BONDS AND CREDIT RATING

|

|

|

- Collin Watson

- 5 years ago

- Views:

Transcription

1 BONDS AND CREDIT RATING

2 Typical Bond Features The indenture - a written agreement between the borrower and a trust company - usually lists Amount of Issue, Date of Issue, Maturity Denomination (Par value) Annual Coupon, Dates of Coupon Payments Security Sinking Funds Call Provisions Covenants Features that may change over time Rating Yield-to-Maturity Market price The general issuance procedure is similar to that of a stock whereby indentures and covenants are not relevant to a stock issuance 2

3 Bond Term Sheet Issue amount Issue date Maturity date Face value Coupon interest Coupon dates Offering price Yield to maturity Call provision Call price Trustee Security Rating $20 million 12/15/98 12/31/18 Bond issue total face value is $20 million Bonds offered to the public in December 1998 Remaining principal is due December 31, 2018 $1,000 Face value denomination is $1,000 per bond $100 per annum Annual coupons are $100 per bond 6/30, 12/31 Coupons are paid semiannually 100 Offer price is 100% of face value 10% Based on stated offer price Callable after 12/31/03 Bonds are call protected for 5 years after issuance 110 before 12/31/08, Callable at 110 percent of par value through 100 thereafter Thereafter callable at par. United Bank of Trustee is appointed to represent Florida bondholders None Bonds are unsecured debenture Moody's A1, S&P A+ Bond credit quality rated upper medium grade by Moody's and S&P's rating 3

4 Protective Covenants Agreements to protect bondholders Negative covenant: Thou shalt not: pay dividends beyond specified amount sell more senior debt & amount of new debt is limited refund existing bond issue with new bonds paying lower interest rate buy another company s bonds Positive covenant: Thou shalt: use proceeds from sale of assets for other assets allow redemption in event of merger or spinoff maintain good condition of assets provide audited financial information 4

5 The Sinking Fund There are many different kinds of sinking-fund arrangements: Most start between 5 and 10 years after initial issuance Some establish equal payments over the life of the bond Most high-quality bond issues establish payments to the sinking fund that are not sufficient to redeem the entire issue Sinking funs provide extra protection to bondholders Sinking funs provide the firm with an option 5

6 Bond Refunding Replacing all or part of a bond issue is called refunding Bond refunding raises two questions: 1. Should firms issue callable bonds? 2. Given that callable bonds have been issued, when should the bonds be called? 6

7 Callable vs Non-Callable Bonds Most bonds are callable Some for the issuer - sensible reasons for call provisions include: Taxes, managerial flexibility and the fact that callable bonds have less interest rate risk If the issuer issues a callable bond then a higher yield has to be paid on it A bond s interest rate is guaranteed only for investors of non-callable bonds until it matures An investor can count on a callable bond s interest rate only until a call date arrives Issuing a callable bonds gives the issuer the right to refinance the debt if either interest rates drop or the credit quality of the issuer improves 7

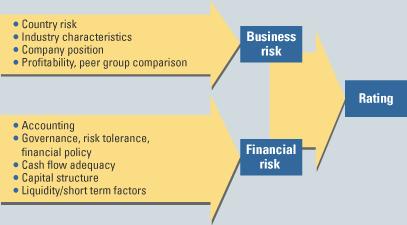

8 Bond Ratings What is rated: The likelihood that the firm will default The protection afforded by the loan contract in the event of default Who pays for ratings: Firms pay to have their bonds rated The ratings are constructed from the financial statements supplied by the firm Ratings can change Rating agencies can disagree 8

9 Bond Ratings Investment Grade Moody's Duff & Phelps S&P's Aaa 1 AAA Aa1 Aa2 2 3 AA+ AA Aa3 A1 A AAA+ A A3 Baa1 7 8 Baa2 9 ABBB + BBB Baa3 10 BBB- Credit Rating Description Highest credit rating, maximum safety High credit quality, investment-grade bonds Upper-medium quality, investment grade bonds Lower-medium quality, investment grade bonds 9

10 Bond Ratings Non-Investment Grade Moody's Duff & Phelps S&P's Credit Rating Description Speculative-Grade Bond Ratings Ba1 11 BB+ Ba2 Ba3 B BB BBB+ B2 B B B- Low credit quality, speculative-grade bonds Very low credit quality, speculative-grade bonds Extremely Speculative-Grade Bond Ratings Caa Ca C 17 CCC + CCC CCCCC C D Extremely low credit standing, high-risk bonds Extremely speculative Bonds in default 10

11 Junk Bonds Anything less than an S&P BB or a Moody s Ba is a junk bond A polite euphemism for junk is high-yield bond There are two types of junk bonds: Original issue junk: Fallen angels: possibly not rated rated Current status of junk bond market Private placement Yield premiums versus default risk 11

12 Different Types of Bonds Callable Bonds Puttable Bonds Convertible Bonds Deep Discount Bonds Income Bonds Floating-Rate Bonds 12

13 Puttable Bonds Put provisions Put price Put date Put deferment Extendible bonds Value of the put feature Cost of the put feature 13

14 Convertible Bonds Why are they issued? Why are they purchased? Conversion ratio: Number of shares of stock acquired by conversion Conversion price: Bond par value / Conversion ratio Conversion value: Price per share of stock x Conversion ratio In-the-money versus out-the-money 14

15 Example of a Convertible Bond 15

16 Exchangeables Exchangeable bonds Convertible into a set number of shares of a third company s common stock Minimum (floor) value of convertible is the greater of Straight or intrinsic bond value Conversion value Conversion option value Bondholders pay for the conversion option by accepting a lower coupon rate on convertible bonds versus otherwise- identical nonconvertible bonds 16

17 Direct Placement vs Public Offering A direct long-term loan avoids the cost of registration with the SEC Direct placement is likely to have more restrictive covenants In the event of default, it is easier to work out a private placement 17

18 Credit Rating 18

19 Intro There is no industry definition or standard to describe credit ratings, and no trade association of Credit Ratings Agencies (CRAs) The US Securities and Exchange Commission (SEC) defines a Credit Rating Agency as a firm that provides its opinion on the creditworthiness of an entity and the financial obligations issued by an entity. Generally, credit ratings distinguish between investment grade and non-investment grade In the Official Journal of the EU in 2006 European Commission (EC) states that CRAs issue opinions on the creditworthiness of a particular issuer or financial instrument. They assess the likelihood that an issuer will default either on its financial obligations generally or on a particular debt or fixed income security 19

20 The Big Three The largest three rating agencies are Standard & Poor's, Moody s and Fitch, they cover approximately 95% of the world market Smaller rating agencies make up the remaining part Many studies have concluded, that this market is a natural oligopoly as the nature of the CRA market makes it complicated for new CRAs to succeed and for existing CRAs to conquer a larger market share Issuers prefer ratings from reputable CRAs, while investors respect CRAs with a history of accurate and timely ratings thus it results in a lack of competition 20

21 The Rise of the CRA Era Credit rating as a profession dates back to the beginning of the 20th century in the USA Three types of businesses emerged in the 19th century: the specialized financial press, credit reporting agencies and investment bankers One of the first publications was The American Railroad Journal, started in 1832, which was transformed in 1949 into a publication for investors in railroads by Henry Poor In the meantime Poor set up his own firm, collecting statistics on US railroad companies. The company published the results annually as the Manual of the Railroads of the US One of the first credit reporting agencies, founded in 1841, was The Mercantile Agency, selling its service to subscribers In 1909, John Moody initiated agency bond ratings in the US, which was a pioneer to include credit risk analysis for rating purposes Originally, this only covered the bonded debt of the US railroad companies 21

