Chapter 2. Time Value of Money (TVOM) Principles of Engineering Economic Analysis, 5th edition

|

|

|

- Randolph Thornton

- 5 years ago

- Views:

Transcription

1 Chapter 2 Time Value of Money (TVOM)

2 Cash Flow Diagrams (EOY)

3 Example 2.1 Cash Flow Profiles for Two Investment Alternatives End of Year (EOY) CF(A) CF(B) CF(B-A) 0 -$100,000 -$100,000 $0 1 $10,000 $50,000 $40,000 2 $20,000 $40,000 $20,000 3 $30,000 $30,000 $0 4 $40,000 $20,000 -$20,000 5 $50,000 $10,000 -$40,000 Sum $50,000 $50,000 $0 Although the two investment alternatives have the same bottom line, there are obvious differences. Which would you prefer, A or B? Why?

4 Principle #7 Consider only differences in cash flows among investment alternatives

5 Inv. B Inv. A

6 Example 2.2 $3,000 $3,000 $3,000 Alternative C (+) 0 (-) $6,000 $3,000 $3,000 $3,000 Alternative D (+) (-) $6,000 Which would you choose?

(-) 0 1 2 3 4 $4000 $3,000 $2,000 $2,000 $1,000")

7 Example 2.3 $2,000 $2,000 $2,000 $3,000 Alternative E (+) (-) $4000 $3,000 $2,000 $2,000 $1,000 Alternative F (+) 0 (-) Alternative E-F $4,000 3 Which would you choose? $1000 $2000 4

8 Simple interest calculation: F n P ( 1 in ) Compound Interest Calculation: F n F n (1 i 1 ) Where P = present value of single sum of money F n = accumulated value of P over n periods i = interest rate per period n = number of periods

9 Example 2.7: simple interest calculation Robert borrows $4,000 from Susan and agrees to pay $1,000 plus accrued interest at the end of the first year and $3,000 plus accrued interest at the end of the fourth year. What should be the size of the payments if 8% simple interest is used? Solution 1 st payment = $1, ($4,000) = $1,320 2 nd payment = $3, ($3,000)(3) = $3,720

10 Simple Interest Cash Flow Diagram $720 $320 $3,000 $1, Principal payment Interest payment $4,000

11 RULES Discounting Cash Flow 1. Money has time value! 2. Cash flows cannot be added unless they occur at the same point(s) in time. 3. Multiply a cash flow by (1+i) to move it forward one time unit. 4. Divide a cash flow by (1+i) to move it backward one time unit.

12 Example 2.8 (Lender s Perspective) Value of $10,000 Investment 10% per year Start of Year Value of Investment Interest Earned End of Year Value of Investment 1 $10, $1, $11, $11, $1, $12, $12, $1, $13, $13, $1, $14, $14, $1, $16,105.10

13 Compounding of Money Beginning of Period Amount Owed Interest Earned End of Period Amount Owed 1 P Pi 1 P(1+i) 2 P(1+i) P(1+i)i 2 P(1+i) 2 3 P(1+i) 2 P(1+i) 2 i 3 P(1+i) 3 4 P(1+i) 3 P(1+i) 3 i 4 P(1+i) 4 5 P(1+i) 4 P(1+i) 4 i 5 P(1+i) n-1 P(1+i) n-2 P(1+i) n-2 i n-1 P(1+i) n-1 n P(1+i) n-1 P(1+i) n-1 i n P(1+i) n......

14 Discounted Cash Flow Formulas F = P (1 + i) n (2.8) F = P (F P i%, n) Vertical line means given P = F (1 + i) -n (2.9) P = F (P F i%, n)

15 Excel DCF Worksheet Functions F = P (1 + i) n (2.1) F = P (F P i%, n) F =FV(i%,n,,-P) P = F (1 + i) -n (2.3) P = F (P F i%, n) P =PV(i%,n,,-F)

16 F = P (1 + i ) n F = P (F P i %,n ) factor F =FV(i %,n,,-p ) single sum, future worth P = F (1 + i ) -n P = F (P F i %,n ) factor P =PV(i %,n,,-f ) single sum, present worth

17 F = P(1+i) n F = P(F P i%, n) F =FV(i%,n,,-P) P = F(1+i) -n P = F(P F i%, n) P =PV(i%,n,,-F) F n-1 n P P occurs n periods before F (F occurs n periods after P)

18 Relationships among P, F, and A P occurs at the same time as A 0, i.e., at t = 0 F occurs at the same time as A n, i.e., at t = n

19 Example 2.9 Dia St. John borrows $1,000 at 12% compounded annually. The loan is to be repaid after 5 years. How much must she repay in 5 years? F = P(F P i, n) F = $1,000(F P 12%,5) F = $1,000(1.12) 5 F = $1,000( ) F = $1, F =FV(12%,5,,-1000) F = $1,762.34

20 Example 2.11 How much must you deposit, today, in order to accumulate $10,000 in 4 years, if you earn 5% compounded annually on your investment? P = F(P F i, n) P = $10,000(P F 5%,4) P = $10,000(1.05) -4 P = $10,000( ) P = $8, P =PV(5%,4,,-10000) P = $

21 Computing the Present Worth of Multiple Cash flows n P A t (1 i ) t (2.12) t 0 P n A t ( P F i %, t ) (2.13) t 0

22 Example 2.12 Determine the present worth equivalent of the CFD shown below, using an interest rate of 10% compounded annually. ( + ) $50,000 $40,000 $30,000 $40,000 $50, End of Year i = 10%/year ( - ) $100,000 End of Year Cash Flow Present Future (P F 10%,n) PV(10%,n,,-CF) (F P 10%,5-n) (n) (CF) Worth Worth FV(10%,5-n,,-CF) 0 -$100, $100, $100, $161, $161, $50, $45, $45, $73, $73, $40, $33, $33, $53, $53, $30, $22, $22, $36, $36, $40, $27, $27, $44, $44, $50, $31, $31, $50, $50, SUM $59, $59, $95, $95, P =NPV(10%,50000,40000,30000,40000,50000) = $59,418.45

23 Example 2.15 Determine the future worth equivalent of the CFD shown below, using an interest rate of 10% compounded annually. ( + ) $50,000 $40,000 $30,000 $40,000 $50, End of Year i = 10%/year ( - ) $100,000 End of Year Cash Flow Present Future (P F 10%,n) PV(10%,n,,-CF) (F P 10%,5-n) (n) (CF) Worth Worth FV(10%,5-n,,-CF) 0 -$100, $100, $100, $161, $161, $50, $45, $45, $73, $73, $40, $33, $33, $53, $53, $30, $22, $22, $36, $36, $40, $27, $27, $44, $44, $50, $31, $31, $50, $50, SUM $59, $59, $95, $95, F =10000*FV(10%,5,,-NPV(10%,5,4,3,4,5)+10) = $95,694.00

