Lectures 11 Foundations of Finance

|

|

|

- Dylan Barton

- 5 years ago

- Views:

Transcription

1 Lectures 11 Foundations of Finance Lecture 11: Futures and Forward Contracts: Valuation. I. Reading. II. Futures Prices. III. Forward Prices: Spot Forward Parity. Lecture 11: Market Efficiency I. Reading. II. Definition of Market Efficiency. III. Features of Market Efficiency. IV. Costly Information Acquisition and Costly Trading. V. Levels of Market Efficiency VI. How efficient are U.S. financial markets. VII. Performance of the U.S. Mutual Fund Industry. VIII. Problems with Testing Market Efficiency IX. Example of Semi-strong Form Inefficiency X. Predictability of Returns. 0

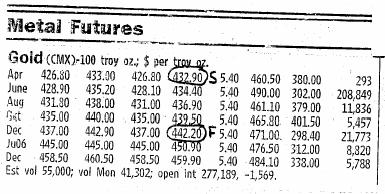

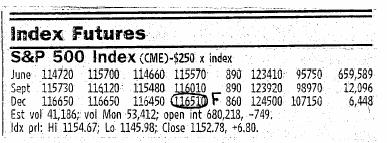

2 Lectures 11 Foundations of Finance Lecture 11: Futures and Forward Contracts: Valuation. I. Reading. A. BKM, Chapter 22, Sections B. BKM, Chapter 23, omit Sections 23.3 and II. Futures Prices. A. Applicability of Spot Forward Parity. 1. In general, the futures price need not equal the forward price and so spot forward parity need not hold exactly for futures contracts. 2. However, spot forward parity can be expected to hold approximately for futures. III. Forward Prices: Spot Forward Parity. A. Introduction. 1. Interested in determining how the forward price is determined. 2. Turns out that no arbitrage implies that the forward price must be related to the spot price in a very particular way. 3. Example. WSJ 4/20/05. Underlying Spot Forward - deliver on 12/05 Growth Rate Gold-1oz % Cotton-100 lb % S&P % Why the differences? 1

3 Lectures 11 Foundations of Finance 2

4 Lectures 11 Foundations of Finance B. The Law of One Price: No Carrying Costs. 1. Example 1: a. Consider a forward contract to deliver 1 oz of gold on 4/06 entered into on the 4/05. The spot price for 1 oz of gold is $400. The price of a U.S. T-bill ($100 face value) maturing on 4/06 is 80. b. What is the relation between the forward price and the spot price? c. Can replicate a forward contract by going long the stock and shorting discount bonds that mature on the settlement date with a face value equal to the forward price. Strategy 4/05 4/06 Buy a forward contract on 4/05 which delivers 1 oz of gold on 4/06 0 S(4/06) - F 1 (4/05) Strategy 4/05 4/06 Buy 1 oz of gold on 4/05 and sell on 4/ S(4/06) Sell 1-yr U.S. T-bills on 4/05 with face value of F 1 (4/05) F 1 (4/05) 0.8 -F 1 (4/05) Net Cash Flow F 1 (4/05) S(4/06) - F 1 (4/05) d. Can see that these two strategies have the same cash flows. e. By definition, no money changes hands today under the forward contract; so the law of one price says F 1 (4/05) = 0; and so F 1 (4/05) = 400 / 0.8 = 500. f. Note: (1) if F 1 (4/05) > 0 (i.e., F 1 (4/05) > 500), the buyer of the forward contract must be paid money today to be induced to enter the contract. (2) if F 1 (4/05) < 0 (i.e., F 1 (4/05) < 500), the buyer of the forward contract would pay money today to be allowed to enter the contract. 3

5 Lectures 11 Foundations of Finance 2. Thus, have shown that the forward price is just the future value of the spot price at the settlement date (invested today in a discount bond maturing at the settlement date): F T (0) = S(0) / d T (0) or F T (0) = S(0) [1 + y* T (0)] T where a. T is time to settlement. b. S(0) be the value of the underlying at time 0. c. d T (0) be the price of a T period discount bond with a $1 face value. d. y* T (0) be the effective 1-period yield on a T period discount bond. e. F T (0) be the time 0 forward price of the underlying for delivery in T periods. 3. So at any point in time expect the forward price of gold to increase as the settlement date becomes more distant since the future value of the spot price increases with maturity. 4

6 Lectures 11 Foundations of Finance C. General Case: Carrying Costs. 1. Suppose there are certain costs associated with holding or carrying an asset between time 0 and the settlement of the forward contract at time T. a. Example: When a physical commodity is the underlying, any storage costs are a carrying cost. b. Example: If the underlying is a stock index, dividend payments by the stocks in the index are a negative carrying cost. 2. Assume the carrying costs are known at time Example 2: a. Consider a forward contract to deliver 100 lb of cotton on 4/06 entered into on the 4/05. The spot price on 4/05 for 100 lb of cotton is $71. The price of a U.S. T-bill ($100 face value) maturing on 4/06 is 80. The cost of storing 100 lb of cotton from 4/05 to 4/06 is $10 payable on 10/05. The price of a U.S. T-bill ($100 face value) maturing on 10/05 is 90. b. What is the relation between the forward price and the spot price? c. Consider the following two investment strategies: Strategy 4/05 10/05 4/06 Buy a forward contract on 4/05 which delivers 100 lb cotton on 4/ S(4/06)-F 1 (4/05) Strategy 4/05 10/05 4/06 Buy 100 lb cotton on 4/05 and sell on 4/ S(4/06) Buy a ½-year discount bond on 4/05 with face value of 10 and close out at maturity Sell a 1 year discount bond on 4/05 with face value of F 1 (4/05) and hold to maturity -10 x F 1 (4/05) 0.8 -F 1 (4/05) Net Cash Flow F 1 (4/05) x S(4/06)-F 1 (4/05) 5

7 Lectures 11 Foundations of Finance d. Can see that these two strategies have the same cash flows. e. By definition, no money changes hands today under the forward contract; so the law of one price says: 0 = F 1 (4/05) x f. So F 1 (4/05) = (71 + 9)/0.8 = Thus, get a relation between the current spot price and the forward price: F T (0) d T (0) = S(0) + C(t c ) d tc (0) or F T (0) 1 [1%y ( T (0)]T ' S(0) % C(t c ) 1 [1%y ( tc (0)]tc where: a. the carrying costs C(t c ) are paid at time t c between times 0 and T (usually will take the settlement date T to be the date at which the costs are paid). b. S(0) be the value of the underlying at time 0. c. d τ (0) be the price of a τ period discount bond with a $1 face value. d. y* τ (0) be the effective 1-period yield on a τ period discount bond. e. F T (0) be the time 0 forward price of the underlying for delivery in T periods. 5. This relation is known as spot forward parity and can be rewritten: F T (0) ' [1%y ( 1 T (0)]T [S(0)% C(t c ) ] [1%y ( tc (0)]tc 6. Can see that a. a positive carrying cost implies a higher forward price. b. a negative carrying cost (e.g., dividend-paying underlying) implies a lower forward price. 7. Example 3: a. The S&P 500 index is 800 on 4/05. The price of a discount bond (face vaue of 100) maturing on 4/06 is 80. The stocks in the index will pay dividends amounting to 40 of index value on 10/05. The price of a discount bond (face vaue of 100) maturing on 10/05 is 90. What is forward price on 4/05 for delivery of the index on 4/06? b. Use spot-forward parity F 1 (4/05) (-40) 0.9 = 800 Y F 1 (4/05) = (800-36)/0.8 =

