2018 FINANCIAL PLANNING CHALLENGE CARL AND NAOMI BERMAN CASE STUDY

|

|

|

- Lambert Moore

- 5 years ago

- Views:

Transcription

1 2018 FINANCIAL PLANNING CHALLENGE CARL AND NAOMI BERMAN CASE STUDY

2 Client Welcome Letter... 3 Executive Summary... 4 Summary of Current Financial Condition... 5 Statement of Net Worth... 5 Statement of Cash Flows... 7 Ratio Analysis... 9 Assumptions SWOT Analysis Strengths, Weaknesses, Opportunities, and Threats Goal Needs Analysis Goal Needs Analysis Summary Life Insurance Needs Analysis Financial Analysis Budget Cash flows and Retirement Income Investment Analysis Recommendations Appendix: Detailed Calculations College Funding - Detailed Calculations and Assumptions Purchase of Harrisburg, VA Home - Detailed Calculations and Assumptions Purchase of Blue Ridge Cabin - Detailed Calculations and Assumptions Social Security - Assumptions... 25

3 CLIENT WELCOME LETTER May 15, 2018 Carl and Naomi Berman Maple Dr Harrisburg, VA Dear Mr. and Mrs. Berman, Thank you for choosing our firm, Sunset Wealth Management, to help you plan your financial journey. We would like to express our appreciation and pleasure in your choice to work with our team full of three experienced advisors on staff. Our team look forwards to the opportunity to build a new relationship as well as provide you with the necessary financial advice that aligns with your goals, needs, and desires in life. We originated in 2011 as a fee-only Registered Investment Advisory (RIA) firm and have helped hundreds of clients in their path towards financial freedom and security. Our approach incorporates providing holistic, high quality, and innovative wealth management services to plan out all the fundamental aspects of our clients financial lives. The philosophy we follow is centered around customization to make sure we create a financial plan and investment portfolio best suited for your goals, risk tolerance, and needs in life. We hold ourselves to a fiduciary standard which entitles us to create a financial plan in your best interest. Our fees are transparent in the sense that we will not charge you hidden costs or push sales to receive commissions. We operate our fee structure as a percentage of your assets we manage and will never charge a hidden fee you are not directly aware of. Thank you again for choosing our firm to guide you through your financial future. We look forward to the opportunity of working with you to help you accomplish all your goals in your financial journey that lies ahead. Sincerely, Sunset Wealth Management

4 EXECUTIVE SUMMARY Carl and Naomi Berman are working professionals in the education field and both earn a healthy income. They have been do it yourselfers in terms of their investment portfolio, saving for retirement, and funding other goals. The Bermans have engaged our firm to perform a complete review and comprehensive financial plan. Thus far, the Bermans have placed focus on saving for the future and now want to know if they are on track to achieve their goals. The Berman s have identified several goals important to them. We have been asked to address college education funding, home purchase practicality, and insurance needs. A major priority is funding the college experience of their two children Matthew (14) and Sarah (11). They have been saving for college for the last 10 years and now want to ensure that fully paying for their children s education is possible. The Berman s currently own a home in Harrisburg, VA; they have revealed major goals of purchasing a home in the historic district of the city one day as well as a small cabin in the Blue Ridge Mountains of Virginia where they could enjoy the outdoors during retirement. The Berman s want to make certain that in the event anything happens to either one of them that the surviving spouse can still fund applicable goals. If Carl were to pass he still would like Naomi to be able to fund all of their goals. If Naomi passes, Carl would want to guarantee coverage for the children s education, but would not purchase the retirement cabin. To that end, our firm is making a thorough recommendation on life and disability insurance. Our firm will also provide counsel on drafting the appropriate estate documents. Upon review of the Berman s financial data, our firm has analyzed the feasibility of the Berman s goals. Our firm has identified strengths and weaknesses associated with the Berman s current financials and life situation as well as opportunities for maximizing their financial health and possible threats to adjust for. Based on our initial analysis and with the implementation of our recommendations the Berman s will be able to achieve all stated goals. Summary of Stated Client Goals & Concerns They hope to use savings to fully fund college expenses for Matthew and Sarah. Is fully funding the kids education an achievable goal? One day owning a home in the historic district of Harrisonburg, VA Keep the original house and rent it for income, or sell it to pay for the new home? Own a small cabin in the Blue Ridge Mountains Insurance review: Life insurance If Carl dies, want Naomi to fund all of their goals If Naomi dies, have kids education funded but do not purchase the cabin Disability insurance Reduction of current lifestyle would be the priority but; They want the income to remain on track with their goals

5 SUMMARY OF CURRENT FINANCIAL CONDITION STATEMENT OF NET WORTH Net Worth Non-Qualified Assets Carl Naomi Joint Total Bank savings $30,281 $30,281 Trading account $107,338 $107,338 Total Non-Qualified Assets $ - $ - $137,619 $137,619 Qualified Assets 0 Carl's Roth $61,431 $61,431 Naomi's Roth $66,550 $66,550 Carl s IRA $153,577 $153,577 Naomi's 401(k) $204,770 $204,770 Carl s 401k $307,155 $307,155 Total Qualified Assets 522 $522,163 $271,320 $ - $793,483 Lifestyle Assets Residence $453,750 $453,750 Total Lifestyle Assets $ - $ - $453,750 $453,750 Total Assets $522,163 $271,320 $591,369 $1,384,852 Liabilities Mortgage -$314,118 -$314,118 Car Loan -$29,787 -$29,787 Credit Card -$7,515 -$7,515 Total Liabilities $ - $ - -$351,420 -$351,420 Total Net Worth $522,163 $271,320 $239,949 $1,033,432

6 Observations on Net Worth Statement: Carl and Naomi have assets worth $1,384,852 and liabilities of only $351,420. After netting the two figures, their net worth totals a positive $1,033,432 at the start of Their assets are sufficiently larger than their debts which is an indicator of great financial health and discipline by saving for their future retirement.

7 STATEMENT OF CASH FLOWS Cash Flow Details As of 12/31/2017 Cash Inflows Carl Naomi Total Earned Income Salary $140,000 $100,000 $240,000 Subtotal $140,000 $100,000 $240,000 Investment Income Interest $386 $386 $772 Dividends $518 $518 $1,036 Long-Term Capital Gains $1,744 $1,744 $3,488 Subtotal $2,648 $2,648 $5,296 Total Cash Inflows $142,648 $102,648 $245,296 Cash Outflows Lifestyle Expenses Discretionary Expenses Fixed Expenses (excluding liabilities) $25,000 $25,000 $50,000 $20,000 $20,000 $40,000 Mortgage Payment $15,000 $15,000 $30,000 Car Loan $3,900 $3,900 $7,800 Credit Card $1,050 $1,050 $2,100 Subtotal $64,950 $64,950 $129,900 Non-qualified Reinvestments Reinvestments $886 $886 $1,772 Reinvested Accrued Investment Expense $1,521 $1,521 $3,042 Subtotal $2,407 $2,407 $4,814 Qualified Savings 401(k) contributions $7,500 $ - $7,500 Subtotal $7,500 $ - $7,500 Taxes Federal Income Tax $21,449 $16,272 $37,721 State Income Tax $5,883 $4,372 $10,255 Social Security Tax - Employment $7,831 $6,200 $14,031 Medicare Taxes $2,030 $1,450 $3,480 Subtotal $37,193 $28,294 $65,487 Total Cash Outflows $112,050 $95,651 $207,701 Surplus/Deficit $30,598 $6,997 $37,595

8 Observations on Cash Flow Statement: Carl and Naomi have annual cash inflows of $245,296 and annual cash outflows of $207,701. When netting these two figure out, our firm can determine that they have an annual cash surplus of $37,595 given their current financial condition. This is a satisfactory surplus of annual inflows for Carl and Naomi which draws the conclusion that their annual income is sufficient enough to cover all their annual expenses. Areas for improvement lie within reducing discretionary spending to $31,500 and utilizing the larger surplus towards fully funding both Carl and Naomi s 401k accounts.

9 RATIO ANALYSIS

10 Observations on Ratio Analysis: As depicted through the image, Carl and Naomi do not have a sufficient annual cash savings balance to keep up with all their annual expenses. In addition, they can improve on maintaining an adequate emergency fund balance of generally 3-6 months of monetary value that would cover monthly expenses in the case of a threatening situation to health, sudden disability, or job loss. Carl and Naomi have a great liquidity ratio comprised of liquid assets well above satisfactory to cover annual expenses in reference to their trading account balance. Their savings ratio is low when considering they jointly earn $240,000 a year. Carl and Naomi have a great debt to asset ratio with assets comprising 75% to liabilities of 25%. One major recommendation we have for Carl and Naomi is to greatly reduce their discretionary expenses as this represents 24% of their total annual expenses. Finally, considering Carl and Naomi s income and tax liability, they are neutral in their effective tax rate and have a 24% marginal tax rate.

