Accounting for Your Marketing Results FBS 2017 USER CONFERENCE

|

|

|

- Lauren Horton

- 5 years ago

- Views:

Transcription

1 Accounting for Your Marketing Results FBS 2017 USER CONFERENCE

2 Course Outline Types of hedges Tax and GAAP reporting differences Definitions Recommended accounts/centers Hand s on case studies (using FBS software) Crop farm Livestock feeding Incorporating cost analysis by period

3 Purpose of a Hedge Provide a change in value of the hedging instrument in the opposite direction of the hedged item. For tax purposes, the gains or losses on from hedging activities are recognized when hedges are lifted For accounting purposes, hedging gains/losses are recognized in the period the gains or losses occur Hedging is consider normal business operation so should be matched to gross revenue and expense

4 Hedging Types and Treatment Three types of hedges Fair value Cash flow Net investment hedge/foreign currency transactions Financial Statement treatment Income Statement -- depends on the hedging type. May be included in net income or may be excluded from net income. Balance Sheet -- No difference in presentation between the two methods.

5 Definitions Realized gains or losses from hedging are computed based on closed hedging transactions. Realized gains and losses appear in a brokerage statement s closed equity position. Recognized gains or losses from hedging are the amounts that flow through the income statement or statement of comprehensive income whether resulting from realized or unrealized gains or losses.

6 Definitions (Continued) Unrealized gains or losses from hedging are based on the mark-to-market rules and value hedging transactions as of the date of the financial statement. Appear in a brokerage statement s open equity position May be recognized as Other Comprehensive Income but not Net Income in respect to Cash Flow Hedges

7 Definitions (Continued) Other comprehensive income (OCI) is unrecognized income that falls outside the scope of net income, and is considered part of an entity s total comprehensive income. Includes the unrealized gains or losses from cash flow hedges that will at some point in the future be reclassified into net income.

8 Definitions (Continued) Accumulated other comprehensive income (AOCI) is the accumulated amount of OCI until reclassified into retained earnings (via the income statement). Unrealized gains and losses are accumulated here for cash flow hedges until the hedged commodity is either sold or priced (and/or the hedge is lifted).

9 Types of Hedges Fair Value Hedge Used to offset changes in the fair value of items with fixed prices Cash Flow Hedge Used to establish a fixed price when future cash flows could vary due to changes In prices

10 Hedge Flow Chart Fair Value Hedge All gains or losses, whether realized or unrealized flow through net income. Cash Flow Hedge Unrealized gains or losses flow into OCI. When hedge is lifted or converted to fair value, realized gain/loss is reflected in net income. Accumulated unrealized gain or loss is reclassified to net income

11 Rule of Thumb If inventories are valued at market, treat as Fair Value Hedge ( Finished goods inventory) If inventories valued at cost, treat as Cash Flow Hedge ( Work In Process inventory) However, you can elect to treat all Cash Flow Hedges as Fair Value Hedges

12 Applications to Agriculture Fair Value Hedges Stored crop inventories Newly-weaned animals Finished Market Gain & Loss goes straight through Income Statement Cash Flow Hedges Growing crop inventories Growing animals Cost Gain & Loss goes to Other Comprehensive Income Then moved to Income Statement when items are sold

13 Accounts Required Hedging Asset One account for each segregated brokerage account Inventory Asset One account for crops; one for livestock Hedging Gain/Loss Income One account for each product or commodity Unrealized Gain/Loss Income One account for all products or commodities Inventory Market Value Gain/Loss Income One account for each product or commodity

14 Additional Cash Flow Hedge Accounts Other Comprehensive Income For recording unrecognized income One account for each product or commodity Accumulated Other Comprehensive Income Equity account for each product or commodity In farmer terms, unrealized gain Use Quantity field to track balance

15 Account Recap Account Name Type Comments Hedging Equity Asset One account for each trading fund Inventory Asset Asset One account for crops/livestock Stored Crop Inventories Feeder Livestock Inventories Hedging G/L Income One account for each commodity Lean Hog G&L Corn G&L Soybean Meal G&L Unrealized Hedging G/L Income Only one account required Inventory Market Value G/L Income Only one account required Commissions Expense Only one account required

16 Cash Flow Hedge Account Recap Account Name Type Comments Other Comprehensive Income Income (OCI) Accumulated Other Comprehensive Income (AOCI) Equity One account for each commodity Lean Hog OCI Corn OCI Soybean Meal OCI One account for each commodity Lean Hog AOCI Corn AOCI Soybean Meal AOCI

17 Centers Required Profit Center Type F/C Farm Financial Standards Managerial Accounting concept Used to post final G&L Alternative to allocating G&L to specific production centers or groups Or Crop Marketing (M) Center for Crops Delivery Period Centers for Livestock Type F By Year / Quarter or Month Used to segregate and park G&L on the balance sheet by delivery period

18 Delivery Period Centers Fair Value Hedges Post directly to the product s Profit or Marketing Center Cash Flow Hedges Post to F Centers corresponding to delivery period Center can used for all commodities matched to sales in delivery period Examples (single flow): Delivery Period Examples By Year HH18 for hog hedges in 2018 By Quarter for first quarter of 2018 By Month for January 2019

19 Delivery Period Centers Cash Flow Hedges Examples (multiple flows): Delivery Period Examples By Quarter (Cattle) C191 for first quarter of 2019 By Quarter (Hogs) H191 for first quarter of 2019 By Month (Cattle) C1901 for January 2019 By Month (Hogs) H1901 for January 2019

20 Marked-To-Market Fair Value Hedges Hedging Gains (Auto-reversing) Accrual (or MV) journal entry Fair Value Hedging Gains Category Debit Credit Hedge Hedging Asset Unrealized Hedging G/L Income Inventories Inventory Market Value G/L Income Crop Inventory Asset

21 Marked-To-Market Fair Value Hedges Hedging Losses (Auto-reversing) Accrual (or MV) journal entry Fair Value Hedging Losses Category Debit Credit Hedge Hedging Gain/Loss Income Hedging Asset Inventories Crop Inventory Asset Inventory Market Value G/L Income

22 Accruing Closed Cash Trades Should be done monthly Management journal entries Reverse cash/tax entries for closed positions Record positive quantity* in Other Comprehensive Income account Delivery Period Delivery Period *Optional Center Debit Credit Hedging Gain Other Comprehensive Income Other Comprehensive Income Hedging Loss

23 Matching Hedging Gain With Animals Sold Should be done monthly Management journal entries Record negative quantity* in Accumulated Other Comprehensive Income account * Optional Center Debit Credit Delivery Period Accumulated Other Comprehensive Income Profit Center Other Comprehensive Income

24 Matching Hedging Loss With Animals Sold Should be done monthly Management journal entries Record negative quantity in Accumulated Other Comprehensive Income account Center Debit Credit Delivery Period Profit Center Other Comprehensive Income Accumulated Other Comprehensive Income

25 December 2019 July 2020 Reverse Tax Hedging G&L July 2020 Delivery Period Center Accumulated Other Comprehensive Income Equity Accounts Hog AOCI Corn AOCI SBM AOCI Hogs 20,000 Head Corn 140,000 Bushels SBM 1,200 Tons Close Out to Other Comprehensive Income Accounts Hog OCI Corn OCI SBM OCI

26 Feed OCI Entries Closing position Zeroes out hedged feed balance Realizes hedging G/L Parks G/L in Delivery Period Center

Reverse Hedging Realized G/L account Record to OCI Unrealized G/L")

27 Feed OCI Entries Reversing entry Management level (one level higher than last entry) Reverse Hedging Realized G/L account Record to OCI Unrealized G/L account

