BASIC IS-LM by John Eckalbar

|

|

|

- Alban Powell

- 5 years ago

- Views:

Transcription

1 BASIC IS-LM by John Eckalbar The idea here is to get some flavor for the way M works in an IS-LM model. We are going to look at the simplest possible case: There are 3 items getting traded: money, final goods, and bonds. There are 3 sectors: households, firms, government. at t. There is no foreign sector, no labor market, prices are exogenous at P, real taxes are fixed Goods market 1. Households demand real consumption goods, c, according to the linear equation c = a + b(y - t), where y is real income and a and b are fixed positive constants, with b < 1 2. Firms demand investment goods according to: i = d - f r, where i is planned real investment, r is the nominal interest rate, and d and f are fixed positive constants. 3. Government buys real output of g and collects real taxes of t. 4. The goods market is in equilibrium when y = c + i + g, or y = a + b(y - t) + d - f r + g, or y(1 - b) = a - b t + d - f r + g, or y = (a - b t + d - f r + g)/(1 - b), or r = (a - b t + d + g)/f -y(1 - b)/f Define the IS curve to be the set of all (y, r) points at which r = (a - b t + d + g)/f - y(1 - b)/f...that is, the set of all r and y points at which the goods market clears. A plot of IS with relevant intercepts and slopes is shown here. Can you list all sources of IS-curve shift? Can you show how IS would shift with changes in g, etc.? If we are at a point like A, are goods in excess demand or excess supply?

2 LM Let nominal money demand be given by Md = k P y + h - j r, where k, h, j > 0 and P is the exogenous price level. Let Ms be the money supply. Money demand equals money supply when: y = (Ms - h + j r)/ (k P) r = (h - Ms)/j + (k P y)/j Define LM to be the set of (y, r) points where Ms = Md. Then LM is as shown below: Again: identify all the ways this can shift. If we are at a point like B, is Md > Ms?

3 The whole story The equilibrium is at ye and re. Be sure you can explain all the factors that would make ye and re change. Where would be move if we happened to be at point X? (Ans.: Assume that if c + i + g > y, then y increases, and if Md > Ms, then r increases. That will let you plot out the vector field...more on this in class.) For what it s worth, though you don t have to be able to derive this. Could you fill this in? Event y r g t M P k h..

4 The big feature of IS-LM is that ye may not be at full employment. If aggregate demand, c + i + g, is low, then ye may well be less than full employment output, yfe. Some have argued that if ye < yfe, then wages will fall...prices will fall...lm will shift right (check this with the equations)...and ye will rise, BUT: 1. Where is the labor market in this model? And how do we treat this analytically? Always be suspect of discussing how a model reacts when something changes that is not explicitly in the model. 2. If P is falling, won t that lead to expectations of further price reductions, and won t this prompt traders to delay spending on c and i, thus causing IS to fall? 3. People with nominally fixed debts may go bankrupt...what does that mean? In any case, the story won t unfold (i.e., falling prices won t lead to full employment) if: 1. Wages are rigid. 2. Md has an interest inelastic segment (liquidity trap). Here s the deal on that: I ll show why in class, but the punch line is that if Ms increases or P falls, LM will slide right, but if IS is down low on the left hand/flat part of LM, then ye will not increase, so monetary policy won t do much.

5 3. If investment demand is interest inelastic, IS will be vertical, and again falling P or rising M won t increase ye, as you see below. These are the so-called Keynesian cases, though Keynes himself would not be happy seeing his name attached to the term.

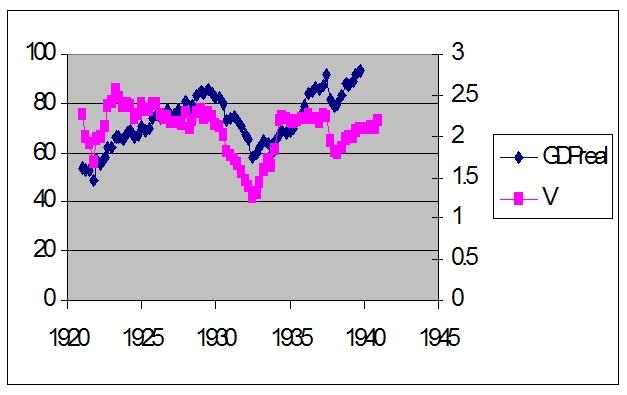

6 What does IS-LM have to say about velocity? By definition, V = P y/ms, so anything that affects P, y, and/or Ms should affect velocity, unless there is some special case at work. For example, if g increased, IS would shift right and ye would increase, so with P and Ms fixed, V would rise. In a sense, IS-LM could be thought of as variable velocity quantity theory, though you don t gain much by thinking of it that way... In effect, V is not particularly interesting in an IS-LM framework. In case you re curious, you can solve to get: V = Note that if a, d, or g increases, V increases. In general, anything that shifts IS to the right will cause V to increase and r to increase...so you might see V and r moving in parallel when IS moves. But if changes in the money demand parameters h, k, or j cause LM to shift, V and r will move in opposite directions. The graph below shows something interesting. We fit an equation for money demand from the period 1959 to 1990 we get M2 = *gdp *OpCost M2, and it gives a good fit over that period. Here is the result. See how actual money demand is a good fit with the equation until about (Though the equation itself is very primitive.) If we continued to use that equation to the period just after 1990, it wanders way off the actual track of M. So it looks like Md shifted or went unstable in about This is about when the Fed quit targeting M2...and this is the reason.

7 More recently, the fitted and actual lines have re-connected somewhat, but the past year or so has shown another break ( FITS1 is the fitted level of money demand according to the equation.):

8 Velocity, Money Demand, and Policy Since V is defined as PQ/M, MV will always equal PQ. This is not a theory, it is a definition. From time to time we will call PQ nominal income or Y. If V were a constant, monetary policy aimed at setting the level of M would (if it succeeded in setting the desired level of M...a big IF) completely determine the value of Y. Note that the split between P and Q is not determined, just the product Y = PQ. In this circumstance there would probably be a theory about how, over the long run, with Q moving roughly along its long run growth path, M growth would determine P growth, or inflation. (With V constant, % M = % P + % Q, so % M - % Q = % P...money growth minus real growth equals inflation. The Fed could pick a target long run average inflation rate, and then set % M to fit the above equation and meet the inflation objective.) Short run effects on Q could also be studied, but extra equations would be necessary. In this circumstance (i.e., if V were constant) people working at the Fed may or (surprisingly) may not need to pay a lot of attention to M. Consider this: Suppose we have a different-looking theory of PQ. Suppose PQ is determined by nominal Aggregate Demand (AD), which consists of the levels of demand coming from C, I, G, and NX (net exports). Suppose further that major components of C and I are dependent upon the interest rate. We could write AD(r) = Y = PQ and use some derivative of the C + I + G + NX and 45-degree line model to determine equilibrium Y, which would depend upon r. This is really just an IS curve when drawn in (r,y)-space Now if the Fed controlled r, it would control Y, even if it paid no attention to M. In theory, nothing whatever rules out having both V constant and AD(r). Both of these models could be true at the same time. All that is needed is a vertical LM curve with a normal IS. If so, when the Fed adjusts r to move on IS and change Y, it is forced to change M according to MV = PQ = Y. Both theories are simultaneously true, and arguments about which is correct are pointless. Note that if V were not constant, but were highly predictable, essentially the same monetary policy could be followed. That is, if V were known to be autonomously growing (i.e., growing due to changes in the efficiency of the payments system, rather than, say, to changes in interest rates) at a rate of, say, 3% per year, the Fed could use % M + % V = % P + % Q. This was Friedman s advice in the late 60s and 70s...For example, if long run % Q = 2.5, % V = 3, and target inflation is 1, then the Fed s monetary policy rule would be to set % M = =.5. Remember from the Cambridge version of the quantity theory that if V is constant and money demand equals money supply, then M = kpq = ky, where k is a constant. This means, and this is important, M demand is a fixed ratio, k, of PQ or Y. And this means that money demand is not a function of interest rates, r. If money demand were a function of r, Md(r), then since in equilibrium V = PQ/Ms = PQ/Md(r)...V would be a function of r...and not a constant. Suppose money demand is a stable function of r and Y in the sense that when money demand equals money supply, we can write M = ky - jr +, where k and j do not vary over time and the error term is small enough to be ignored. This would give us the usual LM curve. If we also had the usual IS curve that derives from a stable AD(r) function, then again, monetary policy could focus either on M or r. If the Fed wanted Y = Y fe = AD(r fe ), where r fe is the interest rate that sets AD(r) = Y fe, the Fed could target M at ky fe - j r fe. But wouldn t it be simpler for the Fed to simply target r at r fe, buying and selling bonds as needed to keep r = r fe. Then markets would automatically move M to ky fe - j r fe. (Keynes has some thoughts on this that we will explore later.) With regard to velocity, if M = ky - j r, V = Y/(kY - jr). Other things (like C, I,