11 ASSUMPTIONS Item Assumption David - Age of Death 90 Naomi - Age of Death 90 Inflation - CPI 3% College Assumptions College inflation Years in college (per child) University of Virginia Tuition + Room & Board / Cost Per Year Today Investment rates of return : Pre-retirement (aggressive) Post-retirement (conservative) 529 Plan Mortgage Assumptions: Insurance/prop taxes built into monthly payment Home appreciation per year Mortgage paid off in 2031 Downtown Harrisburg Home Purchase Cost - Today s Dollars Property appreciation (per year) Blue Ridge Cabin: Purchase Cost - Today s Dollars Property appreciation (per year) Living Expenses: Annual increase in line with CPI Inflation assumption above Salaries: Annual increase in line with CPI Inflation assumption above 4% 4 32,700 8% 6% 8% 4% 400,000 3% 200,000 3%

12 Strengths SWOT ANALYSIS STRENGTHS, WEAKNESSES, OPPORTUNITIES, AND THREATS Saving for their future has been a priority since marriage. Good financial mindset, good behavior Employed, annual income is satisfactory ($140,000 & $100,000) Good health Saving for retirement (401k, Roth, Traditional IRA,) Well diversified, Have a home as an asset. Weaknesses Discretionary spending seems high No 529 Education Savings Plan Bank Savings (Emergency Fund) not sufficient (not 3-6 months of current spending) Lack of Insurance (Life Insurance, Disability, L/T Care Insurance) Lack of Estate Documents, (Trust, Will, Beneficiaries) Has Credit Card debt (not necessary) Cash flow of trading account, low profit Car Loan Debt Opportunities Existing funding within trading account to roll into 529 accounts Sufficient years to accumulate interest and appreciation on 529 accounts Sufficient years to accumulate interest and appreciation on qualified retirement and investment accounts Selling Home (Equity in Home currently, opportunity for Capital Gain once sold) Can adjust discretionary spending to allocate to qualified retirement accounts Conversion to a Roth IRA from a Traditional IRA Threats Death Disability Job loss Market crash Economic recession Discretionary spending Social Security could not be around in the future

13 GOAL NEEDS ANALYSIS Goal PV of $ Needed $ Needed to meet Goal In xx Years Assumed Discount /Growth Rate Pay for full college expenses - Matthew $ (107,849) 146, % Pay for full college expenses - Sarah $ (94,988) 162, % Own a home in Historic District Harrisburg, VA $ (400,000) 553, % Own a small cabin in Blue Ridge Mountains $ (200,000) 350, % Fully fund Retirement spending goal $ (512,821) $2,213, % PV of Financial Goals $ (1,315,659) PV of Current Savings & Investments Trading Account (529 Accounts) $ 107,335 Roth Accounts $ 127, (k) accounts (less: estimated 30% tax burden) $ 465,851 PV of Current Savings & Investments $ 701,067 Surplus/(Shortfall) of Current Funding ASSUMING NO ANNUITIES $ (614,591) Calculations Assuming Annuities PV of Carl s Social Security Benefit Assume $36,000 per year benefit starting at Age 70. Calculate PV of 70, then discount back to today s PV PV of Naomi s Social Security Benefit Assume $30,000 per year benefit starting at Age 70. Calculate PV of 70, then discount back to today s PV Surplus/(Shortfall) of Current Funding ASSUMING Social Security $ 445,391 $989, , % $ 371,159 $824, , % $ 201,959

14 GOAL NEEDS ANALYSIS SUMMARY Observations on Goals Needs Analysis: Carl and Naomi Berman stated several important goals upon meeting with our firm. A main concern was the question of whether fully funding both their children s college experience was possible. Another stated goal was to purchase a home in the Historic District of Harrisburg, VA at some point as well as to purchase a cabin in the Blue Ridge Mountains of Virginia to enjoy during retirement. First, our firm analyzed the amount needed to fully fund their goals at the applicable and recommended years. From that point, assumptions on the either the discount rate or inflation rate were made and used to find the present value needed to fund the Berman s goals. The present value of $1,315,659 was determined as the amount in today s dollars needed to fund the Berman s financial goals. The present value of the Berman s current savings and investments is $701,067. Accounting for the annuity of Social Security paid out, the surplus of the Berman s financial goals is $201,959.

15 LIFE INSURANCE NEEDS ANALYSIS If Carl Dies Immediate Needs Funeral Expenses $ 20,000 Pay Off Car Loan Debt $ 29,787 Pay Off Credit Card $ 7,515 Pay off Mortgage $ 314,118 Subtotal - Immediate Needs $ 371,420 Loss of Income $1,291,516 $ 1,230, years Assume 60% of Carl s Salary discounted Naomi Buy Cabin $ 350,701 College - Son $ 107, ,728 4 years out 8% discount rate College - Daughter $ 94, ,792 7 years out PV of Future Needs $ 1,845,054 Total Insurance Needs In Event of Carl Death $ 2,216,474 If Naomi Dies Immediate Needs Funeral Expenses $ 20,000 Pay Off Car Loan Debt $ 29,787 Pay Off Credit Card $ 7,515 Pay Off Mortgage $ 314,118 Subtotal - Immediate Needs $ 371,420 Loss of Income $ 1,230, years Assume 60% of Naomi s Salary discounted College - Son $ 107, ,728 4 yrs out 8% discount rate College - Daughter $ 94, ,791 7 years out PV of Future Needs $ 1,432,850 Total Insurance Needs In Event of Carl Death $ 1,804,270

16 Observations and Recommendations - Life Insurance Needs Analysis: Buy term life insurance policy in the amount of $2.25 million for a term of 20 years for Carl Berman. Buy term life insurance policy in the amount of $1.8 million for a term of 20 years for Naomi Berman. A term of 20 years will allow the Berman family to fully fund all goals and future needs in case of death of either or both spouses. Once the Bermans reach retirement age and near collecting Social Security, Life insurance will not be necessary as they will have ample qualified retirement accounts and a large trading account to fund any unexpected need.

17 FINANCIAL ANALYSIS BUDGET CASH FLOWS AND RETIREMENT INCOME Spreadsheet 1

18 Spreadsheet 2

19 Spreadsheet 3

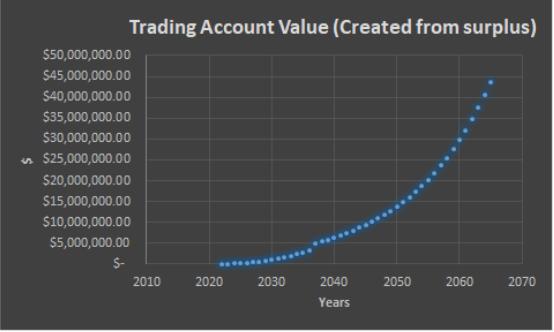

20 Observations on Financial Analysis of Budget Cash Flows and Retirement Income: This spreadsheet which was cut vertically, originally made horizontally, illustrates the complete picture of the financial life of Carl and Naomi Berman. Reaching from today in 2018 to 2065 when Naomi reaches 90 years old, it is an all encompassing view of the Berman s cash inflows, cash outflows, major expenditures, goal achievement, and qualified retirement portfolio. Spreadsheet 1, column 7 features the amount Carl and Naomi will pay into their Qualified Retirement accounts (401k and IRAs) combined, along with what the portfolios will grow to at an established 8% compounding return pre-retirement in column 8. When the Bermans retire they will have a projected $5,354,583 in their qualified retirement accounts. From there, column 9 shows the Qualified Retirement balance as they move through retirement. Post-retirement, these assets will be invested less aggressively and show growth at a 6% rate of return. Column 10, labeled as Qualified Retirement Cashed Out Amount largely shows the amount needed to withdraw to cover basic living expenses. The Bermans will have discretion to withdraw additional funds for travel, leisure, or any other use. Due to the Berman s ample income and surplus once fully funding 529 plans and qualified retirement accounts, Spreadsheet 2 displays the reopening of a trading account in 2022 to accumulate funds for real estate goals and other spending. The trading account is fully funded in 2037 when Carl and Naomi retire and assumes a return of 8% compounding. The trading account grows to a value of $43,746,451 by In column 6 of spreadsheet 2 the total 529 annual contributions for both Matthew and Sarah are shown. The estimated total annual cost of Life, Disability, and Long-term care insurance needed for the Berman family is listed in column 7 of spreadsheet 2 at $15,000 per year. Annual outflow costs are calculated in comuns 8 and 9 of spreadsheet 2. The segment that is spreadsheet 3 focuses on the running total of the surplus/deficit per year. In column 3 of spreadsheet 3, the mortgage is shown running down until it is paid off. As can be seen from this total financial picture of the Berman family, they will have the financials needed to achieve all of their goals. Carl and Naomi Berman will also have amassed a wealth of assets and will be able to spend amply in retirement and transfer wealth to their children through their estate if they so choose. See graphics on next page to (1) Represent the growth (contributions and 8% compounding return) of the Berman s qualified retirement accounts in pre-retirement. (2) The account value and growth (6% compounding return) of the Berman s qualified retirement accounts post-retirement. (3) The value of the trading account that was created from surplus funds in 2022 as it grows over time at a 8% compounding return.

