Defined Benefit System PPA 06 Valuation Coding and Related Topics

|

|

|

- Moris Smith

- 5 years ago

- Views:

Transcription

1 Defined Benefit System PPA 06 Valuation Coding and Related Topics Presented by Dave Roper and Aaron Venouziou TERMINOLOGY FOR PPA Valuations New terminology Funding Target FT Old accrued liability Funding Target Attainment Percentage FTAP Old Funded Current Liability percentage Adjusted Funding Target Attainment Percentage AFTAP FTAP adjusted for annuity payments Funding Shortfall Funding Target minus assets (c) 2008 DATAIR 1

2 TERMINOLOGY FOR PPA Valuations New terminology Carryover Balance COB Old Credit Balance Prefunding Balance PFB New Credit Balance At Risk AFTAP less than 60% Cushion Amount Part of Maximum Deductible Contribution calculation TERMINOLOGY FOR PPA Valuations IRC Sec 436 Proposed Regulation Shutdown benefits (mainly big plans) Limits on amendments increasing benefits Limits on accelerated benefit distributions Limits on benefit accruals (c) 2008 DATAIR 2

3 DB DOS SCREEN CODING Screen 10 Valuation/Allocation Date must be Beginning of Year 1/1/08 or later. No guidance for End of Year valuations DB DOS SCREEN CODING (c) 2008 DATAIR 3

4 DB DOS SCREEN CODING Screen 15 Salary Scale If no salary scale, will still have 1 year increase for increase in accrued benefit for Target Normal Cost Projects salary to retirement to calculate projected accrued benefit for projected Funding Target Difference in funding targets is increase for Funding Target Cushion Amount under 404(o) DB DOS SCREEN CODING FOR PPA 06 Screen 15 Pre-Ret Mortality Table If used must be coordinated with Post Retirement mortality table 08N00 (Non annuitant) with 08A00 (Annuitant) 08C00 (Combined) with 08C00 (Combined) (c) 2008 DATAIR 4

with 08C00 (Combined Do not use 08A00, 08N00, 08C00 as Actuarial Equivalence Sex distinct Suggest not using 08E00 417(e) table may change every year (c) 2008")

5 DB DOS SCREEN CODING DB DOS SCREEN CODING Screen 16 Post-Ret Mortality Table Must be coordinated with Pre-Retirement mortality table 08N00 (Non annuitant) with 08A00 (Annuitant) 08C00 (Combined) with 08C00 (Combined Do not use 08A00, 08N00, 08C00 as Actuarial Equivalence Sex distinct Suggest not using 08E00 417(e) table may change every year (c) 2008 DATAIR 5

6 DB DOS SCREEN CODING DB DOS SCREEN CODING Screen (h) Segment Rates (1st, 2nd, 3rd) Existing Plans Transitional Rates are default For % old rate and 20% new rate New Plans Must use Segment rates (not Transitional Rates) Applicable Month Month that includes valuation date. Default month for segment rates, but have option to elect any of 4 months previous to Applicable Month Recommendation Beginning of Year Valuations use default month End of Year Valuations use 4 th month preceding valuation month Be consistent with all plans (c) 2008 DATAIR 6

2008")

7 DB DOS SCREEN CODING DB DOS SCREEN CODING Screen (e) Segment Rates (1st, 2nd, 3rd) Different segment rates no average For % old rate and 20% new rate IRS publishes the Transitional Rates only (c) 2008 DATAIR 7

Similar to Funding rates (c) 2008 DATAIR 8")

8 DB DOS SCREEN CODING DB DOS SCREEN CODING Screen 16 PBGC Segment Rates (1st, 2nd, 3rd) Similar to Funding rates (c) 2008 DATAIR 8

9 DB DOS SCREEN CODING DB DOS SCREEN CODING Screen 16 You will be responsible for entering all rates DATAIR will publish rates on website. (c) 2008 DATAIR 9

Code 4, fund for annuity Uses Funding Mortality Uses Funding Segment Rates (c) 2008")

10 DB DOS SCREEN CODING DB DOS SCREEN CODING Screen 16 Limit Lump Sum for Funding to 415 Max (0-6) Code 4, fund for annuity Uses Funding Mortality Uses Funding Segment Rates (c) 2008 DATAIR 10

11 DB DOS SCREEN CODING Screen 16 Limit Lump Sum for Funding to 415 Max (0-6) Codes 5 or 6, fund for lump sum. Uses greater of 08E00 and Funding Segment rates. or Actuarial Equivalence Lump Sum and single Funding Segment rate. DB DOS SCREEN CODING (c) 2008 DATAIR 11

= P DB DOS SCREEN CODING (c) 2008 DATAIR")

12 DB DOS SCREEN CODING Screen 19 Actuarial Cost Method (1-9,A-F) = 7 Normal Cost Calculation Method (1-3,P) = P DB DOS SCREEN CODING (c) 2008 DATAIR 12

13 DB DOS SCREEN CODING Screen 19 Recommended contribution Can use other funding methods to generate recommended contribution. DB DOS SCREEN CODING Screen 21 (c) 2008 DATAIR 13

14 New reports Valuation Statement 404(o)(3)(A)(11) CUSHION AMOUNT INCREASE Valuation Results Valuation results Funding Shortfall Minimum Required Contribution Maximum Contribution 2008 Schedule SB Contribution Requirements Report (c) 2008 DATAIR 14

15 (c) 2008 DATAIR 15

16 (c) 2008 DATAIR 16

17 Effective interest rate The SINGLE rate of interest which, if used to determine the Plan s Funding Target, would result in a Funding Target that equals what was calculated using the segment rates (c) 2008 DATAIR 17

18 Shortfall base established (c) 2008 DATAIR 18

19 Minimum Contribution Maximum Contribution (c) 2008 DATAIR 19

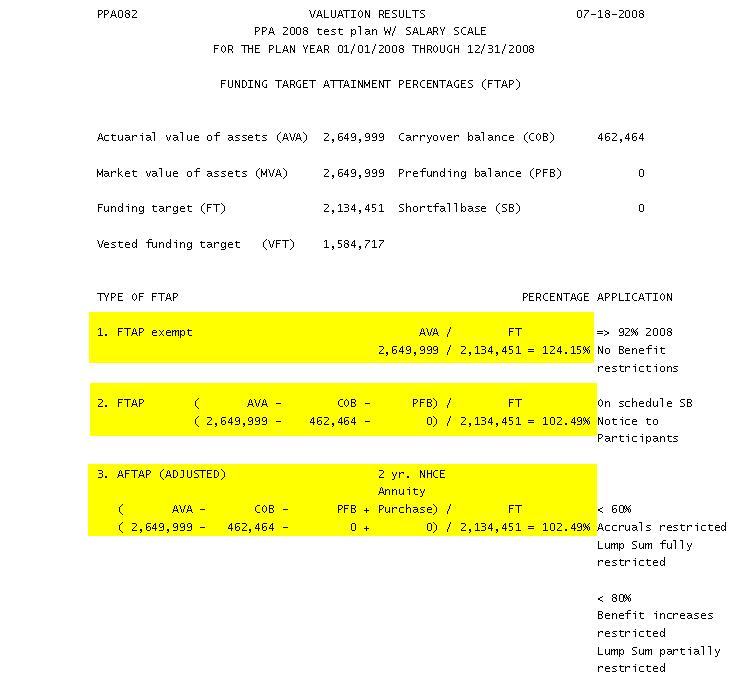

20 Termination Liability 13. Contribution to meet termination liability 1,597,885 Present Value of Accrued Benefits minus Assets C. ACTUARIAL EQUIVALENCE BASIS # VESTED NON-VESTED TOTAL 1. ACTIVE 7 1,640, ,302 2,247, RETIRED DEFERRED VESTED POSTPONED RETIREMENT TERMINATED VESTED TERMINATED NON-VESTED INACTIVE TOTAL 9 1,640, ,302 2,247, Assets (A3) 649,999 No Funding Shortfall (c) 2008 DATAIR 20

21 (c) 2008 DATAIR 21

22 (c) 2008 DATAIR 22

23 (c) 2008 DATAIR 23

24 (c) 2008 DATAIR 24

25 (c) 2008 DATAIR 25

26 (c) 2008 DATAIR 26

27 2008 PBGC Comprehensive Premium Filing DATAIR has approval Filing opened as of July 25, 2008 Filing is electronic Form not filed for illustration only Filing requires Pension Reporter version 1.24f. PR 1.24f will be released soon. PBGC REPORTS PBGC Segment Rates Segment Rates for Month preceding Beginning of Plan Year Calendar Year Plans default to December 2007 Segment Rates May use same Segment Rates as used for funding (c) 2008 DATAIR 27

28 PBGC REPORTS PBGC Unfunded Vested Benefits Accrued Benefits as of Beginning of Premium Payment Year Assets As of Valuation Date Unfunded Vested Benefits As of Valuation Date PBGC REPORTS Who can file now? 2008 Beginning of Year Valuations Retrospective or Prospective Can t use 12/31/2007 valuations no segment rates (c) 2008 DATAIR 28