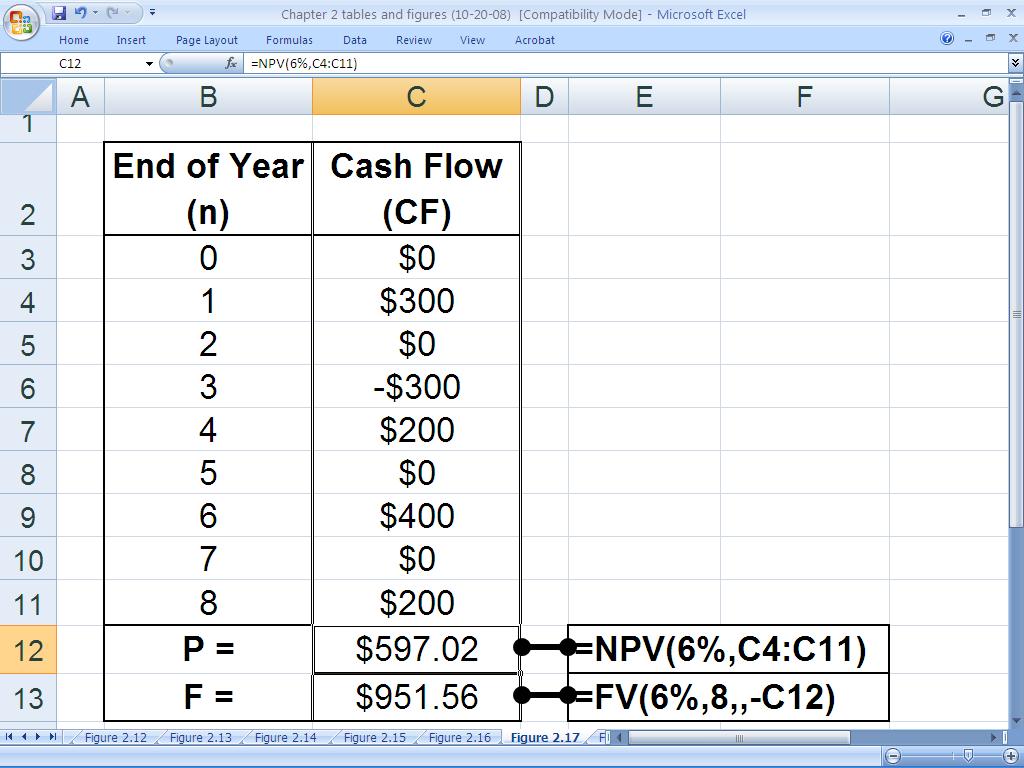

24 Examples 2.13 & 2.16 Determine the present worth equivalent of the following series of cash flows. Use an interest rate of 6% per interest period. End of Period P = $300(P F 6%,1)- $300(P F 6%,3)+$200(P F 6%,4)+$400(P F 6%,6) +$200(P F 6%,8) = $ P =NPV(6%,300,0,-300,200,0,400,0,200) P =$ Cash Flow 0 $0 1 $300 2 $0 3 -$300 4 $200 5 $0 6 $400 7 $0 8 $200

(1 1 1 t n i P F A F i A F n t t t n n t t (2.15) (2.")

25 Computing the Future worth of Multiple cash Flows ) %, ( ) (1 1 1 t n i P F A F i A F n t t t n n t t (2.15) (2.16)

26 Examples 2.14 & 2.16 Determine the future worth equivalent of the following series of cash flows. Use an interest rate of 6% per interest period. F = $300(F P 6%,7)-$300(F P 6%,5)+ $200(F P 6%,4)+$400(F P 6%,2)+$200 F = $ F =FV(6%,8,,-NPV(6%,300,0,-300,200,0,400,0,200)) F =$ End of Period Cash Flow 0 $0 1 $300 2 $0 3 -$300 4 $200 5 $0 6 $400 7 $0 8 $200 (The 3 difference in the answers is due to round-off error in the tables in Appendix A.)

27

28 Some Common Cash Flow Series Uniform Series A t = A t = 1,,n Gradient Series A t = 0 t = 1 = A t-1 +G t = 2,,n = (t-1)g t = 1,,n Geometric Series A t = A t = 1 = A t-1 (1+j) t = 2,,n = A 1 (1+j) t-1 t = 1,,n

29 Uniform Series

30 DCF Uniform Series Formulas A A A A A A P = A[(1+i) n -1]/[i(1+i) n ] P P occurs 1 period before first A P = A(P A i%,n) P = [ =PV(i%,n,-A) ] A = Pi(1+i) n /[(1+i) n -1] A = P(A P i%,n) A =PMT(i%,n,-P)

31 A A A A A A F = A[(1+i) n -1]/i F = A(F A i%,n) F =FV(i%,n,-A) A = Fi/[(1+i) n -1] A = F(A F i%,n) F F occurs at the same time as last A A =PMT(i%,n,,-F)

32 P = A(P A i%,n) = A (2.22) A = P(A P i%,n) = P (2.25) P occurs one period before the first A F = A(F A i%,n) = A (2.28) A = F(A F i%,n) = F (2.30) F occurs at the same time as the last A n n i i i ) (1 1 ) (1 1 ) (1 ) (1 n n i i i i i n 1 ) (1 1 ) (1 n i i

33 Example Troy Long deposits a single sum of money in a savings account that pays 5% compounded annually. How much must he deposit in order to withdraw $2,000/yr for 5 years, with the first withdrawal occurring 1 year after the deposit? P = $2000(P A 5%,5) P = $2000( ) = $ P =PV(5%,5,-2000) P = $

34 Example Troy Long deposits a single sum of money in a savings account that pays 5% compounded annually. How much must he deposit in order to withdraw $2,000/yr for 5 years, with the first withdrawal occurring 3 years after the deposit? P = $2000(P A 5%,5)(P F 5%,2) P = $2000( )( ) = $ P =PV(5%,2,,-PV(5%,5,-2000)) P = $

35 Example Rachel Townsley invests $10,000 in a fund that pays 8% compounded annually. If she makes 10 equal annual withdrawals from the fund, how much can she withdraw if the first withdrawal occurs 1 year after her investment? A = $10,000(A P 8%,10) A = $10,000( ) = $ A =PMT(8%,10,-10000) A = $

36 Example 2.22 Suppose Rachel delays the first withdrawal for 2 years. How much can be withdrawn each of the 10 years? A = $10,000(F P 8%,2)(A P 8%,10) A = $10,000( )( ) A = $ A =PMT(8%,10-FV(8%,2,,-10000)) A = $

37 Example 2.20 A firm borrows $2,000,000 at 12% annual interest and pays it back with 10 equal annual payments. What is the payment? A = $2,000,000(A P 12%,10) A = $2,000,000( ) A = $353,960 A =PMT(12%,10, ) A = $353,968.33

38 Example 2.21 Suppose the firm pays back the loan over 15 years in order to obtain a 10% interest rate. What would be the size of the annual payment? A = $2,000,000(A P 10%,15) A = $2,000,000( ) A = $262,940 A =PMT(10%,15, ) A = $262, Extending the loan period 5 years reduced the payment by $91,020.78

39 Example Luis Jimenez deposits $1,000/yr in a savings account that pays 6% compounded annually. How much will be in the account immediately after his 30 th deposit? F = 1000(F A 6%,30) F = $1000( ) = $79, F =FV(6%,30,-1000) A = $78,058.19

40 Example Andrew Brewer invests $5,000/yr and earns 6% compounded annually. How much will he have in his investment portfolio after 15 yrs? 20 yrs? 25 yrs? 30 yrs? (What if he earns 3%/yr?) F = $5000(F A 6%,15) = $5000( ) = $116, F = $5000(F A 6%,20) = $5000( ) = $183, F = $5000(F A 6%,25) = $5000( ) = $274, F = $5000(F A 6%,30) = $5000( ) = $395, F = $5000(F A 3%,15) = $5000( ) = $92, F = $5000(F A 3%,20) = $5000( ) = $134, F = $5000(F A 3%,25) = $5000( ) = $182, F = $5000(F A 3%,30) = $5000( ) = $237,877.10

41 Example 2.25 If Coby Durham earns 7% on his investments, how much must he invest annually in order to accumulate $1,500,000 in 25 years? A = $1,500,000(A F 7%,25) A = $1,500,000( ) A = $23,715 A =PMT(7%,25,, ) A = $23,715.78

42 Example 2.26 If Crystal Wilson earns 10% on her investments, how much must she invest annually in order to accumulate $1,000,000 in 40 years? A = $1,000,000(A F 10%,40) A = $1,000,000( ) A = $2, A =PMT(10%,40,, ) A = $2,259.41

43 Example 2.27 $500,000 is spent for a SMP machine in order to reduce annual expenses by $92,500/yr. At the end of a 10-year planning horizon, the SMP machine is worth $50,000. Based on a 10% TVOM, a) what single sum at t = 0 is equivalent to the SMP investment? b) what single sum at t = 10 is equivalent to the SMP investment? c) what uniform annual series over the 10-year period is equivalent to the SMP investment? Solution: P = -$500,000 + $92,500(P A 10%,10) + $50,000(P F 10%,10) P = -$500,000 + $92,500( ) + $50,000( ) = $87, P =PV(10%,10,-92500,-50000) = $87,649.62