21

22 INVESTMENT ANALYSIS

23 RECOMMENDATIONS Pay off all the Credit Card Debt in Year 0. Utilize existing bank savings of $30,281 as emergency savings and add to fund in Years 1-5 in increments of $13, per year to total $100,000 in Year 6 to meet a goal of 6 months in expenses. Reduce discretionary expenses from $50,000 to $31,500. Use excess to fully fund 401k accounts. Reallocate entire trading account between two 529 plans for Matthew and Sarah. Superfund Matthew s with $70,000. Superfund Sarah s with $37,338. Max out 401k contributions for both Carl and Naomi at $18,500 each. 401k and 529 contributions will generate approximately $8,000 in tax savings annually. Acquire Life, Disability, Long Term Care Insurance for both Carl and Naomi. Premiums estimated to be $15,000 annually combined. Provide referral to Insurance Broker. Arrange meeting with an Estate Planning Attorney that can provide counsel on Wills, Powers of Attorney, and all the necessary estate items to create a Revocable Living Trust. Consult with CPA to ensure all tax benefits are fully taken advantage of. Pay off the car loan in Year 4. Maintain $7,800 annually to allow for new car purchases and car maintenance. Current mortgage is paid off in Sell current home in 2029 and use equity to purchase new downtown Harrisburg, VA home outright. When Carl begins drawing on retirement accounts, buy Blue Ridge Cabin in Carl retires at age 65 in year 2037, Naomi retires at age 62. Each will begin collecting Social Security when they are 70 years old. In 2037, the year they retire they will cash out 1.25 million in order to purchase Blue Ridge Mountains cabin and provide income cushion until Social Security begins. Consider a Roth IRA conversion for current Traditional IRA accounts. Ask Carl and Naomi to bring information regarding if they are enrolled in a Pension plan at work to the next meeting. Ask Carl and Naomi to bring salary history and most recent annual Social Security Statement to next meeting.

24 APPENDIX: DETAILED CALCULATIONS COLLEGE FUNDING - DETAILED CALCULATIONS AND ASSUMPTIONS College inflation calculations: Assumption is College inflation 4% per year. Expectation is living on campus all 4 years. University of Virginia In state Tuition Today s dollars: $16,800 University of Virginia Room & Board Today s Dollars: $15,900 Total= $32,700 Son (Matthew) Calculation: N=4 i/y=4 PV=32,700 PMT=0 FV=38,254 (first year of son s college) BGN Mode: N=4 i/y= PV=? PMT=-38,784 FV=0, PV=146, <-needed at 18 will continue to grow (1.08/ *100)= Superfund Son with 70,000. What are the monthly contributions needed to have total amount for four years at son s age of 18 if investments are returning 8%? N=48 i/y=8 PV=-70,000 PMT=? FV=146,728.07, PMT= per month Daughter (Sarah) Calculation: N=7 i/4=4 PV=32,700 PMT=0 FV=43,030 (first year of daughter s college) BGN Mode: N=4 i/y= PV=? PMT=-43,030 FV=0, PV=162, <- needed at 18 will continue to grow (1.08/ *100)=3.8462

25 Superfund Daughter with 37,338. What are the monthly contributions needed to have total amount for four years at Daughter s age of 18 if investments are returning 8%? N=84 i/y=8 PV=-37,338 PMT=? FV=158,542.63, PMT= per month PURCHASE OF HARRISBURG, VA HOME - DETAILED CALCULATIONS AND ASSUMPTIONS Assumption is that Historic District Harrisburg Home Costs $400,000 in Today s Dollars. Home prices inflate at 3%. The Historic District Harrisburg Home will be purchased in 2031 when mortgage of current home is paid off and full equity of current home is realized. The estimated price is $553,693.55, but the Berman s have discretion up to $660, which was the equity in their previous home once they sold it also in N=11 i/y=3 PV=400,000 PMT=0 FV=?, FV=$553, <- Purchase Price of Downtown Harrisburg, VA Home in PURCHASE OF BLUE RIDGE CABIN - DETAILED CALCULATIONS AND ASSUMPTIONS Assumption is that Blue Ridge Log Cabin costs $200,000 in today s dollars. Home prices inflate at 3%. The Blue Ridge Log Cabin will be purchased the year the Berman s enter retirement. N=19 i/y=3 PV=200,000 PMT=0 FV=?, FV=$350, <- Purchase price of Log Cabin in SOCIAL SECURITY - ASSUMPTIONS Estimate provided based on current income. Next meeting please provide salary history and most recent annual Social Security statement.

Financial Planning Challenge 2018 Phase 1: Written Financial Planning Case Study

Financial Planning Challenge 2018 Phase 1: Written Financial Planning Case Study The first phase of the competition consists of a financial planning case study for two hypothetical clients. Students must

Financial Planning Challenge 2018 Phase 1: Written Financial Planning Case Study The first phase of the competition consists of a financial planning case study for two hypothetical clients. Students must

PFP Advisors. Financial Planning For Everyone. 123 neat st. Anywhere, USA 12345

PFP Advisors Financial Planning For Everyone. PFP Advisors 123 neat st. Anywhere, USA 12345 1 Table of Contents PFP Advisors 2 Planning Process: 2 Fees: 3 Client Information and Summary 4 Current Financial

PFP Advisors Financial Planning For Everyone. PFP Advisors 123 neat st. Anywhere, USA 12345 1 Table of Contents PFP Advisors 2 Planning Process: 2 Fees: 3 Client Information and Summary 4 Current Financial

Financial Planning Challenge 2018 Phase 1: Written Financial Planning Case Study

Financial Planning Challenge 2018 Phase 1: Written Financial Planning Case Study The first phase of the competition consists of a financial planning case study for two hypothetical clients. Students must

Financial Planning Challenge 2018 Phase 1: Written Financial Planning Case Study The first phase of the competition consists of a financial planning case study for two hypothetical clients. Students must

FINANCIAL PLAN 2018 Prepared for Carl & Naomi Berman. Patrick Yaghoobians Cecilia Mata Taylor Downhour

FINANCIAL PLAN 2018 Prepared for Carl & Naomi Berman Patrick Yaghoobians Cecilia Mata Taylor Downhour Table of Contents Table of Contents 1 Executive Summary 3 Current Financial Situation 4 Cash Inflows

FINANCIAL PLAN 2018 Prepared for Carl & Naomi Berman Patrick Yaghoobians Cecilia Mata Taylor Downhour Table of Contents Table of Contents 1 Executive Summary 3 Current Financial Situation 4 Cash Inflows

ABC FINANCIAL CORP. Retirement Plan. sample. Prepared for: John and Rachel Smith Prepared by: Justin Stanfield, RRC 2/1/2016

ABC FINANCIAL CORP. Retirement Plan sample Prepared for: John and Rachel Smith Prepared by: Justin Stanfield, RRC 2/1/2016 Dear John and Rachel Smith: Choosing to hire a professional to helping you realize

ABC FINANCIAL CORP. Retirement Plan sample Prepared for: John and Rachel Smith Prepared by: Justin Stanfield, RRC 2/1/2016 Dear John and Rachel Smith: Choosing to hire a professional to helping you realize

Wealthcare Financial Plan

Wealthcare Financial Plan PREPARED FOR: Mr. and Mrs. Client August 09, 2014 PREPARED BY: Martin A. Smith, CRPC, AIFA President, Retirement Planning Financial Advisor 4800 Hampden Lane, Suite 200 Bethesda,

Wealthcare Financial Plan PREPARED FOR: Mr. and Mrs. Client August 09, 2014 PREPARED BY: Martin A. Smith, CRPC, AIFA President, Retirement Planning Financial Advisor 4800 Hampden Lane, Suite 200 Bethesda,

p e r s o n a l p r o f i l e

va l u e s a n d g o a l s a s s e s s m e n t p e r s o n a l p r o f i l e personal profile for: Date Representative Representative Number How We Work Together Collect Information and Discuss Your Goals

va l u e s a n d g o a l s a s s e s s m e n t p e r s o n a l p r o f i l e personal profile for: Date Representative Representative Number How We Work Together Collect Information and Discuss Your Goals

BERMAN FINANCIAL PLAN

BERMAN FINANCIAL PLAN Prepared by F.L.S Financial MAY 18, 2018 F.L.S. FINANCIAL April 29, 2018 Carl and Naomi Berman Harrisonburg, VA 22081 Dear Carol and Naomi, It was a pleasure to meet you at our retirement

BERMAN FINANCIAL PLAN Prepared by F.L.S Financial MAY 18, 2018 F.L.S. FINANCIAL April 29, 2018 Carl and Naomi Berman Harrisonburg, VA 22081 Dear Carol and Naomi, It was a pleasure to meet you at our retirement

