FINANCE Performance Standards

Rejuvenate Your Retirement An Educational Course for Retirees

Rejuvenate Your Retirement An Educational Course for Retirees Now being conducted at Location Dates & Times Tuesdays 120 Bloomfield Avenue October 3 & 10 Caldwell, NJ 07006 9:30 a.m. to 11:30 a.m. or Thursdays

Rejuvenate Your Retirement An Educational Course for Retirees Now being conducted at Location Dates & Times Tuesdays 120 Bloomfield Avenue October 3 & 10 Caldwell, NJ 07006 9:30 a.m. to 11:30 a.m. or Thursdays

LESSON 8 -- BUYING A HOME

LESSON 8 -- BUYING A HOME LESSON DESCRIPTION AND BACKGROUND This lesson uses the Better Money Habits video Is Buying a Home Right for You? (www.bettermoneyhabits.com) to help students compare the costs

LESSON 8 -- BUYING A HOME LESSON DESCRIPTION AND BACKGROUND This lesson uses the Better Money Habits video Is Buying a Home Right for You? (www.bettermoneyhabits.com) to help students compare the costs

Federal Student Loan Repayment

Federal Student Loan Repayment The Road to Zero Know your financial goals. Know what you owe. Know what time it is. Know your options. Select your plan. Manage your payments. AccessGroup.org Financial

Federal Student Loan Repayment The Road to Zero Know your financial goals. Know what you owe. Know what time it is. Know your options. Select your plan. Manage your payments. AccessGroup.org Financial

SOCIAL SECURITY CLAIMING GUIDE

the SOCIAL SECURITY CLAIMING GUIDE A guide to the most important financial decision you ll likely make By Steven Sass, Alicia H. Munnell, and Andrew Eschtruth Art direction and design by Ronn Campisi,

the SOCIAL SECURITY CLAIMING GUIDE A guide to the most important financial decision you ll likely make By Steven Sass, Alicia H. Munnell, and Andrew Eschtruth Art direction and design by Ronn Campisi,

Money Matters. financial lessons for life

2013 Money Matters financial lessons for life 92% of parents in Canada want their children to be money-smart* Early conversations about money will improve financial literacy Talk to your kids about money

2013 Money Matters financial lessons for life 92% of parents in Canada want their children to be money-smart* Early conversations about money will improve financial literacy Talk to your kids about money

Closing the Gap Between Belief and Behavior

Closing the Gap Between Belief and Behavior BlackRock s 2010 401(k) Participant Behaviors and Attitudes Study DefinedContribution 2 Closing the Gap Between Belief and Behavior The Blackrock survey: Understanding

Closing the Gap Between Belief and Behavior BlackRock s 2010 401(k) Participant Behaviors and Attitudes Study DefinedContribution 2 Closing the Gap Between Belief and Behavior The Blackrock survey: Understanding

Understanding and Measuring Financial Health

Understanding and Measuring Financial Health Elisabeth Rhyne Managing Director, Center for Financial Inclusion at Accion International Conference on Customer Centric Businesses Mamallapuram, India February

Understanding and Measuring Financial Health Elisabeth Rhyne Managing Director, Center for Financial Inclusion at Accion International Conference on Customer Centric Businesses Mamallapuram, India February

INVESTMENT POLICY GUIDANCE REPORT. Living in Retirement. A Successful Foundation

INVESTMENT POLICY GUIDANCE REPORT Living in Retirement A Successful Foundation Developing Your The process for creating a strategy Plan for the Expected Your Retirement Journey It all starts with you.

INVESTMENT POLICY GUIDANCE REPORT Living in Retirement A Successful Foundation Developing Your The process for creating a strategy Plan for the Expected Your Retirement Journey It all starts with you.

