How is an option priced and what does it mean? Patrick Ceresna, CMT Big Picture Trading Inc.

|

|

|

- Erica Lucas

- 5 years ago

- Views:

Transcription

1 How is an option priced and what does it mean? Patrick Ceresna, CMT Big Picture Trading Inc.

2 Limitation of liability The opinions expressed in this presentation are those of the author(s) and presenter(s) only and do not necessarily represent the views of of the Bourse de Montréal Inc. (the Bourse ) and/or its affiliates. This document is offered for general information purposes only. The information provided in this document, including financial and economic data, quotes and any analysis or interpretation thereof, is provided solely for information purposes and shall not be construed in any jurisdiction as providing any advice or recommendation with respect to the purchase or sale of any derivative instrument, underlying security or any other financial instrument or as providing legal, accounting, tax, financial or investment advice. The Bourse recommends that you consult your own advisors in accordance with your needs. All references in this document to specifications, rules and obligations concerning a product are subject to the rules, policies and procedures of the Bourse and its clearinghouse, the Canadian Derivatives Clearing Corporation, which prevail over this document. Although care has been taken in the preparation of this document, the Bourse and/or its affiliates do not guarantee the accuracy or completeness of the information contained in this document and reserve the right to amend or review the content of this document any time and without prior notice. Neither the Bourse, nor any of its affiliates, directors, officers, employees or agents shall be liable for any damages, losses or costs incurred as a result of any errors or omissions in this document or of the use of or reliance upon any information appearing in this document.

3 02 Outline Black-Scholes Pricing Model The Greeks Delta Gamma Theta Vega Rho Capturing Vega Capturing Theta

4 03 Pricing Models Option pricing models Mathematical formulas Remove subjective decisions from pricing process Assume stock prices in marketplace are random Input Quantifiable factors that create an option s price Output Theoretical values for call and put options Greeks - price sensitivities to changing factors Delta Δ Gamma Γ Theta Θ Vega Κ Rho Ρ

5 04 Option Pricing Factors Quantifiable Underlying stock price Strike price Volatility Time until expiration Risk free interest rate (e.g., T-bill) Dividends Input for any option pricing model

6 05 The Black-Scholes Pricing Model Black-Scholes (1973) Earliest and most widely known European options No dividends Various other pricing models exist Extensions of Black-Scholes we will discuss Cox-Ross-Rubenstein (1979) Binomial model American-style options (regular equity contracts) Accounts for early exercise and dividends

7 06 Assumptions of Black-Scholes European-style contracts Volatility constant Short-term risk free interest rate constant Lognormal distribution of returns No dividends paid No commissions or transaction costs Efficient markets Direction of market or individual stocks not consistently predictable

8 07 Options in the Marketplace Who makes options prices? All market participants (buyers and sellers) Individual and institutional investors Professional market-makers Best bid/ask is consensus of all bids and offers What is an option ultimately worth? What the market is willing to pay Pricing models used as guideline Supply/demand and market dynamics override theoretical values

9 08 The Five Greeks Delta Γ Gamma Θ Theta Κ Vega Ρ Rho Expected change in option value with changing underlying stock price Expected change in option delta with changing underlying stock price Expected change in option value with passage of time (time decay) Expected change in option value with changing implied volatility Expected change in option value with changing risk-free interest rate

10 09 Nature of the Greeks Meaningful only during option s lifetime At expiration they are moot Impact of any Greek is on option s time value An expiring option is worth only intrinsic value (if any) Greeks may affect each other e.g., change in an options theta (time decay) may affect its delta Impact of Greeks differ for each option contract In-the-money vs. at-the-money vs. out-of-the-money Near-term vs. far-term

11 10 Individual Investors With respect to each of the Greeks More important to understand nature of sensitivities being measured Closer look at each will help Value of Greeks Understanding where your risk can come from Balancing risk vs. reward before positions established Setting your expectations Reducing surprises in option price behavior

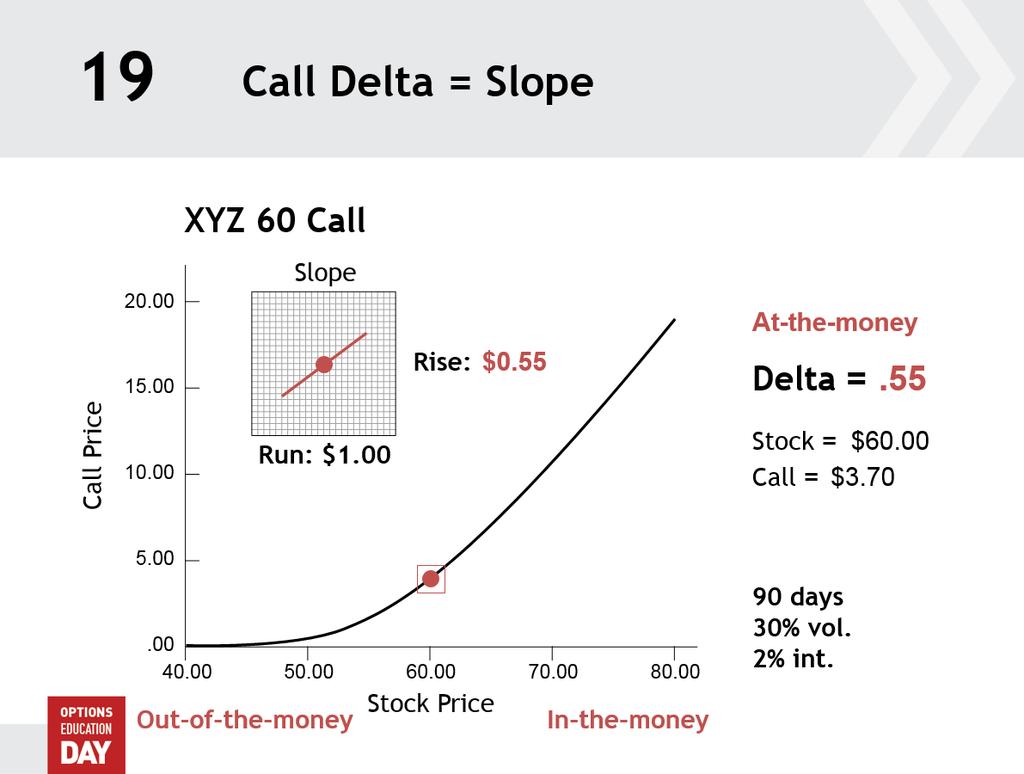

12 12 Delta Delta: Value s sensitivity to stock price Expected percentage change in option value With a short-term $1.00 change up or down in underlying All other pricing factors constant In either decimal form (.50) or whole number (50) Both mean 50% Deltas always range from 0 to 100 or 0 to 100% Each underlying share has a delta of 1.00

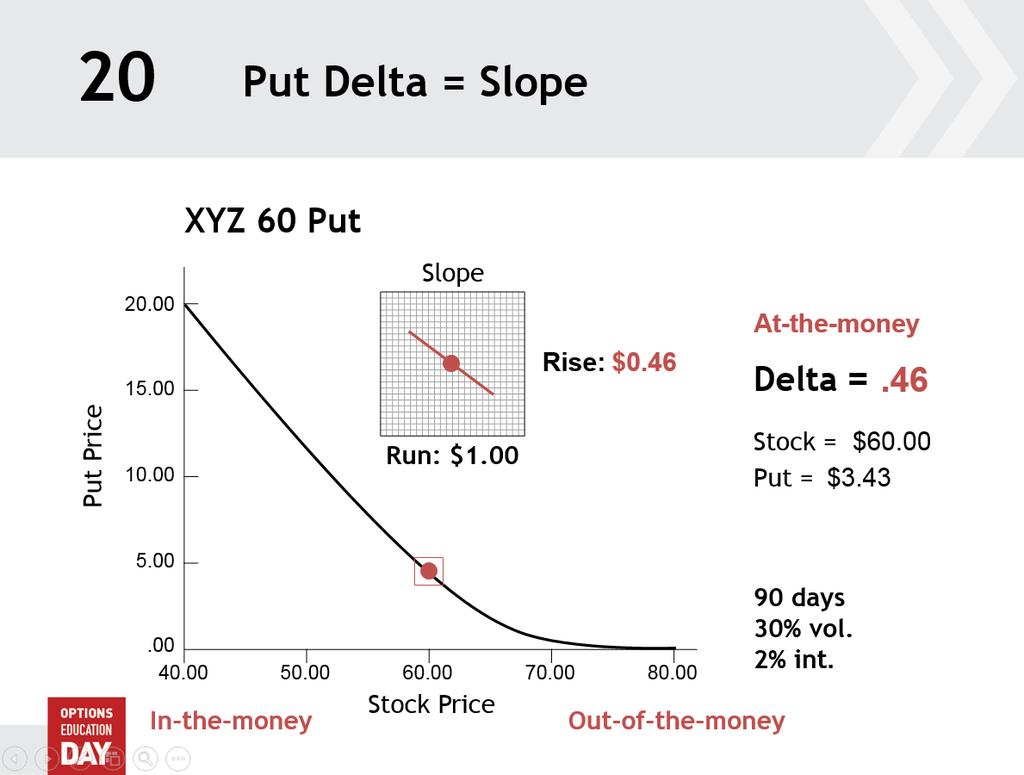

13 13 Delta Characteristics Calls have positive (long) deltas Positive correlation to underlying stock price change Stock price Call price Stock price Call price Call deltas range from 0 to Puts have negative (short) deltas Negative correlation to underlying stock price change Stock price Put price Stock price Put price Put deltas range from 0 to 1.00

14 14 Call Delta Examples On a given day an XYZ call has value $3.50 Delta of.50 (50%) XYZ stock is up $1.00 Call will theoretically increase by 50% of stock move $1.00 x.50 = $0.50 Expected call value = $ $0.50 = $4.00 XYZ stock is up $0.60 Call will theoretically increase by $0.60 x.50 = $0.30 Expected call value = $ $0.30 = $3.80

15 15 Call Delta Examples On a given day an XYZ call has value $2.75 Delta of.40 (40%) XYZ stock is down $1.00 Call will theoretically decrease by 40% of stock move $1.00 x.40 = $0.40 Expected call value = $2.75 $0.40 = $2.35 XYZ stock is down $0.50 Call will theoretically decrease by $0.50 x.40 = $0.20 Expected call value = $2.75 $0.20 = $2.55

16 16 Put Delta Examples On a given day an XYZ put has value $4.50 Delta of.30 (30%) XYZ stock is up $1.00 Put will theoretically decrease by 30% of stock move $1.00 x.30 = $0.30 Expected put value = $4.50 $0.30 = $4.20 XYZ stock is up $0.30 put will theoretically decrease by $0.30 x.30 = $0.09 expected put value = $4.50 $0.09 = $4.41

17 17 Put Delta Examples On a given day an XYZ put has value $2.90 Delta of.45 (45%) XYZ stock is down $1.00 Put will theoretically increase by 45% of stock move $1.00 x.45 = $0.45 Expected put value = $ $0.45 = $3.35 XYZ stock is down $0.60 Put will theoretically increase by $0.60 x.45 = $0.27 Expected put value = $ $0.27 = $3.17