29 PBGC REPORTS Who can file now? 2008 End of Year Valuations 2 Options Option 1 If less than 25 Employees VPR Cap (Variable Rate Premium) Pay $5 per (Employees)^2 Example 10 employees VRP = $5 times 10^2 = $500 PBGC REPORTS Who can file now? 2008 End of Year Valuations Option 2 Wait until End of Year, calculate Unfunded Vested Benefits Pay lesser of VRP Cap or Variable Rate Premium Caution If you use VRP Cap, you may be paying when no Variable Rate Premium is due (c) 2008 DATAIR 29

30 PBGC REPORTS (c) 2008 DATAIR 30

2008 DATAIR")

31 PBGC REPORTS Part I Complete Items 1-4 Part II Check Box only if you elect the Alternative Premium Funding Target Not recommended PBGC REPORTS (c) 2008 DATAIR 31

32 PBGC REPORTS PBGC REPORTS Part III Item 6 Participant count is the same as prior year s 5500 Item 7 If over 25 employees and not exempt (7(a)) complete 7(c) - 7(f) and 7(g)(3) [Enrolled Actuary s signature required] If under 25 employees, Check 7(b), Complete 7(c), 7(g) Pension Reporter will transfer data Pension System and calculate the lesser of the VRP and the VRP Cap 7(d) Enrolled Actuary signature required 7(c)-7(g)(i) omitted, No EA signature required (c) 2008 DATAIR 32

33 PBGC REPORTS Part III Items 8-12 Complete if applicable Part IV Items Complete if applicable Part V Note Items 17 and 18 Signature by Plan Administrator and EA when applicable Note that the Confirmation Number received from the PBGC must be entered in Item 21 PBGC REPORTS (c) 2008 DATAIR 33

2008")

34 PBGC REPORTS PBGC REPORTS (c) 2008 DATAIR 34

35 PBGC REPORTS DB DOS PPA Valuations Recommended Contribution Valuations Level Contributions PPA minimum may be too low PPA Maximum contribution may not be made indefinitely Suggest Individual Aggregate for ongoing plans Suggest Projected Unit Credit for frozen plans (c) 2008 DATAIR 35

36 PPA Valuations 2007 AFTAP Proposed Regulation 1.436(j)(3)(iii)(B) Funded current liability % with numbers from 2007 Schedule B will be used for 08 as the prior year AFTAP after adjustment for annuity purchases PPA Valuations AFTAP AFTAP indicates funding of plan If AFTAP below 80% or 60%, limitations of payments and accruals (Sec. 436) (c) 2008 DATAIR 36

37 PPA Valuations AFTAP If Enrolled Actuary has not issued certification of a plan s 2007 AFTAP, the AFTAP of the 2008 plan year is presumed to be less than 60% until 2007 AFTAP is certified. PPA Valuations AFTAP Until 2008 AFTAP is certified, 2007 AFTAP will be used. BUT, AFTAP will be PRESUMED to be 10 Percentage Points less than 2007 AFTAP unless actual 2008 AFTAP is certified by 1 st day of 4 th month. (c) 2008 DATAIR 37

38 PPA Valuations AFTAP New Plan Exception Limitations do not apply to the first five years (but take into account predecessor plans) However, restrictions on lump sums distributions apply IRC 436(g) PPA Valuations AFTAP Basic Rules 2007 AFTAP greater than 90% - no problem 2007 AFTAP less than 90% but greater than 70% - Limitations on distributions maybe a problem. Watch out! 2007 AFTAP less than 70% - problems (Advanced Valuations for 08 year may be required if AFTAP applicable for current year is 90% or less.) (c) 2008 DATAIR 38

39 PPA Valuations AFTAP 2007 AFTAP only good until 9/30/ AFTAP is required at 10/01/08 or plan is presumed to be less than 60% funded. PPA Valuations AFTAP Example No Burn of Carryover balance (c) 2008 DATAIR 39

40 PPA Valuations AFTAP Example Burn of Carryover balance (c) 2008 DATAIR 40

41 PPA Valuations Topics of Interest Software Symposium with Treasury and IRS Sole Proprietors Beginning of Year Valuations retrospective comp End of Year Valuations IRS did not realize scope of problems with reduction of Earned Income Shortfall amortization costs probably allocated in proportion to Funding Target (c) 2008 DATAIR 41

42 PPA Valuations Topics of Interest Software Symposium with Treasury and IRS End of Year Valuations IRS awaiting Technical Corrections Segment rates for EOY calendar plan will be August December rates. (Be consistent from plan to plan) Default rates will be rates for the applicable month, the month which includes the valuation date. These default rates will be December. Consider using August rates PPA Valuations Topics of Interest Software Symposium with Treasury and IRS Life Insurance Must use Fair Market Value under Rev. Proc Can not use One Year Term cost. Use proportion calculation in 1.430(d)-1(c) (c) 2008 DATAIR 42

43 PPA Valuations Topics of Interest Software Symposium with Treasury and IRS Beginning of Year, Prospective Salary Valuations Treasury and IRS both said not a reasonable funding method Main problem is salary assumption Will not stand up under audit PPA Valuations Topics of Interest Software Symposium with Treasury and IRS 94 GAR mortality table still to be used for 415(b)(2)(E)(ii) adjustments 415 mortality table will be changed in Technical Corrections Schedule SB will not change (c) 2008 DATAIR 43

44 PPA Valuations Topics of Interest Software Symposium with Treasury and IRS Ok to assume 100% probability of lump sum payments Can not use expense load for Early or Disability retirement. Must have decrements May anticipate participation in plan if benefits based upon service Can not use load for administrative expenses unless changed in Technical Corrections PPA Valuations Topics of Interest Software Symposium with Treasury and IRS Use of carryover or prefunding balances to satisfy Quarterly Contribution requirement also satisfies Minimum Contribution requirements. Funding Target may be used as Current Liability for purposes of 1.401(a)(4)-5(B), Payments to restricted participants Remember that 415 and 401(a)(17) annual increases are amendments that may be restricted by Section 436 restrictions (c) 2008 DATAIR 44

45 PPA Valuations Topics of Interest Software Symposium with Treasury and IRS Awaiting Guidance 404 deduction limits At risk funding target Mandatory use of pre-retirement mortality A host of other questions. PPA Valuations Topics of Interest Software Symposium with Treasury and IRS Final Regulations Hopefully end of September 3 releases 5 years worth of mortality tables (c) 2008 DATAIR 45

46 QUESTIONS? (c) 2008 DATAIR 46

DATAIR 401(k) with Cash Balance Plan Design 1

with Cash Balance Plan Design 1") DATAIR 41(k) with Plan Design 1 DATAIR with 4(k) Plan Design 1 For the plan year 1/1/213 through 12/31/213 123 N. Main Street Anytown, IL 1 (63) 325-26 sales@datair.com www.datair.com Three Digit Plan

DATAIR 41(k) with Plan Design 1 DATAIR with 4(k) Plan Design 1 For the plan year 1/1/213 through 12/31/213 123 N. Main Street Anytown, IL 1 (63) 325-26 sales@datair.com www.datair.com Three Digit Plan

Section 436 Rules for DB Plans Monday, April 29, 2013

Section 436 Rules for DB Plans Monday, April 29, 2013 David B. Farber, ASA, COPA, EA, MSPA IRC 436 Overview IRC 436 provides certain restrictions on single and multiple employer defined benefit plans that

Section 436 Rules for DB Plans Monday, April 29, 2013 David B. Farber, ASA, COPA, EA, MSPA IRC 436 Overview IRC 436 provides certain restrictions on single and multiple employer defined benefit plans that

10/9/2015. WS 66 Actuarial 101 for Non-Actuaries. Mary Ann Rocco, EA, MSPA Huntington Beach, CA (714)

") WS 66 Actuarial 101 for Non-Actuaries Mary Ann Rocco, EA, MSPA Huntington Beach, CA (714) 393-8845 mar@roccoea.com 2 1 AGENDA Intro Traditional DB Plan AFTAP PBGC AFN Cash Balance DB Plan AFTAP 3 INTRO

WS 66 Actuarial 101 for Non-Actuaries Mary Ann Rocco, EA, MSPA Huntington Beach, CA (714) 393-8845 mar@roccoea.com 2 1 AGENDA Intro Traditional DB Plan AFTAP PBGC AFN Cash Balance DB Plan AFTAP 3 INTRO

Summary of Practice Problems

Cost methods practice problems 1 Individual level Premium - pay history 2 Individual Aggregate method / Aggregate cost method 3 Aggregate method - with side fund 4 Aggregate method - gain and loss analysis

Cost methods practice problems 1 Individual level Premium - pay history 2 Individual Aggregate method / Aggregate cost method 3 Aggregate method - with side fund 4 Aggregate method - gain and loss analysis

ASC DEFINED BENEFIT SYSTEM SAMPLE REPORTS

ASC DEFINED BENEFIT SYSTEM SAMPLE REPORTS Thank you for your interest in ASC s Defined Benefit Valuation System! ASC offers a fully iterative, comprehensive defined benefit system that administers, values

