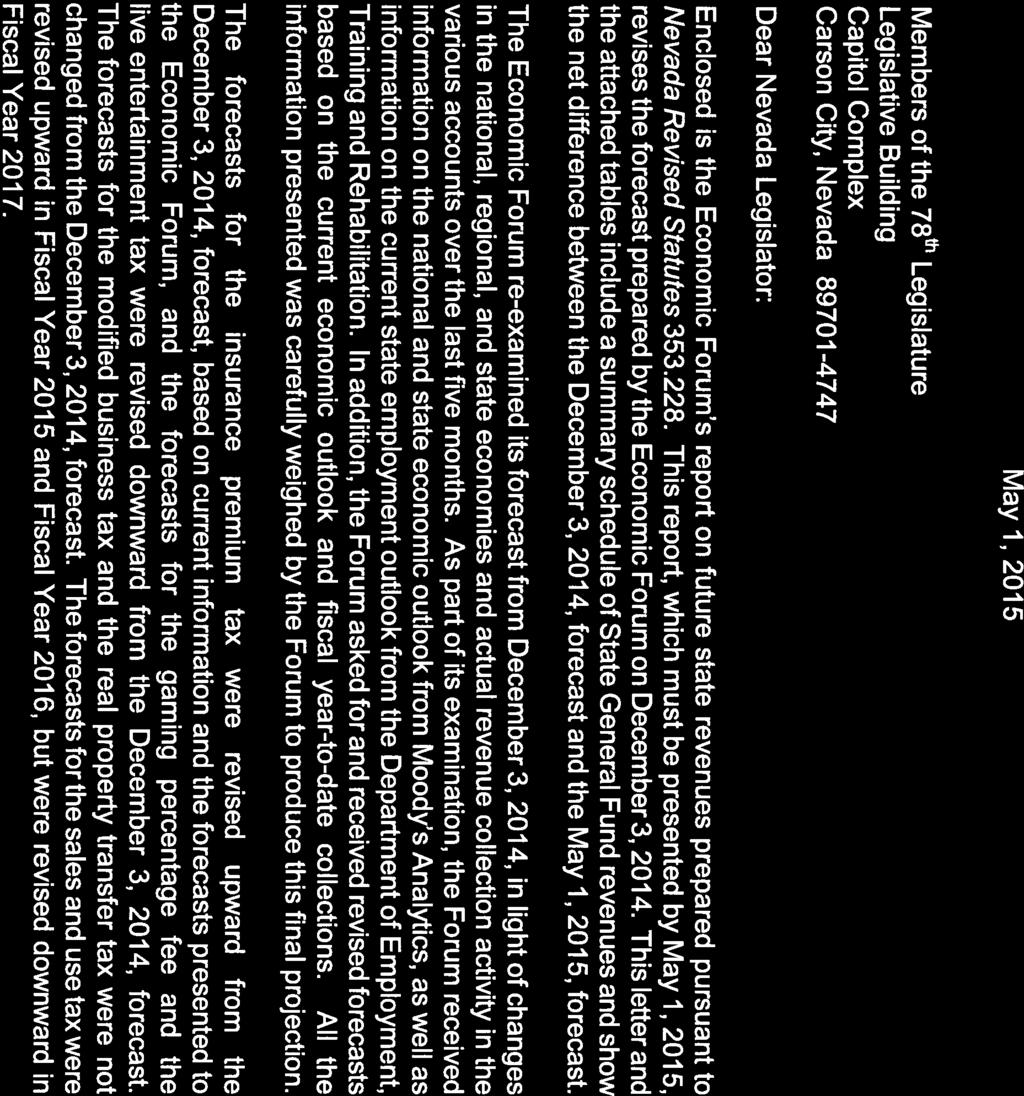

FY 2015 FY 2016 FY 2017 EF May 1 EF May 1 EF May 1 Forecast Forecast Forecast

|

|

|

- Easter Carpenter

- 6 years ago

- Views:

Transcription

1

2

3 A B C D E F G H I J K Line SUMMARY OF THE ECONOMIC FORUM GENERAL FUND REVENUE Economic Forum May 1, 2015, Forecast for,, and Based on Current Statute Biennium Biennium Biennium Comparison Actual EF May 1 EF May 1 EF May 1 Forecast Forecast Forecast Biennium: Actual/Forecast 1 Total General Fund Revenue Forecast Approved by the Economic Forum on May 1, Total General Fund Revenue - Before Tax Credits $3,066,946,360 $3,236,630,323 $3,068,536,235 $3,242,480,185 $6,303,576,683 $6,311,016,420 $7,439,737 3 Estimated Transferrable Tax Credits [1.] $0 -$22,900,000 -$79,300,000 -$76,500,000 -$22,900,000 -$155,800,000 -$132,900,000 4 Total General Fund Revenue - Net of Tax Credits $3,066,946,360 $3,213,730,323 $2,989,236,235 $3,165,980,185 $6,280,676,683 $6,155,216,420 -$125,460,263 5 Total Major General Fund Revenue Forecast Approved by the Economic Forum on May 1, Total Major General Fund Revenue $2,497,638,895 $2,616,593,100 $2,617,362,000 $2,748,905,400 $5,114,231, $5,366,267, $252,035,405 7 Major General Fund Revenue Sources Forecast by the Economic Forum Subject to Sunset Provisions based on Actions from the 2013 Session 8 MBT - Nonfinancial [2.] $361,095,880 $379,528,000 $270,420,000 $283,941,000 $740,623, $554,361, $186,262,880 9 Sales Tax Commissions [3.] $36,386,484 $38,816,100 $39,682,000 $41,859,400 $75,202, $81,541, $6,338, Total-Major Revenue Sources Subject to Sunset $397,482,363 $418,344,100 $310,102,000 $325,800,400 $815,826, $635,902, $179,924, Major General Fund Revenue Sources Forecast by the Economic Forum Not Subject to Sunset Provisions 12 Sales and Use Tax $931,319,687 $999,006,000 $1,057,000,000 $1,114,995,000 $1,930,325, $2,171,995, $241,669, Percentage Fees Tax $682,311,672 $683,708,000 $698,701,000 $716,158,000 $1,366,019, $1,414,859, $48,839, Insurance Premium Tax $263,531,578 $294,420,000 $324,063,000 $355,016,000 $557,951, $679,079, $121,127, Real Property Transfer Tax $60,047,457 $65,405,000 $70,402,000 $76,064,000 $125,452, $146,466, $21,013, LET-Gaming $139,156,240 $131,492,000 $132,125,000 $134,929,000 $270,648, $267,054, $3,594, MBT - Financial $23,789,898 $24,218,000 $24,969,000 $25,943,000 $48,007, $50,912, $2,904, Total-Major Revenue Sources Not Subject to Sunset $2,100,156,532 $2,198,249,000 $2,307,260,000 $2,423,105,000 $4,298,405, $4,730,365, $431,959, Total of All General Fund Revenue Sources Forecast by the Technical Advisory Committee (TAC) on April 27, 2015, and Approved by the Economic Forum on May 1, Total Revenue Sources Forecast by the TAC $569,307,465 $620,037,223 $451,174,235 $493,574,785 $1,189,344, $944,749, $244,595, General Fund Revenue Sources Forecast by the TAC and approved by the Economic Forum Subject to Sunset Provisions Based on Actions from the 2013 Session 22 Net Proceeds of Minerals [4.][5.] $26,221,970 $50,756,000 $0 $34,642,000 $76,977, $34,642, $42,335, Governmental Services Tax [6.] $62,267,322 $62,827,700 $0 $0 $125,095, $ $125,095, Business License Fee [7.] $72,166,482 $74,078,000 $39,947,000 $40,660,000 $146,244, $80,607, $65,637, GST Commissions and Penalites [8.] $0 $24,911,680 $0 $0 $24,911, $ $24,911, Total-Revenue Sources Subject to Sunset $160,655,773 $212,573,380 $39,947,000 $75,302,000 $373,229, $115,249, $257,980, All Other General Fund Revenue Sources Forecast by the TAC and approved by the Economic Forum Not Subject to Sunset Provisions 28 All Other Gaming Taxes and Fees $36,504,394 $29,205,520 $28,107,100 $28,416,650 $65,709, $56,523, $9,186, LET-Nongaming $14,979,978 $15,168,000 $15,825,000 $16,506,000 $30,147, $32,331, $2,183, Cigarette Tax $79,628,983 $79,678,000 $78,484,000 $77,284,000 $159,306, $155,768, $3,538, Liquor Tax $41,838,536 $43,525,000 $44,411,000 $45,346,000 $85,363, $89,757, $4,393, Other Tobacco Tax $11,620,286 $11,296,000 $12,455,000 $12,907,000 $22,916, $25,362, $2,445, Total Secretary of State Revenues $94,922,982 $96,835,300 $98,649,200 $100,399,100 $191,758, $199,048, $7,290, Short-Term Car Rental Fee $46,151,238 $47,538,000 $48,868,400 $50,242,200 $93,689, $99,110, $5,421, Expired Slot Machine Wagers $7,486,068 $8,054,000 $8,228,900 $8,426,900 $15,540, $16,655, $1,115, Court Administrative Assessments $2,511,100 $2,258,200 $0 $0 $4,769, $ $4,769, Unclaimed Property $17,466,436 $11,823,000 $14,438,000 $15,875,000 $29,289, $30,313, $1,023, All Others $55,541,690 $62,082,823 $61,760,635 $62,869,935 $117,624, $124,630, $7,006, Total-All Other Sources Not Subject to Sunset $408,651,692 $407,463,843 $411,227,235 $418,272,785 $816,115, $829,500, $13,384,485 of Total Biennium: Forecast of Total Biennium Difference

