REVENUE Major Vermont Tax Sources

|

|

|

- Osborne Stafford

- 5 years ago

- Views:

Transcription

1 REVENUE DETAILS 39

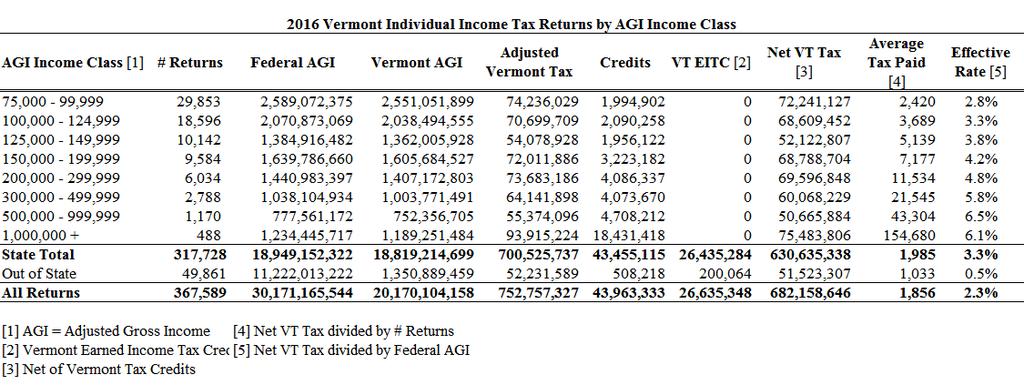

2 REVENUE Major Vermont Tax Sources Vermont has three major funds into which most tax revenue is deposited; the General Fund, the Transportation Fund and the Education Fund. There are also a number of special funds. The revenue from the tax sources described below are dedicated to the General Fund unless otherwise indicated. This section contains brief descriptions of the tax base and rate for each type of tax. Additional detailed information and history is included in other sections for some of the major tax types. The list below is organized by the amount of revenue generated by the tax. The Joint Fiscal Office performs a comprehensive decennial study of Vermont taxes. The most recent study was released in January Individual Income Tax Vermont individual income tax begins at federal taxable income, which is adjusted to calculate Vermont taxable income. Vermont established five state specific tax brackets and rates beginning in Previously, Vermont individual income tax was calculated as a percentage of federal tax liability. Sales & Use Tax Vermont has a 6% general tax on retail sales. The General Fund receives 64% of the revenue and 36% is dedicated to the Education Fund. Vermont also allows a 1% local option sales tax in some municipalities. Meals & Rooms Tax A tax of 9% is imposed on taxable meals and the rent of each room occupancy less than thirty days in length. The alcohol portion of the meals tax is 10%. Vermont also allows a 1% local option sales tax in some municipalities. Corporate Income Tax The net income of C-corporations is taxed according to the state rate and bracket schedule. The apportionment formula includes property, payroll, and is doubled-weighted for sales. Vermont requires unitary combined reporting. 40

3 Major Vermont Tax Sources - continued Cigarette and Tobacco Products Taxes The tax on all cigarettes is $3.08 per pack effective July 1, The tax on tobacco products is at a rate of 92% of the wholesale price, except snuff and new smokeless tobacco which is $2.57 per ounce. The revenue from these excise taxes is dedicated to health care. Both cigarettes and other tobacco products are additionally subject to the sales tax. Insurance Premiums Taxes Traditional insurance companies are taxed at a rate of 2% per year on the gross amount of premiums written in Vermont. Captive insurance companies are taxed on the volume of premiums written for direct premiums and assumed reinsurance premiums. Insurance companies are exempt from the corporate income tax. Property Transfer Tax A real property transfer tax is imposed on the transfer of property located within the state. The first 2% of the revenue collected is retained to the Tax Department. The remaining 98% is distributed as follows: (33%) to the General Fund, (50%) to the Housing and Conservation Trust Fund, and (17%) to the Municipal and Regional Planning Fund. A surcharge of 0.2% is dedicated to the Clean Water Fund. Estate Tax The estate tax is a flat 16% on the value over the exclusion amount of $2.75 million beginning in tax year Any revenue greater than 125% of the previous July forecast is dedicated to the Higher Education Trust Fund. 41

Receipts Tax The telephone property tax is 2.")

4 Major Vermont Tax Sources - continued Liquor Tax A tax based on gross revenues is assessed on the sale of spirituous liquor. Sales tax is also applied to liquor. Bank Franchise Tax The tax rate is % of average monthly deposits is assessed. Banks are exempt from the corporate income tax. Telephone Property Tax and Telephone Co. (Gross) Receipts Tax The telephone property tax is 2.37% of the net book value of all of personal property within VT on the preceding December 31st. The telephone company receipts tax is an alternative tax that may be elected in lieu of the property tax described above for companies with less than $50 million in gross operating receipts and is limited to those that made the election the previous year. The tax is between 2.25% and 5.25% of gross operating revenue. Fuel Tax (formerly Fuel Gross Receipts) A tax of 0.2 cents per gallon on fuel including heating oil and kerosene and propane. Natural gas and coal are 0.75% of gross receipts and electricity is 0.5% of gross receipts. This revenue is dedicated to the Home Weatherization Trust Fund. Beverage Taxes (Wine & Beer) Excise taxes are levied on bottlers and wholesalers of malt and vinous beverages. The beer tax rate is 26.5 cents per gallon and wine is taxed at 55 cents per gallon. Sales tax is also applied to beer and wine. Land Gains Tax This tax is on the gain made from the sale of land located in VT and held by the seller for less than 6 years. The rate is in inverse proportion to the holding period and between 5% and 80% of the gain. 42

5 Major Vermont Tax Sources - continued Land Use Change Tax This tax is assessed if land enrolled in the use value appraisal program (Current Use Program) is developed. Railroad Tax This tax is assessed on the appraised value of property and corporate franchise of each railroad company located in whole or part within VT. The revenue is split between the state and the town where the railroad property is located. Electrical Energy Tax Electric generating facilities with a name plate generating capacity of 200,000 kw or more are subject to this tax. The tax is $ per kwh of electric energy produced and is based on the energy produced in the prior quarter. 43

6 44

7 45

8 46

9 47

10 Education Fund Revenue Sources (Non-Property Tax) General Fund Transfer By statute, the Education Fund receives a transfer from the General Fund. The FY2017 base General Fund transfer of $305.9 million increases annually based on an inflationary adjustment in addition to other changes that the legislature may make on an annual basis. The current-law transfer for FY2019 is $322.9 million. Lottery Transfer All profits from the State lottery are transferred to the Education Fund. The State lottery was created in The Tri-State Lottery was introduced in 1986, and Powerball was introduced in Purchase & Use Tax One-third of the revenue from the purchase & use tax is dedicated to the Education Fund. (See the description of Transportation Fund revenue sources.) Sales & Use Tax Beginning in FY2019, 36% of the revenue from the sales & use tax was dedicated to the Education Fund. (See the description of General Fund revenue sources.) Medicaid Transfer A portion of the federal Medicaid reimbursements received by the State for medically-related services provided to students who are Medicaid-eligible is transferred to the Education Fund. Source: 16 V.S.A