Retirement Planning 1: Basics

Personal Finance: Another Perspective Retirement Planning 1: Basics Updated 2017-03-15 1 Objectives A. Understand how retirement planning impacts your personal financial plan B. Understand the 6 principles

Personal Finance: Another Perspective Retirement Planning 1: Basics Updated 2017-03-15 1 Objectives A. Understand how retirement planning impacts your personal financial plan B. Understand the 6 principles

A Financial Primer: 12 Tips to Help Secure Your Financial Future

A Financial Primer: 12 Tips to Help Secure Your Financial Future What will you do with your earning power and what will you have to show for it in the future? Table of Contents Page Your Earning Power

A Financial Primer: 12 Tips to Help Secure Your Financial Future What will you do with your earning power and what will you have to show for it in the future? Table of Contents Page Your Earning Power

Chapter 6. Learning Objectives. Principals Applies in this Chapter. Time Value of Money

Chapter 6 Time Value of Money 1 Learning Objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate the present and future values of each. 2. Calculate the present value of

Chapter 6 Time Value of Money 1 Learning Objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate the present and future values of each. 2. Calculate the present value of

WELCOME ADDITIONAL DOCUMENTATION PERSONAL INFORMATION

WELCOME We look forward to our initial consultation and appreciate the opportunity to work with you. You may not have all the answers to this questionnaire, but please complete as much as possible. Let

WELCOME We look forward to our initial consultation and appreciate the opportunity to work with you. You may not have all the answers to this questionnaire, but please complete as much as possible. Let

Mapping Your Financial Future

Mapping Your Financial Future Profiles Forecaster Fact Finder Name (please print) Name (please print) Analysis Date Mapping Your Financial Future The best way to achieve financial freedom and peace of

Mapping Your Financial Future Profiles Forecaster Fact Finder Name (please print) Name (please print) Analysis Date Mapping Your Financial Future The best way to achieve financial freedom and peace of

THE FUTURE IS FIDUCIARY

THE FUTURE IS FIDUCIARY INSIDE: Why acting as a fiduciary and taking a lifecycle approach to wealth management can help build trust and deepen relationships POSITION YOUR PRACTICE TO UPHOLD CLIENTS BEST

THE FUTURE IS FIDUCIARY INSIDE: Why acting as a fiduciary and taking a lifecycle approach to wealth management can help build trust and deepen relationships POSITION YOUR PRACTICE TO UPHOLD CLIENTS BEST

CASE STUDY PROTECTING THE FAMILY

CASE STUDY PROTECTING THE FAMILY KNOWLEDGE EXPECTED OF: Both FPSC Level 1 Certificants and CFP Professionals Version 1.0.1, Updated 20180724 Pat, age 33, and Leslie, age 35, are married and have two children,

CASE STUDY PROTECTING THE FAMILY KNOWLEDGE EXPECTED OF: Both FPSC Level 1 Certificants and CFP Professionals Version 1.0.1, Updated 20180724 Pat, age 33, and Leslie, age 35, are married and have two children,

Your Financial Plan. John Smith PREPARED BY: PREPARED FOR: Mark and Lynda Rogers May 05, 2017

Your Financial Plan PREPARED FOR: Mark and Lynda Rogers May 05, 2017 PREPARED BY: John Smith Financial Planner Pruco Securities, LLC, doing business as Prudential Financial Planning Services Prudential,

Your Financial Plan PREPARED FOR: Mark and Lynda Rogers May 05, 2017 PREPARED BY: John Smith Financial Planner Pruco Securities, LLC, doing business as Prudential Financial Planning Services Prudential,

Chapter 26. Retirement Planning Basics 26. (1) Introduction

Introduction") 26. (1) Introduction People are living longer in modern times than they did in the past. Experts project that as life spans continue to increase, the average individual will spend between 20 and 30 years

26. (1) Introduction People are living longer in modern times than they did in the past. Experts project that as life spans continue to increase, the average individual will spend between 20 and 30 years

INVESTMENT POLICY GUIDANCE REPORT. Living in Retirement. A Successful Foundation

INVESTMENT POLICY GUIDANCE REPORT Living in Retirement A Successful Foundation Developing Your The process for creating a strategy Plan for the Expected Your Retirement Journey It all starts with you.

INVESTMENT POLICY GUIDANCE REPORT Living in Retirement A Successful Foundation Developing Your The process for creating a strategy Plan for the Expected Your Retirement Journey It all starts with you.

WHETHER YOUR RETIREMENT IS 40 YEARS AWAY OR ON THE HORIZON, IT IS IMPORTANT TO TAKE STOCK OF YOUR SITUATION AND TAKE CHARGE.

WHETHER YOUR RETIREMENT IS 40 YEARS AWAY OR ON THE HORIZON, IT IS IMPORTANT TO TAKE STOCK OF YOUR SITUATION AND TAKE CHARGE. Industry professionals estimate that some Americans will spend nearly one third

WHETHER YOUR RETIREMENT IS 40 YEARS AWAY OR ON THE HORIZON, IT IS IMPORTANT TO TAKE STOCK OF YOUR SITUATION AND TAKE CHARGE. Industry professionals estimate that some Americans will spend nearly one third

Roth Conversion Tax Idea

Roth Conversion Tax Idea The Concept: Most people do not want to convert to a Roth IRA because of the conversion tax. This program shows the advantages of a surviving spouse using the proceeds of a life

Roth Conversion Tax Idea The Concept: Most people do not want to convert to a Roth IRA because of the conversion tax. This program shows the advantages of a surviving spouse using the proceeds of a life

Financial Plan ADVICENT SAMPLE PREPARED BY: PREPARED FOR: John and Jane Smith May 05, Christopher Moser (414)

") Financial Plan PREPARED FOR: John and Jane Smith May 05, 2014 PREPARED BY: Christopher Moser (414) 555-5555 Table of Contents Cover Page Table of Contents Financial Snapshot Net Worth Summary - Net Worth

Financial Plan PREPARED FOR: John and Jane Smith May 05, 2014 PREPARED BY: Christopher Moser (414) 555-5555 Table of Contents Cover Page Table of Contents Financial Snapshot Net Worth Summary - Net Worth

Building a bridge to the future

An Educational Guide for Families and Individuals Building a bridge to the future Personalized Trust and Wealth Management Services Financial Strategies Managing the details of a friend or family member

An Educational Guide for Families and Individuals Building a bridge to the future Personalized Trust and Wealth Management Services Financial Strategies Managing the details of a friend or family member

A GUIDE TO PREPARING FOR RETIREMENT

A GUIDE TO PREPARING FOR RETIREMENT MaineSaves A Guide to Preparing for Retirement MaineSaves, the State of Maine s voluntary retirement savings plan, is designed to help you move forward on your journey

A GUIDE TO PREPARING FOR RETIREMENT MaineSaves A Guide to Preparing for Retirement MaineSaves, the State of Maine s voluntary retirement savings plan, is designed to help you move forward on your journey

Investment Planning Throughout Retirement

Select Portfolio Management, Inc. David M. Jones, MBA Wealth Advisor 120 Vantis, Suite 430 Aliso Viejo, CA 92656 949-975-7900 dave.jones@selectportfolio.com www.selectportfolio.com Investment Planning

Select Portfolio Management, Inc. David M. Jones, MBA Wealth Advisor 120 Vantis, Suite 430 Aliso Viejo, CA 92656 949-975-7900 dave.jones@selectportfolio.com www.selectportfolio.com Investment Planning

RBC retirement income planning process

Page 1 of 6 RBC retirement income planning process Create income for your retirement At RBC Wealth Management, we believe managing your wealth to produce an income during retirement is fundamentally different

Page 1 of 6 RBC retirement income planning process Create income for your retirement At RBC Wealth Management, we believe managing your wealth to produce an income during retirement is fundamentally different

USING IRA ASSETS TO ADDRESS YOUR WEALTH TRANSFER GOALS

U.S. TRUST FIDUCIARY SERVICES FOR MERRILL LYNCH CLIENTS USING IRA ASSETS TO ADDRESS YOUR WEALTH TRANSFER GOALS Trusteed IRAs from U.S. Trust WHAT S INSIDE Support from Merrill Lynch and U.S. Trust Beyond

U.S. TRUST FIDUCIARY SERVICES FOR MERRILL LYNCH CLIENTS USING IRA ASSETS TO ADDRESS YOUR WEALTH TRANSFER GOALS Trusteed IRAs from U.S. Trust WHAT S INSIDE Support from Merrill Lynch and U.S. Trust Beyond

Introduction. Personal Information. Contact Information. Home Address. Title. First Name. Last Name SSN. Date of Birth. Gender.

Introduction The information you provide will be used to create your financial plan. Your advisor will show you where you currently stand financially and if you are estimated to meet your financial goals

Introduction The information you provide will be used to create your financial plan. Your advisor will show you where you currently stand financially and if you are estimated to meet your financial goals

Mile Marker CONVERSATIONS RETIREMENT ROADMAP TO. Issued by Pruco Life Insurance Company and by Pruco Life Insurance Company of New Jersey.