8 Lectures 11 Foundations of Finance D. Application to Foreign Currency Forward Contracts: Covered Interest Parity. 1. In the case of foreign currency forward contracts, spot forward parity is known as covered interest parity. 2. For a forward contract to deliver a foreign currency in T years, the underlying is the foreign currency. The negative carrying cost is the interest received from investing the foreign currency in a discount bond maturing in T years. 3. Example 4: a. The spot price for a British pound on 4/05 is $1.60: i.e., S $/ (4/05) = The yield on a 1 year discount bond denominated in U.S. dollars is 25% while the yield on a 1 year discount bond denominated in pounds is 10%. What is the forward price on 4/05 for delivery of one on 4/06? b. Consider the following two strategies: Strategy 4/05 4/06 Buy $1 of 1-year $-denominated discount bonds on 4/05 and sell on 4/ Strategy Time 0 Time T Sell a forward contract which delivers [1/1.6][1+ 0.1] = on 4/06 Buy $1 worth of on 4/05 ( 1/1.6) and invest in 1-year -denominated discount bonds and hold til maturity. 0 {F 1 $/ (4/05)- 1} x [1/1.6][1+0.1] = F 1 $/ (4/05) [1/1.6][1+0.1] - [1/1.6][1+0.1] -1 [1/1.6][1+0.1] Net Cash Flow -1 F 1 $/ (4/05) [1/1.6][1+0.1] c. The first strategy is buying a 1-year $-denominated discount bond while the second is creating a synthetic 1-year $-denominated discount bond on 4/05 by: (1) buying pounds on 4/05, (2) investing the proceeds in 1-year -denominated discount bonds, and (3) locking in on 4/05 the exchange rate (the forward rate) at which the pounds can be converted back to dollars on 4/06. 7

9 Lectures 11 Foundations of Finance d. Can see that these two strategies cost $1 on 4/05 and generate a certain dollar cash flow on 4/06. The law of one price says that the certain dollar cash flows on 4/06 must be the same: = F 1 $/ (4/05) [1/1.6][1+0.1] and so F 1 $/ (4/05) = $1.8181/. 4. Thus obtain the following result which is the covered interest parity theorem: [1+y* $ T(0)] T = [1+y* T(0)] T F T $/ (0)/S $/ (0) or [1%y ($ T (0)]T [1%y ( T (0)]T S $/ (0) where a. y* $ T(0) is the effective per period yield on a T period discount bond denominated in U.S. dollars. b. y* T(0) is the effective per period yield on a T period discount bond denominated in. c. S $/ (0) is the spot price of 1 at time 0. $/ d. F T (0) be the forward price at time 0 for 1 delivered in T periods. 5. Can see that: a. if the yield on the foreign currency discount bond is lower than on the dollar-denominated discount bond, the forward price of the foreign currency (in $s) is higher than the spot price (in $s). b. if the yield on the foreign currency discount bond is higher than on the dollar-denominated discount bond, the forward price of the foreign currency (in $s) is lower than the spot price (in $s). ' F $/ T (0) 8

10 Lectures 11 Foundations of Finance E. Spot Forward Parity and Arbitrage. 1. If spot forward parity is violated, there is an arbitrage opportunity. 2. Example 1 (cont): a. Suppose the forward price on 4/05 for delivery of 1 oz of gold on 4/06 is 520 which is greater than the 500 implied by spot forward parity. b. So the forward price is too high which implies that you want to sell forward contracts and buy the underlying: Strategy 4/05 4/06 Sell a forward contract on 4/05 which delivers 1 oz of gold on 4/ S(4/06) Buy 1 oz of gold on 4/05 and sell on 4/ S(4/06) Sell 1-yr U.S. T-bills on 4/05 with face value of x Net Cash Flow 16 0 c. This strategy is an arbitrage opportunity. 3. Example 4 (cont): a. Suppose the forward price on 4/05 for delivery of a on 4/06 is $2 which is higher than $ implied by covered interest parity. b. Want to buy the synthetic 1-year $-denominated discount bond and sell the 1-year $-denominated discount bond: Strategy 4/05 4/06 Sell $1 of 1-year $-denominated discount bonds on 4/05 and close out on 4/06 Sell a forward contract which delivers [1/1.6][1+ 0.1] = on 4/06 Buy $1 worth of on 4/05 ( 1/1.6) and invest in 1-year -denominated discount bonds and hold til maturity {2-1} x =2 x Net Cash Flow 0 2 x = c. This strategy is an arbitrage opportunity. 9

11 Lecture 11 Foundations of Finance Lecture 11: Market Efficiency I. Reading. A. BKM, Chapter 12. Read Sections 12.1 and 12.2 but only skim Sections 12.3 and II. III. Definition of Market Efficiency. A. In an efficient market, the price of a security is an unbiased estimate of its value. B. Notice that the level of efficiency in a market depends on two dimensions: 1. The amount of information incorporated into price. 2. The speed with which new information is incorporated into price. Features of Market Efficiency. A. To assess the level of market efficiency need to know the security s value: 1. Which requires knowing how assets are priced. 2. Need to know the expected return on an asset given the appropriate pricing model for the economy. B. Market efficiency means that over any period: Realized return = Expected Return + Unpredictable Mean-zero Surprise. and so (ignoring dividends): Period-end s Price = Today s Price (1 + Expected Return) + Unpredictable Mean-zero Surprise. C. Market efficiency says that: 1. If a piece of news is always followed by a another piece of news than the market incorporates the likely impact of the second piece of news at the time that the first piece of news becomes available. 2. So even if news is correlated, return surprises will not be. D. Implications of market efficiency for return patterns. 1. If expected returns are constant through time: a. Unpredictable mean-zero return surprises imply unpredictable returns b. So returns will be uncorrelated. 2. If expected returns vary through time. a. Unpredictable mean-zero return surprises do not imply unpredictable returns. b. If past returns forecast future expected returns then returns will be autocorrelated. 3. So autocorrelated returns need not imply market inefficiency 10

12 Lecture 11 Foundations of Finance E. Implications of market efficiency for portfolio manager/investor performance: 1. Need to distinguish skill from luck. 2. In an efficient market: a. expected performance (e.g., Jensen s alpha in a CAPM world) of a manager/investor over any period is zero. b. but in any given period will see really good portfolio performances by some managers/ investors due to chance. 3. Need to be skeptical when someone tells you about good performance. 4. However, the longer the period of good performance, the more likely it s skill and not luck. IV. Costly Information Acquisition and Costly Trading. A. A Contradiction 1. if markets are efficient, all information is reflected in price. 2. but then there is no incentive to gather costly information and trade on it. 3. so how does the information get into price?! B. An Alternate Argument. 1. Could have an equilibrium where some investors choose to gather information and some do not. 2. Those that do earn better returns which offset the costs of acquiring the information and trading on it. 3. The market is not fully efficient in the sense discussed above. 11

13 Lecture 11 Foundations of Finance V. Levels of Market Efficiency A. Weak form. 1. Price reflects all information contained in past prices: so an investor can not use past prices to identify mispriced securities. 2. Technical analysis: a. refers to the practice of using past patterns in stock prices to identify future patterns in prices. b. is not profitable in a market which is at least weak form efficient. B. Semi-strong form. 1. Price reflects all publicly available information: so an investor can not use publicly available information to identify mispriced securities. 2. Fundamental analysis: a. refers to the practice of using financial statements and other publicly available information about firms to pick stocks. b. is not profitable in a market which is at least semi-strong form efficient. 3. If a market is semi-strong form efficient, then it is also weak form efficient since past prices are publicly available. C. Strong form. 1. Price reflects all available information: so an investor can not use any available information to identify mispriced securities. 2. Insider trading: a. refers to the practice of using private information about firms to pick stocks. b. is not profitable in a market which is at least strong form efficient. c. is illegal. 3. If a market is strong form efficient, then it is also semi-strong and weak form efficient since all available information includes past prices and publicly available information. VI. How efficient are U.S. financial markets. A. Probably semi-strong form efficient but not strong form efficient. 1. Can find rare examples of semi-strong form inefficiency. 2. But in general it s difficult to generate abnormally good performance using only publically available information. B. Implications for mutual fund management: 1. Unlikely to be successful using only publicly available information. 2. Need to use smarts or non-public information in forming portfolios to generate good abnormal performance. 12

14 Lecture 11 Foundations of Finance VII. Performance of the U.S. Mutual Fund Industry. A. Performance of funds net of trading costs, expenses and fees relative to Fama- French type pricing models: 1. Average performance is negative a. Carhart, Carpenter, Lynch and Musto (2002) Review of Financial Studies. b. -1.8% per annum abnormal bad performance that is strongly significantly different from zero. 2. More negative for the funds with the highest turnover. 3. More negative for the funds with the highest expense ratios. 13

15 Lecture 11 Foundations of Finance B. Performance persistence 1. Bad performance shows some persistence: likely due to high expenses and turnover. 2. Good performance is not persistent at all: suggests good performance by a fund is most likely due to luck than skill. 14

