1. Classification of Debt and Measurement Issues

|

|

|

- Alan Townsend

- 6 years ago

- Views:

Transcription

1 Chapter 12 Debt Financing 1. Classification and measurement issues associated with debt 2. Accounting for short-term debt 3. Accounting for long-term debt (mortgages) 4. Understand the various types of bonds 5. Compute the price of a bond issue 6. Accounting for the issuance, interest, and redemption of bonds 12-1

2 1. Classification of Debt and Measurement Issues The FASB defined liabilities as probable future sacrifices of economic benefits arising from present obligations to a particular entity to transfer assets or provide services to other entities in the future as a result of past transactions or events. The FASB is currently considering a revision of this liability definition. 12-2

3 Definition of Liabilities A liability is a result of past transactions or events. Thus a liability is not recognized until incurred. This part of the definition excludes contractual obligations from an exchange of promises if performance by both parties is still in the future. Such contracts are referred to as executory contracts. 12-3

4 Classification of Liabilities For reporting purposes liabilities are usually classified as current or noncurrent. If a liability arises in the course of an entity s normal operating cycle, it is considered current if current assets are used to satisfy the obligation within one year or one operating cycle, whichever period is longer. 12-4

5 Classification of Liabilities The classification of a liability as current or noncurrent can impact significantly a company s ability to raise additional funds. When debt classified as noncurrent will mature within the next year, the liability should be reported as a current liability. The distinction between current and noncurrent is important because of the impact on a company s current ratio. 12-5

6 Measurement of Liabilities For measurement purposes, liabilities can be divided into three categories: 1. Liabilities that are definite in amount 2. Estimated liabilities 3. Contingent liabilities The measurement of liabilities always involves some uncertainty because a liability, by definition, involves a future outflow of resources. 12-6

7 2. Accounting for Short-Term Debt The term account payable usually refers to the amount due for the purchase of materials by a manufacturing company or the purchase of merchandise by a wholesaler or retailer. Accounts payable are not recorded when purchase orders are placed but instead when legal title to the goods passes to the buyer. 12-7

8 Short-Term Debt In most cases, debt is evidenced by a promissory note, which is a formal written promise to pay a sum of money in the future, and is usually reflected on the debtor s books as Notes Payable. Notes issued to trade creditors for the purchase of goods or services are called trade notes payable. 12-8

9 Short-Term Debt Nontrade notes payable include notes issued to banks or to officers and stockholders for loans to the company. If a note has no stated rate of interest, or if the stated rate is unreasonable, then the face value of the note would be discounted to the present value to reflect the effective rate of interest implicit in the note. 12-9

10 Short-Term Obligations Expected to be Refinanced A short-term obligation that is expected to be refinanced on a long-term basis should not be reported as a current liability. This applies to the currently maturing portion of a long-term debt and to all other short-term obligations except those arising in the normal course of operations that are due in customary terms

11 Short-Term Obligations Expected to be Refinanced According to FASB ASC Topic 470 (Debt), both of the following conditions must be met before a short-term obligation can be properly excluded from the current liability classification. 1. Management must intend to refinance the obligation on a long-term basis. 2. Management must demonstrate an ability to refinance the obligation

12 Short-Term Obligations Expected to be Refinanced Concerning the second point, the ability to refinance may be demonstrated by either of the following: a) Actually refinancing the obligation during the period between the balance sheet date and the date the statements are issued. b) Reaching a firm agreement that clearly provides for refinancing on a long-term basis

13 Short-Term Obligations Expected to be Refinanced If a $400,000 long-term note is issued to partially refinance $750,000 of short-term obligations, only $400,000 of the shortterm debt can be excluded from current liabilities. If the obligation is paid prior to the actual refinancing but before the issuance of the financial statements, the obligation should be included in current liabilities

14 Short-Term Obligations Expected to be Refinanced According to IAS 1, for the obligation to be classified as long term the refinancing must take place by the balance sheet date, not the later date when the financial statements are finalized. Under the international standard postbalance-sheet date events are NOT considered when determining whether a refinanceable obligation is reported as current or noncurrent

15 Lines of Credit A line of credit is a negotiated arrangement with a lender in which the terms are agreed to prior to the need for borrowing. Please read the example in the textbook on page

16 Lines of Credit The line of credit itself is not a liability. However, once the line of credit is used to borrow money, the company has a formal liability that will be reported as either a current or a long-term liability. Maintaining a line of credit is not costless. Banks typically charge a small amount, a fraction of 1% per year

17 3. Accounting for Long-Term Debt (Mortgages) A mortgage is a loan backed by an asset that serves as collateral for the loan. If the borrower cannot repay the loan, the lender has the legal right to claim the mortgaged asset and sell it in order to recover the loan amount. Mortgages are generally payable in equal installments; a portion of each payment represents interest on the unpaid mortgage balance

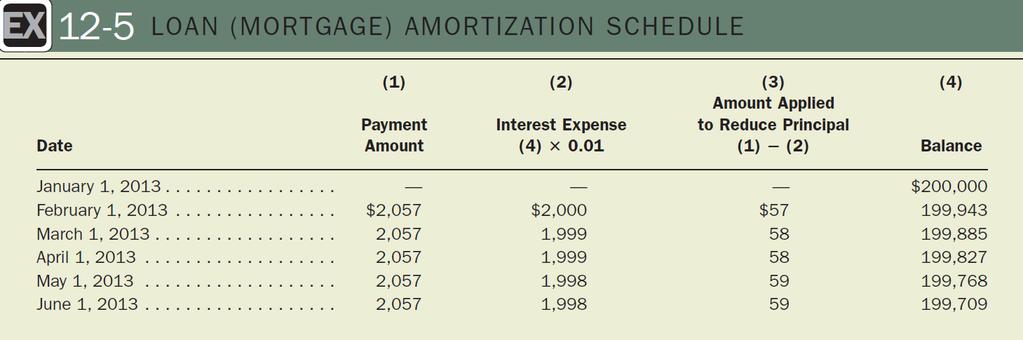

18 Present Value of Long-Term Debt On January 1, 2013, Crystal Michae purchases a house for $250,000 and makes a down payment of $50,000. The remainder is financed with a 12%, 30-year mortgage payable at a rate of $2,057 monthly. The interest rate is compounded monthly, and the first payment is due on February 1,

19 Present Value of Long-Term Debt As the mortgage payments are made, each monthly payment of $2,057 must be divided between principal and interest. On February 1, the interest is $2,000 ($200,000 1/ ), or 1% a month, and the balance of $57 is applied to the principal. In March, the interest is $1,999, 1% of $199,943 ($200,000 $57), and the pattern continues monthly. This loan (or mortgage) amortization is shown in Slide

20 12-20

21 Present Value of Long-Term Debt If Crystal were to maintain a set of personal financial records, she would make the following journal entry on February 1: Interest Expense 2,000 Mortgage Payable 57 Cash 2,057 A secured loan is similar to a mortgage in that it is a loan back by certain assets as collateral

22 4. Various Types of Bonds The long-term financing of a corporation is accomplished either thorough the issuance of long-term debt instruments, usually bonds or notes, or through the sale of additional stock. The issuance of bonds or notes instead of stock may be preferred by management and stockholders for the reasons shown on Slide

23 Financing with Bonds 1. Present owners remain in control of the corporation. 2. Interest is a deductible expense in arriving at taxable income; dividends are not. 3. Current market rates of interest may be favorable relative to stock market prices. 4. The charge against earnings for interest may be less than the amount of expected dividends

24 Understand the Bonds Conceptually, bonds and long-term notes are similar types of debt instruments. The trust indenture (the bond contract) associated with bonds generally provides more extensive detail than the contract terms of a note, often including restrictions on the payment of dividends or incurrence of additional debt

25 Accounting Issues of Bonds There are three main considerations in accounting for bonds: 1. Recording the issuance or purchase 2. Recognizing the applicable interest during the life of the bonds 3. Accounting for retirement of bonds either at maturity or prior to the maturity date 12-25

26 Nature of Bonds Bond certificates, commonly referred to simply as bonds, are frequently issued in denominations of $1,000. The amount printed on the bond is the face value, par value, or maturity value of the bond. The group contract between the corporation and the bondholders is known as the bond indenture

27 Issuers of Bonds Bonds and similar debt instruments are issued by private corporations, the U.S. government, state, county, and local governments, school districts, and government-sponsored organizations. Debt securities issued by state, county, and local governments and their agencies are collectively referred to as municipal debt

28 Types of Bonds Bonds that mature on a single date are called term bonds. Bonds that mature in installments are referred to as serial bonds. Secured bonds offer protection to investors by providing some form of security, such as a mortgage on real estate or the pledge of other collateral

29 Types of Bonds A collateral trust bond is usually secured by stocks and bonds of other corporations owned by the issuing company. Unsecured bonds (frequently termed debenture bonds) are not protected by the pledge of any specific assets. Registered bonds call for the registry of the owner s name on the corporation books

