Credit Cards and Financial Health Member-Exclusive Report from CFSI s Consumer Financial Health Study

|

|

|

- Norman Peters

- 6 years ago

- Views:

Transcription

1 Credit Cards and Financial Health Member-Exclusive Report from CFSI s Consumer Financial Health Study

2 We provide this CFSI Member Exclusive as a resource to create new products, calibrate existing ones, and communicate the benefits of their use to improve consumers financial health. The information is designed for use by product managers, segment managers, marketing managers, and community development/affairs managers to better understand consumers needs. The data and visuals in this presentation are easy to use to inform ideation and business strategies that support consumer financial health. We encourage you to share this asset widely within your organization, and to use the data and visuals in external presentations and communications. When you use an excerpt of this report, please cite CFSI as the source: Credit Cards and Financial Health: Member Exclusive Report from CFSI s Consumer Financial Health Study CFSI, February Per your CFSI Network membership agreement, we ask that you refrain from distributing this report in its entirety outside your organization. If you have any questions about this, please contact your CFSI relationship manager. 2

3 Table of Contents Key Findings... 4 Addressing Customer Needs with Credit Cards..10 Financial Health Recap...14 KF1: Nearly half of credit card holders are struggling financially KF2: A portion of credit card holders struggle with daily finances and resilience..30 KF3: Former credit card holders struggle with debt and poor credit scores..40 Credit Card Holder Demographics

4 Key Findings 1. Credit card holders have higher incomes and more manageable debt levels than non card holders, but nearly half are struggling financially. 2. Credit cards can help consumers weather shocks and balance borrowing and saving. 3. Many former credit card holders struggle with high rates of non-mortgage debt and poor credit scores. Company Logo

5 On average, credit card holders have higher incomes and more sustainable debt levels than non-holders 75% of American adults have a credit card More than half of credit card holders have annual incomes in the top two income quartiles, compared with just a quarter of non credit card holders. Just over a quarter (27%) of credit card holders have a nonmortgage debt-to-income ratio of 40% or more, compared with 37% of non credit card holders. 5

6 Still, nearly half of credit card holders are struggling financially 182 million Americans have credit cards, and 87 million are struggling financially. For more on the financial health segmentation, download the whitepaper, Understanding and Improving Consumer Financial Health in America 6

7 While many credit hard holders thrive, others struggle For more detail, refer to slides:

8 Credit cards can help consumers weather shocks and balance borrowing and saving 15% of credit card holders would first turn to their card to cover a $600 emergency expense and pay it off over time. 19% of non-holders do not know where they would turn to cover a $600 expense. While card holders split about evenly between those who do and do not carry a balance, 39% sometimes leave a balance instead of using savings to pay it off. These customers report a higher frequency of unexpected expenses than their peers who do not report this behavior. Research including the USFD shows that low- to moderate-income consumers need, but often struggle to accumulate, large lump sums. Accumulating lump sums through small contributions over time is a core aim of financial services, formal and informal. This can be accomplished by either saving money gradually or borrowing a lump sum and then paying it off bit by bit. Categorizing a financial vehicle as credit or savings is less important than its ability to aid in accumulating a lump sum for when it is needed. US Financial Diaries Issue Brief, How Households Use Financial Tools of Their Own Making, Morduch & Schneider, August 2014 Credit card providers have an opportunity to enhance products with features that support cash flow management, planning ahead, responsible use of credit, and building resilience key aspects of financial health. For more detail, refer to slides:

9 Many former card holders struggle with high rates of non-mortgage debt and poor credit scores Former credit card holders acknowledge having difficulty managing their cards. These financial challenges are reflected in their levels of debt and credit quality. More than 4 in 10 former card holders report a non-mortgage debt-toincome ratio over 40%, and the same proportion report having poor or very poor credit scores. Credit card providers can leverage robust monitoring and predictive analytics to help customers identify risky behaviors and trends early, so they can adopt strategies to prevent larger financial challenges later. For more detail, refer to slides:

10 What could your financial institution do to help credit card holders improve their financial health? Company Logo

11 Value-Added Tools and Services While credit cards can be an important tool for financial management, those who carry a balance are less likely to be financially healthy. Card holders who carry a balance also budget more than those who do not carry a balance. However, they do not plan for large, irregular expenses a key characteristic of financial health with the same frequency. Many say they would plan ahead if they could, perhaps indicating that they do not have the tools or capabilities to plan. How could you provide tools to help customers plan for large irregular expenses and/or adopt and maintain other financially healthy habits? Benefits include deepening your customer relationships, helping them better manage their financial lives, and contributing to the longevity and long-term profitability of these relationships. 11

12 Guidance and Prevention Consumers who have not owned a credit card before are a source of new business for card providers. However, these customers may not fully understand how to responsibly use the product or the ramifications of misuse. Those who have never had a credit card are the most likely to say they do not know their credit quality or did not know they had a credit score. Young Americans, age 18-25, are most likely to have never had a credit card. Could you provide new card owners with guidance and tools alerts, guardrails, or other features enabling positive credit behavior for your customers and long-term customer relationships for your organization? 12

13 Credit Repair and Rebuilding Many former credit card customers had difficulty managing the product and struggle with indebtedness and poor credit scores. Former credit card holders are four times more likely to have used a payday loan in the last year vs. current card holders and they are more likely to have unhealthy non-mortgage debt-to-income ratios and poor credit quality. Could your organization provide former and at-risk card holders debt repayment plans and tools to rebuild their credit so they can regain access to high-quality, low-cost credit? 13

14 Financial Health Recap Company Logo

15 Recap: Financial Health Financial health comes about when your daily systems help you build resilience and pursue opportunities. Resilience Opportunity Day-to-Day Management Are you prepared for the unexpected? Are you able to pursue your financial aspirations? Do your financial products support resilience and opportunity? 15

16 Recap: Financial Health Segmentation The Consumer Financial Health Study includes a segmentation analysis that groups individuals based upon patterns of responses to a range of survey questions corresponding with subjective and objective indicators of financial health. The seven consumer segments derived from the segmentation analysis were grouped into three tiers: Healthy, Coping and Vulnerable, with the four Coping and Vulnerable segments sometimes referred to in aggregate as the segments comprised of consumers who are struggling financially. Though income significantly influences financial health, consumer behaviors particularly those related to planning ahead and saving also have a significant impact on consumers financial health segment. For more on the financial health segmentation, download the whitepaper, Understanding and Improving Consumer Financial Health in America. For more on the four financially struggling segments, download the segment briefs. 16

17 Recap: Financial Health Segmentation 138 million American adults struggle financially. For more on the financial health segmentation, download the whitepaper, Understanding and Improving Consumer Financial Health in America 17

18 Recap: Financially Healthy Segments Financially Healthy Segments tend to do well across all indicators of financial health. Individuals in these segments are able to manage their day-to-day financial lives; they have a significant financial cushion in case of an emergency; and they are better positioned to seize financial opportunities. They demonstrate the highest rates of checking account, savings account, and credit card ownership of all segments. For more on the financial health segmentation, download the whitepaper, Understanding and Improving Consumer Financial Health in America 18

19 Recap: Financially Coping Segments Financially Coping segments generally exhibit more moderate behaviors and attitudes across the financial health indicators, compared with their Financially Healthy counterparts. These individuals are more likely to struggle in managing their day-to-day financial lives, have less financial cushion for an emergency, and be less well positioned to take advantage of financial opportunities. Individuals in these segments tend to use a variety of financial products and services traditional, nonbank, and new technology-enabled to manage their financial lives. For more on the financial health segmentation, download the whitepaper, Understanding and Improving Consumer Financial Health in America 19

20 Recap: Financially Vulnerable Segments The two Financially Vulnerable segments are doing the least well across financial health indicators. These individuals are more likely to be struggling with their day-today financial lives; they have little or no financial cushion in case of an emergency; and they are not prepared to seize financial opportunities for security and mobility. They are the least likely of all segments to own a credit card and the most likely to be unbanked. For more on the financial health segmentation, download the whitepaper, Understanding and Improving Consumer Financial Health in America 20

21 A closer look at the data Key Finding 1: Credit card holders have higher incomes and more manageable debt levels than non-holders, but nearly half struggle financially. Company Logo

22 Financially Struggling Nearly half of credit card holders struggle financially. Learn more about the financially struggling segments here. For more on the financial health segmentation, download the whitepaper, Understanding and Improving Consumer Financial Health in America 22

23 Financial Stress Nearly 60% of consumers without a card are in a financially vulnerable segment. 58% of them have never owned a credit card. Learn more about the financially struggling segments here. For more on the financial health segmentation, download the whitepaper, Understanding and Improving Consumer Financial Health in America For more on the financial health segmentation, download the whitepaper: bit.ly/consumerfinhealth 23