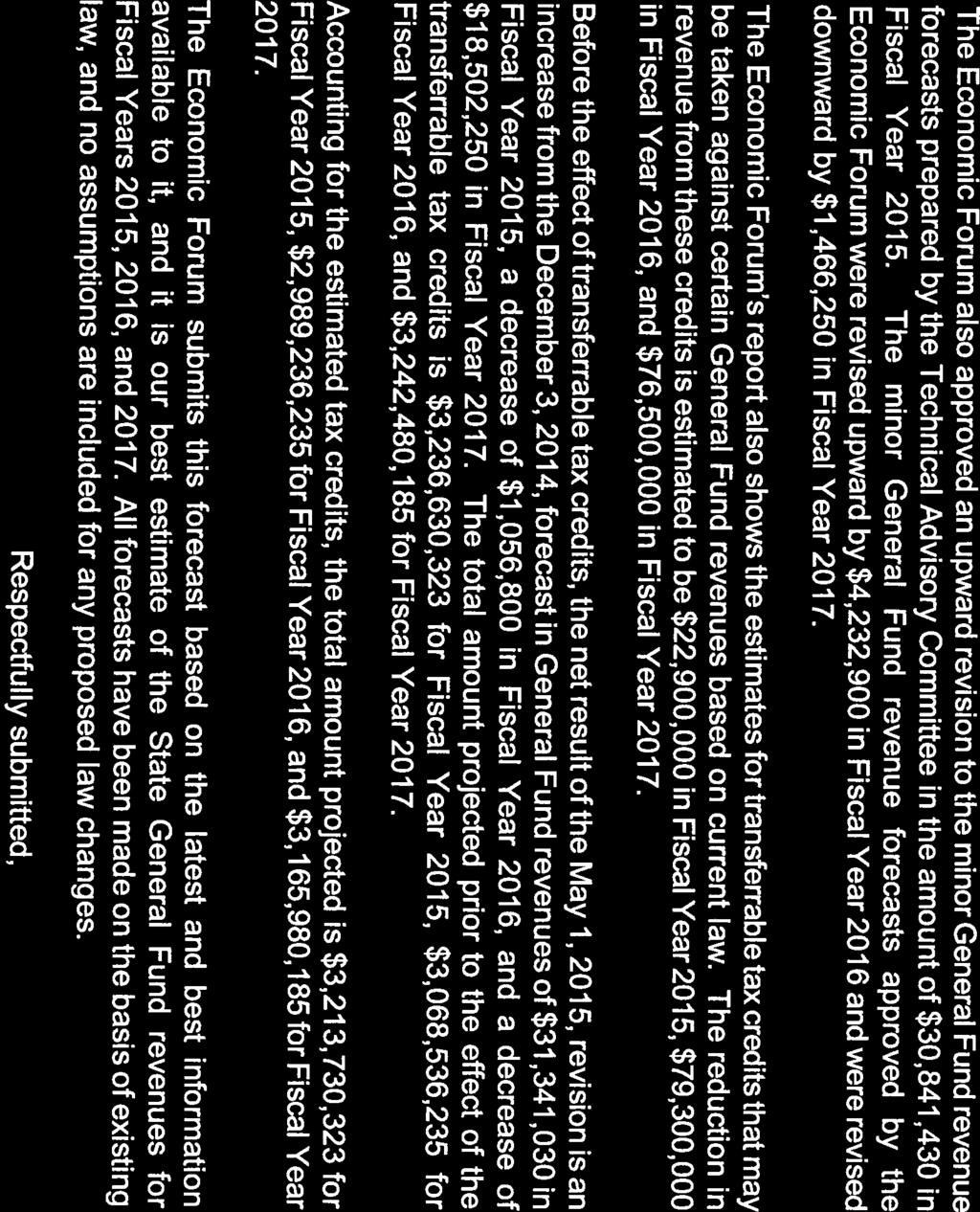

4 Notes: [1.] The amounts listed in this category reflect the current estimate of tax credits that may be issued and taken in each fiscal year as a result of the following programs approved by the Legislature: * Transferrable Film Tax Credits (S.B. 165 of the 2013 Session) * Nevada New Markets Jobs Act Tax Credits (S.B. 357 of the 2013 Session) * Economic Development Transferrable Tax Credits (S.B. 1 of the 28th Special Session) * Nevada Educational Choice Scholarship Program Tax Credits (A.B. 165 of the 2015 Session) [2.] For, the Modified Business Tax on Nonfinancial institutions (MBT Nonfinancial) is imposed at a rate of zero on the first $85,000 of taxable wages in a calendar quarter, and at a rate of 1.17 percent on all taxable wages in excess of $85,000 in that calendar quarter. For and, the tax is imposed at a rate of 0.63 percent on all taxable wages in a calendar quarter. [3.] For, the General Fund s 0.75 percent commission kept to defray costs related to collection and distribution of the Local School Support Tax (LSST) is based on the LSST rate of 2.60 percent. For and, the commission is based on an LSST rate of 2.25 percent. [4.] For, the Net Proceeds of Minerals is collected based on estimated mining activity reported by mining operators for calendar year Beginning on January 1, 2016, the tax paid by a mining operation in a given fiscal year is based on the actual mining activity reported by that operator in the prior fiscal year. Thus, for, there will be no Net Proceeds of Minerals Tax imposed for calendar year 2015 activity, as taxes for that calendar year will have already been paid in. In, Net Proceeds of Minerals Tax revenue will be based on actual mining activity reported for calendar year [5.] For, mining operations may not deduct from gross proceeds the cost of premiums for industrial insurance and the actual cost of hospital and medical attention and accident benefits and group insurance for all employees, when calculating net proceeds for the operation's Net Proceeds of Minerals liability. For and, these costs may be deducted from gross proceeds in determining Net Proceeds of Minerals Tax liability. [6.] For, the portion of the Governmental Services Tax attributable to the 10 percent increase in the depreciation schedule originally approved pursuant to Senate Bill 429 (2009 Session) and extended pursuant to Assembly Bill 491 (2013 Session) is deposited in the State General Fund. For and, this portion is required to be deposited in the State Highway Fund. [7.] For, the Business License Fee imposed on business entities in the state is at an annual rate of $200. For and, the annual rate is reduced to $100. [8.] For, a portion of the commissions and penalties collected by the Department of Motor Vehicles from the imposition of the Governmental Services Tax are deposited in the State General Fund. For and, these proceeds are retained by the Department for deposit in the Motor Vehicle Fund.

5 GENERAL FUND REVENUES - ECONOMIC FORUM MAY 1, 2015 : THROUGH AND : THROUGH ECONOMIC FORUM'S FOR,, AND APPROVED AT THE MAY 1, 2015, MEETING TAXES TOTAL MINING TAXES [3-09][19/20-10][1/2/3-12][1/2-14] $120,425, $111,339, $26,221, $50,801, $45,000 $34,687,000 TOTAL SALES AND USE TAX [1-04][1A/1B-09][1-10][4-12][3-14] $875,596, $923,198, $967,706, $1,037,822, $1,096,682, $1,156,854, TOTAL GAMING TAXES [2/3-04][1-06][5-12] $686,450, $710,525, $718,816, $712,913, $726,808, $744,574, LIVE ENTERTAINMENT TAX [4a/4b-04][2-06] $136,982, $137,416, $154,136, $146,660, $147,950, $151,435, TOTAL INSURANCE TAXES [21-10][1-16] $237,858, $249,389, $264,521, $295,600, $325,110, $356,070, MBT-NONFINANCIAL [10-04][5/6-06][2-10][6-12][4-14][2-16] $348,943, $363,242, $361,095, $379,528, $270,420, $283,941, MBT-FINANCIAL [11-04][5-06][2-16] $20,717, $23,368, $23,789, $24,218, $24,969, $25,943, CIGARETTE TAX [6-04][2-09][3-10] $82,974, $83,017, $79,628, $79,678, $78,484, $77,284, REAL PROPERTY TRANSFER TAX [13-04][8-06] $48,373, $54,989, $60,047, $65,405, $70,402, $76,064, GOVERNMENTAL SERVICES TAX [5-10][5-14] $62,358, $63,503, $62,267, $62,827, LIQUOR TAX [5-04][2-09][7-10] $40,649, $39,884, $41,838, $43,525, $44,411, $45,346, OTHER TOBACCO TAX [7-04][2-09][8-10] $8,274, $10,348, $11,620, $11,296, $12,455, $12,907, HECC TRANSFER $5,000,000 $5,000,000 $5,000,000 $5,000,000 $5,000,000 $5,000,000 BUSINESS LICENSE FEE [8-04][3/4-06][6-10][7-12][6-14] $64,790, $69,010, $72,166, $74,078, $39,947, $40,660, BUSINESS LICENSE TAX [9-04] $ $2, $2, $2, BRANCH BANK EXCISE TAX [12-04][7-06] $3,047, $2,996, $2,788, $3,074, $3,009, $3,017, TOTAL TAXES $2,742,443, $2,847,233, $2,851,648, $2,992,428, $2,845,692, $3,013,783, LICENSES INSURANCE LICENSES $15,646, $16,625, $17,925, $18,463, $19,017, $19,588, MARRIAGE LICENSES $404, $378, $371, $369, $369, $370, TOTAL SECRETARY OF STATE [14-04][9-10][23-10] $93,679, $91,976, $94,922, $96,835, $98,649, $100,399, PRIVATE SCHOOL LICENSES [7-14] $224, $247, $284, $260, $270, $280, PRIVATE EMPLOYMENT AGENCY $11, $11, $11, $11,400 $11,400 $11,400 TOTAL REAL ESTATE [15/16-04] $4,009, $3,411, $1,376, $1,370, $3,649, $3,535, ATHLETIC COMMISSION FEES [24-10] $5,115, $3,867, $5,334, $5,027, $4,599, $4,599,000 TOTAL LICENSES $119,090, $116,518, $120,227, $122,336, $126,565, $128,783, FEES AND FINES VITAL STATISTICS FEES [17-04][25-10][8-14] $1,024, $1,057, DIVORCE FEES $184, $171, $174, $174, $175, $177, CIVIL ACTION FEES $1,389, $1,324, $1,325, $1,275, $1,275, $1,275, INSURANCE FEES $1,431, $1,208, $723, $766, $826, $826,700 MEDICAL PLAN DISCOUNT REGISTRATION FEES $9, $2, TOTAL REAL ESTATE FEES $718, $566, $549, $584, $544, $553, SHORT-TERM CAR LEASE [4-09][10-10][8-12] $44,499, $45,753, $46,151, $47,538, $48,868, $50,242, ATHLETIC COMMISSION LICENSES/FINES $231, $215, $234, $231, $231,500 $231,500 STATE ENGINEER SALES [11-10][9-14] $3,366, $2,617, SUPREME COURT FEES $211, $193, $216, $197, $197,000 $197,000 NOTICE OF DEFAULT FEES [26-10] $2,484, $2,765, $1,706, $1,584, $1,435, $1,300, MISC. FINES/FORFEITURES $2,851, $11,162, $3,125, $8,878, $2,400, $2,400,000 TOTAL FEES AND FINES $58,405, $67,038, $54,207, $61,229, $55,954, $57,203, USE OF MONEY AND PROPERTY OTHER REPAYMENTS [18-04][10-14] $363, $453, $392, $454, $251, $251,935 INTEREST INCOME [9-12] $505, $633, $594, $1,247, $2,575, $4,074, TOTAL USE OF MONEY AND PROPERTY $868, $1,086, $986, $1,702, $2,827, $4,326, ECONOMIC FORUM MAY 1, 2015

6 GENERAL FUND REVENUES - ECONOMIC FORUM MAY 1, 2015 : THROUGH AND : THROUGH ECONOMIC FORUM'S FOR,, AND APPROVED AT THE MAY 1, 2015, MEETING ECONOMIC FORUM MAY 1, 2015 OTHER REVENUE HOOVER DAM REVENUE $300,000 $300,000 $300,000 $300,000 $300,000 $300,000 GST COMMISSIONS AND PENALITIES/DMV [10-12][11-14] $24,678,398 $25,127, $24,911,680 EXPIRED SLOT MACHINE WAGERING VOUCHERS [11-12] $3,134,219 $7,193, $7,486, $8,054, $8,228, $8,426, PROPERTY TAX: 4-CENT OPERATING RATE [13-10] $22 PROPERTY TAX: 5-CENT CAPITAL RATE [14-10] $11 SUPPL. ACCOUNT FOR MED. ASSIST. TO INDIGENT [18-10][12-12] $19,112,621 $19,218, COURT ADMINISTRATIVE ASSESSMENTS [16-10][13-12][12-14] $4,434, $4,118, $2,511, $2,258,200 COURT ADMINISTRATIVE ASSESSMENT FEE [28-10] $2,537, $2,509, $2,335, $2,119,100 $2,127,000 $2,149,500 MISC. SALES AND REFUNDS $870, $867, $894, $877, $868, $861, COST RECOVERY PLAN [13-14] $8,495, $8,470, $8,883, $8,590, $11,534, $10,770, UNCLAIMED PROPERTY [9-06][5-09][12-10][29/30-10][1-11][14-12] $97,397, $32,918, $17,466, $11,823, $14,438, $15,875, TOTAL OTHER REVENUE $160,960, $100,723, $39,877, $58,933, $37,496, $38,382, TOTAL GENERAL FUND REVENUE BEFORE APPLICATION OF TAX CREDITS $3,081,768, $3,132,601, $3,066,946, $3,236,630, $3,068,536, $3,242,480, ESTIMATED TRANSFERRABLE TAX CREDITS ($22,900,000) ($79,300,000) ($76,500,000) TOTAL GENERAL FUND REVENUE - NET OF TAX CREDITS $3,081,768, $3,132,601, $3,066,946, $3,213,730, $2,989,236, $3,165,980,

