17 May 2007 W ork shop for Bank Indu st ry

|

|

|

- Brook Williams

- 6 years ago

- Views:

Transcription

1

2 1. Registration of Participants 2. Introduction to FinScope, Annette Altvater, TD of FSDT 3. Workshop: Findings and Discussion Bob Currin FSDT consultants Oswald Mashindano - ESRF 4. Moving forward, Annette Altvater, FinScope Coordinator

3 Annette Altvater Technical Director FSDT

4

5 First national consumer perception survey: Individuals views of total money management Formal and informal services Attitudes and behaviours Credible, robust, scientific approach Comprehensive market landscape rich to poor for total market understanding Proven multi-nation study within Africa

6 Support for Government development initiatives Insights for commercial service providers (including MFPs), NGOs and development agencies to innovate services and products Allows planning and interventions focused on specific market strata and segments

7 Methodology Sampling Sample achieved Reporting domain Confidence level Field dates Qualitative research Quantitative research National Master Sample Plan national estimates Listing & selection of respondents done by NBS 16+ 4,962 Results weighted to projected population Urban/rural and gender 95% August September 2006

8 Share findings facilitate learning Engage debate Catalyse change and innovation Support effective market development Galvanise market structures

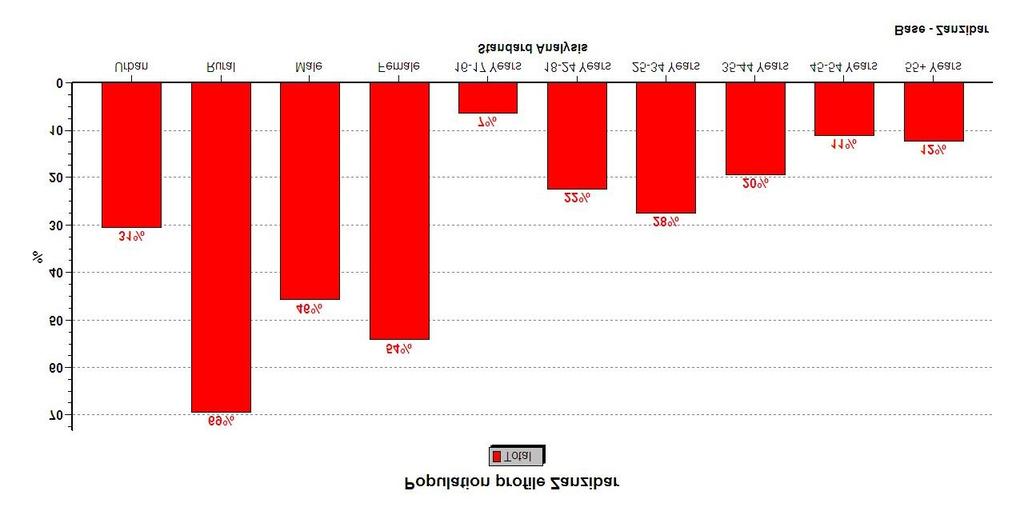

9 Why FinScope? Stratified market intervention MARKET PROVISION STATE PROVISION SAVINGS CREDIT TRANSACTION BANKING ENTERPRISE FINANCE Social Grants Tax Relief Subsidies Development assistance HOUSING FINANCE INSURANCE

10

11 Collected interest areas and queries registration forms and meetings Analysis of data by FSDT, consultants and ESRF Creation of a lens for quick referencing Creation of appropriate context for the information Specific market dynamics reviewed via

12 Population Profile: Population characteristics Geographical concentrations of people & issues Gender issues Perceptions Infrastructure and amenities Rural/Urban perspectives: Semi-formal and informal categories explained Rural population needs & services to reach them Demand and use of credit facilities in rural areas

13 Product & Services contd. In-kind savings and in-kind loans Co-operatives market SACCOs Micro-finance Savings, borrowing Access: Barriers to access physical, non-physical & socio-economic Access costs & perceptions General Money Matters Financial literacy and impact on uptake Policy and legal impacts

14 Poverty Lens Access Strand and frontiers Population profiles & perceptions

15

16 Total adult population 16 years & older = 21 million people 57% of adult population under 34 years of age The urban/rural split of this population group is 28% and 72% There are more women than men in both urban and rural areas

17

18 72% 48% 52% 28% 29% 22% 19% 6% 11% 13% Urban Rural Male Female Years Years Years Years Years 55+ Years

19

20

21 Employed in the formal sector Employed to do other people's domestic chores Employed in the informal sector Agricultural trading-buying and selling produce 4% 4% 5% 6% Employed on other people's farm on a seasonal basis Sell output from my cattle/livestock 8% 9% Sell my livestock Sell own produce from my farm, cash crop 11% 12% Money from family/friends / spouse 28% Running your own business Sell own produce from my farm, food crops 35% 36%

22

23 Total adult population

24 Total adult population

25 Total adult population

26

27

28 Insuring/covering your assets 79% How to manage your money effectively 80% Understanding banks, M FIs or Saccos charges/fees Insuring/covering your life 81% 81% How to open an account in a bank Understand the services/products provided by financial service providers 82% 82% How much of a loan you can afford to apply for 83% How to save more money How interest rates work/calculated 84% 84%

29

30 NGO Office 14% Formal Bank 20% Post Office 25% Secondary School 43% Police Station 43% Produce Market/ Food Market 62% Primary School 95% 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

31

32 Education Fuel for cooking Drinking water Toilet type Material for house construction EQLI

33

34

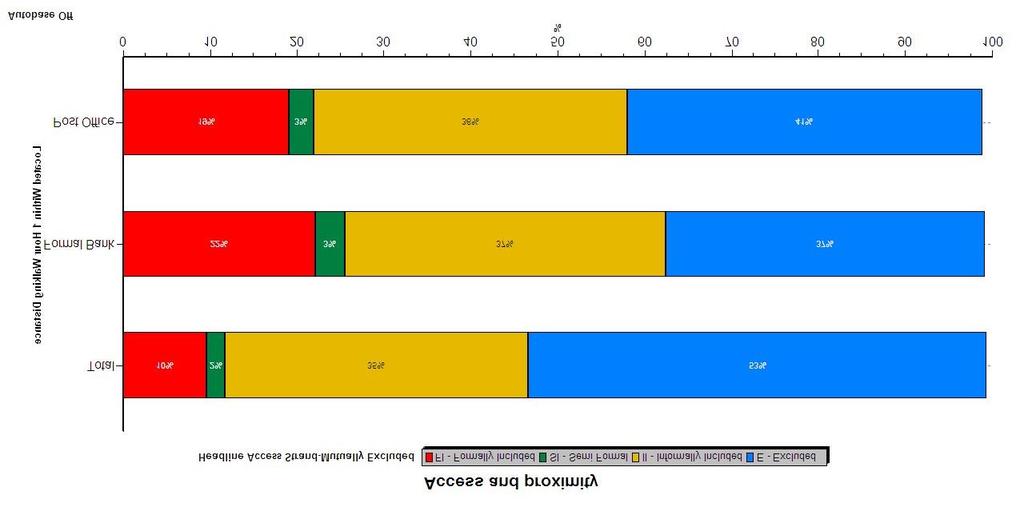

35

36

37

38

39

40

41

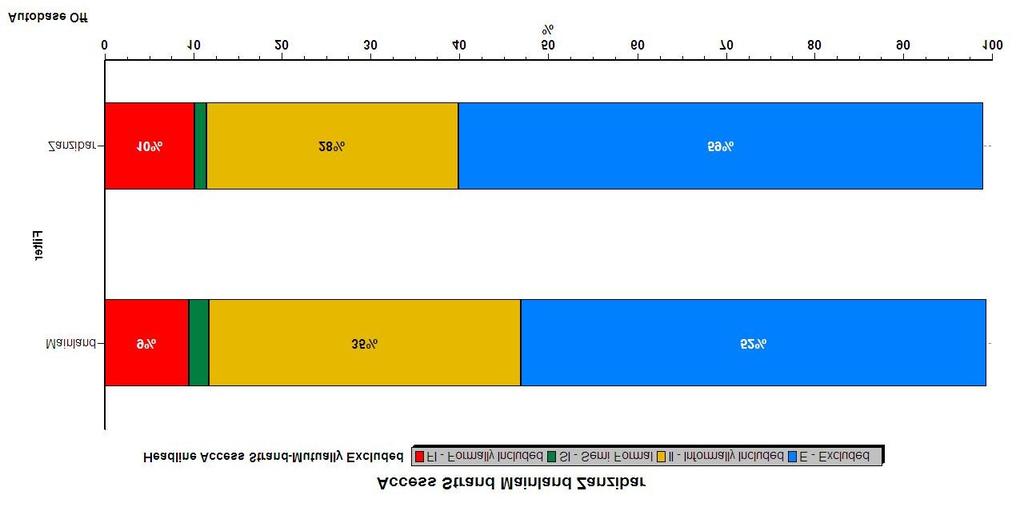

42 Access Strand - Service provider market composition Formally served Formal institutions Semi-formal SACCOs and MFIs Informal associations or groups Financially excluded

43 Access to financial services by categories Formal - 9% Semi-Formal - 2% Informal - 35% Excluded - 54% 1 9% 2% 35% 54%

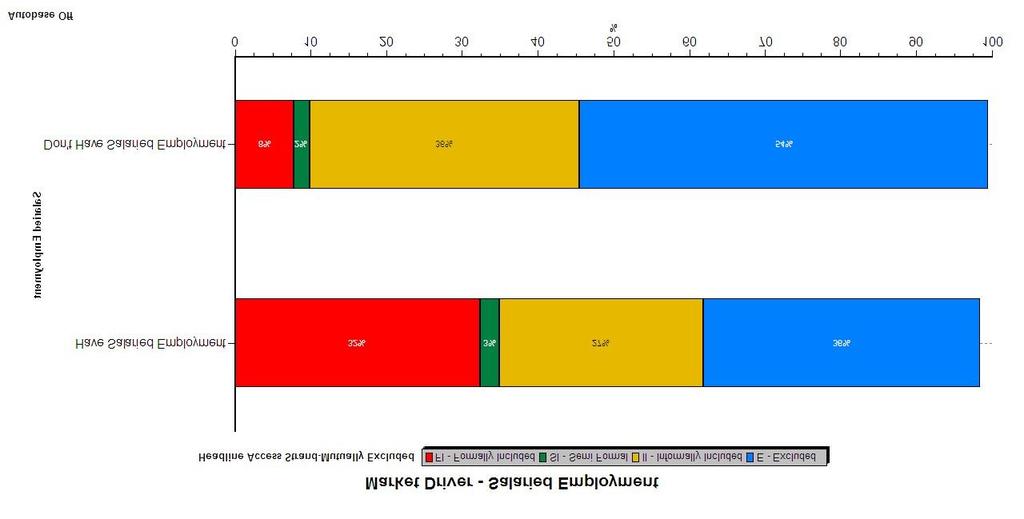

44

45 Access to financial services by segmented categories Formal - BI - 9% Formal Other - 1% Semi-Formal (SACCO) - 2% Semi-Formal (MFI) - 1% Excluded (Totally Unserved) - 34% Informal - 35% Excluded (Non monetary) - 20% 1% 1% 1 9% 35% 20% 34% 2% Percentages rounded up

