Fixed Income Investment

|

|

|

- Jasper Newton

- 5 years ago

- Views:

Transcription

1 Fixed Income Investment Session 1 April, 24 th, 2013 (Morning) Dr. Cesario Mateus c.mateus@greenwich.ac.uk cesariomateus@gmail.com 1

2 Lecture 1 1. A closer look at the different asset classes 2. Bond Market Overview 3. Features in Debt Securities 4. Risks Associated with Investing in Bonds 5. Yield measures, Spot rates and Forward Rates 6. Introduction to the Valuation of Debt Securities 7. The arbitrage-free Approach to Bond Valuation 8. Profiting from Arbitrage Opportunities: Stripping and Reconstituting Bonds 9. Holding Period Yield 2

3 A closer look at the different asset classes What is an Investment? Commitment of funds to assets that will be held over the future time period. Real assets vs. financial assets Real assets are physical, tangible assets such as gold or real estate Financial assets are paper (electronic) claims on some issuer (e.g. corporation or government) Type of financial assets investors are mainly interested in are marketable securities Investment refers in general to financial assets and in particular to marketable securities. Marketable securities are financial assets that are easily traded on the organized exchanges Impersonal trading 3

4 Why Do We Invest? The purpose is to increase one s wealth Wealth = current income or funds + present value of all income in the future We are concerned with monetary wealth Get a return on the money, do not hold cash Opportunity cost Inflation Purchasing power diminishes Protect yourself from inflation, taxes, etc. and MAKE MONEY!!! 4

5 One Classification of Financial Assets Assets with random cashflows: Equity (share, common stock) Type of financial asset that enables the holder to receive dividend payments, after creditors and preference shareholders are paid, and any capital gain (loss) that may arise at the disposal of the asset. Equity holders are residual claimants of a company Shares are irredeemable, thus having an indefinite life A share represents the unit of ownership in the company Not known if investor will receive dividend, as dividends are paid out of earnings 5

6 Assets with known cashflows Fixed income securities (Money Market Instruments, Bonds) Characteristics: coupon rate, principal amount, time to maturity Bond is a promise made by a bond issuer to make regular coupon payments and repay a principal amount at the maturity date to the bondholder. A failure to fulfill that promise results in a default of a bond Assets with contingent cashflows Derivative securities: forwards, futures, options and swaps Cashflows are dependent on the price movements of the underlying assets 6

7 Asset classes and subcategories Equities Fixed Income Cash Alternative Assets UK Equities UK Fixed Income Cash Commodities - Large capitalisation - UK Treasury bonds - Physical holdings - Commodity trading - Mid capitalisation - Municipal - Bank balance advisors (CTAs) - Small capitalisation - Corporate - UK Treasury bills - Physicals: Agricultural, - Micro capitalisation - Mortgage-backed - Municipal notes metal and oil - Growth - Asset-backed - Commercial papers - Options and futures - Value - Options and futures - Certificates of deposit - Blend (Value and Growth) - Repurchase agreement Hedge Funds - Preference shares High Yield - Banker acceptances - Event driven - Options and futures - Non UK instruments - Relative value Convertible Securities - Market neutral Other Developed Markets - Long - short - North America Other Developed Markets - Global macro - Europe - North America - Japan - Europe Private Equity - Options and futures - Japan - Leveraged Buyouts - Options and futures - Venture Capital Emerging Markets - Interest rate swaps - Non UK - Africa - Asia ex Japan Emerging Markets Real Estate - Emerging Europe - Africa - Residential - Latin America - Asia ex Japan - Commercial - Middle East - Emerging Europe - REITs (Real Estate - Options and futures - Latin America Investment Trusts) - Middle East - Options and futures Art 7

8 Fixed Income Rationale for Investment Senior claim Low risk Higher return than cash Portfolio diversifier (Low correlation) Risks and Concerns Lower returns than equity Interest rate risk Inflation risk Credit risk Reinvestment risk Prepayment risk (Callable) 8

9 High yield fixed income Rationale for Investment Risks and Concerns High return Issued to finance leveraged buyouts or ex-investment grade bond consequently downgraded Lower risk than equity Irrational (Inefficient) pricing: Possibility to beat the market Claim senior to equity Credit risk Liquidity risk 9

10 Convertible preference shares and convertible bonds Rationale for Investment Equity-debt hybrid Claim senior to equity Portfolio diversifier (Low correlation with bonds) Risks and Concerns Prepayment risk (Callable) Claim junior to bond Complicated valuation 10

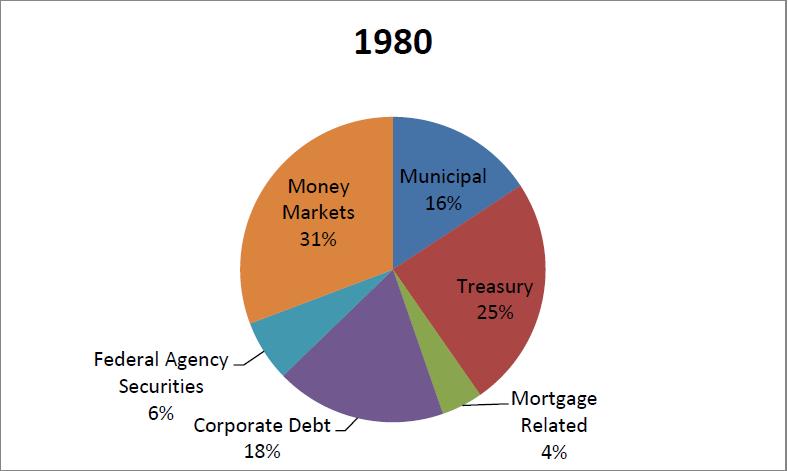

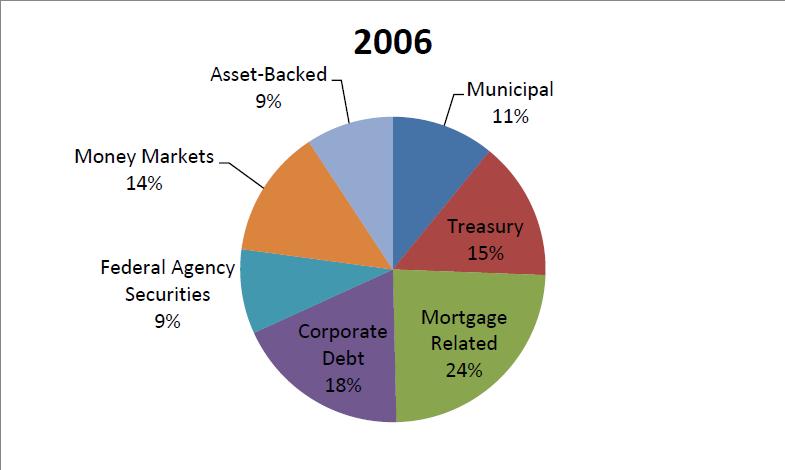

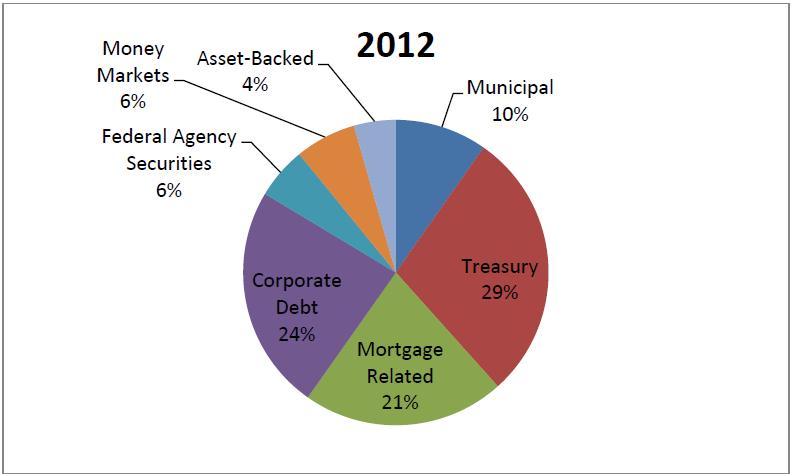

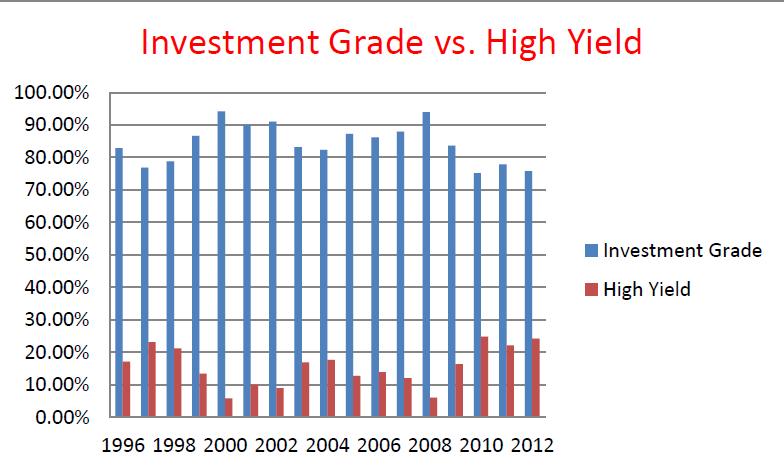

11 Average Real Return UK financial market real returns and risks: % 18% Micro-cap equities 16% 14% 12% High-cap equities Low-cap equities 10% All equities 8% 6% 4% Mid-maturity bonds Long-maturity bonds 2% T-bill 0% 0% 5% 10% 15% 20% 25% 30% Standard Deviation High cap: 90% largest capitalisation stocks Low cap: Next 9% largest stocks Micro cap: 1% smallest stocks Market capitalisation = Number of stocks * Share price Source: Dimson and Marsh,