7 GENERAL FUND REVENUES - ECONOMIC FORUM MAY 1, 2015 : THROUGH AND : THROUGH ECONOMIC FORUM'S FOR,, AND APPROVED AT THE MAY 1, 2015, MEETING ECONOMIC FORUM MAY 1, 2015 TAXES MINING TAX AND MINING CLAIMS FEE 3064 Net Proceeds of Minerals [3-09][19-10][1-12][2-12][1-14][2-14] $120,414, $111,275, $26,221, $50,756, $34,642, Net Proceeds Penalty 3245 Centrally Assessed Penalties $4, $64, $45,000 $45,000 $45, Mining Claims Fee [20-10][3-12] $6,300 TOTAL MINING TAXES AND FEES $120,425, $111,339, $26,221, $50,801, $45,000 $34,687,000 SALES AND USE 3001 Sales & Use Tax [1-04][1A-09][1-10] $842,941, $888,658, $931,319, $999,006, $1,057,000, $1,114,995, State Share - LSST [1-04][1B-09][1-10][4-12][3-14] $8,309, $8,791, $9,194, $9,740, $8,918, $9,407, State Share - BCCRT [1-04][1B-09][1-10] $3,682, $3,893, $4,088, $4,370, $4,624, $4,878, State Share - SCCRT [1-04][1B-09][1-10] $12,884, $13,625, $14,305, $15,297, $16,185, $17,073, State Share - PTT [1-04][1B-09][1-10] $7,778, $8,230, $8,797, $9,407, $9,953, $10,500, TOTAL SALES AND USE $875,596, $923,198, $967,706, $1,037,822, $1,096,682, $1,156,854, GAMING - STATE 3032 Pari-mutuel Tax $2, $3, $2, $2, $3, $3, Racing Fees $11, $8, $9, $7, $7, $7, Racing Fines/Forfeitures $350 $ Percent Fees - Gross Revenue [2-04] $653,672, $678,852, $682,311, $683,708, $698,701, $716,158, Gaming Penalties $459, $1,456, $7,862, $350, $600, $600, Flat Fees-Restricted Slots [3-04][1-06][1-08][5-12] $8,485, $8,403, $8,305, $8,271, $8,249, $8,312, Non-Restricted Slots [1-06][1-08][5-12] $12,628, $12,298, $11,383, $11,195, $10,984, $10,931, Quarterly Fees-Games $6,592, $6,449, $6,410, $6,482, $6,483, $6,632, Advance License Fees $3,996, $1,340, $672, $1,625, $500, $650, Slot Machine Route Operator $36, $40, $37, $35, $36, $36, Gaming Info Systems Annual $18, $18,000 $18,000 $42, $30, $30, Interactive Gaming Fee - Operator $437,500 $604, $500, $500,000 $500, Interactive Gaming Fee - Service Provider $1,000 $27,000 $75, $60, $52, $45, Interactive Gaming Fee - Manufacturer $125,000 $775,000 $700, $200, $225, $225, Equip Mfg. License $264, $273, $290, $280, $279, $282, Race Wire License $38, $34, $29, $31, $33, $34, Annual Fees on Games $116, $106, $105, $120, $124, $126, TOTAL GAMING - STATE $686,450, $710,525, $718,816, $712,913, $726,808, $744,574, LIVE ENTERTAINMENT TAX (LET) 3031G Live Entertainment Tax-Gaming [4b-04] $125,337, $125,709, $139,156, $131,492, $132,125, $134,929, NG Live Entertainment Tax-Nongaming [4b-04][2-06][2-08] $11,644, $11,706, $14,979, $15,168, $15,825, $16,506, TOTAL LET $136,982, $137,416, $154,136, $146,660, $147,950, $151,435, INSURANCE TAXES 3061 Insurance Premium Tax [21-10][1-16] $236,787, $248,512, $263,531, $294,420, $324,063, $355,016, Insurance Retaliatory Tax $396, $242, $234, $302, $223, $223, Captive Insurer Premium Tax $675, $635, $755, $878, $824, $831, TOTAL INSURANCE TAXES $237,858, $249,389, $264,521, $295,600, $325,110, $356,070, MODIFIED BUSINESS TAX (MBT) 3069 MBT - Nonfinancial [10-04][5-06][6-06][3-08][2-10][6-12][4-14][2-16] $348,943, $363,242, $361,095, $379,528, $270,420, $283,941, MBT - Financial [11-04][5-06][2-16] $20,717, $23,368, $23,789, $24,218, $24,969, $25,943, TOTAL MBT $369,660, $386,610, $384,885, $403,746, $295,389, $309,884, CIGARETTE TAX 3052 Cigarette Tax [6-04][2-09][3-10] $82,974, $83,017, $79,628, $79,678, $78,484, $77,284, REAL PROPERTY TRANSFER TAX (RPTT) 3055 Real Property Transfer Tax [13-04][8-06] $48,373, $54,989, $60,047, $65,405, $70,402, $76,064, GOVERMENTAL SERVICES TAX (GST) 3051 Governmental Services Tax [5-10][5-14] $62,358, $63,503, $62,267, $62,827,

8 GENERAL FUND REVENUES - ECONOMIC FORUM MAY 1, 2015 : THROUGH AND : THROUGH ECONOMIC FORUM'S FOR,, AND APPROVED AT THE MAY 1, 2015, MEETING ECONOMIC FORUM MAY 1, 2015 TAXES - CONTINUED OTHER TAXES 3113 Business License Fee [8-04][3-06][4-06][6-10][7-12][6-14] $64,790, $69,010, $72,166, $74,078, $39,947, $40,660, Liquor Tax [5-04][2-09][7-10] $40,649, $39,884, $41,838, $43,525, $44,411, $45,346, Other Tobacco Tax [7-04][2-09][8-10] $8,274, $10,348, $11,620, $11,296, $12,455, $12,907, HECC Transfer $5,000,000 $5,000,000 $5,000,000 $5,000,000 $5,000,000 $5,000, Business License Tax [9-04] $ $2, $2, $2, Branch Bank Excise Tax [12-04][7-06] $3,047, $2,996, $2,788, $3,074, $3,009, $3,017, TOTAL TAXES $2,742,443, $2,847,233, $2,851,648, $2,992,428, $2,845,692, $3,013,783, LICENSES 3101 Insurance Licenses $15,646, $16,625, $17,925, $18,463, $19,017, $19,588, Marriage License $404, $378, $371, $369, $369, $370, SECRETARY OF STATE 3105 UCC [1-02][14-04][23-10] $1,829, $1,685, $1,714, $1,692, $1,695, $1,699, Notary Fees [23-10] $579, $571, $544, $536, $541, $547, Commercial Recordings [14-04][9-10][23-10] $66,693, $65,062, $66,661, $67,665, $68,678, $69,601, Video Service Franchise $8,425 $7, $3, $1, Domestic Partnership Registry Fee [23-10] $33, $43, $51, $40, $26, $13, Securities [14-04][23-10] $24,534, $24,605, $25,947, $26,900, $27,707, $28,538, TOTAL SECRETARY OF STATE $93,679, $91,976, $94,922, $96,835, $98,649, $100,399, Private School Licenses [7-14] $224, $247, $284, $260, $270, $280, Private Employment Agency $11, $11, $11, $11,400 $11,400 $11,400 REAL ESTATE 3161 Real Estate License [15-04] $4,005, $3,408, $1,372, $1,364, $3,645, $3,531, Real Estate Fees $3, $2, $4, $6, $4, $4,000 TOTAL REAL ESTATE $4,009, $3,411, $1,376, $1,370, $3,649, $3,535, Athletic Commission Fees [24-10] $5,115, $3,867, $5,334, $5,027, $4,599, $4,599,000 TOTAL LICENSES $119,090, $116,518, $120,227, $122,336, $126,565, $128,783, FEES AND FINES 3200 Vital Statistics Fees [17-04][25-10][8-14] $1,024, $1,057, Divorce Fees $184, $171, $174, $174, $175, $177, Civil Action Fees $1,389, $1,324, $1,325, $1,275, $1,275, $1,275, Insurance Fines $1,431, $1,208, $723, $766, $826, $826, MD Medical Plan Discount Reg. Fees $9, $2, REAL ESTATE FEES 3107IOS IOS Application Fees $9, $8, $7, $5, $7, $7, Land Co Filing Fees $140, $131, $167, $170, $174, $174, Real Estate Adver Fees $4, $2, $ $ Real Estate Reg Fees $15, $18, $15, $16, $17, $17, Real Estate Exam Fees [19-04] $218, $171, $174, $220, $172, $174, CAM Certification Fee $86, Real Estate Accred Fees $79, $80, $86, $92, $83, $86, Real Estate Penalties $101, $104, $36, $27, $32, $32, A.B. 165, Real Estate Inspectors $63, $50, $60, $52, $58, $61, TOTAL REAL ESTATE FEES $718, $566, $549, $584, $544, $553, Short Term Car Lease [4-09][10-10][8-12] $44,499, $45,753, $46,151, $47,538, $48,868, $50,242, AC Athletic Commission Licenses/Fines $231, $215, $234, $231, $231,500 $231, State Engineer Sales [11-10][9-14] $3,366, $2,617, Supreme Court Fees $211, $193, $216, $197, $197,000 $197, Notice of Default Fee [26-10] $2,484, $2,765, $1,706, $1,584,200 $1,435, $1,300, Misc Fines/Forfeitures $2,851, $11,162, $3,125, $8,878, $2,400, $2,400,000 TOTAL FEES AND FINES $58,405, $67,038, $54,207, $61,229, $55,954, $57,203,

9 GENERAL FUND REVENUES - ECONOMIC FORUM MAY 1, 2015 : THROUGH AND : THROUGH ECONOMIC FORUM'S FOR,, AND APPROVED AT THE MAY 1, 2015, MEETING ECONOMIC FORUM MAY 1, 2015 USE OF MONEY AND PROP OTHER REPAYMENTS 4403 Forestry Nurseries Fund Repayment (05-M27) $20,670 $20,670 $20,670 $20,670 $20,670 $20, Comp/Fac Repayment $23,744 $23,744 $23,744 $23,744 $23,744 $23, CIP 95-M1, Security Alarm $2,998 $2,998 $2,998 $2,998 $2,998 $2, CIP 95-M5, Facility Generator $6,874 $6,874 $6,874 $6,874 $6,874 $6, CIP 95-S4F, Advance Planning $1,000 $1,000 $1,000 $1,000 $1,000 $1, CIP 97-C26, Capitol Complex Conduit System, Phase I $62,542 $62,542 $62,542 $62,542 $62,542 $62, CIP 97-S4H, Advance Planning Addition to Computer Facility $9,107 $9,107 $9,107 $9,107 $9,107 $9, Motor Pool Repay - LV [10-14] $62,500 $125,000 $125,000 $125, State Personnel IFS Repayment; S.B. 201, 1997 Legislature $236,082 $326,659 $202,987 $202, TOTAL OTHER REPAYMENTS $363, $453, $392, $454, $251, $251,935 INTEREST INCOME 3290 Treasurer [9-12] $522, $625, $589, $1,242, $2,570, $4,069, Other ($17,606) $7,723 $4, $5, $5,300 $5,300 TOTAL INTEREST INCOME $505, $633, $594, $1,247, $2,575, $4,074, TOTAL USE OF MONEY & PROP $868, $1,086, $986, $1,702, $2,827, $4,326, OTHER REVENUE 3059 Hoover Dam Revenue $300,000 $300,000 $300,000 $300,000 $300,000 $300,000 MISC SALES AND REFUNDS 4794 GST Commissions and Penalties / DMV [10-12][11-14] $24,678,398 $25,127, $24,911, Expired Slot Machine Wagering Vouchers [11-12] $3,134,219 $7,193, $7,486, $8,054, $8,228, $8,426, Property Tax: 4-cent operating rate (Clark & Washoe) [13-10] $ Property Tax: 5-cent capital rate (Clark & Washoe) [14-10] $ Suppl. Account for Med. Assist. to Indigent [18-10][12-12] $19,112,621 $19,218, Misc Fees $251, $305, $298, $300, $300,000 $300, Court Admin Assessments [16-10][13-12][12-14] $4,434, $4,118, $2,511, $2,258, Court Administrative Assessment Fee [28-10] $2,537, $2,509, $2,335, $2,119, $2,127, $2,149, Declare of Candidacy Filing Fee $68, $37, $92, $11, $40, $16, Fees & Writs of Garnishments $2, $2, $2, $2, $2,400 $2, Nevada Report Sales $5, $8, $3, $7, $2, $5, Excess Property Sales $32, $26, $46, $85, $40, $37, Sale of Trust Property $14, $4, $3, $3, $3,500 $3, Insurance - Misc $432, $390, $416, $437, $450, $464, Misc Refunds $63, $90, $30, $30, $29, $31, Cost Recovery Plan [13-14] $8,495, $8,470, $8,883, $8,590, $11,534, $10,770, TOTAL MISC SALES & REF $63,263, $67,505, $22,110, $46,810, $22,758, $22,207, Unclaimed Property [9-06][5-09][12-10][29-10][30-10][1-11][14-12] $97,397, $32,918, $17,466, $11,823, $14,438, $15,875, TOTAL OTHER REVENUE $160,960, $100,723, $39,877, $58,933, $37,496, $38,382, TOTAL GENERAL FUND REVENUE BEFORE APPLICATION OF TAX CREDITS $3,081,768, $3,132,601, $3,066,946, $3,236,630, $3,068,536, $3,242,480, ESTIMATED TRANSFERRABLE TAX CREDITS ($22,900,000) ($79,300,000) ($76,500,000) TOTAL GENERAL FUND REVENUE - NET OF TAX CREDITS $3,081,768, $3,132,601, $3,066,946, $3,213,730, $2,989,236, $3,165,980,

