Eastern Shore Delegation Breakfast. June 21, 2014

|

|

|

- Margery Haynes

- 5 years ago

- Views:

Transcription

1 Eastern Shore Delegation Breakfast June 21, 2014

2 LARGE COUNTIES 6/21/2014 2

3 6/21/2014 3

4 t 4rth Qtr 2013 latest data available 6/21/2014 4

5 6/21/2014 5

6 6/21/2014 6

7 6/21/2014 7

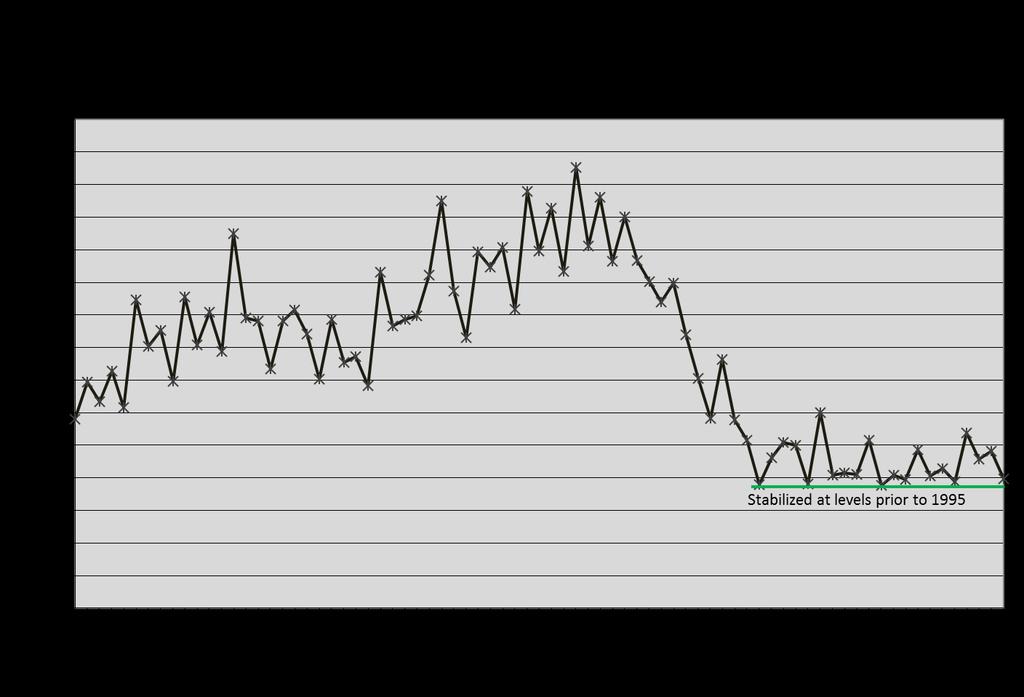

8 Stabilized 6/21/2014 8

9 6/21/2014 9

10 10

11 Wicomico Economic Summary June 2014 Stabilized, but not recovered - Business activity as measured by Sales and Use Tax receipts has improved nearly continuously from September 2011 through May 2014 standing at 24% below the pre-recession level. Employment for county citizens grew strongly for 26 months from November 2010 through December It then declined for 12 consecutive months through December of 2013 forcing the FY14 revenue estimate write-down. As of April 2014 the trend is flat, but FY15 budget target remains attainable. The number of taxable recordation transactions has begun to improve but remains below levels prior to Revenue from the recordation tax is down $3.8 million from the peak in FY06 and is now at 2003 levels. The net taxable real property base declined 18.7% from the peak in FY11 (roughly $1.3 billion); the base is expected to grow by 2.8% from FY15 to FY16 (data provided by the State Department of Assessment and Taxation). Income tax revenue, even after a tax rate increase of 0.01%, is down $5.5 million from peak in FY08 now at 2005 level. Personal property taxes have been the focus of policy decisions designed to stimulate local economic growth. In FY14, the county began a five year phase-out of personal property taxes on business inventory and through State legislative action decoupled the overall personal property tax rate from the real property tax rate. These two initiatives have slowed the growth in revenue from personal property taxes which are now at the levels before 2002: however these changes have been budget neutral since inception. Total revenues from taxes in fiscal 2015 are where they were in 2006, which is roughly $3.8 million less than the peak tax revenue year of FY08. 6/21/

12 12

13 Tax History Summary FY Constant Yield Contant Yield to Tax Rate Levied Tax Rate Levied Tax Rate Year-over- Year Change Revenue Cap Maximum Allowed Tax Levy difference from Cap Allowance $ $ $ $ $ $ $ $ $ $ $ $ $ $ FY $ $ (0.0090) FY $ (0.0020) $ $ (0.0230) (0.0270) FY $ $ $ (0.0060) FY $ $ $ (0.0160) FY $ $ $ (0.0320) FY $ $ $ (0.0510) FY $ $ $ (0.0610) FY $ $ $ (0.0670) FY $ $ $ (0.0550) FY $ $ $ (0.0050) FY $ (0.0284) $ $ (0.0400) FY $ $ $ FY $ $ $ FY $ $ $ Taxes and Rates may be described as follows TAXES have gone down twice since the revenue cap was implemented, FY03 and FY12. The tax RATES declined for 8 consecutive years from FY02 to FY10; but TAXES went up in all of those years, except FY03, because the levied rate was greater than the constant yield rate. The tax RATE stayed the same from FY10 to FY11, but TAXES went up because the flat rate was more than the constant yield rate which had gone down because the assessable base went up. Taxes increased in FY13, FY14 and FY15; that s three consecutive years since the tax decrease in FY12. The tax RATES were increased year-over-year in FY12, FY13, FY14, and FY15: that s four consecutive years since the unchanged rate in FY11. 13

14 Focus on Economic Development Tax Policy FY15 Personal Property Tax Rate set cents LESS THAN what it would have been without the General Assembly s approval of decoupling: businesses are able to save roughly $850K in taxes. FY15 is second year of 5 year phase-out of business inventory tax. Very rough estimate of cumulative savings to businesses is $1M (FY14+FY15). Personal Property Tax Exemption on Manufacturing Equipment is now automatic: streamlined, more business friendly environment. Increase in PP Tax rate of 3.48 cents made these progrowth initiatives slightly revenue positive for FY15 6/21/

15 Focus on Economic Development Proactive Investments FY15 Funded 2 grant programs dedicated to stimulating the construction of single family homes: $387,000 business incubator programs to help new businesses: $157,000 FY15 Funded Henry S. Park Complex improvements to match state grants to further position the county for national and regional sporting events: $1 million to match state grant of $1 million FY15 Funded Wicomico Youth & Civic Center improvements: $1 million to match state grant of $1 million FY14 Funded Wicomico River Multi-Use Terminal Facility Study with John C Martin Associates LLC, Maryland Port Authority Consultant: $53K split 50/50 with Maryland Department of Business and Economic Development FY14 Funded study on providing water service to regional airport; will seek State and Federal grant opportunities. 15

16 Legislative Initiatives & Concerns for /21/

17 Return of HUR #1 Priority HUR was the foundation of Roads budget through FY09 Routine operations now funded by General Fund tax revenue. The property and income tax base cannot support transportation infrastructure renewal costs 6/21/

18 Impact of Dollar and Human Resource Reductions FY15 plan is under development 6/21/

19 Restoration of HUR is our #1 Priority The income tax and property tax revenue cannot sustain the roads infrastructure without detracting from core services such as Education and Public Safety $14 million is a rough estimate for Wicomico County in FY15 based on registered vehicles in county: current allocation is $627K. 6/21/

20 HUR Distribution Estimate State data Registered Vehicles in county 87,726 State data Gasoline tax rate $ cents per gallon State data Diesel $ cents per gallon web average miles driven per year 15,000 web truck mpg 18 web car mpg 23 Computation assumption Milage used 11,000 assumption tax rate $ to reflect some diesel usage assumption mpg 19 more trucks on eastern shore computation miles driven 964,986,000 gallons used 50,788,737 taxes paid $ 14,068,480 20