Ten Things You Should Know About Student Loans

Ten Things You Should Know About Student Loans 1: BORROW ONLY WHAT YOU NEED 4: UNDERSTAND YOUR LOANS There are several different kinds of loans. Here are some key factors to be aware of: 7: MAKE PAYMENTS

Ten Things You Should Know About Student Loans 1: BORROW ONLY WHAT YOU NEED 4: UNDERSTAND YOUR LOANS There are several different kinds of loans. Here are some key factors to be aware of: 7: MAKE PAYMENTS

Making a Roth IRA Conversion

March/April 2019 Making a Roth IRA Conversion If you re nearing or in retirement and concerned that income tax rates will rise, you may want to convert a portion or all of your taxable retirement plan

March/April 2019 Making a Roth IRA Conversion If you re nearing or in retirement and concerned that income tax rates will rise, you may want to convert a portion or all of your taxable retirement plan

Allow us to introduce ourselves.

Allow us to introduce ourselves. We are Zurich. We are part of a global insurance group with Swiss roots. We are one of Ireland s most successful life and pension providers. We believe in building a life

Allow us to introduce ourselves. We are Zurich. We are part of a global insurance group with Swiss roots. We are one of Ireland s most successful life and pension providers. We believe in building a life

STAYING INDEPENDENT. This ebook brought to you by: Buy-Ebook.com

STAYING INDEPENDENT This ebook brought to you by: Buy-Ebook.com Our site has got a great collection of the best ebooks which are sold on the Internet, but at a lower price than on any other site. Earn

STAYING INDEPENDENT This ebook brought to you by: Buy-Ebook.com Our site has got a great collection of the best ebooks which are sold on the Internet, but at a lower price than on any other site. Earn

One BIG Last-Minute Tax Break

March/April 2019 One BIG Last-Minute Tax Break While some of us may worry about getting our tax payments out on time or refunds back, most of us don t use this time to figure out ways to minimize taxes

March/April 2019 One BIG Last-Minute Tax Break While some of us may worry about getting our tax payments out on time or refunds back, most of us don t use this time to figure out ways to minimize taxes

UNDERSTANDING CREDIT. WASFAA Conference Seattle, WA Speakers: Thalassa Naylor, Sallie Mae Anthony Lombardi, Sallie Mae Date: April 10, 2017

UNDERSTANDING CREDIT WASFAA Conference Seattle, WA Speakers: Thalassa Naylor, Sallie Mae Anthony Lombardi, Sallie Mae Date: April 10, 2017 Agenda 2 Credit Management Protect Yourself Understanding Your

UNDERSTANDING CREDIT WASFAA Conference Seattle, WA Speakers: Thalassa Naylor, Sallie Mae Anthony Lombardi, Sallie Mae Date: April 10, 2017 Agenda 2 Credit Management Protect Yourself Understanding Your

20 Steps to Financial Health:

20 Steps to Financial Health: Achieving Lifelong Financial Fitness American Consumer Credit Counseling 130 Rumford Avenue Auburndale, MA 02466 1.800.769.3571 ConsumerCredit.com On behalf of American Consumer

20 Steps to Financial Health: Achieving Lifelong Financial Fitness American Consumer Credit Counseling 130 Rumford Avenue Auburndale, MA 02466 1.800.769.3571 ConsumerCredit.com On behalf of American Consumer

Guide to taking a secure retirement income

Winner of the Gold Standard Award for Retirement the last three years running www.hl.co.uk/annuity Guide to taking a secure retirement income How to boost your income for life One College Square South,

Winner of the Gold Standard Award for Retirement the last three years running www.hl.co.uk/annuity Guide to taking a secure retirement income How to boost your income for life One College Square South,

Set Yourself Up for Retirement Success

Set Yourself Up for Retirement Success Key decisions can help you and your loved ones plan ahead to make your retirement work After years in the workforce, you may be daydreaming about your retirement.

Set Yourself Up for Retirement Success Key decisions can help you and your loved ones plan ahead to make your retirement work After years in the workforce, you may be daydreaming about your retirement.

A Consumer s Guide to

A Consumer s Guide to 401(k) Plans NYSUT Member Benefits wants NYSUT members to be the best-informed consumers in the state. This Consumer Guide is one of our contributions towards achieving that goal.

A Consumer s Guide to 401(k) Plans NYSUT Member Benefits wants NYSUT members to be the best-informed consumers in the state. This Consumer Guide is one of our contributions towards achieving that goal.