12 Number of Years Number of years each UK asset class performed the best ( ) 25 UK bonds beat UK equities: 24% of the time UK equities beat UK bonds: 76% of the time Treasury Bill Mid Maturity Bonds Long Maturity Bonds All Equities High-Cap Equities Micro-cap Equities Low-Cap Equities Asset Class 12

13 13

")

14 Source: SIFMA (Bloomberg, Dealogic, Thomson Reuters, U.S. Treasury, Fannie Mae, Freddie Mac, Ginnie Mae) 14

15 15

16 16

17 17

18 18

19 Features of Debt Securities Fixed income security: financial obligation of an entity that promises to pay a specified sum of money at specified future dates. Issuer of the security: Entity that promises to make the payment (e.g. US government, French government, the city of Rio de Janeiro in Brazil, Corporation such Coca-Cola, Sport Institutions such Porto Football Club or supranational governments such as the World Bank. Fixed Income securities (two general categories): debt obligations and preferred stock Debt Obligations: bonds, mortgage-backed securities, asset backed securities and bank loans. 19

20 Bond indenture (also trust indenture or deed of trust): legal document issued to lenders and describes key terms such as the interest rate, Maturity date, convertibility, pledge, promises, representations, covenants, and other terms of the bond offering. Bond Covenant: designed to protect the interests of both parties. Negative or restrictive covenants forbid the issuer from undertaking certain activities; positive or affirmative covenants require the issuer to meet specific requirements Maturity: Term to maturity: number of years the debt is outstanding or the number of years remaining prior to final principal payment Maturity date: date that the debt will cease to exist Type Maturity Short-term Intermediate-term Long-term 1 to 5 years 5 12 years More than 12 years 20

21 Par Value: Amount that the issuer agrees to repay the bondholder at or by the maturity date (principal value, face value, redemption value or maturity value). Because bonds have different par values, the practice is to quote bonds as a percentage of its par value. Quoted Price Price per $1of par value (rounded) Par value Dollar Price 90 1/ $1, / $5,000 5, / $10,000 7, / $100, ,

22 Coupon Rate (nominal rate): is the interest rate that the issuer agrees to pay each year. Coupon: Annual amount of the interest payments made to bondholders during the term of the bond. Calculated as: Example: 6% coupon rate and a par value of $1,000 Coupon (interest payment) = $60 United States (semi-annual instalments), Mortgage and Asset Backed Securities typically pay interest monthly. Zero-coupon Bonds: the holder realizes interest by buying the bond substantially below its par value 22

23 Provisions for Paying off Bonds Bullet maturity: No principal repayments prior to maturity date. Amortizing Securities: Schedule of partial payments until maturity (e.g. fixed income securities backed by pool of loans, mortgage backed securities and asset-backed securities). Sinking Fund: Repayment of the bond may be arranged to repay only a part of the total by the maturity date. Call provision: guarantee the issuer an option to retire all or part of the issue to the stated maturity date (callable bond). Convertible bond: grants the bondholder the right to convert the bond for a specified number of shares of common stock. Put Provision: grants the bondholder the right to sell issue back to the issuer at a specified price on designed dates. Currency denomination: in the USA, dollar-dominated, nondollar denominated issues and dual-currency issues. 23

24 Risks Associated with Investing in Bonds Interest-rate risk or market risk As interest rates rise, the price of a bond fall (vice-versa) If an investor has to sell a bond prior to the maturity date, an increase in interest rates will mean the realization of a loss (i.e. selling the bond below the purchase price). Example: Consider a 6% 20-year bond with a face value of $100. if the yield investors require to buy this bond is 6%, the price of this bond would be $100 (selling at par). If required yield increase to 6.5%, the price of this bond would decline to $ Thus, for a 50 basis point increase in yield, the bond s price declines by 5.5%. If, instead, the yield declines from 6% to 5.5%, the bond s price will rise by 6.02% to $

25 Coupon rate = yield required by market price = par value Coupon rate < yield required by market price < par value (discount) Coupon rate > yield required by market price > par value (premium) If interest rates increase price of a bond decreases If interest rates decrease price of a bond increases 25

26 Bond Features that affect Interest Rate Risk Maturity: all other factors constant, the longer the bond s maturity, the greater the bond s price sensitivity to changes in interest rates Coupon Rate: all other factors constant, the lower the coupon rate, the greater the bond s price sensitivity to changes in interest rates Embedded Options: Call option: As interest rates decline, the price of a callable bond may not increase as much as an otherwise option-free bond Price of callable bond = price of option-free bond price of embedded call option Yield level: Bond s that trade at a lower yield are more volatile in both percentage price change and absolute price change (as long as the other bond characteristics are the same). Yield curve risk: bond portfolios have different exposures to how the yield curve shifts. 26

27 Call Risk or Prepayment Risk Issuer can retire or call all or part of the issue before the maturity date (Issuer usually retains this right in order to have flexibility to refinance the bond in the future if the market interest rate drops below the coupon rate). Disadvantages from the investor s perspective: 1) The cash flow pattern of a callable bond is not known with certainty because it is not known when the bond is called. 2) Because the issuer is likely to call the bonds when interest rates have declined below the bond s coupon rate, the investor is exposed to reinvestment risk (will have to reinvest the proceeds at a lower interest rate than the bond s coupon rate) 3) The price appreciation potential of the bond will be reduced relative to an otherwise comparable option-free bond (price compression) 27

28 Reinvestment Risk Risk that the proceeds received from the payment of interest and principal that are available for reinvestment must be reinvested at a lower interest rate than the security that generated the proceeds. Credit Risk Three types of credit risk: default risk, credit spread risk and downgrade risk. Default Risk: Risk that issuer will fail to satisfy the term of the obligations with respect to the timely payment of interest and principal (default rate, recovery rate and expected loss). Credit Spread Risk: The part of the risk premium or yield spread attributable to default risk. The price performance and the return over some time period will depend on how the credit spread changes. Downgrade Risk: Risk that the bond issue or issuer credit rating will change. 28

29 Three rating agencies in the United States: Moody s Investors Service Inc, Standard &Poor s Corporation and Fitch Ratings Moody s S&P Fitch Summary Description Investment Grade High Credit Worthiness Aaa AAA AAA Gilt edge, prime, maximum safety Aa1 AA+ AA+ Aa2 AA AA High-grade, high credit quality Aa3 AA- AA- A1 A+ A+ Uper-medium grade A2 A A A3 A- A- Baa1 BBB+ BBB+ Lower-medium Grade Baa2 BBB BBB Baa3 BBB- BBB- 29

30 Moody s S&P Fitch Summary Description Ba1 Ba2 Ba3 B1 B2 BB+ BB BB- B B3 B- Caa Speculative Lower Credit Worthiness Low grade, speculative B+ Highly speculative B Predominantly Speculative, Substantial Risk, or in Default CCC+ CCC CCC+ CCC Substantial Risk, in poor standing Ca CC CC May be in default, very speculative C C C Extremely speculative CI D DDD DD D Income bonds no interest being paid Default 30

31 Liquidity Risk The risk that the investor will have to sell a bond below its indicated value, where the indication is revealed by a recent transaction. The primary measure of liquidity is the size of the spread between the bid price (the price at which the dealer is willing to buy a security) and the ask price (the price at which a dealer is willing to sell a security). The wider the bid-ask spread, the greater the liquidity risk. Exchange Rate or Currency Risk Risk of receiving less of the domestic currency when investing in a bond issue that makes payments in a currency other than the manager s domestic currency. Inflation Risk Risk of decline in the value of a security's cash flows due to inflation. 31

32 Volatility Risk: Risk that the expected yield volatility will change. The greater the expected yield volatility, the greater the value (price) of an option. Price of callable bond = price of option-free bond price of embedded call option Price of Putable bond = price of option-free bond + price of embedded put option Type of embedded option Callable Bonds Putable Bonds Volatility risk due to An increase in expected yield volatility An decrease in expected yield volatility Event Risk 1) Natural disaster (earthquake or hurricane) or an industrial accident. 2) Takeover or corporate restructuring 3) Regulatory change Sovereign Risk: 1) Unwillingness of a foreign government to pay, or 2) inability to pay due to unfavourable economic conditions in the country 32

33 Yield Measures, Spot Rates and Forward Rates Sources of Return 1) The coupon interest payments made by the issuer 2) Any capital gain (or capital loss negative return) when the security matures, is called or is sold. 3) Income from reinvestment of interim cash flows (interest and/or principal payments prior to stated maturity). Current yield Annual dollar coupon interest to a bond s market price Yield to Maturity Interest rate that will make the present value of the bond s cash flows equal to its market price plus accrued interest (is the interest that has accumulated since the previous interest payment 33

34 Yield to Call The yield to call assumes the issuer will call a bond on some assumed call date and that the call price is the price specified in the call schedule. Yield to Put Interest rate that will make the present value of the cash flows to the first put date equal to the price plus accrued interest. Yield to Worst Is the lowest of possible yields (YTM, Yield to call and yield to put). 34

35 Spot Rates A default-free theoretical spot rate curve can be constructed from the observed Treasury yield curve. The approach for creating a theoretical spot rate curve is called bootstrapping. Example: 2-year = 1.71%, 5-year = 3.25%, 10-year = 4.35% and 30-year = 5.21% Then, Interpolated 6-year yield = 3.25% % = 3.47% 7, 8 and 9-years yield, 3.69%, 3.91% and 4.13%, respectively 35