44 Example 2.27 (Solution) F = -$500,000(F P 10%,10) + $92,500(F A 10%,10) + $50,000 F = -$500,000( ) + $92,500( ) + $50,000 = $227, F =FV(10%,10,-92500,500000) = $227, A = -$500,000(A P 10%,10) + $92,500 + $50,000(A F 10%,10) A = -$500,000( ) + $92,500 + $50,000( ) = $14, A =PMT(10%,10,500000,-50000) = $14,264.57

45 P = A A = P F = A A = F [(1 + i) n 1 ] i(1 + i) n [ i(1 + i) n ] (1 + i) n 1 [ ] (1 + i) n 1 i [ i ] (1 + i) n 1 uniform series, present worth factor = A(P A i%,n) =PV(i%,n,-A) uniform series, capital recovery factor = P(A P i%,n) =PMT(i%,n,-P) uniform series, future worth factor = A(F A i%,n) =FV(i%,n,-A) uniform series, sinking fund factor = F(A F i%,n) =PMT(i%,n,,-F)

Chapter 2. Time Value of Money (TVOM) Principles of Engineering Economic Analysis, 5th edition

Principles of Engineering Economic Analysis, 5th edition") Chapter 2 Time Value of Money (TVOM) Cash Flow Diagrams $5,000 $5,000 $5,000 ( + ) 0 1 2 3 4 5 ( - ) Time $2,000 $3,000 $4,000 Example 2.1: Cash Flow Profiles for Two Investment Alternatives (EOY) CF(A)

Chapter 2 Time Value of Money (TVOM) Cash Flow Diagrams $5,000 $5,000 $5,000 ( + ) 0 1 2 3 4 5 ( - ) Time $2,000 $3,000 $4,000 Example 2.1: Cash Flow Profiles for Two Investment Alternatives (EOY) CF(A)

IE463 Chapter 2. Objective. Time Value of Money (Money- Time Relationships)

") IE463 Chapter 2 Time Value of Money (Money- Time Relationships) Objective Given a cash flow (or series of cash flows) occurring at some point in time, the objective is to find its equivalent value at another

IE463 Chapter 2 Time Value of Money (Money- Time Relationships) Objective Given a cash flow (or series of cash flows) occurring at some point in time, the objective is to find its equivalent value at another

Multiple Compounding Periods in a Year. Principles of Engineering Economic Analysis, 5th edition

Multiple Compounding Periods in a Year Example 2.36 Rebecca Carlson purchased a car for $25,000 by borrowing the money at 8% per year compounded monthly. She paid off the loan with 60 equal monthly payments,

Multiple Compounding Periods in a Year Example 2.36 Rebecca Carlson purchased a car for $25,000 by borrowing the money at 8% per year compounded monthly. She paid off the loan with 60 equal monthly payments,

Engineering Economy Chapter 4 More Interest Formulas

Engineering Economy Chapter 4 More Interest Formulas 1. Uniform Series Factors Used to Move Money Find F, Given A (i.e., F/A) Find A, Given F (i.e., A/F) Find P, Given A (i.e., P/A) Find A, Given P (i.e.,

Engineering Economy Chapter 4 More Interest Formulas 1. Uniform Series Factors Used to Move Money Find F, Given A (i.e., F/A) Find A, Given F (i.e., A/F) Find P, Given A (i.e., P/A) Find A, Given P (i.e.,

Engineering Economics

Economic Analysis Methods Engineering Economics Day 3: Rate of Return Analysis Three commonly used economic analysis methods are 1. Present Worth Analysis 2. Annual Worth Analysis 3. www.engr.sjsu.edu/bjfurman/courses/me195/presentations/engeconpatel3nov4.ppt

Economic Analysis Methods Engineering Economics Day 3: Rate of Return Analysis Three commonly used economic analysis methods are 1. Present Worth Analysis 2. Annual Worth Analysis 3. www.engr.sjsu.edu/bjfurman/courses/me195/presentations/engeconpatel3nov4.ppt

CHAPTER 7: ENGINEERING ECONOMICS

CHAPTER 7: ENGINEERING ECONOMICS The aim is to think about and understand the power of money on decision making BREAKEVEN ANALYSIS Breakeven point method deals with the effect of alternative rates of operation

CHAPTER 7: ENGINEERING ECONOMICS The aim is to think about and understand the power of money on decision making BREAKEVEN ANALYSIS Breakeven point method deals with the effect of alternative rates of operation

What is Value? Engineering Economics: Session 2. Page 1

Engineering Economics: Session 2 Engineering Economic Analysis: Slide 26 What is Value? Engineering Economic Analysis: Slide 27 Page 1 Review: Cash Flow Equivalence Type otation Formula Excel Single Uniform

Engineering Economics: Session 2 Engineering Economic Analysis: Slide 26 What is Value? Engineering Economic Analysis: Slide 27 Page 1 Review: Cash Flow Equivalence Type otation Formula Excel Single Uniform

TIME VALUE OF MONEY. Lecture Notes Week 4. Dr Wan Ahmad Wan Omar

TIME VALUE OF MONEY Lecture Notes Week 4 Dr Wan Ahmad Wan Omar Lecture Notes Week 4 4. The Time Value of Money The notion on time value of money is based on the idea that money available at the present

TIME VALUE OF MONEY Lecture Notes Week 4 Dr Wan Ahmad Wan Omar Lecture Notes Week 4 4. The Time Value of Money The notion on time value of money is based on the idea that money available at the present

Time Value of Money and Economic Equivalence

Time Value of Money and Economic Equivalence Lecture No.4 Chapter 3 Third Canadian Edition Copyright 2012 Chapter Opening Story Take a Lump Sum or Annual Installments q q q Millionaire Life is a lottery

Time Value of Money and Economic Equivalence Lecture No.4 Chapter 3 Third Canadian Edition Copyright 2012 Chapter Opening Story Take a Lump Sum or Annual Installments q q q Millionaire Life is a lottery

CE 231 ENGINEERING ECONOMY PROBLEM SET 1

CE 231 ENGINEERING ECONOMY PROBLEM SET 1 PROBLEM 1 The following two cash-flow operations are said to be present equivalent at 10 % interest rate compounded annually. Find X that satisfies the equivalence.

CE 231 ENGINEERING ECONOMY PROBLEM SET 1 PROBLEM 1 The following two cash-flow operations are said to be present equivalent at 10 % interest rate compounded annually. Find X that satisfies the equivalence.

7 - Engineering Economic Analysis

Construction Project Management (CE 110401346) 7 - Engineering Economic Analysis Dr. Khaled Hyari Department of Civil Engineering Hashemite University Introduction Is any individual project worthwhile?

Construction Project Management (CE 110401346) 7 - Engineering Economic Analysis Dr. Khaled Hyari Department of Civil Engineering Hashemite University Introduction Is any individual project worthwhile?

Interest: The money earned from an investment you have or the cost of borrowing money from a lender.

8.1 Simple Interest Interest: The money earned from an investment you have or the cost of borrowing money from a lender. Simple Interest: "I" Interest earned or paid that is calculated based only on the

8.1 Simple Interest Interest: The money earned from an investment you have or the cost of borrowing money from a lender. Simple Interest: "I" Interest earned or paid that is calculated based only on the

Engineering Economics ECIV 5245

Engineering Economics ECIV 5245 Chapter 3 Interest and Equivalence Cash Flow Diagrams (CFD) Used to model the positive and negative cash flows. At each time at which cash flow will occur, a vertical arrow

Engineering Economics ECIV 5245 Chapter 3 Interest and Equivalence Cash Flow Diagrams (CFD) Used to model the positive and negative cash flows. At each time at which cash flow will occur, a vertical arrow

LESSON 2 INTEREST FORMULAS AND THEIR APPLICATIONS. Overview of Interest Formulas and Their Applications. Symbols Used in Engineering Economy

Lesson Two: Interest Formulas and Their Applications from Understanding Engineering Economy: A Practical Approach LESSON 2 INTEREST FORMULAS AND THEIR APPLICATIONS Overview of Interest Formulas and Their

Lesson Two: Interest Formulas and Their Applications from Understanding Engineering Economy: A Practical Approach LESSON 2 INTEREST FORMULAS AND THEIR APPLICATIONS Overview of Interest Formulas and Their

Chapter 8. Rate of Return Analysis. Principles of Engineering Economic Analysis, 5th edition

Chapter 8 Rate of Return Analysis Systematic Economic Analysis Technique 1. Identify the investment alternatives 2. Define the planning horizon 3. Specify the discount rate 4. Estimate the cash flows 5.