11 Description of Transportation Fund Sources Sources for transportation spending consist of (1) the Transportation Fund and (2) the Transportation Infrastructure Bond Fund (TIB Fund). The TIB Fund is a sub-fund of the Transportation Fund whose revenue can only be expended on certain long lived transportation structures (either directly or via payment of debt service on bonds issued for such purposes). The Transportation Fund (excluding the TIB Fund) has six sources of revenue: (1) a fixed cent-per-gallon gasoline tax, (2) a fixed cent-per-gallon diesel fuel tax, (3) a gasoline percentage-of-price assessment with a minimum and maximum cent-per-gallon equivalent, (4) a motor vehicle purchase and use tax (6% split 4% to the Transportation Fund and 2% to the Education Fund), (5) motor vehicle fees, and (6) other revenue (other small transportation related taxes and fees) The TIB fund has 2 sources of revenue: (1) a gasoline percentage of price assessment with a minimum cent-per-gallon equivalent, and (2) a fixed-cent-per-gallon diesel fuel assessment. Gasoline levies State levies on gasoline consist of: (1) a fixed 12.1 cents-per-gallon Transportation Fund tax, (2) a 4% percentage-of-price Transportation Fund assessment with a minimum and maximum cents-per-gallon equivalent of 13.4 cents and 18 cents respectively, (3) a 2% percentage-of-price TIB Fund assessment with a minimum cent-per-gallon equivalent of 3.90 cents, and (4) a 1 cent-per-gallon petroleum clean-up fund fee. Diesel fuel levies State levies on diesel fuel consist of: (1) a fixed 28 cents-per-gallon Transportation Fund tax, (2) a fixed 3 cents-per-gallon TIB Fund assessment and (3) a 1 cent-per-gallon petroleum clean-up fund fee. 49

12 Transportation Fund Sources (continued) Motor Vehicle Purchase and Use-Tax The motor vehicle purchase & use tax applies to (1) motor vehicle sale transactions; and (2) where a sale is not involved, to an owner s initial registration of a vehicle in the state. For sale transactions, the tax is assessed on the vehicle s purchase price less the value of any trade-in which is credited against the purchase price. For non-sale transactions, the tax is assessed on the vehicle s current market value at the time of registration. Sale taxes paid by the owner in another jurisdiction are credited against the tax due. In both cases the tax rate is 6%. For trucks over 10,099 pounds, the tax is capped at $2,075. Vehicles purchased for the short-term rental market are exempt from the purchase tax but each rental transaction is subject to a rental tax equal to 9% of the rental charge. Revenue from the purchase & use tax and short-term rental tax is allocated 2/3 to the Transportation Fund and 1/3 to the Education Fund. Motor Vehicle Fees This category covers a range of fees collected by DMV of which the most important are registration fees and driver license fees. A registration fee is collected on all motor vehicles and trailers. The fee varies depending upon the vehicle type, size, weight, and purpose. All motor vehicle fees are deposited into the Transportation Fund. Relative Contribution to the Transportation Fund The above sources made the following relative contributions to Transportation Fund revenue from FY-13 through FY

13 51

14 52

15 53

A FIELD GUIDE TO THE TAX E S TEXAS

A FIELD GUIDE TO THE TAX E S TEXAS OF DECEMBER GLENN HEGAR TEXAS COMPTROLLER OF PUBLIC ACCOUNTS A FIELD GUIDE TO THE TAXES OF TEXAS The data represented in this report is available in accessible data form

A FIELD GUIDE TO THE TAX E S TEXAS OF DECEMBER GLENN HEGAR TEXAS COMPTROLLER OF PUBLIC ACCOUNTS A FIELD GUIDE TO THE TAXES OF TEXAS The data represented in this report is available in accessible data form

Ohio 2020 Tax Policy Commission

Ohio 2020 Tax Policy Commission Testimony of Tax Commissioner Joe Testa Department of Taxation October 22, 2015 Co-Chairman Senator Peterson, Co-Chairman Representative McClain, and members of the Tax

Ohio 2020 Tax Policy Commission Testimony of Tax Commissioner Joe Testa Department of Taxation October 22, 2015 Co-Chairman Senator Peterson, Co-Chairman Representative McClain, and members of the Tax

CHAPTER 13 STATE TAXES

CHAPTER 13 STATE TAXES Latest Revision 1994 13.01 INTRODUCTION Ohio relies on various taxes to support its governmental activities. Some of these taxes have transfer provisions which accrue to the benefit

CHAPTER 13 STATE TAXES Latest Revision 1994 13.01 INTRODUCTION Ohio relies on various taxes to support its governmental activities. Some of these taxes have transfer provisions which accrue to the benefit

2013 Supplement to the Minnesota Tax Handbook

2013 Supplement to the Minnesota Tax Handbook This supplement to the 2012 Edition of the Minnesota Tax Handbook contains the major tax law changes enacted in 2013. The page references are to the 2012 Edition.

2013 Supplement to the Minnesota Tax Handbook This supplement to the 2012 Edition of the Minnesota Tax Handbook contains the major tax law changes enacted in 2013. The page references are to the 2012 Edition.

CRS Report for Congress Received through the CRS Web

97-331 E CRS Report for Congress Received through the CRS Web Excise Taxes on Alcohol, Tobacco, and Gasoline: History and Inflation Adjusted Rates March 7, 1997 Louis Alan Talley Research Analyst in Taxation

97-331 E CRS Report for Congress Received through the CRS Web Excise Taxes on Alcohol, Tobacco, and Gasoline: History and Inflation Adjusted Rates March 7, 1997 Louis Alan Talley Research Analyst in Taxation

New Hampshire Fiscal Policy Institute 1

New Hampshire Fiscal Policy Institute 1 New Hampshire Fiscal Policy Institute 2 Pays for services that help make our communities stronger Tangible and direct: Roads and bridges Police, fire, and emergency

New Hampshire Fiscal Policy Institute 1 New Hampshire Fiscal Policy Institute 2 Pays for services that help make our communities stronger Tangible and direct: Roads and bridges Police, fire, and emergency

2002 FI$CAL FACT$ VERMONT LEGISLATIVE JOINT FISCAL OFFICE

2002 FI$CAL FACT$ VERMONT LEGISLATIVE JOINT FISCAL OFFICE Joint Fiscal Committee 2001-2002 Legislative Session Chair, Representative Richard Marron Senator Susan Bartlett Senator Ann Cummings Senator Robert

2002 FI$CAL FACT$ VERMONT LEGISLATIVE JOINT FISCAL OFFICE Joint Fiscal Committee 2001-2002 Legislative Session Chair, Representative Richard Marron Senator Susan Bartlett Senator Ann Cummings Senator Robert

State Tax Structures: A Regional Overview Presentation to the Arkansas Tax Reform and Relief Task Force July 11, 2017

EXHIBIT E Strong States, Strong Nation State Tax Structures: A Regional Overview Presentation to the Arkansas Tax Reform and Relief Task Force July 11, 2017 Kathleen Quinn Fiscal Affairs Program National

EXHIBIT E Strong States, Strong Nation State Tax Structures: A Regional Overview Presentation to the Arkansas Tax Reform and Relief Task Force July 11, 2017 Kathleen Quinn Fiscal Affairs Program National

Department of Revenue Analysis of S.F (Pogemiller) Revenue Gain or (Loss) F.Y F.Y F.Y F.Y (000 s)

Revenue Gain or (Loss) F.Y F.Y F.Y F.Y (000 s)") Governor's Tax Proposal February 4, 2002 Separate Official Fiscal Note Requested Fiscal Impact DOR Administrative Costs/Savings Yes No X Department of Revenue Analysis of S.F. 3000 (Pogemiller) Revenue

Governor's Tax Proposal February 4, 2002 Separate Official Fiscal Note Requested Fiscal Impact DOR Administrative Costs/Savings Yes No X Department of Revenue Analysis of S.F. 3000 (Pogemiller) Revenue

Key Elements of the U.S. Tax System

What are the major federal excise taxes, and how much money do they raise? EXCISE TAXES 1/2 Q. What are the major federal excise taxes, and how much money do they raise? A. Federal excise tax revenues

What are the major federal excise taxes, and how much money do they raise? EXCISE TAXES 1/2 Q. What are the major federal excise taxes, and how much money do they raise? A. Federal excise tax revenues

THE COUNTY OF COOK. Competition and Cooperation: Cross-Jurisdictional Issues and Tobacco Taxes

THE COUNTY OF COOK Competition and Cooperation: Cross-Jurisdictional Issues and Tobacco Taxes Table of Contents 1. County s FY2015 Budgeted Revenue and Expenses 2. County s Home Rule Taxes 3. Geographical

THE COUNTY OF COOK Competition and Cooperation: Cross-Jurisdictional Issues and Tobacco Taxes Table of Contents 1. County s FY2015 Budgeted Revenue and Expenses 2. County s Home Rule Taxes 3. Geographical

2017 Supplement to the Minnesota Tax Handbook

2017 Supplement to the Minnesota Tax Handbook This supplement to the 2016 Edition of the Minnesota Tax Handbook contains the major tax law changes enacted in 2017. The page references are to the 2016 Edition.