36 Forward Rates Examples of forward rates: 6-month forward rate six months from now 6-month forward rate three years from now 1-year forward rate one year from now 3-year forward rate two years from now 5-year forward rates three years from now, etc, etc. Deriving 6-month forward rates Arbitrage principle (if two investments have the same cash flows and have the same risk, they should have the same value). Investor with two alternatives: Buy a 1-year Treasury bill or, Buy a 6-month Treasury bill and when it matures in six months, buy another 6-month Treasury bill. 36

37 Spot rate on the 6-month Treasury bill = 3.0% (Z1) Spot rate on the 1-year Treasury bill = 3.3% (Z2) 6-month forward rate on in six months from now =? 37

38 The Valuation Principle The price of a security today is the present value of all future expected cash flows discounted at the appropriate required rate of return (or discount rate) The valuation variables are 1. Current price 2. Future expected cash flows - Face value and/or coupons 3. Yield or required rate of return The valuation problem is to 1. Estimate the price; given the future cash flows and required rate of return, or 2. Estimate the required rate of return; given the future cash flows and price 38

39 Zero Coupon Securities Zero coupon bonds are long-term securities paying the face value at maturity No coupon or interest payment made Issued at deep discount to face value Return earned is based on the appreciation in bond s value (price) over time 39

40 Pricing Zero Coupon Securities 40

41 Coupon Paying Securities Fixed coupon payment, typically every six months Non coupon paying bonds called zero coupon bonds Repayment of face value at maturity Typically issued at face value Examples: Treasury bonds, corporate bonds Market price depends on the rate of return required by investors 41

42 Pricing a Bond Equal to the present value of the expected cash flows from the financial instrument. Determining the price requires: An estimate of the expected cash flows An estimate of the appropriate required yield The price of the bond is the present value of the cash flows, it is determined by adding these two present values: i) The present value of the semi-annual coupon payments ii) The present value of the par or maturity value at the maturity date 42

t = time period when payment is to be received")

43 P = Price n = number of periods (nr of years times 2, if semi-annual) C = semi-annual coupon payment r = periodic interest rate (required annual yield divided by 2, if semi-annual) t = time period when payment is to be received 43

44 Because the semi-annual coupon payments are equivalent to an ordinary annuity, applying the equation for the present value of an ordinary annuity gives the present value of the coupon payments: Consider a 20 year 10% coupon bond with a par value of $1,000. The required yield on this bound is 11%. The PV of the par or maturity value of $1,000 received 40 six-month periods from now, discounted at 5.5%, is $117.46, as follows: Price = PV coupon payments + PV of par (maturity value) $ $ = $

45 The arbitrage-free Approach to Bond Valuation The traditional valuation approach is deficient because it uses a single discount rate (the appropriate YTM) to find the present value of the future cash flows with no regard given to the timing of those cash flows. Cash flows received in year 1 on a 20 year bond are discounted at the same rate as the cash flows received in 20 years! Arbitrage Free Valuation Model This model treats each separate cash flow paid by a fixed-income security as if it were a stand-alone zero-coupon bond. These discount rates are called spot rates. 45

46 Example Give the following Treasury spot rates, calculate the arbitrage-free value of a 5% coupon, 2 year treasury note. Maturity Spot Rate 0.5 years 4.0% % % % The arbitrage-free price of the note is: $2.50 $2.5 $2.5 $102.5 P = + + = $ per $100 of par value (1.020) (1.022) (1.025) (1. 026) 46

47 Profiting from Arbitrage Opportunities: Stripping and Reconstituting Bonds Stripping Suppose the same 2-year, 5% coupon Treasury note is priced at $95.00, which is below its arbitrage-free value of $ What action should arbitrageurs take and what will be the affect of their actions? Because the note is priced below its arbitrage-free value, its zero-coupon cash flow pieces are worth more than the note it self. Therefore, an arbitrage profit could be earned by: Buying the undervalued note at $95.00 Stripping the note of its individual cash flows Selling the individual cash flows pieces as zero-coupon bonds for $99.66 and earning arbitrage profit of $4.66 per $100 of investment. 47

48 As this arbitrage is performed: The increased demand for the notes will cause their prices to increase and their yields maturity to fall The increased supply of zero-coupon bond pieces will cause the prices of zero-coupon bonds to fall and their yields (spot rates) to rise. These forces will quickly eliminate the arbitrage opportunity 48

49 Reconstituting The 2-year, 5% coupon Treasury note is priced at $100. Its arbitrage-free value is $ What action should arbitrageurs take and what will be the effect of their actions? Because the note is priced above its arbitrage-free value, it is overpriced relative to the value of its zero-coupon cash flow pieces. Therefore, an arbitrage profit can be earned by: Buying the zero coupon pieces in the zero-coupon treasury market for $99.66 Reconstituting the note from these zero-coupon Treasuries. Selling the reconstituted note for $100 to earn an arbitrage profit of $0.34 for every $99.66 of original investment. 49

50 As dealers perform this arbitrage: The increased demand for Treasury zero-coupon bonds will drive their prices up and their yields (spot rates) down. The increased supply of reconstituted 2-year, 55 coupon treasuries will drive their prices down and their yields-to-maturity up These forces will quickly eliminate the arbitrage opportunity 50

51 Arbitrage Example We observe two types of bonds: T-bills and coupon bonds. A one-year T-bills pays 1000 in one year, a two year T-bill pay 1000 in two years and a three year T-bill pays 1000 in three years. There are no coupon interests on T-bills. The coupon bond is a 5% three-year bond with a face value of Thus the cash flow from the coupon bond are: In the first year, you receive 50, in the second year 50, and in the last year We observe the following prices: Type of Bond Price Yield One year T-bill Two year T-bill Three year T-bill Coupon bond

52 Pricing using discounted cash flow Assumption: We can borrow funds at the above rates and short sell the securities without any costs No arbitrage profit: Using no wealth, No risk and Positive return The first condition requires a long and short position To satisfy the second condition (no risk) we need to match the cash flows from the long and short positions Short sell (borrow) 20 coupon bonds and buy 1 one year T-bill, 1 two year T-bill and 21 three year T-bills we do not use any of our own wealth. 52

53 Pricing by arbitrage Cash flows from bond transactions Number of Bonds Cash flows at time: Price Coupon Bonds 20 1,000 20,000-1,000-1,000-21,000 Short position - Loan Long Position One year T-bill 1 943,4-943,4 1, Two year T-bill 1 873,44-873,44 0 1,000 0 Three year T-bill ,83-16, ,000 TOTAL 3 1,

54 We have an arbitrage profit of 1,512.73, with no risk and using none of our own funds What will happen: Investors will sell the coupon bonds prices start to drop Investors will buy T-bills price start to increase The price of the coupon bond that is consistent with the no arbitrage condition is

55 Holding Period Yield Example Consider a 30-year zero coupon bond with a face value of $100. If the bond is priced at a yield-to-maturity of 10%, it will cost $5.73 today (the present value of this cash flow). Over the coming 30 years, the price will advance to $100, and the annualized return will be 10%. Suppose that over the first 10 years of the holding period, interest rates decline, and the yield-to-maturity on the bond falls to 7%. With 20 years remaining to maturity, the price of the bond will be $ Even though the yield-to-maturity for the remaining life of the bond is just 7%, and the yield-to-maturity bargained for when the bond was purchased was only 10%, the return earned over the first 10 years is 16.26%. This can be found by evaluating: 55

56 Over the remaining 20 years of the bond, the annual rate earned is not 16.26%, but 7% This can be found by evaluating: Over the entire 30 year holding period, the original $5.73 invested matured to $100, so 10% annually was made, irrespective of interest rate changes in between 56

Corporate Finance. Dr Cesario MATEUS.

Corporate Finance Dr Cesario MATEUS www.cesariomateus.com Session 1 13.03.2015 Module Introduction to Corporate Finance The Objective Function in Corporate Finance Present Value and Related Metrics Risk

Corporate Finance Dr Cesario MATEUS www.cesariomateus.com Session 1 13.03.2015 Module Introduction to Corporate Finance The Objective Function in Corporate Finance Present Value and Related Metrics Risk

Corporate Finance. Dr Cesario MATEUS.

Corporate Finance Dr Cesario MATEUS www.cesariomateus.com Session 1 06.02.2015 Module Introduction to Corporate Finance The Objective Function in Corporate Finance Present Value and Related Metrics Risk

Corporate Finance Dr Cesario MATEUS www.cesariomateus.com Session 1 06.02.2015 Module Introduction to Corporate Finance The Objective Function in Corporate Finance Present Value and Related Metrics Risk

RISKS ASSOCIATED WITH INVESTING IN BONDS

RISKS ASSOCIATED WITH INVESTING IN BONDS 1 Risks Associated with Investing in s Interest Rate Risk Effect of changes in prevailing market interest rate on values. As i B p. Credit Risk Creditworthiness

RISKS ASSOCIATED WITH INVESTING IN BONDS 1 Risks Associated with Investing in s Interest Rate Risk Effect of changes in prevailing market interest rate on values. As i B p. Credit Risk Creditworthiness

I. Asset Valuation. The value of any asset, whether it is real or financial, is the sum of all expected future earnings produced by the asset.

