V aconnor DAVIES ACCOUNTANTS ANO ADVISORS TOWNSHIP OF NORTH BERGEN HUDSON COUNTY, NEW JERSEY REPORT ON EXAMINATION OF ACCOUNTS FOR THE YEARS ENDED

|

|

|

- Michael Richard

- 5 years ago

- Views:

Transcription

1

2 HUDSON COUNTY, NEW JERSEY REPORT ON EXAMINATION OF ACCOUNTS FOR THE YEARS ENDED DECEMBER 31, 2016 AND 2015 r'epkr V aconnor DAVIES ACCOUNTANTS ANO ADVISORS

3 COUNTY OF HUDSON, NEW JERSEY CONTENTS PARTI Independent Auditor's Report Report on Internal Control Over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statement Performed in Accordance with Government Auditing Standards FINANCIAL STATEMENTS CURRENT FUND EXHIBIT A A-1 A-2 A-2a A-2b A-2c A-3 Comparative Balance Sheets.... Comparative Statement of Operations and Change in Fund Balance.... Statement of Revenues Statement of Revenue - Analysis of Miscellaneous Revenue.... Statement of Revenue - Analysis of Taxes..... Statement of Revenue - Analysis of Nonbudget Revenue Statement of Expenditures.... PAGE TRUST FUND B B-1 Comparative Balance Sheets Statement of Trust Fund Balance GENERAL CAPITAL FUND c C-1 Comparative Balance Sheets Statement of Fund Balance PUBLIC ASSISTANCE TRUST FUND D Comparative Balance Sheets CAPITAL FIXED ASSETS F Balance Sheet ii

4 FINANCIAL STATEMENTS (Continued) PAGE NOTES TO FINANCIAL STATEMENTS SUPPLEMENTARY DATA CURRENT FUND EXHIBIT A-4 A-5 A-6 A-7 A-8 A-9 A-10 A-11 A-12 A-13 A-14 A-15 A-16 A-17 A-18 A-19 A-20 A-21 A-22 A-23 A-24 A-25 A-26 A-27 A-28 Cash Receipts and Disbursements Change Fund..... Due from State of New Jersey per Chapter 129, P.L Taxes Receivable and Analysis of Property Tax Levy.... Tax Title Liens Property Acquired for Taxes (At Assessed Valuation) Other Accounts Receivable Other Municipal Liens Revenue Accounts Receivable lnterfunds Receivable.... Deferred Charges Emergency Appropriation.... Appropriation Reserves.... Accounts Payable County Taxes Payable Local School District Taxes Due to the State of New Jersey lnterfunds Payable Federal and State Grant Fund - lnterfunds Due to Claims Fund.... Tax Overpayments Prepaid Taxes.... Other Reserve Accounts Grants Receivable Appropriation Reserves Unappropriated Reserves TRUST FUND B-2 B-3 B-4 Cash Receipts and Disbursements - Treasurer Due from Housing and Urban Development - Community Development Block Grant.... Account Receivable iii

5 SUPPLEMENTARY DATA (Continued) TRUST FUND (Continued) EXHIBIT B-5 B-6 B-7 B-8 B-9 B-10 B-11 B-1 2 B-13 B-14 B-15 lnterfunds - Other Trust Funds Due to State of New Jersey - Animal Control Trust Fund.... Payroll Deductions Payable Due From Current Fund Due to Claims Fund.... lnterfunds Payable Accounts Payable.... Reserve for Animal Control Expenditures.... Special Deposits Reserve for Community Development Block Grant - Department of Housing and Urban Development..... Reserve for Various Insurance Funds PAGE GENERAL CAPITAL FUND C-2 C-3 C-4 C-5 C-6 C-7 C-8 C-9 C-10 C-11 C-12 C-13 C-14 C-15 C-16 C-17 C-18 Cash Receipts and Disbursements - Treasurer.... Analysis of Capital Cash lnterfunds Due from State of New Jersey - Green Acres Trust Program Due From Town of Guttenberg Deferred Charges to Future Taxation - Funded.... Deferred Charges to Future Taxation - Unfunded.... Improvement Authorizations Capital Improvement Fund Reserve for Future Improvements Reserve for State Grants and Other Receivables Green Acres Loans Payable - Green Trust Capital Leases Payable Hudson County Improvement Authority Environmental Infrastructure Loan Payable Bond Anticipation Notes General Serial Bonds.... Bonds and Notes Authorized But Not Issued - General Projects PUBLIC ASSISTANCE TRUST FUND D-1 D-2 D-3 Cash Receipts and Disbursements Reserves for Expenditures - Trust Fund Account..... Due from Claims Fund iv

6 SUPPLEMENTARY DATA (Continued) CLAIMS FUND EXHIBIT E-1 E-2 Cash Receipts and Disbursements - Treasurer lnterfunds PAGE PART II OFFICIALS IN OFFICE AND REPORT ON SURETY BONDS. COMMENTS AND RECOMMENDATIONS Officials in Office and Report on Surety Bonds as of December 31, Comments and Recommendations v

7 PART I REPORT OF EXAMINATION FINANICAL STATEMENTS NOTES TO FINANCIAL STATEMENTS AND SUPPLEMENTARY EXHIBITS FOR THE YEAR ENDED DECEMBER 31, 2016 AND 2015

8 r\9pkr V aconnor DAVIES ACCOUNTANTS AND ADVISORS The Honorable Mayor and Members of the Township Council Township of North Bergen North Bergen, New Jersey Independent Auditors' Report Report on the Financial Statements We have audited the accompanying regulatory-basis financial statements of the various funds and account group of the Township of North Bergen, Hudson County, New Jersey (the ''Township") which comprise the balance sheets as of and for the years ended December 31, 2016 and 2015, and the related statements of revenues, expenditures and changes in fund balances for the years then ended, statements of revenues, statements of expenditures and the related notes to the financial statements, which collectively comprise the Township's basic financial statements as listed in the table of contents. Management's Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with the financial reporting provisions of the Division of Local Government Services, Department of Community Affairs, State of New Jersey (the "Division"). Management is also responsible for the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditors' Responsibility Our responsibility is to express opinions on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America, the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller of the United States; and the audit requirements prescribed by the Division. Those standards and requirements prescribed by the Division require that we plan and perform the audit to obtain reasonable assurance about whether the regulatory-basis financial statements are free of material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the Township's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Township's internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions. PKF O'CONNOR DAVIES, LLP 293 Eisenhower Parkway, Suite 270, Livingston, NJ I Tel: I Fax: I PKF O'Connor Davies, LLP is a member firm of the PKF International Limited network of legally independent firms and does not accept any responsibility or liability for the actions or inactions on the part of any other individual member firm or firms.

9 The Honorable Mayor and Members of the Township Council Township of North Bergen Page 2 Basis for Adverse Opinion on U.S Generally Accepted Accounting Principles As described in Note 2, the financial statements are prepared by the Township on the basis of the financial reporting provisions of the Division to demonstrate compliance with Division's regulatory-basis of accounting, which is a basis of accounting other than accounting principles generally accepted in the United States of America. The effects on the financial statements of the variances between the basis of accounting described in Note 2 and accounting principles generally accepted in the United States of America, although not reasonably determinable, are presumed to be material. Adverse Opinion on U.S. Generally Accepted Accounting Principles In our opinion, because of the significance of the matter discussed in the Basis for the Adverse Opinion on U.S. Generally Accepted Accounting Principles paragraph, the financial statements referred to above do not present fairly in accordance with accounting principles generally accepted in the United States of America the financial position of each fund of the Township as of December 31, 2016 and 2015 and the results of its operations and changes in fund balance, for the years then ended. Unmodified Opinion on Regulatory Basis of Accounting In our opinion, the regulatory-basis financial statements referred to above present fairly, in all material respects, the respective financial position of the various funds and account group of the Township of North Bergen, Hudson County, New Jersey, as of December 31, 2016 and 2015, and the respective results of its operations and changes in fund balance for the years then ended in accordance with the financial reporting provisions of the Division, as described in Note 2 to the financial statements. Report on Supplementary Information as Required by the Division in Accordance with Regulatory Basis Our audit was conducted for the purpose of forming an opinion on the financial statements that collectively comprise the Township's basic financial statements. The supplementary information, as identified as exhibits A-4 through E-2, the comments and recommendations and supplementary information in the table of contents, is presented for purposes of additional analysis as required by the Division and is not a required part of the 2016 regulatory-basis financial statements of the Township. Such information is the responsibility of management and was derived from and relates directly to the underlying accounting and other records used to prepare the basic financial statements. Such information has been subjected to the auditing procedures applied in the audit of the financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the financial statements or to the financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the supplementary information is fairly stated, in all material respects, in relation to the basic financial statements as a whole.

