UNIVERSITY OF SOUTH AFRICA

|

|

|

- Russell Bryan

- 5 years ago

- Views:

Transcription

1 UNIVERSITY OF SOUTH AFRICA

2 Vision Towards the African university in the service of humanity

3 College of Economic and Management Sciences Department of Finance & Risk Management & Banking

4 General information Exam is 2 hours with 40 MCQ s Formula sheet will NOT be provided. (Some of the formulas like Black Scholes and Merton, and FRAs formulas will be provided as part of the exam paper) Formulate the LOS into questions to test your knowledge of the Subject Unit Examination includes both theory and calculations Mark composition: Questions Theory Calculations Total % Percentages

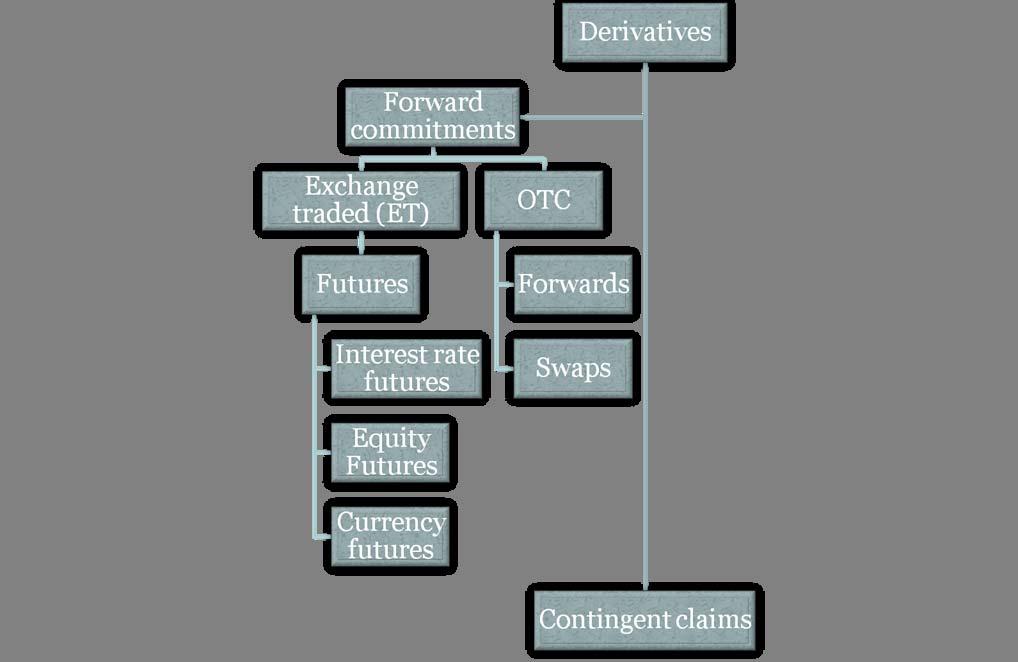

5 INV3703 INVESTMENTS: DERIVATIVES CHAPTER 1 FORWARD MARKETS AND CONTRACTS

6 Read Basic concepts and terminology What is a: Forward contract Futures contract Swap Option Call option Put option Forward commitment Holder has a right but does not impose an obligation

7 Chapter 1 Introduction cont Forward Contracts Contingent Claim No premium paid at inception Premium Paid at inception Question : What is the advantage of a contingent claims over forward commitments? Answer: Permit gain while protecting against losses Why is it so?

8 Chapter 1 Introduction cont If a risk free rate of interest is 7% and an investor enters into a transaction that has no risk, what would be the rate of return the investor should earn in the absence of the risk A. 0% B. between 0% and 7% C. 7% D. Less than 7%

9 Chapter 1 Introduction cont The spot price of Gold is R930 per ounce and the risk free-rate of interest is 5% per annum. Calculate the equilibrium 6-month forward price per ounce of gold. 930 (1+(0.05/2))=R Why divide by 2 (6- months i.e. half a year)

10 INV3703 INVESTMENTS: DERIVATIVES CHAPTER 2 FORWARD MARKETS AND CONTRACTS

11 Definition A forward contract is an agreement between two parties in which one party, the buyer, agrees to buy from the other party, the seller, an underlying asset at a future date at a price established today. The contract is customised and each party is subject to the possibility that the other party will default.

12 Forwards Equity forwards Bond/Fixed-income forwards Interest rate forwards (FRAs) Currency forwards

13 Forwards Futures Over the counter Private Customized Default risk Not marked to market Held until expiration Not liquid Unregulated Futures exchange Public Standardized Default free Marked to market Offset possible Liquid Regulated

14 Differentiate between the positions held by the long and short parties to a forward contract LF (Long Forward) LA Long party SA Short party SF Party that agrees to buy the asset has a long forward position Party that agrees to sell the asset has a short forward position

15 Pricing and valuation of forward contracts Are pricing and valuation not the same thing? The price is agreed on the initiation date (Forward price or forward rate) i.e. pricing means to determining the forward price or forward rate. Valuation, however, means to determine the amount of money that one would need to pay or would expect to receive to engage in the transaction

16 Pricing and valuation of forward contracts cont F(0,T) =S0(1+r)^T The transaction is risk-free and should equivalent to investing S0 Rands in risk free asset

17 Pricing and valuation of forward contracts cont Vo(0,T) = S0 F(0,T)/(1+r)^T For forward contract Vo(0,T) should be ZERO (0) If Vo(0,T) 0 arbitrage would the prevail The forward price that eliminates arbitrage: F(0,T) =S0(1+r)^T

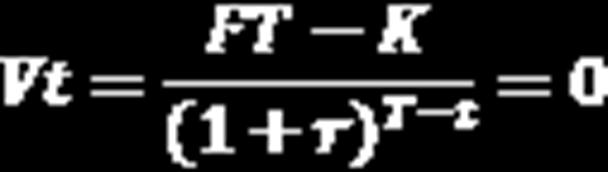

18 Pricing and valuation of forward contracts cont By definition an asset s value is the present value of future value thus, Vt(0,T) = St F(0,T)/(1+r)^(T-t) (T-t) is the remaining time to maturity

19 Pricing and valuation of forward contracts cont F(0,T) =(S0-PV(D,0,T))*(1+r)^T PV (D,0,T) = (Di/(1+r)^(T-ti) When dividends are paid continuously F(0,T) =So ^(- c*t). ^(rc*t) To convert discrete risk-free interest(r) to continuosly compounded equivalent(rc): rc = Ln(1+r)

20 Pricing and valuation of forward contracts cont A portfolio manager expects to purchase a portfolio of stocks in 60 days. In order to hedge against a potential price increase over the next 60 days, she decides to take a long position on a 60-day forward contract on the S&P 500 stock index. The index is currently at The continuously compounded dividend yield is 1.85 percent. The discrete risk-free rate is 4.35 percent. Calculate the no-arbitrage forward price on this contract, the value of the forward contract 28 days into the contract (index value 1225), and the value of the contract at expiration (index value 1235).

21 Decrease the spot index value by the dividend yield and thereafter calculate the future value (first convert the discrete rate to a continuously compounded rate) LN F 0,T 1,150e e $1,154.56

22 The value of a contract is the difference between the discounted current spot price (at the dividend yield) and the discounted forward price (at the converted risk-free rate) for the remaining period LN V 0,T 1,225e 1,154.56e t 1, , $72.76

23 At expiration, the value is simply the difference between the end-period spot index and the forward contract price, as calculated. T V 0,T 1,235 1, $80.44

24 Fixed-Income and interest rate forward contracts Identify the characteristics of forward rate agreements Forward contract to borrow/lend money at a certain rate at some future date Long position Borrows money (pays interest) Benefit when forward rate < market rate Short position Lends money (receives interest) Benefit when forward rate > market rate

25 Calculate and interpret the payment at expiration of a FRA and identify each of the component terms

26 ESKOM P/L is expecting to receive a cash inflow of R20, 000, in 90 days. Short term interest rates are expected to fall during the next 90 days. In order to hedge against this risk, the company decides to use an FRA that expires in 90 days and is based on 90day LIBOR. The FRA is quoted at 6%. At expiration LIBOR is 5%. Indicate whether the company should take a long or short position to hedge interest rate risk. Using the appropriate terminology, identify the type of FRA used here. Calculate the gain or loss to ESKOM P/L as a consequence of entering the FRA.