10 GENERAL FUND REVENUES - ECONOMIC FORUM MAY 1, 2015 : THROUGH AND : THROUGH ECONOMIC FORUM'S FOR,, AND APPROVED AT THE MAY 1, 2015, MEETING ECONOMIC FORUM MAY 1, 2015 NOTES: FY 2004 (Actual collections are not displayed in the table for FY 2004, but notes were retained as they reflect the tax changes approved by the Legislature during the 2003 Regular and Special Sessions. FY 2004 [1-04] A.B. 4 (20th S.S.) reduced the collection allowance provided to the taxpayer for collecting and remitting the sales tax to the state from 1.25 to 0.5, effective July 1, [2-04] S.B. 8 (20th S.S.) increased gross gaming tax rates by 0.5: 3.0 to 3.5 on monthly revenue up to $50,000; 4.0 to 4.5 on revenue over $50,000 and up to $134,000; 6.25 to 6.75 on revenue exceeding $134,000, effective August 1, [3-04] S.B. 8 (20th S.S.) increased quarterly restricted slot fees by 33: from $61 to $81 per machine, up to 5 machines; from $106 to $141 for each machine over 5, up to 15 machines, effective July 22, [4a-04] S.B. 8 (20th S.S.) modified types of establishments and entertainment subject to the 10 Casino Entertainment Tax (CET), effective September 1 to December 31, 2003 [Estimated to generate $4,982,000 additional collections during 4-month period]. [4b-04] S.B. 8 (20th S.S.) repealed CET and replaced by Live Entertainment Tax (LET): 5 of admissions price, if entertainment is in facility with 7,500 or more seats; 10 of admissions price & food, beverage, and merchandise purchased, if facility has more than 300 and up to 7,500 seats; exempt from the tax if facility is a non-gaming establishment with less than 300 seats or is gaming establishment with less than 300 seats and less than 51 slot machines, 6 games, or any combination thereof, effective January 1, [5-04] [6-04] [7-04] [8-04] [9-04] [10-04] [11-04] [12-04] [13-04] [14-04] [15-04] [16-04] [17-04] [18-04] [19-04] FY 2006 [1-06] [2-06] [3-06] [4-06] [5-06] [6-06] [7-06] [8-06] [9-06] S.B. 8 (20th S.S.) increased liquor taxes by 75: beer from 9 cents to 16 cents per gallon; liquor up to 14 alcohol from 40 cents to 70 cents per gallon; liquor over 14 and up to 22 alcohol from 75 cents to $1.30 per gallon; liquor over 22 alcohol from $2.05 (15 cents for alcohol abuse program, 50 cents to local government, and $1.40 to State General Fund) to $3.60 per gallon (15 cents for alcohol abuse program, 50 cents to local government, and $2.95 to State General Fund), effective August 1, [Estimated to generate $13,873,000 in FY 2004 and $15,536,000 in FY 2005]. A.B. 4 (20th S.S.) reduced the collection allowance provided to the taxpayer for collecting and remitting the liquor tax to the state from 3 to 0.5, effective August 1, [Estimated to generate $734,000 in FY 2004 and $822,000 in FY 2005] S.B. 8 (20th S.S.) increased cigarette tax per pack of 20 by 45 cents: from 35 cents per pack (10 cents to Local Government Distribution Fund, 25 cents to State General Fund) to 80 cents per pack (10 cents to Local Government Distribution Fund, 70 cents to State General Fund), effective July 22, [Estimated to generate $63,268,000 in FY 2004 and $70,047,000 in FY 2005] A.B. 4 (20th S.S.) reduced the collection allowance provided to the taxpayer for collecting and remitting the cigarette tax to the state from 3 to 0.5, effective August 1, [Estimated to generate $2,538,000 in FY 2004 and $2,884,000 in FY 2005] A.B. 4 (20th S.S.) reduced collection allowance provided to taxpayer for collecting and remitting tax on other tobacco items from 2.0 to 0.5, effective August 1, S.B. 8 (20th S.S.) changed the $25 one-time annual Business License Fee to an annual fee of $100, effective July 22, S.B. 8 (20th S.S.) repealed the current quarterly $25 per employee tax when the Modified Business Tax comes online, effective October 1, [See Notes 10 and 11] S.B. 8 (20th S.S.) imposes tax on gross payroll of a business less a deduction for health care provided to employees, effective October 1, Tax rate is 0.70 in FY 2004 and 0.65 in FY S.B. 8 (20th S.S.) imposes tax of 2.0 on gross payroll of a financial institution less a deduction for health care provided to employees, effective October 1, S.B. 8 (20th S.S.) imposes excise tax on each bank of $7,000 per year ($1,750 per quarter) on each branch office, effective January 1, S.B. 8 (20th S.S.) imposes tax of $1.30 per $500 of value on the transfers of real property, effective October 1, S.B.2 and A.B. 4 (20th S.S.) makes changes to the rates and structure of the fees collected from entities filing with the Secretary of State's office, effective September 1, 2003 for Securities and UCC fee increases and November 1, 2003 for changes to commercial recording fees. S.B. 428 (2003 Session) increases real estate salesman, broker-salesman, & broker licensing fees by $20 for an original license and $10 for renewal of license (original & renewal license fee varies depending on type of license), effective July 1, A.B. 493 (2003 Session) established that revenues from fees collected by the Division of Financial Institutions of the Department of Business & Industry will be deposited in a separate fund to pay the expenses related to the operations of the Commissioner of Financial Institutions and the Division of Financial Institutions, effective January 1, Previously, the revenues from the fees were deposited in the State General Fund. A.B. 550 (2003 Session) increased state's portion of the fee for issuing copy of a birth certificate by $2 and fee for issuing copy of death certificate by $1, effective October 1, 2003 S.B. 504 (2003 Session) transferred the State Printing Division of the Department of Administration to the Legislative Counsel Bureau and all debt to the State General Fund was forgiven, effective July 1, Beginning in FY 2004, the portion of the fees collected by the Real Estate Division for Real Estate Testing Fees that belong to the general fund are transferred from Category 28 in BA 3823 to GL 4741 in the General Fund. Previously, the revenue from these fees were reverted to the General Fund at the end of the fiscal year. S.B. 357 (2005 Session) allocates $1 per slot machine per quarter in FY 2006 and $2 per slot machine per quarter in FY 2007 from the quarterly fee imposed on restricted and nonrestricted slot machines and sunsets effective June 30, A total of $822,000 in FY 2006 and $1,678,000 is projected to be deposited in the Account to Support Programs for the Prevention and Treatment of Problem Gambling. (FY 2006: $84,666 - Restricted; $737,334 - Nonrestricted and FY 2007: $172,834 - Restricted; $1,505,166 - Nonrestricted) A.B. 554 (2005 Session) lowers the occupancy threshold from 300 to 200, effective July 1, Estimated to generate $3,600,000 in FY 2006 and FY S.B. 3 (22nd S.S.) provides an exemption for entities that have four or fewer rental dwelling units. Estimated to reduce collections by $2,975,000 in FY 2006 and $3,060,000 in FY S.B. 3 (22nd S.S.) allows an entity operating a facility where craft shows, exhibitions, trade shows, conventions, or sporting events to pay the Business License Fee for entities not having a business license as an annual flat fee of $5,000 or on a $1.25 times the number entities without a business license times the number days of the show basis. Estimated to generate $134,420 in FY 2006 and $158,884 in FY S.B. 391 (2005 Session) replaces the NAICS-based approach for defining a financial institution with a structure based on a state or federal licensing or regulatory requirement for conducting financial activities. Collection agencies and pawn shops are not included as financial institutions, but as nonfinancial businesses. The changes are estimated to reduce MBT-Financial collections by $1,801,800 in FY 2006 and $2,047,500 in FY 2007 and increase MBT-Nonfinancial collections by $584,168 in FY 2006 and $621,237 in FY Net effect is a reduction in total MBT collections of $1,217,632 in FY 2006 and $1,426,263 in FY S.B. 523 (2005 Session) reduces the MBT-Nonfinancial institutions tax rate from 0.65 to 0.63 from July 1, 2005 to June 30, Estimated to reduce collections by $6,978,000 in FY 2006 and $7,450,000 in FY S.B. 3 (22nd S.S.) provides an exemption for the first branch bank operated by a bank in each county, replacing the previous exemption for one branch bank only. Estimated to reduce collections by $441,000 in FY 2006 and FY S.B. 390 (2005 Session) increases the collection allowance provided to Clark County and Washoe County from 0.2 to 1.0, effective July 1, 2005, which makes the collection allowance 1.0 in all 17 counties. Estimated to reduce collections by $1,056,292 in FY 2006 and $1,022,504 in FY S.B. 4 (22nd S.S.) allocates $7,600,000 of the Unclaimed Property revenues collected by the State Treasurer to the Millennium Scholarship Trust Fund in FY 2006 and FY 2007.