10 The Honorable Mayor and Members of the Township Council Township of North Bergen Page 3 Other Reporting Required by Government Auditing Standards In accordance with Government Auditing Standards, we have also issued our report dated April 25, 2017 on our consideration of the Township's internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over fi nancial reporting and compliance and the results of that testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the Township's internal control over financial reporting and compliance. Pl(F tj'~ 1auw. LLfJ Livingston, New Jersey Anl~)2017 r/v?-1-7'~ John Lauria, RMA Licensed Registered Municipal Accountant# 403

11 ~ PKF' V aconnor DAVIES ACCOUNTANTS ANO ADVISORS Report on Internal Control Over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance With Government Auditing Standards The Honorable Mayor and Members of the Township Council Township of North Bergen North Bergen, New Jersey Independent Auditors' Report We have audited, in accordance with the auditing standards generally accepted in the United States of America, the standards applicable to financial audits contained in Government Auditing Standards issued by the Comptroller General of the United States and the audit requirements prescribed by the Division of Local Government Services, Department of Community Affairs, State of New Jersey (the "Division"), the regulatory-basis financial statements of the various funds and account group of the Township of North Bergen, Hudson County, New Jersey (the "Township"), as of and for the year ended December 31, 2016, and the related notes to the financial statements, which collectively comprise Township's basic financial statements, and have issued our report thereon dated April 25, 2017, in which we expressed an adverse opinion on the conformity of the statements with accounting principles generally accepted in the United States of America due to the differences between those principles and the financial reporting provisions of the Division. Internal Control Over Financial Reporting In planning and performing our audit of the regulatory basis financial statements, we considered the Township's internal control over financial reporting ("internal control") to determine the audit procedures that are appropriate in the circumstances for the purpose of expressing our opinions on the regulatory basis financial statements, but not for the purpose of expressing an opinion on the effectiveness of the Township's internal control. Accordingly, we do not express an opinion on the effectiveness of the Township's internal control. A deficiency in internal control exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct, misstatements on a timely basis. A material weakness is a deficiency, or a combination of deficiencies, in internal control, such that there is a reasonable possibility that a material misstatement of the entity's financial statements will not be prevented, or detected and corrected on a timely basis. A significant deficiency is a deficiency, or a combination of deficiencies, in internal control that is less severe than a material weakness, yet important enough to merit attention by those charged with governance. Our consideration of internal control was for the limited purpose described in the first paragraph of this section and was not designed to identify all deficiencies in internal control that might be material weaknesses or significant deficiencies. Given these limitations, during our audit we did not identify any deficiencies in internal control that we consider to be material weaknesses. However, material weaknesses may exist that have not been identified. PKF O'CONNOR DAVIES, LLP 293 Eisenhower Parkway, Suite 270, Livingston, NJ I Tel: I Fax: I PKF O'Connor Davies, LLP is a member firm of the PKF International Limited network of legally independent firms and does not accept any responsibility or liability for the actions or inactions on the part of any other individual member firm or firms.

12 The Honorable Mayor and Members of the Township Council Township of North Bergen Page 2 Compliance and Other Matters As part of obtaining reasonable assurance about whether the Township's regulatory-basis financial statements are free from material misstatement, we performed tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements, noncompliance with which could have a direct and material effect on the determination of financial statement amounts. However, providing an opinion on compliance with those provisions was not an objective of our audit, and accordingly, we do not express such an opinion. The results of our tests disclosed no instances of noncompliance or other matters that are required to be reported under Government Auditing Standards. Purpose of this Report The purpose of this report is solely to describe the scope of our testing of internal control and compliance and the results of that testing, and not to provide an opinion on the effectiveness of the entity's internal control or on compliance. This report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the entity's internal control and compliance. Accordingly, this communication is not suitable for any other purpose. Livingston, New Jersey AP:7'~ John Lauria, RMA Licensed Registered Municipal Accountant# 403

13 TOWNSHIP QF NORTH BERGEN CURRENT FUND COMPARATIVE BALANCE SHEETS REGULATORY BASIS DECEMBER AND Sheet# 1 Balance Balance ASSETS Ref. De~mb~r 31, 2Q12 De~m!;!~r~1, 2Q15 Regular Fund Cash - Treasurer A-4 $ 23,393, $ 20,619, Cash - Change Fund A ,394, ,620, Due from State of New Jersey A-6 82, , Receivables and Other Assets with Offsetting Reserves: Delinquent Property Taxes A-7 1,813, ,213, Tax Title Liens A-8 1,401, ,278, Property Acquired for Taxes A-9 6,543, ,543, Other Accounts Receivable A-10 2, , Other Municipal Liens A-11 7, , Revenue Accounts Receivable A , lnterfunds Receivable A-13 16, , ,031, ,307' Deferred Charges: Special Emergency Authorizations: (N.J.S.A. 40A: 4-53) A , ,508, ,288, Fegeral and!!le Grant F!.!nQ Cash A-4 223, , Federal and State Grants Receivable A-26 3,075, ,426, ,299, ,429, $ 36,807, $ 34, 718, See accompanying notes to financial statements. -7-

14 CURRENT FUND COMPARATIVE BALANCE SHEETS REGULATORY BASIS DECEMBER AND Sheet# 2 LIABILITIES. RESERVES AND FUND BALANCE Balance December 31, 2016 Balance December 31, 2015 Regular Fund Appropriation Reserves: Encumbered Unencumbered Accounts Payable County Taxes Payable School Taxes Payable Tax Overpayments Prepaid Taxes Other Reserve Accounts A-3,15 A-3, 15 A-16 A-17 A-18 A-23 A-24 A-25 $ 585, ,766, , , ,217, ,441, ,284, ,316, $ 443, ,484, , , ,672, ,289, ,090, ,276, Reserve for Receivables and Other Assets Fund Balance A-1 10,031, ,160, ,508, ,307, ,704, ,288, Federal and State Grant Fund lnterfunds Payable Due to State of New Jersey Appropriated Reserves Unappropriated Reserves A-21 A-19 A-27 A , , ,587, , , , , ,452, , ,429, $ 36,807, $ 34,718, See accompanying notes to financial statements. -8-

15 CURRENT FUND COMPARATIVE STATEMENTS OF OPERATIONS AND CHANGE IN FUND BALANCE REGULATORY BASIS YEARS ENDED DECEMBER AND 2015 Rev!,lnue and Oth!,lr Income Realized Fund Balance Utilized Miscellaneous Revenue Anticipated Receipts from Delinquent Taxes Receipts from Current Taxes NonbudgetRevenue Other Credits to Income: lnterfunds Liquidated Excess Dog License Fees Appropriation Reserves Lapsed Other Municipal Liens Collected Other Receiveables Liquidated Grant Reserves Canceled Expenditures Budget Appropriations: Operations: Salaries and Wages Other Expenses Deferred Charges and Statutory Expenditures Capital Improvements Municipal Debt Service County Taxes Local School District Taxes Senior Citizen Adjustment - Prior Year Tax Court Judgements lnterfunds Advanced Cancelation of Grant Receivables Refund of Prior Years' Revenue Excess in Revenue Fund Balance Balance, Beginning of Year Decreased by: Utilized as Anticipated Revenue Balance, End of Year Ref. December A-2 $ 3,900, A-2 20,878, A-2b 2,261, A-2b 137,103, A-2c 906, A , A , A-15 2,096, A-11 5, A-10 18, ,428, A-3 24,192, A-3 50,277, A-3 5,368, A-3 150, A-3 6,019, ,007, A-17 27,216, A-18 47,640, A-6 15, A , ,072, ,355, A 10,704, ,060, Above 3,900, A $ 13,160, December $ 2,000, ,466, ,473, ,772, , ,103, , ,745, ,303, ,342, , 105, , ,508, ,402, ,854, ,103, , , , , , ,908, ,836, ,868, ,704, ,000, $ 10,704, See accompanying notes to financial statements. -9-

16 CURRENT FUND STATEMENT OF REVENUES REGULATORY BASIS A-2 YEAR ENDED DECEMBER Sheet #1 (Deficit) or Ref. Budget Realized Excess Fund Balance Appropriated A-1 $ 3,900, $ 3,900, Miscellaneous Revenues Licenses: Alcoholic Beverages A-12 88, , $ (694.00) Other A , , (8,531.00) Fees and Permits A-2a 451, , , Fines and Costs: Municipal Court A-2a 1,723, ,232, , Interest and Cost on Taxes A , , , Interest on Investments and Deposits A , , , Pool Membership Fees A , , , North Bergen Cable Television - Franchise Fees A , , Payment in Lieu of Taxes - Floral Park, Inc. A-2a 642, , (13,908.00) Payment in Lieu of Taxes - North Bergen Housing Auth. A-2a 215, , , Payment in Lieu of Taxes - Fritz Reuter A-2a 174, , Payment in Lieu of Taxes - Avalon Bay A-2a 261, , , Payment in Lieu of Taxes - LWH A-2a 1,121, ,072, (48,642.18) rd Urban Renewal A-2a 258, , , Ambulance Fees A , , (66,536.53) Hotel Tax A , , (15,285.43) Consolidated Municipal Property Tax Relief Aid A-12 1,330, ,330, Energy Receipts Tax (P.L. 1997, Chapters 162 and 167) A-12 5,854, ,854, Uniform Construction Code Fees A-2a 1,355, ,575, , Grants: Clean Communities Program A , , Municipal Alliance on Alcoholism and Drug Abuse A-26 52, , Highway Safety Grant A-26 15, , Drunk Driving Enforcement Fund A-26 6, , DOT - Municipal Aid A , , State Housing Inspection Program: A-26 55, , FEMA - Emergency Management A-26 10, , Pedestrian Safety Grant A-26 16, , Summer Food Program A-26 41, , Bulletproof Vest Program A-26 3, , Body Armor Fund A-26 9, , Alcohol Education and Rehabilitation A-26 3, , Host Fees A , , , Uniform Fire Safety Act A , , (4, ) NJ Transit Tax A , , , MUA -5% of Annual Costs of Operations A , , See accompanying notes to financial statements