28 Cash Flow Hedge OCI Entries For trades to be recognized/allocated to another time period User-Defined Accounting Report for G/L Account Recap by Center Accrual level Note balance for each combination of AOCI Account/ Delivery Period Center not in the current month

29 Cash Flow Hedge OCI Entries Reverse to Accumulated OCI Management level Reverse accumulated amount original G/L Income account to the Unrealized G/L Income account Use the Delivery Period Center from original entry Offset to AOCI Equity account

30 Cash Flow Hedge OCI Entries Allocate to Delivery Period Management level Reverse Accumulated OCI Equity Account Use the Delivery Period Center from original entry Post to OCI Income account

31 Cash Flow Hedge OCI Entries Transaction Recap

32 Cost Analysis Example

33 Analysis Alternatives By ledger account/delivery period center Through contracts / delivery period center Through contracts / specific group/project Through contracts / specific ingredient/input Through contracts / specific ingredient / input / DTN Flow feed hedges through cost of goods Flow feed hedges & livestock hedges through closeouts

34 Feed / Fuel Contracts Ignore center Match on product

35 Crop Hedges Placed through crop marketing center Can be matched against crop project

36 Livestock Hedges Placed through delivery center or profit center

37 Account Settings for Contracts Note Integration types

38 Options On open or close of position? For long puts and calls use positive quantity For short puts and calls use negative quantity

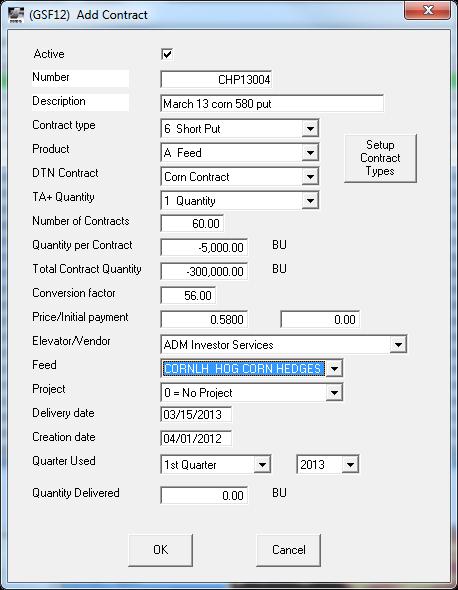

39 Short Options Entry

40 Contract option Matching against feed

41 Lower of Cost/Market Entries Updates from DTN

42 What s Missing? Groups / Projects Automated managerial accounting/wip adjustments and overhead allocations Commissions Reversing MTM journal entries? Contract module Integrated inventories

Hedge Accounting Workshop

Hedge Accounting Workshop AUGUST 26 TH, STONEY CREEK INN, MOLINE, ILLINOIS PAUL NEIFFER, CPA, CLIFTONLARSONALLEN LLP NORM BROWN, CAC, FBS SYSTEMS, INC. Training Materials From the Farm Financial Standards

Hedge Accounting Workshop AUGUST 26 TH, STONEY CREEK INN, MOLINE, ILLINOIS PAUL NEIFFER, CPA, CLIFTONLARSONALLEN LLP NORM BROWN, CAC, FBS SYSTEMS, INC. Training Materials From the Farm Financial Standards

Accounting for Hedging Transactions

CLAconnect.com Accounting for Hedging Transactions Paul Neiffer, CPA Paul Neiffer Bio Paul is an Agribusiness CPA and Principal with CliftonLarsonAllen LLP located in the Kennewick and Yakima, Washington

CLAconnect.com Accounting for Hedging Transactions Paul Neiffer, CPA Paul Neiffer Bio Paul is an Agribusiness CPA and Principal with CliftonLarsonAllen LLP located in the Kennewick and Yakima, Washington

Controller s Corner 2017

Controller s Corner 2017 WIP QUIZ Discussion of WIP in motion We are operating a Wean to Finish hog farm. We have just added a new grower to finish out 5,000 hogs a year. We are paying the new grower

Controller s Corner 2017 WIP QUIZ Discussion of WIP in motion We are operating a Wean to Finish hog farm. We have just added a new grower to finish out 5,000 hogs a year. We are paying the new grower

Buying Hedge with Futures

Buying Hedge with Futures What is a Hedge? A buying hedge involves taking a position in the futures market that is equal and opposite to the position one expects to take later in the cash market. The hedger

Buying Hedge with Futures What is a Hedge? A buying hedge involves taking a position in the futures market that is equal and opposite to the position one expects to take later in the cash market. The hedger

Agricultural Accounting

Agricultural Accounting Steven M. Bragg Chapter 1 Introduction to Agricultural Accounting... 1 Learning Objectives... 1 Introduction... 1 A Note on Terminology... 1 The Economic Entity Concept... 1 Financial

Agricultural Accounting Steven M. Bragg Chapter 1 Introduction to Agricultural Accounting... 1 Learning Objectives... 1 Introduction... 1 A Note on Terminology... 1 The Economic Entity Concept... 1 Financial

HEDGING WITH FUTURES. Understanding Price Risk

HEDGING WITH FUTURES Think about a sport you enjoy playing. In many sports, such as football, volleyball, or basketball, there are two general components to the game: offense and defense. What would happen

HEDGING WITH FUTURES Think about a sport you enjoy playing. In many sports, such as football, volleyball, or basketball, there are two general components to the game: offense and defense. What would happen

Cash Flow Projection

Name Address City, State Preparer Cash Flow Projection Farm Financial Planning Input Forms Farm No. (3 digit) Beginning Cash Flow Date Version 1 Month Year The Cash Flow Projection Program is designed

Name Address City, State Preparer Cash Flow Projection Farm Financial Planning Input Forms Farm No. (3 digit) Beginning Cash Flow Date Version 1 Month Year The Cash Flow Projection Program is designed

TRADING THE CATTLE AND HOG CRUSH SPREADS

TRADING THE CATTLE AND HOG CRUSH SPREADS Chicago Mercantile Exchange Inc. (CME) and the Chicago Board of Trade (CBOT) have signed a definitive agreement for CME to provide clearing and related services

TRADING THE CATTLE AND HOG CRUSH SPREADS Chicago Mercantile Exchange Inc. (CME) and the Chicago Board of Trade (CBOT) have signed a definitive agreement for CME to provide clearing and related services

Accounting for Foreign Currency Transactions. Chapter 10 Foreign Currency Transactions Topic 2: Accounting Fair Value and Cash Flow Hedges

Chapter 10 Foreign Currency Transactions Topic 2: Accounting Fair Value and Cash Flow Hedges Advanced Accounting Dr. Chula King 1 Student Learning Outcomes Account for foreign currency transactions Account

Chapter 10 Foreign Currency Transactions Topic 2: Accounting Fair Value and Cash Flow Hedges Advanced Accounting Dr. Chula King 1 Student Learning Outcomes Account for foreign currency transactions Account

Table of Contents. Introduction

Table of Contents Option Terminology 2 The Concept of Options 4 How Do I Incorporate Options into My Marketing Plan? 7 Establishing a Minimum Sale Price for Your Livestock Buying Put Options 11 Establishing

Table of Contents Option Terminology 2 The Concept of Options 4 How Do I Incorporate Options into My Marketing Plan? 7 Establishing a Minimum Sale Price for Your Livestock Buying Put Options 11 Establishing

Managerial Accounting Using QuickBooks Pro TM

Managerial Accounting Using QuickBooks Pro TM This manual is intended as a reference in furthering knowledge of management accounting for agricultural producers using QuickBooks Pro TM. Historically, agricultural

