Financial Markets & Risk

|

|

|

- Lester Mitchell

- 5 years ago

- Views:

Transcription

1 Financial Markets & Risk Dr Cesario MATEUS Senior Lecturer in Finance and Banking Room QA259 Department of Accounting and Finance

2 Session 3 Derivatives Binomial Trees Black-Scholes Call-Option-Pricing Model Option Greeks Interest Rate Swaps Currency Swaps Forward Rate Agreements May, 21 st,2014 2

3 Binomial Trees Useful and very popular technique for pricing an option. Diagram representing different possible paths that might be followed by the stock price over the life of an option. Underlying assumption: stock price follows a random walk In each time step: Certain probability of moving up or down by a percentage amount In the limit, as the time step becomes smaller, this model leads to the lognormal assumption for stock prices that underlies the Black-Scholes model. Binomial tress can be used to value options using both no-arbitrage arguments and the risk-neutral valuation principle. 3

4 Example Initial stock price = $20 and it is known that at the end of 3 months will be either: $22 or $18. What is the value of an European call option to buy the stock for $21 in 3 months? Stock price = $20 Stock Price = $22 Option price = $1 Stock Price = $18 Option price = $0 Arbitrage opportunities do not exist (assumption) No uncertainty about the value of the portfolio at the end of the 3 months Portfolio has no risk, the return must be equal the risk-free interest rate 4

5 Setting up a Riskless Portfolio Long position in Δ shares of stock and a short position in one call option What is the value of Δ that makes the portfolio riskless? Sock prices moves up from $20 to $22, the value of the shares is 22 Δ The value of the option is 1. Total value of portfolio is 22 Δ -1. Sock prices moves up from $20 to $18, the value of the shares is 18 Δ The value of the option is 0. Total value of portfolio is 18 Δ -0. Portfolio is riskless, if the value of Δ is chosen so that the final value of the portfolio is the same (for both alternatives) Riskless portfolio: long 0.25 shares, short 1 option. 5

6 6

7 Generalization A derivative lasts for time T and is dependent on a stock S 0 = Stock Price ƒ= option price S 0 ƒ S 0 u ƒ u S 0 d ƒ d Portfolio: Long position in Δ shares and a short position in one option Value of the portfolio at the end of life of the option if there is an up movement in the stock price Value of the portfolio at the end of life of the option if there is a down movement in the stock price 7

8 The two are equal when: Portfolio is riskless, no arbitrage opportunities, it must earn the risk-free interest rate. Present value of the portfolio: The cost of setting the portfolio: It follows that: 8

9 The equation can be reduced to: Option Price (one-step binomial tree): 9

10 p as a Probability It is natural to interpret p and 1-p as probabilities of up and down movements The value of a derivative is then its expected payoff in a risk-neutral world discounted at the risk-free rate S 0 u ƒ u S 0 ƒ S 0 d ƒ d 10

11 Risk-Neutral Valuation When the probability of an up and down movements are p and 1-p the expected stock price at time T is S 0 e rt This shows that the stock price earns the risk-free rate Binomial trees illustrate the general result that to value a derivative we can assume that the expected return on the underlying asset is the riskfree rate and discount at the risk-free rate This is known as using risk-neutral valuation 11

12 Two-Step Binomial Trees u = d = 10% X = 21 R = 12% Each time step is 3 months A B C

13 Example with Put S 0 = 50 K = 52 r = 5% u = 1.20 d = 0.8 p = Each time step is one year A 60 B C

14 American Options The value of the option at the final nodes is the same as for European Options. At earlier nodes the value of the option is the greater of: 1. The value given by: 2. The payoff from early exercise 14

15 60 B A C At the initial node A, the value is and the payoff from early exercise is 2 Early exercise is not optimal. 15

16 The Black-Scholes Call-Option-Pricing Model The Concepts Underlying Black-Scholes Model The option price and the stock price depend on the same underlying source of uncertainty We can form a portfolio consisting of the stock and the option which eliminates this source of uncertainty The portfolio is instantaneously riskless and must instantaneously earn the risk-free rate This leads to the Black-Scholes differential equation 16

17 Assumptions Underlying Black-Scholes No dividends Underlying stock returns are normally distributed No transaction costs Risk free interest rate for lending and borrowing Volatility and interest rates are constant up to maturity 17

18 Black and Scholes Formulas rt c S N( d ) Xe N( d ) ln( S0 / X ) [ RF 0.5 Var( R)] T d1 ; d2 d1 T T N(.) is the cumulative distribution function of the standard normal distribution N(d 2 ) is the risk adjusted probability that the option will be exercised. N(d 1 ) always greater than N(d 2 ). N(d 1 ) must not only account for the probability of exercise as given by N(d 2 ) but must also account for the fact that exercise or rather receipt of stock on exercise is dependent on the conditional future values that the stock price takes on the expiry date. 18

19 Example S0 = $60 = market price of the underlying asset (such as the share price of an optioned stock) X = $50 = Exercise (strike) price T = = 4 months = (one third of the year) = the time until the option expires and is worthless. RF=7% = Risk free rate stated at an annual rate Var (R) = = variance of returns = The riskiness of an investment in the optioned asset. d 1 ln($60 / $50) [ ] d

20 Table of Standard Normal Cumulative Distribution Function Φ(z) z

21 rt c S N( d ) Xe N( d ) c0 $ $50e $12.29 X $50 p C S p $12.29 $60 $ r /

22 Forward Use: Black & Scholes in Practice Underlying Price Exercise Price Time-to-Maturity Risk-free Interest Rate Estimated Volatility Backward Use: Black-Scholes Formula OPTION PRICE Underlying Price Exercise Price Time-to-Maturity Risk-free Interest Rate Implied Volatility (forward looking volatility) Black-Scholes Formula OPTION PRICE 22

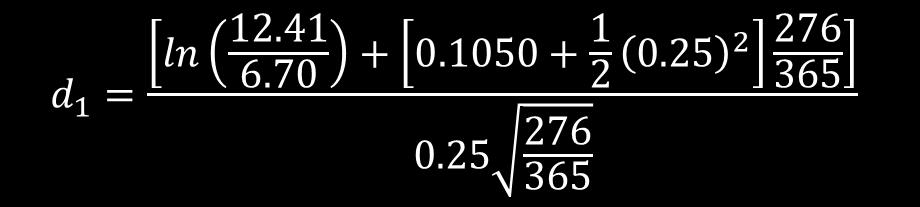

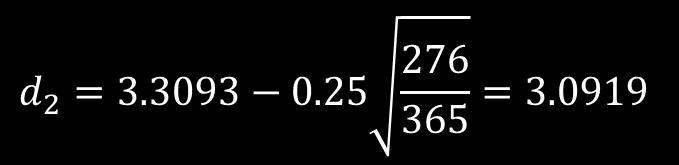

23 Example of option valuation using Black-Scholes What is the value of a European call option with an exercise price of 6.70 and a maturity date of 276 days from now if the current share price is $12.41, standard deviation is 25% p.a. and the risk-free rate is 10.50%. Assume there to be 365 days in a year. Use the Black-Scholes formula to derive your result. rt c P N d Ke N d d ln P K r 2 T d d T T 23

24 24

25 Question The stock of Cloverdale Food Processors currently sells for $40. A European Call option on Cloverdale stock has an expiration date six months in the future and a strike price of $38. The estimate of the annual standard deviation of Cloverdale stock is 45 percent, and the risk-free rate is 6 percent. What is the call worth? 25

26 Answer Question 26

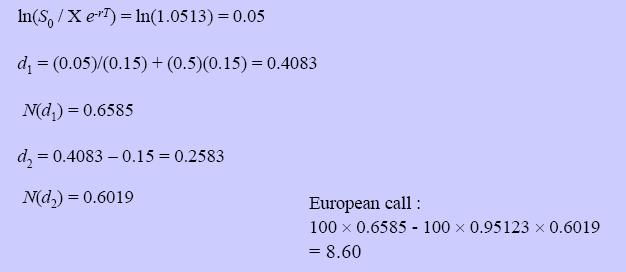

27 Question Stock price S 0 = 100 Exercise Price X = 100 (at the money option) Maturity T = 1 year Interest rate (continuous) r = 5% Volatility σ = 0.15

28 28

29 29

30 Questions A six-month call option with a strike price of $25.00 is selling for $3.50. Assuming the underlying stock price is also $25.00 and the risk-free rate is 6 percent APR, use the following table to determine the volatility (i.e, standard deviation of the return) implied using the option price. (Hint: Price the option using the table to determine which volatility generates a price of $3.50) Volatility N(d1) N(d2) 40% 0,5799 0, % %

