It has been another week of bumpy risk appetite, as both tariff risks and North Korea have entered the frame again.

|

|

|

- Elwin Whitehead

- 5 years ago

- Views:

Transcription

1 It has been another week of bumpy risk appetite, as both tariff risks and North Korea have entered the frame again. We warned a few months back that Auto tariffs would be the obvious next target for Donald Trump (FX weekly: Taxation mirror on the wall, who is the fairest of them all? ) given the discrepancies in the import-taxation of Autos between the US and Europe (and the US and China for that matter). The concept of mirror-taxation that Trump launched at his press meeting on the steel and aluminium tariffs thus stills seems to be at the top of the US president s agenda. While the market overestimated the Trump risks a few months back, we now tend to think that risks are more balanced or even tilted towards Trump re-rocking the market boat. The market repercussions of a renewed focus on tariffs and the breakdown of North Korea talks are relatively clear. If North Korean tensions increase again and if Trump decides to launch auto tariffs, it will take its toll on risk appetite in general and likely also be a game-changer for the current USD positive market environment (at least initially).

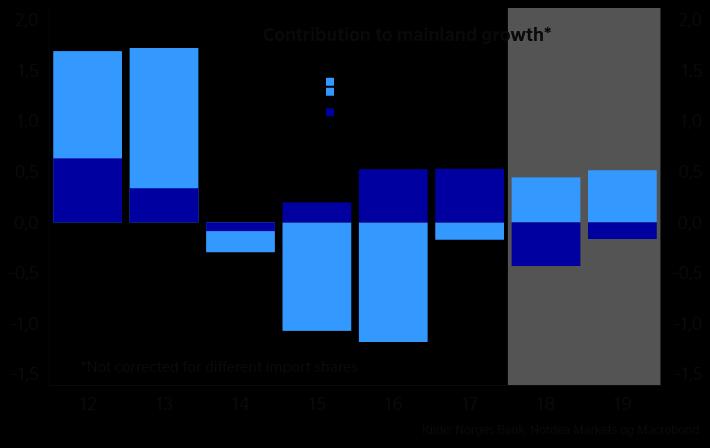

2 While you can read the Fed s tolerance towards overshooting on inflation as dovish news, the primary reason behind the dovish shift in the fed funds pricing in the aftermath of the minutes was the comment on a potential 20 bp hike in the IOER rate instead of a 25 bp hike. The Fed wrote Since the target range was established in December2008, the IOER rate has been set at the top of the target range to help keep the effective federal funds rate within the range. Lately the spread of the IOER rate over the effective federal funds rate had narrowed to only 5 basis points. A technical adjustment of the IOER rate to level 5 basis points below the top of the target range could keep the effective federal funds rate well within the target range. So the re-pricing of the front of the Fed Funds curve was much more about technicalities than actual dovish policy signals. Something that was misinterpreted by many commentators and likely also the reason why the USD did not react negatively to the minutes. The FOMC mentioned the word symmetrical eleven times in the minutes (Fed comment: On track), indicating that they are willing to tolerate overshooting inflation short term. However, we don t consider this a particularly dovish policy signal, but rather see it as prudent risk management from the Fed. As the

3 Fed is obviously not in control of short-term fluctuations in inflation, the FOMC has simply adjusted the language to minimise the negative market impact of the almost certain overshooting inflation. And while this symmetrical inflation focus from the FOMC may sound USD negative at first glance, it is not necessarily bad news for the USD. Since 2016, periods of relative steepening of the USD curve versus the EUR curve have coincided with a stronger USD, as a steeper USD curve invites partially FX hedged international bond flows into US. Our bottom line is that tolerance towards inflation could prove temporarily USD positive via a relative steepening of the USD curve. Recently, the core inflation spread widening between the US and Japan, the UK and the Euro area has been a key driver of the USD gaining versus most peers. Our newly updated G10 forecasts also include a short-term expectation of a stronger USD.

, the updated staff projections could prove unusually interesting.")

.")

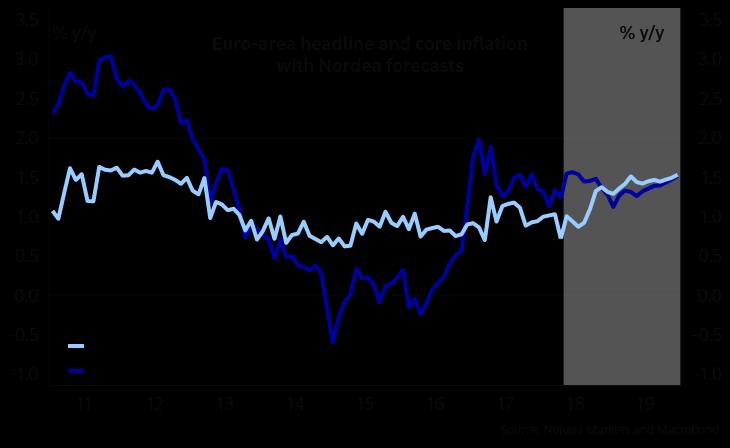

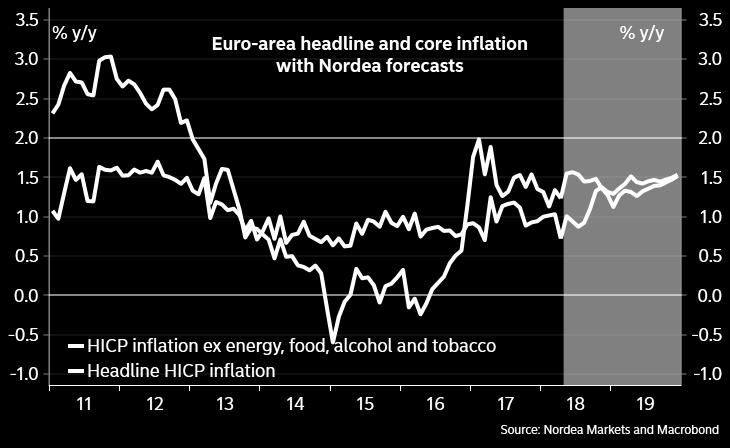

4 On the EUR side of the equation, the ECB meeting in a few weeks time looks increasingly interesting. While our base case is that ECB will refrain from taking any policy actions in June (our base case is July), the updated staff projections could prove unusually interesting. While the rising energy prices will start to surface in EUR headline inflation as early as next week, also the FX developments since the latest projection update in March argue for a higher HICP inflation path in the staff projections (currently as much as 0.25% for 2018 according to the ECB s own methodology). This leaves a potential difficult communication task ahead for the ECB, as they likely want to sound dovish despite a higher inflation forecast.

5 We see elevated risks that markets will put too much emphasis on rising headline inflation in the Euro area over the next months and as the market pricing of the ECB has almost collapsed recently, there is a risk that the market will reprice the ECB hawkishly from the current levels. If a hawkish re-pricing were to arise into the summer, we would prefer to fade such a move. Both core inflation and growth momentum are worrying the ECB and this is maybe also what the EUR/USD currently prices in.

