Locally risk-minimizing vs. -hedging in stochastic vola

|

|

|

- Darleen Newman

- 5 years ago

- Views:

Transcription

1 Locally risk-minimizing vs. -hedging in stochastic volatility models University of St. Andrews School of Economics and Finance August 29, 2007 joint work with R. Poulsen ( Kopenhagen )and K.R.Schenk-Hoppe (Leeds)

2

3 Samuelson model for the dynamics of a stock in continuous time : i.e. S(t) = S(0) exp( µt + σw(t)) log(s(t)) = log(s(0)) + µt }{{} = deterministic effect = random effect + σw(t) }{{} The random effect is decomposed into many similar tiny little random effects which accumulate homogeneous in time and are independent of each other. Central limit theorem W(t) is Brownian motion

4 With µ := µ σ2 S(t) = S(0) exp ((µ 12 ) ) σ2 t + σw(t) In addition to the stock there is a money market account : B(t) = B(0) exp(rt) S(t) and B(t) are the primary tradeable assets. Now consider a European type option with payoff h(s T ), a so called derivative. What is the price of this financial product? How can the seller hedge against the risk?

5 Black, Scholes, Merton approach : assume price of option is C(t, S(t)) construct a riskless portfolio, which consists of buying the option and trading in the stock dc ds = C t dt + C S ds C SSdSdS ds = (C t + 12 ) S2 σ 2 C SS dt + (C s ) ds Substitution of ds = S (µdt + σdw) gives { dc ds = C t + 1 } 2 S2 σ 2 C SS + (C s ) Sµ dt+(c s ) SσdW riskless = C S

6 Substitution gives dc ds = (C t + 12 S2 σ 2 C SS ) dt (1) C S riskless must evolve at the same rate as the money market account dc ds = (C C S S)rdt (2) Combining (1) and (2) leads to the Black-Scholes PDE C r C S S r C t 1 2 S2 σ 2 C S S = 0 C(T, S(T)) = h(s(t)) Black, Scholes, Merton solved this PDE for the case where h(s T ) = max(s T K, 0)

7 To keep in mind : in the BS model it is possible to hedge ( within the model ) against all risk associated with buying or selling a financial derivative every contingent claim can be perfectly replicated by a self financing trading strategy, i.e. C(t, S(t)) = ϕ 0 (t)b(t) + ϕ 1 (t)s(t) =: V ϕ (t) where ϕ 1 (t) = C S is the so called Delta of the option and dv ϕ (t) = ϕ 0 (t)db(t) + ϕ 1 (t)ds(t) in the BS model contingent claims are therefore redundant! hedging based on the Delta of an option is called Delta-hedging

8 The BS-model has several problems, the worst is that it proves itself to be wrong : Curse of implied volatility : Market prices of European call options with different strike s imply different values for σ, which ought to be constant in BS model. More precisely : solve Ch(S BS T )(σ) = Cobs. h(s T ) The solution is called implied volatility σ impl. σ impl. in general depends on the current value of the stock, on time to maturity and on the payoff function h. It is in no way constant as the BS-model suggests.

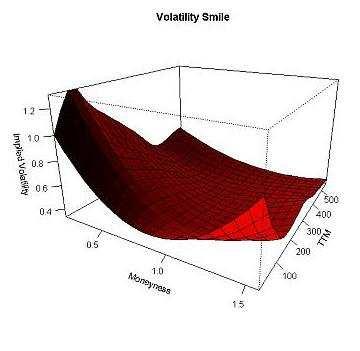

9 Volatility smile :

10 The curse of implied volatility can be partly cured by using so called local volatility models where the local volatility is calibrated by the implied volatilities from the BS-model : ds(t) = S(t)(µdt + σ(t, S(t))dW(t)) But : Some people say, using local volatility models is like substituting the wrong numbers in the wrong formula in order to get the right result. An alternative to BS and local volatility models are stochastic volatility models.

11 returning to Samuelson consideration log(s(t)) = log(s(0)) + µdt + random(t) assume that random(t) is still built up by many little random effects but that they no longer accumulate homogeneous in time, while the accumulation rate is controlled by other random effects alternatively, think of random effects having different magnitudes, compare heteroskedastic time series models dw(t) [ {}}{ ds(t) = S(t) µdt + S(t)γ f (V(t)) 1 ρ 2 dw 1 (t) + ρdw 2 (t)] dv(t) = V(t)(β(V(t))dt + g(v(t))dw 2 (t))

12 Authors & year Specification Remarks Hull-White f (v) = v, Local variance: 1987 β(v) = 0, Geometric Brownian motion. g(v) = σ, Options priced by mixing. ρ = 0, γ = 0 Wiggins f (v) = e v/2, Local volatility: 1987 β(v) = κ(θ v)/v, Ornstein-Uhlenbeck g(v) = σ, in logarithms. ρ = 0, γ = 0 Stein-Stein f (v) = v, Local volatility: 1991 β(v) = κ(θ v)/v, Reflected Ornstein-Uhlenbeck. g(v) = σ/v, ρ = 0, γ = 0 Heston f (v) = v, Local variance: 1993 β(v) = κ(θ v)/v, CIR process. First model with g(v) = σ/ v, correlation. Options priced by ρ [ 1, 1], γ = 0 inversion of characteristic function. Romano-Touzi f (v) = v, Extension of mixing to 1997 β and g are free, correlation. ρ [ 1, 1], γ = 0 SABR f (v) = v Level dependence in volatility β(v) = 0, Options priced perturbation technique Hagan et al. g(v) = σ, ρ [ 1, 1], γ [ 1, 0] Table: Specification of stochastic volatility models.

13 The first ones to consider such models were Hull and White The Pricing of Options on Assets with Stochastic Volatilities. The Journal of Finance, Vol. XLII No. 2, (1987). HW model assumes volatility to be a geometric BM, such as the stock price in BS model. Statistical data show it isn t like this. Nowadays most popular is the Heston model : ( ds(t) = S(t) µdt + ]) V(t)[ 1 ρ 2 dw 1 (t) + ρdw 2 (t) dv(t) = κ(θ V(t)) dt + σ V(t)dW 2 (t)

14 Why is it popular? For European calls there exist closed pricing formulas. Heston, S.L.; A Closed-Form Solution for Options with Stochastic Volatility with Applications to Bond and Currency Options ; Review of Financial Studies, Vol.6, Issue 2 (1993) It can be calibrated effectively to market prices. It produces smiles! are not complete : There are contingent claims, which can not be hedged by a self financing investment strategy in stock and money market account.

15 Option price C = C(t, S, V). Itô s formula dc =...dt + C S ds + C V dv The same approach as Black-Scholes leads to dc ds =...dt + (C S )ds + C V dv }{{} where contains non hedgeable random sources. Main problem caused by incompleteness The No-Arbitrage Principle alone does not determine a unique price for a derivative

16 What to do? Pricing by replication still appears to be a good concept, but in general derivatives are not replicable by self financing investment in the primary assets. One can relax the condition of self financing, allowing non self financing strategies. These strategies come with a cost process Cost ϕ (t) = V ϕ (t) t with V ϕ (t) = ϕ 0 (t) B(t) + ϕ 1 (t) S(t) non self financing hedges always exist : 0 ϕ 0 (s)db(s) ϕ 1 (s)ds(s), ϕ 0 (s) = 0, ϕ 1 (s) = 0 for all s [0, T) and ϕ 0 (T) = h(s T ), ϕ 1 (T) = 0.

17 Obviously the non self financing hedge should be chosen reasonably : classically traders do the following : compute the Delta for the derivative using the corresponding BS-type formula follow Delta-hedging formula, i.e. investing C S S in the stock use market prices to adjust the portfolio from time to time in the money market In order to comply with the last point traders often have to put new money into the market, this is called bleeding. It wouldn t be necessary if the BS model would indeed be the true model, in this case the -hedge would be self financing.

18 Is the -hedging the best one can do? Leaving aside the variances produced by the drift we obtain for the conditional variance of the cost process var t (dcost) = ((C S ) 2 S 2 S 2γ f 2 (V) + C 2 V V 2 g 2 (V) +2(C S )C V SS γ f (V)Vg(V)ρ)dt. This is a quadratic function of, minimized by min = C S + ρ g(v)v f (V)S 1+γ C V, If the agent is interested to minimize the variance in the cost process of his non self financing hedge, i.e. the risk of future bleeding, then he may go for this strategy.