2017 Supplement to the Minnesota Tax Handbook This supplement to the 2016 Edition of the Minnesota Tax Handbook contains the major tax law changes enacted in 2017. The page references are to the 2016 Edition.

Oneida Indian Nation Tax Rules Effective as of March 5, 2014

Oneida Indian Nation Tax Rules Effective as of March 5, 2014 I. RULES OF THE NATION DEPARTMENT OF TAXATION A. The Oneida Nation has authorized the creation of the Nation Department of Taxation with responsibility

Oneida Indian Nation Tax Rules Effective as of March 5, 2014 I. RULES OF THE NATION DEPARTMENT OF TAXATION A. The Oneida Nation has authorized the creation of the Nation Department of Taxation with responsibility

Comprehensive tax reform. 18LSO-0391, 1.3 FISCAL NOTE

FISCAL NOTE FY 2019 FY 2020 FY 2021 NON-ADMINISTRATIVE IMPACT Anticipated Revenue increase/(decrease) GENERAL FUND (1) $0 $108,000,000 $108,000,000 SCHOOL CAP CON ACCOUNT (3) $42,000,000 $42,000,000 $42,000,000

FISCAL NOTE FY 2019 FY 2020 FY 2021 NON-ADMINISTRATIVE IMPACT Anticipated Revenue increase/(decrease) GENERAL FUND (1) $0 $108,000,000 $108,000,000 SCHOOL CAP CON ACCOUNT (3) $42,000,000 $42,000,000 $42,000,000

A Summary of Oregon Taxes

A Summary of Oregon Taxes O R E G O N DEPARTMENT OF REVENUE A Summary of Oregon Taxes provides a brief description of taxes and fees that individuals and businesses can expect to pay in Oregon. This brochure

A Summary of Oregon Taxes O R E G O N DEPARTMENT OF REVENUE A Summary of Oregon Taxes provides a brief description of taxes and fees that individuals and businesses can expect to pay in Oregon. This brochure

Michigan Tax Revenue. Mary Ann Cleary, Director House Fiscal Agency

Michigan Tax Revenue Mary Ann Cleary, Director Michigan State University Institute for Public Policy and Social Research 2016 Legislative Leadership Program December 5, 2016 Major State Taxes 2 Major State

Michigan Tax Revenue Mary Ann Cleary, Director Michigan State University Institute for Public Policy and Social Research 2016 Legislative Leadership Program December 5, 2016 Major State Taxes 2 Major State

1995 Minnesota Tax Incidence Study

1995 Minnesota Tax Incidence Study Who pays Minnesota s household and business taxes? March 1995 MINNESOTA Department of Revenue Tax Research Division MINNESOTA Department of Revenue March 1, 1995 To

1995 Minnesota Tax Incidence Study Who pays Minnesota s household and business taxes? March 1995 MINNESOTA Department of Revenue Tax Research Division MINNESOTA Department of Revenue March 1, 1995 To

$1,516 $925 $19 $2,460 $422 $1,270 $261 $413 $94 = $715 = $274 = $62 = $13 = $555 = $19 = $148 & HWY

OVERVIEW Missouri Transportation Funding Overview Missouri s transportation revenue totaled almost $2.5 billion in fiscal year 2017. As shown below, nearly two-thirds of the revenue came from state user

OVERVIEW Missouri Transportation Funding Overview Missouri s transportation revenue totaled almost $2.5 billion in fiscal year 2017. As shown below, nearly two-thirds of the revenue came from state user

Indiana Tax Descriptions and Receipts

Indiana Tax Descriptions and Receipts All amounts are in thousands. Percentage change reflects increase from FY05 to FY06, unless otherwise indicated. Significant differences reflected in the tax receipts

Indiana Tax Descriptions and Receipts All amounts are in thousands. Percentage change reflects increase from FY05 to FY06, unless otherwise indicated. Significant differences reflected in the tax receipts

Louisiana Tax Study, 2015

Louisiana Tax Study, 2015 The Central Louisiana Chamber of Commerce April 9, 2015 Gregory B. Upton, Jr., Ph.D. Center for Energy Studies Louisiana State University Background 2 Introduction It has been

Louisiana Tax Study, 2015 The Central Louisiana Chamber of Commerce April 9, 2015 Gregory B. Upton, Jr., Ph.D. Center for Energy Studies Louisiana State University Background 2 Introduction It has been

GENERAL FUND Revenues

GENERAL FUND Revenues The General Fund is the general operating fund of the City and encompasses the major activities of the City excluding utilities. The activities of fire and police services, street

GENERAL FUND Revenues The General Fund is the general operating fund of the City and encompasses the major activities of the City excluding utilities. The activities of fire and police services, street

Overview of Gift, Inheritance, Estate, Selected Excise, & Miscellaneous Taxes

Overview of Gift, Inheritance, Estate, Selected Excise, & Miscellaneous Taxes Presentation to Revenue Study Commission Created by SCR 103 of the 2012 Regular Legislative Session October 2, 2012 Presenter

Overview of Gift, Inheritance, Estate, Selected Excise, & Miscellaneous Taxes Presentation to Revenue Study Commission Created by SCR 103 of the 2012 Regular Legislative Session October 2, 2012 Presenter

1999 Minnesota Tax Incidence Study

1999 Minnesota Tax Incidence Study Who pays Minnesota s household and business taxes? March 1999 MINNESOTA Department of Revenue Tax Research Division Mail Station 2230, St. Paul, MN 55146-2230 (612) 296-3425

1999 Minnesota Tax Incidence Study Who pays Minnesota s household and business taxes? March 1999 MINNESOTA Department of Revenue Tax Research Division Mail Station 2230, St. Paul, MN 55146-2230 (612) 296-3425

(S.299) It is hereby enacted by the General Assembly of the State of Vermont: or vinous beverages to the management and staff of businesses who have

It is hereby enacted by the General Assembly of the State of Vermont: or vinous beverages to the management and staff of businesses who have") No. 202. An act relating to sampler flights. (S.299) It is hereby enacted by the General Assembly of the State of Vermont: Sec. 1. PURPOSE The purpose of this act is to allow wholesale dealers to offer

No. 202. An act relating to sampler flights. (S.299) It is hereby enacted by the General Assembly of the State of Vermont: Sec. 1. PURPOSE The purpose of this act is to allow wholesale dealers to offer

Selected Consumer Taxes in the City of Chicago

Selected Consumer Taxes in the City of Chicago A Civic Federation Issue Brief This brief provides a compilation of selected consumer taxes, including rates and descriptions, in place in the City of Chicago

Selected Consumer Taxes in the City of Chicago A Civic Federation Issue Brief This brief provides a compilation of selected consumer taxes, including rates and descriptions, in place in the City of Chicago