1 I. Asset Valuation The value of any asset, whether it is real or financial, is the sum of all expected future earnings produced by the asset. 2 1 II. Bond Features and Prices Definitions Bond: a certificate

1 I. Asset Valuation The value of any asset, whether it is real or financial, is the sum of all expected future earnings produced by the asset. 2 1 II. Bond Features and Prices Definitions Bond: a certificate

A Guide to Investing In Corporate Bonds

A Guide to Investing In Corporate Bonds Access the corporate debt income portfolio TABLE OF CONTENTS What are Corporate Bonds?... 4 Corporate Bond Issuers... 4 Investment Benefits... 5 Credit Quality and

A Guide to Investing In Corporate Bonds Access the corporate debt income portfolio TABLE OF CONTENTS What are Corporate Bonds?... 4 Corporate Bond Issuers... 4 Investment Benefits... 5 Credit Quality and

Economics 173A and Management 183 Financial Markets

Economics 173A and Management 183 Financial Markets Fixed Income Securities: Bonds Bonds Debt Security corporate or government borrowing Also called a Fixed Income Security Covenants or Indenture define

Economics 173A and Management 183 Financial Markets Fixed Income Securities: Bonds Bonds Debt Security corporate or government borrowing Also called a Fixed Income Security Covenants or Indenture define

Questions 1. What is a bond? What determines the price of this financial asset?

BOND VALUATION Bonds are debt instruments issued by corporations, as well as state, local, and foreign governments to raise funds for growth and financing of public projects. Since bonds are long-term

BOND VALUATION Bonds are debt instruments issued by corporations, as well as state, local, and foreign governments to raise funds for growth and financing of public projects. Since bonds are long-term

Chapter 4. Characteristics of Bonds. Chapter 4 Topic Overview. Bond Characteristics

Chapter 4 Topic Overview Chapter 4 Valuing Bond Characteristics Annual and Semi-Annual Bond Valuation Reading Bond Quotes Finding Returns on Bond Risk and Other Important Bond Valuation Relationships Bond

Chapter 4 Topic Overview Chapter 4 Valuing Bond Characteristics Annual and Semi-Annual Bond Valuation Reading Bond Quotes Finding Returns on Bond Risk and Other Important Bond Valuation Relationships Bond

CHAPTER 9 DEBT SECURITIES. by Lee M. Dunham, PhD, CFA, and Vijay Singal, PhD, CFA

CHAPTER 9 DEBT SECURITIES by Lee M. Dunham, PhD, CFA, and Vijay Singal, PhD, CFA LEARNING OUTCOMES After completing this chapter, you should be able to do the following: a Identify issuers of debt securities;

CHAPTER 9 DEBT SECURITIES by Lee M. Dunham, PhD, CFA, and Vijay Singal, PhD, CFA LEARNING OUTCOMES After completing this chapter, you should be able to do the following: a Identify issuers of debt securities;

Fixed-Income Securities: Defining Elements

The following is a review of the Fixed Income: Basic Concepts principles designed to address the learning outcome statements set forth by CFA Institute. Cross-Reference to CFA Institute Assigned Reading

The following is a review of the Fixed Income: Basic Concepts principles designed to address the learning outcome statements set forth by CFA Institute. Cross-Reference to CFA Institute Assigned Reading

Study Session 16. Fixed Income Analysis and Valuation

Study Session 16 Fixed Income Analysis and Valuation 332 Study Session 16 Fixed Income Analysis and Valuation Fixed Income: Analysis and Valuation 56. Valuation of Debt Securities Fixed Income Investments

Study Session 16 Fixed Income Analysis and Valuation 332 Study Session 16 Fixed Income Analysis and Valuation Fixed Income: Analysis and Valuation 56. Valuation of Debt Securities Fixed Income Investments

Fixed Income Securities: Bonds

Economics 173A and Management 183 Financial Markets Fixed Income Securities: Bonds Updated 4/24/17 Bonds Debt Security corporate or government borrowing Also called a Fixed Income Security Covenants or

Economics 173A and Management 183 Financial Markets Fixed Income Securities: Bonds Updated 4/24/17 Bonds Debt Security corporate or government borrowing Also called a Fixed Income Security Covenants or

Bond Valuation. FINANCE 100 Corporate Finance

Bond Valuation FINANCE 100 Corporate Finance Prof. Michael R. Roberts 1 Bond Valuation An Overview Introduction to bonds and bond markets» What are they? Some examples Zero coupon bonds» Valuation» Interest

Bond Valuation FINANCE 100 Corporate Finance Prof. Michael R. Roberts 1 Bond Valuation An Overview Introduction to bonds and bond markets» What are they? Some examples Zero coupon bonds» Valuation» Interest

Chapter 5. Interest Rates and Bond Valuation. types. they fluctuate. relationship to bond terms and value. interest rates

Chapter 5 Interest Rates and Bond Valuation } Know the important bond features and bond types } Compute bond values and comprehend why they fluctuate } Appreciate bond ratings, their meaning, and relationship

Chapter 5 Interest Rates and Bond Valuation } Know the important bond features and bond types } Compute bond values and comprehend why they fluctuate } Appreciate bond ratings, their meaning, and relationship

Study Session 16. Fixed Income Analysis and Valuation

Study Session 16 Fixed Income Analysis and Valuation Fixed Income: Analysis and Valuation 56. Valuation of Debt Securities Fixed Income Investments LOS 56.b Describe CFAI p. 448, Schweser p. 87 Valuation

Study Session 16 Fixed Income Analysis and Valuation Fixed Income: Analysis and Valuation 56. Valuation of Debt Securities Fixed Income Investments LOS 56.b Describe CFAI p. 448, Schweser p. 87 Valuation

Bonds explained. Member of the London Stock Exchange

Bonds explained Member of the London Stock Exchange Killik & Co We pride ourselves on being a relationship firm. Each client has their own dedicated Broker, who acts as the single point of contact to provide

Bonds explained Member of the London Stock Exchange Killik & Co We pride ourselves on being a relationship firm. Each client has their own dedicated Broker, who acts as the single point of contact to provide

COPYRIGHTED MATERIAL FEATURES OF DEBT SECURITIES CHAPTER 1 I. INTRODUCTION

CHAPTER 1 FEATURES OF DEBT SECURITIES I. INTRODUCTION In investment management, the most important decision made is the allocation of funds among asset classes. The two major asset classes are equities

CHAPTER 1 FEATURES OF DEBT SECURITIES I. INTRODUCTION In investment management, the most important decision made is the allocation of funds among asset classes. The two major asset classes are equities

FINC3019 FIXED INCOME SECURITIES

FINC3019 FIXED INCOME SECURITIES WEEK 1 BONDS o Debt instrument requiring the issuer to repay the lender the amount borrowed + interest over specified time period o Plain vanilla (typical) bond:! Fixed

FINC3019 FIXED INCOME SECURITIES WEEK 1 BONDS o Debt instrument requiring the issuer to repay the lender the amount borrowed + interest over specified time period o Plain vanilla (typical) bond:! Fixed

Bond Valuation. Capital Budgeting and Corporate Objectives

Bond Valuation Capital Budgeting and Corporate Objectives Professor Ron Kaniel Simon School of Business University of Rochester 1 Bond Valuation An Overview Introduction to bonds and bond markets» What

Bond Valuation Capital Budgeting and Corporate Objectives Professor Ron Kaniel Simon School of Business University of Rochester 1 Bond Valuation An Overview Introduction to bonds and bond markets» What

I. Introduction to Bonds

University of California, Merced ECO 163-Economics of Investments Chapter 10 Lecture otes I. Introduction to Bonds Professor Jason Lee A. Definitions Definition: A bond obligates the issuer to make specified

University of California, Merced ECO 163-Economics of Investments Chapter 10 Lecture otes I. Introduction to Bonds Professor Jason Lee A. Definitions Definition: A bond obligates the issuer to make specified

A guide to investing in high-yield bonds

A guide to investing in high-yield bonds What you should know before you buy Are high-yield bonds suitable for you? High-yield bonds are designed for investors who: Can accept additional risks of investing

A guide to investing in high-yield bonds What you should know before you buy Are high-yield bonds suitable for you? High-yield bonds are designed for investors who: Can accept additional risks of investing

Chapter Six. Bond Markets. McGraw-Hill /Irwin. Copyright 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter Six Bond Markets Overview of the Bond Markets A bond is is a promise to make periodic coupon payments and to repay principal at maturity; breech of this promise is is an event of default carry

Chapter Six Bond Markets Overview of the Bond Markets A bond is is a promise to make periodic coupon payments and to repay principal at maturity; breech of this promise is is an event of default carry

CHAPTER 8. Valuing Bonds. Chapter Synopsis

CHAPTER 8 Valuing Bonds Chapter Synopsis 8.1 Bond Cash Flows, Prices, and Yields A bond is a security sold at face value (FV), usually $1,000, to investors by governments and corporations. Bonds generally

CHAPTER 8 Valuing Bonds Chapter Synopsis 8.1 Bond Cash Flows, Prices, and Yields A bond is a security sold at face value (FV), usually $1,000, to investors by governments and corporations. Bonds generally

Valuing Bonds. Professor: Burcu Esmer

Valuing Bonds Professor: Burcu Esmer Valuing Bonds A bond is a debt instrument issued by governments or corporations to raise money The successful investor must be able to: Understand bond structure Calculate

Valuing Bonds Professor: Burcu Esmer Valuing Bonds A bond is a debt instrument issued by governments or corporations to raise money The successful investor must be able to: Understand bond structure Calculate

