Understanding and Measuring Financial Health

|

|

|

- Pamela Rodgers

- 5 years ago

- Views:

Transcription

1 Understanding and Measuring Financial Health Elisabeth Rhyne Managing Director, Center for Financial Inclusion at Accion International Conference on Customer Centric Businesses Mamallapuram, India February 2018

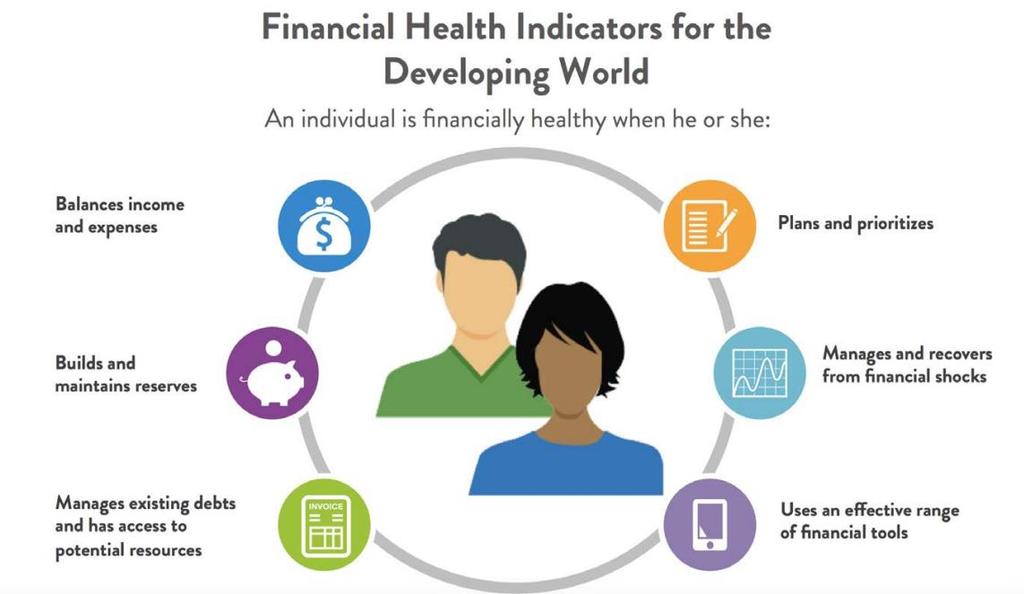

2 What is Financial Health? Financial health has three elements: Balanced daily systems, Resilience ability to weather financial shocks Ability to pursue important life goals Day-to-Day Resilience Goals 2

3 "I spend more than what comes in that s unhealthy Betty Nairobi, Kenya Financial stability is when you don t have to ask other people for help Abraham Nyahruru, Kenya Financial health is when I have what I need every day People across the world use similar words to describe financial health. They desire to manage money effectively to meet day-to-day needs, pursue opportunities, and build resilience. Financial health is when you can pay your bills and have money left over. Phoebe Nairobi, Kenya Financial health is a house and a good salary Rahul Mumbai, India woman from small group Sinnar, India When you have no debt, that s when you re healthy. woman from small group Sinnar, India We will be financially healthy when all of us three brothers start earning and we start earning more Yogesh Sinnar, India

4 Why Is Financial Health So Important? It is an intuitive, universal and robust concept understood by everyone from poor clients to high level policy makers Most people want to be financially healthy and employ financial strategies toward that end If financial services are to have an impact on poverty, it will occur through improvements in financial health Financial health is arguably the core objective of financial inclusion 4

5 5

6 How Financially Healthy Are YOU? Day-to-Day Resilience Goals bit.ly/cfipoll 6

7 Initial Research in Kenya and India Healthy Financial Behaviors, Successful Financial Strategies Across our sample, we saw people managing their finances using these strategies: Shaping Income & Expenses Building Reserves Cultivating Receivable Planning and Prioritization These behaviors are deeply linked to their social and economic endeavors. Jointly conducted by CFSI, CFI and Dalberg

8 Context: Informality Informality was a reality and a methodological hurdle. Social relationships and informal networks formed the backbone of financial strategies Formal services played a limited role. For researchers, this meant: No available checkable numbers (e.g., accounts, loans) Questions and answers are often subjective (see photo) Those who work in the formal sector, earn higher income, and have more formal education tend use more formal financial services.

9 Context: Low and Volatile Incomes Many people s incomes were irregular, unpredictable, and often low. More than any other single factor, income dynamics drove people s financial behaviors. We saw that at some income threshold people struggle just to meet basic food needs. They suffer frequent scarcity and significant financial stress. They have only limited ability to use financial strategies to improve their well-being. We hardly manage food and sleep, why are you talking to us about pensions? - Shruti, Dharavi, Mumbai, India

10 Shaping Income and Expenses People shape income to better cover expenses and pursue their goals. They also work to shape expenses to tailor financial outflows to their income. Ways of shaping income Focus on growing a single source of income through one income generating endeavor Cultivating multiple sources of income to generate more income and hedge against risk of any one dropping Smoothing income by pushing current earnings into the future or borrowing against future earnings Ways of shaping expenses: Earmarking specific income flows to outflows Obligating money to discrete categories of expenses, especially through informal financial networks Budgeting and tracking expenses I m many sided because I have to be. If you can be one-sided you can focus and will perform better, but you need the financing to do it. - Richard, Nyahururu, Kenya Eliminating whole expense categories

11 Building Reserves Reserves are net financial and in-kind assets plus social capital. People build reserves by locking away their money for future use in a manner that balances their needs for liquidity, returns, and security. Saving and investing in diverse instruments and assets as money becomes available Obligating money through informal networks Automating savings through formal accounts Investing in working assets that earn income (e.g. livestock, motorbikes.) Investing in financial assets that earn returns (e.g. interest bearing savings and loans to others.) Locking value in consumable goods to help insure basic needs are met into the future Making social contributions that build social capital and deepen the social safety net.

12 Cultivating Receivables Ability to obtain financial resources when needed. Cultivating formal lines of credit by saving with banks, coops, etc. Cultivating informal credit and saving and investing with informal financial networks Cultivating social safety net by lending and gifts to family, friends, and neighbors "When something happens to a neighbor, there is a oneness in the community. Today it's me, tomorrow it's you. - Michael, Nairobi, Kenya

13 What Can We Say about Financial Health in Kenya? Healthy Balance Income and Expenses 71% say they can afford to live modestly Build and Maintain Reserves Half save regularly Access and Manage Debt 58% have borrowed in the past year Plan and Prioritize A significant minority plan for longer than 6 months 17% have met some of their financial goals Manage and Recover from Financial Shocks 18% could secure more than $300 in an emergency Use a variety of financial tools Many use mobile wallets, savings and credit groups, various financial institutions. Even the very poor use mobile wallets. Non-Healthy Balance Income and Expenses 57% have experienced shortfalls in basic needs (80% of very poor) Build and Maintain Reserves More than half would not be able to live from their reserves for more than a month Access and Manage Debt One third find their debt hard to manage (two thirds of the very poor) 36% borrow to meet basic needs Plan and Prioritize 30% have no plans for old age Half of the very poor make no financial plans Manage and Recover from Financial Shocks For more than half, it would be hard to raise $60 or more in an emergency

14 Debt Burden Comparison: Kenya and India Respondents

15 Financial Health Global Framework Use Cases RESEARCHERS: The financial health framework opens new research avenues, such as the relationship between formal financial services and financial health. For example, does access to a loan or mobile bank account actually improve financial health? PROVIDERS: Providers can use research results to modify product suites, improve functionality, or adapt distribution methods, all with the goal of better serving their existing clients and growing their customer base. POLICYMAKERS: The financial health framework is important to policymakers, who can use it both to gauge the financial health of a country or region s population and to track progress.