27 Identify the characteristics of currency forwards Exchange of currencies Exchange rate specified Manage foreign exchange risk Domestic risk-free rate Foreign risk free rate Interest rate parity (IRP) Covered interest arbitrage

28 Determine the price of a forward contract Initial or delivery price FT =S0(1+r)^T =K Forward price during period FT =St(1+r)^(T-t)

29 Determine the value of a forward contract at initiation, during the life of the contract, and at expiration alternatively

30 Calculate the price and value of a forward contract on a currency Price currency forward Discrete interest Continuous interest

31 Value currency forward Discrete interest

32 Covered interest arbitrage (1 rd ) T (1 rf ) T F S

33 INV3703 INVESTMENTS: DERIVATIVES CHAPTER 3 FUTURES MARKETS AND CONTRACTS

34 Definition A forward contract is an agreement between two parties in which one party, the buyer, agrees to buy from the other party, the seller, an underlying asset at a future date at a price established today. The contract is customized and each party is subject to the possibility that the other party will default. A futures contract is a variation of a forward contract that has essentially the same basic definition, but some clearly distinguishable additional features, the most important being that it is not a private and customized transaction. It is a public, standardized transaction that takes place on a futures exchange.

35

36 Identify the primary characteristics of futures contracts and distinguish between futures and forwards Forwards Over the counter Private Customized Default risk Not marked to market Held until expiration Not liquid Unregulated Futures Futures exchange Public Standardized Default free Marked to market Offset possible Liquid Regulated

37 Describe how a futures contract can be terminated at or prior to expiration by close out, delivery, equivalent cash settlement, or exchange for physicals Close out (prior to expiration) Opposite (offsetting) transaction Delivery Close out before expiration or take delivery Short delivers underlying to long (certain date and location) Cash settlement No need to close out (leave position open) Marked to market (final gain/loss) Exchange for physicals Counterparties arrange alternative delivery

38 Explain why the futures price must converge to the spot price at expiration To prevent arbitrage: ft (T) = ST Spot price (S) current price for immediate delivery Futures price (f) current price for future delivery At expiration f becomes the current price for immediate delivery (S) If : ft (T) < ST Buy contract; take delivery of underlying and pay lower futures price If : ft (T) > ST Sell contract; buy underlying, deliver and receive higher futures price

39 Determine the value of a futures contract Value before m-t-m = gain/loss accumulated since last m-t-m Gain/loss captured through the m-t-m process Contract re-priced at current market price and value = zero 0 t-1 j t T

40 Summary: Value of a futures contract Like forwards, futures have no value at initiation Unlike forwards, futures do not accumulate any value Value always zero after adjusting for day s gain or loss (m-t-m) Value different from zero only during m-t-m intervals Futures value = current price price at last m-t-m time Futures price increase -> value of long position increases Value set back to zero by the end-of-day mark to market

41 No-arbitrage futures prices Cash-and-carry arbitrage: Today: Sell futures contract Borrow money Buy underlying At expiration: Deliver asset and receive futures price Repay loan plus interest Reverse C&C arbitrage: Today: Buy futures contract Sell/short underlying Invest proceeds At expiration: Collect loan plus interest Pay futures price and take delivery

42 No cost or benefit to holding the asset Net cost or benefit to holding an asset Cost-of-carry model + FV CB CB -> cost minus benefit (negative or positive value) Costs exceed benefits (net cost) future value added Benefits exceed costs (net benefit) FV subtracted Financial assets High(er) cash flows -> lower futures

43 Forward price Futures price

44 Contrast backwardation and contango Backwardation Futures price below the spot price Significant benefit to holding asset Net benefit (negative cost of carry) Contango Futures price above spot price Little/no benefit to holding asset Net cost (positive cost of carry)

45 Treasury bond futures Example: Calculate the no-arbitrage futures price of a 1.2 year futures contract on a 7% T-bond with exactly 10 years to maturity and a price of $1,040. The annual risk-free rate is 5%. Assume the cheapest to deliver bond has a conversion factor of 1.13.

46 Answer: The semi-annual coupon is $35. A bondholder will receive two coupons during the contract term i.e., a payment 0.5 years and 1 year from now.

47 Stock futures Example: Calculate the no-arbitrage price for a 120- day future on a stock currently priced at $30 and expected to pay a $0.40 dividend in 15 days and in 105 days. The annual risk-free rate is 5%.

48 Stock index futures Example: The current level of the Nasdaq Index is 1,780. The continuous dividend is 1.1% and the continuously compounded riskfree rate is 3.7%. Calculate the noarbitrage futures price of an 87-day futures contract on this index.

49 Currency futures Example: The risk-free rates are 5% in U.S. Dollars ($) and 6.5% in British pounds ( ). The current spot exchange rate is $1.7301/. Calculate the no-arbitrage $ price of a 6- month futures contract.

50 Currency futures Answer:

51 INV3703 INVESTMENTS: DERIVATIVES CHAPTER 4 OPTION MARKETS AND CONTRACTS

52 Identify the basic elements and characteristics of opti on contracts Call options grant the holder (long position) the opportunity to buy the underlying security at a price below the current market price, provided that the market price exceeds the call strike before or at expiration (specified contingency). Put options grant the holder (long position) the opportunity to sell the underlying security at a price above the current market price, provided that the put strike exceeds the market price before or at expiration (specified contingency). The option seller (short position) in both instances receives a payment (premium) compelling performance at the discretion of the holder.

")

Obligation to buy")

53 Option shapes Long Call (LC) Right to buy Right to sell Long Put (LP) Short Call (SC) Obligation to sell Short Put (SP) Obligation to buy 53

54 JSE Equity Options: Options - Terminology American Style Options: An option that can be exercised at any time prior to expiration is called an American option European Style Options: An option that can only be exercised at expiration is called an European option JSE makes use of both American and European Style Options In the money: S>X You will exercise the option Out the money: S<X You will abandon the option At the money: S=X Strike Price = Underlying Price

55 Call option Put option + At the money + At the money Out of money In the money In the money Out of money Share price =X - Share price =X

56 Identify the different varieties of options in terms of the types of instruments underlying them Financial options Equity options (individual or stock index), bond options, interest rate options, currency options Options on futures Call options long position in futures upon exercise Put options short position in futures upon exercise Commodity options Right to either buy or sell a fixed quantity of physical asset at a (fixed) strike price

57 JSE Equity Options: Call Option - Example You don t have shares in a company but think this dynamic company is going to do well in the future (e.g. new CEO with great vision) The company is currently trading at R100 You buy a call option with a strike price the same as it s current price (R100) at a premium of R12. Scenario 1 Company performed well! On future date the company is R120 Exercise your option and buy the R100 even though it s trading at R120 Profit = R8 (R120 R100 - R12) Scenario 2 Company did NOT perform well! On future date the company is R90 Why would you exercise your option and buy the share at R100 if you can buy it at its current trading price of R90?

58 JSE Equity Options: Put Option - Example You ve got shares in in a company and want to protect yourself as you re worried that this company is not going to do well in the future (e.g. new CEO with different vision) The company is currently trading at R200 You buy a put option with a strike price of R200 at a premium of R20. Scenario 1 Company did not perform well! On future date the company is R160 Exercise your option and sell the R200 even though it s trading at R160 Profit = R20 (R200 R160 R20) Scenario 2 Company performed well! On future date the company is R240 Why would you exercise your option and sell the share at R200 if you can sell it at its current trading price of R240? Loss = Premium of R20

59 JSE Equity Options: Options Compared To Common Stocks Similarities Both options and stocks are listed securities Like stocks, options trade with buyers making bids and sellers making offers. Option investors, like stock investors have the ability to follow price movements, trading volume etc. day by day or even minute by minute Differences Price vs. Premium Unlike common stock, an option has a limited life. Common stock can be held indefinitely, while every option has an expiration date There is not a fixed number of options, as there is with common stock shares available Stock owners have certain voting rights and rights to dividends (if any), option owners participate only in the potential benefit of the stock s price movement

60 Notation and variables Variable Notation State Call option value Put option value Spot price S Increase Increase Decrease Strike price X Higher Lower Higher Volatility Higher Higher Higher Time to maturity t Longer Higher Uncertain Interest rates r Higher Higher Lower Call option C or c max(0; S X) Put option P or p max(0; X S) 60

61 Explain putcall parity for European options and relate arbitrage an d the construction of synthetic instruments Fiduciary call buying a call and investing PV(Payoff is X (otm) or X + (S-X) = S (itm) Protective put buying a put and holding asset Payoff is S (otm) or (X-S) + S = X (itm) Therefore: When call is itm put is otm > payoff is S, - When call is otm, put is itm -> payoff is X S+ p = c+ PV(X) S =c +PV(X) -p P= c +PV(X)- S C=S+ p -PV(X) PV(X)= S+ p -c