MAJOR REVENUES REVENUE FROM LOCAL SOURCES PROPERTY TAX REVENUES

REVENUE FROM LOCAL SOURCES PROPERTY TAX REVENUES Property taxes for FY12 were $41.86M and will increase in FY13 to $44.06M up $2.20M or 5.3%. FY14 projections for property tax revenues are $46.26M a $2.20M

REVENUE FROM LOCAL SOURCES PROPERTY TAX REVENUES Property taxes for FY12 were $41.86M and will increase in FY13 to $44.06M up $2.20M or 5.3%. FY14 projections for property tax revenues are $46.26M a $2.20M

Summaries of Appropriations

Summaries of Appropriations This section includes tables and charts that summarize the Governor's Budget recommendations and highlight significant changes and policy initiatives. THE BUDGET IN BRIEF (thousands

Summaries of Appropriations This section includes tables and charts that summarize the Governor's Budget recommendations and highlight significant changes and policy initiatives. THE BUDGET IN BRIEF (thousands

TAX MEASURES HELP BALANCE STATE BUDGETS A Common and Reasonable Response to Shortfalls By Nicholas Johnson, Andrew C. Nicholas, and Steven Pennington

820 First Street NE, Suite 510 Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org Updated July 9, 2009 TAX MEASURES HELP BALANCE STATE BUDGETS A Common and Reasonable

820 First Street NE, Suite 510 Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org Updated July 9, 2009 TAX MEASURES HELP BALANCE STATE BUDGETS A Common and Reasonable

2016 FAST TAX Tax Summary and Easy Reference Guide

Utah Taxpayers Association SINCE 1922 2016 FAST TAX Tax Summary and Easy Reference Guide Sponsored by Parsons Behle & Latimer A Publication of the Utah Taxpayers Association 656 East 11400 South, Suite

Utah Taxpayers Association SINCE 1922 2016 FAST TAX Tax Summary and Easy Reference Guide Sponsored by Parsons Behle & Latimer A Publication of the Utah Taxpayers Association 656 East 11400 South, Suite

A RIPEC Report on Rhode Island s State and Local Tax System March 25, 2008

A RIPEC Report on Rhode Island s State and Local Tax System March 25, 2008 Compiled as a public service by the Rhode Island Public Expenditure Council A RIPEC Report on Rhode Island s State and Local Tax

A RIPEC Report on Rhode Island s State and Local Tax System March 25, 2008 Compiled as a public service by the Rhode Island Public Expenditure Council A RIPEC Report on Rhode Island s State and Local Tax

STATE MOTOR FUEL TAX INCREASES:

Since 2013, 26 states have increased or adjusted taxes on motor fuel to support needed transportation investments. Twenty-three of those states increased their state gas tax, while three states Kentucky,

Since 2013, 26 states have increased or adjusted taxes on motor fuel to support needed transportation investments. Twenty-three of those states increased their state gas tax, while three states Kentucky,

New York State Senate Finance Committee

New York State Senate Finance Committee 2009 Mid Year Report On Receipts and Disbursements Senator Carl Kruger Chair, Senate Finance Committee Senator Liz Krueger Vice-Chair, Senate Finance Committee Joseph

New York State Senate Finance Committee 2009 Mid Year Report On Receipts and Disbursements Senator Carl Kruger Chair, Senate Finance Committee Senator Liz Krueger Vice-Chair, Senate Finance Committee Joseph

NCSL FISCAL BRIEF: PROJECTED STATE TAX GROWTH IN FY 2012 AND BEYOND

NCSL FISCAL BRIEF: PROJECTED STATE TAX GROWTH IN FY 2012 AND BEYOND December 6, 2011 Fiscal year (FY) 2012 marks the second consecutive year state officials are forecasting state tax growth compared with

NCSL FISCAL BRIEF: PROJECTED STATE TAX GROWTH IN FY 2012 AND BEYOND December 6, 2011 Fiscal year (FY) 2012 marks the second consecutive year state officials are forecasting state tax growth compared with

The Total Impact List: Biennium With an eye on 2017

The Total Impact List: 2015 2016 Biennium With an eye on 2017 The Vermont Chamber has created this highlight of impacts on Vermont s business community as a result of government action during the 2015

The Total Impact List: 2015 2016 Biennium With an eye on 2017 The Vermont Chamber has created this highlight of impacts on Vermont s business community as a result of government action during the 2015

STATE MOTOR FUEL TAX INCREASES:

STATE MOTOR FUEL TAX INCREASES: 2013-2018 Since 2013, 27 states have increased or adjusted taxes on motor fuel to support needed transportation investments. Twenty-four of those states increased their

STATE MOTOR FUEL TAX INCREASES: 2013-2018 Since 2013, 27 states have increased or adjusted taxes on motor fuel to support needed transportation investments. Twenty-four of those states increased their

The Vermont Tax Study

The Vermont Tax Study 2005-2015 Summary Report VERMONT JOINT FISCAL OFFICE 1 Baldwin Street Montpelier, VT 05633-5701 www.leg.state.vt.us/jfo January 17, 2017 The Vermont Tax Study 2005-2015 Summary Report

The Vermont Tax Study 2005-2015 Summary Report VERMONT JOINT FISCAL OFFICE 1 Baldwin Street Montpelier, VT 05633-5701 www.leg.state.vt.us/jfo January 17, 2017 The Vermont Tax Study 2005-2015 Summary Report

The Vermont Tax Study

The Vermont Tax Study 2005-2015 The enabling legislation for this edition of the Vermont Tax Study is Act No. 157 An Act Relating to Miscellaneous Economic Development Provisions of the 2016 session of

The Vermont Tax Study 2005-2015 The enabling legislation for this edition of the Vermont Tax Study is Act No. 157 An Act Relating to Miscellaneous Economic Development Provisions of the 2016 session of

2018 Supplement to the Eighth Edition. December 2018

KANSAS TAX FACTS 2018 Supplement to the Eighth Edition December 2018 Kansas Legislative Research Department Room 68-W State Capitol Building 300 SW Tenth Avenue Phone: (785) 296-3181 Topeka, Kansas 66612-1504

KANSAS TAX FACTS 2018 Supplement to the Eighth Edition December 2018 Kansas Legislative Research Department Room 68-W State Capitol Building 300 SW Tenth Avenue Phone: (785) 296-3181 Topeka, Kansas 66612-1504

CRS Report for Congress Received through the CRS Web

Order Code RS20343 Updated January 10, 2002 CRS Report for Congress Received through the CRS Web Federal Excise Taxes on Tobacco Products: Rates and Revenues Louis Alan Talley Specialist in Taxation Government

Order Code RS20343 Updated January 10, 2002 CRS Report for Congress Received through the CRS Web Federal Excise Taxes on Tobacco Products: Rates and Revenues Louis Alan Talley Specialist in Taxation Government

2017 FI$CAL FACT$ JOINT FISCAL OFFICE VERMONT LEGISLATIVE.

2017 FI$CAL FACT$ VERMONT LEGISLATIVE JOINT FISCAL OFFICE www.leg.state.vt.us/jfo Issue Date: March 2017 THIS PAGE WAS INTENTIONALLY LEFT BLANK 2 Legislative Joint Fiscal Committee 2017-2018 Legislative

2017 FI$CAL FACT$ VERMONT LEGISLATIVE JOINT FISCAL OFFICE www.leg.state.vt.us/jfo Issue Date: March 2017 THIS PAGE WAS INTENTIONALLY LEFT BLANK 2 Legislative Joint Fiscal Committee 2017-2018 Legislative

