Lecture 7 Foundations of Finance

|

|

|

- Virgil Holland

- 5 years ago

- Views:

Transcription

1 Lecture 7: Fixed Income Markets. I. Reading. II. Money Market. III. Long Term Credit Markets. IV. Repurchase Agreements (Repos). 0

2 Lecture 7: Fixed Income Markets. I. Reading. A. BKM, Chapter 2, Sections 2.1 and 2.2. B. BKM, Chapter 14, Sections and II. Money Market. A. Definition. 1. Money market instruments are those with maturities of one year or less. B. U.S. Treasury Bills. 1. Introduction. a. These are obligations backed by the "full faith and credit" of the U.S. government. Among all money market instruments, T-bills are regarded as safest with respect to default risk. b. T-bills (and most money-market instruments) are discount instruments. They do not explicitly pay an interest rate. Instead they are sold below their par (face) value. 2. Maturities. a. Issued weekly with maturities of 91 or 182 days. b. Issued monthly with a maturity of 12 months. 1

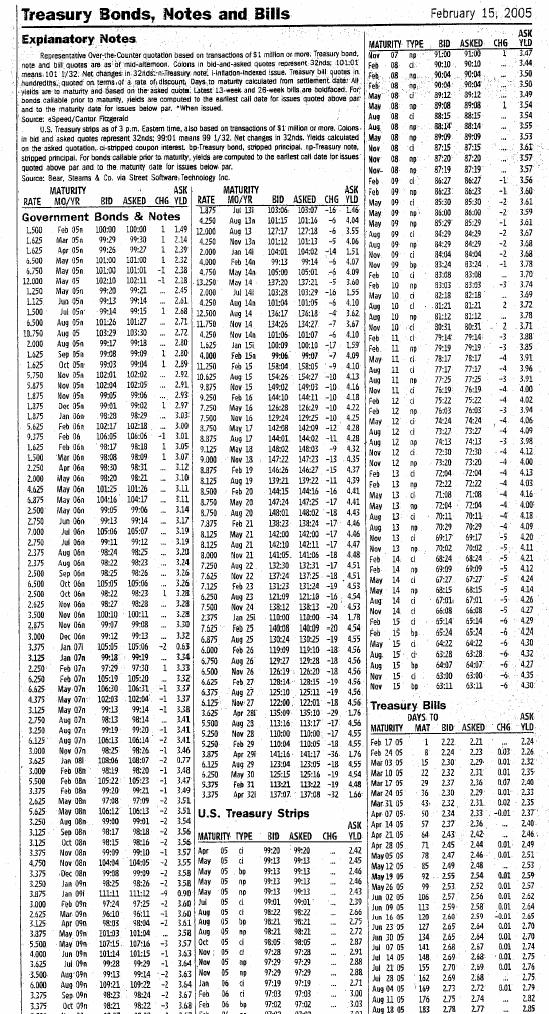

3 Price'Par 3. Bank Discount Rate. a. T-bills are quoted on a 360-day discount basis using the bank discount rate. b. The (bank) discount rate is defined: 1& nr BD 360 Y r BD ' 360 Par&Price n Par where r BD is the quoted discount rate and n is the number of days from settlement to maturity. (A 360-day year is commonly used in pricing money market instruments.) c. The word "discount" is used in many different contexts in finance. It is sometimes used to denote any interest rate used in a present value calculation, as in "the cash flow in year ten was discounted at a rate of 5%." In money market analysis, however, it is used very precisely as the interest rate used to compute the price (as above). d. Example: See WSJ clipping 2/16/05 for Treasury Bills on 2/15/05. Maturity Days to Mat. Bid Asked Chg Ask Yld. Apr Buying at the ask bank discount rate of 2.33% on Tuesday 2/15/05 the trade settles on 2/17/01. Hence 50 days to maturity. The price paid (for $100 face value) is $100 (1 - {50x0.0233/360}) = $

4 R hold (0,n) ' r BEY ' 365 n 4. Holding period return. a. The holding period return from holding a T-bill until maturity is given by: Par & Price Price. b. Example (cont): Apr T-bill, if purchased on 2/15/05, offers a 50 day holding period return of {$100-$99.676}/$ = %. 5. Bond-equivalent yield. a. The bond equivalent yield for n<183 (if not a leap year) can be calculated as follows: R hold (0,n). b. Since there are 365 days in a year, the bond equivalent can be thought of as an annual percentage rate (APR) with n-day compounding. c. The quoted Ask Yield in the WSJ is the bond equivalent yield. d. Example (cont): The bond equivalent yield for the Apr T- bill purchased on 2/15/05 is (365/50)x0.3247% = 2.370% which agrees with the WSJ quote of 2.37%. 3

A non-competitive bid may be entered for an amount up to $1 million. No price is specified. A non-competitive bid is the easiest way for a retail investor to buy T-bills. c.")

5 6. Primary Market. a. T-bills are initially sold at an auction. b. Two sorts of bids are accepted. (1) A competitive bid specifies an amount and a price. (2) A non-competitive bid may be entered for an amount up to $1 million. No price is specified. A non-competitive bid is the easiest way for a retail investor to buy T-bills. c. The Fed arranges the competitive bids in order of descending price (ascending yield). It then works its way down this list until the total amount bid for (plus the non-competitive interest) is equal to the amount it wishes to sell. (1) All successful bids, both competitive and non-competitive, are filled at the lowest competitive bid price that is filled. (2) The auction is single-price: all successful bidders pay the same price. (3) The Treasury does not price discriminate. WSJ 3/16/05 4

6 7. When-issued-market. a. This market trades instruments which obligate the delivery of T- bills not yet issued at a predetermined price at their time of issue. b. So investors can lock in a particular price prior to the auction date. c. This instrument is an example of a forward contract on the T-bill. 8. Secondary Market. a. This is a telephone dealer network. Some quotes are communicated via screens, but there is no centralized trade reporting. b. The Fed has designated some dealers as primary dealers. These are the dealers that the Fed itself uses when conducting open market operations. c. Spreads on T-bills are narrow. 5

7 C. Other Money Market Instruments. 1. Commercial Paper. a. Short-term corporate debt (usually less than one or two months). b. Issued in multiples of $100,000. c. Most issued by finance companies. (1) Captive finance companies (GMAC, Ford Credit, Chrysler Financial, General Electric Credit). (2) Bank (and bank-related) finance companies. (3) Independent finance companies. d. Comparison with T-bills. (1) less liquid. (2) more credit risk. (3) subject to state & local taxation. 2. Certificates of Deposit (CD's). a. CDS are issued by banks. b. Types. (1) Domestic CD's. (2) Eurodollar CD's ($ denominated CDS issued by banks outside of U.S.). (3) Yankee CD's ($ denominated CDS issued by foreign banks with offices in U.S.). c. Large denomination ($ or larger). d. Negotiable/non-negotiable. 3. Federal Reserve Bank reserves. a. In the federal funds market, member banks of the Federal Reserve System with excess reserves lend to those with a shortage. b. These loans which are usually overnight are arranged at a rate of interest called the federal funds rate. 4. London Interbank Offered Rate (LIBOR) Rate. a. Rate on dollar-denominated deposits at large London Banks. b. Used as a reference rate for floating rate loans and in the swap market. 6

8 WSJ 3/16/05 7

9 III. Long Term Credit Markets. A. U.S. Treasury Notes and Bonds. 1. Introduction. a. The distinction between notes and bonds is one of original maturity: notes have an original maturity of 1-10 years; bonds have a maturity>10 years. b. A plain-vanilla bond is characterized by: (1) Maturity: when the bond will be repaid. (2) Par or face value: the amount that will be repaid at maturity. (3) Coupon rate: the rate used in computing the semiannual coupon payments (0.5 x coupon rate x par value gives the semiannual coupon). (4) Coupons are either paid on the 15th or at the end of the month. (5) The quoted prices are on the basis of $100 par, in dollars + 1/32nds. c. Example: See WSJ clipping for Govt Bonds and Notes on 2/15/05. Rate Maturity Mo/Yr Bid Asked Chg Ask Yld. 3 Feb 09n 97:24 97: (1) The time line for this bond: 2/15/05 8/15/05 2/15/06 8/15/08 2/15/ )))))))))))))))))))))))))2)))))))))))))))))))))))))2)... ))2))))))))))))))))))))))))) (2) Coupons for this note are paid on the 15th of the month. (3) The asked price is 97+25/32= (4) Chg is the change in the asked price from the previous day in 32 nd s. 8