6 In terms of the European growth momentum, Mario Draghi and co. should cross their fingers ahead of the Swedish PMIs next week. Sweden is a small open export-dependent country that picks up changes in global demand faster than the Euro area. That is why the Swedish PMI tells us where Euro-area PMI will head a couple of months later. So if the Swedish canary doesn t fly next Friday, it is a sign that the ECB could turn even more dovish than anticipated two to four months from now.

, the signal value could prove to be strong. The tradeweighted krona is still 1% weaker than the Riksbank anticipated for Q2 and 3.")

7 Otherwise it has been a relatively quiet week on the data front from Scandinavia. The most newsworthy story from Sweden is that the Swedish Debt Office will take a position for a stronger krona. While the flow effects are marginal from this decision (7bn SEK), the signal value could prove to be strong. The tradeweighted krona is still 1% weaker than the Riksbank anticipated for Q2 and 3.5% weaker than anticipated for Q3. The Riksbank's KIX forecasts are consistent with EUR/SEK at in Q2 and 9.90 in Q3. In Norway, the AKU unemployment rate came out in line with consensus of 3.9%. But even with the economic surprise index at depressed levels in Norway, we think that the recent patch of data still argues for an unchanged rate path in June. Low inflation and high spreads in the money market argue for a lower rate path. However, higher oil prices pull significantly in the other direction. A September rate hike is still on the table. In addition to the continued developments surrounding the North Korean summit and auto tariffs, next week is relatively data-heavy in both the US and the Euro area. The European inflation print (Wednesday) will be extra closely scrutinised by markets, as the very weak April print caused a dovish shift in market expectations for the ECB. We expect Euro-area core inflation to rebound to 1%, while headline inflation could print at 1.6%.

8 Given the seasonal pattern in Euro-area core inflation for the past ten years, core inflation better rebound in May, otherwise a very weak summer for core inflation could be on the cards. A rebound to 1% alongside headline inflation at 1.6% should limit the need for a further dovish repricing of the ECB short term. We get the first inflationary hints out of Germany already on Tuesday. We will get new clues on whether the US will continue to outpace the rest of the world in terms of economic momentum when the ISM index is published (Friday). The regional surveys point to a rebound in the ISM. While most of this anticipated rebound in the ISM is already priced in (consensus expects a rebound from 57.3 to 58.1), it should still work to emphasise that the US is in the driving seat at the moment. But we still don t judge that there is good risk/reward in betting on a high ISM print. Also the job report will be in focus in the US on Friday afternoon.

.")

9 In Scandinavia, the week will kick off with the Oil Investment Survey from Norway on Monday. Strong growth in oil investment both in 2018 and 2019 is an important reason for ours and Norges Bank s upbeat view on the economy. The rise in oil investment more than counteracts the effect of lower housing activity which follows last year's slowdown in housing prices. We believe in a moderate upward revision of the oil investments this year, which will point to growth at 8-10%. Also Norwegian registered unemployment will be important for Norges Bank (Friday). From Sweden, the first quarter GDP report is due out on Wednesday. We believe that GDP growth moderated in the early months of the year and more than the Riksbank anticipates. Household consumption grew at a healthy pace, while exports flattened. On Friday the Swedish PMI is due. Major forecasts: A temporary return of king USD Swedish Q1 GDP preview: Downside risks to Riksbank forecast Norway preview: Strong growth in oil investment and tighter labour market TRY: Where do we go from here? Should Russia fear US recession?

10

11

12 Swedish and US consumer confidence are the only key releases today. A bunch of central bankers will give speeches, including the Fed s Bullard (dove, non-voter) and ECB members Villeroy (neutral), Mersch (neutral), Lautenschläger (hawk) and Couere (dove).

13

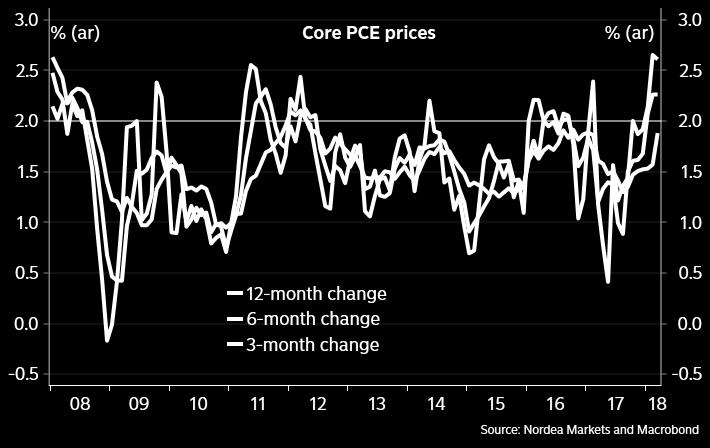

14 Today is the big inflation day as we get both flash Euro-area HICP numbers and the Fed s preferred inflation measure, the core PCE price index. Otherwise, the day will bring official PMIs from China and a couple of speeches from FOMC members Bostic (neutral/dove, voter) and Bullard (dove, non-voter).

15

16 Today s main release is the US job report where focus once again will be on the wage component. The day, however, also brings a lot of important growth and activity indicators, including the ISM index from the US and flash PMIs from China (Caixin), Sweden, Norway, Russia and the UK. Final PMIs from the Euro-area are also due.

17

18

19

Fixed Income and FX Weekly

Fixed Income and FX Weekly Softer growth and renewed sovereign debt focus 23 May, 2011 Bjørn Roger Wilhelmsen Chief Strategist, FX & Fixed Income +47 23 11 62 63 brw@first.no Good morning, A stream of

Fixed Income and FX Weekly Softer growth and renewed sovereign debt focus 23 May, 2011 Bjørn Roger Wilhelmsen Chief Strategist, FX & Fixed Income +47 23 11 62 63 brw@first.no Good morning, A stream of

Leumi. Global Economics Monthly Review. Arie Tal, Research Economist. July 12, Capital Markets Division, Economics Department. leumiusa.

Global Economics Monthly Review July 12, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report

Global Economics Monthly Review July 12, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report

Week ahead: September 5 th 9 th

Week ahead: September 5 th 9 th ECB, BoC, RBA & Riksbank policy meetings, key data in focus Next week s market movers We expect the ECB to hold off from introducing any fresh stimulus. The focus will likely

Week ahead: September 5 th 9 th ECB, BoC, RBA & Riksbank policy meetings, key data in focus Next week s market movers We expect the ECB to hold off from introducing any fresh stimulus. The focus will likely

Nordkinn Market Review & Outlook April 2018

Nordkinn Market Review & Outlook April 2018 Addressed to Nordkinn s Followers on LinkedIn for informational purposes Please note that the content of thetom Nordkinn Market Review & Outlook Report may not

Nordkinn Market Review & Outlook April 2018 Addressed to Nordkinn s Followers on LinkedIn for informational purposes Please note that the content of thetom Nordkinn Market Review & Outlook Report may not

Global Macroeconomic Monthly Review

Global Macroeconomic Monthly Review August 14 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department 1 Please see disclaimer on the last page of this report Key Issues Global

Global Macroeconomic Monthly Review August 14 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department 1 Please see disclaimer on the last page of this report Key Issues Global

Leumi. Global Economics Monthly Review. Arie Tal, Research Economist. May 8, The Finance Division, Economics Department. leumiusa.