ASC DEFINED BENEFIT SYSTEM SAMPLE REPORTS Thank you for your interest in ASC s Defined Benefit Valuation System! ASC offers a fully iterative, comprehensive defined benefit system that administers, values

Funding-Based Benefit Limits for Single Employer Plans (IRC section 436) Full Version

Full Version") Funding-Based Benefit Limits for Single Employer Plans (IRC section 436) Full Version Requirements of IRC section 436 apply only to single employer or multiple employer plans (not multiemployer plans)

Funding-Based Benefit Limits for Single Employer Plans (IRC section 436) Full Version Requirements of IRC section 436 apply only to single employer or multiple employer plans (not multiemployer plans)

MAP-21 Segment Rates. Supplemental reading: Revenue Notice PBGC Technical Updates 12-1 and 12-2

MAP-21 Segment Rates Supplemental reading: Revenue Notice 2012-61 PBGC Technical Updates 12-1 and 12-2 Determination of MAP-21 adjusted segment rates o Each of the 3 segment rates is adjusted (if necessary)

MAP-21 Segment Rates Supplemental reading: Revenue Notice 2012-61 PBGC Technical Updates 12-1 and 12-2 Determination of MAP-21 adjusted segment rates o Each of the 3 segment rates is adjusted (if necessary)

Actuarial 101 for Non-Actuaries. Mary Ann Rocco, EA, MSPA Huntington Beach, CA (714)

") Actuarial 101 for Non-Actuaries Mary Ann Rocco, EA, MSPA Huntington Beach, CA (714) 393-8845 mar@roccoea.com Agenda Intro Traditional DB Plan Benefits Funding AFTAP PBGC AFN Cash Balance DB Plan Benefits

Actuarial 101 for Non-Actuaries Mary Ann Rocco, EA, MSPA Huntington Beach, CA (714) 393-8845 mar@roccoea.com Agenda Intro Traditional DB Plan Benefits Funding AFTAP PBGC AFN Cash Balance DB Plan Benefits

#14 Administrator of the Traditional Defined Benefit Pension Plan Washington, DC 23 Certification of Adjusted Funding Target Attainment Percentage (AFTAP) for the 215 Plan Year The Pension Protection Act

#14 Administrator of the Traditional Defined Benefit Pension Plan Washington, DC 23 Certification of Adjusted Funding Target Attainment Percentage (AFTAP) for the 215 Plan Year The Pension Protection Act

Carryover and Prefunding Balances Post-PPA

Carryover and Prefunding Balances Post-PPA Stephen Parks, EA, MSPA, Chief Actuary, Retirement Systems of California, Inc. Stephen R. Parks, EA, MSPA, Chief Actuary, Retirement Systems of California, Inc.

Carryover and Prefunding Balances Post-PPA Stephen Parks, EA, MSPA, Chief Actuary, Retirement Systems of California, Inc. Stephen R. Parks, EA, MSPA, Chief Actuary, Retirement Systems of California, Inc.

2015 Instructions for Schedule SB (Form 5500) Single-Employer Defined Benefit Plan Actuarial Information

Single-Employer Defined Benefit Plan Actuarial Information") 2015 Instructions for Schedule SB (Form 5500) Single-Employer Defined Benefit Plan Actuarial Information General Instructions Note. Final regulations under certain portions of Code section 430 (sections

2015 Instructions for Schedule SB (Form 5500) Single-Employer Defined Benefit Plan Actuarial Information General Instructions Note. Final regulations under certain portions of Code section 430 (sections

New MAP-21 DB/WIN Features

New DB/WIN Features By Aaron Venouziou, EA, MAAA, MSPA, ACOPA President, DATAIR Employee Benefit Systems, Inc. On July 6, 2012, President Obama signed the Moving Ahead for Progress in the 21st Century

New DB/WIN Features By Aaron Venouziou, EA, MAAA, MSPA, ACOPA President, DATAIR Employee Benefit Systems, Inc. On July 6, 2012, President Obama signed the Moving Ahead for Progress in the 21st Century

415 and 436 Restriction Basics

415 and 436 Restriction Basics Daniel Liss, EA, CEO, Economic Growth Pension Services, Inc. Daniel Liss, EA, CEO, Economic Growth Pension Services, Inc. Daniel began working at EGPS in 2003, where he spent

415 and 436 Restriction Basics Daniel Liss, EA, CEO, Economic Growth Pension Services, Inc. Daniel Liss, EA, CEO, Economic Growth Pension Services, Inc. Daniel began working at EGPS in 2003, where he spent

Items to be covered today..

Defined Benefit System Enhancements: Schedule SB, Discounting Contributions, Carry Over and Pre-Funding Aaron Venouziou, EA John Baratka, EA Dave Roper Sue Evans, EA 1 Items to be covered today.. System

Defined Benefit System Enhancements: Schedule SB, Discounting Contributions, Carry Over and Pre-Funding Aaron Venouziou, EA John Baratka, EA Dave Roper Sue Evans, EA 1 Items to be covered today.. System

QUALIFIED PLAN DESIGN. Salmon Enterprises PENDEAS - Pension Ideas Illustration System Sample DB Reports PREPARED BY:

QUALIFIED PLAN DESIGN FOR Salmon Enterprises PENDEAS - Pension Ideas Illustration System Sample DB Reports PREPARED BY: BLAZE SSI Corp Box 333, Brielle, NJ 08730 732-223-5575 DATE PREPARED: 03/01/2016

QUALIFIED PLAN DESIGN FOR Salmon Enterprises PENDEAS - Pension Ideas Illustration System Sample DB Reports PREPARED BY: BLAZE SSI Corp Box 333, Brielle, NJ 08730 732-223-5575 DATE PREPARED: 03/01/2016

The Final 430 Regulations: Changes in Funding Rules. Larry Deutsch, FSPA President Larry Deutsch Penguin Consulting and Design

The Final 430 Regulations: Changes in Funding Rules Larry Deutsch, FSPA President Larry Deutsch Penguin Consulting and Design Final 430 Regulation On September 9, 2015 Treasury published regulations, primarily

The Final 430 Regulations: Changes in Funding Rules Larry Deutsch, FSPA President Larry Deutsch Penguin Consulting and Design Final 430 Regulation On September 9, 2015 Treasury published regulations, primarily

Understanding the Annual Funding Notice

Date: January 15, 2019 To: The Aerospace Employees' Retirement Plan (AERP or Plan) Participants From: Plan Administrator Subject: The Aerospace Employees' Retirement Plan Funding Notice No Impact on Your

Date: January 15, 2019 To: The Aerospace Employees' Retirement Plan (AERP or Plan) Participants From: Plan Administrator Subject: The Aerospace Employees' Retirement Plan Funding Notice No Impact on Your

Overhead 2018 EA-2F Seminar outline Page # Revised July 25, 2018

01 13 CM-01 CM- CM- CM-16 CM-17 CM-24 CM-25 CM-31 CM-32 CM-33 CM-34 CM-35 CM-36 CM-38 I. INTRODUCTION A. General information B. Summary of past exams C. Summary of Overhead sections II. COST METHODS A.

01 13 CM-01 CM- CM- CM-16 CM-17 CM-24 CM-25 CM-31 CM-32 CM-33 CM-34 CM-35 CM-36 CM-38 I. INTRODUCTION A. General information B. Summary of past exams C. Summary of Overhead sections II. COST METHODS A.

LA Advanced Pension Conference WS 1: Benefit Restrictions Top 25 and IRC 436

LA Advanced Pension Conference WS 1: Benefit Restrictions Top 25 and IRC 436 Lawrence Deutsch, MSPA, MAAA, EA Larry Deutsch Penguin Consulting and Design Andrew W. Ferguson, FSA, EA, MSPA Altman & Cronin

LA Advanced Pension Conference WS 1: Benefit Restrictions Top 25 and IRC 436 Lawrence Deutsch, MSPA, MAAA, EA Larry Deutsch Penguin Consulting and Design Andrew W. Ferguson, FSA, EA, MSPA Altman & Cronin

GRIST InDepth: Funding strategies for DB pension plans to avoid lump sum and accrual restrictions revised

GRIST InDepth: Funding strategies for DB pension plans to avoid lump sum and accrual restrictions revised By Heidi Rackley and Scott Tucker of the Washington Resource Group and Bruce Cadenhead of the New

GRIST InDepth: Funding strategies for DB pension plans to avoid lump sum and accrual restrictions revised By Heidi Rackley and Scott Tucker of the Washington Resource Group and Bruce Cadenhead of the New

Single-Employer Defined Benefit Plan Actuarial Information

SCHEDULE SB (Form 5500) Department of the Treasury Internal Revenue Service Department of Labor Employee Benefits Security Administration Pension Benefit Guaranty Corporation Single-Employer Defined Benefit

SCHEDULE SB (Form 5500) Department of the Treasury Internal Revenue Service Department of Labor Employee Benefits Security Administration Pension Benefit Guaranty Corporation Single-Employer Defined Benefit