31 Option Greeks Delta Measures the exposure of option price to movement of underlying stock price The ratio comparing the change in the price of the underlying asset to the corresponding change in the price of a derivative. Sometimes referred to as the "hedge ratio For example, with respect to call options, a delta of 0.7 means that for every $1 the underlying stock increases, the call option will increase by $

32 Put option deltas, on the other hand, will be negative, because as the underlying security increases, the value of the option will decrease. So a put option with a delta of -0.7 will decrease by $0.70 for every $1 the underlying increases in price. As an in-the-money call option nears expiration, it will approach a delta of 1.00, and as an in-the-money put option nears expiration, it will approach a delta of

33 33

34 Gamma Measures the exposure of the option delta to the movement of the underlying stock price The rate of change for delta with respect to the underlying asset's price. Gamma is an important measure of the convexity of a derivative's value, in relation to the underlying. Mathematically, gamma is the first derivative of delta and is used when trying to gauge the price movement of an option, relative to the amount it is in or out of the money. When the option being measured is deep in or out of the money, gamma is small. When the option is near or at the money, gamma is at its largest. Gamma calculations are most accurate for small changes in the price of the underlying asset. 34

35 Theta Measures the exposure of the option price to the passage of time. A measure of the rate of decline in the value of an option due to the passage of time. Theta can also be referred to as the time decay on the value of an option. If everything is held constant, then the option will lose value as time moves closer to the maturity of the option. For example, if the strike price of an option is $1,150 and theta is 53.80, then in theory the value of the option will drop $53.80 per day. The measure of theta quantifies the risk that time imposes on options as options are only exercisable for a certain period of time. Time has importance for option traders on a conceptual level more than a practical one, so theta is not often used by traders in formulating the value of an option. 35

36 Vega Measures the exposure of the option price to changes in volatility of the underlying The measurement of an option's sensitivity to changes in the volatility of the underlying asset. Vega represents the amount that an option contract's price changes in reaction to a 1% change in the volatility of the underlying asset. 36

37 Swaps Plain vanilla Interest rate swap (most common type of swap). Company agrees to pay cash flows equal to interest at a predetermined fixed rate on a notional principal for a number of years. In return, it receives at a floating rate on the same notional principal for the same period of time. LIBOR (London Interbank Offered Rate): Floating rate used in most interest rate swaps agreements. Rate of interest at which a bank is prepared to deposit money with other banks in the Eurocurrency market. Typically, 1-month, 3-month, 6-month and 12-month (LIBOR is quoted in all major currencies) 37

38 Example 3-year swap initiated in March, 5 th, 2007, between Microsoft and Intel. Microsoft agrees to pay Intel an interest rate of 5% per annum on a principal of $100 million. Intel agrees to pay Microsoft the 6-month LIBOR rate on the same principal. Microsoft: fixed-rate payer Intel: Floating rate payer We assume that payments are to be exchanged every 6-months and that the 5% interest rate is quoted with semi-annual compounding. 38

39 Cash Flows (millions of dollars) to Microsoft in a $100 million 3-year interest rate swap when a fixed rate of 5% is paid and LIBOR received Date Six-month Libor (%) Mar. 5, Floating cash flow received Fixed cash flow paid Net cash flow Sept. 5, Mar. 5, Sept. 5, Mar. 5, Sept. 5, Mar. 5,

40 Using the Swap to Transform a Liability Swap can be used to transform a floating-rate loan into a fixed-rate loan. Suppose: Microsoft has arranged to borrow $100 million at LIBOR plus 10 basis points. Three sets of cash flows: 1. It pays LIBOR plus 0.1% to its outside lenders 2. It receives LIBOR under the terms of the swap 3. It pays 5% under the terms of the swap Microsoft swap have the effect of transforming borrowing at a floating rate of LIBOR plus 10 basis points into borrowings at a fixed rate of 5.1% 40

41 For Intel, the swap could have the effect of transforming a fixed-rate loan into a floating rate loan. Suppose, that Intel has a 3-year $100 million loan outstanding on which it pays 5.2%. After it has entered into the swap, it has the following three sets of cash flows: 1. It pays 5.2% to its outside lenders 2. It pays LIBOR under the terms of the swap 3. It receives 5% under the terms of the swap For Intel, the swap have the effect of transforming borrowings at a fixed rate of 5.2% into borrowings at a floating rate of LIBOR plus 20 basis points. Microsoft and Intel use the Swap to transform a liability 41

42 Using the Swap to Transform an Asset Swaps can also be used to transform the nature of an asset. Consider Microsoft in our example. The swap could have the effect of transforming an asset earning a fixed rate of interest into an asset earning a floating rate of interest. Suppose Microsoft owns $100 million in bonds that will provide interest at 4.7% per annum over the next 3 years. After Microsoft has entered into a swap, it has the following three sets of cash flows: 1. It receives 4.7% on the bonds 2. It receives LIBOR under the terms of the swap 3. It pays 5% under the terms of the swap One possible use of the swap for Microsoft is to transform an asset earning 4.7% into an asset earning LIBOR minus 30 basis points. 42

43 In case of Intel, the swap could have the effect of transforming an asset earning a floating rate of interest into an asset earning a fixed rate of interest. Suppose that Intel has an investment of $100 million that yields LIBOR minus 20 basis points. After it has entered into the swap, has the following three sets of cash flows: 1. It receives LIBOR minus 20 basis points on its investment 2. It pays LIBOR under the terms of the swap 3. It receives 5% under the terms of the swap Possible use of swap for Intel is to transform and asset earning LIBOR minus 20 basis points into an asset earning 4.8%. Microsoft and Intel use the Swap to transform an asset 43

44 Role of Financial Intermediary Usually two nonfinancial companies such as Intel and Microsoft do not get in touch directly to arrange a swap. They each deal with a financial intermediary such as a bank or other financial institution. Plain vanilla fixed-for-floating swaps on US interest rates are usually structured so that the financial institutions earns about 3 or 4 basis points (0.03% or 0.04%) on a pair of offsetting transactions. 44

45 Interest rate swap when financial institution is involved 45

46 Currency Swaps Swap that involves exchanging principal and interest payments in one currency for principal and interest in another. A currency swap agreement requires the principal to be specified in each of the two currencies. Example: Consider a hypothetical 5-year currency swap agreement between IBM and British Petroleum entered into on February, 1, We suppose that IBM pays a fixed rate of interest of 5% in sterling and receives a fixed rate of interest of 6% in dollars from British Petroleum. Interest rate payments are made once a year and the principal amounts are $18 million and 10 million. This is termed a fixed-to-fixed currency swap because the interest rate in both currencies is fixed. 46

47 Date Dollar Cash Flow (millions) Sterling Cash Flow (millions) February, 1, February, 1, February, 1, February, 1, February, 1, February, 1,

48 Use of a Currency Swap to Transform Liabilities A swap can be used to transform borrowings in one currency to borrowings in another. Suppose IBM can issue $18 million of US-dollar-denominated bonds at 6% interest. The swap has the effect of transforming this transaction into one where IBM has borrowed 10 million at 5% interest. The initial exchange of principal converts the proceeds of the bond issue from US dollars to sterling. The subsequent exchanges in the swap have the effect of swapping the interest and principal payments from dollars to sterling 48

49 Use of a Currency Swap to Transform Assets The swap can also be used to transform the nature of assets. Suppose that IBM can invest 10 million in the UK to yield 5% per annum for the next 5 years. However IBM feels the US dollar will strengthen against sterling and prefers US-dollar-denominated investment. The swap has the effect of transforming the UK investment into a $18 million investment in the US yielding 6%. 49

50 Comparative Advantage Currency swaps can be motivated by comparative advantage. Suppose the 5-year fixed-rate borrowing costs to General Electric and Qantas Airways in US dollars (USD) and Australian dollars (AUD) are as below: USD AUD General Electric 5.0% 7.6% Qantas Airways 7.0% 8.0% Australian rates are higher than USD interest rates General Electric is more creditworthy than Qantas Airways From the viewpoint of a swap trader, the interesting aspect is that the spreads between the rates paid by General Electric and Qantas Airways in the two markets are not the same. 50

51 Suppose that General Electric wants to borrow 20 million AUD and Qantas Airways wants to borrow 15 million USD and the current exchange rate (USD per AUD) is General Electric and Qantas Airways each borrow in the market where they have a comparative advantage. General Electric will borrows USD Qantas Airways will borrow AUD They then use a currency swap to transform General Electric s loan into an AUD loan and Qantas Airways loan into USD loan. We expect the total gain to all parties to be 2%-0.4%=1.6% per annum 51