24 Financial Stress Finances Cause Me Significant Stress Almost a quarter of card holders say their finances are a cause of significant stress. Another 30% neither agree nor disagree with that statement. Respondents were asked: On a scale of 1 to 5, where 1 is strongly disagree, 3 is neither agree nor disagree, and 5 is strongly agree, how much do you agree or disagree with the following statement: My finances cause me significant stress. 24

25 Credit Card Fees and Financial Stress 11% of card holders say they were occasionally charged a late fee in the last year due to forgetting to pay. 7% say they were charged a late fee in some months because they did not have the money to pay on time. 4% say they paid an over-the-limit fee for exceeding the credit line. Of these three groups, those who occasionally forget to pay their credit card bill are the least financially stressed (30%). Chart shows: The degree to which credit card owners who were charged a fee for the reasons listed agreed with the statement, My finances cause me significant stress. 25

26 Financial Confidence: Short-Term Goals More than 4 in 10 card holders lack confidence about achieving short-term savings goals. Respondents were asked: On a scale of 1 to 5, where 1 is strongly disagree, 3 is neither agree nor disagree, and 5 is strongly agree, how much do you agree or disagree with the following statement: I am confident that I can meet my short-term saving goals. 26

27 Financial Confidence: Long-Term Goals Half of credit card holders lack confidence about meeting long-term goals for becoming financially secure. Respondents were asked: On a scale of 1 to 5, where 1 is strongly disagree, 3 is neither agree nor disagree, and 5 is strongly agree, how much do you agree or disagree with the following statement: I am confident that I can meet my long-term goals for becoming financially secure. 27

28 Living Paycheck to Paycheck More than a quarter of credit card holders report always living paycheck to paycheck. Another 24% neither agree nor disagree with that statement. Respondents were asked: On a scale of 1 to 5, where 1 is strongly disagree, 3 is neither agree nor disagree, and 5 is strongly agree, how much do you agree or disagree with the following statement: I always find myself living paycheck to paycheck. 28

29 Cash Flow Almost one-third (31%) of credit card holders sometimes run out of money before the end of the month. 29

30 A closer look at the data Key Finding 2: Credit cards can help consumers weather shocks and balance borrowing and saving. Company Logo

31 Credit Card Payments 31

32 Financial Health of Balance-Carriers vs. Non-Carriers Credit card customers who carry a balance are less likely to be financially healthy, compared with those who do not. Balance-carriers were also slightly more likely to have had a health emergency, used savings for bills, or lost a job in the last five years. 3% indicated that they both pay in full and carried a balance; they may have more than one card or simply were not paying close attention. For simplicity, we removed these respondents. Respondents were asked: During the past 5 years, has your household experienced any of the following significant major life changes or financial events? 32

33 Budgeting and Planning: Balance-Carriers vs Non-Carriers While those who carry a balance are just as likely to use a budget as those who do not carry a balance, they feel less able to plan ahead for large, irregular expenses. 3% indicated that they both pay in full and carried a balance; they may have more than one card or simply were not paying close attention. For simplicity, we removed these respondents. 33

; the vast majority (82%) would use savings or a credit card they pay off in full to cover a $600")

34 Credit Card Use: Convenience vs. Cushion Those who do not carry a balance appear to use the card for convenience (and rewards); the vast majority (82%) would use savings or a credit card they pay off in full to cover a $600 emergency. Those who carry a balance would be less likely to turn to savings. Instead, they would use their credit card to weather the shock and pay off the balance over time. Respondents were asked: Thinking about the past 12 months, which of the following describes your experience with credit cards? 34

of those who report having done this in the past year have less than $5,000 in non-retirement savings, more than one-quarter (29%) have more than $20,000 in non-retirement")

35 Balancing Credit and Savings Carrying a credit card balance instead of using savings to pay it off is a practice that consumers with varying levels of savings employ. While nearly half (49%) of those who report having done this in the past year have less than $5,000 in non-retirement savings, more than one-quarter (29%) have more than $20,000 in non-retirement savings. Respondents were asked: About how much money do you and your household have right now in checking, savings, money market accounts, stocks, and bonds? Please do not include any money in formal retirement funds such as Individual Retirement Accounts (IRA), 401k s, Roth IRA s or company retirement funds. 35

36 Balancing Credit and Savings Consumers who carry a balance instead of using savings experience unexpected expenses more frequently and could weather a sudden income drop for less time than those who do not. This sheds light on why and how consumers balance credit and saving to manage their financial lives. Respondents were asked: In the past 12 months, how often have you and your household had an unexpected expense crop up? & How long could your household make ends meet if you faced unemployment, a longer-term illness, job loss, economic downturn, or other emergency that caused a drop in income? 36

37 Non-Retirement Savings Many factors contribute to ability to weather financial ups and downs: savings, access to lowcost credit, and help from family and friends. Credit card holders have accrued significantly more non-retirement savings than non-card holders. More than 62% of card holders have savings balances greater than $5,000, compared with 25% of non-holders. Respondents were asked: About how much money do you and your household have right now in checking, savings, money market accounts, stocks, and bonds? Do not include money in formal retirement funds such as Individual Retirement Accounts (IRA), 401k s, Roth IRA s or company retirement funds. 37

38 Coming Up With $600 in One Week Consistent with card holders having higher incomes and non-retirement savings, more than 6 in 10 would use cash or a credit card they pay off in full to fund a $600 emergency. However, 15% of credit card holders say they would use their credit card and pay off the expense over time. 19% of non-card holders do not know how they would cover the expense, and 13% say they could not meet it. Respondents were asked: If you had one week to pay $600 for an emergency expense, such as a car repair or medical bill, where would you turn first to get the money? 3% of non-credit card holders said they would turn to a credit card, perhaps indicating that they might open an account or that they were simply were not paying close attention. 38

39 Coming Up With $2,000 in One Month Card holders are most confident they could come up with $2,000 in one month for an emergency. However, more than onequarter of card holders are slightly or not at all confident. Former card holders exhibit the least confidence, followed by those who have never owned a credit card. Among never-holders, those who said they don t need or want a card are slightly more confident. Respondents were asked: How confident are you that you could come up with $2,000 if an unexpected need arose within the next month? 39

40 A closer look at the data Key Finding 3: Many former card holders struggle with high rates of non-mortgage debt and poor credit scores. Company Logo

41 Credit Card Ownership 41

42 Never Had A Credit Card Consumers who have never had a credit card are most likely to cite not needing or wanting one. More than one-third say they would qualify for a card, though more than 4 in 10 could not assess their credit quality. 11% indicated that they have excellent or good credit. Respondents were asked: Is each of the following a reason or not a reason why you don t have a credit card? 42

43 No Longer Have a Credit Card Consumers who had a credit card in the past, but no longer do, are most likely to report having had difficulty managing the card. Respondents were asked: Is each of the following a reason or not a reason why you no longer have a credit card? 43

44 Borrowing In the Last Year Card holders are less likely to borrow from members of their social networks. Non-holders are more likely to use payday and pawn loans. Respondents were asked: In the past 12 months, have you and your household used any of the following to borrow money? 44

45 Non-Mortgage Debt-to-Income Ratio The highest proportion of consumers with no nonmortgage debt have never had a card. More than 4 in 10 former credit card holders report a non-mortgage DTI over 40%, the highest of the three groups. Non-mortgage debt-to-income ratio calculated by aggregating a household s student loan debt, medical debt, and other non-mortgage debt, then dividing that number by the household s annual income. A non-mortgage DTI of less than 10% is considered manageable; a ratio between 10% and 40% is considered high but manageable; a ratio over 40% is considered unhealthy. 45

46 Credit Quality: Subjective vs. Objective Card holders are most likely to have both a high credit-quality self-assessment and a prime or super prime VantageScore. Former card holders are most likely to have a low self-assessment and a subprime or deep subprime score. Those who never had a credit card are most likely to not know their credit quality or that they have a credit score; they were also the most likely to be unscorable and unmatchable by Experian.* *Unscorable VantageScore records reflect deceased consumers or those with credit inquiries only. Unmatchable VantageScore records include: (a) consumers who don t have a credit file with the bureau and (b) those for whom Experian did not receive sufficient identifying information. For details see 46