46 Access to financial services by categories Urban/Rural Formal - BI Formal Other Semi-Formal - SACCO Semi-Formal - MFI Informal Excluded - Non monetary Excluded - Totally Unserved 2% 0% Rural 5% 36% 24% 33% 0% 1% 2% Urban 18% 32% 11% 34% 1% Percentages are rounded up

47 Access to financial services by categories - Gender Formal - BI Formal Other Semi-Formal (SACCO) Semi-Formal (MFI) Informal Excluded (Non monetary) Excluded (Totally Unserved) 1% 1% Female 6% 38% 19% 35% 0% 2% 1% Male 12% 31% 21% 32% 1% Percentages rounded up

48 60% 50% 51% 40% 30% 28% 20% 17% 10% 0% Make Decisions Alone In Consultation-Partner In Consultation-Other Family 2% Do Not Make These Decisions

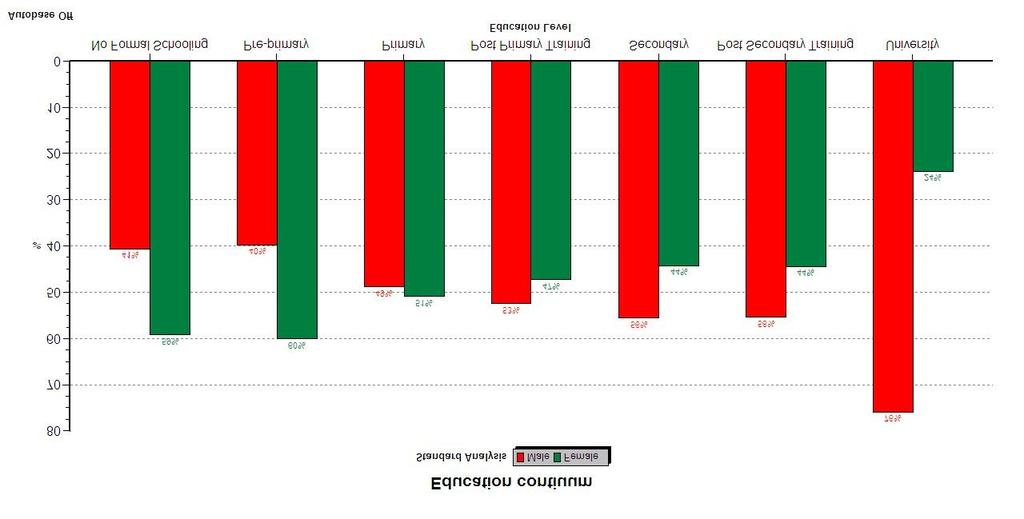

49 Male Female 60% 50% 53% 50% 40% 30% 29% 28% 20% 16% 18% 10% 0% Make Decisions Alone In Consultation-Partner In Consultation-Other Family 2% 3% Do Not Make These Decisions

50 Urban Rural 60% 50% 49% 52% 40% 30% 30% 28% 20% 18% 16% 10% 0% Make Decisions Alone In Consultation-Partner In Consultation-Other Family 2% 2% Do Not Make These Decisions

51 Formally Included Semi Formal Informally Included Excluded In Consultation-Other Family 8% 2% 33% 58% In Consultation-Partner 12% 3% 39% 45% Make Decisions Alone 7% 2% 34% 57% 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

52

53 Pension 1% Domestic work 2% Employed in Formal sector 3% Do not receive income 4% Sub-Letting land/house/rooms 4% Employed in Informal sector 6% Money from Friends/Family 18% Running own business 23% Agriculture related 38% 0% 5% 10% 15% 20% 25% 30% 35% 40%

54 FI - Formally Included SI - Semi Formal II - Informally Included E - Excluded Money from friends and family Selling crops Formal employment Running own business 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

55

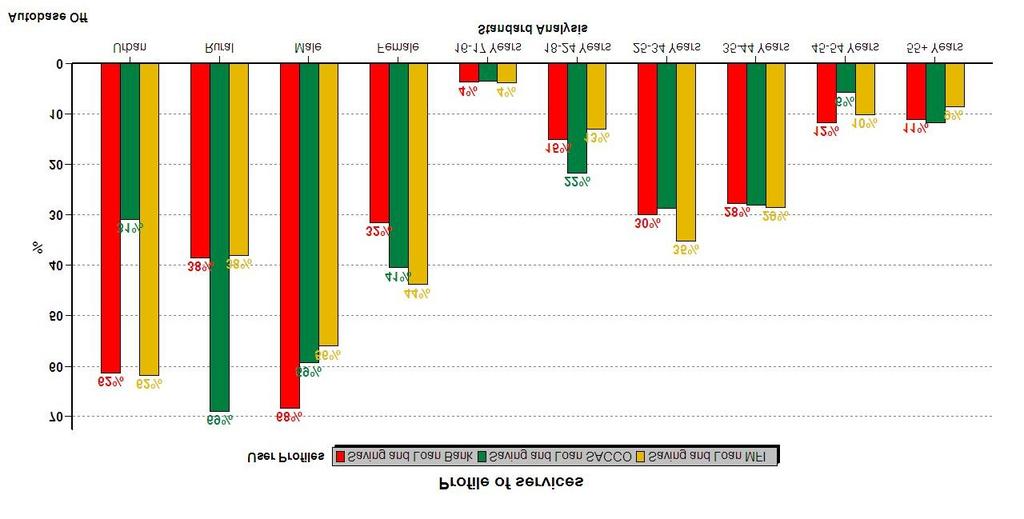

56 FI - Formally Included SI - Semi Formal II - Informally Included E - Excluded University Post Secondary Training Secondary Post Primary Training Primary Pre-primary No Formal Schooling 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

57

58

59

60

61

62 by financial service provider: Banks Saccos MFIs

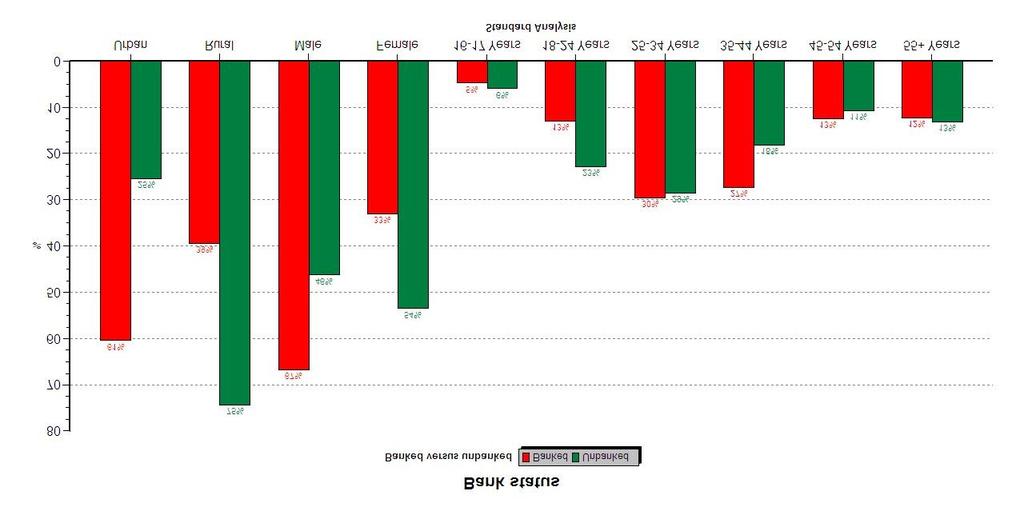

63 Percentage of Tanzanians obtaining saving or loan from: Bank, SACCO or MFI 60% 53% 50% 40% 30% 30% 20% 17% 10% 0% Saving and Loan Bank Saving and Loan SACCO Saving and Loan MFI

64

65

66 People with a bank account who either save or borrow from a SACCO or MFI Saving Loan 25% 20% 15% 10% 5% 0% 22% SACCO 15% 13% MFI 7%

67 Tanzanians with a bank account who are served by informal service providers, MFIs and SACCOs Total Urban Rural 60% 50% 48% 47% 49% 42% 40% 30% 26% 20% 10% 15% 15% 17% 12% 0% Informal financial services % SACCO borrowers and savers % MFI borrowers and savers %

68 Urban - rural split of clients of different categories of financial service providers Urban Rural Informal financial services MFI savers and borrowers Banked SACCO borrowers and savers 30% 71% 55% 45% 61% 39% 31% 69% 0% 20% 40% 60% 80% 100%

69

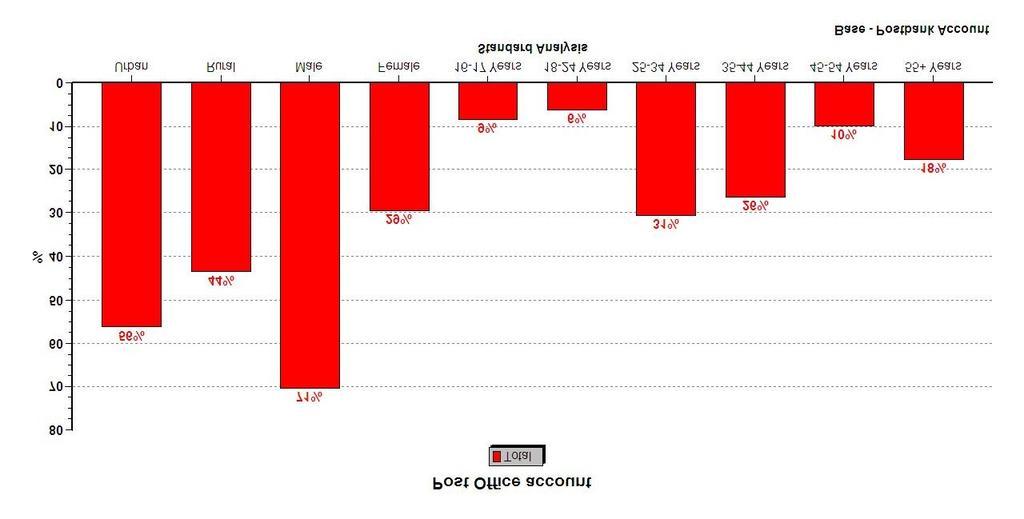

70 Currently Banked Previously Banked Never Banked 1,609, ,976 18,859,849

71

72 Currently Banked Previously Banked Never Banked 55+ Years 12% 13% 26% Years 11% 13% 17% Years 12% 19% 27% Years 29% 28% 30% Years 13% 15% 23% Years 2% 5% 6% 0% 5% 10% 15% 20% 25% 30% 35%

73 Currently Banked Previously Banked Never Banked University 0% 1% 7% Post Secondary Training 0% 8% 19% Secondary 8% 25% 41% Post Primary Training 2% 2% 6% Primary 23% 54% 57% Pre-primary 4% 2% 14% No Formal Schooling 1% 4% 15% 0% 10% 20% 30% 40% 50% 60%

74 Urban Rural 80% 75% 70% 60% 61% 55% 50% 45% 40% 39% 30% 25% 20% 10% 0% Currently Banked Previously Banked Never Banked

75 Currently Banked Previously Banked Never Banked Do not receive income 1% 0% 99% Domestic work 3% 3% 94% Sub-Letting land/house/rooms 6% 21% 73% Running own business 4% 10% 86% Employed in Formal sector 7% 20% 73% Employed in Informal sector 3% 10% 87% Agriculture related 3% 4% 93% Money from Friends/Family 3% 7% 90% Pension 28% 27% 45% 0% 20% 40% 60% 80% 100% 120%