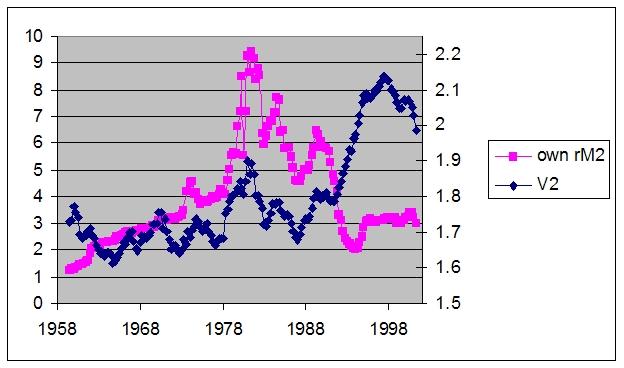

9 G, NX) being equal, you would expect to see V positively correlated with r. In fact this is the way things looked for M1 until about 1980 and for M2 until about If V were wildly erratic and unpredictable, then there would be little to no point in trying to control M., since M would not correlate with any of the Fed s ultimate objectives. In that case, the Fed might as well target the number of goats in Bidwell Park. If instead, the Aggregate Demand had some predictable reaction to r, the Fed would simply target r, and adjust the target as necessary to nudge Y in the desired direction. In fact, when it was clear that V1 was becoming unpredictable starting in the early 80s, the Fed finally gave up on targeting M1. V2 lost its historical relation to r in about 1990, and the Fed quickly gave up on it as well. There is now some evidence that V MZM has a stable relationship with r (actually its opportunity cost), but there is relatively little interest in firmly targeting MZM.

10 IS-LM and Friedman The figure below shows a graphical method of deriving the LM curve. The above figures show what might be called the standard case. Money demand is interest elastic, while Ms is interest inelastic. The end result is that LM has a positive slope. See if you can use the graph to show that if the Md curves were interest inelastic, then LM would be vertical, or interest inelastic. Using the equations from earlier, we see that if the interest elasticity of Md is 0, then j = 0 and the LM is vertical...assuming that Ms also has a zero interest elasticity. If so, the LM would be vertical in this case. What would a vertical LM imply about monetary vs. fiscal policy? Draw some pictures and figure it out. This is important stuff.

11 So if you viewed the world through IS-LM lenses, you would believe that the effectiveness of monetary vs. Fiscal policy depends critically upon the slope of LM. As we look closely at this, what we find is that LM have it s normal upward slope if either Md or Ms is interest elastic. Let us look into these in turn. Interest elasticity of Md. We will look at the theory behind two different reasons for believing that Md is interest elastic. Speculative Money Demand under Certainty Assume a consol pays $1 per year forever. It s market value at time t will be 1/rt, where rt is the interest rate at time t. Any on trader s expected gain from holding a consol for one year would be A little arithmetic shows that We take any one trader s interest expectations as a given and ask whether she/he would want to hold money or bonds at various values of rt. For example, suppose you expected the interest rate to be 5% in one year. Then, and if rt >.476 you want to hold bonds, while if rt <.0476 you want to hold money for speculative purposes. In this case.0476 is the critical interest rate. Your money demand curve will look like this (at left).

12 At the same time, I might expect interest rates to be 7% in one year. Then my critical interest rate is.07/1.07 =.065. In the above graph, me has high interest rate expectations, her has low ones, and you is in the middle. The market-wide total speculative demand curve on the right is the horizontal sum of the three on the left. With many traders, the curve will be smoother in appearance. Of course, all of this is static. We aren t analyzing how interest rate expectations evolve over time or what determines them. This much should be obvious though: 1. There are speculative reasons for holding money. 2..The money demand curve is interest elastic. 3. When peoples interest expectations rise, the money demand curve shifts up or to the right, and this will cause LM to shift up/right. 4. Actual rates depend strongly upon expectations, and expectations depend upon rates. The interest elasticity of transactions demand: Baumol model. Suppose that over a year-long interval you are going to spend a total of T dollars in a steady stream. You have the option of holding cash, which pays no interest or holding, say, a bond that returns r per dollar per year. Every time you go to the broker to get cash, you incur a transaction cost of b dollars per visit. You could withdraw all your cash on January 1 and save a lot on transactions costs by only having to go to the broker once per year, but then you would have to hold an average of T/2 dollars during the year and you interest opportunity cost would be high...it would be rt/2 if we ignore compounding. To save interest opportunity cost you could withdraw money quite often, but then your transaction costs, b, would be high. How do you manage your cash withdrawls? We can figure this out as follows: Let C be the size of each cash withdrawl and assume that all withdrawls are of equal size. It follows that you need to make T/C withdrawls per year, so your total transaction cost will be bt/c. Your average money holding will be C/2, so your annual interest opportunity cost will be rc/2. So your total cost of ready cash is. What you want to do is pick C so as to minimize this total. The technique is to take the derivative of with respect to C, set the result equal to zero, and solve for C. The value of the derivative we seek is. Setting this equal to zero and solving for C we have the optimal cash withdrawl given by

13 . This is the famous square root rule. Since C/2 is in a sense one s average money demand, this equation tells us about the interest elasticity of money demand. Note that if r increases, the optimal C declines. Note also that if b or T increases, money demand rises. Since T will tend to correlate with a person s income, this seems to make one believe that, in our more common notation, Md = f(y, r).

14 Interest Elasticity of Money Supply Even if Md is interest inelastic, if Ms is interest elastic so is LM. I ll give a quick graph and we will explore details in a minute. The figure below shows Md as completely interest inelastic, with Ms as elastic. Note that this give LM the usual shape. Why might Ms be interest elastic? Maybe when r increases people switch from demand deposits to time deposits, and this frees up reserves, or maybe currency flows into the banking system, and this gives banks reserves and allows them to increase loans and deposits.one way to explore this is via the money multiplier. Here s how: 1. M2 = C + D + T 2. C = cr M2 3. T = t M2 4. H = R + C 5. R = RR + XR 6. RR = rr D 7. XR = xr D where C is currency held by the public, D is demand deposits, and T is time deposits Where the currency ratio, cr, is a positive constant Where t, the time deposit ratio, is a positive constant. We assume that 1 - cr - t > 0 Where H is high powered money, with R being bank vault cash or bank reserve deposits at the Fed. H is either reserves or cash, which could be reserves if the public decided to put the cash in the bank. Reserves are either required reserves, RR, or excess reserves, XR Where rr is the required reserve ratio. Time deposits don t have required reserves.

15 If you substitute into equation 4, you get xr is the banking systems excess reserve demand ratio. The idea is that the Fed influences H and rr, while the banks influence xr, and the public determines cr and t. The resulting money supply is end result of all of their actions. To illustrate: Open market purchases of bonds by the Fed will increase H, and this will increase M2, if everything else remains constant. If the Fed increases rr, then M2 should fall, since (1 - c - t) > 0. If the banks want to hold more excess reserves, i.e., xr increases, then mm falls and so does M2 with everything else held constant. When would xr increase? Maybe when interest rates are low, hence the interest elasticity of Ms. If t increases, mm will rise and so will M2. This might happen when interest rates rise hence the interest elasticity of Ms. Exercise: What happens when cr increases? All of these factors point to the interest elasticity of Ms, and therefor a positive slope for LM. Question: How would we use IS-LM if the Fed followed a policy of adjusting Ms in whatever way necessary to hold r = r0?

