Book Review: The Volatility Surface. A Practitioner s Guide (Jim Gatheral, Wiley-Finance, 2006)

|

|

|

- Priscilla Black

- 5 years ago

- Views:

Transcription

1 Book Review: The Volatility Surface. A Practitioner s Guide (Jim Gatheral, Wiley-Finance, 2006) Anatoliy Swishchuk University of Calgary Bankers Hall, Calgary, AB, Canada May 17, 2011 PRMIA Calgary Chapter s Talk

2 Book s Cover

3 Outline of Presentation 1. Introduction to the Book 2. Contents of the Book 3. Review of Chapters Short Description of Chapters Conclusion

4 Intro to the Book: About the Author Jim Gatheral is a Managing Director at Merrill Lynch and also an Adjunct Professor at the Courant Institute of Mathematical Sciences, New York University. Dr. Gatheral obtained a PhD in theoretical physics from Cambridge University in From 1997 to 2005, Dr. Gatheral headed the Equity Quantitative Analytics droup at Merrill Lynch. His current research focus is equity market microstructure and algorithmic trading.

5 Jim Gatheral s Picture

6 Intro to the Book: Purpose The purpose of The Volatility Surface is not to just present results, but to provide you with ways of thinking about and solving practical problems that should have many other areas of application.

7 Intro to the Book: Purpose Understandin the volatility surface is a key objective for both practitioners and academics in the field of finance.

8 Intro to the Book: Purpose Implied volatilities evolve randomly and so models of the volatility surface-which is formed from implied volatilites of all strikes and expirations-need to explicitele reflect this randomness in order to accurately price, trade, and manage the risk of derivative products.

9 Intro to the Book: Focus The first half of the book focuses on setting up the theoretical framework, while the later chapters are oriented towards practical applications.

10 Intro to the Book: Focus The Volatility Surface : Contains a detailed derivation of the Heston model and explanations of many other popular models such as SVJ, SVJJ, SABR, and CreditGrades Discusses the characteristics of various types of exotic options from the humble barrier option to the super exotic Napoleon

11 Contents of the Book Book contains: 11 Chapters Bibliography (74 sources) Index Many figures (47) 12 Tables

12 Chapters 1-3 Short Descriptions Chapter 1 Stochastic Volatility and Local Volatility : Provides an explanation of stochastic (SV) and local volatility (LV); local variance is shown to be the risk-neutral expectation of intantaneous variance, a result that is applied repeatedly in later chapters.

13 Chapters 1-3 Short Descriptions Chapter 2 The Heston Model : Presents the still supremely popular Heston model and derive the Heston European option pricing formula. It s also shown how to simulate the Heston model.

14 Chapters 1-3 Short Descriptions Chapter 3 The Implied Volatility Surface : Derives a powerful representation for implied volatility (IV) in terms of local volatility and applies this to build intuition and derive some properties of the impled volatility surface (VS) generated by the Heston model and compare with the empirically observed SPX surface; deduces that SV cannot be the whole story.

15 Chapters 1-3 Review Book s Cover

16 Chapter 1: Stochastic Volatility (SV) and Local Volatility (LV)

17 Structure of Chapter 1: Stochastic Volatility (SV) and Local Volatility (LV) 1. SV: Derivation of the Valuation Equation 2. LV: History, Brief Review of Dupire s Work 3. LV in Terms of Implied Volatility (IV) 4. LV as a Conditional Expectation of Instantaneous varinace

18 Chapter 1: Stochastic Volatility (SV) and Local Volatlity (LV) In this chapter, author introduces SV-the notion that volatility varies in a random fashion. LV then is then shown to be conditional expectation of the instantaneous variance so that various quantities of interest (such as option prices) may sometimes be computed as though future volatility were detrministic rather than stochastic.

19 Chapter 1: Stochastic Volatility (SV) Sense to model SV as a RV: observations of equity market (the stock market crash of October 1987). SV models are useful because they explain in a self-consistent way why options with different strikes and maturities have different Black-Scholes implied volatilities-that is, the volatility smile. Moreover, unlike alternative models that can fit the smile (such as LV models, e.g.), SV models assume realistic dynamics for the underlying.

20 Chapter 1: Stochastic Volatility (SV) Although SV price processes are sometimes accused by being ad hoc, on the contrary, they can be viewed as arising from Brownian motion subordinated to a random clock. This clock time, often referred to as trading time, may be identified with the volume of trades or the frequency of trading (Clark 1973); the idea is that as trading activity fluctuates, so does volatility.

21 Chapter 1: Stochastic Volatility (SV) From a hedging perspective, traders who use the Balck-Scholes model must continuously change the volatility assumption in order to match market prices. Their hedge ratios change accordingly in an uncontrolled way; SV models bring some order into this chaos. The prices of exotic options given by models based on Black- Scholes assumptions can be widely wrong and dealers in such options are motivated to find models that can take the volatility smile into account.

22 Chapter 1: Stochastic Volatility (SV) In Figure 1.1, the log returns of SPX over a 15-year period is plotted; we see that large moves follow large moves and small moves follow small moves (so-called volatility clustering ).

23 SPX Daily Log Returns (Dec 31, 1984-Dec 31, 2004)

24 Chapter 1: Stochastic Volatility (SV) In Figure 1.2, the frequency distribution of SPX log returns over the 77-year period from 1928 to 2005 is plotted. The distribution is highly peaked and fat-tailed relative to the normal distribution.

25 Frequency Distribution of 77 Years of SPX Daily Log Returns

26 Chapter 1: Stochastic Volatility (SV) The Q-Q plot in Figure 1.3 shows just how extreme the tails of the empirical distribution of returns are relative to the normal distribution. (This plot would be a straight line if the empirical distribution were normal).

27 Q-Q Plot of SPX Daily Log Returns

28 Chapter 1: Stochastic Volatility (SV) Fat tails and the high central peak are characteristics of mixtures of distributions with different variances. This motivates to model variance as a RV. The volatility clustering feature implies that volatility (or variance) is auto-correlated. In the model, this is a consequence of the mean revertion of volatility.

29 Chapter 1: Stochastic Volatility (SV) (Derivation of the Valuation Equation) In this section, author follows Wilmott (2000). Suppose that the stock price S and its variance v satisfy the following SDEs: with ds t = µ t S t dt + v t S t dz 1 dv t = α(s t, v t, t)dt + ηβ(s t, v t, t) v t dz 2 (1) dz 1, dz 2 = ρdt. (2)

30 Chapter 1: Stochastic Volatility (SV) (Derivation of the Valuation Equation) The process S t followed by the stock price is equivalent to the one assumed in the derivation of B-S (1973). This ensures that the standard time-dependent volatility version of the B-S formula (as derived in Sec. 8.6 of Wilmott (2000), e.g.) may be retrieved in the limit η 0. In practical applications, this is a key requirement of a SV option pricing model as practitioners intuition for the behaviour of option prices is invariably expressed within the framework of the B-S formula. No assumption wrt the form of functions α and β.

31 Chapter 1: Stochastic Volatility (SV) (Derivation of the Valuation Equation) In the B-S case, there is only one source of randomness, the stock price, which can be hedged with stock. In the present case, ranom changes in volatility also need to be hedged in order to form a riskless portfolio. So we set up a portfolio Π containing the option being priced, whose value we denote by V (S, v, t), a quantity of the stock and a quantity 1 of another asset whose value V 1 depends on volatility.

32 Chapter 1: Stochastic Volatility (SV) (Derivation of the Valuation Equation) Equation for V has the following form: V t vs2 2 V S 2 + ρηvβs 2 V v S η2 vβ 2 2 V v2 + rs V S rv = (α φβ v) V v, where we have written the arbitrary function of S, v, t as (α φβ v), where α and β are the drift and volatility functions from the SDE (1).

33 Chapter 1: Stochastic Volatility (SV) (Market Price of Volatility Risk) Function φ(s, v, t) is called market price of volatility risk. To see why, we follow Wilmott s argument. Consider the portfolio Π 1 consisting of a delta-hedged option V. Then Π 1 = V V S S and applying Itô s lemma and taking into account of deltahedged option (the coefficient of ds is zero), we have dπ 1 rπ 1 dt = β v V v [φdt + dz 2].

34 Chapter 1: Stochastic Volatility (SV) (Market Price of Volatility Risk) We see that the extra return per unit of volatility risk dz 2 is given by φdt and so in analogy with the CAPM, φ is known as the market price of volatility risk. Defining the risk-neutral drift as α = α β vφ we see that, as far as pricing of options is concerned, we could have started with the risk-neutral SDE for v, dv = α dt + β vdz 2 and got identical results with no explicit price of risk term because we are in the risk neutral world.

35 Chapter 1: Stochastic Volatility (SV) (Risk-Neutral World) In what follows, we always assume that the SDEs for S and v are in risk-neutral terms because we are invariably interested in fitting models to option prices. Effectively, we assume that we are imputing the risk-neutral measure directly by fitting the parameters of the process that we are imposing.

36 Chapter 1: Local Volatility (LV), History Given the computational complexity of SV models and difficulty of fitting parameters to the current prices of vanilla options, practitioners sought a simpler way of pricing exotic options consistently with the volatility skew. Since before Breeden and Litzenberger (1978), it was undestood that the risk-neutral density could be derived from the market prices of European options.

37 Chapter 1: Local Volatility (LV), History The breakthrough came when Dupire (1994) (continuous time version) and Derman and Kani (1994) (discrete time binomial tree version) noted that under risk neutrality, there was a unique diffusion process consistent with these distributions. The corresponding unique state-dependent diffusion coefficient σ L (S, t), consistent with current European option prices, is known as the local volatility function.

38 Chapter 1: Local Volatility (LV), History As if any proof were needed, Dumas, Fleming and Whaley (1998) performed an empirical analysis that confirmed that the dynamics of the implied volatility surface were not consistent with the assumption of constant local volatilities. Later on, we show that LV is indeed an average over instantaneous volatilites, formalizing the intuition of those practitioners who first introduced the concept.

39 Chapter 1: Local Volatility (LV): A Brief Review of Dupire s Work For a given expiration T and current stock price S 0, the collection C(S 0, K, T ) of undiscounted option prices of different strikes yields the risk-neutral density function φ of the final spot S T through the relationship C(S 0, K, T ) = K (S T K)φ(S T, T ; S 0 )ds T.

40 Chapter 1: Local Volatility (LV): A Brief Review of Dupire s Work Differentiate this twice wrt K to obtain φ(s T, T ; S 0 ) = 2 C K 2 so the Arrow-Debreu prices for each expiration may be recovered by twice differentiating the undiscounted option price wrt K.

41 Chapter 1: Local Volatility (LV): A Brief Review of Dupire s Work Given the distribution of final spot prices S T for each time T conditional on some starting spot price S 0, Dupire shows that there is a unique risk neutral diffusion process which generates these distributions. That is, given the set of all European option prices, we may determine the functional form of the diffusion parameter (LV) of the unique risk neutral diffusion process which generates these prices.