16 Lecture 11 Foundations of Finance VIII. Problems with Testing Market Efficiency A. Joint Test Problem. 1. The question whether price fully reflects a given piece of information always depends on the model of asset pricing that the researcher is using. It is always a joint test. 2. Example: a. Know value stocks lie above the SML b. Implies semi-strong market inefficiency if the CAPM is the appropriate pricing model. c. But in an ICAPM world: the high expected return could also be compensation for high covariance with a state variable that individual s care about. B. Data-mining Issue. 1. seek and thou shall find 2. Many researchers and market participants are looking for patterns in returns. 3. Even truly random samples, however, appear to have patterns. 4. In-sample predictability need not imply out-of-sample predictability. 15

17 Lecture 11 Foundations of Finance IX. Example of Semi-strong Form Inefficiency A. Stocks added and deleted from the S&P

18 Lecture 11 Foundations of Finance 17

19 Lecture 11 Foundations of Finance X. Predictability of Returns. A. Can forecast long horizon returns using: 1. Past long horizon returns (negative relation). 2. Information variables related to the business cycle: a. aggregate dividend yield at the start of the return period (positive relation). b. term spread (long term high grade corporate bond yield less one month T-bill rate) which is known at the start of the return period (positive relation). c. these information variables are counter cyclical. B. These findings are consistent with two stories: 1. Time varying expected returns and semistrong market efficiency. 2. Constant expected returns and semistrong market inefficiency. 18

20 Lecture 11 Foundations of Finance 19

Foundations of Finance

Lecture 7: Bond Pricing, Forward Rates and the Yield Curve. I. Reading. II. Discount Bond Yields and Prices. III. Fixed-income Prices and No Arbitrage. IV. The Yield Curve. V. Other Bond Pricing Issues.

Lecture 7: Bond Pricing, Forward Rates and the Yield Curve. I. Reading. II. Discount Bond Yields and Prices. III. Fixed-income Prices and No Arbitrage. IV. The Yield Curve. V. Other Bond Pricing Issues.

CHAPTER 11. The Efficient Market Hypothesis INVESTMENTS BODIE, KANE, MARCUS. Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved.

CHAPTER 11 The Efficient Market Hypothesis McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 11-2 Efficient Market Hypothesis (EMH) Maurice Kendall (1953) found no

CHAPTER 11 The Efficient Market Hypothesis McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 11-2 Efficient Market Hypothesis (EMH) Maurice Kendall (1953) found no

15 Week 5b Mutual Funds

15 Week 5b Mutual Funds 15.1 Background 1. It would be natural, and completely sensible, (and good marketing for MBA programs) if funds outperform darts! Pros outperform in any other field. 2. Except for...

15 Week 5b Mutual Funds 15.1 Background 1. It would be natural, and completely sensible, (and good marketing for MBA programs) if funds outperform darts! Pros outperform in any other field. 2. Except for...

Senior Finance Seminar (FIN 4385) Market Efficiency

Market Efficiency") Senior Finance Seminar (FIN 4385) Market Efficiency Why do we care about Market Efficiency? Market Efficiency is the extent to which prices reflect. If markets are efficient, then what should we conclude

Senior Finance Seminar (FIN 4385) Market Efficiency Why do we care about Market Efficiency? Market Efficiency is the extent to which prices reflect. If markets are efficient, then what should we conclude

Calculating EAR and continuous compounding: Find the EAR in each of the cases below.

Problem Set 1: Time Value of Money and Equity Markets. I-III can be started after Lecture 1. IV-VI can be started after Lecture 2. VII can be started after Lecture 3. VIII and IX can be started after Lecture

Problem Set 1: Time Value of Money and Equity Markets. I-III can be started after Lecture 1. IV-VI can be started after Lecture 2. VII can be started after Lecture 3. VIII and IX can be started after Lecture

Chapter 13. Efficient Capital Markets and Behavioral Challenges

Chapter 13 Efficient Capital Markets and Behavioral Challenges Articulate the importance of capital market efficiency Define the three forms of efficiency Know the empirical tests of market efficiency

Chapter 13 Efficient Capital Markets and Behavioral Challenges Articulate the importance of capital market efficiency Define the three forms of efficiency Know the empirical tests of market efficiency

It is a market where current prices reflect/incorporate all available information.

ECMC49S Market Efficiency Hypothesis Practice Questions Date: Mar 29, 2006 [1] How to define an efficient market? It is a market where current prices reflect/incorporate all available information. [2]

ECMC49S Market Efficiency Hypothesis Practice Questions Date: Mar 29, 2006 [1] How to define an efficient market? It is a market where current prices reflect/incorporate all available information. [2]

CHAPTER 11. The Efficient Market Hypothesis INVESTMENTS BODIE, KANE, MARCUS. Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved.

CHAPTER 11 The Efficient Market Hypothesis McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 11-2 Efficient Market Hypothesis (EMH) Maurice Kendall (1953) found no

CHAPTER 11 The Efficient Market Hypothesis McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 11-2 Efficient Market Hypothesis (EMH) Maurice Kendall (1953) found no

Foundations of Finance

Lecture 5: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Individual Assets in a CAPM World. VI. Intuition for the SML (E[R p ] depending

Lecture 5: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Individual Assets in a CAPM World. VI. Intuition for the SML (E[R p ] depending

Finding outperforming managers

Finding outperforming managers Randolph B. Cohen MIT Sloan School of Management 1 Money Management Skeptics hold that: Managers can t pick stocks and therefore don t beat the market It s impossible to

Finding outperforming managers Randolph B. Cohen MIT Sloan School of Management 1 Money Management Skeptics hold that: Managers can t pick stocks and therefore don t beat the market It s impossible to

The Efficient Market Hypothesis

Efficient Market Hypothesis (EMH) 11-2 The Efficient Market Hypothesis Maurice Kendall (1953) found no predictable pattern in stock prices. Prices are as likely to go up as to go down on any particular

Efficient Market Hypothesis (EMH) 11-2 The Efficient Market Hypothesis Maurice Kendall (1953) found no predictable pattern in stock prices. Prices are as likely to go up as to go down on any particular

MBF2253 Modern Security Analysis

MBF2253 Modern Security Analysis Prepared by Dr Khairul Anuar L8: Efficient Capital Market www.notes638.wordpress.com Capital Market Efficiency Capital market history suggests that the market values of

MBF2253 Modern Security Analysis Prepared by Dr Khairul Anuar L8: Efficient Capital Market www.notes638.wordpress.com Capital Market Efficiency Capital market history suggests that the market values of

Forward and Futures Contracts

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 Forward and Futures Contracts These notes explore forward and futures contracts, what they are and how they are used. We will learn how to price forward contracts

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 Forward and Futures Contracts These notes explore forward and futures contracts, what they are and how they are used. We will learn how to price forward contracts

COMM 324 INVESTMENTS AND PORTFOLIO MANAGEMENT ASSIGNMENT 2 Due: October 20

COMM 34 INVESTMENTS ND PORTFOLIO MNGEMENT SSIGNMENT Due: October 0 1. In 1998 the rate of return on short term government securities (perceived to be risk-free) was about 4.5%. Suppose the expected rate

COMM 34 INVESTMENTS ND PORTFOLIO MNGEMENT SSIGNMENT Due: October 0 1. In 1998 the rate of return on short term government securities (perceived to be risk-free) was about 4.5%. Suppose the expected rate

Lecture 1: Foundation

OPTIONS and FUTURES Lecture 1: Foundation Philip H. Dybvig Washington University in Saint Louis applications big ideas derivatives market players strategy examples Copyright c Philip H. Dybvig 2004 Derivatives

OPTIONS and FUTURES Lecture 1: Foundation Philip H. Dybvig Washington University in Saint Louis applications big ideas derivatives market players strategy examples Copyright c Philip H. Dybvig 2004 Derivatives

Derivation of zero-beta CAPM: Efficient portfolios

Derivation of zero-beta CAPM: Efficient portfolios AssumptionsasCAPM,exceptR f does not exist. Argument which leads to Capital Market Line is invalid. (No straight line through R f, tilted up as far as

Derivation of zero-beta CAPM: Efficient portfolios AssumptionsasCAPM,exceptR f does not exist. Argument which leads to Capital Market Line is invalid. (No straight line through R f, tilted up as far as

Introduction to Futures and Options

Introduction to Futures and Options Pratish Patel Spring 2014 Lecture note on Forwards California Polytechnic University Pratish Patel Spring 2014 Forward Contracts Definition: A forward contract is a

Introduction to Futures and Options Pratish Patel Spring 2014 Lecture note on Forwards California Polytechnic University Pratish Patel Spring 2014 Forward Contracts Definition: A forward contract is a

Lecture 10-12: CAPM.