47 Card Holder Demographics Company Logo

48 Account Mix Credit Card account holders also have 48

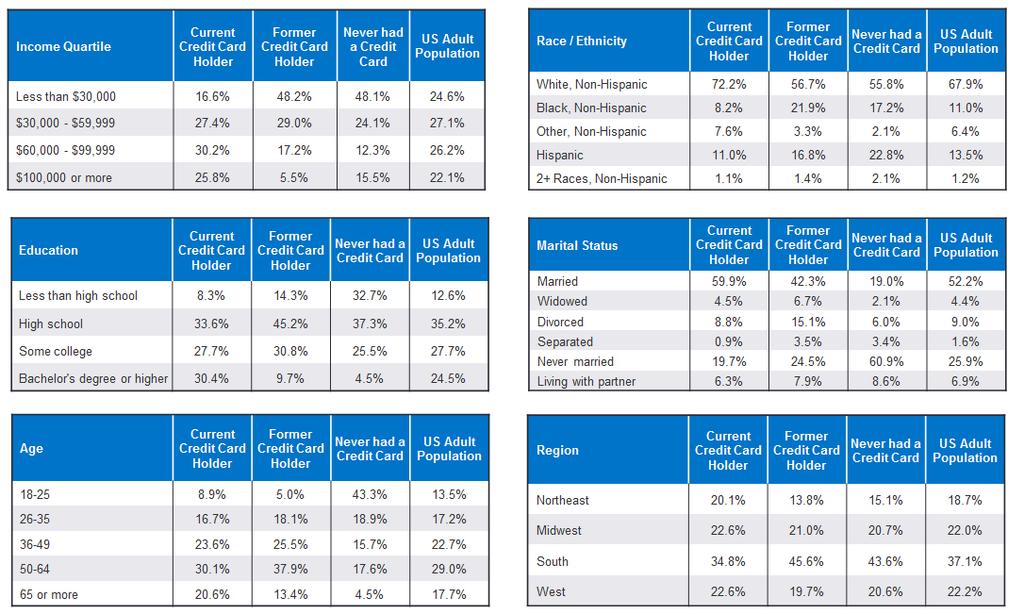

49 Notable Facts About Credit Card Holders Income: 16% earn less than $30,000, compared with 48% of non-holders. Demographics: Black and Hispanic populations represent 40% of non-holders, compared with 19% of card holders. Marital Status: 60% are married, while only 29% of non-holders are. Age: 43% of those who have never owned a credit card are years old, compared with 9% of card holders. 49

50 Demographic Details 50

51 Consumer Financial Health Study The Consumer Financial Health Study survey data was captured from June August The nationally representative survey sample includes more than 7,000 consumers. The Consumer Financial Health Study benefited from the financial support of its funders, which include CFSI founding funder, the Ford Foundation, and MetLife Foundation. Segmentation whitepaper Segment briefs Credit score whitepaper Survey instrument Financial health and child well-being whitepaper MetLife Foundation is a major sponsor of CFSI s ongoing consumer financial health work. 51

52 Consumer Financial Health Study Methodology CFSI partnered with GfK, a global market and consumer research firm, to field the Consumer Financial Health Study survey. invitations were sent to a random sample of GfK s KnowledgePanel participants June-August 2014, yielding 7,152 survey respondents. KnowledgePanel is a large national, probability-based panel that provides a representative sample for online research. The sample is comprised of adults (18 and older) residing in the U.S. at all levels of the income spectrum; consumers with annual incomes under $50,000 were over-sampled to provide a robust set of data on consumers in the lower half of the income distribution. The target over-sample was 1,500 consumers with incomes under $50,000, to augment the generally representative pool of respondents. All data contained in this report has been weighted back to the total U.S. population to ensure that it is nationally representative. Standard, baseline incentives were given to respondents for survey completion; in addition to a sweepstakes entry, respondents each received between 1,000 and 1,500 points. Panelists typically receive 1,000 points for every survey session they complete, which is equal to $1. Respondents were offered a $10 incentive to provide consent to pull their credit score range. For more information about the survey instrument and methodology, download the segmentation whitepaper: bit.ly/consumerfinhealth Segmentation whitepaper Segment briefs Credit score whitepaper Survey instrument Financial health and child well-being whitepaper 52

53 Want More? The Consumer Financial Health Study data set contains a host of demographic, behavioral and product information, in addition to some information about financial institution relationships. Looking for some targeted information to help you make product or marketing decisions? Reach out to your CFSI Relationship Manager to discuss how we can help. 53

54 Chicago New York San Francisco Washington, DC Connect with us #finhealth Linked In: Center for Financial Services Innovation

Checking Accounts and the Financially Struggling Majority. Member Exclusive Report from CFSI s Consumer Financial Health Study

Checking Accounts and the Financially Struggling Majority Member Exclusive Report from CFSI s Consumer Financial Health Study We provide this CFSI Member Exclusive as a resource to create new products,

Checking Accounts and the Financially Struggling Majority Member Exclusive Report from CFSI s Consumer Financial Health Study We provide this CFSI Member Exclusive as a resource to create new products,

The Financial Strains of Small-Dollar Credit Users. Member-Exclusive Report from CFSI s Consumer Financial Health Study

The Financial Strains of Small-Dollar Credit Users Member-Exclusive Report from CFSI s Consumer Financial Health Study CFSI Member Exclusive We provide this CFSI Member Exclusive as a resource to create

The Financial Strains of Small-Dollar Credit Users Member-Exclusive Report from CFSI s Consumer Financial Health Study CFSI Member Exclusive We provide this CFSI Member Exclusive as a resource to create

Eight Ways to Measure Financial Health

Eight Ways to Measure Financial Health April 2016 Leading the Nation in Consumer Financial Health MEMBERSHIP CONSULTING RESEARCH INNOVATION EVENTS IMPACT 8 Ways to Measure Financial Health How Banks, Credit

Eight Ways to Measure Financial Health April 2016 Leading the Nation in Consumer Financial Health MEMBERSHIP CONSULTING RESEARCH INNOVATION EVENTS IMPACT 8 Ways to Measure Financial Health How Banks, Credit

The CFSI Underbanked Consumer Study Underbanked Consumer Overview & Market Segments Fact Sheet

The CFSI Underbanked Consumer Study - Fact Sheet June 8, 28 The CFSI Underbanked Consumer Study Underbanked Consumer Overview & Market Segments Fact Sheet Released: June 8, 28 Introduction The purpose

The CFSI Underbanked Consumer Study - Fact Sheet June 8, 28 The CFSI Underbanked Consumer Study Underbanked Consumer Overview & Market Segments Fact Sheet Released: June 8, 28 Introduction The purpose

The National Credit Union Foundation: Financial Health Check-Up Aggregation

The National Credit Union Foundation: Financial Health Check-Up Aggregation Results excerpt, November 2017 Leading the Nation in Consumer Financial Health MEMBERSHIP CONSULTING RESEARCH INNOVATION Overview

The National Credit Union Foundation: Financial Health Check-Up Aggregation Results excerpt, November 2017 Leading the Nation in Consumer Financial Health MEMBERSHIP CONSULTING RESEARCH INNOVATION Overview

Underbanked 101. Joshua Sledge, Analyst, Innovation and Research, CFSI CFSI Underbanked Financial Services Forum June 13, 2012

2012 2012 Center Center for for Financial Financial Services Services Innovation Innovation Underbanked 101 Joshua Sledge, Analyst, Innovation and Research, CFSI CFSI Underbanked Financial Services Forum

2012 2012 Center Center for for Financial Financial Services Services Innovation Innovation Underbanked 101 Joshua Sledge, Analyst, Innovation and Research, CFSI CFSI Underbanked Financial Services Forum

Segmentation Survey. Results of Quantitative Research

Segmentation Survey Results of Quantitative Research August 2016 1 Methodology KRC Research conducted a 20-minute online survey of 1,000 adults age 25 and over who are not unemployed or retired. The survey

Segmentation Survey Results of Quantitative Research August 2016 1 Methodology KRC Research conducted a 20-minute online survey of 1,000 adults age 25 and over who are not unemployed or retired. The survey

Perceived Helpfulness of Financial Well-being Programs: Results From the 2017 and 2018 Retirement Confidence Surveys

September 2010 No. 346 August 20, 2018 No. 457 Perceived Helpfulness of Financial Well-being Programs: Results From the 2017 and 2018 Retirement Confidence Surveys By Craig Copeland, Ph.D., Employee Benefit

September 2010 No. 346 August 20, 2018 No. 457 Perceived Helpfulness of Financial Well-being Programs: Results From the 2017 and 2018 Retirement Confidence Surveys By Craig Copeland, Ph.D., Employee Benefit

Consumer Financial Services Webinar Series. Webinar #4: Building a Small-Dollar Loan Product September 15, :00 2:00 PM ET

Consumer Financial Services Webinar Series Webinar #4: Building a Small-Dollar Loan Product September 15, 2015 1:00 2:00 PM ET Agenda NEXT Awards and Consumer Financial Services Webinar Series Review CFSI

Consumer Financial Services Webinar Series Webinar #4: Building a Small-Dollar Loan Product September 15, 2015 1:00 2:00 PM ET Agenda NEXT Awards and Consumer Financial Services Webinar Series Review CFSI

Bank of the West 2018 Millennial Study Results

Bank of the West 2018 Millennial Study Results July 2018 Table of Contents Executive Summary 3 Key Findings 5 The Millennial Mindset The American Dream 6 Homeownership 9 Relationship with Debt 17 Investing

Bank of the West 2018 Millennial Study Results July 2018 Table of Contents Executive Summary 3 Key Findings 5 The Millennial Mindset The American Dream 6 Homeownership 9 Relationship with Debt 17 Investing

A Close Look at ETF Households

A Close Look at ETF Households A Report by the Investment Company Institute and Strategic Business Insights SEPTEMBER 2018 Suggested citation: Investment Company Institute and Strategic Business Insights.