21 Fiscal Impacts to the County Generated by the State of Maryland since the start of the Great Recession FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY08-FY15 Cumulative Mandated Expenses - negative is cost to county Support for SDAT functions $ - $ - $ - $ - $ (724,923) $ (755,600) $ (442,018) $ (457,364) $ (2,379,905) Homestead Credit validation fee from SDAT $ - $ - $ - $ (9,593.00) $ (10,797) $ (14,054) $ (18,219) $ (14,441) $ (67,104) Health Department - year-over-year (cost growth)/cost decrease driven by State $ (90,567.00) $ (772,763.00) $ (319,723.00) $ (50,821.93) $ (176,101) $ (252,803) $ (347,749) $ (631,332) $ (2,641,860) Elections Department - year-over-year (cost growth)/cost decrease driven by State $ (30,267.00) $ 79, $ 230, $ (160,533.00) $ (40,284) $ (172,380) $ (337,457) $ (278,728) $ (709,901) Teacher Pension Normal Cost $ - $ - $ - $ - $ - $ (2,173,593) $ (2,755,091) $ (2,719,329) $ (7,648,013) Total Increases in Operating Expenses $ (120,834) $ (693,428) $ (89,310) $ (220,948) $ (952,105) $ (3,368,430) $ (3,900,534) $ (4,101,194) $ (13,446,783) Revenue Reductions - losses Capped Disparity Grant - amount withheld from full formula. FY11,F12,FY13 were capped at the FY10 level of $2,197,041. In FY14 and FY15 the grant was capped at 60% of formula. What is shown is the difference between what was received and 100% of the formula. As a point of reference the full amount in FY09 was $741,624. $ (1,615,958.00) $ (4,162,585) $ (7,168,223) $ (4,435,895) $ (5,494,000) $ (22,876,661) Highway User Revenue - reduction from "historic normal" level of $7M $ 36, $ (729,627.00) $ (6,387,916.00) $ (6,542,429.00) $ (6,687,893) $ (6,464,879) $ (6,377,455) $ (6,373,138) $ (39,526,974) Federal Per Diem for inmates in Detention Center $ (200,823.00) $ (971,882.00) $ (1,394,452) $ (1,376,455) $ (1,399,733) $ (1,411,733) $ (6,755,078) State Per Diem for inmates in Detention Center $ (319,423.00) $ (347,728.00) $ (384,448) $ (262,453) $ (397,858) $ (425,363) $ (2,137,273) Total Decreases in Revenues $ 36,363 $ (729,627) $ (6,908,162) $ (9,477,997) $ (12,629,378) $ (15,272,010) $ (12,610,941) $ (13,704,234) $ (71,295,986) Revenue Enhancements Teacher Retirement Supplement Grant $ - $ - $ - $ - $ - $ 1,567,837 $ 1,567,837 $ 1,567,837 $ 4,703,511 Income tax effect from State deductions change $ 167,000 $ 150,333 $ 133,667 $ 451,000 close IDOT loophole $ 376,000 $ 376,000 $ 376,000 $ 1,128,000 Total Revenue Enhancements $ - $ - $ - $ - $ - $ 2,110,837 $ 2,094,170 $ 2,077,504 $ 6,282,511 Net Effect on the County's ability to fund government functions caused by State Actions from FY08 through FY15 $ (84,471) $ (1,423,055) $ (6,997,472) $ (9,698,945) $ (13,581,483) $ (16,529,603) $ (14,417,305) $ (15,727,924) $ (78,460,258) 6/21/

22 Request restoration of full disparity grant formula. $5.5M 22

23 Mental Health and Addictions Growing Problem Diminishing Resources provided by State Impacting Community Schools Crime Court loading Incarceration cost Will spillover to economy 23

24 Waters of the US Under the Clean Water Act Unwarranted and Unnecessary intrusion by a Federal Regulatory Agency Will complicate State and Local efforts to address already difficult WIP requirements Will drive costs up 24

25 Legislators Discuss Their Priorities and Issues Invite delegation members to vet their ideas for legislative bills/initiatives with local government leadership before formal introduction. Happy to provide fiscal impact analysis and comments. Once a bill is introduced, it can take on a life of its own. 25

26 Airport Water Research and Possible Funding Handout in your package Study completed to identify cost-effective means of providing water service to the airport. Economic Development at the airport will not move ahead without municipal water. Looking for funding partners! 26

27 Community College Collective Bargaining Oppose initiatives to require collective bargaining at community colleges. Expect significant increase in recurring annual funding requirements. New revenue sources would be required to fund resulting cost growth. 27

28 Other Discussion - Questions Thank you

FY15 REVENUES. FY 14 Adopted Taxes. General Fund $ $ $753.50

BROWARD COUNTY BUDGET-IN-BRIEF FY15 REVENUES Overview County services are funded with a variety of revenue sources. These sources include the following: property taxes, miscellaneous taxes and assessments,

BROWARD COUNTY BUDGET-IN-BRIEF FY15 REVENUES Overview County services are funded with a variety of revenue sources. These sources include the following: property taxes, miscellaneous taxes and assessments,

$1,516 $925 $19 $2,460 $422 $1,270 $261 $413 $94 = $715 = $274 = $62 = $13 = $555 = $19 = $148 & HWY

OVERVIEW Missouri Transportation Funding Overview Missouri s transportation revenue totaled almost $2.5 billion in fiscal year 2017. As shown below, nearly two-thirds of the revenue came from state user

OVERVIEW Missouri Transportation Funding Overview Missouri s transportation revenue totaled almost $2.5 billion in fiscal year 2017. As shown below, nearly two-thirds of the revenue came from state user

Understanding H.B. 170: The Transportation Funding Act of 2015

Understanding H.B. 170: The Transportation Funding Act of Recent History in Transportation Funding 2007 Joint Study Committee on Transportation Funding 2009 S.B. 200: Transportation Governance 2010 H.B.

Understanding H.B. 170: The Transportation Funding Act of Recent History in Transportation Funding 2007 Joint Study Committee on Transportation Funding 2009 S.B. 200: Transportation Governance 2010 H.B.

FY16 REVENUES. FY 15 Adopted Taxes. General Fund $ $ $ Voter Approved Debt Service $37.30 $36.90 $37.50

FY16 REVENUES Overview County services are funded with a variety of revenue sources. These sources include the following: property taxes, miscellaneous taxes and assessments, federal and state grants,

FY16 REVENUES Overview County services are funded with a variety of revenue sources. These sources include the following: property taxes, miscellaneous taxes and assessments, federal and state grants,

A Project for The Good Roads Foundation. Arkansas Statewide Likely Voter Survey December 12-13,

A Project for The Good Roads Foundation Arkansas Statewide Likely Voter Survey December 12-13, 2016 1 Methodology The following statewide survey was conducted by Gilmore Strategy Group within the state

A Project for The Good Roads Foundation Arkansas Statewide Likely Voter Survey December 12-13, 2016 1 Methodology The following statewide survey was conducted by Gilmore Strategy Group within the state

THE FISCAL HEALTH OF INDIANA S LARGER MUNICIPALITIES: CITY OF GREENWOOD MUNICIPAL PROFILE

THE FISCAL HEALTH OF INDIANA S LARGER MUNICIPALITIES: CITY OF GREENWOOD MUNICIPAL PROFILE by John Stafford March 2016 1 CITY OF GREENWOOD MUNICIPAL PROFILE MARCH 2016 Introduction This document is a summary

THE FISCAL HEALTH OF INDIANA S LARGER MUNICIPALITIES: CITY OF GREENWOOD MUNICIPAL PROFILE by John Stafford March 2016 1 CITY OF GREENWOOD MUNICIPAL PROFILE MARCH 2016 Introduction This document is a summary

Current Law House (H.R. 1) Senate (S. 1) Conference Agreement NACo Policy. Fully eliminates deductions

Senate (S. 1) Conference Agreement NACo Policy. Fully eliminates deductions") State and Local Tax (SALT) Deduction Tax Exempt Municipal Bonds Any individual or family who itemizes their tax returns may deduct either state and local income taxes or state and local sales taxes paid