PENSION PROTECTION ACT OF 2006

AN OVERVIEW OF THE IMPACT OF THE PENSION PROTECTION ACT OF 2006 ON QUALIFIED RETIREMENT PLANS Indiana Benefits Conference January 16, 2007 Indianapolis, Indiana E. Van Olson Introduction The Pension Protection

AN OVERVIEW OF THE IMPACT OF THE PENSION PROTECTION ACT OF 2006 ON QUALIFIED RETIREMENT PLANS Indiana Benefits Conference January 16, 2007 Indianapolis, Indiana E. Van Olson Introduction The Pension Protection

Schedule SB, Line 24 Changes in Actuarial Assumptions

Schedule SB, Line 24 Changes in Actuarial Assumptions The PEP crediting rate has been updated to reflect current economic conditions as follows: 2016 plan year valuation: 2.95% for 2016; 3.35% for 2017-2021;

Schedule SB, Line 24 Changes in Actuarial Assumptions The PEP crediting rate has been updated to reflect current economic conditions as follows: 2016 plan year valuation: 2.95% for 2016; 3.35% for 2017-2021;

2016 Instructions for Schedule MB (Form 5500) Multiemployer Defined Benefit Plan and Certain Money Purchase Plan Actuarial Information

Multiemployer Defined Benefit Plan and Certain Money Purchase Plan Actuarial Information") 2016 Instructions for Schedule MB (Form 5500) Multiemployer Defined Benefit Plan and Certain Money Purchase Plan Actuarial Information General Instructions Who Must File As the first step, the plan administrator

2016 Instructions for Schedule MB (Form 5500) Multiemployer Defined Benefit Plan and Certain Money Purchase Plan Actuarial Information General Instructions Who Must File As the first step, the plan administrator

HIGHWAY AND TRANSPORTATION FUNDING ACT OF 2014 (HATFA) Presented by: John C. Baratka, EA, MSPA and Sam Venouziou

Presented by: John C. Baratka, EA, MSPA and Sam Venouziou") HIGHWAY AND TRANSPORTATION FUNDING ACT OF 2014 (HATFA) Presented by: John C. Baratka, EA, MSPA and Sam Venouziou HATFA Extends Initial MAP-21 Segment Rate Corridor Through 2017 2 PPA established specific

HIGHWAY AND TRANSPORTATION FUNDING ACT OF 2014 (HATFA) Presented by: John C. Baratka, EA, MSPA and Sam Venouziou HATFA Extends Initial MAP-21 Segment Rate Corridor Through 2017 2 PPA established specific

Talk to your sales representative to upgrade to PE/Win if you haven t already.

TO: DATAIR's Pension System Users FROM: Andrew C. Hoskins DATE: December 31, 2012 RE: Release 3.45 of the PE/DOS PENSION SYSTEM Downloaded from www.datair.com. This release adds the 2013 COLA adjustments.

TO: DATAIR's Pension System Users FROM: Andrew C. Hoskins DATE: December 31, 2012 RE: Release 3.45 of the PE/DOS PENSION SYSTEM Downloaded from www.datair.com. This release adds the 2013 COLA adjustments.

Annual Return/Report of Employee Benefit Plan

Form 55 Department of the Treasury Internal Revenue Service Department of Labor Employee Benefits Security Administration Pension Benefit Guaranty Corporation Part I Annual Return/Report of Employee Benefit

Form 55 Department of the Treasury Internal Revenue Service Department of Labor Employee Benefits Security Administration Pension Benefit Guaranty Corporation Part I Annual Return/Report of Employee Benefit

DB Plans Part I So What Am I Getting? Kevin J Donovan, CPA, EA, MSPA, FCA Managing Member, Pinnacle Plan Design, LLC

DB Plans Part I So What Am I Getting? Kevin J Donovan, CPA, EA, MSPA, FCA Managing Member, Pinnacle Plan Design, LLC Kevin J Donovan, CPA, EA, MSPA, FCA Managing Member, Pinnacle Plan Design, LLC Kevin

DB Plans Part I So What Am I Getting? Kevin J Donovan, CPA, EA, MSPA, FCA Managing Member, Pinnacle Plan Design, LLC Kevin J Donovan, CPA, EA, MSPA, FCA Managing Member, Pinnacle Plan Design, LLC Kevin

Schedule SB Attachments

Schedule SB Attachments Schedule SB, Part V Statement of Actuarial Assumptions and Methods Discount Rates Current plan year PPA effective interest rate (reflecting MAP-21 corridors): 6.82% Prior plan year

Schedule SB Attachments Schedule SB, Part V Statement of Actuarial Assumptions and Methods Discount Rates Current plan year PPA effective interest rate (reflecting MAP-21 corridors): 6.82% Prior plan year

The use of a "standing election" to apply credit balances against minimum funding requirements.

Nov 12, 2009 By Brian Donohue, Senior Vice President, Aon Consulting The IRS recently released a copy of final defined benefit funding regulations that indicate changes made by PPA. In this article, we

Nov 12, 2009 By Brian Donohue, Senior Vice President, Aon Consulting The IRS recently released a copy of final defined benefit funding regulations that indicate changes made by PPA. In this article, we

Insight. DB contribution timing under PPA. Scope. Two funding regimes. Calculating the FTAP and AFTAP

Aug 13, 2009 By Brian Donohue, Senior Vice President, Aon Consulting In the wake of PPA and its new funding rules, both practitioners and plan sponsors have found it more difficult to get their arms around

Aug 13, 2009 By Brian Donohue, Senior Vice President, Aon Consulting In the wake of PPA and its new funding rules, both practitioners and plan sponsors have found it more difficult to get their arms around

Workshop 10: Other Cash Balance Issues

1 Workshop 10: Other Cash Balance Issues Kevin J. Donovan, CPA, EA, MSPA, FCA Pinnacle Plan Design LLC Andrew W. Ferguson, FSA, EA, FCA, MSPA, MAAA Altman & Cronin Benefit Consultants, LLC 2 1. Background

1 Workshop 10: Other Cash Balance Issues Kevin J. Donovan, CPA, EA, MSPA, FCA Pinnacle Plan Design LLC Andrew W. Ferguson, FSA, EA, FCA, MSPA, MAAA Altman & Cronin Benefit Consultants, LLC 2 1. Background

Annual Return/Report of Employee Benefit Plan

Form 5500 Department of the Treasury Internal Revenue Service Department of Labor Employee Benefits Security Administration Pension Benefit Guaranty Corporation Part I Annual Return/Report of Employee

Form 5500 Department of the Treasury Internal Revenue Service Department of Labor Employee Benefits Security Administration Pension Benefit Guaranty Corporation Part I Annual Return/Report of Employee

Outline Table of Contents

Outline Table of Contents Description Page General Rules of Minimum Funding (IRC section 412) 1 Minimum Funding Standards for Single Employer (or Multiple Employer) Plans (IRC section 430) 7 Quarterly

Outline Table of Contents Description Page General Rules of Minimum Funding (IRC section 412) 1 Minimum Funding Standards for Single Employer (or Multiple Employer) Plans (IRC section 430) 7 Quarterly

Session 5 Cash Balance Plans in 2014

Session 5 Cash Balance Plans in 2014 Kevin J. Donovan, CPA, MSPA Sara K. DeFilippo, EA, MSPA Actuarial Symposium, 8/15-8/16/2014 Cash Balance Plans in 2014 This session assumes a basic understanding of

Session 5 Cash Balance Plans in 2014 Kevin J. Donovan, CPA, MSPA Sara K. DeFilippo, EA, MSPA Actuarial Symposium, 8/15-8/16/2014 Cash Balance Plans in 2014 This session assumes a basic understanding of

October 6, Prepared by:

HENRY TALAVERA HUNTON & WILLIAMS LLP FOUNTAIN PLACE 1445 ROSS AVENUE SUITE 3700 DALLAS, TEXAS 75202-2799 CHRISTINA CROCKETT HUNTON & WILLIAMS LLP 1751 PINNACLE DRIVE SUITE 1700 MCLEAN, VA 22102 October

HENRY TALAVERA HUNTON & WILLIAMS LLP FOUNTAIN PLACE 1445 ROSS AVENUE SUITE 3700 DALLAS, TEXAS 75202-2799 CHRISTINA CROCKETT HUNTON & WILLIAMS LLP 1751 PINNACLE DRIVE SUITE 1700 MCLEAN, VA 22102 October

Regulatory Brief: Pension provisions in MAP-21

Regulatory Brief: Pension provisions in MAP-21 Vanguard Strategic Retirement Counsulting September 2012 Charles J. Klose Nathan C. Zahm Executive summary On July 6, 2012, President Obama signed into law

Regulatory Brief: Pension provisions in MAP-21 Vanguard Strategic Retirement Counsulting September 2012 Charles J. Klose Nathan C. Zahm Executive summary On July 6, 2012, President Obama signed into law