19 The derivation above is rather ad hoc : We do not explain where the price C comes from? Under which measure do we compute the variances, subjective? Yes. But C needs to be computed under risk neutral measure! What happens to the drift terms? A more formal approach is due to Foellmer and Schweitzer : Measure for uncertainty in the cost process R ϕ (t) := E[(C ϕ (T) C ϕ (t)) 2 F t ] Note that the expectation is taken under the subjective probability measure

20 call a trading strategy (ψ 0, ψ 1 ) an admissible continuation of (ϕ 0, ϕ 1 ) if ψ 1 (s) = ϕ 1 (s), s t; ψ 0 (s) = ϕ 0 (s), s < t; and V ψ (T) = V ϕ (T) P a Definition We call ϕ R-minimizing if for any t [0, T) and for any admissible continuation ψ of ϕ from t on R ψ (t) R ϕ (t) P a.s. for all t [0, T). It turns out however, that in order to guarantee the existence of such a strategy the criterion has to be localized. This leads to the definition of locally risk minimizing hedging strategies:

21 (δ 0, δ 1 ) is called a small perturbation if both δ 1 and δ 1 (t)s(t) dt are bounded and δ 0 (T) = δ 1 (T) = 0. T 0 for (s, t] [0, T], define the small perturbation δ (s,t] := (δ 0 [s,t), δ1 (s,t] ) with δ0 [s,t) (u, ω) := δ0 (u, ω) 1 [s,t) (u) and δ 1 (s,t] (u, ω) := δ1 (u, ω) 1 (s,t] (u) for τ a partition of [0, T] and δ a small perturbation define r τ (t, ϕ, δ) := R (t ϕ+δ (ti,t i+1 ] i) R ϕ (t i ) ) 1 ti+1 t i τ E( t i S(t) 2 σ(t) 2 (ti,t i+1 ](t). dt F ti Then ϕ is called locally risk-minimizing if, for all δ, lim inf τ 0 rτ (t, ϕ, δ) 0 P-a.s. for all t [0, T].

22 How to find the locally risk minimizing hedge? Complete the original market by introducing a second stock in such a way that the extended (and now complete) market has as its risk premium the one corresponding to the minimal martingale measure, Q min Compute the self-financing hedging strategy in the completed market. Project the hedging strategy from the extended market onto the original market, taking into account the geometry of the market extension A result by Quenez, Peng and ElKaroui guarantees that this gives indeed the locally risk minimizing hedge.

23 Theorem In the stochastic volatility model discussed the risk-minimizing hedge of an h-claim holds where ξ min (t) = C S + ρ g(v(t))v(t) f (V(t))S(t) 1+γ C V units of the stock, (3) C(t, S(t), V(t)) = e r(t t) E min t (h(s(t))). with E min denoting expectation under the minimal martingale measure. The investment in the money market is given by C ξ min (t)s(t).

24 Note : The dynamics of stock and volatility under the minimal martingale measure ( the one chosen for pricing ) are ( [ ]) ds(t) = S(t) rdt + f (V(t))S(t) γ 1 ρ2 dw 1,min (t) + ρdw 2,min (t) ([ dv(t) = V(t) β(v(t)) ρ g(v(t)) ] ) (µ r) dt + g(v(t))dw 2,min (t). f (V(t)) The price of an option h(s T ) therefore will depend on the agents assessment of the expected return rate µ of the stock, quite contrary to the BS model! Should we worry? No, prices are computed under martingale measures and therefore do not lead to arbitrage. Clearly the subjective assessment of the expected return rate influences the agents assessment of the risk in the cost process.

25 Example : Heston model ds(t) = µs(t)dt + V(t)( 1 ρ 2 dw 1 (t) + ρdw 2 (t)) dv(t) = κ(θ V(t))dt + σ V(t)dW 2 (t) The position in the stock for the locally risk minimizing hedge is therefore given by ξ min (t) = C S + ρσ C V S(t) typical parameters : r = 0.04, µ = 0.10, θ = , κ = 4.75, σ = 0.550, ρ = 0.569, S(0) = 100

26 In the first part of our numerical analysis we used simulated prices: Assume the real world is Heston and parameters are r = 0.04, µ = 0.10, θ = , κ = 4.75, σ = 0.550, ρ = 0.569, S(0) = 100 For arbitrary strategy compute the hedge error var hedge error = 100 P (cost(t; n)) e rt E min ([S(T) K] + ). in this model scenario we compared Heston-Delta hedging with locally risk minimizing hedging:

27 Hedge errors in the Heston model relative error (in %) ordinary delta locally risk minimizing # hedge points (per year) Figure: Hedge errors (i.e. standard deviation of cost relative to option value) for the ordinary delta and the locally risk-minimizing hedge strategies of a 1-year forward-at-the-money call option in the Heston model.

28 But maybe the real world is not Heston or it is and the parameters are wrong. We consider four potential scenarios: we use the wrong martingale measure ( parameters κ and θ ) general parameter uncertainty ( including parameters µ, σ and ρ ) using the wrong Greeks ( BS instead of Heston ) wrong data generating process ( real world is different than Heston ) How does the Delta-hedge and the locally risk minimizing hedge compare then?

29 Wrong martingale measure : Martingale measure; Q Minimal Misconceived minimal Market Q-parameters θ κ Hedge error Table: Hedge error under different misspecifications of the volatility model. Quite robust!

30 Parameter Uncertainty : We run the data generating process with a specified set (µ, κ, θ, σ, ρ) and for computing the locally risk minimizing hedge use random samples which are normally distributed around these ( use results of Eraker about standard error of estimated parameters in heston-model ): Hedge frequency Expiry Moneyness monthly weekly daily 3M At-the-money 0.1% 0.2% 0.3% 10% Out-of-the-money 1.1% 1.5% 1.7% 1Y At-the-money 1.2% 2.9 % 3.5% 10% Out-of-the-money 2.8% 3.8% 4.0% Table: Effects of parameter uncertainty on locally risk-minimizing hedges. The table shows the relative increases in hedge error when the hedger uses parameters drawn from the distribution of Eraker s estimator rather than the true parameter.

31 Using BS-Greeks for computing the locally risk minimizing hedge : C S and C V for Heston are not so handy, why not take the corresponding BS values. For these there exist nice formulas!? hedge error (in %) B/S greeks Heston greeks correlation (rho) Figure: Hedge errors when using Black-Scholes resp. Heston Greeks.

32 Wrong data generating process : We assume prices are generated by a SABR process while locally risk minimizing hedges are computed using the formulas for Heston. ds(t)/s(t) = V(t)S γ (t)dw 1 (t), dv(t)/v(t) = νdw 2 (t). The SABR model can generate option prices ( for a specific expiry ) that are quite similar to those in the Heston model. Yet, the model is structurally quite different : The Skew is generated by a level effect rather than correlation

33 Implied volatility Strike Figure: 1-year implied volatilities in the Heston model (circles) and SABR model (solid line). Parameters for the Heston model are as specified in Table?? (except for r = µ = 0). SABR parameter settings are V(0) = 1.92, γ = 1 and ν = 0.2.

34 The investigation of the performance of the locally risk-minimizing hedge and the delta hedge in the (wrong) Heston model is carried out as follows: (1) simulate stock prices and volatilities from the SABR model, (2) for each path implement the Heston-based locally risk-minimizing strategy (using the initially calibrated parameters and the simulated Heston-sense local variance along each path) as well as a delta hedge and (3) implement the SABR model s delta hedge (which, because of zero correlation of the Brownian motions, coincides with the locally risk-minimizing hedge) using the pricing formula given in Hagan et al. (Wilmott Magazine 1 (2002) ) Hedge method SABR RiskMin Heston RiskMin Heston Delta Hedge error Table: Hedge error under a misspecified data-generating process (SABR).

35 Literature : Stochastic Volatility: Risk Minimization and Model Risk. online at http : //papers.ssrn.com/sol3/papers.cfm?abstract id = plus literature in there.