State and Local Tax (SALT) Deduction Tax Exempt Municipal Bonds Any individual or family who itemizes their tax returns may deduct either state and local income taxes or state and local sales taxes paid

TAX AND REVENUE ISSUES IN THE FY 2010 BUDGET

An Affiliate of the Center on Budget and Policy Priorities 820 First Street NE, Suite 460 Washington, DC 20002 (202) 408-1080 Fax (202) 408-1073 www.dcfpi.org Updated September 1, 2009 TAX AND REVENUE

An Affiliate of the Center on Budget and Policy Priorities 820 First Street NE, Suite 460 Washington, DC 20002 (202) 408-1080 Fax (202) 408-1073 www.dcfpi.org Updated September 1, 2009 TAX AND REVENUE

Evaluating Michigan s Options to Increase Road Funding

February 2019 Memorandum 1155 This paper accompanies a longer paper,. That paper is available at https://crcmich.org/evaluating-michigans-options-to-increase-road-funding. Key Takeaways 1. In 2015, Michigan

February 2019 Memorandum 1155 This paper accompanies a longer paper,. That paper is available at https://crcmich.org/evaluating-michigans-options-to-increase-road-funding. Key Takeaways 1. In 2015, Michigan

BUDGET MESSAGE COUNTY OF BLADEN May 23, Bladen County Board of Commissioners: Revenue Overview

BUDGET MESSAGE COUNTY OF BLADEN May 23, 2016 Bladen County Board of Commissioners: I am pleased to present for your consideration, the FY 2016-2017 Proposed Budget for Bladen County, North Carolina. The

BUDGET MESSAGE COUNTY OF BLADEN May 23, 2016 Bladen County Board of Commissioners: I am pleased to present for your consideration, the FY 2016-2017 Proposed Budget for Bladen County, North Carolina. The

METROPOLITAN WATER RECLAMATION DISTRICT FY2019 TENTATIVE BUDGET: Analysis and Recommendations

METROPOLITAN WATER RECLAMATION DISTRICT FY2019 TENTATIVE BUDGET: Analysis and Recommendations December 6, 2018 Table of Contents EXECUTIVE SUMMARY... 4 CIVIC FEDERATION POSITION... 7 ISSUES THE CIVIC FEDERATION

METROPOLITAN WATER RECLAMATION DISTRICT FY2019 TENTATIVE BUDGET: Analysis and Recommendations December 6, 2018 Table of Contents EXECUTIVE SUMMARY... 4 CIVIC FEDERATION POSITION... 7 ISSUES THE CIVIC FEDERATION

Tax Plan Needs Course Correction House Transportation Package Leaves out New Revenues, Could Harm Key Services

Policy Bill Analysis Report Tax Plan Needs Course Correction House Transportation Package Leaves out New Revenues, Could Harm Key Services By Wesley Tharpe, Policy Analyst Georgia needs a sustained commitment

Policy Bill Analysis Report Tax Plan Needs Course Correction House Transportation Package Leaves out New Revenues, Could Harm Key Services By Wesley Tharpe, Policy Analyst Georgia needs a sustained commitment

WHAT ARE THE TAX AND REVENUE CHANGES IN THE FY 2014 BUDGET?

An Affiliate of the Center on Budget and Policy Priorities 820 First Street NE, Suite 510 Washington, DC 20002 (202) 408-1080 Fax (202) 325-8839 www.dcfpi.org WHAT ARE THE TAX AND REVENUE CHANGES IN THE

An Affiliate of the Center on Budget and Policy Priorities 820 First Street NE, Suite 510 Washington, DC 20002 (202) 408-1080 Fax (202) 325-8839 www.dcfpi.org WHAT ARE THE TAX AND REVENUE CHANGES IN THE

Forecast Highlights. HUTD Revenues, FY Biennium Change from EOS '16 Forecast

Forecast Highlights FY 2016-17 HUTD revenues down $45 million (1.1 percent) from 2016 EOS Forecast Gas taxes are up $6 million (0.3 percent), registration taxes are down $32 million (2.2 percent) and motor

Forecast Highlights FY 2016-17 HUTD revenues down $45 million (1.1 percent) from 2016 EOS Forecast Gas taxes are up $6 million (0.3 percent), registration taxes are down $32 million (2.2 percent) and motor

Interested Parties William E. Hamilton Transportation Needs and Revenue Distribution

MEMORANDUM DATE: December 3, 2010 TO: FROM: RE: Interested Parties William E. Hamilton Transportation Needs and Revenue Distribution Introduction Michigan residents rely on a safe efficient transportation

MEMORANDUM DATE: December 3, 2010 TO: FROM: RE: Interested Parties William E. Hamilton Transportation Needs and Revenue Distribution Introduction Michigan residents rely on a safe efficient transportation

Budgets, Tax Rates, & Selected Statistics Fiscal Year 2014

Budgets, Tax Rates, & Selected Statistics Fiscal Year 2014 2 FISCAL YEAR 2014 REPORT OF COUNTY BUDGETS, TAX RATES & SELECTED STATISTICS PREPARED BY THE MARYLAND ASSOCIATION OF COUNTIES (MACO) 169 CONDUIT

Budgets, Tax Rates, & Selected Statistics Fiscal Year 2014 2 FISCAL YEAR 2014 REPORT OF COUNTY BUDGETS, TAX RATES & SELECTED STATISTICS PREPARED BY THE MARYLAND ASSOCIATION OF COUNTIES (MACO) 169 CONDUIT

FIVE-YEAR REVENUE AND COST PROJECTIONS FOR MAJOR OPERATING FUNDS

FIVE-YEAR REVENUE AND COST PROJECTIONS FOR MAJOR OPERATING FUNDS INTRODUCTION AND OVERVIEW This section of the budget outlines in summary form projected revenues and costs for the five fiscal years beyond

FIVE-YEAR REVENUE AND COST PROJECTIONS FOR MAJOR OPERATING FUNDS INTRODUCTION AND OVERVIEW This section of the budget outlines in summary form projected revenues and costs for the five fiscal years beyond

Cobb County School District. FY2007 Budget Development Process

Cobb County School District Process Major Budget Considerations: Revived State of GA Economy FY07 Governor s Education Budget Proposal Cobb County School District Budget Development 1 Revived State of

Cobb County School District Process Major Budget Considerations: Revived State of GA Economy FY07 Governor s Education Budget Proposal Cobb County School District Budget Development 1 Revived State of

Financial Snapshot October 2014

Financial Snapshot October 2014 Financial Snapshot About the Financial Snapshot The Financial Snapshot provides answers to frequently asked questions regarding MoDOT s finances. This document provides

Financial Snapshot October 2014 Financial Snapshot About the Financial Snapshot The Financial Snapshot provides answers to frequently asked questions regarding MoDOT s finances. This document provides

Transportation Funds Forecast November 2017

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp Transportation Funds

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp Transportation Funds

Public School Finance 101

Public School Finance 101 FREQUENTLY ASKED QUESTIONS When were new operating tax levies passed in the Eastwood district? Continuing Operating Property Tax Levies were passed by district voters in 1976,

Public School Finance 101 FREQUENTLY ASKED QUESTIONS When were new operating tax levies passed in the Eastwood district? Continuing Operating Property Tax Levies were passed by district voters in 1976,

21 st Century Transportation Committee Finance Subcommittee

21 st Century Transportation Committee Finance Subcommittee Highway Fund and Highway Trust Fund Transfers Diesel Tax Options January 16, 2008 Outline Funding Sources Department of Transportation s Budget

21 st Century Transportation Committee Finance Subcommittee Highway Fund and Highway Trust Fund Transfers Diesel Tax Options January 16, 2008 Outline Funding Sources Department of Transportation s Budget

REVENUE Major Vermont Tax Sources

REVENUE DETAILS 39 REVENUE Major Vermont Tax Sources Vermont has three major funds into which most tax revenue is deposited; the General Fund, the Transportation Fund and the Education Fund. There are

REVENUE DETAILS 39 REVENUE Major Vermont Tax Sources Vermont has three major funds into which most tax revenue is deposited; the General Fund, the Transportation Fund and the Education Fund. There are