17 CURRENT FUND STATEMENT OF REVENUES REGULATORY BASIS A-2 YEAR ENDED DECEMBER Sheet#2 Excess or Ref. Budget Realized (Deficit) Mi~i.ellaneQ11s R!iMinue~ NJ Meadowlands Lease A-12 $ 201, $ 202, $ 1, General Capital Surplus A , , Parking Authority Building Lease A-12 90, , , Trust Reserves A-12 9, , Parking Authority Surplus A-12 50, , MUA Debt Service Payment A-12 61, , Total Miscellaneous Revenue A-1 19,294, ,878, ,583, Receipts from Delinquent Taxes A-2b 2,250, ,261, , Amount to be Raised by Taxes for Support of Municipal Budget: Local Tax for Municipal Purposes 61,875, Minimum Library Tax 1.715, Total Amount to be Raised by Taxes for Support of Municipal Budget A-2b, A-7 63,591, ,188, , ,035, ,227, , 192, NonbudgetRevenue A-2c 906, , A-3 $ 89,035, $ 93, 134, $ 4,099, See accompanying notes to financial statements

18 CURRENT FUND STATEMENT OF REVENUE ANALYSIS OF MISCELLANEOUS REVENUE REGULA TORY BASIS YEAR ENDED DECEMBER Ref. Other Fees and Permits: Tax Collector Tax Assessor Rent Control Township Clerk HealthNital Statistics Police Returned Check Board of Adjustments Planning Application Fees Record Room Purchasing Less: Refunds A-12 $ 22, A-12 1, A-12 41, A-12 3, A-12 93, A , A A-12 35, A-12 37, A-12 49, A-12 2, A-22 A-2 $ 916, , $ 906, Uniform Construction Code Fees: Collections A-12 Less: Refunds A-22 A-2 Payments in Lieu of Taxes A-12 Less: Refunds A-22 A-2 Municipal Court: Collections A-12 Less: Payments to North Bergen Parking Authority A-22 A-2 $ 1,631, , $ 1,575, $ 2,707, , $ 2,667, $ 3,078, , $ 2,232, See accompanying notes to financial statements

19 CURRENT FUND STATEMENT OF REVENUE ANALYSIS OF TAXES REGULA TORY BASIS YEAR ENDED DECEMBER Allocation of Tax Collection Due from State of New Jersey Collections Tax Title Liens Overpayments Applied Prepaid Taxes Applied Total Revenue Allocated to: County Levy and Added Taxes Local School District Taxes Plus: Reserve for Uncollected Taxes Realized Revenue Amount to be Receipts from Raised by Delinquent Ref. Taxation Taxes A-6, A-7 $ 123, A-7 135,722, $ 2,215, A-8 45, A-7,23 167, A-24 1,090, A-1 137,103, ,261, A-17 (27,216,346.41) A-18 (47,640,510.00) A-3 2,941, A-2 $ 65,188, $ 2,261, Total $ 123, ,937, , , ,090, ,364, (27,216,346.41) (47,640,510.00) 2,941, $ 67,449, See accompanying notes to financial statements

20 CURRENT FUND STATEMENT OF REVENUE ANALYSIS OF NON BUDGET REVENUE REGULATORY BASIS YEAR ENDED DECEMBER Ref. Nonbudget Revenue Prior Year Insurance Reimbursements $ 208, FEMA Reimbursements 135, Administrative Fee - State of N.J. Senior Citizens and Veterans 2, North Bergen Library Reimbursement 181, Board of Education Reimbursements 100, State of New Jersey - Boswell Project 16, Parking Authority Reimbursements 32, NJDMV Reimbursement 5, Community Action Rent 20, Union City Parking Rental 20, Snack Bar - Pool Complex 8, Marriage and Civil Ceremonies 18, State Restitution - Courts 1, Utility Rebates 56, Guttenberg Recreation 11, Bus Shelter Fee 20, Rinaldi Bus Parking 30, Sale of Township Property - Gov. Deals.Com 14, Other 24, A-4 Less: Adjustment A-1, A-2 $ 906, $ 906, See accompanying notes to financial statements. -14-

21 CURRENT FUND A-3 Sheet#1 STATEMENT OF EXPENDITURES REGULATORY BASIS YEAR ENDED DECEMBER ~ Aporooriation Budget Appropriations Modified Budget Paid or Charged Expended ~ Encumbered Unencumbered Unexpended Balance Canceled APPROPRIATIONS WITHIN "CAPS" I -u. DEPARTMENT OF PUBLIC AFFAIRS Directof's Office: Salaries and Wages Other Expenses Purchasing: Salaries and Wages Other Expenses Central Purchasing Township Administrator. Salaries and Wages Other Expenses Township Clerl('s Office: Salaries and Wages Other Expenses North Hudson Council of Mayors: Other Expenses Elections: Other Expenses Public lnfonnation: Other Expenses Printing and Legal Advertising: Other Expenses Consulting Services: Other Expenses Community Services: Salaries and Wages Other Expenses Rent Control: Salaries and Wages Other Expenses Legal Services and Costs: Salaries and Wages Miscellaneous Other Expenses Registrar of Vital Statistics: Salaries and Wages Other Expenses Consumer Affairs Office: Salaries and Wages Board of Health: Salaries and Wages Other Expenses Special Lttigation: Other Expenses License Officer. Salaries and Wages Other Expenses Animal Control: Other Expenses Economic Development : Other Expenses Municipal Court: Salaries and Wages Other Expenses Group Health Insurance Health Benefit Waiver 222, $ 232, , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , ,557, ,557, , , $ 231, , , , , , , , , , , , , , , , , , , , , , , , , , , , , ,301, , $ $ , , , , , , , , , , , , , , , , , , , , , ,256, , See accompanying notes to financial statements.

22 A-3 CURRENT FUN() Sheet #2 STATEMENT OF EXPENDITURES REGULATORY BASIS YEAR ENDED DECEMBER 31, 2016 APPROPRIATIONS WITHIN "CAPS" A~e!oeriations Expended Unexpended Modified Paid or ~ Balance Aporopriation Budget Budget Charged Encumbered Unencumbered Canceled DEPARTMENT OF PUBLIC AFFAIRS Other Insurance $ 1,509, $ 1,509, $ 1,499, $ 9, Unemployment Insurance , Total Department of Public Affairs , ,610, $ 130, ~ DEPARTMENT OF REVENUE AND FINANCE Director's Office: Salartes and Wages 97, , , Other Expenses 6, , , , Tax Collector: Salaries and Wages 275, , , Other Expenses 34, , , , , Tax Assessor. Salaries and Wages 163, , , Other Expenses 34, , , Tax Assessor Consultant: Other Expenses 100, , , , , Financial Administration: Salaries and Wages 271, , , Other Expenses 130, , , , , I Annual Aud~ 112, , , Special Se111ices 100, , , , ~ 29, Housing Inspections: Salaries and Wages 120, , , , Other Expenses 4, , , Postage Total Department of Revenue and Finance , !!Q,, DEPARTMENT OF PUBLIC SAFETY Director's Office: Salaries and Wages 302, , , Other Expenses 7, , , , School Crossing Guards: Salaries and Wages 769, , , , Other Expenses 5, , , , Police: Salaries and Wages 11,561, ,486, ,248, , Other Expenses 571, , , , , Clothing Allowance 81, , , CCTV: Salartes and Wages 275, , , , Ambulance: Salaries and Wages 865, , , , Other Expenses 59, , , , , Traffic Committee: Other Expenses 6, , , , Alarm System: Salartes and Wages 155, , , , Other Expenses 10, , , ABC Board: Other Expenses 40, , , , Chaplains: Other Expenses 2, , , , Un~orm Fire Safety Act: Salaries and Wages 206, , , , See accompanying notes to financial statements.

23 TQWNSHIP OF NORTH BERGEN A-3 CURRENT FUND Sheet #3 STATEMENT OF EXPENDITURES REGULATORY BASIS YEAR ENDED DECEMBER APPROPRIATIONS WITHIN "CAPS" Ae~~ations Ex~nded Unexpended Modified Paid or Reserved Balance Appropriation Budget Budget Charged Encumbered Unencumbered Canceled DEPARTMENT OF PUBLIC SAFETY Municipal Prosecutor. Salaries and Wages $ 97, $ 98, $ 98, $ 1.72 Other Expenses 10, , , , Vehicle Maintenance: Salaries and Wages 532, , , , Other Expenses $ Total Department of Public Safety 16,21 5, ,034, , , , I Other --.J DEPARTMENT OF PUBLIC WORKS Directofs Office: Salaries and Wages 187, , , Other Expenses 10, , , , , Engineering: Other Expenses 85, , , , Streets and Roads: Salaries and Wages 2,644, ,628, ,397, , Other Expenses 850, , , , , Board of Adjustment: Expenses 70, , , , Planning Board: Other Expenses Total Department of Public Wort<s 3,937, ,935, ,335, , , DEPARTMENT OF PARKS AND PUBLIC PROPERTY Directofs Office: Salaries and Wages 192, , , Other Expenses 3, , , , Part<s and Playgrounds: Salaries and Wages 994, , , , Other Expenses 95, , , , , Poot: Salaries and Wages 240, , , Other Expenses 130, , , Public Events: Other Expenses 60, , , , Public Buildings and Grounds: Salaries and Wages 182, , , , Other Expenses 222, , , , , Recreation: Salaries and Wages 702, , , , Other Expenses Total Department of Part<s and Public Property 3,053, ,0?4~246,82 2.W...d2~41_ --~E1_9_ ---~ UNIFORM CONSTRUCTION CODE Chief Administrator of Enforcement Salaries and Wages 90, , , Other Expenses 1, , Building Department: Salaries and Wages 513, , , , Other Expenses 19, , , , , Plumbing Department: Salaries and Wages 127, , , Other Expenses 2, , , , See accompanying notes to financial statements.