A Close Look at ETF Households A Report by the Investment Company Institute and Strategic Business Insights SEPTEMBER 2018 Suggested citation: Investment Company Institute and Strategic Business Insights.

2019 Retirement Confidence Survey Summary Report April 23, 2019

2019 Retirement Confidence Survey Summary Report April 23, 2019 Employee Benefit Research Institute 1100 13 th Street NW, Suite 878 Washington, DC 20005 Phone: (202) 659-0670 Fax: (202) 775-6312 Greenwald

2019 Retirement Confidence Survey Summary Report April 23, 2019 Employee Benefit Research Institute 1100 13 th Street NW, Suite 878 Washington, DC 20005 Phone: (202) 659-0670 Fax: (202) 775-6312 Greenwald

Saving at Work for a Rainy Day Results from a National Survey of Employees

Saving at Work for a Rainy Day Results from a National Survey of Employees Catherine Harvey and David John AARP Public Policy Institute S. Kathi Brown AARP Research September 2018 AARP PUBLIC POLICY INSTITUTE

Saving at Work for a Rainy Day Results from a National Survey of Employees Catherine Harvey and David John AARP Public Policy Institute S. Kathi Brown AARP Research September 2018 AARP PUBLIC POLICY INSTITUTE

Understanding Credit. What it is, why it s important, and how you can maintain it. Brought to you by Sallie Mae and FICO

Understanding Credit What it is, why it s important, and how you can maintain it Brought to you by Sallie Mae and FICO Introduction A student loan may be your first major credit experience. This is a good

Understanding Credit What it is, why it s important, and how you can maintain it Brought to you by Sallie Mae and FICO Introduction A student loan may be your first major credit experience. This is a good

Overconfident and Underprepared: The Disconnect Between Millennials and Their Money Insights from the 2015 National Financial Capability Study

Overconfident and Underprepared: The Disconnect Between Millennials and Their Money Insights from the 2015 National Financial Capability Study About this brief: In June 2015, Annamaria Lusardi, academic

Overconfident and Underprepared: The Disconnect Between Millennials and Their Money Insights from the 2015 National Financial Capability Study About this brief: In June 2015, Annamaria Lusardi, academic

S E P T E M B E R MassMutual African American Middle America Financial Security Study

S E P T E M B E R 2 0 1 7 MassMutual African American Middle America Financial Security Study Background and Methodology Study Objectives To raise awareness of the threats and obstacles to African American

S E P T E M B E R 2 0 1 7 MassMutual African American Middle America Financial Security Study Background and Methodology Study Objectives To raise awareness of the threats and obstacles to African American

T. Rowe Price 2015 FAMILY FINANCIAL TRADE-OFFS SURVEY

T. Rowe Price 2015 FAMILY FINANCIAL TRADE-OFFS SURVEY Contents Perceptions About Saving for Retirement & College Education Respondent College Experience Family Financial Profile Saving for College Paying

T. Rowe Price 2015 FAMILY FINANCIAL TRADE-OFFS SURVEY Contents Perceptions About Saving for Retirement & College Education Respondent College Experience Family Financial Profile Saving for College Paying

Income Stability and Asset Building Tuesday, November 10 4:15 PM - 5:30 PM. Tanya Ladha, Center for Financial Services Innovation

Income Stability and Asset Building Tuesday, November 10 4:15 PM - 5:30 PM Presenters Tony Berkley, Prudential Tanya Ladha, Center for Financial Services Innovation Gwyneth Galbraith, Opportunity Fund

Income Stability and Asset Building Tuesday, November 10 4:15 PM - 5:30 PM Presenters Tony Berkley, Prudential Tanya Ladha, Center for Financial Services Innovation Gwyneth Galbraith, Opportunity Fund

WFSN in Community Colleges. Innovating new financial products and services to support community college student success

WFSN in Community Colleges Innovating new financial products and services to support community college student success Panelists Sarah Griffen, Consultant Ashvin Prakash, CFSI Nancy Castillo, CFSI Wendy

WFSN in Community Colleges Innovating new financial products and services to support community college student success Panelists Sarah Griffen, Consultant Ashvin Prakash, CFSI Nancy Castillo, CFSI Wendy

Why Financial Inclusion Matters: The Household Balance Sheet Perspective

Why Financial Inclusion Matters: The Household Balance Sheet Perspective Promising Pathways to Wealth-Building Financial Services October 25-26, 2012 Ray Boshara, Senior Advisor Federal Reserve Bank of

Why Financial Inclusion Matters: The Household Balance Sheet Perspective Promising Pathways to Wealth-Building Financial Services October 25-26, 2012 Ray Boshara, Senior Advisor Federal Reserve Bank of

Insuring the Way to a Financially Resilient America. Developing Successful Products for LMI Consumers June 2018

Insuring the Way to a Financially Resilient America Developing Successful Products for LMI Consumers June 2018 Financial resilience is fundamental to achieving overall financial health. Yet across CFSI

Insuring the Way to a Financially Resilient America Developing Successful Products for LMI Consumers June 2018 Financial resilience is fundamental to achieving overall financial health. Yet across CFSI

MoneyMinded in the Philippines Impact Report 2013 PUBLISHED AUGUST 2014

in the Philippines Impact Report 2013 PUBLISHED AUGUST 2014 1 Foreword We are pleased to present the Philippines Impact Report 2013. Since 2003, ANZ's flagship adult financial education program, has reached

in the Philippines Impact Report 2013 PUBLISHED AUGUST 2014 1 Foreword We are pleased to present the Philippines Impact Report 2013. Since 2003, ANZ's flagship adult financial education program, has reached

Measuring and Forecasting. Financial Wellness PAGE 1

Measuring and Forecasting Financial Wellness PAGE 1 What does financial wellness have to do with the weather? In both, the ability to measure, track, and forecast its impact leads people to be better prepared.

Measuring and Forecasting Financial Wellness PAGE 1 What does financial wellness have to do with the weather? In both, the ability to measure, track, and forecast its impact leads people to be better prepared.

Saving and Investing Among High Income African-American and White Americans

The Ariel Mutual Funds/Charles Schwab & Co., Inc. Black Investor Survey: Saving and Investing Among High Income African-American and Americans June 2002 1 Prepared for Ariel Mutual Funds and Charles Schwab

The Ariel Mutual Funds/Charles Schwab & Co., Inc. Black Investor Survey: Saving and Investing Among High Income African-American and Americans June 2002 1 Prepared for Ariel Mutual Funds and Charles Schwab

December 2018 Financial security and the influence of economic resources.

December 2018 Financial security and the influence of economic resources. Financial Resilience in Australia 2018 Understanding Financial Resilience 2 Contents Executive Summary Introduction Background

December 2018 Financial security and the influence of economic resources. Financial Resilience in Australia 2018 Understanding Financial Resilience 2 Contents Executive Summary Introduction Background

Millennial Money Mindset Report

Millennial Money Mindset Report 2017 In Partnership with: Data Analysis support by Executive Summary 2017 Millennial Money Mindset Report Previous studies have shown that the expectations of Millennials

Millennial Money Mindset Report 2017 In Partnership with: Data Analysis support by Executive Summary 2017 Millennial Money Mindset Report Previous studies have shown that the expectations of Millennials

Copyright 2005 Freddie Mac. All Rights Reserved. Foreclosure Avoidance Research

Copyright 2005 Freddie Mac. All Rights Reserved. Foreclosure Avoidance Research Purpose & Methodology Over half of the borrowers in foreclosure proceedings have had no contact with their lender. Freddie

Copyright 2005 Freddie Mac. All Rights Reserved. Foreclosure Avoidance Research Purpose & Methodology Over half of the borrowers in foreclosure proceedings have had no contact with their lender. Freddie

DC INVESTOR SURVEY. Biannual Report. Financial stress impedes employees ability to take action and hurts the corporate bottom line.