10 9

11 2. Accrued Interest and the Quoted Price. a. The quoted price does not include accrued interest; so the quoted price is not the invoice price unless a coupon has just been paid. b. To get the invoice price from the quoted price, need to add accrued interest. c. Example (cont): The quoted asked price for the 3 Feb 09 note in the WSJ for 3/1/05 is 96:24 or What would be the accrued interest on the 3 Feb 09 note and the invoice price? (1) Accrued interest is given by w(3/1/05) C/2 = (14/181) x 1.5 = x 1.5 = where C is the coupon rate; and, w(3/1/05) is the period between the last coupon payment and now expressed as a fraction of 6 months (called the accrual period). (2) The quoted asked price for the 3 Feb 09 note in the WSJ of can be converted into the invoice price by adding the accrued interest of to obtain

12 3. Yield to maturity (YTM). a. Definition. (1) YTM is the interest rate such that the present value of the remaining cash flows from the note/bond exactly equals the invoice price. (2) The Ask Yld in the WSJ is the YTM expressed as an APR with semiannual compounding. b. Calculation. (1) Suppose the bond has just paid a coupon. Then the YTM expressed as an APR with semi-annual compounding satisfies: V 0 = C x PVAF YTM/2,N x PVIF YTM/2,N where N is the number of coupon payments to maturity and V 0 is the invoice price today. (2) If the bond has not just paid a coupon, the calculation is more complicated. c. Example (cont): On 2/15/05, the 3 Feb 09 note has just paid a coupon. Thus, can use the formula to get the invoice price which will also equal the quoted price: V 0 = 1.5 x PVAF (3.6/2)%, x PVIF (3.6/2)%,8 = = : Relation of YTM to Coupon Rate: the Impact on Bond Price. a. YTM is expressed as an APR with semi-annual compounding. b. If the bond has just paid a coupon: (1) Coupon Rate<YTM then Par>Price; i.e, the bond is selling at a discount relative to par. (2) Coupon Rate>YTM then Par<Price; i.e., the bond is selling at a premium relative to par. c. Example: See WSJ clipping for Govt Bonds and Notes on 2/15/05. Rate Maturity Mo/Yr Bid Asked Chg Ask Yld. 3.5 Aug 09n 99:13 99: Aug 09n 109:21 109: (1) For 3.5 Aug 09 note, Coupon Rate<YTM and so Par>Price. (2) For 6 Aug 09 note, Coupon Rate>YTM and so Par<Price. 11

13 B. U.S. Treasury Zero Coupon Bonds. 1. Definition. a. "Zeroes" are bonds which have no intermediate payments, and repay the principal amount at maturity. b. In this respect, they are the same as T-bills, except that they are for longer maturities. 2. Creation of Zero Coupon Bonds. a. Zero coupon bonds are created by `stripping' coupon issues: STRIPS (Separate Trading of Registered Interest and Principal Securities). b. Prior to 1982, zero coupon bonds were created by investment banks. A bank would buy coupon bonds, place them in a trust and sell off zero-coupon bonds as claims on the trust. c. In 1982, the U.S. Treasury got into the act by allowing ownership of interest and principal payments to be registered separately. They can then be traded and priced separately. d. Example: WSJ on 2/16/05 reports quotes for Feb 09 principal and for Feb 09 coupon strips separately. 3. A coupon bond can be regarded as a portfolio of zero-coupon bonds, each maturing at a different payment date. This observation is sometimes useful in solving bond pricing problems. 12

14 C. Corporate Bonds. 1. Most are coupon bonds: Usually with semi-annual coupons. 2. Default risk: Can be substantial which is a major difference as compared to treasuries. 3. Seniority: Senior debt gets paid before junior debt in the event of default. 4. Security: Some bond are secured by specified assets of the firm which means that in the event of default the proceeds from those assets are used to pay the secured debt before any other debt is paid 5. Covenants: Some bonds place restrictions on additional issues, dividends, and other corporate actions to increase the likelihood that the bondholders will get paid. 6. Callable bond a. Issuer can repurchase at a specified price, usually par. b. Issuer may want to do this if interest rates are low since it allows the issuer to buy back a bond that otherwise would have a high price. The issuer can refinance at a lower interest rate. 7. Putable bond: After a certain period, bondholder has the right to demand payment of the loan before maturity. 8. Convertible bond. a. Bond is convertible into a number of shares of common stock. The number is fixed at the time the bond is issued. The conversion is one-way : you can convert to stock, but not back to a bond. b. The timing of the conversion is the decision of the bondholder. BUT, the issuer can sometimes force conversion by threatening to call back the bond. c. A conversion feature is attractive, so a convertible bond can generally be issued with a lower coupon rate than straight debt 9. Sinking fund. a. A sinking fund is a provision for the orderly retirement of the debt. It may take one of several forms. (1) Firm must repurchase bonds in the open market. (2) Firm repurchases bonds with call provisions. b. Note that the repurchase is an obligation. 13

15 D. Mortgage-backed Securities 1. Mortgage-backed securities are bonds whose payments are secured by mortgage payments. 2. Two main issuing agencies: Freddie Mac and Fannie Mae, both government-sponsored agencies. 3. Issuance: a. When interest rates go up, banks have a fixed income from their mortgage contracts but need to pay a higher interest rate on deposits, leaving them exposed to interest rate risk b. To reduce this interest rate risk exposure, banks sell their portfolios of mortgages to an issuing agency: i.e., the issuing agency underwrites the mortgages. c. The agency pools these mortgages together and sells them off as securities (mortgage-backed securities) to the general public. 4. Market for mortgage backed securities is currently worth 6 trillion dollars, 50% more than the 4 trillion for government bonds E. Interest Rate Swaps. 1. Basic arrangement. a. An agreement between the buyer and seller of the swap. b. The buyer agrees to pay a fixed rate on the notional principal until maturity of the swap. c. The seller agrees to pay a floating rate (often determined by the LIBOR rate) on the notional principal until maturity. d. No money changes hands at the time that the swap is entered into: so the notional principal never changes hands. e. The fixed rate is referred to as the swap rate. Fixed-rate Payer fixed rate 6 Floating-rate Payer (bought the swap) 7 floating rate (sold the swap) 14

16 IV. Repurchase Agreements (Repos). A. Basic arrangement. 1. Repos are loans collateralized by securities. Initiation: lender 6 ($) borrower (securities) 7 To settle: lender 7($) borrower (securities) 6 B. Terminology. 1. Dealer is the borrower (and so client is the lender): a. "repo". b. "reversing out". c. "selling collateral". 2. Dealer is the lender (and so client is the borrower): a. "reverse repo". b. "reversing in" c. "buying collateral" 3. Explains why Repo rate is less than Reverse Repo rate on Bloomberg. C. Using Repos to sell short. 1. The lender of $ can also be viewed as a borrower of securities (which will be returned when the loan is repaid). 2. Thus, the lender could then sell short the security using the borrowed securities. 3. The dealer uses a reverse repo to sell short the security. 4. The client uses a repo to sell short the security. D. Securities. 1. Historically, the repo market developed for U.S. government securities. 2. Now you can repo practically any kind of fixed income instrument, across currencies. 3. You can also repo risky securities such as emerging market debt. 15

Lectures 1-2 Foundations of Finance

Lectures 1-2: Time Value of Money I. Reading A. RWJ Chapter 5. II. Time Line A. $1 received today is not the same as a $1 received in one period's time; the timing of a cash flow affects its value. B.