52 General Electric borrows USD Qantas Airways borrows AUD Effect of the swap is to transform the USD interest rate of 5% per annum to an AUD interest rate of 6.9% per annum for General electric. General Electric is 0.7% per annum better off than it would be if it went directly to AUD markets. Qantas exchanges an AUD loan at 8% per annum for a USD loan at 6.3% per annum and ends up 0.7% per annum better off than it would be if it went directly to USD markets. 52

53 The financial institution gains 1.3% per annum on its USD cash flows and loses 1.1% per annum on its AUD flows. The financial institution makes a net gain of 0.2% per annum (ignoring the difference between the two currencies). The total gain to all parties is 1.6% per annum. 53

54 Forward Rate Agreements Forward Rate Agreement: is a contract that specifies a cash payment at contract maturity determined by the difference between an agreed interest rate and the realized interest rate at maturity. There are FRAs on Eurodollar deposit rates (LIBOR) and FRAs on euro deposit rates (Euribor). Example: Consider a one-month FRA contract, expiring in 30 days, based on 3-month LIBOR. The underlying rate on the contract is the 3-month LIBOR that will prevail in 30 days. Suppose the two parties to the contract agree on a fixed rate of 2.5%. The buyer of the FRA will receive a payment from the seller if the actual 3-month LIBOR rate at expiration of the FRA contract is greater than 2.5%. The seller of the FRA will receive a payment from the seller if the actual 3-month LIBOR rate at expiration of the FRA contract is less than 2.5%. 54

55 Calculate and Interpret the payoff of a FRA Two parties agree to make a loan to the other at the maturity of the FRA. They enter in a 30-day FRA contract based on 3-month LIBOR with a FRA (fixed) rate of 2.5% and a notional of $100,000,000. This is s 1 4 FRA maturing in 1 month, at which time a 3-month loan will be exchanged (a relationship lasting a total of 4 months). At maturity date (30 days from inception) The seller of the FRA agrees to make a $100 million loan to the buyer at a rate of 2.5% for three months (buyer pays 2.5% interest to the FRA seller). The buyer of the FRA agrees to loan the seller $100 million at whatever 3-month LIBOR is at maturity, again for 3 months. No money actually changes hands at the inception of the FRA. 30 days later, 3 month LIBOR is 2.73%. 55

56 The seller will simply pay the buyer the present value of the difference between the interest payments discounted at the current 3-month LIBOR rate. 56

57 Currency Forward Agreements Currency forwards involve two parties who agree to exchange currencies at a future date and specified exchange rates. Example: Bank A agrees to buy 50,000,000 in six months from Bank B who agrees to sell the pounds at $1.10/. If, in six months, the actual exchange rate is only $1.05/, Bank A will suffer a loss of $2.5 million. Gain or loss calculation: Bank B on the other hand will make a profit of $2.5 million, because it can buy the 50,000,000 in the spot market at $1.05/ and sell it to Bank B at at $1.10/. A forward agreement is a zero-sum game. 57

MBF1243 Derivatives. L7: Swaps

MBF1243 Derivatives L7: Swaps Nature of Swaps A swap is an agreement to exchange of payments at specified future times according to certain specified rules The agreement defines the dates when the cash

MBF1243 Derivatives L7: Swaps Nature of Swaps A swap is an agreement to exchange of payments at specified future times according to certain specified rules The agreement defines the dates when the cash

Swaps 7.1 MECHANICS OF INTEREST RATE SWAPS LIBOR

7C H A P T E R Swaps The first swap contracts were negotiated in the early 1980s. Since then the market has seen phenomenal growth. Swaps now occupy a position of central importance in derivatives markets.

7C H A P T E R Swaps The first swap contracts were negotiated in the early 1980s. Since then the market has seen phenomenal growth. Swaps now occupy a position of central importance in derivatives markets.

Derivatives Questions Question 1 Explain carefully the difference between hedging, speculation, and arbitrage.

Derivatives Questions Question 1 Explain carefully the difference between hedging, speculation, and arbitrage. Question 2 What is the difference between entering into a long forward contract when the forward

Derivatives Questions Question 1 Explain carefully the difference between hedging, speculation, and arbitrage. Question 2 What is the difference between entering into a long forward contract when the forward

Appendix A Financial Calculations

Derivatives Demystified: A Step-by-Step Guide to Forwards, Futures, Swaps and Options, Second Edition By Andrew M. Chisholm 010 John Wiley & Sons, Ltd. Appendix A Financial Calculations TIME VALUE OF MONEY

Derivatives Demystified: A Step-by-Step Guide to Forwards, Futures, Swaps and Options, Second Edition By Andrew M. Chisholm 010 John Wiley & Sons, Ltd. Appendix A Financial Calculations TIME VALUE OF MONEY

Derivative Instruments

Derivative Instruments Paris Dauphine University - Master I.E.F. (272) Autumn 2016 Jérôme MATHIS jerome.mathis@dauphine.fr (object: IEF272) http://jerome.mathis.free.fr/ief272 Slides on book: John C. Hull,

Derivative Instruments Paris Dauphine University - Master I.E.F. (272) Autumn 2016 Jérôme MATHIS jerome.mathis@dauphine.fr (object: IEF272) http://jerome.mathis.free.fr/ief272 Slides on book: John C. Hull,

Chapter 9 - Mechanics of Options Markets

Chapter 9 - Mechanics of Options Markets Types of options Option positions and profit/loss diagrams Underlying assets Specifications Trading options Margins Taxation Warrants, employee stock options, and

Chapter 9 - Mechanics of Options Markets Types of options Option positions and profit/loss diagrams Underlying assets Specifications Trading options Margins Taxation Warrants, employee stock options, and

Derivatives Analysis & Valuation (Futures)

") 6.1 Derivatives Analysis & Valuation (Futures) LOS 1 : Introduction Study Session 6 Define Forward Contract, Future Contract. Forward Contract, In Forward Contract one party agrees to buy, and the counterparty

6.1 Derivatives Analysis & Valuation (Futures) LOS 1 : Introduction Study Session 6 Define Forward Contract, Future Contract. Forward Contract, In Forward Contract one party agrees to buy, and the counterparty

CHAPTER 10 OPTION PRICING - II. Derivatives and Risk Management By Rajiv Srivastava. Copyright Oxford University Press

CHAPTER 10 OPTION PRICING - II Options Pricing II Intrinsic Value and Time Value Boundary Conditions for Option Pricing Arbitrage Based Relationship for Option Pricing Put Call Parity 2 Binomial Option

CHAPTER 10 OPTION PRICING - II Options Pricing II Intrinsic Value and Time Value Boundary Conditions for Option Pricing Arbitrage Based Relationship for Option Pricing Put Call Parity 2 Binomial Option

The Greek Letters Based on Options, Futures, and Other Derivatives, 8th Edition, Copyright John C. Hull 2012

The Greek Letters Based on Options, Futures, and Other Derivatives, 8th Edition, Copyright John C. Hull 2012 Introduction Each of the Greek letters measures a different dimension to the risk in an option

The Greek Letters Based on Options, Futures, and Other Derivatives, 8th Edition, Copyright John C. Hull 2012 Introduction Each of the Greek letters measures a different dimension to the risk in an option

Valuing Stock Options: The Black-Scholes-Merton Model. Chapter 13

Valuing Stock Options: The Black-Scholes-Merton Model Chapter 13 1 The Black-Scholes-Merton Random Walk Assumption l Consider a stock whose price is S l In a short period of time of length t the return

Valuing Stock Options: The Black-Scholes-Merton Model Chapter 13 1 The Black-Scholes-Merton Random Walk Assumption l Consider a stock whose price is S l In a short period of time of length t the return

Lecture Quantitative Finance Spring Term 2015

and Lecture Quantitative Finance Spring Term 2015 Prof. Dr. Erich Walter Farkas Lecture 06: March 26, 2015 1 / 47 Remember and Previous chapters: introduction to the theory of options put-call parity fundamentals

and Lecture Quantitative Finance Spring Term 2015 Prof. Dr. Erich Walter Farkas Lecture 06: March 26, 2015 1 / 47 Remember and Previous chapters: introduction to the theory of options put-call parity fundamentals

2. Futures and Forward Markets 2.1. Institutions

2. Futures and Forward Markets 2.1. Institutions 1. (Hull 2.3) Suppose that you enter into a short futures contract to sell July silver for $5.20 per ounce on the New York Commodity Exchange. The size

2. Futures and Forward Markets 2.1. Institutions 1. (Hull 2.3) Suppose that you enter into a short futures contract to sell July silver for $5.20 per ounce on the New York Commodity Exchange. The size

Appendix: Basics of Options and Option Pricing Option Payoffs

Appendix: Basics of Options and Option Pricing An option provides the holder with the right to buy or sell a specified quantity of an underlying asset at a fixed price (called a strike price or an exercise

Appendix: Basics of Options and Option Pricing An option provides the holder with the right to buy or sell a specified quantity of an underlying asset at a fixed price (called a strike price or an exercise

Derivative Securities Fall 2012 Final Exam Guidance Extended version includes full semester

Derivative Securities Fall 2012 Final Exam Guidance Extended version includes full semester Our exam is Wednesday, December 19, at the normal class place and time. You may bring two sheets of notes (8.5

Derivative Securities Fall 2012 Final Exam Guidance Extended version includes full semester Our exam is Wednesday, December 19, at the normal class place and time. You may bring two sheets of notes (8.5

Econ 174 Financial Insurance Fall 2000 Allan Timmermann. Final Exam. Please answer all four questions. Each question carries 25% of the total grade.