76 Income (groups) of people with a bank account TSHS P/M, 10% TSH 1 to 5,000, 1% TSH 5001 to 20,000, 6% TSH 20,001 to 50,000, 13% TSH 100,001 to P/M, 19% TSH 50,001 to 100,000, 27%

77 8% 7% 7% 6% 5% 4% 3% 2% 2% 2% 1% 1% 1% 0% ATM Card Debit Card Postbank Account Current Account Savings Account 0% Fixed Deposit

78 60% 50% 52% 40% 30% 20% 10% 17% 13% 9% 5% 4% 0% Savings Account ATM Card Postbank Account Debit Card Current Account Fixed Deposit

79 In The Branch Through Cellphone Banking Through An ATM Via The Internet No answer Means Of Drawing A Cheque 88% 0% 5% 1% 6% Means Of Paying Acc To Third Party 83% 3% 8% 2% 4% Means Of Transfering Money Between Banks 87% 0% 5% 6% 1% Means Of Buying Bankers Cheques 81% 1% 5% 0% 12% Means Of Doing Cheque Deposits 89% 0% 4% 0% 6% Means Of Doing Cash Deposits 96% 0% 3% 0% 1% Means Of Doing Cash Witdrawals 76% 0% 22% 0% 1% Means Of Checking Acc Balance 80% 2% 16% 2% 1% 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

80 Perceptions on Banking Operations Would rather deal face to face w ith a person than w ith an electronic device Would rather deal w ith people you know than w ith FI If you save and invest regularly, eventually the sm all amounts w ill mount up You trust your ow n experience/know ledge rather than the advice of others Taking loans should be avoided Can easily live w ithout form al banking institutions Shop around for best interest rates 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% Agree Disagree DK

81 Banks force you to use the ATM Upon receiving an account statement, you check the details Prepared to learn how to use new technology eg ATM Don't trust informal associations Would like to start your ow n business but can't get a loan Most services offered re also available from Non-bank FI Young people know more 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% Agree Disagree DK

82 Financial Products Used

83

84 20% 18% 16% 14% 12% 10% 8% 6% 4% 2% 0% 19% 17% 13% 4% 2% 2% 1% 1% 1% CRDB Bank Tanzania Postal Bank NBC Limited Akiba Commercial Bank Stanbic Bank The People's Bank Of Zanzibar Barclays Bank Dar Es Salaam Community Bank Exim Bank

85 Must Keep Min. Balance In Bank Prefer Alternative Fin.Services Banks Not For People Like Me Don't Need A Bank Account Don't Have A Referee Takes Too Long To Get Money No Documents To Open Acc. Don't Qualify To Open Account Prefer Dealing In Cash Have Too Little Expensive To Have Bank Account Bank Is Too Far From Home Bank Charges Are Too High Don't Know How To Open Account Do Not Have A Job Don't Have Money To Save Don't Have A Regular Income 4% 4% 5% 5% 5% 6% 6% 9% 11% 16% 16% 19% 19% 20% 27% 32% 60% 0% 10% 20% 30% 40% 50% 60% 70%

86

87

88 Banked Unbanked 40% 35% 36% 30% 27% 25% 21% 20% 17% 15% 10% 12% 11% 14% 10% 8% 8% 8% 7% 9% 11% 5% 0% TSh TSh TSh TSh TSh TSh TSh TSh TSh TSh TSh TSh TSh TSh

89 based on education

90

91

92 The concept lines of saving/investing and insuring are blurred

93 Tanzanians save to make provisions or insure themselves in case of certain events Social Reasons (Wedding) Education Of Self, Child and others To Leave Something For Child For Later In Life/Old Age 8% 10% 11% 14% Emergency (Burial Medical 28% Meet HH Needs-Little/No Money 37% 0% 5% 10% 15% 20% 25% 30% 35% 40%

94 How Tanzanians who save keep their savings Other With An ASCA With Group At Workplace Through Insurance Schemes Employer Savings Schemes Businessman For Safekeeping At Microfinance Institution Account At SACCO Complusory Savings Ex NSSF/ZSSF With A Merry -Go- Round Given To Family/Friend To Keep Keep In Secret Hiding Place Savings In Kind Eg. Livestock 2% 2% 2% 2% 2% 3% 3% 6% 6% 12% 15% 54% 68% 0% 10% 20% 30% 40% 50% 60% 70% 80%

95 Forms of savings in-kind of people who save RTA 4% Clothing 9% Agricultural Inputs - Eg. Seeds Household Items - Eg. Salt, Soap Means Of Transport -Eg. Bicycle Entertainment Items-Eg. Radio Food Agricultural Produce 13% 16% 18% 22% 23% 27% Livestock - Eg.Goats And Cows 41% 0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

96 Benefits for keeping savings in-kind of Tanzanians who save Can Avoid Paying Tax RTA Adds To Comfort Of Living Able To Pay For The Goods Makes It Easier To Do Business For Transportation Purposes Security Easier To Meet Your Obligation For News/Entertainment Purposes Can Exchange For Goods/Servicese Better Returns Than Investment To Keep Item&Sell At Later Date 31% 0% 5% 10% 15% 20% 25% 30% 35% 13% 14% 17% 4% 5% 7% 18% 19% 20% 21%

97 Access to financial services of people who save in-kind FI - Formally Included SI - Semi Formal II - Informally Included E - Excluded 1 9.6% 2.6% 47.7% 40.1% 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

98 Demographics of people who save to insure themselves for certain events 80% 73% 70% 60% 50% 48% 52% 40% 30% 20% 10% 27% 5% 22% 32% 19% 11% 11% 0% Urban Rural Male Female Years Years Years Years Years 55+ Years

99 Level of education of Tanzanians between years who save to insure themselves for certain events RTA Post Primary Training Post Secondary Training 2% 2% 3% Pre-primary Secondary No Formal Schooling 8% 12% 12% Primary 60% 0% 10% 20% 30% 40% 50% 60% 70%

100 Reasons for never having saved or invested No Relevant Documentation You Need A Referee Difficult To Use Or Access Too Young To Contract Time Consuming To Participate Cost Of Service/Getting There Can't Qualify Not Available In This Area Unaware Of Products Don't Understand How Serv. Work Facility Not Nearby Live For Today Needing Lump Sum To Start With Poor Or Low Returns Don't Have Start Up Money Having Money To Save 1.60% 2% 2% 2% 2% 2% 2% 3% 3% 4% 4% 5% 6% 15% 20% 22% 0% 5% 10% 15% 20% 25%

101

102 Loan From Informal Lender Personal Loan From A Bank Business Loan 3% 4% 4% Loan From Microfinance Instit. Loan From ASCA 6% 6% Loan From A SACCO 9% Loans In Kind-Eg. Livestock 23% Credit From A Kiosk 33% Loan From Family/Friend 38%

103 Sources of borrowing split by urban/rural 39% Urban Rural 35% 27% 13% 11% 13% 8% 7% 8% 3% 3% 2% Loan From Family/Friend Loans In Kind-Eg. Livestock Loan From A SACCO Loan From Microfinance Instit. Business Loan Personal Loan From A Bank

104

105 Reason for borrowing money Purchase Of Land % Social Reasons % Pay Off Debts % Purchasing Means Of Transport % Increase Your Bank Balance % Expanding Business % Purchase Of Livestock % Emergency % Farming Activities % 2% 2% 3% 3% 3% 4% 4% 4% 6% Building Or Improving A House % Meeting Day To Day Expenses % Setting Up A Business % Educate-Self, child, sibling, other 9% 10% 10% 11% Acquiring Household Goods % 12% 0% 2% 4% 6% 8% 10% 12% 14%

106 Reason for never having applied for a loan Spouse/Partner Won't Allow It Too Young To Qualify Don't Have Identification Don't Have A Guarantor/Referee Don't Believe Paying Interest Don't Have Any Collateral No Place Nearby To Go Get Loan They Charge Too Much Don't Know Where To Get Loan Fear Not Enough Money To Repay Never Needed It Don't Have Enough Money 3% 4% 4% 8% 9% 12% 15% 16% 22% 29% 31% 32% 0% 5% 10% 15% 20% 25% 30% 35%

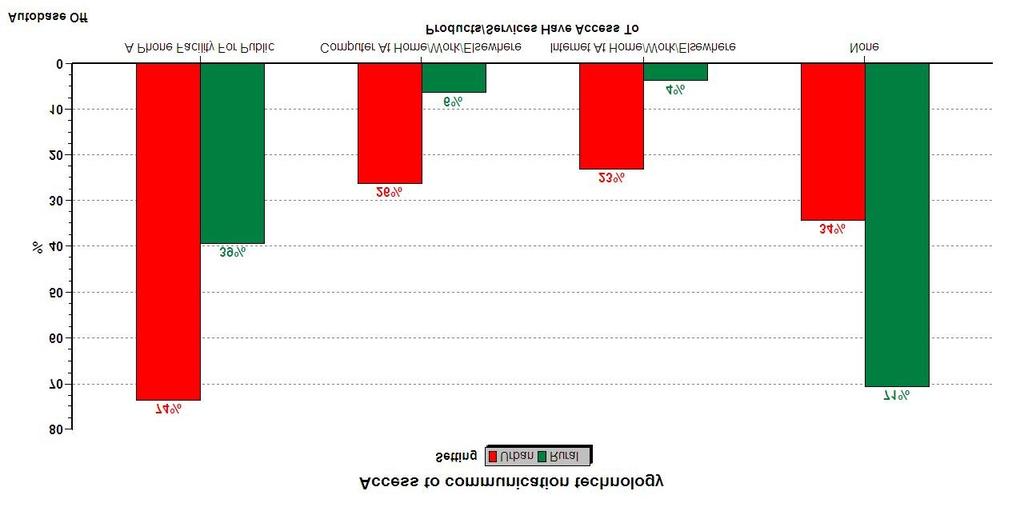

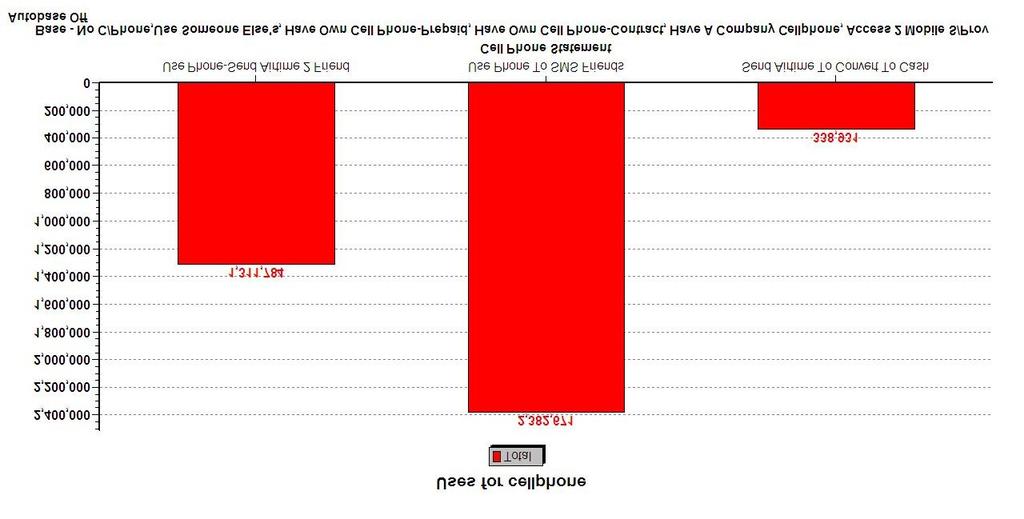

107

108 Saving in Kind Loans in Kind Remittances in Kind 84% 80% 70% 20% 16% 30% Urban Rural

109 24% 16% 14% 13% 10% 9% 8% 5% Livestock - Eg.Goats And Cows Agricultural Produce Food Entertainment Items-Eg. Radio Means Of Transport -Eg. Bicycle Household Items - Eg. Salt Agricultural Inputs - Eg. Seeds Clothing