Lectures 1-2: Time Value of Money I. Reading A. RWJ Chapter 5. II. Time Line A. $1 received today is not the same as a $1 received in one period's time; the timing of a cash flow affects its value. B.

Lectures 2-3 Foundations of Finance

Lecture 2-3: Time Value of Money I. Reading II. Time Line III. Interest Rate: Discrete Compounding IV. Single Sums: Multiple Periods and Future Values V. Single Sums: Multiple Periods and Present Values

Lecture 2-3: Time Value of Money I. Reading II. Time Line III. Interest Rate: Discrete Compounding IV. Single Sums: Multiple Periods and Future Values V. Single Sums: Multiple Periods and Present Values

Markets: Fixed Income

Markets: Fixed Income Mark Hendricks Autumn 2017 FINM Intro: Markets Outline Hendricks, Autumn 2017 FINM Intro: Markets 2/55 Asset Classes Fixed Income Money Market Bonds Equities Preferred Common contracted

Markets: Fixed Income Mark Hendricks Autumn 2017 FINM Intro: Markets Outline Hendricks, Autumn 2017 FINM Intro: Markets 2/55 Asset Classes Fixed Income Money Market Bonds Equities Preferred Common contracted

Chapter 4. Characteristics of Bonds. Chapter 4 Topic Overview. Bond Characteristics

Chapter 4 Topic Overview Chapter 4 Valuing Bond Characteristics Annual and Semi-Annual Bond Valuation Reading Bond Quotes Finding Returns on Bond Risk and Other Important Bond Valuation Relationships Bond

Chapter 4 Topic Overview Chapter 4 Valuing Bond Characteristics Annual and Semi-Annual Bond Valuation Reading Bond Quotes Finding Returns on Bond Risk and Other Important Bond Valuation Relationships Bond

Chapter 8. Money and Capital Markets. Learning Objectives. Introduction

Chapter 8 Money and Capital Markets Learning Objectives Visualize the structure of the government bond market Explain the interaction of Eurodollars, CDs, and Repurchase agreements and their connection

Chapter 8 Money and Capital Markets Learning Objectives Visualize the structure of the government bond market Explain the interaction of Eurodollars, CDs, and Repurchase agreements and their connection

FINC3019 FIXED INCOME SECURITIES

FINC3019 FIXED INCOME SECURITIES WEEK 1 BONDS o Debt instrument requiring the issuer to repay the lender the amount borrowed + interest over specified time period o Plain vanilla (typical) bond:! Fixed

FINC3019 FIXED INCOME SECURITIES WEEK 1 BONDS o Debt instrument requiring the issuer to repay the lender the amount borrowed + interest over specified time period o Plain vanilla (typical) bond:! Fixed

I. Introduction to Bonds

University of California, Merced ECO 163-Economics of Investments Chapter 10 Lecture otes I. Introduction to Bonds Professor Jason Lee A. Definitions Definition: A bond obligates the issuer to make specified

University of California, Merced ECO 163-Economics of Investments Chapter 10 Lecture otes I. Introduction to Bonds Professor Jason Lee A. Definitions Definition: A bond obligates the issuer to make specified

Foundations of Finance

Lecture 7: Bond Pricing, Forward Rates and the Yield Curve. I. Reading. II. Discount Bond Yields and Prices. III. Fixed-income Prices and No Arbitrage. IV. The Yield Curve. V. Other Bond Pricing Issues.

Lecture 7: Bond Pricing, Forward Rates and the Yield Curve. I. Reading. II. Discount Bond Yields and Prices. III. Fixed-income Prices and No Arbitrage. IV. The Yield Curve. V. Other Bond Pricing Issues.

MONEY MARKET FUND GLOSSARY

MONEY MARKET FUND GLOSSARY 1-day SEC yield: The calculation is similar to the 7-day Yield, only covering a one day time frame. To calculate the 1-day yield, take the net interest income earned by the fund

MONEY MARKET FUND GLOSSARY 1-day SEC yield: The calculation is similar to the 7-day Yield, only covering a one day time frame. To calculate the 1-day yield, take the net interest income earned by the fund

Financial Markets 1

318.06 Financial Markets 1 I. Market distinctions (rather than corporate bonds vs government bonds vs mortgages, which may be sold in different physical markets but are very similar) A. Capital market

318.06 Financial Markets 1 I. Market distinctions (rather than corporate bonds vs government bonds vs mortgages, which may be sold in different physical markets but are very similar) A. Capital market

ACCOUNTING - CLUTCH CH LONG TERM LIABILITIES.

!! www.clutchprep.com CONCEPT: INTRODUCTION TO BONDS AND BOND CHARACTERISTICS Bonds Payable are groups of debt securities issued to lenders Example: Company wants to raise $1,000,000. The company can sell

!! www.clutchprep.com CONCEPT: INTRODUCTION TO BONDS AND BOND CHARACTERISTICS Bonds Payable are groups of debt securities issued to lenders Example: Company wants to raise $1,000,000. The company can sell

Debt underwriting and bonds

Debt underwriting and bonds 1 A bond is an instrument issued for a period of more than one year with the purpose of raising capital by borrowing Debt underwriting includes the underwriting of: Government

Debt underwriting and bonds 1 A bond is an instrument issued for a period of more than one year with the purpose of raising capital by borrowing Debt underwriting includes the underwriting of: Government

Collateralized mortgage obligations (CMOs)

") Collateralized mortgage obligations (CMOs) Fixed-income investments secured by mortgage payments An overview of CMOs The goal of CMOs is to provide reliable income passed from mortgage payments. In general,

Collateralized mortgage obligations (CMOs) Fixed-income investments secured by mortgage payments An overview of CMOs The goal of CMOs is to provide reliable income passed from mortgage payments. In general,

COPYRIGHTED MATERIAL FEATURES OF DEBT SECURITIES CHAPTER 1 I. INTRODUCTION

CHAPTER 1 FEATURES OF DEBT SECURITIES I. INTRODUCTION In investment management, the most important decision made is the allocation of funds among asset classes. The two major asset classes are equities

CHAPTER 1 FEATURES OF DEBT SECURITIES I. INTRODUCTION In investment management, the most important decision made is the allocation of funds among asset classes. The two major asset classes are equities

Financial Markets Econ 173A: Mgt 183. Capital Markets & Securities

Financial Markets Econ 173A: Mgt 183 Capital Markets & Securities Financial Instruments Money Market Certificates of Deposit U.S. Treasury Bills Money Market Funds Equity Market Common Stock Preferred

Financial Markets Econ 173A: Mgt 183 Capital Markets & Securities Financial Instruments Money Market Certificates of Deposit U.S. Treasury Bills Money Market Funds Equity Market Common Stock Preferred

Federated Municipal Ultrashort Fund

Statement of Additional Information November 30, 2017 Share Class Ticker A FMUUX Institutional FMUSX Federated Municipal Ultrashort Fund A Portfolio of Federated Fixed Income Securities, Inc. This Statement

Statement of Additional Information November 30, 2017 Share Class Ticker A FMUUX Institutional FMUSX Federated Municipal Ultrashort Fund A Portfolio of Federated Fixed Income Securities, Inc. This Statement

Chap. 15. Government Securities

Reading: Chapter 15 Chap. 15. Government Securities 1. The variety of federal government debt 2. Federal agency debt 3. State and local government debt 4. Authority bonds and Build America bonds 5. Foreign

Reading: Chapter 15 Chap. 15. Government Securities 1. The variety of federal government debt 2. Federal agency debt 3. State and local government debt 4. Authority bonds and Build America bonds 5. Foreign

Asset Classes and Financial Instruments

Chapter 2 Asset Classes and Financial Instruments Bodie, Kane, and Marcus Essentials of Investments Tenth Edition 2.1 Asset Classes 2 2.1 The Money Market: Instruments Treasury Bills Certificates of Deposit

Chapter 2 Asset Classes and Financial Instruments Bodie, Kane, and Marcus Essentials of Investments Tenth Edition 2.1 Asset Classes 2 2.1 The Money Market: Instruments Treasury Bills Certificates of Deposit