State of Arkansas. Tax Relief and Reform Legislative Task Force. State Tax Structures and Recent State Tax Actions EXHIBIT E. December 05, 2017 PFM

EXHIBIT E State of Arkansas Tax Relief and Reform Legislative Task Force State Tax Structures and Recent State Tax Actions December 05, 2017 PFM Group 1735 Market St. (267) 713-0700 Consulting LLC. 43

EXHIBIT E State of Arkansas Tax Relief and Reform Legislative Task Force State Tax Structures and Recent State Tax Actions December 05, 2017 PFM Group 1735 Market St. (267) 713-0700 Consulting LLC. 43

GENERAL FUND PROJECTIONS

GENERAL FUND PROJECTIONS GENERAL FUND REVENUE ESTIMATES AND PROJECTED UNAPPROPRIATED GENERAL FUND BALANCES The 2009 Legislature approved a General Fund operating budget for the 2009-11 biennium that totals

GENERAL FUND PROJECTIONS GENERAL FUND REVENUE ESTIMATES AND PROJECTED UNAPPROPRIATED GENERAL FUND BALANCES The 2009 Legislature approved a General Fund operating budget for the 2009-11 biennium that totals

General Fund Total $761,594 $633,812 $645,863 $657,068. Minnesota Future Resources Fund ($1,022) ($1,055) ($1,001) ($949)

($1,055) ($1,001) ($949)") May 2, 2003 Department of Revenue Analysis of S.F. 1504 (Hottinger), As Amended (A-1) April 30, 2003 Individual Income Tax Corporate Franchise Tax Cigarette and Tobacco Taxes, Others Separate Official

May 2, 2003 Department of Revenue Analysis of S.F. 1504 (Hottinger), As Amended (A-1) April 30, 2003 Individual Income Tax Corporate Franchise Tax Cigarette and Tobacco Taxes, Others Separate Official

STREAMLINED SALES TAX PROJECT TAXES AFFECTED BY SSTP ACT AND AGREEMENT (7/3/02)

") The Project approved moving this paper to the Implementing States on June 14, 2002. Draft Document Not For Publication But For Discussion Purposes Only Nothing contained herein represents a final position

The Project approved moving this paper to the Implementing States on June 14, 2002. Draft Document Not For Publication But For Discussion Purposes Only Nothing contained herein represents a final position

STATE MOTOR FUEL TAXES: NOTES SUMMARY RATES EFFECTIVE 10/01/2018

Tax rates and or notes changed since last report: CT, NJ, OH; IA Rate Updated for Correction; MT Rate Updated for Correction; VA Updated for Method of Calculating Wholesale Tax Other Other Alabama 18.00

Tax rates and or notes changed since last report: CT, NJ, OH; IA Rate Updated for Correction; MT Rate Updated for Correction; VA Updated for Method of Calculating Wholesale Tax Other Other Alabama 18.00

Senate Finance Committee

Presentation to the Senate Finance Committee Review the state's current spending limits and determine if statutory changes are needed to continue restraint of spending growth below the rate of inflation

Presentation to the Senate Finance Committee Review the state's current spending limits and determine if statutory changes are needed to continue restraint of spending growth below the rate of inflation

Financing the Expansion of the

Financing the Expansion of the Children s Health Insurance Program in New Hampshire Presentation to the Children s Health Insurance Commission June 13, 2011 Deborah Fournier, Esq., Policy Analyst Jeff

Financing the Expansion of the Children s Health Insurance Program in New Hampshire Presentation to the Children s Health Insurance Commission June 13, 2011 Deborah Fournier, Esq., Policy Analyst Jeff

Transportation Funds Forecast November 2017

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp Transportation Funds

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp Transportation Funds

Kansas Tax Facts Supplement to the Eighth Edition. December 2016

Kansas Tax Facts 2016 Supplement to the Eighth Edition December 2016 Kansas Legislative Research Department Room 68-W State Capitol Building 300 SW Tenth Avenue Phone: (785) 296-3181/FAX (785) 296-3824

Kansas Tax Facts 2016 Supplement to the Eighth Edition December 2016 Kansas Legislative Research Department Room 68-W State Capitol Building 300 SW Tenth Avenue Phone: (785) 296-3181/FAX (785) 296-3824

Form REG-1 Business Taxes Registration Application

Department of Revenue Services State of Connecticut PO Box 2937 Hartford CT 06104-2937 (Rev. 12/12) Form REG-1 Business Taxes Registration Application 1. Reason for Filing Form REG-1 Check the applicable

Department of Revenue Services State of Connecticut PO Box 2937 Hartford CT 06104-2937 (Rev. 12/12) Form REG-1 Business Taxes Registration Application 1. Reason for Filing Form REG-1 Check the applicable

Indian River County 2030 Comprehensive Plan

2030 Comprehensive Plan Chapter 6 Supplement #15; Adopted December 5, 2017, Ordinance 2017-015 TABLE OF CONTENTS List of Figures... ii List of Tables... iii Introduction... 1 Existing Conditions... 2 Financial

2030 Comprehensive Plan Chapter 6 Supplement #15; Adopted December 5, 2017, Ordinance 2017-015 TABLE OF CONTENTS List of Figures... ii List of Tables... iii Introduction... 1 Existing Conditions... 2 Financial

Forecast Highlights. HUTD Revenues, FY Biennium Change from EOS '16 Forecast

Forecast Highlights FY 2016-17 HUTD revenues down $45 million (1.1 percent) from 2016 EOS Forecast Gas taxes are up $6 million (0.3 percent), registration taxes are down $32 million (2.2 percent) and motor

Forecast Highlights FY 2016-17 HUTD revenues down $45 million (1.1 percent) from 2016 EOS Forecast Gas taxes are up $6 million (0.3 percent), registration taxes are down $32 million (2.2 percent) and motor

Transportation Funds Forecast February 2017

Transportation Funds Forecast February 2017 Released March 3rd, 2017 Forecast Highlights FY 2018-19 HUTD revenues are up $72 million (1.6 percent) from November 2016 Forecast Gas taxes are up $30 million

Transportation Funds Forecast February 2017 Released March 3rd, 2017 Forecast Highlights FY 2018-19 HUTD revenues are up $72 million (1.6 percent) from November 2016 Forecast Gas taxes are up $30 million

STATE AND LOCAL TAXES A Comparison Across States

STATE AND LOCAL TAXES A Comparison Across States INDEPENDENT FISCAL OFFICE FEBRUARY 2018 Methodology This report uses data from the U.S. Census Bureau, the Internal Revenue Service (IRS), the U.S. Bureau

STATE AND LOCAL TAXES A Comparison Across States INDEPENDENT FISCAL OFFICE FEBRUARY 2018 Methodology This report uses data from the U.S. Census Bureau, the Internal Revenue Service (IRS), the U.S. Bureau

Indian River County 2030 Comprehensive Plan

2030 Comprehensive Plan Chapter 6 Adopted:, 2010 DRAFT January 14, 2010 TABLE OF CONTENTS List of Figures... ii List of Tables... ii Introduction... 1 Existing Conditions... 2 Financial Resources... 2

2030 Comprehensive Plan Chapter 6 Adopted:, 2010 DRAFT January 14, 2010 TABLE OF CONTENTS List of Figures... ii List of Tables... ii Introduction... 1 Existing Conditions... 2 Financial Resources... 2

GENERAL FUND Revenues

GENERAL FUND Revenues The General Fund is used to account for general purpose revenues, which are used to fund general governmental services, excluding utilities. Following are descriptions of the City's

GENERAL FUND Revenues The General Fund is used to account for general purpose revenues, which are used to fund general governmental services, excluding utilities. Following are descriptions of the City's