42 Chapter 1: Local Volatility (LV): A Brief Review of Dupire s Work Let us write the process as ds S = µ tdt + σ(s t, t; S 0 )dz. Application of Itô lemma together with risk neutrality, gives rise to a partial DE for functions of the stock price, which is a straightforward generalization of B-S. In particular, the pseudoprobability densities φ = 2 C K 2 must satisfy the Fokker-Planck equation.

43 Chapter 1: Local Volatility (LV): A Brief Review of Dupire s Work This leads to the following equation for the undiscounted option price C in terms of the strike price: C T = σ2 K 2 2 C 2 K 2 + (r t D t )(C K C K ), where r t is the risk-free rate, D t is the dividend yield and C is short for C(S 0, K, T ).

44 Chapter 1: Local Volatility (LV): Derivation of the Dupire Equation Here, φ is the pseudo-probability density of the final spot time T. It evolves according to the Fokker-Planck equation: S 2 T (σ 2 S 2 T ) S (µs T φ) S T = φ T.

45 Chapter 1: Local Volatility (LV): Derivation of the Dupire Equation Differentiting wrt K gives and C + K = ds T φ(s T, T ; S 0 ), K 2 C K 2 = φ.

46 Chapter 1: Local Volatility (LV): Derivation of the Dupire Equation Differentiating C wrt T (and taking into account above φ T ) gives { C + 1 T = 2 } ds T (σ 2 ST 2 K 2 ) S (µs T φ) (S T K). S T S 2 T Integrating by parts twice gives: C T = σ2 K 2 2 C C + µ(t )( K 2 K2 K ) which is the Dupire equation when the underlying stock has riskneutral drift µ.

47 Chapter 1: Local Volatility (LV): Derivation of the Dupire Equation That is, the forward price of the stock at time T is given by F T = S 0 exp( µ tdt). 0 Were we to express the option price as a function of the forward price F T, we would get the same expression minus the drift term. That is, T C T = 1 2 σ2 K 2 2 C K 2, where C = C(F T, K, T ).

48 Chapter 1: Local Volatility (LV): Derivation of the Dupire Equation Inverting this gives σ 2 (K, T, S 0 ) = C T 1 2 K2 2 C K 2 The right-hand side of the last equation can be computed from known European option prices. So, given a complete set of European option prices for all strikes and expirations, LVs are given by the last equation. We can view this equation as a definition of the LV function regardless of what kind of process (SV, e.g.) actually governs the evolution of volatility.

49 Chapter 1: Local Volatility (LV): LV in Terms of Implied Volatility (IV) Market prices of options are quoted in terms of B-S IV σ BS (K, T ; S 0 ). In other words, we may write C(S 0, K, T ) = C BS (S 0, K, σ BS (K, T ; S 0 ), T ). More convenient to work in terms of two dimensionless variables: the B-S implied total variance w defined by and the log-strike y defined by w(s 0, K, T ) := σ 2 BS (K, T ; S 0)T y = log( K F T ), where F T = S 0 exp( T 0 µ t dt) gives the forward price of the stock at time 0.

50 Chapter 1: Local Volatility (LV): LV in Terms of Implied Volatility (IV) In terms of these variables, the B-S formula for the future value of the option price becomes C BS (F T, y, w) = F T [N(d 1 ) e y N(d 2 )] = F T [N( y w + w 2 ) ey N( y w w 2 )] and the Dupire equation becomes C T = v L C 2 [ 2 y 2 C ] + µ(t )C y with v L = σ 2 (S 0, K, T ) representing the LV.

51 Chapter 1: Local Volatility (LV): LV in Terms of Implied Volatility (IV) Using Black-Scholes formula and Dupire equation we get: v L = w T 1 y w w y ( 1 4 w 1 + y2 w 2)( w y ) w y 2

52 Chapter 1: Local Volatility (LV): LV in Terms of Implied Volatility (IV): Special Case: No Skew If the skew w y is zero, we must have (see previous slide) v L = w T. So the LV in this case reduces to the forward B-S IV. The solution to this is w(t ) = T 0 v L(t)dt.

53 Chapter 1: Local Volatility (LV): LV as a Conditional Expectation of Instantaneous Variance This result was origimally independently derived by Dupire (1996) and Derman and Kani (1998). Follwing now the elegant derivation by Derman and Kani, assume the same stochastic process for the stock price ds t = µ t S t dt + v t S t dz but write it in terms of the forward price F t,t = S t exp[ T t µ s ds] : Note that df T,T = ds T. df t,t = v t F t,t dz.

54 Chapter 1: Local Volatility (LV): LV as a Conditional Expectation of Instantaneous Variance The undiscounted value of a European option with strike K expiring at time T is given by C(S 0, K, T ) = E Q [(S T K) + ]. Differentiating once wrt K gives K C = E Q[θ(S T K)], where θ is the Heaviside function. Differentiating again wrt K gives 2 C K 2 = E Q[δ(S T K)], where δ is the Dirac δ function. Now a formal application of Itô s lemma to the terminal payoff of the option (and using df T,T = ds T ) gives the identity d(s T K) + = θ(s T K)dS T v T S 2 T δ(s T K)dT.

55 Chapter 1: Local Volatility (LV): LV as a Conditional Expectation of Instantaneous Variance Taking conditional expectations of each side, and using the fact that F t,t is a martingale, we get dc = de Q [(S T K) + ] = 1 2 E Q[v T S 2 T δ(s T K)]dT. Also, we can write E Q [v T S 2 T δ(s T K)] = E Q [v T S T = K] 1 2 K2 E Q [δ(s T K)] = E Q [v T S T = K] 1 2 K2 2 C K 2.

56 Chapter 1: Local Volatility (LV): LV as a Conditional Expectation of Instantaneous Variance Putting this together, we get C T = E Q[v T S T = K] 1 2 K2 2 C K 2. Comparing this with the definition of LV, we see that σ 2 (S 0, K, T ) = E Q [v T S T = K]. That is, LV is the risk-neutral expectation of the instantaneous variance conditional on the final stock price S T being equal to the strike price K.

57 Chapter 2: The Heston Model Book s Cover

58 Chapter 2: The process (Heston (1993)) with dz 1 t, dz2 t = ρdt. ds t = µ t S t dt + v t S t dz 1 t dv t = λ(v t v)dt + η v t dz 2 t This is an affine process: the drifts and covariance are linear in S t and v t.

59 Chapter 2: The Heston Model (The valuation equation) V t vs2 2 V S 2 + ρηvs 2 V v S η2 v V v + rs V S rv = λ(v v) V v. Note that Gatheral has assumed that the original process is already in the pricing measure.

60 Chapter 2: The Heston Model (European option pricing) The valuation equation rewritten Consider a call option expiring at T with strike price K. Set x = ln F t,t K, where F t,t is the T -forward price of the stock index at time t. Set τ = T t. Write C(τ, x, v) = e rτ V (t, S, v).

61 Chapter 2: The Heston Model (European option pricing) C τ vc xx 1 2 vc x η2 vc vv + ρηvc xv λ(v v)c v = 0 with final time condition C(0, x, v) = K(e x 1) +. According to Duffie, Pan, Singleton (2000), we can look for the solution in the form C(τ, x, v) = K ( e x P 1 (τ, x, v) P 0 (τ, x, v) ).

62 Chapter 2: The Heston Model (European option pricing) P equations: for j = 0, 1 P j τ + 2 v P j x ( 1)j v P j 2 x + η2 v P j 2 v + ρηv 2 P j v x + (a b jv) P j v = 0 where a = λv and b j = λ jρη. Final time conditions: lim τ 0 P j (τ, x, v) = 1 {x>0}.

63 Chapter 2: The Heston Model (Fourier transforms) Set, for j = 0, 1, so that P j (τ, u, v) = P j (τ, x, v) = 1 2π R e iux P j (τ, x, v)dx, R eiux P j (τ, u, v)du.

64 Chapter 2: The Heston Model (Transformed equations) The P equations have constant coefficients in x, and transform into where v[α j P j β j P j v + γ P j v ] + a P j v P j τ = 0, α j = u2 2 iu 2 + iju β j = λ ρηj ρηiu γ = η2 2.

65 Chapter 2: The Heston Model (Transformed equations) We look for solutions of this in the form P j (τ, u, v) = e C j(τ,u)v+d j (τ,u)v P j (0, u, v).

66 Chapter 2: The Heston Model (European option pricing) The result is a set of Riccati equations for C j and D j : where C j τ = λd j; r ± j = β j ± β 2 j 4α jγ 2γ D j τ = γ(d j r + j )(D j r j ), =: β j ± d j η 2. Given that C j (0, u) = D j (0, u) = 0, Gatheral deduces D(τ, u) = r j where g j = r j /r+ j. 1 e d jτ 1 g j e d jτ ; C(τ, u) = λr j τ 2λ η 2 ln 1 g je d jτ 1 g j,

67 Chapter 2: The Heston Model (European option pricing The final step is to compute P j (τ, x, v) = π 0 R e C j(τ,u)v+d j (τ,u)v+iux iu du, and compute the option value via C(τ, x, v) = K ( e x P 1 (τ, x, v) P 0 (τ, x, v) ).

68 Chapter 2: The Heston Model (European option pricing) Next Picture: Black Scholes implied volatilities from Heston option prices

69

70 Chapter 2: Simulation) The Heston Model (European option pricing: The SDE again with dz 1 t, dz2 t = ρdt. ds t = µ t S t dt + v t S t dz 1 t dv t = λ(v t v)dt + η v t dz 2 t

71 Chapter 2: The Heston Model (European option pricing: Euler discretization) The variance process becomes v i+1 = v i λ(v i v) t + η v i tz. The convergence is extremely slow.

72 Chapter 2: The Heston Model (European option pricing: Milstein discretization) Incorporating higher order terms in the Itô-Taylor expansion leads to v i+1 = v i λ(v i v) t + η v i tz + η2 = ( vi + η 2 4 t(z2 1) tz ) 2 λ(vi v) t η2 4 t. The stock process should be discretized in terms of x i = log S i /S 0 : x i+1 = x i v i 2 t + v i tw, where E[ZW ] = ρ.

73 Chapter 3: The Implied Volatility Surface Book s Cover

74 Structure of Chapter 3: The Implied Volatility Surface Ch.1 Brief review Getting Implied Volatilities from Local Volatilities Local Volatility in the Heston Model Implied volatility in the Heston model The SPX Implied Volatility Surface

75 Chapter 3: Main objective - Ch.1 - how to compute local volatilities from implied volatilities - Ch.3 - how to compute implied volatilities from local volatilities: - estimate local volatilities generated by a given SV model using the fact that the local variance (LV) is a conditional expectation of instantaneous variance - given an SV model we can approximate the implied volatility surface - conversely, given the shape of an actual implied volatility surface we can deduce some characteristics of the underlying process

76 Chapter 3: 1. Getting implied volatilities from local volatilities - Understanding implied volatility - Ch.1 derived a formula for local volatility in terms of implied volatility - it is not an easy task to invert this formula - instead, by exploiting the work of Dupire (1998), derive a general path-integral representation of Black-Scholes implied variance

77 Chapter 3: 1. Getting implied volatilities from local volatilities - Understanding implied volatility - Using x t := log S t /S 0 we have: v K,T (t) = v L (x t, t)q(x t )dx t, where q(s t ) looks like a Brownian Bridge density for the stock.