16 Small Group Discussion How can your institution use the financial health concept? Come up with as many specific examples as you can. Be prepared to share the top three 10 minutes

17 Accion Employee Financial Health Survey Results 71 Average Score of Accion Employees Highest: 100 Standard Deviation: 15 Lowest: 26 Through this survey Accion identified emergency savings and student loans as two areas of weakness among its staff.

18 People become financially healthier as they age to a point 73 Over 40 years old years old years old Accion staff survey results

19 Areas for Improvement at Accion Planning Horizon 54% of Accionistas are planning less than six months ahead 24% are not planning ahead at all Perceived debt burden 33% state that they have either far too much or a bit too much debt Emergency Savings 35% could not live off of their savings for 3 months

20 Accion Staff Financial Goals

21 Accion Staff: Areas of Focus

22 Measuring Financial Health: Next Steps Definition Framework Measure Test and Refine Examples : Build Momentum Active Use Grameen Foundation/IPA Poverty Probability Index IPA s Global Financial Health Project The Poverty Stoplight (Fundacion Paraguaya)

23 A New Tool: Building adoption and use Growth of PPI - Scorecards and Users # of PPIs # of users

24 Measuring Global Financial Health Project Overview Our Goal: Building a holistic and quantitative framework from intuitive and easy-to-understand indicators Access to funds as the unifying measurable outcome of financial health: To what extent does finance enable or get in the way of consumption? Key principles for the questions: Capture information beyond income and wealth Monotonic and scorable Aim for measures to be complete and non-overlapping (MECE)

25 Measuring Global Financial Health Project Measurement Framework

26 Measuring Global Financial Health Project Timeline Nov 2017 Kick-off call Nov 2018 Phase 2 Check-in September Preparation March Pilot Test 5 Data Analysis December Dissemination February 2019 PHASE 1 Develop Quantitative Metrics PHASE 2 Test in the Field PHASE 3 Analysis & Dissemination 6 months 9 months 3 months 2 Build Measurement Tool Feb 2018 Phase 1 Check-in 4 Survey at Scale 6 Create Final Tool

27 27

28 Small Group Discussion: Measuring Financial Health (20 minutes) Discuss how you would respond to the following measurement challenges: Informal vs. formal financial lives Extreme income and expense volatility Too poor to be financially healthy Financial role of the individual in the family Debt stress vs. financial health Asking sensitive questions and getting reliable answers Subjective vs. objective questions: How satisfied are you with your financial health? Variation by country and region

29 The Poverty Stoplight 1. Using a list of povery indicators, consumers rate themselves green, yellow or red on each. 2. They set their own goals ( This year I want to turn these three indicators from yellow to green. ) 3. Organizations may intervene to support these goals. 4. Progress is monitored using the same indicators. Benefits for Consumers Visualize and reflect on their own situation motivate behavior change! Take an active and informed role in their lives Break an overwhelming task into manageable fragments Benefits for Organizations Clearly identify status of consumers Collect relevant data More than measurement of the problem part of the solution As outcome measurements, consumer self-assessments offer a self-evident form of validity, even though attribution of changes to interventions is not possible.

30 CFI/MFC Project: Financial Health App With support from the MetLife Foundation A smartphone and tablet application for consumers and financial institutions: Starts with the basic financial health questions motivation! Creates advice modules based on responses priorities and pathways to better financial health Interactive: Keeps customer engaged Financial institution can offer products and support based on results two-way communication Source of information about customers

Credit Cards and Financial Health Member-Exclusive Report from CFSI s Consumer Financial Health Study

Credit Cards and Financial Health Member-Exclusive Report from CFSI s Consumer Financial Health Study We provide this CFSI Member Exclusive as a resource to create new products, calibrate existing ones,

Credit Cards and Financial Health Member-Exclusive Report from CFSI s Consumer Financial Health Study We provide this CFSI Member Exclusive as a resource to create new products, calibrate existing ones,

Checking Accounts and the Financially Struggling Majority. Member Exclusive Report from CFSI s Consumer Financial Health Study

Checking Accounts and the Financially Struggling Majority Member Exclusive Report from CFSI s Consumer Financial Health Study We provide this CFSI Member Exclusive as a resource to create new products,

Checking Accounts and the Financially Struggling Majority Member Exclusive Report from CFSI s Consumer Financial Health Study We provide this CFSI Member Exclusive as a resource to create new products,

Eight Ways to Measure Financial Health

Eight Ways to Measure Financial Health April 2016 Leading the Nation in Consumer Financial Health MEMBERSHIP CONSULTING RESEARCH INNOVATION EVENTS IMPACT 8 Ways to Measure Financial Health How Banks, Credit

Eight Ways to Measure Financial Health April 2016 Leading the Nation in Consumer Financial Health MEMBERSHIP CONSULTING RESEARCH INNOVATION EVENTS IMPACT 8 Ways to Measure Financial Health How Banks, Credit

Developing Financial Capability Over the Life Course

1 / 51 Developing Financial Capability Over the Life Course J. Michael Collins University of Wisconsin-Madison June 3, 2 / 51 Table of Contents 1 2 3 4 5 6 7 3 / 51 Financial Capability Over the Life Course

1 / 51 Developing Financial Capability Over the Life Course J. Michael Collins University of Wisconsin-Madison June 3, 2 / 51 Table of Contents 1 2 3 4 5 6 7 3 / 51 Financial Capability Over the Life Course

The National Credit Union Foundation: Financial Health Check-Up Aggregation

The National Credit Union Foundation: Financial Health Check-Up Aggregation Results excerpt, November 2017 Leading the Nation in Consumer Financial Health MEMBERSHIP CONSULTING RESEARCH INNOVATION Overview

The National Credit Union Foundation: Financial Health Check-Up Aggregation Results excerpt, November 2017 Leading the Nation in Consumer Financial Health MEMBERSHIP CONSULTING RESEARCH INNOVATION Overview

Global Segmentation Framework PAKISTAN WOMEN / SEPTEMBER 2018

Global Segmentation Framework PAKISTAN WOMEN / SEPTEMBER 2018 Contents Approach & Research 3 Segment Overview 18 Social Optimists 21 Confident Planners 49 Careful Strugglers 79 Conservative Individualists

Global Segmentation Framework PAKISTAN WOMEN / SEPTEMBER 2018 Contents Approach & Research 3 Segment Overview 18 Social Optimists 21 Confident Planners 49 Careful Strugglers 79 Conservative Individualists

A positive outlook on auto-enrolment contributions phasing. High

A positive outlook on auto-enrolment contributions phasing High Summary UK businesses are focusing on securing the organisation s future by strengthening their competitive position, increasing revenue

A positive outlook on auto-enrolment contributions phasing High Summary UK businesses are focusing on securing the organisation s future by strengthening their competitive position, increasing revenue

Measuring Graduation: A Guidance Note

Measuring Graduation: A Guidance Note Introduction With the growth of graduation programmes (integrated livelihood programmes that aim to create sustainable pathways out of extreme and chronic poverty)