Chapter 8 Rate of Return Analysis Systematic Economic Analysis Technique 1. Identify the investment alternatives 2. Define the planning horizon 3. Specify the discount rate 4. Estimate the cash flows 5.

Solutions to end-of-chapter problems Basics of Engineering Economy, 2 nd edition Leland Blank and Anthony Tarquin

Solutions to end-of-chapter problems Basics of Engineering Economy, 2 nd edition Leland Blank and Anthony Tarquin Chapter 2 Factors: How Time and Interest Affect Money 2.1 (a) (F/P,10%,20) = 6.7275 (b)

Solutions to end-of-chapter problems Basics of Engineering Economy, 2 nd edition Leland Blank and Anthony Tarquin Chapter 2 Factors: How Time and Interest Affect Money 2.1 (a) (F/P,10%,20) = 6.7275 (b)

TIME VALUE OF MONEY (TVM) IEG2H2-w2 1

IEG2H2-w2 1") TIME VALUE OF MONEY (TVM) IEG2H2-w2 1 After studying TVM, you should be able to: 1. Understand what is meant by "the time value of money." 2. Understand the relationship between present and future value.

TIME VALUE OF MONEY (TVM) IEG2H2-w2 1 After studying TVM, you should be able to: 1. Understand what is meant by "the time value of money." 2. Understand the relationship between present and future value.

??? Basic Concepts. ISyE 3025 Engineering Economy. Overview. Course Focus 2. Have we got a deal for you! 5. Pay Now or Pay Later 4. The Jackpot!

ISyE 3025 Engineering Economy Copyright 1999. Georgia Tech Research Corporation. All rights reserved. Basic Concepts Jack R. Lohmann School of Industrial and Systems Engineering Georgia Institute of Technology

ISyE 3025 Engineering Economy Copyright 1999. Georgia Tech Research Corporation. All rights reserved. Basic Concepts Jack R. Lohmann School of Industrial and Systems Engineering Georgia Institute of Technology

1) Cash Flow Pattern Diagram for Future Value and Present Value of Irregular Cash Flows

Cash Flow Pattern Diagram for Future Value and Present Value of Irregular Cash Flows") Topics Excel & Business Math Video/Class Project #45 Cash Flow Analysis for Annuities: Savings Plans, Asset Valuation, Retirement Plans and Mortgage Loan. FV, PV and PMT. 1) Cash Flow Pattern Diagram for

Topics Excel & Business Math Video/Class Project #45 Cash Flow Analysis for Annuities: Savings Plans, Asset Valuation, Retirement Plans and Mortgage Loan. FV, PV and PMT. 1) Cash Flow Pattern Diagram for

MULTIPLE-CHOICE QUESTIONS Circle the correct answer on this test paper and record it on the computer answer sheet.

M I M E 3 1 0 E N G I N E E R I N G E C O N O M Y Class Test #2 Thursday, 23 March, 2006 90 minutes PRINT your family name / initial and record your student ID number in the spaces provided below. FAMILY

M I M E 3 1 0 E N G I N E E R I N G E C O N O M Y Class Test #2 Thursday, 23 March, 2006 90 minutes PRINT your family name / initial and record your student ID number in the spaces provided below. FAMILY

FE Review Economics and Cash Flow

4/4/16 Compound Interest Variables FE Review Economics and Cash Flow Andrew Pederson P = present single sum of money (single cash flow). F = future single sum of money (single cash flow). A = uniform series

4/4/16 Compound Interest Variables FE Review Economics and Cash Flow Andrew Pederson P = present single sum of money (single cash flow). F = future single sum of money (single cash flow). A = uniform series

ME 353 ENGINEERING ECONOMICS Sample Second Midterm Exam

ME 353 ENGINEERING ECONOMICS Sample Second Midterm Exam Scoring gives priority to the correct formulation. Numerical answers without the correct formulas for justification receive no credit. Decisions

ME 353 ENGINEERING ECONOMICS Sample Second Midterm Exam Scoring gives priority to the correct formulation. Numerical answers without the correct formulas for justification receive no credit. Decisions

3. Time value of money. We will review some tools for discounting cash flows.

1 3. Time value of money We will review some tools for discounting cash flows. Simple interest 2 With simple interest, the amount earned each period is always the same: i = rp o where i = interest earned

1 3. Time value of money We will review some tools for discounting cash flows. Simple interest 2 With simple interest, the amount earned each period is always the same: i = rp o where i = interest earned

FINANCE FOR EVERYONE SPREADSHEETS

FINANCE FOR EVERYONE SPREADSHEETS Some Important Stuff Make sure there are at least two decimals allowed in each cell. Otherwise rounding off may create problems in a multi-step problem Always enter the

FINANCE FOR EVERYONE SPREADSHEETS Some Important Stuff Make sure there are at least two decimals allowed in each cell. Otherwise rounding off may create problems in a multi-step problem Always enter the

Chapter 15B and 15C - Annuities formula

Chapter 15B and 15C - Annuities formula Finding the amount owing at any time during the term of the loan. A = PR n Q Rn 1 or TVM function on the Graphics Calculator Finding the repayment amount, Q Q =

Chapter 15B and 15C - Annuities formula Finding the amount owing at any time during the term of the loan. A = PR n Q Rn 1 or TVM function on the Graphics Calculator Finding the repayment amount, Q Q =

Fin 5413: Chapter 04 - Fixed Interest Rate Mortgage Loans Page 1 Solutions to Problems - Chapter 4 Fixed Interest Rate Mortgage Loans

Fin 5413: Chapter 04 - Fixed Interest Rate Mortgage Loans Page 1 Solutions to Problems - Chapter 4 Fixed Interest Rate Mortgage Loans Problem 4-1 A borrower makes a fully amortizing CPM mortgage loan.

Fin 5413: Chapter 04 - Fixed Interest Rate Mortgage Loans Page 1 Solutions to Problems - Chapter 4 Fixed Interest Rate Mortgage Loans Problem 4-1 A borrower makes a fully amortizing CPM mortgage loan.

3. Time value of money

1 Simple interest 2 3. Time value of money With simple interest, the amount earned each period is always the same: i = rp o We will review some tools for discounting cash flows. where i = interest earned

1 Simple interest 2 3. Time value of money With simple interest, the amount earned each period is always the same: i = rp o We will review some tools for discounting cash flows. where i = interest earned

Lecture 3. Chapter 4: Allocating Resources Over Time

Lecture 3 Chapter 4: Allocating Resources Over Time 1 Introduction: Time Value of Money (TVM) $20 today is worth more than the expectation of $20 tomorrow because: a bank would pay interest on the $20

Lecture 3 Chapter 4: Allocating Resources Over Time 1 Introduction: Time Value of Money (TVM) $20 today is worth more than the expectation of $20 tomorrow because: a bank would pay interest on the $20

IE 343 Midterm Exam 1

IE 343 Midterm Exam 1 Feb 17, 2012 Version A Closed book, closed notes. Write your printed name in the spaces provided above on every page. Show all of your work in the spaces provided. Interest rate tables

IE 343 Midterm Exam 1 Feb 17, 2012 Version A Closed book, closed notes. Write your printed name in the spaces provided above on every page. Show all of your work in the spaces provided. Interest rate tables

Understanding Interest Rates

Money & Banking Notes Chapter 4 Understanding Interest Rates Measuring Interest Rates Present Value (PV): A dollar paid to you one year from now is less valuable than a dollar paid to you today. Why? -

Money & Banking Notes Chapter 4 Understanding Interest Rates Measuring Interest Rates Present Value (PV): A dollar paid to you one year from now is less valuable than a dollar paid to you today. Why? -

Cha h pt p er 2 Fac a t c o t rs r : s : H o H w w T i T me e a n a d I nte t r e e r s e t s A f f e f c e t c t M oney

Chapter 2 Factors: How Time and Interest Affect Money 2-1 LEARNING OBJECTIVES 1. F/P and P/F factors 2. P/A and A/P factors 3. Interpolate for factor values 4. P/G and A/G factors 5. Geometric gradient

Chapter 2 Factors: How Time and Interest Affect Money 2-1 LEARNING OBJECTIVES 1. F/P and P/F factors 2. P/A and A/P factors 3. Interpolate for factor values 4. P/G and A/G factors 5. Geometric gradient

Chapter 4. Discounted Cash Flow Valuation

Chapter 4 Discounted Cash Flow Valuation Appreciate the significance of compound vs. simple interest Describe and compute the future value and/or present value of a single cash flow or series of cash flows

Chapter 4 Discounted Cash Flow Valuation Appreciate the significance of compound vs. simple interest Describe and compute the future value and/or present value of a single cash flow or series of cash flows

Chapter 5. Learning Objectives. Principals Applied in this Chapter. Time Value of Money. Principle 1: Money Has a Time Value.

