NEW TIME AND NEW LOCATION

|

|

|

- Lora Casey

- 5 years ago

- Views:

Transcription

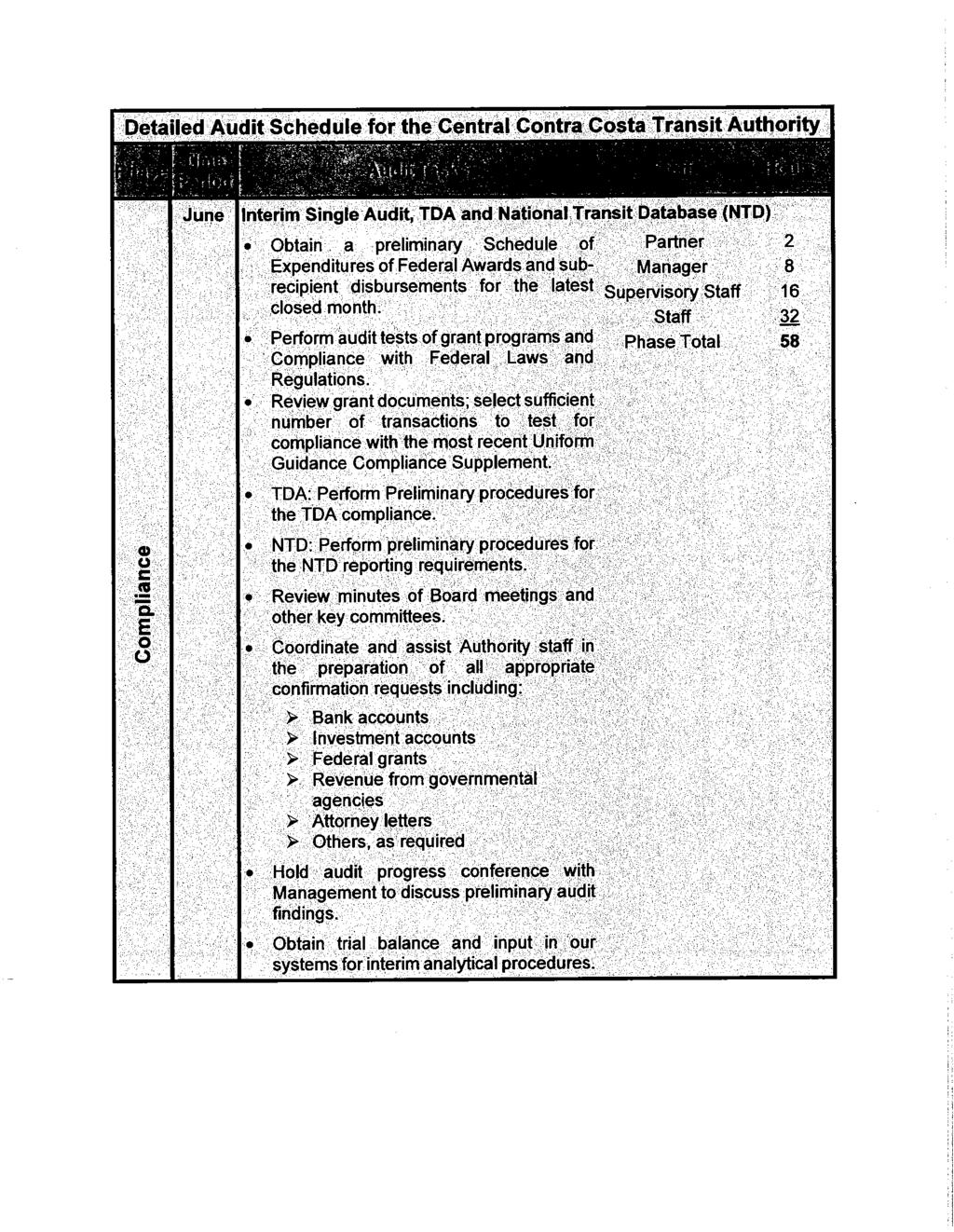

1 ADMINISTRATION & FINANCE COMMITTEE MEETING AGENDA Tuesday, January 8, :30 a.m. Candace Andersen's Office, 3338 Mt. Diablo Blvd. Lafayette, CA NEW TIME AND NEW LOCATION The committee may take action on each item on the agenda. The action may consist of the recommended action, a related action or no action. Staff recommendations are subject to action and/or change by the committee. 1. Approval of Agenda 2. Public Communication 3. Approval of Minutes of December 4, 2018* 4. CCCTA Investment Policy-Quarterly Reporting Requirement* 5. Income Statements for the Three Months Ended September 30, 2018* 6. Independent Accountant s report on Federal Transit Administration National Transit Database Reports* (Staff will request that the committee approve the report and forward to the Board.) 7. Proposal for Financial Audit Services* (Staff will ask for direction to accept or reject the proposal from Brown Armstrong.) 8. Route 99X Promotion* (Information Only) 9. Contra Costa Transportation Authority s Accessible Transportation Strategic (ATS) Plan* (Staff will requests the committee forward this item to the board for discussion, feedback and direction in responding to CCTA s request for feedback regarding the attached MOU prior to the end of January 2019.) *Enclosure **Enclosure for Committee Members ***To be mailed under separate cover ****To be available at the meeting. FY2018/2019 A&F Committee Don Tatzin Lafayette, Al Dessayer-Moraga, Kevin Wilk-Walnut Creek

2 10. Final Fare Restructure Proposal & Title VI Analysis* (Staff will present the final fare proposal and corresponding Title VI analysis. Staff will request the item be forwarded to Board for approval.) 11. February Board Workshop Reminder Verbal Report 12. Review of Vendor Bills, December 2018** 13. Approval of Legal Services Statement, October 2018 General and Labor** 14. Next Scheduled Meeting February 13, Adjournment

3 General Information Public Comment: Each person wishing to address the committee is requested to complete a Speakers Card for submittal to the Committee Chair before the meeting convenes or the applicable agenda item is discussed. Persons who address the Committee are also asked to furnish a copy of any written statement to the Committee Chair. Persons who wish to speak on matters set for Public Hearings will be heard when the Chair calls for comments from the public. After individuals have spoken, the Public Hearing is closed and the matter is subject to discussion and action by the Committee. A period of thirty (30) minutes has been allocated for public comments concerning items of interest within the subject matter jurisdiction of the Committee. Each individual will be allotted three minutes, which may be extended at the discretion of the Committee Chair. Consent Items: All matters listed under the Consent Calendar are considered by the committee to be routine and will be enacted by one motion. There will be no separate discussion of these items unless requested by a committee member or a member of the public prior to when the committee votes on the motion to adopt. Availability of Public Records: All public records relating to an open session item on this agenda, which are not exempt from disclosure pursuant to the California Public Records Act, that are distributed to a majority of the legislative body, will be available for public inspection at 2477 Arnold Industrial Way, Concord, California, at the same time that the public records are distributed or made available to the legislative body. The agenda and enclosures for this meeting are posted also on our website at Accessible Public Meetings: Upon request, County Connection will provide written agenda materials in appropriate alternative formats, or disability-related modification or accommodation, including auxiliary aids or services, to enable individuals with disabilities to participate in public meetings. Please send a written request, including your name, mailing address, phone number and brief description of the requested materials and preferred alternative format or auxiliary aid or service so that it is received by County Connection at least 48 hours before the meeting convenes. Requests should be sent to the Assistant to the General Manager, Lathina Hill, at 2477 Arnold Industrial Way, Concord, CA or hill@countyconnection.com. Shuttle Service: With 24-hour notice, a County Connection LINK shuttle can be available at the BART station nearest the meeting location for individuals who want to attend the meeting. To arrange for the shuttle service, please call Katrina Lewis 925/ , no later than 24 hours prior to the start of the meeting. Currently Scheduled Board and Committee Meetings Board of Directors: Administration & Finance: Advisory Committee: Marketing, Planning & Legislative: Operations & Scheduling: January 17, 9:00 a.m., County Connection Board Room Tuesday, February 13, 9:30 a.m., Supervisor Andersen's Office, 3338 Mt. Diablo Blvd. Lafayette, CA 9454 TBA. County Connection Board Room Thursday, January 10, 8:30 a.m., Supervisor Andersen's Office, 3338 Mt. Diablo Blvd. Lafayette, CA 9454 Friday, January 4, 8:15 a.m. Supervisor Andersen's Office, 3338 Mt. Diablo Blvd. Lafayette, CA 9454 The above meeting schedules are subject to change. Please check the County Connection Website ( or contact County Connection staff at 925/ to verify date, time and location prior to attending a meeting. This agenda is posted on County Connection s Website ( and at the County Connection Administrative Offices, 2477 Arnold Industrial Way, Concord, California

