PFP Advisors. Financial Planning For Everyone. 123 neat st. Anywhere, USA 12345

|

|

|

- Baldwin Dwayne Cooper

- 5 years ago

- Views:

Transcription

1 PFP Advisors Financial Planning For Everyone. PFP Advisors 123 neat st. Anywhere, USA 12345

2 1 Table of Contents PFP Advisors 2 Planning Process: 2 Fees: 3 Client Information and Summary 4 Current Financial Condition 7 College Funding Goal 10 Retirement Funding Goal 11 Real Estate Goals 12 S.W.O.T. Analysis 13 Budgetary Recommendations 13 Investment Recommendations 17 Tax Planning 18 Professional Referrals 19

3 2 Why We Exist: PFP Advisors was founded in 2018 and currently manages over $300 million for individuals and families. We measure our success based on our clients well being and overall satisfaction with our services. We are here to work hard for our clients so that they can spend their valuable time and energy focusing on the other important aspects of life. We Aim to Provide: -Clarity: by simplifying the often complex aspects of financial planning and educating clients along the way. -Confidence: by creating a plan that is unique to each individual, you can rest easy knowing that we are being very thoughtful when creating plans to help our clients reach their goals both financially as well as life goals. -Comfort: by addressing all of our clients goals and risks. As well as by making sure all tax, estate, insurance, and retirement aspects are being planned for. Planning Process: Our job as financial advisors is to look out for our client s best interests. We do this by following detailed steps to create a custom tailored plan for each client. We start by identifying what you value and what your goals are We then start to develop a plan to achieve your goals Next we implement the plan by aligning your financial resources with your goals and making changes Finally, we monitor the plan that has been set in place and make changed when necessary to ensure that we remain on target

4 3 Fees: We aim to be as inclusive as possible. However, we focus on serving individuals and families with investment assets of $1,000,000 and greater. We charge 1.00% of the first $1,000,000 that we manage with a minimum of $2,500 fee per quarter.

5 4 Personal Information Name Carl Berman Naomi Berman Birthday 02/13/ /24/1975 Age Marital Status Married Married SSN # Employer James Madison University Thomas Harrison Middle School Occupation Professor of Law Principal Address 1234 Market St 1234 Market St City Harrisonburg Harrisonburg State Virginia Virginia Dependents Name Relationship Birthdate Age Matthew Berman Son 04/17/ Sarah Berman Daughter 03/12/

6 Financial Information 5

7 6

8 7 Client Summary Carl and Naomi Berman are married and currently living in Harrisonburg, VA. Carl work as a Professor of Law at James Madison University and Naomi is a Principal at Thomas Harrison Middle School in Harrisonburg. They have two children, Matthew and Sarah (14 and 11, respectively). The Berman s have spent their past years traveling and enjoying their time in Virginia with their family. They own their family home in Harrisonburg but are hoping to someday purchase an additional home in the Historic District as well as a cabin in the Blue Ridge Mountains. One of the main goals for Naomi and Carl is to fully fund both Matthew and Sarah s college educations, as education is greatly important to the family. Another goal of the Berman s is to ensure they are both on track for their retirement. As well as to seek consultation regarding their insurance coverage and estate documentation. Financial Goals Funding Matthew and Sarah s Education Funding Carl and Naomi s Retirement Purchasing new home in Historic District Harrisonburg Purchasing cabin in Blue Ridge Mountains Current Financial Condition - Ratio Analysis The following analysis was created using the financial statements you have provided with us. Please note that this analysis is created using standardized benchmarks and is meant to provide a framework for our understanding of your financial condition. Emergency Fund Ratio: 4 ½ months Benchmark - 3 to 6 months This ratio tells us how many months of your non-discretionary, or obligatory expenses, you could cover given your current cash holdings. You could cover about 4 ½ months of these expenses, which is in the middle of the benchmark. However, we would like to see this increase to provide more of a safety net.

9 8 Current Ratio:.83 times Benchmark - 1 to 2 times The current ratio calculates how many times over, you could pay off your current debts if you had to use all of your current, most liquid assets. Right now, you re only able to cover about 83% of your current debts, which is below the benchmark. This is something we would like to work with you to increase as well. Housing Ratio One (Front-End Ratio): 12.5% Benchmark - 25% This ratio tells us what percentage of your income is going towards your housing costs (i.e. mortgage payments). The benchmark for this is to be spending less than 25% of your income on this, your family is spending just 12.5% on this - which is great! Housing Ratio Two (Back-End Ratio): 16.6% Benchmark - 36% This ratio analyzes the percentage of your income which is spent on paying off all debts, including your mortgage, car loan and credit card debt. You re currently spending about 16.6% of your income on these debts, which is far below the benchmark of 36% (or less). Debt to Assets Ratio: 25.4% This ratio analyzes what percentage of your assets are owned by your creditors. While we do not have a specific benchmark for this, ideally this ratio declines more and more with age. For your current ages, this is an appropriate place to be. Net Worth to Assets Ratio: 74.6% This ratio is the opposite of the previous ratio, it tells us what percentage of your assets are owned by you. Again, we do not have a specific benchmark, but we would like to see this continue to increase as you approach retirement.

10 9 Savings Rate: 3.1% Benchmark - Varies with age, approx. 10 to 13% The savings rate calculates the percentage of your annual income that you re saving each year. The benchmark for the savings rate is a minimum of 10-13%, but increases if savings is delayed. Your savings rate is below the benchmark, and is something we would really like to see increase. Investment Assets to Gross Pay: 3.9 times Benchmark - 16 to 20 times (at age 65) This ratio measures your progress towards saving for retirement by analyzing how much you have invested, compared to your income. The benchmark for this ratio is based at age 65, which would be times your gross pay, in invested assets. Since you re not 65 yet, it s okay that you aren t at this number; however, we would like to see this grow as you get closer to retirement. Summary of Ratio Analysis Where are you doing well? Housing Ratio One Housing Ratio Two Debt to Assets Ratio Net Worth to Assets Ratio Where should we focus on? Building up Emergency Fund Increasing Current Ratio Increasing Savings Rate Increasing Investment Assets to Gross Pay Ratio

11 10 College Funding One of your main goals was to fund Matthew and Sarah s college educations. We ve created several present value analysis to illustrate the different routes which we can take to help you fund this goal. The first scenario has assumed both Matthew and Sarah will live on campus for all four years of college. The second scenario funds them living on campus for two years, and then two years of just college tuition. Our final scenario funds two years of tuition at a community college, and two years at a university at full cost. We have used the following assumptions in our calculations. Please note that these are just that, assumptions and will vary depending on what specific university or college Matthew and Sarah attend. These are meant to provide an estimation of what savings are required to meet these goals. Full cost (per year) at an in-state university: $22,987 Tuition cost (per year) at an in-state university: $12,702 Community College tuition (per year): $4,508 Below we have included a table with the current levels of savings needed for both Matthew and Sarah s education fund. Matthew Berman (14) Sarah Berman (11) Total Savings Scenario One $81,445 $71,460 $152,905 Scenario Two $63,565 $61,235 $124,800 Scenario Three $48,100 $46,330 $94,430 We have also included the following graph to visually represent the costs for each child s education.

12 11 Currently, you do not have any savings or accounts dedicated for Matthew or Sarah s education funds - however, you do have the trading account with a balance of over $100,000 which would be a great start for their funds. We have included both investment and budgetary adjustments which will allow you to fully fund both of their educations, using our second analysis. Retirement Funding Another goal of yours was to be able to fund both of your retirements. As you enter retirement, your expenses start to change. For example, in retirement income taxes, commuting expenses and other work related expenses decline; whereas other expenses (such as health-care costs) tend to increase. While there are different methods used to calculate the amount of savings needed for ones retirement, we have opted to use the Wage Replacement method. This approach allows us to calculate a retirement income need, based on your current income. We feel that this is the most appropriate approach given that you are not close enough to retirement age, for us to fully calculate the specific expenses you will have. Similarly to our approach to College Funding, we have created three analyses for different wage replacement levels. Most people find that an 80% wage replacement is appropriate for them in retirement, however we have calculated what your savings needs will be for an 80%, 90% or 100% wage replacement (Scenarios One, Two and Three, respectively). We have used the following assumptions for our calculations:

13 12 Carl will retire at age 65 (19 years from 2018) Naomi will retire at age 65 (22 years from 2018) Carl and Naomi will both live to age 95 No Social Security * 7.5% return on investments *We have chosen to not calculate social security in our calculations. While we feel confident that you will receive some form of a social security benefit we would prefer a conservative estimate of your needed savings. The following table illustrates the current amount of savings needed for each scenario. Carl Berman (46) Naomi Berman (43) Total Savings Scenario One $822,205 $596,975 $1,419,180 Scenario Two $924,980 $624,475 $1,549,455 Scenario Three $1,027,760 $693,860 $1,721,620 Currently you have several investment accounts being utilized for your retirement savings, this includes both Carl and Naomi s 401(k) and IRA accounts. If you continue contributing just $7,500 annually you will not be able to fund your retirement, however we have some recommendations in both budgeting and investing that will allow you to fund your retirement at an 80% wage replacement (the most common). Real Estate Purchasing Aside from funding your retirement and your children s education, you had indicated you would like to make some upcoming real estate purchases. Firstly, you would like to purchase a home in the Historic District of Harrisonburg, VA as well as a small cabin in the nearby Blue Ridge Mountains. Through our research we have found the average price range for 2-4 bedroom homes in the Historic District. Currently, these cost between $250,000 and $450,000. We assumed that you would be interested in purchasing this home at the time of Carl s retirement (in 2037). Given that homes in this region have been appreciating (or rising in price) at about 3.0% per year, we have calculated the price of these homes in At that time, we these homes will most likely cost between $275,000 and $790,000. In regards to the cabin in the Blue Ridge Mountains we have found the price range for small (1-2 bedroom) cabins. Currently the price range is between $95,000 and $100,000 for smaller cabins, without additional acreage. Again we assumed that you would be likely

14 13 to purchase this in 2037, or around that time. Given the same 3.0% per year, price increase these cabins will cost between $104,000 and $175,000. Assuming that you would like to begin saving now for these goals, we are looking at a current savings amount between $345,000 - $550,000. With your current home value being $450,000, we could use this as the basis for funding these future purchases. However, we could also look at other options for funding such as rental income or a second mortgage if necessary. S.W.O.T Analysis Strengths 1. Stable income 2. Several great outcomes from the Ratio Analysis 3. Long timeline between now and retirement (19+ years) Weaknesses 1. Low emergency fund ratio, savings rate 2. Shorter timeline for education funding goal Opportunities 1. Alternative routes for education funding 2. Potential real estate income 3. Potential rental income 4. Potential phased retirement Threats 1. Insurance coverage 2. Job Loss or other major financial emergency Budgetary Recommendation In analyzing your goals, we have determined that currently you do not have enough savings to fully fund your goals without making some adjustments. However, by looking at your cash flow statement we see that there is an annual surplus of $37,497. By allocating this between funding Matthew and Sarah s education, and in conjunction with your current retirement contributions, you ll be able to reach both of your goals. We have separated these adjustments as they are related to each goal.