An Introduction to Bonds

An Introduction to Bonds Agenda Bond basics Different types of bonds Bond features Yield and tax considerations Bond risks Credit quality Bond investing strategies and client suitability Defining Characteristics

An Introduction to Bonds Agenda Bond basics Different types of bonds Bond features Yield and tax considerations Bond risks Credit quality Bond investing strategies and client suitability Defining Characteristics

FRANKLIN TEMPLETON VARIABLE INSURANCE PRODUCTS TRUST

STATEMENT OF ADDITIONAL INFORMATION FRANKLIN TEMPLETON VARIABLE INSURANCE PRODUCTS TRUST May 1, 2017 Franklin Flex Cap Growth VIP Fund Franklin Founding Funds Allocation VIP Fund Franklin Global Real Estate

STATEMENT OF ADDITIONAL INFORMATION FRANKLIN TEMPLETON VARIABLE INSURANCE PRODUCTS TRUST May 1, 2017 Franklin Flex Cap Growth VIP Fund Franklin Founding Funds Allocation VIP Fund Franklin Global Real Estate

CHAPTER 5 Bonds and Their Valuation

5-1 5-2 CHAPTER 5 Bonds and Their Valuation Key features of bonds Bond valuation Measuring yield Assessing risk Key Features of a Bond 1 Par value: Face amount; paid at maturity Assume $1,000 2 Coupon

5-1 5-2 CHAPTER 5 Bonds and Their Valuation Key features of bonds Bond valuation Measuring yield Assessing risk Key Features of a Bond 1 Par value: Face amount; paid at maturity Assume $1,000 2 Coupon

FINA 1082 Financial Management

FINA 1082 Financial Management Dr Cesario MATEUS Senior Lecturer in Finance and Banking Room QA259 Department of Accounting and Finance c.mateus@greenwich.ac.uk www.cesariomateus.com Contents Session 1

FINA 1082 Financial Management Dr Cesario MATEUS Senior Lecturer in Finance and Banking Room QA259 Department of Accounting and Finance c.mateus@greenwich.ac.uk www.cesariomateus.com Contents Session 1

Important Information about Investing in

Robert W. Baird & Co. Incorporated Important Information about Investing in \ Bonds Baird has prepared this document to help you understand the characteristics and risks associated with bonds and other

Robert W. Baird & Co. Incorporated Important Information about Investing in \ Bonds Baird has prepared this document to help you understand the characteristics and risks associated with bonds and other

CHAPTER 14. Bond Characteristics. Bonds are debt. Issuers are borrowers and holders are creditors.

Bond Characteristics 14-2 CHAPTER 14 Bond Prices and Yields Bonds are debt. Issuers are borrowers and holders are creditors. The indenture is the contract between the issuer and the bondholder. The indenture

Bond Characteristics 14-2 CHAPTER 14 Bond Prices and Yields Bonds are debt. Issuers are borrowers and holders are creditors. The indenture is the contract between the issuer and the bondholder. The indenture

Debt markets. International Financial Markets. International Financial Markets

Debt markets Outline Instruments Participants Yield curve Risks 2 Debt instruments Bank loans most typical Reliance on private information Difficult to transfert to third party Government and commercial

Debt markets Outline Instruments Participants Yield curve Risks 2 Debt instruments Bank loans most typical Reliance on private information Difficult to transfert to third party Government and commercial

First Trust Intermediate Duration Preferred & Income Fund Update

1st Quarter 2015 Fund Performance Review & Current Positioning The First Trust Intermediate Duration Preferred & Income Fund (FPF) produced a total return for the first quarter of 2015 of 3.84% based on

1st Quarter 2015 Fund Performance Review & Current Positioning The First Trust Intermediate Duration Preferred & Income Fund (FPF) produced a total return for the first quarter of 2015 of 3.84% based on

A CLEAR UNDERSTANDING OF THE INDUSTRY

A CLEAR UNDERSTANDING OF THE INDUSTRY IS CFA INSTITUTE INVESTMENT FOUNDATIONS RIGHT FOR YOU? Investment Foundations is a certificate program designed to give you a clear understanding of the investment

A CLEAR UNDERSTANDING OF THE INDUSTRY IS CFA INSTITUTE INVESTMENT FOUNDATIONS RIGHT FOR YOU? Investment Foundations is a certificate program designed to give you a clear understanding of the investment

KEY CONCEPTS AND SKILLS

Chapter 5 INTEREST RATES AND BOND VALUATION 5-1 KEY CONCEPTS AND SKILLS Know the important bond features and bond types Comprehend bond values (prices) and why they fluctuate Compute bond values and fluctuations

Chapter 5 INTEREST RATES AND BOND VALUATION 5-1 KEY CONCEPTS AND SKILLS Know the important bond features and bond types Comprehend bond values (prices) and why they fluctuate Compute bond values and fluctuations

Lamar State College - Port Arthur Annual Investment Report (Including Deposits)

") Lamar State College - Port Arthur Annual Investment Report (Including Deposits) August 31, 2017 Market Value Publicly Traded Equity and Similar Investments Common Stock (U.S. and foreign stocks held in

Lamar State College - Port Arthur Annual Investment Report (Including Deposits) August 31, 2017 Market Value Publicly Traded Equity and Similar Investments Common Stock (U.S. and foreign stocks held in

CHAPTER 14. Bond Prices and Yields INVESTMENTS BODIE, KANE, MARCUS. Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved.

CHAPTER 14 Bond Prices and Yields INVESTMENTS BODIE, KANE, MARCUS McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. INVESTMENTS BODIE, KANE, MARCUS 14-2 Bond Characteristics

CHAPTER 14 Bond Prices and Yields INVESTMENTS BODIE, KANE, MARCUS McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. INVESTMENTS BODIE, KANE, MARCUS 14-2 Bond Characteristics

Learn about bond investing. Investor education

Learn about bond investing Investor education The dual roles bonds can play in your portfolio Bonds can play an important role in a welldiversified investment portfolio, helping to offset the volatility

Learn about bond investing Investor education The dual roles bonds can play in your portfolio Bonds can play an important role in a welldiversified investment portfolio, helping to offset the volatility

Fixed income for your portfolio

Fixed income for your portfolio November 2017 2 Fixed income for your portfolio Defence Fixed income investments such as bonds are widely used in portfolios to enhance income and compliment low risk interest

Fixed income for your portfolio November 2017 2 Fixed income for your portfolio Defence Fixed income investments such as bonds are widely used in portfolios to enhance income and compliment low risk interest

BONDS AND CREDIT RATING

BONDS AND CREDIT RATING 2017 1 Typical Bond Features The indenture - a written agreement between the borrower and a trust company - usually lists Amount of Issue, Date of Issue, Maturity Denomination (Par

BONDS AND CREDIT RATING 2017 1 Typical Bond Features The indenture - a written agreement between the borrower and a trust company - usually lists Amount of Issue, Date of Issue, Maturity Denomination (Par

Accrued Interest A currently unpaid amount of interest that has accumulated since the last payment on a bond or other fixed-income security.

Accrued Interest A currently unpaid amount of interest that has accumulated since the last payment on a bond or other fixed-income security. Ad Valorem Tax Translated as according to value, it is a levy

Accrued Interest A currently unpaid amount of interest that has accumulated since the last payment on a bond or other fixed-income security. Ad Valorem Tax Translated as according to value, it is a levy

Bond Prices and Yields

Bond Characteristics 14-2 Bond Prices and Yields Bonds are debt. Issuers are borrowers and holders are creditors. The indenture is the contract between the issuer and the bondholder. The indenture gives

Bond Characteristics 14-2 Bond Prices and Yields Bonds are debt. Issuers are borrowers and holders are creditors. The indenture is the contract between the issuer and the bondholder. The indenture gives

JPMorgan Insurance Trust Class 1 Shares

Prospectus JPMorgan Insurance Trust Class 1 Shares May 1, 2017 JPMorgan Insurance Trust Core Bond Portfolio* * The Portfolio does not have an exchange ticker symbol. The Securities and Exchange Commission

Prospectus JPMorgan Insurance Trust Class 1 Shares May 1, 2017 JPMorgan Insurance Trust Core Bond Portfolio* * The Portfolio does not have an exchange ticker symbol. The Securities and Exchange Commission

Reading. Valuation of Securities: Bonds

Valuation of Securities: Bonds Econ 422: Investment, Capital & Finance University of Washington Last updated: April 11, 2010 Reading BMA, Chapter 3 http://finance.yahoo.com/bonds http://cxa.marketwatch.com/finra/marketd

Valuation of Securities: Bonds Econ 422: Investment, Capital & Finance University of Washington Last updated: April 11, 2010 Reading BMA, Chapter 3 http://finance.yahoo.com/bonds http://cxa.marketwatch.com/finra/marketd

FRANKLIN TEMPLETON VARIABLE INSURANCE PRODUCTS TRUST

STATEMENT OF ADDITIONAL INFORMATION FRANKLIN TEMPLETON VARIABLE INSURANCE PRODUCTS TRUST May 1, 2017 Franklin Flex Cap Growth VIP Fund Franklin Founding Funds Allocation VIP Fund Franklin Global Real Estate

STATEMENT OF ADDITIONAL INFORMATION FRANKLIN TEMPLETON VARIABLE INSURANCE PRODUCTS TRUST May 1, 2017 Franklin Flex Cap Growth VIP Fund Franklin Founding Funds Allocation VIP Fund Franklin Global Real Estate

San Jacinto Community College District Quarterly Investment Report (Including Deposits)