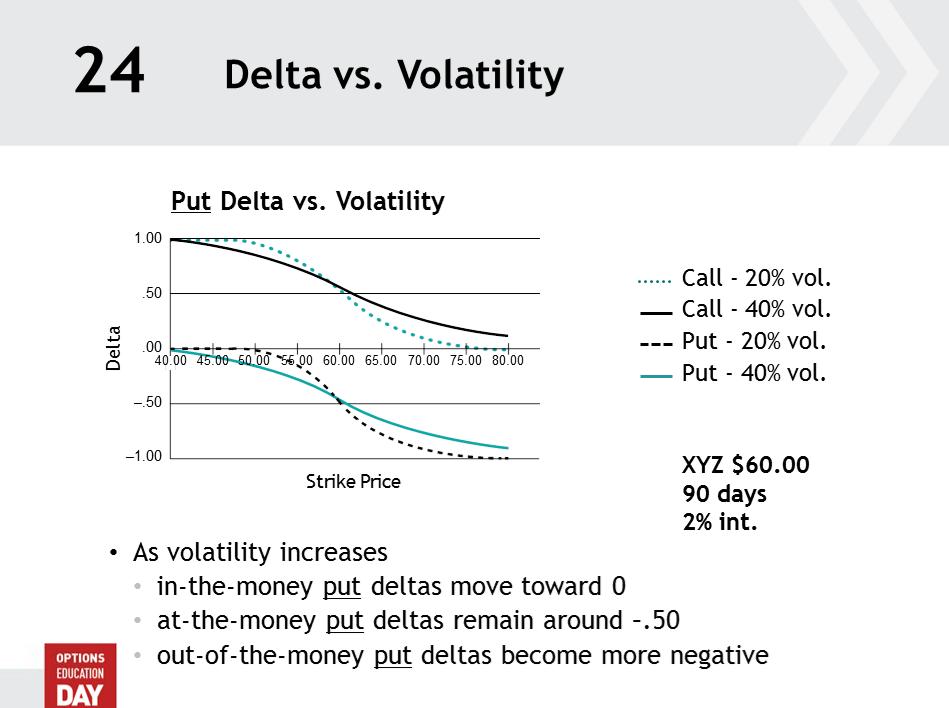

18 18 Deltas Are Not Fixed At-the-money options deltas are generally around.50 In-the-money calls Deltas 1.00 as calls become deep in-the-money When delta = 1.00 become substitute for long stock In-the-money puts Deltas 1.00 as puts become deep in-the-money When delta = 1.00 become substitute for short stock Out-of-the-money options Deltas approach 0 when far out-of-the-money Rate at which delta changes is not constant

19

20

21

22

23

24

25

26

27

28

29

30

31

32

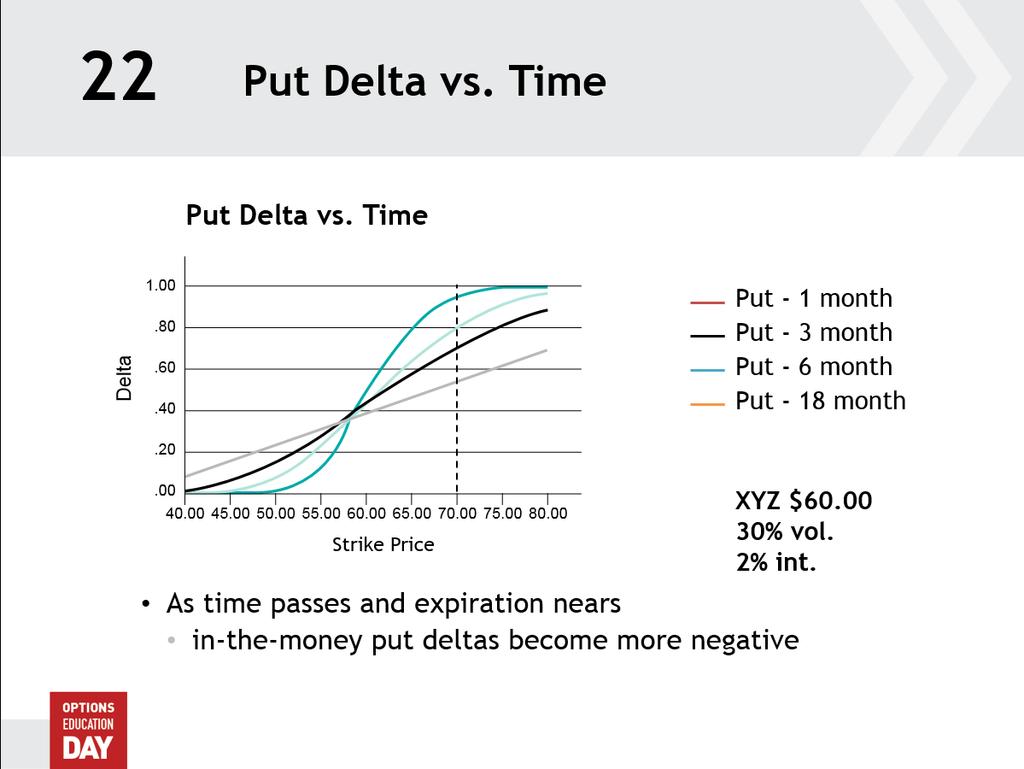

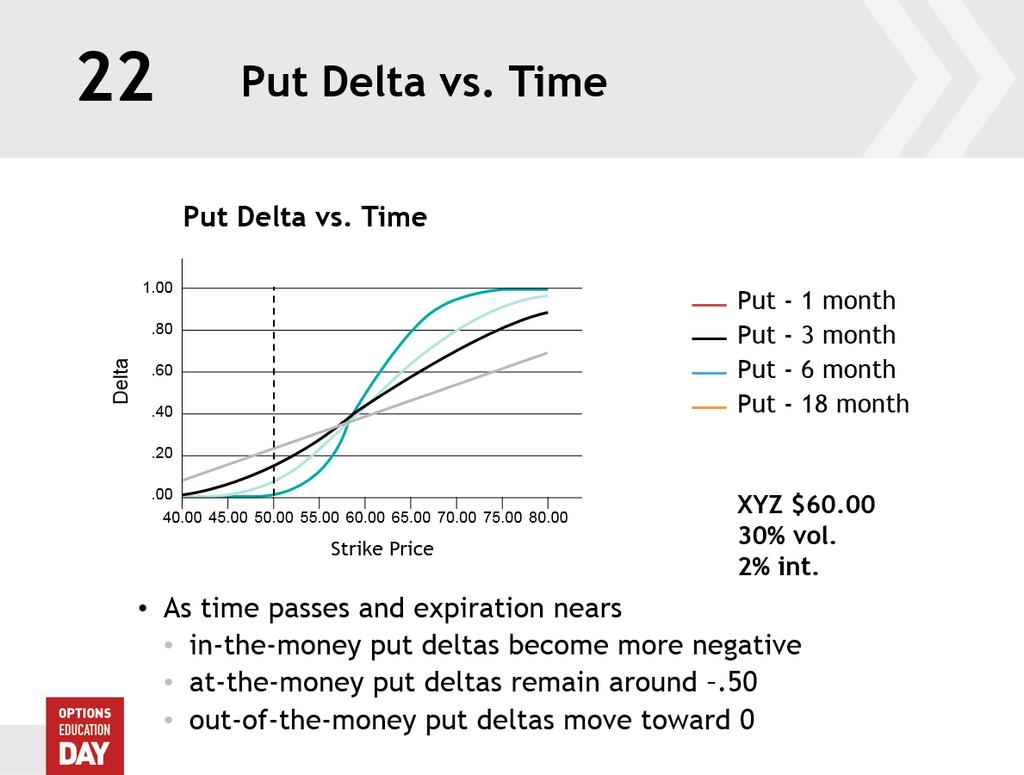

33 23 Delta vs. Time Over time In-the-money options become more sensitive to underlying stock price changes Out-of-the-money options become less sensitive to stock price changes Calls Puts Strike 18 Month 6 Month 3 Month 1 Month XYZ $ % vol. 2% int.

34

35

36 25 Delta as Share Equivalence Another way of using delta is in determining an option position s theoretical underlying share equivalence A single option position or entire option portfolio The calculation: # of options x delta amount x 100 shares (unit of trade) The option position can be expected to perform financially like this equivalent number of underlying shares

37 26 Call Share Equivalence Example Call position: 1 long contract with delta of.40 Share equivalence = 1 x.40 x 100 = 40 shares Call position should perform like 40 long shares Stock up $1.00 Call up $1.00 x.40 x 100 = $ shares up $40.00 Stock down $1.50 Call down $1.50 x.40 x 100 = $ shares down $60.00

38 27 Call Delta as Hedge Ratio Practical application of share equivalence Hedge ratio or Delta hedge To neutralize market risk of a position in that option Call position: 1 short contract that has delta of.45 Share equivalence = 1 x.45 x 100 shares = 45 shares Hedged position: 1 short call hedged by 45 long shares Stock up $1.00 Short call up = $1.00 x.45 x 100 = $45.00 loss 45 long shares = $45.00 profit Net profit/loss = 0

39 28 Netting Position Deltas Deltas from a portfolio of mixed options on same underlying stock Share equivalences are calculated and netted Measures market risk of portfolio in terms of stock Position deltas used for netting depend whether investor is long or short each contract Long call = Positive delta Short call = Negative delta Long put = Negative delta Short put = Positive delta Calculation for each option series # options x delta x 100 shares

40 29 Netting Position Delta Example Position Delta Position Delta Total Position Delta Long 40 Nov calls ,760 Short 45 Nov calls ,565 Long 60 Jan puts ,740 Long 60 Jan calls ,300 Short 2,100 XYZ shares ,100 Net position deltas 345 This portfolio should perform like a position of short 345 XYZ shares Position Delta If Net Positive Value Long shares of stock If Net Negative Value Short shares of stock

41 30 Gamma Γ Gamma: Delta s sensitivity to stock price Expected percentage change in delta s value With a short-term $1.00 change In underlying stock price up or down All other pricing factors constant In decimal form (e.g.,.02) Adjustment to delta Only options have gamma Stock does not

42 31 Gamma Characteristics Gamma amount is same for calls and puts Gamma for calls Stock price Delta by gamma amount Stock price Delta by gamma amount Gamma for puts Stock price Delta by gamma amount Stock price Delta by gamma amount Gamma is what option buyers are paying for Acceleration of delta Delta of the delta

43 32 Call Gamma Examples For purpose of adjusting delta amounts round gamma to two decimal places A call has delta of.54 and gamma of.042 (.04) Stock is up $1.00 Delta will become more positive by gamma amount New delta value:.58 Another call has delta of.75 and gamma of.034 (.03) Stock is down $1.00 Delta will become less positive by gamma amount New delta value:.72

44 33 Put Gamma Examples For purpose of adjusting delta amounts round gamma to two decimal places A put has delta of.54 and gamma of.020 (.02) Stock is up $1.00 Delta will become less negative by gamma amount New delta value:.52 Another put has delta of.27 and gamma of.067 (.07) Stock is down $1.00 Delta will become more negative by gamma amount New delta value:.34

45 34 Gamma Is Not Constant Gamma Delta Gamma vs. Stock Price day option Stock Price Call Delta vs. Stock Price Stock Price Option gamma (call or put) is greatest when stock is at the strike price Option is at-the-money As stock moves up or down (in-the-money or out-of-the-money): Gamma will decrease Delta will change at a decreasing rate 90 days 30% vol. 2% int.

46 35 Gamma Is Not Constant Gamma Gamma vs. Stock Price Gamma of both deep in-the-money and far out-of-the-money options decrease close to zero day option Stock Price Call Delta vs. Stock Price Delta Stock Price 90 days 30% vol. 2% int.

47 36 Gamma s Greatest Impact Gamma Gamma vs. Stock Price week option 1.00 Stock Price XYZ 60 Call Gamma effect greatest on at-the-money options, close to expiration They can move in-themoney to out-of-themoney very quickly Their deltas change the quickest Delta Stock Price 14 days 30% vol. 2% int.