62 Put call parity arbitrage S + p = c+ PV(X) c - p = S-PV(X) c - p >S-PV(X) Sell call; buy put; buy spot; borrow PV(X) c - p < S-PV(X) Buy call; sell put; sell spot; invest PV(X)

63 Determine the minimum and maximum values of European options The lower bound for any option is zero (otm option) Upper bound Lower bound Call options c S c S PV(X) Put options p PV(X) p PV(X) - S

64 Chapter 5 - Swaps Determining the swap rate = pricing of swap As rates change over time, the PV of floating payments will either exceed or be less than the PV of fixed payments Difference = value of swap Market value = difference between bonds Fixed bond minus floating bond Domestic bond minus foreign bond PV (receive) minus PV (pay) 64

65 Equity Swaps Consider an equity swap in which the asset manager receives the return of the Russel 2000 Index in return for paying the return on the DJIA. At the inception of the equity swap, the Russel 2000 is at and the DJIA is at Calculate the market value of the swap a few months later when the Russel 2000 is at and the DJIA is at The notional principal of the swap is $15 million Russel , DJIA , V $15,000, $820,500 pay _DJIA

66 Interest rate swaps Consider a two-year interest rate swap with semi-annual payments. Assume a notional principal of $50 million. Calculate the semi-annual fixed payment and the annualized fixed rate on the swap if the current term structure of LIBOR interest rates is as follows: L 0 (180) = L 0 (360) = L 0 (540) = L 0 (720) =

67 1 B B B B FS0,4, Fixed payment $50,000,000 $1,715,000 Annualized fixed rate 3.43% %

68 Calculate the market value of the swap 120 days later from the point of view of the party paying the floating rate and receiving the fixed rate, and from the point of view of the party paying the fixed rate and receiving the floating rate if the term structure 120 days later is as follows: L 120 (60) = L 120 (240)= L 120 (420)= L 120 (600)=

69 1 B B B B Fixed st 1 Floating payment

70 Ans cont... Discounted with the 60 day present value factor of : Float V $50,000, $145,000 pay _ float V $50,000, $145,000 pay _ fixed

71 Equity and interest rate swap Assume an asset manager enters into a oneyear equity swap in which he will receive the return on the Nasdaq 100 Index in return for paying a floating interest rate. The swap calls for quarterly payments. The Nasdaq 100 is at at the beginning of the swap. Ninety days later, the rate L 90 (90) is Calculate the market value of the swap 100 days from the beginning of the swap if the Nasdaq 100 is at , the notional principal of the swap is $50 million, and the term structure is: L 100 (80) = L 100 (170) = L 100 (260) =

72 1 B Next floating payment Discounted with the 80 day present value factor of : Float , Equity , V $50,000, $1,205,000 pay_float

73 BEST OF LUCK IN YOUR EXAMS

Lecture 2. Agenda: Basic descriptions for derivatives. 1. Standard derivatives Forward Futures Options

Lecture 2 Basic descriptions for derivatives Agenda: 1. Standard derivatives Forward Futures Options 2. Nonstandard derivatives ICON Range forward contract 1. Standard derivatives ~ Forward contracts:

Lecture 2 Basic descriptions for derivatives Agenda: 1. Standard derivatives Forward Futures Options 2. Nonstandard derivatives ICON Range forward contract 1. Standard derivatives ~ Forward contracts:

Risk Management Using Derivatives Securities

Risk Management Using Derivatives Securities 1 Definition of Derivatives A derivative is a financial instrument whose value is derived from the price of a more basic asset called the underlying asset.

Risk Management Using Derivatives Securities 1 Definition of Derivatives A derivative is a financial instrument whose value is derived from the price of a more basic asset called the underlying asset.

Actuarial Models : Financial Economics

` Actuarial Models : Financial Economics An Introductory Guide for Actuaries and other Business Professionals First Edition BPP Professional Education Phoenix, AZ Copyright 2010 by BPP Professional Education,

` Actuarial Models : Financial Economics An Introductory Guide for Actuaries and other Business Professionals First Edition BPP Professional Education Phoenix, AZ Copyright 2010 by BPP Professional Education,

Finance 100 Problem Set 6 Futures (Alternative Solutions)

") Finance 100 Problem Set 6 Futures (Alternative Solutions) Note: Where appropriate, the final answer for each problem is given in bold italics for those not interested in the discussion of the solution.

Finance 100 Problem Set 6 Futures (Alternative Solutions) Note: Where appropriate, the final answer for each problem is given in bold italics for those not interested in the discussion of the solution.

Any asset that derives its value from another underlying asset is called a derivative asset. The underlying asset could be any asset - for example, a

Options Week 7 What is a derivative asset? Any asset that derives its value from another underlying asset is called a derivative asset. The underlying asset could be any asset - for example, a stock, bond,

Options Week 7 What is a derivative asset? Any asset that derives its value from another underlying asset is called a derivative asset. The underlying asset could be any asset - for example, a stock, bond,

INV2601 DISCUSSION CLASS SEMESTER 2 INVESTMENTS: AN INTRODUCTION INV2601 DEPARTMENT OF FINANCE, RISK MANAGEMENT AND BANKING

INV2601 DISCUSSION CLASS SEMESTER 2 INVESTMENTS: AN INTRODUCTION INV2601 DEPARTMENT OF FINANCE, RISK MANAGEMENT AND BANKING Examination Duration of exam 2 hours. 40 multiple choice questions. Total marks

INV2601 DISCUSSION CLASS SEMESTER 2 INVESTMENTS: AN INTRODUCTION INV2601 DEPARTMENT OF FINANCE, RISK MANAGEMENT AND BANKING Examination Duration of exam 2 hours. 40 multiple choice questions. Total marks

Financial Markets & Risk

Financial Markets & Risk Dr Cesario MATEUS Senior Lecturer in Finance and Banking Room QA259 Department of Accounting and Finance c.mateus@greenwich.ac.uk www.cesariomateus.com Session 3 Derivatives Binomial

Financial Markets & Risk Dr Cesario MATEUS Senior Lecturer in Finance and Banking Room QA259 Department of Accounting and Finance c.mateus@greenwich.ac.uk www.cesariomateus.com Session 3 Derivatives Binomial

Introduction, Forwards and Futures

Introduction, Forwards and Futures Liuren Wu Options Markets Liuren Wu ( ) Introduction, Forwards & Futures Options Markets 1 / 31 Derivatives Derivative securities are financial instruments whose returns

Introduction, Forwards and Futures Liuren Wu Options Markets Liuren Wu ( ) Introduction, Forwards & Futures Options Markets 1 / 31 Derivatives Derivative securities are financial instruments whose returns

Appendix A Financial Calculations

Derivatives Demystified: A Step-by-Step Guide to Forwards, Futures, Swaps and Options, Second Edition By Andrew M. Chisholm 010 John Wiley & Sons, Ltd. Appendix A Financial Calculations TIME VALUE OF MONEY

Derivatives Demystified: A Step-by-Step Guide to Forwards, Futures, Swaps and Options, Second Edition By Andrew M. Chisholm 010 John Wiley & Sons, Ltd. Appendix A Financial Calculations TIME VALUE OF MONEY

Introduction to Forwards and Futures

Introduction to Forwards and Futures Liuren Wu Options Pricing Liuren Wu ( c ) Introduction, Forwards & Futures Options Pricing 1 / 27 Outline 1 Derivatives 2 Forwards 3 Futures 4 Forward pricing 5 Interest

Introduction to Forwards and Futures Liuren Wu Options Pricing Liuren Wu ( c ) Introduction, Forwards & Futures Options Pricing 1 / 27 Outline 1 Derivatives 2 Forwards 3 Futures 4 Forward pricing 5 Interest

CHAPTER 17 OPTIONS AND CORPORATE FINANCE

CHAPTER 17 OPTIONS AND CORPORATE FINANCE Answers to Concept Questions 1. A call option confers the right, without the obligation, to buy an asset at a given price on or before a given date. A put option

CHAPTER 17 OPTIONS AND CORPORATE FINANCE Answers to Concept Questions 1. A call option confers the right, without the obligation, to buy an asset at a given price on or before a given date. A put option

Pricing and Valuation of Forward Commitments

Pricing and Valuation of Forward Commitments Professor s Comment: This reading has only four learning outcome statements, but don t be fooled into thinking it is something you can skip. I think you must

Pricing and Valuation of Forward Commitments Professor s Comment: This reading has only four learning outcome statements, but don t be fooled into thinking it is something you can skip. I think you must

OPTION MARKETS AND CONTRACTS

NP = Notional Principal RFR = Risk Free Rate 2013, Study Session # 17, Reading # 63 OPTION MARKETS AND CONTRACTS S = Stock Price (Current) X = Strike Price/Exercise Price 1 63.a Option Contract A contract

NP = Notional Principal RFR = Risk Free Rate 2013, Study Session # 17, Reading # 63 OPTION MARKETS AND CONTRACTS S = Stock Price (Current) X = Strike Price/Exercise Price 1 63.a Option Contract A contract

Derivatives Questions Question 1 Explain carefully the difference between hedging, speculation, and arbitrage.