Global Economics Monthly Review May 8, 2018 Arie Tal, Research Economist The Finance Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report Key

Global Economics Monthly Review May 8, 2018 Arie Tal, Research Economist The Finance Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report Key

Editor: Felix Ewert. The Week Ahead Key Events 2 8 Oct, 2017

Editor: Felix Ewert The Week Ahead Key Events 2 8 Oct, 2017 Monday 2, 08.30 SWE: PMI Manufacturing (Sep) Index SEB Cons. Prev. PMI 60.5 -- 54.7 Manufacturing PMI showed an unexpectedly large fall in August.

Editor: Felix Ewert The Week Ahead Key Events 2 8 Oct, 2017 Monday 2, 08.30 SWE: PMI Manufacturing (Sep) Index SEB Cons. Prev. PMI 60.5 -- 54.7 Manufacturing PMI showed an unexpectedly large fall in August.

Editor: Thomas Nilsson. The Week Ahead Key Events Jul, 2017

Editor: Thomas Nilsson The Week Ahead Key Events 10 16 Jul, 2017 European Sovereign Rating Reviews Recent rating reviews Upcoming rating reviews Source: Bloomberg Monday 10, 08.00 NOR: CPI (Jun) SEB Cons.

Editor: Thomas Nilsson The Week Ahead Key Events 10 16 Jul, 2017 European Sovereign Rating Reviews Recent rating reviews Upcoming rating reviews Source: Bloomberg Monday 10, 08.00 NOR: CPI (Jun) SEB Cons.

Editor: Felix Ewert. The Week Ahead Key Events 6 12 Nov, 2017

Editor: Felix Ewert The Week Ahead Key Events 6 12 Nov, 2017 Monday 6, 09.30 SWE: Industrial production & orders (Sep) % mom/yoy SEB Cons. Prev. Production 2.5/4.1 --- -1.7/7.3 New orders --- --- -1.8/6.3

Editor: Felix Ewert The Week Ahead Key Events 6 12 Nov, 2017 Monday 6, 09.30 SWE: Industrial production & orders (Sep) % mom/yoy SEB Cons. Prev. Production 2.5/4.1 --- -1.7/7.3 New orders --- --- -1.8/6.3

Strategy Bond yield conundrum vol. 2

Investment Research General Market Conditions 30 November 2017 Strategy Bond yield conundrum vol. 2 The big US curve flattening The big theme in the US fixed income market is the flattening of the yield

Investment Research General Market Conditions 30 November 2017 Strategy Bond yield conundrum vol. 2 The big US curve flattening The big theme in the US fixed income market is the flattening of the yield

The Week Ahead Key Events 4 10 Jan, 2016

Editor: Carl Hammer The Week Ahead Key Events 4 10 Jan, 2016 Editor: Benjamin Dousa Monday 4, 08.30 SWE: PMI manufacturing (Dec) Index SEB Cons. Prev PMI 55.0 --- 54.9 Manufacturing confidence according

Editor: Carl Hammer The Week Ahead Key Events 4 10 Jan, 2016 Editor: Benjamin Dousa Monday 4, 08.30 SWE: PMI manufacturing (Dec) Index SEB Cons. Prev PMI 55.0 --- 54.9 Manufacturing confidence according

Global Macroeconomic Monthly Review

Global Macroeconomic Monthly Review October 16 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department Please see disclaimer on the last page of this report 1 Key Issues Global

Global Macroeconomic Monthly Review October 16 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department Please see disclaimer on the last page of this report 1 Key Issues Global

The ECB Survey of Professional Forecasters. First quarter of 2017

The ECB Survey of Professional Forecasters First quarter of 217 January 217 Contents 1 Near-term inflation expectations a little higher, due to oil price rises 3 2 Longer-term inflation expectations unchanged

The ECB Survey of Professional Forecasters First quarter of 217 January 217 Contents 1 Near-term inflation expectations a little higher, due to oil price rises 3 2 Longer-term inflation expectations unchanged

Editor: Thomas Nilsson. The Week Ahead Key Events 31 Jul 6 Aug, 2017

Editor: Thomas Nilsson The Week Ahead Key Events 31 Jul 6 Aug, 2017 European Sovereign Rating Reviews Recent rating reviews Friday, 21 July 2017 Agency previous new action Greece S&P B- / Stable B- /

Editor: Thomas Nilsson The Week Ahead Key Events 31 Jul 6 Aug, 2017 European Sovereign Rating Reviews Recent rating reviews Friday, 21 July 2017 Agency previous new action Greece S&P B- / Stable B- /

Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy February 2017 Global Stock Market Rally likely to Continue with Solid Q4 Earnings & Stronger 2017 Earnings, ECB

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy February 2017 Global Stock Market Rally likely to Continue with Solid Q4 Earnings & Stronger 2017 Earnings, ECB

EMPLOYMENT REPORT (MAY)

") LPL RESEARCH WEEKLY ECONOMIC COMMENTARY May 30 2017 JUNE PREVIEW Matthew E. Peterson Chief Wealth Strategist, LPL Financial Ryan Detrick, CMT Senior Market Strategist, LPL Financial KEY TAKEAWAYS June

LPL RESEARCH WEEKLY ECONOMIC COMMENTARY May 30 2017 JUNE PREVIEW Matthew E. Peterson Chief Wealth Strategist, LPL Financial Ryan Detrick, CMT Senior Market Strategist, LPL Financial KEY TAKEAWAYS June

Fourth Quarter Market Outlook. Kim Huebner, CFA Don Powell, CFA Joseph Styrna, CFA

Fourth Quarter 2017 Market Outlook Kim Huebner, CFA Don Powell, CFA Joseph Styrna, CFA Economic Outlook Growth Increasing, Spending Modest, Low Unemployment 2017 2016 2015 2014 2013 2012 2011 GDP* Q3:

Fourth Quarter 2017 Market Outlook Kim Huebner, CFA Don Powell, CFA Joseph Styrna, CFA Economic Outlook Growth Increasing, Spending Modest, Low Unemployment 2017 2016 2015 2014 2013 2012 2011 GDP* Q3:

Editor: Felix Ewert. The Week Ahead Key Events Mar 2018

Editor: Felix Ewert The Week Ahead Key Events 12 18 Mar 2018 Monday 12, 08.00 SWE: Unemployment, registered (Feb) SEB Cons. Prev. Open 3.9 --- 4.0 Open, seas. adj. 3.8 --- 3.8 Total seas. adj. 7.1 ---

Editor: Felix Ewert The Week Ahead Key Events 12 18 Mar 2018 Monday 12, 08.00 SWE: Unemployment, registered (Feb) SEB Cons. Prev. Open 3.9 --- 4.0 Open, seas. adj. 3.8 --- 3.8 Total seas. adj. 7.1 ---

Ulster Bank Weekly Economic Commentary

Ulster Bank Weekly Economic Commentary Ricardo Amaro Economist 15 June 2018 To subscribe or unsubscribe please contact economics@ulsterbankcm.com Ireland: New housing dwellings revised significantly lower

Ulster Bank Weekly Economic Commentary Ricardo Amaro Economist 15 June 2018 To subscribe or unsubscribe please contact economics@ulsterbankcm.com Ireland: New housing dwellings revised significantly lower

Week Ahead May. Nordea Research, 13 May 2015

Week Ahead 14 22 May Nordea Research, 13 May 2015 Next week s key events US Minutes of the 28-29 April FOMC minutes meeting are expected to signal that the Fed still sees a first rate hike later this year.