24 CURRENT FUND A-3 Sheet#4 STATEMENT OF EXPENDITURES REGULATORY BASIS YEAR ENDED DECEMBER Approoriation Budget Aeeropriations Modified Budget Paid or Charged Ex~nded Reserved Encumbered Unencumbered Unexpended Balance Canceled APPROPRIATIONS WITHIN "CAPS"!.!~IFQRM QQN~TR!,!QTIQ~ QQQ!;!QQNTIN!.!!;QI Fire Protection Officials: Other Expenses Total Un~orm Construction Code $ $ $ $ $ !l., ' QC!,!NCLASSIFIEQ Municipal Utilities Authority Gasoline Electricity Telephone Street Lighting Fire Hydrant Service Water Total Unclassified CQNTINGENT Total Operations Wrthin "CAPS" 6,500, ,500, , , , , , , , , , , ,899, ,444, ,400, ,500, , , , , , ,237, , , , , , , , , , ,577, Detail: Salaries and Wages Other Expenses 24,974, ,976, (),!7Q,480,()Q 3JA_24,10llllL 23,243, ~7_.99],30IJ6_ 732, _585,877,22 2,844, DEFERRED CHARGES AND STATUTORY EXPENQITURES Statutory Expenditures: Contribution to: Social Security System Public Employees' Retirement System Pension Adjustment Fund Police & Fireman's Retirement System Total Deferred Charges and Statutory Expendttures 1, 110, , 154, ,333, ,333, , , , , , 147, ,331, , ~0, ~ , , , Total Appropriations Wrthin "CAPS" 60,488, ,488, ,301, , ,601, APPRQPRIATIQN~!;XQ~!.!Q!;Q FRQM "QAPS" QJHER QPERATIQNS Group Insurance Maintenance of Free Public Library Operations - 911: Salaries and Wages Reserve to Pay Tax Appeals Total Other Operations 227, , ,244, ,244, , , _ 4L092, _4,092,357,00 227, ,244, , ~90, L092, See accompanying notes to financial statements.

25 CURRENT FUND A-3 Sheet#5 STATEMENT OF EXPENDITURES REGULATORY BASIS YEAR ENDED DECEMBER Aopropriation Budget Aeei: E!!i!!tions Modified Budget Paid or Charged E!!Eended ~ Encumbered Unencumbered Unexpended Balance.f.anceled APPROPRIATIONS EXCLUDED FROM "CAPS" INTERLOCAL MUNICIPAL AGREEMENTS North Hudson Regional Fire and Rescue: Other Expenses $ Regional Communications: Other Expenses 14,080, $ 14,080, , $ 13,927, t $ 152,9" ' Summer -\Q Total Other Operations STATE AND FEDERAL PROGRAMS OFFSET!;!Y RfVfN!.!!; Food Program: Other Expenses Salaries and Wages Other Expenses Clean Communities Grant Other Expenses Pedestrian Safety Grant: Other Expenses Bulletproof Vest: Other Expenses Body Armor Fund: Other Expenses Division of Highway Safety: Other Expenses Emergency Management: FEMA Grant Drunk Driving Enforcement Grant State Housing Inspection Program: Other Expenses DOT NJ Transportation Trust: Other Expenses Alcohol Education and Rehabilitation: Other Expenses Matching Funds f0< Grants Matching Funds Drug Alliance ,302, , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , g_ , , See accompanying notes to financial statements.

26 CURRENT FUND A-3 Sheet#6 STATEMENT OF EXPENDITURES REGULATORY BASIS YEAR ENDED DECEMBER AooroOriation BudQet Aee~nalions Modified Budget Paid or Charged Exeended Reserved Encumbered Unencumbered Unexpended Balance Canceled APPROPRIATIONS EXCLUDED FROM "CAPS" Total Operations Excluded from "CAPS" $ $ $ ~~]25.40 Detail: Salaries and Wages Other Expenses 173, , ~~~?._ "15, ~ _1El5, CAPITAL IMPROVEMENTS Capital Improvement Fund 150, , , MUNICIPAL DEBT SERVICE Payment of Bond Principal Payment of Bond Anticipation Notes Interest on Bonds Interest on Notes N ' -= Green Trust Loan Program: ' Loan Repayments for Principal and Interest MUNNJEIT Pipeline Debt NHRF Lease Payable 1,975, , 175, ,353, ,353, ,122, , , , , , , , ,110, , 110, , 175, ,351, , , , , ,109, $ 1, , , , Total Municipal Debt Service 6,061, ,061, ,019, , DEFERRED CHARGES Emergency Authorization Special Emergency Authorizations DEFERRED CHARGES Judgments Total Appropriations Excluded from "CAPS" Sub-Total Appropriations 85,536, ,093, ,654, , , 766, , Reserve for Uncollected Taxes Tota! Appropriations $ $ $ 84,596, $ 585,87722 $ 3,766, $ 86, Adopted Budget Added by Chapter 159 $ 88,478, Above $ 89,035, See accompanying notes to financial statements

27 CURRENT FUND A-3 Sheet#7 STATEMENT OF EXPENDITURES REGULA TORY BASIS YEAR ENDED DECEMBER A-3 Appropriation Ref. Ap~ro~riations Modified Budget Paid or Charged Ex~ended Unexpended Reserved Balance Encumbered Unencumbered Canceled Modified Budget Emergency Appropriation Reserve for Uncollected Taxes Cash Disbursed lnterfunds Receivable, Net lnterfunds Payable Claims Fund Tax Overpayments Encumbered Unencumbered Cancelled A-2 A-14 A-2b A-4 A-1 3 A-20 A-22 A-23 A, A-3 Sheet #Q A, A-3 Sheet #Q A, A-3 Sheet #Q $ 89,035, $ 280, (2,941,596.45) 2,941, ,073, ,915, , ,370, ,490, {86,357.37) $ 585, $ 3,766, $ 86, $ 86,007, $ 84,596, $ 585, $ 3, 766, $ 86, ' N -I Ref. A-1 A-3 Sheet #S A A Above See accompanying notes to financial statements.

28 TRUST FUND COMPARATIVE BALANCE SHEETS REGULATORY BASIS DECEMBER 31 I 2016 AND 2015 B Sheet# 1 ASSETS Animal Control Trust Fund Cash Other Funds Cash Account Receivable Insurance Fund Cash Balance Ref. December B-2 $ 23, B-2 5,253, B-4 919, , 172, B-2 644, Balance December $ 19, ,508, , ,956, , Community Develo12ment Trust Fund Cash B-2 179, Due from Housing and Urban Development B-3 1,285, ,464, Payroll Fund Cash B-2 263, $ 8,569, , ,380, ,387, , $ 8,295, See accompanying notes to financial statements

29 TRUST FUND COMPARATIVE BALANCE SHEETS REGULA TORY BASIS DECEMBER AND 2015 B Sheet# 2 LIABILITIES. RESERVES AND FUND BALANCES Ref. Balance December Balance December Animal Control Trust Fund Due to State of New Jersey Due to Current Fund Reserve for Animal Control Expenditures B-6 B-10 B-12 $ 16, , , $ , , Other Funds lnterfund Payable Reserve for Special Deposits Accounts Payable Fund Balance B-10 B-13 B-13 B-1 788, ,360, , ,172, , ,592, ,956, Insurance Fund Accounts Payable Reserve for: Unemployment Compensation Insurance Self-Insurance B-15 B , , , , , , , Community Development Trust Fund lnterfund Payable Reserve for Community Development Trust Fund: Department of Housing and Urban Development B-10 B , ,356, ,464, , ,281, ,387, Payroll Fund Payroll Deductions Payable B-7 263, , , , $ 8,569, $ 8,295, See accompanying notes to financial statements. -23-

30 TRUST FUND STATEMENT OF TRUST FUND BALANCE REGULATORY BASIS YEAR ENDED DECEMBER Balance, December 31, 2016 and 2015 B Other Trust Fund $ See accompanying notes to financial statements. -24-

31 GENERAL CAPITAL FUND COMPARATIVE BALANCE SHEETS REGULA TORY BASIS DECEMBER AND 2015 g_ Balance Balance A~SETS AND Df;;F!;RREQ CHARGES Ref. December 31, 2016 December 31, 2015 Cash C-2 $ 3,624, $ 2,230, lnterfunds Receivable C-4 1,588, ,160, Due from State of New Jersey: Green Acres Trust Program C-5 1,500, ,500, Due from Town of Guttenberg C-6 338, , Deferred Charges to Future Taxation - Funded C-7 33,717, ,339, Deferred Charges to Future Taxation - Unfunded C-8 30,776, ,302, $ 71,546, $ 69,871, LIABILITIE~ RE~ERY:~~ AND FUND BALA~QE General Serial Bonds C-17 $ 25,347, $ 27,557, Bond Anticipation Notes Payable C-16 28,937, ,463, Capital Leases Payable C-14 6,835, ,689, Green Acres Loans Payable C , , Environmental Infrastructure Loan Payable C-15 1,266, ,787, Capital Improvement Fund 26, Improvement Authorizations: Funded C-9 34, , Unfunded C-9 6,338, ,572, Reserve for Future Improvements C , , Reserve for Grants and Other Receivables C-12 1,838, ,838, Fund Balance C-1 346, , $ 71,546, $ 69,871, Bonds and Notes Authorized but Not Issued C-18 $ 1,838, $ 1,838, See accompanying notes to financial statements

32 GENERAL CAPITAL FUND STATEMENT OF FUND BALANCE REGULA TORY BASIS YEAR ENDED DECEMBER Balance, December 31, 2015 Increased by: Premium on Sale of Notes Ref. c C-2 $ 265, , , Decreased by: Anticipated Revenue C-2 $ 185, Applied to Improvement Authorizations C-9 77, Balance, December 31, 2016 c 262, $ 346, See accompanying notes to financial statements. -26-

33 PUBLIC ASSISTANCE TRUST FUND COMPARATIVE BALANCE SHEETS REGULATORY BASIS DECEMBER AND 2015 D ASSETS Trust Fund Account #1 Cash Balance Ref. December 31, 2016 D-1 $ 5, Balance December 31, 2015 $ 1, LIABILITIES AND FUND BALANCE Trust Fund Account #1 Reserve for Expenditures D-2 $ 5, $ 1, See accompanying notes to financial statements. -27-

34

35 NOTES TO FINANCIAL STATEMENTS

, has been governed under the Walsh Act form of New Jersey municipal government.")