Lecture 10-12: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Minimum Variance Mathematics. VI. Individual Assets in a CAPM World. VII. Intuition

Lecture 10-12: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Minimum Variance Mathematics. VI. Individual Assets in a CAPM World. VII. Intuition

A Random Walk Down Wall Street

FIN 614 Capital Market Efficiency Professor Robert B.H. Hauswald Kogod School of Business, AU A Random Walk Down Wall Street From theory of return behavior to its practice Capital market efficiency: the

FIN 614 Capital Market Efficiency Professor Robert B.H. Hauswald Kogod School of Business, AU A Random Walk Down Wall Street From theory of return behavior to its practice Capital market efficiency: the

Forwards, Futures, Options and Swaps

Forwards, Futures, Options and Swaps A derivative asset is any asset whose payoff, price or value depends on the payoff, price or value of another asset. The underlying or primitive asset may be almost

Forwards, Futures, Options and Swaps A derivative asset is any asset whose payoff, price or value depends on the payoff, price or value of another asset. The underlying or primitive asset may be almost

MARKET EFFICIENCY & MUTUAL FUNDS

MARKET EFFICIENCY & MUTUAL FUNDS Topics: Market Efficiency Random Walks Different Forms of Market Efficiency Investing in Mutual Funds Introduction to mutual funds Evaluating mutual fund performance Evaluating

MARKET EFFICIENCY & MUTUAL FUNDS Topics: Market Efficiency Random Walks Different Forms of Market Efficiency Investing in Mutual Funds Introduction to mutual funds Evaluating mutual fund performance Evaluating

Lecture 8 Foundations of Finance

Lecture 8: Bond Portfolio Management. I. Reading. II. Risks associated with Fixed Income Investments. A. Reinvestment Risk. B. Liquidation Risk. III. Duration. A. Definition. B. Duration can be interpreted

Lecture 8: Bond Portfolio Management. I. Reading. II. Risks associated with Fixed Income Investments. A. Reinvestment Risk. B. Liquidation Risk. III. Duration. A. Definition. B. Duration can be interpreted

Financial Management

Financial Management International Finance 1 RISK AND HEDGING In this lecture we will cover: Justification for hedging Different Types of Hedging Instruments. How to Determine Risk Exposure. Good references

Financial Management International Finance 1 RISK AND HEDGING In this lecture we will cover: Justification for hedging Different Types of Hedging Instruments. How to Determine Risk Exposure. Good references

AFM 371 Winter 2008 Chapter 26 - Derivatives and Hedging Risk Part 2 - Interest Rate Risk Management ( )

") AFM 371 Winter 2008 Chapter 26 - Derivatives and Hedging Risk Part 2 - Interest Rate Risk Management (26.4-26.7) 1 / 30 Outline Term Structure Forward Contracts on Bonds Interest Rate Futures Contracts

AFM 371 Winter 2008 Chapter 26 - Derivatives and Hedging Risk Part 2 - Interest Rate Risk Management (26.4-26.7) 1 / 30 Outline Term Structure Forward Contracts on Bonds Interest Rate Futures Contracts

AFM 371 Winter 2008 Chapter 14 - Efficient Capital Markets

AFM 371 Winter 2008 Chapter 14 - Efficient Capital Markets 1 / 24 Outline Background What Is Market Efficiency? Different Levels Of Efficiency Empirical Evidence Implications Of Market Efficiency For Corporate

AFM 371 Winter 2008 Chapter 14 - Efficient Capital Markets 1 / 24 Outline Background What Is Market Efficiency? Different Levels Of Efficiency Empirical Evidence Implications Of Market Efficiency For Corporate

Futures and Forward Markets

Futures and Forward Markets (Text reference: Chapters 19, 21.4) background hedging and speculation optimal hedge ratio forward and futures prices futures prices and expected spot prices stock index futures

Futures and Forward Markets (Text reference: Chapters 19, 21.4) background hedging and speculation optimal hedge ratio forward and futures prices futures prices and expected spot prices stock index futures

International Finance. Investment Styles. Campbell R. Harvey. Duke University, NBER and Investment Strategy Advisor, Man Group, plc.

International Finance Investment Styles Campbell R. Harvey Duke University, NBER and Investment Strategy Advisor, Man Group, plc February 12, 2017 2 1. Passive Follow the advice of the CAPM Most influential

International Finance Investment Styles Campbell R. Harvey Duke University, NBER and Investment Strategy Advisor, Man Group, plc February 12, 2017 2 1. Passive Follow the advice of the CAPM Most influential

Session 6-8. Efficient Market Hypothesis (EMH) Efficient Market Hypothesis (EMH) Efficient Market Hypothesis (EMH)

Efficient Market Hypothesis (EMH) Efficient Market Hypothesis (EMH)") 2 Efficient Market Hypothesis (EMH) Maurice Kendall (1953) found no predictable pattern in stock prices. Prices are as likely to go up as to go down on any particular day. How do we explain random stock

2 Efficient Market Hypothesis (EMH) Maurice Kendall (1953) found no predictable pattern in stock prices. Prices are as likely to go up as to go down on any particular day. How do we explain random stock

Practice Set #1: Forward pricing & hedging.

Derivatives (3 credits) Professor Michel Robe What to do with this practice set? Practice Set #1: Forward pricing & hedging To help students with the material, eight practice sets with solutions shall

Derivatives (3 credits) Professor Michel Robe What to do with this practice set? Practice Set #1: Forward pricing & hedging To help students with the material, eight practice sets with solutions shall

NAME: ID Number: 3. Lump sum taxes cause effects. a) Do not; wealth b) do; wealth c) do; substitution d) both (b) and (c).

Do not; wealth b) do; wealth c) do; substitution d) both (b) and (c).") NAME: ID Number: Econ 302 Final May 11, 5:05 PM 7:05 PM Instructions: This exam consists of two parts. There are twenty-five multiple choice questions, each worth 2 points (totaling 50 points). The second

NAME: ID Number: Econ 302 Final May 11, 5:05 PM 7:05 PM Instructions: This exam consists of two parts. There are twenty-five multiple choice questions, each worth 2 points (totaling 50 points). The second

EFFICIENT MARKETS HYPOTHESIS

EFFICIENT MARKETS HYPOTHESIS when economists speak of capital markets as being efficient, they usually consider asset prices and returns as being determined as the outcome of supply and demand in a competitive

EFFICIENT MARKETS HYPOTHESIS when economists speak of capital markets as being efficient, they usually consider asset prices and returns as being determined as the outcome of supply and demand in a competitive

Futures and Forwards. Futures Markets. Basics of Futures Contracts. Long a commitment to purchase the commodity. the delivery date.