Derivatives Questions Question 1 Explain carefully the difference between hedging, speculation, and arbitrage. Question 2 What is the difference between entering into a long forward contract when the forward

Derivatives Questions Question 1 Explain carefully the difference between hedging, speculation, and arbitrage. Question 2 What is the difference between entering into a long forward contract when the forward

Financial Markets and Products

Financial Markets and Products 1. Eric sold a call option on a stock trading at $40 and having a strike of $35 for $7. What is the profit of the Eric from the transaction if at expiry the stock is trading

Financial Markets and Products 1. Eric sold a call option on a stock trading at $40 and having a strike of $35 for $7. What is the profit of the Eric from the transaction if at expiry the stock is trading

2. Futures and Forward Markets 2.1. Institutions

2. Futures and Forward Markets 2.1. Institutions 1. (Hull 2.3) Suppose that you enter into a short futures contract to sell July silver for $5.20 per ounce on the New York Commodity Exchange. The size

2. Futures and Forward Markets 2.1. Institutions 1. (Hull 2.3) Suppose that you enter into a short futures contract to sell July silver for $5.20 per ounce on the New York Commodity Exchange. The size

University of Colorado at Boulder Leeds School of Business MBAX-6270 MBAX Introduction to Derivatives Part II Options Valuation

MBAX-6270 Introduction to Derivatives Part II Options Valuation Notation c p S 0 K T European call option price European put option price Stock price (today) Strike price Maturity of option Volatility

MBAX-6270 Introduction to Derivatives Part II Options Valuation Notation c p S 0 K T European call option price European put option price Stock price (today) Strike price Maturity of option Volatility

MCQ on International Finance

MCQ on International Finance 1. If portable disk players made in China are imported into the United States, the Chinese manufacturer is paid with a) international monetary credits. b) dollars. c) yuan,

MCQ on International Finance 1. If portable disk players made in China are imported into the United States, the Chinese manufacturer is paid with a) international monetary credits. b) dollars. c) yuan,

Forwards and Futures

Options, Futures and Structured Products Jos van Bommel Aalto Period 5 2017 Class 7b Course summary Forwards and Futures Forward contracts, and forward prices, quoted OTC. Futures: a standardized forward

Options, Futures and Structured Products Jos van Bommel Aalto Period 5 2017 Class 7b Course summary Forwards and Futures Forward contracts, and forward prices, quoted OTC. Futures: a standardized forward

Finance 402: Problem Set 7 Solutions

Finance 402: Problem Set 7 Solutions Note: Where appropriate, the final answer for each problem is given in bold italics for those not interested in the discussion of the solution. 1. Consider the forward

Finance 402: Problem Set 7 Solutions Note: Where appropriate, the final answer for each problem is given in bold italics for those not interested in the discussion of the solution. 1. Consider the forward

INVESTMENT ANALYSIS AND PORTFOLIO MANAGEMENT. Instructor: Dr. Kumail Rizvi

INVESTMENT ANALYSIS AND PORTFOLIO MANAGEMENT Instructor: Dr. Kumail Rizvi 1 DERIVATIVE MARKETS AND INSTRUMENTS 2 WHAT IS A DERIVATIVE? A derivative is an instrument whose value depends on, or is derived

INVESTMENT ANALYSIS AND PORTFOLIO MANAGEMENT Instructor: Dr. Kumail Rizvi 1 DERIVATIVE MARKETS AND INSTRUMENTS 2 WHAT IS A DERIVATIVE? A derivative is an instrument whose value depends on, or is derived

Financial Markets and Products

Financial Markets and Products 1. Which of the following types of traders never take position in the derivative instruments? a) Speculators b) Hedgers c) Arbitrageurs d) None of the above 2. Which of the

Financial Markets and Products 1. Which of the following types of traders never take position in the derivative instruments? a) Speculators b) Hedgers c) Arbitrageurs d) None of the above 2. Which of the

SOCIETY OF ACTUARIES FINANCIAL MATHEMATICS. EXAM FM SAMPLE QUESTIONS Financial Economics

SOCIETY OF ACTUARIES EXAM FM FINANCIAL MATHEMATICS EXAM FM SAMPLE QUESTIONS Financial Economics June 2014 changes Questions 1-30 are from the prior version of this document. They have been edited to conform

SOCIETY OF ACTUARIES EXAM FM FINANCIAL MATHEMATICS EXAM FM SAMPLE QUESTIONS Financial Economics June 2014 changes Questions 1-30 are from the prior version of this document. They have been edited to conform

Financial Mathematics Principles

1 Financial Mathematics Principles 1.1 Financial Derivatives and Derivatives Markets A financial derivative is a special type of financial contract whose value and payouts depend on the performance of

1 Financial Mathematics Principles 1.1 Financial Derivatives and Derivatives Markets A financial derivative is a special type of financial contract whose value and payouts depend on the performance of

FNCE4830 Investment Banking Seminar

FNCE4830 Investment Banking Seminar Introduction on Derivatives What is a Derivative? A derivative is an instrument whose value depends on, or is derived from, the value of another asset. Examples: Futures

FNCE4830 Investment Banking Seminar Introduction on Derivatives What is a Derivative? A derivative is an instrument whose value depends on, or is derived from, the value of another asset. Examples: Futures

Lecture 8 Foundations of Finance

Lecture 8: Bond Portfolio Management. I. Reading. II. Risks associated with Fixed Income Investments. A. Reinvestment Risk. B. Liquidation Risk. III. Duration. A. Definition. B. Duration can be interpreted

Lecture 8: Bond Portfolio Management. I. Reading. II. Risks associated with Fixed Income Investments. A. Reinvestment Risk. B. Liquidation Risk. III. Duration. A. Definition. B. Duration can be interpreted

Part I: Forwards. Derivatives & Risk Management. Last Week: Weeks 1-3: Part I Forwards. Introduction Forward fundamentals

Derivatives & Risk Management Last Week: Introduction Forward fundamentals Weeks 1-3: Part I Forwards Forward fundamentals Fwd price, spot price & expected future spot Part I: Forwards 1 Forwards: Fundamentals

Derivatives & Risk Management Last Week: Introduction Forward fundamentals Weeks 1-3: Part I Forwards Forward fundamentals Fwd price, spot price & expected future spot Part I: Forwards 1 Forwards: Fundamentals

Financial Management

Financial Management International Finance 1 RISK AND HEDGING In this lecture we will cover: Justification for hedging Different Types of Hedging Instruments. How to Determine Risk Exposure. Good references

Financial Management International Finance 1 RISK AND HEDGING In this lecture we will cover: Justification for hedging Different Types of Hedging Instruments. How to Determine Risk Exposure. Good references

University of Waterloo Final Examination

University of Waterloo Final Examination Term: Fall 2007 Student Name KEY UW Student ID Number Course Abbreviation and Number AFM 372 Course Title Math Managerial Finance 2 Instructor Alan Huang Date of

University of Waterloo Final Examination Term: Fall 2007 Student Name KEY UW Student ID Number Course Abbreviation and Number AFM 372 Course Title Math Managerial Finance 2 Instructor Alan Huang Date of

Fair Forward Price Interest Rate Parity Interest Rate Derivatives Interest Rate Swap Cross-Currency IRS. Net Present Value.