Chapter 5 Time Value of Money Learning Objectives 1. Construct cash flow timelines to organize your analysis of problems involving the time value of money. 2. Understand compounding and calculate the future

Chapter 5 Time Value of Money Learning Objectives 1. Construct cash flow timelines to organize your analysis of problems involving the time value of money. 2. Understand compounding and calculate the future

Chapter 5. Time Value of Money

Chapter 5 Time Value of Money Using Timelines to Visualize Cashflows A timeline identifies the timing and amount of a stream of payments both cash received and cash spent - along with the interest rate

Chapter 5 Time Value of Money Using Timelines to Visualize Cashflows A timeline identifies the timing and amount of a stream of payments both cash received and cash spent - along with the interest rate

Financial institutions pay interest when you deposit your money into one of their accounts.

KEY CONCEPTS Financial institutions pay interest when you deposit your money into one of their accounts. Often, financial institutions charge fees or service charges for providing you with certain services

KEY CONCEPTS Financial institutions pay interest when you deposit your money into one of their accounts. Often, financial institutions charge fees or service charges for providing you with certain services

5.3 Amortization and Sinking Funds

5.3 Amortization and Sinking Funds Sinking Funds A sinking fund is an account that is set up for a specific purpose at some future date. Typical examples of this are retirement plans, saving money for

5.3 Amortization and Sinking Funds Sinking Funds A sinking fund is an account that is set up for a specific purpose at some future date. Typical examples of this are retirement plans, saving money for

REVIEW MATERIALS FOR REAL ESTATE FUNDAMENTALS

REVIEW MATERIALS FOR REAL ESTATE FUNDAMENTALS 1997, Roy T. Black J. Andrew Hansz, Ph.D., CFA REAE 3325, Fall 2005 University of Texas, Arlington Department of Finance and Real Estate CONTENTS ITEM ANNUAL

REVIEW MATERIALS FOR REAL ESTATE FUNDAMENTALS 1997, Roy T. Black J. Andrew Hansz, Ph.D., CFA REAE 3325, Fall 2005 University of Texas, Arlington Department of Finance and Real Estate CONTENTS ITEM ANNUAL

Simple Interest: Interest earned on the original investment amount only. I = Prt

c Kathryn Bollinger, June 28, 2011 1 Chapter 5 - Finance 5.1 - Compound Interest Simple Interest: Interest earned on the original investment amount only If P dollars (called the principal or present value)

c Kathryn Bollinger, June 28, 2011 1 Chapter 5 - Finance 5.1 - Compound Interest Simple Interest: Interest earned on the original investment amount only If P dollars (called the principal or present value)

2. I =interest (in dollars and cents, accumulated over some period)

") A. Recap of the Variables 1. P = principal (as designated at some point in time) a. we shall use PV for present value. Your text and others use P for PV (We shall do it sometimes too!) 2. I =interest (in

A. Recap of the Variables 1. P = principal (as designated at some point in time) a. we shall use PV for present value. Your text and others use P for PV (We shall do it sometimes too!) 2. I =interest (in

Section 5.1 Simple and Compound Interest

Section 5.1 Simple and Compound Interest Question 1 What is simple interest? Question 2 What is compound interest? Question 3 - What is an effective interest rate? Question 4 - What is continuous compound

Section 5.1 Simple and Compound Interest Question 1 What is simple interest? Question 2 What is compound interest? Question 3 - What is an effective interest rate? Question 4 - What is continuous compound

Math 373 Test 2 Fall 2014 March 11, 2014

Math 373 Test 2 Fall 204 March, 204. Rendong is repaying a loan of 0,000 with monthly payments of 400 plus a smaller drop payment. Rendong is paying an annual effective interest rate of %. Determine the

Math 373 Test 2 Fall 204 March, 204. Rendong is repaying a loan of 0,000 with monthly payments of 400 plus a smaller drop payment. Rendong is paying an annual effective interest rate of %. Determine the

Chapter 4 The Time Value of Money

Chapter 4 The Time Value of Money Copyright 2011 Pearson Prentice Hall. All rights reserved. Chapter Outline 4.1 The Timeline 4.2 The Three Rules of Time Travel 4.3 Valuing a Stream of Cash Flows 4.4 Calculating

Chapter 4 The Time Value of Money Copyright 2011 Pearson Prentice Hall. All rights reserved. Chapter Outline 4.1 The Timeline 4.2 The Three Rules of Time Travel 4.3 Valuing a Stream of Cash Flows 4.4 Calculating

ME 353 ENGINEERING ECONOMICS

ME 353 ENGINEERING ECONOMICS Final Exam Sample Scoring gives priority to the correct formulas. Numerical answers without the correct formulas for justification receive no credit. Decisions without numerical

ME 353 ENGINEERING ECONOMICS Final Exam Sample Scoring gives priority to the correct formulas. Numerical answers without the correct formulas for justification receive no credit. Decisions without numerical

FINANCIAL DECISION RULES FOR PROJECT EVALUATION SPREADSHEETS

FINANCIAL DECISION RULES FOR PROJECT EVALUATION SPREADSHEETS This note is some basic information that should help you get started and do most calculations if you have access to spreadsheets. You could

FINANCIAL DECISION RULES FOR PROJECT EVALUATION SPREADSHEETS This note is some basic information that should help you get started and do most calculations if you have access to spreadsheets. You could

hp calculators HP 20b Loan Amortizations The time value of money application Amortization Amortization on the HP 20b Practice amortizing loans

The time value of money application Amortization Amortization on the HP 20b Practice amortizing loans The time value of money application The time value of money application built into the HP 20b is used

The time value of money application Amortization Amortization on the HP 20b Practice amortizing loans The time value of money application The time value of money application built into the HP 20b is used

6.1 Simple and Compound Interest

6.1 Simple and Compound Interest If P dollars (called the principal or present value) earns interest at a simple interest rate of r per year (as a decimal) for t years, then Interest: I = P rt Accumulated

6.1 Simple and Compound Interest If P dollars (called the principal or present value) earns interest at a simple interest rate of r per year (as a decimal) for t years, then Interest: I = P rt Accumulated

Chapter 3 Mathematics of Finance

Chapter 3 Mathematics of Finance Section R Review Important Terms, Symbols, Concepts 3.1 Simple Interest Interest is the fee paid for the use of a sum of money P, called the principal. Simple interest

Chapter 3 Mathematics of Finance Section R Review Important Terms, Symbols, Concepts 3.1 Simple Interest Interest is the fee paid for the use of a sum of money P, called the principal. Simple interest

3.1 Simple Interest. Definition: I = Prt I = interest earned P = principal ( amount invested) r = interest rate (as a decimal) t = time

r = interest rate (as a decimal) t = time") 3.1 Simple Interest Definition: I = Prt I = interest earned P = principal ( amount invested) r = interest rate (as a decimal) t = time An example: Find the interest on a boat loan of $5,000 at 16% for

3.1 Simple Interest Definition: I = Prt I = interest earned P = principal ( amount invested) r = interest rate (as a decimal) t = time An example: Find the interest on a boat loan of $5,000 at 16% for