16 Monetary vs. Fiscal Policy One of the problems with IS-LM as it is conventionally used is that it allows one to ask and get answers to nonsense questions. For example, it is possible to use IS-LM to answer a question like, What happens if we have an increase in g? Or what happens if we have an increase in M? (These may not seem like crazy questions, but they are.) And IS-LM allows us to draw an artificially solid line between monetary and fiscal policy. Why are these nonsense questions? Think of [ g] as an event. We can ask (inside IS- LM), what happens following this event. But this sort of event can never happen. Like every other entity, the government has a budget constraint. The constraint looks like this: g = t + Pb B + M This says that the government s spending must be financed somehow...either by taxes, t, bond sales to the public that bring in Pb B, where Pb is the price of bonds and B is the quantity of bonds held by the public, or by printing money, M. Given this, we can ask about the effects of events like: [ g, t] or [ g, Pb B] or [ g, M], but [ g] makes no sense. This is a big deal. I can t predict what an increase in g will do unless I know how it will be financed.. Here s how all this can give rise to an artificial distinction between monetary and fiscal policy. Consider a few T accounts: 1. The Fed buys bonds from the public. The event is [ M and B ]. This is monetary policy. Since Deposits and Reserves initially increase equally, there will be excess reserves, XR, which prompt banks to make more loans and expand the money supply. So we have M rising and no change in g...looks like monetary policy. 2. What if the treasury increased t and spent the money buying a 747 from Boeing (the public sector)? The event is [ g and t]. Here s what the accts would look like. The financing is above the dashed line and the spending is below. This looks like fiscal policy, since we have g and t changing, but no change in M and not much commotion in financial markets.

17 3. What if the treasury increases g and sold bonds to the public to finance the purchase? The event is [ g and B]. The financing is above the line and the spending is below the line. Note that this involves an increase in g and no change in M, but there will be considerable monetary commotion due to the bond sale. 4. What if the treasury spent more on g by simply running down its deposits at the Fed? The event is [ g and M]. The T acct is just the items below the line in the above figure. This time we get an increase in g and an increase in M. Is this monetary or fiscal policy? 5. Finally, what if the Fed bought a B747 or a new computer system? Is that monetary of fiscal policy? As interest rates drop toward zero here and in Japan, people worry about the ability of Monetary policy aimed at reducing r...one of the options is to have the central bank buy things other than very short T-bills...the further one goes from t-bills, the closer monetary policy comes to being fiscal policy. Do you see now why it isn t proper to ask about the effect of an increase in g with no discussion of financing?

18 The old template was: fiscal change g [ g] change t [ t] Monetary OMO Change discount rate Change reserve req...[ M] but I like:

19

Economics 102 Discussion Handout Week 14 Spring Aggregate Supply and Demand: Summary

Economics 102 Discussion Handout Week 14 Spring 2018 Aggregate Supply and Demand: Summary The Aggregate Demand Curve The aggregate demand curve (AD) shows the relationship between the aggregate price level

Economics 102 Discussion Handout Week 14 Spring 2018 Aggregate Supply and Demand: Summary The Aggregate Demand Curve The aggregate demand curve (AD) shows the relationship between the aggregate price level

Economics 102 Discussion Handout Week 14 Spring Aggregate Supply and Demand: Summary

Economics 102 Discussion Handout Week 14 Spring 2018 Aggregate Supply and Demand: Summary The Aggregate Demand Curve The aggregate demand curve (AD) shows the relationship between the aggregate price level

Economics 102 Discussion Handout Week 14 Spring 2018 Aggregate Supply and Demand: Summary The Aggregate Demand Curve The aggregate demand curve (AD) shows the relationship between the aggregate price level

Test Yourself: Monetary Policy

Test Yourself: Monetary Policy The improvement of understanding is for two ends: first, our own increase of knowledge; second, to enable us to deliver that knowledge to others. John Locke What is the transaction

Test Yourself: Monetary Policy The improvement of understanding is for two ends: first, our own increase of knowledge; second, to enable us to deliver that knowledge to others. John Locke What is the transaction

Professor Christina Romer SUGGESTED ANSWERS TO PROBLEM SET 5

Economics 2 Spring 2017 Professor Christina Romer Professor David Romer SUGGESTED ANSWERS TO PROBLEM SET 5 1. The tool we use to analyze the determination of the normal real interest rate and normal investment

Economics 2 Spring 2017 Professor Christina Romer Professor David Romer SUGGESTED ANSWERS TO PROBLEM SET 5 1. The tool we use to analyze the determination of the normal real interest rate and normal investment

Chapter 9: The IS-LM/AD-AS Model: A General Framework for Macroeconomic Analysis

Chapter 9: The IS-LM/AD-AS Model: A General Framework for Macroeconomic Analysis Cheng Chen SEF of HKU November 2, 2017 Chen, C. (SEF of HKU) ECON2102/2220: Intermediate Macroeconomics November 2, 2017

Chapter 9: The IS-LM/AD-AS Model: A General Framework for Macroeconomic Analysis Cheng Chen SEF of HKU November 2, 2017 Chen, C. (SEF of HKU) ECON2102/2220: Intermediate Macroeconomics November 2, 2017

TWO VIEWS OF THE ECONOMY

TWO VIEWS OF THE ECONOMY Macroeconomics is the study of economics from an overall point of view. Instead of looking so much at individual people and businesses and their economic decisions, macroeconomics

TWO VIEWS OF THE ECONOMY Macroeconomics is the study of economics from an overall point of view. Instead of looking so much at individual people and businesses and their economic decisions, macroeconomics

Chapter 10 Aggregate Demand I CHAPTER 10 0

Chapter 10 Aggregate Demand I CHAPTER 10 0 1 CHAPTER 10 1 2 Learning Objectives Chapter 9 introduced the model of aggregate demand and aggregate supply. Long run (Classical Theory) prices flexible output

Chapter 10 Aggregate Demand I CHAPTER 10 0 1 CHAPTER 10 1 2 Learning Objectives Chapter 9 introduced the model of aggregate demand and aggregate supply. Long run (Classical Theory) prices flexible output

Keynesian Theory (IS-LM Model): how GDP and interest rates are determined in Short Run with Sticky Prices.

: how GDP and interest rates are determined in Short Run with Sticky Prices.") Keynesian Theory (IS-LM Model): how GDP and interest rates are determined in Short Run with Sticky Prices. Historical background: The Keynesian Theory was proposed to show what could be done to shorten

Keynesian Theory (IS-LM Model): how GDP and interest rates are determined in Short Run with Sticky Prices. Historical background: The Keynesian Theory was proposed to show what could be done to shorten

A BOND MARKET IS-LM SYNTHESIS OF INTEREST RATE DETERMINATION

A BOND MARKET IS-LM SYNTHESIS OF INTEREST RATE DETERMINATION By Greg Eubanks e-mail: dismalscience32@hotmail.com ABSTRACT: This article fills the gaps left by leading introductory macroeconomic textbooks

A BOND MARKET IS-LM SYNTHESIS OF INTEREST RATE DETERMINATION By Greg Eubanks e-mail: dismalscience32@hotmail.com ABSTRACT: This article fills the gaps left by leading introductory macroeconomic textbooks

Chapter 6: Supply and Demand with Income in the Form of Endowments

Chapter 6: Supply and Demand with Income in the Form of Endowments 6.1: Introduction This chapter and the next contain almost identical analyses concerning the supply and demand implied by different kinds

Chapter 6: Supply and Demand with Income in the Form of Endowments 6.1: Introduction This chapter and the next contain almost identical analyses concerning the supply and demand implied by different kinds

13 EXPENDITURE MULTIPLIERS: THE KEYNESIAN MODEL* Chapter. Key Concepts

Chapter 3 EXPENDITURE MULTIPLIERS: THE KEYNESIAN MODEL* Key Concepts Fixed Prices and Expenditure Plans In the very short run, firms do not change their prices and they sell the amount that is demanded.

Chapter 3 EXPENDITURE MULTIPLIERS: THE KEYNESIAN MODEL* Key Concepts Fixed Prices and Expenditure Plans In the very short run, firms do not change their prices and they sell the amount that is demanded.

Econ 98- Chiu Spring 2005 Final Exam Review: Macroeconomics

Disclaimer: The review may help you prepare for the exam. The review is not comprehensive and the selected topics may not be representative of the exam. In fact, we do not know what will be on the exam.

Disclaimer: The review may help you prepare for the exam. The review is not comprehensive and the selected topics may not be representative of the exam. In fact, we do not know what will be on the exam.