4 Administration and Finance Committee Summary Minutes December 4, 2018 The meeting was called to order at 9:00 a.m. at the Walnut Creek offices of Hanson Bridgett. Those in attendance were: Committee Members: Director Al Dessayer Director Don Tatzin Director Kevin Wilk Staff: Guests: General Manager Rick Ramacier Chief Financial Officer Erick Cheung Chief Operating Officer Scott Mitchell Accounting Manager Karol McCarty None 1. Approval of Agenda- Approved. 2. Public Communication- None. 3. Approval of Minutes of October 31, Approved. 4. Presentation of the Fiscal Year 2018 Audit Rosalva Flores, the Brown Armstrong partner in charge of the FY 2018 audit, reported by telephone on the audit. She reported that the audit report is unmodified, no findings, no material weaknesses nor deficiencies were identified and no material noncompliance issues were noted. She thanked County Connection s financial staff for working with her staff in completing the audit. Mr. Cheung thanked Ms. Flores and her team, he also thanked finance staff and all of the various County Connection departments involved in the audit. The Committee provided suggestion on the Management Discussion and Analysis (MD&A) section of the financial statements to modify the language of the ballot measure to repeal Senate Bill 1. Mr. Cheung stated that the draft MD&A was completed prior to the election date and was not known at that time the outcome of the proposition and will amend the current draft. The Committee recommended to the Board that the audit report be approved with that suggestion. 5. Issue Request for Proposal Financial Audit Services Mr. Cheung reported the Board extended Brown Armstrong earlier this year to complete the FY 2018 audit and was planning to release a Request for Proposal (RFP). The Committee was complimentary of the services provided by Brown Armstrong, which staff was in concurrence with. Director Dessayer and Director Tatzin discussed the staff time and costs associated with the RFP. The Committee requested that staff ask Brown Armstrong to provide a cost proposal for the next three years, and bring the item back to the Committee for consideration. Mr. Cheung needed to inquire with Ms. Flores of Brown Armstrong on the proposal and possible partner rotation due to State Law. The item is continued till the January meeting. 6. PERS Actuarial Valuation for June 30, 2017; Rate for FY Mr. Cheung reported that the employer rate for PERS retirement for FY 2018 will be 8.313% and unfunded liability payment of $349,903. County Connection s funded status is currently 91.5%, which is up from 88.9% in the previous year due to investment return of 11.2% for FY 2017 over the discount rate of 7.5%. The projections from CalPERS for future years reflects an increase in the unfunded liability payment due to the last couple of years returns of 2.4% for FY 2015 and 0.6% for FY 2016, which has been slightly offset by the 11.2% for FY The unfunded liability payments will be $350K in FY 2020, $548K in FY 2021, $762K in FY 2022, $928K in FY 2023, $980K in FY 2024 and $1.1M in FY This is a net decrease of $1.5 million over a six-year period on the unfunded liability payment in comparison to the previous year estimate. Staff will incorporate the revised payments and contribution rates in the FY 2020 Budget and Ten Year Forecast. Information only. 7. Emergency Procurement for Upgrade and Replacement of Existing Fire Alarm System- Mr. Mitchell reported that during October 2018, Johnson Controls informed County Connection that there are, Deficiencies/impairments in our fire alarm system can result in unintended operation or failure of the system to operate. They strongly recommended immediate correction and provided a quotation in the amount of $179,600 for upgrading and replacing the fire alarm system. County Connection is a member of NJPA (National Joint Powers Alliance) and we are able to utilize the

5 competitive bid of a Johnson Controls system to meet our needs. This project would include replacing all fire panels, horns, lights, pull stations, and wiring throughout the property. The funding for the fire system is from State Proposition 1B. The Committee approved that the Board of Directors authorize the General Manager to enter into a contract with Johnson Controls for the upgrade and replacement of the fire alarm system for consent on the Board agenda. 8. Review of Vendor Bills, November Reviewed. 9. Legal Services Statement, September 2018, General & Labor- Approved. 10. Adjournment- The meeting was adjourned. The next meeting is set for scheduled Tuesday January 8th, and Wednesday February 13 th at 9:30 am at 3338 Mt. Diablo Blvd, Lafayette, CA Erick Cheung, Chief Finance Officer

6 (:puzi[y(prmection TO: Administration & Finance Coinmittee DATE: January 2, 2019 FROM: Rick Ramacier General Manager SUBJECT: CCCTA Investment Policy - Quarterly Reporting Requirement Attached please find CCCTA's Quarterly Investment Policy Reporting Statement for tlie quarter ending September 30, This certifies that the portfolio complies with the CCCTA Investment Policy and that CCCTA has the ability to meet the pool's expenditure requirements (cash flow) for the next six (6) months.

7 CCCTA BANK CASH AND INVESTMENT ACCOUNTS (ROUNDED OFF TO NEAREST $) FINANCIAL INST ACCT # TYPE l PURPOSE FIXED ROUTE UNION BANK CHECKING AP GENERAL UNION BANK CHECKING PAYROLL UNION BANK CHECKING CAPIT AL PURCHASES UNION BANK CHECKING WORKERS' COMP - CORVEL UNION BANK CHECKING PASS SALES PAYPAL 27SAXUUFL9732 CHECKING PAYPAL-PASS SALES TOTAL PARATRANSIT UNION BANK CHECKING AP GENERAL TOTAL LAIF FUND LAIF ACCOUNT INT-INVEST OPERATING FUNDS LAIF ACCOUNT INT-INVEST Rolling Stock LAIF ACCOUNT INT-INVEST Lifeline Bus Stop Access LAIF ACCOUNT INT-INVEST Facility Rehab LAIF ACCOUNT INT-INVEST LCTOP - Martinez Shuttle Ill LAIF ACCOUNT INT-INVEST LCTOP - Martinez Amtrak to BART LAIF ACCOUNT INT-INVEST LCTOP - Electric Trolley I LAIF ACCOUNT INT-INVEST LCTOP - Electric Trolley II LAIF ACCOUNT INT-INVEST Pass-Through CA LAIF ACCOUNT INT-INVEST Safe Harbor Lease Reserve LAIF ACCOUNT FMV ADJ. Fair Market Value Adjustment for Year-End TOTAL CCCTA EMPLOYEE UNION BANK CHECKING EMPLOYEE FITNESS FUND UNION BANK CHECKING EMPLOYEE FUNCTION TOTAL PER BANK PER BANK PER BANK PER GL" MAR 2018 JUN 2018 SEP 2018 SEP 2018 $ 560,811 $ 2,243,592 $ 527,195 $ 543,272 $ 59,363 $ 77,157 $ 54,557 $ 40,460 $ 254,837 $ 248,665 $ 254,681 $ 250,000 $ 122,473 $ 103,721 $ 85,405 $ 48,512 $ 25,052 $ 9,444 $ 11,744 $ 11,744 $ 680 $ 399 $ 870 $ 870 $ 1,023,216 $ 2,682,978 $ 934,452 $ 894,858 $ 687,414 $ 246,831 $ 290,713 $ 293,572 $ 687,414 $ 246,831 $ 290,713 $ 293,572 $ 7,763,798 $ 3,809,256 $ 9,593,541 $ 9,593,541 $ 370,136 $ 371,313 $ 140,277 $ 140,277 $ 84,960 $ 82,197 $ 82,513 $ 82,513 $ 2,944,121 $ 2,930,448 $ 2,931,458 $ 2,931,458 $ 96,404 $ 25,360 $ $ $ $ $ 323,251 $ 323,251 $ 166,147 $ 149,736 $ $ $ $ $ 347,410 $ 347,410 $ $ $ 1,027,959 $ i,ozz,gsg $ 1,470,210 $ 1,475,680 $ 1,482,670 $ 1,482,670 $ $ $ $ $ 12,895,776 $ 8,843,990 $ 15,929,079 $ 15,929,079 $ 10,439 $ 9,878 $ 10,421 $ 10,421 $ 508 $ 508 $ 508 $ 508 $ 10,947 $ 10,386 $ 10,929 $ 10,929 GRAND TOT AL 12/11/2018 I i$ 14,617,353i$ 11,784,185i$ 17,165,173i i$ 17,128,438 KLM " GL balances reduced by oustanding checks and increased by deposits in transit, if any. This is to certify that the portfolio above complies with the CCCTA Investment Policy and that CCCTA has the ability to meet its expeditures (cash flow) for the next six months. Rick Ramacier General Manager

8 To: Administration &Finance Committee Date: January 8, 2019 From: Erick Cheung, Chief Finance Officer SUBJECT: Income Statements for the Three Months Ended September 30, 2018 The attached unaudited County Connection Income Statements for the first three months of FY 2019 are presented for your review. The combined expenses of $8,705,683 for Fixed Route and Paratransit, (Schedule 1), are 7.3% under the budget ($686,262). The expense categories with the most significant variances are: Wages $( 187,630) ( 5.5)% Other wages are lower by $165K due to the Manager of Planning/Community Liaison and Customer Service & Outreach Coordinator positions were vacant during the first quarter but are now filled. The Director of Innovation and Mobility position is vacant with duties reassigned to current planning staff. Fringe Benefits $( 133,146) ( 5.2)% Fringe Benefits are under budget due to vacancies and medical increases will occur on January 1, Services $( 57,978) ( 10.3)% Services are under mainly due to lower than budget for promotions expense ($28K), schedules/graphics expense ($27K), service repairs ($51K), legal ($48K) and various other accounts due to timing. This is offset by Clever Device annual maintenance service paid in September for $239K. Materials & Supplies $( 36,536) ( 5.1)% Materials and supplies are lower due to lower diesel fuel costs ($20K). Contingency $( 200,000) (100.0)% Not needed based on expenses being under budget. Fixed route and Paratransit revenues and expenses are presented on Schedules 2 and 3. Actual expenses are compared to the year-to-date approved budget. Fixed route expenses are -8.8% under budget and Paratransit expenses are 1.0% over budget. The combined revenues are also over/(under) budget. The most significant variances: Passenger fares/special fares $ 40, % Fixed route passenger fares/special fares are $46.0K higher than budget as staff assumed a decrease of 3.0% for fixed route based on past trends. Paratransit fares are ($5.3K) lower than budget. Compared to the same period in the prior year, fixed route is $10K or 1% higher due