Stochastic Volatility: Risk Minimization and Model Risk

Stochastic Volatility: Risk Minimization and Model Risk Christian-Oliver Ewald Rolf Poulsen Klaus Reiner Schenk-Hoppé January 29, 2007 Abstract In this paper locally risk-minimizing hedge strategies for

Stochastic Volatility: Risk Minimization and Model Risk Christian-Oliver Ewald Rolf Poulsen Klaus Reiner Schenk-Hoppé January 29, 2007 Abstract In this paper locally risk-minimizing hedge strategies for

1.1 Basic Financial Derivatives: Forward Contracts and Options

Chapter 1 Preliminaries 1.1 Basic Financial Derivatives: Forward Contracts and Options A derivative is a financial instrument whose value depends on the values of other, more basic underlying variables

Chapter 1 Preliminaries 1.1 Basic Financial Derivatives: Forward Contracts and Options A derivative is a financial instrument whose value depends on the values of other, more basic underlying variables

Advanced Topics in Derivative Pricing Models. Topic 4 - Variance products and volatility derivatives

Advanced Topics in Derivative Pricing Models Topic 4 - Variance products and volatility derivatives 4.1 Volatility trading and replication of variance swaps 4.2 Volatility swaps 4.3 Pricing of discrete

Advanced Topics in Derivative Pricing Models Topic 4 - Variance products and volatility derivatives 4.1 Volatility trading and replication of variance swaps 4.2 Volatility swaps 4.3 Pricing of discrete

Stochastic Processes and Stochastic Calculus - 9 Complete and Incomplete Market Models

Stochastic Processes and Stochastic Calculus - 9 Complete and Incomplete Market Models Eni Musta Università degli studi di Pisa San Miniato - 16 September 2016 Overview 1 Self-financing portfolio 2 Complete

Stochastic Processes and Stochastic Calculus - 9 Complete and Incomplete Market Models Eni Musta Università degli studi di Pisa San Miniato - 16 September 2016 Overview 1 Self-financing portfolio 2 Complete

Risk Minimization in Stochastic Volatility Models: Model Risk and Empirical Performance

Risk Minimization in Stochastic Volatility Models: Model Risk and Empirical Performance Rolf Poulsen Klaus Reiner Schenk-Hoppé Christian-Oliver Ewald September 21, 2007 Abstract In this paper the performance

Risk Minimization in Stochastic Volatility Models: Model Risk and Empirical Performance Rolf Poulsen Klaus Reiner Schenk-Hoppé Christian-Oliver Ewald September 21, 2007 Abstract In this paper the performance

The stochastic calculus

Gdansk A schedule of the lecture Stochastic differential equations Ito calculus, Ito process Ornstein - Uhlenbeck (OU) process Heston model Stopping time for OU process Stochastic differential equations

Gdansk A schedule of the lecture Stochastic differential equations Ito calculus, Ito process Ornstein - Uhlenbeck (OU) process Heston model Stopping time for OU process Stochastic differential equations

Risk Minimization in Stochastic Volatility Models: Model Risk and Empirical Performance

Risk Minimization in Stochastic Volatility Models: Model Risk and Empirical Performance Rolf Poulsen Klaus Reiner Schenk-Hoppé Christian-Oliver Ewald February 26, 2009 Abstract In this paper the performance

Risk Minimization in Stochastic Volatility Models: Model Risk and Empirical Performance Rolf Poulsen Klaus Reiner Schenk-Hoppé Christian-Oliver Ewald February 26, 2009 Abstract In this paper the performance

Hedging under Arbitrage

Hedging under Arbitrage Johannes Ruf Columbia University, Department of Statistics Modeling and Managing Financial Risks January 12, 2011 Motivation Given: a frictionless market of stocks with continuous

Hedging under Arbitrage Johannes Ruf Columbia University, Department of Statistics Modeling and Managing Financial Risks January 12, 2011 Motivation Given: a frictionless market of stocks with continuous

Chapter 15: Jump Processes and Incomplete Markets. 1 Jumps as One Explanation of Incomplete Markets

Chapter 5: Jump Processes and Incomplete Markets Jumps as One Explanation of Incomplete Markets It is easy to argue that Brownian motion paths cannot model actual stock price movements properly in reality,

Chapter 5: Jump Processes and Incomplete Markets Jumps as One Explanation of Incomplete Markets It is easy to argue that Brownian motion paths cannot model actual stock price movements properly in reality,

Illiquidity, Credit risk and Merton s model

Illiquidity, Credit risk and Merton s model (joint work with J. Dong and L. Korobenko) A. Deniz Sezer University of Calgary April 28, 2016 Merton s model of corporate debt A corporate bond is a contingent

Illiquidity, Credit risk and Merton s model (joint work with J. Dong and L. Korobenko) A. Deniz Sezer University of Calgary April 28, 2016 Merton s model of corporate debt A corporate bond is a contingent

M5MF6. Advanced Methods in Derivatives Pricing

Course: Setter: M5MF6 Dr Antoine Jacquier MSc EXAMINATIONS IN MATHEMATICS AND FINANCE DEPARTMENT OF MATHEMATICS April 2016 M5MF6 Advanced Methods in Derivatives Pricing Setter s signature...........................................

Course: Setter: M5MF6 Dr Antoine Jacquier MSc EXAMINATIONS IN MATHEMATICS AND FINANCE DEPARTMENT OF MATHEMATICS April 2016 M5MF6 Advanced Methods in Derivatives Pricing Setter s signature...........................................

Monte Carlo Simulations

Monte Carlo Simulations Lecture 1 December 7, 2014 Outline Monte Carlo Methods Monte Carlo methods simulate the random behavior underlying the financial models Remember: When pricing you must simulate

Monte Carlo Simulations Lecture 1 December 7, 2014 Outline Monte Carlo Methods Monte Carlo methods simulate the random behavior underlying the financial models Remember: When pricing you must simulate

BIRKBECK (University of London) MSc EXAMINATION FOR INTERNAL STUDENTS MSc FINANCIAL ENGINEERING DEPARTMENT OF ECONOMICS, MATHEMATICS AND STATIS- TICS

MSc EXAMINATION FOR INTERNAL STUDENTS MSc FINANCIAL ENGINEERING DEPARTMENT OF ECONOMICS, MATHEMATICS AND STATIS- TICS") BIRKBECK (University of London) MSc EXAMINATION FOR INTERNAL STUDENTS MSc FINANCIAL ENGINEERING DEPARTMENT OF ECONOMICS, MATHEMATICS AND STATIS- TICS PRICING EMMS014S7 Tuesday, May 31 2011, 10:00am-13.15pm

BIRKBECK (University of London) MSc EXAMINATION FOR INTERNAL STUDENTS MSc FINANCIAL ENGINEERING DEPARTMENT OF ECONOMICS, MATHEMATICS AND STATIS- TICS PRICING EMMS014S7 Tuesday, May 31 2011, 10:00am-13.15pm

Lévy models in finance

Lévy models in finance Ernesto Mordecki Universidad de la República, Montevideo, Uruguay PASI - Guanajuato - June 2010 Summary General aim: describe jummp modelling in finace through some relevant issues.

Lévy models in finance Ernesto Mordecki Universidad de la República, Montevideo, Uruguay PASI - Guanajuato - June 2010 Summary General aim: describe jummp modelling in finace through some relevant issues.

Financial Derivatives Section 5

Financial Derivatives Section 5 The Black and Scholes Model Michail Anthropelos anthropel@unipi.gr http://web.xrh.unipi.gr/faculty/anthropelos/ University of Piraeus Spring 2018 M. Anthropelos (Un. of

Financial Derivatives Section 5 The Black and Scholes Model Michail Anthropelos anthropel@unipi.gr http://web.xrh.unipi.gr/faculty/anthropelos/ University of Piraeus Spring 2018 M. Anthropelos (Un. of

CONTINUOUS TIME PRICING AND TRADING: A REVIEW, WITH SOME EXTRA PIECES

CONTINUOUS TIME PRICING AND TRADING: A REVIEW, WITH SOME EXTRA PIECES THE SOURCE OF A PRICE IS ALWAYS A TRADING STRATEGY SPECIAL CASES WHERE TRADING STRATEGY IS INDEPENDENT OF PROBABILITY MEASURE COMPLETENESS,

CONTINUOUS TIME PRICING AND TRADING: A REVIEW, WITH SOME EXTRA PIECES THE SOURCE OF A PRICE IS ALWAYS A TRADING STRATEGY SPECIAL CASES WHERE TRADING STRATEGY IS INDEPENDENT OF PROBABILITY MEASURE COMPLETENESS,

The Black-Scholes Model

IEOR E4706: Foundations of Financial Engineering c 2016 by Martin Haugh The Black-Scholes Model In these notes we will use Itô s Lemma and a replicating argument to derive the famous Black-Scholes formula

IEOR E4706: Foundations of Financial Engineering c 2016 by Martin Haugh The Black-Scholes Model In these notes we will use Itô s Lemma and a replicating argument to derive the famous Black-Scholes formula

The Use of Importance Sampling to Speed Up Stochastic Volatility Simulations

The Use of Importance Sampling to Speed Up Stochastic Volatility Simulations Stan Stilger June 6, 1 Fouque and Tullie use importance sampling for variance reduction in stochastic volatility simulations.