22 The Rise of the CRA Era (cont d) Post war prosperity of 1960s, made CRAs relatively unimportant CRAs expanded rapidly again during the 1970s as the Bretton Woods System collapsed and a new era of financial globalisation emerged together with liberalisation of capital flows and redistribution of OPEC wealth, resulting in a greater number of sovereign states and private corporations, issuing bonds However, the agencies shifted to issuer-pays model This was the point when SEC in 1973 designated certain CRAs as Nationally Recognised Statistical Ratings Organisations (NRSROs), raising further concerns of NRSROs abusing their power for regulatory purposes 22

23 Global Stock and Bond Markets Relative Size 23

24 The Triple A Trouble 24

25 The Triple A Trouble (cont d) Standard & Poor s Moody s 25

26 Credit Rating - Dynamics 26

27 Credit Rating Outlook - Dynamics 27

28 Credit Rating Outlook Dynamics (cont d) 28

29 The Financial Crisis Effect on World s Creditworthiness 29

30 Credit Rating Definition by the Big Three 30

31 Rating Types ESMA (European Securities and Markets Agency) has defined three broad categories of rating types that have been broken down into the following segments: Corporate ratings: financial institutions including banks, brokers, and dealers insurances, other corporate issuers; Structured finance ratings: asset-backed securities (ABS), residential mortgagebacked securities (RMBS), commercial mortgage-backed securities (CMBS), collateralized debt obligations (CDO), asset-backed commercial papers (ABCP); Sovereign and public finance ratings: sovereign, other local governments, municipalities, supranational organizations, and public entities 31

32 Rating Types (cont d) 32

33 Rating Methodologies / Approaches Analyst-Driven Credit Ratings The Big 3 Credit rating agencies that use the analyst-driven approach employ analysts to evaluate and express an opinion on the relative creditworthiness of issuers and the relative credit quality of debt issues Model-Driven Credit Ratings A small number of rating agencies use the model-driven approach, focusing more exclusively on quantitative data that they incorporate into a mathematical model to produce their ratings, which are generally point-in-time assessments 33

34 Typical Process For a New Corporate or Government Rating Contract. The issuer requests a rating and signs an engagement letter. Pre evaluation. CRA assembles a team of analysts to review pertinent information. Management meeting. Analysts meet with management team to review and discuss information. Analysis. Analysts evaluate information and propose the rating to a rating committee. Rating committee. The committee meets to review and discuss the lead analyst s rating recommendation and presentation, including the full analysis and rating rationale, and then votes on the credit rating. Notification. CRA generally provides the issuer with a pre-publication rationale for its credit rating for fact-checking and accuracy purposes. Standard & Poor s may allow for an appeal only if the issuer can provide new and significant information to support a potentially different rating conclusion. Publication. CRA typically publishes a press release announcing the rating and posts the public rating on 34

35 How Agencies Are Paid For Their Services Issuer-Pay Model Under the issuer-pay model, which is the business model used by the Big 3 rating agencies charge issuers and structured finance arrangers a fee for providing credit ratings Critics of the issuer-pay model maintain there is a potential conflict of interest when rating agencies receive payment from the issuers whose securities they are evaluating Subscription Model Some credit ratings agencies use a subscription model and charge investors and other market participants a fee for access to their agencies ratings Critics of this model, however, point out that large investors who subscribe to a rating service, especially sizable investors such as hedge funds who have long and short positions in a variety of securities, may exert an undue influence on the agency s rating results since it is in the investors interest to have the ratings support their investment strategy 35

36 Unsolicited Credit Ratings An unsolicited credit rating is the assessment of a borrower s creditworthiness without any involvement of the borrower itself In particular, the borrower does not pay for the rating assessment. Unsolicited ratings are usually based only on publicly available information about a borrower s credit quality Rating agencies may have an interest in announcing unsolicited ratings to complete their coverage of a specific market or to create access to a market where the agency has not been present before. The observation that unsolicited ratings are often lowly graded has led to the accusation that agencies use this instrument to blackmail borrowers into soliciting (and paying for) a rating assessment Research has shown, however, that low-quality issuers are less willing to pay for a credit rating, receiving instead unsolicited ratings that are low-graded 36

37 Risk Assessment 37

38 Rating of Structured Instruments Structured Finance Instruments or Securitization Bundling or pooling of individual financial assets into a structured vehicle and the sale of separate debt instruments Often with distinct priorities or cash flow allocations, to investors Investors in typical securitized debt instruments have rights to a portion of the cash flows generated by the pool of underlying assets A bond on the other hand depends on a corporation or government for payment 38

")

39 Rating of Structured Instruments (cont d) 39

40 Contact Christian Schopper Private: Business: 40

A Guide to Investing In Corporate Bonds

A Guide to Investing In Corporate Bonds Access the corporate debt income portfolio TABLE OF CONTENTS What are Corporate Bonds?... 4 Corporate Bond Issuers... 4 Investment Benefits... 5 Credit Quality and

A Guide to Investing In Corporate Bonds Access the corporate debt income portfolio TABLE OF CONTENTS What are Corporate Bonds?... 4 Corporate Bond Issuers... 4 Investment Benefits... 5 Credit Quality and

Questions 1. What is a bond? What determines the price of this financial asset?

BOND VALUATION Bonds are debt instruments issued by corporations, as well as state, local, and foreign governments to raise funds for growth and financing of public projects. Since bonds are long-term

BOND VALUATION Bonds are debt instruments issued by corporations, as well as state, local, and foreign governments to raise funds for growth and financing of public projects. Since bonds are long-term

Economics 173A and Management 183 Financial Markets

Economics 173A and Management 183 Financial Markets Fixed Income Securities: Bonds Bonds Debt Security corporate or government borrowing Also called a Fixed Income Security Covenants or Indenture define

Economics 173A and Management 183 Financial Markets Fixed Income Securities: Bonds Bonds Debt Security corporate or government borrowing Also called a Fixed Income Security Covenants or Indenture define

I. Asset Valuation. The value of any asset, whether it is real or financial, is the sum of all expected future earnings produced by the asset.

1 I. Asset Valuation The value of any asset, whether it is real or financial, is the sum of all expected future earnings produced by the asset. 2 1 II. Bond Features and Prices Definitions Bond: a certificate

1 I. Asset Valuation The value of any asset, whether it is real or financial, is the sum of all expected future earnings produced by the asset. 2 1 II. Bond Features and Prices Definitions Bond: a certificate

Chapter. Corporate Bonds. Corporate Bonds. Corporate Bond Basics, I. Corporate Bond Basics, II. Corporate Bond Basics, III. Types of Corporate Bonds

Chapter 18 Corporate Bonds Corporate Bonds Our goal in this chapter is to introduce the specialized knowledge concerning trading corporate bonds. Money managers who buy and sell corporate bonds possess

Chapter 18 Corporate Bonds Corporate Bonds Our goal in this chapter is to introduce the specialized knowledge concerning trading corporate bonds. Money managers who buy and sell corporate bonds possess

Chapter. Investing in Bonds. 3.1 Evaluating Bonds 3.2 Buying and Selling Bonds South-Western, Cengage Learning

Chapter 3 Investing in Bonds 3.1 Evaluating Bonds 3.2 Buying and Selling Bonds Lesson 3.1 Evaluating Bonds Learning Objectives LO 1-1 Describe the characteristics and different types of corporate bonds.

Chapter 3 Investing in Bonds 3.1 Evaluating Bonds 3.2 Buying and Selling Bonds Lesson 3.1 Evaluating Bonds Learning Objectives LO 1-1 Describe the characteristics and different types of corporate bonds.