Chapter 9 The IS LM FE Model: A General Framework for Macroeconomic Analysis

Chapter 9 The IS LM FE Model: A General Framework for Macroeconomic Analysis The main goal of Chapter 8 was to describe business cycles by presenting the business cycle facts. This and the following three

Chapter 9 The IS LM FE Model: A General Framework for Macroeconomic Analysis The main goal of Chapter 8 was to describe business cycles by presenting the business cycle facts. This and the following three

Notes 6: Examples in Action - The 1990 Recession, the 1974 Recession and the Expansion of the Late 1990s

Notes 6: Examples in Action - The 1990 Recession, the 1974 Recession and the Expansion of the Late 1990s Example 1: The 1990 Recession As we saw in class consumer confidence is a good predictor of household

Notes 6: Examples in Action - The 1990 Recession, the 1974 Recession and the Expansion of the Late 1990s Example 1: The 1990 Recession As we saw in class consumer confidence is a good predictor of household

Theory of Consumer Behavior First, we need to define the agents' goals and limitations (if any) in their ability to achieve those goals.

in their ability to achieve those goals.") Theory of Consumer Behavior First, we need to define the agents' goals and limitations (if any) in their ability to achieve those goals. We will deal with a particular set of assumptions, but we can modify

Theory of Consumer Behavior First, we need to define the agents' goals and limitations (if any) in their ability to achieve those goals. We will deal with a particular set of assumptions, but we can modify

Come and join us at WebLyceum

Come and join us at WebLyceum For Past Papers, Quiz, Assignments, GDBs, Video Lectures etc Go to http://www.weblyceum.com and click Register In Case of any Problem Contact Administrators Rana Muhammad

Come and join us at WebLyceum For Past Papers, Quiz, Assignments, GDBs, Video Lectures etc Go to http://www.weblyceum.com and click Register In Case of any Problem Contact Administrators Rana Muhammad

Notes on a Basic Business Problem MATH 104 and MATH 184 Mark Mac Lean (with assistance from Patrick Chan) 2011W

2011W") Notes on a Basic Business Problem MATH 104 and MATH 184 Mark Mac Lean (with assistance from Patrick Chan) 2011W This simple problem will introduce you to the basic ideas of revenue, cost, profit, and demand.

Notes on a Basic Business Problem MATH 104 and MATH 184 Mark Mac Lean (with assistance from Patrick Chan) 2011W This simple problem will introduce you to the basic ideas of revenue, cost, profit, and demand.

a) Calculate the value of government savings (Sg). Is the government running a budget deficit or a budget surplus? Show how you got your answer.

Calculate the value of government savings (Sg). Is the government running a budget deficit or a budget surplus? Show how you got your answer.") Economics 102 Spring 2018 Answers to Homework #5 Due 5/3/2018 Directions: The homework will be collected in a box before the lecture. Please place your name, TA name and section number on top of the homework

Economics 102 Spring 2018 Answers to Homework #5 Due 5/3/2018 Directions: The homework will be collected in a box before the lecture. Please place your name, TA name and section number on top of the homework

International Monetary Policy

International Monetary Policy 7 IS-LM Model 1 Michele Piffer London School of Economics 1 Course prepared for the Shanghai Normal University, College of Finance, April 2011 Michele Piffer (London School

International Monetary Policy 7 IS-LM Model 1 Michele Piffer London School of Economics 1 Course prepared for the Shanghai Normal University, College of Finance, April 2011 Michele Piffer (London School

DEMAND FOR MONEY. Ch. 9 (Ch.19 in the text) ECON248: Money and Banking Ch.9 Dr. Mohammed Alwosabi

ECON248: Money and Banking Ch.9 Dr. Mohammed Alwosabi") Ch. 9 (Ch.19 in the text) DEMAND FOR MONEY Individuals allocate their wealth between different kinds of assets such as a building, income earning securities, a checking account, and cash. Money is what

Ch. 9 (Ch.19 in the text) DEMAND FOR MONEY Individuals allocate their wealth between different kinds of assets such as a building, income earning securities, a checking account, and cash. Money is what

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati Module No. # 03 Illustrations of Nash Equilibrium Lecture No. # 02

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati Module No. # 03 Illustrations of Nash Equilibrium Lecture No. # 02

3Choice Sets in Labor and Financial

C H A P T E R 3Choice Sets in Labor and Financial Markets This chapter is a straightforward extension of Chapter 2 where we had shown that budget constraints can arise from someone owning an endowment

C H A P T E R 3Choice Sets in Labor and Financial Markets This chapter is a straightforward extension of Chapter 2 where we had shown that budget constraints can arise from someone owning an endowment

Putting the Economy Together

Putting the Economy Together Topic 6 1 Goals of Topic 6 Today we will lay down the first layer of analysis of an aggregate macro model. Derivation and study of the IS-LM Equilibrium. The Goods and the

Putting the Economy Together Topic 6 1 Goals of Topic 6 Today we will lay down the first layer of analysis of an aggregate macro model. Derivation and study of the IS-LM Equilibrium. The Goods and the

I. The Money Market. A. Money Demand (M d ) Handout 9

Handout 9") University of California-Davis Economics 1B-Intro to Macro Handout 9 TA: Jason Lee Email: jawlee@ucdavis.edu In the last chapter we developed the aggregate demand/aggregate supply model and used it to

University of California-Davis Economics 1B-Intro to Macro Handout 9 TA: Jason Lee Email: jawlee@ucdavis.edu In the last chapter we developed the aggregate demand/aggregate supply model and used it to

14.02 Principles of Macroeconomics Problem Set 1 Solutions Spring 2003

14.02 Principles of Macroeconomics Problem Set 1 Solutions Spring 2003 Question 1 : Short answer (a) (b) (c) (d) (e) TRUE. Recall that in the basic model in Chapter 3, autonomous spending is given by c

14.02 Principles of Macroeconomics Problem Set 1 Solutions Spring 2003 Question 1 : Short answer (a) (b) (c) (d) (e) TRUE. Recall that in the basic model in Chapter 3, autonomous spending is given by c

Simple Notes on the ISLM Model (The Mundell-Fleming Model)

") Simple Notes on the ISLM Model (The Mundell-Fleming Model) This is a model that describes the dynamics of economies in the short run. It has million of critiques, and rightfully so. However, even though

Simple Notes on the ISLM Model (The Mundell-Fleming Model) This is a model that describes the dynamics of economies in the short run. It has million of critiques, and rightfully so. However, even though

The Government and Fiscal Policy

The and Fiscal Policy 9 Nothing in macroeconomics or microeconomics arouses as much controversy as the role of government in the economy. In microeconomics, the active presence of government in regulating

The and Fiscal Policy 9 Nothing in macroeconomics or microeconomics arouses as much controversy as the role of government in the economy. In microeconomics, the active presence of government in regulating

Part IV: The Keynesian Revolution:

1 Part IV: The Keynesian Revolution: 1945-1970 Objectives for Chapter 13: Basic Keynesian Economics At the end of Chapter 13, you will be able to answer the following: 1. According to Keynes, consumption

1 Part IV: The Keynesian Revolution: 1945-1970 Objectives for Chapter 13: Basic Keynesian Economics At the end of Chapter 13, you will be able to answer the following: 1. According to Keynes, consumption

11 EXPENDITURE MULTIPLIERS* Chapt er. Key Concepts. Fixed Prices and Expenditure Plans1

Chapt er EXPENDITURE MULTIPLIERS* Key Concepts Fixed Prices and Expenditure Plans In the very short run, firms do not change their prices and they sell the amount that is demanded. As a result: The price

Chapt er EXPENDITURE MULTIPLIERS* Key Concepts Fixed Prices and Expenditure Plans In the very short run, firms do not change their prices and they sell the amount that is demanded. As a result: The price

Economics 102 Summer 2014 Answers to Homework #5 Due June 21, 2017

Economics 102 Summer 2014 Answers to Homework #5 Due June 21, 2017 Directions: The homework will be collected in a box before the lecture. Please place your name, TA name and section number on top of the

Economics 102 Summer 2014 Answers to Homework #5 Due June 21, 2017 Directions: The homework will be collected in a box before the lecture. Please place your name, TA name and section number on top of the

Chapter 23. Aggregate Supply and Aggregate Demand in the Short Run. In this chapter you will learn to. The Demand Side of the Economy

Chapter 23 Aggregate Supply and Aggregate Demand in the Short Run In this chapter you will learn to 1. Explain why an exogenous change in the price level shifts the AE curve and changes the equilibrium

Chapter 23 Aggregate Supply and Aggregate Demand in the Short Run In this chapter you will learn to 1. Explain why an exogenous change in the price level shifts the AE curve and changes the equilibrium

ECS2602 www.studynotesunisa.co.za Table of Contents GOODS MARKET MODEL... 4 IMPACT OF FISCAL POLICY TO EQUILIBRIUM... 7 PRACTICE OF THE CONCEPT FROM PAST PAPERS... 16 May 2012... 16 Nov 2012... 19 May/June

ECS2602 www.studynotesunisa.co.za Table of Contents GOODS MARKET MODEL... 4 IMPACT OF FISCAL POLICY TO EQUILIBRIUM... 7 PRACTICE OF THE CONCEPT FROM PAST PAPERS... 16 May 2012... 16 Nov 2012... 19 May/June

Demand for Money MV T = PT,

Demand for Money One of the central questions in monetary theory is the stability of money demand function, i.e., whether and to what extent the demand for money is affected by interest rates and other

Demand for Money One of the central questions in monetary theory is the stability of money demand function, i.e., whether and to what extent the demand for money is affected by interest rates and other

Test Review. Question 1. Answer 1. Question 2. Answer 2. Question 3. Econ 719 Test Review Test 1 Chapters 1,2,8,3,4,7,9. Nominal GDP.