The Use of Importance Sampling to Speed Up Stochastic Volatility Simulations Stan Stilger June 6, 1 Fouque and Tullie use importance sampling for variance reduction in stochastic volatility simulations.

Lecture 8: The Black-Scholes theory

Lecture 8: The Black-Scholes theory Dr. Roman V Belavkin MSO4112 Contents 1 Geometric Brownian motion 1 2 The Black-Scholes pricing 2 3 The Black-Scholes equation 3 References 5 1 Geometric Brownian motion

Lecture 8: The Black-Scholes theory Dr. Roman V Belavkin MSO4112 Contents 1 Geometric Brownian motion 1 2 The Black-Scholes pricing 2 3 The Black-Scholes equation 3 References 5 1 Geometric Brownian motion

Economathematics. Problem Sheet 1. Zbigniew Palmowski. Ws 2 dw s = 1 t

Economathematics Problem Sheet 1 Zbigniew Palmowski 1. Calculate Ee X where X is a gaussian random variable with mean µ and volatility σ >.. Verify that where W is a Wiener process. Ws dw s = 1 3 W t 3

Economathematics Problem Sheet 1 Zbigniew Palmowski 1. Calculate Ee X where X is a gaussian random variable with mean µ and volatility σ >.. Verify that where W is a Wiener process. Ws dw s = 1 3 W t 3

Greek parameters of nonlinear Black-Scholes equation

International Journal of Mathematics and Soft Computing Vol.5, No.2 (2015), 69-74. ISSN Print : 2249-3328 ISSN Online: 2319-5215 Greek parameters of nonlinear Black-Scholes equation Purity J. Kiptum 1,

International Journal of Mathematics and Soft Computing Vol.5, No.2 (2015), 69-74. ISSN Print : 2249-3328 ISSN Online: 2319-5215 Greek parameters of nonlinear Black-Scholes equation Purity J. Kiptum 1,

Quadratic hedging in affine stochastic volatility models

Quadratic hedging in affine stochastic volatility models Jan Kallsen TU München Pittsburgh, February 20, 2006 (based on joint work with F. Hubalek, L. Krawczyk, A. Pauwels) 1 Hedging problem S t = S 0

Quadratic hedging in affine stochastic volatility models Jan Kallsen TU München Pittsburgh, February 20, 2006 (based on joint work with F. Hubalek, L. Krawczyk, A. Pauwels) 1 Hedging problem S t = S 0

Replication and Absence of Arbitrage in Non-Semimartingale Models

Replication and Absence of Arbitrage in Non-Semimartingale Models Matematiikan päivät, Tampere, 4-5. January 2006 Tommi Sottinen University of Helsinki 4.1.2006 Outline 1. The classical pricing model:

Replication and Absence of Arbitrage in Non-Semimartingale Models Matematiikan päivät, Tampere, 4-5. January 2006 Tommi Sottinen University of Helsinki 4.1.2006 Outline 1. The classical pricing model:

Sample Path Large Deviations and Optimal Importance Sampling for Stochastic Volatility Models

Sample Path Large Deviations and Optimal Importance Sampling for Stochastic Volatility Models Scott Robertson Carnegie Mellon University scottrob@andrew.cmu.edu http://www.math.cmu.edu/users/scottrob June

Sample Path Large Deviations and Optimal Importance Sampling for Stochastic Volatility Models Scott Robertson Carnegie Mellon University scottrob@andrew.cmu.edu http://www.math.cmu.edu/users/scottrob June

Hedging Credit Derivatives in Intensity Based Models

Hedging Credit Derivatives in Intensity Based Models PETER CARR Head of Quantitative Financial Research, Bloomberg LP, New York Director of the Masters Program in Math Finance, Courant Institute, NYU Stanford

Hedging Credit Derivatives in Intensity Based Models PETER CARR Head of Quantitative Financial Research, Bloomberg LP, New York Director of the Masters Program in Math Finance, Courant Institute, NYU Stanford

AMH4 - ADVANCED OPTION PRICING. Contents

AMH4 - ADVANCED OPTION PRICING ANDREW TULLOCH Contents 1. Theory of Option Pricing 2 2. Black-Scholes PDE Method 4 3. Martingale method 4 4. Monte Carlo methods 5 4.1. Method of antithetic variances 5

AMH4 - ADVANCED OPTION PRICING ANDREW TULLOCH Contents 1. Theory of Option Pricing 2 2. Black-Scholes PDE Method 4 3. Martingale method 4 4. Monte Carlo methods 5 4.1. Method of antithetic variances 5

Credit Risk : Firm Value Model

Credit Risk : Firm Value Model Prof. Dr. Svetlozar Rachev Institute for Statistics and Mathematical Economics University of Karlsruhe and Karlsruhe Institute of Technology (KIT) Prof. Dr. Svetlozar Rachev

Credit Risk : Firm Value Model Prof. Dr. Svetlozar Rachev Institute for Statistics and Mathematical Economics University of Karlsruhe and Karlsruhe Institute of Technology (KIT) Prof. Dr. Svetlozar Rachev

The Black-Scholes Model

The Black-Scholes Model Liuren Wu Options Markets (Hull chapter: 12, 13, 14) Liuren Wu ( c ) The Black-Scholes Model colorhmoptions Markets 1 / 17 The Black-Scholes-Merton (BSM) model Black and Scholes

The Black-Scholes Model Liuren Wu Options Markets (Hull chapter: 12, 13, 14) Liuren Wu ( c ) The Black-Scholes Model colorhmoptions Markets 1 / 17 The Black-Scholes-Merton (BSM) model Black and Scholes

θ(t ) = T f(0, T ) + σ2 T

= T f(0, T ) + σ2 T") 1 Derivatives Pricing and Financial Modelling Andrew Cairns: room M3.08 E-mail: A.Cairns@ma.hw.ac.uk Tutorial 10 1. (Ho-Lee) Let X(T ) = T 0 W t dt. (a) What is the distribution of X(T )? (b) Find E[exp(

1 Derivatives Pricing and Financial Modelling Andrew Cairns: room M3.08 E-mail: A.Cairns@ma.hw.ac.uk Tutorial 10 1. (Ho-Lee) Let X(T ) = T 0 W t dt. (a) What is the distribution of X(T )? (b) Find E[exp(

Lecture 11: Ito Calculus. Tuesday, October 23, 12

Lecture 11: Ito Calculus Continuous time models We start with the model from Chapter 3 log S j log S j 1 = µ t + p tz j Sum it over j: log S N log S 0 = NX µ t + NX p tzj j=1 j=1 Can we take the limit

Lecture 11: Ito Calculus Continuous time models We start with the model from Chapter 3 log S j log S j 1 = µ t + p tz j Sum it over j: log S N log S 0 = NX µ t + NX p tzj j=1 j=1 Can we take the limit

Bluff Your Way Through Black-Scholes

Bluff our Way Through Black-Scholes Saurav Sen December 000 Contents What is Black-Scholes?.............................. 1 The Classical Black-Scholes Model....................... 1 Some Useful Background

Bluff our Way Through Black-Scholes Saurav Sen December 000 Contents What is Black-Scholes?.............................. 1 The Classical Black-Scholes Model....................... 1 Some Useful Background

Pricing theory of financial derivatives

Pricing theory of financial derivatives One-period securities model S denotes the price process {S(t) : t = 0, 1}, where S(t) = (S 1 (t) S 2 (t) S M (t)). Here, M is the number of securities. At t = 1,

Pricing theory of financial derivatives One-period securities model S denotes the price process {S(t) : t = 0, 1}, where S(t) = (S 1 (t) S 2 (t) S M (t)). Here, M is the number of securities. At t = 1,

Stochastic Differential Equations in Finance and Monte Carlo Simulations

Stochastic Differential Equations in Finance and Department of Statistics and Modelling Science University of Strathclyde Glasgow, G1 1XH China 2009 Outline Stochastic Modelling in Asset Prices 1 Stochastic

Stochastic Differential Equations in Finance and Department of Statistics and Modelling Science University of Strathclyde Glasgow, G1 1XH China 2009 Outline Stochastic Modelling in Asset Prices 1 Stochastic

Definition Pricing Risk management Second generation barrier options. Barrier Options. Arfima Financial Solutions

Arfima Financial Solutions Contents Definition 1 Definition 2 3 4 Contenido Definition 1 Definition 2 3 4 Definition Definition: A barrier option is an option on the underlying asset that is activated

Arfima Financial Solutions Contents Definition 1 Definition 2 3 4 Contenido Definition 1 Definition 2 3 4 Definition Definition: A barrier option is an option on the underlying asset that is activated

Optimizing Bounds on Security Prices in Incomplete Markets. Does Stochastic Volatility Specification Matter?