30 Types of Bonds Bearer bonds, or coupon bonds, are not recorded in the name of the owner; title to these bonds passes with delivery. Zero-interest bonds or deep-discount bonds do not bear interest. Instead, these securities sell at a significant discount. High-risk, high-yield bonds issued by companies that are heavily in debt or otherwise in weak financial condition are referred to as junk bonds

31 Types of Bonds Junk bonds are issued in at least three types of circumstances. 1. They are issued by companies that once had high credit ratings but have fallen on hard times. 2. They are issued by emerging growth companies. 3. They are issued by companies undergoing restructuring, often in conjunction with a leverage buyout

32 Types of Bonds Convertible bonds provide for their conversion into some other security at the option of the bondholder. Commodity-backed bonds may be redeemable in terms of commodities, such as oil or precious metals. Bond indentures frequently give the issuing company the right to call and retire the bonds prior to maturity. Such bonds are termed callable bonds

33 Types of Bonds Mortgage-backed bonds, in many cases, are just a special form of secured bonds. The underlying collateral for these bonds is the collection of mortgages owned by the issuing entity

34 5. Pricing Bonds The amount of interest paid on bonds is a specified percentage of the face value. This percentage is termed the stated rate, or contract rate. If the stated rate exceeds the market rate, the bonds will sell at a bond premium. If the stated rate is less than the market, the bonds will sell at a bond discount. The actual return rate on a bond is known as the market, yield, or effective interest rate

35 Market Price of Bonds Yield 8% Premium Bond Stated Interest Rate 10% 10% Face Value 12% Discount 12-35

36 Market Price of Bonds Ten-year, 8% bonds of $100,000 are to be sold on the bond issue date. The effective interest rate for bonds of similar quality and maturity is 10%, compounded semiannually. The computation of the market price of the bonds may be divided into two parts (as shown in Slide 12-37)

37 Market Price of Bonds Part 1 Present value of principal (maturity value): Maturity value of bonds after 10 years, or 20 semiannual periods $100,000 Effective interest rate: 10% per year, or 5% per semiannual period $37,689 Part 2 Present value of twenty interest payments: Semiannual payment, 4% of $100,000 $4,000 Effective interest rate: 10% per year, or 5% per semiannual period 49,849 Total present value (market price) of bond $87,

38 6. Accounting for Bonds Bonds may be sold directly to investors by the issuer or they may be sold in the open market through security exchanges or through investment bankers. Bonds issued or acquired in exchange for noncash assets or services are recorded at the fair value of the bonds unless the value of the exchanged assets or services is more clearly determinable

39 Issuance of Bonds Each of the bond situations in the following slides will be illustrated using the following data: $100,000, 8%, 10-year bonds are issued; semiannual interest of $4,000 ($100, /12) is payable on January 1 and July

40 Bonds Issued at Par on Interest Date Issuer s Books Jan. 1 Cash 100,000 Bonds Payable 100,000 July 1 Interest Expense 4,000 Cash 4,000 Dec. 31 Interest Expense 4,000 Interest Payable 4,

41 Bonds Issued at Par on Interest Date Investor s Books Jan. 1 Bond Investment 100,000 Cash 100,000 July 1 Cash 4,000 Interest Revenue 4,000 Dec. 31 Interest Receivable 4,000 Interest Revenue 4,

42 Bonds Issued at Discount on Interest Date The bonds were issued on January 1 but the effective rate of interest was 10%, requiring recognition of a discount of $12,462 ($100,000 $87,538)

43 Bonds Issued at Discount on Interest Date Issuer s Books Jan. 1 Cash 87,538 Discount on Bonds Payable 12,462 Bonds Payable 100,000 Investor s Books Jan. 1 Bond Investment 87,538 Cash 87,

44 Bonds Issued at Premium on Interest Date The bonds were issued on January 1 but the effective rate of interest was 7%, requiring recognition of a premium of $7,

45 Bonds Issued at Premium on Interest Date Issuer s Books Jan. 1 Cash 107,106 Premium on Bonds Payable 7,106 Bonds Payable 100,000 Investor s Books Jan. 1 Bond Investment 107,106 Cash 107,

46 Bonds Issued at Par between Interest Date Issuer s Books Mar. 1 Cash 101,333 Bonds Payable 100,000 Interest Payable 1,333 ($100, /12) July 1 Interest Expense 2,667 Interest Payable 1,333 Cash 4,000 ($100, /12) 12-46

47 Bonds Issued at Par between Interest Date Investor s Books Mar. 1 Bond Investment 100,000 Interest Receivable 1,333 Cash 101,333 July 1 Cash 4,000 Interest Receivable 1,333 Interest Revenue 2,

48 Bond Issuance Costs The issuance of bonds normally involves bond issuance costs to the issuer for legal services, printing and engraving, taxes, and underwriting. In Statement of Financial Accounting Concepts No.3, the FASB stated that deferred charges such as bond issuance costs fail to meet the definition of assets

49 Accounting for Bond Interest When bonds are issued at a premium or discount, the market acts to adjust the stated interest rate to a market or effective interest rate. Because the initial premium or discount, the periodic interest payments made over the bond s life by the issuer do not represent the total interest expense involved, an amortization adjustment is made

50 Straight-Line Method The straight-line method provides for the recognition of an equal amount of premium or discount amortization each period. A 10-year, 10% bond issue with a maturity value of $200,000 was sold on the issuance date at 103, the $6,000 premium would be amortized evenly over 120 months until maturity

51 Straight-Line Method To illustrate the accounting for bond interest using straight-line amortization, consider the earlier example of the $100,000, 8%, 10-year bonds issued on January 1. When sold at a $12,462 discount, the appropriate entries to record interest on July 1 and December 31 are shown on Slides and

52 Straight-Line Method Issuer s Books July 1 Interest Expense 4,623 Discount on Bonds Payable 623 Cash 4,000 $12,462/120 6 mo. = $623 (rounded) Dec. 31 Interest Expense 4,623 Discount on Bonds Payable 623 Interest Payable 4,

53 Straight-Line Method Investor s Books July 1 Cash 4,000 Bond Investment 623 Interest Revenue 4,623 Dec. 31 Interest Receivable 4,000 Bond Investment 623 Interest Revenue 4,

54 Straight-Line Method Assume the bonds were sold for $107,106. Issuer s Books July 1 Interest Expense 3,645 Premium on Bonds Payable 355 Cash 4,000 $7,106/120 6 mo. = $355 (rounded) Reflects effective interest of 7% Dec. 31 Interest Expense 3,645 Premium on Bonds Payable 355 Interest Payable 4,

55 Straight-Line Method Investor s Books July 1 Cash 4,000 Bond Investment 355 Interest Revenue 3,645 Dec. 31 Interest Receivable 4,000 Bond Investment 355 Interest Revenue 3,

56 Effective-Interest Method The effective-interest method of amortization uses a uniform interest rate based on a changing loan balance and provides for an increasing premium or discount amortization each period. In order to use this method, the effectiveinterest rate for the bonds must be known

57 Effective-Interest Method Consider once again the $100,000, 8%, 10-year bonds sold for $87,539, based on an effective interest rate of 10%. Bond balance (carrying value) at beginning of year $87,538 Effective rate per semiannual period 5% Stated rate per semiannual period 4% Interest amount based on carrying value and effective rate ($87, ) $ 4,377 Interest payment based on face value and stated rate ($100, ) 4,000 Discount amortization $

58 Effective-Interest Method Assume the $100,000, 8%, 10-year bonds is sold for $107,106, based on an effective interest rate of 7%. The premium amortization for the first 6-month period would be computed as follows: Bond balance (carrying value) at beginning of first period $107,106 Effective rate per semiannual period 3.5% Stated rate per semiannual period 4% Interest payment based on face value and stated rate ($100, ) 4,000 Interest amount based on carrying value and effective rate ($107, ) 3,749 Premium amortization $

59 Effective-Interest Method The second 6-month period would be computed as follows: Bond balance (carrying value) at beginning of second period ($107,106 $251) $106,855 Effective rate per semiannual period 3.5% Stated rate per semiannual period 4% Interest payment based on face value and stated rate ($100, ) 4,000 Interest amount based on carrying value and effective rate ($106,855 x.035) 3,740 Premium amortization $

60 Interest Payment 12-60

61 Retirement of Bonds at Maturity If the bonds are held to maturity, the discount or premium has been eliminated over the life of the bond. The entry for retiring the bond is straightforward. Assume a $100,000 bond matures on July 1. Issuer s Books July 1 Bonds Payable 100,000 Cash 100,

62 Retirement of Bonds at Maturity Investor s Books July 1 Cash 100,000 Bond Investment 100,000 There is no gain or loss on retirement because the carrying value is equal to the maturity value. Any bonds not presented for payment at their maturity date should be moved to Matured Bonds Payable

63 Extinguishment of Debt Prior to Maturity 1. Bonds may be redeemed by the issuer by purchasing the bonds on the open market or by exercising the call provision (if available). 2. Bonds may be converted, that is, exchanged for other securities. 3. Bonds may be refinanced by using the proceeds from the sale of a new bond issue to retire outstanding bonds