March 2015 DC INVESTOR SURVEY Biannual Report Financial stress impedes employees ability to take action and hurts the corporate bottom line i Investor Survey March 2015 ssga.com/definedcontribution About

March 2015 DC INVESTOR SURVEY Biannual Report Financial stress impedes employees ability to take action and hurts the corporate bottom line i Investor Survey March 2015 ssga.com/definedcontribution About

Your Guide to Life Insurance for Families

Your Guide to Life Insurance for Families (800) 827-9990 HealthMarkets.com Your Guide to Life Insurance for Families Contents Does My Family Need Life Insurance? 4 Types of Life Insurance for Families

Your Guide to Life Insurance for Families (800) 827-9990 HealthMarkets.com Your Guide to Life Insurance for Families Contents Does My Family Need Life Insurance? 4 Types of Life Insurance for Families

Understanding and Measuring Financial Health

Understanding and Measuring Financial Health Elisabeth Rhyne Managing Director, Center for Financial Inclusion at Accion International Conference on Customer Centric Businesses Mamallapuram, India February

Understanding and Measuring Financial Health Elisabeth Rhyne Managing Director, Center for Financial Inclusion at Accion International Conference on Customer Centric Businesses Mamallapuram, India February

18 th Annual Transamerica Retirement Survey Influences of Generation on Retirement Readiness. June 2018 TCRS

th Annual Transamerica Retirement Survey Influences of Generation on Retirement Readiness June 0 TCRS -06 Transamerica Institute, 0 Welcome to the th Annual Transamerica Retirement Survey Welcome to this

th Annual Transamerica Retirement Survey Influences of Generation on Retirement Readiness June 0 TCRS -06 Transamerica Institute, 0 Welcome to the th Annual Transamerica Retirement Survey Welcome to this

MUST BE 35 TO 64 TO QUALIFY. ALL OTHERS TERMINATE. COUNTER QUOTA FOR AGE GROUPS.

2016 Puerto Rico Survey Retirement Security & Financial Resilience Labor Force Participants (working or looking for work) age 35 to 64 and current Retirees Total sample n=800, max Retirees (may be current

2016 Puerto Rico Survey Retirement Security & Financial Resilience Labor Force Participants (working or looking for work) age 35 to 64 and current Retirees Total sample n=800, max Retirees (may be current

index The financial stress, challenges and fragility of Canadians from low-income households Financial Health

May 2018 The financial stress, challenges and fragility of Canadians from low-income households Insights from the 2017 Financial Health Index Study May 2018 Financial Health index Definitions Financial

May 2018 The financial stress, challenges and fragility of Canadians from low-income households Insights from the 2017 Financial Health Index Study May 2018 Financial Health index Definitions Financial

Marriage and Money. January 2018

Marriage and Money January 2018 Introduction The broad discussion in many circles about the plight of the non-prime consumer often uses assumptions about how these consumers think, what matters to them,

Marriage and Money January 2018 Introduction The broad discussion in many circles about the plight of the non-prime consumer often uses assumptions about how these consumers think, what matters to them,

S E P T E M B E R MassMutual Hispanic Middle America Financial Security Study

S E P T E M B E R 2 0 1 7 MassMutual Middle America Financial Security Study Background and Methodology Study Objectives To raise awareness of the threats and obstacles to middle-class workers financial

S E P T E M B E R 2 0 1 7 MassMutual Middle America Financial Security Study Background and Methodology Study Objectives To raise awareness of the threats and obstacles to middle-class workers financial

Special Report. Retirement Confidence in America: Getting Ready for Tomorrow EBRI EMPLOYEE BENEFIT RESEARCH INSTITUTE. and Issue Brief no.

December 1994 Jan. Feb. Mar. Retirement Confidence in America: Getting Ready for Tomorrow Apr. May Jun. Jul. Aug. EBRI EMPLOYEE BENEFIT RESEARCH INSTITUTE Special Report and Issue Brief no. 156 Most Americans

December 1994 Jan. Feb. Mar. Retirement Confidence in America: Getting Ready for Tomorrow Apr. May Jun. Jul. Aug. EBRI EMPLOYEE BENEFIT RESEARCH INSTITUTE Special Report and Issue Brief no. 156 Most Americans

Lower savings rates now may have long-term implications for mothers, who are also less engaged in calculating and planning for their retirement.

Mom s retirement A Voya Retirement Research Institute study that looks at financial habits and retirement planning for women who are currently also focused on raising children. The joys and challenges

Mom s retirement A Voya Retirement Research Institute study that looks at financial habits and retirement planning for women who are currently also focused on raising children. The joys and challenges

Measuring and Predicting. Financial Wellness. Do your employees have their financial houses in order? PAGE 1

Measuring and Predicting Financial Wellness Do your employees have their financial houses in order? PAGE 1 We believe being financially well is about more than just dollars and cents. It s also about how

Measuring and Predicting Financial Wellness Do your employees have their financial houses in order? PAGE 1 We believe being financially well is about more than just dollars and cents. It s also about how

Hispanic Personal Finances: Financial Literacy and Decision-making Among College-Educated Hispanics

Hispanic Personal Finances: Financial Literacy and Decision-making Among College-Educated Hispanics Annamaria Lusardi, GFLEC Carlo de Bassa Scheresberg, GFLEC Paul Yakoboski, TIAA-CREF Institute National

Hispanic Personal Finances: Financial Literacy and Decision-making Among College-Educated Hispanics Annamaria Lusardi, GFLEC Carlo de Bassa Scheresberg, GFLEC Paul Yakoboski, TIAA-CREF Institute National

Banking, Saving, and Payday Loans

Banking, Saving, and Payday Loans Lesson 1: Student Activities Ages 14-18 1 Lesson 1: The Payoff Student Activities Lesson Procedures Part 1: Play The Payoff Part 2: Pre-quiz Directions: RESPOND to this

Banking, Saving, and Payday Loans Lesson 1: Student Activities Ages 14-18 1 Lesson 1: The Payoff Student Activities Lesson Procedures Part 1: Play The Payoff Part 2: Pre-quiz Directions: RESPOND to this

17 th Annual Transamerica Retirement Survey Influences of Generation on Retirement Readiness

1 th Annual Transamerica Retirement Survey Influences of Generation on Retirement Readiness December 016 TCRS 1-6 Transamerica Institute, 016 Table of Contents Welcome to the 1 th Annual Transamerica Retirement

1 th Annual Transamerica Retirement Survey Influences of Generation on Retirement Readiness December 016 TCRS 1-6 Transamerica Institute, 016 Table of Contents Welcome to the 1 th Annual Transamerica Retirement

Practice Management Value-Add Programs. TIAA-CREF Asset Management. Silent alarm: Answering investors quiet pleas for help with target-date funds

Practice Management Value-Add Programs TIAA-CREF Asset Management Silent alarm: Answering investors quiet pleas for help with target-date funds Move beyond preconceived notions. A disconnect and missed

Practice Management Value-Add Programs TIAA-CREF Asset Management Silent alarm: Answering investors quiet pleas for help with target-date funds Move beyond preconceived notions. A disconnect and missed

Financial Health of Residents: A City-Level Dashboard

Financial Health of Residents: A City-Level Dashboard Technical Appendix Caroline Ratcliffe, Cary Lou, Diana Elliott, and Signe-Mary McKernan Technical Appendix Creating City Peer Groups We use cluster

Financial Health of Residents: A City-Level Dashboard Technical Appendix Caroline Ratcliffe, Cary Lou, Diana Elliott, and Signe-Mary McKernan Technical Appendix Creating City Peer Groups We use cluster

TURNING EMPLOYEES INTO LIFETIME SAVERS

TURNING EMPLOYEES INTO LIFETIME SAVERS Prudential Retirement Engagement Research Series TURNING EMPLOYEeS INTO LIFETIME SAVERS Key Insights A new program of research from Prudential on Americans motivation

TURNING EMPLOYEES INTO LIFETIME SAVERS Prudential Retirement Engagement Research Series TURNING EMPLOYEeS INTO LIFETIME SAVERS Key Insights A new program of research from Prudential on Americans motivation

Are Early Withdrawals from Retirement Accounts a Problem?