9 to special fares agreements but lower than FY 2017 by $2K; Paratransit is $16.7K higher due to increased ridership but only higher than FY 2017 by $310. TDA revenue earned $( 769,432) ( 20.0)% TDA revenue is lower due to lower than expected expenses. Other revenue $ 100, % Received annual grant revenue for database tracking of $75K in September, prior year received in December. Other operating assistance $( 60,045) ( 13.3)% The difference is mainly due to timing, since State Transit Assistance Lifeline funds are normally received in December. Fixed Route Operator Wages (Schedule 4) Schedule 4 compares various components of operator wages with the budget. Platform (work time) is -2.1% under budget. Overtime is -4.3% under budget. Training is 35.3% over budget. Overall wages for operators are -1.2% under budget. Statistics (Schedule 6) Schedule 6 provides selected statistical information for the current year compared to the last two years: Fixed route: Passenger fares/special fares are 1.0% more than FY 2018 and -0.2% less than FY The farebox recovery ratio is lower compared to FY 2017 and FY The ratio is 14.6% in FY 2019; 15.6% in FY 2018 and 16.1% in FY Operating expenses are 7.7% more than in FY 2018 and 10.1% more than FY As mentioned earlier, Clever Device invoice payment of $239K paid in September and in past years was paid in October. Fixed route revenue hours are 1.1% more than FY 2018 and 0.1% more than FY The cost per revenue hour has increased 3.3% compared to FY 2017 and 1.4% compared to FY Passengers have decreased -2.2% compared to FY 2018 and -8.2% compared to FY The cost per passenger has increased 10.2% compared to FY 2018 and 19.9% compared to FY Passengers per revenue hour has decreased -3.3% compared to FY 2018 and -8.3% compared to FY 2017.

10 Paratransit: Passenger fares have increased 15.9% compared to FY 2018 and 0.3% compared to FY The farebox ratio is more than FY 2018 and less than FY The ratio is 8.2% in FY 2019; 7.6% in FY 2018; and 9.2% in FY Expenses have increased 7.3% compared to FY 2018 and 12.2% compared to FY Due to increase of 3% with First Transit for FY 2019 and revenue hours/passengers increasing as noted below. Revenue hours are 8.1% more than FY 2018 and 5.2% in FY Passengers have increased 1.4% compared to FY 2018 and -0.8% compared to FY The cost per passenger has increased 5.7% since FY 2018 and 13.1% compared to FY Paratransit passengers per revenue hour have decreased -6.6% compared to FY 2018 and -5.6% compared to FY 2017.

11 CENTRAL CONTRA COSTA TRANSIT AUTHORITY FY 2019 Year to Date Comparison of Actual vs Budget Combined Fixed Route and Paratransit Income Statement For the Three Months Ended September 30, 2018 Actual Budget Variance % Variance Revenues Passenger fares $ 781,868 $ 749,874 $ 31, % Special fares 390, ,573 8, % 1,172,128 1,131,447 40, % Advertising 147, ,635 (1,134) -0.8% Safe Harbor lease 8,076 4,413 3, % Other revenue 145,003 44, , % Federal operating 350, ,200 2, % TDA earned revenue 3,495,377 4,255,075 (759,698) -17.9% STA revenue 1,421,285 1,421, % Measure J 1,573,263 1,586,149 (12,886) -0.8% Other operating assistance 392, ,460 (60,045) -13.3% 7,533,555 8,260,499 (726,944) -8.8% Total Revenue $ 8,705,683 $ 9,391,945 $ (686,262) -7.3% Expenses Wages- Operators $ 1,891,197 $ 1,913,427 $ (22,230) -1.2% Wages-Other 1,338,981 1,504,381 (165,400) -11.0% 3,230,178 3,417,808 (187,630) -5.5% Fringe Benefits 2,429,452 2,562,598 (133,146) -5.2% Services 505, ,600 (57,978) -10.3% Materials & Supplies 681, ,738 (36,536) -5.1% Utilities 73,481 95,013 (21,532) -22.7% Insurance 222, ,138 (15,341) -6.4% Taxes 36,355 65,454 (29,099) -44.5% Leases and Rentals 13,395 13, % Miscellaneous 38,932 56,450 (17,518) -31.0% Special Trip Services 1,474,269 1,461,953 12, % Operations 8,705,683 9,191,945 (486,262) -5.3% Contingency Reserve - 200,000 (200,000) % Total Expenses $ 8,705,683 $ 9,391,945 $ (686,262) -7.3% Net Income (Loss) $ - $ - $ - Revenue Hours 75,032 73,054 1, % Cost per Rev Hr $ $ $ (12.53) -9.8% Passengers 859, ,707 (18,235) -2.1% Cost per Passenger $ $ $ (0.57) -5.3% Farebox ratio 13.5% 12.1% 1.4% 11.8% (fares,spec fares/oper exp-w/o contingency-leases) Schedule 1-Combined Fixed Route & Paratransit

12 CENTRAL CONTRA COSTA TRANSIT AUTHORITY FY 2019 Year to Date Comparison of Actual vs Budget Fixed Route Income Statement For the Three Months Ended September 30, 2018 Actual Budget Variance % Variance Revenues Passenger fares $ 660,323 $ 622,999 $ 37, % Special fares 390, ,573 8, % 1,050,583 1,004,572 46, % Advertising 147, ,635 (1,134) -0.8% Safe Harbor lease 8,076 4,413 3, % Other revenue 145,003 44, , % TDA earned revenue 3,084,038 3,853,470 (769,432) -20.0% STA revenue 1,264,098 1,264, % Measure J 1,170,891 1,183,777 (12,886) -1.1% Other operating assistance 350, ,960 (67,476) -16.1% 6,170,091 6,916,610 (746,519) -10.8% Total Revenue $ 7,220,674 $ 7,921,181 $ (700,507) -8.8% Expenses Wages- Operators $ 1,891,197 $ 1,913,427 $ (22,230) -1.2% Wages-Other 1,301,488 1,461,250 (159,762) -10.9% 3,192,685 3,374,677 (181,992) -5.4% Fringe Benefits 2,407,719 2,543,503 (135,784) -5.3% Services 486, ,950 (67,138) -12.1% Materials & Supplies 679, ,638 (36,924) -5.2% Utilities 68,420 88,138 (19,718) -22.4% Insurance 222, ,138 (15,341) -6.4% Taxes 36,355 65,379 (29,024) -44.4% Interest % Leases and Rentals 13,395 13, % Miscellaneous 38,932 56,237 (17,305) -30.8% Purchased Transportation 73,845 71,328 2, % Operations 7,220,674 7,721,181 (500,507) -6.5% Contingency Reserve - 200,000 (200,000) Total Expenses $ 7,220,674 $ 7,921,181 $ (700,507) -8.8% Net Income (Loss) $ - $ - $ - Revenue Hours 56,358 54,760 1, % Cost per Rev Hr $ $ $ (16.53) -11.4% Passengers 824, ,155 (18,732) -2.2% Cost per Passenger $ 8.76 $ 9.39 $ (0.64) -6.8% Passengers per Rev Hr (0.77) -5.0% Farebox recovery ratio 14.6% 13.0% 1.5% 11.8% (fares,spec fares/oper exp-w/o contingency-leases) Schedule 2-Fixed Route

13 CENTRAL CONTRA COSTA TRANSIT AUTHORITY Paratransit Income Statement FY 2019 Year to Date Comparison of Actual vs Budget For the Three Months Ended September 30, 2018 Actual Budget Variance % Variance Revenues Passenger fares (a) $ 121,545 $ 126,875 $ (5,330) -4.2% 121, ,875 (5,330) -4.2% Other revenue 25 (25) % Federal operating 350, ,200 2, % TDA earned revenue 411, ,605 9, % STA revenue 157, , % Measure J 402, , % Other operating assistance 41,931 34,500 7, % 1,363,464 1,343,889 19, % Total Revenue $ 1,485,009 $ 1,470,764 $ 14, % Expenses Wages-Other 37,493 $ 43,131 $ (5,638) -13.1% 37,493 43,131 (5,638) -13.1% Fringe Benefits 21,733 19,095 2, % Services 18,810 9,650 9, % Materials & Supplies 1,488 1, % Utilities 5,061 6,875 (1,814) -26.4% Taxes - 75 (75) % Miscellaneous (213) % Special Trip Services 1,400,424 1,390,625 9, % Total Expenses $ 1,485,009 $ 1,470,764 $ 14, % Net Income (Loss) $ - $ - $ - Revenue Hours 18,674 18, % Cost per Rev Hr $ $ $ (0.87) -1.1% Passengers 35,049 34, % Cost per Passenger $ $ $ (0.20) -0.5% Passengers per Rev Hr (0.01) -0.6% Farebox ratio 8.2% 8.6% -0.4% -5.1% (fares,spec fares/oper exp-leases) Schedule 3- Paratransit