Net Present Value Christopher Ting Christopher Ting http://www.mysmu.edu/faculty/christophert/ : christopherting@smu.edu.sg : 688 0364 : LKCSB 5036 September 16, 016 Christopher Ting QF 101 Week 5 September

Net Present Value Christopher Ting Christopher Ting http://www.mysmu.edu/faculty/christophert/ : christopherting@smu.edu.sg : 688 0364 : LKCSB 5036 September 16, 016 Christopher Ting QF 101 Week 5 September

NATIONAL UNIVERSITY OF SINGAPORE DEPARTMENT OF MATHEMATICS SEMESTER 2 EXAMINATION Investment Instruments: Theory and Computation

NATIONAL UNIVERSITY OF SINGAPORE DEPARTMENT OF MATHEMATICS SEMESTER 2 EXAMINATION 2012-2013 Investment Instruments: Theory and Computation April/May 2013 Time allowed : 2 hours INSTRUCTIONS TO CANDIDATES

NATIONAL UNIVERSITY OF SINGAPORE DEPARTMENT OF MATHEMATICS SEMESTER 2 EXAMINATION 2012-2013 Investment Instruments: Theory and Computation April/May 2013 Time allowed : 2 hours INSTRUCTIONS TO CANDIDATES

FNCE4830 Investment Banking Seminar

FNCE4830 Investment Banking Seminar Introduction on Derivatives What is a Derivative? A derivative is an instrument whose value depends on, or is derived from, the value of another asset. Examples: Futures

FNCE4830 Investment Banking Seminar Introduction on Derivatives What is a Derivative? A derivative is an instrument whose value depends on, or is derived from, the value of another asset. Examples: Futures

FX Options. Outline. Part I. Chapter 1: basic FX options, standard terminology, mechanics

FX Options 1 Outline Part I Chapter 1: basic FX options, standard terminology, mechanics Chapter 2: Black-Scholes pricing model; some option pricing relationships 2 Outline Part II Chapter 3: Binomial

FX Options 1 Outline Part I Chapter 1: basic FX options, standard terminology, mechanics Chapter 2: Black-Scholes pricing model; some option pricing relationships 2 Outline Part II Chapter 3: Binomial

SOCIETY OF ACTUARIES FINANCIAL MATHEMATICS. EXAM FM SAMPLE SOLUTIONS Financial Economics

SOCIETY OF ACTUARIES EXAM FM FINANCIAL MATHEMATICS EXAM FM SAMPLE SOLUTIONS Financial Economics June 2014 changes Questions 1-30 are from the prior version of this document. They have been edited to conform

SOCIETY OF ACTUARIES EXAM FM FINANCIAL MATHEMATICS EXAM FM SAMPLE SOLUTIONS Financial Economics June 2014 changes Questions 1-30 are from the prior version of this document. They have been edited to conform

Gallery of equations. 1. Introduction

Gallery of equations. Introduction Exchange-traded markets Over-the-counter markets Forward contracts Definition.. A forward contract is an agreement to buy or sell an asset at a certain future time for

Gallery of equations. Introduction Exchange-traded markets Over-the-counter markets Forward contracts Definition.. A forward contract is an agreement to buy or sell an asset at a certain future time for

Forwards, Futures, Options and Swaps

Forwards, Futures, Options and Swaps A derivative asset is any asset whose payoff, price or value depends on the payoff, price or value of another asset. The underlying or primitive asset may be almost

Forwards, Futures, Options and Swaps A derivative asset is any asset whose payoff, price or value depends on the payoff, price or value of another asset. The underlying or primitive asset may be almost

Managing Financial Risk with Forwards, Futures, Options, and Swaps. Second Edition

Managing Financial Risk with Forwards, Futures, Options, and Swaps Second Edition Managing Financial Risk with Forwards, Futures, Options, and Swaps Second Edition Fred R. Kaen Contents About This Course

Managing Financial Risk with Forwards, Futures, Options, and Swaps Second Edition Managing Financial Risk with Forwards, Futures, Options, and Swaps Second Edition Fred R. Kaen Contents About This Course

Problems and Solutions Manual

Problems and Solutions Manual to accompany Derivatives: Principles & Practice Rangarajan K. Sundaram Sanjiv R. Das April 2, 2010 Sundaram & Das: Derivatives - Problems and Solutions..................................1

Problems and Solutions Manual to accompany Derivatives: Principles & Practice Rangarajan K. Sundaram Sanjiv R. Das April 2, 2010 Sundaram & Das: Derivatives - Problems and Solutions..................................1

Introduction to Financial Derivatives

55.444 Introduction to Financial Derivatives Week of October 28, 213 Options Where we are Previously: Swaps (Chapter 7, OFOD) This Week: Option Markets and Stock Options (Chapter 9 1, OFOD) Next Week :

55.444 Introduction to Financial Derivatives Week of October 28, 213 Options Where we are Previously: Swaps (Chapter 7, OFOD) This Week: Option Markets and Stock Options (Chapter 9 1, OFOD) Next Week :

Copyright 2009 Pearson Education Canada

CHAPTER NINE Qualitative Questions 1. What is the difference between a call option and a put option? For an option buyer, a call option is the right to buy, while a put option is the right to sell. For

CHAPTER NINE Qualitative Questions 1. What is the difference between a call option and a put option? For an option buyer, a call option is the right to buy, while a put option is the right to sell. For

Eurocurrency Contracts. Eurocurrency Futures

Eurocurrency Contracts Futures Contracts, FRAs, & Options Eurocurrency Futures Eurocurrency time deposit Euro-zzz: The currency of denomination of the zzz instrument is not the official currency of the

Eurocurrency Contracts Futures Contracts, FRAs, & Options Eurocurrency Futures Eurocurrency time deposit Euro-zzz: The currency of denomination of the zzz instrument is not the official currency of the

Lecture 1, Jan

Markets and Financial Derivatives Tradable Assets Lecture 1, Jan 28 21 Introduction Prof. Boyan ostadinov, City Tech of CUNY The key players in finance are the tradable assets. Examples of tradables are:

Markets and Financial Derivatives Tradable Assets Lecture 1, Jan 28 21 Introduction Prof. Boyan ostadinov, City Tech of CUNY The key players in finance are the tradable assets. Examples of tradables are:

Answers to Selected Problems

Answers to Selected Problems Problem 1.11. he farmer can short 3 contracts that have 3 months to maturity. If the price of cattle falls, the gain on the futures contract will offset the loss on the sale

Answers to Selected Problems Problem 1.11. he farmer can short 3 contracts that have 3 months to maturity. If the price of cattle falls, the gain on the futures contract will offset the loss on the sale

Pricing Options with Mathematical Models

Pricing Options with Mathematical Models 1. OVERVIEW Some of the content of these slides is based on material from the book Introduction to the Economics and Mathematics of Financial Markets by Jaksa Cvitanic

Pricing Options with Mathematical Models 1. OVERVIEW Some of the content of these slides is based on material from the book Introduction to the Economics and Mathematics of Financial Markets by Jaksa Cvitanic

ActuarialBrew.com. Exam MFE / 3F. Actuarial Models Financial Economics Segment. Solutions 2014, 2nd edition

ActuarialBrew.com Exam MFE / 3F Actuarial Models Financial Economics Segment Solutions 04, nd edition www.actuarialbrew.com Brewing Better Actuarial Exam Preparation Materials ActuarialBrew.com 04 Please

ActuarialBrew.com Exam MFE / 3F Actuarial Models Financial Economics Segment Solutions 04, nd edition www.actuarialbrew.com Brewing Better Actuarial Exam Preparation Materials ActuarialBrew.com 04 Please

Practice set #3: FRAs, IRFs and Swaps.