Investments 4: Bond Basics

Personal Finance: Another Perspective Investments 4: Bond Basics Updated 2017/06/28 1 Objectives A. Understand risk and return for bonds B. Understand bond terminology C. Understand the major types of

Personal Finance: Another Perspective Investments 4: Bond Basics Updated 2017/06/28 1 Objectives A. Understand risk and return for bonds B. Understand bond terminology C. Understand the major types of

Investments 10th Edition Bodie Test Bank Full Download:

Investments 10th Edition Bodie Test Bank Full Download: http://testbanklive.com/download/investments-10th-edition-bodie-test-bank/ Chapter 02 Asset Classes and Financial Instruments Multiple Choice Questions

Investments 10th Edition Bodie Test Bank Full Download: http://testbanklive.com/download/investments-10th-edition-bodie-test-bank/ Chapter 02 Asset Classes and Financial Instruments Multiple Choice Questions

STATE BOARD OF REGENTS OF THE STATE OF UTAH STUDENT LOAN PURCHASE PROGRAM An Enterprise Fund of the State of Utah

An Enterprise Fund of the State of Utah Financial Statements AN ENTERPRISE FUND OF THE STATE OF UTAH FOR THE THREE MONTHS ENDED SEPTEMBER 30, 2018 TABLE OF CONTENTS Page MANAGEMENT S REPORT 1 FINANCIAL

An Enterprise Fund of the State of Utah Financial Statements AN ENTERPRISE FUND OF THE STATE OF UTAH FOR THE THREE MONTHS ENDED SEPTEMBER 30, 2018 TABLE OF CONTENTS Page MANAGEMENT S REPORT 1 FINANCIAL

CHAPTER 14. Bond Prices and Yields INVESTMENTS BODIE, KANE, MARCUS. Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved.

CHAPTER 14 Bond Prices and Yields INVESTMENTS BODIE, KANE, MARCUS McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. INVESTMENTS BODIE, KANE, MARCUS 14-2 Bond Characteristics

CHAPTER 14 Bond Prices and Yields INVESTMENTS BODIE, KANE, MARCUS McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. INVESTMENTS BODIE, KANE, MARCUS 14-2 Bond Characteristics

Appendix Pricing and Valuation of Securities: Introduction to Common Types of Securities

Page 1 Appendix Pricing and Valuation of Securities: Introduction to Common Types of Securities This handout provides summary information for common security types held by entities in their investment

Page 1 Appendix Pricing and Valuation of Securities: Introduction to Common Types of Securities This handout provides summary information for common security types held by entities in their investment

STATE BOARD OF REGENTS OF THE STATE OF UTAH STUDENT LOAN PURCHASE PROGRAM An Enterprise Fund of the State of Utah

An Enterprise Fund of the State of Utah Financial Statements AN ENTERPRISE FUND OF THE STATE OF UTAH FOR THE NINE MONTHS ENDED MARCH 31, 2018 TABLE OF CONTENTS Page MANAGEMENT S REPORT 1 FINANCIAL STATEMENTS:

An Enterprise Fund of the State of Utah Financial Statements AN ENTERPRISE FUND OF THE STATE OF UTAH FOR THE NINE MONTHS ENDED MARCH 31, 2018 TABLE OF CONTENTS Page MANAGEMENT S REPORT 1 FINANCIAL STATEMENTS:

Federated Municipal High Yield Advantage Fund

Statement of Additional Information October 31, 2017 Share Class Ticker A FMOAX B FMOBX C FMNCX F FHTFX Institutional FMYIX Federated Municipal High Yield Advantage Fund A Portfolio of Federated Municipal

Statement of Additional Information October 31, 2017 Share Class Ticker A FMOAX B FMOBX C FMNCX F FHTFX Institutional FMYIX Federated Municipal High Yield Advantage Fund A Portfolio of Federated Municipal

Powered by TCPDF (www.tcpdf.org) 10.1 Fixed Income Securities Study Session 10 LOS 1 : Introduction (Fixed Income Security) Bonds are the type of long term obligation which pay periodic interest & repay

Powered by TCPDF (www.tcpdf.org) 10.1 Fixed Income Securities Study Session 10 LOS 1 : Introduction (Fixed Income Security) Bonds are the type of long term obligation which pay periodic interest & repay

Test Bank for Investments Global Edition 10th Edition by Zvi Bodie, Alex Kane and Alan J. Marcus

Test Bank for Investments Global Edition 10th Edition by Zvi Bodie, Alex Kane and Alan J. Marcus Link download full: https://digitalcontentmarket.org/download/test-bankfor-investments-global-edition-10th-edition-by-bodie

Test Bank for Investments Global Edition 10th Edition by Zvi Bodie, Alex Kane and Alan J. Marcus Link download full: https://digitalcontentmarket.org/download/test-bankfor-investments-global-edition-10th-edition-by-bodie

Money Markets. Chap. 2 Investment Alternatives. Money Markets. Money Markets. T-Bills. T-Bills

Chap. 2 Investment Alternatives Focus on Marketable Instruments Fixed Income Capital (Bond) markets Equity Derivatives Sept 2003 These are short-term debt obligations - no more than one year in maturity.

Chap. 2 Investment Alternatives Focus on Marketable Instruments Fixed Income Capital (Bond) markets Equity Derivatives Sept 2003 These are short-term debt obligations - no more than one year in maturity.

Introduction to Bond Markets

Wisconsin School of Business December 10, 2014 Bonds A bond is a financial security that promises to pay a fixed (known) income stream in the future Issued by governments, state agencies (municipal bonds),

Wisconsin School of Business December 10, 2014 Bonds A bond is a financial security that promises to pay a fixed (known) income stream in the future Issued by governments, state agencies (municipal bonds),

Investment Policy Fiscal Year

Investment Policy Fiscal Year 2016-17 I. Introduction The investment policies and practices of the Contra Costa Transportation Authority (the Authority) are based on the principles of prudent money management

Investment Policy Fiscal Year 2016-17 I. Introduction The investment policies and practices of the Contra Costa Transportation Authority (the Authority) are based on the principles of prudent money management

CHAPTER 9 DEBT SECURITIES. by Lee M. Dunham, PhD, CFA, and Vijay Singal, PhD, CFA

CHAPTER 9 DEBT SECURITIES by Lee M. Dunham, PhD, CFA, and Vijay Singal, PhD, CFA LEARNING OUTCOMES After completing this chapter, you should be able to do the following: a Identify issuers of debt securities;

CHAPTER 9 DEBT SECURITIES by Lee M. Dunham, PhD, CFA, and Vijay Singal, PhD, CFA LEARNING OUTCOMES After completing this chapter, you should be able to do the following: a Identify issuers of debt securities;

CHAPTER 2: ASSET CLASSES AND FINANCIAL INSTRUMENTS

Chapter 2 - Asset Classes and Financial Instruments CHAPTER 2: ASSET CLASSES AND FINANCIAL INSTRUMENTS PROBLEM SETS 1. Preferred stock is like long-term debt in that it typically promises a fixed payment

Chapter 2 - Asset Classes and Financial Instruments CHAPTER 2: ASSET CLASSES AND FINANCIAL INSTRUMENTS PROBLEM SETS 1. Preferred stock is like long-term debt in that it typically promises a fixed payment

Fixed income security. Face or par value Coupon rate. Indenture. The issuer makes specified payments to the bond. bondholder

Bond Prices and Yields Bond Characteristics Fixed income security An arragement between borrower and purchaser The issuer makes specified payments to the bond holder on specified dates Face or par value

Bond Prices and Yields Bond Characteristics Fixed income security An arragement between borrower and purchaser The issuer makes specified payments to the bond holder on specified dates Face or par value

Mathematics of Financial Derivatives

Mathematics of Financial Derivatives Lecture 11 Solesne Bourguin bourguin@math.bu.edu Boston University Department of Mathematics and Statistics Table of contents 1. Mechanics of interest rate swaps (continued)

Mathematics of Financial Derivatives Lecture 11 Solesne Bourguin bourguin@math.bu.edu Boston University Department of Mathematics and Statistics Table of contents 1. Mechanics of interest rate swaps (continued)

Administration and Projects Committee STAFF REPORT June 4, 2015 Page 2 of 2 Upon review of permitted investments available to the Authority, State law

Administration and Projects Committee STAFF REPORT Meeting Date: June 4, 2015 Subject Approval of the Authority s Investment Policy for FY 2015-16 Summary of Issues Recommendations Financial Implications

Administration and Projects Committee STAFF REPORT Meeting Date: June 4, 2015 Subject Approval of the Authority s Investment Policy for FY 2015-16 Summary of Issues Recommendations Financial Implications

Accrued Interest A currently unpaid amount of interest that has accumulated since the last payment on a bond or other fixed-income security.