Transportation Funds Forecast February 2017

Transportation Funds Forecast February 2017 Released March 3rd, 2017 Forecast Highlights FY 2018-19 HUTD revenues are up $72 million (1.6 percent) from November 2016 Forecast Gas taxes are up $30 million

Transportation Funds Forecast February 2017 Released March 3rd, 2017 Forecast Highlights FY 2018-19 HUTD revenues are up $72 million (1.6 percent) from November 2016 Forecast Gas taxes are up $30 million

Department of Legislative Services

Department of Legislative Services Maryland General Assembly 2008 Session SB 618 FISCAL AND POLICY NOTE Senate Bill 618 Budget and Taxation (Senator Jones, et al.) Property Tax - Homeowners' Property Tax

Department of Legislative Services Maryland General Assembly 2008 Session SB 618 FISCAL AND POLICY NOTE Senate Bill 618 Budget and Taxation (Senator Jones, et al.) Property Tax - Homeowners' Property Tax

THE FISCAL HEALTH OF INDIANA S LARGER MUNICIPALITIES: CITY OF BLOOMINGTON MUNICIPAL PROFILE

THE FISCAL HEALTH OF INDIANA S LARGER MUNICIPALITIES: CITY OF BLOOMINGTON MUNICIPAL PROFILE by John Stafford March 2016 1 CITY OF BLOOMINGTON MUNICIPAL PROFILE MARCH 2016 Introduction This document is

THE FISCAL HEALTH OF INDIANA S LARGER MUNICIPALITIES: CITY OF BLOOMINGTON MUNICIPAL PROFILE by John Stafford March 2016 1 CITY OF BLOOMINGTON MUNICIPAL PROFILE MARCH 2016 Introduction This document is

Proposed Budget. Fiscal Year Revenue Overview

Fiscal Year 1 Revenue Overview Major Revenue Sources T FISCAL YEAR 1 REVENUE OVERVIEW he total estimated revenues from County funds for Fiscal Year 1 is $57 million, a.% increase from Fiscal Year. Total

Fiscal Year 1 Revenue Overview Major Revenue Sources T FISCAL YEAR 1 REVENUE OVERVIEW he total estimated revenues from County funds for Fiscal Year 1 is $57 million, a.% increase from Fiscal Year. Total

TRANSPORTATION-RELATED GOODS AND SERVICES. Cindy Avrette, LAD, NCGA Denise Canada, FRD, NCGA

TRANSPORTATION-RELATED GOODS AND SERVICES Cindy Avrette, LAD, NCGA Denise Canada, FRD, NCGA FUNDING MOST GOVERNMENT SERVICES Variety of Revenue Sources Income Taxes Sales Taxes Excise Taxes Other Principles

TRANSPORTATION-RELATED GOODS AND SERVICES Cindy Avrette, LAD, NCGA Denise Canada, FRD, NCGA FUNDING MOST GOVERNMENT SERVICES Variety of Revenue Sources Income Taxes Sales Taxes Excise Taxes Other Principles

Loveland City Schools FY Revenue

FREQUENTLY ASKED QUESTIONS 1. Where does the Loveland City School District revenue come from? In Ohio, the funding of schools is shared by the state and local school districts. The Ohio General Assembly

FREQUENTLY ASKED QUESTIONS 1. Where does the Loveland City School District revenue come from? In Ohio, the funding of schools is shared by the state and local school districts. The Ohio General Assembly

A City Finance Update

League of California Cities Municipal Finance Institute Monterey 30 November 2016 A City Finance Update Michael Coleman 530.758.3952 coleman@muniwest.com www.facebook.com/munialmanac Twitter: @MuniAlmanac

League of California Cities Municipal Finance Institute Monterey 30 November 2016 A City Finance Update Michael Coleman 530.758.3952 coleman@muniwest.com www.facebook.com/munialmanac Twitter: @MuniAlmanac

Major State Aids &Taxes A COMPARATIVE ANALYSIS, INCLUDING REGIONAL AND COUNTY DATA ON WHERE THE AIDS GO AND WHERE THE TAXES COME FROM

Major State Aids &Taxes A COMPARATIVE ANALYSIS, INCLUDING REGIONAL AND COUNTY DATA ON WHERE THE AIDS GO AND WHERE THE TAXES COME FROM Overview of Presentation I will cover three topics or questions: Why

Major State Aids &Taxes A COMPARATIVE ANALYSIS, INCLUDING REGIONAL AND COUNTY DATA ON WHERE THE AIDS GO AND WHERE THE TAXES COME FROM Overview of Presentation I will cover three topics or questions: Why

Ad Valorem Taxes. Description of Revenue Source. Revenue Assumptions

Ad Valorem Taxes Ad Valorem Taxes are taxes paid on real and personal property located within the Village s corporate limits. Taxes for real and personal property, excluding motor vehicles, are levied

Ad Valorem Taxes Ad Valorem Taxes are taxes paid on real and personal property located within the Village s corporate limits. Taxes for real and personal property, excluding motor vehicles, are levied

THE FISCAL HEALTH OF INDIANA S LARGER MUNICIPALITIES: CITY OF NEW ALBANY MUNICIPAL PROFILE

THE FISCAL HEALTH OF INDIANA S LARGER MUNICIPALITIES: CITY OF NEW ALBANY MUNICIPAL PROFILE by John Stafford March 2016 1 CITY OF NEW ALBANY MUNICIPAL PROFILE MARCH 2016 Introduction This document is a

THE FISCAL HEALTH OF INDIANA S LARGER MUNICIPALITIES: CITY OF NEW ALBANY MUNICIPAL PROFILE by John Stafford March 2016 1 CITY OF NEW ALBANY MUNICIPAL PROFILE MARCH 2016 Introduction This document is a

Ohio 2020 Tax Policy Commission

Ohio 2020 Tax Policy Commission Testimony of Tax Commissioner Joe Testa Department of Taxation October 22, 2015 Co-Chairman Senator Peterson, Co-Chairman Representative McClain, and members of the Tax

Ohio 2020 Tax Policy Commission Testimony of Tax Commissioner Joe Testa Department of Taxation October 22, 2015 Co-Chairman Senator Peterson, Co-Chairman Representative McClain, and members of the Tax

County of Orange. Chairwoman Lisa A. Bartlett, Supervisor, Fifth District Members, Board of Supervisors. Fiscal Year Recommended Budget

TRANSMITTAL LETTER County of Orange TRANSMITTAL LETTER County Executive Office May 9, 2016 To: From: Subject Chairwoman Lisa A. Bartlett, Supervisor, Fifth District Members, Board of Supervisors Frank

TRANSMITTAL LETTER County of Orange TRANSMITTAL LETTER County Executive Office May 9, 2016 To: From: Subject Chairwoman Lisa A. Bartlett, Supervisor, Fifth District Members, Board of Supervisors Frank

Transportation Funding State Comparisons. 21 st Century Transportation Committee August 21, 2008

Transportation Funding State Comparisons 21 st Century Transportation Committee August 21, 2008 State Comparisons State Population 2007 (millions) 1 State-controlled highway miles 2 % of total miles controlled

Transportation Funding State Comparisons 21 st Century Transportation Committee August 21, 2008 State Comparisons State Population 2007 (millions) 1 State-controlled highway miles 2 % of total miles controlled

Michael C. Van Milligen, City Manager

TO: FROM: Michael C. Van Milligen, City Manager Jennifer Larson, Budget Director SUBJECT: Budget and Fiscal Policy Guidelines for Fiscal Year 2020 DATE: December 12, 2018 I am recommending adoption of

TO: FROM: Michael C. Van Milligen, City Manager Jennifer Larson, Budget Director SUBJECT: Budget and Fiscal Policy Guidelines for Fiscal Year 2020 DATE: December 12, 2018 I am recommending adoption of

A FAIR SHARE OF THE TAT ALLOCATION OF TRANSIENT ACCOMMODATIONS TAX (TAT) REVENUE

REVENUE") A FAIR SHARE OF THE TAT ALLOCATION OF TRANSIENT ACCOMMODATIONS TAX (TAT) REVENUE The State took the counties TAT money to cover losses when times were challenging, but failed to make significant adjustments