Workshop #53: Deduction Limits for Defined Benefit and Combo Plans

Workshop #53: Deduction Limits for Defined Benefit and Combo Plans Michael B. Preston, FSPA Preston Actuarial Services, Inc. Angela Barclay, EA Pension Benefits Unlimited, Inc. Overview of Presentation

Workshop #53: Deduction Limits for Defined Benefit and Combo Plans Michael B. Preston, FSPA Preston Actuarial Services, Inc. Angela Barclay, EA Pension Benefits Unlimited, Inc. Overview of Presentation

CITY OF ST. PETE BEACH FIREFIGHTERS RETIREMENT SYSTEM ACTUARIAL IMPACT STATEMENT #2 (MEMBERS USE EXCESS STATE MONIES RESERVE) March 14, 2017

March 14, 2017") CITY OF ST. PETE BEACH FIREFIGHTERS RETIREMENT SYSTEM ACTUARIAL IMPACT STATEMENT #2 (MEMBERS USE EXCESS STATE MONIES RESERVE) March 14, 2017 Attached hereto is a comparison of the impact on the Total Required

CITY OF ST. PETE BEACH FIREFIGHTERS RETIREMENT SYSTEM ACTUARIAL IMPACT STATEMENT #2 (MEMBERS USE EXCESS STATE MONIES RESERVE) March 14, 2017 Attached hereto is a comparison of the impact on the Total Required

IRS Publishes Rules for Single-Employer Pension Plan Funding Relief

IRS Publishes Rules for Single-Employer Pension Plan Funding Relief IRS Notice 2011-3 provides guidance as to how a sponsor of a single-employer defined benefit pension plan may elect one of the two alternative

IRS Publishes Rules for Single-Employer Pension Plan Funding Relief IRS Notice 2011-3 provides guidance as to how a sponsor of a single-employer defined benefit pension plan may elect one of the two alternative

What is your funded status goal?

PRACTICE NOTE What is your funded status goal? James Gannon, EA, FSA, CFA, Director, Asset Allocation and Risk Management ISSUE: Given the number of funded status measures that can be calculated for a

PRACTICE NOTE What is your funded status goal? James Gannon, EA, FSA, CFA, Director, Asset Allocation and Risk Management ISSUE: Given the number of funded status measures that can be calculated for a

DB-A: Defined Benefit Administration

DB-A: Defined Benefit Administration Course This course builds on the material from ASPPA s Administrative Issues of Defined Benefit Plans (DB) exam. That exam deals with basic terms and definitions within

DB-A: Defined Benefit Administration Course This course builds on the material from ASPPA s Administrative Issues of Defined Benefit Plans (DB) exam. That exam deals with basic terms and definitions within

10/17/2016. BOY vs. EOY Valuation Dates. Norman Levinrad & Sheri Alsguth

BOY vs. EOY Valuation Dates Norman Levinrad & Sheri Alsguth 2 1 Coordination of data, val and testing You get data for a plan year, you run a val, and you do testing. EOY: data as of 12/31/16; val for

BOY vs. EOY Valuation Dates Norman Levinrad & Sheri Alsguth 2 1 Coordination of data, val and testing You get data for a plan year, you run a val, and you do testing. EOY: data as of 12/31/16; val for

2018 EA-2L Overheads Page Section Topic

1 INTRODUCTION 2 General Guidelines 3 New exam conditions 4 New exam conditions 4A New exam conditions 4B New exam conditions 5 Implied ranges 6 Recent exam summary 12/07/17 7 Detailed list of recent exam

1 INTRODUCTION 2 General Guidelines 3 New exam conditions 4 New exam conditions 4A New exam conditions 4B New exam conditions 5 Implied ranges 6 Recent exam summary 12/07/17 7 Detailed list of recent exam

Maximum Deductions and Compensation Issues For DB Plans. Kevin J. Donovan, CPA, EA, MSPA, FCA Managing Member, Pinnacle Plan Design, LLC

Maximum Deductions and Compensation Issues For DB Plans Kevin J. Donovan, CPA, EA, MSPA, FCA Managing Member, Pinnacle Plan Design, LLC 1 Kevin J. Donovan, CPA, EA, MSPA, FCA Managing Member, Pinnacle

Maximum Deductions and Compensation Issues For DB Plans Kevin J. Donovan, CPA, EA, MSPA, FCA Managing Member, Pinnacle Plan Design, LLC 1 Kevin J. Donovan, CPA, EA, MSPA, FCA Managing Member, Pinnacle

DB-A: Defined Benefit Administration 2014 Syllabus

Course DB-A: Defined Benefit Administration 2014 Syllabus This course builds on the material learned from ASPPA s Administrative Issues of Defined Benefit Plans (DB) exam. That course deals with basic

Course DB-A: Defined Benefit Administration 2014 Syllabus This course builds on the material learned from ASPPA s Administrative Issues of Defined Benefit Plans (DB) exam. That course deals with basic

Pension Protection Act Series - Single Employer and Cash Balance Plans

Pension Protection Act Series - Single Employer and Cash Balance Plans Dial-in: 800.659.2090 Passcode: 10736696 Mark Boxer John Ferreira Mark Simons September 19 & 21, 2006 How To Print This Presentation

Pension Protection Act Series - Single Employer and Cash Balance Plans Dial-in: 800.659.2090 Passcode: 10736696 Mark Boxer John Ferreira Mark Simons September 19 & 21, 2006 How To Print This Presentation

PENSION PROTECTION ACT. Single-Employer and Multiple-Employer Defined Benefit Plans

August 18, 2006 PENSION PROTECTION ACT President Bush signed the Pension Protection Act of 2006 ("PPA") on August 17, 2006. The PPA contains many changes for both defined contribution plans and defined

August 18, 2006 PENSION PROTECTION ACT President Bush signed the Pension Protection Act of 2006 ("PPA") on August 17, 2006. The PPA contains many changes for both defined contribution plans and defined

Workshop 35 Benefit Restrictions

Workshop 35 Benefit Restrictions Richard A. Block, ASA, FSPA, MAAA, Block Consulting Actuaries, Inc., El Segundo, CA Thomas J. Finnegan, MSPA, CPC, QPA, MAAA, FCA, Principal, The Savitz Organization, Philadelphia,

Workshop 35 Benefit Restrictions Richard A. Block, ASA, FSPA, MAAA, Block Consulting Actuaries, Inc., El Segundo, CA Thomas J. Finnegan, MSPA, CPC, QPA, MAAA, FCA, Principal, The Savitz Organization, Philadelphia,

Federal Agencies Provide Guidance Affecting Multiemployer Defined Benefit Pension Plans

Important Information Plan Administration and Operation June 2008 Federal Agencies Provide Guidance Affecting Multiemployer Defined Benefit Pension Plans WHO'S AFFECTED These developments affect sponsors

Important Information Plan Administration and Operation June 2008 Federal Agencies Provide Guidance Affecting Multiemployer Defined Benefit Pension Plans WHO'S AFFECTED These developments affect sponsors

10/15/2015. PBGC Issues

0/5/205 PBGC Issues Kristina Archeval, Senior Advisor, Corporate Finance & Restructuring Department, PBGC Bela Palli, Manager, Standard Termination Compliance Division, PBGC Amy Viener, Acting Chief Policy

0/5/205 PBGC Issues Kristina Archeval, Senior Advisor, Corporate Finance & Restructuring Department, PBGC Bela Palli, Manager, Standard Termination Compliance Division, PBGC Amy Viener, Acting Chief Policy

Senate passes Pension Protection Act, Bill goes to President

LEGISLATION Senate passes Pension Protection Act, Bill goes to President Seeking to avert a meltdown and taxpayer bailout of traditional private pension plans, Congress has passed a comprehensive pension

LEGISLATION Senate passes Pension Protection Act, Bill goes to President Seeking to avert a meltdown and taxpayer bailout of traditional private pension plans, Congress has passed a comprehensive pension

Short Form Annual Return/Report of Small Employee Benefit Plan

Form 55-SF Department of the Treasury Internal Revenue Service Department of Labor Employee Benefits Security Administration Pension Benefit Guaranty Corporation Part I Short Form Annual Return/Report

Form 55-SF Department of the Treasury Internal Revenue Service Department of Labor Employee Benefits Security Administration Pension Benefit Guaranty Corporation Part I Short Form Annual Return/Report

Solutions to EA-2(A) Examination Fall, 2001

Examination Fall, 2001") Solutions to EA-2(A) Examination Fall, 2001 Question 1 The expected unfunded liability is: eul = (AL 1/1/2000 + Normal cost 1/1/2000 Actuarial assets 1/1/2000 ) 1.07 Contribution 2000 = (800,000 + 50,000

Solutions to EA-2(A) Examination Fall, 2001 Question 1 The expected unfunded liability is: eul = (AL 1/1/2000 + Normal cost 1/1/2000 Actuarial assets 1/1/2000 ) 1.07 Contribution 2000 = (800,000 + 50,000

WS 1 - Regulatory Update August 7, 2015

ACOPA Actuarial Symposium WS 1 - Regulatory Update August 7, 2015 Kyle Brown, IRS Counsel Jim Holland, Cheiron, Inc. Judy Miller, ACOPA Executive Director 1 Agenda IRS Mortality table update Notice 2015-49

ACOPA Actuarial Symposium WS 1 - Regulatory Update August 7, 2015 Kyle Brown, IRS Counsel Jim Holland, Cheiron, Inc. Judy Miller, ACOPA Executive Director 1 Agenda IRS Mortality table update Notice 2015-49

Workshop 13: PBGC / Reportable Events

Workshop 13: PBGC / Reportable Events Lauren R. Okum, MSPA, ASA, EA, MAAA Premier Actuarial Solutions Kurt F. Piper, FSPA, ASA, EA, MAAA Piper Pension & Profit Sharing Background ERISA 4043 requires plan

Workshop 13: PBGC / Reportable Events Lauren R. Okum, MSPA, ASA, EA, MAAA Premier Actuarial Solutions Kurt F. Piper, FSPA, ASA, EA, MAAA Piper Pension & Profit Sharing Background ERISA 4043 requires plan

DB Distributions - Addressing the Common Questions. Daniel Liss, EA, CEO, Economic Growth Pension Services, Inc.