78 Chapter 3: 1. Getting implied volatilities from local volatilities - Understanding implied volatility - This suggests that some Taylor expansion can be written for q (2nd order) and v L (first order) around the peak x t so one can approximate: v K,T (t) v L ( x t, t) so: σ BS (K, T ) 2 1 T T 0 v L ( x t )dt - In words, the BS implied variance of an option with strike K and maturity T is given approximately by the integral from 0 to T of the local variances along the path x t that minimizes the Brownian Bridge density q(x t ).

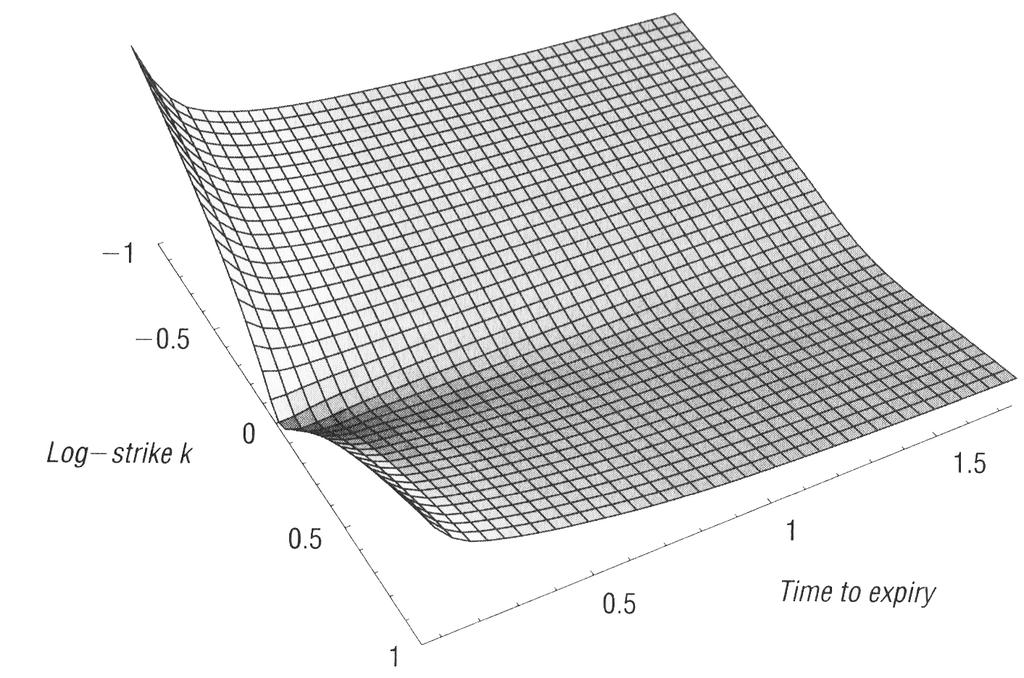

79 Chapter 3: 2. Local volatility in Heston model When µ = 0, we can rewrite the Heston model dynamics: dx t = v t /2dt + v t dz t dv t = λ(v t v)dt + ρη v t dz t + 1 ρ 2 η v t dw t where dw t and dz t are orthogonal. Eliminating v t dz t, we get: dv t = λ(v t v)dt + ρη(dx t + v t /2dt) + 1 ρ 2 η v t dw t Idea: Compute local variances for the Heston model and integrate local variances from valuation date to expiration date using the formula derived previously.

80 Chapter 3: 2. Local volatility in Heston model - The unconditional expected instantaneous variance at time t is: ˆv s := E[v s ] = (v 0 v)e λs + v - The expected total variance to time t is: ŵ t := T 0 ( 1 e λt ˆv s ds = (v 0 v) λ ) + vt Finally we need to compute u t := E[v t x T ].

81 Chapter 3: 2. Local volatility in Heston model - Under some assumptions the last term approaches zero: du t λ (u t v )dt + ρη x T ŵ T ˆv t dt with λ = λ ρη/2 and v = vλ/λ. The solution of this equation is: u T ˆv T + ρη x T ŵ T T 0 ˆv s e λ (T s) ds with ˆv s := (v ˆv)e λ s + v

82 Chapter 3: 2. Local volatility in Heston model - Since from Ch.1 σ 2 (K, T, S 0 ) = E[v T x T ], the above equation gives an accurate approximate for the local variance within the Heston model (extremely accurate when ρ = ±1). We see that in the Heston model, local variance is approximately linear in x : u T = E[v T x T ] = ˆv T + ρη x T ŵ T T 0 ˆv s e λ (T s) ds

83 Chapter Implied volatility in Heston model - Combining the results from 1 and 2 we can now compute the implied variance by integrating the Heston local variance along the most probable stock price path joining the initial stock price to the strike price at expiration. σ BS (K, T ) 2 1 T T σ 2 x t,t dt = 1 T T u t ( x t )dt 0 0

84 Chapter Implied volatility in Heston model - Substituting this into the equation for u T we have: σ BS (K, T ) 2 1 T T u t ( x t )dt 1 T 0 T 0 ˆv tdt + ρη x T 1 ŵ T T T 0 dt t 0 ˆv s e λ (t s) ds

85 Chapter 3: 3. Implied volatility in Heston model - The term structure of Black-Scholes Implied volatility in the Heston model - The at-the-money term structure of BS implied variance in the Heston model is obtained by setting x T = 0. σ BS (K, T ) 2 K=FT 1 T T 0 ˆv tdt = 1 T T 0 [(v v )e λ t + v ] dt = (v v ) 1 e λ T λ + v T - when T 0 the at-the-money BS implied variance converges to the level of instantaneous variance v and as T the atthe-money BS implied variance reverts to v.

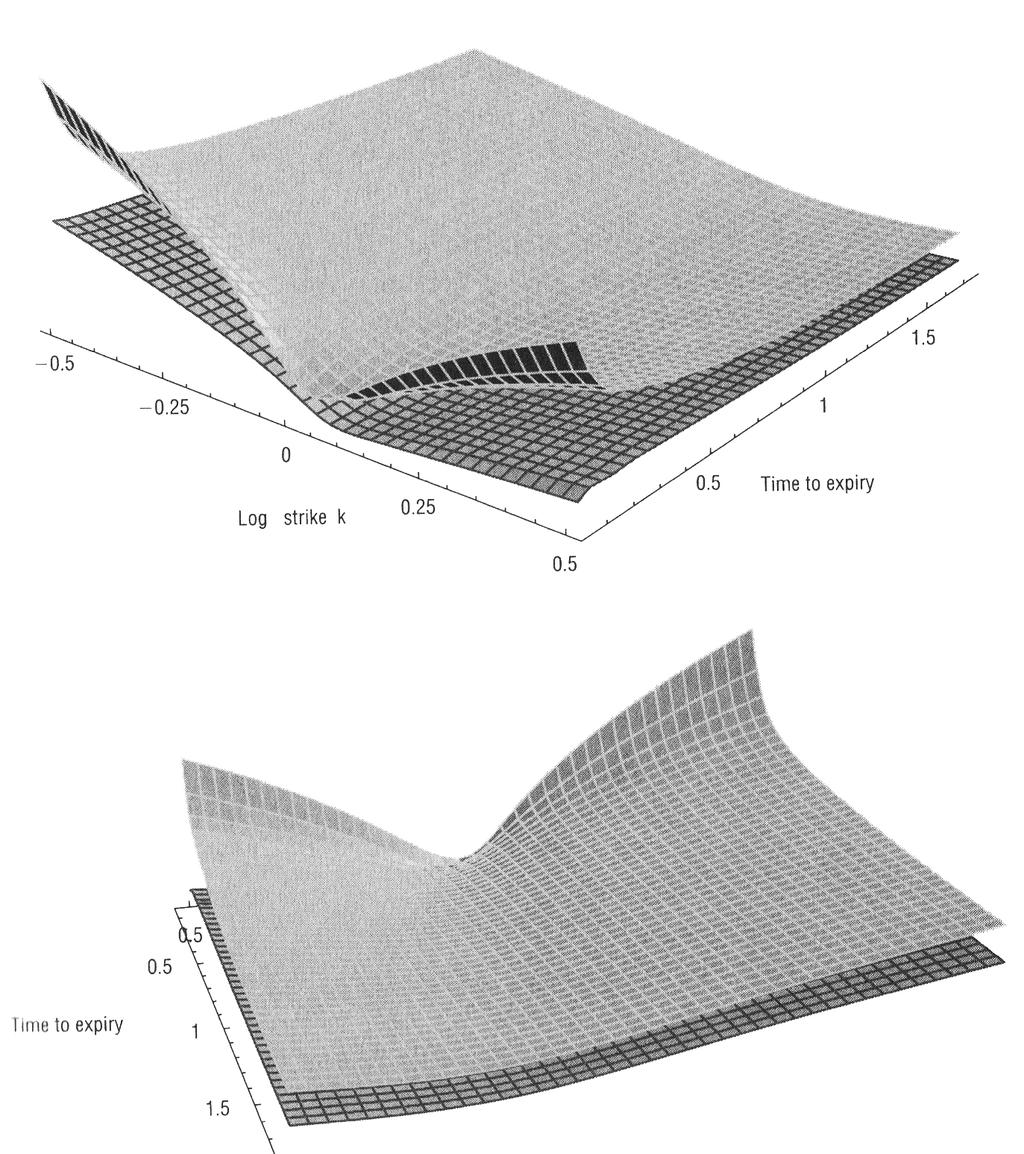

86 Chpater 3: 4. The SPX implied volatility surface - the SVI parametrization - Gatheral (2004) proposes the following stochastic volatility inspired (SVI) parametrization for the volatility smile: σ BS (k) = a + b ( ρ(k m) + (k m) 2 + σ 2) where k is the log-strike and a, b, ρ, σ and m are some parameters depending on the expiration.

87 Chpater 3: 4. The SPX implied volatility surface - the SVI parametrization - Figure 1 below shows the surface from a nonlinear SVI fit to observed implied variance as a function of k for each expiration on September 15, 2005

88

89 Chpater 3: 4. The SPX implied volatility surface - the SVI parametrization - Figure 2 below shows the SVI fit of the SPX implied volatilities for each of the eight listed expirations as of the close on September 15, Strikes are on the x-axis and implied volatilities are on the y-axis. The black and grey diamonds represent bid and offer volatilities respectively and the solid line is the SVI fit.

90

91 Chpater 3: 4. The SPX implied volatility surface - the SVI parametrization - Figure 3 below shows the plot of at-the-money skews as a function of time. The solid and dashed lines show the results of fitting the approximate formula: ρη 1 (1 λ 1 e λ T ) T λ T - The solid line takes all points into account while the dashed line drops the first three time to expirations - The observed variance skew increases faster as T 0 than the one implied by an SV model. Including jumps might solve the problem.