Chapter Six. Bond Markets. McGraw-Hill /Irwin. Copyright 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter Six Bond Markets Overview of the Bond Markets A bond is is a promise to make periodic coupon payments and to repay principal at maturity; breech of this promise is is an event of default carry

Chapter Six Bond Markets Overview of the Bond Markets A bond is is a promise to make periodic coupon payments and to repay principal at maturity; breech of this promise is is an event of default carry

Municipal Bond Basics

Weller Group LLC Timothy Weller, CFP CERTIFIED FINANCIAL PLANNER 6206 Slocum Road Ontario, NY 14519 315-524-8000 tim@wellergroupllc.com www.wellergroupllc.com Municipal Bond Basics March 06, 2016 Page

Weller Group LLC Timothy Weller, CFP CERTIFIED FINANCIAL PLANNER 6206 Slocum Road Ontario, NY 14519 315-524-8000 tim@wellergroupllc.com www.wellergroupllc.com Municipal Bond Basics March 06, 2016 Page

Copyright 2004 Pearson Education, Inc. All rights reserved. Bonds

Copyright 2004 Pearson Education, Inc. All rights reserved. Bonds What is a Bond? Debt securities that may pay a rate of interest based upon the face amount or par value of the bond Bond investors receive

Copyright 2004 Pearson Education, Inc. All rights reserved. Bonds What is a Bond? Debt securities that may pay a rate of interest based upon the face amount or par value of the bond Bond investors receive

FIN 684 Fixed-Income Analysis Corporate Debt Securities

FIN 684 Fixed-Income Analysis Corporate Debt Securities Professor Robert B.H. Hauswald Kogod School of Business, AU Corporate Debt Securities Financial obligations of a corporation that have priority over

FIN 684 Fixed-Income Analysis Corporate Debt Securities Professor Robert B.H. Hauswald Kogod School of Business, AU Corporate Debt Securities Financial obligations of a corporation that have priority over

A guide to investing in high-yield bonds

A guide to investing in high-yield bonds What you should know before you buy Are high-yield bonds suitable for you? High-yield bonds are designed for investors who: Can accept additional risks of investing

A guide to investing in high-yield bonds What you should know before you buy Are high-yield bonds suitable for you? High-yield bonds are designed for investors who: Can accept additional risks of investing

Chapter 5. Valuing Bonds

Chapter 5 Valuing Bonds 5-2 Topics Covered Bond Characteristics Reading the financial pages after introducing the terminologies of bonds in the next slide (p.119 Figure 5-2) Bond Prices and Yields Bond

Chapter 5 Valuing Bonds 5-2 Topics Covered Bond Characteristics Reading the financial pages after introducing the terminologies of bonds in the next slide (p.119 Figure 5-2) Bond Prices and Yields Bond

FUNDAMENTALS OF CREDIT ANALYSIS

FUNDAMENTALS OF CREDIT ANALYSIS 1 MV = Market Value NOI = Net Operating Income TV = Terminal Value RC = Replacement Cost DSCR = Debt Service Coverage Ratio 1. INTRODUCTION CR = Credit Risk Y.S = Yield

FUNDAMENTALS OF CREDIT ANALYSIS 1 MV = Market Value NOI = Net Operating Income TV = Terminal Value RC = Replacement Cost DSCR = Debt Service Coverage Ratio 1. INTRODUCTION CR = Credit Risk Y.S = Yield

KEY CONCEPTS AND SKILLS

Chapter 5 INTEREST RATES AND BOND VALUATION 5-1 KEY CONCEPTS AND SKILLS Know the important bond features and bond types Comprehend bond values (prices) and why they fluctuate Compute bond values and fluctuations

Chapter 5 INTEREST RATES AND BOND VALUATION 5-1 KEY CONCEPTS AND SKILLS Know the important bond features and bond types Comprehend bond values (prices) and why they fluctuate Compute bond values and fluctuations

Chapter 5. Interest Rates and Bond Valuation. types. they fluctuate. relationship to bond terms and value. interest rates

Chapter 5 Interest Rates and Bond Valuation } Know the important bond features and bond types } Compute bond values and comprehend why they fluctuate } Appreciate bond ratings, their meaning, and relationship

Chapter 5 Interest Rates and Bond Valuation } Know the important bond features and bond types } Compute bond values and comprehend why they fluctuate } Appreciate bond ratings, their meaning, and relationship

CHAPTER 14. Bond Prices and Yields INVESTMENTS BODIE, KANE, MARCUS. Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved.

CHAPTER 14 Bond Prices and Yields INVESTMENTS BODIE, KANE, MARCUS McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. INVESTMENTS BODIE, KANE, MARCUS 14-2 Bond Characteristics

CHAPTER 14 Bond Prices and Yields INVESTMENTS BODIE, KANE, MARCUS McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. INVESTMENTS BODIE, KANE, MARCUS 14-2 Bond Characteristics

Chapter 4. Characteristics of Bonds. Chapter 4 Topic Overview. Bond Characteristics

Chapter 4 Topic Overview Chapter 4 Valuing Bond Characteristics Annual and Semi-Annual Bond Valuation Reading Bond Quotes Finding Returns on Bond Risk and Other Important Bond Valuation Relationships Bond

Chapter 4 Topic Overview Chapter 4 Valuing Bond Characteristics Annual and Semi-Annual Bond Valuation Reading Bond Quotes Finding Returns on Bond Risk and Other Important Bond Valuation Relationships Bond

1. An option that can be exercised any time before expiration date is called:

Sample Test Questions for Intermediate Business Finance Ch 20 1. An option that can be exercised any time before expiration date is called: A. an European option B. an American option C. a call option

Sample Test Questions for Intermediate Business Finance Ch 20 1. An option that can be exercised any time before expiration date is called: A. an European option B. an American option C. a call option

Focus on. Fixed Income. Member SIPC 1 MKD-3360L-A-SL EXP 31 JUL EDWARD D. JONES & CO, L.P. ALL RIGHTS RESERVED.

Focus on Fixed Income www.edwardjones.com Member SIPC 1 5 HOW CAN I STAY ON TRACK? 4 HOW DO I GET THERE? 1 WHERE AM I TODAY? MY FINANCIAL NEEDS 3 CAN I GET THERE? 2 WHERE WOULD I LIKE TO BE? 2 Our Objectives

Focus on Fixed Income www.edwardjones.com Member SIPC 1 5 HOW CAN I STAY ON TRACK? 4 HOW DO I GET THERE? 1 WHERE AM I TODAY? MY FINANCIAL NEEDS 3 CAN I GET THERE? 2 WHERE WOULD I LIKE TO BE? 2 Our Objectives

Fixed Income Investment

Fixed Income Investment Session 1 April, 24 th, 2013 (Morning) Dr. Cesario Mateus www.cesariomateus.com c.mateus@greenwich.ac.uk cesariomateus@gmail.com 1 Lecture 1 1. A closer look at the different asset

Fixed Income Investment Session 1 April, 24 th, 2013 (Morning) Dr. Cesario Mateus www.cesariomateus.com c.mateus@greenwich.ac.uk cesariomateus@gmail.com 1 Lecture 1 1. A closer look at the different asset

Bonds explained. Member of the London Stock Exchange

Bonds explained Member of the London Stock Exchange Killik & Co We pride ourselves on being a relationship firm. Each client has their own dedicated Broker, who acts as the single point of contact to provide

Bonds explained Member of the London Stock Exchange Killik & Co We pride ourselves on being a relationship firm. Each client has their own dedicated Broker, who acts as the single point of contact to provide

Bond Valuation. Capital Budgeting and Corporate Objectives

Bond Valuation Capital Budgeting and Corporate Objectives Professor Ron Kaniel Simon School of Business University of Rochester 1 Bond Valuation An Overview Introduction to bonds and bond markets» What

Bond Valuation Capital Budgeting and Corporate Objectives Professor Ron Kaniel Simon School of Business University of Rochester 1 Bond Valuation An Overview Introduction to bonds and bond markets» What