Econ 174 Financial Insurance Fall 2000 Allan Timmermann UCSD Final Exam Please answer all four questions. Each question carries 25% of the total grade. 1. Explain the reasons why you agree or disagree

Econ 174 Financial Insurance Fall 2000 Allan Timmermann UCSD Final Exam Please answer all four questions. Each question carries 25% of the total grade. 1. Explain the reasons why you agree or disagree

FIN FINANCIAL INSTRUMENTS SPRING 2008

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 The Greeks Introduction We have studied how to price an option using the Black-Scholes formula. Now we wish to consider how the option price changes, either

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 The Greeks Introduction We have studied how to price an option using the Black-Scholes formula. Now we wish to consider how the option price changes, either

Homework Assignments

Homework Assignments Week 1 (p 57) #4.1, 4., 4.3 Week (pp 58-6) #4.5, 4.6, 4.8(a), 4.13, 4.0, 4.6(b), 4.8, 4.31, 4.34 Week 3 (pp 15-19) #1.9, 1.1, 1.13, 1.15, 1.18 (pp 9-31) #.,.6,.9 Week 4 (pp 36-37)

Homework Assignments Week 1 (p 57) #4.1, 4., 4.3 Week (pp 58-6) #4.5, 4.6, 4.8(a), 4.13, 4.0, 4.6(b), 4.8, 4.31, 4.34 Week 3 (pp 15-19) #1.9, 1.1, 1.13, 1.15, 1.18 (pp 9-31) #.,.6,.9 Week 4 (pp 36-37)

Mathematics of Financial Derivatives

Mathematics of Financial Derivatives Lecture 11 Solesne Bourguin bourguin@math.bu.edu Boston University Department of Mathematics and Statistics Table of contents 1. Mechanics of interest rate swaps (continued)

Mathematics of Financial Derivatives Lecture 11 Solesne Bourguin bourguin@math.bu.edu Boston University Department of Mathematics and Statistics Table of contents 1. Mechanics of interest rate swaps (continued)

Forwards, Futures, Options and Swaps

Forwards, Futures, Options and Swaps A derivative asset is any asset whose payoff, price or value depends on the payoff, price or value of another asset. The underlying or primitive asset may be almost

Forwards, Futures, Options and Swaps A derivative asset is any asset whose payoff, price or value depends on the payoff, price or value of another asset. The underlying or primitive asset may be almost

Final Exam. Please answer all four questions. Each question carries 25% of the total grade.

Econ 174 Financial Insurance Fall 2000 Allan Timmermann UCSD Final Exam Please answer all four questions. Each question carries 25% of the total grade. 1. Explain the reasons why you agree or disagree

Econ 174 Financial Insurance Fall 2000 Allan Timmermann UCSD Final Exam Please answer all four questions. Each question carries 25% of the total grade. 1. Explain the reasons why you agree or disagree

Mathematics of Finance Final Preparation December 19. To be thoroughly prepared for the final exam, you should

Mathematics of Finance Final Preparation December 19 To be thoroughly prepared for the final exam, you should 1. know how to do the homework problems. 2. be able to provide (correct and complete!) definitions

Mathematics of Finance Final Preparation December 19 To be thoroughly prepared for the final exam, you should 1. know how to do the homework problems. 2. be able to provide (correct and complete!) definitions

The Johns Hopkins Carey Business School. Derivatives. Spring Final Exam

The Johns Hopkins Carey Business School Derivatives Spring 2010 Instructor: Bahattin Buyuksahin Final Exam Final DUE ON WEDNESDAY, May 19th, 2010 Late submissions will not be graded. Show your calculations.

The Johns Hopkins Carey Business School Derivatives Spring 2010 Instructor: Bahattin Buyuksahin Final Exam Final DUE ON WEDNESDAY, May 19th, 2010 Late submissions will not be graded. Show your calculations.

MATH4143: Scientific Computations for Finance Applications Final exam Time: 9:00 am - 12:00 noon, April 18, Student Name (print):

:") MATH4143 Page 1 of 17 Winter 2007 MATH4143: Scientific Computations for Finance Applications Final exam Time: 9:00 am - 12:00 noon, April 18, 2007 Student Name (print): Student Signature: Student ID: Question

MATH4143 Page 1 of 17 Winter 2007 MATH4143: Scientific Computations for Finance Applications Final exam Time: 9:00 am - 12:00 noon, April 18, 2007 Student Name (print): Student Signature: Student ID: Question

Hull, Options, Futures & Other Derivatives Exotic Options

P1.T3. Financial Markets & Products Hull, Options, Futures & Other Derivatives Exotic Options Bionic Turtle FRM Video Tutorials By David Harper, CFA FRM 1 Exotic Options Define and contrast exotic derivatives

P1.T3. Financial Markets & Products Hull, Options, Futures & Other Derivatives Exotic Options Bionic Turtle FRM Video Tutorials By David Harper, CFA FRM 1 Exotic Options Define and contrast exotic derivatives

CHAPTER 9. Solutions. Exercise The payoff diagrams will look as in the figure below.

CHAPTER 9 Solutions Exercise 1 1. The payoff diagrams will look as in the figure below. 2. Gross payoff at expiry will be: P(T) = min[(1.23 S T ), 0] + min[(1.10 S T ), 0] where S T is the EUR/USD exchange

CHAPTER 9 Solutions Exercise 1 1. The payoff diagrams will look as in the figure below. 2. Gross payoff at expiry will be: P(T) = min[(1.23 S T ), 0] + min[(1.10 S T ), 0] where S T is the EUR/USD exchange

Answers to Selected Problems

Answers to Selected Problems Problem 1.11. he farmer can short 3 contracts that have 3 months to maturity. If the price of cattle falls, the gain on the futures contract will offset the loss on the sale

Answers to Selected Problems Problem 1.11. he farmer can short 3 contracts that have 3 months to maturity. If the price of cattle falls, the gain on the futures contract will offset the loss on the sale

Swaps. Chapter 6. Nature of Swaps. Uses of Swaps: Transforming a Liability (Figure 6.2, page 136) Typical Uses of an Interest Rate Swap

Typical Uses of an Interest Rate Swap") 6.1 6.2 Swaps Chapter 6 Nature of Swaps A swap is an agreement to exchange cash flows at specified future times according to specified rules Example: A Plain Vanilla Interest Rate Swap The agreement on

6.1 6.2 Swaps Chapter 6 Nature of Swaps A swap is an agreement to exchange cash flows at specified future times according to specified rules Example: A Plain Vanilla Interest Rate Swap The agreement on

OPTIONS & GREEKS. Study notes. An option results in the right (but not the obligation) to buy or sell an asset, at a predetermined

to buy or sell an asset, at a predetermined") OPTIONS & GREEKS Study notes 1 Options 1.1 Basic information An option results in the right (but not the obligation) to buy or sell an asset, at a predetermined price, and on or before a predetermined

OPTIONS & GREEKS Study notes 1 Options 1.1 Basic information An option results in the right (but not the obligation) to buy or sell an asset, at a predetermined price, and on or before a predetermined

Options Markets: Introduction

17-2 Options Options Markets: Introduction Derivatives are securities that get their value from the price of other securities. Derivatives are contingent claims because their payoffs depend on the value

17-2 Options Options Markets: Introduction Derivatives are securities that get their value from the price of other securities. Derivatives are contingent claims because their payoffs depend on the value

Advanced Topics in Derivative Pricing Models. Topic 4 - Variance products and volatility derivatives