14 CENTRAL CONTRA COSTA TRANSIT AUTHORITY Operator Wages For the Three Months Ended September 30, 2018 Actual Budget Variance % Variance Platform/report/turn in $ 1,511,615 $ 1,544,747 $ (33,133) -2.1% Guarantees 64,700 57,652 7, % Overtime 90,967 95,064 (4,096) -4.3% Spread 50,806 51,253 (447) -0.9% Protection 68,064 67, % Travel 52,544 55,091 (2,546) -4.6% Training 46,801 34,582 12, % Other Misc 5,699 7,435 (1,736) -23.3% $ 1,891,197 $ 1,913,427 $ (22,230) -1.2% Schedule 4- Operator Wages

15 CENTRAL CONTRA COSTA TRANSIT AUTHORITY Other Revenue; Other Operating Assistance; Miscellaneous Expenses For the Three Months Ended September 30, 2018 Other Revenue Investment income (interest) $ 31,385 ADA Database Management revenue 75,000 Paypal Shipping revenue 281 RTC card revenue 752 Various $ 37, ,003 Other Operating Assistance RM2 $ 36,335 BART feeder revenue 206,531 LCTOP 77,827 Homeland Security ITS $ 29, ,484 Miscellaneous Expenses Board Travel Expense $ - Staff Travel Expense 13,763 APTA Dues 8,874 Employee functions 9,554 Employee Awards/pins 1,162 Paypal fees 695 Training 661 Various other $ 4,223 38,932 Schedule 5- Other Revenues/Other Expenses

16 Fixed Route Actual Actual Variance Actual Variance Actual 2019 to Actual 2019 to FY2019 FY2018 Actual 2018 FY2017 Actual 2017 Fares $ 660,323 $ 661, % $ 707, % Special Fares 390, , % 345, % Total Fares $ 1,050,583 $ 1,040, % $ 1,052, % Fares box recovery ratio 14.6% 15.6% -6.3% 16.1% -9.3% Operating Exp (Less leases) $ 7,207,279 $ 6,690, % $ 6,548, % Revenue Hours 56,358 55, % 56, % Cost per Rev Hour $ $ % $ % Passengers 824, , % 898, % Cost per Passenger $ 8.74 $ % $ % Passengers per Rev Hr % % Paratransit CENTRAL CONTRA COSTA TRANSIT AUTHORITY FY 2019 Year to Date Comparison of FY 2018 Actual & FY 2017 Actual Statistics For the Three Months Ended September 30, 2018 Fares $ 121,545 $ 104, % $ 121, % Fares box recovery ratio 8.2% 7.6% 8.0% 9.2% -10.7% Operating Exp (Less leases) $ 1,485,009 $ 1,384, % $ 1,323, % Revenue Hours 18,674 17, % 17, % Cost per Rev Hour $ $ % $ % Passengers 35,049 34, % 35, % Cost per Passenger $ $ % $ % Passengers per Rev Hr % % Schedule 6- Statistics

17 To: Administration and Finance Committee Date: January 8, 2019 From: Erick Cheung, Chief Financial Officer SUBJECT: Proposal For Financial Audit Services Summary of Issues: The Board of Directors approved a one year extension for Brown Armstrong to provide audit services for June 30, Brown Armstrong s contract began in 2012 and has provided County Connection invaluable service over that period of time and has helped staff implement GASB 68 Accounting and Financial Reporting for Pensions in FY 2014 and GASB 75 Accounting for Other Post-Employment Benefits Other Than Pensions in FY Based on the high quality of audit services provided by Brown Armstrong, the A&F Committee directed staff to request a proposal for an additional three fiscal years from FY 2019 through FY Rosalva Flores from Brown Armstrong has provided a proposal (see Attachment A) for the next 3 years with an annual increase of $1,000 or an average of 2.15% shown in the table below. The increases are less than the statewide consumer price index of 3.8% as of October Also, there is an option to change audit partners with the extension or retain Ms. Flores through FY After the FY 2019 audit, Brown Armstrong would be required to rotate partners due to Assembly Bill 1345 which requires lead audit partner rotation after 6 consecutive years. Fiscal Year Amount Increase 2019 $46,500 $1,000 or 2.20% 2020 $47,500 $1,000 or 2.15% 2021 $48,500 $1,000 or 2.11% Recommendation: Provide direction to staff to accept or reject proposal from Brown Armstrong. Options: 1. Accept proposal and recommend to the Board of Directors. 2. Decline proposal and begin Request for Proposal process. 3. Take other action as determined. Attachment A Brown Armstrong Proposal

18 Attachment A

19 Attachment A

20 Attachment A

21 Attachment A

22 Attachment A

23 Attachment A

24 Attachment A

25 To: Administration and Finance Committee Date: January 8, 2019 From: Erick Cheung Chief Finance Officer SUBJECT: Independent Accountant s report on Federal Transit Administration National Transit Database reports SUMMARY OF ISSUES: Annually our independent auditors, Brown Armstrong, CPA s, are required to review the data we report to FTA on Form FFA-10 which is included in the National Transit Database report (NTD). The form reports hours, miles, passengers, passenger miles and total operating expenses. Beginning in fiscal year 2018, the FTA requires a separate report to review appropriate accounting consistent with the NTD Uniform System of Accounts (USOA). We filed the NTD report in October and Brown Armstrong completed their review in December. Brown Armstrong reviewed the data and financial information and issued both reports without exceptions except for a typing error in the FFA-10 (see Item G) which was corrected and resubmitted. FINANCIAL IMPLICATIONS: None. ACTION REQUESTED: Staff requests that the committee approve the report and forward to the Board. ATTACHMENTS: A. Independent Accountant s Report on Applying Agreed-Upon Procedures For Federal Funding Allocation Data Federal Transit Administration B. Independent Accountant s Report on Applying Agreed-Upon Procedures For Financial Data Federal Transit Administration

26 CENTRAL CONTRA COSTA TRANSIT AUTHORITY NATIONAL TRANSIT DATABASE REPORTING INDEPENDENT ACCOUNTANT S REPORT ON APPLYING AGREED-UPON PROCEDURES FOR FEDERAL FUNDING ALLOCATION DATA FEDERAL TRANSIT ADMINISTRATION FOR THE FISCAL YEAR ENDED JUNE 30, 2018 ATTACHMENT A

27 INDEPENDENT ACCOUNTANT S REPORT ON APPLYING AGREED-UPON PROCEDURES To the Administrative and Finance Committee and Board of Directors of Central Contra Costa Transit Authority The Federal Transit Administration (FTA) has established the following standards with regard to the data reported to it in the Federal Funding Allocation Statistics Form (FFA 10) of the Central Contra Costa Transit Authority s (the Authority) annual National Transit Database (NTD) report: A system is in place and maintained for recording data in accordance with NTD definitions. The correct data are being measured and no systematic errors exist. A system is in place to record data on a continuing basis, and the data gathering is an ongoing effort. Source documents are available to support the reported data and are maintained for FTA review and audit for a minimum of three years following FTA s receipt of the NTD report. The data are fully documented and securely stored. A system of internal controls is in place to ensure the data collection process is accurate and that the recording system and reported comments are not altered. Documents are reviewed and signed by a supervisor, as required. The data collection methods are those suggested by FTA or otherwise meet FTA requirements. The deadhead miles, computed as the difference between the reported total actual vehicle miles data and the reported total actual VRM data, appear to be accurate. Data are consistent with prior reporting periods and other facts known about transit agency operations. We have performed the procedures to the Federal Funding Allocation (FFA) 10 described in Attachment A. Such procedures, which were agreed to by Central Contra Costa Transit Authority (the Authority) and specified by the FTA in the Declarations section of the 2018 NTD Policy Manual, were applied solely to assist you in evaluating whether FAX complied with the standards described in the second paragraph of this report and that the information included in the NTD report and that the FFA-10 for the fiscal year ended June 30, 2018 is presented in conformity with the requirements of the Uniform System of Accounts (USOA) and records and Reporting System; Final Rule, as specified in Section 49 Code of Federal Regulations (CFR) Part 630, Federal Register, dated January 15, 1993, and as presented in the 2018 NTD Policy Manual. The Authority s management is responsible for the compliance with those standards. The sufficiency of these procedures is solely the responsibility of those parties specified in the report. Consequently, we make no representation regarding the sufficiency of the procedures described in Attachment A either for the purpose for which this report has been requested or for any other purpose. ATTACHMENT A