Accrued Interest A currently unpaid amount of interest that has accumulated since the last payment on a bond or other fixed-income security. Ad Valorem Tax Translated as according to value, it is a levy

Accrued Interest A currently unpaid amount of interest that has accumulated since the last payment on a bond or other fixed-income security. Ad Valorem Tax Translated as according to value, it is a levy

Financial Markets I The Stock, Bond, and Money Markets Every economy must solve the basic problems of production and distribution of goods and

Financial Markets I The Stock, Bond, and Money Markets Every economy must solve the basic problems of production and distribution of goods and services. Financial markets perform an important function

Financial Markets I The Stock, Bond, and Money Markets Every economy must solve the basic problems of production and distribution of goods and services. Financial markets perform an important function

Chapter 02: Asset Classes and Financial Instruments

Test Bank for Investments and Portfolio Management 9th Edition by Bodie, Kane, Marcus Link download full Test Bank for Investments and Portfolio Management 9th Edition by Bodie, Kane, Marcus: https://digitalcontentmarket.org/download/test-bank-for-investments-and-portfolio-management-

Test Bank for Investments and Portfolio Management 9th Edition by Bodie, Kane, Marcus Link download full Test Bank for Investments and Portfolio Management 9th Edition by Bodie, Kane, Marcus: https://digitalcontentmarket.org/download/test-bank-for-investments-and-portfolio-management-

Chapter 7: Interest Rates and Bond Valuation

Chapter 7: Interest Rates and Bond Valuation Faculty of Business Administration Lakehead University Spring 2003 May 13, 2003 7.1 Bonds and Bond Valuation 7.2 More on Bond Features 7A On Duration 7C Callable

Chapter 7: Interest Rates and Bond Valuation Faculty of Business Administration Lakehead University Spring 2003 May 13, 2003 7.1 Bonds and Bond Valuation 7.2 More on Bond Features 7A On Duration 7C Callable

FEDERAL RESERVE statistical release

FEDERAL RESERVE statistical release H.4.1 Factors Affecting Reserve Balances of Depository Institutions and Condition Statement of Federal Reserve Banks April 20, 2017 1. Factors Affecting Reserve Balances

FEDERAL RESERVE statistical release H.4.1 Factors Affecting Reserve Balances of Depository Institutions and Condition Statement of Federal Reserve Banks April 20, 2017 1. Factors Affecting Reserve Balances

Swap Markets CHAPTER OBJECTIVES. The specific objectives of this chapter are to: describe the types of interest rate swaps that are available,

15 Swap Markets CHAPTER OBJECTIVES The specific objectives of this chapter are to: describe the types of interest rate swaps that are available, explain the risks of interest rate swaps, identify other

15 Swap Markets CHAPTER OBJECTIVES The specific objectives of this chapter are to: describe the types of interest rate swaps that are available, explain the risks of interest rate swaps, identify other

Lecture 2: Swaps. Topics Covered. The concept of a swap

Lecture 2: Swaps 01135532: Financial Instrument and Innovation Nattawut Jenwittayaroje, Ph.D., CFA NIDA Business School National Institute of Development Administration 1 Topics Covered The concept of

Lecture 2: Swaps 01135532: Financial Instrument and Innovation Nattawut Jenwittayaroje, Ph.D., CFA NIDA Business School National Institute of Development Administration 1 Topics Covered The concept of

FEDERAL RESERVE statistical release

FEDERAL RESERVE statistical release H.4.1 Factors Affecting Reserve Balances of Depository Institutions and Condition Statement of Federal Reserve Banks August 20, 2015 1. Factors Affecting Reserve Balances

FEDERAL RESERVE statistical release H.4.1 Factors Affecting Reserve Balances of Depository Institutions and Condition Statement of Federal Reserve Banks August 20, 2015 1. Factors Affecting Reserve Balances

20. Investing 4: Understanding Bonds

20. Investing 4: Understanding Bonds Introduction The purpose of an investment portfolio is to help individuals and families meet their financial goals. These goals differ from person to person and change

20. Investing 4: Understanding Bonds Introduction The purpose of an investment portfolio is to help individuals and families meet their financial goals. These goals differ from person to person and change

MBF1223 Financial Management Prepared by Dr Khairul Anuar

MBF1223 Financial Management Prepared by Dr Khairul Anuar L4 Bonds & Bonds Valuation www.mba638.wordpress.com Bonds - Introduction A bond is a debt instrument issued by a borrower which has borrowed a

MBF1223 Financial Management Prepared by Dr Khairul Anuar L4 Bonds & Bonds Valuation www.mba638.wordpress.com Bonds - Introduction A bond is a debt instrument issued by a borrower which has borrowed a

STATE BOARD OF REGENTS OF THE STATE OF UTAH STUDENT LOAN PURCHASE PROGRAM An Enterprise Fund of the State of Utah

An Enterprise Fund of the State of Utah Financial Statements AN ENTERPRISE FUND OF THE STATE OF UTAH FOR THE NINE MONTHS ENDED MARCH 31, 2014 TABLE OF CONTENTS Page MANAGEMENT S REPORT 1 FINANCIAL STATEMENTS:

An Enterprise Fund of the State of Utah Financial Statements AN ENTERPRISE FUND OF THE STATE OF UTAH FOR THE NINE MONTHS ENDED MARCH 31, 2014 TABLE OF CONTENTS Page MANAGEMENT S REPORT 1 FINANCIAL STATEMENTS:

Fixed Income Investment

Fixed Income Investment Session 1 April, 24 th, 2013 (Morning) Dr. Cesario Mateus www.cesariomateus.com c.mateus@greenwich.ac.uk cesariomateus@gmail.com 1 Lecture 1 1. A closer look at the different asset

Fixed Income Investment Session 1 April, 24 th, 2013 (Morning) Dr. Cesario Mateus www.cesariomateus.com c.mateus@greenwich.ac.uk cesariomateus@gmail.com 1 Lecture 1 1. A closer look at the different asset

Activity Sheet 1: About Bonds

Activity Sheet 1: About Bonds Bonds are issued by corporations, governments and government agencies to raise large amounts of money. Just like any loan, the issuer, or organization trying to sell the bond,

Activity Sheet 1: About Bonds Bonds are issued by corporations, governments and government agencies to raise large amounts of money. Just like any loan, the issuer, or organization trying to sell the bond,

BBM2153 Financial Markets and Institutions Prepared by Dr Khairul Anuar

BBM2153 Financial Markets and Institutions Prepared by Dr Khairul Anuar L5: The Money Markets www. notes638.wordpress.com 5-1 Apple and its $18 billion In its 2013 annual report, Apple listed $18 billion

BBM2153 Financial Markets and Institutions Prepared by Dr Khairul Anuar L5: The Money Markets www. notes638.wordpress.com 5-1 Apple and its $18 billion In its 2013 annual report, Apple listed $18 billion

FUNDING INVESTMENTS FINANCE 238/738, Spring 2008, Prof. Musto Class 1 Introduction and Overview

FUNDING INVESTMENTS FINANCE 238/738, Spring 2008, Prof. Musto Class 1 Introduction and Overview Today: I. Description of course material II. Course mechanics, schedule III. Big picture of funding sources