A FAIR SHARE OF THE TAT ALLOCATION OF TRANSIENT ACCOMMODATIONS TAX (TAT) REVENUE The State took the counties TAT money to cover losses when times were challenging, but failed to make significant adjustments

The Oregon Department of Transportation Budget

19 20 The Oregon Department of Transportation Budget The Oregon Department of Transportation was established in 1969 to provide a safe, efficient transportation system that supports economic opportunity

19 20 The Oregon Department of Transportation Budget The Oregon Department of Transportation was established in 1969 to provide a safe, efficient transportation system that supports economic opportunity

BUDGET MESSAGE FY PROPOSED BUDGET FISCAL YEAR County Manager and Budget Officer

PROPOSED BUDGET FISCAL YEAR 2018-2019 County Manager and Budget Officer Honorable Chairman and Members of the Warren County Board of Commissioners, In accordance with the North Carolina Local Government

PROPOSED BUDGET FISCAL YEAR 2018-2019 County Manager and Budget Officer Honorable Chairman and Members of the Warren County Board of Commissioners, In accordance with the North Carolina Local Government

FISCAL MEMORANDUM HB 534 SB 1221 HB 534 SB April 4, 2017

TENNESSEE GENERAL ASSEMBLY FISCAL REVIEW COMMITTEE FISCAL MEMORANDUM April 4, 2017 SUMMARY OF ORIGINAL BILL: Changes, from July 25 to July 20, the deadline for a person who operates a motor vehicle in

TENNESSEE GENERAL ASSEMBLY FISCAL REVIEW COMMITTEE FISCAL MEMORANDUM April 4, 2017 SUMMARY OF ORIGINAL BILL: Changes, from July 25 to July 20, the deadline for a person who operates a motor vehicle in

THE FISCAL HEALTH OF INDIANA S LARGER MUNICIPALITIES: CITY OF SOUTH BEND MUNICIPAL PROFILE

THE FISCAL HEALTH OF INDIANA S LARGER MUNICIPALITIES: CITY OF SOUTH BEND MUNICIPAL PROFILE by John Stafford March 2016 1 CITY OF SOUTH BEND MUNICIPAL PROFILE MARCH 2016 Introduction This document is a

THE FISCAL HEALTH OF INDIANA S LARGER MUNICIPALITIES: CITY OF SOUTH BEND MUNICIPAL PROFILE by John Stafford March 2016 1 CITY OF SOUTH BEND MUNICIPAL PROFILE MARCH 2016 Introduction This document is a

Hopkins Public Schools #270. December 5, 2017 Presented by John Toop Director of Business Services

Hopkins Public Schools #270 Public Hearing for Taxes Payable in 2018 December 5, 2017 Presented by John Toop Director of Business Services Tax Hearing Presentation State Law Requires Public Meeting: Between

Hopkins Public Schools #270 Public Hearing for Taxes Payable in 2018 December 5, 2017 Presented by John Toop Director of Business Services Tax Hearing Presentation State Law Requires Public Meeting: Between

State of Connecticut

U.S. Public Finance State Rating Report State of Connecticut General Obligation Bonds General Obligation Bonds (2015 Series F) General Obligation Bonds (Green Bonds, 2015 Series G) Analytical Contacts:

U.S. Public Finance State Rating Report State of Connecticut General Obligation Bonds General Obligation Bonds (2015 Series F) General Obligation Bonds (Green Bonds, 2015 Series G) Analytical Contacts:

FY BUDGET MESSAGE

BOARD OF COMMISSIONERS ELMO BUTCH LILLEY, CHAIRMAN TOMMY W. BOWEN, VICE CHAIRMAN RONNIE SMITH DEREK PRICE BOB HYMAN FY 2012-13 BUDGET MESSAGE DAVID B. BONE COUNTY MANAGER MARION B. THOMPSON CLERK TO THE

BOARD OF COMMISSIONERS ELMO BUTCH LILLEY, CHAIRMAN TOMMY W. BOWEN, VICE CHAIRMAN RONNIE SMITH DEREK PRICE BOB HYMAN FY 2012-13 BUDGET MESSAGE DAVID B. BONE COUNTY MANAGER MARION B. THOMPSON CLERK TO THE

John W. Hickenlooper Governor. Henry Sobanet Director. Jason Schrock Chief Economist. Spencer Imel Economist. Laura Blomquist Economist

Table of Contents Summary... Page 2 General Fund Budget... Page 3 General Fund Revenue Forecast... Page 14 Cash Fund Revenue Forecast... Page 21 The Taxpayer's Bill of Rights: Revenue Limit... Page 29

Table of Contents Summary... Page 2 General Fund Budget... Page 3 General Fund Revenue Forecast... Page 14 Cash Fund Revenue Forecast... Page 21 The Taxpayer's Bill of Rights: Revenue Limit... Page 29

Comparison of House and Senate Budget Actions

Teacher Pensions Rejected a Department of Legislative Services (DLS) recommendation to transfer 50 percent of teacher retirement expenses to the local boards of education. However, the Committee did approve

Teacher Pensions Rejected a Department of Legislative Services (DLS) recommendation to transfer 50 percent of teacher retirement expenses to the local boards of education. However, the Committee did approve

and Motor Carrier Tax (IFTA)

") Motor Fuel Tax and Motor Carrier Tax (IFTA) Annual Report Fiscal Year 2014 Comptroller of Maryland To Interested Members of the Motor Fuel and Motor Carrier Industries: I am pleased to present the annual

Motor Fuel Tax and Motor Carrier Tax (IFTA) Annual Report Fiscal Year 2014 Comptroller of Maryland To Interested Members of the Motor Fuel and Motor Carrier Industries: I am pleased to present the annual

Options to Address Minnesota s Budget Deficit

Options to Address Minnesota s Budget Deficit According to the November Forecast, Minnesota faces a deficit of $1.953 billion for the 2002-03 biennium and a structural deficit of $1.234 billion in Fiscal

Options to Address Minnesota s Budget Deficit According to the November Forecast, Minnesota faces a deficit of $1.953 billion for the 2002-03 biennium and a structural deficit of $1.234 billion in Fiscal

Transportation Funds Forecast

Transportation Funds Forecast February 2016 Released March 3,2016 Funds Forecast Executive Summary 2016-17 HUTD revenues down 23 million from Nov 2015 Forecast HUTD Fund revenues in the current 2016-17

Transportation Funds Forecast February 2016 Released March 3,2016 Funds Forecast Executive Summary 2016-17 HUTD revenues down 23 million from Nov 2015 Forecast HUTD Fund revenues in the current 2016-17

UPDATES ON STATE LAW & TAX POLICY

UPDATES ON STATE LAW & TAX POLICY KIMBERLY LEWIS ROBINSON, SECRETARY LOUISIANA DEPARTMENT OF REVENUE 2 0 1 6 T U L A N E TA X I N S T I T U T E N O V E M B E R 1 0, 2 0 1 6 LDR Administration & Department

UPDATES ON STATE LAW & TAX POLICY KIMBERLY LEWIS ROBINSON, SECRETARY LOUISIANA DEPARTMENT OF REVENUE 2 0 1 6 T U L A N E TA X I N S T I T U T E N O V E M B E R 1 0, 2 0 1 6 LDR Administration & Department

Allegheny County Workforce, Spending, and Taxes in the Home Rule Era

Allegheny County Workforce, Spending, and Taxes in the Home Rule Era Eric Montarti, Senior Policy Analyst Allegheny Institute for Public Policy Allegheny Institute Report #16-02 October 2016 by Allegheny

Allegheny County Workforce, Spending, and Taxes in the Home Rule Era Eric Montarti, Senior Policy Analyst Allegheny Institute for Public Policy Allegheny Institute Report #16-02 October 2016 by Allegheny

Michigan Tax Revenue. Mary Ann Cleary, Director House Fiscal Agency

Michigan Tax Revenue Mary Ann Cleary, Director Michigan State University Institute for Public Policy and Social Research 2016 Legislative Leadership Program December 5, 2016 Major State Taxes 2 Major State