DB Distributions - Addressing the Common Questions Daniel Liss, EA, CEO, Economic Growth Pension Services, Inc. 1 Daniel Liss, EA, CEO, Economic Growth Pension Services, Inc. Daniel began working at EGPS

DB Distributions - Addressing the Common Questions Daniel Liss, EA, CEO, Economic Growth Pension Services, Inc. 1 Daniel Liss, EA, CEO, Economic Growth Pension Services, Inc. Daniel began working at EGPS

Pension Protection Act of 2006: Next steps and considerations for plan sponsors of single-employer defined benefit plans *

Pension Protection Act of 2006: Next steps and considerations for plan sponsors of single-employer defined benefit plans * Effective immediately or retroactively Provision Summary of Provision Next Steps

Pension Protection Act of 2006: Next steps and considerations for plan sponsors of single-employer defined benefit plans * Effective immediately or retroactively Provision Summary of Provision Next Steps

ACTEX Learning. Learn Today. Lead Tomorrow. ACTEX Study Manual for EA-2F. Fall 2018 Edition. Michael J. Reilly, ASA, EA, MAAA

Learn Today. Lead Tomorrow. ACTEX Study Manual for EA-2F Fall 2018 Edition Michael J. Reilly, ASA, EA, MAAA ACTEX Study Manual for EA-2F Fall 2018 Edition Michael J. Reilly, ASA, EA, MAAA New Hartford,

Learn Today. Lead Tomorrow. ACTEX Study Manual for EA-2F Fall 2018 Edition Michael J. Reilly, ASA, EA, MAAA ACTEX Study Manual for EA-2F Fall 2018 Edition Michael J. Reilly, ASA, EA, MAAA New Hartford,

University of Puerto Rico Retirement System. Actuarial Valuation Report

University of Puerto Rico Retirement System Actuarial Valuation Report As of June 30, 2016 Cavanaugh Macdonald C O N S U L T I N G, L L C The experience and dedication you deserve May 22, 2017 Retirement

University of Puerto Rico Retirement System Actuarial Valuation Report As of June 30, 2016 Cavanaugh Macdonald C O N S U L T I N G, L L C The experience and dedication you deserve May 22, 2017 Retirement

University of Puerto Rico Retirement System. Actuarial Valuation Valuation Report

University of Puerto Rico Retirement System Actuarial Valuation Valuation Report As of June 30, 2015 Cavanaugh Macdonald C O N S U L T I N G, L L C The experience and dedication you deserve April 11, 2016

University of Puerto Rico Retirement System Actuarial Valuation Valuation Report As of June 30, 2015 Cavanaugh Macdonald C O N S U L T I N G, L L C The experience and dedication you deserve April 11, 2016

Additional Funding Rules for Multiemployer Plans in Endangered or Critical Status (IRC section 432)

") Additional Funding Rules for Multiemployer Plans in Endangered or Critical Status (IRC section 432) A plan is in critical status if one or more of the following conditions exist as of the first day of

Additional Funding Rules for Multiemployer Plans in Endangered or Critical Status (IRC section 432) A plan is in critical status if one or more of the following conditions exist as of the first day of

Funding Stabilization and PBGC Premium Increases

Consulting Retirement Funding Stabilization and PBGC Premium Increases Impact on Plan Sponsors and Participants July 2012 On June 29, 2012, the House and Senate passed H.R. 4348, the Moving Ahead for Progress

Consulting Retirement Funding Stabilization and PBGC Premium Increases Impact on Plan Sponsors and Participants July 2012 On June 29, 2012, the House and Senate passed H.R. 4348, the Moving Ahead for Progress

Stephanie Alden Smithey

Amending Your Qualified Plans for the Pension Protection Act and the Worker, Retiree, and Employer Recovery Act (and Other Pension Laws) September 24, 2009 Presented By: Stephanie Alden Smithey You may

Amending Your Qualified Plans for the Pension Protection Act and the Worker, Retiree, and Employer Recovery Act (and Other Pension Laws) September 24, 2009 Presented By: Stephanie Alden Smithey You may

Workshop 10: Significantly Overfunded and Underfunded DB Plans

1 Workshop 10: Significantly Overfunded and Underfunded DB Plans Presented by: Steven J. Levine, MSPA Thomas J. Finnegan, FSPA 2 1 Use of Pension Surplus Awareness of funding issues Very relevant related

1 Workshop 10: Significantly Overfunded and Underfunded DB Plans Presented by: Steven J. Levine, MSPA Thomas J. Finnegan, FSPA 2 1 Use of Pension Surplus Awareness of funding issues Very relevant related

Annual Return/Report of Employee Benefit Plan

Form 5500 Department of the Treasury Internal Revenue Service Department of Labor Employee Benefits Security Administration Pension Benefit Guaranty Corporation Annual Return/Report of Employee Benefit

Form 5500 Department of the Treasury Internal Revenue Service Department of Labor Employee Benefits Security Administration Pension Benefit Guaranty Corporation Annual Return/Report of Employee Benefit

WHY YOU SHOULD KNOW ABOUT CASH BALANCE PLANS

WHY YOU SHOULD KNOW ABOUT CASH BALANCE PLANS Presented by Steve J. Persons, MSPA, CPA Max E. Wyman, MSPA, CPC Creative Benefit Strategies, Inc. www.creben.com (800) 238-5490 Why should YOU care about Defined

WHY YOU SHOULD KNOW ABOUT CASH BALANCE PLANS Presented by Steve J. Persons, MSPA, CPA Max E. Wyman, MSPA, CPC Creative Benefit Strategies, Inc. www.creben.com (800) 238-5490 Why should YOU care about Defined

PLAN SPONSOR NEWSLETTER

Benefits in Focus January 2018 PLAN SPONSOR NEWSLETTER Retirement Compliance Calendar Retirement plan sponsors are responsible for compliance with many ongoing reporting, disclosure and notice requirements.

Benefits in Focus January 2018 PLAN SPONSOR NEWSLETTER Retirement Compliance Calendar Retirement plan sponsors are responsible for compliance with many ongoing reporting, disclosure and notice requirements.

CITY OF KISSIMMEE MUNICIPAL POLICE OFFICERS RETIREMENT FUND ACTUARIAL VALUATION AS OF OCTOBER 1, 2017

CITY OF KISSIMMEE MUNICIPAL POLICE OFFICERS RETIREMENT FUND ACTUARIAL VALUATION AS OF OCTOBER 1, 2017 CONTRIBUTIONS APPLICABLE TO THE PLAN YEAR ENDED SEPTEMBER 30, 2018, AND THE CITY'S FISCAL YEAR ENDED

CITY OF KISSIMMEE MUNICIPAL POLICE OFFICERS RETIREMENT FUND ACTUARIAL VALUATION AS OF OCTOBER 1, 2017 CONTRIBUTIONS APPLICABLE TO THE PLAN YEAR ENDED SEPTEMBER 30, 2018, AND THE CITY'S FISCAL YEAR ENDED

Compensation measurement period tax year not plan year

404 Deduction Rules for DB/DC Plans Tuesday, April 30, 2013 Kevin J. Donovan, CPA, MSPA Pinnacle Plan Design, LLC Defined Contribution Plans For defined contribution plans deduction limited to 25% of compensation

404 Deduction Rules for DB/DC Plans Tuesday, April 30, 2013 Kevin J. Donovan, CPA, MSPA Pinnacle Plan Design, LLC Defined Contribution Plans For defined contribution plans deduction limited to 25% of compensation

New law impacts multiemployer defined benefit plans

Important information Plan administration and operation New law impacts multiemployer defined benefit plans Who s affected These developments affect sponsors of and participants in qualified multiemployer

Important information Plan administration and operation New law impacts multiemployer defined benefit plans Who s affected These developments affect sponsors of and participants in qualified multiemployer