Optimizing Bounds on Security Prices in Incomplete Markets. Does Stochastic Volatility Specification Matter? Naroa Marroquín-Martínez a University of the Basque Country Manuel Moreno b University of Castilla

Optimizing Bounds on Security Prices in Incomplete Markets. Does Stochastic Volatility Specification Matter? Naroa Marroquín-Martínez a University of the Basque Country Manuel Moreno b University of Castilla

MATH3075/3975 FINANCIAL MATHEMATICS TUTORIAL PROBLEMS

MATH307/37 FINANCIAL MATHEMATICS TUTORIAL PROBLEMS School of Mathematics and Statistics Semester, 04 Tutorial problems should be used to test your mathematical skills and understanding of the lecture material.

MATH307/37 FINANCIAL MATHEMATICS TUTORIAL PROBLEMS School of Mathematics and Statistics Semester, 04 Tutorial problems should be used to test your mathematical skills and understanding of the lecture material.

Analytical formulas for local volatility model with stochastic. Mohammed Miri

Analytical formulas for local volatility model with stochastic rates Mohammed Miri Joint work with Eric Benhamou (Pricing Partners) and Emmanuel Gobet (Ecole Polytechnique Modeling and Managing Financial

Analytical formulas for local volatility model with stochastic rates Mohammed Miri Joint work with Eric Benhamou (Pricing Partners) and Emmanuel Gobet (Ecole Polytechnique Modeling and Managing Financial

AN ANALYTICALLY TRACTABLE UNCERTAIN VOLATILITY MODEL

AN ANALYTICALLY TRACTABLE UNCERTAIN VOLATILITY MODEL FABIO MERCURIO BANCA IMI, MILAN http://www.fabiomercurio.it 1 Stylized facts Traders use the Black-Scholes formula to price plain-vanilla options. An

AN ANALYTICALLY TRACTABLE UNCERTAIN VOLATILITY MODEL FABIO MERCURIO BANCA IMI, MILAN http://www.fabiomercurio.it 1 Stylized facts Traders use the Black-Scholes formula to price plain-vanilla options. An

Stochastic Volatility (Working Draft I)

") Stochastic Volatility (Working Draft I) Paul J. Atzberger General comments or corrections should be sent to: paulatz@cims.nyu.edu 1 Introduction When using the Black-Scholes-Merton model to price derivative

Stochastic Volatility (Working Draft I) Paul J. Atzberger General comments or corrections should be sent to: paulatz@cims.nyu.edu 1 Introduction When using the Black-Scholes-Merton model to price derivative

Rohini Kumar. Statistics and Applied Probability, UCSB (Joint work with J. Feng and J.-P. Fouque)

") Small time asymptotics for fast mean-reverting stochastic volatility models Statistics and Applied Probability, UCSB (Joint work with J. Feng and J.-P. Fouque) March 11, 2011 Frontier Probability Days,

Small time asymptotics for fast mean-reverting stochastic volatility models Statistics and Applied Probability, UCSB (Joint work with J. Feng and J.-P. Fouque) March 11, 2011 Frontier Probability Days,

Dynamic Relative Valuation

Dynamic Relative Valuation Liuren Wu, Baruch College Joint work with Peter Carr from Morgan Stanley October 15, 2013 Liuren Wu (Baruch) Dynamic Relative Valuation 10/15/2013 1 / 20 The standard approach

Dynamic Relative Valuation Liuren Wu, Baruch College Joint work with Peter Carr from Morgan Stanley October 15, 2013 Liuren Wu (Baruch) Dynamic Relative Valuation 10/15/2013 1 / 20 The standard approach

Youngrok Lee and Jaesung Lee

orean J. Math. 3 015, No. 1, pp. 81 91 http://dx.doi.org/10.11568/kjm.015.3.1.81 LOCAL VOLATILITY FOR QUANTO OPTION PRICES WITH STOCHASTIC INTEREST RATES Youngrok Lee and Jaesung Lee Abstract. This paper

orean J. Math. 3 015, No. 1, pp. 81 91 http://dx.doi.org/10.11568/kjm.015.3.1.81 LOCAL VOLATILITY FOR QUANTO OPTION PRICES WITH STOCHASTIC INTEREST RATES Youngrok Lee and Jaesung Lee Abstract. This paper

Risk Neutral Measures

CHPTER 4 Risk Neutral Measures Our aim in this section is to show how risk neutral measures can be used to price derivative securities. The key advantage is that under a risk neutral measure the discounted

CHPTER 4 Risk Neutral Measures Our aim in this section is to show how risk neutral measures can be used to price derivative securities. The key advantage is that under a risk neutral measure the discounted

The Black-Scholes Model

The Black-Scholes Model Liuren Wu Options Markets Liuren Wu ( c ) The Black-Merton-Scholes Model colorhmoptions Markets 1 / 18 The Black-Merton-Scholes-Merton (BMS) model Black and Scholes (1973) and Merton

The Black-Scholes Model Liuren Wu Options Markets Liuren Wu ( c ) The Black-Merton-Scholes Model colorhmoptions Markets 1 / 18 The Black-Merton-Scholes-Merton (BMS) model Black and Scholes (1973) and Merton

Calibration Lecture 4: LSV and Model Uncertainty

Calibration Lecture 4: LSV and Model Uncertainty March 2017 Recap: Heston model Recall the Heston stochastic volatility model ds t = rs t dt + Y t S t dw 1 t, dy t = κ(θ Y t ) dt + ξ Y t dw 2 t, where

Calibration Lecture 4: LSV and Model Uncertainty March 2017 Recap: Heston model Recall the Heston stochastic volatility model ds t = rs t dt + Y t S t dw 1 t, dy t = κ(θ Y t ) dt + ξ Y t dw 2 t, where

Lecture Note 8 of Bus 41202, Spring 2017: Stochastic Diffusion Equation & Option Pricing

Lecture Note 8 of Bus 41202, Spring 2017: Stochastic Diffusion Equation & Option Pricing We shall go over this note quickly due to time constraints. Key concept: Ito s lemma Stock Options: A contract giving

Lecture Note 8 of Bus 41202, Spring 2017: Stochastic Diffusion Equation & Option Pricing We shall go over this note quickly due to time constraints. Key concept: Ito s lemma Stock Options: A contract giving

Completeness and Hedging. Tomas Björk

IV Completeness and Hedging Tomas Björk 1 Problems around Standard Black-Scholes We assumed that the derivative was traded. How do we price OTC products? Why is the option price independent of the expected

IV Completeness and Hedging Tomas Björk 1 Problems around Standard Black-Scholes We assumed that the derivative was traded. How do we price OTC products? Why is the option price independent of the expected

( ) since this is the benefit of buying the asset at the strike price rather

since this is the benefit of buying the asset at the strike price rather") Review of some financial models for MAT 483 Parity and Other Option Relationships The basic parity relationship for European options with the same strike price and the same time to expiration is: C( KT

Review of some financial models for MAT 483 Parity and Other Option Relationships The basic parity relationship for European options with the same strike price and the same time to expiration is: C( KT

Asset Pricing Models with Underlying Time-varying Lévy Processes

Asset Pricing Models with Underlying Time-varying Lévy Processes Stochastics & Computational Finance 2015 Xuecan CUI Jang SCHILTZ University of Luxembourg July 9, 2015 Xuecan CUI, Jang SCHILTZ University

Asset Pricing Models with Underlying Time-varying Lévy Processes Stochastics & Computational Finance 2015 Xuecan CUI Jang SCHILTZ University of Luxembourg July 9, 2015 Xuecan CUI, Jang SCHILTZ University

Advanced topics in continuous time finance

Based on readings of Prof. Kerry E. Back on the IAS in Vienna, October 21. Advanced topics in continuous time finance Mag. Martin Vonwald (martin@voni.at) November 21 Contents 1 Introduction 4 1.1 Martingale.....................................

Based on readings of Prof. Kerry E. Back on the IAS in Vienna, October 21. Advanced topics in continuous time finance Mag. Martin Vonwald (martin@voni.at) November 21 Contents 1 Introduction 4 1.1 Martingale.....................................