Measuring Graduation: A Guidance Note Introduction With the growth of graduation programmes (integrated livelihood programmes that aim to create sustainable pathways out of extreme and chronic poverty)

Prepared by the Office of the Treasurer

Prepared by the Office of the Treasurer The Board s Role in Financial Oversight The Board of Trustees is tasked with financial oversight of the College. The Association of Governing Boards of Universities

Prepared by the Office of the Treasurer The Board s Role in Financial Oversight The Board of Trustees is tasked with financial oversight of the College. The Association of Governing Boards of Universities

Income Stability and Asset Building Tuesday, November 10 4:15 PM - 5:30 PM. Tanya Ladha, Center for Financial Services Innovation

Income Stability and Asset Building Tuesday, November 10 4:15 PM - 5:30 PM Presenters Tony Berkley, Prudential Tanya Ladha, Center for Financial Services Innovation Gwyneth Galbraith, Opportunity Fund

Income Stability and Asset Building Tuesday, November 10 4:15 PM - 5:30 PM Presenters Tony Berkley, Prudential Tanya Ladha, Center for Financial Services Innovation Gwyneth Galbraith, Opportunity Fund

In the previous session we learned about the various categories of Risk in agriculture. Of course the whole point of talking about risk in this

In the previous session we learned about the various categories of Risk in agriculture. Of course the whole point of talking about risk in this educational series is so that we can talk about managing

In the previous session we learned about the various categories of Risk in agriculture. Of course the whole point of talking about risk in this educational series is so that we can talk about managing

MEASURING HOUSEHOLD STRESS

OXFAM PUBLICATION APRIL 208 A working Afghan child herding animal for livelihood in Pulecharkhi, Kabul, November 207. Photo: Joel van Houdt, Oxfam. MEASURING HOUSEHOLD STRESS Introducing the multi-sector

OXFAM PUBLICATION APRIL 208 A working Afghan child herding animal for livelihood in Pulecharkhi, Kabul, November 207. Photo: Joel van Houdt, Oxfam. MEASURING HOUSEHOLD STRESS Introducing the multi-sector

Manulife's Financial Wellness Assessment

Manulife's Financial Wellness Assessment Why having poor financial wellness impacts productivity Manulife s health and wealth research confirms the strong connection between an employee s financial wellness,

Manulife's Financial Wellness Assessment Why having poor financial wellness impacts productivity Manulife s health and wealth research confirms the strong connection between an employee s financial wellness,

paying off student loans

paying off student loans PAYING OFF STUDENT LOANS Student loans are a national crisis impacting millions of people. The class of 2016 borrowed an average of $37,172 in student loans.* Total student loan

paying off student loans PAYING OFF STUDENT LOANS Student loans are a national crisis impacting millions of people. The class of 2016 borrowed an average of $37,172 in student loans.* Total student loan

Measurement of Market Risk

Measurement of Market Risk Market Risk Directional risk Relative value risk Price risk Liquidity risk Type of measurements scenario analysis statistical analysis Scenario Analysis A scenario analysis measures

Measurement of Market Risk Market Risk Directional risk Relative value risk Price risk Liquidity risk Type of measurements scenario analysis statistical analysis Scenario Analysis A scenario analysis measures

Household Debt in America: A Look Across Generations Over Time

Household Debt in America: A Look Across Generations Over Time Carlos Garriga Bryan Noeth Don E. Schlagenhauf Federal Reserve Bank of St. Louis The Center for Household Financial Stability and Research

Household Debt in America: A Look Across Generations Over Time Carlos Garriga Bryan Noeth Don E. Schlagenhauf Federal Reserve Bank of St. Louis The Center for Household Financial Stability and Research

A growing interest in employee financial well-being in India

A growing interest in employee financial well-being in India Insights from the Global Benefits Attitudes Survey 2016 Indian employees satisfaction with their financial state today belies financial worries

A growing interest in employee financial well-being in India Insights from the Global Benefits Attitudes Survey 2016 Indian employees satisfaction with their financial state today belies financial worries

The Art and Science of Multi-Year Planning

The Art and Science of Multi-Year Planning Bethany Pugh Managing Director PFM Financial Advisors LLC www.pfm.com Kevin Kuhar Senior Solutions Consultant PFM Solutions LLC www.whitebrichsoftware.com 1/31

The Art and Science of Multi-Year Planning Bethany Pugh Managing Director PFM Financial Advisors LLC www.pfm.com Kevin Kuhar Senior Solutions Consultant PFM Solutions LLC www.whitebrichsoftware.com 1/31

Al-Amal Microfinance Bank

Impact Brief Series, Issue 1 Al-Amal Microfinance Bank Yemen The Taqeem ( evaluation in Arabic) Initiative is a technical cooperation programme of the International Labour Organization and regional partners

Impact Brief Series, Issue 1 Al-Amal Microfinance Bank Yemen The Taqeem ( evaluation in Arabic) Initiative is a technical cooperation programme of the International Labour Organization and regional partners

KEYNOTE ADDRESS EIOPA S INITIATIVES TO EMPOWER THE PENSIONS SECTOR

Gabriel Bernardino Chairman European Insurance and Occupational Pensions Authority (EIOPA) KEYNOTE ADDRESS EIOPA S INITIATIVES TO EMPOWER THE PENSIONS SECTOR 18 th Handelsblatt Annual Conference on Occupational

Gabriel Bernardino Chairman European Insurance and Occupational Pensions Authority (EIOPA) KEYNOTE ADDRESS EIOPA S INITIATIVES TO EMPOWER THE PENSIONS SECTOR 18 th Handelsblatt Annual Conference on Occupational

Millennial Money Mindset Report

Millennial Money Mindset Report 2017 In Partnership with: Data Analysis support by Executive Summary 2017 Millennial Money Mindset Report Previous studies have shown that the expectations of Millennials

Millennial Money Mindset Report 2017 In Partnership with: Data Analysis support by Executive Summary 2017 Millennial Money Mindset Report Previous studies have shown that the expectations of Millennials

Commodity Risk Management: Supply Chain Best Practices May 24 th,2017: Session Code: JA17

Commodity Risk Management: Supply Chain Best Practices May 24 th,2017: Session Code: JA17 Presented by Michael Irgang Executive Vice President Global Risk Management Corp. 1 Commodity trading is not suitable

Commodity Risk Management: Supply Chain Best Practices May 24 th,2017: Session Code: JA17 Presented by Michael Irgang Executive Vice President Global Risk Management Corp. 1 Commodity trading is not suitable

Mind the Retail Mortgage Gap. To Close More Loans, First Close the Gap

Mind the Retail Mortgage Gap To Close More Loans, First Close the Gap Mind the Retail Mortgage Gap Table of Contents Executive Summary Shifting Lending Landscape............. 2 An Industry Riddled with

Mind the Retail Mortgage Gap To Close More Loans, First Close the Gap Mind the Retail Mortgage Gap Table of Contents Executive Summary Shifting Lending Landscape............. 2 An Industry Riddled with

Capital Speedboat Session 2. Charting your way through troubling waters FARIN & Associates Inc. Agenda

Capital Speedboat 2013 - Session 2 Charting your way through troubling waters 1 Agenda Session 2 Defining Stress Tests Stress vs. Scenario Testing Sensitivity Testing Scenarios Silos Scenario Testing Building

Capital Speedboat 2013 - Session 2 Charting your way through troubling waters 1 Agenda Session 2 Defining Stress Tests Stress vs. Scenario Testing Sensitivity Testing Scenarios Silos Scenario Testing Building

As you can see from this slide, the growth in pension costs has been tremendous.