Futures and Forwards Forward a deferred delivery sale of an asset with the sales price agreed on now. Futures Markets Futures similar to forward but feature formalized and standardized contracts. Key difference

Futures and Forwards Forward a deferred delivery sale of an asset with the sales price agreed on now. Futures Markets Futures similar to forward but feature formalized and standardized contracts. Key difference

INVESTMENTS Lecture 2: Measuring Performance

Philip H. Dybvig Washington University in Saint Louis portfolio returns unitization INVESTMENTS Lecture 2: Measuring Performance statistical measures of performance the use of benchmark portfolios Copyright

Philip H. Dybvig Washington University in Saint Louis portfolio returns unitization INVESTMENTS Lecture 2: Measuring Performance statistical measures of performance the use of benchmark portfolios Copyright

APPENDIX TO LECTURE NOTES ON ASSET PRICING AND PORTFOLIO MANAGEMENT. Professor B. Espen Eckbo

APPENDIX TO LECTURE NOTES ON ASSET PRICING AND PORTFOLIO MANAGEMENT 2011 Professor B. Espen Eckbo 1. Portfolio analysis in Excel spreadsheet 2. Formula sheet 3. List of Additional Academic Articles 2011

APPENDIX TO LECTURE NOTES ON ASSET PRICING AND PORTFOLIO MANAGEMENT 2011 Professor B. Espen Eckbo 1. Portfolio analysis in Excel spreadsheet 2. Formula sheet 3. List of Additional Academic Articles 2011

Overview of Concepts and Notation

Overview of Concepts and Notation (BUSFIN 4221: Investments) - Fall 2016 1 Main Concepts This section provides a list of questions you should be able to answer. The main concepts you need to know are embedded

Overview of Concepts and Notation (BUSFIN 4221: Investments) - Fall 2016 1 Main Concepts This section provides a list of questions you should be able to answer. The main concepts you need to know are embedded

The CAPM. (Welch, Chapter 10) Ivo Welch. UCLA Anderson School, Corporate Finance, Winter December 16, 2016

Ivo Welch. UCLA Anderson School, Corporate Finance, Winter December 16, 2016") 1/1 The CAPM (Welch, Chapter 10) Ivo Welch UCLA Anderson School, Corporate Finance, Winter 2017 December 16, 2016 Did you bring your calculator? Did you read these notes and the chapter ahead of time?

1/1 The CAPM (Welch, Chapter 10) Ivo Welch UCLA Anderson School, Corporate Finance, Winter 2017 December 16, 2016 Did you bring your calculator? Did you read these notes and the chapter ahead of time?

Foundations of Finance

Lecture 9 Lecture 9: Theories of the Yield Curve. I. Reading. II. Expectations Hypothesis III. Liquidity Preference Theory. IV. Preferred Habitat Theory. Lecture 9: Bond Portfolio Management. V. Reading.

Lecture 9 Lecture 9: Theories of the Yield Curve. I. Reading. II. Expectations Hypothesis III. Liquidity Preference Theory. IV. Preferred Habitat Theory. Lecture 9: Bond Portfolio Management. V. Reading.

CHAPTER 12: MARKET EFFICIENCY AND BEHAVIORAL FINANCE

CHAPTER 12: MARKET EFFICIENCY AND BEHAVIORAL FINANCE 1. The correlation coefficient between stock returns for two non-overlapping periods should be zero. If not, one could use returns from one period to

CHAPTER 12: MARKET EFFICIENCY AND BEHAVIORAL FINANCE 1. The correlation coefficient between stock returns for two non-overlapping periods should be zero. If not, one could use returns from one period to

EQUITY RESEARCH AND PORTFOLIO MANAGEMENT

EQUITY RESEARCH AND PORTFOLIO MANAGEMENT By P K AGARWAL IIFT, NEW DELHI 1 MARKOWITZ APPROACH Requires huge number of estimates to fill the covariance matrix (N(N+3))/2 Eg: For a 2 security case: Require

EQUITY RESEARCH AND PORTFOLIO MANAGEMENT By P K AGARWAL IIFT, NEW DELHI 1 MARKOWITZ APPROACH Requires huge number of estimates to fill the covariance matrix (N(N+3))/2 Eg: For a 2 security case: Require

CHAPTER 13 EFFICIENT CAPITAL MARKETS AND BEHAVIORAL CHALLENGES

CHAPTER 13 EFFICIENT CAPITAL MARKETS AND BEHAVIORAL CHALLENGES Answers to Concept Questions 1. To create value, firms should accept financing proposals with positive net present values. Firms can create

CHAPTER 13 EFFICIENT CAPITAL MARKETS AND BEHAVIORAL CHALLENGES Answers to Concept Questions 1. To create value, firms should accept financing proposals with positive net present values. Firms can create

Chapter Ten. The Efficient Market Hypothesis

Chapter Ten The Efficient Market Hypothesis Slide 10 3 Topics Covered We Always Come Back to NPV What is an Efficient Market? Random Walk Efficient Market Theory The Evidence on Market Efficiency Puzzles

Chapter Ten The Efficient Market Hypothesis Slide 10 3 Topics Covered We Always Come Back to NPV What is an Efficient Market? Random Walk Efficient Market Theory The Evidence on Market Efficiency Puzzles

University of Pennsylvania The Wharton School

University of Pennsylvania The Wharton School FNCE 100 PROBLEM SET #5 Fall Term 2005 A. Craig MacKinlay Market Efficiency 1. Money manager Robert J. Betaman of Betaman-Rubin Associates has shown an uncanny

University of Pennsylvania The Wharton School FNCE 100 PROBLEM SET #5 Fall Term 2005 A. Craig MacKinlay Market Efficiency 1. Money manager Robert J. Betaman of Betaman-Rubin Associates has shown an uncanny

Understanding Investments

Understanding Investments Theories and Strategies Nikiforos T. Laopodis j Routledge Taylor & Francis Croup NEW YORK AND LONDON CONTENTS List of Illustrations Preface xxni xxix Parti Chapter 1 INVESTMENT

Understanding Investments Theories and Strategies Nikiforos T. Laopodis j Routledge Taylor & Francis Croup NEW YORK AND LONDON CONTENTS List of Illustrations Preface xxni xxix Parti Chapter 1 INVESTMENT

Efficient capital markets. Skema Business School. Portfolio Management 1. Course Outline

Efficient capital markets bertrand.groslambert@skema.edu Skema Business School Portfolio Management 1 Course Outline Introduction (lecture 1) Presentation of portfolio management Chap.2,3,5 Introduction

Efficient capital markets bertrand.groslambert@skema.edu Skema Business School Portfolio Management 1 Course Outline Introduction (lecture 1) Presentation of portfolio management Chap.2,3,5 Introduction

Lecture 1 Definitions from finance

Lecture 1 s from finance Financial market instruments can be divided into two types. There are the underlying stocks shares, bonds, commodities, foreign currencies; and their derivatives, claims that promise

Lecture 1 s from finance Financial market instruments can be divided into two types. There are the underlying stocks shares, bonds, commodities, foreign currencies; and their derivatives, claims that promise

CHAPTER 7 FOREIGN EXCHANGE MARKET EFFICIENCY

CHAPTER 7 FOREIGN EXCHANGE MARKET EFFICIENCY Chapter Overview This chapter has two major parts: the introduction to the principles of market efficiency and a review of the empirical evidence on efficiency

CHAPTER 7 FOREIGN EXCHANGE MARKET EFFICIENCY Chapter Overview This chapter has two major parts: the introduction to the principles of market efficiency and a review of the empirical evidence on efficiency

Chapter. Return, Risk, and the Security Market Line. McGraw-Hill/Irwin. Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter Return, Risk, and the Security Market Line McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Return, Risk, and the Security Market Line Our goal in this chapter

Chapter Return, Risk, and the Security Market Line McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Return, Risk, and the Security Market Line Our goal in this chapter

P1.T1. Foundations of Risk Management Zvi Bodie, Alex Kane, and Alan J. Marcus, Investments, 10th Edition Bionic Turtle FRM Study Notes

P1.T1. Foundations of Risk Management Zvi Bodie, Alex Kane, and Alan J. Marcus, Investments, 10th Edition Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM www.bionicturtle.com BODIE, CHAPTER

P1.T1. Foundations of Risk Management Zvi Bodie, Alex Kane, and Alan J. Marcus, Investments, 10th Edition Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM www.bionicturtle.com BODIE, CHAPTER

OPTIONS and FUTURES Lecture 5: Forwards, Futures, and Futures Options

OPTIONS and FUTURES Lecture 5: Forwards, Futures, and Futures Options Philip H. Dybvig Washington University in Saint Louis Spot (cash) market Forward contract Futures contract Options on futures Copyright

OPTIONS and FUTURES Lecture 5: Forwards, Futures, and Futures Options Philip H. Dybvig Washington University in Saint Louis Spot (cash) market Forward contract Futures contract Options on futures Copyright

Foundations of Finance. Lecture 8: Portfolio Management-2 Risky Assets and a Riskless Asset.