URBAN INSTITUTE Brief Series No. 27 May 2010 Are Early Withdrawals from Retirement Accounts a Problem? Barbara A. Butrica, Sheila R. Zedlewski, and Philip Issa Policymakers are searching for ways to increase

URBAN INSTITUTE Brief Series No. 27 May 2010 Are Early Withdrawals from Retirement Accounts a Problem? Barbara A. Butrica, Sheila R. Zedlewski, and Philip Issa Policymakers are searching for ways to increase

Preparing for Their Future

Preparing for Their Future AL Look at tthe Financial i lstate t of and Sponsored by The American Savings Education Council and AARP/Divided We Fail Conducted by Mathew Greenwald & Associates Presentation

Preparing for Their Future AL Look at tthe Financial i lstate t of and Sponsored by The American Savings Education Council and AARP/Divided We Fail Conducted by Mathew Greenwald & Associates Presentation

Scottrade Financial Behavior Study. Scottrade Financial Behavior Study 1

2016 Scottrade Financial Behavior Study Scottrade Financial Behavior Study 1 Scottrade Financial Behavior Study Scottrade, Inc. commissioned a survey of investors to explore their attitudes and behaviors

2016 Scottrade Financial Behavior Study Scottrade Financial Behavior Study 1 Scottrade Financial Behavior Study Scottrade, Inc. commissioned a survey of investors to explore their attitudes and behaviors

Refund to Savings: Evidence of Tax- Time Saving in a National Randomized Control Trial

Refund to Savings: Evidence of Tax- Time Saving in a National Randomized Control Trial Dana C. Perantie Michal Grinstein-Weiss May 16, 2014 Note: Statistical compilations disclosed in this document relate

Refund to Savings: Evidence of Tax- Time Saving in a National Randomized Control Trial Dana C. Perantie Michal Grinstein-Weiss May 16, 2014 Note: Statistical compilations disclosed in this document relate

CHAPTER V. PRESENTATION OF RESULTS

CHAPTER V. PRESENTATION OF RESULTS This study is designed to develop a conceptual model that describes the relationship between personal financial wellness and worker job productivity. A part of the model

CHAPTER V. PRESENTATION OF RESULTS This study is designed to develop a conceptual model that describes the relationship between personal financial wellness and worker job productivity. A part of the model

A Complex Portrait: An Examination of Small-Dollar Credit Consumers

A Complex Portrait: An Examination of Small-Dollar Credit Consumers August 2012 By: Rob Levy, Manager, Innovation and Research Joshua Sledge, Analyst, Innovation and Research www.cfsinnovation.com 2012,

A Complex Portrait: An Examination of Small-Dollar Credit Consumers August 2012 By: Rob Levy, Manager, Innovation and Research Joshua Sledge, Analyst, Innovation and Research www.cfsinnovation.com 2012,

2015 SCPC Table of Contents Adoption of Accounts and Payment Instruments

2015 SCPC Table of Contents Adoption of Accounts and Payment Instruments Table 1 Current Ownership of Accounts and Account Access Technologies Table 2 Table 3 Table 4 Table 5a Table 5b Table 6 Table 7

2015 SCPC Table of Contents Adoption of Accounts and Payment Instruments Table 1 Current Ownership of Accounts and Account Access Technologies Table 2 Table 3 Table 4 Table 5a Table 5b Table 6 Table 7

Part 1: 2017 Long-Term Care Research

Part 1: 2017 Long-Term Care Research Findings from Surveys of Advisors and Consumers Lincoln Financial Group and Versta Research February 2018 2018 Lincoln National Corporation Contents Page Research Methods...

Part 1: 2017 Long-Term Care Research Findings from Surveys of Advisors and Consumers Lincoln Financial Group and Versta Research February 2018 2018 Lincoln National Corporation Contents Page Research Methods...

The Voya Retire Ready Index TM

The Voya Retire Ready Index TM Measuring the retirement readiness of Americans Table of contents Introduction...2 Methodology and framework... 3 Index factors... 4 Index results...6 Key findings... 7 Role

The Voya Retire Ready Index TM Measuring the retirement readiness of Americans Table of contents Introduction...2 Methodology and framework... 3 Index factors... 4 Index results...6 Key findings... 7 Role

ASSOCIATED PRESS-LIFEGOESSTRONG.COM BOOMERS SURVEY CONDUCTED BY KNOWLEDGE NETWORKS March 16, 2011

1350 Willow Rd, Suite 102 Menlo Park, CA 94025 www.knowledgenetworks.com Interview dates: March 04 March 13, 2011 Interviews: 1,490 adults, including 1,160 baby boomers Sampling margin of error for a 50%

1350 Willow Rd, Suite 102 Menlo Park, CA 94025 www.knowledgenetworks.com Interview dates: March 04 March 13, 2011 Interviews: 1,490 adults, including 1,160 baby boomers Sampling margin of error for a 50%

Are American Families Becoming More Financially Resilient?

A brief from April 2017 istock Photo Are American Families Becoming More Financially Resilient? Changing household balance sheets and the effects of financial shocks Overview Financial shocks lost income

A brief from April 2017 istock Photo Are American Families Becoming More Financially Resilient? Changing household balance sheets and the effects of financial shocks Overview Financial shocks lost income

Financial Shocks Put Retirement Security at Risk Smart policies can help meet immediate needs without depleting long-term savings

A brief from Oct 2017 Financial Shocks Put Retirement Security at Risk Smart policies can help meet immediate needs without depleting long-term savings Overview Because most households have relatively

A brief from Oct 2017 Financial Shocks Put Retirement Security at Risk Smart policies can help meet immediate needs without depleting long-term savings Overview Because most households have relatively

The 2011 Consumer Financial Literacy Survey Final Report

The 2011 Consumer Financial Literacy Survey Final Report Prepared For: The National Foundation for Credit Counseling March 2011 Prepared By: Harris Interactive Inc. Public Relations Research 1 Summary

The 2011 Consumer Financial Literacy Survey Final Report Prepared For: The National Foundation for Credit Counseling March 2011 Prepared By: Harris Interactive Inc. Public Relations Research 1 Summary

17 th Annual Transamerica Retirement Survey Influences of Gender on Retirement Readiness

1 th Annual Transamerica Retirement Survey Influences of Gender on Retirement Readiness December 2016 TCRS 1335-1216 Transamerica Institute, 2016 Welcome to the 1 th Annual Transamerica Retirement Survey

1 th Annual Transamerica Retirement Survey Influences of Gender on Retirement Readiness December 2016 TCRS 1335-1216 Transamerica Institute, 2016 Welcome to the 1 th Annual Transamerica Retirement Survey

Lessons learned in higher education

Lessons learned in higher education Voya Retirement Research Institute Study focuses on retirement and financial realities for college and university employees Our nation s colleges and universities represent

Lessons learned in higher education Voya Retirement Research Institute Study focuses on retirement and financial realities for college and university employees Our nation s colleges and universities represent

Mind, Body, and Wallet

R Guardian in sync Market Insights Mind, Body, and Wallet Financial Stress Impacts the Emotional and Physical Well-Being of Working Americans Source for all statistics cited is : Fourth Annual, 2016 Life

R Guardian in sync Market Insights Mind, Body, and Wallet Financial Stress Impacts the Emotional and Physical Well-Being of Working Americans Source for all statistics cited is : Fourth Annual, 2016 Life

Alternative Credit Scores: The Key to Financial Inclusion for Consumers

WHITEPAPER Alternative Credit Scores: The Key to Financial Inclusion for Consumers May 2017 WHITEPAPER Alternative Credit Scores: The Key to Financial Inclusion for Consumers May 2017 Executive summary

WHITEPAPER Alternative Credit Scores: The Key to Financial Inclusion for Consumers May 2017 WHITEPAPER Alternative Credit Scores: The Key to Financial Inclusion for Consumers May 2017 Executive summary

17 th Annual Transamerica Retirement Survey Influences of Educational Attainment on Retirement Readiness

th Annual Transamerica Retirement Survey Influences of Educational Attainment on Retirement Readiness December 0 TCRS - Transamerica Institute, 0 Welcome to the th Annual Transamerica Retirement Survey

th Annual Transamerica Retirement Survey Influences of Educational Attainment on Retirement Readiness December 0 TCRS - Transamerica Institute, 0 Welcome to the th Annual Transamerica Retirement Survey

Measuring Client Outcomes. An overview of StepChange Debt Charity s client outcomes measurement pilot project

Measuring Client Outcomes An overview of StepChange Debt Charity s client outcomes measurement pilot project February 2019 2 Measuring Client Outcomes February 2019 Introduction Since 2017, StepChange

Measuring Client Outcomes An overview of StepChange Debt Charity s client outcomes measurement pilot project February 2019 2 Measuring Client Outcomes February 2019 Introduction Since 2017, StepChange

GENDER AND MARITAL STATUS COMPARISONS AMONG WORKERS

2017 RCS FACT SHEET #5 GENDER AND MARITAL STATUS COMPARISONS AMONG WORKERS Are unmarried men and women equally likely to plan and save for retirement? Do they have similar expectations about their needs

2017 RCS FACT SHEET #5 GENDER AND MARITAL STATUS COMPARISONS AMONG WORKERS Are unmarried men and women equally likely to plan and save for retirement? Do they have similar expectations about their needs

Universe expansion. Growth strategies in the evolving consumer market

Growth strategies in the evolving consumer market Executive summary As the economy gains strength, lenders are engaging in an increasingly fierce competition to entice the best candidates to their portfolios

Growth strategies in the evolving consumer market Executive summary As the economy gains strength, lenders are engaging in an increasingly fierce competition to entice the best candidates to their portfolios

The Financial Capability of Young Adults A Generational View

FINRA Foundation Financial Capability Insights March 2014 Author: Gary R. Mottola, Ph.D. This brief was produced in consultation with the United States Department of the Treasury and in support of the

FINRA Foundation Financial Capability Insights March 2014 Author: Gary R. Mottola, Ph.D. This brief was produced in consultation with the United States Department of the Treasury and in support of the

Let me turn it over now and kind of get the one of the questions that s burning in all of our minds is about Social Security and what can we expect.