Chapter 5 - Level 3 - Course FM Solutions

ONLY CERTAIN PROBLEMS HAVE SOLUTIONS. THE REMAINING WILL BE ADDED OVER TIME. 1. Kathy can take out a loan of 50,000 with Bank A or Bank B. With Bank A, she must repay the loan with 60 monthly payments

ONLY CERTAIN PROBLEMS HAVE SOLUTIONS. THE REMAINING WILL BE ADDED OVER TIME. 1. Kathy can take out a loan of 50,000 with Bank A or Bank B. With Bank A, she must repay the loan with 60 monthly payments

Math 373 Test 2 Fall 2013 October 17, 2013

Math 373 Test 2 Fall 2013 October 17, 2013 1. You are given the following table of interest rates: Year 1 Year 2 Year 3 Portfolio Year 2007 0.060 0.058 0.056 0.054 2010 2008 0.055 0.052 0.049 0.046 2011

Math 373 Test 2 Fall 2013 October 17, 2013 1. You are given the following table of interest rates: Year 1 Year 2 Year 3 Portfolio Year 2007 0.060 0.058 0.056 0.054 2010 2008 0.055 0.052 0.049 0.046 2011

The car Adam is considering is $35,000. The dealer has given him three payment options:

Adam Rust looked at his mechanic and sighed. The mechanic had just pronounced a death sentence on his road-weary car. The car had served him well---at a cost of 500 it had lasted through four years of

Adam Rust looked at his mechanic and sighed. The mechanic had just pronounced a death sentence on his road-weary car. The car had served him well---at a cost of 500 it had lasted through four years of

Our Own Problems and Solutions to Accompany Topic 11

Our Own Problems and Solutions to Accompany Topic. A home buyer wants to borrow $240,000, and to repay the loan with monthly payments over 30 years. A. Compute the unchanging monthly payments for a standard

Our Own Problems and Solutions to Accompany Topic. A home buyer wants to borrow $240,000, and to repay the loan with monthly payments over 30 years. A. Compute the unchanging monthly payments for a standard

Solutions to Questions - Chapter 3 Mortgage Loan Foundations: The Time Value of Money

Solutions to Questions - Chapter 3 Mortgage Loan Foundations: The Time Value of Money Question 3-1 What is the essential concept in understanding compound interest? The concept of earning interest on interest

Solutions to Questions - Chapter 3 Mortgage Loan Foundations: The Time Value of Money Question 3-1 What is the essential concept in understanding compound interest? The concept of earning interest on interest

Fin 5413: Chapter 06 - Mortgages: Additional Concepts, Analysis, and Applications Page 1

Fin 5413: Chapter 06 - Mortgages: Additional Concepts, Analysis, and Applications Page 1 INTRODUCTION Solutions to Problems - Chapter 6 Mortgages: Additional Concepts, Analysis, and Applications The following

Fin 5413: Chapter 06 - Mortgages: Additional Concepts, Analysis, and Applications Page 1 INTRODUCTION Solutions to Problems - Chapter 6 Mortgages: Additional Concepts, Analysis, and Applications The following

4: Single Cash Flows and Equivalence

4.1 Single Cash Flows and Equivalence Basic Concepts 28 4: Single Cash Flows and Equivalence This chapter explains basic concepts of project economics by examining single cash flows. This means that each

4.1 Single Cash Flows and Equivalence Basic Concepts 28 4: Single Cash Flows and Equivalence This chapter explains basic concepts of project economics by examining single cash flows. This means that each

Worksheet-2 Present Value Math I

What you will learn: Worksheet-2 Present Value Math I How to compute present and future values of single and annuity cash flows How to handle cash flow delays and combinations of cash flow streams How

What you will learn: Worksheet-2 Present Value Math I How to compute present and future values of single and annuity cash flows How to handle cash flow delays and combinations of cash flow streams How

CAPITAL BUDGETING Shenandoah Furniture, Inc.

CAPITAL BUDGETING Shenandoah Furniture, Inc. Shenandoah Furniture is considering replacing one of the machines in its manufacturing facility. The cost of the new machine will be $76,120. Transportation

CAPITAL BUDGETING Shenandoah Furniture, Inc. Shenandoah Furniture is considering replacing one of the machines in its manufacturing facility. The cost of the new machine will be $76,120. Transportation

MATH 373 Test 2 Fall 2018 November 1, 2018

MATH 373 Test 2 Fall 2018 November 1, 2018 1. A 20 year bond has a par value of 1000 and a maturity value of 1300. The semi-annual coupon rate for the bond is 7.5% convertible semi-annually. The bond is

MATH 373 Test 2 Fall 2018 November 1, 2018 1. A 20 year bond has a par value of 1000 and a maturity value of 1300. The semi-annual coupon rate for the bond is 7.5% convertible semi-annually. The bond is

CHAPTER 4. The Time Value of Money. Chapter Synopsis

CHAPTER 4 The Time Value of Money Chapter Synopsis Many financial problems require the valuation of cash flows occurring at different times. However, money received in the future is worth less than money

CHAPTER 4 The Time Value of Money Chapter Synopsis Many financial problems require the valuation of cash flows occurring at different times. However, money received in the future is worth less than money

Simple Interest. Simple Interest is the money earned (or owed) only on the borrowed. Balance that Interest is Calculated On

only on the borrowed. Balance that Interest is Calculated On") MCR3U Unit 8: Financial Applications Lesson 1 Date: Learning goal: I understand simple interest and can calculate any value in the simple interest formula. Simple Interest is the money earned (or owed)

MCR3U Unit 8: Financial Applications Lesson 1 Date: Learning goal: I understand simple interest and can calculate any value in the simple interest formula. Simple Interest is the money earned (or owed)

A central precept of financial analysis is money s time value. This essentially means that every dollar (or

INTRODUCTION TO THE TIME VALUE OF MONEY 1. INTRODUCTION A central precept of financial analysis is money s time value. This essentially means that every dollar (or a unit of any other currency) received

INTRODUCTION TO THE TIME VALUE OF MONEY 1. INTRODUCTION A central precept of financial analysis is money s time value. This essentially means that every dollar (or a unit of any other currency) received

Copyright 2015 Pearson Education, Inc. All rights reserved.

Chapter 4 Mathematics of Finance Section 4.1 Simple Interest and Discount A fee that is charged by a lender to a borrower for the right to use the borrowed funds. The funds can be used to purchase a house,

Chapter 4 Mathematics of Finance Section 4.1 Simple Interest and Discount A fee that is charged by a lender to a borrower for the right to use the borrowed funds. The funds can be used to purchase a house,

Math 373 Fall 2012 Test 2

Math 373 Fall 2012 Test 2 October 18, 2012 1. Jordan has the option to purchase either of the two bonds below. Both bonds will be purchased to provide the same yield rate. a. A 20-year zero coupon bond

Math 373 Fall 2012 Test 2 October 18, 2012 1. Jordan has the option to purchase either of the two bonds below. Both bonds will be purchased to provide the same yield rate. a. A 20-year zero coupon bond

Chapter 15 Inflation

Chapter 15 Inflation 15-1 The first sewage treatment plant for Athens, Georgia cost about $2 million in 1964. The utilized capacity of the plant was 5 million gallons/day (mgd). Using the commonly accepted

Chapter 15 Inflation 15-1 The first sewage treatment plant for Athens, Georgia cost about $2 million in 1964. The utilized capacity of the plant was 5 million gallons/day (mgd). Using the commonly accepted

Outline of Review Topics

Outline of Review Topics Cash flow and equivalence Depreciation Special topics Comparison of alternatives Ethics Method of review Brief review of topic Problems 1 Cash Flow and Equivalence Cash flow Diagrams

Outline of Review Topics Cash flow and equivalence Depreciation Special topics Comparison of alternatives Ethics Method of review Brief review of topic Problems 1 Cash Flow and Equivalence Cash flow Diagrams

Section 4B: The Power of Compounding

Section 4B: The Power of Compounding Definitions The principal is the amount of your initial investment. This is the amount on which interest is paid. Simple interest is interest paid only on the original

Section 4B: The Power of Compounding Definitions The principal is the amount of your initial investment. This is the amount on which interest is paid. Simple interest is interest paid only on the original

Understanding Interest Rates

Understanding Interest Rates Leigh Tesfatsion (Iowa State University) Notes on Mishkin Chapter 4: Part A (pp. 68-80) Last Revised: 14 February 2011 Mishkin Chapter 4: Part A -- Selected Key In-Class Discussion

Understanding Interest Rates Leigh Tesfatsion (Iowa State University) Notes on Mishkin Chapter 4: Part A (pp. 68-80) Last Revised: 14 February 2011 Mishkin Chapter 4: Part A -- Selected Key In-Class Discussion

An Introduction to Capital Budgeting Methods

An Introduction to Capital Budgeting Methods Econ 466 Spring, 2010 Chapters 9 and 10 Consider the following choice You have an opportunity to invest $20,000 in one of the following capital assets. You

An Introduction to Capital Budgeting Methods Econ 466 Spring, 2010 Chapters 9 and 10 Consider the following choice You have an opportunity to invest $20,000 in one of the following capital assets. You

Full file at https://fratstock.eu

Chapter 2 Time Value of Money ANSWERS TO END-OF-CHAPTER QUESTIONS 2-1 a. PV (present value) is the value today of a future payment, or stream of payments, discounted at the appropriate rate of interest.