SENATE FISCAL OFFICE REPORT 2015 REVENUE REPORT

SENATE FISCAL OFFICE REPORT 2015 REVENUE REPORT FEBRUARY 24, 2015 State House Room 117 Providence, Rhode Island 02903 (401) 222-2480 www.rilin.state.ri.us/senatefinance Senate Committee on Finance Daniel

SENATE FISCAL OFFICE REPORT 2015 REVENUE REPORT FEBRUARY 24, 2015 State House Room 117 Providence, Rhode Island 02903 (401) 222-2480 www.rilin.state.ri.us/senatefinance Senate Committee on Finance Daniel

FY 2018 Revenue Manual CITY OF ST. AUGUSTINE

FY 2018 Revenue Manual CITY OF ST. AUGUSTINE This Revenue Manual was developed to provide a comprehensive reference source for all revenue collected by the City of St. Augustine. The manual is an in depth

FY 2018 Revenue Manual CITY OF ST. AUGUSTINE This Revenue Manual was developed to provide a comprehensive reference source for all revenue collected by the City of St. Augustine. The manual is an in depth

REVENUE MANUAL PALM BEACH COUNTY Edition February 2018

REVENUE MANUAL PALM BEACH COUNTY 218 Edition February 218 TABLE OF CONTENTS About this. 2 Index of Revenues Index of Revenues by Revenue Source Code Index of Revenues by Name. 3 4 1 About this The Palm

REVENUE MANUAL PALM BEACH COUNTY 218 Edition February 218 TABLE OF CONTENTS About this. 2 Index of Revenues Index of Revenues by Revenue Source Code Index of Revenues by Name. 3 4 1 About this The Palm

OVERVIEW OF LOCAL GOVERNMENT REVENUE SOURCES. Joint House and Senate Finance, February 2, 2011 Rodney Bizzell, Fiscal Research Division

OVERVIEW OF LOCAL GOVERNMENT REVENUE SOURCES Joint House and Senate Finance, February 2, 2011 Rodney Bizzell, Fiscal Research Division Sources of Local Revenue 2 Sources of Local Revenue County Municipal

OVERVIEW OF LOCAL GOVERNMENT REVENUE SOURCES Joint House and Senate Finance, February 2, 2011 Rodney Bizzell, Fiscal Research Division Sources of Local Revenue 2 Sources of Local Revenue County Municipal

Transportation Funds Forecast November 2018

Transportation Funds Forecast November 2018 Released December 7th, 2018 Forecast Highlights FY 2018-19 HUTD revenues are up $12.9 million - 0.3 percent Gas tax is up $13.1 million (0.7 percent), registration

Transportation Funds Forecast November 2018 Released December 7th, 2018 Forecast Highlights FY 2018-19 HUTD revenues are up $12.9 million - 0.3 percent Gas tax is up $13.1 million (0.7 percent), registration

Summaries of Appropriations

Summaries of Appropriations This section includes tables and charts that summarize the Governor's Budget recommendations and highlight significant changes and policy initiatives. THE BUDGET IN BRIEF (thousands

Summaries of Appropriations This section includes tables and charts that summarize the Governor's Budget recommendations and highlight significant changes and policy initiatives. THE BUDGET IN BRIEF (thousands

City Council Working Session on FY 2018 General Fund Revenues. Presentation to Petersburg City Council The Robert Bobb Group, LLC March 27, 2017

City Council Working Session on FY 2018 General Fund Revenues Presentation to Petersburg City Council The Robert Bobb Group, LLC March 27, 2017 Work Session Focus: General Fund Revenues We will detail

City Council Working Session on FY 2018 General Fund Revenues Presentation to Petersburg City Council The Robert Bobb Group, LLC March 27, 2017 Work Session Focus: General Fund Revenues We will detail

21 st Century Transportation Committee Finance Subcommittee

21 st Century Transportation Committee Finance Subcommittee Highway Fund and Highway Trust Fund Transfers Diesel Tax Options January 16, 2008 Outline Funding Sources Department of Transportation s Budget

21 st Century Transportation Committee Finance Subcommittee Highway Fund and Highway Trust Fund Transfers Diesel Tax Options January 16, 2008 Outline Funding Sources Department of Transportation s Budget

Revenue-Raising and Cost-Saving Options Option Description Value

Federal Issue: Support the Call for Additional Fiscal Relief for the States At least 48 states are experiencing major budget shortfalls. We urge the NYS Congressional delegation to support additional fiscal

Federal Issue: Support the Call for Additional Fiscal Relief for the States At least 48 states are experiencing major budget shortfalls. We urge the NYS Congressional delegation to support additional fiscal

O Malley s Taxes Tolls and Fees Present

O Malley s Taxes Tolls and Fees 2007 - Present 2013 Increases: 17 GRAND TOTAL: 74 2013 Electricity surcharges HB 226 - Maryland Offshore Wind Energy Act of 2013 2013 Imposes 1% tax collected by wholesalers

O Malley s Taxes Tolls and Fees 2007 - Present 2013 Increases: 17 GRAND TOTAL: 74 2013 Electricity surcharges HB 226 - Maryland Offshore Wind Energy Act of 2013 2013 Imposes 1% tax collected by wholesalers

Connecticut Budget Act and Pending Tax Legislation

M A Y 2 0 1 1 Connecticut Budget Act and Pending Tax Legislation Facing an estimated $3.5 billion budget deficit, both chambers of the Connecticut General Assembly recently approved a modified version

M A Y 2 0 1 1 Connecticut Budget Act and Pending Tax Legislation Facing an estimated $3.5 billion budget deficit, both chambers of the Connecticut General Assembly recently approved a modified version

State Tax Update: July Fiscal Affairs Program National Conference of State Legislatures William T. Pound, Executive Director

State Tax Update: July 2009 Fiscal Affairs Program William T. Pound, Executive Director 7700 East First Place Denver, CO 80230 (303) 364-7700 444 North Capitol Street, N.W., Suite 515 Washington, D.C.

State Tax Update: July 2009 Fiscal Affairs Program William T. Pound, Executive Director 7700 East First Place Denver, CO 80230 (303) 364-7700 444 North Capitol Street, N.W., Suite 515 Washington, D.C.

Primary Sources of County Road Funding

Oklahoma Cooperative Extension Service AGEC-889 Primary Sources of County Road Funding Notie Lansford Extension Economist Introduction Funding for county road and bridge construction, improvement, and/or

Oklahoma Cooperative Extension Service AGEC-889 Primary Sources of County Road Funding Notie Lansford Extension Economist Introduction Funding for county road and bridge construction, improvement, and/or

Briefing Points for Revenue Alternatives, FY 2009 Mary E. Forsberg, Research Director February 2008

137 W. HANOVER ST. TRENTON, NJ 08618 NJPP@NJPP.ORG Briefing Points for Revenue Alternatives, FY 2009 Mary E. Forsberg, Research Director February 2008 We have been told that financial restructuring will

137 W. HANOVER ST. TRENTON, NJ 08618 NJPP@NJPP.ORG Briefing Points for Revenue Alternatives, FY 2009 Mary E. Forsberg, Research Director February 2008 We have been told that financial restructuring will

Ad Valorem Taxes. Description of Revenue Source. Revenue Assumptions

Ad Valorem Taxes Ad Valorem Taxes are taxes paid on real and personal property located within the Village s corporate limits. Taxes for real and personal property, excluding motor vehicles, are levied

Ad Valorem Taxes Ad Valorem Taxes are taxes paid on real and personal property located within the Village s corporate limits. Taxes for real and personal property, excluding motor vehicles, are levied

National Association of Counties. A Look at County Revenue Authority A State by State Report