Mile Marker CONVERSATIONS ROADMAP TO RETIREMENT Issued by Pruco Life Insurance Company and by Pruco Life Insurance Company of New Jersey. 0287505-00003-00 Ed. 04/2017 Knowing what s down the road can help

Mile Marker CONVERSATIONS ROADMAP TO RETIREMENT Issued by Pruco Life Insurance Company and by Pruco Life Insurance Company of New Jersey. 0287505-00003-00 Ed. 04/2017 Knowing what s down the road can help

JOURNEY. Planning for Financial Security SAVING : INVESTING : PLANNING

JOURNEY Planning for Financial Security SAVING : INVESTING : PLANNING Agenda 1 Cash management 2 Investment planning 3 Tax planning 4 Risk management 5 Retirement planning 6 Estate planning SAVING : INVESTING

JOURNEY Planning for Financial Security SAVING : INVESTING : PLANNING Agenda 1 Cash management 2 Investment planning 3 Tax planning 4 Risk management 5 Retirement planning 6 Estate planning SAVING : INVESTING

SERVING A STRONG FUTURE

ENROLLMENT OVERVIEW SERVING A STRONG FUTURE HPOU 457 DEFERRED COMPENSATION PLAN PRODUCTS AND FINANCIAL SERVICES PROVIDED BY AMERICAN UNITED LIFE INSURANCE COMPANY, A ONEAMERICA COMPANY PREPARE FOR YOUR

ENROLLMENT OVERVIEW SERVING A STRONG FUTURE HPOU 457 DEFERRED COMPENSATION PLAN PRODUCTS AND FINANCIAL SERVICES PROVIDED BY AMERICAN UNITED LIFE INSURANCE COMPANY, A ONEAMERICA COMPANY PREPARE FOR YOUR

Worksheet Your Current Investment

Worksheet Your Current Investment Your Current Investment Worksheet Your Current Investment Worksheet How you are invested today checklist Your investment strategy will help determine your ability to reach

Worksheet Your Current Investment Your Current Investment Worksheet Your Current Investment Worksheet How you are invested today checklist Your investment strategy will help determine your ability to reach

A Planning Guide for Participants Nearing Retirement

A Planning Guide for Participants Nearing Retirement What are your plans for retirement? For some, retirement is about living out dreams they didn t have time for during their working years. For others,

A Planning Guide for Participants Nearing Retirement What are your plans for retirement? For some, retirement is about living out dreams they didn t have time for during their working years. For others,

Full-spectrum wealth planning Cover Subhead

Transition and Trust Cover Headline Full-spectrum wealth planning Cover Subhead Wealth Transition Team Planning for wealth transition is about rolling up the complex dynamics of your wealth your retirement

Transition and Trust Cover Headline Full-spectrum wealth planning Cover Subhead Wealth Transition Team Planning for wealth transition is about rolling up the complex dynamics of your wealth your retirement

Rejuvenate Your Retirement

Rejuvenate Your Retirement An Educational Course for Retirees Now being conducted at Rollins College Location Dates & Times Cornell Hall for the Social Sciences, Rm. 134 Thursdays 1000 Holt Avenue March

Rejuvenate Your Retirement An Educational Course for Retirees Now being conducted at Rollins College Location Dates & Times Cornell Hall for the Social Sciences, Rm. 134 Thursdays 1000 Holt Avenue March

Prepared For: Charles Cameron and Mary Johnson. Prepared by: Brian Kobel Oltis Software LLC

Prepared For: Charles Cameron and Mary Johnson Prepared by: Brian Kobel Oltis Software LLC 4035 North St Tucson, AZ 85712 Email: bkobel@financelogix.com Disclosures Disclosures This Investment Analysis

Prepared For: Charles Cameron and Mary Johnson Prepared by: Brian Kobel Oltis Software LLC 4035 North St Tucson, AZ 85712 Email: bkobel@financelogix.com Disclosures Disclosures This Investment Analysis

Enrollment Overview. Heart of CarDon LLC 401(k) Plan

Plan") Enrollment Overview Heart of CarDon LLC 401(k) Plan RETIREMENT PLAN ADMINISTRATIVE AND RECORDKEEPING SERVICES PROVIDED BY MCCREADY AND KEENE, INC., A ONEAMERICA COMPANY Family caring for Family As an employee

Enrollment Overview Heart of CarDon LLC 401(k) Plan RETIREMENT PLAN ADMINISTRATIVE AND RECORDKEEPING SERVICES PROVIDED BY MCCREADY AND KEENE, INC., A ONEAMERICA COMPANY Family caring for Family As an employee

Viewpoint. Using a Trusteed IRA to Protect, Preserve and Control Your IRA Assets

Viewpoint NATALIE B. CHOATE JULY 2017 Using a Trusteed IRA to Protect, Preserve and Control Your IRA Assets The first IRAs were created in 1975 and contained no more than that year s maximum contribution

Viewpoint NATALIE B. CHOATE JULY 2017 Using a Trusteed IRA to Protect, Preserve and Control Your IRA Assets The first IRAs were created in 1975 and contained no more than that year s maximum contribution

Getting ready to retire!

Getting ready to retire! This workbook will help you take actionable steps toward a more secure retirement and provide you with important facts and information you ll need as you continue to plan for a

Getting ready to retire! This workbook will help you take actionable steps toward a more secure retirement and provide you with important facts and information you ll need as you continue to plan for a

4/3/2017. Charting Your Course: A financial guide for women. Today s agenda. Savings challenges women may face. Alicia Brady April 11, 2107

SAVING FOR LIFE S MILESTONES: A TIAA FINANCIAL ESSENTIALS WORKSHOP Charting Your Course: A financial guide for women Alicia Brady April 11, 2107 Today s agenda Evaluate your financial health Set financial

SAVING FOR LIFE S MILESTONES: A TIAA FINANCIAL ESSENTIALS WORKSHOP Charting Your Course: A financial guide for women Alicia Brady April 11, 2107 Today s agenda Evaluate your financial health Set financial

HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR SINGLE, DIVORCED, AND WIDOWED PEOPLE (New York)

") HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR SINGLE, DIVORCED, AND WIDOWED PEOPLE - 2018 (New York) I. Purposes of Estate Planning. A. Providing for the distribution and management of your assets

HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR SINGLE, DIVORCED, AND WIDOWED PEOPLE - 2018 (New York) I. Purposes of Estate Planning. A. Providing for the distribution and management of your assets

HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR MARRIED COUPLES 2019 (New York)

") HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR MARRIED COUPLES 2019 (New York) I. Purposes of Estate Planning. A. Providing for the distribution and management of your assets after your death. B.

HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR MARRIED COUPLES 2019 (New York) I. Purposes of Estate Planning. A. Providing for the distribution and management of your assets after your death. B.

A nd Edition, (Updated: July 25, 2011)

") A-201 2 nd Edition, 2008 (Updated: July 25, 2011) A201 - T1-2 28 Taxation Concepts pertaining to Insurance of Persons The actual amount of assessable dividends 6 is grossed-up by 45% to arrive at a taxable

A-201 2 nd Edition, 2008 (Updated: July 25, 2011) A201 - T1-2 28 Taxation Concepts pertaining to Insurance of Persons The actual amount of assessable dividends 6 is grossed-up by 45% to arrive at a taxable

Personal Financial Plan

Personal Financial Plan Pete and Carrie Mitchell 918 Richmond Street Toronto, Ontario M5N 1V5 Disclaimer This document has been prepared to assist in the analysis of your current financial position, thereby

Personal Financial Plan Pete and Carrie Mitchell 918 Richmond Street Toronto, Ontario M5N 1V5 Disclaimer This document has been prepared to assist in the analysis of your current financial position, thereby

Planning for an Acquisition

Planning for an Acquisition 1 Before Exit Step 1 Establish a Basic Estate Plan Step 2 Outline Your Financial Goals and State of Affairs Step 3 Pre-transition Planning 2 After Exit Step 4 Minimize Tax Impact

Planning for an Acquisition 1 Before Exit Step 1 Establish a Basic Estate Plan Step 2 Outline Your Financial Goals and State of Affairs Step 3 Pre-transition Planning 2 After Exit Step 4 Minimize Tax Impact

Where should my money go First? Here s advice from the financial professionals at Schwab.