International Financial Managment Professor Michel Robe What to do with this practice set? Practice set #3: FRAs, IRFs and Swaps. To help students with the material, seven practice sets with solutions

International Financial Managment Professor Michel Robe What to do with this practice set? Practice set #3: FRAs, IRFs and Swaps. To help students with the material, seven practice sets with solutions

Chapter 1 Introduction. Options, Futures, and Other Derivatives, 8th Edition, Copyright John C. Hull

Chapter 1 Introduction 1 What is a Derivative? A derivative is an instrument whose value depends on, or is derived from, the value of another asset. Examples: futures, forwards, swaps, options, exotics

Chapter 1 Introduction 1 What is a Derivative? A derivative is an instrument whose value depends on, or is derived from, the value of another asset. Examples: futures, forwards, swaps, options, exotics

Answers to Selected Problems

Answers to Selected Problems Problem 1.11. he farmer can short 3 contracts that have 3 months to maturity. If the price of cattle falls, the gain on the futures contract will offset the loss on the sale

Answers to Selected Problems Problem 1.11. he farmer can short 3 contracts that have 3 months to maturity. If the price of cattle falls, the gain on the futures contract will offset the loss on the sale

SOCIETY OF ACTUARIES EXAM IFM INVESTMENT AND FINANCIAL MARKETS EXAM IFM SAMPLE QUESTIONS AND SOLUTIONS DERIVATIVES

SOCIETY OF ACTUARIES EXAM IFM INVESTMENT AND FINANCIAL MARKETS EXAM IFM SAMPLE QUESTIONS AND SOLUTIONS DERIVATIVES These questions and solutions are based on the readings from McDonald and are identical

SOCIETY OF ACTUARIES EXAM IFM INVESTMENT AND FINANCIAL MARKETS EXAM IFM SAMPLE QUESTIONS AND SOLUTIONS DERIVATIVES These questions and solutions are based on the readings from McDonald and are identical

Interest Rates & Credit Derivatives

Interest Rates & Credit Derivatives Ashish Ghiya Derivium Tradition (India) 25/06/14 1 Agenda Introduction to Interest Rate & Credit Derivatives Practical Uses of Derivatives Derivatives Going Wrong Practical

Interest Rates & Credit Derivatives Ashish Ghiya Derivium Tradition (India) 25/06/14 1 Agenda Introduction to Interest Rate & Credit Derivatives Practical Uses of Derivatives Derivatives Going Wrong Practical

Chapter 5. Financial Forwards and Futures. Copyright 2009 Pearson Prentice Hall. All rights reserved.

Chapter 5 Financial Forwards and Futures Introduction Financial futures and forwards On stocks and indexes On currencies On interest rates How are they used? How are they priced? How are they hedged? 5-2

Chapter 5 Financial Forwards and Futures Introduction Financial futures and forwards On stocks and indexes On currencies On interest rates How are they used? How are they priced? How are they hedged? 5-2

Advanced Corporate Finance. 5. Options (a refresher)

") Advanced Corporate Finance 5. Options (a refresher) Objectives of the session 1. Define options (calls and puts) 2. Analyze terminal payoff 3. Define basic strategies 4. Binomial option pricing model 5.

Advanced Corporate Finance 5. Options (a refresher) Objectives of the session 1. Define options (calls and puts) 2. Analyze terminal payoff 3. Define basic strategies 4. Binomial option pricing model 5.

Chapter 8. Swaps. Copyright 2009 Pearson Prentice Hall. All rights reserved.

Chapter 8 Swaps Introduction to Swaps A swap is a contract calling for an exchange of payments, on one or more dates, determined by the difference in two prices A swap provides a means to hedge a stream

Chapter 8 Swaps Introduction to Swaps A swap is a contract calling for an exchange of payments, on one or more dates, determined by the difference in two prices A swap provides a means to hedge a stream

FORWARDS FUTURES Traded between private parties (OTC) Traded on exchange

Traded on exchange") 1 E&G, Ch. 23. I. Introducing Forwards and Futures A. Mechanics of Forwards and Futures. 1. Definitions: Forward Contract - commitment by 2 parties to exchange a certain good for a specific price at a

1 E&G, Ch. 23. I. Introducing Forwards and Futures A. Mechanics of Forwards and Futures. 1. Definitions: Forward Contract - commitment by 2 parties to exchange a certain good for a specific price at a

Profit settlement End of contract Daily Option writer collects premium on T+1

DERIVATIVES A derivative contract is a financial instrument whose payoff structure is derived from the value of the underlying asset. A forward contract is an agreement entered today under which one party

DERIVATIVES A derivative contract is a financial instrument whose payoff structure is derived from the value of the underlying asset. A forward contract is an agreement entered today under which one party

Important Concepts LECTURE 3.2: OPTION PRICING MODELS: THE BLACK-SCHOLES-MERTON MODEL. Applications of Logarithms and Exponentials in Finance

Important Concepts The Black Scholes Merton (BSM) option pricing model LECTURE 3.2: OPTION PRICING MODELS: THE BLACK-SCHOLES-MERTON MODEL Black Scholes Merton Model as the Limit of the Binomial Model Origins

Important Concepts The Black Scholes Merton (BSM) option pricing model LECTURE 3.2: OPTION PRICING MODELS: THE BLACK-SCHOLES-MERTON MODEL Black Scholes Merton Model as the Limit of the Binomial Model Origins

Equity Option Valuation Practical Guide

Valuation Practical Guide John Smith FinPricing Equity Option Introduction The Use of Equity Options Equity Option Payoffs Valuation Practical Guide A Real World Example Summary Equity Option Introduction

Valuation Practical Guide John Smith FinPricing Equity Option Introduction The Use of Equity Options Equity Option Payoffs Valuation Practical Guide A Real World Example Summary Equity Option Introduction

Study Session 16 Sample Questions. Asset Valuation: Derivative Investments

1 Study Session 16 Sample Questions Asset Valuation Derivative Investments 1A Introduction 1. In the theory of finance, a complete market is a market: A. in which any rational price for a financial instrument

1 Study Session 16 Sample Questions Asset Valuation Derivative Investments 1A Introduction 1. In the theory of finance, a complete market is a market: A. in which any rational price for a financial instrument

Introduction to Derivative Instruments

Harvard Business School 9-295-141 Rev. March 4, 1997 Introduction to Derivative Instruments A derivative is a financial instrument, or contract, between two parties that derives its value from some other

Harvard Business School 9-295-141 Rev. March 4, 1997 Introduction to Derivative Instruments A derivative is a financial instrument, or contract, between two parties that derives its value from some other

Introduction to Futures and Options

Introduction to Futures and Options Pratish Patel Spring 2014 Lecture note on Forwards California Polytechnic University Pratish Patel Spring 2014 Forward Contracts Definition: A forward contract is a

Introduction to Futures and Options Pratish Patel Spring 2014 Lecture note on Forwards California Polytechnic University Pratish Patel Spring 2014 Forward Contracts Definition: A forward contract is a

Math 373 Test 4 Fall 2012

Math 373 Test 4 Fall 2012 December 10, 2012 1. ( 3 points) List the three conditions that must be present for arbitrage to exist. 1) No investment 2) No risk 3) Guaranteed positive cash flow 2. (5 points)

Math 373 Test 4 Fall 2012 December 10, 2012 1. ( 3 points) List the three conditions that must be present for arbitrage to exist. 1) No investment 2) No risk 3) Guaranteed positive cash flow 2. (5 points)

Options and Derivative Securities

FIN 614 Options and Other Derivatives Professor Robert B.H. Hauswald Kogod School of Business, AU Options and Derivative Securities Derivative instruments can only exist in relation to some other financial

FIN 614 Options and Other Derivatives Professor Robert B.H. Hauswald Kogod School of Business, AU Options and Derivative Securities Derivative instruments can only exist in relation to some other financial

Final Exam. 5. (24 points) Multiple choice questions: in each case, only one answer is correct.

Multiple choice questions: in each case, only one answer is correct.") Final Exam Fall 06 Econ 80-367 Closed Book. Formula Sheet Provided. Calculators OK. Time Allowed: 3 hours Please write your answers on the page below each question. (0 points) A stock trades for $50. After

Final Exam Fall 06 Econ 80-367 Closed Book. Formula Sheet Provided. Calculators OK. Time Allowed: 3 hours Please write your answers on the page below each question. (0 points) A stock trades for $50. After

Chapter 10: Futures Arbitrage Strategies

Chapter 10: Futures Arbitrage Strategies I. Short-Term Interest Rate Arbitrage 1. Cash and Carry/Implied Repo Cash and carry transaction means to buy asset and sell futures Use repurchase agreement/repo

Chapter 10: Futures Arbitrage Strategies I. Short-Term Interest Rate Arbitrage 1. Cash and Carry/Implied Repo Cash and carry transaction means to buy asset and sell futures Use repurchase agreement/repo

SAMPLE SOLUTIONS FOR DERIVATIVES MARKETS

SAMPLE SOLUTIONS FOR DERIVATIVES MARKETS Question #1 If the call is at-the-money, the put option with the same cost will have a higher strike price. A purchased collar requires that the put have a lower

SAMPLE SOLUTIONS FOR DERIVATIVES MARKETS Question #1 If the call is at-the-money, the put option with the same cost will have a higher strike price. A purchased collar requires that the put have a lower

1- Using Interest Rate Swaps to Convert a Floating-Rate Loan to a Fixed-Rate Loan (and Vice Versa)

") READING 38: RISK MANAGEMENT APPLICATIONS OF SWAP STRATEGIES A- Strategies and Applications for Managing Interest Rate Risk Swaps are not normally used to manage the risk of an anticipated loan; rather,