A Look at County Revenue Authority A State by State Report September 2008 A Look at County Revenue Authority A State by State Report Written by Joshua McLaurin Research Honors Intern Edited by Jacqueline

A Look at County Revenue Authority A State by State Report September 2008 A Look at County Revenue Authority A State by State Report Written by Joshua McLaurin Research Honors Intern Edited by Jacqueline

Minnesota Tax Handbook

Minnesota Tax Handbook A Profile of State and Local Taxes in Minnesota 2000 Edition MINNESOTA DEPARTMENT OF REVENUE Tax Research Division February 2001 The Minnesota Tax Handbook provides general information

Minnesota Tax Handbook A Profile of State and Local Taxes in Minnesota 2000 Edition MINNESOTA DEPARTMENT OF REVENUE Tax Research Division February 2001 The Minnesota Tax Handbook provides general information

CROATIAN TAX SYSTEM (as of January 2018)

") VALUE ADDED Any person who independently carries out any economic activity - Supply of goods and services - Intra-Community acquisition of goods - Importation of goods 5%, 13% and 25% Value Added Tax Act:

VALUE ADDED Any person who independently carries out any economic activity - Supply of goods and services - Intra-Community acquisition of goods - Importation of goods 5%, 13% and 25% Value Added Tax Act:

The Total Impact List

The Total Impact List The Vermont Chamber has developed this list of impacts on Vermont s business community because of government action during the last few years. Email us at govaffairs@vtchamber.com

The Total Impact List The Vermont Chamber has developed this list of impacts on Vermont s business community because of government action during the last few years. Email us at govaffairs@vtchamber.com

Chairman Wathan Spade, Executive Director

- Senator John C. Rafferty, Jr. Chairman Wathan Spade, Executive Director 20 East Wing State Capitol Building Harrisburg, PA I 71 20 Phone: (717) 787-1398 FAX: (717) 783-4587 Bill Summary Senate Bill 1

- Senator John C. Rafferty, Jr. Chairman Wathan Spade, Executive Director 20 East Wing State Capitol Building Harrisburg, PA I 71 20 Phone: (717) 787-1398 FAX: (717) 783-4587 Bill Summary Senate Bill 1

OVERVIEW OF THE FEDERAL TAX SYSTEM AS IN EFFECT FOR 2015

OVERVIEW OF THE FEDERAL TAX SYSTEM AS IN EFFECT FOR 2015 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION March 30, 2015 JCX-70-15 CONTENTS Page INTRODUCTION... 1 I. SUMMARY OF PRESENT-LAW FEDERAL

OVERVIEW OF THE FEDERAL TAX SYSTEM AS IN EFFECT FOR 2015 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION March 30, 2015 JCX-70-15 CONTENTS Page INTRODUCTION... 1 I. SUMMARY OF PRESENT-LAW FEDERAL

Budget FAQ s. Table of Contents

Table of Contents Why is there such a difference between the tax assessment increase in South Berwick (0.74%) and Eliot (3.94%)? How much money per student is Rollinsford paying to our school system to

Table of Contents Why is there such a difference between the tax assessment increase in South Berwick (0.74%) and Eliot (3.94%)? How much money per student is Rollinsford paying to our school system to

FY 08/09 ADOPTED GENERAL FUND REVENUES $224,391,325

GENERAL FUND REVENUES FY 08/09 ADOPTED GENERAL FUND REVENUES $224,391,325 State Revenue 10% Transfers 1% Federal Revenue 2% Fund Balance 0.2% Other Local Revenue 3% Other Local Taxes 22% Gen. Property

GENERAL FUND REVENUES FY 08/09 ADOPTED GENERAL FUND REVENUES $224,391,325 State Revenue 10% Transfers 1% Federal Revenue 2% Fund Balance 0.2% Other Local Revenue 3% Other Local Taxes 22% Gen. Property

Petroleum Taxes in Minnesota was prepared by the Petroleum Tax Unit of the Minnesota Department of Revenue. For additional copies or further

2013 Petroleum Taxes in Minnesota was prepared by the Petroleum Tax Unit of the Minnesota Department of Revenue. For additional copies or further information, contact: Petroleum Tax Unit, Minnesota Department

2013 Petroleum Taxes in Minnesota was prepared by the Petroleum Tax Unit of the Minnesota Department of Revenue. For additional copies or further information, contact: Petroleum Tax Unit, Minnesota Department

Gasoline Excise Taxes,

by Brian Francis 10 10 T he Federal excise tax on gasoline is currently 18. cents per gallon. This excise tax generates over $20 billion per year in tax revenue. Revenues are currently 10 times the amount

by Brian Francis 10 10 T he Federal excise tax on gasoline is currently 18. cents per gallon. This excise tax generates over $20 billion per year in tax revenue. Revenues are currently 10 times the amount

OVERVIEW OF THE FEDERAL TAX SYSTEM AS IN EFFECT FOR 2014

OVERVIEW OF THE FEDERAL TAX SYSTEM AS IN EFFECT FOR 2014 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION March 28, 2014 JCX-25-14 CONTENTS Page INTRODUCTION... 1 I. SUMMARY OF PRESENT-LAW FEDERAL

OVERVIEW OF THE FEDERAL TAX SYSTEM AS IN EFFECT FOR 2014 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION March 28, 2014 JCX-25-14 CONTENTS Page INTRODUCTION... 1 I. SUMMARY OF PRESENT-LAW FEDERAL

FY 2015 FY 2016 FY 2017 EF May 1 EF May 1 EF May 1 Forecast Forecast Forecast

A B C D E F G H I J K Line SUMMARY OF THE ECONOMIC FORUM GENERAL FUND REVENUE Economic Forum May 1, 2015, Forecast for,, and Based on Current Statute 2013-15 Biennium 2015-17 Biennium Biennium Comparison

A B C D E F G H I J K Line SUMMARY OF THE ECONOMIC FORUM GENERAL FUND REVENUE Economic Forum May 1, 2015, Forecast for,, and Based on Current Statute 2013-15 Biennium 2015-17 Biennium Biennium Comparison

FISCAL MEMORANDUM HB 534 SB 1221 HB 534 SB April 4, 2017

TENNESSEE GENERAL ASSEMBLY FISCAL REVIEW COMMITTEE FISCAL MEMORANDUM April 4, 2017 SUMMARY OF ORIGINAL BILL: Changes, from July 25 to July 20, the deadline for a person who operates a motor vehicle in

TENNESSEE GENERAL ASSEMBLY FISCAL REVIEW COMMITTEE FISCAL MEMORANDUM April 4, 2017 SUMMARY OF ORIGINAL BILL: Changes, from July 25 to July 20, the deadline for a person who operates a motor vehicle in

TABLE OF CONTENTS. NOTE... ix FOREWORD... xi I. FLORIDA STATE FINANCES

TABLE OF CONTENTS NOTE... ix FOREWORD... xi I. FLORIDA STATE FINANCES Florida State Treasury Funds... 15 Sources of State Revenue, Sources of General Revenue, 2004-05... 16 Total Appropriations All Funds,

TABLE OF CONTENTS NOTE... ix FOREWORD... xi I. FLORIDA STATE FINANCES Florida State Treasury Funds... 15 Sources of State Revenue, Sources of General Revenue, 2004-05... 16 Total Appropriations All Funds,

2010 Facts Figures How Does Your State Compare?

& 2010 Facts Figures How Does Your State Compare? Table of Contents Number Title Date Taxes and Tax Measures 1 State and Local Tax Burden Per Capita 2008 2 State and Local Tax Burden as a Percentage of