Week Ahead 14 22 May Nordea Research, 13 May 2015 Next week s key events US Minutes of the 28-29 April FOMC minutes meeting are expected to signal that the Fed still sees a first rate hike later this year.

October 2016 Market Update

Market Update (10/2016) Allianz Investment Management LLC October 2016 Market Update Key Points The lack of further easing measures from both the Bank of Japan and the European Central Bank are causing

Market Update (10/2016) Allianz Investment Management LLC October 2016 Market Update Key Points The lack of further easing measures from both the Bank of Japan and the European Central Bank are causing

Strategy The big EUR curve flattening has started

Investment Research General Market Conditions 18 January 2018 Strategy The big EUR curve flattening has started It has been a rocky past month for both the US and the European fixed income market, as 10Y

Investment Research General Market Conditions 18 January 2018 Strategy The big EUR curve flattening has started It has been a rocky past month for both the US and the European fixed income market, as 10Y

Global Macroeconomic Monthly Review

Global Macroeconomic Monthly Review April 2019 Dr. Gil Michael Bufman, Chief Economist Arie Tal, Research Economist Economics Department, Capital Markets Division 1 Please see disclaimer on the last page

Global Macroeconomic Monthly Review April 2019 Dr. Gil Michael Bufman, Chief Economist Arie Tal, Research Economist Economics Department, Capital Markets Division 1 Please see disclaimer on the last page

On The Economy, Wages, Interest Rates & The Yield Curve

On The Economy, Wages, Interest Rates & The Yield Curve May 1, 2018 by Gary D. Halbert of Halbert Wealth Management Overview We touch on several bases today, starting with last Friday s initial estimate

On The Economy, Wages, Interest Rates & The Yield Curve May 1, 2018 by Gary D. Halbert of Halbert Wealth Management Overview We touch on several bases today, starting with last Friday s initial estimate

Diffusion indices of forecast risks in Summary of Economic Projections From September 2016 FOMC to December 2018 FOMC.

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas

Economic Outlook August 2017

Economic Outlook August 2017 Philippe WAECHTER Directeur de la Recherche Economique Compte Twitter: @phil_waechter ou http://twitter.com/phil_waechter SoundCloud http://soundcloud.com/phil_waechter Blog:

Economic Outlook August 2017 Philippe WAECHTER Directeur de la Recherche Economique Compte Twitter: @phil_waechter ou http://twitter.com/phil_waechter SoundCloud http://soundcloud.com/phil_waechter Blog:

Key events in developed markets next week

Economic and Financial Analysis Global Economics Article Key events in developed markets next week It is a data-heavy week in developed markets next week. We'll be watching 1Q growth figures in the US

Economic and Financial Analysis Global Economics Article Key events in developed markets next week It is a data-heavy week in developed markets next week. We'll be watching 1Q growth figures in the US

Diffusion indices of forecast risks in Summary of Economic Projections From September 2016 FOMC to June 2018 FOMC. Mar '17 FOMC

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer

Eurozone - FX EUR/USD

1 Weekly FX 9 September 2013 Eurozone - FX EUR/USD 2-Y spread Germany-US EUR/USD 0.1 1.40-0.1 1.35-0.2 1.30-0.3 1.25-0.4 1.20 Jan 12 Jul 12 Jan 13 Jul 13 2-yr spread Germany-US EUR/USD (rhs) Source: Thomson

1 Weekly FX 9 September 2013 Eurozone - FX EUR/USD 2-Y spread Germany-US EUR/USD 0.1 1.40-0.1 1.35-0.2 1.30-0.3 1.25-0.4 1.20 Jan 12 Jul 12 Jan 13 Jul 13 2-yr spread Germany-US EUR/USD (rhs) Source: Thomson

Editor: Felix Ewert. The Week Ahead Key Events 27 Nov 3 Dec, 2017

Editor: Felix Ewert The Week Ahead Key Events 27 Nov 3 Dec, 2017 Monday 27, 08.00 Swedish CFO Survey and Index The Swedish CFO index rose to 58.2 in the spring which was the highest level since May 2011.

Editor: Felix Ewert The Week Ahead Key Events 27 Nov 3 Dec, 2017 Monday 27, 08.00 Swedish CFO Survey and Index The Swedish CFO index rose to 58.2 in the spring which was the highest level since May 2011.

Ulster Bank Weekly Economic Commentary

Ulster Bank Weekly Economic Commentary Ricardo Amaro Economist 6 th April 2018 To subscribe or unsubscribe please contact economics@ulsterbankcm.com Ireland: PMIs continue to point to healthy growth The

Ulster Bank Weekly Economic Commentary Ricardo Amaro Economist 6 th April 2018 To subscribe or unsubscribe please contact economics@ulsterbankcm.com Ireland: PMIs continue to point to healthy growth The

International Financial Market Report

Financial and Banking Operations Department - International Reserves Management Division - International Financial Market Report (23 27 April 2018) Podgorica, 4 May 2018 FX NEWS EUR/USD The EUR/USD exchange

Financial and Banking Operations Department - International Reserves Management Division - International Financial Market Report (23 27 April 2018) Podgorica, 4 May 2018 FX NEWS EUR/USD The EUR/USD exchange

Swedish krona: A forecast revision

Economic and Financial Analysis 8 May 2018 FX 8 May 2018 Article Swedish krona: A forecast revision We expect the battered Swedish krona to remain under pressure as global trade tensions, domestic politics

Economic and Financial Analysis 8 May 2018 FX 8 May 2018 Article Swedish krona: A forecast revision We expect the battered Swedish krona to remain under pressure as global trade tensions, domestic politics

The ECB Survey of Professional Forecasters. Second quarter of 2017

The ECB Survey of Professional Forecasters Second quarter of 17 April 17 Contents 1 Near-term headline inflation expectations revised up, expectations for HICP inflation excluding food and energy broadly

The ECB Survey of Professional Forecasters Second quarter of 17 April 17 Contents 1 Near-term headline inflation expectations revised up, expectations for HICP inflation excluding food and energy broadly

Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy March 2017 Global Stock Markets Rally likely to Continue, Driven by Strong Earnings & Strengthening GDP Growth.

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy March 2017 Global Stock Markets Rally likely to Continue, Driven by Strong Earnings & Strengthening GDP Growth.