Remarks by Larry Fink National Association of Pension Funds Investment Conference Edinburgh International Conference Centre Edinburgh, Scotland March 5, 2014 (as prepared for delivery) I want to thank

Remarks by Larry Fink National Association of Pension Funds Investment Conference Edinburgh International Conference Centre Edinburgh, Scotland March 5, 2014 (as prepared for delivery) I want to thank

THE BUSINESS OF TREASURY Developing insight, assessing risk, informing strategy

THE BUSINESS OF TREASURY 2018 Developing insight, assessing risk, informing strategy CONTENTS Want to know what s happening in your organisation? Ask a treasurer: how treasurers collaborate in strategy-setting

THE BUSINESS OF TREASURY 2018 Developing insight, assessing risk, informing strategy CONTENTS Want to know what s happening in your organisation? Ask a treasurer: how treasurers collaborate in strategy-setting

NOTTINGHAM CITY HOMES. THE BOARD REPORT OF Ian Rabett Head of Health & Safety 26 November 2015

ITEM 9 NOTTINGHAM CITY HOMES THE BOARD REPORT OF Ian Rabett Head of Health & Safety 26 November 2015 RISK MANAGEMENT 1 SUMMARY 1.1 A review of our risk management arrangements was carried out earlier this

ITEM 9 NOTTINGHAM CITY HOMES THE BOARD REPORT OF Ian Rabett Head of Health & Safety 26 November 2015 RISK MANAGEMENT 1 SUMMARY 1.1 A review of our risk management arrangements was carried out earlier this

Value for Money Research: The voice of the Member Launch: 2 March 2017

Value for Money Research: The voice of the Member Launch: 2 March 2017 Value for Money Research: The voice of the Member Launch: 2 March 2017 Jacqui Reid, Associate Director Sackers David Burns & Jane

Value for Money Research: The voice of the Member Launch: 2 March 2017 Value for Money Research: The voice of the Member Launch: 2 March 2017 Jacqui Reid, Associate Director Sackers David Burns & Jane

MEASURING WOMEN S FINANCIAL INCLUSION

MEASURING WOMEN S FINANCIAL INCLUSION USING FII DATA TO TRACK PROGRESS AND DEVELOP INTERVENTIONS Presented by Nadia van de Walle Women's Financial Inclusion Community of Practice Webinar December 5, 2017

MEASURING WOMEN S FINANCIAL INCLUSION USING FII DATA TO TRACK PROGRESS AND DEVELOP INTERVENTIONS Presented by Nadia van de Walle Women's Financial Inclusion Community of Practice Webinar December 5, 2017

Well-being and Income Poverty

Well-being and Income Poverty Impacts of an unconditional cash transfer program using a subjective approach Kelly Kilburn, Sudhanshu Handa, Gustavo Angeles kkilburn@unc.edu UN WIDER Development Conference:

Well-being and Income Poverty Impacts of an unconditional cash transfer program using a subjective approach Kelly Kilburn, Sudhanshu Handa, Gustavo Angeles kkilburn@unc.edu UN WIDER Development Conference:

Scarcity at the end of the month

Policy brief 31400 December 2017 Emily Breza, Martin Kanz, and Leora Klapper Scarcity at the end of the month A field experiment with garment factory workers in Bangladesh In brief Dealing with sudden,

Policy brief 31400 December 2017 Emily Breza, Martin Kanz, and Leora Klapper Scarcity at the end of the month A field experiment with garment factory workers in Bangladesh In brief Dealing with sudden,

Effective Corporate Budgeting

Effective Corporate Budgeting in 8 Easy Steps This ebook will offer 8 easy and easy and proven steps for improving your corporate budgeting and planning process. You will see that by making a few small

Effective Corporate Budgeting in 8 Easy Steps This ebook will offer 8 easy and easy and proven steps for improving your corporate budgeting and planning process. You will see that by making a few small

Resilience Measurement in the Philippines. March 2015

Resilience Measurement in the Philippines March 2015 WHY FOCUS ON RESILIENCE» Theory of everything» By being all things, resilience risks being nothing new: Theory of everything» Untested assumptions»

Resilience Measurement in the Philippines March 2015 WHY FOCUS ON RESILIENCE» Theory of everything» By being all things, resilience risks being nothing new: Theory of everything» Untested assumptions»

The generation game Savings for the new millennial

Hot topic question The generation game Savings for the new millennial Paul Traynor Head of Insurance International BNY Mellon Financial services providers such as life insurers, asset managers and banks

Hot topic question The generation game Savings for the new millennial Paul Traynor Head of Insurance International BNY Mellon Financial services providers such as life insurers, asset managers and banks

The taxonomy of Sovereign Investment Funds

www.pwc.com/sovereignwealthfunds The taxonomy of Sovereign Investment Funds May 2015 SWF s operating in an evolving political environment The increasing influence and relevance of Sovereign Investors (SIs)

www.pwc.com/sovereignwealthfunds The taxonomy of Sovereign Investment Funds May 2015 SWF s operating in an evolving political environment The increasing influence and relevance of Sovereign Investors (SIs)

Macroeconomics I International Group Course

Learning objectives Macroeconomics I International Group Course 2004-2005 Topic 4: INTRODUCTION TO MACROECONOMIC FLUCTUATIONS We have already studied how the economy adjusts in the long run: prices are

Learning objectives Macroeconomics I International Group Course 2004-2005 Topic 4: INTRODUCTION TO MACROECONOMIC FLUCTUATIONS We have already studied how the economy adjusts in the long run: prices are

Quantitative Trading System For The E-mini S&P

AURORA PRO Aurora Pro Automated Trading System Aurora Pro v1.11 For TradeStation 9.1 August 2015 Quantitative Trading System For The E-mini S&P By Capital Evolution LLC Aurora Pro is a quantitative trading

AURORA PRO Aurora Pro Automated Trading System Aurora Pro v1.11 For TradeStation 9.1 August 2015 Quantitative Trading System For The E-mini S&P By Capital Evolution LLC Aurora Pro is a quantitative trading

By way of background, Carillion (DB) Pension Trustee limited became trustee of the 6 schemes on 1 April I have been chairman since that date.

Pension Trustee limited became trustee of the 6 schemes on 1 April I have been chairman since that date.") Rt Hon Frank Field MP Chair Work and Pensions Committee House of Commons London SW1A 0AA workpencom@parliament.uk By email 26 January 2018 Dear Mr Field Carillion (DB) Pension Trustee Many thanks for your

Rt Hon Frank Field MP Chair Work and Pensions Committee House of Commons London SW1A 0AA workpencom@parliament.uk By email 26 January 2018 Dear Mr Field Carillion (DB) Pension Trustee Many thanks for your

ACCOUNTING 310 COST ACCOUNTING Fall 2009

Dr. Michael Constas CBA 403 mconstas@csulb.edu www.csulb.edu/~mconstas Textbook: Managerial Accounting ACCOUNTING 310 COST ACCOUNTING Fall 2009 ACCT 310 focuses on understanding: (i) the methods in which

Dr. Michael Constas CBA 403 mconstas@csulb.edu www.csulb.edu/~mconstas Textbook: Managerial Accounting ACCOUNTING 310 COST ACCOUNTING Fall 2009 ACCT 310 focuses on understanding: (i) the methods in which

Making Tax Digital A roadmap for small businesses

blow abbott chartered accountants Making Tax Digital A roadmap for small businesses www.blowabbott.com Index Page What is Making Tax Digital? 3 When is it happening? 4 What are the upsides and downsides?

blow abbott chartered accountants Making Tax Digital A roadmap for small businesses www.blowabbott.com Index Page What is Making Tax Digital? 3 When is it happening? 4 What are the upsides and downsides?