SOCIAL SECURITY Financial Literacy GUIDE

SOCIAL SECURITY Financial Literacy GUIDE A guide to the most important financial decision you ll likely make Carl Robinson & David Vinokurov 1 Outline Where does Social Security fit into my overall Financial

SOCIAL SECURITY Financial Literacy GUIDE A guide to the most important financial decision you ll likely make Carl Robinson & David Vinokurov 1 Outline Where does Social Security fit into my overall Financial

Repayment Plans 2.0: Strategies and Insights to Help Borrowers Succeed OASFAA - April 2016

Repayment Plans 2.0: Strategies and Insights to Help Borrowers Succeed OASFAA - April 2016 Latest Report Class of 2014 average student loan debt $28,950 2014 unemployment rate for college graduates 7.2%

Repayment Plans 2.0: Strategies and Insights to Help Borrowers Succeed OASFAA - April 2016 Latest Report Class of 2014 average student loan debt $28,950 2014 unemployment rate for college graduates 7.2%

Budgeting & Debt Basics

Budgeting & Debt Basics Why Have a Budget? Gain control over your finances Get the most out of your money Achieve your financial goals What is a Budget? A plan for saving and spending Allows you to choose

Budgeting & Debt Basics Why Have a Budget? Gain control over your finances Get the most out of your money Achieve your financial goals What is a Budget? A plan for saving and spending Allows you to choose

Guide to Working with

Mutual of Omaha Insurance Company United of Omaha Life Insurance Company Companion Life Insurance Company Guide to Working with Headline Business Owners SUBHEAD 167456 Form No. For producer use only. Not

Mutual of Omaha Insurance Company United of Omaha Life Insurance Company Companion Life Insurance Company Guide to Working with Headline Business Owners SUBHEAD 167456 Form No. For producer use only. Not

GENERAL FINANCING QUESTIONS

GENERAL FINANCING QUESTIONS 1. What is a Mortgage? Tips for Homebuyers Generally speaking, a mortgage is a loan obtained to purchase real estate. The "mortgage" itself is a lien (a legal claim) on the

GENERAL FINANCING QUESTIONS 1. What is a Mortgage? Tips for Homebuyers Generally speaking, a mortgage is a loan obtained to purchase real estate. The "mortgage" itself is a lien (a legal claim) on the

Session Overview. Budgeting Skills Training - Instructor Notes. Thank you for teaching the Budgeting Skills Training Class :D

Session Overview Budgeting Skills Training - Instructor Notes Thank you for teaching the Budgeting Skills Training Class :D The instructor notes contain suggestions for you on how to teach this class.

Session Overview Budgeting Skills Training - Instructor Notes Thank you for teaching the Budgeting Skills Training Class :D The instructor notes contain suggestions for you on how to teach this class.

OVERCOMING THE CREDIT BARRIER. Clearing the Way to Your Financial Goals

OVERCOMING THE CREDIT BARRIER Clearing the Way to Your Financial Goals Overcoming the Credit Barrier: Clearing the Way to Your Financial Goals was written and designed for The National Foundation for Credit

OVERCOMING THE CREDIT BARRIER Clearing the Way to Your Financial Goals Overcoming the Credit Barrier: Clearing the Way to Your Financial Goals was written and designed for The National Foundation for Credit

Introduction Slide SET. Host Organization s Name July 30, Business Smart is a business education series developed by

Introduction Slide Business Smart is a business education series developed by SET Host Organization s Name July 30, 2015 1 Business Smart Workshop 3 Modules READY SET GO 2 Today s Presenter Add Name of

Introduction Slide Business Smart is a business education series developed by SET Host Organization s Name July 30, 2015 1 Business Smart Workshop 3 Modules READY SET GO 2 Today s Presenter Add Name of

Module Summaries

EVERFI @Work Module Summaries Auto Loans Identify different types of auto loan providers Define important components of an auto loan: installment, principal interest, fees Explain the relationship between

EVERFI @Work Module Summaries Auto Loans Identify different types of auto loan providers Define important components of an auto loan: installment, principal interest, fees Explain the relationship between

Financial Well-being. Debt and Credit

Financial Well-being Debt and Credit Debt and Credit When evaluating financial wellness, debt has a real impact on your ability to reach your goals. Debt feels like a four letter word. However, it can

Financial Well-being Debt and Credit Debt and Credit When evaluating financial wellness, debt has a real impact on your ability to reach your goals. Debt feels like a four letter word. However, it can

TAKE CHARGE OF LOAN REPAYMENT!