INVESTMENT OUTLOOK. August 2017

INVESTMENT OUTLOOK August 2017 INVESTMENT OUTLOOK AUGUST 2017 MACRO-ECONOMICS AND CURRENCIES Developed and Emerging Markets A series of comments from major central banks during the month, reminded investors

INVESTMENT OUTLOOK August 2017 INVESTMENT OUTLOOK AUGUST 2017 MACRO-ECONOMICS AND CURRENCIES Developed and Emerging Markets A series of comments from major central banks during the month, reminded investors

Weekly Outlook. 2 nd June 2014 by Richard Perry, Market Analyst. Macro Outlook. Must watch out for: European Central Bank monetary policy

Forex and CFDs are high risk leveraged products that can result in losses greater than your initial deposit and you should therefore only speculate with money you can afford to lose. FX and CFD trading

Forex and CFDs are high risk leveraged products that can result in losses greater than your initial deposit and you should therefore only speculate with money you can afford to lose. FX and CFD trading

Editor: Felix Ewert. The Week Ahead Key Events 29 Jan 4 Feb, 2018

Editor: Felix Ewert The Week Ahead Key Events 29 Jan 4 Feb, 2018 Tuesday 30, 08.00 NOR: Retail sales (Dec) % mom/yoy SEB Cons. Prev. Retail sales exc. autos -0.5/4.5-0.7/--- 2.1/3.5 Retail sales surged

Editor: Felix Ewert The Week Ahead Key Events 29 Jan 4 Feb, 2018 Tuesday 30, 08.00 NOR: Retail sales (Dec) % mom/yoy SEB Cons. Prev. Retail sales exc. autos -0.5/4.5-0.7/--- 2.1/3.5 Retail sales surged

Currencies Daily Report

Currencies Daily Report www.karvycurrency.com Friday 02 Jun 2017 Market Overview Asian shares were mostly higher today with attention on U.S. jobs data later in the day. Overnight, U.S. stocks made a winning

Currencies Daily Report www.karvycurrency.com Friday 02 Jun 2017 Market Overview Asian shares were mostly higher today with attention on U.S. jobs data later in the day. Overnight, U.S. stocks made a winning

Weekly Bulletin November 20, 2017

US data bolster the case for a rate hike. WEEKLY OUTLOOK In the USA, inflation and retail sales in October recorded an upbeat tone. Annual consumer inflation picked up by 2%, while core annual inflation

US data bolster the case for a rate hike. WEEKLY OUTLOOK In the USA, inflation and retail sales in October recorded an upbeat tone. Annual consumer inflation picked up by 2%, while core annual inflation

Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy April 2017 Stock Markets likely to Grind Higher as Expectations of Strong Earnings Growth & Improving Global GDP

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy April 2017 Stock Markets likely to Grind Higher as Expectations of Strong Earnings Growth & Improving Global GDP

Low Inflation and the Symmetry of the 2 Percent Target

Low Inflation and the Symmetry of the 2 Percent Target Charles L. Evans President and Chief Executive Officer Federal Reserve Bank of Chicago UBS European Conference London, England, UK November 15, 2017

Low Inflation and the Symmetry of the 2 Percent Target Charles L. Evans President and Chief Executive Officer Federal Reserve Bank of Chicago UBS European Conference London, England, UK November 15, 2017

Interest Rate Forecast

Interest Rate Forecast Economics January Highlights Global growth firms Waiting for Trumponomics Bank of Canada on hold Recent growth momentum in the global economy continued in December and looks to extend

Interest Rate Forecast Economics January Highlights Global growth firms Waiting for Trumponomics Bank of Canada on hold Recent growth momentum in the global economy continued in December and looks to extend

Diffusion indices of forecast risks in Summary of Economic Projections From September 2016 FOMC to September 2018 FOMC.

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer

Market Outlook 6 12 June 2016

Highlight Treasury Division TMU 0 :(66) 202 TMU 02 :(66) 202 222 TMU 0 :(66) 202 Market Outlook 6 2 June 206 Last Week: The US dollar dropped against major currencies on Friday (/6) after the nonfarm payrolls

Highlight Treasury Division TMU 0 :(66) 202 TMU 02 :(66) 202 222 TMU 0 :(66) 202 Market Outlook 6 2 June 206 Last Week: The US dollar dropped against major currencies on Friday (/6) after the nonfarm payrolls

Developments in inflation and its determinants

INFLATION REPORT February 2018 Summary Developments in inflation and its determinants The annual CPI inflation rate strengthened its upward trend in the course of 2017 Q4, standing at 3.32 percent in December,

INFLATION REPORT February 2018 Summary Developments in inflation and its determinants The annual CPI inflation rate strengthened its upward trend in the course of 2017 Q4, standing at 3.32 percent in December,

Yield Outlook Central banks gradually turning more hawkish

Investment Research General Market Conditions 5 September 207 Yield Outlook Central banks gradually turning more hawkish In the past few editions of Yield Outlook, we have argued that bond yields (represented

Investment Research General Market Conditions 5 September 207 Yield Outlook Central banks gradually turning more hawkish In the past few editions of Yield Outlook, we have argued that bond yields (represented

Market Commentary November 2015

Market Commentary November 2015 The Federal Reserve will, most likely, raise interest rates in December The last time rates were set up was in 2006. It could lead to higher volatility in the short term

Market Commentary November 2015 The Federal Reserve will, most likely, raise interest rates in December The last time rates were set up was in 2006. It could lead to higher volatility in the short term

Risk Insight. The Central Bank Tightening Party: Who Will Be Next To Join? What are the chances... Volume 8, Issue th July 2017.

Inside this issue Big Picture... 1-2 GBPUSD... 3 GBPEUR... 4 Risk Insight Volume 8, Issue 31 24 th July 2017 EURUSD... 5 USDCAD... 6 Economic Data and Market Indicators... 7 Appendix... 8 The Central Bank

Inside this issue Big Picture... 1-2 GBPUSD... 3 GBPEUR... 4 Risk Insight Volume 8, Issue 31 24 th July 2017 EURUSD... 5 USDCAD... 6 Economic Data and Market Indicators... 7 Appendix... 8 The Central Bank

Reading the Markets Sweden

Investment Research - General Market Conditions 13 December 2012 Reading the Markets Sweden How weak is the Swedish economy really? Possible consequences for the curve Danske Banks market view in a nutshell

Investment Research - General Market Conditions 13 December 2012 Reading the Markets Sweden How weak is the Swedish economy really? Possible consequences for the curve Danske Banks market view in a nutshell

Global Data Watch 28 August 1 September 28 August 2017

Economic Research The Week Ahead: Key US data releases and 2Q India GDP in focus US: Labour, personal spending and PCE data releases The US will see a number of important releases at the end of this week.

Economic Research The Week Ahead: Key US data releases and 2Q India GDP in focus US: Labour, personal spending and PCE data releases The US will see a number of important releases at the end of this week.

November 2017 Market Update

Market Update (11/2017) Allianz Investment Management LLC November 2017 Market Update Key Points Equities rallied to fresh all-time highs as the prospects for tax reform continued to move forward. Jay

Market Update (11/2017) Allianz Investment Management LLC November 2017 Market Update Key Points Equities rallied to fresh all-time highs as the prospects for tax reform continued to move forward. Jay

SEB FX Ringside 15 March 2016

SEB FX Ringside 15 March 216 Norges Bank still aiming at seducing markets Author: Erica Blomgren Norges Bank is widely expected to cut rates on March 17. We agree, but the decision isn t set in stone.

SEB FX Ringside 15 March 216 Norges Bank still aiming at seducing markets Author: Erica Blomgren Norges Bank is widely expected to cut rates on March 17. We agree, but the decision isn t set in stone.