Advanced Topics in Derivative Pricing Models Topic 4 - Variance products and volatility derivatives 4.1 Volatility trading and replication of variance swaps 4.2 Volatility swaps 4.3 Pricing of discrete

Advanced Topics in Derivative Pricing Models Topic 4 - Variance products and volatility derivatives 4.1 Volatility trading and replication of variance swaps 4.2 Volatility swaps 4.3 Pricing of discrete

LECTURE 12. Volatility is the question on the B/S which assumes constant SD throughout the exercise period - The time series of implied volatility

LECTURE 12 Review Options C = S e -δt N (d1) X e it N (d2) P = X e it (1- N (d2)) S e -δt (1 - N (d1)) Volatility is the question on the B/S which assumes constant SD throughout the exercise period - The

LECTURE 12 Review Options C = S e -δt N (d1) X e it N (d2) P = X e it (1- N (d2)) S e -δt (1 - N (d1)) Volatility is the question on the B/S which assumes constant SD throughout the exercise period - The

Pricing Options with Mathematical Models

Pricing Options with Mathematical Models 1. OVERVIEW Some of the content of these slides is based on material from the book Introduction to the Economics and Mathematics of Financial Markets by Jaksa Cvitanic

Pricing Options with Mathematical Models 1. OVERVIEW Some of the content of these slides is based on material from the book Introduction to the Economics and Mathematics of Financial Markets by Jaksa Cvitanic

Answers to Selected Problems

Answers to Selected Problems Problem 1.11. he farmer can short 3 contracts that have 3 months to maturity. If the price of cattle falls, the gain on the futures contract will offset the loss on the sale

Answers to Selected Problems Problem 1.11. he farmer can short 3 contracts that have 3 months to maturity. If the price of cattle falls, the gain on the futures contract will offset the loss on the sale

CHAPTER 17 OPTIONS AND CORPORATE FINANCE

CHAPTER 17 OPTIONS AND CORPORATE FINANCE Answers to Concept Questions 1. A call option confers the right, without the obligation, to buy an asset at a given price on or before a given date. A put option

CHAPTER 17 OPTIONS AND CORPORATE FINANCE Answers to Concept Questions 1. A call option confers the right, without the obligation, to buy an asset at a given price on or before a given date. A put option

Advanced Corporate Finance. 5. Options (a refresher)

") Advanced Corporate Finance 5. Options (a refresher) Objectives of the session 1. Define options (calls and puts) 2. Analyze terminal payoff 3. Define basic strategies 4. Binomial option pricing model 5.

Advanced Corporate Finance 5. Options (a refresher) Objectives of the session 1. Define options (calls and puts) 2. Analyze terminal payoff 3. Define basic strategies 4. Binomial option pricing model 5.

Gallery of equations. 1. Introduction

Gallery of equations. Introduction Exchange-traded markets Over-the-counter markets Forward contracts Definition.. A forward contract is an agreement to buy or sell an asset at a certain future time for

Gallery of equations. Introduction Exchange-traded markets Over-the-counter markets Forward contracts Definition.. A forward contract is an agreement to buy or sell an asset at a certain future time for

Corporate Finance, Module 21: Option Valuation. Practice Problems. (The attached PDF file has better formatting.) Updated: July 7, 2005

Updated: July 7, 2005") Corporate Finance, Module 21: Option Valuation Practice Problems (The attached PDF file has better formatting.) Updated: July 7, 2005 {This posting has more information than is needed for the corporate

Corporate Finance, Module 21: Option Valuation Practice Problems (The attached PDF file has better formatting.) Updated: July 7, 2005 {This posting has more information than is needed for the corporate

Financial Management

Financial Management International Finance 1 RISK AND HEDGING In this lecture we will cover: Justification for hedging Different Types of Hedging Instruments. How to Determine Risk Exposure. Good references

Financial Management International Finance 1 RISK AND HEDGING In this lecture we will cover: Justification for hedging Different Types of Hedging Instruments. How to Determine Risk Exposure. Good references

NATIONAL UNIVERSITY OF SINGAPORE DEPARTMENT OF MATHEMATICS SEMESTER 2 EXAMINATION Investment Instruments: Theory and Computation

NATIONAL UNIVERSITY OF SINGAPORE DEPARTMENT OF MATHEMATICS SEMESTER 2 EXAMINATION 2012-2013 Investment Instruments: Theory and Computation April/May 2013 Time allowed : 2 hours INSTRUCTIONS TO CANDIDATES

NATIONAL UNIVERSITY OF SINGAPORE DEPARTMENT OF MATHEMATICS SEMESTER 2 EXAMINATION 2012-2013 Investment Instruments: Theory and Computation April/May 2013 Time allowed : 2 hours INSTRUCTIONS TO CANDIDATES

Economic Risk and Decision Analysis for Oil and Gas Industry CE School of Engineering and Technology Asian Institute of Technology

Economic Risk and Decision Analysis for Oil and Gas Industry CE81.98 School of Engineering and Technology Asian Institute of Technology January Semester Presented by Dr. Thitisak Boonpramote Department

Economic Risk and Decision Analysis for Oil and Gas Industry CE81.98 School of Engineering and Technology Asian Institute of Technology January Semester Presented by Dr. Thitisak Boonpramote Department

Derivatives Options on Bonds and Interest Rates. Professor André Farber Solvay Business School Université Libre de Bruxelles

Derivatives Options on Bonds and Interest Rates Professor André Farber Solvay Business School Université Libre de Bruxelles Caps Floors Swaption Options on IR futures Options on Government bond futures

Derivatives Options on Bonds and Interest Rates Professor André Farber Solvay Business School Université Libre de Bruxelles Caps Floors Swaption Options on IR futures Options on Government bond futures

INSTITUTE OF ACTUARIES OF INDIA

INSTITUTE OF ACTUARIES OF INDIA EXAMINATIONS 10 th November 2008 Subject CT8 Financial Economics Time allowed: Three Hours (14.30 17.30 Hrs) Total Marks: 100 INSTRUCTIONS TO THE CANDIDATES 1) Please read

INSTITUTE OF ACTUARIES OF INDIA EXAMINATIONS 10 th November 2008 Subject CT8 Financial Economics Time allowed: Three Hours (14.30 17.30 Hrs) Total Marks: 100 INSTRUCTIONS TO THE CANDIDATES 1) Please read

CHAPTER 7 INVESTMENT III: OPTION PRICING AND ITS APPLICATIONS IN INVESTMENT VALUATION

CHAPTER 7 INVESTMENT III: OPTION PRICING AND ITS APPLICATIONS IN INVESTMENT VALUATION Chapter content Upon completion of this chapter you will be able to: explain the principles of option pricing theory

CHAPTER 7 INVESTMENT III: OPTION PRICING AND ITS APPLICATIONS IN INVESTMENT VALUATION Chapter content Upon completion of this chapter you will be able to: explain the principles of option pricing theory

Financial Economics 4378 FALL 2013 FINAL EXAM There are 10 questions Total Points 100. Question 1 (10 points)

") Financial Economics 4378 FALL 2013 FINAL EXAM There are 10 questions Total Points 100 Name: Question 1 (10 points) A trader currently holds 300 shares of IBM stock. The trader also has $15,000 in cash.

Financial Economics 4378 FALL 2013 FINAL EXAM There are 10 questions Total Points 100 Name: Question 1 (10 points) A trader currently holds 300 shares of IBM stock. The trader also has $15,000 in cash.

Vanilla interest rate options

Vanilla interest rate options Marco Marchioro derivati2@marchioro.org October 26, 2011 Vanilla interest rate options 1 Summary Probability evolution at information arrival Brownian motion and option pricing

Vanilla interest rate options Marco Marchioro derivati2@marchioro.org October 26, 2011 Vanilla interest rate options 1 Summary Probability evolution at information arrival Brownian motion and option pricing

MORNING SESSION. Date: Wednesday, April 30, 2014 Time: 8:30 a.m. 11:45 a.m. INSTRUCTIONS TO CANDIDATES

SOCIETY OF ACTUARIES Quantitative Finance and Investment Core Exam QFICORE MORNING SESSION Date: Wednesday, April 30, 2014 Time: 8:30 a.m. 11:45 a.m. INSTRUCTIONS TO CANDIDATES General Instructions 1.

SOCIETY OF ACTUARIES Quantitative Finance and Investment Core Exam QFICORE MORNING SESSION Date: Wednesday, April 30, 2014 Time: 8:30 a.m. 11:45 a.m. INSTRUCTIONS TO CANDIDATES General Instructions 1.