92

93 Chapter 3: 4. The SPX implied volatility surface - A Heston fit to the data - The parameters are: v = , v = , η = , ρ = and λ =

94 Chapter 3: 4. The SPX implied volatility surface - A Heston fit to the data - Figure 4 below shows a comparison between the empirical SPX implied volatility surface with the Heston fit on Nov 15. Heston fits well enough long maturity options, but does a poor job for short expirations. The upper surface is the empirical one. The Heston fit surface has been shifted down by five volatility points.

95

96 Contents of the Book: 4-11 Chapters Short Descriptions Book s Cover

97 Contents of the Book: 4-11 Chapters Short Descriptions Chapter 4 The Heston-Nandi Model : Chooses specific numerical values for the parameters of the Heston model, ρ = 1 as originally studied by Heston and Nandi and demonstartes that an approximate formula for implied volatility derived in Chapter 3 works particularly well in this limit. As a result, we are able to find parameters of LV and SV models that generate almost identical European option prices.

98 Contents of the Book: 4-11 Chapters Short Descriptions Chapter 5 Adding Jumps : Explores the modelling of jumps showing first why jumps are required; introduces then characteristic function techniques and applies these to the computation of IV in models with jumps; concludes by showing that the SVJ (SV with jumps in the stock price) is capable of generating a volatility surface that has most of the features of the empirical surface.

99 Contents of the Book: 4-11 Chapters Short Descriptions Chapter 6 Modelling Default Risk : Applies the work on jumps to Merton s jump-to-ruin model of default; explains the Credit- Grades model.

100 Contents of the Book: Chapters Short Descriptions Chapter 7 Volatility Surface Asymptotics : examines the asymptotic properties of the VS showing that all models with SV and jumps generate VS that are roughly the same shape.

101 Contents of the Book: 4-11 Chapters Short Descriptions Chapter 8 Dynamics of the Volatility Surface : shows how the dynamics of V can be deduced from the time series properties of VS; shows also why it is the dynamics of the VS generated by LV models are highly unrealistic.

102 Contents of the Book: 4-11 Chapters Short Descriptions Chapter 9 Barrier Options : presents various types of barrier options (BO) and shows how intuition may be developed for these by studying two simple limiting cases.

103 Contents of the Book: 4-11 Chapters Short Descriptions Chapter 10 Exotic Cliquets : studies in detail three actual exotic cliquet transactions that happen to have matured so that we can explore both pricing and ex post performance, specifically, a locally capped and globally floored cliquet, a reverse cliquet, and a Napoleon.

104 Contents of the Book: 4-11 Chapters Short Descriptions Chapter 11 Volatility Derivatives (the longest of all): focuses on the pricing and hedging of claims whose underlying is quadratic variation, explains why the market in volatility derivatives is suprisingly active and liquid.

105 Conclusion 1. Introduction to the Book 2. Contents of the Book 3. Chapters 1-3 Review 4. Chpaters 4-11 Short Description

106 Acknowledgements: Thank to all our faculty and grad students very much for doing review of this book at the Lunch at the Lab finance seminar (September 2010-March 2011): A. Badescu, D. Sezer, A. Ware, A. Gezahagne, K. Cui, K. Zhao, P. Dovoedo! Many thanks to MITACS for supporting our Lunch at the Lab finance seminar! (For all Chapters review see our Lunch at the Lab finance seminar s web:

107 Acknowledgements: Many thanks to Scott Dalton and PRMIA Calgary Chapter for the opportunity to give this talk!

108 Thank You for Your Time and Attention! Q&A Time!

Lecture 1: Stochastic Volatility and Local Volatility

Lecture 1: Stochastic Volatility and Local Volatility Jim Gatheral, Merrill Lynch Case Studies in Financial Modelling Course Notes, Courant Institute of Mathematical Sciences, Fall Term, 2003 Abstract

Lecture 1: Stochastic Volatility and Local Volatility Jim Gatheral, Merrill Lynch Case Studies in Financial Modelling Course Notes, Courant Institute of Mathematical Sciences, Fall Term, 2003 Abstract

Stochastic Volatility (Working Draft I)

") Stochastic Volatility (Working Draft I) Paul J. Atzberger General comments or corrections should be sent to: paulatz@cims.nyu.edu 1 Introduction When using the Black-Scholes-Merton model to price derivative

Stochastic Volatility (Working Draft I) Paul J. Atzberger General comments or corrections should be sent to: paulatz@cims.nyu.edu 1 Introduction When using the Black-Scholes-Merton model to price derivative

Modeling the Implied Volatility Surface. Jim Gatheral Global Derivatives and Risk Management 2003 Barcelona May 22, 2003

Modeling the Implied Volatility Surface Jim Gatheral Global Derivatives and Risk Management 2003 Barcelona May 22, 2003 This presentation represents only the personal opinions of the author and not those

Modeling the Implied Volatility Surface Jim Gatheral Global Derivatives and Risk Management 2003 Barcelona May 22, 2003 This presentation represents only the personal opinions of the author and not those

A Brief Introduction to Stochastic Volatility Modeling

A Brief Introduction to Stochastic Volatility Modeling Paul J. Atzberger General comments or corrections should be sent to: paulatz@cims.nyu.edu Introduction When using the Black-Scholes-Merton model to

A Brief Introduction to Stochastic Volatility Modeling Paul J. Atzberger General comments or corrections should be sent to: paulatz@cims.nyu.edu Introduction When using the Black-Scholes-Merton model to

1.1 Basic Financial Derivatives: Forward Contracts and Options

Chapter 1 Preliminaries 1.1 Basic Financial Derivatives: Forward Contracts and Options A derivative is a financial instrument whose value depends on the values of other, more basic underlying variables

Chapter 1 Preliminaries 1.1 Basic Financial Derivatives: Forward Contracts and Options A derivative is a financial instrument whose value depends on the values of other, more basic underlying variables

Heston Stochastic Volatility Model of Stock Prices. Peter Deeney. Project Supervisor Dr Olaf Menkens

Heston Stochastic Volatility Model of Stock Prices Peter Deeney Project Supervisor Dr Olaf Menkens School of Mathematical Sciences Dublin City University August 2009 Declaration I hereby certify that this

Heston Stochastic Volatility Model of Stock Prices Peter Deeney Project Supervisor Dr Olaf Menkens School of Mathematical Sciences Dublin City University August 2009 Declaration I hereby certify that this

1 Implied Volatility from Local Volatility

Abstract We try to understand the Berestycki, Busca, and Florent () (BBF) result in the context of the work presented in Lectures and. Implied Volatility from Local Volatility. Current Plan as of March

Abstract We try to understand the Berestycki, Busca, and Florent () (BBF) result in the context of the work presented in Lectures and. Implied Volatility from Local Volatility. Current Plan as of March

Valuation of Volatility Derivatives. Jim Gatheral Global Derivatives & Risk Management 2005 Paris May 24, 2005

Valuation of Volatility Derivatives Jim Gatheral Global Derivatives & Risk Management 005 Paris May 4, 005 he opinions expressed in this presentation are those of the author alone, and do not necessarily

Valuation of Volatility Derivatives Jim Gatheral Global Derivatives & Risk Management 005 Paris May 4, 005 he opinions expressed in this presentation are those of the author alone, and do not necessarily

The Black-Scholes Model

The Black-Scholes Model Liuren Wu Options Markets Liuren Wu ( c ) The Black-Merton-Scholes Model colorhmoptions Markets 1 / 18 The Black-Merton-Scholes-Merton (BMS) model Black and Scholes (1973) and Merton

The Black-Scholes Model Liuren Wu Options Markets Liuren Wu ( c ) The Black-Merton-Scholes Model colorhmoptions Markets 1 / 18 The Black-Merton-Scholes-Merton (BMS) model Black and Scholes (1973) and Merton

Advanced Topics in Derivative Pricing Models. Topic 4 - Variance products and volatility derivatives

Advanced Topics in Derivative Pricing Models Topic 4 - Variance products and volatility derivatives 4.1 Volatility trading and replication of variance swaps 4.2 Volatility swaps 4.3 Pricing of discrete

Advanced Topics in Derivative Pricing Models Topic 4 - Variance products and volatility derivatives 4.1 Volatility trading and replication of variance swaps 4.2 Volatility swaps 4.3 Pricing of discrete

The Black-Scholes Model

The Black-Scholes Model Liuren Wu Options Markets (Hull chapter: 12, 13, 14) Liuren Wu ( c ) The Black-Scholes Model colorhmoptions Markets 1 / 17 The Black-Scholes-Merton (BSM) model Black and Scholes

The Black-Scholes Model Liuren Wu Options Markets (Hull chapter: 12, 13, 14) Liuren Wu ( c ) The Black-Scholes Model colorhmoptions Markets 1 / 17 The Black-Scholes-Merton (BSM) model Black and Scholes

Lecture 3: Asymptotics and Dynamics of the Volatility Skew

Lecture 3: Asymptotics and Dynamics of the Volatility Skew Jim Gatheral, Merrill Lynch Case Studies in Financial Modelling Course Notes, Courant Institute of Mathematical Sciences, Fall Term, 2001 I am

Lecture 3: Asymptotics and Dynamics of the Volatility Skew Jim Gatheral, Merrill Lynch Case Studies in Financial Modelling Course Notes, Courant Institute of Mathematical Sciences, Fall Term, 2001 I am

The Black-Scholes PDE from Scratch

The Black-Scholes PDE from Scratch chris bemis November 27, 2006 0-0 Goal: Derive the Black-Scholes PDE To do this, we will need to: Come up with some dynamics for the stock returns Discuss Brownian motion

The Black-Scholes PDE from Scratch chris bemis November 27, 2006 0-0 Goal: Derive the Black-Scholes PDE To do this, we will need to: Come up with some dynamics for the stock returns Discuss Brownian motion

The Black-Scholes Model

IEOR E4706: Foundations of Financial Engineering c 2016 by Martin Haugh The Black-Scholes Model In these notes we will use Itô s Lemma and a replicating argument to derive the famous Black-Scholes formula

IEOR E4706: Foundations of Financial Engineering c 2016 by Martin Haugh The Black-Scholes Model In these notes we will use Itô s Lemma and a replicating argument to derive the famous Black-Scholes formula

7.1 Volatility Simile and Defects in the Black-Scholes Model

Chapter 7 Beyond Black-Scholes Model 7.1 Volatility Simile and Defects in the Black-Scholes Model Before pointing out some of the flaws in the assumptions of the Black-Scholes world, we must emphasize

Chapter 7 Beyond Black-Scholes Model 7.1 Volatility Simile and Defects in the Black-Scholes Model Before pointing out some of the flaws in the assumptions of the Black-Scholes world, we must emphasize

Local Volatility Dynamic Models

René Carmona Bendheim Center for Finance Department of Operations Research & Financial Engineering Princeton University Columbia November 9, 27 Contents Joint work with Sergey Nadtochyi Motivation 1 Understanding