Michigan Tax Revenue Mary Ann Cleary, Director Michigan State University Institute for Public Policy and Social Research 2016 Legislative Leadership Program December 5, 2016 Major State Taxes 2 Major State

Notes Except where noted otherwise, dollar amounts are expressed in 214 dollars. Nominal (current-dollar) spending was adjusted to remove the effects

spending was adjusted to remove the effects") CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE Public Spending on Transportation and Water Infrastructure, 1956 to 214 MARCH 215 Notes Except where noted otherwise, dollar amounts are expressed

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE Public Spending on Transportation and Water Infrastructure, 1956 to 214 MARCH 215 Notes Except where noted otherwise, dollar amounts are expressed

Transportation Finance Overview. Presentation Contents

Transportation Finance Overview Matt Burress House Research Department matt.burress@house.mn Andy Lee House Fiscal Analysis andrew.lee@house.mn January 5 th & 10 th, 2017 Presentation Contents 2 Part 1:

Transportation Finance Overview Matt Burress House Research Department matt.burress@house.mn Andy Lee House Fiscal Analysis andrew.lee@house.mn January 5 th & 10 th, 2017 Presentation Contents 2 Part 1:

Budget Paper C TAX MEASURES

Budget Paper C TAX MEASURES TAX MEASURES CONTENTS FISCAL SUMMARY OF TAX MEASURES... INTRODUCTION... CARBON TAX... PERSONAL TAX MEASURES... BUSINESS TAX MEASURES... TAX CREDIT EXTENSIONS... ON-GOING TAX

Budget Paper C TAX MEASURES TAX MEASURES CONTENTS FISCAL SUMMARY OF TAX MEASURES... INTRODUCTION... CARBON TAX... PERSONAL TAX MEASURES... BUSINESS TAX MEASURES... TAX CREDIT EXTENSIONS... ON-GOING TAX

The Ward Museum Economic Impact Study. Conducted by:

The Ward Museum Economic Impact Study Conducted by: BEACON of the Franklin P. Perdue School of Business At Salisbury University November 2012 Table of Contents Introduction... 2 Economic Impact Analysis...

The Ward Museum Economic Impact Study Conducted by: BEACON of the Franklin P. Perdue School of Business At Salisbury University November 2012 Table of Contents Introduction... 2 Economic Impact Analysis...

Miami County, Ohio FIVE-YEAR FINANCIAL FORECAST NOTES AND ASSUMPTIONS. For the Fiscal Years Ending June 30, 2013 through 2017

Miami County, Ohio FIVE-YEAR FINANCIAL FORECAST NOTES AND ASSUMPTIONS For the Fiscal Years Ending June 30, 2013 through 2017 May 13, 2013 General The Ohio Constitution assigns the state the responsibility

Miami County, Ohio FIVE-YEAR FINANCIAL FORECAST NOTES AND ASSUMPTIONS For the Fiscal Years Ending June 30, 2013 through 2017 May 13, 2013 General The Ohio Constitution assigns the state the responsibility

5/2/2016 Montgomery County MD - Estimated Real Property Tax System Printed on: 5/2/2016 7:24:02 PM ACCOUNT NUMBER: PROPERTY: OWNER NAME ENG R

5/2/2016 Montgomery County MD - Estimated Real Property Tax System Printed on: 5/2/2016 7:24:02 PM ACCOUNT NUMBER: 01394952 PROPERTY: OWNER NAME ENG RODNEY D TR TAX INFORMATION: Real Property Estimated

5/2/2016 Montgomery County MD - Estimated Real Property Tax System Printed on: 5/2/2016 7:24:02 PM ACCOUNT NUMBER: 01394952 PROPERTY: OWNER NAME ENG RODNEY D TR TAX INFORMATION: Real Property Estimated

Revenues. Property Tax. Property Tax Revenue vs. Assessed Valuations

Property Tax Although property tax has historically been the largest revenue source for the City s General Fund, currently it is a close second to the sales tax revenue. During fiscal year 2012-13, the

Property Tax Although property tax has historically been the largest revenue source for the City s General Fund, currently it is a close second to the sales tax revenue. During fiscal year 2012-13, the

School District of Philadelphia

School District of Philadelphia Fiscal Year 2010-11 (July 2010 June 2011) First Quarter Financial Report October 20, 2010 1 If you have a disability and the format of any material on our web pages interferes

School District of Philadelphia Fiscal Year 2010-11 (July 2010 June 2011) First Quarter Financial Report October 20, 2010 1 If you have a disability and the format of any material on our web pages interferes

2017 State of the Cities

2017 State of the Cities Introduction The League of Minnesota Cities sent the fiscal conditions survey to chief appointed officials in all member cities late last year. Roughly 43 percent of officials

2017 State of the Cities Introduction The League of Minnesota Cities sent the fiscal conditions survey to chief appointed officials in all member cities late last year. Roughly 43 percent of officials

Gerald K. Geist, Executive Director Service and Representation for Town Governments of New York. January 28, 2013

Gerald K. Geist, Executive Director Service and Representation for Town Governments of New York January 28, 2013 PUBLIC HEARING on 2013-2014 Executive Budget Presented to Senate Finance Committee and Assembly

Gerald K. Geist, Executive Director Service and Representation for Town Governments of New York January 28, 2013 PUBLIC HEARING on 2013-2014 Executive Budget Presented to Senate Finance Committee and Assembly

Budget Assumptions and Schedules for the fiscal year

Budget Assumptions and Schedules for the fiscal year 2010 2011 The Honourable Graham Steele Minister of Finance Budget Assumptions and Schedules for the fiscal year 2010 2011 The Honourable Graham Steele

Budget Assumptions and Schedules for the fiscal year 2010 2011 The Honourable Graham Steele Minister of Finance Budget Assumptions and Schedules for the fiscal year 2010 2011 The Honourable Graham Steele

Bringing Virginia s Transportation Funding Up to Speed. August 25, 2014 John W. Lawson Chief Financial Officer

Bringing Virginia s Transportation Funding Up to Speed August 25, 2014 John W. Lawson Chief Financial Officer Virginia Enacts Legislation to Enhance Transportation Revenues After more than a decade of

Bringing Virginia s Transportation Funding Up to Speed August 25, 2014 John W. Lawson Chief Financial Officer Virginia Enacts Legislation to Enhance Transportation Revenues After more than a decade of

2017 Greenwood County. Fiscal Conditions & Trends. Rebecca Bishop John Leatherman

Fiscal Conditions & Trends Rebecca Bishop John Leatherman With the assistance of Luke Willis, Alana McLain, and Aaron Hendrickson 2017 Greenwood County Provided as a service of the Greenwood County Extension

Fiscal Conditions & Trends Rebecca Bishop John Leatherman With the assistance of Luke Willis, Alana McLain, and Aaron Hendrickson 2017 Greenwood County Provided as a service of the Greenwood County Extension

Property Tax Update with Multi- Residential Property Data

#IowaLeague2016 Property Tax Update with Multi- Residential Property Data Erin Mullenix Former League Research Director Handouts and presentations are available through the event app and at www.iowaleague.org.

#IowaLeague2016 Property Tax Update with Multi- Residential Property Data Erin Mullenix Former League Research Director Handouts and presentations are available through the event app and at www.iowaleague.org.

Major State Aids &Taxes DATA ON WHERE THE AIDS GO AND WHERE THE TAXES COME FROM

Major State Aids &Taxes A COMPARATIVE ANALYSIS, INCLUDING REGIONAL AND COUNTY DATA ON WHERE THE AIDS GO AND WHERE THE TAXES COME FROM Overview of Presentation I will cover three topics or questions: Why

Major State Aids &Taxes A COMPARATIVE ANALYSIS, INCLUDING REGIONAL AND COUNTY DATA ON WHERE THE AIDS GO AND WHERE THE TAXES COME FROM Overview of Presentation I will cover three topics or questions: Why

Corporate Income Tax 5.0% Source: The Tax Foundation s State Corporate Income Tax Rates and State Individual Income Tax Rates, 2018.