1 TAKE CHARGE OF LOAN REPAYMENT! Strategies for Managing Your Debt Successfully Spring 2014 Jeffrey Hanson Education Services University of Wisconsin Law School Federal student loans are unique 2 q Flexible

1 TAKE CHARGE OF LOAN REPAYMENT! Strategies for Managing Your Debt Successfully Spring 2014 Jeffrey Hanson Education Services University of Wisconsin Law School Federal student loans are unique 2 q Flexible

Student Loan Ombudsman Caucus

Student Loan Ombudsman Caucus Repayment Plans Selecting the right repayment plan is important in the successful management of your student loan. You can change repayment plans contact your lender/servicer

Student Loan Ombudsman Caucus Repayment Plans Selecting the right repayment plan is important in the successful management of your student loan. You can change repayment plans contact your lender/servicer

PROOF. * pension-plan-limitations-401k-contributionlimitincreasesto for-2018

Loose Change a penny saved is a penny earned March/April 2019 Vol. 26 No. 2 Two Ways to Save Taxes As federal and state tax filing deadlines approach, you may naturally wonder how to minimize your taxes.

Loose Change a penny saved is a penny earned March/April 2019 Vol. 26 No. 2 Two Ways to Save Taxes As federal and state tax filing deadlines approach, you may naturally wonder how to minimize your taxes.

Credit Reports 101. Bill Bufkins, November 3, 2011

Credit Reports 101 Bill Bufkins, November 3, 2011 What is a credit report? A credit report is a record of your past borrowing and repayment activity. The information in your credit report helps determine

Credit Reports 101 Bill Bufkins, November 3, 2011 What is a credit report? A credit report is a record of your past borrowing and repayment activity. The information in your credit report helps determine

Financial Fitness. Taiwanna Smith Chief, Benefits & Work Life Programs Division HROPS, DCPAS 7/20/16 1 FOUO

Financial Fitness Taiwanna Smith Chief, Benefits & Work Life Programs Division HROPS, DCPAS 7/20/16 1 FOUO Agenda Making the Case for Financial Fitness OPM s Requirements for Financial Fitness OPM s Strategy

Financial Fitness Taiwanna Smith Chief, Benefits & Work Life Programs Division HROPS, DCPAS 7/20/16 1 FOUO Agenda Making the Case for Financial Fitness OPM s Requirements for Financial Fitness OPM s Strategy

Name: Hour: Review: 1. What is gross pay? What is net pay? 2. What is FICA? Why are these deductions taken out of your paycheck?

#300051 Name: Hour: VIDEO WORKSHEET Review: After watching each segment of Money Smart, answer the following review questions. EARNING 1. What is gross pay? What is net pay? 2. What is FICA? Why are these

#300051 Name: Hour: VIDEO WORKSHEET Review: After watching each segment of Money Smart, answer the following review questions. EARNING 1. What is gross pay? What is net pay? 2. What is FICA? Why are these

Your Guide to Life Insurance

Your Guide to Life Insurance (800) 827-9990 HealthMarkets.com Your Guide to Life Insurance Contents Life Insurance Basics 4 Do I Need Life Insurance? 9 How Much Life Insurance Do I Need? 11 What Kind of

Your Guide to Life Insurance (800) 827-9990 HealthMarkets.com Your Guide to Life Insurance Contents Life Insurance Basics 4 Do I Need Life Insurance? 9 How Much Life Insurance Do I Need? 11 What Kind of

PRSA Guide. Get to know the advantages of a PRSA

PRSA Guide Get to know the advantages of a PRSA Allow us to introduce ourselves. We are Zurich. We are part of a global insurance group with Swiss roots. We are one of Ireland s most successful life and