FUNDING INVESTMENTS FINANCE 238/738, Spring 2008, Prof. Musto Class 1 Introduction and Overview Today: I. Description of course material II. Course mechanics, schedule III. Big picture of funding sources

AFM 371 Winter 2008 Chapter 26 - Derivatives and Hedging Risk Part 2 - Interest Rate Risk Management ( )

") AFM 371 Winter 2008 Chapter 26 - Derivatives and Hedging Risk Part 2 - Interest Rate Risk Management (26.4-26.7) 1 / 30 Outline Term Structure Forward Contracts on Bonds Interest Rate Futures Contracts

AFM 371 Winter 2008 Chapter 26 - Derivatives and Hedging Risk Part 2 - Interest Rate Risk Management (26.4-26.7) 1 / 30 Outline Term Structure Forward Contracts on Bonds Interest Rate Futures Contracts

Bond Valuation. Lakehead University. Fall 2004

Bond Valuation Lakehead University Fall 2004 Outline of the Lecture Bonds and Bond Valuation Interest Rate Risk Duration The Call Provision 2 Bonds and Bond Valuation A corporation s long-term debt is

Bond Valuation Lakehead University Fall 2004 Outline of the Lecture Bonds and Bond Valuation Interest Rate Risk Duration The Call Provision 2 Bonds and Bond Valuation A corporation s long-term debt is

Lecture 11. SWAPs markets. I. Background of Interest Rate SWAP markets. Types of Interest Rate SWAPs

Lecture 11 SWAPs markets Agenda: I. Background of Interest Rate SWAP markets II. Types of Interest Rate SWAPs II.1 Plain vanilla swaps II.2 Forward swaps II.3 Callable swaps (Swaptions) II.4 Putable swaps

Lecture 11 SWAPs markets Agenda: I. Background of Interest Rate SWAP markets II. Types of Interest Rate SWAPs II.1 Plain vanilla swaps II.2 Forward swaps II.3 Callable swaps (Swaptions) II.4 Putable swaps

Fixed-Income Securities: Defining Elements

The following is a review of the Fixed Income: Basic Concepts principles designed to address the learning outcome statements set forth by CFA Institute. Cross-Reference to CFA Institute Assigned Reading

The following is a review of the Fixed Income: Basic Concepts principles designed to address the learning outcome statements set forth by CFA Institute. Cross-Reference to CFA Institute Assigned Reading

Financial Investment

Financial Investment Dagmar Linnertová Dagmar.linnertova@mail.muni.cz Seminars Excercises in a seminars evaluated by lecturer Questions as a preparation for final test (2, 1 or 0 points) maximum points

Financial Investment Dagmar Linnertová Dagmar.linnertova@mail.muni.cz Seminars Excercises in a seminars evaluated by lecturer Questions as a preparation for final test (2, 1 or 0 points) maximum points

MBF1223 Financial Management Prepared by Dr Khairul Anuar

MBF1223 Financial Management Prepared by Dr Khairul Anuar L4 Bonds & Bonds Valuation www.notes638.wordpress.com Bonds - Introduction A bond is a debt instrument issued by a borrower which has borrowed

MBF1223 Financial Management Prepared by Dr Khairul Anuar L4 Bonds & Bonds Valuation www.notes638.wordpress.com Bonds - Introduction A bond is a debt instrument issued by a borrower which has borrowed

MFE8812 Bond Portfolio Management

MFE8812 Bond Portfolio Management William C. H. Leon Nanyang Business School January 16, 2018 1 / 126 William C. H. Leon MFE8812 Bond Portfolio Management 1 Overview Some Facts 2 Overview General Characteristics

MFE8812 Bond Portfolio Management William C. H. Leon Nanyang Business School January 16, 2018 1 / 126 William C. H. Leon MFE8812 Bond Portfolio Management 1 Overview Some Facts 2 Overview General Characteristics

Lecture #1. Introduction Debt & Fixed Income. BONDS LOANS (Corporate) Chapter 1

Chapter 1") Lecture #1 Introduction Debt & Fixed Income BONDS LOANS (Corporate) Chapter 1 Fed, State, Local BONDS: Six sectors: U.S. Treasury Sector o Issued by U.S. Government o T-Bills, Notes, Bonds o The largest

Lecture #1 Introduction Debt & Fixed Income BONDS LOANS (Corporate) Chapter 1 Fed, State, Local BONDS: Six sectors: U.S. Treasury Sector o Issued by U.S. Government o T-Bills, Notes, Bonds o The largest

Introduction to Bonds. Part One describes fixed-income market analysis and the basic. techniques and assumptions are required.

PART ONE Introduction to Bonds Part One describes fixed-income market analysis and the basic concepts relating to bond instruments. The analytic building blocks are generic and thus applicable to any market.

PART ONE Introduction to Bonds Part One describes fixed-income market analysis and the basic concepts relating to bond instruments. The analytic building blocks are generic and thus applicable to any market.

CHAPTER 14. Bond Prices and Yields INVESTMENTS BODIE, KANE, MARCUS. Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved.

CHAPTER 14 Bond Prices and Yields McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 14-2 Bond Characteristics Bonds are debt. Issuers are borrowers and holders are

CHAPTER 14 Bond Prices and Yields McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 14-2 Bond Characteristics Bonds are debt. Issuers are borrowers and holders are

: Corporate Finance. Corporate Decisions

380.760: Corporate Finance Lecture 6: Corporate Financing Professor Gordon M. Bodnar 2009 Gordon Bodnar, 2009 Corporate Decisions Investment decision vs. financing decision until now we have focused on

380.760: Corporate Finance Lecture 6: Corporate Financing Professor Gordon M. Bodnar 2009 Gordon Bodnar, 2009 Corporate Decisions Investment decision vs. financing decision until now we have focused on

FEDERAL RESERVE statistical release

FEDERAL RESERVE statistical release H.4.1 Factors Affecting Reserve Balances of Depository Institutions and Condition Statement of Federal Reserve Banks August 28, 2014 1. Factors Affecting Reserve Balances

FEDERAL RESERVE statistical release H.4.1 Factors Affecting Reserve Balances of Depository Institutions and Condition Statement of Federal Reserve Banks August 28, 2014 1. Factors Affecting Reserve Balances

Chapter 7. Interest Rate Forwards and Futures. Copyright 2009 Pearson Prentice Hall. All rights reserved.

Chapter 7 Interest Rate Forwards and Futures Bond Basics U.S. Treasury Bills (

Chapter 7 Interest Rate Forwards and Futures Bond Basics U.S. Treasury Bills (

Lecture Materials ASSET/LIABILITY MANAGEMENT YEAR 1

Lecture Materials ASSET/LIABILITY MANAGEMENT YEAR 1 Todd Patrick Senior Vice President - Capital Markets CenterState Bank Atlanta, Georgia tpatrick@centerstatebank.com 770-850-3403 August 7, 2017 Intro

Lecture Materials ASSET/LIABILITY MANAGEMENT YEAR 1 Todd Patrick Senior Vice President - Capital Markets CenterState Bank Atlanta, Georgia tpatrick@centerstatebank.com 770-850-3403 August 7, 2017 Intro

Federated Strategic Value Dividend Fund

Statement of Additional Information December 31, 2017 Share Class Ticker A SVAAX C SVACX Institutional SVAIX R6 SVALX Federated Strategic Value Dividend Fund A Portfolio of Federated Equity Funds This

Statement of Additional Information December 31, 2017 Share Class Ticker A SVAAX C SVACX Institutional SVAIX R6 SVALX Federated Strategic Value Dividend Fund A Portfolio of Federated Equity Funds This

Practice Guidelines for When Issued Trading in GSE Auctioned Securities

Practice Guidelines for When Issued Trading in GSE Auctioned Securities A. Introduction Set forth below are The Bond Market Association s recommended trading practice guidelines ( Guidelines ) for so-called