DB: Basics of Defined Benefit Plans 2017 Syllabus

Course DB: Basics of Defined Benefit Plans 2017 Syllabus This course builds on the material learned from the Retirement Plan Academy Retirement Plan Fundamentals courses (RPF-1 & RPF-2). Those courses

Course DB: Basics of Defined Benefit Plans 2017 Syllabus This course builds on the material learned from the Retirement Plan Academy Retirement Plan Fundamentals courses (RPF-1 & RPF-2). Those courses

INDEX. Enrolled Actuaries Meetings. Compilation of Questions to PBGC and Summary of their Responses 1998,

INDEX Enrolled Actuaries Meetings Compilation of Questions to PBGC and Summary of their Responses 1998, 2000-2016 2016 Enrolled Actuaries Meeting Adapted from material prepared by Mercer A Year-Question

INDEX Enrolled Actuaries Meetings Compilation of Questions to PBGC and Summary of their Responses 1998, 2000-2016 2016 Enrolled Actuaries Meeting Adapted from material prepared by Mercer A Year-Question

CITY OF PENSACOLA FIREFIGHTERS RELIEF AND PENSION FUND ACTUARIAL VALUATION AND REPORT AS OF OCTOBER 1, 2014

CITY OF PENSACOLA FIREFIGHTERS RELIEF AND PENSION FUND ACTUARIAL VALUATION AND REPORT AS OF OCTOBER 1, 2014 CONTRIBUTIONS APPLICABLE TO THE PLAN/ FISCAL YEAR ENDED SEPTEMBER 30, 2016 2 January 20, 2015

CITY OF PENSACOLA FIREFIGHTERS RELIEF AND PENSION FUND ACTUARIAL VALUATION AND REPORT AS OF OCTOBER 1, 2014 CONTRIBUTIONS APPLICABLE TO THE PLAN/ FISCAL YEAR ENDED SEPTEMBER 30, 2016 2 January 20, 2015

THE LIFE OF A PLAN CASE STUDY Cash Balance Plan

THE LIFE OF A PLAN CASE STUDY Cash Balance Plan Charlie Steingas, EA, MSPA, MAAA President, Cash Balance Actuaries, LLC Charlie Steingas, EA, MSPA, MAAA President, Cash Balance Actuaries, LLC Charlie is

THE LIFE OF A PLAN CASE STUDY Cash Balance Plan Charlie Steingas, EA, MSPA, MAAA President, Cash Balance Actuaries, LLC Charlie Steingas, EA, MSPA, MAAA President, Cash Balance Actuaries, LLC Charlie is

Cracking the Code on DB Plan RMDs. Mary Ann Rocco, EA, MSPA Owner and Third-Party Consulting Actuary Mary Ann Rocco

Cracking the Code on DB Plan RMDs Mary Ann Rocco, EA, MSPA Owner and Third-Party Consulting Actuary Mary Ann Rocco Abbreviations RMD: Required Minimum Distribution DCY: Distribution Calendar Year ASD:

Cracking the Code on DB Plan RMDs Mary Ann Rocco, EA, MSPA Owner and Third-Party Consulting Actuary Mary Ann Rocco Abbreviations RMD: Required Minimum Distribution DCY: Distribution Calendar Year ASD:

TYPES OF QUALIFIED PLANS

Chapter 2 by Richard A. Naegele, J.D., M.A. Wickens, Herzer, Panza, Cook & Batista Co. 35765 Chester Road Avon, OH 44011-1262 Phone: (440) 695-8074 Email: RNaegele@WickensLaw.com Website: www.wickenslaw.com

Chapter 2 by Richard A. Naegele, J.D., M.A. Wickens, Herzer, Panza, Cook & Batista Co. 35765 Chester Road Avon, OH 44011-1262 Phone: (440) 695-8074 Email: RNaegele@WickensLaw.com Website: www.wickenslaw.com

7/31/2015. TPA S and Actuaries Working Together. Mary Ann Rocco, EA, MSPA Huntington Beach, CA

1 TPA S and Actuaries Working Together Mary Ann Rocco, EA, MSPA Huntington Beach, CA 714-393-8845 mar@roccoea.com 2 1 TPA S and Actuaries Working Together TPA Clients and your Practice Why bother with

1 TPA S and Actuaries Working Together Mary Ann Rocco, EA, MSPA Huntington Beach, CA 714-393-8845 mar@roccoea.com 2 1 TPA S and Actuaries Working Together TPA Clients and your Practice Why bother with

STATE POLICE RETIREMENT BENEFITS TRUST STATE OF RHODE ISLAND ACTUARIAL VALUATION R E P O R T AS OF J U N E 3 0, 201 6

STATE POLICE RETIREMENT BENEFITS TRUST STATE OF RHODE ISLAND ACTUARIAL VALUATION R E P O R T AS OF J U N E 3 0, 201 6 January 31, 2017 Retirement Board 40 Fountain Street, First Floor Providence, RI 02903-1854

STATE POLICE RETIREMENT BENEFITS TRUST STATE OF RHODE ISLAND ACTUARIAL VALUATION R E P O R T AS OF J U N E 3 0, 201 6 January 31, 2017 Retirement Board 40 Fountain Street, First Floor Providence, RI 02903-1854

Solutions to EA-2(A) Examination Fall, 2005

Examination Fall, 2005") Solutions to EA-2(A) Examination Fall, 2005 Question 1 Section 3.01(1) of Revenue Procedure 2000-40 indicates automatic approval for a change to the unit credit cost method is not available for a cash

Solutions to EA-2(A) Examination Fall, 2005 Question 1 Section 3.01(1) of Revenue Procedure 2000-40 indicates automatic approval for a change to the unit credit cost method is not available for a cash

Workshop 45. Defined Benefit: Ask the Experts

ASPPA 2016 Annual Conference Workshop 45 Defined Benefit: Ask the Experts Tuesday, October 25, 2015 10:45 a.m. 12:00 p.m. Government Participants Linda Marshall, Senior Counsel, Chief Counsel, Qualified

ASPPA 2016 Annual Conference Workshop 45 Defined Benefit: Ask the Experts Tuesday, October 25, 2015 10:45 a.m. 12:00 p.m. Government Participants Linda Marshall, Senior Counsel, Chief Counsel, Qualified

401(a)(26), Top Heavy, and Coverage Basics for Defined Benefit Plans

(26), Top Heavy, and Coverage Basics for Defined Benefit Plans") 401(a)(26), Top Heavy, and Coverage Basics for Defined Benefit Plans Lauren R. Okum, ASA, EA, MAAA, MSPA Owner and Actuary, Premier Actuarial Solutions Page 0 1 Lauren R. Okum, ASA, EA, MAAA, MSPA Owner

401(a)(26), Top Heavy, and Coverage Basics for Defined Benefit Plans Lauren R. Okum, ASA, EA, MAAA, MSPA Owner and Actuary, Premier Actuarial Solutions Page 0 1 Lauren R. Okum, ASA, EA, MAAA, MSPA Owner

PLAN SPONSOR NEWSLETTER

Benefits in Focus January 2019 PLAN SPONSOR NEWSLETTER Retirement Compliance Calendar Retirement plan sponsors are responsible for compliance with many ongoing reporting, disclosure and notice requirements.

Benefits in Focus January 2019 PLAN SPONSOR NEWSLETTER Retirement Compliance Calendar Retirement plan sponsors are responsible for compliance with many ongoing reporting, disclosure and notice requirements.

Cash Balance for Beginners. Kevin J. Donovan, CPA, EA, MSPA, Managing Member, Pinnacle Plan Design, LLC

Cash Balance for Beginners Kevin J. Donovan, CPA, EA, MSPA, Managing Member, Pinnacle Plan Design, LLC 1 Kevin Donovan, CPA, EA, MSPA, Managing Member, Pinnacle Plan Design, LLC Kevin is a shareholder

Cash Balance for Beginners Kevin J. Donovan, CPA, EA, MSPA, Managing Member, Pinnacle Plan Design, LLC 1 Kevin Donovan, CPA, EA, MSPA, Managing Member, Pinnacle Plan Design, LLC Kevin is a shareholder

Cash Balance for Beginners

Cash Balance for Beginners Kevin J. Donovan, CPA, EA, MSPA, Managing Member, Pinnacle Plan Design, LLC 1 Kevin Donovan, CPA, EA, MSPA, Managing Member, Pinnacle Plan Design, LLC Kevin is a shareholder

Cash Balance for Beginners Kevin J. Donovan, CPA, EA, MSPA, Managing Member, Pinnacle Plan Design, LLC 1 Kevin Donovan, CPA, EA, MSPA, Managing Member, Pinnacle Plan Design, LLC Kevin is a shareholder

Audited Financial Statements. Caritas Christi Retirement Plan and Trust. June 30, 2005

Audited Financial Statements Caritas Christi Retirement Plan and Trust June 30, 2005 Audited Financial Statements and Other Financial Information June 30, 2005 INDEPENDENT AUDITORS' REPORT 1 AUDITED FINANCIAL