PRSA Guide Get to know the advantages of a PRSA Allow us to introduce ourselves. We are Zurich. We are part of a global insurance group with Swiss roots. We are one of Ireland s most successful life and

Volume 2 Your Credit Report and Your Rights

Volume 2 Your Credit Report and Your Rights Your Credit Report and Your Rights Take the first step in changing your financial future. Call InCharge Debt Solutions today at 1.877.544.7772 or visit www.incharge.org

Volume 2 Your Credit Report and Your Rights Your Credit Report and Your Rights Take the first step in changing your financial future. Call InCharge Debt Solutions today at 1.877.544.7772 or visit www.incharge.org

LESSONS FROM BEHAVIORAL ECONOMICS FOR PROMOTING RETIREMENT INCOME SECURITY

LESSONS FROM BEHAVIORAL ECONOMICS FOR PROMOTING RETIREMENT INCOME SECURITY Brigitte Madrian Harvard University Retirement Research Consortium Annual Conference, Washington DC August 2, 2018 What is Behavioral

LESSONS FROM BEHAVIORAL ECONOMICS FOR PROMOTING RETIREMENT INCOME SECURITY Brigitte Madrian Harvard University Retirement Research Consortium Annual Conference, Washington DC August 2, 2018 What is Behavioral

THE B WORD. Money in, money out. How do we keep track of it all? But first, why would you keep track of it? Here are the...

Fin Lit Mo 2 BALANCING A BUDGET These materials were created by DailyPay and not your employer. DailyPay is not a financial or investment advisor. The materials presented should be used for informational

Fin Lit Mo 2 BALANCING A BUDGET These materials were created by DailyPay and not your employer. DailyPay is not a financial or investment advisor. The materials presented should be used for informational

RETIREMENT GUIDE. Wise Options For Retirement

RETIREMENT GUIDE Wise Options For Retirement Table of Contents Retirement Phases and Income Needs 3 Retirement Planning Considerations 4 How Much Will You Need To Save? 5 How Long Will Your Savings Last?

RETIREMENT GUIDE Wise Options For Retirement Table of Contents Retirement Phases and Income Needs 3 Retirement Planning Considerations 4 How Much Will You Need To Save? 5 How Long Will Your Savings Last?

I can skip the starter home Truth = skipping the starter home can seriously impact your finances over a long period of time.

Money and Life (the inseparable pair) Money is intertwined with life and how we manage it changes through the course of Life. This defines the financial seasons that occur through Life. We defined this

Money and Life (the inseparable pair) Money is intertwined with life and how we manage it changes through the course of Life. This defines the financial seasons that occur through Life. We defined this

FINANCIAL FITNESS CENTER COURSES

Primary Subject Accounting Accounting Accounting Estate Planning Estate Planning Estate Planning ETFs ETFs Financial Institutions Tutorial Understanding the Balance Sheet Understanding the Income Statement

Primary Subject Accounting Accounting Accounting Estate Planning Estate Planning Estate Planning ETFs ETFs Financial Institutions Tutorial Understanding the Balance Sheet Understanding the Income Statement

Putting Together the Pieces of Your Financial Puzzle Lyons Township Adult & Community Education October 5, 2017

Putting Together the Pieces of Your Financial Puzzle Lyons Township Adult & Community Education October 5, 2017 Kirk A. Kreikemeier, CFP, CFA, FSA 4365 Lawn Avenue, Suite 5 Western Springs, IL 60558 708

Putting Together the Pieces of Your Financial Puzzle Lyons Township Adult & Community Education October 5, 2017 Kirk A. Kreikemeier, CFP, CFA, FSA 4365 Lawn Avenue, Suite 5 Western Springs, IL 60558 708

Note to the Presenter: This slide presentation aims to offer a detailed and comprehensive look at the SSA and its programs. Please feel free to pick

Note to the Presenter: This slide presentation aims to offer a detailed and comprehensive look at the SSA and its programs. Please feel free to pick and choose those slides more relevant to your topic.

Note to the Presenter: This slide presentation aims to offer a detailed and comprehensive look at the SSA and its programs. Please feel free to pick and choose those slides more relevant to your topic.