28 The procedures and associated findings are described in Attachment A. This agreed-upon procedures engagement was conducted in accordance with attestation standards established by the American Institute of Certified Public Accountants. We were not engaged to, and did not, conduct an audit or review, the objective of which would be the expression of an opinion or conclusion, respectively, on the accounting records as of fiscal year ended June 30, Accordingly, we do not express such an opinion or conclusion. Had we performed additional procedures, other matters might have come to our attention that would have been reported to you. This report is intended solely for the information and use of management of the Authoirty and the FTA and is not intended to be, and should not be, used by anyone other than those specified parties. BROWN ARMSTRONG ACCOUNTANCY CORPORATION Bakersfield, California, 2018 ATTACHMENT A

29 CENTRAL CONTRA COSTA TRANSIT AUTHORITY NATIONAL TRANSIT DATABASE REPORTING ATTACHMENT A AGREED UPON PROCEDURES FOR THE FISCAL YEAR ENDED JUNE 30, 2018 The procedures described below, which are referenced in order to correspond to the 2017 National Transit Database (NTD) Policy Manual procedures, were applied separately to each of the information systems used to develop the reported actual vehicle revenue miles, passenger miles traveled, and operating expenses of the Central Contra Costa Transit Authority (the Authority) for the year ended June 30, 2018, for the Motor Bus Service Directly Operated (MBDO) and Demand Response Purchased Transportation (DRPT). Our results and findings are as follows: A. Obtain and read a copy of written system procedures for reporting and maintaining data in accordance with NTD requirements and definitions set forth in 49 Code of Federal Regulations (CFR) Part 630, Federal Register, dated January 15, 1993, and as presented in the 2018 NTD Policy Manual. If there are no procedures available, discuss the procedures with the personnel assigned with the responsibility for supervising the NTD data preparation and maintenance. Result: We discussed procedures related to the system for reporting and maintaining data in accordance with the NTD requirements and definitions set forth in 49 CFR Part 630, Federal Register, dated January 15, 1993, and as presented in the 2018 NTD Policy Manual with the personnel assigned with the responsibility of supervising the preparation and maintenance of NTD data. No exceptions were noted as a result of applying this procedure. B. Discuss the procedures (written or informal) with the personnel assigned with the responsibility for supervising the preparation and maintenance of NTD data to determine: The extent to which the Authority followed the procedures on a continuous basis, and Whether Authority personnel believe such procedures result in accumulation and reporting of data consistent with NTD definitions and requirements set forth in 49 CFR Part 630, Federal Register, dated January 15, 1993, and as presented in the 2018 NTD Policy Manual. Result: We discussed with various personnel the procedures noted in Procedure A above to determine whether the Authority continuously follows the procedures on an ongoing basis and that the procedures result in the accumulation and reporting of data consistent with the NTD requirements and definitions as set forth in the Uniform System of Accounts (USOA) and Records and Reporting System; Final Rule, and specified in the 49 CFR Part 630, Federal Register, dated January 15, 1993, and the most recent 2018 NTD Policy Manual. No exceptions were noted as a result of applying this procedure. C. Ask these same personnel about the retention policy that the Authority follows as to source documents supporting NTD data reported on the Federal Funding Allocation Statistics Form (FFA 10). Result: We noted that the retention policy that is followed by the Authority regarding source documents supporting the FFA 10 data reported are retained for a minimum of three years by the Authority. In addition, we noted that the Authority maintains the computer files more than three years depending on the need of historical data. No exceptions were noted as a result of applying this procedure. ATTACHMENT A

30 D. Based on a description of the Authority s procedures from Procedures A and B above, identify all the source documents that the Authority must retain for a minimum of three years. For each type of source document, select three months out of the year and determine whether the document exists for each of these periods. Result: We identified the source documents that are to be retained by the Authority for a minimum of three years. We randomly selected three months out of the fiscal year ended June 30, 2018, September 2017, January 2018, and April 2018, and verified that each type of source document existed for each of these periods. No exceptions were noted as a result of applying this procedure. E. Discuss the system of internal controls. Inquire whether separate individuals (independent of the individuals preparing source documents and posting data summaries) review the source documents and data summaries for completeness, accuracy, and reasonableness and how often these individuals perform such reviews. Result: We discussed the system of internal control with personnel responsible for supervising and maintaining the NTD data. The method is mostly automated with a few manual procedures. We determined that individuals preparing source documents were independent of individuals posting data summaries, reviewing the source documents, and summarizing data for completeness, accuracy, and reasonableness. No exceptions were noted as a result of applying this procedure. F. Select a random sample of the source documents and determine whether supervisors signatures are present as required by the system of internal controls. If supervisors signatures are not required, inquire how personnel document supervisors reviews. Result: As noted above, the method is mostly automated. As such, there are no physical signatures documenting the supervisors review and approval of the source documents. The software utilized automatically accumulates the data from the Clever Devices Automatic Passenger Counter on each vehicle. Monthly reports are prepared for the Operating and Scheduling Committee and are reviewed by management electronically, as allowed by the 2018 NTD Policy Manual. Approval is given by authorizing the posting of the monthly data to NTD. No exceptions were noted as a result of applying this procedure. G. Obtain the worksheets used to prepare the final data that the Authority transcribes onto the Federal Funding Allocation Statistics Form. Compare the periodic data included on the worksheets to the periodic summaries prepared by the transit agency. Test the arithmetical accuracy of the summaries. Result: We obtained from the Authority s year-end cumulative reports that are used to prepare the FFA 10. We compared the prior year data to the current year data and investigated any changes over 10%. We also compared the source documents to the year-end cumulative report (Form S-10). In addition, we recalculated summarizations of supporting documentation which were tested in (D) above. During our review of the Matrix in comparison to the FFA-10, we noted a difference between the Matrix and the FFA-10, the error was a result of a typing error. The Authority corrected the error and resubmitted the data. H. Discuss the procedure for accumulating and recording passenger miles traveled (PMT) data in accordance with NTD requirements with the Authority s staff. Inquire whether the procedure is one of the methods specifically approved in the 2018 NTD Policy Manual. Result: During fiscal year 2018, the Authority used the procedure of an estimate of passenger miles traveled (PMT) based on statistical sampling, meeting FTA s 95% confidence and +10% precision requirements based on a qualified statistician s determined procedure. No exceptions were noted as a result of applying this procedure. ATTACHMENT A

31 I. Discuss with the Authority s staff (the auditor may wish to list the titles of the persons interviewed) the Authority s eligibility to conduct statistical sampling for PMT data every third year. Determine whether the Authority meets NTD criteria that allow transit agencies to conduct statistical samples for accumulating PMT data every third year rather than annually. Specifically: According to the 2010 Census, the public transit agency serves an urbanized area (UZA) with a population less than 500,000. The public transit agency directly operates fewer than 100 revenue vehicles in all modes in annual maximum revenue service (VOMS) (in any size UZA). Service purchased from a seller is included in the transit agency s NTD report. For transit agencies that meet one of the above criteria, review the NTD documentation for the most recent mandatory sampling year (2017) and determine that statistical sampling was conducted and meets the 95% confidence and ± 10% precision requirements. Determine how the transit agency estimated annual PMT for the current report year. Result: For MBDO, the Authority uses an alternative sampling technique, which is a statistically valid technique, other than 100 percent count, which was certified by a qualified statistician in 2009 when the Authority was testing the method to ensure it met the mandated accuracy and precision levels. We reviewed the certification of the statistician and determined that the individual was qualified and had the proper credentials. We also ensured that the statistician certified that the Authority s alternative technique used the minimal 95% confidence and +10 precision requirements for estimating boarding and passenger miles. We also obtained an understanding of how the Authority collects data, software utilized, and the estimation process. No exceptions were noted as a result of applying this procedure. For DRPT, the Authority does not use estimates, but rather uses the information collected by LINK, the service purchase seller. This data is derived from driver counts and data generated from Trapeze. The information from the Purchase Services Seller is included on the NTD report. No exception noted. J. Obtain a description of the sampling procedure for estimation of PMT data used by the transit agency. Obtain a copy of the transit agency s working papers or methodology used to select the actual sample of runs for recording PMT data. If the transit agency used average trip length, determine that the universe of runs was the sampling frame. Determine that the methodology used to select specific runs from the universe resulted in a random selection of runs. If the transit agency missed a selected sample run, determine that a replacement sample run was random. Determine that the transit agency followed the stated sampling procedure. Result: We obtained a description of the sampling procedure for estimation of PMT data used by the Authority. We obtained a copy of the Authority s working papers and methodology used to select the actual sample of runs for recording PMT data. We determined that the Authority followed the stated sampling procedure. No exceptions were noted as a result of applying this procedure. K. Select a random sample of the source documents for accumulating PMT data and determine that the data are complete (all required data are recorded) and that the computations are accurate. Select a random sample of the accumulation periods and recompute the accumulations for each of the selected periods. List the accumulations periods that were tested. Test the arithmetical accuracy of the summary. Result: We randomly selected three months, September 2017, January 2018, and April We obtained the source documents for accumulating PMT data, determined they were complete, and recomputed the accumulation periods. During our review of the Fixed Route Reports, we noted the data for the month of January 2018 was entered incorrectly on the MBDO report. Per discussion with the Authority, the discrepancy was due to a typing error and was corrected on the MBDO. In addition, we tested a sample of manual routes that are not tracked by the Ridecheck software. We randomly selected trip cards for the months of September 2017, January 2018, and April No exceptions were noted as a result of applying this procedure. ATTACHMENT A