64 Redemption by Purchase of Bonds in the Market Triad, Inc. s $100,000, 8% bonds are not held to maturity. They are redeemed on February 1, 2013, at 97. The carrying value of the bonds is $97,700 as of this date. Interest payment dates are January 31 and July 31. Carrying value of bonds, 2/1/13 $97,700 Redemption Issuer s price Books 97,000 Gain on bond redemption $ 700 Feb. 1 Bonds Payable 100,000 Discount on Bonds Pay. 2,300 Cash 97,000 Gain on Bond Redemption

65 Redemption by Purchase of Bonds in the Market Investor s Books Feb. 1 Cash 97,000 Loss on Sale of Bonds 700 Bond Investment Triad Inc. 97,700 Before the issuance of FASB Statement No. 125 in 1996, early extinguishment of debt could also be accomplished through insubstance defeasance

66 Redemption by Exercise of Call Provision A call provision gives the issuer the option of retiring bonds prior to maturity. Frequently, the call must be made on an interest payment date. When bonds are called, the difference between the amount paid and the bond carrying value is reported as a gain or a loss on both the issuer s and investor s books

67 Convertible Bonds Convertible debt securities usually have the following features: 1. An interest rate lower than the issuer could establish for nonconvertible debt 2. An initial conversion price higher than the market value of the common stock at time of issuance 3. A call option retained by the issuer Convertible debt gives both the issuer and the holder advantages

68 Convertible Bonds Issued with Conversion Feature Nondetachable Assume that 500 ten-year bonds, face value $1,000, are sold at 105 ($525,000). The bonds contain a conversion privilege that provides for exchange of a $1,000 bond for 20 shares of stock, par value $1. It is estimated that without the conversion privilege, the bonds would sell at 96. Assume that a separate value of the conversion feature cannot be determined. Cash 525,000 Bonds Payable 500,000 Premium on Bonds Payable 25,

69 Convertible Bonds Issued with Conversion Feature Nondetachable Cash 525,000 Discount on Bonds Payable 20,000 Bonds Payable 500,000 Paid-In Capital Arising from Bond Conversion Feature 45,000 Par value of bonds (500 $1,000) $500,000 Selling price of bonds without conversion feature ($500,000 x 0.96) 480,000 Discount on bonds w/o conversion $ 20,

70 Convertible Bonds Issued with Conversion Feature Nondetachable Cash 525,000 Discount on Bonds Payable 20,000 Bonds Payable 500,000 Paid-In Capital Arising from Bond Conversion Feature 45,000 Total cash received on sale of bonds $525,000 Selling price of bonds without conversion feature ($500, ) 480,000 Amount applicable to conversion $ 45,

71 Convertible Bonds Issued with Conversion Feature Nondetachable The detachable warrants allow the holder to buy shares of stock at a set price. The FASB has expressed a preliminary preference for ultimately requiring the process of all convertible debt issues to be separated into their debt and equity components

72 Accounting for Conversion Debt According to IAS 32 IAS 32 does not differentiate between convertible debt with nondetachable and detachable conversion features. IAS 32 states that for all convertible debt issues, the issuance proceeds should be allocated between debt and equity

73 Accounting for Conversion HiTec Co. offers bondholders 40 shares of HiTec Co. common stock, $1 par, in exchange for each $1,000, 8% bond held. An investor exchanges bonds of $10,000 (carrying value as of the conversion date, $9,850) for 400 shares of common stock having a market value at the time of the exchange of $26 per share. The exchange took place on an interest payment date after interest had been paid and properly recorded

74 Accounting for Conversion When the bondholders exercise their conversion privileges, the value identified with the obligation is transferred to the common stock that replaces it. The conversion is recorded as follows: Bonds Payable 10,000 Common Stock, $1 par 400 Paid-in Capital in Excess of Par 9,450 Discount on Bonds Payable

75 Accounting for Conversion Assume that, as of the issuance date, the fair value of 40 shares of HiTec Co. common stock was substantially below the issuance price of the convertible bonds. The subsequent unexpected conversion is reported as follows: Bonds Payable 10,000 Loss on Conversion of Bonds 550 Common Stock, $1 par 400 Paid-in Capital in Excess of Par 10,000 Discount on Bonds Payable

76 Accounting for Conversion Bonds Payable 10,000 Loss on Conversion of Bonds 550 Common Stock, $1 par 400 Paid-in Capital in Excess of Par 10,000 Discount on Bonds Payable 150 Market value of stock issued (400 shares at $26) $10,400 Face value of bonds payable $10,000 Less unamortized discount 150 9,850 Loss to company on conversion of bonds $

77 Accounting for Conversion Assume the carrying value is the same on the books of the investor as it is on the books of the issuer. Investor s Books Investment in HiTec Co. Common Stock 10,400 Bond Investment HiTec Co. 9,850 Gain on Conversion of HiTec Co. Bonds 550 Market value of stock issued (400 shares at $26) $10,400 Face value of bonds payable $10,000 Less unamortized discount 150 9,850 Loss to company on conversion of bonds $

78 Bond Refinancing Cash for the retirement of a bond is frequently raised through the sale of a new issue and referred to as bond refinancing. Bond refinancing may take place when an issue matures, or bonds may be refinanced prior to their maturity when the interest rate has dropped and the interest savings on a new issue will more than offset the cost of retiring the old issue

79 Bond Refinancing A corporation has outstanding $1,000,000 of 12% bonds callable at 102 with a remaining 10-year term, and similar 10-year bonds can be marketed currently at an interest rate of only 10%. When refinancing takes place before the maturity date of the old issue, the call premium and unamortized discount and issue costs of the original bonds are considered in computing the gain or loss

PREVIEW OF CHAPTER 14-2

14-1 PREVIEW OF CHAPTER 14 14-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 14 Non-Current Liabilities LEARNING OBJECTIVES After studying this chapter, you should be able to:

14-1 PREVIEW OF CHAPTER 14 14-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 14 Non-Current Liabilities LEARNING OBJECTIVES After studying this chapter, you should be able to:

Reporting and Interpreting Bonds

Reporting and Interpreting Bonds CHAPTER 10 McGraw-Hill/Irwin 2009 The McGraw-Hill Companies, Inc. Not Barry and not James Slide 2 Understanding the Business The mixture of debt and equity used to finance

Reporting and Interpreting Bonds CHAPTER 10 McGraw-Hill/Irwin 2009 The McGraw-Hill Companies, Inc. Not Barry and not James Slide 2 Understanding the Business The mixture of debt and equity used to finance

Bonds and Long-term Notes

Section 11 Bonds & PV Tables (Noncurrent Liabilities) 14-1 Bonds and Long-term Notes The Nature of Long-Term Debt Liabilities signify creditors interest in a company s assets. note payable and note receivable:

Section 11 Bonds & PV Tables (Noncurrent Liabilities) 14-1 Bonds and Long-term Notes The Nature of Long-Term Debt Liabilities signify creditors interest in a company s assets. note payable and note receivable:

ACCOUNTING FOR BONDS

ACCOUNTING FOR BONDS Key Terms and Concepts to Know Bonds are a medium to long-term financing alternative to issuing stock. Bonds are issued or sold face amount or par, at a discount if they pay less than

ACCOUNTING FOR BONDS Key Terms and Concepts to Know Bonds are a medium to long-term financing alternative to issuing stock. Bonds are issued or sold face amount or par, at a discount if they pay less than

ACCT 101 Bonds LECTURE NOTES CH. 10 Prof. Johnson

ACCT 101 Bonds LECTURE NOTES CH. 10 Prof. Johnson BASICS OF BONDS How corporations are financed Corporations raise cash from outside parties by: 1. Equity Financing. This involves issuing common or preferred

ACCT 101 Bonds LECTURE NOTES CH. 10 Prof. Johnson BASICS OF BONDS How corporations are financed Corporations raise cash from outside parties by: 1. Equity Financing. This involves issuing common or preferred

Gleim CPA Test Prep: Financial (137 questions)

") [1] Gleim #: 12.1.1 -- Source: CPA 1189 T-18 Bonds payable issued with scheduled maturities at various dates are called Serial Bonds Term Bonds No Yes No No Yes No Yes Yes [2] Gleim #: 12.1.2 -- Source:

[1] Gleim #: 12.1.1 -- Source: CPA 1189 T-18 Bonds payable issued with scheduled maturities at various dates are called Serial Bonds Term Bonds No Yes No No Yes No Yes Yes [2] Gleim #: 12.1.2 -- Source:

Chapter 11: Liabilities, on and off balance sheet. General issues Long-term debt, contingent liabilities

Chapter 11: Liabilities, on and off balance sheet General issues Long-term debt, contingent liabilities 1 Liabilities, definition and classification present obligations based on past transactions or events

Chapter 11: Liabilities, on and off balance sheet General issues Long-term debt, contingent liabilities 1 Liabilities, definition and classification present obligations based on past transactions or events

Chapter 10 - REPORTING AND ANALYZING LIABILITIES

Revised Summer 2018 Chapter 10 Review 1 Chapter 10 - REPORTING AND ANALYZING LIABILITIES LO 1: Explain how to account for current liabilities. Current Liability: a debt that a company expects to pay 1.