110

111 Urban Rural 19% 11% 11% 6% 2% 4% using an financial institution using a courier company Through a personal contact

112

113

114 Have Own Cell Phone-Contract 6% No C/Phone, don't use others 22% Have own cell Phone-Prepaid 25% No C/Phone, use someone else's 29% Access 2 Mobile S/Prov. Payph. 41%

115

116

117 Area based sampling Allows modelling and mapping of data Overlay supply-side data with demand data Determine market gaps Better utilisation of resources

118 All

119 Summary on Challenges of Financial Markets By Oswald Mashindano Economic & Social Research Foundation (ESRF)

120 Impediments to Financial Markets Low levels of financial literacy Poverty as a barrier Rural dwellers are generally poorer than their urban counterparts Poorly developed infrastructure Roads, communications, electricity, transportation etc

121 A combination of these factors leads to Lower participation and poor financial accessibility Increased transaction costs per monetary unit of financial intermediation; Increased risks for any financial institution attempting to serve rural clients; Formal financial institutions largely avoiding serving rural areas; Financial services available are provided by informal agents or mechanisms which offer a narrow range of financial services to limited customers.

122 1. Summing up 2. Dissemination strategy Annette Altvater FinScope Coordinator FSDT

123 ??

124 The FinScope dataset: contains the universe of information To be used by institutions and individuals able to analyse market research information FinScope key findings: analysis which makes sense of the data Users need information tailored to their specific interests or market challenges

125 Key findings: initial analysis presented at the FinScope Tanzania launch - April 2007 Currently: research institutions and consultants mine the dataset, present more analyses and workshop the application of these analyses Materials are published on the FSDT dgroup website brochure, analyses and presentations. launch

126 Intermediate dissemination between April and June 2007 In-depth analysis and workshops. The FSDT will: host workshops for some market segments facilitate local market research capacity develop the means, (possibly including subsidies), to assist users to buy or use analytical services to apply the findings

127 Date Market segment Subject of analysis Institutions invited 3 May 2007 Donors and development partners Support and promotion of pro poor financial services Donor agencies 4 May 2007 Government Policy and regulatory issues Government agencies 16 May 2007 Insurance industry Client profiles and preferences, useful information for financial sector deepening Insurance companies and Insurance authorities 17 May 2007 Banking industry Client profiles and preferences, useful information for financial sector deepening Commercial Banks and Community Banks, TIOB

128 Date Market segment Subject of analysis Institutions invited 6 June 2007 Cooperative movement Client profiles and preferences, useful information for financial sector deepening Savings- and Credit Co-operative Societies 7 June 2007 Microfinance Client profiles and preferences, useful information for financial sector deepening MicroFinance Institutions 27 June 2007 Research FinScope data and the potential of FinScope market research services Market research service providers 28 June 2007 Mobile telephone industry Usage of mobile telephone services and the potential of mobile payment systems Mobile telephone service providers and regulators

129 from June until the next FinScope survey in 2008 Demand-driven, tailored market research: Market research institutions to offer services to users Feedback from users of information for the next FinScope survey The next FinScope survey may reflect any market innovation implemented in the meantime

130 Register for the workshops with the FSDT Submit questions or issues for mining to: 1. the FSDT dgroup website ( or 2. Juliana, FSDT Office Manager, or

131 Thank you for participating today!

132 This document was created with Win2PDF available at The unregistered version of Win2PDF is for evaluation or non-commercial use only.

FinScope Consumer Survey Malawi 2014

FinScope Consumer Survey Malawi 0 Introduction Malawi Government The Government of Malawi has increasingly recognised that access to financial services can play an important role in poverty alleviation

FinScope Consumer Survey Malawi 0 Introduction Malawi Government The Government of Malawi has increasingly recognised that access to financial services can play an important role in poverty alleviation

Developing a National Financial Literacy Strategy Tanzania

Developing a National Financial Literacy Strategy Tanzania Conference on "Promoting Financial Capability and Consumer Protection : Accra, 8-9 Sept 2009 By: Deogratias P. Macha Real Sector and Microfinance

Developing a National Financial Literacy Strategy Tanzania Conference on "Promoting Financial Capability and Consumer Protection : Accra, 8-9 Sept 2009 By: Deogratias P. Macha Real Sector and Microfinance

FinScope Myanmar 2018 Launch

FinScope Myanmar 2018 Launch Nay Pyi Taw, Myanmar 19 June 2018 Sampling and weighting Respondent profile Universe: Adult population in Myanmar Myanmar residents 18 years and older Coverage and methodology

FinScope Myanmar 2018 Launch Nay Pyi Taw, Myanmar 19 June 2018 Sampling and weighting Respondent profile Universe: Adult population in Myanmar Myanmar residents 18 years and older Coverage and methodology

FinScope Consumer Survey Botswana 2014

FinScope Consumer Survey Botswana 2014 Introduction The government of Botswana in collaboration with the private sector are actively supporting growth and development of the financial sector. Financial

FinScope Consumer Survey Botswana 2014 Introduction The government of Botswana in collaboration with the private sector are actively supporting growth and development of the financial sector. Financial

Exploring market opportunities for savings in Mozambique

1 Exploring market opportunities for savings in Mozambique 3 March 2016 INTERIM RESULTS Eighty20 Consulting 2 Agenda Mozambique a FinScope overview Savings usage Savings access 3 Agenda Mozambique a FinScope

1 Exploring market opportunities for savings in Mozambique 3 March 2016 INTERIM RESULTS Eighty20 Consulting 2 Agenda Mozambique a FinScope overview Savings usage Savings access 3 Agenda Mozambique a FinScope

FinScope Consumer Survey Kingdom of Cambodia Topline findings. July 2016

FinScope Consumer Survey Kingdom of Cambodia 2015 Topline findings July 2016 Contents 1. Overview 2. Understanding people s lives 3. Financial capability 4. Financial inclusion overview 5. Banking and

FinScope Consumer Survey Kingdom of Cambodia 2015 Topline findings July 2016 Contents 1. Overview 2. Understanding people s lives 3. Financial capability 4. Financial inclusion overview 5. Banking and

FinScope Consumer Survey

The Pocket Guide FinScope Consumer Survey Nepal 2014 Introduction The Government of Nepal recognises the importance of a well-functioning financial sector as one of the key drivers in reducing inequality

The Pocket Guide FinScope Consumer Survey Nepal 2014 Introduction The Government of Nepal recognises the importance of a well-functioning financial sector as one of the key drivers in reducing inequality

FinScope Consumer Survey Botswana 2014

FinScope Consumer Survey Botswana 2014 LAUNCH PRESENTATION 14 July 2015 Making financial markets work for the poor Objectives of FinScope Botswana 2014 To describe the levels of financial inclusion (i.e.

FinScope Consumer Survey Botswana 2014 LAUNCH PRESENTATION 14 July 2015 Making financial markets work for the poor Objectives of FinScope Botswana 2014 To describe the levels of financial inclusion (i.e.

Ask Afrika 2010 Making financial markets work for the poor

Ask Afrika 2010 Making financial markets work for the poor Give a man a fish Ask Afrika 2010 Making financial markets work for the poor 2 Ask Afrika 2010 Making financial markets work for the poor 3 Ask

Ask Afrika 2010 Making financial markets work for the poor Give a man a fish Ask Afrika 2010 Making financial markets work for the poor 2 Ask Afrika 2010 Making financial markets work for the poor 3 Ask

By Kasenge Lawrence Economist, Microfinance Department, Ministry Of Finance, Planning And Economic Development, UGANDA

FINANCIAL INCLUSION IN UGANDA A Presentation During the 2nd Meeting of the COMCEC Financial Cooperation Working Group, March 27th, 2014, at Crowne Plaza 0Hotel, in Ankara, Republic of Turkey By Kasenge

FINANCIAL INCLUSION IN UGANDA A Presentation During the 2nd Meeting of the COMCEC Financial Cooperation Working Group, March 27th, 2014, at Crowne Plaza 0Hotel, in Ankara, Republic of Turkey By Kasenge

ANALYSIS OF UNBANKED MOZAMBICANS. Analysis of Unbanked Mozambicans

ANALYSIS OF MOZAMBICANS Analysis of Unbanked Mozambicans ANALYSIS OF MOZAMBICANS Key points ANALYSIS OF MOZAMBICANS THE TOTAL ADULT (+16) IS 11.6 MILLION... 05 07 09 11 13 15 17 WHO ARE THE HOW THE LIVE

ANALYSIS OF MOZAMBICANS Analysis of Unbanked Mozambicans ANALYSIS OF MOZAMBICANS Key points ANALYSIS OF MOZAMBICANS THE TOTAL ADULT (+16) IS 11.6 MILLION... 05 07 09 11 13 15 17 WHO ARE THE HOW THE LIVE

Quick Facts. n n. Total population of Zambia million Total adult population 8.1 million. o o

FinScope Zambia 2015 Quick Facts n n Total population of Zambia 1 15.5 million Total adult population 8.1 million o o 54.8% of adults live in rural areas; 45.2% in urban areas 49.0% of adults are male;

FinScope Zambia 2015 Quick Facts n n Total population of Zambia 1 15.5 million Total adult population 8.1 million o o 54.8% of adults live in rural areas; 45.2% in urban areas 49.0% of adults are male;

REPORT ON WOMEN S ACCESS TO FINANCIAL SERVICES IN ZAMBIA

REPORT ON WOMEN S ACCESS TO FINANCIAL SERVICES IN ZAMBIA WOMEN S ACCESS TO FINANCIAL SERVICES IN ZAMBIA TABLE OF CONTENTS EXECUTIVE SUMMARY 5 PART I BACKGROUND 9 1 Objectives and methodology 9 2 Overview

REPORT ON WOMEN S ACCESS TO FINANCIAL SERVICES IN ZAMBIA WOMEN S ACCESS TO FINANCIAL SERVICES IN ZAMBIA TABLE OF CONTENTS EXECUTIVE SUMMARY 5 PART I BACKGROUND 9 1 Objectives and methodology 9 2 Overview

Although Financial Inclusion is higher amongst females in Cambodia, the income distribution shows a disparity favoring males

Although Financial Inclusion is higher amongst females in Cambodia, the income distribution shows a disparity favoring males 66 % 75 % 73 % 79 % 21 % 78 % headed vs. male headed households (Ownership)