Chapter 2 Time Value of Money ANSWERS TO END-OF-CHAPTER QUESTIONS 2-1 a. PV (present value) is the value today of a future payment, or stream of payments, discounted at the appropriate rate of interest.

CHAPTER 4 SIMPLE AND COMPOUND INTEREST INCLUDING ANNUITY APPLICATIONS. Copyright -The Institute of Chartered Accountants of India

CHAPTER 4 SIMPLE AND COMPOUND INTEREST INCLUDING ANNUITY APPLICATIONS SIMPLE AND COMPOUND INTEREST INCLUDING ANNUITY- APPLICATIONS LEARNING OBJECTIVES After studying this chapter students will be able

CHAPTER 4 SIMPLE AND COMPOUND INTEREST INCLUDING ANNUITY APPLICATIONS SIMPLE AND COMPOUND INTEREST INCLUDING ANNUITY- APPLICATIONS LEARNING OBJECTIVES After studying this chapter students will be able

22.812J Nuclear Energy Economics and Policy Analysis S 04. Classnote: The Time Value of Money

22.812J uclear Energy Economics and Policy Analysis S 04 Classnote: The Time Value of Money 1. Motivating Example To motivate the discussion, we consider a homeowner faced with a decision whether to install

22.812J uclear Energy Economics and Policy Analysis S 04 Classnote: The Time Value of Money 1. Motivating Example To motivate the discussion, we consider a homeowner faced with a decision whether to install

Math 373 Test 1 Spring 2015 February 17, 2015

Math 373 Test 1 Spring 2015 February 17, 2015 1. Hannah is the beneficiary of a trust that will pay her an annual payment of 10,000 with the first payment made twelve years from today. Once the payments

Math 373 Test 1 Spring 2015 February 17, 2015 1. Hannah is the beneficiary of a trust that will pay her an annual payment of 10,000 with the first payment made twelve years from today. Once the payments

Time Value of Money. PV of Multiple Cash Flows. Present Value & Discounting. Future Value & Compounding. PV of Multiple Cash Flows

Chapter 4-6 Time Value of Money Net Present Value Capital Budgeting Konan Chan Financial Management, 2018 Time Value of Money Present values Future values Annuity and Perpetuity APR vs. EAR Five factor

Chapter 4-6 Time Value of Money Net Present Value Capital Budgeting Konan Chan Financial Management, 2018 Time Value of Money Present values Future values Annuity and Perpetuity APR vs. EAR Five factor

Chapter 4-6 Time Value of Money Net Present Value Capital Budgeting. Konan Chan Financial Management, Time Value of Money

Chapter 4-6 Time Value of Money Net Present Value Capital Budgeting Konan Chan Financial Management, 2018 Time Value of Money Present values Future values Annuity and Perpetuity APR vs. EAR Five factor

Chapter 4-6 Time Value of Money Net Present Value Capital Budgeting Konan Chan Financial Management, 2018 Time Value of Money Present values Future values Annuity and Perpetuity APR vs. EAR Five factor

I. Warnings for annuities and

Outline I. More on the use of the financial calculator and warnings II. Dealing with periods other than years III. Understanding interest rate quotes and conversions IV. Applications mortgages, etc. 0

Outline I. More on the use of the financial calculator and warnings II. Dealing with periods other than years III. Understanding interest rate quotes and conversions IV. Applications mortgages, etc. 0

Manual for SOA Exam FM/CAS Exam 2.

Manual for SOA Exam FM/CAS Exam 2. Chapter 2. Cashflows. c 2009. Miguel A. Arcones. All rights reserved. Extract from: Arcones Manual for the SOA Exam FM/CAS Exam 2, Financial Mathematics. Fall 2009 Edition,

Manual for SOA Exam FM/CAS Exam 2. Chapter 2. Cashflows. c 2009. Miguel A. Arcones. All rights reserved. Extract from: Arcones Manual for the SOA Exam FM/CAS Exam 2, Financial Mathematics. Fall 2009 Edition,

Engineering Economic Analysis 9th Edition. Chapter 3 INTEREST AND EQUIVALENCE

Engineering Economic Analysis 9th Edition Chapter 3 INTEREST AND EQUIVALENCE Economic Decision Components Where economic decisions are immediate we need to consider: amount of expenditure taxes Where economic

Engineering Economic Analysis 9th Edition Chapter 3 INTEREST AND EQUIVALENCE Economic Decision Components Where economic decisions are immediate we need to consider: amount of expenditure taxes Where economic

4. Understanding.. Interest Rates. Copyright 2007 Pearson Addison-Wesley. All rights reserved. 4-1

4. Understanding. Interest Rates Copyright 2007 Pearson Addison-Wesley. All rights reserved. 4-1 Present Value A dollar paid to you one year from now is less valuable than a dollar paid to you today Copyright

4. Understanding. Interest Rates Copyright 2007 Pearson Addison-Wesley. All rights reserved. 4-1 Present Value A dollar paid to you one year from now is less valuable than a dollar paid to you today Copyright

Example. Chapter F Finance Section F.1 Simple Interest and Discount

Math 166 (c)2011 Epstein Chapter F Page 1 Chapter F Finance Section F.1 Simple Interest and Discount Math 166 (c)2011 Epstein Chapter F Page 2 How much should be place in an account that pays simple interest

Math 166 (c)2011 Epstein Chapter F Page 1 Chapter F Finance Section F.1 Simple Interest and Discount Math 166 (c)2011 Epstein Chapter F Page 2 How much should be place in an account that pays simple interest

Using an interest rate of 7.42%, calculate the present value of Hannah s payments. PV 10, 000a v 53,

13. Hannah is the beneficiary of a trust that will pay her an annual payment of 10,000 with the first payment made fourteen years from today. Once the payments beginning they will be made forever to Hannah

13. Hannah is the beneficiary of a trust that will pay her an annual payment of 10,000 with the first payment made fourteen years from today. Once the payments beginning they will be made forever to Hannah

Tax Homework. A B C Installed cost $10,000 $15,000 $20,000 Net Uniform annual before 3,000 6,000 10,000

Tax Homework 1. A firm is considering three mutually exclusive alternatives as part of a production improvement program. Management requires that you must select one. The alternatives are: A B C Installed

Tax Homework 1. A firm is considering three mutually exclusive alternatives as part of a production improvement program. Management requires that you must select one. The alternatives are: A B C Installed

Year 10 Mathematics Semester 2 Financial Maths Chapter 15

Year 10 Mathematics Semester 2 Financial Maths Chapter 15 Why learn this? Everyone requires food, housing, clothing and transport, and a fulfilling social life. Money allows us to purchase the things we

Year 10 Mathematics Semester 2 Financial Maths Chapter 15 Why learn this? Everyone requires food, housing, clothing and transport, and a fulfilling social life. Money allows us to purchase the things we

Real Estate. Refinancing

Introduction This Solutions Handbook has been designed to supplement the HP-12C Owner's Handbook by providing a variety of applications in the financial area. Programs and/or step-by-step keystroke procedures