36 NOTES TO FINANCIAL STATEMENTS DECEMBER 31, 2016 AND REPORTING ENTITY Reporting Entity Since 1931, The Township of North Bergen, Hudson County, New Jersey (the "Township"), has been governed under the Walsh Act form of New Jersey municipal government. The government consists of five commissioners elected at large to the Township Committee in non-partisan elections to serve four year terms of office on a concurrent basis. After each election, the Commissioners select one of their members to serve as mayor and each individual is assigned to head one of the five Commissions. The Township's major operations include public safety, road repair and maintenance, sanitation, fire protection, recreation and parks, health services, water and sewer, and general administrative services. 2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES The accounting policies of the Township conform to the accounting principles and practices prescribed by the Division of Local Government Services, Department of Community Affairs, State of New Jersey (the "Division"), which is another reporting framework other than accounting principles generally accepted in the United States of America ("GAAP"). Such principles and practices are designed primarily for determining compliance with legal provisions and budgetary restrictions and as a means of reporting on the stewardship of public officials with respect to public funds. Under this method of accounting, the Borough accounts for its financial transactions through the separate funds, which differ from the fund structure in accordance with GAAP. The Governmental Accounting Standards Board and subsequent Codification (collectively, "GASB") is the accepted standard-setting body for establishing governmental accounting and financial reporting principles for state and local governments. The GASB establishes seven fund types and two account groups to be used by governmental units when reporting financial position and results of operations in accordance with GAAP. GASB has issued Statement No. 14 which requires the financial reporting entity to include both the primary government and those component units for which the primary government is financially accountable. Financial accountability is defined as appointment of a voting majority of the component unit's board, and either a) the ability to impose will by the primary government, or b) the possibility that the component unit will provide a financial benefit to or impose a financial burden on the primary government. However, the municipalities in the State of New Jersey do not prepare financial statements in accordance with GAAP and thus do not comply with all of the GASB pronouncements. The financial statements contained herein include only those boards, bodies, officers or commissions as required by the provisions of N.J.S.A. 40A:5-5. The financial statements of the Township, however, do not include the operations of the Municipal Library, Municipal Parking Authority or the Municipal Utilities Authority, which are separate entities subject to a separate examination. The Township uses funds, as required by the Division, to report on its financial position and the results of its operations. Fund accounting is designed to demonstrate legal compliance and to aid financial administration by segregating transactions related to certain Township functions or activities. An account group, on the other hand, is designed to provide accountability for certain assets and liabilities that are not recorded in those Funds. The Township has the following funds and account groups: Current Fund - Encompasses resources and expenditures for basic governmental operations. Fiscal activity of Federal and State grant programs are also included therein. Trust Funds - The records of receipts, disbursements and custodianship of monies in accordance with the purpose for which each account was created are maintained in Trust Funds. These include the Animal Control Fund, General Trust Fund, Federal Housing and Urban Development Fund, Payroll Account and the Self-Insurance Fund

General Capital Fund - The receipts and expenditure records for the acquisition of general infrastructure and other capital facilities, other")

37 NOTES TO FINANCIAL STATEMENTS (CONTINUED) DECEMBER 31, 2016 AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued) General Capital Fund - The receipts and expenditure records for the acquisition of general infrastructure and other capital facilities, other than those acquired in the Current Fund, are maintained in this Fund, as well as related long-term debt accounts. Public Assistance Trust Fund - Receipts and disbursements of funds that provide assistance to certain residents of the Township which are not covered under the provisions of Title 44 of the New Jersey statutes are maintained in the Public Assistance Trust Fund. General Fixed Assets Account Group - These accounts reflect estimated valuations of land, buildings and certain moveable fixed assets of the Township. Basis of Accounting The Township follows the regulatory basis of accounting. Under this method of accounting, revenues, except for Federal and State Aid, are recognized when received and expenditures are recorded when incurred. The accounting principles and practices prescribed or permitted for municipalities by the Division ("regulatory basis of accounting") differ in certain respects from US GAAP applicable to local government units. The more significant differences are as follows: Property Taxes and Other Revenue Real property taxes are assessed locally, based upon the assessed value of the property. The tax bill includes a levy for Municipal, County, and School purposes. The bills are mailed annually in June for that calendar year's levy. Taxes are payable in four quarterly installments on February 1, May 1, August 1, and November 1. The amounts of the first and second installments are determined as one-quarter of the total tax levied against the property for the preceding year. The installment due the third and fourth quarters is determined by taking the current year levy less the amount previously charged for the first and second installments, with the remainder being divided equally. If unpaid on these dates, the amount due becomes delinquent and subject to interest at 8% per annum, or 18% on any delinquency amount in excess of $1,500. The School levy is turned over to the Board of Education as expenditures are incurred, and the balance, if any, must be transferred as of June 30 of each fiscal year. County taxes are paid quarterly on February 15, May 15, August 15 and November 15, to the County by the Town. When unpaid taxes or any municipal lien, or part thereof, on real property, remains in arrears on April 1 in the year following the calendar year levy when the same became in arrears, the collector in the municipality shall, subject to the provisions of the New Jersey Statutes, enforce the lien by placing the property on a standard tax sale. The Town also has the option when unpaid taxes or any municipal lien, or part thereof, on real property remains in arrears on the 11th day of the 11 1 h month in the fiscal year when the taxes or lien became in arrears, the collector in the municipality shall, subject to the provisions of the New Jersey Statutes, enforce the lien by placing property on an accelerated tax sale, provided that the sale is conducted and completed no earlier than in the last month of the fiscal year. The Town may institute annual in rem tax foreclosure proceedings to enforce the tax collection or acquisition of title to the property. In accordance with the accounting principles prescribed by the State of New Jersey, current and delinquent taxes are realized as revenue when collected. Since delinquent taxes and liens are fully reserved, no provision has been made to estimate that portion of the tax receivable and tax title liens that are uncollectible. US GAAP requires property tax revenues to be recognized in the accounting period when they become susceptible to accrual (i.e., when they are both levied and available), reduced by an allowance for doubtful accounts. Grant and Similar Award Programs Federal and State grants, entitlements or shared revenue received for purposes normally financed through the Current Fund are recognized when anticipated in the Township budget. GAAP requires such revenue to be recognized in the accounting period when they become susceptible to accrual. -30-

Miscellaneous Revenue Miscellaneous revenues are recognized on a cash basis.")

38 NOTES TO FINANCIAL STATEMENTS (CONTINUED) DECEMBER 31, 2016 AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued) Miscellaneous Revenue Miscellaneous revenues are recognized on a cash basis. Receivables for miscellaneous items that are susceptible to accrual are recorded with offsetting reserves on the balance sheet of the Town's Current Fund. US GAAP requires such revenues to be recognized in the accounting period when they become susceptible to accrual (i.e., when they are both measurable and available). Budgets and Budgetary Accounting An annual budget is required to be adopted and integrated into the accounting system to provide budgetary control over revenues and expenditures. Budget amounts presented in the accompanying financial statements represent amounts adopted by the Township and approved by the Division per N.J.S.A. 40A:4 et seq. The Township is not required to adopt budgets for the following funds: Trust Funds General Capital Fund The governing body is required to introduce and approve the annual budget no later than the last day in February of the fiscal year. The budget is required to be adopted no later than April 20, and prior to adoption, must be certified by the Division. The Director of the Division, with the approval of the Local Finance Board, may extend the introduction and approval and adoption dates of the municipal budget. The budget is prepared by fund, function, activity and line item (salary or other expense) and includes information on the previous year. The legal level of control for appropriations is exercised at the individual line item level for all operating budgets adopted. The governing body of the municipality may authorize emergency appropriations and the inclusion of certain special items of revenue to the budget after its adoption and determination of the tax rate. During the last two months of the fiscal year, the governing body may, by a 2/3 vote, amend the budget through line item transfers. Management has no authority to amend the budget without the approval of the governing body. Expenditures may not legally exceed budgeted appropriations at the line item level. Expenditures Expenditures for general operations are generally recorded on the accrual basis. Unexpended appropriation balances, except for amounts which may have been cancelled by the governing body or by statutory regulation, are automatically recorded as liabilities at year end, under the title of "Appropriation Reserves". Amounts unexpended at the end of the second year are lapsed and are recorded as income. Grant appropriations are charged upon budget adoption to create separate spending reserves. Budgeted transfers to the Capital Improvement Fund are recorded as expenditures to the extent permitted by law. Expenditures from Trust and Capital Funds are recorded upon occurrence and charged to accounts statutorily established for specific purposes. Budget Appropriations for interest on General Capital is recognized on the cash basis and is not accrued on the records ; interest on Utility Debt is recognized on the accrual basis and so recorded. GAAP requires expenditures to be recognized in the accounting period in which the fund liability is incurred, if measurable, except for unmatured interest on general long-term debt, which should be recognized when due. -31-

Encumbrances As of January 1, 1986, all local units were required to maintain an encumbrance accounting system.")