Managerial Accounting Using QuickBooks Pro TM This manual is intended as a reference in furthering knowledge of management accounting for agricultural producers using QuickBooks Pro TM. Historically, agricultural

Welcome to a brief discussion of income statements. The income statement is a critical record-keeping tool in evaluating the profitability of your

Welcome to a brief discussion of income statements. The income statement is a critical record-keeping tool in evaluating the profitability of your business. As with the other statements, you may choose

Welcome to a brief discussion of income statements. The income statement is a critical record-keeping tool in evaluating the profitability of your business. As with the other statements, you may choose

INSIGHTS FROM AGRICULTURAL LENDERS. January 11 th, 2019 Top Farmer Conference Beck Agricultural Center Dr. Brady Brewer

INSIGHTS FROM AGRICULTURAL LENDERS January 11 th, 2019 Top Farmer Conference Beck Agricultural Center Dr. Brady Brewer bebrewer@purdue.edu AGRICULTURAL LENDER SURVEY Survey expectations and past results

INSIGHTS FROM AGRICULTURAL LENDERS January 11 th, 2019 Top Farmer Conference Beck Agricultural Center Dr. Brady Brewer bebrewer@purdue.edu AGRICULTURAL LENDER SURVEY Survey expectations and past results

Ending Balance Sheet Page 13 of 21

Farm Name Ending Balance Sheet Page 13 of 21 Current Assets Ending Balance Sheet Date: / / 201 Schedule A: Cash, Savings, and Checking Farm cash, checking and savings account balances as of the balance

Farm Name Ending Balance Sheet Page 13 of 21 Current Assets Ending Balance Sheet Date: / / 201 Schedule A: Cash, Savings, and Checking Farm cash, checking and savings account balances as of the balance

APPENDIX A: EXAMPLE FINANCIAL STATEMENTS

APPENDIX A: EXAMPLE FINANCIAL STATEMENTS This Appendix contains an example of financial statement formats that are intended to assist the reader in the interpretation of the Report. It is impossible for

APPENDIX A: EXAMPLE FINANCIAL STATEMENTS This Appendix contains an example of financial statement formats that are intended to assist the reader in the interpretation of the Report. It is impossible for

ACCRUED INCOME STATEMENT

Iowa Farm Business Association ACCRUED INCOME STATEMENT IOWA STATEWIDE Page: 1 Size 1 Avg Size 2 Avg Size 3 Avg Size 4 Avg Size 5 Avg Group Avg 144 Farms 109 Farms 188 Farms 219 Farms Farms 72 Farms 101

Iowa Farm Business Association ACCRUED INCOME STATEMENT IOWA STATEWIDE Page: 1 Size 1 Avg Size 2 Avg Size 3 Avg Size 4 Avg Size 5 Avg Group Avg 144 Farms 109 Farms 188 Farms 219 Farms Farms 72 Farms 101

Answer each of the following questions by circling True or False (2 points each).

.") Name: Econ 337 Agricultural Marketing, Spring 2019 Exam I; March 28, 2019 Answer each of the following questions by circling True or False (2 points each). 1. True False Some risk transfer premium is appropriate

Name: Econ 337 Agricultural Marketing, Spring 2019 Exam I; March 28, 2019 Answer each of the following questions by circling True or False (2 points each). 1. True False Some risk transfer premium is appropriate

JOHN AND MARY FARMER (Farm Business Only) BALANCE SHEET AS OF 12/31/X1 AND 12/31/X2

BALANCE SHEET AS OF 12/31/X1 AND 12/31/X2") JOHN AND MARY FARMER (Farm Business Only) ASSETS 12/31/X2 12/31/X1 12/31/X2 12/31/X1 LIABILITIES Cash $ 101,743 $ 113,421 Accounts Payable $ 6,578 $ 0 Inventories (Schedule 1) 180,581 149,557 Notes Due

JOHN AND MARY FARMER (Farm Business Only) ASSETS 12/31/X2 12/31/X1 12/31/X2 12/31/X1 LIABILITIES Cash $ 101,743 $ 113,421 Accounts Payable $ 6,578 $ 0 Inventories (Schedule 1) 180,581 149,557 Notes Due

Session 5: Financial Management

Session 5: Financial Management Session 4: Enterprise Budget Develop enterprise budget Decide on Production System How did they decide on pricing Where will they market Fixed cost Revenue = Price X Quantity

Session 5: Financial Management Session 4: Enterprise Budget Develop enterprise budget Decide on Production System How did they decide on pricing Where will they market Fixed cost Revenue = Price X Quantity

Using the Futures Market in Response to Low Market Prices By Gary Schnitkey

Monday, Aug 2, 1999 Using the Futures Market in Response to Low Market Prices By Gary Schnitkey Cash market hog prices have been below $20 per cwt. during late October and November, their lowest levels

Monday, Aug 2, 1999 Using the Futures Market in Response to Low Market Prices By Gary Schnitkey Cash market hog prices have been below $20 per cwt. during late October and November, their lowest levels

1. On Jan. 28, 2011, the February 2011 live cattle futures price was $ per hundredweight.

Econ 339X Spring 2011 Homework Due 2/8/2011 65 points possible Short answer (two points each): 1. On Jan. 28, 2011, the February 2011 live cattle futures price was $107.50 per hundredweight. If the cash

Econ 339X Spring 2011 Homework Due 2/8/2011 65 points possible Short answer (two points each): 1. On Jan. 28, 2011, the February 2011 live cattle futures price was $107.50 per hundredweight. If the cash

Risk Management for Stocker Cattle. R. Curt Lacy, Ph.D. Extension Economist-Livestock University of Georgia

Risk Management for Stocker Cattle R. Curt Lacy, Ph.D. Extension Economist-Livestock University of Georgia Risk Management for Stocker Cattle It is NOT uncertainty! It is the negative outcome associated

Risk Management for Stocker Cattle R. Curt Lacy, Ph.D. Extension Economist-Livestock University of Georgia Risk Management for Stocker Cattle It is NOT uncertainty! It is the negative outcome associated

Balance Sheets- step one for your 2016 farm analysis

1 of 12 Name Address Phone Email Balance Sheets- step one for your 2016 farm analysis The farm s balance sheet is a snapshot, on one day in time, of what the farm business owns, (its assets), and what

1 of 12 Name Address Phone Email Balance Sheets- step one for your 2016 farm analysis The farm s balance sheet is a snapshot, on one day in time, of what the farm business owns, (its assets), and what

Farm Income Statement 2015 Moorhead Farm Business Management Annual Report (Farms Sorted By Net Farm Income) Number of farms

Number of farms") Farm Income Statement Cash Farm Income Barley 5,929 2,010 - - 12,581 14,753 Beans, Black Turtle 350 - - - - 1,723 Beans, Navy 3,627 13,512 - - 5,385 - Corn 168,160 172,777 84,655 79,253 289,902 214,568

Farm Income Statement Cash Farm Income Barley 5,929 2,010 - - 12,581 14,753 Beans, Black Turtle 350 - - - - 1,723 Beans, Navy 3,627 13,512 - - 5,385 - Corn 168,160 172,777 84,655 79,253 289,902 214,568

More information on other ways of forward contracting hogs is available in the module Hog Market Contracting.