Practice Guidelines for When Issued Trading in GSE Auctioned Securities A. Introduction Set forth below are The Bond Market Association s recommended trading practice guidelines ( Guidelines ) for so-called

Chapter 6 : Money Markets

1 Chapter 6 : Money Markets Chapter Objectives Provide a background on money market securities Explain how institutional investors use money markets Explain the globalization of money markets 2 Why so

1 Chapter 6 : Money Markets Chapter Objectives Provide a background on money market securities Explain how institutional investors use money markets Explain the globalization of money markets 2 Why so

Important Information about Investing in

Robert W. Baird & Co. Incorporated Important Information about Investing in \ Bonds Baird has prepared this document to help you understand the characteristics and risks associated with bonds and other

Robert W. Baird & Co. Incorporated Important Information about Investing in \ Bonds Baird has prepared this document to help you understand the characteristics and risks associated with bonds and other

Bond Prices and Yields

Bond Characteristics 14-2 Bond Prices and Yields Bonds are debt. Issuers are borrowers and holders are creditors. The indenture is the contract between the issuer and the bondholder. The indenture gives

Bond Characteristics 14-2 Bond Prices and Yields Bonds are debt. Issuers are borrowers and holders are creditors. The indenture is the contract between the issuer and the bondholder. The indenture gives

Federal Home Loan Mortgage Corporation

Federal Home Loan Mortgage Corporation MULTICLASS CERTIFICATES AGREEMENT AGREEMENT dated as of June 1, 2003 among the Federal Home Loan Mortgage Corporation Freddie Mac ) and Holders of REMIC Certificates,

Federal Home Loan Mortgage Corporation MULTICLASS CERTIFICATES AGREEMENT AGREEMENT dated as of June 1, 2003 among the Federal Home Loan Mortgage Corporation Freddie Mac ) and Holders of REMIC Certificates,

Chapter 8. Swaps. Copyright 2009 Pearson Prentice Hall. All rights reserved.

Chapter 8 Swaps Introduction to Swaps A swap is a contract calling for an exchange of payments, on one or more dates, determined by the difference in two prices A swap provides a means to hedge a stream

Chapter 8 Swaps Introduction to Swaps A swap is a contract calling for an exchange of payments, on one or more dates, determined by the difference in two prices A swap provides a means to hedge a stream

Overview of Financial Instruments and Financial Markets

CHAPTER 1 Overview of Financial Instruments and Financial Markets FRANK J. FABOZZI, PhD, CFA, CPA Professor in the Practice of Finance, Yale School of Management Issuers and Investors 3 Debt versus Equity

CHAPTER 1 Overview of Financial Instruments and Financial Markets FRANK J. FABOZZI, PhD, CFA, CPA Professor in the Practice of Finance, Yale School of Management Issuers and Investors 3 Debt versus Equity

Chapter. Corporate Bonds. Corporate Bonds. Corporate Bond Basics, I. Corporate Bond Basics, II. Corporate Bond Basics, III. Types of Corporate Bonds

Chapter 18 Corporate Bonds Corporate Bonds Our goal in this chapter is to introduce the specialized knowledge concerning trading corporate bonds. Money managers who buy and sell corporate bonds possess

Chapter 18 Corporate Bonds Corporate Bonds Our goal in this chapter is to introduce the specialized knowledge concerning trading corporate bonds. Money managers who buy and sell corporate bonds possess

Chapter 12. The Bond Market

Chapter 12 The Bond Market Chapter Preview In this chapter, we focus on longer-term securities: bonds. Bonds are like money market instruments, but they have maturities that exceed one year. These include

Chapter 12 The Bond Market Chapter Preview In this chapter, we focus on longer-term securities: bonds. Bonds are like money market instruments, but they have maturities that exceed one year. These include

Lecture 8 Foundations of Finance

Lecture 8: Bond Portfolio Management. I. Reading. II. Risks associated with Fixed Income Investments. A. Reinvestment Risk. B. Liquidation Risk. III. Duration. A. Definition. B. Duration can be interpreted

Lecture 8: Bond Portfolio Management. I. Reading. II. Risks associated with Fixed Income Investments. A. Reinvestment Risk. B. Liquidation Risk. III. Duration. A. Definition. B. Duration can be interpreted

Federated Equity Income Fund, Inc.

Statement of Additional Information January 31, 2018 Share Class Ticker A LEIFX B LEIBX C LEICX F LFEIX R FDERX Institutional LEISX Federated Equity Income Fund, Inc. This Statement of Additional Information

Statement of Additional Information January 31, 2018 Share Class Ticker A LEIFX B LEIBX C LEICX F LFEIX R FDERX Institutional LEISX Federated Equity Income Fund, Inc. This Statement of Additional Information

1) Which one of the following is NOT a typical negative bond covenant?

Which one of the following is NOT a typical negative bond covenant?") Questions in Chapter 7 concept.qz 1) Which one of the following is NOT a typical negative bond covenant? [A] The firm must limit dividend payments. [B] The firm cannot merge with another firm. [C] The

Questions in Chapter 7 concept.qz 1) Which one of the following is NOT a typical negative bond covenant? [A] The firm must limit dividend payments. [B] The firm cannot merge with another firm. [C] The

DEBT VALUATION AND INTEREST. Chapter 9

DEBT VALUATION AND INTEREST Chapter 9 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of Value

DEBT VALUATION AND INTEREST Chapter 9 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of Value

A CLEAR UNDERSTANDING OF THE INDUSTRY

A CLEAR UNDERSTANDING OF THE INDUSTRY IS CFA INSTITUTE INVESTMENT FOUNDATIONS RIGHT FOR YOU? Investment Foundations is a certificate program designed to give you a clear understanding of the investment

A CLEAR UNDERSTANDING OF THE INDUSTRY IS CFA INSTITUTE INVESTMENT FOUNDATIONS RIGHT FOR YOU? Investment Foundations is a certificate program designed to give you a clear understanding of the investment

Essential Learning for CTP Candidates NY Cash Exchange 2018 Session #CTP-06

NY Cash Exchange 2018: CTP Track Money Markets S/T Investing & Borrowing Session #6 (Thur. 11:00 am Noon) ETM5-Chapter 5: Money Markets ETM5-Chapter 13: Short-Term Investing and Borrowing Essentials of

NY Cash Exchange 2018: CTP Track Money Markets S/T Investing & Borrowing Session #6 (Thur. 11:00 am Noon) ETM5-Chapter 5: Money Markets ETM5-Chapter 13: Short-Term Investing and Borrowing Essentials of

TEACHING NOTE 01-02: INTRODUCTION TO INTEREST RATE OPTIONS

TEACHING NOTE 01-02: INTRODUCTION TO INTEREST RATE OPTIONS Version date: August 15, 2008 c:\class Material\Teaching Notes\TN01-02.doc Most of the time when people talk about options, they are talking about

TEACHING NOTE 01-02: INTRODUCTION TO INTEREST RATE OPTIONS Version date: August 15, 2008 c:\class Material\Teaching Notes\TN01-02.doc Most of the time when people talk about options, they are talking about

Financial Market Analysis (FMAx) Module 2

Module 2") Financial Market Analysis (FMAx) Module 2 Bond Pricing This training material is the property of the International Monetary Fund (IMF) and is intended for use in IMF Institute for Capacity Development

Financial Market Analysis (FMAx) Module 2 Bond Pricing This training material is the property of the International Monetary Fund (IMF) and is intended for use in IMF Institute for Capacity Development

Debt. Last modified KW

Debt The debt markets are far more complicated and filled with jargon than the equity markets. Fixed coupon bonds, loans and bills will be our focus in this course. It's important to be aware of all of

Debt The debt markets are far more complicated and filled with jargon than the equity markets. Fixed coupon bonds, loans and bills will be our focus in this course. It's important to be aware of all of

Chapter. Bond Basics, I. Prices and Yields. Bond Basics, II. Straight Bond Prices and Yield to Maturity. The Bond Pricing Formula

Chapter 10 Bond Prices and Yields Bond Basics, I. A Straight bond is an IOU that obligates the issuer of the bond to pay the holder of the bond: A fixed sum of money (called the principal, par value, or