Revised Summer 2018 Chapter 10 Review 1 Chapter 10 - REPORTING AND ANALYZING LIABILITIES LO 1: Explain how to account for current liabilities. Current Liability: a debt that a company expects to pay 1.

FAR. Financial Accounting & Reporting. Roger Philipp, CPA

FAR Financial Accounting & Reporting Roger Philipp, CPA FAR Financial Accounting and Reporting Written By: Roger Philipp, CPA Roger CPA Review 1288 Columbus Ave #278 San Francisco, CA 94133 www.rogercpareview.com

FAR Financial Accounting & Reporting Roger Philipp, CPA FAR Financial Accounting and Reporting Written By: Roger Philipp, CPA Roger CPA Review 1288 Columbus Ave #278 San Francisco, CA 94133 www.rogercpareview.com

Long-Term Liabilities C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM

Long-Term Liabilities E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information, in addition to the

Long-Term Liabilities E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information, in addition to the

Lesson 9 Debt and Equity Financing

Lesson 9 Balance Sheet Lesson 9 Debt and Equity Financing Assets: Current Assets: Accounts receivable Less: Allowance for Uncollectible A/R Inventories Prepaid Expenses Long-Term Assets: Property and Equipment

Lesson 9 Balance Sheet Lesson 9 Debt and Equity Financing Assets: Current Assets: Accounts receivable Less: Allowance for Uncollectible A/R Inventories Prepaid Expenses Long-Term Assets: Property and Equipment

Definition: present obligations based on past transactions or events that require either future payment or future performance of services

Liabilities Definition: present obligations based on past transactions or events that require either future payment or future performance of services A liability is a present obligation of the enterprise

Liabilities Definition: present obligations based on past transactions or events that require either future payment or future performance of services A liability is a present obligation of the enterprise

BUS210. Accounting for Financing Decisions: Long-Term Liabilities

BUS210 Accounting for Financing Decisions: Long-Term Liabilities Liabilities Current or Short-term Liabilities Long-term Debt (borrowed funds) Lease Liabilities Deferred Taxes Contingencies and Commitments

BUS210 Accounting for Financing Decisions: Long-Term Liabilities Liabilities Current or Short-term Liabilities Long-term Debt (borrowed funds) Lease Liabilities Deferred Taxes Contingencies and Commitments

Long-Term Liabilities and Investments

Ch 21 Long-Term Liabilities and Investments Understanding bonds Accounting for issuance of bond Retirement of a bond Bond sinking funds Accounting for investments in stocks and bonds Presentation of bonds

Ch 21 Long-Term Liabilities and Investments Understanding bonds Accounting for issuance of bond Retirement of a bond Bond sinking funds Accounting for investments in stocks and bonds Presentation of bonds

John J. Wild Sixth Edition

Financial Accounting John J. Wild Sixth Edition McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 10 Reporting and Analyzing Long-Term Liabilities Conceptual

Financial Accounting John J. Wild Sixth Edition McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 10 Reporting and Analyzing Long-Term Liabilities Conceptual

Long-Term Liabilities. Record and Report Long-Term Liabilities

SECTION Long-Term Liabilities VII OVERVIEW What this section does This section explains transactions, calculations, and financial statement presentation of long-term liabilities, primarily bonds and notes

SECTION Long-Term Liabilities VII OVERVIEW What this section does This section explains transactions, calculations, and financial statement presentation of long-term liabilities, primarily bonds and notes

> DO IT! Chapter 15 Long-Term Liabilities. Bond Terminology. Bond Issuance D-69. Solution. Solution

Chapter 15 Long-Term Liabilities Bond Terminology Review the types of bonds and the basic terms associated with bonds. State whether each of the following statements is true or false. 1. Mortgage bonds

Chapter 15 Long-Term Liabilities Bond Terminology Review the types of bonds and the basic terms associated with bonds. State whether each of the following statements is true or false. 1. Mortgage bonds

ACCOUNTING - CLUTCH CH LONG TERM LIABILITIES.

!! www.clutchprep.com CONCEPT: INTRODUCTION TO BONDS AND BOND CHARACTERISTICS Bonds Payable are groups of debt securities issued to lenders Example: Company wants to raise $1,000,000. The company can sell

!! www.clutchprep.com CONCEPT: INTRODUCTION TO BONDS AND BOND CHARACTERISTICS Bonds Payable are groups of debt securities issued to lenders Example: Company wants to raise $1,000,000. The company can sell

Liabilities. Chapter 10. Learning Objectives. After studying this chapter, you should be able to:

10-1 Chapter 10 Liabilities 10-2 Learning Objectives After studying this chapter, you should be able to: 1. Explain a current liability, and identify the major types of current liabilities. 2. Describe

10-1 Chapter 10 Liabilities 10-2 Learning Objectives After studying this chapter, you should be able to: 1. Explain a current liability, and identify the major types of current liabilities. 2. Describe

B EXERCISES. Instructions Indicate how each of these items should be classified in the financial statements.

B EXERCISES 2 E1-1B (Classification of Liabilities) Presented below are various account balances of Royale Corp. (a) Bonds payable of $12,000,000 maturing January, 2017. (b) Unamortized discount on bonds

B EXERCISES 2 E1-1B (Classification of Liabilities) Presented below are various account balances of Royale Corp. (a) Bonds payable of $12,000,000 maturing January, 2017. (b) Unamortized discount on bonds

Chapter Ten, Debt Financing: Bonds of Introduction to Financial Accounting online text, by Henry Dauderis and David Annand is available under

Chapter Ten, Debt Financing: Bonds of Introduction to Financial Accounting online text, by Henry Dauderis and David Annand is available under Creative Commons Attribution-NonCommercial- ShareAlike 4.0

Chapter Ten, Debt Financing: Bonds of Introduction to Financial Accounting online text, by Henry Dauderis and David Annand is available under Creative Commons Attribution-NonCommercial- ShareAlike 4.0

Original SSAP and Current Authoritative Guidance: SSAP No. 15

Statutory Issue Paper No. 80 Debt STATUS Finalized March 16, 1998 Original SSAP and Current Authoritative Guidance: SSAP No. 15 Type of Issue: Common Area SUMMARY OF ISSUE 1. Current statutory accounting

Statutory Issue Paper No. 80 Debt STATUS Finalized March 16, 1998 Original SSAP and Current Authoritative Guidance: SSAP No. 15 Type of Issue: Common Area SUMMARY OF ISSUE 1. Current statutory accounting

1) Which one of the following is NOT a typical negative bond covenant?

Which one of the following is NOT a typical negative bond covenant?") Questions in Chapter 7 concept.qz 1) Which one of the following is NOT a typical negative bond covenant? [A] The firm must limit dividend payments. [B] The firm cannot merge with another firm. [C] The

Questions in Chapter 7 concept.qz 1) Which one of the following is NOT a typical negative bond covenant? [A] The firm must limit dividend payments. [B] The firm cannot merge with another firm. [C] The

4/10/2012. Liabilities and Interest. Learning Objectives (LO) LO 1 Current Liabilities. LO 1 Current Liabilities. LO 1 Current Liabilities

LO 1 Current Liabilities. LO 1 Current Liabilities. LO 1 Current Liabilities") Learning Objectives (LO) Liabilities and Interest CHAPTER 9 After studying this chapter, you should be able to 1. Account for current liabilities 2. Measure and account for long-term liabilities 3. Account

Learning Objectives (LO) Liabilities and Interest CHAPTER 9 After studying this chapter, you should be able to 1. Account for current liabilities 2. Measure and account for long-term liabilities 3. Account

ACCOUNTING FOR NOTES RECEIVABLE

ACCOUNTING FOR NOTES RECEIVABLE Key Terms and Concepts to Know Notes Receivable: May have any duration from a day or two up to many years. Long-term notes receivable may be used to finance the purchase

ACCOUNTING FOR NOTES RECEIVABLE Key Terms and Concepts to Know Notes Receivable: May have any duration from a day or two up to many years. Long-term notes receivable may be used to finance the purchase

Accrued Interest A currently unpaid amount of interest that has accumulated since the last payment on a bond or other fixed-income security.