48 37 Gamma vs. Time Gamma vs. Time Gamma month 3 month 6 month 18 month Strike Price XYZ $ % vol. 2% int. As expiration nears Gamma of at-the-money calls and puts increases Gammas of both in-the-money and out-of-the-money calls and puts decreases

49 38 Gamma vs. Volatility Gamma vs. Volatility Gamma % volatility 60% volatility Strike Price XYZ $ days 2% int. As volatility decreases Gamma of at-the-money calls and puts increases Gammas of both in-the-money and out-of-the-money calls and puts decreases

50 39 Netting Position Gamma Gammas from a portfolio of mixed options on same underlying stock may be netted May offset or augment an existing position delta Gamma amounts used depends whether investor is long or short each contract All long contracts have positive gamma All short contracts have negative gamma The calculation for each option series # of options x gamma amount x 100 shares

51 40 Netting Position Gamma Position Gamma Position Gamma Total Position Gamma Long 40 Nov calls Short 45 Nov calls Long 60 Jan puts Net XYZ position gamma Position Gamma If Net Positive Value Net long option position If Net Negative Value Net short option position A portfolio with net long position gamma Gets longer to the upside and shorter to the downside The added performance that enhances profits Net short position gamma performs in the opposite manner Gets shorter to the upside and longer to downside Very risky scenario

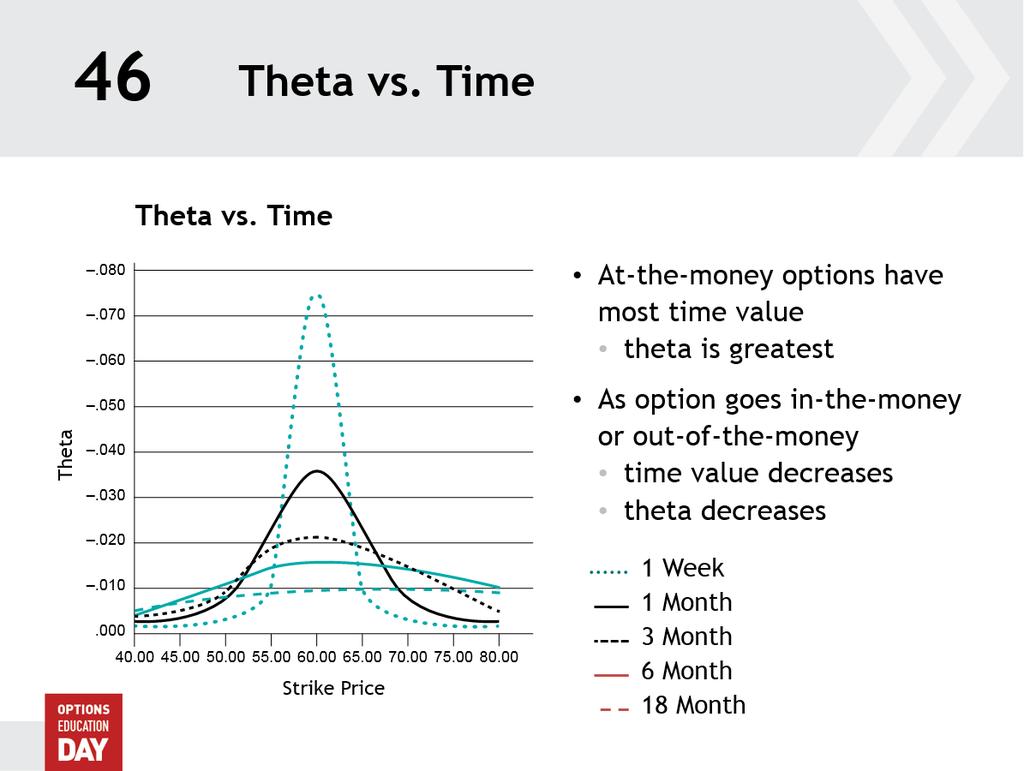

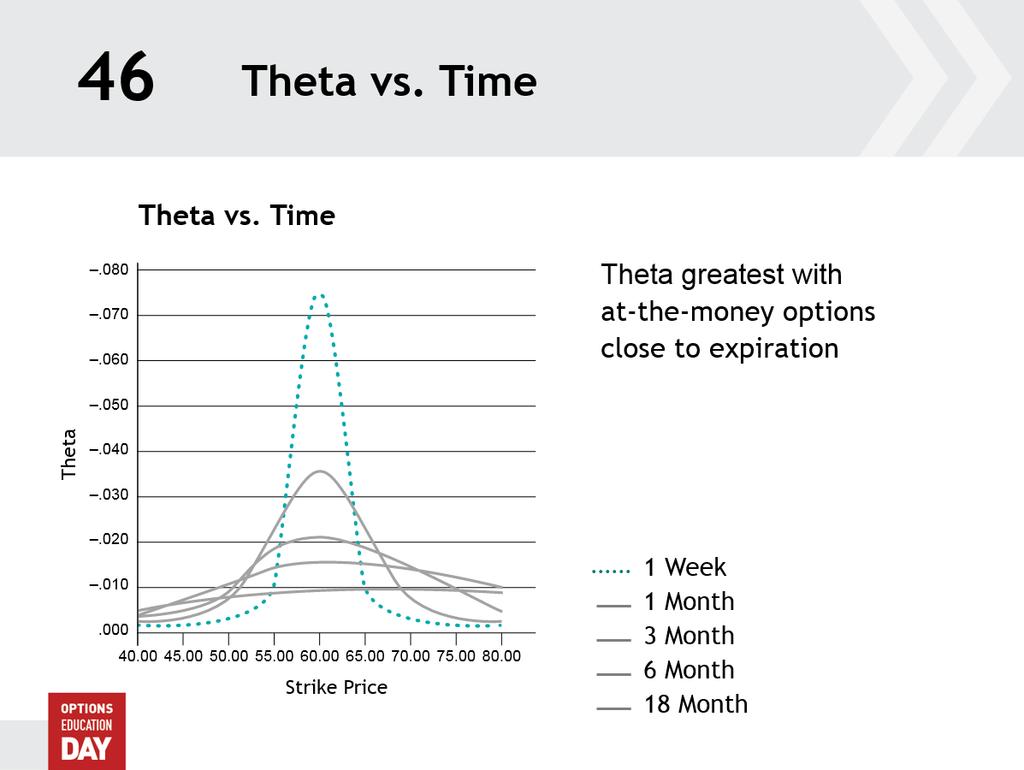

52 41 Theta Θ Theta: Option value s sensitivity to time Expected time decay in option value With the passage of 1 day Expressed in decimal form (.080) Represents cash amount per share All other pricing factors constant Calls and puts both have negative theta amounts

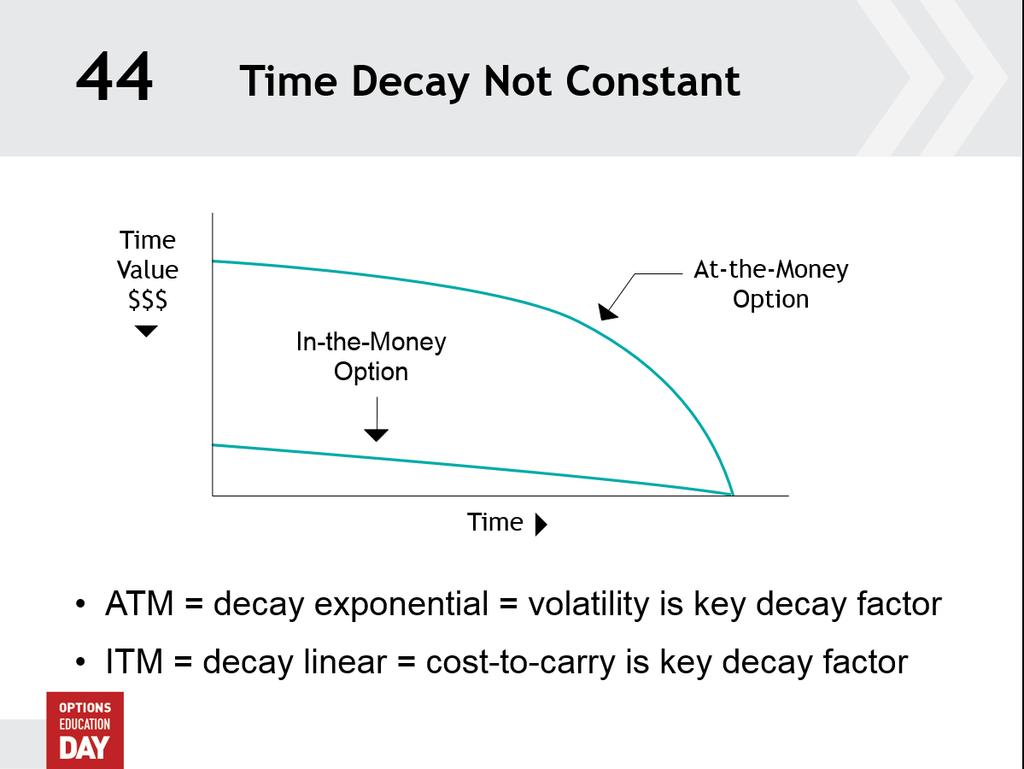

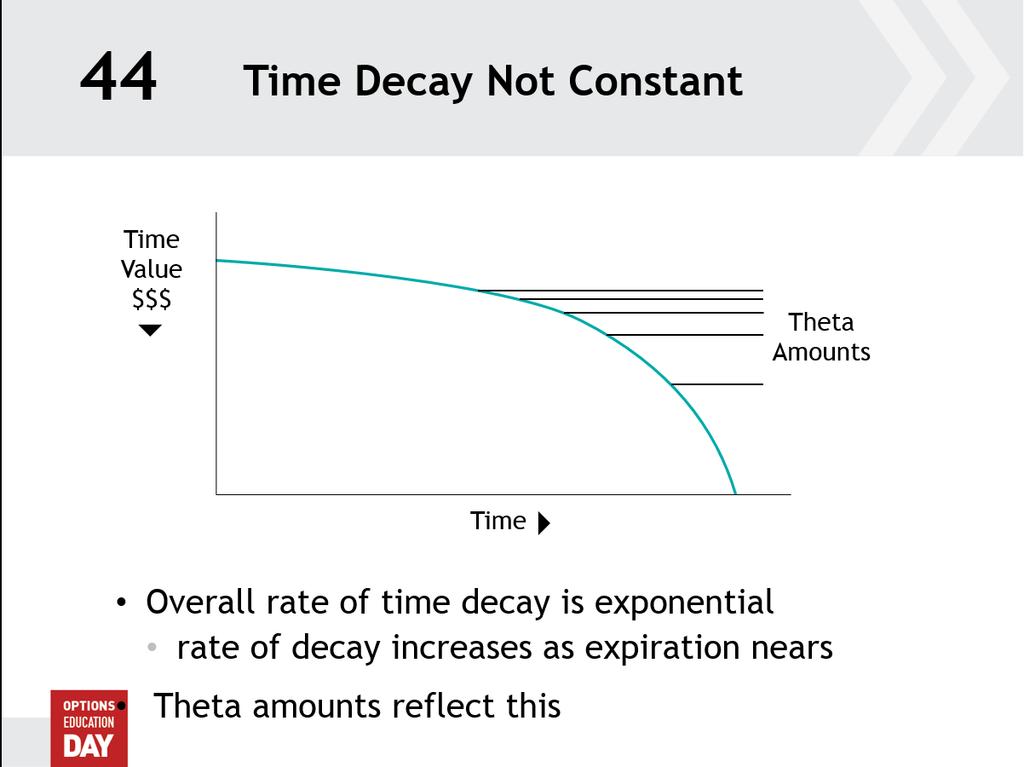

53 42 More on Theta Theta may be measured for periods longer than 1 day e.g., 2-day theta or 10-day theta Decay is per calendar day, not per trading day Theta represents rent buyers pay and writers receive Buyers want time for favorable move in stock price Writers sell that time Buyers hope delta gains will offset theta loss Only time value decays At expiration option worth only intrinsic value (if any)