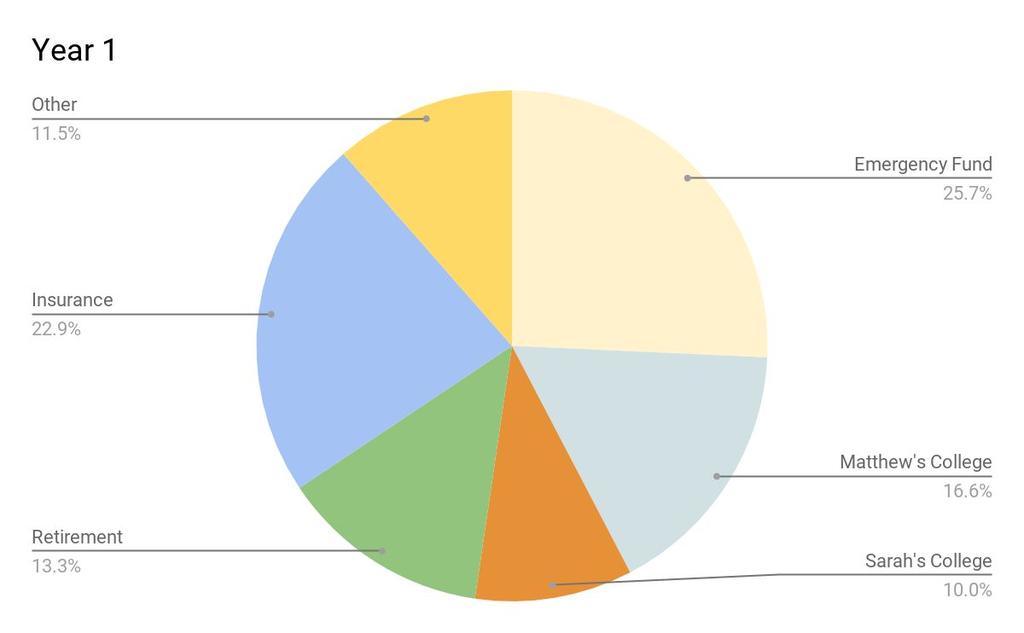

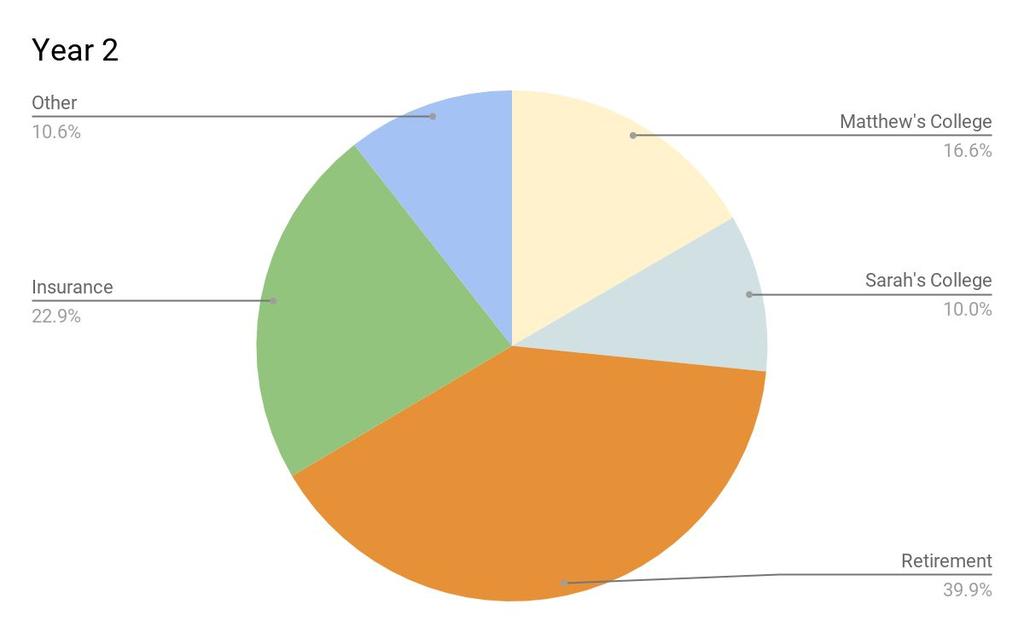

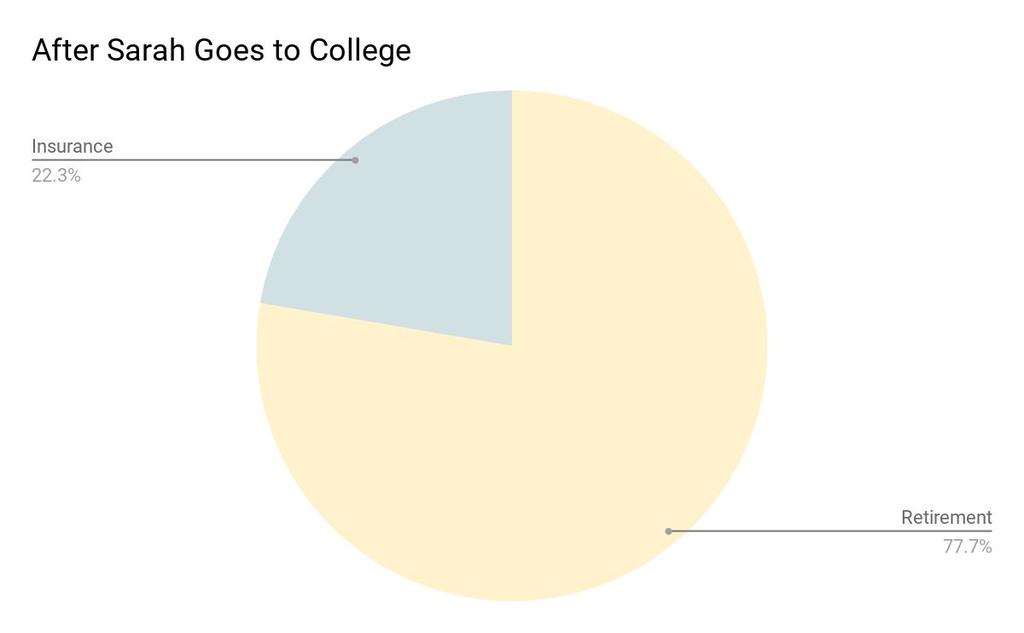

15 14 College Funding With Matthew heading off to school in just 4 years, we wanted to put a greater push to fund his education in these first few years. We ve divided the current trading account between the two kids, delegating $40,000 to Matthew and $30,000 to Sarah. We are able to place these into two, seperate trading accounts where we will be able to invest them. For the next four years, we will be contributing $6,250 annually to Matthew s account and $3,750 to Sarah s. By doing this, at the end of the four years Matthew will have enough to fund four years of tuition and two years of on-campus expenses at an in-state university. In the next two years, we will ramp up Sarah s savings to $9,500 per year. By the end of this she too will have enough in her account to fund four years of tuition and two years of on-campus expenses. Retirement Funding Since we have used the majority of the trading account to be put towards education funding, we are allocating the remaining account balance between your qualified assets. Utilizing the budgetary surplus again, we will allocate a graduating amount towards your retirement savings. This will be in addition to your annual contributions to Carl s 401(k). Your contributions would be scheduled to increase after the first year of working with us (once your emergency fund is at 6 months) and then again after Matthew and Sarah both have entered college. Once Carl retires there will be a major decrease in your household s spending on employment related taxes and these funds can then be contributed towards the retirement accounts. To further illustrate we have created the following diagrams that show how the annual budget surplus will be allocated in the next year, 4 years, 6 years and beyond. You will also note that in the first year we have allocated nearly $10,000 to your emergency fund. By doing this we can ensure that after this first year, you ll have 6 months in your emergency fund. We have also assumed a 7.5% return on investments in our calculations. This is a conservative estimate, and we will go into further detail in regards to your investment possibilities.

16 15

17 16

18 17 Investing for Goals By reviewing your financial statements, we re able to see that you have several accounts that you are currently utilizing to fund your goals. By having these accounts, you re already off to a good start. However, we would like to see these accounts do even more for you through investments. Investing can be great way to boost your annual savings as you work towards your goals. Before we delve into the details of investing and our suggestions for you, we d like to define several terms to help you best understand the world of investments. Asset: Property (Portfolios, savings, Home, Vehicles, etc.) Asset Allocation: Allocation of an investment portfolio across broad asset classes Rate of Return: Gain or loss over a specific period of time, expressed as a percent Inflation: Increasing of prices and decreasing of purchase power Risk: Potential fluctuation of asset worth Portfolio: range of investments Time Horizon: Amount of time an investor is expected to hold on to an investment before pulling from it. Next we d like to go over some of the different kind of assets we will be suggesting for you to invest in. Each different kind of asset has a different potential rate of return, but it also has a different risk. In general, the greater the potential rate of return, the greater the risk of the investment. Risk can seem like a bad thing however, we like to see it as part of the tool box we use for reaching your goals and something that we can mitigate to help protect your assets (or savings). Cash Investments: ex: Money market funds, bank accounts, certificates of deposit Fixed Income: ex: Bonds, ETFs (exchange- traded funds) Stocks: A type of security that signifies ownership in a corporation and represents a claim on part of the corporation's assets and earnings

19 18 Now that we have gone over the kinds of assets you may be invested in, we d like to show you three different allocation options - the different ways you d be invested in. The first option is what we call a Moderate portfolio. This option has the greatest percentage investment in stocks and the least invested in fixed income. We project this will have the greatest rate of return, meaning it has the potential to grow your investments the fastest, however it also has the greatest risk. This kind of allocation is best if you have a long time horizon and a high risk tolerance. Our next option is a conservative portfolio. This option has the lowest percentage invested in stocks, and the most invested in fixed income. This has a lower potential return than the moderate portfolio, but it also has the lowest risk. This allocation can be good for when you don t have a long time horizon and want a lower risk. Our final option is what we like to call the middle man. This is a moderately conservative portfolio. It has more stock than the conservative, but less than the moderate portfolio. This means that the riskiness of this portfolio is about in the middle of the two, but it also has a return that is in the middle. This can be a good allocation if you re comfortable with some risk, but not as much as you may encounter with the moderate portfolio. In order to determine how much risk you are comfortable with, we have attached a survey to help us see where you fall. During all of our calculations we have used an extremely conservative rate of return, assuming an allocation that is more conservative than what we have shown above. Tax Planning Another tool which we will use to help best utilize your assets in order to achieve your goals is taking advantage of the new tax laws that were passed in Some of the new tax laws that were passed are : Allowed to take the deductions for interest up to $1 million mortgage Standard deduction changed to $24,000 (Married Filing Jointly) Gains from sale of home: Up to $250,000 excludable from taxable income Professional Recommendations Professionals that we recommend you seek guidance from are the following. CPA/ Tax Professional- Take advantage of all tax credits that are available to maximize your after tax wealth. Realtor- Help navigate the housing market and find the home you are looking for.

20 19 College Planner- Make sure Matthew and Sarah are taking advantage of all available financial aid. Estate Attorney- Create the will and finalize estate documents. Such as powers of attorney, beneficiaries, and who is in charge of the estate. Insurance Broker- We believe it is important that you obtain coverage for disability, life, perils, as well as a PLUPS policy. You may also want to consider contacting your neighbor for more informations on the appropriate coverage, and what rates are appropriate. We have individuals that we could recommend for all of these areas. Throughout this report we have presented your family with a multitude of goals, ratios and recommendations. We hope that you will take the time to consider our recommendations presented in this plan. We re excited to work with your family and help pursue your financial goals.

2018 FINANCIAL PLANNING CHALLENGE CARL AND NAOMI BERMAN CASE STUDY

2018 FINANCIAL PLANNING CHALLENGE CARL AND NAOMI BERMAN CASE STUDY Client Welcome Letter... 3 Executive Summary... 4 Summary of Current Financial Condition... 5 Statement of Net Worth... 5 Statement of

2018 FINANCIAL PLANNING CHALLENGE CARL AND NAOMI BERMAN CASE STUDY Client Welcome Letter... 3 Executive Summary... 4 Summary of Current Financial Condition... 5 Statement of Net Worth... 5 Statement of

Financial Planning Challenge 2018 Phase 1: Written Financial Planning Case Study

Financial Planning Challenge 2018 Phase 1: Written Financial Planning Case Study The first phase of the competition consists of a financial planning case study for two hypothetical clients. Students must

Financial Planning Challenge 2018 Phase 1: Written Financial Planning Case Study The first phase of the competition consists of a financial planning case study for two hypothetical clients. Students must

Financial Planning Challenge 2018 Phase 1: Written Financial Planning Case Study

Financial Planning Challenge 2018 Phase 1: Written Financial Planning Case Study The first phase of the competition consists of a financial planning case study for two hypothetical clients. Students must

Financial Planning Challenge 2018 Phase 1: Written Financial Planning Case Study The first phase of the competition consists of a financial planning case study for two hypothetical clients. Students must

INSIDE THIS ISSUE. When Is It a Good Time to Sell Investments (p. 1)

") INSIDE THIS ISSUE When Is It a Good Time to Sell Investments (p. 1) Required Minimum Distribution A Primer (p. 4) Equalize Inheritances with Life Insurance (p. 6) Municipals Under the Microscope (p. 7)

INSIDE THIS ISSUE When Is It a Good Time to Sell Investments (p. 1) Required Minimum Distribution A Primer (p. 4) Equalize Inheritances with Life Insurance (p. 6) Municipals Under the Microscope (p. 7)

FINANCIAL PLAN 2018 Prepared for Carl & Naomi Berman. Patrick Yaghoobians Cecilia Mata Taylor Downhour

FINANCIAL PLAN 2018 Prepared for Carl & Naomi Berman Patrick Yaghoobians Cecilia Mata Taylor Downhour Table of Contents Table of Contents 1 Executive Summary 3 Current Financial Situation 4 Cash Inflows

FINANCIAL PLAN 2018 Prepared for Carl & Naomi Berman Patrick Yaghoobians Cecilia Mata Taylor Downhour Table of Contents Table of Contents 1 Executive Summary 3 Current Financial Situation 4 Cash Inflows

SHEDDING LIGHT ON LIFE INSURANCE

SHEDDING LIGHT ON LIFE INSURANCE A practical guide LEARN MORE ABOUT Safeguarding your loved ones Protecting your future Ensuring your dreams live on Life s brighter under the sun About this guide We ve

SHEDDING LIGHT ON LIFE INSURANCE A practical guide LEARN MORE ABOUT Safeguarding your loved ones Protecting your future Ensuring your dreams live on Life s brighter under the sun About this guide We ve

Your Envision profile. Client name:

Your Envision profile Client name: We ll help you live the life you ve imagined... Personal information Name: Spouse/Partner s name: Mailing address: State of primary residence: Date of birth (mm/dd/yyyy):

Your Envision profile Client name: We ll help you live the life you ve imagined... Personal information Name: Spouse/Partner s name: Mailing address: State of primary residence: Date of birth (mm/dd/yyyy):

Introduction. Personal Information. Contact Information. Home Address. Title. First Name. Last Name SSN. Date of Birth. Gender.