Financial Market Introduction

Financial Market Introduction Alex Yang FinPricing http://www.finpricing.com Summary Financial Market Definition Financial Return Price Determination No Arbitrage and Risk Neutral Measure Fixed Income

Financial Market Introduction Alex Yang FinPricing http://www.finpricing.com Summary Financial Market Definition Financial Return Price Determination No Arbitrage and Risk Neutral Measure Fixed Income

Pricing theory of financial derivatives

Pricing theory of financial derivatives One-period securities model S denotes the price process {S(t) : t = 0, 1}, where S(t) = (S 1 (t) S 2 (t) S M (t)). Here, M is the number of securities. At t = 1,

Pricing theory of financial derivatives One-period securities model S denotes the price process {S(t) : t = 0, 1}, where S(t) = (S 1 (t) S 2 (t) S M (t)). Here, M is the number of securities. At t = 1,

Review of Derivatives I. Matti Suominen, Aalto

Review of Derivatives I Matti Suominen, Aalto 25 SOME STATISTICS: World Financial Markets (trillion USD) 2 15 1 5 Securitized loans Corporate bonds Financial institutions' bonds Public debt Equity market

Review of Derivatives I Matti Suominen, Aalto 25 SOME STATISTICS: World Financial Markets (trillion USD) 2 15 1 5 Securitized loans Corporate bonds Financial institutions' bonds Public debt Equity market

Eurocurrency Contracts. Eurocurrency Futures

Eurocurrency Contracts Futures Contracts, FRAs, & Options Eurocurrency Futures Eurocurrency time deposit Euro-zzz: The currency of denomination of the zzz instrument is not the official currency of the

Eurocurrency Contracts Futures Contracts, FRAs, & Options Eurocurrency Futures Eurocurrency time deposit Euro-zzz: The currency of denomination of the zzz instrument is not the official currency of the

Cash Flows on Options strike or exercise price

1 APPENDIX 4 OPTION PRICING In general, the value of any asset is the present value of the expected cash flows on that asset. In this section, we will consider an exception to that rule when we will look

1 APPENDIX 4 OPTION PRICING In general, the value of any asset is the present value of the expected cash flows on that asset. In this section, we will consider an exception to that rule when we will look

Currency Option or FX Option Introduction and Pricing Guide

or FX Option Introduction and Pricing Guide Michael Taylor FinPricing A currency option or FX option is a contract that gives the buyer the right, but not the obligation, to buy or sell a certain currency

or FX Option Introduction and Pricing Guide Michael Taylor FinPricing A currency option or FX option is a contract that gives the buyer the right, but not the obligation, to buy or sell a certain currency

B. Combinations. 1. Synthetic Call (Put-Call Parity). 2. Writing a Covered Call. 3. Straddle, Strangle. 4. Spreads (Bull, Bear, Butterfly).

. 2. Writing a Covered Call. 3. Straddle, Strangle. 4. Spreads (Bull, Bear, Butterfly).") 1 EG, Ch. 22; Options I. Overview. A. Definitions. 1. Option - contract in entitling holder to buy/sell a certain asset at or before a certain time at a specified price. Gives holder the right, but not

1 EG, Ch. 22; Options I. Overview. A. Definitions. 1. Option - contract in entitling holder to buy/sell a certain asset at or before a certain time at a specified price. Gives holder the right, but not

2 f. f t S 2. Delta measures the sensitivityof the portfolio value to changes in the price of the underlying

Sensitivity analysis Simulating the Greeks Meet the Greeks he value of a derivative on a single underlying asset depends upon the current asset price S and its volatility Σ, the risk-free interest rate

Sensitivity analysis Simulating the Greeks Meet the Greeks he value of a derivative on a single underlying asset depends upon the current asset price S and its volatility Σ, the risk-free interest rate

Hull, Options, Futures, and Other Derivatives, 9 th Edition

P1.T4. Valuation & Risk Models Hull, Options, Futures, and Other Derivatives, 9 th Edition Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM and Deepa Sounder www.bionicturtle.com Hull, Chapter

P1.T4. Valuation & Risk Models Hull, Options, Futures, and Other Derivatives, 9 th Edition Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM and Deepa Sounder www.bionicturtle.com Hull, Chapter

UCLA Anderson School of Management Daniel Andrei, Option Markets 232D, Fall MBA Midterm. November Date:

UCLA Anderson School of Management Daniel Andrei, Option Markets 232D, Fall 2013 MBA Midterm November 2013 Date: Your Name: Your Equiz.me email address: Your Signature: 1 This exam is open book, open notes.

UCLA Anderson School of Management Daniel Andrei, Option Markets 232D, Fall 2013 MBA Midterm November 2013 Date: Your Name: Your Equiz.me email address: Your Signature: 1 This exam is open book, open notes.

Risk Management Using Derivatives Securities

Risk Management Using Derivatives Securities 1 Definition of Derivatives A derivative is a financial instrument whose value is derived from the price of a more basic asset called the underlying asset.

Risk Management Using Derivatives Securities 1 Definition of Derivatives A derivative is a financial instrument whose value is derived from the price of a more basic asset called the underlying asset.

Hedging. MATH 472 Financial Mathematics. J. Robert Buchanan

Hedging MATH 472 Financial Mathematics J. Robert Buchanan 2018 Introduction Definition Hedging is the practice of making a portfolio of investments less sensitive to changes in market variables. There

Hedging MATH 472 Financial Mathematics J. Robert Buchanan 2018 Introduction Definition Hedging is the practice of making a portfolio of investments less sensitive to changes in market variables. There

Introduction to Financial Mathematics

Introduction to Financial Mathematics MTH 210 Fall 2016 Jie Zhong November 30, 2016 Mathematics Department, UR Table of Contents Arbitrage Interest Rates, Discounting, and Basic Assets Forward Contracts

Introduction to Financial Mathematics MTH 210 Fall 2016 Jie Zhong November 30, 2016 Mathematics Department, UR Table of Contents Arbitrage Interest Rates, Discounting, and Basic Assets Forward Contracts

CHAPTER 10 INTEREST RATE & CURRENCY SWAPS SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS

CHAPTER 10 INTEREST RATE & CURRENCY SWAPS SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. Describe the difference between a swap broker and a swap dealer. Answer:

CHAPTER 10 INTEREST RATE & CURRENCY SWAPS SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. Describe the difference between a swap broker and a swap dealer. Answer:

Market risk measurement in practice

Lecture notes on risk management, public policy, and the financial system Allan M. Malz Columbia University 2018 Allan M. Malz Last updated: October 23, 2018 2/32 Outline Nonlinearity in market risk Market

Lecture notes on risk management, public policy, and the financial system Allan M. Malz Columbia University 2018 Allan M. Malz Last updated: October 23, 2018 2/32 Outline Nonlinearity in market risk Market

15 American. Option Pricing. Answers to Questions and Problems

15 American Option Pricing Answers to Questions and Problems 1. Explain why American and European calls on a nondividend stock always have the same value. An American option is just like a European option,

15 American Option Pricing Answers to Questions and Problems 1. Explain why American and European calls on a nondividend stock always have the same value. An American option is just like a European option,

Glossary of Swap Terminology

Glossary of Swap Terminology Arbitrage: The opportunity to exploit price differentials on tv~otherwise identical sets of cash flows. In arbitrage-free financial markets, any two transactions with the same

Glossary of Swap Terminology Arbitrage: The opportunity to exploit price differentials on tv~otherwise identical sets of cash flows. In arbitrage-free financial markets, any two transactions with the same

Actuarial Models : Financial Economics

` Actuarial Models : Financial Economics An Introductory Guide for Actuaries and other Business Professionals First Edition BPP Professional Education Phoenix, AZ Copyright 2010 by BPP Professional Education,

` Actuarial Models : Financial Economics An Introductory Guide for Actuaries and other Business Professionals First Edition BPP Professional Education Phoenix, AZ Copyright 2010 by BPP Professional Education,

The Black-Scholes Model

The Black-Scholes Model Inputs Spot Price Exercise Price Time to Maturity Rate-Cost of funds & Yield Volatility Process The Black Box Output "Fair Market Value" For those interested in looking inside the

The Black-Scholes Model Inputs Spot Price Exercise Price Time to Maturity Rate-Cost of funds & Yield Volatility Process The Black Box Output "Fair Market Value" For those interested in looking inside the

Swaps: A Primer By A.V. Vedpuriswar

Swaps: A Primer By A.V. Vedpuriswar September 30, 2016 Introduction Swaps are agreements to exchange a series of cash flows on periodic settlement dates over a certain time period (e.g., quarterly payments