Question 1 Test Review Econ 719 Test Review Test 1 Chapters 1,2,8,3,4,7,9 All of the following variables have trended upwards over the last 40 years: Real GDP The price level The rate of inflation The

Question 1 Test Review Econ 719 Test Review Test 1 Chapters 1,2,8,3,4,7,9 All of the following variables have trended upwards over the last 40 years: Real GDP The price level The rate of inflation The

Chapter 10 Aggregate Demand I

Chapter 10 In this chapter, We focus on the short run, and temporarily set aside the question of whether the economy has the resources to produce the output demanded. We examine the determination of r

Chapter 10 In this chapter, We focus on the short run, and temporarily set aside the question of whether the economy has the resources to produce the output demanded. We examine the determination of r

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

ECON 3312 Mcroeconomics Exam 2 Fall 2016 Prof. Crowder Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) If output is currently 1000 below full

ECON 3312 Mcroeconomics Exam 2 Fall 2016 Prof. Crowder Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) If output is currently 1000 below full

2c Tax Incidence : General Equilibrium

2c Tax Incidence : General Equilibrium Partial equilibrium tax incidence misses out on a lot of important aspects of economic activity. Among those aspects : markets are interrelated, so that prices of

2c Tax Incidence : General Equilibrium Partial equilibrium tax incidence misses out on a lot of important aspects of economic activity. Among those aspects : markets are interrelated, so that prices of

Y C T

Economics 102 Fall 2017 Homework #5 Due 12/12/2017 Directions: The homework will be collected in a box before the lecture. Please place your name, TA name and section number on top of the homework (legibly).

Economics 102 Fall 2017 Homework #5 Due 12/12/2017 Directions: The homework will be collected in a box before the lecture. Please place your name, TA name and section number on top of the homework (legibly).

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati Module No. # 03 Illustrations of Nash Equilibrium Lecture No. # 04

Game Theory and Economics Prof. Dr. Debarshi Das Department of Humanities and Social Sciences Indian Institute of Technology, Guwahati Module No. # 03 Illustrations of Nash Equilibrium Lecture No. # 04

Problem Set #2. Intermediate Macroeconomics 101 Due 20/8/12

Problem Set #2 Intermediate Macroeconomics 101 Due 20/8/12 Question 1. (Ch3. Q9) The paradox of saving revisited You should be able to complete this question without doing any algebra, although you may

Problem Set #2 Intermediate Macroeconomics 101 Due 20/8/12 Question 1. (Ch3. Q9) The paradox of saving revisited You should be able to complete this question without doing any algebra, although you may

The Influence of Monetary and Fiscal Policy on Aggregate Demand P R I N C I P L E S O F. N. Gregory Mankiw. Introduction

C H A P T E R 34 The Influence of Monetary and Fiscal Policy on Aggregate Demand P R I N C I P L E S O F Economics N. Gregory Mankiw Introduction This chapter focuses on the short-run effects of fiscal

C H A P T E R 34 The Influence of Monetary and Fiscal Policy on Aggregate Demand P R I N C I P L E S O F Economics N. Gregory Mankiw Introduction This chapter focuses on the short-run effects of fiscal

ECON Chapter 6: Economic growth: The Solow growth model (Part 1)

") ECON3102-005 Chapter 6: Economic growth: The Solow growth model (Part 1) Neha Bairoliya Spring 2014 Motivations Why do countries grow? Why are there poor countries? Why are there rich countries? Can poor

ECON3102-005 Chapter 6: Economic growth: The Solow growth model (Part 1) Neha Bairoliya Spring 2014 Motivations Why do countries grow? Why are there poor countries? Why are there rich countries? Can poor

3. OPEN ECONOMY MACROECONOMICS

3. OEN ECONOMY MACROECONOMICS The overall context within which open economy relationships operate to determine the exchange rates will be considered in this chapter. It is simply an extension of the closed

3. OEN ECONOMY MACROECONOMICS The overall context within which open economy relationships operate to determine the exchange rates will be considered in this chapter. It is simply an extension of the closed

Part2 Multiple Choice Practice Qs

Part2 Multiple Choice Practice Qs 1. The Keynesian cross shows: A) determination of equilibrium income and the interest rate in the short run. B) determination of equilibrium income and the interest rate

Part2 Multiple Choice Practice Qs 1. The Keynesian cross shows: A) determination of equilibrium income and the interest rate in the short run. B) determination of equilibrium income and the interest rate

Sticky Wages and Prices: Aggregate Expenditure and the Multiplier. 5Topic

Sticky Wages and Prices: Aggregate Expenditure and the Multiplier 5Topic Questioning the Classical Position and the Self-Regulating Economy John Maynard Keynes, an English economist, changed how many economists

Sticky Wages and Prices: Aggregate Expenditure and the Multiplier 5Topic Questioning the Classical Position and the Self-Regulating Economy John Maynard Keynes, an English economist, changed how many economists

Aggregate Demand I: Building the IS -LM Model (continued)

") Chapter 10 Aggregate Demand I: Building the IS -LM Model (continued) slide 0 Exercise: Shifting the IS curve Use the diagram of the Keynesian cross to show how an increase in taxes shifts the IS curve.

Chapter 10 Aggregate Demand I: Building the IS -LM Model (continued) slide 0 Exercise: Shifting the IS curve Use the diagram of the Keynesian cross to show how an increase in taxes shifts the IS curve.

If a model were to predict that prices and money are inversely related, that prediction would be evidence against that model.

The Classical Model This lecture will begin by discussing macroeconomic models in general. This material is not covered in Froyen. We will then develop and discuss the Classical Model. Students should

The Classical Model This lecture will begin by discussing macroeconomic models in general. This material is not covered in Froyen. We will then develop and discuss the Classical Model. Students should

MACROECONOMICS. Aggregate Demand I: Building the IS-LM Model. N. Gregory Mankiw. PowerPoint Slides by Ron Cronovich

11 : Building the IS-LM Model MACROECONOMICS N. Gregory Mankiw PowerPoint Slides by Ron Cronovich 2013 Worth Publishers, all rights reserved IN THIS CHAPTER, YOU WILL LEARN: the IS curve and its relation

11 : Building the IS-LM Model MACROECONOMICS N. Gregory Mankiw PowerPoint Slides by Ron Cronovich 2013 Worth Publishers, all rights reserved IN THIS CHAPTER, YOU WILL LEARN: the IS curve and its relation

a. Fill in the following table (you will need to expand it from the truncated form provided here). Round all your answers to the nearest hundredth.

. Round all your answers to the nearest hundredth.") Economics 102 Summer 2015 Answers to Homework #4 Due Monday, July 13, 2015 Directions: The homework will be collected in a box before the lecture. Please place your name on top of the homework (legibly).

Economics 102 Summer 2015 Answers to Homework #4 Due Monday, July 13, 2015 Directions: The homework will be collected in a box before the lecture. Please place your name on top of the homework (legibly).