32 L. Discuss the procedures for systematic exclusion of charter, school bus, and other ineligible vehicle miles from the calculation of actual vehicle revenue miles with transit agency staff and determine that they follow the stated procedures. Select a random sample of the source documents used to record charter and school bus mileage and test the arithmetical accuracy of the computations. Result: We discussed the procedures for systematic exclusion of charter, school bus, and other ineligible vehicle miles from the calculation of vehicle revenue miles with the Authority staff and determined that stated procedures were not applicable as the Authority does not provide a charter or school bus service. M. For actual vehicle revenue mile (VRM) data, document the collection and recording methodology and determine that deadhead miles are systematically excluded from the computation. This is accomplished as follows: If actual VRMs are calculated from schedules, document the procedures used to subtract missed trips. Select a random sample of the days that service is operated, and recompute the daily total of missed trips and missed VRMs. Test the arithmetical accuracy of the summary. If actual VRMs are calculated from hubodometers, document the procedures used to calculate and subtract deadhead mileage. Select a random sample of the hubodometer readings and determine that the stated procedures for hubodometer deadhead mileage adjustments are applied as prescribed. Test the arithmetical accuracy of the summary of intermediate accumulations. If actual VRMs are calculated from vehicle logs, select random samples of the vehicle logs and determine that the deadhead mileage has been correctly computed in accordance with FTA definitions. Result: We discussed with personnel the procedures for the collection and recording of VRM data and noted that VRMs are calculated upon inception of the route based on the distance between the first stop and last stop, including deadhead miles. We noted that the scheduled deadhead miles are systematically excluded to calculate VRMs. Furthermore, daily trip sheets are used to subtract missed trips and unscheduled deadhead miles. We also discussed the accumulation of VRMs for Demand Response Purchased Transportation (DRPT). We noted that VRMs for DRPT are accumulated and reported by the respective contractors through trip sheets and monthly ridership worksheets by route. These schedules are submitted by the contractors and are reviewed for clerical accuracy by Authority personnel. We recalculated the VRMs and agreed the total VRMs to the Authority s Month-End Ridership Summary report for a sample of trips in the months of September 2017, January 2018, and April No exceptions were noted as a result of applying this procedure. N. For rail modes, review the recording and accumulation sheets for actual VRMs and determine that locomotive miles are not included in the computation. Result: We inquired of personnel the procedures in which the Authority accumulates actual VRMs for rail modes. We noted that the Authority does not provide such service. Therefore, this procedure was not applicable. O. If fixed guideway or High Intensity Bus directional route miles (FG or HIB DRM) are reported, interview the person responsible for maintaining and reporting NTD data whether the operations meet the FTA definition of fixed guideway (FG) or High Intensity Bus (HIB) in that the service is: Rail, trolleybus (TB), ferryboat (FB), or aerial tramway (TR); or Bus (Mode: Bus (MB), Commuter Bus (CB), or Bus Rapid Transit (RB)) service operating over exclusive or controlled access rights-of-way (ROW); and Access is restricted; Legitimate need for restricted access is demonstrated by peak period level of service D or worse on a parallel adjacent highway; and ATTACHMENT A

33 Restricted access is enforced for freeways; priority lanes used by other high occupancy vehicles (HOV) (i.e., vanpools (VP), carpools) must demonstrate safe operation; Result: We inquired of personnel the procedures in which the Authority reports VRMs, passenger miles, and operating expenses for fixed guideways segments. We noted that the Authority does not provide such services. Therefore, this procedure was not applicable. P. Discuss the measurement of FG and HIB DRM with the person reporting NTD data and determine that the he or she computed mileage in accordance with the FTA definitions of FG/HIB and DRM. Inquire of any service changes during the year that resulted in an increase or decrease in DRMs. If a service change resulted in a change in overall DRMs, recompute the average monthly DRMs, and reconcile the total to the FG/HIB DRM reported on the Federal Funding Allocation Statistics Form. Result: We inquired of personnel the procedures in which the Authority measures fixed guideway direction route miles (DRMs). We noted that the Authority does not provide such services. Therefore, this procedure was not applicable. Q. Inquire if any temporary interruptions in transit service occurred during the report year. If these interruptions were due to maintenance or rehabilitation improvements to a FG segment(s), the following apply: Report DRMs for the segment(s) for the entire report year if the interruption is less than 12 months in duration. Report the months of operation on the FG/HIB segments form as 12. The transit agency should document the interruption. If the improvements cause a service interruption on the FG/HIB DRMs lasting more than 12 months, the transit agency should contact its NTD validation analyst to discuss. The FTA will make a determination on how to report the DRMs. Result: We inquired of personnel the procedures in which the Authority measures fixed guideway directional route miles through the use of maps or retracing routes. We noted that the Authority does not provide such services. Therefore, this procedure was not applicable. R. Measure FG/HIB DRM from maps or by retracing route. Result: We inquired of personnel whether other public transit agencies operate service over the same fixed guideway (FG) as the Authority. We noted that the Authority does not provide such service. Therefore, this procedure was not applicable. S. Discuss whether other public transit agencies operate service over the same FG/HIB as the transit agency. If yes, determine that the transit agency coordinated with the other transit agency (or agencies) such that the DRMs for the segment of FG/HIB are reported only once to the NTD on the Federal Funding Allocation Form. Each transit agency should report the actual VRM, PMT, and operating expense (OE) for the service operated over the same FG/HIB. Result: We inquired of personnel the procedures for revenue service for each fixed guideway segment. We noted that the Authority does not provide such service. Therefore, this procedure was not applicable. T. Review the FG/HIB segments form. Discuss the Agency Revenue Service Start Date for any segments added in the 2017 report year with the persons reporting NTD data. This is the commencement date of revenue service for each FG/HIB segment. Determine that the date reported is the date that the agency began revenue service. This may be later than the Original Date of Revenue Service if the transit agency is not the original operator. If a segment was added for the 2017 report year, the Agency Revenue Service Date must occur within the transit agency s 2017 fiscal year. Segments are grouped by like characteristics. Note that for apportionment purposes, under the State of Good Repair ( 5337) and Bus and Bus Facilities ( 5339) programs, the 7-year age requirement for fixed guideway/high Intensity Bus segments is based on the ATTACHMENT A

34 report year when the segment is first reported by any NTD transit agency. This pertains to segments reported for the first time in the current report year. Even if a transit agency can document an Agency Revenue Service Start Date prior to the current NTD report year, the FTA will only consider segments continuously reported to the NTD. Result: We inquired of personnel the procedures for revenue service for each fixed guideway segment. We noted that the Authority does not provide such service. Therefore, this procedure was not applicable. U. Compare operating expenses with audited financial data after reconciling items are removed. Result: We reconciled operating expenses presented to the audited financial statements. No exceptions were noted as a result of applying this procedure. V. If the transit agency purchases transportation services, interview the personnel reporting the NTD data on the amount of purchased transportation (PT)-generated fare revenues. The PT fare revenues should equal the amount reported on the Contractual Relationship form (Form B-30). Result: We compared the data reported on the Form B-30 to the purchased transportation fare revenues. No exceptions were noted as a result of applying this procedure. W. If the transit agency s report contains data for PT services and assurances of the data for those services are not included, obtain a copy of the Independent Auditor Statement (IAS-FFA) regarding data for the PT service. Attach a copy of the statement to the report. Note as an exception if the transit agency does not have an Independent Auditor Statement for the PT data. Result: This procedure is not applicable as assurances over the PT services data are included in Procedures A through V above. X. If the transit agency purchases transportation services, obtain a copy of the PT contract and determine that the contract specifies the public transportation services to be provided; the monetary consideration obligated by the transit agency or governmental unit contracting for the service; the period covered by the contract (and that this period overlaps the entire, or a portion of, the period covered by the transit agency s NTD report); and is signed by representatives of both parties to the contract. Interview the person responsible for retention of the executed contract, and determine that copies of the contracts are retained for three years. Result: We obtained copies of the purchased transportation contracts and noted that all contracts specified the specific mass transportation services to be provided; specified the monetary consideration obligated by the Authority; specified the period covered by the contract and that this period is the same as, or a portion of, the period covered by the Authority s NTD report; and signed by representatives of both parties to the contract. We determined that executed contracts are maintained for a minimum of three years. No exceptions were noted as a result of applying this procedure. Y. If the transit agency provides service in more than one UZA, or between an UZA and a non-uza, inquire of the procedures for allocation of statistics between UZAs and non-uzas. Obtain and review the FG segment worksheets, route maps, and urbanized area boundaries used for allocating the statistics, and determine that the stated procedure is followed and that the computations are correct. Result: We inquired of personnel whether the Authority provides services in more than one UZA, or between a UZA and a non-urbanized area (non-uza). This procedure is not applicable as the Authority does not provide services in more than one UZA. ATTACHMENT A