Lecture 8: Portfolio Management-2 Risky Assets and a Riskless Asset. I. Reading. A. BKM, Chapter 8: read Sections 8.1 to 8.3. II. Standard Deviation of Portfolio Return: Two Risky Assets. A. Formula: σ

Lecture 8: Portfolio Management-2 Risky Assets and a Riskless Asset. I. Reading. A. BKM, Chapter 8: read Sections 8.1 to 8.3. II. Standard Deviation of Portfolio Return: Two Risky Assets. A. Formula: σ

Into a New Dimension. An Alternative View of Smart Beta

Into a New Dimension An Alternative View of Smart Beta Into a New Dimension An Alternative View of Smart Beta Table Of Contents Introduction 4 The alpha/beta debate has a long and evolving history 4 Some

Into a New Dimension An Alternative View of Smart Beta Into a New Dimension An Alternative View of Smart Beta Table Of Contents Introduction 4 The alpha/beta debate has a long and evolving history 4 Some

UNIVERSITY OF SOUTH AFRICA

UNIVERSITY OF SOUTH AFRICA Vision Towards the African university in the service of humanity College of Economic and Management Sciences Department of Finance & Risk Management & Banking General information

UNIVERSITY OF SOUTH AFRICA Vision Towards the African university in the service of humanity College of Economic and Management Sciences Department of Finance & Risk Management & Banking General information

Considerations When Using Grain Contracts

Considerations When Using Grain Contracts Overview The grain industry has developed several new tools to help farmers manage increasing risks and price volatility. Elevators can use grain options markets

Considerations When Using Grain Contracts Overview The grain industry has developed several new tools to help farmers manage increasing risks and price volatility. Elevators can use grain options markets

INV2601 DISCUSSION CLASS SEMESTER 2 INVESTMENTS: AN INTRODUCTION INV2601 DEPARTMENT OF FINANCE, RISK MANAGEMENT AND BANKING

INV2601 DISCUSSION CLASS SEMESTER 2 INVESTMENTS: AN INTRODUCTION INV2601 DEPARTMENT OF FINANCE, RISK MANAGEMENT AND BANKING Examination Duration of exam 2 hours. 40 multiple choice questions. Total marks

INV2601 DISCUSSION CLASS SEMESTER 2 INVESTMENTS: AN INTRODUCTION INV2601 DEPARTMENT OF FINANCE, RISK MANAGEMENT AND BANKING Examination Duration of exam 2 hours. 40 multiple choice questions. Total marks

CIS March 2012 Diet. Examination Paper 2.3: Derivatives Valuation Analysis Portfolio Management Commodity Trading and Futures.

CIS March 2012 Diet Examination Paper 2.3: Derivatives Valuation Analysis Portfolio Management Commodity Trading and Futures Level 2 Derivative Valuation and Analysis (1 12) 1. A CIS student was making

CIS March 2012 Diet Examination Paper 2.3: Derivatives Valuation Analysis Portfolio Management Commodity Trading and Futures Level 2 Derivative Valuation and Analysis (1 12) 1. A CIS student was making

RESEARCH THE SMALL-CAP-ALPHA MYTH ORIGINS

RESEARCH THE SMALL-CAP-ALPHA MYTH ORIGINS Many say the market for the shares of smaller companies so called small-cap and mid-cap stocks offers greater opportunity for active management to add value than

RESEARCH THE SMALL-CAP-ALPHA MYTH ORIGINS Many say the market for the shares of smaller companies so called small-cap and mid-cap stocks offers greater opportunity for active management to add value than

Highly Selective Active Managers, Though Rare, Outperform

INSTITUTIONAL PERSPECTIVES May 018 Highly Selective Active Managers, Though Rare, Outperform Key Takeaways ffresearch shows that highly skilled active managers with high active share, low R and a patient

INSTITUTIONAL PERSPECTIVES May 018 Highly Selective Active Managers, Though Rare, Outperform Key Takeaways ffresearch shows that highly skilled active managers with high active share, low R and a patient

PRINCIPLES of INVESTMENTS

PRINCIPLES of INVESTMENTS Boston University MICHAItL L D\if.\N Griffith University AN UP BASU Queensland University of Technology ALEX KANT; University of California, San Diego ALAN J. AAARCU5 Boston College

PRINCIPLES of INVESTMENTS Boston University MICHAItL L D\if.\N Griffith University AN UP BASU Queensland University of Technology ALEX KANT; University of California, San Diego ALAN J. AAARCU5 Boston College

QR43, Introduction to Investments Class Notes, Fall 2003 IV. Portfolio Choice

QR43, Introduction to Investments Class Notes, Fall 2003 IV. Portfolio Choice A. Mean-Variance Analysis 1. Thevarianceofaportfolio. Consider the choice between two risky assets with returns R 1 and R 2.

QR43, Introduction to Investments Class Notes, Fall 2003 IV. Portfolio Choice A. Mean-Variance Analysis 1. Thevarianceofaportfolio. Consider the choice between two risky assets with returns R 1 and R 2.

Introduction, Forwards and Futures

Introduction, Forwards and Futures Liuren Wu Options Markets Liuren Wu ( ) Introduction, Forwards & Futures Options Markets 1 / 31 Derivatives Derivative securities are financial instruments whose returns

Introduction, Forwards and Futures Liuren Wu Options Markets Liuren Wu ( ) Introduction, Forwards & Futures Options Markets 1 / 31 Derivatives Derivative securities are financial instruments whose returns

Principles of Finance

Principles of Finance Grzegorz Trojanowski Lecture 7: Arbitrage Pricing Theory Principles of Finance - Lecture 7 1 Lecture 7 material Required reading: Elton et al., Chapter 16 Supplementary reading: Luenberger,

Principles of Finance Grzegorz Trojanowski Lecture 7: Arbitrage Pricing Theory Principles of Finance - Lecture 7 1 Lecture 7 material Required reading: Elton et al., Chapter 16 Supplementary reading: Luenberger,

SOCIETY OF ACTUARIES EXAM IFM INVESTMENT AND FINANCIAL MARKETS EXAM IFM SAMPLE QUESTIONS AND SOLUTIONS DERIVATIVES

SOCIETY OF ACTUARIES EXAM IFM INVESTMENT AND FINANCIAL MARKETS EXAM IFM SAMPLE QUESTIONS AND SOLUTIONS DERIVATIVES These questions and solutions are based on the readings from McDonald and are identical

SOCIETY OF ACTUARIES EXAM IFM INVESTMENT AND FINANCIAL MARKETS EXAM IFM SAMPLE QUESTIONS AND SOLUTIONS DERIVATIVES These questions and solutions are based on the readings from McDonald and are identical

CORPORATE FINANCING and MARKET EFFICIENCY FINANCING STRATEGY

CHAPTER 13 CORPORATE FINANCING and MARKET EFFICIENCY FINANCING STRATEGY WE NOW MOVE FROM LEFT-HAND SIDE TO RIGHT HAND SIDE OF THE BALANCE SHEET GIVEN THE FIRM S CURRENT PORTFOLIO OF REAL ASSETS AND ITS

CHAPTER 13 CORPORATE FINANCING and MARKET EFFICIENCY FINANCING STRATEGY WE NOW MOVE FROM LEFT-HAND SIDE TO RIGHT HAND SIDE OF THE BALANCE SHEET GIVEN THE FIRM S CURRENT PORTFOLIO OF REAL ASSETS AND ITS

Lecture Notes 18: Review Sample Multiple Choice Problems

Lecture Notes 18: Review Sample Multiple Choice Problems 1. Assuming true-model returns are identically independently distributed (i.i.d), which events violate market efficiency? I. Positive correlation

Lecture Notes 18: Review Sample Multiple Choice Problems 1. Assuming true-model returns are identically independently distributed (i.i.d), which events violate market efficiency? I. Positive correlation

SAMPLE FINAL QUESTIONS. William L. Silber

SAMPLE FINAL QUESTIONS William L. Silber HOW TO PREPARE FOR THE FINAL: 1. Study in a group 2. Review the concept questions in the Before and After book 3. When you review the questions listed below, make

SAMPLE FINAL QUESTIONS William L. Silber HOW TO PREPARE FOR THE FINAL: 1. Study in a group 2. Review the concept questions in the Before and After book 3. When you review the questions listed below, make

DERIVATIVE SECURITIES Lecture 1: Background and Review of Futures Contracts

DERIVATIVE SECURITIES Lecture 1: Background and Review of Futures Contracts Philip H. Dybvig Washington University in Saint Louis applications derivatives market players big ideas strategy example single-period

DERIVATIVE SECURITIES Lecture 1: Background and Review of Futures Contracts Philip H. Dybvig Washington University in Saint Louis applications derivatives market players big ideas strategy example single-period

Expectations are very important in our financial system.