Hedging Hogs by the Farm Manager Introduction Hog prices can vary significantly from year to year and even day to day. With this volatility in the hog market, forward pricing opportunities arise worthy

Hedging Hogs by the Farm Manager Introduction Hog prices can vary significantly from year to year and even day to day. With this volatility in the hog market, forward pricing opportunities arise worthy

Farm Financial Management Case: Mayer Farm 2013

Farm Financial Management Case: Mayer Farm 2013 The Mayer Farm Case is provided to you as an alternative to using your own financial data. Using the Mayer Farm Case data you can complete the following

Farm Financial Management Case: Mayer Farm 2013 The Mayer Farm Case is provided to you as an alternative to using your own financial data. Using the Mayer Farm Case data you can complete the following

Econ 337 Spring 2016 Midterm 3/8/ points possible

Econ 337 Spring 2016 Midterm 3/8/2016 100 points possible Fill in the blanks (2 points each) 1. A put option contains the right to sell a futures contract. 2. A call option contains the right to buy a

Econ 337 Spring 2016 Midterm 3/8/2016 100 points possible Fill in the blanks (2 points each) 1. A put option contains the right to sell a futures contract. 2. A call option contains the right to buy a

Managing Feed and Milk Price Risk: Futures Markets and Insurance Alternatives

Managing Feed and Milk Price Risk: Futures Markets and Insurance Alternatives Dillon M. Feuz Department of Applied Economics Utah State University 3530 Old Main Hill Logan, UT 84322-3530 435-797-2296 dillon.feuz@usu.edu

Managing Feed and Milk Price Risk: Futures Markets and Insurance Alternatives Dillon M. Feuz Department of Applied Economics Utah State University 3530 Old Main Hill Logan, UT 84322-3530 435-797-2296 dillon.feuz@usu.edu

Reporting of Reclassifications from Accumulated Other Comprehensive Income

Reporting of Reclassifications from Accumulated Other Comprehensive Income The FASB has amended the reporting requirements for reclassifications out of accumulated other comprehensive income. The changes

Reporting of Reclassifications from Accumulated Other Comprehensive Income The FASB has amended the reporting requirements for reclassifications out of accumulated other comprehensive income. The changes

Adecoagro S.A. Condensed Consolidated Interim Financial Statements as of June 30, 2017 and for the six-month periods ended June 30, 2017 and 2016

Condensed Consolidated Interim Financial Statements as of and for the six-month periods ended and 2016 Legal information Denomination: Adecoagro S.A. Legal address: Vertigo Naos Building, 6, Rue Eugène

Condensed Consolidated Interim Financial Statements as of and for the six-month periods ended and 2016 Legal information Denomination: Adecoagro S.A. Legal address: Vertigo Naos Building, 6, Rue Eugène

Risk Management Tools You Can Use

Management Tools You Can Use Categories of Management Tools Financial Production Price Others Rodney Jones OSU NW Area Extension Economist Overall Financial 1) Know costs of production Your number one

Management Tools You Can Use Categories of Management Tools Financial Production Price Others Rodney Jones OSU NW Area Extension Economist Overall Financial 1) Know costs of production Your number one

Summary Results of the 2016 AAEA Outlook Survey

Summary Results of the 2016 AAEA Outlook Survey 8 7 Would you say the farms you are most familiar with are better off, worse off, or just about the same financially as a year ago? 71% 6 5 3 6% Better Off

Summary Results of the 2016 AAEA Outlook Survey 8 7 Would you say the farms you are most familiar with are better off, worse off, or just about the same financially as a year ago? 71% 6 5 3 6% Better Off

Econ 337 Spring 2015 Due 10am 100 points possible

Econ 337 Spring 2015 Final Due 5/4/2015 @ 10am 100 points possible Fill in the blanks (2 points each) 1. Basis = price price 2. A bear thinks prices will. 3. A bull thinks prices will. 4. are willing to

Econ 337 Spring 2015 Final Due 5/4/2015 @ 10am 100 points possible Fill in the blanks (2 points each) 1. Basis = price price 2. A bear thinks prices will. 3. A bull thinks prices will. 4. are willing to

Balance Sheets- step one for your 2018 farm analysis

Page 1 of 21 Name Address Phone Email Balance Sheets- step one for your 2018 farm analysis The farm s balance sheet is a snapshot, on one day in time, of what the farm business owns, (its assets), and

Page 1 of 21 Name Address Phone Email Balance Sheets- step one for your 2018 farm analysis The farm s balance sheet is a snapshot, on one day in time, of what the farm business owns, (its assets), and

PERSONAL TAX INFORMATION WORKSHEET

PERSONAL TAX INFORMATION WORKSHEET Please check the appropriate box: Date Received: I need my taxes done early for my child s financial aid. Most of the information needed to complete this form can be

PERSONAL TAX INFORMATION WORKSHEET Please check the appropriate box: Date Received: I need my taxes done early for my child s financial aid. Most of the information needed to complete this form can be

& is the level of interest which has accumulated on a loan from the last time you paid it up to the date you are doing

,.. Economics 330 Spring 2000 - Exam 2b March 1, 2000 Name U...It LabD~T W Lecture Time 9:00 11:00 R 2:00 Part I: Multiple Choice. (3 points each.) Fill in the correct circle on the accompanying computer

,.. Economics 330 Spring 2000 - Exam 2b March 1, 2000 Name U...It LabD~T W Lecture Time 9:00 11:00 R 2:00 Part I: Multiple Choice. (3 points each.) Fill in the correct circle on the accompanying computer

Grassfed Beef Ranch QuickBooks Setup Accounts

Grassfed Beef Ranch QuickBooks Setup Accounts The business accounting system first must provide the data for compliance reporting following the expense accounts in the Internal Revenue (IRS) Tax Profit

Grassfed Beef Ranch QuickBooks Setup Accounts The business accounting system first must provide the data for compliance reporting following the expense accounts in the Internal Revenue (IRS) Tax Profit

Introduction to Futures Markets

Introduction to Futures Markets History The first U.S. futures exchange was the Chicago Board of Trade (CBOT), formed in 1848. Other U.S. exchanges also began in the last half of the 1800s. Kansas City

Introduction to Futures Markets History The first U.S. futures exchange was the Chicago Board of Trade (CBOT), formed in 1848. Other U.S. exchanges also began in the last half of the 1800s. Kansas City

2008 STATE FFA FARM BUSINESS MANAGEMENT CONTEST

2008 STATE FFA FARM BUSINESS MANAGEMENT CONTEST The information in this section will be used to complete the problem-solving portion of the Farm Management Test. In the balance sheet analysis, you will

2008 STATE FFA FARM BUSINESS MANAGEMENT CONTEST The information in this section will be used to complete the problem-solving portion of the Farm Management Test. In the balance sheet analysis, you will

2017 MN State Farm Business Management Exam MULTIPLE CHOICE (Score 2 points per question)

") 2017 MN State Farm Business Management Exam MULTIPLE CHOICE (Score 2 points per question) Select the most correct answer and bubble it in on your scantron. 1. When local basis increases, it is an indication

2017 MN State Farm Business Management Exam MULTIPLE CHOICE (Score 2 points per question) Select the most correct answer and bubble it in on your scantron. 1. When local basis increases, it is an indication

2017 Farm Tax Worksheet For Clients of Erpelding, Voigt & Co., L.L.P.

2017 Farm Tax Worksheet For Clients of Erpelding, Voigt & Co., L.L.P. INCOME WORKSHEET SALES/COSTS OF LIVESTOCK PURCHASED FOR RESALE: Sold Proceeds Bought Cost Net Calves/fat cattle $ $ $ Calves/fat cattle

2017 Farm Tax Worksheet For Clients of Erpelding, Voigt & Co., L.L.P. INCOME WORKSHEET SALES/COSTS OF LIVESTOCK PURCHASED FOR RESALE: Sold Proceeds Bought Cost Net Calves/fat cattle $ $ $ Calves/fat cattle

Agribusiness Lending Internal Control Questionnaire

Agribusiness Lending Internal Control Questionnaire Completed by: Date Completed: 1. Has the institution established policies that are appropriate for the complexity and scope of the agricultural lending

Agribusiness Lending Internal Control Questionnaire Completed by: Date Completed: 1. Has the institution established policies that are appropriate for the complexity and scope of the agricultural lending

Agricultural Options. November CME Group. All rights reserved.