René Carmona Bendheim Center for Finance Department of Operations Research & Financial Engineering Princeton University Columbia November 9, 27 Contents Joint work with Sergey Nadtochyi Motivation 1 Understanding

Lecture 8: The Black-Scholes theory

Lecture 8: The Black-Scholes theory Dr. Roman V Belavkin MSO4112 Contents 1 Geometric Brownian motion 1 2 The Black-Scholes pricing 2 3 The Black-Scholes equation 3 References 5 1 Geometric Brownian motion

Lecture 8: The Black-Scholes theory Dr. Roman V Belavkin MSO4112 Contents 1 Geometric Brownian motion 1 2 The Black-Scholes pricing 2 3 The Black-Scholes equation 3 References 5 1 Geometric Brownian motion

From Discrete Time to Continuous Time Modeling

From Discrete Time to Continuous Time Modeling Prof. S. Jaimungal, Department of Statistics, University of Toronto 2004 Arrow-Debreu Securities 2004 Prof. S. Jaimungal 2 Consider a simple one-period economy

From Discrete Time to Continuous Time Modeling Prof. S. Jaimungal, Department of Statistics, University of Toronto 2004 Arrow-Debreu Securities 2004 Prof. S. Jaimungal 2 Consider a simple one-period economy

Volatility Smiles and Yield Frowns

Volatility Smiles and Yield Frowns Peter Carr NYU CBOE Conference on Derivatives and Volatility, Chicago, Nov. 10, 2017 Peter Carr (NYU) Volatility Smiles and Yield Frowns 11/10/2017 1 / 33 Interest Rates

Volatility Smiles and Yield Frowns Peter Carr NYU CBOE Conference on Derivatives and Volatility, Chicago, Nov. 10, 2017 Peter Carr (NYU) Volatility Smiles and Yield Frowns 11/10/2017 1 / 33 Interest Rates

Developments in Volatility Derivatives Pricing

Developments in Volatility Derivatives Pricing Jim Gatheral Global Derivatives 2007 Paris, May 23, 2007 Motivation We would like to be able to price consistently at least 1 options on SPX 2 options on

Developments in Volatility Derivatives Pricing Jim Gatheral Global Derivatives 2007 Paris, May 23, 2007 Motivation We would like to be able to price consistently at least 1 options on SPX 2 options on

AN ANALYTICALLY TRACTABLE UNCERTAIN VOLATILITY MODEL

AN ANALYTICALLY TRACTABLE UNCERTAIN VOLATILITY MODEL FABIO MERCURIO BANCA IMI, MILAN http://www.fabiomercurio.it 1 Stylized facts Traders use the Black-Scholes formula to price plain-vanilla options. An

AN ANALYTICALLY TRACTABLE UNCERTAIN VOLATILITY MODEL FABIO MERCURIO BANCA IMI, MILAN http://www.fabiomercurio.it 1 Stylized facts Traders use the Black-Scholes formula to price plain-vanilla options. An

Option Pricing Models for European Options

Chapter 2 Option Pricing Models for European Options 2.1 Continuous-time Model: Black-Scholes Model 2.1.1 Black-Scholes Assumptions We list the assumptions that we make for most of this notes. 1. The underlying

Chapter 2 Option Pricing Models for European Options 2.1 Continuous-time Model: Black-Scholes Model 2.1.1 Black-Scholes Assumptions We list the assumptions that we make for most of this notes. 1. The underlying

Dynamic Relative Valuation

Dynamic Relative Valuation Liuren Wu, Baruch College Joint work with Peter Carr from Morgan Stanley October 15, 2013 Liuren Wu (Baruch) Dynamic Relative Valuation 10/15/2013 1 / 20 The standard approach

Dynamic Relative Valuation Liuren Wu, Baruch College Joint work with Peter Carr from Morgan Stanley October 15, 2013 Liuren Wu (Baruch) Dynamic Relative Valuation 10/15/2013 1 / 20 The standard approach

Multi-asset derivatives: A Stochastic and Local Volatility Pricing Framework

Multi-asset derivatives: A Stochastic and Local Volatility Pricing Framework Luke Charleton Department of Mathematics Imperial College London A thesis submitted for the degree of Master of Philosophy January

Multi-asset derivatives: A Stochastic and Local Volatility Pricing Framework Luke Charleton Department of Mathematics Imperial College London A thesis submitted for the degree of Master of Philosophy January

Stochastic Volatility and Jump Modeling in Finance

Stochastic Volatility and Jump Modeling in Finance HPCFinance 1st kick-off meeting Elisa Nicolato Aarhus University Department of Economics and Business January 21, 2013 Elisa Nicolato (Aarhus University

Stochastic Volatility and Jump Modeling in Finance HPCFinance 1st kick-off meeting Elisa Nicolato Aarhus University Department of Economics and Business January 21, 2013 Elisa Nicolato (Aarhus University

Volatility Smiles and Yield Frowns

Volatility Smiles and Yield Frowns Peter Carr NYU IFS, Chengdu, China, July 30, 2018 Peter Carr (NYU) Volatility Smiles and Yield Frowns 7/30/2018 1 / 35 Interest Rates and Volatility Practitioners and

Volatility Smiles and Yield Frowns Peter Carr NYU IFS, Chengdu, China, July 30, 2018 Peter Carr (NYU) Volatility Smiles and Yield Frowns 7/30/2018 1 / 35 Interest Rates and Volatility Practitioners and

IEOR E4703: Monte-Carlo Simulation

IEOR E4703: Monte-Carlo Simulation Simulating Stochastic Differential Equations Martin Haugh Department of Industrial Engineering and Operations Research Columbia University Email: martin.b.haugh@gmail.com

IEOR E4703: Monte-Carlo Simulation Simulating Stochastic Differential Equations Martin Haugh Department of Industrial Engineering and Operations Research Columbia University Email: martin.b.haugh@gmail.com

Lecture Quantitative Finance Spring Term 2015

and Lecture Quantitative Finance Spring Term 2015 Prof. Dr. Erich Walter Farkas Lecture 06: March 26, 2015 1 / 47 Remember and Previous chapters: introduction to the theory of options put-call parity fundamentals

and Lecture Quantitative Finance Spring Term 2015 Prof. Dr. Erich Walter Farkas Lecture 06: March 26, 2015 1 / 47 Remember and Previous chapters: introduction to the theory of options put-call parity fundamentals

An Overview of Volatility Derivatives and Recent Developments

An Overview of Volatility Derivatives and Recent Developments September 17th, 2013 Zhenyu Cui Math Club Colloquium Department of Mathematics Brooklyn College, CUNY Math Club Colloquium Volatility Derivatives

An Overview of Volatility Derivatives and Recent Developments September 17th, 2013 Zhenyu Cui Math Club Colloquium Department of Mathematics Brooklyn College, CUNY Math Club Colloquium Volatility Derivatives

Asset Pricing Models with Underlying Time-varying Lévy Processes

Asset Pricing Models with Underlying Time-varying Lévy Processes Stochastics & Computational Finance 2015 Xuecan CUI Jang SCHILTZ University of Luxembourg July 9, 2015 Xuecan CUI, Jang SCHILTZ University

Asset Pricing Models with Underlying Time-varying Lévy Processes Stochastics & Computational Finance 2015 Xuecan CUI Jang SCHILTZ University of Luxembourg July 9, 2015 Xuecan CUI, Jang SCHILTZ University

The Volatility Surface

The Volatility Surface A Practitioner s Guide JIM GATHERAL Foreword by Nassim Nicholas Taleb John Wiley & Sons, Inc. Further Praise for The Volatility Surface As an experienced practitioner, Jim Gatheral

The Volatility Surface A Practitioner s Guide JIM GATHERAL Foreword by Nassim Nicholas Taleb John Wiley & Sons, Inc. Further Praise for The Volatility Surface As an experienced practitioner, Jim Gatheral

Copyright Emanuel Derman 2008

E478 Spring 008: Derman: Lecture 7:Local Volatility Continued Page of 8 Lecture 7: Local Volatility Continued Copyright Emanuel Derman 008 3/7/08 smile-lecture7.fm E478 Spring 008: Derman: Lecture 7:Local

E478 Spring 008: Derman: Lecture 7:Local Volatility Continued Page of 8 Lecture 7: Local Volatility Continued Copyright Emanuel Derman 008 3/7/08 smile-lecture7.fm E478 Spring 008: Derman: Lecture 7:Local

The Use of Importance Sampling to Speed Up Stochastic Volatility Simulations

The Use of Importance Sampling to Speed Up Stochastic Volatility Simulations Stan Stilger June 6, 1 Fouque and Tullie use importance sampling for variance reduction in stochastic volatility simulations.

The Use of Importance Sampling to Speed Up Stochastic Volatility Simulations Stan Stilger June 6, 1 Fouque and Tullie use importance sampling for variance reduction in stochastic volatility simulations.

Hedging Credit Derivatives in Intensity Based Models

Hedging Credit Derivatives in Intensity Based Models PETER CARR Head of Quantitative Financial Research, Bloomberg LP, New York Director of the Masters Program in Math Finance, Courant Institute, NYU Stanford

Hedging Credit Derivatives in Intensity Based Models PETER CARR Head of Quantitative Financial Research, Bloomberg LP, New York Director of the Masters Program in Math Finance, Courant Institute, NYU Stanford

MSC FINANCIAL ENGINEERING PRICING I, AUTUMN LECTURE 9: LOCAL AND STOCHASTIC VOLATILITY RAYMOND BRUMMELHUIS DEPARTMENT EMS BIRKBECK

MSC FINANCIAL ENGINEERING PRICING I, AUTUMN 2010-2011 LECTURE 9: LOCAL AND STOCHASTIC VOLATILITY RAYMOND BRUMMELHUIS DEPARTMENT EMS BIRKBECK The only ingredient of the Black and Scholes formula which is

MSC FINANCIAL ENGINEERING PRICING I, AUTUMN 2010-2011 LECTURE 9: LOCAL AND STOCHASTIC VOLATILITY RAYMOND BRUMMELHUIS DEPARTMENT EMS BIRKBECK The only ingredient of the Black and Scholes formula which is

BIRKBECK (University of London) MSc EXAMINATION FOR INTERNAL STUDENTS MSc FINANCIAL ENGINEERING DEPARTMENT OF ECONOMICS, MATHEMATICS AND STATIS- TICS

MSc EXAMINATION FOR INTERNAL STUDENTS MSc FINANCIAL ENGINEERING DEPARTMENT OF ECONOMICS, MATHEMATICS AND STATIS- TICS") BIRKBECK (University of London) MSc EXAMINATION FOR INTERNAL STUDENTS MSc FINANCIAL ENGINEERING DEPARTMENT OF ECONOMICS, MATHEMATICS AND STATIS- TICS PRICING EMMS014S7 Tuesday, May 31 2011, 10:00am-13.15pm

BIRKBECK (University of London) MSc EXAMINATION FOR INTERNAL STUDENTS MSc FINANCIAL ENGINEERING DEPARTMENT OF ECONOMICS, MATHEMATICS AND STATIS- TICS PRICING EMMS014S7 Tuesday, May 31 2011, 10:00am-13.15pm