") San Jacinto Community College District Quarterly Investment Report (Including Deposits) February 28, 2018 Fair Value Publicly Traded Equity and Similar Investments Total Publicly Traded Equity and Similar

San Jacinto Community College District Quarterly Investment Report (Including Deposits) February 28, 2018 Fair Value Publicly Traded Equity and Similar Investments Total Publicly Traded Equity and Similar

Bonds and Their Valuation

Chapter 7 Bonds and Their Valuation Key Features of Bonds Bond Valuation Measuring Yield Assessing Risk 7 1 What is a bond? A long term debt instrument in which a borrower agrees to make payments of principal

Chapter 7 Bonds and Their Valuation Key Features of Bonds Bond Valuation Measuring Yield Assessing Risk 7 1 What is a bond? A long term debt instrument in which a borrower agrees to make payments of principal

LAZARD RETIREMENT SERIES, INC. 30 Rockefeller Plaza New York, New York (800) STATEMENT OF ADDITIONAL INFORMATION May 1, 2018

STATEMENT OF ADDITIONAL INFORMATION May 1, 2018") LAZARD RETIREMENT SERIES, INC. 30 Rockefeller Plaza New York, New York 10112-6300 (800) 823-6300 STATEMENT OF ADDITIONAL INFORMATION May 1, 2018 Lazard Retirement Series, Inc. (the "Fund") is a no-load,

LAZARD RETIREMENT SERIES, INC. 30 Rockefeller Plaza New York, New York 10112-6300 (800) 823-6300 STATEMENT OF ADDITIONAL INFORMATION May 1, 2018 Lazard Retirement Series, Inc. (the "Fund") is a no-load,

JPMorgan Funds statistics report: Mortgage-Backed Securities Fund

NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE JPMorgan Funds statistics report: Mortgage-Backed Securities Fund Must be preceded or accompanied by a prospectus. jpmorganfunds.com Table of contents

NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE JPMorgan Funds statistics report: Mortgage-Backed Securities Fund Must be preceded or accompanied by a prospectus. jpmorganfunds.com Table of contents

FUNDAMENTALS OF CREDIT ANALYSIS

FUNDAMENTALS OF CREDIT ANALYSIS 1 MV = Market Value NOI = Net Operating Income TV = Terminal Value RC = Replacement Cost DSCR = Debt Service Coverage Ratio 1. INTRODUCTION CR = Credit Risk Y.S = Yield

FUNDAMENTALS OF CREDIT ANALYSIS 1 MV = Market Value NOI = Net Operating Income TV = Terminal Value RC = Replacement Cost DSCR = Debt Service Coverage Ratio 1. INTRODUCTION CR = Credit Risk Y.S = Yield

1. An option that can be exercised any time before expiration date is called:

Sample Test Questions for Intermediate Business Finance Ch 20 1. An option that can be exercised any time before expiration date is called: A. an European option B. an American option C. a call option

Sample Test Questions for Intermediate Business Finance Ch 20 1. An option that can be exercised any time before expiration date is called: A. an European option B. an American option C. a call option

CHAPTER 4 Bonds and Their Valuation Key features of bonds Bond valuation Measuring yield Assessing risk

4-1 CHAPTER 4 Bonds and Their Valuation Key features of bonds Bond valuation Measuring yield Assessing risk 4-2 Key Features of a Bond 1. Par value: Face amount; paid at maturity. Assume $1,000. 2. Coupon

4-1 CHAPTER 4 Bonds and Their Valuation Key features of bonds Bond valuation Measuring yield Assessing risk 4-2 Key Features of a Bond 1. Par value: Face amount; paid at maturity. Assume $1,000. 2. Coupon

MUNICIPAL BONDS IN TEXAS and THE BOND SALE PROCESS

MUNICIPAL BONDS IN TEXAS and THE BOND SALE PROCESS Government Treasurers Organization of Texas Winter Seminar December 5, 2017 9:30 AM 10:30 AM Robert W. Baird & Co. Incorporated ( Baird ) is providing

MUNICIPAL BONDS IN TEXAS and THE BOND SALE PROCESS Government Treasurers Organization of Texas Winter Seminar December 5, 2017 9:30 AM 10:30 AM Robert W. Baird & Co. Incorporated ( Baird ) is providing

PRINCIPAL VARIABLE CONTRACTS FUNDS, INC.

PRINCIPAL VARIABLE CONTRACTS FUNDS, INC. Class 1 and Class 2 Shares ("PVC" or the "Fund ) The date of this Prospectus is May 1, 2017, as revised May 2, 2017 and previously supplemented on May 2, 2017.

PRINCIPAL VARIABLE CONTRACTS FUNDS, INC. Class 1 and Class 2 Shares ("PVC" or the "Fund ) The date of this Prospectus is May 1, 2017, as revised May 2, 2017 and previously supplemented on May 2, 2017.

Lecture 7 Foundations of Finance

Lecture 7: Fixed Income Markets. I. Reading. II. Money Market. III. Long Term Credit Markets. IV. Repurchase Agreements (Repos). 0 Lecture 7: Fixed Income Markets. I. Reading. A. BKM, Chapter 2, Sections

Lecture 7: Fixed Income Markets. I. Reading. II. Money Market. III. Long Term Credit Markets. IV. Repurchase Agreements (Repos). 0 Lecture 7: Fixed Income Markets. I. Reading. A. BKM, Chapter 2, Sections

SECTION A: MULTIPLE CHOICE QUESTIONS. 1. All else equal, which of the following would most likely increase the yield to maturity on a debt security?

SECTION A: MULTIPLE CHOICE QUESTIONS 2 (40 MARKS) 1. All else equal, which of the following would most likely increase the yield to maturity on a debt security? 1. Put option. 2. Conversion option. 3.

SECTION A: MULTIPLE CHOICE QUESTIONS 2 (40 MARKS) 1. All else equal, which of the following would most likely increase the yield to maturity on a debt security? 1. Put option. 2. Conversion option. 3.

FUNDAMENTALS OF THE BOND MARKET

FUNDAMENTALS OF THE BOND MARKET Bonds are an important component of any balanced portfolio. To most they represent a conservative investment vehicle. However, investors purchase bonds for a variety of

FUNDAMENTALS OF THE BOND MARKET Bonds are an important component of any balanced portfolio. To most they represent a conservative investment vehicle. However, investors purchase bonds for a variety of

INTEREST RATE SWAP POLICY

INTEREST RATE SWAP POLICY I. INTRODUCTION The purpose of this Interest Rate Swap Policy (Policy) of the Riverside County Transportation Commission (RCTC) is to establish guidelines for the use and management

INTEREST RATE SWAP POLICY I. INTRODUCTION The purpose of this Interest Rate Swap Policy (Policy) of the Riverside County Transportation Commission (RCTC) is to establish guidelines for the use and management

Semper MBS Total Return Fund. Semper Short Duration Fund. Prospectus March 30, 2018

Semper MBS Total Return Fund Class A Institutional Class Investor Class SEMOX SEMMX SEMPX Semper Short Duration Fund Institutional Class Investor Class SEMIX SEMRX (Each a Fund, together the Funds ) Each

Semper MBS Total Return Fund Class A Institutional Class Investor Class SEMOX SEMMX SEMPX Semper Short Duration Fund Institutional Class Investor Class SEMIX SEMRX (Each a Fund, together the Funds ) Each

DEBT POLICY Last Revised October 11, 2013 Last Reviewed October 7, 2016

INTRODUCTION AND PURPOSE This Debt Policy Statement serves to articulate Puget Sound s philosophy regarding debt and to establish a framework to help guide decisions regarding the use and management of

INTRODUCTION AND PURPOSE This Debt Policy Statement serves to articulate Puget Sound s philosophy regarding debt and to establish a framework to help guide decisions regarding the use and management of

BARINGS GLOBAL CREDIT INCOME OPPORTUNITIES FUND Summary Prospectus November 1, 2018

BARINGS GLOBAL CREDIT INCOME OPPORTUNITIES FUND Summary Prospectus November 1, 2018 Class/Ticker Symbol Class A BXIAX Class C BXICX Class I BXITX Class Y BXIYX Before you invest, you may want to review

BARINGS GLOBAL CREDIT INCOME OPPORTUNITIES FUND Summary Prospectus November 1, 2018 Class/Ticker Symbol Class A BXIAX Class C BXICX Class I BXITX Class Y BXIYX Before you invest, you may want to review

A floating-rate portfolio that seeks to deliver attractive income

A floating-rate portfolio that seeks to deliver attractive income An investor should consider the investment objective, risks, and charges and expenses of the Fund carefully before investing. The prospectus

A floating-rate portfolio that seeks to deliver attractive income An investor should consider the investment objective, risks, and charges and expenses of the Fund carefully before investing. The prospectus

Copyright 2004 Pearson Education, Inc. All rights reserved. Bonds

Copyright 2004 Pearson Education, Inc. All rights reserved. Bonds What is a Bond? Debt securities that may pay a rate of interest based upon the face amount or par value of the bond Bond investors receive

Copyright 2004 Pearson Education, Inc. All rights reserved. Bonds What is a Bond? Debt securities that may pay a rate of interest based upon the face amount or par value of the bond Bond investors receive

STATE BOARD OF REGENTS OF THE STATE OF UTAH STUDENT LOAN PURCHASE PROGRAM An Enterprise Fund of the State of Utah

An Enterprise Fund of the State of Utah Financial Statements AN ENTERPRISE FUND OF THE STATE OF UTAH FOR THE NINE MONTHS ENDED MARCH 31, 2014 TABLE OF CONTENTS Page MANAGEMENT S REPORT 1 FINANCIAL STATEMENTS:

An Enterprise Fund of the State of Utah Financial Statements AN ENTERPRISE FUND OF THE STATE OF UTAH FOR THE NINE MONTHS ENDED MARCH 31, 2014 TABLE OF CONTENTS Page MANAGEMENT S REPORT 1 FINANCIAL STATEMENTS:

FIXED INCOME ANALYSIS WORKBOOK

FIXED INCOME ANALYSIS WORKBOOK CFA Institute is the premier association for investment professionals around the world, with over 124,000 members in 145 countries. Since 1963 the organization has developed

FIXED INCOME ANALYSIS WORKBOOK CFA Institute is the premier association for investment professionals around the world, with over 124,000 members in 145 countries. Since 1963 the organization has developed

Morgan Stanley Variable Insurance Fund, Inc. Core Plus Fixed Income Portfolio

Morgan Stanley Variable Insurance Fund, Inc. Core Plus Fixed Income Portfolio Prospectus April 30, 2018 Share Class Class II Ticker Symbol MJIIX Morgan Stanley Variable Insurance Fund, Inc. (the Company

Morgan Stanley Variable Insurance Fund, Inc. Core Plus Fixed Income Portfolio Prospectus April 30, 2018 Share Class Class II Ticker Symbol MJIIX Morgan Stanley Variable Insurance Fund, Inc. (the Company

STATE BOARD OF REGENTS OF THE STATE OF UTAH STUDENT LOAN PURCHASE PROGRAM An Enterprise Fund of the State of Utah

An Enterprise Fund of the State of Utah Financial Statements AN ENTERPRISE FUND OF THE STATE OF UTAH FOR THE THREE MONTHS ENDED SEPTEMBER 30, 2018 TABLE OF CONTENTS Page MANAGEMENT S REPORT 1 FINANCIAL

An Enterprise Fund of the State of Utah Financial Statements AN ENTERPRISE FUND OF THE STATE OF UTAH FOR THE THREE MONTHS ENDED SEPTEMBER 30, 2018 TABLE OF CONTENTS Page MANAGEMENT S REPORT 1 FINANCIAL

STATE BOARD OF REGENTS OF THE STATE OF UTAH STUDENT LOAN PURCHASE PROGRAM An Enterprise Fund of the State of Utah

An Enterprise Fund of the State of Utah Financial Statements AN ENTERPRISE FUND OF THE STATE OF UTAH FOR THE NINE MONTHS ENDED MARCH 31, 2018 TABLE OF CONTENTS Page MANAGEMENT S REPORT 1 FINANCIAL STATEMENTS:

An Enterprise Fund of the State of Utah Financial Statements AN ENTERPRISE FUND OF THE STATE OF UTAH FOR THE NINE MONTHS ENDED MARCH 31, 2018 TABLE OF CONTENTS Page MANAGEMENT S REPORT 1 FINANCIAL STATEMENTS:

FIXED INCOME ANALYSIS WORKBOOK

FIXED INCOME ANALYSIS WORKBOOK Second Edition Frank J. Fabozzi, PhD, CFA John Wiley & Sons, Inc. FIXED INCOME ANALYSIS WORKBOOK CFA Institute is the premier association for investment professionals around

FIXED INCOME ANALYSIS WORKBOOK Second Edition Frank J. Fabozzi, PhD, CFA John Wiley & Sons, Inc. FIXED INCOME ANALYSIS WORKBOOK CFA Institute is the premier association for investment professionals around

BOND NOTES BOND TERMS

BOND NOTES DEFINITION: A bond is a commitment by the issuer (the company that is borrowing the money) to pay a rate of interest for a pre-determined period of time. By selling bonds, the issuing company

BOND NOTES DEFINITION: A bond is a commitment by the issuer (the company that is borrowing the money) to pay a rate of interest for a pre-determined period of time. By selling bonds, the issuing company

The Universal Institutional Funds, Inc.

Class I Prospectus April 29, 2016 The Universal Institutional Funds, Inc. Core Plus Fixed Income Portfolio Above-average total return over a market cycle of three to five years by investing primarily in

Class I Prospectus April 29, 2016 The Universal Institutional Funds, Inc. Core Plus Fixed Income Portfolio Above-average total return over a market cycle of three to five years by investing primarily in

ISS RATHORE INSTITUTE. Strategic Financial Management

1 ISS RATHORE INSTITUTE Strategic Financial Management Solution Booklet By CA. Gaurav Jain 100% Conceptual Coverage Not a Crash Course More than 400 Questions covered in Just 30 Classes Complete Coverage

1 ISS RATHORE INSTITUTE Strategic Financial Management Solution Booklet By CA. Gaurav Jain 100% Conceptual Coverage Not a Crash Course More than 400 Questions covered in Just 30 Classes Complete Coverage

Chapter 5. Valuing Bonds

Chapter 5 Valuing Bonds 5-2 Topics Covered Bond Characteristics Reading the financial pages after introducing the terminologies of bonds in the next slide (p.119 Figure 5-2) Bond Prices and Yields Bond

Chapter 5 Valuing Bonds 5-2 Topics Covered Bond Characteristics Reading the financial pages after introducing the terminologies of bonds in the next slide (p.119 Figure 5-2) Bond Prices and Yields Bond

Lecture #1. Introduction Debt & Fixed Income. BONDS LOANS (Corporate) Chapter 1

Chapter 1") Lecture #1 Introduction Debt & Fixed Income BONDS LOANS (Corporate) Chapter 1 Fed, State, Local BONDS: Six sectors: U.S. Treasury Sector o Issued by U.S. Government o T-Bills, Notes, Bonds o The largest

Lecture #1 Introduction Debt & Fixed Income BONDS LOANS (Corporate) Chapter 1 Fed, State, Local BONDS: Six sectors: U.S. Treasury Sector o Issued by U.S. Government o T-Bills, Notes, Bonds o The largest

Chapter 5. Bonds, Bond Valuation, and Interest Rates

Chapter 5 Bonds, Bond Valuation, and Interest Rates 1 Chapter 5 applies Time Value of Money techniques to the valuation of bonds, defines some new terms, and discusses how interest rates are determined.

Chapter 5 Bonds, Bond Valuation, and Interest Rates 1 Chapter 5 applies Time Value of Money techniques to the valuation of bonds, defines some new terms, and discusses how interest rates are determined.

Financial Markets Econ 173A: Mgt 183. Capital Markets & Securities

Financial Markets Econ 173A: Mgt 183 Capital Markets & Securities Financial Instruments Money Market Certificates of Deposit U.S. Treasury Bills Money Market Funds Equity Market Common Stock Preferred

Financial Markets Econ 173A: Mgt 183 Capital Markets & Securities Financial Instruments Money Market Certificates of Deposit U.S. Treasury Bills Money Market Funds Equity Market Common Stock Preferred

Analysis of Asset Spread Benchmarks. Report by the Deloitte UConn Actuarial Center. April 2008

Analysis of Asset Spread Benchmarks Report by the Deloitte UConn Actuarial Center April 2008 Introduction This report studies the various benchmarks for analyzing the option-adjusted spreads of the major

Analysis of Asset Spread Benchmarks Report by the Deloitte UConn Actuarial Center April 2008 Introduction This report studies the various benchmarks for analyzing the option-adjusted spreads of the major

Coastal Bend College Summary of Investments

1 Coastal Bend College Summary of Investments 2/29/2016 2/29/2016 Book Value Market Value Equity Securities: U.S. Common Stock Equity Mutual Funds Other Equity Securities (list) Total Equities Other Investments:

1 Coastal Bend College Summary of Investments 2/29/2016 2/29/2016 Book Value Market Value Equity Securities: U.S. Common Stock Equity Mutual Funds Other Equity Securities (list) Total Equities Other Investments:

Australia and New Zealand Banking Group Limited New Zealand Branch General Disclosure Statement

Australia and New Zealand Banking Group Limited New Zealand Branch General Disclosure Statement FOR THE YEAR ENDED 30 SEPTEMBER 2010 NUMBER 8 ISSUED NOVEMBER 2010 Australia and New Zealand Banking Group

Australia and New Zealand Banking Group Limited New Zealand Branch General Disclosure Statement FOR THE YEAR ENDED 30 SEPTEMBER 2010 NUMBER 8 ISSUED NOVEMBER 2010 Australia and New Zealand Banking Group

THORNBURG INVESTMENT TRUST Funds Prospectus

THORNBURG INVESTMENT TRUST Funds Prospectus JUNE 15, 2018 RETIREMENT PLAN SHARES Thornburg Limited Term U.S. Government Fund ( Limited Term U.S. Government Fund ) Class R3: LTURX Class R4: LTUGX Class

THORNBURG INVESTMENT TRUST Funds Prospectus JUNE 15, 2018 RETIREMENT PLAN SHARES Thornburg Limited Term U.S. Government Fund ( Limited Term U.S. Government Fund ) Class R3: LTURX Class R4: LTUGX Class

Chapter 11. Section 2: Bonds & Other Financial Assets

Chapter 11 Section 2: Bonds & Other Financial Assets Bonds as Financial Assets Bonds are basically loans, or IOUs, that represent debt that the government or a corporation must repay to an investor. Typically

Chapter 11 Section 2: Bonds & Other Financial Assets Bonds as Financial Assets Bonds are basically loans, or IOUs, that represent debt that the government or a corporation must repay to an investor. Typically