Risk Neutral Valuation

copyright 2012 Christian Fries 1 / 51 Risk Neutral Valuation Christian Fries Version 2.2 http://www.christian-fries.de/finmath April 19-20, 2012 copyright 2012 Christian Fries 2 / 51 Outline Notation Differential

copyright 2012 Christian Fries 1 / 51 Risk Neutral Valuation Christian Fries Version 2.2 http://www.christian-fries.de/finmath April 19-20, 2012 copyright 2012 Christian Fries 2 / 51 Outline Notation Differential

A SUMMARY OF OUR APPROACHES TO THE SABR MODEL

Contents 1 The need for a stochastic volatility model 1 2 Building the model 2 3 Calibrating the model 2 4 SABR in the risk process 5 A SUMMARY OF OUR APPROACHES TO THE SABR MODEL Financial Modelling Agency

Contents 1 The need for a stochastic volatility model 1 2 Building the model 2 3 Calibrating the model 2 4 SABR in the risk process 5 A SUMMARY OF OUR APPROACHES TO THE SABR MODEL Financial Modelling Agency

Hedging Under Jump Diffusions with Transaction Costs. Peter Forsyth, Shannon Kennedy, Ken Vetzal University of Waterloo

Hedging Under Jump Diffusions with Transaction Costs Peter Forsyth, Shannon Kennedy, Ken Vetzal University of Waterloo Computational Finance Workshop, Shanghai, July 4, 2008 Overview Overview Single factor

Hedging Under Jump Diffusions with Transaction Costs Peter Forsyth, Shannon Kennedy, Ken Vetzal University of Waterloo Computational Finance Workshop, Shanghai, July 4, 2008 Overview Overview Single factor

Risk managing long-dated smile risk with SABR formula

Risk managing long-dated smile risk with SABR formula Claudio Moni QuaRC, RBS November 7, 2011 Abstract In this paper 1, we show that the sensitivities to the SABR parameters can be materially wrong when

Risk managing long-dated smile risk with SABR formula Claudio Moni QuaRC, RBS November 7, 2011 Abstract In this paper 1, we show that the sensitivities to the SABR parameters can be materially wrong when

Hedging under Model Uncertainty

Hedging under Model Uncertainty Efficient Computation of the Hedging Error using the POD 6th World Congress of the Bachelier Finance Society June, 24th 2010 M. Monoyios, T. Schröter, Oxford University

Hedging under Model Uncertainty Efficient Computation of the Hedging Error using the POD 6th World Congress of the Bachelier Finance Society June, 24th 2010 M. Monoyios, T. Schröter, Oxford University

TEST OF BOUNDED LOG-NORMAL PROCESS FOR OPTIONS PRICING

TEST OF BOUNDED LOG-NORMAL PROCESS FOR OPTIONS PRICING Semih Yön 1, Cafer Erhan Bozdağ 2 1,2 Department of Industrial Engineering, Istanbul Technical University, Macka Besiktas, 34367 Turkey Abstract.

TEST OF BOUNDED LOG-NORMAL PROCESS FOR OPTIONS PRICING Semih Yön 1, Cafer Erhan Bozdağ 2 1,2 Department of Industrial Engineering, Istanbul Technical University, Macka Besiktas, 34367 Turkey Abstract.

Time-changed Brownian motion and option pricing

Time-changed Brownian motion and option pricing Peter Hieber Chair of Mathematical Finance, TU Munich 6th AMaMeF Warsaw, June 13th 2013 Partially joint with Marcos Escobar (RU Toronto), Matthias Scherer

Time-changed Brownian motion and option pricing Peter Hieber Chair of Mathematical Finance, TU Munich 6th AMaMeF Warsaw, June 13th 2013 Partially joint with Marcos Escobar (RU Toronto), Matthias Scherer

Lecture 3: Review of mathematical finance and derivative pricing models

Lecture 3: Review of mathematical finance and derivative pricing models Xiaoguang Wang STAT 598W January 21th, 2014 (STAT 598W) Lecture 3 1 / 51 Outline 1 Some model independent definitions and principals

Lecture 3: Review of mathematical finance and derivative pricing models Xiaoguang Wang STAT 598W January 21th, 2014 (STAT 598W) Lecture 3 1 / 51 Outline 1 Some model independent definitions and principals

Pricing and hedging in incomplete markets

Pricing and hedging in incomplete markets Chapter 10 From Chapter 9: Pricing Rules: Market complete+nonarbitrage= Asset prices The idea is based on perfect hedge: H = V 0 + T 0 φ t ds t + T 0 φ 0 t ds

Pricing and hedging in incomplete markets Chapter 10 From Chapter 9: Pricing Rules: Market complete+nonarbitrage= Asset prices The idea is based on perfect hedge: H = V 0 + T 0 φ t ds t + T 0 φ 0 t ds

Pricing Barrier Options under Local Volatility

Abstract Pricing Barrier Options under Local Volatility Artur Sepp Mail: artursepp@hotmail.com, Web: www.hot.ee/seppar 16 November 2002 We study pricing under the local volatility. Our research is mainly

Abstract Pricing Barrier Options under Local Volatility Artur Sepp Mail: artursepp@hotmail.com, Web: www.hot.ee/seppar 16 November 2002 We study pricing under the local volatility. Our research is mainly

Unified Credit-Equity Modeling

Unified Credit-Equity Modeling Rafael Mendoza-Arriaga Based on joint research with: Vadim Linetsky and Peter Carr The University of Texas at Austin McCombs School of Business (IROM) Recent Advancements

Unified Credit-Equity Modeling Rafael Mendoza-Arriaga Based on joint research with: Vadim Linetsky and Peter Carr The University of Texas at Austin McCombs School of Business (IROM) Recent Advancements

MSC FINANCIAL ENGINEERING PRICING I, AUTUMN LECTURE 9: LOCAL AND STOCHASTIC VOLATILITY RAYMOND BRUMMELHUIS DEPARTMENT EMS BIRKBECK

MSC FINANCIAL ENGINEERING PRICING I, AUTUMN 2010-2011 LECTURE 9: LOCAL AND STOCHASTIC VOLATILITY RAYMOND BRUMMELHUIS DEPARTMENT EMS BIRKBECK The only ingredient of the Black and Scholes formula which is

MSC FINANCIAL ENGINEERING PRICING I, AUTUMN 2010-2011 LECTURE 9: LOCAL AND STOCHASTIC VOLATILITY RAYMOND BRUMMELHUIS DEPARTMENT EMS BIRKBECK The only ingredient of the Black and Scholes formula which is

Pricing Variance Swaps under Stochastic Volatility Model with Regime Switching - Discrete Observations Case

Pricing Variance Swaps under Stochastic Volatility Model with Regime Switching - Discrete Observations Case Guang-Hua Lian Collaboration with Robert Elliott University of Adelaide Feb. 2, 2011 Robert Elliott,

Pricing Variance Swaps under Stochastic Volatility Model with Regime Switching - Discrete Observations Case Guang-Hua Lian Collaboration with Robert Elliott University of Adelaide Feb. 2, 2011 Robert Elliott,

Lecture 17. The model is parametrized by the time period, δt, and three fixed constant parameters, v, σ and the riskless rate r.

Lecture 7 Overture to continuous models Before rigorously deriving the acclaimed Black-Scholes pricing formula for the value of a European option, we developed a substantial body of material, in continuous

Lecture 7 Overture to continuous models Before rigorously deriving the acclaimed Black-Scholes pricing formula for the value of a European option, we developed a substantial body of material, in continuous

Optimal robust bounds for variance options and asymptotically extreme models

Optimal robust bounds for variance options and asymptotically extreme models Alexander Cox 1 Jiajie Wang 2 1 University of Bath 2 Università di Roma La Sapienza Advances in Financial Mathematics, 9th January,

Optimal robust bounds for variance options and asymptotically extreme models Alexander Cox 1 Jiajie Wang 2 1 University of Bath 2 Università di Roma La Sapienza Advances in Financial Mathematics, 9th January,

last problem outlines how the Black Scholes PDE (and its derivation) may be modified to account for the payment of stock dividends.

may be modified to account for the payment of stock dividends.") 224 10 Arbitrage and SDEs last problem outlines how the Black Scholes PDE (and its derivation) may be modified to account for the payment of stock dividends. 10.1 (Calculation of Delta First and Finest

224 10 Arbitrage and SDEs last problem outlines how the Black Scholes PDE (and its derivation) may be modified to account for the payment of stock dividends. 10.1 (Calculation of Delta First and Finest

2 f. f t S 2. Delta measures the sensitivityof the portfolio value to changes in the price of the underlying

Sensitivity analysis Simulating the Greeks Meet the Greeks he value of a derivative on a single underlying asset depends upon the current asset price S and its volatility Σ, the risk-free interest rate