Agricultural Options November 2018 Ag Option Product Suite Highlights Livestock spread volume on CME Globex hit an all-time high of 35%, led by verticals, 3-ways and delta-hedged options Weekly options

Agricultural Options November 2018 Ag Option Product Suite Highlights Livestock spread volume on CME Globex hit an all-time high of 35%, led by verticals, 3-ways and delta-hedged options Weekly options

Understanding Hedge Accounting & Financial Reporting: Avoiding the Pitfalls PRESENTED BY: BRYAN WRIGHT AND RANDY THROENER

Understanding Hedge Accounting & Financial Reporting: Avoiding the Pitfalls PRESENTED BY: BRYAN WRIGHT AND RANDY THROENER Hedge Accounting - U.S. GAAP 1. Is hedge accounting complicated? NO 2. Are the

Understanding Hedge Accounting & Financial Reporting: Avoiding the Pitfalls PRESENTED BY: BRYAN WRIGHT AND RANDY THROENER Hedge Accounting - U.S. GAAP 1. Is hedge accounting complicated? NO 2. Are the

Income Statement. Are you making a profit? Income Statement Adjustments

The Farm Financial Standards Committee recommends four measures of profitability: 1. Net Farm Income 2. ROA 3. ROE 4. OPMR Income Statement Are you making a profit? The income statement is used to determine

The Farm Financial Standards Committee recommends four measures of profitability: 1. Net Farm Income 2. ROA 3. ROE 4. OPMR Income Statement Are you making a profit? The income statement is used to determine

1. A put option contains the right to a futures contract. 2. A call option contains the right to a futures contract.

Econ 337 Name Midterm Spring 2017 100 points possible 3/28/2017 Fill in the blanks (2 points each) 1. A put option contains the right to a futures contract. 2. A call option contains the right to a futures

Econ 337 Name Midterm Spring 2017 100 points possible 3/28/2017 Fill in the blanks (2 points each) 1. A put option contains the right to a futures contract. 2. A call option contains the right to a futures

2017 NATIONAL FFA FARM AND AGRIBUSINESS MANAGEMENT CAREER DEVELOPMENT EVENT

Participant s Name (please print clearly). Important: Before you start this portion of the event, please write your participant number and state abbreviation on the blanks provided at the top of each page.

Participant s Name (please print clearly). Important: Before you start this portion of the event, please write your participant number and state abbreviation on the blanks provided at the top of each page.

Options Trading in Agricultural Commodities

EC-613 Cooperative Extension Service Purdue University West Lafayette, IN 47907 Options Trading in Agricultural Commodities Steven.P Erickson, Associate Professor Christopher A. Hurt, Assistant Professor

EC-613 Cooperative Extension Service Purdue University West Lafayette, IN 47907 Options Trading in Agricultural Commodities Steven.P Erickson, Associate Professor Christopher A. Hurt, Assistant Professor

2006 Michigan Cash Grain Farm Business Analysis Summary. Eric Wittenberg And Stephen Harsh. Staff Paper December, 2007

2006 Michigan Cash Grain Farm Business Analysis Summary Eric Wittenberg And Stephen Harsh Staff Paper 2007-11 December, 2007 Department of Agricultural Economics MICHIGAN STATE UNIVERSITY East Lansing,

2006 Michigan Cash Grain Farm Business Analysis Summary Eric Wittenberg And Stephen Harsh Staff Paper 2007-11 December, 2007 Department of Agricultural Economics MICHIGAN STATE UNIVERSITY East Lansing,

PLANNING FOR YOUR AGRIPRENEURSHIP BUSINESS

PLANNING FOR YOUR AGRIPRENEURSHIP BUSINESS 1 Creating a basic business plan: Understanding your financials Introduction: Welcome to How to Write Your Business Plan 101! As agricultural entrepreneurs, or

PLANNING FOR YOUR AGRIPRENEURSHIP BUSINESS 1 Creating a basic business plan: Understanding your financials Introduction: Welcome to How to Write Your Business Plan 101! As agricultural entrepreneurs, or

Definitions of Marketing Terms

E-472 RM2-32.0 11-08 Risk Management Definitions of Marketing Terms Dean McCorkle and Kevin Dhuyvetter* Cash Market Cash marketing basis the difference between a cash price and a futures price of a particular

E-472 RM2-32.0 11-08 Risk Management Definitions of Marketing Terms Dean McCorkle and Kevin Dhuyvetter* Cash Market Cash marketing basis the difference between a cash price and a futures price of a particular

2002 Michigan Dairy Farm Business Analysis Summary. Staff Paper No November Eric Wittenberg and Christopher Wolf

2002 Michigan Dairy Farm Business Analysis Summary Staff Paper No. 03-14 November 2003 by Eric Wittenberg and Christopher Wolf Copyright 2003 by Eric Wittenberg and Christopher Wolf. Readers may make verbatim

2002 Michigan Dairy Farm Business Analysis Summary Staff Paper No. 03-14 November 2003 by Eric Wittenberg and Christopher Wolf Copyright 2003 by Eric Wittenberg and Christopher Wolf. Readers may make verbatim

Introduction January 10, 2019

Introduction January 10, 2019 Michael Langemeier Department of Agricultural Economics Purdue University Purdue.edu/commercialag White County Farms Enterprises Corn; 1,500 acres Soybeans; 1,500 acres Owned

Introduction January 10, 2019 Michael Langemeier Department of Agricultural Economics Purdue University Purdue.edu/commercialag White County Farms Enterprises Corn; 1,500 acres Soybeans; 1,500 acres Owned

First Trust Global Tactical Commodity Strategy Fund (FTGC) Consolidated Portfolio of Investments September 30, 2017 (Unaudited) Stated.

Consolidated Portfolio of Investments September 30, 2017 (Unaudited) Stated.") Consolidated Portfolio of Investments Principal Description Stated Coupon Stated Maturity TREASURY BILLS 61.0% $ 30,000,000 U.S. Treasury Bill (a)... (b) 10/19/17 $ 29,987,055 15,000,000 U.S. Treasury

Consolidated Portfolio of Investments Principal Description Stated Coupon Stated Maturity TREASURY BILLS 61.0% $ 30,000,000 U.S. Treasury Bill (a)... (b) 10/19/17 $ 29,987,055 15,000,000 U.S. Treasury

Olericulture Hort 320 Lesson 10, Enterprise Budgets

Olericulture Hort 320 Lesson 10, Enterprise Budgets Jeremy S. Cowan WSU Spokane County Extension 222 N. Havana St. Spokane, WA 99202 Phone: 509-477-2145 Fax: 509-477-2087 Email: jeremy.cowan@wsu.edu Purpose

Olericulture Hort 320 Lesson 10, Enterprise Budgets Jeremy S. Cowan WSU Spokane County Extension 222 N. Havana St. Spokane, WA 99202 Phone: 509-477-2145 Fax: 509-477-2087 Email: jeremy.cowan@wsu.edu Purpose

Commodity products. Grain and Oilseed Hedger's Guide

Commodity products Grain and Oilseed Hedger's Guide In a world of increasing volatility, customers around the globe rely on CME Group as their premier source for price discovery and managing risk. Formed

Commodity products Grain and Oilseed Hedger's Guide In a world of increasing volatility, customers around the globe rely on CME Group as their premier source for price discovery and managing risk. Formed

(Lecture notes for the Week 1 Second session, Wednesday, 2/5/14) Introductory Pricing/Marketing Workshop for Grains, On-Line