39 NOTES TO FINANCIAL STATEMENTS (CONTINUED) DECEMBER 31, 2016 AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued) Encumbrances As of January 1, 1986, all local units were required to maintain an encumbrance accounting system. This directive states that contractual orders outstanding at year end, are reported as expenditures through the establishment of an encumbrance payable. Encumbrances do not constitute expenditures under GAAP. Appropriation Reserves Appropriation reserves are available, until lapsed at the close of the succeeding year, to meet specific claims, commitments or contracts incurred during the preceding year. Lapsed appropriation reserves are recorded as additions to income. Appropriation reserves do not exist under GAAP. Operating Deficits Deficits resulting from expenditures and other debits which exceed cash revenues, other realized revenues and credits to income in such fiscal year, are recorded as deferred charges on the balance sheet of the respective operating fund at year end and are required to be funded in the succeeding year's budget. US GAAP does not permit the deferral of operating deficits at year end. Compensated Absences Expenditures relating to obligations for unused vested accumulated sick pay are not recorded until paid. GAAP requires that the amount that would normally be liquidated with expendable available financial resources be recorded as an expenditure in the operating funds and the remaining obligations be recorded as a long-term obligation. Property Acquired for Taxes Property Acquired for Taxes (Foreclosed Property) is recorded in the Current Fund at the assessed valuation during the year when such property was acquired by deed or foreclosure and is offset by a corresponding reserve account. GAAP requires such property to be recorded in the capital fixed assets at appraised value on the date of acquisition. Self-Insurance Contributions Contributions to self-insurance funds are charged to budget appropriations. GAAP requires that payments be accounted for as an operating transfer and not as an expenditure. lnterfunds Receivable lnterfunds Receivable in the Current Fund are generally recorded with offsetting reserves which are established by charges to operations. Collections are recognized as income in the year that the receivables are realized. lnterfunds Receivable of all other funds are recorded as accrued and are not offset with reserve accounts. lnterfunds Receivable of one fund are offset with lnterfunds Payable of the fund. GAAP does not require the establishment of an offsetting reserve. Inventories of Supplies Materials and supplies purchased by all funds are recorded as expenditures. An annual inventory of materials and supplies for utilities is required, by regulation, to be prepared by Township personnel for inclusion on the Utility Operating Funds' Balance Sheet. Annual changes in valuations, offset with a Reserve Account, are not considered as affecting results of operations. Materials and supplies of other funds are not inventoried nor included on their respective balance sheet. The Township does not maintain a utility. -32-

Deposits Deposits includes amounts on demand deposits, as well as short-term investments with a maturity date within three months of the date")

40 NOTES TO FINANCIAL STATEMENTS (CONTINUED) DECEMBER 31, 2016 AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued) Deposits Deposits includes amounts on demand deposits, as well as short-term investments with a maturity date within three months of the date acquired by the government. Investments are reported at cost and are limited by N.J.S.A. 40A:5-15.I et seq. US GAAP requires that all investments be reported at fair value. Incurred But Not Reported OBNR) Reserves and Claims Pavable The Township has not created a reserve for any potential unreported self-insurance losses which may have taken place. Additionally, the Town has not recorded a liability for those claims filed, but which have not been paid (i.e. claims payable). US GAAP requires that the amount that would normally be liquidated with expendable available financial resources be recorded as an expenditure in the operating funds and the remaining potential claims are recorded as a long-term obligation in the government-wide financial statements, however that is not required under the Division's regulatory-basis of accounting. Tax Appeals and Other Contingent Losses Losses arising from tax appeals and other contingent losses are recognized at the time a decision is rendered by an administrative or judicial body; however, municipalities may establish reserves transferred from tax collections or by budget appropriation for future payments of tax appeal losses. US GAAP requires such amounts to be recorded when it is probable that a loss has been incurred and the amount of such loss can be reasonably estimated. General Fixed Assets In accordance with N.J.A.C. 5:30-5.6, Accounting for Governmental Fixed Assets, the Town has developed a fixed assets accounting and reporting system. Fixed assets are defined by the Town as assets with an initial, individual cost of $2,000 and an estimated useful life in excess of two years. Fixed assets used in governmental operations (general fixed assets) are accounted for in the General Fixed Assets Account Group. Public domain ("infrastructure") general fixed assets consisting of certain improvements other than buildings, such as roads, bridges, curbs and gutters, streets and sidewalks are not capitalized. Fixed Assets purchased after December 31, 1999 are stated at cost. Donated fixed assets are recorded at estimated fair market value at the date of donation. Fixed Assets purchased prior to December 31, 1999 are stated as follows: Land and Buildings Machinery and Equipment Assessed Value Replacement Costs No depreciation has been provided for in the financial statements. Expenditures for construction in progress are recorded in the Capital Funds until such time as the construction is completed and put into operation. Basic Financial Statements The GASS also defines the financial statements of a governmental unit to be presented in the general purpose financial statements to be in accordance with GAAP. The Township presents the financial statements listed in the table of contents, which are required by the Division and which differ from the financial statements required by GAAP. In addition, the Division requires the financial statements listed in the table of contents to be referenced to the supplementary schedules. This practice differs from GAAP. -33-

Recent Pronouncements The GASS issued Statement 75, Accounting and Financial Reporting for Postemployment Benefits Other Than Pensions in June")

41 NOTES TO FINANCIAL STATEMENTS (CONTINUED) DECEMBER 31, 2016 AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued) Recent Pronouncements The GASS issued Statement 75, Accounting and Financial Reporting for Postemployment Benefits Other Than Pensions in June This Statement replaces the requirements of Statement 45 and the primary objective of this Statement is to improve accounting and reporting by state and local governments for postemployment benefits other than pensions (other postemployment benefits or OPES). It also improves information provided by state and local government employers about financial support for OPEB that is provided by other entities. The requirements of this Statement are effective for financial statements for reporting periods beginning after June 15, Management has not yet determined the impact of the Statement on the financial statements. The GASS issued Statement 77, Tax Abatement Disclosures in August This Statement is intended to improve financial reporting by requiring disclosure of tax abatement information about a reporting government's own tax abatement agreements and those that are entered into by other governments and that reduce the reporting government's tax revenues. The requirements of this Statement are effective for financial statements for reporting periods beginning after December 15, The Township has implemented this standard in the current year. The detail is reflected in footnote DEPOSITS AND INVESTMENTS DEPOSITS New Jersey statutes permit the deposit of public funds in institutions located in New Jersey, which are insured by the Federal Deposit Insurance Corporation (FDIC) or any other agencies of the United States that insures deposits or the State of New Jersey Cash Management Fund. Cash on deposit is partially insured by federal deposit insurance in the amount of $250, in each depository. Balances above the federal deposit insurance amount are insured by the Government Unit Deposit Protection Act (GUDPA}, N.J.S.A. 17:941, et seq., which insures all New Jersey governmental units' deposits in excess of the federal deposit insurance maximums. Based on GASB criteria, the Township considers cash and cash equivalents to include petty cash, change funds, demand deposits, money market accounts, short-term investments and cash management money market mutual funds The State of New Jersey Cash Management Fund is authorized by statute and regulations of the State Investment Council to invest in fixed income and debt securities which mature or are redeemed within one year. Twenty-five percent of the Fund may be invested in eligible securities which mature within two years provided, however, the average maturity of all investments in the Fund shall not exceed one year. Collateralization of fund investments is generally not required. In addition, by regulation of the Division, municipalities are allowed to deposit funds in the Municipal Bond Insurance Association (MBIA) through their investment management company, the Municipal Investors Service Corporation. In accordance with the provisions of the Governmental Unit Deposit Protection Act of New Jersey (GUDPA), public depositories are required to maintain collateral for deposits of public funds that exceed insurance limits as follows: The market value of the collateral must equal five percent of the average daily balance of public funds or; If the public funds deposited exceed 75 percent of the capital funds of the depository, the depository must provide collateral having a market value equal to 100 percent of the amount exceeding 75 percent. -34-