How to Get Ahead of Your Student Debt

Client Conversations How to Get Ahead of Your Student Debt WHEN COLLEGE ENDS, YOU RE LEFT WITH A DIPLOMA AND A SENSE OF ACCOMPLISHMENT but you re also probably left with some pretty hefty debt and subsequent

Client Conversations How to Get Ahead of Your Student Debt WHEN COLLEGE ENDS, YOU RE LEFT WITH A DIPLOMA AND A SENSE OF ACCOMPLISHMENT but you re also probably left with some pretty hefty debt and subsequent

Measuring and Forecasting. Financial Wellness PAGE 1

Measuring and Forecasting Financial Wellness PAGE 1 What does financial wellness have to do with the weather? In both, the ability to measure, track, and forecast its impact leads people to be better prepared.

Measuring and Forecasting Financial Wellness PAGE 1 What does financial wellness have to do with the weather? In both, the ability to measure, track, and forecast its impact leads people to be better prepared.

Bank of America Merrill Lynch Banking and Financial Services Conference

Goldman Sachs Presentation to Bank of America Merrill Lynch Banking and Financial Services Conference Comments by Harvey Schwartz, Chief Financial Officer November 12, 2014 Introduction Good morning everyone

Goldman Sachs Presentation to Bank of America Merrill Lynch Banking and Financial Services Conference Comments by Harvey Schwartz, Chief Financial Officer November 12, 2014 Introduction Good morning everyone

Motivation. Research Question

Motivation Poverty is undeniably complex, to the extent that even a concrete definition of poverty is elusive; working definitions span from the type holistic view of poverty used by Amartya Sen to narrowly

Motivation Poverty is undeniably complex, to the extent that even a concrete definition of poverty is elusive; working definitions span from the type holistic view of poverty used by Amartya Sen to narrowly

EBF Response to BCBS Consultative Document (CD) on Interest rate Risk in the Banking Book (IRRBB)

on Interest rate Risk in the Banking Book (IRRBB)") EBF_016518 8 th September 2015 EBF Response to BCBS Consultative Document (CD) on Interest rate Risk in the Banking Book (IRRBB) The European Banking Federation (EBF) is the voice of the European banking

EBF_016518 8 th September 2015 EBF Response to BCBS Consultative Document (CD) on Interest rate Risk in the Banking Book (IRRBB) The European Banking Federation (EBF) is the voice of the European banking

2018 Report. July 2018

2018 Report July 2018 Foreword This year the FCA and FCA Practitioner Panel have, for the second time, carried out a joint survey of regulated firms to monitor the industry s perception of the FCA and

2018 Report July 2018 Foreword This year the FCA and FCA Practitioner Panel have, for the second time, carried out a joint survey of regulated firms to monitor the industry s perception of the FCA and

Monetary Policy under Flexible Inflation Targeting: Thailand s s Experience. Dr. Atchana Waiquamdee Bank of Thailand

Monetary Policy under Flexible Inflation Targeting: Thailand s s Experience Dr. Atchana Waiquamdee Bank of Thailand Overview 2 Introduction Inflation targeting framework in Thailand Challenges ahead and

Monetary Policy under Flexible Inflation Targeting: Thailand s s Experience Dr. Atchana Waiquamdee Bank of Thailand Overview 2 Introduction Inflation targeting framework in Thailand Challenges ahead and

Griffith University. Preparing strata title communities for climate change survey: On line questionnaire findings summary for survey respondents

Griffith University Preparing strata title communities for climate change survey: On line questionnaire findings summary for survey respondents This report provides a summary of findings arising from Griffith

Griffith University Preparing strata title communities for climate change survey: On line questionnaire findings summary for survey respondents This report provides a summary of findings arising from Griffith

The Financial Strains of Small-Dollar Credit Users. Member-Exclusive Report from CFSI s Consumer Financial Health Study

The Financial Strains of Small-Dollar Credit Users Member-Exclusive Report from CFSI s Consumer Financial Health Study CFSI Member Exclusive We provide this CFSI Member Exclusive as a resource to create

The Financial Strains of Small-Dollar Credit Users Member-Exclusive Report from CFSI s Consumer Financial Health Study CFSI Member Exclusive We provide this CFSI Member Exclusive as a resource to create

RISK FACTOR PORTFOLIO MANAGEMENT WITHIN THE ADVICE FRAMEWORK. Putting client needs first

RISK FACTOR PORTFOLIO MANAGEMENT WITHIN THE ADVICE FRAMEWORK Putting client needs first Risk means different things to different people. Everyone is exposed to risks of various types inflation, injury,

RISK FACTOR PORTFOLIO MANAGEMENT WITHIN THE ADVICE FRAMEWORK Putting client needs first Risk means different things to different people. Everyone is exposed to risks of various types inflation, injury,

Automated and High Frequency Trading. Fredrik Hjorth Tieto, Stockholm October 20, 2011

Automated and High Frequency Trading Fredrik Hjorth Tieto, Stockholm October 20, 2011 Present Day Situation 1/2 Post MiFID, 2007 November Many new execution venues for the same instrument Executed number

Automated and High Frequency Trading Fredrik Hjorth Tieto, Stockholm October 20, 2011 Present Day Situation 1/2 Post MiFID, 2007 November Many new execution venues for the same instrument Executed number

Public Financial Management

UNITAR Mustofi Fellowship Hiroshima, Japan 18 22 February 2012! Index! Overview and Objectives! Limitations and Problems! Public Financial Systems! Financial Management System Boundaries! Framework! Government

UNITAR Mustofi Fellowship Hiroshima, Japan 18 22 February 2012! Index! Overview and Objectives! Limitations and Problems! Public Financial Systems! Financial Management System Boundaries! Framework! Government

Evaluation of the Uganda Social Assistance Grants For Empowerment (SAGE) Programme. What s going on?