Accrued Interest A currently unpaid amount of interest that has accumulated since the last payment on a bond or other fixed-income security. Ad Valorem Tax Translated as according to value, it is a levy

Accrued Interest A currently unpaid amount of interest that has accumulated since the last payment on a bond or other fixed-income security. Ad Valorem Tax Translated as according to value, it is a levy

EITF ABSTRACTS. Title: Application of Issue No to Certain Convertible Instruments. Dates Discussed: November 15 16, 2000; January 17 18, 2001

EITF ABSTRACTS Issue No. 00-27 Title: Application of Issue No. 98-5 to Certain Convertible Instruments Dates Discussed: November 15 16, 2000; January 17 18, 2001 References: FASB Statement No. 3, Reporting

EITF ABSTRACTS Issue No. 00-27 Title: Application of Issue No. 98-5 to Certain Convertible Instruments Dates Discussed: November 15 16, 2000; January 17 18, 2001 References: FASB Statement No. 3, Reporting

Copyright 2009 The Learning House, Inc. Income Taxes and Investments Page 1 of 17

Copyright 2009 The Learning House, Inc. Income Taxes and Investments Page 1 of 17 Introduction Taxes are a significant expense for most companies and must be considered when analyzing a company. Differences

Copyright 2009 The Learning House, Inc. Income Taxes and Investments Page 1 of 17 Introduction Taxes are a significant expense for most companies and must be considered when analyzing a company. Differences

2

2 3 4 WOODLANDS FINANCIAL SERVICES COMPANY AND SUBSIDIARIES CONSOLIDATED BALANCE SHEETS DECEMBER 31, 2018 AND 2017 (in thousands except per share amounts) ASSETS 2018 2017 Cash and due from banks $ 6,099

2 3 4 WOODLANDS FINANCIAL SERVICES COMPANY AND SUBSIDIARIES CONSOLIDATED BALANCE SHEETS DECEMBER 31, 2018 AND 2017 (in thousands except per share amounts) ASSETS 2018 2017 Cash and due from banks $ 6,099

CHAPTER 6 ACCOUNTING AND THE TIME VALUE OF MONEY. MULTIPLE CHOICE Conceptual

CHAPTER 6 ACCOUNTING AND THE TIME VALUE OF MONEY MULTIPLE CHOICE Conceptual 21. Which of the following transactions would require the use of the present value of an annuity due concept in order to calculate

CHAPTER 6 ACCOUNTING AND THE TIME VALUE OF MONEY MULTIPLE CHOICE Conceptual 21. Which of the following transactions would require the use of the present value of an annuity due concept in order to calculate

Chapter 15 Long-Term Liabilities

Chapter 15 Long-Term Liabilities CHAPTER OVERVIEW In Chapters 13 and 14 you learned about topics related to shareholders equity. Contributed capital is a major source of funds for corporations. However,

Chapter 15 Long-Term Liabilities CHAPTER OVERVIEW In Chapters 13 and 14 you learned about topics related to shareholders equity. Contributed capital is a major source of funds for corporations. However,

Accounting for Liabilities

CHAPTER 7 Accounting for Liabilities LEARNING OBJECTIVES After you have mastered the material in this chapter, you will be able to: 1 Show how notes payable and related interest expense affect financial

CHAPTER 7 Accounting for Liabilities LEARNING OBJECTIVES After you have mastered the material in this chapter, you will be able to: 1 Show how notes payable and related interest expense affect financial

Click to edit Master title style

1 Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 1 2 15 Bonds Payable and Investments

1 Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 1 2 15 Bonds Payable and Investments

LESTI-bm14-Appendix C. Staff Summary of GAAP for Convertible Instruments

Staff Summary of GAAP for Convertible Instruments 1. Current GAAP for convertible instruments is included in Subtopic 470-20, Debt Debt with Conversion and Other Options. There is a significant amount

Staff Summary of GAAP for Convertible Instruments 1. Current GAAP for convertible instruments is included in Subtopic 470-20, Debt Debt with Conversion and Other Options. There is a significant amount

Equity Financing 13-1

Ch.13 Equity Financing 1. Stock Rights (common and preferred stock) 2. Stock Issuance for cash, noncash assets or for services 3. Treasury stock 4. Stock rights and warrants 5. Compensation expense with

Ch.13 Equity Financing 1. Stock Rights (common and preferred stock) 2. Stock Issuance for cash, noncash assets or for services 3. Treasury stock 4. Stock rights and warrants 5. Compensation expense with

BUS512M Session 9. Accounting for Financing Decisions: Long-Term Liabilities and Stockholders Equity

BUS512M Session 9 Accounting for Financing Decisions: Long-Term Liabilities and Stockholders Equity Liabilities Current or Short-term Liabilities Long-term Debt (borrowed funds) Lease Liabilities Deferred

BUS512M Session 9 Accounting for Financing Decisions: Long-Term Liabilities and Stockholders Equity Liabilities Current or Short-term Liabilities Long-term Debt (borrowed funds) Lease Liabilities Deferred

ASPE AT A GLANCE. Section Financial Instruments

ASPE AT A GLANCE Section 3856 - Financial Instruments December 2014 Section 3856 Financial Instruments Effective Date Fiscal years beginning on or after January 1, 2011 1 SCOPE Applies to all financial

ASPE AT A GLANCE Section 3856 - Financial Instruments December 2014 Section 3856 Financial Instruments Effective Date Fiscal years beginning on or after January 1, 2011 1 SCOPE Applies to all financial

US Financial Reporting - Primary Terms (Definition Report)

") 1 String usfr-gc General Concepts (usfr-gc:generalconcepts) This is a category for storing general concepts. General concepts are high-level business reporting concepts such as "assets" and "liabilities"

1 String usfr-gc General Concepts (usfr-gc:generalconcepts) This is a category for storing general concepts. General concepts are high-level business reporting concepts such as "assets" and "liabilities"

PROFESSOR S CLASS NOTES FOR UNIT 16 COB 241 Sections 13, 14, 15 Class on November 12, 2018

PROFESSOR S CLASS NOTES FOR UNIT 16 COB 241 Sections 13, 14, 15 Class on November 12, 2018 INSTALLMENT LOANS Definition and Comparison to Notes Payable An installment loan is a Promissory Note. It differs

PROFESSOR S CLASS NOTES FOR UNIT 16 COB 241 Sections 13, 14, 15 Class on November 12, 2018 INSTALLMENT LOANS Definition and Comparison to Notes Payable An installment loan is a Promissory Note. It differs

Fixed-Income Securities: Defining Elements

The following is a review of the Fixed Income: Basic Concepts principles designed to address the learning outcome statements set forth by CFA Institute. Cross-Reference to CFA Institute Assigned Reading

The following is a review of the Fixed Income: Basic Concepts principles designed to address the learning outcome statements set forth by CFA Institute. Cross-Reference to CFA Institute Assigned Reading

2 3 Independent Auditor's Report To the Board of Directors and Stockholders Woodlands Financial Services Company and Subsidiaries Williamsport, Pennsylvania Report on the Financial Statements We have audited

2 3 Independent Auditor's Report To the Board of Directors and Stockholders Woodlands Financial Services Company and Subsidiaries Williamsport, Pennsylvania Report on the Financial Statements We have audited

CHAPTER 16. Dilutive Securities and Earnings Per Share 1, 2, 3, 4, 5, 6, 7, Warrants and debt. 3, 8, 9 4, 5 7, 8, 9, 10, 29

CHAPTER 16 Dilutive Securities and Earnings Per Share ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Convertible debt and preference

CHAPTER 16 Dilutive Securities and Earnings Per Share ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Convertible debt and preference

Questions 1. What is a bond? What determines the price of this financial asset?

BOND VALUATION Bonds are debt instruments issued by corporations, as well as state, local, and foreign governments to raise funds for growth and financing of public projects. Since bonds are long-term

BOND VALUATION Bonds are debt instruments issued by corporations, as well as state, local, and foreign governments to raise funds for growth and financing of public projects. Since bonds are long-term

Chapter. Investing in Bonds. 3.1 Evaluating Bonds 3.2 Buying and Selling Bonds South-Western, Cengage Learning

Chapter 3 Investing in Bonds 3.1 Evaluating Bonds 3.2 Buying and Selling Bonds Lesson 3.1 Evaluating Bonds Learning Objectives LO 1-1 Describe the characteristics and different types of corporate bonds.

Chapter 3 Investing in Bonds 3.1 Evaluating Bonds 3.2 Buying and Selling Bonds Lesson 3.1 Evaluating Bonds Learning Objectives LO 1-1 Describe the characteristics and different types of corporate bonds.

Tel: ey.com

Ernst & Young LLP 5 Times Square New York, NY 10036 Tel: +1 212 773 3000 ey.com Ms. Susan M. Cosper Technical Director File Reference No. 2017-200 Financial Accounting Standards Board 401 Merritt 7 P.O.

Ernst & Young LLP 5 Times Square New York, NY 10036 Tel: +1 212 773 3000 ey.com Ms. Susan M. Cosper Technical Director File Reference No. 2017-200 Financial Accounting Standards Board 401 Merritt 7 P.O.