STOCHASTIC CALCULUS AND BLACK-SCHOLES MODEL

STOCHASTIC CALCULUS AND BLACK-SCHOLES MODEL YOUNGGEUN YOO Abstract. Ito s lemma is often used in Ito calculus to find the differentials of a stochastic process that depends on time. This paper will introduce

STOCHASTIC CALCULUS AND BLACK-SCHOLES MODEL YOUNGGEUN YOO Abstract. Ito s lemma is often used in Ito calculus to find the differentials of a stochastic process that depends on time. This paper will introduce

Large Deviations and Stochastic Volatility with Jumps: Asymptotic Implied Volatility for Affine Models

Large Deviations and Stochastic Volatility with Jumps: TU Berlin with A. Jaquier and A. Mijatović (Imperial College London) SIAM conference on Financial Mathematics, Minneapolis, MN July 10, 2012 Implied

Large Deviations and Stochastic Volatility with Jumps: TU Berlin with A. Jaquier and A. Mijatović (Imperial College London) SIAM conference on Financial Mathematics, Minneapolis, MN July 10, 2012 Implied

Youngrok Lee and Jaesung Lee

orean J. Math. 3 015, No. 1, pp. 81 91 http://dx.doi.org/10.11568/kjm.015.3.1.81 LOCAL VOLATILITY FOR QUANTO OPTION PRICES WITH STOCHASTIC INTEREST RATES Youngrok Lee and Jaesung Lee Abstract. This paper

orean J. Math. 3 015, No. 1, pp. 81 91 http://dx.doi.org/10.11568/kjm.015.3.1.81 LOCAL VOLATILITY FOR QUANTO OPTION PRICES WITH STOCHASTIC INTEREST RATES Youngrok Lee and Jaesung Lee Abstract. This paper

A Consistent Pricing Model for Index Options and Volatility Derivatives

A Consistent Pricing Model for Index Options and Volatility Derivatives 6th World Congress of the Bachelier Society Thomas Kokholm Finance Research Group Department of Business Studies Aarhus School of

A Consistent Pricing Model for Index Options and Volatility Derivatives 6th World Congress of the Bachelier Society Thomas Kokholm Finance Research Group Department of Business Studies Aarhus School of

A Moment Matching Approach To The Valuation Of A Volume Weighted Average Price Option

A Moment Matching Approach To The Valuation Of A Volume Weighted Average Price Option Antony Stace Department of Mathematics and MASCOS University of Queensland 15th October 2004 AUSTRALIAN RESEARCH COUNCIL

A Moment Matching Approach To The Valuation Of A Volume Weighted Average Price Option Antony Stace Department of Mathematics and MASCOS University of Queensland 15th October 2004 AUSTRALIAN RESEARCH COUNCIL

Lecture 5: Volatility and Variance Swaps

Lecture 5: Volatility and Variance Swaps Jim Gatheral, Merrill Lynch Case Studies in inancial Modelling Course Notes, Courant Institute of Mathematical Sciences, all Term, 21 I am grateful to Peter riz

Lecture 5: Volatility and Variance Swaps Jim Gatheral, Merrill Lynch Case Studies in inancial Modelling Course Notes, Courant Institute of Mathematical Sciences, all Term, 21 I am grateful to Peter riz

Chapter 15: Jump Processes and Incomplete Markets. 1 Jumps as One Explanation of Incomplete Markets

Chapter 5: Jump Processes and Incomplete Markets Jumps as One Explanation of Incomplete Markets It is easy to argue that Brownian motion paths cannot model actual stock price movements properly in reality,

Chapter 5: Jump Processes and Incomplete Markets Jumps as One Explanation of Incomplete Markets It is easy to argue that Brownian motion paths cannot model actual stock price movements properly in reality,

Pricing and hedging with rough-heston models

Pricing and hedging with rough-heston models Omar El Euch, Mathieu Rosenbaum Ecole Polytechnique 1 January 216 El Euch, Rosenbaum Pricing and hedging with rough-heston models 1 Table of contents Introduction

Pricing and hedging with rough-heston models Omar El Euch, Mathieu Rosenbaum Ecole Polytechnique 1 January 216 El Euch, Rosenbaum Pricing and hedging with rough-heston models 1 Table of contents Introduction

arxiv: v1 [q-fin.pr] 18 Feb 2010

![arxiv: v1 [q-fin.pr] 18 Feb 2010](/thumbs/87/96175643.jpg "arxiv: v1 [q-fin.pr] 18 Feb 2010") CONVERGENCE OF HESTON TO SVI JIM GATHERAL AND ANTOINE JACQUIER arxiv:1002.3633v1 [q-fin.pr] 18 Feb 2010 Abstract. In this short note, we prove by an appropriate change of variables that the SVI implied

CONVERGENCE OF HESTON TO SVI JIM GATHERAL AND ANTOINE JACQUIER arxiv:1002.3633v1 [q-fin.pr] 18 Feb 2010 Abstract. In this short note, we prove by an appropriate change of variables that the SVI implied

Pricing with a Smile. Bruno Dupire. Bloomberg

CP-Bruno Dupire.qxd 10/08/04 6:38 PM Page 1 11 Pricing with a Smile Bruno Dupire Bloomberg The Black Scholes model (see Black and Scholes, 1973) gives options prices as a function of volatility. If an

CP-Bruno Dupire.qxd 10/08/04 6:38 PM Page 1 11 Pricing with a Smile Bruno Dupire Bloomberg The Black Scholes model (see Black and Scholes, 1973) gives options prices as a function of volatility. If an

Rohini Kumar. Statistics and Applied Probability, UCSB (Joint work with J. Feng and J.-P. Fouque)

") Small time asymptotics for fast mean-reverting stochastic volatility models Statistics and Applied Probability, UCSB (Joint work with J. Feng and J.-P. Fouque) March 11, 2011 Frontier Probability Days,

Small time asymptotics for fast mean-reverting stochastic volatility models Statistics and Applied Probability, UCSB (Joint work with J. Feng and J.-P. Fouque) March 11, 2011 Frontier Probability Days,

( ) since this is the benefit of buying the asset at the strike price rather

since this is the benefit of buying the asset at the strike price rather") Review of some financial models for MAT 483 Parity and Other Option Relationships The basic parity relationship for European options with the same strike price and the same time to expiration is: C( KT

Review of some financial models for MAT 483 Parity and Other Option Relationships The basic parity relationship for European options with the same strike price and the same time to expiration is: C( KT

Exploring Volatility Derivatives: New Advances in Modelling. Bruno Dupire Bloomberg L.P. NY

Exploring Volatility Derivatives: New Advances in Modelling Bruno Dupire Bloomberg L.P. NY bdupire@bloomberg.net Global Derivatives 2005, Paris May 25, 2005 1. Volatility Products Historical Volatility

Exploring Volatility Derivatives: New Advances in Modelling Bruno Dupire Bloomberg L.P. NY bdupire@bloomberg.net Global Derivatives 2005, Paris May 25, 2005 1. Volatility Products Historical Volatility

Lecture Note 8 of Bus 41202, Spring 2017: Stochastic Diffusion Equation & Option Pricing

Lecture Note 8 of Bus 41202, Spring 2017: Stochastic Diffusion Equation & Option Pricing We shall go over this note quickly due to time constraints. Key concept: Ito s lemma Stock Options: A contract giving

Lecture Note 8 of Bus 41202, Spring 2017: Stochastic Diffusion Equation & Option Pricing We shall go over this note quickly due to time constraints. Key concept: Ito s lemma Stock Options: A contract giving

Tangent Lévy Models. Sergey Nadtochiy (joint work with René Carmona) Oxford-Man Institute of Quantitative Finance University of Oxford.

Oxford-Man Institute of Quantitative Finance University of Oxford.") Tangent Lévy Models Sergey Nadtochiy (joint work with René Carmona) Oxford-Man Institute of Quantitative Finance University of Oxford June 24, 2010 6th World Congress of the Bachelier Finance Society Sergey

Tangent Lévy Models Sergey Nadtochiy (joint work with René Carmona) Oxford-Man Institute of Quantitative Finance University of Oxford June 24, 2010 6th World Congress of the Bachelier Finance Society Sergey

Preference-Free Option Pricing with Path-Dependent Volatility: A Closed-Form Approach

Preference-Free Option Pricing with Path-Dependent Volatility: A Closed-Form Approach Steven L. Heston and Saikat Nandi Federal Reserve Bank of Atlanta Working Paper 98-20 December 1998 Abstract: This

Preference-Free Option Pricing with Path-Dependent Volatility: A Closed-Form Approach Steven L. Heston and Saikat Nandi Federal Reserve Bank of Atlanta Working Paper 98-20 December 1998 Abstract: This

Math 416/516: Stochastic Simulation

Math 416/516: Stochastic Simulation Haijun Li lih@math.wsu.edu Department of Mathematics Washington State University Week 13 Haijun Li Math 416/516: Stochastic Simulation Week 13 1 / 28 Outline 1 Simulation

Math 416/516: Stochastic Simulation Haijun Li lih@math.wsu.edu Department of Mathematics Washington State University Week 13 Haijun Li Math 416/516: Stochastic Simulation Week 13 1 / 28 Outline 1 Simulation

MASM006 UNIVERSITY OF EXETER SCHOOL OF ENGINEERING, COMPUTER SCIENCE AND MATHEMATICS MATHEMATICAL SCIENCES FINANCIAL MATHEMATICS.

MASM006 UNIVERSITY OF EXETER SCHOOL OF ENGINEERING, COMPUTER SCIENCE AND MATHEMATICS MATHEMATICAL SCIENCES FINANCIAL MATHEMATICS May/June 2006 Time allowed: 2 HOURS. Examiner: Dr N.P. Byott This is a CLOSED

MASM006 UNIVERSITY OF EXETER SCHOOL OF ENGINEERING, COMPUTER SCIENCE AND MATHEMATICS MATHEMATICAL SCIENCES FINANCIAL MATHEMATICS May/June 2006 Time allowed: 2 HOURS. Examiner: Dr N.P. Byott This is a CLOSED

Lecture 11: Stochastic Volatility Models Cont.

E4718 Spring 008: Derman: Lecture 11:Stochastic Volatility Models Cont. Page 1 of 8 Lecture 11: Stochastic Volatility Models Cont. E4718 Spring 008: Derman: Lecture 11:Stochastic Volatility Models Cont.

E4718 Spring 008: Derman: Lecture 11:Stochastic Volatility Models Cont. Page 1 of 8 Lecture 11: Stochastic Volatility Models Cont. E4718 Spring 008: Derman: Lecture 11:Stochastic Volatility Models Cont.