11 GENERAL FUND REVENUES - ECONOMIC FORUM MAY 1, 2015 : THROUGH AND : THROUGH ECONOMIC FORUM'S FOR,, AND APPROVED AT THE MAY 1, 2015, MEETING ECONOMIC FORUM MAY 1, 2015 FY 2008 [1-08] [2-08] [3-08] [4-08] FY 2009 [1A-09] [1B-09] [2-09] [3-09] [4-09] [5-09] FY 2010 [1-10] [2-10] [3-10] [4-10] [5-10] [6-10] [7-10] [8-10] [9-10] [10-10] [11-10] [12-10] [13-10] Per the June 30, 2007, sunset provision of S.B. 357 (2005 Session), the $2 per slot machine per quarter allocated from the quarterly license fee imposed on restricted and nonrestricted slot machines to the Account to Support Programs for the Prevention and Treatment of Problem Gambling ceases and the full amount collected from the quarterly slot fees remains in the General Fund. Per the A.B. 554 (2005 Session), race events that are part of the National Association of Stock Car Auto Racing (NASCAR) Nextel Cup series and all races associated with such an event are exempt from the LET, effective July 1, Per the sunset provision of S.B. 523 (2005 Session), the MBT-Nonfinancial institutions tax rate increases to 0.65 from 0.63, effective July 1, S.B. 165 (2005 Session) requires the State General Fund portion of the petroleum inspection fees imposed pursuant to NRS to be deposited into a separate account for use by the Department of Agriculture, effective July 1, S.B. 2 (25th S.S.) reduced the collection allowance provided to taxpayer for collecting and remitting sales and use taxes to the State from 0.5 to 0.25 effective January 1, 2009 and ending on June 30, During the six months the reduction in the collection allowance is effective in FY 2009, it is estimated that the change will generate $1,087,145 for the State 2 Sales Tax. S.B. 2 (25th S.S.) reduced the collection allowance provided to taxpayer for collecting and remitting sales and use taxes from 0.5 to 0.25 effective January 1, 2009 and ending on June 30, During the six months the reduction in the collection allowance is effective in FY 2009, it is estimated that the General Fund commission of 0.75 retained by the state for collecting and distributing the LSST, BCCRT, SCCRT, and Local Option taxes (LOPT) will generate the following additional General Fund revenue: LSST - $8,859; BCCRT - $1,968; SCCRT - $6,893; and LOPT - $4,275. S.B. 2 (25th S.S.) reduced the collection allowance provided to taxpayer for collecting and remitting cigarette taxes, liquor taxes, and other tobacco taxes to the state from 0.5 to 0.25 effective January 1, 2009 and ending on June 30, During the six months the reduction in the collection allowance is effective in FY 2009, it is estimated to generate the following additional General Fund revenue: Cigarette Tax - $125,955; Liquor Tax - $50,412, and Other Tobacco Tax - $11,209. S.B. 2 (25th S.S.) requires the advance payment on the Net Proceeds of Minerals Tax in FY 2009 based upon estimated net proceeds for the current calendar year. The provisions of S.B. 2 also apply to FY 2010 and FY 2011, but the Net Proceeds of Minerals Tax reverts back to the former method (based on previous calendar year) of taxing net proceeds on July 1, Based on S.B. 2, the Economic Forum's December 1 estimates for Net Proceeds of Minerals Tax for FY 2010 will be collected in FY 2009 and FY 2011 will be collected in FY Thus, S.B. 2 is estimated to increase FY 2009 Net Proceeds of Minerals Tax collections by $28,000,000 and decrease FY 2010 collections by $1,500,000 ($26,500,000 - $28,000,000). There is no revenue impact on FY 2011 as the Net Proceeds of Minerals Tax is estimated to remain at $26,500,000 in FY S.B. 2 (25th S.S.) requires that 1 of the 4 recovery surcharge retained by short-term car rental companies as reimbursement for costs of vehicles licensing fees and taxes to be deposited in the State General Fund effective January 1, 2009, and ending June 30, During the six months that the transfer of 1 of the 4 recovery surcharge to the General Fund is effective in FY 2009, it is estimated that it will generate additional General Fund revenue of $1,779,910. A.B. 549 redirects $7,600,000 to the General Fund of the Unclaimed Property revenues collected by the State Treasurer from the Millennium Scholarship Trust Fund in FY NOTE: Revenue amounts listed in the footnotes for FY 2010 based on legislative actions during the 2009 Session were prepared by the Fiscal Analysis Division using the Economic Forum's forecasts for FY 2010 and FY 2011 produced at its May 1, 2010, meeting. For those revenues for which revised forecasts were produced during January 2010, the effect of the legislative adjustment is included into the revised forecasts for the major General Fund revenue forecasts approved by the Economic Forum at its January 22, 2010, meeting, and the consensus General Fund revenue forecasts for minor revenue sources prepared by the Fiscal Analysis Division and the Budget Division. A.B. 552 lowered the collection allowance provided to a taxpayer for collecting and remitting sales and use taxes from 0.5 to 0.25, effective July 1, A.B. 552 also increased the General Fund commission retained by the Department of Taxation for collecting and distributing the sales and use taxes generated by the BCCRT, SCCRT, and local option taxes (did not apply to the LSST) from 0.75 to 1.75, effective July 1, Collectively, these changes are estimated to generate an additional $16,031,800 in FY 2010 and $16,679,000 in FY [FY State 2: $2,007,000 (TCA); LSST: $1,037,700 (TCA); BCCRT: $1,946,000 (GFC) + $3,700 (TCA); SCCRT: $6,806,700 (GFC) + $12,800 (TCA); LOPT: $4,210,000 (GFC) + $7,900 (TCA) and FY State 2: $2,049,700 (TCA); LSST: $1,081,400 (TCA); BCCRT: $2,028,000 (GFC) + $3,800 (TCA); SCCRT: $7,093,600 (GFC) + $13,300 (TCA); LOPT: $4,400,900 (GFC) + $8,300 (TCA) where GFC represents amount due to General Fund Commission rate change and TCA represents amount due to Taxpayer Collection Allowance change.] S.B. 429 changed the structure and tax rate for the Modified Business Tax on General Business (nonfinancial institutions) by creating a two-tiered tax rate in lieu of the single rate of 0.63, effective July 1, Under S.B. 429, a nonfinancial business pays a tax rate of 0.5 on all taxable wages (gross wages less allowable health care expenses) up to $62,500 per quarter, and a rate of 1.17 on taxable wages exceeding $62,500 per quarter. Estimated to generate an additional $173,330,000 in FY 2010 and $172,393,400 in FY The change to the MBT-General Business sunsets effective June 30, A.B. 552 lowered the collection allowance provided to a taxpayer for collecting & remitting cigarette taxes from 0.5 to 0.25, effective July 1, This change is estimated to generate an additional $236,200 in FY 2010 and $237,300 in FY Initiative Petition 1 (IP1) approved by the 2009 Legislature and allowed to become law by the Governor imposes up to an additional 3 room tax in Clark and Washoe counties but not to exceed a total combined rate of 13 in any area of each county, effective July 1, Under IP1, the revenue from the room tax is deposited in the State General Fund for FY 2010 and FY 2011 and is dedicated to K-12 education beginning in. S.B. 429 increases the depreciation rates for autos and trucks by 10 in the schedules used to determine the value of a vehicle for the purposes of calculating the Governmental Services Tax (GST) due, effective September 1, The portion of the GST generated from the depreciation schedule change is allocated to the State General Fund, which is estimated to generate $42,842,800 in FY 2010 and $51,411,300 in FY Under S.B. 429, additional revenue generated from the GST is deposited in the General Fund until and is then deposited in the State Highway Fund beginning in. S.B. 429 increases the Business License Fee (BLF) by $100 to $200 for initial and annual renewals, effective July 1, Effective October 1, 2009, A.B. 146 transfers the BLF to the Secretary of State from the Department of Taxation as part of the business portal program and requires all entities filing with the Secretary of State under Title 7 to pay the initial and annual renewal $200 BLF. It is estimated to generate an additional $38,254,800 in FY 2010 and $44,802,600 in FY Under S.B. 429, the $100 increase in the BLF sunsets effective June 30, A.B. 552 lowered the collection allowance provided to a taxpayer for collecting and remitting liquor taxes from 0.5 to 0.25, effective July 1, Estimated to generate an additional $100,400 in FY 2010 and $102,800 in FY A.B. 552 lowered the collection allowance provided to a taxpayer for collecting and remitting other tobacco taxes from 0.5 to 0.25, effective July 1, Estimated to generate an additional $23,560 in FY 2010 and $24,270 in FY Effective July 1, 2009, S.B. 53 requires fees collected for expedite services provided by the Secretary of State to business entities to be deposited in the State General Fund. Estimated to generate $2,272,569 in FY 2010 and $1,818,056 in FY Effective October 1, 2009, S.B. 234 increases the state rate imposed on the short-term rental of a vehicle from 6.0 to 10.0 with the proceeds equivalent to 9.0 deposited in the General Fund and 1.0 deposited in the Highway Fund (maintains provisions of A.B. 595 from the 2007 Session). S.B. 234 eliminates the 4.0 recovery surcharge and allows short-term car rental companies to impose a surcharge to recover their vehicle licensing and registration costs. Estimated to generate an additional $9,883,900 in FY 2010 and $13,565,000 in FY A.B. 480 increases various fees collected by the State Engineer for examining and filing applications and issuing and recording permits, effective July 1, Estimated to generate an additional $900,000 in FY 2010 and FY A.B. 562 redirects $3,800,000 to the General Fund of the Unclaimed Property revenues collected by the State Treasurer to the Millennium Scholarship Trust Fund in FY 2010 and FY A.B. 543 requires Clark County and Washoe County to allocate the equivalent of 4-cents worth of property tax generated from their operating rate to the State General Fund in FY 2010 and FY Estimated to generate $36,010,800 in FY 2010 and $32,446,600 in FY (Clark County: $30,380,500 - FY 2010 and $27,329,100 - FY 2011) (Washoe County: $5,630,300 - FY 2010 and $5,117,500 - FY 2011)