Risk and Term Structure of Interest Rates

Risk and Term Structure of Interest Rates Economics 301: Money and Banking 1 1.1 Goals Goals and Learning Outcomes Goals: Explain factors that can cause interest rates to be different for bonds of different

Risk and Term Structure of Interest Rates Economics 301: Money and Banking 1 1.1 Goals Goals and Learning Outcomes Goals: Explain factors that can cause interest rates to be different for bonds of different

Bonds and Their Valuation

Chapter 7 Bonds and Their Valuation Key Features of Bonds Bond Valuation Measuring Yield Assessing Risk 7 1 What is a bond? A long term debt instrument in which a borrower agrees to make payments of principal

Chapter 7 Bonds and Their Valuation Key Features of Bonds Bond Valuation Measuring Yield Assessing Risk 7 1 What is a bond? A long term debt instrument in which a borrower agrees to make payments of principal

Fixed-Income Securities: Defining Elements

The following is a review of the Fixed Income: Basic Concepts principles designed to address the learning outcome statements set forth by CFA Institute. Cross-Reference to CFA Institute Assigned Reading

The following is a review of the Fixed Income: Basic Concepts principles designed to address the learning outcome statements set forth by CFA Institute. Cross-Reference to CFA Institute Assigned Reading

Bond Valuation. FINANCE 100 Corporate Finance

Bond Valuation FINANCE 100 Corporate Finance Prof. Michael R. Roberts 1 Bond Valuation An Overview Introduction to bonds and bond markets» What are they? Some examples Zero coupon bonds» Valuation» Interest

Bond Valuation FINANCE 100 Corporate Finance Prof. Michael R. Roberts 1 Bond Valuation An Overview Introduction to bonds and bond markets» What are they? Some examples Zero coupon bonds» Valuation» Interest

Fixed Income Securities: Bonds

Economics 173A and Management 183 Financial Markets Fixed Income Securities: Bonds Updated 4/24/17 Bonds Debt Security corporate or government borrowing Also called a Fixed Income Security Covenants or

Economics 173A and Management 183 Financial Markets Fixed Income Securities: Bonds Updated 4/24/17 Bonds Debt Security corporate or government borrowing Also called a Fixed Income Security Covenants or

CHAPTER 4 Bonds and Their Valuation Key features of bonds Bond valuation Measuring yield Assessing risk

4-1 CHAPTER 4 Bonds and Their Valuation Key features of bonds Bond valuation Measuring yield Assessing risk 4-2 Key Features of a Bond 1. Par value: Face amount; paid at maturity. Assume $1,000. 2. Coupon

4-1 CHAPTER 4 Bonds and Their Valuation Key features of bonds Bond valuation Measuring yield Assessing risk 4-2 Key Features of a Bond 1. Par value: Face amount; paid at maturity. Assume $1,000. 2. Coupon

STATE STREET GLOBAL ADVISORS GROSS ROLL UP UNIT TRUST

If you are in any doubt about the contents of this Supplement, you should consult your stockbroker, bank manager, solicitor, accountant or other independent financial adviser. The Directors of the Manager

If you are in any doubt about the contents of this Supplement, you should consult your stockbroker, bank manager, solicitor, accountant or other independent financial adviser. The Directors of the Manager

Valuing Bonds. Professor: Burcu Esmer

Valuing Bonds Professor: Burcu Esmer Valuing Bonds A bond is a debt instrument issued by governments or corporations to raise money The successful investor must be able to: Understand bond structure Calculate

Valuing Bonds Professor: Burcu Esmer Valuing Bonds A bond is a debt instrument issued by governments or corporations to raise money The successful investor must be able to: Understand bond structure Calculate

CHAPTER 9 DEBT SECURITIES. by Lee M. Dunham, PhD, CFA, and Vijay Singal, PhD, CFA

CHAPTER 9 DEBT SECURITIES by Lee M. Dunham, PhD, CFA, and Vijay Singal, PhD, CFA LEARNING OUTCOMES After completing this chapter, you should be able to do the following: a Identify issuers of debt securities;

CHAPTER 9 DEBT SECURITIES by Lee M. Dunham, PhD, CFA, and Vijay Singal, PhD, CFA LEARNING OUTCOMES After completing this chapter, you should be able to do the following: a Identify issuers of debt securities;

CHAPTER 5 Bonds and Their Valuation

5-1 5-2 CHAPTER 5 Bonds and Their Valuation Key features of bonds Bond valuation Measuring yield Assessing risk Key Features of a Bond 1 Par value: Face amount; paid at maturity Assume $1,000 2 Coupon

5-1 5-2 CHAPTER 5 Bonds and Their Valuation Key features of bonds Bond valuation Measuring yield Assessing risk Key Features of a Bond 1 Par value: Face amount; paid at maturity Assume $1,000 2 Coupon

Fixed income security. Face or par value Coupon rate. Indenture. The issuer makes specified payments to the bond. bondholder

Bond Prices and Yields Bond Characteristics Fixed income security An arragement between borrower and purchaser The issuer makes specified payments to the bond holder on specified dates Face or par value

Bond Prices and Yields Bond Characteristics Fixed income security An arragement between borrower and purchaser The issuer makes specified payments to the bond holder on specified dates Face or par value

DEBT MANAGEMENT EXAMINATION

1. Duration: a) is a measure of volatility of bond returns. b) is influenced by the coupon rate and yield to maturity. c) provides an approximation of the percentage price change in a bond due to a change

1. Duration: a) is a measure of volatility of bond returns. b) is influenced by the coupon rate and yield to maturity. c) provides an approximation of the percentage price change in a bond due to a change

City of Yuba City. Investment Policy

City of Yuba City Investment Policy January 1, 2017 TABLE OF CONTENTS Page I. PURPOSE... 1 II. SCOPE 1 III. OBJECTIVES... 1 IV. STANDARD OF CARE.... 1 Prudence V. INVESTMENT AUTHORITY AND RESPONSIBILITIES..

City of Yuba City Investment Policy January 1, 2017 TABLE OF CONTENTS Page I. PURPOSE... 1 II. SCOPE 1 III. OBJECTIVES... 1 IV. STANDARD OF CARE.... 1 Prudence V. INVESTMENT AUTHORITY AND RESPONSIBILITIES..

HIGH-YIELD CORPORATE BONDS

HIGH-YIELD (Agreement of Purchaser) Account Name Account Number Rep. No. HY I/We represent and agree as follows: Piper Jaffray Copy Terms. I or me means the client(s). You means Piper Jaffray. High-Yield

HIGH-YIELD (Agreement of Purchaser) Account Name Account Number Rep. No. HY I/We represent and agree as follows: Piper Jaffray Copy Terms. I or me means the client(s). You means Piper Jaffray. High-Yield

MBF1223 Financial Management Prepared by Dr Khairul Anuar

MBF1223 Financial Management Prepared by Dr Khairul Anuar L4 Bonds & Bonds Valuation www.notes638.wordpress.com Bonds - Introduction A bond is a debt instrument issued by a borrower which has borrowed

MBF1223 Financial Management Prepared by Dr Khairul Anuar L4 Bonds & Bonds Valuation www.notes638.wordpress.com Bonds - Introduction A bond is a debt instrument issued by a borrower which has borrowed

ICCCFO FALL CONFERENCE. Bond Basics TAMMIE BECKWITH SCHALLMO SENIOR VICE PRESIDENT PMA SECURITIES, INC.