Cost of Doing Business in The Southeastern United States fast-paced population growth to date, and its anticipated growth, along with the region s manufacturing renaissance, has made it an ideal location

Cost of Doing Business in The Southeastern United States fast-paced population growth to date, and its anticipated growth, along with the region s manufacturing renaissance, has made it an ideal location

MAJOR REVENUE SOURCES - GENERAL FUND

Introduction The City of Geneva has developed a diverse base of revenues to fund its operational and capital needs. The purpose of this section is to describe the major revenue sources and trends and how

Introduction The City of Geneva has developed a diverse base of revenues to fund its operational and capital needs. The purpose of this section is to describe the major revenue sources and trends and how

2018 Greenwood County. Fiscal Conditions & Trends. Rebecca Bishop John Leatherman

Fiscal Conditions & Trends Rebecca Bishop John Leatherman With the assistance of Luke Willis, Alana McLain, Brandon Entz, and Jordan Howard 2018 Greenwood County Provided as a service of the Greenwood

Fiscal Conditions & Trends Rebecca Bishop John Leatherman With the assistance of Luke Willis, Alana McLain, Brandon Entz, and Jordan Howard 2018 Greenwood County Provided as a service of the Greenwood

2018 Cowley County. Fiscal Conditions & Trends. Rebecca Bishop John Leatherman

Fiscal Conditions & Trends Rebecca Bishop John Leatherman With the assistance of Luke Willis, Alana McLain, Brandon Entz, and Jordan Howard 2018 Cowley County Provided as a service of the Cowley County

Fiscal Conditions & Trends Rebecca Bishop John Leatherman With the assistance of Luke Willis, Alana McLain, Brandon Entz, and Jordan Howard 2018 Cowley County Provided as a service of the Cowley County

FY Budget Forecast. January 26, 2010

FY2011-2020 Budget Forecast January 26, 2010 Outline Forecast Document Economic Overview Fund Forecasts General Fund Forecast FY2011 Budget Strategy FY2011 Budget Process Next Steps 2 Forecast Document

FY2011-2020 Budget Forecast January 26, 2010 Outline Forecast Document Economic Overview Fund Forecasts General Fund Forecast FY2011 Budget Strategy FY2011 Budget Process Next Steps 2 Forecast Document

CHAPTER 23 OHIO'S LOCAL GOVERNMENT FUNDS

CHAPTER 23 OHIO'S LOCAL GOVERNMENT FUNDS Local Government Fund (LGF) Local Government Revenue Assistance Fund (LGRAF) Library and Local Government Support Fund (LLGSF) 23.01 INTRODUCTION Latest Revision

CHAPTER 23 OHIO'S LOCAL GOVERNMENT FUNDS Local Government Fund (LGF) Local Government Revenue Assistance Fund (LGRAF) Library and Local Government Support Fund (LLGSF) 23.01 INTRODUCTION Latest Revision

April 30, 2016 Financial Report

2016 April 30, 2016 Financial Report Capital Metropolitan Transportation Authority 6/15/2016 Table of Contents SUMMARY REPORT Budgetary Performance - Revenue 2 - Sales Tax Revenue 6 - Operating Expenses

2016 April 30, 2016 Financial Report Capital Metropolitan Transportation Authority 6/15/2016 Table of Contents SUMMARY REPORT Budgetary Performance - Revenue 2 - Sales Tax Revenue 6 - Operating Expenses

Economic Impact and Policy Analysis of Four Michigan Transportation Investment Proposals

Issued: June 2012 Revised-September 2012 Economic Impact and Policy Analysis of Four Michigan Transportation Investment Proposals Prepared by: Anderson Economic Group, LLC Alex Rosaen, Consultant Colby

Issued: June 2012 Revised-September 2012 Economic Impact and Policy Analysis of Four Michigan Transportation Investment Proposals Prepared by: Anderson Economic Group, LLC Alex Rosaen, Consultant Colby

THE SCHOOL DISTRICT OF PHILADELPHIA

THE SCHOOL DISTRICT OF PHILADELPHIA OFFICE OF THE SUPERINTENDENT 440 NORTH BROAD STREET, SUITE 301 PHILADELPHIA, PENNSYLVANIA 19130 WILLIAM R. HITE, JR., Ed.D. TELEPHONE (215) 400-4100 SUPERINTENDENT FAX

THE SCHOOL DISTRICT OF PHILADELPHIA OFFICE OF THE SUPERINTENDENT 440 NORTH BROAD STREET, SUITE 301 PHILADELPHIA, PENNSYLVANIA 19130 WILLIAM R. HITE, JR., Ed.D. TELEPHONE (215) 400-4100 SUPERINTENDENT FAX

History of State Revenue Sharing

History of State Revenue Sharing Eric Lupher CRC s Director of Local Affairs EMU Urban Planning Studio January 31, 2012 1 Citizens Research Council of Michigan Founded in 1916 Statewide Nonpartisan Private

History of State Revenue Sharing Eric Lupher CRC s Director of Local Affairs EMU Urban Planning Studio January 31, 2012 1 Citizens Research Council of Michigan Founded in 1916 Statewide Nonpartisan Private

TYPICALLY - LESS THAN ONE-THIRD OF THE PROPERTY TAX BILL IS FOR COUNTY GOVERNMENT EXAMPLE FOR RESIDENTIAL TAXPAYER

1 TAX REFORM Where Do Tax Dollars Go? What has the County Done with Additional Property Tax Revenue? How has the State Contributed to the Problem? How will State Tax Cut Proposals Affect our County? Where

1 TAX REFORM Where Do Tax Dollars Go? What has the County Done with Additional Property Tax Revenue? How has the State Contributed to the Problem? How will State Tax Cut Proposals Affect our County? Where

PINELLAS SUNCOAST TRANSIT AUTHORITY KEY BUDGET ASSUMPTIONS FOR FISCAL YEAR 2016

PINELLAS SUNCOAST TRANSIT AUTHORITY KEY BUDGET ASSUMPTIONS FOR FISCAL YEAR 2016 PSTA Budget Forecasting Summary Item Assumption Amount Source 3 Yr. Avg. FY2016 FY2017 FY2018 FY2019 FY2020 Revenues FY15

PINELLAS SUNCOAST TRANSIT AUTHORITY KEY BUDGET ASSUMPTIONS FOR FISCAL YEAR 2016 PSTA Budget Forecasting Summary Item Assumption Amount Source 3 Yr. Avg. FY2016 FY2017 FY2018 FY2019 FY2020 Revenues FY15

Fridley Public Schools, ISD 14

Fridley Public Schools, ISD 14 Public Hearing for Taxes Payable in 2019 DECEMBER 18, 2018 PRESENTED BY: MATTHEW HAMMER, DIRECTOR OF FINANCE Agenda for Hearing 1. State Funding of Schools 2. Information

Fridley Public Schools, ISD 14 Public Hearing for Taxes Payable in 2019 DECEMBER 18, 2018 PRESENTED BY: MATTHEW HAMMER, DIRECTOR OF FINANCE Agenda for Hearing 1. State Funding of Schools 2. Information

Revenue Overview. FY 2018 Proposed Budget

Revenue Overview FY 2018 Proposed Budget County Board Work Session March 2, 2017 General Fund Revenue by Source 2 Local Tax Revenue by Source (General Fund) 3 FY 2017 to FY 2018 Proposed Revenue Changes

Revenue Overview FY 2018 Proposed Budget County Board Work Session March 2, 2017 General Fund Revenue by Source 2 Local Tax Revenue by Source (General Fund) 3 FY 2017 to FY 2018 Proposed Revenue Changes

MPOAC REVENUE STUDY. Study Update Northwest Florida Regional TPO January 18, 2012

Study Update Northwest Florida Regional TPO January 18, 2012 Study History 2008 Florida Senate Bill 1688 Recommend funding mechanism 13 members- 3 governor s, 3 Senate, 3 House, FDOT, MPOAC, FL Association

Study Update Northwest Florida Regional TPO January 18, 2012 Study History 2008 Florida Senate Bill 1688 Recommend funding mechanism 13 members- 3 governor s, 3 Senate, 3 House, FDOT, MPOAC, FL Association