35 Z. Compare the data reported on the Federal Funding Allocation Statistics Form to data from the prior report year and calculate the percentage change from the prior year to the current year. For actual VRM, PMT, or OE data that have increased or decreased by more than 10%, or FG DRM data that have increased or decreased, interview transit agency management regarding the specifics of operations that led to the increases or decreases in the data relative to the prior reporting period. Result: We compared the data reported on the FFA - 10 to comparable data for the prior report year and calculated the percentage change from the prior year to the current year. For VRM, passenger mile, or operating expense data that have increased or decreased by more than 10 percent, we inquired with the Authority management regarding the specifics of operations that led to the increases or decreases in the data relative to the prior reporting period. No exceptions were noted as a result of applying this procedure. AA. The auditor should document the specific procedures followed, documents reviewed, and tests performed in the work papers. The work papers should be available for FTA review for a minimum of three years following the NTD report year. The auditor may perform additional procedures, which are agreed to by the auditor and the transit agency, if desired. The auditor should clearly identify the additional procedures performed in a separate attachment to the statement as procedures that were agreed to by the transit agency and the auditor but not by the FTA. Result: We have documented the specific procedures followed, documents reviewed, and tests performed in the work papers. The work papers are available for FTA review for a minimum of three years following the NTD report year. No exceptions were noted as a result of applying this procedure. ATTACHMENT A

36 CENTRAL CONTRA COSTA TRANSIT AUTHORITY NATIONAL TRANSIT DATABASE REPORTING INDEPENDENT ACCOUNTANT S REPORT ON APPLYING AGREED-UPON PROCEDURES FOR FINANCIAL DATA FEDERAL TRANSIT ADMINISTRATION FOR THE FISCAL YEAR ENDED JUNE 30, 2018 ATTACHMENT B

37 INDEPENDENT ACCOUNTANT S REPORT ON APPLYING AGREED-UPON PROCEDURES To the Administrative and Finance Committee and Board of Directors of Central Contra Costa Transit Authority and the Federal Transit Management We have performed the procedures enumerated below, on the application of the requirements of the Federal Transit Administration (FTA) as set forth in its applicable National Transit Database (NTD) Uniform System of Accounts (USOA) by the Central Contra Costa Transit Authority (the Authority) for the fiscal year ended June 30, Such procedures, which were agreed to by the management of the Authority and the FTA, were performed to assist the Authority and the FTA in determining conformance with USOA requirements based on the following assertion by the Authority s management: The accounting system from which the NTD reports for the fiscal year ended June 30, 2018, were derived, uses the accrual basis of accounting and is directly translated, using a clear audit trail, to the accounting treatment and categories specified by the USOA. The Authority s management is responsible for conformance with the requirements described above. The sufficiency of these procedures is solely the responsibility of the parties specified in this report. Consequently, we make no representation regarding the sufficiency of the procedures described below either for the purpose for which this report has been requested or for any other purpose. This report describes our procedures and findings applied to the data reported to the FTA. Our procedures were applied to the information system used to develop the reported operating revenues and expenses for the Authority for the year ended June 30, 2018, for each of the following Modes: Motor Bus service directly operated (MBDO) Demand Response purchased transportation (DRPT) The agreed-upon procedures and associated findings are as follows: 1. Procedure: NTD Crosswalk a. Obtain the following NTD Reporting Forms prepared by management for the year ended June 30, 2018: NTD Form F-10, Sources of Funds Funds Expended and Funds Earned (USOA Section 2) NTD Form F-20, Uses of Capital (USOA Section 3) NTD Form F-30, Operating Expenses (USOA Section 4, 5, and 6 and Appendix A) NTD Form F-40, Operating Expenses Summary NTD Form F-60, Financial Statement ATTACHMENT B

38 b. Obtain the reconciliation documentation management prepares (referred to as the crosswalk throughout this report) to reconcile the chart of accounts, general ledger, and/or trial balance and other supporting documents such as Excel spreadsheets (collectively referred to as the accounting system) to the respective NTD Reporting Forms identified above. c. Inquire of management as to whether the crosswalk obtained in procedure 1.b is supported by the accounting system. d. For a transit agency that is part of a larger reporting entity, inquire of management as to whether the crosswalk includes the full cost of providing transit service, including costs incurred by the larger reporting entity to specifically support the agency s transit service. e. Inspect the crosswalk to determine that it incorporates NTD reporting using the applicable modes and types of service identified in the bulleted list below: Sources of Funds, Form F-10 Funding sources, passenger fares by mode and service type, passenger fares by passenger paid or by organization paid fares, revenue object class, and funds expended on operations and capital fund types Uses of Capital, Form F-20 - Type of use, asset classifications, and modes and service types Operating Expenses, Form F-30 - Modes, service types, object classes and functions Operating Expenses Summary, Form F-40 - Expense reconciling items Financial Statement, Form F-60 - Current assets, non-current assets, deferred outflows of resources, current liabilities, non-current liabilities, and deferred inflows of resources. Findings: No exceptions were found as a result of this procedure. 2. Procedure: Accrual Accounting a. Obtain the most recent audited financial statements that include the transit agency and inspect the notes to the financial statements to determine whether the accrual basis of accounting was used. b. Inquire of management as to whether the accrual basis of accounting has continued to be used since the last audited reporting period and that it is used for NTD reporting in the current period. c. If the notes to the financial statements indicate that an accrual basis of accounting is not being used, or the results of the inquiry to management in procedure 2.b indicate the accrual basis of accounting is not being used in the current period, inspect the crosswalk to determine that the transit agency made adjustments to convert to an accrual basis for NTD reporting. Findings: No exceptions were found as a result of this procedure. 3. Procedure: Sources of Funds (Form F-10) a. Trace and agree total sources of funds from Form F-10 to revenue reported in the accounting system using the crosswalk. b. Inspect the crosswalk for a written reconciliation between total revenues reported in the audited financial statements or the accounting system and the total revenues reported on Form F-10. c. Trace and agree the two largest directly generated fund passenger fare revenue modes (all service types) from Form F-10 to the accounting system. d. Trace and agree the largest revenue object class (other than passenger fares) in the following major categories of funds from Form F-10 to the accounting system: (1) Local Government; (2) State Government; (3) Federal Funds; and (4) Other Directly Generated Funds (i.e., 4100 and 4200 combined). ATTACHMENT B

39 e. Inspect the crosswalk to determine that it identifies, evaluates, and classifies financial transactions into categories of funds expended on operations and funds expended on capital (USOA Section 2) for the reporting year. Findings: No exceptions were found as a result of this procedure. 4. Procedure: Uses of Capital (Form F-20) a. Obtain accounting system documentation on capital asset additions for the reporting period. b. Trace and agree total uses of capital from Form F-20 to the crosswalk reconciliation of total capital asset additions. c. Trace and agree types of use (existing service and expansion of service) from Form F-20 to the crosswalk or other supporting documentation reflecting the nature of the uses of capital. d. Trace and agree asset classifications (guideway, revenue vehicles, etc.) from Form F-20 to the crosswalk or other documentation reflecting the assets classes of capital additions. e. For the largest mode/service type, trace and agree the type of use classification and asset classification from Form F-20 to the crosswalk or other documentation reflecting the uses of capital. f. If capital projects support multiple modes/types of services or and/or asset classifications, inquire of management as to whether management reported the use of capital considering the predominant use rules as described in the Predominant Use section of the 2018 NTD Policy Manual. g. If capital projects involve: 1) Rehabilitation/Reconstruction/Replacement/Improvement for Existing Service; and 2) Expansion of Service; inquire of management as to whether project costs were allocated between the two project purposes and whether such allocation was documented in the crosswalk or other supporting documentation. Findings: No exceptions were found as a result of this procedure. 5. Procedure: Operating Expenses (Form F-30) a. For the two largest modes/type of services, trace and agree functions (vehicle operations, vehicle maintenance, etc.) from Form F-30 to the crosswalk or other written documentation of functional expenses. b. For the two largest modes/type of services, trace and agree object classes (natural expenses) from Form F-30 to the crosswalk or other written documentation of object class categories. c. If management allocated shared operating expenses, inquire of management as to whether (1) the operating expenses are split between direct and shared costs; (2) shared costs were allocated across modes, services types and functions, (3) the allocation was documented in the crosswalk or other supporting documentation; and (4) the driving variables used are updated annually. Findings: No exceptions were found as a result of this procedure. 6. Procedure: Operating Expenses Summary (Form F-40) a. Obtain total expenses from the accounting system for the reporting period. Trace and agree total expenses from Form F-40 to the accounting system using the crosswalk. ATTACHMENT B

40 b. Trace and agree the reconciling items appearing on Form F-40 through the crosswalk to the accounting system. Findings: No exceptions were found as a result of this procedure. 7. Procedure: Financial Statement (Form F-60) a. Trace and agree (1) Current Assets; (2) Non-Current Assets; (3) Deferred Outflows of Resources; (4) Current Liabilities; (5) Non-Current Liabilities; and (6) Deferred Inflows of Resources appearing on Form F-60 to the crosswalk or other supporting documentation. Findings: No exceptions were found as a result of this procedure. Restriction on Use This agreed-upon procedures engagement was conducted in accordance with attestation standards established by the American Institute of Certified Public Accountants. We were not engaged to, and did not, conduct an examination or review, the objective of which would be the expression of an opinion or conclusion, respectively, on the Authority s conformance with the requirements described above, for the fiscal year ended June 30, Accordingly, we do not express such an opinion or conclusion. Had we performed additional procedures, other matters might have come to our attention that would have been reported to you. This report is intended solely for the information and use of management of the Authority and the FTA and is not intended to be, and should not be, used by anyone other than these specified parties. BROWN ARMSTRONG ACCOUNTANCY CORPORATION Bakersfield, California, 2018 ATTACHMENT B