Programme. What s going on?") Evaluation of the Uganda Social Assistance Grants For Empowerment (SAGE) Programme What s going on? 8 February 2012 Contents The SAGE programme Objectives of the evaluation Evaluation methodology 2 The

Evaluation of the Uganda Social Assistance Grants For Empowerment (SAGE) Programme What s going on? 8 February 2012 Contents The SAGE programme Objectives of the evaluation Evaluation methodology 2 The

Comments on DICK SMITH, FAIR GO. THE AUSSIE HOUSING AFFORDABILITY CRISIS: AN HONEST DEBATE

Introduction Wayne Wanders. The Wealth Navigator has reviewed The Aussie Housing Affordability Crisis: An Honest Debate paper recently issued by Dick Smith s Fair Go Organisation. Whilst Wayne applauds

Introduction Wayne Wanders. The Wealth Navigator has reviewed The Aussie Housing Affordability Crisis: An Honest Debate paper recently issued by Dick Smith s Fair Go Organisation. Whilst Wayne applauds

How to Optimize Your Finances After a Banner Year

How to Optimize Your Finances After a Banner Year By Paul K. Loyacono Jr., WealthPoint Investment Management 2 Are you in a field in which your income fluctuates from year to year? Business owners, sales

How to Optimize Your Finances After a Banner Year By Paul K. Loyacono Jr., WealthPoint Investment Management 2 Are you in a field in which your income fluctuates from year to year? Business owners, sales

Public Trust in Insurance

Opinion survey Public Trust in Insurance cii.co.uk Contents 2 Foreword 3 Research aims and background 4 Methodology 5 The qualitative stage 6 Key themes 7 The quantitative stage 8 Quantitative research

Opinion survey Public Trust in Insurance cii.co.uk Contents 2 Foreword 3 Research aims and background 4 Methodology 5 The qualitative stage 6 Key themes 7 The quantitative stage 8 Quantitative research

The expansion of the U.S. economy continued for the fourth consecutive

Overview The expansion of the U.S. economy continued for the fourth consecutive year in 2005. The President has laid out an agenda to maintain the economy's momentum, foster job creation, and ensure that

Overview The expansion of the U.S. economy continued for the fourth consecutive year in 2005. The President has laid out an agenda to maintain the economy's momentum, foster job creation, and ensure that

Cost Shocks in the AD/ AS Model

Cost Shocks in the AD/ AS Model 13 CHAPTER OUTLINE Fiscal Policy Effects Fiscal Policy Effects in the Long Run Monetary Policy Effects The Fed s Response to the Z Factors Shape of the AD Curve When the

Cost Shocks in the AD/ AS Model 13 CHAPTER OUTLINE Fiscal Policy Effects Fiscal Policy Effects in the Long Run Monetary Policy Effects The Fed s Response to the Z Factors Shape of the AD Curve When the

BOARD OF GOVERNORS FEDERAL RESERVE SYSTEM

BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM WASHINGTON, D.C. 20551 DIVISION OF BANKING SUPERVISION AND REGULATION SR 16-3 March 1, 2016 TO THE OFFICER IN CHARGE OF SUPERVISION AT EACH RESERVE BANK

BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM WASHINGTON, D.C. 20551 DIVISION OF BANKING SUPERVISION AND REGULATION SR 16-3 March 1, 2016 TO THE OFFICER IN CHARGE OF SUPERVISION AT EACH RESERVE BANK

White Paper. Liquidity Optimization: Going a Step Beyond Basel III Compliance

White Paper Liquidity Optimization: Going a Step Beyond Basel III Compliance Contents SAS: Delivering the Keys to Liquidity Optimization... 2 A Comprehensive Solution...2 Forward-Looking Insight...2 High

White Paper Liquidity Optimization: Going a Step Beyond Basel III Compliance Contents SAS: Delivering the Keys to Liquidity Optimization... 2 A Comprehensive Solution...2 Forward-Looking Insight...2 High

How to Strategically Manage Your Debt

Debt. Funny how four little letters can feel so dirty. Most of us have it in one shape or another, but none of us like to talk about it. Debt can get us into trouble, especially if it is unplanned and

Debt. Funny how four little letters can feel so dirty. Most of us have it in one shape or another, but none of us like to talk about it. Debt can get us into trouble, especially if it is unplanned and

Understanding investment risk through drawdown analysis

Understanding investment risk through drawdown analysis A more refined method of managing and mitigating loss Risk is a central theme in the investment world, a counterweight to investor s desire for return.

Understanding investment risk through drawdown analysis A more refined method of managing and mitigating loss Risk is a central theme in the investment world, a counterweight to investor s desire for return.

MAXIMIZE YOUR PERSONAL WEALTH

MAXIMIZE YOUR PERSONAL WEALTH 30 mins This information is provided for educational and general marketing purposes only and should not be construed as a recommendation or suggestion as to the advisability

MAXIMIZE YOUR PERSONAL WEALTH 30 mins This information is provided for educational and general marketing purposes only and should not be construed as a recommendation or suggestion as to the advisability

COMMUNIQUE. Page 1 of 13

COMMUNIQUE 16-COM-001 Feb. 1, 2016 Release of Liquidity Risk Management Guiding Principles The Credit Union Prudential Supervisors Association (CUPSA) has released guiding principles for Liquidity Risk

COMMUNIQUE 16-COM-001 Feb. 1, 2016 Release of Liquidity Risk Management Guiding Principles The Credit Union Prudential Supervisors Association (CUPSA) has released guiding principles for Liquidity Risk

Terms of Reference. Impact Assessment Study of

Terms of Reference For Impact Assessment Study of Partnership in Climate Services for Resilient Agriculture in India (PCSRA) ToR No: ABC122019XYZ Dated: 31-1-2019 Partnership in Climate Services for Resilient

Terms of Reference For Impact Assessment Study of Partnership in Climate Services for Resilient Agriculture in India (PCSRA) ToR No: ABC122019XYZ Dated: 31-1-2019 Partnership in Climate Services for Resilient

Square Mile Managed Portfolio Service Investment Process

For professional advisers only Square Mile Managed Portfolio Service Investment Process www.squaremileresearch.com Follow us: @SquareMileICR Square Mile Investment Consulting & Research Limited INVESTMENT

For professional advisers only Square Mile Managed Portfolio Service Investment Process www.squaremileresearch.com Follow us: @SquareMileICR Square Mile Investment Consulting & Research Limited INVESTMENT

Getting to know your employer s retirement plan

Getting to know your employer s retirement plan It s About You If you re the independent type, you can do your own thing. If you want some help, tools are available to assist you. Confused about investing?

Getting to know your employer s retirement plan It s About You If you re the independent type, you can do your own thing. If you want some help, tools are available to assist you. Confused about investing?

REGULATORY GUIDELINE Liquidity Risk Management Principles TABLE OF CONTENTS. I. Introduction II. Purpose and Scope III. Principles...

REGULATORY GUIDELINE Liquidity Risk Management Principles SYSTEM COMMUNICATION NUMBER Guideline 2015-02 ISSUE DATE June 2015 TABLE OF CONTENTS I. Introduction... 1 II. Purpose and Scope... 1 III. Principles...

REGULATORY GUIDELINE Liquidity Risk Management Principles SYSTEM COMMUNICATION NUMBER Guideline 2015-02 ISSUE DATE June 2015 TABLE OF CONTENTS I. Introduction... 1 II. Purpose and Scope... 1 III. Principles...

Precarious to prosperous: Tackling income volatility in Canada. Bharat Masrani Group President and Chief Executive Officer, TD Bank Group

Precarious to prosperous: Tackling income volatility in Canada Bharat Masrani Group President and Chief Executive Officer, TD Bank Group November 1, 2017 Economic Club Toronto The benefits are welldocumented.

Precarious to prosperous: Tackling income volatility in Canada Bharat Masrani Group President and Chief Executive Officer, TD Bank Group November 1, 2017 Economic Club Toronto The benefits are welldocumented.