Although Financial Inclusion is higher amongst females in Cambodia, the income distribution shows a disparity favoring males 66 % 75 % 73 % 79 % 21 % 78 % headed vs. male headed households (Ownership)

UGANDA WAVE 5 REPORT FIFTH ANNUAL FII TRACKER SURVEY. June Conducted July-August 2017

WAVE 5 REPORT FIFTH ANNUAL FII TRACKER SURVEY Conducted July-August 2017 June 2018 PUTTING THE USER FRONT AND CENTER The Financial Inclusion Insights (FII) program responds to the need identified by multiple

WAVE 5 REPORT FIFTH ANNUAL FII TRACKER SURVEY Conducted July-August 2017 June 2018 PUTTING THE USER FRONT AND CENTER The Financial Inclusion Insights (FII) program responds to the need identified by multiple

MEASURING WOMEN S FINANCIAL INCLUSION

MEASURING WOMEN S FINANCIAL INCLUSION USING FII DATA TO TRACK PROGRESS AND DEVELOP INTERVENTIONS Presented by Nadia van de Walle Women's Financial Inclusion Community of Practice Webinar December 5, 2017

MEASURING WOMEN S FINANCIAL INCLUSION USING FII DATA TO TRACK PROGRESS AND DEVELOP INTERVENTIONS Presented by Nadia van de Walle Women's Financial Inclusion Community of Practice Webinar December 5, 2017

FinScope Consumer Survey Mauritius 2014

FinScope Consumer Survey Mauritius 2014 LAUNCH PRESENTATION October 2014 Making financial markets work for the poor CONTENTS Research Methodology Mauritius Context Income generating activities Incidence

FinScope Consumer Survey Mauritius 2014 LAUNCH PRESENTATION October 2014 Making financial markets work for the poor CONTENTS Research Methodology Mauritius Context Income generating activities Incidence

TANZANIA. QUICKSIGHTS REPORT FII TRACKER SURVEY Conducted September-October December 2015

QUICKSIGHTS REPORT FII TRACKER SURVEY Conducted September-October 2015 December 2015 GLOSSARY Access Access to a bank, NBFI or mobile money account; those with access have used the services either via

QUICKSIGHTS REPORT FII TRACKER SURVEY Conducted September-October 2015 December 2015 GLOSSARY Access Access to a bank, NBFI or mobile money account; those with access have used the services either via

UGANDA 2013 FinScope III SURVEY KEY FINDINGS. Unlocking Barriers to Financial Inclusion

UGANDA 2013 FinScope III SURVEY KEY FINDINGS Unlocking Barriers to Financial Inclusion November 2013 ACKNOWLEDGEMENTS This summary report was prepared by the Economic Policy Research Centre (EPRC) as

UGANDA 2013 FinScope III SURVEY KEY FINDINGS Unlocking Barriers to Financial Inclusion November 2013 ACKNOWLEDGEMENTS This summary report was prepared by the Economic Policy Research Centre (EPRC) as

South African Baseline Study on Financial Literacy

Regional Dissemination Conference on Building Financial Capability South African Baseline Study on Financial Literacy Lyndwill Clarke Head: Consumer Education 30-31 January 2013 Nairobi, Kenya Outline

Regional Dissemination Conference on Building Financial Capability South African Baseline Study on Financial Literacy Lyndwill Clarke Head: Consumer Education 30-31 January 2013 Nairobi, Kenya Outline

Financial Inclusion in SADC

Financial Inclusion in SADC Mbabane, Swaziland December 2017 Contents FinMark Trust FinScope as a tool of Financial Inclusion Current FinScope initiatives in SADC FinScope insights MSME Studies in SADC

Financial Inclusion in SADC Mbabane, Swaziland December 2017 Contents FinMark Trust FinScope as a tool of Financial Inclusion Current FinScope initiatives in SADC FinScope insights MSME Studies in SADC

FinScope Survey Highlights

FinScope Survey Highlights Nepal 2014 Contents Introduction and background 1 About FinMark Trust. About UNCDF. FinScope survey. Survey Objectives. Partnering for a common purpose. Sampling and methodology

FinScope Survey Highlights Nepal 2014 Contents Introduction and background 1 About FinMark Trust. About UNCDF. FinScope survey. Survey Objectives. Partnering for a common purpose. Sampling and methodology

FinScope Consumer Survey Zimbabwe 2011

FinScope Consumer Survey Zimbabwe 2011 Republic of Zimbabwe Introduction The Government of Zimbabwe recognises the role played by the financial sector in facilitating economic growth. In order to develop

FinScope Consumer Survey Zimbabwe 2011 Republic of Zimbabwe Introduction The Government of Zimbabwe recognises the role played by the financial sector in facilitating economic growth. In order to develop

FinScope SA 2013 Consumer Survey

FinScope SA Consumer Survey 1 Contents What did we do? Have people s lives changed? Where is the increase in credit? Are people saving? Is formal insurance replacing the informal? Increasing banking through

FinScope SA Consumer Survey 1 Contents What did we do? Have people s lives changed? Where is the increase in credit? Are people saving? Is formal insurance replacing the informal? Increasing banking through

Under pressure? Ugandans opinions and experiences of poverty and financial inclusion 1. Introduction

Sauti za Wananchi Brief No. 2 March, 2018 Under pressure? Ugandans opinions and experiences of poverty and financial inclusion 1. Introduction Poverty remains an entrenched problem in Uganda. Economic

Sauti za Wananchi Brief No. 2 March, 2018 Under pressure? Ugandans opinions and experiences of poverty and financial inclusion 1. Introduction Poverty remains an entrenched problem in Uganda. Economic

T. Rowe Price 2015 FAMILY FINANCIAL TRADE-OFFS SURVEY

T. Rowe Price 2015 FAMILY FINANCIAL TRADE-OFFS SURVEY Contents Perceptions About Saving for Retirement & College Education Respondent College Experience Family Financial Profile Saving for College Paying

T. Rowe Price 2015 FAMILY FINANCIAL TRADE-OFFS SURVEY Contents Perceptions About Saving for Retirement & College Education Respondent College Experience Family Financial Profile Saving for College Paying

TANZANIA WAVE 5 REPORT FIFTH ANNUAL FII TRACKER SURVEY. June Conducted July-August 2017

WAVE 5 REPORT FIFTH ANNUAL FII TRACKER SURVEY Conducted July-August 2017 June 2018 PUTTING THE USER FRONT AND CENTER The Financial Inclusion Insights (FII) program responds to the need identified by multiple

WAVE 5 REPORT FIFTH ANNUAL FII TRACKER SURVEY Conducted July-August 2017 June 2018 PUTTING THE USER FRONT AND CENTER The Financial Inclusion Insights (FII) program responds to the need identified by multiple

QUICKSIGHTS REPORT FOURTH ANNUAL FII TRACKER SURVEY

QUICKSIGHTS REPORT FOURTH ANNUAL FII TRACKER SURVEY Fieldwork conducted July - August 20 November 20 Key definitions Access to financial accounts Access to a bank account, mobile money account or an NBFI

QUICKSIGHTS REPORT FOURTH ANNUAL FII TRACKER SURVEY Fieldwork conducted July - August 20 November 20 Key definitions Access to financial accounts Access to a bank account, mobile money account or an NBFI

Central Bank of Sudan Microfinance Unit

Central Bank of Sudan Microfinance Unit Role & Mission April 2007 Mutwakil Bakri Why Microfinance Matters? Poverty Map in Sudan: 76% Under Poverty Line,70% in Rural Deprived Areas Demand Gap:only 1-3%

Central Bank of Sudan Microfinance Unit Role & Mission April 2007 Mutwakil Bakri Why Microfinance Matters? Poverty Map in Sudan: 76% Under Poverty Line,70% in Rural Deprived Areas Demand Gap:only 1-3%

NIGERIA WAVE 4 REPORT FII TRACKER SURVEY. June Conducted August October 2016

NIGERIA WAVE 4 REPORT FII TRACKER SURVEY Conducted August October 2016 June 2017 PUTTING THE USER FRONT AND CENTER NIGERIA The Financial Inclusion Insights (FII) program responds to the need identified

NIGERIA WAVE 4 REPORT FII TRACKER SURVEY Conducted August October 2016 June 2017 PUTTING THE USER FRONT AND CENTER NIGERIA The Financial Inclusion Insights (FII) program responds to the need identified

NIGERIA. QUICKSIGHTS REPORT FII TRACKER SURVEY Conducted August-September December 2015

QUICKSIGHTS REPORT FII TRACKER SURVEY Conducted August-September 2015 December 2015 KEY DEFINITIONS Access Access to a bank account or mobile money account means a respondent can use bank/mobile money

QUICKSIGHTS REPORT FII TRACKER SURVEY Conducted August-September 2015 December 2015 KEY DEFINITIONS Access Access to a bank account or mobile money account means a respondent can use bank/mobile money

FINANCIAL ACCESS IN KENYA RESULTS OF THE 2006 NATIONAL SURVEY OCTOBER 2007

FINANCIAL ACCESS IN KENYA RESULTS OF THE 2006 NATIONAL SURVEY OCTOBER 2007 The FinAccess survey was undertaken by Steadman Group and supported by the Financial Access Partnership, with representation from

FINANCIAL ACCESS IN KENYA RESULTS OF THE 2006 NATIONAL SURVEY OCTOBER 2007 The FinAccess survey was undertaken by Steadman Group and supported by the Financial Access Partnership, with representation from

Click to edit Master title style

DIGITAL CREDIT IN TANZANIA: CUSTOMER EXPERIENCES & EMERGING RISKS Click to edit Master title style Photo: Hendri Lombard World Bank Photographer Name, CGAP Photo Contest Michelle Kaffenberger January 2018

DIGITAL CREDIT IN TANZANIA: CUSTOMER EXPERIENCES & EMERGING RISKS Click to edit Master title style Photo: Hendri Lombard World Bank Photographer Name, CGAP Photo Contest Michelle Kaffenberger January 2018

2018/SMEWG/DIA/008 National Financial Inclusion Strategy

2018/SMEWG/DIA/008 National Financial Inclusion Strategy 2016-2020 Submitted by: Centre for Excellence in Financial Inclusion Policy Dialogue on Micro, Small and Medium Enterprises Internationalization

2018/SMEWG/DIA/008 National Financial Inclusion Strategy 2016-2020 Submitted by: Centre for Excellence in Financial Inclusion Policy Dialogue on Micro, Small and Medium Enterprises Internationalization

Impact Evaluation of Savings Groups and Stokvels in South Africa

Impact Evaluation of Savings Groups and Stokvels in South Africa The economic and social value of group-based financial inclusion summary October 2018 SaveAct 123 Jabu Ndlovu Street, Pietermaritzburg,

Impact Evaluation of Savings Groups and Stokvels in South Africa The economic and social value of group-based financial inclusion summary October 2018 SaveAct 123 Jabu Ndlovu Street, Pietermaritzburg,

FINANCIAL EXCLUSION IN KENYA AN ANALYSIS OF FINANCIAL SERVICE USE DECEMBER FSD Kenya Financial Sector Deepening

FINANCIAL EXCLUSION IN KENYA AN ANALYSIS OF FINANCIAL SERVICE USE DECEMBER 2008 FSD Kenya Financial Sector Deepening A Report prepared for the Decentralised Financial Services Project, Kenya and Financial

FINANCIAL EXCLUSION IN KENYA AN ANALYSIS OF FINANCIAL SERVICE USE DECEMBER 2008 FSD Kenya Financial Sector Deepening A Report prepared for the Decentralised Financial Services Project, Kenya and Financial

Financial Capability Tanzania Baseline Survey Findings

Financial Capability Tanzania Baseline Survey Findings November 2014 Acknowledgements This work has been made possible by the Bank of Tanzania and was funded by the Financial Sector Deepening Trust, Tanzania.