Chapter 6 Are Financial Markets Efficient? Chapter Preview Expectations are very important in our financial system. Expectations of returns, risk, and liquidity impact asset demand Inflationary expectations

Chapter 6 Are Financial Markets Efficient? Chapter Preview Expectations are very important in our financial system. Expectations of returns, risk, and liquidity impact asset demand Inflationary expectations

Lecture 1, Jan

Markets and Financial Derivatives Tradable Assets Lecture 1, Jan 28 21 Introduction Prof. Boyan ostadinov, City Tech of CUNY The key players in finance are the tradable assets. Examples of tradables are:

Markets and Financial Derivatives Tradable Assets Lecture 1, Jan 28 21 Introduction Prof. Boyan ostadinov, City Tech of CUNY The key players in finance are the tradable assets. Examples of tradables are:

NAME: Econ 302 Mid-term 3

NAME: Econ 302 Mid-term 3 Instructions: This exam consists of two parts. There are twenty multiple choice questions, each worth 2.5 points (totaling 50 points). The second part consists of 2 problems,

NAME: Econ 302 Mid-term 3 Instructions: This exam consists of two parts. There are twenty multiple choice questions, each worth 2.5 points (totaling 50 points). The second part consists of 2 problems,

ECON FINANCIAL ECONOMICS

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Fall 2017 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Fall 2017 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

Lesson XI: Market Efficiency and FX. Forecasting

Lesson XI: May 15, 2017 Table of Contents Getting Started Market efficiency is an equilibrium condition, such that prices reflect all the available information and no abnormal returns can thus be earned

Lesson XI: May 15, 2017 Table of Contents Getting Started Market efficiency is an equilibrium condition, such that prices reflect all the available information and no abnormal returns can thus be earned

Module 6 Portfolio risk and return

Module 6 Portfolio risk and return Prepared by Pamela Peterson Drake, Ph.D., CFA 1. Overview Security analysts and portfolio managers are concerned about an investment s return, its risk, and whether it

Module 6 Portfolio risk and return Prepared by Pamela Peterson Drake, Ph.D., CFA 1. Overview Security analysts and portfolio managers are concerned about an investment s return, its risk, and whether it

Stock Market Basics. Capital Market A market for intermediate or long-term debt or corporate stocks.

Stock Market Basics Capital Market A market for intermediate or long-term debt or corporate stocks. Stock Market and Stock Exchange A stock exchange is the most important component of a stock market. It

Stock Market Basics Capital Market A market for intermediate or long-term debt or corporate stocks. Stock Market and Stock Exchange A stock exchange is the most important component of a stock market. It

Introduction to Forwards and Futures

Introduction to Forwards and Futures Liuren Wu Options Pricing Liuren Wu ( c ) Introduction, Forwards & Futures Options Pricing 1 / 27 Outline 1 Derivatives 2 Forwards 3 Futures 4 Forward pricing 5 Interest

Introduction to Forwards and Futures Liuren Wu Options Pricing Liuren Wu ( c ) Introduction, Forwards & Futures Options Pricing 1 / 27 Outline 1 Derivatives 2 Forwards 3 Futures 4 Forward pricing 5 Interest

Answers to Selected Problems

Answers to Selected Problems Problem 1.11. he farmer can short 3 contracts that have 3 months to maturity. If the price of cattle falls, the gain on the futures contract will offset the loss on the sale

Answers to Selected Problems Problem 1.11. he farmer can short 3 contracts that have 3 months to maturity. If the price of cattle falls, the gain on the futures contract will offset the loss on the sale

Discussion of Limited Partners and the LB0 Process by Paul Schultz and Sophie Shive

Discussion of Limited Partners and the LB0 Process by Paul Schultz and Sophie Shive Discussion by Adair Morse University of California, Berkeley Southern California Private Equity Conference 2017 Overview

Discussion of Limited Partners and the LB0 Process by Paul Schultz and Sophie Shive Discussion by Adair Morse University of California, Berkeley Southern California Private Equity Conference 2017 Overview

EQUITIES & INVESTMENT ANALYSIS MAF307 EXAM SUMMARY

EQUITIES & INVESTMENT ANALYSIS MAF307 EXAM SUMMARY TOPIC 1 INVESTMENT ENVIRONMENT & FINANCIAL INSTRUMENTS 4 FINANCIAL ASSETS - INTANGIBLE 4 BENEFITS OF INVESTING IN FINANCIAL ASSETS 4 REAL ASSETS 4 CLIENTS

EQUITIES & INVESTMENT ANALYSIS MAF307 EXAM SUMMARY TOPIC 1 INVESTMENT ENVIRONMENT & FINANCIAL INSTRUMENTS 4 FINANCIAL ASSETS - INTANGIBLE 4 BENEFITS OF INVESTING IN FINANCIAL ASSETS 4 REAL ASSETS 4 CLIENTS

6. The Efficient Market Hypothesis

6. The Efficient Market Hypothesis University of Paris 6 Based largely on Bodie, Kane & Markus: Essentials of Investments, 4 th Edition, McGraw Hill International, ch. 9 And Shapiro and Balbirer: Modern

6. The Efficient Market Hypothesis University of Paris 6 Based largely on Bodie, Kane & Markus: Essentials of Investments, 4 th Edition, McGraw Hill International, ch. 9 And Shapiro and Balbirer: Modern

Term Structure of Interest Rates. For 9.220, Term 1, 2002/03 02_Lecture7.ppt

Term Structure of Interest Rates For 9.220, Term 1, 2002/03 02_Lecture7.ppt Outline 1. Introduction 2. Term Structure Definitions 3. Pure Expectations Theory 4. Liquidity Premium Theory 5. Interpreting

Term Structure of Interest Rates For 9.220, Term 1, 2002/03 02_Lecture7.ppt Outline 1. Introduction 2. Term Structure Definitions 3. Pure Expectations Theory 4. Liquidity Premium Theory 5. Interpreting

Financial Markets and Products

Financial Markets and Products 1. Which of the following types of traders never take position in the derivative instruments? a) Speculators b) Hedgers c) Arbitrageurs d) None of the above 2. Which of the

Financial Markets and Products 1. Which of the following types of traders never take position in the derivative instruments? a) Speculators b) Hedgers c) Arbitrageurs d) None of the above 2. Which of the

FINANCE REVIEW. Page 1 of 5

Correlation: A perfect positive correlation means as X increases, Y increases at the same rate Y Corr =.0 X A perfect negative correlation means as X increases, Y decreases at the same rate Y Corr = -.0

Correlation: A perfect positive correlation means as X increases, Y increases at the same rate Y Corr =.0 X A perfect negative correlation means as X increases, Y decreases at the same rate Y Corr = -.0

Syllabus for Capital Markets (FINC 950) Prepared by: Phillip A. Braun Version:

Prepared by: Phillip A. Braun Version:") Syllabus for Capital Markets (FINC 950) Prepared by: Phillip A. Braun Version: 1.15.19 Class Overview Syllabus 3 Main Questions the Capital Markets Class Will Answer This class will focus on answering

Syllabus for Capital Markets (FINC 950) Prepared by: Phillip A. Braun Version: 1.15.19 Class Overview Syllabus 3 Main Questions the Capital Markets Class Will Answer This class will focus on answering

Financial Markets & Institutions. forwards.