Introductory Pricing/Marketing Workshop for Grains, On-Line") (Lecture notes for the Week 1 Second session, Wednesday, 2/5/14) Introductory Pricing/Marketing Workshop for Grains, On-Line Review Futures Market Prices Hilker s version to make some points Think of futures

(Lecture notes for the Week 1 Second session, Wednesday, 2/5/14) Introductory Pricing/Marketing Workshop for Grains, On-Line Review Futures Market Prices Hilker s version to make some points Think of futures

Executive Women in Agriculture

Executive Women in Agriculture FINANCIAL STATEMENT FUNDAMENTALS Understanding what your lender needs 1 OR How can this benefit me? What does 2014 have in store? Lower commodity prices Increasing input

Executive Women in Agriculture FINANCIAL STATEMENT FUNDAMENTALS Understanding what your lender needs 1 OR How can this benefit me? What does 2014 have in store? Lower commodity prices Increasing input

2013 Risk and Profit Conference Breakout Session Presenters. 4. Basics of Futures and Options: Part 1

2013 Risk and Profit Conference Breakout Session Presenters Sean Fox 4. Basics of Futures and Options: Part 1 John A. (Sean) Fox is a native of Ireland and has been on the faculty

2013 Risk and Profit Conference Breakout Session Presenters Sean Fox 4. Basics of Futures and Options: Part 1 John A. (Sean) Fox is a native of Ireland and has been on the faculty

Fall 2017 Crop Outlook Webinar

Fall 2017 Crop Outlook Webinar Chris Hurt, Professor & Extension Ag. Economist James Mintert, Professor & Director, Center for Commercial Agriculture Fall 2017 Crop Outlook Webinar October 13, 2017 50%

Fall 2017 Crop Outlook Webinar Chris Hurt, Professor & Extension Ag. Economist James Mintert, Professor & Director, Center for Commercial Agriculture Fall 2017 Crop Outlook Webinar October 13, 2017 50%

Chapter 4. Agricultural Finance Calum G. Turvey, W.I. Myers Professor of Agricultural Finance

Chapter 4. Calum G. Turvey, W.I. Myers Professor of General Outlook The financial condition of New York s agricultural economy in 2014 is holding steady if not improving over 2013. Although there is some

Chapter 4. Calum G. Turvey, W.I. Myers Professor of General Outlook The financial condition of New York s agricultural economy in 2014 is holding steady if not improving over 2013. Although there is some

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C Form 10-Q

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 10-Q (Mark One) QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 10-Q (Mark One) QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period

GROWMARK, INC. CONSOLIDATED FINANCIAL STATEMENTS YEARS ENDED AUGUST 31, 2017 AND with REPORT OF INDEPENDENT AUDITORS

GROWMARK, INC. CONSOLIDATED FINANCIAL STATEMENTS YEARS ENDED AUGUST 31, 2017 AND 2016 with REPORT OF INDEPENDENT AUDITORS Ernst & Young LLP 155 North Wacker Drive Chicago, Illinois 60606-1787 Tel: (312)

GROWMARK, INC. CONSOLIDATED FINANCIAL STATEMENTS YEARS ENDED AUGUST 31, 2017 AND 2016 with REPORT OF INDEPENDENT AUDITORS Ernst & Young LLP 155 North Wacker Drive Chicago, Illinois 60606-1787 Tel: (312)

6,479,864 (Cost $6,480,320) (c) Net Other Assets and Liabilities 26.1%... 2,286,259 Net Assets 100.0%... $ 8,766,123

(c) Net Other Assets and Liabilities 26.1%... 2,286,259 Net Assets 100.0%... $ 8,766,123") Consolidated Portfolio of Investments Principal TREASURY BILLS 73.9% Description Stated Coupon Stated Maturity $ 1,000,000 U.S. Treasury Bill (a) (b) 4/12/18 $ 999,547 1,500,000 U.S. Treasury Bill (a)

Consolidated Portfolio of Investments Principal TREASURY BILLS 73.9% Description Stated Coupon Stated Maturity $ 1,000,000 U.S. Treasury Bill (a) (b) 4/12/18 $ 999,547 1,500,000 U.S. Treasury Bill (a)

GOLDMAN SACHS 17 TH ANNUAL AGRIBUSINESS CONFERENCE. February 26, 2013

GOLDMAN SACHS 17 TH ANNUAL AGRIBUSINESS CONFERENCE February 26, 2013 DENNIS LEATHERBY, CFO FORWARD-LOOKING STATEMENTS Certain information contained in this presentation may constitute forward-looking statements,

GOLDMAN SACHS 17 TH ANNUAL AGRIBUSINESS CONFERENCE February 26, 2013 DENNIS LEATHERBY, CFO FORWARD-LOOKING STATEMENTS Certain information contained in this presentation may constitute forward-looking statements,

PRODUCTION TOOL. Economic evaluation of new technologies for pork producers: Examples of all-in all-out and segregated early weaning.

PRODUCTION TOOL Economic evaluation of new technologies for pork producers: Examples of all-in all-out and segregated early weaning John D. Lawrence, PhD Summary Objective: To describe a method to evaluate

PRODUCTION TOOL Economic evaluation of new technologies for pork producers: Examples of all-in all-out and segregated early weaning John D. Lawrence, PhD Summary Objective: To describe a method to evaluate

Economics 330 Name Fall 2004 Exam 1 PART I. Multiple Choice. Indicate the best answer. (3 points each)

") Economics 330 Fall 2004 Exam 1 Name PART I. Multiple Choice. Indicate the best answer. (3 points each) 1. We discussed the aspect of establishing S.M.A.R.T. goals. Examples of S.M.A.R.T. goals would include:

Economics 330 Fall 2004 Exam 1 Name PART I. Multiple Choice. Indicate the best answer. (3 points each) 1. We discussed the aspect of establishing S.M.A.R.T. goals. Examples of S.M.A.R.T. goals would include:

First Trust Global Tactical Commodity Strategy Fund (FTGC) Consolidated Portfolio of Investments March 31, 2018 (Unaudited) Stated.

Consolidated Portfolio of Investments March 31, 2018 (Unaudited) Stated.") Consolidated Portfolio of Investments Principal Description Stated Coupon Stated Maturity TREASURY BILLS 80.1% $ 48,000,000 U.S. Treasury Bill (a)... (b) 04/12/18 $ 47,978,254 10,000,000 U.S. Treasury

Consolidated Portfolio of Investments Principal Description Stated Coupon Stated Maturity TREASURY BILLS 80.1% $ 48,000,000 U.S. Treasury Bill (a)... (b) 04/12/18 $ 47,978,254 10,000,000 U.S. Treasury

STANDARDIZED PERFORMANCE ANALYSIS

STANDARDIZED PERFORMANCE ANALYSIS SPA-6 COW-CALF ENTERPRISE FINANCIAL PERFORMANCE MEASURES WORKSHEET (SPA-FCC) * 6-16-06 SPA is a standardized cow-calf enterprise production and financial performance analysis

STANDARDIZED PERFORMANCE ANALYSIS SPA-6 COW-CALF ENTERPRISE FINANCIAL PERFORMANCE MEASURES WORKSHEET (SPA-FCC) * 6-16-06 SPA is a standardized cow-calf enterprise production and financial performance analysis

AGBE 321. Problem Set 6

AGBE 321 Problem Set 6 1. In your own words (i.e., in a manner that you would explain it to someone who has not taken this course) explain how local price risk can be hedged using futures markets? 2. Suppose

AGBE 321 Problem Set 6 1. In your own words (i.e., in a manner that you would explain it to someone who has not taken this course) explain how local price risk can be hedged using futures markets? 2. Suppose