Introduction The information you provide will be used to create your financial plan. Your advisor will show you where you currently stand financially and if you are estimated to meet your financial goals

Introduction The information you provide will be used to create your financial plan. Your advisor will show you where you currently stand financially and if you are estimated to meet your financial goals

Women & Investing: Take Control of Your Wealth

Women & Investing: Take Control of Your Wealth Jerry Jevic Senior Director Investments Financial Advisor Private Client Division Oppenheimer & Co. Inc. 1818 Market Street Philadelphia, PA 19103 Phone:

Women & Investing: Take Control of Your Wealth Jerry Jevic Senior Director Investments Financial Advisor Private Client Division Oppenheimer & Co. Inc. 1818 Market Street Philadelphia, PA 19103 Phone:

Your Guide to Life Insurance for Families

Your Guide to Life Insurance for Families (800) 827-9990 HealthMarkets.com Your Guide to Life Insurance for Families Contents Does My Family Need Life Insurance? 4 Types of Life Insurance for Families

Your Guide to Life Insurance for Families (800) 827-9990 HealthMarkets.com Your Guide to Life Insurance for Families Contents Does My Family Need Life Insurance? 4 Types of Life Insurance for Families

INVESTING FOR YOUR FINANCIAL FUTURE

INVESTING FOR YOUR FINANCIAL FUTURE Saving now, while time is on your side, can help provide you with freedom to do what you want later in life. B B INVESTING FOR YOUR FINANCIAL FUTURE YOUR FINANCIAL FUTURE

INVESTING FOR YOUR FINANCIAL FUTURE Saving now, while time is on your side, can help provide you with freedom to do what you want later in life. B B INVESTING FOR YOUR FINANCIAL FUTURE YOUR FINANCIAL FUTURE

PREPARING FOR A MORE COMFORTABLE RETIREMENT

PREPARING FOR A MORE COMFORTABLE RETIREMENT As financial professionals who specialize in helping government employees transition from work to retirement, we understand that you may have questions about

PREPARING FOR A MORE COMFORTABLE RETIREMENT As financial professionals who specialize in helping government employees transition from work to retirement, we understand that you may have questions about

Planning for an Acquisition

Planning for an Acquisition 1 Before Exit Step 1 Establish a Basic Estate Plan Step 2 Outline Your Financial Goals and State of Affairs Step 3 Pre-transition Planning 2 After Exit Step 4 Minimize Tax Impact

Planning for an Acquisition 1 Before Exit Step 1 Establish a Basic Estate Plan Step 2 Outline Your Financial Goals and State of Affairs Step 3 Pre-transition Planning 2 After Exit Step 4 Minimize Tax Impact

Wealthcare Financial Plan

Wealthcare Financial Plan PREPARED FOR: Mr. and Mrs. Client August 09, 2014 PREPARED BY: Martin A. Smith, CRPC, AIFA President, Retirement Planning Financial Advisor 4800 Hampden Lane, Suite 200 Bethesda,

Wealthcare Financial Plan PREPARED FOR: Mr. and Mrs. Client August 09, 2014 PREPARED BY: Martin A. Smith, CRPC, AIFA President, Retirement Planning Financial Advisor 4800 Hampden Lane, Suite 200 Bethesda,

Retirement. on the Brain. A Woman s Guide to a Financially Secure Future - Workbook

Retirement on the Brain A Woman s Guide to a Financially Secure Future - Workbook Secure your future starting now Women face unique challenges when it comes to saving and investing for the future. We

Retirement on the Brain A Woman s Guide to a Financially Secure Future - Workbook Secure your future starting now Women face unique challenges when it comes to saving and investing for the future. We

Mapping Your Financial Future

Mapping Your Financial Future Profiles Forecaster Fact Finder Name (please print) Name (please print) Analysis Date Mapping Your Financial Future The best way to achieve financial freedom and peace of

Mapping Your Financial Future Profiles Forecaster Fact Finder Name (please print) Name (please print) Analysis Date Mapping Your Financial Future The best way to achieve financial freedom and peace of

Case Study Analysis PERSONAL FINANCE DECATHLON State Competition, April 6

Case Study Analysis 1. Your team is charged with providing financial recommendations to a fictional family based on their current and future financial capability and needs. 2. You are provided with incomplete

Case Study Analysis 1. Your team is charged with providing financial recommendations to a fictional family based on their current and future financial capability and needs. 2. You are provided with incomplete

Solutions A A F M A A. Wealth Management AAFMAA WEALTH MANAGEMENT & TRUST LLC. Financial Planning. Investment Management.

Wealth Management Solutions Financial Planning Investment Management Trust Services A A F M A A COMPASSION TRUST PROTECTION AAFMAA WEALTH MANAGEMENT & TRUST LLC A A F M A A COMPASSION TRUST PROTECTION

Wealth Management Solutions Financial Planning Investment Management Trust Services A A F M A A COMPASSION TRUST PROTECTION AAFMAA WEALTH MANAGEMENT & TRUST LLC A A F M A A COMPASSION TRUST PROTECTION

RETIREMENT QUESTIONS GOVERNMENT EMPLOYEES SHOULD BE ASKING

RETIREMENT QUESTIONS GOVERNMENT EMPLOYEES SHOULD BE ASKING 8/25/16 Preparing For a More Comfortable Retirement As financial professionals who specialize in helping government employees transition from

RETIREMENT QUESTIONS GOVERNMENT EMPLOYEES SHOULD BE ASKING 8/25/16 Preparing For a More Comfortable Retirement As financial professionals who specialize in helping government employees transition from

10 Steps to a SUCCESSFUL RETIREMENT. Chris O Dell. Compliments of

10 Steps to a SUCCESSFUL RETIREMENT Compliments of Chris O Dell Are you approaching retirement? You ve probably been planning for retirement in some way, shape or form for many years. Maybe you participate

10 Steps to a SUCCESSFUL RETIREMENT Compliments of Chris O Dell Are you approaching retirement? You ve probably been planning for retirement in some way, shape or form for many years. Maybe you participate

The Kline Group at Morgan Stanley Smith Barney

The Kline Group at Morgan Stanley Smith Barney We provide comprehensive wealth management advice and help connect all the pieces of your financial life. Our Mission Managing your assets can become not

The Kline Group at Morgan Stanley Smith Barney We provide comprehensive wealth management advice and help connect all the pieces of your financial life. Our Mission Managing your assets can become not

Getting Ready to Retire

How to Prepare for Your Retirement A GUIDE TO: Getting Ready to Retire EDUCATION GUIDE Create a plan now for a more comfortable retirement If you re five years or less from retirement, now is the time

How to Prepare for Your Retirement A GUIDE TO: Getting Ready to Retire EDUCATION GUIDE Create a plan now for a more comfortable retirement If you re five years or less from retirement, now is the time

Program overview October 2011

Program Overview October 2011 Table of Contents Program Overview Important Notices... 3 Summary of Key Features... 4 Account Owner... 5 Contributions... 5 No Guarantee... 5 Account Control... 6 Tax Treatment...

Program Overview October 2011 Table of Contents Program Overview Important Notices... 3 Summary of Key Features... 4 Account Owner... 5 Contributions... 5 No Guarantee... 5 Account Control... 6 Tax Treatment...