Where should my money go First? Here s advice from the financial professionals at Schwab. Start with the basics. In an ideal world, you d have enough money to pay all your bills and save for retirement

Where should my money go First? Here s advice from the financial professionals at Schwab. Start with the basics. In an ideal world, you d have enough money to pay all your bills and save for retirement

INSURANCE PRODUCTS offered through: Page 1 of 16. Presented by: Judson D. MallardCFP, ChFC, CFS

Disclosure Notice The information that follows is intended to serve as a basis for further discussion with your financial, legal, tax and/or accounting advisors. It is not a substitute for competent advice

Disclosure Notice The information that follows is intended to serve as a basis for further discussion with your financial, legal, tax and/or accounting advisors. It is not a substitute for competent advice

Your Financial Well-Being Assessment

Your Financial Well-Being Assessment Congratulations! You are on your way to a better understanding of financial well-being. Downloading this guide is the first step. Now, take some time to review and

Your Financial Well-Being Assessment Congratulations! You are on your way to a better understanding of financial well-being. Downloading this guide is the first step. Now, take some time to review and

LIFETIME INCOME CASE STUDY

Retirement Preparedness: Why 401(k) s Are Essential LIFETIME INCOME CASE STUDY Presented by Financial Sense Advisors, Inc. Registered Investment Advisor Austin & Gloria Kaiser Important Notice: This is

Retirement Preparedness: Why 401(k) s Are Essential LIFETIME INCOME CASE STUDY Presented by Financial Sense Advisors, Inc. Registered Investment Advisor Austin & Gloria Kaiser Important Notice: This is

Helping you reach the future you deserve. The Scripps Health 401(a) Retirement Savings Plan Enrollment Guide

Retirement Savings Plan Enrollment Guide") Helping you reach the future you deserve The Scripps Health 401(a) Retirement Savings Plan Enrollment Guide Invest some of what you earn today for what you plan to accomplish tomorrow. It is our pleasure

Helping you reach the future you deserve The Scripps Health 401(a) Retirement Savings Plan Enrollment Guide Invest some of what you earn today for what you plan to accomplish tomorrow. It is our pleasure

Financial Strategies. From Legal Settlement to. 2 What are Your Hopes and Dreams? 4 Our Approach in Action. 6 A Single Source

2 What are Your Hopes and Dreams? 4 How We Work With Clients 4 Our Approach in Action 6 A Single Source From Legal Settlement to Financial Strategies what are your hopes and dreams? A wrongful death or

2 What are Your Hopes and Dreams? 4 How We Work With Clients 4 Our Approach in Action 6 A Single Source From Legal Settlement to Financial Strategies what are your hopes and dreams? A wrongful death or

Annuities. Stretch Your Assets. Create A Lasting Legacy by Stretching Your IRA Fixed Annuities

Annuities Stretch Your Assets Create A Lasting Legacy by Stretching Your IRA Fixed Annuities There are times in our lives we wish would never end... like special moments with family and friends. There

Annuities Stretch Your Assets Create A Lasting Legacy by Stretching Your IRA Fixed Annuities There are times in our lives we wish would never end... like special moments with family and friends. There

YOUR GUIDE TO GETTING STARTED

Colorado State University 403(b) Plan, # 54192 Invest in your retirement and yourself today, with help from the CSU 403(b) Plan and Fidelity. YOUR GUIDE TO GETTING STARTED Invest some of what you earn

Colorado State University 403(b) Plan, # 54192 Invest in your retirement and yourself today, with help from the CSU 403(b) Plan and Fidelity. YOUR GUIDE TO GETTING STARTED Invest some of what you earn

PersonalFinancialPlan

PersonalFinancialPlan Prepared Exclusively for: Frank and Kathy Married Fairport, New York Prepared by: Kerry Winslow, CFP Fairport, New York October 27, 2004 Linsco/Private Ledger - A Registered Investment

PersonalFinancialPlan Prepared Exclusively for: Frank and Kathy Married Fairport, New York Prepared by: Kerry Winslow, CFP Fairport, New York October 27, 2004 Linsco/Private Ledger - A Registered Investment

YOUR GUIDE TO GETTING STARTED

Albert Einstein College of Medicine, Inc. 403(b) Retirement Income Plan Invest in your retirement and yourself today, with help from the Einstein Retirement Plan and Fidelity. YOUR GUIDE TO GETTING STARTED

Albert Einstein College of Medicine, Inc. 403(b) Retirement Income Plan Invest in your retirement and yourself today, with help from the Einstein Retirement Plan and Fidelity. YOUR GUIDE TO GETTING STARTED

ORGANIZE, PLAN, AND OWN YOUR FUTURE

Be In The Front Seat ORGANIZE, PLAN, AND OWN YOUR FUTURE Making financial health a priority for women HERE S WHAT WE LL COVER: Why now? Getting organized Building your plan Owning your future 2 WHEN IT

Be In The Front Seat ORGANIZE, PLAN, AND OWN YOUR FUTURE Making financial health a priority for women HERE S WHAT WE LL COVER: Why now? Getting organized Building your plan Owning your future 2 WHEN IT

Personal Financial Plan

Personal Financial Plan Pete and Carrie Mitchell 918 Richmond Street Toronto, Ontario M5N 1V5 Disclaimer This document has been prepared to assist in the analysis of your current financial position, thereby

Personal Financial Plan Pete and Carrie Mitchell 918 Richmond Street Toronto, Ontario M5N 1V5 Disclaimer This document has been prepared to assist in the analysis of your current financial position, thereby

Tom and Jane Lundquist

Financial Goal Plan Tom and Jane Lundquist Prepared by: Joe Advisor Financial Consultant December 2, 216 Table Of Contents Expectations and Concerns 1 Summary of Goals and Resources Personal Information

Financial Goal Plan Tom and Jane Lundquist Prepared by: Joe Advisor Financial Consultant December 2, 216 Table Of Contents Expectations and Concerns 1 Summary of Goals and Resources Personal Information

HOW TO ANALYZE A TAX RETURN FOR ELDER LAW ISSUES

HOW TO ANALYZE A TAX RETURN FOR ELDER LAW ISSUES By Keith R. Miles, Esq. The Law Office Of Keith R. Miles, LLC 1755 North Brown Road Suite 200 Lawrenceville, GA 30043 Phone: 1 (888) 758-9640 www.milestaxattorney.com

HOW TO ANALYZE A TAX RETURN FOR ELDER LAW ISSUES By Keith R. Miles, Esq. The Law Office Of Keith R. Miles, LLC 1755 North Brown Road Suite 200 Lawrenceville, GA 30043 Phone: 1 (888) 758-9640 www.milestaxattorney.com

Plan for Your Future. Morgan Stanley Can Help You Achieve Your Financial Goals

Plan for Your Future Morgan Stanley Can Help You Achieve Your Financial Goals 2 MORGAN STANLEY 2016 What Are Your Hopes and Dreams? REGARDLESS OF WHAT STAGE YOUR LIFE IS IN moving ahead in your career,

Plan for Your Future Morgan Stanley Can Help You Achieve Your Financial Goals 2 MORGAN STANLEY 2016 What Are Your Hopes and Dreams? REGARDLESS OF WHAT STAGE YOUR LIFE IS IN moving ahead in your career,

Wealth Management. Organize Analyze Plan

Wealth Management Organize Analyze Plan Who We Are Go confidently in the direction of your dreams. Live the life you have imagined. HENRY DAVID THOREAU We are your financial advocate. We take the time

Wealth Management Organize Analyze Plan Who We Are Go confidently in the direction of your dreams. Live the life you have imagined. HENRY DAVID THOREAU We are your financial advocate. We take the time

REPORT PREPARED FOR Client Sample & Co-client Sample

REPORT PREPARED FOR Client Sample & Co-client Sample by Steve Harvey Steve Harvey LLC Generated on 01/30/2019 Steve Harvey 119 Oronoco Street, Suite 102 Alexandria, Virginia 22314 steve@steveharveyllc.com

REPORT PREPARED FOR Client Sample & Co-client Sample by Steve Harvey Steve Harvey LLC Generated on 01/30/2019 Steve Harvey 119 Oronoco Street, Suite 102 Alexandria, Virginia 22314 steve@steveharveyllc.com

Discover What s Possible

Discover What s Possible Inflation Protector Variable Annuity Inflation Protector Variable Annuity In retirement, you have many ways to spend your time traveling, enjoying hobbies, volunteering, or sharing

Discover What s Possible Inflation Protector Variable Annuity Inflation Protector Variable Annuity In retirement, you have many ways to spend your time traveling, enjoying hobbies, volunteering, or sharing

LIFETIME INCOME CASE STUDY

Real Estate in 2018: The Land of Opportunity? LIFETIME INCOME CASE STUDY Presented by Financial Sense Advisors, Inc. Registered Investment Advisor Stan & Kate Barnett Important Notice: This is a hypothetical

Real Estate in 2018: The Land of Opportunity? LIFETIME INCOME CASE STUDY Presented by Financial Sense Advisors, Inc. Registered Investment Advisor Stan & Kate Barnett Important Notice: This is a hypothetical

Enrollment Overview. for SoutheastHEALTH Retirement Plan. Prepare for the next chapter in life

Prepare for the next chapter in life The Difference is How You re Treated More information available at www.sehealthretirement.com Enrollment Overview for SoutheastHEALTH Retirement Plan Products and financial