Financial Capability Tanzania Baseline Survey Findings November 2014 Acknowledgements This work has been made possible by the Bank of Tanzania and was funded by the Financial Sector Deepening Trust, Tanzania.

UGANDA 2013 FinScope III SURVEY REPORT FINDINGS

ECONOMIC POLICY RESEARCH CENTRE UGANDA 2013 FinScope III SURVEY REPORT FINDINGS Unlocking Barriers to Financial Inclusion MINISTRY OF FINANCE, PLANNING AND ECONOMIC DEVELOPMENT ECONOMIC POLICY RESEARCH

ECONOMIC POLICY RESEARCH CENTRE UGANDA 2013 FinScope III SURVEY REPORT FINDINGS Unlocking Barriers to Financial Inclusion MINISTRY OF FINANCE, PLANNING AND ECONOMIC DEVELOPMENT ECONOMIC POLICY RESEARCH

UGANDA QUICKSIGHTS REPORT FII TRACKER SURVEY WAVE 1. April 2014

QUICKSIGHTS REPORT FII TRACKER SURVEY WAVE 1 April 2014 THE FINANCIAL INCLUSION INSIGHTS (FII) PROGRAM The FII research program responds to the need for timely, demand-side data and practical insights

QUICKSIGHTS REPORT FII TRACKER SURVEY WAVE 1 April 2014 THE FINANCIAL INCLUSION INSIGHTS (FII) PROGRAM The FII research program responds to the need for timely, demand-side data and practical insights

THE LANDSCAPE OF FINANCIAL INCLUSION AND MICROFINANCE IN NIGERIA

THE LANDSCAPE OF FINANCIAL INCLUSION AND MICROFINANCE IN NIGERIA 1 Table of Content 1. About EFInA... 3 2. Background... 3 3. Demographic Profile of Nigerian Adults... 4 4. Landscape of Financial Access

THE LANDSCAPE OF FINANCIAL INCLUSION AND MICROFINANCE IN NIGERIA 1 Table of Content 1. About EFInA... 3 2. Background... 3 3. Demographic Profile of Nigerian Adults... 4 4. Landscape of Financial Access

BANGLADESH QUICKSIGHTS REPORT FIFTH ANNUAL FII TRACKER SURVEY. June Conducted July September 2017

QUICKSIGHTS REPORT FIFTH ANNUAL FII TRACKER SURVEY Conducted July September 2017 June 2018 UNDERSTANDING FINANCIAL INCLUSION What is financial inclusion? Financial inclusion means that individuals and

QUICKSIGHTS REPORT FIFTH ANNUAL FII TRACKER SURVEY Conducted July September 2017 June 2018 UNDERSTANDING FINANCIAL INCLUSION What is financial inclusion? Financial inclusion means that individuals and

BANK OF UGANDA THEME: FINANCIAL INCLUSION AND THE DEVELOPMENT OF THE FINANCIAL SYSTEM

BANK OF UGANDA SPEECH BY GOVERNOR, BANK OF UGANDA AT THE 3 RD GRADUATION CEREMONY OF THE UGANDA INSTITUTE OF BANKING AND FINANCIAL SERVICES ATOM LEADERSHIP CENTRE, MUYENGA FRIDAY 4 TH OCTOBER 2013. THEME:

BANK OF UGANDA SPEECH BY GOVERNOR, BANK OF UGANDA AT THE 3 RD GRADUATION CEREMONY OF THE UGANDA INSTITUTE OF BANKING AND FINANCIAL SERVICES ATOM LEADERSHIP CENTRE, MUYENGA FRIDAY 4 TH OCTOBER 2013. THEME:

Today, 69% of adults around the world have an account Adults with an account (%), 2017

, 2017") Today, 69% of adults around the world have an account Adults with an account (%), 2017 Account ownership rose from 51% to 69% 2011-2017 1.2 billion more banked 2 Women Poor Young Unemployed The gender

Today, 69% of adults around the world have an account Adults with an account (%), 2017 Account ownership rose from 51% to 69% 2011-2017 1.2 billion more banked 2 Women Poor Young Unemployed The gender

BANGLADESH RAPID RESPONSE STUDY ON ATTRITION OF NON-BANK FINANCIAL INSTITUTION ACCOUNTS. July Conducted May June 2017

BANGLADESH RAPID RESPONSE STUDY ON ATTRITION OF NON-BANK FINANCIAL INSTITUTION ACCOUNTS Conducted May June 2017 July 2017 PUTTING THE USER FRONT AND CENTER BANGLADESH The Financial Inclusion Insights (FII)

BANGLADESH RAPID RESPONSE STUDY ON ATTRITION OF NON-BANK FINANCIAL INSTITUTION ACCOUNTS Conducted May June 2017 July 2017 PUTTING THE USER FRONT AND CENTER BANGLADESH The Financial Inclusion Insights (FII)

Financial Access is Not Financial Inclusion:

Financial Access is Not Financial Inclusion: Current Status and issues of Financial Inclusion in Sri Lanka Ganga Tilakaratna Outline Financial Institutions: Diversity and Growth Financial Inclusion: Where

Financial Access is Not Financial Inclusion: Current Status and issues of Financial Inclusion in Sri Lanka Ganga Tilakaratna Outline Financial Institutions: Diversity and Growth Financial Inclusion: Where

Community-Based Savings Groups in Mtwara and Lindi

tanzania Community-Based Savings Groups in Mtwara and Lindi In recent years, stakeholders have increasingly acknowledged that formal financial institutions are not able to address the financial service

tanzania Community-Based Savings Groups in Mtwara and Lindi In recent years, stakeholders have increasingly acknowledged that formal financial institutions are not able to address the financial service

Broad and Deep: The Extensive Learning Agenda in YouthSave

Broad and Deep: The Extensive Learning Agenda in YouthSave Center for Social Development August 17, 2011 Campus Box 1196 One Brookings Drive St. Louis, MO 63130-9906 (314) 935.7433 www.gwbweb.wustl.edu/csd

Broad and Deep: The Extensive Learning Agenda in YouthSave Center for Social Development August 17, 2011 Campus Box 1196 One Brookings Drive St. Louis, MO 63130-9906 (314) 935.7433 www.gwbweb.wustl.edu/csd

Inclusive Insurance Focus Note Series

Inclusive Insurance Focus Note Series Microinsurance Landscape 2015 Contents 03 About 04 Key Highlights 05 Introduction 08 Microinsurance Coverage 10 Distribution 11 Business Case 14 Client Value 15 Industry

Inclusive Insurance Focus Note Series Microinsurance Landscape 2015 Contents 03 About 04 Key Highlights 05 Introduction 08 Microinsurance Coverage 10 Distribution 11 Business Case 14 Client Value 15 Industry

The Status of Agricultural and Rural Financial Services in Southern Africa Zambia Country Report

The Status of Agricultural and Rural Financial Services in Southern Africa Zambia Country Report Lemmy Manje, Melanie Newman Wilkinson Taj Pomodzi Hotel Friday, 13 th December 2013 Making financial markets

The Status of Agricultural and Rural Financial Services in Southern Africa Zambia Country Report Lemmy Manje, Melanie Newman Wilkinson Taj Pomodzi Hotel Friday, 13 th December 2013 Making financial markets

Empowerment of Civil Servants through Savings and Credit Cooperative Society (SACCOS): Evidences from Institute of Accountancy Arusha

: Evidences from Institute of Accountancy Arusha") Empowerment of Civil Servants through Savings and Credit Cooperative Society (SACCOS): Evidences from Institute of Accountancy Arusha Chalicha Sila Arusha-Tanzania csila2004@gmail.com ABSTRACT The aim

Empowerment of Civil Servants through Savings and Credit Cooperative Society (SACCOS): Evidences from Institute of Accountancy Arusha Chalicha Sila Arusha-Tanzania csila2004@gmail.com ABSTRACT The aim

BANGLADESH STEPS TOWARD FINANCIAL INCLUSION 2014 (WAVE 2)

") STEPS TOWARD FINANCIAL INCLUSION 2014 (WAVE 2) PUTTING THE USER FRONT AND CENTER The Financial Inclusion Insights (FII) program responds to the need identified by multiple stakeholders for timely, demand-side

STEPS TOWARD FINANCIAL INCLUSION 2014 (WAVE 2) PUTTING THE USER FRONT AND CENTER The Financial Inclusion Insights (FII) program responds to the need identified by multiple stakeholders for timely, demand-side

PAKISTAN. QUICKSIGHTS REPORT FOURTH ANNUAL FII TRACKER SURVEY Fieldwork completed in October December 2016

QUICKSIGHTS REPORT FOURTH ANNUAL FII TRACKER SURVEY Fieldwork completed in October 206 December 206 Key definitions Access Access to a bank account or mobile money account means an individual can use bank/mobile

QUICKSIGHTS REPORT FOURTH ANNUAL FII TRACKER SURVEY Fieldwork completed in October 206 December 206 Key definitions Access Access to a bank account or mobile money account means an individual can use bank/mobile

FinScope. Consumer Survey Highlights. Madagascar 2016 MAKING ACCESS POSSIBLE

FinScope Consumer Survey Highlights Madagascar 2016 MAKING ACCESS POSSIBLE Partnering for a common purpose The FinScope survey is a research tool which was developed by FinMark Trust. It is a nationally

FinScope Consumer Survey Highlights Madagascar 2016 MAKING ACCESS POSSIBLE Partnering for a common purpose The FinScope survey is a research tool which was developed by FinMark Trust. It is a nationally

ធន គ រជ ត ន កម ព ជ NATIONAL BANK OF CAMBODIA

1 ធន គ រជ ត ន កម ព ជ NATIONAL BANK OF CAMBODIA Financial Inclusion in Cambodia: Issues and Challenges December 7-8, 2017 Presented by: Khou Vouthy (Ph.D.) Deputy Director General The views expressed in

1 ធន គ រជ ត ន កម ព ជ NATIONAL BANK OF CAMBODIA Financial Inclusion in Cambodia: Issues and Challenges December 7-8, 2017 Presented by: Khou Vouthy (Ph.D.) Deputy Director General The views expressed in

Payments in Mozambique. April 2016

1 Payments in Mozambique April 2016 2 Agenda Mozambique a FinScope overview Payments Access According to FinScope 2014 there are 14.43 million adults aged 16 or more in the country; 5 are under the age

1 Payments in Mozambique April 2016 2 Agenda Mozambique a FinScope overview Payments Access According to FinScope 2014 there are 14.43 million adults aged 16 or more in the country; 5 are under the age

TANZANIA DIGITAL PATHWAYS TO FINANCIAL INCLUSION 2015 SURVEY REPORT MARCH 2015

DIGITAL PATHWAYS TO FINANCIAL INCLUSION 2015 SURVEY REPORT MARCH 2015 PUTTING THE USER FRONT AND CENTER The Financial Inclusion Insights (FII) program responds to the need identified by multiple stakeholders