Sensitivity analysis Simulating the Greeks Meet the Greeks he value of a derivative on a single underlying asset depends upon the current asset price S and its volatility Σ, the risk-free interest rate

Application of Stochastic Calculus to Price a Quanto Spread

Application of Stochastic Calculus to Price a Quanto Spread Christopher Ting http://www.mysmu.edu/faculty/christophert/ Algorithmic Quantitative Finance July 15, 2017 Christopher Ting July 15, 2017 1/33

Application of Stochastic Calculus to Price a Quanto Spread Christopher Ting http://www.mysmu.edu/faculty/christophert/ Algorithmic Quantitative Finance July 15, 2017 Christopher Ting July 15, 2017 1/33

Forwards and Futures. Chapter Basics of forwards and futures Forwards

Chapter 7 Forwards and Futures Copyright c 2008 2011 Hyeong In Choi, All rights reserved. 7.1 Basics of forwards and futures The financial assets typically stocks we have been dealing with so far are the

Chapter 7 Forwards and Futures Copyright c 2008 2011 Hyeong In Choi, All rights reserved. 7.1 Basics of forwards and futures The financial assets typically stocks we have been dealing with so far are the

STOCHASTIC INTEGRALS

Stat 391/FinMath 346 Lecture 8 STOCHASTIC INTEGRALS X t = CONTINUOUS PROCESS θ t = PORTFOLIO: #X t HELD AT t { St : STOCK PRICE M t : MG W t : BROWNIAN MOTION DISCRETE TIME: = t < t 1

Stat 391/FinMath 346 Lecture 8 STOCHASTIC INTEGRALS X t = CONTINUOUS PROCESS θ t = PORTFOLIO: #X t HELD AT t { St : STOCK PRICE M t : MG W t : BROWNIAN MOTION DISCRETE TIME: = t < t 1

Volatility Smiles and Yield Frowns

Volatility Smiles and Yield Frowns Peter Carr NYU IFS, Chengdu, China, July 30, 2018 Peter Carr (NYU) Volatility Smiles and Yield Frowns 7/30/2018 1 / 35 Interest Rates and Volatility Practitioners and

Volatility Smiles and Yield Frowns Peter Carr NYU IFS, Chengdu, China, July 30, 2018 Peter Carr (NYU) Volatility Smiles and Yield Frowns 7/30/2018 1 / 35 Interest Rates and Volatility Practitioners and

Lecture 11: Stochastic Volatility Models Cont.

E4718 Spring 008: Derman: Lecture 11:Stochastic Volatility Models Cont. Page 1 of 8 Lecture 11: Stochastic Volatility Models Cont. E4718 Spring 008: Derman: Lecture 11:Stochastic Volatility Models Cont.

E4718 Spring 008: Derman: Lecture 11:Stochastic Volatility Models Cont. Page 1 of 8 Lecture 11: Stochastic Volatility Models Cont. E4718 Spring 008: Derman: Lecture 11:Stochastic Volatility Models Cont.

Lecture on Interest Rates

Lecture on Interest Rates Josef Teichmann ETH Zürich Zürich, December 2012 Josef Teichmann Lecture on Interest Rates Mathematical Finance Examples and Remarks Interest Rate Models 1 / 53 Goals Basic concepts

Lecture on Interest Rates Josef Teichmann ETH Zürich Zürich, December 2012 Josef Teichmann Lecture on Interest Rates Mathematical Finance Examples and Remarks Interest Rate Models 1 / 53 Goals Basic concepts

FINANCIAL PRICING MODELS

Page 1-22 like equions FINANCIAL PRICING MODELS 20 de Setembro de 2013 PhD Page 1- Student 22 Contents Page 2-22 1 2 3 4 5 PhD Page 2- Student 22 Page 3-22 In 1973, Fischer Black and Myron Scholes presented

Page 1-22 like equions FINANCIAL PRICING MODELS 20 de Setembro de 2013 PhD Page 1- Student 22 Contents Page 2-22 1 2 3 4 5 PhD Page 2- Student 22 Page 3-22 In 1973, Fischer Black and Myron Scholes presented

The Uncertain Volatility Model

The Uncertain Volatility Model Claude Martini, Antoine Jacquier July 14, 008 1 Black-Scholes and realised volatility What happens when a trader uses the Black-Scholes (BS in the sequel) formula to sell

The Uncertain Volatility Model Claude Martini, Antoine Jacquier July 14, 008 1 Black-Scholes and realised volatility What happens when a trader uses the Black-Scholes (BS in the sequel) formula to sell

Option Pricing. 1 Introduction. Mrinal K. Ghosh

Option Pricing Mrinal K. Ghosh 1 Introduction We first introduce the basic terminology in option pricing. Option: An option is the right, but not the obligation to buy (or sell) an asset under specified

Option Pricing Mrinal K. Ghosh 1 Introduction We first introduce the basic terminology in option pricing. Option: An option is the right, but not the obligation to buy (or sell) an asset under specified

The Black-Scholes Equation using Heat Equation

The Black-Scholes Equation using Heat Equation Peter Cassar May 0, 05 Assumptions of the Black-Scholes Model We have a risk free asset given by the price process, dbt = rbt The asset price follows a geometric

The Black-Scholes Equation using Heat Equation Peter Cassar May 0, 05 Assumptions of the Black-Scholes Model We have a risk free asset given by the price process, dbt = rbt The asset price follows a geometric

European option pricing under parameter uncertainty

European option pricing under parameter uncertainty Martin Jönsson (joint work with Samuel Cohen) University of Oxford Workshop on BSDEs, SPDEs and their Applications July 4, 2017 Introduction 2/29 Introduction

European option pricing under parameter uncertainty Martin Jönsson (joint work with Samuel Cohen) University of Oxford Workshop on BSDEs, SPDEs and their Applications July 4, 2017 Introduction 2/29 Introduction

Extended Libor Models and Their Calibration

Extended Libor Models and Their Calibration Denis Belomestny Weierstraß Institute Berlin Vienna, 16 November 2007 Denis Belomestny (WIAS) Extended Libor Models and Their Calibration Vienna, 16 November

Extended Libor Models and Their Calibration Denis Belomestny Weierstraß Institute Berlin Vienna, 16 November 2007 Denis Belomestny (WIAS) Extended Libor Models and Their Calibration Vienna, 16 November

The Black-Scholes PDE from Scratch

The Black-Scholes PDE from Scratch chris bemis November 27, 2006 0-0 Goal: Derive the Black-Scholes PDE To do this, we will need to: Come up with some dynamics for the stock returns Discuss Brownian motion

The Black-Scholes PDE from Scratch chris bemis November 27, 2006 0-0 Goal: Derive the Black-Scholes PDE To do this, we will need to: Come up with some dynamics for the stock returns Discuss Brownian motion

Simple Robust Hedging with Nearby Contracts

Simple Robust Hedging with Nearby Contracts Liuren Wu and Jingyi Zhu Baruch College and University of Utah October 22, 2 at Worcester Polytechnic Institute Wu & Zhu (Baruch & Utah) Robust Hedging with

Simple Robust Hedging with Nearby Contracts Liuren Wu and Jingyi Zhu Baruch College and University of Utah October 22, 2 at Worcester Polytechnic Institute Wu & Zhu (Baruch & Utah) Robust Hedging with

PAijpam.eu ANALYTIC SOLUTION OF A NONLINEAR BLACK-SCHOLES EQUATION

International Journal of Pure and Applied Mathematics Volume 8 No. 4 013, 547-555 ISSN: 1311-8080 (printed version); ISSN: 1314-3395 (on-line version) url: http://www.ijpam.eu doi: http://dx.doi.org/10.173/ijpam.v8i4.4

International Journal of Pure and Applied Mathematics Volume 8 No. 4 013, 547-555 ISSN: 1311-8080 (printed version); ISSN: 1314-3395 (on-line version) url: http://www.ijpam.eu doi: http://dx.doi.org/10.173/ijpam.v8i4.4

Option Pricing Under a Stressed-Beta Model

Option Pricing Under a Stressed-Beta Model Adam Tashman in collaboration with Jean-Pierre Fouque University of California, Santa Barbara Department of Statistics and Applied Probability Center for Research

Option Pricing Under a Stressed-Beta Model Adam Tashman in collaboration with Jean-Pierre Fouque University of California, Santa Barbara Department of Statistics and Applied Probability Center for Research

Martingale Approach to Pricing and Hedging

Introduction and echniques Lecture 9 in Financial Mathematics UiO-SK451 Autumn 15 eacher:s. Ortiz-Latorre Martingale Approach to Pricing and Hedging 1 Risk Neutral Pricing Assume that we are in the basic