READING 38: RISK MANAGEMENT APPLICATIONS OF SWAP STRATEGIES A- Strategies and Applications for Managing Interest Rate Risk Swaps are not normally used to manage the risk of an anticipated loan; rather,

Lecture 3: Interest Rate Forwards and Options

Lecture 3: Interest Rate Forwards and Options 01135532: Financial Instrument and Innovation Nattawut Jenwittayaroje, Ph.D., CFA NIDA Business School 1 Forward Rate Agreements (FRAs) Definition A forward

Lecture 3: Interest Rate Forwards and Options 01135532: Financial Instrument and Innovation Nattawut Jenwittayaroje, Ph.D., CFA NIDA Business School 1 Forward Rate Agreements (FRAs) Definition A forward

Chapter 5 Financial Forwards and Futures

Chapter 5 Financial Forwards and Futures Question 5.1. Four different ways to sell a share of stock that has a price S(0) at time 0. Question 5.2. Description Get Paid at Lose Ownership of Receive Payment

Chapter 5 Financial Forwards and Futures Question 5.1. Four different ways to sell a share of stock that has a price S(0) at time 0. Question 5.2. Description Get Paid at Lose Ownership of Receive Payment

22 Swaps: Applications. Answers to Questions and Problems

22 Swaps: Applications Answers to Questions and Problems 1. At present, you observe the following rates: FRA 0,1 5.25 percent and FRA 1,2 5.70 percent, where the subscripts refer to years. You also observe

22 Swaps: Applications Answers to Questions and Problems 1. At present, you observe the following rates: FRA 0,1 5.25 percent and FRA 1,2 5.70 percent, where the subscripts refer to years. You also observe

Part III: Swaps. Futures, Swaps & Other Derivatives. Swaps. Previous lecture set: This lecture set -- Parts II & III. Fundamentals

Futures, Swaps & Other Derivatives Previous lecture set: Interest-Rate Derivatives FRAs T-bills futures & Euro$ Futures This lecture set -- Parts II & III Swaps Part III: Swaps Swaps Fundamentals what,

Futures, Swaps & Other Derivatives Previous lecture set: Interest-Rate Derivatives FRAs T-bills futures & Euro$ Futures This lecture set -- Parts II & III Swaps Part III: Swaps Swaps Fundamentals what,

Final Exam. 5. (21 points) Short Questions. Parts (i)-(v) are multiple choice: in each case, only one answer is correct.

Short Questions. Parts (i)-(v) are multiple choice: in each case, only one answer is correct.") Final Exam Spring 016 Econ 180-367 Closed Book. Formula Sheet Provided. Calculators OK. Time Allowed: 3 hours Please write your answers on the page below each question 1. (10 points) What is the duration

Final Exam Spring 016 Econ 180-367 Closed Book. Formula Sheet Provided. Calculators OK. Time Allowed: 3 hours Please write your answers on the page below each question 1. (10 points) What is the duration

Review of Derivatives I. Matti Suominen, Aalto

Review of Derivatives I Matti Suominen, Aalto 25 SOME STATISTICS: World Financial Markets (trillion USD) 2 15 1 5 Securitized loans Corporate bonds Financial institutions' bonds Public debt Equity market

Review of Derivatives I Matti Suominen, Aalto 25 SOME STATISTICS: World Financial Markets (trillion USD) 2 15 1 5 Securitized loans Corporate bonds Financial institutions' bonds Public debt Equity market

Applying Principles of Quantitative Finance to Modeling Derivatives of Non-Linear Payoffs

Applying Principles of Quantitative Finance to Modeling Derivatives of Non-Linear Payoffs Christopher Ting http://www.mysmu.edu/faculty/christophert/ Christopher Ting : christopherting@smu.edu.sg : 6828

Applying Principles of Quantitative Finance to Modeling Derivatives of Non-Linear Payoffs Christopher Ting http://www.mysmu.edu/faculty/christophert/ Christopher Ting : christopherting@smu.edu.sg : 6828

Swaptions. Product nature

Product nature Swaptions The buyer of a swaption has the right to enter into an interest rate swap by some specified date. The swaption also specifies the maturity date of the swap. The buyer can be the

Product nature Swaptions The buyer of a swaption has the right to enter into an interest rate swap by some specified date. The swaption also specifies the maturity date of the swap. The buyer can be the

Financial Derivatives

Derivatives in ALM Financial Derivatives Swaps Hedge Contracts Forward Rate Agreements Futures Options Caps, Floors and Collars Swaps Agreement between two counterparties to exchange the cash flows. Cash

Derivatives in ALM Financial Derivatives Swaps Hedge Contracts Forward Rate Agreements Futures Options Caps, Floors and Collars Swaps Agreement between two counterparties to exchange the cash flows. Cash

GLOSSARY OF COMMON DERIVATIVES TERMS

Alpha The difference in performance of an investment relative to its benchmark. American Style Option An option that can be exercised at any time from inception as opposed to a European Style option which

Alpha The difference in performance of an investment relative to its benchmark. American Style Option An option that can be exercised at any time from inception as opposed to a European Style option which

MAFS601A Exotic swaps. Forward rate agreements and interest rate swaps. Asset swaps. Total return swaps. Swaptions. Credit default swaps

MAFS601A Exotic swaps Forward rate agreements and interest rate swaps Asset swaps Total return swaps Swaptions Credit default swaps Differential swaps Constant maturity swaps 1 Forward rate agreement (FRA)

MAFS601A Exotic swaps Forward rate agreements and interest rate swaps Asset swaps Total return swaps Swaptions Credit default swaps Differential swaps Constant maturity swaps 1 Forward rate agreement (FRA)

Fixed-Income Options

Fixed-Income Options Consider a two-year 99 European call on the three-year, 5% Treasury. Assume the Treasury pays annual interest. From p. 852 the three-year Treasury s price minus the $5 interest could

Fixed-Income Options Consider a two-year 99 European call on the three-year, 5% Treasury. Assume the Treasury pays annual interest. From p. 852 the three-year Treasury s price minus the $5 interest could

Part II: Futures. Derivatives & Risk Management. Futures vs. Forwards. Futures vs. Forwards. Futures vs. Forwards 3. Futures vs.

Derivatives & Risk Management Previous lecture set: Forward outright positions & payoffs + NDFs Forward price vs. current & future spot prices Part II: Futures This lecture set Part II (Futures) Futures

Derivatives & Risk Management Previous lecture set: Forward outright positions & payoffs + NDFs Forward price vs. current & future spot prices Part II: Futures This lecture set Part II (Futures) Futures

The Good, the Bad and the Ugly: FX Standard and Exotic Options

FIN 700 International Finance FXO: Foreign Exchange Options Professor Robert Hauswald Kogod School of Business, AU The Good, the Bad and the Ugly: FX Standard and Exotic Options The derivative with an

FIN 700 International Finance FXO: Foreign Exchange Options Professor Robert Hauswald Kogod School of Business, AU The Good, the Bad and the Ugly: FX Standard and Exotic Options The derivative with an

Derivatives Analysis & Valuation (Futures)

") 6.1 Derivatives Analysis & Valuation (Futures) LOS 1 : Introduction Study Session 6 Define Forward Contract, Future Contract. Forward Contract, In Forward Contract one party agrees to buy, and the counterparty

6.1 Derivatives Analysis & Valuation (Futures) LOS 1 : Introduction Study Session 6 Define Forward Contract, Future Contract. Forward Contract, In Forward Contract one party agrees to buy, and the counterparty

BOOK 5- DERIVATIVES AND PORTFOLIO MANAGEMENT

BOOK 5- DERIVATIVES AND PORTFOLIO MANAGEMENT Readings and Learning Outcome Statements... 3 Study Session 16- Derivative Investments: Forwards and Futures... 8 Study Session 17 - Derivative Investments:

BOOK 5- DERIVATIVES AND PORTFOLIO MANAGEMENT Readings and Learning Outcome Statements... 3 Study Session 16- Derivative Investments: Forwards and Futures... 8 Study Session 17 - Derivative Investments:

Swaption Product and Vaulation

Product and Vaulation Alan White FinPricing http://www.finpricing.com Summary Interest Rate Swaption Introduction The Use of Swaption Swaption Payoff Valuation Practical Guide A real world example Swaption

Product and Vaulation Alan White FinPricing http://www.finpricing.com Summary Interest Rate Swaption Introduction The Use of Swaption Swaption Payoff Valuation Practical Guide A real world example Swaption