In this chapter, look for the answers to these questions

In this chapter, look for the answers to these questions How does the interest-rate effect help explain the slope of the aggregate-demand curve? How can the central bank use monetary policy to shift the

In this chapter, look for the answers to these questions How does the interest-rate effect help explain the slope of the aggregate-demand curve? How can the central bank use monetary policy to shift the

The Influence of Monetary and Fiscal Policy on Aggregate Demand. Premium PowerPoint Slides by Ron Cronovich

C H A P T E R 34 The Influence of Monetary and Fiscal Policy on Aggregate Demand Economics P R I N C I P L E S O F N. Gregory Mankiw Premium PowerPoint Slides by Ron Cronovich 2009 South-Western, a part

C H A P T E R 34 The Influence of Monetary and Fiscal Policy on Aggregate Demand Economics P R I N C I P L E S O F N. Gregory Mankiw Premium PowerPoint Slides by Ron Cronovich 2009 South-Western, a part

PAPER No. 2: MANAGERIAL ECONOMICS MODULE No.29 : AGGREGATE DEMAND FUNCTION

Subject Paper No and Title Module No and Title Module Tag 2. MANAGERIAL ECONOMICS 29. AGGREGATE DEMAND FUNCTION COM_P2_M29 TABLE OF CONTENTS 1. Learning Outcomes 2. Aggregate Demand 3. Policy Implication

Subject Paper No and Title Module No and Title Module Tag 2. MANAGERIAL ECONOMICS 29. AGGREGATE DEMAND FUNCTION COM_P2_M29 TABLE OF CONTENTS 1. Learning Outcomes 2. Aggregate Demand 3. Policy Implication

Midterm 2 - Economics 101 (Fall 2009) You will have 45 minutes to complete this exam. There are 5 pages and 63 points. Version A.

You will have 45 minutes to complete this exam. There are 5 pages and 63 points. Version A.") Name Student ID Section day and time Midterm 2 - Economics 101 (Fall 2009) You will have 45 minutes to complete this exam. There are 5 pages and 63 points. Version A. Multiple Choice: (16 points total,

Name Student ID Section day and time Midterm 2 - Economics 101 (Fall 2009) You will have 45 minutes to complete this exam. There are 5 pages and 63 points. Version A. Multiple Choice: (16 points total,

Best Reply Behavior. Michael Peters. December 27, 2013

Best Reply Behavior Michael Peters December 27, 2013 1 Introduction So far, we have concentrated on individual optimization. This unified way of thinking about individual behavior makes it possible to

Best Reply Behavior Michael Peters December 27, 2013 1 Introduction So far, we have concentrated on individual optimization. This unified way of thinking about individual behavior makes it possible to

Final Term Papers. Fall 2009 (Session 03a) ECO401. (Group is not responsible for any solved content) Subscribe to VU SMS Alert Service

ECO401. (Group is not responsible for any solved content) Subscribe to VU SMS Alert Service") Fall 2009 (Session 03a) ECO401 (Group is not responsible for any solved content) Subscribe to VU SMS Alert Service To Join Simply send following detail to bilal.zaheem@gmail.com Full Name Master Program

Fall 2009 (Session 03a) ECO401 (Group is not responsible for any solved content) Subscribe to VU SMS Alert Service To Join Simply send following detail to bilal.zaheem@gmail.com Full Name Master Program

Symmetric Game. In animal behaviour a typical realization involves two parents balancing their individual investment in the common

Symmetric Game Consider the following -person game. Each player has a strategy which is a number x (0 x 1), thought of as the player s contribution to the common good. The net payoff to a player playing

Symmetric Game Consider the following -person game. Each player has a strategy which is a number x (0 x 1), thought of as the player s contribution to the common good. The net payoff to a player playing

14.02 Quiz #2 SOLUTION. Spring Time Allowed: 90 minutes

*Note that we decide to not grade #10 multiple choice, so your total score will be out of 97. We thought about the option of giving everyone a correct mark for that solution, but all that would have done

*Note that we decide to not grade #10 multiple choice, so your total score will be out of 97. We thought about the option of giving everyone a correct mark for that solution, but all that would have done

Disputes In Macroeconomics

No G G & T 3-5% Monetary Rule Expectations negate fiscal and monetary Policy. Adam Smith John M. Keynes Milton Friedman Classicals Keynesians Monetarists Robert Lucas Get the G off of our backs. Ronald

No G G & T 3-5% Monetary Rule Expectations negate fiscal and monetary Policy. Adam Smith John M. Keynes Milton Friedman Classicals Keynesians Monetarists Robert Lucas Get the G off of our backs. Ronald

ECON 3312 Macroeconomics Exam 2 Spring 2017 Prof. Crowder

ECON 3312 Macroeconomics Exam 2 Spring 2017 Prof. Crowder Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Suppose the economy is currently

ECON 3312 Macroeconomics Exam 2 Spring 2017 Prof. Crowder Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Suppose the economy is currently

Cosumnes River College Principles of Macroeconomics Problem Set 6 Due April 3, 2017

Spring 2017 Cosumnes River College Principles of Macroeconomics Problem Set 6 Due April 3, 2017 Name: Instructions: Write the answers clearly and concisely on these sheets in the spaces provided. Do not

Spring 2017 Cosumnes River College Principles of Macroeconomics Problem Set 6 Due April 3, 2017 Name: Instructions: Write the answers clearly and concisely on these sheets in the spaces provided. Do not

Problem Set #2. Intermediate Macroeconomics 101 Due 20/8/12

Problem Set #2 Intermediate Macroeconomics 101 Due 20/8/12 Question 1. (Ch3. Q9) The paradox of saving revisited You should be able to complete this question without doing any algebra, although you may

Problem Set #2 Intermediate Macroeconomics 101 Due 20/8/12 Question 1. (Ch3. Q9) The paradox of saving revisited You should be able to complete this question without doing any algebra, although you may

Please choose the most correct answer. You can choose only ONE answer for every question.

Please choose the most correct answer. You can choose only ONE answer for every question. 1. Only when inflation increases unexpectedly a. the real interest rate will be lower than the nominal inflation

Please choose the most correct answer. You can choose only ONE answer for every question. 1. Only when inflation increases unexpectedly a. the real interest rate will be lower than the nominal inflation

Exam #2 Review Answers ECNS 303

Exam #2 Review Answers ECNS 303 Exam #2 will cover all the material we have covered since Exam #1. In addition to working these problems, I would recommend reviewing all of your old class notes and quizzes,

Exam #2 Review Answers ECNS 303 Exam #2 will cover all the material we have covered since Exam #1. In addition to working these problems, I would recommend reviewing all of your old class notes and quizzes,

SIMON FRASER UNIVERSITY Department of Economics. Intermediate Macroeconomic Theory Spring PROBLEM SET 1 (Solutions) Y = C + I + G + NX

Y = C + I + G + NX") SIMON FRASER UNIVERSITY Department of Economics Econ 305 Prof. Kasa Intermediate Macroeconomic Theory Spring 2012 PROBLEM SET 1 (Solutions) 1. (10 points). Using your knowledge of National Income Accounting,

SIMON FRASER UNIVERSITY Department of Economics Econ 305 Prof. Kasa Intermediate Macroeconomic Theory Spring 2012 PROBLEM SET 1 (Solutions) 1. (10 points). Using your knowledge of National Income Accounting,

Professor Christina Romer SUGGESTED ANSWERS TO PROBLEM SET 6

Economics 2 Spring 2017 Professor Christina Romer Professor David Romer SUGGESTED ANSWERS TO PROBLEM SET 6 1.a. The main tool we use to analyze short-run fluctuations in the economy is the Keynesian cross.

Economics 2 Spring 2017 Professor Christina Romer Professor David Romer SUGGESTED ANSWERS TO PROBLEM SET 6 1.a. The main tool we use to analyze short-run fluctuations in the economy is the Keynesian cross.