Audited Financial Statements Caritas Christi Retirement Plan and Trust June 30, 2005 Audited Financial Statements and Other Financial Information June 30, 2005 INDEPENDENT AUDITORS' REPORT 1 AUDITED FINANCIAL

Annual Return/Report of Employee Benefit Plan

Form 55 Department of the Treasury Internal Revenue Service Department of Labor Employee Benefits Security Administration Pension Benefit Guaranty Corporation Part I Annual Return/Report of Employee Benefit

Form 55 Department of the Treasury Internal Revenue Service Department of Labor Employee Benefits Security Administration Pension Benefit Guaranty Corporation Part I Annual Return/Report of Employee Benefit

The Pension Protection Act: the Cost Accounting Standards Harmonization and Implications for Government Contractors

The Pension Protection Act: the Cost Accounting Standards Harmonization and Implications for Government Contractors Paul E. Pompeo, Partner, Government Contracts, 202.942.5723 Mary Cassidy, Counsel, Compensation

The Pension Protection Act: the Cost Accounting Standards Harmonization and Implications for Government Contractors Paul E. Pompeo, Partner, Government Contracts, 202.942.5723 Mary Cassidy, Counsel, Compensation

CITY OF PINELLAS PARK FIREFIGHTERS PENSION FUND ACTUARIAL VALUATION AS OF OCTOBER 1, 2016

CITY OF PINELLAS PARK FIREFIGHTERS PENSION FUND ACTUARIAL VALUATION AS OF OCTOBER 1, 2016 CONTRIBUTIONS APPLICABLE TO THE PLAN/ FISCAL YEAR ENDED SEPTEMBER 30, 2018 January 30, 2017 Board of Trustees City

CITY OF PINELLAS PARK FIREFIGHTERS PENSION FUND ACTUARIAL VALUATION AS OF OCTOBER 1, 2016 CONTRIBUTIONS APPLICABLE TO THE PLAN/ FISCAL YEAR ENDED SEPTEMBER 30, 2018 January 30, 2017 Board of Trustees City

CITY OF HOLLYWOOD FIREFIGHTERS PENSION FUND ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2015

CITY OF HOLLYWOOD FIREFIGHTERS PENSION FUND ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2015 CONTRIBUTIONS APPLICABLE TO THE PLAN/ FISCAL YEAR ENDED SEPTEMBER 30, 2017 June 28, 2016 Board of Trustees c/o

CITY OF HOLLYWOOD FIREFIGHTERS PENSION FUND ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2015 CONTRIBUTIONS APPLICABLE TO THE PLAN/ FISCAL YEAR ENDED SEPTEMBER 30, 2017 June 28, 2016 Board of Trustees c/o

The New York State Teamsters Conference Pension and Retirement Fund Application for Suspension of Benefits under MPRA EXHIBIT 21

The Application for Suspension of Benefits under MPRA EXHIBIT 21 DB1/ 88552986.1 New York State Teamsters Conference Pension and Retirement Fund Actuarial Valuation as of January 1, 2015 November 2, 2015

The Application for Suspension of Benefits under MPRA EXHIBIT 21 DB1/ 88552986.1 New York State Teamsters Conference Pension and Retirement Fund Actuarial Valuation as of January 1, 2015 November 2, 2015

Benefits Handbook Date November 1, Marsh & McLennan Companies Retirement Plan A Marsh & McLennan Companies

Date November 1, 2015 Marsh & McLennan Companies Retirement Plan A Marsh & McLennan Companies Marsh & McLennan Companies Retirement Plan A The (also referred to as the Plan ) is a central part of the Company

Date November 1, 2015 Marsh & McLennan Companies Retirement Plan A Marsh & McLennan Companies Marsh & McLennan Companies Retirement Plan A The (also referred to as the Plan ) is a central part of the Company

STATE POLICE RETIREMENT BENEFITS TRUST STATE OF RHODE ISLAND ACTUARIAL VALUATION R E P O R T AS OF J U N E 3 0, 201 5

STATE POLICE RETIREMENT BENEFITS TRUST STATE OF RHODE ISLAND ACTUARIAL VALUATION R E P O R T AS OF J U N E 3 0, 201 5 February 25, 2016 Retirement Board 40 Fountain Street, First Floor Providence, RI 02903-1854

STATE POLICE RETIREMENT BENEFITS TRUST STATE OF RHODE ISLAND ACTUARIAL VALUATION R E P O R T AS OF J U N E 3 0, 201 5 February 25, 2016 Retirement Board 40 Fountain Street, First Floor Providence, RI 02903-1854

CITY OF KISSIMMEE MUNICIPAL FIREFIGHTERS RETIREMENT PLAN ACTUARIAL VALUATION AS OF OCTOBER 1, 2017

CITY OF KISSIMMEE MUNICIPAL FIREFIGHTERS RETIREMENT PLAN ACTUARIAL VALUATION AS OF OCTOBER 1, 2017 CONTRIBUTIONS APPLICABLE TO THE PLAN YEAR ENDED SEPTEMBER 30, 2018, AND THE CITY'S FISCAL YEAR ENDED SEPTEMBER

CITY OF KISSIMMEE MUNICIPAL FIREFIGHTERS RETIREMENT PLAN ACTUARIAL VALUATION AS OF OCTOBER 1, 2017 CONTRIBUTIONS APPLICABLE TO THE PLAN YEAR ENDED SEPTEMBER 30, 2018, AND THE CITY'S FISCAL YEAR ENDED SEPTEMBER

Workshop 22: Defined Benefit Q&A

Workshop 22: Defined Benefit Q&A Kyle N. Brown, Special Counsel, IRS Chief Counsel TE/GE James E. Holland, Jr., Cheiron Inc. Judy Miller, ASPPA/ACOPA Question 1 Section 401(a)(4): Retroactive Plan Amendments

Workshop 22: Defined Benefit Q&A Kyle N. Brown, Special Counsel, IRS Chief Counsel TE/GE James E. Holland, Jr., Cheiron Inc. Judy Miller, ASPPA/ACOPA Question 1 Section 401(a)(4): Retroactive Plan Amendments

LA Advanced Pension Conference WS 7: Cash Balance Update. Today s Agenda

LA Advanced Pension Conference WS 7: Cash Balance Update Kevin J. Donovan, CPA, EA, MSPA, ACA Pinnacle Plan Design LLC Andrew W. Ferguson, FSA, EA, MSPA Altman & Cronin Benefit Consultants, LLC 1 Today

LA Advanced Pension Conference WS 7: Cash Balance Update Kevin J. Donovan, CPA, EA, MSPA, ACA Pinnacle Plan Design LLC Andrew W. Ferguson, FSA, EA, MSPA Altman & Cronin Benefit Consultants, LLC 1 Today

The Long and Short of the Pension Protection Act of 2006

The Long and Short of the Pension Protection Act of 2006 Long-Term Implications and Short-Term Actions for Plan Sponsors 2006 United States watsonwyatt.com 2 Watson Wyatt Worldwide Table of Contents Single-Employer

The Long and Short of the Pension Protection Act of 2006 Long-Term Implications and Short-Term Actions for Plan Sponsors 2006 United States watsonwyatt.com 2 Watson Wyatt Worldwide Table of Contents Single-Employer

S T A T E P O L I C E R E T I R E M E N T B E N E F I T S T R U S T S T A T E O F R H O D E I S L A N D A C T U A R I A L V A L U A T I O N R E P O R

S T A T E P O L I C E R E T I R E M E N T B E N E F I T S T R U S T S T A T E O F R H O D E I S L A N D A C T U A R I A L V A L U A T I O N R E P O R T A S O F J U N E 3 0, 2 0 0 8 September 2, 2009 Retirement

S T A T E P O L I C E R E T I R E M E N T B E N E F I T S T R U S T S T A T E O F R H O D E I S L A N D A C T U A R I A L V A L U A T I O N R E P O R T A S O F J U N E 3 0, 2 0 0 8 September 2, 2009 Retirement

RE: GASB Statement No. 67 and No. 68 City of Cape Coral Municipal General Employees Retirement Plan

February 21, 2017 Ms. Linda Runkle, Plan Administrator The Resource Centers, LLC P.O. Box 152665 Cape Coral, FL 33915-2665 RE: GASB Statement No. 67 and No. 68 City of Cape Coral Municipal General Employees

February 21, 2017 Ms. Linda Runkle, Plan Administrator The Resource Centers, LLC P.O. Box 152665 Cape Coral, FL 33915-2665 RE: GASB Statement No. 67 and No. 68 City of Cape Coral Municipal General Employees

Workshop 17: 436 Restrictions

Workshop 17: 436 Restrictions James E. Holland, Jr. Lawrence Deutsch 436 Restrictions We should all know by now that under IRC 436, if the AFTAP is less than 80% certain restrictions apply to a plan, and

Workshop 17: 436 Restrictions James E. Holland, Jr. Lawrence Deutsch 436 Restrictions We should all know by now that under IRC 436, if the AFTAP is less than 80% certain restrictions apply to a plan, and