10 Things to Consider in

RETIREMENT INCOME PLANNING for Ages 35 to 50 Compliments of Jennifer & Eric Lahaie Jennifer & Eric Lahaie Eric and Jennifer Lahaie are the owners and founders of JEHM Wealth & Retirement. With years of

RETIREMENT INCOME PLANNING for Ages 35 to 50 Compliments of Jennifer & Eric Lahaie Jennifer & Eric Lahaie Eric and Jennifer Lahaie are the owners and founders of JEHM Wealth & Retirement. With years of

Building Your Portfolio

INVESTMENT POLICY GUIDANCE REPORT Building Your Portfolio A Personalized Approach to Your Investment Portfolio Investing is about more than money. You re investing for a reason maybe it s retirement, sending

INVESTMENT POLICY GUIDANCE REPORT Building Your Portfolio A Personalized Approach to Your Investment Portfolio Investing is about more than money. You re investing for a reason maybe it s retirement, sending

Putting Money to Work - Investing

Chapter 12 Putting Money to Work - Investing J.H. Morley said: In investing money, the amount of interest you want should depend on whether you want to eat well or sleep well. Another man with initials

Chapter 12 Putting Money to Work - Investing J.H. Morley said: In investing money, the amount of interest you want should depend on whether you want to eat well or sleep well. Another man with initials

MANAGED ACCOUNTS. Capital Directions. A guided approach to financial achievement

MANAGED ACCOUNTS Capital Directions A guided approach to financial achievement CAPITAL DIRECTIONS A UNIFIED MANAGED ACCOUNT THAT COMBINES FLEXIBILITY, SIMPLICITY, AND DISCIPLINE With a Capital Directions

MANAGED ACCOUNTS Capital Directions A guided approach to financial achievement CAPITAL DIRECTIONS A UNIFIED MANAGED ACCOUNT THAT COMBINES FLEXIBILITY, SIMPLICITY, AND DISCIPLINE With a Capital Directions

Dear Clients and Friends of The Center,

2016 Dear Clients and Friends of The Center, If you are like us, the end of the year is a natural time to reflect and take stock. Year-end planning also provides the opportunity to develop a sound business

2016 Dear Clients and Friends of The Center, If you are like us, the end of the year is a natural time to reflect and take stock. Year-end planning also provides the opportunity to develop a sound business

Build financial confidence

Build financial confidence One of a series of papers on the Confident Retirement approach For people five or more years away from retirement, achieving financial confidence typically means finding the

Build financial confidence One of a series of papers on the Confident Retirement approach For people five or more years away from retirement, achieving financial confidence typically means finding the

The Griggs Hartman Pattisall Group at Morgan Stanley Smith Barney. A Wealth Management Team

The Griggs Hartman Pattisall Group at Morgan Stanley Smith Barney A Wealth Management Team We are committed to helping our clients through the three stages of wealth: growing, preserving and transferring.

The Griggs Hartman Pattisall Group at Morgan Stanley Smith Barney A Wealth Management Team We are committed to helping our clients through the three stages of wealth: growing, preserving and transferring.

Christopher Eckert, CFP

Christopher Eckert, CFP Senior Vice President Wealth Management Senior Portfolio Manager Financial Advisor Helping You Through Your Most Important Transitions 320 Post Road West Westport, Connecticut 06880

Christopher Eckert, CFP Senior Vice President Wealth Management Senior Portfolio Manager Financial Advisor Helping You Through Your Most Important Transitions 320 Post Road West Westport, Connecticut 06880

BERMAN FINANCIAL PLAN

BERMAN FINANCIAL PLAN Prepared by F.L.S Financial MAY 18, 2018 F.L.S. FINANCIAL April 29, 2018 Carl and Naomi Berman Harrisonburg, VA 22081 Dear Carol and Naomi, It was a pleasure to meet you at our retirement

BERMAN FINANCIAL PLAN Prepared by F.L.S Financial MAY 18, 2018 F.L.S. FINANCIAL April 29, 2018 Carl and Naomi Berman Harrisonburg, VA 22081 Dear Carol and Naomi, It was a pleasure to meet you at our retirement

10 Steps to a SUCCESSFUL RETIREMENT. Robert Trejo. Compliments of

10 Steps to a SUCCESSFUL RETIREMENT Compliments of Robert Trejo Robert Trejo Senior Managing Partner As a young child, Robert Trejo s parents immigrated from El Salvador, bringing him and his two sisters

10 Steps to a SUCCESSFUL RETIREMENT Compliments of Robert Trejo Robert Trejo Senior Managing Partner As a young child, Robert Trejo s parents immigrated from El Salvador, bringing him and his two sisters

About Fred Bowie. Fred Bowie CEO Life & Retirement Guide Canada Retirement Information Centre

About Fred Bowie Fred Bowie CEO Life & Retirement Guide Canada Retirement Information Centre Since May 15, 1980 Fred Bowie and the Life & Retirement Guides at the Canada Retirement Information Centre have

About Fred Bowie Fred Bowie CEO Life & Retirement Guide Canada Retirement Information Centre Since May 15, 1980 Fred Bowie and the Life & Retirement Guides at the Canada Retirement Information Centre have

Your Plan for College

Your Plan for College You can get there. We can help. COLLEGE SAVINGS PLAN TM You can get there. We can help. All parents have hopes and dreams for their children, including a good education. To help you

Your Plan for College You can get there. We can help. COLLEGE SAVINGS PLAN TM You can get there. We can help. All parents have hopes and dreams for their children, including a good education. To help you

MYGAs. Multi-Year Guaranteed Annuities. Annuity Product Guides. A safe, guaranteed and tax-deferred way to grow your retirement savings

Annuity Product s MYGAs Multi-Year Guaranteed Annuities A safe, guaranteed and tax-deferred way to grow your retirement savings Modernizing retirement security through trust, transparency and by putting

Annuity Product s MYGAs Multi-Year Guaranteed Annuities A safe, guaranteed and tax-deferred way to grow your retirement savings Modernizing retirement security through trust, transparency and by putting

Taking an income from your retirement savings The Trust Retirement Guide

Taking an income from your retirement savings The Trust Retirement Guide Your money, your choice The longest holiday of your life - you may have been dreaming of all the things you plan to do when you

Taking an income from your retirement savings The Trust Retirement Guide Your money, your choice The longest holiday of your life - you may have been dreaming of all the things you plan to do when you

What Would Your Family Do Without Your Income?

What Would Your Family Do Without Your Income? Income Protection Option You Know What Matters That s why you work hard to provide for your family. Late nights. Early mornings. Working over the weekend.

What Would Your Family Do Without Your Income? Income Protection Option You Know What Matters That s why you work hard to provide for your family. Late nights. Early mornings. Working over the weekend.

Appendix 1V Baby Boomer Contemplating Retirement

Checkpoint Contents Federal Library Federal Editorial Materials PPC's Tax and Financial Planning Library Retirement Planning Chapter 1 A Step-by-step Planning Approach Appendix 1V Baby Boomer Contemplating

Checkpoint Contents Federal Library Federal Editorial Materials PPC's Tax and Financial Planning Library Retirement Planning Chapter 1 A Step-by-step Planning Approach Appendix 1V Baby Boomer Contemplating

MaineSTART - Saving Today to Afford Retirement Tomorrow. A penny saved is a penny earned. - Benjamin Franklin. A MainePERS Program

A penny saved is a penny earned - Benjamin Franklin A MainePERS Program APRIL 2019 Why Save? While many of us talk about retirement, the truth is that too many of us don t do enough to plan for our retirement.

A penny saved is a penny earned - Benjamin Franklin A MainePERS Program APRIL 2019 Why Save? While many of us talk about retirement, the truth is that too many of us don t do enough to plan for our retirement.

Enrollment Materials. Everything you need to help put your child on the right path to a better future.

Enrollment Materials Everything you need to help put your child on the right path to a better future. www.path2college529.com Path2College 529 Plan, offered by the State of Georgia. Ev e r y j o u r n

Enrollment Materials Everything you need to help put your child on the right path to a better future. www.path2college529.com Path2College 529 Plan, offered by the State of Georgia. Ev e r y j o u r n

Planning for a Good Life. We can help.

Planning for a Good Life We can help. Every successful project starts with a plan. A blueprint to make sure each stage of the process moves the project closer to completion of the final design. So, when

Planning for a Good Life We can help. Every successful project starts with a plan. A blueprint to make sure each stage of the process moves the project closer to completion of the final design. So, when

Saving for Your Future:

Saving for Your Future: Get Advice the Way You Need It Choice. Protection. Clarity. Opportunity. We all have different needs based on our goals, our age, the amount we are able to save, and other factors,

Saving for Your Future: Get Advice the Way You Need It Choice. Protection. Clarity. Opportunity. We all have different needs based on our goals, our age, the amount we are able to save, and other factors,

Secure Your Retirement

4 Creating a Framework 6 Case Study #1: The Dunbars 8 Case Study #2: Professor Harrison 9 Case Study #3: Jane Leahy Advanced Annuity Strategies to Help Secure Your Retirement The Paradigm Has Shifted.