Student Learning Outcomes

Chapter 14: Bonds and Long-Term Notes Part 1 - Bonds Intermediate Accounting II Dr. Chula King Student Learning Outcomes Account for bonds at face value, at a discount, or at a premium using the effective

Chapter 14: Bonds and Long-Term Notes Part 1 - Bonds Intermediate Accounting II Dr. Chula King Student Learning Outcomes Account for bonds at face value, at a discount, or at a premium using the effective

Certain Debt Extinguishment Issues

August 22, 2016 Comments Due: October 28, 2016 Proposed Statement of the Governmental Accounting Standards Board Certain Debt Extinguishment Issues This Exposure Draft of a proposed Statement of Governmental

August 22, 2016 Comments Due: October 28, 2016 Proposed Statement of the Governmental Accounting Standards Board Certain Debt Extinguishment Issues This Exposure Draft of a proposed Statement of Governmental

XTEND, INC. FINANCIAL STATEMENTS September 30, 2017 and 2016

FINANCIAL STATEMENTS Grand Rapids, Michigan FINANCIAL STATEMENTS CONTENTS INDEPENDENT AUDITOR'S REPORT... 1 FINANCIAL STATEMENTS BALANCE SHEETS... 3 STATEMENTS OF INCOME... 4 STATEMENTS OF STOCKHOLDERS'

FINANCIAL STATEMENTS Grand Rapids, Michigan FINANCIAL STATEMENTS CONTENTS INDEPENDENT AUDITOR'S REPORT... 1 FINANCIAL STATEMENTS BALANCE SHEETS... 3 STATEMENTS OF INCOME... 4 STATEMENTS OF STOCKHOLDERS'

LONG-TERM LIABILITIES

Chapter 14 LONG-TERM LIABILITIES PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Winston Kwok, Ph.D.,

Chapter 14 LONG-TERM LIABILITIES PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Winston Kwok, Ph.D.,

LONG-TERM LIABILITIES

Chapter 14 LONG-TERM LIABILITIES PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA McGraw-Hill/Irwin Copyright

Chapter 14 LONG-TERM LIABILITIES PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA McGraw-Hill/Irwin Copyright

Debt Management Policy

Debt Management Policy Policy Number: 01-07 Date: January 9, 2017 Purpose: The City of DeKalb developed this Debt Management Policy to help ensure the City s credit worthiness and to provide a functional

Debt Management Policy Policy Number: 01-07 Date: January 9, 2017 Purpose: The City of DeKalb developed this Debt Management Policy to help ensure the City s credit worthiness and to provide a functional

1. Securities Markets, Investment Securities, and Economic Factors

1. Securities Markets, Investment Securities, and Economic Factors What is a Security Investment of Money In pooled interest With expectation of Profit Managed by third party 2 primary types, and a third

1. Securities Markets, Investment Securities, and Economic Factors What is a Security Investment of Money In pooled interest With expectation of Profit Managed by third party 2 primary types, and a third

Summary of ASPE 3856 Financial Instruments

Purpose and Scope This section establishes standards for: Recognizing and measuring financial assets, financial liabilities and specified contracts to buy or sell non-financial items; The classification

Purpose and Scope This section establishes standards for: Recognizing and measuring financial assets, financial liabilities and specified contracts to buy or sell non-financial items; The classification

Report of Independent Registered Public Accounting Firm 1-2. Consolidated Statements of Comprehensive Income 4

FINANCIAL STATEMENTS FOR THE YEAR ENDED DECEMBER 31, 2016 Contents Report of Independent Registered Public Accounting Firm 1-2 Consolidated Financial Statements Consolidated Balance Sheets 2 Consolidated

FINANCIAL STATEMENTS FOR THE YEAR ENDED DECEMBER 31, 2016 Contents Report of Independent Registered Public Accounting Firm 1-2 Consolidated Financial Statements Consolidated Balance Sheets 2 Consolidated

ntifinancial Reporting Framework for Small- and Medium-Sized E

ntifinancial Reporting Framework for Small- and Medium-Sized E Private Companies Practice Section November 2017 Financial Reporting Framework for Small- and Medium-Sized Entities Presentation and Checklist

ntifinancial Reporting Framework for Small- and Medium-Sized E Private Companies Practice Section November 2017 Financial Reporting Framework for Small- and Medium-Sized Entities Presentation and Checklist

COMBINED FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORT COMMUNITY DEVELOPMENT ADMINISTRATION INFRASTRUCTURE PROGRAM FUNDS JUNE 30, 2013

COMBINED FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORT COMMUNITY DEVELOPMENT ADMINISTRATION INFRASTRUCTURE PROGRAM FUNDS JUNE 30, 2013 TABLE OF CONTENTS PAGE INDEPENDENT AUDITOR S REPORT 3 COMBINED

COMBINED FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORT COMMUNITY DEVELOPMENT ADMINISTRATION INFRASTRUCTURE PROGRAM FUNDS JUNE 30, 2013 TABLE OF CONTENTS PAGE INDEPENDENT AUDITOR S REPORT 3 COMBINED

CITY OF INDUSTRY PUBLIC FACILITIES AUTHORITY (A COMPONENT UNIT OF CITY OF INDUSTRY) For The Year Ended June 30, Financial Statements.

For The Year Ended June 30, Financial Statements.") (A COMPONENT UNIT OF ) For The Year Ended June 30, 2015 Financial Statements With Independent Auditor s Reports (A COMPONENT UNIT OF ) FINANCIAL STATEMENTS WITH INDEPENDENT AUDITOR S REPORTS JUNE 30, 2015

(A COMPONENT UNIT OF ) For The Year Ended June 30, 2015 Financial Statements With Independent Auditor s Reports (A COMPONENT UNIT OF ) FINANCIAL STATEMENTS WITH INDEPENDENT AUDITOR S REPORTS JUNE 30, 2015

ORANGE COUNTY CONVENTION CENTER ORANGE COUNTY, FLORIDA ANNUAL FINANCIAL REPORT. for the years ended September 30, 2006 and 2005

ORANGE COUNTY, FLORIDA ANNUAL FINANCIAL REPORT ANNUAL FINANCIAL REPORT CONTENTS Pages Independent Auditors Report 1-2 Financial Statements: Balance Sheets 3 Statements of Revenues, Expenses and Changes

ORANGE COUNTY, FLORIDA ANNUAL FINANCIAL REPORT ANNUAL FINANCIAL REPORT CONTENTS Pages Independent Auditors Report 1-2 Financial Statements: Balance Sheets 3 Statements of Revenues, Expenses and Changes

Security Analysis. Bond Valuation

Security Analysis Bond Valuation Background on Bonds Bonds represent long-term debt securities Contractual Promise to pay future cash flows to investors The issuer of the bond is obligated to pay: Interest

Security Analysis Bond Valuation Background on Bonds Bonds represent long-term debt securities Contractual Promise to pay future cash flows to investors The issuer of the bond is obligated to pay: Interest

Chapter 14 In a Set of Financial Statements, What Information Is Conveyed about Noncurrent Liabilities Such as Bonds?

This is In a Set of Financial Statements, What Information Is Conveyed about Noncurrent Liabilities Such as, chapter 14 from the book Accounting in the Finance World (index.html) (v. 1.0). This book is

This is In a Set of Financial Statements, What Information Is Conveyed about Noncurrent Liabilities Such as, chapter 14 from the book Accounting in the Finance World (index.html) (v. 1.0). This book is

Name: Class: Date: 1 MULTIPLE CHOICE 11-21

1 MULTIPLE CHOICE 11-21 I certify that I am taking this assessment alone and no help with it other than the use of my textbook and notes. I have not been given these questions in advance, and the results

1 MULTIPLE CHOICE 11-21 I certify that I am taking this assessment alone and no help with it other than the use of my textbook and notes. I have not been given these questions in advance, and the results

Pro-Demnity Insurance Company Summary Financial Statements For the year ended December 31, 2011

Pro-Demnity Insurance Company Summary Financial Statements For the year ended Contents Report of the Independent Auditor's on the Summary Financial Statements 1 Summary Financial Statements Summary Statement

Pro-Demnity Insurance Company Summary Financial Statements For the year ended Contents Report of the Independent Auditor's on the Summary Financial Statements 1 Summary Financial Statements Summary Statement

Financial Instruments: Presentation INTRODUCTION

IAS 32 Financial Instruments: Presentation INTRODUCTION Objective Scope Application The stated objective of IAS 32 is to establish principles for presenting financial instruments as liabilities or equity

IAS 32 Financial Instruments: Presentation INTRODUCTION Objective Scope Application The stated objective of IAS 32 is to establish principles for presenting financial instruments as liabilities or equity

MISSISSIPPI HOME CORPORATION. Audited Financial Statements Year Ended June 30, 2015

Audited Financial Statements Year Ended June 30, 2015 CONTENTS Independent Auditor's Report 1 3 Management's Discussion and Analysis For the Years Ended June 30, 2015 and 2014 4 12 Combined Statement of

Audited Financial Statements Year Ended June 30, 2015 CONTENTS Independent Auditor's Report 1 3 Management's Discussion and Analysis For the Years Ended June 30, 2015 and 2014 4 12 Combined Statement of

ANNUAL REPORT

2 0 1 7 ANNUAL REPORT 2017 Annual Report Table of Contents Independent Auditor s Report... 1 Balance Sheets... 2 Income Statements... 3 Statements of Comprehensive Income... 4 Statements of Changes in

2 0 1 7 ANNUAL REPORT 2017 Annual Report Table of Contents Independent Auditor s Report... 1 Balance Sheets... 2 Income Statements... 3 Statements of Comprehensive Income... 4 Statements of Changes in

2 Glossary. report diluted EPS if the securities in their capital structure are antidilutive; they will report only the basic EPS number.