Introduction This Solutions Handbook has been designed to supplement the HP-12C Owner's Handbook by providing a variety of applications in the financial area. Programs and/or step-by-step keystroke procedures

Lesson FA xx Capital Budgeting Part 2C

- - - - - - Cover Page - - - - - - Lesson FA-20-170-xx Capital Budgeting Part 2C These notes and worksheets accompany the corresponding video lesson available online at: Permission is granted for educators

- - - - - - Cover Page - - - - - - Lesson FA-20-170-xx Capital Budgeting Part 2C These notes and worksheets accompany the corresponding video lesson available online at: Permission is granted for educators

Time Value of Money. Chapter 5 & 6 Financial Calculator and Examples. Five Factors in TVM. Annual &Non-annual Compound

Chapter 5 & 6 Financial Calculator and Examples Konan Chan Financial Management, Fall 2018 Time Value of Money N: number of compounding periods I/Y: periodic rate (I/Y = APR/m) PV: present value PMT: periodic

Chapter 5 & 6 Financial Calculator and Examples Konan Chan Financial Management, Fall 2018 Time Value of Money N: number of compounding periods I/Y: periodic rate (I/Y = APR/m) PV: present value PMT: periodic

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture 09 Future Value Welcome to the lecture series on Time

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture 09 Future Value Welcome to the lecture series on Time

Chapter 2 Applying Time Value Concepts

Chapter 2 Applying Time Value Concepts Chapter Overview Albert Einstein, the renowned physicist whose theories of relativity formed the theoretical base for the utilization of atomic energy, called the

Chapter 2 Applying Time Value Concepts Chapter Overview Albert Einstein, the renowned physicist whose theories of relativity formed the theoretical base for the utilization of atomic energy, called the

Capital Leases I: Present and Future Value

Spreadsheet Models for Managers 9/1 Session 9 Capital Leases I: Present and Future Value Worksheet Functions Non-Uniform Payments Last revised: July 6, 2011 Review of last time: Financial Models 9/2 Three

Spreadsheet Models for Managers 9/1 Session 9 Capital Leases I: Present and Future Value Worksheet Functions Non-Uniform Payments Last revised: July 6, 2011 Review of last time: Financial Models 9/2 Three

Errata and Updates for the 12 th Edition of the ASM Manual for Exam FM/2 (Last updated 5/4/2018) sorted by page

sorted by page") Errata and Updates for the 12 th Edition of the ASM Manual for Exam FM/2 (Last updated 5/4/2018) sorted by page [2/28/18] Page 255, Question 47. The last answer should be 7.98 without the % sign. [7/30/17]

Errata and Updates for the 12 th Edition of the ASM Manual for Exam FM/2 (Last updated 5/4/2018) sorted by page [2/28/18] Page 255, Question 47. The last answer should be 7.98 without the % sign. [7/30/17]

MULTIPLE-CHOICE QUESTIONS Circle the correct answers on this test paper and record them on the computer answer sheet.

#18: /10 #19: /9 Total: /19 VERSION 1 M I M E 3 1 0 E N G I N E E R I N G E C O N O M Y Class Test #2 Wednesday, 12 November, 2008 90 minutes PRINT your family name / initial and record your student ID

#18: /10 #19: /9 Total: /19 VERSION 1 M I M E 3 1 0 E N G I N E E R I N G E C O N O M Y Class Test #2 Wednesday, 12 November, 2008 90 minutes PRINT your family name / initial and record your student ID

Chapter 5 & 6 Financial Calculator and Examples

Chapter 5 & 6 Financial Calculator and Examples Konan Chan Financial Management, Fall 2018 Five Factors in TVM Present value: PV Future value: FV Discount rate: r Payment: PMT Number of periods: N Get

Chapter 5 & 6 Financial Calculator and Examples Konan Chan Financial Management, Fall 2018 Five Factors in TVM Present value: PV Future value: FV Discount rate: r Payment: PMT Number of periods: N Get

Real Estate Investment Analysis using Excel

Graduate Certificate in Real Estate Finance (GCREF) course Real Estate Investment Analysis using Excel Sing Tien Foo Department of Real Estate 27 May 2016 2 Website for sample template http://www.rst.nus.edu.sg/staff/singtienfoo/

Graduate Certificate in Real Estate Finance (GCREF) course Real Estate Investment Analysis using Excel Sing Tien Foo Department of Real Estate 27 May 2016 2 Website for sample template http://www.rst.nus.edu.sg/staff/singtienfoo/

Chapter 9, Mathematics of Finance from Applied Finite Mathematics by Rupinder Sekhon was developed by OpenStax College, licensed by Rice University,

Chapter 9, Mathematics of Finance from Applied Finite Mathematics by Rupinder Sekhon was developed by OpenStax College, licensed by Rice University, and is available on the Connexions website. It is used

Chapter 9, Mathematics of Finance from Applied Finite Mathematics by Rupinder Sekhon was developed by OpenStax College, licensed by Rice University, and is available on the Connexions website. It is used

Mortgage Finance Review Questions 1

Mortgage Finance Review Questions 1 BUSI 221 MORTGAGE FINANCE REVIEW QUESTIONS Detailed solutions are provided at the end of the questions. REVIEW QUESTION 1 Gordon and Helen have recently purchased a

Mortgage Finance Review Questions 1 BUSI 221 MORTGAGE FINANCE REVIEW QUESTIONS Detailed solutions are provided at the end of the questions. REVIEW QUESTION 1 Gordon and Helen have recently purchased a

Chapter 2 Time Value of Money

Chapter 2 Time Value of Money Learning Objectives After reading this chapter, students should be able to: Convert time value of money (TVM) problems from words to time lines. Explain the relationship between

Chapter 2 Time Value of Money Learning Objectives After reading this chapter, students should be able to: Convert time value of money (TVM) problems from words to time lines. Explain the relationship between

Time Value of Money. Part III. Outline of the Lecture. September Growing Annuities. The Effect of Compounding. Loan Type and Loan Amortization

Time Value of Money Part III September 2003 Outline of the Lecture Growing Annuities The Effect of Compounding Loan Type and Loan Amortization 2 Growing Annuities The present value of an annuity in which

Time Value of Money Part III September 2003 Outline of the Lecture Growing Annuities The Effect of Compounding Loan Type and Loan Amortization 2 Growing Annuities The present value of an annuity in which

IE 343 Midterm Exam. March 7 th Closed book, closed notes.

IE 343 Midterm Exam March 7 th 2013 Closed book, closed notes. Write your name in the spaces provided above. Write your name on each page as well, so that in the event the pages are separated, we can still

IE 343 Midterm Exam March 7 th 2013 Closed book, closed notes. Write your name in the spaces provided above. Write your name on each page as well, so that in the event the pages are separated, we can still

Session 1, Monday, April 8 th (9:45-10:45)

") Session 1, Monday, April 8 th (9:45-10:45) Time Value of Money and Capital Budgeting v2.0 2014 Association for Financial Professionals. All rights reserved. Session 3-1 Chapters Covered Time Value of Money:

Session 1, Monday, April 8 th (9:45-10:45) Time Value of Money and Capital Budgeting v2.0 2014 Association for Financial Professionals. All rights reserved. Session 3-1 Chapters Covered Time Value of Money:

Interest and present value Simple Interest Interest amount = P x i x n p = principle i = interest rate n = number of periods Assume you invest $1,000 at 6% simple interest for 3 years. You would earn $180

Interest and present value Simple Interest Interest amount = P x i x n p = principle i = interest rate n = number of periods Assume you invest $1,000 at 6% simple interest for 3 years. You would earn $180

CE 561 Lecture Notes. Engineering Economic Analysis. Set 2. Time value of money. Cash Flow Diagram. Interest. Inflation Opportunity cost

CE 56 Lecture otes Set 2 Engineering Economic Analysis Time value of money Inflation Opportunity cost Cash Flow Diagram P A A PInvestment AYearly Return 0 o. of Years Interest Profit Motive MARR Public

CE 56 Lecture otes Set 2 Engineering Economic Analysis Time value of money Inflation Opportunity cost Cash Flow Diagram P A A PInvestment AYearly Return 0 o. of Years Interest Profit Motive MARR Public