Prepare for the next chapter in life The Difference is How You re Treated More information available at www.sehealthretirement.com Enrollment Overview for SoutheastHEALTH Retirement Plan Products and financial

SAMPLE. John and Jane Smith. LifeView Financial Plan. Prepared by: John Advisor, CFP Financial Advisor. January 04, 2016

LifeView Financial Plan John and Jane Smith Prepared by: John Advisor, CFP Financial Advisor January 04, 2016 Table Of Contents IMPORTANT DISCLOSURE INFORMATION 1-6 Summary of Goals and Resources Personal

LifeView Financial Plan John and Jane Smith Prepared by: John Advisor, CFP Financial Advisor January 04, 2016 Table Of Contents IMPORTANT DISCLOSURE INFORMATION 1-6 Summary of Goals and Resources Personal

FINANCIAL ANALYSIS. Designed For: Martin and Mary Moderate. April 24, 2017

FINANCIAL ANALYSIS Designed For: Martin and Mary Moderate April 24, 217 Prepared By: David M Stitt, CLU, ChFC, CEP, CFP, RFC, CSA, CRFA, MR Financial Planning Building 31 Milton Road Middletown, OH 4542

FINANCIAL ANALYSIS Designed For: Martin and Mary Moderate April 24, 217 Prepared By: David M Stitt, CLU, ChFC, CEP, CFP, RFC, CSA, CRFA, MR Financial Planning Building 31 Milton Road Middletown, OH 4542

CARING FOR TOMORROW BEGINS TODAY

CARING FOR TOMORROW BEGINS TODAY ENROLLMENT OVERVIEW FOR CRAWFORD MEMORIAL HOSPITAL RETIREMENT PLAN TO PROVIDE CARE FOR YOUR TOMORROW, YOU CAN BEGIN TODAY. What do you see yourself doing when you retire?

CARING FOR TOMORROW BEGINS TODAY ENROLLMENT OVERVIEW FOR CRAWFORD MEMORIAL HOSPITAL RETIREMENT PLAN TO PROVIDE CARE FOR YOUR TOMORROW, YOU CAN BEGIN TODAY. What do you see yourself doing when you retire?

Individual income tax provision highlights

Legislative Update Tax Cuts and Jobs Act Individual income tax provision highlights On December 22, 2017, President Trump signed into law the Tax Cuts and Jobs Act (P.L. 115-97). Highlights of the key

Legislative Update Tax Cuts and Jobs Act Individual income tax provision highlights On December 22, 2017, President Trump signed into law the Tax Cuts and Jobs Act (P.L. 115-97). Highlights of the key

TO FOCUS ON RETIREMENT

The Right Time TO FOCUS ON RETIREMENT Equian LLC Retirement Savings Plan Enrollment Overview REVERSED HEADLINE PRODUCTS AND FINANCIAL SERVICES PROVIDED BY AMERICAN UNITED LIFE INSURANCE COMPANY, A ONEAMERICA

The Right Time TO FOCUS ON RETIREMENT Equian LLC Retirement Savings Plan Enrollment Overview REVERSED HEADLINE PRODUCTS AND FINANCIAL SERVICES PROVIDED BY AMERICAN UNITED LIFE INSURANCE COMPANY, A ONEAMERICA

Retirement Tax Strategies for the Affluent. Using Cash Value Life Insurance to Help Design a Secure Future

Retirement Tax Strategies for the Affluent Using Cash Value Life Insurance to Help Design a Secure Future Retirement Tax Strategies for the Affluent Page 1 17-76A In this Guide 1. Introduction 2. Discover

Retirement Tax Strategies for the Affluent Using Cash Value Life Insurance to Help Design a Secure Future Retirement Tax Strategies for the Affluent Page 1 17-76A In this Guide 1. Introduction 2. Discover

ADVISOR HELPING INDIVIDUALS ACCUMULATE WEALTH AND REDUCE TAXES

ADVISOR HELPING INDIVIDUALS ACCUMULATE WEALTH AND REDUCE TAXES RETIREMENT PLANNING FOR IRA OWNERS AND 401(K) PARTICIPANTS By James Lange, Esq., CPA IRA owners and 401(k) participants face a staggering

ADVISOR HELPING INDIVIDUALS ACCUMULATE WEALTH AND REDUCE TAXES RETIREMENT PLANNING FOR IRA OWNERS AND 401(K) PARTICIPANTS By James Lange, Esq., CPA IRA owners and 401(k) participants face a staggering

Joe and Jane Coastal Member

Retirement Plan Joe and Jane Coastal Member Prepared by: Catherine Bryant Financial Advisor Coastal Wealth Management/CUSO FS January 31, 2018 Table Of Contents Personal Information and Summary of Financial

Retirement Plan Joe and Jane Coastal Member Prepared by: Catherine Bryant Financial Advisor Coastal Wealth Management/CUSO FS January 31, 2018 Table Of Contents Personal Information and Summary of Financial

Total Wealth Management

Total Wealth Management Independent, objective advice for building lifelong wealth. Complete integration of all aspects of your financial life, giving you peace of mind to pursue your dreams. Simplify

Total Wealth Management Independent, objective advice for building lifelong wealth. Complete integration of all aspects of your financial life, giving you peace of mind to pursue your dreams. Simplify

ILLINOIS 529 COLLEGE SAVINGS PLAN

ILLINOIS 529 COLLEGE SAVINGS PLAN Your children deserve an opportunity for higher education, and you can help them achieve it. Whether your kids are learning to walk or are in their teenage years, it

ILLINOIS 529 COLLEGE SAVINGS PLAN Your children deserve an opportunity for higher education, and you can help them achieve it. Whether your kids are learning to walk or are in their teenage years, it

Using the Participant Web Site

Using the Participant Web Site https://benefits.paychex.com Participant Resources This site was built with plan participants in mind. With ease, they can: enroll in the plan view account balances get answers

Using the Participant Web Site https://benefits.paychex.com Participant Resources This site was built with plan participants in mind. With ease, they can: enroll in the plan view account balances get answers

CHAPTER 4. The Time Value of Money. Chapter Synopsis

CHAPTER 4 The Time Value of Money Chapter Synopsis Many financial problems require the valuation of cash flows occurring at different times. However, money received in the future is worth less than money

CHAPTER 4 The Time Value of Money Chapter Synopsis Many financial problems require the valuation of cash flows occurring at different times. However, money received in the future is worth less than money

Secure Your Retirement

4 Creating a Framework 6 Case Study #1: The Dunbars 8 Case Study #2: Professor Harrison 9 Case Study #3: Jane Leahy Advanced Annuity Strategies to Help Secure Your Retirement The Paradigm Has Shifted.

4 Creating a Framework 6 Case Study #1: The Dunbars 8 Case Study #2: Professor Harrison 9 Case Study #3: Jane Leahy Advanced Annuity Strategies to Help Secure Your Retirement The Paradigm Has Shifted.

Copyright 2015 by the McGraw-Hill Education (Asia). All rights reserved.

. All rights reserved.") Copyright 2015 by the McGraw-Hill Education (Asia). All rights reserved. Key Concepts and Skills Be able to compute: The future value of an investment made today The present value of cash to be received

Copyright 2015 by the McGraw-Hill Education (Asia). All rights reserved. Key Concepts and Skills Be able to compute: The future value of an investment made today The present value of cash to be received

You ve helped others plan for their future now SourceAmerica can help you prepare for yours.

SourceAmerica Retirement Plan You ve helped others plan for their future now SourceAmerica can help you prepare for yours. ENROLLMENT OVERVIEW PRODUCTS AND FINANCIAL SERVICES PROVIDED BY AMERICAN UNITED

SourceAmerica Retirement Plan You ve helped others plan for their future now SourceAmerica can help you prepare for yours. ENROLLMENT OVERVIEW PRODUCTS AND FINANCIAL SERVICES PROVIDED BY AMERICAN UNITED

Financial Plan. Rona Birenbaum, CFP. PREPARED FOR: October 03, 2017 PREPARED BY: Financial Planner Viviplan Toronto, Ontario (416)

") Financial Plan PREPARED FOR: October 03, 2017 PREPARED BY: Rona Birenbaum, CFP Financial Planner Viviplan Toronto, Ontario (416) 363-8500 Table of Contents Cover Page 1 Table of Contents 2 Objectives 3

Financial Plan PREPARED FOR: October 03, 2017 PREPARED BY: Rona Birenbaum, CFP Financial Planner Viviplan Toronto, Ontario (416) 363-8500 Table of Contents Cover Page 1 Table of Contents 2 Objectives 3

INVESTING FOR YOUR FINANCIAL FUTURE

INVESTING FOR YOUR FINANCIAL FUTURE Saving now, while time is on your side, can help provide you with freedom to do what you want later in life. B B INVESTING FOR YOUR FINANCIAL FUTURE YOUR FINANCIAL FUTURE

INVESTING FOR YOUR FINANCIAL FUTURE Saving now, while time is on your side, can help provide you with freedom to do what you want later in life. B B INVESTING FOR YOUR FINANCIAL FUTURE YOUR FINANCIAL FUTURE