ICCCFO FALL CONFERENCE Bond Basics TAMMIE BECKWITH SCHALLMO SENIOR VICE PRESIDENT PMA SECURITIES, INC. OCTOBER 12, 2016 1 The Official Statement Rating Agency Preparation Refundings Method of Sale 2 The

ICCCFO FALL CONFERENCE Bond Basics TAMMIE BECKWITH SCHALLMO SENIOR VICE PRESIDENT PMA SECURITIES, INC. OCTOBER 12, 2016 1 The Official Statement Rating Agency Preparation Refundings Method of Sale 2 The

MUNICIPAL BONDS IN TEXAS and THE BOND SALE PROCESS

MUNICIPAL BONDS IN TEXAS and THE BOND SALE PROCESS Government Treasurers Organization of Texas Winter Seminar December 5, 2017 9:30 AM 10:30 AM Robert W. Baird & Co. Incorporated ( Baird ) is providing

MUNICIPAL BONDS IN TEXAS and THE BOND SALE PROCESS Government Treasurers Organization of Texas Winter Seminar December 5, 2017 9:30 AM 10:30 AM Robert W. Baird & Co. Incorporated ( Baird ) is providing

Securitization Market Trends Survey Report Issuance Trends in the First Half of Fiscal 2012

November, Japan Securities Dealers Association Japanese Bankers Association Securitization Market Trends Survey Report Issuance Trends in the First Half of Fiscal The following report is a summary of the

November, Japan Securities Dealers Association Japanese Bankers Association Securitization Market Trends Survey Report Issuance Trends in the First Half of Fiscal The following report is a summary of the

Notice to Members. Proposed Rule to Enhance Confirmation Disclosure in Corporate Debt Securities Transactions.

Notice to Members MARCH 2005 SUGGESTED ROUTING Legal and Compliance Operations Registered Representatives Senior Management Technology Training KEY TOPICS REQUEST FOR COMMENT Proposed Rule to Enhance Confirmation

Notice to Members MARCH 2005 SUGGESTED ROUTING Legal and Compliance Operations Registered Representatives Senior Management Technology Training KEY TOPICS REQUEST FOR COMMENT Proposed Rule to Enhance Confirmation

GIOA Conference Moody s Approach to Rating Government Investment Pools: CNAV and Bond Funds. Marty Duffy VP-Managed Investments Group

GIOA Conference 2012 Moody s Approach to Rating Government Investment Pools: CNAV and Bond Funds Marty Duffy VP-Managed Investments Group Local Government Investment Pool Ratings March 21, 2012 Moody s

GIOA Conference 2012 Moody s Approach to Rating Government Investment Pools: CNAV and Bond Funds Marty Duffy VP-Managed Investments Group Local Government Investment Pool Ratings March 21, 2012 Moody s

BOND NOTES BOND TERMS

BOND NOTES DEFINITION: A bond is a commitment by the issuer (the company that is borrowing the money) to pay a rate of interest for a pre-determined period of time. By selling bonds, the issuing company

BOND NOTES DEFINITION: A bond is a commitment by the issuer (the company that is borrowing the money) to pay a rate of interest for a pre-determined period of time. By selling bonds, the issuing company

What makes bonds marketable... or not! And - a program that can help. Patrick Rutledge, AVP / Public Finance Relationship Manager FHLBank Atlanta

What makes bonds marketable... or not! And - a program that can help. Patrick Rutledge, AVP / Public Finance Relationship Manager FHLBank Atlanta 1 Disclaimer Certain information contained herein has been

What makes bonds marketable... or not! And - a program that can help. Patrick Rutledge, AVP / Public Finance Relationship Manager FHLBank Atlanta 1 Disclaimer Certain information contained herein has been

Rating Agencies Love them or hate them they are here to stay

CFA Commentary l A Member of the CFA Institute Global Network of Societies Rating Agencies Love them or hate them they are here to stay By now, anyone in Barbados who reads the newspapers or listens to

CFA Commentary l A Member of the CFA Institute Global Network of Societies Rating Agencies Love them or hate them they are here to stay By now, anyone in Barbados who reads the newspapers or listens to

Appendix Pricing and Valuation of Securities: Introduction to Common Types of Securities

Page 1 Appendix Pricing and Valuation of Securities: Introduction to Common Types of Securities This handout provides summary information for common security types held by entities in their investment

Page 1 Appendix Pricing and Valuation of Securities: Introduction to Common Types of Securities This handout provides summary information for common security types held by entities in their investment

Chapter 11. Section 2: Bonds & Other Financial Assets

Chapter 11 Section 2: Bonds & Other Financial Assets Bonds as Financial Assets Bonds are basically loans, or IOUs, that represent debt that the government or a corporation must repay to an investor. Typically

Chapter 11 Section 2: Bonds & Other Financial Assets Bonds as Financial Assets Bonds are basically loans, or IOUs, that represent debt that the government or a corporation must repay to an investor. Typically

Chapter 10: Answers to Concepts in Review

Chapter 10: Answers to Concepts in Review 1. Bonds are appealing to individual investors because they provide a generous amount of current income and they can often generate large capital gains. These

Chapter 10: Answers to Concepts in Review 1. Bonds are appealing to individual investors because they provide a generous amount of current income and they can often generate large capital gains. These

MBF1223 Financial Management Prepared by Dr Khairul Anuar

MBF1223 Financial Management Prepared by Dr Khairul Anuar L4 Bonds & Bonds Valuation www.mba638.wordpress.com Bonds - Introduction A bond is a debt instrument issued by a borrower which has borrowed a

MBF1223 Financial Management Prepared by Dr Khairul Anuar L4 Bonds & Bonds Valuation www.mba638.wordpress.com Bonds - Introduction A bond is a debt instrument issued by a borrower which has borrowed a

Egan-Jones Ratings Company

Egan-Jones Ratings Company Providing Timely, Accurate Credit Ratings To Institutional Investors Form NRSRO Exhibit #1 Credit ratings performance measurement statistics. March 28, 2016 Overview An Egan-Jones

Egan-Jones Ratings Company Providing Timely, Accurate Credit Ratings To Institutional Investors Form NRSRO Exhibit #1 Credit ratings performance measurement statistics. March 28, 2016 Overview An Egan-Jones

First Trust Intermediate Duration Preferred & Income Fund Update

1st Quarter 2015 Fund Performance Review & Current Positioning The First Trust Intermediate Duration Preferred & Income Fund (FPF) produced a total return for the first quarter of 2015 of 3.84% based on

1st Quarter 2015 Fund Performance Review & Current Positioning The First Trust Intermediate Duration Preferred & Income Fund (FPF) produced a total return for the first quarter of 2015 of 3.84% based on

The State of New York Deferred Compensation Board Stable Income Fund INVESTMENT POLICIES AND GUIDELINES. Table of Contents

The State of New York Deferred Compensation Board Stable Income Fund INVESTMENT POLICIES AND GUIDELINES June 12, 2009 Table of Contents I. Investment Objectives II. Investment Strategy A. Permitted Investments

The State of New York Deferred Compensation Board Stable Income Fund INVESTMENT POLICIES AND GUIDELINES June 12, 2009 Table of Contents I. Investment Objectives II. Investment Strategy A. Permitted Investments

Important Information about Investing in

Robert W. Baird & Co. Incorporated Important Information about Investing in \ Bonds Baird has prepared this document to help you understand the characteristics and risks associated with bonds and other

Robert W. Baird & Co. Incorporated Important Information about Investing in \ Bonds Baird has prepared this document to help you understand the characteristics and risks associated with bonds and other

Chapter Seven 9/25/2018. Chapter 6 The Risk Structure and Term Structure of Interest Rates. Bonds Are Risky!!!