The Dialogue Podcast Episode 1 transcript Climate Risk Disclosure

Date: 15 Jan 2017 Interviewer: Andrew Doughman Guest: Sharanjit Paddam Duration: 18:52 min TRANSCRIPT Andrew: Hello and welcome to your Actuaries Institute dialogue podcast, I'm Andrew Doughman. Now this

Date: 15 Jan 2017 Interviewer: Andrew Doughman Guest: Sharanjit Paddam Duration: 18:52 min TRANSCRIPT Andrew: Hello and welcome to your Actuaries Institute dialogue podcast, I'm Andrew Doughman. Now this

Workplace Insights. 401(k) Wellness Scorecard. Key findings. For quarter ending September 30, 2013

Wellness Scorecard. Key findings. For quarter ending September 30, 2013") RETIREMENT & BENEFIT PLAN SERVICES Workplace Insights 401(k) Wellness Scorecard For quarter ending September 30, 2013 During the third quarter of 2013, data across the participant base showed that the

RETIREMENT & BENEFIT PLAN SERVICES Workplace Insights 401(k) Wellness Scorecard For quarter ending September 30, 2013 During the third quarter of 2013, data across the participant base showed that the

Donald L Kohn: Asset-pricing puzzles, credit risk, and credit derivatives

Donald L Kohn: Asset-pricing puzzles, credit risk, and credit derivatives Remarks by Mr Donald L Kohn, Vice Chairman of the Board of Governors of the US Federal Reserve System, at the Conference on Credit

Donald L Kohn: Asset-pricing puzzles, credit risk, and credit derivatives Remarks by Mr Donald L Kohn, Vice Chairman of the Board of Governors of the US Federal Reserve System, at the Conference on Credit

Ben S Bernanke: Modern risk management and banking supervision

Ben S Bernanke: Modern risk management and banking supervision Remarks by Mr Ben S Bernanke, Chairman of the Board of Governors of the US Federal Reserve System, at the Stonier Graduate School of Banking,

Ben S Bernanke: Modern risk management and banking supervision Remarks by Mr Ben S Bernanke, Chairman of the Board of Governors of the US Federal Reserve System, at the Stonier Graduate School of Banking,

Building Balanced Incentive Scorecards

Building Balanced Incentive Scorecards By Christie Summervill, CEO www.balancedcomp.com Who is BalancedComp? Expert Compensation Consulting and Cloudbased Automated Systems Exclusively for financial institutions

Building Balanced Incentive Scorecards By Christie Summervill, CEO www.balancedcomp.com Who is BalancedComp? Expert Compensation Consulting and Cloudbased Automated Systems Exclusively for financial institutions

Green Climate Fund and the Paris Agreement

Briefing Note February 2016 Green Climate Fund and the Paris Agreement Climate Focus Client Brief on the Paris Agreement V February 2016 Introduction The Paris Agreement and the supporting Decision include

Briefing Note February 2016 Green Climate Fund and the Paris Agreement Climate Focus Client Brief on the Paris Agreement V February 2016 Introduction The Paris Agreement and the supporting Decision include

The EU Reference Budgets Network pilot project

The EU Reference Budgets Network pilot project Towards a method for comparable reference budgets for EU purposes Summary We develop reference budgets that represent the minimum resources that persons need

The EU Reference Budgets Network pilot project Towards a method for comparable reference budgets for EU purposes Summary We develop reference budgets that represent the minimum resources that persons need

Income volatility in Canada: Why it matters and what to do about it. Aug 23, 2017

Income volatility in Canada: Why it matters and what to do about it Aug 23, 2017 Welcome! Thank you for joining the webinar on Income volatility in Canada: Why it matters and what to do about it hosted

Income volatility in Canada: Why it matters and what to do about it Aug 23, 2017 Welcome! Thank you for joining the webinar on Income volatility in Canada: Why it matters and what to do about it hosted

Overview and context

Michael Eves Overview and context Why Are We Talking About This Now? One facet of a long-term reaction to the financial crisis by many stakeholders: Increasing knowledge of models Decreasing confidence

Michael Eves Overview and context Why Are We Talking About This Now? One facet of a long-term reaction to the financial crisis by many stakeholders: Increasing knowledge of models Decreasing confidence

The single most dangerous obstacle to building wealth: Debt.

1 The single most dangerous obstacle to building wealth: Debt. Hey, it s ya girl Candice Marie the Founder of. Before we begin I want to tell you don t be embarrassed about your debt. The last time I checked

1 The single most dangerous obstacle to building wealth: Debt. Hey, it s ya girl Candice Marie the Founder of. Before we begin I want to tell you don t be embarrassed about your debt. The last time I checked

Stocks and corporate bonds not the most important sources of funds for business

Stocks and corporate bonds not the most important sources of funds for business Stocks and corporate bonds not the most important sources of funds for business Indirect finance through financial intermediaries

Stocks and corporate bonds not the most important sources of funds for business Stocks and corporate bonds not the most important sources of funds for business Indirect finance through financial intermediaries

The Strategic Under-Reporting of Bank Risk

Taylor Begley 1 Amiyatosh Purnanandam 2 Kuncheng Zheng 3 1 London Business School 2 University of Michigan 3 Northeastern University December 2015 ACPR Banque de France Motivation Risk measurement is central

Taylor Begley 1 Amiyatosh Purnanandam 2 Kuncheng Zheng 3 1 London Business School 2 University of Michigan 3 Northeastern University December 2015 ACPR Banque de France Motivation Risk measurement is central

July 29, Japanese Bankers Association

July 29, 2008 Comments on "Principles for Sound Liquidity Risk Management and Supervision" June 2008 - Draft for Consultation from the Basel Committee on Banking Supervision Japanese Bankers Association

July 29, 2008 Comments on "Principles for Sound Liquidity Risk Management and Supervision" June 2008 - Draft for Consultation from the Basel Committee on Banking Supervision Japanese Bankers Association

HOW TO ACCELERATE BY USING SOCIAL ACCOUNTABILITY TOOLS

HOW TO ACCELERATE BY USING SOCIAL ACCOUNTABILITY TOOLS Context Social Accountability approach Many governments around the world have acknowledged Right to Water and Sanitation as a basic human rights.

HOW TO ACCELERATE BY USING SOCIAL ACCOUNTABILITY TOOLS Context Social Accountability approach Many governments around the world have acknowledged Right to Water and Sanitation as a basic human rights.

Good morning. Thank you for inviting me here today to deliver a speech at. I have been invited to talk about the finalisation of Basel III.

SPEECH DATE: 15 March 2017 SPEAKER: Governor Stefan Ingves LOCALITY: Bundesbank, Frankfurt SVER IG ES R IK SB AN K SE-103 37 Stockholm (Brunkebergstorg 11) Tel +46 8 787 00 00 Fax +46 8 21 05 31 registratorn

SPEECH DATE: 15 March 2017 SPEAKER: Governor Stefan Ingves LOCALITY: Bundesbank, Frankfurt SVER IG ES R IK SB AN K SE-103 37 Stockholm (Brunkebergstorg 11) Tel +46 8 787 00 00 Fax +46 8 21 05 31 registratorn

CLIENT VALUE & INDEX INSURANCE

CLIENT VALUE & INDEX INSURANCE TARA STEINMETZ, ASSISTANT DIRECTOR FEED THE FUTURE INNOVATION LAB FOR ASSETS & MARKET ACCESS Fairview Hotel, Nairobi, Kenya 4 JULY 2017 basis.ucdavis.edu Photo Credit Goes

CLIENT VALUE & INDEX INSURANCE TARA STEINMETZ, ASSISTANT DIRECTOR FEED THE FUTURE INNOVATION LAB FOR ASSETS & MARKET ACCESS Fairview Hotel, Nairobi, Kenya 4 JULY 2017 basis.ucdavis.edu Photo Credit Goes

Canada s Economy and Household Debt: How Big Is the Problem?