Reading the Markets Norway On track for a March hike

Investment Research 18 February 2019 On track for a March hike Macro: Norges Bank appears determined to hike in March. Fixed income: expensive mid-segment s in ASW terms. NOK FX: utilise NOK setback to

Investment Research 18 February 2019 On track for a March hike Macro: Norges Bank appears determined to hike in March. Fixed income: expensive mid-segment s in ASW terms. NOK FX: utilise NOK setback to

COMMENTARY NUMBER 378 June Retail Sales, PPI, May Trade Deficit. July 14, 2011

COMMENTARY NUMBER 378 June Retail Sales, PPI, May Trade Deficit July 14, 2011 At Best, Inflation-Adjusted Retail Sales Showed No Growth in Second-Quarter 2011 Trade Data Should Offer a Positive Contribution

COMMENTARY NUMBER 378 June Retail Sales, PPI, May Trade Deficit July 14, 2011 At Best, Inflation-Adjusted Retail Sales Showed No Growth in Second-Quarter 2011 Trade Data Should Offer a Positive Contribution

The Yield Curve and Monetary Policy in 2018

The Yield Curve and Monetary Policy in 2018 Christopher Waller Executive Vice President and Director of Research Federal Reserve Bank of St. Louis May 22, 2018 The views expressed here are those of the

The Yield Curve and Monetary Policy in 2018 Christopher Waller Executive Vice President and Director of Research Federal Reserve Bank of St. Louis May 22, 2018 The views expressed here are those of the

Investment Research General Market Conditions 1 December Weakening Nordic housing markets in focus

Investment Research General Market Conditions December 207 Weekly Focus Sweden Weakening Nordic housing markets in focus Market movers ahead In the US, we expect to see a catching up effect for non-farm

Investment Research General Market Conditions December 207 Weekly Focus Sweden Weakening Nordic housing markets in focus Market movers ahead In the US, we expect to see a catching up effect for non-farm

Explore the themes and thinking behind our decisions.

ASSET ALLOCATION COMMITTEE VIEWPOINTS First Quarter 2017 These views are informed by a subjective assessment of the relative attractiveness of asset classes and subclasses over a 6- to 18-month horizon.

ASSET ALLOCATION COMMITTEE VIEWPOINTS First Quarter 2017 These views are informed by a subjective assessment of the relative attractiveness of asset classes and subclasses over a 6- to 18-month horizon.

US Federal Reserve: Feels like the first time

US Federal Reserve: Feels like the first time Economic research note December 17, 2015 The US Federal Reserve (the Fed) has, finally and unanimously, started the monetary policy normalization process by

US Federal Reserve: Feels like the first time Economic research note December 17, 2015 The US Federal Reserve (the Fed) has, finally and unanimously, started the monetary policy normalization process by

Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy John Praveen, PhD Chief Investment Strategist FOR MORE INFORMATION CONTACT: Mayura Hooper Phone: 973-367-7930 Email:

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy John Praveen, PhD Chief Investment Strategist FOR MORE INFORMATION CONTACT: Mayura Hooper Phone: 973-367-7930 Email:

Eurozone. Economic Watch FEBRUARY 2017

Eurozone Economic Watch FEBRUARY 2017 EUROZONE WATCH FEBRUARY 2017 Eurozone: A slight upward revision to our GDP growth projections The recovery proceeded at a steady and solid pace in, resulting in an

Eurozone Economic Watch FEBRUARY 2017 EUROZONE WATCH FEBRUARY 2017 Eurozone: A slight upward revision to our GDP growth projections The recovery proceeded at a steady and solid pace in, resulting in an

Global Inflation. Set to surprise on the upside lifting long-dated inflation pricing. 27 October /

Global Inflation Set to surprise on the upside lifting long-dated inflation pricing Pernille Bomholdt Henneberg Mikael Olai Milhøj Senior Analyst, Euro area macro research Senior Analyst, US and UK macro

Global Inflation Set to surprise on the upside lifting long-dated inflation pricing Pernille Bomholdt Henneberg Mikael Olai Milhøj Senior Analyst, Euro area macro research Senior Analyst, US and UK macro

Themes in this edition:

Strategy Research Sweden: On the radar This publication is a summary of interesting market related topics and observations that have been covered and discussed within the Strategy Research Sweden group,

Strategy Research Sweden: On the radar This publication is a summary of interesting market related topics and observations that have been covered and discussed within the Strategy Research Sweden group,

Financial Market Outlook: Further Stock Gain on Faster GDP Rebound and Earnings Recovery. Year-end Target Raised

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: FurtherStock Gains Likely, Year-end Target Raised. Bond Under Pressure

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: FurtherStock Gains Likely, Year-end Target Raised. Bond Under Pressure

STRONG WEEK AHEAD OF BIG WEEKEND

LPL RESEARCH WEEKLY MARKET COMMENTARY December 3 2018 STRONG WEEK AHEAD OF BIG WEEKEND John Lynch Chief Investment Strategist, LPL Financial Jeffrey Buchbinder, CFA Equity Strategist, LPL Financial KEY

LPL RESEARCH WEEKLY MARKET COMMENTARY December 3 2018 STRONG WEEK AHEAD OF BIG WEEKEND John Lynch Chief Investment Strategist, LPL Financial Jeffrey Buchbinder, CFA Equity Strategist, LPL Financial KEY

US Federal Reserve: Feels like the first time

US Federal Reserve: Feels like the first time Economic research note 17 December 2015 The US Federal Reserve (the Fed) has, finally and unanimously, started the monetary policy normalisation process by

US Federal Reserve: Feels like the first time Economic research note 17 December 2015 The US Federal Reserve (the Fed) has, finally and unanimously, started the monetary policy normalisation process by

Is the Flattening Yield Curve Sending a Message?

Is the Flattening Yield Curve Sending a Message? FEBRUARY 2018 Sean Simko, ChFC Managing Director SEI Fixed Income Portfolio Management SEI Fixed Income Portfolio Management (SFIPM) manages fixed-income

Is the Flattening Yield Curve Sending a Message? FEBRUARY 2018 Sean Simko, ChFC Managing Director SEI Fixed Income Portfolio Management SEI Fixed Income Portfolio Management (SFIPM) manages fixed-income

By John Praveen, Chief Investment Strategist of Prudential International Investments Advisers, LLC.*

By John Praveen, Chief Investment Strategist of Prudential International Investments Advisers, LLC.* For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

By John Praveen, Chief Investment Strategist of Prudential International Investments Advisers, LLC.* For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Eurozone Economic Watch. July 2018

Eurozone Economic Watch July 2018 Eurozone: A shift to more moderate growth with increased downward risks BBVA Research - Eurozone Economic Watch July 2018 / 2 Hard data improved in May but failed to recover

Eurozone Economic Watch July 2018 Eurozone: A shift to more moderate growth with increased downward risks BBVA Research - Eurozone Economic Watch July 2018 / 2 Hard data improved in May but failed to recover

Strategy US stalls while China and Europe strengthen

Investment Research General Market Conditions 18 October 2013 Strategy US stalls while China and Europe strengthen Once again US politicians struck a last-minute deal and once again fears were running

Investment Research General Market Conditions 18 October 2013 Strategy US stalls while China and Europe strengthen Once again US politicians struck a last-minute deal and once again fears were running