4 Creating a Framework 6 Case Study #1: The Dunbars 8 Case Study #2: Professor Harrison 9 Case Study #3: Jane Leahy Advanced Annuity Strategies to Help Secure Your Retirement The Paradigm Has Shifted.

FOR WOMEN: A TIAA FINANCIAL ESSENTIALS WORKSHOP. She s Got It: A woman s guide to savings and investing

FOR WOMEN: A TIAA FINANCIAL ESSENTIALS WORKSHOP She s Got It: A woman s guide to savings and investing Agenda She s got it: A woman s guide to saving and investing Financial goals and strategies Basics

FOR WOMEN: A TIAA FINANCIAL ESSENTIALS WORKSHOP She s Got It: A woman s guide to savings and investing Agenda She s got it: A woman s guide to saving and investing Financial goals and strategies Basics

INVESTING IN YOURSELF

Investment Planning INVESTING IN YOURSELF Women are different from men. So are your financial planning needs. 2 INVESTING IN YOURSELF WOMEN & MONEY There are many reasons why you might require a different

Investment Planning INVESTING IN YOURSELF Women are different from men. So are your financial planning needs. 2 INVESTING IN YOURSELF WOMEN & MONEY There are many reasons why you might require a different

Income for Life #31. Interview With Brad Gibb

Income for Life #31 Interview With Brad Gibb Here is the transcript of our interview with Income for Life expert, Brad Gibb. Hello, everyone. It s Tim Mittelstaedt, your Wealth Builders Club member liaison.

Income for Life #31 Interview With Brad Gibb Here is the transcript of our interview with Income for Life expert, Brad Gibb. Hello, everyone. It s Tim Mittelstaedt, your Wealth Builders Club member liaison.

Fixed Annuities. Annuity Product Guides. A safe, guaranteed and tax-deferred way to grow your retirement savings.

Annuity Product Guides Fixed Annuities A safe, guaranteed and tax-deferred way to grow your retirement savings Modernizing retirement security through trust, transparency and by putting the customer first

Annuity Product Guides Fixed Annuities A safe, guaranteed and tax-deferred way to grow your retirement savings Modernizing retirement security through trust, transparency and by putting the customer first

Total your Time Horizon points: MUGC9288. RISK TOLERANCE The risk you are willing to take in exchange for the possibility of a greater return.

If you re planning to retire in five years or less, your personal situation may require more detailed planning and analysis. Please consult your personal financial advisor. ASSESSMENT In order to choose

If you re planning to retire in five years or less, your personal situation may require more detailed planning and analysis. Please consult your personal financial advisor. ASSESSMENT In order to choose

PRUDENTIAL FINANCIAL PLANNING SERVICES. The Difference Financial Planning Can Make

PRUDENTIAL FINANCIAL PLANNING SERVICES The Difference Financial Planning Can Make Your Current Financial Situation If you re like most people, you ve taken some steps to reach a few of your financial goals.

PRUDENTIAL FINANCIAL PLANNING SERVICES The Difference Financial Planning Can Make Your Current Financial Situation If you re like most people, you ve taken some steps to reach a few of your financial goals.

Six steps to help secure your retirement

Six steps to help secure your retirement The average age for retirement in America is 62.* If you retire at age 65, you can expect to spend 19 years in retirement.** *Source: Gallup **Source: The Wall

Six steps to help secure your retirement The average age for retirement in America is 62.* If you retire at age 65, you can expect to spend 19 years in retirement.** *Source: Gallup **Source: The Wall

Helping your adult kids: How much is too much?

Previous issues New legislation is ending key claiming strategies. What you need to know now. > Read more Roth IRA Financial miscues? Tips to get back on track. Pension > Read more What to consider if

Previous issues New legislation is ending key claiming strategies. What you need to know now. > Read more Roth IRA Financial miscues? Tips to get back on track. Pension > Read more What to consider if

Data Gathering. Questionnaire

Data Gathering Questionnaire Personal Information CLIENT 1 Name Address City, State Zip Phone: Home Work Cell Email Birth date Marital Status Single Married Widowed Are you a citizen of the United States?

Data Gathering Questionnaire Personal Information CLIENT 1 Name Address City, State Zip Phone: Home Work Cell Email Birth date Marital Status Single Married Widowed Are you a citizen of the United States?

WEALTH CARE KIT SM. Investment Planning. A website built by the National Endowment for Financial Education dedicated to your financial well-being.

WEALTH CARE KIT SM Investment Planning A website built by the dedicated to your financial well-being. Do you have long-term goals you re uncertain how to finance? Are you a saver or an investor? Have you

WEALTH CARE KIT SM Investment Planning A website built by the dedicated to your financial well-being. Do you have long-term goals you re uncertain how to finance? Are you a saver or an investor? Have you

THE FUTURE IS FIDUCIARY

THE FUTURE IS FIDUCIARY INSIDE: Why acting as a fiduciary and taking a lifecycle approach to wealth management can help build trust and deepen relationships POSITION YOUR PRACTICE TO UPHOLD CLIENTS BEST

THE FUTURE IS FIDUCIARY INSIDE: Why acting as a fiduciary and taking a lifecycle approach to wealth management can help build trust and deepen relationships POSITION YOUR PRACTICE TO UPHOLD CLIENTS BEST

How to Strategically Manage Your Debt

Debt. Funny how four little letters can feel so dirty. Most of us have it in one shape or another, but none of us like to talk about it. Debt can get us into trouble, especially if it is unplanned and

Debt. Funny how four little letters can feel so dirty. Most of us have it in one shape or another, but none of us like to talk about it. Debt can get us into trouble, especially if it is unplanned and

ALL ABOUT INVESTING. Here is Dave s investing philosophy:

ALL ABOUT INVESTING Knowing how to deal with debt is easy pay it off! Investing, however, isn t quite so simple. Most people have questions about when and how to invest their money, so here s an inside

ALL ABOUT INVESTING Knowing how to deal with debt is easy pay it off! Investing, however, isn t quite so simple. Most people have questions about when and how to invest their money, so here s an inside

ORGANIZE, PLAN, AND OWN YOUR FUTURE

Be In The Front Seat ORGANIZE, PLAN, AND OWN YOUR FUTURE Making financial health a priority for women HERE S WHAT WE LL COVER: Why now? Getting organized Building your plan Owning your future 2 WHEN IT

Be In The Front Seat ORGANIZE, PLAN, AND OWN YOUR FUTURE Making financial health a priority for women HERE S WHAT WE LL COVER: Why now? Getting organized Building your plan Owning your future 2 WHEN IT

15 Questions to ask about Your SOCIAL SECURITY BENEFITS. Questions to ask about Your SOCIAL SECURITY. Benefits. Compliments of.

15 Questions to ask about Your SOCIAL SECURITY Benefits Compliments of David Trombley David Trombley Licensed Insurance Professional Trombley Insurance Agency is a family-owned and -operated firm, offering

15 Questions to ask about Your SOCIAL SECURITY Benefits Compliments of David Trombley David Trombley Licensed Insurance Professional Trombley Insurance Agency is a family-owned and -operated firm, offering

Transcript - The Money Drill: Where and How to Invest for Your Biggest Goals in Life

Transcript - The Money Drill: Where and How to Invest for Your Biggest Goals in Life J.J.: Hi, this is "The Money Drill," and I'm J.J. Montanaro. With the help of some great guest, I'll help you find your

Transcript - The Money Drill: Where and How to Invest for Your Biggest Goals in Life J.J.: Hi, this is "The Money Drill," and I'm J.J. Montanaro. With the help of some great guest, I'll help you find your

UBS Financial Services Inc. Retirement Plan Asset Allocation Guide

ab UBS Financial Services Inc. Retirement Plan Asset Allocation Guide Planning how to invest for your retirement may be one of the most important decisions you ll ever make. Asset allocation is a strategy

ab UBS Financial Services Inc. Retirement Plan Asset Allocation Guide Planning how to invest for your retirement may be one of the most important decisions you ll ever make. Asset allocation is a strategy

Investing in onshore bonds

Investing in onshore bonds Open up your options with our Tailored Investment Bond Before you decide to buy, you need to know what the risks and commitments are. Read our key features document (TNB17).