12 GENERAL FUND REVENUES - ECONOMIC FORUM MAY 1, 2015 : THROUGH AND : THROUGH ECONOMIC FORUM'S FOR,, AND APPROVED AT THE MAY 1, 2015, MEETING ECONOMIC FORUM MAY 1, 2015 FY Continued [14-10] [15-10] [16-10] [17-10] [18-10] A.B. 543 requires Clark County and Washoe County to allocate the equivalent of 3.8 cents in FY 2010 and 3.2 cents in FY 2011 worth of property tax generated from the capital rate imposed pursuant to NRS to the State General Fund in FY 2010 and FY Estimated to generate $34,210,300 in FY 2010 and $25,957,300 in FY (Clark County: $28,861,500 - FY 2010 and $21,863,300 - FY 2011) (Washoe County: $5,348,800 - FY 2010 and $4,094,000 - FY 2011) S.B. 431 requires a portion of the revenue generated from the state 3/8 of 1 room tax revenue provided to the Nevada Commission on Tourism to be allocated to the State General Fund in FY 2010 and FY Estimated to generate $2,334,563 in FY 2010 and $3,265,434 in FY A.B. 531 requires the portion of the revenue generated from Court Administrative Assessment Fees to be deposited in the State General Fund, effective July 1, Estimated to generate $4,763,532 in FY 2010 and $6,133,023 in FY S.B. 431 requires the transfer of the estimated residual amount of revenue generated from Insurance Verification Fees to the State General Fund in FY 2010 and FY Estimated to generate $7,000,000 in FY 2010 and $6,000,000 in FY S.B. 431 requires the transfer of $25,199,365 in FY 2010 and $22,970,977 in FY 2011 from the Supplemental Account for Medical Assistance to Indigent Persons created in the Fund for Hospital Care to Indigent Persons to the State General Fund. FY 2010: Notes 19 to 30 represent legislative actions approved during the 26th Special Session in February [19-10] Based on information provided to the Fiscal Analysis Division regarding the amount of net proceeds that would be reported to the Department of Taxation on March 1, 2010, pursuant to NRS for calendar year 2009 for FY 2010 and information on estimated mining operations for calendar year 2010 and 2011, the Fiscal Analysis Division produced a revised estimate for FY 2010 and FY 2011 for Net Proceeds of Minerals Tax of $71,700,000 and $62,100,000, respectively. These revised estimates were $31,700,000 and $27,100,000 higher than the consensus forecast prepared by the Budget Division/Fiscal Analysis Division on February 1, 2010 of $40,000,000 for FY 2010 and $35,000,000 for FY [20-10] Section 47 of A.B. 6 (26th S.S.) creates a new annual Mining Claims Fee based on a progressive graduated fee per mining claim associated with the total number of mining claims held by an enity in Nevada. This new Mining Claims Fee is estimated to generate $25,700,000 in FY 2011 only as the fee is scheduled to sunset effective June 30, [21-10] The Division of Insurance of the Department of Business and Industry is required to implement a program to perform desk audits of tax returns submitted by insurance companies when filing for the Insurance Premium Tax. This program is estimated to generate an additional $10,000,000 in Insurance Premium Tax collections in FY [22-10] Section 64 of A.B. 6 (26th S.S.) requires the Department of Taxation to conduct a tax amnesty program from July 1, 2010 to September 30, 2010 for all taxes that are required to be reported and paid to the Department. It is estimated that the tax amnesty program will generate $10,000,000 in FY 2011 from all the different applicable taxes, but an estimate of additional revenue expected from each individual revenue source was not prepared. [23-10] A.B. 6 (26th S.S.) increased various fees authorized or imposed in NRS associated with activities of the Secretary of State's Office related to securities, commercial recordings, & UCC filing requirements as well as changed the allocation of the portion to the State General Fund for fees associated with notary training and domestic partnerships. The changes were estimated to generate the following amounts in FY 2010 & FY 2011: UCC: $155,200 - FY 2010 and $465,600 - FY 2011; Commercial Recordings: $354,342 - FY 2010 and $1,063,027 - FY 2011; Notary Fees: $0 - FY 2010 and $153,600 - FY 2011; Securities: $855,314 - FY 2010 and $4,860,193 - FY 2011; and Domestic Partnerships: $0 - FY 2010 and $50,000 - FY [24-10] Section 45 of A.B. 6 (26th S.S.) increases the license fee from 4 to 6 on the gross receipts from admission fees to a live contest or exhibition of unarmed combat, effective July 1, This fee increase is estimated to generate $1,250,000 in additional revenue for FY [25-10] A.B. 6 (26th S.S.) requires the current fees specified in NRS associated with birth and death certificates to continue to be collected by the State Registrar until the State Registrar establishes new higher fees through regulation. The higher fees imposed through regulation are expected to be effective July 1, 2010, and are estimated to generate an additional $368,511 in revenue for FY [26-10] Section 31 of A.B. 6 (26th S.S.) imposes a new fee of $150 per notice of default or election to sell with the proceeds deposited in the State General Fund, effective April 1, This new notice of default fee is estimated to generate additional General Fund revenue of $2,760,000 in FY 2010 and $11,040,000 in FY [27-10] Section 36 of A.B. 6 (26th S.S.) requires the Legislative Commission to transfer the first $100,000 in revenue collected from lobbyist registration fees imposed pursuant to NRS 218H.500 to the State General Fund. The $100,000 transfer to the General Fund is for FY 2011 only as the provisions sunset on June 30, [28-10] Section 34 of A.B. 6 (26th S.S.) increases the adminstrative assessment amount associated with misdemeanor violation fines by $5 effective upon passage and approval of A.B. 6 (March 12, 2010). The proceeds from the additional $5 adminstrative assessment as part of the sentence for a violation of a misdemeanor are deposited in the State General Fund and is estimated to generate an additional $192,544 in FY 2010 and $2,310,530 in FY [29-10] Based on information provided by the Treasurer's Office, the Fiscal Analysis Division revised the estimate for unclaimed property collections to be deposited in the State General Fund to $52,000,000 in FY 2010 and $58,081,000 in FY This revised forecast for unclaimed property proceeds yields an additional $4,018,000 in FY 2010 and $15,000,000 in FY 2011 above the February 1, 2010, consensus forecast of $47,919,000 for FY 2010 and $43,081,000 for FY 2011 prepared by the Budget Division/Fiscal Division based on information provided by the Treasurer's Office. [30-10] Section 1 of A.B. 3 (26th S.S.) redirects the full $7,600,000 to the General Fund of the Unclaimed Property revenues collected by the State Treasurer from the Millennium Scholarship Trust Fund in FY 2010 and FY A.B. 562 (75th Session) redirected $3,800,000 to the General Fund of the Unclaimed Property revenues collected by the State Treasurer to the Millennium Scholarship Trust Fund in FY 2010 and FY The net effect of the provisions of A.B 3 is an additional $3,800,000 in General Fund revenue in FY 2010 and FY 2011 from unclaimed property proceeds. FY 2011 [1-11] The Treasurer's Office provided the Budget Division of the Department of Administration and the Fiscal Analysis Division of the Legislative Counsel Bureau with information on additional unclaimed property for FY 2011, based on more complete information that became available after the Economic Forum May 2, 2011, meeting on actual unclaimed property remitted to the Treasurer's Office. Treasurer's Office estimated an additional $13,630,561 for FY [1-12] S.B. 493 clarifies and eliminates certain deductions allowed against gross proceeds to determine net proceeds for the purpose of calculating the Net Proceeds of Minerals Tax liability. All of the deduction changes are effective beginning with the NPM tax payments due in based on calendar year 2012 mining activity and are permanent, except for the elimination of the deduction for health and industrial insurance expenses, which are effective for and only. Deduction changes are estimated to generate $11,919,643 in addtional revenue in both and. [2-12] A.B. 561 extends the June 30, 2011, sunset (approved in S.B. 429 (2009)) to June 30, 2013, on the Net Proceeds of Minerals Tax, which continues the payment of taxes in the current fiscal year based on the estimated net proceeds for the current calendar year with a true-up against actual net proceeds for the calendar year in the next fiscal year. The two-year extension of the sunset is estimated to yield $69,000,000 in only as tax payments are required in with or without the extension of the sunset. [3-12] S.B 493 repeals the Mining Claims Fee, approved in A.B. 6 (26th Special Session), requiring payment of the fee in FY 2011 only with the June 30, 2011, sunset. S.B. 493 establishes provisions for entities that paid the Mining Claims Fee to apply to the Department of Taxation for a credit against their Modified Business Tax (MBT) liability or for a refund. No estimate of the impact in and from Mining Claims Fee credits was prepared so no adjustment was made to the Economic Forum May 2, 2011 forecast for MBT - Nonfinancial tax collections. [4-12] Extension of the sunset on the 0.35 increase in the Local School Support Tax (LSST) in A.B. 561 from June 30, 2011, to June 30, 2013 generates additional revenue from the 0.75 General Fund Commission assessed against LSST proceeds before distribution to school districts in each county. Estimated to generate $1,052,720 in and $1,084,301 in. [5-12] A.B. 500 reduces the portion of the quarterly licensing fees imposed on restricted and non-restricted slot machines from $2 to $1 per slot machine that is dedicated to the Account to Support Programs for the Prevention and Treatment of Problem Gambling. The other $1 is deposited in the State General Fund in and, due to the June 30, 2013, sunset in A.B Estimated to generate $682,982 in and $692,929 in from non-restricted slot machines and $75,970 in and $77,175 in from restricted slot machines.

GENERAL FUND PROJECTIONS

GENERAL FUND PROJECTIONS GENERAL FUND REVENUE ESTIMATES AND PROJECTED UNAPPROPRIATED GENERAL FUND BALANCES The 2009 Legislature approved a General Fund operating budget for the 2009-11 biennium that totals

GENERAL FUND PROJECTIONS GENERAL FUND REVENUE ESTIMATES AND PROJECTED UNAPPROPRIATED GENERAL FUND BALANCES The 2009 Legislature approved a General Fund operating budget for the 2009-11 biennium that totals

% Change. % Change FY 2015 ACTUAL

GENERAL FUND REVENUES - ECONOMIC FORUM MAY 1, 2017, (UPDATED 10/16/2017) : THROUGH AND : THROUGH ECONOMIC FORUM'S FOR,, AND APPROVED AT THE MAY 1, 2017, MEETING TAXES MINING TAX 3064 Net Proceeds of Minerals

GENERAL FUND REVENUES - ECONOMIC FORUM MAY 1, 2017, (UPDATED 10/16/2017) : THROUGH AND : THROUGH ECONOMIC FORUM'S FOR,, AND APPROVED AT THE MAY 1, 2017, MEETING TAXES MINING TAX 3064 Net Proceeds of Minerals

% Change. % Change FY 2015 ACTUAL

GENERAL FUND REVENUES - ECONOMIC FORUM MAY 1, 2017, : THROUGH AND : THROUGH ECONOMIC FORUM'S FOR,, AND APPROVED AT THE MAY 1, 2017, MEETING TAXES MINING TAX 3064 Net Proceeds of Minerals [1-12][2-12][1-14][2-14][2-16][3-16]

GENERAL FUND REVENUES - ECONOMIC FORUM MAY 1, 2017, : THROUGH AND : THROUGH ECONOMIC FORUM'S FOR,, AND APPROVED AT THE MAY 1, 2017, MEETING TAXES MINING TAX 3064 Net Proceeds of Minerals [1-12][2-12][1-14][2-14][2-16][3-16]

APPENDIX Report of the State of Nevada Economic Forum

269 APPENDIX Report of the State of Nevada Economic Forum Forecast of Future State Revenues December 1, 2010 270 271 STATE OF NEVADA ECONOMIC FORUM OF FUTURE STATE REVENUES December 1, 2010 272 273 274

269 APPENDIX Report of the State of Nevada Economic Forum Forecast of Future State Revenues December 1, 2010 270 271 STATE OF NEVADA ECONOMIC FORUM OF FUTURE STATE REVENUES December 1, 2010 272 273 274

OVERVIEW OF NEVADA S BUDGET PROCESS AND REVENUE FORECAST

OVERVIEW OF NEVADA S BUDGET PROCESS AND REVENUE FORECAST The Office of Fiscal Analysis was created by the 1973 Legislature as a part of the Research and Fiscal Analysis Division. The Legislature authorized

OVERVIEW OF NEVADA S BUDGET PROCESS AND REVENUE FORECAST The Office of Fiscal Analysis was created by the 1973 Legislature as a part of the Research and Fiscal Analysis Division. The Legislature authorized

STATE OF NEVADA ECONOMIC FORUM

STATE OF NEVADA ECONOMIC FORUM OF FUTURE STATE REVENUES December 6, 2016 REPORT TO THE GOVERNOR AND THE LEGISLATURE ON FUTURE STATE REVENUES December 6, 2016 Senate Bill 23 (1993) provided for the

STATE OF NEVADA ECONOMIC FORUM OF FUTURE STATE REVENUES December 6, 2016 REPORT TO THE GOVERNOR AND THE LEGISLATURE ON FUTURE STATE REVENUES December 6, 2016 Senate Bill 23 (1993) provided for the

SECTION II GENERAL FUND PROJECTED FUND BALANCE

19 SECTION II GENERAL FUND PROJECTED FUND BALANCE Senate Bill 23 (1993) established an Economic Forum to forecast State General Fund revenues for use by all state agencies, the Governor and the Legislature

19 SECTION II GENERAL FUND PROJECTED FUND BALANCE Senate Bill 23 (1993) established an Economic Forum to forecast State General Fund revenues for use by all state agencies, the Governor and the Legislature

NEVADA LEGISLATIVE APPROPRIATIONS REPORT

NEVADA LEGISLATIVE APPROPRIATIONS REPORT SEVENTY EIGHTH LEGISLATURE Fiscal Years 2015 16 and 2016 17 Fiscal Analysis Division Legislative Counsel Bureau November 2015 INTRODUCTION The Nevada Legislative

NEVADA LEGISLATIVE APPROPRIATIONS REPORT SEVENTY EIGHTH LEGISLATURE Fiscal Years 2015 16 and 2016 17 Fiscal Analysis Division Legislative Counsel Bureau November 2015 INTRODUCTION The Nevada Legislative

STATE OF NEVADA ECONOMIC FORUM

STATE OF NEVADA ECONOMIC FORUM OF FUTURE STATE REVENUES December 3, 2018 REPORT TO THE GOVERNOR AND THE LEGISLATURE ON FUTURE STATE REVENUES December 3, 2018 Senate Bill (S.B.) 23 (1993) provided for

STATE OF NEVADA ECONOMIC FORUM OF FUTURE STATE REVENUES December 3, 2018 REPORT TO THE GOVERNOR AND THE LEGISLATURE ON FUTURE STATE REVENUES December 3, 2018 Senate Bill (S.B.) 23 (1993) provided for

Multiple Tax Provisions

TAX TOPICS A publication of the Nevada Taxpayers Association, serving the citizens of Nevada since 1922. ISSUE 1-15 ELECTRONIC EDITION JULY 2015 Legislative Enactments Part I: Taxes The following pages

TAX TOPICS A publication of the Nevada Taxpayers Association, serving the citizens of Nevada since 1922. ISSUE 1-15 ELECTRONIC EDITION JULY 2015 Legislative Enactments Part I: Taxes The following pages

STATE OF NEVADA ECONOMIC FORUM

STATE OF NEVADA ECONOMIC FORUM FORECAST OF FUTURE STATE REVENUES December 2, 2002 THE STATE OF NEVADA ECONOMIC FORUM Cary Fisher, Chairman Ron Zideck, Vice Chairman Deborah Pierce Leo Seevers Michael Small

STATE OF NEVADA ECONOMIC FORUM FORECAST OF FUTURE STATE REVENUES December 2, 2002 THE STATE OF NEVADA ECONOMIC FORUM Cary Fisher, Chairman Ron Zideck, Vice Chairman Deborah Pierce Leo Seevers Michael Small

RESTRICTED AND NONRESTRICTED GAMING IN NEVADA MARCH 20, 2013

RESTRICTED AND NONRESTRICTED GAMING IN NEVADA MARCH 20, 2013 Creation of Distinction Between Restricted and Nonrestricted Gaming Licenses C 2 1967: Senate Bill 471 (Taxation) Established flat fee per slot