Glossary accelerated depreciation methods Depreciation methods that allow for higher depreciation charges in the early years and lower charges in later periods. Termed accelerated because these methods

Glossary accelerated depreciation methods Depreciation methods that allow for higher depreciation charges in the early years and lower charges in later periods. Termed accelerated because these methods

Accounting for Long. Different Ways to Finance a Company. u Borrowing from a Bank (Ch 9): Notes Payable More expensive and restrictive than bonds.

: Notes Payable More expensive and restrictive than bonds.") Accounting for Long Term Liabilities Ch 10 Acc 1a Different Ways to Finance a Company u Borrowing from a Bank (Ch 9): Notes Payable More expensive and restrictive than bonds. u Selling Stock (Ch 11): Gives

Accounting for Long Term Liabilities Ch 10 Acc 1a Different Ways to Finance a Company u Borrowing from a Bank (Ch 9): Notes Payable More expensive and restrictive than bonds. u Selling Stock (Ch 11): Gives

IOWA STUDENT LOAN LIQUIDITY CORPORATION. Financial Statements. June 30, 2011 and (With Independent Auditors Reports Thereon)

") Financial Statements (With Independent Auditors Reports Thereon) Table of Contents Page(s) Independent Auditors Report 1 Management s Discussion and Analysis 3 9 Financial Statements: Statements of Net

Financial Statements (With Independent Auditors Reports Thereon) Table of Contents Page(s) Independent Auditors Report 1 Management s Discussion and Analysis 3 9 Financial Statements: Statements of Net

Cash... 16,000,000 Notes payable... 16,000,000. Interest expense ($16,000,000 x 12% x 2/12) ,000 Interest payable ,000

,000 Interest payable ,000") Exercise 13-1 Requirement 1 Cash... 16,000,000 Notes payable... 16,000,000 Requirement 2 Interest expense ($16,000,000 x 12% x 2/12)... 320,000 Interest payable... 320,000 Requirement 3 Interest expense

Exercise 13-1 Requirement 1 Cash... 16,000,000 Notes payable... 16,000,000 Requirement 2 Interest expense ($16,000,000 x 12% x 2/12)... 320,000 Interest payable... 320,000 Requirement 3 Interest expense

Bond problems by Alfredo Garcia December 13, 2004

Bond problems by Alfredo Garcia December 13, 2004 a40.when bonds are sold between interest dates, any accrued interest is credited to a. Interest Payable. b. Interest Revenue. c. Interest Receivable. d.

Bond problems by Alfredo Garcia December 13, 2004 a40.when bonds are sold between interest dates, any accrued interest is credited to a. Interest Payable. b. Interest Revenue. c. Interest Receivable. d.

CBC HOLDING COMPANY AND SUBSIDIARY CONSOLIDATED FINANCIAL STATEMENTS YEAR ENDED DECEMBER 31, 2017

CBC HOLDING COMPANY AND SUBSIDIARY CONSOLIDATED FINANCIAL STATEMENTS TABLE OF CONTENTS Page Independent Auditor s Report... 1 Consolidated Financial Statements Consolidated Balance Sheets... 2 Consolidated

CBC HOLDING COMPANY AND SUBSIDIARY CONSOLIDATED FINANCIAL STATEMENTS TABLE OF CONTENTS Page Independent Auditor s Report... 1 Consolidated Financial Statements Consolidated Balance Sheets... 2 Consolidated

American Airlines Federal Credit Union. Financial Statements December 31, 2016 and 2015

American Airlines Federal Credit Union Financial Statements December 31, 2016 and 2015 Contents Independent auditor s report 1 Financial statements Statements of financial condition 2 Statements of income

American Airlines Federal Credit Union Financial Statements December 31, 2016 and 2015 Contents Independent auditor s report 1 Financial statements Statements of financial condition 2 Statements of income

UTILITY DEBT SECURITIZATION AUTHORITY (A Component Unit of the Long Island Power Authority) Basic Financial Statements

Basic Financial Statements") Basic Financial Statements And Required Supplementary Information (With Independent Auditors Report and Report on Internal Control and Compliance Thereon) Table of Contents Page Section 1 Management s

Basic Financial Statements And Required Supplementary Information (With Independent Auditors Report and Report on Internal Control and Compliance Thereon) Table of Contents Page Section 1 Management s

ACCOUNTING FOR DEBT AND EQUITY INSTRUMENTS IN FINANCING TRANSACTIONS

ACCOUNTING FOR DEBT AND EQUITY INSTRUMENTS IN FINANCING TRANSACTIONS Prepared by: RSM US LLP National Professional Standards Group Faye Miller, Partner, faye.miller@rsmus.com, +1 410 246 9194 Monique Cole,

ACCOUNTING FOR DEBT AND EQUITY INSTRUMENTS IN FINANCING TRANSACTIONS Prepared by: RSM US LLP National Professional Standards Group Faye Miller, Partner, faye.miller@rsmus.com, +1 410 246 9194 Monique Cole,

Lecture. Business Environment & Strategy Analysis. Industry. Strategy. Analysis. Analysis. Financial. Analysis. Analysis. of Sources &Uses of Funds

2 Lecture Industry Analysis Business Environment & Strategy Analysis Strategy Analysis Financial Statement Analysis Accounting Analysis Profitability Analysis Financial Analysis Analysis of Sources &Uses

2 Lecture Industry Analysis Business Environment & Strategy Analysis Strategy Analysis Financial Statement Analysis Accounting Analysis Profitability Analysis Financial Analysis Analysis of Sources &Uses

Dear Friends: Sincerely, Jon P. Conklin President and CEO

Dear Friends: We are pleased to announce the financial results of Woodlands Financial Services Company (Company) for 2016. In addition to several other important strategic initiatives mostly taking place

Dear Friends: We are pleased to announce the financial results of Woodlands Financial Services Company (Company) for 2016. In addition to several other important strategic initiatives mostly taking place

FORM 10-Q FEDERAL DEPOSIT INSURANCE CORPORATION WASHINGTON, D.C

FORM 10-Q FEDERAL DEPOSIT INSURANCE CORPORATION WASHINGTON, D.C. 20429 (X) QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934. For the quarterly period ended March

FORM 10-Q FEDERAL DEPOSIT INSURANCE CORPORATION WASHINGTON, D.C. 20429 (X) QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934. For the quarterly period ended March

CHAPTER 15 12e Update

CHAPTER 15 12e Update Stockholders Equity ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis *1. Stockholders rights; corporate form. 1,

CHAPTER 15 12e Update Stockholders Equity ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis *1. Stockholders rights; corporate form. 1,

Complex Financial Instruments

BDO KNOWS: Complex Financial Instruments A Practice Aid From BDO s National Assurance Practice 4th Edition / Updated May 2010 Complex Financial Instruments Practice Aid 4th Edition This is the fourth edition

BDO KNOWS: Complex Financial Instruments A Practice Aid From BDO s National Assurance Practice 4th Edition / Updated May 2010 Complex Financial Instruments Practice Aid 4th Edition This is the fourth edition

ACCT 652 Accounting. Payroll accounting. Payroll accounting Week 8 Liabilities and Present value

11-1 ACCT 652 Accounting Week 8 Liabilities and Present value Some slides Times Mirror Higher Education Division, Inc. Used by permission 2016, Michael D. Kinsman, Ph.D. 1 1 Payroll accounting I am sure

11-1 ACCT 652 Accounting Week 8 Liabilities and Present value Some slides Times Mirror Higher Education Division, Inc. Used by permission 2016, Michael D. Kinsman, Ph.D. 1 1 Payroll accounting I am sure

Name: ACC 4020 DW Take-Home Test #2

ACC 4020 DW Take-Home Test #2 Name: 1. Of the following items, the one that should be classified as a current asset is a. Trade installment receivables normally collectible in 18 months b. Cash designated

ACC 4020 DW Take-Home Test #2 Name: 1. Of the following items, the one that should be classified as a current asset is a. Trade installment receivables normally collectible in 18 months b. Cash designated

CEBU CPAR CENTER. M a n d a u e C I t y

Page 1 of 11 CEBU CPAR CENTER M a n d a u e C I t y AUDITING PROBLEMS AUDIT OF LIABILITIES PROBLEM NO. 1 In the audit of the Heats Corporation s financial statements at December 31, 2005, the chief accountant

Page 1 of 11 CEBU CPAR CENTER M a n d a u e C I t y AUDITING PROBLEMS AUDIT OF LIABILITIES PROBLEM NO. 1 In the audit of the Heats Corporation s financial statements at December 31, 2005, the chief accountant

NEBRASKA BOOK HOLDINGS, INC. Rule 144(c) Current Public Information Data Sheet and Unaudited Condensed Consolidated Financial Statements