Editor: Lina Fransson. The Week Ahead Key Events 30 Oct 5 Nov, 2017

Editor: Lina Fransson The Week Ahead Key Events 30 Oct 5 Nov, 2017 Monday 30, 08.00 NOR: Retail sales (Sep) % mm/yy change SEB Cons. Prev. Retail sales excl. autos (volume) 0.4/3.1 0.5/--- -0.6/2.6 Retail

Editor: Lina Fransson The Week Ahead Key Events 30 Oct 5 Nov, 2017 Monday 30, 08.00 NOR: Retail sales (Sep) % mm/yy change SEB Cons. Prev. Retail sales excl. autos (volume) 0.4/3.1 0.5/--- -0.6/2.6 Retail

Global Economic and Market Outlook for Gavyn Davies, Chairman, Fulcrum Asset Management

Global Economic and Market Outlook for 2018 Gavyn Davies, Chairman, Fulcrum Asset Management After many years of persistent downgrades to consensus GDP forecasts, 2017 has seen the first upgrades since

Global Economic and Market Outlook for 2018 Gavyn Davies, Chairman, Fulcrum Asset Management After many years of persistent downgrades to consensus GDP forecasts, 2017 has seen the first upgrades since

Minutes of the Monetary Policy Committee meeting, August 2016

The Monetary Policy Committee of the Central Bank of Iceland Minutes of the Monetary Policy Committee meeting, August 2016 Published 7 September 2016 The Act on the Central Bank of Iceland stipulates that

The Monetary Policy Committee of the Central Bank of Iceland Minutes of the Monetary Policy Committee meeting, August 2016 Published 7 September 2016 The Act on the Central Bank of Iceland stipulates that

Summary. Economic Update 1 / 7 December 2017

Economic Update Economic Update 1 / 7 Summary 2 Global Strengthening of the pickup in global growth, with GDP expected to increase 2.9% in 2017 and 3.1% in 2018. 3 Eurozone The eurozone recovery is upholding

Economic Update Economic Update 1 / 7 Summary 2 Global Strengthening of the pickup in global growth, with GDP expected to increase 2.9% in 2017 and 3.1% in 2018. 3 Eurozone The eurozone recovery is upholding

Why is Investor Confidence Lagging?

Veronica Willis Investment Strategy Analyst WEEKLY GUIDANCE ON ECONOMIC AND GEOPOLITICAL EVENTS Why is Investor Confidence Lagging? July 3, 2018 Key takeaways» Typically, late in the economic cycle, we

Veronica Willis Investment Strategy Analyst WEEKLY GUIDANCE ON ECONOMIC AND GEOPOLITICAL EVENTS Why is Investor Confidence Lagging? July 3, 2018 Key takeaways» Typically, late in the economic cycle, we

FRONT BARNETT ASSOCIATES LLC

FRONT BARNETT ASSOCIATES LLC I N V E S T M E N T C O U N S E L September 7, 1999 THE ECONOMIC OUTLOOK: FED HAWKS AND DOVES Despite the Federal Reserve s recent attempts to cool the U.S. economy, business

FRONT BARNETT ASSOCIATES LLC I N V E S T M E N T C O U N S E L September 7, 1999 THE ECONOMIC OUTLOOK: FED HAWKS AND DOVES Despite the Federal Reserve s recent attempts to cool the U.S. economy, business

GLOBAL INVESTMENT OUTLOOK & STRATEGY

May 2018 John Praveen, PhD Managing Director FOLLOW Us ON TWITTER: @prustrategist FOR MORE INFORMATION CONTACT: Kristin Meza Phone: 973-367-4104 Email: kristin.meza@ prudential.com PGIM is the Global Investment

May 2018 John Praveen, PhD Managing Director FOLLOW Us ON TWITTER: @prustrategist FOR MORE INFORMATION CONTACT: Kristin Meza Phone: 973-367-4104 Email: kristin.meza@ prudential.com PGIM is the Global Investment

Markets. Rates. Tuesday, 10 April 2018

Markets Tuesday, April 8 Rates,, -, - Policy Rates,,, -, EURIBOR M / USD LIBOR M ECB FED BOE ECB Deposit EURIBORM USD LIBOR M The US central bank continued its tightening cycle, lifting rates by bps to.%.7%.

Markets Tuesday, April 8 Rates,, -, - Policy Rates,,, -, EURIBOR M / USD LIBOR M ECB FED BOE ECB Deposit EURIBORM USD LIBOR M The US central bank continued its tightening cycle, lifting rates by bps to.%.7%.

Financial Market Outlook: Stock Rally Continues with Faster & Stronger GDP Rebound, Earnings Recovery & Liquidity

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Further Stock Gains with Macro Sweet Spot & Earnings Recovery.

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Further Stock Gains with Macro Sweet Spot & Earnings Recovery.

Market volatility to continue

How much more? Renewed speculation that financial institutions may report increased US subprime-related losses has sent equity markets tumbling. How much more bad news can investors expect going forward?

How much more? Renewed speculation that financial institutions may report increased US subprime-related losses has sent equity markets tumbling. How much more bad news can investors expect going forward?

Yield Forecast Update Fed hike vs. possible further ECB easing

Investment Research General Market Conditions 15 September 215 Fed hike vs. possible further ECB easing One of the most important events for the global fixed income market this autumn will be the FOMC

Investment Research General Market Conditions 15 September 215 Fed hike vs. possible further ECB easing One of the most important events for the global fixed income market this autumn will be the FOMC

file:///c:/users/cathy/appdata/local/microsoft/windows/temporary Int...

1 of 5 9/25/17, 8:57 AM A Publication of the National Association of Manufacturers September 25, 2017 As expected, the Federal Reserve opted to not raise short-term interest rates at its September 19 20

1 of 5 9/25/17, 8:57 AM A Publication of the National Association of Manufacturers September 25, 2017 As expected, the Federal Reserve opted to not raise short-term interest rates at its September 19 20

G10 FX Week Ahead A turning point?

Economic and Financial Analysis 25 May 2018 Article 25 May 2018 G10 FX Week Ahead A turning point? Stable German Ifo provided the first tentative glimmer of hope and if followed by a rise in inflation

Economic and Financial Analysis 25 May 2018 Article 25 May 2018 G10 FX Week Ahead A turning point? Stable German Ifo provided the first tentative glimmer of hope and if followed by a rise in inflation

The Week Ahead. Key Events Apr, 2018

The Week Ahead Key Events 16 22 Apr, 2018 Monday 16, 08.00/13.00 Sweden: Government spring budget Government finances in surplus for the last 3 years, debt falling. Central government debt at the lowest

The Week Ahead Key Events 16 22 Apr, 2018 Monday 16, 08.00/13.00 Sweden: Government spring budget Government finances in surplus for the last 3 years, debt falling. Central government debt at the lowest

Macro Theme. Inflation at an inflection point 2.0

6 November 2018 Macro Theme Inflation at an inflection point 2.0 The lack of inflation has been a defining factor for advanced economies in recent years. A mix of cyclical and structural factors have kept

6 November 2018 Macro Theme Inflation at an inflection point 2.0 The lack of inflation has been a defining factor for advanced economies in recent years. A mix of cyclical and structural factors have kept