EFFICIENT MONTE CARLO ALGORITHM FOR PRICING BARRIER OPTIONS

Commun. Korean Math. Soc. 23 (2008), No. 2, pp. 285 294 EFFICIENT MONTE CARLO ALGORITHM FOR PRICING BARRIER OPTIONS Kyoung-Sook Moon Reprinted from the Communications of the Korean Mathematical Society

Commun. Korean Math. Soc. 23 (2008), No. 2, pp. 285 294 EFFICIENT MONTE CARLO ALGORITHM FOR PRICING BARRIER OPTIONS Kyoung-Sook Moon Reprinted from the Communications of the Korean Mathematical Society

Quadratic hedging in affine stochastic volatility models

Quadratic hedging in affine stochastic volatility models Jan Kallsen TU München Pittsburgh, February 20, 2006 (based on joint work with F. Hubalek, L. Krawczyk, A. Pauwels) 1 Hedging problem S t = S 0

Quadratic hedging in affine stochastic volatility models Jan Kallsen TU München Pittsburgh, February 20, 2006 (based on joint work with F. Hubalek, L. Krawczyk, A. Pauwels) 1 Hedging problem S t = S 0

M5MF6. Advanced Methods in Derivatives Pricing

Course: Setter: M5MF6 Dr Antoine Jacquier MSc EXAMINATIONS IN MATHEMATICS AND FINANCE DEPARTMENT OF MATHEMATICS April 2016 M5MF6 Advanced Methods in Derivatives Pricing Setter s signature...........................................

Course: Setter: M5MF6 Dr Antoine Jacquier MSc EXAMINATIONS IN MATHEMATICS AND FINANCE DEPARTMENT OF MATHEMATICS April 2016 M5MF6 Advanced Methods in Derivatives Pricing Setter s signature...........................................

Pricing theory of financial derivatives

Pricing theory of financial derivatives One-period securities model S denotes the price process {S(t) : t = 0, 1}, where S(t) = (S 1 (t) S 2 (t) S M (t)). Here, M is the number of securities. At t = 1,

Pricing theory of financial derivatives One-period securities model S denotes the price process {S(t) : t = 0, 1}, where S(t) = (S 1 (t) S 2 (t) S M (t)). Here, M is the number of securities. At t = 1,

Economathematics. Problem Sheet 1. Zbigniew Palmowski. Ws 2 dw s = 1 t

Economathematics Problem Sheet 1 Zbigniew Palmowski 1. Calculate Ee X where X is a gaussian random variable with mean µ and volatility σ >.. Verify that where W is a Wiener process. Ws dw s = 1 3 W t 3

Economathematics Problem Sheet 1 Zbigniew Palmowski 1. Calculate Ee X where X is a gaussian random variable with mean µ and volatility σ >.. Verify that where W is a Wiener process. Ws dw s = 1 3 W t 3

Matytsin s Weak Skew Expansion

Matytsin s Weak Skew Expansion Jim Gatheral, Merrill Lynch July, Linking Characteristic Functionals to Implied Volatility In this section, we follow the derivation of Matytsin ) albeit providing more detail

Matytsin s Weak Skew Expansion Jim Gatheral, Merrill Lynch July, Linking Characteristic Functionals to Implied Volatility In this section, we follow the derivation of Matytsin ) albeit providing more detail

Bluff Your Way Through Black-Scholes

Bluff our Way Through Black-Scholes Saurav Sen December 000 Contents What is Black-Scholes?.............................. 1 The Classical Black-Scholes Model....................... 1 Some Useful Background

Bluff our Way Through Black-Scholes Saurav Sen December 000 Contents What is Black-Scholes?.............................. 1 The Classical Black-Scholes Model....................... 1 Some Useful Background

Lecture 17. The model is parametrized by the time period, δt, and three fixed constant parameters, v, σ and the riskless rate r.

Lecture 7 Overture to continuous models Before rigorously deriving the acclaimed Black-Scholes pricing formula for the value of a European option, we developed a substantial body of material, in continuous

Lecture 7 Overture to continuous models Before rigorously deriving the acclaimed Black-Scholes pricing formula for the value of a European option, we developed a substantial body of material, in continuous

FIN FINANCIAL INSTRUMENTS SPRING 2008

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 The Greeks Introduction We have studied how to price an option using the Black-Scholes formula. Now we wish to consider how the option price changes, either

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 The Greeks Introduction We have studied how to price an option using the Black-Scholes formula. Now we wish to consider how the option price changes, either

Queens College, CUNY, Department of Computer Science Computational Finance CSCI 365 / 765 Fall 2017 Instructor: Dr. Sateesh Mane.

Queens College, CUNY, Department of Computer Science Computational Finance CSCI 365 / 765 Fall 2017 Instructor: Dr. Sateesh Mane c Sateesh R. Mane 2017 14 Lecture 14 November 15, 2017 Derivation of the

Queens College, CUNY, Department of Computer Science Computational Finance CSCI 365 / 765 Fall 2017 Instructor: Dr. Sateesh Mane c Sateesh R. Mane 2017 14 Lecture 14 November 15, 2017 Derivation of the

arxiv: v1 [q-fin.pr] 23 Feb 2014

![arxiv: v1 [q-fin.pr] 23 Feb 2014](/thumbs/87/95850189.jpg "arxiv: v1 [q-fin.pr] 23 Feb 2014") Time-dependent Heston model. G. S. Vasilev, Department of Physics, Sofia University, James Bourchier 5 blvd, 64 Sofia, Bulgaria CloudRisk Ltd (Dated: February 5, 04) This work presents an exact solution

Time-dependent Heston model. G. S. Vasilev, Department of Physics, Sofia University, James Bourchier 5 blvd, 64 Sofia, Bulgaria CloudRisk Ltd (Dated: February 5, 04) This work presents an exact solution

Calibration Lecture 4: LSV and Model Uncertainty

Calibration Lecture 4: LSV and Model Uncertainty March 2017 Recap: Heston model Recall the Heston stochastic volatility model ds t = rs t dt + Y t S t dw 1 t, dy t = κ(θ Y t ) dt + ξ Y t dw 2 t, where

Calibration Lecture 4: LSV and Model Uncertainty March 2017 Recap: Heston model Recall the Heston stochastic volatility model ds t = rs t dt + Y t S t dw 1 t, dy t = κ(θ Y t ) dt + ξ Y t dw 2 t, where

4. Black-Scholes Models and PDEs. Math6911 S08, HM Zhu

4. Black-Scholes Models and PDEs Math6911 S08, HM Zhu References 1. Chapter 13, J. Hull. Section.6, P. Brandimarte Outline Derivation of Black-Scholes equation Black-Scholes models for options Implied

4. Black-Scholes Models and PDEs Math6911 S08, HM Zhu References 1. Chapter 13, J. Hull. Section.6, P. Brandimarte Outline Derivation of Black-Scholes equation Black-Scholes models for options Implied

WKB Method for Swaption Smile

WKB Method for Swaption Smile Andrew Lesniewski BNP Paribas New York February 7 2002 Abstract We study a three-parameter stochastic volatility model originally proposed by P. Hagan for the forward swap

WKB Method for Swaption Smile Andrew Lesniewski BNP Paribas New York February 7 2002 Abstract We study a three-parameter stochastic volatility model originally proposed by P. Hagan for the forward swap

Empirical Approach to the Heston Model Parameters on the Exchange Rate USD / COP

Empirical Approach to the Heston Model Parameters on the Exchange Rate USD / COP ICASQF 2016, Cartagena - Colombia C. Alexander Grajales 1 Santiago Medina 2 1 University of Antioquia, Colombia 2 Nacional

Empirical Approach to the Heston Model Parameters on the Exchange Rate USD / COP ICASQF 2016, Cartagena - Colombia C. Alexander Grajales 1 Santiago Medina 2 1 University of Antioquia, Colombia 2 Nacional

Rough volatility models: When population processes become a new tool for trading and risk management

Rough volatility models: When population processes become a new tool for trading and risk management Omar El Euch and Mathieu Rosenbaum École Polytechnique 4 October 2017 Omar El Euch and Mathieu Rosenbaum

Rough volatility models: When population processes become a new tool for trading and risk management Omar El Euch and Mathieu Rosenbaum École Polytechnique 4 October 2017 Omar El Euch and Mathieu Rosenbaum

Copyright Emanuel Derman 2008

E4718 Spring 2008: Derman: Lecture 6: Extending Black-Scholes; Local Volatility Models Page 1 of 34 Lecture 6: Extending Black-Scholes; Local Volatility Models Summary of the course so far: Black-Scholes

E4718 Spring 2008: Derman: Lecture 6: Extending Black-Scholes; Local Volatility Models Page 1 of 34 Lecture 6: Extending Black-Scholes; Local Volatility Models Summary of the course so far: Black-Scholes

Saddlepoint Approximation Methods for Pricing. Financial Options on Discrete Realized Variance

Saddlepoint Approximation Methods for Pricing Financial Options on Discrete Realized Variance Yue Kuen KWOK Department of Mathematics Hong Kong University of Science and Technology Hong Kong * This is

Saddlepoint Approximation Methods for Pricing Financial Options on Discrete Realized Variance Yue Kuen KWOK Department of Mathematics Hong Kong University of Science and Technology Hong Kong * This is

Quantitative Strategies Research Notes

Quantitative Strategies Research Notes January 1994 The Volatility Smile and Its Implied Tree Emanuel Derman Iraj Kani Copyright 1994 Goldman, & Co. All rights reserved. This material is for your private

Quantitative Strategies Research Notes January 1994 The Volatility Smile and Its Implied Tree Emanuel Derman Iraj Kani Copyright 1994 Goldman, & Co. All rights reserved. This material is for your private

Pricing Variance Swaps under Stochastic Volatility Model with Regime Switching - Discrete Observations Case

Pricing Variance Swaps under Stochastic Volatility Model with Regime Switching - Discrete Observations Case Guang-Hua Lian Collaboration with Robert Elliott University of Adelaide Feb. 2, 2011 Robert Elliott,

Pricing Variance Swaps under Stochastic Volatility Model with Regime Switching - Discrete Observations Case Guang-Hua Lian Collaboration with Robert Elliott University of Adelaide Feb. 2, 2011 Robert Elliott,

Constructing Markov models for barrier options

Constructing Markov models for barrier options Gerard Brunick joint work with Steven Shreve Department of Mathematics University of Texas at Austin Nov. 14 th, 2009 3 rd Western Conference on Mathematical

Constructing Markov models for barrier options Gerard Brunick joint work with Steven Shreve Department of Mathematics University of Texas at Austin Nov. 14 th, 2009 3 rd Western Conference on Mathematical

Stochastic modelling of electricity markets Pricing Forwards and Swaps

Stochastic modelling of electricity markets Pricing Forwards and Swaps Jhonny Gonzalez School of Mathematics The University of Manchester Magical books project August 23, 2012 Clip for this slide Pricing

Stochastic modelling of electricity markets Pricing Forwards and Swaps Jhonny Gonzalez School of Mathematics The University of Manchester Magical books project August 23, 2012 Clip for this slide Pricing

MSC FINANCIAL ENGINEERING PRICING I, AUTUMN LECTURE 6: EXTENSIONS OF BLACK AND SCHOLES RAYMOND BRUMMELHUIS DEPARTMENT EMS BIRKBECK