Revenue and Costs for Illinois Grain Crops, Actual for 2012 through 2017, Projected 2018 and 2019

CROP COSTS Department of Agricultural and Consumer Economics University of Illinois Revenue and Costs for Illinois Grain Crops, Actual for 2012 through 2017, Projected 2018 and 2019 Department of Agricultural

CROP COSTS Department of Agricultural and Consumer Economics University of Illinois Revenue and Costs for Illinois Grain Crops, Actual for 2012 through 2017, Projected 2018 and 2019 Department of Agricultural

Revenue and Costs for Corn, Soybeans, Wheat, and Double-Crop Soybeans, Actual for 2011 through 2016, Projected 2017 and 2018

CROP COSTS Department of Agricultural and Consumer Economics University of Illinois Revenue and Costs for Corn, Soybeans, Wheat, and Double-Crop Soybeans, Actual for 2011 through 2016, Projected 2017 and

CROP COSTS Department of Agricultural and Consumer Economics University of Illinois Revenue and Costs for Corn, Soybeans, Wheat, and Double-Crop Soybeans, Actual for 2011 through 2016, Projected 2017 and

MMS EntryInputs. Input Data For MMS's Pro-Forma First-Year Accounting Entries

Input Data For MMS's Pro-Forma First-Year Accounting Entries Pro-forma Model: This Excel model provides pro-forma first-year financial statements, meaning statements that are estimated for planning purposes

Input Data For MMS's Pro-Forma First-Year Accounting Entries Pro-forma Model: This Excel model provides pro-forma first-year financial statements, meaning statements that are estimated for planning purposes

Ranch Accounting and Analysis

Ranch Accounting and Analysis May 16, 2017 Ranch 101 - Ranch Accounting Texas & Southwestern Cattle Raisers Association Ft. Worth, Texas Stan Bevers Retired Professor & Ext. Economist www.ranchkpi.com

Ranch Accounting and Analysis May 16, 2017 Ranch 101 - Ranch Accounting Texas & Southwestern Cattle Raisers Association Ft. Worth, Texas Stan Bevers Retired Professor & Ext. Economist www.ranchkpi.com

The Economics of ARC vs. PLC

University of Nebraska - Lincoln DigitalCommons@University of Nebraska - Lincoln Cornhusker Economics Agricultural Economics Department 2-4-2015 The Economics of ARC vs. PLC Bradley D. Lubben University

University of Nebraska - Lincoln DigitalCommons@University of Nebraska - Lincoln Cornhusker Economics Agricultural Economics Department 2-4-2015 The Economics of ARC vs. PLC Bradley D. Lubben University

FULL TIME OPPORTUNITIES

FULL TIME OPPORTUNITIES 2014-2015 BARTLETT & COMPANY WWW.BARTLETTANDCO.COM/CAREERS ABOUT BARTLETT Bartlett and Company is a diverse, growth-oriented agribusiness company. Our principle businesses are grain

FULL TIME OPPORTUNITIES 2014-2015 BARTLETT & COMPANY WWW.BARTLETTANDCO.COM/CAREERS ABOUT BARTLETT Bartlett and Company is a diverse, growth-oriented agribusiness company. Our principle businesses are grain

ABC Farms 1/1/2013 Balance Sheet

ABC Farms 1/1/2013 Balance Sheet Current Assets Value Current Liabilities Balance Cash and checking 65,579 Prepaid exp. & suppl. (Schd B) 112,225 Growing crops - Accounts receivable - Hedging accounts

ABC Farms 1/1/2013 Balance Sheet Current Assets Value Current Liabilities Balance Cash and checking 65,579 Prepaid exp. & suppl. (Schd B) 112,225 Growing crops - Accounts receivable - Hedging accounts

Farm/Ranch Management Decisions Under Drought

Farm/Ranch Management Decisions Under Drought Frayne Olson, PhD Crop Economist/Marketing Specialist frayne.olson@ndsu.edu 701-231-7377 (o) 701-715-3673 (c) NDSU Extension Service ND Agricultural Experiment

Farm/Ranch Management Decisions Under Drought Frayne Olson, PhD Crop Economist/Marketing Specialist frayne.olson@ndsu.edu 701-231-7377 (o) 701-715-3673 (c) NDSU Extension Service ND Agricultural Experiment

Section II Advanced Pricing Tools

Section II Chapter 13: Options Learning objectives The appeal of options Puts vs. calls Understanding premiums Recognizing if an option is in the money, at the money or out of the money Key terms Call

Section II Chapter 13: Options Learning objectives The appeal of options Puts vs. calls Understanding premiums Recognizing if an option is in the money, at the money or out of the money Key terms Call

Introducing The Income Statement 1

Circular 645 Introducing The Statement 1 P.J. van Blokland 2 Background This publication is one in a series outlining the four basic financial statements used in business today. These statements are the

Circular 645 Introducing The Statement 1 P.J. van Blokland 2 Background This publication is one in a series outlining the four basic financial statements used in business today. These statements are the

December 2018 Monthly Commodity Market Overview Newsletter. Stock Index Futures

December 2018 Monthly Commodity Market Overview Newsletter By the ADMIS Research Team of Steve Freed, Alan Bush, Michael Niemiec & Chris Lehner Stock Index Futures Stock index futures have come under pressure

December 2018 Monthly Commodity Market Overview Newsletter By the ADMIS Research Team of Steve Freed, Alan Bush, Michael Niemiec & Chris Lehner Stock Index Futures Stock index futures have come under pressure

2015 Market Outlook. DTN/The Progressive Farmer 2014 Ag Summit December 9, Darin Newsom DTN Senior Analyst

2015 Market Outlook DTN/The Progressive Farmer 2014 Ag Summit December 9, 2014 Darin Newsom DTN Senior Analyst Here Comes The Sun 2015 Corn Outlook We ve Seen This Show Before Outlook: December 10, 2013

2015 Market Outlook DTN/The Progressive Farmer 2014 Ag Summit December 9, 2014 Darin Newsom DTN Senior Analyst Here Comes The Sun 2015 Corn Outlook We ve Seen This Show Before Outlook: December 10, 2013

Tax Reform Impact on GAAP Accounting Entries

January 2018 Tax Reform Impact on GAAP Accounting Entries On December 22, 2017, the Tax Cuts and Jobs Act of 2017 (the Act) was signed into law. Among other things, the Act reduced the corporate federal

January 2018 Tax Reform Impact on GAAP Accounting Entries On December 22, 2017, the Tax Cuts and Jobs Act of 2017 (the Act) was signed into law. Among other things, the Act reduced the corporate federal

2014 Iowa Farm Business Management Career Development Event. INDIVIDUAL EXAM (150 pts.)

") 2014 Iowa Farm Business Management Career Development Event INDIVIDUAL EXAM (150 pts.) Select the best answer to each of the 75 questions to follow (2 pts. ea.). Code your answers on the answer sheet provided.

2014 Iowa Farm Business Management Career Development Event INDIVIDUAL EXAM (150 pts.) Select the best answer to each of the 75 questions to follow (2 pts. ea.). Code your answers on the answer sheet provided.

2015 Iowa Farm Business Management Career Development Event. INDIVIDUAL EXAM (150 pts.)

") 2015 Iowa Farm Business Management Career Development Event INDIVIDUAL EXAM (150 pts.) Select the best answer to each of the 75 questions to follow (2 pts. ea.). Code your answers on the answer sheet provided.

2015 Iowa Farm Business Management Career Development Event INDIVIDUAL EXAM (150 pts.) Select the best answer to each of the 75 questions to follow (2 pts. ea.). Code your answers on the answer sheet provided.