Chapter Seven Chapter 6 The Risk Structure and Term Structure of Interest Rates Bonds Are Risky!!! Bonds are a promise to pay a certain amount in the future. How can that be risky? 1. Default risk - the

Chapter Seven Chapter 6 The Risk Structure and Term Structure of Interest Rates Bonds Are Risky!!! Bonds are a promise to pay a certain amount in the future. How can that be risky? 1. Default risk - the

Dallas Austin Chicago Houston Miami New York San Antonio San Diego

January 2017 DIMMIT COUNTY, TEXAS Financing 101 Dallas Austin Chicago Houston Miami New York San Antonio San Diego Financing Team Issuer A state, political subdivision, agency or authority which borrows

January 2017 DIMMIT COUNTY, TEXAS Financing 101 Dallas Austin Chicago Houston Miami New York San Antonio San Diego Financing Team Issuer A state, political subdivision, agency or authority which borrows

Fixed Income Update: Structuring Portfolios for a Rising Interest Rate Environment

Fixed Income Update: Structuring Portfolios for a Rising Interest Rate Environment February 16, 2017 Thomas S. Sawyer Sawyer Falduto Asset Management, LLC 630-941-8560 tsawyer@sawyerfalduto.com Introduction

Fixed Income Update: Structuring Portfolios for a Rising Interest Rate Environment February 16, 2017 Thomas S. Sawyer Sawyer Falduto Asset Management, LLC 630-941-8560 tsawyer@sawyerfalduto.com Introduction

CHAPTER 11. Corporate Bonds

CHAPTER 11 Corporate Bonds A corporation issues bonds intending to meet all required payments of interest and repayment of principal. Investors buy bonds believing that the corporation intends to fulfill

CHAPTER 11 Corporate Bonds A corporation issues bonds intending to meet all required payments of interest and repayment of principal. Investors buy bonds believing that the corporation intends to fulfill

RISKS ASSOCIATED WITH INVESTING IN BONDS

RISKS ASSOCIATED WITH INVESTING IN BONDS 1 Risks Associated with Investing in s Interest Rate Risk Effect of changes in prevailing market interest rate on values. As i B p. Credit Risk Creditworthiness

RISKS ASSOCIATED WITH INVESTING IN BONDS 1 Risks Associated with Investing in s Interest Rate Risk Effect of changes in prevailing market interest rate on values. As i B p. Credit Risk Creditworthiness

MONEY MARKET FUND GLOSSARY

MONEY MARKET FUND GLOSSARY 1-day SEC yield: The calculation is similar to the 7-day Yield, only covering a one day time frame. To calculate the 1-day yield, take the net interest income earned by the fund

MONEY MARKET FUND GLOSSARY 1-day SEC yield: The calculation is similar to the 7-day Yield, only covering a one day time frame. To calculate the 1-day yield, take the net interest income earned by the fund

CALIFORNIA BONDS: 101

CALIFORNIA BONDS: 101 A Citizen s Guide to General Obligation Bonds 2016 EDITION JOHN CHIANG CALIFORNIA STATE TREASURER SECTION 1 BONDS 101: Q&A Q. What is a municipal bond? A. A bond is a loan. There

CALIFORNIA BONDS: 101 A Citizen s Guide to General Obligation Bonds 2016 EDITION JOHN CHIANG CALIFORNIA STATE TREASURER SECTION 1 BONDS 101: Q&A Q. What is a municipal bond? A. A bond is a loan. There

Advanced Corporate Finance. 8. Long Term Debt

Advanced Corporate Finance 8. Long Term Debt Objectives of the session 1. Understand the role of debt financing and the various elements involved 2. Analyze the value of bonds with embedded options 3.

Advanced Corporate Finance 8. Long Term Debt Objectives of the session 1. Understand the role of debt financing and the various elements involved 2. Analyze the value of bonds with embedded options 3.

Raising capital. Raising money is not the same as making money

Raising capital Raising money is not the same as making money Types of Financial Instruments Used by All SMEs in Canada Formal financing Percent of total Commercial line of credit 21.65% Commercial credit

Raising capital Raising money is not the same as making money Types of Financial Instruments Used by All SMEs in Canada Formal financing Percent of total Commercial line of credit 21.65% Commercial credit

1) Which one of the following is NOT a typical negative bond covenant?

Which one of the following is NOT a typical negative bond covenant?") Questions in Chapter 7 concept.qz 1) Which one of the following is NOT a typical negative bond covenant? [A] The firm must limit dividend payments. [B] The firm cannot merge with another firm. [C] The

Questions in Chapter 7 concept.qz 1) Which one of the following is NOT a typical negative bond covenant? [A] The firm must limit dividend payments. [B] The firm cannot merge with another firm. [C] The

Chapter 5. Bonds, Bond Valuation, and Interest Rates

Chapter 5 Bonds, Bond Valuation, and Interest Rates 1 Chapter 5 applies Time Value of Money techniques to the valuation of bonds, defines some new terms, and discusses how interest rates are determined.

Chapter 5 Bonds, Bond Valuation, and Interest Rates 1 Chapter 5 applies Time Value of Money techniques to the valuation of bonds, defines some new terms, and discusses how interest rates are determined.

Fixed income for your portfolio

Fixed income for your portfolio November 2017 2 Fixed income for your portfolio Defence Fixed income investments such as bonds are widely used in portfolios to enhance income and compliment low risk interest

Fixed income for your portfolio November 2017 2 Fixed income for your portfolio Defence Fixed income investments such as bonds are widely used in portfolios to enhance income and compliment low risk interest

Third Quarter, 2008 Investor Presentation

CIBC August 27, 2008 Forward Looking Statements From time to time, we make written or oral forward-looking statements within the meaning of certain securities laws, including in this presentation, in other

CIBC August 27, 2008 Forward Looking Statements From time to time, we make written or oral forward-looking statements within the meaning of certain securities laws, including in this presentation, in other

I. Introduction to Bonds

University of California, Merced ECO 163-Economics of Investments Chapter 10 Lecture otes I. Introduction to Bonds Professor Jason Lee A. Definitions Definition: A bond obligates the issuer to make specified

University of California, Merced ECO 163-Economics of Investments Chapter 10 Lecture otes I. Introduction to Bonds Professor Jason Lee A. Definitions Definition: A bond obligates the issuer to make specified

Invesco Emerging Markets Debt Defensive Index Methodology July 2018

Invesco Emerging Markets Debt Defensive Index Methodology July 2018 Invesco Emerging Markets Debt Defensive Index Methodology Table of Contents Description 3 Index Construction 4 Updates 5 Calculation

Invesco Emerging Markets Debt Defensive Index Methodology July 2018 Invesco Emerging Markets Debt Defensive Index Methodology Table of Contents Description 3 Index Construction 4 Updates 5 Calculation

Essential components of an IPS

WELLS FARGO MONEY MARKET FUNDS Primer series A primer on cash investment policy statements An investment policy statement (IPS) is a document that serves as a policy guide to meet the goals and objectives

WELLS FARGO MONEY MARKET FUNDS Primer series A primer on cash investment policy statements An investment policy statement (IPS) is a document that serves as a policy guide to meet the goals and objectives

Accrued Interest A currently unpaid amount of interest that has accumulated since the last payment on a bond or other fixed-income security.