41 To: Administration and Finance Committee Date: 12/19/2018 From: Ruby Horta, Director of Planning & Marketing Reviewed by: SUBJECT: Route 99X Promotion Background: Route 99X is a new route that began service in August The route connects the Martinez Amtrak station to North Concord BART via the Pacheco Transit Hub. The route was designed to serve three primary markets: passengers transferring from Capitol Corridor trains arriving from Solano, Yolo, and Sacramento counties; eastern Contra Costa county residents who work in Martinez, which has several county offices; and Martinez residents living in the medium density multifamily housing along Morello Ave and Arnold Dr. Promotion with 511 Contra Costa: During the first three months of operation, ridership on the route has averaged about 700 passengers per month. In an effort to increase ridership, staff is planning to partner with 511 Contra Costa to run a promotional campaign. As part of this promotion, rides on the route would be free for the month of February. 511 has agreed to reimburse County Connection for fares, and staff is working with legal counsel to develop a formal agreement. Recommendation: For information only. Financial Implications: None. Costs associated with lost fare revenue would be reimbursed by 511 Contra Costa.

42 To: A&F Committee Date: January 2, 2019 From: William Churchill, Assistant General Manager of Admn. Reviewed by: SUBJECT: Contra Costa Transportation Authority s Accessible Transportation Strategic (ATS) Plan Background: Contra Costa Transit Authority (CCTA) was awarded a Caltrans Sustainable Communities Transportation Planning grant to study the potential for a coordinated transportation system for seniors and persons with disabilities. CCTA is calling the new study the Accessible Transportation Strategic (ATS) Plan. The CCTA board authorized their staff at the September 19, 2018 board meeting to reach out to all county public transit operators, the four Regional Transportation Planning Committees (RTPC s) as well as a number of other stakeholders to participate in the study. Additionally, CCTA has requested that each participant in the study sign a Memorandum of Understanding (MOU) prior to the commencement of the study. CCTA has requested each participant review the draft MOU and provide feedback prior to the end of January (Please see attached draft MOU) Staff Analyses of MOU: County Connection staff forwarded the draft MOU to legal for review and has conducted an initial evaluation of the document. Staff has a couple of concerns regarding the document that has the potential to significantly alter the way County Connection provides ADA paratransit services to Central County. Firstly, the document requires the Board to sign off on the final recommendations of the study prior to the study having been completed. Should the study recommend a new Authority be developed that provides ADA services for the whole County, then the MOU would require County Connection use the new entity to provide complimentary paratransit services relinquishing a role it has served since Another concern of significance is the apparent combining of senior s (ambulatory or not) into the definition of Accessible Transportation, significantly broadening the scope of the population transportation services would be provided for. Currently County Connection provides transportation for persons with disabilities as defined by the Federal Transportation Administration (FTA). By adding ambulatory seniors to the group of eligible riders the potential growth in passengers could quickly wipe out existing funding streams.

43 The MOU in its current form does not recognize that each of the groups to be studied (seniors, persons with disabilities and low income individuals) each have a specific set federal regulations that govern how transportation services are to be provided. Summary: While County Connection staff supports CCTA and Contra Costa County s efforts in the development of a centralized and consolidated transportation program for seniors and persons with disabilities, staff also maintains that it is imperative the Authority maintain autonomy and control over decisions of how to provide paratransit services to our community. It may make sense to contract out paratransit services with a potential consolidated transportation provider in the future, then again it may not be financially or operationally advantageous. County Connection should remain in control of decisions regarding how, when and where required paratransit services are to be provided. Staff would like to engage the board in a robust discussion and receive feedback and recommendations in the development of a letter of response to CCTA regarding the proposed MOU. Action Requested: Staff requests the committee forward this memo to the board for discussion, feedback and direction in responding to CCTA s request for feedback regarding the attached MOU prior to the end of January Financial Implications: In the short term the only financial implication will be the investment of County Connection staff time to participate in the study. Long term financial implications are unknown since it is impossible to anticipate the results of the study and the potential expenses associated with using a different entity to provide paratransit services. Attachments: Draft Memorandum of Understanding (MOU)

44 DRAFT FOR REVIEW/COMMENT CCTA AGREEMENT ##.##.## MEMORANDUM OF UNDERSTANDING Between THE CONTRA COSTA TRANSPORTATION AUTHORITY AND LOCAL AGENCIES & ORGANIZATIONS FOR THE ACCESSIBLE TRANSPORTATION STRATEGIC PLAN (Funded by Caltrans: Sustainable Communities - Transportation Planning Grant) 1. Introduction This MEMORANDUM OF UNDERSTANDING (hereafter MOU ), effective as of ******** ##, 2018, is meant to establish a common understanding of: 1) the need for Contra Costa Accessible Transportation Strategic (ATS) Plan (hereafter ATS Plan ), 2) the procedures for the conduct of the ATS Plan, and 3) the collaborative intent of the ATS Plan and parties to this MOU. Parties to this MOU include the Contra Costa Transportation Authority (hereafter CCTA ), a local transportation authority, County of Contra Costa, a political subdivision of the State of California (hereafter COUNTY ), and the following LOCAL AGENCY PARTNERS: [TBD] The ATS Plan: 1) is an assessment of transportation and transportation related services to seniors and persons with disabilities, 2) addresses a diverse array of impacted organizations, 3) implements local and regional plans and policies, 4) is necessary because services to this vulnerable population are being compromised by rising costs, demographic shifts/decreasing public health resulting in increased demand, 5) is intended to address a system that developed unsystematically over a long time frame, and 6) is an implementation action 1 in CCTA s adopted 2017 Countywide Comprehensive Transportation Plan. The need for the ATS Plan and this MOU is further magnified by the intersection of public transit, public health, social service, civil rights interests and philosophies held by the entities and persons using and providing accessible transportation services. It is this complex intersection that results in diffused leadership and authority that further confirms the need for this MOU. The ATS Plan has three broad tasks: 1) Study of existing, individual programs with recommendations. 2) Study of alternative countywide system designs. 3) Development of a phased implementation plan. At every stage, the ATS Plan will include expansive outreach responsive to, and designed for, the subject population CCTA CTP: Table 5-1 Initiate the Accessible Transportation Service Strategic Plan To ensure that services are delivered in a coordinated system

45 2. Definitions A. Accessible Transportation: An umbrella term used to describe the broad range of transportation related services typically provided to seniors and persons with disabilities. For the purposes of this MOU and the ATS Plan, accessible transportation is defined as a range of transportation/transit and related supportive services such as; Americans with Disabilities Act (ADA) mandated public paratransit service, city/community transportation programs, transportation provided by private non-profits, mobility management programs, volunteer based transportation programs, travel training, as well as funding and governance mechanisms associated with the preceding activities. B. Subject Population: The ATS Plan addresses services to the most acutely disadvantaged and fragile communities, seniors and persons with disabilities. These populations are typically also low income. 3. MOU Purpose A. Structure: The system of accessible transportation in Contra Costa County has been described as developed organically with a lack of a structural platform being a major impediment to action 2. Given these characteristics, this MOU (and Oversight Structure referenced herein) provides a temporary structure and forum to more effectively conduct the ATS Plan. The ATS Plan Scope of Work includes a task, Establishment or designation of an organization and/or structure to act as advocate and administrator for this transit transportation sector on an ongoing basis which is intended to address the lack of a structural platform issue once the ATS Plan is complete. B. Understanding: This MOU is intended to ensure consistent understanding of the need for, and the intent of, the ATS Plan. This understanding should be consistent across the range of impacted agencies and organizations as well as across responsible staff and elected decision makers. C. Commitment: In response to the three previous, similar efforts in the past 3, this MOU establishes a commitment of the parties to take formal action relative to the final recommendations of the study as further described in the Understanding section below. 4. Recitals A. During the development of the Measure X Transportation Expenditure Plan (TEP) CCTA conducted substantial outreach and convened the Expenditure Plan Advisory Committee (EPAC) which identified Transportation for Seniors and People with Disabilities as a high priority category 4 in the TEP. B. CCTA and all member agencies (nineteen Cities and the County) unanimously approved the Measure X Transportation Expenditure Plan in Recognizing the aforementioned EPAC prioritization and testimony from advocates, the TEP included a requirement to conduct an Accessible Transportation Service Strategic Plan to ensure services are delivered in a coordinated system that maximizes both service delivery and efficiency.... C. In 2017, with Measure X failing to gain voter approval but recognizing the standing need to improve accessible transportation, CCTA approved the Countywide Comprehensive Transportation Plan which included the following actions, ensure that services are delivered in a coordinated system and Initiate the Accessible Transportation Service Strategic Plan as an implementation activity Contra Costa County Mobility Management Plan Contra Costa County Paratransit Plan, 2004 Contra Costa County Paratransit Improvement Study, 2013 Contra Costa County Mobility Management Study 4 2