Monthly Outlook SEPTEMBER 2013

Monthly Outlook SEPTEMBER 2013 In August, the yield curve of US Treasuries continued to steepen as the likelihood of the US Fed tapering to start before year-end became stronger. Asian Local Currency fund

Monthly Outlook SEPTEMBER 2013 In August, the yield curve of US Treasuries continued to steepen as the likelihood of the US Fed tapering to start before year-end became stronger. Asian Local Currency fund

Macroeconomic Outlook November 2015

Macroeconomic Outlook November 2015 Philippe WAECHTER Head of Economic Research My twitter account @phil_waechter or http://twitter.com/phil_waechter My blog http://philippewaechter.en.nam.natixis.com

Macroeconomic Outlook November 2015 Philippe WAECHTER Head of Economic Research My twitter account @phil_waechter or http://twitter.com/phil_waechter My blog http://philippewaechter.en.nam.natixis.com

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015 Members of the Monetary Policy Council discussed monetary policy against the background of the current and expected

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015 Members of the Monetary Policy Council discussed monetary policy against the background of the current and expected

Norges Bank preview A 25bp rate cut and easing bias

Investment Research 17 March 2015 Norges Bank preview A 25bp rate cut and easing bias We expect Norges Bank (NB) to deliver a 25bp rate cut on Thursday. NB is set to keep the easing bias by presenting

Investment Research 17 March 2015 Norges Bank preview A 25bp rate cut and easing bias We expect Norges Bank (NB) to deliver a 25bp rate cut on Thursday. NB is set to keep the easing bias by presenting

Main Economic & Financial Indicators Eurozone

Main Economic & Financial Indicators Eurozone 7 MAY 2015 AKIKO DARVELL ASSOCIATE ECONOMIST ECONOMIC RESEARCH OFFICE (LONDON) T +44(0)2075771591 E akiko.darvell@uk.mufg.jp The Bank of TokyoMitsubishi UFJ,

Main Economic & Financial Indicators Eurozone 7 MAY 2015 AKIKO DARVELL ASSOCIATE ECONOMIST ECONOMIC RESEARCH OFFICE (LONDON) T +44(0)2075771591 E akiko.darvell@uk.mufg.jp The Bank of TokyoMitsubishi UFJ,

Central banks and rates, the definitive guide

Economic and Financial Analysis 23 October 2017 Article 23 October 2017 Global Economics Central banks and rates, the definitive guide What to expect from the major central banks over the next few months

Economic and Financial Analysis 23 October 2017 Article 23 October 2017 Global Economics Central banks and rates, the definitive guide What to expect from the major central banks over the next few months

UNCERTAINTY DIMS EURO AREA GROWTH

EBF Economic Outlook Nr 44 November 2018 2018 AUTUMN OUTLOOK ON THE EURO AREA ECONOMY IN 2018-2019 UNCERTAINTY DIMS EURO AREA GROWTH EDITORIAL TEAM: Francisco Saravia (author), Helge Pedersen, Chair of

EBF Economic Outlook Nr 44 November 2018 2018 AUTUMN OUTLOOK ON THE EURO AREA ECONOMY IN 2018-2019 UNCERTAINTY DIMS EURO AREA GROWTH EDITORIAL TEAM: Francisco Saravia (author), Helge Pedersen, Chair of

NZ FIXED INTEREST FUND JUNE 2018

NZ FIXED INTEREST FUND JUNE 2018 Contents 1. Economic and market recap 3 2. Performance and attribution 10 3. Attribution 17 4. Strategy 26 Appendix 1. Portfolio composition 30 1. ECONOMIC AND MARKET RECAP

NZ FIXED INTEREST FUND JUNE 2018 Contents 1. Economic and market recap 3 2. Performance and attribution 10 3. Attribution 17 4. Strategy 26 Appendix 1. Portfolio composition 30 1. ECONOMIC AND MARKET RECAP

Economic Outlook and Forecast

Economic Outlook and Forecast Stefano Eusepi Research & Statistics Group January 2017 All views expressed are those of the author only and not necessarily those of the Federal Reserve Bank of New York

Economic Outlook and Forecast Stefano Eusepi Research & Statistics Group January 2017 All views expressed are those of the author only and not necessarily those of the Federal Reserve Bank of New York

Q3/17. Quarterly Market Commentary. Highlights. Canadian & U.S. Fixed Income. U.S. Equities. International Equities.

Q3/17 Highlights Canadian & U.S. Fixed Income The Canadian government bond index declined during Q3/17, underperforming the U.S. government bond index as the Canadian index fell 2.02% Q/Q, compared to

Q3/17 Highlights Canadian & U.S. Fixed Income The Canadian government bond index declined during Q3/17, underperforming the U.S. government bond index as the Canadian index fell 2.02% Q/Q, compared to

Gauging Current Economic Momentum. Dennis Lockhart President and Chief Executive Officer Federal Reserve Bank of Atlanta

Gauging Current Economic Momentum Dennis Lockhart President and Chief Executive Officer Federal Reserve Bank of Atlanta Rotary Club of Knoxville Knoxville, Tennessee August 16, 2016 Atlanta Fed President

Gauging Current Economic Momentum Dennis Lockhart President and Chief Executive Officer Federal Reserve Bank of Atlanta Rotary Club of Knoxville Knoxville, Tennessee August 16, 2016 Atlanta Fed President

Forex and Interest Rate Outlook AIB Treasury Economic Research Unit

Forex and Interest Rate Outlook 7th June 2018 World economy performing quite well, though downside risks are growing Fed sticks to its steady rate tightening path, while other central banks remain cautious

Forex and Interest Rate Outlook 7th June 2018 World economy performing quite well, though downside risks are growing Fed sticks to its steady rate tightening path, while other central banks remain cautious

EUR/USD: Time to question the Quadvergence

EUR/USD: Time to question the Quadvergence - EUR/USD has been supported by growth, inflation, political and policy/yield convergence - We think it s time to question the first two of these factors - EUR/USD

EUR/USD: Time to question the Quadvergence - EUR/USD has been supported by growth, inflation, political and policy/yield convergence - We think it s time to question the first two of these factors - EUR/USD

Monetary Policy Summary and minutes of the Monetary Policy Committee meeting ending on 9 May 2018

Monetary Policy Summary and minutes of the Monetary Policy Committee meeting ending on 9 May 2018 Publication date: 10 May 2018 These are the minutes of the Monetary Policy Committee meeting ending on

Monetary Policy Summary and minutes of the Monetary Policy Committee meeting ending on 9 May 2018 Publication date: 10 May 2018 These are the minutes of the Monetary Policy Committee meeting ending on

Five takeaways from April and five things to watch in May

FOR TRADE PRESS USE AND PROFESSIONAL CLIENTS ONLY Amsterdam, 2 May 2018 Five takeaways from April and five things to watch in May by Kristina Hooper, Chief Global Market Strategist, Invesco Ltd April brought

FOR TRADE PRESS USE AND PROFESSIONAL CLIENTS ONLY Amsterdam, 2 May 2018 Five takeaways from April and five things to watch in May by Kristina Hooper, Chief Global Market Strategist, Invesco Ltd April brought