Swaps: A Primer By A.V. Vedpuriswar September 30, 2016 Introduction Swaps are agreements to exchange a series of cash flows on periodic settlement dates over a certain time period (e.g., quarterly payments

Notes: This is a closed book and closed notes exam. The maximal score on this exam is 100 points. Time: 75 minutes

M339D/M389D Introduction to Financial Mathematics for Actuarial Applications University of Texas at Austin Sample In-Term Exam II - Solutions Instructor: Milica Čudina Notes: This is a closed book and

M339D/M389D Introduction to Financial Mathematics for Actuarial Applications University of Texas at Austin Sample In-Term Exam II - Solutions Instructor: Milica Čudina Notes: This is a closed book and

Term Structure Lattice Models

IEOR E4706: Foundations of Financial Engineering c 2016 by Martin Haugh Term Structure Lattice Models These lecture notes introduce fixed income derivative securities and the modeling philosophy used to

IEOR E4706: Foundations of Financial Engineering c 2016 by Martin Haugh Term Structure Lattice Models These lecture notes introduce fixed income derivative securities and the modeling philosophy used to

I. Reading. A. BKM, Chapter 20, Section B. BKM, Chapter 21, ignore Section 21.3 and skim Section 21.5.

Lectures 23-24: Options: Valuation. I. Reading. A. BKM, Chapter 20, Section 20.4. B. BKM, Chapter 21, ignore Section 21.3 and skim Section 21.5. II. Preliminaries. A. Up until now, we have been concerned

Lectures 23-24: Options: Valuation. I. Reading. A. BKM, Chapter 20, Section 20.4. B. BKM, Chapter 21, ignore Section 21.3 and skim Section 21.5. II. Preliminaries. A. Up until now, we have been concerned

In general, the value of any asset is the present value of the expected cash flows on

ch05_p087_110.qxp 11/30/11 2:00 PM Page 87 CHAPTER 5 Option Pricing Theory and Models In general, the value of any asset is the present value of the expected cash flows on that asset. This section will

ch05_p087_110.qxp 11/30/11 2:00 PM Page 87 CHAPTER 5 Option Pricing Theory and Models In general, the value of any asset is the present value of the expected cash flows on that asset. This section will

Option Pricing. Simple Arbitrage Relations. Payoffs to Call and Put Options. Black-Scholes Model. Put-Call Parity. Implied Volatility

Simple Arbitrage Relations Payoffs to Call and Put Options Black-Scholes Model Put-Call Parity Implied Volatility Option Pricing Options: Definitions A call option gives the buyer the right, but not the

Simple Arbitrage Relations Payoffs to Call and Put Options Black-Scholes Model Put-Call Parity Implied Volatility Option Pricing Options: Definitions A call option gives the buyer the right, but not the

1 Interest Based Instruments

1 Interest Based Instruments e.g., Bonds, forward rate agreements (FRA), and swaps. Note that the higher the credit risk, the higher the interest rate. Zero Rates: n year zero rate (or simply n-year zero)

1 Interest Based Instruments e.g., Bonds, forward rate agreements (FRA), and swaps. Note that the higher the credit risk, the higher the interest rate. Zero Rates: n year zero rate (or simply n-year zero)

Evaluating Options Price Sensitivities

Evaluating Options Price Sensitivities Options Pricing Presented by Patrick Ceresna, CMT CIM DMS Montréal Exchange Instructor Disclaimer 2016 Bourse de Montréal Inc. This document is sent to you on a general

Evaluating Options Price Sensitivities Options Pricing Presented by Patrick Ceresna, CMT CIM DMS Montréal Exchange Instructor Disclaimer 2016 Bourse de Montréal Inc. This document is sent to you on a general

Mathematics of Financial Derivatives. Zero-coupon rates and bond pricing. Lecture 9. Zero-coupons. Notes. Notes

Mathematics of Financial Derivatives Lecture 9 Solesne Bourguin bourguin@math.bu.edu Boston University Department of Mathematics and Statistics Zero-coupon rates and bond pricing Zero-coupons Definition:

Mathematics of Financial Derivatives Lecture 9 Solesne Bourguin bourguin@math.bu.edu Boston University Department of Mathematics and Statistics Zero-coupon rates and bond pricing Zero-coupons Definition:

Pricing Interest Rate Options with the Black Futures Option Model

Bond Evaluation, Selection, and Management, Second Edition by R. Stafford Johnson Copyright 2010 R. Stafford Johnson APPENDIX I Pricing Interest Rate Options with the Black Futures Option Model I.1 BLACK

Bond Evaluation, Selection, and Management, Second Edition by R. Stafford Johnson Copyright 2010 R. Stafford Johnson APPENDIX I Pricing Interest Rate Options with the Black Futures Option Model I.1 BLACK

P-7. Table of Contents. Module 1: Introductory Derivatives

Preface P-7 Table of Contents Module 1: Introductory Derivatives Lesson 1: Stock as an Underlying Asset 1.1.1 Financial Markets M1-1 1.1. Stocks and Stock Indexes M1-3 1.1.3 Derivative Securities M1-9

Preface P-7 Table of Contents Module 1: Introductory Derivatives Lesson 1: Stock as an Underlying Asset 1.1.1 Financial Markets M1-1 1.1. Stocks and Stock Indexes M1-3 1.1.3 Derivative Securities M1-9

University of Colorado at Boulder Leeds School of Business MBAX-6270 MBAX Introduction to Derivatives Part II Options Valuation

MBAX-6270 Introduction to Derivatives Part II Options Valuation Notation c p S 0 K T European call option price European put option price Stock price (today) Strike price Maturity of option Volatility

MBAX-6270 Introduction to Derivatives Part II Options Valuation Notation c p S 0 K T European call option price European put option price Stock price (today) Strike price Maturity of option Volatility

OPTIONS CALCULATOR QUICK GUIDE

OPTIONS CALCULATOR QUICK GUIDE Table of Contents Introduction 3 Valuing options 4 Examples 6 Valuing an American style non-dividend paying stock option 6 Valuing an American style dividend paying stock

OPTIONS CALCULATOR QUICK GUIDE Table of Contents Introduction 3 Valuing options 4 Examples 6 Valuing an American style non-dividend paying stock option 6 Valuing an American style dividend paying stock

Risk Neutral Valuation, the Black-

Risk Neutral Valuation, the Black- Scholes Model and Monte Carlo Stephen M Schaefer London Business School Credit Risk Elective Summer 01 C = SN( d )-PV( X ) N( ) N he Black-Scholes formula 1 d (.) : cumulative

Risk Neutral Valuation, the Black- Scholes Model and Monte Carlo Stephen M Schaefer London Business School Credit Risk Elective Summer 01 C = SN( d )-PV( X ) N( ) N he Black-Scholes formula 1 d (.) : cumulative

JEM034 Corporate Finance Winter Semester 2017/2018

JEM034 Corporate Finance Winter Semester 2017/2018 Lecture #5 Olga Bychkova Topics Covered Today Risk and the Cost of Capital (chapter 9 in BMA) Understading Options (chapter 20 in BMA) Valuing Options

JEM034 Corporate Finance Winter Semester 2017/2018 Lecture #5 Olga Bychkova Topics Covered Today Risk and the Cost of Capital (chapter 9 in BMA) Understading Options (chapter 20 in BMA) Valuing Options

Financial Instruments: Derivatives KPMG. All rights reserved. 1

Financial Instruments: Derivatives 2003 KPMG. All rights reserved. 1 1. Introduction Financial Risk Management data technology strategy Risk tolerance operations Management Infrastructure autorisation

Financial Instruments: Derivatives 2003 KPMG. All rights reserved. 1 1. Introduction Financial Risk Management data technology strategy Risk tolerance operations Management Infrastructure autorisation

Notes for Lecture 5 (February 28)

") Midterm 7:40 9:00 on March 14 Ground rules: Closed book. You should bring a calculator. You may bring one 8 1/2 x 11 sheet of paper with whatever you want written on the two sides. Suggested study questions

Midterm 7:40 9:00 on March 14 Ground rules: Closed book. You should bring a calculator. You may bring one 8 1/2 x 11 sheet of paper with whatever you want written on the two sides. Suggested study questions

Chapter 14. Exotic Options: I. Question Question Question Question The geometric averages for stocks will always be lower.