DIGITAL PATHWAYS TO FINANCIAL INCLUSION 2015 SURVEY REPORT MARCH 2015 PUTTING THE USER FRONT AND CENTER The Financial Inclusion Insights (FII) program responds to the need identified by multiple stakeholders

FinScope SZL. Micro, small and medium enterprises (MSME) survey

survey") FinScope SZL Micro, small and medium enterprises (MSME) survey Swaziland 2017 Partnering for a common purpose FinScope MSME Swaziland was designed to involve a range of stakeholders engaging in a comprehensive

FinScope SZL Micro, small and medium enterprises (MSME) survey Swaziland 2017 Partnering for a common purpose FinScope MSME Swaziland was designed to involve a range of stakeholders engaging in a comprehensive

Microfinance and Energy Clients Win with Partnership Model in Uganda

FIELD BRIEF No. 9 Microfinance and Energy Clients Win with Partnership Model in Uganda A Case Study of FINCA s Microfinance and Renewable Energy Pilot Activity This FIELD Brief is the ninth in a series

FIELD BRIEF No. 9 Microfinance and Energy Clients Win with Partnership Model in Uganda A Case Study of FINCA s Microfinance and Renewable Energy Pilot Activity This FIELD Brief is the ninth in a series

Financial Literacy Report 2015 Summary Rands and Sense: Financial Literacy in South Africa

Financial Literacy Report 2015 Summary Rands and Sense: Financial Literacy in South Africa OVERVIEW OF THE STUDY Background. As part of on-going efforts by the FSB to better understand, monitor and promote

Financial Literacy Report 2015 Summary Rands and Sense: Financial Literacy in South Africa OVERVIEW OF THE STUDY Background. As part of on-going efforts by the FSB to better understand, monitor and promote

BANGLADESH. QUICKSIGHTS REPORT FOURTH ANNUAL FII TRACKER SURVEY Fieldwork completed in September December 2016

QUICKSIGHTS REPORT FOURTH ANNUAL FII TRACKER SURVEY Fieldwork completed in September 016 December 016 Key definitions Access Access to a bank account or mobile money account means an individual can use

QUICKSIGHTS REPORT FOURTH ANNUAL FII TRACKER SURVEY Fieldwork completed in September 016 December 016 Key definitions Access Access to a bank account or mobile money account means an individual can use

Downscaling with CRDB Bank in Tanzania

Downscaling with CRDB Bank in Tanzania Saugata Bandyopadhyay Deputy Managing Director, CRDB Bank Plc Tanzania Financial Inclusion Motivation for Downscaling Disruptive Channel Mobile money & Agent Banking

Downscaling with CRDB Bank in Tanzania Saugata Bandyopadhyay Deputy Managing Director, CRDB Bank Plc Tanzania Financial Inclusion Motivation for Downscaling Disruptive Channel Mobile money & Agent Banking

Strategy for Measuring Financial Inclusion in Mexico

1 Strategy for Measuring Financial Inclusion in Mexico The 2009 Global AFI Policy Forum Nairobi, Kenya September 14, 2009 Raúl Hernández Coss Director General for Access to Finance Vicepresidency of Public

1 Strategy for Measuring Financial Inclusion in Mexico The 2009 Global AFI Policy Forum Nairobi, Kenya September 14, 2009 Raúl Hernández Coss Director General for Access to Finance Vicepresidency of Public

Measuring Financial Inclusion:

Measuring Financial Inclusion: The Global Findex Data Leora Klapper Finance and Private Sector Development Team Development Research Group World Bank GLOBAL FINDEX Financial Inclusion data In depth data

Measuring Financial Inclusion: The Global Findex Data Leora Klapper Finance and Private Sector Development Team Development Research Group World Bank GLOBAL FINDEX Financial Inclusion data In depth data

Pyramids and frontiers of finance measuring access to finance. Forum for the Future. 24 October Mark Napier FinMark Trust

1 Pyramids and frontiers of finance measuring access to finance Forum for the Future Mark Napier FinMark Trust 24 October 2006 2 The concepts Access frontier Finance at the BoP Centrality of the consumer

1 Pyramids and frontiers of finance measuring access to finance Forum for the Future Mark Napier FinMark Trust 24 October 2006 2 The concepts Access frontier Finance at the BoP Centrality of the consumer

The Secret of the Lion

The Secret of the Lion Pay yourself first, live off the rest THE SECRET OF THE LION The lion eats first, ahead of the pack. You too should eat first by arranging an automatic deduction from your salary

The Secret of the Lion Pay yourself first, live off the rest THE SECRET OF THE LION The lion eats first, ahead of the pack. You too should eat first by arranging an automatic deduction from your salary

Rwanda Targeting 80 Per Cent Financial Inclusion in 2017

59 Rwanda Targeting 80 Per Cent Financial Inclusion in 2017 Rugazura Ephraim, Ph.D Scholar, Department of Rural Management, Annamalai University, Annamalainagar ABSTRACT Background: In order to achieve

59 Rwanda Targeting 80 Per Cent Financial Inclusion in 2017 Rugazura Ephraim, Ph.D Scholar, Department of Rural Management, Annamalai University, Annamalainagar ABSTRACT Background: In order to achieve

BANGLADESH WAVE 5 REPORT FIFTH ANNUAL FII TRACKER SURVEY. June Conducted July-September 2017

WAVE 5 REPORT FIFTH ANNUAL FII TRACKER SURVEY Conducted July-September 2017 June 2018 PUTTING THE USER FRONT AND CENTER The Financial Inclusion Insights (FII) program responds to the need identified by

WAVE 5 REPORT FIFTH ANNUAL FII TRACKER SURVEY Conducted July-September 2017 June 2018 PUTTING THE USER FRONT AND CENTER The Financial Inclusion Insights (FII) program responds to the need identified by

INDIA. QUICKSIGHTS REPORT FII TRACKER SURVEY Conducted June through October, January 2016*

QUICKSIGHTS REPORT FII TRACKER SURVEY Conducted June through October, 2015 January 2016* *Revised April 2016 KEY DEFINITIONS Access Access to a bank, NBFI or mobile money account; those with access have

QUICKSIGHTS REPORT FII TRACKER SURVEY Conducted June through October, 2015 January 2016* *Revised April 2016 KEY DEFINITIONS Access Access to a bank, NBFI or mobile money account; those with access have

CÔTE D IVOIRE ANALYTICAL REPORT. October Fieldwork Conducted August - October 2017

ANALYTICAL REPORT Fieldwork Conducted August - October 2017 October 2018 PUTTING THE USER FRONT AND CENTER The Financial Inclusion Insights (FII) program responds to the need identified by multiple stakeholders

ANALYTICAL REPORT Fieldwork Conducted August - October 2017 October 2018 PUTTING THE USER FRONT AND CENTER The Financial Inclusion Insights (FII) program responds to the need identified by multiple stakeholders

National financial inclusion strategies and measurement framework 1

Bank of Morocco CEMLA IFC Satellite Seminar at the ISI World Statistics Congress on Financial Inclusion Marrakech, Morocco, 14 July 2017 National financial inclusion strategies and measurement framework

Bank of Morocco CEMLA IFC Satellite Seminar at the ISI World Statistics Congress on Financial Inclusion Marrakech, Morocco, 14 July 2017 National financial inclusion strategies and measurement framework

BANGLADESH QUICKSIGHTS REPORT FII TRACKER SURVEY WAVE 1. April 2014

QUICKSIGHTS REPORT FII TRACKER SURVEY WAVE 1 April 2014 THE FINANCIAL INCLUSION INSIGHTS (FII) PROGRAM The FII research program responds to the need for timely, demand-side data and practical insights

QUICKSIGHTS REPORT FII TRACKER SURVEY WAVE 1 April 2014 THE FINANCIAL INCLUSION INSIGHTS (FII) PROGRAM The FII research program responds to the need for timely, demand-side data and practical insights

NIGERIA. WAVE 3 REPORT FII TRACKER SURVEY Conducted August-September April 2016

WAVE 3 REPORT FII TRACKER SURVEY Conducted August-September 2015 April 2016 PUTTING THE USER FRONT AND CENTER The Financial Inclusion Insights (FII) program responds to the need identified by multiple

WAVE 3 REPORT FII TRACKER SURVEY Conducted August-September 2015 April 2016 PUTTING THE USER FRONT AND CENTER The Financial Inclusion Insights (FII) program responds to the need identified by multiple

Insurance Awareness Survey

Insurance Awareness Survey Research Report March 2017 Background Several past studies show that insurance awareness levels are low To remedy this AKI 2016-2020 Strategy aims to grow insurance awareness

Insurance Awareness Survey Research Report March 2017 Background Several past studies show that insurance awareness levels are low To remedy this AKI 2016-2020 Strategy aims to grow insurance awareness

41% of Palauan women are engaged in paid employment

Palau 2013/2014 HIES Gender profile Executive Summary 34% 18% 56% of Palauan households have a female household head is the average regular cash pay gap for Palauan women in professional jobs of internet

Palau 2013/2014 HIES Gender profile Executive Summary 34% 18% 56% of Palauan households have a female household head is the average regular cash pay gap for Palauan women in professional jobs of internet

Technology s role in microfinance to improve financial inclusion in the post-conflict regions of Sri Lanka. Mithula Guganeshan Perampalam Suthaharan

Technology s role in microfinance to improve financial inclusion in the post-conflict regions of Sri Lanka Mithula Guganeshan Perampalam Suthaharan Microfinance, a key enabler of financial inclusion Financial

Technology s role in microfinance to improve financial inclusion in the post-conflict regions of Sri Lanka Mithula Guganeshan Perampalam Suthaharan Microfinance, a key enabler of financial inclusion Financial

MAP Zimbabwe Stakeholder Workshop: Key Findings

MAP Zimbabwe Stakeholder Workshop: Key Findings Presentation on the findings from the Making Access Possible (MAP) Diagnostic conducted in Zimbabwe Harare, Zimbabwe 14 December, 2015 Agenda MAP diagnostic

MAP Zimbabwe Stakeholder Workshop: Key Findings Presentation on the findings from the Making Access Possible (MAP) Diagnostic conducted in Zimbabwe Harare, Zimbabwe 14 December, 2015 Agenda MAP diagnostic

Presentation at the Conference <Finance for all: Promoting Financial Inclusion in Central Africa>, COBAC/BEAC/IMF, March 23, 2015

RWANDA s FINANCIAL INCLUSION SUCCESS STORY: UMURENGE SACCO PROGRAM IN RWANDA Presentation at the Conference , COBAC/BEAC/IMF, KAVUGIZO SHYAMBA Kevin OUTLINE 2 I.

RWANDA s FINANCIAL INCLUSION SUCCESS STORY: UMURENGE SACCO PROGRAM IN RWANDA Presentation at the Conference , COBAC/BEAC/IMF, KAVUGIZO SHYAMBA Kevin OUTLINE 2 I.