Applying the Principles of Quantitative Finance to the Construction of Model-Free Volatility Indices

Applying the Principles of Quantitative Finance to the Construction of Model-Free Volatility Indices Christopher Ting http://www.mysmu.edu/faculty/christophert/ Christopher Ting : christopherting@smu.edu.sg

Applying the Principles of Quantitative Finance to the Construction of Model-Free Volatility Indices Christopher Ting http://www.mysmu.edu/faculty/christophert/ Christopher Ting : christopherting@smu.edu.sg

ActuarialBrew.com. Exam MFE / 3F. Actuarial Models Financial Economics Segment. Solutions 2014, 1 st edition

ActuarialBrew.com Exam MFE / 3F Actuarial Models Financial Economics Segment Solutions 04, st edition www.actuarialbrew.com Brewing Better Actuarial Exam Preparation Materials ActuarialBrew.com 04 Please

ActuarialBrew.com Exam MFE / 3F Actuarial Models Financial Economics Segment Solutions 04, st edition www.actuarialbrew.com Brewing Better Actuarial Exam Preparation Materials ActuarialBrew.com 04 Please

Forward and Futures Contracts

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 Forward and Futures Contracts These notes explore forward and futures contracts, what they are and how they are used. We will learn how to price forward contracts

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 Forward and Futures Contracts These notes explore forward and futures contracts, what they are and how they are used. We will learn how to price forward contracts

Types of Foreign Exchange Exposure. Foreign Exchange Exposure

Foreign Exchange Exposure Foreign exchange exposure is a measure of the potential for a firm s profitability, net cash flow, and market value to change because of a change in exchange rates. An important

Foreign Exchange Exposure Foreign exchange exposure is a measure of the potential for a firm s profitability, net cash flow, and market value to change because of a change in exchange rates. An important

Foreign Exchange Exposure

Foreign Exchange Exposure Foreign exchange exposure is a measure of the potential for a firm s profitability, net cash flow, and market value to change because of a change in exchange rates. An important

Foreign Exchange Exposure Foreign exchange exposure is a measure of the potential for a firm s profitability, net cash flow, and market value to change because of a change in exchange rates. An important

Portfolio Management Philip Morris has issued bonds that pay coupons annually with the following characteristics:

Portfolio Management 010-011 1. a. Critically discuss the mean-variance approach of portfolio theory b. According to Markowitz portfolio theory, can we find a single risky optimal portfolio which is suitable

Portfolio Management 010-011 1. a. Critically discuss the mean-variance approach of portfolio theory b. According to Markowitz portfolio theory, can we find a single risky optimal portfolio which is suitable

Table of contents. Slide No. Meaning Of Derivative 3. Specifications Of Futures 4. Functions Of Derivatives 5. Participants 6.

Derivatives 1 Table of contents Slide No. Meaning Of Derivative 3 Specifications Of Futures 4 Functions Of Derivatives 5 Participants 6 Size Of Market 7 Available Future Contracts 9 Jargons 10 Parameters

Derivatives 1 Table of contents Slide No. Meaning Of Derivative 3 Specifications Of Futures 4 Functions Of Derivatives 5 Participants 6 Size Of Market 7 Available Future Contracts 9 Jargons 10 Parameters

TEACHING NOTE 01-02: INTRODUCTION TO INTEREST RATE OPTIONS

TEACHING NOTE 01-02: INTRODUCTION TO INTEREST RATE OPTIONS Version date: August 15, 2008 c:\class Material\Teaching Notes\TN01-02.doc Most of the time when people talk about options, they are talking about

TEACHING NOTE 01-02: INTRODUCTION TO INTEREST RATE OPTIONS Version date: August 15, 2008 c:\class Material\Teaching Notes\TN01-02.doc Most of the time when people talk about options, they are talking about

Currency Futures Trade on YieldX

JOHANNESBURG STOCK EXCHANGE YieldX Currency Futures Currency Futures Trade on YieldX Currency futures are traded on YieldX, the JSE s interest rate market. YieldX offers an efficient, electronic, automatic

JOHANNESBURG STOCK EXCHANGE YieldX Currency Futures Currency Futures Trade on YieldX Currency futures are traded on YieldX, the JSE s interest rate market. YieldX offers an efficient, electronic, automatic

Solutions to Practice Problems

Solutions to Practice Problems CHAPTER 1 1.1 Original exchange rate Reciprocal rate Answer (a) 1 = US$0.8420 US$1 =? 1.1876 (b) 1 = US$1.4565 US$1 =? 0.6866 (c) NZ$1 = US$0.4250 US$1 = NZ$? 2.3529 1.2

Solutions to Practice Problems CHAPTER 1 1.1 Original exchange rate Reciprocal rate Answer (a) 1 = US$0.8420 US$1 =? 1.1876 (b) 1 = US$1.4565 US$1 =? 0.6866 (c) NZ$1 = US$0.4250 US$1 = NZ$? 2.3529 1.2

OPTIONS and FUTURES Lecture 5: Forwards, Futures, and Futures Options

OPTIONS and FUTURES Lecture 5: Forwards, Futures, and Futures Options Philip H. Dybvig Washington University in Saint Louis Spot (cash) market Forward contract Futures contract Options on futures Copyright

OPTIONS and FUTURES Lecture 5: Forwards, Futures, and Futures Options Philip H. Dybvig Washington University in Saint Louis Spot (cash) market Forward contract Futures contract Options on futures Copyright

Options. An Undergraduate Introduction to Financial Mathematics. J. Robert Buchanan. J. Robert Buchanan Options

Options An Undergraduate Introduction to Financial Mathematics J. Robert Buchanan 2014 Definitions and Terminology Definition An option is the right, but not the obligation, to buy or sell a security such

Options An Undergraduate Introduction to Financial Mathematics J. Robert Buchanan 2014 Definitions and Terminology Definition An option is the right, but not the obligation, to buy or sell a security such

Hull, Options, Futures & Other Derivatives

P1.T3. Financial Markets & Products Hull, Options, Futures & Other Derivatives Bionic Turtle FRM Study Notes Sample By David Harper, CFA FRM CIPM and Deepa Raju www.bionicturtle.com Hull, Chapter 1: Introduction

P1.T3. Financial Markets & Products Hull, Options, Futures & Other Derivatives Bionic Turtle FRM Study Notes Sample By David Harper, CFA FRM CIPM and Deepa Raju www.bionicturtle.com Hull, Chapter 1: Introduction

LECTURE 12. Volatility is the question on the B/S which assumes constant SD throughout the exercise period - The time series of implied volatility

LECTURE 12 Review Options C = S e -δt N (d1) X e it N (d2) P = X e it (1- N (d2)) S e -δt (1 - N (d1)) Volatility is the question on the B/S which assumes constant SD throughout the exercise period - The

LECTURE 12 Review Options C = S e -δt N (d1) X e it N (d2) P = X e it (1- N (d2)) S e -δt (1 - N (d1)) Volatility is the question on the B/S which assumes constant SD throughout the exercise period - The

Lecture Notes: Option Concepts and Fundamental Strategies

Brunel University Msc., EC5504, Financial Engineering Prof Menelaos Karanasos Lecture Notes: Option Concepts and Fundamental Strategies Options and futures are known as derivative securities. They derive

Brunel University Msc., EC5504, Financial Engineering Prof Menelaos Karanasos Lecture Notes: Option Concepts and Fundamental Strategies Options and futures are known as derivative securities. They derive

Introduction to Financial Mathematics

Introduction to Financial Mathematics MTH 210 Fall 2016 Jie Zhong November 30, 2016 Mathematics Department, UR Table of Contents Arbitrage Interest Rates, Discounting, and Basic Assets Forward Contracts

Introduction to Financial Mathematics MTH 210 Fall 2016 Jie Zhong November 30, 2016 Mathematics Department, UR Table of Contents Arbitrage Interest Rates, Discounting, and Basic Assets Forward Contracts

Chapter 2: BASICS OF FIXED INCOME SECURITIES

Chapter 2: BASICS OF FIXED INCOME SECURITIES 2.1 DISCOUNT FACTORS 2.1.1 Discount Factors across Maturities 2.1.2 Discount Factors over Time 2.1 DISCOUNT FACTORS The discount factor between two dates, t

Chapter 2: BASICS OF FIXED INCOME SECURITIES 2.1 DISCOUNT FACTORS 2.1.1 Discount Factors across Maturities 2.1.2 Discount Factors over Time 2.1 DISCOUNT FACTORS The discount factor between two dates, t