RESTRICTED AND NONRESTRICTED GAMING IN NEVADA MARCH 20, 2013 Creation of Distinction Between Restricted and Nonrestricted Gaming Licenses C 2 1967: Senate Bill 471 (Taxation) Established flat fee per slot

TAX POLICY BACKGROUND

TAX POLICY TAX POLICY BACKGROUND The 2001 Session of the Legislature convened with clouds across the economic horizon. Stock values had been dropping, most severely in the high-tech sector, and various

TAX POLICY TAX POLICY BACKGROUND The 2001 Session of the Legislature convened with clouds across the economic horizon. Stock values had been dropping, most severely in the high-tech sector, and various

SALES TAX ATTRIBUTABLE TO VISITORS

EXECUTIVE SUMMARY Applied Analysis was retained by the Las Vegas Convention and Visitors Authority (the LVCVA ) to review and analyze the economic impacts associated with its various operations and southern

EXECUTIVE SUMMARY Applied Analysis was retained by the Las Vegas Convention and Visitors Authority (the LVCVA ) to review and analyze the economic impacts associated with its various operations and southern

Volume III Issue III. The Fiscal Impact of Southern Nevada Tourism: The Industry s Contribution to Major Public Revenues 2010 Update

Volume III Issue III Page 1 Applied Analysis was retained by the Las Vegas Convention and Visitors Authority (the LVCVA ) to review and analyze the economic impacts associated with its various operations

Volume III Issue III Page 1 Applied Analysis was retained by the Las Vegas Convention and Visitors Authority (the LVCVA ) to review and analyze the economic impacts associated with its various operations

REVENUE Major Vermont Tax Sources

REVENUE DETAILS 39 REVENUE Major Vermont Tax Sources Vermont has three major funds into which most tax revenue is deposited; the General Fund, the Transportation Fund and the Education Fund. There are

REVENUE DETAILS 39 REVENUE Major Vermont Tax Sources Vermont has three major funds into which most tax revenue is deposited; the General Fund, the Transportation Fund and the Education Fund. There are

CHAPTER 13 STATE TAXES

CHAPTER 13 STATE TAXES Latest Revision 1994 13.01 INTRODUCTION Ohio relies on various taxes to support its governmental activities. Some of these taxes have transfer provisions which accrue to the benefit

CHAPTER 13 STATE TAXES Latest Revision 1994 13.01 INTRODUCTION Ohio relies on various taxes to support its governmental activities. Some of these taxes have transfer provisions which accrue to the benefit

ECONOMIC FORUM. Thursday, November 8, :00 a.m. Legislative Building 401 South Carson Street Carson City, Nevada Room 4100

ECONOMIC FORUM Thursday, November 8, 2018 9:00 a.m. Legislative Building 401 South Carson Street Carson City, Nevada Room 4100 With videoconference to Grant Sawyer State Office Building 555 East Washington

ECONOMIC FORUM Thursday, November 8, 2018 9:00 a.m. Legislative Building 401 South Carson Street Carson City, Nevada Room 4100 With videoconference to Grant Sawyer State Office Building 555 East Washington

Allocation of Money Distributed From the Local Government Tax Distribution Account. Bulletin No Legislative Counsel Bureau

Allocation of Money Distributed From the Local Government Tax Distribution Account Bulletin No. 13-04 Legislative Counsel Bureau January 2013 BULLETIN NO. 13-04 LEGISLATIVE COMMISSION S SUBCOMMITTEE TO

Allocation of Money Distributed From the Local Government Tax Distribution Account Bulletin No. 13-04 Legislative Counsel Bureau January 2013 BULLETIN NO. 13-04 LEGISLATIVE COMMISSION S SUBCOMMITTEE TO

Analysis of Fiscal Policy in Nevada. An Overview of the Approach and Findings of the Governor s Task Force on Tax Policy in Nevada

Analysis of Fiscal Policy in Nevada An Overview of the Approach and Findings of the Governor s Task Force on Tax Policy in Nevada Summary Review ACR 1 s requirements and assumptions provided a general

Analysis of Fiscal Policy in Nevada An Overview of the Approach and Findings of the Governor s Task Force on Tax Policy in Nevada Summary Review ACR 1 s requirements and assumptions provided a general

Ohio 2020 Tax Policy Commission

Ohio 2020 Tax Policy Commission Testimony of Tax Commissioner Joe Testa Department of Taxation October 22, 2015 Co-Chairman Senator Peterson, Co-Chairman Representative McClain, and members of the Tax

Ohio 2020 Tax Policy Commission Testimony of Tax Commissioner Joe Testa Department of Taxation October 22, 2015 Co-Chairman Senator Peterson, Co-Chairman Representative McClain, and members of the Tax

Nevada Commerce Tax Narrative. Prepared by Commerce Tax Division

Nevada Commerce Tax Narrative Prepared by Commerce Tax Division Commerce Tax Highlights Annual tax on business entities engaged in business in Nevada Each business entity engaged in business in Nevada

Nevada Commerce Tax Narrative Prepared by Commerce Tax Division Commerce Tax Highlights Annual tax on business entities engaged in business in Nevada Each business entity engaged in business in Nevada

2013 Supplement to the Minnesota Tax Handbook

2013 Supplement to the Minnesota Tax Handbook This supplement to the 2012 Edition of the Minnesota Tax Handbook contains the major tax law changes enacted in 2013. The page references are to the 2012 Edition.

2013 Supplement to the Minnesota Tax Handbook This supplement to the 2012 Edition of the Minnesota Tax Handbook contains the major tax law changes enacted in 2013. The page references are to the 2012 Edition.

Indiana Tax Descriptions and Receipts

Indiana Tax Descriptions and Receipts All amounts are in thousands. Percentage change reflects increase from FY05 to FY06, unless otherwise indicated. Significant differences reflected in the tax receipts

Indiana Tax Descriptions and Receipts All amounts are in thousands. Percentage change reflects increase from FY05 to FY06, unless otherwise indicated. Significant differences reflected in the tax receipts

2017 Supplement to the Minnesota Tax Handbook

2017 Supplement to the Minnesota Tax Handbook This supplement to the 2016 Edition of the Minnesota Tax Handbook contains the major tax law changes enacted in 2017. The page references are to the 2016 Edition.

2017 Supplement to the Minnesota Tax Handbook This supplement to the 2016 Edition of the Minnesota Tax Handbook contains the major tax law changes enacted in 2017. The page references are to the 2016 Edition.

REPORT ON TAX ABATEMENTS, TAX EXEMPTIONS, TAX INCENTIVES FOR ECONOMIC DEVELOPMENT AND TAX INCREMENT FINANCING IN NEVADA

REPORT ON TAX ABATEMENTS, TAX EXEMPTIONS, TAX INCENTIVES FOR ECONOMIC DEVELOPMENT AND TAX INCREMENT FINANCING IN NEVADA February 2009 REPORT ON TAX ABATEMENTS, TAX EXEMPTIONS, TAX INCENTIVES FOR ECONOMIC

REPORT ON TAX ABATEMENTS, TAX EXEMPTIONS, TAX INCENTIVES FOR ECONOMIC DEVELOPMENT AND TAX INCREMENT FINANCING IN NEVADA February 2009 REPORT ON TAX ABATEMENTS, TAX EXEMPTIONS, TAX INCENTIVES FOR ECONOMIC

Senate File 1209 (Pogemiller, D-Minneapolis) (passed and laid on the table 03/23/05)

(passed and laid on the table 03/23/05)") Summary of 2005 Tax Provisions (Note: This document will be updated from time to time. Please check back periodically. Currently updated through 05.10.05.) The following tables summarize selected provisions

Summary of 2005 Tax Provisions (Note: This document will be updated from time to time. Please check back periodically. Currently updated through 05.10.05.) The following tables summarize selected provisions

FINANCE AND ADMINISTRATION

FINANCE AND ADMINISTRATION Finance and Administration includes those agencies that generally control, coordinate, assist and provide services to other agencies and programs in state government. These agencies

FINANCE AND ADMINISTRATION Finance and Administration includes those agencies that generally control, coordinate, assist and provide services to other agencies and programs in state government. These agencies

FLORIDA REVENUE ESTIMATING CONFERENCE. Long-Term Revenue Analysis FY Through FY Volume 33 Fall, 2017

FLORIDA REVENUE ESTIMATING CONFERENCE Long-Term Revenue Analysis FY 1970-71 Through FY 2026-27 Volume 33 Fall, 2017 Honorable Rick Scott Governor State of Florida Honorable Joe Negron President Florida

FLORIDA REVENUE ESTIMATING CONFERENCE Long-Term Revenue Analysis FY 1970-71 Through FY 2026-27 Volume 33 Fall, 2017 Honorable Rick Scott Governor State of Florida Honorable Joe Negron President Florida

Nevada s Consolidated Tax

Nevada s Consolidated Tax A Review and Analysis of Potential Issues and Restructuring Alternatives in Support of the Assembly Bill 71 (2011) Interim Study 2/6/2013 10:32 AM Assembly Committee: Taxation

Nevada s Consolidated Tax A Review and Analysis of Potential Issues and Restructuring Alternatives in Support of the Assembly Bill 71 (2011) Interim Study 2/6/2013 10:32 AM Assembly Committee: Taxation

FLORIDA REVENUE ESTIMATING CONFERENCE. Long-Term Revenue Analysis FY Through FY

FLORIDA REVENUE ESTIMATING CONFERENCE Long-Term Revenue Analysis FY 1970-71 Through FY 2027-28 Volume 34 Based on the Conference Series held November 5, 2018 through December 21, 2018 Honorable Ron DeSantis

FLORIDA REVENUE ESTIMATING CONFERENCE Long-Term Revenue Analysis FY 1970-71 Through FY 2027-28 Volume 34 Based on the Conference Series held November 5, 2018 through December 21, 2018 Honorable Ron DeSantis

Statewide Initiative Usage. Statewide Initiatives

Statewide Initiative Usage Of Initiatives Passage Rate 166 75 91 45% Statewide Initiatives Year Authorizing the state, counties, and cities to engage in business activities. Authorizing the state to bond

Statewide Initiative Usage Of Initiatives Passage Rate 166 75 91 45% Statewide Initiatives Year Authorizing the state, counties, and cities to engage in business activities. Authorizing the state to bond

Resources. General Fund Resources Available for Appropriation ( biennium, $ in millions)

") Resources The adopted 2004-06 budget includes $27.3 billion in general fund resources available for appropriation. This figure excludes the $300.5 million in existing revenue transferred to the Virginia

Resources The adopted 2004-06 budget includes $27.3 billion in general fund resources available for appropriation. This figure excludes the $300.5 million in existing revenue transferred to the Virginia

NCSL (Summary of States Measures to Balance FY 2010 Budgets - October 21, 2009)

") NCSL (Summary of States Measures to Balance FY 2010 Budgets - October 21, 2009) ACROSS THE BOARD BUDGET CUTS & OTHER MISCELLANEOUS CUTS 13 states have taken across the board budget cuts. The cuts range

NCSL (Summary of States Measures to Balance FY 2010 Budgets - October 21, 2009) ACROSS THE BOARD BUDGET CUTS & OTHER MISCELLANEOUS CUTS 13 states have taken across the board budget cuts. The cuts range

DOR Administrative Costs/Savings Department of Revenue Analysis of H.F (Drazkowski) As Proposed to be Amended (H2716A1 & H2716A2)

As Proposed to be Amended (H2716A1 & H2716A2)") Fair Tax to Replace Income, Sales, and Excise Taxes March 14, 2018 DOR Administrative Costs/Savings Department of Revenue Yes X No Fund Impact F.Y. 2018 F.Y. 2019 F.Y. 2020 F.Y. 2021 (000 s) Individual

Fair Tax to Replace Income, Sales, and Excise Taxes March 14, 2018 DOR Administrative Costs/Savings Department of Revenue Yes X No Fund Impact F.Y. 2018 F.Y. 2019 F.Y. 2020 F.Y. 2021 (000 s) Individual

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 2013 SESSION LAW HOUSE BILL 1050

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 2013 SESSION LAW 2014-3 HOUSE BILL 1050 AN ACT TO AMEND THE REVENUE LAWS, AS RECOMMENDED BY THE REVENUE LAWS STUDY COMMITTEE. The General Assembly of North Carolina

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 2013 SESSION LAW 2014-3 HOUSE BILL 1050 AN ACT TO AMEND THE REVENUE LAWS, AS RECOMMENDED BY THE REVENUE LAWS STUDY COMMITTEE. The General Assembly of North Carolina

New Jersey State Tax News 2009 (Volume 38) INDEX

INDEX") New Jersey State Tax News 2009 (Volume 38) INDEX No. Page No. Page Alcoholic beverage tax Tax Increase (Legislature) 2 11 Amnesty Amnesty Programs in Other States 1 10 2 10 3 10 4 10 New Jersey Establishes

New Jersey State Tax News 2009 (Volume 38) INDEX No. Page No. Page Alcoholic beverage tax Tax Increase (Legislature) 2 11 Amnesty Amnesty Programs in Other States 1 10 2 10 3 10 4 10 New Jersey Establishes

TAX TOPICS A publication of the Nevada Taxpayers Association, serving the citizens of Nevada since 1922.