Launch of Advans Bank Tanzania s SME lending operations

SCBF 2012-07 October 2014 Launch of Advans Bank Tanzania s SME lending operations 1. Development relevance Economic and poverty context: Tanzania is a Sub-Saharan country with a population of 48 million

SCBF 2012-07 October 2014 Launch of Advans Bank Tanzania s SME lending operations 1. Development relevance Economic and poverty context: Tanzania is a Sub-Saharan country with a population of 48 million

BANGLADESH. QUICKSIGHTS REPORT FII TRACKER SURVEY Conducted August-September November 2015

QUICKSIGHTS REPORT FII TRACKER SURVEY Conducted August-September 2015 November 2015 Notable statistics Bangladesh is experiencing a shift in the primary means of financial access. o o o In 2013 and 2014,

QUICKSIGHTS REPORT FII TRACKER SURVEY Conducted August-September 2015 November 2015 Notable statistics Bangladesh is experiencing a shift in the primary means of financial access. o o o In 2013 and 2014,

Swaziland Strives To Reduce Poverty, Empower Women Swaziland Round 5 Release Event 4

WWW.AFROBAROMETER.ORG Swaziland Strives To Reduce Poverty, Empower Women Swaziland Round 5 Release Event 4 What is the Afrobarometer? The Afrobarometer is an independent, nonpartisan research project that

WWW.AFROBAROMETER.ORG Swaziland Strives To Reduce Poverty, Empower Women Swaziland Round 5 Release Event 4 What is the Afrobarometer? The Afrobarometer is an independent, nonpartisan research project that

Indonesia - Global Financial Inclusion (Global Findex) Database 2011

Database 2011") Microdata Library Indonesia - Global Financial Inclusion (Global Findex) Database 2011 Development Research Group, Finance and Private Sector Development Unit - World Bank Report generated on: April 15,

Microdata Library Indonesia - Global Financial Inclusion (Global Findex) Database 2011 Development Research Group, Finance and Private Sector Development Unit - World Bank Report generated on: April 15,

Business Registration Impact Evaluation (BRIE) Malawi

Malawi") Business Registration Impact Evaluation (BRIE) Malawi Informality and Financial Inclusion: Cross-country and experimental evidence Washington, DC, June 2013 Francisco Campos, Africa Financial and Private

Business Registration Impact Evaluation (BRIE) Malawi Informality and Financial Inclusion: Cross-country and experimental evidence Washington, DC, June 2013 Francisco Campos, Africa Financial and Private

FinScope Consumer Survey DRC 2014

FinScope Consumer Survey DRC 2014 LAUNCH PRESENTATION 26 March 2015 Kinshasa, DRC Making financial markets work for the poor Objectives of FinScope DRC 2014 To describe the levels of financial inclusion

FinScope Consumer Survey DRC 2014 LAUNCH PRESENTATION 26 March 2015 Kinshasa, DRC Making financial markets work for the poor Objectives of FinScope DRC 2014 To describe the levels of financial inclusion

Lao PDR - Global Financial Inclusion (Global Findex) Database 2011

Database 2011") Microdata Library Lao PDR - Global Financial Inclusion (Global Findex) Database 2011 Development Research Group, Finance and Private Sector Development Unit - World Bank Report generated on: April 15,

Microdata Library Lao PDR - Global Financial Inclusion (Global Findex) Database 2011 Development Research Group, Finance and Private Sector Development Unit - World Bank Report generated on: April 15,

FinScope. Consumer Survey Highlights. Demand for financial services. Togo 2016 MAKING ACCESS POSSIBLE

FinScope Consumer Survey Highlights Demand for financial services Togo 2016 MAKING ACCESS POSSIBLE Partnering for a common purpose Making Access Possible (MAP) is a diagnostic and programmatic framework

FinScope Consumer Survey Highlights Demand for financial services Togo 2016 MAKING ACCESS POSSIBLE Partnering for a common purpose Making Access Possible (MAP) is a diagnostic and programmatic framework

Interest Payment on Mobile Network Operators Trust Accounts. Term of Reference

Interest Payment on Mobile Network Operators Trust Accounts 1. Introduction Term of Reference The Bank of Tanzania (Directorate of National Payment system) and The Financial Sector Deepening Trust (FSDT)

Interest Payment on Mobile Network Operators Trust Accounts 1. Introduction Term of Reference The Bank of Tanzania (Directorate of National Payment system) and The Financial Sector Deepening Trust (FSDT)

INNOVATIONS FOR POVERTY ACTION S RAINWATER STORAGE DEVICE EVALUATION. for RELIEF INTERNATIONAL BASELINE SURVEY REPORT

INNOVATIONS FOR POVERTY ACTION S RAINWATER STORAGE DEVICE EVALUATION for RELIEF INTERNATIONAL BASELINE SURVEY REPORT January 20, 2010 Summary Between October 20, 2010 and December 1, 2010, IPA conducted

INNOVATIONS FOR POVERTY ACTION S RAINWATER STORAGE DEVICE EVALUATION for RELIEF INTERNATIONAL BASELINE SURVEY REPORT January 20, 2010 Summary Between October 20, 2010 and December 1, 2010, IPA conducted

KENYA QUICKSIGHTS REPORT FIFTH ANNUAL FII TRACKER SURVEY. June Conducted June-July 2017

QUICKSIGHTS REPORT FIFTH ANNUAL FII TRACKER SURVEY Conducted June-July 2017 June 2018 UNDERSTANDING FINANCIAL INCLUSION What is financial inclusion? Financial inclusion means that individuals and businesses

QUICKSIGHTS REPORT FIFTH ANNUAL FII TRACKER SURVEY Conducted June-July 2017 June 2018 UNDERSTANDING FINANCIAL INCLUSION What is financial inclusion? Financial inclusion means that individuals and businesses

INDIA. QUICKSIGHTS REPORT FOURTH ANNUAL FII TRACKER SURVEY Fieldwork Conducted September 2016 through January January 2016

QUICKSIGHTS REPORT FOURTH ANNUAL FII TRACKER SURVEY Fieldwork Conducted September 2016 through January 2017 January 2016 Key definitions Access Access to a bank account or mobile money account means an

QUICKSIGHTS REPORT FOURTH ANNUAL FII TRACKER SURVEY Fieldwork Conducted September 2016 through January 2017 January 2016 Key definitions Access Access to a bank account or mobile money account means an

Financial Inclusion in ASEAN Presentation for the ASEAN Working Group on Financial Inclusion Kuala Lumpur, Malaysia, January 21, 2016

Financial Inclusion in ASEAN Presentation for the ASEAN Working Group on Financial Inclusion Kuala Lumpur, Malaysia, January 21, 2016 Jose De Luna Martinez World Bank Group Contents I. Financial inclusion

Financial Inclusion in ASEAN Presentation for the ASEAN Working Group on Financial Inclusion Kuala Lumpur, Malaysia, January 21, 2016 Jose De Luna Martinez World Bank Group Contents I. Financial inclusion

Case study: Branch. Exploring the potential of alternative data for creating new markets

Case study: Branch Exploring the potential of alternative data for creating new markets Welcome to Branch Learn about your loan offers Your loan has been approved Advancing Financial Inclusion Authors

Case study: Branch Exploring the potential of alternative data for creating new markets Welcome to Branch Learn about your loan offers Your loan has been approved Advancing Financial Inclusion Authors

INDIA WAVE 4 REPORT FII TRACKER SURVEY. June Conducted September 2016 January 2017

INDIA WAVE 4 REPORT FII TRACKER SURVEY Conducted September 2016 January 2017 June 2017 PUTTING THE USER FRONT AND CENTER INDIA The Financial Inclusion Insights (FII) program responds to the need identified

INDIA WAVE 4 REPORT FII TRACKER SURVEY Conducted September 2016 January 2017 June 2017 PUTTING THE USER FRONT AND CENTER INDIA The Financial Inclusion Insights (FII) program responds to the need identified

MEASURING FINANCIAL INCLUSION: THE GLOBAL FINDEX. Asli Demirguc-Kunt & Leora Klapper

MEASURING FINANCIAL INCLUSION: THE Asli Demirguc-Kunt & Leora Klapper OVERVIEW What is the Global Findex? The first individual-level database on financial inclusion that is comparable across countries

MEASURING FINANCIAL INCLUSION: THE Asli Demirguc-Kunt & Leora Klapper OVERVIEW What is the Global Findex? The first individual-level database on financial inclusion that is comparable across countries

Southern Punjab Poverty Alleviation Project (SPPAP)

") Southern Punjab Poverty Alleviation Project (SPPAP) Initial Impact of Community Revolving Funds for Agriculture Input Supply (CRFAIS) ~A Pilot Activity of SPPAP National Rural Support Programme (NRSP)

Southern Punjab Poverty Alleviation Project (SPPAP) Initial Impact of Community Revolving Funds for Agriculture Input Supply (CRFAIS) ~A Pilot Activity of SPPAP National Rural Support Programme (NRSP)

Understanding people's use of financial services in Indonesia

Understanding people's use of financial services in Indonesia Headline Results Report Implemented by For feedback on the contents of this report or to request further information regarding SOFIA, please

Understanding people's use of financial services in Indonesia Headline Results Report Implemented by For feedback on the contents of this report or to request further information regarding SOFIA, please

Tanzania Access to Insurance Diagnostic

Tanzania Access to Insurance Diagnostic Document 8: Understanding consumer needs and segmenting the target market 01/11/12 Final draft VERSION 3 01/11/2012 Diagnostic series authored by Cenfri on behalf

Tanzania Access to Insurance Diagnostic Document 8: Understanding consumer needs and segmenting the target market 01/11/12 Final draft VERSION 3 01/11/2012 Diagnostic series authored by Cenfri on behalf

Overview. Financial Systems approach to microfinance Basic roles and functions of government and donors at various points within the financial sector

Overview Financial Systems approach to microfinance Basic roles and functions of government and donors at various points within the financial sector The Borders of Microfinance are Blurring Khan bank serving

Overview Financial Systems approach to microfinance Basic roles and functions of government and donors at various points within the financial sector The Borders of Microfinance are Blurring Khan bank serving

Survey on Income and Living Conditions (SILC)

") An Phríomh-Oifig Staidrimh Central Statistics Office 15 August 2013 Poverty and deprivation rates of the elderly in Ireland, SILC 2004, 2009, 2010 revised and 2011 At risk of poverty rate Deprivation rate

An Phríomh-Oifig Staidrimh Central Statistics Office 15 August 2013 Poverty and deprivation rates of the elderly in Ireland, SILC 2004, 2009, 2010 revised and 2011 At risk of poverty rate Deprivation rate

Internet use and attitudes Metrics Bulletin

Internet use and attitudes 2014 Metrics Bulletin Research Document Publication date: 7 August 2014 Contents Section Page 1 Introduction 3 2 Internet reach: 2014 9 3 Internet breadth of use 10 4 Internet

Internet use and attitudes 2014 Metrics Bulletin Research Document Publication date: 7 August 2014 Contents Section Page 1 Introduction 3 2 Internet reach: 2014 9 3 Internet breadth of use 10 4 Internet

FinScope. Consumer Survey Highlights. Burkina Faso 2016 MAKING ACCESS POSSIBLE

FinScope Consumer Survey Highlights Burkina Faso 2016 MAKING ACCESS POSSIBLE Partnering for a common purpose Making Access Possible (MAP) is a diagnostic and programmatic framework to support expanding

FinScope Consumer Survey Highlights Burkina Faso 2016 MAKING ACCESS POSSIBLE Partnering for a common purpose Making Access Possible (MAP) is a diagnostic and programmatic framework to support expanding