Remarks by Stephen S. Poloz Governor of the Bank of Canada Yellowknife Chamber of Commerce Yellowknife, Northwest Territories May 1, 2018 Canada s Economy and Household Debt: How Big Is the Problem? Introduction

Remarks by Stephen S. Poloz Governor of the Bank of Canada Yellowknife Chamber of Commerce Yellowknife, Northwest Territories May 1, 2018 Canada s Economy and Household Debt: How Big Is the Problem? Introduction

ENTERPRISE RISK AND STRATEGIC DECISION MAKING: COMPLEX INTER-RELATIONSHIPS

ENTERPRISE RISK AND STRATEGIC DECISION MAKING: COMPLEX INTER-RELATIONSHIPS By Mark Laycock The views and opinions expressed in this paper are those of the authors and do not necessarily reflect the official

ENTERPRISE RISK AND STRATEGIC DECISION MAKING: COMPLEX INTER-RELATIONSHIPS By Mark Laycock The views and opinions expressed in this paper are those of the authors and do not necessarily reflect the official

Aon Defined Contribution. Aon s Global Defined Contribution Points of View

Aon Defined Contribution Aon s Global Defined Contribution Points of View Aon s Global Defined Contribution Points of View Around the globe Aon is helping our clients tackle the challenges that come with

Aon Defined Contribution Aon s Global Defined Contribution Points of View Aon s Global Defined Contribution Points of View Around the globe Aon is helping our clients tackle the challenges that come with

MISOM. Dragline Performance Improvements. Case Study. A MISOM Advanced Solution. M. M. Kahraman & Dr. S. Dessureault

Dragline Performance Improvements Case Study A MISOM Advanced Solution M. M. Kahraman & Dr. S. Dessureault MISOM Mines are investing in equipment monitoring technology with the expectation of gaining large

Dragline Performance Improvements Case Study A MISOM Advanced Solution M. M. Kahraman & Dr. S. Dessureault MISOM Mines are investing in equipment monitoring technology with the expectation of gaining large

CEU Series: Conversations Module 2: Talking About Money With Ourselves, With Our Clients

CEU Series: Conversations Module 2: Talking About Money With Ourselves, With Our Clients CEU Conversations We Weren't Born as Homeopaths! We came to our profession from many backgrounds Communication about

CEU Series: Conversations Module 2: Talking About Money With Ourselves, With Our Clients CEU Conversations We Weren't Born as Homeopaths! We came to our profession from many backgrounds Communication about

HCI: CONTENT LAYOUT. Dr Kami Vaniea

HCI: CONTENT LAYOUT Dr Kami Vaniea 1 2 Affordance and Metaphores 3 Affordance An attribute of an object that allows people to know how to use it. -- ID book To afford means to give a clue It should be

HCI: CONTENT LAYOUT Dr Kami Vaniea 1 2 Affordance and Metaphores 3 Affordance An attribute of an object that allows people to know how to use it. -- ID book To afford means to give a clue It should be

Retirement Solutions. Engaging the Next Generations in Retirement Savings

www.calamos.com Retirement Solutions Engaging the Next Generations in Retirement Savings Improving Retirement Readiness for the Next Generations by Applying Behavioral Finance & Thoughtful Plan Design

www.calamos.com Retirement Solutions Engaging the Next Generations in Retirement Savings Improving Retirement Readiness for the Next Generations by Applying Behavioral Finance & Thoughtful Plan Design

Take control. Help your clients understand the role of risk control in a portfolio A GUIDE TO CONDUCTING A RISK CONTROL REVIEW

A GUIDE TO CONDUCTING A RISK CONTROL REVIEW Take control Help your clients understand the role of risk control in a portfolio MGA-1658740 FOR REGISTERED REPRESENTATIVE USE ONLY. NOT FOR USE BY THE GENERAL

A GUIDE TO CONDUCTING A RISK CONTROL REVIEW Take control Help your clients understand the role of risk control in a portfolio MGA-1658740 FOR REGISTERED REPRESENTATIVE USE ONLY. NOT FOR USE BY THE GENERAL

Optimal Taxation : (c) Optimal Income Taxation

Optimal Income Taxation") Optimal Taxation : (c) Optimal Income Taxation Optimal income taxation is quite a different problem than optimal commodity taxation. In optimal commodity taxation the issue was which commodities to tax,

Optimal Taxation : (c) Optimal Income Taxation Optimal income taxation is quite a different problem than optimal commodity taxation. In optimal commodity taxation the issue was which commodities to tax,

Consumption. Basic Determinants. the stream of income

Consumption Consumption commands nearly twothirds of total output in the United States. Most of what the people of a country produce, they consume. What is left over after twothirds of output is consumed

Consumption Consumption commands nearly twothirds of total output in the United States. Most of what the people of a country produce, they consume. What is left over after twothirds of output is consumed

Evaluating the Mchinji Social Cash Transfer Pilot

Evaluating the Mchinji Social Cash Transfer Pilot Dr. Candace Miller Center for International Health and Development Boston University & Maxton Tsoka Centre for Social Research University of Malawi Benefits

Evaluating the Mchinji Social Cash Transfer Pilot Dr. Candace Miller Center for International Health and Development Boston University & Maxton Tsoka Centre for Social Research University of Malawi Benefits

THIS MATERIAL IS FOR INSTITUTIONAL/BROKER-DEALER USE ONLY. NOT FOR DISTRIBUTION OR USE WITH THE PUBLIC.

Value Price is what people pay, value is what they pay for. You don t get paid for the hour, you get PAID FOR THE VALUE you bring to the hour. WARREN BUFFET Today s objectives 1 Define the real issues

Value Price is what people pay, value is what they pay for. You don t get paid for the hour, you get PAID FOR THE VALUE you bring to the hour. WARREN BUFFET Today s objectives 1 Define the real issues

The CreditRiskMonitor FRISK Score

Read the Crowdsourcing Enhancement white paper (7/26/16), a supplement to this document, which explains how the FRISK score has now achieved 96% accuracy. The CreditRiskMonitor FRISK Score EXECUTIVE SUMMARY

Read the Crowdsourcing Enhancement white paper (7/26/16), a supplement to this document, which explains how the FRISK score has now achieved 96% accuracy. The CreditRiskMonitor FRISK Score EXECUTIVE SUMMARY

LIFE PLANNING IN THE AGE OF LONGEVITY

Stanford Center on Longevity A TOOLKIT SERIES BRIEF LIFE PLANNING IN THE AGE OF LONGEVITY Insights for Gen Xers Steve Vernon, FSA Research Scholar Stanford Center on Longevity Copyright 2017 Stanford Center

Stanford Center on Longevity A TOOLKIT SERIES BRIEF LIFE PLANNING IN THE AGE OF LONGEVITY Insights for Gen Xers Steve Vernon, FSA Research Scholar Stanford Center on Longevity Copyright 2017 Stanford Center

Prosper Marketplace Financial Wellness Survey

Prosper Marketplace Financial Wellness Survey A survey examining the current state and sentiment around personal finance in America FEBRUARY 2016 Summary With both great wealth and extreme poverty, there

Prosper Marketplace Financial Wellness Survey A survey examining the current state and sentiment around personal finance in America FEBRUARY 2016 Summary With both great wealth and extreme poverty, there