& 2010 Facts Figures How Does Your State Compare? Table of Contents Number Title Date Taxes and Tax Measures 1 State and Local Tax Burden Per Capita 2008 2 State and Local Tax Burden as a Percentage of

State Taxes Only See Separate Analysis for Property Taxes and Local Aids

Senate Omnibus Tax Bill April 18, 2008 State Taxes Only See Separate Analysis for Property Taxes and Local Aids DOR Administrative Costs/Savings Yes X No Department of Revenue Analysis of S.F. 2869 (Bakk),

Senate Omnibus Tax Bill April 18, 2008 State Taxes Only See Separate Analysis for Property Taxes and Local Aids DOR Administrative Costs/Savings Yes X No Department of Revenue Analysis of S.F. 2869 (Bakk),

GEORGIA S TAXES A Summary of Major State and Local Government Taxes

GEORGIA S TAXES A Summary of Major State and Local Government Taxes Eleventh Edition February 2005 Fiscal Research Center Andrew Young School of Policy Studies Georgia State University ABOUT THE AUTHORS

GEORGIA S TAXES A Summary of Major State and Local Government Taxes Eleventh Edition February 2005 Fiscal Research Center Andrew Young School of Policy Studies Georgia State University ABOUT THE AUTHORS

OVERVIEW OF STATE TAXATION

DORCHESTER COUNTY, SOUTH CAROLINA TAX & INCENTIVE INFORMATION Dorchester County recognizes that the taxing scheme of a state is an important factor when deciding to locate or expand a business. Often,

DORCHESTER COUNTY, SOUTH CAROLINA TAX & INCENTIVE INFORMATION Dorchester County recognizes that the taxing scheme of a state is an important factor when deciding to locate or expand a business. Often,

STATE MOTOR FUEL TAXES: NOTES SUMMARY RATES EFFECTIVE 04/01/2018

Tax rates and or notes changed since last report: AK, CA, FL, HI, IL, MI, NY, OH, VT Other Other Alabama 18.00 2.91 20.91 39.31 19.00 2.89 21.89 46.29 Alaska 8.95 5.41 14.36 32.76 8.95 5.44 14.39 38.79

Tax rates and or notes changed since last report: AK, CA, FL, HI, IL, MI, NY, OH, VT Other Other Alabama 18.00 2.91 20.91 39.31 19.00 2.89 21.89 46.29 Alaska 8.95 5.41 14.36 32.76 8.95 5.44 14.39 38.79

Petroleum Products 116

www.revenue.state.mn.us Petroleum Products 116 Sales Tax Fact Sheet 116 Fact Sheet What s new in 2018 We clarified when sellers are required to collect local sales taxes. See Local Sales and Use Taxes

www.revenue.state.mn.us Petroleum Products 116 Sales Tax Fact Sheet 116 Fact Sheet What s new in 2018 We clarified when sellers are required to collect local sales taxes. See Local Sales and Use Taxes

Transportation Finance Overview. Presentation Contents

Transportation Finance Overview Matt Burress House Research Department matt.burress@house.mn Andy Lee House Fiscal Analysis andrew.lee@house.mn January 5 th & 10 th, 2017 Presentation Contents 2 Part 1:

Transportation Finance Overview Matt Burress House Research Department matt.burress@house.mn Andy Lee House Fiscal Analysis andrew.lee@house.mn January 5 th & 10 th, 2017 Presentation Contents 2 Part 1:

FY 09/10 ADOPTED GENERAL FUND REVENUES $218,840,522

GENERAL FUND REVENUES FY 09/10 ADOPTED GENERAL FUND REVENUES $218,840,522 State Revenue 11% Transfers Federal Revenue1% 2% Fund Balance 0.1% Other Local Revenue 2% Other Local Taxes 21% Gen. Property Taxes

GENERAL FUND REVENUES FY 09/10 ADOPTED GENERAL FUND REVENUES $218,840,522 State Revenue 11% Transfers Federal Revenue1% 2% Fund Balance 0.1% Other Local Revenue 2% Other Local Taxes 21% Gen. Property Taxes

OVERVIEW OF THE FEDERAL TAX SYSTEM AS IN EFFECT FOR 2013

OVERVIEW OF THE FEDERAL TAX SYSTEM AS IN EFFECT FOR 2013 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION January 8, 2013 JCX-2-13 CONTENTS Page INTRODUCTION... 1 I. SUMMARY OF PRESENT-LAW FEDERAL

OVERVIEW OF THE FEDERAL TAX SYSTEM AS IN EFFECT FOR 2013 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION January 8, 2013 JCX-2-13 CONTENTS Page INTRODUCTION... 1 I. SUMMARY OF PRESENT-LAW FEDERAL

17% 35 $35 and $3/acre above 5 acres 13% and 43% 18,541 $85 and $10/ton. 17% 35 $35 and $3/acre above 5 acres 13% and 43% 18,541 $85 and $10/ton

H.872: 2016 Bill House-Passed Senate-Amended Year Last Current Proposed % Incr New Revenue Proposed % Incr New Revenue Proposed % Incr New Revenue # Of units (if applicable) FY15 FY16 FY17 Row Bill Changed

H.872: 2016 Bill House-Passed Senate-Amended Year Last Current Proposed % Incr New Revenue Proposed % Incr New Revenue Proposed % Incr New Revenue # Of units (if applicable) FY15 FY16 FY17 Row Bill Changed

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project.

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp 2014 Petroleum Taxes

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp 2014 Petroleum Taxes

State Postal Abbreviation Codes

State Postal Areviation Codes State Areviation State Areviation Alaama AL Montana MT Alaska AK Neraska NE Arizona AZ Nevada NV Arkansas AR New Hampshire NH California CA New Jersey NJ Colorado CO New Mexico

State Postal Areviation Codes State Areviation State Areviation Alaama AL Montana MT Alaska AK Neraska NE Arizona AZ Nevada NV Arkansas AR New Hampshire NH California CA New Jersey NJ Colorado CO New Mexico

Government of the District of Columbia Office of the Chief Financial Officer Office of Revenue Analysis. D.C. Tax Facts. As of September 2009

Government of the District of Columbia Office of the Chief Financial Officer Office of Revenue Analysis D.C. Tax Facts As of September 2009 Adrian M. Fenty Mayor Vincent C. Gray, Chair Council of the District

Government of the District of Columbia Office of the Chief Financial Officer Office of Revenue Analysis D.C. Tax Facts As of September 2009 Adrian M. Fenty Mayor Vincent C. Gray, Chair Council of the District

Total Expenditures $ 44,922,702 $ 49,718,336 $ 47,884,092 $ 47,876,610

ALL FUNDS RECOGNIZED IN BUDGET ORDINANCE ITEM 2014-15 Actual 2015-16 Budget 2015-16 Estimated 2016-17 Budget GOVERNMENTAL FUND General Fund Property Taxes $ 20,189,267 $ 20,076,100 $ 20,091,190 $ 19,819,670

ALL FUNDS RECOGNIZED IN BUDGET ORDINANCE ITEM 2014-15 Actual 2015-16 Budget 2015-16 Estimated 2016-17 Budget GOVERNMENTAL FUND General Fund Property Taxes $ 20,189,267 $ 20,076,100 $ 20,091,190 $ 19,819,670

Vermont s Tax Structure

Vermont s Tax Structure Total Revenue and State Revenue, FY2015 Prepared for the Vermont Democratic Caucus Joyce Manchester and Graham Campbell Joint Fiscal Office December 4, 2017 1 Vermont taxes are

Vermont s Tax Structure Total Revenue and State Revenue, FY2015 Prepared for the Vermont Democratic Caucus Joyce Manchester and Graham Campbell Joint Fiscal Office December 4, 2017 1 Vermont taxes are