TAX TOPICS A publication of the Nevada Taxpayers Association, serving the citizens of Nevada since 1922. Issue 2-15 Electronic Edition August 2015 Legislative Enactments Part 2: Fees The following pages

TAX TOPICS A publication of the Nevada Taxpayers Association, serving the citizens of Nevada since 1922. Issue 2-15 Electronic Edition August 2015 Legislative Enactments Part 2: Fees The following pages

CITY OF NORTH LAS VEGAS, NEVADA DEBT MANAGEMENT POLICY IN ACCORDANCE WITH NRS (C)

") CITY OF NORTH LAS VEGAS, NEVADA DEBT MANAGEMENT POLICY IN ACCORDANCE WITH NRS 350.013 1(C) JUNE 30, 2009 TABLE OF CONTENTS Summary of Debt... 2 Affordability of Debt... 8 General Obligation Bonds Supported

CITY OF NORTH LAS VEGAS, NEVADA DEBT MANAGEMENT POLICY IN ACCORDANCE WITH NRS 350.013 1(C) JUNE 30, 2009 TABLE OF CONTENTS Summary of Debt... 2 Affordability of Debt... 8 General Obligation Bonds Supported

Senate Finance Committee

Presentation to the Senate Finance Committee Review the state's current spending limits and determine if statutory changes are needed to continue restraint of spending growth below the rate of inflation

Presentation to the Senate Finance Committee Review the state's current spending limits and determine if statutory changes are needed to continue restraint of spending growth below the rate of inflation

Background & Overview

EXHIBIT C Senate Committee on Revenue and Economic Development Date: 2-14-2017 Total pages: 69 Exhibit begins with: C1 thru: C69 Background & Overview Applied Analysis was retained by the Local Government

EXHIBIT C Senate Committee on Revenue and Economic Development Date: 2-14-2017 Total pages: 69 Exhibit begins with: C1 thru: C69 Background & Overview Applied Analysis was retained by the Local Government

EXHIBIT D-4. Oklahoma Tax Changes. Alterations in Income and Gross Production Taxes and Their Impact on the Oklahoma Tax Base

EXHIBIT D-4 1 Oklahoma Tax Changes Alterations in Income and Gross Production Taxes and Their Impact on the Oklahoma Tax Base 2 Oklahoma s Tax System Eight Major Tax Types Individual Income Tax Corporate

EXHIBIT D-4 1 Oklahoma Tax Changes Alterations in Income and Gross Production Taxes and Their Impact on the Oklahoma Tax Base 2 Oklahoma s Tax System Eight Major Tax Types Individual Income Tax Corporate

CITY OF NORTH LAS VEGAS, NEVADA DEBT MANAGEMENT POLICY IN ACCORDANCE WITH NRS (C)

") CITY OF NORTH LAS VEGAS, NEVADA DEBT MANAGEMENT POLICY IN ACCORDANCE WITH NRS 350.013 1(C) JUNE 30, 2007 TABLE OF CONTENTS DEBT MANAGEMENT POLICY NRS 350.013 Subsection 1(c)... 1 Summary of Debt... 2 Affordability

CITY OF NORTH LAS VEGAS, NEVADA DEBT MANAGEMENT POLICY IN ACCORDANCE WITH NRS 350.013 1(C) JUNE 30, 2007 TABLE OF CONTENTS DEBT MANAGEMENT POLICY NRS 350.013 Subsection 1(c)... 1 Summary of Debt... 2 Affordability

HOUSE COMMITTEE ON APPROPRIATIONS FISCAL NOTE. HOUSE BILL NO. 271 PRINTERS NO PRIME SPONSOR: Ortitay

HOUSE COMMITTEE ON APPROPRIATIONS FISCAL NOTE HOUSE BILL NO. 271 PRINTERS NO. 2652 PRIME SPONSOR: Ortitay REVENUE INCREASE / (DECREASE) FUND FY 2017/18 FY 2018/19 General Fund See Fiscal Impact See Fiscal

HOUSE COMMITTEE ON APPROPRIATIONS FISCAL NOTE HOUSE BILL NO. 271 PRINTERS NO. 2652 PRIME SPONSOR: Ortitay REVENUE INCREASE / (DECREASE) FUND FY 2017/18 FY 2018/19 General Fund See Fiscal Impact See Fiscal

Convention Center Expansion and Renovation Legislative Recommendation Preliminary Draft

Page 1 Legislative Recommendation Preliminary Draft EXPLANATION: Matter in bolded italics is new; matter between brackets [omitted material] is material to be removed. OVERVIEW SECTION 1 amends NRS 244

Page 1 Legislative Recommendation Preliminary Draft EXPLANATION: Matter in bolded italics is new; matter between brackets [omitted material] is material to be removed. OVERVIEW SECTION 1 amends NRS 244

NEVADA TAX REVENUE COMPARED TO THE UNITED STATES

Page 1 EXECUTIVE SUMMARY Applied Analysis was retained by the Las Vegas Convention and Visitors Authority (the LVCVA ) to review and analyze the economic impacts associated with its various operations

Page 1 EXECUTIVE SUMMARY Applied Analysis was retained by the Las Vegas Convention and Visitors Authority (the LVCVA ) to review and analyze the economic impacts associated with its various operations

APPROPRIATIONS REPORT

Kansas Legislature 2017-2019 APPROPRIATIONS REPORT Kansas Legislative Research Department August 2017 TABLE OF CONTENTS General Budget Overview - Fiscal Years 2017, 2018, and 2019 All Funds...1-1 State

Kansas Legislature 2017-2019 APPROPRIATIONS REPORT Kansas Legislative Research Department August 2017 TABLE OF CONTENTS General Budget Overview - Fiscal Years 2017, 2018, and 2019 All Funds...1-1 State

SENATE APPROPRIATIONS COMMITTEE FISCAL NOTE

BILL NO. House Bill 1929 PRINTER NO. 3810 AMOUNT See Fiscal Impact DATE INTRODUCED November 17, 2017 FUND General Fund PRIME SPONSOR Representative Marsico DESCRIPTION AND PURPOSE OF BILL House Bill 1929

BILL NO. House Bill 1929 PRINTER NO. 3810 AMOUNT See Fiscal Impact DATE INTRODUCED November 17, 2017 FUND General Fund PRIME SPONSOR Representative Marsico DESCRIPTION AND PURPOSE OF BILL House Bill 1929

Consolidated Fund Statement Budgetary Basis 2018 November Forecast

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp Consolidated Budgetary

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp Consolidated Budgetary

Chapter 14 MUNICIPALLY IMPOSED TAXES AND FEES

Chapter 14 MUNICIPALLY IMPOSED TAXES AND FEES Some locally-imposed taxes and fees are optional, and a given municipality may have imposed all or portions of their taxing authority under that item. Other

Chapter 14 MUNICIPALLY IMPOSED TAXES AND FEES Some locally-imposed taxes and fees are optional, and a given municipality may have imposed all or portions of their taxing authority under that item. Other

Governor s Tax Bill. March 4, 2005

Governor s Tax Bill March 4, 2005 Department of Revenue Analysis of S.F. 753 (Ortman)/ H.F. 660 (Krinkie) Analysis Revised for Updated Estimates and February 2005 Forecast Separate Official Fiscal Note

Governor s Tax Bill March 4, 2005 Department of Revenue Analysis of S.F. 753 (Ortman)/ H.F. 660 (Krinkie) Analysis Revised for Updated Estimates and February 2005 Forecast Separate Official Fiscal Note

FY 09/10 ADOPTED GENERAL FUND REVENUES $218,840,522

GENERAL FUND REVENUES FY 09/10 ADOPTED GENERAL FUND REVENUES $218,840,522 State Revenue 11% Transfers Federal Revenue1% 2% Fund Balance 0.1% Other Local Revenue 2% Other Local Taxes 21% Gen. Property Taxes

GENERAL FUND REVENUES FY 09/10 ADOPTED GENERAL FUND REVENUES $218,840,522 State Revenue 11% Transfers Federal Revenue1% 2% Fund Balance 0.1% Other Local Revenue 2% Other Local Taxes 21% Gen. Property Taxes

REVISED PROPOSED REGULATION OF THE DEPARTMENT OF MOTOR VEHICLES. LCB File No. R July 17, 2014

REVISED PROPOSED REGULATION OF THE DEPARTMENT OF MOTOR VEHICLES LCB File No. R071-14 July 17, 2014 EXPLANATION Matter in italics is new; matter in brackets [omitted material] is material to be omitted.

REVISED PROPOSED REGULATION OF THE DEPARTMENT OF MOTOR VEHICLES LCB File No. R071-14 July 17, 2014 EXPLANATION Matter in italics is new; matter in brackets [omitted material] is material to be omitted.

Senate Bill 1566 Ordered by the Senate February 15 Including Senate Amendments dated February 15

th OREGON LEGISLATIVE ASSEMBLY--0 Regular Session A-Engrossed Senate Bill Ordered by the Senate February Including Senate Amendments dated February Printed pursuant to Senate Interim Rule. by order of

th OREGON LEGISLATIVE ASSEMBLY--0 Regular Session A-Engrossed Senate Bill Ordered by the Senate February Including Senate Amendments dated February Printed pursuant to Senate Interim Rule. by order of

SENATE BILL 729: Various Changes to the Revenue Laws.

2016-2017 General Assembly SENATE BILL 729: Various Changes to the Revenue Laws. Committee: Senate Finance : April 26, 2016 Introduced by: Sen. Rucho; Sen. Rabon; Sen. Tillman Prepared by: Greg Roney Analysis

2016-2017 General Assembly SENATE BILL 729: Various Changes to the Revenue Laws. Committee: Senate Finance : April 26, 2016 Introduced by: Sen. Rucho; Sen. Rabon; Sen. Tillman Prepared by: Greg Roney Analysis

A FIELD GUIDE TO THE TAX E S TEXAS

A FIELD GUIDE TO THE TAX E S TEXAS OF DECEMBER GLENN HEGAR TEXAS COMPTROLLER OF PUBLIC ACCOUNTS A FIELD GUIDE TO THE TAXES OF TEXAS The data represented in this report is available in accessible data form

A FIELD GUIDE TO THE TAX E S TEXAS OF DECEMBER GLENN HEGAR TEXAS COMPTROLLER OF PUBLIC ACCOUNTS A FIELD GUIDE TO THE TAXES OF TEXAS The data represented in this report is available in accessible data form

: Recodified as by Session Laws 1995, c. 360, s. 1(c).

.") Article 8B. Taxes Upon Insurance Companies. 105-228.3. Definitions. The following definitions apply in this Article: (1) Article 65 corporation. A corporation subject to Article 65 of Chapter 58 of the

Article 8B. Taxes Upon Insurance Companies. 105-228.3. Definitions. The following definitions apply in this Article: (1) Article 65 corporation. A corporation subject to Article 65 of Chapter 58 of the

Senate Bill No. 1 Committee of the Whole

Senate Bill No. 1 Committee of the Whole CHAPTER... AN ACT relating to commerce; providing for the issuance of transferable tax credits and the partial abatement of certain taxes to a project that satisfies