Wi$e Up Webinar Catching On to Retirement September 28, 2007 Speaker 2 Diana Varela Let me turn it over now and kind of get the one of the questions that s burning in all of our minds is about Social Security

Wi$e Up Webinar Catching On to Retirement September 28, 2007 Speaker 2 Diana Varela Let me turn it over now and kind of get the one of the questions that s burning in all of our minds is about Social Security

Raddon Research Insights. The High-Income Market: Trends and Behaviors, 2016

The High-Income Market: Trends and Behaviors, 2016 Contents Introduction 1 Profile of the High-Income Consumer 2 Product Usage: Loans and Deposits 10 Investments 17 Retirement 28 Conclusions 34 Strategies

The High-Income Market: Trends and Behaviors, 2016 Contents Introduction 1 Profile of the High-Income Consumer 2 Product Usage: Loans and Deposits 10 Investments 17 Retirement 28 Conclusions 34 Strategies

18 th Annual Transamerica Retirement Survey Influences of Household Income on Retirement Readiness. June 2018 TCRS

1 th Annual Transamerica Retirement Survey Influences of Household Income on Retirement Readiness June 01 TCRS -01 Transamerica Institute, 01 Welcome to the 1 th Annual Transamerica Retirement Survey Welcome

1 th Annual Transamerica Retirement Survey Influences of Household Income on Retirement Readiness June 01 TCRS -01 Transamerica Institute, 01 Welcome to the 1 th Annual Transamerica Retirement Survey Welcome

Love, Marriage & Debt

Love, Marriage & Debt A Hoyes, Michalos & Associates Inc. Harris/Decima Research Study February, 2014 For more information: Douglas Hoyes, CA, Trustee in Bankruptcy, Hoyes, Michalos & Associates Inc. Email:

Love, Marriage & Debt A Hoyes, Michalos & Associates Inc. Harris/Decima Research Study February, 2014 For more information: Douglas Hoyes, CA, Trustee in Bankruptcy, Hoyes, Michalos & Associates Inc. Email:

Introduction. Salesforce Research 2017 Connected Investor Report / 2

Introduction To explore how Americans manage their money, choose and communicate with financial advisors as well as measure consumer sentiment and trust in financial institutions Salesforce conducted its

Introduction To explore how Americans manage their money, choose and communicate with financial advisors as well as measure consumer sentiment and trust in financial institutions Salesforce conducted its

Curriculum Guide

EverFi @Work Curriculum Guide Table of Contents Overview... 3 Detailed Module Summaries... 4 Auto Loans... 4 Benefits of a Credit Union... 4 Budgeting Tool... 4 Building Emergency Savings... 4 Checking

EverFi @Work Curriculum Guide Table of Contents Overview... 3 Detailed Module Summaries... 4 Auto Loans... 4 Benefits of a Credit Union... 4 Budgeting Tool... 4 Building Emergency Savings... 4 Checking

Participant Preferences in Target Date Funds: An Update

Participant Preferences in Target Date Funds: An Update Examining Perceptions and Expectations Among Target Date Investors and Non-Investors White Paper February 2014 A research study by Voya Investment

Participant Preferences in Target Date Funds: An Update Examining Perceptions and Expectations Among Target Date Investors and Non-Investors White Paper February 2014 A research study by Voya Investment

Educational Matters: The Impact of Educational Attainment on Worker Retirement Outlook

Educational Matters: The Impact of Educational Attainment on Worker Retirement Outlook December 2010 Table of Contents About the Center Page 3 About the Survey Page 4 Methodology Page 5 Educational Matters:

Educational Matters: The Impact of Educational Attainment on Worker Retirement Outlook December 2010 Table of Contents About the Center Page 3 About the Survey Page 4 Methodology Page 5 Educational Matters:

VANTAGESCORE SOLUTIONS INTRODUCES VANTAGESCORE 3.0 MODEL

FOR IMMEDIATE RELEASE Contact: Jeff Richardson VantageScore Solutions 203-363-2170 jeffrichardson@vantagescore.com VANTAGESCORE SOLUTIONS INTRODUCES VANTAGESCORE 3.0 MODEL New Model Sets the Standard for

FOR IMMEDIATE RELEASE Contact: Jeff Richardson VantageScore Solutions 203-363-2170 jeffrichardson@vantagescore.com VANTAGESCORE SOLUTIONS INTRODUCES VANTAGESCORE 3.0 MODEL New Model Sets the Standard for

Melinda Zabritski, Director of Automotive Credit

State of the Automotive Finance Market First Quarter 2012 Melinda Zabritski, Director of Automotive Credit Experian and the marks used herein are service marks or registered trademarks of Experian Information

State of the Automotive Finance Market First Quarter 2012 Melinda Zabritski, Director of Automotive Credit Experian and the marks used herein are service marks or registered trademarks of Experian Information

Minority Workers Remain Confident About Retirement, Despite Lagging Preparations and False Expectations

Issue Brief No. 306 June 2007 Minority Workers Remain Confident About Retirement, Despite Lagging Preparations and False Expectations by Ruth Helman, Mathew Greenwald & Associates; Jack VanDerhei, Temple

Issue Brief No. 306 June 2007 Minority Workers Remain Confident About Retirement, Despite Lagging Preparations and False Expectations by Ruth Helman, Mathew Greenwald & Associates; Jack VanDerhei, Temple

GET SOCIAL WITH US. #vision2016. Tweet, follow, share throughout the session.

GET SOCIAL WITH US Tweet, follow, share throughout the session. 2015 Experian Information Solutions, Inc. All rights reserved. 1 Alternative methods to validate with low portfolio volumes Experian and

GET SOCIAL WITH US Tweet, follow, share throughout the session. 2015 Experian Information Solutions, Inc. All rights reserved. 1 Alternative methods to validate with low portfolio volumes Experian and

2/3 81% 67% Millennials and money. Key insights. Millennials are optimistic despite a challenging start to adulthood

2/3 Proportion of Millennials who believe they will achieve a greater standard of living than their parents 81% Percentage of Millennials who believe they need to pay off their debts before they can begin

2/3 Proportion of Millennials who believe they will achieve a greater standard of living than their parents 81% Percentage of Millennials who believe they need to pay off their debts before they can begin

July 2016 Financial Capability in the United States 2016

July 2016 Financial Capability in the United States 2016 Financial Capability in the United States 2016 1 Contents Introduction 2 1. Making Ends Meet 4 Spending vs. Saving 6 Indicators of Financial Stress

July 2016 Financial Capability in the United States 2016 Financial Capability in the United States 2016 1 Contents Introduction 2 1. Making Ends Meet 4 Spending vs. Saving 6 Indicators of Financial Stress

Lorem ipsum dolor sit amet, consectetur Millennial Financial Literacy and Fin-tech Use adipiscing elit, aliquam tincidunt dui.

Lorem ipsum dolor sit amet, consectetur Millennial Financial Literacy and Fin-tech Use adipiscing elit, aliquam tincidunt dui. Annamaria Lusardi Brussels Month Year November 7, 2018 Lorem ipsum dolor sit

Lorem ipsum dolor sit amet, consectetur Millennial Financial Literacy and Fin-tech Use adipiscing elit, aliquam tincidunt dui. Annamaria Lusardi Brussels Month Year November 7, 2018 Lorem ipsum dolor sit

Taking Control of Your Money. Using Credit Wisely

Taking Control of Your Money Using Credit Wisely Session 4: Using Credit Wisely To help you stay financially healthy you need to understand credit. Credit is access to money that belongs to lenders (e.g.