42 3. DEPOSITS AND INVESTMENTS (CONTINUED) TOWNSHIP OF NORTH BERGEN NOTES TO FINANCIAL STATEMENTS (CONTINUED) DECEMBER 31, 2016 AND 2015 All collateral must be deposited with the Federal Reserve Board, The Federal Home Loan Bank Board or a banking institution that is a member of the Federal Reserve System and has capital funds of not less than $25,000, Cash and cash equivalents have original maturities of three months or less from the date of purchase. Investments are stated at cost, which approximates fair value. At December 31, 2016 and 2015, the book values of the deposits of the Township consisted of the following: Book Balance December 31, December 31, Cash (Demand Accounts) $ 33,611, $ 29,320, Change Funds (On-Hand) Total $ 33,611, $ 29,321, Custodial Credit Risk - Deposits - Custodial credit risk is the risk that in the event of a bank failure, the Township's deposits may not be returned. The government does not have a specific deposit policy for custodial credit risk other than those policies that adhere to the requirements of statute and to deposit all of its funds in banks covered by FDIC and GUDPA. At least five percent of the Township's deposits were fully collateralized by funds held by the financial institution, but not in the name of the Township. Due to the nature of GUDPA, further information is not available regarding the full amount that is collateralized. At December 31, 2016 and 2015 the Township of North Bergen had the following depository accounts. All deposits are carried at cost. $430, and $381, held in agency and payroll accounts for the years ended December 31, 2016 and 2015, respectively are not covered by GUDPA. Depository Account Bank Balance December 31, December 31, FDIC Insured $ 500, $ 500, GUPDA Insured 32,830, , 712, Total $ 33,330, $ 29,212, Investments New Jersey statutes permit the Township to purchase the following types of securities: Bonds or other obligations of the United States of America or obligations guaranteed by the United States of America. This includes instruments such as Treasury bills, notes and bonds. Government money market mutual funds. Any federal agency or instrumentality obligation authorized by Congress that matures within 397 days from the date of purchase, and has a fixed rate of interest not dependent on any index or external factors. -35-

43 3. DEPOSITS AND INVESTMENTS (CONTINUED) TOWNSHIP OF NORTH BERGEN NOTES TO FINANCIAL STATEMENTS (CONTINUED) DECEMBER 31, 2016 AND 2015 Bonds or other obligations of the local unit or school districts of which the local unit is a part. Any other obligations with maturities not exceeding 397 days, as permitted by the Division of Investments. Local government investment pools, such as New Jersey CLASS, and the New Jersey Arbitrage Rebate Management Program. New Jersey State Cash Management Fund. Repurchase agreements of fully collateralized securities, subject to special conditions. The Township did not maintain any investments during 2016 and TAXES AND TAX TITLE LIENS RECEIVABLE Property assessments are determined on true values and taxes are assessed based upon these values. The residential tax bill includes the levies for the Township, County and School purposes. Certified adopted budgets are submitted to the County Board of Taxation (the "Board") by each taxing district. The tax rate is determined by the Board upon the filing of these budgets. Municipalities operating under a calendar fiscal year budget are required by statute to mail tax bills once a year on or about July 20 1 h. Tax installments not paid by the above due dates are subject to interest penalties. The rate of interest is 8% per annum on the first $1, of delinquency and 18% on any delinquency in excess of $1, The resolution also sets a grace period of ten days before interest is calculated. Taxes unpaid on the 11 1 h day of the eleventh month in the fiscal year when the taxes became in arrears are subject to the tax sale provisions of the New Jersey statutes. The municipality may institute in rem foreclosure proceedings after six months from the date of the sale if the lien has not been redeemed. The following is a five year comparison of certain statistical information relative to property taxes and property tax collections: Comparative Schedule of Tax Rates Calendar Year 2016 Calendar Year 2015 Calendar Year 2014 Tax Rate $ $ $ Apportionment of Tax Rate: Municipal (including Library) County School Open Space - County $ $ $

44 NOTES TO FINANCIAL STATEMENTS (CONTINUED) DECEMBER 31, 2016 AND TAXES AND TAX TITLE LIENS RECEIVABLE (continued) Assessed Valuations Calendar Year Amount 2016 $ 2,529,615, ,537, 135, ,485,024, Tax Levies and Collections Percentage Year Tax Lew Collections of Collections CY 2016 $ 139,077, $ 137, 103, % CY ,669, ,772, CY ,389, ,412, Delinquent Taxes and Tax Title Liens Amount of Amount of Percentage Tax Title Delinquent Total of Year Liens Taxes Delinquent Tax Lew CY 2016 $ 1,401, $ 1,813, $ 3,214, % CY ,278, ,213, ,491, CY , 133, ,441, ,574, PROPERTY ACQUIRED BY TAX TITLE LIEN LIQUIDATION The value of properties acquired by tax title lien liquidation is carried at assessed valuation in the year of acquisition, was as follows: Year Amount $ 6,543, ,543, ,543, FUND BALANCES APPROPRIATED Year Balance ut111zed rn Budgets of Succeeding Year Current Fund: CY2016 CY2015 CY2014 $ 13, 160, ,704, ,868, $ 2,500, ,900, ,000,

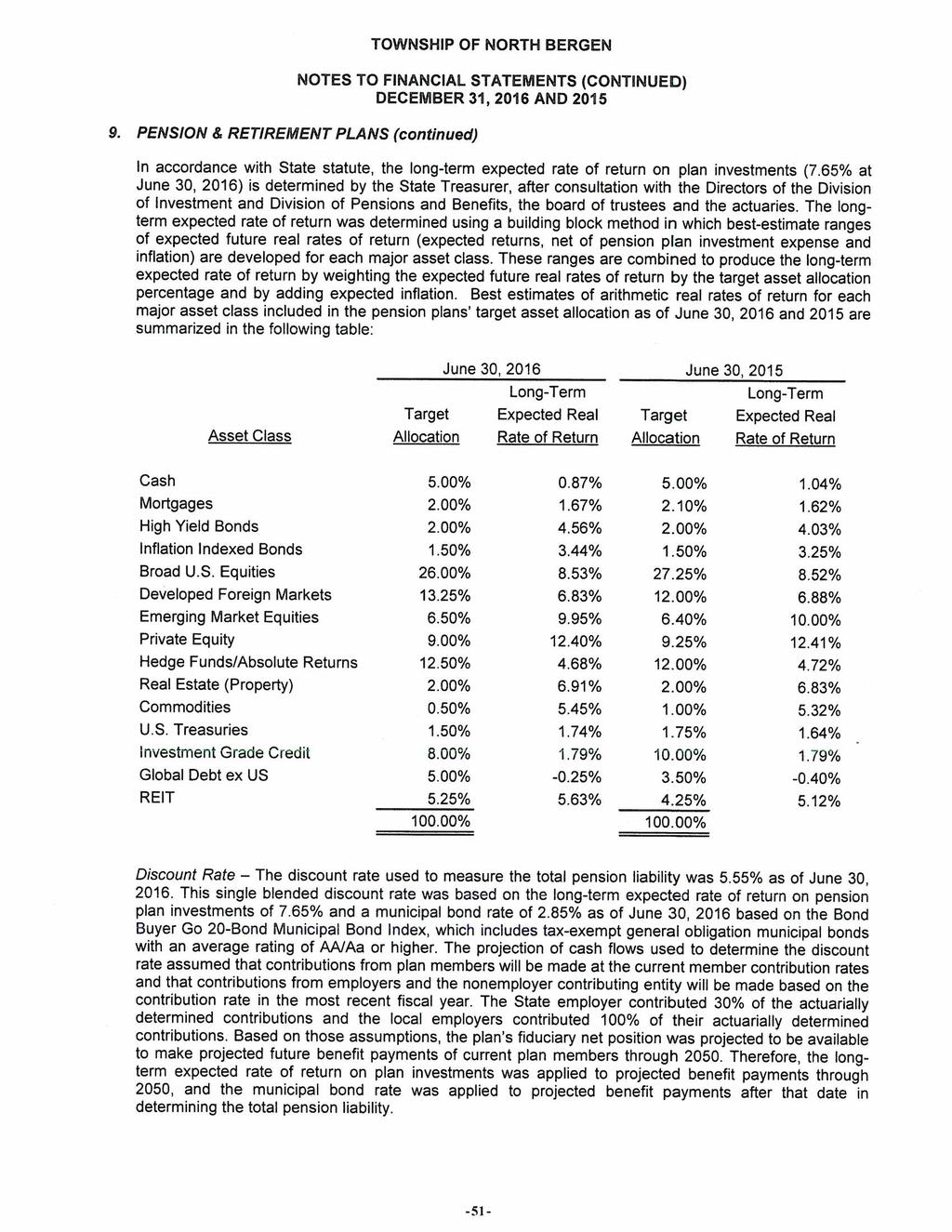

45 NOTES TO FINANCIAL STATEMENTS (CONTINUED) DECEMBER 31, 2016 AND MUNICIPAL DEBT The Local Bond Law governs the issuance of bonds and notes to finance general capital expenditures. All bonds are retired in serial installments within the statutory period of usefulness. Bonds issued by the Township are general obligation bonds, backed by the full faith and credit of the Township. Pursuant to N.J.S.A. 40A:2-8, bond anticipation notes, which are issued to temporarily finance capital projects, cannot be renewed past the third anniversary unless an amount equal to at least the first legal requirement is paid prior to each anniversary and must be paid off within ten years and five months or retired by the issuance of bonds. Summary of Municipal Debt (Excluding Operating and School Debt) Calendar Year2016 Calendar Year2015 Issued General: Bonds and Notes Green Trust Loan Environmental Infrastructure Loan $ 54,284, , ,266, $ 53,020, , ,787, Bonds Issued by Another Public Entity Guaranteed by Municipality Total Issued 49,471, ,291, , 178, ,291, Authorized but Not Issued General: Bonds and Notes 1,838, ,838, Net Bonds and Notes Issued and Authorized but Not Issued $ 107, 130, $ 112, 130, Summary of Statutory Debt Condition - Annual Debt Statement The summary statement of debt condition which follows is prepared in accordance with the required method of setting up the Annual Debt Statement and indicates a statutory net debt of 1.131%. Gross Debt Deductions Net Debt Local School District General Debt $ 3,300, $ 3,300, , 130, ,471, $ 57,659, $ 110,430, $ 52,771, $ 57,659, Net Debt, $57,659,095.79, divided by Equalized Valuation Basis per N.J.S.A. 40A:2-2 as amended,$5,098,733, equals 1.131%.The foregoing is in agreement with the revised annual debt statement submitted with the audit report. -38-