Current Public Information Data Sheet and Unaudited Condensed Consolidated Financial Statements") Rule 144(c) Current Public Information Data Sheet and Unaudited Condensed Consolidated Financial Statements Three and Nine Months Ended The current public information data sheet and unaudited condensed

Rule 144(c) Current Public Information Data Sheet and Unaudited Condensed Consolidated Financial Statements Three and Nine Months Ended The current public information data sheet and unaudited condensed

Terminology of Convertible Bonds

Bellerive 241 P.o. Box CH-8034 Zurich info@fam.ch www.fam.ch T +41 44 284 24 24 Terminology of Convertible Bonds Fisch Asset Management Terminology of Convertible Bonds Seite 2 28 ACCRUED INTEREST 7 ADJUSTABLE-RATE

Bellerive 241 P.o. Box CH-8034 Zurich info@fam.ch www.fam.ch T +41 44 284 24 24 Terminology of Convertible Bonds Fisch Asset Management Terminology of Convertible Bonds Seite 2 28 ACCRUED INTEREST 7 ADJUSTABLE-RATE

FPB FINANCIAL CORP. AND SUBSIDIARIES

FPB FINANCIAL CORP. AND SUBSIDIARIES Audits of Consolidated Financial Statements December 31, 2015 and 2014 Contents Independent Auditor s Report 1-2 Basic Consolidated Financial Statements Consolidated

FPB FINANCIAL CORP. AND SUBSIDIARIES Audits of Consolidated Financial Statements December 31, 2015 and 2014 Contents Independent Auditor s Report 1-2 Basic Consolidated Financial Statements Consolidated

BMO Mutual Funds 2015

BMO Mutual Funds 2015 Semi-Annual Financial Statements BMO Short-Term Income Class NOTICE OF NO AUDITOR REVIEW OF THE SEMI-ANNUAL FINANCIAL STATEMENTS BMO Investments Inc., the Manager of the Fund, appoints

BMO Mutual Funds 2015 Semi-Annual Financial Statements BMO Short-Term Income Class NOTICE OF NO AUDITOR REVIEW OF THE SEMI-ANNUAL FINANCIAL STATEMENTS BMO Investments Inc., the Manager of the Fund, appoints

Sanford Burnham Prebys Medical Discovery Institute

Sanford Burnham Prebys Medical Discovery Institute Financial Statements as of and for the Years Ended June 30, 2016 and 2015, Supplemental Combining Information as of and for the Year Ended June 30, 2016,

Sanford Burnham Prebys Medical Discovery Institute Financial Statements as of and for the Years Ended June 30, 2016 and 2015, Supplemental Combining Information as of and for the Year Ended June 30, 2016,

As of September 30, 2017 and December 31, 2016, and for the Three and Nine Months Ended September 30, 2017 and 2016.

CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED) AND MANAGEMENT S DISCUSSION AND ANALYSIS Ascent Resources Utica Holdings, LLC As of September 30, 2017 and December 31, 2016, and for the Three and

CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED) AND MANAGEMENT S DISCUSSION AND ANALYSIS Ascent Resources Utica Holdings, LLC As of September 30, 2017 and December 31, 2016, and for the Three and

UTILITY DEBT SECURITIZATION AUTHORITY (A Component Unit of the Long Island Power Authority) Basic Financial Statements

Basic Financial Statements") Basic Financial Statements And Required Supplementary Information (With Independent Auditors Report Thereon) Table of Contents Page Section 1 Independent Auditor s Report 1 Management s Discussion and

Basic Financial Statements And Required Supplementary Information (With Independent Auditors Report Thereon) Table of Contents Page Section 1 Independent Auditor s Report 1 Management s Discussion and

Chapter 11. Notes, Bonds, and Leases

1 Chapter 11 Long- Term Liabilities Notes, Bonds, and Leases 2 Long- Term Liabilities Many companies finance their operations and growth opportunities through the use of long term debt instruments: Notes

1 Chapter 11 Long- Term Liabilities Notes, Bonds, and Leases 2 Long- Term Liabilities Many companies finance their operations and growth opportunities through the use of long term debt instruments: Notes

Condensed Consolidated Financial Statements March 31, VIRGIN MEDIA INC Wewatta Street, Suite 1000 Denver, Colorado United States

Condensed Consolidated Financial Statements VIRGIN MEDIA INC. 1550 Wewatta Street, Suite 1000 Denver, Colorado 80202 United States TABLE OF CONTENTS CONDENSED CONSOLIDATED FINANCIAL STATEMENTS Condensed

Condensed Consolidated Financial Statements VIRGIN MEDIA INC. 1550 Wewatta Street, Suite 1000 Denver, Colorado 80202 United States TABLE OF CONTENTS CONDENSED CONSOLIDATED FINANCIAL STATEMENTS Condensed

university of the pacific

university of the pacific Financial Statements (With Independent Auditors Report Thereon) Table of Contents Page(s) Independent Auditors Report 1 2 Financial Statements: Balance Sheet 3 Statement of

university of the pacific Financial Statements (With Independent Auditors Report Thereon) Table of Contents Page(s) Independent Auditors Report 1 2 Financial Statements: Balance Sheet 3 Statement of

First Bancshares of Texas, Inc. and Subsidiary

Report of Independent Auditors and Consolidated Financial Statements Contents Report of Independent Auditors... 1 Consolidated Financial Statements Statements of Financial Condition... 2 Statements of

Report of Independent Auditors and Consolidated Financial Statements Contents Report of Independent Auditors... 1 Consolidated Financial Statements Statements of Financial Condition... 2 Statements of

T A B L E O F C O N T E N T S

T A B L E O F C O N T E N T S PRESIDENT S LETTER... 3 INDEPENDENT AUDITORS REPORT... 4-5 FINANCIAL STATEMENTS Consolidated Balance Sheet... 6 Consolidated Statement of Income... 7 Consolidated Statement

T A B L E O F C O N T E N T S PRESIDENT S LETTER... 3 INDEPENDENT AUDITORS REPORT... 4-5 FINANCIAL STATEMENTS Consolidated Balance Sheet... 6 Consolidated Statement of Income... 7 Consolidated Statement

Superseded by FASB Accounting Standards Codification. APB 21: Interest on Receivables and Payables APB 21 STATUS. Issued: August 1971

APB 21: Interest on Receivables and Payables APB 21 STATUS Issued: August 1971 Effective Date: For transactions on or after October 1, 1971 Affects: Amends ARB 43, Chapter 3A, paragraph 6(g) Amends APS

APB 21: Interest on Receivables and Payables APB 21 STATUS Issued: August 1971 Effective Date: For transactions on or after October 1, 1971 Affects: Amends ARB 43, Chapter 3A, paragraph 6(g) Amends APS

Long Term Liabilities Ch 14 Answers

We have made it easy for you to find a PDF Ebooks without any digging. And by having access to our ebooks online or by storing it on your computer, you have convenient answers with long term liabilities

We have made it easy for you to find a PDF Ebooks without any digging. And by having access to our ebooks online or by storing it on your computer, you have convenient answers with long term liabilities

CONSOLIDATED ANNUAL REPORT. Fleetwood. Bank Corporation. What you want your bank to be

2016 CONSOLIDATED ANNUAL REPORT Fleetwood Bank Corporation & What you want your bank to be CORPORATE MISSION STATEMENT Our educated and motivated team will become the leading provider of financial services

2016 CONSOLIDATED ANNUAL REPORT Fleetwood Bank Corporation & What you want your bank to be CORPORATE MISSION STATEMENT Our educated and motivated team will become the leading provider of financial services

KEY CONCEPTS AND SKILLS

Chapter 5 INTEREST RATES AND BOND VALUATION 5-1 KEY CONCEPTS AND SKILLS Know the important bond features and bond types Comprehend bond values (prices) and why they fluctuate Compute bond values and fluctuations

Chapter 5 INTEREST RATES AND BOND VALUATION 5-1 KEY CONCEPTS AND SKILLS Know the important bond features and bond types Comprehend bond values (prices) and why they fluctuate Compute bond values and fluctuations

SAVI FINANCIAL CORPORATION, INC. AND SUBSIDIARY BURLINGTON, WASHINGTON

SAVI FINANCIAL CORPORATION, INC. AND SUBSIDIARY BURLINGTON, WASHINGTON AUDITED FINANCIAL STATEMENTS AND OTHER FINANCIAL INFORMATION C O N T E N T S AUDITED FINANCIAL STATEMENTS: PAGE Report of Independent

SAVI FINANCIAL CORPORATION, INC. AND SUBSIDIARY BURLINGTON, WASHINGTON AUDITED FINANCIAL STATEMENTS AND OTHER FINANCIAL INFORMATION C O N T E N T S AUDITED FINANCIAL STATEMENTS: PAGE Report of Independent

Purpose of the Capital Market

BOND MARKETS Purpose of the Capital Market Original maturity is greater than one year, typically for long-term financing or investments Best known capital market securities: Stocks and bonds Capital Market

BOND MARKETS Purpose of the Capital Market Original maturity is greater than one year, typically for long-term financing or investments Best known capital market securities: Stocks and bonds Capital Market