Taking Control of Your Money Using Credit Wisely Session 4: Using Credit Wisely To help you stay financially healthy you need to understand credit. Credit is access to money that belongs to lenders (e.g.

Heartland Monitor Poll XXI

National Sample of 1000 AMERICAN ADULTS AGE 18+ (500 on landline, 500 on cell) (Sample Margin of Error for 1,000 Respondents = ±3.1% in 95 out of 100 cases) Conducted October 22 26, 2014 via Landline and

National Sample of 1000 AMERICAN ADULTS AGE 18+ (500 on landline, 500 on cell) (Sample Margin of Error for 1,000 Respondents = ±3.1% in 95 out of 100 cases) Conducted October 22 26, 2014 via Landline and

17 th Annual Transamerica Retirement Survey Influences of Ethnicity on Retirement Readiness

1 th Annual Transamerica Retirement Survey Influences of Ethnicity on Retirement Readiness December 01 TCRS 1-11 Transamerica Institute, 01 Welcome to the 1 th Annual Transamerica Retirement Survey Welcome

1 th Annual Transamerica Retirement Survey Influences of Ethnicity on Retirement Readiness December 01 TCRS 1-11 Transamerica Institute, 01 Welcome to the 1 th Annual Transamerica Retirement Survey Welcome

2018 Retirement Confidence Survey

2018 Retirement Confidence Survey April 24, 2018 Employee Benefit Research Institute 1100 13 th Street NW, Suite 878 Washington, DC 20005 Phone: (202) 659-0670 Fax: (202) 775-6312 Greenwald & Associates

2018 Retirement Confidence Survey April 24, 2018 Employee Benefit Research Institute 1100 13 th Street NW, Suite 878 Washington, DC 20005 Phone: (202) 659-0670 Fax: (202) 775-6312 Greenwald & Associates

Gender And Marital Status Comparisons Among Workers

Page 1 2018 RCS FACT SHEET #5 Gender And Marital Status Comparisons Among Workers Are unmarried men and women equally likely to plan and save for retirement? Do they have similar expectations about their

Page 1 2018 RCS FACT SHEET #5 Gender And Marital Status Comparisons Among Workers Are unmarried men and women equally likely to plan and save for retirement? Do they have similar expectations about their

Foreclosure Avoidance Research II A follow-up to the 2005 benchmark study

Foreclosure Avoidance Research II A follow-up to the 2005 benchmark study Copyright 2008 Freddie Mac. All Rights Reserved. Research Objective Lenders are unable to contact borrowers in more than half of

Foreclosure Avoidance Research II A follow-up to the 2005 benchmark study Copyright 2008 Freddie Mac. All Rights Reserved. Research Objective Lenders are unable to contact borrowers in more than half of

Banking, Saving, and Payday Loans

Banking, Saving, and Payday Loans Lesson 1: Teacher s Guide Ages 14-18 Performance Expectations When making banking and savings decisions during the game, communicate to students that they are to: Check

Banking, Saving, and Payday Loans Lesson 1: Teacher s Guide Ages 14-18 Performance Expectations When making banking and savings decisions during the game, communicate to students that they are to: Check

Universe Expansion: Is the Way You Score Customers State of the Art or State of Denial?

SM MARCH 2014 Universe Expansion: Is the Way You Score Customers State of the Art or State of Denial? Contents In summary 1 Who is typically unscoreable by conventional models? 2 How do these currently

SM MARCH 2014 Universe Expansion: Is the Way You Score Customers State of the Art or State of Denial? Contents In summary 1 Who is typically unscoreable by conventional models? 2 How do these currently

Understanding and Achieving Participant Financial Wellness

Understanding and Achieving Participant Financial Wellness Insights from our research From August 25, 2017 to January 31, 2018, the companies of OneAmerica fielded an online survey to retirement plan participants

Understanding and Achieving Participant Financial Wellness Insights from our research From August 25, 2017 to January 31, 2018, the companies of OneAmerica fielded an online survey to retirement plan participants

BALANCED MONEY WORKBOOK

BALANCED MONEY WORKBOOK 2 Why live in balance? Welcome to the balanced money approach to budgeting! Balance is a concept we hear a lot about eat a balanced diet, keep balance between work and the rest

BALANCED MONEY WORKBOOK 2 Why live in balance? Welcome to the balanced money approach to budgeting! Balance is a concept we hear a lot about eat a balanced diet, keep balance between work and the rest

GREENPATH FINANCIAL WELLNESS SERIES

GREENPATH FINANCIAL WELLNESS SERIES UNDERSTANDING YOUR CREDIT REPORT & SCORE Empowering people to lead financially healthy lives. TABLE OF CONTENTS Understanding credit reports...2 What s in a credit

GREENPATH FINANCIAL WELLNESS SERIES UNDERSTANDING YOUR CREDIT REPORT & SCORE Empowering people to lead financially healthy lives. TABLE OF CONTENTS Understanding credit reports...2 What s in a credit

Universe Expansion: Is the Way You Score Customers State of the Art or State of Denial?

SM MAY 2015 Is the Way You Score Customers State of the Art or State of Denial? Contents In summary 1 Who is typically unscoreable by conventional models? 2 How do these currently unscored consumers score

SM MAY 2015 Is the Way You Score Customers State of the Art or State of Denial? Contents In summary 1 Who is typically unscoreable by conventional models? 2 How do these currently unscored consumers score

Income and Assets of Medicare Beneficiaries,

Income and Assets of Medicare Beneficiaries, 2014 2030 Gretchen Jacobson, Christina Swoope, and Tricia Neuman, Kaiser Family Foundation Karen Smith, Urban Institute Many Medicare, including seniors and

Income and Assets of Medicare Beneficiaries, 2014 2030 Gretchen Jacobson, Christina Swoope, and Tricia Neuman, Kaiser Family Foundation Karen Smith, Urban Institute Many Medicare, including seniors and

Curriculum Guide

EverFi @Work Curriculum Guide Table of Contents Overview... 3 Detailed Module Summaries... 4 Auto Loans... 4 Building Emergency Savings... 4 Checking Accounts... 4 Considering Home Ownership... 5 Credit

EverFi @Work Curriculum Guide Table of Contents Overview... 3 Detailed Module Summaries... 4 Auto Loans... 4 Building Emergency Savings... 4 Checking Accounts... 4 Considering Home Ownership... 5 Credit

AARP-Ad Council Saving for Retirement Campaign - Retirement Attitudes Survey Annotated Questionnaire

AARP-Ad Council Saving for Retirement Campaign - Retirement Attitudes Survey Annotated Questionnaire Methodology: Questionnaire was fielded as part of an omnibus survey from June 2-4, 2017. The sample

AARP-Ad Council Saving for Retirement Campaign - Retirement Attitudes Survey Annotated Questionnaire Methodology: Questionnaire was fielded as part of an omnibus survey from June 2-4, 2017. The sample

Financial Wellness. HOUSEHOLD FINANCIAL CAPABILITY.

Financial Wellness. HOUSEHOLD FINANCIAL CAPABILITY. November 16 Annamaria Lusardi, Ph.D., is the founder and academic director of the Global Financial Literacy Excellence Center (GFLEC) at the George Washington

Financial Wellness. HOUSEHOLD FINANCIAL CAPABILITY. November 16 Annamaria Lusardi, Ph.D., is the founder and academic director of the Global Financial Literacy Excellence Center (GFLEC) at the George Washington

Financial Well-being. Debt and Credit

Financial Well-being Debt and Credit Debt and Credit When evaluating financial wellness, debt has a real impact on your ability to reach your goals. Debt feels like a four letter word. However, it can

Financial Well-being Debt and Credit Debt and Credit When evaluating financial wellness, debt has a real impact on your ability to reach your goals. Debt feels like a four letter word. However, it can

Boomers at Midlife. The AARP Life Stage Study. Wave 2

Boomers at Midlife 2003 The AARP Life Stage Study Wave 2 Boomers at Midlife: The AARP Life Stage Study Wave 2, 2003 Carol Keegan, Ph.D. Project Manager, Knowledge Management, AARP 202-434-6286 Sonya Gross

Boomers at Midlife 2003 The AARP Life Stage Study Wave 2 Boomers at Midlife: The AARP Life Stage Study Wave 2, 2003 Carol Keegan, Ph.D. Project Manager, Knowledge Management, AARP 202-434-6286 Sonya Gross

Young People and Money Report

Young People and Money Report 2018 marks the Year of Young People, a Scottish Government initiative giving young people a platform to voice issues that affect their lives and allowing us to celebrate their

Young People and Money Report 2018 marks the Year of Young People, a Scottish Government initiative giving young people a platform to voice issues that affect their lives and allowing us to celebrate their