54 43 Theta Calculation An option is trading today at $3.50 Theta of $.030 ( $.03) Contract is worth $3.50 x 100 shares = $ Option s expected value tomorrow = $3.50 $.03 = $3.47 Contract is worth $3.47 x 100 shares = $ Theta $.03 $3.00 loss per contract Assuming other pricing factors constant

55

56

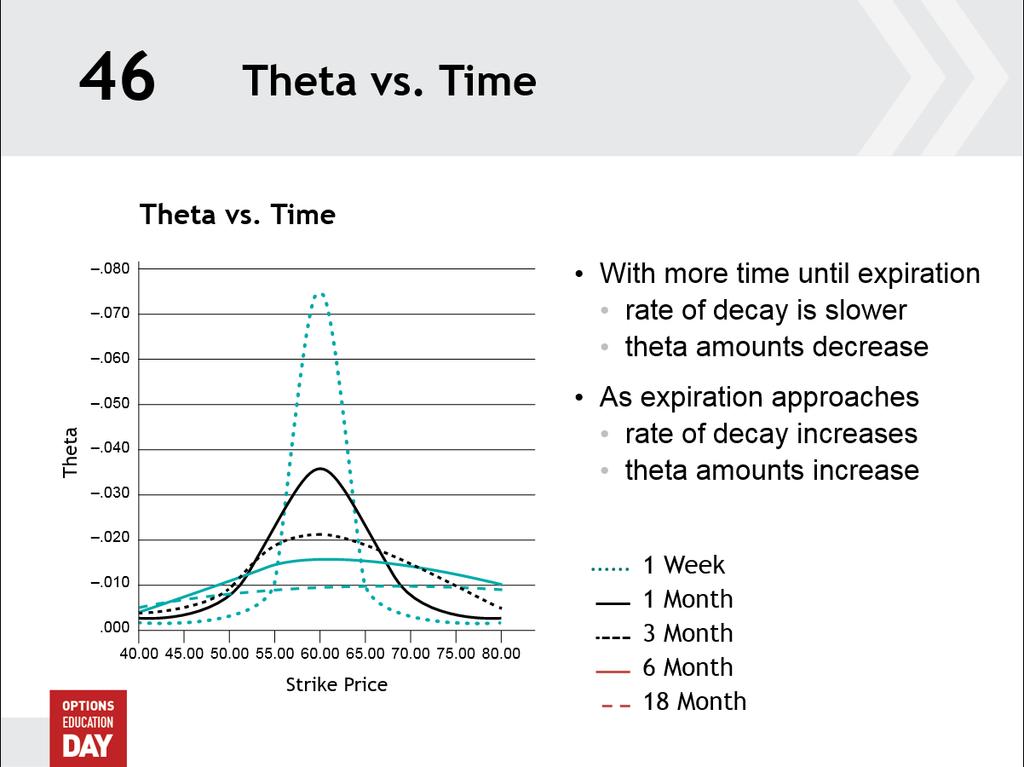

57 45 Theta vs. Volatility Theta vs. Volatility Theta Call - 40% vol. Put - 40% vol. Call - 20% vol. Put - 20% vol Strike Price Implied volatility impacts theta amounts With rising volatility Theta increases With decreasing volatility Theta decreases XYZ $ days 2% int. Higher volatility more time value more to decay by expiration

58 58

59

60

61 47 Netting Position Theta Thetas from a portfolio of mixed options on same underlying stock may be netted Theta amounts used depends whether investor is long or short each contract All long contracts have negative theta All short contracts have positive theta The calculation for each option series # of options x theta amount x 100 shares

62 48 Netting Position Theta Position Theta Position Theta Total Position Theta Long 40 Nov calls Short 45 Nov calls Long 60 Jan puts Net position theta At close of business today, tomorrow this position could expect to see a loss of $93.00 from time decay Position Theta If Net Positive Value Gain from time decay If Net Negative Value Loss from time decay A portfolio with net positive position theta can expect a profit in 1 day of net theta amount A portfolio with net negative position theta can expect a loss in 1 day of net theta amount

63 49 Vega Κ Vega: Option value s sensitivity to volatility Expected change in option value With a 1%-point change in implied volatility up or down Expressed in decimal form (.080) Represents cash amount per share All other pricing factors constant Calls and puts both have positive vega amounts implied option value by vega amount implied option value by vega amount

64 50 Vega Characteristics Also known as kappa (Greek letter) thus symbol K Volatility considered most influential price factor Great impact in dollars on option values possible Changes often occur intra-day Changes may be abrupt and significant Increase in implied or vega does not require change in stock price

65 51 Vega Examples Vega impact greatest In dollar amounts on at-the-money contracts In percentage terms on out-of-the-money contracts Option today valued at $4.50 with vega (.03) volatility 1 pt. option price $ = $4.53 volatility 1 pt. option price $ = $4.47 Option today valued at $2.75 with vega (.02) volatility 1 pt. option price $ = $2.77 volatility 1 pt. option price $ = $2.73

66 52 Vega vs. Time Vega Vega vs. Time month 6 month 3 month 1 month Strike Price More time until expiration Greater the vega Vega size related to amount of time value More time value greater the vega Long term options vega may be significantly higher XYZ $ % vol. 2% int.

67 53 Netting Position Vega Vegas from a portfolio of mixed options on same underlying stock may be netted Vega amounts used depends whether investor is long or short each contract All long contracts have positive vega All short contracts have negative vega The calculation for each option series # of options x vega amount x 100 shares

68 54 Netting Position Vega Position Vega Position Vega Total Position Vega Long 40 Nov calls Short 45 Nov calls Long 60 Jan puts Net position vega If today the implied volatility for XYZ options increased 1 point this portfolio could expect to see profit of $ If the implied volatility decreased 1 point expect to see loss of $ Position Vega If Net Positive Value Gain from implied increase If Net Negative Value Gain from implied decrease A portfolio with net positive position vega (long vega) should expect net vega amount profit with 1 pt. implied increase A portfolio with net negative position vega (short vega) expect net vega amount profit with 1 pt. implied decrease

69 55 Rho Ρ Rho: Option value s sensitivity to interest rate Expected change in option value With a 1% point change in risk-free interest rate up or down Expressed in decimal form (.080) Represents cash amount per share All other pricing factors constant Considered the least significant of all pricing factors Component of cost of carry Small portion of any option s total premium

70 56 Rho Characteristics Rho amounts generated by pricing model Calls have positive rho Puts have negative rho Rho is largest for in-the-money calls and puts Decreases as options move out-of-the-money Rho increases with higher priced underlying stocks Rho increases with more time until expiration For shorter-term options little impact For longer-term options more significant

71 Thank you

72 2017 Bourse de Montréal Inc. All rights reserved. BAX, OBX, ONX, OIS-MX, CGZ, CGF, CGB, LGB, OGB, SXO, SXF, SXM, SCF, SXA, SXB, SXH, SXY, and USX are registered trademarks of the Bourse. OBW, OBY, OBZ, SXK, SXU, SXJ, SXV, Montréal Exchange and the Montréal Exchange logo are trademarks of the Bourse. TMX and TMX Group are registered trademarks of TSX Inc. The S&P/TSX 60 Index, S&P/TSX Composite Index, S&P/TSX Global Gold Index, S&P/TSX Capped Financials Index, S&P/TSX Capped Information Technology Index, S&P/TSX Capped Energy Index, S&P/TSX Composite Index Banks (Industry Group), S&P/TSX Capped Utilities Index (collectively, the Indices ) are products of S&P Dow Jones Indices LLC ( SPDJI ) and TSX Inc. ( TSX ). Standard & Poor s and S&P are registered trademarks of Standard & Poor s Financial Services LLC ( S&P ); Dow Jones is a registered trademark of Dow Jones Trademark Holdings LLC ( Dow Jones ); and TSX is a registered trademark of TSX. SPDJI, Dow Jones, S&P and TSX do not sponsor, endorse, sell or promote any products based on the Indices and none of such parties make any representation regarding the advisability of investing in such product(s) nor do they have any liability for any errors, omissions or interruptions of the Indices or any data related thereto.

73 73

Need help with your options portfolio: Introducing OptionsPlay, a stock and options analysis suite. November 4, 2017

Need help with your options portfolio: Introducing OptionsPlay, a stock and options analysis suite November 4, 2017 Limitation of liability The opinions expressed in this presentation are those of the

Need help with your options portfolio: Introducing OptionsPlay, a stock and options analysis suite November 4, 2017 Limitation of liability The opinions expressed in this presentation are those of the

Option strategies when volatilities are low. Alan Grigoletto, CEO Grigoletto Financial Consulting

Option strategies when volatilities are low Alan Grigoletto, CEO Grigoletto Financial Consulting Limitation of liability The opinions expressed in this presentation are those of the author(s) and presenter(s)

Option strategies when volatilities are low Alan Grigoletto, CEO Grigoletto Financial Consulting Limitation of liability The opinions expressed in this presentation are those of the author(s) and presenter(s)

Options ABCs. Jason Ayres, DMS Director, R N Croft Financial Group

Options ABCs Jason Ayres, DMS Director, R N Croft Financial Group Limitation of liability The opinions expressed in this presentation are those of the author(s) and presenter(s) only and do not necessarily

Options ABCs Jason Ayres, DMS Director, R N Croft Financial Group Limitation of liability The opinions expressed in this presentation are those of the author(s) and presenter(s) only and do not necessarily

Montréal Exchange Quarterly Derivatives Market Activity Update Q1 2018

Montréal Exchange Quarterly Derivatives Market Activity Update Q1 218 Average Daily Volume Montréal Exchange Average Daily Volume & 4, 35, 3, 25, Total volume has more than doubled over the last 1 years

Montréal Exchange Quarterly Derivatives Market Activity Update Q1 218 Average Daily Volume Montréal Exchange Average Daily Volume & 4, 35, 3, 25, Total volume has more than doubled over the last 1 years

Montréal Exchange Quarterly Derivatives Market Activity Update Q3 2017

Montréal Exchange Quarterly Derivatives Market Activity Update 217 Average Daily Volume Montréal Exchange Average Daily Volume & 4, 366,2 391,6 7,, 35, 3, 25, Total volume has more than doubled over the

Montréal Exchange Quarterly Derivatives Market Activity Update 217 Average Daily Volume Montréal Exchange Average Daily Volume & 4, 366,2 391,6 7,, 35, 3, 25, Total volume has more than doubled over the

ETFs in your portfolio?