Introduction and echniques Lecture 9 in Financial Mathematics UiO-SK451 Autumn 15 eacher:s. Ortiz-Latorre Martingale Approach to Pricing and Hedging 1 Risk Neutral Pricing Assume that we are in the basic

Volatility Trading Strategies: Dynamic Hedging via A Simulation

Volatility Trading Strategies: Dynamic Hedging via A Simulation Approach Antai Collage of Economics and Management Shanghai Jiao Tong University Advisor: Professor Hai Lan June 6, 2017 Outline 1 The volatility

Volatility Trading Strategies: Dynamic Hedging via A Simulation Approach Antai Collage of Economics and Management Shanghai Jiao Tong University Advisor: Professor Hai Lan June 6, 2017 Outline 1 The volatility

7.1 Volatility Simile and Defects in the Black-Scholes Model

Chapter 7 Beyond Black-Scholes Model 7.1 Volatility Simile and Defects in the Black-Scholes Model Before pointing out some of the flaws in the assumptions of the Black-Scholes world, we must emphasize

Chapter 7 Beyond Black-Scholes Model 7.1 Volatility Simile and Defects in the Black-Scholes Model Before pointing out some of the flaws in the assumptions of the Black-Scholes world, we must emphasize

Computational Finance. Computational Finance p. 1

Computational Finance Computational Finance p. 1 Outline Binomial model: option pricing and optimal investment Monte Carlo techniques for pricing of options pricing of non-standard options improving accuracy

Computational Finance Computational Finance p. 1 Outline Binomial model: option pricing and optimal investment Monte Carlo techniques for pricing of options pricing of non-standard options improving accuracy

Binomial model: numerical algorithm

Binomial model: numerical algorithm S / 0 C \ 0 S0 u / C \ 1,1 S0 d / S u 0 /, S u 3 0 / 3,3 C \ S0 u d /,1 S u 5 0 4 0 / C 5 5,5 max X S0 u,0 S u C \ 4 4,4 C \ 3 S u d / 0 3, C \ S u d 0 S u d 0 / C 4

Binomial model: numerical algorithm S / 0 C \ 0 S0 u / C \ 1,1 S0 d / S u 0 /, S u 3 0 / 3,3 C \ S0 u d /,1 S u 5 0 4 0 / C 5 5,5 max X S0 u,0 S u C \ 4 4,4 C \ 3 S u d / 0 3, C \ S u d 0 S u d 0 / C 4

Tangent Lévy Models. Sergey Nadtochiy (joint work with René Carmona) Oxford-Man Institute of Quantitative Finance University of Oxford.

Oxford-Man Institute of Quantitative Finance University of Oxford.") Tangent Lévy Models Sergey Nadtochiy (joint work with René Carmona) Oxford-Man Institute of Quantitative Finance University of Oxford June 24, 2010 6th World Congress of the Bachelier Finance Society Sergey

Tangent Lévy Models Sergey Nadtochiy (joint work with René Carmona) Oxford-Man Institute of Quantitative Finance University of Oxford June 24, 2010 6th World Congress of the Bachelier Finance Society Sergey

Robust Stochastic Discount Factors

Robust Stochastic Discount Factors Phelim Boyle Wilfrid Laurier University Shui Feng McMaster University Weidong Tian University of Waterloo Tan Wang University of British Columbia and CCFR When the market

Robust Stochastic Discount Factors Phelim Boyle Wilfrid Laurier University Shui Feng McMaster University Weidong Tian University of Waterloo Tan Wang University of British Columbia and CCFR When the market

1 Introduction. 2 Old Methodology BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM DIVISION OF RESEARCH AND STATISTICS

BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM DIVISION OF RESEARCH AND STATISTICS Date: October 6, 3 To: From: Distribution Hao Zhou and Matthew Chesnes Subject: VIX Index Becomes Model Free and Based

BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM DIVISION OF RESEARCH AND STATISTICS Date: October 6, 3 To: From: Distribution Hao Zhou and Matthew Chesnes Subject: VIX Index Becomes Model Free and Based

Robust Stochastic Discount Factors

Robust Stochastic Discount Factors Phelim Boyle Wilfrid Laurier University Weidong Tian University of Waterloo Shui Feng McMaster University Tan Wang University of British Columbia and CCFR Abstract When

Robust Stochastic Discount Factors Phelim Boyle Wilfrid Laurier University Weidong Tian University of Waterloo Shui Feng McMaster University Tan Wang University of British Columbia and CCFR Abstract When

Multiscale Stochastic Volatility Models

Multiscale Stochastic Volatility Models Jean-Pierre Fouque University of California Santa Barbara 6th World Congress of the Bachelier Finance Society Toronto, June 25, 2010 Multiscale Stochastic Volatility

Multiscale Stochastic Volatility Models Jean-Pierre Fouque University of California Santa Barbara 6th World Congress of the Bachelier Finance Society Toronto, June 25, 2010 Multiscale Stochastic Volatility

Path Dependent British Options

Path Dependent British Options Kristoffer J Glover (Joint work with G. Peskir and F. Samee) School of Finance and Economics University of Technology, Sydney 18th August 2009 (PDE & Mathematical Finance

Path Dependent British Options Kristoffer J Glover (Joint work with G. Peskir and F. Samee) School of Finance and Economics University of Technology, Sydney 18th August 2009 (PDE & Mathematical Finance

Empirical Approach to the Heston Model Parameters on the Exchange Rate USD / COP

Empirical Approach to the Heston Model Parameters on the Exchange Rate USD / COP ICASQF 2016, Cartagena - Colombia C. Alexander Grajales 1 Santiago Medina 2 1 University of Antioquia, Colombia 2 Nacional

Empirical Approach to the Heston Model Parameters on the Exchange Rate USD / COP ICASQF 2016, Cartagena - Colombia C. Alexander Grajales 1 Santiago Medina 2 1 University of Antioquia, Colombia 2 Nacional

Non-semimartingales in finance

Non-semimartingales in finance Pricing and Hedging Options with Quadratic Variation Tommi Sottinen University of Vaasa 1st Northern Triangular Seminar 9-11 March 2009, Helsinki University of Technology

Non-semimartingales in finance Pricing and Hedging Options with Quadratic Variation Tommi Sottinen University of Vaasa 1st Northern Triangular Seminar 9-11 March 2009, Helsinki University of Technology

NEWCASTLE UNIVERSITY SCHOOL OF MATHEMATICS, STATISTICS & PHYSICS SEMESTER 1 SPECIMEN 2 MAS3904. Stochastic Financial Modelling. Time allowed: 2 hours

NEWCASTLE UNIVERSITY SCHOOL OF MATHEMATICS, STATISTICS & PHYSICS SEMESTER 1 SPECIMEN 2 Stochastic Financial Modelling Time allowed: 2 hours Candidates should attempt all questions. Marks for each question

NEWCASTLE UNIVERSITY SCHOOL OF MATHEMATICS, STATISTICS & PHYSICS SEMESTER 1 SPECIMEN 2 Stochastic Financial Modelling Time allowed: 2 hours Candidates should attempt all questions. Marks for each question

Hedging under arbitrage

Hedging under arbitrage Johannes Ruf Columbia University, Department of Statistics AnStAp10 August 12, 2010 Motivation Usually, there are several trading strategies at one s disposal to obtain a given

Hedging under arbitrage Johannes Ruf Columbia University, Department of Statistics AnStAp10 August 12, 2010 Motivation Usually, there are several trading strategies at one s disposal to obtain a given

Basic Arbitrage Theory KTH Tomas Björk

Basic Arbitrage Theory KTH 2010 Tomas Björk Tomas Björk, 2010 Contents 1. Mathematics recap. (Ch 10-12) 2. Recap of the martingale approach. (Ch 10-12) 3. Change of numeraire. (Ch 26) Björk,T. Arbitrage

Basic Arbitrage Theory KTH 2010 Tomas Björk Tomas Björk, 2010 Contents 1. Mathematics recap. (Ch 10-12) 2. Recap of the martingale approach. (Ch 10-12) 3. Change of numeraire. (Ch 26) Björk,T. Arbitrage

Local Volatility Dynamic Models

René Carmona Bendheim Center for Finance Department of Operations Research & Financial Engineering Princeton University Columbia November 9, 27 Contents Joint work with Sergey Nadtochyi Motivation 1 Understanding

René Carmona Bendheim Center for Finance Department of Operations Research & Financial Engineering Princeton University Columbia November 9, 27 Contents Joint work with Sergey Nadtochyi Motivation 1 Understanding