A Quick Guide to the FY 11 Adopted Budget Department of Management and Budget

A Quick Guide to the FY 11 Adopted Budget Department of Management and Budget Introduction The combined Adopted Operating and Capital Budget books are nearly seven hundred pages long and contain a great

A Quick Guide to the FY 11 Adopted Budget Department of Management and Budget Introduction The combined Adopted Operating and Capital Budget books are nearly seven hundred pages long and contain a great

Department of Legislative Services Maryland General Assembly 2008 Session FISCAL AND POLICY NOTE. Property Tax - Charter Counties - Limits

Department of Legislative Services Maryland General Assembly 2008 Session HB 125 FISCAL AND POLICY NOTE House Bill 125 Ways and Means (Delegates Hixson and McIntosh) Property Tax - Charter Counties - Limits

Department of Legislative Services Maryland General Assembly 2008 Session HB 125 FISCAL AND POLICY NOTE House Bill 125 Ways and Means (Delegates Hixson and McIntosh) Property Tax - Charter Counties - Limits

Budgets, Tax Rates, & Selected Statistics Fiscal Year 2018

Budgets, Tax Rates, & Selected Statistics Fiscal Year 2018 1 Fiscal Year 2018 Report of County Budgets, Tax Rates & Selected Statistics Prepared by the Maryland Association of Counties MACo 69 Conduit

Budgets, Tax Rates, & Selected Statistics Fiscal Year 2018 1 Fiscal Year 2018 Report of County Budgets, Tax Rates & Selected Statistics Prepared by the Maryland Association of Counties MACo 69 Conduit

GENERAL FUND Revenues

GENERAL FUND Revenues The General Fund is used to account for general purpose revenues, which are used to fund general governmental services, excluding utilities. Following are descriptions of the City's

GENERAL FUND Revenues The General Fund is used to account for general purpose revenues, which are used to fund general governmental services, excluding utilities. Following are descriptions of the City's

TRANSPORTATION-SPECIFIC SALES TAX REVENUE 23% Visitors Generate Roughly 23 Percent of Taxable Retail Sales

EXECUTIVE SUMMARY Applied Analysis was retained by the Las Vegas Convention and Visitors Authority ( LVCVA ) to review and analyze the economic impacts associated with its various operations and the overall

EXECUTIVE SUMMARY Applied Analysis was retained by the Las Vegas Convention and Visitors Authority ( LVCVA ) to review and analyze the economic impacts associated with its various operations and the overall

Financial. Snapshot An appendix to the Citizen s Guide to Transportation Funding in Missouri

Financial Snapshot An appendix to the Citizen s Guide to Transportation Funding in Missouri November 2017 Financial Snapshot About the Financial Snapshot The Financial Snapshot provides answers to frequently

Financial Snapshot An appendix to the Citizen s Guide to Transportation Funding in Missouri November 2017 Financial Snapshot About the Financial Snapshot The Financial Snapshot provides answers to frequently

February 2016 Financial Report

2016 February 2016 Financial Report Capital Metropolitan Transportation Authority 4/13/2016 Table of Contents SUMMARY REPORT Budgetary Performance - Revenue 2 - Sales Tax Revenue 5 - Operating Expenses

2016 February 2016 Financial Report Capital Metropolitan Transportation Authority 4/13/2016 Table of Contents SUMMARY REPORT Budgetary Performance - Revenue 2 - Sales Tax Revenue 5 - Operating Expenses

CORPORATE TAX REVENUE BUOYANCY

July 2009, Number 196 CORPORATE TAX REVENUE BUOYANCY Introduction Although the tax on corporations is not the largest generator of state tax revenues, its share is too important to ignore. Georgia s tax

July 2009, Number 196 CORPORATE TAX REVENUE BUOYANCY Introduction Although the tax on corporations is not the largest generator of state tax revenues, its share is too important to ignore. Georgia s tax

May 31, 2016 Financial Report

2016 May 31, 2016 Financial Report Capital Metropolitan Transportation Authority 7/13/2016 Table of Contents SUMMARY REPORTS Budgetary Performance - Revenue 2 - Sales Tax Revenue 6 - Operating Expenses

2016 May 31, 2016 Financial Report Capital Metropolitan Transportation Authority 7/13/2016 Table of Contents SUMMARY REPORTS Budgetary Performance - Revenue 2 - Sales Tax Revenue 6 - Operating Expenses

Annual report. KiwiSaver evaluation. July 2011 to June 2012

KiwiSaver evaluation Annual report July 2011 to June 2012 Prepared by: National Research and Evaluation Unit, Inland Revenue for the KiwiSaver Evaluation Steering Group Date: September 2012 1 Contents

KiwiSaver evaluation Annual report July 2011 to June 2012 Prepared by: National Research and Evaluation Unit, Inland Revenue for the KiwiSaver Evaluation Steering Group Date: September 2012 1 Contents

General Fund Revenue Summary

Summary of General Fund Revenues and Expenditures Budget FY 2017-2018 FISCAL YEAR 2017-2018 General Fund Revenue Summary The City of Decatur has 7 broad revenue categories: taxes, licenses and permits,

Summary of General Fund Revenues and Expenditures Budget FY 2017-2018 FISCAL YEAR 2017-2018 General Fund Revenue Summary The City of Decatur has 7 broad revenue categories: taxes, licenses and permits,

State Tax Actions NATIONAL CONFERENCE OF STATE LEGISLATURES JAN 2019

State Tax Actions 2018 NATIONAL CONFERENCE OF STATE LEGISLATURES JAN 2019 2018 State Tax Actions The National Conference of State Legislatures is the bipartisan organization dedicated to serving the lawmakers

State Tax Actions 2018 NATIONAL CONFERENCE OF STATE LEGISLATURES JAN 2019 2018 State Tax Actions The National Conference of State Legislatures is the bipartisan organization dedicated to serving the lawmakers

Total state and local business taxes

Total state and local business taxes State-by-state estimates for fiscal year 2014 October 2015 Executive summary This report presents detailed state-by-state estimates of the state and local taxes paid

Total state and local business taxes State-by-state estimates for fiscal year 2014 October 2015 Executive summary This report presents detailed state-by-state estimates of the state and local taxes paid

DOTD s Response to House Resolution 178 (2016)

") DOTD s Response to House Resolution 178 (2016) Part II: Feasibility of Implementing Local Option Motor Fuel Taxes 2016 HDR, Inc., all rights reserved. National Context Current Events Federal motor fuel

DOTD s Response to House Resolution 178 (2016) Part II: Feasibility of Implementing Local Option Motor Fuel Taxes 2016 HDR, Inc., all rights reserved. National Context Current Events Federal motor fuel

Historical and Projected Population Totals in Maryland,

Growth and Land Use Trends Population Trends From 2000-2030 Maryland will grow by nearly 1.4 million people. Specifically, this growth will mean the difference between 5.3 million people in 2000 to 6.7

Growth and Land Use Trends Population Trends From 2000-2030 Maryland will grow by nearly 1.4 million people. Specifically, this growth will mean the difference between 5.3 million people in 2000 to 6.7

State-Collected Local Taxes: Basis of Distribution

State-Collected Local Taxes: Basis of Distribution PREPARED BY THE NORTH CAROLINA LEAGUE OF MUNICIPALITIES -- MARCH 2018 Powell Bill Funds Distribution Schedule: Powell Bill proceeds are distributed twice

State-Collected Local Taxes: Basis of Distribution PREPARED BY THE NORTH CAROLINA LEAGUE OF MUNICIPALITIES -- MARCH 2018 Powell Bill Funds Distribution Schedule: Powell Bill proceeds are distributed twice

FY 2017 Executive Budget Overview Robert F. Mujica, Budget Director

FY 2017 Executive Budget Overview Robert F. Mujica, Budget Director In the last five years, we have accomplished much and today, the arrows are pointed in the right direction... We went from 50 years of

FY 2017 Executive Budget Overview Robert F. Mujica, Budget Director In the last five years, we have accomplished much and today, the arrows are pointed in the right direction... We went from 50 years of