ALAMEDA COUNTY Annual Investment Policy Calendar Year 2018

ALAMEDA COUNTY Annual Investment Policy Calendar Year 2018 Introduction The Alameda County Board of Supervisors, by Ordinance # O-2017-51 dated, October 24, 2017 has renewed the annual delegation of its

ALAMEDA COUNTY Annual Investment Policy Calendar Year 2018 Introduction The Alameda County Board of Supervisors, by Ordinance # O-2017-51 dated, October 24, 2017 has renewed the annual delegation of its

Dear Shareholder: INVESTMENT OBJECTIVE

2008 ANNUAL REPORT Dear Shareholder: The Puerto Rico AAA Portfolio Bond Fund II, Inc. (the Fund ) is pleased to present its Annual Report to Shareholders for the fiscal year ended June 30, 2008. INVESTMENT

2008 ANNUAL REPORT Dear Shareholder: The Puerto Rico AAA Portfolio Bond Fund II, Inc. (the Fund ) is pleased to present its Annual Report to Shareholders for the fiscal year ended June 30, 2008. INVESTMENT

Fixed income security. Face or par value Coupon rate. Indenture. The issuer makes specified payments to the bond. bondholder

Bond Prices and Yields Bond Characteristics Fixed income security An arragement between borrower and purchaser The issuer makes specified payments to the bond holder on specified dates Face or par value

Bond Prices and Yields Bond Characteristics Fixed income security An arragement between borrower and purchaser The issuer makes specified payments to the bond holder on specified dates Face or par value

MONEY MARKET FUND GLOSSARY

MONEY MARKET FUND GLOSSARY 1-day SEC yield: The calculation is similar to the 7-day Yield, only covering a one day time frame. To calculate the 1-day yield, take the net interest income earned by the fund

MONEY MARKET FUND GLOSSARY 1-day SEC yield: The calculation is similar to the 7-day Yield, only covering a one day time frame. To calculate the 1-day yield, take the net interest income earned by the fund

FIN 6160 Investment Theory. Lecture 9-11 Managing Bond Portfolios

FIN 6160 Investment Theory Lecture 9-11 Managing Bond Portfolios Bonds Characteristics Bonds represent long term debt securities that are issued by government agencies or corporations. The issuer of bond

FIN 6160 Investment Theory Lecture 9-11 Managing Bond Portfolios Bonds Characteristics Bonds represent long term debt securities that are issued by government agencies or corporations. The issuer of bond

MBF1223 Financial Management Prepared by Dr Khairul Anuar

MBF1223 Financial Management Prepared by Dr Khairul Anuar L4 Bonds & Bonds Valuation www.mba638.wordpress.com Bonds - Introduction A bond is a debt instrument issued by a borrower which has borrowed a

MBF1223 Financial Management Prepared by Dr Khairul Anuar L4 Bonds & Bonds Valuation www.mba638.wordpress.com Bonds - Introduction A bond is a debt instrument issued by a borrower which has borrowed a

Corporate Finance. Dr Cesario MATEUS Session

Corporate Finance Dr Cesario MATEUS cesariomateus@gmail.com www.cesariomateus.com Session 4 26.03.2014 The Capital Structure Decision 2 Maximizing Firm value vs. Maximizing Shareholder Interests If the

Corporate Finance Dr Cesario MATEUS cesariomateus@gmail.com www.cesariomateus.com Session 4 26.03.2014 The Capital Structure Decision 2 Maximizing Firm value vs. Maximizing Shareholder Interests If the

DEBT MANAGEMENT EXAMINATION

1. Duration: a) is a measure of volatility of bond returns. b) is influenced by the coupon rate and yield to maturity. c) provides an approximation of the percentage price change in a bond due to a change

1. Duration: a) is a measure of volatility of bond returns. b) is influenced by the coupon rate and yield to maturity. c) provides an approximation of the percentage price change in a bond due to a change

Mutual Funds and Individual Securities

Mutual Funds and Individual Securities A Center for Continuing Education 1465 Northside Drive, Suite 213 Atlanta, Georgia 30318 (404) 355-1921 (800) 344-1921 Fax: (404) 355-1292 Written by Peggy Erland.

Mutual Funds and Individual Securities A Center for Continuing Education 1465 Northside Drive, Suite 213 Atlanta, Georgia 30318 (404) 355-1921 (800) 344-1921 Fax: (404) 355-1292 Written by Peggy Erland.

Powered by TCPDF (www.tcpdf.org) 10.1 Fixed Income Securities Study Session 10 LOS 1 : Introduction (Fixed Income Security) Bonds are the type of long term obligation which pay periodic interest & repay

Powered by TCPDF (www.tcpdf.org) 10.1 Fixed Income Securities Study Session 10 LOS 1 : Introduction (Fixed Income Security) Bonds are the type of long term obligation which pay periodic interest & repay

Guide to investing in municipal securities

Guide to investing in municipal securities What you should know before you buy Before you buy an investment, it is important to review your financial situation, net worth, tax status, investment objectives,

Guide to investing in municipal securities What you should know before you buy Before you buy an investment, it is important to review your financial situation, net worth, tax status, investment objectives,

PRINCIPAL FUNDS, INC. ( PFI )

") PRINCIPAL FUNDS, INC. ( PFI ) Class Institutional Shares The date of this Prospectus is March 10, 2015. Fund Opportunistic Municipal Ticker Symbol by Share Class Institutional POMFX The Securities and

PRINCIPAL FUNDS, INC. ( PFI ) Class Institutional Shares The date of this Prospectus is March 10, 2015. Fund Opportunistic Municipal Ticker Symbol by Share Class Institutional POMFX The Securities and

MS-E2114 Investment Science Lecture 2: Fixed income securities

MS-E2114 Investment Science Lecture 2: Fixed income securities A. Salo, T. Seeve Systems Analysis Laboratory Department of System Analysis and Mathematics Aalto University, School of Science Overview Financial

MS-E2114 Investment Science Lecture 2: Fixed income securities A. Salo, T. Seeve Systems Analysis Laboratory Department of System Analysis and Mathematics Aalto University, School of Science Overview Financial

PIMCO Funds. Effective July 30, 2018, all references to the Fund s name in the Prospectus and the SAI are deleted and replaced with the following:

PIMCO Funds Supplement dated May 18, 2018 to the Bond Funds Prospectus (the Prospectus ), and to the Statement of Additional Information (the SAI ), each dated July 28, 2017, each as supplemented from

PIMCO Funds Supplement dated May 18, 2018 to the Bond Funds Prospectus (the Prospectus ), and to the Statement of Additional Information (the SAI ), each dated July 28, 2017, each as supplemented from

Investment Appendix April 2016

Investment Appendix April 2016 Investment Appendix This is a translation of the original Dutch text. This translation is furnished for the customer s convenience only. The original Dutch text will be binding

Investment Appendix April 2016 Investment Appendix This is a translation of the original Dutch text. This translation is furnished for the customer s convenience only. The original Dutch text will be binding

Australia and New Zealand Banking Group Limited New Zealand Branch Disclosure Statement

Australia and New Zealand Banking Group Limited New Zealand Branch Disclosure Statement FOR THE YEAR ENDED 30 SEPTEMBER 2011 NUMBER 11 ISSUED NOVEMBER 2011 Australia and New Zealand Banking Group Limited

Australia and New Zealand Banking Group Limited New Zealand Branch Disclosure Statement FOR THE YEAR ENDED 30 SEPTEMBER 2011 NUMBER 11 ISSUED NOVEMBER 2011 Australia and New Zealand Banking Group Limited

Senior Floating Rate Loans: The Whole Story

Senior Floating Rate Loans: The Whole Story Mutual fund shares are not guaranteed or insured by the FDIC, the Federal Reserve Board or any other agency. The investment return and principal value of an

Senior Floating Rate Loans: The Whole Story Mutual fund shares are not guaranteed or insured by the FDIC, the Federal Reserve Board or any other agency. The investment return and principal value of an

A WELL-DIVERSIFIED CORE BOND PORTFOLIO

A WELL-DIVERSIFIED CORE BOND PORTFOLIO PRUDENTIAL TOTAL RETURN BOND FUND MORNINGSTAR OVERALL RATING Class A, Q, and Z Class C and R Broad mix of sectors, industries, credit qualities, and maturities Research

A WELL-DIVERSIFIED CORE BOND PORTFOLIO PRUDENTIAL TOTAL RETURN BOND FUND MORNINGSTAR OVERALL RATING Class A, Q, and Z Class C and R Broad mix of sectors, industries, credit qualities, and maturities Research

Franklin Liberty Short Duration U.S. Government ETF

Franklin Liberty Short Duration U.S. Government ETF Prospectus October 1, 2016 Franklin ETF Trust TICKER: EXCHANGE: formerly, Franklin Short Duration U.S. Government ETF FTSD NYSE Arca, Inc. The U.S. Securities

Franklin Liberty Short Duration U.S. Government ETF Prospectus October 1, 2016 Franklin ETF Trust TICKER: EXCHANGE: formerly, Franklin Short Duration U.S. Government ETF FTSD NYSE Arca, Inc. The U.S. Securities

Risk and Term Structure of Interest Rates

Risk and Term Structure of Interest Rates Economics 301: Money and Banking 1 1.1 Goals Goals and Learning Outcomes Goals: Explain factors that can cause interest rates to be different for bonds of different

Risk and Term Structure of Interest Rates Economics 301: Money and Banking 1 1.1 Goals Goals and Learning Outcomes Goals: Explain factors that can cause interest rates to be different for bonds of different