Lesson 12 The Influence of Monetary and Fiscal Policy on Aggregate Demand

Lesson 12 The Influence of Monetary and Fiscal Policy on Aggregate Demand Henan University of Technology Sino-British College Transfer Abroad Undergraduate Programme 0 In this lesson, look for the answers

Lesson 12 The Influence of Monetary and Fiscal Policy on Aggregate Demand Henan University of Technology Sino-British College Transfer Abroad Undergraduate Programme 0 In this lesson, look for the answers

Macroeconomics Mankiw 6th Edition

N. Gregory Mankiw Lecture notes, ECON 1150 Macroeconomics Mankiw 6th Edition 21 & 22 The Influence of Monetary and Fiscal Policy on Aggregate Demand Premium PowerPoint Slides by Ron Cronovich 2012 UPDATE

N. Gregory Mankiw Lecture notes, ECON 1150 Macroeconomics Mankiw 6th Edition 21 & 22 The Influence of Monetary and Fiscal Policy on Aggregate Demand Premium PowerPoint Slides by Ron Cronovich 2012 UPDATE

Chapter 19 Optimal Fiscal Policy

Chapter 19 Optimal Fiscal Policy We now proceed to study optimal fiscal policy. We should make clear at the outset what we mean by this. In general, fiscal policy entails the government choosing its spending

Chapter 19 Optimal Fiscal Policy We now proceed to study optimal fiscal policy. We should make clear at the outset what we mean by this. In general, fiscal policy entails the government choosing its spending

Economics 102 Discussion Handout Week 13 Fall Introduction to Keynesian Model: Income and Expenditure. The Consumption Function

Economics 102 Discussion Handout Week 13 Fall 2017 Introduction to Keynesian Model: Income and Expenditure The Consumption Function The consumption function is an equation which describes how a household

Economics 102 Discussion Handout Week 13 Fall 2017 Introduction to Keynesian Model: Income and Expenditure The Consumption Function The consumption function is an equation which describes how a household

10 AGGREGATE SUPPLY AND AGGREGATE DEMAND* Chapt er. Key Concepts. Aggregate Supply1

Chapt er 10 AGGREGATE SUPPLY AND AGGREGATE DEMAND* Aggregate Supply1 Key Concepts The aggregate supply/aggregate demand model is used to determine how real GDP and the price level are determined and why

Chapt er 10 AGGREGATE SUPPLY AND AGGREGATE DEMAND* Aggregate Supply1 Key Concepts The aggregate supply/aggregate demand model is used to determine how real GDP and the price level are determined and why

The text was adapted by The Saylor Foundation under the CC BY-NC-SA without attribution as requested by the works original creator or licensee

the CC BY-NC-SA without attribution as requested by the works original creator or licensee 1 of 19 Chapter 21 IS-LM C H A P T E R O B J E C T I V E S By the end of this chapter, students should be able

the CC BY-NC-SA without attribution as requested by the works original creator or licensee 1 of 19 Chapter 21 IS-LM C H A P T E R O B J E C T I V E S By the end of this chapter, students should be able

Probability and Stochastics for finance-ii Prof. Joydeep Dutta Department of Humanities and Social Sciences Indian Institute of Technology, Kanpur

Probability and Stochastics for finance-ii Prof. Joydeep Dutta Department of Humanities and Social Sciences Indian Institute of Technology, Kanpur Lecture - 07 Mean-Variance Portfolio Optimization (Part-II)

Probability and Stochastics for finance-ii Prof. Joydeep Dutta Department of Humanities and Social Sciences Indian Institute of Technology, Kanpur Lecture - 07 Mean-Variance Portfolio Optimization (Part-II)

ECON 102 Tutorial 3. TA: Iain Snoddy 18 May Vancouver School of Economics

ECON 102 Tutorial 3 TA: Iain Snoddy 18 May 2015 Vancouver School of Economics Questions Questions 1-3 set-up Y C I G X M 1.00 1.00 0.5 0.7 0.45 0.15 2.00 1.65 0.5 0.7 0.45 0.30 3.00 2.30 0.5 0.7 0.45 0.45

ECON 102 Tutorial 3 TA: Iain Snoddy 18 May 2015 Vancouver School of Economics Questions Questions 1-3 set-up Y C I G X M 1.00 1.00 0.5 0.7 0.45 0.15 2.00 1.65 0.5 0.7 0.45 0.30 3.00 2.30 0.5 0.7 0.45 0.45

This is IS-LM, chapter 21 from the book Finance, Banking, and Money (index.html) (v. 1.1).

(v. 1.1).") This is IS-LM, chapter 21 from the book Finance, Banking, and Money (index.html) (v. 1.1). This book is licensed under a Creative Commons by-nc-sa 3.0 (http://creativecommons.org/licenses/by-nc-sa/ 3.0/)

This is IS-LM, chapter 21 from the book Finance, Banking, and Money (index.html) (v. 1.1). This book is licensed under a Creative Commons by-nc-sa 3.0 (http://creativecommons.org/licenses/by-nc-sa/ 3.0/)

Class 5. The IS-LM model and Aggregate Demand

Class 5. The IS-LM model and Aggregate Demand 1. Use the Keynesian cross to predict the impact of: a) An increase in government purchases. b) An increase in taxes. c) An equal increase in government purchases

Class 5. The IS-LM model and Aggregate Demand 1. Use the Keynesian cross to predict the impact of: a) An increase in government purchases. b) An increase in taxes. c) An equal increase in government purchases

Professor Christina Romer SUGGESTED ANSWERS TO PROBLEM SET 5

Economics 2 Spring 2016 Professor Christina Romer Professor David Romer SUGGESTED ANSWERS TO PROBLEM SET 5 1. The left-hand diagram below shows the situation when there is a negotiated real wage,, that

Economics 2 Spring 2016 Professor Christina Romer Professor David Romer SUGGESTED ANSWERS TO PROBLEM SET 5 1. The left-hand diagram below shows the situation when there is a negotiated real wage,, that

macro macroeconomics Aggregate Demand I N. Gregory Mankiw CHAPTER TEN PowerPoint Slides by Ron Cronovich fifth edition

macro CHAPTER TEN Aggregate Demand I macroeconomics fifth edition N. Gregory Mankiw PowerPoint Slides by Ron Cronovich 2002 Worth Publishers, all rights reserved In this chapter you will learn the IS curve,

macro CHAPTER TEN Aggregate Demand I macroeconomics fifth edition N. Gregory Mankiw PowerPoint Slides by Ron Cronovich 2002 Worth Publishers, all rights reserved In this chapter you will learn the IS curve,

Notes On IS-LM Model Econ3120, Economic Department, St.Louis University

Notes On IS-LM Model Econ3120, Economic Department, St.Louis University Instructor: Xi Wang Introduction In this class notes, I introduce IS-LM Model. For those students have optional textbook, you can

Notes On IS-LM Model Econ3120, Economic Department, St.Louis University Instructor: Xi Wang Introduction In this class notes, I introduce IS-LM Model. For those students have optional textbook, you can

VII. Short-Run Economic Fluctuations

Macroeconomic Theory Lecture Notes VII. Short-Run Economic Fluctuations University of Miami December 1, 2017 1 Outline Business Cycle Facts IS-LM Model AD-AS Model 2 Outline Business Cycle Facts IS-LM

Macroeconomic Theory Lecture Notes VII. Short-Run Economic Fluctuations University of Miami December 1, 2017 1 Outline Business Cycle Facts IS-LM Model AD-AS Model 2 Outline Business Cycle Facts IS-LM

Outline for ECON 701's Second Midterm (Spring 2005)

") Outline for ECON 701's Second Midterm (Spring 2005) I. Goods market equilibrium A. Definition: Y=Y d and Y d =C d +I d +G+NX d B. If it s a closed economy: NX d =0 C. Derive the IS Curve 1. Slope of the

Outline for ECON 701's Second Midterm (Spring 2005) I. Goods market equilibrium A. Definition: Y=Y d and Y d =C d +I d +G+NX d B. If it s a closed economy: NX d =0 C. Derive the IS Curve 1. Slope of the

Chapter 11 Aggregate Demand I: Building the IS -LM Model

Chapter 11 Aggregate Demand I: Building the IS -LM Model Modified by Yun Wang Eco 3203 Intermediate Macroeconomics Florida International University Summer 2017 2016 Worth Publishers, all rights reserved

Chapter 11 Aggregate Demand I: Building the IS -LM Model Modified by Yun Wang Eco 3203 Intermediate Macroeconomics Florida International University Summer 2017 2016 Worth Publishers, all rights reserved

Macroeconomics Sixth Edition

N. Gregory Mankiw Principles of Macroeconomics Sixth Edition 21 The Influence of Monetary and Fiscal Policy on Aggregate Demand Premium PowerPoint Slides by Ron Cronovich 2012 UPDATE In this chapter, look

N. Gregory Mankiw Principles of Macroeconomics Sixth Edition 21 The Influence of Monetary and Fiscal Policy on Aggregate Demand Premium PowerPoint Slides by Ron Cronovich 2012 UPDATE In this chapter, look

Macroeconomics. The Influence of Monetary and Fiscal Policy on Aggregate Demand. Introduction

C H A P T E R 21 The Influence of Monetary and Fiscal Policy on Aggregate Demand P R I N C I P L E S O F Macroeconomics N. Gregory Mankiw Premium PowerPoint Slides by Ron Cronovich 2010 South-Western,