Accrued Interest A currently unpaid amount of interest that has accumulated since the last payment on a bond or other fixed-income security. Ad Valorem Tax Translated as according to value, it is a levy

Accrued Interest A currently unpaid amount of interest that has accumulated since the last payment on a bond or other fixed-income security. Ad Valorem Tax Translated as according to value, it is a levy

JEA TREASURY SERVICES INVESTMENT POLICY AS OF MAY 16, 2017

JEA TREASURY SERVICES INVESTMENT POLICY AS OF MAY 16, 2017 1.0 SCOPE The statement of investment policy and guidelines applies to funds under control of JEA in excess of those required to meet short-term

JEA TREASURY SERVICES INVESTMENT POLICY AS OF MAY 16, 2017 1.0 SCOPE The statement of investment policy and guidelines applies to funds under control of JEA in excess of those required to meet short-term

City of Tucson Finance

City of Tucson Finance Proudly Presented By: Silvia Amparano, CPA, CPFO Finance Director Association of Government Accountants Southern Arizona Chapter October 12, 2016 1 Agenda Governmental Accounting

City of Tucson Finance Proudly Presented By: Silvia Amparano, CPA, CPFO Finance Director Association of Government Accountants Southern Arizona Chapter October 12, 2016 1 Agenda Governmental Accounting

JPMORGAN ETFS (IRELAND) ICAV. USD Ultra-Short Income UCITS ETF. 21 December 2017

ICAV. USD Ultra-Short Income UCITS ETF. 21 December 2017") JPMORGAN ETFS (IRELAND) ICAV USD Ultra-Short Income UCITS ETF 21 December 2017 (A sub-fund of JPMorgan ETFs (Ireland) ICAV, an Irish collective asset-management vehicle constituted as an umbrella fund

JPMORGAN ETFS (IRELAND) ICAV USD Ultra-Short Income UCITS ETF 21 December 2017 (A sub-fund of JPMorgan ETFs (Ireland) ICAV, an Irish collective asset-management vehicle constituted as an umbrella fund

Chapter 6. October Chapter Outline. 6.3 Capital Market Securities: Long-Term Debt. 6.5 Difference between Debt and Equity Capital

Chapter 6 Financial Markets, Institutions and Securities October 2003 Chapter Outline 6.1 Financial Markets and Institutions 6.2 The Money Market 6.3 Capital Market Securities: Long-Term Debt 6.4 Capital

Chapter 6 Financial Markets, Institutions and Securities October 2003 Chapter Outline 6.1 Financial Markets and Institutions 6.2 The Money Market 6.3 Capital Market Securities: Long-Term Debt 6.4 Capital

American Funds Insurance Series Bond Fund

American Funds Insurance Series Bond Fund Summary prospectus Class 1 shares May 1, 2017 Before you invest, you may want to review the fund s prospectus and statement of additional information, which contain

American Funds Insurance Series Bond Fund Summary prospectus Class 1 shares May 1, 2017 Before you invest, you may want to review the fund s prospectus and statement of additional information, which contain

Learn about bond investing. Investor education

Learn about bond investing Investor education The dual roles bonds can play in your portfolio Bonds can play an important role in a welldiversified investment portfolio, helping to offset the volatility

Learn about bond investing Investor education The dual roles bonds can play in your portfolio Bonds can play an important role in a welldiversified investment portfolio, helping to offset the volatility

An Introduction to Bonds

An Introduction to Bonds Agenda Bond basics Different types of bonds Bond features Yield and tax considerations Bond risks Credit quality Bond investing strategies and client suitability Defining Characteristics

An Introduction to Bonds Agenda Bond basics Different types of bonds Bond features Yield and tax considerations Bond risks Credit quality Bond investing strategies and client suitability Defining Characteristics

ALAMEDA COUNTY Annual Investment Policy Calendar Year 2018

ALAMEDA COUNTY Annual Investment Policy Calendar Year 2018 Introduction The Alameda County Board of Supervisors, by Ordinance # O-2017-51 dated, October 24, 2017 has renewed the annual delegation of its

ALAMEDA COUNTY Annual Investment Policy Calendar Year 2018 Introduction The Alameda County Board of Supervisors, by Ordinance # O-2017-51 dated, October 24, 2017 has renewed the annual delegation of its

MET INVESTORS. Pioneer Strategic Income Portfolio. Class A Shares PROSPECTUS. May 1, 2006

MET INVESTORS S E R I E S T R U S T Pioneer Strategic Income Portfolio Class A Shares PROSPECTUS May 1, 2006 Like all securities, these securities have not been approved or disapproved by the Securities

MET INVESTORS S E R I E S T R U S T Pioneer Strategic Income Portfolio Class A Shares PROSPECTUS May 1, 2006 Like all securities, these securities have not been approved or disapproved by the Securities

FINAL TERMS. Part A CONTRACTUAL TERMS. Not Applicable. 4. Issue Price: 100 per cent. of the Aggregate Nominal Amount 100,000

12 June 2017 FINAL TERMS UniCredit S.p.A. (incorporated with limited liability as a Società per Azioni in the Republic of Italy under registered number 00348170101 with registered office at Via A. Specchi

12 June 2017 FINAL TERMS UniCredit S.p.A. (incorporated with limited liability as a Società per Azioni in the Republic of Italy under registered number 00348170101 with registered office at Via A. Specchi

American Funds Insurance Series Attention: Secretary 333 South Hope Street Los Angeles, California Table of Contents

American Funds Insurance Series Part B Statement of Additional Information November 30, 2017 This document is not a prospectus but should be read in conjunction with the current prospectus of American

American Funds Insurance Series Part B Statement of Additional Information November 30, 2017 This document is not a prospectus but should be read in conjunction with the current prospectus of American

Credit Rating Agencies ESMA s investigation into structured finance ratings

Credit Rating Agencies ESMA s investigation into structured finance ratings 16 December 2014 ESMA/2014/1524 Date: 16 December 2014 ESMA/2014/1524 Table of Contents 1 Executive Summary... 4 2 Who should

Credit Rating Agencies ESMA s investigation into structured finance ratings 16 December 2014 ESMA/2014/1524 Date: 16 December 2014 ESMA/2014/1524 Table of Contents 1 Executive Summary... 4 2 Who should

INDEX RULES ECPI GLOBAL BOND INDEX FAMILY

INDEX RULES ECPI GLOBAL BOND INDEX FAMILY NOVEMBER 2017 2 TABLE OF CONTENTS INTRODUCTION... 3 SELECTION CRITERIA... 5 PERIODIC REVIEW... 8 INDEX CALCULATION... 9 HEDGED INDICES... 11 INTRA MONTH EVENTS...

INDEX RULES ECPI GLOBAL BOND INDEX FAMILY NOVEMBER 2017 2 TABLE OF CONTENTS INTRODUCTION... 3 SELECTION CRITERIA... 5 PERIODIC REVIEW... 8 INDEX CALCULATION... 9 HEDGED INDICES... 11 INTRA MONTH EVENTS...

PANAFRICAN CREDIT RATING AGENCY. Tel: +(225) (225) Fax:+(225)

(225) Fax:+(225)") PANAFRICAN CREDIT RATING AGENCY Public Limited Company with a Board of Directors with a share capital of CFAF 100,000,000 Accredited by the Capital Market authority (CMA) of Rwanda Ref/CMA/July/3047/2015

PANAFRICAN CREDIT RATING AGENCY Public Limited Company with a Board of Directors with a share capital of CFAF 100,000,000 Accredited by the Capital Market authority (CMA) of Rwanda Ref/CMA/July/3047/2015

Mapping of the FERI EuroRating Services AG credit assessments under the Standardised Approach

30 October 2014 Mapping of the FERI EuroRating Services AG credit assessments under the Standardised Approach 1. Executive summary 1. This report describes the mapping exercise carried out by the Joint

30 October 2014 Mapping of the FERI EuroRating Services AG credit assessments under the Standardised Approach 1. Executive summary 1. This report describes the mapping exercise carried out by the Joint

House Committee on Oversight

House Committee on Oversight 38 Studios Moral Obligation Bond Repayment May 8, 2014 What is RIPEC? RIPEC is an independent, nonprofit and nonpartisan public policy research and education organization.

House Committee on Oversight 38 Studios Moral Obligation Bond Repayment May 8, 2014 What is RIPEC? RIPEC is an independent, nonprofit and nonpartisan public policy research and education organization.