Financial Markets & Institutions Introduction to derivatives. Futures and forwards. Slides by Emilia Garcia-Appendini The Nature of Derivatives A derivative is an instrument whose value depends on the

Financial Markets & Institutions Introduction to derivatives. Futures and forwards. Slides by Emilia Garcia-Appendini The Nature of Derivatives A derivative is an instrument whose value depends on the

Institutional Finance Financial Crises, Risk Management and Liquidity

Institutional Finance Financial Crises, Risk Management and Liquidity Markus K. Brunnermeier Preceptor: Delwin Olivan Princeton University 1 Overview Efficiency concepts EMH implies Martingale Property

Institutional Finance Financial Crises, Risk Management and Liquidity Markus K. Brunnermeier Preceptor: Delwin Olivan Princeton University 1 Overview Efficiency concepts EMH implies Martingale Property

Problem Set 6. I did this with figure; bar3(reshape(mean(rx),5,5) );ylabel( size ); xlabel( value ); mean mo return %

,5,5) );ylabel( size ); xlabel( value ); mean mo return %") Business 35905 John H. Cochrane Problem Set 6 We re going to replicate and extend Fama and French s basic results, using earlier and extended data. Get the 25 Fama French portfolios and factors from the

Business 35905 John H. Cochrane Problem Set 6 We re going to replicate and extend Fama and French s basic results, using earlier and extended data. Get the 25 Fama French portfolios and factors from the

FORWARDS FUTURES Traded between private parties (OTC) Traded on exchange

Traded on exchange") 1 E&G, Ch. 23. I. Introducing Forwards and Futures A. Mechanics of Forwards and Futures. 1. Definitions: Forward Contract - commitment by 2 parties to exchange a certain good for a specific price at a

1 E&G, Ch. 23. I. Introducing Forwards and Futures A. Mechanics of Forwards and Futures. 1. Definitions: Forward Contract - commitment by 2 parties to exchange a certain good for a specific price at a

Capital Markets (FINC 950) DRAFT Syllabus. Prepared by: Phillip A. Braun Version:

DRAFT Syllabus. Prepared by: Phillip A. Braun Version:") Capital Markets (FINC 950) DRAFT Syllabus Prepared by: Phillip A. Braun Version: 6.29.16 Syllabus 2 Capital Markets and Personal Investing This course develops the key concepts necessary to understand

Capital Markets (FINC 950) DRAFT Syllabus Prepared by: Phillip A. Braun Version: 6.29.16 Syllabus 2 Capital Markets and Personal Investing This course develops the key concepts necessary to understand

Part I: Forwards. Derivatives & Risk Management. Last Week: Weeks 1-3: Part I Forwards. Introduction Forward fundamentals

Derivatives & Risk Management Last Week: Introduction Forward fundamentals Weeks 1-3: Part I Forwards Forward fundamentals Fwd price, spot price & expected future spot Part I: Forwards 1 Forwards: Fundamentals

Derivatives & Risk Management Last Week: Introduction Forward fundamentals Weeks 1-3: Part I Forwards Forward fundamentals Fwd price, spot price & expected future spot Part I: Forwards 1 Forwards: Fundamentals

Performance Measurement and Attribution in Asset Management

Performance Measurement and Attribution in Asset Management Prof. Massimo Guidolin Portfolio Management Second Term 2019 Outline and objectives The problem of isolating skill from luck Simple risk-adjusted

Performance Measurement and Attribution in Asset Management Prof. Massimo Guidolin Portfolio Management Second Term 2019 Outline and objectives The problem of isolating skill from luck Simple risk-adjusted

Lecture Notes: Option Concepts and Fundamental Strategies

Brunel University Msc., EC5504, Financial Engineering Prof Menelaos Karanasos Lecture Notes: Option Concepts and Fundamental Strategies Options and futures are known as derivative securities. They derive

Brunel University Msc., EC5504, Financial Engineering Prof Menelaos Karanasos Lecture Notes: Option Concepts and Fundamental Strategies Options and futures are known as derivative securities. They derive

MBA 203 Executive Summary

MBA 203 Executive Summary Professor Fedyk and Sraer Class 1. Present and Future Value Class 2. Putting Present Value to Work Class 3. Decision Rules Class 4. Capital Budgeting Class 6. Stock Valuation

MBA 203 Executive Summary Professor Fedyk and Sraer Class 1. Present and Future Value Class 2. Putting Present Value to Work Class 3. Decision Rules Class 4. Capital Budgeting Class 6. Stock Valuation

Institutional Finance Financial Crises, Risk Management and Liquidity

Institutional Finance Financial Crises, Risk Management and Liquidity Markus K. Brunnermeier Preceptor: Dong Beom Choi Princeton University 1 Overview Efficiency concepts EMH implies Martingale Property

Institutional Finance Financial Crises, Risk Management and Liquidity Markus K. Brunnermeier Preceptor: Dong Beom Choi Princeton University 1 Overview Efficiency concepts EMH implies Martingale Property

Option Pricing. Based on the principle that no arbitrage opportunity can exist, one can develop an elaborate theory of option pricing.

Arbitrage Arbitrage refers to the simultaneous purchase and sale in different markets to achieve a certain profit. In market equilibrium, there must be no opportunity for profitable arbitrage. Otherwise

Arbitrage Arbitrage refers to the simultaneous purchase and sale in different markets to achieve a certain profit. In market equilibrium, there must be no opportunity for profitable arbitrage. Otherwise

No-Arbitrage and Cointegration

Università di Pavia No-Arbitrage and Cointegration Eduardo Rossi Introduction Stochastic trends are prevalent in financial data. Two or more assets might share the same stochastic trend: they are cointegrated.

Università di Pavia No-Arbitrage and Cointegration Eduardo Rossi Introduction Stochastic trends are prevalent in financial data. Two or more assets might share the same stochastic trend: they are cointegrated.

Answer FOUR questions out of the following FIVE. Each question carries 25 Marks.

UNIVERSITY OF EAST ANGLIA School of Economics Main Series PGT Examination 2017-18 FINANCIAL MARKETS ECO-7012A Time allowed: 2 hours Answer FOUR questions out of the following FIVE. Each question carries

UNIVERSITY OF EAST ANGLIA School of Economics Main Series PGT Examination 2017-18 FINANCIAL MARKETS ECO-7012A Time allowed: 2 hours Answer FOUR questions out of the following FIVE. Each question carries

16. Foreign Exchange

16. Foreign Exchange Last time we introduced two new Dealer diagrams in order to help us understand our third price of money, the exchange rate, but under the special conditions of the gold standard. In

16. Foreign Exchange Last time we introduced two new Dealer diagrams in order to help us understand our third price of money, the exchange rate, but under the special conditions of the gold standard. In

BARUCH COLLEGE DEPARTMENT OF ECONOMICS & FINANCE Professor Chris Droussiotis LECTURE 6. Modern Portfolio Theory (MPT): The Keynesian Animal Spirits

: The Keynesian Animal Spirits") LECTURE 6 Modern Portfolio Theory (MPT): CHALLENGED BY BEHAVIORAL ECONOMICS Efficient Frontier is the intersection of the Set of Portfolios with Minimum Variance (MVS) and set of portfolios with Maximum

LECTURE 6 Modern Portfolio Theory (MPT): CHALLENGED BY BEHAVIORAL ECONOMICS Efficient Frontier is the intersection of the Set of Portfolios with Minimum Variance (MVS) and set of portfolios with Maximum

Real Options. Katharina Lewellen Finance Theory II April 28, 2003

Real Options Katharina Lewellen Finance Theory II April 28, 2003 Real options Managers have many options to adapt and revise decisions in response to unexpected developments. Such flexibility is clearly

Real Options Katharina Lewellen Finance Theory II April 28, 2003 Real options Managers have many options to adapt and revise decisions in response to unexpected developments. Such flexibility is clearly

I. Reading. A. BKM, Chapter 20, Section B. BKM, Chapter 21, ignore Section 21.3 and skim Section 21.5.

Lectures 23-24: Options: Valuation. I. Reading. A. BKM, Chapter 20, Section 20.4. B. BKM, Chapter 21, ignore Section 21.3 and skim Section 21.5. II. Preliminaries. A. Up until now, we have been concerned

Lectures 23-24: Options: Valuation. I. Reading. A. BKM, Chapter 20, Section 20.4. B. BKM, Chapter 21, ignore Section 21.3 and skim Section 21.5. II. Preliminaries. A. Up until now, we have been concerned

Data Analysis and Statistical Methods Statistics 651

Review of previous lecture: Why confidence intervals? Data Analysis and Statistical Methods Statistics 651 http://www.stat.tamu.edu/~suhasini/teaching.html Suhasini Subba Rao Suppose you want to know the

Review of previous lecture: Why confidence intervals? Data Analysis and Statistical Methods Statistics 651 http://www.stat.tamu.edu/~suhasini/teaching.html Suhasini Subba Rao Suppose you want to know the