Chapter 14 Exotic Options: I Question 14.1 The geometric averages for stocks will always be lower. Question 14.2 The arithmetic average is 5 (three 5s, one 4, and one 6) and the geometric average is (5

Chapter 14 Exotic Options: I Question 14.1 The geometric averages for stocks will always be lower. Question 14.2 The arithmetic average is 5 (three 5s, one 4, and one 6) and the geometric average is (5

MATH6911: Numerical Methods in Finance. Final exam Time: 2:00pm - 5:00pm, April 11, Student Name (print): Student Signature: Student ID:

: Student Signature: Student ID:") MATH6911 Page 1 of 16 Winter 2007 MATH6911: Numerical Methods in Finance Final exam Time: 2:00pm - 5:00pm, April 11, 2007 Student Name (print): Student Signature: Student ID: Question Full Mark Mark 1

MATH6911 Page 1 of 16 Winter 2007 MATH6911: Numerical Methods in Finance Final exam Time: 2:00pm - 5:00pm, April 11, 2007 Student Name (print): Student Signature: Student ID: Question Full Mark Mark 1

Lecture 8 Foundations of Finance

Lecture 8: Bond Portfolio Management. I. Reading. II. Risks associated with Fixed Income Investments. A. Reinvestment Risk. B. Liquidation Risk. III. Duration. A. Definition. B. Duration can be interpreted

Lecture 8: Bond Portfolio Management. I. Reading. II. Risks associated with Fixed Income Investments. A. Reinvestment Risk. B. Liquidation Risk. III. Duration. A. Definition. B. Duration can be interpreted

MASM006 UNIVERSITY OF EXETER SCHOOL OF ENGINEERING, COMPUTER SCIENCE AND MATHEMATICS MATHEMATICAL SCIENCES FINANCIAL MATHEMATICS.

MASM006 UNIVERSITY OF EXETER SCHOOL OF ENGINEERING, COMPUTER SCIENCE AND MATHEMATICS MATHEMATICAL SCIENCES FINANCIAL MATHEMATICS May/June 2006 Time allowed: 2 HOURS. Examiner: Dr N.P. Byott This is a CLOSED

MASM006 UNIVERSITY OF EXETER SCHOOL OF ENGINEERING, COMPUTER SCIENCE AND MATHEMATICS MATHEMATICAL SCIENCES FINANCIAL MATHEMATICS May/June 2006 Time allowed: 2 HOURS. Examiner: Dr N.P. Byott This is a CLOSED

Financial Instruments: Derivatives

Financial Instruments: Derivatives KPMG. All rights reserved. 1 1. Introduction Financial Risk Management data technology strategy Risk tolerance operations Management Infrastructure autorisation people

Financial Instruments: Derivatives KPMG. All rights reserved. 1 1. Introduction Financial Risk Management data technology strategy Risk tolerance operations Management Infrastructure autorisation people

Math 181 Lecture 15 Hedging and the Greeks (Chap. 14, Hull)

") Math 181 Lecture 15 Hedging and the Greeks (Chap. 14, Hull) One use of derivation is for investors or investment banks to manage the risk of their investments. If an investor buys a stock for price S 0,

Math 181 Lecture 15 Hedging and the Greeks (Chap. 14, Hull) One use of derivation is for investors or investment banks to manage the risk of their investments. If an investor buys a stock for price S 0,

Advanced Equity Derivatives This course can also be presented in-house for your company or via live on-line webinar

Advanced Equity Derivatives This course can also be presented in-house for your company or via live on-line webinar The Banking and Corporate Finance Training Specialist Course Objectives The broad objectives

Advanced Equity Derivatives This course can also be presented in-house for your company or via live on-line webinar The Banking and Corporate Finance Training Specialist Course Objectives The broad objectives

Section 1: Advanced Derivatives

Section 1: Advanced Derivatives Options, Futures, and Other Derivatives (6th edition) by Hull Chapter Mechanics of Futures Markets (Sections.7-.10 only) 3 Chapter 5 Determination of Forward and Futures

Section 1: Advanced Derivatives Options, Futures, and Other Derivatives (6th edition) by Hull Chapter Mechanics of Futures Markets (Sections.7-.10 only) 3 Chapter 5 Determination of Forward and Futures

Fin 4200 Project. Jessi Sagner 11/15/11

Fin 4200 Project Jessi Sagner 11/15/11 All Option information is outlined in appendix A Option Strategy The strategy I chose was to go long 1 call and 1 put at the same strike price, but different times

Fin 4200 Project Jessi Sagner 11/15/11 All Option information is outlined in appendix A Option Strategy The strategy I chose was to go long 1 call and 1 put at the same strike price, but different times

non linear Payoffs Markus K. Brunnermeier

Institutional Finance Lecture 10: Dynamic Arbitrage to Replicate non linear Payoffs Markus K. Brunnermeier Preceptor: Dong Beom Choi Princeton University 1 BINOMIAL OPTION PRICING Consider a European call

Institutional Finance Lecture 10: Dynamic Arbitrage to Replicate non linear Payoffs Markus K. Brunnermeier Preceptor: Dong Beom Choi Princeton University 1 BINOMIAL OPTION PRICING Consider a European call

STRATEGIC FINANCIAL MANAGEMENT FOREX & OTC Derivatives Summary By CA. Gaurav Jain

1 SFM STRATEGIC FINANCIAL MANAGEMENT FOREX & OTC Derivatives Summary By CA. Gaurav Jain 100% Conceptual Coverage With Live Trading Session Complete Coverage of Study Material, Practice Manual & Previous

1 SFM STRATEGIC FINANCIAL MANAGEMENT FOREX & OTC Derivatives Summary By CA. Gaurav Jain 100% Conceptual Coverage With Live Trading Session Complete Coverage of Study Material, Practice Manual & Previous

MATH 425 EXERCISES G. BERKOLAIKO

MATH 425 EXERCISES G. BERKOLAIKO 1. Definitions and basic properties of options and other derivatives 1.1. Summary. Definition of European call and put options, American call and put option, forward (futures)

MATH 425 EXERCISES G. BERKOLAIKO 1. Definitions and basic properties of options and other derivatives 1.1. Summary. Definition of European call and put options, American call and put option, forward (futures)

P&L Attribution and Risk Management

P&L Attribution and Risk Management Liuren Wu Options Markets (Hull chapter: 15, Greek letters) Liuren Wu ( c ) P& Attribution and Risk Management Options Markets 1 / 19 Outline 1 P&L attribution via the

P&L Attribution and Risk Management Liuren Wu Options Markets (Hull chapter: 15, Greek letters) Liuren Wu ( c ) P& Attribution and Risk Management Options Markets 1 / 19 Outline 1 P&L attribution via the

Asset-or-nothing digitals

School of Education, Culture and Communication Division of Applied Mathematics MMA707 Analytical Finance I Asset-or-nothing digitals 202-0-9 Mahamadi Ouoba Amina El Gaabiiy David Johansson Examinator:

School of Education, Culture and Communication Division of Applied Mathematics MMA707 Analytical Finance I Asset-or-nothing digitals 202-0-9 Mahamadi Ouoba Amina El Gaabiiy David Johansson Examinator:

Queens College, CUNY, Department of Computer Science Computational Finance CSCI 365 / 765 Fall 2017 Instructor: Dr. Sateesh Mane.

Queens College, CUNY, Department of Computer Science Computational Finance CSCI 365 / 765 Fall 2017 Instructor: Dr. Sateesh Mane c Sateesh R. Mane 2017 20 Lecture 20 Implied volatility November 30, 2017

Queens College, CUNY, Department of Computer Science Computational Finance CSCI 365 / 765 Fall 2017 Instructor: Dr. Sateesh Mane c Sateesh R. Mane 2017 20 Lecture 20 Implied volatility November 30, 2017

UNIVERSITY OF SOUTH AFRICA

UNIVERSITY OF SOUTH AFRICA Vision Towards the African university in the service of humanity College of Economic and Management Sciences Department of Finance & Risk Management & Banking General information

UNIVERSITY OF SOUTH AFRICA Vision Towards the African university in the service of humanity College of Economic and Management Sciences Department of Finance & Risk Management & Banking General information

Derivatives: part I 1

Derivatives: part I 1 Derivatives Derivatives are financial products whose value depends on the value of underlying variables. The main use of derivatives is to reduce risk for one party. Thediverse range

Derivatives: part I 1 Derivatives Derivatives are financial products whose value depends on the value of underlying variables. The main use of derivatives is to reduce risk for one party. Thediverse range

B6302 Sample Placement Exam Academic Year

Revised June 011 B630 Sample Placement Exam Academic Year 011-01 Part 1: Multiple Choice Question 1 Consider the following information on three mutual funds (all information is in annualized units). Fund

Revised June 011 B630 Sample Placement Exam Academic Year 011-01 Part 1: Multiple Choice Question 1 Consider the following information on three mutual funds (all information is in annualized units). Fund