Chapter 10 Bond Prices and Yields Bond Basics, I. A Straight bond is an IOU that obligates the issuer of the bond to pay the holder of the bond: A fixed sum of money (called the principal, par value, or

FIN 4140 Financial Markets & Institutions

FIN 4140 Financial Markets & Institutions Lecture 9-10 Money Market Money Market Securities Securities with maturities within one year are referred to as money market securities. They are issued by corporations

FIN 4140 Financial Markets & Institutions Lecture 9-10 Money Market Money Market Securities Securities with maturities within one year are referred to as money market securities. They are issued by corporations

Chapter 07 Interest Rates and Bond Valuation

Chapter 07 Interest Rates and Bond Valuation Multiple Choice Questions 1. Mary just purchased a bond which pays $60 a year in interest. What is this $60 called? A. coupon B. face value C. discount D. call

Chapter 07 Interest Rates and Bond Valuation Multiple Choice Questions 1. Mary just purchased a bond which pays $60 a year in interest. What is this $60 called? A. coupon B. face value C. discount D. call

FEDERAL RESERVE statistical release

FEDERAL RESERVE statistical release Factors Affecting Reserve Balances of Depository Institutions and Condition Statement of Federal Reserve Banks June 8, 2017 1. Factors Affecting Reserve Balances of

FEDERAL RESERVE statistical release Factors Affecting Reserve Balances of Depository Institutions and Condition Statement of Federal Reserve Banks June 8, 2017 1. Factors Affecting Reserve Balances of

UNIVERSITY OF CENTRAL FLORIDA INVESTMENT POLICY AND MANUAL

UNIVERSITY OF CENTRAL FLORIDA INVESTMENT POLICY AND MANUAL TABLE OF CONTENTS INVESTMENT POLICY... 1 INVESTMENT OBJECTIVES... 2 PERFORMANCE MEASUREMENT... 3 PRUDENCE AND ETHICAL STANDARDS... 3 BROKER DEALERS,

UNIVERSITY OF CENTRAL FLORIDA INVESTMENT POLICY AND MANUAL TABLE OF CONTENTS INVESTMENT POLICY... 1 INVESTMENT OBJECTIVES... 2 PERFORMANCE MEASUREMENT... 3 PRUDENCE AND ETHICAL STANDARDS... 3 BROKER DEALERS,

SAN FRANCISCO COUNTY TRANSPORTATION AUTHORITY INVESTMENT POLICY

I. INTRODUCTION II. III. IV. The purpose of this document is to set out policies and procedures that enhance opportunities for a prudent and systematic investment policy and to organize and formalize investment-related

I. INTRODUCTION II. III. IV. The purpose of this document is to set out policies and procedures that enhance opportunities for a prudent and systematic investment policy and to organize and formalize investment-related

I. Asset Valuation. The value of any asset, whether it is real or financial, is the sum of all expected future earnings produced by the asset.

1 I. Asset Valuation The value of any asset, whether it is real or financial, is the sum of all expected future earnings produced by the asset. 2 1 II. Bond Features and Prices Definitions Bond: a certificate

1 I. Asset Valuation The value of any asset, whether it is real or financial, is the sum of all expected future earnings produced by the asset. 2 1 II. Bond Features and Prices Definitions Bond: a certificate

1. Which of the following is not a money market instrument? A. Treasury bill B. commercial paper C. preferred stock D. bankers' acceptance

Student: 1. Which of the following is not a money market instrument? A. Treasury bill B. commercial paper C. preferred stock D. bankers' acceptance 2. T-bills are issued with initial maturities of: I.

Student: 1. Which of the following is not a money market instrument? A. Treasury bill B. commercial paper C. preferred stock D. bankers' acceptance 2. T-bills are issued with initial maturities of: I.

o Securities firms 02 Financial markets facilitating the issuance of new securities are known as

01 Financial markets that facilitate the flow of long-term funds with maturities of more than one year are known as. o money markets o capital markets o primary markets o secondary markets 02 Financial

01 Financial markets that facilitate the flow of long-term funds with maturities of more than one year are known as. o money markets o capital markets o primary markets o secondary markets 02 Financial

Introduction. Master Programmes INTERNATIONAL FINANCE. Szabolcs Sebestyén

Introduction Szabolcs Sebestyén szabolcs.sebestyen@iscte.pt Master Programmes INTERNATIONAL FINANCE Sebestyén (ISCTE-IUL) Introduction International Finance 1 / 43 Outline 1 Why Study Money, Banking, and

Introduction Szabolcs Sebestyén szabolcs.sebestyen@iscte.pt Master Programmes INTERNATIONAL FINANCE Sebestyén (ISCTE-IUL) Introduction International Finance 1 / 43 Outline 1 Why Study Money, Banking, and

Securities Analysis 3FB3 February 25 th, 2014

Chapter 2: Financial Markets and Instruments 2.1 The Money Market The money market is a subsector of the fixed income market. It consists of ST debt securities that usually are highly marketable. Many

Chapter 2: Financial Markets and Instruments 2.1 The Money Market The money market is a subsector of the fixed income market. It consists of ST debt securities that usually are highly marketable. Many

MAFS601A Exotic swaps. Forward rate agreements and interest rate swaps. Asset swaps. Total return swaps. Swaptions. Credit default swaps

MAFS601A Exotic swaps Forward rate agreements and interest rate swaps Asset swaps Total return swaps Swaptions Credit default swaps Differential swaps Constant maturity swaps 1 Forward rate agreement (FRA)

MAFS601A Exotic swaps Forward rate agreements and interest rate swaps Asset swaps Total return swaps Swaptions Credit default swaps Differential swaps Constant maturity swaps 1 Forward rate agreement (FRA)

FINANCING IN INTERNATIONAL MARKETS

FINANCING IN INTERNATIONAL MARKETS 1. INTERNATIONAL BOND MARKETS International Bond Markets The bond market (debt, credit, or fixed income market) is the financial market where participants buy and sell

FINANCING IN INTERNATIONAL MARKETS 1. INTERNATIONAL BOND MARKETS International Bond Markets The bond market (debt, credit, or fixed income market) is the financial market where participants buy and sell

Invesco V.I. Government Securities Fund

Quarterly Schedule of Portfolio Holdings March 31, 2018 invesco.com/us VIGOV-QTR-1 05/18 Invesco Advisers, Inc. Schedule of Investments March 31, 2018 (Unaudited) Principal Amount Value U.S. Government

Quarterly Schedule of Portfolio Holdings March 31, 2018 invesco.com/us VIGOV-QTR-1 05/18 Invesco Advisers, Inc. Schedule of Investments March 31, 2018 (Unaudited) Principal Amount Value U.S. Government

The Goldman Sachs Group, Inc.

1 / 44 Filed Pursuant to Rule 424(b)(2) Registration Statement No. 333-154173 Prospectus Supplement to Prospectus dated April 6, 2009. The Goldman Sachs Group, Inc. Medium-Term Notes, Series D TERMS OF

1 / 44 Filed Pursuant to Rule 424(b)(2) Registration Statement No. 333-154173 Prospectus Supplement to Prospectus dated April 6, 2009. The Goldman Sachs Group, Inc. Medium-Term Notes, Series D TERMS OF

SWAPS. Types and Valuation SWAPS

SWAPS Types and Valuation SWAPS Definition A swap is a contract between two parties to deliver one sum of money against another sum of money at periodic intervals. Obviously, the sums exchanged should

SWAPS Types and Valuation SWAPS Definition A swap is a contract between two parties to deliver one sum of money against another sum of money at periodic intervals. Obviously, the sums exchanged should

Function of Financial Markets

Chapter 2 An Overview of the Financial System Function of Financial Markets Perform the essential function of channeling funds from economic players (households, firms and govt.) that have saved surplus

Chapter 2 An Overview of the Financial System Function of Financial Markets Perform the essential function of channeling funds from economic players (households, firms and govt.) that have saved surplus