Understanding Your Priorities

Understanding Your Priorities The following questionnaire is designed to help us better understand you and your financial priorities. Please indicate the importance of each item by checking the appropriate

Understanding Your Priorities The following questionnaire is designed to help us better understand you and your financial priorities. Please indicate the importance of each item by checking the appropriate

YOUR GUIDE TO GETTING STARTED

Engility Master Savings Plan Invest in your retirement and yourself today, with help from Engility Master Savings Plan and Fidelity. YOUR GUIDE TO GETTING STARTED Invest some of what you earn today for

Engility Master Savings Plan Invest in your retirement and yourself today, with help from Engility Master Savings Plan and Fidelity. YOUR GUIDE TO GETTING STARTED Invest some of what you earn today for

FIDELITY SAMPLE A E- FOR ILLUSTRATIVE PURPOSES ONLY RETIREMENT ANALYSIS

Jake Walter 999 Main Street Anytown, USA, 01752 This sample report, including all graphic representations and data tables, is presented for illustrative purposes only. The data used in this sample report

Jake Walter 999 Main Street Anytown, USA, 01752 This sample report, including all graphic representations and data tables, is presented for illustrative purposes only. The data used in this sample report

10 Steps to a SUCCESSFUL RETIREMENT. Chris O Dell. Compliments of

10 Steps to a SUCCESSFUL RETIREMENT Compliments of Chris O Dell Are you approaching retirement? You ve probably been planning for retirement in some way, shape or form for many years. Maybe you participate

10 Steps to a SUCCESSFUL RETIREMENT Compliments of Chris O Dell Are you approaching retirement? You ve probably been planning for retirement in some way, shape or form for many years. Maybe you participate

Effective Strategies for Wealth Transfer

Effective Strategies for Wealth Transfer The Prudential Insurance Company of America, Newark, NJ. 0265295-00002-00 Ed. 02/2016 Exp. 08/04/2017 UNDERSTANDING WEALTH TRANSFER What strategy to use and when?

Effective Strategies for Wealth Transfer The Prudential Insurance Company of America, Newark, NJ. 0265295-00002-00 Ed. 02/2016 Exp. 08/04/2017 UNDERSTANDING WEALTH TRANSFER What strategy to use and when?

FINANCIAL FITNESS CENTER COURSES

Primary Subject Accounting Accounting Accounting Estate Planning Estate Planning Estate Planning ETFs ETFs Financial Institutions Tutorial Understanding the Balance Sheet Understanding the Income Statement

Primary Subject Accounting Accounting Accounting Estate Planning Estate Planning Estate Planning ETFs ETFs Financial Institutions Tutorial Understanding the Balance Sheet Understanding the Income Statement

Private Client Services. Helping preserve, grow and transfer wealth to the people and causes you care about

Private Client Services Helping preserve, grow and transfer wealth to the people and causes you care about TABLE OF CONTENTS 1 Personalized services delivered by an experienced team 3 Disciplined investment

Private Client Services Helping preserve, grow and transfer wealth to the people and causes you care about TABLE OF CONTENTS 1 Personalized services delivered by an experienced team 3 Disciplined investment

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy Effective November 2016 TABLE OF CONTENTS DISCLOSURE STATEMENT Introduction 3 Section I

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy Effective November 2016 TABLE OF CONTENTS DISCLOSURE STATEMENT Introduction 3 Section I

Rollover Strategies and IRA Distribution Rules.

Rollover Strategies and IRA Distribution Rules. Contents Protecting Your Retirement Plan Nest Egg... 1 Leaving Your Job, Keeping Your Plan Funds... 2 Understanding IRA Rollovers... 6 Understanding IRA

Rollover Strategies and IRA Distribution Rules. Contents Protecting Your Retirement Plan Nest Egg... 1 Leaving Your Job, Keeping Your Plan Funds... 2 Understanding IRA Rollovers... 6 Understanding IRA

SUMMARY PLAN DESCRIPTION FOR. Richmond Public Schools 403(b) Retirement Plan

Retirement Plan") SUMMARY PLAN DESCRIPTION FOR Richmond Public Schools 403(b) Retirement Plan 3-1-2014 Table of Contents Article 1... Introduction Article 2... General Plan Information and Key Definitions Article 3... Description

SUMMARY PLAN DESCRIPTION FOR Richmond Public Schools 403(b) Retirement Plan 3-1-2014 Table of Contents Article 1... Introduction Article 2... General Plan Information and Key Definitions Article 3... Description

10 Steps to a SUCCESSFUL RETIREMENT. Robert Trejo. Compliments of

10 Steps to a SUCCESSFUL RETIREMENT Compliments of Robert Trejo Robert Trejo Senior Managing Partner As a young child, Robert Trejo s parents immigrated from El Salvador, bringing him and his two sisters

10 Steps to a SUCCESSFUL RETIREMENT Compliments of Robert Trejo Robert Trejo Senior Managing Partner As a young child, Robert Trejo s parents immigrated from El Salvador, bringing him and his two sisters

Tax Strategies. Tax-Smart Planning for Every Stage of Life

Tax-Smart Planning for Every Stage of Life General Disclaimer This discussion is based on our understanding of the tax law as it exists as of (date). The information contained in this document is not intended

Tax-Smart Planning for Every Stage of Life General Disclaimer This discussion is based on our understanding of the tax law as it exists as of (date). The information contained in this document is not intended

Sample Comprehensive Financial Plan. Especially Prepared For: John and Jane Doe By: Brad E.S. Tinnon CERTIFIED FINANCIAL PLANNER

Sample Comprehensive Financial Plan Especially Prepared For: By: Brad E.S. Tinnon CERTIFIED FINANCIAL PLANNER September 2013 NET WORTH SUMMARY January 2011 $302,518 September 2012 $375,821 September 2013

Sample Comprehensive Financial Plan Especially Prepared For: By: Brad E.S. Tinnon CERTIFIED FINANCIAL PLANNER September 2013 NET WORTH SUMMARY January 2011 $302,518 September 2012 $375,821 September 2013

14 Reasons Why You Shouldn t Retire Early

14 Reasons Why You Shouldn t Retire Early Early retirement is a goal for many, including physicians. An extra decade or two to travel, pursue hobbies, and volunteer becomes more and more attractive, especially

14 Reasons Why You Shouldn t Retire Early Early retirement is a goal for many, including physicians. An extra decade or two to travel, pursue hobbies, and volunteer becomes more and more attractive, especially

Rejuvenate Your Retirement An Educational Course for Retirees

Rejuvenate Your Retirement An Educational Course for Retirees Now being conducted at Location Dates & Times Tuesdays 120 Bloomfield Avenue October 3 & 10 Caldwell, NJ 07006 9:30 a.m. to 11:30 a.m. or Thursdays

Rejuvenate Your Retirement An Educational Course for Retirees Now being conducted at Location Dates & Times Tuesdays 120 Bloomfield Avenue October 3 & 10 Caldwell, NJ 07006 9:30 a.m. to 11:30 a.m. or Thursdays

Retirement Planning Month

Taylor Financial Group s Monthly Planning Letter March 2018 Retirement Planning Month March is Retirement Planning Month at Taylor Financial Group According to recent Gallup polls, the average American

Taylor Financial Group s Monthly Planning Letter March 2018 Retirement Planning Month March is Retirement Planning Month at Taylor Financial Group According to recent Gallup polls, the average American

Allen & Betty Abbett. Personal Financial Analysis. Sample Financial Plan - TOTAL Goal-Based Planning

Mar 29, 2018 Personal Financial Analysis Allen & Betty Abbett John Smith Asset Advisors Example, LLC A Registered Investment Advisor 2430 NW Professional Drive Corvallis, OR 97330 877-421-9815 www.moneytree.com

Mar 29, 2018 Personal Financial Analysis Allen & Betty Abbett John Smith Asset Advisors Example, LLC A Registered Investment Advisor 2430 NW Professional Drive Corvallis, OR 97330 877-421-9815 www.moneytree.com

Please understand that this podcast is not intended to be legal advice. As always, you should contact your WEALTH TRANSFER STRATEGIES

WEALTH TRANSFER STRATEGIES Hello and welcome. Northern Trust is proud to sponsor this podcast, Wealth Transfer Strategies, the third in a series based on our book titled Legacy: Conversations about Wealth

WEALTH TRANSFER STRATEGIES Hello and welcome. Northern Trust is proud to sponsor this podcast, Wealth Transfer Strategies, the third in a series based on our book titled Legacy: Conversations about Wealth

HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR MARRIED COUPLES 2018 (Connecticut)

") HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR MARRIED COUPLES 2018 (Connecticut) I. Purposes of Estate Planning. A. Providing for the distribution and management of your assets after your death.

HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR MARRIED COUPLES 2018 (Connecticut) I. Purposes of Estate Planning. A. Providing for the distribution and management of your assets after your death.