MSC FINANCIAL ENGINEERING PRICING I, AUTUMN 2010-2011 LECTURE 6: EXTENSIONS OF BLACK AND SCHOLES RAYMOND BRUMMELHUIS DEPARTMENT EMS BIRKBECK In this section we look at some easy extensions of the Black

MSC FINANCIAL ENGINEERING PRICING I, AUTUMN 2010-2011 LECTURE 6: EXTENSIONS OF BLACK AND SCHOLES RAYMOND BRUMMELHUIS DEPARTMENT EMS BIRKBECK In this section we look at some easy extensions of the Black

2 f. f t S 2. Delta measures the sensitivityof the portfolio value to changes in the price of the underlying

Sensitivity analysis Simulating the Greeks Meet the Greeks he value of a derivative on a single underlying asset depends upon the current asset price S and its volatility Σ, the risk-free interest rate

Sensitivity analysis Simulating the Greeks Meet the Greeks he value of a derivative on a single underlying asset depends upon the current asset price S and its volatility Σ, the risk-free interest rate

Multi-factor Stochastic Volatility Models A practical approach

Stockholm School of Economics Department of Finance - Master Thesis Spring 2009 Multi-factor Stochastic Volatility Models A practical approach Filip Andersson 20573@student.hhs.se Niklas Westermark 20653@student.hhs.se

Stockholm School of Economics Department of Finance - Master Thesis Spring 2009 Multi-factor Stochastic Volatility Models A practical approach Filip Andersson 20573@student.hhs.se Niklas Westermark 20653@student.hhs.se

Rough Heston models: Pricing, hedging and microstructural foundations

Rough Heston models: Pricing, hedging and microstructural foundations Omar El Euch 1, Jim Gatheral 2 and Mathieu Rosenbaum 1 1 École Polytechnique, 2 City University of New York 7 November 2017 O. El Euch,

Rough Heston models: Pricing, hedging and microstructural foundations Omar El Euch 1, Jim Gatheral 2 and Mathieu Rosenbaum 1 1 École Polytechnique, 2 City University of New York 7 November 2017 O. El Euch,

The stochastic calculus

Gdansk A schedule of the lecture Stochastic differential equations Ito calculus, Ito process Ornstein - Uhlenbeck (OU) process Heston model Stopping time for OU process Stochastic differential equations

Gdansk A schedule of the lecture Stochastic differential equations Ito calculus, Ito process Ornstein - Uhlenbeck (OU) process Heston model Stopping time for OU process Stochastic differential equations

Greek parameters of nonlinear Black-Scholes equation

International Journal of Mathematics and Soft Computing Vol.5, No.2 (2015), 69-74. ISSN Print : 2249-3328 ISSN Online: 2319-5215 Greek parameters of nonlinear Black-Scholes equation Purity J. Kiptum 1,

International Journal of Mathematics and Soft Computing Vol.5, No.2 (2015), 69-74. ISSN Print : 2249-3328 ISSN Online: 2319-5215 Greek parameters of nonlinear Black-Scholes equation Purity J. Kiptum 1,

Optimal robust bounds for variance options and asymptotically extreme models

Optimal robust bounds for variance options and asymptotically extreme models Alexander Cox 1 Jiajie Wang 2 1 University of Bath 2 Università di Roma La Sapienza Advances in Financial Mathematics, 9th January,

Optimal robust bounds for variance options and asymptotically extreme models Alexander Cox 1 Jiajie Wang 2 1 University of Bath 2 Università di Roma La Sapienza Advances in Financial Mathematics, 9th January,

Numerical schemes for SDEs

Lecture 5 Numerical schemes for SDEs Lecture Notes by Jan Palczewski Computational Finance p. 1 A Stochastic Differential Equation (SDE) is an object of the following type dx t = a(t,x t )dt + b(t,x t

Lecture 5 Numerical schemes for SDEs Lecture Notes by Jan Palczewski Computational Finance p. 1 A Stochastic Differential Equation (SDE) is an object of the following type dx t = a(t,x t )dt + b(t,x t

AMH4 - ADVANCED OPTION PRICING. Contents

AMH4 - ADVANCED OPTION PRICING ANDREW TULLOCH Contents 1. Theory of Option Pricing 2 2. Black-Scholes PDE Method 4 3. Martingale method 4 4. Monte Carlo methods 5 4.1. Method of antithetic variances 5

AMH4 - ADVANCED OPTION PRICING ANDREW TULLOCH Contents 1. Theory of Option Pricing 2 2. Black-Scholes PDE Method 4 3. Martingale method 4 4. Monte Carlo methods 5 4.1. Method of antithetic variances 5

Simulating Stochastic Differential Equations

IEOR E4603: Monte-Carlo Simulation c 2017 by Martin Haugh Columbia University Simulating Stochastic Differential Equations In these lecture notes we discuss the simulation of stochastic differential equations

IEOR E4603: Monte-Carlo Simulation c 2017 by Martin Haugh Columbia University Simulating Stochastic Differential Equations In these lecture notes we discuss the simulation of stochastic differential equations

Pricing Long-Dated Equity Derivatives under Stochastic Interest Rates

Pricing Long-Dated Equity Derivatives under Stochastic Interest Rates Navin Ranasinghe Submitted in total fulfillment of the requirements of the degree of Doctor of Philosophy December, 216 Centre for

Pricing Long-Dated Equity Derivatives under Stochastic Interest Rates Navin Ranasinghe Submitted in total fulfillment of the requirements of the degree of Doctor of Philosophy December, 216 Centre for

Bruno Dupire April Paribas Capital Markets Swaps and Options Research Team 33 Wigmore Street London W1H 0BN United Kingdom

Commento: PRICING AND HEDGING WITH SMILES Bruno Dupire April 1993 Paribas Capital Markets Swaps and Options Research Team 33 Wigmore Street London W1H 0BN United Kingdom Black-Scholes volatilities implied

Commento: PRICING AND HEDGING WITH SMILES Bruno Dupire April 1993 Paribas Capital Markets Swaps and Options Research Team 33 Wigmore Street London W1H 0BN United Kingdom Black-Scholes volatilities implied

Option Pricing with Aggregation of Physical Models and Nonparametric Learning

Option Pricing with Aggregation of Physical Models and Nonparametric Learning Jianqing Fan Princeton University With Loriano Mancini http://www.princeton.edu/ jqfan May 16, 2007 0 Outline Option pricing

Option Pricing with Aggregation of Physical Models and Nonparametric Learning Jianqing Fan Princeton University With Loriano Mancini http://www.princeton.edu/ jqfan May 16, 2007 0 Outline Option pricing

Approximation Methods in Derivatives Pricing

Approximation Methods in Derivatives Pricing Minqiang Li Bloomberg LP September 24, 2013 1 / 27 Outline of the talk A brief overview of approximation methods Timer option price approximation Perpetual

Approximation Methods in Derivatives Pricing Minqiang Li Bloomberg LP September 24, 2013 1 / 27 Outline of the talk A brief overview of approximation methods Timer option price approximation Perpetual

Heston Stochastic Local Volatility Model

Heston Stochastic Local Volatility Model Klaus Spanderen 1 R/Finance 2016 University of Illinois, Chicago May 20-21, 2016 1 Joint work with Johannes Göttker-Schnetmann Klaus Spanderen Heston Stochastic

Heston Stochastic Local Volatility Model Klaus Spanderen 1 R/Finance 2016 University of Illinois, Chicago May 20-21, 2016 1 Joint work with Johannes Göttker-Schnetmann Klaus Spanderen Heston Stochastic

Interest Rate Volatility

Interest Rate Volatility III. Working with SABR Andrew Lesniewski Baruch College and Posnania Inc First Baruch Volatility Workshop New York June 16-18, 2015 Outline Arbitrage free SABR 1 Arbitrage free

Interest Rate Volatility III. Working with SABR Andrew Lesniewski Baruch College and Posnania Inc First Baruch Volatility Workshop New York June 16-18, 2015 Outline Arbitrage free SABR 1 Arbitrage free

arxiv:cond-mat/ v2 [cond-mat.str-el] 5 Nov 2002

![arxiv:cond-mat/ v2 [cond-mat.str-el] 5 Nov 2002](/thumbs/76/73518985.jpg "arxiv:cond-mat/ v2 [cond-mat.str-el] 5 Nov 2002") arxiv:cond-mat/0211050v2 [cond-mat.str-el] 5 Nov 2002 Comparison between the probability distribution of returns in the Heston model and empirical data for stock indices A. Christian Silva, Victor M. Yakovenko

arxiv:cond-mat/0211050v2 [cond-mat.str-el] 5 Nov 2002 Comparison between the probability distribution of returns in the Heston model and empirical data for stock indices A. Christian Silva, Victor M. Yakovenko

A Two Factor Forward Curve Model with Stochastic Volatility for Commodity Prices arxiv: v2 [q-fin.pr] 8 Aug 2017

![A Two Factor Forward Curve Model with Stochastic Volatility for Commodity Prices arxiv: v2 [q-fin.pr] 8 Aug 2017](/thumbs/77/76675488.jpg "A Two Factor Forward Curve Model with Stochastic Volatility for Commodity Prices arxiv: v2 [q-fin.pr] 8 Aug 2017") A Two Factor Forward Curve Model with Stochastic Volatility for Commodity Prices arxiv:1708.01665v2 [q-fin.pr] 8 Aug 2017 Mark Higgins, PhD - Beacon Platform Incorporated August 10, 2017 Abstract We describe

A Two Factor Forward Curve Model with Stochastic Volatility for Commodity Prices arxiv:1708.01665v2 [q-fin.pr] 8 Aug 2017 Mark Higgins, PhD - Beacon Platform Incorporated August 10, 2017 Abstract We describe

Pricing Barrier Options under Local Volatility

Abstract Pricing Barrier Options under Local Volatility Artur Sepp Mail: artursepp@hotmail.com, Web: www.hot.ee/seppar 16 November 2002 We study pricing under the local volatility. Our research is mainly

Abstract Pricing Barrier Options under Local Volatility Artur Sepp Mail: artursepp@hotmail.com, Web: www.hot.ee/seppar 16 November 2002 We study pricing under the local volatility. Our research is mainly

1. What is Implied Volatility?

Numerical Methods FEQA MSc Lectures, Spring Term 2 Data Modelling Module Lecture 2 Implied Volatility Professor Carol Alexander Spring Term 2 1 1. What is Implied Volatility? Implied volatility is: the

Numerical Methods FEQA MSc Lectures, Spring Term 2 Data Modelling Module Lecture 2 Implied Volatility Professor Carol Alexander Spring Term 2 1 1. What is Implied Volatility? Implied volatility is: the

Leverage Effect, Volatility Feedback, and Self-Exciting MarketAFA, Disruptions 1/7/ / 14

Leverage Effect, Volatility Feedback, and Self-Exciting Market Disruptions Liuren Wu, Baruch College Joint work with Peter Carr, New York University The American Finance Association meetings January 7,

Leverage Effect, Volatility Feedback, and Self-Exciting Market Disruptions Liuren Wu, Baruch College Joint work with Peter Carr, New York University The American Finance Association meetings January 7,