C H A P T E R 21 The Influence of Monetary and Fiscal Policy on Aggregate Demand P R I N C I P L E S O F Macroeconomics N. Gregory Mankiw Premium PowerPoint Slides by Ron Cronovich 2010 South-Western,

IN THIS LECTURE, YOU WILL LEARN:

IN THIS LECTURE, YOU WILL LEARN: Am simple perfect competition production medium-run model view of what determines the economy s total output/income how the prices of the factors of production are determined

IN THIS LECTURE, YOU WILL LEARN: Am simple perfect competition production medium-run model view of what determines the economy s total output/income how the prices of the factors of production are determined

The Baumol-Tobin and the Tobin Mean-Variance Models of the Demand

Appendix 1 to chapter 19 A p p e n d i x t o c h a p t e r An Overview of the Financial System 1 The Baumol-Tobin and the Tobin Mean-Variance Models of the Demand for Money The Baumol-Tobin Model of Transactions

Appendix 1 to chapter 19 A p p e n d i x t o c h a p t e r An Overview of the Financial System 1 The Baumol-Tobin and the Tobin Mean-Variance Models of the Demand for Money The Baumol-Tobin Model of Transactions

Quantity Theory II. Graduate Macroeconomics I ECON S. Cunningham

Quantity Theory II Graduate Macroeconomics I ECON 309 -- S. Cunningham The Purpose of the Fed McCandless and Weber (1995) write: The Federal Reserve System was established in 1913 to provide an elastic

Quantity Theory II Graduate Macroeconomics I ECON 309 -- S. Cunningham The Purpose of the Fed McCandless and Weber (1995) write: The Federal Reserve System was established in 1913 to provide an elastic

This is IS-LM, chapter 21 from the book Finance, Banking, and Money (index.html) (v. 2.0).

(v. 2.0).") This is IS-LM, chapter 21 from the book Finance, Banking, and Money (index.html) (v. 2.0). This book is licensed under a Creative Commons by-nc-sa 3.0 (http://creativecommons.org/licenses/by-nc-sa/ 3.0/)

This is IS-LM, chapter 21 from the book Finance, Banking, and Money (index.html) (v. 2.0). This book is licensed under a Creative Commons by-nc-sa 3.0 (http://creativecommons.org/licenses/by-nc-sa/ 3.0/)

ECON 3560/5040 Week 8-9

ECON 3560/5040 Week 8-9 AGGREGATE DEMAND 1. Keynes s Theory - John Maynard Keynes (1936) criticized classical theory for assuming that AS alone capital, labor, and technology determines national income

ECON 3560/5040 Week 8-9 AGGREGATE DEMAND 1. Keynes s Theory - John Maynard Keynes (1936) criticized classical theory for assuming that AS alone capital, labor, and technology determines national income

INTEREST RATES Overview Real vs. Nominal Rate Equilibrium Rates Interest Rate Risk Reinvestment Risk Structure of the Yield Curve Monetary Policy

INTEREST RATES Overview Real vs. Nominal Rate Equilibrium Rates Interest Rate Risk Reinvestment Risk Structure of the Yield Curve Monetary Policy Some of the following material comes from a variety of

INTEREST RATES Overview Real vs. Nominal Rate Equilibrium Rates Interest Rate Risk Reinvestment Risk Structure of the Yield Curve Monetary Policy Some of the following material comes from a variety of

a. What is your interpretation of the slope of the consumption function?

Economics 102 Spring 2017 Homework #5 Due May 4, 2017 Directions: The homework will be collected in a box before the lecture. Please place your name, TA name and section number on top of the homework (legibly).

Economics 102 Spring 2017 Homework #5 Due May 4, 2017 Directions: The homework will be collected in a box before the lecture. Please place your name, TA name and section number on top of the homework (legibly).

14.02 Principles of Macroeconomics Problem Set # 2, Answers

14.0 Principles of Macroeconomics Problem Set #, Answers Part I 1. False. The multiplier is 1/ [1- c 1 (1- t)]. The effect of an increase in autonomous spending is dampened because taxes respond proportionally

14.0 Principles of Macroeconomics Problem Set #, Answers Part I 1. False. The multiplier is 1/ [1- c 1 (1- t)]. The effect of an increase in autonomous spending is dampened because taxes respond proportionally

Chapter 19: Compensating and Equivalent Variations

Chapter 19: Compensating and Equivalent Variations 19.1: Introduction This chapter is interesting and important. It also helps to answer a question you may well have been asking ever since we studied quasi-linear

Chapter 19: Compensating and Equivalent Variations 19.1: Introduction This chapter is interesting and important. It also helps to answer a question you may well have been asking ever since we studied quasi-linear

ECON 3010 Intermediate Macroeconomics Final Exam

ECON 3010 Intermediate Macroeconomics Final Exam Multiple Choice Questions. (60 points; 3 pts each) 1. The returns to scale in the production function YY = KK 0.5 LL 0.5 are: A) decreasing. B) constant.

ECON 3010 Intermediate Macroeconomics Final Exam Multiple Choice Questions. (60 points; 3 pts each) 1. The returns to scale in the production function YY = KK 0.5 LL 0.5 are: A) decreasing. B) constant.

Introduction. What exactly is the statement of cash flows? Composing the statement

Introduction The course about the statement of cash flows (also statement hereinafter to keep the text simple) is aiming to help you in preparing one of the apparently most complicated statements. Most

Introduction The course about the statement of cash flows (also statement hereinafter to keep the text simple) is aiming to help you in preparing one of the apparently most complicated statements. Most

Economics 1012A: Introduction to Macroeconomics FALL 2007 Dr. R. E. Mueller Third Midterm Examination November 15, 2007

Economics 1012A: Introduction to Macroeconomics FALL 2007 Dr. R. E. Mueller Third Midterm Examination November 15, 2007 Answer all of the following questions by selecting the most appropriate answer on

Economics 1012A: Introduction to Macroeconomics FALL 2007 Dr. R. E. Mueller Third Midterm Examination November 15, 2007 Answer all of the following questions by selecting the most appropriate answer on

Chapter 23. The Keynesian Framework. Learning Objectives. Learning Objectives (Cont.)

") Chapter 23 The Keynesian Framework Learning Objectives See the differences among saving, investment, desired saving, and desired investment and explain how these differences can generate short run fluctuations

Chapter 23 The Keynesian Framework Learning Objectives See the differences among saving, investment, desired saving, and desired investment and explain how these differences can generate short run fluctuations

file:///c:/users/moha/desktop/mac8e/new folder (13)/CourseComp...

/CourseComp...") file:///c:/users/moha/desktop/mac8e/new folder (13)/CourseComp... COURSES > BA121 > CONTROL PANEL > POOL MANAGER > POOL CANVAS Add, modify, and remove questions. Select a question type from the Add drop-down

file:///c:/users/moha/desktop/mac8e/new folder (13)/CourseComp... COURSES > BA121 > CONTROL PANEL > POOL MANAGER > POOL CANVAS Add, modify, and remove questions. Select a question type from the Add drop-down

Consider the aggregate production function for Dane County:

Economics 0 Spring 08 Homework #4 Due 4/5/7 Directions: The homework will be collected in a box before the lecture. Please place your name, TA name and section number on top of the homework (legibly).

Economics 0 Spring 08 Homework #4 Due 4/5/7 Directions: The homework will be collected in a box before the lecture. Please place your name, TA name and section number on top of the homework (legibly).

III. 9. IS LM: the basic framework to understand macro policy continued Text, ch 11

Objectives: To apply IS-LM analysis to understand the causes of short-run fluctuations in real GDP and the short-run impact of monetary and fiscal policies on the economy. To use the IS-LM model to analyse

Objectives: To apply IS-LM analysis to understand the causes of short-run fluctuations in real GDP and the short-run impact of monetary and fiscal policies on the economy. To use the IS-LM model to analyse

ECONOMICS QUALIFYING EXAMINATION IN ELEMENTARY MATHEMATICS

ECONOMICS QUALIFYING EXAMINATION IN ELEMENTARY MATHEMATICS Friday 2 October 1998 9 to 12 This exam comprises two sections. Each carries 50% of the total marks for the paper. You should attempt all questions

ECONOMICS QUALIFYING EXAMINATION IN ELEMENTARY MATHEMATICS Friday 2 October 1998 9 to 12 This exam comprises two sections. Each carries 50% of the total marks for the paper. You should attempt all questions