Investing in onshore bonds Open up your options with our Tailored Investment Bond Before you decide to buy, you need to know what the risks and commitments are. Read our key features document (TNB17).

COLLEGE WILL NOT BE EASY, BUT SAVING FOR IT CAN BE.

COLLEGE WILL NOT BE EASY, BUT SAVING FOR IT CAN BE. Why save for college.............. 2 Power of compounding........... 3 Plan highlights..................... 4 Broad investment options........ 6 Other

COLLEGE WILL NOT BE EASY, BUT SAVING FOR IT CAN BE. Why save for college.............. 2 Power of compounding........... 3 Plan highlights..................... 4 Broad investment options........ 6 Other

50% 21%of those INVESTING FOR YOU: 5 CRITICAL QUESTIONS FOR EVERY INVESTOR ... More. than

INVESTING FOR YOU: 5 CRITICAL QUESTIONS FOR EVERY INVESTOR People spend a lot of time worrying about finding the best investment. They pick a bond, mutual fund or stock and then second-guess themselves

INVESTING FOR YOU: 5 CRITICAL QUESTIONS FOR EVERY INVESTOR People spend a lot of time worrying about finding the best investment. They pick a bond, mutual fund or stock and then second-guess themselves

Working with Financial Professionals: Opinions of American Investors. Working with Financial Professionals: Opinions of American Investors

Working with Financial Professionals: Opinions of American Investors Working with Financial Professionals: Opinions of American Investors 1 Goals Understand American investors views on their relationships

Working with Financial Professionals: Opinions of American Investors Working with Financial Professionals: Opinions of American Investors 1 Goals Understand American investors views on their relationships

RBC retirement income planning process

Page 1 of 6 RBC retirement income planning process Create income for your retirement At RBC Wealth Management, we believe managing your wealth to produce an income during retirement is fundamentally different

Page 1 of 6 RBC retirement income planning process Create income for your retirement At RBC Wealth Management, we believe managing your wealth to produce an income during retirement is fundamentally different

Are Your Allocations Right for RMDs?

Are Your Allocations Right for RMDs? Are Your Allocations Right for RMDs? Making sure your IRAs are allocated properly for required minimum distributions (RMDs) once you reach the age at which you must

Are Your Allocations Right for RMDs? Are Your Allocations Right for RMDs? Making sure your IRAs are allocated properly for required minimum distributions (RMDs) once you reach the age at which you must

WEALTH CARE KIT SM. Income Tax Planning. A website built by the National Endowment for Financial Education dedicated to your financial well-being.

WEALTH CARE KIT SM Income Tax Planning A website built by the dedicated to your financial well-being. As the joke goes, figuring out your taxes is pretty easy just add up how much money you made last year

WEALTH CARE KIT SM Income Tax Planning A website built by the dedicated to your financial well-being. As the joke goes, figuring out your taxes is pretty easy just add up how much money you made last year

Why Flagstar Bank for your Retirement Planning Needs?

Section I Why Flagstar Bank for your Retirement Planning Needs? Section I Est. 1987 Member FDIC Page 1 Why Flagstar Bank when saving for retirement? We all understand the importance of saving for retirement.

Section I Why Flagstar Bank for your Retirement Planning Needs? Section I Est. 1987 Member FDIC Page 1 Why Flagstar Bank when saving for retirement? We all understand the importance of saving for retirement.

Hale and Associates Phone: Fax: CA License #0G30788

Hale and Associates Phone: 317-986-6785 Fax: 317-986-6787 www.haleandassociates.net CA License #0G30788 OVERVIEW Most people marvel at the lighthouse. A simple structure that has played such a big role

Hale and Associates Phone: 317-986-6785 Fax: 317-986-6787 www.haleandassociates.net CA License #0G30788 OVERVIEW Most people marvel at the lighthouse. A simple structure that has played such a big role

A guide to your retirement income options with TIAA-CREF

A guide to your retirement income options with TIAA-CREF Helping you make important decisions about your retirement How will I know when the time is right to retire? Making the decision to retire is no

A guide to your retirement income options with TIAA-CREF Helping you make important decisions about your retirement How will I know when the time is right to retire? Making the decision to retire is no

UBS Financial Services Inc. Retirement Plan Asset Allocation Guide

ab UBS Financial Services Inc. Retirement Plan Asset Allocation Guide Planning how to invest for your retirement may be one of the most important decisions you ll ever make. Asset allocation is a strategy

ab UBS Financial Services Inc. Retirement Plan Asset Allocation Guide Planning how to invest for your retirement may be one of the most important decisions you ll ever make. Asset allocation is a strategy

Tax strategies for higher-income taxpayers

Tax strategies for higher-income taxpayers This overview summarizes some of the key areas that you and your tax advisor should assess. Your Financial Advisor can assist in evaluating investment decisions

Tax strategies for higher-income taxpayers This overview summarizes some of the key areas that you and your tax advisor should assess. Your Financial Advisor can assist in evaluating investment decisions

Behavioral Investment Policy Statement. Coddington Family. Prepared on: 25 January 2013

Behavioral Investment Policy Statement Coddington Family Retirement Account Prepared on: 25 January 2013 Based on completion of the: Natural Behavior Discovery on: 14 March 2012 Financial Personality Discovery

Behavioral Investment Policy Statement Coddington Family Retirement Account Prepared on: 25 January 2013 Based on completion of the: Natural Behavior Discovery on: 14 March 2012 Financial Personality Discovery

BUYING YOUR FIRST HOME

BUYING YOUR FIRST HOME Finding the home of your dreams is the tough part, the mortgage process shouldn t be. That s why we ve created a guide to make your first-time home buying experience easier. This

BUYING YOUR FIRST HOME Finding the home of your dreams is the tough part, the mortgage process shouldn t be. That s why we ve created a guide to make your first-time home buying experience easier. This

Investment Progress Toward Goals. Prepared for: Bob and Mary Smith January 19, 2011

Prepared for: Bob and Mary Smith January 19, 2011 Investment Progress Toward Goals Understanding Your Results Introduction I am pleased to present you with this report that will help you answer what may

Prepared for: Bob and Mary Smith January 19, 2011 Investment Progress Toward Goals Understanding Your Results Introduction I am pleased to present you with this report that will help you answer what may

For creating a sound investment strategy.

Five Rules For creating a sound investment strategy. 5 Part one of the two-part guide series Saving Smart for Retirement. The most important decision you will probably ever make concerns the balancing

Five Rules For creating a sound investment strategy. 5 Part one of the two-part guide series Saving Smart for Retirement. The most important decision you will probably ever make concerns the balancing

Your Financial Well-Being Assessment

Your Financial Well-Being Assessment Congratulations! You are on your way to a better understanding of financial well-being. Downloading this guide is the first step. Now, take some time to review and

Your Financial Well-Being Assessment Congratulations! You are on your way to a better understanding of financial well-being. Downloading this guide is the first step. Now, take some time to review and

Churchill Management Group

hurchillmanagement hurchillmanagement Group hurchillmanagement Group ll Management Group hurchillmanagement G hurchillmanagement Group It is the mission of to build wealth for our Clients over the long

hurchillmanagement hurchillmanagement Group hurchillmanagement Group ll Management Group hurchillmanagement G hurchillmanagement Group It is the mission of to build wealth for our Clients over the long

It s easy to get started today.

It s easy to get started today. 1 2 Complete this workbook as accurately and completely as possible. Make an appointment with your Fidelity Workplace Planning and Guidance Consultant to discuss your plan.

It s easy to get started today. 1 2 Complete this workbook as accurately and completely as possible. Make an appointment with your Fidelity Workplace Planning and Guidance Consultant to discuss your plan.