ETFs in your portfolio? Find out how ETF options can enhance your portfolio Jason Ayres, DMS Director, R N Croft Financial Group Limitation of liability The opinions expressed in this presentation are

ETFs in your portfolio? Find out how ETF options can enhance your portfolio Jason Ayres, DMS Director, R N Croft Financial Group Limitation of liability The opinions expressed in this presentation are

OPTIONS CALCULATOR QUICK GUIDE

OPTIONS CALCULATOR QUICK GUIDE Table of Contents Introduction 3 Valuing options 4 Examples 6 Valuing an American style non-dividend paying stock option 6 Valuing an American style dividend paying stock

OPTIONS CALCULATOR QUICK GUIDE Table of Contents Introduction 3 Valuing options 4 Examples 6 Valuing an American style non-dividend paying stock option 6 Valuing an American style dividend paying stock

Evaluating Options Price Sensitivities

Evaluating Options Price Sensitivities Options Pricing Presented by Patrick Ceresna, CMT CIM DMS Montréal Exchange Instructor Disclaimer 2016 Bourse de Montréal Inc. This document is sent to you on a general

Evaluating Options Price Sensitivities Options Pricing Presented by Patrick Ceresna, CMT CIM DMS Montréal Exchange Instructor Disclaimer 2016 Bourse de Montréal Inc. This document is sent to you on a general

Removing the Bias from 5-10 Steepeners

CGF CGB Five-Year Government of Canada Bond Futures Ten-Year Government of Canada Bond Futures Removing the Bias from 5-10 Steepeners Investors that are unfamiliar with yield curve trades should refer

CGF CGB Five-Year Government of Canada Bond Futures Ten-Year Government of Canada Bond Futures Removing the Bias from 5-10 Steepeners Investors that are unfamiliar with yield curve trades should refer

Driven Leverage and Credit Overlay

CGB Ten-Year Government of Canada Bond Futures Driven Leverage and Credit Overlay Recently clients have expressed interest in employing CGB futures and Canadian spread products to replace relatively passive

CGB Ten-Year Government of Canada Bond Futures Driven Leverage and Credit Overlay Recently clients have expressed interest in employing CGB futures and Canadian spread products to replace relatively passive

Z18 - H19 Roll Update

CGF CGB Five-Year Government of Canada Bond Futures Ten-Year Government of Canada Bond Futures Z18 - H19 Roll Update Quarterly Roll Summary Significant roll activity in both CGF and CGB contracts will

CGF CGB Five-Year Government of Canada Bond Futures Ten-Year Government of Canada Bond Futures Z18 - H19 Roll Update Quarterly Roll Summary Significant roll activity in both CGF and CGB contracts will

Selling Call Options

Disclaimer The views and opinions expressed in this presentation reflect those of the individual authors/presenters only and do not represent in any way Bourse de Montréal Inc. s (the Bourse ) opinion

Disclaimer The views and opinions expressed in this presentation reflect those of the individual authors/presenters only and do not represent in any way Bourse de Montréal Inc. s (the Bourse ) opinion

Calendar Spreads Calendar Spreads

Disclaimer The views and opinions expressed in this presentation reflect those of the individual authors/presenters only and do not represent in any way Bourse de Montréal Inc. s (the Bourse ) opinion

Disclaimer The views and opinions expressed in this presentation reflect those of the individual authors/presenters only and do not represent in any way Bourse de Montréal Inc. s (the Bourse ) opinion

How Volatility Influences your Option Value

Disclaimer The views and opinions expressed in this presentation reflect those of the individual authors/presenters only and do not represent in any way Bourse de Montréal Inc. s (the Bourse ) opinion

Disclaimer The views and opinions expressed in this presentation reflect those of the individual authors/presenters only and do not represent in any way Bourse de Montréal Inc. s (the Bourse ) opinion

Index Futures and Options Contract Information

Index Futures and Options Contract Information TMX Group Equities Toronto Stock Exchange TSX Venture Exchange TMX Select Equicom Derivatives Montréal Exchange BOX Options Exchange Montréal Climate Exchange

Index Futures and Options Contract Information TMX Group Equities Toronto Stock Exchange TSX Venture Exchange TMX Select Equicom Derivatives Montréal Exchange BOX Options Exchange Montréal Climate Exchange

MONTRÉAL EXCHANGE Index options and correlation trading

Equity Options MONTRÉAL EXCHANGE Index options and correlation trading Option prices contain important information regarding the market s perception of future risks. The implied probability calculated

Equity Options MONTRÉAL EXCHANGE Index options and correlation trading Option prices contain important information regarding the market s perception of future risks. The implied probability calculated

CANADIAN EQUITY DERIVATIVES

CANADIAN EQUITY DERIVATIVES Quarterly Newsletter - January 2015 MANAGER S COMMENTARY p.3 THE OPTIONS PLAYBOOK Sale of covered call options on XFN Purchase of call options to profit from a rise in XEG p.6

CANADIAN EQUITY DERIVATIVES Quarterly Newsletter - January 2015 MANAGER S COMMENTARY p.3 THE OPTIONS PLAYBOOK Sale of covered call options on XFN Purchase of call options to profit from a rise in XEG p.6

Intrinsic and Time Value

Disclaimer The views and opinions expressed in this presentation reflect those of the individual authors/presenters only and do not represent in any way Bourse de Montréal Inc. s (the Bourse ) opinion

Disclaimer The views and opinions expressed in this presentation reflect those of the individual authors/presenters only and do not represent in any way Bourse de Montréal Inc. s (the Bourse ) opinion

CADerivatives. Table of contents BAX OBX ONX CGZ CGF CGB OGB LGB SCF SXF SXM SXA SXB SXH SXY EQUITY OPTIONS CURRENCY OPTIONS INDEX OPTIONS ETF OPTIONS

The Montréal Exchange s Quarterly Derivatives Newsletter 2011, volume 2 BAX OBX ONX CGZ CGF CGB OGB LGB SCF SXF SXM SXA SXB SXH SXY EQUITY OPTIONS CURRENCY OPTIONS INDEX OPTIONS ETF OPTIONS Table of contents

The Montréal Exchange s Quarterly Derivatives Newsletter 2011, volume 2 BAX OBX ONX CGZ CGF CGB OGB LGB SCF SXF SXM SXA SXB SXH SXY EQUITY OPTIONS CURRENCY OPTIONS INDEX OPTIONS ETF OPTIONS Table of contents

OPTIONS & GREEKS. Study notes. An option results in the right (but not the obligation) to buy or sell an asset, at a predetermined

to buy or sell an asset, at a predetermined") OPTIONS & GREEKS Study notes 1 Options 1.1 Basic information An option results in the right (but not the obligation) to buy or sell an asset, at a predetermined price, and on or before a predetermined

OPTIONS & GREEKS Study notes 1 Options 1.1 Basic information An option results in the right (but not the obligation) to buy or sell an asset, at a predetermined price, and on or before a predetermined

How to Trade Options Using VantagePoint and Trade Management

How to Trade Options Using VantagePoint and Trade Management Course 3.2 + 3.3 Copyright 2016 Market Technologies, LLC. 1 Option Basics Part I Agenda Option Basics and Lingo Call and Put Attributes Profit

How to Trade Options Using VantagePoint and Trade Management Course 3.2 + 3.3 Copyright 2016 Market Technologies, LLC. 1 Option Basics Part I Agenda Option Basics and Lingo Call and Put Attributes Profit

Chapter 9 - Mechanics of Options Markets

Chapter 9 - Mechanics of Options Markets Types of options Option positions and profit/loss diagrams Underlying assets Specifications Trading options Margins Taxation Warrants, employee stock options, and

Chapter 9 - Mechanics of Options Markets Types of options Option positions and profit/loss diagrams Underlying assets Specifications Trading options Margins Taxation Warrants, employee stock options, and

Sample Term Sheet. Warrant Definitions. Risk Measurement

INTRODUCTION TO WARRANTS This Presentation Should Help You: Understand Why Investors Buy s Learn the Basics about Pricing Feel Comfortable with Terminology Table of Contents Sample Term Sheet Scenario

INTRODUCTION TO WARRANTS This Presentation Should Help You: Understand Why Investors Buy s Learn the Basics about Pricing Feel Comfortable with Terminology Table of Contents Sample Term Sheet Scenario

DERIVATIVES CANADIAN EQUITY. Quarterly Newsletter - April 2016 MANAGER S COMMENTARY THE OPTIONS PLAYBOOK

CANADIAN EQUITY DERIVATIVES Quarterly Newsletter - April 2016 MANAGER S COMMENTARY p.3 THE OPTIONS PLAYBOOK Long Gold using the ishares Gold Bullion ETF (CGL) Covered Calls on Franco Nevada (FNV) p.6 GENERAL

CANADIAN EQUITY DERIVATIVES Quarterly Newsletter - April 2016 MANAGER S COMMENTARY p.3 THE OPTIONS PLAYBOOK Long Gold using the ishares Gold Bullion ETF (CGL) Covered Calls on Franco Nevada (FNV) p.6 GENERAL

Introduction to Currency Options

Disclaimer The views and opinions expressed in this presentation reflect those of the individual authors/presenters only and do not represent in any way Bourse de Montréal Inc. s (the Bourse ) opinion

Disclaimer The views and opinions expressed in this presentation reflect those of the individual authors/presenters only and do not represent in any way Bourse de Montréal Inc. s (the Bourse ) opinion

CHANGE IN CLOSING TIME OF SXF, SXM, SCF, SXA, SXB, SXH, SXK, SXU, SXY INDEX FUTURES

CIRCULAR 124-18 July 24, 2018 CHANGE IN CLOSING TIME OF SXF, SXM, SCF, SXA, SXB, SXH, SXK, SXU, SXY INDEX FUTURES Bourse de Montréal Inc. (the Bourse ) hereby announces that, effective on September 24,

CIRCULAR 124-18 July 24, 2018 CHANGE IN CLOSING TIME OF SXF, SXM, SCF, SXA, SXB, SXH, SXK, SXU, SXY INDEX FUTURES Bourse de Montréal Inc. (the Bourse ) hereby announces that, effective on September 24,

Trade a directional bias with a limited and identifiable risk exposure. Protect and preserve investment capital.

Disclaimer The views and opinions expressed in this presentation reflect those of the individual authors/presenters only and do not represent in any way Bourse de Montréal Inc. s (the Bourse ) opinion

Disclaimer The views and opinions expressed in this presentation reflect those of the individual authors/presenters only and do not represent in any way Bourse de Montréal Inc. s (the Bourse ) opinion

Toronto November 4, 2017 Visit the to register

1 Toronto November 4, 2017 Visit the www.m-x.ca to register Disclaimer The views and opinions expressed in this presentation reflect those of the individual authors/presenters only and do not represent

1 Toronto November 4, 2017 Visit the www.m-x.ca to register Disclaimer The views and opinions expressed in this presentation reflect those of the individual authors/presenters only and do not represent

CANADIAN EQUITY DERIVATIVES

CANADIAN EQUITY DERIVATIVES Quarterly Newsletter - July 2014 MANAGER S COMMENTARY p.5 THE OPTIONS PLAYBOOK Collar strategy on Alimentation Couche-Tard Bear call spread on ishares S&P/TSX Capped Financials

CANADIAN EQUITY DERIVATIVES Quarterly Newsletter - July 2014 MANAGER S COMMENTARY p.5 THE OPTIONS PLAYBOOK Collar strategy on Alimentation Couche-Tard Bear call spread on ishares S&P/TSX Capped Financials

REQUEST FOR COMMENTS AMENDMENTS TO THE DAILY SETTLEMENT PRICE PROCEDURES FOR FUTURES CONTRACTS AND OPTIONS ON FUTURES CONTRACTS

CIRCULAR 066-18 May 17 th, 2018 REQUEST FOR COMMENTS AMENDMENTS TO THE DAILY SETTLEMENT PRICE PROCEDURES FOR FUTURES CONTRACTS AND OPTIONS ON FUTURES CONTRACTS The Rules and Policies Committee of Bourse

CIRCULAR 066-18 May 17 th, 2018 REQUEST FOR COMMENTS AMENDMENTS TO THE DAILY SETTLEMENT PRICE PROCEDURES FOR FUTURES CONTRACTS AND OPTIONS ON FUTURES CONTRACTS The Rules and Policies Committee of Bourse

GLOSSARY OF OPTION TERMS

ALL OR NONE (AON) ORDER An order in which the quantity must be completely filled or it will be canceled. AMERICAN-STYLE OPTION A call or put option contract that can be exercised at any time before the

ALL OR NONE (AON) ORDER An order in which the quantity must be completely filled or it will be canceled. AMERICAN-STYLE OPTION A call or put option contract that can be exercised at any time before the

Learn To Trade Stock Options

Learn To Trade Stock Options Written by: Jason Ramus www.daytradingfearless.com Copyright: 2017 Table of contents: WHAT TO EXPECT FROM THIS MANUAL WHAT IS AN OPTION BASICS OF HOW AN OPTION WORKS RECOMMENDED