46 7. MUNICIPAL DEBT (continued) TOWNSHIP OF NORTH BERGEN NOTES TO FINANCIAL STATEMENTS (CONTINUED) DECEMBER 31, 2016 AND 2015 Borrowing Power Under N.J.S.A. 40A:2-6 as Amended 3 1/2% of Equalized Valuation Basis Net Debt $ 178,455, ,659, Remaining Borrowing Capacity $ 120,796, School Debt Deductions _ School debt is deductible up to the extent of 4.0% of the Average Equalized Assessed Valuations of real property for the Local School District. The Board of Education of the Township is a Type fl school district. The members of the Board of Education are elected by the voters of the school district on the third Tuesday in April. At each annual school election, the Board of Education shall submit to the voters of the district the amount of money fixed and determined in its budget, excluding interest and debt redemption charges, to be voted upon for the use of the public schools of the district for the ensuing school year. Long-Term Debt The Township issues general obligation bonds to provide funds for the acquisition and construction of major capital facilities. The full faith and credit of the Township are irrevocably pledged for the payment of the principal of the bonds and interest thereon. As of December 31, 2016 and 2015, the Township's long-term debt is as follows: General Obligation Bonds $11,000,000, 2008 Refunding Bonds, due in annual installments of $580,000 through August 2018, interest at 5.00% $ 1, 160, $ 1, 740, $3,800,000 Tax Appeal Bonds, matured during ,000, $22,472,000, 2009 Bonds, were partially refunded by the 2016 refunding bond. Annual installment of $1,072,000 to $1,390,000 through February 2020 remain due at an interest rate of 4.00% 4,712, ,472, $3, 145,000, 2012 Refunding Bonds, due in annual installments of $385,000 to $395,000 through April 2021, interest 3.00% to 4.00% 1,950, ,345, $17, 725, Refunding Bonds, due in annual installments of$1,360,000 to $1,490,000, interest at 3.00% to 5.00% 17,525, $ 25,347, $ 27,557,

47 7. MUNICIPAL DEBT (continued) 2016 Bonds Refunding TOWNSHIP OF NORTH BERGEN NOTES TO FINANCIAL STATEMENTS (CONTINUED) DECEMBER 31, 2016 AND 2015 Pursuant to a bonds purchase contract entered into between the Township and the underwriter, the bonds are being purchased at an aggregate purchase price of $20,059, (representing the principal amount of the bonds of $17,725,000.00, plus an original issue premium of $2,423, and less the underwriter's discount of $88,625.00). The difference between cash flows required to service the old debt and the cash flows to service the new debt was $834, The economic gain (net present value) resulting from the refunding was $683, As a result of the refunding, $17,760, of the defeased debt is still outstanding at December 31, Changes in Long-Term Municipal Debt The Town's long term capital debt activity for 2016 and 2015 is as follows: Balance December 31, 2015 Increases Reductions Balance December 31, 2016 Due Within One Year General Capital Fund Bonds Payable $ 27,557, $ 17,725, $ 19,935, $ 25,347, $ 2,047, Balance December 31, 2014 Increases Reductions Balance December 31, 2015 Due Within One Year General Capital Fund Bonds Payable $ 29,487, $ ======== $ 1,930, $ 27,557, $ 1,975, A Schedule of Annual Debt Service for Principal and Interest for Bonded Debt is as follows: Fiscal General -- Year Principal Interest Total 2017 $ 2,047, $ 999, $ 3,046, ,070, , ,000, ,540, , ,381, ,780, , ,554, ,745, , ,449, ,300, ,552, ,852, ,420, , ,318, ,445, , ,466, $ 25,347, $ 7, 723, $ 33,070,

48 NOTES TO FINANCIAL STATEMENTS (CONTINUED) DECEMBER 31, 2016 AND MUNICIPAL DEBT (continued) Green Acres Trust Loans The Township was issued loans from the New Jersey Department of Environmental Protection for the purpose of improvements to the Township parks at an interest rate of 2%. Two new loans were issued to the Township in fiscal year 2010 at a zero percent interest rate. Loans payable at December 31, 2016 in the amount of $269, are as follows: Soccer Field $ 5, th Street Park , Ri\eNiew Park , th Street Park , th Street Field , $ 269, The following is a Schedule of Annual Principal and Interest for the Green Acres Trust Loan Year Principal Interest Total 2017 $ 37, $ $ 37, , , , , , , , , , , $ 269, $ $ 269, Environmental Infrastructure Trust Loan The Township has a service contract with the North Bergen Municipal Utility Authority (MUA) in which the MUA provides for the operation of a sewerage system for the Township. The MUA applied for and received an Environmental Infrastructure Trust loan from the State of New Jersey for system upgrades. The Township has agreed to pay fifty percent (50%) of the debt service on the loan. The Township's portion of the loan payable as of December 31, 2016 is as follows: Year Principal Interest Total 2017 $ 113, $ 20, $ 133, , , , , , , , , , , , , , , , , , $ 1,266, $ 89, $ 1,355,

49 7. MUNICIPAL DEBT (continued) TOWNSHIP OF NORTH BERGEN NOTES TO FINANCIAL STATEMENTS (CONTINUED) DECEMBER 31, 2016 AND 2015 Hudson County Improvement Authority (HCIAJ The Township entered into a regional agreement with other municipalities to establish the North Hudson Regional Fire and Rescue. Debt was issued through the HCIA to build fire houses and for other capital expenditures. Each municipality was apportioned a share of the debt. At December 31, 2016 and 2015, the Township's share was $6,835, and $7,689,368.50, respectively. The Township's schedule of capital lease payments at December 31, 2016 are as follows: YEAR AMOUNTS Thereafter 1, 165, ,367, , 165, , 165, , 153, ,785, Total minimum lease payment Less amount representing interest Present value of net future minimum lease payments 8,802, {1,967, ) 6,835, North Bergen Municipal Utilities Authority The Township guarantees the debt of the Utilities Authority. Debt was issued for construction of a wastewater treatment plant and other capital projects. At December 31, 2016 and 2015, the Authority's debt guaranteed by the Township was $49,471, and $55, 178, and, respectively. Bond Anticipation Notes Outstanding Bond Anticipation Notes are summarized as follows: Short Terrm Debt Balance December 31, 2015 Additions Reductions Balance December 31, 2016 Bond Anticipation Notes General Capital Fund $ 25,463, $ 28,937, $ 25,463, $ 28,937, Balance December 31, 2014 Additions Reductions Balance December 31, 2015 Bond Anticipation Notes General Capital Fund $ 24,619, $ 25,463, $ 24,619, $ 25,463,

50 NOTES TO FINANCIAL STATEMENTS (CONTINUED) DECEMBER 31, 2016 AND DEFERRED CHARGES TO BE RAISED IN SUCCEEDING YEARS BUDGET Under N.J.S.A. 40A:4-53, special emergencies, the Township must raise twenty percent each per year for accumulated absences. At December 31, 2015, there were deferred charges totaling $280, The breakdown of the emergency is as follows: Purpose Amount 2011 Accumulated Vacation and Sick Pay $ In 2016, the Township had no deferred charges. 9. PENSION & RETIREMENT PLANS Public Employee Retirement System The Public Employee Retirement System is a cost-sharing, multiple employer defined benefit pension plan as defined in GASB Statement No. 68. The Plan is administered by The New Jersey Division of Pensions and Benefits (Division). The more significant aspects of the PERS Plan are as follows: Plan Membership and Contributing Employers- Substantially all full-time employees of the State of New Jersey or any county, municipality, school district or public agency are enrolled in PERS, provided the employee is not required to be a member of another state-administered retirement system or other state pension fund or other jurisdiction's pension fund. Membership and contributing employers of the defined benefit pension plans consisted of the following at June 30, 2016 and 2015: Inactive plan members or beneficiaries currently receiving benefits Inactive plan members entitled to but not yet receiving benefits Active plan members , , , , 161 Total Contributing Employers - 1, 710 ~ ~ Significant Legislation - For State of New Jersey contributions to PERS, Chapter 1, P.L. 2010, effective May 21, 2010, required the State to resume making actuarially recommended contributions to the pension plan on a phased-in basis over a seven year period beginning in the fiscal year ended June 30, For State fiscal year 2016, the State was required to make a minimum contribution representing 5/ih of the actuarially determined contribution amount based on the July 1, 2014 actuarial valuation. Chapter 19, P.L. 2009, effective March 17, 2009, provided an option for local employers of PERS to contribute 50% of the normal and accrued liability contribution amounts certified for payments due in State Fiscal Year Such an employer will be credited with the full payment and any such amounts will not be included in their unfunded liability. The actuaries will determine the unfunded liability of PERS, by employer, for the reduced normal and accrued liability contributions provided under this law. This unfunded liability will be paid by the employer in level annual payments over a period of 15 years beginning with the payments due in the fiscal year ended June 30, 2012 and will be adjusted by the rate of return on the actuarial value of assets. Pursuant to the provision of Chapter 78, P.L. 2011, COLA increases were suspended for all current and future retirees of PERS. -43-