Frequently Asked Questions (FAQ) on Credit Ratings

on Credit Ratings") TM SEBI Registered RBI Accredited NSIC Empanelled Frequently Asked Questions (FAQ) on Credit Ratings 1. What is a Credit Rating? A Credit Rating is an opinion about whether an issuer of a credit commitment,

TM SEBI Registered RBI Accredited NSIC Empanelled Frequently Asked Questions (FAQ) on Credit Ratings 1. What is a Credit Rating? A Credit Rating is an opinion about whether an issuer of a credit commitment,

1. Classification of Debt and Measurement Issues

Chapter 12 Debt Financing 1. Classification and measurement issues associated with debt 2. Accounting for short-term debt 3. Accounting for long-term debt (mortgages) 4. Understand the various types of

Chapter 12 Debt Financing 1. Classification and measurement issues associated with debt 2. Accounting for short-term debt 3. Accounting for long-term debt (mortgages) 4. Understand the various types of

Annual Investment Policy of the Pooled Investment Fund

SACRAMENTO COUNTY Annual Investment Policy of the Pooled Investment Fund CALENDAR YEAR 2017 Approved by the Sacramento County Board of Supervisors December 6, 2016 Resolution No. 2016-0938 Table of Contents

SACRAMENTO COUNTY Annual Investment Policy of the Pooled Investment Fund CALENDAR YEAR 2017 Approved by the Sacramento County Board of Supervisors December 6, 2016 Resolution No. 2016-0938 Table of Contents

Fixed-Income Insights

Fixed-Income Insights The Appeal of Short Duration Credit in Strategic Cash Management Yields more than compensate cash managers for taking on minimal credit risk. by Joseph Graham, CFA, Investment Strategist

Fixed-Income Insights The Appeal of Short Duration Credit in Strategic Cash Management Yields more than compensate cash managers for taking on minimal credit risk. by Joseph Graham, CFA, Investment Strategist

D I S C L O S U R E M E M O R A N D U M

COLUMBIA TRUST STABLE INCOME FUND D I S C L O S U R E M E M O R A N D U M February 18, 2014 Collective trust funds maintained by Ameriprise Trust Company that seek to preserve principal while maximizing

COLUMBIA TRUST STABLE INCOME FUND D I S C L O S U R E M E M O R A N D U M February 18, 2014 Collective trust funds maintained by Ameriprise Trust Company that seek to preserve principal while maximizing

EMPLOYEES' RETIREMENT SYSTEM AND ELECTED OFFICIALS' RETIREMENT SYSTEM OF THE CITY OF BALTIMORE INVESTMENT OBJECTIVES AND GUIDELINES FIXED INCOME

EMPLOYEES' RETIREMENT SYSTEM AND ELECTED OFFICIALS' RETIREMENT SYSTEM OF THE CITY OF BALTIMORE INVESTMENT OBJECTIVES AND GUIDELINES I. GENERAL This document addresses the investment objectives and guidelines

EMPLOYEES' RETIREMENT SYSTEM AND ELECTED OFFICIALS' RETIREMENT SYSTEM OF THE CITY OF BALTIMORE INVESTMENT OBJECTIVES AND GUIDELINES I. GENERAL This document addresses the investment objectives and guidelines

Supplement. to the Prospectus dated 16 May 2012 UniCredit Bank AG Munich, Federal Republic of Germany

This document constitutes a supplement to the fourteen base prospectuses dated 16 May 2012 (two prospectuses), 20 May 2011, 14 June 2010, 20 May 2010, 20 May 2009, 4 March 2009 (two prospectuses), 11 March

This document constitutes a supplement to the fourteen base prospectuses dated 16 May 2012 (two prospectuses), 20 May 2011, 14 June 2010, 20 May 2010, 20 May 2009, 4 March 2009 (two prospectuses), 11 March

A CLEAR UNDERSTANDING OF THE INDUSTRY

A CLEAR UNDERSTANDING OF THE INDUSTRY IS CFA INSTITUTE INVESTMENT FOUNDATIONS RIGHT FOR YOU? Investment Foundations is a certificate program designed to give you a clear understanding of the investment

A CLEAR UNDERSTANDING OF THE INDUSTRY IS CFA INSTITUTE INVESTMENT FOUNDATIONS RIGHT FOR YOU? Investment Foundations is a certificate program designed to give you a clear understanding of the investment

R E A L. ecap the past. valuate the potential future. djust as needed. earn ACT 10 INVESTMENTS IN THE REAL WORLD

2101 Oregon Pike Lancaster, PA 17601 Tel: (866) 548-8634 Email: rbc-cmg@rbc.com ACT 10 INVESTMENTS IN THE REAL WORLD PASBO 62 ND ANNUAL CONFERENCE AND EXHIBITS, PITTSBURGH March 2017 1 R E A L ecap the

2101 Oregon Pike Lancaster, PA 17601 Tel: (866) 548-8634 Email: rbc-cmg@rbc.com ACT 10 INVESTMENTS IN THE REAL WORLD PASBO 62 ND ANNUAL CONFERENCE AND EXHIBITS, PITTSBURGH March 2017 1 R E A L ecap the

Australia and New Zealand Banking Group Limited New Zealand Branch General Disclosure Statement

Australia and New Zealand Banking Group Limited New Zealand Branch General Disclosure Statement FOR THE YEAR ENDED 30 SEPTEMBER 2010 NUMBER 8 ISSUED NOVEMBER 2010 Australia and New Zealand Banking Group

Australia and New Zealand Banking Group Limited New Zealand Branch General Disclosure Statement FOR THE YEAR ENDED 30 SEPTEMBER 2010 NUMBER 8 ISSUED NOVEMBER 2010 Australia and New Zealand Banking Group

Financial condition. Condensed balance sheets (1) (2) Table 35

(2) Table 35") Financial condition Condensed balance sheets (1) (2) Table 35 As at October 31 (C$ millions) Assets Cash and due from banks $ 13,247 $ 8,440 Interest-bearing deposits with banks 12,181 13,254 Securities

Financial condition Condensed balance sheets (1) (2) Table 35 As at October 31 (C$ millions) Assets Cash and due from banks $ 13,247 $ 8,440 Interest-bearing deposits with banks 12,181 13,254 Securities

Rating Action: Moody's affirms AIIB's Aaa rating; outlook stable 28 Mar 2019

Rating Action: Moody's affirms AIIB's Aaa rating; outlook stable 28 Mar 2019 Singapore, March 28, 2019 -- Moody's Investors Service ("Moody's") has today affirmed the Asian Infrastructure Investment Bank's

Rating Action: Moody's affirms AIIB's Aaa rating; outlook stable 28 Mar 2019 Singapore, March 28, 2019 -- Moody's Investors Service ("Moody's") has today affirmed the Asian Infrastructure Investment Bank's

Senior Floating Rate Loans: The Whole Story

Senior Floating Rate Loans: The Whole Story Mutual fund shares are not guaranteed or insured by the FDIC, the Federal Reserve Board or any other agency. The investment return and principal value of an

Senior Floating Rate Loans: The Whole Story Mutual fund shares are not guaranteed or insured by the FDIC, the Federal Reserve Board or any other agency. The investment return and principal value of an

Dated March 13, 2003 THE GABELLI CONVERTIBLE AND INCOME SECURITIES FUND INC. STATEMENT OF ADDITIONAL INFORMATION

Dated March 13, 2003 THE GABELLI CONVERTIBLE AND INCOME SECURITIES FUND INC. STATEMENT OF ADDITIONAL INFORMATION The Gabelli Convertible and Income Securities Fund Inc. (the "Fund") is a diversified, closed-end

Dated March 13, 2003 THE GABELLI CONVERTIBLE AND INCOME SECURITIES FUND INC. STATEMENT OF ADDITIONAL INFORMATION The Gabelli Convertible and Income Securities Fund Inc. (the "Fund") is a diversified, closed-end