Learn To Trade Stock Options Written by: Jason Ramus www.daytradingfearless.com Copyright: 2017 Table of contents: WHAT TO EXPECT FROM THIS MANUAL WHAT IS AN OPTION BASICS OF HOW AN OPTION WORKS RECOMMENDED

OPTION POSITIONING AND TRADING TUTORIAL

OPTION POSITIONING AND TRADING TUTORIAL Binomial Options Pricing, Implied Volatility and Hedging Option Underlying 5/13/2011 Professor James Bodurtha Executive Summary The following paper looks at a number

OPTION POSITIONING AND TRADING TUTORIAL Binomial Options Pricing, Implied Volatility and Hedging Option Underlying 5/13/2011 Professor James Bodurtha Executive Summary The following paper looks at a number

Bourse de Montréal Inc RULE FOURTEEN DERIVATIVE INSTRUMENTS MISCELLANEOUS RULES ( , , , , ,

Bourse de Montréal Inc. 14-1 RULE FOURTEEN DERIVATIVE INSTRUMENTS MISCELLANEOUS RULES (11.03.80, 13.09.05, 04.03.08, 01.04.13, 09.06.14, 01.10.15) 14001 General (24.04.84, abr. 13.09.05) 14002 Definition

Bourse de Montréal Inc. 14-1 RULE FOURTEEN DERIVATIVE INSTRUMENTS MISCELLANEOUS RULES (11.03.80, 13.09.05, 04.03.08, 01.04.13, 09.06.14, 01.10.15) 14001 General (24.04.84, abr. 13.09.05) 14002 Definition

100% Absolute Return*

A final base shelf prospectus containing important information relating to the securities described in this document has been filed with the securities regulatory authorities in each of the provinces and

A final base shelf prospectus containing important information relating to the securities described in this document has been filed with the securities regulatory authorities in each of the provinces and

Asset-or-nothing digitals

School of Education, Culture and Communication Division of Applied Mathematics MMA707 Analytical Finance I Asset-or-nothing digitals 202-0-9 Mahamadi Ouoba Amina El Gaabiiy David Johansson Examinator:

School of Education, Culture and Communication Division of Applied Mathematics MMA707 Analytical Finance I Asset-or-nothing digitals 202-0-9 Mahamadi Ouoba Amina El Gaabiiy David Johansson Examinator:

CGF Five-Year Government. OGB Options on Ten-Year Government

CGZ Two-Year Government of Canada Bond Futures CGF Five-Year Government of Canada Bond Futures CGB Ten-Year Government of Canada Bond Futures LGB 30-Year Government of Canada Bond Futures OGB Options on

CGZ Two-Year Government of Canada Bond Futures CGF Five-Year Government of Canada Bond Futures CGB Ten-Year Government of Canada Bond Futures LGB 30-Year Government of Canada Bond Futures OGB Options on

Lecture 9: Practicalities in Using Black-Scholes. Sunday, September 23, 12

Lecture 9: Practicalities in Using Black-Scholes Major Complaints Most stocks and FX products don t have log-normal distribution Typically fat-tailed distributions are observed Constant volatility assumed,

Lecture 9: Practicalities in Using Black-Scholes Major Complaints Most stocks and FX products don t have log-normal distribution Typically fat-tailed distributions are observed Constant volatility assumed,

Timely, insightful research and analysis from TradeStation. Options Toolkit

Timely, insightful research and analysis from TradeStation Options Toolkit Table of Contents Important Information and Disclosures... 3 Options Risk Disclosure... 4 Prologue... 5 The Benefits of Trading

Timely, insightful research and analysis from TradeStation Options Toolkit Table of Contents Important Information and Disclosures... 3 Options Risk Disclosure... 4 Prologue... 5 The Benefits of Trading

Bourse de Montréal Inc. Reference Manual. Ten-year. Option on. Ten-year. Government. Government. of Canada. of Canada. Bond Futures.

CGB Ten-year Government of Canada Bond Futures OGB Option on Ten-year Government of Canada Bond Futures Reference Manual Bourse de Montréal Inc. www.boursedemontreal.com Bourse de Montréal Inc. Sales and

CGB Ten-year Government of Canada Bond Futures OGB Option on Ten-year Government of Canada Bond Futures Reference Manual Bourse de Montréal Inc. www.boursedemontreal.com Bourse de Montréal Inc. Sales and

Fin 4200 Project. Jessi Sagner 11/15/11

Fin 4200 Project Jessi Sagner 11/15/11 All Option information is outlined in appendix A Option Strategy The strategy I chose was to go long 1 call and 1 put at the same strike price, but different times

Fin 4200 Project Jessi Sagner 11/15/11 All Option information is outlined in appendix A Option Strategy The strategy I chose was to go long 1 call and 1 put at the same strike price, but different times

Bank of Montreal S&P/TSX Composite Low Volatility Index Fixed Coupon Participation Principal At Risk Notes, Series 3 (CAD), Due October 31, 2022

, Due October 31, 2022") A final base shelf prospectus containing important information relating to the securities described in this document has been filed with the securities regulatory authorities in each of the provinces and

A final base shelf prospectus containing important information relating to the securities described in this document has been filed with the securities regulatory authorities in each of the provinces and

Series 52. NBC Deposit Notes NBC S&P/TSX Composite Low Volatility Index with Low Point Deposit Notes. On or about September 10, 2024

NBC Deposit Notes NBC S&P/TSX Composite Low Volatility Index with Low Point Deposit Notes Series 52 SALES PERIOD: August 13, 2018 to September 4, 2018 ISSUANCE DATE: On or about September 10, 2018 FINAL

NBC Deposit Notes NBC S&P/TSX Composite Low Volatility Index with Low Point Deposit Notes Series 52 SALES PERIOD: August 13, 2018 to September 4, 2018 ISSUANCE DATE: On or about September 10, 2018 FINAL

Naked & Covered Positions

The Greek Letters 1 Example A bank has sold for $300,000 a European call option on 100,000 shares of a nondividend paying stock S 0 = 49, K = 50, r = 5%, σ = 20%, T = 20 weeks, μ = 13% The Black-Scholes

The Greek Letters 1 Example A bank has sold for $300,000 a European call option on 100,000 shares of a nondividend paying stock S 0 = 49, K = 50, r = 5%, σ = 20%, T = 20 weeks, μ = 13% The Black-Scholes

Montreal Exchange. List of Fees

Montreal Exchange List of Fees Effective as of March 1, 2018 A. APPROVED PARTICIPANTS (DOMESTIC & FOREIGN) APPLICATION AND REGULATION 1. Market Regulation Assessments 1.1 Fixed annual assessment 1.1.1

Montreal Exchange List of Fees Effective as of March 1, 2018 A. APPROVED PARTICIPANTS (DOMESTIC & FOREIGN) APPLICATION AND REGULATION 1. Market Regulation Assessments 1.1 Fixed annual assessment 1.1.1

Montreal Exchange. List of Fees

Montreal Exchange List of Fees Effective as of January 1, 2019 A. APPROVED PARTICIPANTS (DOMESTIC & FOREIGN) APPLICATION AND REGULATION 1. Market Regulation Assessments 1.1 Fixed annual assessment 1.1.1

Montreal Exchange List of Fees Effective as of January 1, 2019 A. APPROVED PARTICIPANTS (DOMESTIC & FOREIGN) APPLICATION AND REGULATION 1. Market Regulation Assessments 1.1 Fixed annual assessment 1.1.1

SELFCERTIFICATION NEW PRODUCT: MINI FUTURES CONTRACTS ON THE S&P/TSX 60 INDEX

Trading Interest Rate Derivatives Trading Equity and Index Derivatives Back-office Futures Back-office - Options Technology Regulation MCeX CIRCULAR May 2, 2011 SELFCERTIFICATION NEW PRODUCT: MINI FUTURES

Trading Interest Rate Derivatives Trading Equity and Index Derivatives Back-office Futures Back-office - Options Technology Regulation MCeX CIRCULAR May 2, 2011 SELFCERTIFICATION NEW PRODUCT: MINI FUTURES

Financial Markets & Risk

Financial Markets & Risk Dr Cesario MATEUS Senior Lecturer in Finance and Banking Room QA259 Department of Accounting and Finance c.mateus@greenwich.ac.uk www.cesariomateus.com Session 3 Derivatives Binomial

Financial Markets & Risk Dr Cesario MATEUS Senior Lecturer in Finance and Banking Room QA259 Department of Accounting and Finance c.mateus@greenwich.ac.uk www.cesariomateus.com Session 3 Derivatives Binomial

REQUEST FOR COMMENTS

Trading Interest Rate Derivatives Trading Equity and Index Derivatives Back-office Futures Back-office - Options Technology Regulation CIRCULAR 115-15 September 23, 2015 REQUEST FOR COMMENTS INTRODUCTION

Trading Interest Rate Derivatives Trading Equity and Index Derivatives Back-office Futures Back-office - Options Technology Regulation CIRCULAR 115-15 September 23, 2015 REQUEST FOR COMMENTS INTRODUCTION

INNOVATIVE PORTFOLIOS. for the intelligent advisor

INNOVATIVE PORTFOLIOS for the intelligent advisor FPA INDIANA March 2019 Using Option Strategies for Financial Planning Solutions Dave Gilreath, CFP Co-Founder Chief Investment Officer Innovative Portfolios

INNOVATIVE PORTFOLIOS for the intelligent advisor FPA INDIANA March 2019 Using Option Strategies for Financial Planning Solutions Dave Gilreath, CFP Co-Founder Chief Investment Officer Innovative Portfolios

PROCEDURE FOR THE EXECUTION AND REPORTING OF EXCHANGE FOR PHYSICAL (EFP) AND EXCHANGE FOR RISK (EFR) TRANSACTIONS

AND EXCHANGE FOR RISK (EFR) TRANSACTIONS") PROCEDURE FOR THE EXECUTION AND REPORTING OF EXCHANGE FOR PHYSICAL (EFP) AND EXCHANGE FOR RISK (EFR) TRANSACTIONS The purpose of the following procedure is to explain as fully as possible the requirements

PROCEDURE FOR THE EXECUTION AND REPORTING OF EXCHANGE FOR PHYSICAL (EFP) AND EXCHANGE FOR RISK (EFR) TRANSACTIONS The purpose of the following procedure is to explain as fully as possible the requirements

Europe warms to weekly options

Europe warms to weekly options After their introduction in the US more than a decade ago, weekly options have now become part of the investment toolkit of many financial professionals worldwide. Volume

Europe warms to weekly options After their introduction in the US more than a decade ago, weekly options have now become part of the investment toolkit of many financial professionals worldwide. Volume

REQUEST FOR COMMENTS AMENDMENTS TO THE RULES OF BOURSE DE MONTREAL INC. TO INCREASE THE S&P/TSX 60 INDEX OPTION (SXO) CONTRACT SIZE

CONTRACT SIZE") CIRCULAR 027-19 February 18, 2019 REQUEST FOR COMMENTS AMENDMENTS TO THE RULES OF BOURSE DE MONTREAL INC. TO INCREASE THE S&P/TSX 60 INDEX OPTION (SXO) CONTRACT SIZE The Rules and Policies Committee and

CIRCULAR 027-19 February 18, 2019 REQUEST FOR COMMENTS AMENDMENTS TO THE RULES OF BOURSE DE MONTREAL INC. TO INCREASE THE S&P/TSX 60 INDEX OPTION (SXO) CONTRACT SIZE The Rules and Policies Committee and

Actuarial Models : Financial Economics

` Actuarial Models : Financial Economics An Introductory Guide for Actuaries and other Business Professionals First Edition BPP Professional Education Phoenix, AZ Copyright 2010 by BPP Professional Education,

` Actuarial Models : Financial Economics An Introductory Guide for Actuaries and other Business Professionals First Edition BPP Professional Education Phoenix, AZ Copyright 2010 by BPP Professional Education,