COMPOSED AND SOLVED BY (SADIA ALI) MBA

MBA") MIDTERM EXAMINATION Fall 2009 MGT101- Financial Accounting (Session - 3) Time: 60 min Question No: 1 ( Marks: 1 ) - Please choose one Mr. A sold goods to Mr. B for Rs. 3,000 on October 8, 2008 and Mr.

MIDTERM EXAMINATION Fall 2009 MGT101- Financial Accounting (Session - 3) Time: 60 min Question No: 1 ( Marks: 1 ) - Please choose one Mr. A sold goods to Mr. B for Rs. 3,000 on October 8, 2008 and Mr.

Goldman Sachs. 18 th Annual Agribusiness Conference. March 12, 2014

Goldman Sachs 18 th Annual Agribusiness Conference March 12, 2014 FORWARD-LOOKING STATEMENTS Certain information contained in this presentation may constitute forward-looking statements, such as information

Goldman Sachs 18 th Annual Agribusiness Conference March 12, 2014 FORWARD-LOOKING STATEMENTS Certain information contained in this presentation may constitute forward-looking statements, such as information

Ridley Inc. Reports Financial Results for Fiscal 2012 Third Quarter

NEWS RELEASE RIDLEY Inc. Trading symbol: RCL on The Toronto Stock Exchange FOR IMMEDIATE RELEASE Ridley Inc. Reports Financial Results for Fiscal 2012 Third Quarter MANKATO, MINNESOTA and WINNIPEG, MANITOBA

NEWS RELEASE RIDLEY Inc. Trading symbol: RCL on The Toronto Stock Exchange FOR IMMEDIATE RELEASE Ridley Inc. Reports Financial Results for Fiscal 2012 Third Quarter MANKATO, MINNESOTA and WINNIPEG, MANITOBA

2015 ProSystem Tax Line Conversion Chart by Input Form. Individual. January 2015

2015 ProSystem Conversion Chart by Input Form Individual January 2015 The following chart provides Individual tax line conversion data sorted by form and box number. te: CCH ProSystem fx allows tax lines

2015 ProSystem Conversion Chart by Input Form Individual January 2015 The following chart provides Individual tax line conversion data sorted by form and box number. te: CCH ProSystem fx allows tax lines

As at March 31, 2016 As at April 1, 2015 Balance Sheet as at March 31, 2017 Note No. Rs. Lakhs Rs. Lakhs Rs. Lakhs

As at March 31, 2017 As at March 31, 2016 As at April 1, 2015 Balance Sheet as at March 31, 2017 Note No. ASSETS Non-current assets Property, plant and equipment 1.1 1,379.13 1,674.47 1,510.64 Capital

As at March 31, 2017 As at March 31, 2016 As at April 1, 2015 Balance Sheet as at March 31, 2017 Note No. ASSETS Non-current assets Property, plant and equipment 1.1 1,379.13 1,674.47 1,510.64 Capital

HEDGING WITH FUTURES AND BASIS

Futures & Options 1 Introduction The more producer know about the markets, the better equipped producer will be, based on current market conditions and your specific objectives, to decide whether to use

Futures & Options 1 Introduction The more producer know about the markets, the better equipped producer will be, based on current market conditions and your specific objectives, to decide whether to use

Cross Hedging Agricultural Commodities

Cross Hedging Agricultural Commodities Kansas State University Agricultural Experiment Station and Cooperative Extension Service Manhattan, Kansas 1 Cross Hedging Agricultural Commodities Jennifer Graff

Cross Hedging Agricultural Commodities Kansas State University Agricultural Experiment Station and Cooperative Extension Service Manhattan, Kansas 1 Cross Hedging Agricultural Commodities Jennifer Graff

Agricultural Outlook Forum Presented: Thursday, February 19, 2004 IMPLICATIONS OF EXTENDING CROP INSURANCE TO LIVESTOCK

Agricultural Outlook Forum Presented: Thursday, February 19, 2004 IMPLICATIONS OF EXTENDING CROP INSURANCE TO LIVESTOCK Bruce A. Babcock Center for Agricultural and Rural Development Iowa State University

Agricultural Outlook Forum Presented: Thursday, February 19, 2004 IMPLICATIONS OF EXTENDING CROP INSURANCE TO LIVESTOCK Bruce A. Babcock Center for Agricultural and Rural Development Iowa State University

Econ 337 Spring 2014 Due 10am 100 points possible

Econ 337 Spring 2014 Final Due 5/7/2014 @ 10am 100 points possible Fill in the blanks (2 points each) 1. Price discovery is the process by which and arrive at a specific price for a given lot of produce

Econ 337 Spring 2014 Final Due 5/7/2014 @ 10am 100 points possible Fill in the blanks (2 points each) 1. Price discovery is the process by which and arrive at a specific price for a given lot of produce

2012 Fourth Quarter Financial Results

2012 Fourth Quarter Financial Results February 20, 2013 NYSE: CF Safe Harbor Statement All statements in this communication, other than those relating to historical facts, are forward-looking statements.

2012 Fourth Quarter Financial Results February 20, 2013 NYSE: CF Safe Harbor Statement All statements in this communication, other than those relating to historical facts, are forward-looking statements.

Net farm income is an important

File C3-26 September 2016 www.extension.iastate.edu/agdm Converting Cash to Accrual Net Farm Income Net farm income is an important measure of the financial success of a farm business in a given year.

File C3-26 September 2016 www.extension.iastate.edu/agdm Converting Cash to Accrual Net Farm Income Net farm income is an important measure of the financial success of a farm business in a given year.

Q1. Do you wish for your answers to be entered into the AAEA Extension Forecasting competition? Yes No

2016 AAEA Extension Annual Outlook Survey Welcome to the 2016 AAEA Extension Annual Outlook Survey! If you would like to compete in the AAEA Extension Forecasting Competition, you will need to provide

2016 AAEA Extension Annual Outlook Survey Welcome to the 2016 AAEA Extension Annual Outlook Survey! If you would like to compete in the AAEA Extension Forecasting Competition, you will need to provide

ODAP-S. Ontario Data Analysis Project - Swine FARM SUMMARY. For 2002 Tax Year. Prepared by: Lynn Marchand. Economics and Business Section

ODAP-S Ontario Data Analysis Project - Swine FARM SUMMARY For 22 Tax Year Prepared by: Lynn Marchand Economics and Business Section RIDGETOWN COLLEGE, UNIVERSITY OF GUELPH DECEMBER 23 TABLE OF CONTENTS

ODAP-S Ontario Data Analysis Project - Swine FARM SUMMARY For 22 Tax Year Prepared by: Lynn Marchand Economics and Business Section RIDGETOWN COLLEGE, UNIVERSITY OF GUELPH DECEMBER 23 TABLE OF CONTENTS

ECON 337 Agricultural Marketing Spring Exam I. Answer each of the following questions by circling True or False (2 point each).

.") Name: KEY ECON 337 Agricultural Marketing Spring 2014 Exam I Answer each of the following questions by circling True or False (2 point each). 1. True False Futures and options contracts have flexible sizes

Name: KEY ECON 337 Agricultural Marketing Spring 2014 Exam I Answer each of the following questions by circling True or False (2 point each). 1. True False Futures and options contracts have flexible sizes

Advantage Multiple Currency Support Current Procedures

Advantage Multiple Currency Support Current Procedures Overview: This document explains how to process multiple currencies in a single database; how to convert to a HOME currency and how to consolidate

Advantage Multiple Currency Support Current Procedures Overview: This document explains how to process multiple currencies in a single database; how to convert to a HOME currency and how to consolidate