Determining your investment mix

Determining your investment mix Ten minutes from now, you could know your investment mix. And if your goal is to choose investment options that you can be comfortable with, this is an important step. The

Determining your investment mix Ten minutes from now, you could know your investment mix. And if your goal is to choose investment options that you can be comfortable with, this is an important step. The

New York State Society of Certified Public Accountants IRS Licensed in All States TAX YEAR 2015

David Gitel CPA, EA Certified Public Accountant 1560 Broadway, Suite 1210 New York, NY 10036 Phone: (212) 840-2797 Fax: (212) 840-2817 E-Mail: dgitel@aol.com New York State Society of Certified Public

David Gitel CPA, EA Certified Public Accountant 1560 Broadway, Suite 1210 New York, NY 10036 Phone: (212) 840-2797 Fax: (212) 840-2817 E-Mail: dgitel@aol.com New York State Society of Certified Public

Retirement Strategies for Women RETIREMENT

Retirement Strategies for Women RETIREMENT Contents Retirement Facts for Women... 1 Planning for Retirement...3 Financial Net Worth...4 Cash Flow...5 What Is Important to You?...6 10 Ways to Put Your House

Retirement Strategies for Women RETIREMENT Contents Retirement Facts for Women... 1 Planning for Retirement...3 Financial Net Worth...4 Cash Flow...5 What Is Important to You?...6 10 Ways to Put Your House

Diversification made easy. Asset Allocation Guide

Diversification made easy Asset Allocation Guide 1 First of all, what s asset allocation? To put it simply, asset allocation is the process of spreading your investment dollars over different types of

Diversification made easy Asset Allocation Guide 1 First of all, what s asset allocation? To put it simply, asset allocation is the process of spreading your investment dollars over different types of

Retirement Planning Newsletter Fall 2015

Retirement Planning Newsletter Fall 2015 This issue of Financial Footnotes brings you information to help you meet the challenges of midcareer. Of course, some of the ideas here can also apply if you re

Retirement Planning Newsletter Fall 2015 This issue of Financial Footnotes brings you information to help you meet the challenges of midcareer. Of course, some of the ideas here can also apply if you re

SOCIAL SECURITY WON T BE ENOUGH:

SOCIAL SECURITY WON T BE ENOUGH: 6 REASONS TO CONSIDER AN INCOME ANNUITY How long before you retire? For some of us it s 20 to 30 years away, and for others it s closer to 5 or 0 years. The key here is

SOCIAL SECURITY WON T BE ENOUGH: 6 REASONS TO CONSIDER AN INCOME ANNUITY How long before you retire? For some of us it s 20 to 30 years away, and for others it s closer to 5 or 0 years. The key here is

Give the Gift That Truly Matters A Gift Towards a Child s Retirement

Give the Gift That Truly Matters A Gift Towards a Child s Retirement When you create a RIC-E Trust, you contribute as little as $5,000, and you designate a child or grandchild to receive the money when

Give the Gift That Truly Matters A Gift Towards a Child s Retirement When you create a RIC-E Trust, you contribute as little as $5,000, and you designate a child or grandchild to receive the money when

SAMPLE. Chapter 1 DAVE RAMSEY

Chapter 1 DAVE RAMSEY Case Study Savings Rob and Carol were married recently and both have good jobs coming out of college. Rob was hired by The Lather Group as an assistant designer making a starting

Chapter 1 DAVE RAMSEY Case Study Savings Rob and Carol were married recently and both have good jobs coming out of college. Rob was hired by The Lather Group as an assistant designer making a starting

Planning your investment journey

BASF UK Group Pension Scheme Investment guide Planning your investment journey January 2016 2 BASF UK Group Pension Scheme Contents Planning your journey Types of investments 4 Types of risk 5 Types of

BASF UK Group Pension Scheme Investment guide Planning your investment journey January 2016 2 BASF UK Group Pension Scheme Contents Planning your journey Types of investments 4 Types of risk 5 Types of

Personal Financial Survey

Personal Financial Survey Simplify your financial life so you can spend more time with the people you care about. Enter and Begin with our simple 5-step financial planning process. Financial planning takes

Personal Financial Survey Simplify your financial life so you can spend more time with the people you care about. Enter and Begin with our simple 5-step financial planning process. Financial planning takes

24JAN SIMPLIFIED PROSPECTUS DATED NOVEMBER 17, 2017

No securities regulatory authority has expressed an opinion about these securities and it is an offence to claim otherwise. Your simple guide to investing in Dynamic Funds. DYNAMIC TRUST FUNDS Dynamic

No securities regulatory authority has expressed an opinion about these securities and it is an offence to claim otherwise. Your simple guide to investing in Dynamic Funds. DYNAMIC TRUST FUNDS Dynamic

Invest in Their Future.

CollegeAmerica 9 College Savings Plan June 0, 0 Invest in Their Future. SM A college education can play a crucial part in a loved one s longterm happiness and financial security. College graduates earn

CollegeAmerica 9 College Savings Plan June 0, 0 Invest in Their Future. SM A college education can play a crucial part in a loved one s longterm happiness and financial security. College graduates earn

Spousal Lifetime Access Trust. Transferring wealth and retaining spousal access. Core Stories for Life. learn more about MetLife s

17.75 in. LIFE INSURANCE Equity Advantage Variable Universal Life is offered by prospectus only, which is available from your registered representative. You should carefully consider the product s features,

17.75 in. LIFE INSURANCE Equity Advantage Variable Universal Life is offered by prospectus only, which is available from your registered representative. You should carefully consider the product s features,

INVESTOR INFORMATION GUIDE

INVESTOR INFORMATION GUIDE TABLE OF CONTENTS Important Information Regarding Your HD Vest Account 1 Glossary of Terms 2 Privacy Policy for Individuals 3 Business Continuity Disclosure Statement 5 Guide

INVESTOR INFORMATION GUIDE TABLE OF CONTENTS Important Information Regarding Your HD Vest Account 1 Glossary of Terms 2 Privacy Policy for Individuals 3 Business Continuity Disclosure Statement 5 Guide

Women & Retirement: 3 Unique retirement challenges women face today. Video Transcript

Women & Retirement: 3 Unique retirement challenges women face today Video Transcript Recorded on September 8, 2014 Featuring: Michael Santoli, Senior Columnist, Yahoo! Finance Debra Greenberg, Director

Women & Retirement: 3 Unique retirement challenges women face today Video Transcript Recorded on September 8, 2014 Featuring: Michael Santoli, Senior Columnist, Yahoo! Finance Debra Greenberg, Director

3 Easy Steps to Save for a Child s Education

Savings 3 Easy Steps to Save for a Child s Education Invest Today for a Child s Education Tomorrow Investment Products Offered Are Not FDIC Insured May Lose Value Are Not Bank Guaranteed Education Is One

Savings 3 Easy Steps to Save for a Child s Education Invest Today for a Child s Education Tomorrow Investment Products Offered Are Not FDIC Insured May Lose Value Are Not Bank Guaranteed Education Is One

Mortgage Planning Questionnaire

Mortgage Planning Questionnaire Email: Home: Cell: Birthday: Current Address: 1. How would you like us to stay in contact with you? (Check all that apply) email phone fax mail cell phone 2. Is this a financing

Mortgage Planning Questionnaire Email: Home: Cell: Birthday: Current Address: 1. How would you like us to stay in contact with you? (Check all that apply) email phone fax mail cell phone 2. Is this a financing

Millennium universal life insurance

Millennium universal life insurance Permanent protection that can change with you Millennium universal life insurance Over the years, you ve worked hard to build the lifestyle you enjoy today. You ve made

Millennium universal life insurance Permanent protection that can change with you Millennium universal life insurance Over the years, you ve worked hard to build the lifestyle you enjoy today. You ve made

THE COMMUNIQUE MARCH 2016

THE COMMUNIQUE MARCH 2016 MAJOR INDICES CLOSE MTD QTD YTD S&P 500 1932.23-0.41-5.47-5.47 Dow Jones Industrials 16516.50 0.31-5.21-5.21 NASDAQ Composite 4557.95-1.21-8.98-8.98 U.S. TREASURIES YEILD 5-yr

THE COMMUNIQUE MARCH 2016 MAJOR INDICES CLOSE MTD QTD YTD S&P 500 1932.23-0.41-5.47-5.47 Dow Jones Industrials 16516.50 0.31-5.21-5.21 NASDAQ Composite 4557.95-1.21-8.98-8.98 U.S. TREASURIES YEILD 5-yr

Franklin Templeton 529 College Savings Plan OFFERED NATIONWIDE BY THE NEW JERSEY HIGHER EDUCATION STUDENT ASSISTANCE AUTHORITY

Franklin Templeton 529 College Savings Plan OFFERED NATIONWIDE BY THE NEW JERSEY HIGHER EDUCATION STUDENT ASSISTANCE AUTHORITY What Does the Future Hold? As soon as your child is born, you begin imagining

Franklin Templeton 529 College Savings Plan OFFERED NATIONWIDE BY THE NEW JERSEY HIGHER EDUCATION STUDENT ASSISTANCE AUTHORITY What Does the Future Hold? As soon as your child is born, you begin imagining