Copyright 2018 Craig E. Forman All Rights Reserved. Trading Equity Options Week 2

Copyright 2018 Craig E. Forman All Rights Reserved www.tastytrader.net Trading Equity Options Week 2 Disclosure All investments involve risk and are not suitable for all investors. The past performance

Copyright 2018 Craig E. Forman All Rights Reserved www.tastytrader.net Trading Equity Options Week 2 Disclosure All investments involve risk and are not suitable for all investors. The past performance

Options, Futures, and Other Derivatives, 7th Edition, Copyright John C. Hull

Derivatives, 7th Edition, Copyright John C. Hull 2008 1 The Greek Letters Chapter 17 Derivatives, 7th Edition, Copyright John C. Hull 2008 2 Example A bank has sold for $300,000 000 a European call option

Derivatives, 7th Edition, Copyright John C. Hull 2008 1 The Greek Letters Chapter 17 Derivatives, 7th Edition, Copyright John C. Hull 2008 2 Example A bank has sold for $300,000 000 a European call option

Options 101: The building blocks

PORTFOLIO DISCUSSION J.P. MORGAN U.S. EQUITY GROUP October 2013 Connecting you with our global network of investment professionals IN BRIEF This paper provides an overview of options and describes strategies

PORTFOLIO DISCUSSION J.P. MORGAN U.S. EQUITY GROUP October 2013 Connecting you with our global network of investment professionals IN BRIEF This paper provides an overview of options and describes strategies

Of Option Trading PRESENTED BY: DENNIS W. WILBORN

Of Option Trading PRESENTED BY: DENNIS W. WILBORN Disclaimer U.S. GOVERNMENT REQUIRED DISCLAIMER COMMODITY FUTURES TRADING COMMISSION FUTURES AND OPTIONS TRADING HAS LARGE POTENTIAL REWARDS, BUT ALSO LARGE

Of Option Trading PRESENTED BY: DENNIS W. WILBORN Disclaimer U.S. GOVERNMENT REQUIRED DISCLAIMER COMMODITY FUTURES TRADING COMMISSION FUTURES AND OPTIONS TRADING HAS LARGE POTENTIAL REWARDS, BUT ALSO LARGE

AMENDMENTS TO THE LIST OF FEES OF BOURSE DE MONTRÉAL INC.

Trading Interest Rate Derivatives Trading Equity and Index Derivatives Back-office Futures Back-office Technology Regulation CIRCULAR August 23, 2013 AMENDMENTS TO THE LIST OF FEES OF BOURSE DE MONTRÉAL

Trading Interest Rate Derivatives Trading Equity and Index Derivatives Back-office Futures Back-office Technology Regulation CIRCULAR August 23, 2013 AMENDMENTS TO THE LIST OF FEES OF BOURSE DE MONTRÉAL

OPTIONS TRADING SIMULATOR QUICK GUIDE

OPTIONS TRADING SIMULATOR QUICK GUIDE Orders Trading Market order A market order will be executed at the current marketable price. Limit order Order to buy or sell at a specific price or better. Option

OPTIONS TRADING SIMULATOR QUICK GUIDE Orders Trading Market order A market order will be executed at the current marketable price. Limit order Order to buy or sell at a specific price or better. Option

John W. Labuszewski MANAGING DIRECTOR RESEARCH AND PRODUCT DEVELOPMENT

fx products Managing Currency Risks with Options John W. Labuszewski MANAGING DIRECTOR RESEARCH AND PRODUCT DEVELOPMENT jlab@cmegroup.com cmegroup.com/fx This represents an overview of our currency options

fx products Managing Currency Risks with Options John W. Labuszewski MANAGING DIRECTOR RESEARCH AND PRODUCT DEVELOPMENT jlab@cmegroup.com cmegroup.com/fx This represents an overview of our currency options

OPTIONS ON GOLD FUTURES THE SMARTER WAY TO HEDGE YOUR RISK

OPTIONS ON GOLD FUTURES THE SMARTER WAY TO HEDGE YOUR RISK INTRODUCTION Options on Futures are relatively easy to understand once you master the basic concept. OPTION The option buyer pays a premium to

OPTIONS ON GOLD FUTURES THE SMARTER WAY TO HEDGE YOUR RISK INTRODUCTION Options on Futures are relatively easy to understand once you master the basic concept. OPTION The option buyer pays a premium to

Queens College, CUNY, Department of Computer Science Computational Finance CSCI 365 / 765 Fall 2017 Instructor: Dr. Sateesh Mane.

Queens College, CUNY, Department of Computer Science Computational Finance CSCI 365 / 765 Fall 2017 Instructor: Dr. Sateesh Mane c Sateesh R. Mane 2017 9 Lecture 9 9.1 The Greeks November 15, 2017 Let

Queens College, CUNY, Department of Computer Science Computational Finance CSCI 365 / 765 Fall 2017 Instructor: Dr. Sateesh Mane c Sateesh R. Mane 2017 9 Lecture 9 9.1 The Greeks November 15, 2017 Let

Top Five Things You Should Know Before Buying an Option

Top Five Things You Should Know Before Buying an Option Disclaimers Options involve risks and are not suitable for all investors. Prior to buying or selling options, an investor must receive a copy of

Top Five Things You Should Know Before Buying an Option Disclaimers Options involve risks and are not suitable for all investors. Prior to buying or selling options, an investor must receive a copy of

List of Fees Effective as of July 1, 2015

List of Fees Effective as of July 1, 2015 A. APPROVED PARTICIPANTS (DOMESTIC & FOREIGN) APPLICATION AND REGULATION 1. Market Regulation Assessments 1.1 Fixed annual assessment 1.1.1 Approved participant

List of Fees Effective as of July 1, 2015 A. APPROVED PARTICIPANTS (DOMESTIC & FOREIGN) APPLICATION AND REGULATION 1. Market Regulation Assessments 1.1 Fixed annual assessment 1.1.1 Approved participant

covered warrants uncovered an explanation and the applications of covered warrants

covered warrants uncovered an explanation and the applications of covered warrants Disclaimer Whilst all reasonable care has been taken to ensure the accuracy of the information comprising this brochure,

covered warrants uncovered an explanation and the applications of covered warrants Disclaimer Whilst all reasonable care has been taken to ensure the accuracy of the information comprising this brochure,

The Bull Call Spread. - Debit Spread - Defined Risk - Defined Reward - Mildly Bullish

The Bull Call Spread - Debit Spread - Defined Risk - Defined Reward - Mildly Bullish 1. Bull Call Spread 1.1 General Nature & Characteristics The bull call spread is a long vertical spread made up entirely

The Bull Call Spread - Debit Spread - Defined Risk - Defined Reward - Mildly Bullish 1. Bull Call Spread 1.1 General Nature & Characteristics The bull call spread is a long vertical spread made up entirely

Derivatives Analysis & Valuation (Futures)

") 6.1 Derivatives Analysis & Valuation (Futures) LOS 1 : Introduction Study Session 6 Define Forward Contract, Future Contract. Forward Contract, In Forward Contract one party agrees to buy, and the counterparty

6.1 Derivatives Analysis & Valuation (Futures) LOS 1 : Introduction Study Session 6 Define Forward Contract, Future Contract. Forward Contract, In Forward Contract one party agrees to buy, and the counterparty

FIN FINANCIAL INSTRUMENTS SPRING 2008

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 The Greeks Introduction We have studied how to price an option using the Black-Scholes formula. Now we wish to consider how the option price changes, either

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 The Greeks Introduction We have studied how to price an option using the Black-Scholes formula. Now we wish to consider how the option price changes, either

List of Fees Effective as of October 1, 2014

List of Fees Effective as of October 1, 2014 A. APPROVED PARTICIPANTS (DOMESTIC & FOREIGN) APPLICATION AND REGULATION 1. Market Regulation Assessments 1.1 Fixed annual assessment 1.1.1 Approved participant

List of Fees Effective as of October 1, 2014 A. APPROVED PARTICIPANTS (DOMESTIC & FOREIGN) APPLICATION AND REGULATION 1. Market Regulation Assessments 1.1 Fixed annual assessment 1.1.1 Approved participant

Options & Earnings

0 Joe Burgoyne Director, Options Industry Council Options & Earnings www.optionseducation.org 1 Disclaimer Options involve risks and are not suitable for everyone. Individuals should not enter into options

0 Joe Burgoyne Director, Options Industry Council Options & Earnings www.optionseducation.org 1 Disclaimer Options involve risks and are not suitable for everyone. Individuals should not enter into options

The Poorman s Covered Call. - Debit Spread - Defined Risk - Defined Reward - Mildly Bullish

The Poorman s Covered Call - Debit Spread - Defined Risk - Defined Reward - Mildly Bullish General Nature & Characteristics The Poorman s Covered Call is made up entirely of Call options on the same underlying

The Poorman s Covered Call - Debit Spread - Defined Risk - Defined Reward - Mildly Bullish General Nature & Characteristics The Poorman s Covered Call is made up entirely of Call options on the same underlying

GlobalView Software, Inc.

GlobalView Software, Inc. MarketView Option Analytics 10/16/2007 Table of Contents 1. Introduction...1 2. Configuration Settings...2 2.1 Component Selection... 2 2.2 Edit Configuration Analytics Tab...

GlobalView Software, Inc. MarketView Option Analytics 10/16/2007 Table of Contents 1. Introduction...1 2. Configuration Settings...2 2.1 Component Selection... 2 2.2 Edit Configuration Analytics Tab...

TradeOptionsWithMe.com

TradeOptionsWithMe.com 1 of 18 Option Trading Glossary This is the Glossary for important option trading terms. Some of these terms are rather easy and used extremely often, but some may even be new to

TradeOptionsWithMe.com 1 of 18 Option Trading Glossary This is the Glossary for important option trading terms. Some of these terms are rather easy and used extremely often, but some may even be new to

The Black-Scholes Model

The Black-Scholes Model Inputs Spot Price Exercise Price Time to Maturity Rate-Cost of funds & Yield Volatility Process The Black Box Output "Fair Market Value" For those interested in looking inside the

The Black-Scholes Model Inputs Spot Price Exercise Price Time to Maturity Rate-Cost of funds & Yield Volatility Process The Black Box Output "Fair Market Value" For those interested in looking inside the

Global Journal of Engineering Science and Research Management

THE GREEKS & BLACK AND SCHOLE MODEL TO EVALUATE OPTIONS PRICING & SENSITIVITY IN INDIAN OPTIONS MARKET Dr. M. Tulasinadh*, Dr.R. Mahesh * Assistant Professor, Dept of MBA KBN College-PG Centre, Vijayawada

THE GREEKS & BLACK AND SCHOLE MODEL TO EVALUATE OPTIONS PRICING & SENSITIVITY IN INDIAN OPTIONS MARKET Dr. M. Tulasinadh*, Dr.R. Mahesh * Assistant Professor, Dept of MBA KBN College-PG Centre, Vijayawada

AMENDMENTS TO THE LIST OF FEES OF BOURSE DE MONTRÉAL INC. (EFFECTIVE JULY 1, 2018)

") CIRCULAR 084-18 June 1, 2018 AMENDMENTS TO THE LIST OF FEES OF BOURSE DE MONTRÉAL INC. (EFFECTIVE JULY 1, 2018) Bourse de Montreal Inc. (the Bourse ) hereby announces the following amendments to its list

CIRCULAR 084-18 June 1, 2018 AMENDMENTS TO THE LIST OF FEES OF BOURSE DE MONTRÉAL INC. (EFFECTIVE JULY 1, 2018) Bourse de Montreal Inc. (the Bourse ) hereby announces the following amendments to its list

BANK OF MONTREAL S&P/TSX 60 CANADIAN GROWTH PROTECTED DEPOSIT NOTES TM, Series 9

INFORMATION STATEMENT DATED JUNE 1, 2015 This Information Statement has been prepared solely for assisting prospective purchasers in making an investment decision with respect to the Deposit Notes. This

INFORMATION STATEMENT DATED JUNE 1, 2015 This Information Statement has been prepared solely for assisting prospective purchasers in making an investment decision with respect to the Deposit Notes. This

Spread Adjustments & Time Premium. Disclaimers 10/29/2013

Spread Adjustments & Time Premium Disclaimers Options involve risks and are not suitable for all investors. Prior to buying or selling options, an investor must receive a copy of Characteristics and Risks

Spread Adjustments & Time Premium Disclaimers Options involve risks and are not suitable for all investors. Prior to buying or selling options, an investor must receive a copy of Characteristics and Risks

AMENDMENTS TO THE LIST OF FEES OF BOURSE DE MONTRÉAL INC. (EFFECTIVE SEPTEMBER 1, 2017)

") Trading Interest Rate Derivatives Trading Equity and Index Derivatives Back-office Futures Back-office - Options Technology Regulation CIRCULAR 122-17 August 16, 2017 AMENDMENTS TO THE LIST OF FEES OF

Trading Interest Rate Derivatives Trading Equity and Index Derivatives Back-office Futures Back-office - Options Technology Regulation CIRCULAR 122-17 August 16, 2017 AMENDMENTS TO THE LIST OF FEES OF

AMENDMENTS TO THE LIST OF FEES OF BOURSE DE MONTRÉAL INC. (EFFECTIVE JANUARY 4, 2018)

") Trading Interest Rate Derivatives Back-office - Options Trading Equity and Index Derivatives Technology Back-office Futures Regulation CIRCULAR 184-17 December 20, 2017 AMENDMENTS TO THE LIST OF FEES OF

Trading Interest Rate Derivatives Back-office - Options Trading Equity and Index Derivatives Technology Back-office Futures Regulation CIRCULAR 184-17 December 20, 2017 AMENDMENTS TO THE LIST OF FEES OF

The Greek Letters Based on Options, Futures, and Other Derivatives, 8th Edition, Copyright John C. Hull 2012

The Greek Letters Based on Options, Futures, and Other Derivatives, 8th Edition, Copyright John C. Hull 2012 Introduction Each of the Greek letters measures a different dimension to the risk in an option

The Greek Letters Based on Options, Futures, and Other Derivatives, 8th Edition, Copyright John C. Hull 2012 Introduction Each of the Greek letters measures a different dimension to the risk in an option

AMENDMENTS TO THE LIST OF FEES OF BOURSE DE MONTRÉAL INC. (EFFECTIVE JUNE 1, 2018)

") CIRCULAR 061-18 May 10, 2018 AMENDMENTS TO THE LIST OF FEES OF BOURSE DE MONTRÉAL INC. (EFFECTIVE JUNE 1, 2018) Bourse de Montreal Inc. (the Bourse ) hereby announces the following amendments to its List

CIRCULAR 061-18 May 10, 2018 AMENDMENTS TO THE LIST OF FEES OF BOURSE DE MONTRÉAL INC. (EFFECTIVE JUNE 1, 2018) Bourse de Montreal Inc. (the Bourse ) hereby announces the following amendments to its List

Options Report September 19, 2016

Allergan Inc. Note: The Options Report is not a substitute for the underlying stock s Stock Report which contains information about the underlying stock and basis for the STARS Ranking. Stock Symbol: Stock

Allergan Inc. Note: The Options Report is not a substitute for the underlying stock s Stock Report which contains information about the underlying stock and basis for the STARS Ranking. Stock Symbol: Stock

MODIFICATION TO THE TRADING HOURS

Trading Interest Rate Derivatives Trading Equity and Index Derivatives Back-office Futures Back-office - Options Technology Regulation MODIFICATION TO THE TRADING HOURS CIRCULAR 021-17 February 14, 2017

Trading Interest Rate Derivatives Trading Equity and Index Derivatives Back-office Futures Back-office - Options Technology Regulation MODIFICATION TO THE TRADING HOURS CIRCULAR 021-17 February 14, 2017

Market risk measurement in practice

Lecture notes on risk management, public policy, and the financial system Allan M. Malz Columbia University 2018 Allan M. Malz Last updated: October 23, 2018 2/32 Outline Nonlinearity in market risk Market

Lecture notes on risk management, public policy, and the financial system Allan M. Malz Columbia University 2018 Allan M. Malz Last updated: October 23, 2018 2/32 Outline Nonlinearity in market risk Market

A study on parameters of option pricing: The Greeks

International Journal of Academic Research and Development ISSN: 2455-4197, Impact Factor: RJIF 5.22 www.academicsjournal.com Volume 2; Issue 2; March 2017; Page No. 40-45 A study on parameters of option

International Journal of Academic Research and Development ISSN: 2455-4197, Impact Factor: RJIF 5.22 www.academicsjournal.com Volume 2; Issue 2; March 2017; Page No. 40-45 A study on parameters of option

Equity Derivatives. FAQs & Glossary

Equity Derivatives FAQs & Glossary :. 1. FAQs Q: How do I access the equity derivatives market? Firms can access the market directly by either becoming an accredited derivatives market participant or by

Equity Derivatives FAQs & Glossary :. 1. FAQs Q: How do I access the equity derivatives market? Firms can access the market directly by either becoming an accredited derivatives market participant or by

Using Volatility to Choose Trades & Setting Stops on Spreads

CHICAGO BOARD OPTIONS EXCHANGE Using Volatility to Choose Trades & Setting Stops on Spreads presented by: Jim Bittman, Senior Instructor The Options Institute at CBOE Disclaimer In order to simplify the

CHICAGO BOARD OPTIONS EXCHANGE Using Volatility to Choose Trades & Setting Stops on Spreads presented by: Jim Bittman, Senior Instructor The Options Institute at CBOE Disclaimer In order to simplify the

Lecture Quantitative Finance Spring Term 2015

and Lecture Quantitative Finance Spring Term 2015 Prof. Dr. Erich Walter Farkas Lecture 06: March 26, 2015 1 / 47 Remember and Previous chapters: introduction to the theory of options put-call parity fundamentals

and Lecture Quantitative Finance Spring Term 2015 Prof. Dr. Erich Walter Farkas Lecture 06: March 26, 2015 1 / 47 Remember and Previous chapters: introduction to the theory of options put-call parity fundamentals

GLOSSARY OF COMMON DERIVATIVES TERMS

Alpha The difference in performance of an investment relative to its benchmark. American Style Option An option that can be exercised at any time from inception as opposed to a European Style option which

Alpha The difference in performance of an investment relative to its benchmark. American Style Option An option that can be exercised at any time from inception as opposed to a European Style option which

Valuing Put Options with Put-Call Parity S + P C = [X/(1+r f ) t ] + [D P /(1+r f ) t ] CFA Examination DERIVATIVES OPTIONS Page 1 of 6

![Valuing Put Options with Put-Call Parity S + P C = [X/(1+r f ) t ] + [D P /(1+r f ) t ] CFA Examination DERIVATIVES OPTIONS Page 1 of 6](/thumbs/77/75506899.jpg "Valuing Put Options with Put-Call Parity S + P C = [X/(1+r f ) t ] + [D P /(1+r f ) t ] CFA Examination DERIVATIVES OPTIONS Page 1 of 6") DERIVATIVES OPTIONS A. INTRODUCTION There are 2 Types of Options Calls: give the holder the RIGHT, at his discretion, to BUY a Specified number of a Specified Asset at a Specified Price on, or until, a

DERIVATIVES OPTIONS A. INTRODUCTION There are 2 Types of Options Calls: give the holder the RIGHT, at his discretion, to BUY a Specified number of a Specified Asset at a Specified Price on, or until, a

Mathematics of Financial Derivatives

Mathematics of Financial Derivatives Lecture 8 Solesne Bourguin bourguin@math.bu.edu Boston University Department of Mathematics and Statistics Table of contents 1. The Greek letters (continued) 2. Volatility

Mathematics of Financial Derivatives Lecture 8 Solesne Bourguin bourguin@math.bu.edu Boston University Department of Mathematics and Statistics Table of contents 1. The Greek letters (continued) 2. Volatility

K = 1 = -1. = 0 C P = 0 0 K Asset Price (S) 0 K Asset Price (S) Out of $ In the $ - In the $ Out of the $

0 K Asset Price (S) Out of $ In the $ - In the $ Out of the $") Page 1 of 20 OPTIONS 1. Valuation of Contracts a. Introduction The Value of an Option can be broken down into 2 Parts 1. INTRINSIC Value, which depends only upon the price of the asset underlying the option

Page 1 of 20 OPTIONS 1. Valuation of Contracts a. Introduction The Value of an Option can be broken down into 2 Parts 1. INTRINSIC Value, which depends only upon the price of the asset underlying the option

2 f. f t S 2. Delta measures the sensitivityof the portfolio value to changes in the price of the underlying

Sensitivity analysis Simulating the Greeks Meet the Greeks he value of a derivative on a single underlying asset depends upon the current asset price S and its volatility Σ, the risk-free interest rate

Sensitivity analysis Simulating the Greeks Meet the Greeks he value of a derivative on a single underlying asset depends upon the current asset price S and its volatility Σ, the risk-free interest rate

S&P 500 On Segment Maturity Date* Index Growth Rate*

The Hartford Indexed Universal Life Insurance Product Portfolio Interest Rates Product Name Hartford Frontier Indexed Universal Life Policy Form Numbers ICC10-1342, LA-1342, HL-19288(10)NY Information

The Hartford Indexed Universal Life Insurance Product Portfolio Interest Rates Product Name Hartford Frontier Indexed Universal Life Policy Form Numbers ICC10-1342, LA-1342, HL-19288(10)NY Information

Equity Option Selling Strategies

Interactive Brokers Webcast September 2016 Equity Option Selling Strategies Russell Rhoads, CFA Director of Education CBOE Options Institute Disclosure Options involve risks and are not suitable for all

Interactive Brokers Webcast September 2016 Equity Option Selling Strategies Russell Rhoads, CFA Director of Education CBOE Options Institute Disclosure Options involve risks and are not suitable for all

Trading Options for Potential Income in a Volatile Market

Trading Options for Potential Income in a Volatile Market Dan Sheridan Sheridan Mentoring & Brian Overby TradeKing TradeKing is a member of FINRA & SIPC Disclaimer Options involve risks and are not suitable

Trading Options for Potential Income in a Volatile Market Dan Sheridan Sheridan Mentoring & Brian Overby TradeKing TradeKing is a member of FINRA & SIPC Disclaimer Options involve risks and are not suitable

Understanding Exchange-Traded Funds (ETFs) A guide to TD Asset Management Inc. s (TDAM) ETF solutions

A guide to TD Asset Management Inc. s (TDAM) ETF solutions") Understanding Exchange-Traded Funds (ETFs) A guide to TD Asset Management Inc. s (TDAM) ETF solutions Understanding ETFs Investment in exchange-traded funds (ETFs) has boomed in recent years, with the

Understanding Exchange-Traded Funds (ETFs) A guide to TD Asset Management Inc. s (TDAM) ETF solutions Understanding ETFs Investment in exchange-traded funds (ETFs) has boomed in recent years, with the

Financial Derivatives: A hedging tool 6/21/12

Financial Derivatives: A hedging tool 6/21/12 Agenda We will explore 4 types of OTC and Exchange trades Point-to-point / Call Spread Digital / Binary Long-dated put Variance Swap / Variance Future For

Financial Derivatives: A hedging tool 6/21/12 Agenda We will explore 4 types of OTC and Exchange trades Point-to-point / Call Spread Digital / Binary Long-dated put Variance Swap / Variance Future For